Exhibit (c)(16)

|

Exhibit (c)(16)

Goldman

Sachs

J.Crew Discussion Materials

Goldman, Sachs & Co.

September 2010

[13-September-2010]

|

Goldman

Sachs

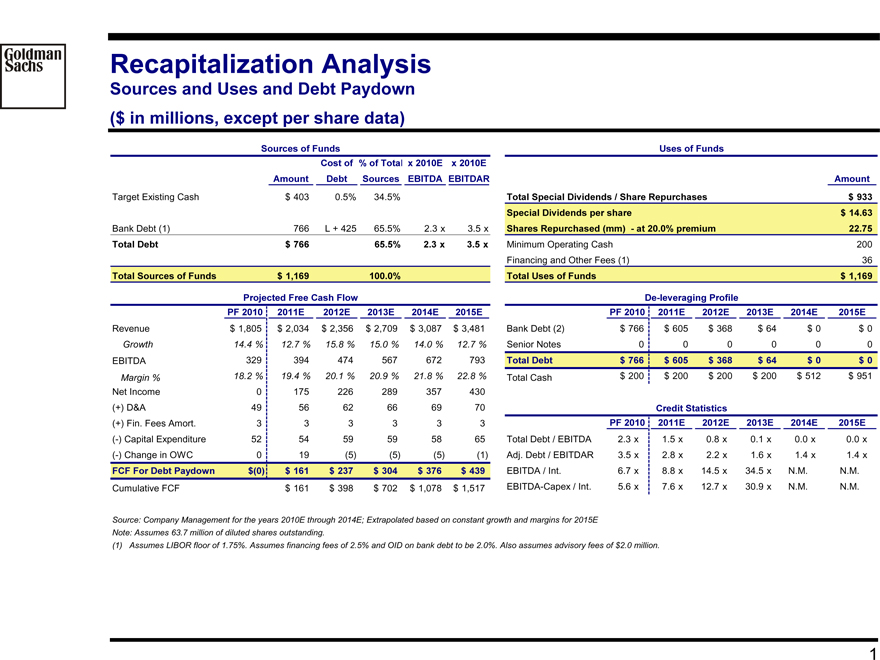

Recapitalization Analysis

Sources and Uses and Debt Paydown ($ in millions, except per share data)

Sources of Funds

Cost of % of Total x 2010E x 2010E

Amount Debt Sources EBITDA EBITDAR

Target Existing Cash $ 403 0.5% 34.5%

Bank Debt (1) 766 L + 425 65.5% 2.3 x 3.5 x

Total Debt $ 766 65.5% 2.3 x 3.5 x

Total Sources of Funds $ 1,169 100.0%

Projected Free Cash Flow

PF 2010 2011E 2012E 2013E 2014E 2015E

Revenue $ 1,805 $ 2,034 $ 2,356 $ 2,709 $ 3,087 $ 3,481

Growth 14.4 % 12.7 % 15.8 % 15.0 % 14.0 % 12.7 %

EBITDA 329 394 474 567 672 793

Margin % 18.2 % 19.4 % 20.1 % 20.9 % 21.8 % 22.8 %

Net Income 0 175 226 289 357 430

(+) D&A 49 56 62 66 69 70

(+) Fin. Fees Amort. 3 3 3 3 3 3

(-) Capital Expenditure 52 54 59 59 58 65

(-) Change in OWC 0 19(5)(5)(5)(1)

FCF For Debt Paydown $(0) $ 161 $ 237 $ 304 $ 376 $ 439

Cumulative FCF $ 161 $ 398 $ 702 $ 1,078 $ 1,517

Uses of Funds

Amount

Total Special Dividends / Share Repurchases $ 933

Special Dividends per share $ 14.63

Shares Repurchased (mm) - at 20.0% premium 22.75

Minimum Operating Cash 200

Financing and Other Fees (1) 36

Total Uses of Funds $ 1,169

De-leveraging Profile

PF 2010 2011E 2012E 2013E 2014E 2015E

Bank Debt (2) $ 766 $ 605 $ 368 $ 64 $ 0 $ 0

Senior Notes 0 0 0 0 0 0

Total Debt $ 766 $ 605 $ 368 $ 64 $ 0 $ 0

Total Cash $ 200 $ 200 $ 200 $ 200 $ 512 $ 951

Credit Statistics

PF 2010 2011E 2012E 2013E 2014E 2015E

Total Debt / EBITDA 2.3 x 1.5 x 0.8 x 0.1 x 0.0 x 0.0 x

Adj. Debt / EBITDAR 3.5 x 2.8 x 2.2 x 1.6 x 1.4 x 1.4 x

EBITDA / Int. 6.7 x 8.8 x 14.5 x 34.5 x N.M. N.M.

EBITDA-Capex / Int. 5.6 x 7.6 x 12.7 x 30.9 x N.M. N.M.

Source: Company Management for the years 2010E through 2014E; Extrapolated based on constant growth and margins for 2015E Note: Assumes 63.7 million of diluted shares outstanding.

(1) Assumes LIBOR floor of 1.75%. Assumes financing fees of 2.5% and OID on bank debt to be 2.0%. Also assumes advisory fees of $2.0 million.

1 |

|

|

Goldman

Sachs

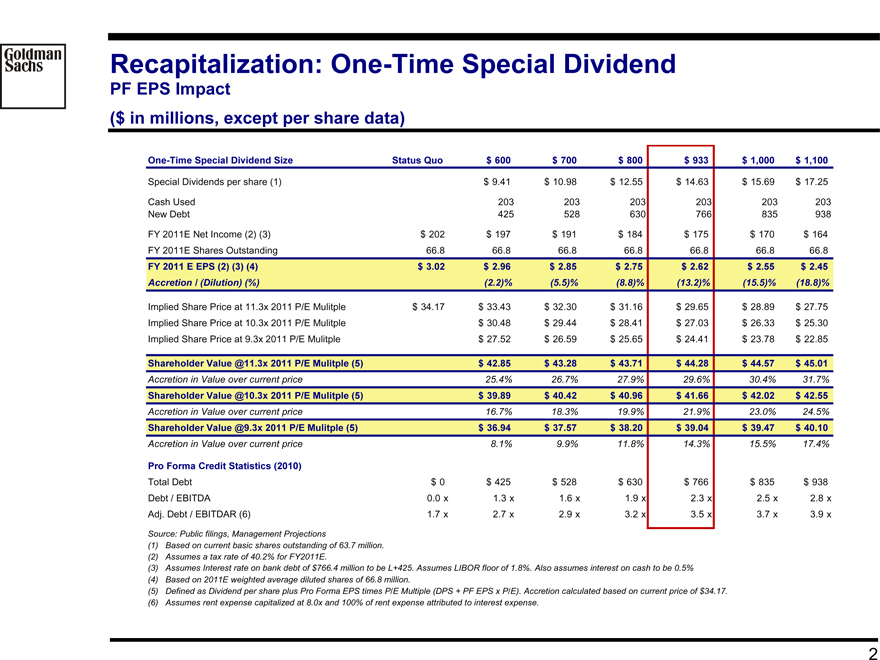

Recapitalization: One-Time Special Dividend

PF EPS Impact

($ in millions, except per share data)

One-Time Special Dividend Size Status Quo $ 600 $ 700 $ 800 $ 933 $ 1,000 $ 1,100

Special Dividends per share (1) $ 9.41 $ 10.98 $ 12.55 $ 14.63 $ 15.69 $ 17.25

Cash Used 203 203 203 203 203 203

New Debt 425 528 630 766 835 938

FY 2011E Net Income (2) (3) $ 202 $ 197 $ 191 $ 184 $ 175 $ 170 $ 164

FY 2011E Shares Outstanding 66.8 66.8 66.8 66.8 66.8 66.8 66.8

FY 2011 E EPS (2) (3) (4) $ 3.02 $ 2.96 $ 2.85 $ 2.75 $ 2.62 $ 2.55 $ 2.45

Accretion / (Dilution) (%)(2.2)%(5.5)%(8.8)%(13.2)%(15.5)%(18.8)%

Implied Share Price at 11.3x 2011 P/E Mulitple $ 34.17 $ 33.43 $ 32.30 $ 31.16 $ 29.65 $ 28.89 $ 27.75

Implied Share Price at 10.3x 2011 P/E Mulitple $ 30.48 $ 29.44 $ 28.41 $ 27.03 $ 26.33 $ 25.30

Implied Share Price at 9.3x 2011 P/E Mulitple $ 27.52 $ 26.59 $ 25.65 $ 24.41 $ 23.78 $ 22.85

Shareholder Value @11.3x 2011 P/E Mulitple (5) $ 42.85 $ 43.28 $ 43.71 $ 44.28 $ 44.57 $ 45.01

Accretion in Value over current price 25.4% 26.7% 27.9% 29.6% 30.4% 31.7%

Shareholder Value @10.3x 2011 P/E Mulitple (5) $ 39.89 $ 40.42 $ 40.96 $ 41.66 $ 42.02 $ 42.55

Accretion in Value over current price 16.7% 18.3% 19.9% 21.9% 23.0% 24.5%

Shareholder Value @9.3x 2011 P/E Mulitple (5) $ 36.94 $ 37.57 $ 38.20 $ 39.04 $ 39.47 $ 40.10

Accretion in Value over current price 8.1% 9.9% 11.8% 14.3% 15.5% 17.4%

Pro Forma Credit Statistics (2010)

Total Debt $ 0 $ 425 $ 528 $ 630 $ 766 $ 835 $ 938

Debt / EBITDA 0.0 x 1.3 x 1.6 x 1.9 x 2.3 x 2.5 x 2.8 x

Adj. Debt / EBITDAR (6) 1.7 x 2.7 x 2.9 x 3.2 x 3.5 x 3.7 x 3.9 x

Source: Public filings, Management Projections

(1) |

| Based on current basic shares outstanding of 63.7 million. (2) Assumes a tax rate of 40.2% for FY2011E. |

(3) Assumes Interest rate on bank debt of $766.4 million to be L+425. Assumes LIBOR floor of 1.8%. Also assumes interest on cash to be 0.5% (4) Based on 2011E weighted average diluted shares of 66.8 million.

(5) Defined as Dividend per share plus Pro Forma EPS times P/E Multiple (DPS + PF EPS x P/E). Accretion calculated based on current price of $34.17. (6) Assumes rent expense capitalized at 8.0x and 100% of rent expense attributed to interest expense.

2 |

|

|

Goldman

Sachs

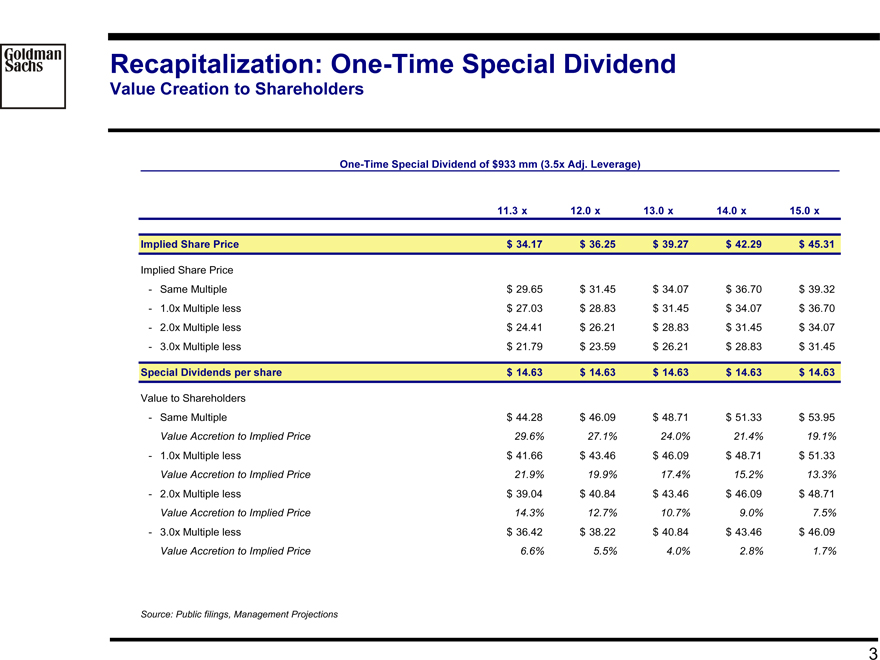

Recapitalization: One-Time Special Dividend

Value Creation to Shareholders

One-Time Special Dividend of $933 mm (3.5x Adj. Leverage)

11.3 |

| x 12.0 x 13.0 x 14.0 x 15.0 x |

Implied Share Price $ 34.17 $ 36.25 $ 39.27 $ 42.29 $ 45.31

Implied Share Price

- Same Multiple $ 29.65 $ 31.45 $ 34.07 $ 36.70 $ 39.32

- 1.0x Multiple less $ 27.03 $ 28.83 $ 31.45 $ 34.07 $ 36.70

- 2.0x Multiple less $ 24.41 $ 26.21 $ 28.83 $ 31.45 $ 34.07

- 3.0x Multiple less $ 21.79 $ 23.59 $ 26.21 $ 28.83 $ 31.45

Special Dividends per share $ 14.63 $ 14.63 $ 14.63 $ 14.63 $ 14.63

Value to Shareholders

- Same Multiple $ 44.28 $ 46.09 $ 48.71 $ 51.33 $ 53.95

Value Accretion to Implied Price 29.6% 27.1% 24.0% 21.4% 19.1%

- 1.0x Multiple less $ 41.66 $ 43.46 $ 46.09 $ 48.71 $ 51.33

Value Accretion to Implied Price 21.9% 19.9% 17.4% 15.2% 13.3%

- 2.0x Multiple less $ 39.04 $ 40.84 $ 43.46 $ 46.09 $ 48.71

Value Accretion to Implied Price 14.3% 12.7% 10.7% 9.0% 7.5%

- 3.0x Multiple less $ 36.42 $ 38.22 $ 40.84 $ 43.46 $ 46.09

Value Accretion to Implied Price 6.6% 5.5% 4.0% 2.8% 1.7%

Source: Public filings, Management Projections

3 |

|

|

Goldman

Sachs

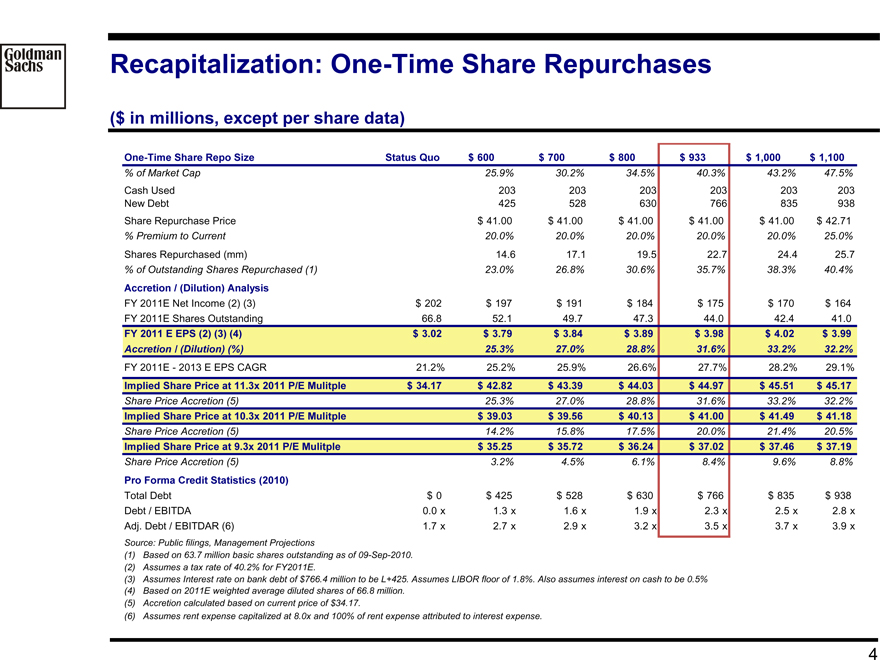

Recapitalization: One-Time Share Repurchases

($ in millions, except per share data)

One-Time Share Repo Size Status Quo $ 600 $ 700 $ 800 $ 933 $ 1,000 $ 1,100

% of Market Cap 25.9% 30.2% 34.5% 40.3% 43.2% 47.5%

Cash Used 203 203 203 203 203 203

New Debt 425 528 630 766 835 938

Share Repurchase Price $ 41.00 $ 41.00 $ 41.00 $ 41.00 $ 41.00 $ 42.71

% Premium to Current 20.0% 20.0% 20.0% 20.0% 20.0% 25.0%

Shares Repurchased (mm) 14.6 17.1 19.5 22.7 24.4 25.7

% of Outstanding Shares Repurchased (1) 23.0% 26.8% 30.6% 35.7% 38.3% 40.4%

Accretion / (Dilution) Analysis

FY 2011E Net Income (2) (3) $ 202 $ 197 $ 191 $ 184 $ 175 $ 170 $ 164

FY 2011E Shares Outstanding 66.8 52.1 49.7 47.3 44.0 42.4 41.0

FY 2011 E EPS (2) (3) (4) $ 3.02 $ 3.79 $ 3.84 $ 3.89 $ 3.98 $ 4.02 $ 3.99

Accretion / (Dilution) (%) 25.3% 27.0% 28.8% 31.6% 33.2% 32.2%

FY 2011E - 2013 E EPS CAGR 21.2% 25.2% 25.9% 26.6% 27.7% 28.2% 29.1%

Implied Share Price at 11.3x 2011 P/E Mulitple $ 34.17 $ 42.82 $ 43.39 $ 44.03 $ 44.97 $ 45.51 $ 45.17

Share Price Accretion (5) 25.3% 27.0% 28.8% 31.6% 33.2% 32.2%

Implied Share Price at 10.3x 2011 P/E Mulitple $ 39.03 $ 39.56 $ 40.13 $ 41.00 $ 41.49 $ 41.18

Share Price Accretion (5) 14.2% 15.8% 17.5% 20.0% 21.4% 20.5%

Implied Share Price at 9.3x 2011 P/E Mulitple $ 35.25 $ 35.72 $ 36.24 $ 37.02 $ 37.46 $ 37.19

Share Price Accretion (5) 3.2% 4.5% 6.1% 8.4% 9.6% 8.8%

Pro Forma Credit Statistics (2010)

Total Debt $ 0 $ 425 $ 528 $ 630 $ 766 $ 835 $ 938

Debt / EBITDA 0.0 x 1.3 x 1.6 x 1.9 x 2.3 x 2.5 x 2.8 x

Adj. Debt / EBITDAR (6) 1.7 x 2.7 x 2.9 x 3.2 x 3.5 x 3.7 x 3.9 x

Source: Public filings, Management Projections

(1) Based on 63.7 million basic shares outstanding as of 09-Sep-2010.

(2) Assumes a tax rate of 40.2% for FY2011E.

(3) Assumes Interest rate on bank debt of $766.4 million to be L+425. Assumes LIBOR floor of 1.8%. Also assumes interest on cash to be 0.5%

(4) Based on 2011E weighted average diluted shares of 66.8 million.

(5) Accretion calculated based on current price of $34.17.

(6) Assumes rent expense capitalized at 8.0x and 100% of rent expense attributed to interest expense.

4

|

Goldman

Sachs

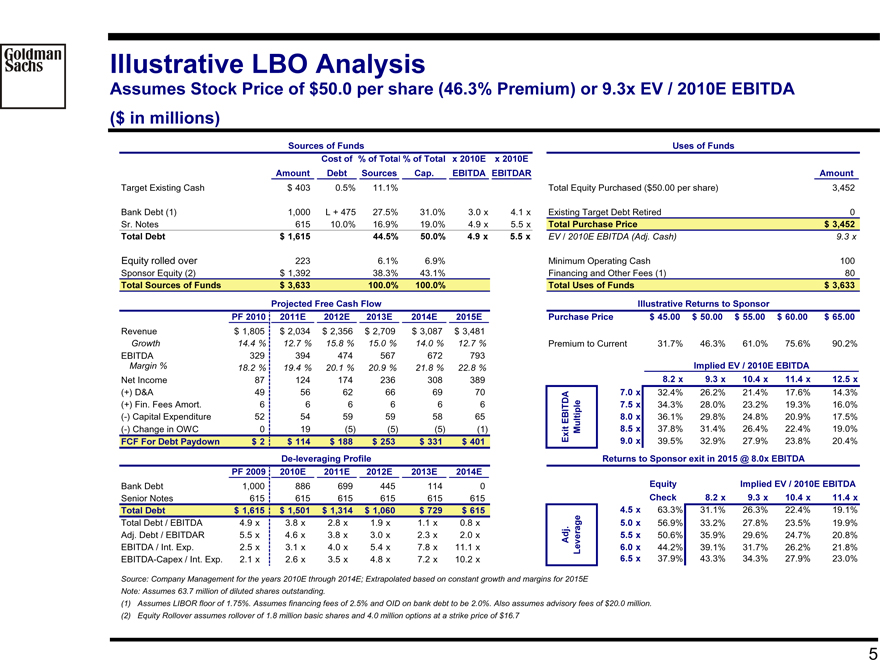

Illustrative LBO Analysis

Assumes Stock Price of $50.0 per share (46.3% Premium) or 9.3x EV / 2010E EBITDA ($ in millions)

Sources of Funds

Cost of % of Total % of Total x 2010E x 2010E

Amount Debt Sources Cap. EBITDA EBITDAR

Target Existing Cash $ 403 0.5% 11.1%

Bank Debt (1) 1,000 L + 475 27.5% 31.0% 3.0 x 4.1 x

Sr. Notes 615 10.0% 16.9% 19.0% 4.9 x 5.5 x

Total Debt $ 1,615 44.5% 50.0% 4.9 x 5.5 x

Equity rolled over 223 6.1% 6.9%

Sponsor Equity (2) $ 1,392 38.3% 43.1%

Total Sources of Funds $ 3,633 100.0% 100.0%

Projected Free Cash Flow

PF 2010 2011E 2012E 2013E 2014E 2015E

Revenue $ 1,805 $ 2,034 $ 2,356 $ 2,709 $ 3,087 $ 3,481

Growth 14.4 % 12.7 % 15.8 % 15.0 % 14.0 % 12.7 %

EBITDA 329 394 474 567 672 793

Margin % 18.2 % 19.4 % 20.1 % 20.9 % 21.8 % 22.8 %

Net Income 87 124 174 236 308 389

(+) D&A 49 56 62 66 69 70

(+) Fin. Fees Amort. 6 6 6 6 6 6

(-) Capital Expenditure 52 54 59 59 58 65

(-) Change in OWC 0 19 (5) (5) (5) (1)

FCF For Debt Paydown $ 2 $ 114 $ 188 $ 253 $ 331 $ 401

De-leveraging Profile

PF 2009 2010E 2011E 2012E 2013E 2014E

Bank Debt 1,000 886 699 445 114 0

Senior Notes 615 615 615 615 615 615

Total Debt $ 1,615 $ 1,501 $ 1,314 $ 1,060 $ 729 $ 615

Total Debt / EBITDA 4.9 x 3.8 x 2.8 x 1.9 x 1.1 x 0.8 x

Adj. Debt / EBITDAR 5.5 x 4.6 x 3.8 x 3.0 x 2.3 x 2.0 x

EBITDA / Int. Exp. 2.5 x 3.1 x 4.0 x 5.4 x 7.8 x 11.1 x

EBITDA-Capex / Int. Exp. 2.1 x 2.6 x 3.5 x 4.8 x 7.2 x 10.2 x

Uses of Funds

Amount

Total Equity Purchased ($50.00 per share) 3,452

Existing Target Debt Retired 0

Total Purchase Price $ 3,452

EV / 2010E EBITDA (Adj. Cash) 9.3 x

Minimum Operating Cash 100

Financing and Other Fees (1) 80

Total Uses of Funds $ 3,633

Illustrative Returns to Sponsor

Purchase Price $ 45.00 $ 50.00 $ 55.00 $ 60.00 $ 65.00

Premium to Current 31.7% 46.3% 61.0% 75.6% 90.2%

Implied EV / 2010E EBITDA

Exit EBITDA Multiple

8.2 |

| x 9.3 x 10.4 x 11.4 x 12.5 x |

7.0 |

| x 32.4% 26.2% 21.4% 17.6% 14.3% |

7.5 |

| x 34.3% 28.0% 23.2% 19.3% 16.0% |

8.0 |

| x 36.1% 29.8% 24.8% 20.9% 17.5% |

8.5 |

| x 37.8% 31.4% 26.4% 22.4% 19.0% |

9.0 |

| x 39.5% 32.9% 27.9% 23.8% 20.4% |

Returns to Sponsor exit in 2015 @ 8.0x EBITDA

Equity Implied EV / 2010E EBITDA

Adj Leverage

Check 8.2 x 9.3 x 10.4 x 11.4 x

4.5 |

| x 63.3% 31.1% 26.3% 22.4% 19.1% |

5.0 |

| x 56.9% 33.2% 27.8% 23.5% 19.9% |

5.5 |

| x 50.6% 35.9% 29.6% 24.7% 20.8% |

6.0 |

| x 44.2% 39.1% 31.7% 26.2% 21.8% |

6.5 |

| x 37.9% 43.3% 34.3% 27.9% 23.0% |

Source: Company Management for the years 2010E through 2014E; Extrapolated based on constant growth and margins for 2015E Note: Assumes 63.7 million of diluted shares outstanding.

(1) Assumes LIBOR floor of 1.75%. Assumes financing fees of 2.5% and OID on bank debt to be 2.0%. Also assumes advisory fees of $20.0 million. (2) Equity Rollover assumes rollover of 1.8 million basic shares and 4.0 million options at a strike price of $16.7

5 |

|

|

Goldman

Sachs

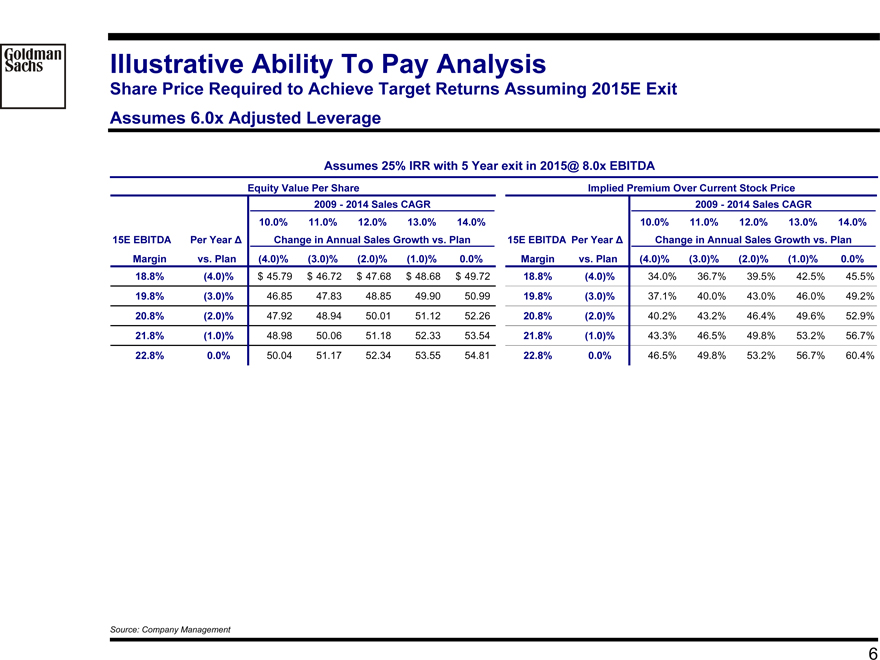

Illustrative Ability To Pay Analysis

Share Price Required to Achieve Target Returns Assuming 2015E Exit Assumes 6.0x Adjusted Leverage

Assumes 25% IRR with 5 Year exit in 2015@ 8.0x EBITDA

Equity Value Per Share Implied Premium Over Current Stock Price

2009 - 2014 Sales CAGR 2009 - 2014 Sales CAGR

10.0% 11.0% 12.0% 13.0% 14.0% 10.0% 11.0% 12.0% 13.0% 14.0%

15E EBITDA Per Year Change in Annual Sales Growth vs. Plan 15E EBITDA Per Year Change in Annual Sales Growth vs. Plan

Margin vs. Plan (4.0)% (3.0)% (2.0)% (1.0)% (0.0)%

18.8% (4.0)% $ 45.79 $ 46.72 $ 47.68 $ 48.68 $ 49.72 18.8% (4.0)% 34.0% 36.7% 39.5% 42.5% 45.5%

19.8% (3.0)% 46.85 47.83 48.85 49.90 50.99 19.8% (3.0)% 37.1% 40.0% 43.0% 46.0% 49.2%

20.8% (2.0)% 47.92 48.94 50.01 51.12 52.26 20.8% (2.0)% 40.2% 43.2% 46.4% 49.6% 52.9%

21.8% (1.0)% 48.98 50.06 51.18 52.33 53.54 21.8% (1.0)% 43.3% 46.5% 49.8% 53.2% 56.7%

22.8% 0.0% 50.04 51.17 52.34 53.55 54.81 22.8% 0.0% 46.5% 49.8% 53.2% 56.7% 60.4%

Source: Company Management

6

|

Goldman

Sachs

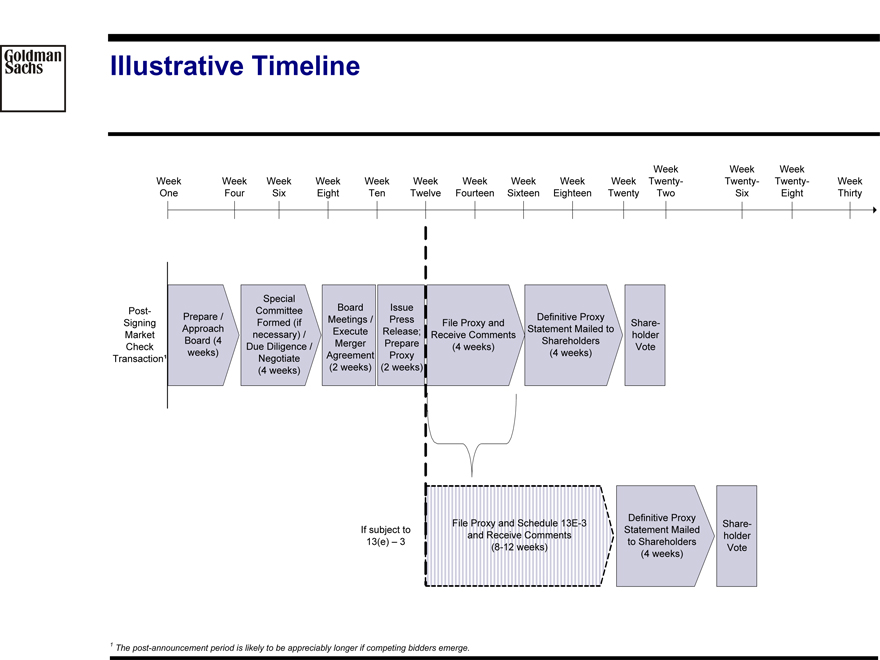

Illustrative Timeline

Week One

Week Four

Week Six

Week Eight

Week Ten

Week Twelve

Week Fourteen

Week Sixteen

Week Eighteen

Week Twenty

Week Twenty-Two

Week Twenty-Six

Week Twenty-Eight

Week Thirty

Post-Signing Market Check Transaction1

Prepare/Approach Board (4 weeks)

Special Committee Formed (if necessary Due Diligence/ Negotiate (4 weeks)

Board Meetings/Execute Merger Agreement (2 weeks)

Issue press Release; Prepare Proxy (2 weeks)

File Proxy and Receive Comments (4 weeks)

Definitive Proxy Statement Mailed to Shareholders (4 weeks)

Share-holder Vote

If subject to 13(e)-3

File Proxy and Schedule 13E-3 and Receive Comments (8-12 weeks)

Definitive Proxy Statement Mailed to Shareholders (4 weeks)

Share-holder Vote

1 The post-announcement period is likely to be appreciably longer if competing bidders emerge.

Exhibit 1

|

Goldman Sachs

J.Crew Back Up Pages

Goldman, Sachs & Co. September 2010

|

Rent Adjusted Debt

Adjusted Debt = Debt +

8XRent EBITDAR = EBITDA + Rent

2010

Adjusted Debt = $1,611 + 8*86= $2297 EBITDAR= $329+$86=$415

Rent Adjusted Leverage = $2297/$415 = 5.5x

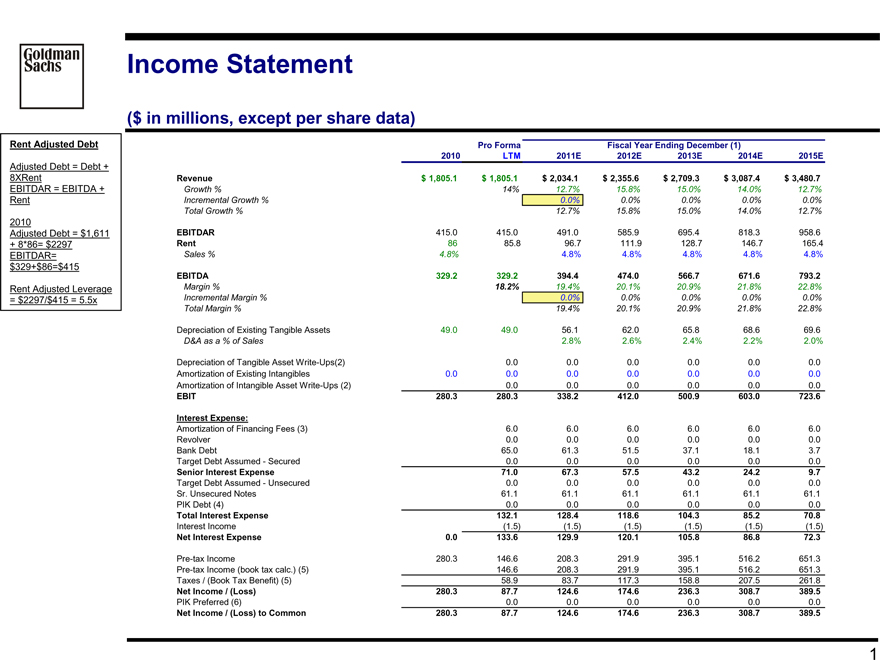

Goldman Sachs

Income Statement

($ in millions, except per share data)

Pro Forma Fiscal Year Ending December (1)

2010 LTM 2011E 2012E 2013E 2014E 2015E

Revenue $ 1,805.1 $ 1,805.1 $ 2,034.1 $ 2,355.6 $ 2,709.3 $ 3,087.4 $ 3,480.7

Growth % 14% 12.7% 15.8% 15.0% 14.0% 12.7%

Incremental Growth % 0.0% 0.0% 0.0% 0.0% 0.0%

Total Growth % 12.7% 15.8% 15.0% 14.0% 12.7%

EBITDAR 415.0 415.0 491.0 585.9 695.4 818.3 958.6

Rent 86 85.8 96.7 111.9 128.7 146.7 165.4

Sales % 4.8% 4.8% 4.8% 4.8% 4.8% 4.8%

EBITDA 329.2 329.2 394.4 474.0 566.7 671.6 793.2

Margin % 18.2% 19.4% 20.1% 20.9% 21.8% 22.8%

Incremental Margin % 0.0% 0.0% 0.0% 0.0% 0.0%

Total Margin % 19.4% 20.1% 20.9% 21.8% 22.8%

Depreciation of Existing Tangible Assets 49.0 49.0 56.1 62.0 65.8 68.6 69.6

D&A as a % of Sales 2.8% 2.6% 2.4% 2.2% 2.0%

Depreciation of Tangible Asset Write-Ups(2) 0.0 0.0 0.0 0.0 0.0 0.0

Amortization of Existing Intangibles 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Amortization of Intangible Asset Write-Ups (2) 0.0 0.0 0.0 0.0 0.0 0.0

EBIT 280.3 280.3 338.2 412.0 500.9 603.0 723.6

Interest Expense:

Amortization of Financing Fees (3) 6.0 6.0 6.0 6.0 6.0 6.0

Revolver 0.0 0.0 0.0 0.0 0.0 0.0

Bank Debt 65.0 61.3 51.5 37.1 18.1 3.7

Target Debt Assumed - Secured 0.0 0.0 0.0 0.0 0.0 0.0

Senior Interest Expense 71.0 67.3 57.5 43.2 24.2 9.7

Target Debt Assumed - Unsecured 0.0 0.0 0.0 0.0 0.0 0.0

Sr. Unsecured Notes 61.1 61.1 61.1 61.1 61.1 61.1

PIK Debt (4) 0.0 0.0 0.0 0.0 0.0 0.0

Total Interest Expense 132.1 128.4 118.6 104.3 85.2 70.8

Interest Income(1.5)(1.5)(1.5)(1.5)(1.5)(1.5)

Net Interest Expense 0.0 133.6 129.9 120.1 105.8 86.8 72.3

Pre-tax Income 280.3 146.6 208.3 291.9 395.1 516.2 651.3

Pre-tax Income (book tax calc.) (5) 146.6 208.3 291.9 395.1 516.2 651.3

Taxes / (Book Tax Benefit) (5) 58.9 83.7 117.3 158.8 207.5 261.8

Net Income / (Loss) 280.3 87.7 124.6 174.6 236.3 308.7 389.5

PIK Preferred (6) 0.0 0.0 0.0 0.0 0.0 0.0

Net Income / (Loss) to Common 280.3 87.7 124.6 174.6 236.3 308.7 389.5

1

|

Goldman Sachs

Cash Flow

($ in millions, except per share data)

Pro Forma Fiscal Year Ending December (1)

2010 LTM 2011E 2012E 2013E 2014E 2015E

Net Income / (Loss) to Common $ 280.3 $ 87.7 $ 124.9 $ 174.9 $ 236.6 $ 309.0 $ 389.8

Additions

Depreciation of Existing Tangible Assets 49.0 49.0 56.1 62.0 65.8 68.6 69.6

Depreciation of Tangible Asset Write-Ups(2) 0.0 0.0 0.0 0.0 0.0 0.0

Amortization of Existing Intangibles 0.0 0.0 0.0 0.0 0.0 0.0

Amortization of Intangible Asset Write-Ups (2) 0.0 0.0 0.0 0.0 0.0

Amortization of Financing Fees (3) 6.0 6.0 6.0 6.0 6.0 6.0

PIK Interest (4) 0.0 0.0 0.0 0.0 0.0 0.0

PIK Dividends (5) 0.0 0.0 0.0 0.0 0.0 0.0

Deferred Taxes (from transaction purchase accounting) (2) (6) 0.0 0.0 0.0 0.0 0.0

Cash Tax Benefit from Loss Carryforwards (6) 0.0 0.0 0.0 0.0 0.0

Other Deferred Taxes 0.0 0.0 0.0 0.0 0.0 0.0

Other Non-Cash Expenses 0.0 0.0 0.0 0.0 0.0 0.0

Total Additions 49.0 55.0 62.2 68.0 71.8 74.6 75.6

Subtractions

Increase / (Decrease) in Working Capital 0.4 0.4 19.3 (4.5) (4.8) (5.1) (1.1)

Reversal of Book Tax Benefit (7) 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Mandatory Capital Expenditures 52.5 52.5 53.9 59.4 59.5 57.7 65.0

Capex as % of Sales 2.6% 2.5% 2.2% 1.9% 1.9%

Discretionary Capital Expenditures 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Total Capital Expenditures 52.5 52.5 53.9 59.4 59.5 57.7 65.0

Total Subtractions 52.9 52.9 73.1 54.9 54.6 52.6 63.9

Free Cash Flow Available for Debt Service 276.4 89.8 113.9 188.0 253.7 331.0 401.5

Cumulative Free Cash Flow 113.9 301.9 555.6 886.7 1,288.2

0.0 0.0 0.0 0.0 0.0

Cash Taxes

Pre-tax Income (book tax calc.) $ 146.6 $ 208.3 $ 291.9 $ 395.1 $ 516.2 $ 651.3

Plus: Reversal of Asset Write-Up D&A for Tax (2) (6) 0.0 0.0 0.0 0.0 0.0 0.0

Less: Goodwill Amortization for Tax (2) (6) 0.0 0.0 0.0 0.0 0.0 0.0

Pre-tax Income before Loss Carryforward (cash tax calc.) $ 146.6 $ 208.3 $ 291.9 $ 395.1 $ 516.2 $ 651.3

Pre-tax Income after Loss Carryforward (cash tax calc.) $ 0.0 $ 208.3 $ 291.9 $ 395.1 $ 516.2 $ 651.3

Tax Loss Carryforward—End of Year $ 0.0 0.0 0.0 0.0 0.0 0.0

2

|

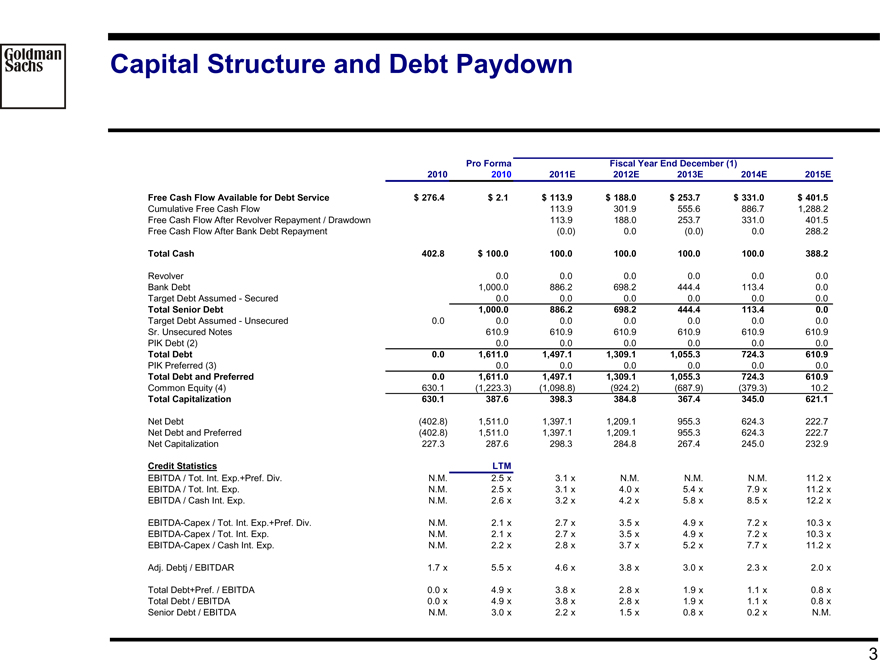

Goldman Sachs

Capital Structure and Debt Paydown

Pro Forma Fiscal Year End December (1)

2010 2010 2011E 2012E 2013E 2014E 2015E

Free Cash Flow Available for Debt Service $ 276.4 $ 2.1 $ 113.9 $ 188.0 $ 253.7 $ 331.0 $ 401.5

Cumulative Free Cash Flow 113.9 301.9 555.6 886.7 1,288.2

Free Cash Flow After Revolver Repayment / Drawdown 113.9 188.0 253.7 331.0 401.5

Free Cash Flow After Bank Debt Repayment (0.0) 0.0 (0.0) 0.0 288.2

Total Cash 402.8 $ 100.0 100.0 100.0 100.0 100.0 388.2

Revolver 0.0 0.0 0.0 0.0 0.0 0.0

Bank Debt 1,000.0 886.2 698.2 444.4 113.4 0.0

Target Debt Assumed - Secured 0.0 0.0 0.0 0.0 0.0 0.0

Total Senior Debt 1,000.0 886.2 698.2 444.4 113.4 0.0

Target Debt Assumed - Unsecured 0.0 0.0 0.0 0.0 0.0 0.0 0.0

Sr. Unsecured Notes 610.9 610.9 610.9 610.9 610.9 610.9

PIK Debt (2) 0.0 0.0 0.0 0.0 0.0 0.0

Total Debt 0.0 1,611.0 1,497.1 1,309.1 1,055.3 724.3 610.9

PIK Preferred (3) 0.0 0.0 0.0 0.0 0.0 0.0

Total Debt and Preferred 0.0 1,611.0 1,497.1 1,309.1 1,055.3 724.3 610.9

Common Equity (4) 630.1(1,223.3)(1,098.8)(924.2)(687.9)(379.3) 10.2

Total Capitalization 630.1 387.6 398.3 384.8 367.4 345.0 621.1

Net Debt (402.8) 1,511.0 1,397.1 1,209.1 955.3 624.3 222.7

Net Debt and Preferred (402.8) 1,511.0 1,397.1 1,209.1 955.3 624.3 222.7

Net Capitalization 227.3 287.6 298.3 284.8 267.4 245.0 232.9

Credit Statistics LTM

EBITDA / Tot. Int. Exp.+Pref. Div. N.M. 2.5 x 3.1 x N.M. N.M. N.M. 11.2 x

EBITDA / Tot. Int. Exp. N.M. 2.5 x 3.1 x 4.0 x 5.4 x 7.9 x 11.2 x

EBITDA / Cash Int. Exp. N.M. 2.6 x 3.2 x 4.2 x 5.8 x 8.5 x 12.2 x

EBITDA-Capex / Tot. Int. Exp.+Pref. Div. N.M. 2.1 x 2.7 x 3.5 x 4.9 x 7.2 x 10.3 x

EBITDA-Capex / Tot. Int. Exp. N.M. 2.1 x 2.7 x 3.5 x 4.9 x 7.2 x 10.3 x

EBITDA-Capex / Cash Int. Exp. N.M. 2.2 x 2.8 x 3.7 x 5.2 x 7.7 x 11.2 x

Adj. Debtj / EBITDAR 1.7 x 5.5 x 4.6 x 3.8 x 3.0 x 2.3 x 2.0 x

Total Debt+Pref. / EBITDA 0.0 x 4.9 x 3.8 x 2.8 x 1.9 x 1.1 x 0.8 x

Total Debt / EBITDA 0.0 x 4.9 x 3.8 x 2.8 x 1.9 x 1.1 x 0.8 x

Senior Debt / EBITDA N.M. 3.0 x 2.2 x 1.5 x 0.8 x 0.2 x N.M.

3 |

|