SCHEDULE 14A

(RULE 14a-101)

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

Filed by the Registrantx Filed by a Party other than the Registrant¨

Check the appropriate box:

| x | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material Under Rule 14a-12 |

SAVVIS Communications Corporation

(Name of Registrant as Specified in its Charter)

(Name of Person(s) Filing Proxy Statement if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11: |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials: |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

NOTICE OF 2005 ANNUAL MEETING OF STOCKHOLDERS

TO BE HELD ON MAY 17, 2005

| Date: | May 17, 2005 | |||

| Time: | 9:00 a.m. CDT | |||

| Place: | SAVVIS Communications Corporation, 1 Savvis Parkway, Town & Country, MO 63017 | |||

| Purpose: | 1. | To elect ten members of the board of directors to serve until the next annual meeting and until their successors have been elected and qualified; | ||

| 2. | To authorize our board of directors to amend our certificate of incorporation to effect a 1-for-15 reverse split of our outstanding common stock, without further approval of our stockholders, upon a determination by our board that such a reverse stock split is in the best interests of our company and our stockholders; | |||

| 3. | To authorize our board of directors to amend our certificate of incorporation to effect a 1-for-20 reverse split of our outstanding common stock, without further approval of our stockholders, upon a determination by our board that such a reverse stock split is in the best interests of our company and our stockholders; | |||

| 4. | To ratify the selection of Ernst & Young LLP as our independent auditors for the fiscal year ending December 31, 2005; and | |||

| 5. | To transact such other business as may properly come before the meeting. | |||

| Record Date: | Holders of record of our common stock and our Series A convertible preferred stock at the close of business on March 31, 2005, are entitled to receive this notice and to vote at the meeting. | |||

It is important that your shares be represented and voted at the meeting. You can vote your shares by completing and returning the enclosed proxy card. Most stockholders can also vote their shares over the Internet or by telephone. If Internet or telephone voting is available to you, voting instructions are printed on the proxy card sent to you. You can revoke a proxy at any time prior to its exercise at the meeting by following the instructions in the accompanying proxy statement. We appreciate your cooperation.

By Order of the Board of Directors |

/s/ Grier C. Raclin |

Grier C. Raclin |

Chief Legal Officer and Corporate Secretary |

April , 2005

SAVVIS COMMUNICATIONS CORPORATION

1 SAVVIS Parkway

Town & Country, Missouri 63017

Phone: (314) 628-7000

PROXY STATEMENT

We will begin mailing this proxy statement and form of proxy card to our stockholders on or about April , 2005.

We are furnishing this proxy statement to our stockholders in connection with a solicitation of proxies by our board of directors for use at our 2005 annual meeting of stockholders to be held on May 17, 2005 at 9:00 a.m. CDT at our principal executive offices at SAVVIS Communications Corporation, 1 Savvis Parkway, Town & Country, Missouri 63017. The purpose of the annual meeting and the matters to be acted on are set forth in the accompanying notice of annual meeting.

Who Can Vote

If you held any shares of our voting stock at the close of business on March 31, 2005, then you will be entitled to notice of and to vote at our 2005 annual meeting. On that date, we had shares of common stock outstanding and entitled to one vote per share and shares of Series A convertible preferred stock outstanding and entitled to an aggregate of approximately votes.

Quorum

The presence, in person or by proxy, of the holders of a majority of the votes represented by our outstanding shares of common stock and Series A convertible preferred stock is necessary to constitute a quorum with respect to the actions listed above. In addition, the presence, in person or by proxy, of the holders of a majority of our outstanding shares of common stock is necessary to constitute a quorum with respect to actions 2 and 3. We will count shares of voting stock present at the meeting that abstain from voting or that are the subject of broker non-votes as present for purposes of determining a quorum. A broker non-vote occurs when a nominee holding common stock for a beneficial owner does not vote on a particular matter because the nominee does not have discretionary voting power with respect to that item and has not received voting instructions from the beneficial owner.

Voting Rights

Each share of our common stock that you hold entitles you to one vote on all matters that come before the annual meeting. Each share of Series A convertible preferred stock that you hold entitles you to a number of votes equal to the number of whole shares of common stock into which the share of Series A convertible preferred stock is convertible as of the record date. As of the record date, the outstanding shares of Series A convertible preferred stock were entitled to an aggregate of approximately votes. Inspectors of election will count votes cast at the annual meeting.

The directors will be elected by a plurality of the votes represented by our outstanding shares of common stock and Series A convertible preferred stock, voting together as a single class, and cast at the annual meeting. Withheld votes and broker non-votes will have no effect on the election of directors.

The affirmative vote of the holders of a majority of the votes represented by our outstanding shares of common stock and Series A convertible preferred stock, voting together as a single class, is required to approve the proposals to authorize our board of directors, in its discretion, to amend our certificate of incorporation to effect a 1-for-15 reverse stock split (proposal 2) and to authorize our board of directors, in its discretion, to amend our certificate of incorporation to effect a 1-for-20 reverse stock split (proposal 3). In addition, the affirmative vote of the holders of a majority of our outstanding shares of common stock, voting as a separate class, is required to approve proposals 2 and 3. Abstentions and broker non-votes will have the effect of a vote against these proposals.

The affirmative vote of the holders of a majority of the votes represented by our outstanding shares of common stock and Series A convertible preferred stock, voting together as a single class, present in person or represented by proxy at the annual meeting and entitled to vote, is required to ratify the selection of Ernst & Young LLP as our independent auditors for the fiscal year ending December 31, 2005 (proposal 4). Abstentions will have the effect of a vote against these proposals and broker non-votes will have no effect.

Granting Your Proxy

Please mark the enclosed proxy card, date and sign it, and mail it in the postage-paid envelope. The shares represented will be voted according to your directions. You can specify how you want your shares voted by marking the appropriate boxes on the proxy card. Please review the voting instructions on the proxy card and read the entire text of the proposals and the position of the board of directors on these proposals in the proxy statement prior to making your vote. If you properly execute and return a proxy in the enclosed form, your stock will be voted as you specify. If your proxy card is signed and returned without specifying a vote or an abstention on any proposal, the proxy representing your common stock will be voted in favor of each of the proposals.

If you hold your shares through a broker, bank or other nominee, you will receive separate instructions from the nominee describing the procedure for voting your shares.

We expect no matter to be presented for action at the annual meeting other than the items described in this proxy statement. The enclosed proxy will, however, confer discretionary authority with respect to any other matter that may properly come before the meeting. If any other matters are presented for action at the meeting, the persons named in the enclosed proxy intend to vote on them in accordance with their best judgment.

2004 Annual Report

A copy of our 2004 annual report, including consolidated financial statements, which is not part of the proxy soliciting material, accompanies this proxy statement. An additional copy will be furnished without charge to beneficial stockholders or stockholders of record upon request by mail to SAVVIS Communications Corporation, Attention: Investor Relations, 12851 Worldgate Drive, Herndon, VA 20170, or by email toinvestor.relations@savvis.net.

Revoking Your Proxy

If you submit a proxy, you can revoke it at any time before it is exercised by giving written notice to our corporate secretary prior to the annual meeting or by timely delivering a properly executed, later-dated proxy. You may also attend the annual meeting in person and vote by ballot, which would cancel any proxy that you previously submitted.

Electronic Access to Proxy Materials and Annual Report

This proxy statement and the 2004 annual report are available on our website at www.savvis.net. Most stockholders can elect to view future proxy statements and annual reports over the Internet instead of receiving paper copies in the mail.

If you are a stockholder of record, you can choose this option and save the company the cost of producing and mailing these documents by following the instructions provided atwww.melloninvestor.com/isd.

If you choose to view future proxy statements and annual reports over the Internet, you will receive a proxy card in the mail next year with instructions containing the Internet address of those materials. Your choice will remain in effect until you cancel it.

2

If you hold your SAVVIS stock through a bank, broker or other nominee, please refer to the information provided by that entity for instructions on how to elect to view future proxy statements and annual reports over the Internet.

Most stockholders who hold their SAVVIS stock through a bank, broker or other nominee and who elect electronic access will receive an e-mail message next year containing the Internet address to use to access our proxy materials and annual report.

Proxy Solicitation

We will pay all expenses of soliciting proxies for the 2005 annual meeting. In addition to solicitations by mail, we have made arrangements for brokers and nominees to send proxy materials to their principals and, upon their request, we will reimburse them for their reasonable expenses in doing so. Certain of our representatives, who will receive no compensation for their services, may also solicit proxies by telephone, telecopy, personal interview or other means.

Stockholder Proposals

If you want us to consider including a stockholder proposal in next year’s proxy statement, you must deliver itin writing to the Corporate Secretary, SAVVIS Communications Corporation, 12851 Worldgate Drive, Herndon, Virginia 20170 by December 14, 2005. SEC rules set forth standards as to which stockholder proposals are required to be included in a proxy statement. Any stockholder who intends to propose any other matter to be acted on at the 2006 annual meeting of stockholders must inform the Corporate Secretary by February 27, 2006. If notice is not provided by that date, the persons named in our proxy for the 2006 annual meeting will be allowed to exercise their discretionary authority to vote upon any such proposal without the matter having been discussed in the proxy statement for the 2006 annual meeting.

3

ELECTION OF DIRECTORS

(Proposal 1)

Our business is managed under the direction of our board of directors. Our bylaws provide that our board determines the number of directors, which is currently set at ten. Our board of directors has designated as nominees for director all ten of the directors presently serving on the board.

Unless marked otherwise, proxies received will be voted “FOR” the election of the nominees named below. In the event any nominee is unable or declines to serve as a director at the time of the annual meeting, the proxies may be voted for any nominee who may be designated by our present board of directors to fill the vacancy. Alternatively, the proxies may be voted for the balance of the nominees, leaving a vacancy. As of the date of this proxy statement, our board of directors is not aware of any nominee who is unable or will decline to serve as a director.

Vote Required.The ten nominees receiving the highest number of affirmative votes of the shares represented by our outstanding shares of common stock and Series A convertible preferred stock, voting together as a single class, and cast at the annual meeting, will be elected directors of our company to serve until the next annual meeting and until their successors have been elected and qualified.

Nominees For Director

The nominees for director are set forth below.The board of directors recommends a vote “FOR” each of the nominees listed below.

Nominee | Age | |||

Robert A. McCormick | 39 | |||

John D. Clark | 40 | |||

John M. Finlayson | 50 | |||

Clifford H. Friedman | 46 | |||

Clyde A. Heintzelman | 66 | |||

Thomas E. McInerney | 63 | |||

James E. Ousley | 59 | |||

James P. Pellow | 43 | |||

Jeffrey H. Von Deylen | 41 | |||

Patrick J. Welsh | 61 |

Executive Officers

Our current executive officers and their positions with our company are set forth below.

Executive Officers | Age | Position and Office | ||

Robert A. McCormick | 39 | Chief Executive Officer and Chairman of the Board | ||

John M. Finlayson | 50 | President, Chief Operating Officer and Director | ||

Jeffrey H. Von Deylen | 41 | Chief Financial Officer and Director | ||

Grier C. Raclin | 52 | Chief Legal Officer and Corporate Secretary | ||

Timothy E. Caulfield | 46 | Managing Director – Global Solutions | ||

Bryan S. Doerr | 41 | Chief Technology Officer | ||

Matthew A. Fanning | 51 | Managing Director – Strategic Accounts | ||

James D. Mori | 49 | Managing Director – Americas | ||

Richard Warley | 39 | Managing Director – EMEA |

Set forth below is a brief description of the principal occupation and business experience of each of our nominees for director and each of our executive officers.

ROBERT A. McCORMICK has served as the Chairman of our board of directors since April 1999 and as our Chief Executive Officer since November 1999. Mr. McCormick served as Executive Vice President and Chief Technical Officer of Bridge Information Systems, Inc. (“Bridge”) from January 1997 to December 1999, and held

4

various engineering, design and development positions at Bridge from 1989 to January 1997. Mr. McCormick was named Best Executive at the International Business Awards in 2004. Mr. McCormick attended the University of Colorado at Boulder.

JOHN M. FINLAYSON has served as our President and Chief Operating Officer since December 1999 and as a director of our company since January 2000. From June 1998 to December 1999, Mr. Finlayson served as Senior Vice President of Global Crossing Holdings, Ltd. and President of Global Crossing International, Ltd. Before joining Global Crossing, Mr. Finlayson was employed by Motorola, Inc. starting in 1994, most recently as Corporate Vice President and General Manager of the Asia Pacific Cellular Infrastructure Group from March 1998 to May 1998. Mr. Finlayson received a B.S. degree in Marketing from LaSalle University, a M.B.A. degree in Marketing and a post-M.B.A. certification in Information Management from St. Joseph University.

JEFFREY H. VON DEYLEN has served as our Chief Financial Officer and a director since March 2003, after joining us as Executive Vice President for Finance in January 2003. From August 2002 to January 2003, Mr. Von Deylen served as Vice President for Corporate Development and Financial Analyst at American Electric Power Company. From June 2001 to June 2002, Mr. Von Deylen served as Chief Financial Officer for KPNQwest N.V. (“KPNQwest”). In 2002, KPNQwest filed a petition for “surseance” (moratorium) in The Netherlands, which moratorium was converted into a bankruptcy shortly thereafter. Before joining KPNQwest, he was employed by Global TeleSystems Inc. (“GTS”) as Senior Vice President of Finance from October 1999 to May 2001. In 2001, GTS filed, in pre-arranged proceedings, a petition for “surseance” (moratorium), offering a composition, in The Netherlands and a voluntary petition for relief under Chapter 11 of Title 11 of the United States Bankruptcy Code, both in connection with the sale of the company to KPNQwest. From June 1998 until September 1999, Mr. Von Deylen served as Vice President and Corporate Controller of Qwest Communications International. Mr. Von Deylen received a B.S. degree in Accountancy from Miami University and holds a C.P.A. certification.

GRIER C. RACLIN has served as our Chief Legal Officer and Corporate Secretary since joining us in January 2003. Mr. Raclin is responsible for our legal and regulatory affairs, as well facilities and procurement. Prior to joining us, Mr. Raclin served as Executive Vice President, Chief Administrative Officer, General Counsel and Corporate Secretary from 2000 to 2002 and as Senior Vice President of Corporate Affairs, General Counsel and Corporate Secretary from 1997 to 2000 of Global TeleSystems Inc. (“GTS”). In 2001, GTS filed, in pre-arranged proceedings, a petition for “surseance” (moratorium), offering a composition, in The Netherlands and a voluntary petition for relief under Chapter 11 of Title 11 of the United States Bankruptcy Code, both in connection with the sale of the company to KPNQwest. Mr. Raclin earned his law degree from Northwestern University Law School in Chicago, Illinois; attended business school at the University of Chicago Executive Program; and earned his B.S. degree in philosophycum laude from Northwestern University.

TIMOTHY E. CAULFIELDhas served as our Managing Director – Global Solutions since joining us in March 2004. Prior to joining us, Mr. Caulfield served as Senior Vice President Consulting and Hosting Services for Cable & Wireless USA, Inc. and Cable & Wireless Internet Services, Inc. (collectively “CWA”) from September 2002 until we acquired CWA in March 2004 after it filed a voluntary petition for relief under Chapter 11 of Title 11 of the United States Bankruptcy Code. From January 2001 to September 2002, Mr. Caulfield led regional and global operations for Exodus Communications (“Exodus”) until it was acquired by CWA after it filed a voluntary petition for relief under Chapter 11 of Title 11 of the United States Bankruptcy Code. Previously, Mr. Caulfield held various leadership positions with ENVIOSNet, an enterprise and service support company, Gateway, Inc., Sequent Computer Systems and Digital Equipment Corporation. Mr. Caulfield received a B.A. degree from Clark University in Worcester, Massachusetts and a M.B.A. degree from the University of Oregon.

BRYAN S. DOERR has served as our Senior Vice President and Chief Technology Officer since October 2003. From February 2002 to October 2003, Mr. Doerr was our Vice President – Software Development. Prior to this, Mr. Doerr has held several positions in management, software technology research and software development at Bridge, The Boeing Company, and Johns Hopkins University Applied Physics Laboratory. Mr. Doerr received his B.S. in Electrical Engineering from the University of Missouri–Columbia, an M.S. degree in Electrical Engineering from Johns Hopkins University and a Masters in Information Management from Washington University in St. Louis, Missouri.

5

MATTHEW A. FANNING joined us in February 2000 and serves as our Managing Director–Strategic Accounts. Mr. Fanning oversees our relationships with Reuters Limited and Moneyline Telerate, our two largest customers. Prior to joining us, from March 1997 to February 2000, Mr. Fanning served as Vice President–Marketing and Sales for Comcast Corporation. Mr. Fanning earned his post-MBA certification in Information System Management and his M.B.A. in Marketing from St. Joseph’s University. He received a B.A. in English Literature from St. Joseph’s College.

JAMES D. MORI has served as our Managing Director–Americas since joining us in October 1999. Mr. Mori is responsible for our sales efforts in the United States, Canada and Latin/South America. Previously, Mr. Mori served as Area Director for Sprint Corporation from February 1997 to October 1999 and in various other sales leadership positions with Sprint Corporation prior to that time. Mr. Mori received a B.S. in business administration from the University of Missouri.

RICHARD WARLEYhas served as our Managing Director – Europe, Middle East and Africa (EMEA) since September 2003. Previously, Mr. Warley held various positions at SAVVIS, including Executive Vice President of Corporate Development and Managing Director – Asia, since joining us in 2000. Prior to joining SAVVIS, Mr. Warley was a director in an investment banking group of Merrill Lynch & Co., Inc. Mr. Warley earned a B.A. and MSc with distinction from the London School of Economics and his law degree from the College of Law, London.

JOHN D. CLARK has served as a director of our company since April 2002. Mr. Clark is a general partner of Welsh, Carson, Anderson & Stowe, a private equity investment firm, and affiliated entities, which collectively are a principal stockholder of our company. Prior to joining Welsh, Carson, Anderson & Stowe in 2000, Mr. Clark was a general partner at Saunders, Karp & Megrue, a private equity firm, where he was employed from 1993 until 2000. Mr. Clark received a B.S. from Princeton University and a M.B.A. from Stanford University Graduate School of Business.

CLIFFORD H. FRIEDMAN has served as a director of our company since July 2002. Since August 1997, Mr. Friedman has served as senior managing director of Constellation Ventures, a Bear Stearns asset management fund. Mr. Friedman also serves as a director of MTM Technologies, Inc. Mr. Friedman earned a B.S. in Electrical Engineering and Computer Science and a M.S. in Electrophysics from Polytechnic Institute of New York, and a M.B.A. in Finance and Investments from Adelphi University.

CLYDE A. HEINTZELMAN has served as a director of our company since December 1998, and is chairman of the board’s audit committee. Mr. Heintzelman served as the chairman of the board of Optelecom, Inc., from February 2000 to June 2003 and as its interim president and chief executive officer from June 2001 to January 2002. From November 1999 to May 2001, he was president of Net2000 Communications, Inc. On November 16, 2001, Net2000 Communications and its subsidiaries filed voluntary petitions for relief under Chapter 11 of Title 11 of the United States Bankruptcy Code. From December 1998 to November 1999, Mr. Heintzelman served as our president and chief executive officer. Mr. Heintzelman serves on the board of TeleCommunication Systems, Inc., where he chairs the compensation committee and also serves as a member of the audit committee. Mr. Heintzelman received a B.A. in marketing from the University of Delaware and did graduate work at Wharton, the University of Pittsburgh, and the University of Michigan.

THOMAS E. MCINERNEY has served as a director of our company since October 1999 and is a member of the board’s compensation committee. Since 1987, Mr. McInerney has been a general partner of Welsh, Carson, Anderson & Stowe, a private equity investment firm, and affiliated entities, which collectively are a principal stockholder of our company. He is also a director of Centennial Communications Corp. and ITC DeltaCom, Inc. Mr. McInerney also served as the chairman of the executive committee of the board of Bridge, which assumed the responsibilities of the chief executive officer of Bridge, from November 2000 until February 2001. Mr. McInerney received a B.A. from St. John’s University and attended New York University Graduate School of Business Administration.

JAMES E. OUSLEY has served as a director of our company since April 2002 and is a member of the board’s audit and compensation committees. Mr. Ousley served as the president and chief executive officer and director of Vytek Corporation from 2001 until April 2004. From 1999 to 2002, he also served as chairman, CEO and president of Syntegra Inc. (USA), a division of British Telecommunications. From September 1991 to August 1999,

6

Mr. Ousley served as president and CEO of Control Data Systems. Mr. Ousley serves on the boards of Activcard Corp., Bell Microproducts, Inc., Datalink, Inc. and CalAmp Corp. Mr. Ousley received a B.S. from the University of Nebraska.

JAMES P. PELLOW has served as a director of our company since April 2002 and is a member of the board’s audit committee. Mr. Pellow has served at St. John’s University as the executive vice president and treasurer since 1999 and from 1998 until 1999 as senior vice president and treasurer. From 1991 to 1998, Mr. Pellow served in various other senior positions at St. John’s University. Mr. Pellow serves on the board of Centennial Communications Corp., where he chairs the audit committee. Mr. Pellow is a C.P.A. and received a B.B.A. and a M.B.A. from Niagara University.

PATRICK J. WELSH has served as a director of our company since October 1999 and is chairman of the board’s compensation committee. Mr. Welsh was a co-founder of the private equity investment firm Welsh, Carson, Anderson & Stowe. He has served as a general partner of Welsh, Carson, Anderson & Stowe and affiliated entities since 1979, which collectively are a principal stockholder of our company. Mr. Welsh received a B.A. from Rutgers University and a M.B.A. from the University of California at Los Angeles.

Pursuant to an investor rights agreement among us, entities and individuals affiliated with Welsh, Carson, Anderson & Stowe VIII, L.P. (“WCAS VIII”), Reuters Holdings Switzerland SA (“Reuters”), a group of funds affiliated with Constellation Ventures (the “Constellation Entities”) and various other entities, we agreed that, among other things, so long as WCAS VIII and its affiliates own voting stock representing more than 50% of the voting power represented by our outstanding voting stock, they have the right to nominate for election to the board of directors at least half of the members of the board. WCAS VIII and its affiliates owned, as of March 1, 2005, approximately 57% of our outstanding voting power, and accordingly have nominated Messrs. Welsh, McInerney, Clark, Finlayson, and Von Deylen for election to the board. Pursuant to the terms of the investor rights agreement, the Constellation Entities are entitled to nominate one person for election to our board of directors, and accordingly have nominated Mr. Friedman. For a more detailed description of the investor rights agreement, see “Certain Relationships and Related Transactions — Transactions with Welsh, Carson” and “— Transactions with the Constellation Entities” beginning on page 22.

Members of our board of directors are elected each year at our annual meeting of stockholders, and serve until the next annual meeting of stockholders and until their respective successors have been elected and qualified. Our officers are elected annually by our board of directors and serve at the board’s discretion.

Independent Directors

Our board of directors has determined that our company is a “Controlled Company,” as defined in the rules of The NASDAQ Stock Market, Inc. (“NASDAQ”), since WCAS VIII and certain entities and individuals affiliated with WCAS VIII are the beneficial owners of more than 50% of our voting power. We therefore are exempt from certain independence requirements of the NASDAQ rules, including the requirement to maintain a majority of independent directors on our board of directors, an independent compensation committee or a standing nominating committee or committee performing a similar function. In addition, because our company is a “Controlled Company,” the board of directors has not adopted a formal policy or process with regard to the consideration of director candidates recommended by stockholders.

Of the ten directors currently serving on the board of directors, the board has determined that Messrs. Heintzelman, Ousley and Pellow are “independent directors” as defined in the NASDAQ rules and also meet the additional independence standards for audit committee members.

7

Board of Directors and Committee Meetings during 2004

The board of directors meets regularly during the year to review matters affecting the company and to act on matters requiring the board’s approval. It also holds special meetings whenever circumstances require and may act by unanimous written consent without a meeting. The board of directors met seven times, including by telephone conference, during fiscal year 2004. All directors attended at least 80% of the meetings of the board of directors and the meetings of the committees on which they served held during the period that they served on the board of directors or such committees. Our board of directors has established an audit committee and a compensation committee.

Audit Committee. Our audit committee consists of Clyde A. Heintzelman, James E. Ousley and James P. Pellow. The board believes that Messrs. Heintzelman, Ousley and Pellow are, “independent directors,” as such term is defined in NASD’s Rule 4200(a)(15). In making this determination, the board considered that Mr. Pellow is the executive vice president and treasurer of St. John’s University and that Mr. McInerney, another of our directors and a general partner of Welsh, Carson, Anderson & Stowe, our principal stockholder, has made significant charitable contributions to St. John’s University in his individual capacity over the last several years. The board of directors determined, after considering the size of the contributions relative to the size of St. John’s University’s revenues and the fact that the contributions were made by Mr. McInerney personally and not by us or Welsh, Carson, Anderson & Stowe, that the existence of such contributions would not interfere with Mr. Pellow’s exercise of independent judgment in carrying out his responsibilities as a director. Separately, the board has determined that Mr. Pellow, one of its independent directors, is an “audit committee financial expert” as defined by the rules and regulations of the U.S. Securities and Exchange Commission.

The responsibilities of our audit committee include:

| • | engaging an independent audit firm to audit our financial statements and to perform services related to the audit; |

| • | reviewing the scope and results of the audit with our independent auditors; |

| • | considering the adequacy of our internal accounting control procedures; and |

| • | considering auditors’ independence. |

The board of directors has adopted a written charter for the audit committee, which is included asAnnex A to this proxy statement. The audit committee held thirteen meetings during fiscal year 2004.

Compensation Committee. Our compensation committee consists of Messrs. Thomas E. McInerney, Patrick J. Welsh and James E. Ousley. The compensation committee is responsible for determining the salaries and incentive compensation of our management and key employees and administering our stock option plan. The compensation committee held five meetings during fiscal year 2004.

Our company does not have a nominating committee or a committee serving a similar function. Nominations are made by and through the full board of directors.

Communications with Board of Directors and Annual Meeting Attendance

The board of directors provides a process for stockholders to send communications to the board or any of the directors. Stockholders may send written communications to the board or any of the directors c/o Corporate Secretary, SAVVIS Communications Corporation, 12851 Worldgate Drive, Herndon, Virginia 20170. All communications will be compiled by the Corporate Secretary of the company and submitted to the board or the individual directors on a periodic basis. This information is also contained on our website atwww.savvis.net.

We do not have a formal policy that directors attend our annual meeting of stockholders. We have determined that the process for stockholders to send written communications to the board is sufficient for our stockholders to discuss matters with the board. One director attended our 2004 annual meeting.

8

Director Compensation

Directors who are also employees of our company or are affiliated with one of our principal stockholders do not receive additional compensation for serving as a director. During 2004, each director who was not an employee of our company and who was not affiliated with one of our principal stockholders received an annual retainer of $10,000. In addition, in 2004, we paid the non-employee/non-affiliated directors as follows for their attendance at board and committee meetings: $1,500 per board meeting attended in person; $750 per committee meeting attended in person; and $250 per board and committee meeting attended by telephone. Directors are also reimbursed for all reasonable expenses incurred in connection with their service. Accordingly, in 2004 in addition to the annual retainer, we paid the following directors the following amounts for meetings they attended: Mr. Heintzelman, $18,250; Mr. Ousley, $19,750; and Mr. Pellow, $ 18,250.

Commencing February 16, 2005, each director who was not an employee of our company and who was not affiliated with one of our principal stockholders will receive an annual retainer of $15,000 and a fee of $1,500 for each regularly scheduled meeting of the board attended in person or by means of conference telephone call. In addition, each non-employee/non-affiliated director that is a member of a standing committee will be paid as follows: the chairman of a standing committee will receive an annual fee of $5,000, and each member of a standing committee will receive $1,000 for each regularly scheduled meeting attended in person and by means of conference telephone call.

9

EXECUTIVE COMPENSATION

The following table provides you with information about compensation earned during each of the last three fiscal years by our chief executive officer and the other four most highly compensated executive officers employed by us in fiscal year 2004, who we refer to as our named executive officers.

Summary Compensation Table (1)

| Long-Term Compensation Awards | |||||||||||||||

Name and Principal Position | Year | Salary | Bonus(4) | Securities Options | All Other Compensation (2) | ||||||||||

Robert A. McCormick | 2004 | $ | 450,000 | $ | — | 1,000,000 | $ | 6,500 | |||||||

Chief Executive Officer and | 2003 | 400,000 | — | — | 2,400 | ||||||||||

Chairman of the Board | 2002 | 400,000 | 88,658 | (3) | 4,734,965 | (3) | 2,400 | ||||||||

John M. Finlayson | 2004 | 420,000 | — | 800,000 | 4,625 | ||||||||||

President and Chief | 2003 | 400,000 | — | — | 2,400 | ||||||||||

Operating Officer | 2002 | 400,000 | 73,882 | (3) | 4,084,553 | (3) | 2,400 | ||||||||

Jeffrey H. Von Deylen(5) | 2004 | 275,000 | — | 650,000 | 4,952 | ||||||||||

Chief Financial Officer | 2003 | 233,502 | 100,000 | 1,000,000 | 75,419 | ||||||||||

Grier C. Raclin(5) | 2004 | 250,000 | — | 650,000 | 2,212 | ||||||||||

Chief Legal Officer | 2003 | 245,000 | 171,500 | 1,000,000 | 2,400 | ||||||||||

James D. Mori | 2004 | 225,000 | — | 400,000 | 6,500 | ||||||||||

Managing Director — | 2003 | 218,000 | 25,000 | — | 2,400 | ||||||||||

Americas | 2002 | 218,000 | 29,553 | (3) | 1,170,486 | (3) | 2,400 | ||||||||

| (1) | In accordance with the rules of the SEC, the compensation described in this table does not include medical, group life insurance or other benefits received by the executive officers that are available generally to all salaried employees and various perquisites and other personal benefits received by the executive officers, which do not exceed the lesser of $50,000 or 10% of any officer’s salary and bonus disclosed in this table. |

| (2) | The amounts in 2004 consist of matching contributions made under our 401(k) plan of $6,500 for Mr. McCormick, $4,625 for Mr. Finlayson, $4,952 for Mr. Von Deylen, $2,212 for Mr. Raclin and $6,500 for Mr. Mori. |

| (3) | Bonuses for fiscal year 2002 were paid partially in cash and the remainder were paid in stock option grants. The cash portion of the bonuses was awarded in April 2003. The stock option grants were awarded in June 2003. These options were fully vested when granted and had an aggregate discount amount (the difference between the fair market value per share of our common stock and the exercise price on the grant date) of $132,988 for Mr. McCormick, $110,823 for Mr. Finlayson and $44,329 for Mr. Mori. Mr. McCormick was granted options for 340,994 shares of common stock at an exercise price of $.39 per share; Mr. Finlayson was granted options for 284,162 shares of common stock at an exercise price of $.39 per share; and Mr. Mori was granted options for 113,665 shares of common stock at an exercise price of $.39 per share. |

| (4) | Cash bonuses for fiscal year 2004 had not been determined prior to distribution of these proxy materials. Cash bonuses for fiscal year 2003 were awarded in February 2004 and paid in April 2004. |

| (5) | Messrs. Von Deylen and Raclin joined our company in January 2003. |

10

Option Grants in Last Fiscal Year

The following table shows grants of stock options to each of our named executive officers during 2004. The percentages in the table below are based on options to purchase a total of 20,743,027 shares of our common stock granted to all our employees and directors in 2004. The numbers are calculated based on the requirements of the SEC and do not reflect our estimate of future stock price growth.

Options Granted In 2004

| Individual Grants | |||||||||||||

Name | Number of Securities Underlying Options Granted | Percent of to | Exercise Price per Share(1) | Expiration Date | Grant Date Value(2) | ||||||||

Robert A. McCormick | 1,000,000 | 4.8 | % | $ | 1.01 | 8/16/2014 | $ | 751,700 | |||||

John M. Finlayson | 800,000 | 3.9 | % | $ | 1.01 | 8/16/2014 | $ | 601,360 | |||||

Jeffrey H. Von Deylen | 650,000 | 3.1 | % | $ | 1.01 | 8/16/2014 | $ | 488,605 | |||||

Grier C. Raclin | 650,000 | 3.1 | % | $ | 1.01 | 8/16/2014 | $ | 488,605 | |||||

James D. Mori | 400,000 | 1.9 | % | $ | 1.01 | 8/16/2014 | $ | 300,680 | |||||

| (1) | All options granted to the named officers were granted on August 16, 2004. The options become exercisable in four equal parts on the first, second, third and fourth anniversaries of the grant date. |

| (2) | Options were valued under the Black-Scholes option pricing methodology, which produces a per share option price of $0.75, using the following assumptions and inputs: expected option life of 4 years, expected price volatility of 110%, dividend yield of zero, and an interest rate of 3% based on the 3-year and 5-year Treasury yield curve rates. The actual value, if any, the employee may realize from these options will depend solely on the gain in stock price over the exercise price when the options are exercised. |

Aggregate Option Exercises in 2004 and Fiscal Year-End Option Values

The following table sets forth as of December 31, 2004, for each of our named executive officers:

| • | the total number of shares received upon exercise of options during 2004; |

| • | the value realized upon that exercise; |

| • | the total number of unexercised options to purchase our common stock; and |

| • | the value of such options which were in-the-money at December 31, 2004. |

Shares on | Value Realized | Number of Securities Underlying | Value of Unexercised In-the-Money Options at | |||||||||||

Name | Exercisable | Unexercisable | Exercisable | Unexercisable | ||||||||||

Robert A. McCormick | — | — | 2,155,986 | 3,919,973 | $ | 1,009,713 | $ | 1,347,189 | ||||||

John M. Finlayson | — | — | 1,849,051 | 3,319,664 | $ | 860,409 | $ | 1,153,062 | ||||||

Jeffrey H. Von Deylen | 100,000 | 260,800 | 87,500 | 1,462,500 | $ | 66,500 | $ | 525,000 | ||||||

Grier C. Raclin | 118,125 | 291,081 | 69,375 | 1,462,500 | $ | 52,725 | $ | 525,000 | ||||||

James D. Mori | — | — | 594,494 | 975,992 | $ | 243,742 | $ | 296,157 | ||||||

| (1) | These values have been calculated on the basis of the last reported sale price of our common stock on the Nasdaq SmallCap Market as reported on December 31, 2004 of $1.16. |

11

Arrangements with Executive Officers

Arrangement with Mr. McCormick. On April 2, 2001, we entered into an agreement with Mr. McCormick, which agreement ratified the terms of Mr. McCormick’s employment arrangements. The agreement provided that Mr. McCormick would serve as our Chairman and Chief Executive Officer effective as of January 3, 2000. Under this agreement, as amended, Mr. McCormick is entitled to a base salary of $450,000 per year. In addition, he is eligible to receive a discretionary annual incentive bonus, which is targeted at 70% of his base salary, but can be greater or less, based on his personal and overall corporate performance. Mr. McCormick is entitled to benefits commensurate with those available to other senior executives.

In connection with his employment, Mr. McCormick received options to purchase 750,000 shares of our common stock at an exercise price of $.50 per share, 500,000 of which were granted on July 22, 1999 and 250,000 of which were granted on December 30, 1999. All of these options vested on the date of their grant. Mr. McCormick will have the right to exercise all options for one year after the termination of his employment, unless his employment was terminated for cause.

In the event we terminate Mr. McCormick’s employment without cause or if he terminates his employment for good reason, he will be entitled to receive a lump sum severance payment equal to his then current base annual salary, which will not be less than his highest annual salary paid by us. In the event of a change in control of our company, Mr. McCormick has agreed to remain with our company for a period of up to twelve months if the new management requests him to do so. A change of control, as defined in the agreement, includes a merger or consolidation of the company or a subsidiary with another company as a result of which more than fifty percent of the outstanding shares of the company after the transaction are owned by stockholders who were not stockholders of the company before the transaction. We will reimburse Mr. McCormick for any parachute payment taxes he would incur under the Internal Revenue Code of 1986, which we refer to as the Internal Revenue Code or Code, as a result of such a change in control. We may terminate Mr. McCormick’s employment for cause at any time without notice, in which case he will not be entitled to any severance benefits.

Arrangement with Mr. Finlayson. On December 28, 1999, we entered into an agreement with Mr. Finlayson pursuant to which he agreed to serve as our President and Chief Operating Officer effective December 31, 1999. Under this agreement, as amended, Mr. Finlayson is entitled to a base salary of $420,000 per year. In addition, he is eligible to receive a discretionary annual incentive bonus, which is targeted at 60% of his base salary, but can be greater or less, based on his personal and overall corporate performance. Mr. Finlayson will be entitled to benefits commensurate with those available to other senior executives.

In connection with his employment, Mr. Finlayson received options to purchase 650,000 shares of our common stock at an exercise price of $.50 per share, all of which have vested. Mr. Finlayson will have the right to exercise all options for one year after the termination of his employment unless his employment was terminated for cause.

In the event we terminate Mr. Finlayson’s employment without cause or if he terminates his employment for good reason, he will be entitled to receive a lump sum severance payment equal to his then current base annual salary, which will not be less than his highest annual salary paid by us. In the event of a change in control of our company, Mr. Finlayson has agreed to remain with our company for a period of up to twelve months if the new management requests him to do so. A change in control, as defined in the agreement, includes a merger or consolidation of the company or a subsidiary with another company as a result of which more than fifty percent of the outstanding shares of the company after the transaction are owned by stockholders who were not stockholders of the company before the transaction. We will reimburse Mr. Finlayson for any parachute payment taxes he would incur under the Internal Revenue Code as a result of such a change in control. We may terminate Mr. Finlayson’s employment for cause at any time without notice, in which case he will not be entitled to any severance benefits.

Arrangement with Mr. Von Deylen. On January 2, 2003, we entered into an agreement with Mr. Von Deylen pursuant to which he became our Chief Financial Officer. Under this agreement, as amended, Mr. Von Deylen is entitled to an annual base salary of $275,000. In addition, he is eligible to receive a discretionary annual

12

incentive bonus, which is targeted at 50% of his base salary, but can be greater or less, based on his personal and overall corporate performance. On January 2, 2003 we granted Mr. Von Deylen options to purchase 750,000 shares of our common stock at an exercise price of $.40 per share, which will vest over four years and options to purchase 250,000 shares of our common stock at an exercise price of $1.49 per share, which will vest over three years commencing in January 2004. In the event of a change of control, which is defined as a company other than Welsh, Carson taking ownership of more than 50% of our voting shares, all granted options will immediately vest. Mr. Von Deylen has also agreed in the event of a change in control to remain with our company for a period of up to six months if the new management requests him to do so. Under this agreement, Mr. Von Deylen is entitled to benefits commensurate with those available to executives of comparable rank.

In the event we terminate Mr. Von Deylen’s employment without cause, Mr. Von Deylen will be entitled to receive his then current base salary for a period of one year, a lump sum payment equal to his pro rated target bonus and any unpaid bonus from the prior year. In addition, the vesting of Mr. Von Deylen’s options will accelerate by one year, and he will have the right to exercise all vested options for a period of twelve months from the date of termination, unless he becomes employed elsewhere during that period, in which case he would only be entitled to exercise his options immediately. Mr. Von Deylen will receive a similar payment if he were to resign as a result of being forced to relocate without his consent from the metropolitan area in which he was living at the time of his resignation, or if he were to be reassigned to a position entailing materially reduced responsibilities or opportunities for compensation.

Arrangement with Mr. Raclin. On January 6, 2003, we entered into an agreement with Mr. Raclin pursuant to which he became our Chief Legal Officer and Corporate Secretary, effective January 1, 2003. Under this agreement, as amended, Mr. Raclin is entitled to an annual base salary of $250,000. In addition, he is eligible to receive a discretionary annual incentive bonus, which is targeted at 50% of his base salary, but can be greater or less, based on his personal and overall corporate performance. For 2003, the agreement provides that Mr. Raclin will receive a bonus equal to no less than 70% of his 2003 annual base salary, which was $245,000, which such bonus he received in April 2004. On January 2, 2003 we granted Mr. Raclin options to purchase 750,000 shares of our common stock at an exercise price of $.40 per share, which will vest over four years and options to purchase 250,000 shares of our common stock at an exercise price of $1.49 per share, which will vest over three years commencing in January 2004. In the event of a change of control, which is defined as a company other than Welsh, Carson taking ownership of more than 50% of our voting shares, all granted options will immediately vest. We will reimburse Mr. Raclin for any parachute payment taxes he would incur under the Internal Revenue Code as a result of such change of control. Under this agreement, Mr. Raclin is entitled to benefits, including severance, commensurate with those available to executives of comparable rank.

In the event we terminate Mr. Raclin’s employment without cause or for reasons other than performance, Mr. Raclin will be entitled to receive benefits at a level not less than those received by other similarly situated senior executive employees of the company, which will at least include a lump sum payment of his then current base salary for a period of one year, the pro rata portion of the prior year’s bonus, and three months’ notice. In addition, all granted options will immediately vest and he will have the right to exercise all vested options for a period of twelve months from the date of termination. Mr. Raclin will receive a similar payment if he were to resign as a result of being forced to relocate without his consent from the metropolitan area in which he was living at the time of his resignation, or if he were to be reassigned to a position entailing materially reduced responsibilities or opportunities for compensation.

Arrangement with Mr. Mori. On September 30, 1999, we entered into an agreement with Mr. Mori pursuant to which he became our Executive Vice President and General Manager for Americas effective October 1, 1999; in 2003 we changed Mr. Mori’s title to Managing Director – Americas. Under this agreement, as amended, Mr. Mori is entitled to an annual base salary of $225,000. In addition, he is eligible to receive a discretionary annual incentive bonus, which is targeted at 50% of his base salary, but can be greater or less, based on his personal and overall corporate performance. On October 29, 1999 and December 30, 1999, we granted Mr. Mori options to purchase 225,000 shares and 75,000 shares of our common stock, respectively, each at an exercise price of $.50 per share. All of these options have vested. Under this agreement, Mr. Mori is entitled to benefits commensurate with those available to executives of comparable rank.

In the event we terminate Mr. Mori’s employment without cause after the second anniversary of his employment, and either we are not a public company or we are a public company and our shares on the date of

13

termination trade at a price less than $15 per share, Mr. Mori will be entitled to receive a payment of $450,000. Mr. Mori will receive a similar payment if he were to resign as a result of an acquisition of more than 30% of our voting shares by an entity other than Bridge, if he were to be forced to relocate without his consent from the St. Louis metropolitan area, or if he were to be reassigned to a position entailing materially reduced responsibilities or opportunities for compensation.

Compensation Committee Interlocks and Insider Participation

Messrs. McInerney and Welsh are general partners of WCAS VIII and affiliated entities, which collectively owned, as of March 1, 2005, 57% of our outstanding voting stock. See “Certain Relationships and Related Transactions — Transactions with Welsh Carson” beginning on page 22.

In 2004, none of our executive officers served as a director or member of the compensation committee of another entity whose executive officers had served on our board of directors or on our compensation committee.

14

Compensation Committee Report on Executive Compensation for 2004

Our compensation committee reviews, analyzes and recommends compensation programs to our board of directors and administers and grants awards under our 1999 stock option plan and our 2003 incentive compensation plan. During 2004, the compensation committee consisted of Messrs. Thomas E. McInerney, Patrick J. Welsh and James E. Ousley. None of these directors are current or former employees of our company.

Compensation Policies Toward Executive Officers

The compensation committee has structured its compensation policies to achieve the following goals:

| • | attract, motivate and retain experienced and qualified executives; |

| • | increase the overall performance of the company; |

| • | increase stockholder value; and |

| • | increase the performance of individual executives. |

To achieve these objectives, the compensation program for our executive officers consists principally of three elements: base salary, cash bonuses and /or stock and long-term incentive compensation in the form of participation in our 1999 stock option plan and our 2003 incentive compensation plan.

The compensation committee seeks to provide competitive salaries based upon individual performance together with cash and/or bonuses awarded based on our overall performance relative to corporate objectives, taking into account individual contributions, teamwork and personal and corporate performance levels. In addition, it is our policy to grant stock options, restricted stock, and/or other incentive compensation awards linked to the performance of our common stock to executives upon their commencement of employment and periodically thereafter in order to strengthen the alliance of interest between such executives and stockholders and to give executives the opportunity to reach the top compensation levels of the competitive market depending on our performance. The following describes in more specific terms the elements of compensation that implement the compensation committee’s compensation policies, with specific reference to compensation reported for 2004:

Base Salaries. Base salaries of executives are initially determined by evaluating the responsibilities of the position, the experience and knowledge of the individual, and the competitive marketplace for executive talent, including a comparison to base salaries for comparable positions at peer public companies in the same geographic region. To ensure retention of qualified management, we have entered into employment agreements with each of our named executive officers. The terms of such agreements were the results of arms-length negotiations between us and each executive officer. You can find further information regarding the employment agreements of the named executive officers under the heading “Arrangements with Executive Officers,” above. The agreements establish the base salary for each officer during the term of the agreement. We will review the salaries for the executives annually and, if appropriate, adjust based on individual performance, increases in general levels of compensation for executives at comparable firms and our overall financial results.

Bonuses. The compensation committee also considers the payment of cash bonuses as part of its compensation program. Annual cash bonuses reflect a policy of requiring a certain level of company financial and operational performance for the prior fiscal year before any cash bonuses are earned by executive officers. In general, the compensation committee has tied potential bonus compensation to performance factors, including the executive officer’s efforts and contributions towards obtaining company objectives and the company’s overall growth. In 2004, the compensation committee established revenue and cash balance targets as the primary factors for determining executive incentive compensation. The employment agreements of each of the executive officers provide that each of these employees will be entitled to a bonus consisting of cash in an amount determined before the conclusion of each fiscal year.

Stock Awards. A third component of executive officers’ compensation is our 1999 stock option plan and 2003 incentive compensation plan, pursuant to which we may grant executive officers and other employees options to purchase shares of our common stock, restricted or unrestricted stock, stock units, or other stock-based awards.

15

The compensation committee grants such awards to executives in order to align their interests with the interests of our stockholders. Such awards are considered by the compensation committee to be an effective long-term incentive because the executives’ gains are linked to increases in the stock value that in turn provides stockholder gains.

The compensation committee generally grants such awards to new executive officers and other key employees upon their commencement of employment with us and periodically thereafter. The option awards generally are granted at an exercise price equal to the market price of our common stock on the date or grant or on the last day of the month following the date of the grant. The full benefit of the awards is realized upon appreciation of the stock price in future periods, thus providing an incentive to create value for our stockholders through appreciation of stock price. We believe that such awards have been helpful in attracting and retaining skilled executive personnel. In 2004, we granted a total of 3,500,000 stock options to our named executive officers. The per share option exercise price of such options was determined to be the fair market value of our common stock on the date of grant.

Other. We have a contributory retirement plan for our employees (including executive officers) age 21 and over. Employees are eligible to begin participation on a quarterly basis. This 401(k) plan provides that each participant may contribute up to 15% of his or her salary (not to exceed the annual statutory limit). We generally make matching contributions to each participant’s account equal to 50% of the participant’s contribution up to 6% of the participant’s annual compensation.

Chief Executive Officer Compensation

The executive compensation policy described above has been applied in setting Mr. McCormick’s 2005 compensation. Mr. McCormick generally participates in the same executive compensation plans and arrangements available to the other executives. Accordingly, his compensation consists of annual base salary, annual bonus, and long-term equity-linked compensation. The compensation committee’s general approach in establishing Mr. McCormick’s compensation is to be competitive with peer companies. In addition, the specific 2004 compensation elements for Mr. McCormick’s compensation were determined in light of his level of responsibility, performance, current salary and other compensation awards and performance of the company. Mr. McCormick’s compensation during the year ended December 31, 2004 included $450,000 in base salary. Mr. McCormick’s base salary for 2004 was consistent with the compensation committee’s policy of being competitive with the compensation of chief executive officers of peer companies. In addition, we granted Mr. McCormick options to purchase 1,000,000 shares of common stock in 2004 at an average exercise price of $1.01 per share which shares vest equally over four years. Mr. McCormick’s base salary for 2005 remains unchanged. For 2005, the compensation committee has established revenue and cash balance targets as the primary factors for determining his incentive compensation, which will be targeted at a percentage of his base salary to be determined by the committee. Mr. McCormick’s incentive compensation for 2005 may be greater or less than this percentage based on whether such targets are met or exceeded.

Compensation Deductibility Policy

Section 162(m) of the Internal Revenue Code generally disallows a tax deduction to public corporations for compensation over $1,000,000 paid for any fiscal year to the corporation’s chief executive officer and four other most highly compensated executive officers as of the end of any fiscal year. However, the statute exempts qualifying performance-based compensation from the deduction limit if specified requirements are met. The board of directors and the compensation committee reserve the authority to award non-deductible compensation in circumstances they deem appropriate. In 2004, stock options granted by the compensation committee under our 1999 stock option plan and 2003 incentive compensation plan did not satisfy the requirements for exemption under Section 162(m) as qualifying performance-based compensation.

Submitted by the Compensation Committee for fiscal year 2004,

Patrick J. Welsh

Thomas E. McInerney

James E. Ousley

16

Audit Committee Report for Fiscal Year 2004

In accordance with its written charter adopted by the board of directors, the audit committee of the board assists the board in fulfilling its responsibility for oversight of the quality and integrity of our accounting, auditing and financial reporting practices. In addition, the audit committee is responsible for overseeing the company’s implementation of the internal controls required under Section 404 of the Sarbanes Oxley Act of 2002. The audit committee has reviewed and discussed our audited financial statements for the fiscal year ended December 31, 2004 with our management. The audit committee has discussed with Ernst & Young LLP, our independent auditors during fiscal year 2004, the matters required to be discussed by Statement on Auditing Standards No. 61. The audit committee has received the written disclosures and the letter from Ernst & Young LLP required by Independence Standards Board Standard No. 1 and discussed with Ernst & Young LLP its independence. Based on the review and discussions described above, the audit committee recommended to the board of directors that our audited financial statements be included in our annual report on Form 10-K for the fiscal year ended December 31, 2004.

Submitted by the Audit Committee,

Clyde A. Heintzelman

James E. Ousley

James P. Pellow

17

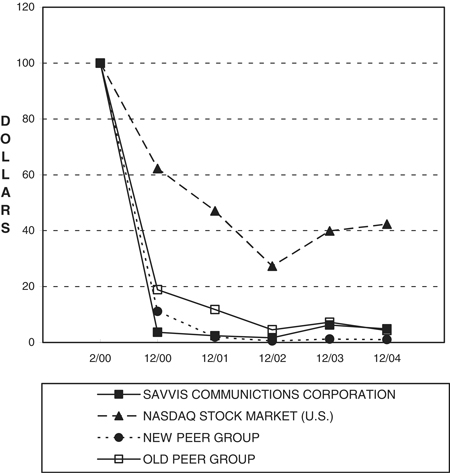

STOCKHOLDER RETURN PERFORMANCE GRAPH

COMPARISON OF 58 MONTH CUMULATIVE TOTAL RETURN*

AMONG SAVVIS COMMUNICATIONS CORPORATION,

THE NASDAQ STOCK MARKET (U.S.) INDEX

A NEW PEER GROUP AND AN OLD PEER GROUP

* $100 invested on 2/15/00 in stock or on 1/31/00 in index-

including reinvestment of dividends

Fiscal year ending December 31.

The peer group in the graph that we refer to as the old peer group (the “Old Peer Group”) is a specially constructed group that we used prior to this year for comparative purposes. This group included the common stocks of Equant N.V., Infonet Services Corp., Interland, Inc. and Internap Network Services Corporation. Two of the companies in this group have announced plans to be acquired by large telecommunications providers: Equant N.V. by France Telecom and Infonet Services Corp. by British Telecom. In addition, our line-of-business changed slightly due to our acquisition of CWA in March 2004. These changes have made the Old Peer Group less relevant for comparative purposes, and we have accordingly adopted a new composite peer group index (the “New Peer Group”), replacing Equant and Infonet Services Corp. with Broadwing, Inc. and Equinix, Inc. We believe this new composite index provides a better basis for performance comparisons than the old index.

The points on the graph represent the following numbers:

| Cumulative Total Return | |||||||||||||

| February 15, 2000 | December 31, 2000 | December 31, 2001 | December 31, 2002 | December 31, 2003 | December 31, 2004 | ||||||||

SAVVIS | $ | 100.00 | 3.65 | 2.38 | 1.67 | 6.23 | 4.83 | ||||||

Nasdaq Stock Market (U.S.) | $ | 100.00 | 62.22 | 47.05 | 27.29 | 39.92 | 42.32 | ||||||

New Peer Group | $ | 100.00 | 11.09 | 1.72 | 0.43 | 1.01 | 0.59 | ||||||

Old Peer Group | $ | 100.00 | 18.88 | 11.76 | 4.54 | 7.20 | 4.24 | ||||||

18

OWNERSHIP OF SECURITIES

Ownership of Our Voting Stock

The following table provides you with information about the beneficial ownership of shares of our voting stock as of March 1, 2005, by:

| • | each person or group that, to our knowledge, beneficially owns more than 5% of the outstanding shares of a class of voting stock; |

| • | each of our directors and executive officers; and |

| • | all of our directors and executive officers as a group. |

The persons named in the table have sole voting and investment power with respect to all shares of voting stock shown as beneficially owned by them, subject to community property laws where applicable and unless otherwise noted in the notes that follow. Shares of common stock subject to options, warrants and convertible preferred stock currently exercisable or convertible, or exercisable or convertible within 60 days of March 1, 2005, are deemed outstanding for purposes of computing the percentage beneficially owned by the person or entity holding such securities but are not deemed outstanding for purposes of computing the percentage beneficially owned by any other person or entity. Percentage of beneficial ownership is based on 178,004,256 shares of common stock and 202,490 shares of Series A preferred stock outstanding as of the close of business on March 1, 2005.

The “Total Voting Power” column reflects each listed individual’s or entity’s percent of actual ownership of all voting securities of our company. As a result, this column excludes any shares of common stock subject to options and warrants, as holders of those securities will not be entitled to vote with respect to such securities unless such securities are exercised.

As of March 1, 2005, we had shares of capital stock outstanding representing 551,909,660 votes.

Unless otherwise indicated below, the address for each listed director and executive officer is SAVVIS Communications Corporation, 1 Savvis Parkway, Town & Country, Missouri 63017.

| Common Stock | Series A Preferred Stock (1) | Total Voting Power | |||||||||||||

Name of Beneficial Owner | # of shares | % of class | # of shares | % of class | (%) | ||||||||||

| 5% Stockholder | |||||||||||||||

Welsh, Carson, Anderson & Stowe | 299,548,297 | (2) | 70 | % | 133,332 | (3) | 66 | % | 54 | % | |||||

Reuters Holdings Switzerland SA | 76,196,469 | (4) | 30 | % | 40,870 | 20 | % | 14 | % | ||||||

Oak Hill Entities | 19,658,660 | (5) | 11 | % | — | — | 4 | % | |||||||

Constellation Entities. | 48,637,694 | (6) | 22 | % | 20,000 | (7) | 10 | % | 8 | % | |||||

JPMorgan Chase & Co. . | 13,030,020 | (8) | 7.3 | % | — | — | 2 | % | |||||||

| Executive Officers and Directors | |||||||||||||||

Robert A. McCormick | 3,473,481 | (9) | * | — | — | * | |||||||||

John M. Finlayson | 3,025,095 | (10) | * | — | — | * | |||||||||

Jeffrey H. Von Deylen | 358,333 | (11) | * | — | — | * | |||||||||

Grier C. Raclin | 340,208 | (12) | * | — | — | * | |||||||||

James D. Mori | 1,191,741 | (13) | * | — | — | * | |||||||||

Clyde A. Heintzelman | 60,000 | (14) | * | — | — | * | |||||||||

Patrick J. Welsh | 301,821,520 | (15) | 71 | % | 134,555 | (16) | 67 | % | 55 | % | |||||

Thomas E. McInerney | 301,795,951 | (17) | 71 | % | 134,422 | (18) | 66 | % | 55 | % | |||||

John D. Clark | 252,751,465 | (19) | 64 | % | 116,115 | (20) | 57 | % | 46 | % | |||||

James E. Ousley | 50,000 | (21) | * | * | * | * | |||||||||

James P. Pellow | 75,000 | (22) | * | * | * | * | |||||||||

Clifford Friedman | 48,637,694 | (23) | 22 | % | 20,000 | 10 | % | 8 | % | ||||||

All executive officers and directors as a group (12 persons) | 361,166,080 | 75 | % | 155,655 | 76 | % | 63 | % | |||||||

| * | Less than one percent. |

19

| (1) | As of March 1, 2005, holders of Series A preferred stock were entitled to an aggregate of approximately 373,905,404 votes. |

| (2) | Includes 25,891,884 shares beneficially held by Welsh, Carson, Anderson & Stowe VI, L.P., which we refer to as WCAS VI, 19,411,038 shares beneficially held by Welsh, Carson, Anderson & Stowe VII, L.P., which we refer to as WCAS VII, 65,357 shares beneficially held by WCAS Information Partners, L.P., which we refer to as WCAS IP, 667,761 shares held by WCAS Capital Partners II, L.P., which we refer to as WCAS CP II, 252,733,029 shares beneficially held by WCAS VIII, and 779,228 shares beneficially held by WCAS Management Corporation, which we refer to as WCAS Management. 18,127,796 of the shares beneficially owned by WCAS VI, 13,590,331 of the shares beneficially owned by WCAS VII, 214,576,549 of the shares beneficially owned by WCAS VIII and 57,278 of the shares beneficially owned by WCAS Management are issuable upon the conversion of the shares of Series A preferred stock, including accrued and unpaid dividends through March 1, 2005, issued by us to these entities under securities purchase agreements dated as of March 6, 2002 and September 18, 2002. The respective sole general partners of WCAS VI, WCAS VII, WCAS IP, WCAS CP II and WCAS VIII are WCAS VI Partners, L.P., WCAS VII Partners, L.P., WCAS INFO Partners, WCAS CP II Partners and WCAS VIII Associates, LLC. |

The individual general partners of each of these partnerships include some or all of Bruce K. Anderson, Russell L. Carson, John D. Clark, Anthony J. de Nicola, D. Scott Mackesy, Thomas E. McInerney, Robert A. Minicucci, James R. Matthews, Paul B. Queally, Jonathan M. Rather, Sanjay Swani and Patrick J. Welsh. The individual general partners who are also directors of the company are Thomas E. McInerney, Patrick J. Welsh and John D. Clark. Each of the foregoing persons may be deemed to be the beneficial owner of the common stock owned by the limited partnerships of whose general partner he or she is a general partner. The address of Welsh, Carson, Anderson & Stowe is 320 Park Avenue, Suite 2500, New York, NY 10022.

| (3) | Includes 9,828 shares of Series A preferred stock held by WCAS VI, 7,368 shares of Series A preferred stock held by WCAS VII, 116,105 shares of Series A preferred stock held by WCAS VIII, and 31 shares of Series A preferred stock held by WCAS Management. |

| (4) | Consists of 76,196,469 shares of common stock issuable upon the conversion of the shares of our Series A preferred stock, including accrued and unpaid dividends through March 1, 2005, acquired by Reuters on March 18, 2002 upon conversion of its 12% convertible senior secured notes due 2005, including accrued and unpaid interest. Such shares of Series A convertible preferred stock are convertible at any time at the holder’s option. According to Schedule 13D filed by Reuters on March 20, 2002, Reuters has both shared voting power and shared disposition power with Reuters Group PLC over the common stock issuable upon the conversion of its shares of our Series A preferred stock. The principal executive offices of Reuters are located at 153 route de Thonon, 1245 Collange-Bellerive, Switzerland. Reuters is an indirect subsidiary of Reuters Group PLC, a public limited liability company registered in England and Wales with its principal executive offices located at 85 Fleet Street, London EC4P 4AJ, England. |

| (5) | Information with respect to the outstanding shares beneficially owned by the Oak Hill Entities is based on a Schedule 13G filed with the SEC on December 20, 2004 by such entities. Consists of shares of common stock held by Oak Hill Special Opportunities Fund, L.P., Oak Hill Special Opportunities Fund (Management), L.P., Oak Hill Securities Fund, L.P., Oak Hills Securities Fund II, L.P., Oak Hill Credit Alpha Fund, L.P., Oak Hill Credit Alpha Fund (Offshore), Ltd., Cardinal Fund I, L.P., FW Savvis Investors, L.P. The principal executive offices of the Oak Hill Entities are located at 201 Main Street, Fort Worth, TX 76102. |

| (6) | Includes 25,719,425 shares of common stock beneficially held by Constellation Venture Capital II, L.P., which we refer to as CVC II, 12,159,334 shares beneficially held by Constellation Venture Capital Offshore II, L.P., which we refer to as CVC Offshore, 10,189,488 shares beneficially held by The BSC Employee Fund IV, L.P., which we refer to as BSC Fund, and 569,447 shares held by CVC II Partners, |

20

L.L.C., which we refer to as CVC II Partners. 36,118,392 of the shares beneficially owned by these entities are issuable upon the conversion of the shares of Series A preferred stock, including accrued and unpaid dividends through March 1, 2005, issued by us to these entities under a securities purchase agreement dated as of June 28, 2002. According to Schedule 13D/A filed by the Constellation Entities on January 11, 2005, all of the Constellation Entities have both shared voting power and shared disposition power with Bear Stearns Asset Management Inc. and CVC II, CVC Offshore and CVC II Partners have both shared voting power and shared disposition power with Constellation Ventures Management II, LLC. The address of the Constellation Entities is 383 Madison Avenue, New York, New York 10179. |

Includes 3,525,227 shares of common stock subject to warrants that are currently exercisable by CVC II, 1,666,620 shares of common stock subject to warrants that are currently exercisable by CVC Offshore, 1,396,610 shares of common stock subject to warrants that are currently exercisable by BSC Fund and 78,210 shares of common stock subject to warrants that are currently exercisable by CVC II Partners.

| (7) | Includes 10,576 shares of Series A preferred stock held by CVC II, 5,000 shares of Series A preferred stock held by CVC Offshore, 4,190 shares of Series A preferred stock held by BSC Fund, and 234 shares of Series A preferred stock held by CVC II Partners. |

| (8) | Information with respect to the outstanding shares beneficially owned by JPMorgan Chase & Co., which we refer to as JPMorgan, is based on a Schedule 13G/A filed with the SEC on February 10, 2005 by such firm. JPMorgan reports that JPMorgan Chase Bank, National Association, its subsidiary, beneficially owns all of the shares. The principal executive offices of JP Morgan are located at 270 Park Ave., New York, NY 10017. |

| (9) | Includes 3,063,481 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (10) | Includes 2,631,495 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005 and 37,500 shares of common stock held in trust for the benefit of Mr. Finlayson’s children. |

| (11) | Includes 358,333 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (12) | Includes 340,208 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005 and 1,200 shares of common stock held by his wife. |

| (13) | Includes 891,741 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (14) | Includes 60,000 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (15) | Includes 299,482,940 shares held by Welsh, Carson, Anderson & Stowe, as described in note 2 above. Also includes 2,259,452 shares issuable upon the conversion of the shares of Series A preferred stock individually held by Mr. Welsh, including accrued and unpaid dividends through March 1, 2005, and 15,000 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (16) | Includes 133,332 shares of Series A preferred stock held by Welsh, Carson, Anderson & Stowe, as described in note 3 above. |

| (17) | Includes 299,548,297 shares held by Welsh, Carson, Anderson & Stowe, as described in note 2 above. Also includes 2,014,178 shares issuable upon the conversion of the shares of Series A preferred stock held by Mr. McInerney, including accrued and unpaid dividends through March 1, 2005, and 15,000 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (18) | Includes 133,332 shares of Series A preferred stock held by Welsh, Carson, Anderson & Stowe, as described in note 3 above. |

21

| (19) | Includes 252,733,029 shares of Series A preferred stock held by WCAS VIII, as described in note 2 above. Includes 18,436 shares issuable upon the conversion of the shares of Series A preferred stock held by Mr. Clark, including accrued and unpaid dividends through March 1, 2005. |

| (20) | Includes 116,105 shares held by WCAS VIII, as described in note 3 above. |

| (21) | Includes 45,000 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (22) | Includes 45,000 shares of common stock subject to options that are exercisable within 60 days of March 1, 2005. |

| (23) | Consists of shares held by the Constellation Entities, as described in notes 6 and 7 above. |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS