Gildan is a vertically-integrated marketer and manufacturer of quality branded basic apparel. The Company is the leading supplier of activewear for the screenprint market in the U.S. and Canada. It is also a leading supplier to this market in Europe, and is establishing a growing presence in Mexico and the Asia-Pacific region. The Company sells T-shirts, sport shirts and fleece in large quantities to wholesale distributors as undecorated “blanks”, which are subsequently decorated by screenprinters with designs and logos. Consumers ultimately purchase the Company’s products, with the Gildan label, in venues such as sports, entertainment and corporate events, and travel and tourism destinations. The Company’s products are also utilized for work uniforms and other end-uses to convey individual, group and team identity. The Company is also a leading supplier of private label and Gildan branded socks primarily sold to mass-market retailers. In addition, Gildan has an objective to become a significant supplier of men’s and boys’ underwear and undecorated activewear products to mass-market retailers in North America.

FINANCIAL HIGHLIGHTS

(in US$ millions, except per share data and ratios)

09

08

07

06

05

04

INCOME STATEMENT

Net sales

1,038.3

1,249.7

964.4

773.2

653.9

533.4

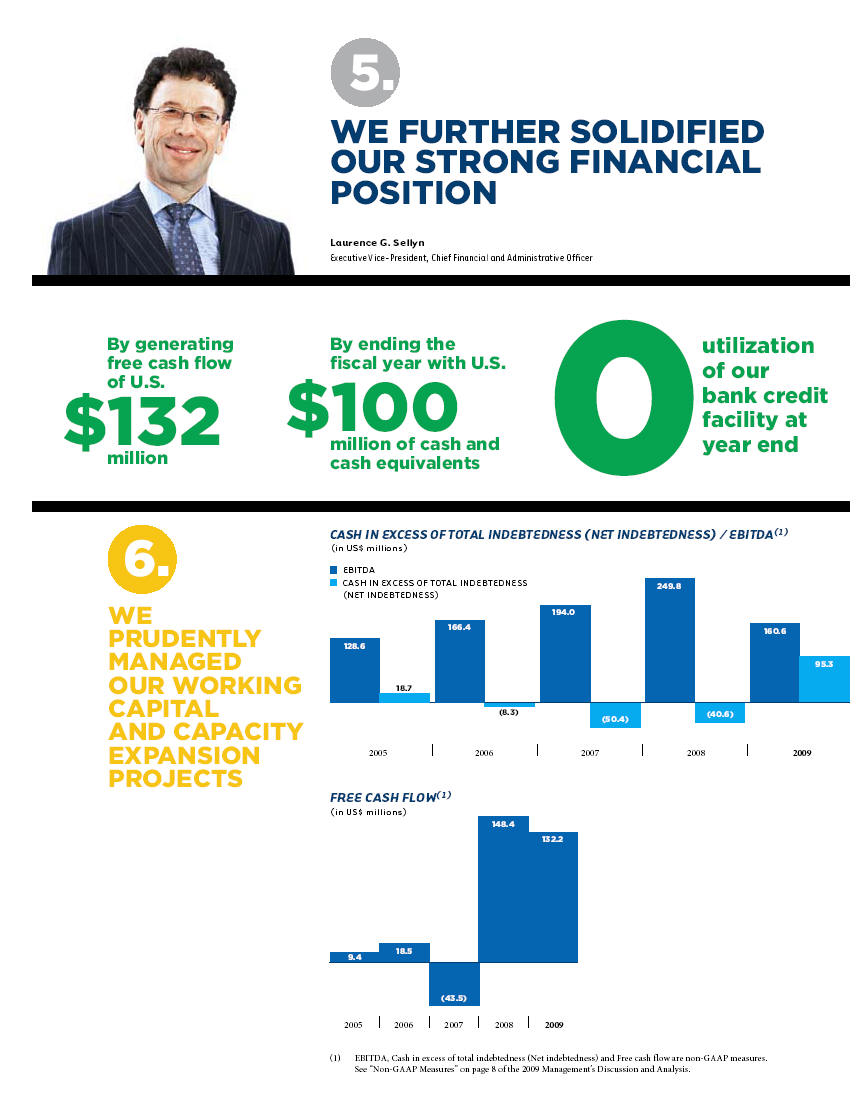

EBITDA(1)

160.6

249.8

194.0

166.4

128.6

98.9

Net earnings(2)

95.3

146.4

129.1

106.3

85.8

59.9

Diluted earnings per share(2)(3)

0.79

1.20

1.06

0.88

0.71

0.50

Adjusted net earnings(1)(2)

99.7

151.3

156.4

126.3

93.8

66.4

Adjusted diluted earnings per share(1)(2)

0.82

1.24

1.29

1.04

0.78

0.56

CASH FLOW

Operating cash flow(2)(4)

159.5

191.2

167.7

158.0

122.0

87.8

Change in non-cash working capital balances(2)

9.7

47.7

(79.1)

(64.6)

(29.6)

(29.6)

Capital expenditures

(44.9)

(97.0)

(134.3)

(80.2)

(86.1)

(53.7)

Free cash flow(1)

132.2

148.4

(43.5)

18.5

9.4

5.1

FINANCIAL POSITION

Total assets(2)

1,082.4

1,095.0

867.7

718.9

596.5

488.1

Long-term debt (including current portion)

4.4

53.0

59.7

33.9

47.1

56.6

Cash in excess of total indebtedness

(Net indebtedness)(1)

95.3

(40.6)

(50.4)

(8.3)

18.7

4.1

Shareholders’ equity(2)

910.8

811.5

661.1

529.0

419.5

326.7

FINANCIAL RATIOS

EBITDA margin

15.5%

20.0%

20.1%

21.5%

19.7%

18.5%

Net debt to EBITDA

n.a

0.2 x

0.3 x

0.0 x

n.a.

0.0 x

Net earnings margin

9.2%

11.7%

13.4%

13.7%

13.1%

11.2%

Return on shareholders’ equity

11.3%

19.8%

22.0%

22.4%

23.5%

20.6%

(1)

EBITDA, Adjusted net earnings, Adjusted diluted earnings per share, Free cash flow and Cash in excess of total indebtedness (Net indebtedness) are non-GAAP measures.

See “Non-GAAP Measures” on page 8 of the 2009 Management’s Discussion and Analysis.

(2)

Reflects the impact of the change in accounting policy as described in Note 1(b) to the 2009 audited Consolidated Financial Statements.

(3)

All per share data reflect the effect of the stock splits in May 2007 and May 2005.

(4)

Cash flows from operating activities before net changes in non-cash working capital balances.

n.a.

Not applicable.

Certain minor rounding variances exist between the financial statements and this summary.

2 GILDAN 2009 Annual Report

“WE WERE PLEASED TO APPOINT TWO NEW BOARD MEMBERS, GEORGE HELLER AND JAMES R. SCARBOROUGH, BOTH OF WHOM HAVE HAD SUCCESSFUL CAREERS AS BUSINESS LEADERS IN THE RETAIL SECTOR.”

A

lthough this has been an extremely challenging year for our industry and for our Company, we are very proud of our progress in 2009 and the important initiatives that have been put in place for the future.

Gildan continues to invest in its commitment to corporate social responsibility and sustainable development. For example, we have spent capital on a major renewable energy project in our Dominican Republic textile facility, which will reduce our environmental footprint and lower our energy consumption and costs. Our initiatives in corporate social responsibility and sustainability are more fully described in the Corporate Citizenship Executive Summary included with this Annual Report.

At our December meeting, we were pleased to appoint two new Board members, George Heller and James R. Scarborough, both of whom have had successful careers as business leaders in the retail sector. We look forward to benefitting from their experience and counsel in the years to come as we pursue the next phase of our major growth initiative to become a full-line supplier of basic family apparel for the retail market. The addition of George and Jim increases the size of the Board from seven to nine directors. We now have eight independent directors. Our ninth director is Glenn Chamandy, who is of course the Company’s founding entrepreneur and a major shareholder.The size of the Board continues to be small, allowing for active participation by all directors, but we have broadened our base of skills and expertise to advise management and provide effective stewardship of your Company.

Finally, we were pleased to again be recognized this year by the Globe and Mail’s Report on Business Annual Corporate Governance Survey as one of the top ten companies of the S&P/TSX Composite Index for our performance in corporate governance. The results of this survey, which is based on a detailed review of the 2008 management proxy circulars of all of the corporations on the index (excluding income trusts), reflect the commitment of both the Board and Gildan’s management to adhere to best practices in corporate governance.

Chairman of the Board

2009 Annual Report GILDAN3

I

n spite of the severe downturn in economic conditions, which resulted in a challenging market environment for the Company, Gildan’s financial results improved markedly in the second half of fiscal 2009 and we ended the year with strong positive momentum for fiscal 2010.

Our main performance highlights for fiscal 2009 included the following:

We continued to significantly increase our market share in all product categories in the U.S. distributor channel, and ended the fiscal year with an overall share of 57.1% compared with 53.4% at the end of fiscal 2008. Our goal is to further increase our market share leadership during fiscal 2010.

We increased our penetration in other target screenprint markets, including imprinted private label customers and our international markets in Europe, Mexico and Asia/Pacific.

NET SALES (in US$ millions)

ADJUSTED DILUTED EARNINGS PER SHARE(1)(2) (in US$)

We made significant progress in positioning the Company to pursue the next phase of our major growth initiative to become a full-line supplier of basic family apparel for retailers. We successfully transitioned the private label brands which we manufacture for our largest retail customer to new highly recognizable consumer brands which are performing well. We have continued to build on the successful performance of our private label sock programs and we have secured new retail programs which will begin shipment in the second quarter of fiscal 2010. In December 2009, we announced that we have been awarded a large strategically important underwear program as well as a smaller underwear program and three further sock programs. The annualized sales revenue from the new programs is currently estimated to be approximately U.S. $70 million. In addition to our private label programs for national mass-retailers, we are continuing to make steady progress in expanding our Gildan branded products with regional retail chains. We are building on existing programs with regional retailers to become a full-line supplier of branded basic family apparel, and leveraging the positioning of our brand in approximately 1,700 retail outlets in North America.

“WE HAVE CONTINUED TO BUILD ON THE SUCCESSFUL PERFORMANCE OF OUR PRIVATE LABEL SOCK PROGRAMS AND WE HAVE SECURED NEW RETAIL PROGRAMS WHICH WILL BEGIN SHIPMENT IN THE SECOND QUARTER OF FISCAL 2010.”

We achieved significant further cost reductions in both manufacturing and distribution, and are continuing to make capital investments to achieve manufacturing cost savings, expand production capacity and reduce our environmental footprint. We are implementing a project in the Dominican Republic to generate energy from biomass and a similar project is planned in fiscal 2010 for Honduras. These projects are expected to contribute to the reduction of our energy costs and reflect our commitment to sustainability. In the first quarter of fiscal 2010, we announced the acquisition

(1)

Adjusted diluted earnings per share is a non-GAAP measure. See “Non-GAAP Measures” on page 8 of the 2009 Management’s Discussion and Analysis.

(2)

Reflects the impact of the change in accounting policy as described in Note 1(b) to the 2009 audited Consolidated Financial Statements.

(3)

Includes income tax benefits of $7.6 million in fiscal 2007 and $6.1 million in fiscal 2009 relating to prior taxation years.

(4)

Includes the impact of a one-time income tax charge of $26.9 million.

4 GILDAN 2009 Annual Report

of a state-of-the-art distribution centre in Charleston, S.C. for approximately U.S. $20 million. This facility will be utilized to support Gildan’s projected sales growth in the mass retail market and is expected to generate cost reductions and improved efficiencies in servicing retail customers as a result of consolidating existing distribution capacity.

In fiscal 2009, we prudently managed our working capital and capital expenditures, and generated U.S. $132 million of free cash flow for the year. We ended the year with cash and cash equivalents of approximately U.S. $100 million.

Our view of the overall economic environment continues to be cautious. However, even in a scenario of continuing economic weakness and low industry demand, Gildan is positioned for strong sales and earnings growth, due to our continuing market share gains, our growth in international and other screenprint markets, our initiatives to enter major new retail markets, and our anticipated further efficiency gains in manufacturing and distribution costs. We believe we will have sufficient inventory and production capacity to be able to capitalize on improved industry demand if an economic turn-around does occur.

We expect to generate free cash flow again in fiscal 2010, after investing approximately U.S. $130 million in capital expenditures. One of our management objectives in fiscal 2010 will be to conduct an analysis of options to utilize our cash balances in order to create maximum value for our shareholders.

In conclusion, we are excited about our opportunities for continuing profitable growth in 2010 and future years. I would like to thank all of our stakeholders who are contributing to Gildan’s continued success, including our dedicated managers and employees, our customers and our supply chain partners.

Glenn J. Chamandy President and Chief Executive Officer

2009 Annual Report GILDAN5

6 GILDAN 2009 Annual Report

EXECUTIVE

MANAGEMENT TEAM

Glenn J. Chamandy

President and Chief Executive Officer

Laurence G. Sellyn

Executive Vice-President, Chief Financial

and Administrative Officer

Michael R. Hoffman

President, Gildan Activewear SRL

Eric Lehman

Executive Vice-President, Supply Chain,

Information Technology and

Operational Excellence

Benito Masi

Executive Vice-President, Manufacturing

Georges Sam Yu Sum

Executive Vice-President, Operations

BOARD

OF DIRECTORS

Robert M. Baylis

Darien, Connecticut, United States

Chairman of the Board of Directors

Chairman of the Corporate

Governance Committee

Director since February 1999

William D. Anderson

Toronto, Ontario, Canada

Chairman of the Audit and Finance Committee

Director since May 2006

Glenn J. Chamandy

Montreal, Quebec, Canada

President and Chief Executive Officer

Director since May 1984

Sheila O’Brien

Calgary, Alberta, Canada

Director since June 2005

Pierre Robitaille

St-Lambert, Quebec, Canada

Director since February 2003

Richard P. Strubel

Chicago, Illinois, United States

Chairman of the Compensation

and Human Resources Committee

Director since February 1999

Gonzalo F. Valdes-Fauli

Key Biscayne, Florida, United States

Director since October 2004

George Heller

Toronto, Ontario, Canada

Director since December 2009

James R. Scarborough

Wolfeboro, New Hampshire, United States

Director since December 2009

2009 Annual Report GILDAN7

FORWARD-LOOKING STATEMENTS Certain statements included in this report constitute “forward-looking statements” within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 and Canadian securities legislation and regulations, and are subject to important risks, uncertainties and assumptions. This forward-looking information includes, amongst others, information with respect to our objectives and the strategies to achieve these objectives, as well as information with respect to our beliefs, plans, expectations, anticipations, estimates and intentions. Forward-looking statements generally can be identified by the use of conditional or forward-looking terminology such as “may”, “will”, “expect”, “intend”, “estimate”, “project”, “assume”, “anticipate”, “plan”, “foresee”, “believe” or “continue” or the negatives of these terms or variations of them or similar terminology. We refer you to the Company’s filings with the Canadian securities regulatory authorities and the U.S. Securities and Exchange Commission, as well as the “Risks and Uncertainties” section and the risks described under the section “Financial Risk Management” of the 2009 Annual MD&A for a discussion of the various factors that may affect the Company’s future results. Material factors and assumptions that were applied in drawing a conclusion or making a forecast or projection are also set out throughout this document.

Forward-looking information is inherently uncertain and the results or events predicted in such forward-looking information may differ materially from actual results or events. Material factors, which could cause actual results or events to differ materially from a conclusion, forecast or projection in such forward-looking information, include, but are not limited to: our ability to implement our growth strategies and plans, including achieving market share gains, implementing cost reduction initiatives and completing and successfully integrating acquisitions; the intensity of competitive activity and our ability to compete effectively; adverse changes in general economic and financial conditions globally or in one or more of the markets we serve; our reliance on a small number of significant customers; the fact that our customers do not commit contractually to minimum quantity purchases; our ability to anticipate changes in consumer preferences and trends; our ability to manage inventory levels effectively in relation to changes in customer demand; fluctuations and volatility in the price of raw materials used to manufacture our products, such as cotton and polyester fibres; our dependence on key suppliers and our ability to maintain an uninterrupted supply of raw materials; the impact of climate, political, social and economic risks in the countries in which we operate, including the current political instability in Honduras; disruption to manufacturing and distribution activities due to labour disruptions, political instability, bad weather, natural disasters and other unforeseen adverse events; changes to international trade legislation that the Company is currently relying on in conducting its manufacturing operations or the application of safeguards thereunder; factors or circumstances that could increase our effective income tax rate, including the outcome of any tax audits or changes to applicable tax laws or treaties; compliance with applicable environmental, tax, trade, employment, health and safety, and other laws and regulations in the jurisdictions in which we operate; our significant reliance on computerized information systems for our business operations; changes in our relationship with our employees or changes to domestic and foreign employment laws and regulations; negative publicity as a result of violation of labour laws or unethical labour or other business practices by the Company or one of its third-party contractors; our dependence on key management and our ability to attract and retain key personnel; changes to and failure to comply with consumer product safety laws and regulations, including the recently enacted U.S. Consumer Product Safety Improvement Act; changes in accounting policies and estimates; and exposure to risks arising from financial instruments, including credit risk, liquidity risk, foreign currency risk and interest rate risk. These factors may cause the Company’s actual performance and financial results in future periods to differ materially from any estimates or projections of future performance or results expressed or implied by such forward-looking statements. Forward-looking statements do not take into account the effect that transactions or non-recurring or other special items announced or occurring after the statements are made, may have on the Company’s business. For example, they do not include the effect of business dispositions, acquisitions, other business transactions, asset write-downs or other charges announced or occurring after forward-looking statements are made. The financial impact of such transactions and non-recurring and other special items can be complex and necessarily depends on the facts particular to each of them.

We believe that the expectations represented by our forward-looking statements are reasonable, yet there can be no assurance that such expectations will prove to be correct. The purpose of the forward-looking statements is to provide the reader with a description of management’s expectations regarding the Company’s fiscal 2010 financial performance and may not be appropriate for other purposes. Furthermore, unless otherwise stated, the forward-looking statements contained in this report are made as of the date of this report, and we do not undertake any obligation to update publicly or to revise any of the included forward-looking statements, whether as a result of new information, future events or otherwise unless required by applicable legislation or regulation. The forward-looking statements contained in this report are expressly qualified by this cautionary statement.

2009

REPORT TO SHAREHOLDERS

December 9, 2009

MD&A:

OUR BUSINESS

2

STRATEGY AND OBJECTIVES

5

OPERATING RESULTS

8

SUMMARY OF QUARTERLY RESULTS

15

FINANCIAL CONDITION

17

CASH FLOWS

19

LIQUIDITY AND CAPITAL RESOURCES

19

LEGAL PROCEEDINGS

21

OUTLOOK

21

FINANCIAL RISK MANAGEMENT

21

CRITICAL ACCOUNTING ESTIMATES

26

CHANGES IN ACCOUNTING POLICIES AND FUTURE ACCOUNTING STANDARDS

28

RELATED PARTY TRANSACTIONS

31

DISCLOSURE CONTROLS

31

INTERNAL CONTROL OVER FINANCIAL REPORTING

32

RISKS AND UNCERTAINTIES

32

DEFINITION AND RECONCILIATION OF NON-GAAP MEASURES

39

FORWARD LOOKING STATEMENTS

41

MANAGEMENT’S RESPONSIBILITY FOR FINANCIAL REPORTING

43

AUDITED CONSOLIDATED FINANCIAL STATEMENTS

44

NOTES TO AUDITED CONSOLIDATED FINANCIAL STATEMENTS

50

MANAGEMENT’S DISCUSSION AND ANALYSIS

This Management’s Discussion and Analysis (MD&A) comments on Gildan’s operations, performance and financial condition as at and for the years ended October 4, 2009 and October 5, 2008, compared to the preceding years. For a complete understanding of our business environment, trends, risks and uncertainties and the effect of accounting estimates on our results of operations and financial condition, this MD&A should be read together with the audited Consolidated Financial Statements and the related notes. This MD&A is dated December 9, 2009. All amounts in this report are in U.S. dollars, unless otherwise noted.

All financial information contained in this MD&A and in the audited Consolidated Financial Statements has been prepared in accordance with Canadian generally accepted accounting principles (GAAP), except for certain information discussed in the paragraph entitled “Non-GAAP Measures” on page 8 of this MD&A. The audited Consolidated Financial Statements and this MD&A were reviewed by Gildan’s Audit and Finance Committee and were approved by our Board of Directors.

Additional information about Gildan, including our 2009 Annual Information Form, is available on our website at www.gildan.com, on the SEDAR website at www.sedar.com, and on the EDGAR section of the U.S. Securities and Exchange Commission website (which includes the Annual Report on Form 40-F) at www.sec.gov.

This document contains forward-looking statements, which are qualified by reference to, and should be read together with, the “Forward-looking Statements” cautionary notice on page 41.

In this MD&A, “Gildan”, the “Company”, or the words “we”, “us”, “our” refer, depending on the context, either to Gildan Activewear Inc. or to Gildan Activewear Inc. together with its subsidiaries and joint venture.

OUR BUSINESS

We are a marketer and vertically-integrated globally cost-competitive manufacturer of basic, non-fashion apparel products for customers requiring an efficient supply chain and consistent product quality for high-volume replenishment programs. We sell activewear products to screenprint markets in North America, Europe and other international markets. Gildan is the leading supplier of activewear for the screenprint channel in the U.S. and Canada, and also a leading supplier for this market in Europe and Mexico. We sell socks and underwear, in addition to our activewear products, to mass market and regional retailers in North America. In the U.S. mass-market retail channel, Gildan is one of the leading suppliers of socks. The Company operates in one business segment, being high-volume, basic, frequently replenished, non-fashion apparel.

Our Products and Markets We have built our core business by manufacturing and selling activewear products through wholesale distributors servicing the screenprint market. Today we sell activewear products to this channel in North America, Europe and other international markets. In more recent years we made our entry into the North American retail channel, with the addition of socks and underwear to our activewear product-line for sale to large mass-market and regional retailers. In fiscal 2006 we acquired Kentucky Derby Hosiery Co., Inc. (Kentucky Derby) and in the first quarter of fiscal 2008 we acquired V.I. Prewett & Son, Inc. (Prewett), two U.S.-based sock manufacturers of basic family socks which provided us with enhanced distribution to major U.S. mass-market retailers.

Our activewear products, namely T-shirts, fleece and sport shirts under the Gildan brand, are sold in large quantities to wholesale distributors as undecorated “blanks”, which are subsequently sold to screenprinters and embroiderers who decorate the products with designs and logos. Screenprinters then sell the imprinted activewear to a highly diversified range of end-use markets, including educational institutions, athletic dealers, event merchandisers, promotional product distributors, charity organizations, entertainment promoters, and travel and tourism venues. Our activewear products are used in a variety of daily activities by individuals, including work and school uniforms and athletic team wear, and for various other purposes to convey individual, group and team identity. We are also growing our private label activewear business to provide undecorated products to large branded apparel companies and retailers which sell imprinted activewear and are currently not supplied by our existing U.S. wholesale distributors. In the North American mass-market and regional retailer channel, we sell a variety of styles of socks, and men’s and boys’ underwear, in addition to our undecorated activewear products, under various retailer private labels and under the Gildan brand.

GILDAN 2009 REPORT TO SHAREHOLDERS P.2

MANAGEMENT’S DISCUSSION AND ANALYSIS

All of our products are made of 100% cotton or of blends of cotton and synthetic fibres. Our products are characterized by low-fashion risk compared to other apparel categories since these products are basic, frequently replenished, and since logos and designs for the screenprint market are not imprinted or embroidered by Gildan. Our value proposition combines consistent quality, competitive pricing and fast and flexible replenishment, due to our geographical proximity to our markets, as well as our leadership in corporate social responsibility and environmental sustainability. As a vertically-integrated manufacturer, Gildan is able to provide premium products to customers in a broad range of sizes, colours and styles with enhanced product features, such as pre-shrunk fabrics, and a selection of fabric weights, blends and construction. Innovations in the manufacturing process of our activewear products have allowed us to ensure colour/shade consistency and high performance of the garments. In addition, innovations in the sock manufacturing process, such as higher needle count machines and seamless toe closing operations have allowed Gildan to deliver enhanced sock product features at lower prices, further improving the value proposition of our activewear and sock products to our customers.

Our Facilities

Textile and Sock Manufacturing To support our sales in the various markets, we have built modern manufacturing facilities located in Central America and the Caribbean Basin where we manufacture T-shirts, fleece, sport shirts, socks and underwear. Our largest manufacturing hub in Central America includes our first vertically-integrated knitting, bleaching, dyeing, finishing and cutting textile facility (Rio Nance 1) to produce activewear fabric and, more recently, underwear fabric. This facility, located in Rio Nance, Honduras, became operational in fiscal 2002. During fiscal 2007, we expanded our operations in Rio Nance to include a new integrated textile facility for the production of activewear fabric (Rio Nance 2) and a new integrated sock manufacturing facility (Rio Nance 3). We have also established a vertically-integrated Caribbean Basin manufacturing hub with a textile facility for the production of activewear fabric in Bella Vista, Dominican Republic, which became operational in fiscal 2005. The Company is also planning further textile capacity expansion in its existing manufacturing hubs in the Dominican Republic and Central America.

In addition to our integrated sock manufacturing facility located in our Central America hub, we operate U.S. sock knitting facilities in Fort Payne, Alabama, purchased as part of the Prewett acquisition in fiscal 2008. During fiscal 2009, we transitioned our U.S. sock finishing operations, which were purchased as part of the Prewett acquisition, to leased sock finishing facilities in Honduras. During fiscal 2010, the Company plans to complete the construction of a second sock manufacturing facility (Rio Nance 4) in Rio Nance, which is expected to begin operations by the end of fiscal 2010. Rio Nance 4 will serve to further consolidate the sock finishing operations and to support our future sales growth in this product category.

Sewing Facilities Our sewing facilities for activewear and underwear are strategically located in close proximity to our textile manufacturing facilities. We operate sewing facilities in Honduras and Nicaragua to support our textile manufacturing hub in Central America. To support our vertically-integrated production in the Dominican Republic, we utilize third-party contractors in Haiti, and we have established a new sewing facility in the Dominican Republic, which began operating during the second quarter of fiscal 2009.

Yarn-Spinning CanAm Yarns, LLC (CanAm), our joint-venture company with Frontier Spinning Mills, Inc. (Frontier), operates yarn-spinning facilities in Georgia and North Carolina. CanAm’s yarn-spinning operations, together with supply agreements currently in place with Frontier and other third-party yarn providers, serve to meet our yarn requirements.

GILDAN 2009 REPORT TO SHAREHOLDERS P.3

MANAGEMENT’S DISCUSSION AND ANALYSIS

Sales, Marketing and Distribution Our global sales and marketing office, which employs approximately 145 full-time employees, is located in St. Michael, Barbados and is responsible for customer-related functions, including sales management, marketing, customer service, credit management, sales forecasting, and inventory control and logistics. The Company also employs a sales group in the U.S. to service its retail customers.

We distribute our activewear products for the screenprint channel primarily out of our distribution centre in Eden, North Carolina, and also use third-party warehouses in the western United States, Canada, Mexico, Europe and Asia to service our customers in these markets. Shipments are also made directly from our third party contractors in Haiti and from our facilities in Honduras. To service the mass-market retail channel, we operate a distribution centre in Martinsville, Virginia. In addition, with our acquisition of Prewett in fiscal 2008, we have two distribution facilities in Fort Payne, Alabama. On November 17, 2009, the Company completed the acquisition of a state-of-the-art distribution centre and office building in Charleston, South Carolina, for approximately $20 million. This facility will be utilized to support the Company’s retail strategy, and is also expected to generate cost reductions and efficiencies as a result of consolidating existing distribution capacity.

Employees and Corporate Offices As of the end of fiscal 2009 we employed more than 19,000 full-time employees worldwide. Our corporate head office is located in Montreal, Canada.

Competitive Environment The apparel market for our products is highly competitive. Competition is generally based upon price, with reliable quality and service also being critical requirements for success. Our competitive strengths include our expertise in building and operating large-scale, vertically-integrated offshore manufacturing hubs which allows us to offer competitive pricing, consistent product quality, and a supply chain which efficiently services replenishment programs with short production/delivery cycle times. Our investments and commitment to our corporate social responsibility programs are also increasingly becoming important factors for our customers. We are focused on providing a more socially and environmentally responsible supply chain for our customers by employing progressive hiring and employment practices in good working conditions, minimizing our environmental footprint and contributing to communities in the countries in which we operate.

Gildan is the leading supplier of activewear products for the screenprint channel in the U.S. and Canada, and also a leading supplier for this market in Europe and Mexico. In the U.S. mass-market retail channel Gildan is one of the leading suppliers of socks. Our primary competitors in North America are the major manufacturers for the screenprint and retail channels, such as Hanesbrands Inc., Berkshire Hathaway Inc. through its subsidiaries Fruit of the Loom, Inc. and Russell Corporation, and smaller U.S.-based manufacturers, including Anvil Knitwear Inc. We also compete with Alstyle Apparel, a division of Ennis Corp., and Delta Apparel Inc. The competition in the European screenprint channel is similar to that in North America, as we compete primarily with the European divisions of the major U.S.-based manufacturers mentioned above. We also face the threat of increasing global competition. In Europe, we also have large competitors that do not have integrated manufacturing operations and source products from suppliers in Asia. In addition, many of Gildan’s U.S. competitors servicing the retail apparel industry currently source products from Asia.

Economic Environment During fiscal 2009, the severe downturn in the overall economic environment resulted in a dramatic curtailment of consumer and corporate spending which negatively impacted demand for our products in the U. S. and other international screenprint markets, and also resulted in significant inventory destocking at the U. S. distributor level. Unit shipments from U.S. wholesale distributors to U.S. screenprinters in fiscal 2009 were down approximately 14.7% based on the S.T.A.R.S. report produced by ACNielsen Market Decisions. In the first quarter of fiscal 2009, inventory destocking occurred as distributors reduced inventory levels on hand at the end of fiscal 2008, and managed their working capital requirements. In the second quarter of fiscal 2009, as a result of the economic slowdown and the financial market crisis, the Company’s largest wholesale distributor, Broder Bros., Co. (Broder) entered into a process to restructure its debt financing which curtailed its ability to replenish its inventory. During the third quarter of fiscal 2009, Broder announced that it had successfully completed its financial restructuring and consequently we began normal replenishment of its inventory requirements. In addition, during fiscal 2009, an unfavourable supply-demand and competitive environment combined with the deflation in cotton and energy prices in the first half of the year resulted in downward pressure on net activewear selling prices. Weaker demand and customer inventory reductions also occurred in the mass-market retail channel.

GILDAN 2009 REPORT TO SHAREHOLDERS P.4

MANAGEMENT’S DISCUSSION AND ANALYSIS

During fiscal 2009, we took a number of steps in response to the downturn in the economy, in order to prudently manage our receivables, inventory levels and capital expenditures. We experienced a significantly higher than usual build-up of activewear inventories in the first half of fiscal 2009 due to the decline in our sales combined with the reduction of inventories at the customer level. As a result, we took production downtime at most of our production facilities in order to better align our inventory levels with projected sales demand. We also achieved significant reductions in our sock inventories, as planned, due in part to improved supply chain efficiencies. We managed our credit risk cautiously, as we balanced short-term market share considerations in relation to increased customer credit exposure, including carefully managing our customer accounts and promotional programs, such as reducing the use of extended payment terms that we typically offer for certain seasonal products in the second half of our fiscal year. We decided to proceed cautiously on capacity expansion projects previously announced and delayed the completion of our Rio Nance 4 sock facility and deferred the construction of our third activewear facility (Rio Nance 5) in Honduras until the economic outlook in support of further major capacity expansion became clearer. At the end of the first quarter of fiscal 2009, we had established a goal to be essentially debt-free by the end of the fiscal year, and we exceeded this goal by accumulating a cash position of approximately $100 million at October 4, 2009.

The Company is currently planning for fiscal 2010 on the basis of the continuation of weak macro economic conditions, although it believes it is in a position to take advantage of any unanticipated improvement in overall industry demand during fiscal 2010. Please refer to the section entitled “Outlook” on page 21.

STRATEGY AND OBJECTIVES Our growth strategy comprises the following initiatives:

1.

Maximize screenprint market penetration and opportunities

While we have achieved a leadership position in the screenprint channel in the U.S. and in Canada, we believe we can continue to further solidify our position in the North American screenprint channel and expand our presence in international screenprint markets. In recent years, we have further developed our integrated manufacturing hubs in Central America and the Caribbean Basin, which we expect will allow us to allocate capacity to service product categories and geographical locations where our growth was previously constrained by capacity availability. We are currently planning to invest further in capacity expansions within our existing manufacturing hubs.

U.S. Screenprint Market

During fiscal 2009, we further increased our leading market share position in the U.S. screenprint channel in all of our product categories as reported in the S.T.A.R.S. report produced by ACNielsen Market Decisions. Our overall total market share in this channel increased to 56.6% for the nine months ended September 30, 2009 compared to 51.9% for the same period last year. We intend to continue gaining market share in all of the product categories that we serve within the U.S. screenprint channel, namely T-shirts, sport shirts and fleece, through our continued focus on delivering consistent high quality products, reliable customer service and competitive pricing. In addition, the introduction of new products such as softer T-shirts and sport shirts made of ring-spun cotton and new styles tailored for women, should enable us to further increase our market share by serving certain niches of the screenprint channel in which we previously did not participate. We also intend to grow our private label activewear business to provide undecorated products to large branded apparel companies and retailers which sell imprinted activewear and are currently not supplied by our existing U.S. wholesale distributors.

GILDAN 2009 REPORT TO SHAREHOLDERS P.5

MANAGEMENT’S DISCUSSION AND ANALYSIS

International Markets We expect to pursue further market penetration primarily within our existing screenprint channels in Europe, Mexico and the Asia/Pacific region. We continue to seek opportunities for growth in Europe, having expanded our product-lines, including the introduction of ring-spun cotton activewear products. In Mexico, we intend to grow our presence in the screenprint channel by building on the sales and distribution infrastructure that we have recently established in the country. In addition, in fiscal 2007, we began selling our products in Japan in both the screenprint and retail channels and during fiscal 2008, we established a sales office in China to position Gildan to service both the screenprint and retail channels in that country. The Company is continuing to evaluate opportunities to further develop its presence in its target markets in China.

2.

Leverage our successful business model to further penetrate the mass-market retail channel

The acquisitions of Kentucky Derby in fiscal 2006 and of Prewett at the beginning of fiscal 2008, combined with the addition of new branded and private label sock programs, have positioned us as a leading supplier of basic family socks in the U.S. mass-market retail channel. We have begun to build on our significant market position in socks to establish a significant presence in the mass-market retail channel with our activewear and underwear product lines. We are leveraging our existing core competencies, successful business model and competitive strengths. Our value proposition in the retail channel as in the screenprint channel combines consistent quality, competitive pricing and fast and flexible replenishment, due to our geographical proximity to our markets, as well as our leadership in corporate social responsibility and environmental sustainability. During fiscal 2009, we strengthened our position with mass-market retailers by positioning ourselves as a strategic private label supplier to mass retailers seeking to consolidate their supply chain with fewer, larger manufacturers.

We have continued to build on the successful performance of our private label sock programs and have been awarded Gildan a major strategic underwear program as well as a smaller underwear program and three further sock programs, which are all expected to begin shipment in the second quarter of fiscal 2010. We are currently in active discussions to secure further opportunities with mass retailers for new programs during fiscal 2010. The annualized full year incremental sales revenue from the additional new mass market retail programs already obtained by the Company in fiscal 2010 is currently estimated to be approximately $70 million.

We have also pursued a strategy of selling our products with the Gildan brand to regional retailers. During fiscal 2009, we continued to further penetrate this channel by adding to our customer base and expanding Gildan branded products with regional retailer chains. We currently sell Gildan branded products in more than 1,700 retail stores.

3.

Continue to generate manufacturing and distribution cost reductions

We seek to continuously improve our manufacturing and distribution processes and cost structure by developing and investing in cost-reduction initiatives. In addition to our continuing consolidation of our manufacturing operations in our Central American and Caribbean Basin hubs, we are implementing other cost reduction initiatives which include, among others, our plans to install biomass facilities as an alternate source of natural renewable energy in order to reduce our reliance on high-cost fossil fuels and further reduce our environmental footprint. We are also planning to achieve further efficiencies in operating our distribution activities.

GILDAN 2009 REPORT TO SHAREHOLDERS P.6

MANAGEMENT’S DISCUSSION AND ANALYSIS

During fiscal 2009, we continued to consolidate our manufacturing operations in our manufacturing hub in Central America as we transitioned our U.S. sock finishing operations, which were purchased as part of the Prewett acquisition, to sock finishing facilities in Honduras. During fiscal 2010, the Company plans to complete the construction of Rio Nance 4, its second sock manufacturing facility in Honduras and begin operating the facility during fiscal 2010.

During fiscal 2009, we began construction of a biomass steam generation system in the Dominican Republic, which is expected to contribute to the reduction of our energy consumption and related costs. The biomass steam generation system is expected to be operational by February 2010. Our current plans for fiscal 2010 also include the initiation of similar biomass steam generation projects at our sock manufacturing facilities in Honduras. We are also planning to implement similar systems for our two textile facilities in Honduras in the future.

In November 2009, we completed the acquisition of a state-of-the-art distribution centre and office building in Charleston, South Carolina. This facility will be utilized to support our retail growth strategy and is also expected to generate cost reductions and improved efficiencies as a result of consolidating existing distribution capacity. Furthermore, we plan to build a new distribution centre in Rio Nance, Honduras to handle value-added labour intensive activities for mass-market retail customers and to support direct shipments to some of our markets.

4.

Re-invest and/or redistribute cash flow We will evaluate opportunities to reinvest our cash flows generated from operations. Our primary use of cash will continue to be to finance our working capital and capital expenditure requirements to support our organic growth, but at the same time we will be open to evaluating complementary strategic acquisition opportunities which meet our return on investment criteria, based on our risk-adjusted cost of capital.

In addition, we will opportunistically consider share repurchases if management and the Board at any time believe that our shares are undervalued, and we also intend, as we have done periodically in the past, to discuss with our Board the possible introduction of a dividend.

We are subject to a variety of business risks that may affect our ability to maintain our current market share and profitability, as well as our ability to achieve our short and long-term strategic objectives. These risks are described under the “Financial Risk Management” and “Risks and Uncertainties” sections of this MD&A.

GILDAN 2009 REPORT TO SHAREHOLDERS P.7

MANAGEMENT’S DISCUSSION AND ANALYSIS

OPERATING RESULTS

OPERATING RESULTS FOR THE YEAR ENDED OCTOBER 4, 2009, COMPARED TO THE YEAR ENDED OCTOBER 5, 2008

Statement of Earnings Classifications Effective the first quarter of fiscal 2009, the Company changed certain classifications of its statement of earnings and comprehensive income with retrospective application to comparative figures presented for prior periods. These new classifications align the results of operations by function and incorporate presentation requirements under the Canadian Institute of Chartered Accountants (CICA) Handbook Section 3031,Inventories, which has been adopted effective the first quarter of fiscal 2009. Pursuant to the requirements of Section 3031, depreciation expense related to manufacturing activities is now included in cost of sales. The remaining depreciation and amortization expense has been reclassified to selling, general and administrative expenses. Depreciation and amortization expense is therefore no longer presented as a separate caption on the statement of earnings and comprehensive income. In addition, the Company reclassified certain other items in its statement of earnings and comprehensive income. Outbound freight to customers, previously classified within selling, general and administrative expenses, is now reported within cost of sales. Also, a new caption is now presented for financial expenses and income, which includes interest income and expenses (including mark-to-market adjustments of interest rate swap contracts), foreign exchange gains and losses (including mark-to-market adjustments of forward foreign exchange contracts), and other financial charges. Interest expense net of interest income was previously reported as a separate caption, while foreign exchange gains and losses were previously included in cost of sales. Other financial charges were previously reflected in selling, general and administrative expenses. For the year ended October 5, 2008 these changes in classification have resulted in a decrease of $63.8 million (2007 - $47.8 million) and $8.7 million (2007 - $11.1 million) in gross profit and selling, general and administrative expenses, respectively, compared to the amounts previously reported. The decrease of $63.8 million (2007 -$47.8 million) in gross profit is due to reclassifications of $44.1 million (2007 - $30.4 million) of depreciation and amortization expense, $20.6 million (2007 - $16.7 million) of outbound freight to customers less $0.9 million (2007 – plus $0.7 million of foreign exchange gain) of foreign exchange loss and other financial income. There was no impact on net earnings as a result of these changes in classification.

For the fourth quarter of fiscal 2008, these changes in classification have resulted in a decrease in amounts previously reported for gross profit of $16.3 million, and a decrease of $1.7 million in selling, general and administrative expenses. The decrease of $16.3 million in gross profit is due to reclassifications of $11.8 million of depreciation and amortization expense, $4.7 million of outbound freight to customers less $0.2 million of foreign exchange loss and other financial income.

Non-GAAP Measures We use non-GAAP measures to assess our operating performance. Securities regulations require that companies caution readers that earnings and other measures adjusted to a basis other than GAAP do not have standardized meanings and are unlikely to be comparable to similar measures used by other companies. Accordingly, they should not be considered in isolation. We use non-GAAP measures including adjusted net earnings, adjusted diluted EPS, EBITDA, free cash flow, total indebtedness and cash in excess of total indebtedness/net indebtedness to measure our performance from one period to the next without the variation caused by certain adjustments that could potentially distort the analysis of trends in our operating performance, and because we believe such measures provide meaningful information on the Company’s financial condition and operating results.

We refer the reader to page 39 for the definition and complete reconciliation of all non-GAAP measures used and presented by the Company to the most directly comparable GAAP measures.

GILDAN 2009 REPORT TO SHAREHOLDERS P.8

MANAGEMENT’S DISCUSSION AND ANALYSIS

Business Acquisition On October 15, 2007, we acquired 100% of the capital stock of Prewett, a U.S. supplier of basic family socks to U.S. mass-market retailers, based in Fort Payne, Alabama. The aggregate purchase price of $128.0 million was comprised of cash consideration of $125.3 million, a deferred payment of $1.2 million, which was disbursed in the fourth quarter of fiscal 2009, and transaction costs of $1.5 million. We accounted for this acquisition using the purchase method and, our results of operations for fiscal 2008 include the operations of Prewett from the date of acquisition. The purchase agreement also provides for an additional purchase consideration of up to $10.0 million contingent on specified future events less amounts reimbursed to Gildan. This amount was paid into escrow by Gildan on October 15, 2007, but events occurring subsequent to the acquisition have resulted in a reduction of the contingent purchase price and escrow balance to $6.0 million as at October 4, 2009. The escrow deposit of $6.0 million (October 5, 2008 - $10.0 million) is included in other assets on the consolidated balance sheet. The remaining contingent purchase price may be subject to further reductions during fiscal 2010 and 2011. The amounts of contingent purchase price ultimately disbursed from the escrow account will be accounted for as additional goodwill. Please refer to Note 2 to the audited Consolidated Financial Statements for a summary of the estimated fair value of the assets acquired and liabilities assumed at the date of acquisition.

SELECTED ANNUAL INFORMATION

2009

2008

2007

(in $ millions, except per share amounts)

Recast(1)

Recast(1)

Net Sales

1,038.3

1,249.7

964.4

Cost of sales

808.0

911.2

705.5

Gross profit

230.3

338.5

258.9

Selling, general and administrative expenses

134.8

142.8

99.9

Restructuring and other charges

6.2

5.5

28.0

Operating income

89.3

190.2

131.0

Financial expense (income), net

(0.3

)

9.2

5.4

Non-controlling interest in consolidated joint venture

0.1

0.2

1.3

Earnings before income taxes

89.5

180.8

124.3

Income taxes

(5.8

)

34.4

(4.8

)

Net earnings and comprehensive income

95.3

146.4

129.1

Basic EPS(2)

0.79

1.21

1.07

Diluted EPS(2)

0.79

1.20

1.06

Total assets

1,082.4

1,095.0

867.7

Total long-term financial liabilities(3)

4.4

53.0

59.7

Certain minor rounding variances exist between the financial statements and this summary.

(1) Reflects the impact of the change in accounting policy as described in Note 1(b) to the audited Consolidated Financial Statementsand the changes to classifications in the statement of earnings and comprehensive income as discussed on page 8.

(2) All earnings per share data reflect the effect of the stock split as described on page 21.

(3) Includes current portion of long-term debt.

Net Sales Net sales in fiscal 2009 totaled $1,038.3 million, down 16.9%, from $1,249.7 million in fiscal 2008. Sales of activewear and underwear in fiscal 2009 were $795.5 million, down 16.9% from $957.1 million last year, and sales of socks were $242.8 million, down 17.0% from $292.7 million in fiscal 2008.

The activewear and underwear sales decline in fiscal 2009 of 16.9% was mainly due to a 9.3% decline in unit sales volumes, unfavourable activewear product-mix as a result of a lower proportion of sales of higher-valued fleece and long-sleeve T-shirts, a 2.9% decrease in net selling prices due to increased promotional activity, and the negative impact of the stronger U.S. dollar on Canadian and international sales for activewear.

GILDAN 2009 REPORT TO SHAREHOLDERS P.9

MANAGEMENT’S DISCUSSION AND ANALYSIS

Demand in the U.S. wholesale distributor channel in fiscal 2009 was negatively impacted by the global economic downturn as overall industry shipments from U.S. distributors to screenprinters declined by 15.4% for the nine months ended September 30, 2009. Gildan’s market share gains partially mitigated the market decline as unit shipments for Gildan products sold by U.S. distributors to U.S. screenprinters declined by 7.2% during the nine months ended September 30, 2009. The unit volume decline in activewear was mainly attributable to the decline in overall industry unit shipments and the significant impact of inventory reductions during the year by U.S. wholesale distributors, particularly in the first half of fiscal 2009. These negative factors more than offset the benefit of Gildan’s increased market share penetration in the U.S. screenprint channel and increased shipments to imprinted private label customers and international markets.

Market growth and share data presented for the U.S. wholesale distributor channel is based on the S.T.A.R.S. report produced by ACNielsen Market Decisions. The table below summarizes the S.T.A.R.S. data for the nine months ended September 30, 2009:

Nine months ended

Nine months ended

September 30,

September 30,

2009

2009

2008

Unit Growth

Market Share

Gildan

Industry

Gildan

All products

(7.2)%

(15.4)%

56.6%

51.9%

T-shirts

(7.3)%

(15.3)%

57.3%

52.7%

Fleece

(2.3)%

(12.5)%

55.6%

50.0%

Sport shirts

(12.4)%

(22.7)%

40.6%

36.0%

During the nine months ended September 30, 2009, Gildan achieved market share gains in all of its product categories and increased its overall market share in the U.S. screenprint channel to 56.6%, up 4.7 percentage points compared to the same period last year. We increased our leading share by 4.6 percentage points in each of the T-shirt and sport shirts product categories and increased our leading market share in fleece products by 5.6 percentage points.

Net sales in Canada and our international markets in fiscal 2009 declined 37.7% and 5.8%, respectively compared to fiscal 2008. Demand in both the Canadian and the international screenprint markets in which we compete was negatively impacted by similar global economic and market conditions as in the U.S. screenprint channel. The decrease in sales from Canada was due to a 16.2% decline in unit volumes combined with inventory reductions by distributors and the negative impact of the decline in the Canadian dollar on sales. The decrease in international sales for the year reflected the negative impact of the decline in the value of local currencies compared to the U.S. dollar and lower unit volume sales in Eastern Europe, partially offset by unit volume gains in Western Europe, the U.K. and Mexico. Although sales in Mexico represent a small portion of our total international business, unit sales volumes more than doubled compared to fiscal 2008, reflecting the benefit from the improved sales and distribution infrastructure that has been implemented.

The decrease in sales of socks for fiscal 2009 was mainly attributable to lower unit volumes primarily due to the elimination of unprofitable sock product-lines and a reduction in inventories carried by retailers, partially offset by the performance of continuing programs. New mass-retailer private label sock brands, which were introduced during fiscal 2009 performed strongly and gained market share.

Gross Profit Effective the first quarter of fiscal 2009, we changed the classification of our statement of earnings and comprehensive income which affected reported gross profit as described on page 8. Gross profit is the result of our net sales less cost of sales. Gross margin reflects gross profit as a percentage of sales. Our cost of sales includes all raw material costs, manufacturing conversion costs, including manufacturing depreciation expense, sourcing costs, transportation costs incurred until the receipt of finished goods at our distribution facilities and outbound freight to customers. Cost of sales also includes costs relating to purchasing, receiving and inspection activities, manufacturing administration, third-party manufacturing services, insurance, internal transfer of inventories, and customs and duties. Our reporting of gross margins may not be comparable to this metric as reported by other companies, since some entities exclude depreciation expense and the cost of shipping goods to customers from cost of sales.

GILDAN 2009 REPORT TO SHAREHOLDERS P.10

MANAGEMENT’S DISCUSSION AND ANALYSIS

Gross profit for fiscal 2009 was $230.3 million, or 22.2% of net sales, compared to $338.5 million, or 27.1% of net sales during fiscal 2008. The decline in gross margins in fiscal 2009 was mainly attributable to lower net selling prices for activewear due to increased promotional discounting, the significant impact of higher cotton costs, the negative effect of currency fluctuations and a more unfavourable activewear product-mix. Also contributing to the decline were the impacts of production downtime taken during fiscal 2009 in order to align our inventory requirements with demand, inefficiencies related to the transition in sock private label brands for Gildan’s largest retail customer, and higher depreciation expense. These negative factors were partially offset by lower manufacturing and energy costs and the non-recurrence of manufacturing inefficiencies in fiscal 2008 related to production constraints.

Selling, General and Administrative Expenses Effective the first quarter of fiscal 2009, we changed the classification of our statement of earnings and comprehensive income which affected reported selling, general and administrative expenses as described on page 8. Selling, general and administrative (SG&A) include warehousing and handling costs, selling and administrative personnel costs, advertising and marketing expenses, costs of leased facilities and equipment, professional fees, non-manufacturing depreciation expense, and other general and administrative expenses. SG&A expenses also include amortization of customer-related intangible assets and bad debt expense.

Selling, general and administrative (SG&A) expenses were $134.8 million, or 13.0% of net sales in fiscal 2009, compared to $142.8 million, or 11.4% of net sales, in fiscal 2008. The decrease in SG&A expenses was primarily due to efficiencies in the management of distribution expenses, as well as reductions due to lower volumes, and the positive impact of the lower-valued Canadian dollar on corporate administrative expenses, partially offset by an increase in variable compensation expense, higher depreciation and amortization expense resulting from capital expenditures related to the relocation of our new corporate head office last year, and higher professional fees.

Restructuring and Other Charges

(in $ millions)

2009

2008

2007

Gain on disposal of assets held for sale

(0.6

)

(0.5

)

(1.5

)

Accelerated depreciation

-

-

3.5

Asset impairment loss and write-down of assets held for sale

1.6

2.7

3.6

Employee termination and other benefits

2.2

0.4

13.6

Carrying and dismantling costs associated with assets held for sale

3.1

3.5

8.8

Adjustment for employment contract

(0.1

)

(0.6

)

-

6.2

5.5

28.0

In fiscal 2006 and 2007, the Company announced the closure, relocation and consolidation of manufacturing and distribution facilities in Canada, the United States and Mexico, as well as the relocation of its corporate office. In fiscal 2008, the Company announced the consolidation of its Haiti sewing operation, which was finalized in the first half of fiscal 2009, and the planned phase out of sock finishing operations in the U.S., which was finalized in the third quarter of fiscal 2009. The costs incurred in connection with these initiatives have been recorded as restructuring and other charges.

For fiscal 2009, restructuring and other charges totalled $6.2 million which included $3.7 million for the closure of the Company's U.S. sock finishing operations in the third quarter, and $3.2 million primarily related to facility closures that occurred in previous fiscal years, including carrying costs and asset write-downs relating to assets held for sale, net of a gain of $0.6 million on the disposal of equipment.

GILDAN 2009 REPORT TO SHAREHOLDERS P.11

MANAGEMENT’S DISCUSSION AND ANALYSIS

Restructuring charges of $5.5 million in fiscal 2008 included $2.1 million relating to the consolidation of the Company's Haiti sewing operation, and $4.5 million relating to facility closures which occurred in previous fiscal years, primarily for carrying and dismantling costs associated with assets held for sale, net of a gain on disposal of assets held for sale of $0.5 million. The Company also had a recovery of $0.6 million from the obligations accrued for the employment contract with the former Chairman and Co-Chief Executive Officer of the Company.

The $28.0 million of restructuring charges incurred in fiscal 2007 relate primarily to the closures of the Company’s textile facilities in Canada and the United States and its sewing facilities in Mexico as well as the relocation of its corporate office, resulting in employee termination costs of $13.6 million, an asset impairment of $3.6 million, an accelerated depreciation charge of $3.5 million, a gain on disposal of assets held for sale of $1.5 million, and other exit costs of $8.8 million.

The Company expects to incur additional carrying costs relating to the closed facilities, which will be accounted for as restructuring charges as incurred and until all property, plant and equipment related to the closures are disposed of. Any gains or losses on the disposal of the assets held for sale will also be accounted for as restructuring charges as incurred.

Financial Expense / Income, net Net financial expense/income includes interest expense, net of interest income, and foreign exchange gains and losses. Net financial income amounted to $0.3 million in fiscal 2009, compared to net financial expense of $9.2 million in fiscal 2008. The decrease of $9.5 million in net financial expense in fiscal 2009 resulted primarily from a decrease in interest expense of $5.4 million and a $4.2 million increase in foreign exchange gains. The decrease in interest expense was due to lower average borrowings and lower average interest rates during fiscal 2009 compared to last year.

Income Taxes The income tax recovery for fiscal 2009 was $5.8 million, compared to an income tax expense of $34.4 million for fiscal 2008. The total income tax recovery for fiscal 2009 include recoveries of $6.1 million relating to the recognition of previously unrecorded tax positions of prior years and $1.8 million related to the impact of restructuring and other charges. The income tax expense for fiscal 2008 included a charge of $26.9 million related to the settlement of the Canada Revenue Agency (CRA) audit, as discussed below. Excluding the income tax recoveries in the current year as well as the impact of restructuring and other charges in both years, and the impact of the CRA audit settlement in fiscal 2008, the effective income tax rate for fiscal 2009 was 2.2%, compared to an effective income tax rate of 4.4% for fiscal 2008. The reduction in the effective income tax rate compared to the prior year reflected a lower proportion of profits earned in higher tax rate jurisdictions.

In the fourth quarter of fiscal 2008, the CRA concluded the audit of our income tax returns for our 2000, 2001, 2002 and 2003 fiscal years, which resulted in a tax reassessment of $26.9 million and a reclassification of $17.3 million of future income tax liabilities to income taxes payable. For a more detailed discussion of the tax reassessment, please refer to the “Operating Results for the Year Ended October 5, 2008 Compared to the Year Ended September 30, 2007” section, under the heading “Income Taxes” on page 14. In the third quarter of fiscal 2009 the CRA completed its audit of the 2004, 2005 and 2006 taxation years and there were no significant adjustments to the Company’s income tax returns.

GILDAN 2009 REPORT TO SHAREHOLDERS P.12

MANAGEMENT’S DISCUSSION AND ANALYSIS

Net Earnings Net earnings for fiscal 2009 were $95.3 million, or $0.79 per share on a diluted basis, down 34.9% and 34.2%, respectively compared with net earnings of $146.4 million, or $1.20 per share on a diluted basis in fiscal 2008. Net earnings included after-tax restructuring and other charges of $4.4 million in fiscal 2009 and $4.9 million in fiscal 2008. Excluding the impact of restructuring charges, adjusted net earnings and adjusted diluted EPS for fiscal 2009 totaled $99.7 million and $0.82 per share compared with adjusted net earnings of $151.3 million, or $1.24 per share for the prior year. The reduction in adjusted net earnings and EPS was primarily due to significantly lower unit sales volumes and gross margins, partially offset by lower SG&A and financial expenses and the non-recurrence of an income tax charge of $26.9 million, or $0.22 per share taken in the fourth quarter of fiscal 2008.

OPERATING RESULTS FOR THE YEAR ENDED OCTOBER 5, 2008 COMPARED TO THE YEAR ENDED SEPTEMBER 30, 2007

Net Sales Net Sales for fiscal 2008 reached $1,249.7 million, up 29.6% from $964.4 million in fiscal 2007. The increase in net sales was due to a $154.5 million increase of sock sales primarily due to the acquisition of Prewett, an increase of approximately 6.7% in activewear selling prices and a 10.2% increase in unit sales volumes for activewear and underwear.

The increase in activewear unit sales was primarily due to continuing market share penetration in all of our product categories in the U.S. distributor channel, as sales of Gildan products from U.S. distributors to screenprinters increased 4.6% for the nine months ended September 30, 2008 according to the S.T.A.R.S. report, while overall industry shipments declined 3.8%. Gildan’s overall leading market share increased to 51.9% for the nine months ended September 30, 2008, compared to 47.8% in the same period last year. Growth in activewear unit volumes and the sale of higher-end products were constrained by lower than anticipated production at our textile facility in the Dominican Republic, including delays in the introduction of new high-value ring-spun T-shirt and sport shirt products. The introduction of more complex product-lines contributed to the shortfall in production output, which also resulted in cost inefficiencies. Despite an improvement in production levels by the end of the year, the lower than anticipated production in the Dominican Republic prevented us from capitalizing on demand for our products, in particular during the peak selling periods in the third and fourth fiscal quarters of the year.

Unit shipments to Canada, Europe, Asia and Mexico in fiscal 2008 increased by 2.5%. Growth in these markets was also constrained, particularly in the second half of the year due to the lack of product availability and the delay of new product introductions attributable to the production shortfall noted above.

The increase in sock sales was partially offset by the impact of exiting less profitable sock product-lines, which did not fit with Gildan’s strategy to focus primarily on high-volume basic sock programs in the U.S. mass-market retail channel which capitalize on Gildan’s modern large-scale manufacturing capacity. In addition, average selling prices for socks were reduced, as selling prices for new sock programs were based on the projected cost structure of Gildan’s new sock facility in Honduras, which was ramping up to full capacity during fiscal 2008.

During fiscal 2008, we continued to make progress within the mass-market retail channel. Although we had some challenges earlier in the year, in completing our systems integration of the operations of a U.S. sock manufacturer acquired in fiscal 2006, the transition was essentially complete by the end of fiscal 2008 and we were pleased with the improvement in our service levels to mass retailers. We continued to implement our strategy to rationalize our sock product-mix, in order to focus on basic higher-volume products and programs which capitalize on Gildan’s modern large-scale manufacturing.

Gross Profit Gross profit for fiscal 2008 and 2007 reflects the impact of the change in statement of earnings classification as described on page 8, and the change in accounting policy as described in Note 1(b) to the audited Consolidated Financial Statements.

Gross profit for fiscal 2008 was $338.5 million, or 27.1% of net sales, compared to $258.9 million, or 26.8% of net sales during fiscal 2007. Gross margins for fiscal 2008 were positively impacted by higher activewear selling prices and lower promotional discounts, together with favourable manufacturing efficiencies resulting from the consolidation of our textile facilities. These positive factors were offset by higher cotton prices, increased freight and energy costs, higher depreciation and amortization, production inefficiencies in our Dominican Republic facility, the impact of inventory write-downs related to the liquidation of discontinued sock product-lines, and the impact of the lower gross margins generated from our Prewett acquisition which generated lower margins than our activewear products. The production inefficiencies affecting our Dominican Republic facility were essentially resolved by the end of the fourth quarter of fiscal 2008.

GILDAN 2009 REPORT TO SHAREHOLDERS P.13

MANAGEMENT’S DISCUSSION AND ANALYSIS

Selling, General and Administrative Expenses Selling, General and Administrative Expenses for fiscal 2008 and 2007 reflect the impact of the change in statement of earnings classification as described on page 8.

SG&A expenses were $142.8 million, or 11.4% of net sales in fiscal 2008, compared to $99.9 million, or 10.4% of net sales in fiscal 2007. The increase in SG&A expenses in fiscal 2008 was due to the acquisition of Prewett, higher distribution and transportation expenses driven by volume increases and higher fuel costs, higher depreciation and amortization, higher bad debt expense, higher corporate costs, including the impact of the higher-valued Canadian dollar during the year, a charge for the disposal of surplus fixed assets, and professional fees for special projects.

Financial Expense / Income, net Net financial expense amounted to $9.2 million during fiscal 2008, up from $5.4 million in fiscal 2007. The increase in net financial expense was due mainly to an increase in net interest expense, resulting from lower investment income and higher borrowings during fiscal 2008, mainly due to the use of funds for the acquisition of Prewett.

Income Taxes The CRA conducted an audit of our income tax returns for our 2000, 2001, 2002 and 2003 fiscal years, the scope of which included a review of transfer pricing and the allocation of income between the Company’s Canadian legal entity and its foreign subsidiaries. In the third quarter of fiscal 2008, management met with the CRA for the first time to discuss preliminary transfer pricing audit issues and, in particular, explain the roles and responsibilities performed in our foreign subsidiaries where the majority of our taxable income is earned. On December 10, 2008, the Company reached a final agreement with the CRA and concluded the audit for the 2000, 2001, 2002 and 2003 fiscal years. In connection with the terms of the agreement, we agreed to a tax reassessment related to the restructuring of our international wholesale business and the related transfer of our assets to our Barbados subsidiary, which occurred in fiscal 1999. The terms of the agreement were accounted for in the fourth quarter of fiscal 2008 through a charge to income tax expense of $26.9 million and a reclassification of $17.3 million of future income tax liabilities to income taxes payable. There were no penalties assessed as part of the agreement and there were no other significant income tax adjustments to reported taxable income for the years under audit.

The Company recorded an income tax expense of $34.4 million in fiscal 2008 compared to an income tax recovery of $4.8 million in fiscal 2007. The income tax expense in fiscal 2008 included a charge of $26.9 million related to the settlement of the CRA audit, as described above. The income tax recovery in fiscal 2007 included the recognition of previously unrecognized tax positions in the amount of $7.6 million relating to a prior taxation year, which became statute-barred during fiscal 2007. Excluding the impact of the CRA audit settlement in fiscal 2008, the impact of restructuring and other charges in both years and the income tax recovery of $7.6 million related to previously unrecognized tax positions of a prior taxation year in fiscal 2007, the effective income tax rate for the year ended October 5, 2008 was 4.4%, compared to an effective income tax rate for fiscal 2007 of 2.3%. The increase in the effective income tax rate in fiscal 2008 compared to fiscal 2007 was mainly due to an income tax recovery of $3.1 million relating to the fiscal 2007 operating losses of Kentucky Derby and an increase in profits generated in higher tax jurisdictions.

GILDAN 2009 REPORT TO SHAREHOLDERS P.14

MANAGEMENT’S DISCUSSION AND ANALYSIS

Net Earnings Net earnings for fiscal 2008 were $146.4 million, or $1.20 per share on a diluted basis, up respectively 13.4% and 13.2% compared to net earnings of $129.1 million, or $1.06 per share on a diluted basis in fiscal 2007. Net earnings for fiscal 2008 included after-tax restructuring and other charges of $4.9 million or $0.04 per share. Net earnings for fiscal 2007 included restructuring and other charges of $27.3 million after tax, or $0.23 per share. Excluding the impact of these restructuring and other charges, adjusted net earnings of $151.3 million, or $1.24 per share on a diluted basis in fiscal 2008, decreased 3.3% and 3.9%, respectively, compared to adjusted net earnings of $156.4 million, or $1.29 per share in fiscal 2007. The decrease in adjusted net earnings and adjusted diluted EPS was due to the one-time income tax charge of $26.9 million, or $0.22 per share related to the settlement of the CRA audit, higher cotton and energy costs, production inefficiencies in the Dominican Republic facility, increased SG&A, depreciation and interest expenses, and the non-recurrence of income tax benefits totaling $7.6 million relating to a prior taxation year which became statute barred in fiscal 2007. These factors more than offset the favourable impact of higher activewear unit sales volumes, increased net selling prices and manufacturing efficiencies resulting from the consolidation of our textile facilities.

SUMMARY OF QUARTERLY RESULTS

The table below sets forth certain summarized unaudited quarterly financial data for the eight most recently completed quarters. This quarterly information is unaudited and has been prepared on the same basis as the annual audited Consolidated Financial Statements. The operating results for any quarter are not necessarily indicative of the results to be expected for any period.

(in $ millions, except per share amounts)(1)

2009

2008

Q4

Q3

Q2

Q1

Q4

Q3

Q2

Q1

Net Sales

301.7

307.8

244.8

184.0

324.7

380.8

293.8

250.5

Net earnings(2)

42.4

41.5

7.1

4.3

21.8

54.5

42.1

27.9

Net earnings per share(2)

Basic EPS(3)

0.35

0.34

0.06

0.04

0.18

0.45

0.35

0.23

Diluted EPS(3)

0.35

0.34

0.06

0.04

0.18

0.45

0.35

0.23

Total assets(2)

1,082.4

1,126.3

1,109.1

1,037.4

1,095.0

1,098.6

1,052.7

988.9

Total long-term financial liabilities

4.4

92.9

121.5

51.2

53.0

108.4

146.3

130.8

Weighted average number of shares outstanding (in ‘000s)

Basic

120,959

120,911

120,799

120,573

120,531

120,492

120,464

120,428

Diluted

121,668

121,483

121,178

121,408

121,558

121,622

121,649

121,656

(1)

Quarterly results reflect the acquisition of Prewett on October 15, 2007 (Q1 2008) from the date of acquisition.

(2)

Net earnings, Net earnings per share and Total assets reflect the impact of the change in accounting policy as described in Note 1(b) to the audited Consolidated Financial Statements.

(3)

Quarterly EPS may not add to year-to-date EPS due to rounding.