www.cemex.com

4Q09 RESULTS

4Q09 RESULTS

January 2010

January 2010

2

2009 achievements

§ Refinanced US$15 billion in debt

§ Issued close to US$2.3 billion in fixed income notes

§ Raised US$2.2 billion in equity and equity-like capital

§ Sold our Australian assets for approximately US$1.7 billion

§ Implemented a US$900 million cost-reduction program

§ Increased use of alternative fuels to 16%, from 10% in 2008

§ On track to achieve 25% reduction in specific CO2 emissions by

2015 from 1990 levels

2015 from 1990 levels

3

4Q09 results highlights

January - December | Fourth Quarter | ||||||||||

2009 | 2008 | % var | l-t-l % var | 2009 | 2008 | % var | l-t-l % var | ||||

Net sales | 14,544 | 20,131 | (28%) | (19%) | 3,444 | 4,148 | (17%) | (20%) | |||

Gross profit | 4,274 | 6,396 | (33%) | (23%) | 911 | 1,262 | (28%) | (31%) | |||

Operating income | 1,165 | 2,327 | (50%) | (38%) | 98 | 346 | (72%) | (75%) | |||

EBITDA | 2,657 | 4,080 | (35%) | (25%) | 474 | 750 | (37%) | (39%) | |||

FCF after maint capex | 1,215 | 2,600 | (53%) | 401 | 474 | (15%) | |||||

Millions US dollars

4

§ 2009 results reflect deconsolidation of Venezuelan assets starting August 2008

§ Australian operations reclassified as “Discontinued Operations” in 2008 and 2009

results

results

Ready Mix | Volume | (23%) | (21%) | (10%) | ||

Price (USD) | (10%) | (1%) | 0% | |||

Price (l-t-l1) | (2%) | (6%) | (2%) |

Aggregates | Volume | (20%) | (16%) | (12%) | ||

Price (USD) | (9%) | 3% | 0% | |||

Price (l-t-l1) | (2%) | (3%) | (2%) |

2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | ||||

Cement | Volume | (14%) | (8%) | (8%) | ||

Price (USD) | (9%) | 0% | (1%) | |||

Price (l-t-l1) | 1% | (4%) | (2%) |

5

Consolidated volumes and prices

1 Like-to-like prices adjusted for investments/divestments and foreign-exchange fluctuations

§ Challenging business environment prevailed during 2009, with some signs of

stabilization in the second half

stabilization in the second half

6

2010 guidance

§ Consolidated volumes expected to increase by 4% for cement and

aggregates and by 2% for ready mix

aggregates and by 2% for ready mix

– Volumes in Mexico flat for cement and growing in excess of 5% for

ready mix

ready mix

– US cement, ready-mix and aggregates volumes to have high-single-digit

increase

increase

– Spanish cement volumes similar to 2009 levels; ready-mix and

aggregates volumes declining by 11% and 2%, respectively

aggregates volumes declining by 11% and 2%, respectively

§ EBITDA to be about US$2.9 billion, on a like-to-like basis, and based

on currently prevailing exchange rates

on currently prevailing exchange rates

§ Free cash flow after maintenance capex to reach close to US$1

billion, reflecting exclusion of Australian operations, higher interest

expense, maintenance capex, and cash taxes, and lower investment

in working capital

billion, reflecting exclusion of Australian operations, higher interest

expense, maintenance capex, and cash taxes, and lower investment

in working capital

§ US$600 million from free cash flow to be used for debt reduction

during the year

during the year

www.cemex.com

REGIONAL

HIGHLIGHTS

HIGHLIGHTS

REGIONAL

HIGHLIGHTS

HIGHLIGHTS

January 2010

January 2010

7

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 3,113 | 3,822 | (19%) | (1%) | 723 | 820 | (12%) | (14%) | |||

EBITDA | 1,160 | 1,453 | (20%) | (3%) | 251 | 302 | (17%) | (18%) | |||

Margin | 37.3% | 38.0% | 34.8% | 36.8% |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (4%) | (10%) | (2%) | |

Ready-mix | (14%) | (28%) | (9%) | |

Aggregates | 4% | (9%) | (6%) |

Price (LC) | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 2% | (3%) | (3%) | |

Ready-mix | 1% | (0%) | (0%) | |

Aggregates | 5% | 10% | 2% |

8

§ Investment in Infrastructure

increased by about 20% in 2009,

partially mitigating contraction in

residential and non-residential

sectors

increased by about 20% in 2009,

partially mitigating contraction in

residential and non-residential

sectors

§ Formal housing affected by bridge

financing constraints; some

recovery expected for 2010

financing constraints; some

recovery expected for 2010

§ Self-construction anticipated to

drop by about 1% in 2010

drop by about 1% in 2010

§ Industrial and commercial sector

expected to grow by 15% in 2010,

after two years of decline

expected to grow by 15% in 2010,

after two years of decline

Mexico

United States

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 2,825 | 4,698 | (40%) | (40%) | 602 | 983 | (39%) | (39%) | |||

EBITDA | 143 | 702 | (80%) | (80%) | (5) | 129 | N/A | N/A | |||

Margin | 5.1% | 14.9% | (0.7%) | 13.1% |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (32%) | (25%) | (14%) | |

Ready-mix | (38%) | (30%) | (12%) | |

Aggregates | (36%) | (29%) | (15%) |

Price (LC) | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (6%) | (7%) | (0%) | |

Ready-mix | (8%) | (13%) | (4%) | |

Aggregates | (7%) | (9%) | (2%) |

9

§ Fourth quarter decline in volumes

reflecting drop in residential and

I&C sectors, as well as poor

weather during December

reflecting drop in residential and

I&C sectors, as well as poor

weather during December

§ Public construction will continue to

be main driver for demand,

supported by ARRA and other

funding

be main driver for demand,

supported by ARRA and other

funding

§ Improvement seen in existing

home sales and inventories;

cement demand from residential

sector expected to have double-

digit growth in 2010 in our markets

home sales and inventories;

cement demand from residential

sector expected to have double-

digit growth in 2010 in our markets

Spain

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 831 | 1,573 | (47%) | (36%) | 194 | 247 | (21%) | (14%) | |||

EBITDA | 204 | 464 | (56%) | (50%) | 44 | 60 | (27%) | (31%) | |||

Margin | 24.6% | 29.5% | 22.4% | 24.3% |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (40%) | (23%) | (16%) | |

Ready-mix | (44%) | (33%) | (19%) | |

Aggregates | (33%) | (15%) | (12%) |

Price (LC) | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (10%) | (14%) | (2%) | |

Ready-mix | (8%) | (11%) | 0% | |

Aggregates | 3% | 0% | (1%) |

10

§ Cement and ready-mix volumes on

a like-to-like basis declined by

30% and 37%, respectively, for

2009

a like-to-like basis declined by

30% and 37%, respectively, for

2009

§ Construction activity affected by

economic slowdown and limited

credit availability

economic slowdown and limited

credit availability

§ Housing starts expected to

decrease to 140-150 thousand in

2009, further decline expected

decrease to 140-150 thousand in

2009, further decline expected

§ Infrastructure relatively stable, but

insufficient to compensate other

sectors

insufficient to compensate other

sectors

United Kingdom

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 1,184 | 1,712 | (31%) | (19%) | 285 | 318 | (10%) | (16%) | |||

EBITDA | 43 | 26 | 62% | 88% | 0 | (19) | 99% | 97% | |||

Margin | 3.6% | 1.5% | (0.1%) | (6.0%) |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (19%) | (14%) | (15%) | |

Ready-mix | (25%) | (23%) | (17%) | |

Aggregates | (19%) | (12%) | (17%) |

Price (LC) | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 8% | 3% | (2%) | |

Ready-mix | 2% | (1%) | (0%) | |

Aggregates | 1% | (2%) | (1%) |

11

§ 2009 results reflected weakness

across all business segments, with

rate of decline decelerating in the

last months of the year

across all business segments, with

rate of decline decelerating in the

last months of the year

§ Mild recovery in the housing sector

expected for 2010

expected for 2010

Rest of Europe

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 3,345 | 4,369 | (23%) | (17%) | 843 | 922 | (9%) | (17%) | |||

EBITDA | 349 | 532 | (34%) | (27%) | 65 | 82 | (20%) | (27%) | |||

Margin | 10.4% | 12.2% | 7.8% | 8.9% |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (17%) | (18%) | (29%) | |

Ready-mix | (17%) | (14%) | (13%) | |

Aggregates | (13%) | (13%) | (15%) |

12

Price (LC)1 | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 4% | 0% | (2%) | |

Ready-mix | 0% | (1%) | 1% | |

Aggregates | 4% | 7% | 1% |

§ In France, ready-mix volume

decreased by 17% and aggregates

volume by 13% during 4Q09

decreased by 17% and aggregates

volume by 13% during 4Q09

§ In Germany, cement volume

decreased by 16% during 4Q09

decreased by 16% during 4Q09

§ In most countries in the region,

infrastructure continues to be the

main driver for volume growth

infrastructure continues to be the

main driver for volume growth

§ In Eastern Europe, 2009 volumes

affected by lower confidence and

tight credit conditions; stabilization

and potential growth expected in

some markets for 2010

affected by lower confidence and

tight credit conditions; stabilization

and potential growth expected in

some markets for 2010

1 Volume-weighted, local-currency average prices

South/Central America and the Caribbean

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 1,368 | 2,023 | (32%) | (13%) | 322 | 378 | (15%) | (18%) | |||

EBITDA | 494 | 658 | (25%) | (4%) | 111 | 121 | (8%) | (13%) | |||

Margin | 36.1% | 32.5% | 34.5% | 31.9% |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | (30%) | (1%) | (5%) | |

Ready-mix | (34%) | (21%) | (10%) | |

Aggregates | (40%) | (27%) | 11% |

13

Price (LC)1 | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 14% | (2%) | (2%) | |

Ready-mix | (3%) | (6%) | (3%) | |

Aggregates | (2%) | (13%) | (3%) |

§ Colombian cement volume

remained flat for the quarter and

ready-mix volume declined by 15%

remained flat for the quarter and

ready-mix volume declined by 15%

§ In Colombia, infrastructure will

continue to be an important

contributor to 2010 volumes;

subsidy in interest rates for new

homes should also contribute to

volume growth

continue to be an important

contributor to 2010 volumes;

subsidy in interest rates for new

homes should also contribute to

volume growth

1 Volume-weighted, local-currency average prices

Africa and Middle East

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 1,049 | 1,071 | (2%) | 2% | 261 | 278 | (6%) | (7%) | |||

EBITDA | 333 | 296 | 12% | 15% | 68 | 72 | (6%) | (7%) | |||

Margin | 31.7% | 27.7% | 25.9% | 25.9% |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 22% | 7% | 1% | |

Ready-mix | (14%) | (8%) | 7% | |

Aggregates | (10%) | 12% | 23% |

14

Price (LC)1 | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 10% | 2% | (1%) | |

Ready-mix | (3%) | (19%) | (4%) | |

Aggregates | 7% | (4%) | 4% |

§ In Egypt, cement volumes

increased by 7% during 4Q09 and

by 13% in 2009

increased by 7% during 4Q09 and

by 13% in 2009

§ The informal housing and

infrastructure sectors will continue

to be main drivers of cement

demand in 2010 in the region

infrastructure sectors will continue

to be main drivers of cement

demand in 2010 in the region

1 Volume-weighted, local-currency average prices

Asia

2009 | 2008 | % var | l-t-l % var | 4Q09 | 4Q08 | % var | l-t-l % var | ||||

Net Sales | 474 | 494 | (4%) | 1% | 122 | 105 | 17% | 14% | |||

EBITDA | 116 | 93 | 25% | 33% | 22 | 15 | 44% | 40% | |||

Margin | 24.5% | 18.8% | 17.8% | 14.5% |

Volume | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 0% | 24% | 1% | |

Ready-mix | (18%) | (9%) | 21% | |

Aggregates | (15%) | 0% | 11% |

15

Price (LC)1 | 2009 vs. 2008 | 4Q09 vs. 4Q08 | 4Q09 vs. 3Q09 | |

Cement | 7% | (2%) | (1%) | |

Ready-mix | 3% | (6%) | (1%) | |

Aggregates | 3% | (3%) | 2% |

1 Volume-weighted, local-currency average prices

www.cemex.com

4Q09 RESULTS

4Q09 RESULTS

January 2010

January 2010

16

EBITDA and free cash flow

January - December | Fourth Quarter | ||||||||||

2009 | 2008 | % var | l-t-l % var | 2009 | 2008 | % var | l-t-l % var | ||||

Net sales | 14,544 | 20,131 | (28%) | (19%) | 3,444 | 4,148 | (17%) | (20%) | |||

EBITDA | 2,657 | 4,080 | (35%) | (25%) | 474 | 750 | (37%) | (39%) | |||

EBITDA margin | 18.3% | 20.3% | (2.0pp) | 13.8% | 18.1% | (4.3pp) | |||||

Cost of sales | 10,270 | 13,735 | (25%) | 2,532 | 2,886 | (12%) | |||||

% sales | 70.6% | 68.2% | 2.4pp | 73.5% | 69.6% | 3.9pp | |||||

SG&A | 3,109 | 4,069 | (24%) | 813 | 916 | (11%) | |||||

% sales | 21.4% | 20.2% | 1.2pp | 23.6% | 22.1% | 1.5pp | |||||

Free cash flow after maintenance capex | 1,215 | 2,600 | (53%) | 401 | 474 | (15%) | |||||

Free cash flow | 805 | 1,040 | (23%) | 334 | 195 | 71% | |||||

US$ million

17

§ Adjusting for Venezuela, divestments and the sale of emission allowances done last

year, EBITDA margin had a slight decline of 0.4pp despite a 19% decline in sales, on a

like-to-like basis

year, EBITDA margin had a slight decline of 0.4pp despite a 19% decline in sales, on a

like-to-like basis

§ Increase in SG&A as a percentage of sales mainly due to lesser economies of scale

due to lower volumes and higher transportation costs, partially offset by savings from

cost-reduction initiatives

due to lower volumes and higher transportation costs, partially offset by savings from

cost-reduction initiatives

§ Free cash flow after maintenance capex reflects lower EBITDA, higher financial

expense and investment in working capital, partially offset by lower maintenance capex

expense and investment in working capital, partially offset by lower maintenance capex

18

Other items

§ Kiln fuel and electricity costs, on a per-ton-of-cement-produced basis,

decreased by 16% for 2009 and expected to increase by 5% for 2010

decreased by 16% for 2009 and expected to increase by 5% for 2010

§ Increase in financial expenses during the quarter reflects new terms

of Financing Agreement

of Financing Agreement

§ Gain on financial instruments during the quarter reflects positive mark

-to-market contribution of our equity derivatives

-to-market contribution of our equity derivatives

§ Income tax resulting from tax losses in many of our operating

jurisdictions due to reduced volumes and local foreign-exchange

losses

jurisdictions due to reduced volumes and local foreign-exchange

losses

§ Estimated impact of the changes in the rules in Mexico for group tax

consolidation : US$799 million

consolidation : US$799 million

– Liability recognized in balance sheet; a deferred tax asset for US$628

million also recognized

million also recognized

– Expected impact on 2010 cash taxes: US$30 million

www.cemex.com

DEBT

INFORMATION

INFORMATION

DEBT

INFORMATION

INFORMATION

January 2010

January 2010

19

20

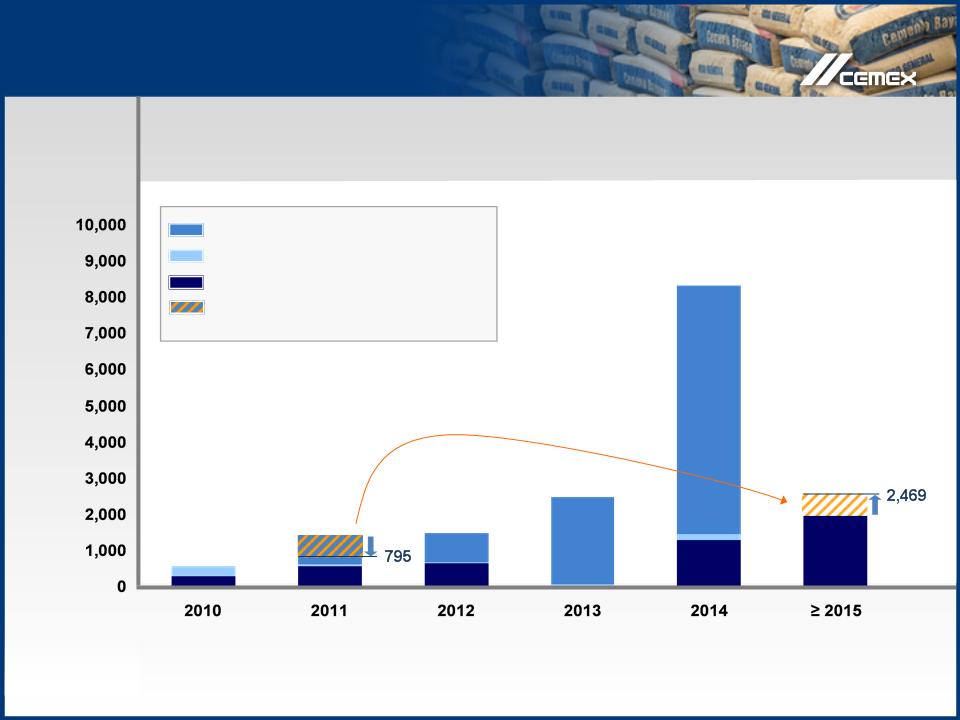

Debt-related activity in the quarter

§ Convertible securities transaction for MXN4.1 billion (approximately

US$320 million); upon conversion will represent about 17.25 million

ADSs

US$320 million); upon conversion will represent about 17.25 million

ADSs

§ Issuance of notes for close to US$2.3 billion

– US-dollar notes for US$1.25 billion (7 years, yield 9.50%) issued in December;

reopening in January for additional US$500 million (yield 8.477%)

reopening in January for additional US$500 million (yield 8.477%)

– Euro notes for €350 million (8 years, yield 9.625%) issued in December

§ Issuance of various short-term notes under our short-term

Certificados Bursátiles program, having an outstanding amount of

MXN800 million at the end of the quarter

Certificados Bursátiles program, having an outstanding amount of

MXN800 million at the end of the quarter

US$ million

Consolidated debt maturity profile

Total debt excluding perpetual debentures as of 4Q09

US$ 16,130

Fixed Income

Financing Agreement Amortizations

Other bank / WC debt

565

1,377

1,455

2,455

8,310

1,969

21

2011 prepayments to Financing

Agreement made during January

Agreement made during January

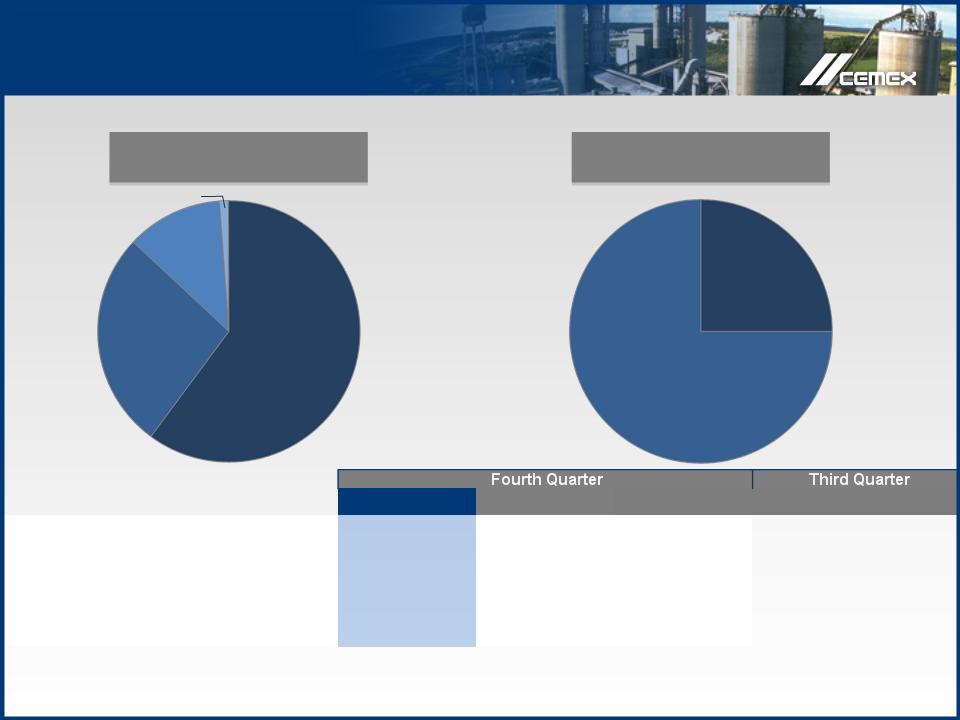

Debt-related information

2009 | 2008 | % Var. | 2009 | ||

Total debt | 16,130 | 18,783 | (14%) | 17,448 | |

Short-term | 4% | 37% | 3% | ||

Long-term | 96% | 63% | 97% | ||

Cash and cash equivalents | 1,077 | 939 | 15% | 363 | |

Fair value cross currency swaps2 | 0 | (114) | 0 | ||

Net debt | 15,053 | 17,958 | (16%) | 17,085 | |

Currency denomination

Interest Rate

22

U.S.

dollar

dollar

60%

Euro

27%

Mexican

peso

peso

12%

other

Variable

75%

Fixed

25%

1 For presentation purposes in the table above, net debt includes the fair value of cross-currency swaps, if any, associated with debt.

This presentation contains certain forward-looking statements and information relating to CEMEX, S.A.B. de

C.V. and its subsidiaries (collectively, “CEMEX”) that are based on the beliefs of its management, as well as

assumptions made by and information currently available to CEMEX. Such statements reflect the current

views of CEMEX with respect to future events and are subject to certain risks, uncertainties, and assumptions.

Many factors could cause the actual results, performance or achievements of CEMEX to be materially

different from any future results, performance or achievements that may be expressed or implied by such

forward-looking statements, including, among others, changes in general economic, political, governmental,

and business conditions globally and in the countries in which CEMEX does business, changes in interest

rates, changes in inflation rates, changes in exchange rates, the level of construction generally, changes in

cement demand and prices, changes in raw material and energy prices, changes in business strategy, and

various other factors. Should one or more of these risks or uncertainties materialize, or should underlying

assumptions prove incorrect, actual results may vary materially from those described herein as anticipated,

believed, estimated, expected or targeted. CEMEX does not intend, and does not assume any obligation, to

update these forward-looking statements.

C.V. and its subsidiaries (collectively, “CEMEX”) that are based on the beliefs of its management, as well as

assumptions made by and information currently available to CEMEX. Such statements reflect the current

views of CEMEX with respect to future events and are subject to certain risks, uncertainties, and assumptions.

Many factors could cause the actual results, performance or achievements of CEMEX to be materially

different from any future results, performance or achievements that may be expressed or implied by such

forward-looking statements, including, among others, changes in general economic, political, governmental,

and business conditions globally and in the countries in which CEMEX does business, changes in interest

rates, changes in inflation rates, changes in exchange rates, the level of construction generally, changes in

cement demand and prices, changes in raw material and energy prices, changes in business strategy, and

various other factors. Should one or more of these risks or uncertainties materialize, or should underlying

assumptions prove incorrect, actual results may vary materially from those described herein as anticipated,

believed, estimated, expected or targeted. CEMEX does not intend, and does not assume any obligation, to

update these forward-looking statements.

UNLESS OTHERWISE NOTED, ALL FIGURES ARE PRESENTED UNDER MEXICAN GAAP

Copyright CEMEX, S.A.B. de C.V. and its subsidiaries.

Forward looking information

23

25

Definitions

EBITDA: Operating income plus depreciation and operating

amortization

amortization

Expansion capital expenditures: consist of expansion spending on

our cement, ready-mix, and other core businesses in existing markets

our cement, ready-mix, and other core businesses in existing markets

LC: Local currency

Like-to-like percentage variation (l-t-l % var): Percentage variations

adjusted for investments/divestments and currency fluctuations

adjusted for investments/divestments and currency fluctuations

Maintenance capital expenditures: consist of maintenance spending

on our cement, ready-mix, and other core businesses in existing

markets

on our cement, ready-mix, and other core businesses in existing

markets

In the United States:

1 877 7CX NYSE

In Mexico:

52 (81) 8888 4292

E-Mail:

ir@cemex.com

Contact Information

26