Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on March 19, 2015

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

o | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | ||

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2014 | |

OR | ||

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

OR | ||

o | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

Commission File Number 001-35370

| LUXFER HOLDINGS PLC (Exact name of Registrant as specified in its charter) |

England and Wales (Jurisdiction of incorporation or organization) |

Anchorage Gateway, 5 Anchorage Quay, Salford, England M50 3XE (Address of principal executive offices) |

Dan Stracner, Investor Relations 3016 Kansas Avenue, Riverside, California, 92507, United States Telephone No. 001 951 341 2375, E-Mail: dan.stracner@luxfer.net (Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person) |

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

Ordinary Shares, nominal value £0.50 each | New York Stock Exchange* | |

American Depositary Shares, each representing an Ordinary Share of nominal value £0.50 each | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report: 26,955,743 Ordinary Shares of £0.50 each and 769,413,708,000 Deferred Ordinary Shares of £0.0001 each.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes o No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer ý | Non-accelerated filer o |

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAPo | International Financial Reporting Standards as issued by the International Accounting Standards Boardý | Othero |

If "Other" has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 o Item 18 o

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No ý

* Not for trading, but only in connection with the registration of American Depositary Shares.

TABLE OF CONTENTS

| | | Page | ||||

|---|---|---|---|---|---|---|

PART I | ||||||

Item 1. | Identity of Directors, Senior Management and Advisers | 1 | ||||

Item 2. | Offer Statistics and Expected Timetable | 1 | ||||

Item 3. | Key Information | 1 | ||||

Item 4. | Information on the Company | 26 | ||||

Item 4a. | Unresolved Staff Comments | 55 | ||||

Item 5. | Operating and Financial Review and Prospects | 55 | ||||

Item 6. | Directors, Senior Management and Employees | 88 | ||||

Item 7. | Major Shareholders and Related Party Transactions | 123 | ||||

Item 8. | Financial Information | 126 | ||||

Item 9. | The Offer and Listing | 127 | ||||

Item 10. | Additional Information | 128 | ||||

Item 11. | Quantitative and Qualitative Disclosures About Market Risk | 133 | ||||

Item 12. | Description of Securities Other Than Equity | 141 | ||||

PART II | ||||||

Item 13. | Defaults, Dividend Arrearages and Delinquencies | 142 | ||||

Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 142 | ||||

Item 15. | Controls and Procedures | 142 | ||||

Item 16. | [Reserved] | 142 | ||||

Item 16a. | Audit Committee Financial Expert | 142 | ||||

Item 16b. | Code of Ethics | 143 | ||||

Item 16c. | Principal Accountant Fees and Services | 143 | ||||

Item 16d. | Exemptions From the Listing Standards for Audit Committees | 143 | ||||

Item 16e. | Purchases of Equity Securities by the Issuer and Affiliated Purchasers | 143 | ||||

Item 16f. | Change in Registrant's Certifying Accountant | 144 | ||||

Item 16g. | Corporate Governance | 144 | ||||

Item 16h. | Mine Safety Disclosure | 145 | ||||

PART III | ||||||

Item 17. | Financial Statements | 146 | ||||

Item 18. | Financial Statements | 146 | ||||

Item 19. | Exhibits | 146 | ||||

GENERAL INFORMATION

In this annual report on Form 20-F ("Annual Report"), references to "Company," "Luxfer," "Group," "Luxfer Group," "we," "us" and "our" are to Luxfer Holdings PLC and, except as the context requires, its consolidated subsidiaries.

PRESENTATION OF FINANCIAL AND OTHER DATA

The consolidated financial statements have been prepared in accordance with International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB") as they apply to the financial statements of the Group. The consolidated financial statements have been prepared on a historical cost basis, except where IFRS requires or permits fair value measurement.

All references in this Annual Report to (i) "U.S. Dollar," "USD" or "$" are to the currency of the United States, (ii) "Pounds Sterling," "GBP sterling," "pence," "p" or "£" are to the currency of the United Kingdom and (iii) "Euro" or "€" are to the currency introduced at the start of the third stage of European economic and monetary union pursuant to the treaty establishing the European Community, as amended.

INFORMATION REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains certain statements, statistics and projections that are, or may be, forward-looking. The accuracy and completeness of all such statements, including, without limitation, statements regarding our future financial position, strategy, plans and objectives for the management of future operations, is not warranted or guaranteed. These statements typically contain words such as "believes," "intends," "expects," "anticipates," "estimates," "may," "will," "should" and words of similar import. By their nature, forward-looking statements involve risk and uncertainty because they relate to events and depend on circumstances that will occur in the future. We undertake no obligation to update any forward-looking statements, whether as a result of new information, future events or otherwise. Although we believe that the expectations reflected in such statements are reasonable, no assurance can be given that such expectations will prove to be correct. There are a number of factors that could cause actual results and developments to differ materially from those expressed or implied by such forward-looking statements. These factors include, but are not limited to, factors identified in "Risk Factors," "Information on the Company" and "Operating and Financial Review and Prospects," or elsewhere in this Annual Report, as well as:

- §

- future revenue being lower than expected;

- §

- increasing competitive pressures in the industry;

- §

- general economic conditions or conditions affecting demand for the services offered by us in the markets in which we operate, both domestically and internationally, being less favorable than expected;

- §

- the significant amount of indebtedness we have incurred and may incur and the obligations to service such indebtedness and to comply with the covenants contained therein;

- §

- restrictions on the ability of Luxfer Holdings PLC to receive dividends or loans from certain of its subsidiaries;

- §

- fluctuations in the price of raw materials and utilities;

- §

- currency fluctuations and hedging risks;

- §

- worldwide economic and business conditions and conditions in the industries in which we operate;

- §

- relationships with our customers and suppliers;

- §

- increased competition from other companies in the industries in which we operate;

- §

- changing technology;

- §

- claims for personal injury, death or property damage arising from the use of products produced by us;

- §

- the occurrence of accidents or other interruptions to our production processes;

- §

- changes in our business strategy or development plans, and our expected level of capital expenditure;

- §

- our ability to attract and retain qualified personnel;

- §

- regulatory, environmental, legislative and judicial developments;

- §

- our intention to pay dividends; and

- §

- factors that are not known to us at this time.

You are urged to read the sections "Risk Factors," "Information on the Company" and "Operating and Financial Review and Prospects" of this Annual Report for a more complete discussion of the factors that could affect our performance and the industry in which we operate.

Item 1. Identity of Directors, Senior Management and Advisers

Not applicable.

Item 2. Offer Statistics and Expected Timetable

Not applicable.

A. Selected Financial Data

The following selected consolidated financial data of Luxfer as of December 31, 2014, 2013, 2012, 2011 and 2010 and for the years ended December 31, 2014, 2013, 2012, 2011 and 2010 have been derived from our audited consolidated financial statements and the related notes appearing elsewhere in this Annual Report, which have been prepared in accordance with IFRS as issued by the IASB. Our historical results are not necessarily indicative of results to be expected for future periods.

This financial data should be read in conjunction with our audited consolidated financial statements and the related notes appearing elsewhere in this Annual Report and Item 5, "Operating and Financial Review and Prospects" below.

1

Consolidated Statement of Income Data

| | Year Ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

| | (In $ million, except share and per share data) | ||||||||||

Continuing operations | |||||||||||

Revenue | $489.5 | $481.3 | $511.6 | $510.8 | $402.7 | ||||||

Cost of sales | (376.6 | ) | (363.5 | ) | (385.7 | ) | (390.4 | ) | (305.1 | ) | |

| | | | | | | | | | | | |

Gross profit | 112.9 | 117.8 | 125.9 | 120.4 | 97.6 | ||||||

Other income/(costs) | — | — | — | 2.0 | 0.1 | ||||||

Distribution costs | (8.1 | ) | (6.5 | ) | (6.9 | ) | (7.3 | ) | (7.4 | ) | |

Administrative expenses | (59.7 | ) | (52.2 | ) | (50.4 | ) | (51.2 | ) | (45.5 | ) | |

Share of results of joint ventures | (0.3 | ) | 0.1 | (0.1 | ) | (0.2 | ) | (0.1 | ) | ||

| | | | | | | | | | | | |

Trading profit(1): | $44.8 | $59.2 | $68.5 | $63.7 | $44.7 | ||||||

Restructuring and other income (expense)(2) | (3.9 | ) | (2.7 | ) | (2.1 | ) | 0.2 | (0.8 | ) | ||

| | | | | | | | | | | | |

Operating profit | $40.9 | $56.5 | $66.4 | $63.9 | $43.9 | ||||||

Acquisition credit / (costs)(3) | 4.5 | (0.1 | ) | (0.6 | ) | — | — | ||||

Disposal costs of intellectual property(4) | — | — | (0.2 | ) | (0.2 | ) | (0.4 | ) | |||

Finance income: | |||||||||||

Interest received | 0.5 | 0.3 | 0.2 | 0.2 | 0.2 | ||||||

Gain on purchase of own debt | — | — | — | — | 0.5 | ||||||

Finance costs: | |||||||||||

Interest costs | (6.6 | ) | (6.2 | ) | (6.7 | ) | (9.2 | ) | (9.6 | ) | |

IAS 19 retirement benefits finance charge | (2.7 | ) | (3.8 | ) | (3.6 | ) | (1.9 | ) | (2.6 | ) | |

Unwind of discount on contingent consideration from acquisitions | (0.3 | ) | — | — | — | — | |||||

| | | | | | | | | | | | |

Profit on operations before taxation | $36.3 | $46.7 | $55.5 | $52.8 | $32.0 | ||||||

Tax expense | (7.1 | ) | (12.6 | ) | (16.0 | ) | (12.5 | ) | (8.9 | ) | |

| | | | | | | | | | | | |

Net income for the year | $29.2 | $34.1 | $39.5 | $40.3 | $23.1 | ||||||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Profit for the year attributable to controlling interests | $29.2 | $34.1 | $39.5 | $40.3 | $23.1 | ||||||

Profit from continuing operations per ordinary share(5): | |||||||||||

Basic | $1.09 | $1.27 | $1.84 | $2.04 | $1.17 | ||||||

Diluted | $1.05 | $1.22 | $1.81 | $2.02 | $1.16 | ||||||

Weighted average ordinary shares outstanding(5): | |||||||||||

Basic | 26,889,330 | 26,814,154 | 21,483,354 | 19,768,290 | 19,702,408 | ||||||

Diluted | 27,735,793 | 28,046,402 | 21,854,892 | 19,960,110 | 19,838,208 | ||||||

Dividends declared and paid during the year per share(6): | $0.40 | $0.40 | $0.30 | — | — | ||||||

2

Segmental information

| | As of December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

| | (In $ million) | ||||||||||

Revenue: | |||||||||||

Elektron | $230.6 | $219.7 | $265.3 | $287.5 | $203.5 | ||||||

Gas Cylinders | 258.9 | 261.6 | 246.3 | 223.3 | 199.2 | ||||||

| | | | | | | | | | | | |

| $489.5 | $481.3 | $511.6 | $510.8 | $402.7 | |||||||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Trading profit(1): | |||||||||||

Elektron | $38.9 | $40.2 | $52.8 | $52.5 | $32.8 | ||||||

Gas Cylinders | 5.9 | 19.0 | 15.7 | 11.2 | 11.9 | ||||||

| | | | | | | | | | | | |

| $44.8 | $59.2 | $68.5 | $63.7 | $44.7 | |||||||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Consolidated Balance Sheet Data

| | As of December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

| | (In $ million) | ||||||||||

Total assets | $459.8 | $396.1 | $390.5 | $364.3 | $296.6 | ||||||

Total liabilities | 284.4 | 204.4 | 241.7 | 299.5 | 231.4 | ||||||

Total equity | 175.4 | 191.7 | 148.8 | 64.8 | 65.2 | ||||||

Cash and short term deposits | 14.6 | 28.4 | 40.2 | 22.2 | 10.3 | ||||||

Non-current bank and other loans | (121.4 | ) | (63.8 | ) | (63.5 | ) | (129.4 | ) | — | ||

Senior Loan Notes due 2012 | — | — | — | — | (106.3 | ) | |||||

Current bank and other loans | — | — | — | (3.1 | ) | (9.6 | ) | ||||

| | | | | | | | | | | | |

Net debt | $(106.8 | ) | $(35.4 | ) | $(23.3 | ) | $(110.3 | ) | $(105.6 | ) | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Non-GAAP Financial Measures

| | Year ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

| | (In $ million) | ||||||||||

Net revenue(7): | |||||||||||

Elektron | $228.4 | $211.3 | $224.8 | $217.7 | $200.3 | ||||||

Gas Cylinders | 258.9 | 261.6 | 246.3 | 223.3 | 199.2 | ||||||

| | | | | | | | | | | | |

| $487.3 | $472.9 | $471.1 | $441.0 | $399.5 | |||||||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Adjusted EBITDA(8): | |||||||||||

Elektron | $50.1 | $49.8 | $61.0 | $60.6 | $40.4 | ||||||

Gas Cylinders | 14.7 | 26.8 | 22.2 | 17.6 | 18.2 | ||||||

| | | | | | | | | | | | |

| $64.8 | $76.6 | $83.2 | $78.2 | $58.6 | |||||||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Adjusted net income(8) | $30.9 | $39.8 | $44.7 | $41.1 | $25.1 | ||||||

Adjusted net income per ordinary share(9): | |||||||||||

Basic | $1.15 | $1.48 | $2.08 | $2.08 | $1.27 | ||||||

Diluted | $1.11 | $1.42 | $2.05 | $2.06 | $1.27 | ||||||

- (1)

- Trading profit is defined as operating profit before restructuring and other income (expense). For the purposes of our divisional segmental analysis, IFRS 8 requires the use of "segment profit" performance measures that are used by our chief operating decision maker. Trading profit is the "segment profit" measure used by our chief operating decision maker for divisional segmental analysis. See "Note 2—Revenue and segmental analysis" in our audited consolidated financial statements included elsewhere in this Annual Report.

3

- (2)

- Restructuring and other income (expense)

| | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | ($ millions) | ||||||||||

(Charged) / Credited to Operating Profit | |||||||||||

Rationalization of operations | (1.7 | ) | (0.5 | ) | (1.3 | ) | — | (0.2 | ) | ||

Environmental costs | (2.0 | ) | — | — | — | — | |||||

IPO related share based compensation charges | (0.2 | ) | (0.5 | ) | (0.8 | ) | — | — | |||

Non-trade legal & professional costs | — | — | — | (1.4 | ) | — | |||||

(Charges)/credits on retirement benefit obligations | — | (1.7 | ) | — | 1.6 | — | |||||

Loss on disposal of property, plant and equipment | — | — | — | — | (0.6 | ) | |||||

| | | | | | | | | | | | |

| $(3.9 | ) | $(2.7 | ) | $(2.1 | ) | $0.2 | $(0.8 | ) | |||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

Rationalization of operations—In 2014, the Gas Cylinders Division incurred $1.1 million of rationalization costs (2013: $0.3million, 2012: $1.1 million, 2011 and 2010: $nil) in relation to restructuring activities, while in the same period the Elektron Division incurred $0.6 million of rationalization costs (2013: $0.2 million, 2012: $0.2 million, 2011: $nil, 2010: $0.2 million) in relation to restructuring activities.

Environmental costs—In 2014, the Elektron Division incurred $2.0 million of costs relating to the discovery of low-level radiation during the routine and on-going remediation of an effluent pond where in the process of removing normal effluent from our U.S. MEL Chemicals plant in Flemington, New Jersey, we encountered uranium contamination. As a result of this, we were required to undertake specific actions to ensure disposal of the effluent material in accordance with Waste Acceptance Criteria, as set out by the New Jersey Department of Environmental Protection, before transportation and disposal. This exercise was completed during 2014.

IPO-related share based compensation charges—In 2014, a charge of $0.2 million (2013: $0.5 million) was recognized in the income statement under IFRS 2 in relation to share options granted as part of the initial public offering.

Non-trade legal and professional costs—In 2011, the Group incurred legal, audit and professional costs of $2.8 million in relation to the IPO and regulatory and legal documentation to support the transaction. Of this, $1.4 million was expensed in the year mainly in relation to historical audit work, and $1.4 million was deferred to be taken against share premium when the IPO took place in 2012.

(Charges) / credits on retirement benefit obligations—In 2013, deferred members of the U.S. pension plan were offered the option of a lump sum in respect of their benefits in the plan. This partial settlement of the pension liabilities resulted in a non-cash charge to the income statement of $1.7 million. In 2011, retired members of the Luxfer Group Pension Plan, the principal defined benefit plan in the U.K., were offered the option of altering the structure of their pension by receiving an immediate increase in their pension in return for giving up rights to a portion of their future inflation-related pension increases. This partial acceptance of the offer resulted in a non-cash gain of $1.6 million.

Loss on disposal of property, plant and equipment—In 2010, a charge of $0.6 million, net of proceeds from a third-party lessee of the building, was made for the demolition of a vacant property owned by the Group.

For further information, see also "Note 5—Other income (expense) items" in our audited consolidated financial statements appearing elsewhere in this Annual Report.

4

- (3)

- Acquisition credit / (costs)—In 2014, a credit of $6.3 million was recognized in the income statement in relation to the remeasurement of deferred contingent consideration arising from acquisitions. Of the $6.3 million, $4.8 million related to the Elektron Division and specifically to the acquisition of the trade and assets of Truetech Inc and Innotech Products Limited (together "Luxfer Magtech") where an element of deferred consideration was considered no longer payable due to the acquired business narrowly failing to achieve a profit trigger as at December 31, 2014. In addition $1.5 million related to the Gas Cylinders Division, being the acquisition of Vexxel Composites LLC and Hypercomp Engineering Inc ("Luxfer Utah") and a subsequent reassessment of the potential profitability of this acquisition in the light of our revised expectations for the demand of compressed natural gas (CNG) systems following the recent fall in oil prices. This was offset in part by acquisition costs of $1.5 million recognized in the Elektron Division in relation to the acquisition of Luxfer Magtech, and $0.3 million of acquisition costs recognized in the Gas Cylinders Division in relation to the acquisition of Luxfer Utah. In 2013, a net acquisition cost of $0.1 million (2012: $0.6 million) was recognized by the Gas Cylinders Division in relation to the acquisition of Dynetek Industries Limited ("Dynetek").

- (4)

- Disposal costs of intellectual property—In 2012, the Elektron Division incurred costs of $0.2 million (2011: $0.2 million, 2010: $0.4 million) in relation to the sale process of intellectual property in the U.S. acquired as part of the 2007 acquisition of Revere Graphics Worldwide.

- (5)

- Basic and diluted earnings per ordinary share—For further information, see "Note 10—Earnings per share" to our audited consolidated financial statements. We calculate earnings per share in accordance with IAS 33. Basic earnings per share is calculated based on the weighted average of ordinary shares outstanding for the period presented. The weighted average of ordinary shares outstanding is calculated by time-apportioning the shares outstanding during the year. For the purpose of calculating diluted earnings per share, the weighted average of ordinary shares outstanding during the period presented has been adjusted for the dilutive effect of all share options granted to employees. In calculating the diluted weighted average of ordinary shares outstanding, there are no shares that have not been included for anti-dilution reasons.

Following the approval of a two-for-one share split at the Annual General Meeting on May 29, 2014, and change in ADR ratio on June 9, 2014, each £0.50 ordinary share represents one American Depositary Share ("ADS"). The share split and ratio change were proposed for administrative convenience and simplicity, in particular to enable us to present earnings per ordinary share equal to earnings per ADS to avoid the complexity of presenting different earnings per share measures, given that previously each £1 ordinary share represented two ADSs.

- (6)

- Dividends declared and paid in the year—In 2014, four interim dividends of $0.10 per share were declared, and payments took place on February 5, May 7, August 6, and November 5. In 2013, four interim dividends of $0.10 per share were declared, and payments took place on February 6, May 8, August 7, and November 6. In 2012, an interim dividend of $0.20 per share was declared and paid on August 10, 2012. A further interim dividend of $0.10 per share was declared and paid on October 25, 2012.

5

- (7)

- Net revenue—Net revenue is defined as revenue excluding rare earth surcharges; the following table presents a reconciliation from revenue to net revenue.

| | Year Ended December 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

| | (In $ million) | ||||||||||

Revenue: | |||||||||||

Elektron | $230.6 | $219.7 | $265.3 | $287.5 | $203.5 | ||||||

Gas Cylinders | 258.9 | 261.6 | 246.3 | 223.3 | 199.2 | ||||||

| | | | | | | | | | | | |

| $489.5 | $481.3 | $511.6 | $510.8 | $402.7 | |||||||

Surcharge | |||||||||||

Elektron | $2.2 | $8.4 | $40.5 | $69.8 | $3.2 | ||||||

Gas Cylinders | — | — | — | — | — | ||||||

| | | | | | | | | | | | |

| $2.2 | $8.4 | $40.5 | $69.8 | $3.2 | |||||||

Net revenue(7): | |||||||||||

Elektron | 228.4 | 211.3 | 224.8 | 217.7 | 200.3 | ||||||

Gas Cylinders | 258.9 | 261.6 | 246.3 | 223.3 | 199.2 | ||||||

| | | | | | | | | | | | |

| $487.3 | $472.9 | $471.1 | $441.0 | $399.5 | |||||||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

- (8)

- Non-GAAP financial measures—The following tables present a reconciliation of adjusted net income and adjusted EBITDA to net income, the most comparable IFRS measure. A reconciliation of adjusted EBITDA to trading profit on a segmental basis is included in "Note 2—Revenue and segmental analysis" in our audited consolidated financial statements included elsewhere in this Annual Report.

| | Year Ended December, 31 | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2012 | 2011 | 2010 | ||||||

| | ($ millions) | ||||||||||

Net income for the year | $29.2 | $34.1 | $39.5 | $40.3 | $23.1 | ||||||

IAS 19 retirement benefits finance charge | 2.7 | 3.8 | 3.6 | 1.9 | 2.6 | ||||||

Acquisition and disposal charges | |||||||||||

Unwind of discount on deferred consideration from acquisitions | 0.3 | — | — | — | — | ||||||

Acquisitions (credit) / costs | (4.5 | ) | 0.1 | 0.6 | — | — | |||||

Amortization on acquired intangibles | 0.6 | — | — | — | — | ||||||

Disposal costs of intellectual property | — | — | 0.2 | 0.2 | 0.4 | ||||||

Restructuring and other income / (expense) | 3.9 | 2.7 | 2.1 | (0.2 | ) | 0.8 | |||||

Gain on purchase of own debt | — | — | — | — | (0.5 | ) | |||||

Other share based compensation charges | 1.6 | 1.3 | — | — | — | ||||||

Tax thereon | (2.9 | ) | (2.2 | ) | (1.3 | ) | (1.1 | ) | (1.3 | ) | |

| | | | | | | | | | | | |

Adjusted net income | $30.9 | $39.8 | $44.7 | $41.1 | $25.1 | ||||||

Add back: | |||||||||||

Tax thereon | 2.9 | 2.2 | 1.3 | 1.1 | 1.3 | ||||||

Tax expense | 7.1 | 12.6 | 16.0 | 12.5 | 8.9 | ||||||

Interest costs | 6.6 | 6.2 | 6.7 | 9.2 | 9.6 | ||||||

Interest received | (0.5 | ) | (0.3 | ) | (0.2 | ) | (0.2 | ) | (0.2 | ) | |

Depreciation & amortization | 18.1 | 15.8 | 14.7 | 14.5 | 13.9 | ||||||

Amortization on acquired intangibles—included in above | (0.6 | ) | — | — | — | — | |||||

Loss on disposal of property, plant and equipment | 0.3 | 0.3 | — | — | — | ||||||

| | | | | | | | | | | | |

Adjusted EBITDA | $64.8 | $76.6 | $83.2 | $78.2 | $58.6 | ||||||

| | | | | | | | | | | | |

| | | | | | | | | | | | |

| | | | | | | | | | | | |

6

Adjusted net income consists of net income adjusted for the post-tax impact of non-trading items, including IAS 19 retirement benefits finance charge, certain accounting charges relating to acquisitions and disposals of businesses (comprising other income / (expense) from acquisitions and disposals of businesses, the unwind of the discount on deferred consideration from acquisitions and the amortization on acquired intangibles), restructuring and other income / (expense), gain on purchase of own debt and other share-based compensation charges.

Adjusted EBITDA is defined as profit for the period before tax expense, finance income (which comprises interest received and gain on purchase of own debt) and costs (which comprises interest costs, IAS 19 retirement benefits finance charges and the unwind of the discount on deferred consideration from acquisitions), other income / (expense) from acquisitions and disposals of businesses, restructuring and other income / (expense), other share-based compensation charges, depreciation and amortization and loss on disposal of property, plant and equipment. Depreciation and amortization amounts include impairments to fixed assets when they are reflected in our financial statements as increases in accumulated depreciation or amortization.

We prepare and present adjusted net income and adjusted EBITDA to eliminate the effect of items that we do not consider indicative of our core operating performance. Management believes that adjusted net income and adjusted EBITDA are key performance indicators used by the investment community and that the presentation of adjusted net income and adjusted EBITDA will enhance an investor's understanding of our results of operations. However, adjusted net income and adjusted EBITDA should not be considered in isolation by investors as an alternative to profit for the year as an indicator of our operating performance or as a measure of our profitability. Adjusted net income and adjusted EBITDA are not measures of financial performance under IFRS, may not be indicative of historic operating results and are not meant to be predictive of potential future results. Adjusted net income and adjusted EBITDA measures presented herein may not be comparable to other similarly titled measures of other companies. While adjusted net income and adjusted EBITDA are not measures of financial performance under IFRS, adjusted net income and adjusted EBITDA presented have been computed using IFRS amounts.

- (9)

- Basic and diluted adjusted earnings per ordinary share—For further information, see "Note 10—Earnings per share" to our audited consolidated financial statements. We believe that the use of non-GAAP financial measures such as adjusted earnings per ordinary share more closely reflects the underlying earnings per ordinary share performance and is a financial measure widely used by both investors and financial analysts of the company's ordinary shares.

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

You should carefully consider the following risk factors described below, together with all of the other information in this Annual Report, including our consolidated financial statements and the related notes appearing elsewhere in this Annual Report, before investing in our American Depositary Shares ("ADSs"). The risks and uncertainties described below are those significant risk factors currently known and specific to us that we believe are relevant to an investment in our securities. If any of these risks materialize, our business, financial condition or results of operations could suffer, the price of our ADSs could decline and you could lose part or all of your investment. Additional risks and uncertainties not currently known to us or those we now deem immaterial may also harm us and adversely affect your investment in our ADSs.

7

Risks Relating to Our Operations

We depend on certain end-markets, including the automotive, alternative fuels, self-contained breathing apparatus, aerospace and defense, medical, and printing and paper end-markets, and an economic downturn or regulatory changes in any of those end-markets could reduce sales.

We have significant exposures to certain key end-markets, including some end-markets that are cyclical in nature or subject to high levels of regulatory control. To the extent that any of these cyclical end-markets are in decline, at a low point in their economic cycle or subject to regulatory change, sales may be adversely affected and thereby negatively affect our ability to fund our business operations and service our indebtedness. It is possible that all or most of these end-markets could be in decline at the same time, such as during a recession, which could significantly harm our financial condition and results of operations due to decreased sales. For example, 16% of our 2014 sales were related to automotive end-markets, 8% to alternative fuels end-markets, 13% to the self-contained breathing apparatus ("SCBA") end-market, 15% to aerospace and defense end-markets, 9% to medical end-markets (including portable oxygen) and 9% to printing and paper end-markets. Together, these six markets accounted for approximately 70% of our 2014 revenue. Dependence of either of our divisions on certain end-markets is even more pronounced. For example, in 2014, excluding rare earth surcharges, 27% of the Elektron Division's sales were to customers in the automotive end-market, which slumped in 2009; although global automotive production, which constitutes a significant driver of sales in our automotive end-market, has since improved, European production has not risen back to pre-recession levels. Moreover, in 2013, 19% of the Gas Cylinders Division's sales were to customers in the alternative fuels end-markets, which dropped to 15% in 2014. Gas Cylinders Division's sales in this end-market were affected by increased competition and more recently falling oil prices, which have led to some customers deferring expenditure in the alternative fuel projects due to the reduced saving on fuel costs when compared to using diesel, along with reduced activities in the oil and gas sector.

Our global operations expose us to economic conditions, political risks and specific regulations in the countries in which we operate, which could have a material adverse impact on our business, financial condition and results of operations.

We derive our revenue and earnings from operations in many countries and are subject to risks associated with doing business internationally. We have wholly-owned facilities in the United Kingdom, the United States, Canada, France, Germany, the Czech Republic and China and joint venture facilities in India, South Korea, Japan and the United States. Doing business in different countries has risks, including the potential for adverse changes in the local political, financial or regulatory climate, difficulty in staffing and managing geographically diverse operations, and the costs of complying with a variety of laws and regulations. Because we have operations in many countries, we are also liable to pay taxes in many fiscal jurisdictions. Our tax burden depends on the interpretation of local tax regulations, bilateral or multilateral international tax treaties and the administrative doctrines in each jurisdiction. Changes in these tax regulations may increase our tax burden.

Moreover, the principal markets for our products are located in North America, Europe and Asia, and any financial difficulties experienced in these markets may have a material adverse impact on our businesses. The maturity of some of our markets, particularly the U.S. medical oxygen cylinder market and the European fire extinguisher market, could require us to increase sales in developing regions, which may involve greater economic and political risks. We cannot provide any assurances that we will be able to expand sales in these regions.

8

Our operations rely on a number of large customers in certain areas of our business, and the loss of any of our major customers could negatively impact our sales.

If we fail to maintain our relationships with our major customers or fail to replace lost customers, or if there is reduced demand from our customers or for products produced by our customers, such failures or reduced demand could reduce our sales and have a material adverse effect on our financial condition and results of operations. In addition, we could experience a reduction in sales if any of our customers fail to perform or default on any payment pursuant to our contracts with them. For example, in certain markets, such as in the gas transportation market for alternative fuels, we contract large single orders, ranging from $2 million to $15 million, which exposes us to individually larger credit risks. For example, in 2014 delays in one particular customer's project resulted in a requirement for a $2 million impairment in the receivable to us due to their financial distress. Long-term relationships with customers are especially important for suppliers of intermediate materials and components such as we are. We often work closely with customers to develop products that meet particular specifications as part of the design of a product intended for an end-user market. The bespoke nature of many of our products could make it difficult to replace lost customers. Our top ten customers accounted for 28% of our revenue in 2014.

Competitive pressures can materially and adversely affect our sales, profit margins, financial condition and results of operations.

The markets for many of our products are now increasingly global and highly competitive, especially in terms of quality, price and service. We could lose market share as a result of these competitive pressures, which could materially and adversely affect our sales, profit margins, financial condition and results of operations.

Because of the highly competitive nature of some markets in which we operate, we may have difficulty raising customer prices to offset increases in costs of raw materials. For example, the U.S. medical oxygen cylinder market has a number of dedicated producers with excess capacity, making it very difficult for us to raise customer prices to offset aluminum cost increases. In addition, rising aluminum prices could lead to the development of alternative products that use lower-cost materials, which could become favored by end-market users.

In recent years, we have also experienced increased competition from developing markets where manufacturers may benefit from lower labor costs. We are also affected by Western-based competitors that have chosen to relocate production to Asia to take advantage of lower labor costs. Competitors with operations in these regions may be able to produce goods at a relatively lower cost, which may enable them to offer highly competitive selling prices.

Competition with respect to less-complex zirconium chemicals has been particularly intense, with Chinese suppliers providing low-cost feedstock to specialist competitors, making it especially difficult to compete in commodity products such as paper-making additives. Chinese magnesium also continues to be imported into Europe in large volumes, which may impact our competitive position in Europe regarding certain magnesium alloys. More generally, we may face potential competition from producers that manufacture products similar to our aluminum-based, magnesium-based and zirconium-based products using other materials, such as steel, plastics, composite materials or other metals, minerals and chemicals. Products manufactured by competitors using different materials might compete with our products in terms of price, weight, engineering characteristics, recyclability or other grounds.

We may also enter new markets with established competitors. We expect to face new and significant challenges in our effort to enter into these highly competitive markets in which we did not have a presence historically. For example, in recent years we have entered markets focused on the containment of compressed natural gas (CNG) and incurred startup costs along with strong competitive pressures from existing providers of similar cylinder technologies. Even if we are able to enter into these new markets

9

initially, we may not be able to sustain the effort on a long term-basis or establish sufficient market share to achieve meaningful returns from our investment.

Other parts of our operations manufacture and sell products that satisfy customer specifications. Competitors may develop lower-cost or better-performing products, and customers may not be willing to pay a premium for advantages offered by our products.

In addition, governments may impose import and export restrictions, grant subsidies to local companies and implement tariffs and other trade-protection regulations and measures that may give competitive advantages to certain of our competitors and adversely affect our business.

We depend upon our larger suppliers for a significant portion of our raw materials, and a loss of one of these suppliers or a significant supply interruption could negatively impact our financial performance.

Failure to maintain relationships with key suppliers or to develop relationships with other suppliers could negatively affect our financial condition or results of operations. We rely, to varying degrees, on major suppliers for some of the principal raw materials of our engineered products, including aluminum, zirconium and carbon fiber. For example, in 2014, we obtained 67% of our aluminum, the largest single raw material purchased by the Gas Cylinders Division, from Rio Tinto Alcan and its associated companies. Moreover, demand for carbon fiber is increasing rapidly, leading to occasional periods of short supply in recent years, with a number of expanding applications competing for the same supply of this specialized raw material. We currently purchase most of our carbon fiber from Toray and Grafil, a subsidiary of Mitsubishi Chemical. For additional details of some of our major suppliers, see "Item 4.B. Business Overview."

We generally purchase raw materials from suppliers on a spot basis under standard terms and conditions. We have recently agreed to a three-year supply contract with Rio Tinto Alcan for a substantial portion of our aluminum requirements. We have also signed both a one-year and a five-year magnesium supply contract with U.S. Magnesium for a portion of our requirements that expire in December 2015 and December 2019, respectively.

An interruption in the supply of essential materials used in our production processes or an increase in the prices of materials due to market shortages, supplier financial difficulties, government quotas or natural disturbances, could significantly affect our ability to provide competitively priced products to customers in a timely manner, and thus have a material adverse effect on our business, results of operations or financial condition. In the event of a significant interruption in the supply of any materials used in our production processes or a significant increase in their prices (as we have experienced, for example, at different times with aluminum, magnesium and rare earths), we may have to purchase these materials from alternative sources, build additional inventory of raw materials, increase our prices, reduce our profit margins or possibly fail to fill customer orders by deadlines required in contracts. We can provide no assurance that we would be able to obtain replacement materials quickly on similar terms or at all.

We are exposed to fluctuations in the prices of the raw materials that are used to manufacture our products, and such fluctuations in raw material prices could lead us to incur unexpected costs and could affect our margins or our results of operations.

The primary raw material we use to manufacture gas cylinders and superformed panels is aluminum supplied in billet and sheet form. The price of aluminum is subject to both significant short-term price fluctuations and to longer-term cyclicality as a result of international supply and demand relationships. In 2014, the London Metal Exchange ("LME") three-month price of aluminum reached a high of just over $2,100 per metric ton and a low of just below $1,700 per metric ton. The delivery premiums added by suppliers to the LME price also fluctuate, for example: the Midwest Aluminum Premium for physical supply of aluminum billet in the United States rose in 2014 from $259 per metric ton to $526 per metric ton. We have experienced significant price increases and volatility in other raw material costs in the last few years,

10

such as primary magnesium, carbon fiber, zircon sand and rare earths. For example, starting in mid-2010, Chinese authorities greatly reduced the export quota for rare earths, which resulted in volatility and an increase in the price of cerium carbonate. See "Item 4.B. Business Overview."

Fluctuations in the prices of these raw materials could affect margins in the businesses in which we use them. See "Item 5. Operating and Financial Review and Prospects." We cannot always pass on price increases or increase our prices to offset raw material price increases immediately or at all, whether because of fixed-price agreements with customers, competitive pressures that restrict our ability to pass on cost increases or increase prices, or other factors. It can be particularly difficult to pass on price increases or increase prices in product areas such as gas cylinders, where competitors offer similar products made from alternative materials, such as steel, if those materials are not subject to the same cost increases. Higher prices necessitated by large increases in raw material costs could make our current or future products unattractive compared to competing products made from alternative materials that have not been so affected by raw material cost increases or compared to products produced by competitors who have not incurred such large increases in their raw material costs. As a result, a substantial increase in raw material costs could have a material adverse effect on our financial condition and results of operations. In such an event, there might be less cash available than necessary to fund our business operations effectively or to service our indebtedness.

If the price of aluminum were to rise, our increased exposure to changes in aluminum prices could have a material adverse impact on our results of operations to the extent that we cannot pass price increases on to our customers or manage exposure effectively through hedging instruments. Currently we use derivative financial instruments to hedge our exposures to fluctuations in aluminum prices. Although it is our treasury policy to enter into these transactions only for hedging and not for speculative purposes, we are exposed to market risk and credit risk with respect to the use of these derivative financial instruments. See "Item 11. Quantitative & Qualitative Disclosures About Market Risk." In addition, if we have hedged our metal position, a fall in the price of aluminum might give rise to hedging margin calls to the detriment of our borrowing position.

In the past several years we have made additional purchases of large stocks of magnesium and some rare earth chemicals in an effort to delay the effect of potentially increased prices in the future (although we have since stopped doing so with respect to rare earth chemicals). However, even though such purchases are not made for speculative purposes, there can be no assurance that prices will move as expected. Moreover, these strategic purchases increase our working capital needs, reducing our liquidity and cash flow and potentially resulting in an increased drawdown on our revolving credit facility (the "Revolving Credit Facility").

We are exposed to fluctuations in prices of utilities that are used in the manufacture of our products, and such fluctuations in utility prices could lead us to incur unexpected costs and could affect our margins or our results of operations.

Our utility costs, which constitute another major input cost of our total expenses and include costs related to electricity, natural gas and water, may be subject to significant variations. The emergence of financial speculators in energy, increased taxation and other factors have contributed to a significant increase in utility costs for us, particularly with respect to the price that we pay for our U.K. energy supplies.

Fluctuations in the prices of these utility costs could affect margins in our businesses in which we use them. We cannot always pass on price increases or increase our prices to offset increases in utility costs immediately or at all, whether because of fixed-price agreements with customers, competitive pressures that restrict our ability to pass on cost increases or increase prices, or other factors. It can be particularly difficult to pass on price increases or increase prices in product areas such as gas cylinders, where competitors offer similar products made from alternative materials, such as steel, if those materials are not subject to the same cost increases. As a result, a substantial increase in utility costs could have a material

11

adverse effect on our financial condition and results of operations. In such an event, there might be less cash available than necessary to fund our business operations effectively or to service our indebtedness.

Changes in foreign exchange rates could reduce margins on our sales, reduce the reported revenue of our non-U.S. operations and have a material adverse effect on our results of operations.

We conduct a large portion of our commercial transactions, purchases of raw materials and sales of goods in various countries and regions, including the United Kingdom, the United States, continental Europe, Australia and Asia. Our manufacturing operations based in the United States, continental Europe and Asia usually purchase raw materials and sell goods denominated in their local currency, but our manufacturing operations in the United Kingdom often purchase raw materials and sell products in different currencies. Changes in the relative values of currencies can decrease the profits of our subsidiaries when they incur costs in currencies that are different from the currencies in which they generate all or part of their revenue. These transaction risks principally arise as a result of purchases of raw materials in U.S. dollars, coupled with sales of products to customers in euros. This impact is most pronounced in our exports to continental Europe from the United Kingdom. In 2014, our U.K. operations sold approximately €41.6 million of goods into the euro zone. Our policy is to hedge a portion of our net exposure to fluctuations in exchange rates with forward foreign currency exchange contracts. Therefore, we are exposed to market risk and credit risk through the use of derivative financial instruments. Moreover, any failure of hedging policies could negatively impact our profits, and thus damage our ability to fund our operations and to service our indebtedness.

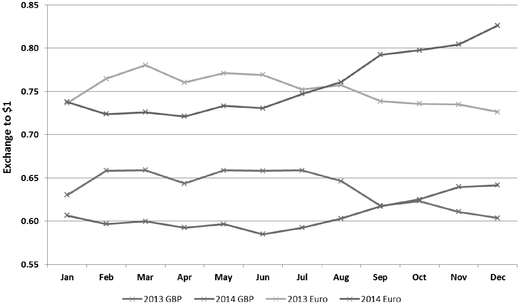

In addition to subsidiaries and joint ventures in the United States, we have subsidiaries located in the United Kingdom, France, Germany, the Czech Republic, Canada and China, as well as joint ventures in Japan and India, whose revenue, costs, assets and liabilities are denominated in local currencies. Because our consolidated accounts are reported in U.S. dollars, we are exposed to fluctuations in those currencies when those amounts are translated to U.S. dollars for purposes of reporting our consolidated accounts, which may cause declines in results of operations. The largest risk is from our operations in the United Kingdom, which in 2014 generated operating profits of $15.8 million from sales revenue of $181.9 million. Fluctuations in exchange rates, particularly between the U.S. dollar and the pound sterling, can have a material effect on our consolidated income statement and balance sheet. In 2014, movements in the average U.S. dollar exchange rate had a positive impact on revenue of $4.3 million, while in 2013, movements in the average U.S. dollar exchange rate had a negative impact on reported revenue of $1.5 million. Changes in translation exchange rates decreased net assets by $10.8 million in 2014 compared to an increase of $3.1 million in 2013. For additional information on these risks and the historical impact on our results see "Item 11. Quantitative & Qualitative Disclosure About Market Risk."

Our defined benefit pension plans have significant funding deficits and are exposed to market forces that could require us to make increased ongoing cash contributions in response to changes in market conditions, actuarial assumptions and investment decisions and that could expose us to significant short-term liabilities if a wind-up trigger occurred in relation to such plans, each of which could have a material adverse effect on our financial condition and results of operations.

We have defined benefit pension arrangements in the United Kingdom, the United States and France. See "Note 29" of the audited consolidated financial statements appearing elsewhere in this Annual Report. Our largest defined benefit plan, the Luxfer Group Pension Plan, which closed to new members in 1998 but remains open for accrual of future benefits based on career-average salary, is funded according to the regulations in effect in the United Kingdom and, as of December 31, 2014, and December 31, 2013, had an IAS 19 accounting deficit of $76.9 million and $61.4 million, respectively. Luxfer Group Limited is the principal employer under the Luxfer Group Pension Plan, and other U.K. subsidiaries also participate under the plan. Our other defined benefit plans are less significant than the Luxfer Group Pension Plan and, as of December 31, 2014, and December 31, 2013, had an IAS 19 accounting deficit of $14.0 million and

12

$6.2 million, respectively. The largest of these additional plans is the BA Holdings, Inc. Pension Plan in the United States, which was closed to further benefit accruals in December 2005. According to the actuarial valuation of the Luxfer Group Pension Plan as at April 5, 2012, the Luxfer Group Pension Plan had a deficit of £50.1 million on the plan-specific basis. Should a wind-up trigger occur in relation to the Luxfer Group Pension Plan, the buy-out deficit of that plan will become due and payable by the employers. The aggregate deficit of the Luxfer Group Pension Plan on a buy-out basis was estimated at £140 million as at April 5, 2012. The trustees have the power to wind-up the Luxfer Group Pension Plan if they consider that in the best interests of members, there is no reasonable purpose in continuing the Luxfer Group Pension Plan.

We are exposed to various risks related to our defined benefit plans, including the risk of loss of market value of the plan assets, the risk of actual investment returns being less than assumed rates of return, the trustees of the Luxfer Group Pension Plan switching investment strategy (which does require consultation with the employer) and the risk of actual experience deviating from actuarial assumptions for such things as mortality of plan participants. In addition, fluctuations in interest rates cause changes in the annual cost and benefit obligations. As a result of the actuarial valuation as at April 5, 2012, we are required to make increased ongoing cash contributions, over and above normal contributions required to meet the cost of future accrual, to the Luxfer Group Pension Plan. These additional payments are intended to reduce the funding deficit. We have agreed with the trustees to a schedule of payments to reduce the deficit. This schedule has been provided to and confirmed by the U.K. Pensions Regulator (the "Pensions Regulator"). The schedule of payments provides for minimum annual contributions of £3.4 million per year, together with additional variable contributions based on one-fifth of net earnings of Luxfer Holdings PLC, in the previous calendar year, in excess of £12 million. The total contributions are subject to an annual cap of £5 million. These contribution rates are to apply until the deficit is eliminated (expected to take between 10 and 12 years from 2012, depending on variable contributions), but in practice the schedule will be reviewed, and may be revised, following the next triennial actuarial valuation. There is a limited ability to delay payments in the event of another severe economic downturn. Regulatory burdens have also proven to be a significant risk, such as the United Kingdom's Pension Protection Fund ("PPF") Levy, which was $0.8 million in 2014. Although they do not carry the same risks to the Company, we have offered new employees membership in defined contribution pension arrangements or 401(k) arrangements following closure of the defined benefit plans described above.

The Pensions Regulator in the United Kingdom has power in certain circumstances to issue contribution notices or financial support directions that, if issued, could result in significant liabilities arising for us.

The Pensions Regulator may issue a contribution notice to the employers that participate in the Luxfer Group Pension Plan or any person who is connected with or is an associate of these employers where the Pensions Regulator is of the opinion that the relevant person has been a party to an act, or a deliberate failure to act, which had as its main purpose (or one of its main purposes) the avoidance of pension liabilities or where such act has a materially detrimental effect on the likelihood of payment of accrued benefits under the Luxfer Group Pension Plan being received. A person holding alone or together with his or her associates directly or indirectly one-third or more of our voting power could be the subject of a contribution notice. The terms "associate" and "connected person," which are taken from the Insolvency Act 1986, are widely defined and could cover our significant shareholders and others deemed to be shadow directors. If the Pensions Regulator considers that a plan employer is "insufficiently resourced" or a "service company" (which terms have statutory definitions), it may impose a financial support direction requiring such plan's employer or any member of the Group, or any person associated or connected with an employer, to put in place financial support in relation to the Luxfer Group Pension Plan. Liabilities imposed under a contribution notice or financial support direction may be up to the difference between the value of the assets of the Luxfer Group Pension Plan and the cost of buying out the benefits of members and other beneficiaries of the Luxfer Group Pension Plan. In practice, the risk of a contribution notice being imposed

13

may restrict our ability to restructure or undertake certain corporate activities. Additional security may also need to be provided to the trustees of the Luxfer Group Pension Plan before certain corporate activities can be undertaken (such as the payment of an unusual dividend), and any additional funding of the Luxfer Group Pension Plan may have an adverse effect on our financial condition and the results of our operations.

Our ability to remain profitable depends on our ability to protect and enforce our intellectual property, and any failure to protect and enforce such intellectual property could have a material adverse impact on our business, financial condition and results of operations.

We cannot ensure that we will always have the ability to protect proprietary information and our intellectual property rights. We protect our intellectual property rights (within the United States, Europe and other countries) through various means, including patents and trade secrets. Because of the difference in foreign trademark, patent and other laws concerning proprietary rights, our intellectual property rights may not receive the same degree of protection in other countries as they would in the United States or the United Kingdom. The patents we own could be challenged, invalidated or circumvented by others and may not be of sufficient scope or strength to provide us with any meaningful protection or commercial advantage. Further, we cannot assure you that competitors will not infringe our patents or that we will have adequate resources to enforce our patents. Our failure to obtain or maintain adequate protection of our intellectual property rights for any reason could have a material adverse effect on our business, results of operations and financial condition. Our patents will only be protected for the duration of the patent. Some of our older key patents have expired and will expire over the next few years. As a result, our competitors may introduce products using the technology previously protected, these products may have lower prices than our products, which may negatively affect our market share. To compete, we may need to reduce our prices for those products. Additionally, the expiry of certain of those patents has reduced and will reduce barriers to entry into products and end-markets. The expiry of our patents therefore could have a significant adverse effect on our business, results of operations and financial condition. For example our European patents covering the use of certain proprietary high strength alloys in the manufacture of high pressure gas cylinders (L7X) expired in Europe in 2014, the expiry of which may lead to competitive products appearing in the European market and consequential price pressures. The US patent expires in 2016.

With respect to our unpatented proprietary technology, it is possible that others will independently develop the same or similar technology or obtain access to our unpatented technology. To protect our trade secrets and other proprietary information, we require employees, consultants, advisors and collaborators to enter into confidentiality agreements. Nevertheless, we cannot assure you that these agreements will provide meaningful protection for our trade secrets, know-how or other proprietary information in the event of any unauthorized use, misappropriation or disclosure of such trade secrets, know-how or other proprietary information. If we are unable to maintain the proprietary nature of our technologies, we could be materially adversely affected. Moreover, we rely on our trademarks, trade names and brand names to distinguish our products from the products of our competitors, and we have registered or applied to register many of these trademarks. Third parties may also oppose our trademark applications, or otherwise challenge our use of the trademarks. In the event that our trademarks are successfully challenged, we could be forced to rebrand our products, which could result in loss of brand recognition and could require us to devote resources to advertising and marketing new brands. Further, we cannot assure you that competitors will not infringe our trademarks or that we will have adequate resources to enforce our trademarks.

Expiration or termination of our right to use certain intellectual property granted by third parties, the right of those third parties to grant the right to use the same intellectual property to our competitors and the right of certain third parties to use certain intellectual property used as part of our business could have a material adverse impact on our business, financial condition and results of operations.

We have negotiated, and may from time to time in the future negotiate, licenses with third parties with respect to third-party proprietary technologies used in certain of our manufacturing processes and products.

14

If any of these licenses expires or terminates, we will no longer retain the rights to use the relevant third-party proprietary technologies in our manufacturing processes and products, which could have a material adverse effect on our business, results of operations and financial condition. Further, the rights granted to us might be non-exclusive, which could result in our competitors gaining access to the same intellectual property.

Some of our patents may cover inventions that were conceived or first reduced to practice under, or in connection with, government contracts or other government funding agreements or grants. With respect to inventions conceived or first reduced to practice under such government funding agreements, a government may retain a non-exclusive, irrevocable, royalty-free license to practice or have practiced for or on behalf of the relevant country the invention throughout the world. In addition, if we fail to comply with our reporting obligations or to adequately exploit the developed intellectual property under these government funding agreements, the relevant country may obtain additional rights to the developed intellectual property, including the right to take title to any patents related to government-funded inventions or to license the same to our competitors. Furthermore, our ability to exclusively license or assign the intellectual property developed under these government funding agreements to third parties may be limited or subject to the relevant government's approval or oversight. These limitations could have a significant impact on the commercial value of the developed intellectual property.

We often enter into research and development agreements with academic institutions whereby they generally retain certain rights to the developed intellectual property. The academic institutions generally retain rights over the technology for use in non-commercial academic and research fields, including in some cases the right to license the technology to third parties for use in those fields. It is difficult to monitor and enforce such non-commercial academic and research uses, and we cannot predict whether the third-party licensees would comply with the use restrictions of these licenses. We could incur substantial expenses to enforce our rights against such licensees. In addition, even though the rights that academic institutions obtain are generally limited to the noncommercial academic and research fields, they may obtain rights to commercially exploit developed intellectual property in certain instances. Under research and development agreements with academic institutions, our rights to intellectual property developed thereunder is not always certain, but instead may be in the form of an option to obtain license rights to such intellectual property. If we fail to exercise our option rights in a timely way and/or we are unable to negotiate a license agreement, the academic institution may offer a license to the developed intellectual property to third parties for commercial purposes. Any such commercial exploitation could adversely affect our competitive position and have a material adverse effect on our business.

If third parties claim that intellectual property used by us infringes upon their intellectual property, our operating profits could be adversely affected.

We may, from time to time, be notified of claims that we are infringing upon patents, copyrights, or other intellectual property rights owned by third parties, and we cannot provide assurances that other companies will not in the future pursue such infringement claims against us or any third-party proprietary technologies we have licensed. If we were found to infringe upon a patent or other intellectual property right, or if we failed to obtain or renew a license under a patent or other intellectual property right from a third party, or if a third party from whom we are licensing technologies was found to infringe upon a patent or other intellectual property rights of another third party, we may be required to pay damages, suspend the manufacture of certain products or re-engineer or rebrand our products, if feasible, or we may be unable to enter certain new product markets. Any such claims could also be expensive and time-consuming to defend and could divert management's attention and resources. Our competitive position could suffer as a result. In addition, if we have omitted to enter into a valid non-disclosure or assignment agreement for any reason, we may not own the invention or our intellectual property and may not be adequately protected.

15

Any failure of our research and development activity to improve our existing products and develop new products could cause us to lose market share and impact our financial position.

Our products are highly technical in nature, and in order to maintain and improve our market position, we depend on successful research and development activity to continue to improve our existing products and develop new products. We cannot be certain that we will have sufficient research and development capability to respond to changes in the industries in which we operate. These changes could include changes in the technological environment in which we currently operate, increased demand for new products or the development of alternatives to our products. For example, the development of lighter-weight steel alloys has made the use of steel in gas cylinders a more competitive alternative to aluminum than it had been previously. In addition, our superformed aluminum components compete with new high-performance composite materials developed for use in the aerospace industry. In our efforts to develop and market new products and enhancements to our existing products, we may fail to identify new product opportunities successfully or develop and timely bring new products to market. We may also experience delays in completing development of, enhancements to or new versions of our products, and product innovations may not achieve the market penetration or price stability necessary for profitability. In addition to benefiting from our research collaboration with universities, we spent $10.6 million, $9.8 million and $8.9 million (including revenue and capital items but before funding grants received) in 2014, 2013 and 2012, respectively, on our own research and development activities. We expect to fund our future capital expenditure requirements through operating profit cash flows and restricted levels of indebtedness, but if operating profit decreases, we may not be able to invest in research and development or continue to develop new products or enhancements.

Without the timely introduction of new products or enhancements to existing products, our products could become obsolete over time, in which case our business, results of operations and financial condition could be adversely affected.

Some of our key operational equipment is relatively old and may require significant capital expenditures for repair or replacement.

We already incur considerable expense on maintenance, including preventative maintenance and repairs. Higher levels of maintenance and repair costs could result from the need to maintain our older plants, property and equipment, and machinery breakdowns could result in interruptions to the business, causing lost production time and reduced output. Machinery breakdowns or equipment failures may hamper or cause delays in the production and delivery of products to our customers and increase our operating costs, thus reducing cash flow from operations. In particular, the breakdown of some of our older equipment, such as the large hot-rolling mill at our Madison, Illinois, plant, could be difficult to repair and would be very costly should it need to be replaced. Any failure to deliver products to our customers in a timely manner could adversely affect our customer relationships and reputation. Any failure to implement required investments, whether because of requirements to divert funds to repair existing physical infrastructure, debt-service obligations, unanticipated liquidity constraints or other factors, could have a material adverse effect on our business and on our ability to service our indebtedness.

Our operations may prove harmful to the environment, and any cleanup or other related costs could have a material adverse effect on our operating results or financial condition.

We are exposed to substantial environmental costs and liabilities, including liabilities associated with divested assets and prior activities performed on sites before we acquired an interest in them. Our operations, including the production and delivery of our products, are subject to a broad range of continually changing environmental laws and regulations in each of the jurisdictions in which we operate. These laws and regulations increasingly impose more stringent environmental protection standards on us with respect to, among other things, air emissions, wastewater discharges, the use and handling of hazardous materials, noise levels, waste-disposal practices, soil and groundwater contamination and

16

environmental cleanup. Complying with these regulations involves significant and recurring costs. See "Item 4.B. Business Overview" for details of our environmental management program and the environmental issues that we are currently addressing.

We cannot predict our future environmental liabilities and cannot assure investors that our management is aware of every fact or circumstance regarding potential liabilities or that the amounts provided and budgeted to address such liabilities will be adequate for all purposes. In addition, future developments, such as changes in regulations, laws or environmental conditions, may increase environmental costs and liabilities and could have a material adverse effect on our operating results and consolidated financial position in any given financial year, which could negatively affect our cash flows and hinder our ability to service our indebtedness.

The health and safety of our employees and the safe operation of our businesses is subject to various health and safety regulations in each of the jurisdictions in which we operate. These regulations impose various obligations on us, including the provision of safe working environments and employee training on health and safety matters. Complying with these regulations involves recurring costs.

Certain of our operations are highly regulated by different agencies that require products to comply with their rules and procedures and can subject our operations to penalties or adversely affect production.

Certain of our operations are in highly regulated industries that require us to maintain regulatory approvals and, from time to time, obtain new regulatory approvals from various countries. This can involve substantial time and expense. In turn, higher costs of compliance reduce our cash flow from operations. For example, manufacturers of gas cylinders throughout the world must comply with high local safety and health standards and obtain regulatory approvals in the markets in which they sell their products. Furthermore, military organizations require us to comply with applicable government regulations and specifications when providing products or services to them directly or as subcontractors. In addition, we are required to comply with U.S. and other export regulations with respect to certain products and materials. The European Union has also passed legislation governing the registration, evaluation and authorization of chemicals, known as REACH, pursuant to which we are required to register chemicals and gain authorization for the use of certain substances. Although we make reasonable efforts to obtain all licenses and certifications that are required by countries in which we operate, there is always a risk that we may be found not to comply with certain required procedures. This risk grows with increased complexity and variance in regulations across the globe. Because regulatory schemes vary by country, we may also be subject to regulations of which we are not presently aware and could be subject to sanctions by a foreign government that could materially and adversely affect our operations in the relevant country.

Governments and their agencies have considerable discretion to determine whether regulations have been satisfied. They may also revoke or limit existing licenses and certifications or change the laws and regulations to which we are subject at any time. If our operations fail to obtain, experience delays in obtaining or lose a needed certification or approval, we may not be able to sell our products to our customers, expand into new geographic markets or expand into new product lines, which will ultimately have a material adverse effect on our business, financial position and results of operations. In addition, new or more stringent regulations, if imposed, could have an adverse effect on our results of operations because we may experience difficulty or incur significant costs in connection with compliance. Non-compliance with these regulations could result in administrative, civil, financial, criminal or other sanctions against us, which could have negative consequences on our business and financial position. Furthermore, if we begin to operate in new countries, we may need to obtain new licenses, certifications and approvals.

Our customers are also often subject to similar regulations and risks. We therefore face the risk that our customers may have the demand for their products reduced as a result of regulatory matters that fall

17

outside our direct control. This would in turn reduce demand for our products and have a negative financial impact on our operating results.

Legislation and regulations to reduce carbon dioxide and other greenhouse gas emissions may have a material adverse impact on our results of operations, financial condition and cash flows.