Table of Contents

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(A) OF THE SECURITIES EXCHANGE ACT OF 1934

Filed by the registrant /x/

Filed by a party other than the registrant /_/

Check the appropriate box:

/_/ Preliminary proxy statement

/_/ Confidential, for Use of the Commission Only (as permitted by Rule

14a-6(e)(2))

/x/ Definitive proxy statement

/_/ Definitive additional materials

/_/ Soliciting material pursuant to Rule 14a-12

Connecticut Bancshares, Inc.

- --------------------------------------------------------------------------------

(Name of Registrant as Specified in Its Charter)

- --------------------------------------------------------------------------------

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of filing fee (Check the appropriate box):

/_/ No fee required.

/x/ Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies: Common

stock, par value $0.01 per share

- --------------------------------------------------------------------------------

(2) Aggregate number of securities to which transactions applies:

12,466,111

- --------------------------------------------------------------------------------

(3) Per unit price or other underlying value of transaction computed pursuant

to Exchange Act Rule 0-11:

$52.00

- --------------------------------------------------------------------------------

(4) Proposed maximum aggregate value of transaction:

$648,237,772

- --------------------------------------------------------------------------------

(5) Total Fee paid:

$129,440

- --------------------------------------------------------------------------------

/x/ Fee paid previously with preliminary materials.

/_/ Check box if any part of the fee is offset as provided by Exchange Act Rule

0-11 (a)(2) and identify the filing for which the offsetting fee was paid

previously. Identify the previous filing by registration statement number,

or the form or schedule and the date of its filing.

(1) Amount previously paid:

N/A

- --------------------------------------------------------------------------------

(2) Form, schedule or registration statement no.:

N/A

- --------------------------------------------------------------------------------

(3) Filing party:

N/A

- --------------------------------------------------------------------------------

(4) Date filed:

N/A

- --------------------------------------------------------------------------------

Table of Contents

[CONNECTICUT BANCSHARES LOGO]

February 19, 2004

Dear Stockholder:

You are cordially invited to attend a special meeting of the stockholders

of Connecticut Bancshares, Inc., the holding company for The Savings Bank of

Manchester. The meeting will be held at The Colonnade Banquet and Conference

Center, 2941 Main Street, Glastonbury, Connecticut, on Tuesday, March 30, 2004,

at 11:00 a.m., local time.

At the special meeting, you will be asked to approve a merger agreement by

and among The New Haven Savings Bank, Connecticut Bancshares and The Savings

Bank of Manchester. Upon completion of the merger, you will be entitled to

receive a cash payment of $52.00 for each share of Connecticut Bancshares stock

that you own.

The completion of the merger is subject to certain conditions, including

the completion of New Haven's conversion from mutual-to-stock form, the receipt

of regulatory approvals and the approval of the merger agreement by the

affirmative vote of a majority of the outstanding shares of Connecticut

Bancshares common stock. We urge you to read the attached proxy statement

carefully. It describes the merger agreement in detail and includes a copy of

the merger agreement as Appendix A.

YOUR BOARD OF DIRECTORS HAS APPROVED THE MERGER AGREEMENT AND RECOMMENDS

THAT YOU VOTE "FOR" APPROVAL OF THE MERGER AGREEMENT BECAUSE THE BOARD BELIEVES

IT TO BE IN THE BEST INTERESTS OF THE CONNECTICUT BANCSHARES STOCKHOLDERS.

YOUR VOTE IS VERY IMPORTANT

Whether or not you plan to attend the special meeting, please complete,

date and sign the enclosed proxy card and return it promptly in the postage-paid

envelope provided or vote over the Internet or by telephone. If you attend the

meeting, you may vote in person even if you have previously mailed a proxy card

or voted over the Internet or by telephone.

On behalf of the board of directors, I thank you for your prompt attention

to this important matter.

Sincerely,

/s/ Richard P. Meduski

Richard P. Meduski

PRESIDENT AND CHIEF EXECUTIVE OFFICER

THIS PROXY STATEMENT DATED FEBRUARY 11, 2004 IS FIRST BEING MAILED TO

CONNECTICUT BANCSHARES' STOCKHOLDERS ON OR ABOUT FEBRUARY 19, 2004.

Table of Contents

CONNECTICUT BANCSHARES, INC.

923 MAIN STREET

MANCHESTER, CONNECTICUT 06040

(860) 646-1700

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON MARCH 30, 2004

A special meeting of stockholders of Connecticut Bancshares, Inc. will be

held at The Colonnade Banquet and Conference Center, 2941 Main Street,

Glastonbury, Connecticut, on Tuesday, March 30, 2004, at 11:00 a.m., local time,

for the following purposes:

1. To consider and vote upon a proposal to approve and adopt the

Agreement and Plan of Merger, dated July 15, 2003, by and among The

New Haven Savings Bank, Connecticut Bancshares, Inc. and The Savings

Bank of Manchester. Upon completion of the merger, you will be

entitled to receive $52.00 in cash for each share of Connecticut

Bancshares common stock that you own. A copy of the merger agreement

is included as Appendix A to the accompanying proxy statement.

2. To transact any other business that may properly come before the

meeting, including adjourning the special meeting to permit, if

necessary, further solicitation of proxies or any adjournment of the

meeting.

The board of directors is not aware of any such other business.

Only stockholders of record at the close of business on February 9, 2004

are entitled to vote at the meeting or any adjournments or postponements of the

meeting.

Remember, if your shares are held in the name of a broker, only your broker

can vote your shares on the merger agreement and only after receiving your

instructions. Please contact the person responsible for your account and

instruct him/her to execute a proxy card on your behalf. You should also sign,

date and mail your instruction card, or, if permitted by your broker, vote on

the Internet or by telephone, at your earliest convenience.

By Order of the Board of Directors

/s/ Carole L. Yungk

Manchester, Connecticut Carole L. Yungk

February 19, 2004 CORPORATE SECRETARY

THE BOARD OF DIRECTORS OF CONNECTICUT BANCSHARES UNANIMOUSLY RECOMMENDS THAT YOU

VOTE "FOR" THE APPROVAL OF THE MERGER AGREEMENT. WHETHER OR NOT YOU PLAN TO

ATTEND THE MEETING, PLEASE COMPLETE, SIGN, DATE AND RETURN THE ENCLOSED PROXY IN

THE ACCOMPANYING PRE-ADDRESSED POSTAGE-PAID ENVELOPE.

Table of Contents

TABLE OF CONTENTS

PAGE

QUESTIONS AND ANSWERS ABOUT THE MERGER.........................................1

SUMMARY TERM SHEET.............................................................3

THE SPECIAL MEETING

Place, Date and Time.......................................................12

Purpose of the Meeting.....................................................12

Who Can Vote at the Meeting; Record Date...................................12

Quorum and Vote Required...................................................12

Shares Held by Directors and Officers of Connecticut Bancshares; Voting

Agreements................................................................13

Voting by Proxy............................................................13

Revocability of Proxies....................................................14

Participants in The Savings Bank of Manchester's ESOP and Savings Plan.....14

THE MERGER

The Parties to the Merger..................................................14

Form of the Merger.........................................................15

Treatment of Connecticut Bancshares Stock Options..........................16

Treatment of Connecticut Bancshares Stock Awards...........................16

Procedures for Surrendering Your Certificates..............................16

Material Federal Income Tax Consequences of the Merger.....................17

Background of the Merger...................................................18

Connecticut Bancshares' Reasons for the Merger.............................21

Opinion of Connecticut Bancshares' Financial Advisor.......................22

Interests of Directors and Officers in the Merger that Are Different

From Your Interests.......................................................29

Approvals Needed to Complete the Merger....................................33

New Haven's Conversion.....................................................34

Financing the Merger.......................................................35

Accounting Treatment of the Merger.........................................35

Dissenters' Appraisal Rights...............................................35

THE MERGER AGREEMENT

When Will the Merger Be Completed..........................................38

Conditions to Completing the Merger........................................39

Other Provisions of the Merger Agreement...................................40

INFORMATION ABOUT NEWALLIANCE BANCSHARES AND NEW HAVEN........................45

STOCK OWNERSHIP...............................................................46

STOCKHOLDER PROPOSALS AND NOMINATIONS.........................................48

SOLICITATION OF PROXIES.......................................................49

WHERE YOU CAN FIND MORE INFORMATION...........................................49

APPENDIX A Agreement and Plan of Merger, dated July 15, 2003 by and among The

New Haven Savings Bank, Connecticut Bancshares, Inc. and The Savings

Bank of Manchester (exhibits omitted)

APPENDIX B Opinion of Sandler O'Neill & Partners, L.P.

APPENDIX C Section 262 of the Delaware General Corporation Law

APPENDIX D Prospectus of NewAlliance Bancshares, Inc., dated February 9, 2004

i

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE MERGER

WHAT AM I BEING ASKED TO VOTE ON AND HOW DOES MY BOARD RECOMMEND THAT I VOTE?

You are being asked to vote FOR the adoption of the Agreement and Plan of

Merger dated as of July 15, 2003, providing for the merger of Connecticut

Bancshares with and into NewAlliance Bancshares, Inc., the newly formed stock

holding company for The New Haven Savings Bank once New Haven completes its

conversion from mutual-to-stock form. The Connecticut Bancshares board of

directors has determined that the proposed merger is in the best interests of

Connecticut Bancshares stockholders, has approved the merger agreement and

recommends that Connecticut Bancshares stockholders vote FOR the adoption of the

merger agreement.

WHAT VOTE IS REQUIRED TO ADOPT THE MERGER AGREEMENT?

The adoption of the merger agreement requires the affirmative vote of at

least a majority of the outstanding shares of Connecticut Bancshares common

stock entitled to vote.

WHAT WILL I RECEIVE IN THE MERGER?

Under the merger agreement, each share of Connecticut Bancshares common

stock you own will be converted into the right to receive $52.00 in cash.

However, if the closing of the merger does not take place on or before March 31,

2004, the per share merger consideration will be increased by the amount that

Connecticut Bancshares' net income exceeds dividends paid for each full month

after that date.

HOW DO I EXCHANGE MY CONNECTICUT BANCSHARES STOCK CERTIFICATES?

You will receive instructions on where and how to surrender your

Connecticut Bancshares stock certificates from the exchange agent, American

Stock Transfer & Trust Company, after the merger is completed. IN ANY EVENT, YOU

SHOULD NOT FORWARD YOUR CONNECTICUT BANCSHARES STOCK CERTIFICATES WITH YOUR

PROXY CARD.

WHAT SHOULD I DO NOW?

After you have carefully read this document, please do one of the

following: (1) indicate on your proxy card how you want to vote and sign, date

and mail the proxy card in the enclosed postage prepaid envelope; (2) vote over

the Internet; or (3) vote by telephone, so that your shares will be represented

at the special meeting. If you do not return a properly executed and dated proxy

card, do not vote over the Internet, do not vote by telephone or do not vote at

the special meeting in person, this will have the same effect as a vote against

the adoption of the merger agreement.

1

Table of Contents

IF MY SHARES ARE HELD IN "STREET NAME" BY MY BROKER, BANK OR NOMINEE, WILL MY

BROKER, BANK OR NOMINEE AUTOMATICALLY VOTE MY SHARES FOR ME?

No. Your broker, bank or nominee will not be able to vote your shares of

Connecticut Bancshares common stock unless you provide instructions on how to

vote. You should instruct your broker, bank or nominee how to vote your shares

by following the procedures your broker, bank or nominee provides. If you do not

provide instructions to your broker, bank or nominee, your shares will not be

voted, and this will have the effect of voting against adoption of the merger

agreement. Please check the voting form used by your broker, bank or nominee to

see if it offers telephone or Internet voting.

WHO CAN HELP ANSWER MY QUESTIONS?

If you want additional copies of this document, or if you want to ask any

questions about the merger or how to submit your proxy, you should contact:

Carole L. Yungk

Corporate Secretary

Connecticut Bancshares, Inc.

923 Main Street

Manchester, Connecticut 06040

Telephone: (860) 646-1700

2

Table of Contents

SUMMARY TERM SHEET

THIS SUMMARY TERM SHEET HIGHLIGHTS SELECTED INFORMATION REGARDING THE

MERGER FROM THIS PROXY STATEMENT AND DOES NOT CONTAIN ALL THE INFORMATION THAT

IS IMPORTANT TO YOU. FOR A MORE COMPLETE DESCRIPTION OF THE TERMS OF THE

PROPOSED MERGER, WE URGE YOU TO READ CAREFULLY THE ENTIRE DOCUMENT AND THE OTHER

DOCUMENTS TO WHICH WE REFER, INCLUDING THE MERGER AGREEMENT, ATTACHED AS

APPENDIX A.

THE COMPANIES

CONNECTICUT BANCSHARES, INC.

THE SAVINGS BANK OF MANCHESTER

923 MAIN STREET

MANCHESTER, CONNECTICUT 06040

(860) 646-1700

We are a Delaware corporation and the parent company of The Savings Bank of

Manchester, a Connecticut-chartered stock savings bank. The Savings Bank of

Manchester operates 28 full-service banking offices in Hartford, Tolland and

Windham Counties, Connecticut. At December 31, 2003, we had total assets of $2.6

billion, deposits of $1.6 billion and stockholders' equity of $263.8 million.

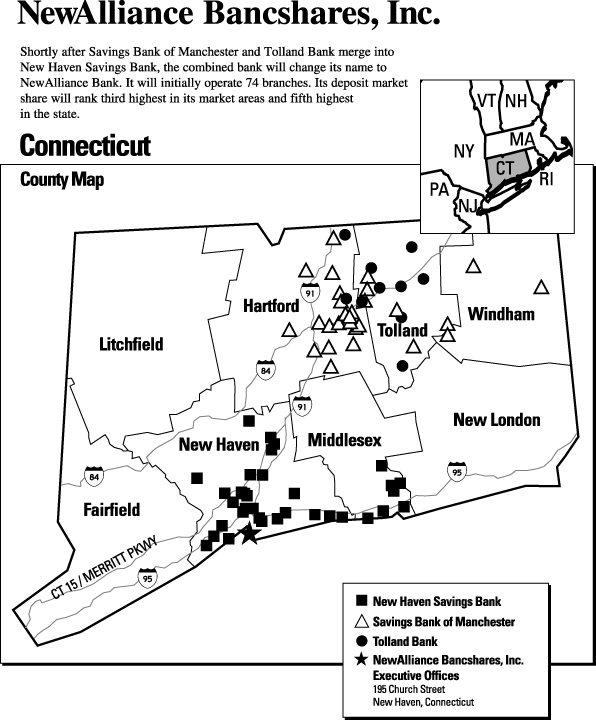

NEWALLIANCE BANCSHARES, INC.

THE NEW HAVEN SAVINGS BANK

195 CHURCH STREET

NEW HAVEN, CONNECTICUT 06510

(203) 787-1111

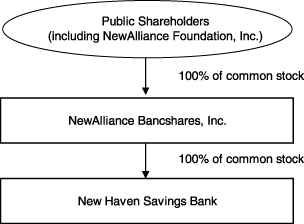

Upon completion of the conversion of The New Haven Savings Bank from

mutual-to-stock form, NewAlliance Bancshares will be the parent company of New

Haven, a Connecticut-chartered stock savings bank. NewAlliance Bancshares is a

Delaware corporation. New Haven operates 36 banking offices located in New Haven

and Middlesex Counties, Connecticut. NewAlliance Bancshares will have no

material assets or liabilities until the completion of the conversion. At

December 31, 2003, New Haven had total assets of $2.5 billion, deposits of $1.8

billion and total equity of $406.0 million.

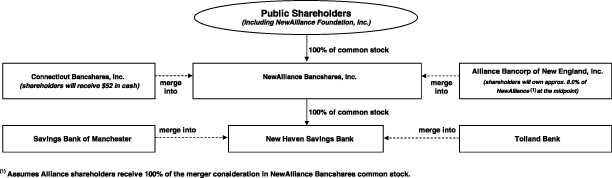

In a separate and unrelated transaction, New Haven is also acquiring Alliance

Bancorp of New England, Inc., a savings and loan holding company organized under

the laws of the State of Delaware in 1997. It operates Tolland Bank, a

Connecticut-charted savings bank that operates nine banking offices in and

around Tolland County. At December 31, 2003, Alliance had total assets of $438.4

million, deposits of $339.0 million and stockholders' equity of $32.8 million.

THE ALLIANCE MERGER DOES NOT REQUIRE THE APPROVAL OF THE STOCKHOLDERS OF

CONNECTICUT BANCSHARES AND THE CONNECTICUT BANCSHARES MERGER DOES NOT DEPEND ON

THE COMPLETION OF THE ALLIANCE MERGER.

THE SPECIAL MEETING

PLACE, DATE AND TIME (PAGE 12)

A special meeting of our stockholders will be held at The Colonnade Banquet and

Conference Center, 2941 Main Street, Glastonbury, Connecticut, on Tuesday, March

30, 2004, at 11:00 a.m., local time.

PURPOSE OF THE MEETING (PAGE 12)

At the special meeting, our stockholders will be asked to approve the merger

agreement with New Haven and to

3

Table of Contents

transact any other business that may properly come before meeting.

WHO CAN VOTE AT THE MEETING (PAGE 12)

You can vote at the special meeting of Connecticut Bancshares stockholders only

if you owned our common stock at the close of business on February 9, 2004. You

will be able to cast one vote for each share of our common stock you owned on

that date. As of February 9, 2004, there were 11,143,133 shares of our common

stock outstanding.

WHAT VOTE IS REQUIRED FOR APPROVAL OF THE MERGER AGREEMENT (PAGE 12)

In order to approve the merger agreement, the holders of at least a majority of

the outstanding shares of our common stock entitled to vote must vote in favor

of the merger agreement. You can vote your shares by attending the special

meeting and voting in person, by completing and mailing the enclosed proxy card,

by voting over the Internet or by voting by telephone. As of February 9, 2004,

the directors and executive officers of Connecticut Bancshares beneficially

owned approximately 5.63% of our outstanding common stock (excluding options).

THE MERGER

OVERVIEW OF THE TRANSACTION (PAGE 15)

We propose a business combination in which we will merge with a wholly owned,

interim subsidiary of NewAlliance Bancshares, with Connecticut Bancshares as the

surviving entity. Immediately after completion of that merger, Connecticut

Bancshares will be merged with and liquidated into NewAlliance Bancshares. Each

of these transactions are conditioned on and will be completed immediately

following the completion of New Haven's conversion from mutual-to-stock form.

EACH CONNECTICUT BANCSHARES SHARE WILL BE EXCHANGED FOR $52.00 IN CASH (PAGE 15)

As our stockholder, upon the closing of the merger, each of your shares of our

common stock will automatically be converted into the right to receive $52.00 in

cash. However, if the closing of the merger does not take place on or before

March 31, 2004, the per share merger consideration will be increased by the

amount that Connecticut Bancshares' net income exceeds dividends paid for each

full month after that date.

HOW TO RECEIVE CASH IN EXCHANGE FOR YOUR CONNECTICUT BANCSHARES STOCK

CERTIFICATES (PAGE 16)

In order to receive cash in exchange for your Connecticut Bancshares stock

certificates, you will need to surrender your Connecticut Bancshares stock

certificates. The exchange agent, American Stock Transfer & Trust Company, will

send you written instructions for surrendering your certificates after we have

completed the merger.

CONNECTICUT BANCSHARES STOCK PRICE

Our common stock trades on the Nasdaq National Market under the symbol "SBMC."

On July 15, 2003, which was the last trading day before we announced the merger,

our

4

Table of Contents

common stock closed at $46.45 per share. On February 11, 2004, which is the last

practicable trading day before the printing of this document, our common stock

closed at $51.90 per share.

TAX CONSEQUENCES OF THE MERGER (PAGE 17)

When you exchange your Connecticut Bancshares shares solely for cash, you

generally should recognize capital gain or loss on the exchange.

THIS TAX TREATMENT MAY NOT APPLY TO ALL CONNECTICUT BANCSHARES STOCKHOLDERS.

DETERMINING THE ACTUAL TAX CONSEQUENCES OF THE MERGER TO YOU CAN BE COMPLICATED.

YOU SHOULD CONSULT YOUR OWN TAX ADVISOR FOR A FULL UNDERSTANDING OF THE MERGER'S

TAX CONSEQUENCES THAT ARE PARTICULAR TO YOU.

CONNECTICUT BANCSHARES' BOARD OF DIRECTORS RECOMMENDS THAT STOCKHOLDERS APPROVE

THE MERGER

Our board of directors believes that the merger is fair and in the stockholders'

best interests, and unanimously recommends that you vote "FOR" the proposal to

approve and adopt the merger agreement.

For a discussion of the circumstances surrounding the merger and the factors

considered by our board of directors in approving the merger agreement, see page

18.

CONNECTICUT BANCSHARES' FINANCIAL ADVISOR BELIEVES THE MERGER CONSIDERATION IS

FAIR TO STOCKHOLDERS (PAGE 22)

Sandler O'Neill & Partners, L.P. has delivered to our board of directors its

opinion that, as of the date of this document, the merger consideration is fair

to the holders of Connecticut Bancshares common stock from a financial point of

view. A copy of this opinion is provided as Appendix B to this document. You

should read it completely to understand the procedures followed, assumptions

made, matters considered, and qualifications and limitations on the review made

by Sandler O'Neill in providing this opinion. We have agreed to pay Sandler

O'Neill approximately $6.1 million, of which $300,000 has been paid as of

February 9, 2004, plus expenses for its services in connection with the merger.

INTERESTS OF CONNECTICUT BANCSHARES' DIRECTORS AND OFFICERS IN THE MERGER THAT

DIFFER FROM YOUR INTERESTS (PAGE 29)

Some of our directors and officers have interests in the merger that are

different from, or are in addition to, their interests as stockholders in

Connecticut Bancshares. The members of our board of directors knew about these

additional interests, and considered them, when they approved the merger. These

include:

.. Termination and Release Agreements with four executive officers (Messrs.

Meduski, Anderson, Pike and Somerville), under which they will receive cash

payments, continued health and welfare benefit coverage, and, as applicable,

vested supplemental retirement benefits in consideration for the termination

of their

5

Table of Contents

employment and supplemental executive retirement agreements with Connecticut

Bancshares and/or The Savings Bank of Manchester and their agreement to take

or refrain from taking certain actions with respect to their restricted stock

awards, stock options, and bonus compensation;

.. Termination and Release Agreements with 12 additional officers (Messrs.

Hartl, Martin, Orenstein, Thomas, Gaucher, Hamby, Lynch, Smith and Ms.

Trainer, McLaughlin, Yungk and Elliott), under which they will receive cash

payments and continued health and welfare benefit coverage in consideration

for the termination of their change in control agreements and their agreement

to refrain from taking certain actions with respect to their outstanding

stock options, restricted stock awards and bonus compensation;

.. Noncompetition Agreements with four executive officers (Messrs. Meduski,

Anderson, Pike and Somerville), under which they will receive cash payments

in exchange for their agreement to refrain, for the period of time set forth

in their agreement, from engaging in competitive business activities within a

certain geographic area and to maintain the confidentiality of information

learned during the course of their employment. Messrs. Meduski, Anderson,

Pike and Somerville will be subject to Noncompetition Agreements for 42

months, 27 months, 12 months and six months, respectively;

.. the vesting of unvested Connecticut Bancshares stock options and restricted

stock awards as a result of completion of the merger;

.. the termination of the Connecticut Bancshares employee stock ownership plan

and allocation of any surplus cash to plan participants following the

repayment of the loan;

.. provisions in the merger agreement relating to the indemnification of

directors and officers and insurance for our directors and officers for

events occurring before the merger; and

.. the offer to two non-employee directors of each of Connecticut Bancshares and

The Savings Bank of Manchester to become directors of NewAlliance Bancshares

and New Haven.

6

Table of Contents

REGULATORY APPROVAL NEEDED TO COMPLETE THE MERGER (PAGE 33)

We cannot complete the merger unless it is first approved by the Federal Deposit

Insurance Corporation and the State of Connecticut Department of Banking and,

unless approval is waived, by the Federal Reserve Board. New Haven has filed the

required applications with these regulatory agencies. As of the date of this

document, all regulatory approvals with respect to the merger and the bank

merger are still pending. While we do not know of any reason why such approvals

can not be obtained in a timely manner, we cannot be certain if or when New

Haven will receive them.

NEW HAVEN'S CONVERSION AND REGULATORY APPROVALS NEEDED TO COMPLETE THE

CONVERSION (PAGE 34)

In connection with the merger, New Haven has adopted a plan of conversion

pursuant to which it will convert from a Connecticut-chartered mutual savings

bank to a Connecticut-chartered stock savings bank. Recently, New Haven has

organized a Delaware holding company, NewAlliance Bancshares, to acquire and

hold all of the capital stock of New Haven to be issued in the conversion.

Consummation of the conversion and/or acquisition of New Haven by NewAlliance

Bancshares requires regulatory approval from the Connecticut Department of

Banking and the Federal Reserve Board and the regulatory non-objection of the

Federal Deposit Insurance Corporation. New Haven has filed applications or

notices with these regulators. As of the date of this proxy statement, the

Connecticut Department of Banking has approved New Haven's plan of conversion

and the Federal Deposit Insurance Corporation has issued its intent not to

object to the plan of conversion. The Federal Reserve Board approval is still

pending.

In connection with the conversion, NewAlliance Bancshares also has filed a

Registration Statement on Form S-1 with the Securities and Exchange Commission.

The Securities and Exchange Commission declared the registration statement

effective on February 9, 2004.

YOU HAVE DISSENTERS' APPRAISAL RIGHTS IN THE MERGER (PAGE 35)

Under Delaware law, if you do not vote in favor of the merger you have the right

to seek an appraisal of the fair value of your Connecticut Bancshares common

stock and receive a cash payment of such fair value. CONNECTICUT BANCSHARES'

STOCKHOLDERS ELECTING TO EXERCISE DISSENTERS' APPRAISAL RIGHTS MUST COMPLY WITH

THE PROVISIONS OF SECTION 262 OF THE DELAWARE GENERAL CORPORATION LAW IN ORDER

TO PERFECT THEIR RIGHTS. WE WILL REQUIRE STRICT COMPLIANCE WITH THE STATUTORY

PROCEDURES. A copy of Section 262 of the Delaware General Corporation Law is

attached as Appendix C.

7

Table of Contents

THE MERGER AGREEMENT

A COPY OF THE MERGER AGREEMENT IS PROVIDED AS APPENDIX A TO THIS PROXY

STATEMENT. PLEASE READ THE ENTIRE MERGER AGREEMENT CAREFULLY. IT IS THE LEGAL

DOCUMENT THAT GOVERNS THE MERGER.

CONDITIONS TO COMPLETING THE MERGER (PAGE 39)

The completion of the merger depends on a number of conditions being met. These

conditions include, among other items:

.. approval of the merger agreement by our stockholders;

.. approval of New Haven's plan of conversion by New Haven's corporators (which

approval was received on September 8, 2003) and any other party as may be

required;

.. completion of New Haven's conversion;

.. approval of the merger and the conversion by regulatory authorities;

.. the continued accuracy of certain representations and warranties made on the

date of the merger agreement;

.. the performance of all obligations and covenants;

.. New Haven's receipt of a "comfort letter" from our independent auditors with

respect to certain financial information regarding us; and

.. the absence of any event or circumstance since January 1, 2003 that has had a

material adverse effect on us.

We cannot be certain when or if the conditions to the merger will be satisfied

or waived, or that the merger will be completed.

AGREEMENT NOT TO SOLICIT OTHER PROPOSALS (PAGE 40)

We have agreed not to initiate, solicit, encourage or facilitate any competing

proposal with a third party.

Despite the agreement not to solicit other competing proposals, we may, at any

time before stockholder approval of the merger, generally negotiate or have

discussions with, or provide information to, a third party who makes an

unsolicited proposal, provided that our board of directors:

.. determines in good faith, based on advice of legal counsel, that such

negotiations or discussions would be required in order to comply with our

directors' fiduciary duties to our stockholders; and

8

Table of Contents

.. determines in good faith, after consultation with our financial advisor, that

a potential "acquisition proposal," if accepted, is at least as reasonably

likely to be consummated and would result in a transaction more favorable to

our stockholders from a financial point of view.

After we receive an "acquisition proposal" from a third party, we must notify

New Haven of the third party offer. If we determine the "acquisition proposal"

is superior, New Haven will have five business days to increase the merger

consideration to an amount at least equal to the "superior proposal."

WE MAY AMEND THE TERMS OF THE MERGER AND WAIVE SOME CONDITIONS (PAGE 42)

We may agree to amend the merger agreement, and each party may waive the right

to require the other party to adhere to the terms and conditions of the merger

agreement, where the law allows. However, if our stockholders approve the merger

agreement, we must obtain their further approval of any amendment or waiver that

reduces or changes the consideration to be received by our stockholders in the

merger.

TERMINATING THE MERGER AGREEMENT (PAGE 42)

We and New Haven may agree at any time not to complete the merger, even if our

stockholders have approved the merger agreement. In addition, either we or New

Haven may decide, without the consent of the other, to terminate the merger

agreement if:

.. there has been a material breach of any of the representations and warranties

by the other party and the breach cannot be cured within 30 days of notice of

breach;

.. there has been a material failure to perform any of the covenants or

agreements on the part of the other party and the breach cannot be cured

within 30 days of notice of breach;

.. our stockholders fail to approve the merger agreement;

.. New Haven's corporators or any other party required to vote on the plan, fail

to approve the plan of conversion;

.. a government entity does not approve the merger agreement or a court or other

governmental authority issues an order prohibiting the merger;

9

Table of Contents

.. a government entity does not approve New Haven's conversion or a court or

other governmental authority issues an order prohibiting New Haven's

conversion; or

.. either party cannot satisfy its obligations to the other party by October 15,

2004 or if the closing has not occurred by October 15, 2004.

We may also terminate the merger agreement if:

.. New Haven has not received all regulatory approvals in connection with the

merger, the bank merger and the conversion and NewAlliance Bancshares' SEC

registration statement is not declared effective by August 16, 2004;

.. New Haven cannot satisfy its conditions to us to consummate the merger or the

bank merger by August 16, 2004; or

.. we enter into an "acquisition agreement" with respect to a "superior

proposal" and sufficient notice has been granted to New Haven allowing it to

match the "superior proposal."

New Haven may also terminate the merger agreement if:

.. our board of directors fails to make its recommendation to our stockholders

or fails to give notice of or convene the stockholders meeting; or

.. a third party commences a tender or exchange offer for 25% or more of our

stock and our board of directors recommends to our stockholders to tender

their shares.

CONNECTICUT BANCSHARES TERMINATION FEE (PAGE 43)

We will pay New Haven a termination fee of $30 million if:

.. New Haven terminates because (i) our board of directors fails to recommend

approval of the merger agreement, (ii) our board of directors fails to call

or convene a meeting of the stockholders, or (iii) a tender offer for 25% or

more of our common stock is commenced and our board of directors recommends

to our stockholders that they tender their shares;

.. New Haven terminates because we materially breach a representation, warranty

or covenant and, before termination, a competing "acquisition proposal" has

been publically announced or made known;

10

Table of Contents

.. either we or New Haven terminate because our stockholders fail to approve the

merger agreement and, before the stockholder vote, a competing "acquisition

proposal" has been publically announced or made known; or

.. before our stockholder meeting, we terminate the merger agreement to accept a

"superior proposal" which New Haven fails to at least match within five

business days after we notify New Haven of the "superior proposal."

For each of the termination events above, except for the last termination event,

we must pay $10 million to New Haven by the third business day following

termination and the balance of $20 million if, within 18 months after

termination, we enter into an agreement with respect to, or consummate, an

"acquisition transaction" with another party. For the last termination event, we

must pay the entire $30 million by the third business day following termination.

NEW HAVEN SPECIAL PAYMENT (PAGE 44)

New Haven must pay us $30 million if (i) New Haven's corporators, or any other

party required to vote on the plan of conversion, fail to approve the plan of

conversion, (ii) New Haven fails to obtain all required regulatory approvals for

the merger and the conversion, (iii) New Haven does not complete the merger by

October 15, 2004 or such later date that we and New Haven may agree upon, or

(iv) we terminate the merger agreement because New Haven has intentionally and

willfully breached any of its representations or warranties or failed to perform

or comply with any of its covenants or agreements to an extent to allow for

termination. New Haven will not have to pay us the $30 million if any of the

above "special payment" events is due to a breach by us of our representations

or warranties or our covenants and such breach is the principal cause of the

"special payment" event.

We must repay to New Haven $15 million of the $30 million special payment if

before the earlier of (a) October 15, 2006 or (b) two years after our demand for

the "special payment," we or any of our subsidiaries enter into a merger

transaction in which our stockholders are entitled to receive merger

consideration in excess of $51.60 per share.

11

Table of Contents

THE SPECIAL MEETING

This proxy statement is furnished in connection with the solicitation of

proxies by the board of directors of Connecticut Bancshares to be used at the

special meeting of stockholders. This proxy statement and the enclosed proxy

card are being first mailed on or about February 19, 2004 to stockholders of

record as of the close of business on February 9, 2004.

PLACE, DATE AND TIME

The special meeting will be held at The Colonnade Banquet and Conference

Center, 2941 Main Street, Glastonbury, Connecticut, on Tuesday, March 30, 2004,

at 11:00 a.m., local time.

PURPOSE OF THE MEETING

The purpose of the meeting is to consider and vote on a proposal to approve

and adopt the merger agreement and to act on any other matters brought before

the meeting.

WHO CAN VOTE AT THE MEETING; RECORD DATE

You are entitled to vote your Connecticut Bancshares common stock only if

you held your shares as of the close of business on February 9, 2004. As of the

close of business on February 9, 2004, a total of 11,143,133 shares of

Connecticut Bancshares' common stock were outstanding. Each share of common

stock has one vote. As provided in Connecticut Bancshares' certificate of

incorporation, record holders of Connecticut Bancshares' common stock who

beneficially own, either directly or indirectly, in excess of 10% of Connecticut

Bancshares' outstanding shares are not entitled to any vote in respect of the

shares held in excess of the 10% limit.

QUORUM AND VOTE REQUIRED

QUORUM. The special meeting will be held only if a majority of the

outstanding shares of common stock entitled to vote (excluding any shares in

excess of the 10% limit) are represented at the meeting. If you return valid

proxy instructions or attend the meeting in person, your shares will be counted

for purposes of determining whether there is a quorum present, even if you

abstain from voting. Broker non-votes also will be counted for purposes of

determining the existence of a quorum. A broker non-vote occurs when a broker,

bank or other nominee holding shares for a beneficial owner does not vote on a

particular proposal because the nominee does not have discretionary voting power

with respect to that item and has not received voting instructions from the

beneficial owner. Under applicable rules, brokers, banks and other nominees may

not exercise their voting discretion on the proposal to approve and adopt the

merger agreement and, for this reason, may not vote shares held for beneficial

owners without specific instructions from the beneficial owners.

VOTE REQUIRED. Approval and adoption of the merger agreement requires the

affirmative vote of the majority of the outstanding shares of Connecticut

Bancshares' common stock entitled to vote. Failure to return a properly executed

and dated proxy card, to vote by Internet or by telephone, or to vote in person,

and abstentions and broker non-votes, will have the same effect as a vote

"Against" the merger agreement.

12

Table of Contents

SHARES HELD BY DIRECTORS AND OFFICERS OF CONNECTICUT BANCSHARES; VOTING

AGREEMENTS

As of February 9, 2004, directors and executive officers of Connecticut

Bancshares owned approximately 5.63% of the shares of Connecticut Bancshares

common stock, not including shares that may be acquired upon the exercise of

stock options. All of the Connecticut Bancshares directors have entered into

voting agreements with New Haven requiring each individual to continue to hold

all shares owned or controlled on and after July 15, 2003 through the date of

the completion of the merger and to vote all of their shares of Connecticut

Bancshares common stock in favor of the proposal to approve the merger

agreement. Notwithstanding the voting agreements, Mr. Meduski's Termination and

Release Agreement requires him to exercise all of his vested stock options and

sell the shares of Connecticut Bancshares common stock acquired upon such

exercise.

VOTING BY PROXY

The board of directors of Connecticut Bancshares is sending you this proxy

statement for the purpose of requesting that you allow your shares of

Connecticut Bancshares common stock to be represented at the special meeting by

the persons named in the enclosed proxy card. If you are a stockholder of record

(I.E., do not hold your shares in street name), you may vote by proxy either by

completing the enclosed proxy card and mailing it in the postage-prepaid

envelope provided, by telephone or by Internet. Please see the enclosed proxy

card for instructions for telephone and Internet proxy voting procedures.

All shares of Connecticut Bancshares' common stock represented at the

special meeting by properly executed and dated proxies will be voted according

to the instructions indicated on the proxy card. If you sign, date and return a

proxy card without giving voting instructions, your shares will be voted as

recommended by Connecticut Bancshares' board of directors. THE BOARD OF

DIRECTORS UNANIMOUSLY RECOMMENDS A VOTE "FOR" APPROVAL OF THE MERGER AGREEMENT.

If any matters not described in this proxy statement are properly presented

at the special meeting, the persons named in the proxy card will use their own

best judgment to determine how to vote your shares. This includes a motion to

adjourn or postpone the special meeting in order to solicit additional proxies.

However, no proxy voted against the proposal to approve the merger agreement

will be voted in favor of an adjournment or postponement to solicit additional

votes in favor of the merger agreement. If the special meeting is postponed or

adjourned, Connecticut Bancshares common stock may be voted by the persons named

in the proxy card on the new special meeting date as well, unless you have

revoked your proxy. Connecticut Bancshares does not know of any other matters to

be presented at the special meeting.

If you hold Connecticut Bancshares common stock in street name, you will

receive instructions from your broker, bank or other nominee that you must

follow in order to have your shares voted. Your broker, bank or other nominee

may allow you to deliver your voting instructions via the telephone or the

Internet. Please see the instruction form provided by your bank, broker or other

nominee that accompanies this proxy statement. If you wish to change your voting

instructions after you have returned your voting instruction form to your broker

or bank, you must contact your broker or bank.

13

Table of Contents

REVOCABILITY OF PROXIES

You may revoke your proxy at any time before the vote is taken at the

meeting. To revoke your proxy you must either advise the Corporate Secretary of

Connecticut Bancshares in writing before your common stock has been voted at the

special meeting, deliver a properly executed and later dated proxy card, or

attend the meeting and vote your shares in person. Attendance at the special

meeting will not in itself constitute revocation of your proxy.

PARTICIPANTS IN THE SAVINGS BANK OF MANCHESTER'S ESOP AND SAVINGS PLAN

If you participate in The Savings Bank of Manchester's Employee Stock

Ownership Plan ("ESOP") or if you hold shares through The Savings Bank of

Manchester's Savings Plan, you will receive a vote authorization form for each

plan that reflects all shares you may vote under the plans. Under the terms of

the ESOP, the ESOP trustee votes all shares held by the ESOP, but each

participant in the ESOP may direct the trustee how to vote the shares of

Connecticut Bancshares common stock allocated to his or her account. The ESOP

trustee, subject to the exercise of its fiduciary duties, will vote all

unallocated shares of common stock held by the ESOP and allocated shares for

which no timely voting instructions are received in the same proportion as

shares for which the trustee has received voting instructions. Under the terms

of the Savings Plan, a participant is entitled to direct the trustee how to vote

the shares of Connecticut Bancshares common stock held in the Connecticut

Bancshares Stock Fund and credited to his or her account. The trustee will vote

all shares of Connecticut Bancshares common stock for which no directions are

given or for which timely instructions were not received in the same proportion

as shares for which the trustee received voting instructions. The deadline for

returning your voting instructions to each plan's trustee is March 22, 2004.

THE MERGER

THE FOLLOWING DISCUSSION OF THE MERGER IS QUALIFIED BY REFERENCE TO THE

MERGER AGREEMENT, WHICH IS ATTACHED TO THIS PROXY STATEMENT AS APPENDIX A. YOU

SHOULD READ THE ENTIRE MERGER AGREEMENT CAREFULLY. IT IS THE LEGAL DOCUMENT THAT

GOVERNS THE MERGER.

THE PARTIES TO THE MERGER

CONNECTICUT BANCSHARES, INC. Connecticut Bancshares was organized in

October 1999 for the purpose of becoming the holding company for The Savings

Bank of Manchester upon the conversion of The Savings Bank of Manchester's

former parent holding company, Connecticut Bancshares, M.H.C., from the

mutual-to-stock form of organization. The conversion was completed on March 1,

2000. As a savings and loan holding company, Connecticut Bancshares is regulated

by the Office of Thrift Supervision. Since its formation, Connecticut

Bancshares' principal activity has been to direct and coordinate the business of

The Savings Bank of Manchester. At December 31, 2003, Connecticut Bancshares had

total assets of $2.6 billion, total deposits of $1.6 billion and stockholders'

equity of $263.8 million.

The Savings Bank of Manchester is a Connecticut-chartered savings bank

headquartered in Manchester, Connecticut. The Savings Bank of Manchester is

regulated by the Connecticut Department of Banking and its deposits are insured

by the Federal Deposit Insurance Corporation up to applicable limits. The

Savings Bank of Manchester is a traditional savings association that accepts

retail deposits from the general public in the areas surrounding its 28

full-service offices.

14

Table of Contents

NEWALLIANCE BANCSHARES. NewAlliance Bancshares is a newly-formed Delaware

corporation that will become the parent company of New Haven upon New Haven's

conversion from mutual-to-stock form. Upon completion of the conversion,

NewAlliance Bancshares will be regulated by the Federal Reserve Board and direct

and coordinate the business of New Haven. NewAlliance Bancshares will have no

material assets or liabilities until the completion of the conversion.

New Haven is a Connecticut-chartered savings bank headquartered in New

Haven, Connecticut. New Haven is regulated by the Connecticut Department of

Banking and its deposits are insured by the Federal Deposit Insurance

Corporation up to applicable limits. New Haven currently operates 36 offices in

the greater New Haven area. At December 31, 2003, New Haven had total assets of

$2.5 billion, total deposits of $1.8 billion and total equity of $406.0 million.

In a separate and unrelated transaction, New Haven is also acquiring

Alliance Bancorp of New England, Inc., a bank holding company organized under

the laws of the State of Delaware in 1997. It operates Tolland Bank, a

Connecticut-charted savings bank that operates nine banking offices in and

around Tolland County. At December 31, 2003, Alliance had total assets of $438.4

million, deposits of $339.0 million and stockholders' equity of $32.8 million.

THE ALLIANCE MERGER DOES NOT REQUIRE THE APPROVAL OF THE STOCKHOLDERS OF

CONNECTICUT BANCSHARES AND THE CONNECTICUT BANCSHARES MERGER DOES NOT DEPEND ON

THE COMPLETION OF THE ALLIANCE MERGER.

FORM OF THE MERGER

Immediately following New Haven's conversion from mutual-to-stock form,

which is a condition precedent to our merger with New Haven, Connecticut

Bancshares will merge with and into a subsidiary of NewAlliance Bancshares, with

Connecticut Bancshares as the surviving entity. In a second step, Connecticut

Bancshares will be merged with and liquidated into NewAlliance Bancshares.

Upon completion of the merger, each share of Connecticut Bancshares common

stock will be converted into the right to receive $52.00 in cash and Connecticut

Bancshares stockholders will no longer have any rights or interests in

Connecticut Bancshares. However, if the closing of the merger does not take

place on or before March 31, 2004, other than as a result of a breach of a

representation, warranty or covenant by Connecticut Bancshares, the per share

merger consideration will be increased by the amount determined by dividing (x)

the Connecticut Bancshares' net income for each full month after March 31, 2004

minus the amount of dividends paid after March 31, 2004 by (y) the sum of (i)

the number of Connecticut Bancshares shares outstanding and (ii) the number of

shares of Connecticut Bancshares stock which may be acquired upon the exercise

of stock options. The adjustment in merger consideration is subject to the

following:

. as soon as possible after the end of each month ending after March 31,

2004, Connecticut Bancshares must deliver to New Haven a consolidated

statement of operations for such month; and

. not later than 5 business days prior to the closing, Connecticut

Bancshares must cause PricewaterhouseCoopers, LLP, or another accounting

firm reasonably acceptable to the parties to review and issue its report

on the consolidated statements of operations of Connecticut Bancshares

for the period ending at the date of the last of such statements

operations. Absent an error in the report, such report will be binding

on the parties for purposes of calculating the adjustment to the merger

consideration.

15

Table of Contents

TREATMENT OF CONNECTICUT BANCSHARES STOCK OPTIONS

Immediately before the closing of the merger, all outstanding options to

purchase shares of Connecticut Bancshares common stock will become immediately

exercisable and vested, to the extent not already exercisable and vested. At or

within five business days after the closing of the merger, all options will be

cancelled and either Connecticut Bancshares or New Haven will pay each holder an

amount equal to the excess of the $52.00 per share merger consideration over the

exercise price per share of each option, net of any cash that must be withheld

under federal and state income and employment tax requirements, and subject to

any increase in the amount of the per share merger consideration as discussed

above.

TREATMENT OF CONNECTICUT BANCSHARES STOCK AWARDS

At the closing of the merger, each share of restricted stock outstanding

and issued under the Connecticut Bancshares 2000 Stock-Based Incentive Plan and

the 2002 Equity Compensation Plan, to the extent not already vested, will vest

and will represent a right to receive the $52.00 per share merger consideration,

subject to any increase in the per share merger consideration as discussed

above.

PROCEDURES FOR SURRENDERING YOUR CERTIFICATES

On or before the closing of the merger, NewAlliance Bancshares will deposit

with the exchange agent (American Stock Transfer & Trust Company) an amount of

cash equal to the aggregate merger consideration. The exchange agent will act as

exchange agent for the benefit of the holders of Connecticut Bancshares common

stock. Each holder of Connecticut Bancshares common stock who properly

surrenders his or her Connecticut Bancshares shares to the exchange agent will

be entitled to receive a cash payment of $52.00 per share of Connecticut

Bancshares common stock, net of any required tax withholding upon acceptance of

the shares by the exchange agent.

No later than five business days after the closing of the merger, the

exchange agent will send you a letter of transmittal that will contain detailed

instructions for surrendering your certificates of Connecticut Bancshares common

stock. If you hold your Connecticut Bancshares common stock in "street name,"

your broker, bank or nominee will send you the letter of transmittal.

YOU SHOULD NOT RETURN YOUR CONNECTICUT BANCSHARES COMMON STOCK CERTIFICATES

WITH THE ENCLOSED PROXY, AND YOU SHOULD NOT SEND YOUR STOCK CERTIFICATES TO THE

EXCHANGE AGENT UNTIL YOU RECEIVE THE LETTER OF TRANSMITTAL.

If your Connecticut Bancshares common stock certificates have been lost,

stolen or destroyed, you will have to prove your ownership of the shares of

common stock evidenced by these certificates and that the certificates were

lost, stolen or destroyed before you receive any payment for your shares.

At any time following the six month period after the closing of the merger,

NewAlliance Bancshares will be entitled at its election to cause the exchange

agent to deliver to NewAlliance Bancshares any funds not disbursed to former

Connecticut Bancshares stockholders. Thereafter, former Connecticut Bancshares

stockholders will be entitled to look to NewAlliance Bancshares with respect to

any merger consideration that may be payable upon surrender of their stock

certificates.

16

Table of Contents

Neither NewAlliance Bancshares, Connecticut Bancshares, the exchange agent

nor any other party to the merger will be liable to any former holder of

Connecticut Bancshares common stock for any funds delivered to a public official

according to applicable abandoned property or escheat laws.

NewAlliance Bancshares or the exchange agent will be entitled to withhold

from the merger consideration payable to any Connecticut Bancshares stockholder

such amounts as either are required to withhold with respect to making such

payments under the Internal Revenue Code of 1986, as amended.

MATERIAL FEDERAL INCOME TAX CONSEQUENCES OF THE MERGER

The following discussion addresses the material United States federal

income tax consequences of the merger to holders of Connecticut Bancshares

common stock. This discussion applies only to Connecticut Bancshares

stockholders that hold their Connecticut Bancshares common stock as a capital

asset within the meaning of Section 1221 of the Internal Revenue Code of 1986,

as amended. This discussion does not address all aspects of United States

federal taxation that may be relevant to a particular stockholder in light of

its personal circumstances or to stockholders subject to special treatment under

the United States federal income tax laws including: banks or trusts; tax-exempt

organizations; insurance companies; dealers in securities or foreign currency;

traders in securities who elect to apply a mark-to-market method of accounting;

pass-through entities and investors in such entities; foreign persons;

stockholders who received their Connecticut Bancshares common stock through the

exercise of employee stock options, through a tax-qualified retirement plan or

otherwise as compensation; and stockholders who hold Connecticut Bancshares

common stock as part of a hedge, straddle, constructive sale, conversion

transaction or other integrated instrument.

This discussion is based on the Internal Revenue Code of 1986, as amended,

Treasury regulations, administrative rulings and judicial decisions, all as in

effect as of the date of this proxy statement and all of which are subject to

change (possibly with retroactive effect) and to differing interpretations. Tax

considerations under state, local and foreign laws are not addressed in this

document. The tax consequences of the merger to you may vary depending upon your

particular circumstances. Therefore, you should consult your tax advisor to

determine the particular tax consequences of the merger to you, including those

relating to state and/or local taxes.

Neither Connecticut Bancshares nor New Haven has requested or will request

a ruling from the Internal Revenue Service as to any of the tax effects to

Connecticut Bancshares' stockholders of the transactions discussed in this proxy

statement, and no opinion of counsel has been or will be rendered to Connecticut

Bancshares's stockholders with respect to any of the tax effects of the merger

to stockholders.

Connecticut Bancshares stockholders will recognize gain or loss for federal

income tax purposes equal to the difference, if any, between the cash received

and such stockholder's aggregate adjusted tax basis in the Connecticut

Bancshares common stock surrendered in exchange for the cash. The gain or loss

will be a capital gain or loss, provided that such shares were held as capital

assets of the Connecticut Bancshares stockholder at the effective time of the

merger. The gain or loss will be long-term capital gain or loss if the

Connecticut Bancshares stockholder's holding period is more than one year;

otherwise, the capital gain or loss will be short-term. The Internal Revenue

Code contains limitations on the extent to which a taxpayer may deduct capital

losses from ordinary income.

THIS TAX TREATMENT MAY NOT APPLY TO ALL CONNECTICUT BANCSHARES

STOCKHOLDERS. DETERMINING THE ACTUAL TAX CONSEQUENCES OF THE MERGER TO YOU CAN

BE COMPLICATED. YOU SHOULD CONSULT YOUR OWN TAX ADVISOR FOR A FULL UNDERSTANDING

OF THE MERGER'S TAX CONSEQUENCES THAT ARE PARTICULAR TO YOU.

17

Table of Contents

BACKGROUND OF THE MERGER

As part of its continuing efforts to improve Connecticut Bancshares'

community banking franchise and enhance stockholder value, Connecticut

Bancshares's board of directors and management, together with its financial and

legal advisors, have periodically reviewed various strategic options available

to Connecticut Bancshares, including, among other things, continued

independence, the acquisition of other institutions and a strategic merger with

or acquisition by another financial institution. As part of this process,

Connecticut Bancshares's legal counsel periodically reviewed with the board of

directors its fiduciary duties in the context of the various strategic

alternatives. Consistent with its periodic reviews of strategic alternatives,

Connecticut Bancshares acquired First Federal Savings and Loan Association of

East Hartford in August 2001.

The initial contact between Connecticut Bancshares and New Haven with

respect to the proposed transaction occurred on November 19, 2002. Peyton R.

Patterson, New Haven's Chairman, President and Chief Executive Officer,

contacted Richard P. Meduski, Connecticut Bancshares's President and Chief

Executive Officer, to request a meeting to discuss New Haven's interest in a

potential business combination with Connecticut Bancshares.

On December 3, 2002, Ms. Patterson, Mr. Meduski and Douglas K. Anderson,

Connecticut Bancshares' Executive Vice President, met along with representatives

of Sandler O'Neill, Connecticut Bancshares' financial advisor. Ms. Patterson

generally discussed New Haven's general business and acquisition strategy and

its interest in a potential business combination with Connecticut Bancshares as

part of New Haven's strategic growth plans, including a potential conversion

from mutual-to-stock form. Although general price parameters relative to

Connecticut Bancshares's trading multiples were discussed, there was no

discussion of a proposed price or a proposed range of prices.

On January 7, 2003, Ms. Patterson contacted Mr. Meduski and discussed

preliminary terms of a proposed transaction, including a proposed price range of

$47 to $50 per share in cash. On January 8, 2003, New Haven's financial advisor

contacted Sandler O'Neill to increase the proposed price range to $48 to $52 per

share in cash.

On January 13, 2003, Connecticut Bancshares's board of directors held its

monthly meeting. Representatives of Sandler O'Neill and legal counsel to

Connecticut Bancshares were present. The board discussed the terms of New

Haven's non-binding expression of interest, including matters relating to New

Haven's proposed conversion transaction, the completion of which would be a

condition precedent to any business combination between New Haven and

Connecticut Bancshares. In addition to reviewing New Haven's non-binding

expression of interest, representatives of Sandler O'Neill also identified and

discussed with the board certain other institutions that, in Sandler O'Neill's

view, would have the capacity and may have an interest in pursuing a business

combination transaction with Connecticut Bancshares. Representatives of these

other institutions had previously expressed to Mr. Meduski their interest in a

potential business combination transaction if and when the board of directors of

Connecticut Bancshares determined to consider such a transaction. Any business

combination between Connecticut Bancshares and any of the identified

institutions would not be subject to a financing contingency analogous to New

Haven's proposed mutual-to-stock conversion. Following discussion, the board

authorized Mr. Meduski to obtain further information about New Haven's

non-binding expression of interest and about the other parties that Sandler

O'Neill discussed as potentially having an interest in a potential business

combination with Connecticut Bancshares. Sandler O'Neill was instructed not to

places any limitations on any party.

18

Table of Contents

On January 27, 2003, Mr. Meduski and Ms. Patterson met and discussed the

proposed transaction.

The board of directors of Connecticut Bancshares met again on February 24,

2003, at which representatives of Sandler O'Neill and legal counsel were

present. After management updated the board of directors relative to the

activity that had taken place since the previous board meeting, the board

authorized management to engage in further exploratory discussions with New

Haven and the other institutions previously discussed by Sandler O'Neill in its

presentation. The board also authorized management to enter into confidentiality

agreements and conduct due diligence investigations.

On February 27, 2003, New Haven executed a confidentiality agreement in

favor of Connecticut Bancshares.

On March 3, 2003, two other interested parties, both large regional

financial institutions who Sandler O'Neill had identified at the January 13,

2003 board meeting, executed separate confidentiality agreements in favor of

Connecticut Bancshares.

From March 5 to 7, 2003, representatives of New Haven conducted preliminary

due diligence on Connecticut Bancshares.

On March 10, 2003, Sandler O'Neill contacted New Haven and the two other

interested parties to request that they submit the final terms of their

non-binding expressions of interest.

On March 12, 2003, representatives of one of the other two interested

parties conducted preliminary due diligence on Connecticut Bancshares.

On March 13, 2003, Connecticut Bancshares executed a confidentiality

agreement in favor of New Haven and representatives of Connecticut Bancshares

conducted preliminary due diligence on New Haven. On the same day,

representatives of the second interested party conducted preliminary due

diligence on Connecticut Bancshares.

On March 19, 2003, one of the other two interested parties submitted to

Sandler O'Neill its non-binding expression of interest. The party proposed part

cash/part stock consideration, which indicated a value of $51 per share.

On March 20, 2003, New Haven and the second interested party submitted to

Sandler O'Neill their respective non-binding expressions of interest. New Haven

initially proposed an all cash price of $50 per share but subsequently increased

it to $52 per share. The other interested party proposed an all cash price of

$49 per share.

On March 24, 2003, Connecticut Bancshares's board of directors held a

special meeting at which representatives of Sandler O'Neill and legal counsel

were present. The board considered the terms of each non-binding expressions of

interest, but deferred any decision until a special board meeting scheduled for

March 31, 2003.

At the special meeting on March 31, 2003, the board of directors again

reviewed with management, representatives of Sandler O'Neill and legal counsel

the non-binding expressions of interest. Following discussion, the board of

directors determined to engage in negotiations with New

19

Table of Contents

Haven toward a definitive agreement containing terms and conditions appropriate

given that the completion of New Haven's mutual-to-stock conversion would be a

condition precedent to the proposed transaction.

On April 8, 2003, Connecticut Bancshares received a draft merger agreement

from New Haven. Representative of Connecticut Bancshares and New Haven

negotiated the merger agreement and other related documents over the next

several days.

On April 17, 2003, representatives of New Haven and Connecticut Bancshares

met to conduct further due diligence.

On April 18, 2003, New Haven's financial advisor contacted Sandler O'Neill

to inform them that New Haven had reduced its proposed price to $48 per share.

On April 28, 2003, the Connecticut Bancshares board of directors met and

adopted resolutions to terminate negotiations with New Haven and to refrain from

initiating or soliciting further contact with New Haven and the other two

interested parties.

On May 16, 2003, Ms. Patterson contacted Mr. Meduski to express New Haven's

desire to resume negotiations at a revised proposed price of $50 per share.

On June 11, 2003, Ms. Patterson contacted Mr. Meduski to express New

Haven's desire to resume negotiations at a revised proposed price of $52 per

share.

On June 17, 2003, the executive committee of the board of directors of

Connecticut Bancshares met to discuss New Haven's most recent proposal and

authorized management to obtain further clarification with respect to certain

proposed terms, including proposed termination terms should New Haven fail to

complete its proposed conversion or to do so in a timely manner.

On June 23, 2003, at a special meeting, the board of directors of

Connecticut Bancshares met to review and discuss New Haven's most recent

non-binding indication of interest. Representatives of Sandler O'Neill and legal

counsel were present. After deliberations, the board of directors authorized

management to resume negotiations with New Haven.

From June 24 to 27, 2003, Connecticut Bancshares representatives conducted

due diligence on New Haven.

On June 26, 2003, Connecticut Bancshares received a revised draft of the

merger agreement from New Haven and representatives of Connecticut Bancshares

and New Haven negotiated the merger agreement and other related documents over

the ensuing days.

At a special meeting of Connecticut Bancshares' board of directors on July

15, 2003, Sandler O'Neill reviewed with the board the financial aspects of the

proposed transaction and delivered its opinion that the merger consideration was

fair to Connecticut Bancshares' stockholders from a financial point of view. The

board of directors considered this opinion carefully as well as Sandler

O'Neill's experience, qualifications and interest in the transaction. In

addition, the board of directors reviewed the merger agreement and all related

documents, copies of which were sent to each director before the date of the

board meeting, at length with legal counsel. After extensive review and

discussion, the merger

20

Table of Contents

agreement was unanimously approved by the directors present and voting and

management was instructed to execute and deliver the merger agreement.

On July 16, 2003, before the opening of the equity markets, Connecticut

Bancshares publicly announced the adoption and approval of the definitive merger

agreement.

CONNECTICUT BANCSHARES' REASONS FOR THE MERGER

Connecticut Bancshares' board of directors voted by unanimous vote of those

directors present and voting to approve the merger agreement and the entire

board of directors unanimously recommends that Connecticut Bancshares

stockholders vote "FOR" the approval of the merger agreement.

Connecticut Bancshares' board of directors has determined that the merger

and the merger agreement are fair to, and in the best interests of, Connecticut

Bancshares and its stockholders. In approving the merger agreement, Connecticut

Bancshares' board of directors also consulted with legal counsel regarding its

legal duties and the terms of the merger agreement, and with Sandler O'Neill

with respect to the financial aspects and fairness of the transaction from a

financial point of view to stockholders. In arriving at its determination,

Connecticut Bancshares' board of directors also considered a number of factors,

including the following:

. the process followed by Connecticut Bancshares and its financial advisor

in connection with the sale helped to ensure that an offer more

favorable than New Haven's offer was not available;

. the board of directors considered the book value and earnings per share

of Connecticut Bancshares' common stock and various pricing and other

data in an attempt to establish Connecticut Bancshares' value in a

merger or sales transaction;

. the opinion of Sandler O'Neill, Connecticut Bancshares' financial

advisor, that the $52.00 merger consideration is fair from a financial

point of view to Connecticut Bancshares' stockholders;

. the review conducted by the board of directors of the strategic options

available to Connecticut Bancshares and the assessment of the board of

directors that none of those options presented superior opportunities or

were likely to create greater value for Connecticut Bancshares

stockholders than the prospects presented by the proposed merger with

New Haven;

. New Haven's indication that it would likely retain most of Connecticut

Bancshares' employees;

. the current and prospective economic, competitive and regulatory

environment facing Connecticut Bancshares, New Haven and the financial

services industry generally;

. the board of directors' assessment that Connecticut Bancshares would

better serve the convenience and needs of its customers and the

communities that it serves through affiliation with a financial

institution such as New Haven that has a larger infrastructure;

21

Table of Contents

. the likelihood of Connecticut Bancshares stockholders approving the

merger;

. the fact that appraisal rights will be available under Delaware law with

respect to the merger;

. the uncertainties of receiving regulatory approval for the merger and

New Haven's conversion;

. the $30 million payment from New Haven in the event New Haven fails to

complete its conversion or consummate this transaction; and

. the appointment of two members of each of Connecticut Bancshares' and

The Savings Bank of Manchester's board of directors to the boards of

directors of NewAlliance Bancshares and New Haven.

The foregoing discussion of the information and factors considered by

Connecticut Bancshares' board of directors is not intended to be exhaustive, but

constitutes all material factors considered by the Connecticut Bancshares board

of directors. In view of the variety of factors considered in connection with

its evaluation of the merger agreement and the transactions contemplated by it,

the Connecticut Bancshares board of directors did not find it practicable to,

and did not, quantify or otherwise attempt to assign relative weights to the

specific factors considered in reaching its determination. In addition,

individual directors may have given different weights to the different factors.

OPINION OF CONNECTICUT BANCSHARES' FINANCIAL ADVISOR

By letter agreement dated as of February 25, 2003, Connecticut Bancshares

retained Sandler O'Neill as an independent financial advisor in connection with

Connecticut Bancshares' consideration of a possible business combination

involving Connecticut Bancshares and a second party. Sandler O'Neill is a

nationally recognized investment banking firm whose principal business specialty

is financial institutions. In the ordinary course of its investment banking

business, Sandler O'Neill is regularly engaged in the valuation of financial

institutions and their securities in connection with mergers and acquisitions

and other corporate transactions.

Sandler O'Neill acted as financial advisor to Connecticut Bancshares in

connection with the proposed merger with New Haven and participated in certain

of the negotiations leading to the merger agreement. At the request of the

Connecticut Bancshares board, representatives of Sandler O'Neill attended the

July 15, 2003 meeting at which the board considered the merger and approved the

merger agreement. At the July 15th meeting, Sandler O'Neill delivered to the

Connecticut Bancshares board its oral opinion, subsequently confirmed in

writing, that, as of such date, the merger consideration was fair to Connecticut

Bancshares' stockholders from a financial point of view. Sandler O'Neill has

updated its July 15th opinion by delivering to the board a written opinion dated

the date of this proxy statement. In rendering its updated opinion, Sandler

O'Neill confirmed the appropriateness of its reliance on the analyses used to

render its earlier opinion by reviewing the assumptions upon which its analyses

were based, performing procedures to update certain of its analyses and

reviewing the other factors considered in rendering its earlier opinion. THE

FULL TEXT OF SANDLER O'NEILL'S UPDATED OPINION IS ATTACHED AS APPENDIX B TO THIS

PROXY STATEMENT. THE OPINION OUTLINES THE PROCEDURES FOLLOWED, ASSUMPTIONS MADE,

MATTERS CONSIDERED AND QUALIFICATIONS AND LIMITATIONS ON THE REVIEW UNDERTAKEN

BY SANDLER O'NEILL IN RENDERING THE OPINION. THE DESCRIPTION OF THE OPINION SET

FORTH BELOW IS QUALIFIED IN ITS

22

Table of Contents

ENTIRETY BY REFERENCE TO THE OPINION. CONNECTICUT BANCSHARES' STOCKHOLDERS ARE

URGED TO READ THE OPINION CAREFULLY AND IN ITS ENTIRETY IN CONNECTION WITH THEIR

CONSIDERATION OF THE PROPOSED MERGER.

Sandler O'Neill's opinion speaks only as of the date of the opinion.

Sandler O'Neill's opinion was directed to the Connecticut Bancshares board and

was provided to the board for its information in considering the merger. The

opinion is directed only to the fairness of the merger consideration to

Connecticut Bancshares stockholders from a financial point of view. It does not

address the underlying business decision of Connecticut Bancshares to engage in

the merger or any other aspect of the merger and is not a recommendation to any

Connecticut Bancshares stockholder as to how such stockholder should vote at the

special meeting with respect to the merger or any other matter.

In connection with rendering its opinion, Sandler O'Neill reviewed and

considered, among other things:

(1) the merger agreement and certain of the exhibits and schedules

thereto;

(2) certain publicly available financial statements and other historical

financial information of Connecticut Bancshares that they deemed

relevant;

(3) certain historical financial information of New Haven that was