As filed with the Securities and Exchange Commission on 23 March 2023

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

☐ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended 31 December 2022

OR

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

☐ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number: 1-15040

PRUDENTIAL PUBLIC LIMITED COMPANY

Exact Name of Registrant as Specified in its Charter)

England and Wales

(Jurisdiction of Incorporation)

13th Floor, One International Financial Centre, 1 Harbour View Street, Central, Hong Kong

(Address of Principal Executive Offices)

Rebecca Wyatt, Chief of Financial & Capital Reporting

+44 20 7220 7588, rebecca.wyatt@prudentialplc.com

1 Angel Court, London EC2R 7AG, England

(Name, telephone, e-mail and/or facsimile number and address of company contact person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| | |||

Title of Each Class |

| Trading Symbol |

| Name of Each Exchange on Which Registered |

| | | ||

American Depositary Shares, each representing 2 Ordinary Shares, 5 pence par value each | PUK | New York Stock Exchange | ||

| | | ||

Ordinary Shares, 5 pence par value each | PUK/D | New York Stock Exchange* | ||

| | | ||

3.125% Senior Notes due 2030 issued by Prudential Funding (Asia) plc | PUK30 | New York Stock Exchange | ||

| | | ||

3.625% Senior Notes due 2032 issued by Prudential Funding (Asia) plc | PUK32 | New York Stock Exchange | ||

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

The number of outstanding shares of each of the issuer’s classes of capital or common stock as of 31 December 2022 was

2,749,669,380 Ordinary Shares, 5 pence par value each

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒ No

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer," "accelerated filer," and "emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☒ Accelerated filer ☐ Non-accelerated filer ☐ Emerging growth company ☐

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected to not use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b).

☐

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP or International Financial Reporting Standards as issued by the International Accounting Standards Board ☒ Other ☐

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

* | Not for trading, but only in connection with the registration of American Depositary Shares. |

† | The term "new or revised financial accounting standard" refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012. |

TABLE OF CONTENTS

1 | |

5 | |

5 | |

6 | |

EEV Basis, New Business Profit, Free Surplus Generation and Group Adjusted Operating Profit | 6 |

7 | |

7 | |

8 | |

9 | |

13 | |

26 | |

26 | |

Summary Consolidated Results and Basis of Preparation Analysis | 27 |

28 | |

34 | |

36 | |

48 | |

48 | |

50 | |

50 | |

52 | |

55 | |

67 | |

67 | |

68 | |

70 | |

75 | |

76 | |

76 | |

77 | |

87 | |

92 | |

96 | |

113 | |

113 | |

115 | |

119 | |

120 | |

120 | |

Summary of proposed changes to the Directors' remuneration Policy | 121 |

124 | |

167 | |

169 | |

170 | |

171 | |

171 | |

188 | |

189 | |

189 | |

190 | |

190 | |

190 | |

191 | |

195 | |

195 | |

196 | |

196 | |

Purchases of Equity Securities by Prudential plc and Affiliated Purchasers | 196 |

197 | |

197 | |

Limitations on Enforcement of US Laws Against Prudential, Its Directors, Management and Others | 197 |

| |

198 | |

198 | |

283 | |

292 | |

304 |

ii

CROSS REFERENCES TO FORM 20-F REQUIREMENTS

Item | 20-F Form Requirements | Section in this Annual Report on Form 20-F | Page |

|---|---|---|---|

Item 1 | Identity of Directors, Senior Management and Advisers | n/a | |

Item 2 | Offer Statistics and Expected Timetable | n/a | |

Item 3 | Key Information | | |

| Capitalisation and indebtedness | n/a | |

| Reasons for the offer and use of proceeds | n/a | |

| Risk Factors | Risk Factors | 171 |

Item 4 | Information on the Company | | |

History and development of the company | ·Our Business at A Glance | 1 | |

·Company Address and Agent | 5 | ||

Business overview | ·Our Strategy | 2 | |

·Our Business Model | 3 | ||

| | ●Recent achievements | 4 |

| | ●Strategic and Operating Review | 8 |

| | ●Competition | 7 |

·Sources | 7 | ||

·Supervision and Regulation of Prudential | 67 | ||

·Investments | 48 | ||

· EEV Basis, New Business Profit, Free Surplus Generation and Group Adjusted Operating Profit | 6 | ||

Organisational structure | ·Our business model | 3 | |

·Significant Subsidiaries | 188 | ||

Property, plants and equipment | Note C11 to the Consolidated Financial Statements | 266 | |

Item 4A | Unresolved Staff Comments | n/a | |

Item 5 | Operating and Financial Review and Prospects | | |

Operating results | · Strategic and Operating Review | 8 | |

| · Note A3 to the Consolidated Financial Statements | 209 | |

· Summary Consolidated Results and Basis of Preparation of Analysis | 27 | ||

· Explanation of Movements in Revenue and Charges | 28 | ||

· Determining Adjusted Operating Profit of Operating Segments | 34 | ||

· Explanation of Performance and Other Financial Measures | 36 | ||

Liquidity and capital resources | · Explanation of Performance and Other Financial Measures | 36 | |

· Additional Information on Liquidity and Capital Resources | 48 | ||

· Note D5 to the Consolidated Financial Statements | 270 | ||

Research and development, patents and licenses, etc | n/a | | |

Trend information | · Strategic and Operating Review | 8 | |

· Explanation of Performance and Other Financial Measures | 36 | ||

Item 6 | Directors, Senior Management and Employees | | |

| Directors and senior management | Board of Directors | 77 |

| Compensation | Compensation and employees: | |

| | · Our Executive Directors’ remuneration at a glance | 120 |

| | · Annual report on remuneration | 124 |

| | · Summary of current Directors’ remuneration policy | 121 |

| | · Additional remuneration disclosure | 167 |

| Board Practices | · How we operate | 87 |

| | · Committee Reports | 96 |

| Employees | Employees | 170 |

| Share ownership | Share ownership | 169 |

Item 7 | Major Shareholders and Related Party Transactions | | |

| Major shareholders | Major Shareholders | 189 |

| Related party transactions | Note D4 to the Consolidated Financial Statements | 269 |

| Interests of Experts and Counsel | n/a | |

iii

Item | 20-F Form Requirements | Section in this Annual Report on Form 20-F | Page |

Item 8 | Financial Information | | |

| Consolidated statements and other financial | · Financial Statements | 198 |

information | · Intellectual Property | 189 | |

| · Legal Proceedings | 190 | |

| Significant changes | n/a | |

Item 9 | The Offer and Listing | Listing Information | 196 |

Item 10 | Additional Information | | |

| Share capital | Memorandum and Articles of Association | 115 |

| Memorandum and Articles of Association | Memorandum and Articles of Association | 115 |

| Material contracts | Material contracts | 190 |

| Exchange controls | Exchange controls | 190 |

| Taxation | Taxation | 191 |

| Dividends and paying agents | n/a | |

| Statement by experts | n/a | |

| Documents on display | Documents on Display | 195 |

| Subsidiary information | n/a | |

| Annual report to security holders | Submitted separately | n/a |

Item 11 | Quantitative and Qualitative Disclosures about Market Risk | · Risk Review | 50 |

· Note C6 to the Consolidated Financial Statements | 257 | ||

Item 12 | Description of Securities Other than Equity Securities | Description of Securities Other than Equity Securities | 196 |

Item 13 | Defaults, Dividend Arrearages and Delinquencies | n/a | |

Item 14 | Material Modifications to the Rights of Security Holders and Use of Proceeds | n/a | |

Item 15 | Controls and Procedures | Controls and Procedures | 195 |

Item 16A | Audit Committee Financial Expert | Audit Committee Financial Expert | 113 |

Item 16B | Code of Ethics | Code of Ethics | 119 |

Item 16C | Principal Accountant Fees and Services | Principal Accountant Fees and Services | 197 |

Item 16D | Exemptions from the Listing Standards for Audit Committees | n/a | |

Item 16E | Purchases of Equity Securities by Prudential plc and Affiliated Purchasers | Purchases of Equity Securities by Prudential plc and Affiliated Purchasers | 196 |

Item 16F | Change in Registrant’s Certifying Accountant | Change in Registrant’s Certifying Accountant | 197 |

Item 16G | Corporate Governance | Differences between Prudential’s Governance Practice and the NYSE Corporate Governance Rules | 113 |

Item 16H | Mine Safety Disclosure | n/a | |

Item 16I | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | n/a | |

Item 17 | Financial Statements | n/a | |

Item 18 | Financial Statements | Financial Statements | 198 |

Item 19 | Exhibits | Exhibits | 304 |

As used in this document, unless the context otherwise requires, the terms ‘Prudential’, ‘Prudential Group’, the ‘Group’, ‘we’, ‘us’ and ‘our’ each refer to Prudential plc together with its subsidiaries, while the terms ‘Prudential plc’, the ‘Company’ and the ‘parent company’ each refer to ‘Prudential plc’.

This 2022 Annual Report may include references to our website. Information on our website or any other website referenced in the Prudential 2022 Annual Report is not incorporated into this Form 20-F and should not be considered to be part of the Form 20-F. We have included any website as an inactive textual reference only.

v

FORWARD-LOOKING STATEMENTS

This document contains ‘forward-looking statements’ with respect to certain of Prudential’s (and its wholly and jointly owned businesses’) plans and its goals and expectations relating to future financial condition, performance, results, strategy and objectives. Statements that are not historical facts, including statements about Prudential’s (and its wholly and jointly owned businesses’) beliefs and expectations and including, without limitation, commitments, ambitions and targets, including those related to ESG, and statements containing the words ‘may’, ‘will’, ‘should’, ‘continue’, ‘aims’, ‘estimates’, ‘projects’, ‘believes’, ‘intends’, ‘expects’, ‘plans’, ‘seeks’ and ‘anticipates’, and words of similar meaning, are forward-looking statements. These statements are based on plans, estimates and projections as at the time they are made, and therefore undue reliance should not be placed on them. By their nature, all forward-looking statements involve risk and uncertainty.

A number of important factors could cause actual future financial condition or performance or other indicated results to differ materially from those indicated in any forward-looking statement. Such factors include, but are not limited to:

| ● | current and future market conditions, including fluctuations in interest rates and exchange rates, inflation (including resulting interest rate rises), sustained high or low interest rate environments, the performance of financial and credit markets generally and the impact of economic uncertainty, slowdown or contraction (including as a result of the Russia-Ukraine conflict and related or other geopolitical tensions and conflicts), which may also impact policyholder behaviour and reduce product affordability; |

| ● | asset valuation impacts from the transition to a lower carbon economy; |

| ● | derivative instruments not effectively mitigating any exposures; |

| ● | global political uncertainties, including the potential for increased friction in cross-border trade and the exercise of laws, regulations and executive powers to restrict trade, financial transactions, capital movements and/or investment; |

| ● | the longer-term impacts of Covid-19, including macro-economic impacts on financial market volatility and global economic activity and impacts on sales, claims, assumptions and increased product lapses; |

| ● | the policies and actions of regulatory authorities, including, in particular, the policies and actions of the Hong Kong Insurance Authority, as Prudential's Group-wide supervisor, as well as the degree and pace of regulatory changes and new government initiatives generally; |

| ● | given Prudential’s designation as an Internationally Active Insurance Group, the impact on Prudential of systemic risk and other group supervision policy standards adopted by the International Association of Insurance Supervisors; |

| ● | the physical, social, morbidity/health and financial impacts of climate change and global health crises, which may impact Prudential's business, investments, operations and its duties owed to customers; |

| ● | legal, policy and regulatory developments in response to climate change and broader sustainability-related issues, including the development of regulations and standards and interpretations such as those relating to ESG reporting, disclosures and product labelling and their interpretations (which may conflict and create misrepresentation risks); |

| ● | the collective ability of governments, policymakers, the Group, industry and other stakeholders to implement and adhere to commitments on mitigation of climate change and broader sustainability-related issues effectively (including not appropriately considering the interests of all Prudential’s stakeholders or failing to maintain high standards of corporate governance and responsible business practices); |

| ● | the impact of competition and fast-paced technological change; |

| ● | the effect on Prudential's business and results from, in particular, mortality and morbidity trends, lapse rates and policy renewal rates; |

| ● | the timing, impact and other uncertainties of future acquisitions or combinations within relevant industries; |

| ● | the impact of internal transformation projects and other strategic actions failing to meet their objectives or adversely impacting the Group’s employees; |

| ● | the availability and effectiveness of reinsurance for Prudential’s businesses; |

| ● | the risk that Prudential's operational resilience (or that of its suppliers and partners) may prove to be inadequate, including in relation to operational disruption due to external events; |

| ● | disruption to the availability, confidentiality or integrity of Prudential's information technology, digital systems and data (or those of its suppliers and partners) including the Pulse platform; |

| ● | the increased non-financial and financial risks and uncertainties associated with operating joint ventures with independent partners, particularly where joint ventures are not controlled by Prudential; |

| ● | the impact of changes in capital, solvency standards, accounting standards or relevant regulatory frameworks, and tax and other legislation and regulations in the jurisdictions in which Prudential and its affiliates operate; and |

| ● | the impact of legal and regulatory actions, investigations and disputes. |

These factors are not exhaustive. Prudential operates in a continually changing business environment with new risks emerging from time to time that it may be unable to predict or that it currently does not expect to have a material adverse effect on its business. In addition, these and other important factors may, for example, result in changes to assumptions used for determining results of operations or re-estimations of reserves for future policy benefits. Further discussion of these and other important factors that could cause actual future financial condition or performance to differ, possibly materially, from those anticipated in Prudential's forward-looking statements can be found under the 'Risk Factors' heading of this Annual Report filed with the US Securities and Exchange Commission on Form 20-F.

vi

Any forward-looking statements contained in this document speak only as of the date on which they are made. Prudential expressly disclaims any obligation to update any of the forward-looking statements contained in this document or any other forward-looking statements it may make, whether as a result of future events, new information or otherwise except as required pursuant to the UK Prospectus Rules, the UK Listing Rules, the UK Disclosure Guidance and Transparency Rules, the Hong Kong Listing Rules, the SGX-ST Listing Rules or other applicable laws and regulations.

Prudential may also make or disclose written and/or oral forward-looking statements in reports filed with or furnished to the SEC, the UK Financial Conduct Authority, the Hong Kong Stock Exchange and other regulatory authorities, as well as in its annual report and accounts to shareholders, periodic financial reports to shareholders, proxy statements, offering circulars, registration statements, prospectuses, prospectus supplements, press releases and other written materials and in oral statements made by directors, officers or employees of Prudential to third parties, including financial analysts. All such forward-looking statements are qualified in their entirety by reference to the factors discussed under the ‘Risk Factors’ heading of this Annual Report filed with the US Securities and Exchange Commission on Form 20-F.

CAUTIONARY STATEMENTS

This document does not constitute or form part of any offer or invitation to purchase, acquire, subscribe for, sell, dispose of or issue, or any solicitation of any offer to purchase, acquire, subscribe for, sell or dispose of, any securities in any jurisdiction nor shall it (or any part of it) or the fact of its distribution, form the basis of, or be relied on in connection with, any contract therefor.

vii

Company Address and Agent

Prudential plc is a public limited company incorporated on 1 November 1978 and registered in England and Wales. Refer to the ‘Memorandum and Articles of Association’ sub-section of the ‘Governance’ section of this report for further information on the constitution of the Company.

Prudential’s registered office is 1 Angel Court, London EC2R 7AG, England (telephone: +44 20 7220 7588). Prudential’s principal address in Hong Kong is 13th Floor, One International Financial Centre, 1 Harbour View Street, Central, Hong Kong. Prudential’s agent in the US for the purposes of this annual report on Form 20-F is Cogency Global Inc, located at 18th Floor, 122 East 42nd Street, New York, NY 10168, United States of America.

Selected Historical Financial Information

The following table sets forth Prudential’s selected consolidated financial data for the years indicated, which is derived from Prudential’s audited consolidated financial statements. This table provides a five year summary overview of the Group and demonstrates trends in the Group’s financial results over the period. This table is only a summary and should be read in conjunction with Prudential’s consolidated financial statements and the related notes included elsewhere in this document.

In the table below, continuing operations reflect the Group’s insurance and asset management businesses in Asia and Africa and central operations. Discontinued operations represent the Group’s US business (Jackson) demerged in September 2021 and the Group’s UK and Europe business (M&G) demerged in November 2019.

IFRS financial results

| | | | | | | | | | | |

Income statement |

| 2022 $m |

| 2021 $m |

| 2020 $m |

| 2019 $m |

| 2018 $m |

|

Continuing operations: |

|

|

|

|

|

|

|

|

|

| |

Gross premiums earned |

| 23,344 |

| 24,217 |

| 23,495 |

| 23,855 |

| 22,039 | |

Outward reinsurance premiums |

| (1,943) |

| (1,844) |

| (1,625) |

| (1,116) |

| (771) | |

Earned premiums, net of reinsurance |

| 21,401 |

| 22,373 |

| 21,870 |

| 22,739 |

| 21,268 | |

Investment return |

| (30,159) |

| 3,486 |

| 13,762 |

| 14,961 |

| (2,723) | |

Other income |

| 539 |

| 641 |

| 615 |

| 639 |

| 465 | |

Total revenue, net of reinsurance |

| (8,219) |

| 26,500 |

| 36,247 |

| 38,339 |

| 19,010 | |

Benefits and claims and movement in unallocated surplus of with-profits funds, net of reinsurance |

| 13,697 |

| (18,911) |

| (28,588) |

| (29,171) |

| (11,690) | |

Acquisition costs and other expenditure |

| (3,880) |

| (4,560) |

| (4,651) |

| (5,908) |

| (5,793) | |

Finance costs: interest on core structural borrowings of shareholder-financed businesses |

| (200) |

| (328) |

| (316) |

| (496) |

| (525) | |

Gain (loss) attaching to corporate transactions |

| 55 |

| (35) |

| (30) |

| (142) |

| (57) | |

Total charges, net of reinsurance |

| 9,672 |

| (23,834) |

| (33,585) |

| (35,717) |

| (18,065) | |

Share of profits from joint ventures and associates net of related tax |

| 29 |

| 352 |

| 517 |

| 397 |

| 319 | |

Profit before tax (being tax attributable to shareholders’ and policyholders’ returns)note (i) |

| 1,482 |

| 3,018 |

| 3,179 |

| 3,019 |

| 1,264 | |

Tax charges attributable to policyholders’ returns |

| (21) |

| (342) |

| (271) |

| (365) |

| (107) | |

Profit before tax attributable to shareholders' returns |

| 1,461 |

| 2,676 |

| 2,908 |

| 2,654 |

| 1,157 | |

Tax charges attributable to shareholders’ returns |

| (454) |

| (462) |

| (440) |

| (316) |

| (235) | |

Profit from continuing operations |

| 1,007 |

| 2,214 |

| 2,468 |

| 2,338 |

| 922 | |

(Loss) profit from discontinued US operations |

| — |

| (5,027) |

| (283) |

| (385) |

| 1,959 | |

(Loss) profit from discontinued UK and Europe operations |

| — |

| — |

| — |

| (1,161) |

| 1,142 | |

Profit (loss) for the year |

| 1,007 |

| (2,813) |

| 2,185 |

| 792 |

| 4,023 | |

| | | | | | | | | | | |

Basic earnings per share (in cents) |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| 2018 | |

Based on profit (loss) for the year attributable to the equity holders of the Company: |

|

|

|

|

|

|

|

|

|

| |

Continuing operations |

| 36.5 | ¢ | 83.4 | ¢ | 94.6 | ¢ | 90.0 | ¢ | 35.6 | ¢ |

Discontinued US operations |

| — | ¢ | (161.1) | ¢ | (13.0) | ¢ | (14.9) | ¢ | 76.1 | ¢ |

Discontinued UK and Europe operations |

| — | ¢ | — | ¢ | — | ¢ | (44.8) | ¢ | 44.3 | ¢ |

Total |

| 36.5 | ¢ | (77.7) | ¢ | 81.6 | ¢ | 30.3 | ¢ | 156.0 | ¢ |

| | | | | | | | | | | |

Dividend per share (in cents) excluding demerger | | | | | | | | | | |

|

dividend |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| 2018 | |

Dividends paid in reporting period | | 17.60 | ¢ | 16.10 | ¢ | 31.34 | ¢ | 63.18 | ¢ | 64.34 | ¢ |

| | | | | | | | | | |

Statement of financial position at 31 Dec |

| 2022 $m |

| 2021 $m |

| 2020 $m |

| 2019 $m |

| 2018 $m |

Total assets |

| 165,942 |

| 199,102 |

| 516,097 |

| 454,214 |

| 647,810 |

Total policyholder liabilities and unallocated surplus of with-profits funds |

| 125,758 |

| 157,299 |

| 446,463 |

| 390,428 |

| 541,466 |

Core structural borrowings of shareholder-financed businesses |

| 4,261 |

| 6,127 |

| 6,633 |

| 5,594 |

| 9,761 |

Total liabilities |

| 148,815 |

| 181,838 |

| 493,978 |

| 434,545 |

| 625,819 |

Total equity |

| 17,127 |

| 17,264 |

| 22,119 |

| 19,669 |

| 21,991 |

5

Other financial information

| | | | | | | | | | |

At 31 Dec |

| 2022 $bn |

| 2021 $bn |

| 2020 $bn |

| 2019 $bn |

| 2018 $bn |

Eastspring funds under management or advicenote (ii) |

| 221.4 |

| 258.5 |

| 247.8 |

| 241.1 |

| 192.7 |

Group shareholder GWS capital surplus (over GPCR)note (iii) |

| 15.6 |

| 17.5 |

| n/a |

| n/a |

| n/a |

Notes

(i) | This measure is the formal profit (loss) before tax measure under IFRS. It is not the result attributable to shareholders. |

(ii) | Eastspring total funds under management or advice comprise funds from external parties, including funds managed on behalf of M&G plc, as well as funds managed or advised for the Group’s insurance operations. |

(iii) | The Group shareholder GWS capital surplus (over GPCR) reflects the Insurance (Group Capital) Rules as set out in the GWS Framework which became effective for Prudential in May 2021.The 2021 comparative information has been re-presented to reflect the impact of HK RBC and C-ROSS II regimes which became effective in the first half of 2022 and after allowing for the impact of the $1.7 billion debt redemption in January 2022 to show total Group GWS capital surplus (over GPCR) on a more comparable basis. Prior to 2021, the Group adopted LCSM basis. Further details of these regulatory updates are provided in the ‘Explanation of Performance and Other Financial Measures’ section. |

Dividend Data

Under UK company law, Prudential plc may pay dividends only if sufficient distributable reserves of the Company are available for that purpose and if the amount of its net assets is greater than the aggregate of its called-up share capital and non-distributable reserves (such as the share premium account) and the payment of the dividend does not reduce the amount of its net assets to less than that aggregate. ‘Distributable reserves’ are accumulated, realised profits not previously distributed or capitalised less accumulated, realised losses not previously written off, on the applicable GAAP basis. For further information about the Company, please refer to the section headed Condensed Financial Information of Registrant (Schedule II).

The retained profit of the Company is principally generated from dividend and interest income received from subsidiaries. Many of its insurance subsidiaries are subject to regulations that restrict the amount of dividends that they can pay to the Company. These restrictions are discussed in more detail in notes C10 and D6.2 to Prudential’s consolidated financial statements. Further information on the Group’s 2022 dividends is provided in note B5 to Prudential’s consolidated financial statements.

Subject to the restrictions referred to above, Prudential plc’s directors have the discretion to determine whether to pay an interim dividend and the amount of any such interim dividend but must take into account the Company’s financial position. The directors also have the discretion to recommend payment of a final dividend, such recommendation to be approved by ordinary resolution of the shareholders. The approved amount may not exceed the amount recommended by the directors.

The following table shows certain information regarding the dividends per share of Prudential plc relating to the years indicated. Prior to the second interim dividend in 2019, the dividends were declared in pence sterling and converted into USD at the noon buying rate in effect on each payment date. First interim dividends for a specific year generally have a record date in August and a payment date in September of that year, and second interim dividends generally have a record date in the following March/April and a payment date in the following May.

| | | | | | | | | | |

US cents per share |

| 2022 |

| 2021 |

| 2020 |

| 2019 |

| 2018 |

First Interim Dividend |

| 5.74 |

| 5.37 |

| 5.37 |

| 20.29 |

| 20.55 |

Second interim Dividend |

| 13.04 |

| 11.86 |

| 10.73 |

| 25.97 |

| 42.89 |

Reflecting the Group’s capital allocation priorities, a portion of capital generation will be retained for reinvestment in the business, and dividends will be determined primarily based on the Group’s operating capital generation after allowing for the capital strain of writing new business and recurring central costs. Dividends are expected to grow broadly in line with the growth in the Group’s operating free surplus generation net of right-sized central costs, and will be set taking into account financial prospects, investment opportunities and market conditions.

The Board has approved a 2022 second interim cash dividend of 13.04 cents per share (2021: 11.86 cents per share). Combined with the first interim cash dividend of 5.74 cents per share (2021: 5.37 cents per share), the Group’s total 2022 cash dividend is 18.78 cents per share (2021: 17.23 cents per share), an increase of 9 per cent.

EEV Basis, New Business Profit, Free Surplus Generation and Group Adjusted Operating Profit

In addition to IFRS basis results, Prudential’s filings with the Financial Conduct Authority, the Stock Exchange of Hong Kong and the Singapore Stock Exchange include reporting by Key Performance Indicators (‘KPIs’). These include results prepared in accordance with the European Embedded Value (‘EEV’) Principles and Guidance issued by the European Insurance CFO Forum in 2016, as well as new business profit and operating free surplus generation measures, which are alternative performance measures.

The EEV basis is a value-based method of reporting in that it reflects the change in the value of in-force long-term business over the accounting period. This value is called the shareholders’ funds on the EEV basis which, at a given point in time, is the value of future cash flows expected to arise from the current book of long-term insurance business plus the net worth (being the net assets on the local regulatory basis with adjustments) of Prudential’s life insurance operations. Prudential publishes its EEV results semi-annually in the UK, Hong Kong and Singapore markets.

6

New business sales are provided as an indicative volume measure of transactions undertaken in the reporting period that have the potential to generate profits for shareholders. New business profitability is a key metric for the Group’s management of the development of the business. New business profit reflects the value of future profit streams which are not fully captured in the year of sale under IFRS reporting. New business margin is shown by reference to annual premium equivalent (APE) which is calculated as the aggregate of regular new business amounts and one-tenth of single new business amounts. The amounts are not, and are not intended to be, reflective of premium income recorded in the IFRS income statement. EEV basis new business profit and margins are also published semi-annually.

Operating free surplus generation is the financial metric we use to measure the internal cash generation of our business operations and for our life operations is generally based (with adjustments) on the capital regimes that apply locally in the various jurisdictions in which the Group operates. It represents amounts emerging from the in-force business during the period, net of amounts reinvested in writing new business. For asset management and other non-insurance operations (including the Group’s central operations), free surplus is taken to be IFRS basis shareholders’ equity, net of goodwill attributable to shareholders, with central Group debt recorded as free surplus to the extent that it is classified as capital resources under the Group’s capital regime.

Prudential’s filings with the Financial Conduct Authority, the Stock Exchange of Hong Kong and the Singapore Stock Exchange also include discussion of the Group adjusted IFRS operating profit based on longer-term investment returns (adjusted operating profit), which is the aggregation of the segment adjusted operating profit and the central expenditure (including restructuring and IFRS 17 implementation costs) discussed in this document.

Competition

There are other significant participants in each of the financial services markets in which Prudential operates. Our competitors include both mutual and stock financial companies. In addition, regulatory and other developments in many of Prudential’s markets have blurred traditional financial service industry lines and opened the market to new competitors and increased competition. In some of Prudential’s markets, other companies may have greater financial resources, allowing them to benefit from economies of scale, and may have stronger brands than Prudential does in that market.

The principal competitive factors affecting the sale of Prudential’s products in its chosen markets are:

– | Price and yields offered; |

– | Financial strength and ratings; |

– | Commission levels, charges and other expenses; |

– | Range of product lines and product quality; |

– | Brand strength, including reputation, quality of service and use of technological advances; |

– | Distribution channels; |

– | Investment management performance; and |

– | Historical bonus/contract enhancement and bonus interest levels. |

Prudential offers different products in its different markets in Asia and Africa and, accordingly, faces different competitors and different types of competition in each market. In all of the markets in which Prudential operates, its products are not unique and, accordingly, it faces competition from market participants who manufacture a varying range of similar and identical products.

The competitive landscape across Asia and Africa differs widely by geographical market, reflecting differing levels of market maturity and regulation. Prudential’s competitors include both the subsidiaries of global life insurers and local domestic (including state-owned) entities. The majority of local domestic life insurers in Asia and Africa remain focused on their core home markets. The developed and liberalised markets of Hong Kong and Singapore are dominated by subsidiaries and branches of global life insurance groups. The developing markets in South-east Asia such as Indonesia, Vietnam and the Philippines also see a high level of participation by global life insurance groups. The large and relatively mature markets, such as Taiwan, are dominated by local domestic insurers. In certain countries, the life insurance markets are dominated by local domestic insurers or by joint venture entities between global insurance groups and local companies.

Prudential’s principal competitors in Asia and Africa include global life insurers together with regional insurers and multinational asset managers. In most markets, there are also local companies that have a material market presence.

Sources

Throughout this annual report, Prudential describes the position and ranking of its overall business and individual business units in various industry and geographic markets. Such data comes from a variety of conventional sources generally accepted as relevant business indicators by members of the financial services industry and which we believe to be reliable. These sources include information available from China Banking and Insurance Regulatory Commission, Insurance Commission of Philippines, the Asia Asset Management Magazine, Indonesian Life Insurance Association, Vietnam Actuarial Network, Fitch, Hong Kong Federation of Insurers, Hong Kong Insurance Authority, HSBC Global Research, Insurance Regulatory and Development Authority of India, Insurance Services Malaysia Berhad, Life Insurance Association of Malaysia, Life Insurance Association of Singapore, Taiwan Insurance Institute, Morningstar, Moody’s, Standard & Poor’s, Thai Life Assurance Association, The Asset Benchmark Research and UBS.

7

STRATEGIC AND OPERATING REVIEW

The following discussion and analysis should be read in conjunction with Prudential’s consolidated financial statements and the related notes for the year ended 31 December 2022 included in this document.

A summary of the critical accounting policies which have been applied in preparing Prudential’s financial statements is set forth in note A3 to the consolidated financial statements.

The results discussed below are not necessarily indicative of the results to be expected in any future periods. This discussion contains forward-looking statements based on current expectations, which involve risks and uncertainties. Actual results and the timing of certain events may differ significantly from those projected in these forward-looking statements due to a number of factors, including those set forth in the ‘Risk Factors’ section and elsewhere in this document

Operating segments and performance measure

The Group's operating and reported segments for financial reporting purposes are defined and presented in accordance with IFRS 8 ‘Operating Segments’ on the basis of the management reporting structure and its financial management information. Under the Group's management and reporting structure, its chief operating decision maker is the Group Executive Committee (GEC), chaired by the Chief Executive Officer.

Adjusted operating profit is management’s primary measure of profitability for each segment and provides an underlying operating result based on longer-term investment returns and excludes non-operating items. Further explanation on the determination of adjusted operating profit is provided in the ‘Determining Adjusted Operating Profit of Operating Segments’ section.

Joint ventures and associates

Under IFRS, the Group accounts for its investments in joint ventures and associates by using the equity method of accounting. The Group’s share of profit or loss of its joint ventures and associates is presented in a single line in the income statement and its share of movements in other comprehensive income is recognised in other comprehensive income, on a net of related tax basis.

For the purpose of segmental reporting on the Group’s other performance metrics such as APE new business sales and adjusted operating profit, the Group’s proportionate share of the results of the joint ventures and associates are included within total Group results and on a pre-tax basis for the segmental analysis of adjusted operating profit, with related tax charges included separately within the Growth markets and other segment.

Currency volatility

Our approach to evaluating the financial performance of the Group is to present percentage growth rates before the impact of the fluctuations in the value of the US dollar against local currencies in our operating markets. In a period of currency volatility this approach allows a more meaningful assessment of underlying performance trends. This is because our businesses receive premiums and pay claims in local currencies and are therefore not exposed to any cross-currency trading effects. To maintain comparability in the discussion below the same basis has been applied. Growth rates based on actual exchange rates (AER) are also shown in the financial tables presented for IFRS measures in this report. Consistent with previous reporting periods, the assets and liabilities of our businesses are translated at year-end exchange rates so the effect of currency movements has been fully incorporated within reported shareholders’ equity.

New business sales

The Group reports APE as a measure of new policies sold in the year, which is a key metric for the Group’s management of the development of the business. APE is calculated as the aggregate of regular premiums and one-tenth of single premiums on new business written during the year for all insurance products, including premiums for contracts designated as investment contracts under IFRS 4. The use of the one-tenth of single premiums is to normalise policy premiums into the equivalent of regular annual payments. This measure is commonly used in the insurance industry to allow comparisons of the amount of new business written in a period by life insurance companies, particularly when the sales contain both single premium and regular premium business. This differs from the IFRS measure of gross premiums earned as shown in the table below:

8

Reconciliation from Gross premiums earned to APE

| | | | | | |

|

| AER | ||||

|

| 2022 $m |

| 2021 $m |

| 2020 $m |

Gross premiums earned |

| 23,344 |

| 24,217 |

| 23,495 |

Less: premiums from in-force renewal business |

| (16,413) |

| (17,593) |

| (18,253) |

Less: 90% of single premiums on new business sold in the period |

| (3,839) |

| (3,602) |

| (2,147) |

Add: APE sales from joint ventures and associates on equity accounting method |

| 1,182 |

| 1,104 |

| 820 |

Other adjustments |

| 119 |

| 68 |

| (107) |

Annual premium equivalent (APE) |

| 4,393 |

| 4,194 |

| 3,808 |

Further explanation of the differences is provided in note II(viii) of the section headed ‘Additional unaudited financial information’. A discussion of the year-on-year movement of gross premiums earned is provided in the ‘Explanation of Movements in Revenue and Charges’ section.

In the remainder of this section, every time we comment on the performance of our businesses, we focus on their performance measured in local currency (presented here by reference to percentage growth expressed on a constant exchange rate (CER) basis) unless otherwise stated. In each such case, the performance of our businesses on an AER basis is explained by the same factors discussed in the comments below, together with the impact of currency movements.

Overview

Following the completion of the Group’s restructuring in 2021, our operations are fully dedicated to the life insurance and asset management opportunities in Asia and Africa. Our headquarters and management of the Group are now based in Hong Kong.

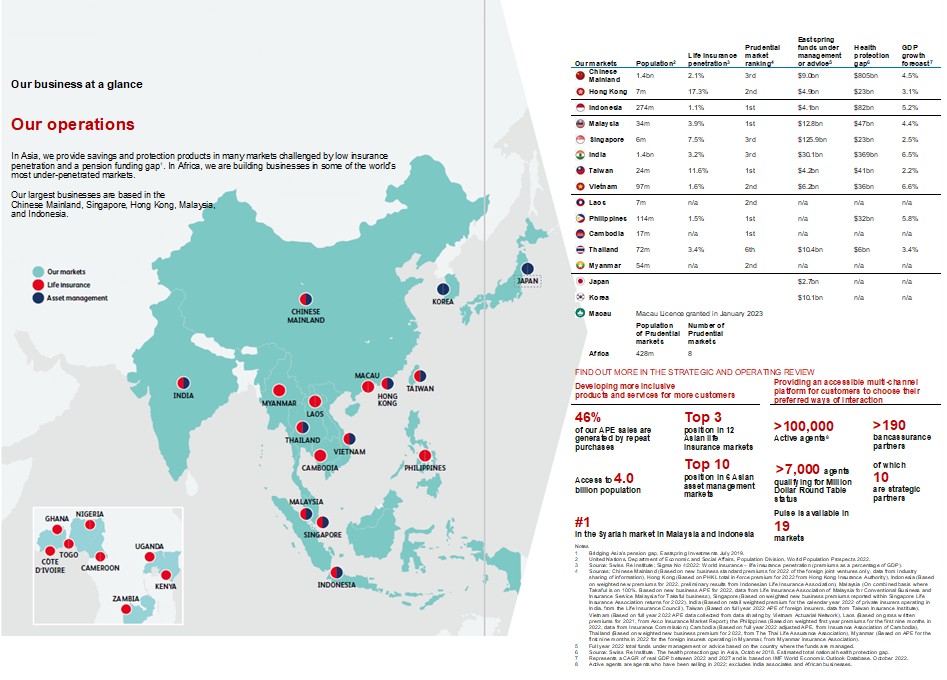

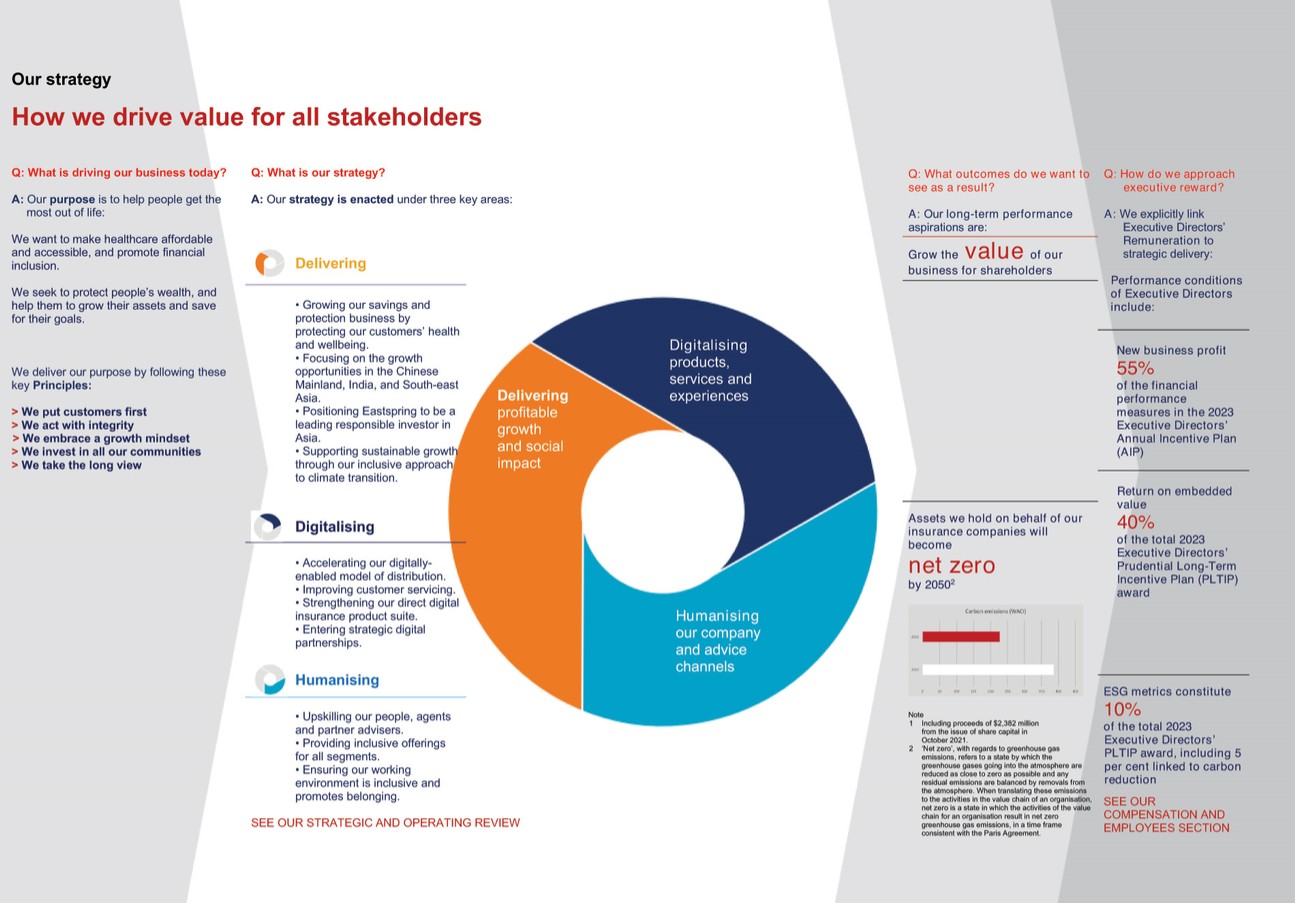

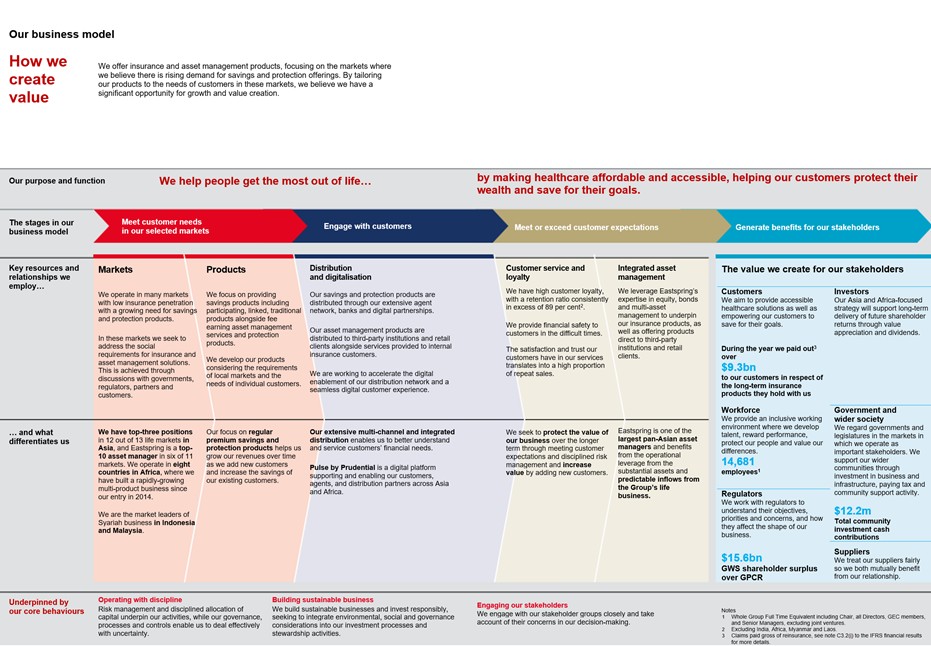

Our strategy is aligned with the long-term structural opportunities in Asia and Africa. Across Asia, the middle class is growing and is forecast to increase by 1.5 billion1 by 2030. Prosperity is also rising across the region2. This, combined with a low level of insurance penetration3 and a high level of out-of-pocket health and protection spending4 is driving an estimated $1.8 trillion health protection gap5. In Africa, the population is expected to double to more than two billion6 people by 2050. These long-term trends underpin increasing demand for savings and protection and create significant opportunities for growth and value creation.

We have set out that our purpose is to help people get the most out of life and we put our customers at the heart of everything we do. We strive to meet the needs of our customers and continue to support the development of the capital markets in which we operate. We believe that it is important to the long-term success of our Group that we play a wider role in the societies in which we operate. In Asia and Africa, we seek to promote financial inclusion and a just and inclusive transition to a low-carbon economy. We will use our investments in both corporate and government sectors to promote long-term sustainable development that is equitable for our markets in the context of their historic carbon emissions. We also aim to fulfil our purpose for our employees, one of our greatest assets. As an employer, we have promised to make Prudential a place where our people can connect, grow and succeed.

To further our purpose, we continue to focus on developing our range of products and investing in our distribution channels as well as enhancing and embedding our digital capabilities. In this way, we expand our capacity to help protect our customers from threats to their health and wellbeing, as well as support them to achieve their savings goals. We also remain focused on investing in our people and systems to ensure we have the resources to deliver on our long-term growth strategy and to enhance our operating model to keep pace with our opportunities.

We have strong franchises and operational expertise in both the more developed markets and developing markets in Asia and Africa. We continue to build on our success in the Chinese Mainland where we see substantial opportunity to deepen our presence across a nationwide footprint. With the newly set up Macau branch of the Hong Kong business, we are strengthening our operations to capture the opportunities in the Greater Bay Area and to fully prepare ourselves for the increase in opportunities following the reopening of the border between Hong Kong and the Chinese Mainland. We also see large growth opportunities in South-east Asia, particularly in Indonesia and Thailand, and also in India. Our focus on selected markets in East and West Africa has provided us with exposure to a growing and fast-changing continent since we re-entered Africa in 2014.

We will allocate capital to those markets that we consider to have attractive size and demographic characteristics, and where we believe we have the ability to build and retain competitive advantage. Through leveraging our scale and expertise in those markets we believe we can achieve attractive returns. We have significant investment appetite and capacity to support organic growth through funding the writing of new business and through adding to our existing capabilities, including distribution. We also remain ready to consider strategic inorganic opportunities.

We seek geographic diversification of our Asia operations among Greater China7, our businesses in South-east Asia8 and India.

9

The first part of 2022 saw Covid-19-related disruption in many of our markets as the Omicron variant increased infection levels and associated social restrictions. Subsequently, most markets have returned to more stable operating conditions, albeit the border between the Chinese Mainland and Hong Kong remained closed throughout 2022. Against this backdrop, APE sales9 increased 9 per cent10 to $4,393 million on a CER basis reflecting growth in the second half of 2022 from both agency and bancassurance channels. Additional commentary on the performance by segment is included in the Operational performance by market section below.

IFRS profit after tax was $1,007 million in 2022 (2021: $2,143 million on a CER basis, $2,214 million on an AER basis). Increases in the underlying life and asset management and segment profitability and lower interest costs following redemption of debt in late 2021 and early 2022 were more than offset by the negative effect of higher interest rates and lower equity markets on the valuation of investments and insurance liabilities. The losses from market volatility were offset in part by the benefit from refinements to the reserving basis following adoption of the Hong Kong Risk-Based Capital regime (HK RBC) as discussed in note C3 of the consolidated financial statements. The Group’s financial performance for the year is further discussed in the Financial Review later in this report.

Customers

Customers are at the heart of everything we do. Our customer-centric strategy has three key pillars:

| 1. | ‘WE Listen to Understand’ the needs of our customers across different segments and build lifelong relationships when we onboard them. For example, our customer segmentation has identified a clear opportunity in further expanding our offering in the family segment leading to the launch of the innovative ‘WE DO Family’ proposition in 2022. Through the application of a data-driven approach, this proposition helps us identify the needs of our customers based on their life events and individual circumstances, helping us to tailor our offerings and build lifelong relationships. More than 30 per cent of our new customers are from the affluent and advanced affluent segments and over 50 per cent of policies issued are health and protection plans to cover for critical illness, to provide medical reimbursement to cover hospital bills and to give protection against loss of income from acute illness or permanent disability. These products and solutions are offered through our multi-channel and integrated distribution and are key to driving long-term business growth. |

| 2. | ‘WE Care’ for our customers to deliver value across all the engagements they have with us. At Prudential, we have well-established core expertise in utilising data and insights to improve customer interactions and make operational improvements to provide a differentiated and personalised experience to our customers. At the point of purchasing, smart underwriting using reflexive methods (an approach to inquiries that generates follow up questions based on the initial answer) enables instant underwriting decisions with confirmation of terms. In 2022, 79 per cent of new policies were auto-underwritten and 41 per cent of policies were issued with no human intervention. At the point of claims, 64 per cent of claims are submitted electronically and 31 per cent of all claims are auto-adjudicated for instantaneous approval. These actions supported 46 per cent11 of total APE sales being generated by customers making a repeat purchase in 2022. |

| 3. | ‘WE Build’ customer advocacy by listening to the voice of customers to understand and address their feedback. We have adopted a systematic approach to understanding customer feedback and then applying the insights gained to continually improve our offerings with the aim of delivering best-in-class customer experiences through each touchpoint and interaction. Customer retention remains high at 89 per cent11. |

We seek to expand and innovate the coverage of our health and financial security products in an inclusive manner. This entails delivering solutions that recognise the evolution and needs of non-nuclear families, women, religious minorities, small and medium-sized enterprises, and lower-income groups. During 2022, we launched strategic propositions that celebrate ‘families of every shape and size’. Across 11 markets, we rolled out a range of new and extended products that are ‘Made For Every Family’ with progressive term definitions (such as ‘Beneficiary’) to offer more tailored protection for extended family members.

Our total life customer base increased to 18.3 million12 (2021: 17.7 million12). New policies13 included 2.4 million14 health and protection cases, an increase of 9 per cent when compared with 2021, reflecting our customers’ increased focus on this area in light of the pandemic. While these policies were generally smaller in size than in previous years14, we believe that the conversion of these customer interactions into sales by our diverse distribution channels is evidence of the power and quality of the Group’s franchise and brand.

Our strategy is to be a customer-centric organisation, driven by customer needs. Customers are active in conducting their own research, for example through search engines and social media; however, when it comes to purchasing decisions on life insurance, given the complexity and emotions, their preferred route is to seek advice. Our multi-channel and integrated distribution strategy enables us to adapt flexibly to changing local market conditions in order to deliver products and services to targeted consumer segments and support our growth ambitions. This distribution network encompasses agency and bancassurance partnerships with a digital platform. Asian and African insurance market distribution dynamics have been significantly affected by Covid-19-related restrictions. Over the last three years, our bancassurance sales have been relatively resilient and agency sales have been limited by mobility.

10

Agency

Agency continues to be an integral part of Prudential’s brand and customer service platform. Across our markets, we have launched and connected a series of agency growth programmes to build capabilities and expand capacity for our agency platform. Prudential’s Futuready Agency programmes aim to give our agency force a defensible competitive advantage by leveraging technology, behavioural science, and analytics to improve their skill sets, capabilities, and external positioning for long-term sustainable growth.

Our Futuready Agency programmes have four areas of emphasis:

| ● | Attracting talent from target segments. PruVenture is Prudential’s signature recruitment programme to attract talent and build a purpose-driven agency force. This has been deployed in seven core agency markets15 and onboarded over 9,800 associates over three years with productivity16 four times higher than standard new recruits. Our profiling assessment, PruDNA, selects individuals with high propensity to succeed. Thirty thousand successful agents went through PruDNA assessment in 2022, prior to joining Prudential. |

| ● | Leading and coaching leaders. PruVerge is Prudential’s signature learning programme for the next generation of leaders to help them attract, recruit, coach and build high-performing teams. This has enrolled over 6,000 Verge leaders over two years, where they learn the science of coaching and development utilising a data-driven decision model. We saw an increase in agent recruitment per leader of 50 per cent for the Verge leaders while overall recruitment was up 9 per cent and agent productivity measured by cases per agent increased 6 per cent in the year. |

| ● | Building a premium career path for purpose-driven agents and offering robust professional development. We had over 7,000 agents with production levels that qualified for the Million Dollar Round Table (MDRT) contributing to 42 per cent17 of APE sales in the relevant markets in 2022. |

| ● | Nurturing prospects by reimagining every aspect of prospecting, engaging, and advising to fit the digital business environment. Agents using PRULeads, our activity and leads management engine, were 30 per cent more productive16 with 32 per cent of agency sales generated using PRULeads18 (2021: circa 30 per cent) from 7.3 million leads19 (2021: 10.2 million) channelled via PRULeads. |

Agency sales were adversely affected by Covid-19-related restrictions in the first half of 2022. Sales through our agency business represent 61 per cent of our total health and protection APE sales. As the impact of Covid-19 subsides and agency activity resumes, we expect the agency contribution to increase while maintaining the diversified distribution mix in line with our strategy.

Bancassurance

Bancassurance plays a key role in our diversified multi-channel platform. We operate the largest independent bancassurance franchise in Asia with access to over 190 bancassurance partners of which 10 are strategic partners. We continue to invest and integrate our insurance solutions into the bank partners’ platforms and ecosystems to enable a seamless customer journey, supporting online to offline, virtual face-to-face and self-directed sales. We also leverage our expertise in selling through bank partners to deepen our customer relationships with an emphasis on health and protection solutions.

Bancassurance was our largest channel in 2022, generating $2,225 million in APE sales. Our strategic partnerships, both regionally and locally, contribute 74 per cent of our overall bancassurance APE sales in 2022.

New health and protection policies sold through the bancassurance channel increased 39 per cent in the year.

Digital

Prudential’s digital platform, Pulse, continues to support and enable our agents, customers and distribution partners across Asia and Africa in 19 of our majority owned markets of operation. We are constantly evolving the Pulse proposition as market conditions and the distribution landscape changes. The agility and flexibility of the platform allows us to provide products and services that meet the changing needs of multiple customer segments locally, while also providing up-to-date customer insights and leads to our distribution network. Pulse also supports a wide variety of modules to assist our agency force such as an integrated training and recruitment solution, ‘real-time’ management information tools and AI-powered analytics. From a technology standpoint, the Pulse platform utilises a one platform approach, allowing Prudential to consolidate and reduce IT investment over the long term as well as accelerate application development and deployment across our many markets. We remain committed to the strategic pillars which have driven our digital transformation and underpin our digital strategy. These are outlined below:

| ● | Accelerating our digitally-enabled model of distribution via PRUForce; |

| ● | Improving servicing of existing and new customers via PRUServices; |

| ● | Strengthening our direct digital insurance suite of products and services; and |

| ● | Nurturing new business verticals and partnerships to drive future customer acquisition opportunities. |

11

PRUForce, our agency tool on the Pulse platform, has allowed our agents to be more efficient, reaching and managing multiple customers at a time, whilst still maintaining a personalised approach. We continue to improve and refine this approach, with PRUForce central to the evolution of our agency network. PRUForce is live in six markets and offers our agents the competitive advantage by allowing them to stay connected with customers, building trust and providing personalised advice.

Accelerating the digital enablement of our distribution network remains critical for Prudential. We provide a full set of digital capabilities enabling agents to interact with customers via a multi-channel approach. The use of data and analytics helps accelerate our aspiration to support and increase sales productivity from those within our organisation, to those of our distribution partners. From a data security perspective, we have developed a common bancassurance gateway which can manage all transactions securely between any bank and Prudential’s businesses, ensuring data security and privacy is always top of mind.

PRUServices is our digital customer servicing platform, allowing customers and agents to access their policy claims, payments, and benefits. Customers and agents can manage policies, from tracking the status of a policy proposal to reinstating a lapsed policy, via self-service features on the platform. PRUServices is live in nine markets. We aim to deliver a seamless digital experience for customers through an effective end-to-end journey. We believe this will strengthen customer affinity toward Prudential, reduce attrition of the in-force policy values and support the value represented by our installed customer base.

Furthermore, the ability to embed insurance products in our ecosystem and in core offerings from our partners is critical. To offer these products dynamically and seamlessly to the broadest possible market is only achievable via a digital platform. We have strengthened our direct product suite, including the launch of endowment products in several markets both via Pulse and through partners’ mobile apps. This has enabled us to capture a larger pool of insurance customers from a wider range of socio-economic segments. Our life insurance joint venture in the Chinese Mainland and our associate in India maintain their own high-quality offerings via digital platforms with further details provided in the relevant sections that follow.

Finally, we have expanded our collaboration with new partners. For example, in October 2022, we entered a strategic partnership with Google Cloud to make healthcare and financial security more accessible across Asia and Africa. This strategic partnership supports our broader digital strategy to leverage AI and advanced analytics to transform the customer and agent experience and lower barriers to accessing financial services.

Asset and wealth management

Eastspring Investments (‘Eastspring’) is the pan-Asia asset management arm of Prudential with a presence in 11 Asian markets20 as well as distribution offices in North America and Europe. Eastspring is a top-10 asset manager in six of these markets21 managing or advising on $221.4 billion in assets22. Eastspring is well placed to address the saving and investment needs of customers across the region through a team of 300 investment professionals with local market expertise. Eastspring also benefits from reliable and stable fund inflows from the Group’s insurance businesses which, together with its broad regional footprint, it can leverage to meet the long-term opportunity to grow mutual fund penetration from the market’s current low base. Eastspring is also playing an important role as an active asset manager and is engaging with investee companies and governments in supporting our commitment to carbon reduction in our insurance company asset portfolio23, allowing us to deliver profitable growth alongside a positive social impact.

During the year, Eastspring’s average funds under management or advice decreased by (5) per cent10 to $229.4 billion (2021: $240.9 billion10), reflecting adverse market movements during the year, partially offset by net inflows, including from the Group’s insurance business.

As a Group, we see opportunities to deepen our share of the wealth market by providing holistic wealth solutions to our high-net-worth and affluent customers. Our large and diverse customer base, well-positioned agency networks, strong intermediary relationships and leading brand name position us well to better serve this segment and deepen our relationship with our existing customers. Fund solutions occupy a central role in the product proposition, and we are focused on offering customer choice and access to top fund managers and innovative portfolio options. Our aim is to distinguish ourselves in this market through our service to customers and additional value-added services, such as consultation with independent panels providing legal and estate planning advice.

People

The Group employs over 14,000 members of staff24. As an employer, we have made a promise to make Prudential a place where our people can Connect, Grow and Succeed. A significant part of that pledge to employees is preparing them for the future of work, so that they can participate in and contribute confidently to our business transformation. We believe in creating a workforce and a workplace that is innovative, inclusive, and customer-centric. During 2022, we focused on equipping our employees with these future-ready skills through a series of webinars and developing our innovation and design thinking capabilities within the organisation.

12

Our goal is to empower our people and deepen belonging at Prudential by respecting and appreciating differences. We maintain a culture where diversity is celebrated, and inclusion assured for our people, customers and partners. Building on the launch of PRUCommunities in 2021, our employee-led networks continued to enhance connections and are key to deepening belonging at Prudential. In 2022, we saw the global launch of various communities including PRU Women Empowered, PRU Young Professionals, Women in Tech, Mental Health First Aiders and the intersectional We DO Wellness, joining the well-established PRUPride. We have been included in the Bloomberg Gender Equality Index 2023, being listed on the index for the third successive year.

Leadership developments

2022 saw a number of leadership changes to support the ongoing evolution of the Group. The internal promotions during the year of James Turner to Group Chief Financial Officer and Avnish Kalra to Group Chief Risk and Compliance Officer, demonstrate Prudential’s bench-strength and ability to focus on operational delivery by leveraging continuity in executive leadership. In addition, the Group continues to benefit from broad based and experienced local leadership teams who are deeply rooted in their markets.

During 2022 Seck Wai-Kwong, CEO, Eastspring; Dennis Tan, CEO, Prudential Singapore; Lilian Ng, CEO, Insurance; and Solmaz Altin, Group Chief Strategy and Transformation Officer, were all promoted to the Group Executive Committee (GEC). Mr Tan, Ms Ng and Mr Altin were promoted to Managing Directors of the Strategic Business Groups, which consist of selected markets. Mr Seck remains responsible for the growth of Eastspring’s business and the delivery of its investment performance. Prudential’s leadership team was further enhanced with the appointment of Lawrence Lam as the new CEO of the Hong Kong insurance business and Bundit Jiamanukoonkit (Kenny) as the new CEO of the Thailand insurance business.

Outlook

We continue to believe that the Group’s multi-channel, digitally enabled distribution model positions us well to capture the opportunities open to us, and this competitive advantage, alongside our distinctive geographical footprint and customer-centric product range enables us to deliver a resilient performance.

There are signs that Covid-19-related impacts in many of our markets have stabilised, albeit operating conditions may continue to be challenging given the volatile macroeconomic environment and increasing risks of inflation. We enter 2023 with a resilient balance sheet and strong capital position, which we believe will enable us to manage these uncertainties and capture the resulting opportunities that arise.

We are encouraged by the year-on-year sales growth we have seen in the first two months of 2023. Our actions to maintain and build agent capacity and our continued innovation to broaden our product proposition mean we stand ready to serve our customers across all our markets. In particular, we are well positioned in Hong Kong and the Chinese Mainland to take advantage of the opportunities that we expect to arise as Covid-19-related restrictions are eased. We have seen a gradual increase in cross-border traffic with sales in the first two months of 2023 driven predominately by savings products.

We remain confident that we have the financial resilience, capital strength and capability to meet the growing protection and savings needs of our customers in Asia and Africa. By doing so, we believe we will deliver on our purpose to help people get the most out of life and also build value for our shareholders over the long term.

Operational performance by market

The following commentary provides an update on the operational capabilities and performance for each of the Group’s segments. Discussion of the financial performance of the Group and its segments, including adjusted operating profit, is contained separately in the Financial review section of this report. Unless otherwise stated, the APE discussion in the following commentary is provided on a CER basis. For the 2021 comparatives to 2022, the CER results were calculated using the 2022 average exchange rates. For the 2020 comparatives to 2021, the CER results were calculated using the 2021 average exchange rates.

Chinese Mainland – CITIC Prudential Life (CPL)

The Chinese Mainland continues to present significant growth opportunities for the Group, with a population of circa 1.4 billion25, with low levels of insurance penetration and an estimated health and protection gap of $805 billion5. Furthermore, a number of factors also support further growth both in health and protection as well as retirement planning products and services. These include regulatory proposals which are conducive to the long-term development of insurance markets as well as favourable demographics such as an ageing population, emerging middle class and rapid urbanisation. The recent announcement made by the China Banking and Insurance Regulatory Commission (CBIRC) to reform private pension schemes offers a significant opportunity for foreign insurers with strong financial capability and deep expertise in retirement planning products.

13

Prudential’s life business in the Chinese Mainland, CPL, is a 50/50 joint venture with CITIC, a leading Chinese state-owned conglomerate. CPL benefits from the strong brands of both shareholders and a balanced distribution network with strength in agency and bancassurance and a well-diversified product range. CPL is a powerful franchise with an extensive footprint across 23 branches. CPL is focused on the affluent and upper affluent segments of the market where there is more stability of income and employment. CPL’s diverse footprint supported its resilient performance with its Greater Bay Area cluster and Beijing performing well, offsetting some softness in Shanghai and surrounding cities which were most affected by Covid-19 surges during the first half of the year. CPL continues to outperform the market. The total Chinese Mainland industry-wide measure of gross written premium increased by 3 per cent in the year, while CPL, on the same basis, saw an increase of 16 per cent26 in 2022. CPL believes that these operational outcomes are due to CPL seeking to put customers first and to enrich their health and wealth journeys. As Covid-19-related controls are progressively removed, CPL will continue to use its multi-distribution platform to serve the insurance needs of customers in terms of health, protection, long-term savings and retirement planning and expects to see a more balanced mix of sales from agency and bancassurance going forward.

New business performance

2022 compared with 2021

Despite isolated lockdowns, CPL achieved APE sales growth of 19 per cent10 to $884 million. This resilient growth has been underpinned by a diversified distribution strategy with a high-quality agency force and strong partnerships with banks delivering customer-centric protection and savings solutions.

The 19 per cent10 growth in APE sales was driven by stronger growth in the bancassurance channel (an increase of 32 per cent10), with the agency business being consolidated with the aim of driving quality throughout 2022 resulting in an overall decrease of (7) per cent10 in the year. In the first half of 2021 agency sales benefited from the effect of regulatory changes in the definition of critical illness coverage, which did not recur in the current year, lowering APE sales by (11) per cent10 in the first half of 2022. Agency APE sales in the second half of 2022 were 6 per cent10 higher than the equivalent period in the prior year.

2021 (AER) compared with 2020 (CER)

CPL’s APE sales grew by 25 per cent to $776 million. Its solid and resilient growth was underpinned by its diversified distribution strategy, with both agency and bancassurance channels delivering double-digit APE sales growth at 25 per cent and 28 per cent respectively in 2021. CPL continued to outgrow the overall sector. In 2021, CPL increased its overall market share to 0.86 per cent, from 0.74 per cent in 2020.

Delivering customer-led solutions

CPL seeks to address customers’ financial security and wellbeing at different life stages, with built-in related services enriching the overall customer propositions. Solutions and services are combined in an ecosystem that provides an integrated experience, which seeks to identify and meet the customers’ needs and so strengthens relationships with them for the long term.

During 2022 CPL continued to develop customised protection solutions. One specialised critical illness product that was specifically developed to meet the needs of customers in the Greater Bay Area of the Chinese Mainland contributed 21 per cent of CPL’s relevant APE sales in that area. Beyond protection, CPL expanded its concierge service network to not only cover healthcare needs, including specialist consultation on treatment options, priority hospital access and mental health rehabilitation services, but also through development of its retirement and planning concierge service. This expansion includes extension of CPL’s retirement village network to cover 17 institutions in seven cities.

CPL is enhancing the digital experience to its customers and distributors, including through its mobile first Xin Yi Tong app. CPL’s ‘Virtual Lounge’ leverages technology to humanise the connection between the agent and the customer. The technology’s ease of use by customers has been recognised by digital media.

Multi-channel distribution

CPL continues to focus on building a professional, high-quality agency force, with a strong understanding of its health, protection and retirement planning products. CPL has over 15,200 agents that serve customers across the country. While CPL’s agency channel continues to go through a period of rationalisation along with the overall industry, CPL’s agency force shows signs of stabilising in numbers as well as improvements in quality, with APE sales per active agent rising 9 per cent. CPL had over 1,000 agents with production levels that qualified for the Million Dollar Round Table (MDRT) in 2022. CPL is providing agents with advanced tools and techniques that help them engage with customers in order to provide solutions tailored to their needs and manage the conversion of leads to completed sales. Over time, as CPL’s agency force continues to mature and build experience, CPL expects this to result in further enhancement in productivity, providing additional support to the growth trajectory in CPL.

14

Meanwhile, CPL also continues to build out its bancassurance distribution network, adding 11 partners. China Merchant Bank has become a significant partner in the Greater Bay Area and beyond. CPL has a network of 59 bancassurance partners with access to over 6,600 branches across the Chinese Mainland. Importantly, these relationships are strengthened and enhanced by 3,200 local insurance specialists catering to customers of the banks. This has resulted in higher levels of new business from the bank channel and supported an improvement in product mix.

Consistent with the ongoing regulatory developments in terms of capital management and customer conduct in the industry, we expect that refinements in the product features may, in the short-term, impact volumes but CPL continues to evolve its product set so that focus remains on meeting customer demands.

Hong Kong

Prudential has a strong and reputable brand in Hong Kong and serves over 1.3 million customers. The fifth wave of the Covid-19 epidemic significantly decreased the amount of economic activity in Hong Kong, especially during the first half of the year with the impact compounded by restrictions on cross-border travel.