UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-10385

Pacific Funds

(Exact name of registrant as specified in charter)

700 Newport Center Drive, P.O. Box 7500, Newport Beach, CA 92660

(Address of principal executive offices)

Robin S. Yonis

Vice President and Investment Counsel of

Pacific Life Insurance Company

700 Newport Center Drive

Post Office Box 9000

Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Jeffrey S. Puretz, Esq.

Dechert LLP

1775 I Street, N.W.

Washington D.C. 20006-2401

Registrant's telephone number, including area code: (949) 219-6767

Date of fiscal year end: March 31

Date of reporting period: April 1, 2004 – March 31, 2005

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Annual Report to Shareholders of the Pacific Funds for the fiscal year ended March 31, 2005. |

|

TABLE OF CONTENTS | |

PACIFIC FUNDS | |

A-1 | |

A-2 | |

B-1 | |

C-1 | |

Financial Statements: | |

D-1 | |

D-7 | |

D-10 | |

E-1 | |

F-1 | |

G-1 | |

H-1 | |

Approval of Investment Advisory Agreement and Management Agreements | H-3 |

H-6 | |

|  |

| Thomas C. Sutton Chairman of the Board | Glenn S. Schafer President |

A-1 |

| Broad-Based Indices | 1-Year Performance as of 3-31-05 | ||||

| Standard & Poor’s 500 Composite Stock Price Index | |||||

| (S&P 500 Index)** (U.S. Stocks) | 6.69 | % | |||

| Morgan Stanley Capital International Europe | |||||

| Australasia Far East Index (MSCI EAFE | |||||

| Index)** (International Stocks) | 15.06 | % | |||

| Lehman Brothers Government/Credit Index** | |||||

| (Fixed Income) | 0.40 | % | |||

| Merrill Lynch 3-Month U.S. T-Bill Index** (Cash) | 1.67 | % | |||

It should be noted that the benchmark indices for the underlying Pacific Funds may differ from the Portfolio Optimization broad-based indices. The Portfolio Optimization funds had investments in the following underlying funds, which helped performance as compared to the broad-based indices above. |

| Underlying Funds | 1-Year Performance as of 3-31-05 | ||||

| PF Van Kampen Mid-Cap Growth Class A* | |||||

| (U.S. Stocks) | 11.49 | % | |||

| PF Van Kampen Comstock Class A* | |||||

| (U.S. Stocks) | 11.08 | % | |||

| PF PIMCO Inflation Managed Class A* | |||||

| (Fixed Income) | 1.99 | % | |||

| PF PIMCO Managed Bond Class A* | |||||

| (Fixed Income) | 0.56 | % | |||

The Portfolio Optimization funds had investments in the following underlying funds, which hurt performance as compared to the broad-based indices above. |

| Underlying Funds | 1-Year Performance as of 3-31-05 | ||||

| PF Goldman Sachs Short Duration Bond | |||||

| Class A* (Fixed Income) | -1.34 | % | |||

| PF AIM Blue Chip Class A* (U.S. Stocks) | -0.49 | % | |||

| PF Salomon Brothers Large-Cap Value | |||||

| Class A* (U.S. Stocks) | 3.78 | % | |||

| PF MFS International Large-Cap Class A* | |||||

| (International Stocks) | 12.73 | % | |||

| A-2 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

PF Portfolio Optimization Model A Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 1.74%* compared to a 6.69%** return for the S&P 500 Index, a 0.40%** return for the Lehman Brothers Government/Credit Index, and a 2.38%(1) return for the Model A Composite Benchmark Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmarks is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 | |||||||||||

| PF Portfolio Optimization Model A | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 1.74 | % | 1.25 | % | 1.18 | % | |||||

| With maximum sales charge*** | -3.85 | % | -3.75 | % | 0.18 | % | |||||

| Lehman Brothers | |||||||||||

| Government/Credit Index** | 0.40 | % | |||||||||

| S&P 500 Index** | 6.69 | % | |||||||||

| Model A Composite Benchmark(1) | 2.38 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 2.61 | % | 2.13 | % | 1.99 | % | |||||

| With maximum sales charge*** | -1.92 | % | -1.07 | % | 1.99 | % | |||||

| Lehman Brothers | |||||||||||

| Government/Credit Index** | 2.78 | % | |||||||||

| S&P 500 Index** | 6.74 | % | |||||||||

| Model A Composite Benchmark(1) | 3.85 | % | |||||||||

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

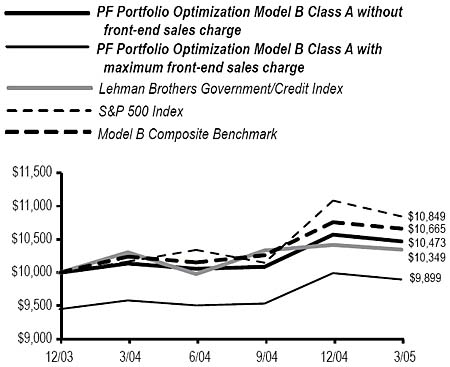

| Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. PF Portfolio Optimization Model A invests primarily in a diverse group of four fixed income funds, with small allocations to domestic and international equity funds. Since its launch on December 31, 2003, the fund’s net assets have grown to over $18 million. The fund’s allocations to the money market and fixed income funds, which represent a combined target allocation of 79% of the overall fund, held back fund performance. Generally, longer maturity issues outperformed shorter maturities over the period. The fund’s significant allocation to the PF Goldman Sachs Short Duration Bond Fund underperformed the Lehman Brothers Government/Credit Index while longer-term investments in the PF PIMCO Inflation Managed Fund helped performance. Overall, the fund’s limited domestic equity allocations, although positive, underperformed when compared to the S&P 500 Index. PF Portfolio Optimization Model B Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 3.28%* compared to a 6.69%** return for the S&P 500 Index, a 0.40%** return for the Lehman Brothers Government/Credit Index, and a 4.12%(2) return for the Model B Composite Benchmark Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmarks is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| A-3 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF Portfolio Optimization Model B | Class A | Class B | Class C | ||||||

| 1 Year Total Return: | |||||||||

| Without sales charge* | 3.28 | % | 2.69 | % | 2.70 | % | |||

| With maximum sales charge*** | -2.40 | % | -2.31 | % | 1.70 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 0.40 | % | |||||||

| S&P 500 Index** | 6.69 | % | |||||||

| Model B Composite Benchmark(2) | 4.12 | % | |||||||

| Since Inception: | |||||||||

| Without sales charge* | 3.77 | % | 3.21 | % | 3.22 | % | |||

| With maximum sales charge*** | -0.81 | % | 0.02 | % | 3.22 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 2.78 | % | |||||||

| S&P 500 Index** | 6.74 | % | |||||||

| Model B Composite Benchmark(2) | 5.29 | % | |||||||

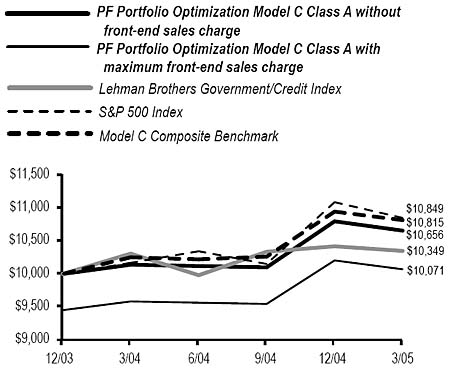

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. PF Portfolio Optimization Model B invests the majority of its assets in a diverse group of four fixed income funds, with the remaining allocations invested in domestic and international equity funds. Since its launch on December 31, 2003, the fund’s net assets have grown to over $41 million. The fund’s allocations to money market and fixed income funds, which represent a combined target allocation of 56% of the overall fund, held back fund performance. Generally, longer maturity issues outperformed shorter maturities during the quarter. The fund’s investment in the PF Goldman Sachs Short Duration Bond Fund underperformed the Lehman Brothers Government/Credit Index, while longer-term investments in the PF PIMCO Inflation Managed Fund and the PF PIMCO Managed Bond Fund helped performance. Overall, the fund’s limited domestic equity allocations, although positive, underperformed when compared to the S&P 500 Index. PF Portfolio Optimization Model C Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 5.09%* compared to a 6.69%** return for the S&P 500 Index, a 0.40%** return for the Lehman Brothers Government/Credit Index, and a 5.50%(3) return for the Model C Composite Benchmark Index. Complete performance information for all classes is included in the following table. |

| Performance Comparison |

| The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmarks is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 | |||||||||

| PF Portfolio Optimization Model C | Class A | Class B | Class C | ||||||

| 1 Year Total Return: | |||||||||

| Without sales charge* | 5.09 | % | 4.55 | % | 4.53 | % | |||

| With maximum sales charge*** | -0.69 | % | -0.45 | % | 3.53 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 0.40 | % | |||||||

| S&P 500 Index** | 6.69 | % | |||||||

| Model C Composite Benchmark(3) | 5.50 | % | |||||||

| Since Inception: | |||||||||

| Without sales charge* | 5.21 | % | 4.70 | % | 4.60 | % | |||

| With maximum sales charge*** | 0.57 | % | 1.52 | % | 4.60 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 2.78 | % | |||||||

| S&P 500 Index** | 6.74 | % | |||||||

| Model C Composite Benchmark(3) | 6.47 | % | |||||||

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

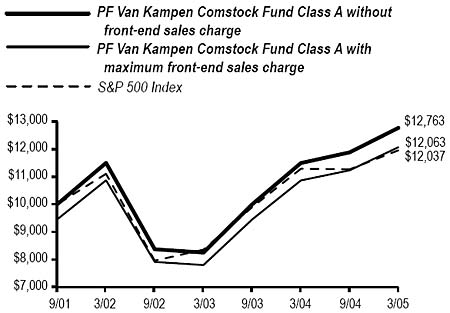

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. PF Portfolio Optimization Model C invests in a diverse group of eight domestic and international equity funds, with smaller allocations to fixed income and money market funds. Since its launch on December 31, 2003, the fund’s net assets have grown to over $125 million. The fund’s domestic equity allocations, representing 45% of the fund’s target allocations, although positive, detracted from fund performance compared to the S&P 500 Index. Generally, value-oriented stocks drove performance during the past year. The fund’s investments in the PF Van Kampen Comstock Fund |

| A-4 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

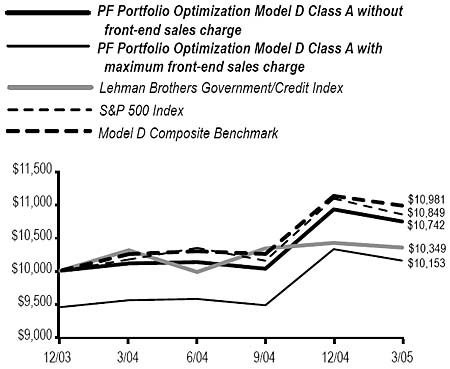

| and the PF Van Kampen Mid-Cap Growth Fund outperformed relative to the S&P 500 Index. The fund’s allocations to the international equity funds, which represent a combined target allocation of 18% of the overall fund, held back fund performance. In particular, the fund’s investment in the PF MFS International Large-Cap Fund underperformed relative to the MSCI EAFE Index. PF Portfolio Optimization Model D Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 6.26%* compared to a 6.69%** return for the S&P 500 Index, a 0.40%** return for the Lehman Brothers Government/Credit Index, and a 7.14%(4) return for the Model D Composite Benchmark Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmarks is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 | |||||||||

| PF Portfolio Optimization Model D | Class A | Class B | Class C | ||||||

| 1 Year Total Return: | |||||||||

| Without sales charge* | 6.26 | % | 5.79 | % | 5.72 | % | |||

| With maximum sales charge*** | 0.40 | % | 0.79 | % | 4.72 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 0.40 | % | |||||||

| S&P 500 Index** | 6.69 | % | |||||||

| Model D Composite Benchmark(4) | 7.14 | % | |||||||

| Since Inception: | |||||||||

| Without sales charge* | 5.90 | % | 5.44 | % | 5.31 | % | |||

| With maximum sales charge*** | 1.23 | % | 2.27 | % | 5.31 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 2.78 | % | |||||||

| S&P 500 Index** | 6.74 | % | |||||||

| Model D Composite Benchmark(4) | 7.77 | % | |||||||

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. PF Portfolio Optimization Model D invests primarily in a diverse group of nine domestic and international equity funds, with small allocations to three fixed income funds. Since its launch on December 31, 2003, the fund’s net assets have grown to over $111 million. The fund’s domestic equity allocations, representing 57% of the fund’s target allocations, although positive, detracted from fund performance compared to the S&P 500 Index. Generally, value-oriented stocks drove performance during the past year. The fund’s investments in the PF Van Kampen Comstock Fund and the PF Van Kampen Mid-Cap Growth Fund outperformed relative to the S&P 500 Index. The fund’s investments in the PF AIM Blue Chip Fund held back performance relative to the S&P 500 Index. The fund’s international equity allocations, representing 25% of the fund’s target allocation, also held back portfolio performance. The fund’s investment in the PF MFS International Large-Cap Fund trailed the MSCI EAFE Index. The fund’s target allocations to fixed income funds, representing 18% of the fund’s target allocations, contributed positively to fund performance relative to the Lehman Brothers Government/Credit Index. |

| A-5 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

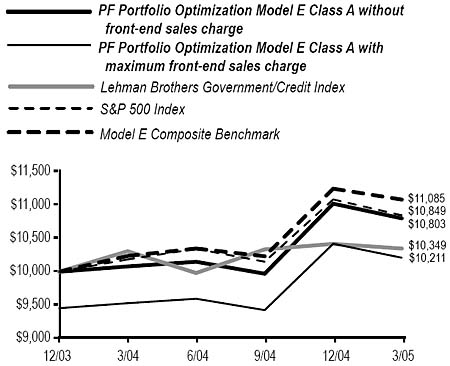

| PF Portfolio Optimization Model E Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 7.17%* compared to a 6.69%** return for the S&P 500 Index, a 0.40%** return for the Lehman Brothers Government/Credit Index, and a 8.28%(5) return for the Model E Composite Benchmark Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmarks is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 | |||||||||

| PF Portfolio Optimization Model E | Class A | Class B | Class C | ||||||

| 1 Year Total Return: | |||||||||

| Without sales charge* | 7.17 | % | 6.75 | % | 6.75 | % | |||

| With maximum sales charge*** | 1.25 | % | 1.75 | % | 5.75 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 0.40 | % | |||||||

| S&P 500 Index** | 6.69 | % | |||||||

| Model E Composite Benchmark(5) | 8.28 | % | |||||||

| Since Inception: | |||||||||

| Without sales charge* | 6.38 | % | 5.95 | % | 5.95 | % | |||

| With maximum sales charge*** | 1.69 | % | 2.79 | % | 5.95 | % | |||

| Lehman Brothers | |||||||||

| Government/Credit Index** | 2.78 | % | |||||||

| S&P 500 Index** | 6.74 | % | |||||||

| Model E Composite Benchmark(5) | 8.59 | % | |||||||

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. PF Portfolio Optimization Model E invests primarily in a diverse group of nine domestic and international equity funds. Since its launch on December 31, 2003, the fund’s net assets have grown to over $41 million. The fund’s domestic equity allocations, representing 68% of the fund’s target allocations, although positive, detracted from fund performance compared to the S&P 500 Index. Generally, value-oriented stocks drove performance during the period. The fund’s investments in the PF Van Kampen Comstock Fund and the PF Van Kampen Mid-Cap Growth Fund outperformed relative to the S&P 500 Index, while the fund’s investments in the PF AIM Blue Chip Fund held back performance relative to the S&P 500 Index. The fund’s international equity allocations, representing 29% of the fund’s target allocation, held back portfolio performance. The fund’s investment in the PF MFS International Large-Cap Fund trailed the MSCI EAFE Index. |

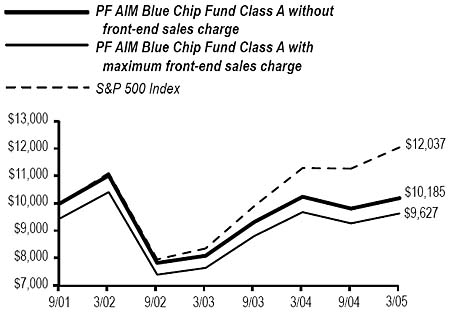

| PF AIM Blue Chip Fund Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned –0.49%* compared to a 6.69%** return for its benchmark, the S&P 500 Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the S&P 500 Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| A-6 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF AIM Blue Chip Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | -0.49 | % | -0.89 | % | -0.89 | % | |||||

| With maximum sales charge*** | -5.94 | % | -5.85 | % | -1.89 | % | |||||

| S&P 500 Index** | 6.69 | % | |||||||||

| 3 Year Total Return: | |||||||||||

| Without sales charge* | -2.56 | % | -3.01 | % | -3.02 | % | |||||

| With maximum sales charge*** | -4.38 | % | -4.33 | % | -3.02 | % | |||||

| S&P 500 Index** | 2.74 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 0.53 | % | 0.04 | % | 0.03 | % | |||||

| With maximum sales charge*** | -1.08 | % | -0.82 | % | 0.03 | % | |||||

| S&P 500 Index** | 5.44 | % |

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. |

| A. During the one-year period ending March 31, 2005, investors started out by focusing on election year politics and the instability in Iraq, and later shifted their attention to the rise in oil prices and fears of inflation. The equity markets posted modest gains, and the U.S. economy grew at a healthy pace. The NASDAQ Composite Stock Index (NASDAQ) posted a slight gain of 0.25%**, the Dow Jones Industrial Average (DJIA) returned 3.79%**, and the S&P 500 Index increased by 6.69%**. The final reading of fourth quarter 2004 GDP growth was unrevised at 3.8%, and early estimates for the first quarter of 2005 predict a growth rate between 3% and 4%. |

| Manufacturing activity was robust as the widely recognized Institute for Supply Management (ISM) index, a measure of manufacturing activity, remained above 50 during the entire one-year period, finishing the month of March at 55.2. Any reading above 50 indicates growth in the sector and March marks the twenty-second consecutive month of growth. Within this most recent report, however, prices paid spiked higher due to rising energy prices. Higher prices were evident in the core finished goods producer price index (Core PPI), which rose in January and February, and increased the twelve-month core finished goods inflation rate to 2.8%, its highest level since May 1992. |

| The overall employment picture improved throughout the year as the unemployment rate fell to 5.2% by the end of March. Job creation improved during this period, although the payroll figures were volatile, ranging dramatically from month to month. |

| Consumer confidence got a boost from the improving employment situation, hitting its highest level since 2002. The Conference Board’s Index of Consumer Confidence finished the period at 102.4 in March, off its July peak, but still quite strong due to a positive consumer outlook. Consumer spending also remained healthy, despite rising energy costs and creeping inflation. |

During the period, the fund’s investment strategy blended two complimentary investment disciplines with a focus on quality market leaders. We at A I M Capital Management, Inc. (AIM) seek companies with attractive growth profiles, focusing on sustainable, long-term earnings growth for the fund. We also seek companies that are trading at attractive valuations relative to their earnings fundamentals and growth prospects. Finally, we focus on high-quality companies that are well-established market leaders, with solid financial positions and strong business franchises. On average, the fund held overweight positions in the information technology and industrials sectors, and held underweight positions in the consumer staples, energy, financials, telecommunication services, and utilities sectors relative to the benchmark during the one-year period. Holdings in information technology stocks were detractors to fund performance, as this was the worst performing sector for this period. Energy stocks performed very well during the one-year period due to the increasing price of oil, but the fund’s underweight position in this sector detracted significantly from relative performance. Stock picks in consumer staples and industrials also detracted from the fund’s return when compared to the benchmark during the period. Although these sectors detracted from relative performance, energy and industrials stocks made the largest positive contributions to the fund’s overall return. |

| Over the past year, the value style of investing continued to significantly outperform the growth style and mid-capitalization stocks continued to outperform large-capitalization stocks. This environment also worked against the fund, as it maintains a consistent, disciplined approach of seeking out high-quality, large-capitalization growth companies that are reasonably priced. |

| The top five contributors to the fund’s return for the one-year period were Exxon Mobil Corp., UnitedHealth Group Inc., Johnson & Johnson, General Electric Co., and Canadian National Railway Co. The top five detractors to fund performance were Pfizer Inc., Cisco Systems, Inc., American International Group, Inc., Wal-Mart Stores, Inc., and Citigroup Inc. |

| A-7 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

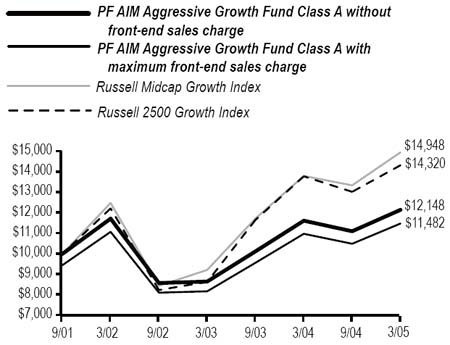

| PF AIM Aggressive Growth Fund |

| Q. How did the fund perform over the year ended March 31, 2005? |

| A. For the year ended March 31, 2005, the fund’s Class A returned 4.54%* compared to a 8.31%** return for its benchmarks, the Russell Midcap Growth Index and a 3.91%** return for the Russell 2500 Growth Index. The fund’s benchmark was changed to the Russell Midcap Growth Index due to the fund’s style of investing in mid-capitalization growth-oriented companies. Complete performance information for all classes is included in the following table. |

| Performance Comparison |

| The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmarks is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF AIM Aggressive Growth Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 4.54 | % | 3.97 | % | 4.06 | % | |||||

| With maximum sales charge*** | -1.20 | % | -1.03 | % | 3.06 | % | |||||

| Russell Midcap Growth Index** | 8.31 | % | |||||||||

| Russell 2500 Growth Index** | 3.91 | % | |||||||||

| 3 Year Total Return: | |||||||||||

| Without sales charge* | 1.20 | % | 0.72 | % | 0.78 | % | |||||

| With maximum sales charge*** | -0.70 | % | -0.61 | % | 0.78 | % | |||||

| Russell Midcap Growth Index** | 6.19 | % | |||||||||

| Russell 2500 Growth Index** | 5.43 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 5.72 | % | 5.20 | % | 5.26 | % | |||||

| With maximum sales charge*** | 4.03 | % | 4.44 | % | 5.26 | % | |||||

| Russell Midcap Growth Index** | 12.17 | % | |||||||||

| Russell 2500 Growth Index** | 10.80 | % |

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. |

| A. During the one-year period ending March 31, 2005, investors started out by focusing on election year politics and the instability in Iraq, and later shifted their attention to the rise in oil prices and fears of inflation. The equity markets posted modest gains, and the U.S. economy grew at a healthy pace. The NASDAQ posted a slight gain of 0.25%**, the DJIA returned 3.79%**, and the S&P 500 Index increased by 6.69%**. Mid-capitalization stocks outperformed large- and small-capitalization stocks, and the value style of investing outperformed the growth style of investing for the one-year period. The final reading of fourth quarter 2004 GDP growth was unrevised at 3.8%, and early estimates for the first quarter of 2005 predict a growth rate between 3% and 4%. |

| Manufacturing activity was robust as the widely recognized ISM index remained above 50 during the entire one-year period, finishing the month of March at 55.2. Any reading above 50 indicates growth in the sector and March marks the twenty-second consecutive month of growth. Within this most recent report, however, prices paid spiked higher due to rising energy prices. Higher prices were evident in the Core PPI, which rose in January and February, and increased the twelve-month core finished goods inflation rate to 2.8%, its highest level since May 1992. |

| The overall employment picture improved throughout the year as the unemployment rate fell to 5.2% by the end of March. Job creation improved during this period, although the payroll figures were volatile, ranging dramatically from month to month. |

| Consumer confidence got a boost from the improving employment situation, hitting its highest level since 2002. The Conference Board’s Index of Consumer Confidence finished the period at 102.4 in March, off its July peak, but still quite strong due to a positive consumer outlook. Consumer spending also remained healthy, despite rising energy costs and creeping inflation. |

| Stock selection in the health care and consumer discretionary sectors were detractors to fund performance during the period. Within the health care sector, stock picks in biotechnology detracted the most from performance when compared to the benchmark, while holdings in hotels, restaurants, and leisure companies detracted the most from performance within the consumer discretionary sector. The fund’s underweight position relative to the benchmark in the energy sector also hurt relative performance, as this sector performed very well during the year. In contrast, the information technology sector contributed significantly to the fund’s return when compared to the benchmark. Within this sector, semiconductors and semiconductor equipment stocks added the most value relative to the benchmark. On an absolute basis, the information technology, financials, and consumer |

| A-8 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

discretionary sectors made the largest contributions to fund performance during the year. |

Sector exposure in the fund is a result of AIM’s bottom-up stock selection process in the context of prudent risk management. During the period, the fund’s holdings in health care and materials stocks were significantly increased, and the number of holdings in consumer discretionary and information technology stocks were decreased. |

The top five contributors to fund performance for the year were Textron Inc., Alliance Data Systems Corp., CB Richard Ellis Group, Inc., Investors Financial Services Corp., and Staples, Inc. The top five detractors to fund performance were Sirva Inc., Corinthian Colleges, Inc., Taro Pharmaceutical Industries Ltd., Omnicare, Inc., and New York Community Bancorp, Inc. |

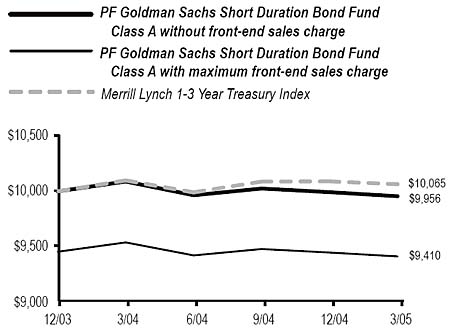

PF Goldman Sachs Short Duration Bond Fund |

Q. How did the fund perform over the year ended March 31, 2005? |

A. For the year ended March 31, 2005, the fund’s Class A returned –1.34%* compared to a –0.35%** return for its benchmark, the Merrill Lynch 1-3 Year Treasury Index. Complete performance information for all classes is included in the following table. |

Performance Comparison |

The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the Merrill Lynch 1-3 Year Treasury Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF Goldman Sachs Short Duration Bond Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | -1.34 | % | -1.77 | % | -1.81 | % | |||||

| With maximum sales charge*** | -6.78 | % | -6.65 | % | -2.78 | % | |||||

| Merrill Lynch 1-3 Year | |||||||||||

| Treasury Index** | -0.35 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | -0.36 | % | -0.79 | % | -0.82 | % | |||||

| With maximum sales charge*** | -4.75 | % | -3.96 | % | -0.82 | % | |||||

| Merrill Lynch 1-3 Year | |||||||||||

| Treasury Index** | 0.52 | % |

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. |

A. The Treasury yield curve flattened dramatically over the reporting period with shorter to intermediate term yields rising more than long-term yields. Consequently, the long end of the curve (ten years and longer) significantly outperformed the short to intermediate portion of the curve. Short-term interest rates rose in response to the Fed’s cumulative 175 basis point increase in the Federal Funds rate and longer-term interest rates rose less, due to mixed economic data, rising oil prices, and continued geopolitical uncertainty. The Federal Funds rate began the reporting period at 1.00% and closed at 2.75%. |

At the beginning of the period, a series of unexpectedly strong monthly non-farm payroll data releases and evidence of inflationary pressures sparked increased optimism of economic growth and drove a sell-off across the broader fixed income market. In response to these indications of economic strength, at its June 30, 2004 meeting, the Fed raised the overnight lending rate by 25 basis points to 1.25%, its first rate hike since April 2000. The markets then turned to rising oil prices as a general theme during the summer months leading into fall, interpreting rising energy prices as a check on growth rather than inflationary. Rising oil prices stemmed from supply uncertainty, hurricane weather, and continued violence in Iraq. Increased concerns over inflationary pressures and expectations of continued (and possibly accelerated) Fed tightening drove interest rates higher at the end of the reporting period. The Fed raised rates a total of seven times over the one-year period. |

A combination of top-down and bottom-up strategies were the primary drivers of fund performance over the period. Top-down strategies for the fund included active sector rotation, duration, and yield curve management. Over the period, the fund was positioned defensively. In particular, a modestly shorter duration was maintained relative to the benchmark, based on Goldman Sachs Asset Management L.P.’s belief that interest rates would move higher. Despite detracting from fund performance in the months that yields rallied on the back of |

| A-9 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

mixed economic data, our short duration strategy was an overall contributor to returns as interest rates ended the period higher. Our sector strategy, which concentrated on the high quality segments of the fixed income market, namely Treasuries and agency debentures, also positively impacted fund returns. The largest weighting in the fund during the period was in the Agency sector where we continue to find attractive values relative to Treasuries. |

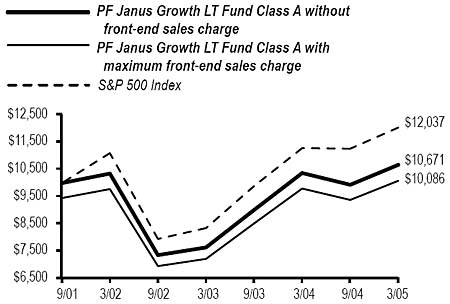

PF Janus Growth LT Fund |

Q. How did the fund perform over the year ended March 31, 2005? |

A. For the year ended March 31, 2005, the fund’s Class A returned 2.90%* compared to a 6.69%** return for its benchmark, the S&P 500 Index. Complete performance information for all classes is included in the following table. |

Performance Comparison |

The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the S&P 500 Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF Janus Growth LT Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 2.90 | % | 2.44 | % | 2.45 | % | |||||

| With maximum sales charge*** | -2.74 | % | -2.56 | % | 1.45 | % | |||||

| S&P 500 Index** | 6.69 | % | |||||||||

| 3 Year Total Return: | |||||||||||

| Without sales charge* | 1.02 | % | 0.61 | % | 0.48 | % | |||||

| With maximum sales charge*** | -0.86 | % | -0.72 | % | 0.48 | % | |||||

| S&P 500 Index** | 2.74 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 1.87 | % | 1.45 | % | 1.36 | % | |||||

| With maximum sales charge*** | 0.24 | % | 0.62 | % | 1.36 | % | |||||

| S&P 500 Index** | 5.44 | % |

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. |

A. We at Janus Capital Management LLC continue to manage the fund for shareholders who want more aggressive long-term exposure to the equity markets. We tend to gravitate to companies that we believe have good growth trends and sustainable competitive advantages within the large- and mid-capitalization areas of the market. During this somewhat volatile period, we made a conscious effort to better balance the fund’s exposure across an assortment of sectors, with the intention of reducing the risk tied to the market’s frequent sector rotations. During the period, the investment team sought out more steady-growth businesses for the fund, as the yield curve on federal debt issues suggested a slow down in the economy. |

|

Detractors to fund performance during the period were a smaller position than the benchmark in the energy sector, which enjoyed increased profits as oil prices spiked to record highs. Weak performances by select holdings in information technology also held back fund performance. Technology leader Cisco Systems, Inc. fell short during the period as a result of sluggish enterprise spending. On the positive side, Cisco continues to aggressively repurchase its own stock, thereby shrinking the number of outstanding shares. This tactic typically helps companies succeed over time. Furthermore, we believe Cisco will be the beneficiary of both a recovery in corporate networking spending where it has leading market share and increasing market share in telecommunications network spending. With this in mind, we are willing to exercise patience with regards to Cisco. |

|

Another weak performer for the twelve-month period was Samsung Electronics Co. Ltd., South Korea’s top electronics and semiconductor chip maker. Though investors have recently shied away from such high-growth and presumably high-risk names, we believe the semiconductor industry has sizable growth potential due to lower inventories and the chance for a rebound in capital spending. As such, during the first quarter of 2005, Samsung posted an impressive gain, rewarding our confidence in semiconductor makers and bouncing past its U.S. counterparts, Texas Instruments Inc. and Intel Corp. While these two companies also had a solid quarter, they did not outperform to the extent that Samsung did. |

|

Meanwhile, a number of the fund’s investments in media stocks, as well as consumer discretionary stocks, contributed to fund performance. The fund’s “fallen-growth” names (former growth companies that currently are either restructuring or refocusing their businesses) by definition require considerable patience. In that group is Liberty Media Corp. “A”. Earlier in 2004, Chief Executive Officer John Malone took steps to simplify the media conglomerate’s complex structure by spinning off its growing stable of international holdings into a new enterprise, Liberty Media International, Inc. “A”. For years, investors had avoided Liberty Media’s stock because it proved too difficult to calculate the value of the company’s myriad |

| A-10 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

assets, which include QVC, the Discovery Channel and News Corp., as well as European and Japanese cable operations. Separating Liberty’s fast-growing, capital-intensive international properties from its mature, cash-generating U.S. businesses has unlocked the upside of each, doubly rewarding the fund. |

Meanwhile, Starwood Hotels & Resorts Worldwide, Inc. moved ahead as interest in another leisure activity - travel - finally started to pick up three years after the September 11 terrorist attacks. With the discretionary income that a stronger economy affords them, Americans are flocking to foreign destinations as near as Canada and as far as India. At the same time, a weak dollar is attracting foreigners eager to visit big-draw East Coast cities like New York, Boston and Orlando. We are pleased to see that Starwood’s 700-plus hotels, operated under several brand names including St. Regis, Sheraton and Westin, are benefiting from this pent-up demand and the increasingly higher room rates that demand is driving. |

As always, the investment team will comb every corner of the market for companies that can further enhance diversification as they help achieve an optimal balance between risk and reward. |

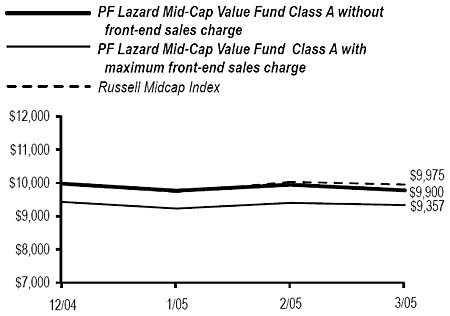

PF Lazard Mid-Cap Value Fund |

Q. How did the fund perform for the period ended March 31, 2005? |

A. The fund commenced operations on December 31, 2004. For the period since inception through March 31, 2005, the fund’s Class A returned –1.00%* compared to a –0.25%** return for its benchmark, the Russell Midcap Index. Complete performance information for all classes is included in the following table. |

Performance Comparison |

The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the Russell Midcap Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Total Returns (Non-Annualized) for the Period Ended March 31, 2005 |

| PF Lazard Mid-Cap Value Fund | Class A | Class B | Class C | ||||||||

| Since Inception: | |||||||||||

| Without sales charge* | -1.00 | % | -1.10 | % | -1.10 | % | |||||

| With maximum sales charge*** | -6.43 | % | -6.05 | % | -2.09 | % | |||||

| Russell Midcap Index** | -0.25 | % |

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| Q. Discuss both positive and negative factors that materially affected the fund’s performance during the period, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. |

A. U.S. markets whipsawed during the quarter, as declines in January 2005 were erased by gains in February, finally ending the quarter modestly negative. During the March Federal Open Market Committee (FOMC) meeting, the Fed cited increasing inflation pressures and evidence of pricing power, which led investors to believe that more aggressive monetary tightening might lie ahead. This renewed fear of inflation caused the market to decline in March, impacting more cyclical stocks, especially commodity producers. Large-capitalization stocks handily outperformed small-capitalization stocks during the quarter. However, mid-capitalization stocks continued to outperform both large- and small-capitalization stocks. Merger activity during the quarter was strong, with about thirty-four mergers greater than $1 billion occurring, totaling over $200 billion combined. From a sector perspective, defensive stocks, such as consumer staples and utilities, held up while pharmaceutical stocks did not. Overall, technology stocks lagged, but semiconductor stocks were stronger as the outlook for demand improved. A profit warning from General Motors Corp. weighed heavily on consumer durables, causing stocks within the auto sector to decline. Once again, energy was the best performing sector as the price of oil rebounded, ending the first quarter of 2005 slightly off its 2004 peak. |

During the period, the fund benefited from stock selection in the telecommunication services sector, as two of the fund’s holdings were takeover targets. Verizon Communications Inc. made a bid for MCI Inc., and Alltel Corp. agreed to purchase Western Wireless Corp. “A”. Conversely, stock selection in the consumer discretionary sector detracted from fund performance as one of the fund’s largest holdings, Westwood One, Inc. declined after reporting disappointing earnings. We at Lazard Asset Management LLC (Lazard) remain positive on the stock’s long-term ability to generate strong returns, and believe that the consensus expectation for long-term growth in radio is too low. Stock selection in the consumer durables sector also hurt fund performance, as Lear Corp. shares declined due to slowing production at General Motors Corp. However, we believe that this situation should improve later in the year as new sport utility vehicle production begins. |

| A-11 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

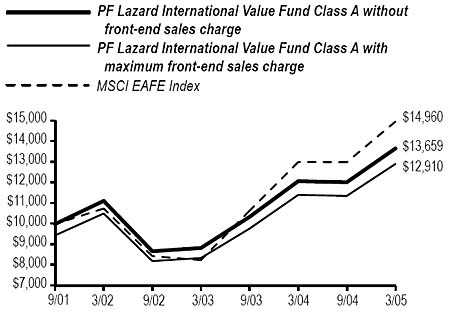

PF Lazard International Value Fund |

Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 13.13%* compared to a 15.06%** return for its benchmark, the MSCI EAFE Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the MSCI EAFE Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF Lazard International Value Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 13.13 | % | 12.59 | % | 12.59 | % | |||||

| With maximum sales charge*** | 6.93 | % | 7.59 | % | 11.59 | % | |||||

| MSCI EAFE Index** | 15.06 | % | |||||||||

| 3 Year Total Return: | |||||||||||

| Without sales charge* | 7.09 | % | 6.53 | % | 6.53 | % | |||||

| With maximum sales charge*** | 5.08 | % | 5.34 | % | 6.53 | % | |||||

| MSCI EAFE Index** | 11.47 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 9.32 | % | 8.75 | % | 8.74 | % | |||||

| With maximum sales charge*** | 7.57 | % | 8.05 | % | 8.74 | % | |||||

| MSCI EAFE Index** | 12.20 | % |

| Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. Over the last twelve months, ending March 31, 2005, the major influences on international stocks were the tightening monetary policy in the U.S., which engendered concerns about rising inflation, uncertainty over the outcome of the U.S. presidential election, rising crude oil prices, and concerns over the sustainability of growth in China. The impact on international markets, regarding the U.S. monetary policy, has been a gradual global reduction in investors’ risk tolerance. International stocks ended flat and slightly negative in the first six months of the period, rallying strongly in the third quarter, before ending the period modestly positive, in local currency terms. Europe managed to generate modest gains in the first six months of the period. In the next six months, the twelve-country euro region was among the benchmark’s best performers, although United Kingdom (U.K.) stocks trailed the other European regions. This rally started right after the U.S. presidential election, as uncertainty over the election’s outcome, as well as its definitiveness, was lifted. Japan’s economic recovery appeared to stall, as Japanese stocks were weak for the first three months of the period, fell sharply during the next three months, and then lagged for the remainder of the year, even as the yen reached a four-year high. Throughout the period, small- and mid-capitalization stocks outperformed larger-capitalization stocks, with small-capitalization stocks continuing their almost five-year run of outperformance. The energy sector was the best performer for the period, although it lagged the broad market in October, November, and December of 2004 when oil prices had crested. During the twelve-month period ending March 31, 2005, the fund benefited from stock selection, particularly in the health care and financials sectors. In health care, GlaxoSmithKline PLC shares rose due to the company’s strong pipeline of new drugs. It also reported a rise in fourth quarter 2004 profits, as an asset sale and reduced spending countered declining Paxil revenues. The company forecast low double-digit earnings growth, thanks to rising sales of drugs such as Avandia and Advair. In financials stocks, Allied Irish Banks PLC (AIB) shares rose as the company benefited from strong loan demand in 2004. The bank’s performance in the second half of 2004 more than doubled, aided by higher lending in Ireland and the U.K., and lower costs. A pick-up in AIB’s Polish unit also helped to counter the impact of the weaker dollar on U.S. earnings. From a sector weight perspective, the fund benefited from an overweight position versus the benchmark in energy stocks and an underweight position in consumer discretionary stocks. In the energy sector, ENI SPA experienced a gradual but steady upward re-rating versus larger European oil companies. A successful shift of capital employed and profit mix from the domestic gas transportation business to a global upstream business has underpinned the re-rating, coupled with capable management guidance, growing reserves and production, attention to unit costs, and a generous dividend. Conversely, lack of exposure to materials and an underweight position in utilities hurt performance. In the past two years, investors have aggressively embraced risk in many forms, emboldened by the extremely accommodative monetary policy in most major economies. This embrace of risk can be seen in the dramatic outperformance of smaller, less profitable, more leveraged companies globally. This environment has been challenging for Lazard’s investment process, which focuses on identifying high quality, financially productive companies trading at attractive valuations. However, as interest rates rise, we believe that investors’ risk tolerance should moderate. We believe that the rebound, during the first quarter of 2005, in larger stocks in the U.S. may spread |

| A-12 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

globally, and lead to an environment where individual company fundamentals drive stock returns. |

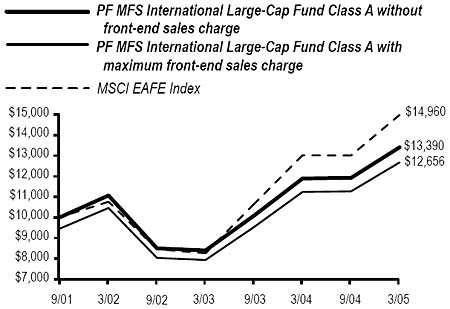

PF MFS International Large-Cap Fund |

Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 12.73%* compared to a 15.06%** return for its benchmark, the MSCI EAFE Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the MSCI EAFE Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF MFS International Large-Cap Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 12.73 | % | 12.18 | % | 12.16 | % | |||||

| With maximum sales charge*** | 6.49 | % | 7.18 | % | 11.16 | % | |||||

| MSCI EAFE Index** | 15.06 | % | |||||||||

| 3 Year Total Return: | |||||||||||

| Without sales charge* | 6.60 | % | 6.03 | % | 6.09 | % | |||||

| With maximum sales charge*** | 4.61 | % | 4.83 | % | 6.09 | % | |||||

| MSCI EAFE Index** | 11.47 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 8.70 | % | 8.12 | % | 8.17 | % | |||||

| With maximum sales charge*** | 6.96 | % | 7.41 | % | 8.17 | % | |||||

| MSCI EAFE Index** | 12.20 | % | |||||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. Stocks experienced considerable volatility during the twelve months ended March 31, 2005. Investors endured skyrocketing oil prices, a volatile and retreating U.S. dollar, record U.S. budget and trade deficits, and war in Iraq. Fundamental economic factors, however, such as corporate spending and earnings, continued to improve around the globe. By the second half of the period, investors seemed to conclude that the global economic recovery, although modest, was still intact. In the end, fundamental economic factors triumphed and most equity markets delivered positive results for the period as a whole. Relative to the fund’s benchmark, leisure, special products and services, and utilities and communications were the sectors that detracted most significantly from fund performance. In all three sectors, stock selection was the key factor that held back results over the period. In the leisure sector, the fund’s position in U.K. satellite television broadcaster British Sky Broadcasting Group PLC declined in price after management said it would boost capital spending to spur growth. We at MFS Investment Management sold the stock because we believed that the change in the company’s business plan would reduce its long-term profitability. Elsewhere in the sector, the fund’s holding in Japanese video game maker Nintendo Co. Ltd. also lost value over the period. Within the special products and services sector, the primary detractor from performance was the fund’s position in NOK Corp., a Japanese producer of auto parts and electrical components. Japanese wireless telecommunications firm KDDI Corp. was the major detractor from results in the utilities and communications area. The stock declined on worries that increased competition would lead to weaker profits and cash flow growth. Fund holdings in other sectors that lost ground during the period and hurt relative fund performance included Samsung SDI Co., Ltd., a Korean maker of digital display screens and rechargeable batteries, U.K.-headquartered financial services company AMVESCAP PLC, and Japanese electronic component firm Murata Manufacturing Co., Ltd. The fund’s cash position also detracted from relative performance. As with nearly all mutual funds, this fund holds some cash to buy new holdings and to provide liquidity. In a period when international equity markets rose sharply, holding any cash hurt performance against the fund’s benchmark, which has no cash position. Relative to the fund’s benchmark, technology and consumer staples were the fund’s strongest-performing sectors over the period. Taken as a group, the fund’s positions in technology stocks delivered slightly positive performance, while the benchmark’s holdings in the sector declined significantly. Stock selection was the key factor in the fund’s strong relative performance in the consumer staples area. U.K.-headquartered Reckitt Benckiser PLC, one of the world’s largest makers of household cleaning products, was the strongest relative contributor in the sector. Fund positions in other sectors that aided relative results included OTP Bank RT in Hungary and Erste Bank der Oesterreichischen Sparkassen AG in Austria, two larger regional banks with exposure to eastern European customers. Holdings in Companhia Vale do Rio Doce (CVRD) in Brazil, the world’s largest miner of iron ore, rose sharply as a result of |

| A-13 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

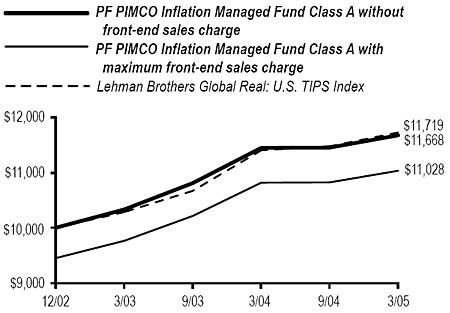

increasing global demand and higher prices for its product. The fund’s position in Canadian National Railway Co. also increased in price. Holding Canadian firm EnCana Corp., one of North America’s largest independent oil and gas producers, proved beneficial to returns as rising energy prices helped the stock perform strongly. Avoiding cellular equipment manufacturer Nokia OYJ, whose stock price sank over the period, contributed to relative returns as well. During the reporting period, shifts in currency valuations were also a significant contributor to performance relative to the benchmark. The base currency of the fund is U.S. dollars and the performance of the fund and its benchmark are presented in terms of this currency. Nevertheless, specific holdings of the fund and the benchmark may be denominated in different currencies and, therefore, present the possibility of currency depreciation or appreciation. Because the exposures of the fund and the benchmark to foreign currency movements may differ from time to time, these movements may have a material impact on relative performance. PF PIMCO Inflation Managed Fund Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 1.99%* compared to a 2.82%** return for its benchmark, the Lehman Brothers Global Real: U.S. TIPS Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the Lehman Brothers Global Real: U.S. TIPS Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF PIMCO Inflation Managed Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 1.99 | % | 1.43 | % | 1.44 | % | |||||

| With maximum sales charge*** | -3.66 | % | -3.37 | % | 0.48 | % | |||||

| Lehman Brothers Global Real: | |||||||||||

| U.S. TIPS Index** | 2.82 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 7.11 | % | 6.55 | % | 6.56 | % | |||||

| With maximum sales charge*** | 4.45 | % | 4.89 | % | 6.56 | % | |||||

| Lehman Brothers Global Real: | |||||||||||

| U.S. TIPS Index** | 7.30 | % |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. After concerns about the durability of the U.S. economy pushed low interest rates lower in the first quarter of 2004, market optimism was revived during the second quarter after a series of robust non-farm payroll growth and inflation releases suggested to investors that the economy indeed was on track. Short-term interest rates increased during the second quarter and fixed income markets sold off, giving back all the gains of the first quarter. The third quarter was essentially a reversal of the previous three months. Economic data releases suggested moderate economic growth, as job numbers, inflation and consumer confidence fell short of analyst expectations, again throwing doubts on the strength of the recovery. Bonds subsequently rallied as the weak employment growth and lower than expected rate of inflation prompted a fall in interest rates. The rally of the third quarter continued into the last three months of 2004 where all major fixed income sectors posted gains, capping a year in which bonds showed unexpected strength. Bonds lost ground during the first quarter of 2005 as volatile interest rates and weakness in credit markets related to concerns about auto issues weighed on fixed income securities. Higher oil prices also fuelled a rise in inflation expectations, which led to nominal yields rising more than real yields. A below benchmark duration from Treasury Inflation Protected Securities (TIPS) during the first six months of the period contributed to fund performance as real yields rose. During the final six months, the fund shifted to slightly longer-than-benchmark duration from TIPS, which was neutral for performance as real yields were essentially unchanged during this period. An overweight position to shorter maturity TIPS during the period was negative for performance as the real yield curve flattened. Exposure to Eurozone nominal interest rates, primarily via German Bund futures, was positive as Eurozone yields fell during the period in contrast to U.S. yields, which rose. An allocation to emerging market bonds was also positive for fund performance as spreads on emerging market debt narrowed during the twelve-month period. |

| A-14 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

With regards to strategy, Pacific Investment Management Co. LLC (PIMCO) will likely employ defensive strategies that enhance yield but protect investors’ capital should global stability erode. Key strategies we expect to employ include: an above benchmark duration from TIPS as real rates in the U.S. are expected to remain lower than historic norms due to excess leverage and other headwinds to economic growth; a below benchmark duration through net short exposure to nominal bonds to limit risk from higher interest rates; exposure to nominal bonds in Europe, where growth and rate pressures will be more muted; an emphasis on short/intermediate maturities, which offer structural advantages given a steep yield curve; forward settled bonds, which can gain even if rates rise as long as the increase is not more than markets expect; and emerging market bonds, which offer relatively high yields and continue to display improving credit fundamentals. PF PIMCO Managed Bond Fund Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 0.56%* compared to a 0.40%** return for its benchmark, the Lehman Brothers Government/Credit Index. Complete performance information for all classes is included in the following table. Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the Lehman Brothers Government/Credit Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF PIMCO Managed Bond Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 0.56 | % | -0.05 | % | 0.04 | % | |||||

| With maximum sales charge*** | -4.99 | % | -4.84 | % | -0.92 | % | |||||

| Lehman Brothers | |||||||||||

| Government/Credit Index** | 0.40 | % | |||||||||

| 3 Year Total Return: | |||||||||||

| Without sales charge* | 6.43 | % | 5.91 | % | 5.94 | % | |||||

| With maximum sales charge*** | 4.45 | % | 4.70 | % | 5.94 | % | |||||

| Lehman Brothers | |||||||||||

| Government/Credit Index** | 6.52 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 5.40 | % | 4.88 | % | 4.90 | % | |||||

| With maximum sales charge*** | 3.72 | % | 4.11 | % | 4.90 | % | |||||

| Lehman Brothers | |||||||||||

| Government/Credit Index** | 5.44 | % |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. After concerns about the durability of the U.S. economy pushed low interest rates lower in the first quarter of 2004, market optimism was revived during the second quarter after a series of robust non-farm payroll growth and inflation releases suggested to investors that the economy indeed was on track. Short-term interest rates increased during the second quarter and fixed income markets sold off, giving back all the gains of the first quarter. The third quarter was essentially a reversal of the previous three months. Economic data releases suggested moderate economic growth, as job numbers, inflation and consumer confidence fell short of analyst expectations, again throwing doubts on the strength of the recovery. Bonds subsequently rallied as the weak employment growth and lower than expected rate of inflation prompted a fall in interest rates. The rally of the third quarter continued into the last three months of 2004 where all major fixed income sectors posted gains, capping a year in which bonds showed unexpected strength. Bonds lost ground during the first quarter of 2005 as volatile interest rates and weakness in credit markets related to concerns about auto issues weighed on fixed income securities. The U.S. yield curve continued to flatten as the Fed tightened interest rates and strong demand from speculative investors and Asian central banks supported longer maturity bonds. A below benchmark duration helped fund returns as interest rates, while volatile, generally trended upwards over the twelve-month period. An underweight position versus the benchmark to longer maturities detracted from fund returns. Longer maturities rallied as demand increased despite the Fed tightening cycle. A mortgage emphasis helped fund performance as spreads versus U.S. Treasuries tightened and the sector outperformed. Underweighting corporate bonds versus the benchmark detracted from returns as the low return environment drove |

| A-15 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |

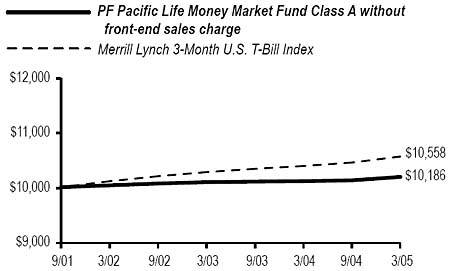

investors to seek yield in the asset class, causing historically tight credit premiums in the sector to tighten even further. A tactical allocation to real return bonds was positive as real yields fell over the period driven by higher energy prices and, thus, higher inflation expectations. Municipal bonds also helped fund returns in the volatile market as a stable base of retail demand supported municipal returns. Diversifying outside the U.S. via exposure to Eurozone issues was positive as rate movements were milder outside the U.S. Emerging markets bonds also added to fund performance as improving credit fundamentals remained and attractive yield premiums drove investor demand. With regards to strategy, PIMCO will likely employ defensive strategies that enhance yield but protect investors’ capital should global stability erode. Key strategies we expect to employ include: a target U.S. duration of neutral to 0.50 year below the benchmark, to limit risk from higher rates, with the flexibility to tactically adjust within these limits as rates near the top or bottom of our forecast range; yield curve exposure near the index, avoiding longer U.S. maturities that have been volatile this year while emphasizing longer maturity Eurozone bonds, which should benefit from demand by pension funds to lengthen their asset duration; and exposure to short-term rates via forward contracts, which offers the potential for gains if interest rates rise less than the market expects. We also expect to cautiously add to the fund’s mortgage holdings to enhance yield and add value via coupon and security selection. We will also plan to look for similar opportunities in corporates, though reduction in corporate underweight versus the benchmark will most likely be smaller than what occurred during the period. We expect to hold TIPS, which should benefit from low and stable real yields, as well as higher inflation expectations; longer maturity municipal securities, another attractive source of income given their high yield ratios versus Treasuries; and emerging market bonds, which offer currently high yields and continue to display improving credit fundamentals. PF Pacific Life Money Market Fund Q. How did the fund perform over the year ended March 31, 2005? A. For the year ended March 31, 2005, the fund’s Class A returned 0.77%* compared to a 1.67%** return for its benchmark, the Merrill Lynch 3-Month U.S. T-Bill Index. Complete performance information for all classes is included in the following table. The current yield measured during the seven-day period ending March 31, 2005 was 1.73%.* Performance Comparison The following graph shows the value as of March 31, 2005 of a $10,000 investment made in Class A shares since the fund began operations. For comparison purposes, the performance of the fund’s benchmark (the Merrill Lynch 3-Month U.S. T-Bill Index) is also shown. Performance data for Class B and C shares will vary due to differences in fees and sales charges. |

|

| Average Annual Total Returns for the Periods Ended March 31, 2005 |

| PF Pacific Life Money Market Fund | Class A | Class B | Class C | ||||||||

| 1 Year Total Return: | |||||||||||

| Without sales charge* | 0.77 | % | 0.35 | % | 0.39 | % | |||||

| Merrill Lynch 3-Month U.S. T-Bill | |||||||||||

| Index** | 1.67 | % | |||||||||

| 3 Year Total Return: | |||||||||||

| Without sales charge* | 0.51 | % | 0.18 | % | 0.19 | % | |||||

| Merrill Lynch 3-Month U.S. T-Bill | |||||||||||

| Index** | 1.47 | % | |||||||||

| Since Inception: | |||||||||||

| Without sales charge* | 0.53 | % | 0.18 | % | 0.19 | % | |||||

| Merrill Lynch 3-Month U.S. T-Bill | |||||||||||

| Index** | 1.56 | % | |||||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities. A. Corresponding with the Fed’s mid-year tightening, the short-term yield environment changed course. Beginning with the June 30, 2004 FOMC meeting, the Fed tightened the Federal Funds target rate by 0.25% at each meeting, leaving the current rate at 2.75%. More rate increases are expected, with the Federal Funds futures predicting a 3.75% rate by year-end. Consequently, the commercial paper (CP), U.S. Treasury Bill and short-term agency markets all followed suit. CP rates have steadily increased, with 30-day CP now trading near 2.8%, 60-day CP near 2.9% and 90-day CP just above 3.0%. Additionally, the CP curve has steepened somewhat, enabling the fund to opportunistically invest in longer maturity instruments in an effort to pick up yield. With the trend for interest rates moving higher, the fund employed a number of strategies to enhance overall yield during the period ended March 31, 2005. Generally, the average maturity was kept short, thus taking advantage of the |

| A-16 | See explanation of symbols and references on A-21 |

| PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued) |