Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-10385

Pacific Life Funds

(Exact name of registrant as specified in charter)

700 Newport Center Drive, P.O. Box 7500

Newport Beach, CA 92660

(Address of principal executive offices) (Zip code)

Robin S. Yonis

Vice President and General Counsel of Pacific Life Funds

700 Newport Center Drive, P.O. Box 9000

Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Anthony H. Zacharski, Esq.

Dechert LLP

90 State House Square

Hartford, CT 06103

Registrant’s telephone number, including area code: 949-219-6767

Date of fiscal year end: March 31

Date of reporting period: April 1, 2012 - March 31, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. Reports to Stockholders.

The following is a copy of the reports transmitted to stockholders pursuant to Rule 30e-1 under the Act (17 CFR 270.30e-1).

Table of Contents

ANNUAL REPORT

AS OF MARCH 31, 2013

TABLE OF CONTENTS | ||

| A-1 | ||

| A-2 | ||

| B-1 | ||

| C-1 | ||

| C-3 | ||

| C-5 | ||

| C-9 | ||

| D-1 | ||

| E-1 | ||

| F-1 | ||

| F-3 | ||

Approval of Investment Advisory Agreement and Fund Management Agreements | F-6 | |

| F-10 |

Table of Contents

We are pleased to share with you the Pacific Life Funds Annual Report dated March 31, 2013. Pacific Life Funds is comprised of thirty-three funds, eleven of which are included in this report (each individually, a “fund” and collectively, the “funds”) and are available for direct investment. Pacific Life Fund Advisors LLC (PLFA), as adviser to the funds, manages the PL Portfolio Optimization Conservative, PL Portfolio Optimization Moderate-Conservative, PL Portfolio Optimization Moderate, PL Portfolio Optimization Moderate-Aggressive and PL Portfolio Optimization Aggressive Funds (PL Portfolio Optimization Funds). Each of the PL Portfolio Optimization Funds is an asset allocation “fund of funds” and invests in certain other funds (PL Underlying Funds) of Pacific Life Funds. PLFA supervises the management of the PL Underlying Funds which are only available for investment by the PL Portfolio Optimization Funds and are included in a separate Annual Report. Please see “Where to Go for More Information” for instructions on how to obtain the PL Underlying Funds’ Annual Report. PLFA also does business under the name “Pacific Asset Management” and manages the PL Short Duration Income, PL Income, PL Strategic Income, PL Floating Rate Income, PL High Income and PL Money Market Funds under that name. The funds and the fund managers as of March 31, 2013 are listed below:

| Fund | Fund Manager | |

| PL Portfolio Optimization Conservative | ||

| PL Portfolio Optimization Moderate-Conservative | ||

| PL Portfolio Optimization Moderate | Pacific Life Fund Advisors LLC (PLFA) | |

| PL Portfolio Optimization Moderate-Aggressive | ||

| PL Portfolio Optimization Aggressive | ||

| PL Short Duration Income | Pacific Asset Management | |

| PL Income | ||

| PL Strategic Income | ||

| PL Floating Rate Income | ||

| PL High Income | ||

| PL Money Market |

We appreciate your confidence in the Pacific Life Funds and look forward to serving your financial needs in the years to come.

Sincerely,

|

| |

| James T. Morris | Mary Ann Brown | |

| Chairman of the Board | Chief Executive Officer | |

| Pacific Life Funds | Pacific Life Funds |

A-1

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION

This Annual Report is provided for the general information of investors with beneficial interests in Pacific Life Funds. This report is not authorized for distribution to prospective investors unless preceded or accompanied by a current Pacific Life Funds’ Prospectus, as supplemented, which contains information about Pacific Life Funds and each of its funds, including their investment objectives, risks, charges and expenses. You should read the Prospectus carefully before investing. There is no assurance that a fund will achieve its investment objective. Each fund is subject to market risk. The net asset value of a fund changes as the values of its assets go up or down. The value of a fund’s shares will fluctuate, and when redeemed, may be worth more or less than their original cost. The total return for each fund (including the 7-day yield for the PL Money Market Fund) includes reinvestment of all dividends and capital gain distributions, if any, and does not include deductions of any applicable sales charges. Past performance is not predictive of future performance. Performance figures for each class reflect the deduction of any applicable maximum front-end sales charge at the time of investment and reflect any applicable contingent deferred sales charge that would be deducted upon redemption at the end of the period presented.

This report shows you the performance of the funds compared to benchmark indices. Index performance is provided for illustrative and comparative purposes only and does not predict or depict the performance of the funds. Indices are unmanaged, do not incur transaction costs and cannot be purchased directly by investors. Index returns on equity securities include reinvested dividends.

The composite benchmarks for the PL Portfolio Optimization Funds are composed using four broad-based indices. The percentage amounts of each broad-based index within each composite benchmark are based on each fund’s target asset class allocations in effect during the reporting period. The percentages attributed to a broad-based index within a composite benchmark will change if a fund’s target asset class allocations change.

PLFA has written the general market conditions commentary which expresses PLFA’s opinions and view on how the market generally performed for the year ended March 31, 2013. All views are subject to change at any time based upon market or other conditions, and Pacific Life Funds, its adviser and the fund managers disclaim any responsibility to update such views. Any references to “we”, “I”, or “ours” are references to the adviser or fund manager. The adviser and fund managers may include statements that constitute “forward-looking statements” under the United States (U.S.) securities laws. Forward-looking statements include information concerning possible or assumed future results of the Pacific Life Funds’ investment operations, asset levels, earnings, expenses, industry or market conditions, regulatory developments and other aspects of the Pacific Life Funds’ operations or general economic conditions. In addition, when used in this report, predictive verbs such as “believes”, “expects”, “anticipates”, “intends”, “plans”, “estimates”, “projects” and future or conditional verbs such as “will”, “may”, “could”, “should”, and “would”, or any other statement that necessarily depends on future events, are intended to identify forward-looking statements. Forward-looking statements are not guarantees of performance or economic results. They involve risks, uncertainties and assumptions. Although such statements are based on expectations that the adviser or fund manager believes to be reasonable, actual results may differ materially from expectations. Investors must not rely on any forward-looking statements.

In connection with any forward-looking statements and any investment in the Pacific Life Funds, investors should carefully consider the investment objectives, policies and risks described in the Pacific Life Funds’ current Prospectus, as supplemented, and Statement of Additional Information, as supplemented, as filed with the Securities and Exchange Commission (SEC), which may be obtained from the SEC’s website at www.sec.gov.

Market Conditions (for the year ended March 31, 2013)

Executive Summary

Over the reporting period, financial markets experienced pockets of volatility but managed to trend higher. While the geopolitical and economic uncertainty that overwhelmed investors lingered during the reporting period, no major disruptions caused the markets to veer off-course for a prolonged period. The short-term “risk-on” and “risk-off” trend persisted over the first half of the reporting period with macro headlines primarily driving market sentiments. However, volatility remained relatively tame and equity markets rallied over the latter half of the reporting period despite the anticipation of challenges coming from of Washington D.C.

Several key events caused volatility to rise in the first half of the reporting period. The euro crisis appeared to have reached peak levels around the start of the reporting period. Amid this challenging environment, European countries saw changes in their political landscape. This included new leaders who pushed for anti-austerity policies. The backlash from anti-austerity supporters (a united front against rampant unemployment and government spending cuts accompanied by strikes and demonstrations) caused additional concerns of unwinding the progress in Europe. Additionally, the economic drag from Europe had global implications that caused global economic growth projections to be revised downward. Concerns over China and its exports to Europe also weighed on its ability to sustain its dominant growth.

Despite the headwinds around the globe, financial markets marched higher over the second-half of the reporting period. The combination of high unemployment rate and lack of evidence of inflation, the Fed continued to provide further support by extending “Operation Twist” (its program to keep long-term rates low by selling its short-term assets and buying long-term Treasuries). The Fed also launched a third round of quantitative easing in September to purchase an additional $40 billion in mortgage-backed securities (MBS) per month. From abroad, the political and economic disturbances in Europe finally led the European Central Bank (ECB) to pledge full support to preserve the euro, which helped unfreeze capital flow throughout the European banking system.

Throughout the reporting period, central banks continued to play a vital role in sustaining the financial market recovery by providing unprecedented liquidity in the global banking system. While such efforts may have helped rejuvenate financial markets, political upheaval introduced uncertainty in the marketplace. Both U.S. and European politicians continued to muddle through their respective fiscal and economic issues. In the U.S., fears of the “fiscal cliff” scenario developed from the inability of Congress to promptly settle budgetary disagreements that led to the implementation of the sequestration budget cuts. In the eurozone, European politicians have struggled to agree and settle on the appropriate policy actions to recover their economies.

| See explanation of symbol and benchmark definitions on page A-20 |

A-2

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

The global economy maintained a steady but slow recovery throughout the reporting period. Various risks continued to linger and influenced markets to varying degrees. The following sections highlight how specific market segments responded to the events that unfolded over the reporting period.

Fixed Income

As the overall market sentiment improved relative to the prior reporting period, the broad fixed income segment fell behind the broad equity market. For the reporting period, the overall fixed income market (as measured by the Barclays U.S. Aggregate Bond Index) gained 3.77%. Short-term Treasuries and credits barely budged over the reporting period as the Fed continued to maintain a near zero interest rate policy for the Federal Funds (Fed Funds). Long-term Treasuries benefited moderately from the Fed’s efforts to keep long-term yields low. Treasury yields (which have an inverse relationship to prices) continued to hit historic low levels, as the 10-Year Treasury yield dipped below 1.50% during the reporting period. The Barclays Long Term U.S. Treasury Index increased 7.31% over the reporting period.

In this environment, the riskier sectors within the fixed income segment performed relatively well. The high yield market experienced a strong rally with lower-rated credits outpacing those in the investment grade tiers. Emerging markets debt also delivered strong results over the reporting period, as the J.P. Morgan Emerging Markets Bond Index Global Diversified Index returned 10.11% over the reporting period. Additionally, the collateralized loan obligation market showed some revival throughout the reporting period, which boded well for bank loans. Throughout this low Treasury yield environment, investors looked across the riskier spectrum to obtain yields.

Domestic Equity

The domestic equity market experienced modest swings throughout the reporting period but managed to finish with a gain of 13.96% for the S&P 500 Index. Results were relatively mixed for the various categories within the domestic equities segment. One common theme among domestic equities was the double-digit returns across the market capitalization and style groups. With respect to market capitalization, mid-capitalization stocks outpaced those of large- and small-capitalizations. Value styles outperformed those of growth, which were primarily driven by the solid performances of the financials sectors over the reporting period. Financials tends to be the largest sector in value indices. The sector’s strong performance followed a dismal year in 2011, which then recovered as the central banks moved aggressively to support the global banking system. On the flipside, information technology, which tends to have heavy representation in growth indices, was the worst performing sector over the reporting period. Other sectors were driven by various reasons. Political factors over the reporting period, especially throughout the presidential election, had a material influence in the stock market. President Obama’s re-election, and his push to pass the Patient Protection and Affordable Healthcare Act, often times referred to as “Obamacare”, helped the healthcare sector experience a strong gain over the reporting period.

International Equity

After a difficult run during the prior reporting period, international stocks in developed markets experienced a healthy recovery over this reporting period. The Morgan Stanley Capital International (MSCI) Europe, Australasia, and Far East (MSCI EAFE) Index and the MSCI Emerging Markets Index returned 11.25% and 1.96%, respectively. Emerging markets equity returns, on the other hand, were less robust, particularly over the first quarter of 2013. Countries such as Brazil and China continued to deal with inflation that led to concerns over monetary tightening to slow their growth. Additionally, the Japanese yen had been devalued sharply, which helps Japan’s exports but threatens the competitiveness of other Asian exporters. Such concerns hurt South Korean stocks, which represent the largest country weighting in the MSCI Emerging Markets Index.

Concluding Remarks

Economic reports indicated that the world economy grew at approximately 3.20% in 2012 (International Monetary Fund—World Economic Outlook Update—April 2013). Emerging markets, particularly China, contributed to that growth. Developed nations, on the other hand, crawled at a sluggish pace or contracted. Despite the dismal economic indicators, equity markets in developed countries thrived over the reporting period. Perhaps, this was driven more out of relief of avoiding meltdown scenarios that markets had feared.

The question remains on the sustainability of the market rise. Over the reporting period, equity valuations had been trading below long-term averages. These trading ranges may have been a reflection of the general market environment. Over the past few years, the world has been dealing with various crises, which may have caused a hesitation to push valuations back to longer-term historic levels. However, these valuation levels have risen closer to the 10-year average over the first quarter of 2013 as U.S. economic reports continued to indicate steady improvements.

More clarity has been developing in 2013, but challenges still linger. The crisis level in the eurozone appears to be manageable, but economic activity is expected to remain weak in the region. Although the situation in the U.S. is relatively better than its developed counterparts in Europe, economic growth is expected to remain modest. The benign economic activity in developed nations is anticipated to dampen demand for exports from emerging markets. This may have some varying implications to these emerging markets nations. Nonetheless, growth in countries such as China is expected to remain healthy.

Performance over the reporting period showed investors that markets can diverge from economic fundamentals. The level of uncertainty and risks throughout the globe may have caused some investors to reduce or avoid equity exposure. However, those investors would have missed out on the impressive performance delivered from equities in developed markets. This validates the importance of proper asset allocation to navigate through various market conditions.

| See explanation of symbol and benchmark definitions on page A-20 |

A-3

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

Performance of the PL Portfolio Optimization Funds

Since the performance of each PL Portfolio Optimization Fund is a composite of the performance of each of the PL Underlying Funds in which each invests (which may include bonds, domestic and/or international equities), there is no one, broad-based industry index to use as a comparison to a PL Portfolio Optimization Fund’s performance. Therefore, we at PLFA have provided information regarding four broad-based indices to use as a comparison to each fund’s performance.

In addition, to assist in performance comparisons, composite benchmarks were constructed for each PL Portfolio Optimization Fund; each is comprised of the four broad-based indices shown below. The composite benchmarks were constructed with allocations to each asset class that correspond to the target allocations for the PL Portfolio Optimization Funds. However, the actual allocation of any PL Portfolio Optimization Fund will naturally vary from these targets as a result of market performance over time. The one-year performance for these broad-based indices is shown in the following table.

Broad Based Indices | One Year (as of 3-31-13) | |||

S&P 500 Index (U.S. Stocks) | 13.96% | |||

Morgan Stanley Capital International (MSCI) EAFE Index (International Stocks) | 11.25% | |||

Barclays U.S. Aggregate Bond Index (Fixed Income) | 3.77% | |||

BofA Merrill Lynch U.S. 3-Month T-Bill Index (Cash) | 0.12% | |||

| See explanation of symbol and benchmark definitions on page A-20 |

A-4

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

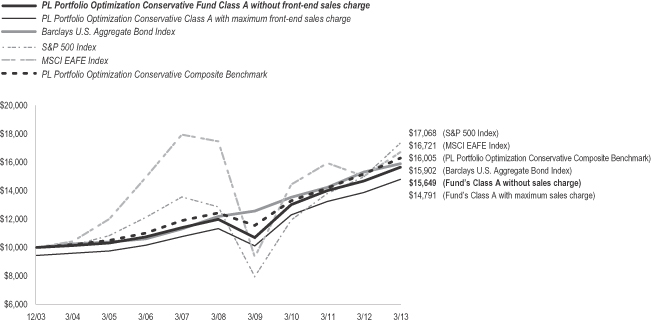

PL Portfolio Optimization Conservative Fund (managed by Pacific Life Fund Advisors LLC)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Portfolio Optimization Conservative Fund’s Class A returned 6.57%, compared to a 3.77% return for its benchmarks, the Barclays U.S. Aggregate Bond Index, a 13.96% return for the S&P 500 Index, a 11.25% return for the MSCI EAFE Index, and a 5.49% return for the PL Portfolio Optimization Conservative Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the fund to its benchmarks for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class B, C, R and Advisor Class shares for the period from inception through March 31, 2013 are also shown in the table below. Performance data for Class B, C, R and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | 5 Years | Since | ||||||||||

Fund’s Class A without sales charge | 6.57% | 5.46% | 4.96% | |||||||||

Fund’s Class A with maximum sales charge | 0.75% | 4.28% | 4.32% | |||||||||

Fund’s Class B without sales charge | 5.89% | 4.74% | 4.39% | |||||||||

Fund’s Class B with maximum sales charge | 0.89% | 4.40% | 4.39% | |||||||||

Fund’s Class C without sales charge | 5.84% | 4.72% | 4.29% | |||||||||

Fund’s Class C with maximum sales charge | 4.84% | 4.72% | 4.29% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.14% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.95% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 5.70% | ||||||||

PL Portfolio Optimization Conservative | 5.49% | 5.16% | 5.21% | |||||||||

| 1 Year | 5 Years | Since | ||||||||||

Fund’s Class R without sales charge | 6.38% | 5.21% | 5.20% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.52% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.53% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 3.28% | ||||||||

PL Portfolio Optimization Conservative | 5.49% | 5.16% | 5.35% | |||||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (12/31/2012) | ||||||||

Fund’s Advisor Class without sales charge | 2.06% | |||||||

Barclays U.S. Aggregate Bond Index | (0.12% | ) | ||||||

S&P 500 Index | 10.61% | |||||||

MSCI EAFE Index | 5.13% | |||||||

PL Portfolio Optimization Conservative Composite Benchmark | 1.90% | |||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| See explanation of symbol and benchmark definitions on page A-20 |

A-5

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

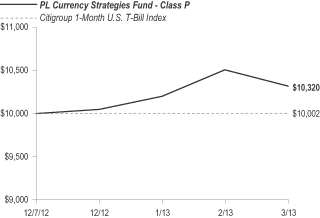

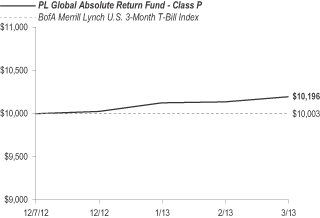

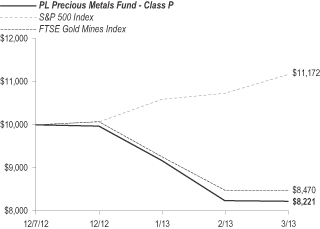

A. The PL Portfolio Optimization Conservative Fund is primarily comprised of various fixed income funds with a small allocation to domestic and international equity funds. The allocation to fixed income funds includes exposure to intermediate-term bonds, short duration securities, inflation-protected bonds, and floating rate loans. The fund’s allocation to equity funds mainly encompasses domestic and foreign large-capitalization funds. Three alternative strategies, the PL Currencies Strategies, PL Global Absolute Return and PL Precious Metals Funds, which commenced operations on December 7, 2012, were added to the fund.

At the broad asset class level, the fund’s fixed income allocations collectively outperformed the Barclays U.S. Aggregate Bond Index. The fund’s domestic and international equity allocation lagged behind the S&P 500 Index and MSCI EAFE Index, respectively.

Within the fund’s fixed income allocation, riskier credit segments performed well over this reporting period. Allocation to riskier, fixed income categories such as the PL Floating Rate Loan and PL Emerging Markets Debt Funds contributed to fund performance. Moreover, the PL Managed Bond and PL Inflation Managed Funds were among the top contributors to fund performance. On the other hand, the PL Short Duration Bond Fund’s subdued returns hampered the fund’s relative performance. This was primarily a result of the Fed’s policy on maintaining the short-term rates near zero percent.

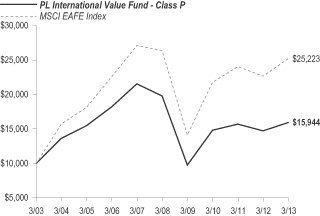

Although the fund’s equity allocation consists of primarily large-capitalization strategies, exposure to the PL Mid-Cap Growth Fund hurt performance. However, the allocation to large-capitalization value strategies (i.e. the PL Comstock and PL Large-Cap Value Funds) helped offset some of the fund’s detractors. Within the international equity segment, the PL International Value Fund mainly detracted from fund performance.

| See explanation of symbol and benchmark definitions on page A-20 |

A-6

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

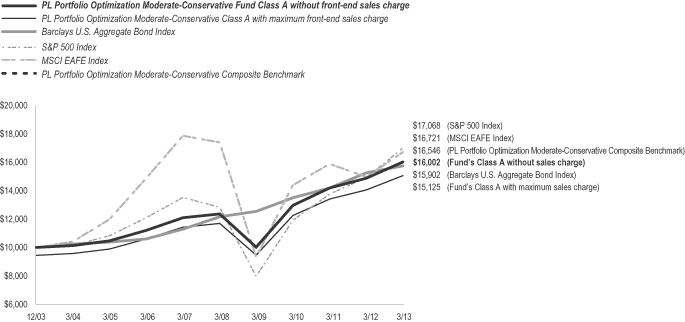

PL Portfolio Optimization Moderate-Conservative Fund (managed by Pacific Life Fund Advisors LLC)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Portfolio Optimization Moderate-Conservative Fund’s Class A returned 7.22%, compared to a 3.77% return for its benchmarks, the Barclays U.S. Aggregate Bond Index, a 13.96% return for the S&P 500 Index, a 11.25% return for the MSCI EAFE Index, and a 7.47% return for the PL Portfolio Optimization Moderate-Conservative Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the fund to its benchmarks for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class B, C, R and Advisor Class shares for the periods from inception through March 31, 2013 are also shown in the table below. Performance data for Class B, C, R and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | 5 Years | Since Inception (12/31/03) | ||||||||||

Fund’s Class A without sales charge | 7.22% | 5.23% | 5.21% | |||||||||

Fund’s Class A with maximum sales charge | 1.35% | 4.05% | 4.57% | |||||||||

Fund’s Class B without sales charge | 6.46% | 4.48% | 4.63% | |||||||||

Fund’s Class B with maximum sales charge | 1.46% | 4.14% | 4.63% | |||||||||

Fund’s Class C without sales charge | 6.41% | 4.48% | 4.54% | |||||||||

Fund’s Class C with maximum sales charge | 5.41% | 4.48% | 4.54% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.14% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.95% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 5.70% | ||||||||

PL Portfolio Optimization Moderate-Conservative Composite Benchmark | 7.47% | 5.12% | 5.59% | |||||||||

| 1 Year | 5 Years | Since Inception (9/30/05) | ||||||||||

Fund’s Class R without sales charge | 6.92% | 4.97% | 5.11% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.52% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.53% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 3.28% | ||||||||

PL Portfolio Optimization Moderate-Conservative Composite Benchmark | 7.47% | 5.12% | 5.47% | |||||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (12/31/2012) | ||||||||

Fund’s Advisor Class without sales charge | 3.60% | |||||||

Barclays U.S. Aggregate Bond Index | (0.12% | ) | ||||||

S&P 500 Index | 10.61% | |||||||

MSCI EAFE Index | 5.13% | |||||||

PL Portfolio Optimization Moderate-Conservative Composite Benchmark | 4.03% | |||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| See explanation of symbol and benchmark definitions on page A-20 |

A-7

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. The PL Portfolio Optimization Moderate-Conservative Fund has a diversified allocation mix that is primarily comprised of an allocation to fixed income funds with a smaller allocation to several domestic and international equity funds. The allocation to fixed income funds includes exposure to intermediate-term bonds as well as short duration securities, inflation-protected bonds, and floating rate loans. The exposure to equity funds is diversified across style (growth/value), market capitalization and region (including an allocation to emerging market funds). Three alternative strategies, the PL Currency Strategies, PL Global Absolute Return and PL Precious Metals Funds, which commenced operations on December 7, 2012, were added to the fund.

At the broad asset class level, the fund’s fixed income allocation collectively outperformed the Barclays U.S. Aggregate Bond Index. The fund’s domestic and international equity allocations lagged behind the S&P 500 Index and MSCI EAFE Index, respectively.

Within the fund’s fixed income allocation, riskier credit segments performed well over this reporting period. Allocation to riskier, fixed income categories such as the PL Floating Rate Loan and PL Emerging Markets Debt Funds contributed to fund performance. Moreover, the PL Managed Bond and PL Inflation Managed Funds were among the top contributors to fund performance. On the other hand, the PL Short Duration Bond Fund’s subdued returns hampered the fund’s relative performance. This was primarily a result of the Fed’s policy on maintaining the short-term rates near zero percent.

Although the fund’s equity allocation consists of primarily large-capitalization strategies, exposure to the PL Mid-Cap Growth Fund hurt performance. However, the allocation to value strategies (i.e. the PL Comstock, PL Large-Cap Value, and PL Small-Cap Value Funds) helped offset some of the fund’s detractors. Within the international equity segment, the PL Emerging Markets and PL International Value Funds primarily detracted from fund performance.

| See explanation of symbol and benchmark definitions on page A-20 |

A-8

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

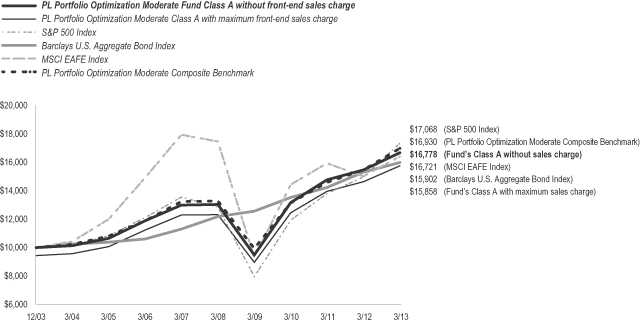

PL Portfolio Optimization Moderate Fund (managed by Pacific Life Fund Advisors LLC)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Portfolio Optimization Moderate Fund’s Class A returned 8.36%, compared to a 13.96% return for its benchmarks, the S&P 500 Index, a 3.77% return for the Barclays U.S. Aggregate Bond Index, a 11.25% return for the MSCI EAFE Index, and a 9.46% return for the PL Portfolio Optimization Moderate Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the fund to its benchmarks for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class B, C, R and Advisor Class shares for the periods from inception through March 31, 2013 are also shown in the table below. Performance data for Class B, C, R and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | 5 Years | Since Inception (12/31/03) | ||||||||||

Fund’s Class A without sales charge | 8.36% | 5.16% | 5.75% | |||||||||

Fund’s Class A with maximum sales charge | 2.42% | 3.98% | 5.11% | |||||||||

Fund’s Class B without sales charge | 7.49% | 4.40% | 5.17% | |||||||||

Fund’s Class B with maximum sales charge | 2.49% | 4.06% | 5.17% | |||||||||

Fund’s Class C without sales charge | 7.50% | 4.41% | 5.07% | |||||||||

Fund’s Class C with maximum sales charge | 6.50% | 4.41% | 5.07% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.95% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.14% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 5.70% | ||||||||

PL Portfolio Optimization Moderate | 9.46% | 4.96% | 5.85% | |||||||||

| 1 Year | 5 Years | Since Inception (9/30/05) | ||||||||||

Fund’s Class R without sales charge | 8.02% | 4.91% | 5.31% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.53% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.52% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 3.28% | ||||||||

PL Portfolio Optimization Moderate | 9.46% | 4.96% | 5.50% | |||||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (12/31/2012) | ||||||||

Fund’s Advisor Class without sales charge | 5.24% | |||||||

S&P 500 Index | 10.61% | |||||||

Barclays U.S. Aggregate Bond Index | (0.12% | ) | ||||||

MSCI EAFE Index | 5.13% | |||||||

PL Portfolio Optimization Moderate | 6.18% | |||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| See explanation of symbol and benchmark definitions on page A-20 |

A-9

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. The PL Portfolio Optimization Moderate Fund has an allocation mix that is primarily comprised of an allocation to domestic and international equity funds with a smaller allocation to fixed income funds. The exposure to equity funds is diversified across style (growth/value), market capitalization and region (including allocations to emerging markets stocks). The allocation to fixed income funds includes exposure to intermediate-term bonds, short duration securities, inflation-protected bonds, and floating rate loans. Three, alternative strategies, the PL Currency Strategies, PL Global Absolute Return and PL Precious Metals Funds, which commenced operations on December 7, 2012, were added to the fund.

At the broad asset class level, the fund’s fixed income allocation collectively outperformed the Barclays U.S. Aggregate Bond Index. The fund’s domestic and international equity allocations lagged behind the S&P 500 Index and MSCI EAFE Index, respectively.

Within the fund’s fixed income allocation, riskier credit segments performed well over this reporting period. Allocation to riskier fixed income categories such as the PL Floating Rate Loan and PL Emerging Markets Debt Funds contributed to fund performance. Moreover, the PL Managed Bond and PL Inflation Managed Funds were among the top contributors to fund performance. On the other hand, the PL Short Duration Bond Fund’s subdued returns hampered the fund’s relative performance. This was primarily a result of the Fed’s policy on maintaining the short-term rates near zero percent.

Although the fund’s equity allocation consists of primarily large-capitalization strategies, exposure to the PL Mid-Cap Growth Fund hurt performance. However, the allocation to value strategies (i.e. the PL Comstock, PL Large-Cap Value, and PL Small-Cap Value Funds) helped offset some of the fund’s detractors. Within the international equity segment, the PL Emerging Markets and PL International Value Funds primarily detracted from fund performance.

While the three alternative strategies were added in December 2012, the continued drop in gold prices over the past couple of quarters had a negative impact on the investments in the PL Precious Metals Fund which in turn detracted from the fund’s performance.

| See explanation of symbol and benchmark definitions on page A-20 |

A-10

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

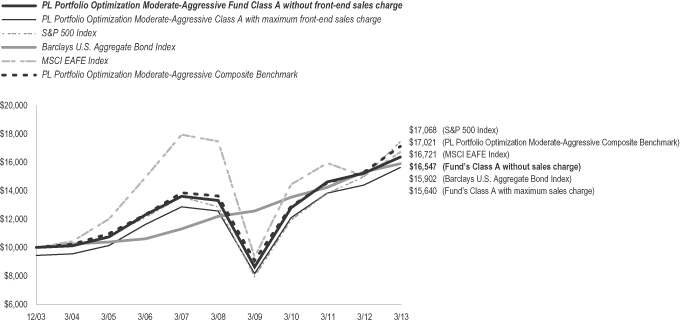

PL Portfolio Optimization Moderate-Aggressive Fund (managed by Pacific Life Fund Advisors LLC)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Portfolio Optimization Moderate-Aggressive Fund’s Class A returned 8.62%, compared to a 13.96% return for its benchmarks, the S&P 500 Index, a 3.77% return for the Barclays U.S. Aggregate Bond Index, a 11.25% return for the MSCI EAFE Index, and a 11.32% return for the PL Portfolio Optimization Moderate-Aggressive Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the fund to its benchmarks for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class B, C, R and Advisor Class shares for the periods from inception through March 31, 2013 are also shown in the table below. Performance data for Class B, C, R and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | 5 Years | Since Inception (12/31/03) | ||||||||||

Fund’s Class A without sales charge | 8.62% | 4.46% | 5.60% | |||||||||

Fund’s Class A with maximum sales charge | 2.67% | 3.28% | 4.95% | |||||||||

Fund’s Class B without sales charge | 7.92% | 3.73% | 5.02% | |||||||||

Fund’s Class B with maximum sales charge | 2.92% | 3.38% | 5.02% | |||||||||

Fund’s Class C without sales charge | 7.95% | 3.72% | 4.93% | |||||||||

Fund’s Class C with maximum sales charge | 6.95% | 3.72% | 4.93% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.95% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.14% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 5.70% | ||||||||

PL Portfolio Optimization Moderate-Aggressive Composite Benchmark | 11.32% | 4.54% | 5.93% | |||||||||

| 1 Year | 5 Years | Since Inception (9/30/05) | ||||||||||

Fund’s Class R without sales charge | 8.38% | 4.21% | 4.90% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.53% | |||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.52% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 3.28% | ||||||||

PL Portfolio Optimization Moderate-Aggressive Composite Benchmark | 11.32% | 4.54% | 5.30% | |||||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (12/31/2012) | ||||||||

Fund’s Advisor Class without sales charge | 6.72% | |||||||

S&P 500 Index | 10.61% | |||||||

Barclays U.S. Aggregate Bond Index | (0.12% | ) | ||||||

MSCI EAFE Index | 5.13% | |||||||

PL Portfolio Optimization Moderate-Aggressive Composite Benchmark | 8.36% | |||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| See explanation of symbol and benchmark definitions on page A-20 |

A-11

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. The PL Portfolio Optimization Moderate-Aggressive Fund has a diversified allocation mix that is primarily comprised of an allocation to domestic and international equity funds and has a moderate allocation to fixed income and sector funds. The exposure to equity funds is diversified across style (growth/value), market capitalization and region (which include allocations to emerging markets stocks). Three alternative strategies, the PL Currency Strategies, PL Global Absolute Return and PL Precious Metals Funds, which commenced operations on December 7, 2012, were added to the fund.

For the reporting period, the fund’s Class A returned 8.62% compared to 11.32% for the PL Portfolio Optimization Moderate-Aggressive Composite Benchmark. At the broad asset class level, the fund’s fixed income allocation collectively outperformed the Barclays U.S. Aggregate Bond Index. The fund’s domestic and international equity allocations lagged behind the S&P 500 Index and MSCI EAFE Index, respectively.

Although the fund’s equity allocation consists of primarily large-capitalization strategies, exposure to the PL Mid-Cap Growth Fund hurt performance. However, the allocation to value strategies (i.e. the PL Comstock, PL Large-Cap Value, and PL Small-Cap Value Funds) helped offset some of the fund’s detractors. Within the international equity segment, the PL Emerging Markets and PL International Value Funds primarily detracted from fund performance.

Within the fund’s fixed income allocation, riskier credit segments performed well over this reporting period. Allocation to riskier, fixed income categories such as the PL Floating Rate Loan Fund contributed to fund performance. Moreover, the PL Managed Bond and PL Inflation Managed Funds were among the top contributors to fund performance. On the other hand, the PL Short Duration Bond Fund’s subdued returns hampered the fund’s relative performance. This was primarily a result of the Fed’s policy on maintaining the short-term rates near zero percent.

While the three alternative strategies were added in December 2012, the continued drop in gold prices over the past couple of quarters had a negative impact on the investments in the PL Precious Metals Fund which in turn detracted from the fund’s performance.

| See explanation of symbol and benchmark definitions on page A-20 |

A-12

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

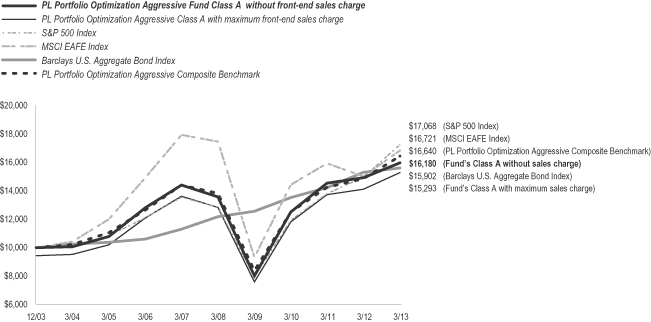

PL Portfolio Optimization Aggressive Fund (managed by Pacific Life Fund Advisors LLC)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Portfolio Optimization Aggressive Fund’s Class A returned 8.30%, compared to a 13.96% return for its benchmarks, the S&P 500 Index, a 11.25% return for the MSCI EAFE Index, a 3.77% return for the Barclays U.S. Aggregate Bond Index, and a 11.88% return for the PL Portfolio Optimization Aggressive Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the fund to its benchmarks for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class B, C, R and Advisor Class shares for the periods from inception through March 31, 2013 are also shown in the table below. Performance data for Class B, C, R and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | 5 Years | Since Inception (12/31/03) | ||||||||||

Fund’s Class A without sales charge | 8.30% | 3.54% | 5.34% | |||||||||

Fund’s Class A with maximum sales charge | 2.35% | 2.38% | 4.70% | |||||||||

Fund’s Class B without sales charge | 7.69% | 2.84% | 4.76% | |||||||||

Fund’s Class B with maximum sales charge | 2.69% | 2.48% | 4.76% | |||||||||

Fund’s Class C without sales charge | 7.71% | 2.86% | 4.71% | |||||||||

Fund’s Class C with maximum sales charge | 6.71% | 2.86% | 4.71% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.95% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 5.70% | ||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.14% | |||||||||

PL Portfolio Optimization Aggressive Composite Benchmark | 11.88% | 3.77% | 5.67% | |||||||||

| 1 Year | 5 Years | Since Inception (9/30/05) | ||||||||||

Fund’s Class R without sales charge | 8.17% | 3.32% | 4.36% | |||||||||

S&P 500 Index | 13.96% | 5.81% | 5.53% | |||||||||

MSCI EAFE Index | 11.25% | (0.89% | ) | 3.28% | ||||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.47% | 5.52% | |||||||||

PL Portfolio Optimization Aggressive Composite Benchmark | 11.88% | 3.77% | 4.81% | |||||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (12/31/2012) | ||||||||

Fund’s Advisor Class without sales charge | 7.56% | |||||||

S&P 500 Index | 10.61% | |||||||

MSCI EAFE Index | 5.13% | |||||||

Barclays U.S. Aggregate Bond Index | (0.12% | ) | ||||||

PL Portfolio Optimization Aggressive Composite Benchmark | 9.27% | |||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

| See explanation of symbol and benchmark definitions on page A-20 |

A-13

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. The PL Portfolio Optimization Aggressive Fund allocates primarily to domestic and international equity funds that are diversified across style (growth/value), market capitalization and region (which include allocations to emerging markets stocks). The fund also has a small allocation to fixed income and sector funds. Three alternative strategies, PL Currency Strategies, PL Global Absolute Return and PL Precious Metals Funds, which commenced operations on December 7, 2012, were added to the fund.

At the broad asset class level, the fund’s fixed income allocation collectively outperformed the Barclays U.S. Aggregate Bond Index. The fund’s domestic and international equity allocations lagged behind the S&P 500 Index and MSCI EAFE Index, respectively.

Although the fund’s equity allocation consists of primarily large-capitalization strategies, exposure to the PL Mid-Cap Growth Fund hurt performance. However, the allocation to value strategies (i.e. the PL Comstock, PL Large-Cap Value, and PL Small-Cap Value Funds) helped offset some of the fund’s detractors. Within the international equity segment, the PL Emerging Markets and PL International Value Funds primarily detracted from fund performance.

While the three alternative strategies were added in December 2012, the continued drop in gold prices over the past couple of quarters had a negative impact on the investments in the PL Precious Metals Fund which in turn detracted from the fund’s performance.

The fund’s fixed income segment is represented by the PL Managed Bond Fund, which contributed to fund performance. The strategy’s overweight exposure to emerging markets debt and riskier credits helped boost its performance.

PL Short Duration Income Fund (managed by Pacific Asset Management)

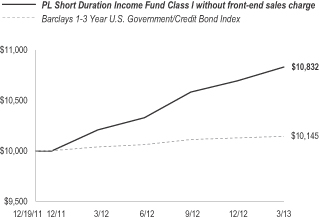

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Short Duration Income Fund’s Class I returned 6.10%, compared to a 1.09% return for its benchmark, the Barclays 1-3 Year U.S. Government/Credit Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the fund to its benchmark for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class A, C and Advisor Class shares for the period from inception through March 31, 2013 are also shown in the table below. Performance data for Class A, C and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | Since Inception (12/19/11) | |||||||

Fund’s Class I without sales charge | 6.10% | 6.43% | ||||||

Barclays 1-3 Year U.S. Government/Credit Bond Index | 1.09% | 1.16% | ||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (6/29/2012) | ||||||

Fund’s Class A without sales charge | 4.78% | |||||

Fund’s Class A with maximum sales charge | 1.60% | |||||

Fund’s Class C without sales charge | 4.28% | |||||

Fund’s Class C with maximum sales charge | 3.28% | |||||

Fund’s Advisor Class without sales charge | 4.85% | |||||

Barclays 1-3 Year U.S. Government/Credit Bond Index | 0.87% | |||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the fund’s Class I outperformed the benchmark. We at Pacific Asset Management manage the fund as a short maturity corporate bond fund that has the flexibility to go up to 30% in non-investment grade securities. The fund outperformed the benchmark during the reporting period primarily due to fixed-income asset allocation and overweights to high yield and floating rate securities. The fund maintained similar overweight allocations through the period in investment-grade corporate debt, floating rate loans, and high-yield bonds, which were all positive contributors to relative performance, as was the underweight to Treasuries. The fund’s duration position was largely unchanged and remains above benchmark.

| See explanation of symbol and benchmark definitions on page A-20 |

A-14

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

PL Income Fund (managed by Pacific Asset Management)

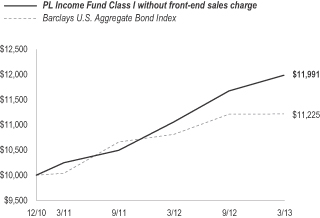

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Income Fund’s Class I returned 8.39%, compared to a 3.77% return for its benchmark, the Barclays U.S. Aggregate Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the fund to its benchmark for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class A, C and Advisor Class shares for the periods from inception through March 31, 2013 are also shown in the table below. Performance data for Class A, C and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | Since Inception (12/31/2010) | |||||||

Fund’s Class A without sales charge | 8.13% | 8.22% | ||||||

Fund’s Class A with maximum sales charge | 3.54% | 6.16% | ||||||

Fund’s Class I without sales charge | 8.39% | 8.41% | ||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.27% | ||||||

| 1 Year | Since Inception (6/30/2011) | |||||||

Fund’s Class C without sales charge | 7.37% | 7.00% | ||||||

Fund’s Class C with maximum sales charge | 6.37% | 7.00% | ||||||

Barclays U.S. Aggregate Bond Index | 3.77% | 5.20% | ||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (6/29/2012) | ||||||

Fund’s Advisor Class without sales charge | 5.97% | |||||

Barclays U.S. Aggregate Bond Index | 1.68% | |||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the fund’s Class I outperformed the benchmark. We at Pacific Asset Management manage the fund as an investment grade corporate bond fund that can invest up to 40% in non-investment grade securities. The fund outperformed the benchmark during the reporting period due to fixed-income asset allocation and a focus on intermediate maturity bonds. The fund outperformed the benchmark during the reporting period due to asset allocation and security selection. The fund maintained similar overweight allocations through the period in investment-grade corporate debt, floating rate loans, and high-yield bonds, which were all positive contributors to the fund’s relative performance, as was the underweight to Treasuries, relative to the benchmark. The fund’s underweight to European banks was a negative to overall fund performance. The fund’s duration position was largely unchanged and remained under the benchmark at the end of the reporting period.

| See explanation of symbol and benchmark definitions on page A-20 |

A-15

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

PL Strategic Income Fund (managed by Pacific Asset Management)

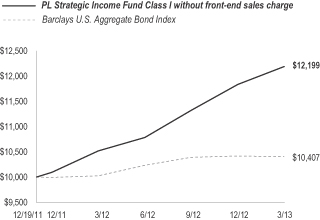

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Strategic Income Fund’s Class I returned 15.94%, compared to a 3.77% return for its benchmark, the Barclays U.S. Aggregate Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the fund to its benchmark for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class A, C and Advisor Class shares for the period from inception through March 31, 2013 are also shown in the table below. Performance data for Class A, C and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | Since Inception (12/19/2011) | |||||||

Fund’s Class I without sales charge | 15.94% | 16.77% | ||||||

Barclays U.S Aggregate Bond Index | 3.77% | 3.16% | ||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (6/29/2012) | ||||||

Fund’s Class A without sales charge | 13.12% | |||||

Fund’s Class A with maximum sales charge | 8.28% | |||||

Fund’s Class C without sales charge | 12.52% | |||||

Fund’s Class C with maximum sales charge | 11.52% | |||||

Fund’s Advisor Class without sales charge | 13.31% | |||||

Barclays U.S Aggregate Bond Index | 1.68% | |||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the fund’s Class I outperformed the benchmark. We at Pacific Asset Management manage the fund using a multi-sector, corporate credit strategy. The fund outperformed the benchmark during the reporting period primarily due to the continued overweight to risk assets and an overweight to high yield bonds. The fund’s structural overweight to high-yield issues was a contributor to the fund’s relative performance for the reporting period, as was the underweight to Treasuries. The fund’s underweight to banking, particularly European Banks, detracted from its performance. The fund marginally increased the weighting of below investment-grade positions, which benefited performance. The allocation of high yield bonds and floating rate loans changed as high yield bond positions were decreased and floating rate loans were increased. The portfolio duration position continues to be moderately higher than the benchmark, but remained consistent during the reporting period.

| See explanation of symbol and benchmark definitions on page A-20 |

A-16

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

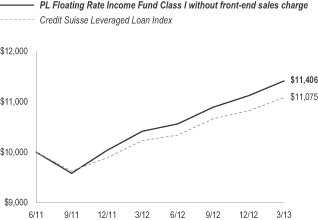

PL Floating Rate Income Fund (managed by Pacific Asset Management)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Floating Rate Income Fund’s Class I returned 9.56%, compared to a 8.27% return for its benchmark, the Credit Suisse Leveraged Loan Index.

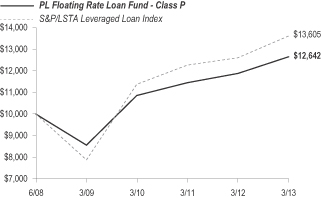

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the fund to its benchmark for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class A, C, P and Advisor Class shares for the periods from inception through March 31, 2013 are also shown in the table below. Performance data for Class A, C, P and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | Since | |||||||

Fund’s Class I without sales charge | 9.56% | 7.79% | ||||||

Credit Suisse Leveraged Loan Index | 8.27% | 6.01% | ||||||

| 1 Year | Since Inception (12/30/2011)~ | |||||||

Fund’s Class A without sales charge | 9.36% | 10.62% | ||||||

Fund’s Class A with maximum sales charge | 6.10% | 8.00% | ||||||

Fund’s Class C without sales charge | 8.56% | 9.88% | ||||||

Fund’s Class C with maximum sales charge | 7.56% | 9.88% | ||||||

Credit Suisse Leveraged Loan Index | 8.27% | 9.51% | ||||||

Total Returns for the Periods Ended March 31, 2013

| Since Inception (6/29/2012) | ||||||

Fund’s Advisor Class without sales charge | 8.13% | |||||

Credit Suisse Leveraged Loan Index | 7.18% | |||||

| Since Inception (12/31/2012) | ||||||

Fund’s Class P without sales charge | 2.74% | |||||

Credit Suisse Leveraged Loan Index | 2.37% | |||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the fund’s Class I outperformed the benchmark. We at Pacific Asset Management manage the fund using a non-investment grade strategy focusing on floating rate debt securities. The fund outperformed its benchmark in the reporting period due to security selection and asset allocation. The fund’s credit quality allocation and emphasis on larger and more liquid loan facilities were neutral to performance. The fund’s underweight to lower rated securities was a negative to performance. The fund’s underweight to the health care sector benefited performance while the underweight to utilities detracted. The fund’s tactical allocation to high yield bonds was a positive contributor to performance during the reporting period.

| See explanation of symbol and benchmark definitions on page A-20 |

A-17

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

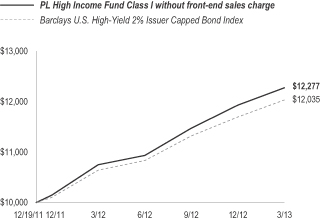

PL High Income Fund (managed by Pacific Asset Management)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL High Income Fund’s Class I returned 14.21%, compared to a 13.08% return for its benchmark, the Barclays U.S. High-Yield 2% Issuer Capped Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the fund to its benchmark for the periods from inception through March 31, 2013. For comparison purposes, the performance of Class A, C and Advisor Class shares for the period from inception through March 31, 2013 are also shown in the table below. Performance data for Class A, C and Advisor Class shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | Since Inception (12/19/2011) | |||||||

Fund’s Class I without sales charge | 14.21% | 17.35% | ||||||

Barclays U.S. High-Yield 2% Issuer Capped Bond Index | 13.08% | 15.55% | ||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (6/29/2012) | ||||||

Fund’s Class A without sales charge | 12.59% | |||||

Fund’s Class A with maximum sales charge | 7.80% | |||||

Fund’s Class C without sales charge | 12.11% | |||||

Fund’s Class C with maximum sales charge | 11.11% | |||||

Fund’s Advisor Class without sales charge | 12.87% | |||||

Barclays U.S. High-Yield 2% Issuer Capped Bond Index | 11.09% | |||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the fund’s Class I outperformed the benchmark. We at Pacific Asset Management manage the fund using a non-investment grade bond strategy. The fund outperformed during the reporting period due to sector allocation and security selection. The fund’s performance was negatively impacted by a mild underweight to B rated and CCC rated issues. The fund was overweight BB rated bonds, which underperformed during the reporting period. The fund’s allocation to larger and more liquid issues were neutral to performance. The fund’s duration position, which is longer than the benchmark, was also neutral to performance.

| See explanation of symbol and benchmark definitions on page A-20 |

A-18

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

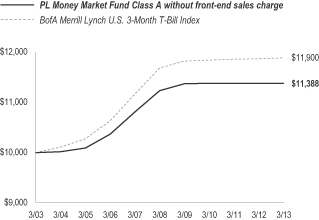

PL Money Market Fund (managed by Pacific Asset Management)

Q. How did the fund perform for the year ended March 31, 2013?

A. For the year ended March 31, 2013, the PL Money Market Fund’s Class A returned 0.00%, compared to a 0.12% return for its benchmark, the BofA Merrill Lynch U.S. 3-Month T-Bill Index. The current yield measured during the seven-day period ended March 31, 2013 was 0.00%.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the fund to its benchmark for the ten-year period ended March 31, 2013. For comparison purposes, the performance of class B and C shares for the period from inception through March 31, 2013 are also shown in the table below. Performance data for Class B and C shares will vary due to differences in fees and sales charges. The fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2013

| 1 Year | 5 Years | 10 Years | ||||||||||

Fund’s Class A without sales charge | 0.00% | 0.26% | 1.31% | |||||||||

BofA Merrill Lynch U.S. 3-Month T-Bill Index | 0.12% | 0.34% | 1.75% | |||||||||

Total Returns for the Period Ended March 31, 2013

| Since Inception (6/29/2012) | ||||||||

Fund’s Class B without sales charge | 0.00% | |||||||

Fund’s Class C without sales charge | 0.00% | |||||||

BofA Merrill Lynch U.S. 3-Month T-Bill Index | 0.09% | |||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on fund distributions or redemption of fund shares. |

Q. Discuss both positive and negative factors that materially affected the fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the fund’s Class A underperformed the benchmark. We at Pacific Asset Management manage the fund with a focus on stability, liquidity, and current income through a consistent, disciplined investment approach emphasizing industry and asset type diversification.

A low Fed Funds target rate and a shrinking supply of commercial paper constrained the absolute return environment for the fund. This environment generated relative outperformance by the longer duration assets in the fund. Citing the slack in the economy and the weakness in the labor force, the Fed remained accommodative throughout the reporting period. The Fed Funds target rate was unchanged, remaining at the range between 0.00% and 0.25%. The three-month London Interbank Offered Rate (LIBOR) was very stable during the reporting period. Fewer companies utilized the commercial paper market during the year, which reduced supply and further lowered available yields. Money market accounts continued to experience outflows, as investor’s deployed cash into higher risk asset classes.

Although the employment picture has started to improve and the economy is strengthening, we believe the Fed is going to remain cautious through the next few years and will want to ensure the recovery is on very solid footing before any tightening of monetary policy. We expect any tightening to be well forecasted to the market and would expect to shorten the fund’s weighted average maturity heading into a rate increase.

| See explanation of symbol and benchmark definitions on page A-20 |

A-19

Table of Contents

PACIFIC LIFE FUNDS PERFORMANCE DISCUSSION (Continued)

Explanation of Symbol for Pacific Life Funds Performance Discussion

| ~ | Due to data limitation, the benchmark since inception return reflects the commencement period from the first calendar day of the month the fund commenced its operations. |

Benchmark Definitions

Barclays 1-3 Year U.S. Government/Credit Bond Index is the 1-3 year component for the U.S. Government/Credit Index. The U.S. Government/Credit Bond Index is the non-securitized component of the U.S. Aggregate Bond Index. The U.S. Government/Credit Bond Index includes U.S. Treasuries, Government-related issues and corporates. The total return is equal to the change in price plus the coupon return.

Barclays U.S. Aggregate Bond Index covers the U.S. dollar-denominated, investment-grade, fixed-rate, taxable bond market of SEC-registered securities. The index includes bonds from the Treasury, government-related, corporate, mortgage-backed securities, asset-backed securities, and corporate mortgage-backed securities sectors. The total return is equal to the change in price plus the coupon return.

Barclays U.S. High-Yield 2% Issuer Capped Bond Index is an index that is an issuer-constrained version for the U.S. Corporate High-Yield Index that coves the U.S. dollar-denominated, non-investment grade fixed-rate taxable corporate bond market and limits issuer exposures to a maximum of 2% and redistributes the excess market value index-wide on a pro-rata basis. The total return is equal to the change in price plus the coupon return.

Barclays Long Term U.S. Treasury Index includes all publicly issued, U.S. Treasury securities that have a remaining maturity of 10 or more years, are rated investment grade, and have $250 million or more of outstanding face value. In addition, the securities must be denominated in U.S. dollars and must be fixed rate and non-convertible.

BofA Merrill Lynch U.S. 3-Month Treasury Bill (T-Bill) Index is an index comprised of a single Treasury bill issue purchased at the beginning of the month and held for a full month, then sold and rolled into a newly selected Treasury bill issue. Results include the reinvestment of all distributions.

Credit Suisse Leveraged Loan Index is an index of U.S. dollar-denominated leveraged loan market securities. The total return is equal to the change in price plus the coupon return.

Morgan Stanley Capital International (MSCI) Europe, Australasia and Far East (EAFE) Index is an index of stocks from 21 countries/regions in Europe, Australia, New Zealand and Asia. Results include reinvested dividends after deducting withholding taxes.

PL Portfolio Optimization Conservative Composite Benchmark is 15% S&P 500; 73% Barclays U.S. Aggregate Bond; 5% MSCI EAFE (Net), and 7% BofA Merrill Lynch U.S. 3-Month Treasury Bill Indices as of March 31, 2013.

PL Portfolio Optimization Moderate-Conservative Composite Benchmark is 30% S&P 500; 55% Barclays U.S. Aggregate Bond; 10% MSCI EAFE (Net), and 5% BofA Merrill Lynch U.S. 3-Month Treasury Bill Indices as of March 31, 2013.

PL Portfolio Optimization Moderate Composite Benchmark is 45% S&P 500; 38% Barclays U.S. Aggregate Bond; 15% MSCI EAFE (Net), and 2% BofA Merrill Lynch U.S. 3-Month Treasury Bill Indices as of March 31, 2013.

PL Portfolio Optimization Moderate-Aggressive Composite Benchmark is 60% S&P 500; 20% Barclays U.S. Aggregate Bond; and 20% MSCI EAFE (Net) Indices as of March 31, 2013.

PL Portfolio Optimization Aggressive Composite Benchmark is 65% S&P 500; 10% Barclays U.S. Aggregate Bond; and 25% MSCI EAFE (Net) Indices as of March 31, 2013.

S&P 500 Index is an index of the stocks of approximately 500 large-capitalization companies traded in U.S. stock markets. Results include reinvested dividends.

A-20

Table of Contents

PACIFIC LIFE FUNDS

PL PORTFOLIO OPTIMIZATION MODERATE-CONSERVATIVE FUND

Schedule of Investments

March 31, 2013

| Value | |||||||

AFFILIATED MUTUAL FUNDS - 100.0% | ||||||||

PL Floating Rate Loan Fund ‘P’ | 3,089,677 | $31,638,296 | ||||||

PL Inflation Managed Fund ‘P’ | 5,195,679 | 50,605,909 | ||||||

PL Managed Bond Fund ‘P’ | 15,817,905 | 175,736,920 | ||||||

PL Short Duration Bond Fund ‘P’ | 7,547,523 | 76,380,934 | ||||||

PL Emerging Markets Debt Fund ‘P’ | 2,315,046 | 24,377,439 | ||||||

PL Comstock Fund ‘P’ | 1,546,801 | 22,273,929 | ||||||

PL Growth LT Fund ‘P’ | 264,406 | 3,683,177 | ||||||

PL Large-Cap Growth Fund ‘P’ | 993,459 | 10,331,969 | ||||||

PL Large-Cap Value Fund ‘P’ | 1,678,744 | 23,435,269 | ||||||

PL Main Street Core Fund ‘P’ | 613,510 | 7,484,816 | ||||||

PL Mid-Cap Equity Fund ‘P’ | 730,071 | 8,030,780 | ||||||

PL Mid-Cap Growth Fund ‘P’ | 556,620 | 4,775,798 | ||||||

PL International Large-Cap Fund ‘P’ | 716,626 | 11,810,003 | ||||||

PL International Value Fund ‘P’ | 789,459 | 7,184,079 | ||||||

PL Currency Strategies Fund ‘P’ * | 1,460,271 | 15,070,002 | ||||||

PL Global Absolute Return Fund ‘P’ | 2,922,175 | 29,776,965 | ||||||

PL Precious Metals Fund ‘P’ | 532,213 | 4,374,793 | ||||||

|

| |||||||

Total Affiliated Mutual Funds | 506,971,078 | |||||||

|

| |||||||

TOTAL INVESTMENTS - 100.0% | 506,971,078 | |||||||

OTHER ASSETS & LIABILITIES, NET - 0.0% | 84,063 | |||||||

|

| |||||||

NET ASSETS - 100.0% | $507,055,141 | |||||||

|

| |||||||

Notes to Schedule of Investments

| (a) | As of March 31, 2013, the fund was diversified as a percentage of net assets as follows: |

Affiliated Fixed Income Funds | 79.6% | |||

Affiliated Equity Funds | 20.4% | |||

|

| |||

| 100.0% | ||||

Other Assets & Liabilities, Net | 0.0% | |||

|

| |||

| 100.0% | ||||

|

|

| Value | |||||||

AFFILIATED MUTUAL FUNDS - 100.0% | ||||||||

PL Floating Rate Loan Fund ‘P’ | 2,933,830 | $30,042,421 | ||||||

PL Inflation Managed Fund ‘P’ | 4,335,266 | 42,225,492 | ||||||

PL Managed Bond Fund ‘P’ | 10,091,364 | 112,115,054 | ||||||

PL Short Duration Bond Fund ‘P’ | 5,472,221 | 55,378,880 | ||||||

PL Emerging Markets Debt Fund ‘P’ | 1,491,770 | 15,708,340 | ||||||

PL Comstock Fund ‘P’ | 2,165,478 | 31,182,878 | ||||||

PL Growth LT Fund ‘P’ | 348,220 | 4,850,711 | ||||||

PL Large-Cap Growth Fund ‘P’ | 1,707,765 | 17,760,751 | ||||||

PL Large-Cap Value Fund ‘P’ | 2,911,588 | 40,645,763 | ||||||

PL Main Street Core Fund ‘P’ | 2,108,282 | 25,721,046 | ||||||

PL Mid-Cap Equity Fund ‘P’ | 930,601 | 10,236,612 | ||||||

PL Mid-Cap Growth Fund ‘P’ | 586,247 | 5,029,999 | ||||||

PL Small-Cap Growth Fund ‘P’ * | 499,727 | 6,641,374 | ||||||

PL Small-Cap Value Fund ‘P’ | 424,831 | 5,161,697 | ||||||

PL Emerging Markets Fund ‘P’ | 589,748 | 8,386,215 | ||||||

PL International Large-Cap Fund ‘P’ | 1,289,349 | 21,248,467 | ||||||

PL International Value Fund ‘P’ | 1,647,084 | 14,988,467 | ||||||

PL Currency Strategies Fund ‘P’ * | 1,352,427 | 13,957,046 | ||||||

PL Global Absolute Return Fund ‘P’ | 2,840,341 | 28,943,076 | ||||||

PL Precious Metals Fund ‘P’ | 1,108,221 | 9,109,580 | ||||||

|

| |||||||

Total Affiliated Mutual Funds | 499,333,869 | |||||||

|

| |||||||

TOTAL INVESTMENTS - 100.0% | 499,333,869 | |||||||

OTHER ASSETS & LIABILITIES, NET - 0.0% | 131,336 | |||||||

|

| |||||||

NET ASSETS - 100.0% | $499,465,205 | |||||||

|

| |||||||

Notes to Schedule of Investments

| (a) | As of March 31, 2013, the fund was diversified as a percentage of net assets as follows: |

Affiliated Fixed Income Funds | 59.8% | |||

Affiliated Equity Funds | 40.2% | |||

|

| |||

| 100.0% | ||||

Other Assets & Liabilities, Net | 0.0% | |||

|

| |||

| 100.0% | ||||

|

|

| (b) | Fair Value Measurements |

The following is a summary of the funds’ investments as categorized under the three-tier hierarchy of inputs used in valuing the funds’ assets and liabilities (See Note 3D in Notes to Financial Statements) as of March 31, 2013:

| Total Value at March 31, 2013 | Level 1 Quoted Price | Level 2 Significant Observable Inputs | Level 3 Significant Unobservable Inputs | |||||||||||||||

PL Portfolio Optimization Conservative Fund | ||||||||||||||||||

Assets | Affiliated Mutual Funds | $506,971,078 | $506,971,078 | $— | $— | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

PL Portfolio Optimization Moderate-Conservative Fund | ||||||||||||||||||

Assets | Affiliated Mutual Funds | $499,333,869 | $499,333,869 | $— | $— | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||