Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORMN-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-10385

Pacific Funds Series Trust

(Exact name of registrant as specified in charter)

700 Newport Center Drive, P.O. Box 7500

Newport Beach, CA 92660

(Address of principal executive offices) (Zip code)

Robin S. Yonis

Vice President, General Counsel and Assistant Secretary of Pacific Funds Series Trust

700 Newport Center Drive, P.O. Box 9000

Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Anthony H. Zacharski, Esq.

Dechert LLP

90 State House Square

Hartford, CT 06103

Registrant’s telephone number, including area code:949-219-6767

Date of fiscal year end: March 31

Date of reporting period:April 1, 2019 -March 31, 2020

FormN-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule30e-1 under the Investment Company Act of 1940 (17 CFR270.30e-1). The Commission may use the information provided on FormN-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by FormN-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in FormN-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule30e-1 under the Act (17 CFR270.30e-1).

Table of Contents

March 31, 2020

ANNUAL REPORT

Table of Contents

PACIFIC FUNDS

ANNUAL REPORT

AS OF MARCH 31, 2020

| A-1 | ||||

| A-2 | ||||

| B-1 | ||||

Financial Statements: | ||||

| C-1 | ||||

| C-4 | ||||

| C-7 | ||||

| C-13 | ||||

| D-1 | ||||

| E-1 | ||||

| F-1 | ||||

| F-2 | ||||

| F-5 | ||||

| F-8 | ||||

| F-9 | ||||

| F-23 | ||||

| F-24 | ||||

Pacific Funds Series Trust, which is a Delaware statutory trust, may be referred to as “Pacific Funds” or the “Trust”.

Beginning January 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of Pacific Funds shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from Pacific Funds or from your financial intermediary (such as a broker-dealer or bank). Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from Pacific Funds electronically by contacting Pacific Funds using one of the methods listed in the Where To Go For More Information section or by contacting your financial intermediary directly.

You may elect to receive all future reports in paper free of charge. You can inform Pacific Funds or your financial intermediary that you wish to continue receiving paper copies by contacting Pacific Funds using one of the methods listed in the Where To Go For More Information section or by contacting your financial intermediary directly. Your election to receive reports in paper will apply to all communications received for all Funds held with Pacific Funds.

Table of Contents

PACIFIC FUNDS

We are pleased to share with you the Annual Report for the fiscal year ended March 31, 2020 for Pacific Funds Series Trust (“Pacific Funds” or the “Trust”). Pacific Funds is comprised of thirty-three Funds, eighteen of which are included in this report (each individually, a “Fund” and collectively, the “Funds”) and are available for direct investment. Pacific Life Fund Advisors LLC (PLFA) is Adviser to the Funds and also directly manages Pacific FundsSM Portfolio Optimization Conservative, Pacific FundsSM Portfolio Optimization Moderate-Conservative, Pacific FundsSM Portfolio Optimization Moderate, Pacific FundsSM Portfolio Optimization Growth and Pacific FundsSM Portfolio Optimization Aggressive-Growth (together, the “Portfolio Optimization Funds”).

Each of the Portfolio Optimization Funds is an asset allocation “Fund of Funds” that invests in Class P shares of certain other funds of the Trust (the “PF Underlying Funds”). PLFA supervises the management of those PF Underlying Funds which are only available for investment by the Portfolio Optimization Funds and are included in a separate PF Underlying Funds Annual Report. Please see “Where to Go for More Information” for instructions on how to obtain the PF Underlying Funds’ Annual Report. During the period, the Portfolio Optimization Funds invested in Class P shares of Pacific FundsSM Core Income, Pacific FundsSM High Income, Pacific FundsSM Floating Rate Income and Pacific FundsSMSmall-Cap Growth.

The Adviser, Pacific Asset Management LLC, Cadence Capital Management LLC and Rothschild & Co Asset Management US Inc. (together, the “Managers”) and their Funds as of March 31, 2020 are listed below:

| Manager(s) | Fund | Page Number | ||

| Pacific Life Fund Advisors LLC (PLFA) | Pacific FundsSM Portfolio Optimization Conservative | A-4 | ||

| Pacific FundsSM Portfolio Optimization Moderate-Conservative | A-5 | |||

| Pacific FundsSM Portfolio Optimization Moderate | A-7 | |||

| Pacific FundsSM Portfolio Optimization Growth | A-8 | |||

| Pacific FundsSM Portfolio Optimization Aggressive-Growth | A-9 | |||

| Pacific Asset Management LLC (Pacific Asset Management) | Pacific FundsSM Ultra Short Income | A-10 | ||

| Pacific FundsSM Short Duration Income | A-11 | |||

| Pacific FundsSM Core Income | A-12 | |||

| Pacific FundsSM Strategic Income | A-13 | |||

| Pacific FundsSM Floating Rate Income | A-14 | |||

| Pacific FundsSM High Income | A-15 | |||

Cadence Capital Management LLC (Cadence) and Pacific Asset Management | Pacific FundsSM Diversified Income | A-16 | ||

| Rothschild & Co Asset Management US Inc. (Rothschild & Co) | Pacific FundsSMLarge-Cap | A-17 | ||

| Pacific FundsSMLarge-Cap Value | A-18 | |||

| Pacific FundsSMSmall/Mid-Cap | A-19 | |||

| Pacific FundsSMSmall-Cap | A-20 | |||

| Pacific FundsSMSmall-Cap Value | A-22 | |||

| Pacific FundsSMSmall-Cap Growth | A-23 | |||

The Adviser and the Managers have prepared a discussion regarding the performance of the Funds of the Trust that they manage, including commentary discussing positive and negative factors affecting performance for the past twelve months.

We appreciate your confidence in Pacific Funds and look forward to serving your financial needs in the years to come.

Sincerely,

|  | |

| James T. Morris | Adrian S. Griggs | |

| Chairman of the Board | Chief Executive Officer | |

| Pacific Funds Series Trust | Pacific Funds Series Trust | |

A-1

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION

This Annual Report is provided for the general information of investors with beneficial interests in the Trust. This report is not authorized for distribution to prospective investors unless preceded or accompanied by a current Trust prospectus, as supplemented, which contains information about the Trust and each of its Funds, including their investment objectives, risks, charges and expenses. You should read the prospectus carefully before investing. There is no assurance that a Fund will achieve its investment objective. Each Fund is subject to market risk. The value of a Fund changes as its asset values go up or down. The value of a Fund’s shares will fluctuate, and when redeemed, may be worth more or less than their original cost. The total return for each Fund of the Trust is net of fees and includes reinvestment of all dividends and capital gain distributions, if any, and does not include deductions of any applicable share class sales charges. Past performance is not predictive of future performance. This report shows you the performance of each of the Funds compared to its benchmark index. Index performance is provided for illustrative and comparative purposes only and does not predict or depict the performance of the Funds. Indices are unmanaged, do not incur transaction costs, do not include fees and expenses, and cannot be purchased directly by investors. Index returns include reinvested dividends.

The composite benchmarks for the Portfolio Optimization Funds are composed of up to four broad-based indices. The percentage amounts of each broad-based index within each composite benchmark are based on each Fund’s target asset class allocations in effect during the reporting period. The percentages attributed to a broad-based index within a composite benchmark will change if a Fund’s target asset class allocations change.

PLFA supervises the management of the Funds contained in this report, subject to the oversight of the Trust’s Board of Trustees (Board). PLFA has written the general market conditions commentary which expresses PLFA’s opinions and views on how the market generally performed for the fiscal year ended March 31, 2020 (the reporting period) as well as separate commentary specific to those Funds that it directly manages that is based on its opinion of how these Funds performed during the year.

All views and opinions expressed in the management discussion of fund performance are subject to change at any time based upon market, economic or other conditions, and the Trust, its Adviser and the Managers disclaim any responsibility to update such views. These views and options may not be relied upon as investment advice or recommendations, or as an offer for any particular security. Any references to “we”, “I”, or “ours” are references to the Managers. Any sectors referenced are provided by the applicable Manager and could be different from the sectors listed in the Schedules of Investments if obtained from another source. The Managers may include statements that constitute “forward-looking statements” under the United States (U.S.) securities laws. Forward-looking statements include information concerning possible or assumed future results of the Trust’s investment operations, asset levels, earnings, expenses, industry or market conditions, regulatory developments and other aspects of the Trust’s operations or general economic conditions. In addition, when used in this report, words such as “believes”, “expects”, “anticipates”, “intends”, “plans”, “estimates”, “projects” and future or conditional verbs such as “will”, “may”, “could”, “should”, and “would”, or any other statement that necessarily depends on future events, are intended to identify forward- looking statements. Forward-looking statements are not guarantees of performance or economic results. They involve risks, uncertainties and assumptions. Although such statements are based on expectations that the Managers believe to be reasonable, actual results may differ materially from expectations. Investors must not rely on any forward-looking statements. Statements of facts and performance data are from sources considered reliable, but no representation or warranty is made as to their completeness or accuracy.

In connection with any forward-looking statements and any investment in the Trust, investors should carefully consider the investment objectives, policies and risks described in the Trust’s current prospectus, as supplemented, and Statement of Additional Information, as supplemented, as filed with the United States (U.S.) Securities and Exchange Commission (SEC), which may be obtained from the SEC’s website atwww.sec.gov.

Market Conditions (for the year ended March 31, 2020)

Executive Summary

While global markets kicked off the new decade with steady gains, risk assets got bombarded in March of 2020 by natural and geopolitical hazards that fueled market volatility. At the start of 2020, economic and business indicators showed that U.S. equities were on track for another positive year. Historically, low employment rates boosted consumer confidence—a key factor behind the rising stock market. This support from American households kept the longest economic expansion in U.S. history going, despite mounting external and operational challenges businesses faced such as rising input costs. However, those stock-market gains over much of the reporting period quickly evaporated with the spread of the coronavirus or “COVID-19”.

Fixed Income

As coronavirus threatened to throw the U.S. economy into a deep recession or worse, the Fed unexpectedly and aggressively lowered the Fed Funds-rate target range from 0% to 0.25% and unleashed multiple credit facilities to maintain ample liquidity in the marketplace. The10-year U.S. Treasury yield slid from nearly 2.5% to 0.70% over the reporting period. The bond market (as defined by the Bloomberg Barclays US Aggregate Bond Index) returned 8.93% for the reporting period. Like equities, spread sectors faced headwinds over the volatile period as the number of coronavirus-related cases and deaths surged, causing elevated risk concerns. Spikes in credit spreads hurt both emerging-market and high-yield bonds, which coincided with the plunge in risk appetite.

Domestic Equity

On the way down, growth stocks continued to outperform value stocks. Value styles and factors tend to have material exposures to financial and energy sectors, both of which performed badly. In the energy sector, a combination of low profit margins, high leverage and tumbling crude prices triggered an outflow of capital. Extremely low interest rates continued to suppress profitability among financial institutions. Amid a flight to quality, investors shifted from small-capitalization stocks to large-capitalization stocks with healthier balance sheets.

A-2

See benchmark definitions on A-24 and A-25

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

International Equity

Internationally, trade tensions between the U.S. and China improved, although the Trump administration maintained most of its tariffs. Russia and Saudi Arabia had been engaging in acrude-oil price war that caused oil prices to plunge as markets prepared for an oncoming glut of oil. Many experts questioned the validity, rationale and strategic motives for engaging in this conflict as well as the possibility of a potential pact between Saudi Arabia and Russia. While Russian President Vladimir Putin maintained a strong interest in the Middle East region, theoil-for-military bilateral relationship between the Saudis and the U.S. has faded over the last several years, particularly after the Crown Prince Mohammed bin Salman become the second most powerful figure in Saudi Arabia behind his father, King Salman.

International equities continued to lag their U.S. counterparts, as both the MSCI EAFE (Europe, Australasia, and Far East) Index (Net) and the MSCI Emerging Markets (EM) Index (Net) experienced double-digit losses(-14.38% and-17.69%, respectively) over the reporting period. International developed- and emerging-market equities tend to have more exposure than U.S. markets to the financial sector, whose performance was lackluster as major central banks maintained exceptionally loose monetary policies. Additionally, both Asian and European economies were hit by the coronavirus outbreak earlier than the U.S., contributing to the relative underperformance.

Concluding Remarks

These unfolding events have caused many countries to take wartime-like measures to fight the spread of the coronavirus and address its effects on the global economy. The Fed and Trump administration unleashed an extraordinary monetary and$2-trillion fiscal-stimulus package in an attempt to offset the snowballing effects ofCOVID-19 and other geopolitical issues.

The Trump administration has found itself simultaneously battling the unprecedented impacts of coronavirus, a trade war with China, falling crude oil prices and cracks in cyber security. We think the$2-trillion stimulus won’t be enough to fully stabilize the economy, and Congress will be forced to pass another package to further bolster markets. We believe the domestic economy and asset prices may begin recovering in the latter half of 2020 if appropriate measures are taken. In particular, we’ll need to see American businesses and consumers regain some optimism after we come out on the other side of the outbreak.

Globally, the energy sector felt the blow delivered by Putin’s drive to regain market share from U.S. shale. Putin also continues to increase Russia’s global influence, especially in the Middle East where the Trump administration has sent mixed messages about the U.S.’s military commitment in the energy-rich region. Russia has been strategically building its key energy infrastructure projects, though construction of its Nord Stream 2 gas pipeline—designed to run from Russia to Germany—has been halted after the U.S. recently announced it would impose sanctions on vessels that help lay the pipeline in the Baltic Sea.

A minefield of issues threatens the European economy. Once the coronavirus crisis fades, the European Union (EU) will still need to finalize terms of Britain’s exit from the EU; deal with a Eurosceptic and battered Italy; and wrestle with political upheavals in Poland and Hungary. The European Union faces these issues with less support from key allies, most notably the U.S. In addition to the coronavirus and geopolitical issues, regulatory pressures to restrict stockholder payouts could add to the mounting headwinds for European dividend-paying stocks such as those in the banking and energy industries, including value sectors, styles and factors.

The economic outlook for Japan, another key international market, remains cloudy. The latest blow was the postponement of the 2020 Summer Olympics to be held in Tokyo Japan due to the coronavirus. Japan’s economic difficulties (e.g. a declining population, perpetual deflation and monumental debt levels) will likely push the government to reluctantly pass another fiscal stimulus package to address some of the challenges.

China appears to be in the early recovery phase from the coronavirus, and the Trump administration has started to show a willingness to lower trade barriers to help revive economic activity. The Trump administration’s actions indicate that it will consider extraordinary measures in an attempt to revive the U.S. equity market. We anticipate that President Trump will place an emphasis on boosting the stock market ahead of November’s presidential election. Those measures could potentially lift risk assets, specifically U.S. and Chinese equities over the medium term.

Forward-lookingprice-to-earnings multiples appear to be fairly reasonable at current levels; however, we have noticed slow downward revisions to analyst earnings estimates amid heightened levels of uncertainty. While the exceptional amount of stimulus could provide a jolt to equity markets, longer-term management of the U.S. government’s finances will likely become a highly complex issue as it will need to address rapidly surging debt levels from bailout packages on top of the Fed’s diminished ability to further loosen monetary policy.

Though the U.S. and other countries currently face multiple headwinds, diligent and careful asset-allocation decisions should help investors navigate through the maze of investment threats and opportunities.

Performance of the Portfolio Optimization Funds

The performance of the Portfolio Optimization Funds are composites of the performance of each of the PF Underlying Funds in which each invests (which may include domestic and/or international equities and bonds). The Portfolio Optimization Funds are compared to two broad-based indices; however, to further assist in performance comparisons, composite benchmarks were constructed for the Portfolio Optimization Funds. Each composite benchmark is comprised of up to four of the broad-based indices shown below. The composite benchmarks were constructed with allocations to each asset class that correspond to the target allocations for Portfolio Optimization Funds. However, the actual allocations of any Portfolio Optimization Fund will naturally vary from these targets as a result of market performance over time. Theone-year performance for these broad-based indices for the year ended March 31, 2020 is shown in the following table:

Broad-Based Indices | ||||

S&P 500 Index (representing U.S. Stocks) | -6.98% | |||

Morgan Stanley Capital International (MSCI) EAFE Index (Net) (International Stocks) | -14.38% | |||

Bloomberg Barclays US Aggregate Bond Index (Fixed Income) | 8.93% | |||

ICE BofAML U.S.3-MonthT-Bill Index (Cash) | 2.25% | |||

| See benchmark definitions on A-24 and A-25 |

A-3

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

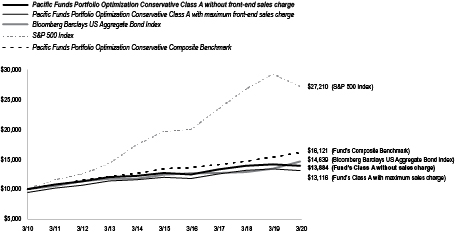

Pacific Funds Portfolio Optimization Conservative (managed by Pacific Life Fund Advisors LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Portfolio Optimization Conservative’s Class A (without sales charge) returned-1.95%, compared to an 8.93% return for the Bloomberg Barclays US Aggregate Bond Index, a-6.98% return for the S&P 500 Index, and a 4.72% return for the Pacific Funds Portfolio Optimization Conservative Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the Fund to its benchmarks for the ten-year period ended March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class C and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | 10 Years | ||||||||||

Fund’s Class A without sales charge | (1.95% | ) | 1.82% | 3.34% | ||||||||

Fund’s Class A with maximum sales charge | (7.38% | ) | 0.68% | 2.75% | ||||||||

Fund’s Class C without sales charge | (2.72% | ) | 1.06% | 2.59% | ||||||||

Fund’s Class C with maximum sales charge | (3.68% | ) | 1.06% | 2.59% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.88% | |||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.53% | ||||||||

Pacific Funds Portfolio Optimization Conservative Composite Benchmark | 4.72% | 3.76% | 4.89% | |||||||||

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | Since Inception (12/31/12) | ||||||||||

Fund’s Advisor Class without sales charge | (1.68% | ) | 2.09% | 2.53% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.06% | |||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.81% | ||||||||

Pacific Funds Portfolio Optimization Conservative Composite Benchmark | 4.72% | 3.76% | 4.31% | |||||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class A underperformed the Pacific Funds Portfolio Optimization Conservative Composite Benchmark. The Pacific Funds Portfolio Optimization Conservative Composite Benchmark is comprised of the Bloomberg Barclays US Aggregate Bond, S&P 500, ICE BofAML U.S.3-MonthT-Bill, and MSCI EAFE (Net) Indices in a weighting that is fixed and specific to the Fund. The Fund was primarily invested in various fixed income strategies, with a smaller allocation to equity, during the reporting period. Fixed income investments included allocations to intermediate-term bond, short duration bond, inflation-indexed bond, emerging markets bond, and floating rate strategies. The equity segment consisted mainly of allocations to domestic and foreign large-capitalization strategies. The Fund’s alternatives allocation consisted of investments in a currency strategy and an equity long/short strategy.

| See benchmark definitions on A-24 and A-25 |

A-4

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

Among the fixed income lineup, high yield and emerging market bonds detracted from performance over the reporting period as riskier asset classes fared poorly amid the global coronavirus pandemic and escalating geopolitical issues. Additionally, the PF Managed Bond Fund, which represented the largest weight in the Fund, underperformed the Bloomberg Barclays US Aggregate Bond Index and detracted from performance over the reporting period.

As for domestic equities, exposures to small-capitalization, value-oriented and real estate-focused stocks dragged performance over the reporting period as growth sectors such as information technology continued to surge past value sectors. Nonetheless, the PF Real Estate Fund outperformed its underlying benchmark and contributed positively to performance.

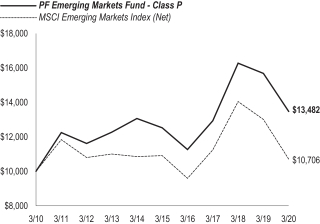

International equities outperformed the MSCI EAFE Index (Net) over the reporting period. An overweight to emerging markets had a positive impact on performance. Additionally, the PF Emerging Markets Fund outpaced its benchmark, the MSCI Emerging Markets Index (Net), which further contributed to performance.

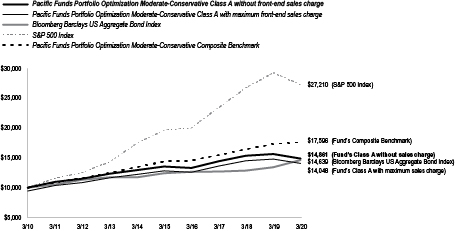

Pacific Funds Portfolio Optimization Moderate-Conservative (managed by Pacific Life Fund Advisors LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Portfolio Optimization Moderate-Conservative’s Class A (without sales charge) returned-4.94%, compared to an 8.93% return for the Bloomberg Barclays US Aggregate Bond Index, a-6.98% return for the S&P 500 Index, and a 1.64% return for the Pacific Funds Portfolio Optimization Moderate-Conservative Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the Fund to its benchmarks for the ten-year period ended March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class C and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | 10 Years | ||||||||||

Fund’s Class A without sales charge | (4.94% | ) | 1.87% | 4.04% | ||||||||

Fund’s Class A with maximum sales charge | (10.15% | ) | 0.73% | 3.46% | ||||||||

Fund’s Class C without sales charge | (5.63% | ) | 1.12% | 3.29% | ||||||||

Fund’s Class C with maximum sales charge | (6.56% | ) | 1.12% | 3.29% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.88% | |||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.53% | ||||||||

Pacific Funds Portfolio Optimization Moderate-Conservative Composite Benchmark | 1.64% | 4.11% | 5.81% | |||||||||

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | Since Inception (12/31/12) | ||||||||||

Fund’s Advisor Class without sales charge | (4.67% | ) | 2.12% | 3.36% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.06% | |||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.81% | ||||||||

Pacific Funds Portfolio Optimization Moderate-Conservative Composite Benchmark | 1.64% | 4.11% | 5.38% | |||||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

| See benchmark definitions on A-24 and A-25 |

A-5

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class A underperformed the Pacific Funds Portfolio Optimization Moderate-Conservative Composite Benchmark. The Pacific Funds Portfolio Optimization Moderate-Conservative Composite Benchmark is comprised of the Bloomberg Barclays US Aggregate Bond, S&P 500, MSCI EAFE (Net), and ICE BofAML U.S.3-MonthT-Bill Indices in a weighting that is fixed and specific to the Fund. The Fund had a diversified allocation mix that was modestly tilted to fixed income during the reporting period. Fixed income investments included intermediate-term bond strategies as well as short duration bond, inflation-indexed bond, high yield bond, emerging markets bond, and floating rate strategies. The Fund’s equity exposure was diversified across style (growth/value), market capitalization and region (including an allocation to foreign small-capitalization and emerging markets strategies). The Fund’s alternatives allocation consisted of investments in a currency strategy and an equity long/short strategy.

Among the fixed income lineup, high yield and emerging market bonds detracted from performance over the reporting period as riskier asset classes fared poorly amid the global coronavirus pandemic and escalating geopolitical issues. Additionally, the PF Managed Bond Fund, which represented the largest weight in the Fund, underperformed the Bloomberg Barclays US Aggregate Bond Index and detracted from performance over the reporting period.

As for domestic equities, exposures to small-capitalization, value-oriented and real estate-focused stocks dragged performance over the reporting period, as growth sectors such as information technology continued to surge past value sectors. Nonetheless, the PF Real Estate Fund outperformed its underlying benchmark and contributed positively to performance.

International equities outperformed the MSCI EAFE Index (Net) over the reporting period. An overweight to emerging markets had a positive impact on performance. Additionally, the PF Emerging Markets Fund outpaced its benchmark, the MSCI Emerging Markets Index (Net), which further contributed to performance.

| See benchmark definitions on A-24 and A-25 |

A-6

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

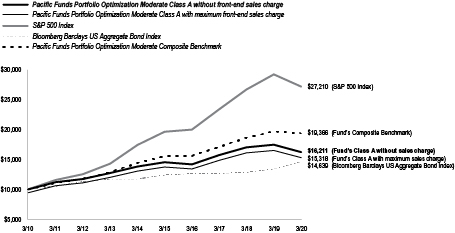

Pacific Funds Portfolio Optimization Moderate (managed by Pacific Life Fund Advisors LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Portfolio Optimization Moderate’s Class A (without sales charge) returned-7.24%, compared to a-6.98% return for the S&P 500 Index, an 8.93% return for the Bloomberg Barclays US Aggregate Bond Index, and a -1.73% return for the Pacific Funds Portfolio Optimization Moderate Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the Fund to its benchmarks for the ten-year period ended March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class C and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | 10 Years | ||||||||||

Fund’s Class A without sales charge | (7.24% | ) | 2.19% | 4.95% | ||||||||

Fund’s Class A with maximum sales charge | (12.35% | ) | 1.03% | 4.36% | ||||||||

Fund’s Class C without sales charge | (7.97% | ) | 1.43% | 4.20% | ||||||||

Fund’s Class C with maximum sales charge | (8.85% | ) | 1.43% | 4.20% | ||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.53% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.88% | |||||||||

Pacific Funds Portfolio Optimization Moderate Composite Benchmark | (1.73% | ) | 4.48% | 6.83% | ||||||||

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | Since Inception (12/31/12) | ||||||||||

Fund’s Advisor Class without sales charge | (7.07% | ) | 2.43% | 4.35% | ||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.81% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.06% | |||||||||

Pacific Funds Portfolio Optimization Moderate Composite Benchmark | (1.73% | ) | 4.48% | 6.58% | ||||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class A underperformed the Pacific Funds Portfolio Optimization Moderate Composite Benchmark. The Pacific Funds Portfolio Optimization Moderate Composite Benchmark is comprised of the S&P 500, Bloomberg Barclays US Aggregate Bond, MSCI EAFE (Net), and ICE BofAML U.S.3-MonthT-Bill Indices in a weighting that is fixed and specific to the Fund. The Fund allocated to a mix of equity and fixed income strategies during the reporting period, with a larger allocation toward equity investments. The equity exposure was diversified across style (growth/value), market capitalization and region (including allocations to foreign small-capitalization and emerging markets stocks). The Fund also maintained exposure to select market sectors such as publicly-traded real estate investment trusts (REITs). Fixed income investments included intermediate-term bond, short duration bond, inflation-indexed bond, emerging markets bond, and floating rate loan strategies. The Fund’s alternatives allocation consisted of investments in a currency strategy and an equity long/short strategy.

Among domestic equities, exposures to small-capitalization, value-oriented and real estate-focused stocks dragged over the reporting period as growth sectors such as information technology continued to surge past value sectors. Nonetheless, the PF Real Estate Fund outperformed its underlying benchmark and contributed positively to performance.

| See benchmark definitions on A-24 and A-25 |

A-7

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

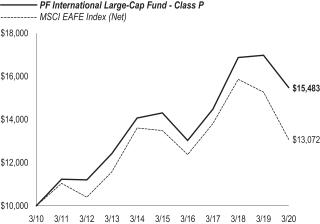

International equities outperformed the MSCI EAFE Index (Net) over the reporting period. An overweight to emerging markets had a positive impact on performance. Additionally, the PF Emerging Markets Fund and the PF InternationalLarge-Cap Fund outpaced their respective benchmarks, which further contributed to performance.

Within the fixed income lineup, high yield and emerging market bonds detracted from performance over the reporting period as riskier asset classes fared poorly amid the global coronavirus pandemic and escalating geopolitical issues. Additionally, the PF Managed Bond Fund, which represented among the top three weights in the Fund, underperformed the Bloomberg Barclays US Aggregate Bond Index and detracted from performance over the reporting period.

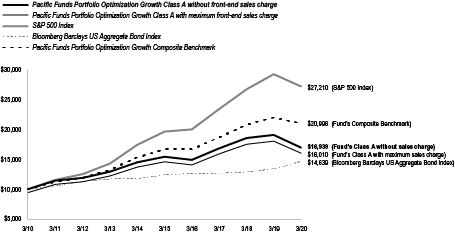

Pacific Funds Portfolio Optimization Growth (managed by Pacific Life Fund Advisors LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Portfolio Optimization Growth’s Class A (without sales charge) returned-11.24%, compared to a-6.98% return for the S&P 500 Index, an 8.93% return for the Bloomberg Barclays US Aggregate Bond Index, and a -4.65% return for the Pacific Funds Portfolio Optimization Growth Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the Fund to its benchmarks for the ten-year period ended March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class C and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | 10 Years | ||||||||||

Fund’s Class A without sales charge | (11.24% | ) | 1.91% | 5.41% | ||||||||

Fund’s Class A with maximum sales charge | (16.11% | ) | 0.77% | 4.82% | ||||||||

Fund’s Class C without sales charge | (11.81% | ) | 1.17% | 4.68% | ||||||||

Fund’s Class C with maximum sales charge | (12.64% | ) | 1.17% | 4.68% | ||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.53% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.88% | |||||||||

Pacific Funds Portfolio Optimization Growth Composite Benchmark | (4.65% | ) | 4.74% | 7.70% | ||||||||

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | Since Inception (12/31/12) | ||||||||||

Fund’s Advisor Class without sales charge | (10.98% | ) | 2.17% | 4.97% | ||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.81% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.06% | |||||||||

Pacific Funds Portfolio Optimization Growth Composite Benchmark | (4.65% | ) | 4.74% | 7.56% | ||||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class A underperformed the Pacific Funds Portfolio Optimization Growth Composite Benchmark. The Pacific Funds Portfolio Optimization Growth Composite Benchmark is comprised of the S&P 500, Bloomberg Barclays US Aggregate Bond Index, and MSCI EAFE (Net) Indices in a weighting that is fixed and specific to the Fund. The Fund had a diversified allocation mix during the reporting period that was tilted to equity. The equity exposure was diversified across style (growth/value), market capitalization and region (including

| See benchmark definitions on A-24 and A-25 |

A-8

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

allocations to foreign small capitalization and emerging markets stocks). The Fund also maintained exposure to select market sectors such as publicly-traded REITs. Fixed income investments included intermediate-term bond strategies as well as specific strategies such as short duration bond, inflation-indexed bond and emerging markets bond strategies. The Fund’s alternatives allocation consisted of investments in a currency strategy and an equity long/short strategy.

Within domestic equities, exposures to small-capitalization, value-oriented and real estate-focused stocks dragged performance over the reporting period as growth sectors such as information technology continued to surge past value sectors. Nonetheless, the PF Real Estate Fund outperformed its underlying benchmark and contributed positively to performance.

International equities outperformed the MSCI EAFE Index (Net) over the reporting period. An overweight to emerging markets had a positive impact on performance. Additionally, the PF Emerging Markets Fund and the PF InternationalLarge-Cap Fund outpaced their respective benchmarks, which further contributed to performance.

Among the fixed income lineup, high yield and emerging market bonds detracted from performance over the reporting period as riskier asset classes fared poorly amid the global coronavirus pandemic and escalating geopolitical issues. Additionally, the PF Managed Bond Fund underperformed the Bloomberg Barclays US Aggregate Bond Index and detracted from performance over the reporting period.

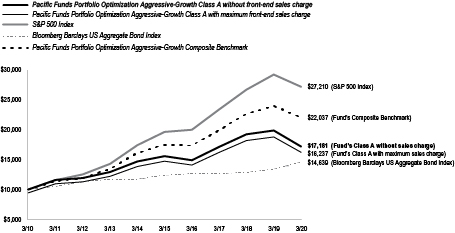

Pacific Funds Portfolio Optimization Aggressive-Growth (managed by Pacific Life Fund Advisors LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Portfolio Optimization Aggressive-Growth’s Class A (without sales charge) returned-13.66%, compared to a-6.98% return for the S&P 500 Index, an 8.93% return for the Bloomberg Barclays US Aggregate Bond Index, and a-8.12% return for the Pacific Funds Portfolio Optimization Aggressive-Growth Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Class A shares of the Fund to its benchmarks for the ten-year period ended March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class C and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | 10 Years | ||||||||||

Fund’s Class A without sales charge | (13.66% | ) | 1.96% | 5.56% | ||||||||

Fund’s Class A with maximum sales charge | (18.41% | ) | 0.81% | 4.97% | ||||||||

Fund’s Class C without sales charge | (14.25% | ) | 1.19% | 4.88% | ||||||||

Fund’s Class C with maximum sales charge | (15.05% | ) | 1.19% | 4.88% | ||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.53% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.88% | |||||||||

Pacific Funds Portfolio Optimization Aggressive-Growth Composite Benchmark | (8.12% | ) | 4.70% | 8.22% | ||||||||

Average Annual Total Returns for the Periods Ended March 31, 2020

| 1 Year | 5 Years | Since Inception (12/31/12) | ||||||||||

Fund’s Advisor Class without sales charge | (13.34% | ) | 2.23% | 5.32% | ||||||||

S&P 500 Index | (6.98% | ) | 6.73% | 10.81% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.06% | |||||||||

Pacific Funds Portfolio Optimization Aggressive-Growth Composite Benchmark | (8.12% | ) | 4.70% | 8.26% | ||||||||

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

| See benchmark definitions on A-24 and A-25 |

A-9

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class A underperformed the Pacific Funds Portfolio Optimization Aggressive-Growth Composite Benchmark. The Pacific Funds Portfolio Optimization Aggressive-Growth Composite Benchmark is comprised of the S&P 500, MSCI EAFE (Net), and Bloomberg Barclays US Aggregate Bond Indices in a weighting that is fixed and specific to the Fund. The Fund primarily allocated to domestic and international equity funds that are diversified across style (growth/value), market capitalization and region (which included allocations to foreign small-capitalization and emerging markets stocks) during the reporting period. The Fund also maintained exposure to select sectors, such as publicly-traded REITs, as well as a small allocation to intermediate-term fixed income securities. The Fund’s alternatives allocation consisted of investments in a currency strategy and an equity long/short strategy.

Within domestic equities, exposures to small-capitalization, value-oriented and real estate-focused stocks dragged performance over the reporting period as growth sectors such as information technology continued to surge past value sectors. Nonetheless, the PF Real Estate Fund outperformed its underlying benchmark and contributed positively to performance.

International equities outperformed the MSCI EAFE Index (Net) over the reporting period. An overweight to emerging markets had a positive impact on performance. Additionally, the PF Emerging Markets Fund and the PF InternationalLarge-Cap Fund outpaced their respective benchmarks, which further contributed to performance.

Among the fixed income lineup, high yield and emerging market bonds detracted from performance over the reporting period as riskier asset classes fared poorly amid the global coronavirus pandemic and escalating geopolitical issues. Additionally, the PF Managed Bond Fund underperformed the Bloomberg Barclays US Aggregate Bond Index and detracted from performance over the reporting period.

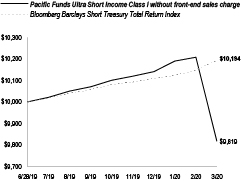

Pacific Funds Ultra Short Income (managed by Pacific Asset Management LLC)

Q. How did the Fund perform for the period ended March 31, 2020?

A. Pacific Funds Ultra Short Income commenced operations on June 28, 2019. For the period from inception through March 31, 2020, Pacific Funds Ultra-Short Income’s Class I (without sales charge) returned-1.81%, compared to a 1.94% return for its benchmark, the Bloomberg Barclays Short Treasury Total Return Index

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the Fund to its benchmark for the period from inception through March 31, 2020. For comparison purposes, the performance of all classes for the period ended March 31, 2020 are also shown in the table below. Performance data for Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Total Returns for the Periods Ended March 31, 2020(1)

| Since Inception (6/28/19) | ||||

Fund’s Class I without sales charge | (1.81% | ) | ||

Fund’s Advisor Class without sales charge | (1.81% | ) | ||

Bloomberg Barclays Short Treasury Total Return Index | 1.94% | |||

| (1) | Pacific Asset Management LLC began managing the Fund effective December 31, 2019. Prior to that date, Pacific Life Fund Advisors LLC doing business under the name Pacific Asset Management managed the Fund. |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the period, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the period from inception through March 31, 2020, the Fund’s Class I underperformed its benchmark. The Fund primarily invests in investment grade short-term fixed and floating rate debt securities Using a fundamental approach with atop-down overlay, Pacific Asset Management’s team of portfolio managers and research analysts look at the relative value of each security and assess the macro environment and marketplace for tailwinds and catalysts in the process of individual investment selection.

| See benchmark definitions on A-24 and A-25 |

A-10

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

The Fund’s focus on corporate debt versus government securities was the primary detractor from performance. The reporting period saw substantial market volatility in short maturity corporate bonds due to the novel Coronavirus and its impacts on corporate earnings and global economic activity. The Fund’s overweight to corporate bonds, notably BBB rated corporate bonds, detracted from performance. The Fund’s overweight to thenon-investment grade bank loan sector and the high yield bond sector detracted from performance. The Fund’s exposure to treasuries that have longer maturities than the index contributed to performance.

The significant spread widening experienced in March 2020 due to the impact of the novel Coronavirus left valuations at attractive levels for corporate debt. However, we are mindful that the duration of Coronavirus and its impacts on corporate earnings and economic activity remain uncertain. Therefore, we are cautious on those sectors most impacted bystay-at-home orders and forced shutdowns including leisure, travel, retail, and energy. Sector and credit selection remain vital as we focus on issuers that are reducing debt, while staying cautious with sectors experiencing more deterioration in credit metrics.

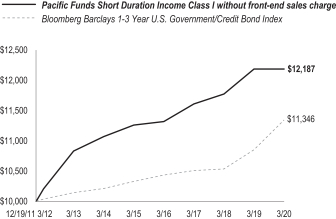

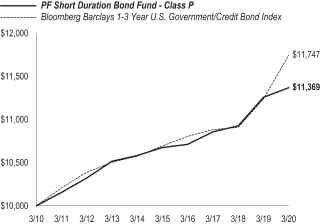

Pacific Funds Short Duration Income (managed by Pacific Asset Management LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Short Duration Income’s Class I (without sales charge) returned 0.03%, compared to a 4.53% return for its benchmark, the Bloomberg Barclays1-3 Year U.S. Government/Credit Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the Fund to its benchmark for the period from inception through March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class A, C and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020(1)

| 1 Year | 5 Years | Since Inception (12/19/11) | ||||||||||

Fund’s Class I without sales charge | 0.03% | 1.60% | 2.42% | |||||||||

Bloomberg Barclays1-3 Year US Government/Credit Bond Index | 4.53% | 1.90% | 1.54% | |||||||||

| 1 Year | 5 Years | Since Inception (6/29/12) | ||||||||||

Fund’s Class A without sales charge | (0.13% | ) | 1.33% | 1.92% | ||||||||

Fund’s Class A with maximum sales charge | (3.13% | ) | 0.72% | 1.52% | ||||||||

Fund’s Class C without sales charge | (0.87% | ) | 0.58% | 1.17% | ||||||||

Fund’s Class C with maximum sales charge | (1.85% | ) | 0.58% | 1.17% | ||||||||

Fund’s Advisor Class without sales charge | 0.02% | 1.58% | 2.16% | |||||||||

Bloomberg Barclays1-3 Year US Government/Credit Bond Index | 4.53% | 1.90% | 1.57% | |||||||||

| (1) | Pacific Asset Management LLC began managing the Fund effective December 31, 2019. Prior to that date, Pacific Life Fund Advisors LLC doing business under the name Pacific Asset Management managed the Fund. |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class I underperformed the benchmark. The Fund uses a short maturity corporate debt focused strategy. Using a fundamental approach with atop-down overlay, Pacific Asset Management’s team of portfolio managers and research analysts look at the relative value of each security and assess the macro environment and marketplace for tailwinds and catalysts in the process of individual investment selection.

The Fund’s focus on income producing corporate debt versus government securities was the primary detractor from relative performance. The reporting period saw substantial market volatility in short maturity corporate bonds due to the novel Coronavirus and its impacts on corporate earnings and global economic activity. Relative to the benchmark, the Fund’s overweight to corporate bonds, notably BBB rated corporate bonds, detracted from performance. The Fund’s overweight to thenon-investment grade bank loan sector and the high yield bond sector detracted from performance. The Fund’s duration was below benchmark, which detracted from performance. Sector overweights to food and beverage, auto Asset-Backed Securities (ABS), and environmental contributed to performance while overweights to independent energy and leisure detracted.

The significant spread widening experienced in March 2020 due to the impact of the novel Coronavirus left valuations at attractive levels for corporate debt. However, we are mindful that the duration of Coronavirus and its impacts on corporate earnings and economic activity remain uncertain. Therefore, we are cautious on those sectors most impacted bystay-at-home orders and forced shutdowns including leisure, travel, retail, and energy. Though we selectively favor bank loans given, in our view, better relative value and downside protection than high yield bonds. The Fund is underweight duration relative to its benchmark.

| See benchmark definitions on A-24 and A-25 |

A-11

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

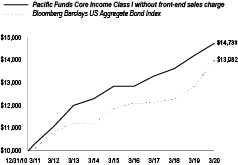

Pacific Funds Core Income (managed by Pacific Asset Management LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Core Income’s Class I (without sales charge) returned 3.81%, compared to an 8.93% return for its benchmark, the Bloomberg Barclays US Aggregate Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the Fund to its benchmark for the period from inception through March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class A, C, P and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020(1)

| 1 Year | 5 Years | Since Inception (12/31/10) | ||||||||||

Fund’s Class I without sales charge | 3.81% | 2.80% | 4.28% | |||||||||

Fund’s Class A without sales charge | 3.51% | 2.49% | 4.01% | |||||||||

Fund’s Class A with maximum sales charge | (0.92% | ) | 1.60% | 3.53% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.69% | |||||||||

| 1 Year | 5 Years | Since Inception (6/30/11) | ||||||||||

Fund’s Class C without sales charge | 2.73% | 1.72% | 2.91% | |||||||||

Fund’s Class C with maximum sales charge | 1.73% | 1.72% | 2.91% | |||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.59% | |||||||||

| 1 Year | 5 Years | Since Inception (6/29/12) | ||||||||||

Fund’s Advisor Class without sales charge | 3.81% | 2.77% | 3.45% | |||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.10% | |||||||||

| 1 Year | Since Inception (4/27/15) | |||||||||||

Fund’s Class P without sales charge | 3.80% | 2.64% | ||||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | ||||||||||

| (1) | Pacific Asset Management LLC began managing the Fund effective December 31, 2019. Prior to that date, Pacific Life Fund Advisors LLC doing business under the name Pacific Asset Management managed the Fund. |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class I underperformed the benchmark. The Fund uses an intermediate term corporate debt focused strategy. Using a fundamental approach with atop-down overlay, Pacific Asset Management’s team of portfolio managers and research analysts look at the relative value of each security and assess the macro environment and marketplace for tailwinds and catalysts in the process of individual investment selection.

The Fund’s focus on corporate debt versus government securities was the primary detractor from relative performance. The reporting period saw substantial market volatility due to the novel Coronavirus and its impacts on corporate earnings and global economic activity. The Fund’s overweight (relative to its benchmark) to corporate bonds, notably BBB rated corporate bonds, detracted from performance. The Fund’s overweight to thenon-investment grade bank loan sector and the high yield bond sector detracted from performance. The Fund’s duration was below that of its benchmark, which detracted from performance. At the security level, Sprint Communications, Bank of America, and Citigroup were the top contributors while Diamondback Energy, NEP Group, and Clubcorp were the top detractors. Sector overweights to banking, electric, and auto ABS contributed to performance while overweights to midstream, leisure, and retailers detracted.

The significant spread widening experienced in March 2020 due to impact of the novel Coronavirus left valuations at particularly attractive levels for corporate debt. However, we are mindful that the duration of Coronavirus and its impacts on corporate earnings and economic activity remain uncertain. Therefore, we are cautious on those sectors most impacted bystay-at-home orders and forced shutdowns including leisure, travel, retail, and energy. We expect to maintain exposure to securitized assets and have looked to add to certain deal structures as they became more attractive due to thesell-off in March 2020.Non-investment grade sectors, bank loans and high yield, are both at attractive levels, though we selectively favor bank loans given, in our view, better relative value and downside protection than high yield bonds. The Fund is underweight duration relative to the benchmark.

| See benchmark definitions on A-24 and A-25 |

A-12

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

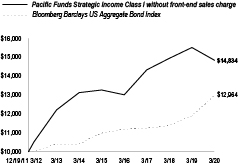

Pacific Funds Strategic Income (managed by Pacific Asset Management LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Strategic Income’s Class I (without sales charge) returned-4.32%, compared to an 8.93% return for its benchmark, the Bloomberg Barclays US Aggregate Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the Fund to its benchmark for the period from inception through March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class A, C and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020(1)

| 1 Year | 5 Years | Since Inception (12/19/11) | ||||||||||

Fund’s Class I without sales charge | (4.32% | ) | 2.26% | 4.88% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.19% | |||||||||

| 1 Year | 5 Years | Since Inception (6/29/12) | ||||||||||

Fund’s Class A without sales charge | (4.58% | ) | 1.97% | 3.93% | ||||||||

Fund’s Class A with maximum sales charge | (8.63% | ) | 1.08% | 3.35% | ||||||||

Fund’s Class C without sales charge | (5.35% | ) | 1.23% | 3.17% | ||||||||

Fund’s Class C with maximum sales charge | (6.27% | ) | 1.23% | 3.17% | ||||||||

Fund’s Advisor Class without sales charge | (4.34% | ) | 2.20% | 4.18% | ||||||||

Bloomberg Barclays US Aggregate Bond Index | 8.93% | 3.36% | 3.10% | |||||||||

| (1) | Pacific Asset Management LLC began managing the Fund effective December 31, 2019. Prior to that date, Pacific Life Fund Advisors LLC doing business under the name Pacific Asset Management managed the Fund. |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class I underperformed the benchmark. Based on our view of the market conditions during the reporting period, we positioned the Fund towardsnon-investment grade securities. Using a fundamental approach with atop-down overlay, Pacific Asset Management’s team of portfolio managers and research analysts look at the relative value of each security and assess the macro environment and marketplace for tailwinds and catalysts in the process of individual investment selection.

The Fund’s underperformance relative to the benchmark for the reporting period was primarily driven by asset allocation. The Fund focused during the reporting period on U.S. credit sectors including bank loans, high yield bonds, and corporate debt. The reporting period saw substantial market volatility due to the novel Coronavirus and its impacts on corporate earnings and global economic activity. The Fund’s overweight relative to its benchmark to corporate bonds, notably BBB rated corporate bonds, detracted from performance. The Fund’s overweight to thenon-investment grade bank loan sector and the high yield bond sector detracted from performance. The Fund’s duration was below benchmark, which detracted from performance. At the security level, Sprint Communications, InBev, and Tesla were the top contributors while Ahern Rentals, Golden Nugget, Energy Transfer Operating LP, and Clubcorp were the top detractors.

The significant spread widening experienced in March 2020 due to the impact of the novel Coronavirus left valuations at attractive levels across the credit spectrum. However, we are mindful that the duration of Coronavirus and its impacts on corporate earnings and economic activity remain uncertain. We have maintained a preference for corporate bonds, especiallyBBB-rated corporates. We have not meaningfully increased our bank loan or high yield allocations at the reduction of corporate bonds. The ultimate path for the credit market remains highly contingent on the path of the virus. We continue to underwrite our credits to stressed scenarios and work closely with our research staff to understand the funding needs of our issuers during this period of economic stress. We expect to be quite flexible from an asset allocation perspective as the market reprices quickly in these volatile times. Security and sector selection remain key as does a need to be flexible.

| See benchmark definitions on A-24 and A-25 |

A-13

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

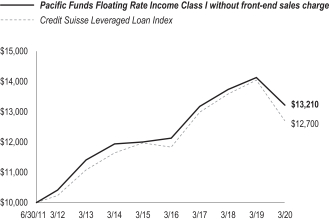

Pacific Funds Floating Rate Income (managed by Pacific Asset Management LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds Floating Rate Income’s Class I (without sales charge) returned-6.49%, compared to a-9.51% return for its benchmark, the Credit Suisse Leveraged Loan Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the Fund to its benchmark for the period from inception through March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class A, C, P and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020(1)

| 1 Year | 5 Years | Since Inception (6/30/11) | ||||||||||

Fund’s Class I without sales charge | (6.49% | ) | 1.94% | 3.23% | ||||||||

Credit Suisse Leveraged Loan Index | (9.51% | ) | 1.21% | 2.77% | ||||||||

| 1 Year | 5 Years | Since Inception (12/30/11) | ||||||||||

Fund’s Class A without sales charge | (6.69% | ) | 1.63% | 3.12% | ||||||||

Fund’s Class A with maximum sales charge | (9.52% | ) | 1.02% | 2.74% | ||||||||

Fund’s Class C without sales charge | (7.31% | ) | 0.92% | 2.38% | ||||||||

Fund’s Class C with maximum sales charge | (8.20% | ) | 0.92% | 2.38% | ||||||||

Credit Suisse Leveraged Loan Index | (9.51% | ) | 1.21% | 3.15% | ||||||||

| 1 Year | 5 Years | Since Inception (6/29/12) | ||||||||||

Fund’s Advisor Class without sales charge | (6.52% | ) | 1.88% | 2.91% | ||||||||

Credit Suisse Leveraged Loan Index | (9.51% | ) | 1.21% | 2.80% | ||||||||

| 1 Year | 5 Years | Since Inception (12/31/12) | ||||||||||

Fund’s Class P without sales charge | (6.49% | ) | 1.90% | 2.40% | ||||||||

Credit Suisse Leveraged Loan Index | (9.51% | ) | 1.21% | 2.24% | ||||||||

| (1) | Pacific Asset Management LLC began managing the Fund effective December 31, 2019. Prior to that date, Pacific Life Fund Advisors LLC doing business under the name Pacific Asset Management managed the Fund. |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class I outperformed the benchmark. Using a fundamental approach with a top down overlay, Pacific Asset Management’s team of portfolio managers and research analysts look for investment opportunities in floating rate loans and floating rate debt securities.

For the reporting period, the Fund’s outperformance relative to the benchmark was driven by sector allocations and credit selection. The reporting period saw some of the highest levels of market volatility since the Global Financial Crisis of 2008, and an underweight to risk as measured by yield to the benchmark contributed to performance. The Fund’s underweights to energy, retail, and metals/minerals were strong contributors to relative performance. Notable was our near zero exposure to energy related securities during the reporting period. Security selection in the food/drug sector detracted from performance.

As of the end of the reporting period, the Fund was underweight risk as measured to our benchmark by yield. We view valuations, given the steepsell-off in March 2020, as attractive. However, we are mindful that the short term path of the novel Coronavirus, and its impacts on earnings and Gross Domestic Product (GDP), remain uncertain. We remain underweight risk, focused on industries and sectors that are less cyclical, and continue to have limited exposure to the sectors most exposed to Coronavirus. We hold limited to no exposure to airlines, hotels, gym/fitness, or department stores. We do hold select gaming sector exposure where we believe the companies have strong balance sheets and good relative value. We are focused on the performing part of the bank loan market. We are overweight service, forest products/containers, and housing (building materials) and underweights energy, metals/minerals, media/telecom, and information technology.

| See benchmark definitions on A-24 and A-25 |

A-14

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

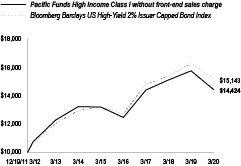

Pacific Funds High Income (managed by Pacific Asset Management LLC)

Q. How did the Fund perform for the year ended March 31, 2020?

A. For the year ended March 31, 2020, Pacific Funds High Income’s Class I (without sales charge) returned-8.36%, compared to a -6.94% return for its benchmark, the Bloomberg Barclays U.S. High-Yield 2% Issuer Capped Bond Index.

The following graph compares the performance of a hypothetical $10,000 investment in Class I shares of the Fund to its benchmark for the period from inception through March 31, 2020. For comparison purposes, the performance of all classes for the periods ended March 31, 2020 are also shown in the table below. Performance data for Class A, C, P and Advisor Class shares will vary due to differences in fees and sales charges. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Average Annual Total Returns for the Periods Ended March 31, 2020(1)

| 1 Year | 5 Years | Since Inception (12/19/11) | ||||||||||

Fund’s Class I without sales charge | (8.36% | ) | 1.81% | 4.52% | ||||||||

Bloomberg Barclays US High-Yield 2% Issuer Capped Bond Index | (6.94% | ) | 2.78% | 5.14% | ||||||||

| 1 Year | 5 Years | Since Inception (6/29/12) | ||||||||||

Fund’s Class A without sales charge | (8.61% | ) | 1.53% | 3.44% | ||||||||

Fund’s Class A with maximum sales charge | (12.52% | ) | 0.64% | 2.86% | ||||||||

Fund’s Class C without sales charge | (9.28% | ) | 0.80% | 2.70% | ||||||||

Fund’s Class C with maximum sales charge | (10.15% | ) | 0.80% | 2.70% | ||||||||

Fund’s Advisor Class without sales charge | (8.38% | ) | 1.78% | 3.69% | ||||||||

Bloomberg Barclays US High-Yield 2% Issuer Capped Bond Index | (6.94% | ) | 2.78% | 4.41% | ||||||||

| 1 Year | 5 Years | Since Inception (1/14/15) | ||||||||||

Fund’s Class P without sales charge | (8.46% | ) | 1.77% | 2.26% | ||||||||

Bloomberg Barclays US High-Yield 2% Issuer Capped Bond Index | (6.94% | ) | 2.78% | 3.18% | ||||||||

| (1) | Pacific Asset Management LLC began managing the Fund effective December 31, 2019. Prior to that date, Pacific Life Fund Advisors LLC doing business under the name Pacific Asset Management managed the Fund. |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |

Q. Discuss both positive and negative factors that materially affected the Fund’s performance during the year, including relevant market conditions, investment strategies and techniques, and particular sectors or securities.

A. For the reporting period, the Fund’s Class I underperformed the benchmark. The Fund seeks a high level of current income by investing innon-investment grade, debt instruments or in instruments with characteristics ofnon-investment grade instruments. Using a fundamental approach with atop-down overlay, Pacific Asset Management’s team of portfolio managers and research analysts look at the relative value of each security and assess the macro environment and marketplace for tailwinds and catalysts.

During the reporting period, the Fund underperformed the benchmark primarily due to sector allocations and an overweight to lower quality securities. Overweights to leisure and midstream and an underweight to technology detracted from performance. Overweights to diversified manufacturing and building materials contributed to performance. At the security level, Golden Nugget, Ahern Rentals and Ascent Resources were the largest detractors. Altice, New Enterprise Stone & Lime, and Howard Hughes Corporation were the top contributors. The Fund’s underweight to BB rated securities and overweight to CCC rated securities also detracted from performance. The Fund held above average cash which benefited performance. The Fund’s duration was shorter than the benchmark, which detracted from relative performance.

As of the end of the reporting period, we believe it is especially important amid current market conditions to continue to maintain our focus on credit selection as the key to our high-yield investment process. The novel Coronavirus, and the duration by which it impacts earnings and GDP, remain uncertain. Current valuations appear attractive, though we remain cautious on many cyclical areas such as retail, energy, and consumer discretionary. The Fund is overweight building materials, leisure, and diversified manufacturing and underweight technology, cable/satellite, and wirelines. The Fund remains underweight exposure to industries in secular decline, which include phone companies in the wirelines sector and hardware companies susceptible to rapid change in the technology sector. The Fund is underweight duration relative to the benchmark.

| See benchmark definitions on A-24 and A-25 |

A-15

Table of Contents

PACIFIC FUNDS PERFORMANCE DISCUSSION (Continued)

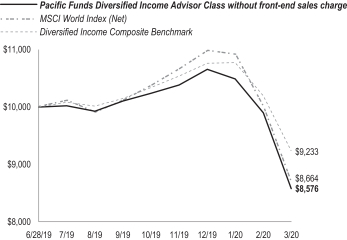

Pacific Funds Diversified Income (co-managed by Cadence Capital Management LLC and Pacific Asset Management LLC)

Q. How did the Fund perform for the period ended March 31, 2020?

A. Pacific Funds Diversified Income commenced operations on June 28, 2019. For the period from inception through March 31, 2020, the Fund’s Advisor Class (without sales charge) returned-14.24%, compared to a-13.36% return for the MSCI World Index (Net) and a-7.67% return for Diversified Income Composite Benchmark.

The following graph compares the performance of a hypothetical $10,000 investment in Advisor Class shares of the Fund to its benchmark for the period from inception through March 31, 2020. The Fund’s performance reflects reinvestments of all dividends and capital gains distributions, if any.

Performance Comparison

Total Returns for the Periods Ended March 31, 2020(1)

| Since Inception (6/28/19) | ||||

Fund’s Advisor Class without sales charge | (14.24% | ) | ||

MSCI World Index (Net) | (13.36% | ) | ||

Diversified Income Composite Benchmark | (7.67% | ) | ||

| (1) | Pacific Asset Management LLC began co-managing the Fund with Cadence effective December 31, 2019. Prior to that date, Pacific Life Fund Advisors LLC doing business under the name Pacific Asset Management co-managed the Fund with Cadence. |

Performance data shown represents past performance. Investment return and principal value will fluctuate so that shares of the Fund when redeemed may be worth more or less than their original cost. Past performance is not predictive of future performance. The table does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or redemption of Fund shares. |