PURSUANT TO RULE 13a-16 OR 15d-16 OF THE

São Paulo, S.P., 05429-900

Federative Republic of Brazil

annual reports under cover Form 20-F or Form 40-F.

Form 20-F ___X___ Form 40-F ______

in paper as permitted by Regulation S-T Rule 101(b)(1)__.

in paper as permitted by Regulation S-T Rule 101(b)(7)__.

Indicate by check mark whether the registrant by furnishing the

information contained in this Form is also thereby furnishing the

information to the Commission pursuant to Rule 12g3-2(b) under

the Securities Exchange Act of 1934.

Yes ______ No ___X___

registrant in connection with Rule 12g3-2(b):

Companhia de Saneamento Básico do Estado de São Paulo - SABESP

Financial Statements as at

December 31, 2019 and 2018

2019 Financial Statements Table of Contents | |||

Independent Auditor’s Report | F-3 | ||

Management Report | F-9 | ||

Statement of Financial Position | F-57 | ||

Income Statements | F-59 | ||

Statements of Comprehensive Income | F-60 | ||

Statements of Changes in Equity | F-61 | ||

Statements of Cash Flows | F-62 | ||

Statements of Value Added | F-64 | ||

Notes to the Financial Statements | F-65 | ||

| 1. | Operations |

|

| 2. | Basis of preparation and presentation of the financial statements |

|

| 3. | Summary of significant accounting policies |

|

| 4. | Changes in accounting practices and disclosures |

|

| 5. | Risk management |

|

| 6. | Key accounting estimates and judgments |

|

| 7. | Cash and cash equivalents |

|

| 8. | Restricted cash |

|

| 9. | Trade receivables |

|

| 10. | Related-party balances and transactions |

|

| 11. | Investments |

|

| 12. | Investment properties |

|

| 13. | Contract asset |

|

| 14. | Intangible assets |

|

| 15. | Property, plant and equipment |

|

| 16. | Borrowings and financing |

|

| 17. | Taxes and contributions |

|

| 18. | Deferred taxes and contributions |

|

| 19. | Provisions |

|

| 20. | Employees benefits |

|

| 21. | Services payable |

|

| 22. | Knowledge Retention Program and Consent Decree |

|

| 23. | Equity |

|

| 24. | Earnings per share |

|

| 25. | Business segment information |

|

| 26. | Insurance |

|

| 27. | Operating income |

|

| 28. | Operating costs and expenses |

|

| 29. | Financial income and expenses |

|

| 30. | Other operating income (expenses), net |

|

| 31. | Commitments |

|

| 32. | Supplemental cash flow information |

|

| 33. | Events after the reporting period |

|

Executive Officers’ Statement | F-172 | ||

Fiscal Council’s Report | F-174 | ||

Audit Committee’s Summarized Annual Report | F-175 | ||

F-2

Independent Auditors` Report on the Financial Statements

(This report is a free translation from the original report issued in Portuguese)

To the Shareholders, Board of Directors and Management of

Companhia de Saneamento Básico do Estado de São Paulo - SABESP

São Paulo – SP

Opinion

We have audited the financial statements of Companhia de Saneamento Básico do Estado de São Paulo - SABESP (“the Company”), which comprise the statement of financial position as at December 31, 2019, the statements of income and other comprehensive income, changes in equity and cash flows for the year then ended, and notes, comprising significant accounting policies and other explanatory information.

In our opinion, the accompanying financial statements present fairly, in all material respects, the financial position of the Companhia de Saneamento Básico do Estado de São Paulo - SABESP as at December 31, 2019, and of its financial performance and its cash flows for the year then ended in accordance with Accounting Practices Adopted in Brazil and with International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB).

Basis for Opinion

We conducted our audit in accordance with Brazilian and International Standards on Auditing. Our responsibilities under those standards are further described in the Auditors’ Responsibilities for the Audit of the Financial Statements section of our report. We are independent of the Company in accordance with the relevant ethical requirements included in the Accountant Professional Code of Ethics (“Código de Ética Profissional do Contador”) and in the professional standards issued by the Brazilian Federal Accounting Council (“Conselho Federal de Contabilidade”) and we have fulfilled our other ethical responsibilities in accordance with these requirements. We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our opinion.

Key Audit Matters

Key audit matters are those matters that, in our professional judgment, were of most significance in our audit of the financial statements of the current period. These matters were addressed in the context of our audit of the financial statements as a whole, and in forming our opinion thereon, and we do not provide a separate opinion on these matters.

F-3

Arrangement with the municipality of Santo André

See notes 3.4, 6 (a) and 9 to the financial statements.

On July 31, 2019, the State of São Paulo, the city of Santo André and SABESP, entered into a concession arrangement for the provision of water supply and sanitary sewage public services in the Municipality of Santo André, under which the States of São Paulo and Santo André assured SABESP the right to explore the provision of such services for a period of 40 years. As a result of such transaction, SABESP recognized R$ 1,337 million as a revenue against intangible assets related to Santo André concession.

The measurement and the accounting recognition was performed considering the negotiation of the transaction, that occurred through the exchange of accounts receivable originated from transactions occurred in previous years for the right to operate the public sanitation services concession of the Municipality of Santo André. The measurement and also the disclosures related to such concession required Company’s management judgment in the analysis of the adequacy of the mentioned measurement and recognition in relation to the following accounting standards: IFRIC 12 – Concession Contracts, IAS 38 – Intangible Assets, IFRS 13 – Fair Value Measurement and IFRS 15 – Revenue from Contracts with Customers.

Due to the relevance of the accounting effects arising from such arrangement with the municipality of Santo André, we consider this matter significant for our audit.

How our audit addressed this matter

Our audit procedures included the understanding and assessment of the design, implementation, and operating effectiveness of the controls related to the accounting of new arrangements/contracts entered into with municipalities whose revenue was obtained through wholesales.

We analyzed the contract entered into with the municipality of Santo André. We tested the reconciliation between the values and documents informed in the contract with the underlying documentation. We obtained the technical memorandum prepared by the Company`s management regarding the accounting treatment adopted and performed our analysis in light of the accounting standards.

We have involved our corporate finance specialists to analyze the intangible assets fair value measurement related to the right to explore the concession services and compared such fair value with the accounts receivable given in the exchange of the concession.

Moreover, we analyzed the accounts receivables records which comprises the accounts receivable formed prior to the signing of the arrangement and performed procedures to evaluate such amount in relation to the expected credit loss recognized due to the lack of payments by Municipality of Santo André until then. We have also evaluated the disclosures to the financial statements.

As a result of the procedures summarized above, we consider the balances recorded in relation to the transaction entered into with the municipality of Santo André and related disclosures, in the context of financial statements taken as a whole for the year ended December 31, 2019, as acceptable.

F-4

Intangible and contract assets

See notes 3.8, 6 (b), 13 and 14 to the financial statements.

During the year of 2019, the Company invested R$ 5,256 million in infrastructure that comprise the basis of concession contracts, intangible and contract assets.

There are several types of transactions that affects the intangible assets caption, such as new concession contracts; evaluation of the classification of existing contracts in the concessions accounting standard; new infrastructures additions, amortization of assets and assessment of construction margin comprising the balance of the infrastructure built.

Due to the relevance of the balances recorded under this caption, the potential financial impact arising from the signing or breaching existing concession contracts, construction of new infrastructures and amortization of such intangible assets, we consider this matter significant for our audit.

How our audit addressed this matter

We have evaluated the design, implementation and operating effectiveness of existing key internal controls related to new infrastructure additions; amortization of intangible assets; administration and management of new and current concession contracts; analysis of the construction margin used by the Company to evaluate the balances recognized as intangible assets.

As a result of evaluating the design and operating effectiveness of internal controls, we planned additional procedures, when applicable, to mitigate any identified risks, primarly in relation to the accounting classification and presentation of the concession itself, the correlated intangible assets and infrastructures under construction, referred as contract assets.

We performed tests on the amortization recognized during the year and compared it with the accounting records; evaluated the transfer of assets under construction classified as contract assets for operation; performed procedures over the amortization rates and the borrowing costs capitalized; to check the construction margin and prepared a technical evaluation to conclude on the compliance of the concession contracts with the respective accounting standard.

We have evaluated the disclosures to the financial statements in relation to the requirements described in the accounting standards relevant to this matter.

Based on the result of the procedures summarized above, we consider the balances of program and concession contracts, recorded as intangible and contract assets and its related disclosures in the context of the financial statements taken as a whole for the year ended December 31, 2019, as acceptable.

Provisions for environmental contingencies

See notes 3.15, 6 (e) and 19 to the financial statements

The Company is a defendant in tax, environmental, labor and civil administrative proceedings and lawsuits, arising from ordinary course of its activities. The environmental lawsuits are related to fines imposed by public and competent bodies on potential environmental damages caused by the Company in the Municipalities where SABESP operates. The Company, with the support and evaluation of its internal and external legal advisors, determines the likelihood of loss and the amounts involved for each lawsuit and records a provision when the criteria for recognition are met, disclosing those assessed as a possible risk (contingent liabilities).

F-5

The likelihood of loss and the estimate of the amounts involved in legal and administrative proceedings of the environmental lawsuits, as well for the other natures, involve the use of judgment by the Company and its legal advisors, expert evaluations, possible changes in case law and other subjective aspects. Thus, we consider this matter significant for our audit.

How our audit addressed this matter

We evaluate the design, implementation and operating effectiveness of existing key internal controls related to: i) the determination of estimates to record a provision; ii) the disclosure of the amounts in accordance with the expected loss on litigation; iii) and how to evaluate that the list contains all litigations; and iv) the updating of the likelihood of loss by the Company.

We obtained confirmation letters from the Company’s legal advisors in relation to the lawsuits, their respective assessment of the likelihood of loss and amounts for the proceedings in the administrative or judicial sphere.

We obtained a sample of environmental lawsuits and involved our legal experts to evaluate the assumptions used by the Company in determining the likelihood of loss, the merits of the lawsuits, similar judgments, recently published information and updates regarding the progress of the lawsuits.

We have assessed the amount of the provision and the disclosures made in the explanatory notes regarding the requirements described in the accounting standards relevant to this matter.

Based on the aforementioned procedures performed and, on the results obtained, we consider the estimates prepared by the Company in the valuation the provisions for environmental contingencies and its related disclosures in the context of the financial statements taken as a whole for the year ended December 31, 2019, as acceptable.

Other matters

Statements of value added

The statements of value added (DVA) for the year ended December 31, 2019, prepared under the responsibility of the Company’s management, and presented herein as supplementary information for IFRS purposes, have been subject to audit procedures jointly performed with the audit of the Company's financial statements. In order to form our opinion, we assessed whether those statements are reconciled with the financial statements and accounting records, as applicable, and whether their format and contents are in accordance with criteria determined in the Technical Pronouncement 09 (CPC 09) - Statement of Value Added issued by the Committee for Accounting Pronouncements (CPC). In our opinion, the statements of value added have been fairly prepared, in all material respects, in accordance with the criteria determined by the aforementioned Technical Pronouncement, and are consistent with the overall financial statements.

Other information accompanying the financial statements and the auditor's report

Management is responsible for the other information comprising the management report.

Our opinion on the financial statements does not cover the other information and we do not express any form of assurance conclusion thereon.

F-6

In connection with our audit of the financial statements, our responsibility is to read the other information and, in doing so, consider whether the other information is materially inconsistent with the financial statements or our knowledge obtained in the audit, or otherwise appears to be materially misstated. If, based on the work we have performed, we conclude that there is a material misstatement of this other information, we are required to report that fact. We have nothing to report in this regard.

Responsibilities of Management and Those Charged with Governance for the Financial Statements

Management is responsible for the preparation and fair presentation of the financial statements in accordance with Accounting Practices Adopted in Brazil and with International Financial Reporting Standards (IFRS), issued by the International Accounting Standards Board (IASB) and for such internal control as management determines is necessary to enable the preparation of financial statements that are free from material misstatement, whether due to fraud or error.

In preparing the financial statements, management is responsible for assessing the Company’s ability to continue as a going concern, disclosing, as applicable, matters related to going concern and using the going concern basis of accounting unless management either intends to liquidate the Company or to cease operations, or has no realistic alternative but to do so.

Those charged with governance are responsible for overseeing the Company’s financial reporting process.

Auditors’ Responsibilities for the Audit of the Financial Statements

Our objectives are to obtain reasonable assurance about whether the financial statements as a whole are free from material misstatement, whether due to fraud or error, and to issue an auditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but is not a guarantee that an audit conducted in accordance with Brazilian and international standards on auditing will always detect a material misstatement when it exists. Misstatements can arise from fraud or error and are considered material if, individually or in the aggregate, they could reasonably be expected to influence the economic decisions of users taken on the basis of these financial statements.

As part of an audit in accordance with Brazilian and international standards on auditing, we exercise professional judgment and maintain professional skepticism throughout the audit.We also:

·Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, design and perform audit procedures responsive to those risks, and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion. The risk of not detecting a material misstatement resulting from fraud is higher than for one resulting from error, as fraud may involve collusion, forgery, intentional omissions, misrepresentations, or the override of internal control.

·Obtain an understanding of internal control relevant to the audit in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control.

·Evaluate the appropriateness of accounting policies used and the reasonableness of accounting estimates and related disclosures made by management.

F-7

·Conclude on the appropriateness of management’s use of the going concern basis of accounting and, based on the audit evidence obtained, whether a material uncertainty exists related to events or conditions that may cast significant doubt on the Company’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to draw attention in our auditors’ report to the related disclosures in the financial statements or, if such disclosures are inadequate, to modify our opinion. Our conclusions are based on the audit evidence obtained up to the date of our auditors’ report. However, future events or conditions may cause the Company to cease to continue as a going concern.

·Evaluate the overall presentation, structure and content of the financial statements, including the disclosures, and whether the financial statements represent the underlying transactions and events in a manner that achieves fair presentation.

·Obtain sufficient appropriate audit evidence regarding the financial information of the entities or business activities within the Group to express an opinion on the financial statements. We are responsible for the direction, supervision and performance of the group audit. We remain solely responsible for our audit opinion.

We communicate with those charged with governance regarding, among other matters, the planned scope and timing of the audit and significant audit findings, including any significant deficiencies in internal control that we identify during our audit.

We also provide those charged with governance with a statement that we have complied with relevant ethical requirements regarding independence, and communicate with them all relationships and other matters that may reasonably be thought to bear on our independence, and where applicable, related safeguards.

From the matters communicated with those charged with governance, we determine those matters that were of most significance in the audit of the financial statements of the current period and are therefore the key audit matters. We describe these matters in our auditors’ report unless law or regulation precludes public disclosure about the matter or when, in extremely rare circumstances, we determine that a matter should not be communicated in our report because the adverse consequences of doing so would reasonably be expected to outweigh the public interest benefits of such communication.

São Paulo, March 26, 2020

KPMG Auditores Independentes

CRC 2SP014428/O-6

(Original report in Portuguese signed by)

Bernardo Moreira Peixoto Neto

Contador CRC RJ-064887/O-8

F-8

Companhia de Saneamento Básico do Estado de São Paulo - SABESP

Management Report 2019

MESSAGE FROM THE CEO

Making progress in benefit of people and the environment

The year of 2019 was marked by the significant progress made within our mission to provide and improve the life quality of people and the environment. We continue to expand the business and our actions always guided by a results-oriented agenda. We began to operate in the municipalities of Santo André, Guarulhos and Aguaí, reaching a total of 372 municipalities under our operations. Additionally, we signed an operating agreement with the municipality of Tapiratiba in October 2019, with operations expected to begin in April 2020.

As part of our vigilance on regulatory and legal security with the granting authority, we renewed our Service Agreement with seventeen municipalities: Espirito Santo do Turvo, Guarujá, São Bernardo do Campo, São Sebastião, Oriente, Bertioga, Itanhaém, Mongaguá, Alambari, Lavrinhas, Peruíbe, Caraguatatuba, Pedra Bela, Vargem, Nazaré Paulista, Águas de São Pedro and Paraguaçu Paulista.

On the operational front, our professionals demonstrated their extreme competence in solving issues regarding the lack of water that, for decades, punished the populations of Guarulhos and Santo André on a weekly basis. Our goal was achieved through interventions that allowed us to interconnect and add water to the distribution systems, putting an end to the recurring shortage of water in the system. We also began to operate the Guarulhos sewage system, which will now provide significant benefits to the city’s population and gradually reduce pollution load dumped in the Tietê river.

The concern for the revitalization of metropolitan water bodies motivated us for the Novo Rio Pinheiros Program challenge launched by the State Government. At the beginning of the year, we elaborated diagnoses and began hiring efforts for the implementation of structures in certain regions, with the goal of providing sewage treatment services to more than 500 thousand properties by the end of 2022.

Given the complexity of the task, we brought important innovations. The contract performance template foresees remuneration based on the number of new properties connected to the sewage treatment system and improvements on the quality of the affluent waters that stream into the Pinheiros river. In terms of technology, we designed equipment that treat affluent waters in regions where there are technical and legal restrictions for for the deployment of conventional networks due to poor and irregular land occupations.

This noble initiative directly impacts the success of an even greater goal: to universalize water and sewage services in the São Paulo Metropolitan Region (SPMR). Initiated 27 years ago by the Tietê Project, this effort has already received investments of over US$ 3 billion in works that havetripled the sewage treatment capacity and expanded sewage collection and treatment to an additional 11 million people, a population similar to Portugal.

F-9

In 2019, we advanced in this project and highlight the progress achieved at the Interceptor Tietê 7 (ITi-7) works, a mega tunnel located under the Tietê highway, with 18 meters in depth, 7.5 km long, 3.4 meters wide and 2.6 meters in height. The structure, which was inaugurated in the beginning of 2020, is integrated with three other key works and began to provide sewage treatment for 2.2 million people, incorporating 350 thousand properties in the city of São Paulo to the collection and treatment service network.

We continue to execute nearly 20 key construction sites for the interception, removal and sewage treatment in 13 metropolitan areas, focusing on the extreme North and East and West regions, in addition to works at the Pró-Billings Program to improve the sewage services of one of our largest metropolitan reservoirs.

Our efforts to expand our sanitation services does not exempt us from permanently striving for stronger water security. Therefore, we continued to execute large infrastructure investments for the transportation, reservation and fight against water loss in light of the severe water crisis we faced in 2014-2015. If these investments had not made, the low rainfall during 2019 would have caused the Cantareira System’s water level to reach zero in November, triggering a new water crisis.

In addition to the robust infrastructure, the consolidation of more rational consumption habits by the population, a behavior that was repeated along 2019, was another important legacy from the previous water crisis.

We also continued to advance in benefit of socially vulnerable areas, where inhabitants receive poor and precarious water supply, through the Água Legal (Legal Water) Program, which was awarded by the Brazil Network of the UN Global Compact. In 2019, we connected 20 thousand properties to our supply network. Since 2017, this initiative has benefited 114 thousand families with quality water supply. We also granted social tariffs to over 71 thousand families, reaching a total of 506 thousand families served by this benefit.

The rebalancing of agreements with the majority of the coastal cities we serve allowed us to restart the environmental sanitation activities of the Onda Limpa (Clean Wave) Program. In the inland regions of the State of São Paulo, we inaugurated six sewage treatment plants (STPs) and are expanding services to communities located remotely from urban centers.

Internally, we concluded the migration of the Health plan, improved the SAP environment (for greater reliability of data management) and advanced with the strengthening of an organizational management aimed at the developing leadership competencies.

The implementation of new Lab Agencies and other improvements in relationship channels demonstrate our ongoing concern to satisfy our customers. We were also recognized for the maturity of our corruption and fraud preventions programs and received theEmpresa Pró-Ética award, granted by the Office of the Comptroller General (CGU).

F-10

��

Finally, we continue to maintain a close eye on the discussions regarding the new basic sanitation framework. For any outcome, we continue to advance in terms of competitiveness by enhancing our human capital, fostering innovation and improving processes, products and services. These strategic efforts reaffirm our perseverance for efficiency and results aimed at the universal access to sanitation services in the operated area.

BENEDITO BRAGA

CEO

F-11

PANEL OF INDICATORS

Indicators | Unit | 2019 | 2018 | 2017 | 2016 | 2015 |

SERVICE | ||||||

Water service ratio |

| Tending towards universalization(1, 2) | ||||

Water coverage ratio | % | Tending towards universalization(1, 2) | ||||

Sewage collection service ratio(2) | % | 84 | 83 | 83 | 82 | 83 |

Sewage collection coverage ratio(2) | % | 91 | 90 | 90 | 89 | 90 |

Ratio of households connected to sewage treatment(3) | % | 78 | 76 | 75 | 74 | 72 |

Resident population supplied with water(4) | Million inhabitants | 27.1 | 25.1 | 24.9 | 24.7 | 24.4 |

Resident population provided with sewage collection(4) | Million inhabitants | 23.8 | 21.8 | 21.6 | 21.3 | 21.0 |

Positive perception of customer satisfaction(5) | % | 86 | 81 | 85 | 82 | 75 |

OPERATIONAL | ||||||

Water connections(6) | Thousands | 9,933 | 9,053 | 8,863 | 8,654 | 8,420 |

Sewage connections(6) | Thousands | 8,326 | 7,495 | 7,302 | 7,091 | 6,861 |

Length of water network(7) | Km | 81,324 | 75,519 | 74,396 | 73,015 | 71,705 |

Length of sewage network(7) | Km | 55,983 | 51,788 | 50,991 | 50,097 | 48,774 |

Water treatment plants (WTP) | Um | 253 | 244 | 240 | 237 | 235 |

Wells | Um | 1,144 | 1,114 | 1,110 | 1,093 | 1,085 |

Sewage treatment plants (STP) | Um | 569 | 565 | 557 | 548 | 539 |

Water loss – billing(8) | % | 18.6 | 19.5 | 20.1 | 20.8 | 16.4 |

Water loss – relating to metering(9) | % | 29.0 | 30.1 | 30.7 | 31.8 | 28.5 |

Water loss per connection(10) | Liters/connection per day | 285 | 293 | 302 | 308 | 258 |

Volume of water produced | Millions of m3 | 2,873 | 2,800 | 2,783 | 2,696 | 2,466 |

Volume of water metered – retail | Millions of m3 | 1,593 | 1,545 | 1,524 | 1,465 | 1,399 |

Volume of water billed – wholesale | Millions of m3 | 82.9 | 263 | 257 | 227 | 216 |

Volume of water billed – retail | Millions of m3 | 2,030 | 1,845 | 1,819 | 1,763 | 1,698 |

Volume of sewage billed | Millions of m3 | 1,767 | 1,641 | 1,617 | 1,552 | 1,481 |

Number of employees(11) | Units | 13,945 | 14,449 | 13,672 | 14,137 | 14,223 |

Operational productivity | Connections/ employee | 1,309 | 1,145 | 1,182 | 1,114 | 1,074 |

FINANCIAL | ||||||

Gross revenues | R$ million | 19,080.6 | 17,056.3 | 15,374.6 | 14,855.1 | 12,283.5 |

Net revenue | R$ million | 17,983.7 | 16,085.1 | 14,608.2 | 14,098.2 | 11,711.6 |

Adjusted EBITDA(12) | R$ million | 7,510.5 | 6,540.6 | 5,269.3 | 4,571.5 | 3,974.3 |

Adjusted EBITDA margin | % of Net Revenue | 41.8 | 40.7 | 36.1 | 32.4 | 33.9 |

Adjusted EBITDA margin excluding construction revenues and costs | % of Net Revenue | 49.5 | 48.8 | 45.4 | 43.3 | 46.6 |

Operating income(13) | R$ million | 5,711.6 | 5,176.7 | 3,961.7 | 3,429.6 | 3,044.0 |

Operating margin (13) | % of Net Revenue | 31.8 | 32.1 | 27.1 | 24.3 | 26.0 |

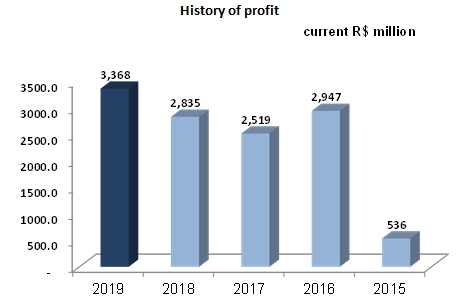

Income (net profit/loss) | R$ million | 3,367.5 | 2,835.1 | 2,519.3 | 2,947.1 | 536.3 |

Net margin | % of Net Revenue | 18.7 | 17.6 | 17.2 | 20.9 | 4.6 |

Net debt over Adjusted EBITDA14) | Multiple | 1.46 | 1.55 | 1.86 | 2.20 | 2.89 |

Net debt over shareholders’ equity(14) | % | 50.8 | 51.8 | 56.1 | 65.4 | 83.7 |

Investment(15) | R$ million | 5,068.0 | 4,177.4 | 3,387.9 | 3,877.7 | 3,481.8 |

(1) For methodological reasons, it includes a variation margin of plus or minus 2 percentage points.

(3) Household is the term used for the building or subdivision of a building, with occupations that are demonstrably independent of each other, collectively using a single water supply and/or sewage connection.

(4) This Indicator Panel’s demographic data takes into account the “Projection for the Population and Households for the Municipalities of the State of São Paulo: 2010-2050”, drawn up by the State Data Analysis System Foundation.

(5) Survey carried out in 2019 by GMR Market Intelligence (9,606 interviews across the entire operating base with a margin of error of 1% and a reliability interval of 95%).

(6) Active and inactive connections and households.

(7) Includes water-mains, branch collectors, interceptors and outfalls.

(8) Includes real (or physical) loss and apparent (or non-physical) loss. The percentage of water loss represents the resulting ratio between (i) Billed Volume Lost and (ii) Volume of water Produced. The Billed Volume Lost corresponds to: Volume of Water Produced MINUS Billed Volume MINUS Volume of Uses. The volume of uses corresponds to: water used in regular maintenance of water mains and reservoirs; water used in municipalities, such as firefighting; and water supplied to irregular settlements.

(9) Includes real (or physical loss) and apparent (or non-physical) loss. The percentage of water loss represents the resulting ratio between the (i) Measured Volume Lost and the (ii) Volume of water Produced. The Measured Volume Lost corresponds to: Volume of water Produced MINUS Measured Volume MINUS Volume of Uses. The volume of uses corresponds to: water used in regular maintenance of water mains and reservoirs; water used in municipalities, such as firefighting; and water supplied to irregular settlements.

(10) Calculated by dividing the Measured Volume Lost in the year by the average amount of active water connections in the year, divided by the number of days in the year.

(11) Internal headcount. Does not include those assigned to other entities. Employees retired due to disability ceased to be taken into account from 2016 onward.

(12) Adjusted EBITDA corresponds to net earnings before: (i) depreciation and amortization expenses; (ii) income tax and social contribution (federal income taxes); (iii) financial income and (iv) other net operating expenses.

(13) Does not include financial income and expenses.

(14) Net debt consists of debt, minus cash and cash equivalents.

(15) Does not include financial commitments assumed in program agreements (R$ 177 million, R$ 6 million, R$ 121 million, R$ 207 million and R$ 331 million in 2015, 2016, 2017, 2018 and 2019, respectively).

F-12

OVERVIEW – AMONG THE LARGEST IN THE WORLD IN TERMS OF POPULATION SERVED

Companhia de Saneamento Básico do Estado de São Paulo - SABESP was founded in 1973 and is the largest sewage company in the Americas and the serves the fourth largest global population. A total of 28.1 million people are served with water supply, with one million residents served in the cities of Mauá, Mogi das Cruzes and São Caetano do Sul - and 27.1 million people are directly served. Of this total amount, approximately 23.8 million people receive sewage collection service.

We provide direct basic and environmental sanitation services in the State of São Paulo and in the supply treated water and wholesale sewage services in the SPMR .

In December 2019, we wereresponsible for water supply, sewage collection and treatment services in372 municipalities in São Paulo, including the cities of Guarulhos, Santo André and Aguaí. We signed a service agreement with the municipality of Tapiratiba in October 2019, with the start of operations expected for the first semester of 2020, when we reach 373 municipalities.

At the same time, we formalized an agreement to continue the water and sewage operation services for at least 30 years in 17 municipalities in the northern coastal region of the State of São Paulo, as well as the regions of Santos, Bragantina and the city of São Bernardo do Campo, in the São Paulo Metropolitan Region (SPMR).

We participate as a minority shareholder in sanitary service companies of four other municipalities, namely: Águas de Castilho S.A., Águas de Andradina S.A., Saneaqua Mairinque S.A. and SESAMM – Serviços de Saneamento de Mogi Mirim S.A.

We also offer consulting services on the rational use of water, as well as planning and financial, commercial and operational management based on the works carried out in Panama. We are qualified to carry out activities in the drainage, urban cleaning services, solid waste and energy management markets in other states and countries.

We also hold equity stakes in companies such as Aquapolo Ambiental (reuse water), Attend Ambiental (non-domestic sewage) and Paulista Geradora de Energia S.A. (electric energy), being the latter in pre-operational phase. For more information on these companies, please refer to Explanatory Note 11 of the Financial Statements.

At the end of2019, we had a total of 13,945 employees, allocated among our head office, administrative units and 17 business units, which operate 81.3 thousand km of water distribution networks and 56 thousand km of sewage collection networks, outfalls and interceptors; 253 water treatment plants (WTPs) and 569 sewage treatment plants (STPs).

In 2019, we invested R$ 5.1 billion and achieved a net revenue of R$ 18.0 billion and a net income of R$ 3.4 billion. Total assets were R$ 46.5 billion and market value was R$41.4billion on December 31, 2019.

Sabesp has been a signatory to the United Nations Global Compact since 2007 and is aligned with the Sustainable Development Goals (SDGs).

F-13

MANAGEMENT GUIDED BY EFFICIENCY, INTEGRITY AND TRANSPARENCY

Sabesp is a mixed capital corporation, controlled by the Government of the State of São Paulo, which owns 50.3% of its shares, and the remaining shares are tradedon theNovo Mercadoof B3 (the São Paulo Stock Exchange) and on the New York Stock Exchange (American Depositary Shares - ADR Level III). The Company operates in a regulated sector and is thus subject to legislation, regulation and sector inspections, both in the Brazilian and the American capital markets, and is also subject to regulations applicable to state-controlled companies.

Compliance with these rules reinforces our robust structure, commitments and corporate governance practices, with differentials that guarantee transparency, equality and accountability for our shareholders and creditors, in addition to quality services for customers and ethics standards in the course of our mission. For details on this structure and the composition of our governance bodies, please visit the Corporate Governance section of our investor relations website.

Integrity, transparency and the adoption of ethical principles and conduct, including the fight and intolerance against any and all forms of fraud and corruption, are part ofSabesp 's culture and reflect its corporate identity.

To guarantee the dissemination of this culture, we have important drivers that establish the principles and practices to be widely adopted, as illustrate below. Through these efforts, we were awarded as a Pro-Ethical Company, an initiative held by the Office of the Comptroller General (CGU), for our Integrity Program model, being the only sanitation company recognized in the 2018/2019 evaluation cycle.

Integrity Program

The Company’s Integrity Program, approved by the Board of Directors and supported by the Compliance Policy, establishes the guidelines, principles and competencies of the Company’s management and employees in order to ensure that they comply with laws, regulations and corporate instruments while preserving the Company’s assets, image, integrity and other ethical values.

Sabesp’s Integrity Program is aligned with the recommendations of theOffice of the Comptroller General (CGU) and the requirement of theBrazilian and North American Anti-Corruption Laws.In addition, the program’s restructuring followed the guidelines of Federal Law 13.303/16, theNovoMercado Regulationsand the best practices recommended by the Brazilian Corporate Governance Code.

Within this scenario, we implement and monitor our compliance to a set of anti-corruption measures that prevent, detect and remedy harmful acts against public administration in two fronts: active corruption and passive corruption.

In 2019, we began a new cycle which includes mapping and analyzing risks, frauds and corruption, as well as undertaking the necessary controls to mitigate them. Currently, 14 critical macroprocesses are being evaluated by means of interviews with the executive board anddirectors in order to identify their perception of fraud and corruption risks linked to strategic guidelines.

F-14

Also in 2019,Sabesp improved its reputational assessment process (Integrity Background Check) for nominating or reappointing Executives and Fiscal Council members, nominations for the independent positions, signing of agreements and constituting new Special Purpose Companies.

Within the compliance practices, we highlight that we encourage our suppliers to adopt integrity measures, foreseen in contractual clauses which also include mandatory compliance with ethical standards and prohibition of fraud and corruption practices, in addition to monitoring transactions between related parties Company.

As a result of our efforts, we did not identify any cases of corruption in 2019. Additionally, we express our public commitment to ethics, through adherence with the Ethos Institute's Business Pact for Integrity and Against Corruption, participation in the working group of the United Nations (UN) Global Anti-Corruption Compact and in the implementation and coordination of the Technical Governance and Legal Chamber of ABES - Brazilian Association of Sanitary and Environmental Engineering.

In order to disseminate and share the ethics and transparency culture with its internal audience,Sabesp, through its business university, Universidade EmpresarialSabesp, developed theConduct and Integrity Learning Trail. This is an ongoing training program with a predefined schedule and learning tools covering the following key matters: integrity, ethics, sexual and moral harassment, diversity, corruption, fraud, conflict of interest, among others.

We also highlight the Ethics Visits project that was carried out in 30 municipalities where we operate and resulted in over 100 lectures given to more than 6,000 employees of all positions. The project was created to reinforce the values and principles ofSabesp 's Code of Ethics and Conduct and is complemented by other actions, such as articles and polls, that are published in internal communication channels.

In 2019,Sabesp also conducted on-site trainings on Preventing and Combating Fraud and Corruption with the aim of providing a reflection on the matter, informing national and international laws on the topic and disseminate best practices, in addition to fostering an integrity culture at the Company. The program’s content includes guidelines for preventing fraud and corruption, as well as on how to act with public agents and address conflicts of interests, risks and control processes, providing concrete examples and cases to help identify the appropriate integrity measure that should be taken. In addition to the internal audience, directors and executives responsible for the compliance areas of special purpose companies, in whichSabesp is a minority shareholder, also participated in the training.

The Executive Board and members of the Fiscal Council also received training on topics related to corporate governance and integrity.

Aside from face-to-face training sessions, over 34,000 hours of virtual training sessions were also held for the topic of integrity and, in 2020,Sabesp expects to increase its actions to include other audiences such as suppliers and business partners.

F-15

In 2019,Sabesp also provided specific training sessions on its whistleblowing channel to employees who work directly with this issue.

Sabesp’s Culture and Integrity Communication Plan is defined annually and formalizes the responsibilities of each division within each phase and the target audience for each communication action. The Plan aims to disseminate the policies and procedures of the Integrity Program, in addition to reinforcing and increasing the use, when applicable, of the Whistleblowing Channel and the principles of the Code of Ethics and Conduct.

In 2019, the plan covered all employees through internal communication channels, such as e-mails, murals and the intranet portal, among others.

Code of Ethics and Conduct

Our Code of Ethics and Conduct,which was initially developed as a collaborative project in 2006 and updated in 2014 and 2018, establishes theground rules for the company’s executives and employees to act in an integrated and coherent way when conducting their relations and business with different counterparties.

The Ethics Committee, which is linked to the Board of Directors, it is responsible for the updating the Code so that it always reflect current scenarios. The committee is also responsible for encouraging executives and employees to engage and commit to the principles established therein.

In order to stimulate dialogues and engage our employees to have ethical behaviors when conducting business activities, we offer atrust channel, which guaranteessecrecy and anonymity foremployees who need to clarify questions. Demands received by the channel are reported every six months to the Ethics Committee and to the Board of Directors on an annual basis.

Whistleblowing Channel

Any interested party can report issues that contradict the principles set out in the Code of Ethics and Conduct, such as fraud, corruption, illegal acts and other violations, by contacting the Whistleblowing Channel, and the procedures for investigating breaches of the Code and events reported to the Whistleblowing Channel are monitored by the Audit Committee.

The internal audit team is responsible for processing complaints and must make every effort to ensure the anonymity of the complainant and protect the confidentiality of the information and of those involved, in order to preserve rights and the neutrality of decisions.

The Whistleblowing Channel recorded 174 incidents in 2019.Out of the total number of complaints considered to be material, penalties were applied to45 employees and third parties, being 20warnings, 2 suspensions and 23 individuals were fired.It should be noted that there were no indications of the Company’s employees being involved in cases of corruption.

Also in 2019, we hired an external channel to address complaints. The initiative will be implemented in 2020 and will allow, in addition to the current reporting options, the possibility of registering complaints electronically.

F-16

Transparency

Transparency is an essential tool for promoting ethics and integrity. Therefore, we provide a Transparency Portal that gathers and discloses clear and updated information on our business. Among them are Institutional Policies, contracts with the granting authorities and suppliers, key developed programs and projects, in addition to minutes of the Company's board and committee meetings.

The Company also has a Citizen Information Service (SIC) channel, which is required by the Access to Information Law.

Risk Management

We have a solid risk management structure that includes bodies, processes and policies that are aligned with the key global and national trends and guided by the principle of mitigation. Thus, we maintain a corporate risk map that allows us toforesee and monitor scenarios that may adversely affect our operations.

The risk management division is linked to the Chief Executive Officer, led by a statutory officer appointed by the Board of Directors, receives support from the internal audit area and establishes direct dialogues with the Fiscal Council, the Audit Committee and the Board of Directors whenever irregular conducts are suspected by the members of the Board of Directors. The risk management division is independent and operates under its own budget.

The Company also has a Corporate Risk Management Committee, comprised by a representative from each operating division and reports to the Collegiate Executive Board.

Our risk management is guided by the Institutional Policy for Corporate Risk Management, which was approved by the Board of Directors and complies with theCOSO – ERM international model – The Committee of Sponsoring Organizations of the Treadway Commission Enterprise Risk Management, as well as the standards issued by ABNT NBR ISO 31.000:2009 and ABNT ISO GUIA 73:2009. The Policy is complemented by the Risk Management Procedure and the Risk Dictionary.

Risks are identified and measured in terms of impact and the probability of occurrence and aresubsequently assessed at the appropriate hierarchical levels in order to define mitigating actions required for each situation, which areupdated annually.Risks are classified in four categories:strategic, financial, operational and compliance. Risks with significant and critical levels are monitored by the Collegiate Board and the Board of Directors. With this, we can develop mitigating actions and minimize the negative impacts of these scenarios, supporting the achievement of our strategic objectives.

A description of the risk factors can be found in item 4 of the Reference Form, which is available on the Company’s Investor Relations website, in the “Financial and Operating Information” section – Reference Form and IAN.

F-17

Internal Controls

Internal controls include adequately elaborating accounting records, preparing financial statements in accordance with the official regulations and properly authorizing transactions for acquiring, using and selling the Company's assets.

We have been promoting a structured and systematic assessment of internal controls for 15 years. Internal controls are currently guided by the internal controls framework of the 2013 Committee of Sponsoring Organizations of the Treadway Commission (COSO), and complies with section 404 of the Sarbanes-Oxley Act (SOX) and Law 13.303. The internal control assessment process is reviewed annually to consider new risks associated with the preparation and disclosure of financial statements and possible significant changes in the computerized processes and systems.

The assessment carried out on the effectiveness of the 2018 internal control environment identified only one significant deficiency related to the service account (support for the ERP system) with privileged access. Management performed tests to the system’s accesses, which indicated that actions taken by the account user were limited to those necessary to maintain the system, without any impacts on the Company's 2018 financial reports. Assessment on the 2019 fiscal year will be concluded in April 2020.

Internal control tests are performed by the internal audit area, which reports directly to the Chief Executive Officer and functionally to the Audit Committee.

External auditors

External auditors are responsible for auditing our financial statements and reviewing quarterly information and financing projects to ensure the reliability of the data presented.

Sabesp respects the principles that preserve the independence of the external auditor as to not audit their own work, exercise management roles and advocate for its client.

The Audit Committee, in line with our Bylaws, is responsible for evaluating the guidelines that provide for the hiring of services by external auditors. The Committee also recommends the Board of Directors on the hiring and dismissal of the external audits, in addition to having the duty to issue an opinion prior to hiring other services by the audit firm, or companies related to it, that are not common audit activities.

KPMG Auditores Independentes has been the Company’s external auditor since the review of the quarterly information (ITR) of June 30, 2016.

In 2019, the Company paid R$ 2.9 million for the audit of the financial statements, the review of the quarterly information and of project financing, among others.During the same period, KPMG provided the revision of Tax Compliance and training on matters that did not conflict with the audit services provided and which did not exceed 5% of the fees paid for the aforesaid services.

In 2019, KPMG Auditores Independentes also provided auditing services to Attend Ambiental S.A.,one of Sabesp’s affiliated companies.

F-18

Management Compensation

The compensation guidelines for management, members of statutory committees and the Fiscal Council are defined by the Compensation Policy. In 2019, the total annual compensation should be approvedby the shareholders at the annual general meeting. In 2019, the gross compensation amount, including legal benefits and charges, totaled R$ 6.7 million, including approximately R$ 1.3 millionrelated to the variable compensation of the executive officers. For more information on compensation, please refer to item 13of the Reference Form, which is available on the Company’s Investor Relations website, in the “Financial and Operating Information” section– Reference Form and IAN.

F-19

STRATEGY AND VISION OF THE FUTURE

Ourmission is to provide water and sewage services, contributing to improve the quality of life and of the environment;with the Company’s goal being to become a worldwide reference in relation to the provision of sanitation services, in a sustainable, competitive and innovative way, with a focus on the customer.

Sabesp’s strategies and guidelines are based on an analysis of risks and opportunities, and in the pursuit of its vision for the future, the Company contributesto ensure the availability of water in its area of operations and to advance with the implementation of structures for the collection and treatment of sewage, with technical and economic feasibility and quality service management.

Since 2018, one of our strategic objectives has been to “Keep and Conquer Markets and New Businesses”. In this sense, during 2019, we added approximately 2 million individuals to our retail operations as a result of services in the municipalities of Guarulhos and Santo André (more details are available in the “Financial Performance – Wholesale Customers” section).

We constantly seek to improve our management processes and, in 2019, we highlight the start of an implementation phase for the opportunities identified in theSabesp Management Model Project (concluded in 2018),which consisted of carrying out the Assisted Self-Assessment based on the National Quality Foundation Management Excellence Model(MEG). The integrated awareness, mentoring activities for developing solutions and new assessments activities scheduled for 2020 will allow us to continue to promote ongoing improvements in management processes in addition to achieving a systemic vision of the business and sharing good practices to obtain excellent performances.

The implementation of a CRM (Customer Relationship Management) system continues underway and it is expected to replace the current commercial information systems by 2021.

Balanced Goals

Within the proposed targets for 2019, we highlight the new water and sewage connections which exceeded our goals by 10% and 4.4%, respectively.

The ratio of households connected to sewage treatment reached 78%, above the 77% expected for the year and did not include the municipalities of Guarulhos and Santo André, which began to operate in 2019. The service and coverage goals were met within the characteristics of their indicators.

In 2019,Sabesp reduced its loss rate by 8 liters per connection per day. Although significant, this reduction was not enough to reach the established goal of 283 liters per connection per day.

F-20

Achievements in 2019 and Targets for 2020-2024 | Achieved | Targets | |||||

| 2019 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 |

Water Supply Service | Tending towards universalization (¹), (2) | Tending towards universalization (¹), (2) | |||||

Sewage Collection | 84 | 85 | 85 | 85 | 86 | 87 | 88 |

Water Supply Coverage (2) | Tending towards universalization(¹), (2) | Tending towards universalization(¹), (2) | |||||

Sewage Collection | 91 | 91 | 92 | 92 | 93 | 94 | 95 |

Ratio of Households Connected to Sewage Treatment (%)(3), (4) | 78 | 77 | 74 | 75 | 82 | 84 | 85 |

New Water Connections (thousands) | 204.8 | 186 | 194 | 187 | 187 | 187 | 177 |

New Sewage Connections (thousands) | 237.0 | 227 | 240 | 240 | 240 | 233 | 233 |

Water Loss per Connection (liters/connection/day) | 285 | 283 | 273 | 267 | 261 | 253 | 249 |

(1) Coverage equal to 98% or more. Service equal to 95% or more.

(2) For methodological reasons, it includes a variation margin of plus or minus 2 percentage points.

(3) Household is the term used for the building or subdivision of a building, with occupations that are demonstrably independent of each other, collectively using a single water supply connection and/or sewage connection.

(4) Excluding Guarulhos and Santo André in 2019.

Research, Development and Innovation

In 2019, the Company invested approximately R$ 17.4 million in its Corporate Research, Technological Development and Innovation Program (RD&I), which aims to organize and integrate its efforts in RD&I and create a portfolio of projects to support research and innovation programs.

Just as the electric energy and piped gas sectors, ARSESP approved in 2018 the use of 0.05% of the direct revenues for RD&I expenses as of 2020 through the Quadrennial Research and Technological Development Program for Innovation in Public Sanitation Services. The Company presented a portfolio of priority projects to be analyzed by ARSESP.

In line with the Company’s corporate planning, RD&I actions adopt the circular economy concept, in which waste is considered an input for new products and cycles. Among them, it is worth mentioning:

- The sequential implementation of integrated actions for liquid, solid and gaseous sewage treatment phases at the STP in Franca. This project aims to optimize processes and transform the plant into a resource recovery station. An additional project has also been implemented at that STP to transform biogas from the sewage treatment process into biomethane, which has been used to supply the Company's vehicle fleet in said municipality. The biomethane project is the result of a technical cooperation agreement with the Fraunhofer Institute in Germany. The STP treats an average of 500 liters per second of sewage and produces approximately 2,500 m³ of biogas on a daily basis, enough to substitute 1,500 liters of gasoline per day.

F-21

· | The plasma gasification system for processing sewage sludge generated at the Barueri STP, which converts sludge into inert glassy waste that can be reused in construction sites significantly reducing the final waste volume generated in the end of the sewage treatment process. The project received funding from the Financier of Studies and Projects (FINEP). |

· | The use of aerators powered by photovoltaic energy, whose objective is to generate clean energy to improve the efficiency of sewage treatments, increasing the removal of organic load. |

· | The use of sludge from the Water Treatment Plant as a raw material for base and sub-base pavements, adding value to a by-product. The project comes from a partnership with the São Paulo State University “Júlio de Mesquita Filho” (UNESP). |

In addition, Biofiltration Units were also developed, with funding from FINEP, for controlling odors in the Pinheiros and Pomar sewage pumping stations.

Technological Innovation destined to research projects in higher education or research institutions in the State of São Paulo, whose themes originated from demands pointed out by the operational areas. Out of the 17 projects to date, the partnership generated seven requests for patents and one request for a software application. The program’s Third Call for Proposals was launched in February 2020.

Sabesp also invests in the development and implementation ofOpen Innovation actions that integrates ideas, thoughts, processes and research from different internal and external segments, aiming at improving their processes, products and services.

The Pitch Sabesp is an example which, through a public call for proposals in late 2018 launched 27 challenges in 5 different areas to select and test innovative solutions for challenges previously determined by the Company. Throughout 2019, areas where solutions will be tested were mapped for the technical conditions necessary for a controlled environment. The conclusion of the technical and financial feasibility assessment for the solutions is scheduled for 2020.

We also have a second Agreement with Fapesp, under the Innovative Research in Small-Sized Companies Program (PIPE), to support scientific and technological research in micro-, small- and medium-sized companies in the São Paulo State, with the objective of accelerating startups aiming at the development of innovative projects that solve challenges faced by the Company.

Sabesp publishes Revista DAE, a quarterly journal with scientific technical articles on sanitary engineering. In 2019, the journal achieved its 220th edition since its first edition and underwent a new assessment which raised it to the B1 category in the Qualis/CAPES system and is in its final publication phase.

F-22

WATER QUALITY AND SUPPLY SAFETY

The areas we operate offer universal access to water supply. However, this requires permanent actions in order to maintain efficient services, water security and follow the geographic and demographic growth of the municipalities. In 2019, we invested R$ 2.5 billion in water supply services.

The Metropolitan Area and its Challenges

With the start of operations in Guarulhos and Santo André, in 2019 we covered 36 of the 39 municipalities that comprise the SPMR , where we are responsible for supplying the 21 million inhabitants, of which 20 million are directly served.

The supply of the SPMR is done through the collection and treatment of water by nine integrated producer systems, with a production capacity of 81.7 m³/s. Large mains transport water to the reservoirs installed in the different regions of the metropolitan area, guaranteeing higher reserves of treated water and constant supply to the regions which are remotely located from the main water systems.

Through long-term planning, theMetropolitan Water Program (PMA) considers variables such as population growth and the production and transportation capacity of water to regions with increasing consumption, in addition to seeking the anticipation of events caused by climate changes that can possibly impact the system, such as changes in rainfall, flows, inflow and availability of water sources.

With nearly 25 years of existence, the program has already promoted the expansion of water production capacity in the SPMR of 23.8m³/s, an increase of 42% compared to a population increase of 28% in the same period.

In 2019, we invested approximately R$ 185.1 million in the program, in which we highlight the conclusion of the first phase of the Genesis System, which aims to bring more security to the water supply of the West region of the greater São Paulo area, in addition to the construction works for networks and pipelines, which expanded the interconnection between systems and reservoirs.

Water Security in the Metropolitan Area was Challenged in 2019

The increase in water security resulting from PMA actions was tested once again, in 2019. The low inflow of the Cantareira System (inflow of only 57% of the historical average) it would have emptied the System if it were not for the two major infrastructure works that began to “import” water from other reservoirs out of the Alto Tietê basin, inthe SPMR.

One of these systems, the São Lourenço Producer System, supplies treated water to regions previously served by Cantareira. The Jaguari-Atibainha interconnection, on the other hand, allowed water to be supplied by the Paraíba do Sul basin to the Cantareira System.

F-23

In operation since the first half of 2018, both systems added 445 million m³ of water to the SPMR , corresponding to 45% of the Cantareira system’s total volume. In 2019 alone, 250 million m³ were added, a volume that is similar to the sum of the capacity of the Guarapiranga and Cachoeira dams, belonging to the Cantareira System (which belongs to the Cantareira System).

In 2019, with the exception of Cantareira System (which registered low inflows), our water systems had satisfactory inflow that resulted in a 14% increase in total water storage volume versus 2018. The improved integration between systems reduced the reliance on the Cantareira System to supply the SPMR . In 2019, the average water volume removed from the System was 24 thousand liters per second, 20% less than the amount permitted by the granting authority.

The consolidation of more rational water consumption habits was reflected in the satisfactory water storage levels of the systems as well in water production (62.6 m³/s). In 2019, residential customers consumed an average of 129 liters per person/day.

Even with a universal supply in the operated areas, many irregular residential settlements still exist with precarious water supply due to improvised connections that are subject to contamination.

To face this problem, we created theÁgua Legal (Legal Water) Program to promote the installation of supply systems in communities with high social vulnerability after necessary legal authorizations are obtains since legislation still prevents services to be offered in irregular land occupations.

During the first three years since the launching of the Program, nearly 115 thousand families living in irregular housing unitsin the SPMR had their water connections regularized.

In addition to offering better health and quality of life, the Program plays an important role in terms of citizenship as it enables residents to have a formal proof of address in addition to qualifying them in the social tariff category. The replacement of irregular networks also contributes to the reduction of water loss, which was greater with the improvised connections.

Protection of water sources in the Metropolitan Area

We promote different initiatives aimed at protecting the main sources of water supply for the metropolitan area. These springs have already scarce resources due to disorganized urban occupation, deforestation of vegetation surrounding their margins and pollution carried by rain into their bodies of water.

In 2019, we planted over 144 thousand seedlings in the vicinity of the Cantareira Reservoir. The initiative is part of theMetropolitan Green Belt Programwhich was created to contribute with the protection of riparian forests and reforestation of regions surrounding these dams, in partnership with theNascentes (Springs) Program of the Government of the São Paulo State.

As a whole, 330 km2 of Atlantic Forest are being preserved in the surrounding areas of water basins, which enables the conservation and preservation of good water quality.

F-24

Through theNossa Guarapiranga (Our Guarapiranga) Program, over the past 9 years we have been cleaning one of the most important metropolitan springs, responsible for supplying water to approximately four million people.

Through the use ofcollecting boats and several eco-barriers, we removed furniture, plastic containers, televisions, and other waste materials that contaminate the reservoir and disrupt water inflows.

From 2011 to 2019,the Program removed a total of178 thousand m³of waste from the reservoir (equivalent to the volume of the lake in Parque Ibirapuera), being 21 thousand m³ in 2019 alone.

Water Supply in the Coastal Region

Afterthe SPMR , the coastal region represents the second biggest challenge for water supply due to the high temperatures and a large number of tourists during the summer periods.

In order to meet higher demand during these peak periods, the service is provided through an integrated system, similar to the concept of the SPMR system.

The water that supplies the nine municipalities of the Baixada Santista region is captured directly from 26 rivers coming from Serra do Mar state park and treated in 16 producing systems, which together have the capacity to treat 11.7 m³/s, and is transported to the 83 sectoral reservoirs to be distributed to approximately three million people, including residents and tourists.

The strengthening of the water production and distribution capacity on the coastal region is part of theÁgua Litoral (Coastal Region Water) Program, which brings together permanent actions to increase security of supply. In 2019, we began the duplication works of the Mambu-Branco Producer System inItanhaém municipality, which is expanding the capacity of the treated water reservoir by creating four reservoirs, with a total capacity of 40 million liters of water.

In Peruíbe municipality, we inaugurated a water treatment Plant (WTPs) with a capacity of 270 liters of water per second and the new Guaraú Reservation Center, thus expanding water security and the quality of the water supplied in the municipality. In Guarujá, we began the implementation of more than 20 km of new networks and pipelines to strengthen the service provided.

We also advanced in the northern coastal region, which has 20 water treatment plants (WTPs) and 51 sectoral reservoirs to supply the systems of the São Sebastião, Caraguatatuba, Ubatuba and Ilhabela municipalities. In 2019, we removed silt from the water collection system, implemented new networks, expanded reserves and sectorized distribution by neighborhoods, aiming at reducing losses and oscillations in the systems.

F-25

Water Supply in the Inland Region

As the water supply situation was resolved in the main operated areas, our actions in the inland regions of the state continues to be focused on operational improvements to increase efficiencies, in addition to execute works that guarantee safety in regions with less water availability.

We highlight the beginning of the construction of the Rio Pardo water dam, which will benefit the municipality of Botucatu. In Cabreúva, located in a region with the lowest water availability in the inland regions of the State of São Paulo, we opened deep wells and pipelines that expanded water availability by 1.3 thousand m³/day, in addition to opening a WTP, reservoirs and elevations.

In Várzea Paulista, we concluded the automation and duplication system for the production capacity of the municipality's WTP, which increased its water availability from 75 l/s to 150 l/s and we initiated works at two reservoirs with capacity for 2 thousand m³/day of treated water each, in addition to substituting 12 km of network.

The start of operations in the municipality of Aguaí, in June 2019, also demanded urgent actions to normalize water supply, such as pipeline networks and drilling of wells.

Combating Water Loss

Another fundamental pillar for promoting water security and supply is the reduction of water loss, which is a permanent challenge to the activity due to aging pipes, equipment and water meters, as well as frauds.

For more than two decades, fighting water loss has been part of our operational routine. In 2009, this work was intensified with the creation of the Corporate Loss Reduction Program.

The total loss indicator is subdivided into two categories: real losses and apparent losses (commercial). Real losses correspond to leaks in the pipelines and amounted to a total of 19% in 2019. Apparent losses – water consumed but not accounted for are the result of fraud, commercial registration failures and inaccurate measurement by the water meters, as a result of their ages – corresponded to 10% in 2019. The sum of these two indicators results in total losses of 29% in 2019. In terms of absolute loss, it corresponded to 285 liters per connection per day.

The target regions for improvement interventions are defined based on technical studies that consider factors such as the age of the networks and leaks incidents. In 2019, R$ 930 million were invested for replacement and maintenance of networks, extensions, water meters, among others. In 2012, the Program began a financial and technological partnership with JICA (Japan International Cooperation Agency).

In 2019, we also began to install 100,000 smart water meters at thelargest customers in the SPMR , which will have their consumption measured remotely by using IoT (Internet of Things) technology, allowing faster identification of consumption anomalies during night period, which indicates leaks in the system.

F-26

Water Reuse at Sewage Treatment Plants (STPs)

Sewage recycling to produce reuse water is an initiative to encourage the sustainable use of water. The use of reuse water for industrial purposes, cleaning streets and irrigating parks and gardens results in significant savings of water that could be used for human consumption but was used for other purposes.

We are installing at the STP in the ABC region, located between the municipalities of São Paulo and São Caetano do Sul, our Aquapolo Ambiental operations, which is jointly managed with GSInima. The plant currently produces on average 360 l/s of reuse water to serve industries in the Capuava Petrochemical Complex, in addition to three other key industries in the ABC region. The plant has a water reuse production capacity of 650 l/s (with an adductor of 1m³/s). The municipalities of Guarulhos and Santo André, which began to be served by Sabesp in 2019, also created new opportunities for the expansion of this segment with new customers.

In addition, we promote the water reuse technology at the ETEs in São Miguel Paulista, Jesus Neto, Parque Novo Mundo and ABC.

Rational Water Use

The PURA (Rational Water Use Program)is an initiative to promote conscious water consumption by readjusting the hydraulic structure of public administration buildings.

Municipal, state or federal schools, hospitals, public restrooms, jails or day care centers who join the program receive low-consumption equipment, new plumbing systems and maintenance support to repair leaks.

At the same time, lectures are held to discuss the conscious use of water, which is aimed at forming multipliers of the sustainability message. We ended 2019 with 11.3 thousand benefited properties. Participants are given a consumption reduction target which, if achieved, entitles them to a 25% discount on their water bills.

Quality Water as a Priority

Along with water security and operational efficiency, quality water is a priority guideline for serving our 28 million customers. The quality of the water distributed complies with the parameters required by Health Ministry Ordinance 2.914/11, which establishes the procedures and standards for human consumption. The measurement of drinking conditions for the water is done from the collection points, which then flows into treatment at stations and is distributed to end consumers.

Our 16 health control laboratories perform nearly 90 types of tests and more than 90 thousand analyses are carried out each month to measure parameters of turbidity, color, chlorine, total coliforms, metals and agrochemicals, among other items. Most of the laboratories are accredited by the National Institute of Metrology, Quality and Technology (Inmetro).

F-27

Since 1996, we have maintained a team of 140 tasters who are qualified to evaluate possible variations in flavor, aroma and coloring. The results guide any preventive or corrective adjustments in the treatment process of the stations.

F-28

EXPANSION OF HEALTH INFRASTRUCTURE AND RECOVERY OF WATER RESOURCES

The sanitation infrastructure directly reflects the reduction of infant mortality, the decrease of hospitalizations due to waterborne diseases and the improvement in the quality of water in rivers and springs, in addition to influencing the creation of jobs and income by improving the tourism and real estate sectors.

In this sense, the ongoing expansions of our sewage collection and treatment services in 372 municipalities in São Paulo placesSabesp as an important driver of environmental sustainability and socioeconomic development in the State.

To support this universe, our infrastructure contains 8.3 million connections and 56 thousand km of collection networks that conducts sewage for treatment at 569 STPs. Jointly, they are capable of treating 57.3 thousand l/s of sewage.

In 2019, we continued to expandsewage collection and treatment services, which required investments of R$ 2.6 billion.

In the municipalities operated in December 2019, weregistered average ratesof 91% for the provision ofa sewage collection network (coverage), 84%for the sewage collection service (effective connections in the networks) and 78% (not including Guarulhos and Santo André)of households connected to the sewage treatment network.

The São Paulo Metropolitan Region (SPMR) and its Sanitation Challenges

We are responsible for sanitation services in 36 of the 39 municipalities that make up the SPMR, considered one of the largest urban agglomerations in the world. Characteristics such as overpopulation, large territorial extension and disorganized housing occupations resulting from little or no urban planning, place this region at the top of the list of the most challenging areas for the expansion of sewage services.

Operating in this environment requires concentrated efforts to enable the ongoing expansion of collection and sewage treatment services aimed at improving the population’s life quality and progressively revitalizing urban rivers.

The Tietê Project

To face this challenge, we continue with the structural interventions at the Tietê Project which, given the volume of investments and required construction works, it is considered the largest environmental sanitation program in the country. Since the beginning of the project, in 1992, we have taken sewage collection and treatment services to more than 11 million people in the SPMR.

F-29

Over these 27 years, the program used its own resources and financing from the IDB(Interamerican Development Bank),BNDES (National Bank for Economic and Social Development) and Caixa Econômica Federal (Federal Savings Bank) to expand its network of interceptors, trunk collectors and its sewage collection and transportation system from the metropolitan area to the treatment plants, with installed treatment capacity leaping from 8.5 thousand liters per second, in 1992, to the current 26 thousand liters per second.With the expansion of the collection and transportation infrastructure, the effective treatment increased from 4 thousand liters per second to the current 20.6 thousand liters per second during the same period.