Exhibit 99.1

2021 Annual Report Building for a sustainable future

III IV Algonquin Power & Utilities Corp. 2021 annual report Corporate profile Letter to shareholders 2021 stats at a glance VI VII VII VIII X XII XIV 1 71 72 75 83 Renewable Energy Group Regulated Services Group Financial highlights Growth Pillar Sustainability Pillar Operational Excellence Pillar Appendices Management Discussion & Analysis Management’s Report Independent Auditor’s Report Consolidated Financial Statements Notes to the Consolidated Statements Financial Algonquin’s leadership Corporate info 149 BC II

Corporate profile Algonquin Power & Utilities Corp. (“AQN”, the “Company”, or “we”), parent company of Liberty, is a diversified international generation, transmission, and distribution utility with over $16 billion of total assets. Through its two business groups, the Regulated Services Group and the Renewable Energy Group, AQN is committed to providing safe, secure, reliable, cost-effective, and sustainable energy and water solutions through its portfolio of electric generation, transmission, and distribution utility investments to over one million customer connections, largely in the United States and Canada. AQN is a global leader in renewable energy through its portfolio of long-term contracted wind, solar, and hydroelectric generating facilities. AQN owns, operates, and/or has net interests in over 4 GW of installed renewable energy capacity. AQN is committed to delivering growth and the pursuit of operational excellence in a sustainable manner through an expanding global pipeline of renewable energy and electric transmission development projects, organic growth within its rate-regulated generation, distribution, and transmission businesses, and the pursuit of accretive acquisitions and value enhancing recycling of assets. Forward-looking information This document contains statements that constitute “forward-looking statements” or “forward-looking information” within the meaning of applicable securities legislation (collectively, “forward-looking information”). The words “will”, “anticipates”, “expects”, “intends”, “may”, “pending”, “target”, “could”, “would”, “plans”, “potential”, and similar words and expressions are often intended to identify forward-looking statements, although not all forward-looking information contains these identifying words. Specific forward-looking information in this document includes, but is not limited to: expected future growth, earnings, and results of operations; ongoing and planned acquisitions, projects, and initiatives, including expected increases in customer connections from acquisitions; statements regarding the Company’s sustainability and environmental, social, and governance goals, including its net-zero by 2050 target; expectations regarding future "greening the fleet" initiatives, including with respect to Kentucky Power Company; expected generating capacity of renewable energy projects and facilities; expectations regarding the completion and pending closing of Kentucky Power acquisition; and expected customer benefits. Readers are advised that all forward-looking information in this document is provided subject to the ”Caution Concerning Forward-Looking Statements and Forward-Looking Information” section of the Management Discussion & Analysis section of this Annual Report. AlgonquinPowerandUtilities.com TSX/NYSE: AQN III Algonquin | 2021 Annual Report

"In 2021, Algonquin successfully delivered on many of its strategic initiatives, including the continued execution of several new renewable projects and further advancement of sustainability goals, all underpinned by our three strategic pillars." Kenneth Moore, Chair of the Board Arun Banskota, President and Chief Executive Officer IV

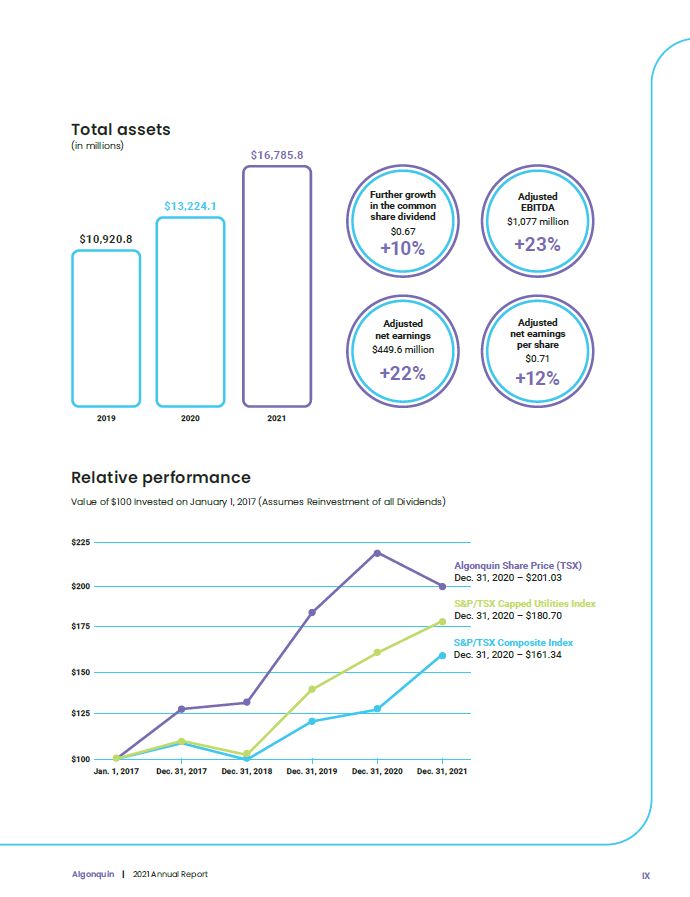

Letter from the Chair, and President and Chief Executive Officer Dear fellow shareholder, 2021 marked an exciting year of growth, innovation, and success, and laying the foundations for long-term value creation. Our employees made significant progress in 2021, and these successes are a testament to our entrepreneurial spirit, owner mindset, and customer-centric approach. This, combined with our culture of teamwork and inclusion, translates into delivered results that we are pleased to share with you. 2021 was a busy year for AQN, with approximately 1,200 MW of new renewable projects added. We announced an agreement to acquire Kentucky Power Company and AEP Kentucky Transmission Company, Inc., which would represent the largest acquisition in the Company’s history and would add approximately 228,000 new customer connections upon closing. On the sustainability front, we announced our target to achieve net-zero by 2050 for scope 1 and 2 greenhouse gas emissions across AQN’s business operations. These accomplishments were underpinned by our three strategic pillars of Growth, Operational Excellence, and Sustainability, which serve as a key foundation as we continue to build the business. Strength in Diversity Whether through diversification of assets, modality, geography or talent, diversity at AQN has been an important factor in the Company’s resiliency and success. In 2021, AQN showcased its strength in diversity on both the acquisition and ESG fronts. During the year, AQN completed the acquisition of the North Fork Ridge, Kings Point, and Neosho Ridge Wind Facilities. As a result, the Regulated Services Group successfully completed the construction and acquisition of all the wind facilities related to its Midwest 'greening the fleet' initiative. This diversification of assets and modalities consisted of 600 MW of new wind energy generation which is expected to provide long-term benefits to electricity customers. At AQN, we are also committed to fostering a more inclusive and equitable workplace. We are proud that AQN has been included in the Bloomberg Gender Equality Index for the third year in a row and in the Globe and Mail’s Women Lead Here benchmark for the second year in a row. In the third quarter of 2021, we welcomed Helen Bremner, Executive Vice President, Strategy and Sustainability, to our Executive Management Team. At the end of 2021, we are delighted to report that AQN’s Board of Directors and Executive Management Team are now comprised of 38% and 40% of female leadership, respectively. Strong Financial Results We are pleased to report another solid year of financial results for 2021, which saw year-over-year growth in a number of the Company’s key financial metrics. As a testament to our strong growth program, asset growth increased 27% year-over-year, as AQN recorded over $16 billion in total assets for the year ended 2021. The Company's financial performance supported a 10% increase in our common share dividend, which has seen over ten consecutive years of double-digit growth. AQN has a history of providing long-term value to shareholders. Over the five- and ten-year periods ended December 31, 2021, AQN has delivered 101% and 350%, respectively, of total shareholder returns on the Toronto Stock Exchange, outperforming key market and utility sector peer group averages. Also, over the five-year period ended December 31, 2021, AQN delivered a compound annual growth rate of 11.1% for Adjusted Net Earnings per Share1 and 4.4% for net earnings attributable to shareholders. The Path Ahead At our 2021 Analyst and Investor Day, we discussed the Company’s updated five-year strategic and capital expenditure plan, with approximately $12.4 billion of growth opportunities allocated across the regulated and renewable business groups from 2022 through 2026. In our regulated business, we are focused on the pending acquisition of Kentucky Power Company and AEP Kentucky Transmission Company, Inc., while continuing to invest in the rate base to improve the safety, security, reliability, and resiliency of our utilities. In our renewables business, we converted 600 MW from our inaugural prospective greenfield pipeline into our new five-year capital plan, while growing the Company’s updated greenfield pipeline to 3,800 MW. Another important initiative establishing a strong foundation for future growth is the Company’s 1,700 MWhr pipeline of prospective energy storage projects. We continue to remain focused on the execution of these strategic growth plans and are excited about the prospects for AQN’s regulated and renewables businesses, which are well-positioned to contribute to and benefit from the ongoing decarbonization transformation. Of course, we could not have done this without the continued support of our stakeholders. We are grateful to our diverse team of employees for their perseverance, professionalism, and entrepreneurial spirit. Our sincere gratitude also goes to our Board of Directors for their invaluable guidance. Finally, we would like to offer a heartful thank you to our valued shareholders for the ongoing trust and support as we continue to deliver on our vision for the Company: sustaining energy and water for life. Yours Sincerely, Kenneth Moore, Chair of the Board Arun Banskota, President and Chief Executive Officer 1) “Adjusted Net Earnings per Share” is not a recognized measure under U.S. GAAP (as defined herein). Please refer to note 1 under the heading “Financial highlights” on page VIII for more information about this Non-GAAP Measure. V Algonquin | 2021 Annual Report

2021 stats at a glance1 1) Data in this report is provided as of December 31, 2021 unless otherwise stated. Dollar figures herein are presented in U.S. dollars unless otherwise stated. ~307,000 electric customer connections Founded in 1988 8,773 miles of gas distribution lines ~373,000 natural gas customer connections Over $16 billion total assets 14,310 miles of electricity distribution lines ~413,000 water and wastewater customer connections ~$9.7 billion market cap (NYSE) 5,318 miles of water distribution mains 55 hydroelectric generators 1,217,680 solar panels Headquartered in Greater Toronto Area, Ontario 1,541 wind turbines 3,400+ employees VI

Renewable Energy Group connections ~1,093,000 2 228,000 additional anticipated connections3 ~$10.5 billion regulated utility assets 13 U.S. states, 1 Canadian province, Bermuda, and Chile 41 renewable and clean energy facilities ~2.3 GW gross installed capacity ~1.4 GW net generating capacity investments ~$6.1 billion non-regulated power generation assets1 Does not include 125,000 customer connections added upon acquisition of New York American Water Company, Inc, effective January 1, 2022. Reflects pending acquisition of Kentucky Power Company and AEP Kentucky Transmission Company, Inc. 1) Includes a proportionate amount based on AQN’s ~44% equity interest in Atlantica Sustainable Infrastructure plc’s wind and solar assets as of December 31, 2021. The Renewable Energy Group generates and sells electrical energy produced by its diverse portfolio of renewable and clean power generation facilities primarily located across Canada and the United States. Its directly owned and operated diversified fleet of hydroelectric, wind, solar, and thermal facilities have a combined gross generating capacity of approximately 2.3 GW. Approximately 82% of the electrical output is sold pursuant to long-term contractual agreements which have a production-weighted average remaining contract life of approximately 12 years. In addition to its directly owned and operated assets, the Renewable Energy Group has investments in generating assets with approximately 1.4 GW of net generating capacity, including AQN’s interest in Atlantica Sustainable Infrastructure plc. Regulated Services Group The Regulated Services Group operates a diversified portfolio of regulated electric, natural gas, water and wastewater collection utility systems, and transmission operations, which collectively serve approximately 1,093,000 customer connections located in the United States, Canada, Bermuda, and Chile. The Regulated Services Group seeks to provide safe, high-quality, and reliable services to its customers and to deliver stable and predictable earnings to AQN. In addition to encouraging and supporting organic growth within its service territories, the Regulated Services Group seeks to deliver continued growth through accretive acquisitions of additional utility systems. VII Algonquin | 2021 Annual Report

Twelv Months Ended December 31 2021 2020 2019 Revenue Renewable Energy Group 268.0 256.0 256.5 Regulated Services Group 1,944.2 1,386.0 1,368.4 Corporate - - 1.5 Total Revenue 2,212.1 1,642.0 1,626.4 Net Earnings attributable to shareholders 264.9 782.5 530.9 Adjusted EBITDA1 1,076.9 869.5 838.6 Earnings, Funds from Operations and Dividends Cash provided by operating activities 157.5 505.2 611.3 Adjusted Funds from Operations1 757.9 600.2 566.2 Adjusted Net Earnings1 449.6 365.8 321.3 Per Share1 0.71 0.64 0.63 Dividends to Shareholders 423.0 344.4 277.8 Per Share 0.67 0.61 0.55 Balance Sheet Data Total Assets 16,785.8 13,224.1 10,920.8 Long Term Debt (includes current portion) 6,211.7 4,538.8 3,932.2 Number of Shares outstanding as of Dec. 31 671,960,276 597,142,219 524,233,323 Renewable energy production (% of long term average) 90% 91% 95% Utility Connections 1,093,000 1,086,000 804,000 Financial highlights (in USD millions except per share information) 1. The terms “Adjusted EBITDA”, “Adjusted Net Earnings”, “Adjusted Net Earnings per Share” and “Adjusted Funds from Operations” (together, the “Non-GAAP Measures”) are used in this Annual Report. The Non-GAAP Measures are not recognized measures under United States generally accepted accounting principles (“U.S. GAAP”). There is no standardized measure of the Non-GAAP Measures. Consequently, AQN’s method of calculating the Non-GAAP Measures may differ from methods used by other companies and therefore may not be comparable to similar measures presented by other companies. An explanation and analysis of the Non-GAAP Measures and a reconciliation to the most comparable U.S. GAAP measure can be found in the Management Discussion & Analysis section of this Annual Report under the headings “Caution Concerning Non-GAAP Measures” and “Non-GAAP Financial Measures”. VIII

Algonquin Share Price (TSX) Dec. 31, 2020 – $201.03 $225 $200 $150 $175 $125 $100 Jan. 1, 2017 Dec. 31, 2017 Dec. 31, 2018 Dec. 31, 2019 Dec. 31, 2020 Dec. 31, 2021 S&P/TSX Capped Utilities Index Dec. 31, 2020 – $180.70 S&P/TSX Composite Index Dec. 31, 2020 – $161.34 2019 $10,920.8 $13,224.1 $16,785.8 2020 2021 Adjusted net earnings $449.6 million +22% Adjusted EBITDA $1,077 million +23% Adjusted net earnings per share $0.71 +12% Further growth in the common share dividend $0.67 +10% Total assets (in millions) Relative performance Value of $100 Invested on January 1, 2017 (Assumes Reinvestment of all Dividends) IX Algonquin | 2021 Annual Report

X

Growth Pillar Advancing our strategic plan 2021 saw the successful execution of previously announced strategic growth plans. In 2021, AQN successfully completed the construction and acquisition of all the wind facilities related to its inaugural 'greening the fleet' initiative. The initiative consisted of 600 MW of new strategically located wind energy generation which is expected to provide benefits to the Regulated Services Group's electric customers in Missouri, Arkansas, Oklahoma, and Kansas. In the third quarter of 2021, AQN entered into an agreement to acquire Kentucky Power Company and AEP Kentucky Transmission Company, Inc. (the “Kentucky Acquisition”). Upon closing, the Kentucky Acquisition is expected to add approximately 228,000 new customer connections. The Kentucky Acquisition is well aligned with the Company's three Strategic Pillars of Growth, Operational Excellence, and Sustainability. On Growth, the Kentucky Acquisition is expected to add over $2.0 billion of regulated rate base assets in a favourable regulatory jurisdiction. Consistent with the Company's Sustainability pillar, AQN intends to leverage its ‘greening the fleet’ capabilities as a renewable energy developer, with an opportunity to explore the potential to replace over 1 GW of fossil fuel generation capacity with renewables. Leveraging its expertise in financing, development, and construction, the Company continued to execute on its partnerships with commercial and industrial customers to help them achieve their corporate targets for cleaner energy. In 2021, the Renewable Energy Group achieved full commercial operations at its Maverick Creek Wind Facility (“Maverick Creek”) and Altavista Solar Facility (“Altavista”). Maverick Creek is the Renewable Energy Group's 14th wind powered electric generating facility and is expected to generate approximately 1,920 GWhr of energy per year with the majority of output being sold through two long-term power purchase agreements with investment grade rated entities. Altavista is the Renewable Energy Group's sixth solar powered electric generating facility and is expected to generate approximately 174 GWhr of energy per year with the majority of output being sold to Facebook Operations, LLC, a wholly-owned subsidiary of Meta. Finally, 2021 was a record year for AQN with approximately 1,200 MW of new renewable projects added. This achievement in the midst of the COVID-19 pandemic, and supply chain challenges, is a testament to the hard work and entrepreneurial culture of the Company’s employees. XI Algonquin | 2021 Annual Report

XII

Sustainability Pillar Leader in sustainability With more than 30 years of experience developing and operating renewable and clean energy facilities, sustainability has long been part of AQN’s DNA and is embedded in the Company’s business strategy. Sustainability is not a top-down directive in our organization but is embraced by our employees across the business. Our dedicated regional sustainability councils have demonstrated a deep-rooted commitment to sustainability through the development of robust regional plans and grassroots initiatives that operationalize our ESG strategy on a local level. In 2021, we made meaningful progress in driving sustainable practices across each of the Company’s business segments, resulting in the reduction of the Company’s annual carbon emissions by more than 1 million metric tons relative to 2017 levels. By implementing pipeline upgrades in the Company’s natural gas distribution business, the Company has achieved a total reduction of 1,500 metric tons in aggregate methane emissions in that business since 2017. In addition, this past year AQN recharged more than 2.4 million litres of water back into the water table and enabled the reuse of approximately 2.1 million litres of recycled water. AQN further embedded sustainability into its business strategy by announcing a commitment to achieve net-zero emissions by 2050 for scope 1 and scope 2 emissions. This target is expected to serve as a strategic guardrail for AQN’s business groups and drive alignment across the business for long-term planning and strategy development. As we approach the end of the timeframe for the Company’s nine 2023 ESG-linked goals, established in 2019, the Company intends to launch a new set of interim targets to support its decarbonization initiatives on the pathway to 2050. With accountability and transparency at the heart of AQN’s sustainability commitments, we continue to improve our ESG disclosures each year. In October, AQN released its 2021 ESG Report. The Company also developed an ESG data hub on its website to improve user experience and centralize the availability of enhanced ESG data. Finally, AQN continues to be recognized for its sustainability performance. For the third year in a row, AQN has been included in the Bloomberg Gender Equality Index. AQN’s inclusion in this index is a testament to its continued commitment to improve gender equality and transparency as it targets above-market gender representation at the board and executive levels. These achievements, along with many more, come together to underscore AQN’s commitment to ESG leadership and sustainable business practices to build a cleaner energy future. XIII Algonquin | 2021 Annual Report

Operational Excellence Pillar Operational excellence in action At AQN, our vision of operational excellence is focused on safety, security, and reliability. AQN has and continues to demonstrate ongoing resiliency, while keeping the health, safety, and well-being of our employees, customers, and communities a top priority. We also have an exceptional track record of smooth integration of our utility acquisitions. 2021 marked the first full year of contribution from ESSAL and BELCO to the Company's utility portfolio, with both utilities having been successfully integrated into AQN’s operations. ~60 point improvement in J.D. Power Customer Satisfaction Scores over 2017 levels 100% improvement in Safety Lost Time Injury Rate over 2017 levels 17% improvement in Reliability 5-year System Average Interruption Frequency Index over 2017 levels XIV

Management Discussion & Analysis

Management of Algonquin Power & Utilities Corp. (“AQN” or the “Company” or the “Corporation”) has prepared the following discussion and analysis to provide information to assist its shareholders’ understanding of the financial results for the three and twelve months ended December 31, 2021. This Management Discussion & Analysis (“MD&A”) should be read in conjunction with AQN’s annual consolidated financial statements for the years ended December 31, 2021 and 2020. This material is available on SEDAR at www.sedar.com, on EDGAR at www.sec.gov/edgar, and on the AQN website at www.AlgonquinPowerandUtilities.com. Additional information about AQN, including the most recent Annual Information Form (“AIF”), can be found on SEDAR at www.sedar.com and on EDGAR at www.sec.gov/edgar.

Unless otherwise indicated, financial information provided for the years ended December 31, 2021 and 2020 has been prepared in accordance with generally accepted accounting principles in the United States (“U.S. GAAP”). As a result, the Company's financial information may not be comparable with financial information of other Canadian companies that provide financial information on another basis.

All monetary amounts are in U.S. dollars, except where otherwise noted. We denote any amounts denominated in Canadian dollars with "C$" immediately prior to the stated amount.

Capitalized terms used herein and not otherwise defined will have the meanings assigned to them in the Company's most recent AIF.

This MD&A is based on information available to management as of March 3, 2022.

| 2 | |

| 4 | |

| 6 | |

| 9 | |

| 12 | |

| 13 | |

| 15 | |

| 17 | |

| 18 | |

| 19 | |

| 29 | |

| 35 | |

| 37 | |

| 39 | |

| 40 | |

| 42 | |

| 46 | |

| 48 | |

| 49 | |

| 66 | |

| 67 | |

| 68 |

This document may contain statements that constitute "forward-looking information" within the meaning of applicable securities laws in each of the provinces and territories of Canada and the respective policies, regulations and rules under such laws and/or "forward-looking statements" within the meaning of the U.S. Private Securities Litigation Reform Act of 1995 (collectively, “forward-looking information”). The words “anticipates”, “believes”, “budget”, “could”, “estimates”, “expects”, “forecasts”, “intends”, “may”, “might”, “plans”, “projects”, “schedule”, “should”, “will”, “would” and similar expressions are often intended to identify forward-looking information, although not all forward-looking information contains these identifying words. Specific forward-looking information in this document includes, but is not limited to, statements relating to: expected future growth, earnings (including 2022 Adjusted Net Earnings per common share) and results of operations; liquidity, capital resources and operational requirements; sources of funding, including adequacy and availability of credit facilities, debt maturation and future borrowings; expectations regarding the impact of the 2019 novel coronavirus (“COVID-19”) on the Company; expectations regarding the use of proceeds from financings; ongoing and planned acquisitions, projects and initiatives, including expectations regarding costs, financing, results, ownership structures, offtake arrangements, regulatory matters, in-service dates and completion dates; expectations regarding the anticipated closing of the Kentucky Power Transaction (as defined herein); expectations regarding the purchase price for the Kentucky Power Transaction and the expected financing thereof; the anticipated benefits of the Kentucky Power Transaction, including the impact of the Kentucky Power Transaction on the Corporation’s business, operations, financial condition, cash flows and results of operations; expectations regarding the Corporation’s and Kentucky Power’s (as defined herein) rate base; business mix and sustainability objectives following completion of the Kentucky Power Transaction; expectations regarding the timing for the transfer or retirement (for rate-making purposes in Kentucky) of the Mitchell Plant (as defined herein); expectations regarding cost recovery of amounts incurred by Empire in connection with the Midwest Extreme Weather Event (as defined herein) and retirement of the Asbury coal plant; expectations regarding the Company's corporate development activities and the results thereof, including the expected business mix between the Regulated Services Group and Renewable Energy Group; expectations regarding regulatory hearings, motions, filings, appeals and approvals, including rate reviews, and the impacts and outcomes thereof; expected future generation of the Company’s energy facilities; expected timing for signing a General Interconnection Agreement at the Neosho Ridge Wind Facility; statements regarding the Company’s sustainability and environmental, social and governance goals, including its net-zero by 2050 target; expected future capital investments, including expected timing, investment plans, sources of funds and impacts; expectations regarding future "greening the fleet" initiatives, including with respect to Kentucky Power; expectations regarding opportunities for the development of renewable natural gas facilities and cost recovery thereof; expectations regarding generation availability, capacity and production; expectations regarding the outcome of existing or potential legal and contractual claims and disputes; strategy and goals; dividends to shareholders; expectations regarding the impact of tax reforms; credit ratings and equity credit from rating agencies; anticipated customer benefits; the future impact on the Company of actual or proposed laws, regulations and rules; accounting estimates; interest rates and currency exchange rates. All forward-looking information is given pursuant to the “safe harbor” provisions of applicable securities legislation.

The forecasts and projections that make up the forward-looking information contained herein are based on certain factors or assumptions which include, but are not limited to: the receipt of applicable regulatory approvals and requested rate decisions; the absence of a material increase in the costs of compliance with environmental laws following the completion of the Kentucky Power Transaction; the absence of material adverse regulatory decisions being received and the expectation of regulatory stability; the absence of any material equipment breakdown or failure; availability of financing (including tax equity financing and self-monetization transactions for U.S. federal tax credits) on commercially reasonable terms and the stability of credit ratings of the Corporation and its subsidiaries; the absence of unexpected material liabilities or uninsured losses; the continued availability of commodity supplies and stability of commodity prices; the absence of sustained interest rate increases or significant currency exchange rate fluctuations; the absence of significant operational, financial or supply chain disruptions or liability; the continued ability to maintain systems and facilities to ensure their continued performance; the absence of a severe and prolonged downturn in general economic, credit, social or market conditions; the successful and timely development and construction of new projects; the closing of pending acquisitions substantially in accordance with the expected timing for such acquisitions; the absence of capital project or financing cost overruns; sufficient liquidity and capital resources; the continuation of long term weather patterns and trends; the absence of significant counterparty defaults; the continued competitiveness of electricity pricing when compared with alternative sources of energy; the realization of the anticipated benefits of the Corporation’s acquisitions and joint ventures; the absence of a change in applicable laws, political conditions, public policies and directions by governments, materially negatively affecting the Corporation; the ability to obtain and maintain licenses and permits; maintenance of adequate insurance coverage; the absence of material fluctuations in market energy prices; the absence of material disputes with taxation authorities or changes to applicable tax laws; continued maintenance of information technology infrastructure and the absence of a material breach of cybersecurity; favourable relations with external stakeholders; favourable labour relations; the realization of the anticipated benefits of the Kentucky Power Transaction, including that it will be accretive to the Corporation’s Adjusted Net Earnings per common share; that the Corporation will be able to successfully integrate newly acquired entities, and the absence of any material adverse changes to such entities prior to closing; the successful transfer of operational control over the Mitchell Plant to Wheeling Power Company; the transfer of the Mitchell Plant being implemented in accordance with the Corporation’s expectations; the absence of

undisclosed liabilities of entities being acquired; that such entities will maintain constructive regulatory relationships with state regulatory authorities; the ability of the Corporation to retain key personnel of acquired entities and the value of such employees; no adverse developments in the business and affairs of the sellers during the period when transitional services are provided to the Corporation in connection with any acquisition; the ability of the Corporation to satisfy its liabilities and meet its debt service obligations following completion of any acquisition; the absence of any reputational harm to the Corporation as a result of any acquisition; and the ability of the Corporation to successfully execute future “greening the fleet” initiatives. Given the continued uncertainty and evolving circumstances surrounding the COVID-19 pandemic and related response from governments, regulatory authorities, businesses, suppliers and customers, there is more uncertainty associated with the Corporation’s assumptions and expectations as compared to periods prior to the onset of COVID-19.

The forward-looking information contained herein is subject to risks, uncertainties and other factors that could cause actual results to differ materially from historical results or results anticipated by the forward-looking information. Factors which could cause results or events to differ materially from current expectations include, but are not limited to: changes in general economic, credit, social or market conditions; changes in customer energy usage patterns and energy demand; global climate change; the incurrence of environmental liabilities; natural disasters, diseases, pandemics and other force majeure events; critical equipment breakdown or failure; supply chain disruptions; the failure of information technology infrastructure and cybersecurity; physical security breach; the loss of key personnel and/or labour disruptions; seasonal fluctuations and variability in weather conditions and natural resource availability; reductions in demand for electricity, gas and water due to developments in technology; reliance on transmission systems owned and operated by third parties; issues arising with respect to land use rights and access to the Corporation’s facilities; terrorist attacks; fluctuations in commodity prices; capital expenditures; reliance on subsidiaries; the incurrence of an uninsured loss; a credit rating downgrade; an increase in financing costs or limits on access to credit and capital markets; increases in interest rates; currency exchange rate fluctuations; restricted financial flexibility due to covenants in existing credit agreements; an inability to refinance maturing debt on commercially reasonable terms; disputes with taxation authorities or changes to applicable tax laws; failure to identify, acquire, develop or timely place in service projects to maximize the value of tax credits; requirement for greater than expected contributions to post-employment benefit plans; default by a counterparty; inaccurate assumptions, judgments and/or estimates with respect to asset retirement obligations; failure to maintain required regulatory authorizations; changes in, or failure to comply with, applicable laws and regulations; failure of compliance programs; failure to identify attractive acquisition or development candidates necessary to pursue the Corporation’s growth strategy; failure to dispose of assets (at all or at a competitive price) to fund the Company’s operations and growth plans; delays and cost overruns in the design and construction of projects, including as a result of COVID-19; loss of key customers; failure to complete or realize the anticipated benefits of acquisitions or joint ventures; Atlantica (as defined herein) or a third party joint venture partner acting in a manner contrary to the Corporation’s interests; a drop in the market value of Atlantica's ordinary shares; facilities being condemned or otherwise taken by governmental entities; increased external-stakeholder activism adverse to the Corporation’s interests; fluctuations in the price and liquidity of the Corporation’s common shares and the Corporation's other securities; the severity and duration of the COVID-19 pandemic and its collateral consequences, including the disruption of economic activity, volatility in capital and credit markets and legislative and regulatory responses; impact of significant demands placed on the Corporation as a result of pending acquisitions or growth strategies; potential undisclosed liabilities of any entities being acquired by the Corporation; uncertainty regarding the length of time required to complete pending acquisitions; the failure to implement the Corporation’s strategic objectives or achieve expected benefits relating to acquisitions; Kentucky Power’s failure to receive regulatory approval for the construction of new renewable generation facilities; indebtedness of any entity being acquired by the Corporation; reputational harm and increased costs of compliance with environmental laws as a result of announced or completed acquisitions; unanticipated expenses and/or cash payments as a result of change of control and/or termination for convenience provisions in agreements to which any entity being acquired is a party; and the reliance on third parties for certain transitional services following the completion of an acquisition. Although the Corporation has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward- looking information, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. Some of these and other factors are discussed in more detail under the heading Enterprise Risk Management in this MD&A and under the heading Enterprise Risk Factors in the Corporation's most recent AIF.

Forward-looking information contained herein (including any financial outlook) is provided for the purposes of assisting the reader in understanding the Corporation and its business, operations, risks, financial performance, financial position and cash flows as at and for the periods indicated and to present information about management’s current expectations and plans relating to the future and the reader is cautioned that such information may not be appropriate for other purposes. Forward-looking information contained herein is made as of the date of this document and based on the plans, beliefs, estimates, projections, expectations, opinions and assumptions of management on the date hereof. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such forward-looking information. Accordingly, readers should not place undue reliance on forward-looking information. While subsequent events and developments may cause the Corporation’s views to change, the Corporation disclaims any obligation to update any forward-looking information or to explain any material

difference between subsequent actual events and such forward-looking information, except to the extent required by applicable law. All forward-looking information contained herein is qualified by these cautionary statements.

AQN uses a number of financial measures to assess the performance of its business lines. Some measures are calculated in accordance with U.S. GAAP, while other measures do not have a standardized meaning under U.S. GAAP. These non-GAAP measures include non-GAAP financial measures and non-GAAP ratios, each as defined in Canadian National Instrument 52-112 Non-GAAP and Other Financial Measures Disclosure. AQN’s method of calculating these measures may differ from methods used by other companies and therefore may not be comparable to similar measures presented by other companies.

The terms “Adjusted Net Earnings”, “Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization” (“Adjusted EBITDA”), “Adjusted Funds from Operations”, "Net Energy Sales", "Net Utility Sales" and "Divisional Operating Profit", which are used throughout this MD&A, are non-GAAP financial measures. An explanation of each of these non-GAAP financial measures is set out below and a reconciliation to the most directly comparable U.S. GAAP measure, in each case, can be found in this MD&A. In addition, “Adjusted Net Earnings” is presented throughout this MD&A on a per share basis. Adjusted Net Earnings per common share is a non-GAAP ratio and is calculated by dividing Adjusted Net Earnings by the weighted average number of common shares outstanding during the applicable period.

Adjusted EBITDA

Adjusted EBITDA is a non-GAAP financial measure used by many investors to compare companies on the basis of ability to generate cash from operations. AQN uses these calculations to monitor the amount of cash generated by AQN. AQN uses Adjusted EBITDA to assess the operating performance of AQN without the effects of (as applicable): depreciation and amortization expense, income tax expense or recoveries, acquisition costs, certain litigation expenses, interest expense, gain or loss on derivative financial instruments, write down of intangibles and property, plant and equipment, earnings attributable to non-controlling interests, non-service pension and post-employment costs, cost related to tax equity financing, costs related to management succession and executive retirement, costs related to prior period adjustments due to changes in tax law, costs related to condemnation proceedings, financial impacts on the Company's Senate Wind Facility from the significantly elevated pricing that persisted in the Electric Reliability Council of Texas market over several days (the "Market Disruption Event") as a result of the February 2021 extreme winter storm conditions experienced in Texas and parts of the central U.S. (the “Midwest Extreme Weather Event”), gain or loss on foreign exchange, earnings or loss from discontinued operations, changes in value of investments carried at fair value, and other typically non-recurring or unusual items. AQN adjusts for these factors as they may be non-cash, unusual in nature and are not factors used by management for evaluating the operating performance of the Company. AQN believes that presentation of this measure will enhance an investor’s understanding of AQN’s operating performance. Adjusted EBITDA is not intended to be representative of cash provided by operating activities or results of operations determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Adjusted EBITDA to net earnings, see Non-GAAP Financial Measures starting on page 37 of this MD&A.

Adjusted Net Earnings

Adjusted Net Earnings is a non-GAAP financial measure used by many investors to compare net earnings from operations without the effects of certain volatile primarily non-cash items that generally have no current economic impact or items such as acquisition expenses or certain litigation expenses that are viewed as not directly related to a company’s operating performance. AQN uses Adjusted Net Earnings to assess its performance without the effects of (as applicable): gains or losses on foreign exchange, foreign exchange forward contracts, interest rate swaps, acquisition costs, one-time costs of arranging tax equity financing, certain litigation expenses and write down of intangibles and property, plant and equipment, earnings or loss from discontinued operations (excluding sale of assets in the course of normal operations), unrealized mark-to-market revaluation impacts (other than those realized in connection with the sales of development assets), costs related to management succession and executive retirement, costs related to prior period adjustments due to changes in tax law, costs related to condemnation proceedings, financial impacts from the Market Disruption Event on the Company's Senate Wind Facility, changes in value of investments carried at fair value, and other typically non-recurring or unusual items as these are not reflective of the performance of the underlying business of AQN. AQN believes that analysis and presentation of net earnings or loss on this basis will enhance an investor’s understanding of the operating performance of its businesses. Adjusted Net Earnings is not intended to be representative of net earnings or loss determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Adjusted Net Earnings to net earnings, see Non-GAAP Financial Measures starting on page 38 of this MD&A.

Adjusted Funds from Operations

Adjusted Funds from Operations is a non-GAAP financial measure used by investors to compare cash flows from operating activities without the effects of certain volatile items that generally have no current economic impact or items such as acquisition expenses that are viewed as not directly related to a company’s operating performance. AQN uses Adjusted

Funds from Operations to assess its performance without the effects of (as applicable): changes in working capital balances, acquisition expenses, certain litigation expenses, cash provided by or used in discontinued operations, financial impacts from the Market Disruption Event on the Company's Senate Wind Facility, and other typically non-recurring items affecting cash from operations as these are not reflective of the long-term performance of the underlying businesses of AQN. AQN believes that analysis and presentation of funds from operations on this basis will enhance an investor’s understanding of the operating performance of its businesses. Adjusted Funds from Operations is not intended to be representative of cash flows from operating activities as determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Adjusted Funds from Operations to cash flows from operating activities, see Non-GAAP Financial Measures starting on page 39 of this MD&A.

Net Energy Sales

Net Energy Sales is a non-GAAP financial measure used by investors to identify revenue after commodity costs used to generate revenue where such revenue generally increases or decreases in response to increases or decreases in the cost of the commodity used to produce that revenue. AQN uses Net Energy Sales to assess its revenues without the effects of fluctuating commodity costs as such costs are predominantly passed through either directly or indirectly in the rates that are charged to customers. AQN believes that analysis and presentation of Net Energy Sales on this basis will enhance an investor’s understanding of the revenue generation of the Renewable Energy Group. It is not intended to be representative of revenue as determined in accordance with U.S. GAAP. For a reconciliation of Net Energy Sales to revenue, see Renewable Energy Group - 2021 Renewable Energy Group Operating Results on page 31 of this MD&A.

Net Utility Sales

Net Utility Sales is a non-GAAP financial measure used by investors to identify utility revenue after commodity costs, either natural gas or electricity, where these commodity costs are generally included as a pass through in rates to its utility customers. AQN uses Net Utility Sales to assess its utility revenues without the effects of fluctuating commodity costs as such costs are predominantly passed through and paid for by utility customers. AQN believes that analysis and presentation of Net Utility Sales on this basis will enhance an investor’s understanding of the revenue generation of the Regulated Services Group. It is not intended to be representative of revenue as determined in accordance with U.S. GAAP. For a reconciliation of Net Utility Sales to revenue, see Regulated Services Group - 2021 Regulated Services Group Operating Results on page 22 of this MD&A.

Divisional Operating Profit

Divisional Operating Profit is a non-GAAP financial measure . AQN uses Divisional Operating Profit to assess the operating performance of its business groups without the effects of (as applicable): depreciation and amortization expense, corporate administrative expenses, income tax expense or recoveries, acquisition costs, certain litigation expenses, interest expense, gain or loss on derivative financial instruments, write down of intangibles and property, plant and equipment, gain or loss on foreign exchange, earnings or loss from discontinued operations (excluding the sale of assets in the course of normal operations), non-service pension and post-employment costs, financial impacts from the Market Disruption Event on the Company's Senate Wind Facility, and other typically non-recurring or unusual items. AQN adjusts for these factors as they may be non-cash, unusual in nature and are not factors used by management for evaluating the operating performance of the divisional units. Divisional Operating Profit is calculated inclusive of interest, dividend and equity income earned from indirect investments, and Hypothetical Liquidation at Book Value (“HLBV”) income, which represents the value of net tax attributes earned in the period from electricity generated by certain of its U.S. wind power and U.S. solar generation facilities. AQN believes that presentation of this measure will enhance an investor’s understanding of AQN’s divisional operating performance. Divisional Operating Profit is not intended to be representative of cash provided by operating activities or results of operations determined in accordance with U.S. GAAP, and can be impacted positively or negatively by these items. For a reconciliation of Divisional Operating Profit to revenue for AQN's main business units, see Regulated Services Group - 2021 Regulated Services Group Operating Results on page 22 and Renewable Energy Group - 2021 Renewable Energy Group Operating Results on page 31 of this MD&A

AQN is incorporated under the Canada Business Corporations Act. AQN owns and operates a diversified portfolio of regulated and non-regulated generation, distribution, and transmission utility assets which are expected to deliver predictable earnings and cash flows. AQN seeks to maximize total shareholder value through real per share growth in earnings and cash flows to support a growing dividend and share price appreciation. AQN strives to achieve these results while also seeking to maintain a business risk profile consistent with its BBB flat investment grade credit ratings and a strong focus on Environmental, Social and Governance factors.

AQN’s current quarterly dividend to shareholders is $0.1706 per common share or $0.6824 per common share per annum. Based on the Bank of Canada exchange rate on March 2, 2022, the quarterly dividend is equivalent to C$0.2161 per common share or C$0.8644 per common share per annum. AQN believes its annual dividend payout allows for both an immediate return on investment for shareholders and retention of sufficient cash within AQN to fund growth opportunities. Changes in the level of dividends paid by AQN are at the discretion of AQN’s Board of Directors (the “Board”), with dividend levels being reviewed periodically by the Board in the context of AQN’s financial performance and growth prospects.

AQN’s operations are organized across two primary business units consisting of: the Regulated Services Group, which primarily owns and operates a portfolio of regulated assets in the United States, Canada, Bermuda and Chile, and the Renewable Energy Group, which primarily operates a diversified portfolio of owned renewable generation assets.

AQN pursues investment opportunities with an objective of maintaining the current business mix between its Regulated Services Group and Renewable Energy Group and with leverage consistent with its current credit ratings1. The business mix target may from time to time require AQN to grow its Regulated Services Group or implement other strategies in order to pursue investment opportunities within its Renewable Energy Group.

The Company also undertakes development activities for both business units, working with a global reach to identify, develop, acquire, or invest in renewable power generating facilities, regulated utilities and other complementary infrastructure projects. See additional discussion in Corporate Development Activities.

Summary Structure of the Business

The following chart depicts, in summary form, AQN’s key businesses. A more detailed description of AQN’s organizational structure can be found in the most recent AIF.

1 See Treasury Risk Management -Downgrade in the Company's Credit Rating Risk.

Regulated Services Group

The Regulated Services Group operates a diversified portfolio of regulated utility systems throughout the United States, Canada, Bermuda and Chile serving approximately 1,093,000 customer connections as at December 31, 2021 (using an average of 2.5 customers per connection, this translates into approximately 2,733,000 customers). The Regulated Services Group seeks to provide safe, high quality, and reliable services to its customers and to deliver stable and predictable earnings to AQN. In addition to encouraging and supporting organic growth within its service territories, the Regulated Services Group seeks to deliver growth through accretive acquisitions of additional utility systems.

The Regulated Services Group's regulated electrical distribution utility systems and related generation assets are located in the U.S. States of California, New Hampshire, Missouri, Kansas, Oklahoma, and Arkansas, as well as in Bermuda, which together served approximately 307,000 electric customer connections as at December 31, 2021. The group also owns and operates generating assets with a gross capacity of approximately 2.0 GW and has investments in generating assets with approximately 0.3 GW of net generation capacity.

The Regulated Services Group's regulated natural gas distribution utility systems are located in the U.S. States of Georgia, Illinois, Iowa, Massachusetts, New Hampshire, Missouri, and New York, and in the Canadian Province of New Brunswick, which together served approximately 373,000 natural gas customer connections as at December 31, 2021.

The Regulated Services Group's regulated water distribution and wastewater collection utility systems are located in the

U.S. States of Arizona, Arkansas, California, Illinois, Missouri, and Texas as well as in Chile which together served approximately 413,000 customer connections as at December 31, 2021. With the acquisition of New York American Water Company, Inc. (subsequently renamed Liberty Utilities (New York Water) Corp. (“Liberty NY Water”)), the Regulated Services Group added an additional approximately 125,000 customer connections in the state of New York effective January 1, 2022.

Below is a breakdown of the Regulated Services Group’s Revenue by geographic area for the twelve months ended December 31, 2021.

Renewable Energy Group

The Renewable Energy Group generates and sells electrical energy produced by its diverse portfolio of renewable power generation and clean power generation facilities primarily located across the United States and Canada. The Renewable Energy Group seeks to deliver growth through development of new power generation projects and accretive acquisitions of additional power generation facilities, as well as the acquisition and development of other complementary projects, such as renewable natural gas (“RNG”) and energy storage.

The Renewable Energy Group directly owns and operates hydroelectric, wind, solar, and thermal facilities with a combined gross generating capacity of approximately 2.3 GW. Approximately 82% of the electrical output is sold pursuant to long term contractual arrangements which as of December 31, 2021 had a production-weighted average remaining contract life of approximately 12 years.

In addition to directly owned and operated assets, the Renewable Energy Group has investments in generating assets with approximately 1.4 GW of net generating capacity which includes the Company’s approximately 44% interest in Atlantica Sustainable Infrastructure plc (“Atlantica”). Atlantica owns and operates a portfolio of international clean energy and water infrastructure assets under long term contracts with a Cash Available for Distribution (CAFD) weighted average remaining contract life of approximately 15 years as of December 31, 2021.

Below is a breakdown of the Renewable Energy Group’s generating capacity by geographic area as of December 31, 2021, which was comprised of gross generating capacity of facilities owned and operated and net generating capacity of investments including the Company’s approximately 44% interest in Atlantica.

Operating Results

AQN operating results relative to the same period last year are as follows:

Three months ended December 31 | Twelve months ended December 31 | |||||

| (all dollar amounts in $ millions except per share information) | 2021 | 2020 | Change | 2021 | 2020 | Change |

| Net earnings attributable to shareholders | $175.6 | $504.2 | (65)% | $264.9 | $782.5 | (66)% |

Adjusted Net Earnings1 | $136.3 | $127.0 | 7% | $449.6 | $365.8 | 23% |

Adjusted EBITDA1 | $297.6 | $253.1 | 18% | $1,076.9 | $869.5 | 24% |

| Net earnings per common share | $0.27 | $0.84 | (68)% | $0.41 | $1.38 | (70)% |

Adjusted Net Earnings per common share1 | $0.21 | $0.21 | —% | $0.71 | $0.64 | 11% |

1 See Caution Concerning Non-GAAP Measures.

Declaration of 2022 First Quarter Dividend of $0.1706 (C$0.2161) per Common Share

AQN currently targets annual growth in dividends payable to shareholders underpinned by increases in earnings and cash flow. In setting the appropriate dividend level, the Board considers the Company’s current and expected growth in earnings per share as well as a dividend payout ratio as a percentage of earnings per share and cash flow per share.

On March 3, 2022, AQN announced that the Board declared a first quarter 2022 dividend of $0.1706 per common share payable on April 14, 2022 to shareholders of record on March 31, 2022.

Based on the Bank of Canada exchange rate on March 2, 2022, the Canadian dollar equivalent for the first quarter 2022 dividend is C$0.2161 per common share.

The previous four quarter U.S and Canadian dollar equivalent dividends per common share have been as follows:

| Q2 2021 | Q3 2021 | Q4 2021 | Q1 2022 | Total | |||||||||

| U.S. dollar dividend | $ | 0.1706 | $ | 0.1706 | $ | 0.1706 | $ | 0.1706 | $0.6824 | ||||

| Canadian dollar equivalent | $ | 0.2094 | $ | 0.2134 | $ | 0.2124 | $ | 0.2161 | $0.8513 | ||||

Agreement to Acquire Kentucky Power Company and AEP Kentucky Transmission Company

On October 26, 2021, Liberty Utilities Co. (“Liberty Utilities”), an indirect subsidiary of AQN, entered into an agreement with American Electric Power Company, Inc. and AEP Transmission Company, LLC to acquire Kentucky Power Company (“Kentucky Power”) and AEP Kentucky Transmission Company, Inc. (“Kentucky TransCo”) for a total purchase price of approximately $2.846 billion, including the assumption of approximately $1.221 billion in debt (the “Kentucky Power Transaction”).

Kentucky Power is a state rate-regulated electricity generation, distribution and transmission utility serving approximately 228,000 active customer connections in 20 eastern Kentucky counties and operating under a cost of service framework. Kentucky TransCo is an electricity transmission business operating in the Kentucky portion of the transmission infrastructure that is part of the Pennsylvania – New Jersey – Maryland regional transmission organization, PJM Interconnection, L.L.C.. Kentucky Power and Kentucky TransCo are both regulated by the U.S. Federal Energy Regulatory Commission (“FERC”).

Closing of the Kentucky Power Transaction is subject to receipt of certain regulatory and governmental approvals, including the expiration or termination of any applicable waiting period under the Hart-Scott-Rodino Antitrust Improvements Act of 1976 (which has expired), clearance of the Kentucky Power Transaction by the Committee on Foreign Investment in the United States (which has been obtained), the approval by each of the Kentucky Public Service Commission and FERC with respect to the Kentucky Power Transaction and the termination and replacement of the existing operating agreement for the Mitchell coal generating facility (in which Kentucky Power owns a 50% interest, representing 780 MW) (the “Mitchell Plant”), and the approval of the Public Service Commission of West Virginia with respect to the termination and replacement of the existing operating agreement for the Mitchell Plant, and the satisfaction of other customary closing conditions. If the acquisition agreement is terminated in certain circumstances, including due to a failure to receive required regulatory approvals (other than the approval of the Kentucky Public Service Commission, FERC or the Public Service Commission of West Virginia for the termination and replacement of the existing operating agreement for the Mitchell Plant), the Corporation may be required to pay a termination fee of $65 million. The Kentucky Power Transaction is expected to close in mid-2022.

The Kentucky Power Transaction is expected to add over $2.0 billion of regulated rate base assets in a favourable regulatory jurisdiction. AQN expects the Kentucky Power Transaction to be accretive to Adjusted Net Earnings per common share in the first full year of ownership, generate mid-single digit percentage Adjusted Net Earnings per common share accretion thereafter, and support growth in AQN’s Adjusted Net Earnings per common share over the long term (see Caution Concerning Non-GAAP Measures). Near and medium term planned retirements (for Kentucky rate-making purposes) or transitions of over 1 GW of fossil fuel generation owned by Kentucky Power are expected to provide the Company with an opportunity to leverage its “greening the fleet” capabilities as a renewable energy developer and target to replace this generation capacity with renewable energy.

Acquisition of Liberty NY Water (formerly New York American Water Company, Inc.)

Effective January 1, 2022, Liberty Utilities (Eastern Water Holdings) Corp., a wholly-owned subsidiary of Liberty Utilities, closed the previously-announced acquisition of Liberty NY Water from American Water Works Company, Inc. for a purchase price of approximately $608 million.

Headquartered in Merrick, NY, Liberty NY Water is a regulated water and wastewater utility serving over 125,000 customer connections across seven counties in southeastern New York. Liberty NY Water’s operations include approximately 1,270 miles of water mains and distribution lines, with 98% of customers located in Nassau County on Long Island.

Completion of Renewable Construction Projects

Completion of Midwest Greening the Fleet Initiative

On January 27, 2021, The Empire District Electric Company (“Empire”) closed its acquisition of the North Fork Ridge Wind Facility and, on May 5, 2021, Empire closed the acquisitions of the Kings Point and Neosho Ridge Wind Facilities (collectively, the “Empire Wind Facilities”.) As a result, the Regulated Services Group has successfully completed the construction and acquisition of all the wind facilities related to its Midwest ‘greening the fleet’ initiative. The initiative consisted of 600 MWs of new strategically located wind energy generation which is expected to provide benefits to the Regulated Services Group's electric customers in Missouri, Arkansas, Oklahoma and Kansas. The initiative also resulted in the early retirement of the 200 MW Asbury Coal Facility (Asbury”) on March 1, 2020, approximately 15 years ahead of its original retirement schedule.

The early retirement of Asbury is expected to provide long term benefits to customers and has reduced the Company's CO2e emissions by more than 900,000 metric tons, bringing the Company’s total reduction of greenhouse gas (“GHG”) emissions to over 1 million metric tons since 2017. The early retirement has also contributed to the reduction in the Company’s total Scope 1 GHG emissions as well as reductions in emission intensity per dollar of revenue since 2017, the year in which the Company acquired Empire, which owns Asbury. See Regulatory Proceedings.

Completion of the Maverick Creek Wind Project

On April 21, 2021, the Renewable Energy Group achieved full commercial operations (“COD”) at its 492 MW Maverick Creek Wind Facility, located in Concho County, Texas. The Maverick Creek Wind Facility is the Renewable Energy Group's 14th wind powered electric generating facility and is expected to generate approximately 1,920 GW-hrs of energy per year with the majority of output being sold through two long-term power purchase agreements (“PPA”s) with investment grade rated entities.

Completion of the Altavista Solar Project

On June 1, 2021, the Renewable Energy Group achieved COD at its 80 MW Altavista Solar Facility, located in Campbell County, Virginia. The Altavista Solar Facility is the Renewable Energy Group’s sixth solar powered electric generating facility and is expected to generate approximately 174 GW-hrs of energy per year with the majority of output being sold to Facebook Operations, LLC, a wholly-owned subsidiary of Meta, pursuant to a PPA.

Acquisition of Majority Interest in Texas Coastal Wind Facilities

In the first quarter of 2021, the Renewable Energy Group closed the acquisitions of a 51% interest in three of four wind facilities (collectively the “Texas Coastal Wind Facilities”) that it had previously agreed to purchase from RWE Renewables Americas, LLC, a subsidiary of RWE AG. The acquisition of a 51% interest in the fourth wind facility closed in the third quarter of 2021 when that facility achieved COD. The four Texas Coastal Wind Facilities have a total generating capacity of approximately 861 MW.

Agreement to Acquire Renewable Natural Gas Development Platform

On December 13, 2021, Liberty (RNG), LLC, a wholly-owned subsidiary of AQN, entered into an agreement to acquire Sandhill Advanced Biofuels, LLC (“Sandhill”). Sandhill is a renewable natural gas ("RNG") development platform specializing in anaerobic digestion projects located on dairy farms with a portfolio of four projects in the state of Wisconsin, two of which are currently under construction and the remaining two are in late-stage development. The existing projects are expected to produce RNG at a rate of approximately 500 one million British thermal units (“MMBTU”) per day. The transaction is expected to close in the first half of 2022. If successfully completed, the acquisition will represent the Company’s first investment in the non-regulated renewable natural gas space.

Corporate Financings Completed

Issuance of C$400 Million of Green Senior Unsecured Debentures

On April 9, 2021, the Renewable Energy Group issued C$400.0 million of green senior unsecured debentures bearing interest at 2.85% and with a maturity date of July 15, 2031 (the “Debentures”). Concurrent with the offering of the Debentures, the Renewable Energy Group entered into a cross currency interest rate swap to convert the proceeds into U.S. dollars with an effective interest rate throughout the term of the Debentures of approximately 2.82%. The net proceeds from the offering of the Debentures were or will be, as applicable, used in accordance with AQN’s Green Financing Framework.

Inaugural Issuance of Green Equity Units

On June 23, 2021, the Company closed an underwritten marketed public offering of 20,000,000 equity units (the “Green Equity Units”) for total gross proceeds of $1.0 billion. The underwriters subsequently exercised their option to purchase an additional 3,000,000 Green Equity Units on the same terms, bringing total gross proceeds including the over-allotment to

$1.15 billion.

Each Green Equity Unit consists of a 1/20 or 5% undivided beneficial interest in a $1,000 principal amount remarketable senior note of the Company due June 15, 2026, and a contract to purchase AQN common shares on June 15, 2024 based on a reference price determined by the volume-weighted average AQN common share price over the preceding 20 day trading period. Total annual distributions on the Green Equity Units are at the rate of 7.75%. The net proceeds from the Offering have been or will be, as applicable, used to finance or refinance investments in renewable energy generation or facilities or other clean energy technologies in accordance with the Company’s Green Financing Framework. See additional discussion in Long Term Debt.

Common Equity Financing

On November 8, 2021, AQN closed a bought deal common equity offering for gross proceeds of approximately C$800 million (the “Common Equity Offering”). The Company intends to use the net proceeds of the Common Equity Offering to partially finance the Kentucky Power Transaction provided that, in the short-term, prior to closing of the Kentucky Power Transaction, the Company has used such net proceeds to reduce amounts outstanding under existing credit facilities.

Issuance of approximately $1.1 Billion of Subordinated Notes

Subsequent to quarter-end on January 18, 2022, the Company closed (i) an underwritten public offering in the United States (the “U.S. Note Offering”) of $750 million aggregate principal amount of 4.75% fixed-to-fixed reset rate junior subordinated notes series 2022-B due January 18, 2082 (the “U.S. Notes”); and (ii) an underwritten public offering in Canada (the “Canadian Note Offering” and, together with the U.S. Note Offering, the “Note Offerings”) of C$400 million aggregate principal amount of 5.25% fixed-to-fixed reset rate junior subordinated notes series 2022-A due January 18, 2082 (the “Canadian Notes” and, together with the U.S. Notes, the “Notes”). The Company intends to use the net proceeds of the Note Offerings to partially finance the Kentucky Power Transaction provided that, in the short-term, prior to closing of the Kentucky Power Transaction, the Company has used a portion of, and expects to use the remainder of such net proceeds to repay certain indebtedness of the Corporation and its subsidiaries. Concurrent with the pricing of the Note Offerings, the Company entered into a cross currency interest rate swap, to convert the Canadian dollar denominated proceeds from the Canadian Note Offering into U.S. dollars and a forward starting swap to fix the interest rate for the second five year term of the U.S. Notes. resulting in an anticipated effective interest rate to the Company of approximately 4.95% throughout the first ten year period of the Notes.

Net-Zero Goals and 2021 ESG Report

On October 5, 2021, the Company announced its target to achieve net-zero (scope 1 and 2 GHG) by 2050. Concurrently, the Company released its 2021 ESG Report, which details AQN’s progress with respect to environmental, social and governance matters.

Impact of COVID-19 on Operating Results

For the three and twelve months ended December 31, 2021, the Company’s operating results were not materially impacted by the COVID-19 pandemic. Approximately 60% of the Company’s workforce continues to work remotely and the Company continues to employ operational measures intended to protect the health and safety of its employees and customers. Over the coming months the Company is planning a return to base operations as the impacts of the pandemic further diminish.

The Company’s business, financial condition, cash flows and results of operations continue to be subject to actual and potential future impacts resulting from COVID-19, the full extent of which are not currently known. The extent of the future impact of the COVID-19 pandemic on the Company will depend on, among other things, the duration of the pandemic, the extent of the related public health measures taken in response to the pandemic and the Company’s efforts to mitigate the impact on its operations.

For a discussion of the risks the Company faces related to COVID-19 please refer to Enterprise Risk Management.

The following discussion should be read in conjunction with the Forward-Looking Statements and Forward-Looking Information section in this MD&A. Actual results may differ materially from the estimates below. Accordingly, investors are cautioned not to place undue reliance on these estimates.

Estimated 2022 Adjusted Net Earnings Per Common Share

The Company estimates that its Adjusted Net Earnings per common share will be within a range of $0.72-$0.77 for the 2022 fiscal year, as compared to Adjusted Net Earnings per common share of $0.71 for the 2021 fiscal year (see Caution Concerning Non-GAAP Measures).

The Company’s 2022 Adjusted Net Earnings per common share estimate is based on the following key assumptions, as well as those set out under Forward-Looking Statements and Forward-Looking Information:

| • | normalized weather patterns in the geographical areas in which the Company operates or has projects; |

| • | rate decisions in line with expectations; |

| • | renewable energy production and realized pricing consistent with long-term averages; |

| • | no impacts from COVID-19 on operations; and |

| • | closing of the Kentucky Power Transaction in mid-2022. |

Capital Investment Expectations

The Company anticipates making capital investments of between approximately $4.34 billion and $4.68 billion in 2022. See 2022 Capital Investments for a more detailed discussion of the Company’s 2022 capital investment estimates.

The Company has also announced an approximately $12.4 billion capital plan for the period from 2022 through the end of 2026, with approximately 70% expected to be invested by the Regulated Services Group and approximately 30% expected to be invested by the Renewable Energy Group (see Corporate Development).

| Key Financial Information | Three months ended December 31 | ||||||

| (all dollar amounts in $ millions except per share information) | 2021 | 2020 | |||||

| Revenue | $ | 594.8 | $ | 491.3 | |||

| Net earnings attributable to shareholders | 175.6 | 504.2 | |||||

| Cash provided by operating activities | 126.5 | 174.0 | |||||

Adjusted Net Earnings1 | 136.3 | 127.0 | |||||

Adjusted EBITDA1 | 297.6 | 253.1 | |||||

Adjusted Funds from Operations1 | 221.2 | 179.3 | |||||

| Dividends declared to common shareholders | 115.5 | 93.1 | |||||

| Weighted average number of common shares outstanding | 653,728,621 | 597,165,849 | |||||

| Per share | |||||||

| Basic net earnings | $ | 0.27 | $ | 0.84 | |||

| Diluted net earnings | $ | 0.26 | $ | 0.83 | |||

Adjusted Net Earnings1 | $ | 0.21 | $ | 0.21 | |||

| Dividends declared to common shareholders | $ | 0.17 | $ | 0.16 | |||

1 See Caution Concerning Non-GAAP Measures.

For the three months ended December 31, 2021, AQN experienced an average exchange rate of Canadian to U.S. dollars of approximately 0.7937 as compared to 0.7675 in the same period in 2020. As such, any quarter over quarter variance in revenue or expenses, in local currency, at any of AQN’s Canadian entities is affected by a change in the average exchange rate upon conversion to AQN’s reporting currency.

For the three months ended December 31, 2021, AQN reported total revenue of $594.8 million as compared to $491.3 million during the same period in 2020, an increase of $103.5 million or 21.1%. The major factors impacting AQN’s revenue in the three months ended December 31, 2021 as compared to the same period in 2020 are set out as follows:

| (all dollar amounts in $ millions) | Three months ended December 31 | ||

| Comparative Prior Period Revenue | $ | 491.3 | |

| REGULATED SERVICES GROUP | |||

| Existing Facilities | |||

| Electricity: Increase is primarily due to higher pass through commodity costs at the Empire Electric System, partially offset by higher operating costs at the CalPeco Electric System. | 0.4 | ||

| Gas: Increase is primarily due to higher pass through commodity costs across all the Company’s gas systems and new connections at the New Brunswick Gas System. | 33.8 | ||

| Water: Increase is due to higher consumption and organic growth at the Beardsley and Litchfield Park Water Systems, partially offset by lower pass though commodity costs at the Park Water System. | 0.8 | ||

| Other: Decrease is primarily due to a reduction in projects at Ft. Benning. | (1.2 | ) | |

| 33.8 | |||

| New Facilities | |||

| Electricity: Acquisition of Liberty Group Limited (formerly Ascendant Group Limited (“Ascendant”)) (November 2020) and the Empire Wind Facilities (2021). | 50.1 | ||

| Water: Acquisition of Empresa de Servicios Sanitarios de Los Lagos S.A.(“ESSAL”) (October 2020). | 2.6 | ||

| 52.7 | |||

| Rate Reviews | |||

| Electricity: Increase is primarily due to implementation of new rates at the CalPeco and Granite State Electric Systems. | 2.9 | ||

| Gas: Increase is primarily due to implementation of new rates at the EnergyNorth and Midstates Gas Systems. | 0.5 | ||

| Water: Increase is due to implementation of new rates at the Park Water and Apple Valley Water Systems. | 1.5 | ||

| 4.9 | |||

Estimated Impact of COVID-19 on comparative period results1 | 0.7 | ||

| RENEWABLE ENERGY GROUP | |||

Existing Facilities Hydro: Decrease is primarily due to lower production in the Ontario and Quebec Region, partially offset by favourable pricing in the Western Region. | (0.5 | ) | |

| Wind Canada: Decrease is primarily due to lower production for the St. Damase, Morse and Amherst Wind Facilities. | (0.7 | ) | |

| Wind U.S.: Decrease is primarily due to lower production for the Minonk, Shady Oaks, and Deerfield Wind Facilities along with unfavourable energy pricing, partially offset by higher renewable energy credit (“REC”) revenue across the U.S. Wind Facilities. | (1.9 | ) | |

| Solar: Decrease is primarily due to lower REC revenue for the Great Bay I & II Solar Facilities, partially offset by favourable capacity rates and higher availability revenue as well as the receipt of an insurance payment for the Bakersfield I Solar Facility. | (0.6 | ) | |

| Thermal: Increase is primarily due to favourable pricing at the Windsor Locks Thermal Facility, partially offset by unfavourable capacity pricing for the Sanger Thermal Facility. | 0.3 | ||

| Other: Decrease is primarily due to higher administrative fees received in 2020 from joint venture construction projects. | (0.2 | ) | |

| (3.6 | ) | ||

| New Facilities | |||

| Wind U.S.: Sugar Creek Wind Facility (full COD in November 2020) and Maverick Creek Wind Facility (full COD in April 2021). | 11.6 | ||

| Solar: Altavista Solar Facility (full COD in June 2021) and Croton Solar Facility (full COD in December 2021). | 1.3 | ||

| Other: Increase is due to Congestion Revenue Rights (“CRRs”) Revenue | 1.3 | ||

| 14.2 | |||

| Foreign Exchange | 0.8 | ||

| Current Period Revenue | $ | 594.8 | |

| 1 | The impacts of COVID-19 were estimated by normalizing sales in both periods for changes in weather and attributing the remaining variances to COVID-19. |

| Key Financial Information | Twelve months ended December 31 | ||||||||

| (all dollar amounts in $ millions except per share information) | 2021 | 2020 | 2019 | ||||||

| Revenue | $ | 2,285.5 | $ | 1,677.0 | $ | 1,624.9 | |||

| Net earnings attributable to shareholders | 264.9 | 782.5 | 530.9 | ||||||

| Cash provided by operating activities | 157.5 | 505.2 | 611.3 | ||||||

Adjusted Net Earnings1 | 449.6 | 365.8 | 321.3 | ||||||

Adjusted EBITDA1 | 1,076.9 | 869.5 | 838.6 | ||||||

Adjusted Funds from Operations1 | 757.9 | 600.2 | 566.2 | ||||||

| Dividends declared to common shareholders | 423.0 | 344.4 | 277.8 | ||||||

| Weighted average number of common shares outstanding | 622,347,677 | 559,633,275 | 499,910,876 | ||||||

| Per share | |||||||||

| Basic net earnings | $ | 0.41 | $ | 1.38 | $ | 1.05 | |||

| Diluted net earnings | $ | 0.41 | $ | 1.37 | $ | 1.04 | |||

Adjusted Net Earnings1 | $ | 0.71 | $ | 0.64 | $ | 0.63 | |||

| Dividends declared to common shareholders | $ | 0.67 | $ | 0.61 | $ | 0.55 | |||

| Total assets | 16,785.8 | 13,224.1 | 10,920.8 | ||||||

Long term debt2 | 6,211.7 | 4,538.8 | 3,932.2 | ||||||

1 See Caution Concerning Non-GAAP Measures.

2 Includes current and long-term portion of debt and convertible debentures per the annual consolidated financial statements