UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-21335

Exact name of registrant as specified in charter:

Optimum Fund Trust

Address of principal executive offices:

2005 Market Street

Philadelphia, PA 19103

Name and address of agent for service:

David F. Connor, Esq.

2005 Market Street

Philadelphia, PA 19103

Registrant’s telephone number, including area code: (800) 523-1918

Date of fiscal year end: March 31

Date of reporting period: March 31, 2007

Item 1. Reports to Stockholders

| | ||

| Optimum Fund Trust | ||

| May 30, 2007 | ||

This brochure accompanies an annual report for the information of Optimum Fund Trust shareholders, but it may be used with prospective investors when preceded or accompanied by a current prospectus for Optimum Fund Trust. You should consider the investment objectives, risks, charges, and expenses of the investment company carefully before investing. The prospectus contains this and other important information about the Funds. Prospectuses for Optimum Fund Trust are available from your financial advisor, online at www.optimummutualfunds.com, or by phone at 800 914-0278. Please read the prospectus carefully before you invest or send money. The figures in the annual report for Optimum Fund Trust represent past results, which are not a guarantee of future results. The return and principal value of an investment in a Fund will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. | ||

| | |||

| Optimum Fixed Income Fund* | |||

| Optimum International Fund | |||

| Optimum Large Cap Growth Fund | |||

| Optimum Large Cap Value Fund | |||

| Optimum Small Cap Growth Fund | |||

| Optimum Small Cap Value Fund | |||

| Annual Report | |||

| March 31, 2007 | |||

* | The Fund’s prospectus supplement contains important information regarding the investment manager for the Fund. A prospectus, which contains a complete copy of the supplement, may be obtained by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. | ||

Table of contents

| > Portfolio management review | ||

| Optimum Fixed Income Fund | 1 | |

| Optimum International Fund | 6 | |

| Optimum Large Cap Growth Fund | 10 | |

| Optimum Large Cap Value Fund | 14 | |

| Optimum Small Cap Growth Fund | 18 | |

| Optimum Small Cap Value Fund | 22 | |

| > Disclosure of Fund expenses | 28 | |

| > Sector/Country allocations, | ||

| credit quality breakdown and top 10 holdings | 30 | |

| > Financial statements | ||

| Statements of net assets | 34 | |

| Statements of assets and liabilites | 72 | |

| Statements of operations | 73 | |

| Statements of changes in net assets | 74 | |

| Financial highlights | 77 | |

| Notes to financial statements | 101 | |

| > Report of independent registered public | ||

| accounting firm | 112 | |

| > Board of trustees and officers addendum | 113 | |

| > About the organization | 115 |

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management

Business Trust, which is a registered investment advisor.

© 2007 Delaware Distributors, L.P.

Portfolio management review

> Optimum Fixed Income Fund

April 10, 2007

Advisor

Delaware Management Company (DMC)

Sub-advisor

Aberdeen Asset Management Inc. (AAMI)

Optimum Fixed Income Fund seeks a high level of income and may also seek growth of capital. The Fund’s advisor, Delaware Management Company, manages one portion of the Fund. It also has selected a sub-advisor, AAMI, to manage another portion of the Fund’s assets.

DMC and AAMI are responsible for day-to-day investment management of a portion of the Fund’s assets. They select investments for their portion of the Fund based on their own investment style and strategy. For more information on the investment approach of the advisor and sub-advisor, please see the Fund’s prospectus.

Within its portion of the Fund, DMC allocates investments principally among the fixed income markets:

- U.S. investment grade

- U.S. high yield

- International developed markets

- International emerging markets

The strategy employed by AAMI is predicated on an investment philosophy that the best way to consistently add value is through a strictly bottom-up approach capitalizing on the inefficiencies inherent in the bond market. Therefore, the sub-advisor focuses its efforts on a disciplined process of individual security selection and avoids such techniques as interest rate forecasting.

Optimum Fixed Income Fund returned +7.58% at net asset value and +2.77% at maximum offer price for the fiscal year ended March 31, 2007 (both figures reflect performance for Class A shares with all distributions reinvested). For complete annualized performance, please see the table on page 4. By comparison, the Fund’s benchmark — the Lehman Brothers Aggregate Bond Index — gained +6.59% for the period.

During the fiscal year, the U.S. Federal Reserve ended its policy of monetary tightening. After 17 consecutive interest rate increases of 0.25 percentage points, including two last spring, the Fed paused after its June 2006 meeting. Since then the Fed funds rate has been anchored at 5.25%. In reaction to the Fed’s pause last summer, Treasuries rallied as the market priced-in interest rate cuts expected in 2007. Treasury yields have retreated, with the benchmark 10-year Treasury yielding 4.65% on March 31, 2007, versus 4.85% a year prior.

A quest for higher yields drove some investors to lower-quality assets. This increase in risk appetite, combined with the excess demand fueled by increased leverage, has pressured yields lower and, despite a deteriorating credit outlook, has compressed the difference, or spread, between yields on high- and low-quality bonds.

Against this backdrop, the Lehman Aggregate Bond Index returned 6.59% for the 12 months ended March 31, 2007. Based on total returns for Lehman Brothers sector indices, credit gained 7.08%, mortgage-backed securities (MBS) 6.94%, commercial mortgage-backed securities (CMBS) 6.85%, and asset-backed securities (ABS) 5.91%.

The sections below provide additional information about the portion of the Fund managed by the advisor and sub-advisor.

AAMI

Q: What influenced performance in your portion of the Fund?

A: We remain focused on the hard work of identifying and appropriately valuing the existing risks in individual bonds. The discipline of consistently adhering to our valuation approach has historically been a governor of our overall risk positioning, our present positioning not excepted. Given our view that valuations were full across the board at period end, we were finding more selling opportunities than buying opportunities. However, we generally believe this type of environment can be nearly as fertile as any other for generating returns.

We ended the period slightly underweight versus the Lehman Aggregate Bond Index in corporate bonds, having trimmed exposure during the year as bond prices reached our target valuations. An area of particular emphasis within our corporate positioning, as well as within headlines recently, is the broadly defined hybrid capital securities market. This market underperformed early

The views expressed are current as of the date of this report and are subject to change.

1

in the period when the regulatory treatment of these securities came under review, and appeared to cause consternation among buyers. In recent months, hybrid capital securities have regained that lost performance and then some, after it appeared that views held by market participants and regulators moved toward our own view with regard to their creditworthiness and structural integrity. Additionally, holdings in cable/media, telecommunications, and property and casualty insurance were among our better performers. Investments in gaming companies detracted from results.

Mortgage-backed securities benefited from muted volatility during much of the period. Our MBS portfolio remains largely concentrated in structured bonds (hybrid adjustable-rate mortgages and planned amortization class bonds) that are less prepayment-sensitive than the pass-throughs that comprise the MBS index. Although these securities dampened performance at times during the year when volatility eased, overall they have aided results and we believe they currently remain attractively valued in the intermediate part of the yield curve.

The other high-grade sectors of the market such as CMBS and ABS performed well during the year. Commercial real estate valuations fared better than residential mortgages, leading to positive performance during the period. Recent headlines about subprime mortgage lending notwithstanding, ABS as a market segment also posted positive results for the period. Our ABS holdings remain concentrated in high-quality (AAA-rated by Standard & Poor’s), short-duration securities. The current turmoil in subprime mortgages has negatively impacted the sector of late; however, we believe that our defensive posture has helped to minimize the effect on the portfolio.

DMC

Q: What influenced performance in your portion of the Fund?

A: The portfolio managed by Delaware Management Company uses our “core plus” fixed income investment strategy. In a core plus strategy, we invest the core of the assets under our management in domestic investment grade securities, then tactically allocate other assets to “plus” sectors of the fixed income markets. These plus sectors include domestic high yield bonds as well as both established and emerging international markets.

During the year, high yield, emerging markets, and non-dollar debt performed well, aiding performance of a core plus strategy against the Lehman Brothers Aggregate Bond Index.

Throughout the year, we focused diligently on credit selection when analyzing U.S. corporate bonds. We believed the specter of risk from highly leveraged transactions increasingly loomed over the investment-grade space during much of the year. When considering new investment grade corporate bond issues, the team tended to favor subordinated securities in capital structures of issuers that we fundamentally favor, rather than stretching for higher yields by sacrificing credit quality. Our research efforts generally have been aimed at avoiding the isolated, but now increasing situations such as leveraged buyouts (LBOs), management buyouts, leveraged recapitalizations, and mergers, which generally tend to be unfriendly to bondholders.

During the fiscal year, higher-risk securities such as emerging market bonds and U.S. high yield bonds generally outperformed lower-risk assets. Especially during the late-2006 rally, lower-rated bonds outperformed as investors continued to search for yield, with total returns among credit ratings often showing significant differences based on Lehman Brothers credit indices.

We continued to focus on security selection within our allocation to high yield bonds. Although the economic climate and other big-picture factors were influential in the high yield market, company-specific characteristics and influences generally played larger roles in overall performance. As such, we generally avoided making significant sector bets, preferring instead to focus on our in-depth research efforts to uncover attractively valued securities throughout the high yield universe. We continually paid attention to the new issue LBO market, as large deals were often priced at attractive levels.

After several years of double-digit advances, the market for emerging market bonds underwent a significant correction in the second calendar quarter of 2006, but roared back to life when fixed income assets rallied as a whole in the summer months. We believe that steady world economic growth and continued strong pricing among commodities kept demand strong for both dollar-denominated and local currency–denominated bonds. During the year, our emerging markets team attempted to add value through both the corporate emerging markets area and local currency–denominated bonds that are issued by foreign governments.

2

Performance summary

> Optimum Fixed Income Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com.

You should consider the Fund’s investment objectives, risks, charges, and expenses carefully before investing. The Optimum Fixed Income Fund prospectus contains this and other important information about the Fund. Please request a prospectus through your financial advisor or by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Read the prospectus carefully before you invest or send money.

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted below.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

An expense limitation was in effect for all classes during the periods shown below and on the next page. Performance would have been lower had the expense limitation not been in effect.

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 4.50% and have an annual distribution and service fee of up to 0.35% of average daily net assets.

Class B shares are sold with a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Effective at the close of business on July 31, 2007, no new or subsequent investments will be allowed in Class B shares of each portfolio in Optimum Fund Trust, except through a reinvestment of dividends or permitted exchanges. Please see the prospectus supplement for additional information.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Please see the fee table in the prospectus and your financial professional for a more complete explanation of sales charges.

Management has contracted to reimburse expenses and/or waive its management fees through Aug. 1, 2007.

The most recent Fund prospectus designates the Fund’s net expense ratios for Class A, B, C, and Institutional Class shares as 1.25%, 1.90%, 1.90%, and 0.90%, respectively, and the total operating expenses for Class A, B, C, and Institutional Class shares as 1.67%, 2.32%, 2.32%, and 1.32%, respectively. Please see the fee table in the Fund’s prospectus for more information.

The average annual total returns for the one-year and lifetime periods ended March 31, 2007, for Optimum Fixed Income Fund Institutional Class shares were +8.09% and +5.34%, respectively. Institutional Class shares were first made available on Aug. 1, 2003, for certain retirement plan products. They are sold (without a sales charge or asset-based distribution charges) only to certain eligible investors.

A rise or fall in interest rates can have a significant impact on bond prices and the NAV (net asset value) of the Fund.

Foreign investments are subject to risks not ordinarily associated with domestic investments, such as currency, economic and political risks, and different accounting standards. Investing in emerging markets can be riskier than investing in well-established foreign markets.

High yielding noninvestment grade bonds involve higher risk than investment grade bonds. Adverse conditions may affect the issuer’s ability to pay interest and principal on these securities.

Fund Performance

Average Annual Total Returns | ||

| Through March 31, 2007 | 1 Year | Lifetime |

| Class A (Est. Aug. 1, 2003) | ||

| Excluding Sales Charge | +7.58% | +4.96% |

| Including Sales Charge | +2.77% | +3.66% |

| Class B (Est. Aug. 1, 2003) | ||

| Excluding Sales Charge | +7.01% | +4.31% |

| Including Sales Charge | +3.01% | +3.95% |

| Class C (Est. Aug. 1, 2003) | ||

| Excluding Sales Charge | +6.88% | +4.31% |

| Including Sales Charge | +5.88% | +4.31% |

The performance table above and the graph on the next page do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

4

| Fund basics |

| As of March 31, 2007 |

| Fund objective |

| The Fund seeks a high level of income and may also seek growth of capital. |

| Total fund net assets |

| $749 million |

| Number of holdings |

| 1,039 |

| Fund start date | ||

| Aug. 1, 2003 | ||

| Nasdaq symbols | CUSIPs | |

| Class A | OAFIX | 246118681 |

| Class B | OBFIX | 246118673 |

| Class C | OCFIX | 246118665 |

| Institutional Class | OIFIX | 246118657 |

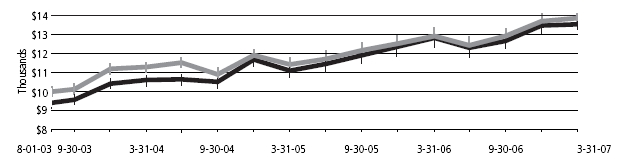

Performance of a $10,000 Investment

Aug. 1, 2003 (Fund’s inception) through March 31, 2007

| Starting value (Aug. 1, 2003) | Ending value (March 31, 2007) | ||

| Lehman Brothers Aggregate Bond Index | $10,000 | $11,732 | |

| Optimum Fixed Income Fund — Class A Shares | $9,550 | $11,408 |

Chart assumes $10,000 invested on Aug. 1, 2003 and includes the effect of a 4.50% front-end sales charge and the reinvestment of all distributions.

Performance of other Fund classes will vary due to different charges and expenses.

The chart also assumes $10,000 invested in the Lehman Brothers Aggregate Bond Index as of Aug. 1, 2003. The Lehman Brothers Aggregate Bond Index is an unmanaged composite that tracks the broad U.S. bond markets. An index does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index.

Past performance is not a guarantee of future results.

5

Portfolio management review

> Optimum International Fund

April 10, 2007

Advisor

Delaware Management Company (DMC)

Sub-advisors

AllianceBernstein L.P. (Alliance)

Mondrian Investments Partners Ltd. (Mondrian)

Optimum International Fund seeks long-term growth of capital. The Fund may also seek income. The Fund’s advisor, Delaware Management Company, selected two sub-advisors, each of whom is responsible for day-to-day investment management of a portion of the Fund’s assets. Each sub-advisor selects investments for its portion of the Fund based on its own investment style and strategy. For more information on the investment approach of the sub-advisors, please see the Fund’s prospectus.

For the fiscal year ending March 31, 2007, the Morgan Stanley Capital International Europe, Australasia, Far East Index (MSCI EAFE Index) gained +20.20%, as strong global economic growth and a falling U.S. dollar helped international equity returns outpace domestic returns in the U.S. By comparison, Optimum International Fund had a total return of +21.26% at net asset value and +14.30% at its maximum offer price. Both figures reflect performance for Class A shares with all distributions reinvested. For complete annualized returns, please see page 8.

International equity markets were again very strong, as most markets showed gains in local currency terms for the year, and currency movements added to returns in U.S. dollars for all EAFE markets except Japan and Hong Kong. For the year ended March 31, 2007, Singapore benefited from strong domestic economic growth, strong international trade, and rising property prices and returned 45.7%, making it the strongest market in the MSCI EAFE Index (all country returns based on MSCI country indices). Another strong Pacific market was Australia, up 35.0%. Conversely, the largest pacific market, Japan, had the lowest return in EAFE, up just 3.0%. Among the European markets, Spain had the highest performance at 38.3%, followed by a 37.0% rise in the Danish market. The U.K. had a reasonable 24.3% rise, but Finland’s 19.9% gain was the weakest European figure.

The utilities sector, despite its defensive reputation, had the highest performance, rising 40.0% for the year ended March 31, 2007. Merger and acquisition activity, rumored and actual, helped drive this sector. Having lagged for some time, the telecommunication sector surged in the latter half of the 12 months, making it another strong performing sector with a return of 31.0%. The weakest sector was information technology, up just 3.1%, and the former market darling, the energy sector, rose just 8.4%.

The sections below provide additional information about the portion of the Fund managed by each sub-advisor.

Alliance

Q: Please describe your approach to the Fund’s positioning during the course of the fiscal year.

A: We took advantage of the February 2007 market decline to increase some of our holdings in companies whose valuations we believed were unjustly punished during the indiscriminate sell off. We also accelerated planned purchases of shares in other companies that our research had already identified as potentially attractive value opportunities.

Financial stocks remained the single largest sector position in our portion of the Fund, but for different reasons in different markets and geographical locations.

ING Groep fell on exposure to the U.S. subprime market through bonds held by the Dutch financial service company’s life insurance subsidiary. We continued to hold significant stakes in some oil companies. We believed that strong demand from emerging economies and the commercial transportation sector, together with only gradual increases in supply, could keep oil prices higher for longer than most investors expect. We also maintained significant positions in several transport, capital equipment, and technology companies.

Q: What factors influenced performance in a positive way during the fiscal year?

A: When comparing our sector positioning and returns to the MSCI EAFE Index, both our heavier weighting and stock selection within the materials sector contributed to Fund returns. Our metal and mining stocks, including JFE Holdings, Voestalpine, and Xstrata benefited from ongoing expectations of industry consolidation.

The views expressed are current as of the date of this report and are subject to change.

6

Our consumer staples holdings also were strong performers. In the United Kingdom, the stock of food retailer J Sainsbury was buoyed by private equity interest. Meanwhile, Japan Tobacco outperformed after the company confirmed plans to purchase its smaller rival, the Gallaher Group, based in the U.K.

Q: What factors influenced performance in a negative way?

A: In our portion of the Fund, an overweight exposure to the energy sector compared to the benchmark was the main detractor from returns during the period.

Also affecting returns negatively was stock selection among healthcare companies, particularly positions in Sanofi-Aventis, a French pharmaceutical firm, and AstraZeneca. Shares of Sanofi-Aventis traded lower amid uncertainty about an ongoing U.S. patent dispute investigation regarding the firm’s blood-thinning drug, Plavix. Also detracting was our position in European aerospace and defense firm European Aeronautic Defence & Space (EADS) because of delays in the new A380 airplane. The position has since been sold.

Mondrian

Q: What global economic factors influenced your approach to the MSCI EAFE markets?

A: For the fiscal year that ended on March 31, 2007, market contribution was helped by underweight position versus the EAFE Index in the underperforming Japanese market and overweight positions in the strongest markets, Singapore and Spain. An underweight position in the Swedish and Danish markets held returns back a little. Sector weighting was also helpful because our portion of the Fund was overweight in two of the three strongest sectors. The overweight position in energy, however, was not beneficial. Also for the fiscal year stocks that did not perform well include the South African stock Sasol, which was down 8% (having risen 65.7% in the year ending on March 31, 2006) Millea Holdings, the Japanese insurer was down by more than 6% for the period ended March 31, 2007. Strongly outperforming stocks included Coles Group, Compass Group, and Bayer, the German pharmaceutical company, each up in excess of 60% for the same period. In Australia, Coles Group, one of the two main retail groups was approached in the second half of 2006 by a private equity firm with a conditional bid.

Compass Group in the U.K. gained market confidence with better-than-expected results during the year and with the appointment of a new CEO and chairman, which signaled positive change.

An underweight position in the Danish and Swedish kronor was not helpful. However, currency contribution was helped greatly by an underweight position in the underperforming Japanese yen and Swiss franc, and an overweight position in the outperforming Australian and New Zealand dollars.

Q: What transactions are noteworthy for shareholders?

A: During the fiscal year, new stocks purchased for the Fund included Astellas Pharmaceutical in Japan, France Telecom in France, and Deutsche Telekom in Germany. Astellas is one of the largest Japanese pharmaceutical companies and has recently announced a new strategy, which involves more active balance sheet management that we believe could potentially lead to a substantial improvement in shareholder returns over the long term.

The telecommunications sector has suffered from negative sentiment as a result of increasing competition and regulation and technological risks. Incumbent telecom operators such as France Telecom and Deutsche Telekom have seen their share prices hit hard. At Mondrian, we believe that these companies currently have attractive valuations, even if we assume significant market share losses and weaker pricing. These and other new positions have been funded by taking profits and selling certain positions. We liquidated our entire position in our portion of the fund of stocks including the British industrial gases company BOC, Brambles, the Anglo-Australian distribution business, and Rio Tinto, Anglo-Australian resources company.

Q: What were the main highlights of your strategy as the period ended?

A: The main highlights of the strategy adopted for Mondrian’s portion of Optimum International Fund included an underweight position in the Japanese market, an overweight position in the Australasian and smaller Asian markets, an overweight in selected European markets, and a defensive currency hedge out of sterling.

7

Performance summary

> Optimum International Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com.

You should consider the Fund’s investment objectives, risks, charges, and expenses carefully before investing. The Optimum International Fund prospectus contains this and other important information about the Fund. Please request a prospectus through your financial advisor or by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Read the prospectus carefully before you invest or send money.

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted below, and they are subject to change.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

An expense limitation was in effect for all classes during the periods shown below and on the next page. Performance would have been lower had the expense limitation not been in effect.

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 5.75% and have an annual distribution and service fee of up to 0.35% of average daily net assets.

Class B shares are sold with a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Effective at the close of business on July 31, 2007, no new or subsequent investments will be allowed in Class B shares of each portfolio in Optimum Fund Trust, except through a reinvestment of dividends or permitted exchanges. Please see the prospectus supplement for additional information.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Please see the fee table in the prospectus and your financial professional for a more complete explanation of sales charges.

Management has contracted to reimburse expenses and/or waive its management fees through Aug. 1, 2007.

The most recent Fund prospectus designates the Fund’s net expense ratios for Class A, B, C, and Institutional Class shares as 2.01%, 2.66%, 2.66%, and 1.66%, respectively, and the total operating expenses for Class A, B, C, and Institutional Class shares as 2.19%, 2.84%, 2.84%, and 1.84%, respectively. Please see the fee table in the Fund’s prospectus for more information.

The average annual total returns for the one-year and lifetime periods ended March 31, 2007, for Optimum International Fund Institutional Class shares were +21.68% and +22.54%, respectively. Institutional Class shares were first made available on Aug. 1, 2003, for certain retirement plan products. They are sold (without a sales charge or asset-based distribution charges) only to certain eligible investors.

Instances of high double-digit returns are unusual, cannot be sustained, and were achieved primarily during favorable market conditions.

Foreign investments are subject to risks not ordinarily associated with domestic investments, such as currency, economic and political risks, and different accounting standards.

Fund Performance

Average Annual Total Returns | ||

| Through March 31, 2007 | 1 Year | Lifetime |

| Class A (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +21.26% | +22.12% |

| Including sales charge | +14.30% | +20.16% |

| Class B (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +20.44% | +21.33% |

| Including sales charge | +16.44% | +20.96% |

| Class C (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +20.51% | +21.35% |

| Including sales charge | +19.51% | +21.35% |

The performance table above and the graph on the next page do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

8

| Fund basics |

| As of March 31, 2007 |

| Fund objective |

| The Fund seeks long-term growth of capital and may also seek income. |

| Total fund net assets |

| $276 million |

| Number of holdings |

| 165 |

| Fund start date | ||

| Aug. 1, 2003 | ||

| Nasdaq symbols | CUSIPs | |

| Class A | OAIEX | 246118731 |

| Class B | OBIEX | 246118723 |

| Class C | OCIEX | 246118715 |

| Institutional Class | OIIEX | 246118699 |

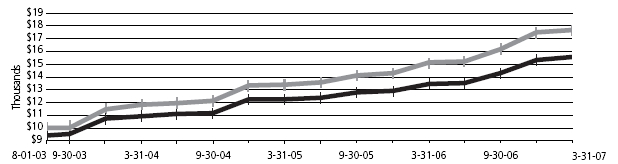

Performance of a $10,000 Investment

Aug. 1, 2003 (Fund’s inception) through March 31, 2007

![]()

| Starting value (Aug. 1, 2003) | Ending value (March 31, 2007) | ||

| MSCI EAFE Index | $10,000 | $22,485 | |

| Optimum International Fund — Class A Shares | $9,425 | $19,616 |

Chart assumes $10,000 invested on Aug. 1, 2003 and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions.

Performance of other Fund classes will vary due to different charges and expenses.

The chart also assumes $10,000 invested in the MSCI EAFE Index as of Aug. 1, 2003. The MSCI EAFE is an unmanaged composite of stocks in established markets within Europe, Australasia, and the Far East. An index does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index.

Past performance is not a guarantee of future results.

9

Portfolio management review

> Optimum Large Cap Growth Fund

April 10, 2007

Advisor

Delaware Management Company (DMC)

Sub-advisors

Marsico Capital Management LLC (Marsico Capital) T. Rowe Price Associates Inc. (T. Rowe Price)

Optimum Large Cap Growth Fund seeks long-term growth of capital. The Fund’s advisor, Delaware Management Company, selected two sub-advisors, each of whom is responsible for day-to-day investment management of a portion of the Fund’s assets. Each sub-advisor selects investments for its portion of the Fund based on its own investment style and strategy. For more information on the investment approach of the sub-advisors, please see the Fund’s prospectus.

For the year ending March 31, 2007, the S&P 500 Index and Russell 1000 Growth Index had total returns of 11.83% and 7.06%, respectively. At an economic sector level, gains were widespread. All 10 Global Industry Classification Standard sectors of the Russell 1000 Growth Index had positive returns. Utilities, materials, telecommunication services, consumer staples, and financials were the economic sectors with the highest performance for the 12-month period with gains of more than 10%. The information technology sector was the weakest performing area with a return of 3%. In terms of investment style, large-capitalization value stocks, as represented by the Russell 1000 Value Index, solidly outperformed growth stocks, as represented by the Russell 1000 Growth Index — by more than 9% during the period.

U.S. stocks produced solid gains for the year ended March 31, 2007. Despite a housing-led economic slowdown, stocks rallied thanks to robust corporate earnings growth, declining energy prices, and significant merger and acquisition activity, particularly a marked increase in buyouts by private equity firms. A stable interest rate policy by the U.S. Federal Reserve over the last nine months of the period also contributed to the positive sentiment in the market. However, volatility increased late in the period as troubles in the subprime mortgage-lending industry worsened.

Optimum Large Cap Growth Fund underperformed its benchmark, the Russell 1000 Growth Index, for the year ended March 31, 2007. The Fund had a total return of +5.75% at net asset value and -0.30% at its maximum offer price. Both figures reflect performance for Class A shares with all distributions reinvested. For complete annualized returns, please see page 12.

The sections below provide additional information about the portion of the Fund managed by each sub-advisor.

Marsico Capital

Q: What sectors were among the largest detractors from performance?

A: Stock selection in the healthcare sector was the largest performance detractor for the Marsico portion of the Fund during the year. Pharmaceutical, biotechnology, and life sciences companies Amylin Pharmaceuticals and Genentech posted negative returns. Healthcare services provider UnitedHealth Group, one of the Fund’s largest individual holdings, declined 5% during the reporting period.

The Fund’s homebuilding and home improvement retailing positions, including KB Home, Home Depot, Lennar, and Lowe’s struggled, in part because of a softening housing market and concerns about retail spending. Of these companies, only Lowe’s was held in our portion of the Fund as of March 31, 2007.

For much of the year, the Marsico-managed portion of the Fund generally maintained a smaller allocation than the Russell 1000 Growth Index to the energy sector, an area of strong performance for the index. Stock selection in energy was weak. In particular, price declines in Peabody Energy and Halliburton hurt the Fund prior to those stocks being sold. Information technology positions Qualcomm and Texas Instruments were among the weakest performing individual positions in our portion of the Fund. Both were sold during the period.

The views expressed are current as of the date of this report and are subject to change.

10

Q: What sectors were among the largest contributors to performance?

A: Stock selection in the consumer discretionary sector was a leading positive contributor to performance. Hotel and casino operators MGM Mirage, Las Vegas Sands, and Wynn Resorts posted strong returns. Media company Comcast also performed well during the annual period and remained a holding in the Fund as of March 31, 2007.

Another significant performance contributor for the Fund was stock selection and posture in the diversified financials industry. Goldman Sachs Group was among the Fund’s strongest individual positions. A larger weighting in the strong-performing diversified financials industry versus the benchmark index also had a positive impact. Certain capital goods positions performed well, including Lockheed Martin and General Dynamics. The Fund had less exposure than the index to information technology companies, a position that aided our relative performance because information technology was the weakest sector of the index.

As of March 31, 2007, our economic sector allocations emphasized consumer discretionary, industrials, financials, and healthcare. The Fund had little exposure in areas such as utilities.

T. Rowe Price

Q: What were the positive aspects of performance for your portion of the Fund during the fiscal year?

A: Optimum Large Cap Growth Fund as a whole underperformed the benchmark, but in seven of the ten sectors in the Fund, our holdings contributed to performance compared to the Russell 1000 Growth Index during the fiscal year.

Our stock selection added the most value in the consumer discretionary sector, where choices among gaming companies and retailers contributed favorably to relative results. Stock selection also paid off among telecommunication services stocks, as did an overweight versus the index in the sector. Other sectors where stock picks enhanced results included healthcare — particularly healthcare services providers — and energy.

Liberty Media Capital, which owns interests in private and publicly held media and telecommunications companies, was among our holdings with the highest performance. Liberty benefited from an agreement to trade its shares in News Corp. for a large stake in satellite television provider DirecTV. Other strong contributors in this sector included casino operator MGM Mirage and retailer Kohl’s.

Q: What were the negative aspects of performance in your portion of the Fund?

A: Three sectors detracted from our performance relative to the benchmark index — utilities, consumer staples, and materials. Our underweight in each of these sectors was the reason for their underperformance. We tend to be underweight in this sector because long-term growth prospects are generally below our target.

Stock selection detracted from our results compared to our peers in the information technology and financial sectors, especially among semiconductor manufacturers and capital markets firms. The stocks of Marvell Technology and Maxim Integrated both suffered from options back-dating concerns and inventory growth in a moderating economy.

Financials sector stocks SLM and E-Trade also hurt relative performance. But our favorable underweight in technology and overweight in financials more than offset the negative impact of stock selection.

11

Performance summary

> Optimum Large Cap Growth Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com.

You should consider the Fund’s investment objectives, risks, charges, and expenses carefully before investing. The Optimum Large Cap Growth Fund prospectus contains this and other important information about the Fund. Please request a prospectus through your financial advisor or by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Read the prospectus carefully before you invest or send money.

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted below, and they are subject to change.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

An expense limitation was in effect for all classes during the periods shown below and on the next page. Performance would have been lower had the expense limitation not been in effect.

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 5.75% and have an annual distribution and service fee of up to 0.35% of average daily net assets.

Class B shares are sold with a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Effective at the close of business on July 31, 2007, no new or subsequent investments will be allowed in Class B shares of Optimum Fund Trust, except through a reinvestment of dividends or permitted exchanges. Please see the prospectus for additional information.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Please see the fee table in the prospectus and your financial professional for a more complete explanation of sales charges.

Management has contracted to reimburse expenses and/or waive its management fees through Aug. 1, 2007.

The most recent Fund prospectus designates the Fund’s net expense ratios for Class A, B, C, and Institutional Class shares as 1.69%, 2.34%, 2.34%, and 1.34%, respectively, and the total operating expenses for Class A, B, C, and Institutional Class shares as 1.83%, 2.48%, 2.48%, and 1.47%, respectively. Please see the fee table in the Fund’s prospectus for more information.

The average annual total returns for the one-year and lifetime periods ended March 31, 2007, for Optimum Large Cap Growth Fund Institutional Class shares were +6.13% and +10.76%, respectively. Institutional Class shares were first made available on Aug. 1, 2003, for certain retirement plan products. They are sold without a sales charge or asset-based distribution charges only to certain eligible investors.

Fund Performance

Average Annual Total Returns | ||

| Through March 31, 2007 | 1 Year | Lifetime |

| Class A (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +5.75% | +10.36% |

| Including sales charge | -0.30% | +8.59% |

| Class B (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +5.14% | +9.66% |

| Including sales charge | +1.14% | +9.18% |

| Class C (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +5.14% | +9.66% |

| Including sales charge | +4.14% | +9.66% |

The performance table above and the graph on the next page do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

12

| Fund basics |

| As of March 31, 2007 |

| Fund objective |

| The Fund seeks long-term growth of capital. |

| Total fund net assets |

| $789 million |

| Number of holdings |

| 147 |

| Fund start date | ||

| Aug. 1, 2003 | ||

| Nasdaq symbols | CUSIPs | |

| Class A | OALGX | 246118707 |

| Class B | OBLGX | 246118806 |

| Class C | OCLGX | 246118889 |

| Institutional Class | OILGX | 246118871 |

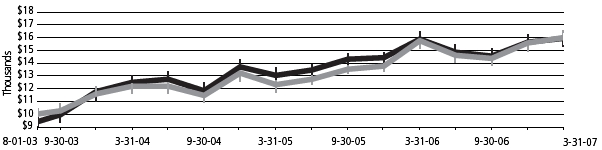

Performance of a $10,000 Investment

Aug. 1, 2003 (Fund’s inception) through March 31, 2007

| Starting value (Aug. 1, 2003) | Ending value (March 31, 2007) | ||

| Russell 1000 Growth Index | $10,000 | $13,825 | |

| Optimum Large Cap Growth Fund — Class A Shares | $9,425 | $13,531 |

Chart assumes $10,000 invested on Aug. 1, 2003 and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions.

Performance of other Fund classes will vary due to different charges and expenses.

The chart also assumes $10,000 invested in the Russell 1000 Growth Index as of Aug. 1, 2003. The Russell 1000 Growth Index is an unmanaged composite that includes performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values. An index does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index.

Past performance is not a guarantee of future results.

13

Portfolio management review

> Optimum Large Cap Value Fund

April 10, 2007

Advisor

Delaware Management Company (DMC)

Sub-advisors

Massachusetts Financial Services Company (MFS)

TCW Investment Management Company (TCW)

Optimum Large Cap Value Fund seeks long-term growth of capital and it may also seek income. The Fund’s advisor, Delaware Management Company, chose two sub-advisors to manage the Fund’s assets. Each is responsible for day-to-day investment management of a portion of the Fund’s assets and selects investments for its portion based on its own investment style and strategy.

Based on changing projections for inflation during the year, the U.S. Federal Reserve’s direction on monetary policy remained a topic of speculation and drove market volatility. As the summer of 2006 progressed, inflation concerns began to cool because of weaker housing data and a turnaround in oil prices — a steady drop. The fiscal year ended with a period of slowing economic growth overall.

Optimum Large Cap Value Fund returned +15.65% at net asset value and +9.01% at maximum offer price for the fiscal year ending March 31, 2007 (both figures reflect performance for Class A shares with all distributions reinvested). For complete annualized returns, please see page 16.

The Fund’s performance slightly trailed the Russell 1000 Value Index return of +16.84%.

The sections below provide additional information about the portion of the Fund managed by each sub-advisor.

MFS

Q: What are some of the factors important to understanding the performance of your portion of the Fund?

A: All of the investment decisions made by MFS are driven by the fundamentals of each individual opportunity. It is common for our Fund to have different currency exposure than the benchmark. During the reporting period ended March 31, 2007, the Fund’s currency exposure was a plus factor for relative performance.

Q: What were the areas of strength regarding your portion of the Fund’s holdings?

A: Stock selection in the financial services sector was the principal source of strength in our portion of the Fund. Leading contributors in this sector included investment banking firm Goldman Sachs and insurance company MetLife. Not owning American International Group (AIG) also bolstered comparative results, as this stock significantly underperformed the benchmark.

Stock selection in the industrial goods and services sector also aided relative returns. Defense contractor Lockheed Martin, which is not a benchmark constituent, and agricultural equipment manufacturer Deere & Co. were strong contributors in this sector. A lesser position compared to the Russell 1000 Value Index in industrial conglomerate General Electric, a relatively weak performer, was another positive factor in relative results. Stock selection and, to a lesser extent, an overweight position in the strong-performing consumer staples sector also helped. Tobacco company Altria Group was a leading contributor.

Q: What were areas of weakness regarding your portion of the Fund’s holdings?

A: A combination of stock selection and an underweight position in the strong-performing utilities and communications sectors held back results relative to the benchmark. Wireless services provider Sprint Nextel was among the top detractors. Underweighting telecommunications service company AT&T, and not owning BellSouth, hurt relative performance because both stocks outperformed the benchmark.

Stock selection in the energy sector also detracted from results. The Fund’s underweight positions in integrated oil and gas companies Exxon Mobil and Chevron, both of which yielded higher returns than the benchmark, dampened relative returns.

The views expressed are current as of the date of this report and are subject to change.

14

Stocks in other sectors that negatively affected relative performance included home improvement products maker Masco, healthcare products maker Johnson & Johnson, and defense contractor Northrop Grumman.

TCW

Q: What factors in the marketplace and elements of your strategy had a significant impact on the Fund?

A: During the period under review, large-cap value stocks significantly outperformed large-cap growth, with the Russell 1000 Value Index more than doubling the Russell 1000 Growth Index return of +7.06%. Although it is dividend-focused, our strategy is not deep value, and the Fund captured more than 93% of the Russell 1000 Value’s strong performance during the year ending March 31, 2007.

We believe the prospect of capital appreciation plus dividend income made the strategy an attractive investment vehicle for long-term, conservative investors. Our strategy is to select securities with outstanding performance based primarily on fundamental stock selection discipline and placing less emphasis on the impact of economic trends. In addition, we continued our search for value securities that we believe were poised for growth.

Q: What factors influenced the Fund’s performance in a negative way?

A: Relative to the Russell 1000 Value Index, the underweight in both the energy and utilities sectors in our portion of the portfolio detracted from performance for the year ending March 31, 2007. Stock selection in the healthcare sector dampened returns. Underperformers for the year in the healthcare sector include Watson Pharmaceuticals, Tenet Healthcare, and Boston Scientific, which was sold after hitting our downside sell discipline price target.

Q: What factors influenced the Fund’s performance in a positive way?

A: Relative to the Russell 1000 Value Index, stock selection within the consumer discretionary sector and the Fund’s underweight position in financials had a positive impact on performance for the year ending March 31, 2007. Top performers in the consumer discretionary sector included General Motors, Comcast, and Sears Holdings. Sears was completely sold during the year as the stock reached its target price.

15

Performance summary

> Optimum Large Cap Value Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com.

You should consider the Fund’s investment objectives, risks, charges, and expenses carefully before investing. The Optimum Large Cap Value Fund prospectus contains this and other important information about the Fund. Please request a prospectus through your financial advisor or by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Read the prospectus carefully before you invest or send money.

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted below and they are subject to change.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

An expense limitation was in effect for all classes during the periods shown below and on the next page. Performance would have been lower had the expense limitation not been in effect.

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with maximum a front-end sales charge of up to 5.75% and have an annual distribution and service fee of up to 0.35% of average daily net assets.

Class B shares are sold with a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Effective at the close of business on July 31, 2007, no new or subsequent investments will be allowed in Class B shares of the Optimum Fund Trust, except through a reinvestment of dividends or permitted exchanges. Please see the prospectus supplement for additional information.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Please see the fee table in the prospectus and your financial professional for a more complete explanation of sales charges.

Management has contracted to reimburse expenses and/or waive its management fees through Aug. 1, 2007.

The most recent Fund prospectus designates the Fund’s net expense ratios for Class A, B, C, and Institutional Class shares as 1.55%, 2.20%, and 2.20%, 1.20%, respectively, and the total operating expenses for Class A, B, C, and Institutional Class shares as 1.82%, 2.47%, 2.47%, and 1.47%, respectively. Please see the fee table in the Fund’s prospectus for more information.

The average annual total returns for the one-year and lifetime periods ended March 31, 2007, for Optimum Large Cap Value Fund Institutional Class shares were +16.12% and +15.08%, respectively. Institutional Class shares were first made available on Aug. 1, 2003, for certain retirement plan products. They are sold without a sales charge or asset-based distribution charges only to certain eligible investors.

Fund Performance

Average Annual Total Returns | ||

| Through March 31, 2007 | 1 Year | Lifetime |

| Class A (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +15.65% | +14.68% |

| Including sales charge | +9.01% | +12.83% |

| Class B (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +14.97% | +13.94% |

| Including sales charge | +10.97% | +13.51% |

| Class C (Est. Aug. 1, 2003) | ||

| Excluding sales charge | +14.88% | +13.92% |

| Including sales charge | +13.88% | +13.92% |

The performance table above and the graph on the next page do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

16

| Fund basics |

| As of March 31, 2007 |

| Fund objective |

| The Fund seeks long-term growth of capital and may also seek income. |

| Total fund net assets |

| $794 million |

| Number of holdings |

| 136 |

| Fund start date | ||

| Aug. 1, 2003 | ||

| Nasdaq symbols | CUSIPs | |

| Class A | OALVX | 246118863 |

| Class B | OBLVX | 246118855 |

| Class C | OCLVX | 246118848 |

| Institutional Class | OILVX | 246118830 |

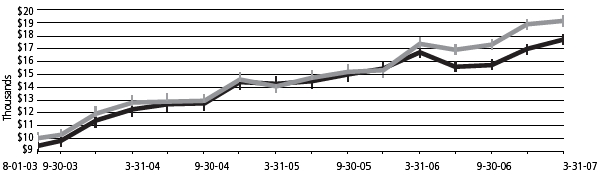

Performance of a $10,000 Investment

Aug. 1, 2003 (Fund’s inception) through March 31, 2007

| Starting value (Aug. 1, 2003) | Ending value (March 31, 2007) | ||

| Russell 1000 Value Index | $10,000 | $17,723 | |

| Optimum Large Cap Value Fund — Class A Shares | $9,425 | $15,573 |

Chart assumes $10,000 invested on Aug. 1, 2003 and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions.

Performance of other Fund classes will vary due to different charges and expenses.

The chart also assumes $10,000 invested in the Russell 1000 Value Index as of Aug. 1, 2003. The Russell 1000 Value Index measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values. An index is unmanaged and does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index.

Past performance is not a guarantee of future results.

17

Portfolio management review

> Optimum Small Cap Growth Fund

April 10, 2007

Advisor

Delaware Management Company (DMC)

Sub-advisors

Columbia Wanger Asset Management L.P. (CWAM)

Oberweis Asset Management, Inc. (Oberweis)

Optimum Small Cap Growth Fund seeks long-term growth of capital. The Fund’s advisor, Delaware Management Company, selected two sub-advisors, each of whom is responsible for day-to-day investment management of a portion of the Fund’s assets. Each sub-advisor selects investments for its portion of the Fund based on its own investment style and strategy. For more information on the investment approach of the sub-advisors, please see the Fund’s prospectus.

The Fund experienced negative performance during the first half of the fiscal year ending March 31, 2007, but performed well compared to its benchmark, the Russell 2000 Growth Index. For the full year, Optimum Small Cap Growth Fund gained 0.37% at net asset value and returned -5.37% at maximum offer price (both figures are for Class A shares and include distributions reinvested during the fiscal year); by comparison, the benchmark gained 1.56%. For complete annualized performance for the Fund, please see the table on page 20.

During the first two quarters of the fiscal year, stocks of small companies pulled back after a large surge during the first quarter of calendar year 2006. Housing prices, consumer debt loads, the war in Iraq, and the threat of terrorism weighed heavily on investors’ minds. Overlooked amid the apparent pessimism, in our opinion, was the resiliency of the U.S. economy. While respected stock market watchers and the financial press warned of an economic slowdown, the market was in one of the longest stretches of double-digit profit growth in history.

The calendar year 2006 ended much the same way it began, with a large run-up in the more speculative companies of the small-cap market, including micro-caps and stocks with no earnings. As oil prices retreated and worries about the health of the consumer and the housing market abated, lesser-quality stocks surged. These trends hurt the Fund’s performance relative to its benchmark.

The sections below provide additional information about the portion of the Fund managed by each sub-advisor.

Columbia Wanger Asset Management

Q: What factors in your investment strategy influenced returns for your portion of the Fund?

A: In the final quarter of the fiscal year, U.S. markets were jolted by turbulence overseas as a steep decline in the Chinese market spread globally. In our opinion investors suddenly seemed more focused on risk. Within the small-cap market, the lower-quality and smaller-company stocks lost favor in the marketplace. This played into our strength — our attention to risk — and the Fund outpaced the benchmark during the final period of the year.

Q: Can you describe some areas that detracted from performance?

A: The largest detractors from a sector standpoint were healthcare and retail. The Fund’s healthcare stocks were down 10% more than the benchmark during the period. The largest detractor was Neurocrine Bioscience stock, which collapsed when the FDA withheld full approval for the high dosage of its sleep medication Indiplon. We sold the stock, taking a 66% loss for the year, and it later fell another 50%.

The Fund maintained a healthy overweight within the consumer discretionary sector at 4% above the benchmark. Fund performance for retail stocks was slightly better than the benchmark although retail stocks in general reported sluggish performance. A large detractor within the retail space was Chico’s FAS, a women’s specialty retailer. Chico’s lost 21% during the year because its fall lineup was off the mark, and sales came in below expectations.

The views expressed are current as of the date of this report and are subject to change.

18

| Q: | Can you describe some areas that aided performance? |

A: Information technology and telecom had the highest performance in the Fund. Good stock selection in both sectors added value. The Fund’s technology stocks were up 9% versus a slight loss for the benchmark. Fueling strong performance in this sector was bar-code scanner manufacturer Symbol Technologies, which received a buyout offer from Motorola and was up 39% before the acquisition was completed in January 2007.

The Fund’s telecommunications holdings were up 10% over the benchmark performance. Time Warner Telecom, an owner of fiber optic networks connected to more than 6,000 office buildings was up because of strong sales growth. American Tower also posted strong annual gains. As cellular minute usage grows, cellular service providers continued to turn to the company for antenna space.

Oberweis Asset Management

| Q: | What factors influenced returns for your portion of the Fund? |

A: As value-oriented investments continued to dominate the small-cap market during the year, our portfolio of high-growth companies fared poorly relative to the rest of the small-cap marketplace. Investors continued to overlook opportunities in the high earnings and high growth space. Although our style struggled during the first three quarters of 2006, returns were favorable in the calendar fourth quarter.

| Q: | What aspect of your strategy had a significant impact on the Fund during the fiscal year? |

A: Oberweis invests in small-cap companies with high earnings growth rates. However, within our small-cap universe, high-growth companies had lower performance during the year. On a valuation basis, we believe stocks within our high-growth, small-cap universe are currently inexpensive relative to their longer term averages. On a relative basis, valuations of high-growth, small-cap equities appear much more attractive than valuations of small-cap value-oriented equities. High-growth equities have underperformed value equities in recent periods. When this situation has occurred in the past, the cycle generally reversed course over time.

As a result of our strict high-growth discipline, we are generally more heavily invested in sectors such as technology, healthcare, and consumer discretionary, and we have less exposure to slower growth sectors such as financial services, utilities, and producer durables.

| Q: | What factors influenced the Fund’s performance in a negative way? |

A: On a sector basis, technology and healthcare accounted for most of the strategy’s shortfall relative to the Russell 2000 Growth Index. Our portion of the Fund tends to be consistently more invested in these two growth-oriented sectors. At the stock level, two of the leading detractors for the year were ASV and Openwave Systems. The two top-performing sectors over the fiscal year, consumer staples and utilities, were slower-growing sectors in which we maintained minimal exposure.

| Q: | What factors influenced the Fund’s performance in a positive way? |

A: The largest contributors to performance from a sector standpoint were energy and “other.” The latter sector is comprised of recent IPOs or companies that are not yet included in the Russell 2000 Growth Index. Over the past fiscal year, healthcare carried a slightly higher average weight versus the Russell 2000 Growth Index. Technology also averaged higher than the benchmark. At the stock level, two of the top contributors for the year were Vasco Data Security International and Focus Media Holding.

19

Performance summary

> Optimum Small Cap Growth Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com.

You should consider the Fund’s investment objectives, risks, charges, and expenses carefully before investing. The Optimum Small Cap Growth Fund prospectus contains this and other important information about the Fund. Please request a prospectus through your financial advisor or by calling 800 914-0278 or visiting our Web site at www.optimummutualfunds.com. Read the prospectus carefully before you invest or send money.

Returns reflect the reinvestment of all distributions and any applicable sales charges as noted below, and they are subject to change.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

An expense limitation was in effect for all classes during the periods shown below and on the next page. Performance would have been lower had the expense limitation not been in effect.

The Fund offers Class A, B, C, and Institutional Class shares. Class A shares are sold with a maximum front-end sales charge of up to 5.75% and have an annual distribution and service fee of up to 0.35% of average daily net assets.

Class B shares are sold with a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Effective at the close of business on July 31, 2007, no new or subsequent investments will be allowed in Class B shares of each portfolio in the Optimum Fund Trust, except through a reinvestment of dividends or permitted exchanges. Please see the prospectus supplement for additional information.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Please see the fee table in the prospectus and your financial professional for a more complete explanation of sales charges.

Management has contracted to reimburse expenses and/or waive its management fees through Aug. 1, 2007.

The most recent Fund prospectus designates the Fund’s net expense ratios for Class A, B, C, and Institutional Class shares as 1.95%, 2.60%, 2.60%, and 1.60%, respectively, and the total operating expenses for Class A, B, C, and Institutional Class shares as 2.46%, 3.11%, 3.11%, and 2.11%, respectively. Please see the fee table in the Fund’s prospectus for more information.

The average annual total returns for the one-year and lifetime periods ended March 31, 2007, for Optimum Small Cap Growth Fund Institutional Class shares were +0.72% and +15.84%, respectively. Institutional Class shares were first made available on Aug. 1, 2003, for certain retirement plan products. They are sold without a sales charge or asset-based distribution charges only to certain eligible investors.

Funds that invest in small and/or medium-sized company stocks typically involve greater risk, particularly in the short term, than those investing in larger, more established companies.

| Fund Performance | ||||

| Average Annual Total Returns | ||||

| Through March 31, 2007 | 1 Year | Lifetime | ||

| Class A (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | +0.37% | +15.45% | ||

| Including sales charge | -5.37% | +13.59% | ||

| Class B (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | -0.27% | +14.74% | ||

| Including sales charge | -4.17% | +14.31% | ||

| Class C (Est. Aug. 1, 2003) | ||||

| Excluding sales charge | -0.27% | +14.74% | ||

| Including sales charge | -1.25% | +14.74% |

The performance table above and the graph on the next page do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

20

| Fund basics |

| As of March 31, 2007 |

| Fund objective |

| The Fund seeks long-term growth of capital. |

| Total fund net assets |

| $140 million |

| Number of holdings |

| 184 |

| Fund start date | ||

| Aug. 1, 2003 | ||

| Nasdaq symbols | CUSIPs | |

| Class A | OASGX | 246118822 |

| Class B | OBSGX | 246118814 |

| Class C | OCSGX | 246118798 |

| Institutional Class | OISGX | 246118780 |

Performance of a $10,000 Investment

Aug. 1, 2003 (Fund’s inception) through March 31, 2007

| Starting value (Aug. 1, 2003) | Ending value (March 31, 2007) | ||

| Russell 2000 Growth Index | $10,000 | $16,002 | |

| Optimum Small Cap Growth Fund — Class A Shares | $9,425 | $15,960 |

Chart assumes $10,000 invested on Aug. 1, 2003 and includes the effect of a 5.75% front-end sales charge and the reinvestment of all distributions.

Performance of other Fund classes will vary due to different charges and expenses.

The chart also assumes $10,000 invested in the Russell 2000 Growth Index as of Aug. 1, 2003. The Russell 2000 Growth Index is an unmanaged index that generally tracks the performance of those stocks in the Russell 2000 Index that have higher price-to-book ratios and higher forecasted growth values. An index does not reflect the costs of operating a mutual fund, such as the costs of buying, selling, and holding securities. You cannot invest directly in an index.

Past performance is not a guarantee of future results.

21

Portfolio management review

> Optimum Small Cap Value Fund

April 10, 2007

Advisor

Delaware Management Company (DMC)

Sub-advisors

Delafield Asset Management (Delafield)

Hotchkis and Wiley Capital Management, L.L.C. (H&W)

The Killen Group, Inc. (Killen)

Optimum Small Cap Value Fund seeks long-term growth of capital. The Fund’s advisor, Delaware Management Company, selected three sub-advisors, each of whom is responsible for day-to-day investment management of a portion of the Fund’s assets. Each sub-advisor selects investments for its portion of the Fund based on its own investment style and strategy. For more information on the investment approach of the sub-advisors, please see the Fund’s prospectus.

At the beginning of the fiscal year, gross domestic product data and corporate profits remained strong, but commodity price inflation and excessive liquidity had the U.S. Federal Reserve in a tightening mode. As the year progressed, concerns arose about the growth rate of corporate earnings, as well as the higher and thus less attractive price-to-earnings ratios that come with a market rally. These concerns began to weigh on the market and produced lower but still positive returns. Interest rates remained unchanged after June 2006, and in the latter months of the fiscal period major weaknesses in the mortgage lending and homebuilding areas threatened the economic outlook.

For the fiscal year ended March 31, 2007, the overall return for Optimum Small Cap Value Fund was +5.93% at net asset value and -0.17% at maximum offer price. Both figures reflect performance for Class A shares with all distributions reinvested. For complete annualized returns for the fund, please see page 26.

For the same period, the Russell 2000 Value Index gained 10.38%.

The sections below provide additional information about the portion of the Fund managed by each sub-advisor.

Delafield

| Q: | What market factors influenced performance in your portion of the Fund? |

A: Overall, Delafield’s focus remained on finding special situations. Such investments tend to have performance that more closely parallels the underlying events of the individual company rather than the broad markets. This can cause our performance quarter-to-quarter to be out of sync with the overall market.

Following the basic Delafield discipline, we invested in appropriately priced securities that we believed to have low market risk. During the year, the significant cash position in our portion of the Fund detracted from performance.

| Q: | What contributed to positive performance in your portion of the Fund? |

A: During the fiscal year, eight of the Fund’s investments received takeover proposals, which positively impacted returns. Among our better-performing stocks were Novelis, which was up 95%; Lydall, up 70%; and Standard Motor Products, which was sold prior to year end to lock in gains, after a 57% increase. In general, holdings benefiting from cyclical growth contributed to the Fund’s overall performance.

| Q: | What elements of performance in your portion of the Fund had a negative effect? |

A: On the negative side, education curriculum materials provider ProQuest fell 30% because of concerns arising after accounting irregularities forced a restatement of financials, followed closely by Furniture Brands International, down 28%. ProQuest is no longer a holding in the portfolio. Furniture Brands remains a core holding, but has been negatively affected by the consumer slowdown in spending on big-ticket items. Combined, these stocks impaired the portfolio returns by about 2.5 percentage points.

The views expressed are current as of the date of this report and are subject to change.

22

H & W

| Q: | What market factors influenced performance in your portion of the Fund? |

A: Toward the end of 2006, the Chicago Board of Options Exchange Volatility Index, which generally reflected fears of a market downturn, hit a 12-year low. This index can be viewed as a measure of market expectations, where a low reading indicates a high level of complacency among investors. In general, we believe it is imperative to identify potential risk factors as opposed to discounting them.

We prefer to own shares that are trading at a low multiple of sustainable normal earnings rather than make a bet that good times will be everlasting. Clearly, our disciplined, value-oriented process has caused us to miss some of the lavish returns in the market. However, we remain confident due in part to the fact that many of our holdings at period end exhibited attractive valuations relative to the market.

| Q: | What were the negative factors that affected your investments during the period? |

A: Nearly all of our relative underperformance versus the Russell 2000 Value Index was concentrated in the consumer discretionary sector, and to a lesser degree industrials, energy, and financials. Within the consumer discretionary sector, homebuilders Beazer Homes USA and WCI Communities, and publisher Valassis Communications, were sources of negative performance. Within the industrials sector, equipment manufacturer Flowserve and defense manufacturer EDO posted losses. In the financials sector, mortgage REIT Fieldstone Investment and insurers Conseco, Hanover Insurance Group, and KMG America were all weak performers.

Within the energy sector, the performance of coal producers Foundation Coal Holdings and Alpha Natural Resources lagged behind other securities.

| Q: | What were the positive factors that affected your investments? |

A: Strength came primarily from positive sector allocation with regard to information technology sector and strong stock selection within the materials sector. Within materials, chemicals manufacturers CF Industries and Agrium were standouts. We sold our position in CF Industries in January 2007 when it reached its target valuation. Apparel manufacturer Warnaco, staffing company Kelly Services, shipping company Overseas Shipholding Group, and real estate company MI Developments were leading contributors to performance.

Killen

| Q: | How favorable or unfavorable was your investment approach given the year’s market backdrop? |