UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number: | 811-21335 | |

| Exact name of registrant as specified in charter: | Optimum Fund Trust | |

| Address of principal executive offices: | 2005 Market Street | |

| Philadelphia, PA 19103 | ||

| Name and address of agent for service: | David F. Connor, Esq. | |

| 2005 Market Street | ||

| Philadelphia, PA 19103 | ||

| Registrant’s telephone number, including area code: | (800) 523-1918 | |

| Date of fiscal year end: | March 31 | |

| Date of reporting period: | March 31, 2013 |

Item 1. Reports to Stockholders

| | |||

Optimum Fixed Income Fund | |||

Optimum International Fund | |||

| Optimum Large Cap Growth Fund | |||

| Optimum Large Cap Value Fund | |||

| Optimum Small-Mid Cap Growth Fund | |||

| Optimum Small-Mid Cap Value Fund | |||

| Annual Report | |||

| March 31, 2013 | |||

Carefully consider the Funds’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Funds’ prospectus and, if available, their summary prospectus, which may be obtained by visiting optimummutualfunds.com or calling 800 914-0278. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

Table of contents

| Portfolio management review | |

| Optimum Fixed Income Fund | 1 |

| Optimum International Fund | 3 |

| Optimum Large Cap Growth Fund | 6 |

| Optimum Large Cap Value Fund | 9 |

| Optimum Small-Mid Cap Growth Fund | 12 |

| Optimum Small-Mid Cap Value Fund | 14 |

| Performance summary | |

| Optimum Fixed Income Fund | 18 |

| Optimum International Fund | 22 |

| Optimum Large Cap Growth Fund | 24 |

| Optimum Large Cap Value Fund | 26 |

| Optimum Small-Mid Cap Growth Fund | 28 |

| Optimum Small-Mid Cap Value Fund | 30 |

| Disclosure of Fund expenses | 32 |

| Security type/sector/country allocations | |

| and top 10 equity holdings | 34 |

| Financial statements | |

| Statements of net assets | 38 |

| Statements of assets and liabilities | 86 |

| Statements of operations | 87 |

| Statements of changes in net assets | 88 |

| Financial highlights | 91 |

| Notes to financial statements | 115 |

| Report of independent | |

| registered public accounting firm | 131 |

| Other Fund information | 132 |

| Board of trustees and officers addendum | 133 |

| About the organization | 135 |

Investments in Optimum Fixed Income Fund, Optimum International Fund, Optimum Large Cap Growth Fund, Optimum Large Cap Value Fund, Optimum Small-Mid Cap Growth Fund, and Optimum Small-Mid Cap Value Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies, and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Funds, the repayment of capital from the Funds, or any particular rate of return.

Unless otherwise noted, views expressed herein are current as of March 31, 2013, and subject to change. Holdings are as of the date indicated and subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Funds’ distributor, Delaware Distributors, L.P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

All third-party marks cited are the property of their respective owners.

© 2013 Delaware Management Holdings, Inc.

Portfolio management review

Optimum Fixed Income Fund

April 9, 2013

| Performance review (for the year ended March 31, 2013) | ||||

| Optimum Fixed Income Fund (Class A shares) | 1-year return | +5.47% | ||

| Optimum Fixed Income Fund (Institutional Class shares) | 1-year return | +5.72% | ||

| Barclays U.S. Aggregate Index (benchmark) | 1-year return | +3.77% |

Past performance does not guarantee future results. |

Advisor

Delaware Management Company (DMC)

Sub-advisor

Pacific Investment Management Company LLC (PIMCO)

Market overview

The 12 months ended March 31, 2013 were defined in part by a dynamic global political process. The year began with a focus on Europe, as the situation in Greece fueled speculation of when, not if, the European Union (EU) would see its membership shrink. In late July 2012, a few determined statements from the European Central Bank (ECB) — later reinforced by the ECB Governing Council — stabilized markets and helped result in no sovereign exits from the EU during the period. The markets spent the remainder of 2012 weighing the costs of the Greek austerity commitment, the bailout package for Cyprus, and Spanish financial system stability against the benefits of safeguarding the European monetary union.

Despite this, the U.S. political climate often relegated geopolitical instability and uprising to second-page news. Markets confronted an evolving monetary policy that produced a third quantitative easing mortgage purchase program, targeted Treasury purchases, and significantly increased the Federal Reserve balance sheet. Risk assets generally benefited from these actions, while yields on intermediate and long-term Treasurys moved temporarily higher.

The start of 2013 brought rallies in the U.S. equity markets despite news that the world’s largest economy unexpectedly shrank during the fourth quarter of 2012. U.S. economic indicators were generally solid, as employment, manufacturing, auto sales, consumer spending, and housing statistics showed strength. Volatility followed, however, as investors tried to make sense of major political events in the U.S. and Europe. In the U.S., for example, Congress failed to reach a budget, which triggered the so-called “sequester”, invoking $1.2 trillion in automatic spending cuts over the next decade. In Europe, the surprise outcome of the Italian elections, in which no party managed to secure a governing majority, heightened concerns about the country’s commitment to the reform agenda of outgoing Prime Minister Mario Monti.

Fund performance

For the fiscal year, Optimum Fixed Income Fund (Class A shares with all dividends reinvested and excluding the applicable sales charge) outperformed its benchmark index, the Barclays U.S. Aggregate Index. The following remarks describe several factors that affected performance within the two respective portions of the Fund.

DMC

Positioning that was in place during the Fund’s fiscal year included:

- an underweight position in Treasury securities

- an overweight allocation to investment grade corporate bonds

- productive positions in emerging markets

(continues) 1

Portfolio management review

Optimum Fixed Income Fund

Generally speaking, DMC spent the fiscal year transitioning its portion of the Fund from being long versus the benchmark index (in terms of duration) to being short. Its small position in U.S. Treasury notes detracted from relative performance, and investment grade positions helped performance.

The most notable positive performance factors came from the Fund’s positioning in the high grade corporate sector. DMC maintained an overweight allocation to this sector. Emerging markets investments also garnered strong returns. Notable gains were likewise registered in the high yield corporate and developed market segments.

On the other hand, significant detractors from performance within DMC’s portion of the Fund came from hedges in European credit derivative indices, high yield credit derivative indices, and hedges on the euro. These hedges were in place throughout most of the Fund’s fiscal year. DMC began reducing the hedge positions in September 2012, and removed the last of these in December 2012 (except for the euro hedge).

DMC’s portion of the Fund had an overweight exposure to the 7- and 10-year maturity groups via corporate investments. This positioning served the portfolio well, as the 5- to 10-year maturity points of the curve recorded small rallies for the full fiscal year.

DMC also used interest rate futures in its portion of the Fund to adjust interest rate sensitivity levels during the Fund’s fiscal year. These instruments had a neutral effect on performance.

PIMCO

The PIMCO portion of the Fund maintained an underweight allocation to U.S. duration, which detracted from returns as rates fell over the 12-month period. However, tactical curve positioning, including an overweight allocation to the intermediate portion of the yield curve, where rates fell the most, more than offset the negative U.S. duration positioning. Duration exposure in other developed markets, particularly Australia and Canada, contributed to returns as interest rates also fell in these countries over the fiscal year.

An underweight allocation to corporate bonds also detracted from returns, but this was more than offset by an emphasis on the bonds of banks and other financial institutions as these securities outperformed the broader corporate market on renewed risk appetite. Within the mortgage-backed securities (MBS) sector, an underweight to agency MBS hindered returns as rates dropped due to the Federal Reserve’s quantitative-easing purchases (QE3) and investor demand for these securities, which was brought on by signs of recovery in the housing market. Exposure to nonagency MBS helped performance amid strong demand for higher-yielding assets.

Beyond the core sectors, holdings of taxable Build America Bonds (BABs) contributed to returns as the sector outpaced like-duration Treasurys due to supply technicals. Positions within the high yield corporate sector designed to benefit from the widening of European credit spreads detracted from performance as European credit spreads compressed during the period due to the risk-on environment. Performance within PIMCO’s portion of the Fund also benefited from exposure to external debt in Asia and the Middle East as spreads tightened and to Brazilian local rates as yields fell. Select developed-market currency positioning, including strategies designed to benefit from a decline in the euro and exposure to a narrow basket of emerging market currencies, added to returns as the U.S. dollar appreciated relative to the euro and depreciated relative to these emerging markets.

Derivatives, including government futures and interest rate swaps as well as credit default swaps, were used to manage duration and credit risk. These positions were used in conjunction with physical securities to tactically manage credit exposure and to focus on the intermediate portion of the yield curve; this was a net contributor for performance.

2

Optimum International Fund

April 9, 2013

| Performance review (for the year ended March 31, 2013) | ||||

| Optimum International Fund (Class A shares) | 1-year return | +8.10% | ||

| Optimum International Fund (Institutional Class shares) | 1-year return | +8.41% | ||

| MSCI EAFE Index (gross) (benchmark) | 1-year return | +11.81% | ||

| MSCI EAFE Index (net) (benchmark) | 1-year return | +11.27% |

Past performance does not guarantee future results. |

Advisor

Delaware Management Company (DMC)

Sub-advisors

BlackRock Advisors, LLC (BlackRock)

Mondrian Investment Partners Ltd. (Mondrian)

Market overview

Major headwinds to growth — namely the ongoing euro crisis, concerns over a stalling Chinese economy, and moderating U.S. economic growth — collectively began to subside during the Fund’s fiscal year, leading to a more favorable market environment. While no single catalyst was responsible for turning the table, a series of positive policy-related outcomes and further central bank easing measures, most notably an announcement by the European Central Bank, fueled an updraft in risk assets.

Concurrently, key economic indicators related to U.S. housing continued to convalesce, while last-minute U.S. “fiscal cliff” negotiations proved to be more political drama than anything of substance. Japan also garnered much attention toward the end of the Fund’s fiscal year as the new prime minister, Shinzõ Abe, began to promote aggressive monetary tactics and higher inflation targets, measures intended to weaken the yen and boost overall economic output.

Additional notes on regional developments during the Fund’s fiscal year:

- Despite the euro crisis, European equity markets were generally strong. The Belgian and Swiss equity markets rose 27.7% and 21.6%, respectively, during the period, while the French, German, and U.K. markets were each up more than 8.0%.

- Italy was one of the worst-performing markets, down 6.8%, with most of the declines taking place since its inconclusive election in late February 2013.

- In March 2013, protracted and fraught negotiations over a financial support package for Cyprus eventually produced an agreement which imposed the burden of recapitalizing Cypriot banks on bank bondholders and uninsured depositors. This situation put pressure on other peripheral markets’ banking sectors.

- In the Asia-Pacific region, New Zealand and Australia were the strongest-performing equity markets, up 22.7% and 22.2%, respectively, while the Japanese equity market only amassed 8.5%.

Fund performance

Optimum International Fund posted a positive return for its fiscal year but trailed its benchmark, the MSCI EAFE (Europe, Australasia, Far East) Index (both gross and net figures).

BlackRock

When the fiscal year began, BlackRock maintained an optimistic outlook on equity markets, based on what the firm deemed to be reasonable valuations, as well as on expectations that larger policy risks — namely a potential euro-zone breakup and the worst-case scenario of the U.S. fiscal cliff — would begin to fade.

(continues) 3

Portfolio management review

Optimum International Fund

As a result, BlackRock’s risk-reward analysis by sector led to an overweight bias toward cyclical subsectors such as asset management, construction equipment, chemicals, heavy trucks, and oil and gas services. This approach, combined with a large allocation to European names (58% on average), contributed to Fund performance during the year. Conversely, stocks selection in the energy and semiconductor sector detracted from Fund performance.

At the individual stock level, BlackRock was particularly attracted to well-run European businesses where valuations still did not reflect enhanced margin potential after years of either restructuring or successful penetration into higher growth parts of the world, like China and ASEAN (Association of Southeast Asian Nations) regions. For example, Deutsche Lufthansa is a holding that BlackRock believes stands out as a prime beneficiary of massive consolidation in the European airline industry where the gains from cost cutting are only now being realized in higher stock valuations. Similarly, exposure to Svenska Cellulosa, a Swedish tissue and packaging company, contributed meaningfully to Fund performance as investors shifted their focus to the potential for its steadier, highly cash-generative household products business (following a recent divesture of its more cyclical forest products segment).

Stock selection in energy was a negative factor, due in part to holdings in select Asian coal names. As an example, Adaro Energy, an Indonesian mining company no longer held in the Fund’s portfolio, came under pressure on account of lower production levels and lackluster coal pricing tied to a slowdown in China. Elsewhere, performance volatility in semiconductors hurt relative results as Avago Technologies, a key component supplier to the Apple iPhone platform, suggested softer forward-looking demand trends in the wireless market.

Now that global equities have repriced, although not necessarily rerated upward, it seems plausible to expect a pullback in the near term. However, BlackRock’s core thesis remains that the combination of proactive policy responses, combined with an extraordinary investment replacement cycle and still-low intrinsic valuations versus long-term history, make equities the place to continue the hunt for opportunities in the foreseeable future.

Mondrian

Overall, country allocations across Mondrian’s portion of the Fund were broadly in line with the benchmark for the fiscal year. In Europe, overweight positions toward Spain, Italy, and France held back returns while exposure to the Japanese and Taiwanese markets helped offset their effects.

At the sector level, the healthcare and consumer staples sectors were among the strongest-performing sectors, up 25.5% and 20.6% respectively during the Fund’s fiscal year. The financial sector was also strong, gaining 20.3% as European banks benefited from reduced refinancing risks following two substantial liquidity injections by the European Central Bank (ECB). In the utilities sector, ongoing regulatory concerns continued to dampen returns in the sector as it fell 2.4% for the period. Energy and materials were the worst-performing sectors, falling 5.7% and 3.3%, respectively. Lower prices for many commodities affected certain large companies in the metals and mining subindex as well.

Looking back, an additional feature of the past year was investors’ intolerance for companies whose results failed to live up to expectations. Certain stocks in Mondrian’s portion of the Fund experienced this fate. They included a diverse range of companies such as BG Group, the British oil and gas company, which fell 24.9% following a profits warning due to revised production expectations for 2013. This did not change the company’s longer-term production guidance. Canon, the Japanese printer manufacturer, fell 21.0% as slowing demand growth for office equipment weighed on the company in addition to market concerns regarding Hewlett-Packard’s strategy and commitment to laser printers. Additionally, France

4

Telecom and Telefonica fell 19.5% and 12.6%, respectively, as a result of higher-than-expected sensitivity to weak economic environments and fears of dividend cuts.

On a positive note, stocks that performed well during the Fund’s fiscal year included Sanofi, a France-based pharmaceutical company. For the period, the company’s share price gained 35.7% on the back of stronger-than-expected results and as concerns surrounding its insulin drug Lantus were reduced. Unilever, the Anglo-Dutch consumer products company, appreciated 31.8% following consistent financial results and continued profitable growth in emerging markets. Finally, Toyota Motor, the Japanese automobile manufacturer, benefited from the weaker yen and better-than-expected sales in the United States, and gained 20.6% during the Fund’s fiscal year.

(continues) 5

Portfolio management review

Optimum Large Cap Growth Fund

April 9, 2013

| Performance review (for the year ended March 31, 2013) | ||||

| Optimum Large Cap Growth Fund (Class A shares) | 1-year return | +7.76% | ||

| Optimum Large Cap Growth Fund (Institutional Class shares) | 1-year return | +8.25% | ||

| Russell 1000® Growth Index (benchmark) | 1-year return | +10.08% |

Past performance does not guarantee future results. |

Advisor

Delaware Management Company (DMC)

Sub-advisors

Fred Alger Management, Inc. (Alger)

T. Rowe Price Associates, Inc. (T. Rowe Price)

Marsico Capital Management, LLC (Marsico)

Market overview

Domestic stocks generated solid gains during the Fund’s fiscal year ended March 31, 2013. Generally, American corporations’ ongoing ability to show solid earnings growth, generate strong cash flows, and maintain healthy balance sheets boosted stock prices. The Federal Reserve’s accommodative monetary policies also firmed investors’ confidence in stocks during the fiscal year.

These factors largely helped domestic markets overcome a range of macroeconomic headwinds throughout the fiscal year, including yearlong uncertainty about the direction of U.S. fiscal policy and concerns about slow economic growth in the United States and Europe, coupled with ongoing concerns surrounding the debt crisis in the euro zone.

Within the equity markets, mid- and small-cap shares generally outpaced large-caps, and value stocks strongly outperformed growth stocks.

Fund performance

Optimum Large Cap Growth Fund lagged its benchmark index for the fiscal year, due in part to underperformance within the healthcare sector across the portions of the Fund that Alger and T. Rowe Price manage. Returns within the consumer discretionary and energy sectors detracted from performance for the portion of the Fund that Marsico manages.

Alger

One of Alger’s long-standing priorities has been to achieve exposure to high-quality U.S. companies that might benefit from strong emerging market demand. Alger believes it owned these types of companies within the consumer discretionary and financial sectors during the fiscal year, both of which benefited performance within Alger’s portion of the Fund. The most significant detractors to portfolio performance within Alger’s portion of the Fund came from the consumer staples and healthcare sectors. In both instances, stock selection led to disappointing performance.

Among individual stocks, eBay was the largest individual contributor to positive performance (on a relative basis) within Alger’s portion of the Fund. The company brings together millions of buyers and sellers every day on a local, national, and international basis through an array of websites. Alger looked favorably upon the shares as the company improved its pace of innovation and leveraged its core assets into the mobile landscape, leading to accelerated growth in e-commerce. Alger believes eBay can see improved growth driving long-term margin expansion, if eBay retakes share in e-commerce and grows its online payment processing businesses.

6

News Corp. was another important contributor to Alger’s portion of the Fund. News Corp. is a diversified global media company with operations across a wide array of industry segments. Alger continued to own shares in the company as of the end of the fiscal year because it was the fastest growing network, bolstered by sports, news, and international programming, each of which was in growth mode.

Apple, whose shares posted a 27% decline during the Fund’s fiscal year, was the largest detractor from Alger’s portion of the Fund. Apple suffered some margin compression during the fiscal year as it introduced several new products, reported somewhat disappointing earnings as customers waited for the newest versions of the iPhone, and lost some market share to its strongest competitor, Samsung. With net cash of more than $140 per share, a current annual dividend of $11 per share, and free cash flow generation of more than $50 per share annually, Alger believed that Apple’s shares were attractively valued at the end of the Fund’s fiscal year. As a result, it maintained its position in the stock.

Caterpillar was another relatively large detractor from Alger’s portion of the Fund during the fiscal year, as shares of the company registered a double-digit loss. Caterpillar is the world’s largest manufacturer of construction and earthmoving equipment. A weakening environment within the mining industry, inventory buildups in China, and diminished agricultural demand in North America combined to hurt Caterpillar during the fiscal year.

Looking forward, however, Alger believes that the company can potentially achieve strong growth in the coming years, based on its forecast of 3%-plus gross domestic product growth in the U.S., a healthy Chinese economy, and a recovering European economy. As a result, Alger maintained a position in the company as of the end of the fiscal year.

T. Rowe Price

The consumer discretionary sector was the largest relative detractor within T. Rowe Price’s portion of the Fund. Within this sector, priceline.com and Chipotle Mexican Grill were the greatest individual detractors. Concerns over the health of the euro-zone economy, combined with worries that higher payroll taxes in the U.S. would reduce domestic consumer spending, weighed on share prices of online travel company priceline.com. Chipotle was hurt by slowing sales and higher food costs, a combination that also drove down the share prices of many other chain restaurants in the U.S.

T. Rowe Price’s position within the healthcare sector, and particularly its underweight position in the strong-performing pharmaceuticals industry during the fiscal year, also detracted from performance within its portion of the Fund. Its positions within the healthcare providers and services industry also hurt its relative performance, as many managed-care companies were affected by concerns that Medicare reimbursements would be cut as costs rose.

Information technology was the top performer within T. Rowe Price’s portion of the Fund. Within this sector, shares of Google moved higher as the company profited from the popularity of smartphones running on its Android operating system. Google has expanded its efforts to increase mobile-use monetization, and has attracted advertisers by offering a single package that utilizes both mobile and personal-computer endpoints.

Telecommunication services holdings also contributed to the performance of T. Rowe Price’s portion of the Fund. Specifically within this sector, holding Crown Castle International benefited, as did other wireless communication tower companies, from strong demand for higher data capacity to support smartphone technology.

Marsico

The Marsico investment approach seeks stocks of companies that have potential for long-term capital appreciation. Marsico’s investment process combines top-down macroeconomic and industry analysis with individual stock selection.

During the Fund’s fiscal year, stock selection in the consumer discretionary and energy sectors was the primary source of underperformance within Marsico’s

(continues) 7

Portfolio management review

Optimum Large Cap Growth Fund

portion of the Fund. A portion of its consumer discretionary stocks were positioned in companies with high-end brands in an attempt to benefit from growing high-net-worth populations in emerging markets. Early in the Fund’s fiscal year, however, concerns about a global economic slowdown negatively affected some of the Fund’s consumer stocks. In particular, positions in luxury goods retailers Cie Financiere Richemont and Coach, which produce significant revenues from Asia, were pressured. Marsico sold both positions from its portion of the Fund during the fiscal year.

Marsico believes that a paradigm shift is taking place in energy production as advances in horizontal drilling and hydraulic fracturing techniques have allowed for energy exploration companies to drill for previously unreachable natural gas and crude oil. One of the ways in which Marsico chose to participate in the energy theme was through positions in oilfield services companies National Oilwell Varco and Halliburton. However, both stocks were hurt by low natural gas prices, which prompted drillers to reduce their land rig count in the U.S. While Marsico believes in the long-term tailwinds of this theme, it did not see a likely recovery in rig count until the back half of 2013 at the earliest, and sold its positions in both stocks.

The information technology sector was a contributor to Marsico’s portion of the Fund. A particular benefit to performance came from Marsico’s sale of Apple during the fiscal year. It began selling the position in 2012 and was completely out of the stock prior to Apple’s announcement of quarterly earnings in January 2013, at which time the stock price fell further. Marsico exited the position because it was concerned that Apple’s product pipeline was lacking a major catalyst and a recurring revenue stream.

Another bright spot for Marsico’s portion of the Fund came from healthcare stocks. Several biotechnology and pharmaceutical companies stood out for their strong returns during the fiscal year, including Biogen Idec, Gilead Sciences, and Bristol-Myers Squibb. These companies introduced products during the fiscal year that have large markets. Marsico believes these companies have distinguished themselves as a result of the innovative science they are using to perform drug research.

8

Optimum Large Cap Value Fund

April 9, 2013

| Performance review (for the year ended March 31, 2013) | |||

| Optimum Large Cap Value Fund (Class A shares) | 1-year return | +12.48% | |

| Optimum Large Cap Value Fund (Institutional Class shares) | 1-year return | +12.92% | |

| Russell 1000® Value Index (benchmark) | 1-year return | +18.77% |

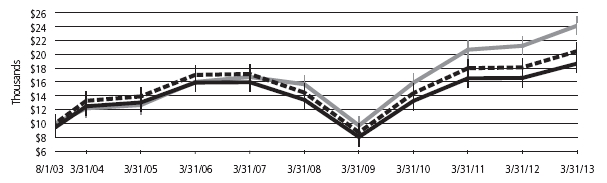

For complete, annualized performance for Optimum Large Cap Value Fund, please see the table on page 26.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible investors.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Herndon Capital Management, LLC (Herndon)

Massachusetts Financial Services Company (MFS)

Market overview

The beginning of the Fund’s fiscal year was characterized by a risk-on sentiment as a result of additional liquidity measures by the U.S. Federal Reserve and the European Central Bank (ECB), as well as a commensurate improvement in macroeconomic conditions. During this time, global equity valuations rose, credit spreads contracted, and high-quality sovereign yields increased modestly.

Within a couple of months, however, conditions worsened, driven by broadly weaker global macroeconomic indicators, as well as renewed concerns over the euro zone’s capacity and determination to address its ongoing crisis. Despite this deterioration, broad market sentiment remained relatively resilient as equity markets generally maintained gains and credit spreads did not indicate deterioration.

However, this renewed weakness in the fundamentals precipitated a further round of monetary easing by both the Fed (through a third round of quantitative easing) and the ECB (through a new bond-purchase facility) in the middle of the Fund’s fiscal year, which helped instill additional confidence in risk markets. Nonetheless, toward the end of 2012, weaker equity earnings reports and declining forward guidance caused market sentiment to soften. In addition, fiscal-cliff negotiations between congressional Republicans and President Obama were a particular source of market attention, as the uncertainty surrounding the fiscal negotiations continued right up to the Dec. 31 deadline. A last-minute political agreement averted the worst-case scenario and markets gravitated toward risk assets again; however, heading into 2013, the implementation of the U.S. budget sequester, combined with the uncertainty surrounding the Italian election results, inserted a greater degree of caution as the fiscal year ended.

Fund performance

Optimum Large Cap Value Fund underperformed its benchmark primarily due to weak returns by several high-profile holdings in the Fund. The holdings, which represented a number of sectors and were held by different sub-advisors for the Fund, included Cliffs Natural Resources, Coach, Philip Morris International, and Western Union.

Herndon

Herndon’s approach in this market environment has been to identify what it views as value-creating opportunities, and this approach led to positive returns during the fiscal year, though they lagged those of the benchmark index. These results may not be surprising, given the current environment in which the market continues to be as much affected by macro events and sentiment as by company fundamentals.

The two sectors that contributed most to the performance of Herndon’s portion of the Fund were healthcare and energy. Over the course of the Fund’s fiscal year, nine of Herndon’s holdings in the healthcare sector generated returns exceeding 40% (versus just a 20% gain from the

(continues) 9

Portfolio management review

Optimum Large Cap Value Fund

benchmark’s healthcare holdings). The positive effects from stock selection offset a slight negative effect from allocation. An overweight allocation and outperformance in the energy sector proved beneficial to Herndon’s portion of the Fund as its energy names made significant gains (versus slight gains from the benchmark’s energy stocks).

The two sectors that detracted the most from the performance of Herndon’s portion of the Fund were consumer discretionary and materials. In both cases, along with negative absolute returns (due principally to two stocks in each sector), an overweight position in these sectors exacerbated the negative results. Investments in high-end retailer Coach and for-profit education company Apollo Group proved less than profitable, especially when compared to the consumer discretionary stocks within the benchmark, which gained almost 30%. And while the benchmark’s materials sector gained less than 5% for the Fund’s fiscal year (the worst of any sector), Herndon’s holdings failed to keep up as well. Underperformance coupled with an overweight allocation to the sector proved unfavorable.

Two names that performed quite well and contributed to Herndon’s portion of the Fund were Marathon Petroleum and Health Management Associates. These stocks remain in the portfolio as they continue to meet Herndon’s criteria for value-creating opportunities.

Marathon Petroleum sells refined products through a nationwide network of branded gas stations. It also holds stakes in pipelines and is one of the largest asphalt and light-oil product terminal operators in the United States. Improvements in revenue, earnings, and profit margins helped propel the stock’s performance.

Health Management Associates is an owner of more than 65 hospitals and acute healthcare facilities in suburban and rural markets primarily in the southeastern U.S. — the stock’s strong performance was primarily due to fewer concerns over corporate governance and management. Also, the stock has benefited as many investors have become enthusiastic that new healthcare regulations will likely lead to more patients.

Two stocks that significantly detracted from Herndon’s portion of the Fund during the fiscal year were Cliffs Natural Resources and Herbalife. Cliffs Natural Resources is an international mining and natural resources company that produces iron ore and metallurgical coal in the U.S., Canada, and Australia. The company’s recent disappointing earnings results, coupled with a dividend cut and new share issuance leading to dilution for current shareholders, have disappointed long-only investors in this stock. Herndon continues to hold the stock, given that Cliffs has reduced debt, lowered its dividend, disposed of noncore assets, and refinanced near-term debt maturities. Cliffs management’s actions to maintain financial flexibility — while somewhat discomforting for the short term — seem to be prudent measures to help the company execute on its long-term plans for future organic growth and expansion.

Herbalife manufactures and distributes weight-control products including meal replacements, snacks, and “enhancers.” It also offers nutritional supplements, energy drinks, and skincare products. In 2013, Herbalife found itself at the center of an ugly skirmish between two hedge-fund heavyweights. While the company’s fundamentals and growth story appear to be intact, concerns over valuation, its risk-reward profile, and weak relative performance led Herndon to exit the position at the end of the Fund’s fiscal year.

MFS

The management team at MFS continues to believe that focusing on investing in high-quality, undervalued stocks can give the best potential for delivering long-term, strong risk-adjusted returns. The market environment did, however, present headwinds for MFS’s strategy given the outperformance of companies with high betas (that is, stocks considered to have higher volatility in relation to the market) and low return on equities as compared to those with low betas and high return on equities (which is more consistent with those owned in MFS’s portion of the Fund). This continued to present some attractive investment opportunities, in the team’s opinion,

10

in a number of larger-capitalization, higher-quality companies. The team continued to add to these types of companies throughout the Fund’s fiscal year.

Security selection in the consumer staples sector detracted from the Fund’s relative performance. MFS’s holdings of tobacco companies Philip Morris International and Lorillard hurt relative performance as both stocks underperformed the benchmark during the fiscal year.

An underweight allocation and poor stock selection within the strong-performing utilities-and-communications sector also weakened relative performance. Within this sector, the Fund’s avoidance of telecommunications services provider Verizon Communications at the beginning of the period detracted from performance within MFS’s portion of the Fund.

Stock selection in both the retail and financial services sectors detracted from relative returns. Within the financial services sector, holdings of poor-performing money transfer services firm Western Union held back relative performance.

Elsewhere, MFS’s holdings of diversified technology products and services company International Business Machines (IBM) and cardiovascular medical device maker St. Jude Medical, and its lack of a position in strong-performing integrated oil company Phillips 66, had a negative effect on relative performance.

Cash and cash equivalents were another detractor from relative performance. MFS strives to be fully invested and generally holds cash to buy new holdings and to provide liquidity. In a period when equity markets rose, as measured by the Fund’s benchmark, holding cash hurt performance versus the benchmark, which does not have a cash component.

Stock selection in the basic materials sector contributed to relative performance. Holdings of protective and decorative coatings manufacturer PPG Industries boosted performance as the stock outpaced the benchmark over the course of the Fund’s fiscal year.

The Fund’s position in poorly performing integrated oil and gas company Exxon Mobil was the largest individual detractor from performance. Elsewhere, the Fund’s holdings of alcoholic beverage producer Diageo, insurance company St. Paul Travelers, media company Viacom, automotive supplier Delphi Automotive, paint retailer Sherwin Williams, and an underweight position in network equipment company Cisco Systems, had a positive impact on relative performance. Avoiding shares of weak-performing health insurance provider UnitedHealth Group and oil & gas producer Devon Energy also helped performance.

(continues) 11

Portfolio management review

Optimum Small-Mid Cap Growth Fund

April 9, 2013

| Performance review (for the year ended March 31, 2013) | |||

| Optimum Small-Mid Cap Growth Fund (Class A shares) | 1-year return | +12.50% | |

| Optimum Small-Mid Cap Growth Fund (Institutional Class shares) | 1-year return | +12.94% | |

| Russell 2500™ Growth Index (benchmark) | 1-year return | +13.69% |

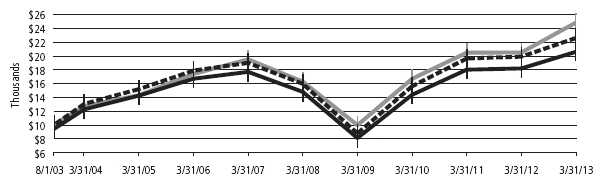

For complete, annualized performance for Optimum Small-Mid Cap Growth Fund, please see the table on page 28.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible investors.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Wellington Management Company, LLP (Wellington)

Columbia Wanger Asset Management, LLC (Columbia WAM)

Market overview

Global equity markets performed well over the Fund’s fiscal year ended March 31, 2013. The global slow-growth environment did not appear to diminish investor appetite for equities, particularly as several downside risks seemed to abate during the fiscal year. Concerns about the euro zone generally remained in check as policy makers seemed committed to saving the euro. Additionally, numerous central banks around the globe continued their aggressive monetary stimulus policies in an effort to jumpstart sustainable economic recovery from the financial crisis that remains fresh on many investors’ minds. China, a major engine of global growth, also showed signs that its economy would not experience a “hard landing.”

Despite concerns about the so-called fiscal cliff and sequestration cuts in the United States, domestic investors bid up risk assets amid signs of improvement in the U.S. housing market, for the first time in approximately seven years. Housing prices in the U.S. began 2013 with the largest 12-month advance since August 2006. Better-than-expected corporate earnings and generally improving economic data also provided tailwinds for stocks.

Fund performance

Optimum Small-Mid Cap Growth Fund underperformed its benchmark index for the Fund’s fiscal year, due in part to poor performance by information technology holdings in the portfolios of both sub-advisors.

Wellington

Wellington’s portion of the Fund generated strong absolute gains but underperformed the Fund’s benchmark index for the fiscal year. Weak security selection within the information technology and financial sectors drove underperformance within Wellington’s portion of the Fund, while strong performance in the energy, healthcare, and consumer discretionary sectors contributed to relative results for the fiscal year ended March 31, 2013.

At the individual security level, top relative contributors for Wellington’s portion of the Fund included companies in the industrials, consumer discretionary, and healthcare sectors. Shares of DigitalGlobe, a digital imaging products and service provider for defense, intelligence, and industrial applications, increased during the year after DigitalGlobe reached a resolution on a merger agreement with former competitor GeoEye. Wellington continued to hold its position in this stock as of the end of the Fund’s fiscal year. U.S. homebuilder PulteGroup was another contributor to Wellington’s portion of the Fund. This stock’s price rose during the Fund’s fiscal year as signs of stabilization began to turn investor sentiment positive toward housing in the first half of 2012. Following many years of decline, investors began contemplating future home-price appreciation as the combination of record home affordability, an improving jobs picture, and very low levels of new home construction provided a powerful backdrop for U.S. homebuilders. The investment team at Wellington exited its position as PulteGroup’s shares approached the team’s target price. Finally, Gen-Probe, a biotechnology firm specializing in molecular diagnostics products, also contributed to performance. Share prices rose after the company announced that it would be acquired by Hologic, a leading

12

manufacturer and supplier of diagnostic, surgical, and medical imaging equipment and products. Wellington eliminated its position in Gen-Probe after the stock passed the investment team’s target price.

VeriFone Systems, a company that designs, markets, and services electronic payment solutions worldwide, was one of the top detractors from Wellington’s portion of the Fund. Weak macroeconomic conditions in Europe, lower revenue from Brazil-based business, and delays in customer projects caused the company to lower earnings estimates, which may have contributed to a decrease in share price. Wellington eliminated its position in the stock during the Fund’s fiscal year. Riverbed Technology, a wide-area networks (WAN) optimization provider that offers cloud computing services, was another detractor from Wellington’s portion of the Fund. Wellington eliminated its position in Riverbed during the year as shares in the company declined based on soft earnings and concerns about the ongoing impact of a weak demand environment. In the healthcare sector, Abiomed also detracted from performance. Shares of Abiomed, a cardiac treatment-focused medical device manufacturer, declined because of controversy regarding the efficacy and labeling of the company’s Impella ventricular support treatment. Wellington eliminated its position in Abiomed during the year.

Columbia WAM

During the Fund’s fiscal year, Columbia WAM continued to employ its low-turnover, bottom-up, fundamental strategy to the portion of the Fund that it manages. The investment team works to identify reasonably priced growth companies that it believes are positioned to grow over the next three to five years.

At the sector level, the team lowered its allocations in the energy and telecom sectors and increased its allocation to financials during the Fund’s fiscal year. Columbia WAM lowered its energy allocation due to its perception of changing supply-demand dynamics within the sector. Specifically, energy supply has increased due to new technology, while demand has decreased due to conservation efforts.

Consumer discretionary and healthcare companies were strong contributors to performance during the Fund’s fiscal year. A variety of different companies linked to the consumer discretionary sector performed well for Columbia WAM’s portion of the Fund as U.S. consumers became more confident in the economic recovery, due in part to the housing recovery and an improving stock market. Within the healthcare sector, Columbia WAM generally stayed away from areas that could potentially be affected by healthcare reform and government reimbursement risk.

Underweight allocations to the financials and real estate sectors were the largest detractors from Columbia WAM’s portion of the Fund during the fiscal year. Financial stocks were surprisingly strong performers, while real estate also performed well as investors continued to seek yield in a low interest rate environment.

At the individual stock level, Ryman Hospitality Properties, formerly Gaylord Entertainment, was a top contributor to Columbia WAM’s portion of the Fund. The stock’s performance surged during the Fund’s fiscal year as the company converted its status as a hotel, resort, entertainment, and media company to a real estate investment trust (REIT) that specializes in group-oriented, destination hotel assets in urban and resort markets. Avis Budget Group, a leading global provider of vehicle rental services, was the second-largest contributor to performance. The stock’s performance was likely boosted by high fleet utilization as well as what Columbia WAM viewed as a positive new pricing trend within the rental car industry.

The largest detractors from Columbia WAM’s portion of the Fund during the fiscal year came from technology stocks. Share prices of Informatica, a data integration software company, declined during the fiscal year after the company reported disappointing earnings that likely came as a result of a slowdown in sales to European customers. Atmel was another notable detractor from performance during the fiscal year. The company manufactures microcontrollers that are used in the industrial, consumer, security, communications, computing, and automotive markets. Its stock was likely affected by declining revenues and a lost contract bid.

(continues) 13

Portfolio management review

Optimum Small-Mid Cap Value Fund

April 9, 2013

| Performance review (for the year ended March 31, 2013) | |||

| Optimum Small-Mid Cap Value Fund (Class A shares) | 1-year return | +13.23% | |

| Optimum Small-Mid Cap Value Fund (Institutional Class shares) | 1-year return | +13.56% | |

| Russell 2500™ Value Index (benchmark) | 1-year return | +21.17% |

For complete, annualized performance for Optimum Small-Mid Cap Value Fund please see the table on page 30.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible investors.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

The Delafield Group, a division of Tocqueville Asset Management L.P. (Tocqueville)

The Killen Group, Inc. (Killen)

Westwood Management Corp. (Westwood)

Market overview

Despite a mostly unchanged global economic landscape and uncertainty regarding the outcome of the U.S. presidential election, equity markets generally achieved strong gains during the Fund’s fiscal year ended March 31, 2013. In general, investors seemed buoyed by directionally favorable, albeit modest, improvements in U.S. economic data along with reasonably positive corporate earnings reports, and the Federal Reserve’s announcement in September 2012 that it would engage in new, and open-ended, quantitative easing measures.

Toward the end of 2012, however, investors’ worries were rekindled on several fronts that included the European sovereign debt crisis and the fiscal cliff standoff in the United States. Global markets had a mixed response as a result, although the Fund’s benchmark (the Russell 2500 Value Index) registered a solid gain during the last three months of 2012, compared to the broad stock market’s decline. Despite reminders of the fragile status of Europe’s economies (most recently in Cyprus), investors cheered a last-minute deal for the so-called fiscal cliff to start the new calendar year. Improved U.S. housing and jobs market data reports and relative stability in the U.S. fiscal situation drove strong market returns to close out the Fund’s fiscal year on a high note.

Fund performance

Security selection by two of Optimum Small-Mid Cap Value Fund’s sub-advisors across the consumer staples, energy, consumer discretionary, and real estate investment trusts (REITs) sectors was a leading factor in the Fund’s underperformance versus its benchmark. An underweight allocation to the strong-performing financials sector by one of the sub-advisors was another notable detractor.

Tocqueville

Despite the uncertain macroeconomic environment, Tocqueville stayed true to its investment strategy throughout the Fund’s fiscal year, as it continued to employ its bottom-up (stock-by-stock) approach. Tocqueville generally seeks to hold stocks of companies whose management teams it believes are taking action to position their businesses for the long term.

Tocqueville’s limited exposure to the financial sector detracted from relative performance, as the financial sector outperformed the overall index for the Fund’s fiscal year and also constituted the largest component of the index. Additionally, Tocqueville held no utilities stocks during this period, which also detracted from relative returns within its portion of the Fund.

Tocqueville’s stock selection was mixed during the Fund’s fiscal year. Its holdings in the materials sector strongly outperformed comparable index positions and, owing to an overweight allocation in the space, contributed to performance of Tocqueville’s portion of the Fund.

14

In contrast, investments in its other large areas of exposure, namely industrials and information technology, underperformed the index for the fiscal year.

PolyOne was the top contributor to the performance of Tocqueville’s portion of the Fund. This company reported solid earnings and continued to demonstrate a successful expansion of its product offerings to include custom-engineered structure and packaging solutions. Sealed Air, a packaging producer, was another large contributor to performance, benefiting from stabilized earnings trends and senior management appointments that the market generally viewed as favorable.

Tocqueville’s investments in ACCO Brands and Plexus were the largest detractors from performance within its portion of the Fund. ACCO, a supplier of branded office products, experienced disappointing earnings results and Plexus, a provider of electronic manufacturing services, was battered after announcing the loss of its largest customer. Despite the stocks’ recent challenges, Tocqueville continued to hold them. It continues to view ACCO’s May 2011 merger with MeadWestvaco’s office products business positively, with the belief that, over time, the combined businesses should realize improved earnings power as well as substantial free cash flow and debt reduction. With respect to the Plexus investment, Tocqueville believes the long-term financial model for the company — specifically, its targets of 10% gross margins and 5% operating margins — remains achievable. Further, with a modest net cash position and more than $100 million in estimated free cash flow in fiscal 2013, Tocqueville believes that Plexus could be well positioned to accelerate an opportunistic share repurchase program that its board has authorized.

Killen

Killen’s strategy seeks overlooked and undervalued businesses. During the Fund’s fiscal year, it found contrarian investment opportunities in a number of disparate sectors, including consumer discretionary, industrials, information technology, healthcare, and telecom services. The market’s weakness during the first few months of the fiscal year allowed Killen to opportunistically deploy cash reserves that had risen during the preceding quarters. In similar fashion, cash rose once again during the second half of the Fund’s fiscal year as valuations became somewhat extended, in Killen’s view.

As a value-based, bottom-up investment manager, Killen does not change or adapt its approach to the economic environment. While remaining cognizant of the broader economic conditions, it uses a company-by-company approach, looking at the long-term potential for each business and judging its valuation based on that analysis. Additionally, Killen believes its valuation discipline can help mitigate portfolio risk, as it is willing to maintain cash when investments are sold if it cannot find replacements at suitable valuations.

During the Fund’s fiscal year, Killen’s allocations to specific sectors were attributable to its value-oriented stock selection process, and not consciously targeted. Nevertheless, Killen derived positive contributions from the financials, information technology, materials, industrials, and consumer discretionary sectors. The solid returns from these sectors were primarily the result of one or more stocks performing well in each sector, rather than from sector positioning.

Killen underperformed the benchmark index for the Fund’s fiscal year in the consumer staples and energy sectors. Killen’s lagging performance in both sectors was mainly a result of stock-specific factors.

Winnebago Industries, a manufacturer of recreational vehicles, and Stewart Information Services, a title insurance company, were notable contributors to performance within Killen’s portion of the Fund. Winnebago benefited from a number of developing trends, such as an improving economic outlook, pent-up demand, and the return of financing availability. Stewart rallied from depressed levels on the strength of refinancing activity and the general improvement in housing.

Portfolio management review

Optimum Small-Mid Cap Value Fund

SkyWest, a regional airline carrier that serves as a feeder to hubs of major airlines, and Gulf Island Fabrication, a manufacturer of offshore drilling platforms and other structures used primarily in oil and gas exploration, were examples of detractors within Killen’s portion of the Fund. Each stock fell more than 20% for the Fund’s fiscal year.

SkyWest suffered from a decline in revenues as a result of increased training costs and a challenging integration of an acquired rival. Consequently, Killen felt the management team was not able to deliver on its margin and revenue growth targets, and projected that the company’s fundamentals would deteriorate. In keeping with its sell discipline, Killen completely exited the holding during the fiscal year. Gulf Island Fabrication suffered more as a result of company-specific issues, including the bankruptcy of a client with an existing contract and cost overruns on another contract. Killen believes that Gulf Island remains financially strong, and maintained its position within the Fund.

Westwood

Throughout the Fund’s fiscal year, Westwood continued to use the consistent and disciplined investment approach that it employs through all market environments; that is, Westwood focuses on what it views as high-quality companies with strong fundamental characteristics and visible earnings prospects.

Security selection in the technology and utilities sectors helped the relative performance of Westwood’s portion of the Fund. Utilities generally benefited from the demand for safety and yield during the first part of the Fund’s fiscal year, while technology companies gained from secular growth trends in storage, enterprise software, and cloud services.

Security selection in the consumer discretionary and REIT sectors detracted from relative performance within Westwood’s portion of the Fund. The economically-sensitive consumer discretionary sector was hurt by uncertainty in the U.S. and global economies in the earlier part of the fiscal year. In addition, Westwood’s underweight allocation to REITs, which are similarly sensitive to macroeconomic factors, was a drag on performance as the economy gained strength and investors seemed to gain confidence.

j2 Global, a provider of cloud-based communications and storage services to businesses, was the top-performing security for Westwood’s portion of the Fund for the fiscal year. The company reported strong results during its second and fourth fiscal quarters that highlighted its attractive growth opportunities and investor demand for companies with attractive dividend yields. Packaging Corporation of America, a manufacturer and seller of packaging materials for industrial and consumer use, also added to returns within Westwood’s portion of the Fund. The stock rose after the company reported a second-quarter earnings surprise, resulting from revenue growth that exceeded expectations.

Navistar International manufactures and markets medium and heavy trucks, school buses, midrange diesel engines, and service parts worldwide. This company, which fell on the announcement of a slowdown of global heavy truck orders, was the worst-performing security for Westwood’s portion of the Fund during the fiscal year. Based on the company’s declining fundamentals, Westwood ultimately sold the stock.

Swift Energy, an independent oil and gas company that explores, acquires, and operates oil and gas properties, declined as a result of falling crude oil prices and expectations for weaker commodity demand. While Westwood is optimistic about oil and gas commodity prices over the medium and longer term, it was not comfortable with Swift’s increased spending and lack of defensive hedging. Westwood felt that both could be damaging in the event of a rebound in commodity prices. As a result, Westwood exited the position during the Fund’s fiscal year, seeking a company with a better natural gas hedge and balance sheet.

16

Performance summary

Optimum Fixed Income Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our website at optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.

| Fund performance1, 2 | |||||||||

| Average annual total returns | |||||||||

| Through March 31, 2013 | 1 year | 3 years | 5 years | Lifetime | |||||

| Class A (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +5.47% | +6.40% | +7.32% | +6.05% | |||||

| Including sales charge | +0.70% | +4.77% | +6.34% | +5.55% | |||||

| Class B (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +4.69% | +5.72% | +6.65% | +5.49% | |||||

| Including sales charge | +0.69% | +5.04% | +6.42% | +5.49% | |||||

| Class C (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +4.69% | +5.72% | +6.62% | +5.37% | |||||

| Including sales charge | +3.69% | +5.72% | +6.62% | +5.37% | |||||

| Institutional Class (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +5.72% | +6.76% | +7.70% | +6.42% | |||||

| Including sales charge | +5.72% | +6.76% | +7.70% | +6.42% |

1Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 19. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.35% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Lifetime performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible investors.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

2The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total annual fund operating expenses (excluding certain other expenses) from exceeding 1.00% of the Fund’s average daily net assets from July 27, 2012, through July 29, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

18

| Fund expense ratios | Class A | Class B | Class C | Institutional Class | ||||

| Total annual operating expenses | ||||||||

| (without fee waivers) | 1.44% | 2.09% | 2.09% | 1.09% | ||||

| Net expenses | ||||||||

| (including fee waivers, if any) | 1.35% | 2.00% | 2.00% | 1.00% | ||||

| Type of waiver | Contractual | Contractual | Contractual | Contractual |

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds. The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for the Fund to obtain precise valuations of the high yield securities in its portfolio.

If and when we invest in forward foreign currency contracts or use other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

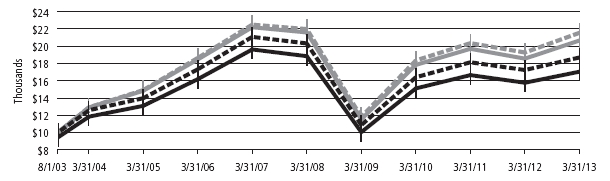

Performance of a $10,000 Investment1

Average annual total returns from Aug. 1, 2003 (Fund’s inception) through March 31, 2013

| Starting value (Aug. 1, 2003) | Ending value (March 31, 2013) | ||||

| Optimum Fixed Income Fund — Institutional Class shares | $10,000 | $18,244 | |||

| Optimum Fixed Income Fund — Class A shares | $9,550 | $16,856 | |||

| Barclays U.S. Aggregate Index | $10,000 | $16,482 |

(continues) 19

Performance summary

Optimum Fixed Income Fund

The chart also assumes $10,000 invested in the Barclays U.S. Aggregate Index as of Aug. 1, 2003. The Barclays U.S. Aggregate Index is a broad composite that tracks the investment grade domestic bond market.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Stock symbols and CUSIP numbers | ||||

| Nasdaq symbols | CUSIPs | |||

| Class A | OAFIX | 246118681 | ||

| Class B | OBFIX | 246118673 | ||

| Class C | OCFIX | 246118665 | ||

| Institutional Class | OIFIX | 246118657 |

20

Performance summary

Optimum International Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our website at optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.

| Fund performance1,2 | |||||||||

| Average annual total returns | |||||||||

| Through March 31, 2013 | 1 year | 3 years | 5 years | Lifetime | |||||

| Class A (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +8.10% | +4.10% | -1.98% | +6.32% | |||||

| Including sales charge | +1.84% | +2.07% | -3.13% | +5.67% | |||||

| Class B (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +7.38% | +3.41% | -2.63% | +5.74% | |||||

| Including sales charge | +3.38% | +2.55% | -3.03% | +5.74% | |||||

| Class C (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +7.37% | +3.44% | -2.62% | +5.63% | |||||

| Including sales charge | +6.37% | +3.44% | -2.62% | +5.63% | |||||

| Institutional Class (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +8.41% | +4.45% | -1.66% | +6.68% | |||||

| Including sales charge | +8.41% | +4.45% | -1.66% | +6.68% |

1Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 23. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 5.75%, and have an annual distribution and service fee of 0.35% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Lifetime performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Performance for Class B and C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible investors.

The “Fund performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

2The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the following “Fund expense ratios” table. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total annual fund operating expenses, (excluding certain other expenses) from exceeding 1.40% of the Fund’s average daily net assets from July 27, 2012, through July 29, 2013. Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

22

| Fund expense ratios | Class A | Class B | Class C | Institutional Class | |||

| Total annual operating expenses | |||||||

| (without fee waivers) | 1.84% | 2.49% | 2.49% | 1.49% | |||

| Net expenses | |||||||

| (including fee waivers, if any) | 1.75% | 2.40% | 2.40% | 1.40% | |||

| Type of waiver | Contractual | Contractual | Contractual | Contractual |

International investments entail risks not ordinarily associated with U.S. investments including fluctuation in currency values, differences in accounting principles, or economic or political instability in other nations. Investing in emerging markets can be riskier than investing in established foreign markets due to increased volatility and lower trading volume.

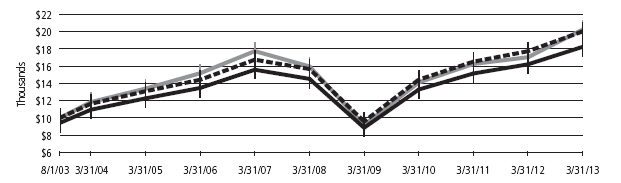

Performance of a $10,000 Investment1

Average annual total returns from Aug. 1, 2003 (Fund’s inception) through March 31, 2013

| Starting value (Aug. 1, 2003) | Ending value (March 31, 2013) | |||||

| MSCI EAFE Index (gross) | $10,000 | $21,542 | ||||

| MSCI EAFE Index (net) | $10,000 | $20,649 | ||||

| Optimum International Fund — Institutional Class shares | $10,000 | $18,690 | ||||

| Optimum International Fund — Class A shares | $9,425 | $17,042 |

1The “Performance of a $10,000 investment” graph assumes $10,000 invested in Class A and Institutional Class shares of the Fund on Aug. 1, 2003, and includes the effect of a 5.75% front-end sales charge (for Class A shares) and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table above. Please note additional details on pages 22 through 23.

The chart also assumes $10,000 invested in the MSCI EAFE Index as of Aug. 1, 2003. The MSCI EAFE Index measures equity market performance across developed market countries in Europe, Australasia, and the Far East. Index “gross” return approximates the maximum possible dividend reinvestment. Index “net” return approximates the minimum possible dividend reinvestment, after deduction of withholding tax at the highest possible rate.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

| Stock symbols and CUSIP numbers | ||||

| Nasdaq symbols | CUSIPs | |||

| Class A | OAIEX | 246118731 | ||

| Class B | OBIEX | 246118723 | ||

| Class C | OCIEX | 246118715 | ||

| Institutional Class | OIIEX | 246118699 |

(continues) 23

Performance summary

Optimum Large Cap Growth Fund

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our website at optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.

| Fund performance1, 2 | |||||||||

| Average annual total returns | |||||||||

| Through March 31, 2013 | 1 year | 3 years | 5 years | Lifetime | |||||

| Class A (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +7.76% | +10.94% | +5.30% | +6.19% | |||||

| Including sales charge | +1.58% | +8.77% | +4.07% | +5.54% | |||||

| Class B (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +7.07% | +10.22% | +4.63% | +5.62% | |||||

| Including sales charge | +3.07% | +9.46% | +4.25% | +5.62% | |||||

| Class C (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +7.15% | +10.22% | +4.63% | +5.50% | |||||

| Including sales charge | +6.15% | +10.22% | +4.63% | +5.50% | |||||

| Institutional Class (Est. Aug. 1, 2003) | |||||||||

| Excluding sales charge | +8.25% | +11.33% | +5.68% | +6.57% | |||||

| Including sales charge | +8.25% | +11.33% | +5.68% | +6.57% |

1Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund performance” chart. The current expenses for each class are listed on the “Fund expense ratios” table on page 25. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 5.75%, and have an annual distribution and service fee of 0.35% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class B shares may be purchased only through dividend reinvestment and certain permitted exchanges as described in the prospectus. Please see the prospectus for additional information on Class B shares. Class B shares have a contingent deferred sales charge that declines from 4.00% to zero depending on the period of time the shares are held. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets. Class B shares will automatically convert to Class A shares on a quarterly basis approximately eight years after purchase. Lifetime performance figures for Class B shares reflect conversion to Class A shares after approximately eight years.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.