UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number: | 811-21335 | |

| Exact name of registrant as specified in charter: | Optimum Fund Trust | |

| Address of principal executive offices: | 2005 Market Street | |

| Philadelphia, PA 19103 | ||

| Name and address of agent for service: | David F. Connor, Esq. | |

| 2005 Market Street | ||

| Philadelphia, PA 19103 | ||

| Registrant’s telephone number, including area code: | (800) 523-1918 | |

| Date of fiscal year end: | March 31 | |

| Date of reporting period: | March 31, 2015 |

Item 1. Reports to Stockholders

Table of Contents

Optimum Fixed Income Fund

Optimum International Fund

Optimum Large Cap Growth Fund

Optimum Large Cap Value Fund

Optimum Small-Mid Cap Growth Fund

Optimum Small-Mid Cap Value Fund

Annual report

March 31, 2015

|

Carefully consider the Funds’ investment objectives, risk factors, charges, and expenses before investing. This and other information can be found in the Funds’ prospectus and, if available, their summary prospectus, which may be obtained by visiting optimummutualfunds.com or calling 800 914-0278. Investors should read the prospectus and, if available, the summary prospectus carefully before investing.

Table of Contents

| 1 | ||||

| 4 | ||||

| 7 | ||||

| 9 | ||||

| 11 | ||||

| 13 | ||||

| 16 | ||||

| 19 | ||||

| 22 | ||||

| 25 | ||||

| 28 | ||||

| 31 | ||||

| 34 | ||||

Security type / sector / country allocations and top 10 equity holdings | 36 | |||

Financial statements | ||||

| 41 | ||||

| 97 | ||||

| 99 | ||||

| 101 | ||||

| 104 | ||||

| 122 | ||||

| 148 | ||||

| 149 | ||||

| 152 | ||||

| 154 | ||||

Investments in Optimum Fixed Income Fund, Optimum International Fund, Optimum Large Cap Growth Fund, Optimum Large Cap Value Fund, Optimum Small-Mid Cap Growth Fund, and Optimum Small-Mid Cap Value Fund are not and will not be deposits with or liabilities of Macquarie Bank Limited ABN 46 008 583 542 and its holding companies, including their subsidiaries or related companies, and are subject to investment risk, including possible delays in repayment and loss of income and capital invested. No Macquarie Group company guarantees or will guarantee the performance of the Funds, the repayment of capital from the Funds, or any particular rate of return.

Unless otherwise noted, views expressed herein are current as of March 31, 2015, and subject to change for events occurring after such a date. Holdings are as of the date indicated and subject to change.

Funds are not FDIC insured and are not guaranteed. It is possible to lose the principal amount invested.

Mutual fund advisory services provided by Delaware Management Company, a series of Delaware Management Business Trust, which is a registered investment advisor. Delaware Investments, a member of Macquarie Group, refers to Delaware Management Holdings, Inc. and its subsidiaries, including the Funds’ distributor, Delaware Distributors, L. P. Macquarie Group refers to Macquarie Group Limited and its subsidiaries and affiliates worldwide.

All third-party marks cited are the property of their respective owners.

© 2015 Delaware Management Holdings, Inc.

Table of Contents

April 7, 2015

Performance review (for the year ended March 31, 2015) | ||||||

Optimum Fixed Income Fund (Class A shares) | 1-year return | +4.21% | ||||

Optimum Fixed Income Fund (Institutional Class shares) | 1-year return | +4.47% | ||||

Barclays U.S. Aggregate Index (benchmark) | 1-year return | +5.72% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Fixed Income Fund, please see the table on page 16.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisor

Pacific Investment Management Company LLC (PIMCO)

Market overview

Risk appetite returned through much of the Fund’s fiscal year. Generally, global equity markets posted gains and bonds rallied as central banks remained accommodative.

The U.S. job gains stabilized, economic growth was robust, and consumer confidence rose. With inflation low, the U.S. Federal Reserve continued its dovish bias, reaffirming that the fed funds rate would remain near zero for a “considerable time” after the end of its quantitative easing (QE) program. As QE came to an end in October 2014, the U.S. dollar quickly strengthened and oil prices fell sharply, causing speculation that Fed rate hikes would be delayed further. By the first quarter of 2015, however, improving economic conditions signaled that the Fed seemed to remain on track to raise rates in the summer or fall of 2015.

The European Central Bank (ECB) rolled out a series of easing measures, including a negative rate on deposits, a policy rate cut, and targeted long-term refinancing to spur business lending. Euro-zone growth weakened, German business confidence fell, and geopolitical tensions created uncertainty. Inflationary expectations fell, feeding expectations for a full-scale QE. In January 2015, 14 central banks eased policies, but the ECB took center stage as it unveiled its plan to deploy quantitative easing. While markets largely expected the move, the program exceeded expectations in terms of its size, pace, and open-ended design.

Emerging markets experienced episodes of heightened volatility and weakness. Geopolitical headlines and country-specific events drove markets. Sanctions against Russia and a sharp decline in oil prices caused the ruble to tumble, forcing the Russian central bank to raise rates to 17% as of December 2014.

Source: Bloomberg

Fund performance

For the fiscal year, Optimum Fixed Income Fund underperformed its benchmark index, the Barclays U.S. Aggregate Index. In particular, DMC’s diversified floating-rate component and PIMCO’s low duration component both detracted from the Fund’s overall performance versus the Fund’s benchmark index. The following remarks describe factors that affected performance within the Fund’s respective portions.

DMC

Note: The portfolio-level discussion presented below appears in two sections. The first section covers DMC’s portion of the Fund that focused on a multisector strategy, while the second section covers its portion of the Fund that focused on a short duration strategy.

Intermediate-term component

For the year ended March 31, 2015, DMC’s fixed-rate, intermediate-term portion of Optimum Fixed Income Fund underperformed the Fund’s benchmark, the Barclays U.S. Aggregate Index.

The U.S. Treasury sector had strong gains, and longer-maturity instruments performed better than short maturities as the yield curve flattened. The Fed’s tapering of bond purchases tightened monetary conditions, and inflation remained benign. DMC’s portion of the Fund had low allocations to this sector in an attempt to capture extra income in the credit sectors. The fixed-rate portfolio had an average exposure of 8% to U.S. Treasury investments in the first quarter of 2015. The portfolio’s significant underweight to Treasurys detracted from relative performance for the year. This was offset partially by the use of U.S. Treasury futures to balance yield curve exposure and add some duration.

DMC’s most successful strategies were in its investment grade corporate bond exposure, which returned 8.15%, outpacing the 6.74% return of corporate bonds in the Barclays benchmark index. High-quality corporate bonds represented DMC’s largest exposure within this component of the Fund, at 35%. The financial services sector contained some of the leading performers, as bank credits outperformed index returns.

| (continues | ) | 1 |

Table of Contents

Portfolio management reviews

Optimum Fixed Income Fund

DMC’s mortgage position (19% of this component of the Fund) produced mixed results. Although its security selection outperformed the index, its underweight allocation (10 percentage points less than the index) slightly detracted from performance. DMC’s investments in commercial mortgage-backed securities (CMBS), although only a 3% exposure, added to relative returns.

High yield bond investments were a drag on results, as this segment had a return of 0.52% for the period — below that of the benchmark sector’s 1.98% return.

Energy sector bonds also detracted 43 basis points from the Fund’s relative performance for the period as oil prices declined significantly in the second half of 2014. (One basis point is a hundredth of a percentage point.) DMC held several shale-drilling names and water-drilling service names that were adversely affected.

Emerging market investments accounted for 8% of DMC’s intermediate-term portion of the Fund and returned 2.35%. Significant moves in both currencies and commodities prices challenged emerging markets. DMC’s U.S. dollar–denominated (USD) sovereign investments did well, but results in USD corporate investments, and in local currency exposures disappointed. Additionally, investments in developed-market international bonds took 3 basis points away from index returns, as surprisingly good payroll numbers continued to boost the U.S. dollar versus many developed-market currencies.

DMC employed derivatives in the intermediate-term strategy. In addition to the U.S. Treasury futures mentioned earlier, it hedged currency losses with strict stop-loss mitigation tactics. Total currency hedging in the intermediate-term portfolio clawed back 17 basis points from the index deficit.

Diversified floating-rate component

In managing its diversified floating-rate portion of the Fund’s assets, DMC principally invests in a diversified group of floating-rate securities. During the fiscal year, those assets made up about 5% of the total DMC-managed assets within the Fund.

The diversified floating-rate component of DMC’s portion of the Fund outperformed the London interbank offered rate (Libor) — DMC’s internal benchmark for this component — and returned 0.80%. During the 12-month period, DMC’s primary objective was to maintain a duration of about three months within its diversified floating-rate segment.

Investment grade credit represented the largest segment (averaging more than half) of this portion of the Fund. An 18% exposure to financials returned 0.86%, contributing 26 basis points to performance. Industrials were the largest sector exposure within high-grade credit but underperformed the benchmark. Utilities and noncorporate positions contributed little to overall performance.

Emerging markets, with a 3% weighting within this component, detracted from performance, due largely to security selection.

Performance was mixed for assets rated below investment grade. The Fund benefited from having 30% exposure to bank loans, which returned 1.41%. However, exposure to the energy sector broadly detracted from results.

On average, DMC maintained a 5% exposure to AAA-rated asset-backed securities within this component, which help provide liquidity and risk management flexibility. This holding outperformed Libor with a 0.41% total return.

DMC used interest rate swaps in the diversified floating-rate strategy to hedge its allocation to fixed-rate bonds. These positions declined in value as rates fell.

Overall, the use of derivatives in DMC’s portion of the Fund had a slight negative effect on overall performance but was not material. It is worth noting that the use of derivatives in the diversified floating-rate component was used to hedge fixed-rate bonds.

PIMCO

Note: The portfolio-level discussion presented below appears in two sections. The first section covers PIMCO’s portion of the Fund that focused on an intermediate-term strategy, while the second section covers its portion of the Fund that focused on a low duration strategy.

Intermediate-term component

The intermediate-term component of PIMCO’s portion of the Fund returned 6.28% (before fees), outperforming its benchmark, the Barclays U.S. Aggregate Index by 56 basis points for the Fund’s fiscal year. An underweight to U.S. duration detracted from performance, as yields on U.S. Treasurys generally fell. Additionally, yield curve positioning with an underweight to longer-dated Treasurys hurt performance, as intermediate and long rates fell the most.

Overall spread sector strategies added to returns during the 12-month period. An average underweight to agency mortgage-backed securities (MBS) modestly detracted from returns. However, positive security selection within agency collateralized mortgage obligations (CMOs) more than offset this. An allocation to nonagency MBS was positive for returns, as the sector benefited from strong demand and limited supply. An underweight to investment grade credit and security selection within high yield financials and industrials was positive for performance. Holdings of Treasury inflation-protected securities (TIPS) detracted from performance, as break-even levels tightened. Lastly, a long U.S. dollar bias versus the euro and Japanese yen helped performance, as these currencies depreciated relative to the U.S. dollar.

2

Table of Contents

Low duration component

The low duration component of PIMCO’s portion of the Fund returned 2.08% (before fees), outperforming PIMCO’s internal benchmark, the BofA Merrill Lynch

1–3 Year U.S. Treasury Index by 1.08% for the Fund’s fiscal year. An underweight to U.S. duration detracted from performance, as yields on U.S. Treasurys generally fell. However, yield curve positioning more than offset the underweight position. In this portion of the Fund, PIMCO concentrated its underweight on the short end of the yield curve, where rates rose, and had an allocation to intermediate rates, where yields fell. Short exposure to core European rates detracted from returns, as yields fell in this region.

Overall spread sector strategies contributed to returns during the fiscal year. An allocation to nonagency MBS helped, as the sector benefited from strong demand and limited supply. Exposure to investment grade credit was negative, as the sector underperformed, but this was more than offset by positive security selection within financials and industrials. Exposure to U.S. dollar–denominated Brazilian debt within the energy sector detracted from performance since declining oil prices hurt this sector. Lastly, a long dollar bias versus the euro and yen boosted performance, as these currencies depreciated relative to the dollar.

Currency forwards held within PIMCO’s intermediate-term and low duration portions of the Fund had a positive material effect on performance. PIMCO used currency forwards to short the euro and yen, which depreciated against the U.S. dollar during the fiscal year. Its use of money market and government futures, interest rate swaps, and credit default swaps did not have a material impact on performance, nor did the use of options and interest rate swaps.

| (continues | ) | 3 |

Table of Contents

Portfolio management reviews

April 7, 2015

Performance review (for the year ended March 31, 2015) | ||||||

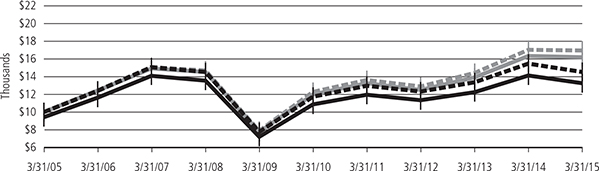

Optimum International Fund (Class A shares) | 1-year return | – 6.25% | ||||

Optimum International Fund (Institutional Class shares) | 1-year return | – 6.04% | ||||

MSCI EAFE Index (gross) (benchmark) | 1-year return | – 0.48% | ||||

MSCI EAFE Index (net) (benchmark) | 1-year return | – 0.92% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum International Fund, please see the table on page 19.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Acadian Asset Management LLC (Acadian)

EARNEST Partners LLC (EARNEST)

The Board of Trustees of the Fund approved the appointment of Acadian Asset Management LLC (“Acadian”) as a sub-advisor to the Fund during the fiscal year. Acadian replaced BlackRock Advisors, LLC (“BlackRock”) as a sub-advisor to Optimum International Fund. Please see the supplement to the Fund’s prospectus, dated Dec. 22, 2014, for more information.

Market overview

The fiscal year ended March 31, 2015, was a tough one for international markets and investors. Economies worldwide were buffeted by cross currents that were difficult to navigate. The fiscal year began with a profound rotation from growth into value and also featured a major strengthening of the U.S. dollar, a historic drop in oil prices, increased geopolitical tensions in Ukraine and the Middle East, and the continued focus on the divergent central bank policies in different markets as a key driver of results.

Through the end of 2014, weak European economic data, more dovish commentary from the European Central Bank and the Bank of Japan, and continued expectations for monetary tightening by the U.S. Federal Reserve drove the U.S. dollar higher. At the same time, the drop in oil prices exacerbated the already-tenuous deflationary environments in both Europe and Japan.

However, by the beginning of 2015, a nascent recovery emerged in Europe, particularly in Germany, as the effects of lower oil prices, the euro’s drop, and quantitative easing combined to provide an inflection point.

A similar phenomenon occurred in Japan where the yen weakened 15% over the fiscal year relative to the dollar. Exports ranging from semiconductors to pick-up trucks increased. Strong corporate earnings from the nation’s exporters and fourth-quarter gross domestic product recovery (following two quarters of contraction) benefited Japanese equities.

Emerging markets remained mixed. Chinese equities continued to rise even as signs of slowing mounted. There were signs of trouble in Brazil, Russia, India, China, and South Africa (BRICS) and, in general, emerging markets underperformed their developed — market counterparts.

Source: Bloomberg

Fund performance

Optimum International Fund declined in a tough year for international equities, and trailed its benchmark, the MSCI EAFE (Europe, Australia, Far East) Index, which also declined. In Acadian’s case, an underweight in financial services was a detractor. EARNEST underperformed in the energy sector; its underweight to Japan was also a detractor. For BlackRock, stock selection in industrials and financials detracted from performance within its portion of the Fund.

Acadian

Acadian managed its portion of the Fund from Jan. 26, 2015 to March 31, 2015. During this period, Acadian outperformed the MSCI EAFE Index.

On a sector level, Acadian added value via its overweight position in information technology. During the fiscal period, many technology companies reported earnings that exceeded consensus estimates and returned money to investors in the form of dividends and share repurchases. Acadian’s underweight position in energy was also a contributor, as slumping oil prices and a stronger U.S. dollar hurt the sector.

4

Table of Contents

Financial services was the only notable performance detractor from Acadian’s portion of the Fund during the fiscal period. Acadian maintained an underweight position in this sector and, subsequently, underperformed when several financial institutions received approval from the Fed in March 2015 to initiate stock buy-back programs and raise dividends — developments that seemed to provide a boost to overall sector performance.

In security selection, two holdings that contributed to Acadian’s portion of the Fund were Delhaize Group and Alps Electric. Shares of Delhaize Group advanced after the Belgian supermarket operator reported solid fourth-quarter results, including double-digit sales growth at its Hannaford and Food Lion chains. Meanwhile, shares of Alps Electric rallied after Morgan Stanley upgraded its rating for the Japanese electronics manufacturer to “overweight” from “equal weight.”

In contrast, two holdings that detracted from performance within Acadian’s portion of the Fund were Deutsche Lufthansa and Hindustan Unilever. Shares of Deutsche Lufthansa dropped after the German air carrier suspended its 2014 dividend. The company cited several factors, including poor full-year earnings brought on by the sale of the company’s information technology unit, an increase in pension liabilities, and fuel-hedging provisions. In India, shares of Hindustan Unilever retreated after this leading provider of consumer goods reported a fiscal third quarter net loss.

BlackRock

During the period that BlackRock was a sub-advisor to the Fund, its portion of the Fund posted a negative return and underperformed the benchmark. Stock selection in the financials and industrials sectors was the main detractor. An overweight allocation and good stock selection in the healthcare sector helped dampen losses. Holdings in the information technology sector also outperformed.

Within the financials sector, BlackRock’s holdings in the real estate services sub-industry led detractors due to its position in U. K.-based Foxtons Group. A steep decline in prices and volumes in the London property market negatively affected this residential real estate company.

BlackRock’s security selection in the industrials sector also detracted from relative returns, led by a position in Osram Licht. Based in Germany, Osram is one of the world’s two leading lighting product manufacturers. The stock sold off over the fiscal period, ignited by poor operational execution, decreased capital expenditures, and excessive cost cutting.

On the plus side, BlackRock’s overweight allocation and stock selection in the healthcare sector contributed to its portion of the Fund. BlackRock consistently focuses on companies that have positioned themselves to benefit from innovation, mergers-and-acquisitions activity, and healthcare reform. More specifically,

positioning in the pharmaceuticals subindustry led to gains for the sector, driven by a holding in Novartis. Based in Basel, Switzerland, Novartis is one of the elite innovators in the pharmaceutical industry, and BlackRock’s portion of the Fund benefited from Novartis’ strong pipeline of drugs for the treatment of psoriasis, heart failure, and respiratory-related illnesses. BlackRock’s security selection in information technology also contributed to gains, led by holdings in the internet software and services subindustry. Baidu, a Chinese developer of search engines and related products, was a strong performer. Baidu traded significantly higher after reporting exponential growth above expectations, resulting from widening profit margins and continued demand for internet search engines in China.

The use of derivatives in BlackRock’s portion of the Fund was small during the period, but deliberate in risk management decisions. Derivatives were used in the form of forward currency transactions to hedge currency exposure of its holdings back to the exposure of the benchmark but they had little effect on performance.

EARNEST

During the period, EARNEST’s portion of the Fund posted a negative return, trailing the MSCI EAFE Index.

EARNEST’s underperformance stemmed largely from its overweight to the energy sector. The spot price of oil fell more than 50% over the last nine months of the period (from approximately $100 to $50 a barrel). EARNEST’s allocation was a headwind as its portion of the Fund had twice the weighting to energy than the benchmark (13% versus 6.5%). Additionally, EARNEST’s Japanese holdings trailed, and its underweight to Japan also detracted as the Nikkei Index was up more than 10% for the period.

The industrials and healthcare sectors were the largest contributors to EARNEST’s portion of the Fund during the fiscal year, primarily due to stock selection. That said, one of EARNEST’s strongest performers was a financial services company. ICICI Bank is India’s largest private-sector bank by assets. The company reported strong net profits, driven by strength in its retail franchise, which saw loan growth of 25% at the end of 2014. ICICI has also been able to maintain its asset quality. This was an area of concern for the market in 2013 as investors had expected loan quality to deteriorate in light of India’s macroeconomic problems. ICICI’s notable customer service, however, fostered continued growth, and shares were up more than 20% for the period.

ICON is a global contract research organization, with headquarters in Ireland. The company provides outsourced phase I-IV clinical trial management and laboratory services for pharmaceutical and biotech companies. Outsourcing is a growing trend, and pharmaceutical companies are consolidating their relationships with fewer strategic partners. As such, ICON has seen steady earnings growth in excess of expectations. Shares rose close to 50% during the fiscal year.

| (continues | ) | 5 |

Table of Contents

Portfolio management reviews

Optimum International Fund

As noted earlier, investments in Japan and in the energy sector were the largest detractors during the fiscal year. Hitachi is the well-known Japanese conglomerate with a diversified revenue stream ranging from thermal power systems, water recycling systems, and electronic materials, to automotive components, telecom services, and home appliances. During the most recent quarter, management reported revenues in excess of expectations; however, operating profits disappointed, despite being above management’s guidance. The stock was down more than 5% for the fiscal year. Statoil is one of the world’s largest oil and gas companies and is the largest oil producer in its home country of Norway. The stock fell more than 30% during the fiscal year, driven by an approximately 50% decline in Brent oil prices. However, Statoil withstood the fall in oil price due to investor appreciation of Statoil’s focus on generating free cash flow and improving its return on invested capital.

Overall, Optimum International Fund used derivatives, including foreign currency exchange contracts, during the fiscal year. However, these had a minimal effect on performance.

6

Table of Contents

April 7, 2015

Performance review (for the year ended March 31, 2015) | ||||||

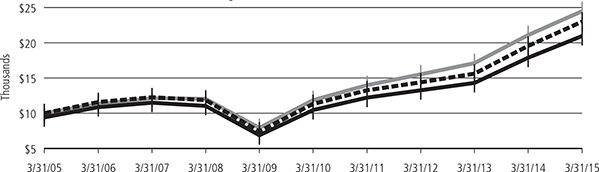

Optimum Large Cap Growth Fund (Class A shares) | 1-year return | +17.27% | ||||

Optimum Large Cap Growth Fund (Institutional Class shares) | 1-year return | +17.55% | ||||

Russell 1000® Growth Index (benchmark) | 1-year return | +16.09% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Large Cap Growth Fund, please see the table on page 22.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Fred Alger Management, Inc. (Alger)

T. Rowe Price Associates, Inc. (T. Rowe Price)

Market overview

U.S. stock market indices posted strong gains during the fiscal year ended March 31, 2015, as the global economy continued to gradually improve. Major market indices climbed to record highs during the period with large- and mid-cap stocks outperforming small-caps. As measured by Russell indices, growth stocks outperformed value across all market capitalizations. In the United States, an accommodative U.S. Federal Reserve kept interest rates at historically low levels even as continued employment gains, lower energy prices, and steady economic growth raised investor expectations for an interest rate increase.

Europe continued to show signs of stabilization, and as the fiscal year progressed, increasing economic strength in Germany and the United Kingdom spread to other European countries. Lower interest rates, a weakening euro that helped European export markets, and the European Central Bank’s aggressive quantitative-easing program supported this stabilization. Japan, China, and many Southeast Asian emerging markets continued to experience reasonably positive gross domestic product growth due in part to lower energy prices, Japan’s own quantitative-easing program, and China’s steady bank effort to restore liquidity. Amid this slow-but-steady progression of global economic growth, corporate profits generally continued to strengthen.

The strong market environment was also supported by an increase in global merger and acquisition activity, shareholder activism, attractive equity valuations, and a strengthening U.S. dollar that helped drive down commodity costs and shore up consumer income.

Source: Bloomberg

Fund performance

Optimum Large Cap Growth Fund delivered positive double-digit returns for the fiscal year, outperforming its benchmark. Sector allocation was the primary contributor to performance within the portions of the Fund managed by Alger and T. Rowe Price. Stock selection was a secondary but still significant factor during the fiscal year. The healthcare sector was the most significant contributor in both Alger’s and T. Rowe Price’s portions of the Fund. Also within Alger’s portion of the Fund, the information technology sector was a leading contributor while industrials and financials detracted. T. Rowe Price’s portion of the Fund saw a significant contribution from industrials; its detractors included information technology and consumer discretionary sectors.

Alger

With its strategy of investing in companies undergoing “positive dynamic change, “ Alger seeks what it views as high-quality, domestic growth stocks that can potentially generate strong earnings growth and free cash flow.

An overweight in the healthcare sector was a strong contributor to performance in Alger’s portion of the Fund, as its holdings in the sector outperformed the healthcare companies in the benchmark index. Many of Alger’s favored companies in this sector posted strong earnings increases, raised dividends to shareholders, generated strong levels of free cash flow, and authorized substantial share repurchase programs. Additionally, several of the healthcare companies in Alger’s portion of the Fund achieved advancements in drug trials and regulatory approvals. Another significant contributor to performance was Alger’s overweight in information technology, as these companies within its portion of the Fund on average gained more than 25% for the fiscal year.

In the industrials sector, Alger’s underweight allocation was largely responsible for its underperformance in the sector. In financials, an overweight versus the benchmark, combined with weak stock selection, detracted from performance in Alger’s portion of the Fund.

| (continues | ) | 7 |

Table of Contents

Portfolio management reviews

Optimum Large Cap Growth Fund

At the individual security level, Actavis was a leading contributor to overall results in Alger’s portion of the Fund. Actavis manufactures and distributes generic pharmaceuticals and branded pharmaceutical products focused on urology, nephrology, and women’s health globally. The shares gained more than 45% during the Fund’s fiscal year. The company is a leading global generic pharmaceutical company with one of the industry’s most profitable and sustainable generic pipelines that includes many first-to-file and difficult-to-manufacture drugs. Actavis also is aggressive with patent challenges, has what Alger believes is a leading management team, and appears positioned to cut costs across the company, allowing for greater merger-and-acquisition and pipeline investment.

NXP Semiconductors was another notable contributor to Alger’s portion of the Fund, which gained more than 65% during the fiscal year. NXP Semiconductors is one of the leading suppliers of motion co-processors and the near field communication (NFC) controller chip used in mobile payment systems. The company has benefited from the growth in mobile adoption and usage. A key driver has been its proprietary hardware and customized software capabilities, in addition to its product innovation.

The largest relative detractor in Alger’s portion of the Fund was industrials company Precision Castparts. The company manufactures and sells metal components and products used for aircraft engines, industrial gas turbine engines, medical implants, aerial vehicles, and other industrial applications. Although the company did not execute effectively over the last 12 months, Alger remains positive given the company’s growth prospects and management team. Alger’s average allocation to the stock was overweight the benchmark index, which seemed to magnify the effect of the company’s underperformance.

Within the financials sector, Carlyle Group detracted from performance in Alger’s portion of the Fund as the shares declined sharply in the fourth quarter of 2014. Slowed earnings growth and consequently, significant outflows in assets under management, were to blame. Overall, Alger remains positive on the company and the sector and believes that relative valuations are attractive.

T. Rowe Price

T. Rowe Price’s portion of the Fund contributed to Fund performance relative to the benchmark. Overall, sector allocations were the principal reason for this relative performance, though stock selection was also notably positive.

Healthcare, driven mainly by stock selection, was by far the leading relative outperformer in T. Rowe Price’s portion of the Fund. A significant overweight allocation to this strongest-performing sector also helped. Shares of Pharmacyclics surged after the biotechnology company announced better-than-expected revenue forecasts for its leukemia drug Imbruvica, which the U.S. Food and Drug Administration also approved for the additional treatment of a rare type of lymphoma. Shares surged later after AbbVie agreed to acquire the company in a $21 billion deal.

Industrials and business services outperformed on stock selection. Shares of American Airlines Group experienced a difficult third quarter in 2014 but rebounded sharply, helped by solid fundamental results, progress on its merger integration with US Airways, and falling crude oil prices. The company does not hedge fuel, which allowed it to take full advantage of the decline in oil prices.

Furthermore, American Airlines has more transatlantic traffic than its peers, allowing the airline to benefit from its competitive position.

Consumer discretionary was the largest relative detractor in T. Rowe Price’s portion of the Fund, largely due to stock selection. Wynn Resorts detracted from relative performance as its Macau revenues continued to decline. Though its VIP and high-end mass-gaming business in Macau continued to slide, the casino operator’s share of the mass-business market experienced an increase relative to last year.

Stock selection in information technology, including a limited allocation to Apple, hurt relative performance in T. Rowe Price’s portion of the Fund. Apple’s shares were up during the fiscal year as investors anticipated the iPhone 6 upgrade cycle, and the company subsequently reported strong quarterly results driven by iPhone sales that exceeded expectations. However, the company is slowly losing share in the tablet market, and T. Rowe Price believes that the law of large numbers and a decelerating product cycle could eventually hamper iPhone growth. The tech firm is generating solid gross margins, remains financially sound, and has become more committed to returning value to shareholders via buybacks. T. Rowe Price is also encouraged by the potential market effect to two new products, Apple Watch and Apple Pay, a mobile payment option for iPhone and Watch users.

Overall, Optimum Large Cap Growth Fund used derivatives, including foreign currency exchange contracts, during the fiscal year. However, these had a minimal effect on performance.

8

Table of Contents

April 7, 2015

Performance review (for the year ended March 31, 2015) | ||||||

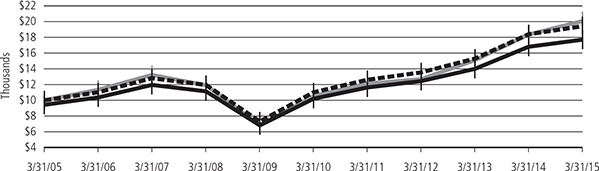

Optimum Large Cap Value Fund (Class A shares) | 1-year return | +5.34% | ||||

Optimum Large Cap Value Fund (Institutional Class shares) | 1-year return | +5.60% | ||||

Russell 1000® Value Index (benchmark) | 1-year return | +9.33% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Large Cap Value Fund, please see the table on page 25.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Herndon Capital Management, LLC (Herndon)

Massachusetts Financial Services Company (MFS)

Market overview

A generally risk-friendly environment persisted from early in the Fund’s fiscal year until mid-2014. While geopolitical tensions flared in the Middle East and Ukraine, any market setbacks were short-lived. Improving economic growth within the United States and the potential for a looser monetary policy in regions with slowing growth such as Japan, Europe, and China, supported price-sensitive investments, or risk assets. The European Central Bank (ECB), for example, cut policy interest rates below zero. Expectations were subsequently high for additional rate cuts and additional nonconventional easing measures. Similarly, toward the middle of the fiscal year, and on the heels of lackluster growth trends, the Bank of Japan surprised markets with fresh stimulus measures. The related decline in government bond yields and credit spreads within developed markets also supported equity markets during this period.

A dominant trend during the second half of the Fund’s fiscal year was the ongoing rise in U.S. equities alongside a decline in U.S. bond yields. The uptrend in U.S. corporate margins and profits continued throughout the second half of 2014, but a rising dollar and a sharp decline in commodity prices, particularly crude oil prices, negatively affected credit markets. This was particularly true among U.S. high yield and emerging market debt. The higher weightings of oil and gas credits in these asset classes resulted in widening spreads and increased volatility. Toward the end of this period, declining inflation and inflation expectations caused a mini-wave of global quantitative easing (QE). In particular, the ECB initiated a potentially open-ended phase of QE, a move that appeared to support both risk assets and government bond prices. Meanwhile, the U.S. dollar continued to

benefit from the perception that the U.S. Federal Reserve could tighten its monetary policy in mid to late 2015.

Source: Bloomberg

Fund performance

Optimum Large Cap Value Fund generated solid absolute gains but underperformed its benchmark, the Russell 1000 Value Index, for the fiscal year. A dramatic decline in oil prices, combined with weak-performing stocks within financials, were significant detractors for Herndon’s portion of the Fund. Holdings in healthcare and an underweight position in technology detracted from performance within MFS’s portion of the Fund.

Herndon

Herndon’s approach to managing its portion of the Fund remained consistent throughout the fiscal year. The management team seeks value-creating opportunities at the individual stock level and subsequently aggregates individual stock information to determine sector weightings. Each market sector presents both risks and opportunities; the team seeks adequate compensation for risks taken. The team seeks stocks that it believes offer value-creating opportunities, which it defines as those exhibiting both attractive fundamental and valuation characteristics.

From a sector perspective, the strongest performance relative to the benchmark came from the materials and telecommunications sectors. Telecommunications companies in general suffered during the Fund’s fiscal year, and Herndon’s portion of the Fund held just one stock from the sector, global broadband and cell phone leader Verizon Communications, which had positive returns. Positive stock selection within the materials sector also helped bolster returns, particularly from NewMarket Corporation, parent company for several petroleum additives businesses, and CF Industries, agricultural fertilizer producer and distributor.

| (continues | ) | 9 |

Table of Contents

Portfolio management reviews

Optimum Large Cap Value Fund

The primary performance detractors within Herndon’s portion of the Fund came from the energy and financial sectors. Unexpected dramatic declines in oil prices, particularly during the fourth quarter of 2014, substantially affected returns, and blindsided many investors. Within the financial sector, increased investor pessimism dragged down performance of residential mortgage provider Nationstar Mortgage Holdings and asset manager and financial planning firm Waddell & Reed. Despite negative performance during the fiscal year, Herndon believes both holdings maintain solid long-term fundamentals and therefore it continues to hold each.

From an individual stock perspective, consumer electronics leader Apple advanced by more than 65% during the Fund’s fiscal year, due primarily to its consumer-needs driven focus. The company has surprised the market by maintaining a culture of innovation, even several years after it transitioned leadership from its late founder Steve Jobs to former COO and current CEO Tim Cook. Another key contributor to Herndon’s portion of the Fund was off-price department store chain Ross Stores. The company reclaimed investor attention as it continued to deliver quality goods at fair value, particularly as consumers remained cost conscious. Herndon views each of these as a value creating opportunity and therefore continues to hold them in the Fund.

In terms of laggards, U.S. shale producer Oasis Petroleum suffered a 70% loss during the Fund’s fiscal year. More than 50% of that drop was attributable to factors outside the dramatic decrease in oil prices. Herndon eliminated its position in this stock in early 2015 as part of an overarching adjustment to sector weightings. Another performance detractor, Waddell & Reed, was plagued by negative investor sentiment during the fiscal year amid turnover within its portfolio management. Even so, Herndon believes the market’s reaction was overstated and therefore it continues to hold the stock in its portion of the Fund.

MFS

MFS’s investment philosophy and approach for its portion of the Fund remain consistent during all market environments. The management team seeks to identify high-quality, undervalued stocks that offer the best potential for healthy long-term, risk-adjusted returns.

From a sector perspective, performance for MFS’s portion of the Fund relative to the benchmark was enhanced by an underweight allocation to energy stocks, which suffered dramatic losses during the fiscal year. Most notably, MFS held an underweight position in integrated oil and gas company ExxonMobil, a strategy that benefited performance relative to the benchmark. Stock selection within the industrial goods and services and basic materials sectors also contributed to performance.

An underweight position in the technology industry, which posted strong results during the fiscal year, detracted from performance within MFS’s portion of the Fund, as did weak stock selection within the sector. MFS’s portion of the Fund did not hold several strong benchmark performers, including network equipment company Cisco Systems and computer and personal electronics maker Apple. Further, MFS’s position in diversified technology products and services company IBM, which is not held within the benchmark, also detracted from performance.

At the individual stock level, a position in defense contractor Lockheed Martin (which was not represented within the benchmark) contributed to relative performance within MFS’s portion of the Fund. Conversely, MFS did not hold positions in industrial conglomerate General Electric or financial services firm Bank of America — lack of exposure to these names enhanced performance relative to the benchmark. Overweight positions in diversified technology company 3M, retail giant Target, insurance company St. Paul Travelers, and drugstore retailer CVS Health also contributed to relative performance. Other stock holdings that aided performance within MFS’s portion of the Fund included management consulting firm Accenture and semiconductor company Texas Instruments, neither of which was represented within the benchmark index.

At the individual stock level, an overweight position in tobacco company Philip Morris International detracted from performance. Other performance detractors included positions in Diageo, an international manufacturer and distributer of premium drinks, and media giant Viacom. Overweight positions in insurance provider MetLife, investment management firm Franklin Resources, oil and gas exploration and production company Occidental Petroleum, also hurt performance relative to the benchmark.

MFS’s portion of the Fund also benefited from its currency exposure during the fiscal year, which resulted primarily from differences between the Fund’s and benchmark’s exposures to holdings of securities dominated in foreign currencies. All of MFS’s investment decisions are driven by the fundamentals of each individual opportunity and, as such, it is common for the mutual funds that MFS advises to have different currency exposure than that of the benchmark.

Overall, Optimum Large Cap Value Fund used derivatives, including foreign currency exchange contracts, during the fiscal year. However, these had a minimal effect on performance.

10

Table of Contents

Optimum Small-Mid Cap Growth Fund

April 7, 2015

Performance review (for the year ended March 31, 2015) | ||||||

Optimum Small-Mid Cap Growth Fund (Class A shares) | 1-year return | +8.93% | ||||

Optimum Small-Mid Cap Growth Fund (Institutional Class shares) | 1-year return | +9.18% | ||||

Russell 2500™ Growth Index (benchmark) | 1-year return | +13.83% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Small-Mid Cap Growth Fund, please see the table on page 28.

The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions. Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

Columbia Wanger Asset Management, LLC (Columbia WAM)

Wellington Management Company, LLP (Wellington)

Market overview

During the Fund’s fiscal year ended March 31, 2015, domestic equity markets continued to gain, although at a slower pace than the previous year. Larger company stocks generally outperformed those of small companies, with growth stocks outperforming core and value stocks.

Though the overall market trend throughout the year was upward, with the S&P 500® Index passing through the 2,000 level for the first time and the NASDAQ making a brief return to 5,000, the pattern of volatility that began in 2013 continued. However, it was the specter of rising interest rates rather than the end of quantitative easing that repeatedly roiled the markets during the fiscal year. International concerns also arose throughout year, including heightened tension in Ukraine and the Middle East, the plunging price of oil, continued economic weakness in Europe and Japan, and a rapid strengthening of the U.S. dollar. On the positive side, the economy in the United States continued to grow as new-job creation picked up, unemployment declined, and interest rates remained low.

Interest rate sensitive areas such as utilities and real estate investment trusts (REITs) beat the overall market as investors clamored for the yield these stocks offered. In addition, biotech stocks performed well during the 12-month period. Energy stocks declined the most as oil prices were down nearly 50% in the last six months of 2014. Industrial company stocks also lagged the market. Because smaller-cap industrial companies tend to have a higher amount of revenues outside the U.S., the stronger U.S. dollar and

lower growth in emerging markets negatively affected many of these stocks.

Source: Bloomberg

Fund performance

Optimum Small-Mid Cap Growth Fund underperformed its benchmark index for the Fund’s fiscal year due, in part, to poor stock selection in the healthcare sector by both sub-advisors. Additionally, within one sub-advised portion of the Fund, an overweight and weak relative performance of companies in the industrials sector was a notable detractor.

Wellington

Wellington’s portion of the Fund generated strong gains on an absolute basis but underperformed the benchmark for the fiscal year. Generally, weak security selection within information technology weighed on relative performance, as did selection within healthcare. Stronger selection within energy, consumer discretionary, and materials helped to partially offset this weakness.

Among the strongest contributors to Wellington’s portion of the Fund were companies in energy, pharmaceuticals, and information technology (the problem with otherwise poor stock selection in that last sector notwithstanding). Shares of Mobileye — the leading designer of driver-assistance systems that seek to increase driver safety and comfort — were purchased prior to the company’s initial public offering and subsequently climbed. Later in the fiscal year, Wellington exited the position. Shares of Athlon, an exploration and production company focused on the Permian Basin, gained after it was acquired by natural gas producer Encana. Wellington also exited that position during the fiscal year. Shares of Anacor Pharmaceuticals, a biopharmaceutical company focused on discovering, developing, and commercializing novel small-molecule therapeutics, rose as the market responded favorably when the company highlighted its two lead compounds in development during a presentation to analysts. Wellington initiated its position during the 12-month period and continued to hold it as of the end of the Fund’s fiscal year. Wellington’s investment in several privately held companies also contributed to relative performance in aggregate.

| (continues | ) | 11 |

Table of Contents

Portfolio management reviews

Optimum Small-Mid Cap Growth Fund

Web.com Group, an internet service provider focused primarily on small- and medium-sized businesses, was one of the largest detractors from Wellington’s portion of the Fund. Its shares declined following weak results brought about by increased competition in the company’s “do-it-for-me” web design and service business. Wellington exited the position during the fiscal year. Shares of zulily, an e-commerce company focused on children’s and women’s apparel, and other product categories, also declined. The company faced significant challenges related to marketing promotions, specifically flash sales driving customer traffic. The lack of a position in healthcare company Intermune, a strong-performing constituent of the Russell 2500 Growth Index, also detracted from relative results in Wellington’s portion of the Fund.

As of the end of the fiscal year, Wellington’s portion of the Fund had significant exposure to the information technology, industrials, and healthcare sectors, and no exposure to utilities and telecommunication services.

Columbia WAM

Columbia WAM’s portion of the Fund gained on an absolute basis, but underperformed the benchmark, reflecting the stronger performance of growth-oriented investments during the fiscal year. Columbia WAM employs a low-turnover, bottom-up (stock-by-stock), fundamental investment strategy and made no significant adjustments to its portion of the Fund during the 12-month period. The company seeks to identify reasonably priced growth companies that it believes are positioned to grow over the next three to five years. During much of the fiscal year, more reasonably priced companies underperformed both high-priced momentum stocks and value stocks, resulting in significant relative underperformance for Columbia WAM’s portion of the Fund.

The consumer discretionary and telecommunication sectors were the two most significant contributors to Columbia WAM’s portion of the Fund. During the fiscal year, it maintained an underweight in consumer discretionary and an overweight in telecommunications. These weighting decisions had little effect on performance. Instead, positive results were largely attributable to strong stock selection in both sectors.

Consumer discretionary stocks generally outperformed the overall benchmark index return while Columbia WAM’s selections in this sector outperformed the benchmark index by nearly 5% during the period. Columbia WAM’s allocation to telecommunications, roughly 2% as of the end of the Fund’s fiscal year, was greater than that of the benchmark. While telecommunications overall was a laggard for

the Fund’s fiscal year, Columbia’s telecommunications stocks gained more than 50% during the fiscal year versus just more than 5% for the benchmark.

The two sectors that detracted most from performance in Columbia WAM’s portion of the Fund were healthcare and industrials. Industrials accounted for the largest absolute and relative weight. With industrials lagging for the fiscal year, the weighting decision resulted in below-benchmark performance. Additionally, several of these industrial stocks derive a fair amount of revenue from outside the U.S. With the U.S. dollar strengthening throughout the 12-month period, prices rose for industrial goods outside the U.S. while demand from end users slowed.

Columbia WAM’s portion of the Fund was underweight the healthcare sector on average during the fiscal year. At the same time, healthcare stocks (in particular pharmaceuticals and biotechnology) were among the strongest performers within the benchmark. The combination of the underweight and Columbia WAM’s stock selection — which failed to keep pace with the torrid 36% return of the benchmark healthcare stocks during the period — was the culprit in Columbia WAM’s underperformance in this sector.

At the individual stock level, Akorn and Infinera were the two strongest contributors to performance in Columbia WAM’s portion of the Fund. Both stocks more than doubled during the Fund’s fiscal year.

Akorn is a developer of specialty generic drugs and has experienced strong revenue growth from new products. Infinera is an optical networking equipment company. Internet service providers deploy its networks as users increase data transmission. Infinera’s Cloud Xpress product appears to have strong potential.

During the fiscal year, the two largest detractors were Rosetta Resources and Chicago Bridge & Iron. Rosetta Resources, an energy exploration company, fell more than 64% during the fiscal year, reflecting the hefty decline in oil prices and the anticipated lower level of production that lower prices will induce.

Chicago Bridge & Iron is a multinational engineering and construction company that specializes in natural gas and petrochemical projects. Falling energy prices were partly responsible for the stock’s decline, as well as potential cost overruns at two nuclear power plant projects. For these reasons, Columbia WAM exited that position during the fiscal year.

Overall, Optimum Small-Mid Cap Growth Fund used derivatives, including foreign currency exchange contracts, during the fiscal year. However, these had a minimal effect on performance.

12

Table of Contents

Optimum Small-Mid Cap Value Fund

April 7, 2015

Performance review (for the year ended March 31, 2015) | ||||||

Optimum Small-Mid Cap Value Fund (Class A shares) | 1-year return | – 0.69% | ||||

Optimum Small-Mid Cap Value Fund (Institutional Class shares) | 1-year return | – 0.53% | ||||

Russell 2500™ Value Index (benchmark) | 1-year return | +6.59% |

Past performance does not guarantee future results.

For complete, annualized performance for Optimum Small-Mid Cap Value Fund please see the table on page 31. The performance of Class A shares excludes the applicable sales charge and reflects the reinvestment of all distributions.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts. Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index.

Advisor

Delaware Management Company (DMC)

Sub-advisors

The Delafield Group, a division of Tocqueville Asset

Management L.P. (Tocqueville)

The Killen Group, Inc. (Killen)

Westwood Management Corp. (Westwood)

Market overview

The Fund’s fiscal year ended March 31, 2015 was marked by rising volatility, with investors keenly sensitive to the actions of global central banks. A significant decline in crude oil prices, which began in the third quarter of 2014, also contributed to the volatile environment. The fiscal year began with many investors pulling back from equities on the release of weaker-than-expected first-quarter 2014 domestic economic data that was due, in part, to severe weather. Improved consumer confidence, job numbers, and housing reports then seemed to be the tonic for a jittery market, despite renewed geopolitical flare-ups in the Middle East and Ukraine.

Challenges remained, however, as investors anticipated a near-term rise in interest rates. Despite the U.S. Federal Reserve’s October 2014 decision to complete its quantitative easing (QE) program, investors seemed encouraged by continued signs of strength in the U.S. economy and solid earnings reports.

In early 2015, the markets experienced persistent volatility as oil prices continued to drop, the U.S. dollar surged, and worries about international economic activity, particularly in China, resurfaced. In late January, the European Central Bank embarked on its own version of QE, which resulted in an equity rally, particularly for European stocks. For the balance of the Fund’s fiscal year, investors’ optimism won out, with fundamental economic and corporate data supporting indices just shy of record highs.

Source: Bloomberg

Fund performance

Optimum Small-Mid Cap Value Fund underperformed the Fund’s benchmark for the fiscal year. In Killen’s case, weak-performing stocks in the consumer discretionary sector were a significant factor. For Tocqueville, the two weakest detractors were holdings in the industrials and materials sectors. The third sub-advisor, Westwood, underperformed in the energy and producer durables sectors, while its holdings in materials & processing and increased exposure to healthcare stocks helped performance.

Tocqueville

Tocqueville’s investment approach remained consistent throughout the fiscal year, which resulted in performance that was out of step with the market. During this period, the Russell 2500 Value Index favored larger-tier companies, and financials and healthcare over basic industry. Tocqueville’s bottom-up (stock-by-stock), value-driven investment approach did not uncover attractive opportunities in the financial and healthcare sectors. While these two sectors comprised nearly 44% of the benchmark’s holdings — and contributed more than six percentage points of total return to the index during the fiscal year — Tocqueville’s portion of the Fund had virtually no exposure to these stocks during the fiscal year.

Tocqueville’s holdings in the industrials sector, followed by materials, were the most detrimental to its performance. In industrials, its portion of the Fund underperformed the benchmark’s sector holdings, while Tocqueville’s large weighting compounded the weak performance. In materials, Tocqueville’s absolute returns were essentially in-line with those of the benchmark, but an overweight there hurt relative performance. Within the industrials segment, two of the poorest performers were Aegion and Civeo. Both declined on weaker outlooks, largely due to the rapid decline in energy prices. Tocqueville ultimately sold Civeo after the company decided against the real estate investment trust (REIT) conversion that Tocqueville had anticipated. A number of Tocqueville’s holdings in the industrials and materials sectors experienced tangential energy price-related

| (continues | ) | 13 |

Table of Contents

Portfolio management reviews

Optimum Small-Mid Cap Value Fund

declines. Some, like Dover and Wesco International were the result of end-market exposure; others, like Eastman Chemical, were a function of energy-related input cost variations.

In contrast, Tocqueville’s overweight in the information technology (IT) sector was a bright spot. Its stock selection outperformed the benchmark’s IT holdings for the fiscal year. Tocqueville’s electronic manufacturing service stocks contributed favorably on the strength of solid earnings reports and improved outlooks.

Flextronics International was the strongest contributor to the performance of Tocqueville’s portion of the Fund. The company reported solid earnings throughout the fiscal year, exhibited robust free-cash-flow generation, and strategically created shareholder value through substantial share repurchase activity. Staples was Tocqueville’s second-strongest contributor to performance. The stock showed modest improvement midway through the fiscal year on stabilized earnings trends, and then jumped following confirmed reports that the company was in advanced merger talks with Office Depot.

Energy XXI was the largest individual detractor from performance. Tocqueville invested in the company believing that its anticipated acquisition of EPL Oil & Gas would consolidate its position in the Gulf Coast shelf and lead to efficiencies of operation and substantial free cash flow. However, due to unexpected operating inefficiencies, the sharp decline in the price of oil, and tax-loss selling late in 2014, shares declined radically. Tocqueville sold the stock during the fiscal year. Carpenter Technology was Tocqueville’s next-biggest detractor from performance. Shares declined on missed earnings, a lowered outlook on a slower-than-expected ramp-up of its Athens, Ga., facility, and lower specialty steel prices.

Killen

The Killen Group’s value style strategy seeks to invest in what it views as overlooked and undervalued businesses. During the Fund’s fiscal year, Killen found contrarian investment opportunities in a number of sectors, including consumer discretionary, materials, and industrials. Killen’s allocations to specific sectors result from its bottom-up stock selection process rather than from a sector-weighting strategy.

The fiscal year was particularly challenging for the Fund’s asset class, as small-cap stocks underperformed the S&P 500 Index. In addition, the strong dollar darkened the outlook for many manufacturing companies, and the severe drop in oil and other commodity prices affected the near-term earnings potential of a number of holdings in Killen’s portion of the Fund. Despite these challenges, Killen’s portion of the Fund experienced strong performance within information technology, financials, and telecommunications. Double-digit returns from these sectors were primarily the result of large gains in one or more stocks.

For the 12-month period, Killen’s portion of the Fund posted negative returns within the energy, consumer discretionary, and industrials sectors. In aggregate, Killen underperformed the Fund’s benchmark, the Russell 2500 Value Index, for the same period.

KMG Chemicals, a manufacturer of specialty chemicals, and Methode Electronics, a manufacturer of electronic components used in automobiles and other industrial equipment, were strong performers within Killen’s portion of the Fund. KMG benefited from cost-savings initiatives and its divestment of a noncore business. In Methode’s case, improved manufacturing efficiencies and continued strong automotive segment sales for its center consoles played a large role in the stock’s strong showing.

Two of Killen’s holdings fell more than 50% for the Fund’s fiscal year. Vaalco Energy, an oil and gas exploration and development company, was hit by both rapidly declining oil prices and an unsuccessful exploration-drilling program. Even with a new CEO who Killen believes is focused on the correct strategy, the company faces structural issues that are likely to persist; therefore, Killen is in the process of exiting this position. LeapFrog Enterprises, a manufacturer of children’s electronic toys, has been tested by sales and operating margin pressure as its educational products have fallen out of favor with the marketplace. Killen believes that although LeapFrog is attractively priced and carries a strong balance sheet, the competitive pressures are too great for the company’s management team to overcome. Therefore, Killen plans to exit this position over the coming fiscal year.

Westwood

Westwood employs a consistent and disciplined approach throughout all market environments that seeks to protect capital in unfavorable market periods and provide attractive risk-adjusted returns over the long term. Stock selection priority is driven by extensive research to attempt to identify companies that have limited downside risk from strong fundamental underpinnings but that are also attractively valued.

Westwood’s security selection in the materials & processing and healthcare sectors aided both absolute and relative performance in Westwood’s portion of the Fund during the Fund’s fiscal year. Westwood’s materials & processing holdings benefited from improvements in the demand for housing-related materials and from moves to unlock value by several companies. Over the past two years, Westwood has increased exposure in the healthcare sector through the acquisition of companies with good earnings visibility that Westwood believes are unlikely to be affected by legislation-associated healthcare pricing pressures. This approach proved favorable for performance in its portion of the Fund during the fiscal year.

| 14 |

Table of Contents

Security selection in the energy and producer durables sectors hurt performance in Westwood’s portion of the Fund. Holdings in both sectors were hampered by the unexpected and dramatic decline in crude oil prices in the second half of 2014. Energy producers and industrial companies connected to energy production performed poorly in this environment. During the fiscal year, a number of companies held in Westwood’s portion of the Fund underwent corporate actions — including mergers and breakups — that unlocked a great deal of value and contributed strong returns. Westwood views this trend as a confirmation of the unrealized value it seeks to identify through its fundamental research process. Healthcare firms Hospira, acquired by Pfizer, and CareFusion, acquired by Becton, Dickinson & Co., both benefited from such corporate actions.

Energy exploration and production holdings were the worst performers in Westwood’s portion of the Fund during the 12-month period. Investors were forced to price the impact of a 50% decline in West Texas Intermediate crude during the last six months of 2014 into their valuations of these companies, and the result was a material drop in the stock prices of many companies. Two such holdings affected by this repricing were Rex Energy and Oasis Petroleum. Westwood exited both positions during the fiscal year.

Overall, Optimum Small-Mid Cap Value Fund used derivatives, including foreign currency exchange contracts, during the fiscal year. However, these had a minimal effect on performance.

| (continues | ) | 15 |

Table of Contents

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our website at optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | ||||||||||||

| Average annual total returns through March 31, 2015 | 1 year | 5 years | 10 years | |||||||||

| ||||||||||||

Class A (Est. Aug. 1, 2003) | ||||||||||||

Excluding sales charge | +4.21% | +4.35% | +5.17% | |||||||||

Including sales charge | – 0.49% | +3.39% | +4.68% | |||||||||

| ||||||||||||

Class C (Est. Aug. 1, 2003) | ||||||||||||

Excluding sales charge | +3.44% | +3.66% | +4.47% | |||||||||

Including sales charge | +2.44% | +3.66% | +4.47% | |||||||||

| ||||||||||||

Institutional Class (Est. Aug. 1, 2003) | ||||||||||||

Excluding sales charge | +4.47% | +4.70% | +5.52% | |||||||||

Including sales charge | +4.47% | +4.70% | +5.52% | |||||||||

| ||||||||||||

Barclays U.S. Aggregate Index | +5.72% | +4.41% | +4.93% | |||||||||

1Returns reflect the reinvestment of all distributions and are presented both with and without the applicable sales charges described below. Returns do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

Expense limitations were in effect for certain classes during some or all of the periods shown in the “Fund and benchmark performance” graph. The current expenses for each class are listed on the “Fund expense ratios” table on the next page. Performance would have been lower had expense limitations not been in effect.

Class A shares are sold with a maximum front-end sales charge of 4.50%, and have an annual distribution and service fee of 0.25% of average daily net assets. Performance for Class A shares, excluding sales charges, assumes that no front-end sales charge applied.

Class C shares are sold with a contingent deferred sales charge of 1.00% if redeemed during the first 12 months. They are also subject to an annual distribution and service fee of 1.00% of average daily net assets.

Performance for Class C shares, excluding sales charges, assumes either that contingent deferred sales charges did not apply or that the investment was not redeemed.

Institutional Class shares are available without sales or asset-based distribution charges only to certain eligible institutional accounts.

The “Fund and benchmark performance” table and the “Performance of a $10,000 investment” graph do not reflect the deduction of taxes the shareholder would pay on Fund distributions or redemptions of Fund shares.

2 The Fund’s expense ratios, as described in the most recent prospectus, are disclosed in the “Fund expense ratios” table on the next page. Delaware Management Company has agreed to reimburse certain expenses and/or waive certain fees in order to prevent total fund operating expenses (excluding any 12b-1 fees and certain other expenses) from exceeding 0.95% of the Fund’s average daily net assets from July 29, 2014, through July 29, 2015.* Please see the most recent prospectus and any applicable supplement(s) for additional information on these fee waivers and/or reimbursements.

16

Table of Contents

| Fund expense ratios | Class A | Class C | Institutional Class | |||

| Total annual operating expenses | 1.27% | 2.02% | 1.02% | |||

| (without fee waivers) | ||||||

| Net expenses (including fee | 1.20% | 1.95% | 0.95% | |||

| waivers, if any) | ||||||

| Type of waiver | Contractual | Contractual | Contractual |

* The contractual waiver period is from July 29, 2014 to July 29, 2015. Prior to July 29, 2014, the contractual waiver was 1.00%.

Fixed income securities and bond funds can lose value, and investors can lose principal, as interest rates rise. They also may be affected by economic conditions that hinder an issuer’s ability to make interest and principal payments on its debt.

The Fund may also be subject to prepayment risk, the risk that the principal of a fixed income security that is held by the Fund may be prepaid prior to maturity, potentially forcing the Fund to reinvest that money at a lower interest rate.

High yielding, noninvestment grade bonds (junk bonds) involve higher risk than investment grade bonds. The high yield secondary market is particularly susceptible to liquidity problems when institutional investors, such as mutual funds and certain other financial institutions, temporarily stop buying bonds for regulatory, financial, or other reasons. In addition, a less liquid secondary market makes it more difficult for the Fund to obtain precise valuations of the high yield securities in its portfolio.

If and when we invest in forward foreign currency contracts or use other investments to hedge against currency risks, the Fund will be subject to special risks, including counterparty risk.

The Fund may invest in derivatives, which may involve additional expenses and are subject to risk, including the risk that an underlying security or securities index moves in the opposite direction from what the portfolio manager anticipated. A derivative transaction depends upon the counterparties’ ability to fulfill their contractual obligations.

The Fund may experience portfolio turnover in excess of 100%, which could result in higher transaction costs and tax liability.

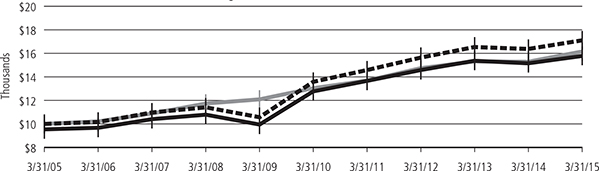

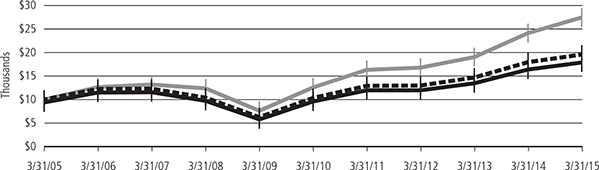

Performance of a $10,000 Investment1

Average annual total returns from March 31, 2005 through March 31, 2015

| Starting value (March 31, 2005) Ending value (March 31, 2015) | ||||||

| $10,000 | $17,107 | ||||

| $10,000 | $16,174 | ||||

| $9,550 | $15,801 | ||||

Optimum Fixed Income Fund — Institutional Class shares

Optimum Fixed Income Fund — Institutional Class shares Barclays U.S. Aggregate Index

Barclays U.S. Aggregate Index Optimum Fixed Income Fund — Class A shares

Optimum Fixed Income Fund — Class A shares1The “Performance of $10,000 investment” graph assumes $10,000 invested in Class A and Institutional Class shares of the Fund on March 31, 2005, and includes the effect of a 4.50% front-end sales charge (for Class A shares) and the reinvestment of all distributions. The graph does not reflect the deduction of taxes the shareholders would pay on Fund distributions or redemptions of Fund shares. Expense

| (continues | ) | 17 |

Table of Contents

Performance summaries

Optimum Fixed Income Fund

Performance of a $10,000 Investment1 (continued)

limitations were in effect for some or all of the periods shown. Performance would have been lower had expense limitations not been in effect. Current expenses are listed in the “Fund expense ratios” table on page 17. Please note additional details on pages 16 through 18.

The graph also assumes $10,000 invested in the Barclays U.S. Aggregate Index as of March 31, 2005. The Barclays U.S. Aggregate Index measures the performance of publicly issued investment grade (Baa3/BBB- or better) corporate, U.S. government, mortgage- and asset-backed securities with at least one year to maturity and at least $250 million par amount outstanding.

The BofA Merrill Lynch 1–3 Year U.S. Treasury Index, mentioned on page 3, generally tracks the market for U.S. Treasury securities with maturities of one to three years.

Index performance returns do not reflect any management fees, transaction costs, or expenses. Indices are unmanaged and one cannot invest directly in an index. Past performance is not a guarantee of future results.

Performance of other Fund classes will vary due to different charges and expenses.

Stock symbols and CUSIP numbers | ||||||

| Nasdaq symbols | CUSIPs | |||||

Class A | OAFIX | 246118681 | ||||

Class C | OCFIX | 246118665 | ||||

Institutional Class | OIFIX | 246118657 |

18

Table of Contents

The performance data quoted represent past performance; past performance does not guarantee future results. Investment return and principal value will fluctuate so your shares, when redeemed, may be worth more or less than their original cost. Please obtain the performance data for the most recent month end by calling 800 914-0278 or visiting our website at optimummutualfunds.com. Current performance may be lower or higher than the performance data quoted.

| Fund and benchmark performance1,2 | ||||||||||||||

| Average annual total returns through March 31, 2015 | 1 year | 5 years | 10 years | |||||||||||

Class A (Est. Aug. 1, 2003) | ||||||||||||||

Excluding sales charge | –6.25% | +4.05% | +3.47% | |||||||||||

Including sales charge | –11.66% | +2.82% | +2.86% | |||||||||||

Class C (Est. Aug. 1, 2003) | ||||||||||||||