Exhibit 99.1

MAG SILVER CORP.

Suite 770, 800 West Pender Street

Vancouver, British Columbia V6C 2V6

NOTICE OF ANNUAL GENERAL AND SPECIAL MEETING AND

MANAGEMENT INFORMATION CIRCULAR

relating to the

2013 ANNUAL GENERAL AND SPECIAL

MEETING OF SHAREHOLDERS

TO BE HELD ON JUNE 18, 2013

Dated May 14, 2013

THIS PAGE INTENTIONALLY LEFT BLANK

NOTICE OF ANNUAL GENERAL AND SPECIAL MEETING

NOTICE IS HEREBY GIVEN that the annual general and special meeting (the “Meeting”) of shareholders of MAG Silver Corp. (the “Company”) will be held at The Fairmont Waterfront, 900 Canada Place Way, Vancouver, British Columbia, Canada V6C 3L5 at 9:00 a.m. (Pacific time) on Tuesday, June 18, 2013 for the following purposes:

| · | To receive the report of the directors of the Company; |

| · | To receive the audited financial statements of the Company for the financial year ended December 31, 2012 and accompanying report of the auditor; |

| · | To elect the directors of the Company for the ensuing year; |

| · | To appoint Deloitte & Touche LLP, Chartered Accountants, as the auditor of the Company for the ensuing year and to authorize the directors to fix their remuneration; |

| · | To approve the continuation of the Shareholder Rights Plan of the Company; and |

| · | To transact such other business as may properly come before the Meeting or any adjournment or postponement thereof. |

The details of all matters proposed to be put before shareholders at the Meeting are set forth in the management information circular accompanying this Notice of Meeting. At the Meeting, shareholders will be asked to approve each of the foregoing items.

The directors of the Company have fixed May 14, 2013 as the record date for the Meeting (the “Record Date”). Only Shareholders of record at the close of business on the Record Date are entitled to vote at the Meeting or any adjournment thereof.

If you are a registered shareholder of the Company and unable to attend the Meeting in person, please exercise your right to vote by completing and returning the accompanying form of proxy and deposit it with Computershare Investor Services Inc., 3rd Floor, 510 Burrard Street, Vancouver, British Columbia, Canada V6C 3B9 by 9:00 a.m. (Pacific time) on Friday, June 14, 2013 or at least 48 hours (excluding Saturdays, Sundays and holidays) before the time that the Meeting is to be reconvened after any adjournment of the Meeting. The deadline for the deposit of proxies may be waived or extended by the Chairman of the Meeting at the Chairman’s discretion without notice.

If you are a non-registered shareholder of the Company and received this Notice of Meeting and accompanying materials through a broker, a financial institution, a participant, a trustee or administrator of a self-administered retirement savings plan, retirement income fund, education savings plan or other similar self-administered savings or investment plan registered under the Income Tax Act (Canada), or a nominee of any of the foregoing that holds your security on your behalf (the “Intermediary”), please complete and return the materials in accordance with the instructions provided to you by your Intermediary.

DATED at Vancouver, British Columbia May 14, 2013.

MAG SILVER CORP.

“Daniel MacInnis”

by: _____________________________

Daniel MacInnis

President and Chief Executive Officer

TABLE OF CONTENTS

| Page | |

| SOLICITATION OF PROXIES | 1 |

| PROXIES AND VOTING RIGHTS | 1 |

| RECORD DATE, VOTING SECURITIES AND PRINCIPAL HOLDERS THEREOF | 4 |

| RECEIPT OF DIRECTORS’ REPORT AND FINANCIAL STATEMENTS | 5 |

| PARTICULARS OF OTHER MATTERS TO BE ACTED UPON | 5 |

| ELECTION OF DIRECTORS | 5 |

| APPOINTMENT AND REMUNERATION OF AUDITOR | 10 |

| APPROVAL OF SHAREHOLDERS RIGHTS PLAN | 10 |

| STATEMENT OF EXECUTIVE COMPENSATION | 15 |

| SECURITIES AUTHORIZED FOR ISSUANCE UNDER EQUITY COMPENSATION PLANS | 41 |

| DISCLOSURE OF CORPORATE GOVERNANCE PRACTICES | 44 |

| INDEBTEDNESS OF DIRECTORS AND EXECUTIVE OFFICERS | 51 |

MANAGEMENT CONTRACTS | 52 |

| INTEREST OF INFORMED PERSONS IN MATERIAL TRANSACTIONS | 52 |

| INTEREST OF CERTAIN PERSONS OR COMPANIES IN MATTERS TO BE ACTED UPON | 52 |

| ADDITIONAL INFORMATION | 53 |

| APPROVAL OF THE BOARD OF DIRECTORS | 53 |

MAG SILVER CORP.

SUITE 770, 800 WEST PENDER STREET

VANCOUVER, BRITISH COLUMBIA V6C 2V6

MANAGEMENT INFORMATION CIRCULAR

Dated May 14, 2013

This Management Information Circular (“Information Circular”) accompanies the Notice of Annual General and Special Meeting (the “Meeting”) of the shareholders of MAG Silver Corp. (the “Company”) to be held on Tuesday, June 18, 2013 at the time and place and for the purposes set out in the accompanying Notice of Meeting. This Information Circular is furnished in connection with the solicitation of proxies by management of the Company for use at the Meeting and at any adjournment or postponement of the Meeting.

PROXIES AND VOTING RIGHTS

General

It is expected that solicitations of proxies will be made primarily by mail but proxies may also be solicited by telephone or other personal contact by directors, officers and employees of the Company without special compensation. The Company may reimburse shareholders’ nominees or agents (including brokers holding shares on behalf of clients) for the costs incurred in obtaining authorization to execute forms of proxies from their principals. The Company will be using the services of Kingsdale Shareholder Services Inc. (“Kingsdale”) to provide the following services in connection with the Meeting: review and analysis of the information circular, recommending corporate governance best practices where applicable, liaising with proxy advisory firms, developing and implementing shareholder proxies, and the solicitation of proxies including contacting shareholders by telephone. Shareholders needing assistance completing a form of proxy or voting instruction form should contact Kingsdale toll free in North America at 1-866-481-2532. The estimated cost of such service is $55,000 plus charges for any telephone calls. The costs of solicitation will be borne by the Company.

Only a shareholder whose name appears on the certificate(s) representing its shares (a “Registered Shareholder”) or its duly appointed proxy nominee is permitted to vote at the Meeting. A shareholder is a non-registered shareholder (a “Non-Registered Shareholder”) if its shares are registered in the name of an intermediary, such as an investment dealer, bank, trust company, trustee, custodian, or other nominee, or a clearing agency in which the intermediary participates. Accordingly, most shareholders of the Company are “Non-Registered Shareholders” because the shares they own are not registered in their names but are instead registered in the name of the brokerage firm, bank or trust company through which they purchased the shares. More particularly, a person is a Non-Registered Shareholder in respect of shares which are held on behalf of that person, but which are registered either: (a) in the name of an intermediary (an “Intermediary”) that the Non-Registered Shareholder deals with in respect of the shares (Intermediaries include, among others, banks, trust companies, securities dealers or brokers and trustees or administrators of self-administered RRSPs, RRIFs, RESPs and similar plans); or (b) in the name of a clearing agency (such as The Canadian Depository for Securities Limited (“CDS”)) of which the Intermediary is a participant. In Canada, the vast majority of such shares are registered under the name of CDS, which company acts as nominee for many Canadian brokerage firms. Shares so held by brokers or their nominees can only be voted (for or against resolutions) upon the instructions of the Non-Registered Shareholder. Without specific instructions, brokers/nominees are prohibited from voting shares held for Non-Registered Shareholders.

These shareholder materials are being sent to both Registered Shareholders and Non-Registered Shareholders. If the Company or its agent has sent these materials directly to a Non-Registered Shareholder, such Non-Registered Shareholder’s name and address and information about its holdings of securities have been obtained in accordance with applicable securities regulatory requirements from the Intermediary holding the securities on such Non-Registered Shareholder’s behalf.

Non-Registered Shareholders who have not objected to their Intermediary disclosing certain information about them to the Company are referred to as “NOBOs”, whereas Non-Registered Shareholders who have objected to their Intermediary disclosing ownership information about them to the Company are referred to as “OBOs”. In accordance with National Instrument 54-101 – Communication with Beneficial Owners of Securities of a Reporting Issuer, the Company has elected to send the Notice of Meeting, this Information Circular and the related form of proxy or voting instruction form (collectively, the “Meeting Materials”) directly to the NOBOs, and indirectly to the OBOs through their Intermediaries. By choosing to send the Meeting Materials directly to NOBOs, the Company (and not the Intermediary holding shares on behalf of the NOBOs), has assumed responsibility for (i) delivering the Meeting Materials to the NOBOs, and (ii) executing their proper voting instructions.

Appointment of Proxies

Registered Shareholders

The persons named in the accompanying form of proxy are nominees of the Company’s management. A shareholder has the right to appoint a person (who need not be a shareholder) to attend and act for and on the shareholder’s behalf at the Meeting other than the persons designated as proxyholders in the accompanying form of proxy. To exercise this right, the shareholder must either:

| (a) | on the accompanying form of proxy, strike out the printed names of the individuals specified as proxyholders and insert the name of the shareholder’s nominee in the blank space provided; or |

(b) complete another proper form of proxy.

In either case, to be valid, a proxy must be dated and signed by the shareholder or by the shareholder’s attorney authorized in writing. In the case of a corporation, the proxy must be signed by a duly authorized officer of, or attorney for, the corporation.

The completed proxy, together with the power of attorney or other authority, if any, under which the proxy was signed or a notarially certified copy of the power of attorney or other authority, must be delivered to Computershare Investor Services Inc. (“Computershare”), 3rd Floor, 510 Burrard Street, Vancouver, British Columbia, Canada V6C 3B9, or by telephone, internet or facsimile, by 9:00 a.m. (Pacific time) on Friday, June 14, 2013 or at least 48 hours (excluding Saturdays, Sundays and holidays) before the time that the Meeting is to be reconvened after any adjournment of the Meeting. The deadline for the deposit of proxies may be waived or extended by the Chairman of the Meeting at the Chairman’s discretion without notice.

- 2 -

Non-Registered Shareholders

Only Registered Shareholders or duly appointed proxyholders for Registered Shareholders are permitted to vote at the Meeting. Non-Registered Shareholders (whether NOBOs or OBOs) are advised that only proxies from shareholders of record can be recognized and voted at the Meeting.

Non-Registered Shareholders that are NOBOs should complete and return the voting instruction form (as opposed to the form of proxy) accompanying this Information Circular as specified in the voting instruction form.

With respect to Non-Registered Shareholders that are OBOs, the Intermediary holding shares on behalf of an OBO is required to forward the Meeting Materials to such OBO (unless such OBO has waived its right to receive the Meeting Materials) and to seek such OBO’s instructions as how to vote its shares in respect of each of the matters described in this Information Circular to be voted on at the Meeting. Each Intermediary has its own procedures which should be carefully followed by OBOs to ensure that their Shares are voted by the Intermediary on their behalf at the Meeting. The instructions for voting will be set out in the form of proxy or voting instruction form provided by the Intermediary. OBOs should contact their Intermediary and carefully follow the voting instructions provided by such Intermediary. Alternatively, OBOs who wish to vote their Shares in person at the Meeting may do so by appointing themselves as the proxy nominee by writing their own name in the space provided on the form of proxy or voting instruction form provided to them by the Intermediary and following the Intermediary's instructions for return of the executed form of proxy or voting instruction form.

All references to shareholders in this Information Circular and the accompanying Notice of Meeting and form of proxy are to shareholders of record unless specifically stated otherwise.

Shareholders needing assistance completing and returning a proxy or VIF may call Kingsdale Shareholder Services Inc. toll free at 1-866-481-2532.

Revocation of Proxies

A shareholder who has given a proxy may revoke it at any time before the proxy is exercised:

| (a) | by an instrument in writing that is: |

| (i) | signed by the shareholder, the shareholder’s legal personal representative or trustee in bankruptcy or, where the shareholder is a corporation, a duly authorized representative of the corporation; and |

| (ii) | delivered to Computershare Investor Services Inc., 3rd Floor, 510 Burrard Street, Vancouver, British Columbia, Canada V6C 0A3 or to the registered office of the Company located at Suite 1600 – 925 West Georgia Street, Vancouver, British Columbia, Canada V6C 3L2 at any time up to and including the last business day preceding the day of the Meeting or any adjournment of the Meeting; |

| (b) | by sending another proxy form with a later date to Computershare before 9:00 a.m. (Pacific time) on Friday, June 14, 2013 or at least 48 hours (excluding Saturdays, Sundays and holidays) before any adjourned or postponed Meeting; |

| (c) | by attending the Meeting and notifying the Chairman of the Meeting prior to the commencement of the Meeting that the shareholder has revoked its proxy; or |

| (d) | in any other manner provided by law. |

- 3 -

A revocation of a proxy does not affect any matter on which a vote has been taken prior to the revocation.

Voting and Exercise of Discretion by Proxyholders

A shareholder may indicate the manner in which the persons named in the accompanying form of proxy are to vote with respect to a matter to be acted upon at the Meeting by marking the appropriate space. If the instructions as to voting indicated in the proxy are certain, the shares represented by the proxy will be voted or withheld from voting in accordance with the instructions given in the proxy on any ballot that may be called for.

If the shareholder specifies a choice in the proxy with respect to a matter to be acted upon, then the shares represented will be voted or withheld from the vote on that matter accordingly. If no choice is specified in the proxy with respect to a matter to be acted upon, it is intended that the proxyholder named by management in the accompanying form of proxy will vote the shares represented by the proxy in favour of each matter identified in the proxy and for the nominees of the Company’s board of directors for directors and auditor.

The accompanying form of proxy also confers discretionary authority upon the named proxyholder with respect to amendments or variations to the matters identified in the accompanying Notice of Meeting and with respect to any other matters which may properly come before the Meeting. As of the date of this Information Circular, management of the Company is not aware of any such amendments or variations, or any other matters that will be presented for action at the Meeting other than those referred to in the accompanying Notice of Meeting. If, however, other matters that are not now known to management properly come before the Meeting, then the persons named in the accompanying form of proxy intend to vote on them in accordance with their best judgment.

RECORD DATE, VOTING SECURITIES AND PRINCIPAL HOLDERS THEREOF

The authorized capital of the Company consists of an unlimited number of common shares. As at May 14, 2013, the Company had 60,141,718 common shares issued and outstanding.

In accordance with applicable laws, the board of directors of the Company has provided notice of and fixed the record date as of May 14, 2013 (the “Record Date”) for the purposes of determining shareholders entitled to receive notice of, and to vote at, the Meeting, and has obtained a list of all persons who are Registered Shareholders at the close of business on the Record Date and the number of common shares registered in the name of each Registered Shareholder on that date. Each Registered Shareholder as at the close of business on the Record Date will be entitled to receive notice of the Meeting and will be entitled to one vote at the Meeting for each common share registered in his or her name as it appears on the list.

To the knowledge of the directors and executive officers of the Company, as at the Record Date, only the following shareholder beneficially owns, directly or indirectly, or exercises control or direction over, common shares carrying 10% or more of the voting rights attached to all outstanding voting securities of the Company:

| Name | Number of Shares | Percentage of Outstanding Shares |

Fresnillo plc(1)(2) | 9,746,193 | 16.21%(3) |

| Notes: |

| (1) | The information above has been obtained by the Company from the System for Electronic Disclosure by Insiders (SEDI) as of the date of this Information Circular. |

| (2) | The common shares in this table are held by Fresnillo plc (“Fresnillo”) and its affiliates. |

| (3) | The percentage shown has been calculated based on the number of issued and outstanding common shares of the Company as at May 14, 2013. |

- 4 -

RECEIPT OF DIRECTORS’ REPORT AND FINANCIAL STATEMENTS

The Directors’ Report and the consolidated financial statements of the Company for the financial year ended December 31, 2012 and accompanying auditor’s report will be presented at the Meeting and have been previously filed under the Company’s profile on SEDAR at www.sedar.com.

PARTICULARS OF MATTERS TO BE ACTED UPON

Election of Directors

The board of directors of the Company presently consists of nine directors. The term of office of each of the present directors expires at the Meeting. At the Meeting, the shareholders will consider and, if deemed advisable, pass an ordinary resolution to set the number of directors at nine and to elect nine directors for the ensuing year.

The Company’s board of directors recently adopted a majority voting policy. This policy provides that any nominee for election as a director who has more votes withheld than votes for his or her election at the Meeting must tender his or her resignation to the Chairman following the meeting. This policy applies only to uncontested elections. The board shall consider any resignation tendered pursuant to the policy and whether or not it should be accepted. The board will disclose its decision via press release within 90 days of the Meeting. If a resignation is accepted, the board may appoint a new director to fill any vacancy created by the resignation. A copy of the Company’s majority voting policy may be obtained under the Company’s profile on SEDAR at www.sedar.com.

The Company’s board of directors proposes to nominate the persons named in the table below for election as directors of the Company. Each director elected will hold office until the next annual general meeting of the Company or until his or her successor is duly elected or appointed, unless the office is earlier vacated in accordance with the Articles of the Company or the Business Corporations Act (British Columbia) or he or she becomes disqualified to act as a director.

The table below sets forth for each management nominee for election as director, (i) their name, (ii) the province or state and country where they reside, (iii) all offices of the Company now held by each of them, including committees on which they serve, (iv) their principal occupations, businesses or employments, (v) the period of time during which each has been a director of the Company, and (vi) the number of common shares of the Company beneficially owned, directly or indirectly, or controlled or directed, as of the date of this Information Circular. The Company’s board of directors recommends a vote “FOR” the appointment of each of the following nominees as directors. In the absence of a contrary instruction, the persons designated by management of the Company in the enclosed form of proxy intend to vote FOR the election of the directors set out in the following table.

Name, Position, Province / State and Country of Residence(1) | Principal Occupation and Occupations during the past 5 years (1) | Director Since | Number of Shares Beneficially Owned, Controlled or Directed (1) |

Daniel T. MacInnis (7) British Columbia, Canada President, CEO and Director | President and CEO of the Company since February 1, 2005. Mr. MacInnis is also a director of MAX Resources Corp. | February 1, 2005 | 301,300 |

Frank R. Hallam (5)(7)(8) British Columbia, Canada Director | April 2003 to June 22, 2010, CFO of MAG Silver Corp., 2002 to present, CFO and director of Platinum Group Metals Ltd., a company building a platinum mine in South Africa and exploring properties in Canada and South Africa; 1996 to 2007, CFO Callinan Mines Ltd.; 2006 to 2009, director of West Timmins Mining Inc. and CFO 2006 to 2008; 2009 to present, director Lake Shore Gold Corp.; 2009 to present, director and CFO of West Kirkland Mining Inc. Mr. Hallam is also a director of Nextraction Energy Corp. | June 22, 2010 | Nil |

- 5 -

Name, Position, Province / State and Country of Residence(1) | Principal Occupation and Occupations during the past 5 years (1) | Director Since | Number of Shares Beneficially Owned, Controlled or Directed (1) |

Eric H. Carlson (3)(4) British Columbia, Canada Director | Founder and CEO of Anthem Properties Group Ltd. and its affiliates, including Anthem Works Ltd., a reporting issuer, together comprising a real estate investment and development group of companies operating under the Anthem brand, from July 1994 to present; 1992 to 2008, President of Kruger Capital Corp.; and director of West Timmins Mining Inc. from 2006 to 2009. Mr. Carlson is also a director of Platinum Group Metals Ltd., West Kirkland Mining Inc., and Nextraction Energy Corp. | June 11, 1999 | 1,325,500 |

Dr. Peter K. Megaw(7) Arizona, USA Director | President of IMDEX and co-founder of Minera Cascabel S.A. DE C.V. since 1988, a geological consulting company; consulting geologist for the Company since its inception in 2003. Dr. Megaw is also a director of Candente Gold Corp and Minaurum Gold Corp. | February 6, 2006 | 287,591(6) |

Jonathan A. Rubenstein (4)(5) British Columbia, Canada Chairman and Director | Professional Director. Director of Detour Gold 2009 to present; director of Eldorado Gold 2009 to present; director of Troon Ventures 2009 to present; director of Roxgold Inc. 2012 to present; director of Aurelian Gold 2006 to 2008; director of Rio Novo Gold 2010 to 2012; Former lawyer in private practice, with focus on corporate and securities law. | February 26, 2007 | 1,000 |

- 6 -

Name, Position, Province / State and Country of Residence(1) | Principal Occupation and Occupations during the past 5 years (1) | Director Since | Number of Shares Beneficially Owned, Controlled or Directed (1) |

Richard M. Colterjohn(2)(3)(5)(8) Ontario, Canada Director | Managing Partner at Glencoban Capital Management Inc., a merchant banking firm, since 2002. Founder, president, CEO and director of Centenario Copper Corporation from 2004 to 2009; director of Cumberland Resources Ltd from 2003 to 2007; director of Explorator Resources Ltd. from 2009 to 2011. Mr. Colterjohn also currently serves as a director of AuRico Gold Inc. (since 2010) and Roxgold Inc. (since 2012). | October 16, 2007 | 10,000 |

Derek C. White(2) British Columbia, Canada Director | CEO and President since September 2012, and Executive Vice President – Corporate Development since September 2007, of KGHM International Limited, a company constructing and operating mines in Canada, the USA and Chile; CFO of Quadra Mining from April 2004 to November 2007. Mr. White holds an undergraduate degree in Geological Engineering and is a Chartered Accountant. Mr. White is also a director of Magellan Mineral Limited and Laurentian Goldfields Ltd. | October 16, 2007 | Nil |

Peter D. Barnes(2)(4)(8) British Columbia, Canada Director | Corporate Director and a private investor. Director of CB Gold Inc. since April 2010, where he is the non-executive Chairman and a member of the Audit Committee and the Governance Committee. Former CEO and director of Silver Wheaton Corp from 2006 to 2011, and one of Silver Wheaton’s founders in 2004, a silver streaming company. Executive Vice President and CFO of Goldcorp Inc. from 2005 to 2006. Director of Avanti Mining Inc. from June 2007 to April 2012. Member of the Institute of Corporate Directors and was a member of the Silver Institute’s Board of Directors from 2009 to 2011. | October 5, 2012 | 5,000 |

Richard P. Clark(3)(5)(7) British Columbia, Canada Director | CEO since October 2011 and director since 1994 of Sirocco Mining Inc., a mining company holding an interest in mines in South America, and exploring resource sector opportunities in West Africa and South America. Senior executive with the Lundin Group of Companies for past 10 years. Former CEO, President and a director of Red Back Mining Inc. from 2004 until the company’s takeover by Kinross Gold Corporation in 2010. Mr. Clark served as a director of Kinross Gold Corporation from November 2010 until July 2011, Fortuna Silver Mines Inc. from August 2008 to June 2010, Corriente Resources Inc. from 1996 until its acquisition in 2010, Minera Andes Inc. from 2008 to 2009, Sanu Resources Ltd. from 2004 until its acquisition by Canadian Gold Hunter Corp. in 2009, and Sunridge Gold Corp. from 2007 to 2008. Mr. Clark also currently serves as director of Lucara Diamond Corp. and Orca Gold Inc. | October 5, 2012 | Nil |

- 7 -

| Notes: |

| (1) | Information as to the place of residence, principal occupation and shares beneficially owned, directly or indirectly, or controlled or directed has been furnished by the respective nominees individually. |

| (2) | Member of the Company’s Audit Committee. |

| (3) | Member of the Company’s Compensation Committee. |

| (4) | Member of the Company’s Governance and Nomination Committee. |

| (5) | Member of the Company’s Special Committee. |

| (6) | Of these holdings, 11,085 shares are held by Minera Cascabel S.A. de C.V., of which Dr. Megaw is a 33.33% owner. |

| (7) | Member of the Company’s Disclosure Committee. |

| (8) | Member of the Company’s Finance Committee. |

Management of the Company does not contemplate that any of the proposed nominees will be unable to serve as a director; however, if for any reason any of the proposed nominees do not stand for election or are unable to serve as such, the common shares represented by properly executed proxies given in favour of management’s nominee(s) may be voted by the person designated by management of the Company in the enclosed form of proxy, in their discretion, in favour of another nominee.

None of the management nominees is currently, or has been within the past ten years, (A) a director, chief executive officer or chief financial officer of any company that (i) was subject to an order that was issued while such person was acting in the capacity as director, chief executive officer or chief financial officer, or (ii) was subject to an order that was issued after such person ceased to be a director, chief executive officer or chief financial officer and which resulted from an event that occurred while such person was acting as a director, chief executive officer or chief financial officer, or (B) a director or executive officer of any company that, while such person was acting in such capacity, or within a year of such person ceasing to act in such capacity, became bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency or was subject to or instituted any proceedings, arrangement or compromise with creditors or had a receiver, receiver manager or trustee appointed to hold its assets. None of the management nominees has within the past ten years become bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency, or become subject to or instituted any proceedings, arrangement or compromise with creditors, or had a receiver, receiver manager or trustee appointed to hold the assets of such person. None of the management nominees has been subject to (1) any penalties or sanctions imposed by a court relating to securities legislation or by a securities regulatory authority or has entered into a settlement agreement with a securities regulatory authority or (2) any other penalties or sanctions imposed by a court or regulatory body that would likely be considered important to a reasonable security holder in deciding whether to vote for such person.

- 8 -

On August 23, 2012 the Company’s board of directors adopted an advance notice policy subsequently ratified, confirmed and approved by Shareholders at the October 5, 2012 Annual General and Special Meeting of Shareholders. The policy provides shareholders, directors and management of the Company with a clear framework for nominating directors. The Advance Notice Policy fixes a deadline by which holders of record of common shares of the Company must submit director nominations to the Company prior to any annual or special meeting of shareholders and sets forth the information that a shareholder must include in the notice to the Company for the notice to be in proper written form in order for any director nominee to be eligible for election at any annual or special meeting of shareholders. A copy of the Company’s advance notice policy may be obtained under the Company’s profile on SEDAR at www.sedar.com.

Director Share Ownership Requirement

In an effort to align the interests of members of the Board with those of MAG’s shareholders, in 2013 MAG adopted a minimum share ownership requirement for directors, under which directors are required to own MAG Common Shares or equity linked securities other than options (collectively “MAG Securities”) having a value established by the Board. The minimum MAG Securities ownership requirement for non-executive directors is a value equivalent to three times the annual cash retainer paid to the non-executive director. Directors are required to achieve these thresholds by the later of (a) three years from the date the individual became a director; and (b) three years from the date of the minimum equities holding policy (dated May 13, 2013). If a retainer is increased, directors shall have two years to reach the new resulting ownership requirement from the date of such increase. Ownership levels are calculated based on the greater of the initial acquisition cost and the 200-day volume-weighted average price (“VWAP”) of MAG Securities on the TSX as at December 31, provided that any other change in the market value of MAG Securities will not be considered in determining the minimum holdings of MAG Securities required by this policy.

Each director is required to maintain his or her minimum ownership level throughout his or her tenure as a director.

Given that the Company’s share ownership requirement for directors was adopted May 13, 2013, each of the Company’s directors has until May 13, 2016 under the policy to meet the director share ownership requirement.

Share Ownership Position and Requirement of Non-Executive Directors

| Eligible MAG Securities Holdings | 2012 Retainer ($) | Minimum Equity Holding (“MEH”) ($) | Value of Holdings as Multiple of Retainer | Deadline to Meet Requirement | |||

| Name | Number of Common Shares(1) | Value Per Share(2) ($) | Value of Holdings ($) | ||||

| Frank Hallam | Nil | 10.03 | Nil | 20,000 | 60,000 | 0x | May 13, 2016 |

| Eric Carlson | 1,325,500 | 10.03 | 13,294,765 | 20,000 | 60,000 | 664.74x | May 13, 2016 |

| Peter Megaw | 287,591 | 10.03 | 2,884,538 | 20,000 | 60,000 | 144.23x | May 13, 2016 |

| Jonathan Rubenstein | 1,000 | 10.03 | 10,030 | 30,000 | 90,000 | 0.33x | May 13, 2016 |

| Richard Colterjohn | 10,000 | 10.03 | 100,300 | 20,000 | 60,000 | 5.02x | May 13, 2016 |

| Derek White | Nil | 10.03 | Nil | 20,000 | 60,000 | 0x | May 13, 2016 |

- 9 -

| Eligible MAG Securities Holdings | 2012 Retainer ($) | Minimum Equity Holding (“MEH”) ($) | Value of Holdings as Multiple of Retainer | Deadline to Meet Requirement | ||

| Name | Number of Common Shares(1) | Value Per Share(2) ($) | Value of Holdings ($) | |||

| Peter Barnes | 5,000 | 11.36 | 56,800 | 20,000 | 60,000 | 2.84x | May 13, 2016 |

| Richard Clark | Nil | 10.03 | Nil | 20,000 | 60,000 | 0x | May 13, 2016 |

Notes:

| (1) | Includes Common Shares held as at December 31, 2012. |

| (2) | Value per share is calculated as the greater of the initial acquisition value per common share and the 200-day volume weighted average MAG Common Share price on the TSX as at December 31, 2012 of $10.03. |

Appointment and Remuneration of Auditor

The shareholders will be asked to vote for the appointment of Deloitte & Touche LLP, Chartered Accountants, as the auditor of the Company to hold office until the next annual general meeting of shareholders of the Company and to authorize the directors to fix their remuneration. The Company’s board of directors recommends a vote “FOR” the appointment of Deloitte & Touche LLP, Chartered Accountants, as the auditor of the Company to hold office until the close of the next annual meeting of shareholders and to authorize the directors to fix their remuneration. In the absence of a contrary instruction, the persons designated by management of the Company in the enclosed form of proxy intend to vote FOR the appointment of Deloitte & Touche LLP, Chartered Accountants, as the auditor of the Company to hold office until the close of the next annual meeting of shareholders and to authorize the directors to fix their remuneration.

Approval of Shareholder Rights Plan

On August 3, 2007, the Board approved a shareholder rights plan for the Company. On January 18, 2008, the Company’s shareholders ratified and confirmed the shareholder rights plan, which was amended, with the approval of 87.06% of the Company’s shareholders (excluding Fresnillo), on March 24, 2009 (the “Rights Plan”). The Company and Computershare Investor Services Inc. then entered into an amended and restated shareholder rights plan agreement dated March 24, 2009 to reflect the amendments (the “Rights Agreement”). On June 22, 2010, the Company’s shareholders approved the confirmation, ratification and continuation of the Rights Plan with 65.20% of the shareholder votes cast at the meeting. The Rights Plan will expire at the end of the Meeting, unless the shareholders of the Company vote to approve its continuation.

At the Meeting, the shareholders will be asked to confirm, ratify and continue the Rights Plan. A summary of the key terms of the Rights Plan is set out below. This summary is qualified in its entirety by reference to the full text of the Rights Plan, which may be obtained under the Company’s profile on SEDAR at www.sedar.com. A copy of the Rights Plan may also be obtained upon request made in writing to the Company at Suite 770, 800 West Pender Street, Vancouver, B.C., V6C 2V6. Capitalized terms used in this section and not otherwise defined herein have the meanings assigned to them in the Rights Plan.

Rationale

The purpose of the Rights Plan is to encourage the fair treatment of shareholders in connection with any take-over bid for the Company. The Rights Plan seeks to provide shareholders with adequate time to properly assess a take-over bid without undue pressure. It is also intended to provide the board of directors with more time to fully consider an unsolicited take-over bid and, if considered appropriate, to identify, develop and negotiate other alternatives to maximize shareholder value.

- 10 -

The Rights Plan generally provides that if a bidder acquires or announces an intention to acquire more than 20% of the issued and outstanding common shares of the Company (“Shares”), other than by way of a “Permitted Bid” or a “Shareholder Endorsed Insider Bid” or with the approval of the board of directors, the share capital of the Company would be considerably diluted if the bidder proceeds with its bid, thereby making its bid prohibitively expensive.

Term

If the Rights Plan is confirmed, ratified and continued by the shareholders of the Company at the Meeting, the Rights Plan will continue in force up to the end of the Company’s third annual meeting of shareholders following such approval.

Issue of Rights

On August 3, 2007, the Board implemented the Rights Plan by authorizing the issue of one right (a “Right”) in respect of each outstanding Share to holders of record as at the Record Time. The Board also authorized the issue of one Right in respect of each Share issued after the Record Time and prior to the Separation Time (as defined below) and the Expiration Time (as defined in the Rights Plan).

Exercise of Rights

The Rights are not exercisable initially. The Rights will separate from the Shares and become exercisable at the close of business on the tenth business day after the earlier of the first public announcement of facts indicating that a person has acquired Beneficial Ownership of 20% or more of the Shares or the commencement of, or first public announcement of, the intent of any person to commence a take-over bid which would result in such person Beneficially Owning 20% or more of the Shares, or the date upon which a Permitted Bid or Competing Permitted Bid ceases to be such, or such later time as the Board may determine in good faith (in any such case, the “Separation Time”). After the Separation Time, but prior to the occurrence of a Flip-in Event (as defined below), each Right may be exercised to purchase one Share at an exercise price per Right of $75.

The exercise price payable and the number of securities issuable upon the exercise of the Rights are subject to adjustment from time to time upon the occurrence of certain corporate events affecting the Shares.

Flip-in Event and Exchange Option

Subject to certain customary exceptions, upon the acquisition by any person (an “Acquiring Person”) of 20% or more of the Shares (a “Flip-in Event”) and following the Separation Time, each Right, other than a Right Beneficially Owned by an Acquiring Person, its affiliates and associates, their respective joint actors and certain transferees, may be exercised to purchase that number of Shares which have a market value equal to two times the exercise price of the Rights. Rights beneficially owned by an Acquiring Person, its affiliates and associates, their respective joint actors and certain transferees will be void. The Rights Plan provides that a person (a “Grandfathered Person”) who was the Beneficial Owner of 20% or more of the outstanding Shares determined as at 4:00 p.m. on August 3, 2007 (the “Record Time”) shall not be an Acquiring Person unless, after the Record Time, that person becomes the Beneficial Owner of any additional Shares. To the best of the Company’s knowledge, there is no Grandfathered Person under the Rights Plan.

- 11 -

In addition, the Rights Plan permits the Board to authorize the Company, after a Flip-in Event has occurred, to issue or deliver, in return for the Rights and on payment of the relevant exercise price or without charge, debt, equity or other securities or assets of the Company or a combination thereof.

Certificates and Transferability

Prior to the Separation Time, certificates for Shares will also evidence one Right for each Share represented by the certificate. Certificates issued after August 3, 2007 will bear a legend to this effect.

Prior to the Separation Time, Rights will not be transferable separately from the associated Shares. From and after the Separation Time, the Rights will be evidenced by Rights certificates which will be transferable and trade separately from the Shares.

Permitted Bids

Under the Rights Plan, a Permitted Bid or Competing Permitted Bid will not trigger the Rights Plan. A Permitted Bid is one that: (i) is made by means of a take-over bid circular, (ii) is made to all holders of Shares for all Shares held by them; (iii) is open for at least 60 days; (iv) contains a condition that no Shares will be taken up and paid for until at least 50% of the independent shareholders have tendered and not withdrawn, (v) contains a condition that Shares may be deposited at any time and withdrawn until they are taken up and paid for, and (vi) contains a provision that, if 50% of the independent shareholders tender, the bidder will make an announcement to that effect and keep the bid open for at least ten more business days.

Shareholder Endorsed Insider Bid

As a result of the shareholder approved amendment to the Rights Plan, the Rights Plan now also permits a bidder who together with its affiliates or associates and joint actors has beneficial ownership of securities of the Company carrying 10% or more of the voting rights attached to all of the Shares (an “Insider”) to proceed with a “Shareholder Endorsed Insider Bid” without triggering the Rights Plan. This feature is in addition to the ability of an Insider to proceed with a Permitted Bid or with prior approval of the Board without triggering the Rights Plan.

A Shareholder Endorsed Insider Bid is a take-over bid made by an Insider by way of take-over bid circular to all registered holders of common shares of the Company, other than the Insider, for all common shares held by them, and in respect of which:

| (a) | more than 50% of the common shares held by shareholders (other than the Insider and its joint actors) have been tendered to the take-over bid at the time of first take-up under the take-over bid; |

| (b) | the date of such first take-up occurs not later than the 120th calendar day following the date on which the take-over bid is commenced; and |

| (c) | immediately prior to or contemporaneously with such first take-up, the Insider makes a public announcement (i) informing shareholders of such take-up and the number and percentage of common shares then owned or controlled by the Insider and its joint actors, and (ii) confirming that the Insider has extended or will extend its take-over bid for not less than 10 business days in order to allow the remaining shareholders to tender their common shares to the bid if they choose to do so. |

- 12 -

The requirements for a Shareholder Endorsed Insider Bid are similar to, but not as stringent as, the requirements for a Permitted Bid. A Permitted Bid must be open for not less than 60 days while a Shareholder Endorsed Insider Bid is not required to be open for a minimum period of time (but will be subject to a minimum bid period of 35 days in accordance with applicable securities laws). A Permitted Bid must contain an irrevocable minimum tender condition of 50% of the common shares held by shareholders (other than common shares held by the bidder and certain related persons) and an irrevocable provision that if such minimum tender is achieved and common shares are taken up, the bidder must extend the bid for not less than 10 business days. A Shareholder Endorsed Insider Bid is not required to contain such irrevocable condition and provision at the outset of the bid, rather, it must have achieved such result at the time of first take up under the bid. The date of first take up under a Shareholder Endorsed Insider Bid must occur not later than the 120th calendar day following the day on which the bid is commenced, while a Permitted Bid is not subject to a similar restriction.

The Shareholder Endorsed Insider Bid is a novel concept that was introduced by the Company, and adopted by way of amendment to the Rights Plan in 2009, in the face of the announced intention by an Insider of the Company to launch a take-over bid for all the outstanding shares of the Company not already owned by it and its affiliates at an offer price that represented a discount to the closing price of the Shares on the NYSE MKT (formerly NYSE Alternext) on the day preceding such announcement.

The Board’s intention in introducing this concept to the Rights Plan was not to thwart take-over bids by Insiders, but rather to provide Insiders who are otherwise legally entitled to make a take-over bid for the Company with an additional avenue to proceed with a take-over bid in a manner that is fair and non-coercive to shareholders (in addition to making a Permitted Bid or proceeding with board approval) without triggering the Rights Plan. Although introduced in the face of an unsolicited bid by an Insider, the provision would apply equally to any take-over bid by an Insider.

Under Canadian securities laws, where an Insider proceeds with a take-over bid and shareholders holding more than a majority of the common shares reject it, the Insider has the ability to waive any minimum tender condition and take up any common shares that are tendered to the bid. Because of the Insider’s already sizeable share position, it can, by purchasing only a relatively small percentage of additional common shares, take up enough common shares to vest de facto control over the Company in the hands of the Insider without the Insider having had to pay a premium that is sufficient to induce shareholders holding a majority of the common shares not held by the Insider and certain related persons to tender to its bid. This potentially coercive conduct, if it occurs, could be extremely damaging to both the short-term and long-term financial interests of that large body of shareholders who choose not to tender to the Insider’s bid. Among other things, adopting a coercive strategy of this nature could make it practically impossible for any subsequent competing offer to succeed. As trading liquidity in the common shares diminishes, the Insider could choose not to acquire further common shares or to time any further acquisition it does elect to proceed with on a basis that may allow it to pay substantially less for the common shares that are not tendered to its bid than for those that were tendered. A shareholder may feel compelled to tender to a take-over bid which it considers to be inadequate out of a concern that failing to tender may result in the shareholder being left with illiquid or discounted shares.

In the context of shareholder rights plans, it is common practice in Canada for unsolicited bidders to launch a bid that is not a Permitted Bid and then apply to Canadian securities regulators for an order that has the effect of rendering the rights plan inoperative in respect of its bid. Typically, absent compelling unusual circumstances, Canadian securities regulators have been prepared to grant such orders within approximately 45 to 70 days following commencement of the bid, based on the premise that shareholders should not be denied the ability to respond to the bid.

An Insider could, if it is otherwise legally entitled to make a take-over bid for the Company, follow the coercive practice described above.

- 13 -

If an Insider does not wish to make a Permitted Bid, the Rights Plan provides an Insider with the ability to make a bid directly to shareholders and complete a Shareholder Endorsed Insider Bid (on terms less stringent than Permitted Bids) without triggering the Rights Plan and without prior board approval for the bid, and avoid applying to Canadian securities regulators to render the Rights Plan inoperative in a process that is costly for the Company, the Insider and the regulators. If an Insider chooses not to do so and instead elects to apply to Canadian securities regulators for an order that has the effect of rendering the Rights Plan inoperative despite its ability to complete a Shareholder Endorsed Insider Bid without triggering the Rights Plan, the board of directors believes that the ability of an Insider to complete a Shareholder Endorsed Insider Bid (which allows shareholders to respond directly to the bid through a process that is fair and non-coercive) should allow the Company to make a compelling submission to the regulators not to grant such an order in certain circumstances.

In effect, by voting in favour of the resolution approving the Rights Plan, shareholders will be endorsing, among other things, the following key principles:

| (a) | they acknowledge the increased risk of coercive conduct where a take-over bid is launched by an Insider; and |

| (b) | they reject the notion that an Insider should be allowed to adopt a coercive strategy of taking up Shares under a bid in one or more take-ups so that, over an extended period of time, the Insider acquires a sufficient number of Shares to provide it with de facto control over the Company even though the price offered by the Insider was insufficient to secure the tender of a majority of the outstanding shares not already owned by the Insider or its joint actors at the commencement of the bid. |

Redemption and Waiver

The Rights may be redeemed by the Board at a redemption price of $0.0001 per Right at any time prior to the occurrence of a Flip-in Event without the prior approval of the holders of Shares or Rights. The Board will be deemed to have elected to redeem the Rights if a person who has made a take-over bid, in respect of which the Board has waived the application of the Rights Plan, takes up and pays for Shares pursuant to the terms and conditions of such take-over bid.

The provisions of the Rights Plan which apply upon the occurrence of a Flip-in Event may be waived at the option of the Board and without the prior approval of the holders of Shares or Rights in certain circumstances prior to the occurrence of a Flip-in Event. The Board would, however, by virtue of such waiver be deemed to have waived the Rights Plan with respect to any other Flip-in Event. In addition, the operation of the Rights Plan may be waived where a person has inadvertently become an Acquiring Person and has reduced its beneficial ownership of Shares such that it is no longer an Acquiring Person.

Amendment of the Rights Plan

Amendments to the Rights Agreement, other than those required to correct clerical or typographical errors or to maintain the validity of the Rights Plan as a result of a change of law, will require the approval of Independent Shareholders (as defined in the Rights Plan).

Shareholder Approval

The continuation of the Rights Plan is required to be approved by a majority of the votes cast by Independent Shareholders (as defined in the Rights Plan) of the Company present in person or represented by proxy at the Meeting. To the best of the knowledge of the Company, all shareholders of the Company as of the Record Date are Independent Shareholders within the meaning of the Rights Plan. The text of the Rights Plan Resolution is set out below.

- 14 -

Resolution Approving the Rights Plan

The resolution to approve the and continuation of the Rights Plan which will be presented at the Meeting and, if deemed appropriate, adopted with or without variation is as follows:

“IT IS RESOLVED THAT:

| 1. | The continuation of the shareholder rights plan of the Company containing the terms and conditions substantially set forth in the shareholder rights plan agreement between MAG Silver Corp. and Computershare Investor Services Inc. dated as of August 3, 2007, as amended and restated on March 24, 2009, is hereby approved; and |

| 2. | Any one director or officer of the Company is authorized and directed on behalf of the Company to execute all documents and to do all such other acts and things as such director or officer may determine to be necessary or advisable to give effect to the foregoing provisions of this resolution.” |

If the Rights Plan is not continued at the Meeting, then the Rights Plan and all Rights issued thereunder will cease to have any force and effect following the termination of the Meeting.

The board of directors of the Company has determined that the Rights Plan is still in the best interests of shareholders and recommends that shareholders vote FOR the resolutions approving the continuation of the Rights Plan. Common shares represented by proxies in favour of management will be voted FOR the continuation of the Rights Plan, unless a shareholder has specified in his or her proxy that his or her common shares are to be voted against the approval of the continuation of the Rights Plan.

Other Business

Management knows of no other matter to come before the Meeting other than the matters referred to in the accompanying Notice of Meeting and this Information Circular.

STATEMENT OF EXECUTIVE COMPENSATION

A. Named Executive Officers

For the purposes of this Information Circular, a Named Executive Officer (“NEO”) of the Company means each of the following individuals:

| (a) | a chief executive officer (“CEO”) of the Company; |

| (b) | a chief financial officer (“CFO”) of the Company; |

| (c) | each of the Company’s three most highly compensated executive officers, or the three most highly compensated individuals acting in a similar capacity, other than the CEO and CFO, at the end of the most recently completed financial year whose total compensation was, individually, more than $150,000, as determined in accordance with subsection 1.3(6) of Form 51-102F6, for that financial year; and |

- 15 -

| (d) | each individual who would be an NEO under paragraph (c) above but for the fact that the individual was neither an executive officer of the Company, nor acting in a similar capacity, at the end of that financial year. |

The Company’s NEOs for the fiscal year ending December 31, 2012 were:

- Daniel MacInnis, President and Chief Executive Officer (“CEO”);

- Larry Taddei, Chief Financial Officer (“CFO”);

- Michael Petrina, former Vice President Operations (“VP Operations”);

- Gordon Neal, former Vice President Corporate Development (“VP Corporate Development”); and

- Jody Harris, Corporate Secretary.

Effective March 15, 2013, Mr. Gordon Neal resigned from the Company for personal reasons. Mr. Petrina, the Company’s VP Operations announced his resignation effective April 15, 2013 in order to relocate to Ontario.

B. Compensation Discussion and Analysis

The Compensation Committee of the Company’s board of directors (the “Compensation Committee”), which is comprised exclusively of independent directors, is responsible for ensuring that the Company has in place an appropriate plan for executive compensation and for making recommendations to the board with respect to the compensation of the Company’s executive officers. The Compensation Committee has a pay-for-performance philosophy and its compensation programs are designed to attract and retain executive officers with the talent and experience necessary for the success of the Company. The Compensation Committee ensures that the total compensation paid to all NEOs is fair and reasonable and is consistent with the Company’s compensation philosophy.

Compensation plays an important role in achieving short and long-term business objectives that ultimately drive business success. The Company’s compensation philosophy includes fostering entrepreneurship at all levels of the organization by making long term equity-based incentives, through the granting of stock options, a significant component of executive compensation. This approach is based on the assumption that the performance of the Company’s common share price over the long term is an important indicator of long term performance.

The Company’s principal goal is to create value for its shareholders. The Company’s compensation philosophy reflects this goal, and is based on the following fundamental principles:

| 1. | Compensation programs align with shareholder interests – the Company aligns the goals of executives with maximizing long term shareholder value; |

| 2. | Performance sensitive – compensation for executive officers should fluctuate and be linked to: |

| (a) | operating performance of the Company, considering ongoing exploration and corporate successes; and |

- 16 -

| (b) | market performance of the Company, considering current market conditions and market performance against peers; and |

| 3. | Offer market competitive compensation to attract and retain talent – the compensation program should provide market competitive pay in terms of value and structure in order to retain existing employees who are performing according to their objectives and to attract new individuals of the highest caliber. |

The objectives of the compensation program in compensating all NEOs were developed based on the above-mentioned compensation philosophy and are as follows:

| · | to attract and retain highly qualified executive officers; |

| · | to align the interests of executive officers with shareholders’ interests and with the execution of the Company’s business strategy; |

| · | to evaluate executive performance on the basis of key measurements that correlate to long-term shareholder value; and |

| · | to tie compensation directly to those measurements and rewards based on achieving and exceeding predetermined objectives. |

Competitive Compensation

The Company is dependent on individuals with specialized skills and knowledge related to the exploration for and development of mineral prospects, corporate finance and management. Therefore, the Company seeks to attract, retain and motivate highly skilled and experienced executive officers by providing competitive aggregate compensation. As discussed more fully below, the Compensation Committee reviews compensation practices of similarly situated companies in determining compensation policy. Although the Compensation Committee reviews each element of compensation for market competitiveness, and it may weigh a particular element more heavily based on a particular NEO’s role within the Company, it is primarily focused on remaining competitive in the market with respect to overall compensation.

The Compensation Committee reviews data related to compensation levels and programs of various companies that are both similar in size to the Company and operate within the mining exploration and development industry, prior to making its decisions. These companies are used as the Company’s primary peer group because they have similar business characteristics or because they compete with the Company for employees and investors. The Compensation Committee also periodically engages independent executive compensation consulting firms to conduct peer group compensation analysis, and provide comparative analysis of relevant industry compensation levels. Lastly, the Compensation Committee relies on the experience of its members as officers and/or directors at other companies in similar lines of business as the Company in assessing compensation levels. These other companies are identified below under the heading “Disclosure of Corporate Governance Practices – Directorships”. The purpose of this process is to:

| · | understand the competitiveness of current pay levels for each executive position relative to companies with similar operations and business characteristics; |

| · | identify and understand any gaps that may exist between actual compensation levels and market compensation levels; and |

- 17 -

| · | establish a basis for developing salary adjustments and short-term and long-term incentive awards for the Compensation Committee’s approval. |

Comparator Group

Comparative data for the Company’s peer group is accumulated from a number of external sources including the use of independent compensation consultants.

In 2010, the Compensation Committee engaged Lane Caputo Compensation Inc. (“Lane Caputo”). Lane Caputo worked with the Compensation Committee to assemble a comparable industry peer group, and then undertook a comparative compensation analysis of the peer group, including director compensation, and reported back to the Compensation Committee with an Executive Compensation Report (“2010 Executive Compensation Report”). The Compensation Committee re-engaged Lane Caputo in July 2012 to update the Company’s peer group analysis and prepare a 2012 Executive & Director Compensation report, with a comparative analysis of the Company’s 2011 executive and board compensation against peers (“2012 Executive Compensation Report”). The Compensation Committee then recently re-engaged Lane Caputo in April 2013 to update the 2012 Executive Compensation report for a comparison of the Company’s 2012 executive and board compensation against peers (“2013 Executive Compensation Report”).

Both the 2012 and 2013 Executive Compensation Reports used the same peer group of comparator companies (the “Peer Group”), which was updated from the peer group used in the 2010 Executive Compensation Report to better reflect the evolving business of the Company and the emergence of new comparators. Lane Caputo used various considerations in establishing the comparator group, including similar stage of development, industry focus and range of market capitalization.

Based on these considerations, Lane Caputo determined MAG’s Peer Group to be comprised of the following 21 companies:

Alexco Resources Inc. Asanko Gold Inc. (formerly Keegan Resources Inc.) Banro Corp. Bear Creek Mining Corp. Chesapeake Gold Corp. Colossus Minerals Inc. Continental Gold Ltd. Copper Fox Metals Inc. Extorre Gold Mines Ltd. Guyana Goldfields Inc. NovaGold Resources Inc. | Premier Gold Mines Ltd. Pretium Resources Inc. Queenston Mining Inc. Rainy River Resources Ltd. Rio Alto Mining Ltd. Romarco Minerals Inc. Rubicon Minerals Corp. Sabina Gold & Silver Corp. Seabridge Gold Inc. Torex Gold Resources Inc. |

The results of the 2010 Executive Compensation Report were used by and assisted the Compensation Committee in establishing compensation levels for 2012.

The results of the 2012 Executive Compensation Report was used by and assisted the Compensation Committee in determining 2012 annual incentives (bonuses) for the NEO’s and their 2013 compensation levels.

The results of the 2013 Executive Compensation Report will be used by the Compensation Committee in establishing 2013 annual incentives (bonuses) for the NEO’s and their 2014 compensation levels. However, for purposes of this Information Circular, the Company has included some analysis comparing the Company’s 2012 pay levels to the 2012 compensation levels of the Peer Group in the interest of providing shareholders with a more current benchmarking analysis of the Company’s overall compensation and pay practices (see “Benchmarking of NEO Compensation Relative to the Company’s Peer Group” below).

- 18 -

Aligning the Interests of the NEOs with the Interests of the Company’s Shareholders

The Company believes that transparent, objective and easily verified corporate goals, combined with individual performance goals, play an important role in creating and maintaining an effective compensation strategy for the NEOs. The Company’s objective is to establish benchmarks and targets for its NEOs which, if achieved, will enhance shareholder value.

A combination of fixed and variable compensation is used to motivate executives to achieve overall corporate goals. For the 2012 financial year, the three basic components of the executive officer compensation program were:

| · | Base (fixed) salary; |

| · | Annual incentives (cash bonus); and |

| · | Long term (option based) compensation. |

Base salary comprises a portion of the total cash-based compensation and is paid semi-monthly; however, annual incentives and option based compensation represent compensation that is “at risk” and thus may or may not be paid to the respective executive officer depending on: (i) whether the executive officer is able to meet or exceed his or her applicable performance targets; (ii) whether the Company has met its operational performance targets; and (iii) market performance of the Company’s common shares relative to the market and peer common share performance.

To date, no specific formulae have been developed to assign a specific weighting to each of these components. Instead, the Compensation Committee meets at least twice annually to consider performance targets and the Company’s performance, and assigns compensation based on its subjective assessment of the accomplishments of the executive relative to these performance metrics and makes recommendations to the board for consideration.

Base Salary

The base salary for each NEO is reviewed annually by the Compensation Committee, with recommendations made to the board for final approval. The base salary review for each NEO is based on an assessment of factors such as current competitive market conditions, compensation levels within the peer group and particular skills, such as leadership ability and management effectiveness, experience, responsibility and proven or expected performance of the particular individual.

The Compensation Committee, using the 2010 and 2012 Executive Compensation Reports and other available peer group information, together with budgetary guidelines and other internally generated planning and forecasting tools, performed annual assessments of the compensation of all executive and employee compensation levels.

2012 Base Salary

During the financial year ended December 31, 2011, Daniel MacInnis, Larry Taddei and Michael Petrina were awarded a 5.1%, 5.0% and 5.0% increase in base salary, respectively, effective January 1, 2012, in order to better align their respective salary levels with those of peers with similar roles and responsibilities (see “Benchmarking of NEO Compensation Relative to the Company’s Peer Group” below). The Company also awarded a 2.9% increase in base salary to Gordon Neal and Jody Harris, effective January 1, 2012, as a cost of living increase consistent with the consumer price index. In the case of Gordon Neal, his salary (with mutual agreement) was adjusted to 70% of his base to reflect that he commits up to 30% of his time to other activities outside of MAG.

- 19 -

2013 Base Salary

During the financial year ended December 31, 2012, Daniel MacInnis, Larry Taddei and Jody Harris were awarded a 12.5%, 9.5% and 4.0% increase in base salary, respectively, effective January 1, 2013, in order to continue to align their respective salary levels with those of peers with similar roles and responsibilities. The Company also awarded a 1.2% increase in base salary to Gordon Neal, effective January 1, 2013, as a cost of living increase consistent with the consumer price index. Michael Petrina did not receive a base salary increase for 2013, as he had provided the Company notice that he would be leaving the Company in early 2013.

Annual Incentives

To motivate executives to achieve short-term corporate goals, the NEOs participate in an annual incentive plan. Awards under the annual incentive plan are made by way of cash bonuses which are based in part on the Company’s success in reaching its objectives and in part on individual performance. A target bonus is set for each of the CEO, CFO and VP Operations, based on a percentage of Base Salary. The Compensation Committee and the board of directors approve all annual incentives.

Executive management together with the Compensation Committee set certain individual and corporate performance objectives each year. These corporate objectives are generally qualitative in nature given the exploration and predevelopment stage of the Company. In 2012, the principal individual and corporate objectives related primarily to the continued advancement of the Company’s two principal projects (the 44% owned Juanicipio project and the 100% owned Cinco de Mayo project), and maintaining an adequate treasury for the Company. Specific objectives included:

CEO

| 1. | Advancement of the 44% owned Juanicipio Project, in conjunction with the Company’s Joint Venture partner, Fresnillo, including the finalization of an Updated Preliminary Economic Assessment (“UPEA”); implementation of an approved 2012/2013 mine permitting and underground development budget; and continued exploration on the Juanicipio Project; |

| 2. | The continued assessment and advancement of the 100% owned Cinco de Mayo project, including aggressive drilling of the silver-zinc-lead deposit targets, completion of an initial 43-101 mineral resource estimate on the Upper Manto zone, and an extensive metallurgical test program on the Pozo Seco molybdenum-gold deposit in advance of a planned Preliminary Economic Assessment (“PEA”); |

| 3. | Create market awareness and value for the Cinco de Mayo project; and, |

| 4. | Increasing investor interest in, and analyst coverage with respect to, the Company. |

CFO

| 1. | Evaluate and monitor financial needs of the Company and ensure financing strategies are in place; |

- 20 -

| 2. | Implementation of successful transition to a US$ reporting currency effective January 1, 2012; |

| 3. | Review Juanicipio UPEA model mechanics and tax review(s); and |

| 4. | Manage the Company's corporate structure and analyze and implement any changes thereto as deemed advisable by the board of directors. |

VP Operations

| 1. | Advancement of the 44% owned Juanicipio Project, in conjunction with the Company’s Joint Venture partner, Fresnillo, including the oversight/finalization of an UPEA and associated parallel studies, and continued exploration; |

| 2. | The continued assessment of the 100% owned Cinco de Mayo project, specifically with respect to an extensive metallurgical test program on the Pozo Seco molybdenum-gold deposit in advance of a planned PEA; and |

| 3. | Identifying and advancing value-add merger and acquisition opportunities. |

The CEO and CFO review the performance of the VP Corporate Development and the Corporate Secretary and recommend a bonus to the Compensation Committee based on their subjective assessment of these NEO’s performance. The Compensation Committee can then choose to accept, reject or modify the bonus recommended by the CEO and CFO. In addition, the CEO provides the Compensation Committee with his assessment and recommendations for both the CFO and the VP Operations.

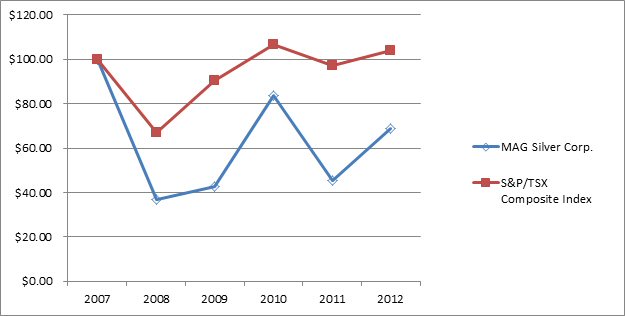

The Compensation Committee does not set “share price targets” and hold the NEOs accountable to such targets, given the numerous uncontrollable factors that can affect the Company’s share price (commodity prices, threats of global economic country failures, etc.) However the Compensation Committee and the other board members are aware of the Company’s share price performance against peer performance and against various market indices (see “Performance Graph” below). In addition, the Company’s financial advisor is often asked to provide insight into the Company’s share performance, including share price as a multiple of the Company���s ‘Net Asset Value’ (“NAV”) relative to peers. This information provides the backdrop against which the corporate successes achieved by the NEOs are evaluated, and subjectively is factored into the discretionary compensation rewards earned by the NEOs.

The more objective factors considered in the determination of annual bonus are the success of NEOs in achieving their individual objectives and their respective contributions to the Company in reaching its overall goals. The Compensation Committee assesses the performance of each NEO on the basis of his or her respective contribution to the achievement of the predetermined objectives, as well as to needs of the Company that arise on a day to day basis (see “Compensation and Measurements of Performance” below). This assessment is used by the Compensation Committee in developing its recommendations to the board of directors with respect to the determination of annual bonuses for the NEOs. Where the Compensation Committee cannot unanimously agree, the matter is referred to the full board for decision. The board relies heavily on the recommendations of the Compensation Committee in granting annual incentives.

The Compensation Committee, by recommendation to the board of directors, may increase the bonus payment beyond the targeted amount in circumstances where the NEO achieves all targets and exceeds the expectations for his or her position. This discretion was exercised with respect to the CEO and CFO’s 2012 bonus paid which exceeded target by 5% and 5.7% respectively of salary.

- 21 -

Compensation and Measurements of Performance

With the recommendations from the Compensation Committee, the board of directors approves targeted annual incentives for all NEO’s for each financial year. Achievement of individual and corporate objectives would generally lead to payment of the target bonus, while performance above or below target would correspondingly result in a bonus payment above or below the target level.

In 2012, the targeted incentives and incentives paid were as follows for each of the NEOs:

| NEO | Target as % of Base Salary | Targeted Bonus ($) | Actual Bonus ($) Paid |

| Daniel MacInnis – CEO | 40% | $115,600 | $130,000 |

| Larry Taddei – CFO | 30% | $ 63,000 | $ 75,000 |

| Michael Petrina – former VP Operations | 30% | $ 63,000 | $ 50,000 |

| Gordon Neal – former VP Corporate Development | n/a (1) | n/a (1) | $ 40,000 |

| Jody Harris – Corporate Secretary | n/a (1) | n/a (1) | $ 27,500 |

Notes:

(1) Target bonus levels are not set for the VP Corporate Development and Corporate Secretary. Rather, the Compensation Committee looks to the CEO and CFO to provide them with their evaluation and bonus recommendations for these positions, and then makes a final bonus determination.

The above targeted amounts were pre-determined by the Compensation Committee based on market research and an assessment of compensation levels within the Company’s peer group (using the 2010 Executive Compensation Report), and were then approved by the board of directors.

Achieving predetermined individual and/or corporate targets and objectives, as well as general performance in day to day corporate activities, triggers the award of a bonus payment to the NEOs. The NEOs will receive a partial or full incentive payment depending on the number of the predetermined targets met and the Compensation Committee’s and the board’s assessment of overall performance. Included in this assessment, is an evaluation of how the NEO’s managed any unexpected or unforeseen events during the period. The determination as to whether a target has been met is ultimately made by the board and the board reserves the right to make positive or negative adjustments to any bonus payment if they consider them to be appropriate.

Before paying out the annual incentives, the Compensation Committee and the board of directors consider all annual incentives carefully in light of the achieved individual and corporate targets and objectives, respective performance, analysis of external market conditions and competitive needs to retain its qualified personnel. In conducting this assessment, the board of directors and Compensation Committee retain the discretion to increase or decrease bonus payments, regardless of attainment of objectives, due principally to their recognition that the achievement of milestones and objectives relating to its Juanicipio Project are heavily co-dependent on the actions of Fresnillo, its joint venture partner and operator of the project.

For 2012, the Compensation Committee and the board of directors concluded that each NEO broadly met or (in the case of the CEO and CFO) exceeded their target objectives, including the achievement of the following key 2012 milestones:

| · | At the Juanicipio Project, the finalization of a robust Updated Preliminary Economic Assessment (“UPEA”) lead to the implementation of an approved 2012/2013 mine permitting and underground development budget of US$25.4 million; |

- 22 -

| · | Drilling at the Cinco de Mayo project resulted in the discovery of hole CM-431 (the new “Pegaso Zone”) substantiating the exploration model theory previously put forth by senior management and the exploration team; |

| · | Completed initial 43-101 mineral resource estimate at Cinco de Mayo (Upper Manto zone); and, |

| · | Closed a $33 million financing in a very difficult capital market environment. |

In addition, the Compensation Committee and board factored into their performance assessments the manner in which the CEO and the CFO managed several unexpected and significant challenges that arose in 2012, including dealing and negotiating with a dissident group of MAG shareholders which collectively held approximately 9.76% of MAG's outstanding shares. The Company ultimately reached an agreement on September 4, 2012 whereby the Company agreed to nominate Richard Clark and Peter Barnes for election at the annual and special meeting (“Annual Meeting”) of shareholders held on October 5, 2012.

On this basis, the board of directors determined that annual 2012 incentives to the CEO and CFO’s be increased by 5% and 5.7% respectively to reflect performance beyond targeted expectations, resulting in Daniel MacInnis and Larry Taddei receiving 2012 bonuses of $130,000 and $75,000 respectively.