EXHIBIT 99.2

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

OPERATIONS AND FINANCIAL CONDITION

FOR THE YEAR ENDED DECEMBER 31, 2013

TABLE OF CONTENTS

| Page | |||

| 1. | Core Business | ||

| 2. | Highlights | ||

| 3. | Outlook and Strategy | ||

| 4. | Summary of Financial and Operating Statistics | ||

| 4.1: | Annual Financial Statistics | ||

| 4.2: | Annual Operating Statistics | ||

| 4.3: | Quarterly Financial Statistics | ||

| 4.4: | Quarterly Operating Statistics | ||

| 5. | Overview of Annual Results | ||

| 5.1: | Overview of Annual Financial Results | ||

| 5.2: | Overview of Annual Operating Results | ||

| 5.3: | Overview of Quarterly Financial Results | ||

| 5.4: | Overview of Quarterly Operating Results | ||

| 6. | Operating Mines | ||

| 7. | Construction, Development and Exploration | ||

| 8. | Mineral Reserves and Mineral Resources | ||

| 9. | Liquidity, Capital Resources and Contractual Commitments | ||

| 10. | Income Taxes | ||

| 11. | Economic Trends, Risks and Uncertainties | ||

| 12. | Contingencies | ||

| 13. | Critical Accounting Policies and Estimates | ||

| 14. | Non-GAAP Measures | ||

| 15. | Selected Quarterly Financial and Operating Summary | ||

| 16. | Disclosures Controls and Procedures | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF OPERATIONS AND FINANCIAL CONDITION

(All figures are in United States Dollars unless otherwise specified and are in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). This Management’s Discussion and Analysis of Operations and Financial Condition should be read in conjunction with the Company’s most recently issued annual consolidated financial statements for the year ended December 31, 2013 ("Consolidated Annual Financial Statements").

Cautionary notes regarding forward-looking statements follow this Management’s Discussion and Analysis of Operations and Financial Condition.

1. CORE BUSINESS

Yamana Gold Inc. (the “Company” or “Yamana”) is a Canadian-headquartered gold producer engaged in gold mining and related activities including exploration, extraction, processing and reclamation. The Company has significant precious metal properties and land positions throughout the Americas including in Brazil, Chile, Argentina and Mexico.

The Company plans to continue to build on its current production base through existing operating mine expansions and development of new mines, advancement of its exploration properties and by targeting other gold consolidation opportunities with a primary focus in the Americas.

Note 34(a) Related Parties to the most recently audited Consolidated Annual Financial Statements lists Yamana’s significant subsidiaries with 100% equity interest. The Company does not have any material off-balance sheet arrangements, except as noted in Note 32 Contractual Commitments to the Consolidated Annual Financial Statements.

Yamana is listed on the Toronto Stock Exchange (Symbol: YRI) and the New York Stock Exchange (Symbol: AUY).

2. HIGHLIGHTS

The Company’s focus continues to be on ensuring a balance between costs and production, margin preservation and on the generation and protection of cash flow. The Company continues to believe this balanced approach is appropriate and prudent to create value in the prevailing commodity price environment.

Financial

For the year ended December 31, 2013

| • | Revenues of $1.84 billion. |

| • | Net loss(a) of $446.2 million or $0.59 loss per share, after impairment charges related to mineral properties of $546.1 million, net of taxes. |

| • | Adjusted earnings(b) of $273.4 million or $0.36 adjusted basic and diluted earnings per share(b). |

| • | Mine operating earnings of $540.8 million. |

| • | Cash flows from operating activities after changes in non-cash working capital of $653.1 million and cash flows from operating activities before changes in non-cash working capital* of $707.9 million. |

For the three months ended December 31, 2013

| • | Revenues of $420.7 million. |

| • | Net loss(a) of $583.9 million or $0.78 loss per share, after impairment charges related to mineral properties of $535.8 million, net of taxes. |

| • | Adjusted earnings(b) of $36.7 million or $0.05 adjusted basic and diluted earnings per share(b). |

| • | Mine operating earnings of $70.1 million. |

| • | Cash flows from operating activities after changes in non-cash working capital of $184.8 million and cash flows from operating activities before changes in non-cash working capital* of $165.3 million. |

________________________________________

(a) Attributable to Yamana equity holders, after deducting non-controlling interest’s share of non-recurring impairment charge.

(b) A non-GAAP measure - Refer to Section 14.

1

Operational

For the year ended December 31, 2013

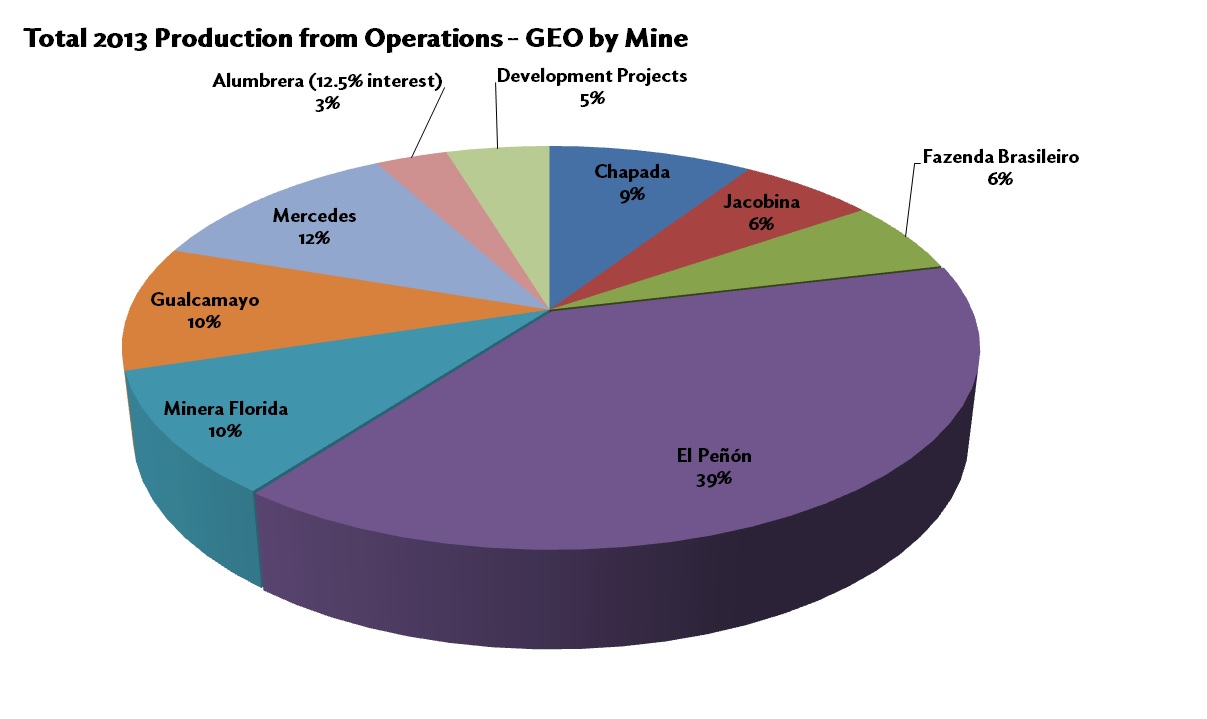

| • | Production of 1.20 million gold equivalent ounces ("GEO")(a). |

| • | Commercial production of 1.14 million GEO. |

| • | Production from operating mines is summarized as follows: |

| For the years ended December 31, | ||||||

| (In GEO) | 2013 | 2012 | ||||

| Chapada | 110,618 | 128,171 | ||||

| El Peñón | 467,523 | 462,496 | ||||

Mercedes (d) | 141,618 | 126,010 | ||||

| Gualcamayo | 120,337 | 147,310 | ||||

| Jacobina | 73,695 | 116,863 | ||||

| Minera Florida | 118,590 | 105,679 | ||||

| Fazenda Brasileiro | 70,079 | 67,130 | ||||

Ernesto/Pau-a-Pique (b) | 27,571 | 1,274 | ||||

C1 Santa Luz (b) | 12,997 | — | ||||

Pilar (b) | 15,374 | — | ||||

| Alumbrera (12.5%) | 39,157 | 46,077 | ||||

| Total | 1,197,559 | 1,201,010 | ||||

| • | Production of 8.4 million silver ounces. |

| • | Copper production from Chapada of 130.2 million pounds. |

| • | By-product cash costs(c) of $410 per GEO. |

| • | Co-product cash costs(c) of $596 per GEO and $1.65 per pound of copper from Chapada. |

| • | All-in sustaining cash costs(c) of $814 per GEO on a by-product basis and $947 per GEO on a co-product basis. |

| • | Average all-in sustaining cash cost on a co-product basis for the last three quarters was below $925 per GEO exceeding expectations of the cost containment initiative implemented in the second quarter. |

| • | Jacobina, Brazil — Production met the revised goals that were set in the first quarter of 2013 and more importantly, the near term objectives relating to the improvement of costs and underground development were met. |

| • | Mercedes, Mexico — GEO production was 12% higher than 2012. |

| • | Minera Florida, Chile — GEO production was 12% higher than 2012 with new production from the tailings retreatment plant that started in September 2012. |

For the three months ended December 31, 2013

| • | Production of 303,768 GEO. |

| • | Commercial production of 277,447 GEO. |

| • | Production from operating mines is summarized as follows: |

| For the three months ended December 31, | ||||||

| (In GEO) | 2013 | 2012 | ||||

| Chapada | 29,817 | 32,498 | ||||

| El Peñón | 101,364 | 128,119 | ||||

| Mercedes | 31,716 | 39,443 | ||||

| Gualcamayo | 34,929 | 31,502 | ||||

| Jacobina | 19,519 | 28,337 | ||||

| Minera Florida | 30,513 | 32,797 | ||||

| Fazenda Brasileiro | 18,270 | 18,251 | ||||

Ernesto/Pau-a-Pique (b) | 9,707 | 1,274 | ||||

C1 Santa Luz (b) | 6,120 | — | ||||

Pilar (b) | 10,494 | — | ||||

| Alumbrera (12.5%) | 11,319 | 10,769 | ||||

| Total | 303,768 | 322,990 | ||||

2

| • | Production of 2.2 million silver ounces. |

| • | Copper production from Chapada of 36.0 million pounds. |

| • | By-product cash costs(c) of $417 per GEO. |

| • | Co-product cash costs(c) of $647 per GEO and $1.53 per pound of copper from Chapada. |

| • | All-in sustaining cash costs(c) of $754 per GEO on a by-product basis and $935 per GEO on a co-product basis. |

| • | Minera Florida, Chile — GEO production increased each consecutive quarter; fourth quarter production was 11% higher than the third quarter and 15% higher than the second quarter of 2013 with decreases in co-product costs by 22% and 35% for the corresponding periods. |

| • | Gualcamayo, Argentina — Gold production was 26% higher than the third quarter of 2013 with December and January 2014 production averaging over 14,000 ounces per month, consistent with plan and production objectives for the expanded operation. |

| • | Fazenda Brasileiro, Brazil — Gold production was 9.3% higher than the third quarter of 2013. |

| • | El Peñón, Chile & Mercedes, Mexico — Production levels decreased according to normal sequencing of mine plan to contain costs and better position those mines for 2014, although both produced at above guidance expectations. |

| • | Pilar and Ernesto/Pau-a-Pique production increased by 115% and 46% respectively in the fourth quarter over third quarter levels with significant improvements occurring in December. |

| • | Pilar, Brazil — Commissioning continued in the quarter. An infill drilling program is currently underway with a focus to ensure higher grade ore shoots can be mined efficiently. Additionally, the Company has elected to take Maria Lazarus through the development cycle on an expedited basis as the exploration drilling results to date indicate possible contribution to future production. Completion of commissioning is expected in the third quarter of 2014. New low-profile equipment arrived on site early in 2014. |

| • | C1 Santa Luz, Brazil — Commissioning continued in the quarter. The gradual ramp-up at C1 Santa Luz was due to permitting, availability of equipment and the need to ensure sufficient water reserves for continuous operations, which are now in place. |

| • | Ernesto/Pau-a-Pique, Brazil — The project (operation) was originally planned as a combination of an open-pit at Ernesto and an underground operation at Pau-a-Pique with a common plant. A plan has been developed which continues to include an underground operation at Pau-a-Pique but now contemplates a near-to-surface underground operation at Ernesto. These alternatives are under consideration. |

______________________________

(a) GEO assumes gold plus the gold equivalent of silver using a ratio of 50:1 for all periods presented.

(b) Commissioning production as the mine is not yet in commercial operation.

| (c) | A non-GAAP measure - refer to Section 14. |

(d) Includes commissioning production of 8,959 GEO in January of 2012, commercial production started on February 1, 2012.

Construction and Development

| • | Chapada, Brazil — The Company continues to advance programs relating to the optimization of production that include the installation of an in-pit crusher and modifications to the grinding circuit. These initiatives will increase throughput and facilitate the development of new ore bodies including Corpo Sul in the fourth quarter of 2014. This will enable future production to continue at a rate of at least 130,000 GEO and 130 million pounds of copper annually. |

| • | Cerro Moro, Argentina — Work continued at Cerro Moro toward the completion of its updated feasibility study including pre-development work and drilling to support the study and to grow the mineral resource base as well as further advancing the project for a reduced-scale operation. Subject to a positive feasibility study and market conditions, the Company plans to make a construction decision with a goal of initial production in 2016. |

| • | Suyai, Argentina — The Company plans to apply for environmental permits in 2014. A number of relevant studies have already been completed and others are ongoing, which would position the Company well to apply for permitting this year. The current plan being evaluated includes an underground operation without any chemical processing onsite that will produce a precious metal concentrate that could be sold to third parties or potentially processed at Cerro Moro. |

| • | Gualcamayo, Argentina — The QDD Lower West ("QDDLW") underground mine has started to contribute to production. Completion of the underground conveyor is expected in the second quarter and production is expected to ramp-up each quarter during the year. |

Exploration

| • | Gualcamayo, Argentina — Exploration at Gualcamayo has focused on drilling targets surrounding the Rodado and QDD Lower West (“QDDLW”) systems. Positive assays received from drilling in the fourth quarter continued to expand the mineral envelope of Rodado southwest and the potential orebody, which remains open along strike and down dip. |

3

| • | Minera Florida, Chile — The near mine exploration program completed 4,510 metres distributed in 29 holes during the fourth quarter of 2013. The program tested targets within Mina Este such as Triangulo Mineralizado, Lisset and PVO and additional targets including Tribuna, Victoria and Hallazgo. Assay results continue to show positive results from most targets. |

| • | C1 Santa Luz, Brazil — During the fourth quarter of 2013, the near-mine and district exploration drill programs completed 1,634 metres in eight holes. The near-mine program tested the up-dip extension of the southwestern deep target and completed infill holes and tested the northern extensions at Antas III. The regional program tested the Gravata and Rancho do Carneiro targets. Results from both programs are in-line with prior results and are being evaluated for economic potential. |

| • | Ernesto/Pau-a-Pique, Brazil — A total of 13,928 meters were completed in 95 drill holes at the mine during the year to test near-mine targets and extensions. Several new mineral traps were discovered that host potential ore grade gold mineralization which could increase mineral resources and extend the life of mine. |

| • | Pilar, Brazil — Underground mapping at Caiamar and sampling along with computer modeling of drill data has identified moderate to high grade inferred mineral resource ore shoots that will be drill-tested from the surface during 2014 to expand the mineral resource and mineral reserve base at Pilar. |

| • | Cerro Moro, Argentina — The focus of the 2013 exploration program was to develop and test new targets that are both within and outside of the known mineralized structural blocks. During the fourth quarter, 1,077 metres in five holes were drilled to complete the 2013 exploration drill program. This drilling tested the Carlita, Patricia and Margarita veins in an effort to build and expand the known mineralization envelopes. The final hole of the year drilled at the southeast end of the Margarita system cut important gold and silver values leaving the structure open to the southeast and to depth. |

3. OUTLOOK AND STRATEGY

The Company continues to strive to deliver sustainable value. In doing so, the Company remains focused on cost control, operational performance and sustainable volume growth, always with a "simple to understand" objective of performing financially and maximizing cash flows. Emphasis remains on comparatively low costs to drive margins and cash flows, delivery of higher quality ounces and projects while maintaining disciplined capital spending, along with our commitment to adhere to the best practices for health, safety and environmental protection.

In response to the current volatile gold price environment which puts margins at risk, the Company has initiated cost containment and margin reclamation initiatives to focus on quality of ounces produced measured by contribution to cash flows instead of production volume alone. The cost containment and margin reclamation initiatives are consistent with the Company's established focus on cash flow generation. The Company believes prioritizing financial performance over production is an approach that will deliver value, particularly in periods of volatile and uncertain metal prices.

These initiatives have progressed since they were announced in the second quarter. Cost savings are being realized through reductions in operating costs, capital expenditures, exploration costs, and general and administrative costs, in addition to other areas. The Company's progress in executing its cost containment and margin reclamation initiatives is evidenced by a reduction of its all-in sustaining co-product cash costs per gold equivalent ounce ("GEO"). Average all-in sustaining cash costs ("AISC") for the last three quarters was below $925 per GEO on a co-product basis. The reduction in AISC on a co-product basis was primarily driven by:

| • | General and administrative expenses were $66 per GEO in the fourth quarter, compared to $88 per GEO in the second quarter, representing a 25% decrease. |

| • | Sustaining capital expenditures were $197 per GEO in the fourth quarter, compared to $260 per GEO in the second quarter, representing a 24% decrease. Compared to the previous guidance of sustaining capital expenditure at $310 per GEO for 2013, the reduction was in excess of 55%. |

Given the current metal price environment and significant precious metal price volatility, the Company continues to align its production expectation with the new price environment. As marginal ounces are at risk of eroding margins, the Company will be diligent in protecting margins through creating a base production level at a sustainable contained cost structure that will generate cash flow in the current and lower price environments. The Company will not sacrifice margin, or compromise cost structure, for volume growth until costs are believed to be contained so that new production will generate margins in current and lower metal price environments. With costs stabilizing at lower levels, the focus is now returning to maximizing production growth, while generating cash flows and free cash flows will always be the core focus.

The Company has budgeted production of 1.4 million GEO in 2014 at AISC below $850 per GEO on a by-product basis and $925 per GEO on a co-product basis. Silver production is expected to be approximately 8.8 million ounces in 2014 which is included in GEO. Estimated cash costs for 2014 are forecast to be in line with 2013 on both a co-product and by-product basis.

4

Cash costs on a by-product basis are calculated after base metal by-product credits, which assumes a price forecast for copper of $3.20 per pound.

As part of the annual budgeting process, the Company has performed various evaluations to maximize the level of confidence and reliability in the forecast production, costs and cash flow generation capacity at every operation. These evaluations identify ounces that the Company considers to have a lower level of certainty or reliability on any of: production, costs or cash flow generation. For budgeted production in 2014, all of these ounces relate to new operations as they progress to full capacity. The Company considers 70,000 production ounces, or less than five per cent, of its budgeted production for 2014 to be within this category and most of these ounces would be in pre-commercial production and as such not impact its cash flow expectations for the year.

The Company strives to achieve budgeted production and conducts these evaluations for the purposes of stress testing its business plan and for evaluation of the proper balance between production and costs and other factors that may influence or affect cash flow. While the Company will make every effort to produce at budget levels, this approach provides a reasonable tool for assessing downside risk to production or where costs are at risk or where the level of reliability for certain production is below the level of total of its expected production. The Company remains focused on the generation and maximization of cash flow.

The table below provides the mine-by-mine 2014 production expectations according to budget.

| (in GEO) | 2014 Estimate | |

Chapada (i) | 103,000 | |

El Peñón (i) | 448,000 | |

Mercedes (i) | 129,000 | |

| Gualcamayo | 170,000 | |

| Jacobina | 89,000 | |

Minera Florida (i) | 114,000 | |

| C1 Santa Luz | 90,000 | |

| Ernesto/Pau-a-Pique | 58,000 | |

| Pilar | 90,000 | |

| Fazenda Brasileiro | 64,000 | |

| Alumbrera (12.5% interest) | 45,000 | |

| Total GEO | 1,400,000 | |

| Total Copper - Chapada (millions of pounds) | 134 | |

________________________________________________________

(i) Silver production is reported as GEO at a ratio of 50:1.

Production in 2015 is expected to further increase. The Company is evaluating proposed plans for production increases in light of its philosophy of balancing production with costs.

Copper production is expected to be approximately 134 million pounds in 2014. This estimate reflects the production from Chapada and does not include the attributable copper production from the Company’s 12.5% interest in Alumbrera.

Expansionary capital spending for 2014 is expected to be approximately $150 million (excluding capitalized interest), which is significantly lower than 2013 as the Company’s newest operations ramp-up to commercial production and the Company continues to allocate capital to those opportunities that can most readily contribute to cash flow.

The Company expects to spend approximately $70 million on exploration in 2014. The 2014 exploration program will continue to focus on increasing mineral reserves and mineral resources with its near-mine and regional exploration programs, as well as continuing to explore identified greenfield targets and generate new targets.

In 2014, sustaining capital expenditures are expected to be in the range of $320 million to $340 million or approximately $250 per GEO. This allocates all capital to gold ounces with no consideration for copper. The Company treats copper as a by-product and applies all sustaining capital to GEOs. Sustaining capital expenditures are expected to decline in future years as a result, in part, of the cost saving initiatives related to maintenance and the expected growth in gold production. Sustaining capital is included in AISC.

5

For 2014, depreciation, depletion and amortization ("DD&A") is expected to be approximately $340 per GEO when excluding any allocation to copper as the Company treats copper as a by-product and applies all DD&A to GEO. General and administrative expenses are expected to be below $140 million, in line with 2013 levels. The effective tax rate for 2014 is forecast to be between 30% to 32%.

The Company continues to work toward the stated target of 1.5 million to 1.7 million GEO which it believes remains achievable with its existing portfolio of assets. However, with an extended timetable, this further growth can more efficiently be delivered at better costs. Exploration results continue to support the higher level of sustainable production through its producing mines. Details of the exploration program year to date can be found in Section 7 Construction, Development and Exploration.

The Company had approximately $830 million of available cash and undrawn credit at December 31, 2013.

6

4. SUMMARY OF FINANCIAL AND OPERATING STATISTICS

4.1 Annual Financial Statistics

| For the years ended | |||||||||||

| Dec 31, 2013 | Dec 31, 2012 | Dec 31, 2011 | |||||||||

| (Loss)/earnings per share attributable to Yamana equity holders - basic & diluted | $ | (0.59 | ) | $ | 0.59 | $ | 0.74 | ||||

Adjusted earnings per share (i) - basic and diluted | $ | 0.36 | $ | 0.93 | $ | 0.96 | |||||

| Dividends declared per share | $ | 0.260 | $ | 0.240 | $ | 0.155 | |||||

| Dividends paid per share | $ | 0.260 | $ | 0.225 | $ | 0.135 | |||||

Weighted average number of common shares outstanding - basic ( in thousands) | 752,697 | 748,095 | 744,600 | ||||||||

Weighted average number of common shares outstanding - diluted (in thousands) | 752,697 | 749,591 | 746,144 | ||||||||

| (In thousands of United States Dollars; unless otherwise noted) | |||||||||||

| Net (loss)/earnings attributable to Yamana equity holders | $ | (446,247 | ) | $ | 442,064 | $ | 548,294 | ||||

Adjusted earnings (i) | $ | 273,358 | $ | 694,333 | $ | 712,896 | |||||

| Revenues | $ | 1,842,682 | $ | 2,336,762 | $ | 2,173,325 | |||||

| Mine operating earnings | $ | 540,778 | $ | 1,121,270 | $ | 1,099,874 | |||||

| Cash flows from operating activities | $ | 653,135 | $ | 1,158,057 | $ | 1,225,782 | |||||

Cash flows from operating activities before changes in non-cash working capital (i) | $ | 707,861 | $ | 1,044,946 | $ | 1,266,373 | |||||

| Cash flows to investing activities | $ | (1,053,410 | ) | $ | (1,498,030 | ) | $ | (846,075 | ) | ||

| Cash flows (to)/from financing activities | $ | 283,843 | $ | 146,399 | $ | (142,678 | ) | ||||

Average realized gold price per ounce (ii) | $ | 1,408 | $ | 1,670 | $ | 1,567 | |||||

Average realized copper price per pound (ii) | $ | 3.28 | $ | 3.60 | $ | 3.93 | |||||

Average realized silver price per ounce (ii) | $ | 23.73 | $ | 30.46 | $ | 35.19 | |||||

Average market gold price per ounce (iii) | $ | 1,411 | $ | 1,669 | $ | 1,573 | |||||

Average market copper price per pound (iii) | $ | 3.32 | $ | 3.61 | $ | 4.00 | |||||

Average market silver price per ounce (iii) | $ | 23.85 | $ | 31.17 | $ | 35.32 | |||||

| As at | |||||||||||

| Dec 31, 2013 | Dec 31, 2012 | Dec 31, 2011 | |||||||||

| Total assets | $ | 11,410,717 | $ | 11,800,163 | $ | 10,769,940 | |||||

| Total long-term liabilities | $ | 3,615,242 | $ | 3,269,266 | $ | 2,783,786 | |||||

| Total equity | $ | 7,158,105 | $ | 7,861,878 | $ | 7,491,523 | |||||

| Working capital | $ | 81,093 | $ | 255,134 | $ | 608,021 | |||||

_____________________________

| (i) | A cautionary note regarding non-GAAP measures and their respective reconciliations are included in Section 14 including a discussion and definition of Adjusted Earnings, Adjusted Earnings per Share, and additional measures. |

| (ii) | Realized prices based on gross sales compared to market prices for metals may vary due to infrequent shipments and depending on timing of the sales. |

| (iii) | Source of information: Bloomberg. |

7

4.2 Annual Operating Statistics

| For the years ended | |||||||

| Dec 31, 2013 | Dec 31, 2012 | ||||||

Gold Equivalent Ounces (GEO) Production (i) | |||||||

| Brazil | |||||||

Chapada (ii) | 110,618 | 128,171 | |||||

| Jacobina | 73,695 | 116,863 | |||||

| Fazenda Brasileiro | 70,079 | 67,130 | |||||

| Chile | |||||||

El Peñón (ii) | 467,523 | 462,496 | |||||

Minera Florida (ii) | 118,590 | 103,818 | |||||

| Argentina | |||||||

| Gualcamayo | 120,337 | 147,310 | |||||

Alumbrera (iii) | 39,157 | 46,077 | |||||

| Mexico | |||||||

Mercedes (ii)(v) | 141,618 | 117,051 | |||||

Total commercial GEO production (i) | 1,141,617 | 1,188,916 | |||||

Commissioning GEO (i)(v) | 55,942 | 12,094 | |||||

Total GEO production (i) | 1,197,559 | 1,201,010 | |||||

By-product Cash Costs per GEO (i) (iv) | |||||||

| Brazil | |||||||

| Chapada | $ | (1,296 | ) | $ | (1,865 | ) | |

| Jacobina | 1,174 | 747 | |||||

| Fazenda Brasileiro | 808 | 872 | |||||

| Chile | |||||||

| El Peñón | 485 | 440 | |||||

| Minera Florida | 747 | 797 | |||||

| Argentina | |||||||

| Gualcamayo | 772 | 536 | |||||

Alumbrera (iii) | (252 | ) | (1,203 | ) | |||

| Mexico | |||||||

| Mercedes | 496 | 485 | |||||

By-product cash costs per GEO produced (i) (iv) | $ | 410 | $ | 230 | |||

Co-product cash costs per GEO produced (i) (iv) | $ | 596 | $ | 525 | |||

Co-product cash costs per pound of copper produced (iv) | $ | 1.75 | $ | 1.48 | |||

All-in sustaining cash costs per GEO, by-product basis (i) (iv) | $ | 814 | n/a | ||||

All-in sustaining cash costs per GEO, co-product basis (i) (iv) | $ | 947 | n/a | ||||

| Concentrate Production | |||||||

| Chapada concentrate production (tonnes) | 239,811 | 268,135 | |||||

| Chapada copper contained in concentrate production (millions of lbs) | 130.2 | 150.6 | |||||

Chapada co-product cash costs per pound of copper (iv) | $ | 1.65 | $ | 1.40 | |||

Alumbrera attributable concentrate production (tonnes) (iii) | 55,115 | 65,140 | |||||

Alumbrera attributable copper contained in concentrate production (millions of lbs) (iii) | 30.2 | 37.4 | |||||

Alumbrera co-product cash costs per lb of copper (iii) (iv) | $ | 2.21 | $ | 1.81 | |||

| Gold Equivalent Ounces Breakdown | |||||||

| Gold ounces produced | 1,029,863 | 1,019,969 | |||||

| Silver ounces produced (millions) | 8.4 | 9.0 | |||||

| Sales | |||||||

| Total GEO sales (including 12.5% interest in Alumbrera) | 1,178,972 | 1,186,991 | |||||

| - Total gold sales (ounces) | 1,013,697 | 1,007,414 | |||||

| - Total silver sales (millions of ounces) | 8.3 | 9.0 | |||||

| Chapada concentrate sales (tonnes) | 242,681 | 263,704 | |||||

| Chapada payable copper contained in concentrate sales (millions of lbs) | 126.0 | 139.0 | |||||

______________________________

8

(i) | Silver production is treated as a gold equivalent. Gold equivalent ounce calculations are based on an average historical silver to gold ratio (50:1) which is used and presented solely for period-over-period comparative purposes only. |

(ii) | 2013 gold production: El Peñón — 338,231 ounces; Minera Florida — 99,000 ounces, Chapada — 104,096 ounces, and Mercedes — 129,327 ounces; and 2013 silver production: El Peñón — 6.5 million ounces; Minera Florida — 1.0 million ounces, Chapada — 0.3 million ounces and Mercedes — 0.6 million ounces. |

(iii) | The Company holds a 12.5% equity interest in Alumbrera. |

(iv) | A cautionary note regarding non-GAAP measures and their respective reconciliations are included in Section 14 including a discussion and definition of Cash Costs. |

(v) | Commissioning is ongoing at Ernesto/Pau-a-Pique, C1 Santa Luz and Pilar. Commissioning at Mercedes started in 2011 and concluded on February 1, 2012. |

4.3 Quarterly Financial Statistics

| For the three months ended | ||||||||

| Dec 31, 2013 | Dec 31, 2012 | |||||||

| (Loss)/earnings per share attributable to Yamana equity holders - basic | $ | (0.78 | ) | $ | 0.23 | |||

| (Loss)/earnings per share attributable to Yamana equity holders - diluted | $ | (0.78 | ) | $ | 0.22 | |||

Adjusted earnings per share (i) - basic and diluted | $ | 0.05 | $ | 0.26 | ||||

| Dividends declared per share | $ | 0.065 | $ | 0.065 | ||||

| Dividends paid per share | $ | 0.065 | $ | 0.055 | ||||

Weighted average number of common shares outstanding - basic ( in thousands) | 752,995 | 751,780 | ||||||

Weighted average number of common shares outstanding - diluted (in thousands) | 752,995 | 753,325 | ||||||

| (In thousands of United States Dollars; unless otherwise noted) | ||||||||

| Net (loss)/earnings attributable to Yamana equity holders | $ | (583,936 | ) | $ | 169,161 | |||

Adjusted earnings (i) | $ | 36,719 | $ | 197,368 | ||||

| Revenues | $ | 420,663 | $ | 629,505 | ||||

| Mine operating earnings | $ | 70,113 | $ | 322,082 | ||||

| Cash flows from operating activities | $ | 184,845 | $ | 367,881 | ||||

Cash flows from operating activities before changes in non-cash working capital (i) | $ | 165,315 | $ | 298,064 | ||||

| Cash flows to investing activities | $ | (259,992 | ) | $ | (375,544 | ) | ||

| Cash flows to/(from) financing activities | $ | 66,711 | $ | (44,467 | ) | |||

Average realized gold price per ounce (ii) | $ | 1,277 | $ | 1,692 | ||||

Average realized copper price per pound (ii) | $ | 3.37 | $ | 3.54 | ||||

Average realized silver price per ounce (ii) | $ | 20.63 | $ | 31.37 | ||||

Average market gold price per ounce (iii) | $ | 1,272 | $ | 1,718 | ||||

Average market copper price per pound (iii) | $ | 3.25 | $ | 3.59 | ||||

Average market silver price per ounce (iii) | $ | 20.80 | $ | 32.58 | ||||

_____________________________

(i) | A cautionary note regarding non-GAAP measures and their respective reconciliations are included in Section 14 including a discussion and definition of Adjusted Earnings, Adjusted Earnings per Share, and additional measures. |

(ii) | Realized prices based on gross sales compared to market prices for metals may vary due to infrequent shipments and depending on timing of the sales. |

(iii) | Source of information: Bloomberg. |

9

4.4 Quarterly Operating Statistics

| For the three months ended | |||||||

| Dec 31, 2013 | Dec 31, 2012 | ||||||

Gold Equivalent Ounces (GEO) Production (i) | |||||||

| Brazil | |||||||

Chapada (ii) | 29,817 | 32,498 | |||||

| Jacobina | 19,519 | 28,337 | |||||

| Fazenda Brasileiro | 18,270 | 18,251 | |||||

| Chile | |||||||

El Peñón (ii) | 101,364 | 128,119 | |||||

Minera Florida (ii) | 30,513 | 32,797 | |||||

| Argentina | |||||||

| Gualcamayo | 34,929 | 31,502 | |||||

Alumbrera (iii) | 11,319 | 10,769 | |||||

| Mexico | |||||||

Mercedes (ii)(v) | 31,716 | 39,443 | |||||

Total commercial GEO production (i) | 277,447 | 321,716 | |||||

Commissioning GEO (i)(v) | 26,321 | 1,274 | |||||

Total GEO production (i) | 303,768 | 322,990 | |||||

| By-product Cash Costs per GEO (i) (iv) | |||||||

| Brazil | |||||||

| Chapada | $ | (1,547 | ) | $ | (2,021 | ) | |

| Jacobina | 1,140 | 825 | |||||

| Fazenda Brasileiro | 809 | 856 | |||||

| Chile | |||||||

| El Peñón | 593 | 415 | |||||

| Minera Florida | 592 | 805 | |||||

| Argentina | |||||||

| Gualcamayo | 825 | 485 | |||||

Alumbrera (iii) | (261 | ) | (2,012 | ) | |||

| Mexico | |||||||

| Mercedes | 656 | 435 | |||||

By-product cash costs per GEO produced (i) (iv) | $ | 417 | $ | 198 | |||

Co-product cash costs per GEO produced (i) (iv) | $ | 647 | $ | 517 | |||

Co-product cash costs per pound of copper produced (iv) | $ | 1.58 | $ | 1.51 | |||

All-in sustaining cash costs per GEO, by-product basis (i) (iv) | $ | 754 | n/a | ||||

All-in sustaining cash costs per GEO, co-product basis (i) (iv) | $ | 935 | n/a | ||||

| Concentrate Production | |||||||

| Chapada concentrate production (tonnes) | 67,395 | 72,518 | |||||

| Chapada copper contained in concentrate production (millions of lbs) | 36.0 | 40.5 | |||||

Chapada co-product cash costs per pound of copper (iv) | $ | 1.53 | $ | 1.38 | |||

Alumbrera attributable concentrate production (tonnes) (iii) | 17,547 | 14,669 | |||||

Alumbrera attributable copper contained in concentrate production (millions of lbs) (iii) | 9.6 | 8.5 | |||||

Alumbrera co-product cash costs per lb of copper (iii) (iv) | $ | 1.75 | $ | 2.15 | |||

| Gold Equivalent Ounces Breakdown | |||||||

| Gold ounces produced | 260,187 | 276,373 | |||||

| Silver ounces produced (millions) | 2.2 | 2.3 | |||||

| Sales | |||||||

| Total GEO sales (including 12.5% interest in Alumbrera) | 305,376 | 317,615 | |||||

| - Total gold sales (ounces) | 263,031 | 272,524 | |||||

| - Total silver sales (millions of ounces) | 2.1 | 2.3 | |||||

| Chapada concentrate sales (tonnes) | 67,616 | 69,589 | |||||

| Chapada payable copper contained in concentrate sales (millions of lbs) | 34.5 | 37.3 | |||||

______________________________

10

(i) | Silver production is treated as a gold equivalent. Gold equivalent ounce calculations are based on an average historical silver to gold ratio (50:1) which is used and presented solely for quarter-over-quarter comparative purposes only. |

(ii) | Three-month gold production for the periods ended December 31, 2013: El Peñón — 68,246 ounces; Minera Florida — 24,539 ounces, Chapada — 28,223 ounces, and Mercedes — 28,821 ounces; and three-month silver production: El Peñón — 1.7 million ounces; Minera Florida — 298,696 ounces, Chapada — 79,696 ounces, and Mercedes — 144,715 ounces. |

(iii) | The Company holds a 12.5% equity interest in Alumbrera. |

(iv) | A cautionary note regarding non-GAAP measures and their respective reconciliations are included in Section 14 including a discussion and definition of Cash Costs. |

(v) | Commissioning is ongoing at Ernesto/Pau-a-Pique, C1 Santa Luz and Pilar. Commissioning at Mercedes started in 2011 and concluded on February 1, 2012. |

5. OVERVIEW OF RESULTS

5.1 Overview of Annual Financial Results

| For the years ended December 31, | |||||||

| (In thousands of United States Dollars; unless otherwise noted) | 2013 | 2012 | |||||

| Revenues | $ | 1,842,682 | $ | 2,336,762 | |||

| Cost of sales excluding depletion, depreciation and amortization | (900,789 | ) | (831,754 | ) | |||

| Gross margin | 941,893 | 1,505,008 | |||||

| Depletion, depreciation and amortization | (401,115 | ) | (383,738 | ) | |||

| Mine operating earnings | 540,778 | 1,121,270 | |||||

Other expenses (i) | (249,841 | ) | (289,100 | ) | |||

| Equity (loss)/earnings from associate | (3,905 | ) | 50,642 | ||||

| Impairment of mineral properties and other assets | (682,273 | ) | (67,684 | ) | |||

| Earnings from operations before income taxes | (395,241 | ) | 815,128 | ||||

| Income tax expense | (79,110 | ) | (373,064 | ) | |||

| Net (loss) earnings | $ | (474,351 | ) | $ | 442,064 | ||

Earnings adjustments (ii): | |||||||

| Non-cash unrealized foreign exchange losses | 45,709 | 64,648 | |||||

| Reorganization costs | 3,969 | — | |||||

| Share-based payments/mark-to-market of deferred share units | 7,683 | 26,292 | |||||

| Impact of change in Mexican tax rates on non-cash deferred tax expense | 28,323 | — | |||||

| Impact of change in Chilean tax rates on non-cash deferred tax expense | — | 83,830 | |||||

| Deferred income tax expense on translation of intercompany debt | — | (2,983 | ) | ||||

| Impairment of mineral properties | 682,273 | — | |||||

| Impairment of investment in available-for-sale securities and other assets | 70,285 | 67,684 | |||||

| Other non-cash and non-recurring losses | 44,566 | 16,592 | |||||

| Adjusted earnings before income tax effect | 408,457 | 698,127 | |||||

| Income tax effect of adjustments | (135,099 | ) | (3,794 | ) | |||

Adjusted earnings (ii) | $ | 273,358 | $ | 694,333 | |||

Net (loss) earnings per share attributable to Yamana Gold Inc. equity holders - basic and diluted | $ | (0.59 | ) | $ | 0.59 | ||

Adjusted earnings per share (ii) - basic and diluted | $ | 0.36 | $ | 0.93 | |||

______________________________

| (i) | For 2013, other expenses represent the aggregate of the following expenses: general and administrative of $135.3 million (2012 - $145.9 million), exploration and evaluation of $30.2 million (2012 - $58.0 million), other operating expenses of $78.1 million (2012 - $99.3 million) and net finance expense of 6.3 million (2012 - expense $53.5 million). |

| (ii) | A cautionary note regarding non-GAAP measures and their respective reconciliations are included in Section 14 including a discussion and definition of Adjusted Earnings and Adjusted Earnings per Share. |

11

Impairment

The Company assesses at the end of each reporting period whether there is any indication, from external and internal sources of information, that an asset or cash generating unit (“CGU”) may be impaired. Impairment testing is performed using life of mine after-tax cash flow projections. During the second quarter, the Company updated its after-tax life of mine cash flow projections with updated economic assumptions as a result of the decline in metal prices towards the latter half of the second quarter of 2013. Based on its assessment during the second quarter, the Company concluded that there were no impairment charges in respect to its mineral properties as at June 30, 2013 as a result of the decline in metal prices at that time. Adverse changes in metal price assumptions were partially offset by other inputs that resulted in lower costs and updated mine plans. The recoverable values in the impairment assessment in the second quarter were calculated assuming long-term prices of $1,375 per ounce of gold and $3.00 per pound of copper.

In early October of 2013, after the spot price for gold returned to the $1,350 per ounce level, it started a continuous decline during the fourth quarter and dipped below $1,200 per ounce by late December. During the fourth quarter, the Company performed its impairment test updating its life of mine after-tax cash flow projections for updated reasonable estimates of future metal prices, production based on current estimates of recoverable mineral reserves and mineral resources, recent operating and exploration results, exploration potential, future operating costs, capital expenditures, inflation and long-term foreign exchange rates. The Company examined future cash flows, the intrinsic value beyond proven and probable mineral reserves, value of land holdings, as well as other factors, which are determinants of commercial viability of each mining property in its portfolio, and concluded that a total of $672.0 million ($563.9 million, net of taxes) of impairment charges should be recognized. The impairment charges in the fourth quarter include the following:

| For the periods ended December 31, 2013 | ||||||||||||||||

| (in million dollars) | Three months | Twelve months | ||||||||||||||

| Mine/Project | Impairment | After-tax Impairment | Impairment | After-tax Impairment | ||||||||||||

| Jacobina (goodwill) | $ | 55.0 | $ | 55.0 | $ | 55.0 | $ | 55.0 | ||||||||

| Ernesto/Pau-a-Pique | 175.0 | 168.2 | 175.0 | 168.2 | ||||||||||||

| Alumbrera (12.5% Interest) | 70.0 | 70.0 | 70.0 | 70.0 | ||||||||||||

Jeronimo (a) | 110.0 | 88.0 | 110.0 | 88.0 | ||||||||||||

| Exploration properties | $ | 262.0 | $ | 182.8 | $ | 272.3 | $ | 193.0 | ||||||||

Impairment on mineral properties (b) | $ | 672.0 | $ | 563.9 | $ | 682.3 | $ | 574.2 | ||||||||

| Less: Non-controlling interest (43.3%) - Jeronimo | (28.1 | ) | (28.1 | ) | ||||||||||||

| Impact on net earnings | $ | 535.8 | $ | 546.1 | ||||||||||||

_________________

| (a) | The Company holds 56.7% interest in the Agua de La Falda ("ADLF") project. The ADLF project is an exploration project which includes the Jeronimo deposit and is located in northern Chile. |

| (b) | An impairment charge of $10.3 million was recognized in the second quarter of 2013. |

The Company expects there is further or additional value in these properties over and above what they are being written down to but not at the metal price assumptions used in the impairment testing. The valuation of impairment is based on current forecasts for long-term metal prices which have been influenced by the recent decline in spot prices over the last nine months of 2013. These metal price assumptions are then held constant over mine lives which in some cases are in excess of fifteen years. The fair values in the impairment assessment in the fourth quarter were calculated assuming long-term prices of $1,300 per ounce of gold and $3.00 per pound of copper. The historical three-year average gold price was approximately $1,550 per ounce well in excess of the long-term gold price assumption used in its impairment testing. The Company believes that it is prudent to update its metal price assumption used in its impairment testing to reflect current forecasts and it does not rely on higher prices to drive its business plans, however, the Company remains positive on the long-term price fundamentals for its metals. The Company will continue to monitor the valuation of its assets and the impact of changes in economic assumptions and mine plans on these valuations. Higher prices in the future could result in greater volatility in earnings, as the Company reassesses the fair value of its mineral properties and could potentially reverse a portion or all of the impairment charges taken.

In addition to the impairment charges mentioned above, an additional $10.3 million (before and net of taxes) related to minor exploration properties was recognized during the year on the decision of not proceeding with further exploration and/or disposition in the prior quarters of 2013, bringing the impairment charges against mineral properties for the year to a total of $682.3 million (574.2 million, net of taxes).

12

For the year ended December 31, 2013

Cash flows from operating activities before changes in non-cash working capital for the year ended December 31, 2013 were $653.1 million compared to $1.16 billion for the year ended December 31, 2012. Cash flows from operating activities before changes in non-cash working capital items (a non-GAAP measure, see Section 14) for the year ended December 31, 2013 were $707.9 million compared to $1.04 billion for the year ended December 31, 2012. Cash and cash equivalents as at December 31, 2013 were $220.0 million compared to $349.6 million as at December 31, 2012.

Net loss for the year 2013 was $446.2 million or $0.59 per share(a), compared with net earnings of $442.1 million or basic and diluted earnings per share of $0.59 for the year 2012. Net loss for the year includes an impairment charge of $574.2 million, net of taxes in respect to certain mineral properties. Adjusted earnings were $273.4 million or $0.36 per share in 2013, compared with $694.3 million or $0.93 per share in 2012. Lower adjusted earnings were mainly attributed to the decline in metal prices and lower sales volume of gold, copper and silver, combined with inflationary impacts on costs and lower equity earnings from the Company's 12.5% of interest in Alumbrera.

Revenues were $1.84 billion in 2013 compared with $2.3 billion in 2012. Mine operating earnings were $540.8 million, compared with $1.12 billion in 2012. Lower revenues and mine operating earnings were due to lower metal prices and lower sales volumes of gold, copper in concentrate and silver. Higher cost of sales, including depletion, depreciation and amortization expenses, was mainly related to higher cost inflation relative to that of 2012.

The average realized gold price in 2013 was $1,408 per ounce versus $1,670 per ounce in 2012 or 16% lower. The average realized copper price was $3.28 per pound versus $3.60 per pound in 2012 or 9% lower. The average realized silver price was $23.73 per ounce compared to $30.46 per ounce in 2012 or 22% lower.

Revenues for 2013 were generated from the sale of 925,496 ounces of gold, 8.3 million ounces of silver and 126.0 million pounds of copper, excluding Alumbrera which is accounted for as an equity investment. This compares to sales, excluding Alumbrera, of 963,833 ounces of gold, 9.0 million ounces of silver and 139.0 million pounds of copper in 2012.

Revenues for the year are comprised of the following:

| For the years ended December 31, | 2013 | 2012 | |||||||||||||

| (In thousands of United States Dollars; unless otherwise noted) | Quantity Sold (ii) | Realized Price | Revenues | Revenues | |||||||||||

Gold (i) | 925,496 | oz | $ | 1,408 | $ | 1,302,687 | $ | 1,609,172 | |||||||

| Silver | 8,263,729 | oz | $ | 23.73 | 196,129 | 273,455 | |||||||||

| Total precious metals | 1,090,771 | GEO | 1,498,816 | 1,882,627 | |||||||||||

Copper (i) | 125,999,185 | lbs | $ | 3.28 | 413,609 | 499,895 | |||||||||

| Gross Revenues | $ | 1,912,425 | $ | 2,382,522 | |||||||||||

| Add (deduct): | |||||||||||||||

- Treatment and refining charges of gold and copper concentrate | $ | (33,163 | ) | $ | (30,099 | ) | |||||||||

| - Sales taxes | (26,417 | ) | (36,718 | ) | |||||||||||

| - Metal price adjustments related to concentrate revenues | (10,493 | ) | 19,325 | ||||||||||||

| - Other adjustments | 330 | 1,732 | |||||||||||||

Revenues (ii) | $ | 1,842,682 | $ | 2,336,762 | |||||||||||

______________________________

| (i) | Includes payable copper and gold contained in concentrate. |

| (ii) | Excludes Alumbrera which is accounted for as an equity investment. |

Cost of sales excluding depletion, depreciation and amortization for 2013 was $900.8 million compared with $831.8 million in the same period of 2012. The increase in cost of sales was mainly due to higher co-product cash costs as a result of inflationary pressures in the countries where the Company operates.

The following table provides a reconciliation of the co-product cash costs to the cost of sales excluding depletion, depreciation and amortization for the year:

13

| 2013 | 2012 | ||||||||||||||

| For the years ended December 31, | GEO or Pounds of Copper Produced | Co-product Cash Cost per Unit | Total Costs | Total Costs | |||||||||||

| (In thousands of United States Dollars; unless otherwise noted) | |||||||||||||||

Chapada — GEO (i) | 110,618 | oz | $ | 400 | $ | 44,297 | $ | 42,681 | |||||||

| Chapada — Copper | 130,239,902 | lbs | 1.65 | 214,481 | 210,072 | ||||||||||

El Peñón — GEO (i) | 467,523 | oz | 485 | 226,628 | 203,724 | ||||||||||

| Jacobina | 73,695 | oz | 1,174 | 86,488 | 87,316 | ||||||||||

| Gualcamayo | 120,337 | oz | 772 | 92,844 | 78,952 | ||||||||||

Minera Florida — GEO (i) | 118,590 | oz | 747 | 88,621 | 82,793 | ||||||||||

| Fazenda Brasileiro | 70,079 | oz | 808 | 56,622 | 58,554 | ||||||||||

Mercedes — GEO (i) | 141,618 | oz | 496 | 70,301 | 60,915 | ||||||||||

Co-product cash cost of sales (ii) | $ | 880,282 | $ | 825,007 | |||||||||||

| Add (deduct): | |||||||||||||||

| - Inventory movements and adjustments | 21,005 | 5,278 | |||||||||||||

| - Chapada concentrate treatment and refining charges | (33,163 | ) | (32,369 | ) | |||||||||||

| - Commercial & other costs | 16,108 | 17,795 | |||||||||||||

| - Overseas freight for Chapada concentrate | 16,557 | 16,043 | |||||||||||||

| Cost of sales excluding depletion, depreciation and amortization | $ | 900,789 | $ | 831,754 | |||||||||||

______________________________

| (i) | Silver ounces reported from Chapada, El Peñón, Minera Florida and Mercedes are treated as gold equivalent ounces ("GEO"). |

| (ii) | A cautionary note regarding non-GAAP measures is included in Section 14 of this Management’s Discussion and Analysis of Operations and Financial Condition. |

Depletion, depreciation and amortization (“DDA”) expense for the year 2013 was $401.1 million, compared to $383.7 million in the same period of 2012. The increase in DDA is attributable to higher levels of depletable capital expenditures and higher cost ore bodies being depleted.

Other expenses including general and administrative, exploration and evaluation, other operating and net finance expenses were $249.8 million in the year ended December 31, 2013, compared to $289.1 million in the year ended December 31, 2012. The net decrease in other expenses is detailed below:

General and administrative expenses were $135.3 million in 2013 compared to $145.9 million in the year ended December 31, 2012. General and administrative expenses have declined mainly as a result of the Company's cost containment initiative introduced in May 2013, and are expected to be maintained at these lower levels in 2014.

Exploration and evaluation expenses were $30.2 million in 2013, compared to $58.0 million incurred in 2012 as a result of the Company's reduced focus on greenfield exploration.

Other operating expenses were $78.1 million in the year compared to $99.3 million in 2012. Lower other operating expenses reflect lower impairment of investments in available-for-sale securities of $16.3 million for the year compared to $67.7 million in 2012, an $18.1 million write-off of long-term tax credits and a loss of $38.4 million incurred on the sale of non-core exploration properties with no 2012 comparative.

Net finance expenses were $6.3 million for the year compared with net finance expenses of $53.5 million in the same period of 2012. Lower net finance expense was mainly due to higher foreign exchange gains in the amount of $17.7 million compared to a foreign exchange loss of $25.9 million in the comparative period.

Equity loss from associate was $3.9 million for 2013 compared with earnings of $50.6 million in 2012. The equity loss was driven by lower revenues as a result of lower metal prices and lower sales volume of copper and gold concentrate due to lower production from Alumbrera. Cash dividends from the Company’s equity investment in Alumbrera during 2013 were $27.9 million compared to $nil in 2012. During the year, the Company also received loan proceeds of $44.6 million from Alumbrera.

The Company recorded an income tax expense of $79.1 million in 2013 compared to $373.1 million in the same period of 2012. The decrease in the income tax expense is a result of lower earnings relative to the comparative year. The income tax provision for the year ended December 31, 2013 reflects a current income tax expense of $140.6 million compared to current tax expense of $265.5 million in 2012, and a deferred income tax recovery of $61.5 million compared to deferred tax expense of $107.6 million. The effective tax rate on adjusted earnings for the year of 2013 was 30.0% compared to 25.0% for 2012.

14

_______________

(a) Attributable to Yamana equity holders.

5.2 Overview of Annual Operating Results

For the year ended December 31, 2013

Total production for the Company was 1.20 million GEO comparable to 2012 production level of 1.20 million GEO. Total production for the year consisted of 1.03 million ounces of gold and 8.4 million ounces of silver, representing an increase of 1% in gold production and a 7% decrease in silver production over the period of 2012. Total production included the Company’s attributable production from Alumbrera of 39,157 ounces of gold and production during commissioning from Ernesto/Pau-a-Pique, C1 Santa Luz and Pilar of 55,942 ounces of gold. This compares with total production in 2012 of 1.20 million GEO that consisted of 1.01 million ounces of gold and 9.0 million ounces of silver. The 2012 production also included commissioning production of 12,094 GEO from Mercedes, Minera Florida and Ernesto/Pau-a-Pique.

Commercial production for the year consisted of 1.14 million GEO compared with 1.19 million GEO produced in 2012. Commercial production for 2013 consisted of 973,921 ounces of gold and 8.38 million ounces of silver, representing a 1% increase in gold production and a 7% decrease in silver production over the commercial production of 733,910 ounces of gold and 8.93 million ounces of silver in 2012.

By-product cash costs (a non-GAAP measure, see Section 14) for the year averaged $410 per GEO, compared with $230 per GEO in the same period of 2012. By-product cash costs were impacted by a lower copper credit contribution due to lower copper market prices and lower copper sales volume. The average market price for copper in 2013 was 8% lower than the average of 2012. By-product cash costs for 2013 exceeded the Company's previous guidance for a 2013 year-average of below $365 per GEO, which assumed a copper price of $4.00 per pound compared to average market price for the year of $3.32 per pound and the Company's average realized price of $3.28 per pound.

Co-product cash costs (a non-GAAP measure, see Section 14) for the year were $596 per GEO compared with $525 per GEO in 2012.

15

Effective January 1, 2013, the Company began reporting all-in sustaining cash costs (a non-GAAP measure, see Section 14), which seeks to represent total sustaining expenditures of producing gold equivalent ounces from current operations, based on by-product and co-product cash costs, including cost components of mine sustaining capital expenditures, corporate general and administrative expense excluding stock-based compensation and exploration and evaluation expense. For 2013, all-in sustaining cash costs were $814 per GEO on a by-product basis and $947 per GEO on a co-product basis. Average all-in sustaining cash cost on a co-product basis for the last three quarters was below $925 per GEO meeting expectations of the cost containment initiative implemented in the second quarter.

Copper production for the year was 130.2 million pounds from the Chapada mine, compared with 150.6 million pounds for the same period of 2012. Chapada copper production was lower primarily as a result of expected lower copper grade and recovery rate compared with 2012. A total of 30.2 million pounds of copper produced from Alumbrera were attributable to the Company in 2013, compared to 37.4 million pounds for the year ended December 31, 2012. Total copper production for 2013 was 160.5 million pounds, compared with 188.0 million pounds in 2012. The new orebody, Corpo Sul, and the regrinding project at Chapada are expected to contribute to future gold and copper production.

Co-product cash costs per pound of copper (a non-GAAP measure, see Section 14) averaged $1.65 per pound from the Chapada mine in 2013, compared with $1.40 per pound in the year ended December 31, 2012. Co-product cash costs per pound of copper for the year including the Company’s interest in the Alumbrera mine were $1.75 per pound compared to $1.48 per pound for the year ended December 31, 2012.

The Company's total proven and probable mineral reserves including all projects were 18.5 million GEO compared to 19.3 million GEO in 2012 representing a decrease of 4%. This is offset by significant increases in measured and indicated mineral resources, almost all of which are at existing operations. Total measured and indicated mineral resources increased from 2012 mainly due to the addition of mineral resources from Gualcamayo, El Peñón and Chapada, partly offset the reduction of measured and indicated mineral resources at Cerro Moro, which had been upgraded to an initial proven and probable mineral reserves estimate. Total measured and indicated mineral resources including all projects were 17.3 million GEO compared to 15.6 million GEO in 2012, representing an increase in contained ounces of 10%. Total inferred mineral resources increased by 32% to 15.0 million GEO (contained gold - 13.4 million ounces; contained silver - 81.2 million ounces). The overall focus of the exploration program for 2014 will be on the upgrade of the increases in mineral resources in 2013 to mineral reserves and the extension of mine life.

Refer to Section 8 - “Mineral Reserve and Mineral Resource Estimates” for a detailed discussion on the Company's mineral reserve and mineral resource estimates and metal price assumptions. Complete information relating to mineral reserves and mineral resources is also contained in a mineral reserve and mineral resource table which indicates complete information on tonnage and grade. This mineral reserve and mineral resource table accompanies the 2013 annual report and is also available on the Company's website, www.yamana.com.

16

5.3 Overview of Quarterly Financial Results

| For the three months ended | ||||||||

| (In thousands of United States Dollars; unless otherwise noted) | Dec 31, 2013 | Dec 31, 2012 | ||||||

| Revenues | $ | 420,663 | $ | 629,505 | ||||

| Cost of sales excluding depletion, depreciation and amortization | (239,030 | ) | (207,228 | ) | ||||

| Gross margin | 181,633 | 422,277 | ||||||

| Depletion, depreciation and amortization | (111,520 | ) | (100,195 | ) | ||||

| Mine operating earnings | 70,113 | 322,082 | ||||||

Other expenses (i) | (62,708 | ) | (66,934 | ) | ||||

| Equity earnings from associate | (5,086 | ) | 18,147 | |||||

| Impairment of mineral properties | (672,000 | ) | (10,896 | ) | ||||

| Earnings from operations before income taxes | (669,681 | ) | 262,399 | |||||

| Income tax expense | 57,641 | (93,238 | ) | |||||

| Net (loss) earnings | $ | (612,040 | ) | $ | 169,161 | |||

Earnings adjustments (ii): | ||||||||

| Non-cash unrealized foreign exchange losses | (284 | ) | 12,371 | |||||

| Reorganization costs | 842 | — | ||||||

| Share-based payments/mark-to-market of deferred share units | 3,474 | 4,086 | ||||||

| Impact of change in Mexican tax rates on non-cash deferred tax expense | 28,323 | — | ||||||

| Impairment of mineral properties | 672,000 | — | ||||||

| Impairment of investment in available-for-sale securities and other assets | 29,271 | 10,896 | ||||||

| Other non-cash and non-recurring losses | 43,649 | 1,064 | ||||||

| Adjusted earnings before income tax effect | 165,235 | 197,578 | ||||||

| Income tax effect of adjustments | (128,516 | ) | (210 | ) | ||||

Adjusted earnings (ii) | $ | 36,719 | $ | 197,368 | ||||

| Net (loss) earnings per share attributable to Yamana Gold Inc. equity holders - basic | $ | (0.78 | ) | $ | 0.23 | |||

| Net (loss) earnings per share attributable to Yamana Gold Inc. equity holders - diluted | $ | (0.78 | ) | $ | 0.22 | |||

Adjusted earnings per share (ii) - basic and diluted | $ | 0.05 | $ | 0.26 | ||||

______________________________

(i) | For the three-months ended December 31, 2013, other expenses represent the aggregate of the following expenses: general and administrative of $29.8 million (2012 - 39.0 million), exploration and evaluation of $8.0 million (2012 - $15.1 million), other operating expense of $47.1 million (2012 - $5.8 million) and net finance income of $22.1 million (2012 - expense $7.0 million). |

(ii) | A cautionary note regarding non-GAAP measures and their respective reconciliations are included in Section 14 including a discussion and definition of Adjusted Earnings and Adjusted Earnings per Share. |

For the three months ended December 31, 2013

Cash flows from operating activities before changes in non-cash working capital (a non-GAAP measure, see Section 14) for the quarter ended December 31, 2013 were $165.3 million, lower than the $298.1 million generated for the same period of 2012. Lower cash flows from operating activities compared to that of the same quarter in the prior year were mainly due to a decline in revenue as a result of a decline in metal prices and lower sale volumes. However, cash flows from operating activities before changes in non-cash working capital were 10% above levels in the second quarter when the Company’s cost savings and containment program was initiated. Cash flows from operating activities after taking into effect changes in non-cash working capital items for the three month period ended December 31, 2013 were inflows of $184.8 million, compared to inflows of $367.9 million for the three month period ended December 31, 2012, which reflects a decrease in trade receivables.

Net loss for the quarter was $583.9 million or $0.78 per share(a), compared with net earnings of $169.2 million or basic earnings per share of $0.23 and diluted earnings per share of $0.22 for the three months ended December 31, 2012. Net loss for the year includes an impairment charge of 535.8 million, net of taxes in respect to certain mineral properties. Adjusted earnings were $36.7 million or $0.05 per share in the fourth quarter, compared with $197.4 million or $0.26 per share in the fourth quarter of 2012. Lower adjusted earnings were attributed to lower realized metal prices, lower volume of metal sales, higher cash costs and an equity loss from the Company's 12.5% of interest in Alumbrera.

17

Revenues were $420.7 million in the fourth quarter compared with $629.5 million in the fourth quarter of 2012. Mine operating earnings were $70.1 million, compared with $322.1 million in the fourth quarter of 2012. Lower revenues and mine operating earnings were primarily due to lower metal prices in addition to lower volume of gold and copper sales. Lower metal prices accounted for 58% of the variance in revenues in comparison to the fourth quarter of 2012 representing approximately $0.16 per share in earnings. Lower cost of sales, including depletion, depreciation and amortization expenses, corresponded to lower sales volumes of gold and copper.

Revenues for the fourth quarter were generated from the sale of 218,223 ounces of gold, 2.1 million ounces of silver and 34.5 million pounds of copper, excluding Alumbrera which is accounted for as an equity investment. This compares to sales, excluding Alumbrera, of 258,978 ounces of gold, 2.3 million ounces of silver and 37.3 million pounds of copper in the three months ended December 31, 2012.

The average realized price of gold in the fourth quarter of 2013 was $1,277 per ounce compared to $1,692 per ounce in the same quarter of 2012, representing a decrease of 24%. The average realized price of copper was $3.37 per pound compared to $3.54 per pound in the fourth quarter of last year, representing a decrease of 5%, and the average realized silver price was $20.63 per ounce compared to $31.37 per ounce in the fourth quarter of 2012, representing a decrease of 33%.

Revenues for the year are comprised of the following:

| For the three months ended December 31, | 2013 | 2012 | |||||||||||||

| (In thousands of United States Dollars; unless otherwise noted) | Quantity Sold (ii) | Realized Price | Revenues | Revenues | |||||||||||

Gold (i) | 218,223 | oz | $ | 1,277 | $ | 278,744 | $ | 438,199 | |||||||

| Silver | 2,117,273 | oz | $ | 20.63 | 43,670 | 70,721 | |||||||||

| Total precious metals | 260,568 | GEO | 322,414 | 508,920 | |||||||||||

Copper (i) | 34,510,774 | lbs | $ | 3.37 | 116,247 | 131,875 | |||||||||

| Gross Revenues | $ | 438,661 | $ | 640,795 | |||||||||||

| Add (deduct): | |||||||||||||||

- Treatment and refining charges of gold and copper concentrate | $ | (8,717 | ) | $ | (8,913 | ) | |||||||||

| - Sales taxes | (5,205 | ) | (7,246 | ) | |||||||||||

| - Metal price adjustments related to concentrate revenues | (136 | ) | 4,053 | ||||||||||||

| - Other adjustments | (3,940 | ) | 816 | ||||||||||||

Revenues (ii) | $ | 420,663 | $ | 629,505 | |||||||||||

______________________________

(i) | Includes payable copper and gold contained in concentrate. |

(ii) | Excludes Alumbrera which is accounted for as an equity investment. |

18

The following table provides a reconciliation of the co-product cash costs to the cost of sales excluding depletion, depreciation and amortization for the year:

| 2013 | 2012 | ||||||||||||||

| For the three months ended December 31, | GEO or Pounds of Copper Produced | Co-product Cash Cost per Unit | Total Costs | Total Costs | |||||||||||

| (In thousands of United States Dollars; unless otherwise noted) | |||||||||||||||

Chapada — GEO (i) | 29,817 | oz | $ | 377 | $ | 11,253 | $ | 11,327 | |||||||

| Chapada — Copper | 35,958,765 | lbs | 1.53 | 55,148 | 55,857 | ||||||||||

El Peñón — GEO (i) | 101,364 | oz | 593 | 60,062 | 53,187 | ||||||||||

| Jacobina | 19,519 | oz | 1,140 | 22,254 | 23,384 | ||||||||||

| Gualcamayo | 34,929 | oz | 825 | 28,816 | 15,271 | ||||||||||

| Minera Florida — GEO (i) | 30,513 | oz | 592 | 18,069 | 26,416 | ||||||||||

| Fazenda Brasileiro | 18,270 | oz | 809 | 14,771 | 15,615 | ||||||||||

| Mercedes — GEO (i) | 31,716 | oz | 656 | 20,792 | 17,154 | ||||||||||

Co-product cash cost of sales (ii) | $ | 231,165 | $ | 218,211 | |||||||||||

| Add (deduct): | |||||||||||||||

| - Inventory movements and adjustments | 8,707 | (8,984 | ) | ||||||||||||

| - Chapada concentrate treatment and refining charges | (8,717 | ) | (8,913 | ) | |||||||||||

| - Commercial & other costs | 2,943 | 3,262 | |||||||||||||

| - Overseas freight for Chapada concentrate | 4,933 | 3,652 | |||||||||||||

| Cost of sales excluding depletion, depreciation and amortization | $ | 239,031 | $ | 207,228 | |||||||||||

______________________________

(i) | Silver ounces reported for Chapada, El Peñón, Minera Florida and Mercedes are treated as gold equivalent ounces ("GEO"). |

(ii) | A cautionary note regarding non-GAAP measures is included in Section 14 of this Management’s Discussion and Analysis of Operations and Financial Condition. |

Cost of sales excluding depletion, depreciation and amortization for the fourth quarter of 2013 was $239.0 million compared with $207.2 million in same quarter of 2012. Cost of sales excluding depletion, depreciation and amortization was higher compared to the same period in 2012 was mainly due to the higher co-product cash cost of production.

Depletion, depreciation and amortization (“DDA”) expense for the quarter was $111.5 million, compared to $100.2 million in the fourth quarter of 2012. The increase was attributable to higher DDA at Gualcamayo from AIM which contributed to production levels in 2013 and DDA from the tailings retreatment plant at Minera Florida which also started to contribute to production in 2013.

Other expenses including of general and administrative, exploration and evaluation, other operating and net finance expenses were $62.7 million in the quarter, compared to $66.9 million in the three months ended December 31, 2012. The net decrease in other expenses is detailed below:

General and administrative expenses were $29.8 million in the fourth quarter compared to $39.0 million in the same quarter of 2012. It is expected that general and administrative expenses will continue to be maintained at current levels as a result of the cost containment initiatives undertaken by the Company.

Exploration and evaluation expenses were $8.0 million, compared to $15.1 million incurred in the fourth quarter of 2012 as a result of the Company's reduced focus on greenfield exploration relative to 2012.

Other operating expenses were $47.1 million in the quarter compared to $5.8 million in the fourth quarter of 2012. The increase in other operating expenses primarily reflects a $38.4 million loss on sale of non-core exploration properties during the quarter.

Net finance income was $22.1 million mainly related to foreign exchange gains in the quarter compared to net finance expenses of $7.0 million in the fourth quarter of 2012. Foreign exchange gains resulted from favourable exchange rates of country currencies with which the Company settled its mine operating expenses compared to foreign exchange losses in the comparative period of 2012.

Equity loss from associate was $5.1 million for the quarter compared with earnings of $50.6 million in the fourth quarter of 2012. The lower equity earnings were mainly due to lower revenues as a result of lower metal prices and lower sales volume of concentrate in addition to higher co-product cash costs from Alumbrera. Lower volume of concentrate produced was due to mining in lower

19

grade areas. Cash dividends from the Company’s equity investment in Alumbrera received in the quarter were $6.8 million compared to $nil in the fourth quarter of 2012.

The Company recorded an income tax recovery of $57.6 million in the fourth quarter of 2013 compared to tax expense of $93.2 million in the same quarter of 2012. The lower income tax expense in the fourth quarter of 2013 is attributable to lower earnings relative to that of the fourth quarter of 2012. The income tax provision for the fourth quarter of 2013 reflects a current income tax expense of $40.7 million compared to current tax expense of $106.1 million in the same quarter of 2012, and a deferred income tax recovery of $98.3 million compared to deferred tax recovery of $12.9 million. During the quarter, the exchange rates of Brazilian Real and Argentinean Peso devalued against the US Dollar increased. As a result for local purposes, a reduction of $2.4 million relating to unrealized foreign exchange gain was recorded in the deferred tax expense. The impact of these foreign exchange movements on taxes are non-cash and as such excluded from adjusted earnings. The adjusted tax rate for the fourth quarter of 2013 was 22.3% compared to 29.7% for the fourth quarter of 2012. See Note 29 to the Condensed Consolidated Interim Financial Statements for a breakdown of the foreign exchange and interest and penalties charged to the income tax expense.

____________________

(a) Attributable to Yamana equity holders.

5.4 Overview of Quarterly Operating Results

For the three months ended December 31, 2013

Total production for the fourth quarter of 2013 was 303,768 GEO, a decrease of 6% from the 322,990 GEO produced in the fourth quarter of 2012. Total fourth quarter production consisted of 260,187 ounces of gold and 2.2 million ounces of silver, compared to 276,373 ounces of gold and 2.3 million ounces of silver produced in the same quarter of 2012. Total production included the Company’s attributable production from Alumbrera of 11,319 ounces of gold and production during commissioning from Ernesto/Pau-a-Pique, C1 Santa Luz and Pilar of 26,321 ounces of gold.

Commercial production for the fourth quarter comprised of 277,447 GEO compared with 321,716 GEO produced in the fourth quarter of 2012. Total commercial production consisted of 233,866 of gold and 2.2 million ounces of silver, compared to commercial production of 264,888 ounces of gold and 2.2 million ounces of silver in the same quarter of 2012. The decrease in gold production was mainly due to the decreased production levels from Chapada, Jacobina, El Peñón, Minera Florida and Mercedes, partly offset by increased production levels from Gualcamayo and Alumbrera.

20

By-product cash costs (a non-GAAP measure, see Section 14) for the fourth quarter of 2013 averaged $417 per GEO, compared with $198 per GEO in the fourth quarter of 2012. By-product cash costs were impacted by a lower copper credit contribution from Chapada and Alumbrera due to the decline in the copper price and lower copper sales volume. The average market price for copper in the fourth quarter of 2013 was 9% lower than the average of the same quarter in 2012.

Co-product cash costs (a non-GAAP measure, see Section 14) for the fourth quarter averaged $647 per GEO, compared to $517 per GEO for the fourth quarter of 2012. Planned lower grades at certain mines and higher input costs during the quarter relative to the same quarter of 2012 impacted costs compared to the three months ended December 31, 2012. In comparison to the third quarter of 2013, production levels at El Peñón and Mercedes were tapered to contain increasing costs and better position those mines for 2014.

All-in sustaining cash costs (a non-GAAP measure, see Section 14) were $754 per GEO on a by-product basis well below the guidance level of $850 per GEO and $935 per GEO on a co-product basis for the fourth quarter of 2013 in line with the guidance level of $925 per GEO on a co-product basis.

Copper production for the quarter was 36.0 million pounds from the Chapada mine, compared with 40.5 million pounds for same quarter of 2012. Chapada copper production was lower primarily as a result of expected lower copper grade compared to the fourth quarter of 2012. A total of 9.6 million pounds of copper produced from Alumbrera were attributable to the Company, compared with 8.5 million pounds for the quarter ended December 31, 2012 mainly due to higher copper feed grade. Total copper production for the fourth quarter of 2013 was 45.6 million pounds, compared with 49.0 million pounds in the fourth quarter of 2012.

Co-product cash costs per pound of copper (a non-GAAP measure, see Section 14) averaged $1.53 per pound from the Chapada mine compared to $1.38 per pound of copper in the same quarter of 2012. Co-product cash costs per pound of copper for the quarter including the Company’s interest in Alumbrera were $1.58 per pound compared to $1.51 per pound for the fourth quarter of 2012.

6. OPERATING MINES

CHAPADA, BRAZIL

21

| For the three months ended December 31, | For the years ended December 31, | ||||||||||||||

| Operating Statistics | 2013 | 2012 | 2013 | 2012 | |||||||||||

| Production | |||||||||||||||

| Concentrate (tonnes) | 67,395 | 72,518 | 239,811 | 268,135 | |||||||||||

GEO contained in concentrate production (i) | 29,817 | 32,498 | 110,618 | 128,171 | |||||||||||

| Gold contained in concentrate (ounces) | 28,223 | 30,121 | 104,096 | 119,655 | |||||||||||

| Silver contained in concentrate (ounces) | 79,696 | 118,874 | 326,087 | 425,805 | |||||||||||

| Copper contained in concentrate (millions of pounds) | 36.0 | 40.5 | 130.2 | 150.6 | |||||||||||

By-product cash costs per GEO produced (ii) | $ | (1,547 | ) | $ | (2,021 | ) | $ | (1,296 | ) | $ | (1,865 | ) | |||

Co-product cash costs per GEO produced (ii) | $ | 377 | $ | 349 | $ | 400 | $ | 333 | |||||||

Co-product cash costs per pound of copper produced (ii) | $ | 1.53 | $ | 1.38 | $ | 1.65 | $ | 1.40 | |||||||

| Ore mined (tonnes) | 5,753,649 | 5,924,456 | 21,833,258 | 22,490,266 | |||||||||||

| Ore processed (tonnes) | 5,540,262 | 5,734,592 | 21,347,439 | 21,591,482 | |||||||||||

| Gold feed grade (g/t) | 0.28 | 0.28 | 0.26 | 0.29 | |||||||||||

| Copper feed grade (%) | 0.37 | 0.40 | 0.35 | 0.39 | |||||||||||

| Concentrate grade - gold (g/t) | 13.03 | 12.92 | 13.50 | 13.88 | |||||||||||

| Concentrate grade - copper (%) | 24.20 | 25.33 | 24.63 | 25.47 | |||||||||||

| Gold recovery rate (%) | 57.5 | 59.4 | 57.9 | 59.4 | |||||||||||

| Copper recovery rate (%) | 80.4 | 81.1 | 79.7 | 82.2 | |||||||||||

Sales (iii) | |||||||||||||||

| Concentrate (tonnes) | 67,616 | 69,589 | 242,681 | 263,704 | |||||||||||

| Payable gold contained in concentrate (ounces) | 26,805 | 27,692 | 98,680 | 115,443 | |||||||||||

| Payable silver contained in concentrate (ounces) | 45,103 | 81,949 | 166,917 | 279,371 | |||||||||||

| Payable copper contained in concentrate (millions of pounds) | 34.5 | 37.3 | 126.0 | 139.0 | |||||||||||

| Depletion, depreciation and amortization | |||||||||||||||