YAMANA GOLD INC.

ANNUAL INFORMATION FORM

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2014

March 27, 2015

200 Bay Street, Suite 2200

Royal Bank Plaza, North Tower

Toronto, Ontario M5J 2J3

TABLE OF CONTENTS

| INTRODUCTORY NOTES | 3 | |

| Cautionary Note Regarding Forward-Looking Statements | 3 | |

| Cautionary Note to United States Investors Concerning Estimates of Mineral Reserves and Mineral Resources | 4 | |

| Currency Presentation And Exchange Rate Information | 4 | |

| CORPORATE STRUCTURE | 5 | |

| GENERAL DEVELOPMENT OF THE BUSINESS | 7 | |

| Overview of Business | 7 | |

| History | 8 | |

| DESCRIPTION OF THE BUSINESS | 11 | |

| Principal Products | 11 | |

| Competitive Conditions | 11 | |

| Operations | 11 | |

| Environment and Communities | 12 | |

| Risks of the Business | 14 | |

| Technical Information | 31 | |

| Cautionary Note to United States Investors Concerning Estimates of Measured, Indicated and Inferred Mineral Resources | 33 | |

| Mineral Projects | 35 | |

| Summary of Mineral Reserve and Mineral Resource Estimates | 35 | |

| Material Mineral Properties | 38 | |

| Chapada Mine | 38 | |

| El Peñón Mine | 47 | |

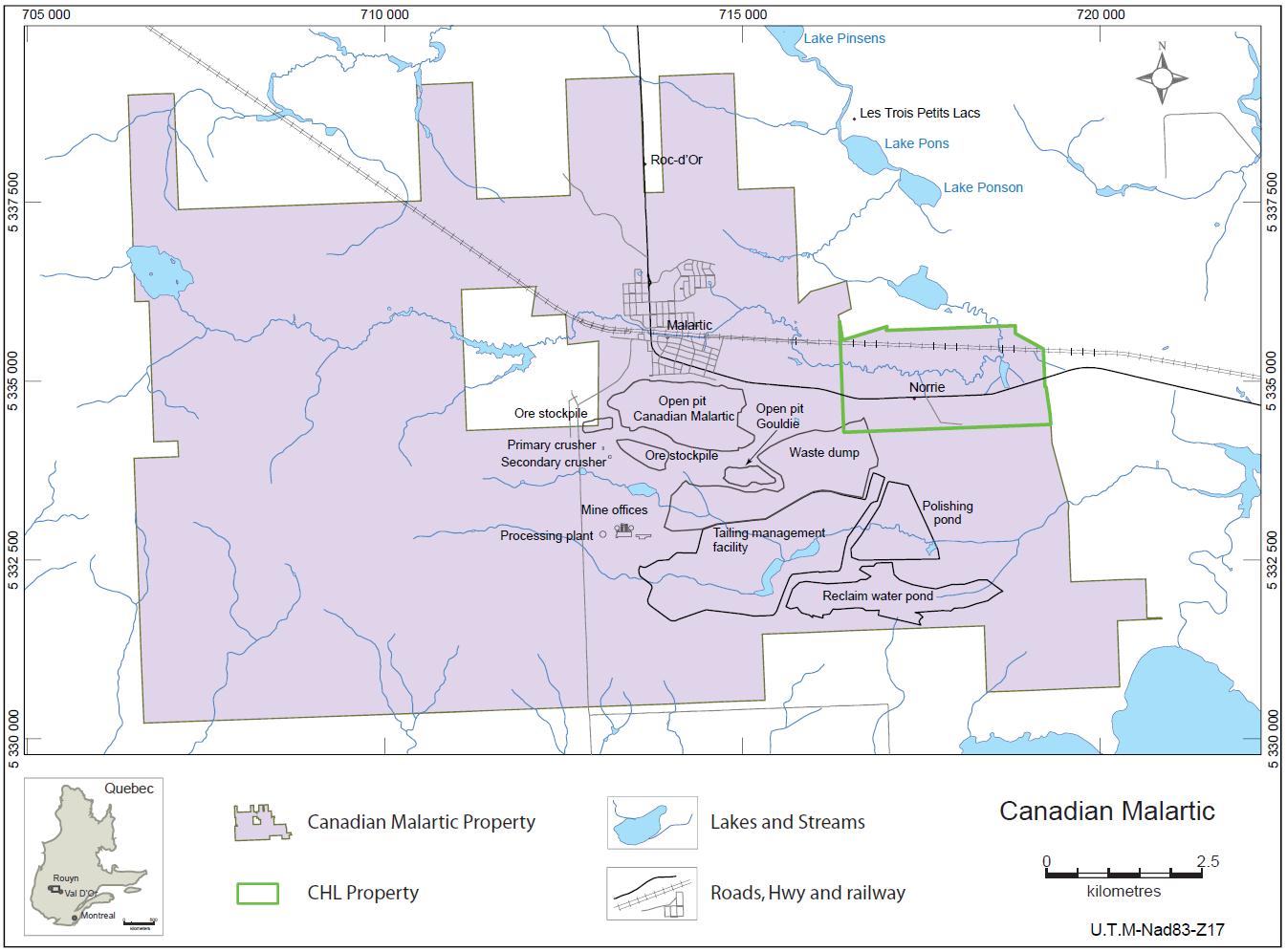

| Canadian Malartic Mine | 56 | |

| Other Producing Mines | 63 | |

| Mercedes Mine | 63 | |

| Gualcamayo Mine | 65 | |

| Jacobina Mining Complex | 66 | |

| Minera Florida Mine | 67 | |

| Alumbrera Mine | 68 | |

| Additional Projects | 69 | |

| Cerro Moro Project | 69 | |

| Agua Rica Project | 69 | |

| Suyai Project | 70 | |

| Brio Gold Projects | 70 | |

| Fazenda Brasileiro Mine | 71 | |

| Pilar Project | 71 | |

| C1 Santa Luz Project | 72 | |

| DIVIDENDS | 72 | |

| DESCRIPTION OF CAPITAL STRUCTURE | 73 | |

| MARKET FOR SECURITIES | 74 | |

| DIRECTORS AND OFFICERS | 74 | |

| PROMOTER | 80 | |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 80 | |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 81 | |

| TRANSFER AGENTS AND REGISTRAR | 81 | |

| MATERIAL CONTRACTS | 81 | |

| AUDIT COMMITTEE | 82 | |

| INTERESTS OF EXPERTS | 84 | |

| ADDITIONAL INFORMATION | 85 | |

| SCHEDULE “A” — CHARTER OF THE AUDIT COMMITTEE | 86 | |

2

ITEM 1

INTRODUCTORY NOTES

Cautionary Note Regarding Forward-Looking Statements

This annual information form contains “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information” under applicable Canadian securities legislation. Except for statements of historical fact relating to the Company (as defined herein), information contained herein constitutes forward-looking statements, including, but not limited to, any information as to the Company’s strategy, plans or future financial or operating performance. Forward-looking statements are characterized by words such as “plan”, “expect”, “budget”, “target”, “project”, “intend”, “believe”, “anticipate”, “estimate” and other similar words, or statements that certain events or conditions “may” or “will” occur. Forward-looking statements are based on the opinions, assumptions and estimates of management considered reasonable at the date the statements are made, and are inherently subject to a variety of risks and uncertainties and other known and unknown factors that could cause actual events or results to differ materially from those projected in the forward-looking statements. These factors include the Company’s expectations in connection with the production and exploration, development and expansion plans at the Company’s projects discussed herein being met, the impact of proposed optimizations at the Company’s projects, the impact of the proposed new mining law in Brazil, the new tax reform bill in Mexico, the amended federal income tax statute in Argentina and the new Chilean tax reform package, and the impact of general domestic and foreign business, economic and political conditions, global liquidity and credit availability on the timing of cash flows and the values of assets and liabilities based on projected future conditions, fluctuating metal prices (such as gold, copper, silver and zinc), currency exchange rates (such as the Brazilian real, the Chilean peso, the Argentine peso, the Mexican peso and the Canadian dollar versus the United States dollar), interest rates, possible variations in ore grade or recovery rates, changes in the Company’s hedging program, changes in accounting policies, changes in Mineral Resources (as defined herein) and Mineral Reserves (as defined herein), risks related to non-core mine disposition, Yamana’s expectations relating to the Osisko Acquisition (as defined herein), including with respect to anticipated benefits thereof and the magnitude of synergies therefrom, and the performance of the assets acquired from Osisko Mining Corporation (“Osisko”), and risks related to other acquisitions, changes in project parameters as plans continue to be refined, changes in project development, construction, production and commissioning time frames, risks related to joint venture operations, the possibility of project cost overruns or unanticipated costs and expenses, potential impairment charges, higher prices for fuel, steel, power, labour and other consumables contributing to higher costs and general risks of the mining industry, including but not limited to, failure of plant, equipment or processes to operate as anticipated, unexpected changes in mine life, final pricing for concentrate sales, unanticipated results of future studies, seasonality and unanticipated weather changes, costs and timing of the development of new deposits, success of exploration activities, permitting timelines, environmental and government regulation and the risk of government expropriation or nationalization of mining operations, risks related to relying on local advisors and consultants in foreign jurisdictions, environmental risks, unanticipated reclamation expenses, title disputes or claims, limitations on insurance coverage and timing and possible outcome of pending and outstanding litigation and labour disputes, risks related to enforcing legal rights in foreign jurisdictions, vulnerability of information systems, as well as those risk factors discussed or referred to herein and in the Company’s annual management’s discussion and analysis filed with the securities regulatory authorities in all provinces of Canada and available under the Company’s SEDAR profile at www.sedar.com. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. The Company undertakes no obligation to update forward-looking statements if circumstances or management’s estimates, assumptions or opinions should change, except as required by applicable law. The reader is cautioned not to place undue reliance on forward-looking statements. The forward-looking information contained herein is presented for the purpose of assisting investors in understanding the Company’s expected financial and operational performance and results as at and for the periods ended on the dates presented in the Company’s plans and objectives and may not be appropriate for other purposes.

Cautionary Note to United States Investors Concerning Estimates of Mineral Reserves and Mineral Resources

- 3 -

This annual information form has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ in certain material respects from the disclosure requirements of United States securities laws. The terms “Mineral Reserve”, “Proven Mineral Reserve” and “Probable Mineral Reserve” are Canadian mining terms as defined in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”) and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) - CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended (the “CIM Standards”). These definitions differ significantly from the definitions in the disclosure requirements promulgated by the Securities and Exchange Commission (the “Commission”) and contained in Industry Guide 7 (“Industry Guide 7”) under the United States Securities Act of 1933, as amended (the “Securities Act”). In particular, under Industry Guide 7 standards, a “final” or “bankable” feasibility study is required to report Mineral Reserves, the three-year historical average price is used in any Mineral Reserve or cash flow analysis to designate Mineral Reserves and the primary environmental analysis or report must be filed with the appropriate governmental authority. In addition, Industry Guide 7 applies different standards in order to classify mineralization as a mineral reserve. As a result, the definitions of Proven Mineral Reserves (as defined herein) and Probable Mineral Reserves (as defined herein) used in NI 43-101 differ from the definitions used in Industry Guide 7. Under Commission standards, mineralization may not be classified as a mineral reserve unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the mineral reserve determination is made. Among other things, all necessary permits would be required to be in hand or the issuance must be imminent in order to classify mineralized material as mineral reserves under the Commission’s standards. Accordingly, Mineral Reserve estimates contained in this annual information form may not qualify as mineral reserves under Commission standards.

In addition, the terms “Mineral Resource”, “Measured Mineral Resource”, “Indicated Mineral Resource” and “Inferred Mineral Resource” are defined in and required to be disclosed by NI 43-101. However, the Commission does not recognize Mineral Resources and United States companies are generally not permitted to disclose Mineral Resources of any category in documents they file with the Commission. Investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into Mineral Reserves as defined in NI 43-101 or Industry Guide 7. Further, Inferred Mineral Resources (as defined herein) have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility. Under Canadian rules, estimates of Inferred Mineral Resources may not form the basis of feasibility or pre-feasibility studies. Investors are cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable, or that all or any part of Measured Mineral Resources (as defined herein), Indicated Mineral Resources (as defined herein), or Inferred Mineral Resources will ever be upgraded to a higher category. In addition, disclosure of “contained ounces” in a Mineral Resource is permitted disclosure under Canadian regulations. In contrast, the Commission only permits United States companies to report mineralization that does not constitute Mineral Reserves by Commission standards as in place tonnage and grade, without reference to unit measures. Investors are cautioned that information contained in this annual information form may not be comparable to similar information made public by United States companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations of the Commission thereunder.

Currency Presentation And Exchange Rate Information

This annual information form contains references to both United States dollars and Canadian dollars. All dollar amounts referenced, unless otherwise indicated, are expressed in United States dollars and Canadian dollars are referred to as “Canadian dollars” or “Cdn$”.

The closing, high, low and average exchange rates for the United States dollar in terms of Canadian dollars for the years ended December 31, 2014, December 31, 2013, December 31, 2012, and December 31, 2011 based on the noon spot rate reported by the Bank of Canada, were as follows:

- 4 -

| Year-Ended December 31 | ||||

| 2014 | 2013 | 2012 | 2011 | |

| Closing | Cdn$1.16 | Cdn$1.06 | Cdn$0.99 | Cdn$1.02 |

| High | 1.16 | 1.07 | 1.04 | 1.06 |

| Low | 1.06 | 0.98 | 0.97 | 0.94 |

Average(1) | 1.10 | 1.03 | 1.00 | 0.99 |

(1)Calculated as an average of the daily noon rates for each period.

On March 26, 2015, the Bank of Canada noon rate of exchange was $1.00 = Cdn$1.2471 or Cdn$1.00 = $0.8019.

ITEM 2

CORPORATE STRUCTURE

Yamana Gold Inc. (the “Company” or “Yamana”) was continued under the Canada Business Corporations Act by Articles of Continuance dated February 7, 1995. On February 7, 2001, pursuant to Articles of Amendment, the Company created and authorized the issuance of a maximum of 8,000,000 first preference shares, Series 1. On July 30, 2003, pursuant to Articles of Amendment, the name of the Company was changed from Yamana Resources Inc. to Yamana Gold Inc. On August 12, 2003, the authorized capital of the Company was altered by consolidating all of the then issued and outstanding common shares of the Company on the basis of one new common share for 27.86 existing common shares.

The Company’s head office is located at 200 Bay Street, Royal Bank Plaza, North Tower, Suite 2200, Toronto, Ontario M5J 2J3 and its registered office is located at 2100 Scotia Plaza, 40 King Street West, Toronto, Ontario M5H 3C2.

The corporate chart that follows on the next page illustrates the Company’s principal subsidiaries (collectively, the “Subsidiaries”), together with the jurisdiction of incorporation of each company and the percentage of voting securities beneficially owned, controlled or directed, directly or indirectly, by the Company. As used in this annual information form, except as otherwise required by the context, reference to the “Company” or “Yamana” means Yamana Gold Inc. and the Subsidiaries.

- 5 -

- 6 -

ITEM 3

GENERAL DEVELOPMENT OF THE BUSINESS

Overview of Business

Yamana is a Canadian-based gold producer with significant gold production, gold development stage properties, exploration properties and land positions in Brazil, Chile, Argentina, Mexico and Canada. Yamana plans to continue to build on this base through existing operating mine expansions, throughput increases, development of new mines, advancement of its exploration properties and by targeting other gold consolidation opportunities with a primary focus in the Americas.

The Company’s portfolio includes: (i) seven operating gold mines considered as core assets, including the Company’s three material producing mines - namely Chapada (copper/gold), El Peñón (gold/silver) and a 50% indirect interest in the Canadian Malartic Mine (gold/silver) - as well as Mercedes (gold/silver), Gualcamayo (gold), Jacobina (gold) and Minera Florida (gold/silver/zinc); (ii) a 12.5% indirect interest in the Alumbrera mine (copper/gold/molybdenum); (iii) various advanced and near development stage projects and exploration properties in Brazil, Chile, Argentina, Mexico and Canada; and (iv) Fazenda Brasileiro, Pilar and C1 Santa Luz, along with some related exploration concessions, which are held by the Company’s subsidiary, Brio Gold Inc. (“Brio Gold”).

Set out below is a list of Yamana’s main properties and mines:

Material Producing Mines

| • | Chapada Mine (Brazil) |

| • | El Peñón Mine (Chile) |

| • | Canadian Malartic Mine (Canada) - 50% indirect interest |

Other Producing Mines

| • | Mercedes Mine (Mexico) |

| • | Gualcamayo Mine (Argentina) |

| • | Jacobina Mining Complex (Brazil) |

| • | Minera Florida Mine (Chile) |

| • | Alumbrera Mine (Argentina) - 12.5% indirect interest |

Additional Projects

| • | Cerro Moro Project (Argentina) |

| • | Agua Rica Project (Argentina) |

| • | Suyai Project (Argentina) |

Brio Gold Projects

| • | Fazenda Brasileiro Mine (Brazil) |

| • | Pilar Project (Brazil) |

| • | C1 Santa Luz Project (Brazil) |

History

Over the three most recently completed financial years, the following events contributed materially to the development of the Company’s business:

- 7 -

Dividend Reinvestment Plan

On February 18, 2015, the Company announced the implementation of a dividend reinvestment plan (the ��DRIP”), effective for the first quarter dividend of 2015 forward, which provides eligible holders of the Company’s common shares with the option of reinvesting all or a portion of the dividends paid to them as shareholders (less any withholding tax) to purchase addition common shares of the Company. Participation in the DRIP is optional. The common shares acquired on behalf of eligible participants by the DRIP agent, CST Trust Company, will, at the sole option of the Company, be common shares issued from the treasury of the Company or common shares acquired on the open market through the facilities of the Toronto Stock Exchange (the “TSX”), the New York Stock Exchange (the “NYSE”) or any other stock exchange on which the common shares of the Company are then listed (each a “Listed Market”). The purchase price of the common shares purchased under the DRIP shall be the volume weighted average price of the common shares on the applicable Listed Market for the five (5) trading days preceding the dividend payment date.

Cerro Moro Construction Decision

In February 2015, the Company announced that it would proceed with the construction of the Cerro Moro Project. The current plan indicates average annual production in the first three years of full production of 135,000 ounces of gold and 6.7 million ounces of silver. After various optimization studies, the Company decided to pursue a single-stage plant scenario with an increased capacity of 1,000 tonnes per day (“tpd”). The single stage plant construction provides the project with less project execution, inflation and timing risk by completing the project in a shorter time frame with the same work force. The 1,000 tpd of throughput is considered the optimal project size to maximize throughput and value. The current mine design focuses the highest grade production into the first years of the production to decease the time for project payback. See “Description of the Business - Additional Projects - Cerro Moro Project”.

Public Offering

On February 3, 2015, the Company closed a bought deal offering (the “Public Offering”) of common shares of the Company. A total of 56,465,000 common shares were issued at a price of Cdn$5.30 per share, for aggregate gross proceeds of Cdn$299,264,500 (which included the full exercise by the underwriters of the over-allotment option for 7,365,000 common shares). The common shares of the Company were sold pursuant to an underwriting agreement (the “Underwriting Agreement”) dated January 15, 2015 between the Company and a syndicate of underwriters led by Canaccord Genuity Corp. and National Bank Financial Inc., and including CIBC World Markets Inc., RBC Dominion Securities Inc., Scotia Capital Inc., TD Securities Inc., Merrill Lynch Canada Inc., Credit Suisse Securities (Canada), Inc., Raymond James Ltd., Citigroup Global Markets Canada Inc., Cormark Securities Inc., Macquarie Capital Markets Canada Ltd., Morgan Stanley Canada Limited, and Barclays Capital Canada Inc. The net proceeds of the Public Offering were used to repay amounts under the Company’s $1 billion revolving credit facility, in order to reduce the Company’s debt position and further strengthen its balance sheet. See “Material Contracts”.

Copper Hedge Program

Late in 2014, the Company entered into a hedging program for its 2015 copper production. The Company has hedged 73 million pounds of copper, approximately 60% of expected production from the Chapada Mine for 2015, at a price of $3.00 per pound. This program is consistent with the Company’s focus on cash flow as it will provide an increased level of certainty for cash flows given the current environment of increased volatility in metal prices.

Strategic Initiatives Update

On December 10, 2014, the Company provided an update on strategic initiatives relating to non-core assets, including the Fazenda Brasileiro Mine, the Pilar Project and the C1 Santa Luz Project. The Company is advanced in the process of structuring its intercorporate holdings to form a new subsidiary company, Brio Gold, that will hold the Fazenda Brasileiro Mine, the Pilar Project and the C1 Santa Luz Project as well as some related exploration concessions. See “Description of the Business - Brio Gold Projects”.

- 8 -

In October 2014, the Company entered into a Memorandum of Understanding (“MOU”) with the provincial Government of Catamarca, Argentina (the “Catamarca Government”), represented by the provincial mining company Catamarca Mineria y Energetica Sociedad del Estado (“CAMYEN”), with respect to the creation of the Catamarca Mining District. The MOU established the groundwork for the Company and the Catamarca Government to work together to consolidate important mining projects and prospective properties in the province, currently consisting of the Agua Rica Project and the Cerro Atajo prospect. On February 27, 2015, a formal agreement was entered into among the parties to the MOU. This agreement forms the basis of a working relationship between the Catamarca Government through CAMYEN, other mining companies and the Company and is expected to help advance the Agua Rica Project and the Cerro Atajo prospect. The formal agreement also establishes a maximum ownership interest of up to 5% for CAMYEN of a combined entity, including the Agua Rica Project and Cerro Atajo prospect, and some exploration and infrastructure spending during the term of the agreement. The formal agreement does not restrict the Company’s ability to continue with Agua Rica, although it provides a framework of cooperation that would see Agua Rica advance to development more efficiently and on an expedited timeline. Presently, the Company is considering the development of Agua Rica in conjunction with other financial and mining industry participants. See “Description of the Business - Additional Projects - Agua Rica Project”.

On September 10, 2014, the Company announced that, after careful and extensive review, and having allowed a sufficient period of time for optimization efforts, the optimal plan for its C1 Santa Luz Project would be to temporarily suspend ramp-up activities and put the project on care and maintenance while several identified alternative metallurgical processes are evaluated. The C1 Santa Luz Project is now on care and maintenance. See “Description of the Business - Brio Gold Projects - C1 Santa Luz Project”.

Dividend Policy

In October 2014, the Company’s board of directors amended the Company’s dividend policy to set the quarterly dividends paid per common share at $0.015 commencing in the fourth quarter of 2014. Payment of any future dividends will be at the discretion of the Company’s board of directors after taking into account many factors, including the Company’s operating results, financial condition, comparability of the dividend yield to peer group gold companies and current and anticipated cash needs.

Board and Management Updates

On September 2, 2014, the Company announced the appointment of two new directors to the board of directors, namely Christiane Bergevin and Jane Sadowsky. The Company also announced additions to its senior management team which reflect an important pivot in the focus of management and supplemented existing management. Daniel Racine was appointed Senior Vice President, Northern Operations, which better aligns the Company’s technical and jurisdictional expertise with its property portfolio that now includes the Canadian Malartic Mine, Kirkland Lake and other Canadian exploration assets. Barry Murphy was appointed as Senior Vice President, Technical Services, which the Company believes increases the technical depth of its management as the Company continues to advance its development projects.

Note Exchange Offer

On June 30, 2014, the Company issued $500 million aggregate principal amount of 4.95% Senior Notes due 2024 (the “Initial Notes”) in a transaction that was exempt from registration under the Securities Act, and resold to qualified institutional buyers in reliance on Rule 144A and non-U.S. persons outside the United States in reliance on Regulation S. In connection with the issuance of the Initial Notes, the Company entered into a registration rights agreement, dated as of June 30, 2014, with the initial purchasers of the Initial Notes, providing for the issuance of new notes in exchange for a like aggregate principal amount of Initial Notes. Subsequently, in October 2014, the Company commenced an exchange offer which expired on November 20, 2014, pursuant to which new notes (the “New Notes”) were issued in exchange for an equal aggregate principal amount of outstanding Initial Notes validly tendered and accepted in the exchange offer. The terms of the New Notes are substantially identical to the terms of the Initial Notes, except that, among other things, the New Notes are registered under the Securities Act and do not contain restrictions on transfer.

- 9 -

In connection with the issuance of the Initial Notes, the Company entered into a trust indenture, dated as of June 30, 2014, as supplemented by the first supplemental indenture dated as of June 30, 2014 (collectively, the “Indenture”). Pursuant to the terms of the Indenture, the New Notes are unsecured, unsubordinated obligations of Yamana evidencing the same continuing indebtedness as the Initial Notes and will mature on July 15, 2024. The New Notes bear interest at the rate of 4.95% per annum from and including the most recent interest payment date to which interest has been paid or provided for, or if no interest has been paid or provided for, from June 30, 2014. Interest on the New Notes is payable semi-annually in arrears on January 15 and July 15 of each year, beginning on January 15, 2015, to the persons in whose names the New Notes are registered at the close of business on the preceding January 1 or July 1, as the case may be. See “Material Contracts”.

Canadian Malartic Mine - Acquisition

On June 16, 2014, the Company and Agnico Eagle Mines Limited (“Agnico Eagle”) jointly acquired 100% of all issued and outstanding common shares (with each company owning 50%) of Osisko (the “Osisko Acquisition”). Osisko operated the Canadian Malartic Mine in the Abitibi Gold Belt, immediately south of the Town of Malartic located in the province of Québec, Canada. Additionally, Osisko conducted advanced exploration activities at the Kirkland Lake and Hammond Reef properties in Northern Ontario, Canada and additional exploration projects located in the Americas. As of December 31, 2014, the estimated global Measured Mineral Resources and Indicated Mineral Resources for Canadian Malartic stood at 10.6 million ounces of gold, inclusive of Proven Mineral Reserves and Probable Mineral Reserves of 8.66 million ounces of gold. The estimated gold Inferred Mineral Resources are 1.11 million ounces. See “Description of the Business - Mineral Projects - Summary of Mineral Reserve and Mineral Resource Estimates”. Total consideration paid by Yamana consisted of approximately $0.5 billion in cash and $1.0 billion in common shares of the Company (based on a share price of $8.18 per share).

Since the date of the Osisko Acquisition, the Company’s 50% share of production for 2014 is 143,008 ounces of gold. See “Description of the Business - Material Producing Mines - Canadian Malartic Mine”.

Cerro Moro Project - Acquisition

On August 22, 2012, the Company acquired all the issued and outstanding common shares of Extorre Gold Mines Limited (“Extorre”). Each Extorre shareholder received $4.28 per share comprised of $3.50 in cash and 0.0467 of a Yamana common share for each Extorre common share held. Total consideration paid was approximately $451.5 million, comprised of 4.7 million common shares, transaction costs and issued options.

With the completion of the acquisition, the Company added several exploration and development stage precious metals projects, the most advanced of which is Cerro Moro, an advanced stage, high grade epithermal gold and silver deposit located in the Santa Cruz province of Argentina. The Cerro Moro Project covers 177 square kilometres and is located approximately 70 kilometres southwest of the coastal port city of Puerto Deseado, and 130 kilometres east of the Cerro Vanguardia gold silver mine.

In February 2015, the Company announced that it would proceed with the construction of the Cerro Moro Project. The current plan indicates average annual production in the first three years of full production of 135,000 ounces of gold and 6.7 million ounces of silver. See “Description of the Business - Additional Projects - Cerro Moro Project”.

ITEM 4

DESCRIPTION OF THE BUSINESS

Yamana is a Canadian-based gold producer with significant gold production, gold development stage properties, exploration properties and land positions in Brazil, Chile, Argentina, Mexico and Canada. Yamana plans to continue to build on this base through existing operating mine expansions, throughput increases, development of new mines, advancement of its exploration properties and by targeting other gold consolidation opportunities with a primary focus in the Americas.

- 10 -

Principal Products

The Company’s principal product is gold, with gold production forming a significant part of revenues. There is a global gold market into which Yamana can sell its gold and, as a result, the Company is not dependent on a particular purchaser with regard to the sale of the gold that it produces.

The Company produces gold-copper concentrate at its Chapada Mine, gold and silver doré bars at its El Peñón Mine and Mercedes Mine, gold doré bars at its Jacobina Mining Complex (the “JMC”), Gualcamayo Mine and Fazenda Brasileiro Mine, and gold and silver doré bars and zinc concentrate at its Minera Florida Mine. Additionally, the Company has a 50% indirect interest in the Canadian Malartic Mine which produces gold and silver doré bars, and a 12.5% indirect interest in the Alumbrera Mine which produces copper and gold concentrate and gold doré bars. The Company has contracts with a number of smelters, refineries and trading companies to sell gold and silver doré and gold-copper and zinc concentrate.

Competitive Conditions

The precious metal mineral exploration and mining business is a competitive business. The Company competes with numerous other companies and individuals in the search for and the acquisition of attractive precious metal mineral properties. The ability of the Company to acquire precious metal mineral properties in the future will depend not only on its ability to develop its present properties, but also on its ability to select and acquire suitable producing properties or prospects for precious metal development or mineral exploration.

Operations

Employees

As at December 31, 2014, the Company had the following employees and contractors at its operations:

| Country | Employees | Contractors | Total |

| Canada | 94 | 10 | 104 |

| Canada, Canadian Malartic (50% indirect interest) | 738 | 250 | 988 |

| Argentina | 1,148 | 355 | 1,503 |

| Brazil | 2,581 | 2,048 | 4,629 |

| Chile | 1,895 | 2,105 | 4,000 |

| Mexico | 515 | 185 | 700 |

| United States | 13 | 3 | 16 |

Domestic and Foreign Operations

The Company’s mine and mineral projects are located in Brazil, Chile, Argentina, Mexico and Canada. See “General Development of the Business - Overview of Business” for a summary of the Company’s projects. Any changes in regulations or shifts in political attitudes in any of these jurisdictions, or other jurisdictions in which Yamana has projects from time to time, are beyond the control of the Company and may adversely affect its business. Future development and operations may be affected in varying degrees by such factors as government regulations (or changes thereto) with respect to the restrictions on production, export controls, income taxes, expropriation of property, repatriation of profits, environmental legislation, land use, water use, land claims of local people, mine safety and receipt of necessary permits. The effect of these factors cannot be accurately predicted. See “- Risks of the Business”.

- 11 -

Environment and Communities

In common with other natural resources and mineral processing companies, the Company’s operations generate hazardous and non-hazardous waste, effluent and emissions into the atmosphere, water and soil in compliance with local and international regulations and standards. There are numerous environmental laws in Brazil, Chile, Argentina, Mexico, the United States, Canada and elsewhere in the Americas that apply to the Company’s operations, exploration, development projects and land holdings. These laws address such matters as protection of the natural environment, air and water quality, emissions standards and disposal of waste.

Yamana’s operating mine sites seek to adopt the best environmental practices programs to manage environmental matters and compliance with local and international legislation. Programs include: promotion of rational water use; solid waste management; control of emissions and fossil fuel consumption; rationing of energy; soil and biodiversity protection; archaeological sites identification and rescue and ruins preservation and monitoring; environmental education; surface and groundwater monitoring; air monitoring; land reclamation and revegetation; native seedlings production; and native forest conservation.

In 2014, Yamana continued its attention towards environmental performance indicators and continued to track its consumption of diesel, electricity, fresh water and its non-mineral solid waste generation. In 2014, consumption of diesel, electricity and non-mineral solid waste generation has decreased as follows: diesel (l/gold equivalent ounce (“GEO”)) by 4%; electricity (MWh/GEO) by 0.3%; generation of non-mineral solid waste (t/GEO) by 5%. In 2014, Yamana increased fresh water consumption (m³/GEO) by 8%.

In 2014, Yamana continued its focus on greenhouse gas emissions - comprised of both direct and indirect emissions. Yamana’s total greenhouse gas emissions were approximately 700,000 (t/CO2e), representing an aggregate increase for both direct and indirect emissions of 3% over 2013. Direct emissions at Yamana’s operations increased 2% in 2014. Increases in direct emissions were primarily due to the acquisition of additional equipment, changes in the location of waste rock piles that resulted in longer distances to be covered, and the resulting increase in fuel consumption. Indirect emissions increased 11% in 2014. Increases in indirect emissions were primarily due to new plant and mine ventilation equipment as well as the fact that Brazil is experiencing an historic drought. Less rainfall in Brazil has required increased use of thermal power plants which are more carbon intensive than hydroelectric power.

Yamana has a corporate integrated management system for Safety, Health, Environment and Community (“SHEC”) Relations and Social Responsibility (the “YMS”) which was created in October 2006. This system was developed based on the best practices and international standards - ISO 14001 - Environmental Management System, OHSAS 18001 - Occupational Health and Safety Management System and SA 8000 - Social Accountability, the International Cyanide Management Code (the “ICMC”) and local laws.

In early 2009, the Company was added to the Jantzi Social Index (“JSI”). Companies included in the JSI must pass a set of broadly based environmental, social and governance criteria. Inclusion in this index is a testament to the Company’s social, environmental, health and safety management programs which are considered by JSI to be above average. To date, seven of the Company’s wholly-owned operating mines have achieved ISO 14001 certification for their Environmental Management Systems and six wholly-owned operating mines have achieved OHSAS 18001 certification for their Occupational Health and Safety Management Systems. This exceeds the industry average.

The YMS involves: corporate policies, standards and procedures; risk assessment; identification of all legal and contractual requirements; definition of Company objectives and targets; and also includes internal auditing systems to ensure that Yamana operates in compliance with its policies and management programs. The implementation of the YMS commenced in Brazil in 2007 and in Chile in 2008. Yamana has continued to consolidate YMS across existing operations and has extended this consolidation to both exploration and construction areas. In order to verify compliance with the YMS, internal corporate audits have been conducted at each mine site, exploration project and construction project since 2009. Over the last five years the compliance with YMS increased 15.5%, including an increase from 86.4% compliance in 2013 to 87.8% compliance in 2014.

Yamana has mapped all environmental risks at its mine sites as part of the YMS. High level risks, including those associated with tailings dam facilities, waste rock dumps, heap leach piles or cyanide usage, have enhanced and

- 12 -

specific management measures in order to be better able to mitigate potential failures, spills or slides. These systems are based on the permanent monitoring of the particular structure, using specific tools that assist in monitoring such risks. In addition, reports on tailings dam facilities are prepared by third party consultants on a monthly basis and reviewed periodically by the Company.

Geomechanical, geotechnical and geochemical risks are also assessed periodically by third party consultants in order to minimize related risks, such as rock falls, as well as environmental contamination. These, and other high level risks, are dealt with as part of Yamana’s emergency response plan with emergency simulation tests being conducted during the year to evaluate the plan’s effectiveness.

Each of the Company’s mining operations has established a SHEC committee (collectively, the “SHEC Committees”) which are chaired by the General Manager at each mine. The SHEC Committees meet at least once a month to discuss issues and solutions related to SHEC relations and other operational practices. The goal of each SHEC Committee is to measure the effectiveness and performance of the Company’s sustainability programs. Yamana also maintains a corporate SHEC Committee (the “Corporate SHEC Committee”), comprised of certain executives and employees of the Company, to discuss strategic SHEC issues and to deliberate solutions for the various mine sites.

Since 2012, as part of the YMS, the Company defined a process to help mitigate, prevent and avoid negative environmental and safety incidents, and to prevent environmental and property damage. The general process with respect to key risks were reviewed and approved by the Corporate SHEC Committee, with local SHEC Committees at the Company’s mining operations evaluating the effective management of particular risks associated with the respective operations. Local SHEC Committees review major risks and processes, along with what actions have been taken to address and mitigate risks to an acceptable level (which actions are checked during corporate auditing and technical visits).

Certain of the Company’s mining operations utilize cyanide. These mines include the JMC and Fazenda Brasileiro Mines in Brazil; the El Peñün and Minera Florida Mines in Chile, the Mercedes Mine in Mexico; the Gualcamayo Mine in Argentina; and the Canadian Malartic Mine in Canada. Yamana is signatory to the ICMC and, with exception of the Canadian Malartic Mine, all of the mine sites noted immediately above are ICMC certified.

The Company has also made several investments in connection with infrastructure improvements to enhance community relations in the locations where it operates. The Company’s social responsibility programs are focused on local development, income generation and improvements in quality of life in the local communities. Through programs such as the Partnership Seminar Program, the Integration Program and the Open Doors Program, Yamana has provided support to local communities in many different areas such as education, culture, health, environment and the generation of employment and income. To further develop these programs, the Company conducts various education projects and cultural activities in each of the communities where the Company operates.

The Company’s compliance with its environmental policies and obligations is overseen by the Sustainability Committee.

Risks of the Business

The operations of the Company are speculative due to the high-risk nature of its business, which is the acquisition, financing, exploration, development and operation of mining properties. These risk factors could materially affect the Company’s future operating results and could cause actual events to differ materially from those described in forward-looking statements relating to the Company.

- 13 -

Gold, Copper and Silver Prices

The Company’s profitability and long-term viability depend, in large part, upon the market price of metals that may be produced from its properties, primarily gold, copper and silver. Market price fluctuations of these commodities could adversely affect profitability of the Company’s operations and lead to impairments and write downs of mineral properties. Metal prices fluctuate widely and are affected by numerous factors beyond the Company’s control, including:

| • | global and regional supply and demand for industrial products containing metals generally; |

| • | changes in global or regional investment or consumption patterns; |

| • | increased production due to new mine developments and improved mining and production methods; |

| • | decreased production due to mine closures; |

| • | interest rates and interest rate expectation; |

| • | expectations with respect to the rate of inflation or deflation; |

| • | fluctuations in the value of the United States dollar and other currencies; |

| • | availability and costs of metal substitutes; |

| • | global or regional political or economic conditions; and |

| • | sales by central banks, holders, speculators and other producers of metals in response to any of the above factors. |

There can be no assurance that metal prices will remain at current levels or that such prices will improve. A decrease in the market prices could adversely affect the profitability of the Company’s existing mines and projects as well as its ability to finance the exploration and development of additional properties, which would have a material adverse effect on the Company’s results of operations, cash flows and financial position. A decline in metal prices may require the Company to write-down Mineral Reserve and Mineral Resource estimates by removing ores from reserves that would not be economically processed at lower metal prices and revise life-of-mine plans (“LOM Plans”), which could result in material write-downs of investments in mining properties. Any of these factors could result in a material adverse effect on the Company’s results of operations, cash flows and financial position. Further, if revenue from metal sales declines, the Company may experience liquidity difficulties. Its cash flow from mining operations may be insufficient to meet its operating needs, and as a result the Company could be forced to discontinue production and could lose its interest in, or be forced to sell, some or all of its properties.

In addition to adversely affecting Mineral Reserve and Mineral Resource estimates and the Company’s results of operations, cash flows and financial position, declining metal prices can impact operations by requiring a reassessment of the feasibility of a particular project. Even if a project is ultimately determined to be economically viable, the need to conduct such a reassessment may cause substantial delays and/or may interrupt operations until the reassessment can be completed, which may have a material adverse effect on the Company’s results of operations, cash flows and financial position. In addition, lower metal prices may require the Company to reduce funds available for exploration with the result that the depleted reserves may not be replaced.

Asset Impairment Charges

Yamana assesses at the end of each reporting period whether there are any indicators, from external and internal sources of information that an asset or cash generating unit (“CGU”) may be impaired requiring an adjustment to the carrying value in order not to exceed its recoverable amount. A CGU is defined as the smallest identifiable group of mineral assets that generates independent cash flows. External sources of information considered could include changes in market conditions, the economic and legal environment in which the Company operates that are not within its control and the impact these changes may have on the recoverable amount. Internal sources of information include the manner in which the mineral properties are being used or are expected to be used and indications of the economic performance of the assets. The recoverable amounts of CGUs are based on each CGU’s future after-tax cash flows expected to be derived from Yamana’s mining properties. Reductions in metal price forecasts, increases in estimated future costs of production, increases in estimated future capital costs and reductions in the amount of recoverable reserves and resources are each examples of factors and estimates that could each result in a write-down of the carrying amount of the Company’s mineral properties. Although management makes its best estimates, it is possible that material changes could occur which may adversely affect management’s estimate of the net cash flows expected to be generated from its properties.

- 14 -

Any impairment estimates, which are based on applicable key assumptions and sensitivity analysis, are based on management’s best knowledge of the amounts, events or actions at such time, and the actual future outcomes may differ from any estimates that are provided by the Company. Any impairment charges on the Company’s mineral projects could adversely affect its results of operations.

The Company had a review of assets in 2014, including engaging in a detailed review of its LOM Plans and an evaluation of capital expenditures and expected returns. As a result of this process, in the third quarter, certain impairments were recognized on certain assets. The carrying values of assets are highly dependent on several factors including metal prices and the prevailing cost environment, and the carrying values of some properties are more sensitive to metal prices than others. The Company will continue to review at each period end whether there are any indications that a further impairment or reversal is required.

Exploration, Development and Operating Risks

Mining operations are inherently dangerous and generally involve a high degree of risk. Yamana’s operations are subject to all the hazards and risks normally encountered in the exploration, development and production of gold, copper and silver, including, without limitation, unusual and unexpected geologic formations, seismic activity, rock bursts, cave-ins, flooding, pit wall failure and other conditions involved in the drilling and removal of material, any of which could result in damage to, or destruction of, mines and other producing facilities, personal injury or loss of life, damage to property and environmental damage, all of which may result in possible legal liability. Although the Company expects that adequate precautions to minimize risk will be taken, mining operations are subject to hazards such as fire, rock falls, geomechanical issues, equipment failure or failure of retaining dams around tailings disposal areas which may result in environmental pollution and consequent liability. The occurrence of any of these events could result in a prolonged interruption of the Company’s operations that would have a material adverse effect on its business, financial condition, results of operations and prospects.

The exploration for and development of mineral deposits involves significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. While the discovery of an ore body may result in substantial rewards, few properties that are explored are ultimately developed into producing mines. Major expenses may be required to locate and establish Mineral Reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site. It is impossible to ensure that the exploration or development programs planned by Yamana will result in a profitable commercial mining operation. Whether a mineral deposit will be commercially viable depends on a number of factors, some of which are: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; metal prices that are highly cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. The exact effect of these factors cannot be accurately predicted, but the combination of these factors may result in Yamana not receiving an adequate return on invested capital.

There is no certainty that the expenditures made by Yamana towards the search and evaluation of mineral deposits will result in discoveries or development of commercial quantities of ore.

Health, Safety and Environmental Risks and Hazards

Mining, like many other extractive natural resource industries, is subject to potential risks and liabilities due to accidents that could result in serious injury or death and/or material damage to the environment and Company assets. The impact of such accidents could affect the profitability of the operations, cause an interruption to operations, lead to a loss of licenses, affect the reputation of the Company and its ability to obtain further licenses, damage community relations and reduce the perceived appeal of the Company as an employer.

All phases of the Company’s operations are subject to environmental regulation in the various jurisdictions in which it operates. These regulations mandate, among other things, water quality standards and land reclamation and regulate the generation, transportation, storage and disposal of hazardous waste. Environmental legislation is evolving in a manner that will require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects and a heightened degree of responsibility for companies and their officers, directors and employees. There is no assurance that the Company has been or will at all times be in full

- 15 -

compliance with all environmental laws and regulations or hold, and be in full compliance with, all required environmental and health and safety permits. The potential costs and delays associated with compliance with such laws, regulations and permits could prevent the Company from proceeding with the development of a project or the operation or further development of a project, and any non-compliance therewith may adversely affect the Company’s business, financial condition and results of operations.

At the Alumbrera Mine, in which Yamana holds a 12.5% interest, a sulphate seepage plume has developed in the natural groundwater downstream of the tailings facility, currently within the mining concession. After completing the original model, an initial pump back well mesh was designed and completed before start up, in order to capture the seepage, which is characterized by high levels of dissolved calcium and sulphate. It will be necessary to augment the pump-back wells over the life of the mine in order to contain the plume within the concession and to provide for monitoring wells for the Vis Vis River. Based on the latest groundwater model, the pump-back system will need to be operated for several years after mine closure. The concentrate pipeline at the Alumbrera Mine crosses areas of mountainous terrain, significant rivers, high rainfall and active agriculture. Although various control structures and monitoring programs have been implemented, any rupture of the pipeline poses an environmental risk from spillage of concentrate. Yamana does not have any indemnities from the previous vendors of its interests in the Alumbrera Mine against any potential environmental liabilities that may arise from operations, including, but not limited to, potential liabilities that may arise from the seepage plume or a rupture of the pipeline.

Environmental hazards may also exist on the properties on which the Company holds interests that are unknown to the Company at present and that have been caused by previous or existing owners or operators of the properties.

Government environmental approvals and permits are currently, or may in the future be, required in connection with the Company’s operations. To the extent such approvals are required and not obtained, the Company may be curtailed or prohibited from proceeding with planned exploration or development of mineral properties.

Failure to comply with applicable laws, regulations and permitting requirements may result in enforcement actions, including orders issued by regulatory or judicial authorities causing operations to cease or be curtailed, and may include corrective measures requiring capital expenditures, installation of additional equipment, or remedial actions. Parties engaged in mining operations, including the Company, may be required to compensate those suffering loss or damage by reason of the mining activities and may have civil or criminal fines or penalties imposed for violations of applicable laws or regulations.

In 2013, Osisko received 41 notices of non-compliance pertaining to exceeding noise level parameters, NOx gas production and surpassing limits for over pressure and vibrations during blasting operations, exceeding noise levels and blast-induced vibrations at the Canadian Malartic Mine in which Yamana now owns a 50% interest. As a result of the Osisko Acquisition, the Company may face administrative fines or other charges in connection with such notices, Osisko’s other former operations or the properties that the Company acquired in the Osisko Acquisition.

Amendments to current laws, regulations and permits governing operations and activities of mining companies, or more stringent implementation thereof, could have a material adverse impact on the Company and cause increases in exploration expenses, capital expenditures or production costs, reduction in levels of production at producing properties, or abandonment or delays in development of new mining properties.

In certain jurisdictions, the Company may be required to submit, for government approval, a reclamation plan for each of its mining/project sites. The reclamation plan establishes the Company’s obligation to reclaim property after minerals have been mined from the sites. In some jurisdictions, bonds or other forms of financial assurances are required as security to ensure performance of the required reclamation activities. The Company may incur significant reclamation costs which may materially exceed the provisions the Company has made for such reclamation. In addition, the potential for additional regulatory requirements relating to reclamation or additional reclamation activities may have a material adverse effect on the Company’s financial condition, liquidity or results of operations. When a previously unrecognized reclamation liability becomes known or a previously estimated cost is increased, the amount of that liability or additional cost may be expensed, which may materially reduce net income in that period.

- 16 -

Production at certain of the Company’s mines involves the use of cyanide which is toxic material if not handled properly. Should cyanide leak or otherwise be discharged from the containment system, the Company could suffer a material impact on its business, financial condition and results of operations. The Company became a signatory to the ICMC in September 2008. Further information regarding the ICMC can be found at the International Cyanide Management Institute website located at www.cyanidecode.org.

The mineral exploration activities of the Company are subject to various laws governing prospecting, development, production, taxes, labour standards and occupational health, mine safety, toxic substances and other matters. Although the Company believes that its exploration activities are currently carried out in accordance with all applicable rules and regulations, new rules and regulations may be enacted or existing rules and regulations may be applied in a manner that could limit or curtail production or development of the Company’s properties. Amendments to current laws and regulations governing the operations and activities of the Company or more stringent implementation thereof could have a material adverse effect on the Company’s business, financial condition and results of operations. See “- Foreign Operations and Political Risk”.

Nature and Climatic Condition Risk

The Company and the mining industry are facing continued geotechnical challenges, which could adversely impact the Company’s production and profitability. Unanticipated adverse geotechnical and hydrological conditions, such as landslides, droughts, pit wall failures and rock fragility may occur in the future and such events may not be detected in advance. Geotechnical instabilities and adverse climatic conditions can be difficult to predict and are often affected by risks and hazards outside of the Company’s control, such as severe weather and considerable rainfall, which may lead to periodic floods, mudslides, wall instability and seismic activity, which may result in slippage of material.

Geotechnical failures could result in limited or restricted access to mine sites, suspension of operations, government investigations, increased monitoring costs, remediation costs, loss of ore and other impacts, which could cause one or more of the Company’s projects to be less profitable than currently anticipated and could result in a material adverse effect on the Company’s results of operations and financial position.

Counterparty, Credit, Liquidity and Interest Rate Risks and Access to Financing

The Company is exposed to various counterparty risks including, but not limited to: (i) financial institutions that hold the Company’s cash and short term investments; (ii) companies that have payables to the Company, including concentrate and bullion customers; (iii) providers of its risk management services (including hedging arrangements); (iv) shipping service providers that move the Company’s material; (v) the Company’s insurance providers; and (vi) the Company’s lenders. The Company seeks to limit counterparty risk by entering into business arrangements with high credit-quality counterparties, limiting the amount of exposure to each counterparty and monitoring the financial condition of counterparties. For cash, cash equivalents and accounts receivable, credit risk is represented by the carrying amount on the balance sheet. For derivatives, the Company assumes no credit risk when the fair value of the instruments is negative. When the fair value of the instruments is positive, this is a reasonable measure of credit risk. The Company is also exposed to liquidity risks in meeting its operating and capital expenditure requirements in instances where cash positions are unable to be maintained or appropriate financing is unavailable. Under the terms of the Company’s trading agreements, counterparties cannot require the Company to immediately settle outstanding derivatives except upon the occurrence of customary events of default. The Company mitigates liquidity risk through the implementation of its capital management policy by spreading the maturity dates of derivatives over time, managing its capital expenditures and operation cash flows, and by maintaining adequate lines of credit. The Company is exposed to interest rate risk on its variable rate debt and enters into interest rate swap agreements to hedge this risk. These factors may impact the ability of the Company to obtain loans and other credit facilities and refinance existing facilities in the future and, if obtained, on terms favourable to the Company. Such failures to obtain loans and other credit facilities could require the Company to take measures to conserve cash and could adversely affect its access to the liquidity needed for the business in the longer term.

The development of the Company’s projects and the construction of mining facilities and commencement of mining operations may require substantial additional financing. Failure to obtain sufficient financing will result in a delay or indefinite postponement of exploration, development or production on any or all of the Company’s properties

- 17 -

or even a loss of a property interest. Additional financing may not be available when needed, or if available, the terms of such financing might not be favorable to the Company. Failure to raise capital when needed would have a material adverse effect on the Company’s business, financial condition and results of operations.

Construction and Start-up of New Mines

The success of construction projects and the start-up of new mines by the Company is subject to a number of factors including the availability and performance of engineering and construction contractors, mining contractors, suppliers and consultants, the receipt of required governmental approvals and permits in connection with the construction of mining facilities and the conduct of mining operations (including environmental permits), the successful completion and operation of ore passes, the adsorption/desorption/recovery plants and conveyors to move ore, among other operational elements. Any delay in the performance of any one or more of the contractors, suppliers, consultants or other persons on which the Company is dependent in connection with its construction activities, a delay in or failure to receive the required governmental approvals and permits in a timely manner or on reasonable terms, or a delay in or failure in connection with the completion and successful operation of the operational elements in connection with new mines could delay or prevent the construction and start-up of new mines as planned. There can be no assurance that current or future construction and start-up plans implemented by the Company will be successful, that the Company will be able to obtain sufficient funds to finance construction and start-up activities, that personnel and equipment will be available in a timely manner or on reasonable terms to successfully complete construction projects, that the Company will be able to obtain all necessary governmental approvals and permits or that the completion of the construction, the start-up costs and the ongoing operating costs associated with the development of new mines will not be significantly higher than anticipated by the Company. Any of the foregoing factors could adversely impact the operations and financial condition of the Company.

Some of the Company’s projects have no operating history upon which to base estimates of future cash flow. The capital expenditures and time required to develop new mines or other projects are considerable and changes in costs or construction schedules can affect project economics. Thus, it is possible that actual costs may change significantly and economic returns may differ materially from the Company’s estimates.

As an example, C1 Santa has significantly underperformed. As such, during the third quarter of 2014, the Company suspended commissioning activities at C1 Santa Luz and placed the project on care and maintenance, and also reduced the carrying value of C1 Santa Luz. While commercial production at Pilar was declared effective October 1, 2014, this project has also been met with challenges during commissioning and now has a decreased production expectation relative to feasibility levels and, as such, the Company has reduced the carrying value of this project as well.

Commercial viability of a new mine or development project is predicated on many factors. Mineral Reserves and Mineral Resources projected by feasibility studies and technical assessments performed on the projects may not be realized, and the level of future metal prices needed to ensure commercial viability may not materialize. Consequently, there is a risk that start-up of new mine and development projects may be subject to write-down and/or closure as they may not be commercially viable.

Uncertainty in the Estimation of Mineral Reserves and Mineral Resources

To extend the lives of its mines and projects, ensure the continued operation of the business and realize its growth strategy, it is essential that the Company continues to realize its existing identified Mineral Reserves, convert Mineral Resources into Mineral Reserves, increase its Mineral Resource base by adding new Mineral Resources from areas of identified mineralized potential, and/or undertake successful exploration or acquire new Mineral Resources.

No assurance can be given that the anticipated tonnages and grades in respect of Mineral Reserves and Mineral Resources contained in this annual information form will be achieved, that the indicated level of recovery will be realized or that Mineral Reserves will be mined or processed profitably. Actual Mineral Reserves may not conform to geological, metallurgical or other expectations, and the volume and grade of ore recovered may differ from estimated levels. There are numerous uncertainties inherent in estimating Mineral Reserves and Mineral Resources, including

- 18 -

many factors beyond the Company’s control. Such estimation is a subjective process, and the accuracy of any Mineral Reserve or Mineral Resource estimate is a function of the quantity and quality of available data and of the assumptions made and judgments used in engineering and geological interpretation. Short-term operating factors relating to the Mineral Reserves, such as the need for orderly development of the ore bodies or the processing of new or different ore grades, may cause the mining operation to be unprofitable in any particular accounting period. In addition, there can be no assurance that gold recoveries in small scale laboratory tests will be duplicated in larger scale tests under on-site conditions or during production. Lower market prices, increased production costs, reduced recovery rates and other factors may result in a revision of its Mineral Reserve estimates from time to time or may render the Company’s Mineral Reserves uneconomic to exploit. Mineral Reserve data is not indicative of future results of operations. If the Company’s actual Mineral Reserves and Mineral Resources are less than current estimates or if the Company fails to develop its Mineral Resource base through the realization of identified mineralized potential, its results of operations or financial condition may be materially and adversely affected. Evaluation of Mineral Reserves and Mineral Resources occurs from time to time and they may change depending on further geological interpretation, drilling results and metal prices. The category of Inferred Mineral Resource is often the least reliable Mineral Resource category and is subject to the most variability. The Company regularly evaluates its Mineral Resources and it often determines the merits of increasing the reliability of its overall Mineral Resources.

Replacement of Depleted Mineral Reserves

Given that mines have limited lives based on Proven Mineral Reserves and Probable Mineral Reserves, the Company must continually replace and expand its Mineral Reserves at its mines. The life-of-mine estimates included in this annual information form may not be correct. The Company’s ability to maintain or increase its annual production will be dependent in part on its ability to bring new mines into production and to expand Mineral Reserves at existing mines.

Uncertainty Relating to Mineral Resources

Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. Due to the uncertainty which may attach to Inferred Mineral Resources, there is no assurance that Inferred Mineral Resources will be upgraded to Proven Mineral Reserves and Probable Mineral Reserves as a result of continued exploration.

Commodity Prices

The profitability of the Company’s operations will be dependent upon the cost and availability of commodities which are consumed or otherwise used in connection with the Company’s operations and projects, including, but not limited to, diesel, fuel, natural gas, electricity, steel, concrete and cyanide. Commodity prices fluctuate widely and are affected by numerous factors beyond the control of the Company. Further, as many of the Company’s mines are in remote locations and energy is generally a limited resource, the Company faces the risk that there may not be sufficient energy available to carry out mining activities efficiently or that certain sources of energy may not be available.

Joint Ventures

Yamana holds an indirect 12.5% interest in the Alumbrera Mine, the other 37.5% and 50% interests being held by Goldcorp Inc. (“Goldcorp”) and Glencore plc (“Glencore”), respectively. The Company accounts for this investment under the equity method of accounting. The Company’s interest in the Alumbrera Mine is subject to the risks normally associated with the conduct of joint ventures. The existence or occurrence of one or more of the following circumstances and events, for example, could have a material adverse impact on Company’s profitability or the viability of its interests held through joint ventures, which could have a material adverse impact on future cash flows, earnings, results of operations and financial condition, disagreement with joint venture partners on how to develop and operate mines efficiently; inability of joint venture partners to meet their obligations to the joint venture or third parties; or litigation arising between joint venture partners regarding joint venture matters.

- 19 -

Infrastructure

Mining, processing, development and exploration activities depend, to one degree or another, on adequate infrastructure. Reliable roads, bridges, power sources and water supply are important determinants that affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect the Company’s operations, financial condition and results of operations.

Permitting

The Company’s operations are subject to receiving and maintaining permits from appropriate governmental authorities. There is no assurance that delays will not occur in connection with obtaining all necessary renewals of permits for the Company’s existing operations, additional permits for any possible future changes to operations, or additional permits associated with new legislation. Prior to any development on any of its properties, the Company must receive permits from appropriate governmental authorities. There can be no assurance that the Company will continue to hold all permits necessary to develop or continue operating at any particular property. Any of these factors could have a material adverse effect on the Company’s results of operations and financial position.

Insurance and Uninsured Risks

Yamana’s business is subject to a number of risks and hazards generally, including adverse environmental conditions, industrial accidents, labour disputes, unusual or unexpected geological conditions, ground or slope failures, cave-ins, catastrophic equipment failures or unavailability of materials and equipment, changes in the regulatory environment and natural phenomena such as inclement weather conditions, floods and earthquakes. Such occurrences could result in damage to mineral properties or production facilities, personal injury or death, environmental damage to the Company’s properties or the properties of others, delays in mining, monetary losses and possible legal liability.

Yamana’s insurance will not cover all the potential risks associated with the Company’s operations. Even if available, Yamana may also be unable to maintain insurance to cover these risks at economically feasible premiums. Insurance coverage may not continue to be available or may not be adequate to cover any resulting liability. Moreover, insurance against risks such as environmental pollution or other hazards as a result of exploration and production (such as underground coverage) is not generally available to Yamana or to other companies in the mining industry on acceptable terms. Yamana might also become subject to liability for pollution or other hazards that may not be insured against or that Yamana may elect not to insure against because of premium costs or other reasons. Losses from these events could cause Yamana to incur significant costs that could have a material adverse effect upon its financial performance and results of operations. Should the Company be unable to fully fund the cost of remedying an environmental problem, the Company might be required to suspend operations or enter into interim compliance measures pending completion of the required remedy, which may have a material adverse effect. The Company may suffer a material adverse effect on its business, results of operations, cash flows and financial position if it incurs a material loss related to any significant event that is not covered, or adequately covered, by its insurance policies.

Foreign Operations and Political Risk

The Company holds mining and exploration properties in Brazil, Argentina, Chile, Mexico and Canada, exposing it to the socioeconomic conditions as well as the laws governing the mining industry in those countries. Inherent risks with conducting foreign operations include, but are not limited to: high rates of inflation; military repression; war or civil war; social and labour unrest; organized crime; hostage taking; terrorism; violent crime; extreme fluctuations in currency exchange rates; expropriation and nationalization; renegotiation or nullification of existing concessions, licenses, permits and contracts; illegal mining; changes in taxation policies; restrictions on foreign exchange and repatriation; and changing political norms, currency controls and governmental regulations that favour or require the Company to award contracts in, employ citizens of, or purchase supplies from, a particular jurisdiction.

Changes, if any, in mining or investment policies or shifts in political attitude in any of the jurisdictions in which the Company operates may adversely affect the Company’s operations or profitability. Operations may be

- 20 -

affected in varying degrees by government regulations with respect to, but not limited to, restrictions on production, price controls, export controls, currency remittance, importation of parts and supplies, income and other taxes, expropriation of property, foreign investment, maintenance of claims, environmental legislation, land use, land claims of local people, water use and mine safety.

Failure to comply strictly with applicable laws, regulations and local practices relating to mineral right applications and tenure could result in loss, reduction or expropriation of entitlements, or the imposition of additional local or foreign parties as joint venture partners with carried or other interests. In addition, changes in government laws and regulations, including taxation, royalties, the repatriation of profits, restrictions on production, export controls, changes in taxation policies, environmental and ecological compliance, expropriation of property and shifts in the political stability of the country, could adversely affect the Company’s exploration, development and production initiatives in these countries.

In efforts to tighten capital flows and protect foreign exchange reserves, the Argentine government issued a foreign exchange resolution with respect to export revenues. This resulted in a temporary suspension of export sales of concentrate at the Alumbrera Mine during the second quarter of 2012 as management evaluated how to comply with the new resolution. The Argentine government subsequently announced an amendment to the foreign exchange resolution which extended the time for exporters to repatriate net proceeds from export sales, enabling the Alumbrera Mine to resume exports in July 2012. The Argentine government has also introduced certain protocols relating to the importation of goods and services and providing, where possible, for the substitution of Argentine produced goods and services. During 2012, the Alumbrera Mine was unable to obtain permission to repatriate dividends even though certain accommodations have since been made to permit distribution of profits from Argentina. Discussions between the joint venture and the Argentine government on approval to remit dividends are ongoing.

On September 23, 2013, Argentina’s federal income tax statute was amended to include a 10% income tax withholding on dividend distributions by Argentine corporations. On September 26, 2014, the Chilean government enacted a tax reform package. The Chilean reform progressively increases the Company’s cash taxes from 2014 to 2017 and also impacts the Company’s non-cash deferred tax liability. In addition to the rate changes, the Company is evaluating the impact of the Chilean tax reform package on its taxes.