EXHIBIT 99.1

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

OPERATIONS AND FINANCIAL CONDITION

FOR THE THREE AND NINE MONTHS ENDED SEPTEMBER 30, 2015

TABLE OF CONTENTS

| Page | ||||

| 1. | Core Business | |||

| 2. | Highlights | |||

| 3. | Outlook and Strategy | |||

| 4. | Summary of Financial and Operating Statistics | |||

| 4.1: | Financial Statistics | |||

| 4.2: | Operating Statistics | |||

| 5. | Overview of Results | |||

| 5.1: | Overview of Financial Results | |||

| 5.2: | Overview of Operating Results | |||

| 6. | Operating Mines | |||

| 7. | Construction, Development and Exploration | |||

| 8. | Liquidity, Capital Resources and Contractual Commitments | |||

| 9. | Income Taxes | |||

| 10. | Economic Trends, Business Risks and Uncertainties | |||

| 11. | Contingencies | |||

| 12. | Critical Accounting Policies and Estimates | |||

| 13. | Non-GAAP Measures | |||

| 14. | Selected Quarterly Financial and Operating Summary | |||

| 15. | Disclosure Controls and Procedures | |||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF OPERATIONS AND FINANCIAL CONDITION

(All figures are in United States Dollars ("US Dollars") unless otherwise specified and are in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS”). This Management’s Discussion and Analysis of Operations and Financial Condition ("MD&A") should be read in conjunction with the Company’s most recently issued annual consolidated financial statements for the year ended December 31, 2014 ("Consolidated Financial Statements").

Cautionary notes regarding forward-looking statements and mineral reserves and mineral resources follow this MD&A.

1. CORE BUSINESS

Yamana Gold Inc. (TSX:YRI and NYSE:AUY) (the “Company” or “Yamana”) is a Canadian-headquartered gold producer with significant precious metal properties in Brazil, Chile, Argentina, Mexico and Canada.

Note 3(a) Significant Accounting Policies - Basis of Consolidation to the most recently audited Consolidated Annual Financial Statements lists Yamana’s significant subsidiaries with 100% equity interest and its joint operation of the Canadian Malartic mine. The Company does not have any material off-balance sheet arrangements, except as noted in Note 33 Contractual Commitments to the Consolidated Financial Statements.

2. HIGHLIGHTS

For the three months ended September 30, 2015 (unless otherwise specified)

Financial

| • | Revenue from continuing operations of $448.9 million on the sale of 317,859 ounces of gold, 2.2 million ounces of silver, and 29.1 million pounds of copper(i). |

| • | Net loss from continuing operations of $115.0 million or $0.12 per share basic and diluted, after a $132.7 million charge arising from a non-cash tax expense relating to unrealized foreign exchange rate fluctuations, partially offset by unrealized foreign exchange gains of $38.4 million. After eliminating the impact of the aforementioned exchange rate fluctuations, Adjusted loss(ii) from continuing operations was $20.2 million or $0.02 per share. |

| • | Mine operating earnings from continuing operations of $49.7 million. |

| • | Cash flows of $77.6 million from operating activities from continuing operations after changes in non-cash working capital and cash flows of $127.6 million from operating activities before changes in non-cash working capital(ii). |

| • | General and Administrative ("G&A") expenses were $28.5 million, compared to $32.0 million for the second quarter of 2015, representing a decrease of 11%. G&A for the nine months ended September 30, 2015 were $89.9 million, compared to $93.0 million for the same period of 2014 or 3% lower. |

The non-cash tax expense referred to above, is notional only and results from foreign exchange rate fluctuations in the quarter, which was determined at a low point of the Brazilian Real exchange rate, vis-à-vis the US Dollar. Results on calculations of foreign exchange and taxes on foreign exchange are subject to high volatility and may swing favourably or unfavourably from period to period. If the Brazilian Real was to strengthen to previous levels, the Company would experience a tax recovery. In either case, they are notional and non-cash. Due to the unrealized, non-cash nature of these charges, it is the Company’s policy to exclude them from adjusted earnings.

Operational

| • | Gold production from continuing operations of 325,897 ounces of gold, in line with the third quarter of 2014, with gold production from core assets(iii) of 281,915 ounces of gold, also in line with the third quarter of 2014. |

| • | Individual mine highlights include the following: |

| ◦ | Record quarterly production from Canadian Malartic of 76,603 ounces of gold, representing an 18% increase in production over the third quarter of 2014 and a 12% increase over the second quarter of 2015. |

| ◦ | Quarterly production from Chapada of 32,029 ounces of gold, representing an 11% increase in production over the third quarter of 2014 and a 6% increase over the second quarter of 2015. |

| ◦ | Quarterly production from Jacobina of 28,080 ounces of gold, representing a 33% increase in production over the third quarter of 2014 and a 32% increase over the second quarter of 2015. |

1

| ◦ | Quarterly production from Minera Florida of 28,989 ounces of gold, representing a 29% increase in production over the third quarter of 2014 and a 10% increase over the second quarter of 2015. |

| ◦ | Increase in production at Gualcamayo to 44,076 ounces of gold, representing a 2% increase in production over the third quarter of 2014 and a 17% increase over the second quarter of 2015. |

| ◦ | Increase in production from Brio Gold Inc.(iv) ("Brio Gold") to 38,430 ounces of gold, representing a 9% increase in production over the second quarter of 2015 and in the case of Fazenda Brasileiro, a 21% increase over the second quarter of 2015. |

| • | Cash costs(ii)of $594 per ounce of gold ($653 per ounce of gold on a co-product basis). |

| • | All-in sustaining costs(ii) ("AISC") of $841 per ounce of gold, 3% lower than the third quarter of 2014 ($856 per ounce of gold on a co-product basis, 12% lower than the third quarter of 2014). |

| • | Silver production of 2.2 million ounces at cash costs of $7.37 per ounce and AISC of $11.32 per ounce. |

| • | Copper production from Chapada of 34.0 million pounds at cash costs of $1.41 per pound of copper, representing a decrease in costs of 11% over the third quarter of 2014. |

| • | Given the advancement of the Brio Gold monetization plan, the table below has been provided to give a preview of the Company's cost profile for its core mines, Brio Gold and continuing operations, all other inputs remaining equal. Additionally, the table shows that in the absence of the foreign exchange hedges, that will be extinguished by year end, the Company's cash costs, AISC and cash costs on a co-product basis would have come in at lower levels. |

Core Mines(1)(iii) | Cash cost per ounce | AISC per ounce | Gold co-product cash cost per ounce | ||||||

| Costs including hedge impact | $ | 570 | $ | 748 | $ | 652 | |||

Impact of hedge (4) | (40 | ) | (40 | ) | (18 | ) | |||

| Costs excluding hedge impact | $ | 530 | $ | 708 | $ | 634 | |||

Brio Gold(2)(iv) | |||||||||

| Costs including hedge impact | $ | 658 | $ | 866 | $ | 658 | |||

Impact of hedge (4) | — | — | — | ||||||

| Costs excluding hedge impact | $ | 658 | $ | 866 | $ | 658 | |||

Continuing Operations(3) | |||||||||

| Costs including hedge impact | $ | 594 | $ | 841 | $ | 653 | |||

Impact of hedge (4) | (35 | ) | (35 | ) | (16 | ) | |||

| Costs excluding hedge impact | $ | 559 | $ | 806 | $ | 637 | |||

______________________________

| (1) | Based on gold production of 281,915 ounces from the Company's core mines. |

| (2) | Based on gold production of 38,430 ounces from Brio Gold. Brio Gold costs exclude impact of copper by-product credits, as those are attributable to Chapada, which is part of the Company's core mines. |

| (3) | Based on gold production of 325,897 ounces from the Company's continuing operations. |

| (4) | Based on realized foreign exchange hedges settled during the third quarter of 2015. |

Strategic Developments and Updates

| • | Subsequent to the quarter end, the Company announced a streaming transaction with Sandstorm Gold Ltd, for which Sandstorm has paid the Company an advanced payment of $148 million and has issued the Company 15 million common share purchase warrants with a strike price of $3.50 and a term of five years (valued at approximately $15-20 million, depending on valuation assumptions used). Sandstorm will also pay the Company an additional $4 million in six months. The metal purchase agreements include a silver purchase transaction related to production from Cerro Moro, Minera Florida and Chapada, a copper purchase transaction related to production from Chapada, and a gold purchase transaction related to production from Agua Rica. The full amount of the advanced payment will be used by the Company to reduce the balance outstanding on its revolving credit facility. |

| • | Subsequent to the quarter end, the Company announced the engagement of an investment bank in the United States to pursue several alternatives relating to the monetization of Brio Gold. |

Construction and Development

2

| • | Continued with detailed engineering of the processing plant and mine at Cerro Moro, with preparations underway including the mobilization of the bulk earthworks construction contractor, whose site activities are expected to commence in late 2015. The Company is concurrently investigating various modifications to the development timetable and capital schedule in order to enhance the overall value of, and further de-risk the Cerro Moro project. For all the new development scenarios under consideration, production is expected to commence towards the end of the first quarter of 2018. A final decision on the development timetable and capital schedule is expected in the first quarter of 2016. |

Exploration

| • | El Peñón, Chile - Drilling at the Ventura vein advanced with results continuing to support the economic potential of the target and the objective of upgrading the mineral resources. |

| • | Chapada, Brazil - Drilling at Sucupira continued, supporting a 1.5 kilometre high grade extension of the mineralization previously identified from the southwest limits of the Cava Norte Pit with the aim of upgrading mineral resources. |

| • | Jacobina, Brazil - Drilling continued at the Canavieras North and South, Morro do Vento and João Belo mines, with results continuing to support the higher grades in the mineral resource and mineral reserve models. Infilling drilling during the quarter returned above average grades and widths at all targets. |

| • | Minera Florida, Chile - Drilling program continued with positive results at Manda, Lisset, Lorena, Falla Hallazgo, Florencia, Mina Este and Polvorin. The positive assay results continue to support the objective of upgrading mineral resources and mineral reserves replacement. |

| • | Fazenda Brasileiro, Brazil - Drilling advanced at E388 East with preliminary results that are similar in thickness and grade to those seen in the early years of the mine, and support the potential for mineral resource expansion. |

______________________________

| (i) | Excluding attributable sales from Alumbrera. |

| (ii) | A non-GAAP measure - Refer to Section 13. |

| (iii) | "Core assets" or "core operations" include Chapada, El Peñón, Gualcamayo, Mercedes, Canadian Malartic, Minera Florida and Jacobina. |

| (iv) | Brio Gold holdings include Fazenda Brasileiro, Pilar and C1 Santa Luz. Currently, C1 Santa Luz is on care and maintenance. |

3

3. OUTLOOK AND STRATEGY

The Company strives to maximize production with the lowest level of capital and operating costs, with the objective of generating sustainable and increasing cash flow.

In 2015, the Company expects to deliver gold production in line with previous guidance. Annual copper production is expected to exceed guidance of 120 million pounds, while silver production is expected to come in under guidance of 9.6 million ounces, driven mostly by lower than expected silver grades at the El Peñón mine. Consistent with prior years, the Company expects higher gold production in the second half of the year compared to the first half of the year, which was evidenced by the increase in production at most mines during the third quarter. Consolidated fourth quarter production levels are also expected to exceed third quarter production levels. The expected increases will come from increases in production improvements at Mercedes, El Peñón, Gualcamayo and Chapada.

With respect to costs, the table below summarizes company-wide cash costs and AISC for the third quarter, first nine months of the year and projections for the second half of 2015, clearly demonstrating the positive trend in costs over the first nine months of the year:

| Third Quarter | Third Quarter YTD | Second Half Projection | |

| Cash costs for continuing operations per ounce of gold | $594 | $616 | $570 |

| AISC for continuing operations per ounce of gold | $841 | $876 | $820 |

With the advancement of the Brio Gold monetization plan, the table below provides a preview of the Company's profile excluding the non-core operations. The impact of the consolidated costs for the Company’s seven core mines for the same periods demonstrate an even more favourable trend, summarized as follows:

| Third Quarter | Third Quarter YTD | Second Half Projection | |

| Cash costs for core mines per ounce of gold | $570 | $581 | $560 |

| AISC for core mines per ounce of gold | $748 | $766 | $740 |

Consistent with expected gold production increases, cash costs are expected to be lower in the second half of the year compared to the first half of the year, with a further decrease expected in the fourth quarter from that of the third quarter.

For Brio Gold, estimated cash costs for 2015 are forecast to be approximately $710 per ounce of gold, and AISC approximately $905 per ounce of gold. However, on a go forward basis costs are expected to be lower as evidenced by third quarter results showing cash costs and AISC at $658 and $866 per ounce of gold, respectively.

In the absence of the foreign exchange hedges, that will be extinguished by year end, the Company's cash costs on a co-product basis, cash costs and AISC would have improved as follows:

| Third Quarter | Third Quarter YTD | |

| Co-product cash costs per ounce of gold | $16/oz | $13/oz |

| Co-product cash costs per pound of copper | $0.18/lb | $0.16/lb |

| Cash cost and AISC per ounce of gold | $35/oz | $28/oz |

| Cash cost and AISC per ounce of gold of core mines | $40/oz | $32/oz |

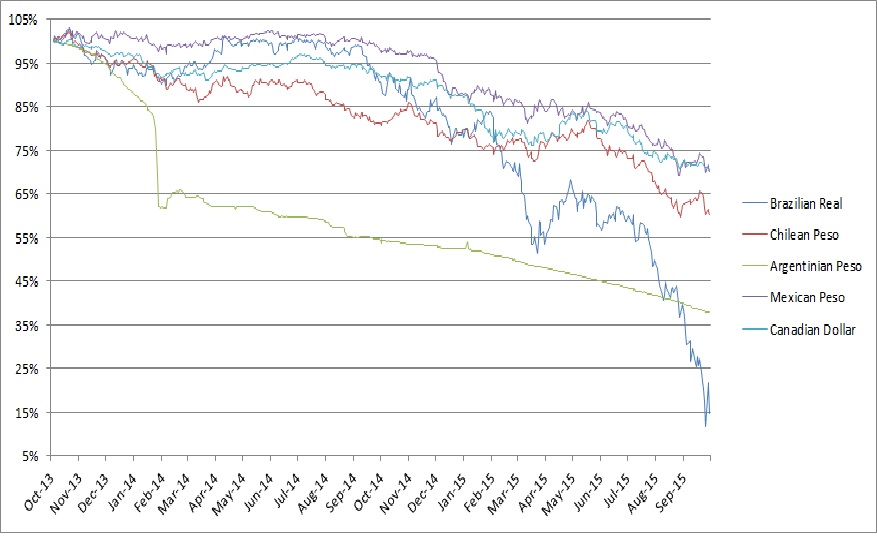

The expiry of the hedges in the fourth quarter will fuel lower cash costs starting in January of 2016 for gold and will coincide with an improving production profile and cost structure at certain mining operations. For Brazilian operations, the average exchange rate for the quarter and the first nine months of 2015 was 3.54 and 3.17 Reais per US Dollar, respectively. This compares to an after-hedge realized rate of 3.13 and 2.90 Reais per US Dollar, which had an unfavourable impact on cash costs. Should the exchange rate remain at the 3.95 Reais per US Dollar level observed at the end of the quarter, the Company will continue to benefit from a lower costing structure, partially offset by the remaining hedges in place for the fourth quarter. Starting in 2016, the Company will begin to fully benefit from the expected weaker foreign currency.

For the second half of 2015, projected cash costs and AISC are generally in line with the levels guided for full year cash costs of $545 per ounce of gold and AISC at between $800 and $830 per ounce of gold. Cash costs and AISC for 2015 are impacted by lower than expected copper by-product credits during the second half of the year. By-product credits for purposes of cost guidance

4

used a $3.00 per pound assumption. However, realized copper prices for the quarter were $2.85 per pound, and for the nine months ended, averaged at $2.88 per pound. Forecasted copper prices are expected to be lower in the fourth quarter. The lower cash costs and AISC costs associated with the Company's core operation vis-à-vis its consolidated operations, provide insight over the positive impact on cash costs expected subsequent to the pending monetization of Brio Gold.

In terms of other non-production related targets, results in the first nine months of the year support the Company's ability to meet or report below previous guidance, as follows:

| • | Sustaining capital to come in under $265 million (which represents approximately $176 per ounce of gold and $2.75 per ounce of silver); |

| • | Expansionary capital spending expected to be at the low end of the $90 to $140 million range previously provided; |

| • | Exploration spending to come in under $98 million; |

| • | Depreciation, depletion and amortization to come in under $570 million (which represents approximately $395 per ounce of gold and $6 per ounce of silver); and |

| • | G&A expense which is expected to be approximately $120 million in 2015 with potential for further reductions beginning in 2016, resulting from additional savings related to the streamlining of management, the downsizing and relocation of its Brazilian and other South American offices, and the disposition of Brio Gold. |

Overall, the Company expects improved operating results for the remainder of 2015 and production growth into the next several years. As previously announced, the Company made a construction decision for the Cerro Moro project in early 2015. Cerro Moro is a high quality project that has the potential to add significantly to the Company’s production growth at a low cost. The Company remains committed to advancing the project in a prudent manner and decided to de-risk project ramp-up by advancing the underground mining ahead of the original schedule. Project capital expenditures are expected to be approximately $25 million for 2015 comprised of costs related to detailed engineering and pre-development. The expenditures for 2016 are expected to be $56 million. Including these expenditures, the Company expects its expansionary capital to not exceed the levels observed in 2015. The development timetable has been adjusted to accommodate the aforementioned works and now reflects a capital schedule which maximizes cash preservation in 2016. Simultaneously, this allows for a more thorough evaluation of the economic factors in Argentina, including the impact of the currency in relation to the outcome of the presidential ballot in the November 2015 election. Furthermore, this approach allows for further exploration drilling to take place to increase the size of the Cerro Moro mineral resources, in addition to improving the current mineral resource categorization. Production is expected to commence in the first quarter of 2018.

Several other developing projects that are not as advanced as Cerro Moro are advancing through technical and economical evaluation. One of these projects is Upper Beaver, in relation to which the Company is completing an internal Preliminary Economic Assessment which is expected to be completed by the end of the year. The Deep Carbonates project at Gualcamayo is also similar. The Company undertook the initial technical and financial analysis which is complete and supports a viable project with recoverable gold currently estimated at more than 1.1 million ounces. The Company’s ongoing work is considering a number of mining method alternatives to further improve the capital spend profile and de-risk the project. The results to date and the ongoing work are expected to support a decision in 2016 to advance the project to the pre-feasibility stage.

Importantly, the Company is first and foremost focused on its core assets, which include its cornerstone operations of Chapada, Canadian Malartic and El Peñón, and opportunities which have the best prospects for exploration successes, optimization and cash flow generation. The corollary is that the Company is also committed to rationalizing its portfolio which includes monetizing non-core assets. Consistent with this strategy, the Company continues to pursue its planned monetization of Brio Gold and is currently advancing on a number of strategic alternatives. These alternatives include an initial public offering, reverse takeover, joint venture with private equity firms, a disposition to, or merger with, other companies, and other financing and liquidity options. The Company has an emphasis on transactions that could be completed on an accelerated timeline and may allow Brio Gold to continue to operate as a private company in the short term. Additionally, the Company continues to advance its efforts at realizing value from other non-producing assets including Agua Rica.

While the Company is focused on operations and deriving significant and increasing cash flow and earnings before interest, taxes depreciation and amortization ("EBITDA") from its operations, a strategic objective has been to also focus on monetization initiatives, which serve as catalysts to reducing debt and increasing cash balances. As part of this strategy, the Company has committed to reducing the outstanding balance on its revolving credit facility to zero and holding sufficient funds for some or all of the scheduled debt repayments in 2016 and 2017. The Company's monetization initiatives are on track to achieve this strategic objective before the end of 2015 with the first of which, the metal purchasing arrangements, having already been completed, resulting in a sizable cash inflow. With the completion of these catalysts, the Company will be well positioned to focus entirely on operations, having secured a stronger balance sheet, and maximizing cash flow and EBITDA as noted above.

5

6

4. SUMMARY OF FINANCIAL AND OPERATING STATISTICS

4.1 Financial Statistics

| For the three months ended | For the nine months ended | |||||||||||

| September 30, 2015 | September 30, 2014 | September 30, 2015 | September 30, 2014 | |||||||||

| Net loss per share attributable to Yamana equity holders - basic and diluted | $ | (0.12 | ) | $ | (1.17 | ) | $ | (0.29 | ) | $ | (1.31 | ) |

| Net loss per share from continuing operations attributable to Yamana equity holders - basic and diluted | $ | (0.12 | ) | $ | (1.00 | ) | $ | (0.28 | ) | $ | (1.12 | ) |

Adjusted (loss)/earnings per share (i) from continuing operations attributable to Yamana Gold Inc. equity holders. - basic and diluted | $ | (0.02 | ) | $ | — | $ | (0.07 | ) | $ | 0.07 | ||

| Dividends declared per share | $ | 0.0150 | $ | 0.0375 | $ | 0.0450 | $ | 0.1125 | ||||

| Dividends paid per share | $ | 0.0150 | $ | 0.0375 | $ | 0.0450 | $ | 0.1400 | ||||

| Weighted average number of common shares outstanding - basic (in thousands) | 946,563 | 877,551 | 933,180 | 801,613 | ||||||||

| Weighted average number of common shares outstanding - diluted (in thousands) | 946,563 | 877,551 | 933,180 | 801,613 | ||||||||

| (In millions of United States Dollars; unless otherwise noted) | ||||||||||||

| Net loss from continuing operations attributable to Yamana equity holders | $ | (115.0 | ) | $ | (879.6 | ) | $ | (257.2 | ) | $ | (895.4 | ) |

Adjusted (loss)/earnings from continuing operations attributable to Yamana Gold Inc. equity holders (i) | $ | (20.2 | ) | $ | (1.3 | ) | $ | (65.9 | ) | $ | 58.4 | |

| Revenues | $ | 448.9 | $ | 494.4 | $ | 1,361.9 | $ | 1,292.2 | ||||

| Mine operating earnings | $ | 49.7 | $ | 84.2 | $ | 148.3 | $ | 198.1 | ||||

| Cash flows from operating activities from continuing operations | $ | 77.6 | $ | 156.6 | $ | 203.1 | $ | 330.2 | ||||

Cash flows from operating activities before changes in non-cash working capital (i) | $ | 127.6 | $ | 180.7 | $ | 373.0 | $ | 419.4 | ||||

| Cash flows to investing activities from continuing operations | $ | (65.7 | ) | $ | (197.3 | ) | $ | (240.3 | ) | $ | (930.8 | ) |

| Cash flows from/(used in) financing activities from continuing operations | $ | 9.0 | $ | 34.1 | $ | (11.8 | ) | $ | 550.6 | |||

Average realized gold price per ounce (ii) | $ | 1,122 | $ | 1,276 | $ | 1,176 | $ | 1,286 | ||||

Average realized silver price per ounce (ii) | $ | 14.88 | $ | 19.27 | $ | 15.99 | $ | 19.79 | ||||

Average realized copper price per pound (ii) | $ | 2.85 | $ | 3.14 | $ | 2.88 | $ | 3.16 | ||||

Average market gold price per ounce (iii) | $ | 1,124 | $ | 1,282 | $ | 1,178 | $ | 1,288 | ||||

Average market silver price per ounce (iii) | $ | 14.91 | $ | 19.71 | $ | 15.99 | $ | 19.94 | ||||

Average market copper price per pound (iii) | $ | 2.39 | $ | 3.17 | $ | 2.59 | $ | 3.15 | ||||

_____________________________

| (i) | A cautionary note regarding non-GAAP measures is included in Section 13 of this Management’s Discussion and Analysis. Comparatives have been restated to conform to the change in presentation adopted in the current period. |

| (ii) | Realized prices based on gross sales compared to market prices for metals may vary due to infrequent shipments and depending on timing of the sales. |

| (iii) | Source of information: LBMA p.m. price and LME Cash. |

7

4.2 Operating Statistics

| For the three months ended September 30, | 2015 | 2014 | 2015 | 2014 | ||||||||

| Ounces of Production | Gold | Silver | ||||||||||

| Chapada | 32,029 | 28,847 | 69,067 | 83,769 | ||||||||

| El Peñón | 51,983 | 70,111 | 1,914,356 | 2,349,577 | ||||||||

| Canadian Malartic | 76,603 | 64,761 | — | — | ||||||||

| Gualcamayo | 44,076 | 43,060 | — | — | ||||||||

| Mercedes | 20,155 | 28,459 | 88,456 | 103,642 | ||||||||

| Minera Florida | 28,989 | 22,402 | 124,865 | 409,676 | ||||||||

| Jacobina | 28,080 | 21,112 | — | — | ||||||||

Alumbrera (i) | 5,552 | 7,520 | — | — | ||||||||

Brio Gold (ii) | 38,430 | 40,327 | — | — | ||||||||

| Total from continuing operations | 325,897 | 326,599 | 2,196,744 | 2,946,664 | ||||||||

Ernesto/Pau-a-Pique (discontinued operations) | — | 5,745 | — | — | ||||||||

| Total production | 325,897 | 332,344 | 2,196,744 | 2,946,664 | ||||||||

Cash costs from continuing operations per ounce (iii) | ||||||||||||

| Chapada | $ | (420 | ) | $ | (1,173 | ) | $ | (31.69 | ) | $ | (66.95 | ) |

| El Peñón | $ | 676 | $ | 567 | $ | 8.39 | $ | 7.30 | ||||

Canadian Malartic (i) | $ | 544 | $ | 735 | $ | — | $ | — | ||||

| Gualcamayo | $ | 892 | $ | 867 | $ | — | $ | — | ||||

| Mercedes | $ | 865 | $ | 671 | $ | 8.00 | $ | 11.02 | ||||

| Minera Florida | $ | 710 | $ | 745 | $ | 12.86 | $ | 3.56 | ||||

| Jacobina | $ | 712 | $ | 981 | $ | — | $ | — | ||||

Alumbrera (i) | $ | 1,347 | $ | (205 | ) | $ | — | $ | — | |||

Brio Gold (ii) | $ | 658 | $ | 844 | $ | — | $ | — | ||||

Cash costs from continuing operations per ounce produced (iii) | $ | 594 | $ | 528 | $ | 7.37 | $ | 4.80 | ||||

Co-product cash costs from continuing operations per ounce produced (iii) | $ | 653 | $ | 695 | $ | 8.46 | $ | 6.84 | ||||

All-in sustaining costs from continuing operations per ounce (iii) | $ | 841 | $ | 867 | $ | 11.32 | $ | 8.80 | ||||

All-in sustaining co-product costs from continuing operations per ounce (iii) | $ | 856 | $ | 971 | $ | 11.67 | $ | 9.99 | ||||

| Concentrate Production | 2015 | 2014 | ||||||||||

| Chapada concentrate production (tonnes) | 63,259 | 69,279 | ||||||||||

| Chapada copper contained in concentrate production (millions of lbs) | 34.0 | 38.0 | ||||||||||

Chapada co-product cash costs per pound of copper (iii) | $ | 1.41 | $ | 1.59 | ||||||||

Co-product cash costs per pound of copper produced (iii) | $ | 1.68 | $ | 1.73 | ||||||||

| Sales Included in Revenue (excluding 12.5% interest in Alumbrera) | 2015 | 2014 | ||||||||||

| Gold (ounces) | 317,859 | 281,681 | ||||||||||

| Silver (ounces) | 2,247,068 | 2,690,232 | ||||||||||

| Chapada concentrate (tonnes) | 55,460 | 70,288 | ||||||||||

| Chapada payable copper contained in concentrate (millions of lbs) | 29.1 | 35.7 | ||||||||||

____________________

| (i) | The Company holds a 12.5% equity interest in Alumbrera and a 50% interest in Canadian Malartic. |

| (ii) | Brio Gold holdings include Fazenda Brasileiro, Pilar and C1 Santa Luz. Currently, C1 Santa Luz is on care and maintenance. Commissioning production related to Brio Gold is included in the respective balance. |

| (iii) | A cautionary note regarding non-GAAP measures is included in Section 13 of this Management’s Discussion and Analysis. Comparatives have been restated to conform to the change in presentation adopted in the current period. |

8

| For the nine months ended September 30, | 2015 | 2014 | 2015 | 2014 | ||||||||

| Ounces of Production | Gold | Silver | ||||||||||

| Chapada | 84,561 | 78,177 | 203,987 | 223,645 | ||||||||

| El Peñón | 167,914 | 205,506 | 6,108,532 | 6,188,184 | ||||||||

Canadian Malartic (iv) | 212,937 | 76,639 | — | — | ||||||||

| Gualcamayo | 127,811 | 134,404 | — | — | ||||||||

| Mercedes | 63,731 | 74,847 | 280,827 | 290,741 | ||||||||

| Minera Florida | 83,400 | 72,123 | 458,354 | 790,915 | ||||||||

| Jacobina | 67,988 | 54,741 | — | — | ||||||||

Alumbrera (i) | 15,969 | 25,946 | — | — | ||||||||

Brio Gold (ii) | 104,819 | 106,193 | — | — | ||||||||

| Total from continuing operations | 929,130 | 828,576 | 7,051,700 | 7,493,485 | ||||||||

Ernesto/Pau-a-Pique (discontinued operations) | 460 | 16,503 | — | — | ||||||||

| Total production | 929,590 | 845,079 | 7,051,700 | 7,493,485 | ||||||||

| Cash costs from continuing operations per ounce (iii) | ||||||||||||

| Chapada | $ | (556 | ) | $ | (821 | ) | $ | (35.71 | ) | $ | (52.52 | ) |

| El Peñón | $ | 648 | $ | 548 | $ | 8.13 | $ | 7.86 | ||||

Canadian Malartic (iv) | $ | 593 | $ | 717 | $ | — | $ | — | ||||

| Gualcamayo | $ | 820 | $ | 765 | $ | — | $ | — | ||||

| Mercedes | $ | 899 | $ | 703 | $ | 8.28 | $ | 10.82 | ||||

| Minera Florida | $ | 727 | $ | 695 | $ | 10.33 | $ | 5.54 | ||||

| Jacobina | $ | 864 | $ | 1,123 | $ | — | $ | — | ||||

Alumbrera (i) | $ | 1,563 | $ | (530 | ) | $ | — | $ | — | |||

Brio Gold (ii) | $ | 746 | $ | 907 | $ | — | $ | — | ||||

Cash costs from continuing operations per ounce produced (iii) | $ | 616 | $ | 518 | $ | 7.01 | $ | 5.93 | ||||

Co-product cash costs from continuing operations per ounce produced (iii) | $ | 683 | $ | 676 | $ | 8.14 | $ | 7.64 | ||||

All-in sustaining costs from continuing operations per ounce (iii) | $ | 876 | $ | 875 | $ | 10.81 | $ | 10.86 | ||||

All-in sustaining co-product costs from continuing operations per ounce (iii) | $ | 899 | $ | 981 | $ | 11.32 | $ | 11.87 | ||||

| Concentrate Production | 2015 | 2014 | ||||||||||

| Chapada concentrate production (tonnes) | 172,268 | 181,824 | ||||||||||

| Chapada copper contained in concentrate production (millions of lbs) | 94.4 | 98.5 | ||||||||||

Chapada co-product cash costs per pound of copper (iii) | $ | 1.52 | $ | 1.71 | ||||||||

Co-product cash costs per pound of copper produced (iii) | $ | 1.79 | $ | 1.83 | ||||||||

| Sales Included in Revenue (excluding 12.5% interest in Alumbrera) | 2015 | 2014 | ||||||||||

| Gold (ounces) | 906,208 | 721,928 | ||||||||||

| Silver (ounces) | 7,017,562 | 7,106,716 | ||||||||||

| Chapada concentrate (tonnes) | 166,252 | 175,044 | ||||||||||

| Chapada payable copper contained in concentrate (millions of lbs) | 87.4 | 89.7 | ||||||||||

____________________

| (i) | The Company holds a 12.5% equity interest in Alumbrera. |

| (ii) | Brio Gold holdings include Fazenda Brasileiro, Pilar and C1 Santa Luz. Currently, C1 Santa Luz is on care and maintenance. Commissioning production related to Brio Gold is included. |

| (iii) | A cautionary note regarding non-GAAP measures is included in Section 13 of this Management’s Discussion and Analysis. Comparatives have been restated to conform to the change in presentation adopted in the current period. |

| (iv) | The Company holds a 50% interest in Canadian Malartic, the acquisition of which closed June 16, 2014. |

9

5. OVERVIEW OF RESULTS

5.1 Overview of Financial Results

| For the three months ended | For the nine months ended | |||||||||||

| (In millions of United States Dollars; unless otherwise noted) | September 30, 2015 | September 30, 2014 | September 30, 2015 | September 30, 2014 | ||||||||

| Revenues | $ | 448.9 | $ | 494.4 | $ | 1,361.9 | $ | 1,292.2 | ||||

| Cost of sales excluding depletion, depreciation and amortization | (266.0 | ) | (275.0 | ) | (818.2 | ) | (727.2 | ) | ||||

| Gross margin excluding depletion, depreciation and amortization | 182.9 | 219.4 | 543.7 | 565.0 | ||||||||

| Depletion, depreciation and amortization | (133.2 | ) | (135.2 | ) | (395.4 | ) | (366.9 | ) | ||||

| Mine operating earnings | 49.7 | 84.2 | 148.3 | 198.1 | ||||||||

Other expenses (i) | (41.1 | ) | (65.6 | ) | (194.5 | ) | (219.8 | ) | ||||

| Equity loss from associate | (6.3 | ) | (12.1 | ) | (17.2 | ) | (10.7 | ) | ||||

| Impairment of mineral properties | — | (539.9 | ) | — | (539.9 | ) | ||||||

| Income/(Loss) before income taxes | 2.3 | (533.4 | ) | (63.4 | ) | (572.3 | ) | |||||

| Income tax expense | (117.3 | ) | (346.2 | ) | (193.8 | ) | (323.1 | ) | ||||

| Net loss from continuing operations | (115.0 | ) | (879.6 | ) | (257.2 | ) | (895.4 | ) | ||||

| Net income/(loss) from discontinued operations | 2.0 | (143.7 | ) | (15.4 | ) | (152.4 | ) | |||||

| Net loss attributable to Yamana Gold Inc. equity holders | $ | (113.0 | ) | $ | (1,023.3 | ) | $ | (272.6 | ) | $ | (1,047.8 | ) |

Adjustments (ii): | ||||||||||||

| Net loss from continuing operations | $ | (115.0 | ) | $ | (879.6 | ) | $ | (257.2 | ) | $ | (895.4 | ) |

| Non-cash unrealized foreign exchange gain | (38.4 | ) | (18.2 | ) | (38.0 | ) | (19.6 | ) | ||||

| Share-based payments/mark-to-market of deferred share units | (1.5 | ) | (1.6 | ) | 3.6 | 7.8 | ||||||

| Demobilization and reorganization costs | 6.3 | 14.7 | 6.8 | 16.6 | ||||||||

| Mark-to-market of investment in available-for-sale securities and other assets | (7.6 | ) | 6.0 | (8.0 | ) | 12.7 | ||||||

| Impairment of mineral properties | — | 539.9 | — | 539.9 | ||||||||

| (Gain)/loss on sale of assets | (0.4 | ) | 3.9 | (0.5 | ) | 4.6 | ||||||

| Transaction costs related to the Osisko acquisition | — | — | — | 32.4 | ||||||||

| Other non-recurring adjustments | 4.4 | 17.9 | 18.3 | 22.2 | ||||||||

| Adjusted loss before income tax effect | $ | (152.2 | ) | $ | (317.0 | ) | $ | (275.0 | ) | $ | (278.8 | ) |

| Non-cash tax on unrealized foreign exchange gains | 132.7 | 33.3 | 209.4 | 51.4 | ||||||||

| Income tax effect of adjustments | (0.7 | ) | 282.4 | (0.3 | ) | 285.8 | ||||||

Adjusted (loss)/earnings from continuing operations (ii) | $ | (20.2 | ) | $ | (1.3 | ) | $ | (65.9 | ) | $ | 58.4 | |

| Net loss per share from continuing operations attributable to Yamana Gold Inc. equity holders - basic and diluted | $ | (0.12 | ) | $ | (1.00 | ) | $ | (0.28 | ) | $ | (1.12 | ) |

| Net loss per share attributable to Yamana Gold Inc. equity holders - basic and diluted | $ | (0.12 | ) | $ | (1.17 | ) | $ | (0.29 | ) | $ | (1.31 | ) |

Adjusted (loss)/earnings per share from continuing operations attributable to Yamana Gold Inc. equity holders (ii)- basic and diluted | $ | (0.02 | ) | $ | — | $ | (0.07 | ) | $ | 0.07 | ||

Adjusted Operating Cash Flows (ii): | ||||||||||||

| Cash flows from operating activities before non-cash working capital | $ | 127.6 | $ | 180.7 | $ | 373.0 | $ | 419.4 | ||||

| Reorganization costs | 6.3 | — | 6.3 | 2.0 | ||||||||

| Demobilization costs | — | — | — | 9.6 | ||||||||

| Transaction costs related to the Osisko acquisition | — | — | — | 32.4 | ||||||||

| Adjusted Operating Cash Flows | $ | 133.9 | $ | 180.7 | $ | 379.3 | $ | 463.4 | ||||

______________________________

| (i) | For the three and nine month periods ended September 30, 2015, other expenses represent the aggregate of the following expenses: general and administrative of $28.5 million and $89.9 million (2014 - $24.9 million and $93.0 million), exploration and evaluation of $6.6 million and $16.1 million (2014 - $5.2 million and $14.1 million), other expenses of $7.4 million and $34.2 million, (2014 - $39.3 million and $90.2 million) and net finance income of $1.4 million and net finance expense $54.3 million (2014 - finance income $3.8 million and finance expense $22.5 million), and charges related to impairment of mineral properties of $nil and $nil (2014 - $539.9 million and $539.9 million). |

| (ii) | A cautionary note regarding non-GAAP measures and their respective reconciliations are included in Section 13. |

10

For the three months ended September 30, 2015

Net loss from continuing operations attributable to Yamana equity holders for the three months ended September 30, 2015 was $115.0 million or $0.12 per share basic, compared to a net loss from continuing operations attributable to Yamana equity holders of $879.6 million or $1.00 per share basic and diluted for the three months ended September 30, 2014. Net loss was impacted by a higher income tax expense and an equity loss from Alumbrera (12.5% interest). The income tax expense for the quarter reflects the impact of the non-cash tax relating to unrealized foreign exchange gains of $132.7 million as during the period, the Brazilian Real, Argentinean Peso and Mexican Peso devalued significantly against the US Dollar. The following chart outlines the components of the income tax expense including the foreign exchange impact for the quarter.

| In millions of United States Dollars | Current Taxes | Deferred Taxes | September 30, 2015 | September 30, 2014 | ||||||||

| Income tax expense/(recovery) before foreign exchange in taxes | $ | 41.3 | $ | (56.7 | ) | $ | (15.4 | ) | $ | 353.5 | ||

| Non-cash tax expense/(recovery) related to unrealized foreign exchange | (3.2 | ) | 135.9 | 132.7 | (7.3 | ) | ||||||

| Income tax expense | 38.1 | 79.2 | 117.3 | 346.2 | ||||||||

The impact of these foreign exchange movements on taxes are non-cash and, as such, are excluded from adjusted earnings.

Adjusted loss (a non-GAAP measure, see Section 13) from continuing operations was $20.2 million or $0.02 per share basic for the three months ended September 30, 2015, compared to adjusted loss of $1.3 million or $nil per share for the same period of 2014. Mine operating earnings for the three months ended September 30, 2015 were $49.7 million, compared to $84.2 million for the same period of 2014. Adjusted loss and mine operating earnings for the period were primarily impacted by lower realized metal prices than the same quarter of 2014 by approximately 12% for gold, 23% for silver and 9% for copper, partially offset by higher sales volume for gold. Revenue for the three months ended September 30, 2015 was lower by $45.5 million compared to the same period last year largely due to lower metal prices.

Cash flows from operating activities from continuing operations for the three months ended September 30, 2015, after and before (a non-GAAP measure, see Section 13) changes in non-cash working capital, were $77.6 million and $127.6 million, respectively. The Company generated $0.30 of adjusted operating cash flows before changes in non-cash working capital for every dollar of revenue generated during the period, notwithstanding lower metal prices in 2015. This compares to $0.34 for the same period of 2014 which was lower predominantly related to the lower metal prices during the period.

Revenue for the three months ended September 30, 2015 was $448.9 million, lower compared to $494.4 million for the same period of 2014 as increase in gold and copper sales volumes were more than offset by a decline in metal prices. Revenue for the third quarter of 2015 was generated from the sale of 317,859 ounces of gold, 2.2 million ounces of silver and 29.1 million pounds of copper, excluding attributable sales from Alumbrera which is accounted for as an equity investment. This compares to sales, excluding Alumbrera, of 281,681 ounces of gold, 2.7 million ounces of silver and 35.7 million pounds of copper for the three months ended September 30, 2014.

The average realized price of gold for the quarter was $1,122 per ounce, compared to $1,276 per ounce for the same quarter in 2014, or 12% lower and the average realized silver price was $14.88 per ounce, compared to $19.27 per ounce for the same quarter in 2014, or 23% lower. The average realized price of copper was $2.85 per pound, compared to the $3.14 per pound for the same quarter in 2014, or 9% lower.

11

Revenue for the quarter was comprised of the following:

| For the three months ended September 30, | 2015 | 2014 | ||||||||||

| (In millions of Dollars; unless otherwise noted) | Quantity Sold (ii) | Realized Prices (iii) | Revenue | Revenue | ||||||||

Gold (i) | 317,859 | oz | $ | 1,122 | $ | 356.6 | $ | 359.4 | ||||

Silver (i) | 2,247,068 | oz | 14.88 | 33.4 | 51.8 | |||||||

Copper (i) | 29,136,112 | lbs | 2.85 | 83.0 | 112.1 | |||||||

| Gross revenue | $ | 473.0 | $ | 523.3 | ||||||||

| (Deduct)/add: | ||||||||||||

- Treatment and refining charges of gold and copper concentrate | (8.7 | ) | (10.4 | ) | ||||||||

| - Sales taxes | (6.6 | ) | (7.8 | ) | ||||||||

| - Metal price adjustments related to concentrate revenue | (8.8 | ) | (7.4 | ) | ||||||||

| - Other adjustments | — | (3.3 | ) | |||||||||

Revenue (ii) | $ | 448.9 | $ | 494.4 | ||||||||

______________________________

| (i) | Includes payable gold, silver and copper contained in concentrate. |

| (ii) | Excludes Alumbrera which is accounted for as an equity investment and Ernesto/Pau-a-Pique which is a discontinued operation. |

| (iii) | Realized prices based on gross sales compared to market prices for metals may vary due to infrequent shipments and depending on timing of the sales. Realized price for copper of $2.85 is higher than market price reflecting the settlements on copper forward contracts entered into by the Company. |

Cost of sales excluding depletion, depreciation and amortization for the three months ended September 30, 2015 was $266.0 million, compared to $275.0 million for the same period in 2014. Cost of sales excluding depletion, depreciation and amortization for the third quarter was lower than that of the same period in 2014, despite higher sales volume for gold, reflecting cost reduction initiatives implemented by Company and the impact of the depreciation of foreign currency rates from the strengthening of the US Dollar against the Brazilian Real, the Argentinean Peso, the Mexican Peso and the Canadian Dollar.

The following table provides a reconciliation of the co-product cash cost (a non-GAAP measure, see Section 13) to the cost of sales excluding depletion, depreciation and amortization for the quarter:

| For the three months ended September 30, | 2015 | 2014 | ||||||||||

| (In millions of Dollars; unless otherwise noted) | Gold/Silver Ounces or Pounds of Copper Produced (i) | Co-product Cash Cost per Unit (ii) | Total Costs | Total Costs | ||||||||

| Chapada — Gold | 32,029 | oz | $ | 307 | $ | 9.8 | $ | 12.0 | ||||

| Chapada — Silver | 69,067 | oz | 3.20 | 0.2 | 0.4 | |||||||

| Chapada — Copper | 33,950,544 | lbs | 1.41 | 48.0 | 60.3 | |||||||

| El Peñón — Gold | 51,983 | oz | 676 | 35.2 | 39.8 | |||||||

| El Peñón — Silver | 1,914,356 | oz | 8.39 | 16.1 | 17.2 | |||||||

| Gualcamayo — Gold | 44,076 | oz | 892 | 39.3 | 37.4 | |||||||

| Mercedes — Gold | 20,155 | oz | 865 | 17.4 | 19.1 | |||||||

| Mercedes — Silver | 88,456 | oz | 8.00 | 0.7 | 1.1 | |||||||

Canadian Malartic — Gold (50% interest) | 76,603 | oz | 544 | 41.6 | 47.6 | |||||||

| Minera Florida — Gold | 28,989 | oz | 710 | 20.6 | 16.7 | |||||||

| Minera Florida — Silver | 124,865 | oz | 13.00 | 1.6 | 1.5 | |||||||

| Jacobina — Gold | 28,080 | oz | 712 | 20.0 | 20.7 | |||||||

| Brio Gold — Gold | 38,430 | oz | 658 | 25.3 | 14.0 | |||||||

Co-product cash cost of sales (ii) | $ | 275.8 | $ | 287.8 | ||||||||

| Add (deduct): | ||||||||||||

| - Inventory movements and adjustments | (2.6 | ) | (6.6 | ) | ||||||||

- Treatment and refining charges of gold and copper concentrate | (8.7 | ) | (10.5 | ) | ||||||||

| - Commercial and other costs | (1.5 | ) | 1.5 | |||||||||

| - Overseas freight for Chapada concentrate | 3.0 | 2.8 | ||||||||||

Cost of sales excluding depletion, depreciation and amortization (i) | $ | 266.0 | $ | 275.0 | ||||||||

______________________________

12

| (i) | Excludes Alumbrera which is accounted for as an equity investment and Ernesto/Pau-a-Pique which is a discontinued operation. |

| (ii) | A cautionary note regarding non-GAAP measures is included in Section 13 of this Management’s Discussion and Analysis of Operations and Financial Condition. |

Depletion, depreciation and amortization ("DDA") expense for the three months ended September 30, 2015 was $133.2 million, in line with the $135.2 million for the same period of 2014.

G&A, exploration and evaluation, other and net finance income were $41.1 million for the three months ended September 30, 2015, compared to $65.6 million for the same period in 2014, representing a decrease of 37%, a breakdown of which is as follows:

| • | G&A expenses were $28.5 million, compared to $24.9 million for the same period in 2014. Higher G&A than in the comparative period of 2014 resulted mainly from adjustments on stock based compensation and other recoveries for which there is no current period comparative. The Company has continued to implement cost saving initiatives resulting in a decrease of 11% in G&A from that of the second quarter of 2015. |

| • | Exploration and evaluation expenses were $6.6 million, compared to $5.2 million for the same period of 2014 mainly from additional exploration and evaluation on new properties acquired. |

| • | Other expenses were $7.4 million, compared to $39.3 million for the same period of 2014 or 81% lower. Other expenses in the comparative period included provisions, demobilization and reorganization costs relating to C1 Santa Luz with no current period comparative. |

| • | Net finance income was $1.4 million, compared to net finance income of $3.8 million for the same period of 2014, predominantly from higher foreign exchange gains partly offset by a loss on derivatives compared to a gain in the same period of 2014. Additionally, included in net finance income are proceeds of $12.4 million following the closeout of forward copper derivative contracts during the period. The realized contracts associated with the copper price protection program for the period and the closeout of the fourth quarter contracts during the period, generated total cash proceeds of $24.8 million. Of the total proceeds, $12.4 million was related to third quarter production and was included in revenue and the remainder in net finance income. |

Equity loss from Alumbrera was $6.3 million for the three months ended September 30, 2015, compared to equity loss of $12.1 million for the three months ended September 30, 2014. The equity loss was a result of lower metal prices and planned reduced production from Alumbrera as the mine is near the end of its life. No cash dividends were received during the three months ended September 30, 2015 from the Company’s equity investment in Alumbrera compared to $12.4 million of the same period of 2014.

For the nine months ended September 30, 2015

Net loss from continuing operations attributable to Yamana equity holders for the nine months ended September 30, 2015 was $257.2 million or $0.28 per share, impacted by higher income tax expense and a higher equity loss from Alumbrera. This compares to net loss from continuing operations attributable to Yamana equity holders of $895.4 million or $1.12 per share basic for the nine months ended September 30, 2014. The income tax expense for the first nine months reflects the impact of non-cash tax of $209.4 million relating to unrealized foreign exchange gains, as during the period the Brazilian Real, Argentinean Peso and Mexican Peso devalued against the US Dollar (for a detailed discussion, see Section 9).

Adjusted loss (a non-GAAP measure, see Section 13) from continuing operations was $65.9 million or $0.07 per share basic for the nine months ended September 30, 2015, compared to adjusted earnings of $58.4 million or $0.07 per share for the same period of 2014. Mine operating earnings for the nine months ended September 30, 2015 were $148.3 million, compared to $198.1 million for the same period of 2014. Adjusted loss and mine operating earnings for the period were impacted by lower realized metal prices of approximately 9% for gold, 19% for silver and 9% for copper, higher costs and DDA offset by higher gold sales volume. Mine operating earnings was impacted by higher costs and DDA on higher sales volume and also included additional depletion, depreciation and amortization as a result of the acquisition of Canadian Malartic in the third quarter of 2014 and Pilar which completed commissioning in the third quarter of 2014.

Cash flows from operating activities from continuing operations for the nine months ended September 30, 2015, after and before (a non-GAAP measure, see Section 13) changes in non-cash working capital, were $203.1 million and $373.0 million, respectively. The Company generated $0.28 of adjusted operating cash flows before changes in non-cash working capital for every dollar of revenue generated during the period notwithstanding lower metal prices in 2015. This compares to $0.33 for the same period of 2014, not including dividends from Alumbrera. The decrease was predominantly related to the lower metal prices during the period.

Revenue for the nine months ended September 30, 2015 of $1,361.9 million, compared to $1,292.2 million for the same period of 2014 as a result of higher sales quantities driven by the contribution from Canadian Malartic acquired at the end of the second

13

quarter of 2014, offset by lower metal prices. Revenue for the first nine months of 2015 was generated from the sale of 906,208 ounces of gold, 7.0 million ounces of silver and 87.4 million pounds of copper, excluding attributable sales from Alumbrera which is accounted for as an equity investment. This compares to sales, excluding Alumbrera, of 721,928 ounces of gold, 7.1 million ounces of silver and 89.7 million pounds of copper for the nine months ended September 30, 2014. The average realized price of gold for the nine months ended September 30, 2015 was $1,176 per ounce, compared to $1,286 per ounce for the same period in 2014, or 9% lower and the average realized silver price was $15.99 per ounce, compared to $19.79 per ounce for the same period in 2014, or 19% lower. The average realized price of copper was $2.88 per pound, compared to the $3.16 per pound for the same period in 2014, or 9% lower.

Revenue for the period was comprised of the following:

| For the nine months ended September 30, | 2015 | 2014 | ||||||||||

| (In millions of Dollars; unless otherwise noted) | Quantity Sold (ii) | Realized Prices (iii) | Revenue | Revenue | ||||||||

Gold (i) | 906,208 | oz | $ | 1,176 | $ | 1,066.0 | $ | 928.6 | ||||

Silver (i) | 7,017,562 | oz | 15.99 | 112.2 | 141.0 | |||||||

Copper (i) | 87,371,179 | lbs | 2.88 | 252.0 | 283.7 | |||||||

| Gross revenue | $ | 1,430.2 | $ | 1,353.3 | ||||||||

| (Deduct)/add: | ||||||||||||

- Treatment and refining charges of gold and copper concentrate | (27.2 | ) | (26.1 | ) | ||||||||

| - Sales taxes | (19.8 | ) | (23.6 | ) | ||||||||

| - Metal price adjustments related to concentrate revenue | (21.3 | ) | (7.7 | ) | ||||||||

| - Other adjustments | — | (3.7 | ) | |||||||||

Revenue (ii) | $ | 1,361.9 | $ | 1,292.2 | ||||||||

______________________________

| (i) | Includes payable gold, silver and copper contained in concentrate. |

| (ii) | Excludes Alumbrera which is accounted for as an equity investment and Ernesto/Pau-a-Pique which is a discontinued operation. |

| (iii) | Realized prices based on gross sales compared to market prices for metals may vary due to infrequent shipments and depending on timing of the sales. Realized price for copper of $2.88 is higher than market price reflecting the settlements on copper forward contracts entered into by the Company. |

Cost of sales excluding depletion, depreciation and amortization for the nine months ended September 30, 2015 was $818.2 million, compared to $727.2 million for the same period in 2014. Cost of sales excluding depletion, depreciation and amortization for the third quarter was higher than that of the same period in 2014 due to higher sales volume and higher cash costs partly offset by the strengthening of the US Dollar against the foreign currencies in which the Company operates.

The following table provides a reconciliation of the co-product cash cost (a non-GAAP measure, see Section 13) to the cost of sales excluding depletion, depreciation and amortization for the period:

14

| For the nine months ended September 30, | 2015 | 2014 | ||||||||||

| (In millions of Dollars; unless otherwise noted) | Gold/Silver Ounces or Pounds of Copper Produced (i) | Co-product Cash Cost per Unit (ii) | Total Costs | Total Costs | ||||||||

| Chapada — Gold | 84,561 | oz | $ | 352 | $ | 29.7 | $ | 33.9 | ||||

| Chapada — Silver | 203,987 | oz | 3.23 | 0.7 | 1.1 | |||||||

| Chapada — Copper | 94,413,310 | lbs | 1.52 | 143.2 | 168.8 | |||||||

| El Peñón — Gold | 167,914 | oz | 648 | 108.8 | 112.7 | |||||||

| El Peñón — Silver | 6,108,532 | oz | 8.13 | 49.7 | 48.6 | |||||||

| Gualcamayo — Gold | 127,811 | oz | 820 | 104.8 | 102.8 | |||||||

| Mercedes — Gold | 63,731 | oz | 899 | 57.3 | 52.6 | |||||||

| Mercedes — Silver | 280,827 | oz | 8.28 | 2.3 | 3.1 | |||||||

Canadian Malartic — Gold (50% interest) | 212,937 | oz | 593 | 126.2 | 64.3 | |||||||

| Minera Florida — Gold | 83,400 | oz | 727 | 60.7 | 50.1 | |||||||

| Minera Florida — Silver | 458,354 | oz | 10.33 | 4.7 | 4.4 | |||||||

| Jacobina — Gold | 67,988 | oz | 864 | 58.7 | 61.5 | |||||||

| Brio Gold — Gold | 104,819 | oz | 746 | 78.2 | 39.0 | |||||||

Co-product cash cost of sales (ii) | $ | 825.0 | $ | 742.9 | ||||||||

| Add (deduct): | ||||||||||||

| - Inventory movements and adjustments | 7.8 | (13.6 | ) | |||||||||

- Treatment and refining charges of gold and copper concentrate | (27.2 | ) | (26.0 | ) | ||||||||

| - Commercial and other costs | 3.8 | 12.6 | ||||||||||

| - Overseas freight for Chapada concentrate | 8.8 | 11.3 | ||||||||||

Cost of sales excluding depletion, depreciation and amortization (i) | $ | 818.2 | $ | 727.2 | ||||||||

______________________________

| (i) | Excludes Alumbrera which is accounted for as an equity investment and Ernesto/Pau-a-Pique which is a discontinued operation. |

| (ii) | A cautionary note regarding non-GAAP measures is included in Section 13 of this Management’s Discussion and Analysis of Operations and Financial Condition. |

Depletion, depreciation and amortization ("DDA") expense for the nine months ended September 30, 2015 was $395.4 million, compared to $366.9 million for the same period of 2014. Higher DDA was attributed to additional DDA following the acquisition of Canadian Malartic which closed at the end of the third quarter of 2014 including DDA on the amount of purchase price in excess of historical cost. Furthermore, additional DDA was recognized relative to the comparative period in 2014 from Pilar which completed commissioning effective October 1, 2014.

G&A, exploration and evaluation, other and net finance expenses were $194.5 million for the nine months ended September 30, 2015, lower by 12% compared to $219.8 million for the same period in 2014, a breakdown of which is as follows:

| • | G&A expenses were $89.9 million, compared to $93.0 million for the same period in 2014, or 3% lower. |

| • | Exploration and evaluation expenses were $16.1 million, compared to $14.1 million for the same period of 2014 mainly from additional exploration and evaluation on new properties acquired. |

| • | Other expenses were $34.2 million, compared to $90.2 million for the same period of 2014, or 62% lower, as other expenses for the 2014 period include transaction costs on the acquisition of Canadian Malartic, provisions, demobilization and restructuring costs with no current period comparative cost. |

| • | Net finance expense was $54.3 million, compared to net finance expense of $22.5 million for the same period of 2014. Higher net finance expense resulted from higher interest expense on additional long-term debt following the acquisition of Canadian Malartic. It was further impacted by the reduced amount of interest capitalized following the completion of mine commissioning, partially offset by a higher net foreign exchange gain. |

Equity loss from Alumbrera was $17.2 million for the nine months ended September 30, 2015, compared to equity loss of $10.7 million for the nine months ended September 30, 2014. Equity loss was mainly a result of lower metal prices and reduced production from Alumbrera as the mine is near the end of its life. No cash dividends were received during the nine months ended September 30, 2015 from the Company’s equity investment in Alumbrera compared to $40.5 million of the same period of 2014.

5.2 Overview of Operating Results

15

For the three months ended September 30, 2015

Gold production for the third quarter was in line with the comparative period in 2014 and lower for silver. Production at most mines was generally in line with or above targets, except for El Peñón and Mercedes. The Company continues to expect to be in line with overall annual gold production guidance. For the third quarter, El Peñón's production continued to be impacted by lower grades from the more erratic areas in the periphery of higher grade ore bodies encountered during the second quarter, while at Mercedes, operational improvements including measures to improve dilution control began to take effect towards the end of the quarter as evidenced by higher production at lower cash costs relative to the second quarter of 2015. Production at these mines will continue to improve for the remainder of the year.

Gold

Third quarter gold production from continuing operations of 325,897 ounces was in line with the 326,599 ounces of gold in the third quarter of 2014. Production from core assets for the quarter was 281,915 ounces of gold and compares to 278,750 ounces of gold in the third quarter of 2014, representing a 1% increase. The most notable production increases from the third quarter of 2014 was a 33% increase at Jacobina, a 29% increase at Minera Florida, an 11% increase at Chapada and an 18% increase at Canadian Malartic. Production increases from the second quarter of 2015 included a 32% increase at Jacobina, a 17% increase at Gualcamayo, a 12% increase at Canadian Malartic (which also achieved at fifth consecutive quarterly record), a 10% increase at Minera Florida, a 6% increase at Chapada and a 9% increase at Brio Gold. The Company is well positioned for higher production for the remainder of 2015 with the largest impact at mines that contribute most significantly to the operating cash flow generation of the Company.

The following summarizes total production of gold ounces by mine for the third quarter relative to the comparative quarter in 2014:

| (i) | The Company holds a 50% interest in Canadian Malartic, the acquisition of which closed June 16, 2014. |

Cash costs (a non-GAAP measure, see Section 13) for the third quarter were $594 per ounce of gold, compared to $528 per ounce of gold in the same quarter of 2014. Cash costs were impacted by a 9% decline in the realized price of copper and lower sales volume resulting in lower by-product credits for the quarter. On a co-product basis, cash costs (a non-GAAP measure, see Section 13) for the third quarter were $653 per ounce of gold or 6% lower, compared to the $695 per ounce of gold in the third quarter of 2014. Relative to the second quarter of 2015, cash costs on a co-product basis were 7% lower reflecting the impact of higher

16

production. Late in the quarter, further improvements in co-product cash costs occurred due to further weakening of the currencies in the countries in which the Company operates. The Company expects this trend to continue into the fourth quarter.

All-in sustaining costs ("AISC", a non-GAAP measure, see Section 13) were $841 per ounce of gold, compared to $867 per ounce of gold for the third quarter of 2014 and $896 per ounce of gold for the second quarter of 2015. On a co-product basis, AISC were $856 per ounce of gold for the third quarter compared to $971 per ounce of gold for the third quarter of 2014 and $949 per ounce of gold for the second quarter of 2015. AISC from core assets were $790 per ounce of gold on a co-product basis or 15% and 10% lower than the third quarter of 2014 and the second quarter of 2015, respectively.

Lower cash costs overall reflect the implementation of several mine specific cost reduction initiatives implemented during the period and the depreciation of foreign currencies against the US Dollar, partly offset by planned lower grades at some mines.

Silver

Third quarter silver production was 2.2 million ounces compared to the 2.9 million ounces of silver in the third quarter of 2014 as mine plan in certain locations called for mining from areas with lower silver grades and was also impacted by lower grades from the more erratic areas in the periphery of higher grade ore bodies at El Peñón. Cash costs for the third quarter of 2015 were $7.37 per ounce of silver, impacted by lower production and lower by-product copper credits when compared to $4.80 per ounce of silver in the third quarter of 2014. Cash costs on a co-product basis for the third quarter were $8.46 per ounce of silver, compared to $6.84 per ounce of silver in the third quarter of 2014.

Copper

Total copper production for the three months ended September 30, 2015 was 38.0 million pounds, compared to 43.5 million pounds for the same period of 2014. Copper production for the three months ended September 30, 2015 was 34.0 million pounds from the Chapada mine, compared to 38.0 million pounds for the same period of 2014. Lower copper production compared to the third quarter of 2014 was due to planned lower copper feed grades and lower throughput. Cash costs per pound of copper on a co-product basis were $1.41 per pound from the Chapada mine compared to $1.59 per pound of copper in the third quarter of 2014.

For the nine months ended September 30, 2015

Production for the first nine months of the year was higher than 2014 levels. Overall, production was in line with target, positioning the Company towards achieving its annual gold production guidance.

Gold

Production in the first nine months of 2015 was 929,590 ounces of gold of which 929,130 ounces were gold from continuing operations or 10% and 12% higher than the 845,079 ounces of gold and 828,576 ounces of gold from continuing operations in the same period of 2014, respectively. Production from core assets of 808,341 ounces of gold was 16% higher than the 696,437 ounces of gold in the same period of 2014. Higher production included a 24% increase at Jacobina, a 16% increase at Minera Florida and an 8% increase at Chapada as well as the attributable ounces from Canadian Malartic.

The following summarizes the cumulative effect of gold production at each mine for the current and comparative period of 2014:

17

| (i) | Canadian Malartic acquisition closed June 16, 2014. |

Cash costs from continuing operations in the first nine months of 2015 were $616 per ounce of gold, compared to $518 per ounce of gold in the same period of 2014. While production increased 12% compared to the first nine months of 2014, cash costs were impacted by a 9% decline in the realized price of copper resulting in lower by-product credits for the first nine months of the year. On a co-product basis, cash costs from continuing operations for the first nine months of 2015 were $683 per ounce of gold, in line with the $676 per ounce of gold in the same period of 2014.

In the first nine months of 2015, AISC were $876 per ounce of gold, compared to $875 per ounce of gold for the same period of 2014. On a co-product basis, AISC from continuing operations were $899 per ounce of gold for the first nine months of 2015, compared to $981 per ounce of gold for the same period of 2014. All-in sustaining costs from core assets of $826 per ounce of gold a co-product basis for the first nine months of 2015, or 10% lower compared with the same period of 2014.

Lower cash costs overall reflect the implementation of several cost reduction initiatives during the period and the depreciation of foreign currencies against the US Dollar.

Silver

Silver production for the first nine months of 2015 was 7.1 million ounces compared to 7.5 million ounces of silver for the same period of 2014. Cash costs from continuing operations for the first nine months of 2015 were $7.01 per ounce of silver, impacted by lower by-product copper credits when compared to $5.93 per ounce of silver in the same period of 2014. Cash costs from continuing operations on a co-product basis were $8.14 per ounce of silver, compared to $7.64 per ounce of silver in the first nine months of 2014.

Copper

Copper production for the first nine months of 2015 was 104.3 million pounds including Alumbrera, compared to 117.7 million pounds for the same period of 2014. Copper production for the first nine months of 2015 was 94.4 million pounds from the Chapada mine, in line with the 98.5 million pounds for the same period of 2014. Cash costs per pound of copper on a co-product basis were $1.52 per pound from the Chapada mine compared to $1.71 per pound of copper in the first nine months of 2014.

18

6. OPERATING MINES

CHAPADA, BRAZIL

| For the three months ended September 30, | For the nine months ended September 30, | |||||||||||||

| Operating Statistics | 2015 | 2014 | 2015 | 2014 | ||||||||||

| Production | ||||||||||||||

| Concentrate (tonnes) | 63,259 | 69,279 | (9)% | 172,268 | 181,824 | (5)% | ||||||||

| Gold contained in concentrate (ounces) | 32,029 | 28,847 | 11% | 84,561 | 78,177 | 8% | ||||||||

| Silver contained in concentrate (ounces) | 69,067 | 83,769 | (18)% | 203,987 | 223,645 | (9)% | ||||||||

| Copper contained in concentrate (millions of pounds) | 34.0 | 38.0 | (11)% | 94.4 | 98.5 | (4)% | ||||||||

Cash costs per gold ounce produced (ii) | $ | (420 | ) | $ | (1,173 | ) | (64)% | $ | (556 | ) | $ | (821 | ) | (32)% |

Cash costs per silver ounce produced (ii) | $ | (31.69 | ) | $ | (66.95 | ) | (53)% | $ | (35.71 | ) | $ | (52.52 | ) | (32)% |

Co-product cash costs per gold ounce produced (ii) | $ | 307 | $ | 416 | (26)% | $ | 352 | $ | 434 | (19)% | ||||

| Co-product cash costs per silver ounce produced (ii) | $ | 3.20 | $ | 4.58 | (30)% | $ | 3.23 | $ | 4.81 | (33)% | ||||

Co-product cash costs per pound of copper produced (ii) | $ | 1.41 | $ | 1.59 | (11)% | $ | 1.52 | $ | 1.71 | (11)% | ||||

| Ore mined (tonnes) | 5,388,684 | 5,449,798 | (1)% | 13,818,088 | 14,178,447 | (3)% | ||||||||

| Ore processed (tonnes) | 5,215,213 | 5,440,264 | (4)% | 14,475,375 | 15,319,507 | (6)% | ||||||||

| Gold feed grade (g/t) | 0.34 | 0.28 | 22% | 0.31 | 0.27 | 15% | ||||||||

| Copper feed grade (%) | 0.36 | 0.39 | (7)% | 0.37 | 0.36 | 3% | ||||||||

| Concentrate grade - gold (g/t) | 15.75 | 12.95 | 22% | 15.27 | 13.37 | 14% | ||||||||

| Concentrate grade - copper (%) | 24.34 | 24.85 | (2)% | 24.86 | 24.57 | 1% | ||||||||

| Gold recovery rate (%) | 56.1 | 59.3 | (5)% | 58.0 | 59.4 | (2)% | ||||||||

| Copper recovery rate (%) | 81.0 | 81.2 | —% | 80.5 | 80.3 | —% | ||||||||

Sales (iii) | ||||||||||||||

| Concentrate (tonnes) | 55,460 | 70,288 | (21)% | 166,252 | 175,044 | (5)% | ||||||||

| Payable ounces contained in concentrate | ||||||||||||||

| Payable gold contained in concentrate (ounces) | 31,138 | 26,284 | 18% | 80,323 | 66,242 | 21% | ||||||||

| Payable silver contained in concentrate (ounces) | 54,072 | 42,258 | 28% | 144,219 | 86,065 | 68% | ||||||||

| Payable copper contained in concentrate (millions of pounds) | 29.1 | 35.7 | (18)% | 87.4 | 89.7 | (3)% | ||||||||

| Depletion, depreciation and amortization | ||||||||||||||

| Per gold ounces sold | $ | 82 | $ | 103 | (20)% | $ | 107 | $ | 118 | (9)% | ||||

| Per silver ounces sold | $ | 1.09 | $ | 1.53 | (29)% | $ | 1.47 | $ | 1.87 | (21)% | ||||

| Per copper pound sold | $ | 0.17 | $ | 0.26 | (35)% | $ | 0.24 | $ | 0.29 | (17)% | ||||

______________________________

| (i) | A cautionary note regarding non-GAAP measures is included in Section 13 of this Management’s Discussion and Analysis. Comparatives have been restated to conform to the change in presentation adopted in the current period. |

| (ii) | Quantities sold include quantity adjustment on provisional and final invoice settlements. |

Chapada continued to deliver on expectations in the third quarter of 2015, following a strong first half. Gold production continued sequential quarter-over-quarter increases in 2015, exceeding targets and was higher compared to the third quarter of 2014. Gold and silver production are expected to further increase in the fourth quarter with copper production expected to be in line with the third quarter of 2015.

Higher gold production, compared to the third quarter of 2014 and to the second quarter of 2015, was due to planned higher gold feed grades partially offset by lower recoveries. Payable ounces of gold also increased due to higher ore grade. Lower copper

19

production compared to the third quarter of 2014 was due to planned lower copper feed grades and lower throughput. Silver production was in line with the second quarter of 2015 and lower compared to the third quarter of 2014.

Throughput at Chapada increased compared to the second quarter of 2015 due to more efficient flow of material through the crushers, partly offset by the unplanned maintenance to a feeder. As a result of increased throughput, Chapada produced approximately 6,200 dry metric tonnes of concentrate inventory in excess of plan. Due to the fixed schedule of shipments versus the aforementioned increased production, inventory levels increased during the third quarter, which will be sold during the fourth quarter. The approximate market value at the end of the period, related to the increased inventory that was not sold, was $9.3 million. Efforts to further improve operational performance continue at the site, with targets to increase recoveries and throughput in addition to the implementation of cost improvement initiatives.

Cash costs were impacted by a 9% decline in the realized price of copper and lower sales volume, resulting in a lower by-product credit for the third quarter of 2015 compared to the third quarter of 2014. Lower co-product cash costs for gold compared to the third quarter of 2014 were due to increased production and the depreciation of the Brazilian Real. Co-product cash costs for copper were lower compared to the third quarter of 2014 due to the depreciation of the Brazilian Real.

In the absence of the foreign exchange hedges, the third quarter co-product cash costs would have improved by $51 per gold ounce and by $0.20 per copper pound, or $19 per gold ounce and $0.07 per copper pound in the comparative period. Cash costs and AISC, net of by-product credits, for the third quarter would have improved by $260 per gold ounce and $110 per gold ounce for the comparative period. The average exchange rate for the quarter and the first nine months of 2015 was 3.54 and 3.17 Reais per US Dollar, respectively. This compares to an after-hedge realized rate of 3.00 and 2.82 Reais per US Dollar for Chapada, which had a unfavourable impact on cash costs. Should the exchange rate remain at the 3.95 Reais per US Dollar level observed at the end of the quarter, the Company will continue to benefit from a lower costing structure, partially offset by the remaining hedges in place. Starting in 2016, the Company will begin to fully benefit from the expected weaker foreign currency resulting in a lower cash cost for both gold and copper.

The Company periodically uses forward contracts to economically hedge against the risk of declining copper prices for a portion of Chapada's forecast copper concentrate sales. Settlements for the period are reflected on the effective realized copper price of $2.85 and $2.88 per pound as compared to average market copper prices of $2.39 and $2.59 per pound, for the three and nine months ended September 30, 2015, respectively. During the third quarter the Company bought back 18 million pounds of fourth quarter copper contracts that were previously entered into with a contract price of $3.00 per pound. Upon the closeout of these contracts the Company received proceeds of $12.4 million.

In the third quarter of 2015, Chapada produced 32,029 ounces of gold and 69,067 ounces of silver compared to 28,847 ounces of gold and 83,769 ounces of silver for the same quarter of 2014. Co-product cash costs were $307 per ounce of gold and $3.20 per ounce of silver in the third quarter, compared to $416 per ounce of gold and $4.58 per ounce of silver in the same quarter of 2014.

Copper production was 34.0 million pounds in the third quarter of 2015, compared to production of 38.0 million pounds of copper for the same quarter of 2014. Co-product cash costs for copper were $1.41 per pound in the third quarter compared to $1.59 per pound for the same quarter of 2014.

Chapada produced 84,561 ounces of gold and 203,987 ounces of silver in the first nine months of 2015, compared to 78,177 ounces of gold and 223,645 ounces of silver in the same period of 2014. Co-product cash costs were $352 per ounce of gold and $3.23 per ounce of silver in the first nine months of 2015, compared to $434 per ounce of gold and $4.81 per ounce of silver in the same period of 2014.

Copper production was 94.4 million pounds in the first nine months of 2015, compared to production of 98.5 million pounds of copper for the same period of 2014. Co-product cash costs for copper were $1.52 per pound in the first nine months of 2015, compared to $1.71 per pound for the same period of 2014.

20

EL PEÑÓN, CHILE

| For the three months ended September 30, | For the nine months ended September 30, | |||||||||||||

| Operating Statistics | 2015 | 2014 | 2015 | 2014 | ||||||||||

| Production | ||||||||||||||

| Gold production (ounces) | 51,983 | 70,111 | (26)% | 167,914 | 205,506 | (18)% | ||||||||

| Silver production (ounces) | 1,914,356 | 2,349,577 | (19)% | 6,108,532 | 6,188,184 | (1)% | ||||||||

Co-product cash costs per gold ounce produced (i) | $ | 676 | $ | 567 | 19% | $ | 648 | $ | 548 | 18% | ||||

Co-product cash costs per silver ounce produced (i) | $ | 8.39 | $ | 7.30 | 15% | $ | 8.13 | $ | 7.86 | 3% | ||||

| Ore mined (tonnes) | 265,966 | 389,115 | (32)% | 881,145 | 1,129,158 | (22)% | ||||||||

| Ore processed (tonnes) | 331,793 | 375,507 | (12)% | 1,075,049 | 1,093,663 | (2)% | ||||||||

| Gold feed grade (g/t) | 5.15 | 6.19 | (17)% | 5.21 | 6.26 | (17)% | ||||||||

| Silver feed grade (g/t) | 203.97 | 227.73 | (10)% | 203.01 | 210.59 | (4)% | ||||||||

| Gold recovery rate (%) | 94.2 | 93.7 | 1% | 93.3 | 93.5 | —% | ||||||||

| Silver recovery rate (%) | 87.5 | 85.2 | 3% | 87.2 | 83.5 | 4% | ||||||||

| Sales | ||||||||||||||

| Gold (ounces) | 52,633 | 67,775 | (22)% | 168,045 | 201,385 | (17)% | ||||||||

| Silver (ounces) | 1,970,069 | 2,201,354 | (11)% | 6,130,827 | 5,968,393 | 3% | ||||||||

| Depletion, depreciation and amortization | ||||||||||||||

| Per gold ounce sold | $ | 396 | $ | 356 | 11% | $ | 405 | $ | 367 | 10% | ||||

| Per silver ounce sold | $ | 5.26 | $ | 5.39 | (2)% | $ | 5.51 | $ | 5.65 | (2)% | ||||

______________________________

| (i) | A cautionary note regarding non-GAAP measures is included in Section 13 of this Management’s Discussion and Analysis. Comparatives have been restated to conform to the change in presentation adopted in the current period. |