MANAGEMENT'S DISCUSSION AND ANALYSIS FOR THE PERIOD ENDED JUNE 30, 2021 |

This Management Discussion and Analysis ("MD&A") should be read in conjunction with the condensed consolidated interim financial statements of Endeavour Silver Corp. ("Endeavour" or "the Company") for the three months and six ended June 30, 2021 and the related notes contained therein, which were prepared in accordance with IAS34 Interim financial reporting of the International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB"). The Company uses certain non-IFRS financial measures in this MD&A as described under "Non-IFRS Measures". Additional information relating to the Company, including the most recent Annual Information Form (the "Annual Information Form"), is available on SEDAR at www.sedar.com, and the Company's most recent annual report on Form 40-F has been filed with the U.S. Securities and Exchange Commission (the "SEC"). This MD&A contains "forward-looking statements" that are subject to risk factors set out in a cautionary note contained herein. All dollar ($) amounts are expressed in United States ("$.") dollars and tabular amounts are expressed in thousands of U.S. dollars unless Canadian dollars (CAN$) are otherwise indicated. This MD&A is dated as of August 4, 2021 and all information contained is current as of August 4, 2021 unless otherwise stated.

Cautionary Note to U.S. Investors Regarding Mineral Reserves and Resources

This Management Discussion and Analysis has been prepared in accordance with the requirements of Canadian provincial securities laws, which differ from the requirements of U.S. securities laws. Unless otherwise indicated, all mineral reserve and mineral resource estimates included have been prepared in accordance with Canadian National Instrument 43-101- Standards of Disclosure for Mineral Projects ("NI 43-101") and the Canadian Institute of Mining, Metallurgy and Petroleum (the "CIM") - CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. NI 43-101 is an instrument developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. These definitions differ from the definitions in requirements under United States securities laws adopted by the United States Securities and Exchange Commission.

Under Canadian rules, estimates of inferred mineral resources may not form the basis of feasibility or pre-feasibility studies, except in rare cases. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. An "inferred mineral resource" is that part of a mineral resource for which quantity and grade or quality are estimated on the basis of limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An inferred mineral resource has a lower level of confidence than that applying to an indicated mineral resource and must not be converted to a mineral reserve. It is reasonably expected that the majority of inferred mineral resources could be upgraded to indicated mineral resources with continued exploration.

Investors are cautioned not to assume that all or any part of mineral reserves and mineral resources determined in accordance with NI 43-101 and CIM standards will qualify as, or be identical to, mineral reserves and mineral resources estimated under the standards of the SEC applicable to U.S. companies. The SEC has adopted amendments to its disclosure rules to modernize the mineral property disclosure requirements for issuers whose securities are registered with the SEC. As a foreign private issuer that files its annual report on Form 40-F with the SEC pursuant to the multi-jurisdictional disclosure system, the Company is not required to provide disclosure on its mineral properties under the SEC's new rules and will continue to provide disclosure under NI 43-101 and the CIM standards. If the Company ceases to be a foreign private issuer or lose its eligibility to file its annual report on Form 40-F pursuant to the multi-jurisdictional disclosure system, then the Company will be subject to the SEC's new rules, which differ from the requirements of NI 43-101 and the CIM standards.

Accordingly, information contained in this Management Discussion and Analysis that contain descriptions of the Corporation's mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

Forward-Looking Statements

This MD&A contains "forward-looking statements" within the meaning of the U.S. Securities Litigation Reform Act of 1995, as amended and "forward-looking information" within the meaning of applicable Canadian securities legislation. Such forward-looking statements and information include, but are not limited to, statements regarding Endeavour's anticipated performance in 2021, including silver and gold production, financial results, timing and expenditures to develop new silver mines and mineralized zones, silver and gold grades and recoveries, cash costs per ounce, capital expenditures and sustaining capital and the impact of the COVID 19 pandemic on operations. Forward-looking statements are frequently characterized by words such as "plan", "expect", "forecast", "project", "intend", "believe", "anticipate", "outlook" and other similar words, or statements that certain events or conditions "may" or "will" occur. Forward- looking statements are based on the opinions and estimates of management at the dates the statements are made, and are subject to a variety of risks and uncertainties and other factors that could cause actual events or results to differ materially from those projected in the forward-looking statements.

The Company does not intend to, and does not assume any obligation to, update such forward-looking statements or information, other than as required by applicable law. Forward-looking statements or information involve known and unknown risks, uncertainties and other factors and are based on assumptions that may cause the actual results, level of activity, performance or achievements of the Company and its operations to be materially different from those expressed or implied by such statements. Such factors and assumptions include, among others: the ultimate impact of the COVID 19 pandemic on operations and results, fluctuations in the prices of silver and gold, fluctuations in the currency markets (particularly the Mexican peso, Chilean peso, Canadian dollar and U.S. dollar); changes in national and local governments, legislation, taxation, controls, regulations and political or economic developments in Canada and Mexico; operating or technical difficulties in mineral exploration, development and mining activities; risks and hazards of mineral exploration, development and mining (including, but not limited to environmental hazards, industrial accidents, unusual or unexpected geological conditions, pressures, cave-ins and flooding); inadequate insurance, or inability to obtain insurance; availability of and costs associated with mining inputs and labour; the speculative nature of mineral exploration and development, diminishing quantities or grades of mineral reserves as properties are mined; the ability to successfully integrate acquisitions; risks in obtaining necessary licenses and permits, and challenges to the Company's title to properties; as well as those factors described under "Risk Factors" in the Company's Annual Information Form. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking statements or information, there may be other factors that cause results to be materially different from those anticipated, described, estimated, assessed or intended. There can be no assurance that any forward-looking statements or information will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements or information. Accordingly, readers should not place undue reliance on forward-looking statements or information.

Qualified Person

The scientific and technical information contained in this MD&A relating to the Company's mines and mineral projects has been reviewed and approved by Dale Mah, B.Sc., P.Geo., Vice President Corporate Development of Endeavour, a Qualified Person within the meaning of NI 43-101.

TABLE OF CONTENTS

OPERATING HIGHLIGHTS

Three Months Ended June 30 | Q1 2021 Highlights | Six Months Ended June 30 | ||||

2021 | 2020 | % Change | 2021 | 2020 | % Change | |

|

|

| Production |

|

|

|

1,073,724 | 596,545 | 80% | Silver ounces produced | 2,121,824 | 1,454,204 | 46% |

11,166 | 5,817 | 92% | Gold ounces produced | 22,275 | 14,293 | 56% |

1,062,267 | 590,618 | 80% | Payable silver ounces produced | 2,098,977 | 1,440,409 | 46% |

10,955 | 5,717 | 92% | Payable gold ounces produced | 21,849 | 14,037 | 56% |

1,967,004 | 1,061,905 | 85% | Silver equivalent ounces produced(1) | 3,903,824 | 2,597,644 | 50% |

13.03 | 2.78 | 369% | Cash costs per silver ounce(2)(3) | 10.48 | 5.77 | 82% |

19.55 | 10.33 | 89% | Total production costs per ounce(2)(4) | 17.51 | 13.88 | 26% |

25.39 | 14.91 | 70% | All-in sustaining costs per ounce(2)(5) | 22.69 | 16.96 | 34% |

242,018 | 114,120 | 112% | Processed tonnes | 451,471 | 313,447 | 44% |

119.94 | 102.02 | 18% | Direct operating costs per tonne(2)(6) | 116.43 | 98.76 | 18% |

141.61 | 109.74 | 29% | Direct costs per tonne(2)(6) | 134.48 | 104.59 | 29% |

18.52 | 10.16 | 82% | Silver co-product cash costs(7) | 16.89 | 10.99 | 54% |

1,288 | 1,111 | 16% | Gold co-product cash costs(7) | 1,116 | 1,175 | (5%) |

|

|

| Financial | |||

47.7 | 20.2 | 136% | Revenue ($ millions) | 82.2 | 42.1 | 95% |

1,120,266 | 634,839 | 76% | Silver ounces sold | 1,743,645 | 1,300,339 | 34% |

9,810 | 5,218 | 88% | Gold ounces sold | 20,473 | 12,672 | 62% |

26.82 | 17.04 | 57% | Realized silver price per ounce | 26.95 | 16.16 | 67% |

1,866 | 1,862 | 0% | Realized gold price per ounce | 1,781 | 1,727 | 3% |

6.7 | (3.3) | 302% | Net earnings (loss) ($ millions) | 18.9 | (19.2) | 198% |

0.8 | (3.3) | 126% | Adjusted net earnings (loss) (11) ($ millions) | (3.7) | (19.2) | 81% |

10.2 | 3.1 | 228% | Mine operating earnings (loss) ($ millions) | 15.9 | 0.2 | 6800% |

17.2 | 7.6 | 125% | Mine operating cash flow ($ millions)(8) | 30.5 | 11.9 | 156% |

8.7 | 1.9 | 358% | Operating cash flow before working capital changes(9) | 13.9 | (3.1) | 551% |

15.9 | 1.2 | 1214% | Earnings before ITDA(10) ($ millions) | 39.8 | (5.5) | 823% |

146.8 | 44.6 | 229% | Working capital ($ millions) | 146.8 | 44.6 | 229% |

|

|

| Shareholders | |||

0.04 | (0.02) | 300% | Earnings (loss) per share - basic | 0.12 | (0.13) | 192% |

0.01 | (0.02) | 123% | Adjusted earnings (loss) per share - basic(8) | (0.02) | (0.13) | 83% |

0.05 | 0.01 | 302% | Operating cash flow before working capital changes per share(9) | 0.08 | (0.02) | 499% |

168,383,755 | 147,862,393 | 14% | Weighted average shares outstanding | 164,051,368 | 144,836,300 | 13% |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-product revenue on a payable silver basis, total production costs per ounce, all-in sustaining costs per ounce, direct production costs per tonne, silver co-product cash costs and gold co-product cash costs in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliations to IFRS beginning on page 19.

(3) Cash costs net of by-product revenue per payable silver ounce include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 21 & 22.

(4) Total production costs per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 21 & 22.

(5) All-in sustaining cost per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 22 & 23.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne include all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 21 & 22.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 24 & 25.

(8) Mine operating cash flow is calculated by adding back amortization, depletion, inventory write-downs and share-based compensation to mine operating earnings. Mine operating earnings and mine operating cash flow are before taxes. See Reconciliation to IFRS on page 19.

(9) See Reconciliation to IFRS on page 20 for the reconciliation of operating cash flow before working capital changes and for the operating cash flow before working capital changes per share.

(10) See Reconciliation of Earnings before interest, taxes, depreciation and amortization on page 20.

(11) Adjusted net earnings is calculated by adding back the reversal of impairment on non-current assets that are held for sale which had a significant effect on reported earnings. See Reconciliation to IFRS on page 19.

The above highlights are key measures used by management, however they should not be the sole measures used in determining the performance of the Company's operations.

HISTORY AND STRATEGY

The Company is engaged in silver mining in Mexico and related activities including property acquisition, exploration, development, mineral extraction, processing, refining and reclamation. The Company is also engaged in exploration activities in Chile. Since 2002, the Company's business strategy has been to focus on acquiring advanced-stage silver mining properties in Mexico. Mexico, despite its long and prolific history of metal production, appears to be relatively under-explored using modern exploration techniques and offers promising geological potential for precious metals exploration and production.

The Company's Guanaceví and Bolañitos mines acquired in 2004 and 2007, respectively, demonstrate its business model of acquiring fully built and permitted silver mines that were about to close for lack of ore. By bringing the money and expertise needed to find new silver ore-bodies, the Company successfully re-opened and expanded these mines to develop their full potential. The benefit of acquiring fully built and permitted mining and milling infrastructure is that, if new exploration efforts are successful, the mine development cycle from discovery to production only takes a matter of months instead of the several years normally required in the traditional mining business model.

In addition to operating the Guanaceví and Bolañitos mines, the Company commissioned the El Compas mine in March 2019. The Company is advancing the Terronera development project and several exploration projects in order to achieve its goal to become a premier senior producer in the silver mining sector. In 2012, the Company acquired the El Cubo silver-gold mine located in Guanajuato, Mexico, which operated until November 2019.

On March 17, 2021, the Company signed a definitive agreement to sell the El Cubo mine and related assets to VanGold Mining Corp. ("VanGold") for a combination of cash and share payments plus additional contingency payments. On April 9, 2021, VanGold purchased the El Cubo assets for total consideration of $19.7 million and the Company recognizing a gain on disposal of $5.8 million.

The Company has historically funded its acquisition, exploration and development activities through equity financings, debt facilities and convertible debentures. In recent years, the Company has financed most of its acquisition, exploration, development and operating activities from production cash flows, treasury and equity financings. The Company may choose to undertake equity, debt, convertible debt or other financings, on an as-needed basis, in order to facilitate its growth.

On March 31, 2020, the Mexican government declared a national health emergency with extraordinary measures due to the COVID-19 pandemic. Numerous health precautions were decreed, including the suspension of non-essential businesses, with only essential services to remain open. At March 31, 2020, mining did not qualify as an essential service so for the protection of the Company's staff, employees, contractors and communities, the Company suspended its three mining operations in Mexico as of April 1, 2020 as mandated by the Mexican government. The Company retained essential personnel at each mine site during the suspension period to maintain safety protocols, environmental monitoring, security measures and equipment maintenance. Essential personnel followed the Company's strict COVID-19 safety protocols and non-essential employees were sent home to self-isolate and stay healthy, while continuing to receive their base pay. The suspension of activities ceased in May 2020 as mining was declared an essential business.

The Company implemented measures to minimize the risks of the COVID-19 virus, both to employees and to the business. At each site, the Company is following government health protocols and is closely monitoring the pandemic with local health authorities. The Company has posted health advisories to educate employees about the COVID-19 symptoms, best practices to avoid contracting and spreading the virus, and procedures to follow if symptoms are experienced.

As the COVID-19 global pandemic is dynamic and, given that the ultimate duration and severity of the pandemic remains uncertain, the impact on the Company's 2021 production and costs has greater uncertainty. Globally, and in Mexico, positive COVID-19 continues to spread at a significant rate, while the duration of vaccine distributions and effectiveness remain uncertain. A local outbreak, an impediment to supply or market logistics or change in government health orders remains a significant risk.

The Company's long-term business could be significantly adversely affected by the on-going effects of the COVID-19 pandemic. The Company cannot accurately predict the impact COVID-19 will have on third parties' ability to meet their obligations with the Company, including due to uncertainties relating to the ultimate geographic spread of the virus, the severity of the disease, the duration of the outbreak, the duration of vaccine distribution and the length of travel and quarantine restrictions imposed by governments of affected countries.

In particular, the continued spread of COVID-19 globally could materially and adversely impact the Company's business including without limitation, employee health, limitations on travel, the availability of industry experts and personnel, on-going restrictions to mining and processing operations and drill programs, and other factors that will depend on future developments beyond the Company's control. In addition, the COVID 19 pandemic could adversely affect the economies and financial markets of many countries (including those in which the Company operates), resulting in an economic downturn that could negatively impact the Company's operating results and ability to raise capital.

As of June 30, 2021, the Company held $125.2 million in cash and $146.8 million in working capital. Management believes there is sufficient working capital to meet the Company's current obligations, however the ultimate duration and severity of the COVID pandemic remains uncertain and could impact the financial liquidity of the Company.

REVIEW OF OPERATING RESULTS

The Company operates the Guanaceví, Bolañitos and El Compas mines.

Consolidated Production Results for the Three and Six Months Ended June 30, 2021 and 2020

Three Months Ended June 30 | CONSOLIDATED | Six Months Ended June 30 | ||||

2021 | 2020 | % Change |

| 2021 | 2020 | % Change |

242,018 | 114,120 | 112% | Ore tonnes processed | 451,471 | 313,447 | 44% |

163 | 188 | (14%) | Average silver grade (gpt) | 170 | 167 | 2% |

84.9 | 86.3 | (2%) | Silver recovery (%) | 85.8 | 86.2 | (1%) |

1,073,724 | 596,545 | 80% | Total silver ounces produced | 2,121,824 | 1,454,204 | 46% |

1,062,267 | 590,618 | 80% | Payable silver ounces produced | 2,098,977 | 1,440,409 | 46% |

1.63 | 1.84 | (11%) | Average gold grade (gpt) | 1.76 | 1.66 | 6% |

87.9 | 86.3 | 2% | Gold recovery (%) | 87.2 | 85.3 | 2% |

11,166 | 5,817 | 92% | Total gold ounces produced | 22,275 | 14,293 | 56% |

10,955 | 5,717 | 92% | Payable gold ounces produced | 21,849 | 14,037 | 56% |

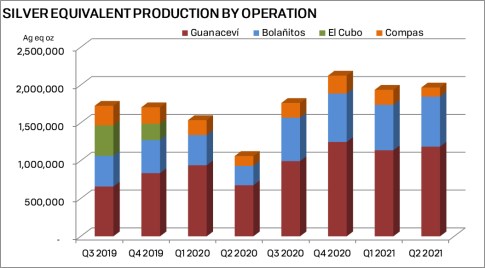

1,967,004 | 1,061,905 | 85% | Silver equivalent ounces produced(1) | 3,903,824 | 2,597,644 | 50% |

13.03 | 2.78 | 369% | Cash costs per silver ounce(2)(3) | 10.48 | 5.77 | 82% |

19.55 | 10.33 | 89% | Total production costs per ounce(2)(4) | 17.51 | 13.88 | 26% |

25.39 | 14.91 | 70% | All in sustaining cost per ounce (2)(5) | 22.69 | 16.96 | 34% |

119.94 | 102.02 | 18% | Direct operating costs per tonne(2)(6) | 116.43 | 98.76 | 18% |

141.61 | 109.74 | 29% | Direct costs per tonne(2)(6) | 134.48 | 104.59 | 29% |

18.52 | 10.16 | 82% | Silver co-product cash costs(7) | 16.89 | 10.99 | 54% |

1,288 | 1,111 | 16% | Gold co-product cash costs(7) | 1,116 | 1,175 | (5%) |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-product revenue on a payable silver basis, total production costs per ounce, all-in sustaining costs per ounce, direct production costs per tonne, silver co-product cash costs and gold co-product cash costs in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliations to IFRS on 19.

(3) Cash costs net of by-product revenue per payable silver ounce include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 21 & 22.

(4) Total production costs per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 21 & 22.

(5) All-in sustaining costs per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 22 & 23.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne include all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 21 & 22.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 24 & 25.

|

| (1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio. |

Consolidated Production

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Consolidated silver production during Q2, 2021 was 1,073,724 ounces (oz), an increase of 80% compared to 596,545 oz in Q2, 2020, and gold production was 11,166 oz, an increase of 92% compared to 5,817 oz in Q2, 2020. Plant throughput was 242,018 tonnes at average grades of 163 grams per tonne (gpt) silver and 1.63 gpt gold, a throughput increase of 112% compared to 114,120 tonnes at average grades of 188 gpt silver and 1.84 gpt gold in Q2, 2020. The 80% increase in silver production and 92% increase in gold production compared to Q1, 2020 is primarily due to the suspension of the Guanaceví, Bolañitos and El Compas mines during Q2 2020 due to the COVID-19 pandemic, offset by slightly lower grades in Q2 2021. There was a 14% decrease in the average silver grade driven by lower grades at Bolañitos and El Compas, slightly offset by higher grades at Guanaceví, and an 11% decrease in gold grades driven by lower grades at Guanaceví and El Compas, slightly offset by higher gold grades at Bolañitos.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Consolidated silver production during the first half of 2021 was 2,121,824 ounces (oz), an increase of 46% compared to 1,454,204 oz in the first half of 2020, and gold production was 22,275 oz, an increase of 56% compared to 14,293 oz in Q2, 2020. Plant throughput was 451,471 tonnes at average grades of 170 grams per tonne (gpt) silver and 1.76 gpt gold, a throughput increase of 44% compared to 313,447 tonnes at average grades of 167 gpt silver and 1.66 gpt gold in the first half of 2020. The 46% increase in silver production and 56% increase in gold production compared to 2020 is primarily due to the suspension of the Guanaceví, Bolañitos and El Compas mines during Q2 2020 due to the COVID-19 pandemic. Silver grades have been consistent with 2020 and there has been a 6% increase in gold grades with recoveries for both consistent with 2020.

For the first half of 2021, silver equivalent production was in line with guidance. The COVID-19 pandemic remains prevalent in Mexico, and at the Company's business locations, process and protocols remain in place to ensure staff and workers as well as our communities remain as safe as possible.

Consolidated Operating Costs

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Direct operating costs per tonne in Q2, 2021 increased 18%, to $119.94 compared with Q2, 2020 due to higher operating costs at Guanaceví, Bolañitos and El Compas. Guanaceví, Bolañitos and El Compas have seen increased labour costs and at Guanaceví, increased third party ore purchased and operating development have increased compared to prior year. There has also been an increase in the Mexican Peso foreign exchange rates comparative to the US Dollar, which increase expenses denominated in that currency. Including royalties and special mining duty, direct costs per tonne increased 29% to $141.61. Royalties increased 420% to $4.3 million as increased production from the El Curso and El Porvenir concessions at Guanaceví and higher prices substantially increased the royalty expense. The higher prices and higher grades increased special mining duty expense to $0.7 million for Q2, 2021.

Consolidated cash costs per oz, net of by-product credits (a non-IFRS measure and a standard of the Silver Institute) increased to $13.03 due to higher direct costs per tonne and lower silver and gold grades. All-in sustaining costs (also a non-IFRS measure) increased 70% to $25.39 per oz in Q2, 2021 as a result of higher cash costs, higher corporate general and administrative costs, increased mine site expensed exploration and increased capital expenditures at Guanaceví to accelerate mine development within the El Curso ore body. In Q2, 2021 corporate general and administrative included a $1.6 million mark to market expense of cash settled deferred share units expense, whereas the mark to market expense was $1.1 million in 2020, due to period end changes in the Company's share price.

On a co-product cash costs basis silver cost per ounce increased 82% and gold cost per ounce increased 16% compared to the Q2, 2020. The silver co-product cost per ounce decreased due to reduced silver ore grade, lower silver recoveries and higher operating, royalty and special mining duty costs primarily at the Guanaceví mine. Gold co-product cash costs increased due to lower gold ore grades, and the higher operating costs at Guanaceví offset by an increase in gold recovery.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Direct operating costs per tonne in 2021 increased 18%, to $116.43 compared with 2020 due to higher operating costs at Guanaceví, Bolañitos and El Compas. Guanaceví, Bolañitos and El Compas have seen increased labour costs and at Guanaceví, increased third party ore purchased and operating development have increased compared to the prior year. There has also been a 7% increase in the average Mexican Peso to US Dollar foreign exchange rate compared to the prior period, which increase expenses denominated in that currency. Including royalties and special mining duty, direct costs per tonne increased 29% to $134.48. Royalties increased 302% to $6.8 million as increased production from the El Curso and El Porvenir concessions at Guanaceví and higher prices substantially increased the royalty expense. The higher prices and higher grades increased special mining duty expense to $0.9 million for Q2, 2021.

Consolidated cash costs per oz, net of by-product credits (a non-IFRS measure and a standard of the Silver Institute) was increased to $10.48 due to the higher direct costs per tonne, offset by higher grades and higher gold prices. All-in sustaining costs (also a non-IFRS measure) increased 34% to $22.69 per oz in 2021 as a result of higher cash costs, higher corporate general and administrative costs, increased mine site expensed exploration and increased capital expenditures at Guanaceví to accelerate mine development within the El Curso ore body. In 2021 corporate general and administrative included a $1.4 million mark to market expense of cash settled deferred share units expense, whereas the mark to market expense was $0.1 million in 2020, due to period end changes in the Company's share price.

On a co-product cash costs basis silver cost per ounce increased 54% and gold cost per ounce decreased 5% compared to the 2020. The improved silver ore grade was offset by higher operating, royalty and special mining duty costs primarily at the Guanaceví mine. Gold co-product cash costs decreased due to higher gold ore grades, higher gold recoveries offset by the higher operating costs at Bolañitos.

GUANACEVÍ OPERATIONS

The Guanaceví operation is currently producing from three underground silver-gold mines along a five kilometre length of the prolific Santa Cruz vein. Guanaceví provides steady employment to over 500 people and engages over 390 contractors.

During 2019, the Company acquired a 10-year right to explore and exploit the El Porvenir and El Curso concessions from Ocampo Mining SA de CV ("Ocampo"), a subsidiary of Grupo Frisco. The Company agreed to meet certain minimum production targets from the properties, subject to various terms and conditions and pay Ocampo a $12 fixed per tonne production payment plus a floating net smelter return royalty based on the spot silver price. The Company pays a 4% royalty on sales below $15.00 per ounce, 9% above $15.00 per ounce 13% above $20.00 per silver ounce, and a maximum 16% above $25 per silver ounce, based on the then current realized prices.

The development of two new orebodies, Milache and SCS and the acquisition of the Ocampo concession rights have provided sufficient ore and flexibility to increase mine output and to reach designed plant capacity.

Production Results for the Three and Six Months Ended June 30, 2021 and 2020

Three Months Ended June 30 | GUANACEVÍ | Six Months Ended June 30 | ||||

2021 | 2020 | % Change |

| 2021 | 2020 | % Change |

111,893 | 62,231 | 80% | Ore tonnes processed | 200,525 | 156,438 | 28% |

308 | 304 | 1% | Average silver grade (g/ t) | 335 | 289 | 16% |

84.8 | 86.7 | (2%) | Silver recovery (%) | 86.0 | 87.5 | (2%) |

939,241 | 527,347 | 78% | Total silver ounces produced | 1,857,458 | 1,272,461 | 46% |

936,424 | 525,766 | 78% | Payable silver ounces produced | 1,851,886 | 1,268,764 | 46% |

0.98 | 1.05 | (7%) | Average gold grade (g/ t) | 1.01 | 0.94 | 7% |

87.5 | 87.9 | (0%) | Gold recovery (%) | 89.5 | 90.4 | (1%) |

3,084 | 1,847 | 67% | Total gold ounces produced | 5,827 | 4,274 | 36% |

3,075 | 1,842 | 67% | Payable gold ounces produced | 5,810 | 4,263 | 36% |

1,185,961 | 675,107 | 76% | Silver equivalent ounces produced(1) | 2,323,618 | 1,614,381 | 44% |

17.06 | 8.48 | 101% | Cash costs per silver ounce(2)(3) | 14.19 | 8.79 | 61% |

19.98 | 12.43 | 61% | Total production costs per ounce(2)(4) | 17.01 | 12.02 | 42% |

24.68 | 15.00 | 65% | All in sustaining cost per ounce (2)(5) | 21.93 | 14.77 | 48% |

149.81 | 113.72 | 32% | Direct operating costs per tonne(2)(6) | 145.86 | 107.73 | 35% |

193.09 | 126.13 | 53% | Direct costs per tonne(2)(6) | 182.33 | 117.55 | 55% |

18.72 | 10.76 | 74% | Silver co-product cash costs(7) | 16.30 | 10.63 | 53% |

1,303 | 1,176 | 11% | Gold co-product cash costs(7) | 1,077 | 1,137 | (5%) |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-product revenue on a payable silver basis, total production costs per ounce, all-in sustaining costs per ounce and direct production costs per tonne, in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliation to IFRS on page 19.

(3) Cash costs net of by-product revenue per payable silver ounce include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 21 & 22.

(4) Total production costs per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 21 & 22.

(5) All-in sustaining cost per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 22 & 23.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne includes all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 21 & 22.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 24 & 25.

Guanaceví Production Results

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Silver production at the Guanaceví mine during Q2, 2021 was 939,241 oz, an increase of 78% compared to 527,347 oz in Q2, 2020, and gold production was 3,084 oz, an increase of 67% compared to 1,847 oz in Q2, 2020. Plant throughput was 111,893 tonnes at average grades of 308 gpt silver and 0.98 gpt gold, compared to 62,231 tonnes at average grades of 304 gpt silver and 1.05 gpt gold in Q2, 2020. The 78% increase in silver production and 67% increase in gold production compared to Q2, 2020 is primarily due to the suspension of the Guanaceví mine during Q2 2020 due to the COVID-19 pandemic. Production also increased due to higher throughput, as the plant reached its 1,200 tonnes per day capacity in Q2, 2021, and higher ore grades partially offset by lower recoveries. Stockpiled ore inventory increased slightly during the quarter as the mine output is ahead of plan. With the higher metal prices, the purchase of local third-party ores continued to supplement mine production, amounting to 11% of quarterly throughput, and contributed to the higher ore grades.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Silver production at the Guanaceví mine during 2021 was 1,857,458 oz, an increase of 46% compared to 1,272,461 oz in 2020, and gold production was 5,827 oz, an increase of 36% compared to 4,274 oz in 2020. Plant throughput was 200,525 tonnes at average grades of 335 gpt silver and 1.01 gpt gold, compared to 156,438 tonnes at average grades of 289 gpt silver and 0.94 gpt gold in Q2, 2020. The 46% increase in silver production and 36% increase in gold production compared to 2020 is primarily due to the suspension of the Guanaceví mine during Q2, 2020 due to the COVID-19 pandemic. Production also increased due to higher throughput, as the plant reached its 1,200 tonnes per day capacity in Q2, 2021, and higher ore grades partially offset by lower recoveries. Stockpiled ore inventory increased during the first half of the year as the mine output is ahead of plan. The purchase of local third-party ores continued to supplement mine production, amounting to 11% of quarterly throughput, and contributed to the higher ore grades.

Guanaceví Operating Costs

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Direct operating costs per tonne for the three months ended June 30, 2021 increased 32% to $149.81 compared with the same period in 2020, resulting from increased purchase of local third-party ores, increased labour costs, the expensing of development costs at El Porvenir, as there are no reserves to allow for capitalization, and an increase in operating development. Including royalty and special mining duty costs, direct cost per tonne increased 53% to $193.09 compared with the same period in 2020. Increased production from the El Curso and El Porvenir concessions and higher prices significantly increased the royalties paid during the quarter. The increased metal prices and ore grades resulted in improved profitability and higher special mining duty payable to the Mexican government.

Cash costs per oz, net of by-product credits (a non-IFRS measure and a standard of the Silver Institute) were $17.06 compared to $8.48 due to the higher cost per tonne and lower gold grades. Similarly, all-in sustaining costs (also a non-IFRS measure) increased 65% to $24.68 from $15.00 per oz for the three months ended June 30, 2021. The increase in cash costs per oz was the primary driver of the higher all in sustaining costs, while higher capital and exploration expenditures and general and administration expenses contributed to the higher costs compared to the same period in 2020. In Q2, 2020 there was a reduction in capital and exploration expenditures due to the suspension of activities due to COVID-19. Mine development advancement exceeded plan in Q2, 2021 increasing development expenditures in Q2, 2021 compared to Q2, 2020.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Direct operating costs per tonne in 2021 increased 35% to $145.86 compared with the same period in 2020, as a result of increased purchase of local third-party ores, increased labour costs, the expensing of development costs at El Porvenir, as there are no reserves to allow for capitalization, and an increase in operating development. Including royalty and special mining duty costs direct cost per tonne increased 55% to $182.33 compared with the same period in 2020. Increased production from the El Curso and El Porvenir concessions and higher prices significantly increased the royalties paid during the quarter. The increased metal prices and ore grades resulted in improved profitability and higher special mining duty payable to the Mexican government.

Cash costs per oz, net of by-product credits (a non-IFRS measure and a standard of the Silver Institute) were $14.19, 61% higher due to the higher cost per tonne, offset by the higher metal grades and higher gold credit. Similarly, all-in sustaining costs (also a non-IFRS measure) increased 48% to $21.93 per oz for the six months ended June 30, 2021. The increase in cash costs per oz was the primary driver of the higher all in sustaining costs, while higher capital and exploration expenditures and general and administration expenses contributed to the higher costs compared to the same period in 2020. In Q2, 2020 there was a sharp reduction in capital and exploration expenditures due to the suspension of activities due to COVI-19. Mine development advancement exceeded plan during the six months ended June 30, 2021 increasing development expenditures in 2021 compared to 2020.

BOLAÑITOS OPERATIONS

The Bolañitos operation encompasses three underground silver-gold mines and a flotation plant. Bolañitos provides steady employment for over 380 people and engages over 250 contractors.

Production Results for the Three Months and Six Months Ended June 30, 2021 and 2020

Three Months Ended June 30 | BOLAÑITOS | Six Months Ended June 30 | ||||

2021 | 2020 | % Change |

| 2021 | 2020 | % Change |

107,912 | 41,680 | 159% | Ore tonnes processed | 205,604 | 124,897 | 65% |

39 | 47 | (17%) | Average silver grade (g/ t) | 39 | 43 | (9%) |

88.7 | 88.4 | 0% | Silver recovery (%) | 87.8 | 82.1 | 7% |

120,044 | 55,682 | 116% | Total silver ounces produced | 226,271 | 141,807 | 60% |

112,456 | 51,912 | 117% | Payable silver ounces produced | 211,444 | 132,918 | 59% |

2.14 | 2.10 | 2% | Average gold grade (g/ t) | 2.15 | 1.84 | 17% |

91.0 | 89.1 | 2% | Gold recovery (%) | 91.0 | 87.0 | 5% |

6,753 | 2,508 | 169% | Total gold ounces produced | 12,935 | 6,430 | 101% |

6,584 | 2,446 | 169% | Payable gold ounces produced | 12,612 | 6,263 | 101% |

660,284 | 256,322 | 158% | Silver equivalent ounces produced(1) | 1,261,071 | 656,207 | 92% |

(30.39) | (30.20) | (1%) | Cash costs per silver ounce(2)(3) | (27.16) | (16.26) | (67%) |

4.76 | (8.73) | 154% | Total production costs per ounce(2)(4) | 9.73 | 8.55 | 14% |

19.56 | 29.79 | (34%) | All in sustaining cost per ounce (2)(5) | 22.05 | 38.55 | (43%) |

78.66 | 76.46 | 3% | Direct operating costs per tonne(2)(6) | 77.99 | 70.96 | 10% |

81.69 | 77.02 | 6% | Direct costs per tonne(2)(6) | 80.65 | 71.44 | 13% |

14.94 | 9.74 | 53% | Silver co-product cash costs(7) | 15.34 | 10.76 | 43% |

1,040 | 1,064 | (2%) | Gold co-product cash costs(7) | 1,014 | 1,150 | (12%) |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-product revenue on a payable silver basis, total production costs per ounce, all-in sustaining costs per ounce and direct production costs per tonne, in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliation to IFRS on page 19.

(3) Cash costs net of by-product revenue per payable silver ounce include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 21 & 22.

(4) Total production costs per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 21 & 22.

(5) All-in sustaining cost per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 22 & 23.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne includes all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 21 & 22.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 24 & 25.

Bolañitos Production Results

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Silver production at the Bolañitos mine was 120,044 oz in Q2, 2021, an increase of 116% compared to 55,682 oz in Q2, 2020, and gold production was 6,753 oz in Q2, 2021, an increase of 169% compared to 2,508 oz in Q2, 2020. Plant throughput in Q2, 2021 was 107,912 tonnes at average grades of 39 gpt silver and 2.14 gpt gold, compared to 41,680 tonnes at average grades of 47 gpt silver and 2.10 gpt gold. The 116% increase in silver production and 169% increase in gold production compared to Q2, 2020 is primarily due to the suspension of the Bolañitos mine during Q2 2020 due to the COVID-19 pandemic. There was a 17% reduction in silver grade and a 2% increase in gold grade and both silver and gold recoveries improved in Q2, 2021 compared to Q2, 2020. Recoveries improved as the operations improved ore blending to maximize recoveries compared to the prior period.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Silver production at the Bolañitos mine was 226,271 oz in 2021, an increase of 60% compared to 141,807 oz in 2020, and gold production was 12,935 oz in 2021, an increase of 101% compared to 6,430 oz in 2020. Plant throughput in 2021 was 205,604 tonnes at average grades of 39 gpt silver and 2.15 gpt gold, compared to 124,897 tonnes at average grades of 43 gpt silver and 1.84 gpt gold. There was a 9% reduction in silver grade and a 17% increase in gold grade and silver and gold recoveries improved in 2021 compared to 2020. Recoveries improved as the operations improved ore blending to maximize recoveries compared to the prior period.

Bolañitos Operating Costs

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Direct production costs per tonne in Q1, 2021 increased 6% to $81.69 per tonne due to higher waste tonnes handled during the quarter, and higher labour costs. Cash costs net of by-product credits (which is a non-IFRS measure and a standard of the Silver Institute), were negative $30.39 per oz of payable silver in Q2, 2021 compared to negative $30.20 per oz in Q2, 2020 as the proportion of gold production increased compared to the same period in prior year. All-in sustaining costs (also a non-IFRS measure) decreased in Q2, 2021 to $19.56 per oz due to lower operating cost per oz, partially offset by higher sustaining capital expenditures and higher corporate general and administrative charges.

On a co-product cash costs basis, silver cost per ounce increased compared to Q2, 2020. Silver co-product cash costs increased 53%, while gold co-product costs fell 2% to $14.94 per silver ounce and $1,040 per gold ounce respectively. The deterioration in the silver cost on a co-product basis was primarily driven by the higher direct costs per tonne and the variation in ore, while the lower gold costs on a co-product basis was driven by the higher ore gold grades, partially offset by the higher direct costs per tonne.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Direct production costs per tonne in 2021 increased 13% to $80.65 per tonne due to higher waste tonnes handled during the period, and higher labour costs. Cash costs net of by-product credits (which is a non-IFRS measure and a standard of the Silver Institute), were negative $27.16 per oz of payable silver in 2021 compared to negative $16.26 per oz in 2020 as the proportion of gold production increased compared to the same period in prior year and there was a 3% increase in the realized gold price. All-in sustaining costs (also a non-IFRS measure) decreased in 2021 to $22.05 per oz due to lower operating cost per oz, partially offset by higher sustaining capital expenditures higher corporate general and administrative charges.

On a co-product cash costs basis, silver cost per ounce increased compared to 2020. Silver co-product cash costs increased 43%, while gold co-product costs fell 12% to $15.34 per silver ounce and $1,014 per gold ounce respectively. The deterioration in the silver cost on a co-product basis was primarily driven by the higher direct costs per tonne and the variation in ore, while the lower gold costs on a co-product basis was driven by the higher ore gold grades, partially offset by the higher direct costs per tonne.

EL COMPAS OPERATIONS

The El Compas operation is a small but high grade, permitted gold-silver mine with a small leased flotation plant in the historic silver mining district of Zacatecas, with good exploration potential to expand resources and scale up production. There is also potential for the Company to acquire other properties in the area to consolidate resources and exploration targets in the district. El Compas has a nominal plant capacity of 250 tonnes per day.

El Compas currently employs close to 200 people and engages over 55 contractors and achieved commercial production during Q1, 2019. The December resource was sufficient to support mining until mid-2021, while management has elected to suspend mining and milling operations during Q3, 2021.

There remain several brownfield exploration opportunities on concessions owned by the Company, however further resource definition and evaluation is required to recommence production. Temporary closure costs are estimated to be $1.3 million for 2021, including demobilization costs of $0.1 million, and severance cost of $1.0 million.

Production Results for the Three Months and Six Months Ended June 30, 2021 and 2020

Three Months Ended June 30 | El Compas | Six Months Ended June 30 | ||||

2021 | 2020 | % Change |

| 2021 | 2020 | % Change |

22,213 | 10,209 | 118% | Ore tonnes processed | 45,342 | 32,112 | 41% |

30 | 60 | (50%) | Average silver grade (g/ t) | 39 | 59 | (34%) |

67.4 | 68.6 | (2%) | Silver recovery (%) | 67.0 | 65.6 | 2% |

14,439 | 13,516 | 7% | Total silver ounces produced | 38,095 | 39,936 | (5%) |

13,387 | 12,940 | 3% | Payable silver ounces produced | 35,647 | 38,727 | (8%) |

2.45 | 5.55 | (56%) | Average gold grade (g/ t) | 3.30 | 4.50 | (27%) |

76.0 | 80.3 | (5%) | Gold recovery (%) | 73.0 | 77.3 | (6%) |

1,329 | 1,462 | (9%) | Total gold ounces produced | 3,513 | 3,589 | (2%) |

1,296 | 1,429 | (9%) | Payable gold ounces produced | 3,427 | 3,511 | (2%) |

120,759 | 130,476 | (7%) | Silver equivalent ounces produced(1) | 319,135 | 327,056 | (2%) |

96.21 | (96.83) | 199% | Cash costs per silver ounce(2)(3) | 41.01 | (17.64) | 333% |

114.59 | 1.62 | 6973% | Total production costs per ounce(2)(4) | 89.38 | 93.06 | (4%) |

123.73 | (48.25) | 356% | All in sustaining cost per ounce (2)(5) | 66.07 | 14.50 | 356% |

170.04 | 134.98 | 26% | Direct operating costs per tonne(2)(6) | 160.51 | 163.18 | (2%) |

173.37 | 143.50 | 21% | Direct costs per tonne(2)(6) | 166.93 | 170.31 | (2%) |

36.02 | 8.45 | 326% | Silver co-product cash costs(7) | 28.01 | 12.91 | 117% |

2,506 | 924 | 171% | Gold co-product cash costs(7) | 1,851 | 1,380 | 34% |

(1) Silver equivalents are calculated using an 80:1 (Ag/Au) ratio.

(2) The Company reports non-IFRS measures which include cash costs net of by-products on a payable silver basis, total production costs per ounce, all-in sustaining costs per ounce and direct production costs per tonne, in order to manage and evaluate operating performance at each of the Company's mines. These measures, some established by the Silver Institute (Production Cost Standards, June 2011), are widely used in the silver mining industry as a benchmark for performance, but do not have a standardized meaning. These measures are reported on a production basis. See Reconciliation to IFRS on page 19.

(3) Cash costs net of by-product revenue per payable silver ounce include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead, net of gold credits. See Reconciliation to IFRS on pages 21 & 22.

(4) Total production costs per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, amortization, depletion and amortization at the operation sites net of by product revenues. See Reconciliation to IFRS on pages 21 & 22.

(5) All-in sustaining cost per ounce include mining, processing (including smelting, refining, transportation and selling costs), direct overhead, corporate general and administration, on-site exploration, share-based compensation, reclamation and sustaining capital net of gold credits. See Reconciliation to IFRS on pages 22&23.

(6) Direct operating costs per tonne include mining, processing (including smelting, refining, transportation and selling costs) and direct overhead at the operation sites. Direct cost per tonne includes all direct operating costs, royalties and special mining duty. See Reconciliation to IFRS on pages 21 & 22.

(7) Silver co-product cash cost and gold co-product cash cost include mining, processing (including smelting, refining, transportation and selling costs), and direct overhead allocated on pro-rated basis of realized metal value. See Reconciliation to IFRS on pages 24 & 25.

El Compas Production Results

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Silver production at the El Compas mine was 14,439 oz and gold production was 1,329 oz in Q2, 2021 compared to 13,516 silver oz and gold 1,462 gold oz in Q2, 2020. Plant throughput in Q2, 2021 was 22,213 tonnes at average grades of 30 gpt silver and 2.45 gpt gold compared to 10,209 tonnes at average grades of 60 gpt silver and 5.55 gpt gold. El Compas production was close to plan with higher throughput offset by lower silver and gold grades. The increase in throughput compared to Q2, 2020 is primarily due to the suspension of the El Compas mine during Q2 2020 due to the COVID-19 pandemic. Although throughput has increased, both silver and gold grades have decreased as the mine has approached the end of its economic reserve life, resulting in lower proportional production.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Silver production at the El Compas mine was 38,095 oz and gold production was 3,513 oz in 2021 compared to 39,936 silver oz and 3,589 gold oz in 2020. Plant throughput in 2021 was 45,342 tonnes at average grades of 39 gpt silver and 3.3 gpt gold compared to 32,112 tonnes at average grades of 59 gpt silver and 4.5 gpt gold. El Compas production was close to plan with higher throughput offset by lower silver and gold grades. The increase in throughput compared to Q2, 2020 is primarily due to the suspension of the El Compas mine during Q2 2020 due to the COVID-19 pandemic. Although throughput remained steady, both silver and gold grades have decreased as the mine has approached the end of its estimated reserve life resulting in lower proportional production.

El Compas Operating Costs

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

Direct production costs were $173.37 per tonne in Q2, 2021, a 21% increase from Q2, 2020. Silver cash costs net of by-product credits (which is a non-IFRS measure and a standard of the Silver Institute), were $96.21 per oz of payable silver in Q2, 2021 compared to negative $96.83 per oz in Q2, 2020. The increased costs per tonne and the decrease in grades were the primary drivers in the high cash cost metric compared to 2020. The decrease in costs per tonne was a result of normal variations in costs incurred.

On a co-product cash costs basis, both silver and gold co-product costs per ounce rose 326% and 171% higher respectively due to higher operating costs on a per tonne basis and significantly lower grades.

All-in sustaining costs (also a non-IFRS measure) increased in Q2, 2021 to $123.73 per oz compared to negative $48.25 per ounce in the same period ended in 2020. The higher all-in sustaining costs is a function of the higher operating costs and significantly lower silver and gold grades compared to 2020.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

Direct production costs were $166.93 per tonne in 2021, a 2% decrease from 2020. Silver cash costs net of by-product credits (which is a non-IFRS measure and a standard of the Silver Institute), were $41.01 per oz of payable silver in 2021 compared to negative $17.64 per oz in 2020. The significantly lower gold grade was the primary driver in the increase in cash costs in 2021 compared to 2020. The decrease in costs per tonne was a result of normal variations in costs incurred.

On a co-product cash costs basis, both silver cost per ounce and gold co-product costs per ounce increased to $28.01 per ounce and $1,851 per ounce, respectively compared to 2020. The silver co-product cost per ounce increased due to the lower silver grade ore partially offset by the lower operating costs on a per tonne basis. The gold co-product cost per ounce increased due to the lower gold grade ore partially offset by the lower operating costs on a per tonne basis.

All-in sustaining costs (also a non-IFRS measure) increased in 2021 to $66.07 per oz compared to $14.50 per ounce in the same period ended in 2020. The higher all-in sustaining costs is a function of the lower silver and gold grades.

The Company retained essential personnel at El Compas during the 2020 suspension period to maintain safety protocols, environmental monitoring, security measures and day-to-day maintenance. Non-essential employees were sent home to self-isolate and continued to receive their base pay.

EL CUBO OPERATIONS

The El Cubo operation included two previously operating underground silver-gold mines and a flotation plant. which employed over 350 people and engaged over 200 contractors until the suspension of operations at the end of November 2019 as the mineral reserves had been exhausted. The mine, plant and tailings facilities were on care and maintenance until the sale of the El Cubo mine and related assets in April 2021.

Company management and contract personnel maintained the security of the mine, plant and tailings facilities until the sale. For the six months ended June 30, 2021 the Company incurred $0.6 million (2020 - $2.0 million) in legal, administrative and care and maintenance expenses. In 2020 $0.3 million severance costs and $1.5 million in legal, administrative and care and maintenance expenses were incurred and $0.2 million in building and office depreciation.

On March 17, 2021, the Company signed a definitive agreement to sell the El Cubo mine and related assets to VanGold Mining Corp. ("VanGold") for $15.0 million in cash and share payments plus additional contingency payments. On April 9, 2021, VanGold purchased the El Cubo assets for the following gross consideration:

- $7.5 million cash (paid)

- $9.8 million paid in shares with 21,331,058 shares of VanGold with a fair value of CDN $0.58 per share on April 9, 2021. Total fair value of the shares at the time of agreement was $5.0 million priced at CDN$0.30

- $2.4 million paid by unsecured promissory note with a face value of $2.5 million due and payable April 9, 2022

VanGold is required to pay the Company up to an additional $3.0 million in contingent payments based on the following events:

- $1.0 million upon VanGold producing 3.0 million silver equivalent ounces from the El Cubo mill

- $1.0 million if the price of gold closes at or above US$2,000 dollars per ounce for 20 consecutive days prior to April 9, 2023.

- $1.0 million if the price of gold closes at or above US$2,200 dollars per ounce for 20 consecutive days prior to April 9, 2023.

On sale of the El Cubo assets the Company recognized a $16.8 million reversal of prior year impairments and $5.8 million gain on disposal for totaling $22.6 million impact on earnings in the first half of 2021.

DEVELOPMENT ACTIVITIES

Terronera Project

The Terronera project, located 40 kilometres northeast of Puerto Vallarta in the state of Jalisco, Mexico, features a high-grade silver-gold mineral resource in the Terronera vein, which is now over 1,400 metres long, 400 metres deep, 3 to 16 metres thick, and remains open along strike to the southeast and down dip.

In 2020, the Company engaged an external consultant to update a previous Preliminary Feasibility Study based on updated information gathered in 2019 and 2020. In Q3, 2020 the Company completed an updated summary of the project's economics and published the NI 43-101 Technical Report ("2020 PFS").

The 2020 PFS included significant changes to the operations plan, capital and operating costs compared to the previous study and, as a result, project economics improved with higher certainty on a number of assumptions. The external consultant reviewed all aspects of the previous studies, while further cost-benefit initiatives will continue to be evaluated.

The 2020 PFS base case assumes a two-year trailing average silver price of $15.97 per oz and a gold price of $1,419 per oz. At base case prices, the improved economics estimates a net present value (NPV) of $137 million at a 5% discount rate, internal rate of return (IRR) of 30.0%, and payback period of 2.7 years. Initial capital expenditures are estimated to be $99 million with life of mine capital expenditures estimated to be $60 million. The 10-year life of mine is estimated to produce an average of 3 million silver oz and 32,800 gold ounces per year generating $315 million pre-tax, $217 million after-tax, free cash flow over the life of the project.

The Company is working to complete a Feasibility Study in Q3, 2021 at an estimated cost of $1.8 million. The Company is evaluating a number of opportunities to further enhance the value of the project, including exploration drilling to expand the known resources and to test multiple veins within the district. Additionally, the Company has defined an engineering, procurement and construction strategy and is planning commencement of various early work items. An engineering team is being assembled and a $11.0 million budget has been approved for sourcing equipment and machinery and early work items, including temporary camp construction and earthworks.

EXPLORATION RESULTS

In 2021, the Company plans to spend $10.2 million drilling 50,000 metres of core on brownfields projects, greenfields exploration and development engineering across its portfolio of mines and properties. At the Guanaceví and Bolañitos operating mines, 11,500 metres of core drilling are planned at a cost of $2.0 million and $1.9 million, respectively to replace reserves and expand resources.

On the exploration and development projects, expenditures of $6.3 million are planned to fund 27,000 metres of core drilling at the Terronera project to test multiple regional targets, the Parral project to continue drilling the San Patricio and Veta Colorada vein systems and the Paloma project in Chile. The Company is currently permitting of the Cerro Marquez and Aida projects and will continue to map and sample to prioritize targets for drilling.

At Guanaceví, in 2021 the Company drilled 9,989 metres in 39 holes to delineate the extension of the Porvenir Cuatro and Milache ore bodies. Drilling confirmed expectations and intersected significant mineralization with similar ore grades and vein widths similar to the 2020 intersections. The remaining drilling is planned to connect the Porvenir Cuatro (previously mined), El Curso and Milache ore bodies forming one continuous orebody over a 1,500 m length by 400 m vertical extent.

At Bolañitos, in 2021 the Company drilled 7,343 metres in 38 holes to target the Melladito vein, the Plateros vein and the Belen vein. The Company intersected significant mineralization with ore grades over mineable widths. Management is currently interpreting the results and will continue to drill these veins throughout 2021.

At Terronera the Company commenced the 2021 drill program targeting the southeast area near the Terronera vein and regional area acquired in 2020. A total of 10,117 metres were drilled in 37 holes intersecting high grade silver-gold mineralization in a number of structures near the Terronera vein, highlighting the potential of the area. Four structures, the San Simon, Fresno, Pendencia and Lindero veins are located immediately to the southeast of the Terronera vein, and the Los Cuates vein is located approximately 10 kilometers to the northwest of the Terronera Project. The drill results represent ongoing exploration work at the Terronera Project, with a plan to complete 16,000 metres of drilling by the end of the year. Key targets include extensions of the Terronera vein, which hosts most of the reserves in the Terronera Feasibility Study that is planned to be completed in Q3, 2021, and more regional targets to grow resources in the district. As the Feasibility Study is nearing completion, all 2021 drill results will not be included as part of the development plan.

At Parral the Company commenced the drill program in March, drilling 19 holes totaling 4,715 metres in untested areas of the Colorada vein. The 2021 drill program is on-going with results and interpretation expected in Q3, 2021.

In Chile, the Company completed initial drilling on the Paloma properties targeting a bulk tonnage, sulfidation epithermal deposit relate to intrusive domes or the tops of porphyry systems located in the Chilean Miocene deposit belt, 180 kilometers southeast of the city of Calama, 5,000 metres above sea level. The Company has an option to acquire up to 70% ownership of 5,100 hectares from Compañía Minera del Pacifico. To date, Endeavour completed 5,945 metres of diamond drilling in 13 drill holes. Drilling confirmed widespread alteration and low-grade gold mineralization. Highlights include 0.4 grams per tonne of gold over 46 metres true width, however it is interpreted that the drilling did not reach the core of the system. The exploration team is currently analyzing the drill results to develop the next phase drill program to test for the possibility of higher-grade mineralization.

CONSOLIDATED FINANCIAL RESULTS

Three months ended June 30, 2021 (compared to the three months ended June 30, 2020)

In Q2, 2021, the Company's mine operating earnings was $10.2 million (Q2, 2020: $3.1 million) on net revenue of $47.7 million (Q2, 2020: $20.2 million) with cost of sales of $37.5 million (Q2, 2020: $17.1 million).

In Q2, 2021, the Company had operating earnings of $0.8 million (Q2, 2020: operating loss $4.6 million) after exploration costs of $5.0 million (Q2, 2020: $1.7 million), general and administrative costs of $4.3 million (Q2, 2020: $3.1 million), care and maintenance expense for the El Cubo operation of $0.1 million (Q2, 2020: $0.7 million) and in Q2 2020 there was an additional $2.2 million in care and maintenance costs related to the temporary suspension of the Guanaceví, Bolañitos and El Compas operations due to COVID-19.

The earnings before taxes for Q2, 2021 was $8.9 million (Q2, 2020: loss before taxes $3.6 million) after finance costs of $0.2 million (Q2, 2020: $0.4 million), a foreign exchange gain of $0.7 million (Q2, 2020: $0.7 million), gain on disposal of assets of $5.8 million (Q2, 2020: $nil) and investment and interest income of $1.8 million (Q2, 2020: $0.7 million). The Company realized net earnings for the period of $6.7 million (Q2, 2020: net loss of $3.3 million) after an income tax expense of $2.2 million (Q2, 2020: income tax recovery of $0.3 million).

Net revenue of $47.7 million in Q2, 2021, net of $0.6 million of smelting and refining costs, increased by 136% compared to $20.2 million, net of $0.3 million of smelting and refining costs in Q2, 2020. Gross sales of $48.3 million in Q2, 2021 represented a 136% increase over the $20.5 million for the same period in 2020. There was a 76% increase in silver ounces sold and a 57% increase in the realized silver price resulting in a 179% increase to silver sales. There was an 88% increase in gold ounces sold with no change in realized gold prices resulting in a 88% increase in gold sales. During the period, the Company sold 1,120,266 oz silver and 9,810 oz gold, for realized prices of $26.82 and $1,866 per oz respectively, compared to sales of 634,839 oz silver and 5,218 oz gold, for realized prices of $17.04 and $1,862 per oz, respectively, in the same period of 2020. For the three months ended June 30, 2021, the realized prices of silver were within approximately 1% to London spot prices and the realized prices of gold were within approximately 3% to London spot prices. During the same period, silver and gold spot prices averaged $26.69 and $1,816, respectively.

The Company slightly decreased its finished goods silver and increased its gold inventory to 471,817 oz and 2,835 oz, respectively at June 30, 2021 compared to 529,817 oz silver and 1,689 oz gold at March 31, 2021. The cost allocated to these finished goods was $10.1 million at June 30, 2021, compared to $8.0 million at March 31, 2021. At June 30, 2021, the finished goods inventory fair market value was $17.3 million, compared to $15.9 million at March 31, 2021.

Cost of sales for Q2, 2021 was $37.5 million, an increase of 119% over the cost of sales of $17.1 million for the same period of 2020. The increase in cost of sales was primarily related to significantly higher labour costs and royalty costs partially offset by improved productivity at the Guanaceví and Bolañitos operations and the temporary suspension of the Guanaceví, Bolañitos and El Compas operations due to COVID-19 during Q2 2020, which significantly affected sales and costs of sales in the prior period. Royalties increased 420% to $4.3 million due to higher realized prices and the increased mining of the high grade Porvenir and Porvenir Cuatro extensions at the Guanaceví operation which is subject to the significantly higher royalty rates.

During Q2, 2021 the Company's operations experienced higher costs than budgeted due to global supply constraints creating inflationary pressure, labour costs are tracking higher than guidance and increased operating development at Guanaceví.

Exploration and evaluation expenses increased in Q2, 2021 to $5.0 million from $1.7 million for the same period of 2020 primarily based on additional expenditures to advance the Terronera Feasibility Study and the timing of drill programs as drilling was also suspended during Q2 2020 due to COVID-19. General and administrative expenses increased to $4.3 million in Q2, 2021 compared to $3.1 million for the same period of 2020, due to mark-to-market fluctuations for director's deferred share units which comparatively increased costs by $0.4 million, additional salary costs as during early 2020 senior management took voluntary pay reductions and received lower bonuses and the impact on the strengthening of the Canadian dollar increasing the US dollar amount of Canadian dollar expenditures.

The Company incurred a foreign exchange gain of $0.7 million in Q2, 2021 compared to a foreign exchange gain of $0.7 million in Q2, 2020 due to the strengthening of the Mexican Peso at the end of Q2, 2021 and Q2, 2020 compared to the prior quarters which resulted in higher valuations of peso denominated tax receivables and cash balances. The Company incurred $0.2 million in finance charges primarily related to mobile equipment purchased in 2019 and early 2020 compared to $0.4 million in the same period in 2020. The decrease is a result of the decrease in the loan balances. The Company recognized $1.8 million in investment and other income compared to $0.6 million in Q1, 2020 with the majority of the other income derived from the gain on marketable securities and interest received on IVA collections. During Q2, 2021, the Company also recognized a gain on the sale of the El Cubo mine of $5.8 million.

Income tax expense was $2.2 million in Q2, 2021 compared to an income tax recovery of $0.3 million in Q2, 2020. The $2.2 million tax expense is comprised of $1.1 million in current income tax expense (Q2, 2020: $0.2 million) and $1.1 million in deferred income tax expense (Q2, 2020: deferred income tax recovery of $0.5 million). The current income tax expense consists of $0.9 million of special mining duty taxes and $0.2 million of income taxes. The deferred income tax expense of $1.1 million is due to the use of loss carry forwards to offset taxable income generated at the Guanaceví operations.

The recoverable amounts of the Company's cash-generating units (CGUs), which include mining properties, plant and equipment are determined at the end of each reporting period, if impairment indicators are identified. In previous years, commodity price declines led the Company to determine there were impairment indicators and assessed the recoverable amounts of its CGUs. The recoverable amounts were based on each CGUs future cash flows expected to be derived from the Company's mining properties and represent each CGU's value in use. The cash flows were determined based on the life-of-mine after-tax cash flow forecast which incorporates management's best estimates of future metal prices, production based on current estimates of recoverable reserves and resources, exploration potential, future operating costs and non-expansionary capital expenditures discounted at risk adjusted rates based on the CGUs weighted average cost of capital.

Six months ended June 30, 2021 (compared to the six months ended June 30, 2020)

For the six-month period ended June 30, 2021, the Company's mine operating earnings was $15.9 million (2020: $0.2 million) on net revenue of $82.2 million (2020: $42.1 million) with cost of sales of $66.3 million (2020: $41.9 million).

The Company had operating earnings of $15.1 million (2020: operating loss $13.2 million) after exploration costs of $9.2 million (2020: $4.1 million), general and administrative costs of $7.8 million (2020: $5.1 million), care and maintenance expense for the El Cubo operation of $0.6 million (2020: $2.0 million) and an impairment reversal of $16.8 million as a result of the valuation assessment done as a result of the El Cubo mine and related assets a liabilities classification as held for sale. In Q2 2020 there was an additional $2.2 million in care and maintenance costs related to the temporary suspension of the Guanaceví, Bolañitos and El Compas operations due to COVID-19.

The earnings before taxes was $24.9 million (2020: loss before taxes $17.4 million) after finance costs of $0.5 million (2020: $0.7 million), a foreign exchange loss of $35 thousand (2020 $4.2 million), a gain on disposal of the El Cubo assets of $5.8 million (2020: $nil) and investment and interest income of $4.5 million (2020: $0.7 million) . The Company realized net earnings for the period of $18.9 million (2020: net loss of $19.2 million) after an income tax expense of $6.0 million (2020: $1.8 million).

Net revenue of $82.2 million in for the first half of 2021, net of $1.2 million of smelting and refining costs, increased by 95% compared to $42.1 million, net of $0.8 million of smelting and refining costs in 2020. Gross sales of $83.4 million in 2021 represented a 94% increase over the $42.9 million for the same period in 2020. There was a 34% increase in silver ounces sold and a 67% increase in the realized silver price resulting in a 124% increase to silver sales. There was a 62% increase in gold ounces sold with a 3% increase in realized gold prices resulting in a 66% increase in gold sales. During the period, the Company sold 1,743,645 oz silver and 20,473 oz gold, for realized prices of $26.95 and $1,781 per oz respectively, compared to sales of 1,300,339 oz silver and 12,672 oz gold, for realized prices of $16.16 and $1,727 per oz, respectively, in the same period of 2020. For the six months ended June 30, 2021, the realized prices of silver and gold were within approximately 2% to London spot prices. During the same period, silver and gold spot prices averaged $26.47 and $1,805, respectively.