Exhibit 99.1

| 20_13 ANNUAL REPORT Making Our Mark in 2013 LAKE SHORE GOLD CORP. |

| TABLE OF CONTENTS 2 Letter to Shareholders 4 Performance Against 2013 Objectives 4 Objectives for 2014 5 Reserves and Resources 6 Management’s Discussion & Analysis 34 Management’s Responsibility for Financial Reporting 35 Management’s Report on Internal Controls Over Financial Reporting 36 Report of Independent Registered Public Accounting Firm 37 Consolidated Statements of Financial Position 38 Consolidated Statements of Comprehensive Loss 39 Consolidated Statements of Cash Flows 40 Consolidated Statements of Changes in Equity 41 Notes to the Consolidated Financial Statements 82 Corporate Information CORPORATE PROFILE Lake Shore Gold Corp. is a Canadian gold producer that is generating net free cash flow from its wholly owned operations in the Timmins Gold Camp of Northern Ontario. The Company is in production at both the Timmins West and Bell Creek mines, which combined for 134,600 ounces of gold production in 2013, a 57% increase from 2012. The completion of a mill expansion during the third quarter of 2013 marked the end of a multi-year growth capital program aimed at establishing mining and milling operations capable of producing over 3,000 tonnes per day. The target production rate was met, and exceeded, beginning in September 2013, with the Company entering 2014 positioned to process between 3,200 and 3,300 tonnes per day and produce between 160,000 and 180,000 ounces of gold during the year. In addition to current operations, the Company has a number of highly prospective projects and exploration targets located in and around the Timmins Camp and, in many cases, situated in close proximity to existing operations. The Company’s common shares trade on the TSX and NYSE MKT under the symbol LSG. MINING OPERATIONS Lake Shore Gold is in production at both the Timmins West Mine (photo above) and Bell Creek Mine. Timmins West Mine, located 18 kilometres west of Timmins, Ontario, is the Company’s flagship asset. In 2013, production at the mine totaled 107,100 ounces and is expected to grow to over 130,000 ounces in 2014. The mine is well constructed with excellent infrastructure and significant potential to grow resources and extend mine life. Bell Creek Mine, located 20 kilometres east of Timmins, produced 27,500 ounces in 2013 using a surface ramp with production targeted to grow to over 30,000 ounces in 2014. With the majority of resources below current mining, considerable opportunity exists to grow the size and scale of mining operations at Bell Creek with additional investment. |

| LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 1 MILL EXPANSION In 2013, Lake Shore Gold made its mark by completing a major expansion, increasing production, improving unit costs, reducing capital requirements, managing its balance sheet and generating net free cash flow during the fourth quarter. Making Our Mark in 2013 1 LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 A major milestone was achieved during the third quarter of 2013 when the Company completed an expansion of its milling facility to a production rate of over 3,000 tonnes per day. The Bell Creek Mill is a conventional gold milling circuit that has consistently achieved average recoveries of over 95%. Following completion of the expansion, the Company averaged 3,500 tonnes per day in the fourth quarter of 2013 as the mill processed both mine production and ore stockpiled during mill commissioning. While the Company anticipates averaging between 3,200 and 3,300 tonnes per day in 2014, the fact that the mill has performed well at higher throughput levels is a reflection of the excellent quality of the new milling infrastructure and the opportunity it provides for future growth. |

| LETTER TO SHAREHOLDERS In 2013, YOUR COMPANY COMPLETED A MULTI-YEAR GROWTH CAPITAL PROGRAM AND MET OR EXCEEDED ITS KEY PERFORMANCE TARGETS. WE INCREASED PRODUCTION, IMPROVED UNIT COSTS, REDUCED CAPITAL REQUIREMENTS, MANAGED OUR BALANCE SHEET AND GENERATED NET FREE CASH FLOW DURING THE FOURTH QUARTER. VERY IMPORTANTLY, WE IMPROVED OUR SAFETY PERFORMANCE, MAKING LAKE SHORE GOLD ONE OF THE SAFEST MINING COMPANIES IN ONTARIO. Lake Shore Gold had a very successful 2013. We completed our mill expansion and brought our production rate to well over 3,000 tonnes per day. For the year, we increased production 57% to 134,600 ounces, improved our cash operating costs(1) per ounce sold by 23% and reduced our capital expenditures. We made debt repayments of approximately $20 million and commenced generating net free cash flow in the fourth quarter. Our cash earnings from mine operations(1) rose 60% from 2012. Our net loss for the year reflected non-cash items, most significantly a $225 million impairment charge. The charge largely resulted from lower gold prices, which affected the estimated net carrying value of our assets as well as our levels of resources and reserves. A very important area of progress in 2013 was safety. We achieved the best safety performance in our history, improving our Total Medical Injury Frequency Rate to 2.6, among the best in the province. If cash flow is the fuel that drives our future, operating safely and responsibly provides the driver’s license that keeps us on the road. Looking back over 2013, our stock price reached a low in June. Among the contributing factors was a gold price that had corrected by over US$300 per ounce from a few months earlier. In addition, we were still investing considerable capital on our mill expansion and ramping up production. As a result, we were drawing down our cash at a time of declining gold prices and our share price was affected by market concern over our debt and debt covenants. How did your company respond? We effectively managed our debt and remained in compliance with our debt covenants throughout the year. We also extended the maturity of the standby line of credit in December and negotiated improvements to our debt covenants, providing us with greater flexibility. 2 LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 |

| At the same time, we remained focused on our capital program and business objectives. We completed our mill expansion during the third quarter and, by the fourth quarter, were operating at well over 3,000 tonnes per day. Our production increased significantly, totaling 51,700 ounces in the fourth quarter, ahead of target levels. Our unit costs improved each quarter of 2013, with cash operating costs for the full year averaging US$766 per ounce, better than our guidance of US$800 to US$875 per ounce. Our capital requirements declined sharply, falling to $10.3 million in the fourth quarter and totaling $90.4 million for the year, in line with our guidance. And, we increased our cash and bullion during the fourth quarter by $18.8 million to $34.0 million at year end. Looking forward, we entered 2014 positioned for a record year including production of 160,000 – 180,000 ounces of gold, cash operating costs of between US$675 and US$775 per ounce sold and all-in sustaining costs(1) of US$950 – US$1,050 per ounce sold. We expect to generate significant free cash flow assuming our budget price of $1,300 (Canadian) per ounce and are highly leveraged to gold prices above that level. We are off to a good start in the year. In the first two months of 2014 our production totaled 29,500 ounces and, with an average selling price of $1,406 per ounce, our cash position increased by approximately $7.0 million. We also entered 2014 with a renewed commitment to exploration. In March, we announced a reduction in our resources and reserves. The reduction largely reflected lower gold prices and the fact that we have focused our drilling over the last two years within existing resources in support of mining activities rather than on identifying and adding new ounces. We have now entered a replenishing phase with a new drilling program in progress. The program is focused on high-potential targets at both our Timmins West and Bell Creek mines. We have already announced some encouraging drill results at Bell Creek, which included identifying new, high-grade structures within 100 metres of current mining activities. It is an exciting time for Lake Shore Gold. It is a time when the return on a lot of hard work and investment has started to be realized. It is also a time when we have resumed the build out of our existing deposits and can consider future growth through evaluation of our large, wholly owned projects. Through our Gold River, Bell Creek Deep, Vogel and Fenn-Gib projects, we have a number of attractive opportunities for future growth located in close proximity to our existing mining operations. I want to thank the people of Lake Shore Gold, our employees, suppliers and contractors, for their hard work and commitment over the last year. I also want to thank our shareholders for their ongoing support and belief in our future. We have come through the challenging development phase of building a low-cost gold producer. We have invested our capital well, achieved target production levels and are well positioned to create value going forward. Tony Makuch President & CEO 3 LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 |

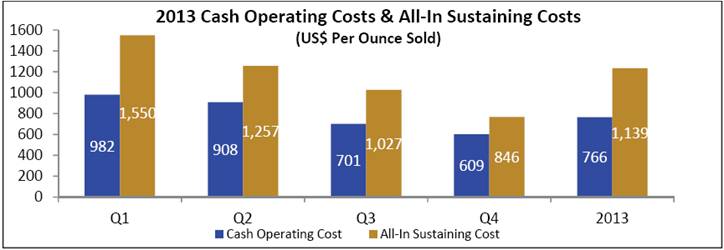

| LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 4 Q1 2013 Production (Ounces) 23,200 Q2 Q3 Q4 2013 30,800 28,900 51,700 134,600 Q1 2013 Cash Operating Costs & All-In Sustaining Costs (US$ Per Ounce Sold) 982 1,550 Q2 Q3 Q4 2013 908 1,257 701 1,027 609 849 766 1,139 Q1 Mill Throughput (Tonnes Per Day) 2,200 Q2 Q3 Q4 2013 2,540 2,200 3,500 2,610 ALL-IN SUSTAINING COSTS CASH OPERATING COSTS Q1 Capital Investment ($ Millions) 38.2 Q2 Q3 Q4 2013 27.7 14.2 10.3 90.4 Achieve at least 40% growth in production to 120,000 to 135,000 ounces of gold. Production increased 57% to 134,600 ounces. The Company set a quarterly record for production in the second quarter of 2013, with mill throughput averaging over 2,500 tonnes per day for the first time. Following completion of Phase 2 of the Company’s mill expansion during the third quarter, production reached a new record of 51,700 ounces in the fourth quarter, with average mill throughput of 3,500 tonnes per day resulting from processing both mine production and ore from stockpiles built up during mill commissioning. Improve cash operating costs(1) to between US$800 and US$875 per ounce. Cash operating costs in 2013 averaged US$766 per ounce sold, a 23% improvement from 2012 and better than the target range. Cash operating costs improved each quarter during the year and reached a low of US$609 per ounce sold during the fourth quarter. In the second quarter of 2013, the Company adopted a new unit cost measure, all-in sustaining costs(1) or “AISC”. The Company defines AISC as the sum of production costs, sustaining capital, corporate general and administrative expenses, in-mine exploration expenses and reclamation cost accretion related to current operations. AISC in 2013 averaged US$1,139 per ounce sold, a 37% improvement from 2012. Reduce capital investment by close to 50%, to $90 million. Total capital investment in 2013 totaled $90.4 million, a reduction of 47% from 2012 and in line with the Company’s guidance. Investment levels decreased each quarter of 2013 and declined dramatically starting in the third quarter with the completion and commissioning of Phase 2 of the Company’s mill expansion. Complete Phase 2 mill expansion to a production rate of over 3,000 tonnes per day during the second quarter. Commissioning of Phase 2 of the mill expansion commenced in July with the target processing rate achieved, and exceeded, for the first time in September, when mill throughput averaged 3,370 tonnes per day. During the fourth quarter, throughput averaged 3,500 tonnes per day, in excess of target levels. The expansion was completed in the third quarter rather than on the original schedule reflecting the need to manage the timing of cash outflows during a period of declining gold prices. (1) cash operating costs, all-in sustaining costs and cash earnings from mine operations are examples of non-Gaap measures. a discussion of non-Gaap measures is provided in the Non-Gaap Measures section of the Management’s Discussion & Analysis beginning on page 23 of this annual report. Objectives for 2014 Performance Against 2013 Objectives • Increase production to 160,000 – 180,000 ounces of gold • Achieve cash operating costs of between US$675 and US$775 per ounce sold • Reduce AISC to within a range of US$950 and US$1,050 per ounce sold • Achieve average mill throughput of 3,200 – 3,300 tonnes per day • Make debt repayments of between $20 and $25 million 4 LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 |

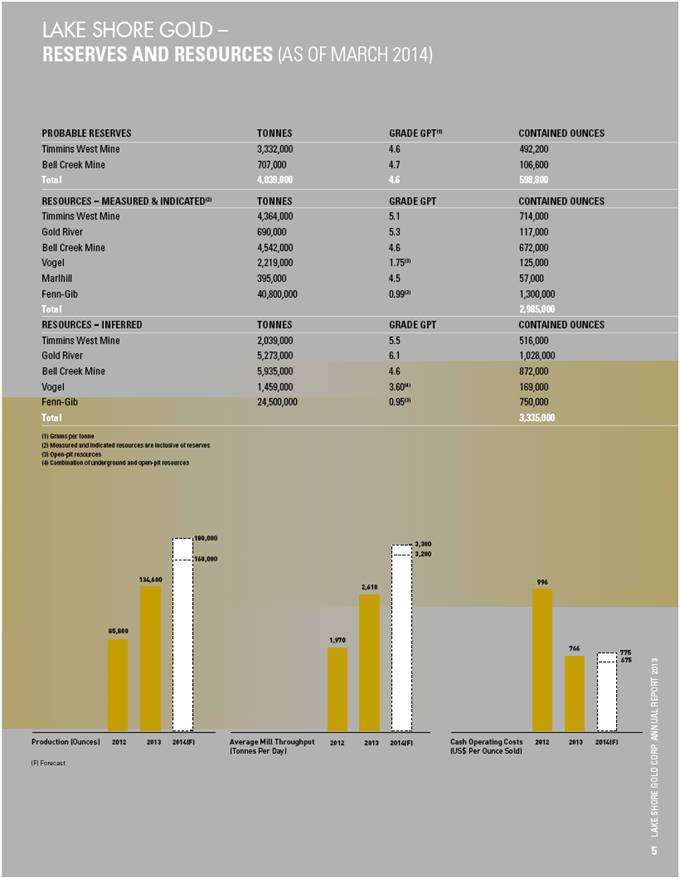

| LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 5 LAKE SHORE GOLD – RESERVES AND RESOURCES (AS OF MARCH 2014) PROBABLE RESERVES TONNES GRADE GPT(1) CONTAINED OUNCES Timmins West Mine 3,332,000 4.6 492,200 Bell Creek Mine 707,000 4.7 106,600 Total 4,039,000 4.6 598,800 RESOURCES – MEASURED & INDICATED(2) TONNES GRADE GPT CONTAINED OUNCES Timmins West Mine 4,364,000 5.1 714,000 Gold River 690,000 5.3 117,000 Bell Creek Mine 4,542,000 4.6 672,000 Vogel 2,219,000 1.75(3) 125,000 Marlhill 395,000 4.5 57,000 Fenn-Gib 40,800,000 0.99(3) 1,300,000 Total 2,985,000 RESOURCES – INFERRED TONNES GRADE GPT CONTAINED OUNCES Timmins West Mine 2,039,000 5.5 516,000 Gold River 5,273,000 6.1 1,028,000 Bell Creek Mine 5,935,000 4.6 872,000 Vogel 1,459,000 3.60(4) 169,000 Fenn-Gib 24,500,000 0.95(3) 750,000 Total 3,335,000 (1) Grams per tonne (2) Measured and indicated resources are inclusive of reserves (3) Open-pit resources (4) Combination of underground and open-pit resources Production (Ounces) 2014(F) 2013 2012 85,800 134,600 180,000 160,000 Cash Operating Costs (US$ Per Ounce Sold) 2014(F) 2013 2012 996 766 775 675 Average Mill Throughput (Tonnes Per Day) 2014(F) 2013 2012 1,970 2,610 3,200 3,300 (F) Forecast 5 LAKE SHORE GOLD CORP. ANNUAL REPORT 2013 |

Management’s Responsibility for Financial Reporting

The accompanying consolidated financial statements have been prepared by management and are in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IASB”). Other information contained in this document has also been prepared by management and is consistent with the data contained in the consolidated financial statements. A system of internal controls has been developed and is maintained by management to provide reasonable assurance that assets are safeguarded and financial information is accurate and reliable.

The Board of Directors approves the financial statements and ensures that management discharges its financial reporting responsibilities. The Board’s review is accomplished principally through the audit committee, which is composed of non-executive directors. The audit committee meets periodically with management and the auditors to review financial reporting and control matters.

/signed Anthony Makuch | | /signed Philip C. Yee |

| | |

Anthony Makuch | | Philip C. Yee |

Chief Executive Officer | | Vice President and Chief Financial Officer |

| | |

March 18, 2014 | | |

Toronto, Canada | | |

2

Management’s Report on Internal Controls Over Financial Reporting

The management of Lake Shore Gold Corp. (the “Company”) is responsible for establishing and maintaining adequate internal controls over financial reporting. The Company’s internal controls over financial reporting are reviewed and approved by the Chief Executive Officer and the Vice President and Chief Financial Officer with the expectation of providing reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with International Financial Reporting Standards as issued by the IASB.

Due to its inherent limitations, internal controls over financial reporting may not prevent or detect misstatements on a timely basis. Also, projections regarding the effectiveness of these controls applicable to future periods are subject to risk and may not be sufficient to meet the degree of compliance required to comply with the policies or procedures in the future.

Management conducted an assessment of the Company’s internal controls over financial reporting based on the “Internal Control-Integrated Framework (1992)” established by the Committee of Sponsoring Organizations of the Treadway Commission (“COSO”). Based on that assessment, the Chief Executive Officer and Vice President and Chief Financial Officer concluded the Company’s internal controls over financial reporting were effective as of December 31, 2013. There were no material weaknesses identified by management as of December 31, 2013.

/signed Anthony Makuch | | /signed Philip C. Yee |

| | |

Anthony Makuch | | Philip C. Yee |

Chief Executive Officer | | Vice President and Chief Financial Officer |

| | |

March 18, 2014 | | |

Toronto, Canada | | |

3

Report of Independent Registered Public Accounting Firm

To the Shareholders and Board of Directors of Lake Shore Gold Corp.

We have audited the accompanying consolidated financial statements of Lake Shore Gold Corp. and subsidiaries (the “Company”), which comprise the consolidated statements of financial position as at December 31, 2013 and 2012 and the consolidated statements of comprehensive loss, consolidated statements of changes in equity and consolidated statements of cash flows for the years ended December 31, 2013 and December 31, 2012, and a summary of significant accounting policies and other explanatory information.

Management’s Responsibility for the Consolidated Financial Statements

Management is responsible for the preparation and fair presentation of these consolidated financial statements in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board, and for such internal control as management determines is necessary to enable the preparation of consolidated financial statements that are free from material misstatement, whether due to fraud or error.

Auditor’s Responsibility

Our responsibility is to express an opinion on these consolidated financial statements based on our audits. We conducted our audits in accordance with Canadian generally accepted auditing standards. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the consolidated financial statements are free from material misstatement. We were not engaged to perform an audit of the Company’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting, accordingly we express no such opinion.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the consolidated financial statements. The procedures selected depend on the auditor’s judgment, including the assessment of the risks of material misstatement of the consolidated financial statements, whether due to fraud or error. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the consolidated financial statements.

We believe that the audit evidence we have obtained in our audits is sufficient and appropriate to provide a basis for our audit opinion.

Opinion

In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as at December 31, 2013 and 2012 and its financial performance and its cash flows for the years ended December 31, 2013 and December 31, 2012 in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board.

“Deloitte LLP” |

|

Chartered Professional Accountants, Chartered Accountants |

Licensed Public Accountants |

|

March 18, 2014 |

Toronto, Canada |

4

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

(in thousands of Canadian dollars)

As at | | Note | | December 31, 2013 | | December 31, 2012 | |

| | | | | | | |

Assets | | | | | | | |

Current assets | | | | | | | |

Cash and cash equivalents | | | | $ | 33,120 | | $ | 48,715 | |

Receivables and prepaids | | 10 | | 3,589 | | 7,736 | |

Inventories and stockpiled ore | | 11 | | 20,378 | | 27,626 | |

Assets held for sale | | 9(i)(a) | | — | | 2,432 | |

| | | | 57,087 | | 86,509 | |

Non-current assets | | | | | | | |

Available for sale financial assets and warrant investments | | 12 | | 416 | | 810 | |

Investments in associates | | 13 | | 1,749 | | 5,361 | |

Restricted cash | | 14 | | 7,095 | | 7,095 | |

Mining interests | | 15 | | 531,585 | | 719,888 | |

Deferred financing costs | | 19(a) | | — | | 3,352 | |

| | | | $ | 597,932 | | $ | 823,015 | |

| | | | | | | |

Liabilities | | | | | | | |

Current liabilities | | | | | | | |

Accounts payable and accrued liabilities | | 17 | | $ | 21,619 | | $ | 33,867 | |

Current portion of finance lease obligations | | 18 | | 3,446 | | 6,324 | |

Current portion of long term debt | | 19 | | 13,339 | | 18,219 | |

| | | | 38,404 | | 58,410 | |

Non-current liabilities | | | | | | | |

Finance lease obligations | | 18 | | 6,150 | | 2,812 | |

Long term debt | | 19 | | 116,686 | | 100,334 | |

Share-based liabilities | | 20 | | 754 | | 479 | |

Environmental rehabilitation provision | | 21 | | 4,770 | | 5,257 | |

| | | | 128,360 | | 108,882 | |

| | | | | | | |

Shareholders’ Equity | | | | | | | |

Share capital | | | | 1,017,262 | | 1,016,524 | |

Equity portion of convertible debentures | | | | 14,753 | | 14,753 | |

Reserves | | | | 31,388 | | 23,212 | |

Deficit | | | | (632,235 | ) | (398,766 | ) |

| | | | 431,168 | | 655,723 | |

| | | | $ | 597,932 | | $ | 823,015 | |

Commitments and contractual obligations (note 29)

See accompanying notes to the consolidated financial statements

Approved by the Board

/signed Alan Moon | | /signed Arnold Klassen |

Alan C. Moon | | Arnold Klassen |

Director | | Director |

5

CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS

(in thousands of Canadian dollars, except per share amounts)

For the years ended December 31, | | Note | | 2013 | | 2012 | |

| | | | | | | |

Revenue | | | | $ | 192,647 | | $ | 133,012 | |

Production costs | | 6 | | (107,491 | ) | (80,037 | ) |

Depletion and depreciation | | | | (60,205 | ) | (42,641 | ) |

Impairment charge | | 16 | | (225,000 | ) | (231,000 | ) |

Loss from mine operations | | | | (200,049 | ) | (220,666 | ) |

| | | | | | | |

General and administrative | | | | (12,555 | ) | (11,467 | ) |

Exploration and evaluation | | 15 | | (1,313 | ) | (3,769 | ) |

Write down of investments in associates and available for sale investment | | 12,13,28 | | (3,874 | ) | (7,529 | ) |

Share of loss of investments in associates | | 13 | | (1,833 | ) | (2,738 | ) |

Loss from operations and associates | | | | (219,624 | ) | (246,169 | ) |

Other income (loss), net | | 7 | | 5,133 | | (518 | ) |

Finance items | | 8 | | | | | |

Finance income | | | | 706 | | 552 | |

Finance expense | | | | (15,382 | ) | (3,283 | ) |

Loss before taxes | | | | (229,167 | ) | (249,418 | ) |

Deferred mining tax recovery | | 16,22 | | — | | 3,029 | |

Loss from continuing operations | | | | (229,167 | ) | (246,389 | ) |

Loss from discontinued operations | | 9(i) | | (4,302 | ) | (71,543 | ) |

Net loss | | | | $ | (233,469 | ) | $ | (317,932 | ) |

Other comprehensive income (loss) | | | | | | | |

Items that may be reclassified subsequently to profit or loss | | | | | | | |

Other comprehensive income (loss) from continuing operations, net of tax | | | | | | | |

Unrealized loss on available for sale investments, net of tax | | 9(ii),12 | | 1,786 | | (2,560 | ) |

Other comprehensive income from discontinued operations | | | | | | | |

Exchange differences on translation of foreign operations | | 9(i(b)) | | 3,967 | | 3,712 | |

Comprehensive loss from continuing operations | | | | $ | (227,381 | ) | $ | (248,949 | ) |

Comprehensive loss from discontinued operations | | | | $ | (335 | ) | $ | (67,831 | ) |

Total comprehensive loss | | | | $ | (227,716 | ) | $ | (316,780 | ) |

Basic and diluted loss per share | | 23(c) | | | | | |

Loss per share from continuing operations | | | | $ | (0.55 | ) | $ | (0.60 | ) |

Loss per share | | | | $ | (0.56 | ) | $ | (0.77 | ) |

| | | | | | | |

Weighted average number of common shares outstanding (in 000’s) | | 23(c) | | | | | |

Basic and Diluted | | | | 416,536 | | 411,334 | |

See accompanying notes to the consolidated financial statements

6

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands of Canadian dollars)

For the years ended December 31, | | Note | | 2013 | | 2012 | |

| | | | | | | |

Operating Activities | | | | | | | |

| | | | | | | |

Loss from continuing operations | | | | $ | (229,167 | ) | $ | (246,389 | ) |

Impairment charge | | | | 225,000 | | 231,000 | |

Depletion and depreciation | | | | 60,316 | | 42,812 | |

Share-based payments expense | | | | 2,621 | | 4,136 | |

Share of loss of investments in associates | | | | 1,833 | | 2,738 | |

Write down of investment in associates and available for sale investment | | | | 3,874 | | 7,529 | |

Other (income) loss, net | | | | (5,133 | ) | 518 | |

Finance income | | | | (706 | ) | (552 | ) |

Interest received | | | | 629 | | 531 | |

Finance expense | | | | 15,382 | | 3,283 | |

Interest paid | | | | (10,120 | ) | (2,260 | ) |

Deferred mining tax recovery | | | | — | | (3,029 | ) |

Change in non-cash operating working capital | | 25 | | 6,118 | | (10,434 | ) |

Net cash flow provided by continuing operating activities | | | | 70,647 | | 29,883 | |

Net cash flow used by discontinued operating activities | | | | — | | (43 | ) |

| | | | | | | |

Investing Activities | | | | | | | |

| | | | | | | |

Additions to mining interests, net of pre-production sales and movements in working capital | | | | (99,901 | ) | (161,888 | ) |

Restricted cash | | | | — | | (1,441 | ) |

Proceed from sale of available for sale investment | | 12 | | — | | 1,017 | |

Proceeds from sale of mining interest | | | | 200 | | — | |

Net cash flow used in investing activities of continuing operations | | | | (99,701 | ) | (162,312 | ) |

Net cash flow used in investing activities of discontinued operations | | | | — | | — | |

| | | | | | | |

Financing Activities | | | | | | | |

| | | | | | | |

Proceeds from long term debt, net of transaction costs | | 19(a,b) | | 33,450 | | 132,435 | |

Proceeds from sale lease back | | 18 | | 7,300 | | — | |

Long term debt payments | | 19(a,c) | | (21,454 | ) | (49,055 | ) |

Payment of finance lease obligations | | | | (5,739 | ) | (8,598 | ) |

Proceeds from sale of royalty interest, net of transaction costs | | 15 | | — | | 34,704 | |

Common shares issued for cash (net of share issue costs) | | | | — | | 14,881 | |

Exercise of stock options and warrants | | | | 23 | | 68 | |

Net cash flow provided by financing activities of continuing operations | | | | 13,580 | | 124,435 | |

Net cash flow provided by financing activities of discontinued operations | | 15 | | — | | 1,151 | |

| | | | | | | |

Impact of foreign exchange on cash balances | | | | $ | (121 | ) | (358 | ) |

| | | | | | | |

Decrease in cash and cash equivalents during the year | | | | (15,595 | ) | (7,244 | ) |

Cash and cash equivalents at beginning of year | | | | 48,715 | | 55,959 | |

Cash and cash equivalents at end of year | | | | $ | 33,120 | | $ | 48,715 | |

Supplemental cash flow information note 25

See accompanying notes to the consolidated financial statements

7

LAKE SHORE GOLD CORP.

CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(in thousands of Canadian dollar except for share information)

| | | | | | | | | | Reserves | | | | | |

| | | | Share capital | | Equity portion | | | | | | Currency | | Investment | | | | | |

| | Note | | Shares

(‘000s) | | Amount | | of convertible

debentures | | Warrants | | Share-based

payments | | translation

adjustment | | revaluation

reserve | | Deficit | | Shareholders’

equity | |

At January 1, 2013 | | | | 415,654 | | 1,016,524 | | $ | 14,753 | | $ | 2,469 | | $ | 26,259 | | $ | (3,967 | ) | $ | (1,549 | ) | $ | (398,766 | ) | $ | 655,723 | |

Shares issued as part of agreements (net of share issue costs of $30) | | 23(a) | | 936 | | 702 | | — | | — | | — | | — | | — | | — | | 702 | |

Share based payments | | 23(b(iv)) | | — | | — | | — | | — | | 2,436 | | — | | — | | — | | 2,436 | |

Stock-options exercised (including transfer from share based payments reserve of $13) | | 23(b(ii)) | | 30 | | 36 | | — | | — | | (13 | ) | — | | — | | — | | 23 | |

Net loss | | | | | | | | | | | | | | | | | | $ | (233,469 | ) | (233,469 | ) |

Other comprehensive income, net of tax | | | | | | | | | | | | | | 3,967 | | 1,786 | | — | | 5,753 | |

Total comprehensive income | | | | | | | | | | | | | | 3,967 | | 1,786 | | (233,469 | ) | (227,716 | ) |

At December 31, 2013 | | | | 416,620 | | 1,017,262 | | $ | 14,753 | | $ | 2,469 | | $ | 28,682 | | $ | — | | $ | 237 | | $ | (632,235 | ) | $ | 431,168 | |

| | | | | | | | | | Reserves | | | | | |

| | | | Share capital | | Equity portion of | | | | | | Currency | | Investment | | | | | |

| | Note | | Shares

(‘000s) | | Amount | | convertible

debentures | | Warrants | | Share-based

payments | | translation

adjustment | | revaluation

reserve | | Deficit | | Shareholders’

equity | |

At January 1, 2012 | | | | 400,169 | | $ | 992,318 | | $ | — | | $ | 2,469 | | $ | 21,543 | | $ | (7,679 | ) | $ | 1,011 | | $ | (80,834 | ) | $ | 928,828 | |

Shares issued as part of agreements (net of share issue costs of $119) | | 23(a) | | 15,401 | | 19,742 | | — | | — | | — | | — | | — | | — | | 19,742 | |

Equity portion of convertible debentures (net of transaction costs of $988) | | 19(b) | | — | | — | | 20,000 | | — | | — | | — | | — | | — | | 20,000 | |

Share based payments | | 23(b(iv)) | | — | | — | | — | | — | | 4,744 | | — | | — | | — | | 4,744 | |

Stock-options exercised (including transfer from share based payments reserve of $28) | | 23(b(ii)) | | 84 | | 96 | | — | | — | | (28 | ) | — | | — | | — | | 68 | |

Change in deferred tax assets (liabilities) | | 22 | | — | | 4,368 | | (5,247 | ) | — | | — | | — | | — | | — | | (879 | ) |

Net loss | | | | — | | — | | — | | — | | — | | — | | — | | (317,932 | ) | (317,932 | ) |

Other comprehensive income (loss), net of tax | | | | — | | — | | — | | — | | — | | 3,712 | | (2,560 | ) | — | | 1,152 | |

Total comprehensive income | | | | | | | | | | | | | | 3,712 | | (2,560 | ) | (317,932 | ) | (316,780 | ) |

At December 31, 2012 | | | | 415,654 | | 1,016,524 | | $ | 14,753 | | $ | 2,469 | | $ | 26,259 | | $ | (3,967 | ) | $ | (1,549 | ) | $ | (398,766 | ) | $ | 655,723 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

See accompanying notes to the consolidated financial statements

8

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

1. DESCRIPTION OF BUSINESS AND NATURE OF OPERATIONS

Lake Shore Gold Corp. (“Lake Shore Gold” or the “Company”) is a publicly listed company, incorporated in Canada; the Company’s shares are traded on the Toronto Stock Exchange and on the NYSE MKT stock exchange. The head office, principal address and record office are located at 181 University Avenue, Suite 2000, Toronto, Ontario, Canada, M5H 3M7. The Company is primarily engaged in the operation, exploration and development of three gold complexes located in the Timmins Gold Camp in Timmins, Ontario; the Company also has certain exploration properties in Quebec. The Company is in commercial production at its Timmins West Mine and Bell Creek Mine.

2. BASIS OF PREPARATION

Statement of Compliance

These consolidated financial statements have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”). The consolidated financial statements were approved by the Board of Directors of the Company on March 18, 2014.

These consolidated financial statements have been prepared under the historical cost convention, except for certain financial instruments measured at fair value, as set out in the accounting policies in note 3.

The preparation of financial statements in accordance with IFRS requires the use of certain critical accounting estimates. It also requires management to exercise its judgment in the process of applying the Company’s accounting policies. The areas involving a higher degree of judgment or complexity, or areas where assumptions and estimates are significant to the consolidated financial statements are disclosed in note 4.

3. SIGNIFICANT ACCOUNTING POLICIES

The principal accounting policies are set out below:

a) Basis of presentation and consolidation

The consolidated financial statements incorporate the financial statements of the Company and its subsidiaries. Subsidiaries are those entities controlled by the Company. Control exists when the Company is exposed or has rights to the variable returns from the subsidiary and has the ability to affect those returns through its power over the subsidiary. Power is defined as existing rights that give the Company the ability to direct the relevant activities of the subsidiary. The financial statements of the subsidiaries are included in the consolidated financial statements from the date that control is transferred to the Company to the date control ceases. All intercompany transactions, balances, income and expenses are eliminated in full upon consolidation.

An associate is an entity in which the Company or any of its subsidiaries have significant influence, and that is neither a subsidiary nor an interest in a joint venture. Significant influence is the power to participate in the financial and operating policy decisions of the investee but is not control or joint control over those

9

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

policies and is presumed to exist when the Company holds between 20 and 50 percent of the voting power of another entity.

The subsidiaries and associates of the Company as at December 31, 2013 and their principal activities are described below:

Name | | Place of

Incorporation | | Proportion of

Ownership Interest | | Principal Activity | |

Subsidiaries | | | | | | | |

LSG Holdings Corp. | | British Columbia | | 100 | % | Not active* | |

1583908 Alberta Limited | | Alberta | | 100 | % | Not active* | �� |

Associates | | | | | | | |

Northern Superior Resources | | British Columbia | | 23.8 | % | Exploration | |

Revolution Resources Corp. | | British Columbia | | 22.5 | % | Exploration | |

*In process of winding-up

The financial statements of subsidiaries are prepared for the same reporting periods as the Company, using consistent accounting policies. Where necessary, adjustments are made to bring the accounting policies of the Company’s associates in line with those of the Company. All intercompany balances and transactions have been eliminated upon consolidation.

b) Investment in associates

The Company’s investments in associates are accounted for using the equity method of accounting. Under the equity method, the Company’s investment in an associate is initially recognized at cost and subsequently increased or decreased to recognize the Company’s share of earnings and losses of the associate and for impairment losses after the initial recognition date. The Company’s share of an associate’s losses that are in excess of its investment in the associate are recognized only to the extent that the Company has incurred legal or constructive obligations or made payments on behalf of the associate. The Company’s share of earnings and losses of associates are recognized in net loss during the period.

After application of the equity method, the Company determines whether it is necessary to recognize an impairment loss on the Company’s investment in its associates. The Company determines at each statement of financial position date whether there is any objective evidence that the investment in the associate is impaired. If this is the case the Company calculates the amount of impairment as the difference between the recoverable amount of the associate and its carrying value and recognizes the amount in net loss. When a group entity transacts with an associate of the Company, profit and losses are eliminated to the extent of the Company’s interest in the relevant associate.

10

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

c) Non-current assets held for sale and discontinued operations

Non-current assets and disposal group are classified as held for sale if their carrying amount will be recovered principally through a sale transaction rather than through continuing use. This condition is regarded as met only when the sale is highly probable and the non-current asset (or disposal group) is available for sale in its present condition. Management must be committed to the sale, which should be expected to qualify for recognition as a completed sale within one year from the date of classification.

When the Company is committed to a sale plan involving loss of control of a subsidiary, all of the assets and liabilities of that subsidiary are classified as held for sale when the criteria described in the above paragraph are met, regardless of whether the Company will retain a non-controlling interest in its former subsidiary after the sale.

A discontinued operation is a component of an entity that either has been disposed of, or that is classified as held for sale, and represents a separate major line of business or geographical area of operations, is a part of a single coordinated plan to dispose of a separate major line of business or geographical area of operations, or is a subsidiary acquired exclusively with a view to resale.

Non-current assets (and disposal group) classified as held for sale and discontinued operations are measured at the lower of carrying amount or fair value less costs to sell. Any gain or loss from disposal of a business, together with the results of these operations until the date of disposal, is reported separately as discontinued operations. The financial information of discontinued operations is excluded from the respective captions in the Consolidated financial statements and related notes for all years presented.

d) Foreign currency translation

The functional currency for each entity consolidated with the Company is determined by the currency of the primary economic environment in which it operates (the “functional currency”). The consolidated financial statements are presented in Canadian dollars, which is the Company’s functional and reporting currency.

In preparing the financial statements of the individual entities, transactions in currencies other than the entity’s functional currency (foreign currencies) are recognized at the rates of exchange prevailing at the dates of the transactions. At the end of each reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at that date. Non-monetary items carried at fair value that are denominated in foreign currencies are translated at the rates prevailing at the date when the fair value was determined. Non-monetary items that are measured in terms of historical cost in a foreign currency are translated at the rate on the date of transaction.

Foreign operations are translated from their functional currencies into Canadian dollars on consolidation by applying the exchange rate at period-end for assets and liabilities and the average exchange rate for profit and loss items. Exchange differences, including differences that arise relating to long-term intercompany balances that form part of the net investment in a foreign operation, are recognized in other comprehensive income (as exchange differences on translation of foreign operations). Fair value adjustments arising on the acquisition of a foreign entity are treated as assets and liabilities of the foreign entity and translated at

11

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

the closing rate. On the disposal of a foreign operation the accumulated exchange differences in respect of that operation are reclassified to net loss.

e) Financial instruments

Financial assets and liabilities are recognized when the Company or its subsidiaries become party to the contracts that give rise to them and are classified as loans and receivables, financial instruments fair valued through profit or loss, held-to-maturity, available-for-sale financial assets and other liabilities, as appropriate. The Company considers whether a contract contains an embedded derivative when the entity first becomes a party to it. The embedded derivatives are separated from the host contract if the host contract is not measured at fair value through profit or loss and when the economic characteristics and risks are not closely related to those of the host contract. Reassessment only occurs if there is a change in the terms of the contract that significantly modifies the cash flows that would otherwise be required.

Financial assets at fair value through profit or loss (“FVTPL”)

Financial assets at FVTPL include financial assets held for trading and financial assets designated upon initial recognition as at FVTPL. A financial asset is classified in this category principally for the purpose of selling in the short term or if so designated by management. The Company holds warrants in certain public companies; the warrants are considered derivatives and measured at fair value, with changes in fair value at each period end recorded in net loss. Transaction costs are expensed as incurred.

Available-for-sale financial assets

Available-for-sale (“AFS”) financial assets are those non-derivative financial assets that are designated as such or are not classified as loans and receivables, held-to-maturity investments or financial assets at FVTPL. AFS financial assets are measured at fair value upon initial recognition and at each period end, with unrealized gains or losses being recognized as a separate component of equity in other comprehensive income until the investment is derecognized or until the investment is determined to be impaired at which time the cumulative gain or loss previously reported in equity is included in net loss. The Company has classified its investments in certain public companies as available-for-sale.

Loans and receivables

Trade receivables, loans and other receivables that have fixed or determinable payments that are not quoted in an active market are classified as loans and receivable. Loans and receivable are initially recognized at the transaction value and subsequently carried at amortized cost using the effective interest method if the time value of money is significant. Gains and losses are recognized in the statement of comprehensive loss when the loans and receivables are derecognized or impaired, as well as through the amortization process. Interest income is recognized by applying the effective interest rate, except for short term receivables when the recognition of interest would be immaterial.

12

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

Other financial liabilities

Other financial liabilities, including borrowings, are recognized initially at fair value, net of transaction costs. After initial recognition, interest bearing loans and borrowings are subsequently measured at amortized cost using the effective interest method. Gains and losses are recognized in net loss when the liabilities are derecognized as well as through the amortization process. Borrowings are classified as current liabilities unless the Company has an unconditional right to defer settlement of the liability for at least 12 months after the statement of financial position date, and are derecognized when, and only when, the Company’s obligations are discharged or they expire.

Derivative instruments

Derivative instruments, including embedded derivatives, are recorded at fair value on initial recognition and at each subsequent reporting period. Any gains or losses arising from changes in fair value on derivatives are recorded in the statement of comprehensive loss.

Fair values

The fair value of quoted investments is determined by reference to market prices at the close of business on the statement of financial position date. Where there is no active market, fair value is determined using valuation techniques. These include using recent arm’s length market transactions; reference to the current market value of another instrument which is substantially the same; discounted cash flow analysis and pricing models.

Financial instruments that are measured subsequent to initial recognition are grouped into a hierarchy based on the degree to which the fair value is observable as follows:

Level 1 fair value measurements are quoted prices (unadjusted) in active markets for identical assets or liabilities;

Level 2 fair value measurements are those derived from inputs other than quoted prices included within Level 1 that are observable for the asset or liability either directly (i.e. as prices) or indirectly (i.e. derived from prices); and

Level 3 fair value measurements are those derived from valuation techniques that include inputs for the asset or liability that are not based on observable market data (unobservable inputs).

Impairment of financial assets

Financial assets, other than those recorded at FVTPL, are assessed for indicators of impairment at each period end. A financial asset is considered impaired when there is objective evidence that, as a result of one or more events that occurred after the initial recognition of the financial asset, the estimated future cash flows of the investments have been adversely impacted.

If an available-for-sale asset is impaired, an amount comprising the difference between its cost (net of any principal payment and amortization) and its fair value is transferred from equity to net loss, and cumulative

13

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

gains or losses previously recognized in other comprehensive income or loss are reclassified to net loss in the period. Reversals of impairment in respect of equity instruments classified as available-for-sale are not recognized in net loss but included in other comprehensive income.

f) Cash and cash equivalents

Cash and cash equivalents includes cash and short-term money market instruments that are readily convertible to cash with original terms of three months or less.

g) Inventories and stockpiled ore

Inventories are valued at the lower of cost or net realizable value. Inventories include stockpiled ore, gold in circuit and bullion inventories as well as materials and supplies inventory. Cost is determined using the weighted average method. The cost of ore inventories is based on the average cost of production. For this purpose, the costs of production include: (i) materials, equipment, labour and contractor expenses which are directly attributable to the extraction and processing of ore; (ii) depletion and depreciation of property, plant and equipment used in the extraction and processing of ore; and (iii) related production overheads (based on normal operating capacity).

Net realizable value is the estimated selling price in the ordinary course of business, less all estimated costs of completion and costs necessary to make the sale.

h) Mining interests

Mining interests represent capitalized expenditures related to the development of mining properties, related plant and equipment and expenditures arising from property acquisitions. Upon disposal or abandonment, the carrying amounts of mining interests are derecognized and any associated gains or losses are recognized in net loss.

Mining properties

Purchased mining properties are recognized as assets at their cost of acquisition or at fair value if purchased as part of a business combination. Mineral exploration costs are charged to net income (loss) in the year in which they are incurred (“green field exploration”), unless any of the conditions listed as (i) and (ii) are present in any of the mineral properties, in which case the costs of further exploration and development on the property are capitalized:

(i) The Company establishes a National Instrument (“NI”) 43-101 technical report with resources and/or reserves in a property; and/or

(ii) The Board of Directors of the Company approves the start of an advanced exploration program on a property, which requires surface or/and underground work (such as an open pit or underground drifts, shafts and other works, other than exploration drilling and analysis).

14

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

Mining properties and process facility assets are amortized upon commencement of commercial production either on a unit-of-production basis over measured and indicated resources included in the mine plan or the life of mine.

Revenues realized before commencement of commercial production (“pre-production revenues”), which are not incidental but are necessary to bring the mine to the condition required to be operating in the manner intended by management, are recorded as a reduction of the respective mining asset.

Commercial production

Capitalization of costs incurred ceases when the related mining property has reached operating levels intended by management. Costs incurred prior to this point, including depreciation of related plant and equipment, are capitalized and proceeds from sales during this period are offset against costs capitalized.

Operating levels intended by management are considered to be reached when operational commissioning of major mine and plant components is complete, operating results are achieved consistently for a period of time and there are indications that these operating results will be continued. Other factors include one or more of the following:

(iii) a significant portion of plant/mill capacity is achieved;

(iv) a significant portion of available funding is directed towards operating activities;

(v) a pre-determined, reasonable period of time has passed;

(vi) a development project significant to the primary business objective of the Company has been completed in terms of significant milestones being achieved; or

(vii) the Company has filed a NI 43-101 technical report for the property.

Costs incurred to maintain current production are included in mine operating costs. These costs include the development and access (tunneling) costs of production drifts to develop the ore body in the current production cycle. During the production phase of a mine, costs incurred that provide access to reserves and resources that will be produced in future periods that would not have otherwise been accessible are capitalized and included in the carrying amount of the related mining property. Capitalized stripping costs are depleted over the estimated recoverable ounces contained in reserves and resources that directly benefit from the stripping activities. Costs for regular waste removal that do not give rise to future economic benefits are included in mine operating costs in the period they are incurred.

Plant and equipment

Plant and equipment is stated at cost less accumulated depreciation and impairment losses. The cost capitalized for plant and equipment includes borrowing costs incurred that are attributable to qualifying plant and equipment as noted in note 3(i). The carrying amounts of plant and equipment are depreciated

15

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

using either the straight-line or unit-of-production method over the estimated useful lives of the related assets.

The significant classes of depreciable plant and equipment and their estimated useful lives are as follows:

Category | | Rates |

| | |

Mill and related infrastructure | | 20 years or unit-of-production |

Underground infrastructure | | Life of mine |

Vehicles and mobile equipment | | 3-10 years |

Office equipment | | 20% |

Computer equipment | | 30% |

Assets under construction are carried at cost less any recognized impairment loss. Cost includes cost of equipment, cost of labour and installation, project management cost and other indirect costs specifically for assets under construction. When the asset is completed and ready for intended use, the Company reclassifies it from assets under construction to plant and equipment or depletable assets.

Leased assets

Leases in which the Company assumes substantially all risks and rewards of ownership are classified as finance leases. Assets held under finance leases are recognized at the lower of the fair value and the present value of minimum lease payments at inception of the lease, less accumulated depreciation and impairment losses. Lease payments are accounted for as discussed in note 3(k).

Assets held under finance leases are depreciated over their expected useful lives on the same basis as owned assets.

i) Borrowing costs

Borrowing costs directly attributable to the acquisition, construction or production of a qualifying asset (i.e. an asset that necessarily takes a substantial period of time to get ready for its intended use or sale) are capitalized as part of the cost of the asset. All other borrowing costs are expensed in the period they occur.

j) Impairment of assets

Assets that have an indefinite useful life are not subject to amortization and are tested annually for impairment or whenever other indicators exist. Assets that are subject to amortization or depreciation are reviewed for impairment whenever events or changes in circumstances indicate that the carrying amount may not be recoverable. An impairment loss is recognized for the amount by which the asset’s carrying amount exceeds its recoverable amount. The recoverable amount of assets is the greater of their fair value less costs to sell and value in use. Fair value is based on an estimate of the amount that the Company may obtain in a sale transaction on an arm’s-length basis. In assessing value in use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset. For an asset that does not

16

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

generate cash inflows largely independent of those from other assets, the recoverable amount is determined for the cash-generating unit to which the asset belongs. The Company’s cash generating units are the lowest level of identifiable groups of assets that generate cash inflows that are largely independent of the cash inflows from other assets or groups of assets. Where a reasonable and consistent basis of allocation can be identified, corporate assets are also allocated to individual cash-generating units, otherwise they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can be identified.

An impairment loss is reversed if there has been a change in the estimates used to determine the recoverable amount. An impairment loss is reversed only to the extent that the asset’s carrying amount does not exceed the carrying amount that would have been determined, net of depreciation or amortization, if no impairment loss had been recognized.

k) Leases

Assets held under finance leases are recognized as discussed in note 3(h). The corresponding liability is recognized as a finance lease obligation. Lease payments are apportioned between finance charges and reduction of the lease obligation to achieve a constant rate of interest on the remaining liability. Finance charges are recorded as a finance expense to profit and loss, unless they are attributable to qualifying assets, in which case they are capitalized.

Operating lease payments are recognized as an expense on a straight-line basis over the lease term, except where another systematic basis is more representative of the time pattern in which economic benefits from the leased asset are consumed.

The Company engages in sales and leaseback transactions as part of the Company’s financing strategy. Where a sale and leaseback transaction results in a finance lease, any excess of sales proceeds over the carrying amount is deferred and amortized over the lease term. Where a sale and leaseback transaction results in an operating lease, and it is clear that the transaction is established at fair value, any profit or loss is recognized immediately. If the sales price is below fair value, the shortfall is recognized in income immediately, except that, if the loss is compensated for by future lease payments at below market price, it is deferred and amortized in proportion to the lease payments over the period for which the asset is expected to be used. If the sale price is above fair value, the excess over fair value is deferred and amortized over the period the asset is expected to be used.

l) Provisions

Provisions are recognized when the Company or its subsidiaries have a present obligation (legal or constructive) as a result of a past event, it is probable that an outflow of resources will be required to settle the obligation and a reliable estimate can be made of the amount of the obligation. The amount recognized as a provision is the best estimate of the consideration required to settle the present obligation at the end of the reporting period. If the effect of the time value of money is material, provisions are determined by discounting the expected future cash flows at a pre-tax rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability. Where discounting is used, the increase in the provision due to the passage of time is recognized as a finance cost.

17

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

Contingent liabilities are not recognized in the consolidated financial statements, if not estimable and probable, and are disclosed in notes to the financial information unless their occurrence is remote. Contingent assets are not recognized in the consolidated financial statements, but are disclosed in the notes if their recovery is deemed probable.

Environmental rehabilitation

Provisions for environmental rehabilitation are made in respect of the estimated future costs of closure and restoration and for environmental rehabilitation costs (which include the dismantling and demolition of infrastructure, removal of residual materials and remediation of disturbed areas) in the accounting period when the related environmental disturbance occurs. The provision is discounted using a pre-tax rate, and the unwinding of the discount is included in finance costs. At the time of establishing the provision, a corresponding asset is capitalized and is depreciated over future production from the mining property to which it relates. The provision is reviewed on an annual basis for changes in cost estimates, discount rates and operating lives.

Changes to estimated future costs are recognized in the statement of financial position by adjusting the rehabilitation asset and liability. Increases in estimated costs related to mine production become part of ore inventory. For closed sites, changes to estimated costs are recognized immediately in the profit and loss.

m) Share-based payments

The fair value of the estimated number of stock options awarded to employees, officers and directors that will eventually vest, is recognized as share-based compensation expense over the vesting period of the stock options with a corresponding increase to equity. The fair value of each stock option granted is estimated on the date of the grant using the Black-Scholes option-pricing model and is expensed over the vesting period, based on the Company’s estimate of equity instruments that will eventually vest. At the end of each reporting period, the Company revises its estimate of the number of equity instruments expected to vest. The impact of the revision of the original estimates, if any, is recognized in net loss or capitalized in mining properties such that the accumulated expense reflects the revised estimate, with a corresponding adjustment to the share-based payment reserve. The share based payment cost is recognized in net loss or capitalized in mining properties (options granted to individuals involved on specific projects).

Performance share units (“PSUs”) awarded to eligible executives are settled in cash. The fair value of the estimated number of PSUs awarded expected to vest is recognized as share-based compensation expense over the vesting period of the PSUs with a corresponding amount set up as a liability. Until the liability is settled, the fair value of the PSUs is re-measured at the end of each reporting period and at the date of settlement, with changes in fair value recognized as share-based compensation expense or recovery over the vesting period. The fair value of PSUs is estimated using the Monte-Carlo simulation pricing model to determine the expected market value of the underlying Lake Shore Gold shares on settlement date, multiplied by the expected target settlement percentage (multiplier).

Deferred share units (“DSUs”) awarded to non-executive directors can be settled in cash, shares or a combination of both as elected by the directors. In the case of a payment in shares, the Company will purchase the shares on the open market, through a broker, on behalf of the directors. The fair value of the

18

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

DSUs awarded is recognized as share-based compensation expense at grant date with a corresponding amount set up as a liability. Until the liability is settled, the fair value of the DSUs is re-measured at the end of each reporting period and at the date of settlement, with changes in fair value recognized as share-based compensation expense or recovery in the period. The fair value of DSUs is estimated using the Black-Scholes option-pricing model to determine the expected market value of the underlying Lake Shore Gold shares on settlement date.

n) Defined contribution pension plan

The Company has a defined contribution pension plan which covers all of the Company’s employees. Under the plan provisions, the Company contributes a fixed percentage of the employees’ salaries to the pension plan. The employees are able to direct the contributions into a variety of investment funds offered by the plan. Pension costs associated with the Company’s required contributions under the plan are recognized as an expense when the employees have rendered service entitling them to the contribution and are charged to profit or loss, or capitalized to mining interests for employees directly involved in the specific projects.

o) Deferred income and mining taxes

Taxes, comprising both income taxes and mining taxes accounted for as income taxes, are recognized in net loss, except where they relate to items recognized in other comprehensive income or directly in equity, in which case the related taxes are recognized in other comprehensive income or equity. Deferred income taxes are provided using the balance sheet liability method, providing for unused tax losses, unused tax credits and temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. As an exception, deferred tax assets and liabilities are not recognized if the temporary differences arise from the initial recognition of goodwill or an asset or liability in a transaction (other than in a business combination) that affects neither accounting profit or taxable profit.

Deferred tax assets and liabilities are measured at the tax rates that are expected to apply to the period when the asset is realized or the liability is settled based on the tax rates (and tax laws) that have been enacted or substantively enacted at the statement of financial position date.

A deferred tax asset is recognized only to the extent that it is probable that future taxable profits will be available against which the asset can be utilized. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit will be realized.

Deferred tax assets and liabilities are offset when there is a legally enforceable right to set off current tax assets against current tax liabilities and when they relate to income taxes levied by the same taxation authority and the Company intends to settle its current assets and liabilities on a net basis.

p) Share capital

Common shares issued by the Company are classified as equity. Incremental costs directly attributable to the issue of new common shares are recognized in equity, net of tax, as a deduction from the share proceeds (share issue costs).

19

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

q) Revenue recognition

Revenue is measured at the fair value of the consideration received or receivable and represents amounts received for goods sold in the normal course of business, net of discounts and sales related taxes. Revenue from gold sales is recognized to the extent that it is probable that economic benefits will flow to the Company, the revenue can be reliably measured and when all significant risks and rewards of ownership are transferred to the customer, which is when title has passed to the customer. Revenue from by-product sales is recorded as a reduction of production costs.

r) Finance income and costs

Finance income and costs comprise interest income on funds invested, interest expense on borrowings and the accumulation of interest on provisions. Interest income is recognized as it accrues, taking into account the effective yield on the asset.

s) Earnings (loss) per share

Basic earnings (loss) per share is computed by dividing net earnings (loss) available to common shareholders by the weighted average number of outstanding common shares for the period. In computing diluted earnings per share, an adjustment is made for the dilutive effect of the exercise of stock options and warrants. The number of additional shares is calculated by assuming that outstanding stock options, debentures and warrants are exercised and that the proceeds from such exercises were used to acquire common shares at the average market price during the reporting periods. In periods where a net loss is reported, all outstanding options and warrants are excluded from the calculation of diluted loss per share, as they are anti-dilutive.

t) Deferred financing charges

Costs of arranging a loan facility are recorded in the statement of financial position net of the respective facility obligation and amortized using the effective interest method over the term of the respective facility agreement.

u) Other comprehensive income (loss)

Other comprehensive income (loss) is the change in the Company’s net assets that results from transactions, events and circumstances from sources other than the Company’s shareholders and includes items that are not included in net profits such as unrealized gains and losses on financial assets classified as available-for-sale, net of income taxes, gain or losses on certain derivative instruments and foreign currency exchange gains or losses related to foreign subsidiaries which functional currency is different than the functional currency of the Company.

20

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

v) Segment reporting

An operating segment is a component of an entity:

(i) that engages in business activities from which it may earn revenues and incur expenses (including revenues and expenses relating to transactions with other components of the same entity);

(ii) whose operating results are regularly reviewed by the entity’s chief operating decision maker to make decisions about resources to be allocated to the segment and assess its performance; and

(iii) for which discrete financial information is available.

The Company’s operating segments are its mining operations segment and exploration and advanced exploration segments.

4. CRITICAL ACCOUNTING JUDGMENTS AND KEY SOURCES OF ESTIMATION UNCERTAINTY

In the application of the Company’s accounting policies, which are described in note 3, management is required to make judgments, estimates and assumptions about the carrying amount and classification of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimate is revised if the revisions affect only that period, or in the period of the revision and future periods, if the revision affects both current and future periods.

The following are the critical judgments and areas involving estimates, that management have made in the process of applying the Company’s accounting policies and that have the most significant effect on the amounts recognized in the consolidated financial statements.

CRITICAL JUDGMENTS IN APPLYING ACCOUNTING POLICIES

Commercial production - Operating levels intended by management

Prior to reaching operating levels intended by management, costs incurred are capitalized as part of costs of the related mining property and proceeds from sales are offset against costs capitalized. Depletion of capitalized costs for mining properties begins when operating levels intended by management have been reached. Management considers several factors in determining when a mining property has reached the operating levels intended by management.

21

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

Determination of functional currency

In accordance with International Accounting Standards (“IAS”) 21, The Effects of Changes in Foreign Exchange Rates, management determined that the functional currency of its Canadian entities (the Company and its Canadian subsidiaries — note 3(a)) is the Canadian dollar and Mexico pesos for the Company’s subsidiary in Mexico (Minera Golondrina S. de R.L. de C.V. or the “Mexico entity”). The Company disposed of its Mexico entity on May 8, 2013 (note 9).

KEY SOURCES OF ESTIMATION UNCERTAINTIES

Useful life of plant and equipment

As discussed in note 3(h), the Company reviews the estimated lives of its plant and equipment at the end of each reporting period. There were no material changes in the lives of plant and equipment for the years ended December 31, 2013 and 2012.

Determination of ore reserves and resources

Reserves and resources are used in the units of production calculation for depreciation and depletion calculations and in the determination of the timing of environmental rehabilitation costs as well as in the impairment analysis.

There are numerous uncertainties inherent in estimating ore reserves and resources. Assumptions that are valid at the time of estimation may change significantly when new information becomes available. Changes in the forecast prices of commodities, exchange rates, production costs, or recovery rates as well as new drilling results may change the economic status of reserves and resources and may result in the reserves and resources being revised.

Deferred income taxes

Judgment is required in determining whether deferred tax assets are recognized on the statement of financial position. Deferred tax assets, including those arising from unutilized tax losses require management to assess the likelihood that the Company and/or its subsidiaries will generate taxable earnings in future periods, in order to utilize recognized deferred tax assets. Estimates of future taxable income are based on forecast cash flows from operations and the application of existing tax laws in each jurisdiction. To the extent that future cash flows and taxable income differ significantly from estimates, the ability of the Company and/or its subsidiaries to realize the net deferred tax assets recorded at the statement of financial position date could be impacted. Additionally, future changes in tax laws in the jurisdictions in which the Company and its subsidiaries operates could limit the ability of the Company to obtain tax deductions in future periods.

22

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)

Impairment of assets

The carrying amounts of mining properties and plant and equipment are reviewed for impairment if events or changes in circumstances indicate that the carrying value may not be recoverable. If there are indicators of impairment, an exercise is undertaken to determine whether the carrying values are in excess of their recoverable amount. Such review is undertaken on an asset by asset basis, except where such assets do not generate cash flows independent of other assets, and then the review is undertaken at the cash generating unit level (“CGU”).

The assessment requires the use of estimates and assumptions such as, but not limited to, long-term commodity prices, foreign exchange rates, discount rates, future capital requirements, resource estimates, exploration potential and operating performance as well as the CGU definition. It is possible that the actual fair value could be significantly different from those assumptions, and changes in these assumptions will affect the recoverable amount of the mining interests. In the absence of any mitigating valuation factors, adverse changes in valuation assumptions or declines in the fair values of the Company’s CGUs or other assets may, over time, result in impairment charges causing the Company to record material losses.

Environmental rehabilitation

Significant estimates and assumptions are made in determining the environmental rehabilitation costs as there are numerous factors that will affect the ultimate liability payable. These factors include estimates of the extent and costs of rehabilitation activities, technological changes, regulatory changes, cost increases, and changes in discount rates.

Those uncertainties may result in actual expenditures in the future being different from the amounts currently provided. The provision represents management’s best estimate of the present value of the future rehabilitation costs required.

Share-based payments

Management assesses the fair value of stock options granted, PSUs and DSUs in accordance with the accounting policy stated in note 3(m). The fair value of stock options granted and DSUs is measured using the Black-Scholes option valuation model; the fair value of PSUs is measured using the Monte Carlo simulation valuation model. The fair value of stock options granted, PSUs and DSUs using valuation models is only an estimate of their potential value and requires the use of estimates and assumptions.

23

LAKE SHORE GOLD CORP.

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

FOR THE YEARS ENDED DECEMBER 31, 2013 AND 2012

(in thousands of Canadian dollars, except per share amounts)