UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21515

TS&W / Claymore Tax-Advantaged Balanced Fund

(Exact name of registrant as specified in charter)

2455 Corporate West Drive, Lisle, IL 60532

(Address of principal executive offices) (Zip code)

J. Thomas Futrell

2455 Corporate West Drive, Lisle, IL 60532

(Name and address of agent for service)

Registrant's telephone number, including area code: (630) 505-3700

Date of fiscal year end: December 31

Date of reporting period: January 1, 2010 - June 30, 2010

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

Item 1. Reports to Stockholders.

The registrant's semi-annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows:

www.claymore.com/tyw

... home port for the LATEST,

most up-to-date INFORMATION about the

TS&W/Claymore Tax-Advantaged Balanced Fund

The shareholder report you are reading right now is just the beginning of the story. Online at www.claymore.com/tyw, you will find:

| · | Daily, weekly and monthly data on share prices, distributions and more |

| · | Portfolio overviews and performance analyses |

| · | Announcements, press releases and special notices |

| · | Fund and adviser contact information |

Thompson, Siegel & Walmsley LLC, SMC Fixed Income Management, LP and Claymore are continually updating and expanding shareholder information services on the Fund’s website, in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more way we are working to keep you better informed about your investment in the Fund.

2 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund

Dear Shareholder|

We thank you for your investment in the TS&W/Claymore Tax-Advantaged Balanced Fund (the “Fund”).This report covers the Fund’s performance for the semiannual period ended June 30, 2010.

The Fund’s investment objective is to provide a high level of total after-tax return, including attractive tax-advantaged income.The Fund focuses its investments mainly on (i) municipal securities, the interest on which is exempt from regular Federal income tax, and which is not a preference item for purposes of the alternative minimum tax (such securities referred to generally as “municipal securities”) and (ii) common stocks and preferred securities that are eligible to pay dividends which, for individual shareholders, qualify for the long-term capital gains rate.The portfolio is comprised primarily of municipal securities, equity securities, preferred securities and high-yield debt securities and real estate investment trusts.

Claymore Advisors, LLC is the investment adviser (“Adviser”) to the Fund and is responsible for managing the Fund’s overall asset allocation. Claymore entities provided supervision, management or servicing on approximately $15.3 billion in assets as of June 30, 2010.Two Investment Sub-Advisers are responsible for day-to-day management of the Fund’s investments.Thompson, Siegel & Walmsley LLC (“TS&W”) manages the Fund’s equity portfolio and other non-municipal income-producing securities.As of June 30, 2010,TS&W managed or supervised approximately $7.2 billion in assets. SMC Fixed Income Management, LP (“SMC”) is responsible for the Fund’s portfolio of municipal securities.As of June 30, 2010, SMC managed or supervised approximately $1.2 billion in assets. Collectively ,TS&W and SMC are also referred to as the “Sub-Advisers.”

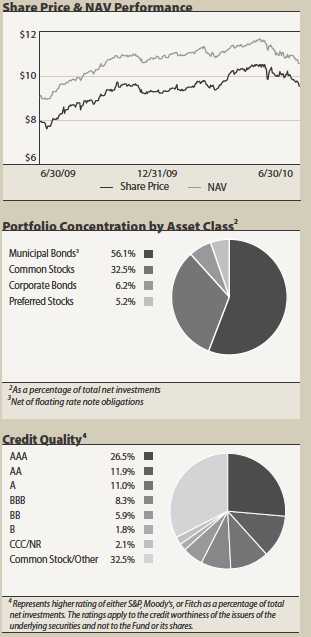

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the six months ended June 30, 2010, the Fund provided a total return based on market price of 3.52% and a total return based on NAV of -0.91%.As of June 30, 2010, the Fund’s market price of $9.53 per share represented a discount of 9.75% to its NAV of $10.56 per share. Past performance is not a guarantee of future results.The market price of the Fund’s shares fluctuates from time to time, and it may be higher or lower than the Fund’s NAV.

The Fund paid quarterly dividends of $0.1800 on March 31 and June 30, 2010.The most recent dividend represents an annualized distribution rate of 7.56% based on the Fund’s closing market price of $9.53 on June 30, 2010.This translates to a tax-advantaged distribution rate of 10.94% for investors in the 35% federal income tax bracket, based on the 2009 tax characteristics of distributions paid. However, there is no guarantee that this level of income will be maintained.

On October 15, 2009, Guggenheim Partners, LLC, a global diversified financial services firm, and Claymore Group Inc. (“Claymore”), the parent company of the Fund’s adviser, announced the completion of a previously announced merger.As a result of the transaction, Claymore and its associated entities, including Claymore Securities, Inc., Claymore Advisors, LLC and Claymore Investments, Inc. (in Canada), are now indirect wholly-owned subsidiaries of Guggenheim Partners, LLC, a global diversified financial services firm with more than $100 billion in assets under supervision.

On February 19, 2010, the Fund announced that it had entered into a new investment advisory agreement with Claymore Advisors, LLC and new investment sub-advisory agreements with TS&W and SMC upon receiving the necessary shareholder approval.These new agreements were necessary because the former agreements were automatically terminated upon the merger of Claymore with Guggenheim Partners.

In an effort to enhance shareholder value, the Fund announced on January 2, 2009, the adoption of an open-market share repurchase plan (the “Plan”) authorizing the purchase of up to 5% of its outstanding common shares in the open market on a quarterly basis, subject to applicable

Semiannual Report | June 30, 2010 | 3

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Dear Shareholder continued

regulatory and legal restrictions and in consideration of certain operational and market factors, including the size of the market price discount to net asset value of the Fund.There is no assurance that the Fund will purchase shares at any particular discount levels or in any particular amounts.There is also no assurance that the market price of the Fund’s shares, either absolutely or relative to the net asset value, will increase as a result of any share repurchases.

We encourage shareholders to consider the opportunity to reinvest their distributions from the Fund through the Dividend Reinvestment Plan (“DRIP”), which is described in detail on page 29 of the Fund’s semiannual report.When shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the quarterly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at NAV, subject to an IRS limitation that the purchase price cannot be more than 5% below the market price per share.The DRIP provides a cost-effective means to accumulate additional shares and enjoy the benefits of compoundin g returns over time. Since the Fund endeavors to maintain a steady quarterly distribution rate, the DRIP plan effectively provides an income averaging technique, which causes shareholders to accumulate a larger number of Fund shares when the market price is depressed than when the price is higher.

To learn more about the Fund’s performance and investment strategy, we encourage you to read the Questions & Answers section of the report, which begins on page 5. You will find information about what impacted the performance of the Fund during the first half of 2010 and the Adviser’s and Sub-Advisers’ views on the market environment.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at www.claymore.com/tyw.

Sincerely,

J. Thomas Futrell

Chief Executive Officer

TS&W/ClaymoreTax-Advantaged Balanced Fund

4 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund

Questions & Answers|

The TS&W/Claymore Tax-Advantaged Balanced Fund (the “Fund”) is managed jointly by Thompson, Siegel &Walmsley LLC (“TS&W”) and SMC Fixed Income Management, LP (“SMC”).The portfolio management teams apply their specialized experience to different sleeves within the Fund, but work closely with one another to collectively guide the overall operations of the Fund.The individuals named below are responsible for managing the Fund.

Vincent R. Giordano, Portfolio Manager, Managing Member SMC Fixed Income Management, LP

Mr. Giordano is a Managing Member of SMC. He leads SMC’s municipal fixed-income investment management team and co-manages the Fund’s municipal securities portfolio. Prior to joining SMC, Mr. Giordano was employed by Claymore Advisors, LLC (“Claymore”) and Merrill Lynch. He has more than 30 years of investment experience.

RobertoW. Roffo, Portfolio Manager, Managing Director SMC Fixed Income Management, LP

Mr. Roffo co-manages the Fund’s municipal securities portfolio. He has more than 15 years of investment management experience focused on the municipal securities market. Prior to joining SMC, Mr. Roffo was employed by Claymore and Merrill Lynch. He has worked closely with Mr. Giordano throughout his career. He holds a Bachelor’s Degree from the University of Massachusetts.

Paul A. Ferwerda, CFA, Portfolio Manager, Senior Vice President –Domestic Equity and Research Thompson, Siegel &Walmsley LLC

Mr. Ferwerda is responsible for the day-to-day management of the Fund’s common stock portfolio. He has been with TS&W for over 20 years and has more than 25 years of investment experience. Mr. Ferwerda has extensive equity research experience within the financial sector and holds an MBA from Duke University.

William M. Bellamy, CFA, Portfolio Manager, Vice President Thompson, Siegel &Walmsley LLC

Mr. Bellamy joined TS&W in 2002. He has over 20 years of investment industry experience focused on the fixed-income markets. Mr. Bellamy is responsible for managing the Fund’s taxable fixed-income securities. He holds an MBA from Duke University.

In the following interview, Claymore,TS&W and SMC share their thoughts on the market and discuss the factors that influenced the Fund’s performance for the six months ended June 30, 2010.

Please remind us of this Fund’s objective and strategy.

The Fund’s investment objective is to provide a high level of total after-tax return, including attractive tax-advantaged income.The Fund seeks to achieve its objective by investing in a portfolio of assets consisting primarily of (i) municipal securities, the interest on which is exempt from regular Federal income tax, and which is not a preference item for purposes of the alternative minimum tax (such securities referred to generally as “municipal securities”) and (ii) common stocks and preferred securities that are eligible to pay dividends which, for individual shareholders, qualify for the long-term capital gains rate.The portfolio is comprised primarily of municipal securities, equity securities, preferred securities, high-yield debt securities and real estate investment trusts.

How did the Fund perform during the first six months of 2010?

All Fund returns cited—whether based on net asset value (“NAV”) or market price—assume the reinvestment of all distributions. For the six months ended June 30, 2010, the Fund provided a total return based on market price of 3.52% and a total return based on NAV of -0.91%.As of June 30, 2010, the Fund’s market price of $9.53 per share represented a discount of 9.75% to its NAV of $10.56 per share.The market value of the Fund’s shares fluctuates from time to time and it may be higher or lower than the Fund’s NAV. Past performance is not a guarantee of future results.

For NAV performance comparison purposes, the municipal bond market, as measured by the Barclays Capital U.S. Municipal Long Bond Index (“Barclays Muni Index”), a widely used measure of the municipal bond market as a whole, returned 4.50% for the six months ended June 30, 2010.The broad equity market, as measured by the Standard & Poor’s 500 Index (“S&P 500”), returned -6.65%.The high-yield bond market, as measured by the Merrill Lynch HighYield Master II Index, returned 4.74% for the period, and the Merrill Lynch Fixed Rate Preferred Securities Index returned 4.68%.

The Fund paid quarterly dividends of $0.1800 on March 31 and June 30, 2010.The most recent dividend represents an annualized distribution rate of 7.56% based on the Fund’s closing market price of $9.53 on June 30, 2010.This translates to a tax-advantaged distribution rate of 10.94% for investors in the 35% federal income tax bracket, based on the 2009 tax characteristics of distributions paid. However, there is no guarantee that this level of income will be maintained.

Semiannual Report | June 30, 2010 | 5

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Questions & Answers continued

How are assets allocated among the various asset classes?

The Fund invests at least 50%, and may invest up to 60%, of its total assets in municipal securities.As of June 30, 2010, approximately 56.1% of the Fund’s portfolio was invested in municipal securities. Of the remaining assets in the Fund’s portfolio as of June 30, 2010, approximately 32.5% were invested in equity securities consisting primarily of large-cap dividend-paying stocks, and approximately 11.4% were invested in other taxable income-producing securities, which include but are not limited to high-yield bonds, preferred stocks and real estate investment trusts. From time to time, assets are rebalanced to maintain at least 50% of the Fund’s total assets in municipal securities.

How has the Fund’s leverage strategy affected performance?

The Fund utilizes leverage (borrowing) as part of its investment strategy, to finance the purchase of additional securities that provide increased income and potentially greater appreciation potential to common shareholders than could be achieved from a portfolio that is not leveraged. Of course, leverage results in greater NAV volatility and entails more downside risk than an unleveraged portfolio. Leverage adds to performance only when the cost of leverage is less than the total return generated by investments. During the six months ended June 30, 2010, the cost of leverage was less than the return of the Fund’s investments before the impact of the Fund’s operating expenses; accordingly, leverage contributed positively to the Fund’s total return.

As of June 30, 2010, the Fund had $105 million of leverage outstanding in the form of Auction Market Preferred Shares (“AMPSSM”).The Fund has two series of AMPS, one 7-day series and one 28-day series.AMPS holders receive a dividend that is reset every 7 or 28 days, depending on the tranche.1 The broad auction-rate preferred securities market remains essentially frozen, as it has been since February 2008.The auctions for nearly all auction-rate preferred shares, including those issued by the Fund, continue to fail. Investors need to be aware that a failed auction is not a default, nor does it require the redemption of a fund’s auction-rate preferred shares. Provi sions in the offering documents of the Fund’s AMPS provide a mechanism to set a maximum rate in the event of a failed auction, and, thus, investors will continue to be entitled to receive payment for holding these AMPS.This maximum rate is determined based upon a multiple of or a spread to LIBOR2, whichever is greater. During the six months ended June 30, 2010, established maximum rates were based on a spread of 125 basis points over the applicable LIBOR rates, with the maximum rates ranging from 1.46% to 1.60%.

There is no guarantee that the Fund’s leverage strategy will be successful, and the Fund’s use of leverage may cause the Fund’s NAV and market price of common shares to be more volatile. Leverage adds value only when the return on securities purchased exceeds the cost of leverage.

The following questions are related to the municipal securities portfolio and are answered by Portfolio Managers Vincent R. Giordano and Roberto W. Roffo, who have managed the municipal securities portfolio since the Fund’s inception.

Please provide an overview of the municipal securities market during the first six months of 2010.

In the Fund’s last annual report, dated December 31, 2009, SMC pointed out that it did not seem reasonable to expect the unusually strong overall performance of municipal securities in 2009 to be repeated in 2010. During the first half of 2010, municipal securities have continued to provide attractive returns, but the returns were a bit lower than returns on taxable bonds. For the six months ended June 30, 2010, return of the Barclays Muni Index, which measures performance of the U.S. municipal market, was 4.50%. Some of that return was price appreciation, but the majority of it was income.

For comparison, return of the Barclays Capital U.S.Aggregate Bond Index, which measures performance of the U.S. taxable bond market, was 5.33%, and return of the Barclays U.S.Treasury Index was 5.86%.Treasury securities have performed well because of a flight to quality, as credit crises in several states, as well as problems with sovereign debt of several European nations, have made investors wary of credit risk.

Interest rates remained quite low during the first half of 2010, as the Federal Reserve’s stimulative monetary policy kept short-term rates at historically low levels. Individual investors, who are usually the main buyers of municipal securities, were reluctant to commit to bonds with very low coupons, and that has put some pressure on municipal securities.

How did the municipal securities portion of the Fund perform in this environment and what decisions drove that performance?

The Fund’s municipal securities portfolio performed well, and the positive impact of leverage made the total return even higher.

| 1 | The term tranche is used to describe a specific series of AMPS. The Fund has issued two tranches of AMPS. |

| 2 | LIBOR is the interest rate that banks charge one another in the short-term international interbank market. |

6 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Questions & Answers continued

Since the majority of the return on bonds during the period came from income, the Fund’s performance benefited from a focus on increasing the average coupon.The portfolio is structured with a significantly higher average coupon than the Barclays Muni Index.

SMC’s practice of carefully analyzing each bond under consideration has made it possible to achieve a high level of income while also maintaining high credit quality. In a market environment that is challenging for issuers, some bonds have been offered at what might seem to be a higher than normal coupon for reasons that really have little to do with credit quality.A good example is a City of Detroit Sewer Disposal bond with a 7.0% coupon, maturing in 2027. SMC feels is a very solid AAA rated security, plus it is insured by Assured Guaranty Municipal, the only remaining AAA-rated insurer. Just because the issuer is a Detroit entity, and investors mentally connect Detroit with the rust belt and the troubled automotive industry, the 7% coupon was necessary to get the deal done.The portfolio includes a number of bonds with attractive i ncome streams and similar situations.

Most of the bonds in the portfolio performed well. Notable contributors to performance were relatively large positions in AAA-rated Texas Permanent School Fund (“PSF”) bonds and a Rhode Island State Health & Educational Corp. hospital bond with an A rating on the underlying credit that is insured by Assured Guaranty.

With regard to duration, most of the bonds that have been added to the portfolio during the period are priced to the first call date. (Duration is a measure of a bond’s price sensitivity to changes in interest rates.) In the expectation that interest rates are unlikely to move lower, and will eventually rise, the duration has been kept fairly short.The duration of the municipal securities portfolio is approximately eight years, much shorter than the duration of the Barclays Muni Index, which is approximately 14 years.As bonds have rallied a bit in 2010, this shorter duration has hurt the portfolio’s performance relative to the index, but this was more than offset by the advantage of the portfolio’s higher coupon on average compared to the index.Another negative trend was that spreads widened on some of the Fund’s l ower rated credits, such as BBB tobacco bonds and a BB hospital bond, and that was detrimental for performance.

How are municipal securities selected for the Fund?

SMC begins by analyzing broad macroeconomic trends and developments affecting the fixed-income markets, including the economic outlook, market conditions and perceived effects on interest rates and yield curves. From there, a bottom-up and top-down analysis is incorporated to help construct a portfolio that SMC believes optimizes federally tax-exempt income while seeking to avoid undue credit risk and market timing risk.While SMC monitors interest rates very closely and acts quickly to adjust the portfolio to changing market rates, positions in the portfolio are not traded in search of incremental gains that could be achieved by active trading based on daily changes in rates. SMC’s proprietary unbiased research makes it possible to identify undervalued sectors that are considered to have the potential for ratings upgrades and capita l appreciation; however, there is no guarantee that such events will occur.

What is the outlook for the municipal securities market and what does this mean for the Fund?

SMC believes it is unlikely that interest rates will move significantly lower.With the massive amounts of stimulus provided by the government plus some other positive trends, economic activity is expected to pick up eventually.Although certain states and European nations definitely have credit issues, current concerns of some investors seem overblown. Since bond prices generally move in the opposite directions of interest rates, SMC does not expect that bond prices will move significantly higher. Accordingly, the current focus is on income and increasing the average coupon of the portfolio. Ongoing efforts will be made to purchase bonds that can provide an attractive level of income such as the Detroit Sewer bonds mentioned earlier.

The Fund’s equity portfolio and taxable fixed-income securities are managed by TS&W.The following questions are related to those portions of the portfolio and are answered by Portfolio Managers Paul A. Ferwerda and William M. Bellamy.

Please provide an overview of the U.S. equity and high-yield bond markets during the six months ended June 30, 2010.

Market conditions in first half of 2010 are difficult to characterize concisely because there was so much variation within the period. As the year began, there was a fair amount of enthusiasm, and the rally that began in 2009 continued into the first quarter. Investors exhibited high hopes that the economic recovery was well

Semiannual Report | June 30, 2010 | 7

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Questions & Answers continued

underway and was becoming more entrenched as the government stimulus had a positive impact.Then in April that sentiment shifted to a more sober view, as investors seemed to lose confidence that there would be a smooth transition from a stimulus-fueled recovery to sustained economic growth driven by the private sector.The considerable uncertainty about the strength of the economy created substantial volatility in capital markets in the second quarter of 2010.

For the six-month period ended June 30, 2010, the broad equity market, as measured by the S&P 500, was down, with a return of -6.65%. Performance of sectors and industry groups was rather odd, with some of the sectors normally considered defensive performing poorly; for example, food and staples retailing was one of the worst performing groups. Other economically sensitive sectors, such as materials and processing, were down, as would be expected when economic concerns are affecting the market. Energy stocks were dragged down by concerns about the oil spill in the Gulf of Mexico.Technology and communications were weak, and many health care stocks were down, even though recent legislation removed some of the uncertainty that had been plaguing that sector. In contrast, some sectors that are generally considered to be sensitive to econom ic conditions performed relatively well. Banks, real estate and transportation were among the better performing sectors in the first half of 2010. Other relatively strong sectors were defensive groups such as food, beverage and tobacco and household and personal products.

Another unusual characteristic of the equity market during this period was that small to mid-cap stocks were generally stronger than large-cap. Ordinarily, when the market is weak, the more defensive large-cap stocks perform better.As would be expected, growth stock indices were down more than value indices.

In the bond market, the most notable feature was a significant decline in interest rates: the rate on the 10-year U.S.Treasury note went from approximately 4% at the beginning of the period to approximately 3% as of June 30.This meant that in the investment-grade market, most of the performance was driven by lower interest rates.Treasury securities performed very well, as investors who worried about European credits sought the safety of U.S. Treasury securities.The return of the Barclays U.S.Treasury Index was 5.86% for the six months ended June 30, 2010.

In the high-yield bond market, credit quality was a much more important determinant of performance than interest rates. High-yield bonds performed relatively well; return of the Merrill Lynch HighYield Master II Index was 4.74%.Within the high-yield category, bonds with lower credit ratings generally performed better than higher rated bonds. Bond issuers’ balance sheets seem to be fairly healthy, and there have been few defaults.

Please describe how equity and high-yield securities are selected for the Fund.

TS&W’s investment process is value-driven and team-oriented. On the equity side, a proprietary quantitative valuation model is applied to more than 400 stocks.This directs TS&W’s review process toward companies believed to have the highest expected return potential over a multi-year period.TS&W’s in-house research analysts are responsible for validating the model inputs for companies under their coverage and monitoring them over the holding period. Buys and sells are discussed at weekly research meetings or more frequently as needed.TS&W’s fixed-income team is responsible for overall bond market strategy as well as security selection. In-house analysts are used to support the credit review process.

How did the equity portfolio perform over this period, and what were the main determinants of this performance?

The common equity portion of the portfolio, including some perpetual preferreds, had a return of approximately -7.6% (excluding the effect of leverage) for the six months ended June 30, 2010.This was below the Russell 1000Value Index, which returned -5.12%, and the S&P 500 Index, which returned -6.65%.

The portfolio’s pattern of performance was generally as would be expected, since it is designed to be a defensive portfolio: it outperformed during the periods when the market was down, and underperformed when the market was up. However, in part because of the disappointing performance of several of the industry groups that are generally regarded as defensive, the Fund’s return for the period as a whole was below that of its benchmarks.

The main source of the underperformance was a large position in BP PLC (0.3% of total net investment at the end of the reporting period), an international oil company that is now best known for the massive oil spill in the Gulf of Mexico and its handling the aftermath of the spill.TS&W continued to hold the stock, which was an attractive source of dividend income, until the dividend was suspended.While TS&W believes that BP has the financial resources to pay the dividend, the matter has become so

8 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Questions & Answers continued

politicized that it now appears that the dividend will not be reinstated until the company believes it can do so without incurring public criticism and political pressure.The decision was therefore made to begin selling the stock with approximately 60% of the position disposed of prior to the end of the reporting period.

Also negative was a position in Noble Corp., (0.7% of total net investments) an offshore drilling company that had nothing to do with the oil spill disaster, although the drilling moratorium will have some impact. Noble just announced the acquisition of a privately owned offshore drilling company and also a major joint venture with Royal Dutch Shell PLC (1.2% of total net investments), an international oil company that was another detractor from performance, as the entire energy group sold off. TS&W continues to believe that both of these stocks represent good value.

Looking to decisions that contributed to performance in the equity portfolio, an underweight in the technology sector, which performed poorly, contributed to performance relative to the S&P 500.Also, an overweight in the financials sector relative to the S&P 500 contributed to performance, as this sector performed well despite concerns about financial reform legislation.

One of the best performing holdings was Rayonier, Inc. (0.6% of total net investments), a real estate investment trust that is an international forest products company. Several stocks in the consumer discretionary sector were major contributors, including Nintendo Co., Ltd., a Japanese manufacturer of computer games and game consoles, andYum! Brands Inc., a quick service restaurant company; both of these stocks were sold on strength and are not in the portfolio at period end. Other holdings that contributed to performance include H.J. Heinz Co. (not held in the portfolio at period end), a global branded food company;The Chubb Corp. (0.9% of total net investments), a property and casualty insurance company; Republic Services, Inc. (not held in the portfolio at period end), a waste management company; and Bristol-Myers Squibb Co., (1.0% of total net investments), a global pharmaceutical company.

How did the portfolio’s high-yield bonds and preferred stocks perform?

As the high-yield bond market continued to recover, this portion of the Fund’s portfolio had a return of 4.57% in the first half of 2010, slightly below the 4.74% return of the Merrill Lynch High Yield Master II Index (the “HighYield Index”), which measures return of the high-yield market as a whole. Since this portion of the portfolio includes both high-yield bonds and preferred stock, a blended benchmark which is 67% the HighYield Index and 33% the Merrill Lynch Fixed Rate Preferred Securities Index (the “Preferred Index”) is helpful in evaluating performance.The Preferred Index returned 4.68% for the six-month period, and the return of the blended benchmark was 4.72%.

While the portfolio’s return was very close to that of the blended benchmark, the slight underperformance resulted mainly from a bias toward higher quality during a period when lower rated credits generally performed better than higher rated issues.This was the case with both high-yield bonds and preferred stocks. While it is always desirable to outperform the benchmark,TS&W is more concerned about being confident that the holdings in the portfolio have the financial strength and staying power to pay the interest and principal than about short-term performance.

Among the better performing holdings were several health care names, which benefited from the elimination of some uncertainty when the recent health care legislation was passed.These include Omega Healthcare Investors, Inc., a real estate investment trust that invests in long-term health care facilities; Community Health Systems, Inc. a hospital operator; and Omnicare, Inc., a pharmaceutical services company (0.2%, 0.2% and 0.1% of total net investments, respectively).The worst performing issues in the portfolio, though still with good income and positive total returns, were several oil companies that were hurt by the fallout from the Gulf oil spill, even though they had no direct involve-ment.These include Tesoro Corp., an oil refiner; and McMoRan Exploration Co., an offshore driller (0.1% and 0.2% of total net investments, respectively) .

What is the outlook for the equity and high-yield markets in the months ahead, and what is the portfolio’s strategy for that outlook?

TS&W believes that the recent weakness in the equity market may indicate that investors who began the year with a very optimistic view may not have fully appreciated the extent to which the early stages of the recovery were driven by government stim-

Semiannual Report | June 30, 2010 | 9

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Questions & Answers continued

ulus and the huge amounts of liquidity injected by the Federal Reserve.A big question now is whether there will be a smooth transition into a period of economic growth driven by the consumer spending and business investment.At this point, with the stimulus in place for about a year, year-over-year comparisons have become more difficult.TS&W does not expect that the economy will slip back into recession, but it seems likely that growth will be tepid.

Nonetheless,TS&W believes that valuations are compelling for many equities and especially for higher quality companies with ample free cash flow and little debt on their balance sheets. In a slow growth economy, many of these companies have the opportunity to perform very well. Some recent additions to the portfolio include economically sensitive companies with improving fundamentals that are selling at low multiples of price to earnings, book value and cash flow.These include Corning, Inc., which produces specialty glass and ceramics products; electronics retailer Best Buy Co.; and Freeport-McMoRan Copper & Gold, Inc., a mining company (0.6%, 0.7% and 0.5% of total net investments, respectively). In addition to the appeal of each of these stocks on their own merits, these stocks are expected to increase the portfolio’s beta (sensitivity to broad market movements), which should help performance as the market recovers from the recent weakness.

10 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Questions & Answers continued

Index Definitions

Indices are unmanaged and it is not possible to invest directly in an index.

Barclays Capital U.S. Municipal Long Bond Index is a rules-based, market-value-weighted index engineered for the long-term (22+ years) tax-exempt bond market.

The S&P 500 is an unmanaged, capitalization-weighted index of 500 stocks.The index is designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The Merrill Lynch HighYield Master II Index is a commonly used benchmark index for high yield corporate bonds and is a measure of the broad high yield market.

The Merrill Lynch Fixed Rate Preferred Securities Index is designed to replicate the total return of a diversified group of investment-grade preferred securities.The Index is rebalanced on a monthly basis.

Barclays Capital U.S.Aggregate Bond Index represents securities that are U.S. domestic, taxable, and dollar denominated.The index covers the U.S. investment grade fixed rate bond market, with index components for government and corporate securities, mortgage pass-through securities, and asset-backed securities.

Barclays Capital U.S.Treasury Index is an unmanaged index of prices of U.S.Treasury bonds with maturities of one to 30 years.

The Russell 1000®Value Index measures the performance of those Russell 1000 companies with lower price-to-book ratios and lower forecasted growth values, while the Russell 1000 Growth Index measures the performance of those Russell 1000 companies with higher price-to-book ratios and higher forecasted growth values.

TYW Risks and Other Considerations

The views expressed in this report reflect those of the portfolio managers only through the report period as stated on the cover. These views are subject to change at any time, based on market and other conditions and should not be construed as a recommendation of any kind.The material may also include forward looking statements that involve risk and uncertainty, and there is no guarantee that any predictions will come to pass.There can be no assurance that the Fund will achieve its investment objectives. The value of the Fund will fluctuate with the value of the underlying securities. Historically, closed-end funds often trade at a discount to their net asset value. There can be no assurance that the Fund will achieve its investment objective. The value of the Fund will fluctuate with the value of the underlying securities. The Fund is s ubject to investment risk, including the possible loss of the entire amount that you invest.

Municipal Securities Market Risk. The yields on and market prices of municipal securities are dependent on a variety of factors, including general conditions of the municipal securities market, the size of a particular offering, the maturity of the obligation and the rating of the issue. The value of outstanding municipal securities will vary as a result of changing evaluations of the ability of their issuers to meet interest and principal payments. Such values will also change in response to changes in the interest rates payable on new issues of municipal securities and changes in general interest rate levels. Changes in the value of the municipal securities held in the Fund’s portfolio arising from these or other factors will cause changes in the Fund’s net asset val ue per share.

Income and Interest Rate Risk. The income shareholders receive from the Fund is based primarily on the dividends and interest earned by the Fund from its investments, which can vary widely over the short and long term. The dividend income from the Fund’s investment in equity securities will be influenced by both general economic activity and issuer-specific factors. In the event of a recession or adverse events effecting a specific industry or issuer, the issuers of the common stocks held by the Fund may reduce the dividends paid on such common stocks. Interest rate risk is the risk that municipal securities and other debt (and, in certain cases, equity) securities in which the Fund invests (and the Fund’s net assets) will decline in value because of changes in interest r ates.

Lower Grade Securities. Investment in fixed income securities of below-investment grade quality (commonly known as “Junk bonds”) involves substantial risk of loss.They are considered predominantly speculative with respect to the issuer’s ability to pay interest and repay principal and are susceptible to default or decline in market value due to adverse economic and business developments. Debt securities in the lowest investment grade category may also be considered to have speculative characteristics by certain ratings agencies.The market values for fixed income securities of below investment grade quality tend to be more volatile, and these securities are less liquid, than investment grade debt securities.

Common Stock Risk. The common stocks and other equity securities in which the Fund invests may experience substantial volatility in their market value. Although common stocks typically provide higher returns than debt securities, they are also more susceptible to adverse changes in market value due to issuer-specific events. The market values of common stocks

Semiannual Report | June 30, 2010 | 11

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Questions & Answers continued

are also sensitive to changes in investor perceptions as well as general movements in the equities markets.

State Concentration Risk. To the extent the Fund concentrates its investments in municipal bonds, the Fund may be significantly impacted by political, economic, or regulatory developments that affect issuers and their ability to pay principal and interest on their obligations.

Leverage Risk. Certain risks are associated with the leveraging of common stock. Both the net asset value and the market value of shares of common stock may be subject to higher volatility and a decline in value.

AMPS Risk. There also risks associated with investing in Auction Market Preferred Shares or AMPS.The AMPS are redeemable, in whole or in part, at the option of the Fund on any dividend payment date for the AMPS, and will be subject to mandatory redemption in certain circumstances. The AMPS will not be listed on an exchange. You may only buy or sell AMPS through an order placed at an auction with or through a broker-dealer that has entered into an agreement with the auction agent and the Fund or in a secondary market maintained by certain broker dealers. These broker-dealers are not required to maintain this market, and it may not provide you with liquidity. The federal tax advice contained herein was not intended or written to be used, and it cannot be used by any taxpayer, for th e purpose of avoiding penalties that may be imposed on the taxpayer; the advice was written to support the promotion or marketing of the matters addressed; and the taxpayers should seek advice based on the taxpayer’s particular circumstances from an independent tax advisor.

Equity Risk. A principal risk of investing in the Fund is equity risk, which is the risk that the value of the securities held by the Fund will fall due to general market and economic conditions, perceptions regarding the industries in which the issuers of securities held by the Fund participate, or factors relating to specific companies in which the Fund invests. For example, an adverse event, such as an unfavorable earnings report, may depress the value of equity securities of an issuer held by the Fund; the price of common stock of an issuer may be particularly sensitive to general movements in the stock market; or a drop in the stock market may depress the price of most or all of the common stocks and other equity securities held by the Fund. In addition, common stock of an is suer in the Fund’s portfolio may decline in price if the issuer fails to make anticipated dividend payments because, among other reasons, the issuer of the security experiences a decline in its financial condition. Common stock is subordinated to preferred stocks, bonds and other debt instruments in a company’s capital structure, in terms of priority to corporate income, and therefore will be subject to greater dividend risk than preferred stocks or debt instruments of such issuers. In addition, while broad market measures of common stocks have historically generated higher average returns than fixed income securities, common stocks have also experienced significantly more volatility in those returns.

Preferred Securities Risk These securities are inherently more risky than the bonds and other debt instruments of the issuer, but typically less risky than its common stock. They may be significantly less liquid than many other securities, such as U.S. Government securities, corporate debt and common stock.

Taxable Debt Securities. The value of debt securities, including corporate debt securities, can be expected to vary inversely with interest rates. Income payments received by the Fund on debt securities will not be eligible for treatment as tax-qualified dividends.

High Yield Risk: CEFs that invest in high yield securities and unrated securities of similar credit quality (commonly known as “junk bonds”) may be subject to greater levels of credit and liquidity risk than funds that do not invest in such securities. These securities are considered predominately speculative with respect to the issuer’s continuing ability to make principal and interest payments. An economic downturn or period of rising interest rates could adversely affect the market for these securities and reduce the fund’s ability to sell these securities. If the issuer of a security is in default with respect to interest or principal payments, the fund may lose its entire investment.

In addition to the risks described above, the Fund is also subject to: Investment Risk, Common Share Market Risk, Tax Risk, Credit Risk, Geographical and Sector Risk, Interest Rate and Hedging Transactions Risk, Value Investing Risk, Illiquid Investments Risk, Foreign Securities Risk, Small- and Medium-Sized Company Risk, Fund Distribution Risk, Market Discount Risk, Portfolio Turnover, and Current Developments. Please see www.claymore.com/tyw for a more detailed discussion about Fund risks and considerations.

12 | Semiannual Report | June 30, 2010

| |

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |

Fund Summary | As of June 30, 2010 (unaudited) |

| | | |

| Fund Statistics | | |

| Share Price | | $9.53 |

| Common Share Net Asset Value | | $10.56 |

| Premium/(Discount) to NAV | | -9.75% |

| Net Asset Applicable to Common Shareholders ($000) | $162,740 |

Total Returns | | |

| (Inception 4/28/04) | Market | NAV |

| Six Month | 3.52% | -0.91% |

| One Year | 29.35% | 24.13% |

| Three Year - average annual | -5.29% | -6.57% |

| Five Year - average annual | 1.12% | 0.08% |

| Since Inception - average annual | 0.59% | 2.19% |

| Returns for periods of less than one year are not annualized. | |

| | | |

| Top Ten Holdings | % of Total |

Municipal Portfolio1 | Net Investments |

| Birmingham Special Care Facilities Financing Authority | | |

Health Care Facilities Revenue, ASSURED Insured, AAA, | | |

| Aa3, 6.00%, 6/1/2039 | | 3.2% |

| Frisco Texas Independent School District, School Improvements, | | |

Series A, PSF Guaranteed, NR, Aaa, 6.00%, 8/15/2038 | | 2.9% |

| Louisiana State Citizens Property Insurance Corp. Assessment Revenue, | |

Series C-2-RMKT, ASSURED Insured, AAA, Aa3, 6.75%, 6/1/2026 | 2.9% |

| Fomey Independent School District, Unlimited Tax School | | |

Building Bonds, Series A, PSF Guaranteed, AAA, NR, 6.00%, 8/15/2037 | 2.8% |

| Detroit Michigan Sewer Disposal Revenue | | |

Rols RR II R 11841-1, AGM Insured, AAA, NR, 14.21%, 7/1/2017 | 2.6% |

| Rhode Island State Health & Educational Building Corp. Revenue | |

Hospital Financing Lifespan Obligation, ASSURED Insured, | | |

Series A, AAA, NR, 13.29%, 5/15/2017 | | 2.6% |

| Detroit Michigan Sewer Disposal Revenue | | |

Refunding-Senior Lien-Series C-1-RMKT, AGM Insured, | | |

AAA, Aa3, 7.00%, 7/1/2027 | | 2.1% |

| Metropolitan Transportation Authority Revenue | | |

| Transportation - Series 2008C, A, A2, 6.50%, 11/15/2028 | | 2.1% |

| North Texas Tollway Authority Revenue | | |

Rols RR II R-11392-1, BHAC Insured, NR, Aa1, 10.82%, 1/1/2016 | 2.1% |

| New York State Dormitory Authority Income Tax Revenue, | | |

PIT Education - Series B, AAA, NR, 5.75%, 3/15/2036 | | 2.1% |

1 Excludes short-term | | |

| | |

| Top Ten Holdings | % of Total |

| Equity and Income Portfolio | Net Investments |

| AT&T, Inc. | 1.4% |

| Verizon Communications, Inc. | 1.3% |

| Waste Management, Inc. | 1.3% |

| Royal Dutch Shell PLC, ADR - Class B (United Kingdom) | 1.2% |

| ITT Corp. | 1.2% |

| Kimberly-Clark Corp. | 1.1% |

| Chevron Corp. | 1.0% |

| Pfizer, Inc. | 1.0% |

| Merck & Co., Inc. | 1.0% |

| Bristol-Myers Squibb Co. | 1.0% |

Securities and holdings are subject to change daily. For more current information, please visit www.claymore.com/tyw. The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results.

| | |

| | % of Total |

| Top Ten Sectors | Net Investments |

| Health Care | 15.2% |

| Special Tax | 11.1% |

| General Obligation | 9.0% |

| Water & Sewer | 8.1% |

| Insurance | 5.0% |

| Telecommunications | 4.4% |

| Pharmaceuticals | 3.7% |

| General Funds | 3.6% |

| Oil&Gas | 3.6% |

| Diversified Financial Services | 3.5% |

Semiannual Report | June 30, 2010 | 13

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund

Portfolio of Investments | June 30, 2010 (unaudited)

| | | | | |

| Principal | | | Optional Call | |

| Amount | | Description | Provisions | Value |

| | | Long-Term Municipal Bonds — 95.0% | |

| | | Alabama — 5.4% | | |

| $ 8,150,000 | | Birmingham Special Care Facilities Financing Authority, | | |

| | | Health Care Facilities Revenue, ASSURED Insured, AAA, Aa3 | |

| | | 6.00%, 6/1/2039 | 6/1/19 @ 100.00 | $ 8,850,003 |

| | | Arizona — 2.0% | | |

| 3,000,000 | | Glendale Western Loop 101, Public Facilities Corp., | | |

| | | Third Lien Excise Tax Revenue, Series A, AA, A1 | | |

| | | 7.00%, 7/1/2033 | 1/1/14 @ 100.00 | 3,226,470 |

| | | California — 8.3% | | |

| 4,610,000 | | Alhambra Certificates of Participation, | | |

| | | Police Facilities 91-1-RMK, AMBAC Insured, NR, NR | | |

| | | 6.75%, 9/1/2023 | N/A | 5,279,925 |

| 2,000,000 | | California Statewide Communities Development Authority, | |

| | | American Baptist Homes West, BBB-, NR | | |

| | | 6.25%, 10/1/2039 | 10/1/19 @ 100.00 | 1,986,480 |

| 2,500,000 | | Golden State Tobacco Securitization Corp., | | |

| | | Tobacco Settlement Asset-Backed Bonds, Series 2007A-1, BBB, Baa3 | |

| | | 5.75%, 6/1/2047 | 6/1/17 @ 100.00 | 1,789,550 |

| 4,600,000 | | Manhattan Beach California Unified School District, | | |

| | | Capital Appreciation-Election 2008, Series B, AA, Aa2 | | |

| | | 6.50%, 9/1/2045 (a) | 9/1/35 @ 100.00 | 1,672,238 |

| 2,500,000 | | M-S-R Energy Authority, | | |

| | | Natural Gas Revenue, Series B, A, NR | | |

| | | 7.00%, 11/1/2034 | N/A | 2,845,525 |

| | | | | 13,573,718 |

| | | District of Columbia — 0.7% | | |

| 1,000,000 | | District of Columbia Water & Sewer Authority, | | |

| | | Public Utility Revenue, Series A, AA, Aa2 | | |

| | | 6.00%, 10/1/2035 | 10/1/18 @ 100.00 | 1,122,890 |

| | | Indiana— 2.2% | | |

| 3,500,000 | | Evansville Industrial Redevelopment Authority, | | |

| | | Build America Bonds, Series B, A, Aa3 | | |

| | | 7.21%, 2/1/2039 (b) | 8/1/20 @ 100.00 | 3,626,455 |

| | | Kentucky — 3.6% | | |

| 2,700,000 | | Kentucky Economic Development Finance Authority, | | |

| | | Owensboro Medical Health System, Series A, NR, Baa2 | | |

| | | 6.375%, 6/1/2040 | 6/1/20 @ 100.00 | 2,768,607 |

| 3,050,000 | | Kentucky Economic Development Finance Authority, | | |

| | | Owensboro Medical Health System, Series B, NR, Baa2 | | |

| | | 6.375%, 3/1/2040 | 6/1/20 @ 100.00 | 3,134,393 |

| | | | | 5,903,000 |

| | | Louisiana — 4.8% | | |

| 6,980,000 | | Louisiana State Citizens Property Insurance Corp. Assessment Revenue, | |

| | | Series C-2-RMKT, ASSURED Insured, AAA, Aa3 | | |

| | | 6.75%, 6/1/2026 | 6/1/18 @ 100.00 | 7,861,714 |

| | | Massachusetts — 1.0% | | |

| 1,820,000 | | Massachusetts Development Finance Agency Revenue, | | |

| | | Evergreen Center, BBB-, NR | | |

| | | 5.50%, 1/1/2035 | 1/1/15 @ 100.00 | 1,578,450 |

| | | |

| | | | | |

| Principal | | | Optional Call | |

| Amount | | Description | Provisions | Value |

| | | Michigan — 14.5% | | |

| $ 5,150,000 | | Detroit Michigan Sewer Disposal Revenue, | | |

| | | Rols RR II R 11841-1, AGM Insured, AAA, NR | | |

| | | (Underlying Obligor: Detroit Michigan Sewer Disposal) | | |

| | | 14.21%, 7/1/2017 (c) | N/A | $ 7,205,365 |

| 5,000,000 | | Detroit Michigan Sewer Disposal Revenue, | | |

| | | Refunding-Senior Lien-Series C-1-RMKT, AGM Insured, AAA, Aa3 | |

| | | 7.00%, 7/1/2027 | 7/1/19 @ 100.00 | 5,816,350 |

| 5,000,000 | | Detroit Michigan Water Supply System Revenue, | | |

| | | Refunding-Senior Lien-Series C-RMKT, BHAC/FGIC Insured, AA+, Aa1 | |

| | | 5.75%, 7/1/2026 | 7/1/18 @ 100.00 | 5,419,650 |

| 2,265,000 | | Detroit Michigan Water Supply System Revenue, | | |

| | | Second Lien-Series B-RMKT, AGM Insured, AAA, NR | | |

| | | 7.00%, 7/1/2036 | 7/1/19 @ 100.00 | 2,607,921 |

| 2,500,000 | | Michigan Public Educational Facilities Authority Revenue, | |

| | | Refunding-Limited, Obligation-Landmark Academy, BBB-, NR | |

| | | 7.00%, 12/1/2039 | 6/1/20 @ 100.00 | 2,569,925 |

| | | | | 23,619,211 |

| | | New Jersey — 2.9% | | |

| 4,150,000 | | Newark Housing Authority Revenue, | | |

| | | South Ward Police Facility, ASSURED Insured, NR, Aa3 | | |

| | | 6.75%, 12/1/2038 | 12/1/19 @ 100.00 | 4,726,892 |

| | | New York — 16.1% | | |

| 3,000,000 | | Long Island Power Authority Revenue, | | |

| | | Electrical Light and Power Improvements, Series A, A-, A3 | |

| | | 6.25%, 4/1/2033 | 4/1/19 @ 100.00 | 3,460,590 |

| 5,000,000 | | Metropolitan Transportation Authority Revenue, | | |

| | | Transportation - Series 2008C, A, A2 | | |

| | | 6.50%, 11/15/2028 | 11/15/18 @ 100.00 | 5,804,600 |

| 5,000,000 | | New York State Dormitory Authority Income Tax Revenue, | |

| | | PIT Education - Series B, AAA, NR | | |

| | | 5.75%, 3/15/2036 | 3/15/19 @ 100.00 | 5,657,400 |

| 1,000,000 | | New York State Dormitory Authority Revenue, | | |

| | | The Bronx-Lebanon Hospital Center, NR, Aa2 | | |

| | | 6.50%, 8/15/2030 | 2/15/19 @ 100.00 | 1,099,570 |

| | | New York State Dormitory Authority Revenue, | | |

| | | Health, Hospital & Nursing Home Improvements, FHA, AAA, Aa2 | |

| 4,500,000 | | 6.25%, 8/15/2034 | 8/15/19 @ 100.00 | 4,998,330 |

| 2,500,000 | | 6.00%, 8/15/2038 | 8/15/19 @ 100.00 | 2,717,475 |

| 2,220,000 | | New York State Dormitory Authority Revenue, | | |

| | | School Districts Financing Program, ASSURED Insured, Series A, AAA, Aa3 | |

| | | 5.625%, 10/1/2029 | 10/1/19 @ 100.00 | 2,415,915 |

| | | | | 26,153,880 |

| | | Ohio — 1.4% | | |

| 2,900,000 | | Buckeye Tobacco Settlement Financing Authority, | | |

| | | Tobacco Settlement Asset-Backed Bonds, Series 2007A-2, BBB, Baa3 | |

| | | 6.50%, 6/1/2047 | 6/1/17 @ 100.00 | 2,275,224 |

| | | Pennsylvania — 1.2% | | |

| 2,500,000 | | Allegheny County Hospital Development Authority Health System Revenue, | |

| | | West Penn, Series 2007A, BB-, B1 | | |

| | | 5.375%, 11/15/2040 | 11/15/17 @ 100.00 | 1,883,725 |

See notes to financial statements.

14 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Portfolio of Investments (unaudited) continued

| | | | | |

| Principal | | | Optional Call | |

| Amount | | Description | Provisions | Value |

| | | Puerto Rico — 7.7% | | |

| $ 2,500,000 | | Puerto Rico Highway and Transportation Authority Revenue, | |

| | | Refunding Bonds, Series AA-1-RMKT, AGM Insured, AAA, Aa3 | |

| | | 4.95%, 7/1/2026 | 7/1/20 @ 100.00 | $ 2,525,550 |

| | | Puerto Rico Sales Tax Financing Revenue, | | |

| | | Public Improvements, First Sub-Series A, A+, A1 | | |

| 2,000,000 | | 6.00%, 8/1/2042 | 8/1/19 @ 100.00 | 2,120,540 |

| 5,000,000 | | 6.50%, 8/1/2044 | 8/1/19 @ 100.00 | 5,549,750 |

| 2,000,000 | | Puerto Rico Sales Tax Financing Revenue, | | |

| | | Public Improvements, First Sub-Series C, A+, A1 | | |

| | | 6.50%, 8/1/2035 | 8/1/20 @ 100.00 | 2,253,860 |

| | | | | 12,449,700 |

| | | Rhode Island — 4.7% | | |

| 5,500,000 | | Rhode Island State Health & Educational Building Corp. Revenue, | |

| | | Hospital Financing Lifespan Obligation, ASSURED Insured, Series A, AAA, NR | |

| | | (Underlying Obligor: Rhode Island State Health and Educational Building Corp.) | |

| | | 13.29%, 5/15/2017 (c) | N/A | 7,167,820 |

| 500,000 | | Rhode Island State Health & Educational Building Corp. Revenue, | |

| | | Hospital Financing Lifespan Obligation, A-, A3 | | |

| | | 6.375%, 8/15/2021 | 8/15/12 @ 100.00 | 517,635 |

| | | | | 7,685,455 |

| | | Texas — 16.8% | | |

| 6,700,000 | | Forney Independent School District, | | |

| | | Unlimited Tax School Building Bonds, Series A, PSF Guaranteed, AAA, NR | |

| | | 6.00%, 8/15/2037 (d) | N/A | 7,651,333 |

| | | Forney Independent School District, | | |

| | | Property Tax School Building Bonds, PSF Guaranteed, AAA, NR | |

| 3,030,000 | | 5.50%, 8/15/2038 | 8/15/20 @ 100.00 | 3,351,998 |

| 2,310,000 | | 5.50%, 8/15/2040 | 8/15/20 @ 100.00 | 2,545,458 |

| 7,000,000 | | Frisco Texas Independent School District, | | |

| | | School Improvements, Series A, PSF Guaranteed, NR, Aaa | | |

| | | 6.00%, 8/15/2038 (d) | N/A | 8,025,360 |

| 5,000,000 | | North Texas Tollway Authority Revenue, | | |

| | | Rols RR II R-11392-1, BHAC Insured, NR, Aa1 | | |

| | | (Underlying Obligor: North Texas Tollway Authority) | | |

| | | 10.82%, 1/1/2016 (c) | N/A | 5,775,300 |

| | | | | 27,349,449 |

| | | Wisconsin — 1.7% | | |

| 2,000,000 | | Wisconsin State Health & Educational Facilities Authority Revenue, | |

| | | Aurora Health Care, Series A, NR, A3 | | |

| | | 5.60%, 2/15/2029 | 2/15/11 @ 100.00 | 1,974,820 |

| 750,000 | | Wisconsin State Health & Educational Facilities Authority Revenue, | |

| | | Blood Center Southeastern Project, A-, NR | | |

| | | 5.75%, 6/1/2034 | 6/1/14 @ 100.00 | 762,300 |

| | | | | 2,737,120 |

| | | Total Long-Term Municipal Bonds — 95.0% | | |

| | | (Cost $147,657,327) | | 154,623,356 |

| | | | |

| Number | | | |

| of Shares | | Description | Value |

| | | Common Stocks — 54.9% | |

| | | Aerospace & Defense — 3.1% | |

| 27,500 | | General Dynamics Corp. | $ 1,610,400 |

| 75,000 | | ITT Corp. | 3,369,000 |

| | | | 4,979,400 |

| | | Beverages — 0.7% | |

| 17,500 | | Diageo PLC, ADR (United Kingdom) | 1,097,950 |

| | | Capital Markets — 0.8% | |

| 55,000 | | Morgan Stanley | 1,276,550 |

| | | Chemicals — 0.6% | |

| 16,000 | | CF Industries Holdings, Inc. | 1,015,200 |

| | | Commercial Banks — 0.3% | |

| 20,000 | | Wells Fargo & Co. | 512,000 |

| | | Commercial Services & Supplies — 3.5% | |

| 100,000 | | Pitney Bowes, Inc. | 2,196,000 |

| 110,000 | | Waste Management, Inc. | 3,441,900 |

| | | | 5,637,900 |

| | | Communications Equipment — 0.5% | |

| 38,500 | | Cisco Systems, Inc. (e) | 820,435 |

| | | Computers & Peripherals — 0.4% | |

| 35,000 | | EMC Corp. (e) | 640,500 |

| | | Containers & Packaging — 0.4% | |

| 25,000 | | Bemis Co., Inc. | 675,000 |

| | | Diversified Financial Services — 1.2% | |

| 52,500 | | JPMorgan Chase & Co. | 1,922,025 |

| | | Diversified Telecommunication — 5.0% | |

| 155,000 | | AT&T, Inc. | 3,749,450 |

| 125,000 | | Verizon Communications, Inc. | 3,502,500 |

| 85,000 | | Windstream Corp. | 897,600 |

| | | | 8,149,550 |

| | | Electric Utilities — 0.6% | |

| 30,000 | | Southern Co. | 998,400 |

| | | Electronic Equipment & Instruments — 1.0% | |

| 100,000 | | Corning, Inc. | 1,615,000 |

| | | Energy Equipment & Services — 1.2% | |

| 62,500 | | Noble Corp. (Switzerland) (e) | 1,931,875 |

| | | Food Products — 2.2% | |

| 77,700 | | Kraft Foods, Inc. - Class A | 2,175,600 |

| 50,000 | | Unilever NV (Netherlands) | 1,366,000 |

| | | | 3,541,600 |

| | | Health Care Equipment & Supplies — 0.8% | |

| 20,000 | | Becton, Dickinson and Co. | 1,352,400 |

See notes to financial statements.

Semiannual Report | June 30, 2010 | 15

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Portfolio of Investments (unaudited) continued

| | | | |

| Number | | | |

| of Shares | | Description | Value |

| | | Hotels, Restaurants & Leisure — 0.4% | |

| 15,000 | | Darden Restaurants, Inc. | $ 582,750 |

| | | Household Durables — 0.5% | |

| 29,475 | | Garmin Ltd. (Switzerland) | 860,081 |

| | | Household Products — 1.9% | |

| 50,000 | | Kimberly-Clark Corp. | 3,031,500 |

| | | Industrial Conglomerates — 1.2% | |

| 22,500 | | Siemens AG, ADR (Germany) | 2,014,425 |

| | | Insurance — 4.4% | |

| 50,000 | | Chubb Corp. | 2,500,500 |

| 60,000 | | MetLife, Inc. | 2,265,600 |

| 50,000 | | Travelers Cos., Inc. (The) | 2,462,500 |

| | | | 7,228,600 |

| | | IT Services — 1.3% | |

| 16,500 | | IBM Corp. | 2,037,420 |

| | | Metals & Mining— 0.9% | |

| 25,000 | | Freeport-McMoRan Copper & Gold, Inc. - Class B | 1,478,250 |

| | | Multiline Retail — 2.3% | |

| 75,000 | | Macy’s, Inc. | 1,342,500 |

| 50,000 | | Target Corp. | 2,458,500 |

| | | | 3,801,000 |

| | | Multi-Utilities — 2.5% | |

| 150,000 | | Centerpoint Energy, Inc. | 1,974,000 |

| 75,000 | | NiSource, Inc. | 1,087,500 |

| 24,225 | | PG&E Corp. | 995,648 |

| | | | 4,057,148 |

| | | Oil, Gas & Consumable Fuels — 4.3% | |

| 30,000 | | BP PLC, ADR (United Kingdom) | 866,400 |

| 40,000 | | Chevron Corp. | 2,714,400 |

| 70,719 | | Royal Dutch Shell PLC, ADR - Class B (United Kingdom) | 3,414,313 |

| | | | 6,995,113 |

| | | Pharmaceuticals — 7.3% | |

| 105,000 | | Bristol-Myers Squibb Co. | 2,618,700 |

| 55,000 | | Eli Lilly & Co. | 1,842,500 |

| 37,500 | | Johnson & Johnson | 2,214,750 |

| 75,000 | | Merck & Co., Inc. | 2,622,750 |

| 185,000 | | Pfizer, Inc. | 2,638,100 |

| | | | 11,936,800 |

| | | Real Estate Investment Trusts — 0.9% | |

| 35,000 | | Rayonier, Inc. | 1,540,700 |

| | | Semiconductors — 1.3% | |

| 105,000 | | Intel Corp. | 2,042,250 |

| | | | | |

| Number | | | | |

| of Shares | | Description | | Value |

| | | Software — 1.1% | | |

| 125,000 | | Symantec Corp. (e) | | $ 1,735,000 |

| | | Specialty Retail — 1.2% | | |

| 57,500 | | Best Buy Co., Inc. | | 1,946,950 |

| | | Tobacco — 1.1% | | |

| 35,000 | | Reynolds American, Inc. | | 1,824,200 |

| | | Total Common Stocks — 54.9% | | |

| | | (Cost $96,742,060) | | 89,277,972 |

| | | | |

| Principal | | | Optional Call | |

| Amount | | Description | Provisions | Value |

| | | Corporate Bonds — 10.4% | | |

| | | Aerospace & Defense — 0.7% | | |

| $ 875,000 | | Alliant Techsystems, Inc., BB-, B1 | | |

| | | 6.75%, 4/1/2016 | 4/1/11 @ 103.38 | 857,500 |

| 350,000 | | Triumph Group, Inc., B+, B1 | | |

| | | 8.00%, 11/15/2017 | 11/15/13 @ 104.00 | 334,250 |

| | | | | 1,191,750 |

| | | Banks — 0.1% | | |

| 100,000 | | FCB/NC Capital Trust I, BB, Baa2 | | |

| | | 8.05%, 3/1/2028 | 3/1/11 @ 102.82 | 96,144 |

| | | Building Materials — 0.1% | | |

| 239,000 | | Boise Cascade LLC, B+, Caa1 | | |

| | | 7.125%, 10/15/2014 | 10/15/10 @ 102.38 | 224,959 |

| | | Commercial Services — 0.8% | | |

| 600,000 | | Hertz Corp. (The), CCC+, B2 | | |

| | | 8.875%, 1/1/2014 | 1/1/11 @ 102.22 | 607,500 |

| 668,000 | | Valassis Communications, Inc., BB-, Ba3 | | |

| | | 8.25%, 3/1/2015 | 3/1/11 @ 104.13 | 689,710 |

| | | | | 1,297,210 |

| | | Containers & Packaging — 0.4% | | |

| 600,000 | | Greif, Inc., BB+, Ba2 | | |

| | | 7.75%, 8/1/2019 | N/A | 618,000 |

| | | Diversified Financial Services — 0.7% | | |

| 750,000 | | Ford Motor Credit Co. LLC, B-, Ba3 | | |

| | | 8.70%, 10/1/2014 | N/A | 781,642 |

| 500,000 | | Goldman Sachs Capital II, BBB, Baa2 | | |

| | | 5.793%, 6/1/2043 (f) (g) | 6/1/12 @ 100.00 | 377,500 |

| | | | | 1,159,142 |

| | | Diversified Telecommunications — 0.9% | | |

| 541,000 | | Frontier Communications Corp., BB, Ba2 | | |

| | | 7.125%, 3/15/2019 | N/A | 500,425 |

| 425,000 | | NII Capital Corp., BB-,B1 | | |

| | | 10.00%, 8/15/2016 | 8/15/13 @ 105.00 | 447,312 |

| 500,000 | | Windstream Corp., B+, Ba3 | | |

| | | 8.625%, 8/1/2016 | 8/1/11 @ 104.31 | 503,750 |

| | | | | 1,451,487 |

See notes to financial statements.

16 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund |Portfolio of Investments (unaudited) continued

| | | | | |

| Principal | | | Optional Call | |

| Amount | | Description | Provisions | Value |

| | | Food — 0.6% | | |

| $ 1,015,000 | | Dean Foods Co., B, B2 | | |

| | | 7.00%, 6/1/2016 | N/A | $ 949,025 |

| | | Health Care — 0.8% | | |

| 550,000 | | Community Health Systems, Inc., B, B3 | | |

| | | 8.875%, 7/15/2015 | 7/15/11 @ 104.44 | 567,187 |

| 740,000 | | DaVita, Inc., B, B2 | | |

| | | 7.25%, 3/15/2015 | 3/15/11 @ 102.42 | 740,000 |

| | | | | 1,307,187 |

| | | Independent Power Producers — 0.3% | | |

| 520,000 | | NRG Energy, Inc., BB-, B1 | | |

| | | 8.50%, 6/15/2019 | 6/15/14 @ 104.25 | 528,450 |

| | | Insurance — 0.5% | | |

| 500,000 | | Genworth Financial, Inc., BB+, Ba1 | | |

| | | 6.15%, 11/15/66 (f) | 11/15/16 @ 100.00 | 341,250 |

| 445,000 | | White Mountain Re Group Ltd. (Bermuda), BBB-, Baa3 | | |

| | | 6.375%, 3/20/17 (h) | N/A | 445,474 |

| | | | | 786,724 |

| | | Internet & Catalog Retail — 0.3% | | |

| 500,000 | | NetFlix, Inc., BB-, Ba2 | | |

| | | 8.50%, 11/15/2017 | 11/15/13 @ 104.25 | 520,000 |

| | | Iron/Steel — 0.2% | | |

| 350,000 | | Allegheny Technologies, Inc., BBB-, Baa3 | | |

| | | 9.375%, 6/1/2019 | N/A | 413,271 |

| | | IT Services — 0.3% | | |

| 425,000 | | Unisys Corp., B, Caa1 | | |

| | | 12.50%, 1/15/2016 | 1/15/12 @ 106.25 | 459,000 |

| | | Office/Business Equipment — 0.6% | | |

| 1,000,000 | | Xerox Capital Trust I, BB, Baa3 | | |

| | | 8.00%, 2/1/2027 | 2/1/11 @ 101.47 | 1,005,383 |

| | | Oil, Gas & Consumable Fuels — 0.5% | | |

| 500,000 | | McMoRan Exploration Co., B, Caa1 | | |

| | | 11.875%, 11/15/2014 | 11/15/11 @ 105.94 | 510,000 |

| 425,000 | | Tesoro Corp., BB+, Ba1 | | |

| | | 6.625%, 11/1/2015 | 11/1/11 @ 102.21 | 398,438 |

| | | | | 908,438 |

| | | Pharmaceuticals — 0.2% | | |

| 325,000 | | Omnicare, Inc., BB, Ba2 | | |

| | | 7.75%, 6/1/2020 | 6/1/15 @ 103.88 | 331,500 |

| | | Real Estate Investment Trusts — 0.3% | | |

| 500,000 | | Omega Healthcare Investors, Inc., BB+, Ba3 | | |

| | | 7.00%, 1/15/2016 | 1/15/11 @ 103.50 | 493,750 |

| | | Real Estate Management Services — 0.4% | | |

| 525,000 | | CB Richard Ellis Services, Inc., B+, Ba3 | | |

| | | 11.625%, 6/15/2017 | 6/15/13 @ 105.81 | 588,000 |

| | | | | |

| Principal | | | Optional Call | |

| Amount | | Description | Provisions | Value |

| | | Retail — 0.6% | | |

| $ 700,000 | | Dillards, Inc., B+, B3 | | |

| | | 7.13%, 8/1/2018 | N/A | $ 658,000 |

| 315,000 | | Foot Locker, Inc., B+, B1 | | |

| | | 8.50%, 1/15/2022 | N/A | 296,100 |

| | | | | 954,100 |

| | | Transportation — 1.1% | | |

| 500,000 | | Kansas City Southern Railway, BB-, B2 | | |

| | | 8.00%, 6/1/2015 | 6/1/12 @ 104.00 | 515,000 |

| | | Overseas Shipholding Group, Inc., BB-, Ba3 | | |

| 850,000 | | 8.75%, 12/1/2013 | N/A | 873,375 |

| 350,000 | | 8.125%, 3/30/2018 | N/A | 343,875 |

| | | | | 1,732,250 |

| | | Total Corporate Bonds — 10.4% | | |

| | | (Cost $17,030,759) | | 17,015,770 |

| Number | | | | |

| of Shares | | Description | | Value |

| | | Preferred Stocks — 8.8% | | |

| | | Diversified Financial Services — 2.8% | | |

| 7,500 | | Ameriprise Financial, Inc., 7.75%, A, A3 | | 199,200 |

| 50,000 | | Bank of America Corp., Series 3, 6.375%, BB, Ba3 | | 962,500 |

| 56,000 | | Bank of America Corp., Series MER, 8.625%, BB, Ba3 | | 1,394,960 |

| 23,060 | | BB&T Capital Trust VI, 9.60%, BBB, A3 | | 627,693 |

| 31,650 | | Deutsche Bank Contingent Capital Trust II, 6.55%, BBB+, Baa2 | 653,256 |

| 60,000 | | RBS Capital Funding Trust VII, Series G, 6.08%, CC, B3 | | 732,000 |

| | | | | 4,569,609 |

| | | Electric — 0.3% | | |

| 20,000 | | Dominion Resources, Inc., Series A, 8.375%, BBB, Baa3 | | 556,000 |

| | | Insurance — 3.5% | | |

| 50,000 | | Aegon NV (Netherlands), 6.50%, BBB, Baa2 | | 881,000 |

| 51,240 | | Allianz SE (Germany), 8.375%, A+, A3 | | 1,295,414 |

| 25,000 | | Aspen Insurance Holdings Ltd. (Bermuda), 7.401%, BBB-, Ba1 (f) | 564,250 |

| 33,200 | | ING Groep NV (Netherlands), 7.375%, BB, Ba1 | | 623,164 |

| 50,000 | | Metlife, Inc., Series B, 6.50%, BBB-, Baa2 | | 1,163,000 |

| 48,600 | | Prudential PLC (United Kingdom), 6.50%, A-, Baa1 | | 1,132,380 |

| | | | | 5,659,208 |

See notes to financial statements.

Semiannual Report | June 30, 2010 | 17

TYW l TS&W/Claymore Tax-Advantaged Balanced Fund |Portfolio of Investments (unaudited) continued

| | | | | |

| Number | | | | |

| of Shares | | Description | | Value |

| | | Real Estate Investment Trusts — 2.2% | | |

| 15,480 | | Apartment Investment & Management Co., Series T, 8.00%, B+, Ba3 | $ 363,780 |

| 19,000 | | Brandywine Realty Trust, Series C, 7.50%, NR, NR | | 447,070 |

| 11,000 | | Capital Automotive REIT, Series A, 7.50%, NR, NR | | 221,719 |

| 10,000 | | CBL & Associates Properties, Inc., Series C, 7.75%, NR, NR | | 223,000 |

| 10,000 | | First Industrial Realty Trust, Inc., Series J, 7.25%, B-, B2 | | 169,800 |

| 6,700 | | Health Care REIT, Inc., Series D, 7.875%, BB, Baa3 | | 168,639 |

| 13,000 | | Kimco Realty Corp., Series G, 7.75%, BBB-, Baa2 | | 330,590 |

| 12,000 | | PS Business Parks, Inc., Series H, 7.00%, BB+, Baa3 | | 273,840 |

| 24,500 | | Public Storage, Series M, 6.625%, BBB, Baa1 | | 596,820 |

| 15,200 | | Regency Centers Corp., Series D, 7.25%, BB+, Baa3 | | 350,816 |

| 15,000 | | Vornado Realty Trust, Series E, 7.00%, BBB-, Baa3 | | 349,650 |

| | | | | 3,495,724 |

| | | Total Preferred Stocks — 8.8% | | |

| | | (Cost $16,466,812) | | 14,280,541 |

| | | Total Long-Term Investments - 169.1% | | |

| | | (Cost $277,896,958) | | 275,197,639 |

| Principal | | | Optional Call | |

| Amount | | Description | Provisions | Value |

| | | Short-Term Investments — 3.7% | | |

| | | Municipal Bonds — 3.7% | | |

| | | Tennessee — 3.7% | | |

| $ 6,000,000 | | Blount County Public Building Authority, | | |

| | | Local Government Public Improvements-A-4-A, NR, Aa1 | | |

| | | 1.41%, 6/1/2032 (i) | 9/1/10 @ 100.00 | |

| | | (Cost $6,000,000) | | 6,000,000 |

| | | Total Investments — 172.8% | | |

| | | (Cost $283,896,958) | | 281,197,639 |

| | | Floating Rate Note Obligations — (4.2%) | | |

| (6,850,000) | | Notes with interest rates ranging from 0.31% to 0.32% on June 30, 2010, | |

| | | and contractual maturities of collateral from 2016 to 2037. | | |

| | | (Cost ($6,850,000)) | | (6,850,000) |

| | | Total Net Investments — 168.6% | | |

| | | (Cost $277,046,958) | | 274,347,639 |

| | | Liabilities in excess of Other Assets — (4.1%) | | (6,607,349) |

| | | Preferred Shares, at Liquidation Value — (-64.5% of Net Assets | |

| | | Applicable to Common Shareholders or -37.3% of Total Investments) | (105,000,000) |

| | | Net Assets Applicable to Common Shareholders — 100.0% | $ 162,740,290 |

| | | |

| ADR | | American Depositary Receipt |

| AG | | Stock Corporation |

| AGM | Assured Guaranty Municipal Corp. |

| AMBAC | Ambac Assurance Corporation |

| ASSURED | Assured Guaranty Corporation |

| BHAC | Berkshire Hathaway Assurance Corporation |

| FGIC | | Financial Guaranty Insurance Company |

| FHA | | Guaranteed by Federal Housing Administration |

| LLC | | Limited Liability Corporation |

| N/A | | Not Applicable |

| NV | | Publicly Traded Company |

| PLC | | Public Limited Company |

| PSF | | Permanent School Fund (Texas) |

| REIT | | Real Estate Investment Trust |

| (a) | Security has a step coupon and a convertible feature effective after September 1, 2026 . |

| (b) | Taxable municipal bond issued as part of the Build America Bond program. |

| (c) | Inverse floating rate investment. Interest rate shown is that in effect at June 30, 2010. |

| (d) | Underlying security related to inverse floating rate investment entered into by the Fund. |

| (e) | Non-income producing security. |

| (f) | Floating or variable rate coupon. The rate shown is as of June 30, 2010. |

| (g) | Security is a hybrid bond that will convert to a preferred stock on the first call date. |

| (h) | Securities are exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be |

| | resold in transactions exempt from registration, normally to qualified institutional buyers. At June 30, 2010, these |

| | securities amounted to $445,474, which represents 0.27% of net assets applicable to common shares. |

| (i) | Security has a maturity of more than one year, but has variable rate and demand features which qualify it as a |

| | short-term security. The rate shown is that earned by the Fund as of June 30, 2010. |

Ratings shown are per Standard & Poor’s and Moody’s. Securities classified as NR are not rated.

All percentages shown in the Portfolio of Investments are based on Net Assets Applicable to Common Shareholders unless otherwise noted.

See notes to financial statements.

18 | Semiannual Report | June 30, 2010

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund

Statement of Assets and Liabilities| June 30, 2010 (unaudited)

| Assets | | |

| Investments in securities, at value (cost $283,896,958) | $ | 281,197,639 | |

| Interest receivable | | 2,946,607 | |

| Dividends receivable | | 290,501 | |

| Other assets | | 13,743 | |

Total assets | | 284,448,490 | |

| Liabilities | | | |

| Floating rate note obligations | | 6,850,000 | |

| Payable for securities purchased | | 6,702,221 | |

| Custodian bank | | 2,830,810 | |

| Advisory fee payable | | 156,944 | |

| Administration fee payable | | 5,717 | |

| Dividend payable - preferred shares | | 5,298 | |

| Accrued expenses and other liabilities | | 157,210 | |

| Total liabilities | | 16,708,200 | |

| Preferred Shares, at Redemption Value | | | |

| $.01 par value per share; 4,200 Auction Market Preferred Shares authorized, | | | |

| issued and outstanding at $25,000 per share liquidation preference | | 105,000,000 | |

| Net Assets Applicable to Common Shareholders | $ | 162,740,290 | |

| Composition of Net Assets Applicable to Common Shareholders | | | |

| Common stock, $.01 par value per share; unlimited number of shares authorized, 15,407,000 shares issued and outstanding | $ | 154,070 | |

| Additional paid-in capital | | 218,557,393 | |

| Accumulated net realized loss on investments and swaps | | (53,127,199 | ) |

| Net unrealized depreciation on investments | | (2,699,319 | ) |

| Accumulated distributions in excess of net investment income | | (144,655 | ) |

| Net Assets Applicable to Common Shareholders | $ | 162,740,290 | |

Net Asset Value Applicable to Common Shareholders (based on 15,407,000 common shares outstanding) | $ | 10.56 | |

See notes to financial statements.

Semiannual Report | June 30, 2010 | 19

TYW | TS&W/Claymore Tax-Advantaged Balanced Fund

Statement of Operations | For the Six Months Ended June 30, 2010 (unaudited)

| | | |

| Investment Income | | |

| Interest | $ 4,692,914 | |

| Dividends (net of foreign withholding taxes of $2,073) | 2,214,613 | |

Total income | | $ 6,907,527 |

| Expenses | | |