united states

securities and exchange commission

washington, d.c. 20549

form n-csr

certified shareholder report of registered management

investment companies

Investment Company Act file number 811-21872

Mutual Fund Series Trust

(Exact name of registrant as specified in charter)

4221 North 203rd Street, Suite 100 Elkhorn, Nebraska 68022-3474

(Address of principal executive offices) (Zip code)

Ultimus Fund Solutions ___

80 Arkay Drive, Suite 110, Hauppauge, NY 11788

(Name and address of agent for service)

Registrant's telephone number, including area code: 866-447-4228

Date of fiscal year end: 3/31

Date of reporting period: 3/31/23

ITEM 1. REPORTS TO SHAREHOLDERS.

Annual Report

AlphaCentric Income Opportunities Fund

Class A: IOFAX Class C: IOFCX Class I: IOFIX

AlphaCentric Premium Opportunity Fund

Class A: HMXAX Class C: HMXCX Class I: HMXIX

AlphaCentric Robotics and Automation Fund

Class A: GNXAX Class C: GNXCX Class I: GNXIX

AlphaCentric Symmetry Strategy Fund

Class A: SYMAX Class C: SYMCX Class I: SYMIX

AlphaCentric LifeSci Healthcare Fund

Class A: LYFAX Class C: LYFCX Class I: LYFIX

AlphaCentric SWBC Municipal Opportunities Fund

Class A: MUNAX Class C: MUNCX Class I: MUNIX

AlphaCentric Strategic Income Fund

Class A: SIIAX Class C: SIICX Class I: SIIIX

March 31, 2023

AlphaCentric Advisors LLC

53 Palmeras Street, Suite 601

San Juan, PR 00901

1-844-223-8637

March 31, 2023

Dear AlphaCentric Income Opportunities Fund (“the Fund”) Investor:

To say that the last year has been eventful is an understatement, and to that end we hope you have been able to weather the volatility in the markets as well as the world in general!

Few asset classes were spared over the last year, with the Fund’s holdings being no exception: returns were -19.90% (Class I shares), versus -4.78% for the Bloomberg US Aggregate Bond Index.

The Federal Reserve (“Fed”) continued its vigilant battle against inflation all last year and into 2023, raising rates every meeting at a pace not seen prior. The war in Ukraine persisted and dragged, requiring more and more US financial and military support and contributing to a deep risk-off mentality, with investors effectively remaining on the sidelines all year. Even the turn of the calendar year, which allowed participants to “start with a clean slate” and begin January 2023 with higher yields and bounce-back prospects aplenty, was met with a very strong jobs number and persistent inflation indicators. This quickly led to additional Fed hike fears and thus reluctance to deploy capital.

However, spillover effects from the rapid rise in rates plus apparent missteps in Fed monitoring led to turmoil at Silicon Valley Bank (SVB) in early March. As other regional banks were swept up into the resultant deposit run, an effective “lid” on further Fed hike action was priced into the market; incremental calm and stability in bonds resulted; and broad fixed income performance has improved.

Our sector presently remains relatively cheap, but activity has been increasing and we feel that the Fund is poised to potentially rally in response. Interestingly, collateral and fundamentals have not been an issue at all and have steadily improved. We believe that the clearing-up of poor bond technicals should produce much better conditions.

Further, the Fund’s dividend was increased in November to reflect higher interest generated from the floating-rate holdings of the Fund.

We thank you for your support of the Fund during this difficult period, and hope for more favorable market conditions this year!

Sincerely,

Garrison Point Fund Management Team

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

1

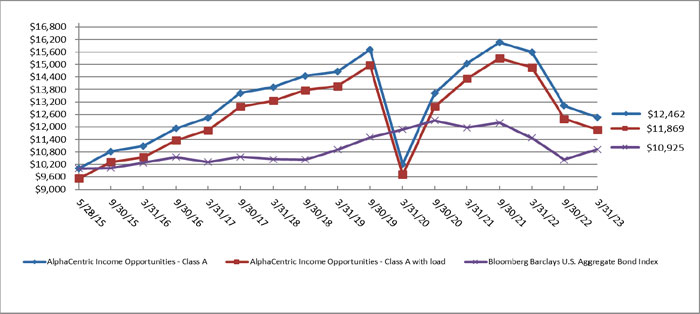

The Fund’s returns for the fiscal year ended 3/31/23 and for the period since inception through 3/31/23, as compared to the Benchmark Index, were as follows:

| Since Inception | ||

| Fiscal Year Ended 3/31/2023 | 5/28/2015 | |

| Class I | -19.90 | 3.11 |

| Class A | -20.13 | 2.85 |

| Class A w/ Sales Charge | -23.91 | 2.21 |

| Class C | -20.74 | 2.08 |

| Bloomberg US Agg Bond Index (1) | -4.78 | 1.13 |

| (1) | Bloomberg US Aggregate Bond Index: A market capitalization-weighted index that is designed to measure the performance of the U.S. investment grade bond market with maturities of more than one year. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 4.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 1-844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 5436-NLD-05052023

2

AlphaCentric Income Opportunities Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2023

The Fund’s performance figures* for the periods ended March 31, 2023, compared to its benchmark:

| Annualized | ||||

| Annualized | Annualized | Since Inception + - | ||

| One Year | Three Years | Five Years | March 31, 2023 | |

| Class A (IOFAX) | (20.13)% | 6.88% | (2.18)% | 2.85% |

| Class A (IOFAX) with 4.75% load | (23.91)% | 5.15% | (3.13)% | 2.21% |

| Class C (IOFCX) | (20.74)% | 6.07% | (2.92)% | 2.08% |

| Class I (IOFIX) | (19.90)% | 7.15% | (1.93)% | 3.11% |

| Bloomberg U.S. Aggregate Bond Index ** | (4.78)% | (2.77)% | 0.91% | 1.13% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 4.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 31, 2023. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s manager has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2023, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.74%, 2.49% and 1.49% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the manager from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus were 1.94%, 2.70% and 1.69% for the Fund’s Class A, Class C, and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus were 1.75%, 2.50% and 1.50% for the Fund’s Class A, Class C, and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The Bloomberg U.S. Aggregate Bond Index is commonly used as a benchmark by both passive and active investors to measure portfolio performance relative to the U.S. dollar-denominated investment grade fixed-rate taxable bond market. It is also an informational measure of broad market returns commonly applied to fixed income instruments. Investors cannot invest directly in an index. |

| + | The AlphaCentric Income Opportunities Fund commenced operations on May 28, 2015. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type | % of Net Assets | |||

| Non-Agency Residential Mortgage Backed Securities | 106.4 | % | ||

| Liabilities In Excess Of Other Assets | (6.4 | )% | ||

| 100.0 | % | |||

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

3

March 31, 2023

Dear AlphaCentric Premium Opportunity Fund (“the Fund”) Investor:

We are pleased to provide our Annual Letter to Shareholders. Thank you for your support and for being an investor in the Fund.

Investment Strategy

The portfolio strategy utilized by the Fund seeks to achieve capital appreciation with lower overall volatility than the equity market. The strategy attempts to achieve its objective by investing in a systematically managed portfolio of long and short call and put options and futures on the Standard & Poor’s 500 Index (the “Index”) and/or other securities that represent the return of the Index (such as exchange traded funds), as well as investments tied to measures of market volatility such as volatility exchange traded funds and futures on the VIX Index, which reflect the market’s expected fluctuation (volatility).

In terms of positioning, the strategy generally aims to earn 40% to 60% of the stock market upside over a full market cycle but also employs options selling and other strategies to help reduce risk and mitigate the downside risk, aiming for 50% to 100% coverage during periods of severe market declines like March 2020.

In addition to option strategies such as call ratios, strangles and straddles, the strategy uses futures, options on futures, and a variety of derivative instruments in an attempt to achieve capital efficiency. Relying on the embedded leverage of these markets, the Fund aims to hold between 70% and 85% of assets in U.S. Treasury bills or similar investments.

Treasury bills act as a source of both safety and potential upside, aligning with the overall dual mandate of balancing offense and defense. The income they generate, especially in a higher rate environment, helps enhance risk-adjusted returns for investors.

Fund Performance

For the fiscal year ended March 31, 2023, the Fund returned -4.32% (Class I shares). This compares to a -7.73% return for the S&P 500 Index.

While the Fund’s strategy can and will be able to post positive returns in certain down-market environments thanks to its long VIX components, the 2022 market selloff occurred with the decline of the VIX, starting around 20, then averaging just 23 for the period before finishing below where it started, falling to 18.70. In comparison, March 2020 saw the VIX move from around 15 up to 75.

Additionally, volatility seemed to have a stubborn floor throughout the period, averaging 23 instead of falling back into the teens as was the pattern for much of the 2010 to 2020 period. This ceiling/floor phenomenon essentially put a cap on the opportunity available to the type of option trades the Fund employs. This kept the model alternating between its falling market/falling volatility quadrant and falling

4

market/rising volatility quadrant, which created a bit of drag as positions were adjusted and pivoted to the new quadrant, then back to the previous quadrant, then back to the other, and so on.

That sort of movement is not unexpected, but it is rarer to see than the typical pattern of markets finishing a falling market/rising volatility regime with a rising market/falling volatility regime. This was finally seen in January of 2023 and the Fund was quick to pivot and participate in the upside as it came into Q1 of 2023.

Market Outlook

Looking ahead, the market appears at an important turning point with many uncertainties remaining around risks such as recession, interest rates, inflation, and geopolitical issues.

Will the economy enter a downturn, or will growth continue at a steady pace? The Federal Reserve may have raised rates for the last time this cycle. But how long will they stay there, and how will that impact risk assets, valuations, and economic growth? For the first time since the COVID-19 pandemic first hit, it really feels like there are reasonable arguments on both the bull and bear sides. The future could unfold as a tale of either steady growth and healthy markets or deceleration, tightening monetary policy, and falling asset prices. Staying positioned to benefit no matter how events actually play out is the approach we’ll follow. The Fund aims to do just that through a strategy designed to earn solid returns through participation in up markets while also defending capital when volatility rises. With decades of experience, a time-tested process, and close monitoring of risks, the goal is making the most of opportunities to generate attractive risk-adjusted performance no matter the environment.

Sincerely,

Russell Kellites

Portfolio Manager

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

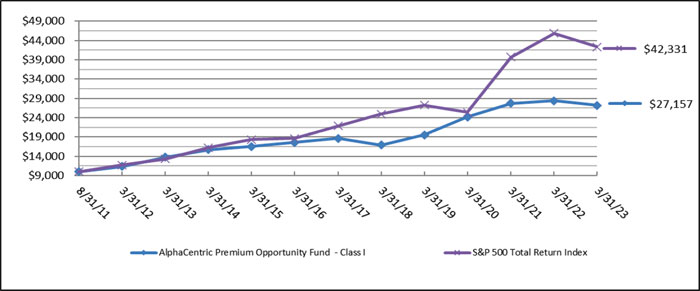

The Fund’s returns for the fiscal year ended 3/31/23 and for the period since inception through 3/31/23, as compared to the Benchmark Index, were as follows:

| Fiscal Year Ended 3/31/2023 | Since Inception* | |

| Class A | -4.53 | 6.12 |

| Class A with Sales Charge | -10.01 | 5.16 |

| Class C | -5.24 | 5.44 |

| S&P 500 TR Index (1) | -7.73 | 12.37 |

| Class I | -4.32 | 9.01 |

| S&P 500 TR Index (1) | -7.73 | 13.27 |

5

| * | Fund Inception: 9/1/2011 (Class I) & 9/30/2016 (Class A & C). The Performance shown before September 30, 2016, is for the Fund’s Predecessor Fund (Theta Funds, L.P.) The Fund’s management practices, investment goals, policies, objectives, guidelines and restrictions are, in all material respects, equivalent to the predecessor limited partnership. From its inception date, the predecessor limited partnership was not subject to certain investment restrictions, diversification requirements and other restrictions of the Investment Company Act of 1940, as amended, if they had been applicable, it might have adversely affected its performance. In addition, the predecessor limited partnership was not subject to sales loads that would have adversely affected performance. Performance of the predecessor fund is not an indicator of future results. |

| (1) | The S&P 500 Total Return Index by Standard & Poor’s Corp. is a capitalization-weighted index comprising 500 widely held common stocks listed on various exchanges, representing the performance of the stock market generally. Please note that indices do not take into account any fees and expenses of investing in the individual securities that they track, and individuals cannot invest directly in any index, although individuals may invest in exchange traded funds or other investment vehicles that attempt to track the performance of an index. The Fund may or may not purchase the types of securities represented by the S&P 500 Total Return Index. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Dividends are not assured. Investments in mutual funds involve risks. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 5447-NLD-05102023

6

AlphaCentric Premium Opportunity Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2023

The Fund’s performance figures* for the periods ended March 31, 2023, compared to its benchmark:

| Annualized | Annualized | |||||

| Annualized | Annualized | Annualized | Since Inception + - | Since Inception ++ - | ||

| One Year | Three Years | Five Years | Ten Years | March 31, 2023 | March 31, 2023 | |

| Class A (HMXAX) without load | (4.53)% | 3.67% | 9.66% | — | 6.12% | — |

| Class A (HMXAX) with 5.75% load | (10.01)% | 1.65% | 8.37% | — | 5.16% | — |

| Class C (HMXCX) | (5.24)% | 2.89% | 8.95% | — | 5.44% | — |

| Class I (HMXIX) +++ | (4.32)% | 3.92% | 9.92% | 7.06% | — | 9.01% |

| S&P 500 Total Return Index ** | (7.73)% | 18.60% | 11.19% | 12.24% | 12.37% | 13.27% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 31, 2023. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s manager has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2023, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 2.24%, 2.99% and 1.99% for the Fund’s Class A, Class C and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the manager from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus were 2.44%, 3.19% and 2.20% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus were 2.43%, 3.18%, and 2.18% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index. |

| + | The AlphaCentric Premium Opportunity Fund Class A and Class C commenced operations on September 30, 2016. |

| ++ | The AlphaCentric Premium Opportunity Fund Class I, formerly a private fund, commenced operations on August 31, 2011. |

| +++ | The Fund acquired all of the assets and liabilities of Theta Funds, L.P. (the “Predecessor Fund”) in a tax-free reorganization on September 30, 2016. In connection with this acquisition, shares of the Predecessor Fund were exchanged for Class I shares of the Fund, so the Predecessor Fund became the Class I shares of the Fund. The Fund’s investment objective, policies and guidelines are, in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies and guidelines. The Predecessor Fund commenced operations on August 31, 2011. Updated performance information will be available at no cost by calling 1-844-ACFUNDS (844-223-8637) or visiting the Fund’s website at www.AlphaCentricFunds.com. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type ** | % of Net Assets | |||

| U.S. Government & Agencies | 44.0 | % | ||

| Short-Term Investments | 27.6 | % | ||

| Future Options Purchased | 1.1 | % | ||

| Index Options Purchased | 0.0 | %* | ||

| Written Future Options | (1.0 | )% | ||

| Other Assets in Excess of Liabilities | 28.3 | % | ||

| 100.0 | % | |||

* - Less than 0.05%

** - Does not include derivative investments.

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

7

March 31, 2023

Dear AlphaCentric Robotics and Automation Fund (the “Fund”) Investor:

The highest inflation rates in four decades led to the fastest monetary policy tightening cycle in U.S. history. That in turn drove a 27% peak-to-trough decline in the S&P 500 during 2022. The major averages posted interim lows in mid-October and have since recovered approximately 50% of the aforementioned drop. Headline inflation data has receded sharply from the peak levels recorded last summer, but core inflation remains sticky, with the latest core Personal Consumption Expenditures report holding at 4.6% for the month ended February 2023. This remains well above the Federal Reserve’s 2.0% target rate, suggesting that the central bank may be inclined to raise rates further and potentially hold them there for a prolonged period. Complicating the situation is the fact that the held-to-maturity assets on many bank balance sheets have been substantially impaired by the rise in interest rates. This condition has already resulted in the failure of three regional banks in the U.S. – most notably Silicon Valley Bank. An impending credit crunch is expected as lending standards tighten in response to less liquid conditions, thus raising the odds of a recession later this year.

March 31, 2023 marked the end of the fiscal year of the Fund. Since the end of the last fiscal year, the Fund posted a -12.46% (Class I shares) decline. The S&P 500 TR Index during the same period reported a loss of -7.73%. The macro environment described above has put excessive pressure on the valuations of emerging growth and disruptive technology companies despite sound underlying fundamentals and robust execution. Due to this fact, the Fund experienced a relative performance deficit over the year ended March 31, 2023 versus the benchmark index.

Notably, despite the continuing conflict in Ukraine, energy prices and supply chains have normalized. As such, capex spending priorities have resumed their focus on robotics and automation solutions. It is our view that the mandate to improve operational efficiencies will remain front and center as companies large and small adapt to the new realities of a post-COVID world. Indeed, the Fund’s strategy of focusing on leading edge technologies and the core end-market beneficiaries of the automation theme has already begun to recover in the form of M&A. Two of the Fund’s former core portfolio holdings were acquired in 2022 – Kuka AG and Cyberoptics Corp – at substantial premiums to our cost basis. Both buyers were industrial manufacturers who saw significant value in the underlying businesses of these two technology innovators.

The Fund’s top performing position during the fiscal year was another German company by the name of Krones AG. The company posted a 43.1% gain for the year ended March 31, 2023. Krones is a packaging and bottling machine manufacturer. They are perhaps best known for their cutting-edge packing and filling process technologies used in the beer, soft drink, and spirits industries. But they have also become dominant in the juice, water, milk, and plant-based drinks arenas as well. Their solutions extend to include blow molding, filling and capping, tempering, labelling, palletizing, inspecting, cleaning, and conveying.

Allied Motion Technologies was the second largest contributor to the Fund’s results last year. The stock gained 29.9% during the period. The company is a leader in precision and specialty motion control

8

components and systems used in robotics and automation applications for a variety of end markets including industrial, medical, aerospace and defense, and autonomous vehicle technologies.

And lest we forget, the 20% gain from one of the Fund’s largest holdings – Infineon Technologies AG, was the Fund’s third largest driver of performance. The company, a spinoff from Siemens AG in 1999, has since become the largest semiconductor manufacturer in Germany. Their products make robotics possible. They are the world leader in high reliability motor control integrated circuits across all subcategories, microcontrollers, and ASICs serving the automotive, consumer, and industrial machinery end markets.

While these are just a few positions that were important to the Fund’s fiscal year results, they are representative of the broad array of companies and technologies that populate our portfolio. From smart warehouses, automated manufacturing, and robotic process automation to tele-medicine and surgical robotics, to autonomous vehicles, artificial intelligence and machine learning technologies, the Fund remains laser-focused on identifying and capitalizing upon advances and innovative technologies that are changing the world by investing in the companies that are driving this change.

Thank you for your support and participation in the Fund.

Sincerely,

Brian Gahsman, Portfolio Manager

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

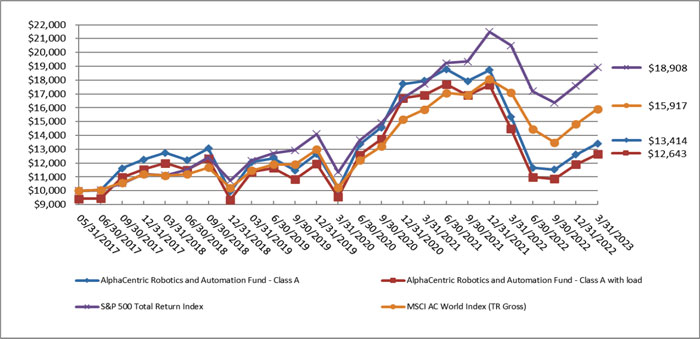

The Fund’s returns for the fiscal year ended 3/31/23 and for the period since inception through 3/31/23, as compared to the Benchmark Index, were as follows:

| Fiscal Year Ended | ||

| 3/31/2023 | Since Inception 5/31/17 | |

| Class I | -12.46 | 5.43 |

| Class A | -12.64 | 5.16 |

| Class A w/Sales Charge | -17.64 | 4.10 |

| Class C | -13.28 | 4.39 |

| S&P 500 Total Return Index(1) | -7.73 | 11.54 |

| MSCI AC World Index TR Gross(2) | -6.96 | 8.29 |

| (1) | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index. |

9

| (2) | The MSCI AC World Index TR Gross represents the Modern Index Strategy and captures all sources of equity returns in 23 developed and 24 emerging markets. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 6220-NLD-05052023

10

AlphaCentric Robotics and Automation Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2023

The Fund’s performance figures* for the periods ended March 31, 2023, compared to its benchmarks:

| Annualized | ||||

| Annualized | Annualized | Since Inception + - | ||

| One Year | Three Years | Five Years | March 31, 2023 | |

| Class A (GNXAX) without load | (12.64)% | 9.80% | 1.05% | 5.16% |

| Class A (GNXAX) with 5.75% load | (17.64)% | 7.64% | (0.14)% | 4.10% |

| Class C (GNXCX) | (13.28)% | 8.97% | 0.29% | 4.39% |

| Class I (GNXIX) | (12.46)% | 10.04% | 1.28% | 5.43% |

| S&P 500 Total Return Index ** | (7.73)% | 18.60% | 11.19% | 11.54% |

| MSCI AC World Index (TR Gross) *** | (6.96)% | 15.90% | 7.46% | 8.29% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 31, 2023. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s manager has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2023, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.65%, 2.40% and 1.40% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the manager from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus for the Fund’s period of operation are 2.03%, 2.79% and 1.79% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses shown in the August 1, 2022 prospectus for the Fund’s period of operation are 1.66%, 2.41% and 1.41% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index. |

| *** | The MSCI AC World Index (TR Gross) represents the Modern Index Strategy and captures all sources of equity returns in 23 developed and 24 emerging markets. Investors cannot invest directly in an index. |

| + | The AlphaCentric Robotics and Automation Fund Class A, Class C and Class I commenced operations on May 31, 2017. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type | % of Net Assets | |||

| Common Stocks | 97.4 | % | ||

| Investment Purchased as Securities Lending Collateral | 28.0 | % | ||

| Money Market Fund | 2.4 | % | ||

| Liabilities In Excess Of Other Assets | (27.8 | )% | ||

| 100.0 | % | |||

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

11

March 31, 2023

Dear AlphaCentric Symmetry Strategy Fund (“the Fund”) Investor:

The Fund was down -2.65% (Class I shares) for fiscal year 2023, outperforming the blended MSCI World/U.S. Aggregate Bond Blended Index which returned -6.80%. The traditional portfolio, that invests in stocks and credit detracted from performance as both equity and bond markets fell over the period, with the S&P 500 falling -7.75% over the period and the Bloomberg Aggregate falling -4.78%. The alternative portfolio which invests in commodities, fixed income and currencies, added to performance over the period, with short positions in fixed income futures and long positions in the USD helping to offset equity losses as the Fund’s trend following strategies captured the move to higher global yields. Adaptability is important.

Those hoping for a quiet start to the new year after the rollercoaster that was 2022 were disappointed in the first quarter of 2023. Our favorite of the once-in-a-black-swan statistics: in the past 25 years the US 2-Year yield had moved 25bps or more 17 times; in March 2023 it happened 6 times in a row. Strong US inflation and payroll data for January caused US yields to rapidly move to the highest levels in 15 years, increasing the 2-Year yield almost 100bps from 4.20% at the end of February to 5.07% in early March. After a bank failure over a weekend, it reversed 110bps lower in just 3 sessions.

The Federal Reserve has found itself in a difficult position. Inflation has been stubbornly high as it is officially reported while the channel through which they expect tighter policy to work – the labor market – remains strong. At the same time, the most interest rate sensitive sectors of the economy have slowed, in some places meaningfully so. Housing prices and rents are clearly dropping. This is not in the official CPI data yet but will show up in due course, easing the inflation trajectory. Commercial real estate is showing signs of stress as well, partly due to post-pandemic working habits and partly due to financing cost increases. Some additional areas of the banking system are also stressed, which have implications for credit standards, loan growth and loan availability in the coming quarters.

Moving on to less-volatile things than the 2-Year bond – commodity markets. Not quite, but it sure feels that way. Our alternative strategies fit so well with traditional equity exposures as they generally thrive on volatility in markets. Traditional markets abhor volatility. What drives volatility in commodity markets? Deficit markets moving to surplus and surplus markets moving to deficits. Balanced markets are no fun for anyone. We sometimes hear the refrain that futures markets are price predictions of where things will trade. This is not right; they are arbitrage-free prices. Commodity markets can move further and more quickly than stock and bond markets as they must live in the here and now, unable to do too much discounting of what may happen in the out years. Take copper for example, the current price may be stable as we aren’t currently in the thick of a supply demand crunch, but that crunch is certainly building. Green revolutions will need a lot of copper. There are many markets with the potential for large moves as growth recovers, leading to higher demand than available supply – grains and energy markets may also come to fit this bill. But, if the slowdown in the economy continues, the strategy will move into short positions in due course as commodity demand falls away. Again, adaptability is important.

12

The traditional side of the portfolio spent much of 2022 with reduced risk exposures, having reduced meaningfully in late 2021 and ending the fiscal year about 50% net long. The strategy spent the majority of the fiscal year ended 2023 short global bonds and long the USD, both of which helped as rising yields driven by improving economies and inflation fears pushed all yields higher. Commodity exposures were more mixed, as the immediate price spike environment caused by the Ukraine war at the start of the Fund’s fiscal year subsided as the world evolved to manage as best it could through the supply disruptions. By way of example, energy markets stabilized in part due to releases from the Strategi Petroleum Reserve, and natural gas markets calmed as Europe in particular was fortunate to experience a fairly mild winter season.

Should equity and credit markets continue to stabilize and rebound after the battering of 2022, we believe the Fund is positioned to benefit. The Fund’s equity positions are cheap to a variety of fundamentals we analyze and look to have long runways ahead. During the first quarter of 2023, we saw some deal flow in a few names the Fund holds as other strategic buyers see the same thing, particularly in the energy space. We look for that to continue.

Thank you for your support, and we hope that you stay healthy and safe in 2023.

Sincerely,

Mount Lucas Management LP Team

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

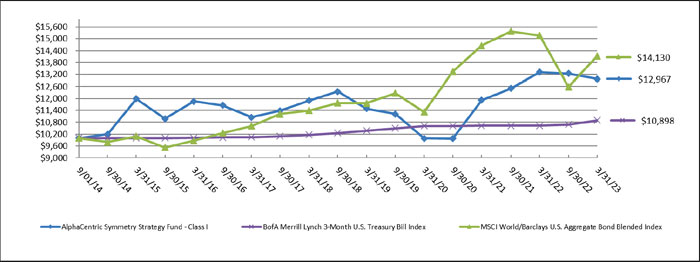

The Fund’s returns for the fiscal year ended 3/31/23 and for the period since inception through 3/31/23, as compared to the Benchmark Index, were as follows:

| Fiscal Year | ||

| Ended | ||

| 3/31/2023 | Since Inception* | |

| Class A | -2.86 | 3.67 |

| Class A w/ Sales Charge | -8.46 | 2.00 |

| Class C | -3.53 | 2.88 |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (1) | 2.53 | 1.11 |

| MSCI World/Bloomberg U.S. Aggregate Bond Blended Index (2) | -6.80 | 4.26 |

| Class I | -2.65 | 3.08 |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index (1) | 2.53 | 1.01 |

| MSCI World/Bloomberg U.S. Aggregate Bond Blended Index (2) | -6.80 | 4.11 |

| * | Inception (annualized): 9/1/14 (I Share) | 8/9/19 (A & C Shares) |

13

The Fund acquired all of the assets and liabilities of MLM Symmetry Fund, LP (the “Predecessor Fund”) in a tax-free reorganization on August 9, 2019. In connection with this acquisition, shares of the Predecessor Fund were exchanged for Class I shares of the Fund. The Fund’s investment objectives, policies, restrictions, and guidelines are, in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies, restrictions, and guidelines. The Fund’s sub-advisor was the adviser to the Predecessor Fund.

| (1) | BofA Merrill Lynch 3-Month U.S. Treasury Bill Index is an unmanaged market index of U.S. Treasury securities maturing in 90 days that assumes reinvestment of all income. Investors cannot invest directly in an index. |

| (2) | MSCI World Index is a broad global equity index that represents large and mid-cap equity performance across all 23 developed markets countries. It covers approximately 85% of the free float-adjusted market capitalization in each country. The Bloomberg U.S. Aggregate Bond index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Dividends are not assured. Investments in mutual funds involve risks. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 5446-NLD-05102023

14

AlphaCentric Symmetry Strategy Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2023

The Fund’s performance figures* for the periods ended March 31, 2023, compared to its benchmarks:

| Annualized | Annualized | ||||

| Annualized | Annualized | Since Inception + - | Since Inception ++ - | ||

| One Year | Three Years | Five Years | March 31, 2023 | March 31, 2023 | |

| Class A (SYMAX) without load | (2.86)% | 8.88% | — | 3.67% | — |

| Class A (SYMAX) with 5.75% load | (8.46)% | 6.77% | — | 2.00% | — |

| Class C (SYMCX) | (3.53)% | 8.01% | — | 2.88% | — |

| Class I (SYMIX) +++ | (2.65)% | 9.10% | 1.73% | — | 3.08% |

| BofA Merrill Lynch 3-Month U.S. Treasury Bill Index ** | 2.53% | 0.90% | 1.41% | 1.11% | 1.01% |

| MSCI World/Bloomberg U.S. Aggregate Bond Blended Index *** | (6.80)% | 7.64% | 4.40% | 4.26% | 4.11% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 31, 2023. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s manager has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2023, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.85%, 2.60% and 1.60% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the manager from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus are 2.49%, 3.23% and 2.23% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses shown in the August 1, 2022 prospectus are 1.98%, 2.73% and 1.73% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | BofA Merrill Lynch 3-Month U.S. Treasury Bill Index tracks the performance of the U.S. dollar denominated U.S. Treasury Bills publicly issued in the U.S. domestic market with a remaining term to final maturity of less than 3 months. Investors cannot invest directly in an index. |

| *** | MSCI World/Bloomberg U.S. Aggregate Bond Blended Index reflects an unmanaged portfolio of 60% of the MSCI World Index and 40% of the Bloomberg U.S. Aggregate Bond Index. Investors cannot invest directly in an index. |

| + | The AlphaCentric Symmetry Strategy Fund Class A, Class C commenced operations on August 8, 2019. |

| ++ | The AlphaCentric Symmetry Strategy Fund Class I, formerly a private fund, commenced operations on September 1, 2014. |

| +++ | The Fund acquired all of the assets and liabilities of MLM Symmetry Fund, LP (the “Predecessor Fund”) in a tax-free reorganization on August 9, 2019. In connection with this acquisition, shares of the Predecessor Fund were exchanged for Class I shares of the Fund. The Fund’s investment objectives, policies, restrictions, and guidelines are, in all material respects, equivalent to the Predecessor Fund’s investment objectives, policies, restrictions, and guidelines. The Fund’s sub-advisor was the adviser to the Predecessor Fund. The financial statements for the Predecessor Fund can be found in the Fund’s SAI. The performance information set forth below reflects the historical performance of the Predecessor Fund shares. Updated performance information will be available at no cost by calling 1-844-ACFUNDS (844-223-8637) or visiting the Fund’s website at www.AlphaCentricFunds.com |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type * | % of Net Assets | |||

| Exchange-Traded Funds | 35.5 | % | ||

| Common Stocks | 29.6 | % | ||

| U.S. Government & Agencies | 16.6 | % | ||

| Short-term Investment | 11.1 | % | ||

| Other Assets in Excess of Liabilities | 7.2 | % | ||

| 100.0 | % | |||

* Does not include derivative investments.

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

15

March 31, 2023

Dear AlphaCentric LifeSci Healthcare Fund (“the Fund”) Investor:

PERFORMANCE

The Fund offered significant outperformance through the fiscal year ended March 31, 2023 with a return of +3.22% (Class I shares) that was driven by fundamental, thesis-driven stock picking. The S&P Biotechnology Select Index (“Index”) one-year return for the period ended March 31, 2023 was -15.60%. The Fund created alpha from holdings benefiting from M&A transactions, favorable earnings announcements, positive fundamental company-specific news and avoidance of negative clinical or regulatory developments. The Fund remains nimble and continues to seek asymmetric risk/reward opportunities for the portfolio that are poised to create value regardless of the trajectory of the broader economic environment.

MARKET OVERVIEW

The Index remains in the midst of the longest and deepest bear market in its history. The divergence from the S&P 500 seemingly widened in response to turmoil in the banking system following the collapse of Silicon Valley Bank (“SVB”) and negative headlines on coming price controls from the so-called Inflation Reduction Act. The US drug pricing outlook seems to compare favorably to the rest of the world though, as China reduced average prices for drugs by 56% during the most recent centralized procurement process. The Index entered 2023 following its two worst years on record and more than 50% off highs set in early 2021. Reset valuations set the stage for asymmetric upside in a subset of companies with differentiated profiles, while a growing number of companies are falling by the wayside as capital becomes scarce for marginal assets. Clearly, this environment strongly favors fundamental, thesis-driven stock selection.

The quarter ended March 31, 2023 got off on the right foot with announcement at the JP Morgan Healthcare conference of three >$1 billion bolt-on M&A transactions, seemingly indicating deal count will be trending higher in 2023. Shock and awe M&A followed later in the quarter with a pair of eyebrow-raising valuations. Pfizer (PFE) announced the acquisition of Seagen (SGEN) for ~$43 billion or $229 per share, a ~33% premium to the prior day’s closing price. The deal values SGEN at ~20x current revenue of ~$2.2 billion, but PFE projects the 2030 revenue contribution from SGEN’s assets will be >$10 billion. Notably, PFE’s projections are well ahead of 2030 Wall Street numbers of ~$8 billion and are perhaps the only way they could justify the lofty valuation of the deal. PFE does not expect the deal to be accretive until 2028, and some analysts project the deal may never be accretive. PFE’s willingness to pay a very high price for unprofitable SGEN signals the desperate need for large players to augment revenues and should benefit the valuations of other stand-alone commercial biotechs.

Loss of exclusivity (patent expiration) is a growing theme as Jefferies projects there will be $170 billion of branded product revenue lost by 2028, prompting urgency for M&A. To be sure, Merck (MRK), Bristol Myers (BMY) and Abbvie (ABBV) will all be losing their patent protection on top selling drug(s) Keytruda, Revlimid and Humira, respectively. Pending price controls from the Inflation Reduction Act will only

16

exacerbate the situation and further encourage M&A. Getting a drug over the goal line can be difficult, let alone proving differentiation from an often-crowded competitive landscape, potentially leading to significant premiums for the most differentiated assets.

Regulatory sentiment was also bolstered with several new watershed drug approvals. Bluebird bio’s (BLUE) Zynteglo made history as the first gene therapy approved for patients with beta-thalassemia. BLUE plans to launch the drug with a $2.8 million price tag, making it the most expensive therapy in the US. Regulators further surprised investors to the upside by approving Bristol Myers Squibb’s (BMY) oral TYK2 inhibitor deucravacitinib (Sotyktu) in psoriasis without an expected ‘black box’ warning. Amylyx Pharmaceuticals’ (AMLX) secured FDA approval for their controversial Amyotrophic Lateral Sclerosis (ALS) therapy following a favorable Advisory Committee meeting vote. FDA continues to show flexibility to allow new treatment options to come to market that serve small populations of patients with severe conditions and no other alternatives.

Culling of the biotech herd continued as Neoleukin Therapeutics (NLTX) announced the CEO was stepping down and a 70% reduction in force (RIF), a.k.a. layoffs. Likewise, RIF announcements were also made by Century Therapeutics (IPSC, 25% RIF), Editas Medicine (EDIT, 20% RIF), Elevation Oncology (ELEV, 30% RIF), TCR2 Therapeutics (TCRR, 40% RIF), Applied Molecular Transport (AMTI, 57% RIF), Cyteir Therapeutics (CYT, 70% RIF) and Y-Mabs Therapeutics (YMAB, 35% RIF). More extreme measures were taken at Calithera Biosciences (CALA) as the board approved the complete liquidation and dissolution of the company after concluding they were “unable to complete a transaction that would allow us to continue the development of our clinical programs and enhance shareholder value.” CALA has an accumulated deficit of ~$500 million, reminding investors of the downside risks inherent in drug discovery and development. Rubius Therapeutics (RUBY) was another former highflyer to announce a dissolution plan after unsuccessful attempts on alternatives. RUBY had been valued at >$2 billion during the sector’s peak in 1Q 2021. Mei Pharma (MEIP) and Infinity Pharmaceuticals (INFI) announced a merger to combine resources and extend the operating runway for the combined company. Codiak Biosciences (CDAK) also filed for Chapter 11 bankruptcy.

FUND OVERVIEW

The Fund materially benefited from biotech M&A in the quarter with exposure to two of the three deals announced at the JP Morgan Healthcare conference. Specifically, Chiesi Farmaceutici S.p.A. (certified B Corp) agreed to acquire portfolio holding Amryt Pharma Plc (AMYT) for $14.50 upfront cash or $1.25 billion representing a ~107% premium to the prior close, plus a $2.50 contingent value right (CVR) for up to an additional ~$225 million in payments based on pipeline progress. AstraZeneca PLC (AZN) agreed to buy portfolio holding CinCor Pharma (CINC) for $1.3 billion upfront or $26 per share representing a >100% premium to the prior close. The deal also included a $10 per share CVR for an additional $500 million, based on a regulatory submission for the lead asset, baxdrostat. CINC had been trading at a negative enterprise value (EV = market capitalization net of cash and debt) following mixed results in a mid-stage clinical trial last November. The Fund entered the position due to the asymmetric risk/reward potential. The upfront deal price was essentially the same value that CINC was trading at before the mixed data release, and well below the 2022 high of ~$43 per share.

The Fund also materially benefited from Amgen’s (AMGN) announcement it was purchasing Horizon Therapeutics (HZNP) for $116.50 per share or ~$28 billion. The acquisition represented a 48% premium to HZNP’s closing price before the announcement of a possible deal under Irish takeover law. Analysts

17

expect the deal to be accretive near term and bolster AMGN against loss of exclusivity risk in 2026 through the end of the decade. HZNP was one of the top holdings of the Fund going into the deal announcement. In addition, the Fund holding Sierra Oncology (SRRA) was acquired by Glaxosmithkline PLC (GSK) for $1.9 billion, a 39% premium to prior close and 63% to VWAP over 30 days. The transaction was focused on SRRA’s myelofibrosis drug momelotinib, which had positive pivotal data from the phase 3 MOMENTUM trial reported earlier in the year. SRRA raised $135 million immediately following the data announcement in January at $27, making the takeout price of $55 a 104% premium for the investors who participated in the offering. Analysts viewed the deal as a win/win as investors get to cash out at an estimated peak sales multiple of ~3x prior to approval/launch while GSK gets strategic synergy and potential accretion in 2024-2025. The Fund also filed in the past on holding Turning Point Therapeutics (TPTX) that was acquired by Bristol Myers Squibb (BMY) for $4 billion. The deal was a 122% premium to the prior close and showed the continued interest of big pharma for differentiated targeted oncology assets. TPTX was recently granted a breakthrough therapy designation by the FDA for lead drug candidate repotrectinib, a small molecule kinase inhibitor targeting the ROS1 and TRK oncogenic drivers of non-small cell lung cancer and advanced solid tumors.

The Fund continued to benefit from an overweight exposure to companies with robust revenue and cash flow growth profiles expected to be resilient in an economic downturn. Aurinia Pharmaceuticals (AUPH) reminded investors alpha is often found at the intersection of oversold conditions and good news. Shares rallied nearly 40% on news they entered into a settlement agreement with a patent challenger in January. AUPH stock was punished in 2022, falling >80% to near cash value as the patent overhang shook out weak hands and emboldened shorts. Shares ended the quarter up ~100%. Exelixis (EXEL) flexed its cash flow strength to announce a $550 million share repurchase program that will retire ~10% of outstanding shares in 2023. EXEL’s small molecule kinase inhibitor Cabometyx is expected to generate >$1.5 billion in revenue this year, providing the company the ability to return capital to shareholders as well as advance pipeline development programs. Activist investors are engaged with the company in an attempt to further enhance capital return to shareholders. A number of other commercial stage portfolio companies provided numbers ahead of consensus, including Lantheus Holdings (LNTH), Collegium Pharmaceuticals (COLL), Revance Therapeutics (RVNC), 2seventy bio (TSVT), and Embecta Corp (EMBC). Strong fundamentals will be critical to enable companies to successfully navigate through this period of increasing cost of capital and broad economic uncertainty.

Positive developments extended to big pharmas as well with GSK PLC (GSK) and Sanofi (SNY) posting strong numbers, with the latter benefiting from a ~10% currency tailwind. Further, GSK and SNY added an additional >$15 billion in combined market capitalization when the US District Court Judge in the Southern District of Florida for the multidistrict litigation (MDL) granted summary judgment for the pharma defendants, striking all plaintiffs’ evidence Zantac causes cancer. Analysts viewed this outcome as a best-case scenario since the MDL ruling is expected to clear a majority of the liability from the class action Zantac litigation. The Fund opportunistically increased exposure to both GSK and SNY during the prior quarter when they were being indiscriminately sold off due to fear of significant liability from the pending litigation.

Positive clinical and regulatory updates from Fund holdings also provided alpha generation. Specifically, the Fund benefited from the following positive program updates.

18

Acadia Pharmaceuticals (ACAD) announced the approval of the first drug for Rett Syndrome, DAYBUE (trofinetide). Rett is a rare genetic disease that severely impairs brain development and may be lethal, providing a basis for ACAD’s ~$400k estimated annual cost of therapy.

Viridian Therapeutics (VRDN) reached an all-time high on additional favorable updated data from their thyroid eye disease (TED) program.

Intra-cellular Therapies (ITCI) rallied on positive topline results from Study 403 evaluating lumateperone as monotherapy in the treatment of major depressive episodes in patients with mixed features. Peak revenue estimates for ITCI’s lead drug now exceed $2.5 billion.

Avoidance of negative clinical and regulatory events was also an important contributor to allowing the Fund to generate a positive return while the primary benchmark lost ground.

OUTLOOK

The Index continues to consolidate above the 2022 lows as green shoots push through the scorched earth. Full protection of SVB’s uninsured depositors enabled life sciences investors to focus on fundamental clinical/regulatory developments instead of potential capital impairment/recovery. Favorable regulatory developments continue to furnish a pathway to market for innovative therapies, even those with a measure of controversary. The therapeutics business model continues to perform independent of broader economic headwinds with a growing number of products beating financial projections. Reset valuations, cash flush pharma balance sheets and the strategic imperative for growth heighten expectations for M&A. For the rest of the sector, capital efficiency and a high bar for program advancement are coming back into vogue as the era of infinite money printing has come to an end. Creative destruction will continue to cull the herd of aspiring development stage SMID innovators, but the resulting group continues to offer an improving risk/reward profile. Although it’s not yet apparent at the Index level, good news is starting to pile up for a growing number of individual components. We continue to believe the setup for a fundamental, thesis-driven life sciences portfolio is as attractive as ever.

Sincerely,

Mark Charest, Ph.D.

Founding Partner and Portfolio Manager

LifeSci Fund Management

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

19

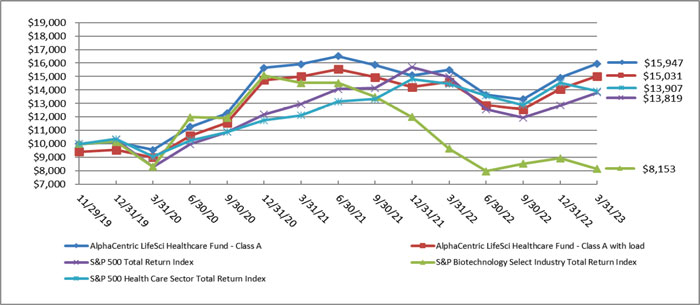

The Fund’s returns for the fiscal year ended 3/31/23 and for the period since inception through 3/31/23, as compared to the Benchmark Index, were as follows:

| Fiscal Year Ended | Since Inception | |

| 3/31/2023 | 11/29/2019 | |

| Class I | 3.22 | 15.25 |

| Class A | 3.00 | 15.01 |

| Class A w/ Sales Charge | -2.95 | 12.99 |

| Class C | 2.26 | 14.41 |

| S&P Biotechnology Select Industry Index (1) | -15.60 | -5.94 |

| (1) | The S&P Biotechnology Select Industry Index represents the biotechnology sub-industry portion of the S&P Total Markets Index (S&P TMI). The S&P TMI tracks all the U.S. common stocks listed on the NYSE, NYSE American, NASDAQ National Market and NASDAQ Small Cap exchanges. The S&P Biotechnology Select Industry Index is a modified equal weight index and typically consists of approximately 70 companies. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 5.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information or the Fund’s prospectus please call the Fund, toll free at 1-844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com. 1553-NLD-04-28-2023

20

AlphaCentric LifeSci Healthcare Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2023

The Fund’s performance figures* for the periods ended March 31, 2023, compared to its benchmarks:

| Annualized | |||

| Annualized | Since Inception + - | ||

| One Year | Three Years | March 31, 2023 | |

| Class A (LYFAX) without load | 3.00% | 18.64% | 15.01% |

| Class A (LYFAX) with 5.75% load | (2.95)% | 16.33% | 12.99% |

| Class C (LYFCX) | 2.26% | 17.95% | 14.41% |

| Class I (LYFIX) | 3.22% | 18.91% | 15.25% |

| S&P 500 Total Return Index ** | (7.73)% | 18.60% | 10.18% |

| S&P Biotechnology Select Industry Total Return Index *** | (15.60)% | (0.58)% | (5.94)% |

| S&P 500 Health Care Sector Total Return Index **** | (3.70)% | 15.41% | 10.39% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 5.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 31, 2023. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s manager has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2023, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.65%, 2.40% and 1.40% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the manager from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus are 2.11%, 2.86% and 1.86% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus are 1.66%, 2.41% and 1.41% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The S&P 500 Total Return Index, a registered trademark of McGraw-Hill Co., Inc., is a market capitalization-weighted index of 500 widely held common stocks. Investors cannot invest directly in an index. |

| *** | S&P Biotechnology Select Industry Total Return Index is designed to measure the performance of narrow GICS® sub-industries. The Index comprises stocks in the S&P Total Market Index that are classified in the GICS biotechnology sub-industry. Investors cannot invest directly in an index. |

| **** | S&P 500 Health Care Sector Total Return Index is designed to measure the performance of narrow GICS® health care sub-industries. The Index comprises stocks in the S&P Total Market Index that are classified in the GICS health care sub-industry. Investors cannot invest directly in an index. |

| + | The AlphaCentric LifeSci Healthcare Fund Class A, Class C and Class I commenced operations on November 29, 2019. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type | % of Net Assets | |||

| Common Stocks | 93.7 | % | ||

| Short-term Investments | 7.3 | % | ||

| Liabilities In Excess Of Other Assets | (1.0 | )% | ||

| 100.0 | % | |||

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

21

March 31, 2023

Dear AlphaCentric SWBC Municipal Opportunities Fund (the “Fund”) Investor:

The fiscal year ended 03/31/2023 was an extremely volatile 12-month period. The municipal market endured an extreme rise in interest rates and a historic outflow of investor cash. The first two quarters of the fiscal year proved to be an extremely difficult environment for fixed income securities as inflation increased more than almost anyone predicted, and the Federal Reserve continued its aggressive tightening campaign. The third quarter of the fiscal year saw a peak in long-term interest rates and the beginning of the downtrend in inflation indicators. The value in fixed income, which was created by the devastating prior two quarters, offered an entrance point for investors, and the market rallied significantly going into the fourth quarter of the fiscal year.

From March 31, 2022, to the lows on October 27, 2022, the various municipal indices were showing historically negative returns for the market. The Bloomberg Municipal Aggregate Index was -7.17%. The Bloomberg Long Term Municipal Index was -14.34% and the First Trust Municipal Closed End Fund Index was -18.69%. The Fund at this point was -14.83% (Class I shares). As sentiment began to change from October 27, 2022, to January 31, 2023, the Bloomberg Municipal Aggregate had an 8.11% return. The Bloomberg Long Term Municipal Index had a 12.97% return and the First Trust Municipal Closed End Fund Index returned 14.69%. The Fund had a 12.47% (Class I shares) return during this period.

The fourth quarter of the fiscal year started out with a bang as January showed the best first month municipal performance dating back to 1993. Due to sentiment change on how much more aggressive the Federal Reserve was going to be, February was decidedly negative with the worst performing February dating back to 2008. To top off the extreme volatility, the market suffered through a bank crisis in March, which caused a flight to safety trade, in which Treasury securities outperformed all other fixed income securities.

The fiscal year ended with the Bloomberg Municipal Aggregate Index at 0.26%; the Bloomberg Long Term Municipal Index at -3.64%; and the First Trust Municipal Closed End Fund Index at -9.60%. The Fund finished the fiscal year at -6.63% (Class I shares), with the overlay contributing approximately 2.80%. Since this is an income-oriented fund, the Fund paid an average annual dividend of approximately 3.90% which is a tax equivalent of 6.45%. This payout was in the top three of an internal peer group consisting of 39 of the largest and most well-known municipal bond funds.

Looking forward, management is optimistic for the overall fixed income market and specifically for the municipal bond market.

While the Federal Reserve may not be done hiking short-term interest rates yet, we believe they are close. The previous hikes in interest rates are starting to trickle into the economy and should speed up the process of moderating both inflation and employment going into the latter part of the year. We believe the combination of the Federal Reserve pausing its aggressive tightening and a moderating economy should cause interest rates to fall.

22

Municipal bonds should outperform their taxable counterparts as interest rates decline as some tax-free yields on the long end of the curve are higher than taxable interest rates. The municipal market should also benefit from strong fundamentals as the overall credit environment remains strong.

Additionally, new issuance is on track to come in much lower than projected with only $350 billion anticipated for 2023, while maturing bonds, bonds being called, and dividends are projected to equal approximately $525 billion for the year.

Thank you for your support.

Sincerely,

The SWBC Management Team

This report is intended for the Fund’s shareholders. It may not be distributed to prospective investors unless it is preceded or accompanied by the current Fund prospectus. To obtain a prospectus or other information about the Fund, please visit www.AlphaCentricFunds.com or call 844-ACFUNDS (844-223-8637). Please read the prospectus carefully before investing.

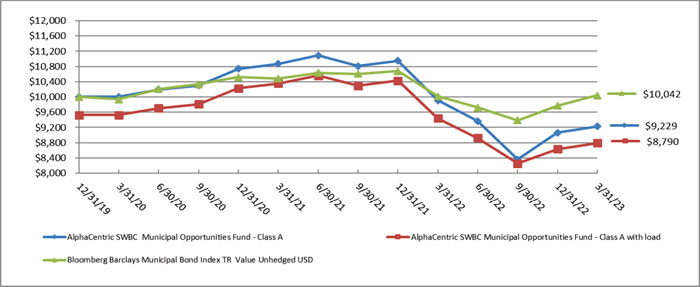

The Fund’s returns for the fiscal year ended 3/31/23 and for the period since inception through 3/31/23, as compared to the Benchmark Index, were as follows:

| Fiscal Year Ended 3/31/2023 | Since Inception* | |

| Class A | -6.86 | -2.44 |

| Class A w/ Sales Charge | -11.31 | -3.89 |

| Class C | -7.51 | -2.87 |

| Class I | -6.63 | -2.21 |

| Bloomberg Municipal Bond Index Value Unhedged USD (1) | 0.26 | 0.13 |

| (1) | Bloomberg Municipal Bond Index TR Value Unhedged covers the USD-denominated long-term tax-exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. Investors cannot invest directly in an index. |

The Fund’s maximum sales charge for Class “A” shares is 4.75%. Performance is historic and does not guarantee future results. Investment return and principal value will fluctuate with changing market conditions so that when redeemed, shares may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. To obtain the most recent month end performance information please call the Fund, toll free at 1-844-ACFUNDS (844-223-8637). You can also obtain a prospectus at www.AlphaCentricFunds.com.

The First Trust Municipal Closed End Fund Index is a capitalization weighted index designed to provide a broad representation of the U.S. municipal closed-end fund universe. 6222-NLD-05082023

23

AlphaCentric SWBC Municipal Opportunities Fund

PORTFOLIO REVIEW (Unaudited)

March 31, 2023

The Fund’s performance figures* for the periods ended March 31, 2023, compared to its benchmark:

| Annualized | |||

| Annualized | Since Inception + - | ||

| One Year | Three Years | March 31, 2023 | |

| Class A (MUNAX) without load | (6.86)% | (2.64)% | (2.44)% |

| Class A (MUNAX) with 4.75% load | (11.31)% | (4.21)% | (3.89)% |

| Class C (MUNCX) | (7.51)% | (3.20)% | (2.87)% |

| Class I (MUNIX) | (6.63)% | (2.49)% | (2.21)% |

| Bloomberg Municipal Bond Index Total Return Value Unhedged USD** | 0.26% | 0.35% | 0.13% |

| * | The performance data quoted here represents past performance. Current performance may be lower or higher than the performance data quoted above. Investment return and principal value will fluctuate, so that shares, when redeemed, may be worth more or less than their original cost. Class A is subject to a maximum applicable sales charge of 4.75% and a maximum deferred sales charge of 1.00% on investments at or above the $1 million breakpoint (where you do not pay a sales charge) on shares redeemed within 18 months of purchase. Total returns are calculated using the net asset value (“NAV”) on March 31, 2023. The returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or on the redemptions of Fund shares. Past performance is no guarantee of future results. Performance figures for periods greater than 1 year are annualized. The Fund’s manager has contractually agreed to reduce its fees and/or absorb expenses of the Fund, at least until July 31, 2023, to ensure that the net annual fund operating expenses (excluding brokerage costs; borrowing costs, such as (a) interest and (b) dividends on securities sold short; taxes; costs of investing in underlying funds and extraordinary expenses) will not exceed 1.50%, 2.25% and 1.25% for the Fund’s Class A, Class C, and Class I shares, respectively, subject to possible recoupment from the Fund in future years. Fee waivers and expense reimbursements are subject to possible recoupment by the manager from the Fund in future years on a rolling three-year basis (within three years after the fees have been waived or reimbursed) if such recoupment can be achieved within the foregoing expense limits and any expense limits in place at the time of recoupment. Without these waivers, the Fund’s total annual operating expenses as shown in the August 1, 2022 prospectus are 3.68%, 4.43% and 3.43% for the Fund’s Class A, Class C and Class I shares, respectively. After fee waivers, the Fund’s total annual operating expenses shown in the August 1, 2022 prospectus are 1.98%, 2.73% and 1.73% for the Fund’s Class A, Class C and Class I shares, respectively. Please review the Fund’s most recent prospectus for more detail on the expense waiver. For more current information on the Fund’s expense ratio, please see the Financial Highlights. For performance information current to the most recent month-end, please call toll-free 1-844-223-8637. |

| ** | The Bloomberg Municipal Bond Index Total Return Value Unhedged USD covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds. Investors cannot invest directly in an index. |

| + | The AlphaCentric SWBC Municipal Opportunities Fund Class A, Class C and Class I commenced operations on December 31, 2019. |

Comparison of the Change in value of a $10,000 investment

| Holdings by Security Type * | % of Net Assets | |||

| Municipal Bonds | 84.4 | % | ||

| Closed End Funds | 6.7 | % | ||

| Exchange-Traded Funds | 5.2 | % | ||

| Short-term Investment | 0.3 | % | ||

| Other Assets in Excess of Liabilities | 3.4 | % | ||

| 100.0 | % | |||

* Does not include derivative investments.

Please refer to the Schedule of Investments in this Annual Report for a detailed listing of the Fund’s holdings.

24

March 31, 2023

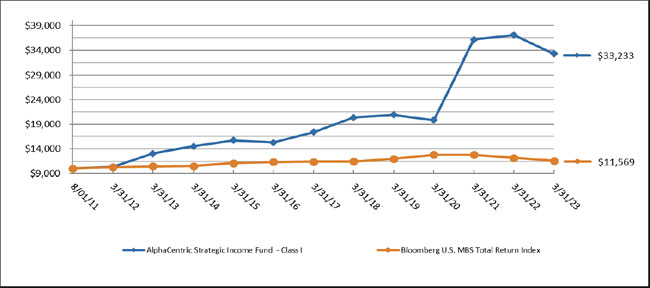

Dear AlphaCentric Strategic Income Fund (“the Fund”) Investor:

The Fund’s performance for the year ended March 31, 2023 was -10.29% (for the Class I Shares) versus -19.08% for the S&P US REIT Index. The Fund also outperformed most other funds in Morningstar’s Real Estate Fund category for the same period. In addition to achieving attractive total returns, our goal is to protect client capital in volatile periods. We believe the Fund’s flexibility shift between residential and commercial real estate exposure as well as the Fund’s ability to invest across the capital structure, in bonds and equities of publicly traded real estate securities, helped to limit the drawdown of the Fund in the context of broad financial asset price declines. We believe the Fund’s outperformance versus the S&P US REIT Index is attributable to the Fund’s differentiated approach and ability to take advantage of evolving dislocations in the market for real estate related securities.

As 2022 progressed, it became obvious that inflation was deeply imbedded in goods and services and the word “transitory” may need to be suspended from the English lexicon. Russia’s tragic and unexpected invasion of Ukraine early in the year certainly exacerbated upward price pressures although many commodity prices ended 2022 around pre-invasion levels. As the Federal Reserve (Fed) changed its tune on inflation, it hiked the Fed Funds rate over 400 basis points (bps) by year-end and ceased purchasing Agency MBS. Hawkish actions by several central banks sent global markets into a tailspin, losing more than $30 trillion in value. A rapidly strengthening dollar created pressure on other currencies with the UK bond market requiring a temporary government bailout. Growth stocks and speculative areas of the market like cryptocurrency got clobbered and even relatively short duration bonds proved an ill-conceived hiding spot.