Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box

¨ | Preliminary Proxy Statement | ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |||

x | Definitive Proxy Statement | |||||

¨ | Definitive Additional Materials | |||||

¨ | Soliciting Material Pursuant to §240 14a-12 |

BREITBURN ENERGY PARTNERS L.P.

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required |

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(l) and 0-11 |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| ¨ | Fee paid previously with preliminary materials |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing Party: |

| (4) | Date Filed: |

Table of Contents

BREITBURN ENERGY PARTNERS L.P.

515 South Flower Street

Suite 4800

Los Angeles, California 90071

ANNUAL MEETING OF LIMITED PARTNERS

The Annual Meeting of Limited Partners of BreitBurn Energy Partners L.P. will be held at

The Wilshire Grand Hotel

Sierra Room

930 Wilshire Boulevard

Los Angeles, California 90017

on June 23, 2011, at 10:00 a.m., Pacific Daylight Time

YOUR VOTE IS IMPORTANT!

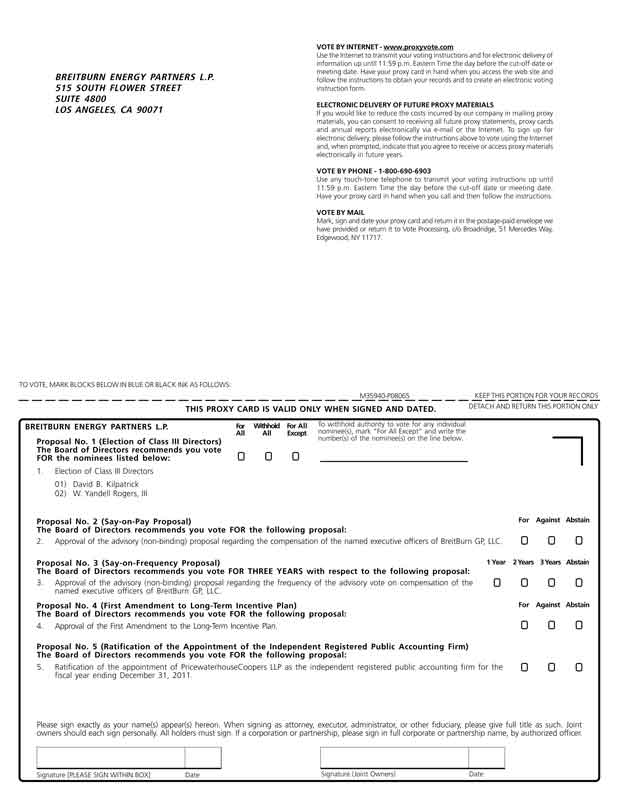

Whether or not you expect to attend the Annual Meeting in person, we urge you to vote your common units by phone, via the Internet, or by signing, dating, and returning the enclosed proxy card at your earliest convenience. This will ensure the presence of a quorum at the Annual Meeting. Submitting your proxy now will not prevent you from voting your common units at the Annual Meeting if you desire to do so, as your vote by proxy is revocable at your option.

Voting by theInternet ortelephone is fast, convenient, and your vote is immediately confirmed and tabulated. Most important, by using the Internet or telephone, you help us reduce our postage and proxy tabulation costs. If you prefer, you can vote by mail by returning the enclosed proxy card in the enclosed addressed, prepaid envelope.

VOTE BY INTERNET | VOTE BY TELEPHONE | |

http://www.proxyvote.com/ 24 hours a day / 7 days a week | 1-800-690-6903 via touch-tone phone toll-free 24 hours a day / 7 days a week | |

| INSTRUCTIONS: | INSTRUCTIONS: | |

Read the accompanying proxy statement and Go to the following website: http://www.proxyvote.com | Read the accompanying proxy statement and Call the toll-free 800 number provided on your | |

| Use the Internet to transmit your voting instructions and for electronic delivery of information up until 11:59 p.m. (EDT) the day before the Annual Meeting date. Have your proxy card in hand when you access the website and follow the instructions to obtain your records and to create an electronic voting instruction form. | Use any touch-tone telephone to transmit your voting instructions up until 11:59 p.m. (EDT) the day before the Annual Meeting date. Have your proxy card in hand when you call and follow the instructions. | |

PLEASE DO NOT RETURN THE ENCLOSED PAPER PROXY IF YOU ARE VOTING OVER THE INTERNET OR BY TELEPHONE.

Table of Contents

BREITBURN ENERGY PARTNERS L.P.

515 South Flower Street

Suite 4800

Los Angeles, California 90071

April 29, 2011

TO THE LIMITED PARTNERS OF BREITBURN ENERGY PARTNERS L.P.:

We cordially invite you to the Annual Meeting of Limited Partners (the “Annual Meeting”) of BreitBurn Energy Partners L.P. (the “Partnership”). The Annual Meeting will be held on June 23, 2011, at 10:00 a.m., Pacific Daylight Time, at The Wilshire Grand Hotel, Sierra Room, 903 Wilshire Boulevard, Los Angeles, California 90017.

The following pages contain the formal Notice of the Annual Meeting and the Proxy Statement. At the Annual Meeting, you will be asked to vote on (1) the election of two directors to the Board of Directors of BreitBurn GP, LLC, the general partner of the Partnership (the “General Partner”), to serve for a three-year term that will expire in 2014 at the 2014 annual meeting of limited partners (“Class III Directors”), or until their successors are duly elected and qualified; (2) the approval of an advisory (non-binding) proposal regarding the compensation of our General Partner’s named executive officers (the “Say-on-Pay Proposal”); (3) the approval of an advisory (non-binding) proposal regarding the frequency of the advisory vote on compensation of our General Partner’s named executive officers (the “Say-on-Frequency Proposal”); (4) the approval of the First Amendment to the First Amended and Restated BreitBurn Energy Partners L.P. 2006 Long-Term Incentive Plan (the “Long-Term Incentive Plan”) which increases the aggregate number of common units that may be delivered with respect to awards under the Long-Term Incentive Plan by an additional 3,000,000 units; and (5) the ratification of the appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm for the year ending December 31, 2011. You will also be asked to transact such other business as may properly come before the Annual Meeting, or any postponements or adjournments thereof.

Our General Partner’s Board of Directors unanimously recommends that you vote “FOR ALL” of the Class III Directors nominated for reelection, “FOR” the Say-on-Pay Proposal, for “THREE YEARS” with respect to the Say-on-Frequency Proposal, “FOR” the approval of the First Amendment to our Long-Term Incentive Plan, and “FOR” the ratification of the appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm.

To be certain that your common units are voted at the Annual Meeting, whether or not you plan to attend in person, you should vote your common units as soon as possible. Your vote is important. You may vote by telephone, Internet or mail. To vote by telephone, call 1-800-690-6903 using a touch-tone phone to transmit your voting instructions up until 11:59 p.m. (EDT) the day before the Annual Meeting date. Your proxy card has a control number that you must have to receive access to vote. Have your proxy card in hand when you call and follow the instructions. To vote electronically, accesshttp://www.proxyvote.com over the Internet to transmit your voting instructions and for electronic delivery of information up until 11:59 p.m. (EDT) the day before the Annual Meeting date. Your proxy card has a control number that you must have to receive access to vote. Have your proxy card in hand when you access the website and follow the instructions to obtain your records and to create an electronic voting instruction form. To vote by mail, mark, sign and date your proxy card and return it in the postage-paid envelope we have provided or return it to Vote Processing, c/o Broadridge Financial Solutions, 51 Mercedes Way, Edgewood, NY 11717.

At the Annual Meeting, our management team will review our performance during the past year and discuss our plans for the future. An opportunity will be provided for questions by the unitholders. You will have an additional opportunity to meet with management. I hope you will be able to join us.

Sincerely, |

|

John R. Butler, Jr. |

Chairman of the Board of BreitBurn GP, LLC, general partner of BreitBurn Energy Partners L.P. |

Table of Contents

BREITBURN ENERGY PARTNERS L.P.

515 South Flower Street

Suite 4800

Los Angeles, California 90071

NOTICE OF ANNUAL MEETING OF LIMITED PARTNERS

April 29, 2011

TO THE LIMITED PARTNERS OF BREITBURN ENERGY PARTNERS L.P.:

You are invited to the Annual Meeting of Limited Partners (the “Annual Meeting”) of BreitBurn Energy Partners L.P. (the “Partnership”), which will be held at 10:00 a.m., Pacific Daylight Time, on June 23, 2011, at The Wilshire Grand Hotel, Sierra Room, 930 Wilshire Boulevard, Los Angeles, California 90017, for the following purposes:

| 1. | To elect two directors to the Board of Directors of BreitBurn GP, LLC, the general partner of BreitBurn Energy Partners L.P. (the “General Partner”), to serve for a three-year term that will expire in 2014 at the 2014 annual meeting of limited partners (“Class III Directors”), or until their successors are duly elected and qualified; |

| 2. | To approve an advisory (non-binding) proposal regarding the compensation of our General Partner’s named executive officers (the “Say-on-Pay Proposal”); |

| 3. | To approve an advisory (non-binding) proposal regarding the frequency of the advisory vote on compensation of our General Partner’s named executive officers (the “Say-on-Frequency Proposal”); |

| 4. | To approve the First Amendment to the First Amended and Restated BreitBurn Energy Partners L.P. Long-Term Incentive Plan (the “Long-Term Incentive Plan”) which increases the aggregate number of common units that may be delivered with respect to awards under the Long-Term Incentive Plan by an additional 3,000,000 units; |

| 5. | To ratify the appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm for the year ending December 31, 2011; and |

| 6. | To transact such other business as may properly come before the Annual Meeting, or any postponements or adjournments thereof. |

The Board of Directors of our General Partner has fixed the close of business on April 25, 2011 as the record date for the determination of unitholders entitled to notice of, and to vote at, the Annual Meeting. Only unitholders of record as of the close of business on such date are entitled to notice of, and to vote at, the Annual Meeting.

We encourage you to take part in the affairs of the Partnership either by voting in person, by telephone, by Internet or by executing and returning the enclosed proxy.

| By Order of the Board of Directors of the General Partner, |

|

| Gregory C. Brown |

| Executive Vice President and General Counsel of BreitBurn GP, LLC, general partner of BreitBurn Energy Partners L.P. |

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF PROXY MATERIALS FOR THE ANNUAL MEETING OF LIMITED PARTNERS TO BE HELD ON JUNE 23, 2011

The Notice of Annual Meeting of Limited Partners, the Proxy Statement for the Annual Meeting |

Table of Contents

BREITBURN ENERGY PARTNERS L.P.

515 South Flower Street

Suite 4800

Los Angeles, California 90071

| 1 | ||||

| 2 | ||||

| 9 | ||||

| 12 | ||||

| 24 | ||||

| 29 | ||||

| 36 | ||||

| 37 | ||||

| 38 | ||||

| 46 | ||||

| 56 | ||||

| 57 | ||||

| 69 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 70 | |||

| 72 | ||||

| 72 | ||||

| 72 | ||||

| A-1 | ||||

i

Table of Contents

BREITBURN ENERGY PARTNERS L.P.

515 South Flower Street

Suite 4800

Los Angeles, California 90071

References in this proxy statement to “the Partnership,” “we,” “our,” “us” or like terms refer to BreitBurn Energy Partners L.P. and its subsidiaries. References in this proxy statement to “BEC” or the “Predecessor” refer to BreitBurn Energy Company L.P., our predecessor, and its predecessors and subsidiaries. References in this proxy statement to the “General Partner” refer to BreitBurn GP, LLC, our general partner and our wholly owned subsidiary as of June 17, 2008. References in this proxy statement to the “Board” refer to the Board of Directors of the General Partner. References in this proxy statement to “Provident” refer to Provident Energy Trust. References in this proxy statement to “Pro GP” refer to Pro GP Corp., BEC’s former general partner up to August 26, 2008 and indirect subsidiary of Provident. References in this proxy statement to “Pro LP” refer to Pro LP Corp., BEC’s former limited partner and indirect subsidiary of Provident. References in this proxy statement to “BreitBurn Corporation” refer to BreitBurn Energy Corporation, a corporation owned by Halbert S. Washburn and Randall H. Breitenbach, the Chief Executive Officer and President of the General Partner, respectively. References in this proxy statement to “BreitBurn Management” refer to BreitBurn Management Company, LLC, our administrative manager, and wholly owned subsidiary as of June 17, 2008. References in this proxy statement to “BOLP” refer to BreitBurn Operating L.P., our wholly owned operating subsidiary. References in this proxy statement to “BOGP” refer to BreitBurn Operating GP, LLC, the general partner of BOLP. References in this proxy statement to “Quicksilver” refer to Quicksilver Resources Inc. References in this proxy statement to the “Partnership Agreement” refer to our First Amended and Restated Agreement of Limited Partnership, dated as of October 10, 2006, as amended by Amendment No. 1, dated as of June 17, 2008, Amendment No. 2, dated as of April 7, 2009, Amendment No. 3, dated as of August 27, 2009, and Amendment No. 4, dated as of April 5, 2010. References in this proxy statement to “common units” refer to common units representing limited partner interests in the Partnership. References in this proxy statement to “unitholders” or “limited partners” refer to limited partners of the Partnership owning our common units.

This proxy statement contains information related to our Annual Meeting of Limited Partners to be held on June 23, 2011 (the “Annual Meeting”), beginning at 10:00 a.m., Pacific Daylight Time, at The Wilshire Grand Hotel, Sierra Room, 930 Wilshire Boulevard, Los Angeles, California 90017, and at any postponements or adjournments thereof. This proxy statement and the accompanying proxy card, which are accompanied by our annual report to unitholders, will first be mailed to unitholders on or about May 9, 2011. Our annual report to unitholders includes our Annual Report on Form 10-K for the fiscal year ended December 31, 2010 (the “2010 Annual Report”). Unitholders are referred to the 2010 Annual Report for financial and other information about our business. The 2010 Annual Report is not incorporated by reference into this proxy statement and is not deemed to be a part of this proxy statement.

1

Table of Contents

Who sent me this proxy statement?

The Board sent you this proxy statement and proxy card. We will pay for the solicitation of your proxy. In addition to this solicitation by mail, proxies may be solicited by the directors, officers and other employees of our General Partner and our affiliates by telephone, Internet, facsimile, in person or otherwise. These people will not receive any additional compensation for assisting in the solicitation. We may also request brokerage firms, nominees, custodians and fiduciaries to forward proxy materials to the beneficial owners of our common units. We will reimburse those people and our transfer agent for their reasonable out-of-pocket expenses in forwarding such material. We will also bear the entire cost of the preparation, assembly, printing and mailing of this proxy statement, the proxy card, and any additional information furnished to unitholders. We have retained Broadridge Financial Solutions, Inc., a proxy soliciting firm, to assist in the solicitation of proxies, provide voting and tabulation services and serve as inspector of election at the Annual Meeting for an estimated cost of $50,000.

Why did I receive this proxy statement and proxy card?

You received this proxy statement and proxy card from us because you owned our common units as of the record date, April 25, 2011, and, as a result, you are entitled to elect directors to serve on the Board and to vote on the other proposals to be voted on at the Annual Meeting. This proxy statement contains important information for you to consider when deciding whether and/or how to vote on the various proposals to be voted on at the Annual Meeting, including the election of directors and ratification of the selection of our independent registered public accounting firm. Please read this proxy statement carefully.

What is a proxy?

A proxy is your legal designation of another person to vote the common units that you own. That other person is also called a proxy. If you designate someone as your proxy in a written document, that document is also called a proxy or a proxy card. Halbert S. Washburn and Randall H. Breitenbach, or either of them, each with power of substitution, have been appointed by the Board as proxies for the Annual Meeting.

What is a proxy statement?

A proxy statement is a document that the regulations of the Securities and Exchange Commission (“SEC”) require us to give you when we ask you to sign a proxy card designating proxies to vote on your behalf. The proxy statement includes information about the proposals to be considered at the Annual Meeting and other required disclosures, including information about the Board.

What does it mean if I receive more than one proxy card?

Your receipt of more than one proxy card means that you have multiple accounts with our transfer agent and/or with a brokerage firm, bank or other nominee. If voting by mail, please sign and return all proxy cards to ensure that all of your common units are voted. Each proxy card represents a discrete number of common units and it is the only means by which those particular common units may be voted by proxy.

What is the purpose of the Annual Meeting?

At the Annual Meeting, our unitholders will act upon the matters outlined in the Notice of Annual Meeting, including the election of the Class III Directors, the Say-on-Pay Proposal, the Say-on-Frequency Proposal, the First Amendment to our Long-Term Incentive Plan and the ratification of the appointment of our independent registered public accounting firm, as well as such other business as may properly come before the Annual Meeting, or any postponements or adjournments thereof.

2

Table of Contents

What is the difference between a unitholder of record and a unitholder who holds common units in “street name”?

Most of our unitholders hold their common units through a brokerage firm, bank or other nominee rather than directly in their own name. As summarized below, there are some distinctions between common units held of record and those held beneficially through a brokerage account, bank or other nominee.

| • | Unitholder of Record.If your common units are registered directly in your name with our transfer agent, you are considered, with respect to those common units, the “unitholder of record,” and these proxy materials are being sent directly to you by us. As the unitholder of record, you have the right to grant your voting proxy directly or to vote in person at the Annual Meeting. We have enclosed a proxy card for you to use. |

| • | Street Name.If your common units are held in a brokerage account or by a bank or other nominee, you are considered the beneficial owner of common units held in “street name,” and these proxy materials are being forwarded to you by your broker or nominee, which is considered, with respect to those common units, the unitholder of record. As the beneficial owner, you have the right to direct your broker how to vote and are also invited to attend the Annual Meeting. However, since you are not the unitholder of record, you may not vote these common units in person at the Annual Meeting unless you obtain a signed proxy from the record holder giving you the right to vote the common units. Your broker or nominee has enclosed or provided a voting instruction card for you to use in directing the broker or nominee how to vote your common units. |

What is the record date and what does it mean?

The record date established by the Board for the Annual Meeting is April 25, 2011. Unitholders of record at the close of business on the record date are entitled to:

| • | receive notice of the Annual Meeting; and |

| • | vote at the Annual Meeting and any adjournments or postponements of the Annual Meeting. |

Who is entitled to vote at the Annual Meeting?

Each of our common units Outstanding (as defined in the Partnership Agreement) as of the close of business on April 25, 2011, the record date, is entitled to one vote per common unit at the Annual Meeting, subject to certain exceptions as described below under the heading “Voting Requirements for the Annual Meeting.”

As of the record date, 59,039,933 of our common units were Outstanding, all of which are entitled to vote at the Annual Meeting.

Who can attend the Annual Meeting?

All unitholders as of the record date, or their duly appointed proxies, may attend the Annual Meeting.

Common units held directly in your name as the unitholder of record can be voted in person at the Annual Meeting. Common units held in street name (for example, at your brokerage account) may be voted in person by you only if you obtain a signed proxy from the record holder giving you the right to vote the common units. In addition, if you plan to vote in person at the Annual Meeting, please bring the enclosed proxy card or proof of identification.

Even if you currently plan to attend the Annual Meeting in person, we recommend that you also submit your proxy as described below so that your vote will be counted if you later decide not to attend the Annual Meeting.

3

Table of Contents

What constitutes a quorum?

The holders of a majority of the Outstanding common units on the record date, represented in person or by proxy, will constitute a quorum, subject to certain exceptions as described below under the heading “Voting Requirements for the Annual Meeting.” As of April 25, 2011, there were 59,039,933 outstanding common units. Consequently, holders of at least 29,519,967 common units must be present either in person or by proxy to establish a quorum for the Annual Meeting. Proxies received but marked as abstentions and broker non-votes will be included in the number of common units considered to be present at the Annual Meeting for purposes of establishing a quorum.

How do I vote?

If you complete and properly sign the accompanying proxy card and return it to us, or properly transmit your vote by telephone or electronically as described below, your common units will be voted as you direct. If you are a unitholder of record and attend the Annual Meeting, you may deliver your completed proxy card in person or vote by ballot using a form provided at the Annual Meeting. Street name unitholders who wish to vote at the Annual Meeting will need to obtain a proxy form from the institution that holds their common units. Even if you plan to attend the Annual Meeting, your plans may change; thus, we recommend you complete, sign and return your proxy card or vote by telephone or electronically in advance of the Annual Meeting.

You may vote by telephone by calling 1-800-690-6903 using a touch-tone phone to transmit your voting instructions up until 11:59 p.m. (EDT) the day before the Annual Meeting date. Your proxy card has a control number that you must have to receive access to vote. Have your proxy card in hand when you call and follow the instructions. To vote electronically, accesshttp://www.proxyvote.com over the Internet to transmit your voting instructions and for electronic delivery of information up until 11:59 p.m. (EDT) the day before the Annual Meeting date. Your proxy card has a control number that you must have to receive access to vote. Have your proxy card in hand when you access the website and follow the instructions to obtain your records and to create an electronic voting instruction form. To vote by mail, mark, sign and date your proxy card and return it in the postage-paid envelope we have provided or return it to Vote Processing, c/o Broadridge Financial Solutions, 51 Mercedes Way, Edgewood, NY 11717.

May I vote confidentially?

Yes. We treat all unitholder meeting proxies and ballots confidentially if the unitholder has requested confidentiality on the proxy or ballot.

Can I change my vote after I return my proxy card?

Yes. If you are a unitholder of record, you may revoke a previously submitted proxy at any time before the polls close at the Annual Meeting by:

| • | timely submitting a proxy with new voting instructions using the telephone or Internet voting system; |

| • | timely delivering a valid, later-dated executed proxy card; |

| • | giving written notice of revocation to BreitBurn Energy Partners L.P., Attention: Investor Relations, 515 South Flower Street, Suite 4800, Los Angeles, California 90071, no later than later than 11:59 p.m. (EDT), on June 22, 2011; or |

| • | attending the Annual Meeting and voting your common units in person; however, attending the Annual Meeting will not by itself have the effect of revoking a previously submitted proxy. |

If you are a street name unitholder, you must follow the instructions on revoking your proxy, if any, provided by your bank or broker.

4

Table of Contents

What are the recommendations of the Board?

Unless you give other instructions on your proxy card, the persons named as proxy holders on the proxy card will vote in accordance with the recommendations of the Board. The recommendations of the Board are set forth together with the description of each item in this proxy statement. In summary, the Board recommends a vote:

| • | “FOR ALL” of the Class III Directors nominated for reelection to the Board; |

| • | “FOR” approval of the Say-on-Pay Proposal; |

| • | “FOR THREE YEARS” with respect to the Say-on-Frequency Proposal; |

| • | “FOR” the approval of the First Amendment to our Long-Term Incentive Plan to increase the number of common units that may be delivered with respect to awards under the Long-Term Incentive Plan by 3,000,000 units; and |

| • | “FOR” the ratification of the appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm for the year ending December 31, 2011. |

With respect to any other matter that properly comes before the Annual Meeting, the proxy holders will vote as recommended by the Board or, if no recommendation is given, at their own discretion.

What are “abstentions” and “broker non-votes” and how are these votes treated?

An “abstention” occurs when a unitholder is present at the Annual Meeting but fails to vote or voluntarily withholds his or her vote for any of the matters upon which the unitholders are voting. Abstentions are considered “present” and are included in the quorum calculations.

If you hold your common units in street name, you will receive instructions from your brokers or other nominees describing how to vote your common units yourself or, in the alternative, how to direct your brokers or other nominees to vote your common units held in street name. If you do not vote your common units held in street name yourself and if you do not instruct your brokers or nominees how to vote your common units, they may vote your common units as they decide as to each matter for which they have discretionary authority under the rules of The NASDAQ Stock Market LLC. The election of directors (Proposal 1), the Say-on-Pay and Say-on-Frequency Proposals (Proposals 2 and 3, respectively), and the approval of the First Amendment to our Long-Term Incentive Plan (Proposal 4) are non-discretionary matters for which brokers and other nominees do not have discretionary authority to vote unless they receive timely instructions from you. As such, for Proposals 1, 2, 3 and 4 to be voted on at the Annual Meeting, you must provide timely instructions on how the broker or other nominee should vote your common units. When a broker or other nominee does not have discretion to vote on a particular matter, you have not given timely instructions on how the broker or other nominee should vote your common units, and the broker or other nominee indicates it does not have authority to vote such common units on its proxy, a “broker non-vote” results. Although any broker non-vote would be counted as present at the meeting for purposes of determining a quorum, it would be treated as not entitled to vote with respect to non-discretionary matters, and, as such, broker non-votes will not be counted as a vote “FOR” or “AGAINST” the election of directors, the Say-on-Pay and Say-on-Frequency Proposals and the proposal to amend our Long-Term Incentive Plan. The ratification of the appointment of our independent registered public accounting firm as our independent auditors for the year ending December 31, 2011 (Proposal 5) is a discretionary matter on which brokers and other nominees may vote in the absence of timely instructions from you.

What are my voting choices when voting for Class III Director nominees and what vote is needed to elect the nominees?

In the vote on the election of the Class III Director nominees, you may:

| • | vote “FOR ALL” as to all nominees; |

| • | vote “WITHHOLD ALL” as to all nominees; or |

5

Table of Contents

| • | vote “FOR ALL EXCEPT” as to specific nominees. |

The Board recommends a vote “FOR ALL”of the nominees.

Please see “Voting Requirements for the Annual Meeting” for an explanation of the vote needed to elect the Class III Directors.

What are my voting choices when voting on the Say-on-Pay Proposal and what vote is needed to approve the proposal?

In the vote on the Say-on-Pay Proposal, you may:

| • | vote “FOR” the proposal; |

| • | vote “AGAINST” the proposal; or |

| • | “ABSTAIN” from voting on the proposal. |

The Board recommends a vote “FOR” the proposal.

Please see “Voting Requirements for the Annual Meeting” for an explanation of the vote needed to approve the Say-on-Pay Proposal.

What are my voting choices when voting on the Say-on-Frequency Proposal and what vote is needed to approve the proposal?

In the vote on the Say-on-Frequency Proposal, you may:

| • | vote “FOR ONE YEAR” with respect to the proposal; |

| • | vote “FOR TWO YEARS” with respect to the proposal; |

| • | vote “FOR THREE YEARS” with respect to the proposal; or |

| • | “ABSTAIN” from voting on the proposal. |

The Board recommends a vote “FOR THREE YEARS” with respect to the Say-on-Frequency proposal.

Please see “Voting Requirements for the Annual Meeting” for an explanation of the vote needed to approve the Say-on-Frequency Proposal.

What are my voting choices when voting on the First Amendment to the Partnership’s Long-Term Incentive Plan and what vote is needed to approve the amendment?

In the vote on the approval of the First Amendment to our Long-Term Incentive Plan, you may:

| • | vote “FOR” the amendment; |

| • | vote “AGAINST” the amendment; or |

| • | “ABSTAIN” from voting on the amendment. |

The Board recommends a vote “FOR” the amendment.

Please see “Voting Requirements for the Annual Meeting” for an explanation of the vote needed to approve the First Amendment to our Long-Term Incentive Plan.

6

Table of Contents

What are my voting choices when voting on the ratification of the Audit Committee’s appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm for the year ending December 31, 2011, and what vote is needed to ratify their appointment?

In the vote on the ratification of the appointment of PricewaterhouseCoopers LLP, you may:

| • | vote “FOR” the ratification; |

| • | vote “AGAINST” the ratification; or |

| • | vote “ABSTAIN” on the ratification. |

The Board recommends a vote “FOR”the ratification of the appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm for the year ending December 31, 2011.

Please see “Voting Requirements for the Annual Meeting” for an explanation of the vote needed to approve this proposal.

What if I do not specify a choice for a matter when returning my proxy?

You should specify your choice for each matter on the enclosed proxy. If you sign and return your proxy but do not give specific instructions, your proxy will be voted “FOR ALL”of the Class III Director nominees, “FOR” the Say-on-Pay proposal, “FOR THREE YEARS” with respect to the Say-on-Frequency proposal, “FOR” the approval of the First Amendment to our Long-Term Incentive Plan, and “FOR” the proposal to ratify the appointment of Pricewaterhouse Coopers LLP as our independent registered public accounting firm for the year ending December 31, 2011.

Do I have dissenters’ rights of appraisal?

We were formed as a limited partnership under the laws of the State of Delaware, including the Delaware Revised Uniform Limited Partnership Act. Under those laws, dissenters’ rights are not available to our unitholders with respect to the matters to be voted upon at the Annual Meeting.

Who counts the votes?

Broadridge Financial Solutions will tabulate the votes and will act as the independent inspector of election.

Whom should I contact with questions?

If you have any questions about this proxy statement or the Annual Meeting, please contact our Investor Relations Department in writing at 515 South Flower Street, Suite 4800, Los Angeles, California 90071 or by telephone at (213) 225-5900.

Where may I obtain additional information about BreitBurn Energy Partners L.P.?

We refer you to our 2010 Annual Report for additional information about us. Our 2010 Annual Report is included with your proxy materials. You may receive additional copies of our 2010 Annual Report at no charge through the Investor Relations section of our website athttp://www.breitburn.com. This proxy statement, a form of proxy and our 2010 Annual Report are also available athttp://www.proxyvote.com. You may receive additional copies of our 2010 Annual Report or proxy statement at no charge, or request to receive any additional information or directions to the Annual Meeting to be able to vote in person, by contacting our Investor Relations Department in writing at 515 South Flower Street, Suite 4800, Los Angeles, California 90071 or by telephone at (213) 225-5900. In order to facilitate timely delivery of such additional proxy materials, such a request must be made by June 9, 2011, as we are unable to guarantee the timely delivery of additional proxy materials for requests made after this date.

7

Table of Contents

How do I get to the Annual Meeting?

The Annual Meeting will be held at The Wilshire Grand Hotel, Sierra Room, 930 Wilshire Boulevard, Los Angeles, California 90017, which is located in downtown Los Angeles. The hotel is bounded on the west by Francisco Street, on the east by Figueroa Street, on the north by Wilshire Boulevard and on the south by Seventh Street.

IMPORTANT NOTICE REGARDING THE AVAILABILITY OF

PROXY MATERIALS FOR THE ANNUAL MEETING OF LIMITED PARTNERS

TO BE HELD ON JUNE 23, 2011

The Notice of Annual Meeting of Limited Partners, the Proxy Statement for the Annual Meeting, including a form of proxy and the 2010 Annual Report to Unitholders, which includes the Annual Report on Form 10-K

for the year ended December 31, 2010, are available athttp://www.proxyvote.com.

8

Table of Contents

VOTING REQUIREMENTS FOR THE ANNUAL MEETING

Right to Vote and Related Matters

Only those record holders of our common units on April 25, 2011, the record date for the Annual Meeting (subject to the limitations contained in the definition of “Outstanding” and in Section 13.4(b) in the Partnership Agreement), are entitled to notice of, and to vote at, the Annual Meeting, or to act with respect to matters as to which the holders of the Outstanding common units have the right to vote or to act. All references in this proxy statement to votes of, or other acts that may be taken by, the Outstanding common units are deemed to be references to the votes or acts of the record holders of such Outstanding common units. As of the record date, 59,039,933 of our common units were Outstanding, all of which are entitled to vote at the Annual Meeting.

Pursuant to the Partnership Agreement, each holder of our Outstanding common units as of the close of business on the record date is entitled to one vote per unit at the Annual Meeting, subject to the exceptions described below. As defined in the Partnership Agreement, “Outstanding” means, with respect to Partnership Securities (as defined in the Partnership Agreement), all Partnership Securities that are issued by the Partnership and reflected as outstanding on the Partnership’s books and records as of the date of determination; provided, however, that if at any time any person or group (other than our General Partner or its affiliates) beneficially owns 20% or more of the Outstanding Partnership Securities of any class then Outstanding, all Partnership Securities owned by such person or group can not be voted on any matter and are not considered to be Outstanding when sending notices of a meeting of limited partners to vote on any matter (unless otherwise required by law), calculating required votes, determining the presence of a quorum or for other similar purposes under the Partnership Agreement, except that common units so owned are considered to be Outstanding for purposes of Section 11.1(b)(iv) of the Partnership Agreement relating to the voluntary withdrawal of our General Partner (such common units are not, however, treated as a separate class of Partnership Securities for purposes of the Partnership Agreement). However, the foregoing limitation does not apply to (1) any person or group who acquired 20% or more of the Outstanding Partnership Securities of any class then Outstanding directly from our General Partner or its affiliates, (2) any person or group who acquired 20% or more of the Outstanding Partnership Securities of any class then Outstanding directly or indirectly from a person or group described in clause (1) provided that our General Partner has notified such person or group in writing that such limitation does not apply, or (3) any person or group who acquired 20% or more of any Partnership Securities issued by the Partnership with the prior approval of the Board. Quicksilver is not subject to the 20% limitation described in this paragraph since Quicksilver acquired its common units with the prior approval of the Board.

With respect to the election of directors to the Board, (1) we and our General Partner will not be entitled to vote common units that are otherwise entitled to vote at any meeting of the limited partners, and (2) with the exception of Quicksilver, if at any time any person or group beneficially owns 20% or more of the Outstanding Partnership Securities of any class then Outstanding, then all Partnership Securities owned by such person or group in excess of 20% of the Outstanding Partnership Securities of the applicable class may not be voted, and in each case, the foregoing common units will not be counted when calculating the required votes for such matter and will not be deemed to be Outstanding for purposes of determining a quorum for such meeting. Such common units will not be treated as a separate class of Partnership Securities for purposes of the Partnership Agreement. Pursuant to our Settlement Agreement with Quicksilver entered into as of April 5, 2010 (the “Quicksilver Settlement Agreement”), Quicksilver is not subject to the 20% limitation described in this paragraph with respect to the common units currently held by Quicksilver. Quicksilver has agreed to vote in favor of the Class III Directors nominated by the Board for election at the Annual Meeting. For additional information, see “Certain Relationships and Related Transactions — Quicksilver Settlement Agreement.”

With respect to common units that are held for a person’s account by another person (such as a broker, dealer, bank, trust company or clearing corporation, or an agent of any of the foregoing) in whose name such common units are registered, such other person must, in exercising the voting rights in respect of such common units on any matter, and unless the arrangement between such persons provides otherwise, vote such common units in favor of, and at the direction of, the person who is the beneficial owner, and the Partnership is entitled to assume it is so acting without further inquiry.

9

Table of Contents

Quorum

Subject to the 20% limitations described above, the holders of a majority of the Outstanding common units on the record date, represented in person or by proxy, will constitute a quorum at the Annual Meeting, unless any such action by the limited partners requires approval by holders of a greater percentage of such common units, in which case the quorum will be such greater percentage. Proxies received but marked as abstentions and broker non-votes will be included in the number of common units considered to be present at the Annual Meeting. The limited partners present at a duly called or held meeting at which a quorum is present may continue to transact business until adjournment, notwithstanding the withdrawal of enough limited partners to leave less than a quorum, if any action taken (other than adjournment) is approved by the required percentage of Outstanding common units specified in the Partnership Agreement (including Outstanding common units deemed owned by our General Partner, if any). In the absence of a quorum, the Annual Meeting may be adjourned from time to time by the affirmative vote of holders of at least a majority of the Outstanding common units entitled to vote at the Annual Meeting (including Outstanding common units deemed owned by our General Partner, if any) represented either in person or by proxy, but no other business may be transacted, except as otherwise provided in the Partnership Agreement.

Required Vote for the Election of Class III Directors

Pursuant to the Partnership Agreement, the directors of the Board of our General Partner are elected by a plurality of the votes cast by the unitholders entitled to vote at the Annual Meeting. This means that the two Class III Director nominees receiving the highest number of affirmative votes at the Annual Meeting will be elected. Withholding votes, abstentions and broker non-votes will be counted for purposes of determining the presence or absence of a quorum but otherwise will have no effect on the election of a director nominee. You may not cumulate your votes in the election of directors.

Required Vote for the Say-on-Pay Proposal

Pursuant to the Partnership Agreement, the Say-on-Pay Proposal will require approval by the holders of a majority of the Outstanding common units entitled to vote and present in person or by proxy at the Annual Meeting. Abstentions will have the same effect as votes “AGAINST” the proposal, while broker non-votes will not be entitled to vote with respect to the Say-on-Pay Proposal and, therefore, will not be considered in determining whether the required vote on this proposal has been obtained.

Required Vote for the Say-on-Frequency Proposal

Pursuant to the Partnership Agreement, the Say-on-Frequency Proposal will require approval by the holders of a majority of the Outstanding common units entitled to vote and present in person or by proxy at the Annual Meeting. Abstentions will have the same effect as votes “AGAINST” the proposal, while broker non-votes will not be entitled to vote with respect to the Say-on-Frequency Proposal and, therefore, will not be considered in determining whether the required vote on this proposal has been obtained. With respect to this proposal, if none of the frequency alternatives (one year, two years or three years) receives a majority of the votes cast, we will consider the frequency that receives the highest number of votes by unitholders to be the frequency that has been selected by our unitholders.

Required Vote for the Approval of the First Amendment to the Partnership’s Long-Term Incentive Plan

Pursuant to applicable NASDAQ rules and our Long-Term Incentive Plan, the First Amendment to our Long-Term Incentive Plan will require approval by a majority of the total votes cast on the proposal. Pursuant to the Partnership Agreement, this proposal also will require approval by the holders of a majority of the Outstanding common units entitled to vote and present in person or by proxy at the Annual Meeting. As a result, abstentions will have the same effect as votes “AGAINST” the proposal, while broker non-votes will not be entitled to vote and will not be counted as votes with respect to the proposal and, therefore, will not be considered in determining whether the required vote on this proposal has been obtained.

10

Table of Contents

Required Vote for the Ratification of the Audit Committee’s Appointment of PricewaterhouseCoopers LLP as Our Independent Registered Public Accounting Firm for the Year Ending December 31, 2011

Pursuant to the Partnership Agreement, the proposal to ratify the appointment of PricewaterhouseCoopers LLP as our independent registered public accounting firm for the year ending December 31, 2011 will require approval by the holders of a majority of the Outstanding common units entitled to vote and present in person or by proxy at the Annual Meeting. Abstentions will have the same effect as votes “AGAINST” the proposal. Because brokers and other nominees will have discretion to vote common units without the direction of their clients with respect to this proposal, there will not be any broker non-votes with respect to this proposal.

11

Table of Contents

PROPOSALS PRESENTED FOR UNITHOLDER VOTE

PROPOSAL 1:

ELECTION OF TWO CLASS III DIRECTORS TO SERVE A THREE-YEAR TERM UNTIL THE 2014 ANNUAL MEETING

The Board is comprised of six directors. The Board has been divided into three classes: Class I, Class II and Class III. The directors designated in the Fourth Amended and Restated Limited Liability Company Agreement of our General Partner (the “Limited Liability Company Agreement”) to Class I are serving a term that expires at the annual meeting to be held in 2012. The directors designated to Class II are serving a term that expires at the annual meeting to be held in 2013. The directors designated to Class III are serving for an initial term that expires at the Annual Meeting. Successors to the class of directors whose term expires at an annual meeting will be elected for a three-year term, or until their successors are duly elected and qualified.

The two Class III Board members whose terms expire at the Annual Meeting are David B. Kilpatrick and W. Yandell Rogers, III. The Board recommends the approval of the election of Messrs. Kilpatrick and Rogers to serve as Class III Directors for a term of three years, until the Partnership’s annual meeting to be held in 2014, or until their successors are duly elected and qualified. Certain individual qualifications and skills of our directors that contribute to the Board’s effectiveness as a whole are described below in each director’s biographical information under the heading “Board of Directors and Executive Officers.”

Unless otherwise indicated on the proxy, the persons named as proxies in the enclosed proxy will vote “FOR ALL” of the nominees listed above. We did not pay any third-party fees to assist in the process of identifying or evaluating Class III Director candidates nor did we receive a recommended Class III Director nominee from any unitholder.Although we have no reason to believe that any of the nominees will be unable to serve if elected, should any of the nominees become unable to serve prior to the Annual Meeting, the proxies will be voted for the election of such other persons as may be nominated by the Board. Unitholders may not cumulate their votes in the election of directors.

THE BOARD UNANIMOUSLY RECOMMENDS A VOTE “FOR ALL” OF THE CLASS III DIRECTOR NOMINEES.

12

Table of Contents

PROPOSAL 2:

ADVISORY VOTE ON EXECUTIVE COMPENSATION

Background

Section 14A of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) requires that we provide our unitholders the opportunity to vote on an advisory (non-binding) basis to approve the compensation of the named executive officers of our General Partner as reported in this proxy statement.

Summary

We are asking our unitholders to provide advisory approval of the compensation of the named executive officers (which consist of the Chief Executive Officer, the Chief Financial Officer and the next three highest paid executives) of our General Partner, as such compensation is described in the “Compensation Discussion and Analysis” section, the tabular disclosure regarding such compensation and the accompanying narrative disclosure set forth in this proxy statement. The Board believes that our long-term success depends in large measure on our ability to attract and retain qualified personnel. Our executive compensation program plays a significant role in our ability to attract, retain and motivate the highest quality executives. The program directly links executive compensation to performance, aligning the interests of the executive officers with those of our unitholders through long-term incentive awards in the form of unit-based awards granted under our long-term incentive plan and annual cash bonuses awarded under our short-term incentive plan. The following is a summary of some of the key elements of our executive compensation program. Unitholders are urged to read and review carefully the “Compensation Discussion and Analysis” section of this proxy statement and the tabular and other disclosures on executive compensation that follow, which discuss in detail how our compensation policies and procedures implement our compensation philosophy.

We emphasize pay-for-performance. We believe that a significant portion of the compensation of our General Partner’s executives should be variable and at risk and tied to performance. The short-term incentive plan rewards annual performance based on the Compensation and Governance Committee’s evaluation of Partnership and individual performance. Based on our performance in 2010, we achieved the following objectives under the short-term incentive plan:

| • | in October 2010, we successfully issued $305 million in aggregate principal amount of 8.625% Senior Notes due 2020 at a price of 98.358% (the “Senior Notes”); |

| • | we significantly reduced our outstanding bank debt under our credit facility by $331 million during 2010, from $559 million at December 31, 2009 to $228 million at December 31, 2010, by applying $290 million of the net proceeds from the issuance of the Senior Notes and using cash flow from operating activities to repay amounts outstanding under our credit facility; |

| • | we continued to reduce general and administrative expenses and lease operating expenses through cost-cutting initiatives throughout the Partnership; |

| • | we increased production levels over 2009 production; |

| • | we reinstated distributions beginning with the first quarter of 2010 at an annualized rate of $1.50 per common unit and our fourth quarter distribution has increased the annualized rate to $1.65; |

| • | in April 2010, we entered into the Quicksilver Settlement Agreement; |

| • | our total return per common unit for 2010 was 101%; |

| • | the Partnership significantly exceeded budgeted performance for reduction of lease operating expenses, and general and administrative expenses; and |

| • | capital efficiency and safety goals exceeded target levels and production goals met budget levels. |

13

Table of Contents

We believe that our compensation programs strongly align our executives’ interests with those of our unitholders. We place a strong emphasis on the use of equity-based awards as a key component of our compensation program. We believe that unit-based awards reward long-term performance and align the interests of management with those of our unitholders. We have used CPUs and RPUs (as described in the “Compensation Discussion and Analysis — Components of Compensation — Long-Term Incentive Plan” section of this proxy statement) as key equity incentive vehicles because the executives are primarily responsible for our operating results, and therefore, the amount of distributions we make to holders of our common units which directly affects the value of the CPUs and RPUs. As a result, CPUs and RPUs are effective tools for meeting our compensation goal of increasing long-term unitholder value by tying the value of these awards to our future performance.

In addition to linking compensation value to unitholder value, CPUs and RPUs generally require continued service over a multi-year period as a condition to full vesting, creating a strong retention incentive and ensuring the continuity of our operations.

We are committed to having strong governance standards and best practices for our compensation programs. As part of its commitment to strong corporate governance and best practices, the Compensation and Governance Committee engaged and received advice on the compensation program from an independent, third-party compensation consultant, which provided no other services to us in 2009 and 2010 other than those provided directly to or on behalf of the Compensation and Governance Committee. The Compensation and Governance Committee oversees risk management as it relates to our compensation plans, policies and practices. The Compensation and Governance Committee consistently reviews our executive compensation program to ensure that it not only provides competitive pay opportunities, but also reflects best practices.

Recommendation

The Board believes that the information provided above and within the “Compensation Discussion and Analysis” section of this proxy statement demonstrates that our executive compensation program was designed appropriately and is working to ensure that the executives’ interests are aligned with our unitholders’ interests to support long-term value creation.

Accordingly, at the Annual Meeting, unitholders are being asked to vote on the following advisory resolution:

“RESOLVED, that the unitholders of the Partnership advise that they approve the compensation paid to the named executive officers of the Partnership’s General Partner, as disclosed pursuant to the compensation disclosure rules set forth in Item 402 of Regulation S-K, which disclosure shall include the Compensation Discussion and Analysis, the compensation tables, narrative discussion and any related material.”

While this vote is advisory and, therefore, non-binding, the Board and the Compensation and Governance Committee, which is comprised of independent directors, will review the voting results in connection with their ongoing evaluation of our compensation program and expect to take into account the outcome of this vote in considering future executive compensation arrangements.

THE BOARD UNANIMOUSLY RECOMMENDS A VOTE “FOR” THIS SAY-ON-PAY PROPOSAL.

14

Table of Contents

PROPOSAL 3:

ADVISORY VOTE ON THE FREQUENCY OF ADVISORY VOTES ON EXECUTIVE COMPENSATION

Background

Section 14A of the Exchange Act also enables unitholders to indicate how frequently they believe we should seek an advisory vote on the compensation of the named executive officers of our General Partner. We are seeking an advisory, non-binding determination from unitholders as to the frequency with which unitholders would have an opportunity to provide an advisory approval of our executive compensation program. We are providing unitholders the option of selecting a frequency of every one, two or three years, or abstaining.

Summary

For the reasons described below, the Board recommends that unitholders select a frequency of three years (triennially). We believe that this frequency is appropriate for the following reasons:

| • | Our executive compensation programs are designed to support long-term value creation. A triennial vote will allow unitholders to better judge our compensation programs in relation to our long-term performance. |

| • | A triennial vote will provide the Compensation and Governance Committee and the Board sufficient time to thoughtfully evaluate the results of the most recent advisory vote on executive compensation, to discuss the implications of the vote with unitholders and to develop and implement any changes to our executive compensation programs that may be appropriate in light of the vote. |

| • | A triennial vote will allow for any changes to our executive compensation programs to be in place long enough for unitholders to see and evaluate the effectiveness of these changes. |

| • | We have in the past been, and will in the future continue to be, engaged with our unitholders on a number of topics and in a number of forums. Thus, we view the advisory vote on executive compensation as an additional, but not exclusive, opportunity for our unitholders to communicate with us regarding their views on our executive compensation programs. |

Recommendation

Based on the factors discussed, the Board recommends that future advisory votes on executive compensation occur every three years until the next frequency vote. Unitholders are not being asked to approve or disapprove the Board’s recommendation, but rather to indicate their choice among the following say-on-pay frequency options: every one year, every two years or every three years, or to abstain from voting.

While this vote is advisory and, therefore, non-binding, the Board and the Compensation and Governance Committee, which is comprised of independent directors, will take into account the outcome of this vote in considering the frequency of future advisory votes with respect to executive compensation.

THE BOARD UNANIMOUSLY RECOMMENDS A VOTE OF “FOR THREE YEARS” WITH RESPECT TO THIS SAY-ON-FREQUENCY PROPOSAL.

15

Table of Contents

PROPOSAL 4:

APPROVAL OF THE FIRST AMENDMENT TO THE FIRST AMENDED AND RESTATED BREITBURN ENERGY PARTNERS L.P. 2006 LONG-TERM INCENTIVE PLAN

The Board is recommending that unitholders approve the First Amendment (the “First Amendment”) to the Long-Term Incentive Plan at the Annual Meeting. A copy of the First Amendment is attached to this proxy statement as Appendix A. The First Amendment amends the Long-Term Incentive Plan to increase the aggregate number of common units that may be delivered with respect to awards under the Long-Term Incentive Plan by an additional 3,000,000 units, from 6,702,064 units to a total of 9,702,064 units. On April 27, 2011, the Compensation and Governance Committee adopted the First Amendment to the Long-Term Incentive Plan, subject to unitholder approval. The Long-Term Incentive Plan is integral to the Partnership’s compensation strategies and programs, and the Board believes that the increase in the aggregate number of units that may be delivered with respect to awards under the Long-Term Incentive Plan provides the flexibility that the Partnership and our General Partner need to keep pace with our competitors and to effectively recruit, motivate and retain the caliber of employees and directors essential for achievement of our success.

A summary of the principal provisions of the Long-Term Incentive Plan, as amended by the First Amendment, is set forth below. The summary is qualified in its entirety by reference to the full text of the Long-Term Incentive Plan and the First Amendment.

General

The purpose of the Long-Term Incentive Plan is to promote the interests of the Partnership and our General Partner by providing our employees, consultants and directors incentive compensation awards based on common units of the Partnership in order to encourage superior performance. The Long-Term Incentive Plan is also contemplated to enhance the ability of our General Partner and its affiliates to attract and retain the services of individuals who are essential for the growth and profitability of the Partnership, our General Partner and their affiliates and to encourage such individuals to devote their best efforts to advancing the business of the Partnership, our General Partner and their affiliates. The Long-Term Incentive Plan provides for the grant to eligible individuals of options, restricted units, phantom units, unit appreciation rights (“UARs”), unit awards, distribution equivalent rights and other unit-based awards.

The BreitBurn Energy Partners, L.P. 2006 Long-Term Incentive Plan was originally adopted as of October 9, 2006 (the “Original Plan”). The Original Plan was amended and restated in its entirety by the Long-Term Incentive Plan effective on October 29, 2009. As of April 25, 2011, grants covering approximately 3,148,868 units were outstanding under the Long-Term Incentive Plan, and 2,093,897 units remained available for issuance under the Long-Term Incentive Plan.

Administration

The Long-Term Incentive Plan is administered by our Compensation and Governance Committee, which currently consists of four directors, each of whom qualifies as a non-employee director pursuant to Rule 16b-3 of the Exchange Act and an “independent director” under the rules of The NASDAQ Stock Market LLC.

Eligibility

Persons eligible to participate in the Long-Term Incentive Plan include (i) employees of our General Partner or any of its affiliates; (ii) any individuals who render consulting services to the Partnership, our General Partner or either of their affiliates; and (iii) members of the Board or of the board of directors of any affiliate of the Partnership or our General Partner, in each case as determined by the plan administrator. As of April 25, 2011, approximately 104 individuals were eligible under our compensation policy to receive equity awards under the Long-Term Incentive Plan.

16

Table of Contents

Limitation on Awards and Units Available

Subject to certain adjustments set forth in the Long-Term Incentive Plan as described below, the aggregate number of units that may be delivered with respect to awards under the Long-Term Incentive Plan, without giving effect to the First Amendment increasing the number of units available for grant thereunder, is 6,702,064 units. If the First Amendment is approved by our unitholders, the aggregate number of units that may be delivered with respect to awards under the Long-Term Incentive Plan will be increased by an additional 3,000,000 units to 9,702,064 units. Units deliverable pursuant to an award under the Long-Term Incentive Plan may be units acquired in the open market, from any affiliate of the Partnership or our General Partner, from the Partnership, from any other person, or any combination of the foregoing, as determined by the plan administrator in its discretion.

Units withheld from an award to either satisfy the tax withholding obligations of the Partnership, our General Partner or either of their affiliates with respect to the award or to pay the exercise price of an award will not be considered to be units delivered under the Long-Term Incentive Plan. Similarly, to the extent that an award under the Long-Term Incentive Plan is forfeited, cancelled, exercised, paid or otherwise terminates or expires without the actual delivery of units pursuant to such award, the units subject to such award will again be available for awards under the Long-Term Incentive Plan.

There is no limitation on the number of awards under the Long-Term Incentive Plan that may be paid in cash. As of April 25, 2011, the closing price of our common units on the Nasdaq Global Select Market was $21.64 per unit.

Awards

The Long-Term Incentive Plan provides for the grant of options, UARs, restricted units, phantom units, unit awards, distribution equivalent rights and other unit-based awards.

Options

The Long-Term Incentive Plan permits the grant of options to purchase common units. The plan administrator may make grants of options containing such terms as it shall determine that are consistent with the terms of the Long-Term Incentive Plan. The exercise price of an option may not be less than the fair market value of a common unit on the date of the grant. Options will become vested and exercisable over a period determined by the plan administrator.

Unit Appreciation Rights

The Long-Term Incentive Plan permits the grant of UARs. A UAR is the right to receive payment of an amount equal to the excess of the fair market value of a common unit on the exercise date over the exercise price established for the UAR. Such excess will be paid in cash, common units, or in a combination of cash and common units as determined by the plan administrator. The plan administrator may make grants of UARs containing such terms as it shall determine that are consistent with the terms of the Long-Term Incentive Plan. The exercise price of a UAR may not be less than the fair market value of a common unit on the date of the grant. UARs will become vested and exercisable over a period determined by the plan administrator.

Restricted Units

A restricted unit is a common unit that is subject to a restricted period established by the plan administrator during which the common unit remains subject to forfeiture. The plan administrator may make grants of restricted units containing such terms as it shall determine that are consistent with the terms of the Long-Term Incentive Plan, including the period over which restricted units will become vested and nonforfeitable. To the extent provided by the plan administrator, in its discretion, a grant of restricted stock units may provide that distributions made by the Partnership with respect to the restricted stock units may be subjected to the same or different forfeiture and other restrictions as the restricted units to which such distributions relate.

17

Table of Contents

Phantom Units

A phantom unit is a notional unit that upon vesting entitles the grantee to receive a common unit or, in the discretion of the plan administrator, an amount in cash equivalent to the fair market value of a common unit. The plan administrator may make grants of phantom units containing such terms as it shall determine that are consistent with the terms of the Long-Term Incentive Plan, including the period over which phantom units will vest.

Distribution Equivalent Rights

The plan administrator may, in its discretion, grant distribution equivalent rights (“DERs”) with respect to phantom unit awards. DERs are rights to receive the equivalent value (in cash or additional awards) of the amount of any cash distributions made by the Partnership during the period the phantom unit is outstanding. Payment of a DER may be subject to the same vesting terms as the award to which it relates or differing vesting terms, as determined by the plan administrator in its discretion.

Unit Awards

The Long-Term Incentive Plan permits the grant of units that are not subject to vesting restrictions. Unit awards may be in lieu of or in addition to other compensation payable to the individual. Grants of unit awards and the amounts of such grants are in the discretion of the Compensation and Governance Committee.

Other Unit-Based Awards

The Long-Term Incentive Plan permits the grant of other unit-based awards, which are awards that are based, in whole or in part, on the value of performance of a common unit. Vested and other unit-based awards may be paid in common units (including restricted units), cash or a combination thereof, as provided in the applicable grant agreement.

Changes in Control and Anti-Dilution Adjustments

Upon the occurrence of a “change of control,” as defined in the Long-Term Incentive Plan, any change in applicable law or regulation affecting the Long-Term Incentive Plan or awards thereunder, or any change in accounting principles affecting the financial statements of the Partnership, the plan administrator, in its sole discretion, without the consent of any participant or holder of an award, may take certain actions to prevent dilution or enlargement of the benefits or potential benefits intended to be made available under the Long-Term Incentive Plan or an outstanding award, including the acceleration, cash-out, termination or replacement of awards, the assumption or exchange of awards by a successor or survivor entity, and adjustments to outstanding awards and awards available for issuance under the Long-Term Incentive Plan.

In the event of certain corporate transactions and changes in capitalization, the plan administrator will equitably adjust the terms and conditions of any outstanding awards, including the number and type of common units covered by each award, and the number and type of common units (or other securities or property) with respect to which awards may be granted after such event. With respect to any such event that would not result in an accounting charge under ASC 718 if the adjustment to awards with respect to such event were subject to discretionary action, the plan administrator will have complete discretion to adjust awards in such manner as it deems appropriate with respect to such other event.

Transferability

Awards under the Long-Term Incentive Plan are generally non-transferable other than by will or the laws of descent and distribution, and stock options and UARs generally may be exercised, during a participant’s lifetime, only by the participant, subject to exceptions for estate planning or as otherwise provided under the Long-Term Incentive Plan.

18

Table of Contents

Amendment and Termination

The Board or an authorized committee thereof may amend, alter, suspend, discontinue or terminate the Long-Term Incentive Plan in any manner, without the consent of any person, except as otherwise required by the rules of the principle securities exchange on which the common units are traded. In addition, the plan administrator may amend the terms of any outstanding awards, provided that no change, other than as described above under the section entitled “Changes in Control and Anti-Dilution Adjustments,” in any award may materially reduce the rights or benefits of a participant with respect to an award without the consent of such participant.

The Long-Term Incentive Plan will terminate on the earliest of (i) the date the Long-Term Incentive Plan is terminated by the Board or an authorized committee thereof; (ii) the date all common units available under the Long-Term Incentive Plan have been delivered to participants; or (iii) October 9, 2016 (which is the tenth anniversary of the date on which the Original Plan was approved by our General Partner), provided that outstanding awards at such time will generally remain in effect subject to the terms of the Long-Term Incentive Plan.

U.S. Federal Income Tax Consequences

The Federal income tax consequences of the Long-Term Incentive Plan under current federal income tax law are summarized in the following discussion which deals with the general federal income tax principles applicable to the Long-Term Incentive Plan and is intended for general information only. The following discussion of federal income tax consequences does not purport to be a complete analysis of all of the potential tax effects of the Long-Term Incentive Plan. It is based upon laws, regulations, rulings and decisions now in effect, all of which are subject to change. Certain kinds of taxes, such as state, local and foreign income taxes and federal employment taxes, are not discussed (except, with respect to federal employment taxes, to the limited extent discussed below under “— Potential Self Employment Consequences”). The following discussion does not address the tax consequences that may apply to a participant as a holder of common units issued pursuant to any award under the Long-Term Incentive Plan (except to the limited extent discussed below under “— Additional Tax Consequences for Holders of Units” and“— Potential Self Employment Consequences”). The following discussion also does not address all aspects of U.S. Federal income taxation that may be relevant in light of a participant’s particular circumstances. Furthermore, the grant, vesting, exercise, settlement or other taxable event relating to an award under the Long-Term Incentive Plan may require the participant to recognize taxable income without the participant’s receipt of cash.

Options.If a participant is granted an option under the Long-Term Incentive Plan, the participant should not have taxable income on the grant of the option. The participant generally will recognize ordinary income at the time of exercise in an amount equal to the aggregate fair market value of the common units purchased at such time, less the aggregate exercise price paid for such Common Units. The participant’s initial basis in each common unit generally will be the fair market value of a common unit on the date the participant exercises the option.

Unit Appreciation Rights. Generally, no taxable income will be recognized by the participant upon the grant of a unit appreciation right, but, upon exercise of the unit appreciation right, the cash or the fair market value of the common units received generally will be taxable as ordinary income to the recipient in the year of such exercise.

Restricted Units. For purposes of this summary, we have assumed that any restricted units granted under the Long-Term Incentive Plan will be capital interests and that each participant to whom such units are transferred will file a timely election under Section 83(b) of the Internal Revenue Code of 1986, as amended (the “Code”), with respect to the transfer to the participant of such units. Accordingly, a participant who receives restricted units that constitute capital interests generally will recognize ordinary income at the time the participant is issued such restricted units in an amount equal to their fair market value on such date less the amount, if any, that the participant paid for them. The participant generally will not recognize any additional ordinary income as and when the restrictions applicable to such restricted units lapse. The tax consequences would be different for participants who do not file a timely election under Section 83(b) of the Code. The Partnership has not granted restricted units that constitute profits interests.

19

Table of Contents

Phantom Units. A recipient of phantom units generally will not have taxable income at the time of grant. However, at the time the award is settled, whether in cash or in common units, the participant generally will recognize ordinary income equal to the value received.

Distribution Equivalent Rights, Unit Distribution Rights and Performance Distribution Rights.A participant who receives distribution equivalent rights, unit distribution rights or performance distribution rights generally will not recognize taxable income at the time of grant. However, at the time such an award is settled, whether in cash or in common units, the participant generally will recognize ordinary income equal to the value received.

Unit Awards. A participant who receives a unit award that constitutes a capital interest generally will recognize ordinary income in an amount equal to the fair market value of the common units received. The Partnership has not granted unit awards that constitute profits interests.

Other Unit-Based Awards. A participant who receives other unit-based awards, such as convertible phantom units, generally should not recognize taxable income at the time of the grant of the award. When the award is settled, whether in cash or common units, the participant generally should recognize ordinary income equal to the value received.

Additional Tax Consequences for Holders of Units. To the extent a participant receives common units, there will be additional tax consequences to the participant as a unitholder, which may be material to such participant. In particular, each unitholder of the Partnership is required to report on his or her individual income tax return his or her allocable share of income, gains, losses and deductions of the Partnership in computing his or her federalincome tax liability, regardless of whether cash distributions are made by the Partnership. Distributions by the Partnership to a unitholder generally are not taxable unless the amount of cash distributed is in excess of the unitholder’s adjusted basis in his or her Common Units. Tax consequences to unitholders are very complex and are beyond the scope of this summary.