UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

Amendment No. 1

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2012

or

| o | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from ___ to ___

Commission file number 001-33055

BreitBurn Energy Partners L.P.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 74-3169953 |

| (State or Other Jurisdiction of | (I.R.S. Employer |

| Incorporation or Organization) | Identification No.) |

| 515 South Flower Street, Suite 4800 | |

| Los Angeles, California | 90071 |

| (Address of Principal Executive Offices) | (Zip Code) |

Registrant’s telephone number, including area code: (213) 225-5900

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| Common Units Representing Limited Partner Interests | The NASDAQ Stock Market LLC | |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer x Accelerated filer o Non-accelerated filer o (Do not check if a smaller reporting company) Smaller reporting company o

Indicate by check-mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No x

The aggregate market value of the Common Units held by non-affiliates was approximately $1.1 billion on June 30, 2012, the last business day of the registrant’s most recently completed second fiscal quarter, based on $16.58 per unit, the last reported sales price on The NASDAQ Global Select Market on such date.

As of February 27, 2013, there were 99,679,796 Common Units outstanding.

Documents Incorporated By Reference: Certain information called for in Items 10, 11, 12, 13 and 14 of Part III are incorporated by reference from the registrant’s definitive proxy statement for the 2013 annual meeting of unitholders to be held on June 19, 2013.

EXPLANATORY NOTE

BreitBurn Energy Partners L.P. (the “Partnership,” “we,” “us” or “our”) is filing this Amendment No. 1 on Form 10-K/A (this “Amendment”) to amend its Annual Report on Form 10-K for the year ended December 31, 2012, filed with the Securities and Exchange Commission (the “SEC”) on February 28, 2013 (the “Original 10-K”).

This Amendment is being filed to amend the Original 10-K as follows:

(a) Revised the reconciliation of Adjusted EBITDA to net income (loss) attributable to the partnership table in Part II-Item 6 “Selected Financial Data” to remove the amount shown as “Net operating cash flow from acquisitions, effective date through closing date,” and to replace the unrealized derivative gain or loss row with a row for the add back of derivative gain or loss and a row for derivative contract settlement amounts. In footnotes, disclosed (i) the amount of deferred premiums settled during the periods presented; (ii) the amount of premiums for derivative contracts paid in earlier periods that apply to contracts settled during the periods presented; and (iii) the amount of crude oil, natural gas and interest rate settlements received or paid during the periods presented.

(b) Part II-Item 7 - “Executive Overview” - amended the section under “Operational Focus” related to realized sales prices to delete the discussion of realized prices including the effect of commodity derivative instruments.

(c) Part II-Item 7 - “Results of Operations” - (i) amended the results of operations table to combine “Realized gain (loss) on commodity derivatives” and “Unrealized gain (loss) on commodity derivatives” into a new row titled “Gain on commodity derivatives” and to exclude the effect of commodity derivative instruments from the average realized sales prices; (ii) replaced the section titled “Revenues” with separate sections titled “Oil, natural gas and NGL sales” and “Gain on commodity derivatives” to discuss sales revenues separately from gain (loss) on commodity derivatives including a discussion of settlements received or paid during the periods presented; and (iii) amended the section titled “Interest expense, net of amounts capitalized” and added “Loss on interest rate swaps” to discuss interest expense separately from loss on interest rate swaps.

(d) Part II-Item 7 - “Liquidity and Capital Resources” - revised the discussion in the first paragraph of the section titled “Cash Flows” “Operating activities” to replace the words “realized gains” with “settlements received” during the period.

(e) Revised the Consolidated Statements of Cash Flows in Part IV-Item 15 to remove the row titled “Unrealized (gain) loss on derivative instruments” under the header “Adjustments to reconcile to cash flow from operating activities” and replace it by a row titled “Gain on derivative instruments” that combines settled and mark-to-market gains on derivative instruments. Added a new row titled “Derivative instrument settlements” under the same header that includes cash attributable to commodity derivative instruments that settled during the periods. Added new rows titled “Prepaid premiums on derivative instruments” and “Settlement payments on terminated derivative instruments” under this same header to reflect actual payments made or received relating to these items during the periods.

(f) Part IV-Item 15 - Note 4 “Acquisitions” - revised the pro forma revenue and net income (loss) table for material acquisitions - (i) revised the years ended December 31, 2011 and 2012 were to include aggregated pro forma information for our 2012 insignificant subsidiary acquisitions; and (ii) corrected the year ended December 31, 2010, which was incorrectly reported in the Original 10-K.

(g) Part IV-Item 15 - Note 5 “Financial Instruments and Fair Value Measurements” - revised the tables presenting gain and loss on derivative instruments not designated as hedging instruments to remove the “Realized gain (loss)” and “Unrealized gain (loss)” rows and combine these amounts in a new row titled “Net gain (loss).” Revised the tables setting forth a reconciliation of changes in fair value of our derivative instruments classified as Level 3 to remove the “Realized gain” and “Unrealized loss” rows and combine these amounts in a new row titled “Gain (loss).”

This Amendment includes new certifications by our Principal Executive Officer and Principal Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002, filed as Exhibits 31.1, 31.2, 32.1 and 32.2, hereto. Each certification was true and correct as of the date of the filing of the Original 10-K.

Pursuant to interpretation 246.14 in the Regulation S-K section of the SEC’s “Compliance & Disclosure Interpretations,” we are filing Parts II and IV of the Original 10-K in their entirety as part of this Amendment. The information included in the Original 10-K was complete and correct as of the date of the filing of the Original 10-K.

Except as described above, we have not modified or updated other disclosures contained in the Original 10-K. Accordingly, this Amendment, with the exception of the foregoing, does not reflect events occurring after the date of filing of the Original 10-K, or modify or update those disclosures affected by subsequent events. Consequently, all other information not affected by the corrections described above is unchanged and reflects the disclosures and other information made at the date of the filing of the Original 10-K and should be read in conjunction with our filings with the SEC subsequent to the filing of the Original 10-K, including amendments to those filings, if any.

BREITBURN ENERGY PARTNERS L.P. AND SUBSIDIARIES

TABLE OF CONTENTS

| Page | ||

| No. | ||

| PART II | ||

| PART IV | ||

GLOSSARY OF OIL AND GAS TERMS, DESCRIPTION OF REFERENCES

The following is a description of the meanings of some of the oil and gas industry terms that may be used in this report. The definitions of proved developed reserves, proved reserves and proved undeveloped reserves have been abbreviated from the applicable definitions contained in Rule 4-10(a)(6), (22) and (31) of Regulation S-X.

API: The specific gravity or density of oil expressed in terms of a scale devised by the American Petroleum Institute.

Bbl: One stock tank barrel, or 42 U.S. gallons of liquid volume, of crude oil or other liquid hydrocarbons.

Bbl/d: Bbl per day.

Bcf: One billion cubic feet of natural gas.

Bcfe: One billion cubic feet equivalent, determined using the ratio of one Bbl of crude oil to six Mcf of natural gas.

Boe: One barrel of oil equivalent. Natural gas is converted on the basis of six Mcf of gas per one barrel of oil equivalent. This ratio reflects an energy content equivalency and not a price or revenue equivalency. Given commodity price disparities, the price for a barrel of oil equivalent for natural gas is significantly less than the price for a barrel of oil.

Boe/d: Boe per day.

Btu: British thermal unit, which is the quantity of heat required to raise the temperature of a one-pound mass of water by one degree Fahrenheit.

completion: The installation of permanent equipment for the production of oil or natural gas, or in the case of a dry hole, the reporting of abandonment to the appropriate agency.

development well: A well drilled within the proved area of a natural gas or oil reservoir to the depth of a stratigraphic horizon known to be productive.

differential: The difference between a benchmark price of oil and natural gas, such as the NYMEX crude oil price, and the wellhead price received.

dry hole or well: A well found to be incapable of producing either oil or gas in sufficient quantities to justify completion as an oil or gas well.

economically producible: A resource which generates revenue that exceeds, or is reasonably expected to exceed, the costs of the operation.

exploitation: A drilling or other project which may target proven or unproven reserves (such as probable or possible reserves), but which generally has a lower risk than that associated with exploration projects.

exploratory well: A well drilled to find a new field or to find a new reservoir in a field previously found to be productive of oil or gas in another reservoir. Generally, an exploratory well is not a development well.

field: An area consisting of a single reservoir or multiple reservoirs all grouped on or related to the same individual geological structural feature and/or stratigraphic condition.

gross acres or gross wells: The total acres or wells, as the case may be, in which a working interest is owned.

ICE: Intercontinental Exchange.

LIBOR: London Interbank Offered Rate.

MBbls: One thousand barrels of crude oil or other liquid hydrocarbons.

1

MBoe: One thousand barrels of oil equivalent.

MBoe/d: One thousand barrels of oil equivalent per day.

Mcf: One thousand cubic feet of natural gas.

Mcf/d: One thousand cubic feet of natural gas per day.

Mcfe: One thousand cubic feet of natural gas equivalent, determined using the ratio of one Bbl of crude oil to six Mcf of natural gas.

MichCon: Michigan Consolidated Gas Company.

MMBbls: One million barrels of crude oil or other liquid hydrocarbons.

MMBoe: One million barrels of oil equivalent.

MMBtu: One million British thermal units.

MMBtu/d: One million British thermal units per day.

MMcf: One million cubic feet of natural gas.

MMcfe: One million cubic feet of natural gas equivalent, determined using the ratio of one Bbl of crude oil to six Mcf of natural gas.

MMcfe/d: One million cubic feet of natural gas equivalent per day, determined using the ratio of one Bbl of crude oil to six Mcf of natural gas.

net acres or net wells: The sum of the fractional working interests owned in gross acres or gross wells, as the case may be.

NGLs: The combination of ethane, propane, butane and natural gasolines that when removed from natural gas become liquid under various levels of higher pressure and lower temperature.

NYMEX: New York Mercantile Exchange.

oil: Crude oil, condensate and natural gas liquids.

productive well: A well that is producing or that is mechanically capable of production.

proved developed reserves: Proved reserves that can be expected to be recovered (i) through existing wells with existing equipment and operating methods or in which the cost of the required equipment is relatively minor compared to the cost of a new well, and (ii) through installed extraction equipment and infrastructure operational at the time of the reserves estimate if the extraction is by means not involving a well. This definition of proved developed reserves has been abbreviated from the applicable definition contained in Rule 4-10(a)(6) of Regulation S-X.

proved reserves: The estimated quantities of crude oil, natural gas and natural gas liquids that geological and engineering data demonstrate with reasonable certainty to be economically producible in future years from known reservoirs under existing economic and operating conditions and government regulations. The project to extract the hydrocarbons must have commenced or the operator must be reasonably certain that it will commence the project within a reasonable time. This definition of proved reserves has been abbreviated from the applicable definition contained in Rule 4-10(a)(22) of Regulation S-X.

2

proved undeveloped reserves or PUDs: Proved reserves that are expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for recompletion. This definition of proved undeveloped reserves has been abbreviated from the applicable definitions contained in Rule 4-10(a)(31) of Regulation

S-X.

recompletion: The completion for production of an existing wellbore in another formation from that which the well has been previously completed.

reserve: Estimated remaining quantities of mineral deposits anticipated to be economically producible, as of a given date, by application of development projects to known accumulations.

reservoir: A porous and permeable underground formation containing a natural accumulation of producible oil and/or natural gas that is confined by impermeable rock or water barriers and is individual and separate from other reservoirs.

standardized measure: The present value of estimated future net revenue to be generated from the production of proved reserves, determined in accordance with the rules and regulations of the SEC (using prices and costs in effect as of the date of estimation), less future development, production and income tax expenses, and discounted at 10% per annum to reflect the timing of future net revenue. Standardized measure does not give effect to derivative transactions.

undeveloped acreage: Lease acreage on which wells have not been drilled or completed to a point that would permit the production of economic quantities of natural gas and oil regardless of whether such acreage contains proved reserves.

West Texas Intermediate (“WTI”): Light, sweet crude oil with high API gravity and low sulfur content used as the benchmark for U.S. crude oil refining and trading. WTI is deliverable at Cushing, Oklahoma to fill NYMEX futures contracts for light, sweet crude oil.

working interest: The operating interest that gives the owner the right to drill, produce and conduct operating activities on the property and to receive a share of production.

workover: Operations on a producing well to restore or increase production.

_____________________________________

References in this report to “the Partnership,” “we,” “our,” “us” or like terms refer to BreitBurn Energy Partners L.P. and its subsidiaries. References in this filing to “PCEC” or the “Predecessor” refer to Pacific Coast Energy Company LP, formerly named BreitBurn Energy Company L.P., our predecessor, and its predecessors and subsidiaries. References in this filing to “BreitBurn GP” or the “General Partner” refer to BreitBurn GP, LLC, our general partner and our wholly owned subsidiary. References in this filing to “BreitBurn Corporation” refer to BreitBurn Energy Corporation, a corporation owned by Randall Breitenbach and Halbert Washburn, the President (until December 31, 2012) and Chief Executive Officer, respectively, of our general partner. References in this filing to “BreitBurn Management” refer to BreitBurn Management Company, LLC, our administrative manager and wholly owned subsidiary. References in this filing to “BOLP” or “BreitBurn Operating” refer to BreitBurn Operating L.P., our wholly owned operating subsidiary. References in this filing to “BOGP” refer to BreitBurn Operating GP, LLC, the general partner of BOLP. References in this filing to “Quicksilver” refer to Quicksilver Resources Inc. from whom we acquired oil and gas properties and facilities in Michigan, Indiana and Kentucky on November 1, 2007. References in this filing to “BEPI” refer to BreitBurn Energy Partners I, L.P. References in this filing to “Utica” refer to BreitBurn Collingwood Utica LLC, our wholly owned subsidiary formed September 17, 2010. References in this filing to “Cabot” refer to Cabot Oil & Gas Corporation, from whom we acquired oil and natural gas properties primarily located in Wyoming on October 6, 2011. References in this filing to “NiMin” refer to NiMin Energy Corp., from whom we acquired oil properties located in Wyoming on June 28, 2012. References in this filing to “Element” refer to Element Petroleum, LP, from whom we acquired oil and natural gas properties located in Texas on July 2, 2012. References in this filing to “CrownRock” refer to CrownRock, L.P., from whom we acquired oil and natural gas properties located in Texas on July 2, 2012 and December 28, 2012. References in this filing to “AEO” refer to American Energy Operations, Inc., from whom we acquired principally oil gas properties located in California on November 30, 2012. References in this filing to “Lynden” refer to Lynden USA Inc., from whom we acquired oil and natural gas properties located in Texas on December 28, 2012. References in this filing to “Piedra” refer to Piedra Energy I, LLC, from whom we acquired oil and natural gas properties located in Texas on December 28, 2012.

3

PART II

Item 5. Market for Registrant’s Common Equity, Related Unitholder Matters and Issuer Purchases of Equity Securities.

Our Common Units trade on the NASDAQ Global Select Market under the symbol “BBEP.” As of December 31, 2012, based upon information received from our transfer agent and brokers and nominees, we had approximately 61,000 common unitholders of record.

The following table sets forth high and low sales prices per Common Unit and cash distributions to common unitholders for the periods indicated. The last reported sales price for our Common Units on February 27, 2013 was $19.60 per unit.

| Price Range | Cash Distribution | Date | ||||||||||||

| Period | High | Low | Per Common Unit | Paid | ||||||||||

| First Quarter 2011 | $ | 23.14 | $ | 19.50 | $ | 0.4175 | 5/13/2011 | |||||||

| Second Quarter 2011 | 22.69 | 19.01 | 0.4225 | 8/12/2011 | ||||||||||

| Third Quarter 2011 | 20.00 | 15.00 | 0.4350 | 11/14/2011 | ||||||||||

| Fourth Quarter 2011 | 19.17 | 15.75 | 0.4500 | 2/14/2012 | ||||||||||

| First Quarter 2012 | 20.19 | 18.65 | 0.4550 | 5/14/2012 | ||||||||||

| Second Quarter 2012 | 19.20 | 16.06 | 0.4600 | 8/14/2012 | ||||||||||

| Third Quarter 2012 | 19.85 | 16.51 | 0.4650 | 11/14/2012 | ||||||||||

| Fourth Quarter 2012 | 20.47 | 16.90 | 0.4700 | 2/14/2013 | ||||||||||

We intend to make cash distributions to unitholders on a quarterly basis, although there is no assurance as to future cash distributions since they are dependent upon future earnings, cash flows, capital requirements, financial condition and other factors. Our credit agreement restricts us from making cash distributions unless, after giving effect to such distribution, we remain in compliance with all terms and conditions of our credit facility. See Item 7 “—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Credit Facility” and Note 10 to the consolidated financial statements in this report.

For the quarters for which we declare a distribution, distributions of available cash are made within 45 days after the end of the quarter to unitholders of record on the applicable record date. Available cash, as defined in our partnership agreement, generally is all cash on hand, including cash from borrowings, at the end of the quarter after the payment of our expenses and the establishment of reserves for future capital expenditures and operational needs.

Equity Compensation Plan Information

See Part III—Item 12 “—Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters” for information regarding securities authorized for issuance under equity compensation plans.

Unregistered Sales of Equity Securities and Use of Proceeds

The information required by this item is included in our Current Report on Form 8-K filed on November 27, 2012. See also Note 15 of the consolidated financial statements included in this report.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers

There were no purchases of our Common Units by us or any affiliated purchasers during the fourth quarter of 2012.

4

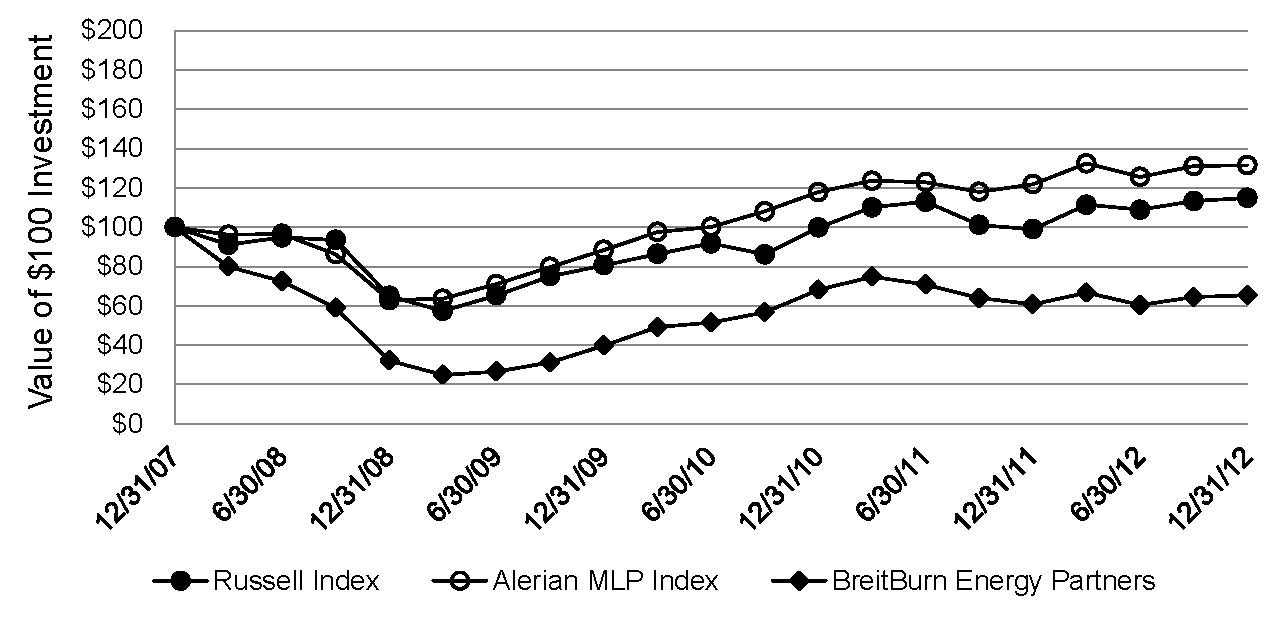

Common Unit Performance Graph

The graph below compares our cumulative total unitholder return on our Common Units over the past five years, with the cumulative total returns over the same period of the Russell 2000 index and the Alerian MLP index. The graph assumes that the value of the investment in our Common Units, in the Russell 2000 index and in the Alerian MLP index was $100 on December 31, 2007. Cumulative return is computed assuming reinvestment of dividends.

Comparison of Cumulative Total Return among the Partnership, the Russell 2000 Index and the Alerian MLP Index

The information in this report appearing under the heading “Common Unit Performance Graph” is being furnished pursuant to Item 2.01(e) of Regulation S-K and shall not be deemed to be “soliciting material” or to be “filed” with the SEC or subject to Regulation 14A or 14C, other than as provided in Item 2.01(e) of Regulation S-K, or to the liabilities of Section 18 of the Securities Exchange Act of 1934, as amended.

5

Item 6. Selected Financial Data.

Set forth below is selected historical consolidated financial data for the past five years.

The selected consolidated financial data presented is derived from our audited financial statements. In 2008, we acquired Provident’s interest in BreitBurn Management, BreitBurn Corporation contributed its interest in BreitBurn Management to us, and BreitBurn Management contributed its interest in the General Partner to us, resulting in BreitBurn Management and the General Partner becoming our wholly owned subsidiaries. In 2009, we completed the sale of the Lazy JL field for $23 million in cash. In 2011, we completed the Greasewood Acquisition on July 28, 2011 for approximately $57 million and the Cabot Acquisition on October 6, 2011 for approximately $281 million. In 2012, we completed the NiMin Acquisition on June 28, 2012 for approximately $95 million, the Element and CrownRock acquisitions on July 2, 2012 for approximately $148 million and $70 million, respectively, the AEO Acquisition on November 30, 2012 for approximately $38 million in cash and approximately 3 million Common Units, and the CrownRock II and Lynden acquisitions on December 28, 2012 for approximately $167 million and approximately $25 million, respectively. See Note 4 to the consolidated financial statements in this report for further details about our 2011 and 2012 acquisitions. Effective April 1, 2012, our ownership interest in properties at two California fields decreased from approximately 95% to approximately 62%. See Note 16 to the consolidated financial statements in this report.

You should read the following selected financial data in conjunction with Part II—Item 7 “—Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes in this report.

The selected financial data table presents a non-GAAP financial measure, “Adjusted EBITDA,” which we use in our business. This measure is not calculated or presented in accordance with generally accepted accounting principles (“GAAP”). We reconcile this measure to the most directly comparable financial measure calculated and presented in accordance with GAAP.

We believe the presentation of Adjusted EBITDA provides useful information to investors to evaluate the operations of our business excluding certain items and for the reasons set forth below. Adjusted EBITDA should not be considered an alternative to net income, operating income, cash flow from operating activities or any other measure of financial performance presented in accordance with GAAP. Our Adjusted EBITDA may not be comparable to similarly titled measures of another company because all companies may not calculate Adjusted EBITDA in the same manner.

We use Adjusted EBITDA to assess:

| • | the financial performance of our assets, without regard to financing methods, capital structure or historical cost basis; |

| • | our operating performance and return on capital as compared to those of other companies in our industry, without regard to financing or capital structure; |

| • | the viability of acquisitions and capital expenditure projects and the overall rates of return on alternative investment opportunities; and |

| • | the ability of our assets to generate cash sufficient to pay interest costs and support our indebtedness. |

6

Selected Financial Data

| Year Ended December 31, | ||||||||||||||||||||

| Thousands of dollars, except per unit amounts | 2012 | 2011 | 2010 | 2009 | 2008 | |||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||

| Oil, natural gas and natural gas liquid sales | $ | 413,867 | $ | 394,393 | $ | 317,738 | $ | 254,917 | $ | 467,381 | ||||||||||

| Gain (loss) on commodity derivative instruments, net | 5,580 | 81,667 | 35,112 | (51,437 | ) | 332,102 | ||||||||||||||

| Other revenue, net | 3,548 | 4,310 | 2,498 | 1,382 | 2,920 | |||||||||||||||

| Total revenue | 422,995 | 480,370 | 355,348 | 204,862 | 802,403 | |||||||||||||||

| Operating income (loss) | 21,700 | 153,809 | 63,743 | (82,811 | ) | 429,354 | ||||||||||||||

| Net income (loss) | (40,739 | ) | 110,698 | 34,913 | (107,257 | ) | 378,424 | |||||||||||||

| Less: Net income attributable to noncontrolling interest | (62 | ) | (201 | ) | (162 | ) | (33 | ) | (188 | ) | ||||||||||

| Net income (loss) attributable to the partnership | $ | (40,801 | ) | $ | 110,497 | $ | 34,751 | $ | (107,290 | ) | $ | 378,236 | ||||||||

| Basic net income (loss) per unit | $ | (0.56 | ) | $ | 1.80 | $ | 0.61 | $ | (2.03 | ) | $ | 6.29 | ||||||||

| Diluted net income (loss) per unit | $ | (0.56 | ) | $ | 1.79 | $ | 0.61 | $ | (2.03 | ) | $ | 6.28 | ||||||||

| Cash Flow Data: | ||||||||||||||||||||

| Net cash provided by operating activities | $ | 191,782 | $ | 128,543 | $ | 182,022 | $ | 224,358 | $ | 226,696 | ||||||||||

| Net cash used in investing activities | (697,159 | ) | (414,573 | ) | (68,286 | ) | (6,229 | ) | (141,039 | ) | ||||||||||

| Net cash provided by (used in) financing activities | 504,556 | 287,728 | (115,872 | ) | (214,909 | ) | (89,040 | ) | ||||||||||||

| Balance Sheet Data (at period end): | ||||||||||||||||||||

| Cash | $ | 4,507 | $ | 5,328 | $ | 3,630 | $ | 5,766 | $ | 2,546 | ||||||||||

| Other current assets | 109,158 | 167,492 | 121,674 | 136,675 | 138,020 | |||||||||||||||

| Net property, plant and equipment | 2,711,893 | 2,072,759 | 1,722,295 | 1,741,089 | 1,840,341 | |||||||||||||||

| Other assets | 89,936 | 85,270 | 82,568 | 87,499 | 235,927 | |||||||||||||||

| Total assets | $ | 2,915,494 | $ | 2,330,849 | $ | 1,930,167 | $ | 1,971,029 | $ | 2,216,834 | ||||||||||

| Current liabilities | 115,240 | 89,889 | 101,317 | 91,890 | 79,990 | |||||||||||||||

| Long-term debt | 1,100,696 | 820,613 | 528,116 | 559,000 | 736,000 | |||||||||||||||

| Other long-term liabilities | 110,022 | 93,133 | 91,477 | 91,338 | 47,413 | |||||||||||||||

| Partners' equity | 1,589,536 | 1,326,764 | 1,208,803 | 1,228,373 | 1,352,892 | |||||||||||||||

| Noncontrolling interest | — | 450 | 454 | 428 | 539 | |||||||||||||||

| Total liabilities and partners' equity | $ | 2,915,494 | $ | 2,330,849 | $ | 1,930,167 | $ | 1,971,029 | $ | 2,216,834 | ||||||||||

| Cash dividends declared per unit outstanding: | $ | 1.8300 | $ | 1.6875 | $ | 1.1475 | $ | 0.5200 | $ | 1.9925 | ||||||||||

7

The following table presents a reconciliation of Adjusted EBITDA to net income (loss) attributable to the partnership, our most directly comparable GAAP financial performance measure, for each of the periods indicated.

| Year Ended December 31, | ||||||||||||||||||||

| Thousands of dollars | 2012 | 2011 | 2010 | 2009 | 2008 | |||||||||||||||

| Reconciliation of consolidated net income (loss) to Adjusted EBITDA: | ||||||||||||||||||||

| Net income (loss) attributable to the partnership | $ | (40,801 | ) | $ | 110,497 | $ | 34,751 | $ | (107,290 | ) | $ | 378,236 | ||||||||

| Gain (loss) on commodity derivative instruments (a) | (5,580 | ) | (81,667 | ) | (35,112 | ) | 51,437 | (332,102 | ) | |||||||||||

| Commodity derivative instrument settlements (b)(c)(d) | 87,605 | (16,067 | ) | 74,825 | 167,683 | (55,946 | ) | |||||||||||||

| Depletion, depreciation and amortization (e) | 149,565 | 107,503 | 102,758 | 106,843 | 179,933 | |||||||||||||||

| Write-down of crude oil inventory | — | — | — | — | 1,172 | |||||||||||||||

| Interest expense and other financing costs | 61,206 | 39,165 | 24,552 | 18,827 | 29,147 | |||||||||||||||

| Loss on interest rate swaps (f) | 1,101 | 2,777 | 4,490 | 7,246 | 20,035 | |||||||||||||||

| Settlement payments (receipts) on terminated derivatives | — | 36,779 | — | (70,587 | ) | — | ||||||||||||||

| (Gain) loss on sale of assets | 486 | (111 | ) | 14 | 5,965 | — | ||||||||||||||

| Income tax expense (benefit) | 84 | 1,188 | (204 | ) | (1,528 | ) | 1,939 | |||||||||||||

| Amortization of intangibles | — | — | 495 | 2,771 | 3,131 | |||||||||||||||

| Non-cash unit based compensation | 22,184 | 22,002 | 20,331 | 13,619 | 7,481 | |||||||||||||||

| Adjusted EBITDA | $ | 275,850 | $ | 222,066 | $ | 226,900 | $ | 194,986 | $ | 233,026 | ||||||||||

| (a) The Partnership enters into certain derivative instrument contracts such as put options that require the payment of premiums at contract inception. Gain (loss) on commodity derivative instruments includes the reduction of premium value for derivative instruments over time. The Partnership’s calculation of adjusted EBITDA does not include premiums paid for derivative instruments at contract inception as these payments pertain to future contract settlement periods. | ||||||||||||||||||||

| (b) Includes net cash settlements on derivative instruments: | ||||||||||||||||||||

| - Crude oil settlements received (paid) of: | $ | 3,855 | $ | (70,398 | ) | $ | 11,252 | $ | 66,176 | $ | (35,146 | ) | ||||||||

| - Natural gas settlements received (paid) of: | $ | 83,750 | $ | 54,331 | $ | 63,573 | $ | 101,507 | $ | (20,800 | ) | |||||||||

| (c) Includes premiums deferred and paid at the time of derivative contract settlements each period of: | $ | — | $ | — | $ | 1,820 | $ | 1,116 | $ | 154 | ||||||||||

| (d) Excludes premiums paid at contract inception related to those derivative contracts that settled during the periods of: | $ | 859 | $ | — | $ | — | $ | — | $ | — | ||||||||||

| (e) Includes impairments and price-related depletion, depreciation and amortization expense adjustments of: | $ | 12,313 | $ | 648 | $ | 6,286 | $ | — | $ | 86,385 | ||||||||||

| (f) Includes settlements paid on interest rate derivatives of: | $ | 5,469 | $ | 3,257 | $ | 11,087 | $ | 13,115 | $ | 2,721 | ||||||||||

8

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis should be read in conjunction with the “Selected Financial Data” and the financial statements and related notes included elsewhere in this report. The following discussion contains forward-looking statements that reflect our future plans, estimates, beliefs and expected performance. The forward-looking statements are dependent upon events, risks and uncertainties that may be outside our control. Our actual results could differ materially from those discussed in these forward-looking statements. Factors that could cause or contribute to such differences are discussed in “Risk Factors” contained in Part I—Item 1A of this report. In light of these risks, uncertainties and assumptions, the forward-looking events discussed may not occur. See “Cautionary Statement Regarding Forward-Looking Information” in the front of this report.

Executive Overview

We are an independent oil and gas partnership focused on the acquisition, exploitation and development of oil and gas properties in the United States. Our objective is to manage our oil and gas producing properties for the purpose of generating cash flow and making distributions to our unitholders. Our assets consist primarily of producing and non-producing crude oil and natural gas reserves located primarily in the Antrim Shale and other non-Antrim formations in Michigan, the Evanston Green River, Wind River, Big Horn and Powder River Basins in Wyoming, the Los Angeles and San Joaquin Basins in California, the Permian Basin in Texas, the Sunniland Trend in Florida and the New Albany Shale in Indiana and Kentucky.

Our core investment strategy includes the following principles:

| • | acquire long-lived assets with low-risk exploitation and development opportunities; |

| • | use our technical expertise and state-of-the-art technologies to identify and implement successful exploitation techniques to optimize reserve recovery; |

| • | reduce cash flow volatility through commodity price and interest rate derivatives; and |

| • | maximize asset value and cash flow stability through operating and technical expertise. |

2012 Acquisitions

In June 2012, we completed the NiMin Acquisition, to acquire oil properties located in Park County in the Big Horn Basin of Wyoming for approximately $95 million in cash. The properties are 100% oil.

In July 2012, we completed the acquisitions of oil and natural gas properties in the Permian Basin in Texas from Element and CrownRock for approximately $148 million and $70 million in cash, respectively. In December 2012, we completed the acquisitions of additional oil and natural gas properties in the Permian Basin in Texas from CrownRock, Lynden and Piedra for approximately $167 million, $25 million and $10 million, respectively. The Permian Basin properties were approximately 79% oil as of December 31, 2012.

In November 2012, we completed the AEO Acquisition to acquire principally oil properties located in the Belridge Field in Kern County, California for approximately $38 million in cash and approximately 3 million Common Units valued at $56 million. The properties were approximately 85% oil as of December 31, 2012

During 2012, we completed other smaller acquisitions of oil and natural gas properties located in California and Michigan. In the aggregate, we paid approximately $9.6 million in total consideration for these properties.

We used borrowings under our credit facility to fund the cash portion of our 2012 acquisitions.

9

2012 Highlights

In 2012, we paid cash distributions to unitholders totaling $127.7 million. On February 14, 2013, we paid a cash distribution to unitholders of $39.8 million for the fourth quarter of 2012. We increased our quarterly cash distributions from $0.4500 per Common Unit for the fourth quarter of 2011 to $0.4700 per Common Unit for the fourth quarter of 2012.

In 2012, our oil and natural gas capital expenditures, including capitalized engineering costs and excluding acquisitions, totaled approximately $153 million, compared with approximately $75 million in 2011. We spent approximately $47 million in California, $46 million in Florida, $32 million in Wyoming, $16 million in Texas and $12 million in Michigan, Indiana and Kentucky. We drilled and completed 11 new wells, 27 recompletions and six workovers in Michigan and Indiana. We drilled and completed 20 new wells, 20 workovers and six recompletions in Wyoming. We drilled and completed 20 new wells, 14 workovers and one recompletion in California, 18 new wells in Texas and four new wells in Florida. Primarily as a result of our 2012 acquisitions and our capital spending, our 2012 production was 8,318 MMBoe, which was 18% higher than our 2011 production.

In January 2012, we and BreitBurn Finance Corporation, and certain of our subsidiaries as guarantors, issued $250 million in aggregate principal amount of 7.875% Senior Notes due 2022 (the “Initial Notes”) at a price of 99.154%. We received net proceeds of approximately $242.3 million and used the proceeds to reduce borrowings under our credit facility.

In February 2012, we sold 9.2 million Common Units at a price to the public of $18.80, resulting in proceeds net of underwriting discounts and estimated offering expenses of $166.0 million, which we used to reduce borrowings under our credit facility.

In May 2012, we entered into the Fifth Amendment to our $1.5 billion bank credit facility (the “Second Amended and Restated Credit Agreement”), which increased the permitted amount of senior unsecured notes we may issue from $700 million to $1 billion.

In September 2012, we sold 11.5 million of our Common Units at a price to the public of $18.51 per Common Unit, resulting in proceeds net of underwriting discount and offering expenses of $204.1 million, which we used to reduce borrowings under our credit facility.

In September 2012, we issued an additional $200 million aggregate principal amount of our 7.875% Senior Notes due 2022 (the “Additional Notes”) (the Additional Notes and the Initial Notes collectively referred to as the “2022 Senior Notes”). The Additional Notes were issued at a premium of 103.500%, or $207.0 million. We used the net proceeds from the Additional Notes offering of approximately $202.8 million, after financing fees and expenses, to reduce borrowings under our credit facility.

In October 2012, we entered into the Sixth Amendment to the Second Amended and Restated Credit Agreement (the “Sixth Amendment”), which increased our borrowing base to $1 billion and increased our total commitments from existing lenders to $900 million. The Sixth Amendment also provided us with the ability to increase our total commitments up to the $1 billion borrowing base upon lender approval.

In December 2012, we filed a registration statement for the offer to exchange the 2022 Senior Notes for substantially identical notes that are registered under the Securities Act of 1933, as amended. On December 27, 2012, the exchange registration statement became effective, and we commenced the exchange offer, which was completed on February 7, 2013.

Outlook

In 2013, our crude oil and natural gas capital spending program, including capitalized engineering costs and excluding acquisitions, is expected to be approximately $261 million, compared with approximately $153 million in 2012. In 2013, we anticipate spending approximately 84% principally on oil projects in California, Florida and Texas and approximately 16% principally on oil projects in Michigan, Wyoming, Indiana and Kentucky. We anticipate 89% of

10

our total capital spending will be focused on drilling and rate-generating projects that are designed to increase or add to production or reserves. Without considering potential acquisitions, we expect our 2013 production to be approximately 9.8 MMBoe.

Commodity hedging remains an important part of our strategy to reduce cash flow volatility. We use swaps, collars and options for managing risk relating to commodity prices. As of February 27, 2013, we had hedged approximately 77% of our expected 2013 production. For 2013, we had 11,038 Bbl/d of oil and 58,100 MMBtu/d of natural gas hedged at average prices of approximately $92.93 and $5.87, respectively. For 2014, we had 11,114 Bbl/d of oil and 52,100 MMBtu/d of natural gas hedged at average prices of approximately $95.17 and $4.99, respectively. For 2015, we had 9,489 Bbl/d of oil and 52,200 MMBtu/d of natural gas hedged at average prices of approximately $95.61 and $5.00, respectively. For 2016, we had 5,911 Bbl/d of oil and 25,200 MMBtu/d of natural gas hedged at average prices of approximately $93.15 and $4.30, respectively. For 2017, we had 1,769 Bbl/d of oil and 5,571 MMBtu/d hedged at average prices of approximately $88.20 and $4.51, respectively.

Consistent with our long-term business strategy, we intend to continue to actively pursue oil and natural gas acquisition opportunities in 2013.

Operational Focus

We use a variety of financial and operational measures to assess our performance. Among these measures are the following: volumes of oil and natural gas produced, reserve replacement, realized prices, operating expenses and general and administrative expenses (”G&A”).

As of December 31, 2012, our total estimated proved reserves were 149.4 MMBoe, of which approximately 53% was crude oil and 47% was natural gas. As of December 31, 2011, our total estimated proved reserves were 151.1 MMBoe, of which approximately 35% was crude oil and 65% was natural gas.

Our total estimated reserve additions in 2012 from acquisitions of 33.7 MMBoe were offset by reserve revisions of 27.1 MMBoe and 8.3 MMBoe of production, resulting in a net decrease of 1.7 MMBoe from 2011. The decrease in 2012 was primarily the result of a 30.9MMBoe (185.6 Bcf) decrease in natural gas reserves driven primarily by a decrease in natural gas prices. Price-related reserve revisions were partially offset by drilling, recompletions, workovers, addition of new drilling locations and revised estimates of existing reserves. The unweighted average first-day-of-the-month crude oil and natural gas prices used to determine our total estimated proved reserves as of December 31, 2012 were $94.71 per Bbl of oil and $2.76 per MMBtu of natural gas, compared to $95.97 per Bbl of oil and $4.12 per MMBtu of gas in 2011. The unweighted average first-day-of-the-month crude oil and natural gas prices used to determine our total estimated proved reserves as of December 31, 2010 were $79.40 per Bbl of oil $4.38 per MMBtu of gas.

Of our total estimated proved reserves as of December 31, 2012, 35% were located in Michigan, 26% in Wyoming, 17% in California, 15% in Texas and 7% in Florida, with less than 1% in Indiana and Kentucky. On a net production basis, we operated approximately 84% of our production in 2012.

Our revenues and net income are sensitive to oil and natural gas prices. Our operating expenses are highly correlated to oil prices, and as oil prices rise and fall, our operating expenses will directionally rise and fall. Significant factors that will impact near-term commodity prices include global demand for oil and natural gas, political developments in oil producing countries, including, without limitation, the extent to which members of the OPEC and other oil exporting nations are able to manage oil supply through export quotas and variations in key North American natural gas and refined products supply and demand indicators.

In 2012, the NYMEX WTI spot price averaged approximately $94 per Bbl, compared with approximately $95 per Bbl a year earlier. In 2012, crude oil prices ranged from a monthly average low of $82 per Bbl in June to a monthly average high of $106 per Bbl in March. In 2011, prices ranged from a monthly average low of $86 per Bbl in September to a monthly average high of $110 per Bbl in April. In 2013 to date, the NYMEX WTI spot price averaged $95 per Bbl.

Prices for natural gas have historically fluctuated widely and in many markets are aligned both with supply and demand conditions in their respective regional markets and with the overall U.S. market. Natural gas prices are also

11

typically higher during the winter period when demand for heating is greatest in the U.S. Since January 2010, monthly average natural gas spot prices at Henry Hub ranged from a low of $1.95 per MMBtu in April 2012 to a high of $5.83 per MMBtu in January 2010. During 2012, the natural gas spot price at Henry Hub ranged from a low of $1.82 per MMBtu to a high of $3.77 per MMBtu, with the monthly average ranging from a low of $1.95 per MMBtu in April to a high of $3.54 per MMBtu in November, and averaged approximately $2.75 per MMBtu for the year. During 2011, the natural gas spot price at Henry Hub ranged from a low of $2.84 per MMBtu to a high of $4.92 per MMBtu, and averaged approximately $4.00 per MMBtu. In 2013 to date, the natural gas spot price at Henry Hub averaged approximately $3.32 per MMBtu.

Excluding the effect of derivatives, our average realized oil and NGL price for 2012 decreased $0.15 per Boe to $89.77 per Boe as compared to $89.92 per Boe in 2011. Excluding the effect of derivatives, our realized natural gas price for 2012 decreased $1.18 per Mcf to $3.00 per Mcf as compared to $4.18 per Mcf in 2011.

While our commodity price risk management program is intended to reduce our exposure to commodity prices and assist with stabilizing cash flow and distributions, to the extent we have hedged a significant portion of our expected production and the cost for goods and services increases, our margins would be adversely affected.

In evaluating our production operations, we frequently monitor and assess our operating and general and administrative expenses per Boe produced. These measures allow us to better evaluate our operating efficiency and are used in reviewing the economic feasibility of a potential acquisition or development project.

Operating expenses are the costs incurred in the operation of producing properties. Expenses for utilities, direct labor, water injection and disposal, production taxes and materials and supplies comprise the most significant portion of our operating expenses. A majority of our operating cost components are variable and increase or decrease along with our levels of production. For example, we incur power costs in connection with various production related activities such as pumping to recover oil and gas, separation and treatment of water produced in connection with our oil and gas production, and re-injection of water produced into the oil producing formation to maintain reservoir pressure. Although these costs typically vary with production volumes, they are driven not only by volumes of oil and gas produced but also volumes of water produced. Consequently, fields that have a high percentage of water production relative to oil and gas production, also known as a high water cut, will experience higher levels of power costs for each Boe produced. Certain items, however, such as direct labor and materials and supplies, generally remain relatively fixed across broad production volume ranges but can fluctuate depending on activities performed during a specific period. For instance, repairs to our pumping equipment or surface facilities result in increased expenses in periods during which they are performed. Our operating expenses are highly correlated to oil prices, and we experience upward or downward pressure on material and service costs depending on how oil prices change. These costs include specific expenditures such as lease fuel, electricity, drilling services and severance and property taxes. Lease operating expenses, including processing fees, were $19.15 per Boe in 2012 and $19.39 per Boe in 2011. The decrease in per Boe lease operating expenses was primarily due to lower operating costs from our acquisitions in Wyoming and Texas.

Production taxes vary by state. All states in which we operate impose ad valorem taxes on our oil and gas properties. Various states regulate the drilling for, and the production, gathering and sale of, oil and natural gas, including imposing severance taxes and requirements for obtaining drilling permits. Currently, Wyoming, Michigan, Indiana, Kentucky and Florida impose severance taxes on oil and gas producers at rates ranging from 1% to 9% of the value of the gross product extracted. Wyoming wells that reside on Indian or federal land are subject to an additional tax of 8.5%. California does not currently impose a severance tax; rather it imposes an ad valorem tax based in large part on the value of the mineral interests in place. See Part I—Item 1A “—Risk Factors” — “Risks Related to Our Business — We are subject to complex federal, state, local and other laws and regulations that could adversely affect the cost, manner or feasibility of conducting our operations” in this report.

G&A, excluding unit based compensation, was $4.00 per Boe in 2012 and $4.45 per Boe in 2011. The decrease in per Boe G&A, excluding unit based compensation, was primarily due to additional production from our 2012 acquisitions.

12

BreitBurn Management

BreitBurn Management operates our assets and performs other administrative services for us such as accounting, corporate development, finance, land administration, legal and engineering. All of our employees, including our executives, are employees of BreitBurn Management. BreitBurn Management also operates the assets of PCEC, our Predecessor. In addition to a monthly fee for indirect expenses, BreitBurn Management charges PCEC for all direct expenses including incentive plan costs and direct payroll and administrative costs related to PCEC’s properties and operations.

On January 6, 2012, Pacific Coast Oil Trust (the “Trust”), which was formed by PCEC, filed a registration statement on Form S-1 with the SEC in connection with an initial public offering by the Trust. On May 8, 2012, the Trust completed its initial public offering (the “Trust IPO”). We have no direct or indirect ownership interest in PCEC or the Trust. As part of the Trust IPO, PCEC conveyed net profits interests in its oil and natural gas production from certain of its properties to the Trust in exchange for Trust units. PCEC’s assets consist primarily of producing and non-producing crude oil reserves located in Santa Barbara, Los Angeles and Orange Counties in California, including certain interests in the East Coyote and Sawtelle Fields. Prior to the Trust IPO, PCEC operated the East Coyote and Sawtelle Fields for the benefit of itself and us, who owned the non-operated interests in the East Coyote and Sawtelle Fields. PCEC owned an average working interest of approximately 5% in the two fields and held a reversionary interest in both fields.

Effective April 1, 2012 and pursuant to an agreement with us, PCEC’s ownership interest in these properties was increased. As a result of that agreement, our average working interest in the properties decreased from approximately 95% to approximately 62%.

On May 8, 2012, BreitBurn Management entered into the Third Amended and Restated Administrative Services Agreement with PCEC, pursuant to which the parties agreed to increase the monthly fee charged by BreitBurn Management to PCEC for indirect costs.

Prior to the Trust IPO, the 2012 monthly fee charged by BreitBurn Management to PCEC for indirect costs was set at $571,000, and the two parties agreed to increase that monthly fee to $700,000. The new monthly fee will be in effect from April 1, 2012 through August 31, 2014 and will be redetermined biannually thereafter. In connection with the Trust IPO, we also amended the Omnibus Agreement with PCEC to remove our right of first offer with respect to the sale of assets by PCEC.

For information on potential conflicts between us and PCEC, see Part I—Item 1A “—Risk Factors”— “Risks Related to Our Structure — Certain of the directors and officers of our General Partner, including our Chief Executive Officer, our President and other members of our senior management, own interests in PCEC, which is managed by our subsidiary, BreitBurn Management. Conflicts of interest may arise between PCEC, on the one hand, and us and our unitholders, on the other hand. Our partnership agreement limits the remedies available to you in the event you have a claim relating to conflicts of interest.”

See Note 6 to the consolidated financial statements in this report for more information regarding our relationship with BreitBurn Management and PCEC.

13

Results of Operations

The table below summarizes certain of the results of operations and period-to-period comparisons attributable to our operations for the periods indicated. These results are presented for illustrative purposes only and are not indicative of our future results. The data reflect our results as they are presented in our consolidated financial statements.

| Year Ended December 31, | Increase / decrease % | |||||||||||||||||

| Thousands of dollars, except as indicated | 2012 | 2011 | 2010 | 2012-2011 | 2011-2010 | |||||||||||||

| Total production (MBoe) (a) | 8,318 | 7,037 | 6,699 | 18 | % | 5 | % | |||||||||||

| Oil and NGL (MBoe) | 3,652 | 3,255 | 3,157 | 12 | % | 3 | % | |||||||||||

| Natural gas (MMcf) | 27,997 | 22,697 | 21,251 | 23 | % | 7 | % | |||||||||||

| Average daily production (Boe/d) | 22,726 | 19,281 | 18,354 | 18 | % | 5 | % | |||||||||||

| Sales volumes (MBoe) | 8,334 | 7,106 | 6,663 | 17 | % | 7 | % | |||||||||||

| Average realized sales price (per Boe) (b) (c) | $ | 49.57 | $ | 55.41 | $ | 47.71 | (11 | )% | 16 | % | ||||||||

| Oil and NGL (per Boe) (c) | 89.77 | 89.92 | 70.71 | — | 27 | % | ||||||||||||

| Natural gas (per Mcf) | 3.00 | 4.18 | 4.57 | (28 | )% | (9 | )% | |||||||||||

| Oil, natural gas and NGL sales (d) | $ | 413,867 | $ | 394,393 | $ | 317,738 | 5 | % | 24 | % | ||||||||

| Gain on commodity derivative instruments (e) | 5,580 | 81,667 | 35,112 | (93 | )% | 133 | % | |||||||||||

| Other revenues, net | 3,548 | 4,310 | 2,498 | (18 | )% | 73 | % | |||||||||||

| Total revenues | 422,995 | 480,370 | 355,348 | (12 | )% | 35 | % | |||||||||||

| Lease operating expenses including processing fees | 159,289 | 136,441 | 122,512 | 17 | % | 11 | % | |||||||||||

| Production and property taxes (f) | 33,634 | 26,599 | 20,510 | 26 | % | 30 | % | |||||||||||

| Total lease operating expenses | 192,923 | 157,787 | 138,964 | 22 | % | 14 | % | |||||||||||

| Purchases and other operating costs | 1,577 | 961 | 328 | 64 | % | 193 | % | |||||||||||

| Change in inventory | 1,279 | 1,968 | (825 | ) | (35 | )% | n/a | |||||||||||

| Total operating costs | $ | 195,779 | $ | 165,969 | $ | 142,525 | 18 | % | 16 | % | ||||||||

| Lease operating expenses pre-taxes per Boe (g) | 19.15 | 19.39 | 18.29 | (1 | )% | 6 | % | |||||||||||

| Production and property taxes per Boe | 4.04 | 3.78 | 3.06 | 7 | % | 23 | % | |||||||||||

| Total lease operating expenses per Boe | 23.19 | 23.17 | 21.35 | — | % | 9 | % | |||||||||||

| Depletion, depreciation and amortization | $ | 149,565 | $ | 107,503 | $ | 102,758 | 39 | % | 5 | % | ||||||||

| (a) Natural gas is converted on the basis of six Mcf of gas per one Bbl of oil equivalent. This ratio reflects an energy content equivalency and not a price or revenue equivalency. Given commodity price disparities, the price for a Bbl of oil equivalent for natural gas is significantly less than the price for a Bbl of oil. | ||||||||||||||||||

| (b) Excludes the effect of commodity derivative settlements. | ||||||||||||||||||

| (c) Includes the per Boe price effect of crude oil purchases. For 2010, amount excludes the per Boe price effect of amortization of an intangible asset related to crude oil sales contracts. | ||||||||||||||||||

| (d) 2010 amount includes $495 of amortization of an intangible asset related to crude oil sales contracts. | ||||||||||||||||||

| (e) Includes the effects of the early termination of commodity derivative contracts terminated in 2011 for a cost of $36,779. | ||||||||||||||||||

| (f) Includes ad valorem and severance taxes. | ||||||||||||||||||

| (g) Includes lease operating expenses, district expenses, transportation expenses and processing fees. | ||||||||||||||||||

14

Comparison of Results of Operations for the Years Ended December 31, 2012, 2011 and 2010

The variances in our results of operations were due to the following components:

Production

For the year ended December 31, 2012 compared to the year ended December 31, 2011, production volumes increased by 1,281 MBoe, or 18%, primarily due to a 1,112 MBoe increase from a full year of production from our southwest Wyoming properties acquired in October 2011, a 155 MBoe increase from a full year of production from our eastern Wyoming properties acquired in July 2011, 315 MBoe from our Permian Basin properties acquired in July and December 2012, 92 MBbl of oil from our central Wyoming properties acquired in June 2012, 28 MBoe from our properties in the San Joaquin Basin in California acquired in November 2012 and 42 MBbl higher Florida production from new wells partially offset by 411 MBoe lower Michigan production due to lower natural gas prices and natural field declines. The remaining decrease was primarily due to natural field declines at our legacy Wyoming properties, and a reduction in our ownership interest in two California fields, partially offset by higher production from a field in California due to additional drilling. In 2012, natural gas, crude oil and natural gas liquids accounted for 56%, 42% and 2% of our production, respectively.

For the year ended December 31, 2011 compared to the year ended December 31, 2010, production volumes increased by 338 MBoe, or 5%, primarily due to 368 MBoe from our southwestern Wyoming properties acquired in October 2011, 88 MBoe from our eastern Wyoming properties acquired in July 2011 and 41 MBoe higher Florida production from new wells partially offset by 129 MBoe lower Michigan natural gas production due to natural field declines. In 2011, natural gas, crude oil and natural gas liquids accounted for 54%, 44% and 2% of our production, respectively.

Oil, natural gas and NGL sales

Total oil, natural gas liquids (“NGL”) and natural gas sales revenues increased $19.5 million for the year ended December 31, 2012 compared to the year ended December 31, 2011. Crude oil and NGL revenues increased $30.6 million due to higher sales volumes, primarily due to oil production from our 2012 acquisitions in Texas, California and Wyoming. Natural gas revenues decreased $11.1 million primarily due to lower natural gas prices partially offset by higher natural gas production primarily from our 2012 acquisitions in Texas. Realized prices for crude oil and NGLs, excluding the effect of derivative instruments, decreased $0.15 per Boe, or less than 1%, for the year ended December 31, 2012 compared to the year ended December 31, 2011. Realized prices for natural gas, excluding the effect of derivative instruments, decreased $1.18 per Mcf, or approximately 28%, for the year ended December 31, 2012 compared to the year ended December 31, 2011.

Total oil, NGLs and natural gas sales revenues increased $76.7 million for the year ended December 31, 2011 compared to the year ended December 31, 2010. Crude oil and NGL revenues increased $78.9 million due to higher crude oil prices and sales volumes, primarily due to oil production from our 2011 acquisitions in Wyoming. Natural gas revenues decreased $2.2 million primarily due to lower natural gas prices partially offset by higher natural gas production. Realized prices for crude oil and NGLs, excluding the effect of derivative instruments, increased $19.21 per Boe, or 27%, for the year ended December 31, 2011 compared to the year ended December 31, 2010. Realized prices for natural gas, excluding the effect of derivative instruments, decreased $0.39 per Mcf, or 9%, for the year ended December 31, 2011 compared to the year ended December 31, 2010.

Gain on commodity derivative instruments

Gain on commodity derivative instruments for the year ended December 31, 2012 was $5.6 million compared to a gain of $81.7 million for the year ended December 31, 2011. Commodity derivative instrument settlements received for the year ended December 31, 2012 were $87.6 million compared to derivative settlements paid of $16.1 million for the year ended December 31, 2011, which included $36.8 million paid to terminate commodity hedge contracts in the fourth quarter of 2011.

15

Gain on commodity derivatives instruments for the year ended December 31, 2011 was $81.7 million compared to a gain of $35.1 million the year ended December 31, 2010. Commodity derivative instrument settlements paid for the year ended December 31, 2011 were $16.1 million, which included $36.8 million paid to terminate hedge contracts in the fourth quarter of 2011. Commodity derivative instrument settlements received for the year ended December 31, 2010 were $74.8 million.

Lease operating expenses

Pre-tax lease operating expenses, including processing fees, for the year ended December 31, 2012 totaled $159.3 million, $22.8 million higher than 2011. The increase in pre-tax lease operating expenses reflects our newly acquired Wyoming and Texas properties, higher California well service costs, higher Florida fuel and utilities costs and higher transportation expenses. The increase in California well services was partially offset by lower lease operating expenses at the East Coyote and Sawtelle fields as a result of the reduction in our working interests from 95% to 62% attributable to a payout reversion that was effective April 1, 2012. On a per Boe basis, lease operating expenses were 1% lower than 2011.

Production and property taxes for the year ended December 31, 2012 totaled $33.6 million, or $4.04 per Boe, which was 7% higher per Boe than the year ended December 31, 2011. The per Boe increase in production and property taxes compared to 2011 was primarily due to higher per Boe production and property taxes on our newly acquired Permian Basin assets and an increase in per Boe Florida taxes.

Pre-tax lease operating expenses, including processing fees, for the year ended December 31, 2011 totaled $136.4 million or $19.39 per Boe, which was 6% higher per Boe than 2010. The increase was primarily attributable to an increase in crude oil prices, higher Florida production costs related to new wells and higher transportation expenses, well services, compression repairs and maintenance.

Production and property taxes for the year ended December 31, 2011 totaled $26.6 million, or $3.78 per Boe, which was 23% higher per Boe than the year ended December 31, 2010. The per Boe increase in production and property taxes compared to 2010 was primarily due to higher commodity prices in 2011.

Change in inventory

In Florida, our crude oil sales are a function of the number and size of crude oil shipments in each year and thus crude oil sales do not always coincide with volumes produced in a given year. Sales occur on average every six to eight weeks. We match production expenses with crude oil sales. Production expenses associated with unsold crude oil inventory are credited to operating costs through the change in inventory account. Production expenses are charged to operating costs through the change in inventory account when they are sold. In 2012 and 2011, the change in inventory account amounted to a charge of $1.3 million and $2.0 million, respectively, reflecting the higher amount of barrels sold than produced during the periods, compared to a credit of $0.8 million in 2010, reflecting the higher amount of barrels produced than sold during the period.

Depletion, depreciation and amortization

Depletion, depreciation and amortization (“DD&A”) expense totaled $149.6 million, or $17.98 per Boe, for the year ended December 31, 2012, compared to DD&A of $15.28 per Boe for the year ended December 31, 2011. Included in DD&A for the year ended December 31, 2012 are $12.3 million in impairments primarily related to uneconomic proved properties in Michigan, Indiana and Kentucky due to a decrease in expected future natural gas prices. Included in DD&A for the year ended December 31, 2011 are $0.6 million in impairments related to uneconomic proved properties in Michigan. Excluding the impact of impairments, DD&A per Boe for 2012 and 2011 was $16.50 and $15.18, respectively. The increase in DD&A excluding impairments was primarily due to higher DD&A rates on our newly acquired properties.

DD&A expense totaled $107.5 million, or $15.28 per Boe, for the year ended December 31, 2011, which was in line with DD&A of $15.34 per Boe for the year ended December 31, 2010. Included in DD&A for the year ended December 31, 2011 are $0.6 million in impairments related to uneconomic proved properties in Michigan. Included in DD&A for

16

the year ended December 31, 2010 are $6.3 million in impairments related to our Eastern region properties, including a $4.2 million write-down of uneconomic proved properties and a $2.1 million write-down of expired unproved lease properties. Excluding the impact of impairments, DD&A per Boe for 2011 and 2010 was $15.18 and $14.40, respectively. The increase in DD&A per Boe excluding impairments was primarily due to higher DD&A rates reflecting lower natural gas reserves as a result of a decrease in natural gas prices, and investment additions related to new wells in Florida.

General and administrative expenses

Our G&A expenses totaled $55.5 million and $53.3 million in 2012 and 2011, respectively. This included $22.2 million and $22.0 million, respectively, in unit-based compensation expense related to employee incentive plans. For 2012, G&A expenses, excluding unit-based compensation, were $33.3 million, which was $2.0 million higher than 2011. The increase was primarily due to additional activity related to our 2012 acquisitions. On a per Boe basis, G&A expenses, excluding unit-based compensation, were $4.00, a 10% decrease from the prior year.

Our G&A expenses totaled $53.3 million and $44.9 million in 2011 and 2010, respectively, including $22.0 million and $20.4 million, respectively, in unit-based compensation expense related to employee incentive plans. The increase in non-cash unit-based compensation expense was primarily due to new equity awards granted in the first quarter of 2011. For 2011, G&A expenses, excluding unit-based compensation, were $31.3 million, which was $6.8 million higher than 2010. The increase was primarily due to acquisition and integration costs related to our 2011 acquisitions, higher employee related costs and higher short-term incentive compensation expense.

Interest expense, net of amounts capitalized

Our interest expense totaled $61.2 million for the year ended December 31, 2012, net of less than $0.1 million of capitalized interest, an increase of $22.0 million from 2011. This increase in interest expense was primarily attributable to an additional $23.0 million associated with our 2022 Senior Notes and slightly higher amortization of debt issuance costs, partially offset by $1.2 million lower interest expense on our credit facility due to a lower credit facility debt balance.

Our interest expense totaled $39.2 million for the year ended December 31, 2011 net of $0.1 million of capitalized interest, an increase of $14.6 million from 2010. This increase in interest expense was primarily attributable to an additional $19.9 million in interest expense associated with our 2020 Senior Notes, partially offset by $4.8 million lower interest expense on our credit facility due to a lower credit facility debt balance and $0.7 million lower amortization of debt issuance costs.

Loss on interest rate swaps

We are subject to interest rate risk associated with loans under our credit facility that bear interest based on floating rates. See Part II-Item 7A “-Quantitative and Qualitative Disclosures About Market Risk” in this report for a discussion of our interest rate risk. Loss on interest swaps for the year ended December 31, 2012 was $1.1 million compared to a loss of $2.8 million for the year ended December 31, 2011. The higher loss in 2011 compared to 2012 reflects higher average interest rates on our swap contracts in 2011 compared to 2012.

Loss on interest swaps for the year ended December 31, 2011 was $2.8 million compared to a loss of $4.5 million for the year ended December 31, 2010. The higher loss in 2010 primarily reflects higher average interest rates on our swap contracts in 2010 compared to 2011.

Liquidity and Capital Resources

Our primary sources of liquidity are cash generated from operations, amounts available under our credit facility and cash from the issuance of unsecured long-term debt and partnership units. Historically, our primary uses of cash have been for our operating expenses, capital expenditures, cash distributions to unitholders and unit repurchase transactions. To fund certain acquisition transactions, we have also sourced the private placement markets and have issued equity as

17

partial consideration for the acquisition of oil and natural gas properties. As market conditions have permitted, we have also engaged in asset sale transactions.

Natural gas prices have fluctuated substantially in the last two years from a high monthly average Henry Hub price of $4.54 per MMBtu in June 2011 to a low of $1.95 per MMBtu in April 2012, with an average of $3.32 in 2013 to date. Henry Hub prices averaged $4.00 and $2.75 in 2011 and 2012, respectively. We have hedged more than 68% of our expected natural gas production in 2013 and 2014 at average prices of $5.87 and $4.99, respectively. As of February 27, 2013, we had approximately $77.0 million in borrowings outstanding under our credit facility and total lender commitments of $900 million. However, sustained low prices for natural gas may reduce the amounts we would otherwise have available to pay expenses, make distributions to our unitholders and service our indebtedness.

In 2013, our crude oil and natural gas capital spending program, including capitalized engineering and excluding acquisitions, is expected to be approximately $261 million.

In 2012, we spent $562.4 million on acquisitions in Texas, Wyoming and California and issued approximately 3 million Common Units.

Equity Offerings

In February 2011, we sold approximately 4.9 million Common Units at a price to the public of $21.25, resulting in proceeds net of underwriting discounts and expenses of $100 million. In February 2012, we sold 9.2 million Common Units at a price to the public of $18.80, resulting in proceeds net of underwriting discounts and estimated offering expenses of $166.0 million. In September 2012, we sold 11.5 million of our Common Units at a price to the public of $18.51 per Common Unit, resulting in proceeds, net of underwriting discount and offering expenses, of $204.1 million. In February 2013, we sold 14.95 million Common Units at a price to the public of $19.86, resulting in proceeds net of underwriting discounts and expenses of $285.0 million. We used the proceeds from these offerings to reduce borrowings under our credit facility.

Senior Notes

On October 6, 2010, we and BreitBurn Finance Corporation, and certain of our subsidiaries as guarantors, issued $305 million in aggregate principal amount of 8.625% senior notes due 2020 at a price of 98.358%. We received net proceeds of approximately $291.2 million, after deducting estimated fees and offering expenses, and used $290 million of the net proceeds to repay amounts outstanding under our credit facility.

On January 13, 2012, we and BreitBurn Finance Corporation, and certain of our subsidiaries, as guarantors, issued $250 million in aggregate principal amount of 7.875% senior notes due 2022 at a price of 99.154%. We received net proceeds of approximately $242.3 million, after deducting estimated fees and offering expenses, and used the proceeds to reduce borrowings under our credit facility.

In September 2012, we issued an additional $200 million aggregate principal amount of our 7.875% Senior Notes due 2022. These notes were offered as an addition to our existing 7.875% Senior Notes due 2022 at a premium of 103.500%. We received net proceeds of approximately $202.8 million, after deducting estimated fees and offering expenses, and used the proceeds to reduce borrowings under our credit facility.

The use of proceeds from the issuance of these senior notes to repay amounts outstanding under our credit facility increased the borrowing availability under our credit facility, which gives us additional flexibility to finance future acquisitions.

Credit Facility

As of December 31, 2011, our Second Amended and Restated Credit Agreement had a maturity date of May 9, 2016 and a borrowing base of $850 million.

18

In May 2012, we entered into the Fifth Amendment to the Second Amended and Restated Credit Agreement, which increased the permitted amount of senior unsecured notes we may issue from $700 million to $1 billion.

In October 2012, we entered into the Sixth Amendment to the Second Amended and Restated Credit Agreement, which increased our borrowing base to $1.0 billion and increased our total commitments from existing lenders to $900 million. The Sixth Amendment also provided us with the ability to increase our total commitments up to the $1 billion borrowing base upon lender approval.

We had outstanding borrowings under our credit facility of $345.0 million as of December 31, 2012 and $77.0 million as of February 27, 2013.

As of December 31, 2012, the lending group under the Second Amended and Restated Credit Agreement included 14 banks. Of the $900 million in total commitments under the credit facility, Wells Fargo Bank National Association held approximately 18.8% of the commitments. Ten banks held between 5% and 8% of the commitments, including Union Bank, N.A., Bank of Montreal, The Bank of Nova Scotia, Houston Branch, Citibank, N.A., Royal Bank of Canada, U.S. Bank National Association, Bank of Scotland plc, Barclays Bank PLC, The Royal Bank of Scotland plc and Credit Suisse AG, Cayman Islands Branch, with each of the remaining lenders holding less than 5% of the commitments. In addition to our relationships with these institutions under the credit facility, from time to time we engage in other transactions with a number of these institutions. Such institutions or their affiliates may serve as underwriter or initial purchaser of our debt and equity securities and/or serve as counterparties to our commodity and interest rate derivative agreements.

The Second Amended and Restated Credit Agreement contains customary covenants, including restrictions on our ability to: incur additional indebtedness, make certain investments, loans or advances, make distributions to our unitholders or repurchase units, make dispositions or enter into sales and leasebacks, or enter into a merger or sale of our property or assets, including the sale or transfer of interests in our subsidiaries.

The Second Amended and Restated Credit Agreement includes the restriction on our ability to make distributions unless after giving effect to such distribution, we remain in compliance with all terms and conditions of our credit facility. In addition, the Second Amended and Restated Credit Agreement requires us to maintain a leverage ratio (defined as the ratio of total debt to EBITDAX) as of the last day of each quarter, on a last twelve month basis of no more than 4.00 to 1.00 and a current ratio as of the last day of each quarter, of not less than 1.00 to 1.00. As of December 31, 2012, we were in compliance with these covenants.