Table of Contents

As filed with the Securities and Exchange Commission on March 7, 2007

Registration No. 333-140831

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

Form F-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Gafisa S.A.

(Exact name of Registrant as specified in its charter)

| Federative Republic of Brazil | 1520 | Not Applicable | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

Av. Nações Unidas No. 4777, 9th floor

São Paulo, SP, 05477-000

Federative Republic of Brazil

+55 (11) 3025 9000

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

National Corporate Research, Ltd.

225 W. 34th Street, Suite 910

New York, New York 10122

1-800-221-0102

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| Manuel Garciadiaz Davis Polk & Wardwell 450 Lexington Avenue New York, N.Y. 10017 Phone: (212) 450-4000 Fax: (212) 450-4800 | Sara Hanks Clifford Chance US LLP Phone: (212) 878-8000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, please check the following box.¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.¨

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We and the selling shareholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated March 7, 2007

PROSPECTUS

39,676,600 Common Shares

including Common Shares in the form of American Depositary Shares

We are selling American Depositary Shares, or ADSs, and the selling shareholders named in this prospectus are selling an additional ADSs. Each ADS represents two common shares. In addition, the selling shareholders are concurrently offering common shares in the Federative Republic of Brazil, or Brazil, through Brazilian underwriters using a Portuguese-language prospectus. The closings of this offering and the Brazilian offering are conditioned upon each other.

Prior to this offering, no public market existed for the ADSs. We have applied to have the ADSs listed on the New York Stock Exchange under the symbol “GFA.” Our common shares are listed on the São Paulo Stock Exchange (Bolsa de Valores de São Paulo), or the BOVESPA, under the symbol “GFSA3.” The closing price of our common shares on the BOVESPA on February 21, 2007 was R$35.30 per common share, which is equivalent to approximately US$16.97 per common share, based upon an exchange rate of R$2.0802 to US$ 1.00 reported by the Central Bank of Brazil (Banco Central do Brasil), or the Central Bank, on February 21, 2007.

This global offering will be registered with the Brazilian Securities Commission (Comissão de Valores Mobiliários), or the CVM. The CVM has not approved or disapproved of these securities or determined if this prospectus (or the Portuguese-language prospectus referred to above) is truthful or complete.

Investing in the common shares and ADSs involves risks. See “Risk Factors” beginning on page 13 of this prospectus.

| Per ADS | Total | |||||

Public offering price | US$ | US$ | ||||

Underwriting discounts | US$ | US$ | ||||

Proceeds, before expenses, to us | US$ | US$ | ||||

Proceeds, before expenses, to the selling shareholders | US$ | US$ | ||||

Merrill Lynch, Pierce, Fenner & Smith Incorporated, upon agreement with Itaú Securities Inc. and Citigroup Global Markets Inc., may also purchase up to 5,951,490 additional common shares in the form of ADSs from one of the selling shareholders, minus the number of common shares sold by one of the other selling shareholders pursuant to the Brazilian underwriters’ over-allotment option referred to in this prospectus, within 30 days from the date of this prospectus to cover overallotments, if any, in the international offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The ADSs will be ready for delivery on or about , 2007.

| Merrill Lynch & Co. | Banco Itaú BBA | Citigroup |

| HSBC | UBS Investment Bank |

The date of this prospectus is , 2007.

Table of Contents

| Page | ||

| 1 | ||

| 13 | ||

| 25 | ||

| 26 | ||

| 28 | ||

| 29 | ||

| 33 | ||

| 34 | ||

| 36 | ||

| 38 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 43 | |

| 72 | ||

| 84 | ||

| 115 | ||

| 125 | ||

| 127 | ||

| 128 | ||

| 141 | ||

| 150 | ||

| 155 | ||

| 162 | ||

| 167 | ||

| 168 | ||

| 168 | ||

| 168 | ||

| 169 | ||

| F-1 |

In this prospectus, the terms “Gafisa,” “we,” “us,” “our” and “our company” mean Gafisa S.A. and its consolidated subsidiaries, unless otherwise indicated. The term “selling shareholders” means Brazil Development Equity Investments, LLC, Emerging Markets Capital Investments, LLC, EIP Brazil Holdings Godo Kaisha, EI Fund II Brazil Godo Kaisha, EIP Brazil Holdings, LLC, Mr. Renato de Albuquerque and Mr. Nuno Luís de Carvalho Lopes Alves.

You should rely only on the information contained in this prospectus. We, the selling shareholders and the international underwriters have not authorized any other person to provide you with different or additional information. If anyone provides you with different or additional information, you should not rely on it. Each of Gafisa, the selling shareholders and the international underwriters is not making an offer to sell the common shares or ADSs in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus, regardless of the time of delivery of this prospectus or any sale of the common shares or ADSs. Our business, financial condition, results of operations and prospects may have changed since the date on the front cover of this prospectus.

i

Table of Contents

This prospectus is being used in connection with the offering of common shares, including common shares in the form of ADSs, in the United States and other countries outside Brazil.

This offering of ADSs is being made in the United States and elsewhere outside Brazil solely on the basis of the information contained in this prospectus. We and the selling shareholders are also offering common shares in Brazil using a Portuguese-language prospectus. The Brazilian prospectus, which has been filed with the CVM, is in a format different from that of this prospectus and contains information not generally included in documents such as this prospectus.

No offer or sale of ADSs may be made to the public in Brazil except in circumstances that do not constitute a public offer or distribution under Brazilian laws and regulations. Any offer or sale of ADSs in Brazil to non-Brazilian residents may be made only under circumstances that do not constitute a public offer or distribution under Brazilian laws and regulations.

ii

Table of Contents

This summary highlights selected information about us and the ADSs that we and the selling shareholders are offering. It may not contain all of the information that may be important to you. Before investing in the ADSs, you should read this entire prospectus carefully for a more complete understanding of our business and this offering, including our audited consolidated financial statements and the related notes, and the sections entitled “Risk Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus.

Overview

We are one of Brazil’s leading homebuilders. Over the last 50 years, we have been recognized as one of the foremost professionally-managed homebuilders, having completed and sold more than 924 developments and constructed over 37 million square meters of housing, with 900 developments and over 10 million square meters under our Gafisa brand and 24 developments and 27 million square meters under our Alphaville brand, which we believe is more than any other residential development company in Brazil. We believe “Gafisa” and “Alphaville” are two of the best-known brands in the Brazilian real estate development market, enjoying a reputation among potential homebuyers, brokers, lenders, landowners and competitors for quality, consistency and professionalism.

Our core business is the development of high-quality residential buildings in attractive locations. For the year ended December 31, 2006, approximately 65% of our launches were derived from our middle and upper-income residential developments. We are also engaged in the development of land subdivisions, also known as residential communities, and affordable entry-level housing. In addition, we provide construction services to third parties.

We are one of Brazil’s most geographically-diversified homebuilders currently operating in 35 markets, including São Paulo, Rio de Janeiro, Salvador, Fortaleza, Natal, Curitiba, Belo Horizonte, Manaus, Porto Alegre and Belém, across 16 states, representing approximately 86% of the national population and 89% of the gross domestic product. See “Business — Our Markets.” For the year ended December 31, 2006, approximately 27% of our launches were derived from our operations outside São Paulo and Rio de Janeiro.

Our Competitive Strengths

We believe that our competitive strengths in this industry include the following:

Geographic and Product Diversification. We are one of Brazil’s most geographically-diversified homebuilders with developments in 35 markets across 16 states. Many of these developments are located in markets with significant demand for premium middle and upper income residential units where few large, well-capitalized competitors currently operate, allowing us to sell at higher margins. We are also one of the most product-diversified homebuilders in Brazil, engaging in the development of a wide range of real estate products, including residential buildings, land subdivisions, and affordable entry-level housing, which allow us to identify and undertake a broader range of projects offering the most attractive returns.

Strong Management Team Backed by Institutional Shareholders. We have a professional and committed senior management team consisting of eight persons with five to 34 years of experience in the Brazilian real estate industry. In addition, our management has been backed by two institutional shareholders with a successful track record: Equity International, one of the largest real estate investment companies in the United States and GP, one of Brazil’s leading private equity investment firms.

1

Table of Contents

Managerial Systems and Unique Organizational Structure. Our managerial systems and organizational structure are based on our results-oriented culture. We develop and market our projects through business units, which serve as separate profit centers in each of the regions we operate to provide maximum value to clients while keeping our focus on cost control, operating margins, and working capital. We believe the scalability of our platform will support our future expansion plans in a focused, efficient and flexible manner.

Strong Brand Recognition. We believe “Gafisa” and “Alphaville” are two of the best-known brands in the Brazilian real estate development industry, enjoying a solid reputation among potential homebuyers, brokers, lenders, landowners and competitors. We are widely recognized in the markets in which we operate for our consistency, on-time delivery, customer satisfaction and innovative products.

Efficient Business Model. Our objective is to minimize our working capital requirements while maximizing returns. We seek to finance our activities primarily with proceeds from the sale of units and below-market rate government regulated loans. On average, we enter into contracts with customers to sell approximately 70% of our units before the start of construction. Our reputation and sales velocity allow us to minimize land acquisition costs through partnerships with other developers and exchanges of units for land.

Low Operating Costs. We are constantly focused on reducing and maintaining low costs. Our activities are fully integrated and our processes standardized, allowing us to manage all stages of the real estate development process in an efficient manner. Due to our low operating costs, we are also able to generate additional income by providing construction services to many of our competitors.

Strategic Land Bank in Premium Locations. Our existing land reserves represent approximately two to three years of future development at current rates of development. We believe our land reserves comprise prime locations in all of the markets we operate, which are ideally located, diversified and difficult to replicate by competitors.

Our Strategy

We intend to implement the following strategies by building on our competitive strengths:

Capitalize on Growth Potential. We believe that the increase in the availability of affordable home financing, lower interest rates in Brazil and recently enacted government incentives, high rates of population growth and the reduction of unemployment in Brazil present a unique opportunity to expand our homebuilding activities in the country’s major metropolitan areas and other regions.

Continue to Focus on High Return Opportunities. Our strategy is to identify and target high return opportunities. We plan to continue focusing on high-quality middle and upper-income residential developments. We will also maintain and expand our foothold position in the affordable, entry-level residential market to capitalize on any potential improvement in the availability of housing financing in this type of developments.

Increase Land Acquisitions and New Developments. We aim to accelerate the rate of new developments through (1) increased acquisition of prime tracts of land and their subsequent developments and (2) strategic partnerships or selected acquisitions of other developers and builders. Swaps, where we exchange land for units in our future developments, will continue to be our preferred method for land acquisition. However, we will continue to purchase land in prime locations with cash.

Maintain Conservative Financial Position. We plan to continue operating with a conservative approach to indebtedness while maximizing the use of working capital. We will seek to optimize our capital structure to deliver maximum value to our shareholders while maintaining financial costs and risks at appropriate levels.

2

Table of Contents

Recent Developments

In October 2006, we entered into an agreement to acquire 100% of Alphaville Urbanismo S.A., or Alphaville, the largest residential community development company in Brazil focused on the identification, development and sale of high quality residential communities in the metropolitan regions throughout Brazil targeted at upper and upper-middle income families. On January 8, 2007, we successfully completed the acquisition of 60% of Alphaville’s shares for R$198.4 million, of which R$20 million was paid in cash and the remaining R$178.4 million was paid in exchange for 6.4 million common shares of Gafisa. The acquisition agreement provides that we will purchase the remaining 40% over the next five years (20% within three years from the acquisition date and the remaining 20% within five years from the acquisition date) in cash or shares, at our sole discretion. Alphaville is operating as one of our subsidiaries based in the city of Barueri, within the metropolitan region of São Paulo. See “Business — History and Ownership Structure.”

On February 14, 2007, we entered into an agreement with Odebrecht Empreendimentos Imobiliários Ltda to form a partnership for the development, construction and management of low income residential projects each with more than 1,000 units. In connection with the partnership, we will form a holding company in respect of which we and Odebrecht Empreendimentos will each own 50% of the equity stake. Upon the formation of such holding company, we intend to enter into a shareholders agreement with Odebrecht Empreendimentos which will govern, among other matters, our respective voting rights and management of the partnership.

Risks Related to Our Business

Prospective investors should carefully consider the matters described under “Risk Factors,” including that our business and results of operations are related to and may be adversely affected by weakness in general economic, real estate and other conditions; the real estate industry in Brazil is highly competitive; problems with the construction and timely completion of our real estate projects may decrease our profitability; our inability to acquire adequate capital to finance our projects could delay the launch of new projects; changing market conditions may adversely affect our ability to sell our land and home inventories at expected prices; we are subject to risks associated with granting of as well as obtaining financing; we may fail to comply with or become subject to more onerous government regulations; we may experience difficulties in finding desirable land tracts and increases in the price of raw materials may increase our cost of sales and reduce our earnings. One or more of these matters could negatively impact our business and our ability to implement our business strategy successfully.

Our principal executive offices are located at Av. Nações Unidas No. 4777, 9th floor, 05477-000, São Paulo, SP, Brazil, and our general telephone number is +55 11 3025-9000. Our website is www.gafisa.com.br. Information contained on, or accessible through, our website is not incorporated by reference in, and shall not be considered part of, this prospectus.

3

Table of Contents

THE OFFERING

Issuer | Gafisa S.A. |

Selling shareholders | Brazil Development Equity Investments, LLC, Emerging Markets Capital Investments, LLC, EIP Brazil Holdings Godo Kaisha, EI Fund II Brazil Godo Kaisha, EIP Brazil Holdings, LLC, Mr. Renato de Albuquerque and Mr. Nuno Luís de Carvalho Lopes Alves. |

Global offering | The global offering consists of the international offering and the concurrent Brazilian offering. |

International offering | We are offering ADSs representing two common shares, and the selling shareholders are offering ADSs representing two common shares, through the international underwriters in the United States and other countries outside Brazil. |

Brazilian offering | Concurrently with the international offering, the selling shareholders are offering common shares through Brazilian underwriters in Brazil to Brazilian investors. The common shares purchased by any investor outside Brazil will be cleared and settled in Brazil and paid for inreais, and the offering of these common shares is being underwritten by the Brazilian underwriters named elsewhere in this prospectus. Any investor outside Brazil purchasing common shares must be authorized to invest in Brazilian securities under the requirements established by the CMN and the CVM. |

Primary offering | We are offering 18,761,992 common shares, including in the form of ADSs. |

Secondary offering | The selling shareholders are offering 20,914,608 common shares, including in the form of ADSs. |

ADSs | Each ADS represents two common shares. ADSs may be evidenced by American depositary receipts, or “ADRs.” The ADSs will be issued under a deposit agreement among us, Citibank, N.A. as depositary, and the holders and beneficial owners from time to time of ADSs issued thereunder. |

Offering price | US$ per ADS. |

Overallotment options | One of the selling shareholders, Brazil Development Equity Investments, LLC, has granted Merrill Lynch, Pierce, Fenner & Smith Incorporated, upon agreement with Itaú Securities Inc. and Citigroup |

4

Table of Contents

Global Markets Inc., the right to purchase up to an additional 5,951,490 common shares in the form of ADSs, minus the number of common shares sold by EIP Brazil Holdings, LLC pursuant to the Brazilian underwriters’ overallotment option referred to below, within 30 days from the date of this prospectus to cover overallotments, if any, in the international offering. |

One of the selling shareholders, EIP Brazil Holdings, LLC, has also granted the Brazilian underwriters the right to purchase up to an additional 5,951,490 common shares, minus the number of common shares in the form of ADSs sold by Brazil Development Equity Investments, LLC pursuant to the overallotment option of Merrill Lynch, Pierce, Fenner & Smith Incorporated, upon agreement with Itaú Securities Inc. and Citigroup Global Markets Inc., within 30 days from the date of this prospectus to cover overallotments, if any, in the Brazilian offering. |

Use of proceeds | We estimate that the net proceeds to us from the global offering (before deducting transaction expenses) will be approximately US$310.4 million. We intend to use the net proceeds from this offering and the Brazilian offering as follows: (1) approximately $124.2 million to acquire land; (2) approximately $62.1 million to pursue strategic partnerships and acquisitions; (3) approximately $62.1 million to launch new developments; (4) approximately $46.6 million to provide for working capital; and (5) any remaining amounts, to invest in existing operations. See “Use of Proceeds.” |

We will not receive any proceeds from the sale of our common shares, including common shares in the form of ADSs, by the selling shareholders. |

Share capital before and after global offering | Our share capital consists of 109,882,466 common shares as of the date of this prospectus (excluding 3,124,972 treasury shares). |

Immediately after the global offering, we will have 128,644,458 common shares outstanding, assuming no exercise of the underwriters’ overallotment options. |

Voting rights | Holders of our common shares are entitled to one vote per common share in all shareholders’ meetings. See “Description of Capital Stock—Rights of Common Shares.” |

5

Table of Contents

Holders of ADSs are entitled to instruct the depositary how to vote underlying common shares, subject to the terms of the applicable deposit agreement. See “Description of American Depositary Shares—Voting Rights.” |

Dividends | The Brazilian corporation law and our bylaws require us to distribute at least 25% of our annual adjusted net income, as calculated under Brazilian GAAP and the Brazilian corporation law (which differs significantly from net income as calculated under U.S. GAAP), unless the payment of dividends is suspended by our board of directors, having concluded that such distribution would be incompatible with our financial condition. |

Holders of the ADSs will be entitled to receive dividends to the same extent as the owners of our common shares, subject to the deduction of the fees of the depositary and the costs of foreign exchange conversion. For 2002, 2003, 2004 and 2005, we have not distributed dividends but we have determined to distribute dividends for the fiscal year 2006. See “Dividends and Dividend Policy” and “Description of Capital Stock.” |

Listing | We have applied to have the ADSs listed on the New York Stock Exchange, or NYSE, under the symbol “GFA.” Our common shares are listed on the BOVESPA under the symbol “GFSA3.” |

Lock-up agreements | We have agreed with the underwriters, subject to certain exceptions, not to offer, sell, or dispose of any shares of our share capital or securities convertible into or exchangeable or exercisable for any shares of our share capital during the 90-day period following the date of this prospectus. Our selling shareholders, members of our board of directors and our executive officers have agreed to substantially similar lock-up provisions, subject to certain exceptions. |

ADR Depositary | Citibank, N.A. |

Risk factors | See “Risk Factors” and the other information included in this prospectus for a discussion of factors you should consider before deciding to invest in the ADSs or common shares. |

6

Table of Contents

Expected timetable for the global offering (subject to change): |

Commencement of marketing of the global offering | February 23, 2007 |

Announcement of offer price | March 15, 2007 |

Settlement and delivery of ADSs and common shares | March 21, 2007 |

Unless otherwise indicated, all information contained in this prospectus assumes no exercise of the option granted to Merrill Lynch, Pierce, Fenner & Smith Incorporated, to be exercise upon agreement with Itaú Securities Inc. and Citigroup Global Markets Inc., to purchase up to 5,951,490 additional common shares in the form of ADSs from Brazil Development Equity Investments, LLC, minus the number of common shares sold by EIP Brazil Holdings, LLC pursuant to the Brazilian underwriters’ overallotment option referred to below, to cover overallotments of ADSs, if any, and the option of the Brazilian underwriters to purchase up to 5,951,490 additional common shares from EIP Brazil Holdings, LLC, minus the number of common shares in the form of ADSs sold by Brazil Development Equity Investments, LLC pursuant to the overallotment option of Merrill Lynch, Pierce, Fenner & Smith Incorporated, upon agreement with Itaú Securities Inc. and Citigroup Global Markets Inc., to cover overallotments, if any, in the Brazilian offering.

7

Table of Contents

SUMMARY FINANCIAL AND OPERATING DATA

The following table presents our summary financial and operating data and was extracted from our audited financial statements. The financial data as of the years ended December 31, 2006, 2005 and 2004 and for the three years ended December 31, 2006 have been derived from our audited consolidated financial statements included in this prospectus. The financial data as of December 31, 2003 and 2002 and for the two years ended December 31, 2003 have been derived from audited consolidated financial statements of our company that are not included in this prospectus.

Our financial statements are prepared in accordance with Brazilian GAAP, which differs in significant respects from U.S. GAAP. For a discussion of the significant differences relating to these consolidated financial statements and a reconciliation of net income and shareholders’ equity from Brazilian GAAP to U.S. GAAP, see notes to our audited consolidated financial statements. In 2006, we changed the Brazilian GAAP accounting practice adopted with respect to the deferral of selling expenses and presentation of construction costs and have amended our Brazilian GAAP financial statements for years ended December 31, 2005, 2004, 2003 and 2002; see Notes 3 (t)(u) to our financial statements included elsewhere in this prospectus for this amendment and other reclassifications to our Brazilian GAAP financial statements. All periods presented have been modified to reflect such new accounting practices.

The statements of income, shareholders’ equity and earnings per share as at and for the year ended December 31, 2005 under U.S. GAAP were restated as follows: (i) a charge to financial expenses and adjustment to deferral of selling expenses which increased net income for 2005 from R$33.3 million to R$34.4 million, and; (ii) following the exchange of Class A for Class G preferred shares, the excess of the fair value of the consideration transferred to the holders of the Class G preferred shares over the carrying amount of the Class A preferred shares, totaling R$9.6 million was allocated to the preferred shares before apportioning the remaining undistributed earnings to the common and preferred shareholders in the calculation of earnings per share; and (iii) following the change in accounting principle for deferred selling expenses for Brazilian GAAP, we discovered that certain selling expenses deferred under Brazilian GAAP were improperly adjusted for U.S. GAAP purposes. We recorded a credit of R$4.6 million, net of tax, to general, selling and administrative expenses to correct the amount of project specific advertising, marketing and selling costs that had been previously recorded for U.S. GAAP purposes (see Note 19(a)(xii) to our financial statements included elsewhere in this prospectus).

The financial and operating information presented in this section do not reflect Alphaville’s operations, which we acquired on January 8, 2007. See “Business — History and Ownership Structure.”

This financial information should be read in conjunction with our audited financial statements and the related notes and the sections entitled “Selected Financial and Operating Data”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Presentation of Financial and Other Information” included elsewhere in this prospectus.

8

Table of Contents

| As of and For the Year Ended December 31, | ||||||||||||||||||||||||

| 2006(1) | 2006 | 2005 | 2004(2) | 2003 | 2002 | |||||||||||||||||||

| (in thousands except per share and per ADS data)(4) | ||||||||||||||||||||||||

Statement of income data: | ||||||||||||||||||||||||

Brazilian GAAP: | ||||||||||||||||||||||||

Gross operating revenue | US$ | 323,210 | R$ | 691,023 | R$ | 480,774 | R$ | 439,254 | R$ | 428,721 | R$ | 321,780 | ||||||||||||

Net operating revenue | 310,500 | 663,847 | 457,024 | 416,876 | 410,621 | 306,853 | ||||||||||||||||||

Operating costs | (217,865 | ) | (465,795 | ) | (318,211 | ) | (292,391 | ) | (268,672 | ) | (192,375 | ) | ||||||||||||

Gross profit | 92,635 | 198,052 | 138,813 | 124,485 | 141,949 | 114,478 | ||||||||||||||||||

Operating expenses, net(3) | (49,916 | ) | (106,721 | ) | (82,545 | ) | (59,688 | ) | (70,952 | ) | (53,478 | ) | ||||||||||||

Stock issuance expenses | (12,773 | ) | (27,308 | ) | — | — | — | — | ||||||||||||||||

Financial income (expenses), net | (5,586 | ) | (11,943 | ) | (27,972 | ) | (34,325 | ) | (17,095 | ) | (13,500 | ) | ||||||||||||

Non-operating income (expenses), net | — | — | (1,024 | ) | (1,450 | ) | — | 29 | ||||||||||||||||

Income before taxes on income | 24,360 | 52,080 | 27,272 | 29,022 | 53,902 | 47,528 | ||||||||||||||||||

Taxes on income | (2,818 | ) | (6,024 | ) | 3,405 | (5,575 | ) | (10,471 | ) | (5,488 | ) | |||||||||||||

Net income | 21,542 | 46,056 | 30,677 | 23,447 | 43,431 | 42,041 | ||||||||||||||||||

Share and ADS data(4): | ||||||||||||||||||||||||

Earnings per share—R$ per thousand shares | 208.39 | 445.54 | 1,245.69 | 1,218.82 | 2,257.62 | 1,998.36 | ||||||||||||||||||

Number of preferred shares outstanding as at end of period | — | — | 16,222,209 | 11,037,742 | 11,037,742 | 11,037,742 | ||||||||||||||||||

Number of common shares outstanding as at end of period | 103,369,950 | 103,369,950 | 8,404,185 | 8,199,743 | 8,199,743 | 10,000,006 | ||||||||||||||||||

Earnings per ADS—R$ per thousand ADS (pro forma)(5) | 416.78 | 891.08 | 2,491.38 | 2,437.64 | 4,515.24 | 3,996.72 | ||||||||||||||||||

U.S. GAAP(6) | Restated | |||||||||||||||||||||||

Net operating revenue | 315,594 | 674,740 | 439,011 | 442,913 | — | — | ||||||||||||||||||

Operating costs | (235,347 | ) | (503,172 | ) | (329,775 | ) | (339,653 | ) | — | — | ||||||||||||||

Gross profit | 80,247 | 171,568 | 109,236 | 103,260 | — | — | ||||||||||||||||||

Operating expenses, net(3) | (65,102 | ) | (139,188 | ) | (77,305 | ) | (52,770 | ) | — | — | ||||||||||||||

Financial income (expenses), net | 1,881 | 4,022 | (17,684 | ) | (31,645 | ) | — | — | ||||||||||||||||

Income before income taxes, equity in results and minority interest | 17,026 | 36,402 | 14,247 | 18,845 | — | — | ||||||||||||||||||

Taxes on income | (5,232 | ) | (11,187 | ) | (1,886 | ) | (3,530 | ) | — | — | ||||||||||||||

Equity in results | 418 | 894 | 22,593 | 11,674 | — | — | ||||||||||||||||||

Minority interest | (526 | ) | (1,125 | ) | (571 | ) | 252 | — | — | |||||||||||||||

Cumulative effect of a change in an accounting principle: Stock option | (73 | ) | (157 | ) | — | — | — | — | ||||||||||||||||

Net income(7) | 11,612 | 24,827 | 34,383 | 27,241 | — | — | ||||||||||||||||||

Per share and ADS data(4): | ||||||||||||||||||||||||

Per preferred share data—R$ per thousand shares: | Restated | |||||||||||||||||||||||

Earnings per share—Basic | 70.99 | 151.77 | 605.57 | 491.04 | — | — | ||||||||||||||||||

Earnings per share—Diluted | 70.04 | 149.75 | 602.28 | 491.04 | — | — | ||||||||||||||||||

Per common share data—R$ per thousand shares: | ||||||||||||||||||||||||

Earnings per share—Basic | 116.31 | 248.68 | 346.92 | 446.40 | — | — | ||||||||||||||||||

Earnings per share—Diluted | 114.97 | 245.81 | 345.34 | 446.40 | — | — | ||||||||||||||||||

Per ADS data—R$ per thousand ADS (5): | ||||||||||||||||||||||||

Earnings per ADS —Basic (pro forma) (5) | 232.63 | 497.36 | 693.84 | 892.80 | — | — | ||||||||||||||||||

Earnings per ADS—Diluted (pro forma) (5) | 229.94 | 491.62 | 690.68 | 892.80 | — | — | ||||||||||||||||||

Balance sheet data: | ||||||||||||||||||||||||

Brazilian GAAP | ||||||||||||||||||||||||

Cash, bank and financial investments | US$ | 124,489 | R$ | 266,159 | R$ | 133,891 | R$ | 45,888 | R$ | 34,382 | R$ | 33,205 | ||||||||||||

Properties for sale | 206,262 | 440,989 | 304,329 | 237,113 | 177,169 | 86,609 | ||||||||||||||||||

Working capital(8) | 476,534 | 1,018,829 | 497,948 | 205,972 | 192,087 | 165,643 | ||||||||||||||||||

Total assets | 698,885 | 1,494,217 | 944,619 | 748,508 | 856,308 | 700,330 | ||||||||||||||||||

Total debt(9) | 138,187 | 295,443 | 316,933 | 151,537 | 194,400 | 104,726 | ||||||||||||||||||

Total shareholders’ equity | 380,770 | 814,087 | 270,187 | 146,469 | 122,503 | 105,806 | ||||||||||||||||||

U.S. GAAP | ||||||||||||||||||||||||

Cash, bank and financial investments | 122,039 | 260,919 | 136,153 | 42,803 | — | — | ||||||||||||||||||

Properties for sale | 226,104 | 483,411 | 376,613 | 245,055 | — | — | ||||||||||||||||||

Working capital (8) | 398,393 | 851,764 | 507,155 | 195,392 | — | — | ||||||||||||||||||

Total assets | 764,212 | 1,633,886 | 901,387 | 601,220 | — | — | ||||||||||||||||||

Total debt(9) | 135,368 | 289,416 | 294,149 | 141,476 | — | — | ||||||||||||||||||

Total shareholders’ equity | 371,960 | 795,251 | 290,604 | 160,812 | — | — | ||||||||||||||||||

Other financial data: | ||||||||||||||||||||||||

EBITDA(10) | 31,958 | 68,325 | 58,852 | 69,489 | 76,328 | 63,711 | ||||||||||||||||||

Net debt(11) | 13,697 | 29,284 | 183,042 | 105,649 | 160,018 | 71,521 | ||||||||||||||||||

Cash flow provided by (used in): | ||||||||||||||||||||||||

Brazilian GAAP | ||||||||||||||||||||||||

Operating activities | (143,238 | ) | (306,243 | ) | (112,947 | ) | 23,616 | — | ||||||||||||||||

Investing activities | (4,012 | ) | (8,577 | ) | (5,576 | ) | (1,509 | ) | — | — | ||||||||||||||

Financing activities | 209,115 | 447,087 | 206,526 | 10,601 | — | — | ||||||||||||||||||

Operating data: | ||||||||||||||||||||||||

Number of new developments | — | 30 | 21 | 11 | 20 | 25 | ||||||||||||||||||

Total sales value of developments launched (Gafisa’s proportional share) (12) | 470,098 | 1,005,069 | 651,815 | 206,942 | 377,356 | 387,542 | ||||||||||||||||||

Number of units launched(13) | — | 3,755 | 2,446 | 1,132 | 1,790 | 2,298 | ||||||||||||||||||

Launched usable area (m2)(14) | — | 586,653 | 514,068 | 233,393 | 179,437 | 256,575 | ||||||||||||||||||

Total sales value(15) (Gafisa’s proportional share) | 465,423 | 995,074 | 450,153 | 253,826 | 325,248 | 333,478 | ||||||||||||||||||

Sold usable area (m2)(14) | — | 427,309 | 408,676 | 181,777 | 185,273 | 256,190 | ||||||||||||||||||

Units sold | — | 3,391 | 1,994 | 1,192 | 1,595 | 2,179 | ||||||||||||||||||

Average sales price (R$/m2)(14)(16) | 1,420 | 3,037 | 2,878 | 2,934 | 2,822 | 1,972 | ||||||||||||||||||

(footnotes on following page)

9

Table of Contents

| (1) | Translated using the exchange rate as reported by the Central Bank as of December 31, 2006 forreais into U.S. dollars of R$2.1380 to US$1.00. |

| (2) | The financial information in relation to receivables from clients, properties for sale, real estate development obligations, other current liabilities, working capital, total assets and unearned income from property sales from 2004 and thereafter is not comparable to prior periods as a result of the adoption of CFC Resolution No. 963 for real estate developments launched after January 1, 2004. |

| (3) | Excludes stock issuance expenses. |

| (4) | On January 26, 2006 all preferred shares were converted into common shares. On January 27, 2006, a stock split of our common shares was approved, giving effect to the split of one existing share into three newly issued shares, increasing the number of shares from 27,774,775 to 83,324,316. All information relating to the numbers of shares and ADSs have been adjusted retrospectively to reflect the share split on January 27, 2006. All U.S. GAAP earnings per share and ADS amounts have been adjusted retrospectively to reflect the share split on January 27, 2006. Brazilian GAAP earnings per share and ADS amounts have not been adjusted retrospectively to reflect the share split on January 27, 2006. |

| (5) | Earnings per ADS is calculated based on each ADS representing two common shares. The ADSs will be issued upon deposit of the common shares with the custodian. See “Description of American Depositary Shares.” |

| (6) | As discussed in Note 19(a)(xii) to our consolidated financial statements included elsewhere in the prospectus, we restated our U.S. GAAP statement of income and earnings per share for the year ended December 31, 2005. |

| (7) | The following table sets forth reconciliation from US GAAP net income to US GAAP net income available to common shareholders: |

| 2006 | 2005 | 2004 | |||||||

restated | |||||||||

Reconciliation from US GAAP net income to US GAAP net income available to common shareholders (Basic): | |||||||||

US GAAP net income (Basic) | 24,827 | 34,383 | 27,241 | ||||||

Preferred Class G exchange* | — | (9,586 | ) | — | |||||

Undistributed earnings for Preferred Shareholders (Basic earnings) | (258 | ) | (16,334 | ) | (16,260 | ) | |||

US GAAP net income available to common shareholders (Basic earnings) | 24,569 | 8,463 | 10,981 | ||||||

Reconciliation from US GAAP net income to US GAAP net income available to common shareholders (Diluted): | |||||||||

US GAAP net income | 24,827 | 34,383 | 27,241 | ||||||

Preferred Class G exchange* | — | (9,586 | ) | — | |||||

Undistributed earnings for Preferred Shareholders (Diluted earnings) | (259 | ) | (16,373 | ) | (16,260 | ) | |||

US GAAP net income available to common shareholders (Diluted earnings) | 24,568 | 8,424 | 10,981 | ||||||

* Pursuant to EITF Topic D-42 “The Effect on the Calculation of Earnings per Share for the Redemption or Induced Conversion of Preferred Stock”, following the exchange of Class A for Class G Preferred shares, the excess of the fair value of the consideration transferred to the holders of the preferred stock over the carrying amount of the preferred stock in the balance sheet was subtracted from net income to arrive at net earnings available to common shareholders in the calculation of earnings per share. For purposes of displaying earnings per share, the amount is treated in a manner similar to the treatment of dividends paid to the holders of the preferred shares. The conceptual return or dividends on preferred shares are deducted from net earnings to arrive at net earnings available to common shareholders.

(footnotes continued on following page)

10

Table of Contents

| (8) | Working capital equals current assets less current liabilities. |

| (9) | Total debt comprises loans, financings and short term and long term debentures. Amounts exclude loans from real estate development partners. |

| (10) | We define and calculate EBITDA as Brazilian GAAP net income before financial expenses, net, income tax expense, depreciation and non-operating expenses. We use EBITDA as a supplemental measure of financial performance as well as of our ability to generate cash from operations. EBITDA is not a Brazilian GAAP or U.S. GAAP measurement, does not represent cash flows for the periods presented and should not be considered an alternative to net income as an indicator of liquidity. EBITDA does not have a standardized meaning and our definition of EBITDA may not be comparable to EBITDA as used by other companies. We understand that although EBITDA is frequently used by securities analysts, lenders and others in their evaluation of companies, EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for analysis of our results as reported under Brazilian and U.S. GAAP. Some of these limitations are: |

| Ÿ | EBITDA does not reflect our cash expenditures, or future requirements for capital expenditures or contractual commitments; |

| Ÿ | EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| Ÿ | EBITDA does not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debts; and |

| Ÿ | Although depreciation is a non-cash charge, the assets being depreciated will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements. |

| The following table is a reconciliation of our Brazilian GAAP net income to EBITDA: |

| As of and For the Year Ended December 31, | |||||||||||||

| 2006(1) | 2006 | 2005 | 2004 | 2003 | 2002 | ||||||||

| (in thousands of US$) | (in thousands of R$) | ||||||||||||

Brazilian GAAP | |||||||||||||

Net income | 21,542 | 46,056 | 30,677 | 23,447 | 43,431 | 42,041 | |||||||

Financial expenses, net | 5,586 | 11,943 | 27,972 | 34,325 | 17,095 | 13,500 | |||||||

Income tax expense | 2,818 | 6,024 | (3,405 | ) | 5,575 | 10,471 | 5,488 | ||||||

Non operating expense | — | — | 1,024 | 1,450 | — | — | |||||||

Depreciation | 2,012 | 4,302 | 2,584 | 4,702 | 5,331 | 2,099 | |||||||

EBITDA | 31,958 | 68,325 | 58,852 | 69,499 | 76,328 | 63,128 | |||||||

| Stock issuance expenses in the year ended December 31, 2005 and 2006 were R$410 thousand and R$27,308 thousand, respectively. |

(footnotes continued on following page)

11

Table of Contents

| The table below sets forth a reconciliation of our Brazilian GAAP net cash from operating activities to EBITDA(a): |

| 2006(1) | 2006 | 2005 | 2004 | |||||||||

| (in thousands of US$) | (in thousands of R$) | |||||||||||

Brazilian GAAP | ||||||||||||

Net cash provided by (used in) operating activities | (142,702 | ) | (306,243 | ) | (112,947 | ) | 23,616 | |||||

Amortization of negative goodwill | 7,196 | 15,387 | 2,721 | — | ||||||||

Provision for contingencies | 148 | 317 | (1,994 | ) | 449 | |||||||

Decrease (increase) in assets | ||||||||||||

Receivables from clients | 76,138 | 162,785 | (23,305 | ) | (91,919 | ) | ||||||

Properties for sale | 63,920 | 136,660 | 33,511 | 21,818 | ||||||||

Deferred selling and prepaid expenses | 4,943 | 10,569 | (2,230 | ) | 4,736 | |||||||

Other | 26,576 | 56,926 | (6,579 | ) | 16,838 | |||||||

Increase (decrease) in liabilities | ||||||||||||

Real estate development obligations | 27,110 | 57,963 | 133,481 | 66,310 | ||||||||

Obligations for purchase of land | (33,996 | ) | (72,684 | ) | (4,463 | ) | 7,285 | |||||

Taxes and contributions | 4,844 | 10,355 | (5,713 | ) | (8,807 | ) | ||||||

Unearned income from property sales | (13,992 | ) | 25,168 | 65,553 | 76,492 | |||||||

Other | 11,773 | (28,878 | ) | (19,183 | ) | (47,319 | ) | |||||

EBITDA | 31,958 | 68,325 | 58,852 | 69,499 | ||||||||

(a) | Statements of cash flows were not prepared for the years ended December 2003 and 2002. |

| (11) | Net debt consists of loans and financing and debentures, net of cash, bank and financial investments. Net debt is not a Brazilian GAAP measurement. |

| (12) | Total sales value of developments launched is the aggregate nominal value of the units that we launched sales campaigns for in a given project. |

| (13) | The units delivered in exchange for land pursuant to swap agreements are not included. |

| (14) | One square meter is equal to approximately 10.76 square feet. |

| (15) | Total sales value represents the monetary amount of all sales contracts executed by us as a result of the sale of our residential units, regardless of the stage of the development (i.e., whether the development is under construction or completed). Total sales value is calculated by multiplying the number of units sold in a development by the unit sales price. Gross operating revenues, on the other hand, are calculated by applying the percentage of costs incurred to the total sales value of the units sold. Because of the long cycle of our business activities, there is usually a lag between the execution of our sales contracts and the recognition of the sales value as gross operating revenues on our financial statements. For that reason, total sales value is used as an indicator of current operating performance. We also review other indicators of current operating performance such as total sales value of developments launched, number of units launched, units sold and sold usable area. |

| Total sales value is different from total sales value of development launched in that the former accounts for the amount of sales contracts executed in the indicated period while the latter accounts for the amount of the units that were launched in sales campaigns in the indicated period. The former is an indicator of current operating performance and the latter is an indicator of sales activities. |

| (16) | The average sales price inreaisper square meter excludes land subdivisions. The average sales value inreais per square meter, including land subdivisions, was R$2,752, R$1,291, R$2,061, R$2,580 and R$1,852 in 2006, 2005, 2004, 2003 and 2002, respectively. |

12

Table of Contents

You should carefully consider the risks described below, as well as the other information in this prospectus, before deciding to purchase our common shares and ADSs. Our business, results of operations, financial condition or prospects could be adversely affected if any of these risks occurs, and as a result, the market price of our common shares and the ADSs could decline and you could lose all or part of your investment. The risks described below are those known to us and that we currently believe may materially affect us.

Risks Relating to Our Business and to the Brazilian Real Estate Industry

Our business and results of operations may be adversely affected by weaknesses in general economic, real estate and other conditions.

The residential homebuilding and land development industry is cyclical and is significantly affected by changes in general and local economic conditions, such as:

| Ÿ | employment levels; |

| Ÿ | population growth; |

| Ÿ | consumer confidence and stability of income levels; |

| Ÿ | availability of financing for land home site acquisitions, and the availability of construction and permanent mortgages; |

| Ÿ | inventory levels of both new and existing homes; |

| Ÿ | supply of rental properties; and |

| Ÿ | conditions in the housing resale market. |

Furthermore, the market value of undeveloped land, buildable lots and housing inventories held by us can fluctuate significantly as a result of changing economic and real estate market conditions. If there are significant adverse changes in economic or real estate market conditions, we will have to sell homes at a loss or hold land in inventory longer than planned. For example, in 2003 and 2004, high interest rates in Brazil adversely affected consumer confidence which negatively impacted the sales of our units. Inventory carrying costs can be significant and can result in losses in a poorly performing project or market. We may be particularly affected by changes in local market conditions in São Paulo and Rio de Janeiro, where we derive a large portion of our revenue.

The real estate industry in Brazil is highly competitive. Failure to compete successfully could have a material adverse effect on our business, financial condition and results of operations.

The Brazilian real estate industry is highly competitive and fragmented. We compete with Brazilian as well as international developers on availability and location of land, price, funding, design, quality, reputation and partnerships with other developers. Because our industry does not have high barriers to entry, new competitors, including international companies working in partnerships with Brazilian developers, may enter into the industry, further intensifying this competition. Some of our current potential competitors may have greater financial and other resources than we do. Furthermore, a significant portion of our real estate development and construction activities is conducted in the states of São Paulo and Rio de Janeiro, areas where the real estate market is highly competitive due to a scarcity of properties in desirable locations and the relatively large number of local competitors. If we are not able to compete effectively, our business, financial condition and results of operations could be adversely affected.

13

Table of Contents

Problems with the construction and timely completion of our real estate projects may damage our reputation, expose us to civil liability and decrease our profitability.

The quality of work in the construction of our real estate projects and the timely completion of these projects are major factors that determine our reputation, and therefore our sales and growth. Delays in the construction of our projects or defects in materials and/or workmanship may occur. Any defects could delay the completion of our real estate projects, or, if such defects are discovered after completion, expose us to civil lawsuits by purchasers or tenants. Construction projects often involve delays in obtaining, or the inability to obtain, permits or approvals from the relevant authorities. In the past, we have encountered circumstances where we had obtained the necessary environmental permits from state authorities, but we were prevented from commencing our construction due to investigations by the local prosecutor’s office in response to complaints regarding our tree-cutting activities. Such investigations delayed the start of construction by us and the delivery of completed units to our customers. In addition, construction projects may also encounter delays due to adverse weather conditions, natural disasters, fires, delays in the provision of materials or labor, accidents, labor disputes, unforeseen engineering, environmental or geological problems, disputes with contractors and subcontractors, or other events. In addition, we may encounter previously unknown conditions at or near our construction sites, that may delay or prevent construction of a particular project. If we encounter a previously unknown condition at or near a site, we may be required to correct the condition prior to continuing construction and there may be a delay in the construction of a particular project. The occurrence of any one or more of these problems in our real estate projects could adversely affect our reputation and our future sales.

Construction delays, cost overruns and addressing newly discovered conditions may increase project development costs. In addition, delays in the completion of a project may result in a delay in the commencement of cash flow, which would increase our capital needs. We may also incur construction and other development costs for a project that exceed our original estimates due to increases over time in interest rates, material costs, labor costs or other costs. We may not be able to pass these increased costs on to purchasers and thus the increases may decrease our profitability.

Our inability to acquire adequate capital to finance our projects could delay the launch of new projects.

We expect that the continuing expansion and development of our business will require significant capital, which we may be unable to obtain on acceptable terms, or at all, to fund our capital expenditures and operating expenses, including working capital needs. We may fail to generate sufficient cash flow from our operations to meet our cash requirements. Furthermore, our capital requirements may vary materially from those currently planned if, for example, our revenues do not reach expected levels or we have to incur unforeseen capital expenditures and make investments to maintain our competitive position. If this is the case, we may require additional financing sooner than anticipated, or we may have to delay some of our new development and expansion plans or otherwise forego market opportunities. We may not be able to obtain future equity or debt financing on favorable terms, if at all. Future borrowing instruments such as credit facilities are likely to contain restrictive covenants and may require us to pledge assets as security for borrowings under those facilities. Our inability to obtain additional capital on satisfactory terms may delay or prevent the expansion of our business.

Changing market conditions may adversely affect our ability to sell our land and home inventories at expected prices, which could reduce our margins.

As a homebuilder, we must constantly locate and acquire new tracts of land for development and development home sites to support our homebuilding operations. There is a lag between the time we acquire land for development or developed home sites and the time that we can bring the properties to market and sell homes. Lag time varies on a project-by-project basis; however, historically, we have experienced a lag time of 24 to 36 months. As a result, we face the risk that demand for housing may decline, costs of labor or materials may increase, interest rates may increase, currencies may fluctuate and political uncertainties may occur during this period and that we will not be able to dispose of developed properties or undeveloped land or home sites acquired

14

Table of Contents

for development at expected prices or profit margins or within anticipated time frames or at all. Significant expenditures associated with investments in real estate, such as maintenance costs, construction costs and debt payments, cannot generally be reduced if changes in the economy cause a decrease in revenues from our properties. The market value of home inventories, undeveloped land, and developed home sites can fluctuate significantly because of changing market conditions. In addition, inventory carrying costs (including interest on funds unused to acquire land or build homes) can be significant and can adversely affect our performance. Because of these factors, we may be forced to sell homes or other property at a loss or for prices that generate lower profit margins than we anticipate. We may also be required to make material write-downs of the book value of our real estate assets in accordance with Brazilian GAAP if values decline.

We are subject to risks normally associated with permitting our purchasers to make payments in installments; if there are higher than anticipated defaults or if our costs of providing that financing increase, then our profitability could be adversely affected.

As is common in our industry, we and the special purpose entities or SPEs in which we participate permit some purchasers of the units in our projects to make payments in installments. As a result, we are subject to the risks associated with this financing, including the risk of default in the payment of principal or interest on the loans we make as well as the risk of increased costs for the funds raised by us. As of December 31, 2006, our receivables relating to such financing amounted to R$1,319.8 million. Our customer default rate in the last five years was 2% and as a result, on average, we recovered 98 cents of every dollar loaned that is overdue. In addition to the 12% per annum fixed rate component of the interest payments, our term sales agreements usually provide for an inflation adjustment linked to the National Index of Construction Cost (Índice Nacional de Custo da Construção), or INCC, during the construction phase of the projects and to the General Market Price Index (Índice Geral de Preços—Mercado), or IGP-M, after completion. If the rate of inflation increases, the loan payments under these term sales agreements may increase, which may lead to a higher rate of payment default. If the default rate among our purchasers increases, our cash generation and, therefore, our profitability could be adversely affected.

In the case of a payment default after the delivery of financed units, Brazilian law provides for the filing of a collection claim to recover the amount owed or to repossess the unit following specified procedures. The collection of overdue amounts or the repossession of the property is a lengthy process, which usually takes two years, and involves additional costs. It is uncertain that we can recover the full amount owed to us or that if we repossess the unit, we can re-sell the unit at favorable terms or at all.

If we or the SPEs in which we participate fail to comply with or become subject to more onerous government regulations, our business could be adversely affected.

We and the SPEs we participate in are subject to various federal, state and municipal laws and regulations, including those relating to construction, zoning, use of soil, environmental protection, historical patrimony and consumer protection. We are required to obtain, maintain and renew on a regular basis permits, licenses and authorizations from various governmental authorities in order to carry out our projects. We strive to maintain compliance with these laws and regulations. If we are unable to maintain or achieve compliance with these laws and regulations, we could be subject to fines, project shutdowns, cancellation of licenses and revocation of authorizations or other restrictions on our ability to develop our projects, which could have an adverse impact on our financial condition. In addition, our contractors and subcontractors are required to comply with various labor and environmental regulations and tax obligations. Because we are secondary obligors to these contractors and subcontractors, if they fail to comply with these regulations or obligations, we may be subject to penalties by the relevant regulatory bodies.

Regulations governing the Brazilian real estate industry as well as environmental laws have tended to become more restrictive over time. We cannot assure you that new and stricter standards will not be adopted or become applicable to us, or that stricter interpretations of existing laws and regulations will not occur. For

15

Table of Contents

example, we have encountered circumstances where we had obtained the necessary environmental permits from state authorities, but subsequently became subject to investigations by the local prosecutor’s office in response to complaints regarding our tree-cutting activities based on a different interpretation of the applicable regulations. Any such event may require us to spend additional funds to achieve compliance with such new rules and therefore make the development of our projects more costly.

If there is a scarcity of financing and/or increased interest rates, this may decrease the demand for real estate properties, which could negatively affect our business.

The scarcity of financing and/or an increase in interest rates may adversely affect the ability or willingness of prospective buyers to purchase our products and services. A majority of the bank financing obtained by prospective buyers comes from the Housing Financial System (Sistema Financeiro de Habitação), or SFH, which is financed by funds raised from savings account deposits. The CMN often changes the amount of such funds that banks are required to make available for real estate financing. If the CMN restricts the amount of available funds that can be used to finance the purchase of real estate properties, or if there is an increase in interest rates, there may be a decrease in the demand for our residential and commercial properties and for the development of lots of land, which may adversely affect our financial position and results of operations.

Because we recognize sales income from our real estate properties under the percentage of completion method of accounting, an adjustment in the cost of a development project may reduce or eliminate previously reported revenue and income.

We recognize income from the sale of units in our properties based on the percentage of completion method of accounting, which requires us to recognize income as we incur the cost of construction. Revenue and total cost estimates are revised on a regular basis as the work progresses, and adjustments based upon the percentage of completion are reflected in contract revenue in the period when these estimates are revised. To the extent that these adjustments result in an increase, a reduction or an elimination of previously reported income, we will recognize a credit to or a charge against income, which could have an adverse effect on our previously reported revenue and income.

Our participation in SPEs creates additional risks, including potential problems in our financial and business relationships with our partners.

We invest in SPEs, with other real estate developers and construction companies in Brazil. The risks involved with SPEs include the potential bankruptcy of our SPE partners and the possibility of diverging or inconsistent economic or business interests between us and our partners. If an SPE partner fails to perform or is financially unable to bear its portion of the required capital contributions, we could be required to make additional investments and provide additional services in order to make up for our partner’s shortfall in return for an increased share in the venture. In 2002, one of our SPE partners had financial difficulties and was unable to fulfill its financial obligations under the SPE. As a result we were required to make additional investments of approximately R$800,000 in return for an increased share in the SPE. In addition, under Brazilian law, the partners of an SPE may be liable for obligations of an SPE in particular areas, including tax, labor, environmental and consumer protection.

We may experience difficulties in finding desirable land tracts and increases in the price of land may increase our cost of sales and decrease our earnings.

Our continued growth depends in large part on our ability to continue to acquire land and to do so at a reasonable cost. As more developers enter or expand their operations in the Brazilian home building industry, land prices could rise significantly and suitable land could become scarce due to increased demand or decreased supply. A resulting rise in land prices may increase our cost of sales and decrease our earnings. We may not be able to continue to acquire suitable land at reasonable prices in the future.

16

Table of Contents

Increases in the price of raw materials may increase our cost of sales and reduce our earnings.

The basic raw materials used in the construction of our homes include concrete, concrete block, steel, bricks, windows, doors, roof tiles and plumbing fixtures. Increases in the price of these and other raw materials, including increases that may occur as a result of shortages, duties, restrictions, or fluctuations in exchange rates, could increase our cost of sales. From 2003 to 2005, for instance, the price of steel increased approximately 36% which increased our cost of sales. Any such cost increases could reduce our earnings to the extent we are unable to pass on these increased costs to our buyers.

If we are not able to implement our growth strategy as planned or at all our business, financial condition and results of operations could be adversely affected.

We plan to grow our business by selectively expanding to meet the growth potential of the Brazilian residential market. We believe that there is increasing competition for suitable real estate development sites. We may not find suitable additional sites for development of new projects or other suitable expansion opportunities.

We anticipate that we will need additional financing to implement our expansion strategy and we may not have access to the funding required for the expansion of our business or such funding may not be available to us on acceptable terms. We may finance the expansion of our business with additional indebtedness or by issuing additional equity securities. We could face financial risks associated with incurring additional indebtedness, such as reducing our liquidity and access to financial markets and increasing the amount of cash flow required to service such indebtedness, or associated with issuing additional stock, such as dilution of ownership and earnings.

Our level of indebtedness could have an adverse effect on our financial health, diminish our ability to raise additional capital to fund our operations and limit our ability to react to changes in the economy or the real estate industry.

As of December 31, 2006, our total debt was R$295.4 million. For the fiscal year 2006, our annual debt service obligation was approximately R$136.3 million.

Our level of indebtedness could have important negative consequences for us. For example, it could:

| Ÿ | require us to dedicate a large portion of our cash flow from operations to fund payments on our debt, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; |

| Ÿ | increase our vulnerability to adverse general economic or industry conditions; |

| Ÿ | limit our flexibility in planning for, or reacting to, changes in our business or the industry in which we operate; |

| Ÿ | limit our ability to raise additional debt or equity capital in the future or increase the cost of such funding; |

| Ÿ | restrict us from making strategic acquisitions or exploring business opportunities; |

| Ÿ | make it more difficult for us to satisfy our obligations with respect to our debt; and |

| Ÿ | place us at a competitive disadvantage compared to our competitors that have less debt. |

A portion of our indebtedness has variable interest rates. At December 31, 2006, the principal amount of our aggregate outstanding variable rate indebtedness was R$295.4 million. A hypothetical 1% adverse change in interest rates would have had an annualized unfavorable impact of approximately R$2.9 million on our earnings and cash flows, based on the debt level at December 31, 2006.

17

Table of Contents

Risks Relating to Brazil

Brazilian economic, political and other conditions, and Brazilian government policies or actions in response to these conditions, may negatively affect our business and results of operations and the market price of our common shares.

The Brazilian economy has been characterized by frequent and occasionally extensive intervention by the Brazilian government and unstable economic cycles. The Brazilian government has often changed monetary, taxation, credit, tariff and other policies to influence the course of Brazil’s economy. For example, the government’s actions to control inflation have at times involved setting wage and price controls, blocking access to bank accounts, imposing exchange controls and limiting imports into Brazil. We have no control over, and cannot predict, what policies or actions the Brazilian government may take in the future.

Our business, results of operations, financial condition and prospects, as well as the market prices of our common shares or the ADSs, may be adversely affected by, among others, the following factors:

| Ÿ | exchange rate movements; |

| Ÿ | exchange control policies; |

| Ÿ | expansion or contraction of the Brazilian economy, as measured by rates of growth in gross domestic product, or “GDP”; |

| Ÿ | inflation; |

| Ÿ | tax policies; |

| Ÿ | other economic, political, diplomatic and social developments in or affecting Brazil; |

| Ÿ | interest rates; |

| Ÿ | energy shortages; |

| Ÿ | liquidity of domestic capital and lending markets; and |

| Ÿ | social and political instability. |

Uncertainty over whether the Brazilian government may implement changes in policy or regulations may contribute to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets as well as securities issued abroad by Brazilian issuers. As a result, these uncertainties and other future developments in the Brazilian economy may adversely affect us and our business and results of operations and the market price of our common shares.

Inflation and government measures to curb inflation, may adversely affect the Brazilian economy, the Brazilian securities market, our business and operations and the market prices of our common shares or the ADSs.

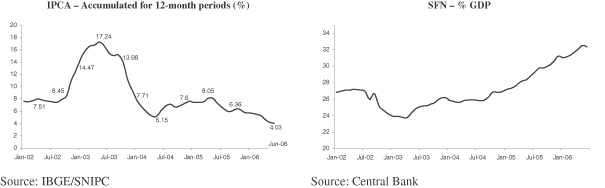

At times in the past, Brazil has experienced high rates of inflation. According to the General Market Price Index (Índice Geral de Preços—Mercado) or “IGP-M,” a general price inflation index, the inflation rates in Brazil were 10.4% in 2001, 25.3% in 2002, 8.7% in 2003, 12.4% in 2004, 1.2% in 2005 and 3.8% in 2006. In addition, according to the National Extended Consumer Price Index (Índice Nacional de Preços ao Consumidor Amplo), or “IPCA,” published by the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística) or “IBGE”, the Brazilian price inflation rates were 7.7% in 2001, 12.5% in 2002, 9.3% in 2003, 7.6% in 2004, 5.7% in 2005 and 3.1% in 2006. The Brazilian government’s measures to control inflation have often included maintaining a tight monetary policy with high interest rates, thereby restricting availability of credit and reducing economic growth. Inflation, actions to combat inflation and public speculation about possible

18

Table of Contents

additional actions have also contributed materially to economic uncertainty in Brazil and to heightened volatility in the Brazilian securities markets.

Brazil may experience high levels of inflation in future periods. Periods of higher inflation may slow the rate of growth of the Brazilian economy, which could lead to reduced demand for our products in Brazil and decreased net sales. Inflation is also likely to increase some of our costs and expenses, which we may not be able to pass on to our customers and, as a result, may reduce our profit margins and net income. In addition, high inflation generally leads to higher domestic interest rates, and, as a result, the costs of servicing ourreais-denominated debt may increase, resulting in lower net income. Inflation and its effect on domestic interest rates can, in addition, lead to reduced liquidity in the domestic capital and lending markets, which could affect our ability to refinance our indebtedness in those markets. Any decline in our net sales or net income and any deterioration in our financial condition would also likely lead to a decline in the market price of the ADSs.

Fluctuations in interest rates may have an adverse effect on our business and the market prices of the ADSs.

The Central Bank establishes the basic interest rate target for the Brazilian financial system by reference to the level of economic growth of the Brazilian economy, the level of inflation and other economic indicators. From February to July 17, 2002, the Central Bank reduced the basic interest rate from 18.75% to 18.00%. From October 2002 to February 2003, the Central Bank increased the basic interest rate by 8.5 percentage points, to 26.5% by February 19, 2003. The basic interest rate continued to increase to 26% in June 2003 when the Central Bank started to decrease it. Subsequently, the basic interest rate suffered further fluctuations, and, in June 2006, the basic interest rate was 15.25%.

At December 31, 2006, all of our indebtedness was denominated inreais and subject to Brazilian floating interest rates, such as the Long-Term Interest Rate (Taxa de Juros de Longo Prazo), or TJLP, and the Interbank Deposit Certificate Rate (Certificado de Depósito Interbancário), or CDI rate. Any increase in the TJLP rate or the CDI rate may have an adverse impact on our financial expenses and our results of operations.

Restrictions on the movement of capital out of Brazil may adversely affect your ability to receive dividends and distributions on, or the proceeds of any sale of the ADSs.

Brazilian law permits the Brazilian government to impose temporary restrictions on conversions of Brazilian currency into foreign currencies and on remittances to foreign investors of proceeds from their investments in Brazil, whenever there is a serious imbalance in Brazil’s balance of payments or there are reasons to expect a pending serious imbalance. The Brazilian government last imposed remittance restrictions for approximately six months in 1989 and early 1990. The Brazilian government may take similar measures in the future. Any imposition of restrictions on conversions and remittances could hinder or prevent holders of our common shares or the ADSs from converting into U.S. dollars or other foreign currencies and remitting abroad dividends, distributions or the proceeds from any sale in Brazil of our common shares. Exchange controls could also prevent us from making payments on our U.S. dollar-denominated debt obligations and hinder our ability to access the international capital markets. As a result, exchange controls restrictions could reduce the market prices of our common shares and the ADSs.

Changes in tax laws may increase our tax burden and, as a result, adversely affect our profitability.

The Brazilian government regularly implements changes to tax regimes that may increase our and our customers’ tax burdens. These changes include modifications in the rate of assessments and, on occasion, enactment of temporary taxes, the proceeds of which are earmarked for designated governmental purposes. In April 2003, the Brazilian government presented a tax reform proposal, which was mainly designed to simplify tax assessments, to avoid internal disputes within and between the Brazilian states and municipalities, and to redistribute tax revenues. The tax reform proposal provided for changes in the rules governing the federal Social

19

Table of Contents

Integration Program (Programa de Integração Social), or “PIS,” the federal Contribution for Social Security Financing (Contribuição para Financiamento da Seguridade Social), or “COFINS,” the federal Tax on Bank Account Transactions (Contribuição Provisória sobre Movimentação ou Transmissão de Valores e de Créditos e Direitos de Natureza Financeira), or “CPMF,” the state Tax on the Circulation of Merchandise and Services (Imposto Sobre a Circulação de Mercadorias e Serviços), or “ICMS,” and some other taxes. The effects of these proposed tax reform measures and any other changes that result from enactment of additional tax reforms have not been, and cannot be, quantified. However, some of these measures, if enacted, may result in increases in our overall tax burden, which could negatively affect our overall financial performance.

Risks Relating to Our ADSs

Developments and the perception of risks in other countries, especially emerging market countries, may adversely affect the market prices of the ADSs.