UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 20-F

(Mark One)

¨ REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2008

OR

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

¨ SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report:

For the transition period from _______________ to _______________

Commission file number 333-143914

COMANCHE CLEAN ENERGY CORPORATION

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant's name into English)

Cayman Islands

(Jurisdiction of incorporation or organization)

Rua do Rocio 84, 11th Floor

Sao Paulo SP CEP 04552-000, Brazil

(Address of principal executive offices)

Thomas Cauchois

Greenwich Administrative Services, LLC

One Dock Street

Stamford, Connecticut 06902

T:203-326-4570, E: tcauchois@comanchecleanenergy.com, F: 203-326-4578

(Name, Telephone, E-mail and/or Facsimile number and Address, of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act: None

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Ordinary Voting Shares

(Title of Class)

Indicate the number of outstanding shares of each of the issuer's classes of capital or common stock as of the close of the period covered by the annual report.

There were 25,474,813 ordinary shares outstanding on June 9, 2008.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

¨ Yes x No

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). o Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

¨ Large accelerated filer ¨ Accelerated filer x Non-accelerated filer

Indicate by check which basis of accounting the registrant has used to prepare the financial statements included in this filing:

US GAAP x International Financial Reporting Standards as issued by the International

Accounting Standards Board ¨ Other ¨

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes x No

TABLE OF CONTENTS

| Cautionary Note Regarding Forward Looking Statements | 3 |

| Part I |

| | | |

| Item 1. | Identity of Directors, Senior Management and Advisers | 4 |

| Item 2. | Offer Statistics and Expected Timetable | 4 |

| Item 3. | Key Information | 4 |

| Item 4. | Information on the Company | 35 |

| Item 4A. | Unresolved Staff Comments | 76 |

| Item 5. | Operating and Financial Review and Prospects | 76 |

| Item 6. | Directors, Senior Management and Employees | 102 |

| Item 7. | Major Shareholders and Related Party Transactions | 112 |

| Item 8. | Financial Information | 118 |

| Item 9. | The Offer and Listing | 121 |

| Item 10. | Additional Information | 121 |

| Item 11. | Quantitative and Qualitative Disclosures About Market Risk | 128 |

| Item 12. | Description of Other Securities Other Than Equity Securities | 129 |

| |

| Part II |

| | | |

| Item 13. | Defaults, Dividend Arrearages and Delinquencies | 129 |

| Item 14. | Material Modifications to the Rights of Security Holders and Use of Proceeds | 129 |

| Item 15. | Controls and Procedures | 129 |

| Item 16. | Reserved | 131 |

| Item 16A | Audit Committee Financial Expert | 132 |

| Item 16B | Code of Ethics | 132 |

| Item 16C | Principal Accountant Fees and Services | 132 |

| Item 16D | Exemptions from the Listing Standards for Audit Committees. | 133 |

| Item 16E | Purchases of Equity Securities by the Issuer and Affiliated Purchasers. | 133 |

| Item 16F | Changes in Registrant’s Certifying Accountant | 133 |

| Item 16G | Corporate Governance | 133 |

| Part III |

| | | |

| Item 17. | Financial Statements | 133 |

| Item 18. | Financial Statements | 133 |

| Item 19. | Exhibits | 133 |

| | | |

| Financial Statements | F-1 |

| | | |

| Signature Page | 138 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 20-F contains or incorporates by reference forward-looking statements. All statements, other than statements of historical facts, that address activities, events or developments that we intend, expect, project, believe or anticipate will or may occur in the future are forward-looking statements. Such statements are characterized by terminology such as “anticipates,” “believes,” “expects,” “future,” “intends,” “assuming,” “projects,” “plans,” “will,” “should” and similar expressions or the negative of those terms or other comparable terminology. These forward-looking statements, which include statements about the growth of the alternative fuels industry; market size, share and demand; performance; our expectations, objectives, anticipations, intentions and strategies regarding the future, expected operating results, revenues and earnings and current and potential litigation are not guarantees of future performance and are subject to risks and uncertainties, including those risks described under the heading “Risk Factors” set forth herein, or in the documents incorporated by reference herein, that could cause actual results to differ materially from the results contemplated by the forward-looking statements.

Investors are cautioned that our forward-looking statements are not guarantees of future performance and the actual results or developments may differ materially from the expectations expressed in the forward-looking statements.

As for the forward-looking statements that relate to future financial results and other projections, actual results will be different due to the inherent uncertainty of estimates, forecasts and projections may be better or worse than projected. Given these uncertainties, you should not place any reliance on these forward-looking statements. These forward-looking statements also represent our estimates and assumptions only as of the date that they were made. We expressly disclaim a duty to provide updates to these forward-looking statements, and the estimates and assumptions associated with them, after the date of this filing to reflect events or changes in circumstances or changes in expectations or the occurrence of anticipated events.

We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future events or otherwise. You are advised, however, to consult any additional disclosures we make in our reports on Form 20-F and Form 6-K, or their successors. We also note that we have provided a cautionary discussion of risks and uncertainties under the caption "Risk Factors" in this Annual Report. These are factors that we think could cause our actual results to differ materially from expected results. Other factors besides those listed here could also adversely affect us.

Information regarding market and industry statistics contained in this Annual Report is included based on information available to us which we believe is accurate. We have not reviewed or included data from all sources, and cannot assure stockholders of the accuracy or completeness of the data included in this Annual Report. Forecasts and other forward-looking information obtained from these sources are subject to the same qualifications and the additional uncertainties accompanying any estimates of future market size, revenue and market acceptance of products and services.

PART I

| Item1. | Identity of Directors, Senior Management and Advisers |

| Item2. | Offer Statistics and Expected Timetable |

Not applicable.

| 3.A. | Selected Financial Data |

The following selected consolidated financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and related notes included elsewhere in these statements. The selected consolidated financial data presented below are derived from our audited consolidated financial statements as of December 31, 2008, and 2007 and for the period from June 8, 2006 (date of inception) to December 31, 2006, and the consolidated financial statements of the Company as of December 31, 2008 and 2007, and for the twelve months then ended, which are prepared in accordance with accounting principles generally accepted in the United States of America (“US GAAP”).

| | | | | | | | | Jun. 8, 2006 | |

| | | Jan. 1, 2008 | | | Jan. 1, 2007 | | | (date of | |

| Income Statement Data (000's except shares | | to | | | to | | | inception) to | |

| and per share data) | | Dec. 31, 2008 | | | Dec. 31, 2007 | | | Dec. 31, 2006 | |

| Net sales | | $ | 50,350 | | | $ | 7,473 | | | $ | - | |

| Impairment charge | | $ | (13,824 | ) | | $ | - | | | $ | - | |

| Operating loss | | $ | (35,119 | ) | | $ | (7,494 | ) | | $ | (1,096 | ) |

| Loss on extinguishment of debt | | $ | (28,004 | ) | | $ | - | | | $ | - | |

| Net loss | | $ | (78,600 | ) | | $ | (19,018 | ) | | $ | (1,172 | ) |

| Net loss per share, basic and diluted | | $ | (4.23 | ) | | $ | (3.39 | ) | | $ | (586,000 | ) |

| Number of shares, basic and diluted | | | 18,577,251 | | | | 5,604,859 | | | | 2 | |

| Balance Sheet Data ($000's) | | Dec. 31, 2008 | | | Dec. 31, 2007 | | | Dec. 31, 2006 | |

| Total assets | | $ | 153,755 | | | $ | 153,308 | | | $ | 1,963 | |

| Total debt | | $ | 113,760 | | | $ | 108,288 | | | $ | 2,399 | |

| Additional paid-in capital | | $ | 143,131 | | | $ | 43,470 | | | $ | 685 | |

| Accumulated other comprehensive income (loss) | | $ | (33,133 | ) | | $ | 8,968 | | | $ | 34 | |

| | | | | | | | | Jun. 8, 2006 | |

| | | Jan. 1, 2008 | | | Jan. 1, 2007 | | | (date of | |

| | | to | | | to | | | inception) to | |

| Sales Data | | Dec. 31, 2008 | | | Dec. 31, 2007 | | | Dec. 31, 2006 | |

| Biodiesel | | | | | | | | | |

| Volume (millions of liters) | | | 21.80 | | | | 3.30 | | | | - | |

| Average selling price per liter | | $ | 1.18 | | | $ | 1.06 | | | $ | - | |

| | | | | | | | | | | | | |

| Ethanol | | | | | | | | | | | | |

| Volume (millions of liters) | | | 55.20 | | | | 9.20 | | | | - | |

| Average selling price per liter | | $ | 0.38 | | | $ | 0.38 | | | $ | - | |

Except as may be otherwise indicated, all dollar amounts are stated in U.S. dollars, the Registrant’s reporting currency. The following tables set out the exchange rates, based on the data from the website www.Oanda.com , for the conversion of the Brazilian real (R$) into one United States dollar (US$). The average exchange rates are based on the average of the daily closing exchange rates during such periods:

| | | Average | | | High | | | Low | | | Close | |

| Fiscal Year Ended 12/31/08 | | | 1.84 | | | | 2.61 | | | | 1.55 | | | | 2.36 | |

| Fiscal Year Ended 12/31/07 | | | 1.95 | | | | 2.16 | | | | 1.72 | | | | 1.77 | |

| Fiscal Year Ended 12/31/06 | | | 2.18 | | | | 2.37 | | | | 1.95 | | | | 2.14 | |

The closing exchange rate on June 29, 2009 was 1.95 Brazilian reais per one US dollar.

| 3.B. | Capitalization and Indebtedness |

Not applicable.

| 3.C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

You should carefully consider the following risk factors and all other information contained in this Report before purchasing our shares. We have assembled these risk factors based upon both publicly available information, our own analysis and our own beliefs relative to our understanding of our business. If any of the following risks occur, our business, financial condition or results of operations could be materially and adversely affected, in which case, the value of our shares could decline, and you may lose some or all of your investment.

General Risks Relating to Our Business

We are a recently formed company and still yet developing our management team and adjusting our internal controls; our inexperience could have detrimental effects on our business.

The Company was formed in 2006 and made its original acquisitions in 2007. Our operating businesses today consist of our ownership interests in two operating ethanol plants, Comanche Biocombustivieis de Canitar Ltda. (“Canitar”), and Comanche Biocombustivies de Santa Anita Ltda. (“Santa Anita”), along with related land, sugarcane plantings, rolling stock and storage tanks and our biodiesel business, Comanche Biocombustiveis de Bahia Ltda. (“Bahia”). During 2008, these acquired assets were significantly enlarged or rebuilt. While all of our plants are now fully operational, we are still a young and fast growing company, and are continuing to work (both internally and with outside consultants) to improve internal controls, production and logistics controls and management information system platforms. These will require continuing adjustments to achieve better control over and visibility into our operations and financials so as to avoid material weaknesses in our controls. Improvement and development efforts are ongoing and not yet complete.

We have made a number of substantial changes to our senior Brazilian management, principally by promoting from within the Company, and while we believe that the persons who have taken senior positions are qualified and committed, their performance is as yet not fully proven, and we may require further adjustments. Hiring or retaining capable experienced professionals may be difficult and if we are unable to hire and retain qualified personnel on a timely basis our business may be adversely affected.

We operate in a commodity based business in which the demand and the market price for our products are very cyclical and are affected by government policies, substitute products, the presence of large competitors and general economic conditions in Brazil and the world, all of which can augment the volatility of our revenues and such volatility could have adverse effects on our business.

The ethanol and biodiesel industries, both globally and in Brazil, have historically been and are expected to continue to be cyclical and volatile, sensitive to domestic and international changes in supply and demand, whether caused by changes in economic conditions or government policies. The current world economic crisis has both sharply reduced demand for many products and caused liquidity issues for many producers, including us. Our current product set, fuel ethanol and biodiesel, are very basic commodities and vulnerable to many competitive pressures, such as alternative products, producer overcapacity, weak demand and changes in government policies. As we are a small producer in these markets, we are subject to continual pricing pressure, exacerbated by a combination of over-capacity and weak demand worldwide that have created an environment of low prices and margins for our industry during most of 2008 and the first half of 2009.

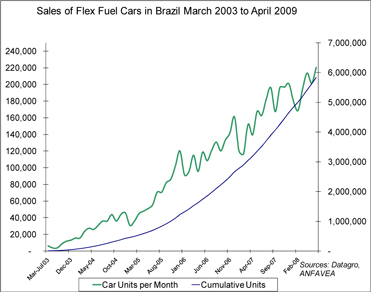

Ethanol is marketed as a fuel additive to reduce vehicle emissions from gasoline, as a blending agent to improve the octane rating of gasoline and as a substitute fuel for gasoline. As a result, ethanol prices are influenced by the supply and demand for gasoline and cars as well as government policy toward fuel usage, and our business and financial performance may be materially adversely affected if fuel demand or price decreases. For example, in Brazil, the demand for ethanol as a fuel is driven by the sales of flex-fuel cars, which in turn benefit from lower taxation, since 2002, as compared to gasoline-only cars. Approximately one-half of all fuel ethanol in Brazil is used to fuel automobiles that run on a blend of anhydrous ethanol and gasoline; the remainder is used in either flex fuel vehicles or vehicles powered by hydrous ethanol alone. If this favorable tax treatment of car sales is eliminated at some point, the production of flex fuel cars may decrease, which could adversely affect demand for fuel ethanol.

Our ethanol and biodiesel operations also compete with producers of other fuel sources and fuel additives made from raw materials having similar British thermal unit (“BTU”), octane and oxygenate values. Many of our potential competitors, including the major oil companies, have significantly greater resources than we have to develop alternative products and to influence the legislation and public perception of biofuels. In Brazil, Petrobras has enormous influence over the fuel markets and legislation pertaining thereto, so by virtue of Petrobras’ dominant position in Brazil, we may be exposed to further pricing risks, cost pressures or their changes in business strategy.

The domestic biodiesel market in Brazil is new and has already experienced periods of significant feedstock versus pricing mismatch—causing industry profit margins to decrease—while at the same time an expansion in the industry has resulted in overcapacity— further affecting industry profit margins.

Fluctuations in prices for ethanol or biodiesel may occur as a result of many factors beyond our control, such as fluctuations in fuel prices, changes in the production capacities of our competitors and the availability and price of substitute goods for the fuels we produce. In addition, like other agricultural commodities, biofuels are also subject to many other factors beyond our control, such as significant cost and sales price fluctuations resulting from the cost of growing and/or purchasing feedstocks, weather, natural disasters, harvest levels, agricultural investments, government policies and programs for the agricultural sector, domestic and foreign trade policies, shifts in supply and demand, increasing purchasing power, and global production of similar or competing products. In addition, as to those feedstocks that we do not grow ourselves, such as biodiesel feedstocks, we are subject to cost pressures arising from speculation in commodity markets that may result in price peaks or secular cost increases.

A change in governmental policies regarding biofuels blending mandates, relative taxation, environmental or overall policy in Brazil or worldwide may materially adversely affect our business.

Some studies and commentators have challenged whether ethanol and or biodiesel are an appropriate source of fuel or fuel additives because of concerns about energy efficiency, potential health effects, competition for food resources, the indirect effects of land-use. competition for water, cost and impact on air and water quality, and impact on worker well-being. At this time the energy policies of governments in several countries strongly support biofuel production. However, if a consensus develops that these or other concerns are well-founded and that biofuel production does not enhance such countries’ overall energy, social or environmental policies, our ability to economically produce and market ethanol and/or biodiesel could be materially and adversely affected.

For example, governmental authorities of several countries, including Brazil and certain states of the United States (“US”), currently require the use of ethanol as an additive to gasoline. Since 1997, the Brazilian Sugar and Alcohol Interministerial Council (Conselho Interministerial do Açúcar e Álcool) has set the percentage of anhydrous ethanol that must be used as an additive to gasoline (currently, at 25% by volume). According to the United States Department of Energy, (“DOE”), total annual gasoline consumption in the United States is approximately 140 billion gallons and total annual ethanol consumption represented less than 7% of this amount in 2008, driven by mandates. The US market should achieve a total volume of 36 billion gallons of ethanol annually under the new US national Renewable Fuel Standards, (“RFS”), by 2022. The European Union (“EU”) promotes the production of biofuels and has set a target of 5.75% share of biofuels in the transport section for all EU Member States by 2010, and a target of 10% to be reached by 2020. According to Cosan S. A. (“Cosan”), some areas of China require the addition of 10% ethanol to gasoline, Japan requires the addition of 3% of ethanol to gasoline, increasing such requirement to 10% in 2010 and nine states and four union territories in India require the addition of 5% of ethanol to gasoline. Other countries have similar governmental policies requiring various blends of anhydrous ethanol and gasoline. Changes in these government policies and blending mandates in Brazil or elsewhere could have a dramatic affect on the demand for ethanol from Brazil, which could affect our ability to develop an export market for our products in the future.

There are other government policies in Brazil that might have a material effect on our business. For example, an increase in the levels at which flex fuel vehicles are taxed in Brazil, a stimulus to the demand for natural gas and other fuels as an alternative to ethanol, or Brazilian government mandated lowering of gasoline prices or taxes on gasoline are policy measures which may cause demand for ethanol to decline.

In January 2007, the State of California established a Low-Carbon Fuel Standard (LCFS) by Executive Order. This greenhouse gas (GHG) standard for transportation fuels may dramatically change the relative competitiveness of certain types of biofuels, or may result in a fundamental change in how biofuels are produced and where they are produced. We expect that the LCFS will be adopted by other states in the US and may be adopted by a number of European countries in one form or another. Such new and evolving standards may have material impacts on our business model that are hard to anticipate at this time.

In the case of biodiesel, Brazilian law 11.097 of January 13, 2005 required that the biodiesel participation in total diesel sales be at least 2% by January 2008. On April 27, 2009, the CNPE (Conselho Nacional de Política Energética) of Brazil increased the minimum percent participation to 4% effective July 1, 2009. The law calls for a 5% blending requirement by 2013. In addition, Law 11.116 of 2005 reduces substantially the gross turnover taxes (PIS and COFINS) levied on the sale of biodiesel produced with certain raw materials and under certain conditions. In addition, the National Petroleum Agency (“ANP”) licenses new plants. Thus, government policy can have a very material effect on both demand as well as supply of biodiesel, causing our business margin pressures and additional competition.

There can be no assurance that, among other factors, competition from alternative sources of ethanol or biodiesel, gasoline or diesel, changes in world or Brazilian agricultural or trade policy or developments relating to international trade, including those under the World Trade Organization (“WTO”), will not directly or indirectly result in lower domestic or global fuel, ethanol or biodiesel prices.

The global credit crisis has significantly limited our access to capital markets and our ability to borrow for working capital. The acquisition or planting and harvesting of feedstocks for production of ethanol and biodiesel requires substantial amounts of working capital to meet both our production objectives and our contractual commitments and our inability to obtain financing to purchase such feedstocks has limited and may continue to limit our ability to operate our plants at planned levels of production and may also adversely affect our margins.

The global credit crisis has dramatically reduced credit for most businesses worldwide. Agriculturally based industries, such as ours, are constantly in need of both working capital and planting credits. In addition, credit in Brazil for companies such as ours, while never plentiful, has become more limited and more expensive since the third quarter of 2008. We have limited cash and credit resources and may not be able to fund the planting and harvesting or acquisition of sufficient feedstocks to meet our projected volumes of ethanol and biodiesel production or the volumes required under our contracts, or we may be unable to negotiate for feedstocks on the same terms as are available to producers with better cash and credit resources. Our anticipated margins, or our ability to continue to perform under our supply contracts, may be adversely affected as a result.

The acquisition of biodiesel feedstock requires substantial working capital and lack of working capital in our ethanol business may force us to sell ethanol as it is produced, which may be during periods of seasonal low prices. Availability of working capital financing for these two uses has affected our results in 2008 and 2009 and may continue to significantly affect our financial results.

Our ability to maintain and grow our business could be adversely affected if we are unable to obtain additional financing on acceptable terms. In carrying out our recent expansions, we incurred liabilities with vendors that we have not been able to satisfy on a timely basis to date because of the unavailability of capital; as a result we risk incurring ill will and we have incurred legal actions from some of our suppliers.

We will seek additional debt or equity financing to finance our existing operations and future acquisitions or expansions. Such financing may not be available on acceptable terms and our failure to obtain additional financing when needed could negatively impact our growth, financial condition and results of operations. In addition, we incurred liabilities with vendors in connection with the Canitar construction that we have not been able to satisfy on a timely basis because of the unavailability of capital. While we are in the process of negotiating these vendor liabilities, we are attempting to pay installments from operating cash flow, which, dependent on the amortization, has caused us to be delinquent on other obligations. We may risk ill will from suppliers who are necessary to our continuing operations, or face potential legal actions from suppliers. This has made availability of borrowing more difficult and more expensive than it would be otherwise during this period.

Obtaining of additional equity financing may be dilutive to the holders of our shares, and debt financing, if available, may involve significant cash payment obligations and covenants that restrict our ability to operate our business. The availability of credit inside Brazil is limited, especially to a new business, and the ability to access credit internationally may be impaired by the condition of global credit markets. Our ability to access the limited local credit may be adversely affected by poor payment history reports from our vendors to local Brazilian credit bureaus. While all of these factors and the ones described in our financial statements raise substantial doubt about the Company’s ability to continue as a going concern, management has taken certain steps to raise external capital, manage our cash position and improve profitability, as described below in Item 5.Operating and Financial Review and Prospects, “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

.

We may not successfully achieve the expansions of product mix that we are working on and we may not be able to successfully acquire or develop additional production capacity through acquisitions, new projects or expansion of existing facilities, affecting our ability to grow our margins and to grow the overall scale of our business.

Our business model is to produce clean, renewable chemicals from agriculture, in the first phase, producing only basic biofuels and over time also producing enhanced products, such as electricity, non-fuel types of renewable chemicals, and advanced biofuels as defined by the United States Government,. Advanced biofuels, under U.S. law have a series of tax credits associated with them, that may more than offset the current U.S. tariff against Brazilian ethanol. The U.S. government is still in the process of refining the definitions of advanced biofuels. However our ability to produce these enhanced products is dependent on our continued ability to attract capital on reasonable terms (see the risk factor entitled “The global credit crisis has affected substantially limited our access to capital markets…” above) to build or expand our operating facilities to produce such additional products, to sign contracts with off-take purchasers, and to have the operational expertise to manufacture these products successfully. Thus, our growth strategy to expand our product mix to include such higher value added products such as chemicals and electricity may not be realized because we fail to have access to sufficient capital or technology or markets. In addition, our intention to eventually produce advanced biofuels is subject to many technical, environmental and policy issues, as well as clarification of the product specifications as policies evolve. We may have neither the technical expertise, understanding or financial resources to produce such products.

We have little significant prior experience in planning, developing and managing alcohol based chemical or energy generation projects. We may need to invest significant amounts to overcome any operating difficulties, while there are many competitors with more experience and more capital both in Brazil and worldwide competing in these products. We will need to identify and negotiate contracts with customers for these products; we may have difficulty to do so, and such contracts may provide for penalties for non-performance. We may be subject to governmental regulation affecting our ability to change our product mix; for example, the Brazilian government regulates the electricity sector extensively. We may not be able to satisfy all the requirements necessary to acquire new contracts or to otherwise comply with Brazilian energy regulation. Changes to the current energy regulation or federal authorization programs may adversely affect the implementation of this element of our business strategy.

We are also continually exploring opportunities to increase our conventional production capacity and throughput, so as to enhance our ability to produce our basic product line and future enhanced products through acquisitions, new projects and expansion of existing facilities or strategic alliances. However, our management is unable to predict whether or when any prospective acquisitions or strategic alliances will occur, or the likelihood of a certain transaction being completed or financed on favorable terms and conditions. Even if we are able to identify expansion or acquisition targets and obtain the necessary financing to make these investments, we could financially overextend ourselves, especially if an investment is followed by a period of lower than projected biofuel prices.

Our failure to successfully integrate, operate and manage such new products and plants or to manage any new alliances successfully, could adversely affect our business and financial performance.

The integration of new products, new businesses or expansions may result in unforeseen operating difficulties and may require significant financial and managerial resources that would otherwise be available for the ongoing development or expansion of our existing operations. In addition, such new products, new businesses or expansions may not enhance our financial performance.

Many of our competitors have substantially greater financial and other resources than we do and also may be pursuing growth through acquisitions and alliances. This may reduce the likelihood that we will be successful in completing expansions, acquisitions and alliances necessary for the expansion of our business. Acquisitions also pose the risk that we may be exposed to successor liability relating to actions involving an acquired company, its management or contingent liabilities incurred before the acquisition. The due diligence we conduct in connection with an acquisition, and any contractual guarantees or indemnities that we receive from the sellers of acquired companies, may not be sufficient to protect us from, or compensate us for, actual liabilities. A material liability associated with an acquisition could adversely affect our business and results of operations and reduce the benefits of the acquisition.

We may not be successful at reducing our operating costs and increasing our operating efficiencies and this would negatively affect our financial performance.

Our projections assume that we will continue to reduce costs and increase operating efficiencies. We may not be able to reduce operating costs by applying processes, equipment, technology and cost controls and increasing our operating efficiencies to achieve improved operating results in the future because we could have inadequate management, lack necessary capital and other resources, have anticipated technical improvements that we do not achieve or for other reasons. We cannot assure you that we will be able to achieve all of the cost savings initiatives that we expect to realize from our assets, or we may be unable to successfully implement one or more of our initiatives. In addition, we may experience unexpected cost increases that offset the savings that we achieve. Our failure to realize cost savings may adversely affect our competitiveness and results of operations.

We may invest in innovative technologies or alternative feedstock for the production of ethanol, biodiesel or enhanced products, and such investments might not have the anticipated results, leading to a partial or complete loss of such investments. Alternatively, such investment by others in such technological developments could make other sources of ethanol or biodiesel less expensive and give others a competitive advantage over us.

Various technologies or alternative feedstocks could increase plant utilization, lead to different processing technologies to increase the yield from feedstocks, such as cellulosic technology, or make feasible the use of entirely new feedstocks, among other things. For example, although at present ethanol produced from sugarcane is competitive with that produced from other feedstocks, various technologies are under development that could improve the efficiency of production from corn or that can make possible the economic production of ethanol from agricultural sources not presently used for ethanol production, and such developments would have an adverse effect on the market for ethanol derived from sugarcane. Similarly, there could be significant technological breakthroughs in the production processes of or feedstock for biodiesel. These technologies could create a vastly different competitive landscape for us and our products.

There could also occur technological developments for the production of sugar cane ethanol or biodiesel to which we might not have access. Other producers may have access to such developments, allowing them to produce more efficiently, reducing our competitiveness and causing a decline in our market share, sales and/or profitability.

We face significant competition in our business, which may adversely affect our market share and profitability.

The agricultural sector in Brazil, including ethanol and biodiesel industries, is very competitive and some existing producers have substantially greater production, financial, research and development, personnel and marketing resources than we do. As a result, our competitors may be able to compete more aggressively, influence market conditions, and sustain that competition over a longer period of time. Our lack of resources relative to some of our competitors may cause us to fail to anticipate or respond adequately to new developments and other competitive pressures. This failure could reduce our competitiveness and cause a decline in market share, sales and/or profitability.

In Brazil, we compete with more than 275 individual ethanol producers in the Center South, according to data from the União da Indústria de Cana-de-açúcar (“UNICA”). Despite increased consolidation, the Brazilian sugar and ethanol industries remain highly fragmented. Major competitors in the ethanol sector in Brazil, according to Cosan, are Cosan itself, Louis Dreyfus, Grupo São Martinho, Vale do Rosario (acquired by Louis Dreyfus), Carlos Lyra, Grupo Zillo Lorenzetti, Alto Alegre, Grupo Irmaos Biaggi, J. Pessoa & Co., and Nova America (acquired by Cosan), among others. A number of other sugar and ethanol producers in Brazil market their sugar products through cooperatives. Today, our major competitors in the biodiesel sector include Brasil Ecodiesel, Granol, Biocapital, ADM, Oleoplan and Agrenco, as well a Petrobras itself, among others.

Many factors influence our competitive position, including the cost of capital, agricultural productivity, industrial productivity, location relative to transportation, the availability, quality and cost of fertilizer, energy, water, chemical products and labor, and in the case of biodiesel, third party feedstock. In addition, a number of our competitors have substantially greater financial and marketing resources, a larger customer base and a greater breadth of products than we do. They may be able to sustain low market prices for a longer time than we can. If we are unable to remain competitive with these producers in the future, our profitability may be adversely affected.

Our competitors may open new plants that will expand the Brazilian sugarcane-related or biodiesel industries, and such expansion could result in overcapacity and competitive pricing pressures or competition for human and material resources causing risks to our business.

Expansion in these sectors could result in oversupply, inability of infrastructure to sustain larger volumes, and pressure on limited production resources. The Brazilian internal market might not absorb the volume or timing of additional production, bringing prices down and forcing producers to export ethanol or biodiesel. The Brazilian infrastructure for exports is currently limited and requires additional investments, and may not be able to absorb additional volumes. It is also possible that the domestic infrastructure of rail and roads might be insufficient to support large scale increases in demand for such infrastructure. There may be limited availability of equipment, or delays in delivering or installing newly contracted equipment due to an increased demand for processing equipment, which could affect expansion plans. There may be limited availability of agricultural and industrial workers—the sugarcane industry, for example, presently employs over 1 million people according to the website of Cosan and depending on the rate of mechanization of the fields, the industry will have to attract a significant number of workers. We might face difficulties in hiring trained experienced industrial workers at our plants, and for the production of feedstocks, we will need to attract experienced agricultural workers and train workers for mechanical harvesting. It is also possible that the growth of the Brazilian economy generally will create a demand for the same production resources that we require.

As a biofuel producer, the cost basis of our product relies on agricultural productivity, weather, availability of fertilizers and pesticides and other input factors, that are generally out of our control and our output prices are affected by seasonality.

For example, our ethanol production depends on the volume and sucrose content of the sugarcane that we cultivate or that is supplied to us by growers located in the vicinity of our mills. Crop yields and sucrose content depend primarily on weather conditions such as rainfall and temperature, which vary. Our biodiesel feedstocks suffer from susceptibility to similar adverse weather patterns. Weather conditions have historically caused volatility in the biofuel industries by causing crop failures or reduced harvests. Flood, drought or frost can adversely affect the supply and pricing of the agricultural commodities that we sell and use in our business. Future weather patterns may reduce the amount of sugar or sugarcane that we can recover in a given harvest or its sucrose content. In addition, our ethanol business is subject to seasonal trends based on the sugarcane growing cycle in the Center-South region of Brazil.

The annual sugarcane harvesting period in the Center-South region of Brazil begins in April/May and ends in November/December. This creates fluctuations in our inventory, usually peaking in November to cover sales between crop harvests (i.e., December through April), and a degree of seasonality in our gross profit. Seasonality and any reduction in the volumes of sugar recovered could have a material adverse effect on our business and financial performance.

We rely on a limited number of production plants, and any interruption on the production of those plants would affect us.

Interruptions in the operations of the plants might be caused by, among other things, technical difficulties, accidents, operating flaw, weather, natural or environmental disasters, strikes, poor judgment of management, and lack of skill or our personnel, diminishing or interrupting our output and resulting in material losses. Our insurance coverage might not be sufficient or appropriate to compensate for such interruptions, or not cover unpredicted events or weather. Our lack of diversification may subject us to numerous economic, competitive and regulatory developments, any or all of which may have a substantial adverse impact.

The agricultural sector is highly susceptible to governmental influence and policies.

Changes in rules or more restrictive rules for the agricultural sector could negatively affect our results. Industry specific increases in taxation, price-control policies, land use restrictions, import-export restrictions or rulings by environmental agencies could broadly affect the agricultural industry as a whole, and therefore our results.

We require permits from Brazilian Governmental authorities with control over certain aspects of our business. Failure to obtain permits on a timely basis or to maintain permits in proper order could materially affect our ability to operate.

We are subject to various Brazilian federal, state and local environmental protection and health and safety laws and regulations governing, among other matters, land use limitations, the generation, storage, handling, use and transportation of hazardous materials; the emission and discharge of hazardous materials into the ground, air or water; and the health and safety of our employees.

We are also required to obtain permits from governmental authorities for certain aspects of our operations. Following the Canitar facility lightening strike, we started the reconstruction of the facility based on the understanding that we were authorized to proceed to reconstruct according to the current operating license for 300,000 tons, until CETESB ( Companhia de Tecnologia de Saneamento Ambiental ), the state of Sao Paulo regulatory authorities, analyzed our applications for the expansion. Subsequently, the Company’s Canitar unit negotiated with CETESB with respect to the issuance of environmental licenses for our Canitar facility at its expanded 1.2 million ton capacity (expressed in terms of 6,000 tons per day, the capacity depends on days utilized) in the form of a Termo de Ajuste de Conduta (an Agreement for amending the licensing process and our compliance, a “TAC”) that covers the granting of provisional, installation and operating licenses for Canitar. While such negotiation is complete, the TAC has not been executed. While the TAC requires some additional expenditures to comply with its terms, these further expenditures are not material. If the TAC were not to be entered into, or if after entering into the TAC Canitar were to fail to perform thereunder, Canitar could be exposed to penalties for failure to be properly licensed, or could be required to cease operations pending the receipt of necessary licenses. Our filing of an environmental impact report with respect to the expansion of the capacity of our Santa Anita facility from its licensed 300,000 tons to 1.2 million tons has been delayed as regulators determine how zoning maps will be applied in the case of Santa Anita. While we believe that these licenses will be granted as a matter of course, the granting of licenses is subject to administrative discretion and the performance of ministerial acts and receipt of necessary licenses may be delayed. We may at times proceed to install facilities or operate based on provisional licenses, prior licenses, licenses for lesser capacities or in anticipation of receipt of a full complement of licenses. In addition, we will be required to file environmental impact statements for expansions beyond 1.5 million tons of processing capacity. We are subject to regulation by the Brazilian National Petroleum Agency in the case of operation and expansion of our biodiesel facilities. Our current license is for 120 million liters of capacity. Due to the possibility of changes to environmental regulations, permit regulations and other unanticipated changes, the amount and timing of future environmental or regulatory expenditures may vary substantially from those currently anticipated. We could be subject to civil penalties for non-compliance with certain laws or regulations under Brazilian law or other international laws. We could be held liable for any and all consequences arising out of human exposure to hazardous substances or other environmental damage. We cannot assure you that our costs of complying with current and future environmental and health and safety laws, permit laws, and our liabilities arising from past or future releases of, or exposure to, hazardous substances will not adversely affect our business, results of operations or financial condition. Violations of these laws and regulations or permit conditions can result in substantial fines, criminal sanctions, revocations of operating permits and/or shutdowns of our facilities.

Our costs of complying with current and future environmental and health and safety laws, and our liabilities arising from failure to comply with environmental laws, including past or future releases of, or exposure to, hazardous substances, could adversely affect our business or financial performance.

Government laws and regulations governing the burning of sugarcane could have a material adverse impact on our business or financial performance.

Today, although we are able to achieve 100% mechanization at our Canitar plant and 50% at our Santa Anita plant on our own sugarcane, many of our external suppliers are not mechanized and so overall, approximately 43% of our sugarcane supply for Canitar is harvested mechanically and approximately 47% of our sugarcane supply for Santa Anita is harvested mechanically. The balance of our sugarcane is currently harvested by burning the crop, which removes leaves and destroys insects and other pests. The State of São Paulo and some local governments have established laws and regulations that limit our ability to burn sugarcane or that reduce and/or entirely prohibit the burning of sugarcane in certain areas by 2012. In addition, we bear co-responsibility with certain of our suppliers in terms of mechanization. Any failure to comply with these laws and regulations may subject us to legal and administrative actions. These actions can result in civil or criminal penalties, including a requirement to pay penalties or fines, which may range from R$50.00 to R$50.0 million (approximately $25 to $25 million based on an exchange rate as of R$2 to $1) and could be doubled or tripled in case of recidivism, an obligation to make capital and other expenditures or an obligation to materially change or cease some operations.

We manage our business on a local basis and our ongoing implementation and improvement of our management information system is subject to functionality and adequacy risks, which we may not be able to fully control, thus our operations and internal controls may be materially adversely affected by this inadequacies in this implementation, failures of functionality or training and/or inconsistent management practices.

We manage our business in Brazil with local and regional management retaining responsibility for day-to-day operations, profitability and the growth of the business. Our operating approach may make it difficult for us to implement strategic decisions and coordinated practices and procedures throughout our extended operations, including implementing and maintaining effective internal controls Company-wide. Our decentralized operating approach could result in inconsistent management practices and procedures and adversely affect our overall profitability, and ultimately our business, results of operations, financial condition and prospects.

We have installed an enterprise resource management (“ERP”) information technology system that will control and report on all of our enterprise operations. We are continually working on implementing, training, data collection and broadening the use of our ERP system, however, our system may not be sufficient to fully control our current or anticipated operations over time, or may not meet the requirements that are imposed upon our internal control procedures to accomplish our Sarbanes Oxley Act of 2002 requirements. In addition, ERP systems are dependent upon communications providers, web browsers, telephone systems and other aspects of the Internet infrastructure, which have experienced significant system failures and electrical outages in the past. Our systems are susceptible to outages due to fire, floods, power loss, telecommunications failures, break-ins and similar events. Despite our implementation of network security measures, our servers are vulnerable to computer viruses, break-ins and similar disruptions from unauthorized tampering with our computer systems. Unplanned systems outages or unauthorized access to our systems could materially and adversely affect our business.

We may be adversely affected by the failure to perform, or even the dishonesty, of persons or entities with whom we deal. We rely on contracts with many third party suppliers or purchasers. Breaches of these contracts may have a material adverse effect on our business.

We may rely heavily on the performance and integrity of representations made by suppliers, the sellers of assets, or our personnel in making our acquisition and purchasing decisions. Although, we have implemented a company-wide code of ethics, it is difficult to measure progress in the adoption of this code. Also, because there may be generally little or no publicly available information about other entities, such as suppliers, we may not be able to confirm independently or verify the information provided for use in such decisions. In addition, we rely on the performance and integrity of suppliers, customers or vendors, whose employees or partners may take actions which are not permitted by the relevant agreements.

Both our own agricultural production and third party feedstock production require extensive use of third party contracts to maintain our operations. We buy ethanol from third parties periodically, and to the extent that such third parties breach their obligations, such as occurred in with the Nelson Cury family sugarcane businesses our financial results could be adversely affected and we may be required to resort to litigation to enforce our rights. In December, 2007 the Company’s Canitar unit entered into a trading transaction with this group pursuant to which Canitar advanced an aggregate of approximately R$10 million (approximately $5.6 million at average exchange rates in effect in December 2007), the repayment of which was to be satisfied by delivery to Canitar’s designee of ethanol during 2008. Approximately R$8 million (approximately $4.17 million at average exchange rates in effect for 2008) remains unsatisfied under such contracts and R$5.3 million (approximately $2.9 million at average 2008 exchange rates) has been paid. See Item 8.A.7. Such results require us to enter into litigation to enforce our rights. We also buy transportation services, and a contract breach caused a nearly complete stoppage at our Santa Anita facility for several days in June of 2008 due to a failure to supply such services. Since then we have diversified suppliers and bought trucks to better protect against such a future event. Similarly, we sell biofuels to third parties, and while most such contracts have been undertaken without problems,

the ability to enforce contracts in Brazil through the Brazilian legal system is time consuming and without certain results.

We are subject to acts of nature. Our products are flammable and combustible and our production processes involve risk of fire and explosion and other dangers.

Lightning, wind, earth movements, floods and other acts of nature could interrupt our production or our markets, and damage our assets. Our insurance coverage might not be sufficient to compensate for such losses, or not cover unpredicted events. For example, in September, 2007, storage tanks at Canitar in which Santa Anita had stored ethanol were hit by lightning, and the resulting explosion and fire caused the death of one worker, injuries to others, and a total loss of the stored fuel. Liability for the death and injuries is covered by insurance, and is the subject of labor claims aggregating approximately R$762,000, which are expected to be settled in conjunction with Canitar’s liability insurer. Santa Anita had acquired insurance coverage for its fuel with a policy limit of approximately R$6,000,000, approximating the value at the time of the stored fuel. However, the insurance carrier has maintained that the coverage applies to Canitar, not Santa Anita, and that as the value of the coverage was less than the value of the facility, the pro-ratio provisions of the policy permit the insurer to pay only a pro-rated part of the loss. Hence, approximately R$2,842,741 of the loss remains unpaid, and the Company will cause Santa Anita to continue to claim for such payment. However, the Company’s financial statements in 2007 and 2008 reflected the loss and insurance payments received to date. See also Item 8.A.7.

Fire, explosion or malfunction of equipment could cause injury or death to employees or other persons, damage to our installations and/or loss to our finished products or our inventory in the future. Fire, whether naturally occurring or resulting from uncontrolled crop-burning, could cause injury or death to employees or other persons, burn planted crops or could damage agricultural equipment. Such events could also result in civil liability to third parties, or subject us to regulatory sanctions and our management to criminal liability.

We maintain third-party insurance over a certain range of risks to our business and assets, and our results of operations and financial condition may be affected by the cost of uninsured risks.

We have obtained insurance for our business and assets which we believe is comparable to that obtained by other similar companies in Brazil. However, since the Brazilian insurance market is closed and the ability to place insurance is somewhat limited, this may address only a limited range of risks and may not cover a variety of risks that might be covered by other types of businesses in other developed country markets. We might not cover all risks to which we are exposed or acquire sufficient coverage, and insurers may challenge our claims in connection with losses. As a result, our results of operations and financial condition may be affected by the cost of uninsured risks.

Hedging transactions, or lack of hedging, involve risks that can harm our financial performance.

We are exposed to market risks arising from the conduct of our business activities—in particular, market risks arising from changes in commodity prices, exchange rates or interest rates. For example, the bulk of our long-term debt is denominated in US dollars, and our cash flows are primarily in Reais. During 2008, we did not hedge foreign exchange rates or soy oil for our biodiesel operations. Both decisions had an adverse effect on our financial results and ability to service our debt. While in the future, we may attempt to minimize the effects of volatility of ethanol prices, feedstock prices and exchange rates on our cash flows by engaging in hedging transactions involving commodities and exchange rate futures, options, forwards and swaps, such operations have intrinsic risks including basis risk, risk of inappropriate or incomplete hedges, counterparty risks or risk where there is a change in the expected differential between the underlying price in the hedging agreement and the actual settlement price of commodities or exchange rate. We may also choose not to engage in hedging transactions in the future, due to the perceived risk or lack of financial capability, which could adversely affect our financial performance or ability to service our debt during periods in which commodities prices or exchange rates suffer from high volatility and unexpected sharp increases or decreases.

As a holding company, we may face limitations on our ability to receive distributions from our subsidiaries.

We conduct all of our operations through subsidiaries and are dependent upon dividends or other inter-company transfers of funds from our subsidiaries to meet our obligations, including financial obligations. For example, Brazilian law permits the Brazilian government to impose temporary restrictions on conversions of Brazilian currency into foreign currencies and on remittances to foreign investors of proceeds from their investments in Brazil, whenever there is a serious imbalance in Brazil’s balance of payments or there are reasons to expect a pending serious imbalance. The Brazilian government last imposed remittance restrictions for approximately six months in 1989 and early 1990. The Brazilian government may take similar measures in the future. Any imposition of restrictions on conversions and remittances could hinder or prevent us from converting into U.S. dollars or other foreign currencies and remitting abroad dividends, distributions or the proceeds from any sale in Brazil of common shares of our Brazilian subsidiaries. We currently conduct all of our operations through our Brazilian subsidiaries. As a result, any imposition of exchange controls restrictions could reduce the market price of our Ordinary Shares.

Risks Specifically Relating to Our Ethanol Business

Sugarcane is the primary input into our ethanol business. We are exposed to market prices for a portion of our raw materials and we may be adversely affected by a shortage of sugarcane, high third party sugarcane costs or changes in the costs of inputs to the growing process.

Sugarcane is our principal raw material used for the production of ethanol. We grow sugarcane ourselves, enter into grower partnerships and purchase sugarcane from third party suppliers. For 2009, approximately 48% of our sugarcane needs were from our own sugarcane on company owned or leased land and grower partnerships and 52% will be acquired from third party suppliers under long-term or spot contracts. Our ability to increase the percentage of owned sugarcane depends on our ability to lease or purchase land and to develop plantations or to obtain long-term contracts on economic terms. As of June 1, 2009, we also leased approximately 7,600 hectares under approximately 100 land lease contracts with an average remaining term of four years, with renewal provisions. Any shortage in sugarcane supply or increase in sugarcane prices in the near future, including as a result of the termination of supply contracts or lease agreements representing a material reduction in the sugarcane available to us for processing or increase in sugarcane prices may adversely affect our business and financial performance.

To the extent that we purchase feedstock at market prices from third parties or our contracts have market pricing provisions, this could have a negative effect on our margins, depending on prices relative to ethanol prices. To the extent that we produce our own feedstock and market prices of feedstock, for whatever reason, fall below our cost of feedstock production, then we may miss an opportunity to improve our margins and we cannot be certain that we will recover any specific margin over our cost of feedstock or that we will not suffer a loss from the sale at variable prices in the future.

Both our own agricultural production and third party feedstock production require extensive use of fertilizers and pesticides to maintain yield and productivity. The unavailability of such inputs or excessively high prices, as occurred in mid 2008, can dramatically affect our yields and costs.

We rely on a number of land leasing or agricultural partnership agreements to meet a large portion of our land and feedstock needs. Sugarcane transportation costs are an important part of our cost structure.

Interruptions in sugarcane supply by our third party suppliers, or termination or expiration of our leasing or sugarcane partnership agreements, might affect our processing forecasts. We acquire sugarcane from suppliers to meet the balance of our sugarcane needs. Contract issues or contract defaults could have a materially negative effect on our business. We grow sugarcane on land leased through multi-year land leasing agreements, which in the case of sugarcane in Sao Paulo state typically have a five or six year term, which is shorter than the useful life of our production facilities, and therefore we are exposed to the risks of relying on the availability, renewal and enforceability of contracts to control our feedstock production.

Transportation is an important cost to us, so we must lease our land within a limited area of influence for sugarcane, forcing us to negotiate our leasing contracts with a limited number of properties and land owners, which could result in higher leasing rates. We have focused our land strategy on regions where currently there is availability of land for lease. However, competitors might install themselves or expand their area of influence and dispute land with us, or land-use regulations could limit the availability of land for planting, changing the market dynamics and affecting either our ability to lease land or the price of the leasing contracts. Market conditions for alternative crops or uses of land, or regulatory considerations, might change and affect either our ability to lease land or the price of the leasing contracts.

We may be adversely affected by seasonality or changing weather patterns.

Our business is subject to seasonal trends based on the growing cycles in the regions where we produce in Brazil. The annual sugarcane harvesting period in the Center-South region of Brazil begins in April/May and ends in November/December. This can create fluctuations in our inventory, usually peaking in December to cover sales between crop harvests ( i.e. , January through April), and a degree of seasonality in our gross profit, with sugar and ethanol sales significantly lower in the last quarter of the fiscal year. Similarly, oil crops in the Northeast of Brazil, which are used as feedstock for our biodiesel, have a certain growing season, and we may need to store material or inventory outside of these seasons. This seasonality could have a material adverse effect on our results of operations for the last quarter of each fiscal year.

A significant change in expected or historical rain patterns for the regions where we have our plantations might diminish our ethanol output. Our ability to harvest and transport sugarcane from the fields to the production facility is reduced or impeded during rainy periods. Therefore, the rainy season of the year defines our harvesting period, and rain-intensive periods during the production period forces us to have idle plants or operate below capacity even during the production period. A significantly rainy year might reduce our ethanol output. Even though we keep agricultural experts to control our sugarcane plantations, uncommon plagues might affect our plantations, impacting our feedstock supply.

We have limited time periods within the year to plant crops and perform maintenance or expansion, so significant delays in the execution of planting or maintenance or expansion or weather or unavailability of fertilizers, could have a material effect on our anticipated future financial performance.

We are planting more sugarcane in 2009, as well as negotiating third-party sugarcane supply contracts, to meet our sugarcane feedstock needs for our 2009-2010 business plan. Our ability to meet plan objectives will be dependent on the availability of leased land or third-party supply in locations near to our mills, and tractors, harvesters, fertilizer and good weather conditions to meet our feedstock objectives. Maintenance and any planned upgrades of our sugarcane mills must be done between harvesting seasons, so we must order equipment that may have long lead times and we will have a limited time period to perform maintenance and upgrades.

We are not yet fully mechanized in our harvesting process and manual harvesting is a labor-intensive activity, so we are highly dependent on seasonal workers to complete the balance of our harvest.

We might face difficulties in hiring the number of workers we may need, and/or we, or the industry, might face difficult negotiations with the unions which generally represent all workers in the sector. We are migrating to mechanized harvesting to the extent of our resources to fund the acquisition of mechanical harvesters and related equipment. However, we have limited capital and credit, the availability of mechanical harvesters might be subject to a backlog, and the changeover to mechanized harvesting may cause tensions with manual sugarcane workers and their unions.

Ethanol prices have been correlated to the price of sugar historically. Accordingly, a decline in the price of sugar could lead to overproduction of ethanol and adversely affect our ethanol business.

A majority of ethanol in Brazil is produced at sugarcane mills that produce both ethanol and sugar. These millers are able to alter their product mix in response to the relative prices of ethanol and sugar, and this results in the prices of both products being correlated. Moreover, because sugar prices in Brazil are determined by prices in the world market, there can be a strong correlation between Brazilian ethanol prices and world sugar prices. Accordingly, a decline in sugar prices may also have an adverse effect on our ethanol business.

Our ethanol products are sold to a small number of customers which may be able to exercise significant bargaining power concerning pricing and other sale terms.

A substantial portion of our ethanol production is sold to a small number of customers that acquire large portions of our production and thus may be able to exercise significant bargaining power concerning pricing and other sale terms. In fiscal year 2008, we had 13 ethanol customers with four accounting for 56% of our sales.

Risks Specifically Relating to Our Biodiesel Business

Biodiesel is a relatively new market worldwide, the business is new in Brazil and thus the demand cannot be forecasted with great accuracy. A change in the Brazilian Government's policy that biodiesel be added to the sales of all diesel may materially adversely affect our business.

Our revenue will be derived in part from the production and sales of biodiesel. We expect that sales of biodiesel may constitute approximately 42% of our revenues in 2009, but that such percentage will decline in future years. This industry is relatively new in Brazil and the world, so there is not the length and depth of experience in the biodiesel industry that the ethanol industry has.

Furthermore, the industry is dependent on mandates to mix biodiesel into regular diesel both in Brazil and worldwide. The initial mandate for Brazil took effect in January 2008 at a 2% level and has been changed upwards twice. Most recently it was changed to a 4% mandate effective July 1, 2009. The law calls for a 5% mandate by 2013. Any changes in these mandates by the Brazilian Government could materially affect our biodiesel business operations by reducing overall demand within Brazil for biodiesel.

Our current contracts for biodiesel are at a fixed price, whereas our feedstock is for the most part purchased at market prices.

Our contracts with Petrobras extend for three months from their date, and are at fixed prices. These are granted pursuant to a series of reverse auctions to supply Petrobras. We are exposed to the risk that the cost of feedstock may be greater than that which we projected at the time that we bid for the Petrobras contracts, and may not be able to or may choose not to hedge against rising cost of feedstock. Future contracts with Petrobras are expected also to be for fixed prices. The pattern of the auctions and sales process exposes us to significant margin squeezes. We did not make any income on this operation in 2008 and there is no assurance that with this structure of the market that we will have any profitability in the future. Margin squeezes are caused by a combination of sharp commodity feedstock price volatility, relative to fixed off-take prices, and poorly executed government policies at the beginning of the industry. To the extent that we purchase our feedstock and such pricing falls below our cost of feedstock production, then it will have a material adverse effect on our results of operations. We expect this margin pressure to continue and government policies (with potentially detrimental effects) to continue to evolve for the foreseeable future.

While in the future, we could attempt to minimize the effects of volatility of feedstock prices by engaging in hedging transactions, such transactions involve a degree of risk. See the risk factor “Hedging transactions, or lack of hedging, involve risks that can harm our financial performance” above.

Our biodiesel products are sold to a small number of customers which may be able to exercise significant bargaining power concerning pricing and other sale terms. Our biodiesel sales contracts expose us to the risk of significant penalties and of cancellation.

The Company’s Bahia subsidiary has entered into various contracts with Petrobras for the delivery of biodiesel to only one customer, Petrobras S.A. pursuant to the current Brazilian industry framework. We anticipate that we might enter into bilateral contracts with other producers in 2010. To sell to Petrobras, we have entered into contracts pursuant to price auctions held by the ANP to sell up to 21 million liters of biodiesel in the first six months of 2009 to Petrobrás providing for an aggregate sales price of R$55.4 million (approximately $26 million at an exchange rate of R$2 per US$1). Those contracts can be terminated by Petrobrás, and also provide for large penalties in the event of default. If we fail to observe the operating provisions of those contracts, including such matters as meeting environmental or safety requirements, delay or failure in making deliveries, failure to program anticipated deliveries properly, fail to satisfy inspection requirements or delivery or operating standards, or if delivered product fails to meet quality standards, or we fail to pay or reimburse applicable taxes, we could be penalized by up to 0.033% of the contract value for each day of default. If we fail to deliver biodiesel timely, we could be penalized up to 100% of the contracted for value of the undelivered fuel, and we could be disqualified from participating in further auctions.

In connection with the contract entered into in the first semester of 2008, Petrobras failed to collect certain contracted for volumes and failed to pay the purchase price timely. As such failures created significant cash flow difficulties for the Company, the Bahia unit made a claim against Petrobras for indemnity payments (multas) applicable under the sales contract in the case of such failures, aggregating approximately $8.8 million (based on average exchange rates in effect during the first half of 2008). In the case of subsequent contracts with Petrobras for the delivery of biodiesel, the Bahia unit has failed to make full delivery of contracted for volumes. Although the Company believes that Bahia’s failure to deliver is excused under the relevant contracts, it is possible that Petrobras may make a claim for multas against Bahia, and while no such claim has been threatened, it is possible that if Bahia continues to press its claim against Petrobras to recover multas claimed by Bahia against Petrobras, or independent of the Company’s claim, Petrobras may seek to make claims against Bahia for multas by reason of Bahia’s failure to deliver, and such multas may aggregate to approximately $2.6 million (based on average exchange rates in effect during the first half of 2008. Moreover, Petrobras has notified Bahia that Petrobras proposes to to terminate the quarterly contract with Bahia expiring June 30, 2009 by reason of Bahia’s failure to deliver contracted for volumes. Such termination, should it occur, will have no practical effect on the contract as it would occur at or near the end of its term, however, it may disqualify Bahia from bidding to supply Petrobras in the auction for supply in the fourth quarter of 2009. The Company would cause Bahia to defend against such disqualification on the basis that Bahia’s non-performance was excused by force majeure and on other bases, and Bahia would not be precluded by such termination from participating in Petrobras’s anticipated auction for emergency supply of biodiesel in the northeast region of Brazil. See also Item 8.A.7.

If we are unable to obtain sufficient adequate feedstock, or if feedstock prices make the production of biodiesel at the prices provided for in the contracts uneconomical, we may be unable to deliver the contracted for product or we may be unable to operate so as to produce the contracted for product because of equipment breakdown or operator error, electricity outage or other circumstances not meeting the definition of an “act of God” within the terms of the contracts. We may thus be exposed to such non-delivery penalties or be disqualified from further auctions. Also, if Petrobrás were to cancel the contracts in whole or in part or disqualify us from future auctions after we had acquired feedstock, and we were unable to contract for the sale of biodiesel produced from that feedstock at the same or better price than in the Petrobrás contracts, we would be exposed to the risk of producing at a lesser margin than anticipated or to the risk of loss in the event that we were to resell such feedstock at a lower price than our acquisition price.

Our biodiesel business is subject to a number of sales, income and other tax exemptions granted by the Brazilian state and federal governments.

These exemptions are granted pursuant to law or special tax zone regulations. However, any repeal of such exemptions could materially affect our cost competitiveness in the biodiesel business. Some Brazilian states have not yet developed specific tax legislation for biodiesel, and the entire tax regime at different stages for biodiesel could change. Any changes in such legislation could negatively affect our biodiesel profitability. Some of these tax exemptions are related to the Social Fuel Seal program of the Brazilian Ministry of Agricultural Development, which seeks to encourage purchases of agricultural feedstocks from family farms of twelve hectares or less. We must maintain our certification in the Social Fuel Seal program to maintain these benefits.

Developing and administering agricultural projects that include a social service component may require skills that we do not possess, may be more costly than we project and may expose us to political or social pressures or criticism.