UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF

REGISTERED MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number: | 811-22132 |

| Exact name of registrant as specified in charter: | Aberdeen Funds |

| Address of principal executive offices: | 1900 Market Street, Suite 200 |

| Philadelphia, PA 19103 | |

| Name and address of agent for service: | Ms. Andrea Melia |

| abrdn Inc. | |

| 1900 Market Street, Suite 200 | |

| Philadelphia, PA 19103 | |

| Registrant’s telephone number, including area code: | 866-667-9231 |

| Date of fiscal year end: | October 31 |

| Date of reporting period: | October 31, 2021 |

Item 1. Reports to Shareholders.

Aberdeen Funds

Equity Series

Annual Report

October 31, 2021

Aberdeen China A Share Equity Fund

Class A – GOPAX ■ Class C – GOPCX ■ Class R – GOPRX ■ Institutional Class – GOPIX ■ Institutional Service Class – GOPSX

Aberdeen Dynamic Dividend Fund

Class A – ADAVX ■ Institutional Class – ADVDX

Aberdeen Emerging Markets Fund

Class A – GEGAX ■ Class C – GEGCX ■ Class R – GEMRX ■ Institutional Class – ABEMX ■ Institutional Service Class – AEMSX

Aberdeen Emerging Markets Sustainable Leaders Fund (formerly, Aberdeen International Equity Fund)

Class A – GIGAX ■ Class C – GIGCX ■ Class R – GIRRX ■ Institutional Class – GIGIX ■ Institutional Service Class – GIGSX

Aberdeen Global Equity Fund

Class A – GLLAX ■ Class C – GLLCX ■ Class R – GWLRX ■ Institutional Class – GWLIX ■ Institutional Service Class – GLLSX

Aberdeen Global Infrastructure Fund

Class A – AIAFX ■ Institutional Class – AIFRX

Aberdeen International Real Estate Equity Fund

Class A – EGALX ■ Institutional Class – EGLRX

Aberdeen International Small Cap Fund

Class A – WVCCX ■ Class C – CPVCX ■ Class R – WPVAX ■ Institutional Class – ABNIX

Aberdeen Realty Income & Growth Fund

Class A – AIAGX ■ Institutional Class – AIGYX

Aberdeen U.S. Small Cap Equity Fund

Class A – GSXAX ■ Class C – GSXCX ■ Class R – GNSRX ■ Institutional Class – GSCIX ■ Institutional Service Class – GSXIX

Aberdeen U.S. Sustainable Leaders Fund (formerly, Aberdeen U.S. Multi-Cap Equity Fund)

Class A – GXXAX ■ Class C – GXXCX ■ Institutional Class – GGLIX ■ Institutional Service Class – GXXIX

Aberdeen U.S. Sustainable Leaders Smaller Companies Fund (formerly, Aberdeen Focused U.S. Equity Fund)

Class A – MLSAX ■ Class C – MLSCX ■ Class R – GLSRX ■ Institutional Class – GGUIX ■ Institutional Service Class – AELSX

Table of Contents

| Market Review | Page 1 |

| Aberdeen China A Share Equity Fund | Page 3 |

| Aberdeen Dynamic Dividend Fund | Page 9 |

| Aberdeen Emerging Markets Fund | Page 16 |

| Aberdeen Emerging Markets Sustainable Leaders Fund | Page 22 |

| Aberdeen Global Equity Fund | Page 29 |

| Aberdeen Global Infrastructure Fund | Page 35 |

| Aberdeen International Real Estate Equity Fund | Page 41 |

| Aberdeen International Small Cap Fund | Page 47 |

| Aberdeen Realty Income & Growth Fund | Page 53 |

| Aberdeen U.S. Small Cap Equity Fund | Page 58 |

| Aberdeen U.S. Sustainable Leaders Fund | Page 64 |

| Aberdeen U.S. Sustainable Leaders Smaller Companies Fund | Page 70 |

| Financial Statements | Page 76 |

| Notes to Financial Statements | Page 121 |

| Report of Independent Registered Public Accounting Firm | Page 144 |

| Other Tax Information | Page 145 |

| Shareholder Expense Examples | Page 147 |

| Supplemental Information | Page 149 |

| Liquidity Risk Management Program | Page 152 |

| Management of the Funds | Page 153 |

Investors should carefully consider a fund's investment objectives, risks, fees, charges and expenses before investing any money. To obtain this and other fund information, please call 866-667-9231 to request a prospectus, or download a prospectus at https://www.abrdn.com/en-us/us/investor/fund-centre#literature. Please read it carefully before investing any money.

Investing in mutual funds involves risk, including possible loss of principal.

Aberdeen Funds is distributed by Aberdeen Fund Distributors LLC, Member FINRA, 1900 Market Street, Suite 200, Philadelphia, PA 19103.

Aberdeen Standard Investments Inc. (ASII) has been registered as an investment adviser under the Investment Advisers Act of 1940 since August 23, 1995.

The complete schedule of portfolio holdings for each fund of Aberdeen Funds (each a "Fund" and collectively, the "Funds") is included in the Funds' semi-annual and annual reports to shareholders. Aberdeen Funds also files complete schedules of portfolio holdings for each Fund with the Securities and Exchange Commission (the "Commission") for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Funds' Form N-PORT filings are available on the Commission's website at http://www.sec.gov and the Funds make the information on the exhibit to Form N-PORT available to shareholders upon request without charge by calling 1-866-667-9231.

Statement Regarding Availability of Proxy Voting Record.

Information regarding the policies and procedures that the Funds use to determine how to vote proxies relating to portfolio securities is available without charge, upon request, by calling 1-866-667-9231. The information is also included in the Funds' Statement of Additional Information, which is available on the Funds' website at https://www.abrdn.com/en-us/us/investor/fund-centre#literature and on the Commission's website at www.sec.gov.

Information relating to how each Fund voted proxies relating to portfolio securities held during the most recent twelve months ended June 30 is available by August 30 of the relevant year: (i) upon request and without charge by calling 1-866-667-9231; and (ii) on the Commission's website at www.sec.gov.

abrdn

abrdn plc, formerly known as Standard Life Aberdeen plc, was renamed on September 27, 2021. In connection with this re-branding, the entities within abrdn plc group, including investment advisory entities, have been or will be renamed in the near future. In addition, the fund names are anticipated to be re-branded over the next year.

Market Review

Global financial markets mainly recorded positive returns despite bouts of significant volatility over the 12-month reporting period ended October 31, 2021. Global developed-market equities, as represented by the MSCI AC World Index,1 returned 37.3% for the period. Supportive monetary and fiscal policies were prevalent over the period. The U.S. Federal Reserve (Fed) maintained the federal funds rate at near 0% throughout the reporting period, while providing support through its bond-buying program. Elsewhere, the European Central Bank ramped up its original €1.35 trillion (US$1.57 trillion) stimulus plan to €1.85 trillion (US$2.15 trillion) in December 2020. The U.S. Congress passed two additional stimulus packages during the reporting period, with a cumulative total of roughly $2.8 trillion. In August 2021, the U.S. Senate passed the $1 trillion infrastructure deal.

At the beginning of the reporting period in November 2020, news of three major COVID-19 vaccines buoyed investor sentiment. This persisted through to the end of 2020 due to the launch of vaccination programs, the approval of stimulus packages, and the UK and the European Union reaching a Brexit trade deal.

Momentum stalled in January and February 2021, as global bond markets experienced a significant selloff, spurring worries that this could impact the fragile global recovery. The downturn in bond markets also had a negative impact on equities. However, stock markets resumed their upward momentum, driven by economic optimism, vaccine rollouts, central banks' continued accommodative monetary policies, and a strong corporate earnings reporting season. The MSCI AC World Index reached a record high in August 2021, but sold off in September amid investors' growing concerns over inflation and possible interest-rate hikes from central banks. Uneasiness about the global economy led to a selloff across most equity markets across the globe. In October 2021, upbeat company results, along with comments that demand remained strong, eased investors' concerns about stagflation,* supply-chain pressures, spiraling energy prices and higher interest rates.

Emerging-market (EM) equities posted notable gains over the reporting period, with the exception of China. The MSCI Emerging Markets Index2 returned 17.0% for the period. Stock prices initially rallied on investors' optimism regarding the COVID-19 vaccine rollout, which allowed the reopening of economies worldwide. Upbeat corporate earnings, driven by an e-commerce boom, a multi-year technology upgrading cycle and pent-up infrastructure demand also bolstered investor sentiment. Increasing adoption of climate-change goals by governments globally also fueled interest in clean-energy themes. These positive factors outweighed investors' concerns over supply-chain disruptions caused by a shortage of semiconductors, shipping gridlocks, and an energy crunch. However, the spread of the more contagious Delta variant of coronavirus capped the stock market gains in some EM economies due to their relatively slower vaccine rollouts.

In the global fixed-income markets, government bond prices moved lower during the reporting period, with the ICE bank of America (BofA) Global Government Index3 returning –2.5%. Lockdown restrictions heightened investors' fears of a deep recession, with the

"risk-off" environment boosting government bond prices as investors fled to their perceived safety. However, rising optimism about vaccines and concerns that an economic recovery would fuel sharp rises in inflation led to a drop in government bond prices. Bond prices continued to decline later in the reporting period as expectations of a withdrawal of support from central banks globally, along with inflation fears, triggered a selloff. Corporate bonds, as measured by the ICE BofA Corporate Index, returned 2.1% for the reporting period as government monetary and fiscal stimuli measures and rising investor optimism helped bolster the corporate fixed-income markets. However, corporate bond prices subsequently fell modestly as investors' fears of forthcoming central bank action increased. The global high-yield fixed income market, as represented by the ICE BofA Global High Yield Constrained Index,4 performed well over the reporting period, returning 8.9%, as the COVID-19 vaccine rollout and resulting economic reopening and reflation narrative bolstered risk assets throughout the first half of 2021. However, the high-yield market's performance was tempered towards the end of the summer of 2021, as it became increasingly evident that supply-side pressures were building, perhaps unsurprisingly after entire economies and industries had been shut down and were reopening.

The global real estate market performed relatively well during the reporting period. The Financial Times Stock Exchange European Public Real Estate Association/National Association of Real Estate Investment Trusts (FTSE EPRA/NAREIT) Global ex U.S. Index5 and the FTSE EPRA NAREIT U.S. Index6 returned 23.4% and 53.5%, respectively, over the period. Real estate investment trusts (REITs) typically are more resistant to inflationary pressures due to the ability to raise rents, offset the impact of rising interest rates. While the overall performance of the REIT market was very robust during the reporting period, there was a wide disparity in returns. Those sectors that had materially underperformed in 2020 because their tenants were at the epicenter of the COVID-19-induced lockdowns (i.e., retail and urban apartments), posted extremely strong gains as economic activity rebounded and investors sought value-oriented sectors exposed to the reopening. Meanwhile, those "safe-haven" sectors where cash flows held up during the pandemic but were trading at elevated price/earnings multiples,7 such as data centers and cell towers, underperformed as investors rotated into more value-oriented sectors. Additionally, as the reporting period progressed, the industrial and storage sectors, which had garnered accelerating earnings growth and true pricing power in the form of rising rents, also were strong outperformers.

Outlook

When bond yields rally, investors tend to take profits and sell highly valued companies. Time will tell whether this proves shortsighted this time around. From our conversations with various industry participants, it appears that some of the supply bottlenecks emanating from manufacturing hubs such as Vietnam, Thailand and Malaysia are now easing. Some raw material costs, noticeably metals, are also decreasing. This is due to a mix of government price caps and a slowdown in demand. It is worth noting that China's manufacturing

2021 Annual Report 1

Market Review (concluded)

purchasing managers' index for September recorded a reading of 49.6, a marginal contraction from the previous month.

From our perspective, the most recent corporate earnings reports generally were positive, indicating that most companies have been successful in passing through higher costs. While this is a positive factor for fixed-income securities in the short term, we think that it is emblematic of the inflationary environment that currently exists. Over the longer term, if inflation remains high, central banks globally most likely will need to act more decisively, risking a slowdown in global economic growth. Therefore, we think that the market may be especially sensitive to economic data over the next several months as investors look to divine the direction of inflation and growth, while simultaneously gauging the reaction function of central bankers. Overall, we believe that the credit fundamentals of the market are solid, and we anticipate that companies will be well-positioned to weather modestly slower growth, keeping default rates relatively low.

In the U.S. and Western Europe, we are waiting to see the effect of the withdrawal of government support schemes on labor participation. These factors suggest that, as we head towards the end of the year, pressure on the supply chain could start to moderate. Overall, we think that the performance of equity markets may be tempered by gradual monetary policy normalisation and the potential impact of increased taxation.

COVID-19

Beginning in the first quarter of 2020, the illness caused by a novel coronavirus, COVID-19, has resulted in a global pandemic and major disruption to economies and markets around the world, including the United States. Financial markets have experienced extreme volatility and severe losses. Some sectors of the economy and individual issuers have experienced particularly large losses. These circumstances may continue for an extended period of time, and as a result may affect adversely the value and liquidity of the Fund's investments. The rapid

development and fluidity of this situation precludes any prediction as to the ultimate adverse impact of COVID-19 on economic and market conditions, and, as a result, present uncertainty and risk with respect to the Fund and the performance of its investments and ability to pay distributions. The full extent of the impact and effects of COVID-19 will depend on future developments, including, among other factors, the duration and spread of the outbreak, along with related travel advisories, quarantines and restrictions, the recovery time of the disrupted supply chains and industries, the impact of labor market interruptions, the impact of government interventions, and uncertainty with respect to the duration of the global economic slowdown.

abrdn

| 1 | The MSCI AC World Index is an unmanaged index considered representative of stock markets of developed and emerging markets. Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index. |

| 2 | The MSCI Emerging Markets Index is an unmanaged index considered representative of stocks of developing countries. |

| 3 | The ICE BofA Global Government Index tracks the performance of investment-grade sovereign debt publicly issued and denominated in the issuer's own domestic market and currency. |

| 4 | The ICE BofA Global High Yield Constrained Index tracks the performance of U.S. dollar-, Canadian dollar-, British pound- and euro-denominated below-investment-grade corporate debt publicly issued in the major domestic or eurobond markets. |

| 5 | The FTSE EPRA/NAREIT Global ex U.S. Index is an unmanaged index considered representative of real estate companies and REITs outside the U.S. |

| 6 | The FTSE EPRA NAREIT U.S. Index is a free-float adjusted, market capitalization-weighted index of U.S. equity REITs. |

| 7 | A price/earnings multiple is calculated by dividing the current market price of a stock by the earnings per share. Price/earnings multiples often are used to compare companies in the same industry, or to assess the historical performance of an individual company. |

2 2021 Annual Report

Aberdeen China A Share Equity Fund (Unaudited)

Aberdeen China A Share Equity Fund (Institutional Class shares net of fees) returned 13.33% for the 12-month reporting period ended October 31, 2021, versus the 16.66% return of its benchmark, the Morgan Stanley Capital International (MSCI) China A Onshore Index (net dividends), over the same period.

Market/Economic Review

Chinese equities posted gains over the 12-month period ended October 31, 2021. Healthy economic data and the rapid recovery of corporate earnings in the market initially supported share prices. Investors cheered the COVID-19 vaccine rollout globally and drove a rotation out of higher-quality stocks, which had performed well amid the pandemic, into cyclical and undervalued sectors. However, as the reporting period progressed, expectations of tighter monetary policy to control inflation and excessive debt, new government regulations and a potential debt default by property developer China Evergrande Group (which the Fund did not hold as of the end of the reporting period) weighed on China's equity markets.

Throughout the reporting period, China's central bank, the People's Bank of China, maintained its accommodative monetary policy and prioritized its focus on consumer spending and investment over rising inflation. However, the tougher regulatory environment capped gains as the Chinese government stepped up scrutiny of the country's internet and education sector, alongside the tightening of regulations for the real estate and banking sectors. The Chinese Communist Party marked the centennial of its founding on July 1, 2021, with President Xi Jinping warning that China would not tolerate any sovereignty infringements. U.S.-China relations remained tense, reflecting continuing issues around trade, competition in the technology space, as well as their respective geopolitical interests.

In mid-2021, China's equity markets became turbulent, characterized by frenetic and unexpected regulatory intervention focusing on the technology sector. This later spread to other areas, including media and entertainment, with threats of further regulatory action at one point decreasing the market value of Chinese stocks by up to US$500 billion. This occurred as part of a broader government crackdown and determination to regain control of the economy and reduce the wealth gap in an effort to create "common prosperity." In September 2021, the volatility and uncertainty triggered investors' concerns about debt-ridden China Evergrande Group, one of China's largest property developers. Swift action by the People's Bank of China averted a collapse of the company on fears that it would miss a scheduled debt repayment. Chinese A-share equity prices rebounded at the end of the reporting period in October 2021 despite new outbreaks of COVID-19, which led to the government reimposing lockdowns in several regions of the country.

Fund Performance Review

The Fund's underperformance relative to its benchmark, the MSCI China A Onshore Index, over the 12-month reporting period was

attributable to negative overall asset allocation. Conversely, stock selection had a positive impact on Fund performance.

Overweight allocations versus the benchmark to the consumer staples and industrials sectors weighed on Fund performance for the reporting period. The largest individual stock detractor was pharmaceutical company Jiangsu Hengrui Medicine Co., Ltd.

The Fund's underweight positioning in the materials sector was the primary detractor from the relative performance for the reporting period. However, the Fund's holding in Yunnan Energy New Material Co. Ltd., a manufacturer of lithium-ion battery separators, contributed positively to performance. The company benefited from a supply shortage and raised its earnings expectations for the second quarter of its 2021 fiscal year, due to an increase in demand, continued capacity growth and operational efficiency.

An underweight allocation to the financials sector hampered Fund performance during the reporting period. The position in Ping An Insurance hampered Fund performance as the insurance company's stock price moved lower due to concerns within the life insurance industry and about the firm's exposure to China's real estate sector. The Fund's holding in electrical appliance manufacturer Midea Group Co. Ltd. also detracted from performance after its shares declined amid a tighter credit stance and weaker-than-expected retail data.

Overweight positions in the healthcare and consumer discretionary sectors bolstered the Fund's relative performance over the reporting period. Specifically, the shares of China Tourism Group Duty Free Corporation Ltd., which sells duty-free goods,* moved higher doing the reporting period due the Chinese government's favorable tax-policy changes.

In the healthcare sector, Chinese companies' increasing research and development spending in drug research benefited the Fund's holding in contract research organization Hangzhou Tigermed Consulting Co. Ltd. Aier Eye Hospital Group Co. Ltd. posted rapid earnings growth over the reporting period amid greater demand for eyecare due to work-from-home lifestyles, while its hospital network expanded to more cities in China.

The holding in Nari Technology Co. Ltd., which develops and manufactures power-grid automation and industrial control products, benefited from an upgrade of a massive electricity grid covering about 90% of the country by its state-owned parent, State Grid Corp. of China. We like Nari Technology's leading position in secondary power equipment and software given China's ambitions in renewable energy. We believe that its growth areas include charging infrastructure for new energy vehicles, power trading and global energy internet.

During the reporting period, we initiated several holdings in companies that we believe are positioned to benefit from China's drive for carbon neutrality, including solar wafer manufacturer Longi Green Energy Technology Co. and lithium-ion battery maker Contemporary Amperex Technology Co., Ltd. We also established new positions in pharmaceutical company Jiangsu Hengrui Medicine Co., Ltd., Apple AirPods assembler Luxshare Precision Industry Co. Ltd. and

* Consumers are able to purchase duty-free goods in particular circumstances without paying import, sales, value-added, or other taxes.

2021 Annual Report 3

Aberdeen China A Share Equity Fund (Unaudited) (concluded)

China International Capital Corp. Ltd., China's largest investment bank.

Additionally, we initiated holdings in enterprise software company Yonyou Network Co. Ltd., Hundsun Technologies Inc, a provider of software products and services and financial data for financial institutions, and By-health Co. Ltd., a distributor of nutrition supplements. In our view, these companies have clear competitive advantages, which we believe will enable them to defend their market leadership over the long term. We also purchased shares of Shenzhen Inovance Technology Co. Ltd., and Sungrow Power Supply Co. Ltd. over the reporting period. Shenzhen Inovance is a leader in China's industrial automation sector with a strong track record, competitive products, diversified revenue streams and cost advantage underpinned by effective supply-chain management. We believe that Sungrow Power Supply is well-positioned to benefit from multi-year growth in demand for solar energy, as the company is a leading producer of solar inverters and a solar energy performance certificate farm operator, as well as energy storage.

During the reporting period, we exited the Fund's positions in Hangzhou Hikvision Digital Technology Co. Ltd., a provider of video surveillance systems, pharmaceutical firm China Resources Sanjiu Medical & Pharmaceutical Co. Ltd.; electrical appliances manufacturers Hangzhou Robam Appliances Company Ltd. and Haier Smart Home Co. Ltd.; financial services companies China Construction Bank Corp. and Industrial and Commercial Bank of China; supermarket chain operator Yonghui Superstores Co. Ltd.; airport operator Shenzhen Airport Co. Ltd.; and China Life Insurance Co. Ltd.

Outlook

The Chinese government's imposition of regulatory measures on numerous segments of the economy – including education, technology, real estate and gaming – came as a surprise to investors. However, we don't think that this is the end of capitalism in China; we believe that these changes should be seen in the context of a fast-changing technology landscape. Regulators are trying to keep pace with innovation, but in our view, a heavy-handed clamp down on all private new-economy sectors is unlikely. The new economy is a vital component of China's vision for a modern consumption-led economy. Furthermore, the private sector retains a critical role in ensuring that the Chinese economy continues to innovate and prosper, and that the government reaches its goal of being a moderately prosperous nation by 2035. We think that China still needs well-functioning capital markets to help propel growth.

We feel that investors overreacted to the regulatory measures and that the indiscriminate selling will create investment opportunities. In our view, companies that can adapt to changing regulatory frameworks and align with policy objectives such as digital innovation, green technology, access to affordable healthcare and improved welfare, have a bright outlook. Moreover, we think that investors are likely to refocus on company-specific factors in the

upcoming corporate earnings-reporting seasons, which we believe should benefit the Fund's high-quality company holdings.

Portfolio Management:

Asian Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to https://www.abrdn.com/en-us/us/investor/fund-centre.

Investing in mutual funds involves risk, including the possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Risk Considerations

Deteriorating market conditions might cause a general weakness in the market that reduces the prices, or yield, of securities in those markets in which the Fund invests.

The value of a security may decline for reasons directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer's goods or services.

The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company, to the industry in which the company is engaged, or to the market as a whole.

The Fund is subject to the risk that the Adviser or Subadviser may make poor security selections.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and currency exchange rate, political and economic risks. The Fund focuses its investments in China and Hong Kong, which may subject the Fund to more volatility and greater risk of loss than geographically diverse mutual funds. Additional risks associated with investments in China and Hong Kong include exposure to currency fluctuations, less liquidity, expropriation, confiscatory taxation, nationalization, exchange control regulations (including currency blockage), trading halts, imposition of tariffs, limitations on repatriation and differing legal standards. Trading in China A Shares through Stock Connect and the QFII Programs involves additional risks.

The risks that apply to foreign investments are greater for securities of companies in emerging market countries because the countries may have less stable governments, more volatile currencies and less established markets.

Please read the prospectus for more detailed information regarding these and other risks.

4 2021 Annual Report

Aberdeen China A Share Equity Fund (Unaudited)

| Average Annual Total Return1 (For periods ended October 31, 2021) | 1 Yr. | 5 Yr. | 10 Yr. | |||

| Class A | w/o SC | 12.95% | 17.24% | 8.64% | ||

| w/SC2 | 6.45% | 15.85% | 8.00% | |||

| Class C | w/o SC | 12.23% | 16.46% | 7.88% | ||

| w/SC3 | 11.23% | 16.46% | 7.88% | |||

| Class R4 | w/o SC | 12.60% | 16.86% | 8.27% | ||

| Institutional Service Class4 | w/o SC | 13.21% | 17.52% | 8.90% | ||

| Institutional Class4 | w/o SC | 13.33% | 17.63% | 8.96% | ||

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible because it has the most significant effect on performance data. The total returns shown above do not include the impact of financial statement rounding of the net asset value (NAV) per share and/or financial statement adjustments.

| 1 | The Fund changed its investment strategies effective June 13, 2019. Performance information for periods prior to June 13, 2019 does not reflect the current investment strategy. In connection with the change in investment strategy, the Fund changed its name from Aberdeen China Opportunities Fund to Aberdeen China A Share Equity Fund. Please consult the Fund's prospectus for more detail. |

| 2 | A 5.75% front-end sales charge was deducted. |

| 3 | A 1.00% contingent deferred sales charge (CDSC) was deducted from the one year return because it is charged when Class C shares are sold within the first year after purchase. |

| 4 | Not subject to any sales charges. |

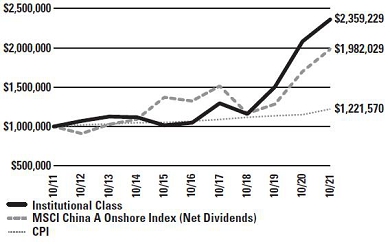

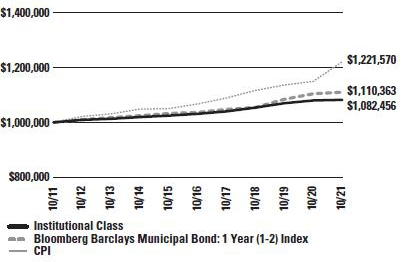

Performance of a $1,000,000 Investment* (as of October 31, 2021)

* Minimum Initial Investment

Performance of $1,000,000 invested in Institutional Class shares of the Aberdeen China A Share Equity Fund, MSCI China A (Onshore) Index (Net Dividends) and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2021. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses, or sales charges. Investors cannot invest directly in market indexes.

The MSCI China A (Onshore) Index captures large and mid cap representation across China securities listed on the Shanghai and Shenzhen exchanges

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and Performance graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Total returns reflect waivers and reimbursements in effect, without which returns would have been lower.

| 2021 Annual Report | 5 |

Aberdeen China A Share Equity Fund (Unaudited)

Portfolio Summary (as a percentage of net assets)

October 31, 2021 (Unaudited)

| Asset Allocation | ||

| Common Stocks | 95.9% | |

| Short-Term Investment | 2.3% | |

| Exchange-Traded Funds | 2.0% | |

| Liabilities in Excess of Other Assets | (0.2%) | |

| 100.0% | ||

The following table summarizes the composition of the Fund's portfolio, in S&P Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets as of October 31, 2021.

| Top Sectors | ||

| Consumer Staples | 18.9% | |

| Industrials | 18.0% | |

| Information Technology | 15.2% | |

| Financials | 12.9% | |

| Consumer Discretionary | 12.4% | |

| Health Care | 11.3% | |

| Materials | 5.6% | |

| Real Estate | 1.6% | |

| Energy | –% | |

| Other | 4.1% | |

| 100.0% | ||

Amounts listed as "–" are 0% or round to 0%.

| Top Holdings* | ||

| China Tourism Group Duty Free Corp. Ltd., A Shares (Stock Connect) | 7.2% | |

| Kweichow Moutai Co. Ltd., A Shares (Stock Connect) | 7.1% | |

| China Merchants Bank Co. Ltd., A Shares | 5.2% | |

| Contemporary Amperex Technology Co. Ltd., A Shares | 5.1% | |

| LONGi Green Energy Technology Co. Ltd., A Shares | 3.9% | |

| Shenzhen Mindray Bio-Medical Electronics Co. Ltd., A Shares | 3.3% | |

| Wuliangye Yibin Co. Ltd., A Shares | 3.2% | |

| NARI Technology Co. Ltd., A Shares (Stock Connect) | 3.1% | |

| Glodon Co. Ltd., A Shares | 3.0% | |

| Centre Testing International Group Co. Ltd., A Shares (Stock Connect) | 2.8% | |

| Other | 56.1% | |

| 100.0% | ||

* For the purpose of listing top holdings, Short-Term Investments are included as part of Other.

| Top Countries | ||

| China | 95.9% | |

| United States | 4.3% | |

| Other | (0.2%) | |

| 100.0% | ||

| 6 | 2021 Annual Report |

Statement of Investments

October 31, 2021

Aberdeen China A Share Equity Fund

| Shares or Principal Amount | Value | ||||

| COMMON STOCKS (95.9%) | |||||

| CHINA (95.9%) | |||||

| Consumer Discretionary (12.4%) | |||||

| China Tourism Group Duty Free Corp. Ltd., A Shares (Stock Connect) (a) | 151,695 | $ | 6,345,130 | ||

| Fuyao Glass Industry Group Co. Ltd., A Shares (a) | 293,841 | 2,266,841 | |||

| Midea Group Co. Ltd., A Shares (Stock Connect) (a) | 219,842 | 2,355,086 | |||

| 10,967,057 | |||||

| Consumer Staples (18.9%) | |||||

| By-health Co. Ltd., A Shares (a) | 345,688 | 1,374,293 | |||

| Chacha Food Co. Ltd., A Shares (a) | 174,000 | 1,547,823 | |||

| Foshan Haitian Flavouring & Food Co. Ltd., A Shares (a) | 130,412 | 2,384,892 | |||

| Inner Mongolia Yili Industrial Group Co. Ltd., A Shares (a) | 199,500 | 1,335,742 | |||

| Kweichow Moutai Co. Ltd., A Shares (Stock Connect) (a) | 21,863 | 6,230,669 | |||

| Proya Cosmetics Co. Ltd., A Shares (a) | 31,300 | 981,113 | |||

| Wuliangye Yibin Co. Ltd., A Shares (a) | 82,237 | 2,775,282 | |||

| 16,629,814 | |||||

| Energy (0.0%) | |||||

| G3 Exploration Ltd. (b)(c)(d) | 53,000 | – | |||

| Financials (12.9%) | |||||

| Bank of Ningbo Co. Ltd., A Shares (a) | 357,015 | 2,125,608 | |||

| China International Capital Corp. Ltd., H Shares (e) | 359,600 | 890,286 | |||

| China Merchants Bank Co. Ltd., A Shares (a) | 547,532 | 4,605,939 | |||

| Ping An Bank Co. Ltd., A Shares (a) | 603,300 | 1,835,267 | |||

| Ping An Insurance Group Co. of China Ltd., A Shares (a) | 249,737 | 1,926,580 | |||

| 11,383,680 | |||||

| Health Care (11.3%) | |||||

| Aier Eye Hospital Group Co. Ltd., A Shares (a) | 310,358 | 2,344,103 | |||

| Hangzhou Tigermed Consulting Co. Ltd., A Shares (a) | 82,767 | 2,200,470 | |||

| Hangzhou Tigermed Consulting Co. Ltd., H Shares (e) | 29,400 | 573,407 | |||

| Jiangsu Hengrui Medicine Co. Ltd., A Shares (a) | 252,095 | 1,934,069 | |||

| Shenzhen Mindray Bio-Medical Electronics Co. Ltd., A Shares (a) | 49,610 | 2,903,238 | |||

| 9,955,287 | |||||

| Industrials (18.0%) | |||||

| Centre Testing International Group Co. Ltd., A Shares (Stock Connect) (a) | 564,388 | 2,429,712 | |||

| Contemporary Amperex Technology Co. Ltd., A Shares (a) | 45,079 | 4,509,771 | |||

| Guangzhou Baiyun International Airport Co. Ltd., A Shares (a) | 315,200 | 582,420 | |||

| Shares or Principal Amount | Value | ||||

| NARI Technology Co. Ltd., A Shares (Stock Connect) (a) | 449,560 | $ | 2,733,769 | ||

| Shanghai International Airport Co. Ltd., A Shares (Stock Connect) (a)(b) | 101,910 | 841,615 | |||

| Shanghai M&G Stationery, Inc., A Shares (a) | 167,680 | 1,659,838 | |||

| Shenzhen Inovance Technology Co. Ltd., A Shares (a) | 136,789 | 1,391,901 | |||

| Sungrow Power Supply Co. Ltd., A Shares (Stock Connect) (a) | 65,278 | 1,675,689 | |||

| 15,824,715 | |||||

| Information Technology (15.2%) | |||||

| Beijing Sinnet Technology Co. Ltd., A Shares (a) | 287,489 | 592,642 | |||

| Glodon Co. Ltd., A Shares (a) | 230,989 | 2,677,938 | |||

| Hundsun Technologies, Inc., A Shares (a) | 159,850 | 1,567,405 | |||

| LONGi Green Energy Technology Co. Ltd., A Shares (a) | 227,920 | 3,470,561 | |||

| Luxshare Precision Industry Co. Ltd., A Shares (a) | 386,870 | 2,336,539 | |||

| Venustech Group, Inc., A Shares (a) | 427,100 | 1,699,176 | |||

| Yonyou Network Technology Co. Ltd., A Shares (a) | 202,800 | 1,005,312 | |||

| 13,349,573 | |||||

| Materials (5.6%) | |||||

| Anhui Conch Cement Co. Ltd., A Shares (a) | 187,756 | 1,112,325 | |||

| Wanhua Chemical Group Co. Ltd., A Shares (a) | 109,017 | 1,799,092 | |||

| Yunnan Energy New Material Co. Ltd., A Shares (Stock Connect) (a) | 45,220 | 2,059,616 | |||

| 4,971,033 | |||||

| Real Estate (1.6%) | |||||

| China Vanke Co. Ltd., A Shares (a) | 497,273 | 1,412,031 | |||

| 84,493,190 | |||||

| Total Common Stocks | 84,493,190 | ||||

| EXCHANGE-TRADED FUNDS (2.0%) | |||||

| UNITED STATES (2.0%) | |||||

| KraneShares Bosera MSCI China A Shares ETF | 37,077 | 1,725,564 | |||

| Total Exchange-Traded Funds | 1,725,564 | ||||

| SHORT-TERM INVESTMENT (2.3%) | |||||

| UNITED STATES (2.3%) | |||||

| State Street Institutional U.S. Government Money Market Fund, Premier Class, 0.03% (f) | 1,993,668 | 1,993,668 | |||

| Total Short-Term Investment | 1,993,668 | ||||

| Total Investments (Cost $88,051,584) (g)—100.2% | 88,212,422 | ||||

| Liabilities in Excess of Other Assets—(0.2)% | (138,964) | ||||

| Net Assets—100.0% | $ | 88,073,458 | |||

See accompanying Notes to Financial Statements.

| 2021 Annual Report | 7 |

Statement of Investments (concluded)

October 31, 2021

Aberdeen China A Share Equity Fund

| (a) | China A Shares. These shares are issued in local currency, traded in the local stock markets and are held through either a Qualified Foreign Institutional Investor (QFII) license or the Shanghai or Shenzhen Hong-Kong Stock Connect program. |

| (b) | Non-income producing security. |

| (c) | Illiquid security. |

| (d) | Delisted. Fair Value is determined pursuant to procedures approved by the Fund's Board of Trustees. See Note 2(a) of the accompanying Notes to Financial Statements. |

| (e) | Denotes a security issued under Regulation S or Rule 144A. |

| (f) | Registered investment company advised by State Street Global Advisors. The rate shown is the 7 day yield as of October 31, 2021. |

| (g) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| ETF | Exchange-Traded Fund |

See accompanying Notes to Financial Statements.

| 8 | 2021 Annual Report |

Aberdeen Dynamic Dividend Fund (Unaudited)

Aberdeen Dynamic Dividend Fund (Institutional Class shares net of fees) returned 35.36% for the 12-month reporting period ended October 31, 2021, versus the 37.28% return of its benchmark, the Morgan Stanley Capital International (MSCI) All Country (AC) World Index (Net Dividends), during the same period.

Major global equity market indices moved sharply higher despite bouts of significant market volatility over the 12-month period ended October 31, 2021. Supportive monetary and fiscal policies were prevalent over the period. The U.S. Federal Reserve (Fed) maintained the federal funds rate at near 0% throughout the reporting period, while providing support through its bond-buying program. Elsewhere, the European Central Bank ramped up its original €1.35 trillion (US$1.57 trillion) stimulus plan to €1.85 trillion (US$2.15 trillion) in December 2020. The U.S. Congress passed two additional stimulus packages during the reporting period, with a cumulative total of roughly $2.8 trillion. In August 2021, the U.S. Senate passed the $1 trillion infrastructure deal.

At the beginning of the reporting period in November 2020, news of three major COVID-19 vaccines buoyed investor sentiment. This persisted through to the end of 2020 due to the launch of vaccination programs, the approval of stimulus packages, and the UK and the European Union reaching a Brexit trade deal.

Momentum stalled in January and February 2021, as global bond markets experienced a significant selloff, spurring worries that this could impact the fragile global recovery. The downturn in bond markets also had a negative impact on equities. However, stock markets resumed their upward momentum, driven by economic optimism, vaccine rollouts, central banks' continued accommodative monetary policies, and a strong corporate earnings reporting season. The MSCI AC World Index reached a record high in August 2021, but sold off in September amid investors' growing concerns over inflation and possible interest-rate hikes from central banks. Uneasiness about the global economy led to a selloff across most equity markets across the globe. In October, upbeat company results, along with comments that demand remained strong, eased investors' concerns about stagflation,* supply-chain pressures, spiraling energy prices and higher interest rates.

The Fund's underperformance relative to the benchmark for the reporting period was attributable mainly to stock selection in the industrials and real estate sectors. At the individual stock level, key detractors from performance included holdings in Canada-based gold and copper mining company Barrick Gold Corp. and multi-lines insurer Ping An Insurance Group of China Ltd., as well as the absence of a position in electric vehicle (EV) manufacturer and renewable energy company Tesla Inc.

Barrick Gold Corp. reported solid results early in the reporting period, but this was offset by 2021 financial guidance that was slightly disappointing in terms of production and costs. The market has been disappointed that the company's earnings growth has lagged that of its peers. Furthermore, the price of gold declined over the reporting

period. Shares of Ping An Insurance moved lower over the reporting period due to investors' concerns regarding the life insurance industry and about the firm's property exposure in China. As of the date of this report, the Fund does not hold Tesla as the company does not pay a dividend.

Conversely, stock selection in the consumer discretionary, communication services and healthcare sectors bolstered the Fund's relative performance over the reporting period. The largest contributors to performance were the lack of exposure to Chinese e-commerce giant Alibaba Group Holding Ltd., along with positons in two U.S.-based companies: alternative asset manager Blackstone Inc. and diversified financial services company Goldman Sachs Group Inc.

The absence of a holding in Alibaba Group benefited Fund performance over the reporting period as its shares declined after Chinese regulators opened an anti-trust investigation into the company. Blackstone Inc. consistently reported strong quarterly results during the reporting period. The alternative asset manager benefited from both good financial performance and strong fund inflows.

The company is profiting from its investments in retail and is raising a significant amount of capital in its Blackstone Real Estate Income Trust (BREIT) and Blackstone Private Credit (BCRED) funds. In addition, Blackstone continues to grow its asset management business for insurance clients, as the company recently reached an agreement to manage assets for AIG (which the Fund did not hold as of the end of the reporting period). Diversified financial services company Goldman Sachs Group saw healthy year-over-year revenue growth over the reporting period, buoyed mainly by notable strength in its Asset Management, Investment Banking and Global Markets units. Investors viewed this as evidence that the new management team is on the path to improving shareholder returns over the medium term through various revenue and expense initiatives.

Regarding the use of derivatives, we continued to hedge a portion of the Fund's currency exposure to the euro during the reporting period.

The Fund earns income through a combination of investing in companies that pay dividends and implementing a dividend-capture strategy. In a dividend-capture trade, the Fund sells a stock on or shortly after the stock's ex-dividend date and reinvests the sales proceeds into one or more other stocks that are expected to pay dividends before the next dividend payment on the stock that it is selling. While employing this strategy, the Fund purchases companies that pay regular and/or special dividends. Over the 12-month period ended October 31, 2021, the Fund issued total distributions of $x.xx per share.

When bond yields rally, investors tend to take profits and sell highly valued companies. Time will tell whether this proves shortsighted this time around. As we move through the upcoming corporate earnings season, we maintain our preference for what we believe are well-run companies with a clear competitive advantage.

| * | Stagflation refers to an economic environment of stagnant activity and accelerating inflation. |

| 2021 Annual Report | 9 |

Aberdeen Dynamic Dividend Fund (Unaudited) (concluded)

From our conversations with various industry participants, it appears that some of the supply bottlenecks emanating from manufacturing hubs such as Vietnam, Thailand and Malaysia are now easing. Some raw material costs, noticeably metals, are also decreasing. This is due to a mix of government price caps and a slowdown in demand. It is worth noting that China's manufacturing purchasing managers' index for September recorded a reading of 49.6, a marginal contraction from the previous month.

In the U.S. and Western Europe, we are waiting to see the effect of the withdrawal of government support schemes on labor participation. These factors suggest that, as we head towards the end of the year, pressure on the supply chain could start to moderate. Overall, we think that the performance of equity markets may be tempered by gradual monetary policy normalization and the potential impact of increased taxation.

We remain committed to our fundamental analysis-based stock-picking strategies. This is supported by our proprietary research platform staffed by an experienced team that has successfully navigated past crises. Therefore, we continue to seek what we believe are attractively valued companies with resilient, well-run businesses that adapt well to the changing landscape, and also are poised for a recovery in economic growth. We are actively engaging with management in an effort to ensure robust corporate governance and environmental sustainability standards.

Portfolio Management:

Global Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to https://www.abrdn.com/en-us/us/investor/fund-centre.

Investing in mutual funds involves risk, including possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Risk Considerations

Deteriorating market conditions might cause a general weakness in the market that reduces the prices, or yield, of securities in those markets in which the Fund invests.

The value of a security may decline for reasons directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer's goods or services.

The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company, to the industry in which the company is engaged, or to the market as a whole.

The Fund is subject to the risk that the Adviser or Subadviser may make poor security selections.

The Fund's emphasis on dividend paying stocks could cause the Fund to underperform similar funds that invest without consideration of a company's track record of paying dividends or ability to pay dividends in the future. Dividend-paying stocks may not participate in a broad market advance to the same degree as other stocks, and a sharp rise in interest rates or economic downturn could cause a company to unexpectedly reduce or eliminate its dividend.

Foreign securities are more volatile, harder to price and less liquid than U.S. securities. They are subject to different accounting and regulatory standards, and currency exchange rate, political and economic risks.

The value of foreign currencies relative to the U.S. Dollar fluctuates in response to market, economic, political, regulatory, geopolitical or other conditions. Fluctuations in currency exchange rates may impact a Fund's returns more greatly to the extent the Fund does not hedge currency exposure or hedging techniques are unsuccessful.

Please read the prospectus for more detailed information regarding these and other risks.

| 10 | 2021 Annual Report |

Aberdeen Dynamic Dividend Fund (Unaudited)

| Average Annual Total Return1 (For periods ended October 31, 2021) | 1 Yr. | 5 Yr. | 10 Yr. | ||||||

| Class A | w/o SC | 35.40% | 12.57% | N.A. | |||||

| w/SC2 | 27.77% | 11.27% | N.A. | ||||||

| Institutional Class3 | w/o SC | 35.36% | 12.85% | 9.64% |

All figures showing the effect of a sales charge (SC) reflect the maximum charge possible because it has the most significant effect on performance data. The total returns shown above do not include the impact of financial statement rounding of the net asset value (NAV) per share and/or financial statement adjustments.

| 1 | Returns prior to May 7, 2018 reflect the performance of a predecessor fund (the "Predecessor Fund"). Returns of the Predecessor Fund have not been adjusted to reflect the expenses applicable to the respective classes. The Fund and the Predecessor Fund have substantially similar investment objectives and strategies. Please consult the Fund's prospectus for more detail. |

| 2 | A 5.75% front-end sales charge was deducted. |

| 3 | Not subject to any sales charges. |

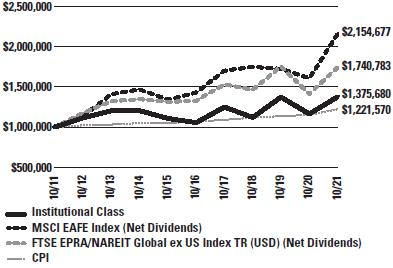

Performance of a $1,000,000 Investment* (as of October 31, 2021)

* Minimum Initial Investment

Comparative performance of $1,000,000 invested in Institutional Class shares of the Aberdeen Dynamic Dividend Fund, Morgan Stanley Capital International All Country World Index (MSCI ACWI) (Net

Dividends) and the Consumer Price Index (CPI) over a 10-year period ended October 31, 2021. Unlike the Fund, the returns for these unmanaged indexes do not reflect any fees, expenses or sales charges. Investors cannot invest directly in market indexes.

The MSCI ACWI captures large and mid cap representation across 23 Developed Markets (DM) and 27 Emerging Markets (EM) countries. With 2,986 constituents, the index covers approximately 85% of the global investable equity opportunity set. DM countries in the Index are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the UK and the US. EM countries in the Index are: Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Russia, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey and United Arab Emirates.

The CPI is a measure of the average change over time in the prices paid by urban consumers for a market basket of consumer goods and services.

Investment return and principal value will fluctuate, and when redeemed, shares may be worth more or less than original cost. Past performance is no guarantee of future results. The Average Annual Total Return table and Performance graph do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Investing in mutual funds involves market risk, including loss of principal. Performance returns assume the reinvestment of all distributions. Total returns reflect waivers and reimbursements in effect, without which returns would have been lower.

| 2021 Annual Report | 11 |

Aberdeen Dynamic Dividend Fund (Unaudited)

Portfolio Summary (as a percentage of net assets)

October 31, 2021 (Unaudited)

| Asset Allocation | |||

| Common Stocks | 96.8% | ||

| Short-Term Investment | 1.9% | ||

| Preferred Stocks | 1.4% | ||

| Liabilities in Excess of Other Assets | (0.1%) | ||

| 100.0% | |||

The following table summarizes the composition of the Fund's portfolio, in S&P Global Industry Classification Standard (GICS) sectors, expressed as a percentage of net assets as of October 31, 2021.

| Top Sectors | |||

| Information Technology | 17.3% | ||

| Financials | 16.2% | ||

| Health Care | 12.5% | ||

| Consumer Discretionary | 9.6% | ||

| Industrials | 9.1% | ||

| Consumer Staples | 8.5% | ||

| Communication Services | 6.7% | ||

| Utilities | 5.1% | ||

| Materials | 4.9% | ||

| Real Estate | 4.3% | ||

| Other | 5.8% | ||

| 100.0% | |||

| Top Holdings* | |||

| Apple, Inc. | 3.1% | ||

| Microsoft Corp. | 2.5% | ||

| Alphabet, Inc., Class C | 2.3% | ||

| Broadcom, Inc. | 1.7% | ||

| Bank of America Corp. | 1.7% | ||

| Tryg A/S | 1.5% | ||

| AbbVie, Inc. | 1.5% | ||

| Target Corp. | 1.5% | ||

| Lowe's Cos., Inc. | 1.5% | ||

| Enbridge, Inc. | 1.4% | ||

| Other | 81.3% | ||

| 100.0% | |||

| * | For the purpose of listing top holdings, Short-Term Investments are included as part of Other. |

| Top Countries | |||

| United States | 54.5% | ||

| France | 5.9% | ||

| United Kingdom | 5.2% | ||

| Germany | 4.7% | ||

| Switzerland | 3.3% | ||

| China | 3.0% | ||

| Canada | 2.4% | ||

| South Korea | 2.4% | ||

| Netherlands | 2.3% | ||

| Brazil | 2.2% | ||

| Other | 14.1% | ||

| 100.0% | |||

| 12 | 2021 Annual Report |

Statement of Investments

October 31, 2021

Aberdeen Dynamic Dividend Fund

| Shares or Principal Amount | Value | |||||||

| COMMON STOCKS (96.8%) | ||||||||

| AUSTRALIA (0.9%) | ||||||||

| Materials (0.9%) | ||||||||

| Rio Tinto PLC, ADR | 18,158 | $ | 1,148,857 | |||||

| BRAZIL (2.2%) | ||||||||

| Industrials (1.4%) | ||||||||

| CCR SA | 873,100 | 1,768,229 | ||||||

| Materials (0.8%) | ||||||||

| Vale SA, ADR | 78,700 | 1,001,851 | ||||||

| 2,770,080 | ||||||||

| CANADA (2.4%) | ||||||||

| Energy (1.4%) | ||||||||

| Enbridge, Inc. | 43,500 | 1,820,910 | ||||||

| Materials (1.0%) | ||||||||

| Barrick Gold Corp. | 70,800 | 1,300,596 | ||||||

| 3,121,506 | ||||||||

| CHINA (3.0%) | ||||||||

| Communication Services (1.1%) | ||||||||

| Tencent Holdings Ltd. | 22,500 | 1,368,670 | ||||||

| Financials (1.0%) | ||||||||

Ping An Insurance Group Co. of China Ltd., H Shares | 184,000 | 1,317,942 | ||||||

| Real Estate (0.9%) | ||||||||

| China Vanke Co. Ltd., H Shares | 472,000 | 1,102,795 | ||||||

| 3,789,407 | ||||||||

| DENMARK (1.5%) | ||||||||

| Financials (1.5%) | ||||||||

| Tryg A/S | 83,333 | 1,977,751 | ||||||

| FINLAND (2.1%) | ||||||||

| Financials (1.1%) | ||||||||

| Nordea Bank Abp | 121,400 | 1,486,763 | ||||||

| Information Technology (1.0%) | ||||||||

| Nokia OYJ (a) | 214,500 | 1,231,124 | ||||||

| 2,717,887 | ||||||||

| FRANCE (5.9%) | ||||||||

| Consumer Discretionary (1.2%) | ||||||||

| LVMH Moet Hennessy Louis Vuitton SE | 1,900 | 1,489,831 | ||||||

| Consumer Staples (1.1%) | ||||||||

| Danone SA | 21,700 | 1,414,531 | ||||||

| Energy (1.3%) | ||||||||

| TOTAL SE, ADR | 34,200 | 1,713,762 | ||||||

| Health Care (1.2%) | ||||||||

| Sanofi | 15,100 | 1,516,706 | ||||||

| Shares or Principal Amount | Value | |||||||

| Industrials (1.1%) | ||||||||

| Alstom SA | 38,322 | $ | 1,365,711 | |||||

| 7,500,541 | ||||||||

| GERMANY (4.7%) | ||||||||

| Financials (1.0%) | ||||||||

| Deutsche Boerse AG | 8,000 | 1,328,057 | ||||||

| Information Technology (1.2%) | ||||||||

| Infineon Technologies AG | 33,900 | 1,587,582 | ||||||

| Materials (1.2%) | ||||||||

| Linde PLC | 4,700 | 1,512,161 | ||||||

| Utilities (1.3%) | ||||||||

| RWE AG | 41,900 | 1,612,800 | ||||||

| 6,040,600 | ||||||||

| HONG KONG (0.9%) | ||||||||

| Financials (0.9%) | ||||||||

| Hong Kong Exchanges & Clearing Ltd. | 18,700 | 1,126,520 | ||||||

| INDONESIA (1.2%) | ||||||||

| Communication Services (1.2%) | ||||||||

| Telkom Indonesia Persero Tbk PT | 5,575,800 | 1,490,331 | ||||||

| ITALY (1.0%) | ||||||||

| Utilities (1.0%) | ||||||||

| Enel SpA | 155,000 | 1,297,626 | ||||||

| JAPAN (2.0%) | ||||||||

| Financials (1.1%) | ||||||||

| Mitsubishi UFJ Financial Group, Inc. | 263,900 | 1,447,094 | ||||||

| Real Estate (0.9%) | ||||||||

| GLP J-REIT | 700 | 1,141,742 | ||||||

| 2,588,836 | ||||||||

| NETHERLANDS (2.3%) | ||||||||

| Consumer Staples (1.3%) | ||||||||

| Heineken NV | 14,600 | 1,616,060 | ||||||

| Information Technology (1.0%) | ||||||||

| ASML Holding NV | 1,600 | 1,300,639 | ||||||

| 2,916,699 | ||||||||

| NORWAY (0.9%) | ||||||||

| Communication Services (0.9%) | ||||||||

| Telenor ASA | 76,700 | 1,211,899 | ||||||

| SINGAPORE (1.2%) | ||||||||

| Financials (1.2%) | ||||||||

| Oversea-Chinese Banking Corp. Ltd. | 168,155 | 1,469,982 | ||||||

| SOUTH KOREA (1.0%) | ||||||||

| Materials (1.0%) | ||||||||

| LG Chem Ltd. | 1,840 | 1,320,301 | ||||||

See accompanying Notes to Financial Statements.

| 2021 Annual Report | 13 |

Statement of Investments (continued)

October 31, 2021

Aberdeen Dynamic Dividend Fund

| Shares or Principal Amount | Value | |||||||

| COMMON STOCKS (continued) | ||||||||

| SPAIN (1.3%) | ||||||||

| Industrials (1.3%) | ||||||||

| Ferrovial SA | 53,626 | $ | 1,692,868 | |||||

| SWITZERLAND (3.3%) | ||||||||

| Consumer Staples (1.1%) | ||||||||

| Nestle SA | 10,300 | 1,358,644 | ||||||

| Financials (1.0%) | ||||||||

| Zurich Insurance Group AG | 2,900 | 1,285,339 | ||||||

| Health Care (1.2%) | ||||||||

| Roche Holding AG | 4,000 | 1,549,576 | ||||||

| 4,193,559 | ||||||||

| TAIWAN (1.2%) | ||||||||

| Information Technology (1.2%) | ||||||||

| Taiwan Semiconductor Manufacturing Co. Ltd., ADR | 13,700 | 1,557,690 | ||||||

| UNITED KINGDOM (5.2%) | ||||||||

| Communication Services (1.2%) | ||||||||

| Vodafone Group PLC, ADR | 103,300 | 1,544,335 | ||||||

| Consumer Staples (0.8%) | ||||||||

| Unilever PLC | 19,600 | 1,049,273 | ||||||

| Health Care (2.3%) | ||||||||

| AstraZeneca PLC, ADR | 28,000 | 1,746,640 | ||||||

| Dechra Pharmaceuticals PLC | 17,500 | 1,226,222 | ||||||

| 2,972,862 | ||||||||

| Industrials (0.9%) | ||||||||

| Melrose Industries PLC | 532,326 | 1,148,517 | ||||||

| 6,714,987 | ||||||||

| UNITED STATES (52.6%) | ||||||||

| Communication Services (2.3%) | ||||||||

| Alphabet, Inc., Class C (a) | 1,000 | 2,965,410 | ||||||

| Consumer Discretionary (8.4%) | ||||||||

| Aptiv PLC (a) | 9,300 | 1,607,877 | ||||||

| Genuine Parts Co. | 13,000 | 1,704,430 | ||||||

| Hanesbrands, Inc. | 60,600 | 1,032,624 | ||||||

| Las Vegas Sands Corp. (a) | 32,600 | 1,265,206 | ||||||

| Lowe's Cos., Inc. | 8,100 | 1,893,942 | ||||||

| Target Corp. | 7,400 | 1,921,188 | ||||||

| TJX Cos., Inc. (The) | 19,900 | 1,303,251 | ||||||

| 10,728,518 | ||||||||

| Consumer Staples (4.2%) | ||||||||

| Coca-Cola Co. (The) | 24,900 | 1,403,613 | ||||||

| Kraft Heinz Co. (The) | 32,300 | 1,159,247 | ||||||

| Mondelez International, Inc., Class A | 25,600 | 1,554,944 | ||||||

| PepsiCo, Inc. | 8,200 | 1,325,120 | ||||||

| 5,442,924 | ||||||||

| Shares or Principal Amount | Value | |||||||

| Energy (1.3%) | ||||||||

| Williams Cos., Inc. (The) | 57,900 | $ | 1,626,411 | |||||

| Financials (7.4%) | ||||||||

| Bank of America Corp. | 44,500 | 2,126,210 | ||||||

| Blackstone, Inc., Class A | 9,500 | 1,314,990 | ||||||

| Goldman Sachs Group, Inc. (The) | 3,800 | 1,570,730 | ||||||

| Huntington Bancshares, Inc. | 90,900 | 1,430,766 | ||||||

| Intercontinental Exchange, Inc. | 11,600 | 1,606,136 | ||||||

| JPMorgan Chase & Co. | 8,500 | 1,444,065 | ||||||

| 9,492,897 | ||||||||

| Health Care (7.8%) | ||||||||

| AbbVie, Inc. | 17,103 | 1,961,201 | ||||||

| Baxter International, Inc. | 17,400 | 1,373,904 | ||||||

| Bristol-Myers Squibb Co. | 28,300 | 1,652,720 | ||||||

| Eli Lilly & Co. | 6,000 | 1,528,560 | ||||||

| Medtronic PLC | 13,600 | 1,630,096 | ||||||

| UnitedHealth Group, Inc. | 3,900 | 1,795,833 | ||||||

| 9,942,314 | ||||||||

| Industrials (4.4%) | ||||||||

| FedEx Corp. | 6,300 | 1,483,839 | ||||||

| Lockheed Martin Corp. | 2,700 | 897,264 | ||||||

| Norfolk Southern Corp. | 5,600 | 1,641,080 | ||||||

| Schneider Electric SE | 9,400 | 1,620,730 | ||||||

| 5,642,913 | ||||||||

| Information Technology (11.5%) | ||||||||

| Analog Devices, Inc. | 7,600 | 1,318,524 | ||||||

| Apple, Inc. | 26,800 | 4,014,640 | ||||||

| Avast PLC (b) | 174,100 | 1,333,329 | ||||||

| Broadcom, Inc. | 4,000 | 2,126,680 | ||||||

| Cisco Systems, Inc. | 26,800 | 1,499,996 | ||||||

| Fidelity National Information Services, Inc. | 11,500 | 1,273,510 | ||||||

| Microsoft Corp. | 9,700 | 3,216,714 | ||||||

| 14,783,393 | ||||||||

| Real Estate (2.5%) | ||||||||

| American Tower Corp., REIT | 4,600 | 1,297,062 | ||||||

| Digital Realty Trust, Inc. | 4,100 | 647,021 | ||||||

| Gaming and Leisure Properties, Inc., REIT | 26,000 | 1,260,740 | ||||||

| 3,204,823 | ||||||||

| Utilities (2.8%) | ||||||||

| CMS Energy Corp. | 11,300 | 681,955 | ||||||

| FirstEnergy Corp. | 31,100 | 1,198,283 | ||||||

| NextEra Energy, Inc. | 19,500 | 1,663,935 | ||||||

| 3,544,173 | ||||||||

| 67,373,776 | ||||||||

| Total Common Stocks | 124,021,703 | |||||||

See accompanying Notes to Financial Statements.

| 14 | 2021 Annual Report |

Statement of Investments (concluded)

October 31, 2021

Aberdeen Dynamic Dividend Fund

| Shares or Principal Amount | Value | |||||||

| PREFERRED STOCKS (1.4%) | ||||||||

| SOUTH KOREA (1.4%) | ||||||||

| Information Technology (1.4%) | ||||||||

| Samsung Electronics Co. Ltd. | 32,000 | $ | 1,757,952 | |||||

| Total Preferred Stocks | 1,757,952 | |||||||

| SHORT-TERM INVESTMENT (1.9%) | ||||||||

| UNITED STATES (1.9%) | ||||||||

| State Street Institutional U.S. Government Money Market Fund, Premier Class, 0.03% (c) | 2,493,808 | 2,493,808 | ||||||

| Total Short-Term Investment | 2,493,808 | |||||||

| Total Investments (Cost $94,646,611) (d)—100.1% | 128,273,463 | |||||||

| Liabilities in Excess of Other Assets—(0.1)% | (121,436 | ) | ||||||

| Net Assets—100.0% | $ | 128,152,027 | ||||||

| (a) | Non-income producing security. |

| (b) | Denotes a security issued under Regulation S or Rule 144A. |

| (c) | Registered investment company advised by State Street Global Advisors. The rate shown is the 7 day yield as of October 31, 2021. |

| (d) | See accompanying Notes to Financial Statements for tax unrealized appreciation/(depreciation) of securities. |

| ADR | American Depositary Receipt |

| PLC | Public Limited Company |

| REIT | Real Estate Investment Trust |

At October 31, 2021, the Fund's open forward foreign currency exchange contracts were as follows:

| Sale Contracts Settlement Date | Counterparty | Amount Purchased | Amount Sold | Fair Value | Unrealized Depreciation | |||||||||

United States Dollar/Euro | ||||||||||||||

| 01/13/2022 | Royal Bank of Canada (UK) | USD 3,009,305 | EUR 2,600,000 | $3,011,319 | $(2,014 | ) | ||||||||

See accompanying Notes to Financial Statements.

| 2021 Annual Report | 15 |

Aberdeen Emerging Markets Fund (Unaudited)

Aberdeen Emerging Markets Fund (Institutional Class shares net of fees) returned 21.45% for the 12-monh reporting period ended October 31, 2021, versus the 16.96% return of its benchmark, the Morgan Stanley Capital International (MSCI) Emerging Markets Index, during the same period.

Emerging-market (EM) equities posted notable gains over the reporting period, with the exception of China. Stock prices initially rallied on investors' optimism regarding the COVID-19 vaccine rollout, which allowed the reopening of economies worldwide. Upbeat corporate earnings, driven by an e-commerce boom, a multi-year technology upgrading cycle and pent-up infrastructure demand also bolstered investor sentiment. Increasing adoption of climate-change goals by governments globally also fueled interest in clean-energy themes. These positive factors outweighed investors' concerns over supply-chain disruptions caused by a shortage of semiconductors, shipping gridlocks, and an energy crunch. However, the spread of the more contagious Delta variant of COVID-19 capped the stock market gains in some EM economies due to their relatively slower vaccine rollouts.

In China, the government's efforts to promote "common prosperity" led to a tougher regulatory environment for some business models. Stock prices fell as the government increased its focus on sustainable development issues, including: excessive real estate debt, the high cost of living, education, gaming, worker welfare, technology giants' antitrust issues, data-privacy practices and climate change.

Elsewhere in Asia, Indian equities scaled all-time highs despite the country's struggles against a deadly wave of COVID-19 cases in the first half of the reporting period. The Indian government's pro-business policies exceeded the market's expectations and buoyed investor sentiment. Share prices also were lifted by the Indian government's decision not to implement a nationwide lockdown, as this sustained the corporate earnings recovery. The Taiwanese and South Korean markets performed well over the reporting period because of their dominance in the electronics supply chain.

The markets in Latin America and Russia benefited over the reporting period from bullish commodity prices and hopes that massive fiscal stimulus in the U.S. would further boost their exports. Central banks in Brazil, Mexico and Russia began to raise their respective benchmark interest rates in an effort to control inflationary pressures.

The Fund's outperformance relative to its benchmark, the MSCI Emerging Markets Index, for the reporting period was attributable mainly to strong stock selection in the information technology and consumer discretionary sectors. Conversely, the exposure to travel-related stocks, as well as the transportation and automobiles and components subsectors, weighed on Fund performance. Within the regional markets, the Fund's holdings in China were key contributors to performance, while positions in the Netherlands, South Korea, Latin America and Russia also had a positive impact. Conversely, stock selection in South Africa and an underweight allocation to Taiwan detracted from Fund performance for the reporting period.

Given the global chip shortage, demand for foundry operations boosted shares of leading semiconductor companies during the reporting period, including three Fund holdings: multinational technology company Samsung Electronics Co. Ltd., Dutch chip-maker ASML Holding NV, and Taiwan Semiconductor Manufacturing Co. (TSMC). In China, the holdings in power-grid company Nari Technology Co. Ltd., and solar energy company Longi Green Energy Technology Co. enhanced Fund performance due to their alignment to national clean energy objectives. In Russia, natural gas producer and distributor Novatek PJSC benefited from its exposure to soaring spot energy prices and expectations for better valuation of liquefied natural gas (LNG) projects, which form the bedrock of the company's future growth. The Fund's position in Brazilian mining company Vale SA also performed well amid surging iron ore prices.

Conversely, the Fund's education and gaming holdings – New Oriental Education & Technology Group Inc. and Sands China Ltd. – detracted from Fund performance for the reporting period, as both companies were in the crosshairs of the Chinese government's policy tightening.

Regarding key portfolio activity over the reporting period, we initiated holdings in sporting goods maker Li Ning Co. Ltd.; clean energy company Sungrow Power Supply Co. Ltd.; and Yunnan Energy New Material Co. Ltd., a supplier of film, packaging and printing products. We also initiated positions in platinum producer Anglo American Platinum Ltd. (Amplats); electronics manufacturer Hon Hai Precision Industry Co., Ltd.; and conglomerate Grupo Mexico SAB de C.V. Additionally, we initiated a holding in clean energy company Xinjiang Goldwind Science & Technology Co., Ltd., and subsequently exited the position later in the reporting period.

Chinese government regulation in the education sector impaired the investment case for New Oriental Education & Technology to such an extent that we sold the Fund's holding in the company. We exited the Fund's position in Shanghai International Airport Co. Ltd., as its stock price performed poorly due to revisions to its duty-free contract. We also sold the Fund's shares in Ping An Insurance Co. of China Ltd.; online auto retailer Autohome Inc; China Merchants Bank; hotel-chain operator Huazhu Group Ltd.; and Petobras, Brazil's state-owned oil company. Furthermore, the Fund no longer holds global internet company Naspers Ltd. following a recent corporate action in which the majority of the position was exchanged for shares of Prosus NV. We believe that Prosus offers a more attractive valuation opportunity to access the portfolio of technology businesses owned by the company, including internet and technology company Tencent Holdings Ltd.

We initiated more holdings that we believe will benefit from various structural trends, such as the accelerating adoption of 5G, cloud computing, artificial intelligence and the Internet of Things.1 In the hardware segment, we initiated a holding in ASM International NV, a semiconductor wafer equipment maker, and Delta Electronics, a diversified global supplier of electronics components. We established new positions in several software companies, including Globant SA, a

1 The Internet of Things refers to a system of interrelated, internet-connected objects that are able to collect and transfer data over a wireless network without human intervention.

| 16 | 2021 Annual Report |

Aberdeen Emerging Markets Fund (Unaudited) (concluded)

software and user-experience consultancy which we believe has an upbeat growth outlook as more companies adopt digital solutions. In China, we initiated a holding in GDS Holdings Ltd., one of the largest providers of high-performance internet data centers, as we believe that the company is well-placed to benefit from policies supporting cloud adoption in that country. We also established new positions in several internet-oriented companies, including Kakao Corp., South Korea's top online platform, and Sea Ltd., which operates e-commerce, gaming and fintech platforms that benefit from accelerating digital penetration trends. We also initiated a holding in Russian fintech company TCS Group Holding PLC. Furthermore, we established several new Fund positions outside of the technology sector over the reporting period. In our view, sock exchange operator B3 SA offers attractive exposure to Brazil's rising capital markets penetration. We think that Rumo, Brazil's largest independent railroad operator, has an appealing growth profile. Maruti Suzuki India Ltd., India's largest passenger-vehicle manufacturer, has a dominant market share in the four-wheeler market and, in our view, an unparalleled distribution network. We believe that Zhongsheng Group Holdings Ltd., a major Chinese automotive dealer, benefits from a strong portfolio of premium car brands, recurring cash flows from its after-sales business, and scale2 advantage with its ability to make accretive acquisitions.

Despite China's regulatory agenda related to social equality, data security and environmental sustainability, we believe that the government remains pro-innovation and, in the long term, a greater focus on social equality should put the economy on a more sustainable footing. It is a similar story with the shift in the country's growth model to have less reliance on the property sector. We also feel that the global economic recovery is supported by accelerating COVID-19 vaccination rates that allow an easing of mobility restrictions. In our view, this should mitigate the pockets of inflationary pressure in parts of EMs tied to rising energy prices and near-term supply-chain disruptions. With central banks across EMs on the front foot and external balances3 mostly in good shape, we view the risks associated with the U.S. Federal Reserve's tapering as manageable for most of the EM equities asset class.

We think that valuations in EMs are now looking more supportive and, as stock-pickers, we remain focused on what we believe are attractively valued companies with pricing power and sustainable economic moats4 that drive long-term returns. In our view, EM stocks remain attractive due to the diversity of high-quality companies underpinned by structural growth drivers, including healthy demographics, a growing middle class, and reasonable valuations. We believe that, by maintaining our disciplined, bottom-up investment

approach, the Fund's holdings should deliver sustainable returns to shareholders over the longer term.

Portfolio Management:

Global Emerging Markets Equity Team

PAST PERFORMANCE DOES NOT GUARANTEE FUTURE RESULTS.

The performance data quoted represents past performance and current returns may be lower or higher. Class A Shares have up to a 5.75% front-end sales charge and a 0.25% 12b-1 fee. The investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than the original cost. To obtain performance information current to the most recent month-end, which may be higher or lower than the performance shown above, please call 866-667-9231 or go to https://www.abrdn.com/en-us/us/investor/fund-centre.

Investing in mutual funds involves risk, including the possible loss of principal.

Indexes are unmanaged and have been provided for comparison purposes only. No fees or expenses are reflected. You cannot invest directly in an index.

Risk Considerations

Deteriorating market conditions might cause a general weakness in the market that reduces the prices, or yield, of securities in those markets in which the Fund invests.

The value of a security may decline for reasons directly related to the issuer, such as management performance, financial leverage and reduced demand for the issuer's goods or services.

The stock or other security of a company may not perform as well as expected, and may decrease in value, because of factors related to the company, to the industry in which the company is engaged, or to the market as a whole.

The Fund is subject to the risk that the Adviser or Subadviser may make poor security selections.

The risks that apply to foreign investments are greater for securities of companies in emerging market countries because the countries may have less stable governments, more volatile currencies and less established markets.