Obfuscation and Misdirection at TPC Group Inc.:

Analysis of the Process and Alternatives for TPCG

by Sandell Asset Management Corp.

Analysis of the Process and Alternatives for TPCG

by Sandell Asset Management Corp.

October 2012

SAMC Analysis of TPC Group Inc.

2

DISCLAIMER

THIS PRESENTATION WITH RESPECT TO TPC GROUP INC (“TPCG”, “TPCG GROUP” OR THE “COMPANY”) IS FOR GENERAL INFORMATIONAL PURPOSES

ONLY. IT DOES NOT HAVE REGARD TO THE SPECIFIC INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY OR PARTICULAR NEED OF ANY

SPECIFIC PERSON WHO MAY RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION.

THE VIEWS EXPRESSED HEREIN REPRESENT THE OPINIONS OF SANDELL ASSET MANAGEMENT CORP. (“SAMC”), AND ARE BASED ON PUBLICLY

AVAILABLE INFORMATION AND SAMC ANALYSES. CERTAIN FINANCIAL INFORMATION AND DATA USED HEREIN HAVE BEEN DERIVED OR OBTAINED FROM

FILINGS MADE WITH THE SEC BY THE COMPANY, AFFILIATES OR ENTITIES WITHIN THE GROUP OR OTHER COMPANIES CONSIDERED COMPARABLE, AND

FROM OTHER THIRD PARTY REPORTS. NO REPRESENTATION OR WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED OR OBTAINED

FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE, AND SAMC SHALL NOT BE RESPONSIBLE OR HAVE ANY LIABILITY FOR

ANY MISINFORMATION CONTAINED IN ANY SEC FILING OR THIRD PARTY REPORT.

ONLY. IT DOES NOT HAVE REGARD TO THE SPECIFIC INVESTMENT OBJECTIVE, FINANCIAL SITUATION, SUITABILITY OR PARTICULAR NEED OF ANY

SPECIFIC PERSON WHO MAY RECEIVE THIS PRESENTATION, AND SHOULD NOT BE TAKEN AS ADVICE ON THE MERITS OF ANY INVESTMENT DECISION.

THE VIEWS EXPRESSED HEREIN REPRESENT THE OPINIONS OF SANDELL ASSET MANAGEMENT CORP. (“SAMC”), AND ARE BASED ON PUBLICLY

AVAILABLE INFORMATION AND SAMC ANALYSES. CERTAIN FINANCIAL INFORMATION AND DATA USED HEREIN HAVE BEEN DERIVED OR OBTAINED FROM

FILINGS MADE WITH THE SEC BY THE COMPANY, AFFILIATES OR ENTITIES WITHIN THE GROUP OR OTHER COMPANIES CONSIDERED COMPARABLE, AND

FROM OTHER THIRD PARTY REPORTS. NO REPRESENTATION OR WARRANTY IS MADE THAT DATA OR INFORMATION, WHETHER DERIVED OR OBTAINED

FROM FILINGS MADE WITH THE SEC OR FROM ANY THIRD PARTY, ARE ACCURATE, AND SAMC SHALL NOT BE RESPONSIBLE OR HAVE ANY LIABILITY FOR

ANY MISINFORMATION CONTAINED IN ANY SEC FILING OR THIRD PARTY REPORT.

SAMC HAS NOT SOUGHT OR OBTAINED CONSENT FROM ANY THIRD PARTY TO USE ANY STATEMENTS OR INFORMATION INDICATED HEREIN AS HAVING

BEEN OBTAINED OR DERIVED FROM A THIRD PARTY. ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT

OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN.

BEEN OBTAINED OR DERIVED FROM A THIRD PARTY. ANY SUCH STATEMENTS OR INFORMATION SHOULD NOT BE VIEWED AS INDICATING THE SUPPORT

OF SUCH THIRD PARTY FOR THE VIEWS EXPRESSED HEREIN.

THERE IS NO ASSURANCE OR GUARANTEE WITH RESPECT TO THE PRICES AT WHICH ANY SECURITIES OF THE ISSUER WILL TRADE, AND SUCH

SECURITIES MAY NOT TRADE AT PRICES THAT MAY BE IMPLIED HEREIN. THE ESTIMATES, PROJECTIONS, PRO FORMA INFORMATION AND POTENTIAL

IMPACT OF SAMC’S ACTION PLAN SET FORTH HEREIN ARE BASED ON ASSUMPTIONS THAT SAMC BELIEVES TO BE REASONABLE, BUT THERE CAN BE NO

ASSURANCE OR GUARANTEE THAT ACTUAL RESULTS OR PERFORMANCE OF THE COMPANY WILL NOT DIFFER, AND SUCH DIFFERENCES MAY BE

MATERIAL. THIS PRESENTATION DOES NOT RECOMMEND, AND SHOULD NOT BE CONSIDERED AS AN OFFER FOR, THE PURCHASE OR SALE OF ANY

SECURITY. SAMC RESERVES THE RIGHT TO CHANGE ANY OF ITS OPINIONS EXPRESSED HEREIN AT ANY TIME AS IT DEEMS APPROPRIATE. SAMC

DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN.

SECURITIES MAY NOT TRADE AT PRICES THAT MAY BE IMPLIED HEREIN. THE ESTIMATES, PROJECTIONS, PRO FORMA INFORMATION AND POTENTIAL

IMPACT OF SAMC’S ACTION PLAN SET FORTH HEREIN ARE BASED ON ASSUMPTIONS THAT SAMC BELIEVES TO BE REASONABLE, BUT THERE CAN BE NO

ASSURANCE OR GUARANTEE THAT ACTUAL RESULTS OR PERFORMANCE OF THE COMPANY WILL NOT DIFFER, AND SUCH DIFFERENCES MAY BE

MATERIAL. THIS PRESENTATION DOES NOT RECOMMEND, AND SHOULD NOT BE CONSIDERED AS AN OFFER FOR, THE PURCHASE OR SALE OF ANY

SECURITY. SAMC RESERVES THE RIGHT TO CHANGE ANY OF ITS OPINIONS EXPRESSED HEREIN AT ANY TIME AS IT DEEMS APPROPRIATE. SAMC

DISCLAIMS ANY OBLIGATION TO UPDATE THE INFORMATION CONTAINED HEREIN.

PRIVATE INVESTMENT FUNDS ADVISED BY SAMC CURRENTLY HOLD SHARES OF COMMON STOCK REPRESENTING AGGREGATE OWNERSHIP OF

APPROXIMATELY 7% OF THE OUTSTANDING COMMON STOCK OF THE COMPANY. SAMC MANAGES INVESTMENT FUNDS THAT ARE IN THE BUSINESS OF

TRADING - BUYING AND SELLING - PUBLIC SECURITIES. IT IS POSSIBLE THAT THERE WILL BE DEVELOPMENTS IN THE FUTURE THAT CAUSE SAMC AND/OR

ONE OR MORE OF THE INVESTMENT FUNDS IT MANAGES, FROM TIME TO TIME (IN OPEN MARKET OR PRIVATELY NEGOTIATED TRANSACTIONS OR

OTHERWISE), TO SELL ALL OR A PORTION OF THEIR SHARES (INCLUDING VIA SHORT SALES), BUY ADDITIONAL SHARES OR TRADE IN OPTIONS, PUTS,

CALLS OR OTHER DERIVATIVE INSTRUMENTS RELATING TO SUCH SHARES. SAMC AND SUCH INVESTMENT FUNDS ALSO RESERVE THE RIGHT TO TAKE

ANY ACTIONS WITH RESPECT TO THEIR INVESTMENTS IN THE COMPANY AS THEY MAY DEEM APPROPRIATE, INCLUDING, BUT NOT LIMITED TO,

COMMUNICATING WITH MANAGEMENT OF THE COMPANY, THE BOARD OF DIRECTORS OF THE COMPANY AND OTHER INVESTORS AND THIRD PARTIES,

AND CONDUCTING A PROXY SOLICITATION WITH RESPECT TO THE ELECTION OF PERSONS TO THE BOARD OF DIRECTORS OF THE COMPANY.

APPROXIMATELY 7% OF THE OUTSTANDING COMMON STOCK OF THE COMPANY. SAMC MANAGES INVESTMENT FUNDS THAT ARE IN THE BUSINESS OF

TRADING - BUYING AND SELLING - PUBLIC SECURITIES. IT IS POSSIBLE THAT THERE WILL BE DEVELOPMENTS IN THE FUTURE THAT CAUSE SAMC AND/OR

ONE OR MORE OF THE INVESTMENT FUNDS IT MANAGES, FROM TIME TO TIME (IN OPEN MARKET OR PRIVATELY NEGOTIATED TRANSACTIONS OR

OTHERWISE), TO SELL ALL OR A PORTION OF THEIR SHARES (INCLUDING VIA SHORT SALES), BUY ADDITIONAL SHARES OR TRADE IN OPTIONS, PUTS,

CALLS OR OTHER DERIVATIVE INSTRUMENTS RELATING TO SUCH SHARES. SAMC AND SUCH INVESTMENT FUNDS ALSO RESERVE THE RIGHT TO TAKE

ANY ACTIONS WITH RESPECT TO THEIR INVESTMENTS IN THE COMPANY AS THEY MAY DEEM APPROPRIATE, INCLUDING, BUT NOT LIMITED TO,

COMMUNICATING WITH MANAGEMENT OF THE COMPANY, THE BOARD OF DIRECTORS OF THE COMPANY AND OTHER INVESTORS AND THIRD PARTIES,

AND CONDUCTING A PROXY SOLICITATION WITH RESPECT TO THE ELECTION OF PERSONS TO THE BOARD OF DIRECTORS OF THE COMPANY.

SAMC Analysis of TPC Group Inc.

3

Executive Summary

u Sandell Asset Management Corp. (SAMC) holds 7.0% of the outstanding shares of TPC Group (TPCG). Upon reading the preliminary

proxy statement, we stand by our belief that the sale process was flawed and tainted by ‘self-dealing’, the projections

employed were low-balled to the benefit of First Reserve & SK Capital (PE Buyers) and management, and the Exit Multiple

needs to be re-rated upwards to reflect the MLP-qualifying nature of TPCG’s stable, processing-based cash flows.

proxy statement, we stand by our belief that the sale process was flawed and tainted by ‘self-dealing’, the projections

employed were low-balled to the benefit of First Reserve & SK Capital (PE Buyers) and management, and the Exit Multiple

needs to be re-rated upwards to reflect the MLP-qualifying nature of TPCG’s stable, processing-based cash flows.

u With a thorough reading of the preliminary proxy, we believe that potential strategic bidders were unquestionably at a

disadvantage compared to financial bidders. This despite the overwhelming evidence that strategic acquirers usually pay more given

operational and financial synergies. We stand by our initial belief that this process was flawed and tainted by ‘self-dealing’.

Given the level of strategic interest, the fact that a ‘go-shop’ period was not negotiated to ensure that shareholders receive the

maximum value for their shares evidences the self-interest which poisoned this process.

disadvantage compared to financial bidders. This despite the overwhelming evidence that strategic acquirers usually pay more given

operational and financial synergies. We stand by our initial belief that this process was flawed and tainted by ‘self-dealing’.

Given the level of strategic interest, the fact that a ‘go-shop’ period was not negotiated to ensure that shareholders receive the

maximum value for their shares evidences the self-interest which poisoned this process.

u Upon analyzing the Fairness Opinion valuation methodologies, we believe the opinion was biased towards a low valuation for

TPCG, justifying the inadequate transaction price and thereby enabling a high return for the PE Buyers and management.

TPCG, justifying the inadequate transaction price and thereby enabling a high return for the PE Buyers and management.

l TPCG is repeatedly and incorrectly compared to volatile, commodity chemicals companies - this is in contrast to management

who has guided investors to compare TPCG to stable industrial gas suppliers such as Praxair, Air Products and Airgas. We

believe the PE Buyers would project out-sized IRRs of 55%+ when using the correct multiples.

who has guided investors to compare TPCG to stable industrial gas suppliers such as Praxair, Air Products and Airgas. We

believe the PE Buyers would project out-sized IRRs of 55%+ when using the correct multiples.

l We believe that projections being used for the core business and Project Phoenix are low-balled (similar to the most conservative

sell-side estimate) and are well below what management communicated to shareholders as recently as July 2012.

sell-side estimate) and are well below what management communicated to shareholders as recently as July 2012.

l Management incentive agreements have purposefully ‘not been negotiated’ as of the time of the transaction to keep shareholders

ignorant about the significant mis-alignment of incentives between management and the shareholders.

ignorant about the significant mis-alignment of incentives between management and the shareholders.

u Lastly, we believe, based on the preliminary proxy and discussions with our own MLP counsel, that there is little doubt that the cash

flows generated from the C4 processing business (2/3 of current EBITDA) and those cash flows expected from the de-hydro projects

are MLP-qualifying, providing another lever for shareholder value creation. We believe that the projections / Exit Multiple should be

adjusted upwards, reflecting the value of a fee-based processing business with MLP-qualifying income.

flows generated from the C4 processing business (2/3 of current EBITDA) and those cash flows expected from the de-hydro projects

are MLP-qualifying, providing another lever for shareholder value creation. We believe that the projections / Exit Multiple should be

adjusted upwards, reflecting the value of a fee-based processing business with MLP-qualifying income.

Sandell intends to vote against the deal, encourages fellow shareholders to do the same

and seeks to have the Company run a proper auction to maximize shareholder values.

and seeks to have the Company run a proper auction to maximize shareholder values.

SAMC Analysis of TPC Group Inc.

4

Process Was Flawed And Tainted By Self-Dealing; SC Failed to Negotiate a Go-Shop

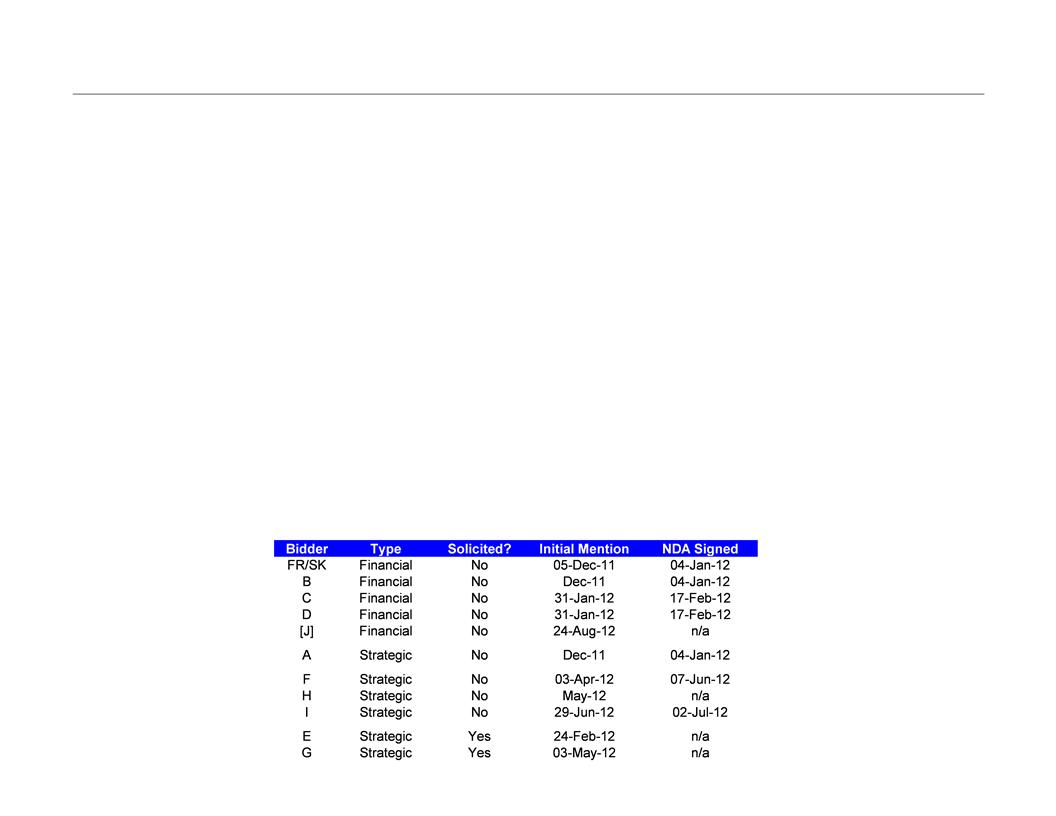

u The significant number of unsolicited, incoming calls suggest an uncontrolled, shadow auction for the company over the course of

nine months with the PE Buyers heavily favored given their accelerated access to the data room and negotiations. Out of the 11

interested parties, 9 contacted TPCG in an unsolicited manner - this is highly unusual, and likely created an uneven playing

field. This reflects, we believe, management putting its self-interest ahead of the best interests of all shareholders.

nine months with the PE Buyers heavily favored given their accelerated access to the data room and negotiations. Out of the 11

interested parties, 9 contacted TPCG in an unsolicited manner - this is highly unusual, and likely created an uneven playing

field. This reflects, we believe, management putting its self-interest ahead of the best interests of all shareholders.

u Strategic bidders were not clearly encouraged in the process - despite strategic bidders being in the most likely position to offer

the best price to shareholders. Of the 6 strategic bidders, 4 had to contact TPCG in an unsolicited manner and only 2 accessed

the data room - this also is highly unusual as strategic bidders have the most to gain from data room access. Given this haphazard

process, it is particularly disheartening that a go-shop period was not negotiated to ensure the maximization of shareholder value.

the best price to shareholders. Of the 6 strategic bidders, 4 had to contact TPCG in an unsolicited manner and only 2 accessed

the data room - this also is highly unusual as strategic bidders have the most to gain from data room access. Given this haphazard

process, it is particularly disheartening that a go-shop period was not negotiated to ensure the maximization of shareholder value.

u The Special Committee (SC) only discussed potential strategic bidders a full 2 months after first contact from the PE Buyers and 4

parties having started due diligence - at one meeting, the SC determined to “postpone” negotiations with strategic bidders “until

more definitive bids were obtained from the financial buyers”, and a week later determined not to pursue a public auction due to

“routine business contract negotiations” and “negotiations [related to] the strategic growth projects”. This is not a credible rationale

as target companies regularly hold controlled auctions while conducting contract negotiations.

parties having started due diligence - at one meeting, the SC determined to “postpone” negotiations with strategic bidders “until

more definitive bids were obtained from the financial buyers”, and a week later determined not to pursue a public auction due to

“routine business contract negotiations” and “negotiations [related to] the strategic growth projects”. This is not a credible rationale

as target companies regularly hold controlled auctions while conducting contract negotiations.

u Lastly, despite Perella’s indication that the “universe of potential strategic bidders was small”, the subsequent avalanche of strategic

interest (a majority of which was unsolicited) and the initial indication of another 20 potential strategic bidders plus more from the SC,

we believe, reflects the willful favoritism of the SC and the management to ‘cash-out’ and provide management with

employment and upside as TPCG executes its growth plan privately.

interest (a majority of which was unsolicited) and the initial indication of another 20 potential strategic bidders plus more from the SC,

we believe, reflects the willful favoritism of the SC and the management to ‘cash-out’ and provide management with

employment and upside as TPCG executes its growth plan privately.

SAMC Analysis of TPC Group Inc.

5

u Fairness Opinions are valuation analyses that can be tailored considerably for a client by cherry-picking EBITDA figures, multiples and

comparable figures to obtain the desired effect. We believe that the Fairness Opinion for TPCG is considerably more egregious

than most. The most obvious faults are:

comparable figures to obtain the desired effect. We believe that the Fairness Opinion for TPCG is considerably more egregious

than most. The most obvious faults are:

l Using publicly traded comps that are commodity chemical businesses, while the management has repeatedly made the

claim on public conference calls that the majority of TPCG’s cash flows are ‘fee-based’ and not related to commodity prices;

claim on public conference calls that the majority of TPCG’s cash flows are ‘fee-based’ and not related to commodity prices;

l Using LTM EBITDA (approximately $110m) vs 2013E ($160m) to emphasize the ‘high’ multiple paid, despite ample evidence

that LTM EBITDA reflects reduced C4 volumes as a result of ethylene cracker turnarounds which will not repeat. Also, the

2013E figures reflect service fee increases that have been discussed at length by management;

that LTM EBITDA reflects reduced C4 volumes as a result of ethylene cracker turnarounds which will not repeat. Also, the

2013E figures reflect service fee increases that have been discussed at length by management;

l Using a depressed LTM Exit Multiple range of 4.5x-5.5x when the business is being taken private at a 7.7x trailing EBITDA

multiple. Furthermore, this multiple does not consider the ‘fee-based’ and MLP-qualifying nature of TPCG as of 2016;

multiple. Furthermore, this multiple does not consider the ‘fee-based’ and MLP-qualifying nature of TPCG as of 2016;

l Using a 9% interest rate for the almost $682m in senior notes (in the LBO analysis), which is significantly above market for

comparable notes given TPCG’s asset profile and currently low spreads and interest rates;

comparable notes given TPCG’s asset profile and currently low spreads and interest rates;

l Using July 24th and June 25th trading prices for the ‘premium paid’ analysis, notwithstanding the fact that TPCG traded

near $40/share between those dates and traded above $40/share for almost 2 months in 2012 and 2011. Furthermore, TPCG

closed at a high of $47.03/share as recently as March 2012.

near $40/share between those dates and traded above $40/share for almost 2 months in 2012 and 2011. Furthermore, TPCG

closed at a high of $47.03/share as recently as March 2012.

Fairness Opinion Valuation Undervalues Company

SAMC Analysis of TPC Group Inc.

6

u Management has spent significant effort in explaining the fee-based nature of TPCG’s business (see comments below) and has

also commented that TPCG’s processing, service and distribution business should be valued similarly to industrial gas

companies such as Praxiar, Air Products and Airgas that trade in the 8x-10x EBITDA range.

also commented that TPCG’s processing, service and distribution business should be valued similarly to industrial gas

companies such as Praxiar, Air Products and Airgas that trade in the 8x-10x EBITDA range.

u Based on these comments and TPCG’s underlying business, it is clear that its cash flows are not related to commodity prices and

therefore TPCG should not be valued as a commodity chemical business. It is a processing business, taking limited risk to the

underlying price of butadiene (BD).

therefore TPCG should not be valued as a commodity chemical business. It is a processing business, taking limited risk to the

underlying price of butadiene (BD).

u We believe that the Fairness Opinion and several statements made in the background incorrectly characterize TPCG as a commodity

chemical business to intentionally dissuade potential bidders and hand the company to First Reserve and SK Capital as

preferred bidders without maximizing shareholder value.

chemical business to intentionally dissuade potential bidders and hand the company to First Reserve and SK Capital as

preferred bidders without maximizing shareholder value.

TPCG is a Fee-Based Processing Business Not a Commodity Chemical Business

SAMC Analysis of TPC Group Inc.

7

Projections For Core Business and Project Phoenix Are Low-Balled

u EBITDA estimates presented in the Fairness Opinion are near the estimates of the most bearish sell-side analyst; however, they are

noticeably lower than other sell-side estimates.

noticeably lower than other sell-side estimates.

u Furthermore, Fairness Opinion EBITDA estimates are well below long run estimates given by current management in October 2011

and communicated to various shareholders in July 2012. These differences most likely reflect the changing motivation of

management once an LBO is being contemplated.

and communicated to various shareholders in July 2012. These differences most likely reflect the changing motivation of

management once an LBO is being contemplated.

u As an example, management is now talking down real values - as evidenced by a sell-side research piece published by Macquarie

on September 10th, 2012, stating previously undisclosed information to encourage shareholders to vote for the current deal.

Some negative management comments from this note:

on September 10th, 2012, stating previously undisclosed information to encourage shareholders to vote for the current deal.

Some negative management comments from this note:

l “capital cost required to restart its two offline de-hydro assets sum to a total greater than the market cap of TPC Group

and more than 20% higher than our prior estimation”; and

and more than 20% higher than our prior estimation”; and

l “issues with sourcing mixed C4s due to increased competitive pressure from underutilized C4 processors at integrated cracker

operators are a real concern for 2H12 and 2013”

operators are a real concern for 2H12 and 2013”

u Lastly, there seems to be a discrepancy in TPCG’s unlevered free cash flow (UFCF) estimates. As shown below, UFCF for the Core

TPCG business is significantly below what would be estimated using D&A and Maintenance Capex figures provided by management.

It is unclear what this $96m and $62m cash flow discrepancy in 2013 and 2014 could be; however, in our LBO analysis we

have conservatively included these ‘mystery’ cash costs.

TPCG business is significantly below what would be estimated using D&A and Maintenance Capex figures provided by management.

It is unclear what this $96m and $62m cash flow discrepancy in 2013 and 2014 could be; however, in our LBO analysis we

have conservatively included these ‘mystery’ cash costs.

SAMC Analysis of TPC Group Inc.

8

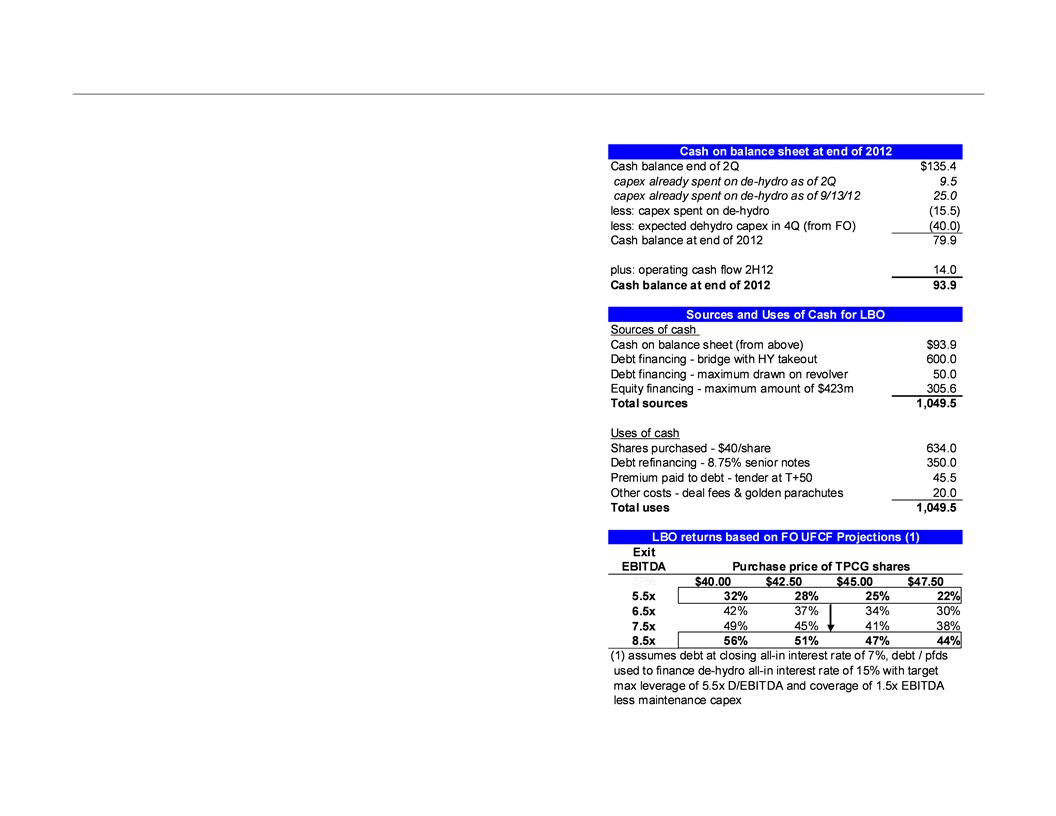

Even Using Low-Ball Projections, LBO Returns For PE Buyers Could Be Considerable

u Using given unlevered free cash flow estimates and Project Phoenix,

IRRs for the PE Buyers could be 32% to 56% at $40/share:

IRRs for the PE Buyers could be 32% to 56% at $40/share:

l Assumes full 35% cash taxes although up to 80% of EBITDA

in 2016 is most likely MLP-qualifying;

in 2016 is most likely MLP-qualifying;

l Does not include any upside from the 2nd de-hydro project -

which is considered by some to be more valuable than the 1st

de-hydro project;

which is considered by some to be more valuable than the 1st

de-hydro project;

l Includes $96.4m and $62.0m of ‘mystery’ cash costs in 2013

and 2014;

and 2014;

l Estimates cash balances at end of 2012 (at closing) and sources

and uses of cash based on the Fairness Opinion and recent

press releases from the company;

and uses of cash based on the Fairness Opinion and recent

press releases from the company;

l Targeting a maximum Debt + Pfds / EBITDA of 5.5x and

coverage ratio of 1.5x of EBITDA less maintenance capex;

coverage ratio of 1.5x of EBITDA less maintenance capex;

l The High LBO price range reflects the maximum drawdown on

the PE Buyers Equity Commitment of $423m.

the PE Buyers Equity Commitment of $423m.

u As in most valuations, the key determinant is the Exit Multiple figure -

using a range of 5.5x to 8.5x, the IRR increases substantially.

using a range of 5.5x to 8.5x, the IRR increases substantially.

l We believe that given the fee-based, processing nature of

TPCG’s cash flows plus the potential upside of those cash flows

being MLP-qualifying necessitates using an 8.5x Exit Multiple.

TPCG’s cash flows plus the potential upside of those cash flows

being MLP-qualifying necessitates using an 8.5x Exit Multiple.

l The best comp for this Exit Multiple would be a discount multiple

to industrial gas suppliers (PX, APD or ARG) or the EBITDA

multiple for PetroLogistics MLP (PDH), a variable-dividend

paying, de-hydro asset.

to industrial gas suppliers (PX, APD or ARG) or the EBITDA

multiple for PetroLogistics MLP (PDH), a variable-dividend

paying, de-hydro asset.

SAMC Analysis of TPC Group Inc.

9

80% of TPCG’s Income is MLP-Qualifying, Increasing Exit Valuation

u There is ample disclosure regarding the evaluation of TPCG as an MLP. Based on our read of the preliminary proxy, the cash

flows from the C4 business (2/3 of current EBITDA) are MLP-qualifying. Furthermore, with PetroLogistics (PDH) as a public

comparable, we also believe all the EBITDA generated from the de-hydro projects will be MLP-qualifying.

flows from the C4 business (2/3 of current EBITDA) are MLP-qualifying. Furthermore, with PetroLogistics (PDH) as a public

comparable, we also believe all the EBITDA generated from the de-hydro projects will be MLP-qualifying.

u Given the complexities surrounding structuring and developing an MLP structure (the pacing required to ‘drop-down’ assets into the

MLP, the tax concerns as a result of the low tax basis of the assets, the expected capital projects in front of TPCG, etc.), the SC

decided not to pursue the MLP option. However, the PE Buyers will be able to take advantage of the MLP-qualifying nature of

TPCG’s cash flows through this hold period, away from the view of public shareholders.

MLP, the tax concerns as a result of the low tax basis of the assets, the expected capital projects in front of TPCG, etc.), the SC

decided not to pursue the MLP option. However, the PE Buyers will be able to take advantage of the MLP-qualifying nature of

TPCG’s cash flows through this hold period, away from the view of public shareholders.

u We believe that the Exit Multiple should reflect this significant change in the business as MLP-qualifying income in an MLP

structure is extremely valuable to other MLPs and can serve to reduce TPCG’s cash tax costs and lower its cost of capital.

structure is extremely valuable to other MLPs and can serve to reduce TPCG’s cash tax costs and lower its cost of capital.

u PetroLogistics (PDH) would be the best comparable company to TPCG as an MLP. It processes propane into propylene and

generates variable-dividend paying MLP-qualifying income. Other variable-dividend paying entities are fertilizer MLPs (shown below)

as well as refining MLPs and other processors that have oil, natural gas, NGLs or crude C4 as a feedstock.

generates variable-dividend paying MLP-qualifying income. Other variable-dividend paying entities are fertilizer MLPs (shown below)

as well as refining MLPs and other processors that have oil, natural gas, NGLs or crude C4 as a feedstock.