Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number: 811-22375

PIMCO Equity Series

(Exact name of registrant as specified in charter)

840 Newport Center Drive, Newport Beach, CA 92660

(Address of principal executive offices)

John P. Hardaway

Treasurer and Principal Financial Officer

PIMCO Equity Series

840 Newport Center Drive

Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Brendan C. Fox

Dechert LLP

1900 K Street, N.W.

Washington, D.C. 20006

Registrant’s telephone number, including area code: (888) 877-4626

Date of fiscal year end: June 30

Date of reporting period: June 30, 2013

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Table of Contents

Item 1. | Reports to Stockholders. | |||||||

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30e-1).

| • | PIMCO Equity Series—Institutional, P, Administrative, D, A, C and R Classes |

Table of Contents

Your Global Investment Authority

PIMCO Equity Series®

Annual Report

June 30, 2013

PIMCO Dividend and Income Builder Fund

PIMCO EqS® Dividend Fund

PIMCO EqS® Emerging Markets Fund

PIMCO EqS® Long/Short Fund

PIMCO Emerging Multi-Asset Fund

PIMCO EqS Pathfinder Fund®

Share Classes

| n | Institutional |

| n | P |

| n | Administrative |

| n | D |

| n | A |

| n | C |

| n | R |

Table of Contents

| Page | ||||||

| 2 | ||||||

| 3 | ||||||

| 26 | ||||||

| 28 | ||||||

| 34 | ||||||

| 36 | ||||||

| 38 | ||||||

| 39 | ||||||

| 40 | ||||||

| 41 | ||||||

| 42 | ||||||

| 80 | ||||||

| 100 | ||||||

| 101 | ||||||

| 102 | ||||||

| 103 | ||||||

| 105 | ||||||

| Fund | Insights from the Portfolio Managers | Fund Summary | Schedule of Investments | |||||||||

| 4 | 7 | 43 | ||||||||||

| 8 | 11 | 52 | ||||||||||

| 12 | 14 | 57 | ||||||||||

| 15 | 17 | 65 | ||||||||||

| 18 | 21 | 69 | ||||||||||

| 22 | 25 | 73 | ||||||||||

This material is authorized for use only when preceded or accompanied by the current PIMCO Equity Series prospectus.

Table of Contents

Dear Shareholder,

Please find enclosed the Annual Report for the PIMCO Equity Series covering the twelve-month reporting period ended June 30, 2013. On the following pages are specific details about the investment performance of each fund and a discussion of the factors that influenced performance during the reporting period. In addition, the letters from the portfolio managers provide a further review of such factors as well as an overview of each fund’s investment strategy.

Over most of the reporting period, intervention by the Federal Reserve (“Fed”) and other developed market central banks including the European Central Bank, Bank of England and Bank of Japan, largely succeeded in suppressing market volatility and encouraged investors to move into riskier assets such as equities and high yield bonds. As a result, prices on these asset classes rose considerably through April 2013, propped up by aggressive central bank policies rather than strong economic fundamentals.

However, conditions in financial markets deteriorated rapidly beginning in mid-May as investors reacted to signals by the Fed that it might begin to slow the pace of its asset purchases later this year. Fed Chairman Ben Bernanke outlined a plan for eventually tapering quantitative easing (“QE”) purchases of U.S. Treasuries and mortgage-backed securities (“MBS”) as the U.S. economy begins to meet certain growth targets. In particular, this shift in tone fueled a broad-based sell-off within fixed income assets, undermining market liquidity and sending yields higher across the risk spectrum.

Highlights of the financial markets during our twelve-month reporting period include:

| n | Developed market equities posted strong performance and touched record highs in the early part of 2013. U.S. equities, as measured by the S&P 500 Index, returned 20.60%. Global equities, as represented by the MSCI All Country World Index Net USD and MSCI World Index, returned 16.57% and 18.58%, respectively. Emerging market (“EM”) equities, as represented by the MSCI Emerging Markets Index (Net Dividends in USD), returned 2.87%. EM equities were impacted by declining earnings growth and rising U.S. interest rates towards the latter part of the period which placed pressure on local EM currencies. Concerns over growth and financial risk in China, worsening economic conditions in Brazil, and political turmoil in Turkey also weighed on EM equity returns. |

| n | After reaching historic lows in July 2012, yields on U.S. Treasuries beyond two years in maturity rose considerably beginning in mid-May through the end of the period primarily due to the possibility that the Fed would begin considering tapering its asset purchase program. As a result, bond markets sold off with yields increasing and bond prices declining. The benchmark ten-year U.S. Treasury note yielded 2.49% at the end of the reporting period, as compared to 1.64% on June 30, 2012. The Barclays U.S. Aggregate Index, a widely used index of U.S. investment-grade bonds, declined 0.69% for the period. |

All of our active equity strategies are global, high-conviction portfolios that are unconstrained by geography, benchmark or market capitalization and incorporate downside risk management. Each strategy is managed by experienced equity investors who benefit from PIMCO’s global investment resources and macroeconomic insights. We believe the long-term potential of equities to grow earnings and dividends is an important component of an investor’s overall portfolio.

If you have any questions regarding the PIMCO Equity Series, please contact your account manager or financial adviser, or call one of our shareholder associates at 888.87.PIMCO (888.877.4626). We also invite you to visit our website at www.pimco.com/investments to learn more about our views and global thought leadership.

Thank you again for the trust you have placed in us. We value your commitment and will continue to work diligently to meet your broad investment needs.

| Sincerely,

Brent R. Harris Chairman of the Board, PIMCO Equity Series

July 25, 2013 |

| 2 | PIMCO EQUITY SERIES |

Table of Contents

Important Information About the Funds

PIMCO Equity Series (the “Trust”) is an open-end management investment company currently consisting of six separate investment portfolios (the “Funds”). Each Fund is an actively managed equity strategy. While we believe that equity funds have an important role to play in a well diversified investment portfolio, they are subject to notable risks. Among other things, equity and equity-related securities may decline in value due to both real and perceived general market, economic, and industry conditions.

The Funds may be subject to various risks as described in the Funds’ prospectus. Some of these risks may include, but are not limited to, the following: allocation risk, Acquired Fund risk, equity risk, dividend-oriented stocks risk, value investing risk, foreign (non-U.S.) investment risk, emerging markets risk, market risk, issuer risk, interest rate risk, credit risk, high yield and distressed company risk, cash holdings risk, currency risk, real estate risk, liquidity risk, leveraging risk, management risk, small-cap and mid-cap company risk, arbitrage risk, derivatives risk, mortgage-related and other asset-backed risk, short sale risk, commodity risk, convertible securities risk, tax risk, subsidiary risk and issuer non-diversification risk. A complete description of these risks and other risks is contained in the Funds’ prospectus. The Funds may use derivative instruments for hedging purposes or as part of an investment strategy. Use of these instruments may involve certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, management risk, leverage risk, mispricing or improper valuation risk and the risk that the Funds could not close out a position when it would be most advantageous to do so. Certain derivative transactions may have a leveraging effect on a Fund. For example, a small investment in a derivative instrument may have a significant impact on a Fund’s exposure to interest rates, currency exchange rates or other investments. As a result, a relatively small price movement in a derivative instrument may cause an immediate and substantial loss or gain. A Fund may engage in such transactions regardless of whether

the Fund owns the asset, instrument or components of the index underlying the derivative instrument. A Fund may invest a significant portion of its assets in these types of instruments. If it does, the Fund’s investment exposure could far exceed the value of its portfolio securities and its investment performance could be primarily dependent upon securities it does not own.

On each individual Fund Summary page in this Annual Report (“Shareholder Report”), the Average Annual Total Return table and Cumulative Returns chart measure performance assuming that any dividend and capital gain distributions were reinvested. Class A shares are subject to an initial sales charge. A Contingent Deferred Sales Charge (“CDSC”) may be imposed in certain circumstances on Class A shares that are purchased without an initial sales charge and then redeemed during the first 18 months after purchase. The Cumulative Returns chart reflects only Institutional Class performance. Performance for Class P, Administrative Class, Class D, Class A, Class C and Class R shares is typically lower than Institutional Class performance due to the lower expenses paid by Institutional Class shares. Performance shown is net of fees and expenses. A Fund’s total annual operating expense ratios on each individual Fund summary page are as of the currently effective prospectus, as supplemented to date. The Cumulative Returns chart assumes the initial investment of $1,000,000 was made at the end of the month that the Institutional Class of the relevant Fund commenced operations. The minimum initial investment amount for Institutional Class, Class P or Administrative Class shares is $1,000,000. The minimum initial investment amount for Class A, Class C and Class D shares is $1,000. There is no minimum initial investment for Class R shares. Each Fund measures its performance against a broad-based securities market index (benchmark index). The benchmark index does not take into account fees, expenses, or taxes. A Fund’s past performance, before and after taxes, is not necessarily an indication of how the Fund will perform in the future.

The following table discloses the inception dates of each Fund and its respective share classes:

| Fund Name | Fund Inception | Institutional Class | Class P | Administrative Class | Class D | Class A | Class C | Class R | ||||||||||||||||||||||||||

PIMCO Dividend and Income Builder Fund | 12/14/11 | 12/14/11 | 12/14/11 | — | 12/14/11 | 12/14/11 | 12/14/11 | 12/14/11 | ||||||||||||||||||||||||||

PIMCO EqS® Dividend Fund | 12/14/11 | 12/14/11 | 12/14/11 | — | 12/14/11 | 12/14/11 | 12/14/11 | 12/14/11 | ||||||||||||||||||||||||||

PIMCO EqS® Emerging Markets Fund | 03/22/11 | 03/22/11 | 03/22/11 | 04/19/11 | 03/22/11 | 03/22/11 | 03/22/11 | 03/22/11 | ||||||||||||||||||||||||||

PIMCO EqS® Long/Short Fund | 04/20/12 | 04/20/12 | 04/30/12 | — | 04/30/12 | 04/30/12 | 04/30/12 | — | ||||||||||||||||||||||||||

PIMCO Emerging Multi-Asset Fund | 04/12/11 | 04/12/11 | 04/12/11 | 04/19/11 | 04/12/11 | 04/12/11 | 04/12/11 | 04/12/11 | ||||||||||||||||||||||||||

PIMCO EqS Pathfinder Fund® | 04/14/10 | 04/14/10 | 04/14/10 | — | 04/14/10 | 04/14/10 | 04/14/10 | 04/14/10 | ||||||||||||||||||||||||||

For periods prior to the inception date of the Class P, Administrative Class, Class D, Class A, Class C and Class R shares (if applicable), performance information shown is based on the performance of the Fund’s Institutional Class shares. The prior Institutional Class performance has been adjusted to reflect the distribution and/or service fees and other expenses paid by the Class P, Administrative Class, Class D, Class A, Class C and Class R shares, respectively.

An investment in a Fund is not a bank deposit and is not guaranteed or insured by the Federal Deposit Insurance Corporation (“FDIC”) or any other government agency. It is possible to lose money on investments in a Fund.

PIMCO has adopted written proxy voting policies and procedures (“Proxy Policy”) as required by Rule 206(4)-6 under the Investment Advisers Act of 1940, as amended. The Proxy Policy has been adopted by PIMCO Equity Series as the policies and procedures that PIMCO will use when voting proxies on behalf of a Fund. A description of the policies and procedures that PIMCO uses to vote proxies relating to portfolio securities of a Fund, and information about how the Fund

voted proxies relating to portfolio securities held during the most recent twelve-month period ended June 30th, are available without charge, upon request, by calling the Trust at (888) 87-PIMCO, on the Fund’s website at http://www.pimco.com/investments, and on the Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov.

PIMCO Equity Series files a complete schedule of each Fund’s portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. A copy of a Fund’s Form N-Q is available on the SEC’s website at http://www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. A Fund’s Form N-Q will also be available without charge, upon request, by calling the Trust at (888) 87-PIMCO and on the Fund’s website at http://www.pimco.com/investments. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

| ANNUAL REPORT | JUNE 30, 2013 | 3 |

Table of Contents

Insights from the Portfolio Managers PIMCO Dividend and Income Builder Fund

Dear Shareholder,

We appreciate your investment in the PIMCO Dividend and Income Builder Fund (the “Fund”). In the following letter, please find a discussion of the recent market environment and a review of portfolio performance.

Market overview

During the twelve months ended June 30, 2013, the MSCI All Country World Index Net USD (the “Index”), which tracks the performance of stocks in developed and emerging markets countries, returned 16.57%. While overall market performance was positive, the intra-period performance was volatile due to political uncertainty in the U.S. and Europe.

Global equity market performance was strong during most of the third quarter of 2012 after Mario Draghi, President of the European Central Bank, vowed on July 26 to do “whatever it takes” to stabilize Europe. Following the U.S. Federal Reserve’s (“Fed”) announcement of plans for more stimulus action in mid-September, however, global equity markets declined and remained volatile through October, possibly implying a decreasing effectiveness of Fed actions. Global equity markets resumed the decline during the first half of November following the U.S. presidential election as the focus turned to the “fiscal cliff” in the U.S. Markets began to rally in mid-November as hope grew that U.S. lawmakers could reach an agreement that would avoid the $600 billion of automatic tax hikes and spending cuts that were scheduled to take effect in the new year. Market performance faded at the end of December as hope for an agreement waned.

Markets steadily rose in January 2013 after U.S. politicians finally passed and signed legislation that avoided much of the so-called “fiscal cliff,” although the legislation fell far short of the “grand bargain” that some had hoped for, leaving looming fiscal policy fights ahead. After reaching five-year highs, equity markets fell in February 2013 in response to weak U.S. and European economic data. They bounced back at the end of February and rallied through mid-March 2013, led by Japanese equities as investors anticipated that the Bank of Japan’s new governor would push forward very aggressive monetary easing policies. Markets fell slightly in mid-March after the small European country of Cyprus requested a bailout of its financial system, raising concerns about economic stability in Europe.

Following some bumpy first weeks in April 2013, markets rose until May 21, when Federal Reserve chairman Ben Bernanke indicated that the Fed might begin tapering quantitative easing in 2013 if employment improved. Markets then fell, particularly in June 2013 after Bernanke, at a press conference, clarified his earlier remarks regarding tapering. Markets rose slightly during the last week of the quarter after the U.S., European, and Chinese central banks all

delivered remarks aimed at assuaging investor concerns about liquidity, noting that “tapering” referred to less accommodative, not most restrictive, monetary policies. Performance was also helped by positive U.S. macro data, which suggested, among other things, that the housing market was improving.

Global equity market performance was positive in each of the ten Global Industry Classification Standard (“GICS”) sectors except the materials sector. Performance was strongest in consumer discretionary, health care, and financials. Materials, utilities, and energy were the poorest performing sectors. Japan and the U.S. were the strongest performing regions globally, while emerging markets, particularly Brazil, lagged.

Fund review

Over time, we seek to grow the total dividends paid by the Fund each year, while pursuing our other goals of providing an attractive current yield and total returns. During the twelve months ended June 30, 2013, the Fund paid ordinary quarterly dividends of 42.1 cents per share on its Institutional Class shares. The dividend per share was slightly lower for the other share classes, to account for varying class specific expenses. The Fund’s net asset value increased by $1.13 per share (from $10.47 to $11.60) over the reporting period, bringing the twelve-month total return to 15.17% (net of fees).

On a relative basis, the Fund outperformed its benchmark (a blend of 75% MSCI All Country World Index Net USD/25% Barclays Global Aggregate (USD Unhedged) Index), which returned 11.63%. Overall security selection within equities was positive, and was particularly strong in the health care, energy, and telecommunication services sectors. Security selection was negative in the materials and industrials sectors.

At the security level, the Fund’s position in Marathon Petroleum, a U.S. oil refining and marketing company, was the largest contributor to relative performance. Marathon’s stock outperformed as the company continued to profit from above-average crack spreads and growing oil production in America’s heartland, and Marathon announced favorable quarterly earnings results in both November 2012 and January 2013. The company also announced that it had entered into a $500 million share repurchase program. These positive developments prompted Moody’s to upgrade Marathon’s credit rating in March 2013.

Enagás was another contributor to performance. The Spanish natural gas utility outperformed as the outlook for the regulatory environment in Spain became more favorable, and after reporting positive quarterly earnings results which were driven by the contribution of new assets as well as by cost controls. Enagás also grew its semiannual dividend in April 2013.

The largest detractor for the period was the Fund’s holding of Gold Fields. The South African precious metals miner underperformed in sympathy with gold, the price of which declined during the period as

| 4 | PIMCO EQUITY SERIES |

Table of Contents

the economic environment appeared to stabilize and investor demand for gold declined. At the same time, Gold Fields’ production difficulties led to earnings disappointments. Given these increased risks, the Fund exited the position.

Poseidon Concepts was another detractor from performance. The Canada-based fluid management company underperformed after announcing disappointing quarterly earnings results in November 2012. The disappointment was due mainly to a decline in water tank utilization, lower North American rig counts, and a revision on the company’s ability to collect accounts receivable fully. Our concerns, including that the company might eliminate its dividend, prompted the Fund to exit the position.

The Fund’s fixed income allocation performed positively, driven mainly by overweight positions to investment grade, high yield, and emerging markets credit securities, as these sectors outperformed during the reporting period.

Investment process and portfolio construction

Our bottom-up investment strategy is focused on providing attractive income today and long-term capital appreciation. As we seek to achieve these goals, we employ fundamental research that aims to identify attractively priced companies exhibiting the ability and willingness to increase dividend payments. We then construct a portfolio that is diversified across three types of businesses:

| n | Consistent Earners are blue-chip industry leaders that consistently create value year after year. |

| n | Basic Value companies are traditional value companies such as cyclicals, turnarounds, and companies with low valuations. |

| n | Emerging Franchises are companies with the potential to be significantly larger over time. |

Our total return focused approach to dividend investing means that we do not advocate selecting equity investments based on yield alone. Instead, we believe that an investment process that seeks out attractively valued income generating opportunities is critical in an environment where certain sectors commonly targeted by investors for yield are expensive relative to history. Additionally, we believe that dividend growth is a vital ingredient to investment success with benefits including excess returns over the broad market and an increasing yield on cost over time.

Conclusion

Over the reporting period, we “derisked” the portfolio by decreasing our allocation to “Consistent Earners” (i.e. stable, blue-chip companies) that had appreciated in value during the market rally. We also increased our allocations to “Basic Value” (i.e. more cyclical) companies and

“Emerging Franchises” (i.e. growth companies) as the market volatility provided opportunities to initiate positions in some very compelling investments. At the sector level, we reduced our allocation to health care and materials and increased our allocation to financials.

Going forward, we maintain our long-term view that dividend-paying equities have the potential to be an attractive long-term investment solution, especially given a secular outlook for lower returns across asset classes. With ten-year U.S. Treasury yields currently near historical lows, the dividend yield on global stocks can be particularly attractive albeit with additional volatility and potential for loss. As always, however, we continue to emphasize valuation in a market that has recently been characterized by overreactions to both positive and negative news.

We thank you for your investment in the Fund.

Sincerely,

|  | |

|  | |

| Brad Kinkelaar | Cliff Remily, CFA | |

| Co-Portfolio Manager | Co-Portfolio Manager | |

| ||

| ||

| Eve Tournier | ||

| Fixed Income Portfolio Manager | ||

| ANNUAL REPORT | JUNE 30, 2013 | 5 |

Table of Contents

Insights from the Portfolio Managers PIMCO Dividend and Income Builder Fund (Cont.)

Top 10 Holdings1

KeyCorp | 3.4% | |||||

JPMorgan Chase & Co. | 3.4% | |||||

Kohl’s Corp. | 3.3% | |||||

Cisco Systems, Inc. | 3.2% | |||||

Walgreen Co. | 3.2% | |||||

Microsoft Corp. | 3.0% | |||||

ProSafe SE | 2.5% | |||||

Enagas S.A. | 2.5% | |||||

Nippon Telegraph & Telephone Corp. | 2.4% | |||||

Total S.A. | 2.3% |

Geographic Breakdown1

United States | 42.5% | |||||

United Kingdom | 8.8% | |||||

France | 4.3% | |||||

Brazil | 3.8% | |||||

Japan | 3.6% | |||||

South Africa | 3.6% | |||||

Switzerland | 3.3% | |||||

Spain | 3.0% | |||||

Netherlands | 2.6% | |||||

Cyprus | 2.5% | |||||

Australia | 2.4% | |||||

Canada | 2.0% | |||||

Other | 9.3% |

Sector Breakdown1

Financials | 23.1% | |||||

Health Care | 10.4% | |||||

Energy | 9.6% | |||||

Consumer Discretionary | 9.1% | |||||

Industrials | 9.1% | |||||

Information Technology | 8.2% | |||||

Telecommunication Services | 7.4% | |||||

Consumer Staples | 5.5% | |||||

Utilities | 6.0% | |||||

Mortgage-Backed Securities | 1.5% | |||||

Other | 1.7% |

| 1 | % of Total Investments as of 06/30/2013. Top Holdings, Geographic and Sector Breakdown solely reflect long positions. Securities sold short, financial derivative instruments and short-term instruments are not taken into consideration. |

| 6 | PIMCO EQUITY SERIES |

Table of Contents

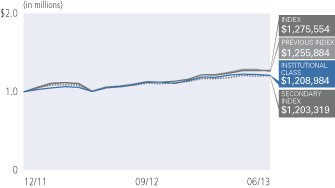

PIMCO Dividend and Income Builder Fund

| Institutional Class - PQIIX | Class A - PQIZX | |

| Class P - PQIPX | Class C - PQICX | |

| Class D - PQIDX | Class R - PQIBX |

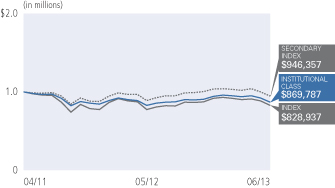

Cumulative Returns Through June 30, 2013

| Average Annual Total Return for the period ended June 30, 2013 | ||||||||||

| 1 Year | Fund Inception (12/14/11) | |||||||||

| PIMCO Dividend and Income Builder Fund Institutional Class | 15.17% | 14.59% | |||||||

| PIMCO Dividend and Income Builder Fund Class P | 15.15% | 14.61% | ||||||||

| PIMCO Dividend and Income Builder Fund Class D | 14.91% | 14.29% | ||||||||

| PIMCO Dividend and Income Builder Fund Class A | 14.91% | 14.29% | ||||||||

| PIMCO Dividend and Income Builder Fund Class A (adjusted) | 8.59% | 10.18% | ||||||||

| PIMCO Dividend and Income Builder Fund Class C | 14.08% | 13.40% | ||||||||

| PIMCO Dividend and Income Builder Fund Class C (adjusted) | 13.08% | 13.40% | ||||||||

| PIMCO Dividend and Income Builder Fund Class R | 14.66% | 14.04% | ||||||||

| MSCI All Country World Index Net USD± | 16.57% | 17.06% | |||||||

| MSCI World Index** | 18.58% | 18.79% | |||||||

| 75% MSCI All Country World Index Net USD/25% Barclays Global Aggregate USD Unhedged±± | 11.63% | 12.72% | |||||||

All Fund returns are net of fees and expenses.

± The MSCI All Country World Index Net USD is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The Index consists of 45 country indices comprising 24 developed and 21 emerging market country indices. It is not possible to invest directly in an unmanaged index.

±± The benchmark is a blend of 75% MSCI All Country World Index Net USD/25% Barclays Global Aggregate USD Unhedged. The MSCI All Country World Index Net USD is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The Index consists of 45 country indices comprising 24 developed and 21 emerging market country indices. Barclays Global Aggregate (USD Unhedged) Index provides a broad-based measure of the global investment-grade fixed income markets. The three major components of this index are the U.S. Aggregate, the Pan-European Aggregate, and the Asian-Pacific Aggregate Indices. The index also includes Eurodollar and Euro-Yen corporate bonds, Canadian Government securities, and USD investment grade 144A securities. It is not possible to invest directly in an unmanaged index.

** The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of 24 developed market country indices. It is not possible to invest directly in an unmanaged index.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1.00% CDSC on Class C shares. The Fund’s total annual operating expense ratio as stated in the Fund’s current prospectus, as supplemented to date, is 0.99% for the Institutional Class shares, 1.09% for the Class P shares, 1.34% for the Class D shares, 1.34% for the Class A shares, 2.09% for the Class C shares and 1.59% for the Class R shares. Details regarding any Fund’s operating expenses can be found in the Fund’s prospectus. For performance current to the most recent month-end, visit www.pimco.com/investments.

Portfolio Insights

| » | The PIMCO Dividend and Income Builder Fund seeks to provide current income that exceeds the average yield on global stocks, and to provide a growing stream of income per share over time, with a secondary objective to seek to provide long-term capital appreciation, by investing under normal circumstances at least 80% of its assets in a diversified portfolio of income-producing investments, and will typically invest at least 50% of its assets in equity and equity-related securities. The Fund’s investments in equity and equity-related securities include common and preferred stock (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred stock), as well as securities issued by real estate investment trusts, master limited partnerships and other equity trusts and depositary receipts. |

| » | The Fund’s Institutional Class shares returned 15.17% after fees, and the Fund’s benchmark index, a blend of 75% MSCI All Country World Index Net USD/25% Barclays Global Aggregate (USD Unhedged) Index, returned 11.63%. |

| » | During the reporting period, the Fund paid ordinary quarterly dividends of 42.1 cents per share on its Institutional Class shares. The dividend per share was slightly lower for the other share classes, to account for varying class specific expenses. The net asset value of the Fund’s Institutional Class shares increased by $1.13 per share (from $10.47 to $11.60) over the reporting period, bringing the twelve-month total return to 15.17%. |

| » | Security selection contributed to performance. The largest single contributor to relative performance was the Fund’s holding of Marathon Petroleum, the U.S.-based oil refining and marketing company. |

| » | The largest single detractor from relative performance was the Fund’s holding of Gold Fields. The South African precious metals miner underperformed as the price of gold declined during the reporting period. |

| » | The Fund’s defensive sector positioning, specifically the Fund’s underweights to consumer discretionary and financials, detracted from relative performance. |

| » | The Fund’s fixed income allocation performed positively, driven mainly by overweights to investment grade, high yield, and emerging markets credit securities, as these sectors outperformed during the reporting period. |

| ANNUAL REPORT | JUNE 30, 2013 | 7 |

Table of Contents

Insights from the Portfolio Managers PIMCO EqS® Dividend Fund

Dear Shareholder,

We appreciate your investment in the PIMCO EqS® Dividend Fund (the “Fund”). In the following letter, please find a discussion of the recent market environment and a review of portfolio performance.

Market overview

During the twelve months ended June 30, 2013, the MSCI All Country World Index Net USD (the “Index”), which tracks the performance of stocks in developed and emerging markets countries, returned 16.57%. While overall market performance was positive, the intra-period performance was volatile due to political uncertainty in the U.S. and Europe.

Global equity market performance was strong during most of the third quarter of 2012 after Mario Draghi, President of the European Central Bank, vowed on July 26 to do “whatever it takes” to stabilize Europe. Following the U.S. Federal Reserve’s (“Fed”) announcement of plans for more stimulus action in mid-September, however, global equity markets declined and remained volatile through October, possibly implying a decreasing effectiveness of Fed actions. Global equity markets resumed the decline during the first half of November following the U.S. presidential election as the focus turned to the “fiscal cliff” in the U.S. Markets began to rally in mid-November as hope grew that U.S. lawmakers could reach an agreement that would avoid the $600 billion of automatic tax hikes and spending cuts that were scheduled to take effect in the new year. Market performance faded at the end of December as hope for an agreement waned.

Markets steadily rose in January 2013 after U.S. politicians finally passed and signed legislation that avoided much of the so-called “fiscal cliff,” although the legislation fell far short of the “grand bargain” that some had hoped for, leaving looming fiscal policy fights ahead. After reaching five-year highs, equity markets fell in February 2013 in response to weak U.S. and European economic data. They bounced back at the end of February and rallied through mid-March 2013, led by Japanese equities as investors anticipated that the Bank of Japan’s new governor would push forward very aggressive monetary easing policies. Markets fell slightly in mid-March after the small European country of Cyprus requested a bailout of its financial system, raising concerns about economic stability in Europe.

Following some bumpy first weeks in April 2013, markets rose until May 21, when Federal Reserve chairman Ben Bernanke indicated that the Fed might begin tapering quantitative easing in 2013 if employment improved. Markets then fell, particularly in June 2013 after Bernanke, at a press conference, clarified his earlier remarks regarding tapering. Markets rose slightly during the last week of the quarter after the U.S., European, and Chinese central banks all delivered remarks aimed at assuaging investor concerns about

liquidity, noting that “tapering” referred to less accommodative, not most restrictive, monetary policies. Performance was also helped by positive U.S. macro data, which suggested, among other things, that the housing market was improving.

Global equity market performance was positive in each of the ten Global Industry Classification Standard (“GICS”) sectors except the materials sector. Performance was strongest in consumer discretionary, health care, and financials. Materials, utilities, and energy were the poorest performing sectors. Japan and the U.S. were the strongest performing regions globally, while emerging markets, particularly Brazil, lagged.

Fund review

Over time, we seek to provide attractive current yield and total returns. During the twelve months ended June 30, 2013, the Fund paid ordinary quarterly dividends of 37.1 cents per share on its Institutional Class shares. The dividend per share was slightly lower for the other share classes, to account for varying class specific expenses. The Fund’s net asset value increased by $1.40 per share (from $10.47 to $11.87) over the reporting period, bringing the twelve-month total return to 17.32% (net of fees).

On a relative basis, the Fund outperformed the MSCI All Country World Index Net USD, which returned 16.57%. Overall security selection was positive, and was particularly strong in the health care, energy, and telecommunication services sectors. Security selection was negative in the materials and industrials sectors.

At the security level, the Fund’s position in Marathon Petroleum, a U.S. oil refining and marketing company, was the largest contributor to relative performance. Marathon’s stock outperformed as the company continued to profit from above-average crack spreads and growing oil production in America’s heartland, and Marathon announced favorable quarterly earnings results in both November 2012 and January 2013. The company also announced that it had entered into a $500 million share repurchase program. These positive developments prompted Moody’s to upgrade Marathon’s credit rating in March 2013.

Enagás was another contributor to performance. The Spanish natural gas utility outperformed as the outlook for the regulatory environment in Spain became more favorable, and after reporting positive quarterly earnings results which were driven by the contribution of new assets as well as by cost controls. Enagás also grew its semiannual dividend in April 2013.

The largest detractor for the period was the Fund’s holding of Gold Fields. The South African precious metals miner underperformed in sympathy with gold, the price of which declined during the period as

| 8 | PIMCO EQUITY SERIES |

Table of Contents

the economic environment appeared to stabilize and investor demand for gold declined. At the same time, Gold Fields’ production difficulties led to earnings disappointments. Given these increased risks, the Fund exited the position.

Poseidon Concepts was another detractor from performance. The Canada-based fluid management company underperformed after announcing disappointing quarterly earnings results in November 2012. The disappointment was due mainly to a decline in water tank utilization, lower North American rig counts, and a revision on the company’s ability to collect accounts receivable fully. Our concerns, including that the company might eliminate its dividend, prompted the Fund to exit the position.

Investment process and portfolio construction

Our bottom-up investment strategy is focused on providing attractive income today and long-term capital appreciation. As we seek to achieve these goals, we employ fundamental research that aims to identify attractively priced companies exhibiting the ability and willingness to increase dividend payments. We then construct a portfolio that is diversified across three types of businesses:

| n | Consistent Earners are blue-chip industry leaders that consistently create value year after year. |

| n | Basic Value companies are traditional value companies such as cyclicals, turnarounds, and companies with low valuations. |

| n | Emerging Franchises are companies with the potential to be significantly larger over time. |

Our total return focused approach to dividend investing means that we do not advocate selecting equity investments based on yield alone. Instead, we believe that an investment process that seeks out attractively valued income generating opportunities is critical in an environment where certain sectors commonly targeted by investors for yield are expensive relative to history. Additionally, we believe that dividend growth is a vital ingredient to investment success with benefits including excess returns over the broad market and an increasing yield on cost over time.

Conclusion

Over the reporting period, we “derisked” the portfolio by decreasing our allocation to “Consistent Earners” (i.e. stable, blue-chip companies) that had appreciated in value during the market rally. We also increased our allocations to “Basic Value” (i.e. more cyclical) companies and “Emerging Franchises” (i.e. growth companies) as the market volatility provided opportunities to initiate positions in some very compelling investments. At the sector level, we reduced our allocation to health care and materials and increased our allocation to financials.

Going forward, we maintain our long-term view that dividend-paying equities have the potential to be an attractive long-term investment solution, especially given a secular outlook for lower returns across asset classes. With ten-year U.S. Treasury yields currently near historical lows, the dividend yield on global stocks can be particularly attractive albeit with additional volatility and potential for loss. As always, however, we continue to emphasize valuation in a market that has recently been characterized by overreactions to both positive and negative news.

We thank you for your investment in the Fund.

Sincerely,

| | |

|  | |

Brad Kinkelaar Co-Portfolio Manager | Cliff Remily, CFA Co-Portfolio Manager | |

Top 10 Holdings1

Walgreen Co. | 4.2% | |||||

JPMorgan Chase & Co. | 4.0% | |||||

Cisco Systems, Inc. | 4.0% | |||||

KeyCorp | 3.9% | |||||

Kohl’s Corp. | 3.7% | |||||

Microsoft Corp. | 3.5% | |||||

Nippon Telegraph & Telephone Corp. | 2.9% | |||||

Enagas S.A. | 2.8% | |||||

Intel Corp. | 2.5% | |||||

Total S.A. | 2.5% |

Geographic Breakdown1

United States | 46.3% | |||||

United Kingdom | 9.1% | |||||

France | 4.3% | |||||

Japan | 4.3% |

| ANNUAL REPORT | JUNE 30, 2013 | 9 |

Table of Contents

Insights from the Portfolio Managers PIMCO EqS® Dividend Fund (Cont.)

Geographic Breakdown1 (Cont.)

Brazil | 4.1% | |||||

South Africa | 4.0% | |||||

Switzerland | 3.7% | |||||

Canada | 2.8% | |||||

Spain | 2.8% | |||||

Cyprus | 2.5% | |||||

Netherlands | 2.5% | |||||

Australia | 2.3% | |||||

Other | 7.3% |

Sector Breakdown1

Financials | 24.1% | |||||

Health Care | 12.1% | |||||

Energy | 11.7% | |||||

Consumer Discretionary | 10.3% | |||||

Information Technology | 10.0% | |||||

Telecommunication Services | 8.9% | |||||

Consumer Staples | 7.0% | |||||

Industrials | 6.7% | |||||

Utilities | 5.3% |

| 1 | % of Total Investments as of 06/30/2013. Top Holdings, Geographic and Sector Breakdown solely reflect long positions. Securities sold short, financial derivative instruments and short-term instruments are not taken into consideration. |

| 10 | PIMCO EQUITY SERIES |

Table of Contents

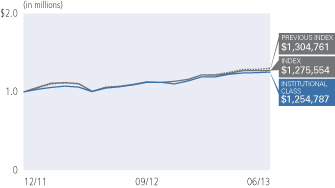

| Institutional Class - PQDIX | Class A - PQDAX | |

| Class P - PQDPX | Class C - PQDCX | |

| Class D - PQDDX | Class R - PQDRX |

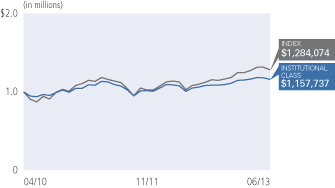

Cumulative Returns Through June 30, 2013

Average Annual Total Return for the period ended June 30, 2013 | ||||||||||

| 1 Year | Fund Inception (12/14/11) | |||||||||

| PIMCO EqS® Dividend Fund Institutional Class | 17.32% | 15.82% | |||||||

| PIMCO EqS® Dividend Fund Class P | 17.21% | 15.78% | ||||||||

| PIMCO EqS® Dividend Fund Class D | 16.85% | 15.46% | ||||||||

| PIMCO EqS® Dividend Fund Class A | 16.95% | 15.52% | ||||||||

| PIMCO EqS® Dividend Fund Class A (adjusted) | 10.52% | 11.37% | ||||||||

| PIMCO EqS® Dividend Fund Class C | 16.14% | 14.53% | ||||||||

| PIMCO EqS® Dividend Fund Class C (adjusted) | 15.14% | 14.53% | ||||||||

| PIMCO EqS® Dividend Fund Class R | 16.71% | 15.21% | ||||||||

| MSCI All Country World Index Net USD± | 16.57% | 17.06% | |||||||

| MSCI World Index** | 18.58% | 18.79% | |||||||

All Fund returns are net of fees and expenses.

± The MSCI All Country World Index Net USD is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The Index consists of 45 country indices comprising 24 developed and 21 emerging market country indices. It is not possible to invest directly in an unmanaged index.

** The MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed markets. The MSCI World Index consists of 24 developed market country indices. It is not possible to invest directly in an unmanaged index.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1.00% CDSC on Class C shares. The Fund’s total annual operating expense ratio as stated in the Fund’s current prospectus, as supplemented to date, is 0.99% for the Institutional Class shares, 1.09% for the Class P shares, 1.34% for the Class D shares, 1.34% for the Class A shares, 2.09% for the Class C shares and 1.59% for the Class R shares. Details regarding any Fund’s operating expenses can be found in the Fund’s prospectus. For performance current to the most recent month-end, visit www.pimco.com/investments.

Portfolio Insights

| » | The PIMCO EqS® Dividend Fund seeks to provide current income that exceeds the average yield on global stocks, and as a secondary objective, seeks to provide long-term capital appreciation, by investing under normal circumstances at least 75% of its assets in equity and equity-related securities, including common and preferred stock (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred stock), as well as securities issued by real estate investment trusts, master limited partnerships and other equity trusts and depositary receipts. |

| » | The Fund’s Institutional Class shares returned 17.32% after fees, and the Fund’s benchmark index, the MSCI All Country World Index Net USD, returned 16.57%. |

| » | During the reporting period, the Fund paid ordinary quarterly dividends of 37.1 cents per share on its Institutional Class shares. The dividend per share was slightly lower for the other share classes to account for varying class specific expenses. The net asset value of the Fund’s Institutional Class shares increased by $1.40 per share (from $10.47 to $11.87) over the reporting period, bringing the twelve-month total return to 17.32%. |

| » | Security selection contributed to performance. The largest single contributor to relative performance was the Fund’s holding of Marathon Petroleum, the U.S.-based oil refining and marketing company. |

| » | The largest single detractor from relative performance was the Fund’s holding of Gold Fields. The South African precious metals miner underperformed as the price of gold declined during the reporting period. |

| » | The Fund’s defensive sector positioning, specifically the Fund’s underweights to consumer discretionary and financials, detracted from relative performance. |

| ANNUAL REPORT | JUNE 30, 2013 | 11 |

Table of Contents

Insights from the Portfolio Managers PIMCO EqS® Emerging Markets Fund

Dear Shareholder,

We appreciate your investment in the PIMCO EqS® Emerging Markets Fund (the “Fund”). In the following letter, please find a discussion of the recent market environment and a review of portfolio performance.

Market Overview

While developed market equities rallied strongly over the twelve-month reporting period, emerging market (“EM”) equities delivered modest returns, with the MSCI Emerging Markets Index increasing 2.87%, underperforming its developed market counterpart, the MSCI World Index, by over 15%.

With emerging market equities performing roughly in-line with developed markets during the latter half of 2012, the difference in performance has been driven by events in 2013. While earnings growth continues to be slow, a more optimistic outlook for the U.S. economy and unprecedented monetary stimulus in Japan has helped trigger a re-rating of multiples in equity markets. At the same time as sentiment has become more positive for developed economies, it has become more negative for emerging markets. Companies have been struggling to grow earnings in an environment of moderate global growth, and concerns over slowing growth in China have weighed on equity market returns. Furthermore, both emerging market equities and fixed income have been vulnerable to the influence of developed market monetary policy, with the asset classes suffering from a sell-off in May and June following comments from the Federal Reserve (“Fed”) that it may unwind its program of bond purchases earlier than expected. This talk of so-called “Fed tapering” sparked an increase in U.S. interest rates and a subsequent fall in EM local currencies.

Looking forward, our view is that a more negative outlook on emerging markets, given lower growth in China, earnings weakness and higher U.S. interest rates, is offset by long-term economic advantages, and historically low valuations. We continue to believe that emerging market growth rates will exceed that of developed markets, as structural advantages such as higher current account balances, higher foreign currency reserves, lower degrees of indebtedness, and better demographic profiles, remain. In our view, these growth dynamics should continue to provide long-term support for emerging market companies. At the same time, we think many short-term concerns may already be reflected in market prices, particularly in sectors such as energy and materials, which on a price-to-book basis, are trading close to or below valuation troughs reached in 2008. These valuations may in turn provide attractive entry points for investors taking a long-term approach to the asset class.

Fund Review

Over the twelve-month reporting period, the Fund’s Institutional Class shares returned 4.68% net of fees, outperforming its benchmark index, the MSCI Emerging Markets Index, by 1.81% on an after fees basis.

Against a backdrop of low global economic growth, a focus on businesses with long-term secular growth drivers, as opposed to short-term cyclical return drivers, was a major factor in the Fund’s performance. High quality consumer discretionary firms performed particularly well, benefiting from growing demand in end markets. Top performers included Melco Crown Entertainment, a Macau gaming company, which benefits from a combination of expanding demand, driven by wage growth, and constrained supply, which is limited by regulation. Other top contributors to performance included Thai Beverage, which performed strongly after the company successfully acquired food and beverage assets from Singaporean conglomerate, Fraser and Neave.

With low growth sustaining low interest rates in developed markets (at least until recent months), businesses with more consistent earnings profiles offering attractive dividend yields also outperformed. Two examples of this were MegaFon, a Russian telecom company, and KCell, a Kazakhstani telecoms company, which the Fund purchased for their “ultra” high dividend yields of between 10% and 15%, and which re-rated over the reporting period.

While businesses with sustainable growth drivers and consistent earnings profiles outperformed, those more exposed to short-term cyclical swings, and in particular to resources and commodities, suffered. The Fund’s avoidance of many of the largest companies in this sector was positive for relative returns; however, the areas of the portfolio where we had more cyclical exposure detracted on an absolute basis. Underperformers in this area included China Shenhua Energy, a Chinese coal producer, and Turquoise Resources, a Mongolia-based subsidiary of mining company, Rio Tinto. The share prices of both of these companies suffered in line with falling commodity prices.

Conclusion

Mid-way through 2013, we are mindful of the short-term headwinds facing emerging markets, while remaining optimistic on the long-term growth potential of these economies. We believe that emerging market equities remain attractively valued on a historical basis and that real wage growth and an emerging consuming class should drive equity returns. To take advantage of these trends we continue to adopt an unconstrained approach, investing in both emerging market stocks, and developed market stocks with emerging market growth drivers. We also continue to employ an active approach to currency management, an area that may be particularly important in light of the recent volatility seen in emerging market currencies. From a stock perspective, we are focused on consumer sectors, where we are gaining exposure through what we believe are high quality consumer discretionary firms, while avoiding more expensively valued staples firms. We are also finding attractive opportunities in more cyclical sectors trading at low valuations.

| 12 | PIMCO EQUITY SERIES |

Table of Contents

Again, we thank you for your continued investment in the Fund and look forward to serving your investment needs.

Sincerely,

Maria (Masha) Gordon Portfolio Manager |

Top 10 Holdings1

Kia Motors Corp. | 3.3% | |||||

Itau Unibanco Holding S.A. SP—ADR | 3.1% | |||||

Samsung Electronics Co. Ltd. | 2.9% | |||||

Israel Chemicals Ltd. | 2.5% | |||||

JPMorgan Chase & Co., Chinese Exchange | 2.4% | |||||

China Mobile Ltd. | 2.4% | |||||

MegaFon OAO GDR | 2.4% | |||||

Samsung Electronics Co. Ltd.—Preferred Stock | 2.3% | |||||

AIA Group Ltd. | 2.2% | |||||

Bolsa Mexicana de Valores S.A.B. de C.V. | 2.1% |

Geographic Breakdown1

China | 10.6% | |||||

Brazil | 10.3% | |||||

South Korea | 8.5% | |||||

Russia | 8.1% | |||||

Hong Kong | 6.4% | |||||

India | 6.1% | |||||

United Kingdom | 3.7% | |||||

Israel | 3.5% | |||||

Japan | 3.2% |

Geographic Breakdown1 (Cont.)

Peru | 2.8% | |||||

South Africa | 2.6% | |||||

Indonesia | 2.3% | |||||

Cyprus | 2.3% | |||||

Thailand | 2.2% | |||||

Mexico | 2.1% | |||||

Italy | 2.0% | |||||

Kazakhstan | 2.0% | |||||

Macau | 1.9% | |||||

Denmark | 1.9% | |||||

Turkey | 1.7% | |||||

Luxembourg | 1.6% | |||||

Australia | 1.6% | |||||

Cambodia | 1.6% | |||||

Other | 6.9% |

Sector Breakdown1

Financials | 20.9% | |||||

Consumer Discretionary | 16.9% | |||||

Consumer Staples | 16.0% | |||||

Telecommunication Services | 9.8% | |||||

Materials | 8.8% | |||||

Information Technology | 7.7% | |||||

Industrials | 5.8% | |||||

Energy | 5.6% | |||||

Exchange-Traded Funds | 1.6% | |||||

Utilities | 1.6% | |||||

Health Care | 1.0% |

| 1 | % of Total Investments as of 06/30/2013. Top Holdings, Geographic and Sector Breakdown solely reflect long positions. Securities sold short, financial derivative instruments and short-term instruments are not taken into consideration. |

| ANNUAL REPORT | JUNE 30, 2013 | 13 |

Table of Contents

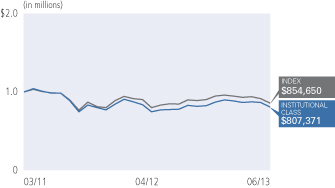

PIMCO EqS® Emerging Markets Fund

| Institutional Class - PEQWX | Class A - PEQAX | |

| Class P - PEQQX | Class C - PEQEX | |

| Administrative Class - PEQTX | Class R - PEQHX | |

| Class D - PEQDX |

Cumulative Returns Through June 30, 2013

| Average Annual Total Return for the period ended June 30, 2013 | ||||||||||

1 Year | Fund Inception | |||||||||

| PIMCO EqS® Emerging Markets Fund Institutional Class | 4.68% | -7.51% | |||||||

PIMCO EqS® Emerging Markets Fund Class P | 4.46% | -7.60% | ||||||||

PIMCO EqS® Emerging Markets Fund Administrative Class | 4.36% | -7.79% | ||||||||

PIMCO EqS® Emerging Markets Fund Class D | 4.31% | -7.87% | ||||||||

PIMCO EqS® Emerging Markets Fund Class A | 4.23% | -7.93% | ||||||||

PIMCO EqS® Emerging Markets Fund Class A (adjusted) | -1.48% | -10.18% | ||||||||

PIMCO EqS® Emerging Markets Fund Class C | 3.54% | -8.51% | ||||||||

PIMCO EqS® Emerging Markets Fund Class C (adjusted) | 2.54% | -8.51% | ||||||||

PIMCO EqS® Emerging Markets Fund Class R | 4.04% | -8.07% | ||||||||

| MSCI Emerging Markets Index (Net Dividends in USD)± | 2.87% | -4.81% | |||||||

All Fund returns are net of fees and expenses.

± The MSCI Emerging Markets Index (Net Dividends in USD) is a free float-adjusted market capitalization index that is designed to measure equity market performance of emerging markets. The MSCI Emerging Markets Index consists of the following 21 emerging market country indices: Brazil, Chile, China, Colombia, Czech Republic, Egypt, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Morocco, Peru, Philippines, Poland, Russia, South Africa, Taiwan, Thailand, and Turkey. It is not possible to invest directly in an unmanaged index.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1.00% CDSC on Class C shares. The Fund’s total annual operating expense ratio as stated in the Fund’s current prospectus, as supplemented to date, is 1.49% for the Institutional Class shares, 1.59% for the Class P shares, 1.74% for the Administrative Class shares, 1.84% for the Class D shares, 1.84% for the Class A shares, 2.59% for the Class C shares and 2.09% for the Class R shares. Details regarding any Fund’s operating expenses can be found in the Fund’s prospectus. For performance current to the most recent month-end, visit www.pimco.com/investments.

Portfolio Insights

| » | The PIMCO EqS® Emerging Markets Fund seeks capital appreciation by investing under normal circumstances at least 80% of its assets in a diversified portfolio of investments economically tied to emerging market countries. The Fund will invest a substantial portion of its assets in equity and equity-related securities, including common and preferred stock (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred stock). The Fund may also invest in fixed income securities, including debt securities issued by both corporate and government issuers. The Fund may invest in commodity related instruments, including exchange-traded funds, futures and other investment companies. The Fund may also invest in derivative instruments, such as options, futures contracts or swap agreements. |

| » | The Fund’s Institutional Class shares returned 4.68% after fees, and the Fund’s benchmark index, the MSCI Emerging Markets Index, returned 2.87%. |

| » | From a sector perspective, stock selection in the consumer discretionary and telecommunications sectors contributed to relative performance. In consumer discretionary, positions in companies benefiting from strong secular growth in gaming and retail were the top contributors. In telecommunications, mobile phone operators with high dividend yields and stable earnings streams in Russia and Kazakhstan performed well. |

| » | On the downside, an underweight to information technology detracted from returns as the sector outperformed the Fund’s benchmark index. Stock selection in information technology and industrials also detracted from returns, with the former driven by both underperformance of portfolio holdings and avoidance of large benchmark weights which outperformed. |

| » | From a country perspective, stock selection in Brazil and Korea, together with exposure to Japanese companies with emerging market growth drivers, was positive for performance. |

| » | On the downside, stock selection in Russia and China detracted from returns as these securities underperformed. |

| » | Currency positioning and cash holdings were positive contributors to performance over the reporting period. |

| 14 | PIMCO EQUITY SERIES |

Table of Contents

Insights from the Portfolio Managers PIMCO EqS® Long/Short Fund

Dear Shareholder,

We appreciate your investment in the PIMCO EqS® Long/Short Fund (the “Fund”). In the following letter, please find a discussion of the recent market environment and a review of recent portfolio performance.

Market Overview

U.S. equities rallied over the twelve-month reporting period, reaching an all-time high in May 2013 before retreating in June. The rally was largely driven by coordinated monetary easing on behalf of the Federal Reserve, the European Central Bank (“ECB”) and the Bank of Japan. In late 2012 in particular, positive sentiment increased due to a perceived reduction in the risk of a severe left tail event in Europe, following the ECB’s announcement of plans to purchase government bonds in early September.

Markets experienced a slight pull back in June 2013 as investors began to speculate as to the speed and magnitude of the Federal Reserve’s tapering and eventual exit of its supportive monetary policies. Investor sentiment continued to not be affected by continuing concerns out of Europe, viewing these concerns largely as localized events without impairing the region’s access to capital markets. Economic data in the U.S. has been mixed as employment and payroll numbers continue to be modest. Although risks remain, slow growth, as opposed to severe crisis, now appears to be the consensus view.

Fund Review

Over the twelve-month reporting period, the Fund returned 14.66% net of fees, outperforming its benchmark, 3-Month USD LIBOR by 14.31% on an after fees basis.

The Fund’s position in Spirit Airlines was the top contributor to performance. Shares were down in 2012 after a beneficial tax expired causing an increase in fares and hurricane Sandy impacted flights. Spirit Airlines rebounded in 2013 and has added to the Fund’s performance overall since we initiated a position. The company reported solid earnings for its fourth fiscal quarter and has resumed its attractive growth rate. The other area of contribution was the Fund’s positions with high yields and upside potential including several companies that are undergoing real estate investment trust (“REIT”) conversions. This included prison operators Geo Group and Corrections Corp. of America and records management company Iron Mountain. We believe this process can enhance cash generative businesses as the markets reassess intrinsic value after conversion based on different metrics than non-REIT businesses.

The Fund’s investment in Domino’s Pizza, consistent with the theme of consumers trading down in a moderate growth environment, also contributed to performance for the reporting period. The company

reported higher earnings driven by rapid international expansion of its asset-light franchise model, which keeps capital expenditure intensity and commodity risk (i.e. wheat and cheese) low and enhances cash generation. A combination of product innovation and low ticket prices has kept developed-world consumers coming back and rising discretionary incomes have driven emerging market sales. We sold out of the position after shares appreciated and we felt there was less upside potential.

These positive results were partially offset by the Fund’s position in Herbalife, which detracted from returns. Our original thesis on Herbalife was that the company had attractive growth prospects, but a depressed valuation multiple versus its peer group after an earnings disappointment earlier in the year has changed our view. Since that time, multiples for Herbalife’s peers have also contracted and we believe the controversial headlines for the company make it less likely that the multiple expands in the near future. As a result, we believe the opportunity is less compelling and have decided to exit the position.

In addition, our short positions detracted in aggregate due to the strong equity market rally. Our approach to shorting is to generate alpha as opposed to simply hedging market risk. We believe that stock market exposure represents an important expected driver of long-term capital appreciation for many investors. However, equity markets do not always deliver positive returns and often are characterized by periods of high volatility. Consequently, we believe investors can benefit from a strategy that seeks to provide exposure to the long-term growth benefits of owning stocks, while allowing for better downside risk mitigation. To help meet these needs, the Fund aims to provide a positive return with lower volatility than the equity market over the long term. Although the Fund does not explicitly aim to manage short-term volatility, we believe it has greater ability than many traditional long-only strategies to manage downside risk, which provides the opportunity for strong risk-adjusted returns over a full market cycle. While detracting over the one year period, these positions did serve to reduce the volatility of the portfolio in periods when the market pulled back, and we believe can still generate alpha over the full market cycle.

Conclusion

Mid-way through 2013, much of the strong equity market performance this year has been driven by multiple expansions rather than earnings growth, suggesting central bank activity, rather than underlying fundamentals, has been driving returns. As macroeconomic events continue to create inflection points and heightened equity market volatility, we believe an emphasis on downside risk mitigation will be critical. As a result, we have been very selective on both the long and short side of the portfolio while also carefully managing our net equity

| ANNUAL REPORT | JUNE 30, 2013 | 15 |

Table of Contents

Insights from the Portfolio Managers PIMCO EqS® Long/Short Fund (Cont.)

market exposure. While we believe earnings growth will continue to be moderate, certain areas of the U.S. economy appear to be in recovery. In particular, we are seeking to benefit from strengthening in the U.S. housing market, construction and recovering financials.

Again, we thank you for your continued investment in the Fund and look forward to serving your investment needs.

Sincerely,

Geoffrey Johnson, CFA

Portfolio Manager

Top 10 Holdings1

Kirby Corp. | 6.0% | |||||

DST Systems, Inc. | 5.6% | |||||

Spirit Airlines, Inc. | 5.4% | |||||

American International Group, Inc. | 4.8% | |||||

Enstar Group Ltd. | 4.1% | |||||

Methanex Corp. | 3.9% | |||||

SNC-Lavalin Group, Inc. | 3.6% | |||||

Genworth Financial, Inc. ‘A’ | 3.3% | |||||

Gilead Sciences, Inc. | 3.2% | |||||

Express Scripts Holding Co. | 3.0% |

Sector Breakdown2

Industrials | 22.2% | |||||

Financials | 12.3% | |||||

Health Care | 7.9% | |||||

Consumer Discretionary | 7.3% | |||||

Consumer Staples | 5.9% | |||||

Information Technology | 3.8% | |||||

Exchange-Traded Funds | (1.2% | ) | ||||

Materials | (3.4% | ) | ||||

Energy | (7.8% | ) |

| 1 | % of Total Investments as of 06/30/2013. Top Holdings solely reflect long positions. Securities sold short, financial derivative instruments and short-term instruments are not taken into consideration. |

| 2 | % of net exposure (Total Investments less Securities Sold Short) as of 06/30/2013. Financial derivative instruments and short-term instruments are not taken into consideration. |

| 16 | PIMCO EQUITY SERIES |

Table of Contents

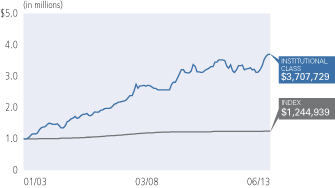

| Institutional Class - PMHIX | Class A - PMHAX | |

| Class P - PMHBX | Class C - PMHCX | |

| Class D - PMHDX |

Cumulative Returns Through June 30, 2013

Average Annual Total Return for the period ended June 30, 2013* | ||||||||||||||||||

| 1 Year | 5 Year | 10 Year | Fund Inception (01/01/03) | |||||||||||||||

| PIMCO EqS® Long/Short Fund Institutional Class | 14.66% | 6.84% | 12.27% | 13.43% | |||||||||||||

| PIMCO EqS® Long/Short Fund Class P | 14.77% | 6.75% | 12.17% | 13.33% | ||||||||||||||

| PIMCO EqS® Long/Short Fund Class D | 14.31% | 6.47% | 11.88% | 13.04% | ||||||||||||||

| PIMCO EqS® Long/Short Fund Class A | 14.27% | 6.46% | 11.88% | 13.04% | ||||||||||||||

| PIMCO EqS® Long/Short Fund Class A (adjusted) | 8.03% | 5.26% | 11.24% | 12.43% | ||||||||||||||

| PIMCO EqS® Long/Short Fund Class C | 13.41% | 5.67% | 11.04% | 12.19% | ||||||||||||||

| PIMCO EqS® Long/Short Fund Class C (adjusted) | 12.41% | 5.67% | 11.04% | 12.19% | ||||||||||||||

| 3 Month USD LIBOR Index±± | 0.35% | 0.76% | 2.16% | 2.12% | |||||||||||||

All Fund returns are net of fees and expenses.

±± 3 Month USD LIBOR (London Interbank Offered Rate) Index is an average interest rate, determined by the British Bankers Association, that banks charge one another for the use of short-term money (3 months) in England’s Eurodollar market. It is not possible to invest directly in an unmanaged index.

Performance quoted represents past performance. Past performance is not a guarantee or a reliable indicator of future results. Current performance may be lower or higher than performance shown. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Returns shown do not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. The adjusted returns take into account the maximum sales charge of 5.50% on Class A shares and 1.00% CDSC on Class C shares. The Fund’s total annual operating expense ratio as stated in the Fund’s current prospectus, as supplemented to date, is 1.61% for the Institutional Class shares, 1.71% for the Class P shares, 1.96% for the Class D shares, 1.96% for the Class A shares, and 2.71% for the Class C shares. Details regarding any Fund’s operating expenses can be found in the Fund’s prospectus. For performance current to the most recent month-end, visit www.pimco.com/investments.

* For periods prior to April 20, 2012, the Fund’s performance reflects the performance when the Fund was a partnership, net of actual fees and expenses charged to individual partnership accounts in the aggregate. If the performance had been restated to reflect the applicable fees and expenses of each share class, the performance may have been higher or lower. The Fund began operations as a partnership on January 1, 2003 and, on April 20, 2012, was reorganized into a newly-formed fund that was registered as an investment company under the Investment Company Act of 1940. Prior to the reorganization, the Fund had an investment objective, investment strategies, investment guidelines, and restrictions that were substantially similar to those currently applicable to the Fund; however, the Fund was not registered as an investment company under the Investment Company Act of 1940 and was not subject to its requirements or requirements imposed by the Internal Revenue Code of 1986 which, if applicable, may have adversely affected its performance. The performance of Class P, D, A and C shares for the period from April 20, 2012 to April 30, 2012 is based on the performance of the Institutional Class shares of the Fund. The performance of each class of shares will differ as a result of the different levels of fees and expenses applicable to each class of shares.

Portfolio Insights

| » | The PIMCO EqS® Long/Short Fund seeks long-term capital appreciation by investing under normal circumstances in long and short positions of equity and equity-related securities, including common and preferred stock (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred stock), utilizing a fundamental investing style that integrates bottom-up and top-down research. The Fund will normally invest a substantial portion of its assets in equity and equity-related securities. The Fund may also invest in fixed income securities of varying maturities, cash and cash equivalents. |

| » | The Fund’s Institutional Class shares returned 14.66% after fees, and the Fund’s benchmark index, the 3-Month USD LIBOR Index, returned 0.35%. |

| » | The Fund’s long equity positions contributed to absolute returns as equity markets rallied and the stocks held in the Fund outperformed the broad equity markets. |

| » | The Fund’s short equity positions detracted from performance in aggregate as the overall equity markets rose during the reporting period. |

| » | Within the Fund, the two investment themes that contributed most on the long side were investing in high yielding equities, specifically companies undergoing real estate investment trust (“REIT”) conversions, and companies that benefit from U.S. consumers seeking bargain products and services. |

| » | The Fund’s cash position, which includes currency hedging, detracted from performance. |

| ANNUAL REPORT | JUNE 30, 2013 | 17 |

Table of Contents

Insights from the Portfolio Managers PIMCO Emerging Multi-Asset Fund

Dear Shareholder,

We appreciate your investment in the PIMCO Emerging Multi-Asset Fund (the “Fund”). Below is our annual update that includes a discussion of our investment outlook with a focus on emerging markets (“EM”) as well as an update on the portfolio over the twelve-month reporting period ended June 30, 2013.

Emerging Market Asset Classes Benefit from Central Bank Provisions

Central bank actions have driven returns across EM asset classes over the reporting period. Generous central bank-provided liquidity and worldwide easing measures helped spur strong positive returns across EM during the second half of 2012. Gains have largely been erased in 2013, as EM, both equities and fixed income, had losses in May and June following comments from the Federal Reserve (“Fed”) that it may unwind its program of bond purchases earlier than expected. This talk of so-called “Fed tapering” sparked an increase in U.S. interest rates and a subsequent fall in EM local currencies.

EM equities (as represented by the MSCI Emerging Markets Index) returned 2.87% over the reporting period, trailing its developed market (“DM”) counterpart (as represented by the MSCI World Index) by over 15%. The divergence in returns has largely occurred in 2013. While earnings growth continues to be slow, a more optimistic outlook for the U.S. economy and unprecedented monetary stimulus in Japan has helped trigger a re-rating of multiples in developed equity markets. Sentiment has become more positive for developed economies and more negative for emerging markets. EM companies have been struggling to grow earnings in an environment of moderate global growth, and concerns over slowing growth in China have weighed on EM equity market returns. We have tactically moved to a neutral position to EM equities, as we believe EM equities will continue to suffer from a weaker corporate and macroeconomic outlook and may be prone to the influence of DM monetary policy in the near term. Nevertheless, we believe EM valuations look favorable versus DM and we will be monitoring conditions to deploy risk into the EM equity space.

EM external debt (as represented by the JPMorgan Emerging Markets Bond Index (EMBI) Global) returned 1.24% over the reporting period. Early in the period, the approval of a Greek aid package, a compromise over the U.S. fiscal cliff, and strong inflows into EM debt from investors seeking yield led to significant spread compression and record-low yields. The asset class turned sharply negative in May and June as U.S. Treasury yields spiked following talk of Fed tapering. Spread widening due to lower investor risk appetite, a drop in liquidity and idiosyncratic country-specific factors further impacted returns. We will look to maintain an underweight position in EM spread duration, with overweights focused on those EM countries with the most durable growth drivers and seek opportunities within the more strongly positioned countries to earn additional compensation by

substituting what we believe are high quality quasi-sovereign and corporate credits for sovereign issuers.

EM local debt markets (as represented by the JPMorgan Government Bond Index-Emerging Markets Global Diversified Index Unhedged) returned 1.32% during the period, as the high nominal and real yields, relative to those found in developed markets, drove inflows and performance during the second half of 2012. Similar to other EM asset classes, EM local markets and currencies sold-off during the second half of the reporting period with losses concentrated in May and June. Rising yields following Fed tapering talk, a stronger U.S. dollar, and heavy foreign ownership of local markets vulnerable to swings in market sentiment weighed on returns. We continue to hold a slight overweight to local duration at the overall portfolio level, which should allow our investors to benefit from any continued declines in nominal yields and also benefit from the high relative carry of this asset class.

Ripple Effects from Central Banks