Exhibit 99.1

SMART Technologies Inc. 2011 Annual Report

We built our company on an idea. Today, our technology solutions have a profound impact on learning and collaboration around the world.

It has been a year of milestones for SMART. We completed our IPO and celebrated the 20th anniversary of the SMART Board interactive whiteboard. Those 20 years have been rich with progress and growth. Recently, we installed our two millionth SMART Board interactive whiteboard.

When we introduced the SMART Board interactive whiteboard in 1991, no one knew about interactive whiteboards, much less why they might want or need one. Educators were among the first to recognize the depth of its potential, and soon students began learning in more visual, hands-on ways. Teachers noticed that even the most reticent children were up at the interactive whiteboard, presenting to peers and solving problems. Administrators noticed upward trends in achievement. Students found that learning was simply more interesting and engaging.

Today, the SMART Board interactive whiteboard remains the world’s most popular brand. We now offer solutions for businesses to help their teams collaborate in interactive and visual ways. All of these advances and milestones demonstrate our ongoing commitment to innovation. We acknowledge and thank the thousands of educators and business professionals who have worked with us through the years, helping us develop solutions that improve the way the world works and learns.

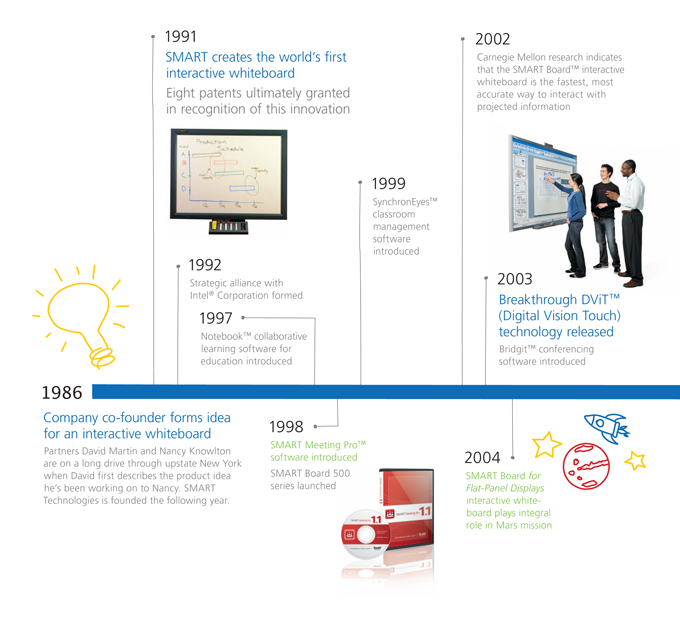

Our Evolution

1991

SMART creates the world’s first interactive whiteboard Eight patents ultimately granted in recognition of this innovation

1992

Strategic alliance with Intel® Corporation formed

1997

Notebook™ collaborative learning software for education introduced

1999

SynchronEyes™ classroom management software introduced

2002

Carnegie Mellon research indicates that the SMART Board™ interactive whiteboard is the fastest, most accurate way to interact with projected information

2003

Breakthrough DViT™ (Digital Vision Touch) technology released

Bridgit™ conferencing software introduced

Company co-founder forms idea for an interactive whiteboard

Partners David Martin and Nancy Knowlton are on a long drive through upstate New York when David first describes the product idea he’s been working on to Nancy. SMART Technologies is founded the following year.

1998

SMART Meeting Pro™ software introduced SMART Board 500 series launched

2004

SMART Board for Flat-Panel Displays interactive white-board plays integral role in Mars mission

2005

SMART Board 600 series launched

Receives the Lifetime Achievement Canada Export Award Database of K–12 lesson activities correlated to state standards released AirLiner™ wireless slate introduced

2008

First interactive table developed for primary education announced

One millionth SMART Board interactive whiteboard shipped SMART Document Camera™ launched SMART Board interactive display frame introduced

2010

Initial public offering completed July 20

Multiuser, multitouch SMART Board 800 series introduced Entry-level SMART Board 400 series introduced SMART Board 8070i interactive display launched Acquisition of NextWindow enhances optical touch patent portfolio

2006

New

Sympodium™ interactive pen display products launched Named one of Canada’s 50 Best Managed Companies for eighth consecutive year

2007

Senteo™ interactive response

system introduced Unifi™ projector introduced

2009

SMART world headquarters and research center opened SMART Exchange™ website for educators launched Patented DViT technology licensed

2011

20th anniversary of the SMART Board interactive whiteboard

Two millionth SMART Board interactive whiteboard shipped Global reach continues to expand

• Products now used in over 175 countries

• SMART Notebook™ software now offered in 50 languages

• 71 patents currently issued in the United States and 85 in the rest of the world, with about 600 patents pending

SMART Technologies Inc. 2011 Annual Report

Message from the CEO and Chairman

David Martin, Executive Chairman

Nancy Knowlton, President and Chief Executive Officer

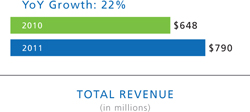

Total revenue increased 22% year over year despite a challenging second half.

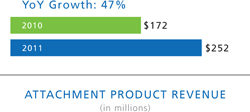

Revenue from attachment products increased 47% year over year.

Fiscal 2011 was an exciting year for SMART. We are very pleased with the company’s financial performance, particularly in light of the challenging environment that developed as the year progressed. As the category creator and market share leader for interactive , SMART’s recognized brand and easy-to-use collaboration solutions have made it the standard in education and the emerging business and government sectors.

Our solid execution enabled us to grow revenues by 22% over fiscal 2010 and ship record unit volumes despite the strong head winds in education spending that emerged in the second half of the year. In addition, the completion of our initial public offering in July 2010 was a significant milestone for our company as it led to greater brand awareness and provided access to further resources to execute our strategy. We look forward to leveraging the strong foundation we have built over the past 20 years as we execute our growth plan and take SMART to the next level as a public company.

Fiscal 2011 Financial Highlights

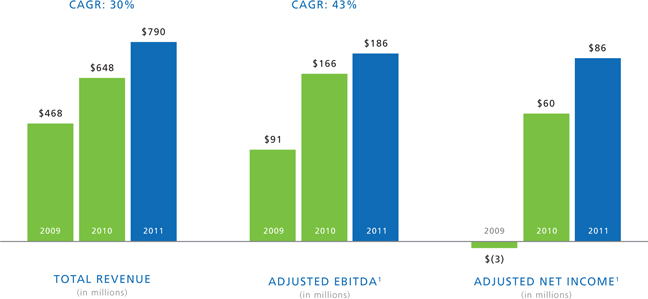

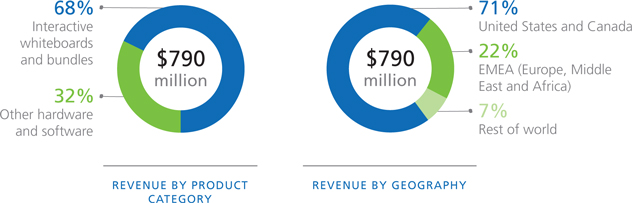

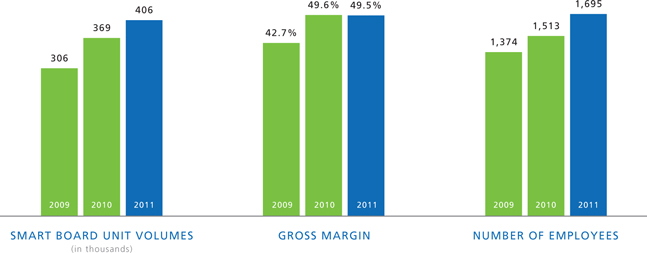

Total revenues increased 22% to $790 million due to the combination of 10% unit growth of interactive whiteboards, 47% growth of attachment product revenue and strength in our business and government markets. We are very pleased with our ability to maintain growth in North America and EMEA (Europe, Middle East and Africa) despite education funding challenges that increased as the year progressed. We continued to deliver best-in-class profitability levels, achieving Adjusted EBITDA of $186 million and Adjusted Net Income of $86 million, up 12% and 44% respectively compared to fiscal 2010. At the same time, we generated $85 million in cash flow from operations and ended the year in a strong financial position with $119 million of cash. Our strong performance demonstrates our ability to adapt to changing market conditions and execute our plan in a difficult operating environment.

2

SMART Technologies Inc. 2011 Annual Report

We help educators achieve better results with technology products that support student- centered learning. We help businesses become more productive with easy-to-use solutions that facilitate collaboration.

Strategy Execution

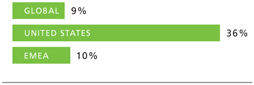

The market environment changed rapidly during the year, with strong year-over-year revenue growth of 31% in the first half followed by growth of only 12% in the second half of the year. This was due to education funding issues at the state and local level in the United States and austerity measures in other countries around the world. Despite these challenges, SMART outperformed its competitors and increased the company’s interactive whiteboard category share in its key markets of the United States and EMEA.

First, we increased sales of our core products into the education market, where classroom interactive whiteboard penetration in the United States increased from 28% to 36%, and in EMEA increased from 8% to 10%. Nearly half of the approximately 895,000 interactive whiteboards sold globally in calendar 2010 were SMART Board interactive whiteboards. We continued our global expansion during the year, with SMART products now used in over 175 countries.

PENETRATION RATES1

Second, we executed our strategy of selling attachment products to our existing installed base as customers are recognizing the value of the fully integrated SMART solution. These products represented 32% of our total revenue for the year, and sales of these products increased 47% over fiscal 2010.

Third, we continued to accelerate adoption in the business and government sectors, which represented approximately 15% of our revenue in fiscal 2011.

Finally, we continued to further develop our leadership in interactive touch technologies with the acquisition of NextWindow in April 2010. This acquisition enhanced our optical touch patent portfolio, which we are leveraging in a number of recently announced SMART products and in the all-in-one computer segment.

The above four strategies remain our focus in the year ahead.

| 1 | Futuresource Consulting Ltd., May 2011 (data as of December 31, 2010) |

3

SMART Technologies Inc. 2011 Annual Report

Market Dynamics

Since SMART introduced the world’s first interactive white-board in 1991, we have shipped more than two million interactive whiteboards, establishing our company as the clear leader in this product category. In education, we now estimate that at least 40 million students and teachers currently use SMART Board interactive whiteboards and other SMART products worldwide. The growth has been driven primarily by our broad, integrated suite of collaboration solutions, ease of use and the value for both students and teachers. Third-party research suggests that interactive whiteboards in the classroom can have a positive effect on student engagement and motivation, while accommodating a variety of learning styles (including those of students with special needs). As a result, these collaboration products have become a high priority for teachers, administrators and parents.

An October 2010 survey indicated that interactive whiteboards were the #2 education technology spending priority next to a classroom computer with Internet access.

The survey also indicated that 30% of U.S. districts were aiming for 100% adoption of interactive whiteboards in their classrooms over the next 3–5 years.

Despite current challenges with education funding, we remain optimistic about the long-term growth prospects of our business. Customer interest in our products is as high as ever. In fact, in the fall of 2010, we commissioned a third-party survey of approximately 375 of the largest school districts in the United States, which indicated that interactive whiteboards with short-throw projectors and document cameras remain high-priority future purchases. Furthermore, during the next five years, over half of these districts have plans to move to interactive whiteboard adoption levels in excess of 75%, including 30% of districts aiming for 100% adoption.

Of an estimated 35 million teaching spaces globally, only 9% currently have an interactive whiteboard.

According to Futuresource Consulting, global classroom penetration of interactive whiteboards was only 9% as of December 31, 2010. In combination with our other products for the classroom, this leaves significant runway in the education market alone.

In addition, although we are still in the early stages of penetrating the business and government sectors, we believe that SMART is well positioned to benefit from the significant long-term growth opportunity in unified communications as businesses continue to realize the benefits of technology for collaboration and quick decision making.

4

SMART Technologies Inc. 2011 Annual Report

Innovation

Innovation remains a cornerstone of our strategy, and our significant investment in research and development and focus on customer needs have enabled us to maintain our competitive edge. At the heart of our advantage is our touch technology and portfolio of integrated solutions, including SMART Notebook and SMART Meeting Pro software, which have not only differentiated the company in the marketplace, but allowed us to increase penetration in our core education market and in the business sector. A relentless focus on ease of use and the customer experience has been at SMART’s core from the beginning.

In fiscal 2011, we launched a significant number of new products and product upgrades that have expanded and enhanced our collaboration solutions portfolio. In October, we launched the SMART Board 800 series interactive whiteboard, which offers true collaboration through multiuser writing and common multitouch gestures. Shortly after, we introduced the SMART Board 400 series interactive whiteboard, a cost-effective, entry-level interactive whiteboard system that leveraged NextWindow’s optical touch technology and components.

In addition, we launched two new interactive products designed specifically for business users – the SMART Board 885ix interactive whiteboard system and the SMART Board 8070i interactive display. When used in conjunction with SMART Bridgit™ conferencing software and SMART Meeting Pro Premium software, meeting participants can connect and collaborate from anywhere in the world to share and interact with digital information, minimizing the cost and hassle of travel.

Since the company’s inception, we have invested over $185 million in R&D, resulting in over 150 issued patents and approximately 600 patents pending. We remain committed to investing in the company to support future growth in an effort to strengthen our technology and product leadership position in our core education sector and to build our presence in the business and government sectors.

Conclusion

We are proud of SMART’s strong execution during fiscal 2011, and we remain excited about the opportunity ahead. Despite the near-term challenges in the education marketplace, we are confident in our ability to grow and increase shareholder value over the long term. We plan to strengthen our leadership position through continued innovation and a strong focus on improving collaboration in the classroom and meeting room.

We are honored to work with our staff worldwide, who continue to have an unwavering commitment to excellence. We would also like to extend our sincere appreciation to our customers, resellers, suppliers and shareholders for their ongoing support of SMART.

Sincerely,

| | |

| |  |

| |

| NANCY KNOWLTON | | DAVID MARTIN |

| President and Chief Executive Officer | | Executive Chairman |

5

SMART Technologies Inc. 2011 Annual Report

Financial Highlights

| 1 | Adjusted EBITDA and Adjusted Net Income are non-GAAP measures and are not substitutes for GAAP equivalents. For a full reconciliation of Adjusted EBITDA and Adjusted Net Income to their most comparable GAAP measures, please refer later in this document to Management’s Discussion and Analysis for the year ended March 31, 2011. |

6

SMART Technologies Inc. 2011 Annual Report

In fiscal 2011, we increased our interactive whiteboard category share in our key markets in the United States and EMEA. We continue to make investments in areas we believe are large future growth opportunities, such as emerging international markets and the business sector.

INTERACTIVE WHITEBOARD CATEGORY SHARE2

| 2 | Futuresource Consulting Ltd., May 2011 (trailing 12-month data to March 31, 2011) |

7

SMART Technologies Inc. 2011 Annual Report

Education Solutions

When SMART created the world’s first interactive white-board in 1991, educators were among the first to recognize its potential. Since then, the education community has made SMART the global leader in the interactive whiteboard product category – over 40 million teachers and students in over 1.7 million K–12 classrooms around the world use a SMART Board interactive whiteboard. Educators trust SMART solutions because they help them achieve an immediate and lasting impact on learning.

Helping Education Evolve

Schools are changing. Classrooms today are increasingly interactive, student-centered, technology-rich environments. This shift demands new pedagogical strategies and versatile technology products. Educators around the world are choosing SMART solutions to help give students the skills they need to succeed in a knowledge-based society.

Integrated Products for Flexible Teaching

SMART solutions are designed to facilitate the dynamic learning environments preferred by today’s educators. SMART products are designed to work together, so they help teachers move easily between a variety of activities and learning environments.

Using SMART Notebook collaborative learning software, teachers can create compelling multimedia lessons that engage students of all learning styles. Once they’ve taught the lesson to the whole class on the SMART Board interactive whiteboard, teachers can reinforce the concept for small groups with the SMART Table™ interactive learning center. To assess knowledge, teachers can take a quick poll right from SMART Notebook software, with the SMART Response™ interactive response system.

Comprehensive Solutions for Long-Term Success

SMART solutions begin with innovative products. We have more than 300 researchers and developers who ensure that teachers find our products relevant and simple to use. This commitment to innovation has paid off. Our products have been proven around the world to create enthusiasm for teaching and learning.

To help educators realize the full potential of SMART products, we provide the support needed to ensure our products will be used, and used well. SMART solutions include the following three key elements that help educators improve student learning outcomes.

8

SMART Technologies Inc. 2011 Annual Report

Professional development and training – We offer programs and sites that help teachers gain the confidence to make SMART products part of everyday curriculum.

High-quality digital resources– Through the SMART Exchange website, we offer extensive collections of subject-specific, curriculum-correlated resources to help teachers find content that’s right for them. We also link teachers to a vast online community, providing them with access to advice, product information, support and ideas from around the world.

Strong support – Administrators can access consultative services to plan and execute the implementation of SMART products. Along with our extensive network of resellers, we provide excellent technical support.

Comprehensive SMART solutions help ensure that teachers adopt our products enthusiastically, knowing the right resources and services are at their fingertips. When teachers become passionate leaders of technology adoptions, administrators achieve their two main goals – improved student achievement and an excellent return on their investment.

“Twenty-first century learning skills are necessary for the success of our students and the economic prosperity of our nation. These skills begin with installing a SMART Board in every classroom.”

Anthony Mullen

2009 National Teacher of the Year

United States

“Teachers who had 35 years’ experience but very little technology skill are now doing integrated technology lessons in their classrooms with SMART Board interactive whiteboards.”

David C. Harding

Superintendent

Willington Public Schools, United States

“The growing interest shown by the teachers in our school and their widespread use of the SMART Board inside classrooms confirms the great education value of the SMART Board interactive whiteboard. It gives students the opportunity to mature, consolidate and express the multiple and simultaneous skills required for communication.”

Alma Perucca

Teacher

Croce-Morelli Public Middle School, Italy

9

SMART Technologies Inc. 2011 Annual Report

Business Solutions

For 20 years, SMART has been designing products that change the way people share and work with digital information, turning workplaces into interactive collaboration spaces where teamwork can thrive. True collaboration – when people share their ideas, skills, experiences and inspiration to work toward common goals – can help virtually any business reach its objectives. And it can strengthen the relationships with colleagues, customers and suppliers upon which businesses are built.

A New Way to Collaborate

In a SMART-equipped workspace, every meeting becomes an opportunity to share information, brainstorm ideas, capture feedback and clearly document next steps. Our interactive whiteboards and displays, software, services and support all work together so that people can share information and ideas in visual and interactive ways. Teams can easily access their digital resources – files, applications, websites and multimedia – and open them on a SMART Board interactive whiteboard or display. They can write notes in digital ink, save them into their files and share them instantly via e-mail. They can switch from writing notes to navigating applications and back to writing with a simple touch. And they can share screens instantly with remote participants, so everyone can see and contribute to the work in real time – regardless of location.

Collaboration Solutions for Any Business

Because our products are designed to streamline the exchange of information and make meetings more productive, they can benefit virtually any organization. SMART solutions have been implemented by businesses in various industries, from architecture to manufacturing to telecommunications. We’ve helped our customers find innovative ways to work together across distances, accelerate decision making, enhance cross-functional collaboration, engage clients and stakeholders, train personnel and respond to emergency situations – all by making it easier to share information and communicate ideas.

“We now have the ability to give the client a collaborative experience with us, and we don’t have to get on an airplane to do it. SMART business solutions have eliminated the competitive disadvantage of being remote from our clients.”

Johnny Anderson

Vice President, Business Development

Bulldog Solutions

10

SMART Technologies Inc. 2011 Annual Report

Why Businesses Choose SMART Products

We understand the needs of business today and deliver solutions that help our customers deliver exceptional results. We recognize that business people don’t have time to focus on technology when they have urgent challenges and opportunities. Our business solutions offer the following five key benefits.

Ease of use – SMART products are designed with the user in mind. They are highly intuitive and easy to use, so teams can quickly incorporate them into collaborative work sessions.

Interactivity – Team members can control applications with a simple touch and write over applications in digital ink, so collaboration is highly visual and interactive.

Distance collaboration – You can share content on your desktops or displays and write notes in digital ink for everyone to see, regardless of location.

Integration with everyday software – Our products integrate easily with a growing list of preferred software applications, allowing users to save notes and markups directly into their original files.

Support – SMART solutions include world-class customer service and technical support. Our extensive global network of resellers also offers excellent support.

“Our new SMART collaboration capability enables people to meet, regardless of where they are in the world, and interact as if they were in the same room. This has had a massive impact on travel costs and reduced our carbon footprint significantly.”

Bola Oshisanwo

Director, Agile Development Centre

BT

“With the SMART Board interactive whiteboard, we can very easily demonstrate what works and what doesn’t. The evolution of a plan can take place right there, when normally it would take three meetings.”

Helma Gansen

President

Gansen Lindsay Design Consultants Inc.

11

Looking Ahead

When we think of the future, we envision classrooms and meeting rooms where images, applications and information are literally at people’s fingertips. We envision students around the world, experiencing the rewards of learning, whether they learn best by seeing, hearing or doing. We envision teams collaborating simultaneously around the world, at home and in offices, developing ideas on SMART Board interactive whiteboards, making decisions quickly and minimizing the barrier of distance.

We are passionate about our vision. Our motivation comes from educators and business professionals who tell us they can’t imagine working without SMART solutions. Students who once struggled have found their stride, teachers have rediscovered their love for learning and business teams have found new ways to collaborate and become more productive.

That’s what drives SMART staff around the world to invest their energy in innovation. Our teams are united in their desire to create intuitive products that help educators and business people achieve their goals.

2011 marks the 20th anniversary of the SMART Board interactive whiteboard – a milestone that reminds us of the long-lasting and profound impact our solutions have had on our customers. Over the next 20 years, we’re committed to further innovation to deliver on our vision of changing the way the world works and learns.

SMART Technologies Inc. 2011 Annual Report

13

SMART Technologies Inc. 2011 Annual Report

Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following annual management’s discussion and analysis (“MD&A”) should be read in conjunction with our audited consolidated financial statements and the accompanying notes of SMART Technologies Inc. (the “Company”) for the fiscal year ended March 31, 2011. The consolidated financial statements have been presented in United States (“U.S.”) dollars and have been prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”). Unless the context otherwise requires, any reference to the “Company”, “SMART Technologies”, “we”, “our”, “us” or similar terms refers to SMART Technologies Inc. and its subsidiaries. Because our fiscal year ends on March 31, references to a fiscal year refer to the fiscal year ended March 31 of the same calendar year. For example, when we refer to fiscal 2011, we mean our fiscal year ended March 31, 2011. Unless otherwise indicated, all references to “$” and “dollars” in this discussion and analysis mean U.S. dollars. The following table sets forth the period end and period average exchange rates for U.S. dollars expressed in Canadian dollars that are used in the preparation of our audited consolidated financial statements and this MD&A. These rates are based on the closing rates published by the Bank of Canada.

| | | | |

| | | Period End Rate | | Period Average Rate |

Year ended March 31, 2011 | | 0.9696 | | 1.0167 |

Year ended March 31, 2010 | | 1.0158 | | 1.0906 |

Year ended March 31, 2009 | | 1.2613 | | 1.1260 |

This MD&A includes forward-looking statements which reflect our current views with respect to future events and financial performance. These statements include forward-looking statements both with respect to us specifically and the technology product industry and business, demographic and other matters in general. Statements which include the words “expect”, “intend”, “plan”, “believe”, “project”, “estimate”, “anticipate”, “may”, “will”, “continue”, “further”, “seek”, and similar words or statements of a future or forward-looking nature identify forward-looking statements for purposes of the applicable securities laws or otherwise. In particular and without limitation, this MD&A contains forward-looking statements pertaining to general market conditions, our future growth strategy and prospects, including growth of the education, business and government markets for our products, our plans and objectives for future operations, our future financial performance and financial condition, the addition of new products to our portfolio and enhancements to current products, our industry, opportunities in the business and government markets and licensing opportunities, working capital requirements, integration of our acquisition of NextWindow, our acquisition strategy, regulation, exchange rates and income tax considerations.

All forward-looking statements address matters that involve risks, uncertainties and assumptions. Accordingly, there are or will be important factors and assumptions that could cause our actual results and other circumstances and events to differ materially from those indicated in these statements, as discussed more fully in the sections “Risks Related to Our Business” and “Capital Structure Risks”. These risk factors and assumptions include, but are not limited to, the following:

| | • | | competition in our industry; |

| | • | | our ability to successfully obtain patents or registration for other intellectual property rights or protect, maintain and enforce such rights; |

| | • | | our ability to manage our growth; |

| | • | | third-party claims of infringement or violation of, or other conflicts with, intellectual property rights by us; |

| | • | | our ability to enhance current products and develop and introduce new products; |

| | • | | the development of the market for interactive learning and collaboration products; |

| | • | | reduced spending by our customers due to changes in the spending policies or budget priorities for government funding; |

| | • | | our ability to grow our sales in foreign markets; |

| | • | | our ability to manage risks inherent in foreign operations; |

| | • | | our ability to protect our brand; |

| | • | | our ability to obtain components and products from suppliers on a timely basis and on favorable terms; |

| | • | | our ability to manage our component and product assembly and logistical services successfully; |

| | • | | the reliability of component supply and product assembly and logistical services provided by third parties; |

| | • | | possible changes in the demand for our products; |

| | • | | our ability to successfully execute our strategy to grow in the business and government markets; |

14

SMART Technologies Inc. 2011 Annual Report

| | • | | our ability to integrate the operations of the various businesses we acquire; |

| | • | | our ability to establish new relationships and to build on our existing relationships with our dealers and distribu- tors; and |

| | • | | our ability to manage cash flow, foreign exchange risk and working capital. |

Overview

We design, develop and sell interactive technology products and integrated solutions that enhance learning and enable people to collaborate in innovative and effective ways. We are the global leader in the interactive whiteboard product category, which is the core of our collaboration solutions. We introduced the world’s first commercial interactive whiteboard in 1991 and as of March 31, 2011, we have shipped over 1.9 million of our SMART Board™ interactive whiteboards worldwide.

SMART Board interactive whiteboards combine the simplicity of a whiteboard and the power of a computer. By touching the surface of a SMART Board interactive whiteboard, the user can control computer applications, access the Internet, write in digital ink and save and share work. Our interactive whiteboards are designed to serve as the focal point of a broad technology platform in classrooms and meeting rooms.

We complement our interactive whiteboards with a comprehensive range of modular and integrated interactive technology products for easy-to-use, touch- and gesture-enabled solutions that facilitate effective learning and collaboration. Our line of interactive whiteboards currently ranges from the 400 series, our latest entry-level product, to the 600 series, our most popular product in education, to the 800 series, our feature- and functionality-rich multi-user interactive whiteboard. We also have a line of SMART Board interactive displays and the SMART Table™ interactive learning center, as well as a variety of related attachment products and services.

We generate our revenue from the sale of these interactive technology products and integrated solutions, including hardware, software and services. Our global expansion has led to our products being used in more than 175 countries worldwide through our distributor and dealer network to the education, business and government markets. Although we do not sell to them directly, we consider these end-users to be our customers. We estimate that approximately 85% of our sales are to customers in the education market and the other 15% to customers in the business and government markets.

Our company operates in a very competitive global environment with products based on rapidly changing technologies. As we continue to focus on expanding our markets and further developing our portfolio of collaboration solutions, we plan to build on our position as the global leader in the interactive whiteboard product category.

We believe the interactive whiteboard market is in the early stages of adoption and that significant opportunities exist beyond the traditional education markets we have penetrated. Our strategy includes acquiring new customers in the education market, specifically in markets we are developing such as Europe, Middle East and Africa (“EMEA”), that have seen recent growth. We have expanded operations in continental Europe, Asia and in other countries where we believe average penetration rates are currently lower than in the United Kingdom, U.S., Mexico and Canada. We have broadened our geographical focus to support our distribution channel by opening offices in additional countries, by continuing to hire additional personnel in our current global locations and by increasing our global distribution network.

We have been successful at penetrating the education market by providing integrated solutions that enhance the interactive whiteboard experience with improved collaboration. Our portfolio of products has expanded to include related attachment products that provide this collaboration solution, including SMART Response™, SMART Slate™, SMART Document Camera™, SMART Table, SMART Audio™ and SMART Classroom Suite™. We have also increased the depth and quality of the digital content offered by us and third parties for use on our interactive whiteboards through a combination of both free and premium content.

Our company plans to accelerate the adoption of our products in the business and government markets, leveraging on our existing distribution network and other strategic relationships to penetrate these markets. Our growth strategy focuses on the simplicity and ease of use of our products, while fully integrating them with critical business processes and products for a superior collaborative business solution. We have expanded our staffing and research and development team in these areas to develop new solutions and improve existing solutions for these markets.

15

SMART Technologies Inc. 2011 Annual Report

Management’s Discussion and Analysis of Financial Condition and Results of Operations(continued)

We have supported our focus of expanding globally and further penetrating the education, business and government markets by developing different series of collaboration solutions designed to meet the specific requirements of our target markets. Our 400 series is a cost-effective, entry-level product recently introduced to respond to the growing needs of markets such as EMEA, Asia Pacific and Latin America. Our 600 series is our leading product and continues to evolve to meet changing market needs. The 800 series was recently introduced as a premium solution for next-generation classrooms and corporate meeting rooms requiring enhanced collaboration, using our DViT™ (Digital Vision Touch) technology to enable many of the enhanced features of this interactive whiteboard.

Significant 2011 Financial Transactions

During fiscal 2011, we completed several significant transactions, including the acquisition of Next Holdings Limited (“NextWindow”), a reorganization of the capital of the company that we refer to as the “2010 Reorganization”, our initial public offering (“IPO”), and significant repayments of our debt. The details of each of these transactions are as follows.

As part of our strategy to expand our market position in optical touch technology, we acquired NextWindow on April 21, 2010. NextWindow designs and manufactures components for optical touch screens for integration into electronic displays, including PC displays. We are integrating NextWindow’s technologies within our products to accelerate the introduction of new products, including the new SMART Board 400 series interactive whiteboard. The acquisition consideration for NextWindow consisted of $82.0 million funded from our available cash, net of $8.0 million of cash held by NextWindow at the date of acquisition.

On May 13, 2010, in preparation for our IPO, our Board of Directors approved a reorganization of the capital of the Company. Through a series of transactions, the 2010 Reorganization resulted in the repayment of $8.0 million of the shareholder note payable and the effective conversion of the remaining shareholder note payable and cumulative preferred shares, together with all accrued interest and accumulated dividends thereon, as well as all our other outstanding shares into Class B Shares, Class A Subordinate Voting Shares and Class A Preferred Shares. The 2010 Reorganization was completed prior to and in conjunction with the closing of our IPO on July 20, 2010. At this time, the newly created Class A Preferred Shares were converted into Class B Shares and Class A Subordinate Voting Shares and are therefore no longer outstanding.

Upon the completion of our IPO on July 20, 2010, we issued 8,800,000 Class A Subordinate Voting Shares resulting in proceeds received of $134.3 million, net of underwriting commissions and other offering expenses. Concurrently, existing shareholders sold an aggregate of 30,030,000 Class A Subordinate Voting Shares in the offering. In July 2010, we repaid $19.2 million of our term construction facility and $40.0 million of our unsecured term loan with proceeds from the offering. In conjunction with our IPO, we implemented an Equity Incentive Plan which provides for the grant of options, restricted share units and deferred share units to directors, officers, employees, consultants and service providers of our Company and its subsidiaries. During the year ended March 31, 2011, we granted 1,444,500 stock options to purchase the Company’s Class A Subordinate Voting Shares at a weighted average exercise price of $16.22. Of these options, 1,140,000 were granted on July 15, 2010 in conjunction with the IPO at an exercise price of $17.00.

In September 2010, the remaining balances of the unsecured term loan, the term construction facility and the construction loan of $42.4 million, $29.8 million and $1.4 million, respectively, were repaid in full. During the remainder of fiscal 2011, $55.0 million of the Second lien facility was repaid. Using interest rates and the debt level at March 31, 2011, we expect that future interest expense will be approximately $16.3 million annually.

Sources of Revenue and Expenses

Revenue

We generate our revenue from the sale of interactive technology products and solutions, including hardware, software and services. Our distribution and sales channel includes dealers in North America and distributors in Europe, the Middle East and Africa, Caribbean and Latin America and the Asia Pacific regions. We complement and support our sales channel with sales and support staff who work either directly with prospective customers or in coordination with our sales channel to promote and provide products and solutions that address the needs of the end-user. Revenue is recognized at the time we transfer the risks and rewards to our sales channel according to contractual terms. Our practice with end-users usually involves multiple elements including post-contract technical support, software

16

SMART Technologies Inc. 2011 Annual Report

upgrades and updates, although we are not contractually required to do so. Revenue from product sales is allocated to each element based on relative fair values with any discount allocated proportionately. Revenue attributable to undelivered elements is deferred and recognized ratably over the estimated term of provision of these elements.

Cost of Sales

Our cost of sales is primarily comprised of the cost of materials and components purchased from our suppliers, assembly labor and overhead costs, inventory provisions and write offs, warranty costs, product transportation costs and other supply chain management costs. Our standard warranty period on interactive whiteboards extends up to five years and on other hardware products from one to three years. At the time product revenue is recognized, an accrual for estimated warranty costs is recorded as a component of cost of sales based on prior claims experience. Depreciation of assembly equipment is included in cost of sales. To the extent that our sales increase, we expect our cost of sales to also increase in absolute dollars.

Selling, Marketing and Administration Expenses

Our selling and marketing expenses consist primarily of costs relating to our sales and marketing activities, including salaries and related expenses, customer order management activities, customer support, advertising, trade shows and other promotional activities. We offer various cooperative marketing programs to assist our sales channel to market and sell our products which are included as part of selling and marketing expenses. Our administration expenses consist of costs relating to people services, information systems, legal and finance functions, professional fees, insurance, stock-based compensation and other corporate expenses. During fiscal 2011, our selling, marketing and administration expenses increased in absolute dollars as a result of hiring additional personnel, expanding internationally and becoming a public company. We do not expect these expenses to change materially from prior years as a percentage of revenue.

Research and Development Expenses

Research and development expenses consist primarily of salaries and related expenses for software and hardware engineering and technical personnel as well as materials and consumables used in product development. We incur most of our research and development expenses in Canada and New Zealand, and are eligible to receive Scientific Research and Experimental Development investment tax credits for certain eligible expenditures. Investment tax credits are netted against our provision for income taxes for financial statement presentation purposes. We expect research and development expenses to continue to grow in absolute dollars as we focus on enhancing and expanding our product offerings, although we do not expect these expenses to change materially from prior years as a percentage of revenue.

Interest Expense

In August 2007, shareholders of our predecessor company (SMART Technologies (Holdings) Inc.) signed an agreement with Apax Partners to effect a corporate reorganization, pursuant to which the shareholders of our predecessor company reduced their combined ownership interest to 50.1% and Apax Partners acquired a 49.9% interest in the Company. As part of this corporate reorganization, we issued $465.0 million of term bank debt and CDN$338.9 million (equivalent to $319.2 million when issued) of related party debt, consisting of the shareholder note payable and cumulative preferred shares. Our increased interest expense from this 2007 corporate reorganization was one of the principal reasons for our net loss in fiscal 2009. Interest expense has declined significantly in fiscal 2011 as a result of the 2010 Reorganization described under “Significant 2011 Financial Transactions” above, which resulted in the conversion of the shareholder note payable and cumulative preferred shares into equity during the first quarter of fiscal 2011. Interest expense has also declined due to the significant debt repayments made in the last three quarters of 2011.

Foreign Exchange Gains & Losses

We report our financial results in U.S. dollars allowing us to assess our business performance in comparison to the financial results of other companies in the technology industry. Our Canadian operations and marketing support subsidiaries around the world have the Canadian dollar as their functional currency. Our U.S. and New Zealand operating subsidiaries have the U.S. dollar as their functional currency, our German operating subsidiary has the Euro as its functional currency, and our Japanese operating subsidiary has the Japanese Yen as its functional currency. The financial results of these operating subsidiaries are converted to Canadian dollars for consolidation purposes and then the Canadian consolidated financial results are converted from Canadian dollars to U.S. dollars

17

SMART Technologies Inc. 2011 Annual Report

Management’s Discussion and Analysis of Financial Condition and Results of Operations(continued)

for reporting purposes. During the first quarter of fiscal 2012, our Germany operating subsidiary will discontinue its distribution activities and become a marketing support subsidiary for EMEA, at which point the Canadian dollar will become its functional currency.

Our foreign exchange exposure is primarily between the Canadian dollar and both the U.S. dollar and the Euro. This exposure relates to our U.S. dollar-denominated assets and liabilities, including our external debt, the sale of our products to customers globally and purchases of goods and services in foreign currencies. Gains and losses on our U.S. dollar-denominated debt prior to its maturity or redemption are non-cash in nature.

Results of Operations

The following table sets forth certain consolidated statement of operations data and other data for the periods indicated in millions of dollars, except for percentages, shares, per share amounts, units and average selling prices.

| | | | | | | | | | | | |

Fiscal Year Ended March 31, | | 2011 | | | 2010 | | | 2009 | |

Consolidated Statement of Operations | | | | | | | | | | | | |

Revenue | | $ | 790.1 | | | $ | 648.0 | | | $ | 468.2 | |

Cost of sales | | | 399.2 | | | | 326.5 | | | | 268.2 | |

| | | | | | | | | | | | |

Gross margin | | | 390.9 | | | | 321.5 | | | | 200.0 | |

Operating expenses | | | | | | | | | | | | |

Selling, marketing and administration | | | 180.8 | | | | 138.8 | | | | 99.7 | |

Research and development | | | 53.0 | | | | 33.6 | | | | 25.0 | |

Depreciation and amortization | | | 31.8 | | | | 15.9 | | | | 5.8 | |

| | | | | | | | | | | | |

Operating income | | | 125.3 | | | | 133.2 | | | | 69.5 | |

Non-operating expenses | | | | | | | | | | | | |

Other income, net | | | (0.5 | ) | | | (0.2 | ) | | | (0.8 | ) |

Interest | | | 31.6 | | | | 64.9 | | | | 78.6 | |

Foreign exchange (gain) loss | | | (10.5 | ) | | | (91.8 | ) | | | 94.0 | |

| | | | | | | | | | | | |

Income (loss) before income taxes | | | 104.7 | | | | 160.3 | | | | (102.3 | ) |

Income tax expense | | | 35.3 | | | | 18.3 | | | | 4.3 | |

| | | | | | | | | | | | |

Net income (loss) | | $ | 69.4 | | | $ | 142.0 | | | $ | (106.6 | ) |

| | | | | | | | | | | | |

Earnings (loss) per share | | | | | | | | | | | | |

Basic and diluted earnings (loss) per share | | $ | 0.53 | | | $ | 0.81 | | | $ | (0.63 | ) |

Weighted average number of shares outstanding | | | 130,775,288 | | | | 176,322,584 | | | | 170,096,497 | |

Period end number of shares outstanding | | | 123,772,791 | | | | 181,053,688 | | | | 170,096,497 | |

| | | | | | | | | | | | |

Selected Data | | | | | | | | | | | | |

Revenue by geographic location | | | | | | | | | | | | |

North America | | $ | 558.4 | | | $ | 457.3 | | | $ | 314.3 | |

Europe, Middle East and Africa | | | 175.5 | | | | 149.9 | | | | 131.5 | |

Rest of World | | | 56.2 | | | | 40.8 | | | | 22.4 | |

| | | | | | | | | | | | |

| | $ | 790.1 | | | $ | 648.0 | | | $ | 468.2 | |

| | | | | | | | | | | | |

Revenue growth(1) | | | 21.9 | % | | | 38.4 | % | | | 23.7 | % |

As a percent of revenue | | | | | | | | | | | | |

Gross margin | | | 49.5 | % | | | 49.6 | % | | | 42.7 | % |

Selling, marketing and administration | | | 22.9 | % | | | 21.4 | % | | | 21.3 | % |

Research and development | | | 6.7 | % | | | 5.2 | % | | | 5.3 | % |

Adjusted EBITDA(2) | | $ | 185.8 | | | $ | 166.3 | | | $ | 90.9 | |

Adjusted EBITDA as a percentage of revenue(2)(3) | | | 23.1 | % | | | 25.1 | % | | | 19.4 | % |

Adjusted Net Income(4) | | $ | 85.5 | | | $ | 59.5 | | | $ | (2.5 | ) |

Adjusted Net Income per share(4)(5) | | $ | 0.65 | | | $ | 0.34 | | | $ | (0.01 | ) |

Total number of SMART Board interactive whiteboards sold | | | 406,314 | | | | 369,489 | | | | 306,234 | |

Average selling price of SMART Board interactive whiteboards sold(6) | | $ | 1,324 | | | $ | 1,289 | | | $ | 1,146 | |

18

SMART Technologies Inc. 2011 Annual Report

| (1) | Revenue growth is calculated as a percentage by comparing the increase in revenue in the period to revenue during the same period in the immediately preceding fiscal year. |

| (2) | Adjusted EBITDA is a non-GAAP measure that is described and reconciled to net income in the next section and is not a substitute for the GAAP equivalent. |

| (3) | Adjusted EBITDA as a percentage of revenue is calculated by dividing Adjusted EBITDA by revenue after adding back the net change in deferred revenue. |

| (4) | Adjusted Net Income is a non-GAAP measure that is described and reconciled to net income in the next section and is not a substitute for the GAAP equivalent. |

| (5) | Adjusted Net Income per share is calculated by dividing Adjusted Net Income by the average number of basic shares outstanding during the period. |

| (6) | Average selling price is calculated by dividing the total revenue from the sale of SMART Board interactive whiteboards and SMART Board interactive whiteboards with integrated projectors by the total number of units sold. |

Non-GAAP Measures

We define Adjusted EBITDA as net income before interest, income taxes, depreciation and amortization, as well as adjusting for the following items: foreign exchange gains or losses, net change in deferred revenue, stock-based compensation, acquisition costs and other income. We define Adjusted Net Income as net income before stock-based compensation, acquisition costs, foreign exchange gains or losses, net change in deferred revenue and amortization of intangible assets, all net of tax.

Adjusted EBITDA and Adjusted Net Income are non-GAAP measures and should not be considered as an alternative to net income or any other measure of financial performance calculated and presented in accordance with GAAP. Adjusted EBITDA, Adjusted Net Income and other non-GAAP measures have inherent limitations and therefore, you should not place undue reliance on them.

We use Adjusted EBITDA as a key measure to assess the core operating performance of our business removing the effects of our leveraged capital structure and the volatility associated with the foreign exchange on our U.S. dollar-denominated debt. We also use Adjusted Net Income to assess the performance of the business removing the after-tax impact of stock-based compensation, acquisition costs, foreign exchange gains and losses, revenue deferral and amortization of intangible assets. We use both of these measures to assess business performance when we evaluate our results in comparison to budgets, forecasts, prior-year financial results and other companies in our industry. Many of these companies use similar non-GAAP measures to supplement their GAAP disclosures but such measures may not be directly comparable. In addition to its use by management in the assessment of business performance, Adjusted EBITDA is used by our Board of Directors and by our lenders in assessing management’s performance and is a key metric in the determination of incentive plan payments. We believe Adjusted EBITDA and Adjusted Net Income may be useful to investors in evaluating our operating performance because securities analysts use metrics similar to Adjusted EBITDA and Adjusted Net Income as supplemental measures to evaluate the overall operating performance of companies.

Some of the limitations of Adjusted EBITDA are that it does not reflect:

| | • | | depreciation and amortization; |

| | • | | foreign exchange gains or losses; |

| | • | | changes in deferred revenue which, in accordance with our revenue recognition policy described under “Critical Accounting Policies and Estimates – Revenue Recognition” below, represents the portion of our sales that we do not recognize in the period less amounts recognized from prior periods; |

| | • | | stock-based compensation expense; |

| | • | | other income, including interest income and gains or losses related to the sale of property and equipment. |

Adjusted Net Income has the same limitations as Adjusted EBITDA discussed above, with the exception that it does reflect income taxes, depreciation and amortization of property and equipment, interest expense and other income.

We compensate for the inherent limitations associated with using Adjusted EBITDA and Adjusted Net Income through disclosure of such limitations, presentation of our financial statements in accordance with GAAP and reconciliation of Adjusted EBITDA and Adjusted Net Income to the most directly comparable GAAP measure, net income (loss).

19

SMART Technologies Inc. 2011 Annual Report

Management’s Discussion and Analysis of Financial Condition and Results of Operations(continued)

The following table sets forth the reconciliation of net income to Adjusted EBITDA in millions of dollars.

| | | | | | | | | | | | |

Fiscal Year Ended March 31, | | 2011 | | | 2010 | | | 2009 | |

Adjusted EBITDA | | | | | | | | | | | | |

Net income (loss) | | $ | 69.4 | | | $ | 142.0 | | | $ | (106.6 | ) |

Income tax expense | | | 35.3 | | | | 18.3 | | | | 4.3 | |

Depreciation in cost of sales | | | 4.1 | | | | 2.0 | | | | 3.9 | |

Depreciation and amortization | | | 31.8 | | | | 15.9 | | | | 5.8 | |

Interest expense | | | 31.6 | | | | 64.9 | | | | 78.6 | |

Foreign exchange (gain) loss | | | (10.5 | ) | | | (91.8 | ) | | | 94.0 | |

Change in deferred revenue(1) | | | 14.8 | | | | 13.4 | | | | 11.7 | |

Stock-based compensation | | | 8.7 | | | | — | | | | — | |

Acquisition costs | | | 1.1 | | | | 1.8 | | | | — | |

Other income, net | | | (0.5 | ) | | | (0.2 | ) | | | (0.8 | ) |

| | | | | | | | | | | | |

Adjusted EBITDA | | $ | 185.8 | | | $ | 166.3 | | | $ | 90.9 | |

| | | | | | | | | | | | |

| (1) | Change in deferred revenue is calculated as the difference between deferred revenue and deferred revenue recognized. In accordance with our revenue recognition policy, deferred revenue represents the portion of our sales that we do not recognize in the period. Deferred revenue recognized represents the portion of our revenue deferred in a prior period that we recognized in the current period. We deferred revenue of $44.2 million, $36.9 million and $31.1 million in the years ended March 31, 2011, 2010 and 2009, respectively. |

The following table sets forth the reconciliation of net income to Adjusted Net Income and basic and diluted earnings per share to Adjusted Net Income per share in millions of dollars, except per share amounts.

| | | | | | | | | | | | |

Fiscal Year Ended March 31, | | 2011 | | | 2010 | | | 2009 | |

Adjusted Net Income | | | | | | | | | | | | |

Net income (loss) | | $ | 69.4 | | | $ | 142.0 | | | $ | (106.6 | ) |

Adjustments to net income (loss) | | | | | | | | | | | | |

Amortization of intangible assets | | | 9.0 | | | | — | | | | — | |

Foreign exchange (gain) loss | | | (10.5 | ) | | | (91.8 | ) | | | 94.0 | |

Change in deferred revenue | | | 14.8 | | | | 13.4 | | | | 11.7 | |

Stock-based compensation | | | 8.7 | | | | — | | | | — | |

Acquisition costs | | | 1.1 | | | | 1.8 | | | | — | |

| | | | | | | | | | | | |

| | | 23.1 | | | | (76.6 | ) | | | 105.7 | |

Tax impact on adjustments(1) | | | 7.0 | | | | 5.9 | | | | (1.6 | ) |

| | | | | | | | | | | | |

Adjustments to net income (loss), net of tax | | | 16.1 | | | | (82.5 | ) | | | 104.1 | |

| | | | | | | | | | | | |

Adjusted Net Income | | $ | 85.5 | | | $ | 59.5 | | | $ | (2.5 | ) |

| | | | | | | | | | | | |

Adjusted Net Income per share | | | | | | | | | | | | |

Basic and diluted earnings (loss) per share | | $ | 0.53 | | | $ | 0.81 | | | $ | (0.63 | ) |

Adjustments to net income (loss), net of tax, per share | | | 0.12 | | | | (0.47 | ) | | | 0.62 | |

| | | | | | | | | | | | |

Adjusted Net Income per share | | $ | 0.65 | | | $ | 0.34 | | | $ | (0.01 | ) |

| | | | | | | | | | | | |

| (1) | Reflects the tax impact on the adjustments to net income (loss). A key driver of our foreign exchange (gain) loss is the conversion of our U.S. dollar-denominated debt that was originally incurred at an average rate of 1.05. When the unrealized foreign exchange amount on U.S. dollar-denominated debt is in a net gain position as measured against the original exchange rate, the gain is tax-effected at current rates. When the unrealized foreign exchange amount on the U.S. dollar-denominated debt is in a net loss position as measured against the original exchange rate, a valuation allowance is taken against it and as a result no net tax effect is recorded. |

20

SMART Technologies Inc. 2011 Annual Report

Results of Operations – Fiscal 2011 Compared to Fiscal 2010

Revenue

Revenue increased by $142.1 million, or 21.9%, from $648.0 million in fiscal 2010 to $790.1 million in fiscal 2011. Sales volumes for SMART Board interactive whiteboards for fiscal 2011 were 406,314 units, an increase of 36,825 units, or 10.0%, from 369,489 units in fiscal 2010. The majority of this growth was driven by market demand in the education sector in both North America and EMEA. In North America, revenue increased by $101.1 million as a result of continued adoption of interactive whiteboards in the education market, and increased sales of related attachment products. In EMEA, revenue increased by $25.6 million as a result of our expansion in this region during fiscal 2011.

Gross Margin

Gross margin increased by $69.4 million from $321.5 million in fiscal 2010 to $390.9 million in fiscal 2011. The gross margin percentage in fiscal 2011 was 49.5%, compared to 49.6% in fiscal 2010. Although we continue to focus on lowering assembly costs of certain key components in our product offering as well as logistics and transportation costs, improvements were offset by higher warranty provisions on certain attachment products. The increase in gross margin was partially offset by a negative foreign exchange impact of approximately $6.1 million as a result of the year-over-year weakening of the Euro relative to the U.S. dollar, which impacted our revenue, and the strengthening of the Canadian dollar relative to the U.S. dollar, which impacted our cost of sales.

Operating Expenses

Selling, Marketing and Administration Expenses

Selling, marketing and administration expenses increased by $42.0 million, or 30.3%, from $138.8 million in fiscal 2010 to $180.8 million in fiscal 2011. Approximately $9.0 million of the increase is related to growth in North American employee levels and $8.1 million is related to stock-based compensation expense from the Participant Equity Loan Plan and the Equity Incentive Plan. Approximately $7.4 million of the increase related to increased consulting fees and other costs primarily related to our information systems, the acquisition of NextWindow and the additional costs related to being a public company. Internationally, our expansion in Europe, as part of our global strategy, accounted for approximately $4.3 million of the increase and selling, marketing and administration expenses of NextWindow accounted for approximately $5.7 million of the increase. Lastly, the strengthening in the value of the Canadian dollar compared to the U.S. dollar contributed approximately $8.8 million of the increase.

Research and Development Expenses

Our research and development expenses increased by $19.4 million, or 57.7%, from $33.6 million in fiscal 2010 to $53.0 million in fiscal 2011. These increases reflect our continued commitment to innovation and investment in product development for the education and business markets, including an increase in the number of software developers, engineers and technicians required to support this development, as well as the acquisition of NextWindow. Also, the strengthening in the value of the Canadian dollar compared to the U.S. dollar contributed approximately $3.1 million of the increase.

Depreciation and Amortization

Depreciation and amortization of property and equipment increased by $6.9 million from $15.9 million in fiscal 2010 to $22.8 million in fiscal 2011. This reflects higher depreciation from our continued investment in systems to support our business growth.

Amortization of intangible assets reflects amortization of $8.6 million on $50.1 million of intangible assets recorded upon the acquisition of NextWindow on April 21, 2010. The weighted average amortization period for the intangible assets is 5.6 years.

21

SMART Technologies Inc. 2011 Annual Report

Management’s Discussion and Analysis of Financial Condition and Results of Operations(continued)

Non-Operating Expenses

Interest Expense

Interest expense declined by $33.3 million, or 51.3%, from $64.9 million in fiscal 2010 to $31.6 million in fiscal 2011. Interest expense declined as a result of the 2010 Reorganization described under “Significant 2011 Financial Transactions” above, which resulted in the conversion of the shareholder note payable and cumulative preferred shares into equity during the first quarter of fiscal 2011, as well as the debt repayments made in the last three quarters of fiscal 2011. Using interest rates and the debt level at March 31, 2011, we expect that future interest expense will be approximately $16.3 million annually.

Foreign Exchange Gains

Foreign exchange gains decreased by $81.3 million, from $91.8 million in fiscal 2010 to $10.5 million in fiscal 2011. In prior years, foreign exchange gains and losses have primarily resulted from the conversion of our U.S. dollar-denominated long-term debt into our functional currency of Canadian dollars. From March 31, 2010 to March 31, 2011, the U.S. dollar weakened by approximately 4.5% against the Canadian dollar from CDN$1.0158 to CDN$0.9696, resulting in an unrealized foreign exchange gain on our U.S. dollar-denominated debt of $10.4 million in the year. This compares to a $105.7 million gain reported in fiscal 2010 when the U.S. dollar weakened by approximately 19.5% compared to the Canadian dollar. Although U.S. dollar-denominated debt will continue to be a key driver of foreign exchange gains and losses, the debt repayments during fiscal 2011 and the year-over-year increase in U.S. dollar-denominated cash and accounts receivable have significantly offset the impact of the revaluation of U.S. dollar-denominated debt.

Provision for Income Taxes

Income tax expense increased by $17.0 million from $18.3 million in fiscal 2010 to $35.3 million in fiscal 2011. Our tax provision is weighted towards Canadian income tax rates as substantially all our taxable income is Canadian-based. In calculating the tax provision we adjust income before income taxes by the unrealized foreign exchange (gain) loss from the revaluation of the U.S. dollar-denominated debt. This is treated as a capital item for income tax purposes. We take a valuation allowance if the conversion of U.S. dollar-denominated debt is in a net foreign exchange loss position due to the uncertainty that we will be able to utilize the capital loss in the future. The increase in income tax expense in fiscal 2011 compared to fiscal 2010 was due to a reduction in the valuation allowance against unrealized capital losses on U.S. dollar-denominated debt and utilization of non-capital losses occurring in fiscal 2010. The tax provision also includes investment tax credits for fiscal 2011 and fiscal 2010 of $4.4 million and $4.6 million, respectively.

Net Income (Loss)

Net income decreased by $72.6 million from $142.0 million in fiscal 2010 to $69.4 million in fiscal 2011. This change is due to the increase in gross margin of $69.4 million and decrease in interest expense of $33.3 million, offset by an increase in operating expenses of $77.3 million, income taxes of $17.0 million and the impact of the volatility of the U.S. dollar relative to the Canadian dollar on our U.S. dollar-denominated debt, which resulted in an $81.3 million decrease in year-over-year foreign exchange gains.

Adjusted EBITDA

Adjusted EBITDA increased by $19.5 million, or 11.7%, from $166.3 million in fiscal 2010 to $185.8 million in fiscal 2011 due to continued revenue growth in the adoption of SMART Board interactive whiteboards and related attachment products. This was offset by a negative foreign exchange impact of approximately $17.7 million as a result of the year-over-year strengthening of the Canadian dollar relative to the U.S. dollar.

22

SMART Technologies Inc. 2011 Annual Report

Equity Incentive Plan

In June 2010, we implemented an Equity Incentive Plan which provides for the grant of options, restricted share units and deferred share units to directors, officers, employees, consultants and service providers of the Company and its subsidiaries. During fiscal 2011, we granted 1,444,500 stock options to purchase an equivalent number of the Company’s Class A Subordinate Voting Shares at a weighted average exercise price of $16.22. Of these options, 1,140,000 were granted on July 15, 2010, in conjunction with our IPO, at an exercise price of $17.00. These options will vest over various periods ranging between three and four years. We expect stock-based compensation in selling, marketing and administration and research and development expenses to be approximately $1.7 million in fiscal 2012 as a result of these issuances.

Participant Equity Loan Plan

In August 2010, the Board of Directors approved a change to the Participant Equity Loan Plan (the “Plan”) whereby 40% of performance-based Class A Subordinate Voting Shares that did not become unrestricted as part of the IPO transaction on July 20, 2010, representing 24% of total shares under the Plan, will become unrestricted in two equal installments on each of the next two anniversary dates of the IPO. This has been treated as a change in the Plan for accounting purposes and we expect stock-based compensation in selling, marketing and administration and research and development expenses will be approximately $5.8 million for fiscal 2012 as a result of this change.

Results of Operations – Fiscal 2010 Compared to Fiscal 2009

Revenue

Revenue for fiscal 2010 increased by $179.8 million, or 38.4%, from $468.2 million in fiscal 2009 to $648.0 million in fiscal 2010. This was due primarily to higher product sales volumes in North America driven by the continued adoption of interactive whiteboard technology and related products in the U.S. education market. Demand for our core products increased as a result of a general expansion of the market for interactive whiteboards and related attachment products. In addition, the education market, which represents an estimated 85% of our revenue base, was aided by various government economic stimulus programs in fiscal 2010 as governments undertook spending initiatives to improve public infrastructure and to help alleviate the effects of the global recession.

Gross Margin

Gross margin for fiscal 2010 increased by $121.5 million from $200.0 million in fiscal 2009 to $321.5 million in fiscal 2010. The gross margin percentage in fiscal 2010 was 49.6% compared to 42.7% in fiscal 2009. The improvement in gross margin as a percentage of revenue reflects the redesign and lower assembly cost of certain key components in our product offering, including interactive whiteboards and integrated projectors, and a general focus on cost reduction in other areas, including logistics and transportation. The increase in gross margin was partially offset by a negative foreign exchange impact of approximately $5.0 million as a result of the year-over-year weakening of the Euro relative to the U.S. dollar, which impacted our revenue, and the strengthening of the Canadian dollar relative to the U.S. dollar, which impacted our cost of sales.

Operating Expenses

Selling, Marketing and Administration Expenses

Selling, marketing and administration expenses increased by $39.1 million, or 39.2%, from $99.7 million in fiscal 2009 to $138.8 million in fiscal 2010. Approximately $12.1 million of the increase related to our expansion into Europe as part of our overall global strategy. Growth in North American employee levels accounted for approximately $4.5 million of the increase. Approximately $5.8 million related to sales and marketing expenses to support additional product offerings and our growing revenue profile and the remaining expenses related to remediation efforts for our enterprise resource planning, or ERP, system and increased expenses for administrative support in finance, information systems and legal required to meet the business growth.

23

SMART Technologies Inc. 2011 Annual Report

Management’s Discussion and Analysis of Financial Condition and Results of Operations(continued)

Research and Development Expenses

Research and development expenses increased by $8.6 million, or 34.4%, from $25.0 million in fiscal 2009 to $33.6 million in fiscal 2010. The increase reflects our continued focus on investing in product development for the education and business markets, including an increase in the number of software developers, engineers and technicians required to support this development.

Depreciation and Amortization

Depreciation and amortization expense increased by $10.1 million, or 174.1%, from $5.8 million in fiscal 2009 to $15.9 million in fiscal 2010. The increase relates to the first full year of depreciation recorded on our new headquarters building which was substantially completed on January 1, 2009, amortization for the information technology infrastructure which was put into place in the new building and amortization of the implemented components of our new ERP system. Because the building was under construction in fiscal 2009, depreciation was recorded only for the fourth quarter of fiscal 2009.

Non-Operating Expenses

Interest Expense

Interest expense declined by $13.7 million, or 17.4%, from $78.6 million in fiscal 2009 to $64.9 million in fiscal 2010. The decrease corresponds with the year-over-year decrease in the U.S. LIBOR rate, which is the rate on which our floating rate term bank debt is based. For example, three-month LIBOR declined from an average of 2.4% in fiscal 2009 to an average of 0.4% in fiscal 2010.

Foreign Exchange Loss (Gain)

Foreign exchange loss (gain) for fiscal 2010 changed by $185.8 million, from a loss of $94.0 million in fiscal 2009 to a gain of $91.8 million in fiscal 2010. These foreign exchange gains and losses primarily resulted from the conversion of our U.S. dollar denominated long-term debt into our functional currency of Canadian dollars. From the end of fiscal 2009 to the end of fiscal 2010, the U.S. dollar weakened by approximately 19.5% against the Canadian dollar from CDN$1.2613 to CDN$1.0158, resulting in an unrealized foreign exchange gain on our U.S. dollar denominated debt of $105.7 million. This gain reversed the loss reported in the same period in 2009 when the U.S. dollar strengthened by approximately 22.9% compared to the Canadian dollar.

Provision for Income Taxes

Income tax expense increased by $14.0 million, from $4.3 million in fiscal 2009 to $18.3 million in fiscal 2010. This was primarily due to an increase in taxable income. Our tax provision is weighted towards Canadian income tax rates as substantially all our taxable income is Canadian-based. In calculating the tax provision we add back the unrealized foreign exchange loss (gain) from the revaluation of the U.S. dollar denominated debt to net income (loss) before income taxes. This is treated as a capital item for income tax purposes. The tax provision also includes investment tax credits for fiscal 2010 and fiscal 2009 of $4.6 million and $3.5 million, respectively.

Net Income (Loss)

Net income increased by $248.6 million from a net loss of $106.6 million in fiscal 2009 to a net income of $142.0 million in fiscal 2010. The primary factors driving the change in net income (loss) were the impact of the volatility of the U.S. dollar relative to the Canadian dollar on our U.S. dollar denominated debt, which resulted in an unrealized foreign exchange gain of $91.8 million in fiscal 2010 compared to a loss of $94.0 million in fiscal 2009. This accounted for $185.8 million of the increase, and continued growth in Adjusted EBITDA accounted for the remainder.

Adjusted EBITDA

Adjusted EBITDA increased by $75.4 million, or 82.9%, from $90.9 million in fiscal 2009 to $166.3 million in fiscal 2010. This was due to continued growth in the adoption of SMART Board interactive whiteboards and related attachment products and the improvement in gross margin.

24

SMART Technologies Inc. 2011 Annual Report

Selected Quarterly Financial Data

The following tables set forth the Company’s unaudited quarterly consolidated results of operations, reconciliation of net income to Adjusted EBITDA and reconciliation to Adjusted Net Income for each of the eight most recent quarters. The information in the table below has been derived from our unaudited interim consolidated financial statements. Our quarterly operating results have varied substantially in the past and may vary substantially in the future. Accordingly, the information below is not necessarily indicative of future results. Data for the periods are indicated in millions of dollars, except for shares, per share amounts, units and average selling prices.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Fiscal Year 2011 | | | Fiscal Year 2010 | |

| | | Fourth

Quarter | | | Third

Quarter | | | Second

Quarter | | | First

Quarter | | | Fourth

Quarter | | | Third

Quarter | | | Second

Quarter | | | First

Quarter | |

Consolidated Statement of Operations | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenue | | $ | 167.3 | | | $ | 180.9 | | | $ | 222.7 | | | $ | 219.2 | | | $ | 155.6 | | | $ | 156.1 | | | $ | 177.8 | | | $ | 158.5 | |

Cost of sales | | | 89.6 | | | | 94.5 | | | | 106.6 | | | | 108.5 | | | | 75.9 | | | | 79.5 | | | | 92.7 | | | | 78.4 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Gross margin | | | 77.7 | | | | 86.4 | | | | 116.1 | | | | 110.7 | | | | 79.7 | | | | 76.6 | | | | 85.1 | | | | 80.1 | |

Operating expenses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Selling, marketing and administration expenses | | | 52.1 | | | | 45.5 | | | | 41.4 | | | | 41.8 | | | | 41.9 | | | | 35.7 | | | | 33.4 | | | | 27.9 | |

Research and development expenses | | | 14.7 | | | | 13.8 | | | | 12.7 | | | | 11.8 | | | | 9.9 | | | | 9.0 | | | | 7.5 | | | | 7.1 | |

Depreciation and amortization | | | 7.9 | | | | 7.2 | | | | 8.1 | | | | 8.6 | | | | 6.7 | | | | 3.9 | | | | 3.0 | | | | 2.3 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating income | | | 3.0 | | | | 19.9 | | | | 53.9 | | | | 48.5 | | | | 21.2 | | | | 28.0 | | | | 41.2 | | | | 42.8 | |

Non-operating expenses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Other (income) loss, net | | | (0.1 | ) | | | (0.1 | ) | | | (0.1 | ) | | | (0.2 | ) | | | (0.2 | ) | | | (0.2 | ) | | | — | | | | 0.2 | |

Interest expense | | | 4.8 | | | | 5.3 | | | | 8.0 | | | | 13.5 | | | | 17.8 | | | | 16.2 | | | | 16.0 | | | | 14.9 | |

Foreign exchange (gain) loss | | | (13.6 | ) | | | (3.2 | ) | | | (14.7 | ) | | | 21.0 | | | | (8.2 | ) | | | (8.7 | ) | | | (38.9 | ) | | | (36.0 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income before income taxes | | | 11.9 | | | | 17.9 | | | | 60.7 | | | | 14.2 | | | | 11.8 | | | | 20.7 | | | | 64.1 | | | | 63.7 | |

Income tax expense | | | 4.3 | | | | 5.4 | | | | 16.4 | | | | 9.2 | | | | 1.3 | | | | 0.8 | | | | 7.4 | | | | 8.8 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 7.6 | | | $ | 12.5 | | | $ | 44.3 | | | $ | 5.0 | | | $ | 10.5 | | | $ | 19.9 | | | $ | 56.7 | | | $ | 54.9 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Certain reclassifications have been made to prior periods’ figures to conform to the current period’s presentation.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Fiscal Year 2011 | | | Fiscal Year 2010 | |

| | | Fourth

Quarter | | | Third

Quarter | | | Second

Quarter | | | First

Quarter | | | Fourth

Quarter | | | Third

Quarter | | | Second

Quarter | | | First

Quarter | |

Adjusted EBITDA | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income | | $ | 7.6 | | | $ | 12.5 | | | $ | 44.3 | | | $ | 5.0 | | | $ | 10.5 | | | $ | 19.9 | | | $ | 56.7 | | | $ | 54.9 | |

Income tax expense | | | 4.3 | | | | 5.4 | | | | 16.4 | | | | 9.2 | | | | 1.3 | | | | 0.8 | | | | 7.4 | | | | 8.8 | |

Depreciation in cost of sales | | | 0.9 | | | | 0.9 | | | | 0.5 | | | | 1.8 | | | | (1.0 | ) | | | 1.1 | | | | 1.0 | | | | 0.9 | |

Depreciation and amortization | | | 7.9 | | | | 7.2 | | | | 8.1 | | | | 8.6 | | | | 6.7 | | | | 3.9 | | | | 3.0 | | | | 2.3 | |

Interest expense | | | 4.8 | | | | 5.3 | | | | 8.0 | | | | 13.5 | | | | 17.8 | | | | 16.2 | | | | 16.0 | | | | 14.9 | |