UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22497

Strategy Shares

(Exact name of registrant as specified in charter)

36 North New York Avenue, Huntington, NY 11743

(Address of principal executive offices) (Zip code)

Citi Fund Services Ohio, Inc., 4400 Easton Commons, Suite 200, Columbus, OH 43219

(Name and address of agent for service)

Registrant’s telephone number, including area code: (855) 477-3837

Date of fiscal year end: April 30

Date of reporting period: April 30, 2023

Item 1. Reports to Stockholders.

![]()

Annual Shareholder Report

Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR)

Strategy Shares Gold-Hedged Bond ETF (GLDB)

Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL)

Strategy Shares Halt Climate Change ETF (NZRO)

Strategy Shares Newfound/Resolve Robust Momentum ETF (ROMO)

April 30, 2023

You may elect to receive shareholder reports in paper free of charge. You can contact your financial intermediary to request that you receive paper copies of your reports. Your election to receive reports in paper will apply to all funds held with your financial intermediary.

![]()

TABLE OF CONTENTS

| Page | ||

| Management’s Discussion of Fund Performance | ||

| Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) | 1 | |

| Strategy Shares Gold-Hedged Bond ETF (GLDB) | 4 | |

| Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL) | 6 | |

| Strategy Shares Halt Climate Change ETF (NZRO) | 9 | |

| Strategy Shares Newfound/ReSolve Robust Momentum ETF (ROMO) | 11 | |

| Expense Examples | 13 | |

| Portfolios of Investments | ||

| Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) | 14 | |

| Strategy Shares Gold-Hedged Bond ETF (GLDB) | 15 | |

| Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL) | 17 | |

| Strategy Shares Halt Climate Change ETF (NZRO) | 18 | |

| Strategy Shares Newfound/ReSolve Robust Momentum ETF (ROMO) | 20 | |

| Statements of Assets and Liabilities | 21 | |

| Statements of Operations | 23 | |

| Statements of Changes in Net Assets | 25 | |

| Financial Highlights | 28 | |

| Notes to Financial Statements | 30 | |

| Report of Independent Registered Public Accounting Firm | 38 | |

| Additional Information | 40 | |

| Trustees and Officers | 44 |

| Strategy Shares Nasdaq 5HANDL™ Index ETF (Unaudited) | April 30, 2023 |

Management’s Discussion of Fund Performance

Dear Shareholder:

Income Investors who focus purely on yield when evaluating potential investments do so at their own risk. Metrics that fail to incorporate risk are not meaningful when used to compare duration-managed bond pools, multi-asset income funds, REITS, MLPS, and high dividend stocks. The HANDLS™ solution uses the teachings of modern portfolio theory to seek to deliver income-oriented investment solutions to investors. By building well-diversified, balanced portfolios of low-cost ETFs and using moderate amounts of leverage to achieve enhanced returns, investors seeking income can seek to minimize the idiosyncratic risk posed by concentrated investments and earn higher risk-adjusted returns.

The Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) seeks investment results that correlate generally, before fees and expenses, to the price and yield performance of the NASDAQ 5 HANDL™ Index, which has the goal but not the guarantee, of achieving a total return sufficient, over time and after expenses, to support a five percent (5.0%) annual distribution rate. Nasdaq HANDLS™ Indexes have risk characteristics similar to the broad US capital markets and can be expected to generally rise and fall with prevailing market conditions. For the fiscal year ended April 30, 2023, FIVR generated a total return of +0.04% at net asset value and -0.15% at market value. During this same period, the Fund’s underlying index, the Nasdaq 5HANDL™ Index, returned +0.74%; the Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index, returned -0.43%.

In order to allow shareholders of the Fund to realize a predictable, but not assured, level of cash flow, FIVR has adopted a policy (which may be modified at any time by its Board of Trustees) to pay monthly distributions on Fund shares at a target rate that represents an annualized payout of approximately 5.0% on the Fund’s per-share net asset value on the date of a distribution’s declaration. For the fiscal year ended April 30, 2023, FIVR paid out total distributions of $1.06 per share between May 2022 and April 2023, during which period the average NAV on the distribution calculation date was $21.18.

To accomplish its objective, HANDLS™ allocates across 19 exchange-traded Funds (“ETFs”) and is split into two components, with a 50% allocation to fixed income and equity ETFs (the “Core Portfolio”) and a 50% allocation to ETFs of 12 asset categories using a proprietary Nasdaq Dorsey Wright algorithm (the “Explore Portfolio”) that have historically provided high levels of income. Because the Index is comprised of securities issued by other investment companies, FIVR operates as a “fund of funds.”

| For the year, the five best performing holdings were: | Category | Return |

| Alerian MLP ETF (AMLP) | US Alternative | 11.32% |

| JPMorgan Equity Premium Income ETF (JEPI) | US Alternative | 5.83% |

| Vanguard Dividend Appreciation ETF (VIG) | US Equity | 4.54% |

| Invesco QQQ Trust Series 1 (QQQ) | US Equity | 3.76% |

| iShares Core S&P 500 ETF (IVV) | US Equity | 2.70% |

| And the five weakest performing holdings were: | Category | Return |

| Schwab U.S. REIT ETF (SCHH) | US Equity | -16.09% |

| Global X US Preferred ETF (PFFD) | US Fixed Income | -2.52% |

| WisdomTree US Efficient Core Fund (NTSX) | US Blend | -1.09% |

| iShares MBS ETF (MBB) | US Fixed Income | -0.76% |

| Vanguard Mortgage-Backed Securities ETF (VMBS) | US Fixed Income | -0.69% |

Annual Shareholder Report | 1

Strategy Shares Nasdaq 5HANDL™ Index ETF (Unaudited) (Continued)

Investors have different risk appetites, but we believe diversification remains the best path to high risk-adjusted returns. The launch of the Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) is a complement to our 7HANDL Index ETF (HNDL). Both the 5HANDL™ and 7HANDL™ ETF seek to deliver high current income using a common, well-diversified portfolio seeking high risk-adjusted returns. The primary difference is that the 5HANDL ETF uses no leverage, pays a lower managed distribution, and, by design, is expected to experience about 23% less volatility over time.

For investors looking to fund their day-to-day lives, we believe HANDLS™ offers a better approach; one that focuses on maximizing risk-adjusted returns and manufacturing a distribution. High managed distribution rates provide an additional benefit to investors by minimizing the need to manage cash reserves and make piecemeal asset sales to finance lifestyle needs.

We are pleased with the Fund’s performance relative to its benchmark and remain convinced that Investors are best served by relying upon diversified portfolios to maximize risk-adjusted returns; even when those market returns are negative.

We appreciate your confidence and thank you for your continued interest in the Fund.

Sincerely,

David Miller and Charles Ashley

Portfolio Manager

Nasdaq 5HANDL™ Index ETF

The views and opinions expressed in management’s discussion of Fund performance are those of Rational Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Rational Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Must be preceded or accompanied by a prospectus.

All investments involve risk, including loss of principal. Past performance is no guarantee of future results. Please see the Fund’s prospectus for specific details regarding investment objectives, risks, performance, and other important information. Review this information carefully before you make any investment decision. Investors cannot invest directly in an index, and unmanaged index returns do not reflect any fees, expenses or sales charges.

The Fund is distributed by Foreside Fund Services, LLC.

2 | Annual Shareholder Report

Strategy Shares Nasdaq 5HANDL™ Index ETF (Unaudited) (Continued)

Investment Objective

Strategy Shares Nasdaq 5HANDL™ Index ETF seeks to achieve investment results that correlate generally, before fees and expenses, to the price and yield performance of the Nasdaq 5HANDL™ Index.

Fund Performance (as of 4/30/23)

| Average Annual Total Returns | Expense Ratios(a) | |||||||

| One Year | Inception(b) | Gross | Net | |||||

| Strategy Shares Nasdaq 5HANDL™ Index ETF - Total Return (at Net Asset Value)(c) | 0.04% | -7.12% | 0.90% | 0.88% | ||||

| Strategy Shares Nasdaq 5HANDL™ Index ETF - Total Return (at Market Value)(d) | -0.15% | -7.17% | 0.90% | 0.88% | ||||

| Nasdaq 5HANDL™ Index | 0.74% | -6.36% | N/A | N/A | ||||

| Bloomberg U.S. Aggregate Bond Index(e) | -0.43% | -7.46% | N/A | N/A | ||||

Hypothetical Growth of a $10,000 Investment (*)

Past performance does not guarantee future results. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The performance data quoted represent past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would be lower. To obtain performance information current to the most recent month-end, please call 855-477-3837 or visit http://strategysharesetfs.com/

| * | The chart represents historical performance of a hypothetical investment of $10,000 in Strategy Shares Nasdaq 5HANDL™ Index ETF and represents the reinvestment of of dividends and capital gains in the Fund. | |

| (a) | The expense ratios reflect the expense ratios as reported in the Fund’s Prospectus dated September 1, 2022. However, the Advisor has agreed to contractual waivers in effect through August 31, 2023 and has agreed to limit total annual fund operating expenses to the net expense ratios shown. Please see the Fund’s most recent prospectus for details. Additional information pertaining to the Fund’s expense ratio as of April 30, 2023 can be found in the Financial Highlights. | |

| (b) | Commencement of operations: December 28, 2021. | |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. | |

| (d) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from the Fund’s listing market (e.g., Nasdaq) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. | |

| (e) | The Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid ARM pass-throughs), asset-backed securities and collateralized mortgage-backed securities (agency and non-agency). An investor cannot invest directly in an index. |

Annual Shareholder Report | 3

| Strategy Shares Gold-Hedged Bond ETF (Unaudited) | April 30, 2023 |

Management’s Discussion of Fund Performance

Dear Shareholder,

The Strategy Shares Gold-Hedged Bond ETF (GLDB) seeks investment results that correlate, before fees and expenses, to the performance of the Solactive Gold-Backed Bond Index (the “Index”). The Fund was designed on the belief that the best way for investors to generate income that maintains its purchasing power is to combine bonds and a gold overlay within one portfolio. The Index seeks to provide 100% exposure to the U.S. dollar-denominated investment grade corporate bond sector (the “Bond Component”) plus a gold inflation hedge with a notional value designed to correspond to the value of the Bond Component, with such notional value reset on a monthly basis (the “Gold Hedge Component”). The Bond Index aims to mirror the performance of investment grade corporate bonds issued in U.S. dollars. The Gold Hedge Index tracks the performance of the near month gold futures contracts listed on the Chicago Mercantile Exchange.

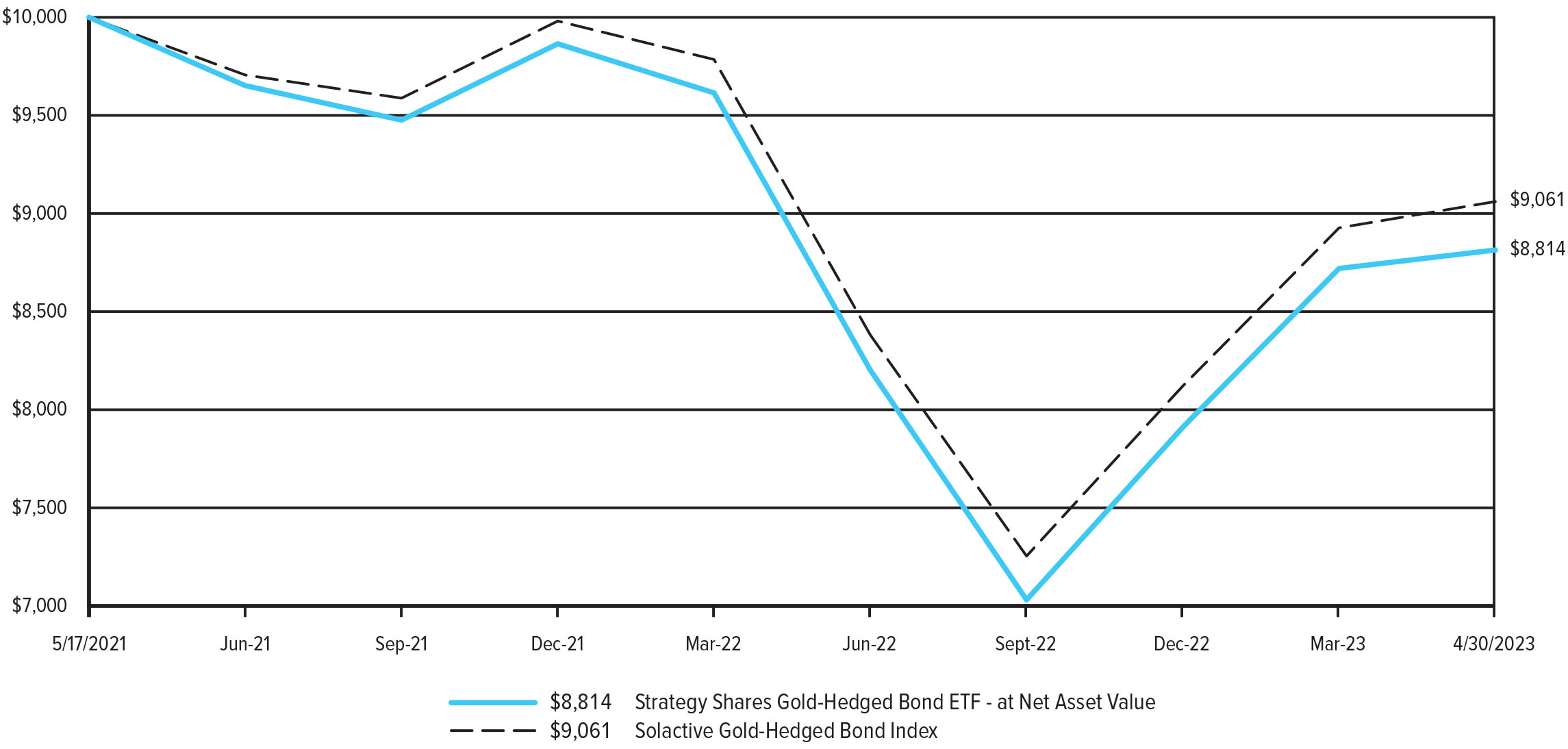

For the fiscal year ended April 30, 2023, GLDB generated a total return of +0.09% at net asset value and -0.79% at market value. During this same period, the Fund’s benchmark and underlying index, the Solactive Gold Backed Bond Index, returned -0.35%.

The Fund’s exposure to gold futures contracts was the primary source of positive contribution during the fiscal year. We continue to believe that an investment in gold can potentially provide a hedge against inflation for a bond. The best performing bonds during the fiscal year were BA 5.15 05/01/30 (CUSIP: 097023CY9, Sector: Industrials), ORCL 5 ⅜ 07/15/40 (CUSIP: 68389XAM7, Sector: Information Technology), ABIBB 4.7 02/01/36 (CUSIP: 03522AAH3, Sector: Consumer Staples), PCG 4.55 07/01/30 (CUSIP: 694308JM0, Sector: Utilities) and GE 5 ⅞ 01/14/38 (CUSIP: 36962G3P7, Sector: Industrials). The worst performing bonds were VZ 4.522 09/15/48 (CUSIP: 92343VCX0, Sector: Communication Services), DOW 3.6 11/15/50 (CUSIP: 260543DD2, Sector: Materials), NTRS 1.95 05/01/30 (CUSIP: 665859AV6, Sector: Financials), RDSALN 6 ⅜ 12/15/38 (CUSIP: 822582AD4, Sector: Energy) and HD 5 ⅞ 12/16/36 (CUSIP: 437076AS1, Sector: Consumer Discretionary).

We appreciate your confidence and continued interest in the Fund.

Sincerely,

David Miller and Charles Ashley

Co-Portfolio Managers

Strategy Shares Gold-Hedged Bond ETF

The views and opinions expressed in management’s discussion of Fund performance are those of Rational Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Rational Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Must be preceded or accompanied by a prospectus.

All investments involve risk, including loss of principal. Past performance is no guarantee of future results. Please see the Fund’s prospectus for specific details regarding investment objectives, risks, performance, and other important information. Review this information carefully before you make any investment decision. Investors cannot invest directly in an index, and unmanaged index returns do not reflect any fees, expenses or sales charges.

The Fund is distributed by Foreside Fund Services, LLC.

4 | Annual Shareholder Report

Strategy Shares Gold-Hedged Bond ETF (Unaudited) (Continued)

Investment Objective

Strategy Shares Gold-Hedged Bond ETF seeks to provide investment returns that correspond, before fees and expenses, to the performance of the Solactive Gold Backed Bond Index.

Fund Performance (as of 4/30/23)

| Average Annual Total Returns | Expense Ratios(a) | |||||||

| One Year | Inception(b) | Gross | Net | |||||

| Strategy Shares Gold-Hedged Bond ETF - Total Return (at Net Asset Value)(c) | 0.09% | -6.26% | 0.79% | 0.79% | ||||

| Strategy Shares Gold-Hedged Bond ETF - Total Return (at Market Value)(d) | -0.79% | -6.26% | 0.79% | 0.79% | ||||

| Solactive Gold-Backed Bond Index(e) | -0.35% | -4.92% | N/A | N/A | ||||

Hypothetical Growth of a $10,000 Investment (*)

Past performance does not guarantee future results. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The performance data quoted represent past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would be lower. To obtain performance information current to the most recent month-end, please call 855-477-3837 or visit http://strategysharesetfs.com/

| * | The chart represents historical performance of a hypothetical investment of $10,000 in Strategy Shares Gold-Hedged Bond ETF and represents the reinvestment of dividends and capital gains in the Fund. | |

| (a) | The expense ratios reflect the expense ratios as reported in the Fund’s Prospectus dated September 1, 2022. Please see the Fund’s most recent prospectus for details. Additional information pertaining to the Fund’s expense ratio as of April 30, 2023 can be found in the Financial Highlights. | |

| (b) | Commencement of operations: May 17, 2021. | |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. | |

| (d) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from the Fund’s listing market (e.g., Cboe) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. | |

| (e) | Solactive Gold-Backed Bond Index replicates the performance of a hypothetical investment in the Investment Grade Corporate Bond Sector, with the return stream denominated in Gold rather than dollars. The index consists of a 1x exposure to the Investment Grade Corporate Bond Sector along with a 1x exposure to the Gold Sector. An investor cannot invest directly in an index. |

Annual Shareholder Report | 5

| Strategy Shares Nasdaq 7HANDL™ Index ETF (Unaudited) | April 30, 2023 |

Management’s Discussion of Fund Performance

Dear Shareholder:

Income Investors who focus purely on yield when evaluating potential investments do so at their own risk. Metrics that fail to incorporate risk are not meaningful when used to compare duration-managed bond pools, multi-asset income funds, REITS, MLPS, and high dividend stocks. The HANDLS™ solution uses the teachings of modern portfolio theory to seek to deliver income-oriented investment solutions to investors. By building well-diversified, balanced portfolios of low-cost ETFs and using moderate amounts of leverage to achieve enhanced returns, investors seeking income can seek to minimize the idiosyncratic risk posed by concentrated investments and earn higher risk-adjusted returns.

The Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL) seeks investment results that correlate generally, before fees and expenses, to the price and yield performance of the NASDAQ 7 HANDL™ Index, which has the goal but not the guarantee, of achieving a total return sufficient, over time and after expenses, to support a seven percent (7.0%) annual distribution rate. Nasdaq HANDLS™ Indexes have risk characteristics similar to the broad US capital markets and can be expected to generally rise and fall with prevailing market conditions. For the fiscal year ended April 30, 2023, HNDL generated a total return of -1.83% at net asset value and -2.19% at market value. During this same period, the Fund’s underlying index, the Nasdaq 7HANDL™ Index, returned ¬-0.37%. The Fund’s benchmark, the Bloomberg U.S. Aggregate Bond Index, returned -0.43%.

In order to allow shareholders of the Fund to realize a predictable, but not assured, level of cash flow, HNDL has adopted a policy (which may be modified at any time by its Board of Trustees) to pay monthly distributions on Fund shares at a target rate that represents an annualized payout of approximately 7.0% on the Fund’s per-share net asset value on the date of a distribution’s declaration. For the fiscal year ended April 30, 2023, HNDL paid out total distributions of $1.44 per share between May 2022 and April 2023, during which period the average NAV on the distribution calculation date was $20.63.

To accomplish its objective, HANDLS™ allocates across 19 exchange-traded Funds (“ETFs”) and is split into two components, with a 50% allocation to fixed income and equity ETFs (the “Core Portfolio”) and a 50% allocation to ETFs of 12 asset categories using a proprietary Nasdaq Dorsey Wright algorithm (the “Explore Portfolio”) that have historically provided high levels of income. Because the Index is comprised of securities issued by other investment companies, HNDL operates as a “fund of funds.”

| For the year, the five best performing holdings were: | Category | Return |

| Alerian MLP ETF (AMLP) | US Alternative | 11.32% |

| JPMorgan Equity Premium Income ETF (JEPI) | US Alternative | 5.83% |

| Vanguard Dividend Appreciation ETF (VIG) | US Equity | 4.54% |

| Invesco QQQ Trust Series 1 (QQQ) | US Equity | 3.76% |

| iShares Core S&P 500 ETF (IVV) | US Equity | 2.70% |

| And the five weakest performing holdings were: | Category | Return |

| Schwab U.S. REIT ETF (SCHH) | US Equity | -16.09% |

| Global X US Preferred ETF (PFFD) | US Fixed Income | -2.52% |

| WisdomTree US Efficient Core Fund (NTSX) | US Blend | -1.09% |

| iShares MBS ETF (MBB) | US Fixed Income | -0.76% |

| Vanguard Mortgage-Backed Securities ETF (VMBS) | US Fixed Income | -0.69% |

6 | Annual Shareholder Report

Strategy Shares Nasdaq 7HANDL™ Index ETF (Unaudited) (Continued)

Investors have different risk appetites, but we believe diversification remains the best path to high risk-adjusted returns. Recently, we launched the Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR), a complement to our 7HANDL Index ETF (HNDL). Both the 5HANDL™ and 7HANDL™ ETF seek to deliver high current income using a common, well-diversified portfolio seeking high risk-adjusted returns. The primary difference is that the 5HANDL ETF uses no leverage, pays a lower managed distribution, and, by design, is expected to experience about 23% less volatility.

For investors looking to fund their day-to-day lives, we believe HANDLS™ offers a better approach; one that focuses on maximizing risk-adjusted returns, and manufacturing a distribution. High managed distribution rates provide an additional benefit to investors by minimizing the need to manage cash reserves and make piecemeal asset sales to finance lifestyle needs.

We are pleased with the Fund’s performance relative to its benchmark and remain convinced that Investors are best served by relying upon diversified portfolios to maximize risk-adjusted returns; even when those market returns are negative.

We appreciate your confidence and thank you for your continued interest in the Fund.

Sincerely,

David Miller and Charles Ashley

Portfolio Manager

Nasdaq 7HANDL™ Index ETF

The views and opinions expressed in management’s discussion of Fund performance are those of Rational Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Rational Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Must be preceded or accompanied by a prospectus.

All investments involve risk, including loss of principal. Past performance is no guarantee of future results. Please see the Fund’s prospectus for specific details regarding investment objectives, risks, performance, and other important information. Review this information carefully before you make any investment decision. Investors cannot invest directly in an index, and unmanaged index returns do not reflect any fees, expenses or sales charges.

The Fund is distributed by Foreside Fund Services, LLC.

Annual Shareholder Report | 7

Strategy Shares Nasdaq 7HANDL™ Index ETF (Unaudited) (Continued)

Investment Objective

Strategy Shares Nasdaq 7HANDL™ Index ETF seeks to achieve investment results that correlate generally, before fees and expenses, to the price and yield performance of the Nasdaq 7HANDL™ Index.

Fund Performance (as of 4/30/23)

| Average Annual Total Returns | Expense Ratios(a) | |||||||||

| One Year | Five Year | Inception(b) | Gross | Net | ||||||

| Strategy Shares Nasdaq 7HANDL™ Index ETF - Total Return (at Net Asset Value)(c) | -1.83% | 3.96% | 3.15% | 0.98% | 0.98% | |||||

| Strategy Shares Nasdaq 7HANDL™ Index ETF - Total Return (at Market Value)(d) | -2.19% | 3.87% | 3.11% | 0.98% | 0.98% | |||||

| Nasdaq 7HANDL™ Index | -0.37% | 5.43% | 4.62% | N/A | N/A | |||||

| Bloomberg U.S. Aggregate Bond Index(e) | -0.43% | 1.18% | 0.78% | N/A | N/A | |||||

Hypothetical Growth of a $10,000 Investment (*)

Past performance does not guarantee future results. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The performance data quoted represent past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would be lower. To obtain performance information current to the most recent month-end, please call 855-477-3837 or visit http://strategysharesetfs.com/

| * | The chart represents historical performance of a hypothetical investment of $10,000 in Strategy Shares Nasdaq 7HANDL™ Index ETF and represents the reinvestment of dividends and capital gains in the Fund. | |

| (a) | The expense ratios reflect the expense ratios as reported in the Fund’s Prospectus dated September 1, 2022. However, the Advisor has agreed to contractual waivers in effect through August 31, 2023 and has agreed to limit total annual fund operating expenses to the net expense ratios shown. Please see the Fund’s most recent prospectus for details. Additional information pertaining to the Fund’s expense ratio as of April 30, 2023 can be found in the Financial Highlights. | |

| (b) | Commencement of operations: January 16, 2018. | |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. | |

| (d) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from the Fund’s listing market (e.g., Nasdaq) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. | |

| (e) | The Bloomberg U.S. Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. This includes Treasuries, government-related and corporate securities, mortgage-backed securities (agency fixed-rate and hybrid ARM pass-throughs), asset-backed securities and collateralized mortgage-backed securities (agency and non-agency). An investor cannot invest directly in an index. |

8 | Annual Shareholder Report

| Strategy Shares Halt Climate Change ETF (Unaudited) | April 30, 2023 |

Management’s Discussion of Fund Performance

Dear Shareholder,

The Strategy Shares Halt Climate Change ETF invests in companies that, in our view, are committed to curbing or mitigating the deleterious effects of climate change. Strategy Shares invests profits into private initiatives focused on halting and reversing the impact of climate change on behalf of the Fund. The Fund invests in the equity securities of climate conscious and environmentally friendly companies with clear sustainability goals. We believe that investing in an ETF that not only screens for climate conscious companies but also takes an active approach in reversing climate change through outside initiatives is an important way to help in the fight for carbon neutrality.

For the fiscal year ended April 30, 2023, NZRO generated a total return of -0.82% at net asset value and -3.66% at market value. During this same period, the Fund’s benchmark, the Russell 3000 Index, returned +1.50%. During the period, the Fund maintained a large exposure to Information Technology and Health Care companies. The Fund’s overweight exposure to Industrials and underweight exposure to Energy, because of the Fund’s objective, contributed to the underperformance relative to the benchmark.

The Fund’s exposure to alternative energy and information technology equities was the primary source of positive performance during the fiscal year. We continue to remain allocated to a wide range of companies with direct net zero commitments that meet our rigorous green criteria. The best performing holdings were Array Technologies Inc (Ticker: ARRY, Sector: Industrials), First Solar Inc (Ticker: FSLR, Sector: Information Technology), Maxeon Solar Technologies Ltd (Ticker: MAXN, Sector: Information Technology), Shoals Technologies Group Inc (Ticker: SHLS, Sector: Industrials) and Fluence Energy Inc (Ticker: FLNC, Sector: Industrials). The worst performing holdings were Arcimoto Inc (Ticker: FUV, Sector: Consumer Discretionary), Nikola Corp (Ticker: NKLA, Sector: Industrials), Canoo Inc (Ticker: GOEV, Sector: Consumer Discretionary), Aemetis Inc (Ticker: AMTX, Sector: Energy) and Enviva Inc (Ticker: EVA, Sector: Energy).

We are optimistic regarding the potential for future performance of our portfolio, as we believe our investments in companies that are working to be active leaders in the fight against climate change are well-positioned for the future. We appreciate your confidence and continued interest in the Fund.

Sincerely,

David Miller and Charles Ashley

Portfolio Managers

Strategy Shares Halt Climate Change ETF

The views and opinions expressed in management’s discussion of Fund performance are those of Rational Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Rational Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Must be preceded or accompanied by a prospectus.

All investments involve risk, including loss of principal. Past performance is no guarantee of future results. Please see the Fund’s prospectus for specific details regarding investment objectives, risks, performance, and other important information. Review this information carefully before you make any investment decision. Investors cannot invest directly in an index, and unmanaged index returns do not reflect any fees, expenses or sales charges.

The Fund is distributed by Foreside Fund Services, LLC.

Annual Shareholder Report | 9

Strategy Shares Halt Climate Change ETF (Unaudited) (Continued)

Investment Objective

Strategy Shares Halt Climate Change ETF seeks long-term capital appreciation.

Fund Performance (as of 4/30/23)

| Average Annual Total Returns | Expense Ratios(a) | |||||||

| One Year | Inception(b) | Gross | Net | |||||

| Strategy Shares Halt Climate Change ETF - Total Return (at Net Asset Value)(c) | -0.82% | -12.66% | 0.95% | 0.95% | ||||

| Strategy Shares Halt Climate Change ETF - Total Return (at Market Value)(d) | -3.66% | -12.71% | 0.95% | 0.95% | ||||

| Russell 3000 Index(e) | 1.50% | -8.08% | N/A | N/A | ||||

Hypothetical Growth of a $10,000 Investment (*)

Past performance does not guarantee future results. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The performance data quoted represent past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would be lower. To obtain performance information current to the most recent month-end, please call 855-477-3837 or visit http://strategysharesetfs.com/

| * | The chart represents historical performance of a hypothetical investment of $10,000 in Strategy Shares Halt Climate Change ETF and represents the reinvestment of dividends and capital gains in the Fund. | |

| (a) | The expense ratios reflect the expense ratios as reported in the Fund’s Prospectus dated September 1, 2022. Please see the Fund’s most recent prospectus for details. Additional information pertaining to the Fund’s expense ratio as of April 30, 2023 can be found in the Financial Highlights. | |

| (b) | Commencement of operations: January 10, 2022. | |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. | |

| (d) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from the Fund’s listing market (e.g., Nasdaq) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. | |

| (e) | The Russell 3000 Index is a market-capitalization-weighted equity index maintained by FTSE Russell that provides exposure to the entire U.S. stock market. The index tracks the performance of the 3,000 largest U.S.-traded stocks, which represent about 97% of all U.S.-incorporated equity securities. An investor cannot invest directly in an index. |

10 | Annual Shareholder Report

| Strategy Shares Newfound/ReSolve Robust Momentum ETF (Unaudited) | April 30, 2023 |

Management’s Discussion of Fund Performance

Dear Shareholder,

The Strategy Shares Newfound/ReSolve Robust Momentum ETF (ROMO) seeks to provide investment returns that correspond, before fees and expenses, to the performance of the Newfound/ReSolve Robust Equity Momentum Index. The Index generally consists of exchange traded funds (ETFs) that track regional equity indices, representative of U.S. equities, developed international equities and emerging market equities, as well as ETFs that track U.S. Treasury market indices. Because the Index is comprised of securities issued by other investment companies, ROMO operates as a “fund of funds.”

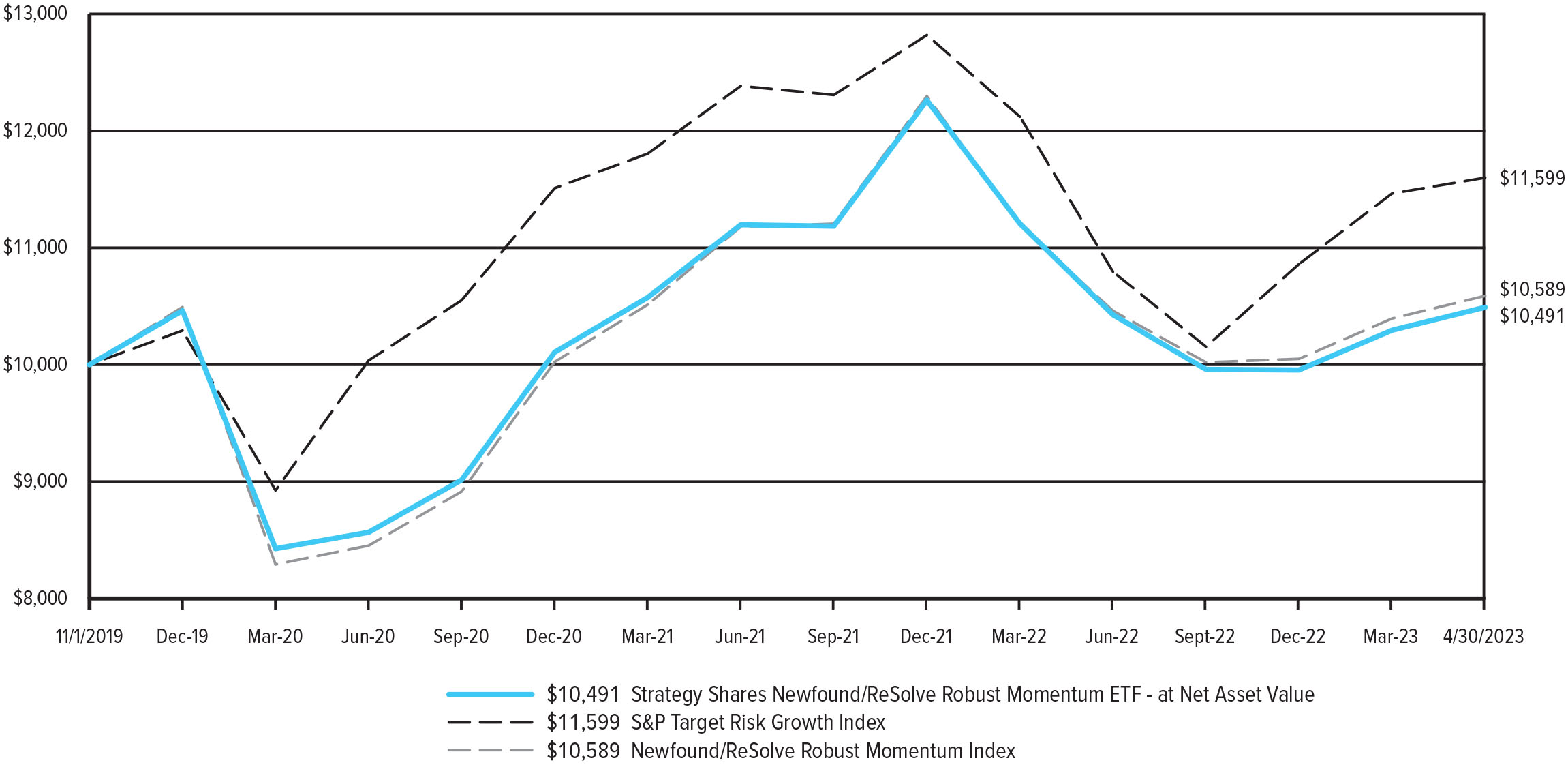

For the fiscal year ended April 30, 2023, ROMO generated a total return of -0.89% at net asset value and -1.04% at market value. During this same period, the Fund’s underlying index, the Newfound/ReSolve Robust Equity Momentum Index, returned -0.09% and the Fund’s benchmark, the S&P Target Risk Growth Index, returned +1.99%.

The Fund’s exposure to intermediate-term US treasury ETFs was the primary source of underperformance relative to its benchmark during the fiscal year. The negative trend in the equity markets for most of the trailing year positioned the Fund with a heavier allocation to treasury ETFs and limited the Fund’s allocations to equity ETFs. The best performing holdings were iShares Core MSCI EAFE ETF (Ticker: IEFA, Category: International Equity), iShares Core S&P 500 ETF (Ticker: IVV, Category: US Equity) and iShares 1-3 Year Treasury Bond ETF (Ticker: SHY, Category: US Fixed Income). The worst performing holding was iShares 7-10 Year Treasury Bond ETF (Ticker: IEF, Category: US Fixed Income).

We are pleased with the performance of the Fund and its underlying index. We appreciate your confidence and continued interest in the Fund.

Sincerely,

David Miller & Charles Ashley

Co-Portfolio Managers

Strategy Shares Newfound/ReSolve Robust Momentum ETF

The views and opinions expressed in management’s discussion of Fund performance are those of Rational Advisers, Inc. and its affiliates. These views and opinions are subject to change at any time based on factors such as market and economic conditions. These views and opinions may not be relied upon as investment advice or recommendations, or as an offer for a particular security. The information is not a complete analysis of every aspect of any market, country, industry, security or the Fund. Statements of fact are from sources considered reliable, but Rational Advisers, Inc. makes no representation or warranty as to their completeness or accuracy. Although historical performance is no guarantee of future results, these insights may help you understand our investment management philosophy.

Must be preceded or accompanied by a prospectus.

All investments involve risk, including loss of principal. Past performance is no guarantee of future results. Please see the Fund’s prospectus for specific details regarding investment objectives, risks, performance, and other important information. Review this information carefully before you make any investment decision. Investors cannot invest directly in an index, and unmanaged index returns do not reflect any fees, expenses or sales charges.

The Fund is distributed by Foreside Fund Services, LLC.

Annual Shareholder Report | 11

Strategy Shares Newfound/ReSolve Robust Momentum ETF (Unaudited) (Continued)

Investment Objective

Strategy Shares Newfound/ReSolve Robust Momentum ETF seeks to provide investment returns that correspond, before fees and expenses, to the performance of the Newfound/ReSolve Robust Equity Momentum Index.

Fund Performance (as of 4/30/23)

| Average Annual Total Returns | Expense Ratios(a) | |||||||

| One Year | Inception(b) | Gross | Net | |||||

| Strategy Shares Newfound/ReSolve Robust Momentum ETF - Total Return (at Net Asset Value)(c) | -0.89% | 1.38% | 0.94% | 0.87% | ||||

| Strategy Shares Newfound/ReSolve Robust Momentum ETF - Total Return (at Market Value)(d) | -1.04% | 1.37% | 0.94% | 0.87% | ||||

| Newfound/ReSolve Robust Equity Momentum Index | -0.09% | 1.65% | N/A | N/A | ||||

| S&P Target Risk Growth Index(e) | 1.99% | 4.34% | N/A | N/A | ||||

Hypothetical Growth of a $10,000 Investment (*)

Past performance does not guarantee future results. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on Fund distributions or on the redemption of Fund shares. The performance data quoted represent past performance and current returns may be lower or higher. The investment return and principal value will fluctuate so that an investor’s shares, when redeemed may be worth more or less than the original cost. The performance above reflects any fee reductions during the applicable periods. If such fee reductions had not occurred, the quoted performance would be lower. To obtain performance information current to the most recent month-end, please call 855-477-3837 or visit http://strategysharesetfs.com/

| * | The chart represents historical performance of a hypothetical investment of $10,000 in Strategy Shares Newfound/ReSolve Robust Momentum ETF and represents the reinvestment of dividends and capital gains in the Fund. | |

| (a) | The expense ratios reflect the expense ratios as reported in the Fund’s Prospectus dated September 1, 2022. However, the Advisor has agreed to contractual waivers in effect through August 31, 2023 and has agreed to limit total annual fund operating expenses to the net expense ratios shown. Please see the Fund’s most recent prospectus for details. Additional information pertaining to the Fund’s expense ratio as of April 30, 2023 can be found in the Financial Highlights. | |

| (b) | Commencement of operations: November 1, 2019. | |

| (c) | Net asset value total return is calculated assuming an initial investment made at the net asset value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at net asset value. This percentage is not an indication of the performance of a shareholder’s investment in the Fund based on market value due to differences between the market price of the shares and the net asset value per share of the Fund. | |

| (d) | Market value total return is calculated assuming an initial investment made at the market value at the beginning of the period, reinvestment of all distributions, including dividends and return of capital, at net asset value during the period, if any, and redemption on the last day of the period at market value. Market value is determined by the composite closing price. Composite closing security price is defined as the last reported sale price from the Fund’s listing market (e.g., Cboe) or participating regional exchanges or markets. The composite closing price is the last reported sale price from any of the eligible sources, regardless of volume and not an average price and may have occurred on a date prior to the close of the reporting period. Market value may be greater or less than net asset value, depending on the Fund’s closing price on the listing market. | |

| (e) | The S&P Target Risk Growth Index is designed to measure the performance of equity allocations, while seeking to provide limited fixed income exposure to diversify risk. An investor cannot invest directly in an index. |

12 | Annual Shareholder Report

| Expense Examples (Unaudited) | April 30, 2023 |

As a Fund shareholder, you may incur two types of costs: (1) transaction costs, including commissions on trading, as applicable; and (2) ongoing costs, including advisory fees and other Fund expenses. These examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The expense examples below are based on an investment of $1,000 invested at November 1, 2022 and held through the period ended April 30, 2023.

The Actual Expense figures in the table below provide information about actual account values and actual expenses. You may use this information, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the table under the heading entitled “Actual Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

The Hypothetical Expense figures in the table below provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in your Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the examples are useful in comparing ongoing costs only and will not help you determine the relative total cost of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Fund | Beginning Account Value 11/1/22 | Actual Ending Account Value 4/30/23 | Hypothetical Value | Actual Expenses Paid During the Period(2) | Hypothetical Expenses Paid During the Period(1)(2) | Annualized Net Expense Ratio During the Period | ||||||

| Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) | $1,000.00 | $1,062.80 | $1,021.27 | $3.63 | $3.56 | 0.71% | ||||||

| Strategy Shares Gold-Hedged Bond ETF (GLDB) | 1,000.00 | 1,286.60 | 1,020.88 | 4.48 | 3.96 | 0.79% | ||||||

| Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL) | 1,000.00 | 1,071.10 | 1,020.88 | 4.06 | 3.96 | 0.79% | ||||||

| Strategy Shares Halt Climate Change ETF (NZRO) | 1,000.00 | 996.70 | 1,020.08 | 4.70 | 4.76 | 0.95% | ||||||

| Strategy Shares Newfound/ReSolve Robust Momentum ETF (ROMO) | 1,000.00 | 1,057.60 | 1,021.03 | 3.88 | 3.81 | 0.76% |

| (1) | Represents the hypothetical 5% annual return before expenses. | |

| (2) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period multiplied by 181/365 (to reflect the one half year period). |

Annual Shareholder Report | 13

| Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) | April 30, 2023 |

Portfolio of Investments Summary Table

| Percentage of Value | |||

| Exchange-Traded Funds | 100.0% | ||

| Total | 100.0% | ||

Portfolio holdings and allocations are subject to change. As of April 30, 2023, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth in the following Portfolio of Investments which are computed using the Fund’s total net assets.

Portfolio of Investments

| Shares | Value | |||||||

| Exchange-Traded Funds — 99.7% | ||||||||

| 4,180 | Alerian MLP ETF | $ | 164,065 | |||||

| 948 | Dimensional Core Fixed Income ETF | 40,404 | ||||||

| 3,380 | Fidelity MSCI Utilities Index ETF | 150,376 | ||||||

| 4,744 | Global X U.S. Preferred ETF | 94,548 | ||||||

| 488 | Invesco QQQ Trust | 157,409 | ||||||

| 1,000 | Invesco Taxable Municipal Bond ETF | 27,030 | ||||||

| 1,512 | iShares Broad USD High Yield Corporate Bond ETF | 53,585 | ||||||

| 124 | iShares Core S&P 500 ETF | 51,790 | ||||||

| 2,460 | iShares Core U.S. Aggregate Bond ETF | 245,902 | ||||||

| 140 | iShares MBS ETF | 13,283 | ||||||

| 2,220 | JPMorgan Equity Premium Income ETF | 122,988 | ||||||

| 5,220 | Schwab U.S. Aggregate Bond ETF | 245,653 | ||||||

| 1,084 | Schwab U.S. Large-Cap ETF | 53,105 | ||||||

| 4,144 | Schwab U.S. REIT ETF | 80,974 | ||||||

| 872 | Vanguard Dividend Appreciation ETF | 137,401 | ||||||

| 836 | Vanguard Intermediate-Term Corporate Bond ETF | 67,340 | ||||||

| 136 | Vanguard S&P 500 ETF | 51,959 | ||||||

| 3,320 | Vanguard Total Bond Market ETF | 245,946 | ||||||

| 3,072 | WisdomTree U.S. Efficient Core Fund | 109,117 | ||||||

| Total Exchange-Traded Funds (Cost $2,224,581) | $ | 2,112,875 | ||||||

| Total Investments — 99.7% (Cost $2,224,581) | $ | 2,112,875 | ||||||

| Other Assets less Liabilities — 0.3% | 5,684 | |||||||

| Net Assets — 100.0% | $ | 2,118,559 | ||||||

ETF — Exchange-Traded Fund

MBS — Mortgage-Backed Security

MLP — Master Limited Partnership

REIT — Real Estate Investment Trust

S&P — Standard and Poor’s

USD — United States Dollar

(See notes which are an integral part of the Financial Statements)

14 | Annual Shareholder Report

| Strategy Shares Gold-Hedged Bond ETF (GLDB) | April 30, 2023 |

Portfolio of Investments Summary Table

| Percentage of Value | |||

| Communication Services | 11.2% | ||

| Consumer Discretionary | 6.1% | ||

| Consumer Staples | 12.8% | ||

| Energy | 5.2% | ||

| Financials | 26.4% | ||

| Health Care | 8.5% | ||

| Industrials | 8.5% | ||

| Information Technology | 8.3% | ||

| Materials | 3.1% | ||

| Real Estate | 3.8% | ||

| Utilities | 6.1% | ||

| Total | 100.0% | ||

Portfolio holdings and allocations are subject to change. As of April 30, 2023, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth in the following Portfolio of Investments which are computed using the Fund’s total net assets.

Portfolio of Investments*

| Principal Amount | Value | |||||||

| Corporate Bonds — 74.9% | ||||||||

| Communication Services — 6.3% | ||||||||

| $ | 532,000 | Verizon Communications, Inc., 4.52%, 9/15/48 | $ | 480,921 | ||||

| 504,000 | Walt Disney Co. (The), 2.65%, 1/13/31 | 446,751 | ||||||

| 927,672 | ||||||||

| Consumer Discretionary — 4.9% | ||||||||

| 448,000 | Amazon.com, Inc., 1.50%, 6/03/30 | 374,471 | ||||||

| 308,000 | Home Depot, Inc. (The), 5.88%, 12/16/36 | 347,399 | ||||||

| 721,870 | ||||||||

| Consumer Staples — 10.2% | ||||||||

| 476,000 | Anheuser-Busch Companies LLC / Anheuser-Busch InBev Worldwide, Inc., 4.70%, 2/01/36 | 478,893 | ||||||

| 392,000 | BAT Capital Corp., 3.56%, 8/15/27 | 366,850 | ||||||

| 420,000 | Coca-Cola Co. (The), 1.38%, 3/15/31 | 344,357 | ||||||

| 364,000 | Costco Wholesale Corp., 1.60%, 4/20/30 | 309,614 | ||||||

| 1,499,714 | ||||||||

| Energy — 4.1% | ||||||||

| 364,000 | Chevron Corp., 2.24%, 5/11/30 | 324,484 | ||||||

| 336,000 | MPLX LP, 2.65%, 8/15/30 | 287,083 | ||||||

| 611,567 | ||||||||

| Financials — 18.6% | ||||||||

| 140,000 | Capital One Financial Corp., 3.80%, 1/31/28 | 130,777 | ||||||

| 476,000 | Citigroup, Inc., 4.41%, 3/31/31 | 454,453 | ||||||

| 364,000 | Fiserv, Inc., 3.50%, 7/01/29 | 339,041 | ||||||

| 504,000 | Goldman Sachs Group, Inc. (The), 1.99%, 1/27/32 | 403,534 | ||||||

| 448,000 | JPMorgan Chase & Co., 4.49%, 3/24/31 | 436,466 | ||||||

| 392,000 | MetLife, Inc., 4.55%, 3/23/30 | 392,873 | ||||||

| 168,000 | Northern Trust Corp., 1.95%, 5/01/30 | 142,104 | ||||||

| 476,000 | Wells Fargo & Co., 3.00%, 10/23/26 | 447,958 | ||||||

| 2,747,206 | ||||||||

| Principal Amount | Value | |||||||

| Health Care — 6.8% | ||||||||

| $ | 392,000 | AbbVie, Inc., 3.20%, 11/21/29 | $ | 362,238 | ||||

| 308,000 | Amgen, Inc., 2.20%, 2/21/27 | 284,947 | ||||||

| 364,000 | CVS Health Corp., 4.30%, 3/25/28 | 359,543 | ||||||

| 1,006,728 | ||||||||

| Industrials — 6.9% | ||||||||

| 392,000 | Boeing Co. (The), 5.15%, 5/01/30 | 395,017 | ||||||

| 280,000 | General Electric Co., 5.88%, 1/14/38 | 306,847 | ||||||

| 308,000 | Southwest Airlines Co., 5.13%, 6/15/27 | 310,491 | ||||||

| 1,012,355 | ||||||||

| Information Technology — 6.6% | ||||||||

| 336,000 | Apple, Inc., 3.35%, 2/09/27 | 328,335 | ||||||

| 336,000 | Broadcom Corp. / Broadcom Cayman Finance, Ltd., 3.88%, 1/15/27 | 326,463 | ||||||

| 336,000 | Oracle Corp., 5.38%, 7/15/40 | 323,695 | ||||||

| 978,493 | ||||||||

| Materials — 2.5% | ||||||||

| 252,000 | Dow Chemical Co. (The), 3.60%, 11/15/50 | 192,029 | ||||||

| 196,000 | Sherwin-Williams Co. (The), 2.95%, 8/15/29 | 177,278 | ||||||

| 369,307 | ||||||||

| Real Estate — 3.1% | ||||||||

| 504,000 | Equinix, Inc., 3.20%, 11/18/29 | 452,681 | ||||||

| Utilities — 4.9% | ||||||||

| 448,000 | NextEra Energy Capital Holdings, Inc., 2.25%, 6/01/30 | 380,274 | ||||||

| 364,000 | Pacific Gas and Electric Co., 4.55%, 7/01/30 | 338,272 | ||||||

| 718,546 | ||||||||

| Total Corporate Bonds (Cost $11,589,683) | $ | 11,046,139 | ||||||

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report | 15

| Strategy Shares Gold-Hedged Bond ETF (GLDB) (Continued) | April 30, 2023 |

| Principal Amount | Value | |||||||

| Yankee Dollars — 5.1% | ||||||||

| Communication Services — 2.7% | ||||||||

| $ | 308,000 | Orange SA, 9.00%, 3/01/31 | $ | 388,902 | ||||

| Financials — 2.4% | ||||||||

| 308,000 | Shell International Finance BV, 6.38%, 12/15/38 | 358,629 | ||||||

| Total Yankee Dollars (Cost $796,172) | $ | 747,531 | ||||||

| Total Investments — 80.0% | ||||||||

| (Cost $12,385,855) | $ | 11,793,670 | ||||||

| Other Assets less Liabilities — 20.0% | 2,953,043 | |||||||

| Net Assets — 100.0% | $ | 14,746,713 | ||||||

| * | Portfolio of Investments is presented on a consolidated basis. See Note 2.A. in the Notes to Financial Statements. |

LLC — Limited Liability Corporation

LP — Limited Partnership

Total Return Swap Agreements

| Pay/ Receive | Financing Rate | Description | Counterparty | Payment Frequency | Expiration Date | Notional Amount | Value and Unrealized Appreciation/ (Depreciation) | |||||||||||

| Receive | Effective Federal Funds Rate(a) + 85 bps | iShares Gold Trust | BNP Paribas SA | Monthly | 5/23/23 | $ | 15,594,370 | $ | (64,801 | ) | ||||||||

| Receive | Effective Federal Funds Rate(a) + 85 bps | iShares IBoxx $ Investment Grade Corporate Bond | BNP Paribas SA | Monthly | 5/23/23 | 2,598,304 | 29,149 | |||||||||||

| $ | (35,652 | ) | ||||||||||||||||

| (a) | The Effective Federal Funds Rate at April 30, 2023 was 4.83%. |

SA — Societe Anonyme (French public limited company)

The derivative instruments outstanding as of April 30, 2023, as disclosed in the Portfolio of Investments and the amounts of realized and changes in unrealized gains and losses on swaps during the period as disclosed in the Statements of Operations serve as indicators of the volume of derivative activity for the Fund.

(See notes which are an integral part of the Financial Statements)

16 | Annual Shareholder Report

| Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL) | April 30, 2023 |

Portfolio of Investments Summary Table

| Percentage of Value | |||

| Exchange-Traded Funds | 100.0% | ||

| Total | 100.0% | ||

Portfolio holdings and allocations are subject to change. As of April 30, 2023, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth in the following Portfolio of Investments which are computed using the Fund’s total net assets.

Portfolio of Investments

| Shares | Value | |||||||

| Exchange-Traded Funds — 89.8% | ||||||||

| 1,915,263 | Alerian MLP ETF | $ | 75,174,073 | |||||

| 434,805 | Dimensional Core Fixed Income ETF | 18,531,389 | ||||||

| 1,548,330 | Fidelity MSCI Utilities Index ETF | 68,885,202 | ||||||

| 2,176,146 | Global X U.S. Preferred ETF | 43,370,590 | ||||||

| 224,826 | Invesco QQQ Trust | 72,519,875 | ||||||

| 458,136 | Invesco Taxable Municipal Bond ETF | 12,383,416 | ||||||

| 693,567 | iShares Broad USD High Yield Corporate Bond ETF | 24,580,014 | ||||||

| 57,267 | iShares Core S&P 500 ETF | 23,918,135 | ||||||

| 1,126,251 | iShares Core U.S. Aggregate Bond ETF | 112,580,050 | ||||||

| 63,630 | iShares MBS ETF | 6,037,214 | ||||||

| 1,015,959 | JPMorgan Equity Premium Income ETF | 56,284,129 | ||||||

| 2,392,488 | Schwab U.S. Aggregate Bond ETF | 112,590,485 | ||||||

| 496,314 | Schwab U.S. Large-Cap ETF | 24,314,423 | ||||||

| 1,898,295 | Schwab U.S. REIT ETF | 37,092,684 | ||||||

| 400,869 | Vanguard Dividend Appreciation ETF | 63,164,928 | ||||||

| 383,901 | Vanguard Intermediate-Term Corporate Bond ETF | 30,923,226 | ||||||

| 63,630 | Vanguard S&P 500 ETF | 24,309,842 | ||||||

| 1,520,757 | Vanguard Total Bond Market ETF | 112,657,678 | ||||||

| 1,408,344 | WisdomTree U.S. Efficient Core Fund | 50,024,379 | ||||||

| Total Exchange-Traded Funds (Cost $1,031,232,135) | $ | 969,341,732 | ||||||

| Total Investments — 89.8% (Cost $1,031,232,135) | $ | 969,341,732 | ||||||

| Other Assets less Liabilities — 10.2% | 110,099,716 | |||||||

| Net Assets — 100.0% | $ | 1,079,441,448 | ||||||

ETF — Exchange-Traded Fund

MBS — Mortgage-Backed Security

MLP — Master Limited Partnership

REIT — Real Estate Investment Trust

S&P — Standard and Poor’s

USD — United States Dollar

Total Return Swap Agreements

| Pay/ Receive | Financing Rate | Description | Counterparty | Payment Frequency | Expiration Date | Notional Amount | Value and Unrealized Appreciation/ (Depreciation) | |||||||||||

| Receive | Effective Federal Funds Rate(a) + 85 bps | Nasdaq 7HANDL™ Index | BNP Paribas SA | Monthly | 1/12/24 | $ | 428,246,945 | $ | 1,225,053 | |||||||||

| (a) | The Effective Federal Funds Rate at April 30, 2023 was 4.83%. |

SA — Societe Anonyme (French public limited company)

The derivative instruments outstanding as of April 30, 2023, as disclosed in the Portfolio of Investments and the amounts of realized and changes in unrealized gains and losses on swaps during the period as disclosed in the Statements of Operations serve as indicators of the volume of derivative activity for the Fund.

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report | 17

| Strategy Shares Halt Climate Change ETF (NZRO) | April 30, 2023 |

Portfolio of Investments Summary Table

| Percentage of Value | |||

| Communication Services | 6.0% | ||

| Consumer Discretionary | 2.2% | ||

| Consumer Staples | 4.5% | ||

| Energy | 0.3% | ||

| Financials | 6.3% | ||

| Health Care | 24.6% | ||

| Industrials | 15.8% | ||

| Information Technology | 28.5% | ||

| Materials | 1.9% | ||

| Real Estate | 0.6% | ||

| Utilities | 9.3% | ||

| Total | 100.0% | ||

Portfolio holdings and allocations are subject to change. As of April 30, 2023, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth in the following Portfolio of Investments which are computed using the Fund’s total net assets.

Portfolio of Investments

| Shares | Value | |||||||

| Common Stocks — 96.1% | ||||||||

| Communication Services — 5.9% | ||||||||

| 200 | Alphabet, Inc., Class C † | $ | 21,644 | |||||

| 98 | Meta Platforms, Inc., Class A † | 23,551 | ||||||

| 46 | Netflix, Inc. † | 15,177 | ||||||

| 60,372 | ||||||||

| Consumer Discretionary — 2.1% | ||||||||

| 6 | Arcimoto, Inc. † | 9 | ||||||

| 1,366 | Canoo, Inc. † | 1,031 | ||||||

| 590 | Fisker, Inc. † | 3,800 | ||||||

| 96 | Tesla, Inc. † | 15,774 | ||||||

| 910 | Workhorse Group, Inc. † | 857 | ||||||

| 21,471 | ||||||||

| Consumer Staples — 4.3% | ||||||||

| 126 | Beyond Meat, Inc. † | 1,706 | ||||||

| 88 | Ingredion, Inc. | 9,343 | ||||||

| 90 | McCormick & Co., Inc. | 7,907 | ||||||

| 476 | Unilever PLC ADR | 26,432 | ||||||

| 45,388 | ||||||||

| Energy — 0.3% | ||||||||

| 278 | Aemetis, Inc. † | 617 | ||||||

| 120 | Enviva, Inc. | 2,580 | ||||||

| 3,197 | ||||||||

| Financials — 6.1% | ||||||||

| 180 | Hannon Armstrong Sustainable Infrastructure Capital, Inc. | 5,108 | ||||||

| 68 | Mastercard, Inc., Class A | 25,842 | ||||||

| 10 | MSCI, Inc. | 4,825 | ||||||

| 116 | Visa, Inc., Class A | 26,997 | ||||||

| 62,772 | ||||||||

| Health Care — 23.6% | ||||||||

| 188 | Abbott Laboratories | 20,768 | ||||||

| 188 | AbbVie, Inc. | 28,411 | ||||||

| 112 | Amgen, Inc. | 26,851 | ||||||

| 102 | Baxter International, Inc. | 4,863 | ||||||

| 126 | Beam Therapeutics, Inc. † | 3,869 | ||||||

| 404 | Boston Scientific Corp. † | 21,057 | ||||||

| Shares | Value | |||||||

| Common Stocks — (Continued) | ||||||||

| Health Care — (Continued) | ||||||||

| 140 | Edwards Lifesciences Corp. † | $ | 12,317 | |||||

| 240 | Gilead Sciences, Inc. | 19,730 | ||||||

| 66 | IQVIA Holdings, Inc. † | 12,424 | ||||||

| 118 | Moderna, Inc. † | 15,681 | ||||||

| 460 | Pfizer, Inc. | 17,889 | ||||||

| 72 | The Cigna Group | 18,237 | ||||||

| 56 | UnitedHealth Group, Inc. | 27,557 | ||||||

| 26 | Waters Corp. † | 7,809 | ||||||

| 22 | West Pharmaceutical Services, Inc. | 7,947 | ||||||

| 245,410 | ||||||||

| Industrials — 15.1% | ||||||||

| 128 | Ameresco, Inc., Class A † | 5,325 | ||||||

| 254 | Aris Water Solution, Inc., Class A | 1,847 | ||||||

| 618 | Array Technologies, Inc. † | 12,639 | ||||||

| 748 | Ballard Power Systems, Inc. † | 3,306 | ||||||

| 370 | Blink Charging Co. † | 2,638 | ||||||

| 458 | Bloom Energy Corp., Class A † | 7,626 | ||||||

| 108 | Casella Waste Systems, Inc. † | 9,612 | ||||||

| 518 | Chargepoint Holdings, Inc. † | 4,491 | ||||||

| 22 | Cintas Corp. | 10,026 | ||||||

| 478 | Emeren Group, Ltd. ADR † | 1,950 | ||||||

| 112 | EnerSys | 9,293 | ||||||

| 318 | Fluence Energy, Inc. † | 5,743 | ||||||

| 910 | Freyr Battery SA † | 6,434 | ||||||

| 1,696 | FuelCell Energy, Inc. † | 3,188 | ||||||

| 386 | GreenPower Motor Co., Inc. † | 1,089 | ||||||

| 98 | Heritage-Crystal Clean, Inc. † | 3,426 | ||||||

| 216 | Johnson Controls International PLC | 12,925 | ||||||

| 86 | ManpowerGroup, Inc. | 6,511 | ||||||

| 860 | Nikola Corp. † | 762 | ||||||

| 348 | Plug Power, Inc. † | 3,142 | ||||||

| 408 | Shoals Technologies Group, Inc., Class A † | 8,523 | ||||||

| 152 | Stericycle, Inc. † | 6,939 | ||||||

| 456 | SunPower Corp. † | 6,028 | ||||||

| 276 | Sunrun, Inc. † | 5,807 | ||||||

(See notes which are an integral part of the Financial Statements)

18 | Annual Shareholder Report

| Strategy Shares Halt Climate Change ETF (NZRO) (Continued) | April 30, 2023 |

| Shares | Value | |||||||

| Common Stocks — (Continued) | ||||||||

| Industrials — (Continued) | ||||||||

| 1,076 | Sunworks, Inc. † | $ | 873 | |||||

| 218 | TPI Composites, Inc. † | 2,694 | ||||||

| 46 | Watts Water Technologies, Inc. | 7,440 | ||||||

| 76 | Xylem, Inc. | 7,891 | ||||||

| 158,168 | ||||||||

| Information Technology — 27.4% | ||||||||

| 50 | Adobe, Inc. † | 18,878 | ||||||

| 188 | Apple, Inc. | 31,900 | ||||||

| 64 | Autodesk, Inc. † | 12,467 | ||||||

| 296 | Canadian Solar, Inc. † | 11,076 | ||||||

| 418 | Cisco Systems, Inc. | 19,751 | ||||||

| 60 | Enphase Energy, Inc. † | 9,852 | ||||||

| 104 | First Solar, Inc. † | 18,988 | ||||||

| 30 | Gartner, Inc. † | 9,074 | ||||||

| 44 | Intuit, Inc. | 19,534 | ||||||

| 46 | Keysight Technologies, Inc. † | 6,653 | ||||||

| 242 | Maxeon Solar Technologies, Ltd. † | 6,803 | ||||||

| 104 | Microsoft Corp. | 31,955 | ||||||

| 94 | NetApp, Inc. | 5,912 | ||||||

| 290 | Oracle Corp. | 27,469 | ||||||

| 112 | Salesforce, Inc. † | 22,217 | ||||||

| 44 | ServiceNow, Inc. † | 20,214 | ||||||

| 36 | SolarEdge Technologies, Inc. † | 10,283 | ||||||

| 283,026 | ||||||||

| Materials — 1.8% | ||||||||

| 74 | Ecolab, Inc. | 12,420 | ||||||

| 1,016 | PureCycle Technologies, Inc. † | 6,675 | ||||||

| 19,095 | ||||||||

| Real Estate — 0.6% | ||||||||

| 82 | CBRE Group, Inc., Class A † | 6,286 | ||||||

| Utilities — 8.9% | ||||||||

| 52 | American Water Works Co., Inc. | 7,710 | ||||||

| 260 | Atlantica Sustainable Infrastructure PLC | 6,921 | ||||||

| 262 | Brookfield Renewable Corp., Class A | 8,753 | ||||||

| 130 | California Water Service Group | 7,290 | ||||||

| 262 | Clearway Energy, Inc., Class C | 7,957 | ||||||

| 188 | Global Water Resources, Inc. | 2,062 | ||||||

| 902 | Montauk Renewables, Inc. † | 5,998 | ||||||

| 114 | NextEra Energy Partners LP | 6,556 | ||||||

| 298 | NextEra Energy, Inc. | 22,836 | ||||||

| 116 | Ormat Technologies, Inc. | 9,955 | ||||||

| 374 | Sunnova Energy International, Inc. † | 6,717 | ||||||

| 92,755 | ||||||||

| Total Common Stocks (Cost $1,194,729) | $ | 997,940 | ||||||

| Total Investments — 96.1% | ||||||||

| (Cost $1,194,729) | $ | 997,940 | ||||||

| Other Assets less Liabilities — 3.9% | 40,807 | |||||||

| Net Assets — 100.0% | $ | 1,038,747 | ||||||

ADR — American Depositary Receipt

LP — Limited Partnership

PLC — Public Liability Company

| † | Non-income producing security |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report | 19

| Strategy Shares Newfound/ReSolve Robust Momentum ETF (ROMO) | April 30, 2023 |

Portfolio of Investments Summary Table

| Percentage of Value | |||

| Exchange-Traded Funds | 100.0% | ||

| Total | 100.0% | ||

Portfolio holdings and allocations are subject to change. As of April 30, 2023, percentages in the table above are based on total investments. Such total investments may differ from the percentages set forth in the following Portfolio of Investments which are computed using the Fund’s total net assets.

Portfolio of Investments

| Shares | Value | ||||||

| Exchange-Traded Funds — 99.8% | |||||||

| 72,688 | iShares 1-3 Year Treasury Bond ETF | $ | 5,973,500 | ||||

| 36,883 | iShares 7-10 Year Treasury Bond ETF | 3,678,342 | |||||

| 543,620 | iShares Core MSCI EAFE ETF | 37,384,746 | |||||

| 5,236 | iShares Core S&P 500 ETF | 2,186,868 | |||||

| Total Exchange-Traded Funds (Cost $47,062,943) | $ | 49,223,456 | |||||

| Total Investments — 99.8% (Cost $47,062,943) | $ | 49,223,456 | |||||

| Other Assets less Liabilities — 0.2% | 124,407 | ||||||

| Net Assets — 100.0% | $ | 49,347,863 | |||||

ETF — Exchange-Traded Fund

MSCI EAFE — MSCI Europe, Australasia and Far East

S&P — Standard and Poor’s

(See notes which are an integral part of the Financial Statements)

20 | Annual Shareholder Report

| Statements of Assets and Liabilities | April 30, 2023 |

| Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) | Strategy Shares Gold-Hedged Bond ETF (GLDB)(a) | Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL) | ||||||||||

| Assets: | ||||||||||||

| Investments, at value (Cost $2,224,581, $12,385,855 and $1,031,232,135) | $ | 2,112,875 | $ | 11,793,670 | $ | 969,341,732 | ||||||

| Cash and Cash Equivalents | 13,447 | 1,865,746 | 54,986,959 | |||||||||

| Segregated cash balances for swap agreements with custodian | - | 1,010,000 | 55,000,000 | |||||||||

| Dividends and interest receivable | - | 122,686 | - | |||||||||

| Receivable for investments sold | - | - | 2,285,105 | |||||||||

| Unrealized appreciation on swap agreements | - | 29,149 | 1,225,053 | |||||||||

| Receivable from Advisor | 9,668 | - | - | |||||||||

| Prepaid expenses | 5,428 | - | 42,013 | |||||||||

| Total Assets | 2,141,418 | 14,821,251 | 1,082,880,862 | |||||||||

| Liabilities: | ||||||||||||

| Payable for capital shares redeemed | - | - | 2,545,085 | |||||||||

| Unrealized depreciation on swap agreements | - | 64,801 | - | |||||||||

| Payable to counterparties for swap agreements | - | - | 82,189 | |||||||||

| Accrued expenses: | ||||||||||||

| Advisory | - | 9,737 | 537,338 | |||||||||

| Administration | 3,368 | - | 33,874 | |||||||||

| Related parties | 2,500 | - | 26,259 | |||||||||

| Compliance services | - | (b) | - | 2 | ||||||||

| Custodian | 93 | - | 4,526 | |||||||||

| Fund accounting | 29 | - | 29 | |||||||||

| Other | 16,869 | - | 210,112 | |||||||||

| Total Liabilities | 22,859 | 74,538 | 3,439,414 | |||||||||

| Net Assets | $ | 2,118,559 | $ | 14,746,713 | $ | 1,079,441,448 | ||||||

| Net Assets consist of: | ||||||||||||

| Paid in Capital | $ | 2,400,519 | $ | 15,793,774 | $ | 1,235,219,219 | ||||||

| Total Distributable Earnings / (Loss) | (281,960 | ) | (1,047,061 | ) | (155,777,771 | ) | ||||||

| Net Assets | $ | 2,118,559 | $ | 14,746,713 | $ | 1,079,441,448 | ||||||

| Net Assets: | $ | 2,118,559 | $ | 14,746,713 | $ | 1,079,441,448 | ||||||

| Shares of Beneficial Interest Outstanding (unlimited number of shares authorized, no par value): | 100,000 | 700,000 | 53,025,000 | |||||||||

| Net Asset Value (offering and redemption price per share): | $ | 21.19 | $ | 21.07 | $ | 20.36 | ||||||

| (a) | Statement has been consolidated. See Note 2.A. in the Notes to Financial Statements for the basis of consolidation. | |

| (b) | Amount is less than $0.50. |

(See notes which are an integral part of the Financial Statements)

Annual Shareholder Report | 21

| Statements of Assets and Liabilities | April 30, 2023 |

| Strategy Shares Halt Climate Change (NZRO) | Strategy Shares Newfound/ReSolve Robust Momentum | |||||||

| Assets: | ||||||||

| Investments, at value (Cost $1,194,729 and $47,062,943) | $ | 997,940 | $ | 49,223,456 | ||||

| Cash and Cash Equivalents | 41,211 | 158,578 | ||||||

| Dividends and interest receivable | 417 | - | ||||||

| Prepaid expenses | - | 4,288 | ||||||

| Total Assets | 1,039,568 | 49,386,322 | ||||||

| Liabilities: | ||||||||

| Accrued expenses: | ||||||||

| Advisory | 821 | 13,420 | ||||||

| Administration | - | 5,400 | ||||||

| Related parties | - | 2,500 | ||||||

| Custodian | - | 264 | ||||||

| Fund accounting | - | 5 | ||||||

| Other | - | 16,870 | ||||||

| Total Liabilities | 821 | 38,459 | ||||||

| Net Assets | $ | 1,038,747 | $ | 49,347,863 | ||||

| Net Assets consist of: | ||||||||

| Paid in Capital | $ | 1,250,686 | $ | 51,763,172 | ||||

| Total Distributable Earnings / (Loss) | (211,939 | ) | (2,415,309 | ) | ||||

| Net Assets | $ | 1,038,747 | $ | 49,347,863 | ||||

| Net Assets: | $ | 1,038,747 | $ | 49,347,863 | ||||

| Shares of Beneficial Interest Outstanding (unlimited number of shares authorized, no par value): | 50,000 | 1,925,000 | ||||||

| Net Asset Value (offering and redemption price per share): | $ | 20.77 | $ | 25.64 | ||||

(See notes which are an integral part of the Financial Statements)

22 | Annual Shareholder Report

| Statements of Operations | For the Periods Indicated |

| Strategy Shares Nasdaq 5HANDL™ Index ETF (FIVR) | Strategy Shares Gold-Hedged Bond ETF (GLDB)(a) | Strategy Shares Nasdaq 7HANDL™ Index ETF (HNDL) | ||||||||||

Year Ended April 30, | Year Ended April 30, | Year Ended April 30, | ||||||||||

| Investment Income: | ||||||||||||

| Dividend income | $ | 81,916 | $ | - | $ | 38,056,294 | ||||||

| Interest income | - | 468,235 | 8,133 | |||||||||

| Total Investment Income | 81,916 | 468,235 | 38,064,427 | |||||||||

| Expenses: | ||||||||||||

| Advisory | 10,869 | 108,857 | 7,401,121 | |||||||||

| Administration | 31,313 | - | 439,712 | |||||||||

| Related parties | 30,000 | - | 341,773 | |||||||||

| Fund accounting | 340 | - | 333 | |||||||||

| Custodian | 452 | - | 58,566 | |||||||||

| Trustee | 15,451 | - | 15,451 | |||||||||

| Compliance services | 7,936 | - | 39,174 | |||||||||

| Legal and audit | 29,716 | - | 142,703 | |||||||||

| Printing | 3,616 | - | 494,081 | |||||||||

| Nasdaq licensing | 1,181 | - | 616,212 | |||||||||

| Other fees | 4,980 | - | 58,334 | |||||||||

| Offering costs | 4,082 | - | - | |||||||||

| Total Expenses before fee reductions | 139,936 | 108,857 | 9,607,460 | |||||||||

| Expenses contractually waived or reimbursed by the Advisor | (123,173 | ) | - | - | ||||||||

| Total Net Expenses | 16,763 | 108,857 | 9,607,460 | |||||||||

| Net Investment Income | 65,153 | 359,378 | 28,456,967 | |||||||||

| Realized and Unrealized Gains (Losses): | ||||||||||||

| Net realized gains (losses) from investment transactions | (137,562 | ) | (419,224 | ) | (79,253,310 | ) | ||||||

| Net realized gains (losses) from in-kind transactions | 12,807 | - | (3,473,331 | ) | ||||||||

| Net realized gains (losses) from swap agreements | - | (878,240 | ) | (54,198,122 | ) | |||||||

| Change in unrealized appreciation/depreciation on investments | 71,610 | 208,966 | 37,069,325 | |||||||||

| Change in unrealized appreciation/depreciation on swap agreements | - | 708,007 | 31,089,734 | |||||||||