Exhibit 99.2

POSTMEDIA NETWORK CANADA CORP.

INTERIM MANAGEMENT’S DISCUSSION AND ANALYSIS

FOR THE THREE MONTHS ENDED NOVEMBER 30, 2013 AND 2012

Issued: January 9, 2014

MANAGEMENT’S DISCUSSION AND ANALYSIS

This management’s discussion and analysis of financial condition and results of operations of Postmedia Network Canada Corp. and its subsidiary Postmedia Network Inc. (collectively, “we”, “our”, “us”, or “Postmedia”) should be read in conjunction with the interim condensed consolidated financial statements and related notes of Postmedia for the three months ended November 30, 2013 and 2012 and the annual audited consolidated financial statements and related notes for the years ended August 31, 2013, 2012 and 2011. The interim condensed consolidated financial statements of Postmedia for the three months ended November 30, 2013 and 2012 and the annual audited consolidated financial statements for the years ended August 31, 2013, 2012 and 2011 are available on SEDAR at www.sedar.com and on the EDGAR system maintained by the U.S. Securities and Exchange Commission at www.sec.gov.

This discussion contains statements that are not historical facts and are forward-looking statements. These statements are subject to a number of risks described in the section entitled “Risk Factors” contained in our annual management’s discussion and analysis for the years ended August 31, 2013, 2012 and 2011. Risks and uncertainties may cause actual results to differ materially from those contained in such forward-looking statements. Such statements reflect management’s current views and are based on certain assumptions. They are only estimates of future developments, and actual developments may differ materially from these statements due to a number of factors. Investors are cautioned not to place undue reliance on such forward-looking statements. No forward-looking statement is a guarantee of future results. We have tried, where possible, to identify such statements by using words such as “believe”, “expect”, “estimate”, “anticipate”, “will”, “could” and similar expressions in connection with any discussion of future operating or financial performance. Except as required by law, we undertake no obligation to publicly update or revise any forward-looking statements or information, whether written or oral, that may be as a result of new information, future events or otherwise.

All amounts are expressed in Canadian dollars unless otherwise noted. The interim condensed consolidated financial statements of Postmedia for the three months ended November 30, 2013 and 2012 have been prepared in accordance with International Financial Reporting Standards (“IFRS”) and International Accounting Standard (“IAS”) 34 – Interim Financial Reporting.

This management’s discussion and analysis is dated January 9, 2014 and does not reflect changes or information subsequent to this date. Additional information in respect of Postmedia is available on SEDAR at www.sedar.com and EDGAR at www.sec.gov.

Overview and Background

We are the largest publisher by circulation of paid English-language daily newspapers in Canada, according to Newspapers Canada’s 2012 Circulation Data Report. We have the highest weekly print readership of paid English-language daily newspapers in Canada, based on the NADbank 2012 survey data. Our business consists of news and information gathering and dissemination operations, with products offered in major Canadian markets and a number of regional and local markets in Canada through a variety of print, web, tablet and smartphone platforms. The combination of these distribution platforms provides readers with a variety of mediums through which to access and interact with our content. The breadth of our reach and the diversity of our content enable advertisers to reach their target audiences on a local, regional or national scale through the convenience of a single provider.

For financial reporting purposes we have one operating segment, the Newspaper segment which publishes daily and non-daily newspapers and operates digital media and online assets including the canada.com website, each newspaper’s online website and Infomart, our media monitoring service.

Recent developments

In August 2013, we outsourced the production of the Edmonton Journal and entered into a print outsourcing agreement for the production of the Calgary Herald, which began in November 2013. On September 9, 2013, we announced our intention to sell two of our real estate holdings. The net proceeds from these potential sales will be used to make an offer to redeem an equal amount of our 8.25% Senior Secured Notes due 2017 (“First-Lien Notes”). In addition, in November 2013, we committed to third party outsourcing contracts for the production of both The Vancouver Sun and The Province.

Key Factors Affecting Operating Results

Revenue is earned primarily from advertising, circulation and digital sources. Print advertising revenue is a function of the volume, or linage, of advertising sold and rates charged. Print circulation revenue is derived from home-delivery subscriptions for newspapers, single copy sales at retail outlets and vending machines and is a function of the number of newspapers sold and the price per copy. Digital revenue consists of revenue from national and local display advertising on our newspaper and other websites, including canada.com, revenue from e-Papers and digital access subscriptions, as well as subscription revenue generated through Infomart, our media monitoring service.

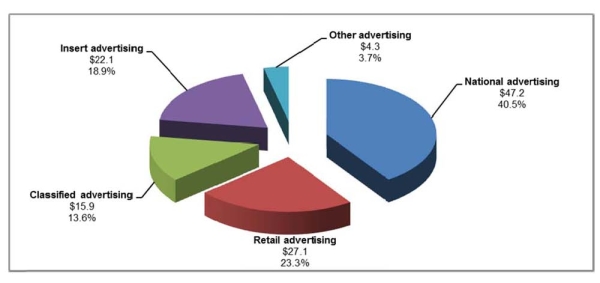

Print advertising revenue was $116.6 million for the three months ended November 30, 2013, representing 60.1% of total revenue. The following chart summarizes our print advertising revenue by category for the three months ended November 30, 2013 ($ in millions):

Print advertising is influenced by both the overall strength of the economy and significant structural changes in the newspaper industry and media in general. In recent years and continuing to date, economic uncertainty and structural changes in the industry have resulted in significant declines in print advertising as well as a continuing shift in advertising dollars from print advertising to advertising in other formats, particularly online and other digital platforms such as search and social media websites. This shift is expected to continue and may be permanent. We anticipate the print advertising market to remain challenging and expect current trends to continue throughout the remainder of fiscal 2014. During the three months ended November 30, 2013, we experienced print advertising revenue declines of 12.2% as compared to the same period in the prior year. The decline in print advertising revenue in the three months ended November 30, 2013 relates to weakness in all major advertising categories including classified, retail and national.

Print circulation revenue was $49.6 million for the three months ended November 30, 2013, representing 25.6% of total revenue. Declines in circulation volumes have been experienced over the last few years and this trend continued in the three months ended November 30, 2013. Circulation volume declines have been offset by price increases resulting in a 0.6% increase in print circulation revenue in the three months ended November 30, 2013 as compared to the same period in the prior year. We expect print circulation revenue to remain stable throughout the remainder of fiscal 2014.

Digital revenue was $23.6 million for the three months ended November 30, 2013, representing 12.1% of total revenue. Digital revenues decreased 5.1% in the three months ended November 30, 2013, as compared to the same period in the prior year as a result of decreases in local digital advertising revenue and digital classified revenue. We continue to believe digital revenue represents a future growth opportunity for Postmedia and as a result we are focused on various new products and initiatives in this area.

Our principal expenses consist of compensation, newsprint, and distribution. These composed 50.0%, 6.2% and 17.8%, respectively, of total operating expenses excluding depreciation, amortization and restructuring for the three months ended November 30, 2013. During this period we experienced declines in compensation, newsprint and distribution expenses of 11.0%, 24.7% and 6.7%, respectively, as compared to the same period in the prior year.

We are in the process of implementing a three year business transformation program which was announced in July 2012 (“Transformation Program”) that will focus on the development of our digital products and is expected to result in net operating cost savings of 15% to 20%. During the three months ended November 30, 2013 as part of our Transformation Program we implemented initiatives which are expected to result in an additional $5 million of net annualized cost savings. In total, we have implemented net annualized cost savings of approximately $87 million, or 12.5% of operating costs, since the Transformation Program was announced.

Our operating results are affected by variations in the cost and availability of newsprint. Newsprint is the principal raw material used in the production of our daily newspapers and other print publications. It is a commodity that is generally subject to price volatility. We take advantage of the purchasing power that comes with the large volume of newsprint we purchase, as well as our proximity to paper mills across Canada, to minimize our total newsprint expense. Changes in newsprint prices can significantly affect our operating results. A $50 per tonne increase or decrease in the price of newsprint would be expected to affect our newsprint expense by approximately $3.0 million on an annualized basis. We don’t expect a material change in newsprint prices throughout the remainder of fiscal 2014. Our distribution is primarily outsourced to third party suppliers. The key drivers of our distribution expenses are fuel costs and circulation and insert volumes. Our distribution expenses have decreased during the three months ended November 30, 2013 as a result of Transformation Program initiatives as well as decreased circulation and insert volumes.

Additional IFRS Measures

We use operating income before depreciation, amortization and restructuring, as presented in the condensed consolidated statements of operations for the three months ended November 30, 2013 and 2012 and described in note 3 thereto, to assist in assessing our financial performance. Management and the Board of Directors of Postmedia use this measure to evaluate consolidated operating results and to assess Postmedia’s ability to incur and service debt. In addition, this measure is used to make operating decisions as it is an indicator of how much cash is being generated by Postmedia and assists in determining the need for additional cost reductions, evaluation of personnel and resource allocation decisions. Operating income before depreciation, amortization and restructuring is referred to as an additional IFRS measure and may not be comparable to similar measures presented by other companies.

Other Factors

Seasonality

Revenue has experienced, and is expected to continue to experience, significant seasonality due to seasonal advertising patterns and seasonal influences on media consumption habits. Typically, our advertising revenue is highest in the first and third fiscal quarters, while expenses are relatively constant throughout the fiscal year. These seasonal variations may lead to increased borrowing needs at certain points within the fiscal year.

Critical accounting estimates

The preparation of financial statements in accordance with IFRS requires management to make estimates, assumptions and judgements that affect the reported amounts of assets and liabilities, related amounts of revenues and expenses, and disclosure of contingent assets and liabilities. Although these estimates, assumptions and judgements are based upon management’s best knowledge of the amount, event or actions; actual results could differ from those estimates, assumptions and judgements. The critical accounting estimates used in our interim condensed consolidated financial statements for the three months ended November 30, 2013 and 2012 are not materially different from those disclosed in our annual management’s discussion and analysis and annual audited consolidated financial statements for the years ended August 31, 2013, 2012 and 2011 except as described below:

Employee future benefits

The cost of defined benefit pension benefit plans, post-retirement benefit plans and other long-term employee benefit plans and the present value of the defined benefit obligation are determined using actuarial valuations. An actuarial valuation involves making various assumptions including mortality rates. In July 2013, the Canadian Institute of Actuaries (“CIA”) issued a draft report proposing new mortality tables for use in the valuation of Canadian pension and benefit plans. On October 31, 2013 the CIA announced that the use of current mortality tables without adjustment would only be appropriate if supported by credible experience, the characteristics of the specific plan, or other quantifiable experience. As a result, during the three months ended November 30, 2013, the Company has modified the mortality tables used to value the defined benefit pension benefit and post-retirement benefit obligations. During the three months ended November 30, 2013, this change in mortality rate assumptions has resulted in an estimated actuarial loss of $15.6 million recorded in other comprehensive income with an offsetting increase in other non-current liabilities. The change in mortality rate assumptions is expected to result in increased funding valuations as well as increased defined benefit plan expense in future years.

Changes in accounting policies

We have adopted the following new and amended standards effective September 1, 2013. The comparative interim condensed consolidated financial statements have been revised as applicable to reflect the adopted standards as described below.

(i) IFRS 13 – Fair Value Measurement

IFRS 13 – Fair Value Measurement establishes a single source of guidance for fair value measurement across all IFRS standards. IFRS 13 defines fair value, provides guidance on measurement and introduces certain disclosure requirements. We adopted IFRS 13 on September 1, 2013 on a prospective basis. The adoption of IFRS 13 did not result in any measurement adjustments or changes to the valuation techniques used. We have included the interim disclosure requirements in note 11 of our interim condensed consolidated financial statements for the three months ended November 30, 2013 and 2012.

(ii) IAS 19 – Employee Benefits (Amended)

IAS 19 – Employee Benefits (Amended) includes a number of changes related to the recognition and measurement of defined benefit employee benefit plans and termination benefits. The amendments introduce a net interest approach that replaces the expected return on plan assets and interest costs on the defined benefit obligation with a single net interest component which will be determined based on the application of the discount rate on the net defined benefit obligation. As a result the discount rate previously used to calculate the interest costs on plan obligations is now also being used to calculate the expected return on plan assets. The amendments also require the recognition of all past service costs in profit or loss when the employee benefit plan is amended. We adopted IAS 19 on September 1, 2013 on a retrospective basis back to September 1, 2011. The adoption of IAS 19 has resulted in an adjustment to the opening deficit as at September 1, 2011 to reflect previously unrecognized past service costs. Additionally, the comparative figures in the interim condensed consolidated financial statements for the three months ended November 30, 2013 and 2012 have been revised as illustrated in the tables below to reflect the new standard. In addition, the amended standard clarifies when an employer offers voluntary termination benefits that the obligating event under such termination benefits is deemed to have occurred when an entity can no longer withdraw the offer. This resulted in a decrease to restructuring and other items of $10.5 million in the three months ended May 31, 2013 and a corresponding increase to restructuring and other items of $10.5 million in the three months ended August 31, 2013.

| | | | |

| | The following tables provide the impact on the comparative financial information in the interim condensed consolidated financial statements for the three months ended November 30, 2013 and 2012. Effect on comprehensive loss attributable to equity holders of the Company |

| | | | |

| | | | Three months ended November 30, 2012 | |

| | | | | |

| | Net earnings attributable to equity holders of the Company as previously reported | | | 8,304 | |

| | | | | | |

| | IAS 19 amendments decreasing reported net earnings | | | | |

| | Compensation | | | (119 | ) |

| | Net financing expense relating to employee benefit plans | | | (1,481 | ) |

| | Total IAS 19 amendments decreasing reported net earnings | | | (1,600 | ) |

| | Net earnings attributable to equity holders of the Company revised (1) | | | 6,704 | |

| | | | | | |

| | Comprehensive loss attributable to equity holders of the Company as previously reported | | | (1,314 | ) |

| | | | | | |

| | IAS 19 amendments (increasing) decreasing reported comprehensive loss | | | | |

| | Impact of IAS 19 amendments to net earnings | | | (1,600 | ) |

| | Net actuarial losses on employee benefits | | | 1,662 | |

| | Total IAS 19 amendments decreasing reported comprehensive loss | | | 62 | |

| | Comprehensive loss attributable to equity holders of the Company revised | | | (1,252 | ) |

| | | | | | |

| | (1) These adjustments reduced basic and diluted net earnings per share attributable to equity holders of the Company by $0.04 per share. |

| | Effect on the consolidated statements of financial position | | | | | | | | |

| | Increase (decrease) | | August 31, 2013 | | | August 31, 2012 | | | September 1, 2011 | |

| | | | | | | | | | | |

| | Other non-current liabilities | | | 1,675 | | | | 1,923 | | | | 2,171 | |

| | Deficit | | | 1,675 | | | | 1,923 | | | | 2,171 | |

| | | | | | | | | | | | | | |

| | (iii) IFRS 10 – Consolidated Financial Statements IFRS 10 – Consolidated Financial Statements replaces SIC-12 Consolidation – Special Purposes Entities and parts of IAS 27 – Consolidated and Separate Financial Statements and introduces a new definition of control that is intended to provide more consistent guidance in the determination of whether control exists and whether or not an entity should be included within the consolidated financial statements. The adoption of this standard did not have an impact on our interim condensed consolidated financial statements. |

The following table provides our fiscal 2013 quarterly and full year consolidated statements of operations, revised for the adoption of IAS 19:

| | | Fiscal 2013 (revised) |

| | | | Q1 | | | | Q2 | | | | Q3 | | | | Q4 | | | Total | |

| | | | | | | | | | | | | | | | | | | | |

| Revenues | | | | | | | | | | | | | | | | | | | |

| Print advertising | | | 132,741 | | | | 105,443 | | | | 113,395 | | | | 93,968 | | | | 445,547 | |

| Print circulation | | | 49,276 | | | | 47,863 | | | | 49,401 | | | | 49,359 | | | | 195,899 | |

| Digital | | | 24,813 | | | | 21,292 | | | | 24,093 | | | | 21,408 | | | | 91,606 | |

| Other | | | 4,842 | | | | 4,220 | | | | 4,895 | | | | 4,574 | | | | 18,531 | |

| Total revenues | | | 211,672 | | | | 178,818 | | | | 191,784 | | | | 169,309 | | | | 751,583 | |

| Expenses | | | | | | | | | | | | | | | | | | | | |

| Compensation | | | 83,067 | | | | 81,291 | | | | 83,075 | | | | 73,791 | | | | 321,224 | |

| Newsprint | | | 12,108 | | | | 9,856 | | | | 10,147 | | | | 8,791 | | | | 40,902 | |

| Distribution | | | 28,192 | | | | 26,365 | | | | 27,542 | | | | 25,806 | | | | 107,905 | |

| Other operating | | | 39,318 | | | | 36,240 | | | | 38,268 | | | | 37,800 | | | | 151,626 | |

| Operating income before depreciation, amortization, impairment and restructuring | | | 48,987 | | | | 25,066 | | | | 32,752 | | | | 23,121 | | | | 129,926 | |

| Depreciation | | | 6,890 | | | | 6,740 | | | | 6,706 | | | | 9,613 | | | | 29,949 | |

| Amortization | | | 10,734 | | | | 10,834 | | | | 11,111 | | | | 10,646 | | | | 43,325 | |

| Impairments | | | - | | | | - | | | | 93,883 | | | | 6,100 | | | | 99,983 | |

| Restructuring and other items | | | 4,797 | | | | 1,814 | | | | 6,305 | | | | 21,255 | | | | 34,171 | |

| Operating income (loss) | | | 26,566 | | | | 5,678 | | | | (85,253 | ) | | | (24,493 | ) | | | (77,502 | ) |

| Interest expense | | | 16,167 | | | | 15,606 | | | | 14,994 | | | | 15,133 | | | | 61,900 | |

| Net financing expense relating to employee benefit plans | | | 1,864 | | | | 1,863 | | | | 1,863 | | | | 1,868 | | | | 7,458 | |

| (Gain) loss on disposal of property and equipment and intangible assets | | | 268 | | | | (1,055 | ) | | | (202 | ) | | | (16 | ) | | | (1,005 | ) |

| Loss on derivative financial instruments | | | 697 | | | | 1,193 | | | | 760 | | | | 4,656 | | | | 7,306 | |

| Foreign currency exchange losses | | | 866 | | | | 3,832 | | | | 588 | | | | 1,779 | | | | 7,065 | |

| Earnings (loss) before income taxes | | | 6,704 | | | | (15,761 | ) | | | (103,256 | ) | | | (47,913 | ) | | | (160,226 | ) |

| Provision for income taxes | | | - | | | | - | | | | - | | | | - | | | | - | |

| Net earnings (loss) attributable to equity holders of the Company | | | 6,704 | | | | (15,761 | ) | | | (103,256 | ) | | | (47,913 | ) | | | (160,226 | ) |

Operating Results

Postmedia’s operating results for the three months ended November 30, 2013 as compared to the three months ended November 30, 2012

| | | 2013 | | | 2012 | |

| | | | | | (revised) (1) | |

| Revenues | | | | | | |

| Print advertising | | | 116,605 | | | | 132,741 | |

| Print circulation | | | 49,588 | | | | 49,276 | |

| Digital | | | 23,554 | | | | 24,813 | |

| Other | | | 4,231 | | | | 4,842 | |

| Total revenues | | | 193,978 | | | | 211,672 | |

| Expenses | | | | | | | | |

| Compensation | | | 73,958 | | | | 83,067 | |

| Newsprint | | | 9,120 | | | | 12,108 | |

| Distribution | | | 26,308 | | | | 28,192 | |

| Other operating | | | 38,581 | | | | 39,318 | |

| Operating income before depreciation, amortization and restructuring | | | 46,011 | | | | 48,987 | |

| Depreciation | | | 13,227 | | | | 6,890 | |

| Amortization | | | 10,412 | | | | 10,734 | |

| Restructuring and other items | | | 20,113 | | | | 4,797 | |

| Operating income | | | 2,259 | | | | 26,566 | |

| Interest expense | | | 15,733 | | | | 16,167 | |

| Net financing expense relating to employee benefit plans | | | 1,404 | | | | 1,864 | |

| (Gain) loss on disposal of property and equipment | | | (14 | ) | | | 268 | |

| (Gain) loss on derivative financial instruments | | | (4,054 | ) | | | 697 | |

| Foreign currency exchange losses | | | 995 | | | | 866 | |

| Earnings (loss) before income taxes | | | (11,805 | ) | | | 6,704 | |

| Provision for income taxes | | | - | | | | - | |

| Net earnings (loss) attributable to equity holders of the Company | | | (11,805 | ) | | | 6,704 | |

(1) See “Other Factors – Changes in accounting policies”.

Revenue

Print advertising

Print advertising revenue decreased $16.1 million, or 12.2%, to $116.6 million for the three months ended November 30, 2013, as compared to the same period in the prior year. A decrease was experienced in all of our major categories of print advertising revenue, including decreases from national advertising of 11.3%, retail advertising of 11.7% and classified advertising of 24.2%. The total print advertising linage and average line rate related to national, retail and classified advertising decreased 10.8% and 3.6%, respectively, during the three months ended November 30, 2013, as compared to the same period in the prior year.

Print circulation

Print circulation revenue increased $0.3 million to $49.6 million for the three months ended November 30, 2013 as compared to the same period in the prior year. Paid circulation volume decreased 13.4% during this period, as compared to the same period in the prior year, but was offset by price increases.

Digital

Digital revenue decreased $1.3 million, or 5.1%, to $23.6 million for the three months ended November 30, 2013, as compared to the same period in the prior year. The decline in digital revenue is primarily as a result of decreases in local digital advertising revenue of $0.9 million and digital classified revenue of $0.6 million, partially offset by increases in digital circulation revenue of $0.3 million.

Other

Other revenue decreased $0.6 million, or 12.6%, to $4.2 million for the three months ended November 30, 2013, as compared to the same period in the prior year. The decline in other revenue is primarily as a result of declines in commercial print revenue and commission revenue on third party advertising sales.

Expenses

Compensation

Compensation expenses decreased $9.1 million, or 11.0%, to $74.0 million for the three months ended November 30, 2013, as compared to the same period in the prior year. The decrease is primarily due to lower salary and benefits expense of $7.7 million as a result of a reduction in employees due to the Transformation Program initiatives, a decrease in employee benefit plan expense of $0.7 million and a decrease in non-cash share-based and other long-term incentive plan compensation expense of $0.7 million. Excluding non-cash share-based and other long-term incentive plan compensation expense, compensation expense decreased $8.4 million, or 10.2%.

Newsprint

Newsprint expenses decreased $3.0 million, or 24.7%, to $9.1 million for the three months ended November 30, 2013, as compared to the same period in the prior year. Newsprint expense decreases are primarily a result of consumption decreases of 23.2% due to continued usage reduction efforts, reduced publishing days and lower newspaper circulation volumes, combined with a decrease in newsprint cost per tonne of 1.9%. Newsprint expenses include newsprint purchased for production at both our owned and outsourced production facilities.

Distribution

Distribution expenses decreased $1.9 million, or 6.7%, to $26.3 million for the three months ended November 30, 2013, as compared to the same period in the prior year. Decreases in distribution expenses are primarily a result of a reduction in newspaper circulation volumes, the elimination of unprofitable circulation and other cost reduction initiatives.

Other operating

Other operating expenses decreased $0.7 million, or 1.9%, to $38.6 million for the three months ended November 30, 2013, as compared to the same period in the prior year. Decreases in other operating expenses are primarily a result of ongoing cost savings initiatives, partially offset by an increase in production costs as a result of the outsourced newspaper production described earlier in “Recent developments”.

Operating income before depreciation, amortization and restructuring

Operating income before depreciation, amortization and restructuring decreased $3.0 million, or 6.1%, to $46.0 million for the three months ended November 30, 2013, as compared to the same period in the prior year. The decrease relates primarily to decreases in revenue, partially offset by decreases in expenses as discussed above. Excluding non-cash share-based and other long-term incentive plan compensation expense, operating income before depreciation, amortization and restructuring decreased $3.7 million, or 7.4%.

Depreciation

Depreciation expense increased $6.3 million to $13.2 million for the three months ended November 30, 2013, as compared to the same period in the prior year. The increase relates primarily to a change in the estimate of the useful lives of certain production assets as a result of production outsourcing.

Amortization

Amortization expense decreased $0.3 million to $10.4 million for the three months ended November 30, 2013, as compared to the same period in the prior year.

Restructuring and other items

Restructuring and other items expense increased $15.3 million to $20.1 million for the three months ended November 30, 2013 as compared to the same period in the prior year. Restructuring and other items expense for the three months ended November 30, 2013 consists of severance costs, which include both involuntary terminations and voluntary buyouts. Restructuring and other items expense for the three months ended November 30, 2012 included an estimated expense of $3.9 million related to changes made to an employee benefit plan as a result of an arbitrator’s ruling. Additionally, included in restructuring and other items for the three months ended November 30, 2012 were $0.9 million of severance costs, which included both involuntary terminations and voluntary buyouts.

Operating income

Operating income was $2.3 million for the three months ended November 30, 2013, as compared to $26.6 million for the same period in the prior year primarily as a result of decreased operating income before depreciation, amortization and restructuring, increased depreciation expense and increased restructuring and other items expense, all as discussed above.

Interest expense

Interest expense decreased $0.4 million, or 2.7%, to $15.7 million for the three months ended November 30, 2013, as compared to the same period in the prior year. Interest expense primarily relates to interest on our long-term debt that is recognized using the effective interest rate method, which amortizes the initial debt issuance costs and includes both cash and non-cash interest. The decrease in interest expense relates to a decrease in cash interest expense of $0.6 million during the three months ended November 30, 2013, as compared to the same period in the prior year due to lower first-lien debt, partially offset by an increase in non-cash interest of $0.2 million.

Net financing expense relating to employee benefit plans

Net financing expense relating to employee benefit plans decreased $0.5 million to $1.4 million for the three months ended November 30, 2013, as compared to the same period in the prior year. The decrease relates primarily to a reduction in the net defined benefit plan obligations.

(Gain) Loss on disposal of property and equipment

During the three months ended November 30, 2013, we disposed of property and equipment and realized a nominal gain. During the three months ended November 30, 2012, we disposed of property and equipment and realized a loss of $0.3 million.

(Gain) loss on derivative financial instruments

Gain on derivative financial instruments for the three months ended November 30, 2013 was $4.1 million as compared to a loss of $0.7 million during the same period in the prior year. The gain for the three months ended November 30, 2013 and the loss for the three months ended November 30, 2012 both relate to the change in fair value of our variable prepayment option embedded derivatives on the First-Lien Notes and 12.5% Senior Secured Notes due 2017 (“Second-Lien Notes”).

Foreign currency exchange losses

Foreign currency exchange losses for the three months ended November 30, 2013 were $1.0 million as compared to $0.9 million during the same period in the prior year. For the three months ended November 30, 2013 and 2012 foreign currency exchange losses consist primarily of unrealized losses of $0.9 million and $0.8 million, respectively, related to the non-swapped portion of the Second-Lien Notes.

Earnings (loss) before income taxes

Loss before income taxes was $11.8 million for the three months ended November 30, 2013, as compared to earnings of $6.7 million for the same period in the prior year. The increase in loss before income taxes is primarily the result of decreased operating income partially offset by gains on derivative financial instruments, both as discussed above.

Provision for income taxes

We have not recorded a current or deferred tax expense or recovery for the three months ended November 30, 2013 or 2012. Current taxes payable or recoverable result in a decrease or increase, respectively, to our tax loss carryforward balances. The cumulative tax loss carryforward balances have not been recognized as a net deferred tax asset on the consolidated statement of financial position.

Net earnings (loss) attributable to equity holders of the Company

Net loss for the three months ended November 30, 2013 was $11.8 million as compared to net earnings of $6.7 million for the same period in the prior year, as a result of the factors described above in earnings (loss) before income taxes.

Consolidated quarterly financial information

| | | Fiscal 2014 | | Fiscal 2013 | | | Fiscal 2012 |

| ($ in thousands of Canadian dollars, except per share information) | | Q1 | | | | Q4 | | | | Q3 | | | | Q2 | | | | Q1 | | | | Q4 | | | | Q3 | | | | Q2 | |

| | | | | | | ----------------------------------------- revised (1) ----------------------------------------- | |

| Total revenues | | | 193,978 | | | | 169,309 | | | | 191,784 | | | | 178,818 | | | | 211,672 | | | | 190,124 | | | | 212,021 | | | | 198,642 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net earnings (loss) attributible to equity holders of the Company | | | (11,805 | ) | | | (47,913 | ) | | | (103,256 | ) | | | (15,761 | ) | | | 6,704 | | | | (28,921 | ) | | | (12,707 | ) | | | (11,635 | ) |

| Basic | | $ | (0.29 | ) | | $ | (1.19 | ) | | $ | (2.57 | ) | | $ | (0.39 | ) | | $ | 0.17 | | | $ | (0.72 | ) | | $ | (0.32 | ) | | $ | (0.29 | ) |

| Diluted | | $ | (0.29 | ) | | $ | (1.19 | ) | | $ | (2.57 | ) | | $ | (0.39 | ) | | $ | 0.16 | | | $ | (0.72 | ) | | $ | (0.32 | ) | | $ | (0.29 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Cash flows from operating activities | | | 4,223 | | | | (11,562 | ) | | | 15,975 | | | | 20,706 | | | | 13,228 | | | | (7,472 | ) | | | 24,046 | | | | 16,045 | |

(1) See “Other Factors – Changes in accounting policies”.

Liquidity and capital resources

Our principal uses of funds are for working capital requirements, debt servicing and capital expenditures. Based on our current and anticipated level of operations, we believe that our cash on hand, cash flows from operations and available borrowings under our senior secured asset-based revolving credit facility (“ABL Facility”) will enable us to meet our working capital, capital expenditure, debt servicing and other funding requirements. However, our ability to fund our working capital needs, debt servicing and other obligations depends on our future operating performance and cash flows. There are a number of factors which may adversely affect our operating performance and our ability to meet these obligations. See “Key Factors Affecting Operating Results”. Our cash flows from operating activities may be impacted by, among other things, the overall strength of the economy, competition from other newspapers and alternative forms of media and competition from alternative emerging technologies. In addition, in recent years there has been a growing shift in advertising dollars from newspaper advertising to other advertising formats, particularly online and other digital platforms such as search and social media websites. Although we expect to fund our capital needs with our available cash, cash generated from operations and available borrowings under the ABL Facility, our indebtedness could adversely affect our financial condition and prevent us from fulfilling our obligations under our debt agreements. The ABL Facility will terminate on July 13, 2014 and we are still in the process of determining if it will be renewed. We have not relied on the ABL Facility since its inception and based on our current forecasts we believe we can adequately fund our future obligations without the ABL Facility. As at November 30, 2013, no amounts were drawn under the ABL Facility. See “Risk Factor - We may not be able to refinance our ABL Facility on attractive terms, or at all” contained in our annual management’s discussion and analysis for the years ended August 31, 2013, 2012 and 2011.

Sources of Cash

Cash flows from operating activities

Our principal sources of liquidity are cash flows from operating activities. For the three months ended November 30, 2013, our cash flows from operating activities were inflows of $4.2 million (2012 – $13.2 million). Cash flows from operating activities decreased $9.0 million for the three months ended November 30, 2013, as compared to the same period in the prior year due to a decrease in operating income before depreciation, amortization and restructuring as well as increased interest and restructuring payments. Partially offsetting these items was the absence of a settlement of a foreign currency interest rate swap designated as a cash flow hedge in the three months ended November 30, 2013.

As at November 30, 2013 we had cash of $35.1 million (August 31, 2013 - $40.8 million) and our ABL Facility remained undrawn (August 31, 2013 – nil). Availability under the ABL Facility as at November 30, 2013 was $40.4 million (August 31, 2013 - $20.7 million).

Cash flows from investing activities

For the three months ended November 30, 2013, our cash flows from investing activities were outflows of $3.7 million (2012 – inflows of $21.1 million). The net cash outflows from investing activities during the three months ended November 30, 2013 include outflows on capital expenditures related to property and equipment of $3.0 million and intangible assets of $0.7 million. The net cash inflows from investing activities during the three months ended November 30, 2012, included the net proceeds received on the sale of property and equipment and asset held-for-sale of $24.7 million, offset by outflows on capital expenditures related to property and equipment of $2.6 million and intangible assets of $1.0 million.

Uses of Cash

Cash flows from financing activities

Cash outflows from financing activities for the three months ended November 30, 2013, were $6.3 million (2012 – $23.3 million), and were related to our indebtedness as discussed below.

Indebtedness

As of November 30, 2013, we have $211.7 million First-Lien Notes and US$268.6 million Second-Lien Notes outstanding (August 31, 2013 - $218.0 million and US$268.6 million, respectively). During the three months ended November 30, 2013 and 2012, we redeemed $6.3 million and $23.2 million, respectively, of aggregate principal amount of First-Lien Notes at par in accordance with the terms and conditions of the First-Lien Notes indenture.

The following tables set out the principal and carrying amount of our long-term debt outstanding as at November 30, 2013 and August 31, 2013. The first column of the table translates, where applicable, our US dollar debt to the Canadian equivalent based on foreign exchange rates specified in our foreign currency swap agreements for swapped debt and at the closing foreign exchange rate on November 30, 2013 and August 31, 2013, respectively, for our non-swapped debt.

| | | As at November 30, 2013 | |

| ($ in thousands of Canadian dollars) | | Principal Outstanding (US$ Debt translated at swapped or period end rates) | | | Principal Outstanding (US$ Debt translated at period end exchange rates) | | | Financing fees, discounts and other | | | Carrying Value | |

| First-Lien Notes (CDN$211.7M) | | | 211,710 | | | | 211,710 | | | | 5,560 | | | | 206,150 | |

| Second-Lien Notes (swapped) (US$167.5M) | | | 173,363 | | | | 177,885 | | | | 4,824 | | | | 173,061 | |

| Second-Lien Notes (non-swapped) (US$101.1M) | | | 107,405 | | | | 107,405 | | | | 2,912 | | | | 104,493 | |

| | | | 492,478 | | | | 497,000 | | | | 13,296 | | | | 483,704 | |

| | | As at August 31, 2013 | |

| ($ in thousands of Canadian dollars) | | Principal Outstanding (US$ Debt translated at swapped or period end rates) | | | Principal Outstanding (US$ Debt translated at period end exchange rates) | | | Financing fees, discounts and other | | | Carrying Value | |

| First-Lien Notes (CDN$218.0M) | | | 217,960 | | | | 217,960 | | | | 5,927 | | | | 212,033 | |

| Second-Lien Notes (swapped) (US$167.5M) | | | 173,363 | | | | 176,378 | | | | 5,005 | | | | 171,373 | |

| Second-Lien Notes (non-swapped) (US$101.1M) | | | 106,495 | | | | 106,495 | | | | 3,021 | | | | 103,474 | |

| | | | 497,818 | | | | 500,833 | | | | 13,953 | | | | 486,880 | |

Financial position as at November 30, 2013 and August 31, 2013

| ($ in thousands of Canadian dollars) | | As at November 30, 2013 | | | As at August 31, 2013 | |

| | | | | | | |

| Current assets | | | 155,653 | | | | 138,200 | |

| Total assets | | | 864,147 | | | | 862,797 | |

| Current liabilities | | | 144,866 | | | | 130,860 | |

Total liabilities (revised) (1) | | | 731,930 | | | | 728,564 | |

Equity (revised) (1) | | | 132,217 | | | | 134,233 | |

(1) See “Other Factors – Changes in accounting policies”.

The increase in our current assets at November 30, 2013 as compared to August 31, 2013 is primarily due to an increase in accounts receivable due to the seasonality of our business partially offset by a decrease in cash. Total assets at November 30, 2013 increased compared to August 31, 2013, as a result of the increase in current assets previously described, partially offset by the decrease in the carrying value of property and equipment and intangible assets as a result of depreciation and amortization during the three months ended November 30, 2013. Current liabilities have increased due to increases in both accrued interest payable on long-term debt and increased restructuring provisions as a result of the Transformation Program. The increase in total liabilities is due to the increase in current liabilities previously described, partially offset by a decrease in other non-current liabilities as a result of a decrease in the carrying value of our net defined benefit plan obligations.

Financial Instruments and Financial Instruments Risk Management

The financial instruments and financial risk management policies and related risks are the same as disclosed in the audited consolidated financial statements for the years ended August 31, 2013, 2012 and 2011.

Guarantees and Off-Balance Sheet Arrangements

We do not have any significant guarantees or off-balance sheet arrangements.

Future Accounting Standards

IFRS 9 – Financial Instruments, a future accounting standard that is issued but not yet effective, is described in our annual management’s discussion and analysis and annual audited consolidated financial statements for the years ended August 31, 2013, 2012 and 2011. We have not yet assessed the impact of the standard or determined whether we will adopt the standard earlier than its current effective date.

Risk Factors

The risks relating to our business are described in the section entitled “Risk Factors” included in our annual management’s discussion and analysis for the years ended August 31, 2013, 2012 and 2011, which section is incorporated by reference herein.

Internal Controls

Disclosure controls and procedures within the Company have been designed to provide reasonable assurance that all relevant information is identified to its management, including the President and Chief Executive Officer (“CEO”) and the Executive Vice President and Chief Financial Officer (“CFO”), as appropriate, to allow required disclosures to be made in a timely fashion.

Internal controls over financial reporting have been designed by management, under the supervision of and with the participation of the CEO and CFO, to provide reasonable assurance regarding the reliability of the Company’s financial reporting and the preparation of financial statements for external purposes in accordance with IFRS.

The CEO and CFO have evaluated whether there were changes to Postmedia's internal control over financial reporting during the three months ended November 30, 2013, that have materially affected, or are reasonably likely to materially affect, internal control over financial reporting. There were no changes identified during their evaluation.

Share Capital

As at January 6, 2014 we had the following number of shares and options outstanding:

Class C voting shares | | | 951,661 | |

Class NC variable voting shares | | | 39,257,958 | |

Total shares outstanding | | | 40,209,619 | |

| | | | | |

Total options and restricted share units outstanding (1) | | | 1,800,000 | |

(1) The total options and restricted share units outstanding are convertible into 1,730,000 Class C voting shares and 70,000 Class NC variable voting shares. The total options and restricted share units outstanding include 1,280,000 options that are vested and 520,000 options that are unvested.

16