| FREE WRITING PROSPECTUS | ||

| FILED PURSUANT TO RULE 433 | ||

| REGISTRATION FILE NO.: 333-227784-05 | ||

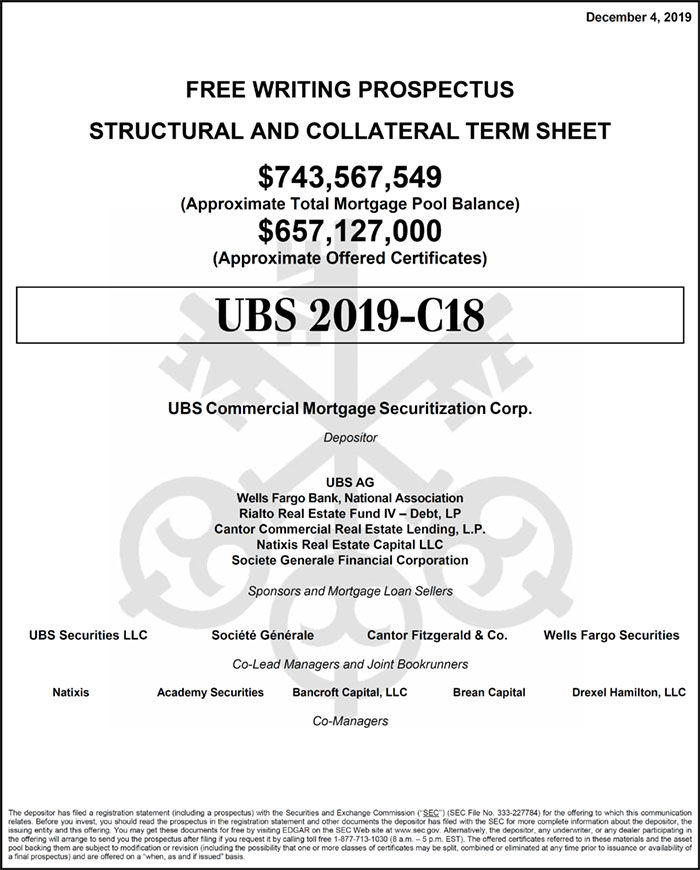

December 4, 2019 FREE WRITING PROSPECTUS STRUCTURAL AND COLLATERAL TERM SHEET $743,567,549 (Approximate Total Mortgage Pool Balance)$657,127,000(Approximate Offered Certificates) UBS 2019-C18 UBS Commercial Mortgage Securitization Corp.DepositorUBS AG Wells Fargo Bank, National Association Rialto Real Estate Fund IV – Debt, LP Cantor Commercial Real Estate Lending, L.P. Natixis Real Estate Capital LLC Societe Generale Financial CorporationSponsors and Mortgage Loan SellersUBS Securities LLC Société Générale Cantor Fitzgerald & Co. Wells Fargo SecuritiesCo-Lead Managers and Joint BookrunnersNatixis Academy Securities Bancroft Capital, LLC Brean Capital Drexel Hamilton, LLCCo-ManagersThe depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-227784) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-877-713-1030 (8 a.m. – 5 p.m. EST). The offered certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis.

1

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

Nothing in this document constitutes an offer of securities for sale in any jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered prior to the time of sale and ultimately by the final prospectus relating to the offered certificates. These materials are subject to change, completion, supplement or amendment from time to time.

This free writing prospectus has been prepared by the underwriters for information purposes only and does not constitute, in whole or in part, a prospectus for the purposes of Directive 2003/71/EC (as amended) and/or Part VI of the Financial Services and Markets Act 2000, as amended, or other offering document.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward- looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) that have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of the offered certificates. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the offered certificates may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of UBS Securities LLC, Wells Fargo Securities, LLC, SG Americas Securities, LLC, Cantor Fitzgerald & Co., Natixis Securities Americas LLC, Academy Securities, Inc., Bancroft Capital, LLC, Brean Capital, LLC or Drexel Hamilton, LLC or any of their respective affiliates, make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the offered certificates. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

Wells Fargo Securities is the trade name for the capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including but not limited to Wells Fargo Securities, LLC, a member of NYSE, FINRA, NFA and SIPC, Wells Fargo Prime Services, LLC, a member of FINRA, NFA and SIPC, and Wells Fargo Bank, N.A. Wells Fargo Securities, LLC and Wells Fargo Prime Services, LLC are distinct entities from affiliated banks and thrifts.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The offered certificates described herein are not suitable investments for all investors. In particular, you should not purchase any class of offered certificates unless you understand and are able to bear the prepayment, credit, liquidity and market risks associated with such class of certificates. For those reasons and for the reasons set forth under the heading “Risk Factors” in the Preliminary Prospectus, the yield to maturity and the aggregate amount and timing of distributions on the offered certificates are subject to material variability from period to period and give rise to the potential for significant loss over the life of such certificates. The interaction of these factors and their effects are impossible to predict and are likely to change from time to time. As a result, an investment in the offered certificates involves substantial risks and uncertainties and should be considered only by sophisticated institutional investors with substantial investment experience with similar types of securities and who have conducted appropriate due diligence on the mortgage loans and the certificates. Potential investors are advised and encouraged to review the Preliminary Prospectus in full and to consult with their legal, tax, accounting and other advisors prior to making any investment in the offered certificates described in this free writing prospectus.

This free writing prospectus is not to be construed as an offer to sell or the solicitation of any offer to buy any security in any jurisdiction where such an offer or solicitation would be illegal. The information contained in this free writing prospectus may not pertain to any securities that will actually be sold. The information contained in this free writing prospectus may be based on assumptions regarding market conditions and other matters as reflected in this free writing prospectus. We make no representations regarding the reasonableness of such assumptions or the likelihood that any of such assumptions will coincide with actual market conditions or events, and this free writing prospectus should not be relied upon for such purposes. The underwriters and their respective affiliates, officers, directors, partners and employees, including persons involved in the preparation or issuance of this free writing prospectus may, from time to time, have long or short positions in, and buy or sell, the offered certificates mentioned in this free writing prospectus or derivatives thereof (including options). Information contained in this free writing prospectus is current as of the date appearing on this free writing prospectus only. None of UBS Securities LLC, Wells Fargo Securities, LLC, SG Americas Securities, LLC, Cantor Fitzgerald & Co., Natixis Securities Americas LLC, Academy Securities, Inc., Bancroft Capital, LLC, Brean Capital, LLC or Drexel Hamilton, LLC provides accounting, tax or legal advice.

2

The issuing entity will be relying upon an exclusion or exemption from the definition of “investment company” under the Investment Company Act of 1940, as amended (the “Investment Company Act”), contained in Section 3(c)(5) of the Investment Company Act or Rule 3a-7 under the Investment Company Act, although there may be additional exclusions or exemptions available to the issuing entity. The issuing entity is being structured so as not to constitute a “covered fund” for purposes of the Volcker Rule under the Dodd-Frank Act (both as defined in “Risk Factors—Other Risks Relating to the Certificates—Legal and Regulatory Provisions Affecting Investors Could Adversely Affect the Liquidity of the Offered Certificates” in the Preliminary Prospectus). See also “Legal Investment” in the Preliminary Prospectus.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) any representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

3

UBS 2019-C18

Capitalized terms used but not defined herein have the meanings assigned to them in the preliminary prospectus expected to be dated December 4, 2019 relating to the offered certificates (hereinafter referred to as the “Preliminary Prospectus”).

| KEY FEATURES OF SECURITIZATION |

| Offering Terms: | |

| Co-Lead Managers and Joint Bookrunners: | UBS Securities LLC Wells Fargo Securities, LLC SG Americas Securities, LLC Cantor Fitzgerald & Co. |

| Co-Managers: | Natixis Securities Americas LLC Academy Securities, Inc. Bancroft Capital, LLC Brean Capital, LLC Drexel Hamilton, LLC |

| Mortgage Loan Sellers: | UBS AG, by and through its branch office at 1285 Avenue of the Americas, New York, New York (“UBS AG”) (45.1%), Wells Fargo Bank, National Association (“WFB”) (14.8%), Rialto Real Estate Fund IV – Debt, LP (“RREF”) (13.1%), Cantor Commercial Real Estate Lending, L.P. (“CCRE”) (12.9%), Natixis Real Estate Capital LLC (“Natixis”) (8.4%) and Societe Generale Financial Corporation (“SG”) (5.7%) |

| Master Servicer: | Wells Fargo Bank, National Association |

| Operating Advisor: | Park Bridge Lender Services LLC |

| Asset Representations Reviewer: | Park Bridge Lender Services LLC |

| Special Servicer: | Rialto Capital Advisors, LLC |

| Trustee: | Wilmington Trust, National Association |

| Certificate Administrator: | Wells Fargo Bank, National Association |

| Rating Agencies: | Fitch Ratings, Inc., Kroll Bond Rating Agency, Inc. and Moody’s Investors Service, Inc. |

| U.S. Credit Risk Retention: | RREF, the retaining sponsor, intends to satisfy the U.S. credit risk retention requirement through the purchase by one or more of its “majority-owned affiliates” (as defined in the credit risk retention rules), from the underwriters and initial purchasers, on the Closing Date, of (i) an “eligible horizontal residual interest” comprised of the Class NR-RR certificates that are not part of the VRR Interest and (ii) an “eligible vertical interest” comprised of a certain percentage of the certificate balance, notional amount or percentage interest in each class of certificates (other than the Class R certificates) (the “VRR Interest”). The aggregate estimated fair value of the “eligible horizontal residual interest” will equal approximately 0.81279% of the estimated fair value of all of the certificates (other than the Class R certificates) issued by the issuing entity and the VRR Interest will consist of the portion of each class of certificates (other than the Class R certificates) necessary to satisfy the credit risk retention rules. As RREF is retaining its right to sell the “eligible horizontal residual interest” to a subsequent third party purchaser in accordance with the provisions of the credit risk retention rules, the pooling and servicing agreement will include the required provisions applicable to an operating advisor necessary for the securitization to comply with the credit risk retention rules utilizing the “third party purchaser” option. See “Operating Advisor” below. For further discussion on the manner in which the U.S. credit risk retention requirements will be satisfied see “Credit Risk Retention” in the Preliminary Prospectus. |

| EU Credit Risk Retention: | None of the sponsors, the depositor, the issuing entity, the underwriters or any other person is required or intends to retain a material net economic interest in the securitization constituted by the issue of the Offered Certificates, or to take any other action in respect of such securitization, in a manner prescribed or contemplated by the European Union’s Securitization Regulation (Regulation (EU) 2017/2402). In particular, no person undertakes to take any action which may be required by any investor for the purposes of their compliance with such regulations or similar requirements. |

| Determination Date: | The 11th day of each month, or if such 11th day is not a business day, the succeeding business day, commencing in January 2020. |

| Distribution Date: | The 4th business day following the Determination Date in each month, commencing in January 2020. |

| Cut-off Date: | The mortgage loans will be considered part of the trust fund as of their respective cut-off dates. The cut-off date with respect to each mortgage loan is the respective due date for the monthly debt service payment that is due in December 2019 (or, in the case of any mortgage loan that has its first due date after December 2019, the date that would have been its due date in December 2019 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). |

| Closing Date: | On or about December 20, 2019 |

| Settlement Terms: | DTC, Euroclear and Clearstream, same day funds, with accrued interest. |

| ERISA Eligible: | All of the offered certificates are expected to be ERISA eligible. |

| SMMEA Eligible: | None of the offered certificates will be SMMEA eligible. |

| Day Count: | 30/360 |

| Tax Treatment: | REMIC |

| Rated Final Distribution Date: | December 2052 |

| Minimum Denominations: | $10,000 (or $1,000,000 with respect to the Class X-A and Class X-B Certificates) and in each case in multiples of $1 thereafter. |

| Clean-up Call: | 1.0% |

| Distribution of Collateral by Property Type |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

UBS 2019-C18

| TRANSACTION HIGHLIGHTS |

| Mortgage Loan Sellers | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Initial Outstanding Pool Balance(1) | ||||

| UBS AG | 19 | 80 | $335,051,250 | 45.1% | ||||

| Wells Fargo Bank, National Association | 8 | 8 | $110,349,639 | 14.8% | ||||

| Rialto Real Estate Fund IV – Debt, LP(2) | 12 | 19 | $97,310,000 | 13.1% | ||||

| Cantor Commercial Real Estate Lending, L.P. | 9 | 10 | $96,128,049 | 12.9% | ||||

| Natixis Real Estate Capital LLC | 3 | 6 | $62,128,611 | 8.4% | ||||

| Societe Generale Financial Corporation | 4 | 4 | $42,600,000 | 5.7% | ||||

| Total | 55 | 127 | $743,567,549 | 100.0% | ||||

| Pooled Collateral Facts: | |

| Initial Outstanding Pool Balance: | $743,567,549 |

| Number of Mortgage Loans: | 55 |

| Number of Mortgaged Properties: | 127 |

| Average Mortgage Loan Cut-off Date Balance: | $13,519,410 |

| Average Mortgaged Property Cut-off Date Balance: | $5,854,863 |

| Weighted Average Mortgage Rate: | 3.966% |

| Weighted Average Mortgage Loan Original Term to Maturity Date or ARD (months)(3): | 114 |

| Weighted Average Mortgage Loan Remaining Term to Maturity Date or ARD (months)(3): | 113 |

| Weighted Average Mortgage Loan Seasoning (months): | 1 |

| % of Mortgage Loans Secured by a Property or a Portfolio of Mortgaged Properties Leased to a Single Tenant: | 12.2% |

| Credit Statistics | |

| Weighted Average Mortgage Loan U/W NCF DSCR(4): | 2.33x |

| Weighted Average Mortgage Loan Cut-off Date LTV(4)(5): | 59.5% |

| Weighted Average Mortgage Loan Maturity Date or ARD LTV(3)(4)(5): | 53.2% |

| Weighted Average U/W NOI Debt Yield(4): | 11.4% |

| Amortization Overview | |

| % Mortgage Loans which pay Interest Only through Maturity Date or ARD(3): | 48.6% |

| % Mortgage Loans with Amortization through Maturity Date: | 28.7% |

| % Mortgage Loans which pay Interest Only followed by Amortization through Maturity Date: | 22.8% |

| Weighted Average Remaining Amortization Term (months)(6): | 341 |

| Loan Structural Features | |

| % Mortgage Loans with Upfront or Ongoing Tax Reserves: | 66.4% |

| % Mortgage Loans with Upfront or Ongoing Replacement Reserves(7): | 69.9% |

| % Mortgage Loans with Upfront or Ongoing Insurance Reserves: | 62.3% |

| % Mortgage Loans with Upfront or Ongoing TI/LC Reserves(8): | 63.1% |

| % Mortgage Loans with Upfront Engineering Reserves: | 46.8% |

| % Mortgage Loans with Upfront or Ongoing Other Reserves: | 51.9% |

| % Mortgage Loans with In Place Hard Lockboxes: | 55.0% |

| % Mortgage Loans with Cash Traps Triggered at DSCR Levels ≥ 1.05x: | 84.7% |

| % Mortgage Loans with Defeasance Only After a Lockout Period and Prior to an Open Period: | 79.3% |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge Only After a Lockout Period and Prior to an Open Period: | 12.0% |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge or Defeasance After a Lockout Period and Prior to an Open Period: | 4.4% |

| % Mortgage Loans with Prepayment with a Yield Maintenance Charge or Defeasance After a Prepayment with a Yield Maintenance Charge Period Prior to an Open Period: | 4.3% |

Please see footnotes on the following page.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

UBS 2019-C18

| TRANSACTION HIGHLIGHTS |

| (1) | Unless otherwise indicated, all references to “% of Initial Outstanding Pool Balance” in this Term Sheet reflect a percentage of the aggregate principal balance of the mortgage pool as of the Cut-off Date, after application of all payments of principal due during or prior to December 2019. |

| (2) | Rialto Real Estate Fund IV – Debt, LP acquired each of the mortgage loans it is selling to the depositor from BSPRT CMBS Finance, LLC, Ladder Capital Finance LLC, or CIBC Inc. Such mortgage loans were re-underwritten pursuant to Rialto Real Estate Fund IV – Debt, LP’s underwriting guidelines. |

| (3) | For any mortgage loan with an anticipated repayment date, calculated to or as of, as applicable, that anticipated repayment date. |

| (4) | With respect to any mortgage loan that is part of a whole loan, unless otherwise indicated, LTV, DSCR and Debt Yield calculations in this Term Sheet include any relatedpari passu companion loans and exclude any subordinate companion loans, as applicable. Additionally, LTV, DSCR and Debt Yield figures in this Term Sheet are calculated for mortgage loans without regard to any additional indebtedness that may be incurred at a future date. See “Description of the Mortgage Pool—Mortgage Pool Characteristics” in the Preliminary Prospectus and Annex A-1 to the Preliminary Prospectus. |

| (5) | The Cut-off Date LTV and Maturity Date or ARD LTV for the following mortgage loans are based on an appraised value for one or more mortgaged properties that is not an “As-Is” appraised value. |

With respect to the mortgage loan secured by the portfolio of mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as Wyndham National Hotel Portfolio, the Cut-off Date LTV, Maturity Date or ARD LTV, and appraised value are based on the aggregate sum of the available "As-Is" and “As-Complete” appraised value of $215,000,000, as of August 1, 2019, which assumes the completion of all renovations for which the lender reserved for at origination. The sum of the “As-Is” appraised values on a stand-alone basis is $209,900,000. The Cut-off Date LTV and Maturity Date or ARD LTV based on the appraised value representing the sum of the “As-Is” appraised values are 69.1% and 47.8%, respectively.

With respect to the mortgage loan identified on Annex A-1 to the Preliminary Prospectus as Holiday Inn Express Lincoln CA, the Cut-off Date LTV, Maturity Date or ARD LTV, and appraised value are based on the “As-Complete Value” appraised value of $15,000,000, as of October 1, 2020, which assumes the completion of all renovations for which the lender reserved for at origination. The “As-Is” appraised value is $13,400,000. The Cut-off Date LTV and Maturity Date or ARD LTV based on the “As-Is” appraised values are 67.2% and 60.3%, respectively.

With respect to the mortgage loan identified on Annex A-1 to the Preliminary Prospectus as 530 West 136th Street, the Cut-off Date LTV, Maturity Date or ARD LTV, and appraised value are based on the "As-Stabilized" appraised value of $10,400,000, as of September 13, 2019, which assumes the completion of all renovations for which the lender reserved for at origination. The "As-Is" appraised value is $10,300,000 as of September 13, 2019. The Cut-off Date LTV and Maturity Date or ARD LTV based on the "As-Is" appraised values are 63.3% and 63.3%, respectively.

With respect to the mortgage loan identified on Annex A-1 to the Preliminary Prospectus as BNSF Logistics, the Cut-off Date LTV, Maturity Date or ARD LTV, and appraised value are based on the “As-Complete Value” appraised value of $8,300,000, as of November 3, 2019, which assumes the completion of all renovations for which the lender reserved for at origination. The “As-Is” appraised value is $7,000,000. The Cut-off Date LTV and Maturity Date or ARD LTV based on the “As-Is” appraised values are 77.1% and 65.8%, respectively.

With respect to the mortgage loan identified on Annex A-1 to the Preliminary Prospectus as Brickyard Plaza, the Cut-off Date LTV, Maturity Date or ARD LTV, and appraised value are based on the conclusion of $6,400,000, which assumes the lease-up costs for recently signed leases are escrowed and available to any potential purchaser at origination. The “As-Is” appraised value is $5,150,000. The Cut-off Date LTV and Maturity Date or ARD LTV based on the “As-Is” appraised values are 77.7% and 77.7%, respectively.

| (6) | Excludes mortgage loans that are interest-only for the full loan term to maturity or the related anticipated repayment date. |

| (7) | Includes FF&E Reserves. |

| (8) | Represents the percent of the allocated aggregate principal balance of the mortgage pool as of the Cut-off Date of only the office, retail, industrial, mixed use properties and the mortgage loan identified on Annex A-1 to the Preliminary Prospectus as Chroma Apartments. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

UBS 2019-C18

| STRUCTURE OVERVIEW |

OFFERED CERTIFICATES

| Class(1) | Ratings(2) (Fitch/KBRA/Moody’s) | Approx. Initial Certificate Principal Balance or Notional Amount(3) | Approx. Initial Available Certificate Principal Balance or Notional Amount(3) | Approx. Initial Retained Certificate Principal Balance or Notional Amount(3)(4) | Initial Subordination Levels | Expected Weighted Average Life (years)(5) | Principal Window (months)(5) | Certificate Principal to Value Ratio(6) | Underwritten NOI Debt Yield(7) |

| Class A-1 | AAAsf / AAA(sf) / Aaa(sf) | $29,089,000 | $27,865,000 | $1,224,000 | 30.000%(8) | 2.81 | 1 - 58 | 41.7% | 16.3% |

| Class A-2 | AAAsf / AAA(sf) / Aaa(sf) | $69,160,000 | $66,250,000 | $2,910,000 | 30.000%(8) | 4.88 | 58 - 60 | 41.7% | 16.3% |

| Class A-SB | AAAsf / AAA(sf) / Aaa(sf) | $35,630,000 | $34,130,000 | $1,500,000 | 30.000%(8) | 7.21 | 60 - 111 | 41.7% | 16.3% |

| Class A-3 | AAAsf / AAA(sf) / Aaa(sf) | (9) | (9) | (9) | 30.000%(8) | (9) | (9) | 41.7% | 16.3% |

| Class A-4 | AAAsf / AAA(sf) / Aaa(sf) | (9) | (9) | (9) | 30.000%(8) | (9) | (9) | 41.7% | 16.3% |

| Class X-A(10) | AAAsf / AAA(sf) / Aaa(sf) | $520,497,000(11) | $498,596,000 | $21,901,000 | N/A | N/A | N/A | N/A | N/A |

| Class X-B(10) | A-sf / AAA(sf) / NR | $136,630,000(11) | $130,880,000 | $5,750,000 | N/A | N/A | N/A | N/A | N/A |

| Class A-S | AAAsf / AAA(sf) / Aa2(sf) | $72,498,000 | $69,447,000 | $3,051,000 | 20.250% | 9.99 | 120 - 120 | 47.5% | 14.3% |

| Class B | AA-sf / AA(sf) / NR | $33,460,000 | $32,052,000 | $1,408,000 | 15.750% | 9.99 | 120 - 120 | 50.2% | 13.5% |

| Class C | A-sf / A(sf) / NR | $30,672,000 | $29,381,000 | $1,291,000 | 11.625% | 9.99 | 120 - 120 | 52.6% | 12.9% |

NON-OFFERED CERTIFICATES(12)

| Class(1) | Ratings(2) (Fitch/KBRA/Moody’s) | Approx. Initial Certificate Amount(3) | Approx. Initial Available Certificate Principal Balance or Notional Amount(3) | Approx. Initial Retained Certificate Principal Balance or Notional Amount(3)(4) | Initial Subordination Levels | Expected Weighted Average Life (years)(5) | Principal Window (months)(5) | Certificate Value Ratio(6) | Underwritten NOI Debt Yield(7) |

| Class X-D(10) | BBB-sf / BBB(sf) / NR | $36,249,000(11) | $34,723,000 | $1,526,000 | N/A | N/A | N/A | N/A | N/A |

| Class X-F(10) | BB-sf / BB(sf) / NR | $14,872,000(11) | $14,246,000 | $626,000 | N/A | N/A | N/A | N/A | N/A |

| Class X-G(10) | B-sf / B(sf) / NR | $7,435,000(11) | $7,122,000 | $313,000 | N/A | N/A | N/A | N/A | N/A |

| Class D | BBBsf / BBB+(sf) / NR | $20,448,000 | $19,587,000 | $861,000 | 8.875% | 9.99 | 120 - 120 | 54.3% | 12.5% |

| Class E | BBB-sf / BBB(sf) / NR | $15,801,000 | $15,136,000 | $665,000 | 6.750% | 9.99 | 120 - 120 | 55.5% | 12.2% |

| Class F | BB-sf / BB(sf) / NR | $14,872,000 | $14,246,000 | $626,000 | 4.750% | 9.99 | 120 - 120 | 56.7% | 12.0% |

| Class G | B-sf / B(sf) / NR | $7,435,000 | $7,122,000 | $313,000 | 3.750% | 9.99 | 120 - 120 | 57.3% | 11.8% |

| Class NR-RR | NR / NR / NR | $27,884,548 | $26,710,548 | $1,174,000 | 0.000% | 9.99 | 120 - 120 | 59.5% | 11.4% |

Please see footnotes on the following page.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

UBS 2019-C18

| STRUCTURE OVERVIEW |

| (1) | Theper annum pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class NR-RR Certificates (collectively, the “principal balance certificates”) will, in each case, equal one of: (i) a fixed rateper annum, (ii) a variable rateper annum equal to the weighted average of the net mortgage interest rates on the mortgage loans for the related distribution date adjusted as necessary to a 30/360 basis (the “WAC Rate”), (iii) a variable rateper annum equal to the lesser of (a) a fixed rate and (b) the WAC Rate or (iv) a variable rateper annum equal to the WAC Rate minus a specified percentage. |

| (2) | Ratings shown are those of Fitch Ratings, Inc. (“Fitch”), Kroll Bond Rating Agency, Inc. (“KBRA”) and Moody’s Investors Service, Inc. (“Moody’s”). Certain nationally recognized statistical rating organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended, or otherwise to rate the certificates. There can be no assurance as to what ratings a non-hired nationally recognized statistical rating organization would assign. See “Risk Factors—Other Risks Relating to the Certificates—Nationally Recognized Statistical Rating Organizations May Assign Different Ratings to the Certificates; Ratings of the Certificates Reflect Only the Views of the Applicable Rating Agencies as of the Dates Such Ratings Were Issued; Ratings May Affect ERISA Eligibility; Ratings May Be Downgraded” and “Ratings” in the Preliminary Prospectus. Fitch, KBRA and Moody’s have informed us that the “sf” designation in their ratings represents an identifier for structured finance product ratings. |

| (3) | Approximate; subject to a permitted variance of plus or minus 5% on the Closing Date, including in connection with any variation in the portion of the certificate balances and notional amounts of the classes comprising the VRR Interest following the calculation of the actual fair value of the certificates (other than the Class R certificates) issued by the issuing entity, and further subject to the discussion in footnote (9) below. In addition, the notional amounts of each class of Class X Certificates may vary depending upon the final pricing of all classes of principal balance certificates whose certificate balances comprise such notional amounts and, if as a result of such pricing the pass-through rate of the Class X Certificates, as applicable, would be equal to zero, such class of certificates may not be issued on the Closing Date of this securitization. |

| (4) | On the Closing Date, the certificates (other than the Class R certificates) (collectively, the “VRR Interest”) with the Initial Certificate Principal Balances or Notional Amounts, as applicable, set forth in the above table under “Approx. Initial Retained Certificate Principal Balance or Notional Amount” are expected to be sold by theunderwriters and the initial purchasersto RREF or a majority-owned affiliate of RREF as described in “Credit Risk Retention—General” in the Preliminary Prospectus. |

| (5) | The principal window is expressed in months following the Closing Date and reflects the period during which distributions of principal would be received under the assumptions set forth in the following sentence. The expected weighted average life and principal window figures set forth above are based on the following assumptions, among others: (i) no defaults or subsequent losses on the mortgage loans; (ii) no extensions of maturity dates of the mortgage loans; (iii) payment in full on the stated maturity date or on the anticipated repayment date; and (iv) no prepayments of the mortgage loans prior to maturity or the anticipated repayment date. See the structuring assumptions set forth under “Yield and Maturity Considerations—Weighted Average Life” in the Preliminary Prospectus. |

| (6) | “Certificate Principal to Value Ratio” for any class of principal balance certificates is calculated as the product of (a) the weighted average Cut-off Date LTV Ratio of the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial certificate balance of such class of principal balance certificates and all other classes of principal balance certificates that are senior to such class, and the denominator of which is the total initial certificate balance of all the principal balance certificates. The Certificate Principal to Value Ratios of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (7) | “Underwritten NOI Debt Yield” for any class of principal balance certificates is calculated as the product of (a) the weighted average UW NOI Debt Yield for the mortgage pool, multiplied by (b) a fraction, the numerator of which is the total initial certificate balance of all the principal balance certificates, and the denominator of which is the total initial certificate balance of such class of principal balance certificates and all other classes of principal balance certificates, if any, that are senior to such class. The Underwritten NOI Debt Yields of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates are calculated in the aggregate for those classes as if they were a single class. |

| (8) | The initial subordination levels for the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates represent the approximate credit support for those classes in the aggregate. |

| (9) | The exact initial certificate balances of the Class A-3 and Class A-4 certificates are unknown and will be determined based on the final pricing of those classes of certificates. However, the respective initial certificate balances, assumed final distribution date, weighted average lives and principal windows of the Class A-3 and Class A-4 certificates are expected to be within the applicable ranges reflected in the following chart. The aggregate initial certificate balance of the Class A-3 and Class A-4 certificates is expected to be approximately $386,618,000 subject to a variance of plus or minus 5%. In the event that the Class A-3 Certificates are issued at $386,618,000, the Class A-4 Certificates will not be issued. |

Class of Certificates | Expected Range of Approximate Initial Certificate Balance | Expected Range of Assumed Final Distribution Date | Expected Range of Weighted Average Life (Years) | Expected Range of Principal Window (Months) | ||||

| Class A-3 | $25,000,000 - $386,618,000 | Mar 2029 / Dec 2029 | 9.24 / 9.87 | 111-111 / 111-120 | ||||

| Class A-4 | $211,618,000 - $361,618,000 | Dec 2029 / Dec 2029 | 9.91 / 9.96 | 111-120 / 119-120 |

| (10) | The pass-through rate for the Class X-A certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the WAC Rate, over (b) the weighted average of the pass-through rates on the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates for the related distribution date, weighted on the basis of their respective certificate balances outstanding immediately prior to that distribution date. The pass-through rate for the Class X-B certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the WAC Rate, over (b) the weighted average of the pass-through rates on the Class A-S, Class B and Class C certificates for the related distribution date, weighted on the basis of their respective certificate balances outstanding immediately prior to that distribution date. The pass-through rate for the Class X-D certificates for any distribution date will be aper annumrate equal to the excess, if any, of (a) the WAC Rate, over (b) the weighted average of the pass-through rates on the Class D and Class E certificates for the related distribution date, weighted on the basis of their respective certificate balances outstanding immediately prior to that distribution date. The pass-through rate for the Class X-F certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the WAC Rate, over (b) the pass-through rate on the Class F certificate for the related distribution date. The pass-through rate for the Class X-G certificates for any distribution date will be aper annum rate equal to the excess, if any, of (a) the WAC Rate, over (b) the pass-through rate on the Class G certificates for the related distribution date. |

| (11) | The Class X-A, Class X-B, Class X-D, Class X-F and Class X-G certificates (collectively, the “Class X Certificates”) are notional amount certificates and will not be entitled to distributions of principal. The notional amount of the Class X-A certificates will be equal to the aggregate certificate balance of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates. The notional amount of the Class X-B certificates will be equal to the aggregate certificate balance of the Class A-S, Class B and Class C certificates. The notional amount of the Class X-D will be equal to the aggregate certificate balance of the Class D and Class E certificates. The notional amount of the Class X-F will be equal to the certificate balance of the Class F certificates. The notional amount of the Class X-G will be equal to the certificate balance of the Class G certificates. |

| (12) | Not offered pursuant to the Preliminary Prospectus or this Term Sheet. Information provided in this Term Sheet regarding the characteristics of these certificates is provided only to enhance your understanding of the offered certificates. The non-offered certificates also include the Class Z and Class R certificates, which do not have a certificate balance, notional amount, pass-through rate, rating or rated final distribution date, and which are not shown in the chart. The Class Z certificates represent the entitlement to distributions of excess interest accrued on the mortgage loans with an anticipated repayment date, as further described in the Preliminary Prospectus. The Class R certificates represent the beneficial ownership of the residual interest in each of the real estate mortgage investment conduits, as further described in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

UBS 2019-C18

| STRUCTURE OVERVIEW |

| Class A-2 Principal Paydown(1) |

| Class | Mortgage Loan Seller | Mortgage Loan | Property Type | Cut-off Dates Balance | Remaining Term to Maturity (Mos.) | Cut-off Date LTV Ratio | U/W NCF DSCR | U/W NOI Debt Yield |

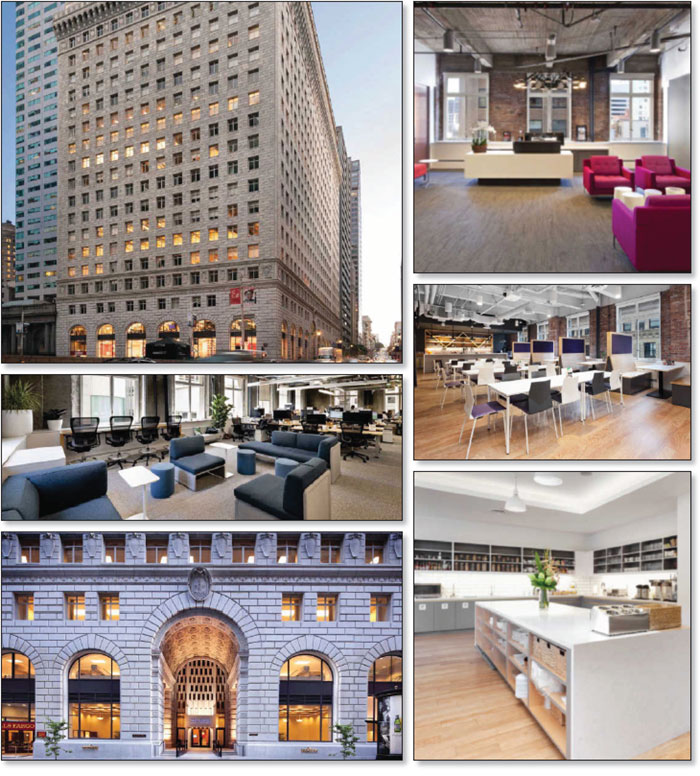

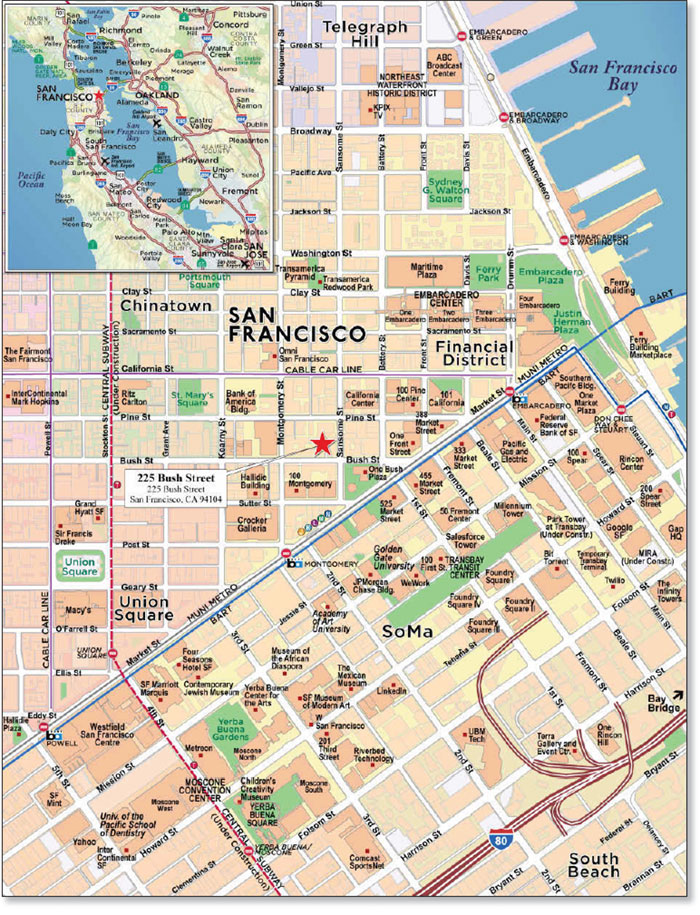

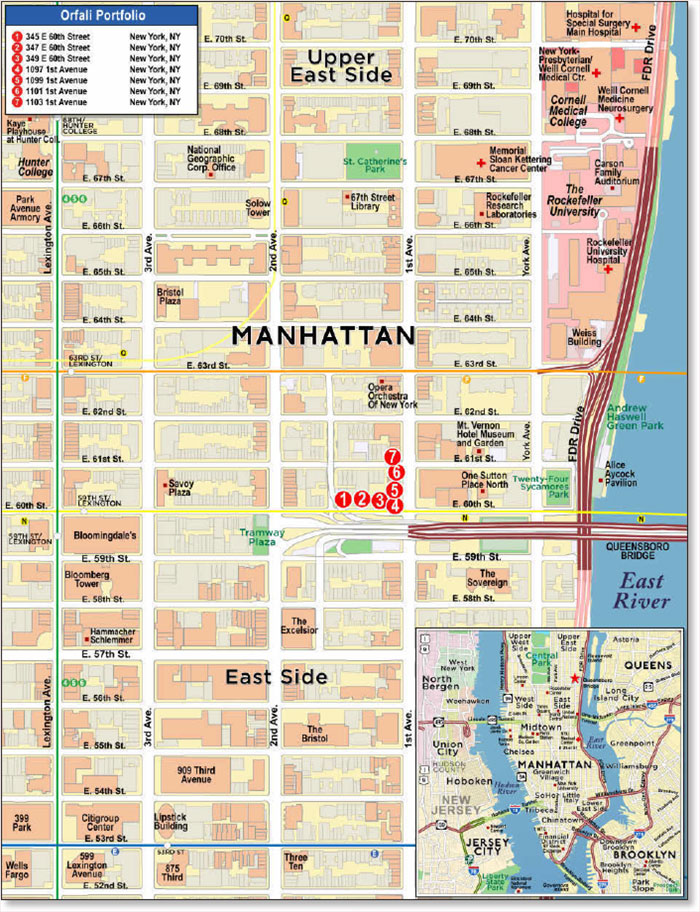

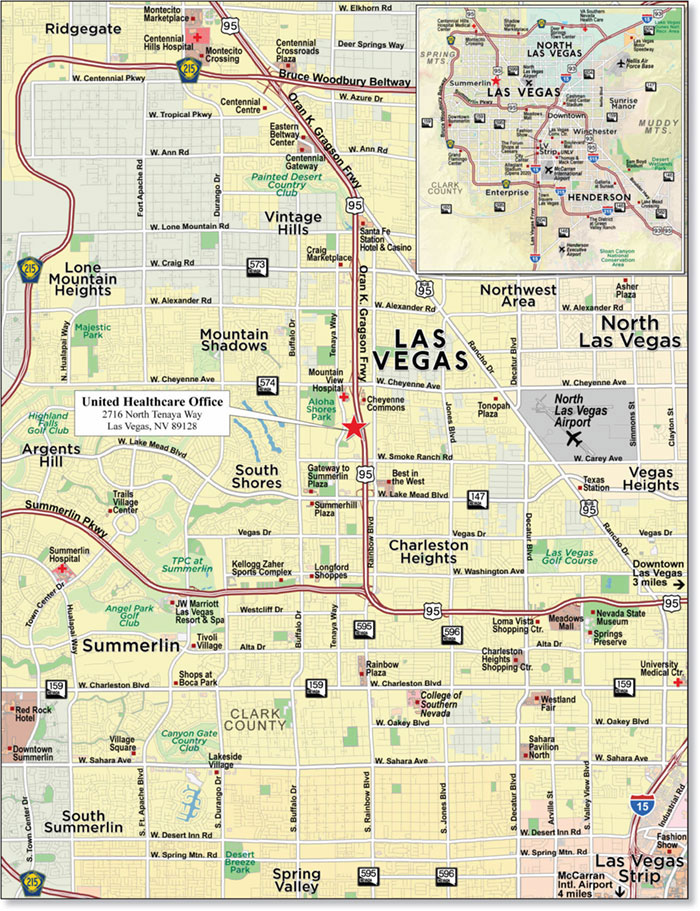

| A-2 | UBS AG | 225 Bush | Office | $35,000,000 | 59 | 34.6% | 3.85x | 13.4% |

| A-2 | UBS AG | United Healthcare Office | Office | $26,800,000 | 58 | 66.7% | 1.56x | 10.2% |

| A-2 | WFB | CubeSmart Penn's Landing | Self Storage | $8,550,000 | 60 | 66.4% | 1.97x | 9.4% |

| (1) | This table reflects the mortgage loan whose balloon payment will be applied to pay down the Class A-2 certificates, assuming (i) that none of the mortgage loans experience prepayments (prior to maturity or anticipated repayment date, as applicable), defaults or losses, (ii) there are no extensions of maturity dates or anticipated repayment dates, as applicable and (iii) each mortgage loan is paid in full on its stated maturity date. See “Yield and Maturity Considerations—Yield Considerations” in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

UBS 2019-C18

| STRUCTURE OVERVIEW |

| Principal Distributions: | Payments in respect of principal of the certificates will be distributed, first, to the Class A-SB Certificates, until the certificate balance of such class is reduced to the planned principal balance for the related Distribution Date set forth on Annex E to the Preliminary Prospectus, then, to the Class A-1, Class A-2, Class A-3, Class A-4, Class A-SB, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class NR-RR Certificates, in that order, until the certificate balance of each such class is reduced to zero. Notwithstanding the foregoing, if the aggregate certificate balances of the Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class NR-RR Certificates have been reduced to zero as a result of the allocation of mortgage loan losses to those certificates distributions in respect of principal of the certificates will be distributed,first, to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates, on apro ratabasis, based on the certificate principal balance of each such class, then, to the extent of any recoveries on realized losses, to the Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class NR-RR Certificates, in that order, in each case until the certificate balance of each such class is reduced to zero (or previously allocated realized losses have been fully reimbursed).

The Class X Certificates will not be entitled to receive distributions of principal; however, (i) the notional amount of the Class X-A Certificates will be reduced by the aggregate amount of principal distributions and realized losses, if any, allocated to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates, (ii) the notional amount of the Class X-B Certificates will be reduced by the aggregate amount of principal distributions and realized losses, if any, allocated to the Class A-S, Class B and Class C Certificates, (iii) the notional amount of the Class X-D Certificates will be reduced by the aggregate amount of principal distributions and realized losses, if any, allocated to the Class D and Class E Certificates, (iv) the notional amount of the Class X-F Certificates will be reduced by the principal distributions and realized losses if any, allocated to the Class F Certificates and (v) the notional amount of the Class X-G Certificates will be reduced by the principal distributions and realized losses if any, allocated to the Class G Certificates.

|

| Interest Distributions: | On each Distribution Date, interest accrued for each class of the certificates at the applicable pass-through rate will be distributed in the following order of priority, to the extent of available funds:first, to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class X-A, Class X-B, Class X-D, Class X-F and Class X-G Certificates, on apro rata basis, based on the accrued and unpaid interest on each such class and then, to the Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class NR-RR Certificates, in that order, in each case until the interest payable to each such class is paid in full.

Theper annum pass-through rates applicable to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class C, Class D, Class E, Class F, Class G and Class NR-RR Certificates for each Distribution Date will equal one of: (i) a fixed rateper annum, (ii) the WAC Rate, (iii) a variable rate equal to the lesser of (a) a fixed rate and (b) the WAC Rate, or (iv) a variable rate equal to the WAC Rate less a specified percentage.

As further described in the Preliminary Prospectus, theper annum pass-through rate on the Class X-A Certificates will generally be equal to the excess, if any, of (a) the WAC Rate, over (b) the weighted average of the pass-through rates of the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates, weighted on the basis of their respective certificate balances outstanding immediately prior to that Distribution Date as described in the Preliminary Prospectus. Theper annum pass-through rate on the Class X-B Certificates will generally be equal to the excess, if any, of (a) the WAC Rate, over (b) the weighted average of the pass-through rates of the Class A-S, Class B and Class C Certificates, weighted on the basis of their respective certificate balances outstanding immediately prior to that Distribution Date as described in the Preliminary Prospectus. Theper annum pass-through rate on the Class X-D Certificates will generally be equal to the excess, if any, of (a) the WAC Rate, over (b) the weighted average of the pass-through rates of the Class D and Class E Certificates, weighted on the basis of their respective certificate balances outstanding immediately prior to that Distribution Date as described in the Preliminary Prospectus. Theper annum pass-through rate on the Class X-F Certificates will generally be equal to the excess, if any, of (a) the WAC Rate, over (b) the pass-through rate of the Class F Certificates as described in the Preliminary Prospectus. Theper annum pass-through rate on the Class X-G Certificates will generally be equal to the excess, if any, of (a) the WAC Rate, over (b) the pass-through rate of the Class G Certificates as described in the Preliminary Prospectus. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

UBS 2019-C18

| STRUCTURE OVERVIEW |

| Prepayment Interest Shortfalls: | Prepayment interest shortfalls will be allocatedpro ratabased on interest entitlements, in reduction of the interest otherwise payable with respect to each of the interest-bearing classes of certificates. |

| Realized Loss Allocation: | On each distribution date, immediately following the distributions to be made to the Certificateholders on that date, the certificate administrator is required to calculate the amount, if any, by which (i) the aggregate stated principal balance of the mortgage loans, including any REO loans, expected to be outstanding immediately following that distribution date is less than (ii) the then-aggregate Certificate Balance of the Principal Balance Certificates after giving effect to distributions of principal on that distribution date. Such amount will be applied to the Class NR-RR, Class G, Class F, Class E, Class D, Class C, Class B and Class A-S certificates, in that order, in each case until the related Certificate Balance has been reduced to zero, and then to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates,pro rata based upon their respective Certificate Balances, until their respective Certificate Balances have been reduced to zero. |

| Prepayment Premiums/Yield Maintenance Charges: | If any yield maintenance charge or prepayment premium is collected during any particular collection period with respect to any mortgage loan, then on the distribution date corresponding to that collection period, the certificate administrator will pay that yield maintenance charge or prepayment premium, net of any liquidation fees or workout fees payable therefrom, in the following manner: (a) to the holders of each of the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class C, Class D and Class E certificates, the product of (x) such yield maintenance charge or prepayment premium, (y) the related Base Interest Fraction for such class, and (z) a fraction, the numerator of which is equal to the amount of principal distributed to such class for that distribution date, and the denominator of which is the total amount of principal distributed to such classes of Principal Balance Certificates for that distribution date, (b) to the holders of the Class X-A certificates, the excess, if any, of (x) the product of (1) such yield maintenance charge or prepayment premium and (2) a fraction, the numerator of which is equal to the amount of principal distributed to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 certificates for that distribution date, and the denominator of which is the total amount of principal distributed to the Class A-1, Class A-2, Class A-SB, Class A-3, Class A-4, Class A-S, Class B, Class C, Class D and Class E certificates for that distribution date, over (y) the amount of such yield maintenance charge or prepayment premium distributed to the Class A-1, Class A-2, Class A-SB, Class A-3 and Class A-4 Certificates as described above, and (c) to the holders of the Class X-B certificates, any remaining portion of such yield maintenance charge or prepayment premium not distributed as described above.

No prepayment premiums or yield maintenance charges will be distributed to the holders of the Class X-D, Class X-F, Class X-G, Class F, Class G, Class NR-RR, Class Z or Class R Certificates.

“Base Interest Fraction” means, with respect to any principal prepayment of any mortgage loan that provides for the payment of a yield maintenance charge or prepayment premium, and with respect to any class of Principal Balance Certificates, a fraction (A) the numerator of which is the greater of (x) zero and (y) the difference between (i) the pass-through rate on that class, and (ii) the applicable discount rate and (B) the denominator of which is the difference between (i) the mortgage interest rate on the related mortgage loan and (ii) the applicable discount rate;provided,however, that: under no circumstances will the Base Interest Fraction be greater than one; if the applicable discount rate is greater than or equal to the mortgage interest rate on the related mortgage loan and is greater than or equal to the pass-through rate on that class, then the Base Interest Fraction will equal zero; and if the applicable discount rate is greater than or equal to the mortgage interest rate on the related mortgage loan and is less than the pass-through rate on that class, then the Base Interest Fraction will be equal to 1.0.

Consistent with the foregoing, the Base Interest Fraction is equal to:

(Pass-Through Rate - Discount Rate)

|

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

UBS 2019-C18

| STRUCTURE OVERVIEW |

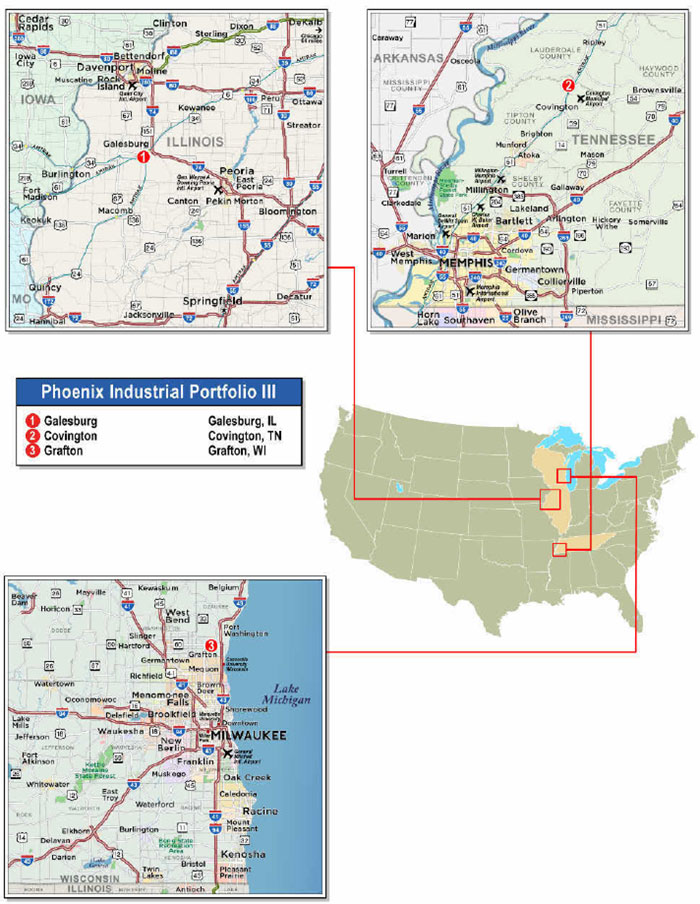

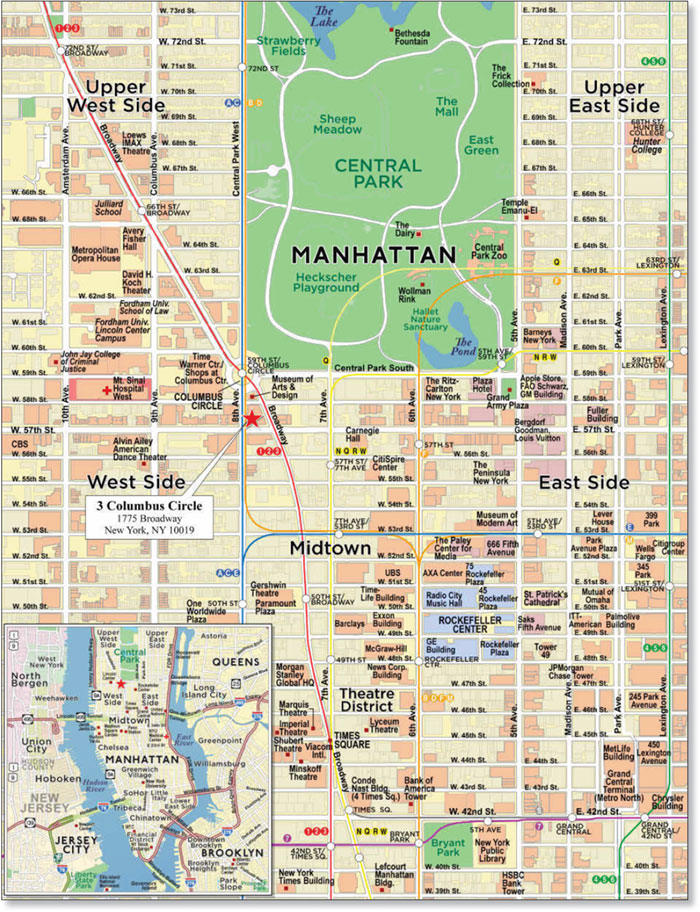

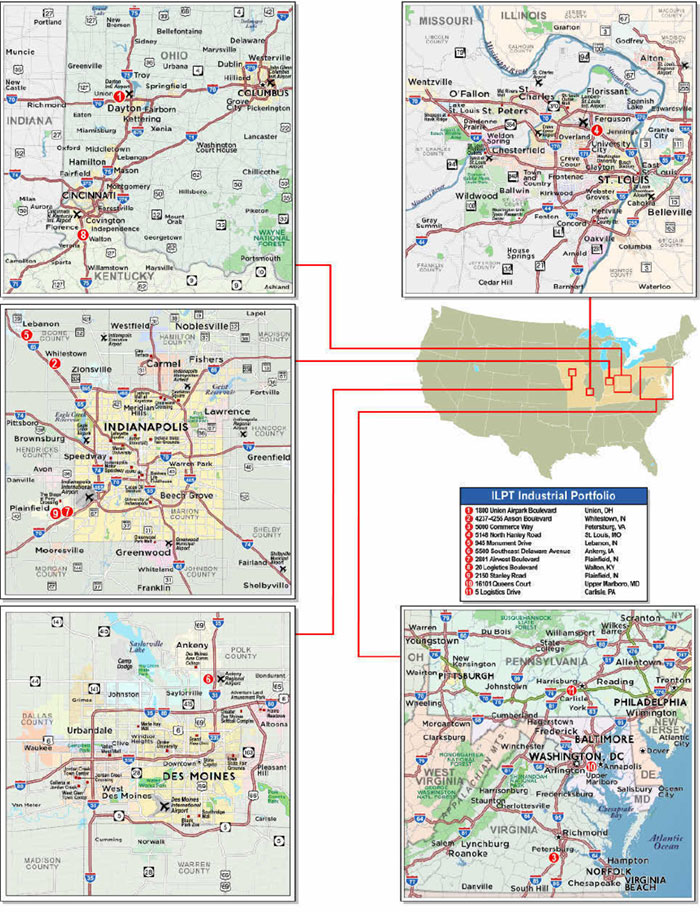

| Whole Loans: | The mortgaged properties identified on Annex A-1 to the Preliminary Prospectus as 225 Bush, Chroma Apartments, Wyndham National Hospitality Portfolio, 3 Columbus Circle, ILPT Industrial Portfolio, DoubleTree New York Times Square West Leased Fee, United Healthcare Office, 4041 Central, Century Plaza Towers, Crimson Retail Portfolio, Redwood Technology Center, 7105 - 7115 37th Avenue, Shoppes at Parma, Global Payments, Inc. and Airport Square, each secure both a mortgage loan to be included in the trust fund and one or more other mortgage loans that will not be included in the trust fund, each of which will bepari passu or subordinate in right of payment with the related mortgage loan included in the trust fund. We refer to each such group of mortgage loans as a “whole loan”. The Chroma Apartments whole loan, the Wyndham National Hospitality Portfolio whole loan, the United Healthcare Office whole loan, the 4041 Central whole loan, the Redwood Technology Center whole loan and the 7105 - 7115 37th Avenue whole loan will be principally serviced under the PSA for the UBS 2019-C18 securitization (each, a “Serviced Whole Loan”). The 225 Bush whole loan is serviced under the pooling and servicing agreement for the Benchmark 2019-B14 securitization. The 3 Columbus Circle whole loan is serviced under the pooling and servicing agreement for the Benchmark 2019-B10 securitization. The ILPT Industrial Portfolio whole loan is serviced under the pooling and servicing agreement for the MSC 2019-L3 securitization. The Century Plaza Towers whole loan is serviced under the trust and servicing agreement for the CPTS 2019-CPT securitization. The Crimson Retail Portfolio whole loan and Redwood Technology Center whole loan are each expected to be serviced under the pooling and servicing agreement for the CSAIL 2019-C18 securitization. The Global Payments, Inc. whole loan is serviced under the pooling and servicing agreement for the WFCM 2019-C54 securitization. The Airport Square whole loan is expected to be serviced under the pooling and servicing agreement for the CF 2019-CF3 securitization. The DoubleTree New York Times Square West Leased Fee whole loan and Shoppes at Parma whole loan (each, a “Servicing Shift Whole Loan” and collectively, the “Servicing Shift Whole Loans”) are each expected to initially be serviced under the UBS 2019-C18 PSA until the date of securitization of the related controllingpari passu note (each, a “Servicing Shift Securitization Date”), after which the related whole loan will be serviced under the pooling and servicing agreement related to the securitization of the related controllingpari passu note (each, a “Servicing Shift PSA”). The master servicer and special servicer under the related Servicing Shift PSA will be identified in a notice, report or statement to holders of the UBS 2019-C18 certificates after the securitization of the related controllingpari passu note.

As of the Closing Date, thepari passucompanion loans in the whole loans are expected to be held by the party identified below under “Overview of Mortgage Pool Characteristics—Pari Passu Companion Loan Summary”.

|

| Control Rights and Directing Certificateholder: | The “Directing Certificateholder” (i) with respect to a Servicing Shift Mortgage Loan, will be the related Loan-Specific Directing Certificateholder, and (ii) with respect to each Serviced Mortgage Loan (other than a Servicing Shift Mortgage Loan), will be the Controlling Class Certificateholder (or its representative) selected by more than 50% of the Controlling Class Certificateholders, by Certificate Balance, as determined by the certificate registrar from time to time;provided,however, that (for the purposes of clause (ii) above in this definition) (1) absent that selection, (2) until a Directing Certificateholder is so selected, or (3) upon receipt of a notice from a majority of the Controlling Class Certificateholders, by Certificate Balance, that a Directing Certificateholder is no longer designated, the Controlling Class Certificateholder that owns the largest aggregate Certificate Balance of the Controlling Class (or its representative) will be the Directing Certificateholder;provided,however, that (i) in the case of this clause (3), in the event no one holder owns the largest aggregate Certificate Balance of the Controlling Class, then there will be no Directing Certificateholder until appointed in accordance with the terms of the PSA, and (ii) the certificate administrator and the other parties to the PSA will be entitled to assume that the identity of the Directing Certificateholder has not changed until such parties receive written notice of a replacement of the Directing Certificateholder from a party holding the requisite interest in the Controlling Class (as confirmed by the certificate registrar), or the resignation of the then-current Directing Certificateholder.

The Directing Certificateholder will be entitled to direct the Special Servicer to take, or refrain from taking certain actions with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. Furthermore, the Directing Certificateholder will also have the right to receive notice and consent to certain material actions that the Master Servicer and the Special Servicer proposes to take with respect to each Serviced Mortgage Loan and any related Serviced Companion Loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

UBS 2019-C18

| STRUCTURE OVERVIEW |

It is expected that RREF IV-D UBSCM 2019-C18 MOA-HRR, LLC, or its affiliate, will be the initial Directing Certificateholder with respect to each Serviced Mortgage Loan (other than a Servicing Shift Mortgage Loan) and any related Serviced Companion Loans.

With respect to the DoubleTree New York Times Square West Leased Fee mortgage loan and the 7105 - 7115 37th Avenue mortgage loan, the rights of the Directing Certificateholder will be subject to the rights of the holder of the related subordinate companion loan. For a description of the rights of the holder of the subordinate companion loans with respect to the DoubleTree New York Times Square West Leased Fee whole loan and the 7105 - 7115 37th Avenue whole loan (each, a “Serviced AB Whole Loan” and collectively, the “Serviced AB Whole Loans”), see “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loans—The DoubleTree New York Times Square West Leased Fee Whole Loan” and “—The 7105 - 7115 37th Avenue Whole Loan” in the Preliminary Prospectus. With respect to the DoubleTree New York Times Square West Leased Fee mortgage loan, the rights of the Directing Certificateholder described above will be subject to the consultation rights of the holders of the relatedpari passucompanion loans as described below. With respect to the Servicing Shift Whole Loans, prior to the related Servicing Shift Securitization Date, the rights of the Directing Certificateholder described above will be, in each such case, subject to the control rights of the related controllingpari passu companion loan as described below.

Notwithstanding any contrary description set forth above, with respect to the Chroma Apartments mortgage loan, the Wyndham National Hospitality Portfolio mortgage loan, the United Healthcare Office mortgage loan, the 4041 Central mortgage loan and the Redwood Technology Center mortgage loan, the holder of the relatedpari passu companion loan (or its representative, including any directing certificateholder under any securitization of suchpari passu companion loan(s)) will have consultation rights with respect to asset status reports and material special servicing actions involving the related whole loan, as provided for in the related intercreditor agreement and as described in the Preliminary Prospectus, and those rights will be in addition to the rights of the directing certificateholder in this transaction described above.

Notwithstanding any contrary description set forth above, with respect to the 225 Bush mortgage loan, the 3 Columbus Circle mortgage loan, the ILPT Industrial Portfolio mortgage loan, the Century Plaza Towers mortgage loan, the Crimson Retail Portfolio Tower mortgage loan, the Global Payments, Inc. mortgage loan and the Airport Square mortgage loan, in general the related whole loan will be serviced under the pooling and servicing agreement or trust and servicing agreement as indicated in the “Pari Passu Companion Loan Summary” table below, which grants the related directing certificateholder (or, in the case of a Servicing Shift Whole Loan prior to the securitization of the related controllingpari passunote, the related controlling noteholder) under the related securitization control rights that may include the right to approve or disapprove various material servicing actions involving the related whole loan. The directing certificateholder for this securitization (so long as no Consultation Termination Event has occurred and is occurring) will nonetheless have the right to be consulted on a non-binding basis with respect to such actions. For purposes of the servicing of the related whole loan, the occurrence and continuance of a Control Termination Event or Consultation Termination Event under this securitization will not limit the control or other rights of the directing certificateholder (or equivalent) under the related securitization.

Notwithstanding any contrary description set forth above, with respect to the DoubleTree New York Times Square West Leased Fee mortgage loan and Shoppes at Parma mortgage loan, in general, the related whole loan will be serviced (i) prior to the applicable Servicing Shift Securitization Date, under the pooling and servicing agreement for this securitization and (ii) after the applicable Servicing Shift Securitization Date, under the related Servicing Shift PSA, which grants, or is expected to grant, to the related controlling noteholder or its representative control rights that include the right to approve or disapprove various material servicing actions involving the related whole loan. The Directing Certificateholder for this securitization (so long as no Consultation Termination Event has occurred and is occurring) will nonetheless have the right to be consulted on a non-binding basis with respect to such actions. For purposes of the servicing of each Servicing Shift Whole Loan, the occurrence and continuance of a Control Termination Event or Consultation Termination Event under this securitization will not limit the control or other rights of the controlling noteholder, and the securitization of each related controllingpari passu companion loan will not limit the consultation rights of the Directing Certificateholder under this securitization. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

UBS 2019-C18

| STRUCTURE OVERVIEW |

| For a description of the directing holder for each Non-Serviced Whole Loan, see “Description of the Mortgage Pool—The Whole Loans” and “Pooling and Servicing Agreement—The Directing Certificateholder—Rights of the Directing Certificateholder appointed by the Controlling Class with respect to Non-Serviced Mortgage Loans or a Servicing Shift Whole Loan” in the Preliminary Prospectus. | |

| Control Eligible Certificates: | Class G and Class NR-RR Certificates. |

| Controlling Class: | The “Controlling Class” will be, as of any time of determination, the most subordinate class of Control Eligible Certificates then-outstanding that has an aggregate Certificate Balance (as notionally reduced by any Cumulative Appraisal Reduction Amounts (as defined below) allocable to such class) at least equal to 25% of the initial Certificate Balance of that class;provided,however, that if at any time the Certificate Balances of the certificates other than the Control Eligible Certificates have been reduced to zero as a result of principal payments on the mortgage loans, then the Controlling Class will be the most subordinate class of Control Eligible Certificates that has a Certificate Balance greater than zero without regard to any Cumulative Appraisal Reduction Amounts. The Controlling Class as of the Closing Date will be the Class NR-RR certificates. |

| Appraised-Out Class: | An “Appraised-Out Class” is any class of Control Eligible Certificates that is determined at any time of determination to no longer be the Controlling Class as a result of the application of any Appraisal Reduction Amounts or Collateral Deficiency Amounts to notionally reduce the Certificate Balance of the constituent classes. No Appraised-Out Class may exercise any direction, control, consent and/or similar rights of the Controlling Class until such time, if any, as such class is reinstated as the Controlling Class, and the rights of the Controlling Class will be exercised by the next most senior class of Control Eligible Certificates that is not an Appraised-Out Class, if any, during such period.

With respect to each Serviced AB Whole Loan, the holder of the related controlling subordinate companion loan may in certain circumstances post collateral to avoid a change of control as described in “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loans—The DoubleTree New York Times Square West Leased Fee Whole Loan” and “—The 7105 - 7115 37th Avenue Whole Loan” in the Preliminary Prospectus.

|

| Remedies Available to Holders of an Appraised-Out Class: | The holder of the majority (by Certificate Balance) of an Appraised-Out Class will have the right, at its sole expense, to require the Special Servicer to order a second appraisal of any mortgage loan (or Serviced Whole Loan) for which an appraisal reduction event has occurred or as to which there exists a Collateral Deficiency Amount (such holders, the “Requesting Holders”). The Special Servicer will use its reasonable best efforts to ensure that such appraisal is delivered within 30 days from receipt of the Requesting Holders’ written request and will ensure that such appraisal is prepared on an “as-is” basis by an MAI appraiser. Upon receipt of such supplemental appraisal, the Special Servicer will be required to determine, in accordance with the Servicing Standard, whether, based on its assessment of such supplemental appraisal, any recalculation of the applicable Appraisal Reduction Amount or Collateral Deficiency Amount, as applicable, is warranted and, if so warranted, will recalculate such Appraisal Reduction Amount or Collateral Deficiency Amount, as applicable, based upon such supplemental appraisal and receipt of information requested by the Special Servicer from the Master Servicer. If required by any such recalculation, the applicable Appraised-Out Class will be reinstated as the Controlling Class and each other Appraised-Out Class will, if applicable, have its related Certificate Balance notionally restored to the extent required by such recalculation of the Appraisal Reduction Amount or Collateral Deficiency Amount, if applicable. The Certificate Administrator, the Operating Advisor and the Master Servicer will be entitled to conclusively rely on the Special Servicer’s calculation or determination of any Collateral Deficiency Amount. |

| Control Rights: | Subject to the rights of the holder of the related controllingpari passu companion loan or subordinate companion loan, as applicable, with respect to a Servicing Shift Whole Loan, prior to a Control Termination Event, the Directing Certificateholder appointed by the Controlling Class Certificateholder will have certain consent and consultation rights under the PSA with respect to certain major decisions and other matters. A “Control Termination Event” will occur when (i) the Class G certificates have a Certificate Balance (taking into account the application of any Cumulative Appraisal Reduction Amounts to notionally reduce the Certificate Balance of such class) of less than 25% of the initial Certificate |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

UBS 2019-C18

| STRUCTURE OVERVIEW |

Balance of such class; or (ii) a holder of the Class G certificates is the majority Controlling Class Certificateholder and has irrevocably waived its right, in writing, to exercise any of the rights of the Controlling Class Certificateholder and such rights have not been reinstated to a successor Controlling Class Certificateholder;provided that no Control Termination Event may occur with respect to a Loan-Specific Directing Certificateholder and the term “Control Termination Event” will not be applicable to a Loan-Specific Directing Certificateholder;provided, further,that a Control Termination Event will not be deemed continuing in the event that the Certificate Balances of the Certificates other than the Control Eligible Certificates have been reduced to zero as a result of principal payments on the mortgage loans.

After the occurrence of a Control Termination Event but prior to the occurrence of a Consultation Termination Event, the Directing Certificateholder appointed by the Controlling Class Certificateholder will not have any consent rights, but such Directing Certificateholder will have certain non-binding consultation rights under the PSA with respect to certain major decisions and other matters. A “Consultation Termination Event” will occur when (i) there is no class of Control Eligible Certificates that has a then-outstanding Certificate Balance at least equal to 25% of the initial Certificate Balance of that class, in each case, without regard to the application of any Cumulative Appraisal Reduction Amounts; or (ii) a holder of the Class G certificates is the majority Controlling Class Certificateholder and has irrevocably waived its right, in writing, to exercise any of the rights of the Controlling Class Certificateholder and such rights have not been reinstated to a successor Controlling Class Certificateholder (providedthat no Consultation Termination Event resulting solely from the operation of clause (ii) will be deemed to have existed or be in continuance with respect to a successor holder of the Class G certificates that has not irrevocably waived its right to exercise any of the rights of the Controlling Class Certificateholder);provided,further, that no Consultation Termination Event may occur with respect to a Loan-Specific Directing Certificateholder and the term “Consultation Termination Event” will not be applicable to a Loan-Specific Directing Certificateholder;provided,further, that a Consultation Termination Event will not be deemed continuing in the event that the Certificate Balances of the certificates other than the Control Eligible Certificates have been reduced to zero as a result of principal payments on the mortgage loans.

After the occurrence of a Consultation Termination Event, the Directing Certificateholder appointed by the Controlling Class Certificateholder will not have any consent or consultation rights, except with respect to any rights expressly set forth in the PSA.

Notwithstanding the proviso to the definitions of “Control Termination Event” and “Consultation Termination Event,” a Control Termination Event and a Consultation Termination Event will be deemed to have occurred with respect to any Excluded Loan with respect to the Directing Certificateholder or the holder of the majority of the Controlling Class, and neither the Directing Certificateholder nor any Controlling Class Certificateholder will have any consent or consultation rights with respect to the servicing of such Excluded Loan.

An “Excluded Loan” means (a) with respect to the Directing Certificateholder or the holder of the majority of the Controlling Class, a mortgage loan or whole loan with respect to which, as of any date of determination, the Directing Certificateholder or the holder of the majority of the Controlling Class is a Borrower Party or (b) with respect to the Risk Retention Consultation Party or the holder of the majority of the VRR Interest, a mortgage loan or whole loan with respect to which, as of any date of determination, the Risk Retention Consultation Party or the holder of the majority of the VRR Interest is a Borrower Party. As of the Closing Date, it is expected that there will be no Excluded Loans with respect to this securitization.

“Borrower Party” means a borrower, a mortgagor, a manager of a mortgaged property, a mezzanine lender under a mezzanine loan that has been accelerated or as to which foreclosure or enforcement proceedings have been commenced against the equity collateral pledged to secure the related mezzanine loan, or any Borrower Party Affiliate.

“Borrower Party Affiliate” means, with respect to a borrower, a mortgagor, a manager of a mortgaged property or a mezzanine lender under a mezzanine loan that has been accelerated or as to which foreclosure or enforcement proceedings have been commenced against the equity collateral pledged to secure the related mezzanine loan, (a) any other |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

UBS 2019-C18

| STRUCTURE OVERVIEW |

person controlling or controlled by or under common control with such borrower, mortgagor, manager or mezzanine lender under a mezzanine loan that has been accelerated or as to which foreclosure or enforcement proceedings have been commenced against the equity collateral pledged to secure the related mezzanine loan, as applicable, or (b) any other person owning, directly or indirectly, 25% or more of the beneficial interests in such borrower, mortgagor, manager or mezzanine lender under a mezzanine loan that has been accelerated or as to which foreclosure or enforcement proceedings have been commenced against the equity collateral pledged to secure the related mezzanine loan, as applicable. For the purposes of this definition, “control” when used with respect to any specified person means the power to direct the management and policies of such person, directly or indirectly, whether through the ownership of voting securities, by contract or otherwise and the terms “controlling” and “controlled” have meanings correlative to the foregoing. Notwithstanding any of the foregoing to the contrary, if any mortgage loan is part of a whole loan, the consent and/or consultation rights of a Controlling Class Certificateholder with respect thereto may be limited as described in the Preliminary Prospectus. In particular, with respect to each Non-Serviced Whole Loan, the Directing Certificateholder will only have certain consultation rights with respect to certain “major decisions” and other matters related to such whole loan, in each case only prior to a Control Termination Event or Consultation Termination Event, as applicable, and the controlling noteholder (or its representative) will be entitled to similar consent and/or consultation rights with respect to such whole loan. | |

| Operating Advisor Consultation Event: | An “Operating Advisor Consultation Event” will occur when the Certificate Balance of the Class NR-RR Certificates (taking into account the application of any Cumulative Appraisal Reduction Amounts to notionally reduce the Certificate Balances of such classes) is reduced to 25% or less of the initial Certificate Balances of such class. |

| Appointment and Replacement of Special Servicer: | The Directing Certificateholder will appoint the initial Special Servicer as of the Closing Date. Prior to the occurrence and continuance of a Control Termination Event, the Directing Certificateholder generally may replace the Special Servicer with or without cause at any time.

Upon the occurrence and during the continuance of a Control Termination Event, the Directing Certificateholder appointed by the Controlling Class Certificateholder will no longer have the right to replace the Special Servicer and such replacement will occur based on a vote of holders of all voting eligible classes of certificates as described in “Replacement of Special Servicer by Vote of Certificateholders” below.

Notwithstanding the foregoing, with respect to a Serviced AB Whole Loan, prior to the occurrence of a Control Appraisal Period with respect to the related subordinate companion loan, and with respect to a Servicing Shift Whole Loan, the Directing Certificateholder appointed by the Controlling Class Certificateholder will not be entitled to exercise the above-described rights and the holder of such subordinate companion loan will be entitled to replace the Special Servicer with or without cause in accordance with the PSA and the related intercreditor agreement. However, during a Control Appraisal Period with respect to a Serviced AB Whole Loan, the Directing Certificateholder appointed by the Controlling Class Certificateholder will have generally similar (although not necessarily identical) rights (including the rights described above) with respect to such Serviced AB Whole Loan as it does for the other mortgage loans in the issuing entity. See “Description of the Mortgage Pool—The Whole Loans—The Serviced AB Whole Loans—The DoubleTree New York Times Square West Leased Fee Whole Loan” and “—The 7105 - 7115 37th Avenue Whole Loan” in the Preliminary Prospectus.