Issuer Free Writing Prospectus

Filed Pursuant to Rule 433

Registration Statement No.: 333-172366

|  |

Free Writing Prospectus

Structural and Collateral Term Sheet

$1,091,143,971

(Approximate Aggregate Cut-off Date Balance of Mortgage Pool)

$763,800,000

(Approximate Aggregate Principal Balance of Offered Certificates)

WFRBS Commercial Mortgage Trust 2011-C5

as Issuing Entity

Wells Fargo Commercial Mortgage Securities, Inc.

as Depositor

The Royal Bank of Scotland

Wells Fargo Bank, National Association

Basis Real Estate Capital II, LLC

C-III Commercial Mortgage LLC

General Electric Capital Corporation

as Sponsors and Mortgage Loan Sellers

Commercial Mortgage Pass-Through Certificates

Series 2011-C5

October 24, 2011

| WELLS FARGO SECURITIES | RBS | |

Co-Lead Manager and Co-Bookrunner | Co-Lead Manager and Co-Bookrunner | |

Citigroup | Goldman, Sachs & Co. | |

| Co-Manager | Co-Manager |

STATEMENT REGARDING THIS FREE WRITING PROSPECTUS

The depositor has filed a registration statement (including a prospectus) with the Securities and Exchange Commission (‘‘SEC’’) (SEC File No. 333-172366) for the offering to which this communication relates. Before you invest, you should read the prospectus in the registration statement and other documents the depositor has filed with the SEC for more complete information about the depositor, the issuing entity and this offering. You may get these documents for free by visiting EDGAR on the SEC Web site at www.sec.gov. Alternatively, the depositor, any underwriter, or any dealer participating in the offering will arrange to send you the prospectus after filing if you request it by calling toll free 1-800-745-2063 (8 a.m. – 5 p.m. EST) or by emailing wfs.cmbs@wellsfargo.com.

Nothing in this document constitutes an offer of securities for sale in any other jurisdiction where the offer or sale is not permitted. The information contained herein is preliminary as of the date hereof, supersedes any such information previously delivered to you and will be superseded by any such information subsequently delivered and ultimately by the final prospectus relating to the securities. These materials are subject to change, completion, supplement or amendment from time to time.

STATEMENT REGARDING ASSUMPTIONS AS TO SECURITIES, PRICING ESTIMATES AND OTHER INFORMATION

The attached information contains certain tables and other statistical analyses (the “Computational Materials”) which have been prepared in reliance upon information furnished by the Mortgage Loan Sellers. Numerous assumptions were used in preparing the Computational Materials, which may or may not be reflected herein. As such, no assurance can be given as to the Computational Materials’ accuracy, appropriateness or completeness in any particular context; or as to whether the Computational Materials and/or the assumptions upon which they are based reflect present market conditions or future market performance. The Computational Materials should not be construed as either projections or predictions or as legal, tax, financial or accounting advice. You should consult your own counsel, accountant and other advisors as to the legal, tax, business, financial and related aspects of a purchase of these securities. Any weighted average lives, yields and principal payment periods shown in the Computational Materials are based on prepayment and/or loss assumptions, and changes in such prepayment and/or loss assumptions may dramatically affect such weighted average lives, yields and principal payment periods. In addition, it is possible that prepayments or losses on the underlying assets will occur at rates higher or lower than the rates shown in the attached Computational Materials. The specific characteristics of the securities may differ from those shown in the Computational Materials due to differences between the final underlying assets and the preliminary underlying assets used in preparing the Computational Materials. The principal amount and designation of any security described in the Computational Materials are subject to change prior to issuance. None of Wells Fargo Securities, LLC (“WFS”), RBS Securities Inc. (“RBSSI”), Citigroup Global Markets Inc., Goldman, Sachs & Co. or any of their respective affiliates make any representation or warranty as to the actual rate or timing of payments or losses on any of the underlying assets or the payments or yield on the securities. The information in this presentation is based upon management forecasts and reflects prevailing conditions and management’s views as of this date, all of which are subject to change. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Mortgage Loan Sellers or which was otherwise reviewed by us.

This free writing prospectus contains certain forward-looking statements. If and when included in this free writing prospectus, the words “expects”, “intends”, “anticipates”, “estimates” and analogous expressions and all statements that are not historical facts, including statements about our beliefs or expectations, are intended to identify forward-looking statements. Any forward-looking statements are made subject to risks and uncertainties which could cause actual results to differ materially from those stated. Those risks and uncertainties include, among other things, declines in general economic and business conditions, increased competition, changes in demographics, changes in political and social conditions, regulatory initiatives and changes in customer preferences, many of which are beyond our control and the control of any other person or entity related to this offering. The forward-looking statements made in this free writing prospectus are made as of the date stated on the cover. We have no obligation to update or revise any forward-looking statement.

Wells Fargo Securities is the trade name for certain capital markets and investment banking services of Wells Fargo & Company and its subsidiaries, including Wells Fargo Securities, LLC, member FINRA and SIPC, and Wells Fargo Bank, National Association.

RBS is a trade name for the investment banking business of RBSSI. Securities, syndicated loan arranging, financial advisory and other investment banking activities are performed by RBSSI and their securities affiliates. Lending, derivatives and other commercial banking activities are performed by The Royal Bank of Scotland plc and their banking affiliates. RBSSI is a member of SIPC, FINRA and the NYSE.

IRS CIRCULAR 230 NOTICE

THIS TERM SHEET IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING U.S. FEDERAL, STATE OR LOCAL TAX PENALTIES. THIS TERM SHEET IS WRITTEN AND PROVIDED BY THE DEPOSITOR IN CONNECTION WITH THE PROMOTION OR MARKETING BY THE DEPOSITOR AND THE CO-LEAD BOOKRUNNING MANAGERS OF THE TRANSACTION OR MATTERS ADDRESSED HEREIN. INVESTORS SHOULD SEEK ADVICE BASED ON THEIR PARTICULAR CIRCUMSTANCES FROM AN INDEPENDENT TAX ADVISOR.

IMPORTANT NOTICE REGARDING THE OFFERED CERTIFICATES

The Offered Certificates referred to in these materials and the asset pool backing them are subject to modification or revision (including the possibility that one or more classes of certificates may be split, combined or eliminated at any time prior to issuance or availability of a final prospectus) and are offered on a “when, as and if issued” basis. Prospective investors should understand that, when considering the purchase of the Offered Certificates, a contract of sale will come into being no sooner than the date on which the relevant class of certificates has been priced and the underwriters have confirmed the allocation of certificates to be made to investors; any “indications of interest” expressed by any prospective investor, and any “soft circles” generated by the underwriters, will not create binding contractual obligations for such prospective investors, on the one hand, or the underwriters, the depositor or any of their respective agents or affiliates, on the other hand.

As a result of the foregoing, a prospective investor may commit to purchase certificates that have characteristics that may change, and each prospective investor is advised that all or a portion of the certificates referred to in these materials may be issued without all or certain of the characteristics described in these materials. The underwriters’ obligation to sell certificates to any prospective investor is conditioned on the certificates and the transaction having the characteristics described in these materials. If the underwriters determine that a condition is not satisfied in any material respect, such prospective investor will be notified, and neither the depositor nor the underwriters will have any obligation to such prospective investor to deliver any portion of the Offered Certificates which such prospective investor has committed to purchase, and there will be no liability between the underwriters, the depositor or any of their respective agents or affiliates, on the one hand, and such prospective investor, on the other hand, as a consequence of the non-delivery.

Each prospective investor has requested that the underwriters provide to such prospective investor information in connection with such prospective investor’s consideration of the purchase of the certificates described in these materials. These materials are being provided to each prospective investor for informative purposes only in response to such prospective investor’s specific request. The underwriters described in these materials may from time to time perform investment banking services for, or solicit investment banking business from, any company named in these materials. The underwriters and/or their affiliates or respective employees may from time to time have a long or short position in any security or contract discussed in these materials.

The information contained herein supersedes any previous such information delivered to any prospective investor and will be superseded by information delivered to such prospective investor prior to the time of sale.

IMPORTANT NOTICE RELATING TO AUTOMATICALLY-GENERATED EMAIL DISCLAIMERS

Any legends, disclaimers or other notices that may appear at the bottom of any email communication to which this free writing prospectus is attached relating to (1) these materials not constituting an offer (or a solicitation of an offer), (2) no representation that these materials are accurate or complete and may not be updated or (3) these materials possibly being confidential, are not applicable to these materials and should be disregarded. Such legends, disclaimers or other notices have been automatically generated as a result of these materials having been sent via Bloomberg or another system.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

2

| WFRBS Commercial Mortgage Trust 2011-C5 | Certificate Structure |

I. Certificate Structure

| Class | Expected Ratings (Fitch/Moody’s)(1) | Approximate Initial Certificate Balance or Notional Amount(2) | Approx. Initial Credit Support(3) | Pass- Through Rate Description | Weighted Average Life (Years)(4) | Expected Principal Window(4) | Certificate Principal to Value Ratio(5) | Certificate Principal U/W NOI Debt Yield(6) | ||||||||||||||

| Offered Certificates | ||||||||||||||||||||||

| A-1 | AAA(sf)/Aaa(sf) | $66,527,000 | 30.000% | (7) | 2.45 | 12/2011 – 7/2016 | 43.5% | 16.0% | ||||||||||||||

| A-2 | AAA(sf)/Aaa(sf) | $118,410,000 | 30.000% | (7) | 4.75 | 7/2016 – 11/2016 | 43.5% | 16.0% | ||||||||||||||

| A-3 | AAA(sf)/Aaa(sf) | $107,908,000 | 30.000% | (7) | 7.42 | 11/2016 – 7/2021 | 43.5% | 16.0% | ||||||||||||||

| A-4 | AAA(sf)/Aaa(sf) | $470,955,000 | 30.000% | (7) | 9.72 | 7/2021 – 9/2021 | 43.5% | 16.0% | ||||||||||||||

| Non-Offered Certificates | ||||||||||||

| X-A | AAA(sf)/Aaa(sf) | $849,728,000(8) | N/A | Variable(9) | N/A | N/A | N/A | N/A | ||||

| X-B | NR/Aaa(sf) | $241,415,970(10) | N/A | Variable(11) | N/A | N/A | N/A | N/A | ||||

| A-S | AAA(sf)/Aaa(sf) | $85,928,000 | 22.125% | (7) | 9.81 | 9/2021 – 9/2021 | 48.4% | 14.4% | ||||

| B | AA(sf)/Aa2(sf) | $54,557,000 | 17.125% | (7) | 9.86 | 9/2021 – 10/2021 | 51.5% | 13.5% | ||||

| C | A(sf)/A2(sf) | $40,918,000 | 13.375% | (7) | 9.90 | 10/2021 – 10/2021 | 53.8% | 12.9% | ||||

| D | BBB+(sf)/Baa1(sf) | $25,915,000 | 11.000% | (7) | 9.90 | 10/2021 – 10/2021 | 55.3% | 12.6% | ||||

| E | BBB-(sf)/Baa3(sf) | $49,101,000 | 6.500% | (7) | 9.92 | 10/2021 – 11/2021 | 58.1% | 12.0% | ||||

| F | BB(sf)/Ba2(sf) | $17,731,000 | 4.875% | (7) | 9.98 | 11/2021 – 11/2021 | 59.1% | 11.8% | ||||

| G | B(sf)/B2(sf) | $16,367,000 | 3.375% | (7) | 9.98 | 11/2021 – 11/2021 | 60.0% | 11.6% | ||||

| H | NR/NR | $36,826,970 | 0.000% | (7) | 9.98 | 11/2021 – 11/2021 | 62.1% | 11.2% | ||||

Notes: | ||

| (1) | The expected ratings presented are those of Fitch, Inc. (“Fitch”) and Moody’s Investors Service, Inc. (“Moody’s”) which the depositor hired to rate the rated offered certificates. One or more other nationally recognized statistical ratings organizations that were not hired by the depositor may use information they receive pursuant to Rule 17g-5 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), to rate or provide market reports and/or published commentary related to the offered certificates. We cannot assure you as to what ratings a non-hired nationally recognized statistical ratings organization would assign or that its reports will not express differing, possibly negative, views of the mortgage loans and/or the offered certificates. See “Risk Factors—Risks Related to the Offered Certificates—Ratings of the Certificates Have Substantial Limitations” and “Ratings” in the free writing prospectus, dated October 24, 2011 (the “Free Writing Prospectus”). Fitch, Inc. and Moody’s Investors Service, Inc. have indicated generally that the “(sf)” designation in their ratings is an identifier for structured finance product ratings. For general information about ratings definitions and the “(sf)” designation, prospective investors may register and log onto www.moodys.com and www.fitchratings.com. We and the underwriters have not verified, do not adopt and accept no responsibility for any statements made by the rating agencies on those websites. | |

(2) | The principal balances and notional amounts set forth in the table are approximate. The actual initial principal balances and notional amounts may be larger or smaller depending on the aggregate cut-off date principal balance of the mortgage loans definitively included in the pool of mortgage loans, which aggregate cut-off date principal balance may be as much as 5% larger or smaller than the amount presented in the Free Writing Prospectus. | |

(3) | The approximate initial credit support with respect to the Class A-1, A-2, A-3 and A-4 Certificates represents the approximate credit enhancement for the Class A-1, A-2, A-3 and A-4 Certificates in the aggregate. | |

(4) | Weighted Average Lives and Expected Principal Windows are calculated based on an assumed prepayment rate of 0% CPR and the “Structuring Assumptions” described under “Glossary” in the Free Writing Prospectus. | |

(5) | The Certificate Principal to Value Ratio for each Class of Certificates (other than the Class A-1, A-2, A-3 and A-4 Certificates) is calculated by dividing the aggregate principal balance of such class of certificates and all classes of certificates senior to such class by the aggregate appraised value of $1,755,784,000 (calculated as described in the Free Writing Prospectus) for the mortgaged properties securing the mortgage loans. The Certificate Principal to Value Ratios for each of the Class A-1, A-2, A-3 and A-4 Certificates are calculated by dividing the aggregate principal balance of the Class A-1, A-2, A-3 and A-4 Certificates by such aggregate appraised value. However, excess mortgaged property value associated with a mortgage loan will not be available to offset losses on any other mortgage loan (unless such mortgage loans are cross-collateralized). | |

| (6) | The Certificate Principal U/W NOI Debt Yield for each Class of Certificates (other than the Class A-1, A-2, A-3 and A-4 Certificates) is calculated by dividing the underwritten net operating income for the mortgage pool of $122,198,104 (calculated as described in the Free Writing Prospectus) by the aggregate certificate balance of such class of certificates and all classes of certificates senior to such class of certificates. The Underwritten NOI Debt Yield for each of the Class A-1, A-2, A-3 and A-4 Certificates is calculated by dividing such mortgage pool underwritten net operating income by the aggregate principal balance of the Class A-1, A-2, A-3 and A-4 Certificates. However, cash flow from each mortgaged property supports only the related mortgage loan and will not be available to support any other mortgage loan (unless such mortgage loans are cross-collateralized). | |

(7) | The pass-through rates for the Class A-1, A-2, A-3, A-4, A-S, B, C, D, E, F, G and H Certificates in each case will be one of the following: (i) a fixed rate per annum, (ii) the WAC Rate (as defined in the Free Writing Prospectus) for the related distribution date, (iii) a variable rate per annum equal to the lesser of (a) a fixed rate and (b) the WAC Rate for the related distribution date or (iv) a variable rate per annum equal to the WAC Rate for the related distribution date minus a specified percentage. | |

| (8) | The Class X-A Certificates are notional amount certificates. The Notional Amount of the Class X-A Certificates will be equal to the aggregate principal balance of the Class A-1, A-2, A-3, A-4 and A-S Certificates outstanding from time to time. The Class X-A Certificates will not be entitled to distributions of principal. | |

(9) | The pass-through rate for the Class X-A Certificates for any distribution date will equal the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class A-1, A-2, A-3, A-4 and A-S Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. | |

(10) | The Class X-B Certificates are notional amount certificates. The Notional Amount of the Class X-B Certificates will be equal to the aggregate principal balance of the Class B, C, D, E, F, G and H Certificates outstanding from time to time. The Class X-B Certificates will not be entitled to distributions of principal. | |

| (11) | The pass-through rate for the Class X-B Certificates for any distribution date will equal the excess, if any, of (a) the WAC Rate for the related distribution date, over (b) the weighted average of the pass-through rates on the Class B, C, D, E, F, G and H Certificates for the related distribution date, weighted on the basis of their respective aggregate principal balances outstanding immediately prior to that distribution date. | |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

3

| WFRBS Commercial Mortgage Trust 2011-C5 | Transaction Highlights |

II. Transaction Highlights

Mortgage Loan Sellers:

Mortgage Loan Seller | Number of Mortgage Loans | Number of Mortgaged Properties | Aggregate Cut-off Date Balance | % of Cut-off Date Pool Balance | |||||||||||

The Royal Bank of Scotland(1) | 21 | 28 | $ 741,132,025 | 67.9 | % | ||||||||||

| Wells Fargo Bank, National Association | 18 | 33 | 152,584,580 | 14.0 | |||||||||||

| Basis Real Estate Capital II, LLC | 12 | 13 | 88,774,741 | 8.1 | |||||||||||

| C-III Commercial Mortgage LLC | 13 | 13 | 55,675,107 | 5.1 | |||||||||||

General Electric Capital Corporation | 11 | 11 | 52,977,517 | 4.9 | |||||||||||

| Total | 75 | 98 | $ | 1,091,143,971 | 100.0 | % | |||||||||

| (1) | The mortgage loan seller referred to herein as The Royal Bank of Scotland is comprised of two affiliated companies: The Royal Bank of Scotland plc and RBS Financial Products Inc. With respect to the mortgage loans being sold to the trust by The Royal Bank of Scotland (a) 18 mortgage loans, having an aggregate cut-off date principal balance of $664,662,678 and representing 60.9% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date, are being sold to the trust only by The Royal Bank of Scotland plc and (b) 3 mortgage loans, having an aggregate cut-off date principal balance of $76,469,347 and representing 7.0% of the aggregate principal balance of the pool of mortgage loans as of the cut-off date are being sold to the trust only by RBS Financial Products Inc. |

Loan Pool:

| Cut-off Date Balance: | $1,091,143,971 | |||

| Number of Mortgage Loans: | 75 | |||

| Average Cut-off Date Balance per Mortgage Loan: | $14,548,586 | |||

| Number of Mortgaged Properties: | 98 | |||

Average Cut-off Date Balance per Mortgaged Property(1): | $11,134,122 | |||

| Weighted Average Mortgage Interest Rate: | 5.744% | |||

| Ten Largest Mortgage Loans as % of Cut-off Date Pool Balance: | 57.0% | |||

| Weighted Average Original Term to Maturity (months): | 112 | |||

| Weighted Average Remaining Term to Maturity (months): | 110 | |||

Weighted Average Original Amortization Term (months)(2): | 345 | |||

Weighted Average Remaining Amortization Term (months)(2): | 343 | |||

Weighted Average Seasoning (months): | 2 |

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in related loan documents. | |

| (2) | Excludes any mortgage loan that does not amortize. |

Credit Statistics:

Weighted Average U/W Net Cash Flow DSCR(1): | 1.47x | |||

Weighted Average U/W Net Operating Income Debt Yield Ratio(1): | 11.2% | |||

Weighted Average Cut-off Date Loan-to-Value Ratio(1): | 63.0% | |||

Weighted Average Balloon Loan-to-Value Ratio(1): | 53.8% | |||

| % of Mortgage Loans with Additional Debt: | 9.4% | |||

% of Mortgage Loans with Single Tenants(2): | 6.8% | |||

| (1) | Information regarding mortgage loans secured by multiple properties is based on an allocation according to relative appraised values or the allocated loan amounts or property-specific release prices set forth in related loan documents. | |

| (2) | Excludes mortgage loans that are secured by multiple single-tenant properties. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

4

| WFRBS Commercial Mortgage Trust 2011-C5 | Transaction Highlights |

Loan Structural Features:

Amortization: Based on the Cut-off Date Balance, 97.5% of the mortgage pool (73 mortgage loans) has scheduled amortization, as follows:

83.3% (67 mortgage loans) requires amortization during the entire loan term

14.3% (6 mortgage loans) provides for an interest-only period followed by an amortization period

Interest-Only: Based on the Cut-off Date Balance, 2.5% of the mortgage pool (2 mortgage loans) provides for interest-only payments during the entire loan term.

Hard Lockboxes: Based on the Cut-off Date Balance, 82.4% of the mortgage pool (38 mortgage loans) has hard lockboxes in place.

Reserves: The mortgage loans require amounts to be escrowed monthly as follows (excluding any mortgage loans with springing provisions):

| Real Estate Taxes: | 86.0% of the pool |

| Insurance Premiums: | 54.9% of the pool |

| Capital Replacements: | 87.6% of the pool |

| TI/LC: | 79.6% of the pool* |

* The percentage of Cut-off Date Balance for loans with TI/LC reserves is based on the aggregate principal balance allocable to office, retail, mixed-use and industrial properties. | |

Call Protection/Defeasance: Based on the Cut-off Date Balance, the mortgage pool has the following call protection and defeasance features:

89.3% of the mortgage pool (61 mortgage loans) features a lockout period, then defeasance only until an open period

9.9% of the mortgage pool (13 mortgage loans) features a lockout period, then greater of a prepayment premium or yield maintenance until an open period

0.8% of the mortgage pool (1 mortgage loan) features a lockout period, then the greater of a prepayment premium or yield maintenance, then defeasance until an open period

Please refer to Annex A-1 to the Free Writing Prospectus for further description of individual loan call protection.

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

5

| WFRBS Commercial Mortgage Trust 2011-C5 | Issue Characteristics |

III. Issue Characteristics

| Securities Offered: | $763,800,000 approximate monthly pay, multi-class, commercial mortgage REMIC pass-through certificates consisting of four classes (Classes A-1, A-2, A-3 and A-4), which are offered pursuant to a registration statement filed with the SEC. | |

| Mortgage Loan Sellers: | The Royal Bank of Scotland (“RBS”); Wells Fargo Bank, National Association (“WFB”); Basis Real Estate Capital II, LLC (“Basis”); C-III Commercial Mortgage LLC (“CIIICM”); and General Electric Capital Corporation (“GECC”). | |

| Co-lead Bookrunning Managers: | Wells Fargo Securities, LLC and RBS Securities Inc. | |

| Co-Managers: | Citigroup Global Markets Inc. and Goldman, Sachs & Co. | |

| Rating Agencies: | Fitch, Inc. and Moody’s Investors Service, Inc. | |

| Master Servicer: | Wells Fargo Bank, National Association | |

| Special Servicer: | Midland Loan Services, a division of PNC Bank, National Association | |

| Certificate Administrator: | Wells Fargo Bank, National Association | |

| Trustee: | Deutsche Bank Trust Company Americas | |

| Trust Advisor: | TriMont Real Estate Advisors, Inc. | |

| Cut-off Date: | The Cut-off Date with respect to each mortgage loan is the due date for the monthly debt service payment that is due in November 2011 (or, in the case of any mortgage loan that has its first due date in December 2011, the date that would have been its due date in November 2011 under the terms of that mortgage loan if a monthly debt service payment were scheduled to be due in that month). | |

| Expected Closing Date: | On or about November 22, 2011. | |

| Determination Dates: | The 11th day of each month (or if that day is not a business day, the next succeeding business day), commencing in December 2011. | |

| Distribution Dates: | The fourth business day following the Determination Date in each month, commencing in December 2011. | |

| Rated Final Distribution Date: | The Distribution Date in November 2044. | |

| Interest Accrual Period: | With respect to any Distribution Date, the calendar month preceding the month in which such Distribution Date occurs. | |

| Day Count: | The Offered Certificates will accrue interest on a 30/360 basis. | |

| Minimum Denominations: | $25,000 for each Class of Offered Certificates. Investments may also be made in any whole dollar denomination in excess of the applicable minimum denomination. | |

| Clean-up Call: | 1% | |

| Delivery: | DTC, Euroclear and Clearstream Banking. | |

| ERISA/SMMEA Status: | Each Class of Offered Certificates is expected to be eligible for exemptive relief under ERISA. No Class of Offered Certificates will be SMMEA eligible. | |

| Risk Factors: | THE CERTIFICATES INVOLVE CERTAIN RISKS AND MAY NOT BE SUITABLE FOR ALL INVESTORS. SEE THE “RISK FACTORS” SECTION OF THE FREE WRITING PROSPECTUS. | |

| Bond Analytics Information: | The Certificate Administrator will generally be required to make distribution date settlements, CREFC reports and certain supplemental reports (other than confidential information) available to certain financial modeling and data provision services, including Bloomberg L.P., Trepp LLC, Intex Solutions, Inc., Markit Group Limited and BlackRock Financial Management Inc. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

6

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

IV. Characteristics of the Mortgage Pool

A. Ten Largest Mortgage Loans

Mortgage Loan Seller | Mortgage Loan Name | City | State | Number of Mortgage Loans / Mortgaged Properties | Mortgage Loan Cut-off Date Balance ($) | % of Cut- off Date Balance (%) | Property Type | Number of SF or Rooms | Cut-off Date Balance Per SF or Room ($) | Cut-off Date LTV Ratio (%) | Balloon LTV Ratio (%) | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | |||||||||||||||||||||

| RBS | The Domain | Austin | TX | 1 / 1 | $207,550,029 | 19.0 | % | Retail | 878,974 | $236 | 53.4 | % | 44.6 | % | 1.35 | x | 9.7 | % | ||||||||||||||||

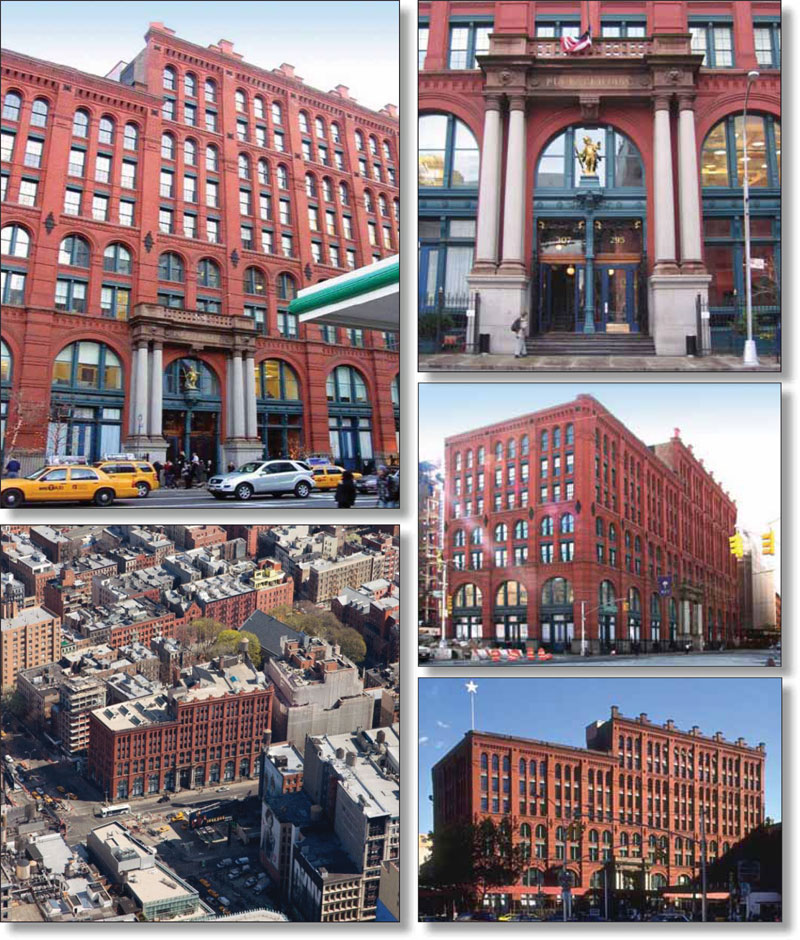

| RBS | Puck Building | New York | NY | 1 / 1 | 85,000,000 | 7.8 | Mixed Use | 206,693 | 411 | 60.7 | 56.3 | 1.25 | 8.5 | |||||||||||||||||||||

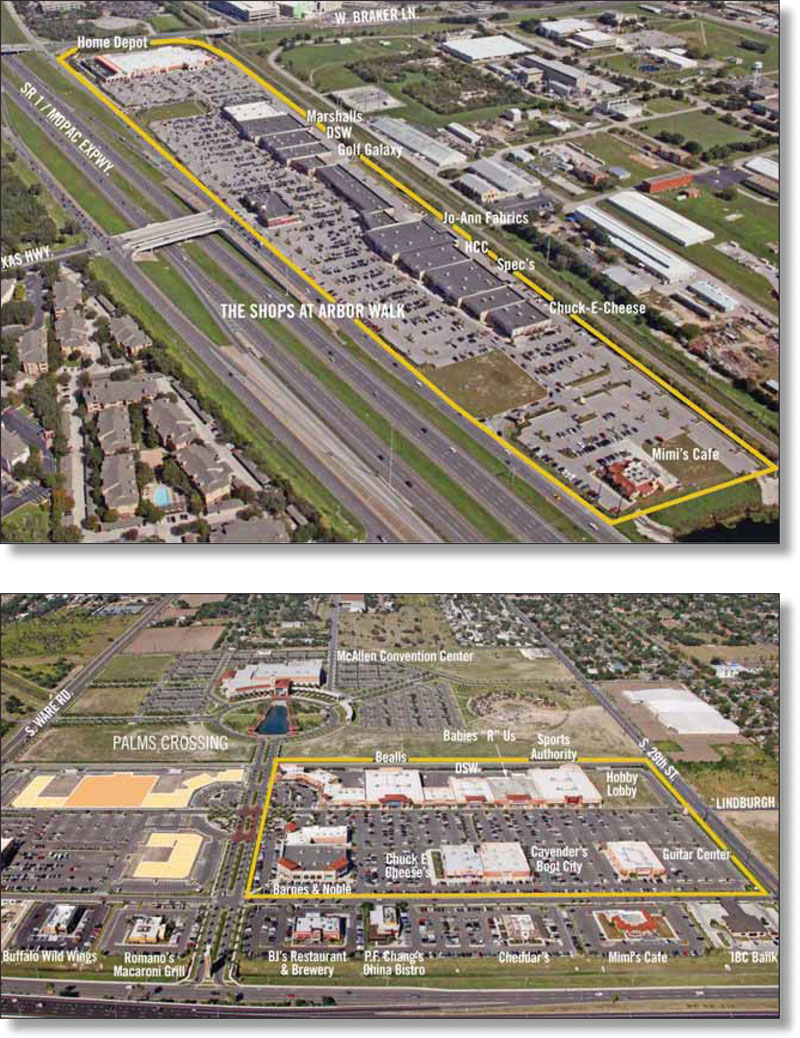

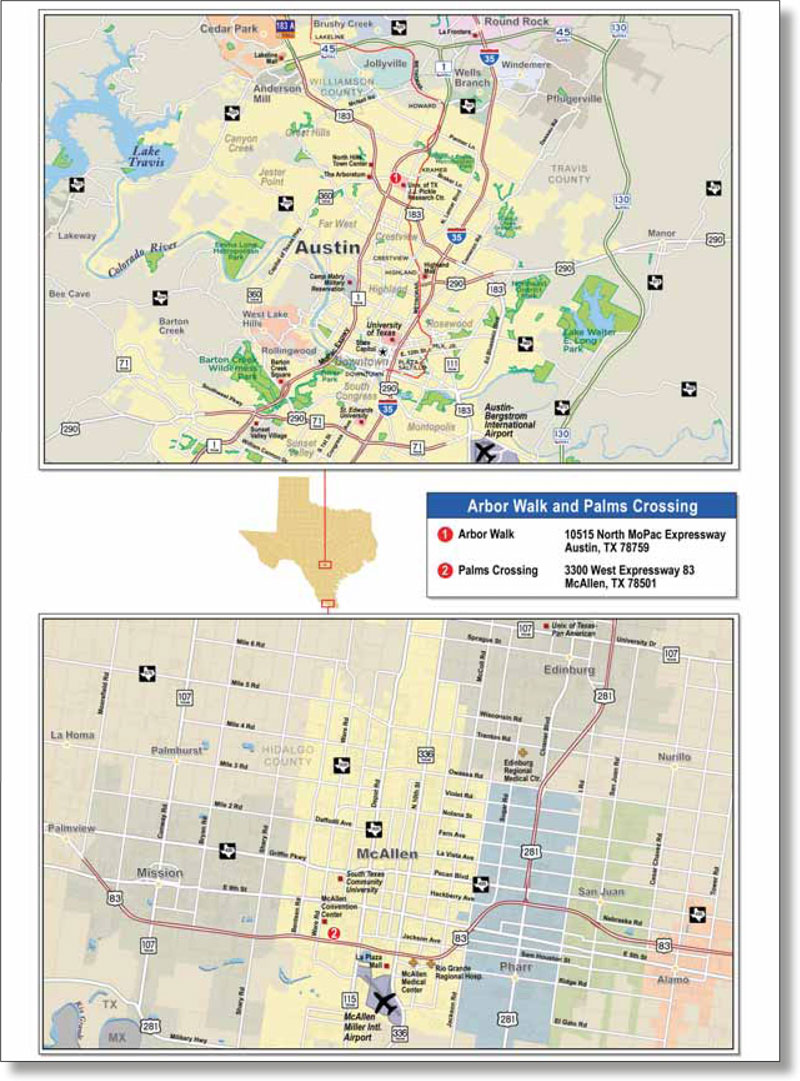

| RBS | Arbor Walk and Palms Crossing | Various | TX | 1 / 2 | 81,547,453 | 7.5 | Retail | 792,758 | 103 | 68.5 | 57.4 | 1.38 | 10.4 | |||||||||||||||||||||

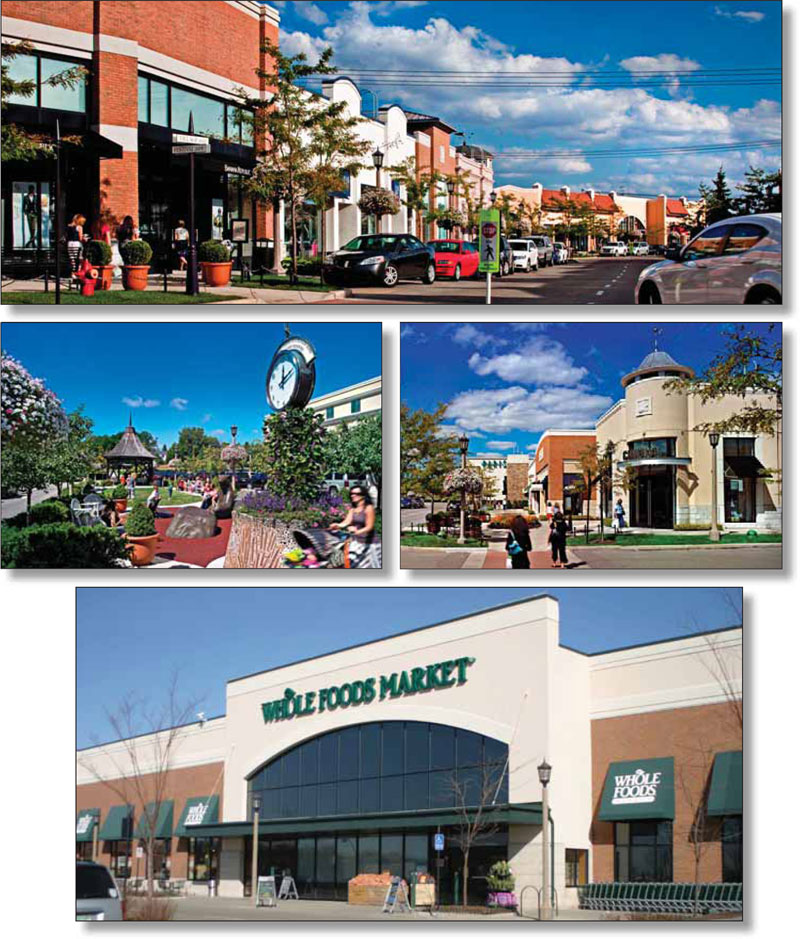

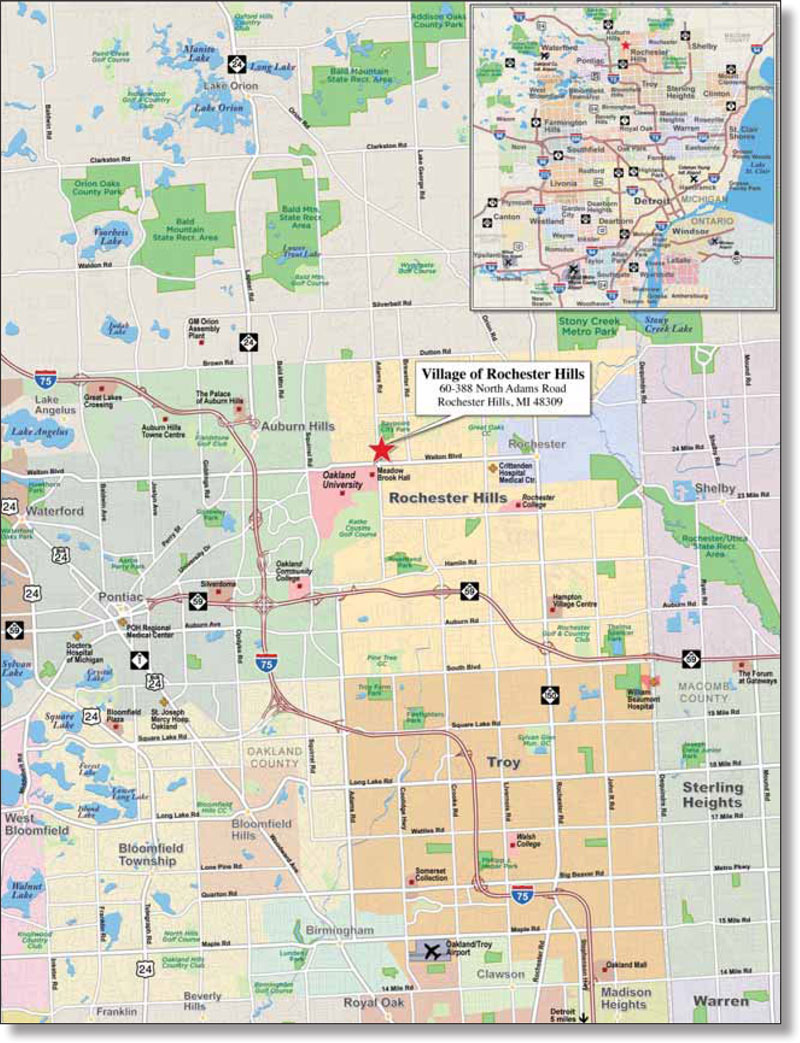

| RBS | Village of Rochester Hills | Rochester Hills | MI | 1 / 1 | 51,000,000 | 4.7 | Retail | 254,596 | 200 | 65.7 | 58.0 | 1.60 | 11.6 | |||||||||||||||||||||

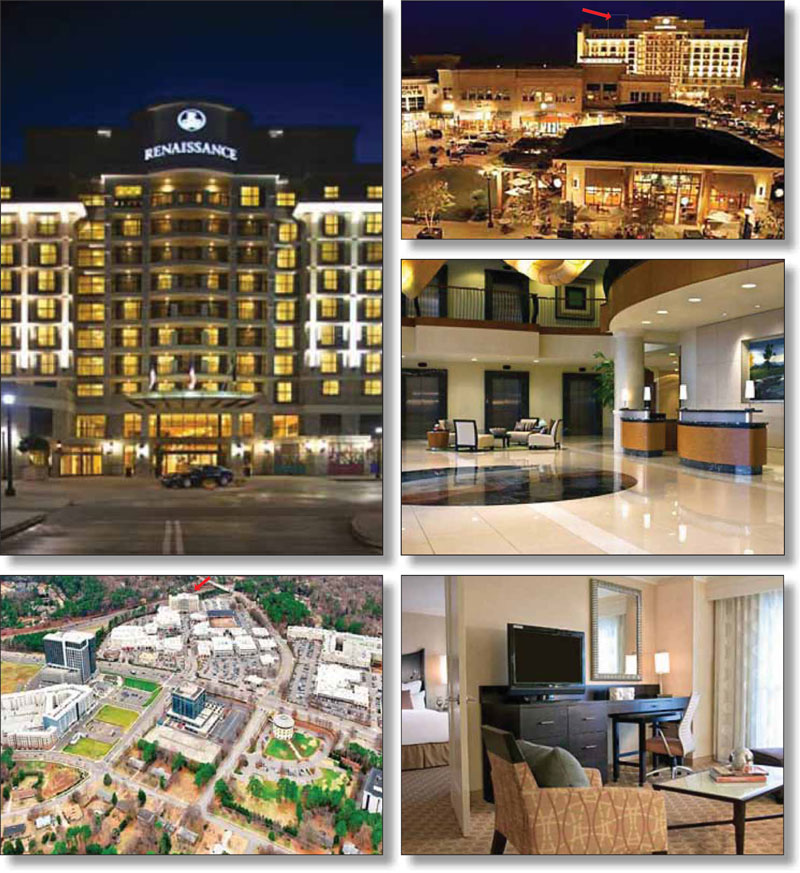

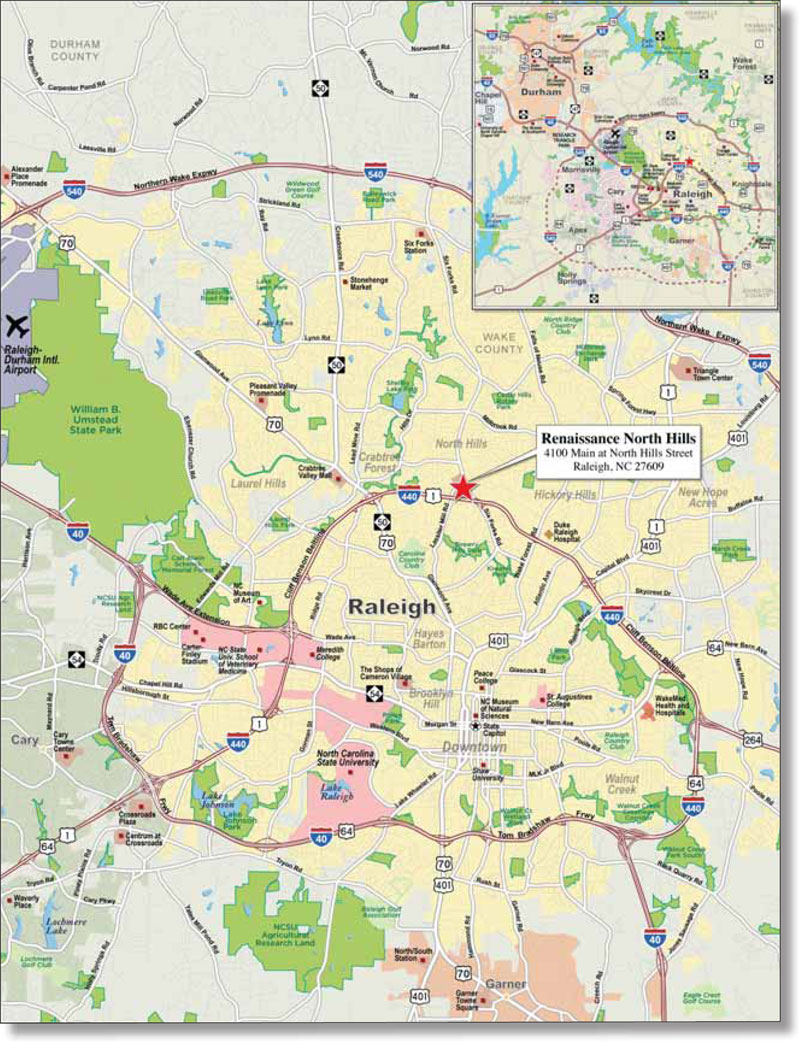

| RBS | Renaissance North Hills | Raleigh | NC | 1 / 1 | 47,411,949 | 4.3 | Hospitality | 229 | 207,039 | 69.7 | 59.1 | 1.63 | 13.0 | |||||||||||||||||||||

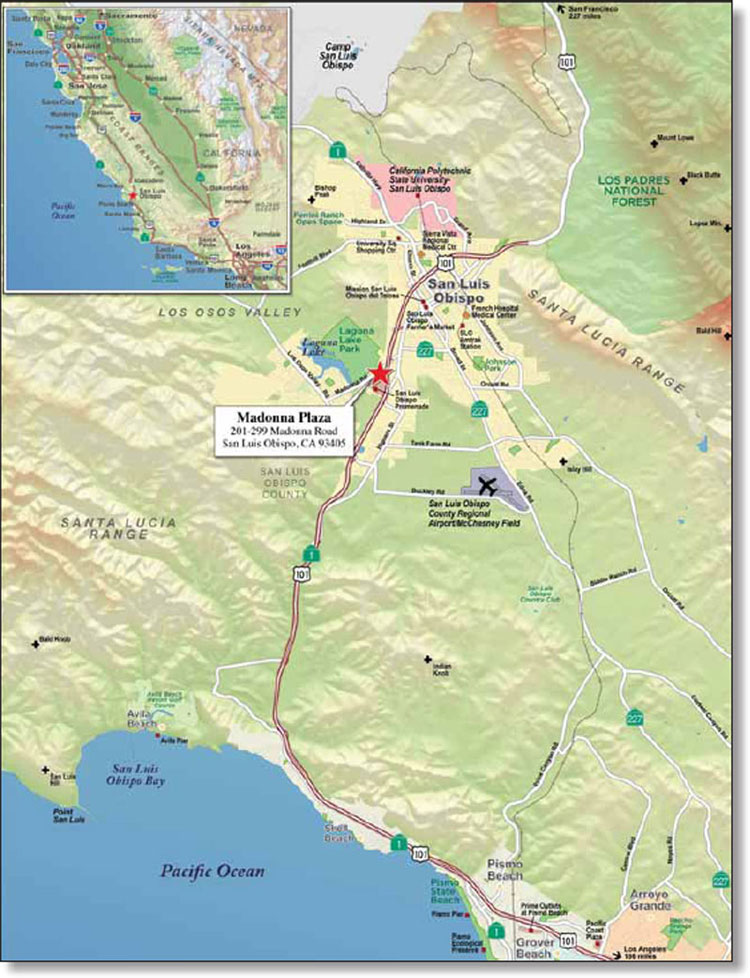

| RBS | Madonna Plaza | San Luis Obispo | CA | 1 / 1 | 40,000,000 | 3.7 | Retail | 318,514 | 126 | 68.0 | 57.4 | 1.28 | 9.6 | |||||||||||||||||||||

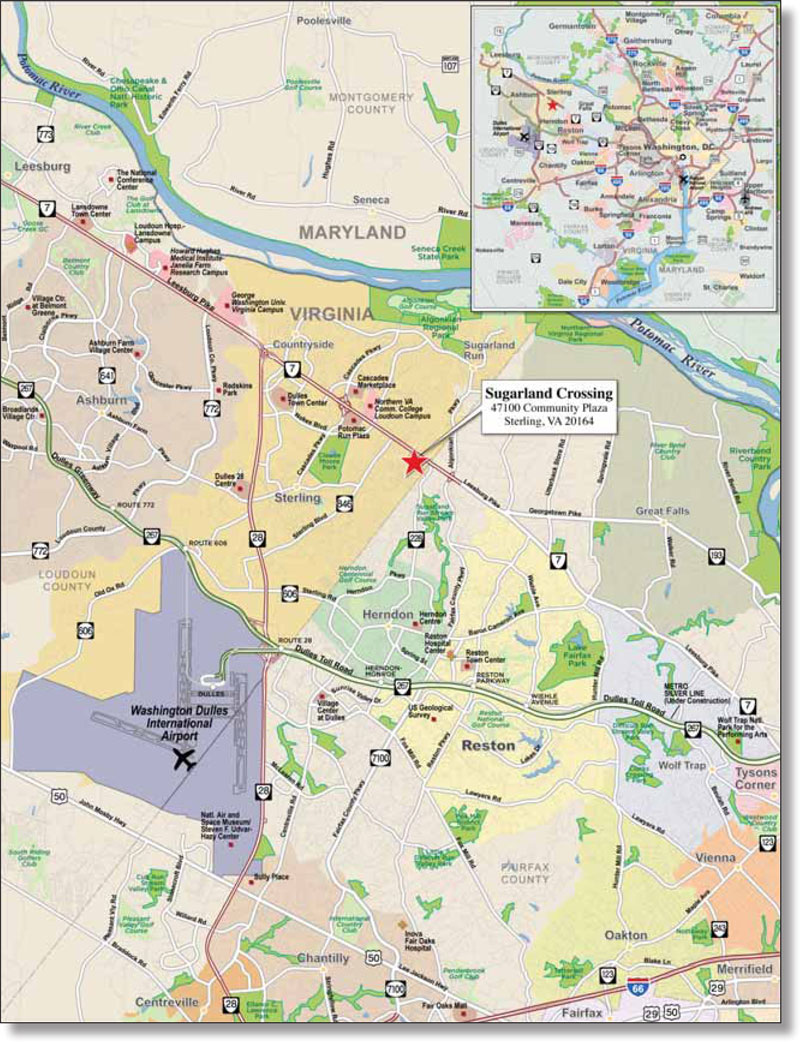

| RBS | Sugarland Crossing | Sterling | VA | 1 / 1 | 29,918,786 | 2.7 | Retail | 256,623 | 117 | 72.1 | 61.2 | 1.41 | 10.8 | |||||||||||||||||||||

| RBS | 919 Congress | Austin | TX | 1 / 1 | 27,918,559 | 2.6 | Office | 164,718 | 169 | 68.9 | 58.0 | 1.32 | 9.9 | |||||||||||||||||||||

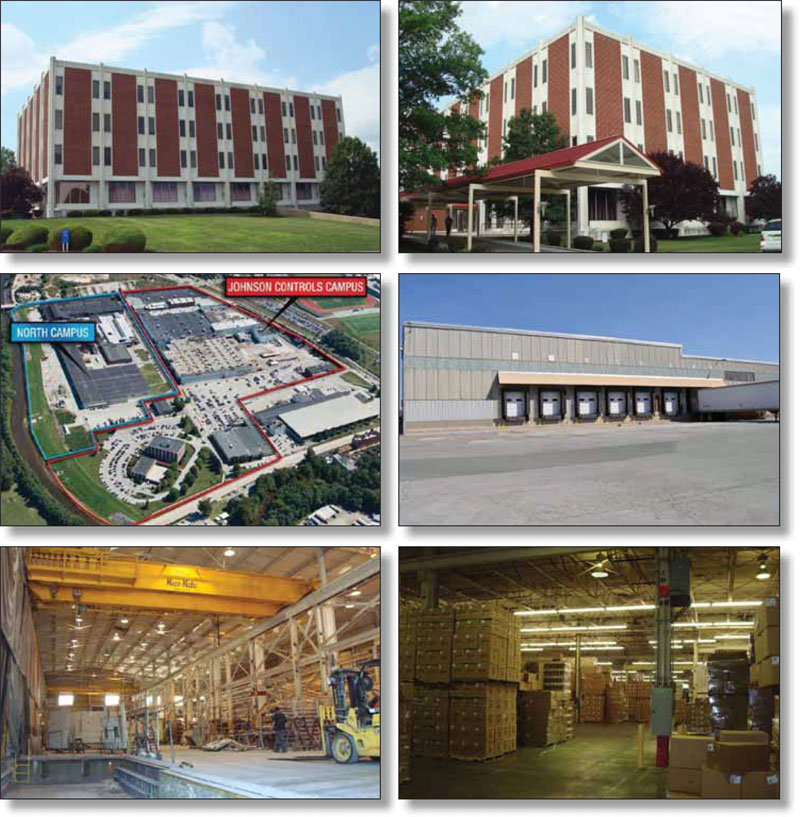

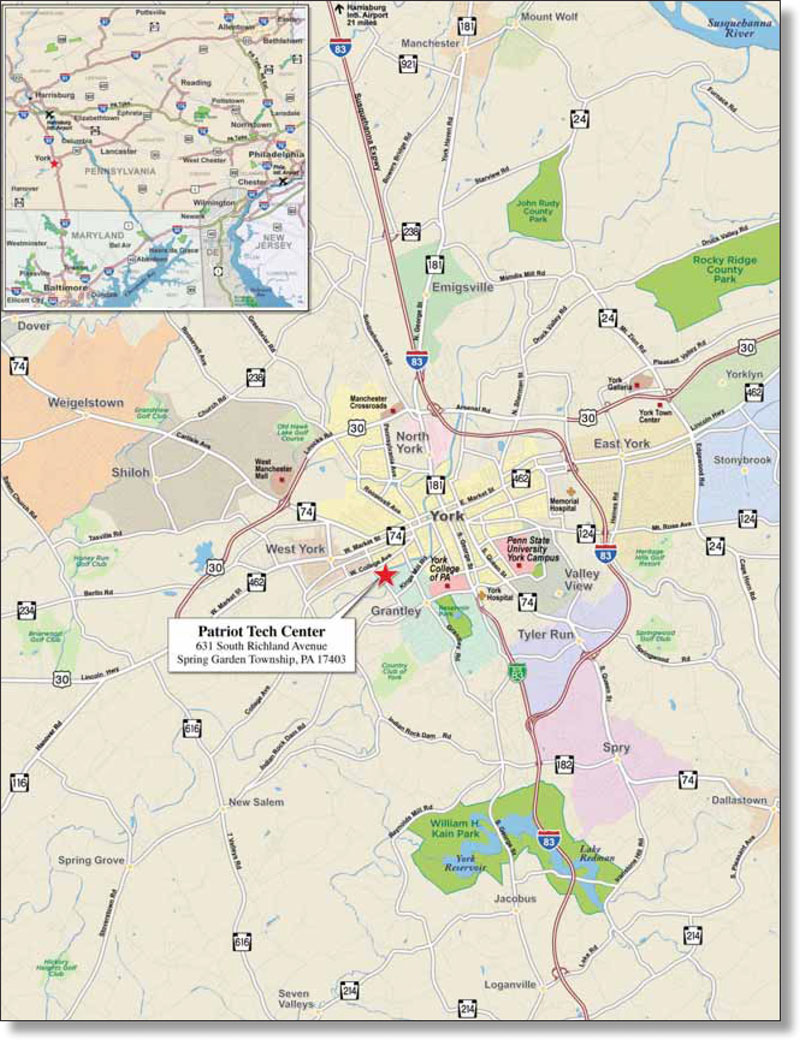

| RBS | Patriot Tech Center | Spring Garden Township | PA | 1 / 1 | 27,477,803 | 2.5 | Industrial | 1,539,290 | 18 | 60.2 | 51.2 | 1.31 | 11.5 | |||||||||||||||||||||

| RBS | Ascent Hotel Portfolio | Various | Various | 1 / 4 | 24,468,913 | 2.2 | Hospitality | 325 | 75,289 | 60.1 | 46.7 | 1.79 | 15.1 | |||||||||||||||||||||

| Top Three Total / Weighted Average | 3 / 4 | $374,097,482 | 34.3 | % | 58.4 | % | 50.0 | % | 1.33 | x | 9.6 | % | ||||||||||||||||||||||

| Top Five Total / Weighted Average | 5 / 6 | $472,509,430 | 43.3 | % | 60.3 | % | 51.8 | % | 1.39 | x | 10.1 | % | ||||||||||||||||||||||

| Top Ten Total / Weighted Average | 10 / 14 | $622,293,491 | 57.0 | % | 61.7 | % | 52.7 | % | 1.39 | x | 10.4 | % | ||||||||||||||||||||||

B. Mortgage Loans with Additional Secured and Mezzanine Financing(1)

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | Mortgage Loan Cut-off Date Balance ($) | % of Cut- off Date Balance (%) | Non-Trust Mortgage Loan Cut-off Date Balance ($) | Mezzanine Debt Cut-off Date Balance ($) | Total Debt Interest Rate (%) | Mortgage Loan U/W NCF DSCR (x) | Total Debt U/W NCF DSCR (x) | Mortgage Loan Cut- off Date U/W NOI Debt Yield (%) | Total Debt Cut-off Date U/W NOI Debt Yield (%) | Mortgage Loan Cut-off Date LTV Ratio (%) | Total Debt Cut-off Date LTV Ratio (%) | |||||||||||||||||||||||||

| 2 | RBS | Puck Building(2) | $85,000,000 | 7.8 | % | $0 | $10,000,000 | 5.842 | % | 1.25 | x | 1.06 | x | 8.5 | % | 7.6 | % | 60.7 | % | 67.9 | % | |||||||||||||||||

| 14 | WFB | Overlook at the Rim(3) | 18,000,000 | 1.6 | 0 | 5,000,000 | 4.650 | 3.12 | 1.99 | 15.0 | 11.7 | 54.8 | 70.0 | |||||||||||||||||||||||||

| Total/Weighted Average | $103,000,000 | 9.4 | % | $0 | $15,000,000 | 1.58 | x | 1.22 | x | 9.6 | % | 8.4 | % | 59.7 | % | 68.3 | % | |||||||||||||||||||||

| (1) | In addition, the borrowers under certain of the mortgage loans also have incurred unsecured additional debt as described in the Free Writing Prospectus. |

| (2) | For mortgage loan #2 (Puck Building), the mezzanine loan bears interest at an interest rate that increases to 12.000% after 36 months following origination. The combined U/W NCF DSCR based on the mortgage loan and the mezzanine loan assuming a 10.000% rate for the life of the mezzanine loan is 1.06x and the combined U/W NCF DSCR based on the mortgage loan and the mezzanine loan assuming a 12.000% rate for the life of the mezzanine loan is 1.03x. |

| (3) | For mortgage loan #14 (Overlook at the Rim), the mezzanine loan has an interest rate that increases to 10.000% if the mezzanine loan is not paid off on or prior to December 31, 2011. The combined U/W NCF DSCR based on the mortgage loan and the mezzanine loan assuming a 4.650% rate for the life of the mezzanine loan is 2.44x and the combined U/W NCF DSCR based on the mortgage loan and the mezzanine loan assuming a 10.000% rate for the life of the mezzanine loan is 1.95x. In addition, if the mezzanine debt is not retired on or prior to December 31, 2011, all excess cash flow after all debt service payments will be applied toward amortizing the mezzanine debt. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

7

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

| C. Previous Securitization History(1) | |

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | City | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Previous Securitization | ||||||||

| 2 | RBS | Puck Building | New York | NY | Mixed Use | $85,000,000 | 7.8% | Various(2) | ||||||||

| 4 | RBS | Village of Rochester Hills | Rochester Hills | MI | Retail | 51,000,000 | 4.7 | CSFB 2002-CP5 | ||||||||

| 7 | RBS | Sugarland Crossing | Sterling | VA | Retail | 29,918,786 | 2.7 | JPMCC 2002-CIBC4 | ||||||||

| 8 | RBS | 919 Congress | Austin | TX | Office | 27,918,559 | 2.6 | GCCFC 2005-GG3 | ||||||||

| 11 | RBS | Torrance Plaza East | Torrance | CA | Office | 21,082,280 | 1.9 | LBUBS 2001-C7 | ||||||||

| 12 | WFB | Flagship Storage Portfolio - Indiana | Indianapolis | IN | Self Storage | 20,247,005 | 1.9 | Various(3) | ||||||||

| 13 | WFB | PetSmart | Phoenix | AZ | Industrial | 19,950,045 | 1.8 | BSCMS 2002-TOP8 | ||||||||

| 16 | RBS | Residence Inn Atlanta Midtown | Atlanta | GA | Hospitality | 15,432,583 | 1.4 | GCCFC 2006-GG7 | ||||||||

| 17 | RBS | Torrance Plaza West | Torrance | CA | Office | 15,387,067 | 1.4 | LBUBS 2001-C7 | ||||||||

| 21 | RBS | Brookwood Village | Erie | PA | Multifamily | 12,225,727 | 1.1 | CSFB 2002-CKPI | ||||||||

| 22 | WFB | Del Monte Portfolio | Various | Various | Industrial | 11,267,922 | 1.0 | Various(4) | ||||||||

| 24 | Basis | H-Mart Portfolio | Various | Various | Retail | 11,072,477 | 1.0 | Various(5) | ||||||||

| 25 | WFB | Flagship Storage Portfolio - Ohio | Various | OH | Self Storage | 10,672,067 | 1.0 | Various(6) | ||||||||

| 29 | RBS | Silver Springs Pointe | Oklahoma City | OK | Retail | 8,800,000 | 0.8 | WBCMT 2002-C1 | ||||||||

| 30 | RBS | Poughkeepsie Galleria II | Poughkeepsie | NY | Retail | 8,464,724 | 0.8 | FUNB 2001-C3 | ||||||||

| 31 | WFB | Sprint Center | Rio Rancho | NM | Office | 8,438,918 | 0.8 | SBM7 2001-C2 | ||||||||

| 32 | CIIICM | Hampton Inn Jacksonville | Jacksonville | FL | Hospitality | 7,318,278 | 0.7 | FUBOA 2001-C1 | ||||||||

| 33 | RBS | Dayton Park | Dayton | MN | Manufactured Housing Community | 7,244,455 | 0.7 | ASC 1996-D2 | ||||||||

| 35 | Basis | 354 Mountain View Drive | Colchester | VT | Office | 6,978,388 | 0.6 | BACM 2006-5 | ||||||||

| 37 | CIIICM | 1680-1700 East Touhy Avenue | Des Plaines | IL | Industrial | 6,692,023 | 0.6 | BACM 2001-PB1 | ||||||||

| 38 | Basis | 356 Mountain View Drive | Colchester | VT | Office | 6,305,472 | 0.6 | BACM 2006-5 | ||||||||

| 41 | GECC | American Self Storage - Palo Alto | East Palo Alto | CA | Self Storage | 5,982,007 | 0.5 | BACM 2004-5 | ||||||||

| 44 | WFB | Boardwalk Apartments | Houston | TX | Multifamily | 5,734,989 | 0.5 | DLJMA 1996-CF2 | ||||||||

| 46 | GECC | Boulder Bins Self Storage | Boulder | CO | Self Storage | 5,483,506 | 0.5 | Various(7) | ||||||||

| 47 | GECC | Ross Valley Self Storage | Kentfield | CA | Self Storage | 5,383,806 | 0.5 | BACM 2004-5 | ||||||||

| 49 | GECC | Lock It San Diego Self Storage | San Diego | CA | Self Storage | 4,985,638 | 0.5 | DLJCM 2000-CKP1 | ||||||||

| 50 | GECC | Burlington Self Storage | West Palm Beach | FL | Self Storage | 4,461,000 | 0.4 | CD 2005-CD1 | ||||||||

| 55 | CIIICM | Royal Highlander | Peoria | IL | Manufactured Housing Community | 3,888,500 | 0.4 | JPMCC 2006-LDP8 | ||||||||

| 57 | GECC | Country Estates MHC | Grants Pass | OR | Manufactured Housing Community | 3,678,873 | 0.3 | BACM 2006-4 | ||||||||

| 58 | Basis | 180 West Washington Office | Chicago | IL | Office | 3,596,363 | 0.3 | LBCMT 1999-C1 | ||||||||

| 59 | GECC | Castle Rock Self Storage | Castle Rock | CO | Self Storage | 3,494,612 | 0.3 | LBUBS 2004-C6 | ||||||||

| 60 | CIIICM | American Mini Storage I & II | Sierra Vista | AZ | Self Storage | 3,447,588 | 0.3 | BACM 2001-PB1 | ||||||||

| 62 | CIIICM | Mimi’s Plaza | Tustin | CA | Retail | 2,997,674 | 0.3 | BSCMS 2001-TOP4 | ||||||||

| 65 | CIIICM | Mill Creek Village | Buford | GA | Retail | 2,698,047 | 0.2 | JPMCC 2001-CIBC3 | ||||||||

| 66 | Basis | New Market Square | Varina | VA | Retail | 2,689,372 | 0.2 | LBUBS 2001-C7 |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

8

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

| Previous Securitization History (cont’d) | ||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | City | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Previous Securitization | ||||||||

| 67 | CIIICM | Pecan Valley Estates | Bossier City | LA | Manufactured Housing Community | $2,598,119 | 0.2% | DLJCM 2000-CF1 | ||||||||

| 68 | WFB | Metro Storage | Taylor | MI | Self Storage | 2,446,219 | 0.2 | WBCMT 2005-C18 | ||||||||

| 70 | CIIICM | First American Self Storage - River Oaks | River Oaks | TX | Self Storage | 2,158,473 | 0.2 | BSCMS 2006-TOP22 | ||||||||

| 72 | WFB | 2 Claire Road | East Brunswick Township | NJ | Industrial | 2,144,368 | 0.2 | CSFB 2001-CK6 | ||||||||

| 73 | WFB | Georgetown South Apartments | Sharpsville | PA | Multifamily | 2,089,268 | 0.2 | MSDWC 2001-TOP3 | ||||||||

| (1) | The table above represents the most recent securitization with respect to the mortgaged property securing the related mortgage loan, based on information provided by the related borrower or obtained through TREPP searches. The information has not otherwise been confirmed by the mortgage loan sellers. |

| (2) | The debt on the mortgaged property was securitized in two separate transactions: CCMSC 1997-1 and MLMT 2003-KEY1. |

| (3) | The debt on seven of the eight mortgaged properties was securitized in one transaction: LBUBS 2004-C8 (8270 Michigan Road, 2251 Shadeland Avenue, 5425 North Tacoma Avenue, 9685 Fall Creek Road, 3601 West 96th Street, 551 East Stover Avenue and 920 County Line Road). |

| (4) | The debt on one of the three mortgaged properties (Del Monte – Mendota) was securitized in a previous transaction: MSDWC 2001-TOP5. |

| (5) | The debt on one of the two mortgaged properties (H Mart – Carrollton) was securitized in three separate transactions: GSMS 2005-FL7A, GSMS 2006-FL8A and CGCMT 2006-FL2. |

| (6) | The debt on two of the seven mortgaged properties (1500 Brush Road and 23640 Lakeland Boulevard) was securitized in one transaction: LBUBS 2000-C5. |

| (7) | The debt on the mortgaged property was securitized in two separate transactions: BACM 2004-5 and FULB 1997-C1. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

9

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

D. Mortgage Loans with Scheduled Balloon Payments and Related Classes

Class A-2(1)

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-2 Certificate Principal Balance (%) | Units/ SF/ Rooms | Loan per Unit/ SF/ Room | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) | ||||||||||||||||||||||||||||||

| 14 | WFB | Overlook at the Rim | TX | Office | $18,000,000 | 1.6 | % | $18,000,000 | 15.2 | % | 145,025 | $124 | 3.12 | x | 15.0 | % | 54.8 | % | 54.8 | % | 56 | 56 | ||||||||||||||||||||||||

| 16 | RBS | Residence Inn Atlanta Midtown | GA | Hospitality | 15,432,583 | 1.4 | 13,918,463 | 11.8 | 160 | 96,454 | 1.49 | 12.6 | 59.4 | 53.5 | 0 | 57 | ||||||||||||||||||||||||||||||

| 19 | WFB | 24 Hour Fitness - Pleasanton | CA | Retail | 13,539,491 | 1.2 | 11,509,162 | 9.7 | 56,206 | 241 | 1.42 | 12.2 | 66.5 | 56.6 | 0 | 58 | ||||||||||||||||||||||||||||||

| 22 | WFB | Del Monte Portfolio | Various | Industrial | 11,267,922 | 1.0 | 9,480,882 | 8.0 | 724,600 | 16 | 1.35 | 12.8 | 46.4 | 39.0 | 0 | 57 | ||||||||||||||||||||||||||||||

| 31 | WFB | Sprint Center | NM | Office | 8,438,918 | 0.8 | 7,106,999 | 6.0 | 94,730 | 89 | 1.66 | 15.6 | 56.6 | 47.7 | 0 | 57 | ||||||||||||||||||||||||||||||

| 32 | CIIICM | Hampton Inn Jacksonville | FL | Hospitality | 7,318,278 | 0.7 | 6,696,322 | 5.7 | 118 | 62,019 | 1.54 | 14.1 | 69.7 | 63.8 | 0 | 57 | ||||||||||||||||||||||||||||||

| 34 | Basis | Westchase Corporate Park | TX | Office | 6,987,393 | 0.6 | 6,555,289 | 5.5 | 176,977 | 39 | 1.34 | 11.5 | 69.9 | 65.6 | 0 | 58 | ||||||||||||||||||||||||||||||

| 35 | Basis | 354 Mountain View Drive | VT | Office | 6,978,388 | 0.6 | 6,491,324 | 5.5 | 59,523 | 117 | 1.63 | 12.7 | 66.5 | 61.8 | 0 | 57 | ||||||||||||||||||||||||||||||

| 36 | Basis | Hilton Garden Inn | WI | Hospitality | 6,819,062 | 0.6 | 6,140,309 | 5.2 | 128 | 53,274 | 1.75 | 14.5 | 69.6 | 62.7 | 0 | 56 | ||||||||||||||||||||||||||||||

| 37 | CIIICM | 1680-1700 East Touhy Avenue | IL | Industrial | 6,692,023 | 0.6 | 6,091,177 | 5.1 | 252,000 | 27 | 1.95 | 17.2 | 57.7 | 52.5 | 0 | 59 | ||||||||||||||||||||||||||||||

| 38 | Basis | 356 Mountain View Drive | VT | Office | 6,305,472 | 0.6 | 5,865,375 | 5.0 | 50,949 | 124 | 1.43 | 10.7 | 70.8 | 65.9 | 0 | 57 | ||||||||||||||||||||||||||||||

| 50 | GECC | Burlington Self Storage | FL | Self Storage | 4,461,000 | 0.4 | 4,290,882 | 3.6 | 69,861 | 64 | 1.41 | 10.1 | 73.7 | 70.9 | 22 | 58 | ||||||||||||||||||||||||||||||

| 55 | CIIICM | Royal Highlander | IL | Manufactured Housing Community | 3,888,500 | 0.4 | 3,650,024 | 3.1 | 280 | 13,888 | 1.47 | 11.2 | 70.7 | 66.4 | 0 | 60 | ||||||||||||||||||||||||||||||

| 57 | GECC | Country Estates MHC | OR | Manufactured Housing Community | 3,678,873 | 0.3 | 3,325,272 | 2.8 | 104 | 35,374 | 1.37 | 10.4 | 67.8 | 61.2 | 0 | 56 | ||||||||||||||||||||||||||||||

| 66 | Basis | New Market Square | VA | Retail | 2,689,372 | 0.2 | 2,509,357 | 2.1 | 40,200 | 67 | 1.67 | 12.8 | 64.0 | 59.7 | 0 | 56 | ||||||||||||||||||||||||||||||

| Total/Weighted Average | $122,497,276 | 11.2 | % | $111,630,834 | 94.3 | % | 1.76 | x | 13.2 | % | 62.0 | % | 56.6 | % | 9 | 57 | ||||||||||||||||||||||||||||||

| (1) | The table above presents the mortgage loans whose balloon payments would be applied to pay down the principal balance of the Class A-2 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-2 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

10

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

Class A-3(1) | |||||||||||||||||||||||||||||||||||||||||||||||

| Loan No. | Mortgage Loan Seller | Mortgage Loan Name | State | Property Type | Mortgage Loan Cut-off Date Balance ($) | % of Cut-off Date Balance (%) | Mortgage Loan Balance at Maturity ($) | % of Class A-3 Certificate Principal Balance (%) | Units/ SF/ Rooms | Loan per Unit/ SF/ Room | U/W NCF DSCR (x) | U/W NOI Debt Yield (%) | Cut-off Date LTV Ratio (%) | Balloon LTV Ratio (%) | Rem. IO Period (mos.) | Rem. Term to Maturity (mos.) | |||||||||||||||||||||||||||||||

| 20 | WFB | Merit Medical Systems | UT | Mixed Use | $12,984,987 | 1.2 | % | $10,775,582 | 10.0 | % | 193,449 | 67 | 1.43 | x | 13.0 | % | 65.3 | % | 54.1 | % | 0 | 101 | |||||||||||||||||||||||||

| 21 | RBS | Brookwood Village | PA | Multifamily | 12,225,727 | 1.1 | 10,991,152 | 10.2 | 135 | 90,561 | 1.37 | 9.8 | 73.8 | 66.4 | 0 | 82 | |||||||||||||||||||||||||||||||

| 48 | RBS | Candlewood Suites Houston, TX | TX | Hospitality | 4,994,401 | 0.5 | 4,345,908 | 4.0 | 81 | 61,659 | 1.49 | 13.5 | 62.4 | 54.3 | 0 | 83 | |||||||||||||||||||||||||||||||

| Total/Weighted Average | $30,205,116 | 2.8 | % | $26,112,643 | 24.2 | % | 1.42 | x | 11.8 | % | 68.3 | % | 59.1 | % | 0 | 90 | |||||||||||||||||||||||||||||||

| (1) | The table above presents the mortgage loans whose balloon payments would be applied to pay down the principal balance of the Class A-3 Certificates, assuming a 0% CPR and applying the “Structuring Assumptions” described in the Free Writing Prospectus, including the assumptions that (i) none of the mortgage loans in the pool experience prepayments, defaults or losses; (ii) there are no extensions of maturity dates of any mortgage loans in the pool; and (iii) each mortgage loan in the pool is paid in full on its stated maturity date. Each class of Certificates, including the Class A-3 Certificates, evidences undivided ownership interests in the entire pool of mortgage loans. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

11

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

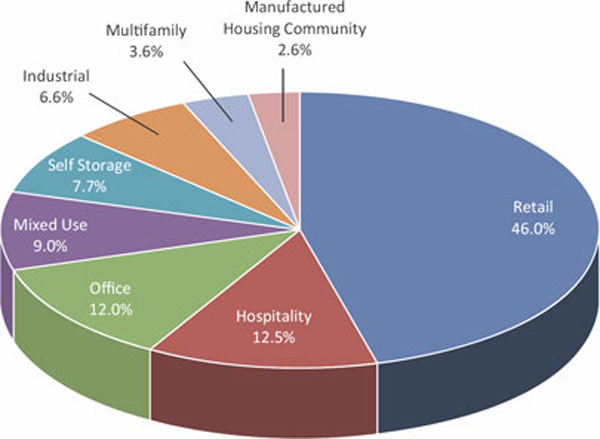

E. Property Type Distribution

| Property Type | Number of Mortgaged Properties | Aggregate Cut- off Date Balance ($)(1) | % of Cut-off Date Balance (%) | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | |||||||||||||||||||||||||||

| Retail | 20 | $ | 501,891,318 | 46.0 | % | 61.7 | % | 52.3 | % | 1.43 | x | 10.5 | % | 9.9 | % | 5.630 | % | |||||||||||||||||||

| Anchored | 9 | 238,178,634 | 21.8 | 67.8 | 58.1 | 1.46 | 10.8 | 10.1 | 5.741 | |||||||||||||||||||||||||||

| Regional Mall | 2 | 216,014,753 | 19.8 | 53.4 | 44.6 | 1.37 | 9.8 | 9.2 | 5.430 | |||||||||||||||||||||||||||

| Single Tenant | 4 | 27,599,449 | 2.5 | 69.9 | 58.1 | 1.44 | 11.9 | 11.3 | 5.779 | |||||||||||||||||||||||||||

| Unanchored | 5 | 20,098,482 | 1.8 | 67.0 | 57.3 | 1.61 | 12.7 | 11.9 | 6.259 | |||||||||||||||||||||||||||

| Hospitality | 12 | 136,855,466 | 12.5 | 66.0 | 55.1 | 1.61 | 13.6 | 12.2 | 6.026 | |||||||||||||||||||||||||||

| Limited Service | 10 | 78,296,786 | 7.2 | 63.7 | 53.1 | 1.61 | 13.9 | 12.5 | 6.031 | |||||||||||||||||||||||||||

| Full Service | 1 | 47,411,949 | 4.3 | 69.7 | 59.1 | 1.63 | 13.0 | 11.7 | 5.941 | |||||||||||||||||||||||||||

| Extended Stay | 1 | 11,146,732 | 1.0 | 67.1 | 52.7 | 1.55 | 13.7 | 12.4 | 6.357 | |||||||||||||||||||||||||||

| Office | 10 | 130,975,264 | 12.0 | 64.6 | 56.7 | 1.66 | 12.0 | 10.9 | 5.605 | |||||||||||||||||||||||||||

| Suburban | 8 | 99,460,342 | 9.1 | 63.5 | 56.5 | 1.76 | 12.5 | 11.3 | 5.576 | |||||||||||||||||||||||||||

| CBD | 2 | 31,514,922 | 2.9 | 68.3 | 57.3 | 1.35 | 10.4 | 9.5 | 5.699 | |||||||||||||||||||||||||||

| Mixed Use | 2 | 97,984,987 | 9.0 | 61.3 | 56.0 | 1.27 | 9.1 | 8.8 | 5.505 | |||||||||||||||||||||||||||

| Office/Retail | 1 | 85,000,000 | 7.8 | 60.7 | 56.3 | 1.25 | 8.5 | 8.4 | 5.353 | |||||||||||||||||||||||||||

| Office/Warehouse/Medical | 1 | 12,984,987 | 1.2 | 65.3 | 54.1 | 1.43 | 13.0 | 11.6 | 6.500 | |||||||||||||||||||||||||||

| Self Storage | 31 | 84,302,538 | 7.7 | 66.5 | 55.0 | 1.54 | 11.8 | 11.4 | 5.996 | |||||||||||||||||||||||||||

| Self Storage | 31 | 84,302,538 | 7.7 | 66.5 | 55.0 | 1.54 | 11.8 | 11.4 | 5.996 | |||||||||||||||||||||||||||

| Industrial | 8 | 71,863,557 | 6.6 | 54.8 | 45.2 | 1.36 | 12.4 | 10.6 | 6.017 | |||||||||||||||||||||||||||

| Warehouse | 5 | 37,909,990 | 3.5 | 50.2 | 41.6 | 1.40 | 13.0 | 11.2 | 5.968 | |||||||||||||||||||||||||||

| Flex | 3 | 33,953,567 | 3.1 | 60.0 | 49.3 | 1.32 | 11.7 | 9.8 | 6.071 | |||||||||||||||||||||||||||

| Multifamily | 7 | 39,072,575 | 3.6 | 72.7 | 62.6 | 1.36 | 10.4 | 9.8 | 5.861 | |||||||||||||||||||||||||||

| Garden | 5 | 27,522,575 | 2.5 | 72.1 | 61.3 | 1.39 | 10.9 | 10.1 | 5.867 | |||||||||||||||||||||||||||

| Student Housing | 2 | 11,550,000 | 1.1 | 74.3 | 65.6 | 1.27 | 9.2 | 9.0 | 5.846 | |||||||||||||||||||||||||||

| Manufactured Housing Community | 8 | 28,198,265 | 2.6 | 66.6 | 58.4 | 1.47 | 11.3 | 10.9 | 6.267 | |||||||||||||||||||||||||||

| Manufactured Housing Community | 8 | 28,198,265 | 2.6 | 66.6 | 58.4 | 1.47 | 11.3 | 10.9 | 6.267 | |||||||||||||||||||||||||||

| Total/ Weighted Average | 98 | $ | 1,091,143,971 | 100.0 | % | 63.0 | % | 53.8 | % | 1.47 | x | 11.2 | % | 10.4 | % | 5.744 | % | |||||||||||||||||||

| (1) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents). |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

12

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

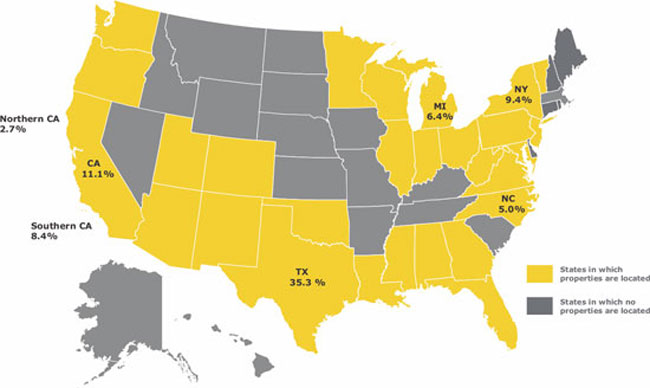

F. Geographic Distribution*

Location(1) | Number of Mortgaged Properties | Aggregate Cut-off Date Balance ($)(2) | % of Cut- off Date Balance | Weighted Average Cut-off Date LTV Ratio (%) | Weighted Average Balloon LTV Ratio (%) | Weighted Average U/W NCF DSCR (x) | Weighted Average U/W NOI Debt Yield (%) | Weighted Average U/W NCF Debt Yield (%) | Weighted Average Mortgage Rate (%) | ||||||||||||||||||||||||||

| Texas | 13 | $ | 385,037,285 | 35.3 | % | 59.9 | % | 50.7 | % | 1.44 | x | 10.3 | % | 9.6 | % | 5.512 | % | ||||||||||||||||||

| California | 11 | 121,383,751 | 11.1 | 64.5 | 54.1 | 1.44 | 11.1 | 10.4 | 5.802 | ||||||||||||||||||||||||||

| Southern | 7 | 92,147,049 | 8.4 | 65.1 | 55.1 | 1.40 | 10.8 | 9.9 | 5.884 | ||||||||||||||||||||||||||

| Northern | 4 | 29,236,701 | 2.7 | 62.4 | 51.1 | 1.56 | 12.4 | 11.9 | 5.542 | ||||||||||||||||||||||||||

| New York | 3 | 102,939,924 | 9.4 | 60.7 | 55.0 | 1.32 | 9.3 | 9.0 | 5.430 | ||||||||||||||||||||||||||

| Michigan | 9 | 69,845,283 | 6.4 | 66.6 | 57.5 | 1.58 | 11.8 | 11.3 | 5.896 | ||||||||||||||||||||||||||

| North Carolina | 3 | 55,055,499 | 5.0 | 69.4 | 58.8 | 1.61 | 12.9 | 11.7 | 5.998 | ||||||||||||||||||||||||||

Other States(3) | 59 | 356,882,229 | 32.7 | 64.9 | 55.2 | 1.50 | 12.3 | 11.2 | 5.996 | ||||||||||||||||||||||||||

| Total/ Weighted Average | 98 | $ | 1,091,143,971 | 100.0 | % | 63.0 | % | 53.8 | % | 1.47 | x | 11.2 | % | 10.4 | % | 5.744 | % | ||||||||||||||||||

| * | The Mortgaged Properties are located in 28 states. |

| (1) | For purposes of determining whether a mortgaged property is in Northern California or Southern California, Northern California includes areas with zip codes above 93600 and Southern California includes areas with zip codes of 93600 and below. |

(2) | Because this table presents information relating to the mortgaged properties and not the mortgage loans, the information for mortgage loans secured by more than one mortgaged property is based on allocated amounts (allocating the mortgage loan principal balance to each of those properties according to the relative appraised values of the mortgaged properties or the allocated loan amounts or property-specific release prices set forth in the related mortgage loan documents). |

| (3) | Includes 23 other states. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

13

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

| G. | Characteristics of the Mortgage Pool |

| CUT-OFF DATE BALANCE | LOAN PURPOSE | |||||||||||||||

Range of Cut-off Date Balances ($) | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Cut-off Date Balance | Loan Purpose | Number of Mortgage Loans | Aggregate Cut- off Date Balance | % of Cut-off Date Balance | |||||||||

| 1,290,156 - 2,000,000 | 2 | $ | 2,933,706 | 0.3% | Refinance | 58 | $ | 945,746,647 | 86.7% | |||||||

| 2,000,001 - 3,000,000 | 12 | 30,158,865 | 2.8 | Acquisition | 17 | 145,397,323 | 13.3 | |||||||||

| 3,000,001 - 4,000,000 | 7 | 25,314,408 | 2.3 | Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||

| 4,000,001 - 5,000,000 | 7 | 31,363,271 | 2.9 | |||||||||||||

| 5,000,001 - 6,000,000 | 8 | 46,073,301 | 4.2 | MORTGAGE RATE | ||||||||||||

| 6,000,001 - 7,000,000 | 6 | 39,964,774 | 3.7 | Number of | ||||||||||||

| 7,000,001 - 8,000,000 | 2 | 14,562,733 | 1.3 | Range of Mortgage Rates | Mortgage | Aggregate Cut- | % of Cut-off | |||||||||

| 8,000,001 - 9,000,000 | 3 | 25,703,642 | 2.4 | (%) | Loans | off Date Balance | Date Balance | |||||||||

| 9,000,001 - 10,000,000 | 3 | 28,498,200 | 2.6 | 4.650 - 4.750 | 1 | $ | 18,000,000 | 1.6% | ||||||||

| 10,000,001 - 15,000,000 | 8 | 97,897,775 | 9.0 | 4.751 - 5.000 | 2 | 19,706,840 | 1.8 | |||||||||

| 15,000,001 - 20,000,000 | 5 | 85,050,518 | 7.8 | 5.001 - 5.250 | 1 | 8,800,000 | 0.8 | |||||||||

| 20,000,001 - 30,000,000 | 6 | 151,113,346 | 13.8 | 5.251 - 5.500 | 12 | 436,823,939 | 40.0 | |||||||||

| 30,000,001 - 50,000,000 | 2 | 87,411,949 | 8.0 | 5.501 - 5.750 | 9 | 83,226,262 | 7.6 | |||||||||

| 50,000,001 - 70,000,000 | 1 | 51,000,000 | 4.7 | 5.751 - 6.000 | 13 | 234,558,341 | 21.5 | |||||||||

| 80,000,001 - 90,000,000 | 2 | 166,547,453 | 15.3 | 6.001 - 6.250 | 16 | 163,606,873 | 15.0 | |||||||||

| 90,000,001 - 207,550,029 | 1 | 207,550,029 | 19.0 | 6.251 - 6.500 | 15 | 102,574,053 | 9.4 | |||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | 6.501 - 6.750 | 6 | 23,847,661 | 2.2 | ||||||||

Average: | $14,548,586 | Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||||

| Weighted Average: | 5.744% | |||||||||||||||

| UNDERWRITTEN NOI DEBT SERVICE COVERAGE RATIO | ||||||||||||||||

| Number of | UNDERWRITTEN NOI DEBT YIELD | |||||||||||||||

Range of U/W NOI | Mortgage | Aggregate Cut- | % of Cut-off | Number of | ||||||||||||

| DSCRs (x) | Loans | off Date Balance | Date Balance | Range of U/W NOI | Mortgage | Aggregate Cut- | % of Cut-off | |||||||||

| 1.27 - 1.30 | 3 | $ | 96,359,989 | 8.8% | Debt Yields (%) | Loans | off Date Balance | Date Balance | ||||||||

| 1.31 - 1.40 | 4 | 51,977,155 | 4.8 | 8.5 - 9.0 | 1 | $ | 85,000,000 | 7.8% | ||||||||

| 1.41 - 1.50 | 15 | 363,165,919 | 33.3 | 9.1 - 10.0 | 6 | 299,244,316 | 27.4 | |||||||||

| 1.51 - 1.60 | 17 | 241,470,724 | 22.1 | 10.1 - 11.0 | 13 | 190,048,113 | 17.4 | |||||||||

| 1.61 - 1.70 | 15 | 146,424,654 | 13.4 | 11.1 - 12.0 | 18 | 223,719,323 | 20.5 | |||||||||

| 1.71 - 1.80 | 5 | 29,974,757 | 2.7 | 12.1 - 13.0 | 18 | 148,890,181 | 13.6 | |||||||||

| 1.81 - 1.90 | 6 | 67,449,734 | 6.2 | 13.1 - 14.0 | 8 | 53,731,383 | 4.9 | |||||||||

| 1.91 - 2.00 | 5 | 49,366,616 | 4.5 | 14.1 - 15.0 | 7 | 47,913,127 | 4.4 | |||||||||

| 2.01 - 2.25 | 3 | 18,154,422 | 1.7 | 15.1 - 16.0 | 3 | 35,905,505 | 3.3 | |||||||||

| 2.76 - 3.00 | 1 | 8,800,000 | 0.8 | 17.1 - 17.2 | 1 | 6,692,023 | 0.6 | |||||||||

| 3.01 - 3.17 | 1 | 18,000,000 | 1.6 | Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | Weighted Average: | 11.2% | ||||||||||

Weighted Average: | 1.58x | |||||||||||||||

| UNDERWRITTEN NCF DEBT YIELD | ||||||||||||||||

| UNDERWRITTEN NCF DEBT SERVICE COVERAGE RATIO | Number of | |||||||||||||||

| Number of | Range of U/W NCF | Mortgage | Aggregate Cut- | % of Cut-off | ||||||||||||

| Range of U/W NCF | Mortgage | Aggregate Cut- | % of Cut-off | Debt Yields (%) | Loans | off Date Balance | Date Balance | |||||||||

| DSCRs (x) | Loans | off Date Balance | Date Balance | 8.4 - 9.0 | 3 | $ | 130,625,000 | 12.0% | ||||||||

| 1.20 | 1 | $ | 5,734,989 | 0.5% | 9.1 - 10.0 | 12 | 416,508,864 | 38.2 | ||||||||

| 1.21 - 1.30 | 6 | 160,831,442 | 14.7 | 10.1 - 11.0 | 22 | 202,207,568 | 18.5 | |||||||||

| 1.31 - 1.40 | 16 | 444,239,181 | 40.7 | 11.1 - 12.0 | 16 | 195,533,999 | 17.9 | |||||||||

| 1.41 - 1.50 | 21 | 193,069,335 | 17.7 | 12.1 - 13.0 | 15 | 72,615,094 | 6.7 | |||||||||

| 1.51 - 1.60 | 12 | 112,912,011 | 10.3 | 13.1 - 14.0 | 5 | 48,961,422 | 4.5 | |||||||||

| 1.61 - 1.70 | 7 | 73,570,907 | 6.7 | 14.1 - 15.0 | 1 | 18,000,000 | 1.6 | |||||||||

| 1.71 - 1.80 | 4 | 40,708,454 | 3.7 | 15.1 - 15.6 | 1 | 6,692,023 | 0.6 | |||||||||

| 1.81 - 1.90 | 5 | 26,585,628 | 2.4 | Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||

| 1.91 - 2.00 | 1 | 6,692,023 | 0.6 | Weighted Average: | 10.4% | |||||||||||

| 2.51 - 3.00 | 1 | 8,800,000 | 0.8 | |||||||||||||

| 3.01 - 3.12 | 1 | 18,000,000 | 1.6 | |||||||||||||

Total/Weighted Average: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||||||

Weighted Average: | 1.47x | |||||||||||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

14

| WFRBS Commercial Mortgage Trust 2011-C5 | Characteristics of the Mortgage Pool |

| ORIGINAL TERM TO MATURITY | CUT-OFF DATE LOAN-TO-VALUE RATIO | |||||||||||||||||

| Number of | Number of | |||||||||||||||||

| Range of Original Terms to | Mortgage | Aggregate Cut- | % of Cut-off | Range of Cut-off Date LTV | Mortgage | Aggregate Cut- | % of Cut-off | |||||||||||

| Maturity (months) | Loans | off Date Balance | Date Balance | Ratios (%) | Loans | off Date Balance | Date Balance | |||||||||||

| 60 | 15 | $ | 122,497,276 | 11.2% | 46.4 - 50.0 | 4 | $ | 37,654,114 | 3.5% | |||||||||

| 61 - 84 | 2 | 17,220,129 | 1.6 | 50.1 - 55.0 | 4 | 242,814,753 | 22.3 | |||||||||||

| 85 - 120 | 58 | 951,426,566 | 87.2 | 55.1 - 60.0 | 9 | 54,046,277 | 5.0 | |||||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | 60.1 - 65.0 | 11 | 174,921,276 | 16.0 | ||||||||||

Weighted Average: | 112 | 65.1 - 70.0 | 33 | 467,368,931 | 42.8 | |||||||||||||

| 70.1 - 75.0 | 14 | 114,338,620 | 10.5 | |||||||||||||||

| REMAINING TERM TO MATURITY | Total: | 75 | $ | 1,091,143,971 | 100.0% | |||||||||||||

Weighted Average: | 63.0% | |||||||||||||||||

| Number of | ||||||||||||||||||

| Range of Remaining Terms | Mortgage | Aggregate Cut- | % of Cut-off | BALLOON LOAN-TO-VALUE RATIO | ||||||||||||||

| to Maturity (months) | Loans | off Date Balance | Date Balance | |||||||||||||||

| 56 - 60 | 15 | $ | 122,497,276 | 11.2% | Number of | |||||||||||||

| 61 - 84 | 2 | 17,220,129 | 1.6 | Range of Balloon LTV | Mortgage | Aggregate Cut- | % of Cut-off | |||||||||||

| 85 - 120 | 58 | 951,426,566 | 87.2 | Ratios (%) | Loans | off Date Balance | Date Balance | |||||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | 39.0 - 40.0 | 3 | $ | 35,549,364 | 3.3% | |||||||||

Weighted Average: | 110 | 40.1 - 45.0 | 4 | 216,973,656 | 19.9 | |||||||||||||

| 45.1 - 50.0 | 8 | 58,672,849 | 5.4 | |||||||||||||||

| ORIGINAL AMORTIZATION TERM | 50.1 - 55.0 | 21 | 195,104,401 | 17.9 | ||||||||||||||

| 55.1 - 60.0 | 21 | 444,458,075 | 40.7 | |||||||||||||||

| Range of Original | Number of | 60.1 - 65.0 | 12 | 100,892,533 | 9.2 | |||||||||||||

| Amortization Terms | Mortgage | Aggregate Cut- | % of Cut-off | 65.1 - 70.0 | 5 | 35,032,092 | 3.2 | |||||||||||

| (months) | Loans | off Date Balance | Date Balance | 70.1 - 70.9 | 1 | 4,461,000 | 0.4 | |||||||||||

| Non-Amortizing | 2 | $ | 26,800,000 | 2.5% | Total: | 75 | $ | 1,091,143,971 | 100.0% | |||||||||

| 240 | 5 | 40,565,209 | 3.7 | Weighted Average: | 53.8% | |||||||||||||

| 241 - 300 | 20 | 178,729,321 | 16.4 | |||||||||||||||

| 301 - 360 | 48 | 845,049,441 | 77.4 | AMORTIZATION TYPE | ||||||||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||||||||

Weighted Average:* | 345 | Number of | ||||||||||||||||

| * | Excludes the non-amortizing loans. | Mortgage | Aggregate Cut- | % of Cut-off | ||||||||||||||

| Type of Amortization | Loans | off Date Balance | Date Balance | |||||||||||||||

REMAINING AMORTIZATION TERM(1) | Amortizing Balloon | 67 | $ | 908,562,971 | 83.3% | |||||||||||||

| Interest-only, Amortizing | ||||||||||||||||||

| Range of Remaining | Number of | Balloon | 6 | 155,781,000 | 14.3 | |||||||||||||

| Amortization Terms | Mortgage | Aggregate Cut- | % of Cut-off | Interest-only, Balloon | 2 | 26,800,000 | 2.5 | |||||||||||

| (months) | Loans | off Date Balance | Date Balance | Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||||

| Non-Amortizing | 2 | $ | 26,800,000 | 2.5% | ||||||||||||||

| 237 - 240 | 5 | 40,565,209 | 3.7 | ORIGINAL TERM OF INTEREST-ONLY PERIOD FOR PARTIAL IO LOANS* | ||||||||||||||

| 241 - 300 | 20 | 178,729,321 | 16.4 | |||||||||||||||

| 301 - 360 | 48 | 845,049,441 | 77.4 | Number of | ||||||||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | Mortgage | Aggregate Cut- | % of Cut-off | |||||||||||

Weighted Average:(2) | 343 | IO Term (months) | Loans | off Date Balance | Date Balance | |||||||||||||

| (1) | The remaining amortization term shown for any mortgage loan that is interest-only for part of its term does not include the number of months in its interest-only period and reflects only the number of months as of the commencement of amortization remaining from the end of such interest-only period. | 19 - 24 | 5 | $ | 70,781,000 | 6.5% | ||||||||||||

| 49 - 60 | 1 | 85,000,000 | 7.8 | |||||||||||||||

| Total: | 6 | $ | 155,781,000 | 14.3% | ||||||||||||||

| Weighted Average: | 44 | |||||||||||||||||

(2) | Excludes the non-amortizing loans. | * | Excludes non-amortizing loans and amortizing loans that do not provide for a partial interest-only period. | |||||||||||||||

| LOCKBOXES | ||||||||||||||||||

| SEASONING | ||||||||||||||||||

| Number of | ||||||||||||||||||

| Mortgage | Aggregate Cut- | % of Cut-off | Number of | |||||||||||||||

| Type of Lockbox | Loans | off Date Balance | Date Balance | Mortgage | Aggregate Cut- | % of Cut-off | ||||||||||||

| Hard/Springing Cash Management | 29 | $ | 794,102,922 | 72.8% | Seasoning (months) | Loans | off Date Balance | Date Balance | ||||||||||

| Hard/Upfront Cash Management | 9 | 104,933,345 | 9.6 | 0 | 5 | $ | 103,718,500 | 9.5% | ||||||||||

| None | 21 | 102,728,816 | 9.4 | 1 - 3 | 59 | 842,517,226 | 77.2 | |||||||||||

| Soft/Springing Cash Management | 6 | 35,310,513 | 3.2 | 4 | 11 | 144,908,245 | 13.3 | |||||||||||

| Springing (With Established | Total: | 75 | $ | 1,091,143,971 | 100.0% | |||||||||||||

| Account) | 7 | 31,537,259 | 2.9 | Weighted Average: | 2 | |||||||||||||

| Springing (Without Established | ||||||||||||||||||

| Account) | 3 | 22,531,116 | 2.1 | |||||||||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||||||||

| PREPAYMENT PROVISION SUMMARY | ||||||||||||||||||

| Number of | % of Cut- | |||||||||||||||||

| Mortgage | Aggregate Cut- | off Date | ||||||||||||||||

| Prepayment Provision | Loans | off Date Balance | Balance | |||||||||||||||

| Lockout/ Defeasance/ Open | 61 | $ | 974,384,643 | 89.3% | ||||||||||||||

| Lockout/ YM%/ Open | 13 | 108,294,603 | 9.9 | |||||||||||||||

| Lockout/ YM%/ Defeasance/ Open | 1 | 8,464,724 | 0.8 | |||||||||||||||

Total: | 75 | $ | 1,091,143,971 | 100.0% | ||||||||||||||

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

15

| WFRBS Commercial Mortgage Trust 2011-C5 | Certain Terms and Conditions |

V. Certain Terms and Conditions

| Interest Entitlements: | The interest entitlement of each Class of Offered Certificates on each Distribution Date generally will be the interest accrued during the related Interest Accrual Period on the related Certificate Principal Balance or Notional Amount at the related pass-through rate, net of any prepayment interest shortfalls allocated to that Class for such Distribution Date as described below. If prepayment interest shortfalls arise from voluntary prepayments (without special servicer consent) on non-specially serviced mortgage loans during any collection period, the Master Servicer is required to make a compensating interest payment to offset those shortfalls, generally up to an amount equal to the portion of its master servicing fees that accrues at three basis points per annum. The remaining amount of prepayment interest shortfalls will be allocated to reduce the interest otherwise distributable on all Classes of Certificates (other than the Class X-A and Class X-B Certificates), pro rata, based on their respective amounts of accrued interest for the related Distribution Date. If a Class receives less than the entirety of its interest entitlement on any Distribution Date, then the shortfall will be added to its interest entitlement for the next succeeding Distribution Date. Interest entitlements on the Class B, C, D and E Certificates, in that order, may be reduced by certain Trust Advisor expenses. |

| Principal Distribution Amount: | The Principal Distribution Amount for each Distribution Date generally will be the aggregate amount of principal received or advanced in respect of the mortgage loans, net of any nonrecoverable advances and interest thereon that are reimbursed to the Master Servicer, the Special Servicer or the Trustee during the related collection period. Nonrecoverable advances and interest thereon are reimbursable from principal collections and advances before reimbursement from other amounts. The Principal Distribution Amount may also be reduced, with a corresponding loss to the Class E, D, C, B and A-S Certificates, then to the Class A-1, A-2, A-3 and A-4 Certificates (with any losses on the Class A-1, A-2, A-3 and A-4 Certificates allocated pro rata according to their respective Certificate Principal Balances immediately prior to that Distribution Date), in that order, in connection with certain Trust Advisor expenses to the extent that interest entitlements on the Class B, C, D and E Certificates are insufficient to absorb the effect of the expense on any particular Distribution Date. |

| Distributions: | On each Distribution Date, funds available for distribution from the mortgage loans, net of specified trust fees, expenses and reimbursements will generally be distributed in the following amounts and order of priority (in each case to the extent of remaining available funds): |

1. Class A-1, A-2, A-3, A-4, X-A and X-B Certificates: To interest on the Class A-1, A-2, A-3, A-4, X-A and X-B Certificates, pro rata, according to their respective interest entitlements. | |

2. Class A-1, A-2, A-3 and A-4 Certificates: To principal on the Class A-1, A-2, A-3 and A-4 Certificates in the following amounts and order of priority: (i) first, to principal on the Class A-1 Certificates until their Certificate Principal Balance is reduced to zero, up to the Principal Distribution Amount for such Distribution Date; (ii) second, to principal on the Class A-2 Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date; (iii) third, to principal on the Class A-3 Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date; (iv) fourth, to principal on the Class A-4 Certificates until their Certificate Principal Balance is reduced to zero, up to the remainder of the Principal Distribution Amount for such Distribution Date. However, if the Certificate Principal Balance of each and every Class of Principal Balance Certificates other than the Class A-1, A-2, A-3 and A-4 Certificates has been reduced to zero as a result of the allocation of Mortgage Loan losses and expenses and any of the Class A-1, A-2, A-3 and/or A-4 Certificates remain outstanding, then the Principal Distribution Amount will be distributed on the Class A-1, A-2, A-3 and A-4 Certificates, pro rata, based on their respective outstanding Certificate Principal Balances, until their Certificate Principal Balances have been reduced to zero. | |

3. Class A-1, A-2, A-3 and A-4 Certificates: To reimburse the holders of the Class A-1, A-2, A-3 and A-4 Certificates, pro rata, for any previously unreimbursed losses (other than certain Trust Advisor expenses) on the mortgage loans that were previously allocated in reduction of the Certificate Principal Balances of such Classes. |

THE INFORMATION IN THIS STRUCTURAL AND COLLATERAL TERM SHEET IS NOT COMPLETE AND MAY BE AMENDED PRIOR TO THE TIME OF SALE. THIS TERM SHEET IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT A SOLICITATION OF AN OFFER TO BUY THESE SECURITIES IN ANY JURISDICTION WHERE THE OFFER OR SALE IS NOT PERMITTED.

16

| WFRBS Commercial Mortgage Trust 2011-C5 | Certain Terms and Conditions |

4. Class A-S Certificates: To make distributions on the Class A-S Certificates as follows: (a) first, to interest on Class A-S Certificates in the amount of the interest entitlement for that Class; (b) next, to the extent of the portion of the Principal Distribution Amount remaining after distributions in respect of principal to each Class with a higher distribution priority (in this case, the Class A-1, A-2, A-3 and A-4 Certificates), to principal on Class A-S Certificates until their Certificate Principal Balance is reduced to zero; and (c) next, to reimburse the holders of the Class A-S Certificates for any previously unreimbursed losses (other than certain Trust Advisor expenses) on the mortgage loans that were previously allocated to that Class in reduction of its Certificate Principal Balance. | |

5. After the Class A-1, A-2, A-3, A-4 and A-S Certificates are paid all amounts to which they are entitled, the remaining funds available for distribution will be used to pay interest, principal and loss reimbursement amounts (other than certain Trust Advisor expenses) on the Class B, C, D, E, F, G and H Certificates sequentially in that order in a manner analogous to the Class A-S Certificates. | |

| Allocation of Yield Maintenance and Prepayment Premiums: | If any yield maintenance charges and prepayment premiums are collected during any particular collection period with respect to any mortgage loan, then on the distribution date corresponding to that collection period, the certificate administrator will pay a portion of the yield maintenance charges and prepayment premiums (net of liquidation fees payable therefrom) in the following manner: (1) pro rata, between the (x) the group (the “YM Group A”) of the Class A-1, A-2, A-3, A-4, A-S and X-A Certificates, and (y) the group (the “YM Group B” and, collectively with the YM Group A, the “YM Groups”) of the Class B, C, D, E and X-B Certificates, based upon the aggregate amount of principal distributed to the classes of principal balance certificates in each YM Group for that distribution date, and (2) among the classes of certificates in each YM Group, in the following manner, up to an amount equal to the product of (a) the yield maintenance or prepayment premium allocated to such YM Group, (b) the related Base Interest Fraction (as defined in the Free Writing Prospectus), and (c) a fraction, which in no event may be greater than 1.0, the numerator of which is equal to the amount of principal distributed to the holder(s) of such class for that distribution date, and the denominator of which is the aggregate amount of principal distributed to all the certificates in that YM Group for that distribution date. Any yield maintenance charges or prepayment premium allocated to such YM Group remaining after such distributions will be distributed to the Class X-A and/or Class X-B Certificates, as applicable, in such YM Group. |

No prepayment premiums or yield maintenance charges will be distributed to the holders of the Class F, G, H or R Certificates. The holders of the Class X-B Certificates will be entitled to all prepayment premiums and yield maintenance charges collected after the Class A-1, A-2, A-3, A-4, A-S, B, C, D and E Certificates are retired. For a description of when prepayment premiums and yield maintenance charges are generally required on the mortgage loans, see Annex A-1 to the Free Writing Prospectus. See also “Certain Legal Aspects of Mortgage Loans — Enforceability of Certain Provisions” in the Free Writing Prospectus. Prepayment premiums and yield maintenance charges will be distributed on each Distribution Date only to the extent they are actually received on the mortgage loans as of the related Determination Date. | |