| 1 1 Independence Contract Drilling, Inc. August 8, 2022 EnerCom Denver The Energy Investment Conference |

| 2 2 2 Various statements contained in this presentation, including those that express a belief, expectation or intention, as well a s t hose that are not statements of historical fact, are forward - looking statements. These forward - looking statements may include projections and estimates concerning the timing and success of specific projects and our future revenues, income and capital spe nding. Our forward - looking statements are generally accompanied by words such as “ estimate, ” “ project, ” “ predict, ” “ believe, ” “ expect, ” “ anticipate, ” “ potential, ” “ plan, ” “ goal, ” “ will ” or other words that convey the uncertainty of future events or outcomes. The forward - looking statements in this presentation spe ak only as of the date of this presentation; we disclaim any obligation to update these statements unless required by law, and we caution you not to rely on them unduly. We hav e based these forward - looking statements on our current expectations and assumptions about future events. While our management considers these expectations and assumptions to be reasonable, they are inherently subject to significant business , e conomic, competitive, regulatory and other risks, contingencies and uncertainties, most of which are difficult to predict and many of which are beyond our control. These and other important factors, including those discussed under “ Risk Factors ” and “ Management ’ s Discussion and Analysis of Financial Condition and Results of Operations ” included in the Company ’ s filings with the Securities and Exchange Commission, including the Company ’ s Annual Report on Form 10 - K, may cause our actual results, performance or achievements to differ materially from any future results, performance or ach ie vements expressed or implied by these forward - looking statements. These risks, contingencies and uncertainties include, but are not limited to, th e following: • inability to predict the duration or magnitude of the effects of the COVID - 19 pandemic on our business, operations, and financial condition and when or if worldwide oil demand will stabilize and begin to improve ; • decline in or substantial volatility of crude oil and natural gas commodity prices • a decrease in domestic spending by the oil and natural gas exploration and production industry ; • fluctuation of our operating results and volatility of our industry ; • inability to maintain or increase pricing of our contract drilling services, or early termination of any term contract for which early termination compensation is not paid ; • our backlog of term contracts declining rapidly ; • the loss of any of our customers, financial distress or management changes of potential customers or failure to obtain contract renewals and additional customer contracts for our drilling services ; • overcapacity and competition in our industry ; • an increase in interest rates and deterioration in the credit markets ; • our inability to comply with the financial and other covenants in debt agreements that we may enter into as a result of reduced revenues and financial performance ; • unanticipated costs, delays and other difficulties in executing our long - term growth strategy ; • the loss of key management personnel ; • new technology that may cause our drilling methods or equipment to become less competitive ; • labor costs or shortages of skilled workers ; • the loss of or interruption in operations of one or more key vendors ; • the effect of operating hazards and severe weather on our rigs, facilities, business, operations and financial results, and limitations on our insurance coverage ; • increased regulation of drilling in unconventional formations ; • the incurrence of significant costs and liabilities in the future resulting from our failure to comply with new or existing environmental regulations or an accidental release of hazardous substances into the environment ; and • the potential failure by us to establish and maintain effective internal control over financial reporting .. All forward - looking statements are necessarily only estimates of future results, and there can be no assurance that actual resul ts will not differ materially from expectations, and, therefore, you are cautioned not to place undue reliance on such statements. Any forward - looking statements are qualified in their entirety by reference to the factors discussed throughout this presentation and in the Company ’ s filings with the Securities and Exchange Commission, including the Company ’ s Annual Report on Form 10 - K. Further, any forward - looking statement speaks only as of the date of this presentation, and we undertake no obligation to up date any forward - looking statement to reflect events or circumstances after the date on which the statement is made or to reflect the occurrence of unanticipated events. Adjusted Net Income or Loss, EBITDA and adjusted EBITDA are supplemental non - GAAP financial measures that are used by management and external users of the Company ’ s financial statements, such as industry analysts, investors, lenders and rating agencies. The Company ’ s management believes adjusted Net Income or Loss, EBITDA and adjusted EBITDA are useful because such measures allow the Comp any and its stockholders to more effectively evaluate its operating performance and compare the results of its operations from period to period and against its peers without regard to its financing methods or capital str ucture. See non - GAAP financial measures at the end of this presentation for a full reconciliation of Net Income or Loss to adjus ted Net Income or Loss, EBITDA and adjusted EBITDA. Preliminary Matters |

| 3 3 3 US Land Drilling’s Only Publicly - Traded, Pure - Play, Pad - Optimal, Super - Spec, Growth Story Highest Asset Quality 100% Pad - Optimal, Super - Spec Fleet Premier Customer Base Rapidly Expanding Margins/Cash Flows Driven by Strategic Investments and Market Conditions Significant Investment Opportunity - Meaningful Current Valuation Discount to Market Based Upon Both Asset Values and Cash Flow Multiples Fleet 100% Dual - Fuel Enabled / Electric Hi - Line Capable: Substantial GHG Reduction / Elimination Recognized Industry Leader for Service and Professionalism Ideal Geographic Focus on Most Prolific Oil and Natural Gas Producing Regions |

| 4 4 4 1. Company Background: Pure - Play, 100 % Pad - Optimal, Super - Spec U.S. Land Contract Driller 2. Very Constructive Market Dynamics and Outlook 3. Drivers of Returns and Free Cash Flow in Current Market 4. Balance Sheet / Recent Debt Re - Financing Untaps Imbedded Value 5. ESG 6. Conclusion Presentation Outline |

| 5 5 5 COMPANY BACKGROUND Pure - Play, 100% Pad - Optimal, Super - Spec U.S. Land Contract Driller |

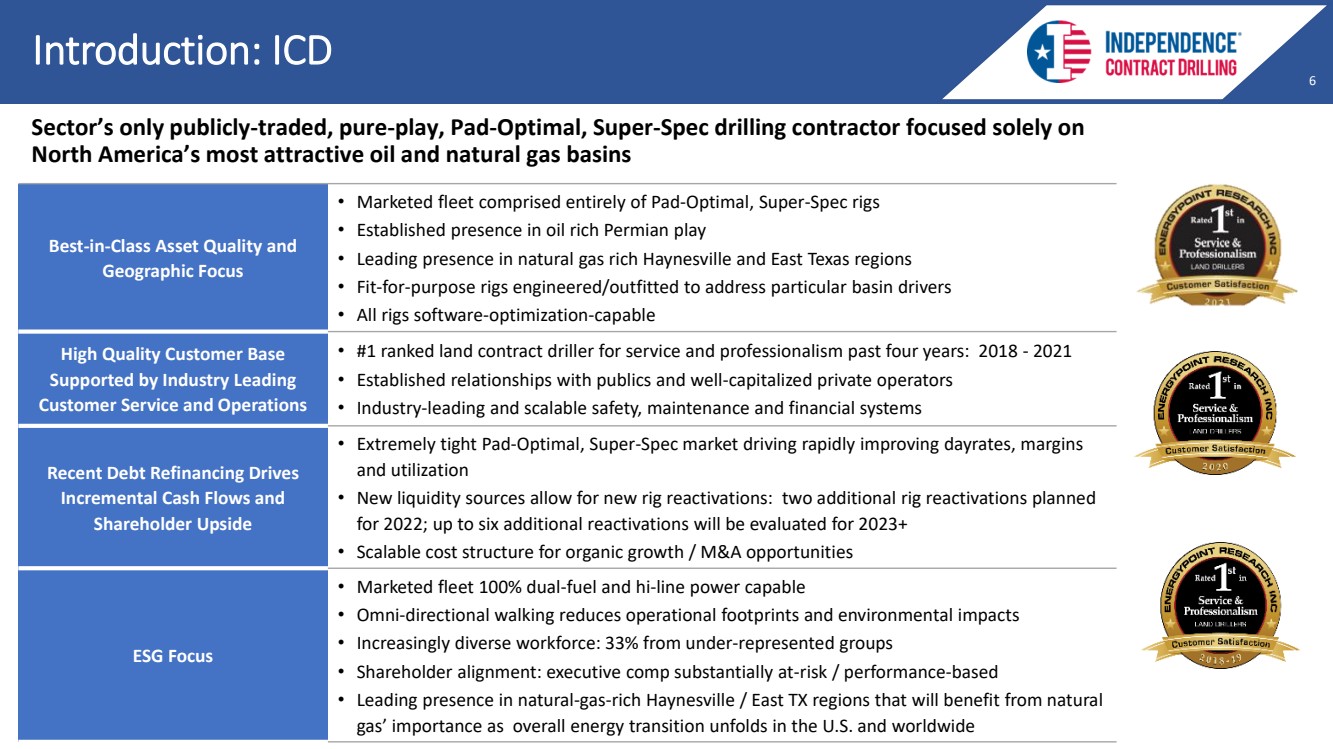

| 6 6 6 Introduction: ICD Best - in - Class Asset Quality and Geographic Focus • Marketed fleet comprised entirely of Pad - Optimal, Super - Spec rigs • Established presence in oil rich Permian play • Leading presence in natural gas rich Haynesville and East Texas regions • Fit - for - purpose rigs engineered/outfitted to address particular basin drivers • All rigs software - optimization - capable High Quality Customer Base Supported by Industry Leading Customer Service and Operations • #1 ranked land contract driller for service and professionalism past four years: 2018 - 2021 • Established relationships with publics and well - capitalized private operators • Industry - leading and scalable safety, maintenance and financial systems Recent Debt Refinancing Drives Incremental Cash Flows and Shareholder Upside • Extremely tight Pad - Optimal, Super - Spec market driving rapidly improving dayrates, margins and utilization • New liquidity sources allow for new rig reactivations: two additional rig reactivations planned for 2022; up to six additional reactivations will be evaluated for 2023+ • Scalable cost structure for organic growth / M&A opportunities ESG Focus • Marketed fleet 100% dual - fuel and hi - line power capable • Omni - directional walking reduces operational footprints and environmental impacts • Increasingly diverse workforce: 33% from under - represented groups • Shareholder alignment: executive comp substantially at - risk / performance - based • Leading presence in natural - gas - rich Haynesville / East TX regions that will benefit from natural gas’ importance as overall energy transition unfolds in the U.S. and worldwide Sector’s only publicly - traded, pure - play, Pad - Optimal, Super - Spec drilling contractor focused solely on North America’s most attractive oil and natural gas basins |

| 7 7 7 • 17 rigs operating throughout the quarter • 18 th rig commenced operations early August ‘22 • Future rig reactivations - 19 th rig: scheduled for early Q4’22 - 20 th rig: scheduled for mid - to - late Q4 ’22 - 21 st rig: planned for early Q1 ’23 - 22 nd - 26 th rigs: TBD (2023+) • Rapidly expanding margins and EBITDA operating leverage - Sequential margin increase of 56% and sequential adjusted EBITDA increase of 156% - Forecasting Q3’22 and Q4’22 margin per day of $10,250 and $11,750, respectively, at midpoint of guidance range, representing 14% and 31% increases over reported 2Q’22 margin per day - Quarterly sequential adjusted EBITDA growth will outpace percentage growth in margin per day based upon significant operating leverage and increasing fleet utilization - Announcement of 200 - to - 300 Series rig conversion program and increase in marketed rig fleet to 26 rigs 2Q ’22 Conference Call Highlights |

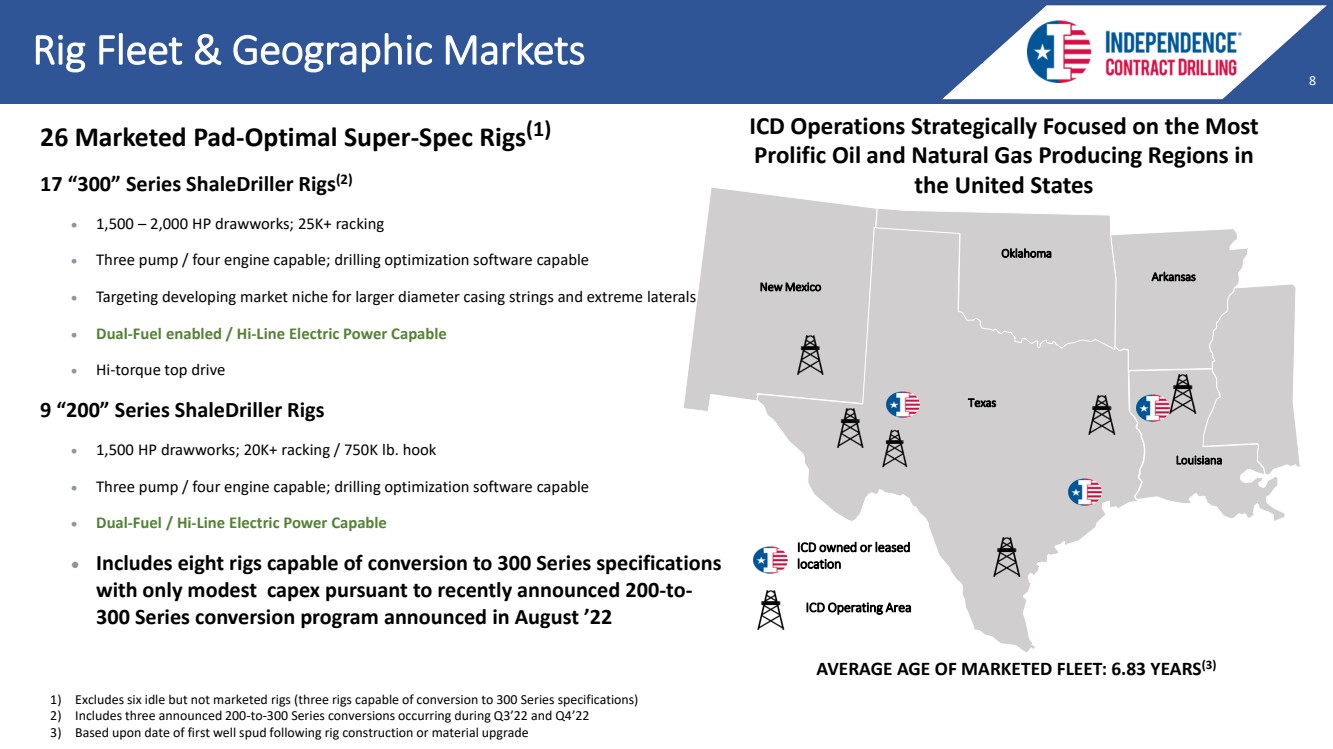

| 8 8 8 Rig Fleet & Geographic Markets Texas Oklahoma Arkansas Louisiana New Mexico ICD owned or leased location ICD Operating Area AVERAGE AGE OF MARKETED FLEET: 6.83 YEARS (3) 26 Marketed Pad - Optimal Super - Spec Rigs (1) 17 “300” Series ShaleDriller Rigs (2) • 1,500 – 2,000 HP drawworks ; 25K+ racking • Three pump / four engine capable; drilling optimization software capable • Targeting developing market niche for larger diameter casing strings and extreme laterals • Dual - Fuel enabled / Hi - Line Electric Power Capable • Hi - torque top drive 9 “200” Series ShaleDriller Rigs • 1,500 HP drawworks; 20K+ racking / 750K lb. hook • Three pump / four engine capable; drilling optimization software capable • Dual - Fuel / Hi - Line Electric Power Capable • Includes eight rigs capable of conversion to 300 Series specifications with only modest capex pursuant to recently announced 200 - to - 300 Series conversion program announced in August ’22 1) Excludes six idle but not marketed rigs (three rigs capable of conversion to 300 Series specifications) 2) Includes three announced 200 - to - 300 Series conversions occurring during Q3’22 and Q4’22 3) Based upon date of first well spud following rig construction or material upgrade ICD Operations Strategically Focused on the Most Prolific Oil and Natural Gas Producing Regions in the United States |

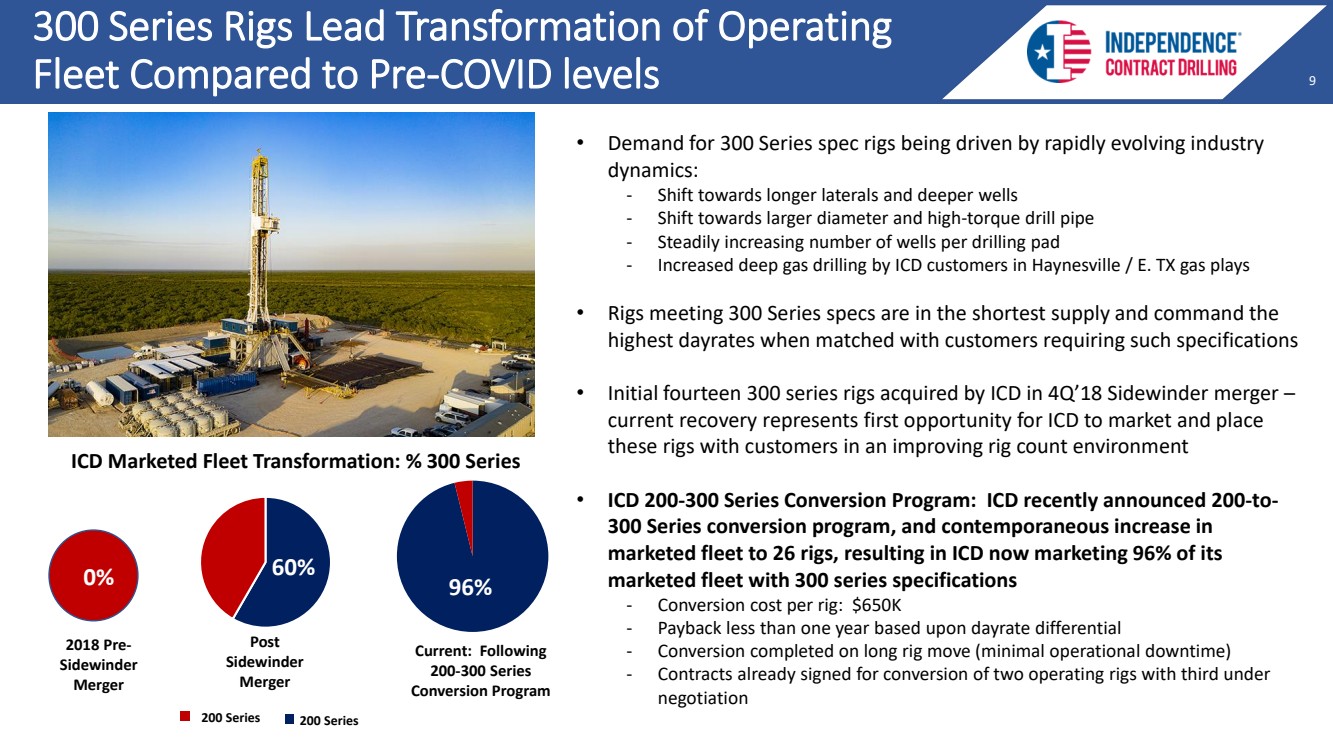

| 9 9 9 300 Series Rigs Lead Transformation of Operating Fleet Compared to Pre - COVID levels • Demand for 300 Series spec rigs being driven by rapidly evolving industry dynamics: - Shift towards longer laterals and deeper wells - Shift towards larger diameter and high - torque drill pipe - Steadily increasing number of wells per drilling pad - Increased deep gas drilling by ICD customers in Haynesville / E. TX gas plays • Rigs meeting 300 Series specs are in the shortest supply and command the highest dayrates when matched with customers requiring such specifications • Initial fourteen 300 series rigs acquired by ICD in 4Q’18 Sidewinder merger – current recovery represents first opportunity for ICD to market and place these rigs with customers in an improving rig count environment • ICD 200 - 300 Series Conversion Program: ICD recently announced 200 - to - 300 Series conversion program, and contemporaneous increase in marketed fleet to 26 rigs, resulting in ICD now marketing 96% of its marketed fleet with 300 series specifications - Conversion cost per rig: $650K - Payback less than one year based upon dayrate differential - Conversion completed on long rig move (minimal operational downtime) - Contracts already signed for conversion of two operating rigs with third under negotiation 2018 Pre - Sidewinder Merger Post Sidewinder Merger Current: Following 200 - 300 Series Conversion Program 0% 60% 96% ICD Marketed Fleet Transformation: % 300 Series 200 Series 200 Series |

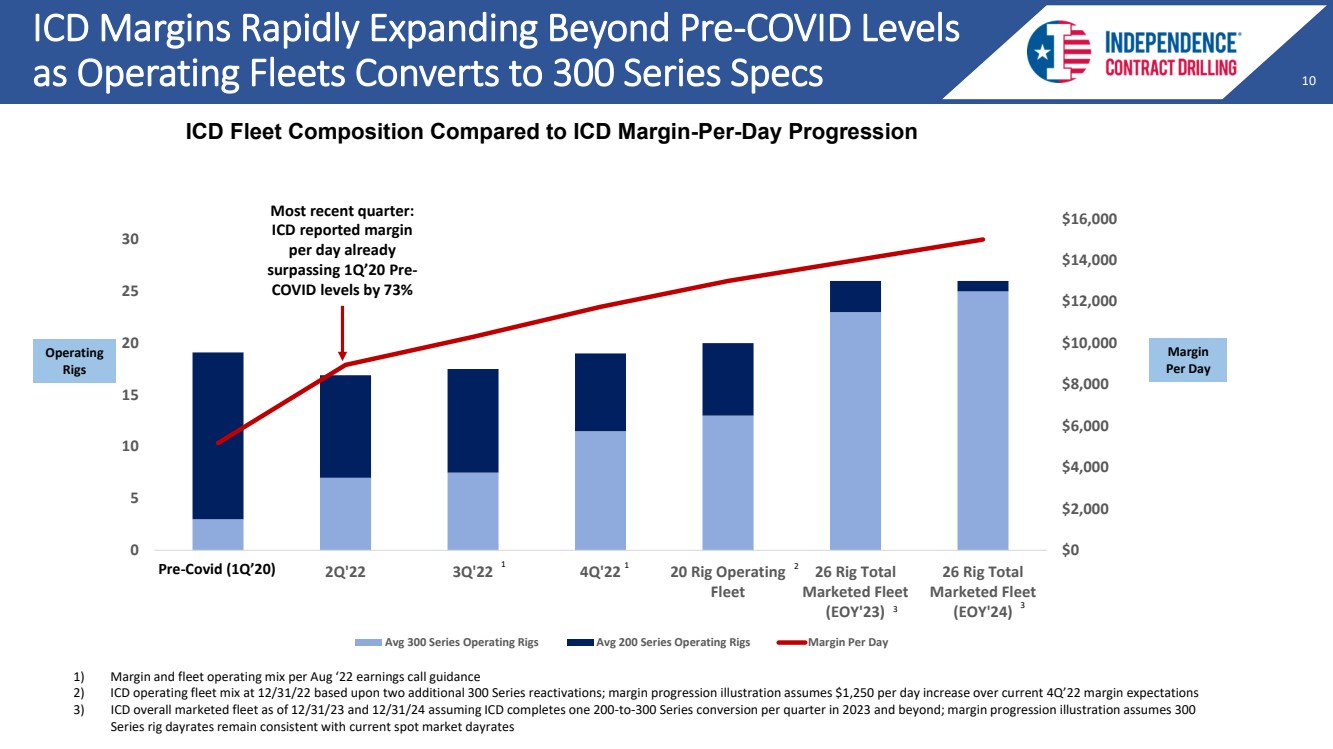

| 10 10 10 ICD Margins Rapidly Expanding Beyond Pre - COVID Levels as Operating Fleets Converts to 300 Series Specs ICD Fleet Composition Compared to ICD Margin - Per - Day Progression 1 1) Margin and fleet operating mix per Aug ‘22 earnings call guidance 2) ICD operating fleet mix at 12/31/22 based upon two additional 300 Series reactivations; margin progression illustration assum es $1,250 per day increase over current 4Q’22 margin expectations 3) ICD overall marketed fleet as of 12/31/23 and 12/31/24 assuming ICD completes one 200 - to - 300 Series conversion per quarter in 2023 and beyond; margin progression illustration assumes 300 Series rig dayrates remain consistent with current spot market dayrates Margin Per Day Operating Rigs 2 1 3 3 Most recent quarter: ICD reported margin per day already surpassing 1Q’20 Pre - COVID levels by 73% $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 0 5 10 15 20 25 30 Pre Covid (1Q'20) 2Q'22 3Q'22 4Q'22 20 Rig Operating Fleet 26 Rig Total Marketed Fleet (EOY'23) 26 Rig Total Marketed Fleet (EOY'24) Avg 300 Series Operating Rigs Avg 200 Series Operating Rigs Margin Per Day Pre - Covid (1Q’20) |

| 11 11 11 Maximizing Returns By Strategically Marketing ICD Fleet Across Target Markets Texas Oklahoma Arkansas Louisiana New Mexico Permian – Midland Basin 200 Series Target Market Eagle Ford/STX 200 Series Target Market Haynesville/ETX 300 Series Target Market Permian – Delaware Basin 300 Series Target Market |

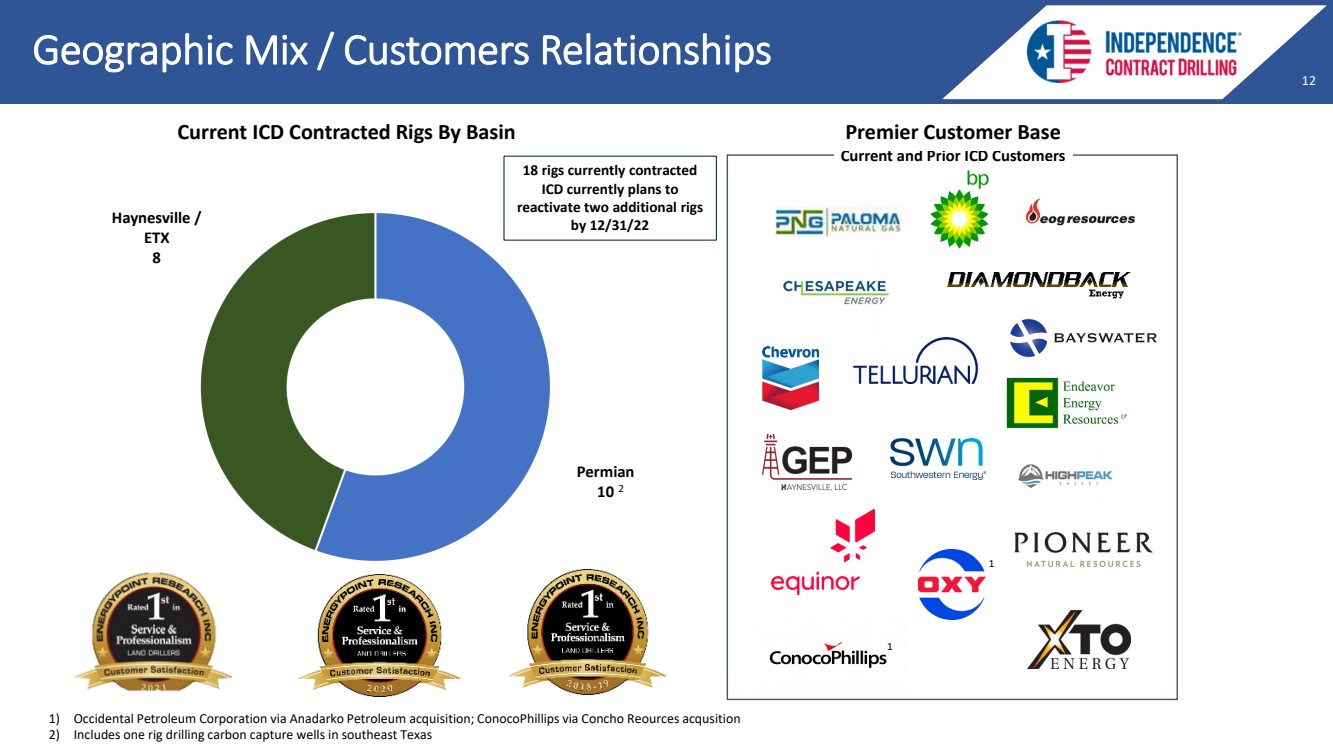

| 12 12 12 Geographic Mix / Customers Relationships Current and Prior ICD Customers Premier Customer Base Current ICD Contracted Rigs By Basin 1) Occidental Petroleum Corporation via Anadarko Petroleum acquisition; ConocoPhillips via Concho Reources acqusition 2) Includes one rig drilling carbon capture wells in southeast Texas Permian 10 Haynesville / ETX 8 1 1 18 rigs currently contracted ICD currently plans to reactivate two additional rigs by 12/31/22 2 |

| 13 13 13 Very Constructive Market Dynamics and Outlook |

| 14 14 14 Defining a Pad - Optimal, Super - Spec Rig Omni - Directional Walking 1500 HP Drawworks High - Pressure Mud Systems (7500 psi) Fast Moving AC Programmable Fleet must have flexibility to provide differing equipment packages to meet particular requirements of E&Ps’ drilling programs • Three pump / four engine: 100% of ICD marketed fleet • High - Torque top drive: 96% of ICD marketed fleet • Enhanced racking (25K ft) : 96% of ICD marketed fleet • Drilling optimization software capable: 100% of marketed fleet • Dual - fuel / Electric Hi - line capable : 100% of marketed fleet Total U.S. Pad - Optimal Super - Spec Supply: ̴ 620 Rigs ( 1 ) 474 Pad Optimal Rigs 146 Upgradeable Rigs (2) 1) Source: Enverus and Company estimates. Includes AC, 1500HP+, 750,000lb+ hookload ; excludes rigs not operating since 2018 and rigs owned by non - operating entities 2) 1500HP AC rigs with skidding systems upgradeable to omni - directional walking (capex estimated at $7M+ per rig) |

| 15 15 15 Accelerating rig count with improving fundamentals Constructive oil supply / natural gas demand fundamentals Depleted drilled - but - uncompleted (DUC) inventories Spare Pad - Optimal, Super - Spec capacity consolidating within small number of players U.S. Pad - Optimal, Super - Spec fleet utilization exceeding 90% Drivers for Expected Improvements in Pad - Optimal, Super - Spec Utilization / Dayrates |

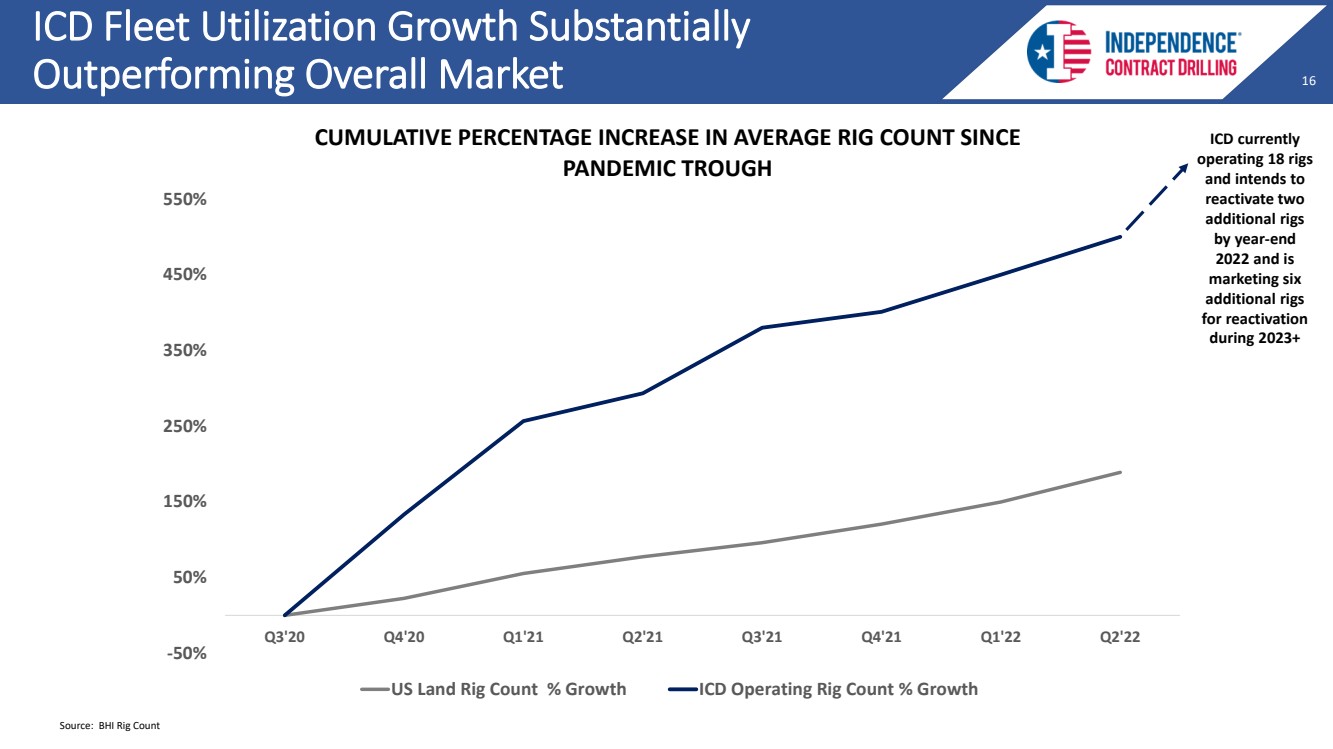

| 16 16 16 ICD Fleet Utilization Growth Substantially Outperforming Overall Market -50% 50% 150% 250% 350% 450% 550% Q3'20 Q4'20 Q1'21 Q2'21 Q3'21 Q4'21 Q1'22 Q2'22 CUMULATIVE PERCENTAGE INCREASE IN AVERAGE RIG COUNT SINCE PANDEMIC TROUGH US Land Rig Count % Growth ICD Operating Rig Count % Growth Source: BHI Rig Count ICD currently operating 18 rigs and intends to reactivate two additional rigs by year - end 2022 and is marketing six additional rigs for reactivation during 2023+ |

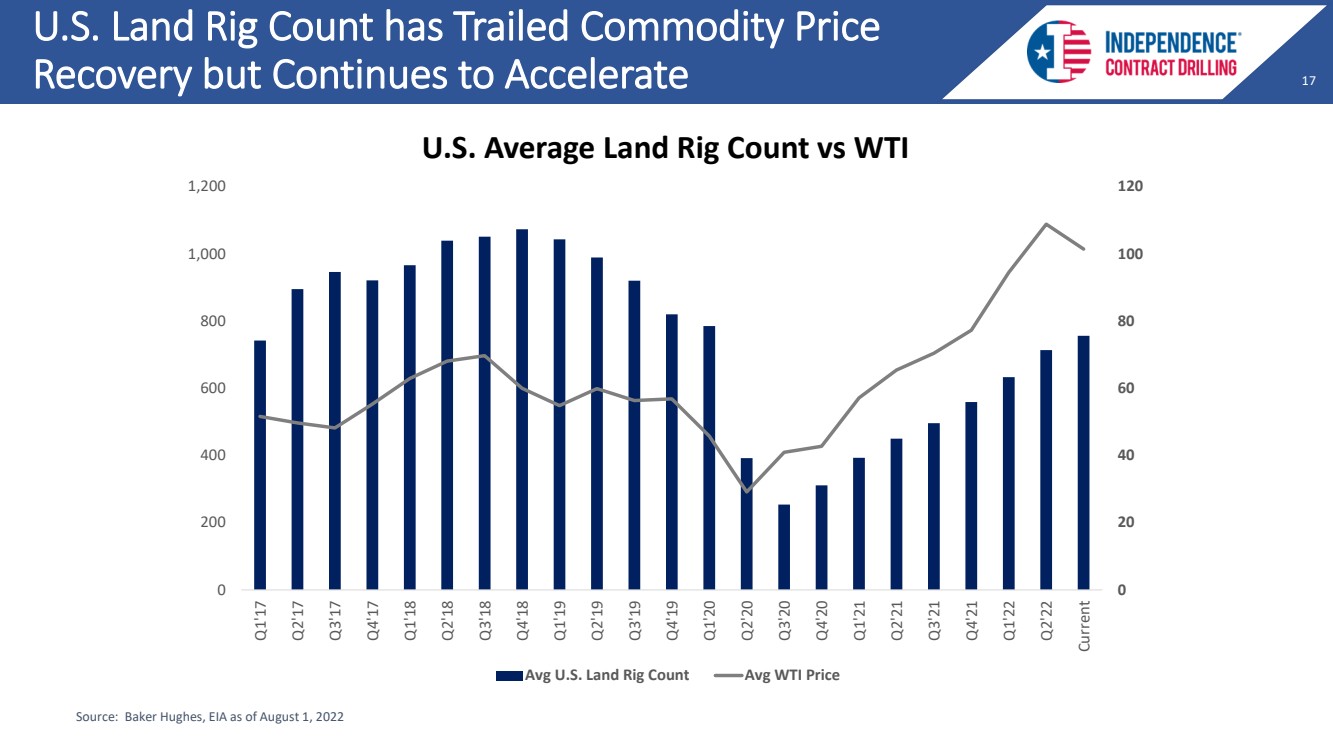

| 17 17 17 U.S. Land Rig Count has Trailed Commodity Price Recovery but Continues to Accelerate 0 20 40 60 80 100 120 0 200 400 600 800 1,000 1,200 Q1'17 Q2'17 Q3'17 Q4'17 Q1'18 Q2'18 Q3'18 Q4'18 Q1'19 Q2'19 Q3'19 Q4'19 Q1'20 Q2'20 Q3'20 Q4'20 Q1'21 Q2'21 Q3'21 Q4'21 Q1'22 Q2'22 Current U.S. Average Land Rig Count vs WTI Avg U.S. Land Rig Count Avg WTI Price Source: Baker Hughes, EIA as of August 1, 2022 |

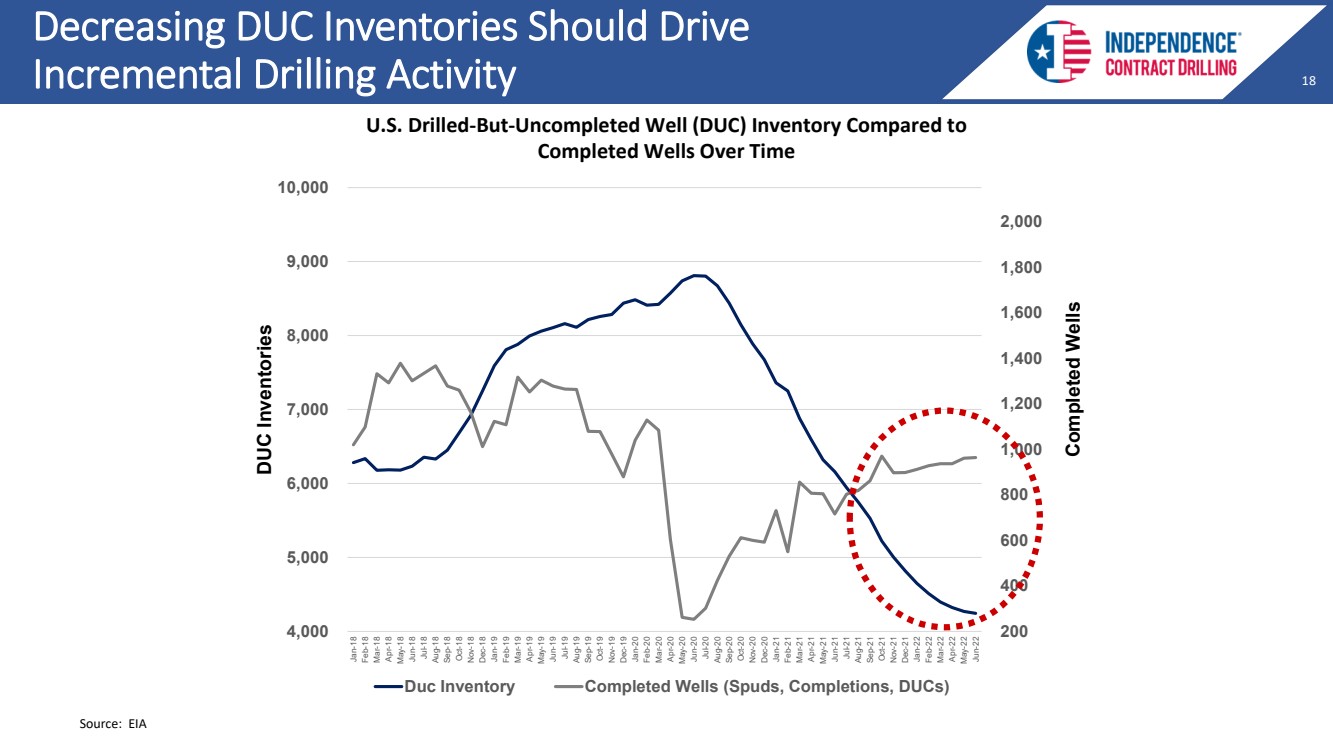

| 18 18 18 Decreasing DUC Inventories Should Drive Incremental Drilling Activity 200 400 600 800 1,000 1,200 1,400 1,600 1,800 2,000 4,000 5,000 6,000 7,000 8,000 9,000 10,000 Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20 Jul-20 Aug-20 Sep-20 Oct-20 Nov-20 Dec-20 Jan-21 Feb-21 Mar-21 Apr-21 May-21 Jun-21 Jul-21 Aug-21 Sep-21 Oct-21 Nov-21 Dec-21 Jan-22 Feb-22 Mar-22 Apr-22 May-22 Jun-22 Duc Inventory Completed Wells (Spuds, Completions, DUCs) U.S. Drilled - But - Uncompleted Well (DUC) Inventory Compared to Completed Wells Over Time DUC Inventories Completed Wells Source: EIA |

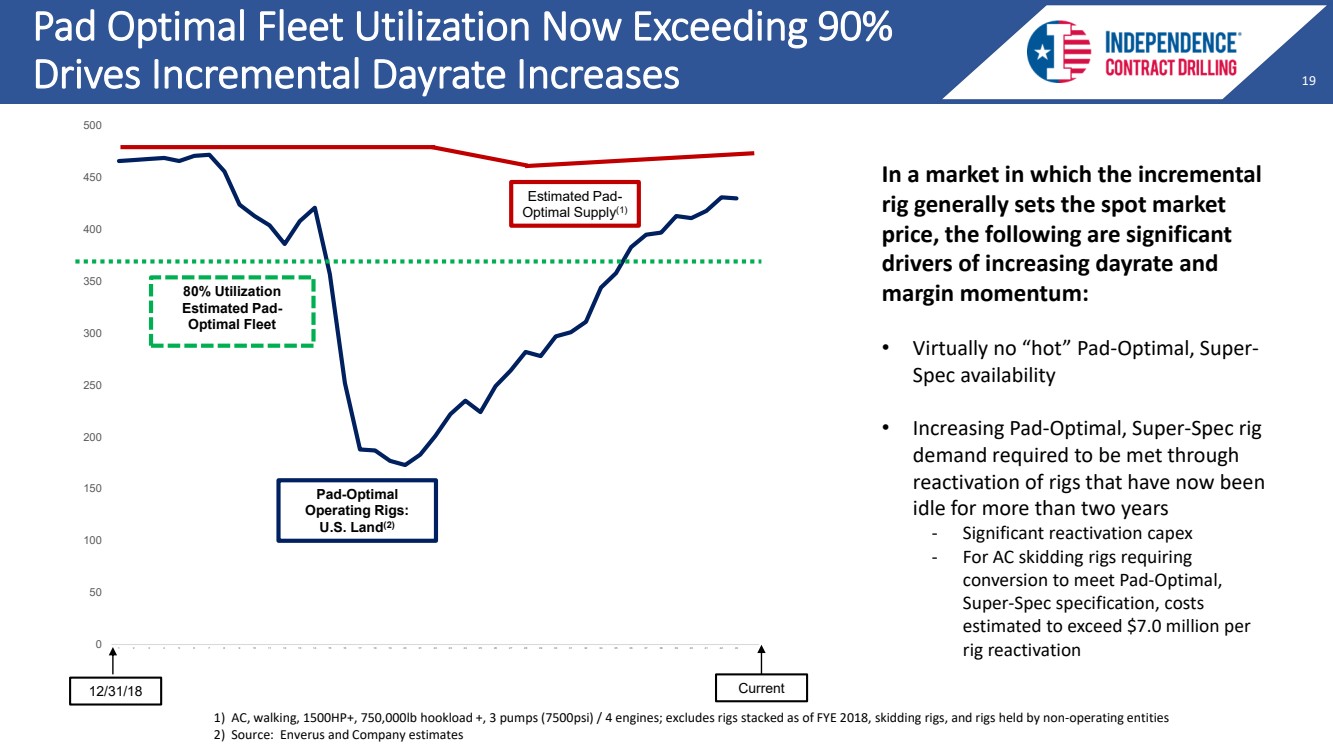

| 19 19 19 Pad Optimal Fleet Utilization Now Exceeding 90% Drives Incremental Dayrate Increases 0 50 100 150 200 250 300 350 400 450 500 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 30 31 32 34 35 36 37 38 39 40 41 42 43 80% Utilization Estimated Pad - Optimal Fleet Pad - Optimal Operating Rigs: U.S. Land ( 2 ) Estimated Pad - Optimal Supply (1) 12/31/18 In a market in which the incremental rig generally sets the spot market price, the following are significant drivers of increasing dayrate and margin momentum: • Virtually no “hot” Pad - Optimal, Super - Spec availability • Increasing Pad - Optimal, Super - Spec rig demand required to be met through reactivation of rigs that have now been idle for more than two years - Significant reactivation capex - For AC skidding rigs requiring conversion to meet Pad - Optimal, Super - Spec specification, costs estimated to exceed $7.0 million per rig reactivation 1) AC, walking, 1500HP+, 750,000lb hookload +, 3 pumps (7500psi) / 4 engines; excludes rigs stacked as of FYE 2018, skidding ri gs, and rigs held by non - operating entities 2) Source: Enverus and Company estimates Current |

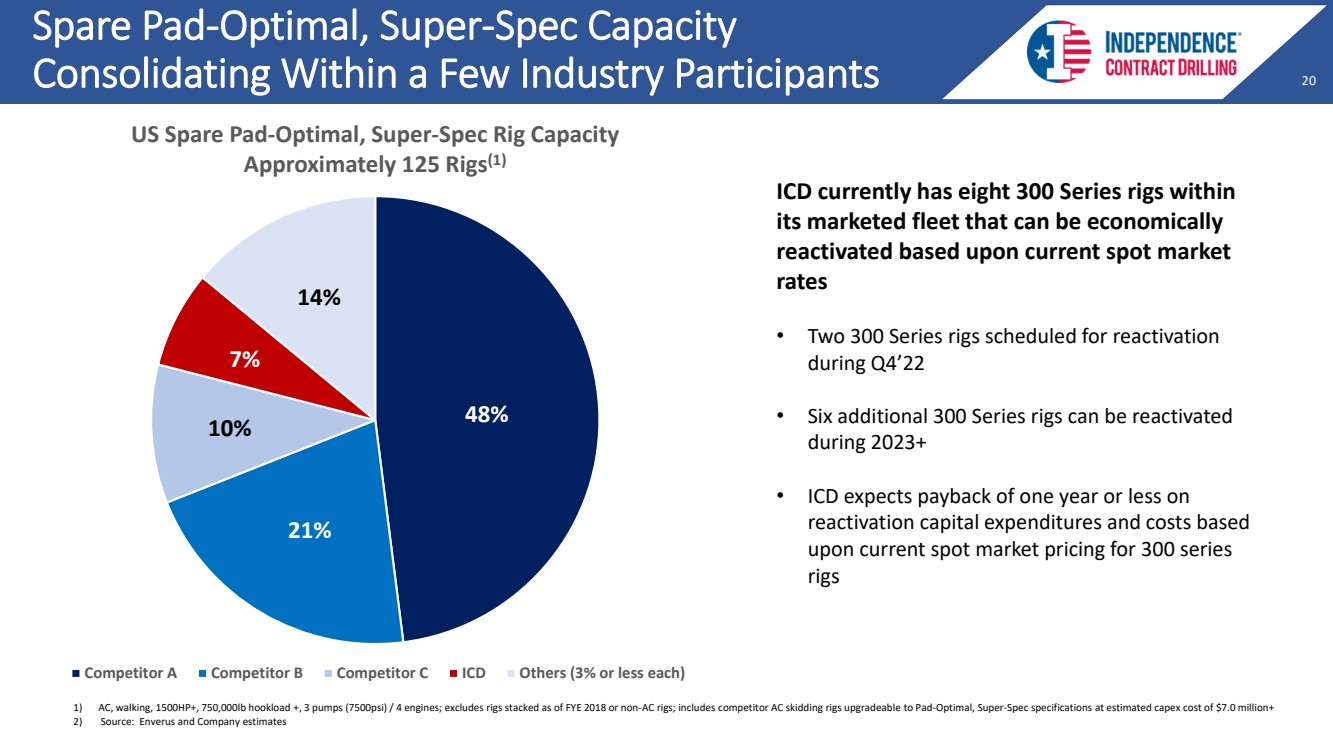

| 20 20 20 48% 21 % 10% 7% 14% US Spare Pad - Optimal, Super - Spec Rig Capacity Approximately 125 Rigs (1) Competitor A Competitor B Competitor C ICD Others (3% or less each) Spare Pad - Optimal, Super - Spec Capacity Consolidating Within a Few Industry Participants ICD currently has eight 300 Series rigs within its marketed fleet that can be economically reactivated based upon current spot market rates • Two 300 Series rigs scheduled for reactivation during Q4’22 • Six additional 300 Series rigs can be reactivated during 2023+ • ICD expects payback of one year or less on reactivation capital expenditures and costs based upon current spot market pricing for 300 series rigs 1) AC, walking, 1500HP+, 750,000lb hookload +, 3 pumps (7500psi) / 4 engines; excludes rigs stacked as of FYE 2018 or non - AC rigs; includes competitor AC skidding rigs upgradeable to Pad - Optimal, Super - Spec specifications at estimated capex cost of $7.0 milli on+ 2) Source: Enverus and Company estimates |

| 21 21 21 Drivers of Returns and Free Cash Flow in Current Market |

| 22 22 22 Drivers of Returns /FCF Through Oil and Gas Cycle Improving Fleet Utilization • Recent refinancing unlocks ICD ability to reactivate Pad - Optimal, Super - Spec rigs into an extremely tight, constructive market • 18 th rig commenced operations August 1, 2022, on one - year contract; two additional reactivations planned for 2022; six additional rig reactivations to be evaluated in 2023+ • All ICD reactivations will be 300 Series rigs, which are in shortest supply Increasing Dayrate and Margin Momentum • Dayrates and margins expanding in very tight, constructive Pad Optimal, Super - Spec market • U.S. Pad - Optimal, Super - Spec fleet utilization exceeding 90% with continuing improvements in U.S. rig count expected • Increasing 300 Series market penetration drives sequential dayrate improvements • Short - term contract structures allow ICD to steadily reprice contracts into an improving dayrate environment Scalable Cost Structure Drives Substantial Improvements in Cash Flows • Costs to operate a rig do not fluctuate meaningfully with increases in dayrates - dayrate improvements fall directly to bottom line driving incremental margins and cash flows • Contract terms and short - term contract structures allow ICD to pass through labor and other cost increases • Scalable SG&A cost structure: minimal increases in SG&A as operating fleet and revenues increase |

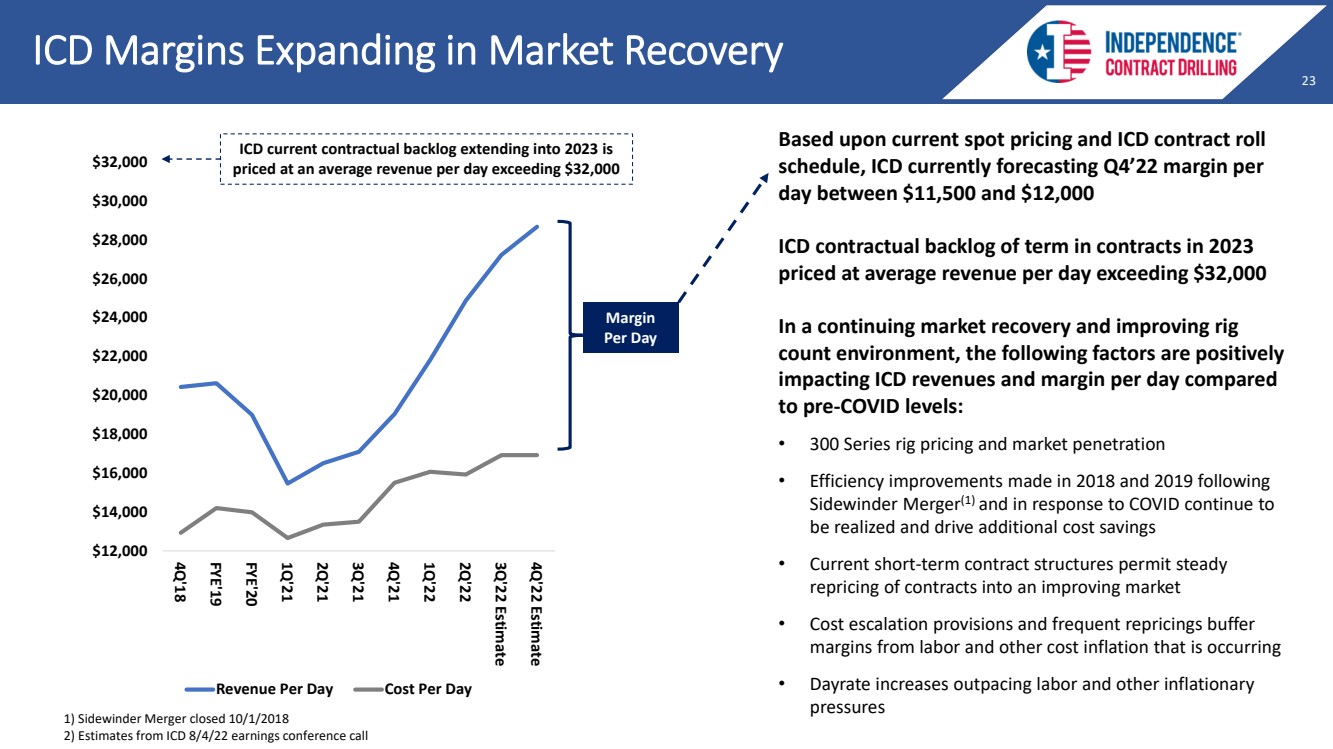

| 23 23 23 ICD Margins Expanding in Market Recovery Based upon current spot pricing and ICD contract roll schedule, ICD currently forecasting Q4’22 margin per day between $11,500 and $12,000 ICD contractual backlog of term in contracts in 2023 priced at average revenue per day exceeding $32,000 In a continuing market recovery and improving rig count environment, the following factors are positively impacting ICD revenues and margin per day compared to pre - COVID levels: • 300 Series rig pricing and market penetration • Efficiency improvements made in 2018 and 2019 following Sidewinder Merger (1) and in response to COVID continue to be realized and drive additional cost savings • Current short - term contract structures permit steady repricing of contracts into an improving market • Cost escalation provisions and frequent repricings buffer margins from labor and other cost inflation that is occurring • Dayrate increases outpacing labor and other inflationary pressures $12,000 $14,000 $16,000 $18,000 $20,000 $22,000 $24,000 $26,000 $28,000 $30,000 $32,000 4Q'18 FYE'19 FYE'20 1Q'21 2Q'21 3Q'21 4Q'21 1Q'22 2Q'22 3Q'22 Estimate 4Q'22 Estimate Revenue Per Day Cost Per Day 1) Sidewinder Merger closed 10/1/2018 2) Estimates from ICD 8/4/22 earnings conference call Margin Per Day ICD current contractual backlog extending into 2023 is priced at an average revenue per day exceeding $32,000 |

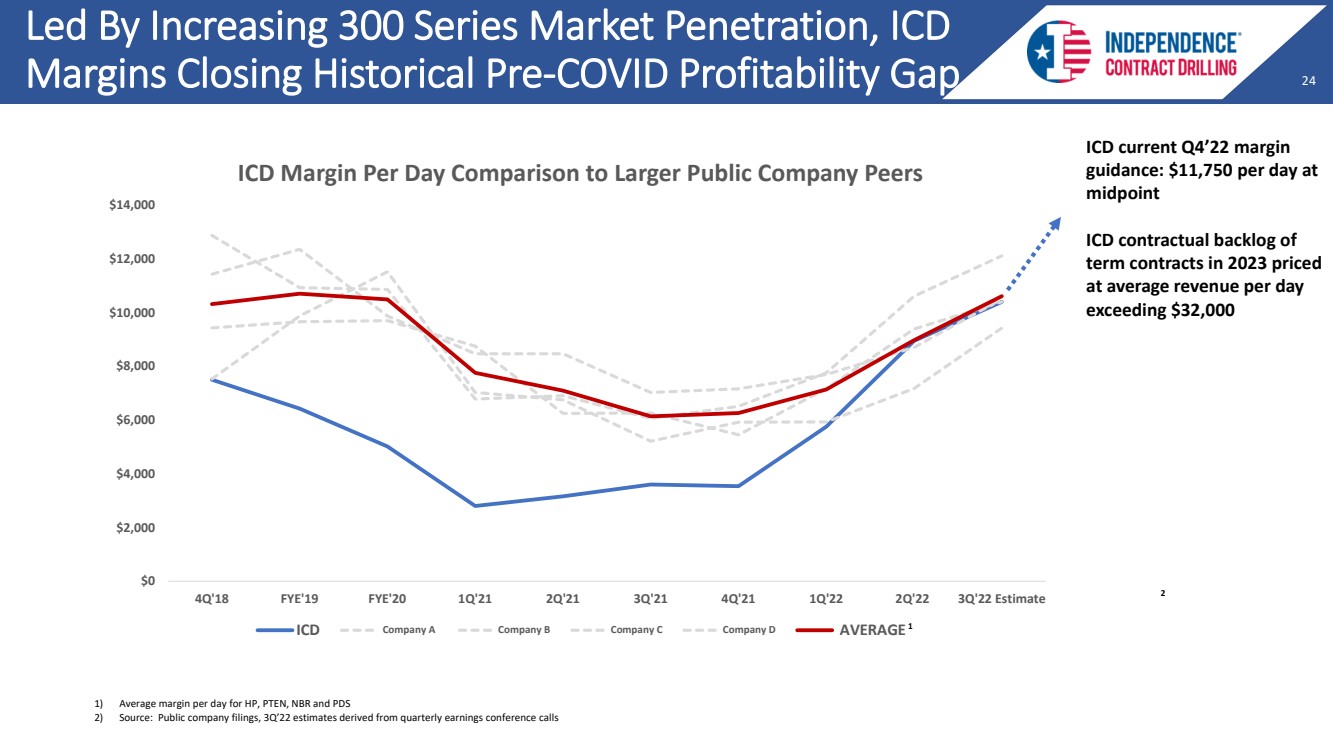

| 24 24 24 Led By Increasing 300 Series Market Penetration, ICD Margins Closing Historical Pre - COVID Profitability Gap $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 4Q'18 FYE'19 FYE'20 1Q'21 2Q'21 3Q'21 4Q'21 1Q'22 2Q'22 3Q'22 Estimate ICD Margin Per Day Comparison to Larger Public Company Peers ICD Company A Company B Company C Company D AVERAGE 1 1) Average margin per day for HP, PTEN, NBR and PDS 2) Source: Public company filings, 3Q’22 estimates derived from quarterly earnings conference calls 2 ICD current Q4’22 margin guidance: $11,750 per day at midpoint ICD contractual backlog of term contracts in 2023 priced at average revenue per day exceeding $32,000 |

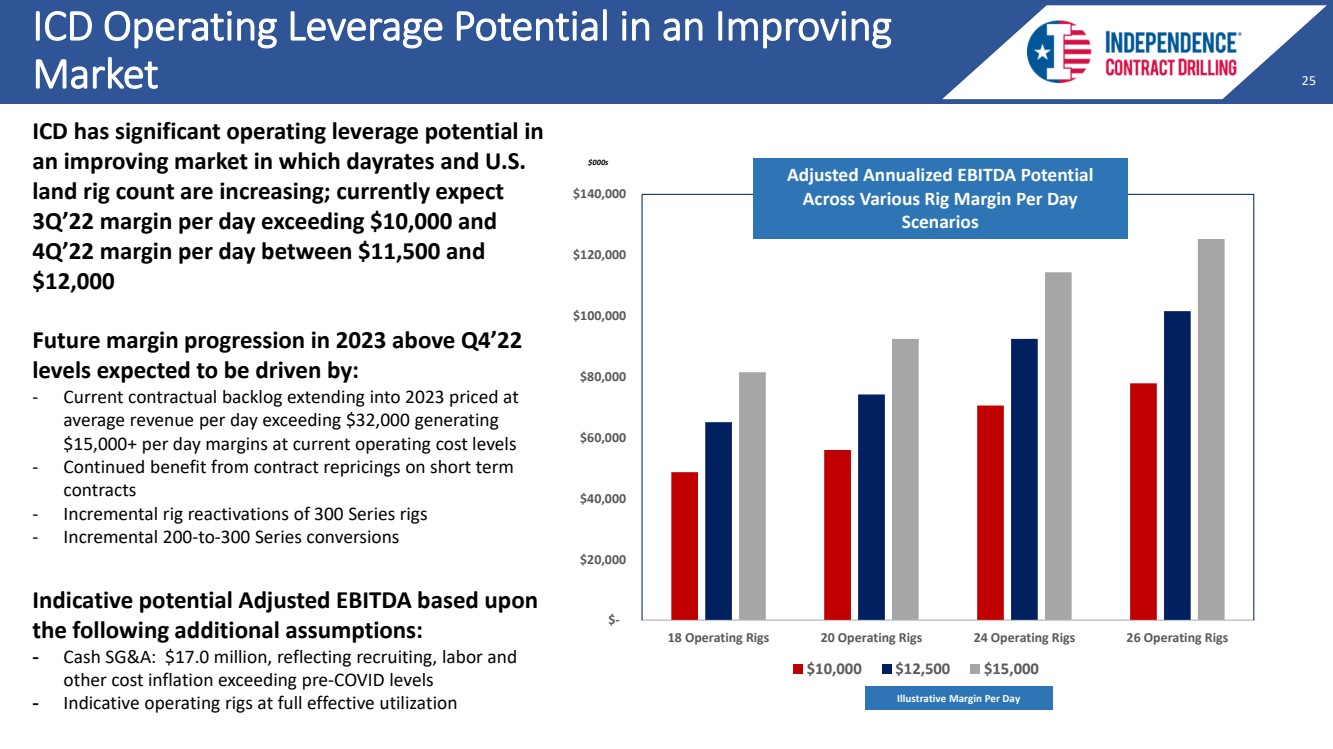

| 25 25 25 ICD Operating Leverage Potential in an Improving Market $- $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 $140,000 18 Operating Rigs 20 Operating Rigs 24 Operating Rigs 26 Operating Rigs $10,000 $12,500 $15,000 Adjusted Annualized EBITDA Potential Across Various Rig Margin Per Day Scenarios ICD has significant operating leverage potential in an improving market in which dayrates and U.S. land rig count are increasing; currently expect 3Q’22 margin per day exceeding $10,000 and 4Q’22 margin per day between $11,500 and $12,000 Future margin progression in 2023 above Q4’22 levels expected to be driven by: - Current contractual backlog extending into 2023 priced at average revenue per day exceeding $32,000 generating $15,000+ per day margins at current operating cost levels - Continued benefit from contract repricings on short term contracts - Incremental rig reactivations of 300 Series rigs - Incremental 200 - to - 300 Series conversions Indicative potential Adjusted EBITDA based upon the following additional assumptions: - Cash SG&A: $17.0 million, reflecting recruiting, labor and other cost inflation exceeding pre - COVID levels - Indicative operating rigs at full effective utilization $000s Illustrative Margin Per Day |

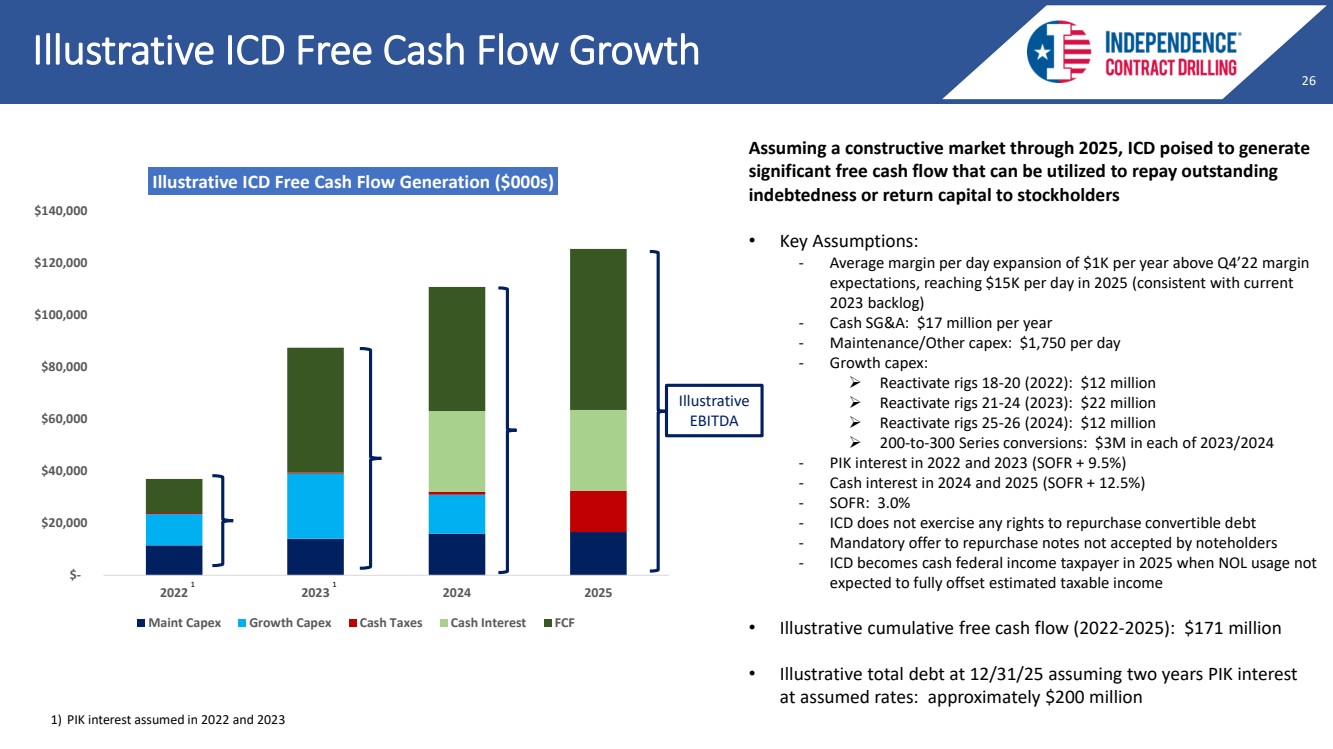

| 26 26 26 Illustrative ICD Free Cash Flow Growth $- $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 $140,000 2022 2023 2024 2025 Illustrative ICD Free Cash Flow Generation ($000s) Maint Capex Growth Capex Cash Taxes Cash Interest FCF Assuming a constructive market through 2025, ICD poised to generate significant free cash flow that can be utilized to repay outstanding indebtedness or return capital to stockholders • Key Assumptions: - Average margin per day expansion of $1K per year above Q4’22 margin expectations, reaching $15K per day in 2025 (consistent with current 2023 backlog) - Cash SG&A: $17 million per year - Maintenance/Other capex: $1,750 per day - Growth capex: ➢ Reactivate rigs 18 - 20 (2022): $12 million ➢ Reactivate rigs 21 - 24 (2023): $22 million ➢ Reactivate rigs 25 - 26 (2024): $12 million ➢ 200 - to - 300 Series conversions: $3M in each of 2023/2024 - PIK interest in 2022 and 2023 (SOFR + 9.5%) - Cash interest in 2024 and 2025 (SOFR + 12.5%) - SOFR: 3.0% - ICD does not exercise any rights to repurchase convertible debt - Mandatory offer to repurchase notes not accepted by noteholders - ICD becomes cash federal income taxpayer in 2025 when NOL usage not expected to fully offset estimated taxable income • Illustrative cumulative free cash flow (2022 - 2025): $171 million • Illustrative total debt at 12/31/25 assuming two years PIK interest at assumed rates: approximately $200 million Illustrative EBITDA 1 1 1 ) PIK interest assumed in 2022 and 2023 |

| 27 27 27 Balance Sheet / Recent Debt Financing Untaps Imbedded Value |

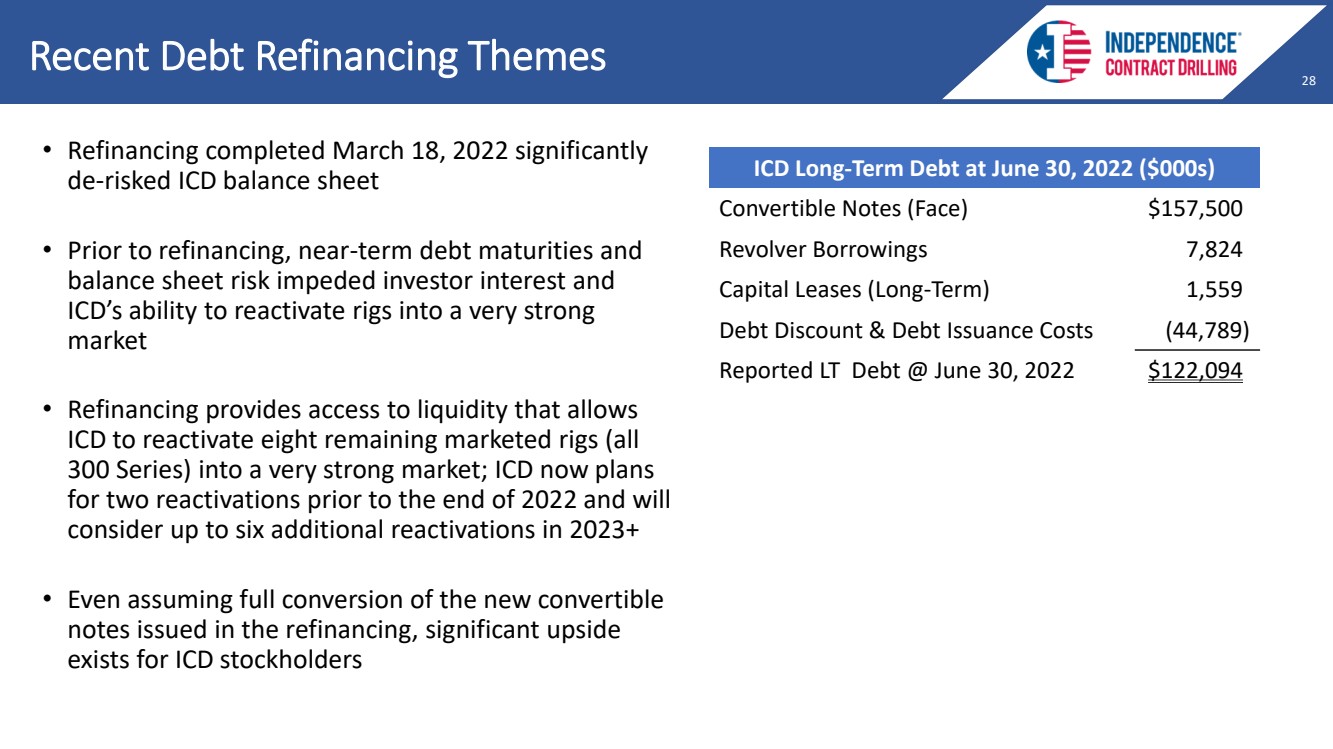

| 28 28 28 Recent Debt Refinancing Themes • Refinancing completed March 18, 2022 significantly de - risked ICD balance sheet • Prior to refinancing, near - term debt maturities and balance sheet risk impeded investor interest and ICD’s ability to reactivate rigs into a very strong market • Refinancing provides access to liquidity that allows ICD to reactivate eight remaining marketed rigs (all 300 Series) into a very strong market; ICD now plans for two reactivations prior to the end of 2022 and will consider up to six additional reactivations in 2023+ • Even assuming full conversion of the new convertible notes issued in the refinancing, significant upside exists for ICD stockholders ICD Long - Term Debt at June 30, 2022 ($000s) Convertible Notes (Face) $157,500 Revolver Borrowings 7,824 Capital Leases (Long - Term) 1,559 Debt Discount & Debt Issuance Costs (44,789) Reported LT Debt @ June 30, 2022 $122,094 |

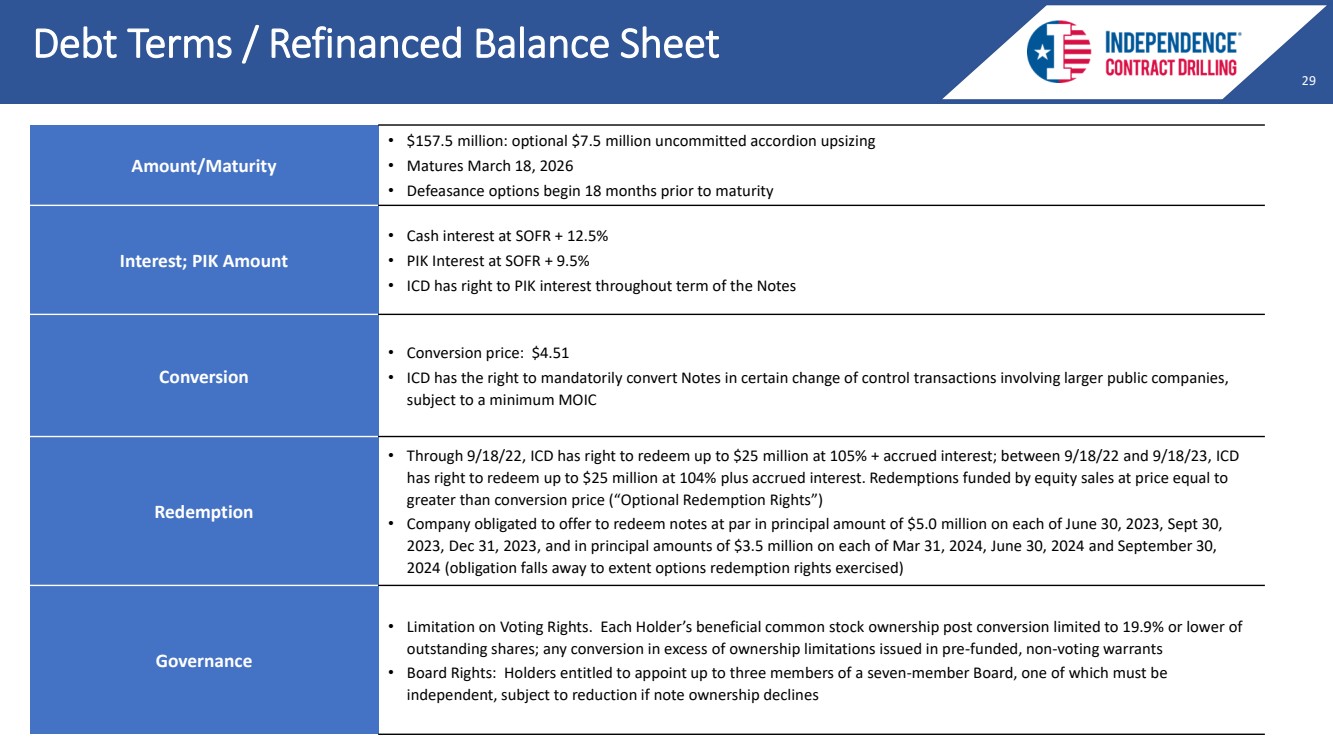

| 29 29 29 Debt Terms / Refinanced Balance Sheet Amount/Maturity • $157.5 million: optional $7.5 million uncommitted accordion upsizing • Matures March 18, 2026 • Defeasance options begin 18 months prior to maturity Interest; PIK Amount • Cash interest at SOFR + 12.5% • PIK Interest at SOFR + 9.5% • ICD has right to PIK interest throughout term of the Notes Conversion • Conversion price: $4.51 • ICD has the right to mandatorily convert Notes in certain change of control transactions involving larger public companies, subject to a minimum MOIC Redemption • Through 9/18/22, ICD has right to redeem up to $25 million at 105% + accrued interest; between 9/18/22 and 9/18/23, ICD has right to redeem up to $25 million at 104% plus accrued interest. Redemptions funded by equity sales at price equal to greater than conversion price (“Optional Redemption Rights”) • Company obligated to offer to redeem notes at par in principal amount of $5.0 million on each of June 30, 2023, Sept 30, 2023, Dec 31, 2023, and in principal amounts of $3.5 million on each of Mar 31, 2024, June 30, 2024 and September 30, 2024 (obligation falls away to extent options redemption rights exercised) Governance • Limitation on Voting Rights. Each Holder’s beneficial common stock ownership post conversion limited to 19.9% or lower of outstanding shares; any conversion in excess of ownership limitations issued in pre - funded, non - voting warrants • Board Rights: Holders entitled to appoint up to three members of a seven - member Board, one of which must be independent, subject to reduction if note ownership declines |

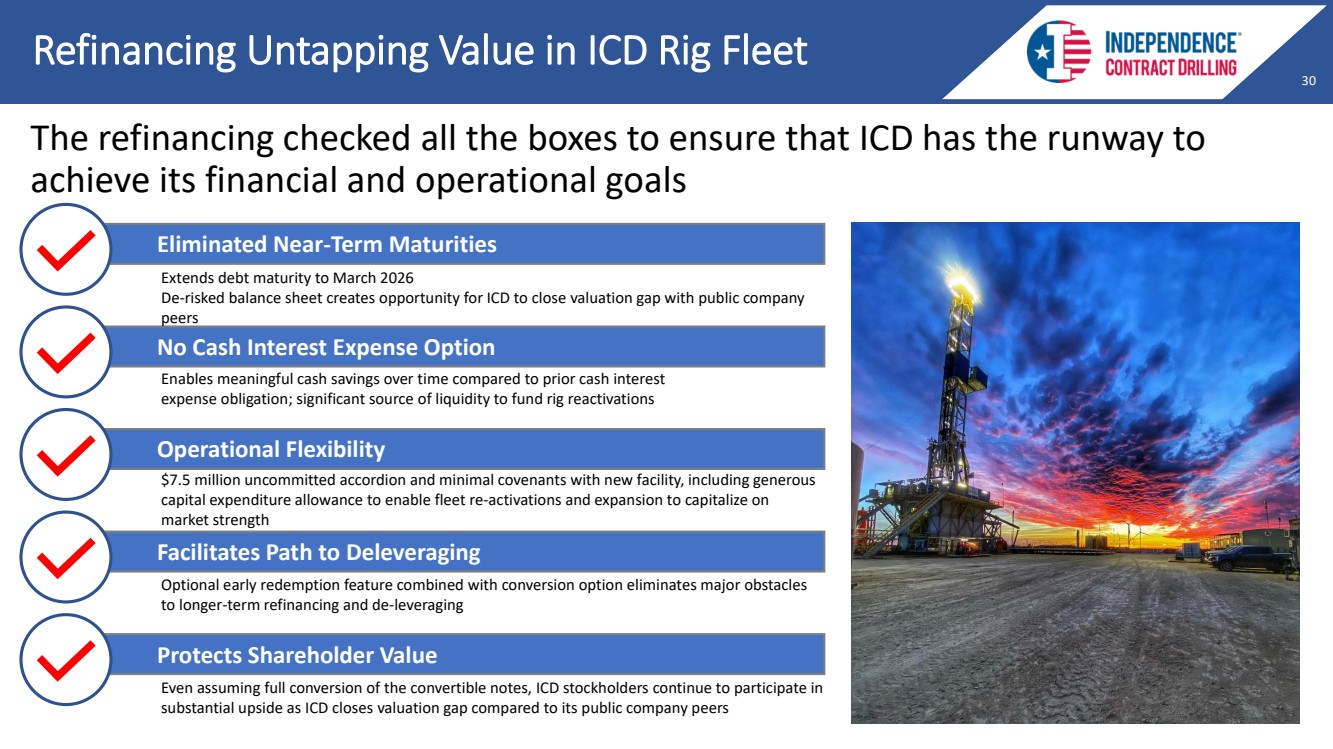

| 30 30 30 The refinancing checked all the boxes to ensure that ICD has the runway to achieve its financial and operational goals Refinancing Untapping Value in ICD Rig Fleet Eliminated Near - Term Maturities No Cash Interest Expense Option Operational Flexibility Facilitates Path to Deleveraging Protects Shareholder Value Extends debt maturity to March 2026 De - risked balance sheet creates opportunity for ICD to close valuation gap with public company peers Enables meaningful cash savings over time compared to prior cash interest expense obligation; significant source of liquidity to fund rig reactivations $7.5 million uncommitted accordion and minimal covenants with new facility, including generous capital expenditure allowance to enable fleet re - activations and expansion to capitalize on market strength Optional early redemption feature combined with conversion option eliminates major obstacles to longer - term refinancing and de - leveraging Even assuming full conversion of the convertible notes, ICD stockholders continue to participate in substantial upside as ICD closes valuation gap compared to its public company peers |

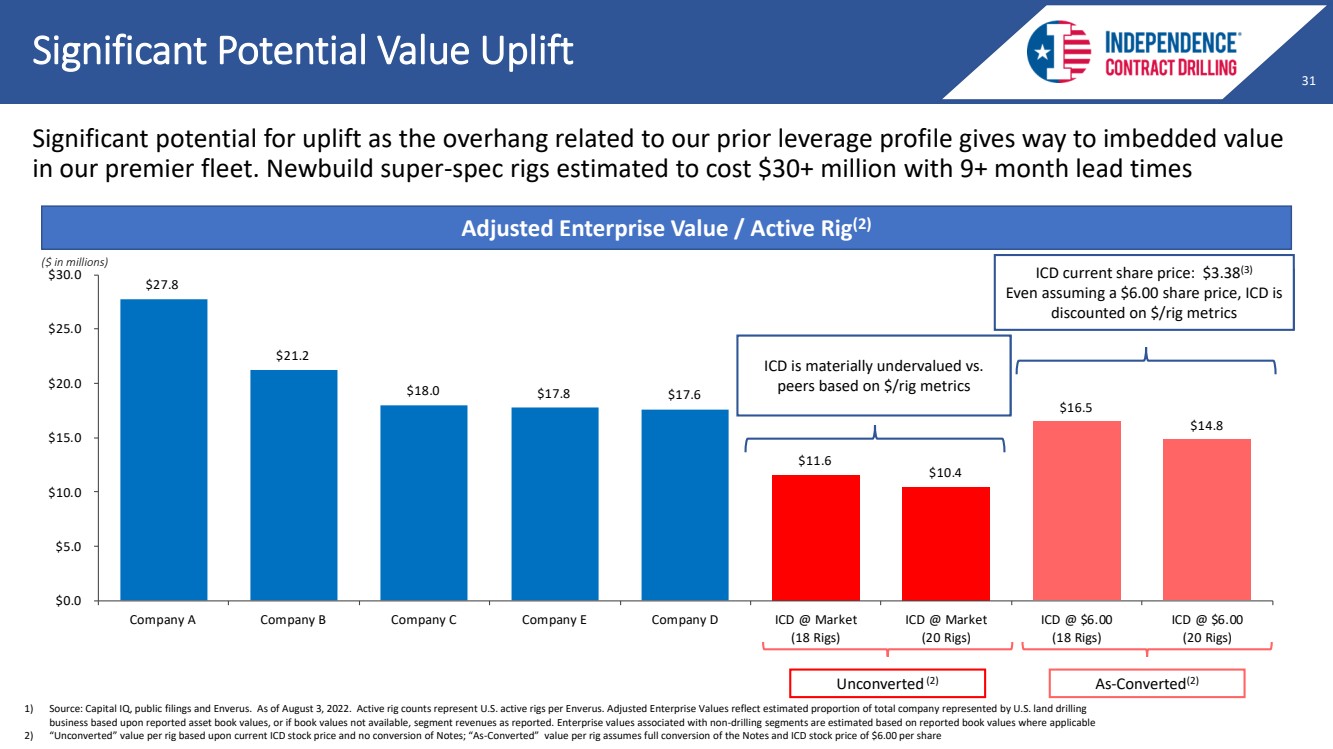

| 31 31 31 Significant potential for uplift as the overhang related to our prior leverage profile gives way to imbedded value in our premier fleet. Newbuild super - spec rigs estimated to cost $30+ million with 9+ month lead times Adjusted Enterprise Value / Active Rig (2) ($ in millions) Significant Potential Value Uplift 1) Source: Capital IQ, public filings and Enverus. As of August 3, 2022. Active rig counts represent U.S. active rigs per Env erus. Adjusted Enterprise Values reflect estimated proportion of total company represented by U.S. land drilling business based upon reported asset book values, or if book values not available, segment revenues as reported. Enterprise val ues associated with non - drilling segments are estimated based on reported book values where applicable 2) “Unconverted” value per rig based upon current ICD stock price and no conversion of Notes; “As - Converted” value per rig ass umes full conversion of the Notes and ICD stock price of $6.00 per share ICD is materially undervalued vs. peers based on $/rig metrics Unconverted (2) As - Converted (2) Even assuming a $6.00 share price, ICD is discounted on $/rig metrics $27.8 $21.2 $18.0 $17.8 $17.6 $11.6 $10.4 $16.5 $14.8 $0.0 $5.0 $10.0 $15.0 $20.0 $25.0 $30.0 Company A Company B Company C Company E Company D ICD @ Market (18 Rigs) ICD @ Market (20 Rigs) ICD @ $6.00 (18 Rigs) ICD @ $6.00 (20 Rigs) ICD current share price: $3.38 (3) Even assuming a $6.00 share price, ICD is discounted on $/rig metrics ICD is materially undervalued vs. peers based on $/rig metrics |

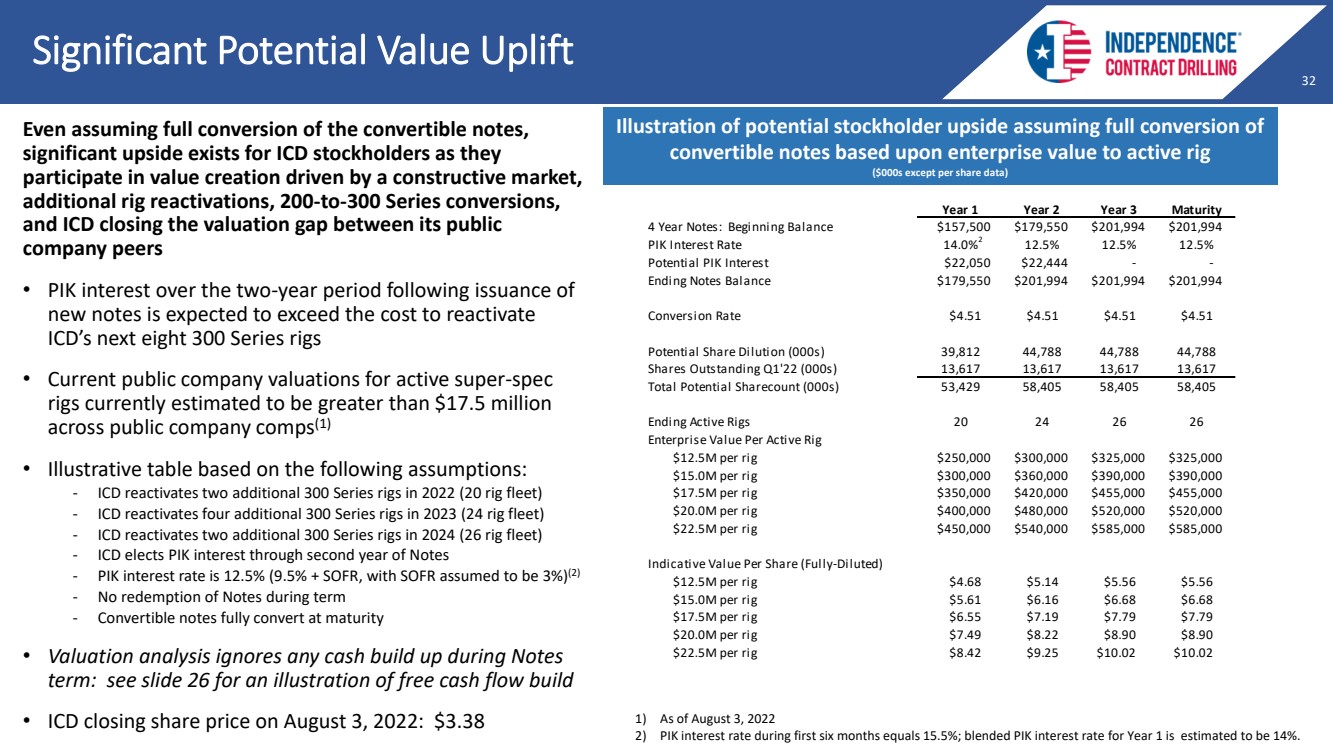

| 32 32 32 Even assuming full conversion of the convertible notes, significant upside exists for ICD stockholders as they participate in value creation driven by a constructive market, additional rig reactivations, 200 - to - 300 Series conversions, and ICD closing the valuation gap between its public company peers • PIK interest over the two - year period following issuance of new notes is expected to exceed the cost to reactivate ICD’s next eight 300 Series rigs • Current public company valuations for active super - spec rigs currently estimated to be greater than $17.5 million across public company comps (1) • Illustrative table based on the following assumptions: - ICD reactivates two additional 300 Series rigs in 2022 (20 rig fleet) - ICD reactivates four additional 300 Series rigs in 2023 (24 rig fleet) - ICD reactivates two additional 300 Series rigs in 2024 (26 rig fleet) - ICD elects PIK interest through second year of Notes - PIK interest rate is 12.5% (9.5% + SOFR, with SOFR assumed to be 3%) (2) - No redemption of Notes during term - Convertible notes fully convert at maturity • Valuation analysis ignores any cash build up during Notes term: see slide 26 for an illustration of free cash flow build • ICD closing share price on August 3, 2022: $3.38 Significant Potential Value Uplift Illustration of potential stockholder upside assuming full conversion of convertible notes based upon enterprise value to active rig ($000s except per share data) 1) As of August 3, 2022 2) PIK interest rate during first six months equals 15.5%; blended PIK interest rate for Year 1 is estimated to be 14%. Year 1 Year 2 Year 3 Maturity 4 Year Notes: Beginning Balance $157,500 $179,550 $201,994 $201,994 PIK Interest Rate 14.0% 12.5% 12.5% 12.5% Potential PIK Interest $22,050 $22,444 - - Ending Notes Balance $179,550 $201,994 $201,994 $201,994 Conversion Rate $4.51 $4.51 $4.51 $4.51 Potential Share Dilution (000s) 39,812 44,788 44,788 44,788 Shares Outstanding Q1'22 (000s) 13,617 13,617 13,617 13,617 Total Potential Sharecount (000s) 53,429 58,405 58,405 58,405 Ending Active Rigs 20 24 26 26 Enterprise Value Per Active Rig $12.5M per rig $250,000 $300,000 $325,000 $325,000 $15.0M per rig $300,000 $360,000 $390,000 $390,000 $17.5M per rig $350,000 $420,000 $455,000 $455,000 $20.0M per rig $400,000 $480,000 $520,000 $520,000 $22.5M per rig $450,000 $540,000 $585,000 $585,000 Indicative Value Per Share (Fully-Diluted) $12.5M per rig $4.68 $5.14 $5.56 $5.56 $15.0M per rig $5.61 $6.16 $6.68 $6.68 $17.5M per rig $6.55 $7.19 $7.79 $7.79 $20.0M per rig $7.49 $8.22 $8.90 $8.90 $22.5M per rig $8.42 $9.25 $10.02 $10.02 2 |

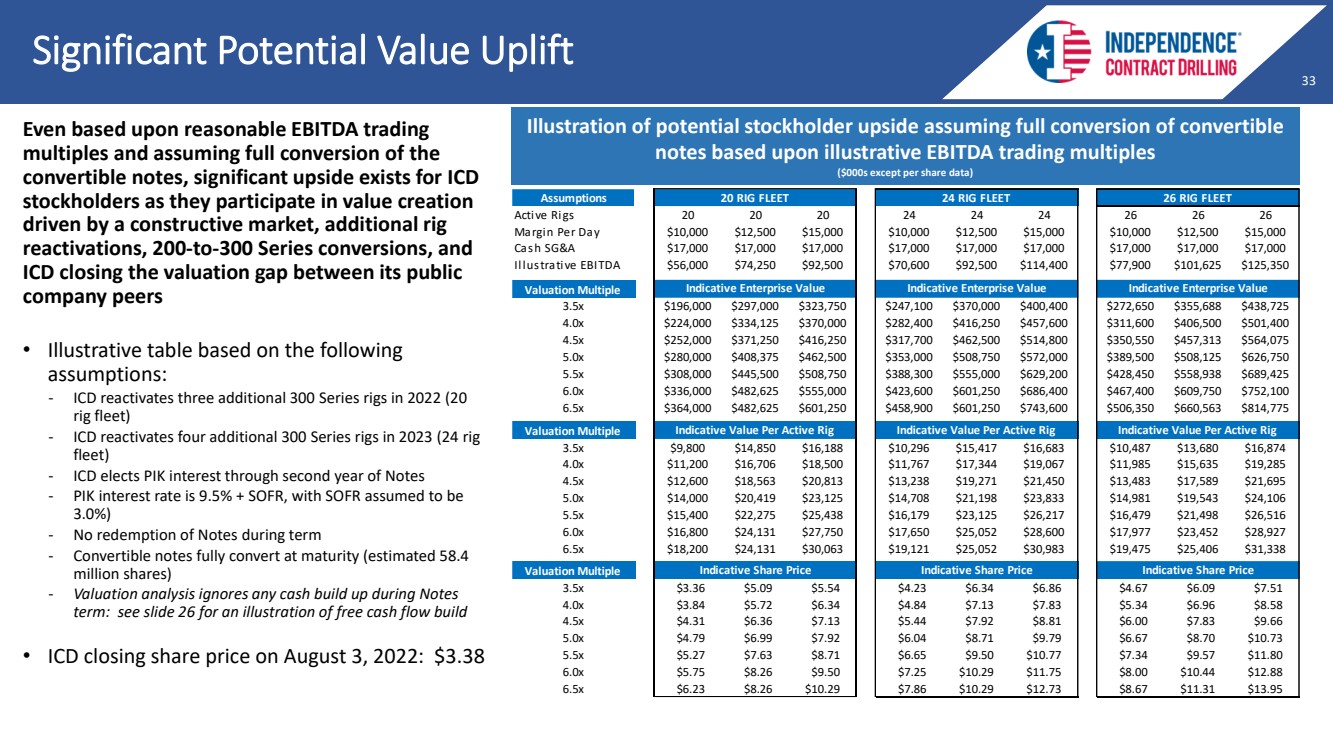

| 33 33 33 Significant Potential Value Uplift Illustration of potential stockholder upside assuming full conversion of convertible notes based upon illustrative EBITDA trading multiples ($000s except per share data) Even based upon reasonable EBITDA trading multiples and assuming full conversion of the convertible notes, significant upside exists for ICD stockholders as they participate in value creation driven by a constructive market, additional rig reactivations, 200 - to - 300 Series conversions, and ICD closing the valuation gap between its public company peers • Illustrative table based on the following assumptions: - ICD reactivates three additional 300 Series rigs in 2022 (20 rig fleet) - ICD reactivates four additional 300 Series rigs in 2023 (24 rig fleet) - ICD elects PIK interest through second year of Notes - PIK interest rate is 9.5% + SOFR, with SOFR assumed to be 3.0%) - No redemption of Notes during term - Convertible notes fully convert at maturity (estimated 58.4 million shares) - Valuation analysis ignores any cash build up during Notes term: see slide 26 for an illustration of free cash flow build • ICD closing share price on August 3, 2022: $3.38 Assumptions 20 RIG FLEET 24 RIG FLEET 26 RIG FLEET Active Rigs 20 20 20 24 24 24 26 26 26 Margin Per Day $10,000 $12,500 $15,000 $10,000 $12,500 $15,000 $10,000 $12,500 $15,000 Cash SG&A $17,000 $17,000 $17,000 $17,000 $17,000 $17,000 $17,000 $17,000 $17,000 Illustrative EBITDA $56,000 $74,250 $92,500 $70,600 $92,500 $114,400 $77,900 $101,625 $125,350 Valuation Multiple 3.5x $196,000 $297,000 $323,750 $247,100 $370,000 $400,400 $272,650 $355,688 $438,725 4.0x $224,000 $334,125 $370,000 $282,400 $416,250 $457,600 $311,600 $406,500 $501,400 4.5x $252,000 $371,250 $416,250 $317,700 $462,500 $514,800 $350,550 $457,313 $564,075 5.0x $280,000 $408,375 $462,500 $353,000 $508,750 $572,000 $389,500 $508,125 $626,750 5.5x $308,000 $445,500 $508,750 $388,300 $555,000 $629,200 $428,450 $558,938 $689,425 6.0x $336,000 $482,625 $555,000 $423,600 $601,250 $686,400 $467,400 $609,750 $752,100 6.5x $364,000 $482,625 $601,250 $458,900 $601,250 $743,600 $506,350 $660,563 $814,775 Valuation Multiple 3.5x $9,800 $14,850 $16,188 $10,296 $15,417 $16,683 $10,487 $13,680 $16,874 4.0x $11,200 $16,706 $18,500 $11,767 $17,344 $19,067 $11,985 $15,635 $19,285 4.5x $12,600 $18,563 $20,813 $13,238 $19,271 $21,450 $13,483 $17,589 $21,695 5.0x $14,000 $20,419 $23,125 $14,708 $21,198 $23,833 $14,981 $19,543 $24,106 5.5x $15,400 $22,275 $25,438 $16,179 $23,125 $26,217 $16,479 $21,498 $26,516 6.0x $16,800 $24,131 $27,750 $17,650 $25,052 $28,600 $17,977 $23,452 $28,927 6.5x $18,200 $24,131 $30,063 $19,121 $25,052 $30,983 $19,475 $25,406 $31,338 Valuation Multiple 3.5x $3.36 $5.09 $5.54 $4.23 $6.34 $6.86 $4.67 $6.09 $7.51 4.0x $3.84 $5.72 $6.34 $4.84 $7.13 $7.83 $5.34 $6.96 $8.58 4.5x $4.31 $6.36 $7.13 $5.44 $7.92 $8.81 $6.00 $7.83 $9.66 5.0x $4.79 $6.99 $7.92 $6.04 $8.71 $9.79 $6.67 $8.70 $10.73 5.5x $5.27 $7.63 $8.71 $6.65 $9.50 $10.77 $7.34 $9.57 $11.80 6.0x $5.75 $8.26 $9.50 $7.25 $10.29 $11.75 $8.00 $10.44 $12.88 6.5x $6.23 $8.26 $10.29 $7.86 $10.29 $12.73 $8.67 $11.31 $13.95 Indicative Enterprise Value Indicative Value Per Active Rig Indicative Share Price Indicative Value Per Active Rig Indicative Share Price Indicative Enterprise Value Indicative Enterprise Value Indicative Value Per Active Rig Indicative Share Price |

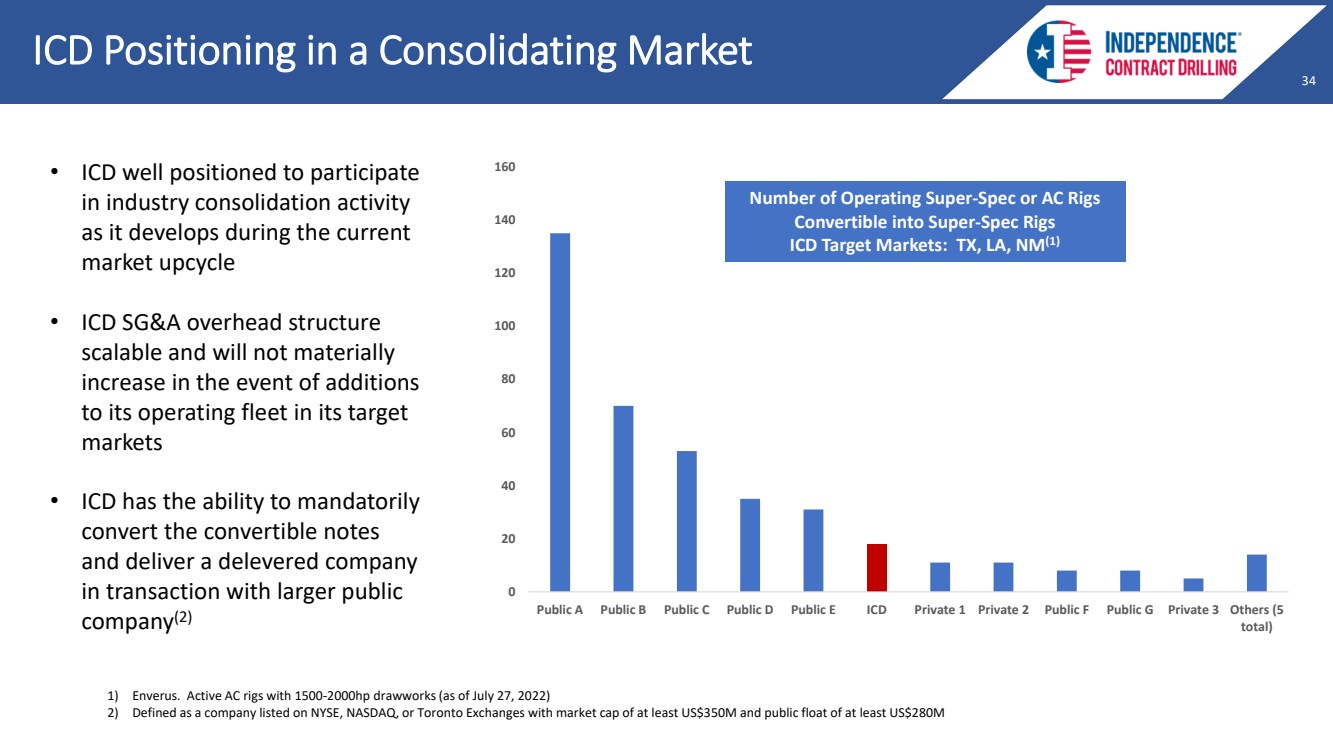

| 34 34 34 ICD Positioning in a Consolidating Market 0 20 40 60 80 100 120 140 160 Public A Public B Public C Public D Public E ICD Private 1 Private 2 Public F Public G Private 3 Others (5 total) Number of Operating Super - Spec or AC Rigs Convertible into Super - Spec Rigs ICD Target Markets: TX, LA, NM (1) 1) Enverus .. Active AC rigs with 1500 - 2000hp drawworks (as of July 27, 2022) 2) Defined as a company listed on NYSE, NASDAQ, or Toronto Exchanges with market cap of at least US$350M and public float of at lea st US$280M • ICD well positioned to participate in industry consolidation activity as it develops during the current market upcycle • ICD SG&A overhead structure scalable and will not materially increase in the event of additions to its operating fleet in its target markets • ICD has the ability to mandatorily convert the convertible notes and deliver a delevered company in transaction with larger public company (2) |

| 35 35 35 ESG |

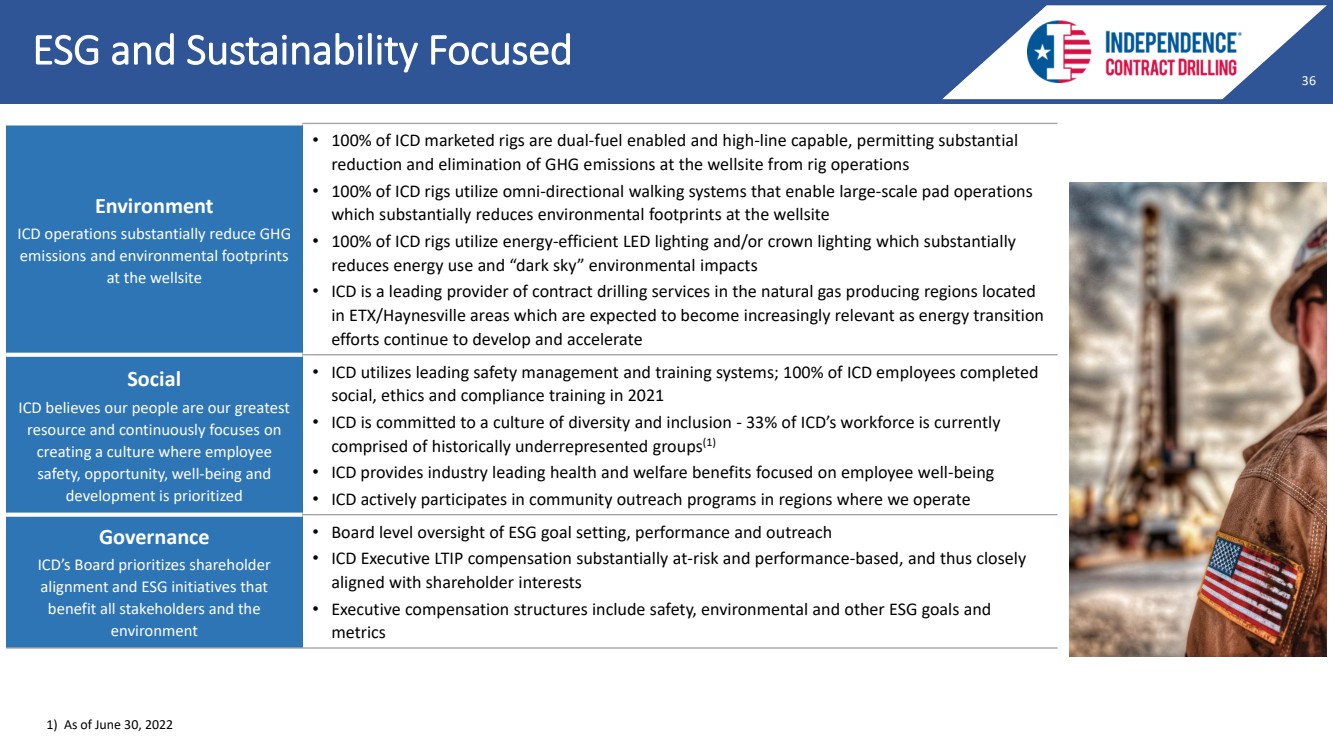

| 36 36 36 ESG and Sustainability Focused Environment ICD operations substantially reduce GHG emissions and environmental footprints at the wellsite • 100% of ICD marketed rigs are dual - fuel enabled and high - line capable, permitting substantial reduction and elimination of GHG emissions at the wellsite from rig operations • 100% of ICD rigs utilize omni - directional walking systems that enable large - scale pad operations which substantially reduces environmental footprints at the wellsite • 100% of ICD rigs utilize energy - efficient LED lighting and/or crown lighting which substantially reduces energy use and “dark sky” environmental impacts • ICD is a leading provider of contract drilling services in the natural gas producing regions located in ETX/Haynesville areas which are expected to become increasingly relevant as energy transition efforts continue to develop and accelerate Social ICD believes our people are our greatest resource and continuously focuses on creating a culture where employee safety, opportunity, well - being and development is prioritized • ICD utilizes leading safety management and training systems; 100% of ICD employees completed social, ethics and compliance training in 2021 • ICD is committed to a culture of diversity and inclusion - 33% of ICD’s workforce is currently comprised of historically underrepresented groups (1) • ICD provides industry leading health and welfare benefits focused on employee well - being • ICD actively participates in community outreach programs in regions where we operate Governance ICD’s Board prioritizes shareholder alignment and ESG initiatives that benefit all stakeholders and the environment • Board level oversight of ESG goal setting, performance and outreach • ICD Executive LTIP compensation substantially at - risk and performance - based, and thus closely aligned with shareholder interests • Executive compensation structures include safety, environmental and other ESG goals and metrics 1) As of June 30, 2022 |

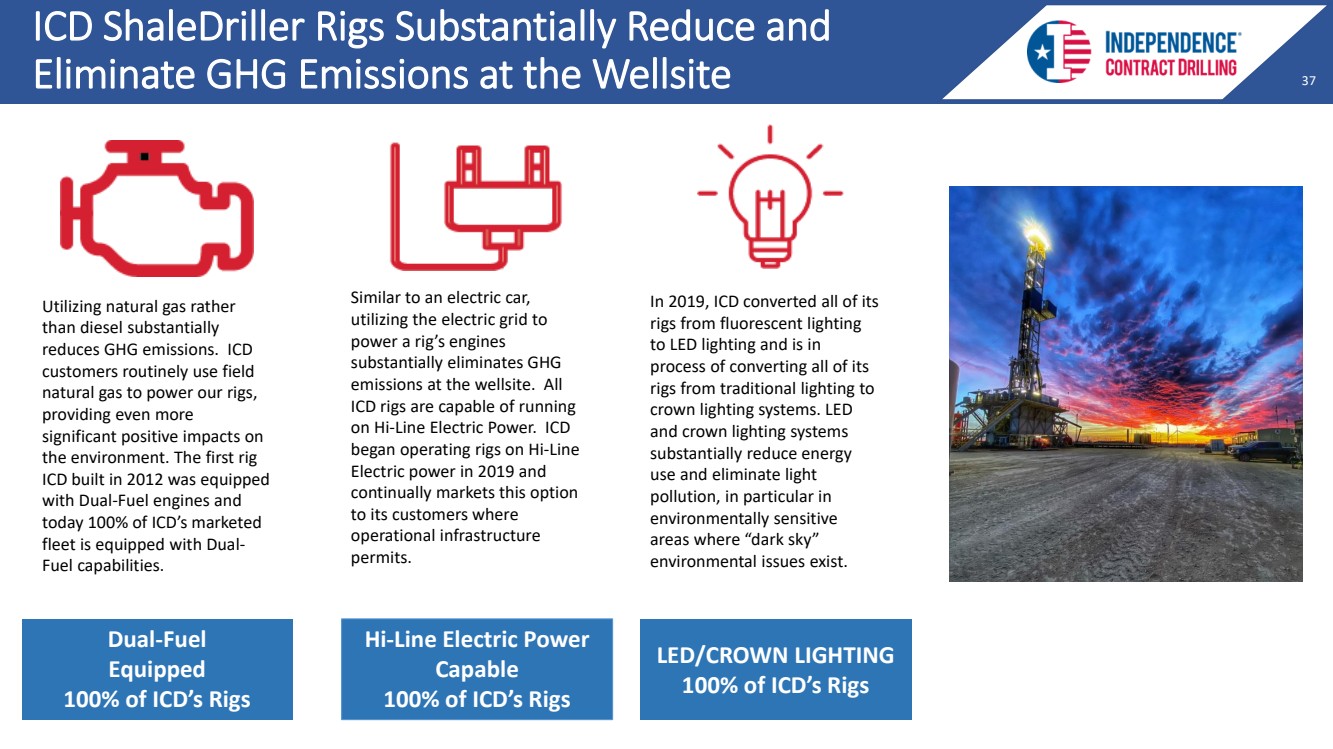

| 37 37 37 ICD ShaleDriller Rigs Substantially Reduce and Eliminate GHG Emissions at the Wellsite Utilizing natural gas rather than diesel substantially reduces GHG emissions. ICD customers routinely use field natural gas to power our rigs, providing even more significant positive impacts on the environment. The first rig ICD built in 2012 was equipped with Dual - Fuel engines and today 100% of ICD’s marketed fleet is equipped with Dual - Fuel capabilities. Dual - Fuel Equipped 100% of ICD’s Rigs Similar to an electric car, utilizing the electric grid to power a rig’s engines substantially eliminates GHG emissions at the wellsite. All ICD rigs are capable of running on Hi - Line Electric Power. ICD began operating rigs on Hi - Line Electric power in 2019 and continually markets this option to its customers where operational infrastructure permits. Hi - Line Electric Power Capable 100% of ICD’s Rigs LED/CROWN LIGHTING 100% of ICD’s Rigs In 2019, ICD converted all of its rigs from fluorescent lighting to LED lighting and is in process of converting all of its rigs from traditional lighting to crown lighting systems. LED and crown lighting systems substantially reduce energy use and eliminate light pollution, in particular in environmentally sensitive areas where “dark sky” environmental issues exist. |

| 38 38 38 US Land Drilling’s Only Publicly - Traded, Pure - Play, Pad - Optimal, Super - Spec, Growth Story Highest Asset Quality 100% Pad - Optimal, Super - Spec Fleet Premier Customer Base Rapidly Expanding Margins/Cash Flows Driven by Strategic Investments and Market Conditions Significant Investment Opportunity - Meaningful Current Valuation Discount to Market Based Upon Both Asset Values and Cash Flow Multiples Fleet 100% Dual - Fuel Enabled / Electric Hi - Line Capable: Substantial GHG Reduction / Elimination Recognized Industry Leader for Service and Professionalism Ideal Geographic Focus on Most Prolific Oil and Natural Gas Producing Regions |

| 39 39 39 Investor Contact Information Email inquiries: investor.relations@icdrilling.com Phone inquiries: (281) 878 - 8710 |

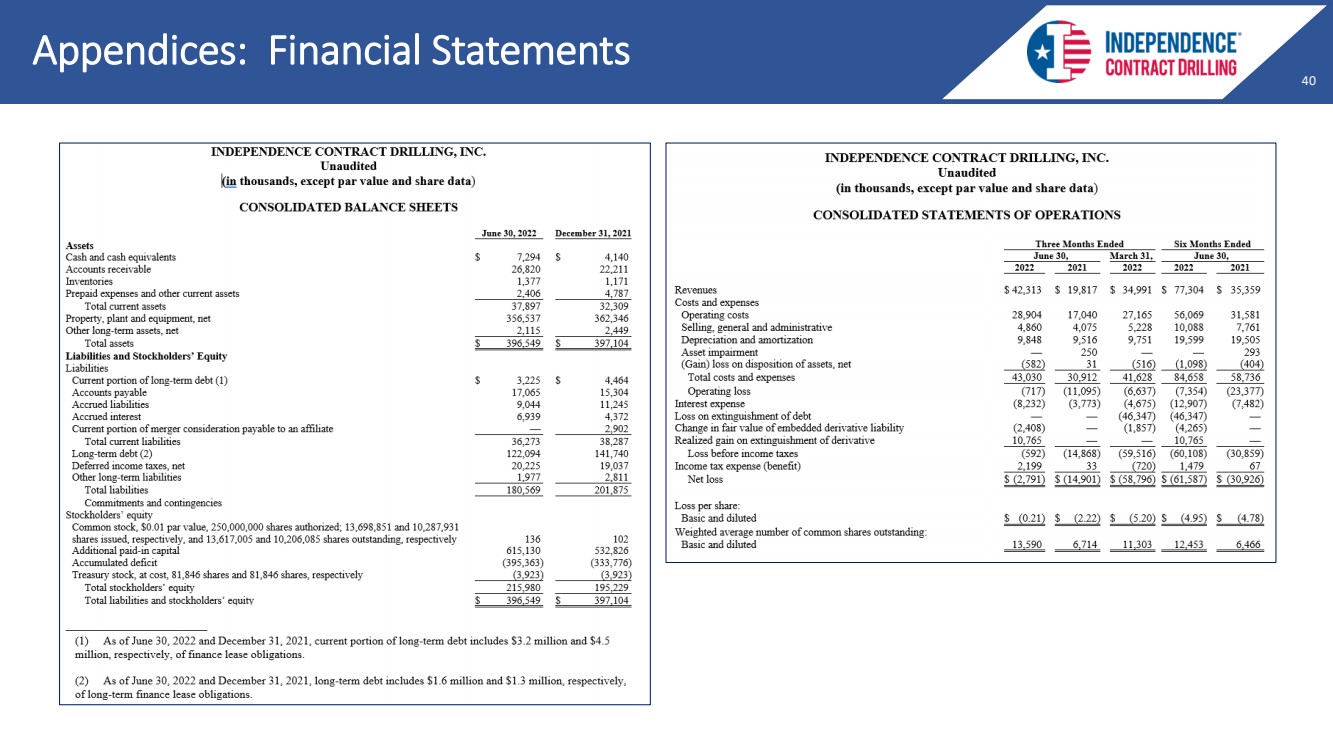

| 40 40 40 Appendices: Financial Statements |

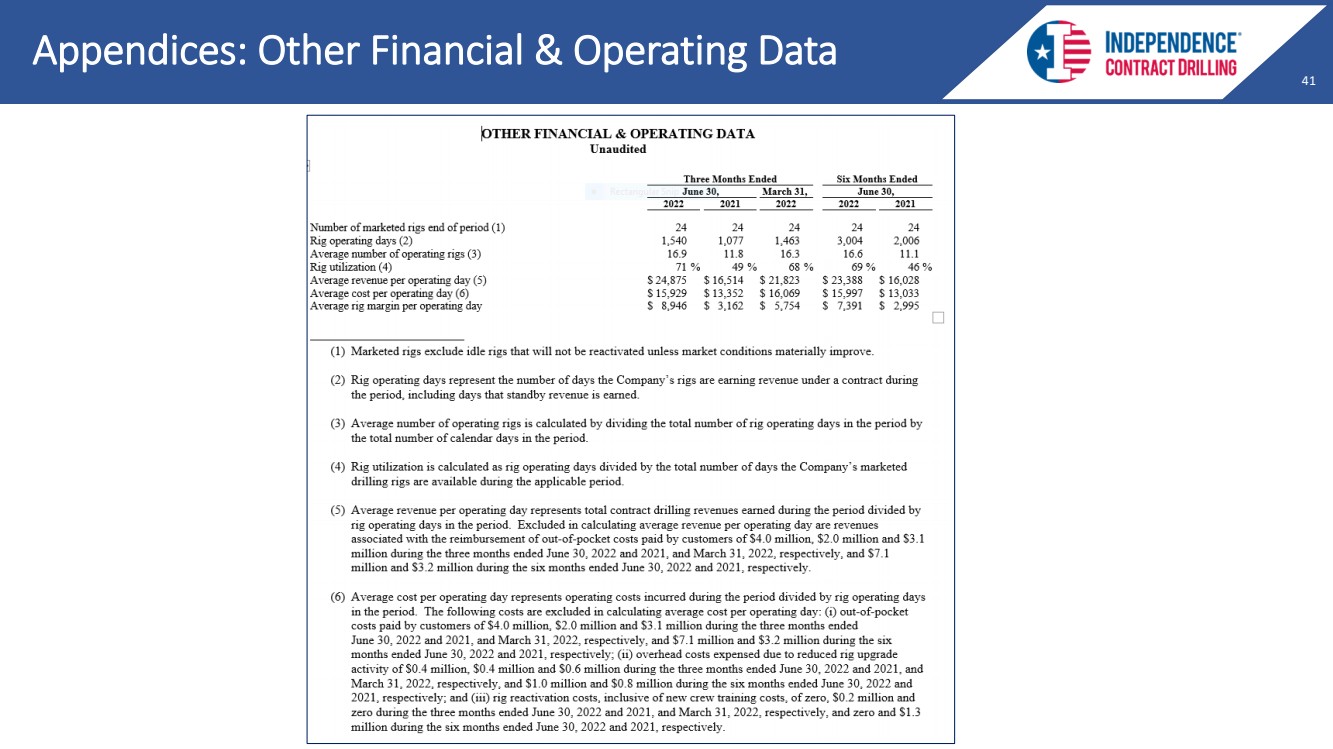

| 41 41 41 Appendices: Other Financial & Operating Data |

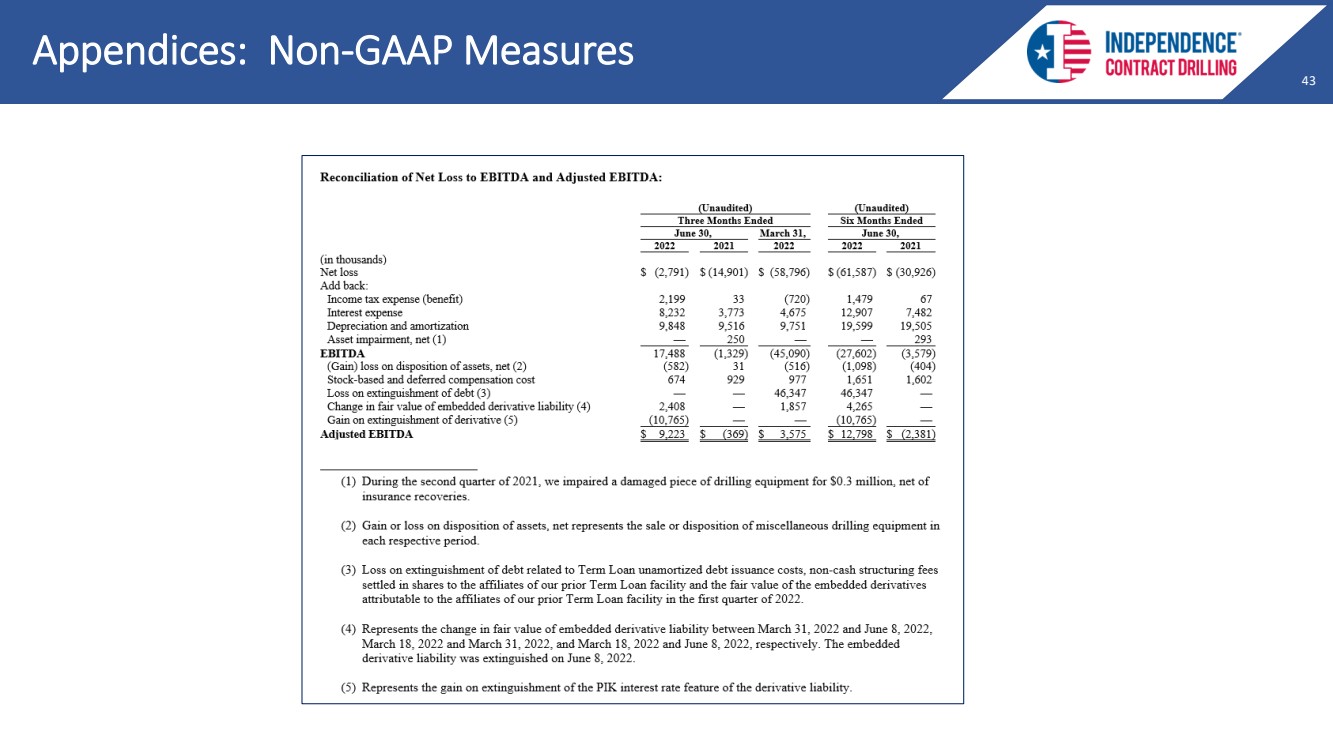

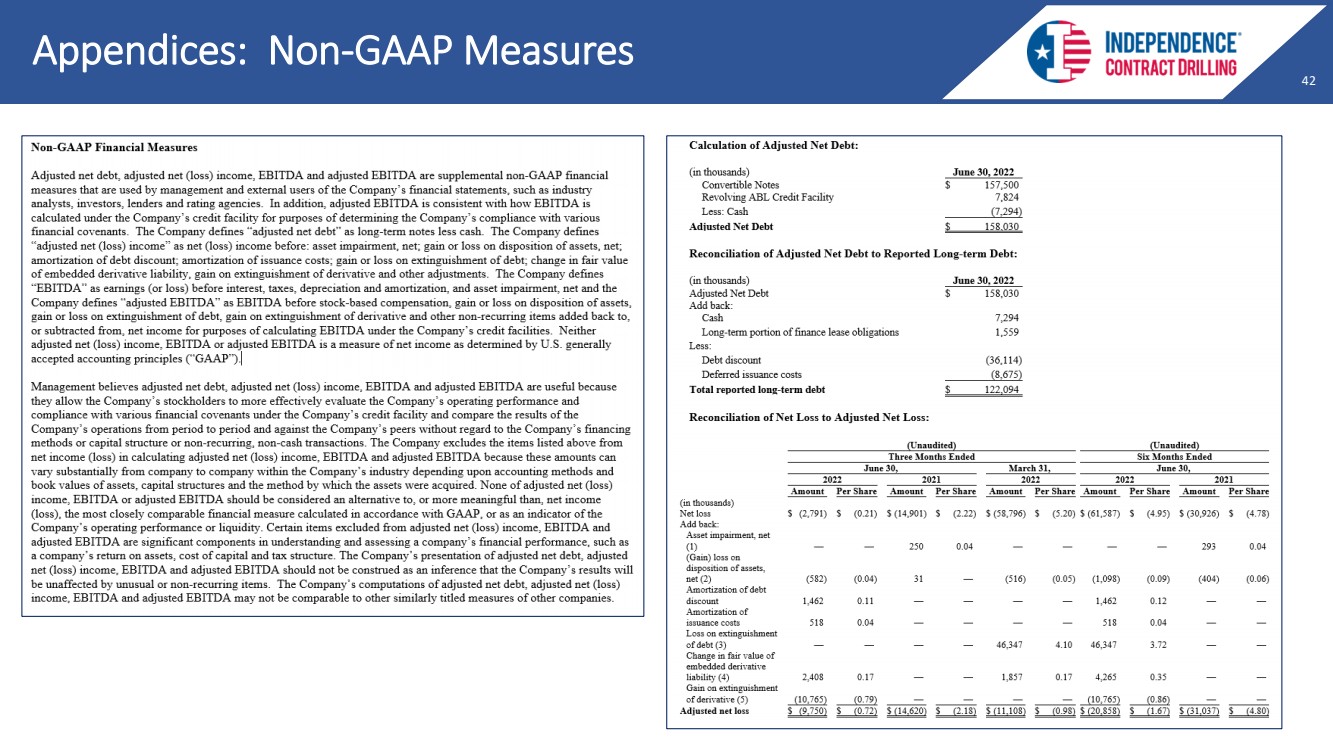

| 42 42 42 Appendices: Non - GAAP Measures |

| 43 43 43 Appendices: Non - GAAP Measures |