UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22747

ALPS SERIES TRUST

(Exact name of registrant as specified in charter)

1290 Broadway, Suite 1100, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

303.623.5277

(Registrant’s telephone number, including area code)

Richard C. Noyes, Esq., Secretary

ALPS Series Trust

1290 Broadway, Suite 1100

Denver, CO 80203

(Name and address of agent for service)

Date of fiscal year end: September 30

Date of reporting period: October 1, 2017 – September 30, 2018

Item 1. Reports to Stockholders.

Table of Contents

| Shareholder Letter | 1 |

| Portfolio Updates | 3 |

| Disclosure of Fund Expenses | 11 |

| Portfolio of Investments | 12 |

| Statements of Assets and Liabilities | 19 |

| Statements of Operations | 20 |

| Statements of Changes in Net Assets | 22 |

| Financial Highlights | 24 |

| Notes to Financial Statements | 28 |

| Report of Independent Registered Public Accounting Firm | 38 |

| Additional Information | 39 |

| Privacy Policy | 42 |

| Trustees & Officers | 44 |

| American Independence Funds | Shareholder Letter |

September 30, 2018 (Unaudited)

Dear Shareholder,

We are pleased to present you with the Annual Report for the American Independence Global Tactical Allocation Fund and the American Independence Kansas Tax-Exempt Bond Fund (each a “Fund” and collectively “Funds”) for the year ended September 30, 2018. The Annual Report period is a shorter period as a result of the reorganization of the Funds into a series of ALPS Series Trust (“AST”).

In the fiscal 11 months, we’ve seen the strongest corporate profits in seven years, which drove the drove the equity market higher, while volatility dramatically increased in February, and continued rising interest rates constrained bond returns. Though the market’s appetite for risk remained, it was moderated as risk-taking was tempered somewhat, as shorter term, higher quality securities led the bond market and U.S. equities outperformed most international stock markets.

Relatively strong equity performance worldwide was driven by synchronized economic growth across the most influential economies and industry sectors. However, volatility around the globe rose, as U. S. and China trade relations and debt concerns weighed heavily on stock markets.

In addition, the following factors were of concern: (i) there were increased tensions between the U.S. and China that affected the Chinese stock market, (ii) Turkey became embroiled in a currency crisis shortly after the end of the reporting period, and (iii) Brexit concerns and uncertainties remain in the market.

In terms of interest rates, short-term interest rates for U.S. Treasuries rose the fastest, while longer-term rates slightly increased, heading to a negative return for long-term U.S. Treasuries and a substantial flattening of the yield curve. As discussed by industry commentators, many investors are concerned that the flattening of the yield curve is as a harbinger of a possible recession. But, given the extraordinary monetary measures and fiscal policy in the last decade, we believe a more accurate barometer of the economy are returns along the “risk spectrum” in stock and bond markets. Although the fundamentals in credit markets remained relatively solid, investment grade bonds declined slightly, and high-yield and tax-exempt bonds posted moderate returns.

In response to rising growth inflation, the U.S. Federal Reserve (“Fed”) increased short-term interest rates four times during the reporting period. Meanwhile, the European Central Bank announced a bond purchase program that would conclude at year end of 2018, while also expressing its commitment to low interest rates. In contrast, the Bank of Japan continued to expand its balance sheet through bond purchasing while lowering its expectation for inflation.

The U.S. economy continued to gain momentum despite the Fed’s reduction of economic stimulus. The national unemployment rate has continued to decline, with wages increasing and the number of job openings reaching record highs.

While U.S. monetary policy is seeking to restrain growth and inflation, fiscal policy has produced new sources of growth that could nourish the economy for the next few years. Corporate tax cuts and lower individual tax cuts could encourage the robust job market and refresh consumer spending.

We continue to believe the primary risks to economic expansion are trade protectionism, rapidly rising interest rates, and geo-political tensions. Given the deflationary forces of technology and globalization, we are encouraged. In this environment, investors need to think globally, extend their scope of diversification across an array of asset classes and be nimble with downside protection products.

We encourage you to talk to your financial advisor for further insights about investing in today’s markets.

As always, our mission is to continue to provide quality investment outcomes for clients and shareholders. The Funds’ sub-advisers bring expertise in significant disciplines – including macroeconomics, behavioral finance, and asset allocations using Exchange Traded Funds (ETFs) – to provide a unique lineup of investment solutions for shareholders, advisors, and institutions.

Portfolio reviews written by each sub-adviser follow this letter.

Thank you for your continued support.

Sincerely,

Jane A. Kanter

Managing Partner and Chief Counsel

Manifold Partners LLC

| Annual Report | September 30, 2018 | 1 |

| American Independence Funds | Shareholder Letter |

September 30, 2018 (Unaudited)

Basis Points: One hundredth of one percent.

Yield Curve: a line that plots the interest rates, at a set point in time, of bonds having equal credit quality but differing maturity dates.

Diversification does not eliminate the risk of experiencing investment losses.

The views and information discussed in this commentary are as of the date of publication, are subject to change, and may not reflect the writer’s current views. The views expressed are those of the Adviser only, and represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund(s) or any securities or any sectors mentioned in this letter. The subject matter contained in this letter has been derived from several sources believed to be reliable and accurate at the time of compilation. Neither the Fund nor the Adviser accepts any liability for losses either direct or consequential caused by the use of this information.

Not FDIC Insured – No Bank Guarantee – May Lose Value

Past performance does not guarantee future results.

ALPS Distributors, Inc. is not affiliated with Manifold Partners LLC, the investment adviser to the Funds.

| 2 | www.americanindependence.com |

| American Independence Global Tactical Allocation Fund | Portfolio Update |

September 30, 2018 (Unaudited)

2018 Commentary

The Institutional Class of the American Independence Global Tactical Allocation Fund (“GTA Fund” or “Fund”) returned 1.53% for the 11-month fiscal year ended September 30, 2018. Over the same period, the GTA Fund’s benchmark, the MSCI All Country World Index (“MSCI ACWI”), returned 7.54% and the Blended Benchmark (a monthly rebalanced mix comprised of 60% of the MSCI ACWI and 40% of the Bloomberg Barclays US Aggregate Bond Index) returned 4.03%.

The GTA Fund invests in equities and fixed income, targeting exposures in five regions for equities as well as global and domestic fixed income indices. It uses a quantitative model to determine the portfolio balances among these asset classes that best fits the current market climate. All non-cash positions are invested in exchange traded funds (“ETFs”), which gives the GTA Fund significant flexibility in terms of low-cost asset allocation.

Year in Review

Fiscal 2018 was notably a transition year for the markets, and it was also a transition year for the management of the Fund. As of January 19, 2018, Manifold Fund Advisors, LLC (“MFA”), the prior adviser to the Fund, assumed sole responsibility for the management of the Fund and the prior sub-adviser to the Fund continued to provide advice to MFA as to the management of the Fund on an interim basis. As of March 24, 2018, MFA managed the Fund without advice from the Fund’s prior sub-adviser and began to accept research suggestions and trading signals from Lee Capital Management (“LCM”). On September 24, 2018, LCM assumed the role of sub-adviser to the Fund, in connection with the reorganization of the Fund as a series of ALPS Series Trust, and Manifold Partners LLC became the adviser to the Fund. Management of the Fund’s assets did not change as a result of the reorganization of the Fund into the ALPS Series Trust, and the GTA Fund continues to have substantially the same objective, strategies and risks as it did prior to the reorganization.

On the market side, the last several years’ relatively tranquil appreciation in global equities, supported by historically low capital market interest rates, persisted through January of 2018. However, that benign environment gave way for the rest of the fiscal year to higher bond yields and elevated equity volatility as central banks in major economies around the world went about removing, or making preparations to remove, the extraordinary monetary stimulus that was put in place following the global financial crisis of 2008. In early February, the accumulated increases in interest rates and anticipation of further monetary policy tightening led to a major spike of volatility. This ushered in declines in domestic and global equity markets that persisted for over two months; the start of the decline coincided with the start of Jerome Powell’s tenure as chairman of the Federal Reserve. Evidence of ebbing speculative enthusiasm was exhibited by dramatic (and widely reported) reversals in the prices of crypto-currencies such as Bitcoin, and later disclosure that margin borrowing in January (reported by U.S. securities dealers) had peaked at a level that exceeded the previous record (dating back to early 2000) before backing down as the markets declined.

November 2017 to March 2018

The Fund’s positioning at the start of the fiscal year showed relative caution, particularly with respect to bond yields, with 10% set aside as a cash cushion, 35% in fixed income, and 50% in equities (evenly split between domestic and international). Over the three months leading up to February’s selloff, equity exposure crept up to 55%, but the defensive “alternatives” allocation was doubled from 5% to 10% by adding diversified commodity exposure to the Fund’s longstanding position in gold, while the fixed income exposure and cash buffer were reduced to 30% and 5%, respectively.

What became clear during the February selloff was that the Fund’s fixed income allocation was no longer providing a defensive ballast to the portfolio’s equity positions. This challenge to maintaining stable performance through a relatively steady balance of stocks and bonds was exacerbated by the lackluster (or worse) performance of other “defensive” positions, in gold and other commodities. Based on guidance and advice from LCM, in late March, the Fund’s allocation to equity securities was significantly increased and all fixed income and alternatives holdings in the Fund were sold. The Fund’s new 75% equity allocation was split between 45% domestic and 30% international, and cash was raised to 25%, effectively assuming the defensive role formerly played by fixed income and alternatives. This repositioning of the Fund’s assets resulted in the realization of capital gains by the Fund, which will be passed through to the Fund’s shareholders.

Fund Changes

In addition to the changes to the Fund’s portfolio described above, there were some other changes to the Fund’s investments, although the objective, strategy, goals and restrictions of the Fund remained constant. The two most significant changes are that (i) the Fund no longer utilized alternative investments (such as commodities) and (ii) positions in the Fund would no longer be updated on a fixed monthly schedule. In contrast to the prior methodology’s monthly allocation procedure, the Fund’s new approach continually reviews market developments, meaning that the Fund can rebalance holdings on any day, as needed. This decision to engage in more frequent trading also contributed to more portfolio turnover and increased trading costs and tax consequences.

| Annual Report | September 30, 2018 | 3 |

| American Independence Global Tactical Allocation Fund | Portfolio Update |

September 30, 2018 (Unaudited)

LCM believes that although risky assets, such as fixed income and equity, are almost certainly profitable in the long run, there are periods in which the risk of certain assets is not justified. During these periods, LCM seeks to reallocate in favor of other asset classes or cash.

April 2018 to September 2018

There was a consistent underweight in the Fund to fixed income securities throughout the final six months of the Fund’s fiscal year. Only briefly, for a few days in early July, did the portfolio approach its normal (calm market) fixed income weight of 40%. On average, the fixed income weight was just under 19% for the six months ended September 30, 2018.

In general, this was a successful positioning, as the Bloomberg Barclays US Aggregate was close to flat over the period (down -0.14%) while equities rose sharply (S&P 500 up 12.95%, MSCI All Country World up 5.22%).

In contrast, the US equity allocation for the Fund, although variable, averaged under its normal weighting of 30% for US equity securities, at 25% for the six months, reached its allowed maximum of 45% in April and went as low as just over 14% in early August.

Although a larger allocation of the GTA Fund’s assets to US equity securities would have been more beneficial to the Fund, LCM believes that the significant exposure to US stocks had a positive impact on performance.

Emerging Market and Asia ex-Japan equity securities both spent April through July at or above their normal weightings of 6%. Then, in early and mid-August, as “trade war” concerns began to weigh heavily on export-driven economies, the Fund reduced its allocations to assets in both of those jurisdictions to approximately 1% of the portfolio, where both remained through September.

As measured by the MSCI Pacific ex-Japan Index, Asia ex-Japan equities gained 1.81% over the April-July (inclusive) period, and then fell -2.42% in August and September. The MSCI Emerging Markets Index declined in both periods, by -5.64% and -3.16% respectively.

The remaining equity asset classes, Japan and developed Europe, spent nearly the entire April to September period fully invested, with weightings between their normal targets and their maximums. The MSCI Japan Index gained 1.61% over the six months, while the MSCI Europe was almost perfectly flat, losing -0.03%.

Except for a brief period in early April, the Fund held meaningful cash positions throughout April to September, reaching a peak of over 40% in late May, and averaging approximately 20% throughout the period. Much of this cash holding was due to the underweighting of fixed income securities in the Fund, although it could also be said that had LCM’s view been more positive on equities, cash holdings would have been smaller. Relative to fixed income, the cash positioning had a neutral effect on performance, while relative to equity it was largely a drag.

LCM’s Outlook

As the fourth calendar quarter begins, LCM believes that storm clouds are gathering on the horizon. Central banks worldwide seem to have become comfortable with tightening what had been notably lax and long-standing monetary policy. Fixed income markets appear to be settling in for years of rate increases.

Non-US equity appears to be under pressure. In Europe, Italian political and budgetary woes weigh heavily, and a disaster-averting Brexit deal continues to be elusive. Asia and Emerging markets are threatened by trade disputes with the United States.

LCM believes that the US equity market remains the only bright spot, and then partially by elimination. There are certainly reasons to suspect that the almost decade long bull market is showing its age. Media talk of “peak earnings” underlines the unspecific feeling that this is as good as it gets, that conditions cannot improve further so can only deteriorate.

LCM’s outlook for the coming fiscal year is the same as its outlook for most years: cautious optimism. Markets are more likely to be higher in a year than lower, but the wise investor understands that there are no guarantees and stands ready to exit if conditions make a turn for the worse.

| 4 | www.americanindependence.com |

| American Independence Global Tactical Allocation Fund | Portfolio Update |

September 30, 2018 (Unaudited)

| Average Annual Total Returns (as of September 30, 2018) | ||||

| 1 Year | 3 Year | 5 Year | Since Inception* | |

| American Independence Global Tactical Allocation Fund - Institutional Class | 2.81% | 7.81% | 5.89% | 5.69% |

| American Independence Global Tactical Allocation Fund - Class A | 2.38% | 7.43% | 5.50% | 5.31% |

| MSCI All Country World Index(a) | 9.77% | 13.40% | 8.67% | 8.33% |

| 60% MSCI ACWI / 40% Bloomberg Barclays US Agg Bond Index(b) | 5.35% | 8.53% | 6.15% | 5.99% |

The performance data quoted above represents past performance. Past performance is not a guarantee of future results. Investment return and value of the Fund shares will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Performance may be lower or higher than performance data quoted. Fund performance current to the most recent month-end is available by calling (833) 287-7933 or by visiting www.americanindependence.com.

| * | The Fund commenced operations on September 20, 2013. The Predecessor Fund, American Independence JAForlines Global Tactical Allocation Fund, managed by Manifold Fund Advisors, LLC, was reorganized into the American Independence Global Tactical Allocation Fund on September 24, 2018. Manifold Partners, LLC has been the Fund’s investment adviser since September 24, 2018, with Lee Capital Management, L.P. serving as sub-adviser. Fund performance prior to September 24, 2018 is reflective of the past performance of the Predecessor Fund. |

| (a) | The MSCI All Country World Index (“ACWI”) is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI consists of 46 country indexes comprising 23 developed and 23 emerging market country indexes. |

| (b) | The Bloomberg Barclays U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market, including Treasuries, government-related and corporate securities, MBS (agency fixed-rate and hybrid ARM pass-throughs), ABS, and CMBS (agency and non-agency). The index is not actively managed and does not reflect any deductions for fees, expenses or taxes. |

Returns of less than 1 year are cumulative.

Indices are not actively managed and do not reflect deduction for fees, expenses or taxes. An investor cannot invest directly in an index.

The returns shown above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares.

The total annual operating expenses and total annual operating expenses after fee waivers and/or reimbursement you may pay as an investor in the Fund’s Institutional Class and Class A shares (as reported in the September 24, 2018 Prospectus) are 1.44% and 1.27% and 1.69% and 1.52%, respectively. The Fund’s investment adviser has contractually agreed to limit expenses through January 31, 2021.

Performance of $3,000,000 Initial Investment (as of September 30, 2018)

The graph shown above represents historical performance of a hypothetical investment of $3,000,000 in the Institutional Class. Due to differing expenses, performance of Class A will vary. Past performance does not guarantee future results. Returns do not reflect the deduction of fees, sales charges, or taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

| Annual Report | September 30, 2018 | 5 |

| American Independence Global Tactical Allocation Fund | Portfolio Update |

September 30, 2018 (Unaudited)

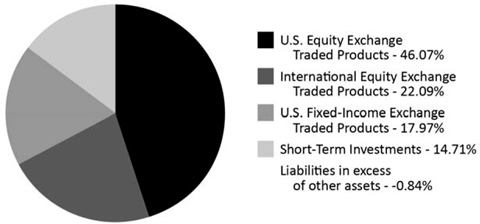

Portfolio Diversification (% of Net Assets as of September 30, 2018)

| 6 | www.americanindependence.com |

| American Independence Kansas Tax-Exempt Bond Fund | Portfolio Update |

September 30, 2018 (Unaudited)

2018 Commentary

2018 will likely be defined by several factors, including (i) much-improved economic conditions, (ii) record low unemployment, (iii) increasing wage growth, and (iv) rising U.S. interest rates. However, many questions remain unanswered including how far will the Federal Reserve (Fed) raise short-term interest rates year and what steps may be taken to achieve the Fed’s goal of “normalization”? Will these Fed moves create an “inverted” yield curve? And, ultimately, will a meaningful rise in interest rates bring an end to the U.S. equity markets’ 9-year bull run?

There have been a handful of noticeable “fits and starts” to U.S. equity markets so far this calendar year. Over that time, interest rates have tended to grind higher, albeit slowly. The yield on the 10- year U.S. Treasury Bond ended both fiscal 2017 and calendar 2017 at a yield of about 2.40% and was approximately 65 basis points higher (3.05%) at the end of September 2018. The 2-year to 10-year yield spread for U.S. Treasuries stood at just +25 basis points, close to its tightest this year.

Municipal bond yields tended to drift higher in sympathy with U.S. Treasuries. However, the municipal bond market has historically been driven more by supply and demand dynamics, than by interest rates specifically. Municipal bond new issuance set records in the fourth quarter of 2017 due to forward looking uncertainty about advance refundings [Pre Res] and marginal tax rates. The supply in 2018 has been relatively modest - far below annual averages – while demand has remained robust. Thus, municipal bonds have tended to be “rich” compared to U.S. Treasuries (lower yields relative to Treasuries than historical averages), especially in the short-end of the yield curve (inside 5 years). The 2-year-to 10-year spread in municipal bonds at the end of the third quarter of 2018 was much wider than that for U.S. Treasuries at +65 basis points.

In 2018, rating agencies such as Moody’s and S&P both issued reports noting solid improvements to municipal credit at the state and local levels, with the recovery in property values, higher tax receipts, increased reserves, stable direct debt, and accelerating economic growth all key factors.

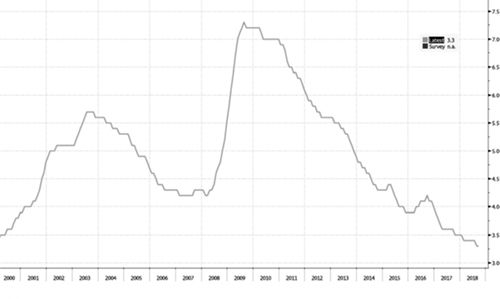

In Kansas, the challenges to the various local economies mirror many of those at the national level, with “trade wars” and tariffs now taking center stage. Unemployment across the state has fallen to 3.3% with major strides coming specifically from nonfarm employment.

Unemployment Rate – State of Kansas [through 09/30/18]

Source: Bloomberg

The Kansas manufacturing sector has been a bright spot so far in 2018. Export sales in transportation and food products were major contributors, as were higher soybean exports. One thing to note: agriculture, while still a solid contributor to Gross Domestic Product ("GDP"), has decreased by over 40% over the last 5 years.

There is growing concern that tariffs might dampen productivity, and cause wages and personal income growth to stagnate. In late July, the Federal Reserve Bank of Kansas City’s monthly manufacturing survey reported strong activity and increased optimism, while labor shortages and tariffs remained top-of-mind.

Annual Report | September 30, 2018 | 7 |

American Independence Kansas | Portfolio Update |

September 30, 2018 (Unaudited)

One important issue to note is the state’s budget deficit. Kansas will continue to battle potential spending cuts, while trying to keep K-12 education funding a top priority. Thus, we would expect school districts across the state to continue to issue municipal bonds for that funding.

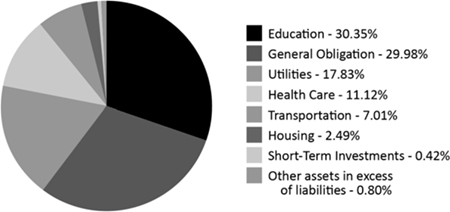

The Kansas Tax-Exempt Bond Fund focuses on preservation of capital while producing cash flows that are fully exempt from Federal taxes and Kansas state tax. The Fund continues to seek premium coupon general obligation (GO) and essential service revenue bonds in the investment grade rating category. Representative bond issues in the Fund include Kansas Department of Transportation Revenue, City of Wichita GO, Topeka Utility Revenue, Kansas Department of Finance Authority Revenue, and Wichita Water & Sewer Revenue. The Fund’s largest sector allocations are to School Districts (21%), Pre-Refunded bonds (16%), Utility Revenue bonds (13%), and General Obligation bonds (11%).

The Fund’s modified duration is 4.35 years, which is slightly longer than a year ago. We may look to alter the Fund’s duration over the next several quarters should value-added opportunities arise. The Fund holds 179 different bond issues, and over 60% of those are rated AA or better. The Institutional Share Class (I shares) return was essentially unchanged over the 12 month period ending September 30, 2018. Over this same time period, however, the Barclays Capital 7 year Municipal Bond Index returned a negative -0.59%. Over a 5-year time horizon, the I shares returned an average of 2.76% (annualized), compared to the comparable Barclays Index 2.62% annual average return.

The Fund did not employ any derivative investments during the fiscal year ending September 30, 2018.

8 | www.americanindependence.com |

American Independence Kansas | Portfolio Update |

September 30, 2018 (Unaudited)

| Average Annual Total Returns (as of September 30, 2018) | ||||||||||||||||

| 1 Year | 5 Year | 10 Year | Since Inception* | |||||||||||||

| American Independence Kansas Tax | ||||||||||||||||

| Exempt Bond Fund - Institutional Class | 0.00% | 2.76% | 3.63% | 4.50% | ||||||||||||

| American Independence Kansas Tax | ||||||||||||||||

| Exempt Bond Fund – Class A | -0.39% | 2.37% | 3.23% | 4.16% | ||||||||||||

| Bloomberg Barclays US Municipal | ||||||||||||||||

| Bond: 7 Year (6-8) Index(a) | -0.59% | 2.62% | 4.20% | 2.43% | ||||||||||||

The performance data quoted above represents past performance. Past performance is not a guarantee of future results. Investment return and value of the Fund shares will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Performance may be lower or higher than performance data quoted. Fund performance current to the most recent month-end is available by calling (833) 287-7933 or by visiting www.americanindependence.com.

| * | The Fund commenced operations on May 22, 2007. The Predecessor Fund, American Independence Kansas Tax-Exempt Bond Fund, managed by Manifold Fund Advisors, LLC, was reorganized into the American Independence Kansas Tax-Exempt Bond Fund on September 24, 2018. Manifold Partners, LLC has been the Fund’s investment adviser since September 24, 2018, with Carret Asset Management, LLC serving as sub-adviser. Fund performance prior to September 24, 2018, is reflective of the past performance of the Predecessor Fund. |

| (a) | The Bloomberg Barclays 7-Year Municipal Bond Index is a total return performance benchmark for the investment-grade, geographically unrestricted 7-year tax-exempt bond market, consisting of municipal bonds with maturities of 6 to 8 years. |

Returns of less than 1 year are cumulative.

Indices are not actively managed and do not reflect deduction for fees, expenses or taxes. An investor cannot invest directly in an index.

The returns shown above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares.

The total annual operating expenses and total annual operating expenses after fee waivers and/or reimbursement you may pay as an investor in the Fund’s Institutional Class and Class A shares (as reported in the September 24, 2018 Prospectus) are 0.57% and 0.48% and 0.82% and 0.73%, respectively. The Fund’s investment adviser has contractually agreed to limit expenses through January 31, 2021.

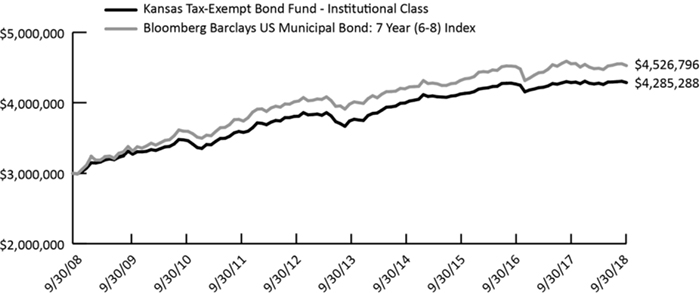

Performance of $3,000,000 Initial Investment (as of September 30, 2018)

The graph shown above represents historical performance of a hypothetical investment of $3,000,000 in the Institutional Class. Due to differing expenses, performance of Class A will vary. Past performance does not guarantee future results. Returns do not reflect the deduction of fees, sales charges, or taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Annual Report | September 30, 2018 | 9 |

American Independence Kansas | Portfolio Update |

September 30, 2018 (Unaudited)

Portfolio Diversification (% of Net Assets as of September 30, 2018)

10 | www.americanindependence.com |

American Independence Funds | Disclosure of Fund Expenses |

September 30, 2018 (Unaudited)

Examples. As a shareholder of the American Independence Global Tactical Allocation Fund or American Independence Kansas Tax-Exempt Bond Fund, you incur two types of costs: (1) transaction costs, including applicable redemption fees; and (2) ongoing costs, including management fees, distribution and service (12b-1) fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on April 1, 2018 and held through September 30, 2018.

Actual Expenses. The first line under each class in the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period April 1, 2018 – September 30, 2018” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line under each class in the table below provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not each Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in each Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing Fund costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the second line under each class in the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Beginning Account Value April 1, 2018 | Ending Account Value September 30, 2018 | Expense Ratio(a) | Expenses Paid During Period April 1, 2018 - September 30, 2018(b) | |

| American Independence Global Tactical Allocation Fund | ||||

| Institutional Class | ||||

| Actual | $ 1,000.00 | $999.20 | 1.11% | $5.56 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $1,019.50 | 1.11% | $5.62 |

| Class A | ||||

| Actual | $ 1,000.00 | $996.60 | 1.49% | $7.46 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $1,017.60 | 1.49% | $7.54 |

| American Independence Kansas Tax-Exempt Bond Fund | ||||

| Institutional Class | ||||

| Actual | $ 1,000.00 | $1,002.20 | 0.64% | $3.21 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $1,021.86 | 0.64% | $3.24 |

| Class A | ||||

| Actual | $ 1,000.00 | $1,000.20 | 1.03% | $5.16 |

| Hypothetical (5% return before expenses) | $ 1,000.00 | $1,019.90 | 1.03% | $5.22 |

| (a) | Each Fund's expense ratios have been annualized based on the Fund's actual expenses for the 6 month period ending September 30, 2018. |

| (b) | Expenses are equal to the annualized expense ratio shown above for the applicable class, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (183), divided by 365. |

Annual Report | September 30, 2018 | 11 |

| American Independence Global Tactical Allocation Fund | Portfolio of Investments |

September 30, 2018

| Security Description | Shares | Value (Note 2) | ||||||

| EXCHANGE TRADED PRODUCTS (86.13%) | ||||||||

| International Equity Exchange Traded Products (22.09%) | ||||||||

| Global X Scientific Beta Asia ex-Japan ETF | 8,800 | $ | 219,983 | |||||

| Global X Scientific Beta Europe ETF | 43,594 | 1,181,031 | ||||||

| Global X Scientific Beta Japan ETF | 34,600 | 1,067,465 | ||||||

| iShares® Europe ETF | 104,600 | 4,714,322 | ||||||

| iShares® MSCI Emerging Markets ETF | 11,500 | 493,580 | ||||||

| iShares® MSCI Japan ETF | 30,900 | 1,861,107 | ||||||

| iShares® MSCI Pacific ex Japan ETF | 1,000 | 45,420 | ||||||

| 9,582,908 | ||||||||

| U.S. Equity Exchange Traded Products (46.07%) | ||||||||

| Global X Scientific Beta US ETF(a) | 444,245 | 14,710,329 | ||||||

| SPDR® Doubleline Total Return Tactical ETF | 59,300 | 2,801,925 | ||||||

| SPDR® S&P 500® ETF Trust | 8,500 | 2,471,120 | ||||||

| 19,983,374 | ||||||||

| U.S. Fixed-Income Exchange Traded Products (17.97%) | ||||||||

| iShares® Core U.S. Aggregate Bond ETF | 73,900 | 7,797,928 | ||||||

| Total Exchange Traded Products (Cost $37,033,487) | 37,364,210 | |||||||

| 7 - Day Yield | Shares | Value | ||||||||||

| SHORT TERM INVESTMENT (14.71%) | ||||||||||||

| Money Market Fund (14.71%) | ||||||||||||

| Federated Government Obligations Fund, Premier Shares | 1.939 | % | 6,380,332 | 6,380,332 | ||||||||

| TOTAL SHORT TERM INVESTMENT (Cost $6,380,332) | 6,380,332 | |||||||||||

| TOTAL INVESTMENTS (100.84%) (Cost $43,413,819) | $ | 43,744,542 | ||||||||||

| Total Liabilities in Excess of Other Assets (-0.84%) | (365,297 | ) | ||||||||||

| NET ASSETS (100.00%) | $ | 43,379,245 | ||||||||||

| (a) | Represents an investment greater than 25% of the Fund's net assets. Performance of the Fund may be adversely impacted by concentrated investments in securities. The financial statements and portfolio holdings for these securities can be found at www.sec.gov. |

Summary of Abbreviations

ETF - Exchange Traded Funds

See Notes to Financial Statements.

| 12 | www.americanindependence.com |

| American Independence Kansas Tax-Exempt Bond Fund | Portfolio of Investments |

September 30, 2018

| Security Description | Principal | Value (Note 2) | ||||||

| MUNICIPAL BONDS (98.78%) | ||||||||

| Education (30.35%) | ||||||||

| Barton Community College, Certificate Participation, | ||||||||

| 4.00%, 12/01/32 | $ | 555,000 | $ | 584,298 | ||||

| 4.00%, 12/01/34 | 250,000 | 259,780 | ||||||

| Bourbon County Unified School District No. 234-Fort Scott, General Obligation Unlimited, | ||||||||

| 5.00%, 09/01/25 | 355,000 | 398,108 | ||||||

| Butler County Unified School District No. 385 Andover, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/30 | 690,000 | 737,472 | ||||||

| 4.00%, 09/01/31 | 500,000 | 530,795 | ||||||

| 5.00%, 09/01/34 | 2,000,000 | 2,282,220 | ||||||

| Butler County Unified School District No. 490 El Dorado, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/36 | 500,000 | 515,395 | ||||||

| Dodge City Community College, Higher Education, Revenue Bonds, 5.13%, 04/01/30 | 250,000 | 261,315 | ||||||

| Douglas County Unified School District No. 497 Lawrence, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/31 | 1,500,000 | 1,609,245 | ||||||

| 4.00%, 09/01/33 | 500,000 | 517,835 | ||||||

| Finney County Unified School District No. 457 Garden City, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/31 | 500,000 | 519,945 | ||||||

| Ford County Unified School District No. 443 Dodge City, General Obligation Unlimited, | ||||||||

| 4.00%, 03/01/34 | 1,000,000 | 1,034,670 | ||||||

| Franklin County Unified School District No. 290 Ottawa, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/40 | 250,000 | 253,770 | ||||||

| 5.00%, 09/01/31 | 1,715,000 | 1,926,545 | ||||||

| 5.00%, 09/01/32 | 150,000 | 168,204 | ||||||

| 5.00%, 09/01/33 | 1,000,000 | 1,119,380 | ||||||

| Geary County Unified School District No. 475, General Obligation Unlimited, 4.00%, | ||||||||

| 09/01/38 | 2,000,000 | 2,049,760 | ||||||

| Hutchinson Community College & Area Vocational School, Certificate Participation, 4.00%, | ||||||||

| 10/01/37 | 1,700,000 | 1,720,128 | ||||||

| Johnson & Miami Counties Unified School District No. 230 Spring Hills, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/33 | 1,000,000 | 1,044,130 | ||||||

| 4.00%, 09/01/35 | 1,000,000 | 1,030,790 | ||||||

| 5.25%, 09/01/29 | 1,500,000 | 1,620,465 | ||||||

| Johnson County Unified School District No. 231 Gardner - Edgerton, General Obligation Unlimited, | ||||||||

| 2.00%, 10/01/18 | 185,000 | 185,000 | ||||||

| 4.00%, 10/01/18 | 200,000 | 200,000 | ||||||

| Johnson County Unified School District No. 233 Olathe, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/31 | 1,000,000 | 1,060,550 | ||||||

| 4.00%, 09/01/33 | 175,000 | 182,677 | ||||||

| 4.00%, 09/01/33 | 730,000 | 759,967 | ||||||

| 4.00%, 09/01/35 | 790,000 | 818,472 | ||||||

| 4.00%, 09/01/36 | 480,000 | 495,806 | ||||||

| Johnson County Unified School District No. 512 Shawnee Mission, General Obligation | ||||||||

| Unlimited, 5.00%, 10/01/32 | 1,000,000 | 1,152,640 | ||||||

| Kansas Development Finance Authority, Revenue Bonds, | ||||||||

| 4.00%, 05/01/34 | 1,000,000 | 1,034,380 | ||||||

| 5.00%, 05/15/35 | 330,000 | 336,161 | ||||||

| 5.38%, 03/01/30 | 1,000,000 | 1,043,800 | ||||||

See Notes to Financial Statements.

| Annual Report | September 30, 2018 | 13 |

| American Independence Kansas Tax-Exempt Bond Fund | Portfolio of Investments |

September 30, 2018

| Security Description | Principal | Value (Note 2) | ||||||

| Leavenworth County Unified School District No. 453, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/36 | $ | 1,000,000 | $ | 1,034,280 | ||||

| 4.75%, 03/01/25 | 535,000 | 548,690 | ||||||

| 5.25%, 09/01/23 | 60,000 | 61,751 | ||||||

| Leavenworth County Unified School District No. 458, General Obligation Unlimited, | ||||||||

| 5.00%, 09/01/29 | 395,000 | 405,815 | ||||||

| 5.00%, 09/01/30 | 215,000 | 220,887 | ||||||

| Rice County Unified School District No. 376 Sterling, General Obligation Unlimited, | ||||||||

| 5.25%, 09/01/35 | 165,000 | 169,693 | ||||||

| 5.25%, 09/01/35 | 335,000 | 344,527 | ||||||

| Riley County Unified School District No. 383 Manhattan-Ogden, General Obligation | ||||||||

| Unlimited, 5.00%, 09/01/23 | 1,000,000 | 1,026,190 | ||||||

| Scott County Unified School District No. 466 Scott City, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/37 | 1,000,000 | 1,004,780 | ||||||

| Sedgwick County Unified School District No. 259 Wichita, General Obligation Unlimited, | ||||||||

| 3.00%, 10/01/21 | 500,000 | 511,540 | ||||||

| 5.00%, 10/01/21 | 30,000 | 30,000 | ||||||

| 5.00%, 10/01/21 | 55,000 | 55,000 | ||||||

| Sedgwick County Unified School District No. 260 Derby, General Obligation Unlimited, | ||||||||

| 5.00%, 10/01/29 | 340,000 | 377,063 | ||||||

| Sedgwick County Unified School District No. 261 Haysville, General Obligation Unlimited, | ||||||||

| 5.00%, 11/01/19 | 20,000 | 20,050 | ||||||

| 5.00%, 11/01/23 | 5,000 | 5,012 | ||||||

| Sedgwick County Unified School District No. 262 Valley Center, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/30 | 500,000 | 520,840 | ||||||

| 5.00%, 09/01/33 | 750,000 | 831,143 | ||||||

| Sedgwick County Unified School District No. 264 Clearwater, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/29 | 530,000 | 558,286 | ||||||

| Sedgwick County Unified School District No. 265 Goddard, General Obligation Unlimited, | ||||||||

| 4.50%, 10/01/24 | 250,000 | 250,000 | ||||||

| 5.00%, 10/01/24 | 370,000 | 421,219 | ||||||

| Sedgwick County Unified School District No. 266 Maize, General Obligation Unlimited, | ||||||||

| 5.00%, 09/01/21 | 500,000 | 539,150 | ||||||

| Seward County Unified School District No. 480 Liberal, General Obligation Unlimited, | ||||||||

| 5.00%, 09/01/29 | 1,500,000 | 1,684,035 | ||||||

| Shawne County Unified School District No. 437 Auburn - Washburn, General Obligation | ||||||||

| Unlimited, 3.95%, 09/01/28 | 825,000 | 854,576 | ||||||

| Sumner County Unified School District No. 353 Wellington, General Obligation Unlimited, | ||||||||

| 5.00%, 09/01/26 | 230,000 | 254,297 | ||||||

| University of Kansas Hospital Authority, Revenue Bonds, | ||||||||

| 5.00%, 09/01/28 | 250,000 | 283,173 | ||||||

| 5.00%, 09/01/30 | 350,000 | 393,638 | ||||||

| 5.00%, 09/01/31 | 500,000 | 560,680 | ||||||

| Washburn University/Topeka, Revenue Bonds, | ||||||||

| 4.00%, 07/01/41 | 330,000 | 334,274 | ||||||

| 5.00%, 07/01/35 | 500,000 | 556,450 | ||||||

| Wyandotte County Unified School District No. 500 Kansas City, General Obligation | ||||||||

| Unlimited, 5.00%, 09/01/30 | 500,000 | 571,105 | ||||||

| 41,881,847 | ||||||||

See Notes to Financial Statements.

| 14 | www.americanindependence.com |

| American Independence Kansas Tax-Exempt Bond Fund | Portfolio of Investments |

September 30, 2018

| Security Description | Principal | Value (Note 2) | ||||||

| General Obligation (29.98%) | ||||||||

| Ashland Public Building Commission, Revenue Bonds, | ||||||||

| 4.00%, 09/01/19 | $ | 100,000 | $ | 100,974 | ||||

| 4.00%, 09/01/20 | 110,000 | 112,028 | ||||||

| 5.00%, 09/01/35 | 720,000 | 748,872 | ||||||

| City of Abilene, General Obligation Unlimited, | ||||||||

| 4.30%, 09/01/27 | 150,000 | 156,358 | ||||||

| 4.60%, 09/01/30 | 500,000 | 523,995 | ||||||

| City of Abilene, Revenue Bonds, | ||||||||

| 4.00%, 12/01/29 | 325,000 | 344,172 | ||||||

| 4.00%, 12/01/31 | 445,000 | 466,569 | ||||||

| City of Dodge City, Revenue Bonds, 4.00%, 06/01/24 | 230,000 | 246,475 | ||||||

| City of Haysville, Certificate Participation, 4.13%, 11/01/32 | 460,000 | 465,203 | ||||||

| City of Junction City, General Obligation Unlimited, 4.50%, 09/01/31 | 1,000,000 | 1,027,300 | ||||||

| City of Lawrence, General Obligation Unlimited, | ||||||||

| 4.00%, 09/01/30 | 470,000 | 505,969 | ||||||

| 4.00%, 09/01/31 | 445,000 | 476,782 | ||||||

| City of Leawood, General Obligation Unlimited, 5.00%, 09/01/25 | 665,000 | 775,915 | ||||||

| City of Manhattan, General Obligation Unlimited, 5.00%, 11/01/25 | 570,000 | 660,733 | ||||||

| City of Merriam, General Obligation Unlimited, 5.00%, 10/01/27 | 1,670,000 | 1,995,617 | ||||||

| City of Newton, General Obligation Unlimited, 4.00%, 09/01/23 | 250,000 | 267,235 | ||||||

| City of Olathe, General Obligation Unlimited, | ||||||||

| 4.00%, 10/01/28 | 1,315,000 | 1,434,258 | ||||||

| 5.00%, 10/01/24 | 535,000 | 603,362 | ||||||

| City of Park City, General Obligation Unlimited, | ||||||||

| 5.38%, 12/01/25 | 495,000 | 514,053 | ||||||

| 5.38%, 12/01/25 | 5,000 | 5,101 | ||||||

| City of Phillipsburg, Revenue Bonds, 4.50%, 10/01/28 | 545,000 | 564,380 | ||||||

| City of Shawnee, General Obligation Unlimited, 4.00%, 12/01/27 | 425,000 | 456,917 | ||||||

| City of Topeka, General Obligation Unlimited, 4.50%, 08/15/30 | 450,000 | 457,875 | ||||||

| City of Wichita, General Obligation Unlimited, | ||||||||

| 4.00%, 06/01/26 | 475,000 | 493,938 | ||||||

| 4.00%, 06/01/27 | 780,000 | 811,099 | ||||||

| 4.00%, 12/01/29 | 250,000 | 261,025 | ||||||

| 4.00%, 06/01/30 | 820,000 | 889,298 | ||||||

| 5.00%, 12/01/25 | 500,000 | 579,730 | ||||||

| County of Clay, General Obligation Unlimited, 4.00%, 10/01/36 | 750,000 | 775,875 | ||||||

| County of Johnson, General Obligation Unlimited, | ||||||||

| 3.00%, 09/01/30 | 400,000 | 391,344 | ||||||

| 4.00%, 09/01/28 | 1,125,000 | 1,222,571 | ||||||

| County of Scott, General Obligation Unlimited, 5.00%, 04/01/28 | 500,000 | 522,090 | ||||||

| County of Sedgwick / County of Shawnee, Revenue Bonds, 6.70%, 06/01/29 | 5,000 | 5,038 | ||||||

| Crawford County Public Building Commission, Revenue Bonds, 5.38%, 09/01/24 | 1,300,000 | 1,339,390 | ||||||

| Johnson County Public Building Commission, Revenue Bonds, | ||||||||

| 4.00%, 09/01/24 | 500,000 | 517,340 | ||||||

| 4.00%, 09/01/29 | 650,000 | 703,092 | ||||||

| 4.00%, 09/01/31 | 1,500,000 | 1,611,510 | ||||||

| 4.50%, 09/01/27 | 955,000 | 1,008,891 | ||||||

See Notes to Financial Statements.

| Annual Report | September 30, 2018 | 15 |

| American Independence Kansas Tax-Exempt Bond Fund | Portfolio of Investments |

September 30, 2018

| Security Description | Principal | Value (Note 2) | ||||||

| Kansas Development Finance Authority, Revenue Bonds, | ||||||||

| 4.00%, 10/01/20 | $ | 250,000 | $ | 258,547 | ||||

| 4.00%, 03/01/27 | 775,000 | 781,177 | ||||||

| 4.75%, 09/01/34 | 360,000 | 367,924 | ||||||

| 5.00%, 11/01/18 | 200,000 | 200,502 | ||||||

| 5.00%, 04/01/25 | 800,000 | 884,576 | ||||||

| 5.00%, 04/01/26 | 1,485,000 | 1,641,326 | ||||||

| 5.00%, 11/01/29 | 2,060,000 | 2,121,450 | ||||||

| 5.00%, 04/01/31 | 1,000,000 | 1,098,120 | ||||||

| 5.00%, 04/01/34 | 2,000,000 | 2,177,660 | ||||||

| 5.13%, 11/01/25 | 100,000 | 100,269 | ||||||

| 5.25%, 11/15/21 | 25,000 | 25,849 | ||||||

| 5.25%, 11/15/21 | 1,275,000 | 1,317,878 | ||||||

| 5.25%, 11/01/28 | 305,000 | 305,851 | ||||||

| 5.50%, 11/15/22 | 20,000 | 20,734 | ||||||

| 5.50%, 11/15/22 | 980,000 | 1,017,985 | ||||||

| Overland Park Transportation Development District, Revenue Bonds, 5.90%, 04/01/32 | 1,025,000 | 1,052,429 | ||||||

| Unified Government of Greeley County, General Obligation Unlimited, | ||||||||

| 4.00%, 12/01/29 | 250,000 | 260,102 | ||||||

| 4.00%, 12/01/32 | 100,000 | 102,439 | ||||||

| Wyandotte County-Kansas City Unified Government, General Obligation Unlimited, | ||||||||

| 4.00%, 08/01/30 | 500,000 | 516,505 | ||||||

| 4.00%, 08/01/31 | 930,000 | 972,650 | ||||||

| 5.00%, 08/01/29 | 1,000,000 | 1,051,230 | ||||||

| Wyandotte County-Kansas City Unified Government, Revenue Bonds, | ||||||||

| 4.88%, 10/01/28 | 415,000 | 411,278 | ||||||

| 5.00%, 12/01/23 | 570,000 | 638,320 | ||||||

| 41,367,175 | ||||||||

| Health Care (11.12%) | ||||||||

| Allen County Public Building Commission, Revenue Bonds, | ||||||||

| 5.05%, 12/01/31 | 1,310,000 | 1,458,292 | ||||||

| 5.15%, 12/01/36 | 500,000 | 558,580 | ||||||

| City of Manhattan, Revenue Bonds, 5.00%, 11/15/29 | 680,000 | 734,502 | ||||||

| City of Olathe, Revenue Bonds, | ||||||||

| 4.00%, 09/01/30 | 450,000 | 461,695 | ||||||

| 5.25%, 09/01/25 | 580,000 | 596,652 | ||||||

| City of Wichita, Revenue Bonds, | ||||||||

| 4.75%, 11/15/24 | 810,000 | 834,430 | ||||||

| 5.00%, 11/15/29 | 3,070,000 | 3,332,546 | ||||||

| County of Franklin, Certificate Participation, 4.75%, 09/01/21 | 525,000 | 525,494 | ||||||

| Kansas Development Finance Authority, Revenue Bonds, | ||||||||

| 4.00%, 04/01/24 | 230,000 | 235,688 | ||||||

| 4.50%, 04/01/22 | 225,000 | 232,918 | ||||||

| 5.00%, 02/01/22 | 555,000 | 575,624 | ||||||

| 5.00%, 11/15/27 | 1,000,000 | 1,030,210 | ||||||

| 5.00%, 04/01/29 | 650,000 | 677,839 | ||||||

| 5.00%, 11/15/32 | 1,500,000 | 1,618,695 | ||||||

| 5.00%, 11/15/34 | 350,000 | 376,568 | ||||||

| 5.25%, 01/01/25 | 200,000 | 207,532 | ||||||

| 5.25%, 11/15/30 | 250,000 | 258,323 | ||||||

| Lyon County Public Building Commission, Revenue Bonds, 5.00%, 12/01/35 | 1,335,000 | 1,475,068 | ||||||

| Pawnee County Public Building Commission, Revenue Bonds, 4.00%, 02/15/31 | 145,000 | 146,544 | ||||||

| 15,337,200 | ||||||||

See Notes to Financial Statements.

| 16 | www.americanindependence.com |

| American Independence Kansas Tax-Exempt Bond Fund | Portfolio of Investments |

September 30, 2018

| Security Description | Principal | Value (Note 2) | ||||||

| Housing (2.49%) | ||||||||

| La Cygne Public Building Commission, Revenue Bonds, 5.00%, 11/01/29 | $ | 375,000 | $ | 385,616 | ||||

| Pratt County Public Building Commission, Revenue Bonds, 3.25%, 12/01/32 | 655,000 | 649,099 | ||||||

| Topeka Public Building Commission, Revenue Bonds, 5.00%, 06/01/27 | 2,355,000 | 2,407,328 | ||||||

| 3,442,043 | ||||||||

| Transportation (7.01%) | ||||||||

| Kansas Turnpike Authority, Revenue Bonds, 4.00%, 09/01/26 | 1,000,000 | 1,023,880 | ||||||

| State of Kansas Department of Transportation, Revenue Bonds, | ||||||||

| 5.00%, 09/01/23 | 200,000 | 225,944 | ||||||

| 5.00%, 09/01/24 | 500,000 | 574,240 | ||||||

| 5.00%, 09/01/28 | 1,500,000 | 1,780,815 | ||||||

| 5.00%, 09/01/29 | 1,000,000 | 1,147,550 | ||||||

| 5.00%, 09/01/31 | 1,000,000 | 1,172,460 | ||||||

| 5.00%, 09/01/34 | 1,260,000 | 1,428,034 | ||||||

| 5.00%, 09/01/34 | 2,000,000 | 2,320,960 | ||||||

| 9,673,883 | ||||||||

| Utilities (17.83%) | ||||||||

| City of Lawrence Water & Sewage System, Revenue Bonds, | ||||||||

| 4.00%, 11/01/38 | 1,000,000 | 1,023,520 | ||||||

| 4.30%, 11/01/22 | 235,000 | 235,477 | ||||||

| City of Olathe Water & Sewer System, Revenue Bonds, 4.00%, 07/01/24 | 250,000 | 269,602 | ||||||

| City of Topeka Combined Utility, Revenue Bonds, | ||||||||

| 3.38%, 08/01/32 | 1,335,000 | 1,329,834 | ||||||

| 3.50%, 08/01/33 | 2,285,000 | 2,286,531 | ||||||

| 4.00%, 08/01/26 | 2,600,000 | 2,716,740 | ||||||

| 4.50%, 08/01/33 | 650,000 | 659,847 | ||||||

| City of Wichita Water & Sewer Utility, Revenue Bonds, | ||||||||

| 3.25%, 10/01/31 | 1,070,000 | 1,065,506 | ||||||

| 4.00%, 10/01/20 | 500,000 | 519,085 | ||||||

| 4.00%, 10/01/29 | 1,000,000 | 1,039,170 | ||||||

| 4.00%, 10/01/30 | 1,000,000 | 1,039,170 | ||||||

| 5.00%, 10/01/25 | 1,000,000 | 1,079,270 | ||||||

| 5.00%, 10/01/28 | 2,650,000 | 2,855,296 | ||||||

| Kansas Power Pool, Revenue Bonds, | ||||||||

| 5.00%, 12/01/19 | 600,000 | 621,222 | ||||||

| 5.00%, 12/01/23 | 200,000 | 218,324 | ||||||

| 5.00%, 12/01/28 | 700,000 | 784,350 | ||||||

| 5.00%, 12/01/31 | 1,000,000 | 1,061,230 | ||||||

| Kansas Rural Water Finance Authority, Revenue Bonds, 4.10%, 09/01/34 | 270,000 | 271,350 | ||||||

| Wyandotte County-Kansas City Unified Government Utility System, Revenue Bonds, | ||||||||

| 4.25%, 09/01/23 | 500,000 | 512,355 | ||||||

| 5.00%, 09/01/24 | 800,000 | 810,456 | ||||||

| 5.00%, 09/01/27 | 1,300,000 | 1,393,795 | ||||||

| 5.00%, 09/01/31 | 850,000 | 949,229 | ||||||

| 5.00%, 09/01/31 | 500,000 | 561,725 | ||||||

| 5.00%, 09/01/32 | 1,090,000 | 1,185,462 | ||||||

| 5.00%, 09/01/33 | 100,000 | 111,279 | ||||||

| 24,599,825 | ||||||||

| TOTAL MUNICIPAL BONDS (Cost $135,491,962) | 136,301,973 | |||||||

See Notes to Financial Statements.

| Annual Report | September 30, 2018 | 17 |

| American Independence Kansas Tax-Exempt Bond Fund | Portfolio of Investments |

September 30, 2018

7 - Day Yield | Shares | Value | ||||||||||

| SHORT TERM INVESTMENT (0.42%) | ||||||||||||

| Money Market Fund (0.42%) | ||||||||||||

| Federated Treasury Obligations Fund, Institutional Shares | 1.936 | % | 579,959 | $ | 579,959 | |||||||

| TOTAL SHORT TERM INVESTMENT (Cost $579,959) | 579,959 | |||

| TOTAL INVESTMENTS (99.20%) (Cost $136,071,921) | $ | 136,881,932 | ||

| Other Assets in Excess of Liabilities (0.80%) | 1,101,598 | |||

| NET ASSETS (100.00%) | $ | 137,983,530 |

See Notes to Financial Statements.

| 18 | swww.americanindependence.com |

| American Independence Funds | Statements of Assets and Liabilities |

| September 30, 2018 |

| AMERICAN INDEPENDENCE GLOBAL TACTICAL ALLOCATION FUND | AMERICAN INDEPENDENCE KANSAS TAX- EXEMPT BOND FUND | |||||||

| ASSETS: | ||||||||

| Investments, at value (Cost $43,413,819 and $136,071,921) | $ | 43,744,542 | $ | 136,881,932 | ||||

| Cash | 10,003 | 4,297 | ||||||

| Receivable for shares sold | 6,980 | 54,824 | ||||||

| Receivable due from adviser | 6,243 | – | ||||||

| Dividends and interest receivable | 11,591 | 1,553,618 | ||||||

| Other Assets | 1,309 | 1,137 | ||||||

| Total Assets | 43,780,668 | 138,495,808 | ||||||

| LIABILITIES: | ||||||||

| Distributions payable | – | 321,898 | ||||||

| Administration and transfer agency fees payable | 30,504 | 21,521 | ||||||

| Payable for shares redeemed | 276,608 | 7,398 | ||||||

| Payable to adviser | – | 16,847 | ||||||

| Payable for distribution and service fees | 14,022 | 6,188 | ||||||

| Payable for printing | 2,681 | 3,979 | ||||||

| Payable for professional fees | 36,454 | 47,990 | ||||||

| Payable to trustees | 54 | 168 | ||||||

| Payable to Chief Compliance Officer | 1,975 | 2,938 | ||||||

| Accrued expenses and other liabilities | 39,125 | 83,351 | ||||||

| Total Liabilities | 401,423 | 512,278 | ||||||

| NET ASSETS | $ | 43,379,245 | $ | 137,983,530 | ||||

| NET ASSETS CONSIST OF: | ||||||||

| Paid-in capital (Note 5) | $ | 37,753,000 | $ | 136,710,892 | ||||

| Total distributable earnings (Note 3) | 5,626,245 | 1,272,638 | ||||||

| NET ASSETS | $ | 43,379,245 | $ | 137,983,530 | ||||

| PRICING OF SHARES | ||||||||

| Institutional Class: | ||||||||

| Net Asset Value, offering and redemption price per share | $ | 11.83 | $ | 10.59 | ||||

| Net Assets | $ | 31,417,371 | $ | 133,235,166 | ||||

| Shares of beneficial interest outstanding | 2,655,093 | 12,584,917 | ||||||

| Class A: | ||||||||

| Net Asset Value, offering and redemption price per share | $ | 11.75 | $ | 10.59 | ||||

| Net Assets | $ | 11,961,874 | $ | 4,748,364 | ||||

| Shares of beneficial interest outstanding | 1,017,731 | 448,473 | ||||||

| Maximum offering price per share(a) | $ | 12.47 | $ | 11.06 | ||||

| (a) | Net Asset Value/100% minus maximum sales charge of net asset value, 5.75% and 4.25% respectively for the Funds, adjusted to the nearest cent. |

| See Notes to Financial Statements. |

| Annual Report | September 30, 2018 | 19 |

| American Independence Global Tactical Allocation Fund | Statements of Operations |

| For the Period Ended September 30, 2018(a) | For the Year Ended October 31, 2017 | |||||||

| INVESTMENT INCOME: | ||||||||

| Dividends | $ | 2,186,914 | $ | 3,269,954 | ||||

| Interest | 120,298 | 15,501 | ||||||

| Total Investment Income | 2,307,212 | 3,285,455 | ||||||

| EXPENSES: | ||||||||

| Investment advisory fees (Note 6) | 676,287 | 849,169 | ||||||

| Accounting fees | – | 38,239 | ||||||

| Administration fees | 150,025 | 141,528 | ||||||

| Shareholder service fees | ||||||||

| Class A | 85,340 | 134,254 | ||||||

| Class C | 7,228 | 11,192 | ||||||

| Distribution fees | ||||||||

| Class A | 85,917 | 134,254 | ||||||

| Class C | 21,685 | 33,575 | ||||||

| Custodian fees | 18,083 | 22,621 | ||||||

| Legal fees | 49,349 | 6,928 | ||||||

| Audit and tax fees | 25,980 | 31,679 | ||||||

| Transfer agent fees | 185,377 | 188,528 | ||||||

| Trustees fees and expenses | 17,575 | 16,053 | ||||||

| Registration and filing fees | 50,540 | 46,649 | ||||||

| Printing fees | 20,093 | 18,026 | ||||||

| Chief Compliance Officer fees | 26,374 | 17,371 | ||||||

| Insurance expense | 38,716 | 10,577 | ||||||

| Other expenses | 12,604 | 5,660 | ||||||

| Total Expenses | 1,471,173 | 1,706,303 | ||||||

| Expenses reduced by: Adviser (Note 6) | (370,184 | ) | (317,597 | ) | ||||

| Distribution/service fees (Class A) (Note 6) | (40,963 | ) | (64,442 | ) | ||||

| Net Expenses | 1,060,026 | 1,324,264 | ||||||

| NET INVESTMENT INCOME | 1,247,186 | 1,961,191 | ||||||

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | ||||||||

| Net realized gain/(loss) on: | ||||||||

| Investments | 10,687,068 | 3,920,283 | ||||||

| Long-term capital gain distributions from other investment companies | 6,094 | – | ||||||

| Net realized gain | 10,693,162 | 3,920,283 | ||||||

| Change in unrealized appreciation/(depreciation) on: | ||||||||

| Investments | (10,162,136 | ) | 9,660,783 | |||||

| Net change | (10,162,136 | ) | 9,660,783 | |||||

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS | 531,026 | 13,581,066 | ||||||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 1,778,212 | $ | 15,542,257 | ||||

| (a) | Effective September 24, 2018, the American Independence Global Tactical Allocation Fund merged with and into a clone series of ALPS Series Trust. The Funds were previously advised by Manifold Fund Advisors, LLC. In connection with the merger, the fiscal year-end changed from October 31 to September 30. |

| See Notes to Financial Statements. |

| 20 | www.americanindependence.com |

| American Independence Kansas Tax-Exempt Bond Fund | Statements of Operations |

| For the Period Ended September 30, 2018(a) | For the Year Ended October 31, 2017 | |||||||

| INVESTMENT INCOME: | ||||||||

| Dividends | $ | 3,444 | $ | – | ||||

| Interest | 4,800,452 | 6,308,485 | ||||||

| Total Investment Income | 4,803,896 | 6,308,485 | ||||||

| EXPENSES: | ||||||||

| Investment advisory fees (Note 6) | 429,057 | 552,112 | ||||||

| Accounting fees | – | 86,478 | ||||||

| Administration fees | 251,944 | 230,047 | ||||||

| Shareholder service fees | ||||||||

| Class A | 18,403 | 28,725 | ||||||

| Class C | 1,179 | 2,418 | ||||||

| Distribution fees | ||||||||

| Class A | 18,630 | 28,725 | ||||||

| Class C | 3,536 | 7,256 | ||||||

| Custodian fees | 28,623 | 36,824 | ||||||

| Legal fees | 86,175 | 13,882 | ||||||

| Audit and tax fees | 26,422 | 35,355 | ||||||

| Transfer agent fees | 50,888 | 51,405 | ||||||

| Trustees fees and expenses | 23,110 | 26,794 | ||||||

| Registration and filing fees | 28,142 | 16,230 | ||||||

| Printing fees | 16,670 | 15,964 | ||||||

| Chief Compliance Officer fees | 33,951 | 23,954 | ||||||

| Insurance expense | 91,159 | 21,243 | ||||||

| Other expenses | 7,551 | 9,762 | ||||||

| Total Expenses | 1,115,440 | 1,187,174 | ||||||

| Expenses reduced by: Adviser (Note 6) | (271,478 | ) | (236,681 | ) | ||||

| Distribution/service fees (Class A) (Note 6) | (8,097 | ) | (12,639 | ) | ||||

| Net Expenses | 835,865 | 937,854 | ||||||

| NET INVESTMENT INCOME | 3,968,031 | 5,370,631 | ||||||

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | ||||||||

| Net realized gain/(loss) on: | ||||||||

| Investments | 1,077,483 | (244,507 | ) | |||||

| Net realized gain/(loss) | 1,077,483 | (244,507 | ) | |||||

| Change in unrealized appreciation/(depreciation) on: | ||||||||

| Investments | (5,413,242 | ) | (3,649,118 | ) | ||||

| Net change | (5,413,242 | ) | (3,649,118 | ) | ||||

| NET REALIZED AND UNREALIZED LOSS ON INVESTMENTS | (4,335,759 | ) | (3,893,625 | ) | ||||

| NET INCREASE/(DECREASE) IN NET ASSETS RESULTING FROM OPERATIONS | $ | (367,728 | ) | $ | 1,477,006 | |||

| (a) | Effective September 24, 2018, the American Independence Kansas Tax-Exempt Bond Fund merged with and into a clone series of ALPS Series Trust. The Funds were previously advised by Manifold Fund Advisors, LLC. In connection with the merger, the fiscal year-end changed from October 31 to September 30. |

| See Notes to Financial Statements. |

| Annual Report | September 30, 2018 | 21 |

| American Independence Global Tactical Allocation Fund | Statements of Changes in Net Assets |

| For the Period Ended September 30, 2018(a) | For the Year Ended October 31, 2017 | For the Year Ended October 31, 2016 | ||||||||||

| OPERATIONS: | ||||||||||||

| Net investment income | $ | 1,247,186 | $ | 1,961,191 | $ | 1,887,661 | ||||||

| Net realized gain/(loss) on investments | 10,693,162 | 3,920,283 | (869,006 | ) | ||||||||

| Net change in unrealized appreciation/(depreciation) on investments | (10,162,136 | ) | 9,660,783 | 1,212,214 | ||||||||

| Net increase in net assets resulting from operations | 1,778,212 | 15,542,257 | 2,230,869 | |||||||||

| TOTAL DISTRIBUTIONS TO SHAREHOLDERS:(b) | ||||||||||||

| Institutional Class | (2,800,890 | ) | (720,260 | ) | (484,129 | ) | ||||||

| Class A(c) | (2,261,503 | ) | (563,180 | ) | (680,507 | ) | ||||||

| Class C(c) | (145,462 | ) | (17,786 | ) | (69,943 | ) | ||||||

| Total distributions | (5,207,855 | ) | (1,301,226 | ) | (1,234,579 | ) | ||||||

| BENEFICIAL SHARE TRANSACTIONS (Note 5): | ||||||||||||

| Institutional Class | ||||||||||||

| Shares sold | 24,535,873 | 30,834,298 | 30,189,836 | |||||||||

| Dividends reinvested | 1,859,235 | 490,606 | 367,108 | |||||||||

| Shares redeemed | (65,522,791 | ) | (11,783,964 | ) | (5,318,822 | ) | ||||||

| Net increase/(decrease) from beneficial share transactions | (39,127,683 | ) | 19,540,940 | 25,238,122 | ||||||||

| Class A (c) | ||||||||||||

| Shares sold | 9,225,330 | 24,876,625 | 32,234,644 | |||||||||

| Dividends reinvested | 1,790,835 | 281,975 | 281,631 | |||||||||

| Shares redeemed | (59,181,296 | ) | (26,350,301 | ) | (14,830,497 | ) | ||||||

| Net increase/(decrease) from beneficial share transactions | (48,165,131 | ) | (1,191,701 | ) | 17,685,778 | |||||||

| Class C (c) | ||||||||||||

| Shares sold | 221,432 | 540,680 | 2,075,353 | |||||||||

| Dividends reinvested | 116,345 | 15,079 | 57,172 | |||||||||

| Shares redeemed | (4,373,476 | ) | (2,146,016 | ) | (2,168,925 | ) | ||||||

| Net decrease from beneficial share transactions | (4,035,699 | ) | (1,590,257 | ) | (36,400 | ) | ||||||

| Net increase/(decrease) in net assets | (94,758,156 | ) | 31,000,013 | 43,883,790 | ||||||||

| NET ASSETS: | ||||||||||||

| Beginning of year | 138,137,401 | 107,137,388 | 63,253,598 | |||||||||

| End of period(b) | $ | 43,379,245 | $ | 138,137,401 | $ | 107,137,388 | ||||||

| (a) | Effective September 24, 2018, the American Independence Global Tactical Allocation Fund merged with and into a clone series of ALPS Series Trust. The Funds were previously advised by Manifold Fund Advisors, LLC. In connection with the merger, the fiscal year-end changed from October 31 to September 30. |

| (b) | For the prior year ended October 31, 2017, American Independence Global Tactical Allocation Fund had Total Distributions consisting of Net Investment Income of $1,301,226, and Net Realized Gains of $0 and Net Assets included accumulated net investment income of $798,190. For the prior year ended October 31, 2016, The Fund had Total Distributions consisting of Net Investment Income of $1,234,579, and Net Realized Gains of $0 and Net Assets included accumulated net investment income of $406,016. |

| (c) | Class C shares were merged into Class A on September 24, 2018. The amounts presented represent the results of the Class A shares for the periods prior to the merger and the results of the combined share class for the period subsequent the merger. As a result of the merger, Shareholder equity in Class A increased by $2,040,463 and 172,662 shares |

| See Notes to Financial Statements. |

| 22 | www.americanindependence.com |

| American Independence Kansas Tax-Exempt Bond Fund | Statements of Changes in Net Assets |

| For the Period Ended September 30, 2018(a) | For the Year Ended October 31, 2017 | For the Year Ended October 31, 2016 | ||||||||||

| OPERATIONS: | ||||||||||||

| Net investment income | $ | 3,968,031 | $ | 5,370,631 | $ | 5,686,354 | ||||||

| Net realized gain/(loss) on investments | 1,077,483 | (244,507 | ) | 3,335 | ||||||||

| Net change in unrealized depreciation on investments | (5,413,242 | ) | (3,649,118 | ) | (477,351 | ) | ||||||

| Net increase/(decrease) in net assets resulting from operations | (367,728 | ) | 1,477,006 | 5,212,338 | ||||||||

| TOTAL DISTRIBUTIONS TO SHAREHOLDERS:(b) | ||||||||||||

| Institutional Class | (3,771,175 | ) | (5,057,517 | ) | (5,380,356 | ) | ||||||

| Class A(c) | (180,929 | ) | (294,193 | ) | (287,049 | ) | ||||||

| Class C(c) | (8,545 | ) | (18,921 | ) | (20,356 | ) | ||||||

| Total distributions | (3,960,649 | ) | (5,370,631 | ) | (5,687,761 | ) | ||||||

| BENEFICIAL SHARE TRANSACTIONS (Note 5): | ||||||||||||

| Institutional Class | ||||||||||||

| Shares sold | 28,106,930 | 28,351,865 | 32,270,430 | |||||||||

| Dividends reinvested | 384,039 | 453,721 | 326,415 | |||||||||

| Shares redeemed | (58,543,555 | ) | (48,557,589 | ) | (23,352,111 | ) | ||||||

| Net increase/(decrease) from beneficial share transactions | (30,052,586 | ) | (19,752,003 | ) | 9,244,734 | |||||||

| Class A (c) | ||||||||||||

| Shares sold | 651,534 | 381,419 | 1,874,639 | |||||||||

| Dividends reinvested | 113,411 | 164,729 | 168,088 | |||||||||

| Shares redeemed | (7,251,264 | ) | (374,573 | ) | (1,131,127 | ) | ||||||

| Net increase/(decrease) from beneficial share transactions | (6,486,319 | ) | 171,575 | 911,600 | ||||||||

| Class C (c) | ||||||||||||

| Shares sold | 27,246 | 1,536 | 231,744 | |||||||||

| Dividends reinvested | 4,246 | 8,118 | 12,414 | |||||||||

| Shares redeemed | (710,429 | ) | (459,797 | ) | (152,035 | ) | ||||||

| Net increase/(decrease) from beneficial share transactions | (678,937 | ) | (450,143 | ) | 92,123 | |||||||

| Net increase/(decrease) in net assets | (41,546,219 | ) | (23,924,196 | ) | 9,773,034 | |||||||

| NET ASSETS: | ||||||||||||

| Beginning of year | 179,529,749 | 203,453,945 | 193,680,911 | |||||||||

| End of period(b) | $ | 137,983,530 | $ | 179,529,749 | $ | 203,453,945 | ||||||

| (a) | Effective September 24, 2018, the American Independence Kansas Tax-Exempt Bond Fund merged with and into a clone series of ALPS Series Trust. The Funds were previously advised by Manifold Fund Advisors, LLC. In connection with the merger, the fiscal year-end changed from October 31 to September 30. |

| (b) | For the prior year ended October 31, 2017, American Independence Kansas Tax-Exempt Bond Fund had Total Distributions consisting of Net Investment Income of $5,370,631, and Net Realized Gains of $0 and Net Assets included accumulated net investment income of $72,211. For the prior year ended October 31, 2016, The Fund had Total Distributions consisting of Net Investment Income of $5,687,761, and Net Realized Gains of $0 and Net Assets included accumulated net investment income of $72,211. |

| (c) | Class C shares were merged into Class A on September 24, 2018. The amounts presented represent the results of the Class A shares for the periods prior to the merger and the results of the combined share class for the period subsequent the merger. As a result of the merger, Shareholder equity in Class A increased by $342,954 and 32,402 shares. |

| See Notes to Financial Statements. |

| Annual Report | September 30, 2018 | 23 |

| American Independence Global Tactical Allocation Fund | Financial Highlights |

| Institutional Class | For a Share Outstanding Throughout the Periods Presented |

| For the Period Ended September 30, 2018(a) | For the Year Ended October 31, 2017 | For the Year Ended October 31, 2016 | For the Year Ended October 31, 2015 | For the Year Ended October 31, 2014 | For the Period Ended October 31, 2013(b) | |||||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 12.09 | $ | 10.68 | $ | 10.52 | $ | 10.69 | $ | 10.18 | $ | 10.00 | ||||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||||||

| Net investment income(c) | 0.17 | 0.22 | 0.26 | 0.32 | 0.21 | 0.01 | (d) | |||||||||||||||||

| Net realized and unrealized gain/(loss) on investments | 0.01 | (e) | 1.34 | 0.09 | (0.10 | ) | 0.35 | 0.17 | ||||||||||||||||

| Total from investment operations | 0.18 | 1.56 | 0.35 | 0.22 | 0.56 | 0.18 | ||||||||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||||||||||

| From net investment income | (0.15 | ) | (0.15 | ) | (0.19 | ) | (0.39 | ) | (0.05 | ) | – | |||||||||||||

| From net realized gains on investments | (0.29 | ) | – | – | – | – | – | |||||||||||||||||

| Total Distributions | (0.44 | ) | (0.15 | ) | (0.19 | ) | (0.39 | ) | (0.05 | ) | – | |||||||||||||

| NET INCREASE/(DECREASE) IN NET ASSET VALUE | (0.26 | ) | 1.41 | 0.16 | (0.17 | ) | 0.51 | 0.18 | ||||||||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 11.83 | $ | 12.09 | $ | 10.68 | $ | 10.52 | $ | 10.69 | $ | 10.18 | ||||||||||||

| TOTAL RETURN(f) | 1.53 | % | 14.78 | % | 3.34 | % | 2.10 | % | 5.52 | % | 1.80 | % | ||||||||||||

| SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of period (in 000s) | $ | 31,417 | $ | 72,454 | $ | 45,813 | $ | 20,028 | $ | 6,329 | $ | 6,934 | ||||||||||||

| RATIOS TO AVERAGE NET ASSETS | ||||||||||||||||||||||||

| Operating expenses excluding reimbursement/waiver | 1.42 | %(g) | 1.23 | % | 1.27 | % | 1.33 | % | 1.73 | % | 10.18 | %(g) | ||||||||||||

| Operating expenses including reimbursement/waiver | 1.01 | %(g) | 0.95 | % | 0.95 | % | 0.94 | % | 0.90 | % | 0.90 | %(g) | ||||||||||||

| Net investment income including reimbursement/waiver | 1.52 | %(g) | 1.93 | % | 2.48 | % | 2.98 | % | 2.00 | % | 6.14 | %(g)(h) | ||||||||||||

| PORTFOLIO TURNOVER RATE(i) | 193 | % | 138 | % | 129 | % | 98 | % | 166 | % | 19 | % | ||||||||||||

| (a) | Effective September 24, 2018, the American Independence Global Tactical Allocation Fund merged with and into a clone series of ALPS Series Trust. The Funds were previously advised by Manifold Fund Advisors, LLC. In connection with the merger, the fiscal year-end changed from October 31 to September 30. |

| (b) | Commenced operations on September 20, 2013. |

| (c) | Per share amounts are based upon average shares outstanding, unless otherwise noted. |

| (d) | Calculated based on ending shares outstanding during the period. |

| (e) | Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions for the period. |

| (f) | Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are for the period indicated and have not been annualized. Total returns would have been lower had certain expenses not been waived during the period. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (g) | Annualized. |

| (h) | Due to the short life of the Fund and significant cash inflows into the Institutional Class at the end of the year in question; the ratio of net investment income is not indicative of future results. |

| (i) | Portfolio turnover rate for periods less than one full year have not been annualized. |

See Notes to Financial Statements.

| 24 | www.americanindependence.com |

| American Independence Global Tactical Allocation Fund | Financial Highlights |

| Class A | For a Share Outstanding Throughout the Periods Presented |

| For the Period Ended September 30, 2018(a)(b) | For the Year Ended October 31, 2017 | For the Year Ended October 31, 2016 | For the Year Ended October 31, 2015 | For the Year Ended October 31, 2014 | For the Period Ended October 31, 2013(c) | |||||||||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 12.04 | $ | 10.64 | $ | 10.50 | $ | 10.65 | $ | 10.18 | $ | 10.00 | ||||||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||||||||||

| Net investment income(d) | 0.14 | 0.18 | 0.23 | 0.29 | 0.24 | 0.00 | (e)(f) | |||||||||||||||||

| Net realized and unrealized gain/(loss) on investments | 0.00 | (g)(h) | 1.33 | 0.08 | (0.10 | ) | 0.27 | 0.18 | ||||||||||||||||

| Total from investment operations | 0.14 | 1.51 | 0.31 | 0.19 | 0.51 | 0.18 | ||||||||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||||||||||

| From net investment income | (0.14 | ) | (0.11 | ) | (0.17 | ) | (0.34 | ) | (0.04 | ) | – | |||||||||||||

| From net realized gains on investments | (0.29 | ) | – | – | – | – | – | |||||||||||||||||

| Total Distributions | (0.43 | ) | (0.11 | ) | (0.17 | ) | (0.34 | ) | (0.04 | ) | – | |||||||||||||

| NET INCREASE/(DECREASE) IN NET ASSET VALUE | (0.29 | ) | 1.40 | 0.14 | (0.15 | ) | 0.47 | 0.18 | ||||||||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 11.75 | $ | 12.04 | $ | 10.64 | $ | 10.50 | $ | 10.65 | $ | 10.18 | ||||||||||||

| TOTAL RETURN(i) | 1.19 | % | 14.34 | % | 2.99 | % | 1.75 | % | 5.07 | % | 1.80 | % | ||||||||||||

| SUPPLEMENTAL DATA: | ||||||||||||||||||||||||

| Net assets, end of period (in 000s) | $ | 11,962 | $ | 61,546 | $ | 56,135 | $ | 38,019 | $ | 21,684 | $ | 3,876 | ||||||||||||

| RATIOS TO AVERAGE NET ASSETS | ||||||||||||||||||||||||

| Operating expenses excluding reimbursement/waiver | 1.91 | %(j) | 1.73 | % | 1.77 | % | 1.75 | % | 2.23 | % | 10.77 | %(j) | ||||||||||||

| Operating expenses including reimbursement/waiver | 1.37 | %(j) | 1.33 | % | 1.33 | % | 1.28 | % | 1.28 | % | 1.28 | %(j) | ||||||||||||

| Net investment income including reimbursement/waiver | 1.25 | %(j) | 1.59 | % | 2.23 | % | 2.70 | % | 2.32 | % | 0.25 | %(j)(k) | ||||||||||||

| PORTFOLIO TURNOVER RATE(l) | 193 | % | 138 | % | 129 | % | 98 | % | 166 | % | 19 | % | ||||||||||||

| (a) | Effective September 24, 2018, the American Independence Global Tactical Allocation Fund merged with and into a clone series of ALPS Series Trust. The Funds were previously advised by Manifold Fund Advisors, LLC. In connection with the merger, the fiscal year-end changed from October 31 to September 30. |

| (b) | Class C shares were merged into Class A on September 24, 2018. The amounts presented represent the results of the Class A shares for the periods prior to the merger and the results of the combined share class for the period subsequent the merger. |

| (c) | Commenced operations on September 20, 2013. |

| (d) | Per share amounts are based upon average shares outstanding, unless otherwise noted. |

| (e) | Calculated based on ending shares outstanding during the period. |

| (f) | Amount less than $0.005 per share. |

| (g) | Less than $0.005 per share. |

| (h) | Realized and unrealized gains and losses per share in this caption are balancing amounts necessary to reconcile the change in net asset value per share for the period and may not reconcile with the aggregate gains and losses in the Statement of Operations due to share transactions for the period. |