UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-22747

ALPS SERIES TRUST

(Exact name of registrant as specified in charter)

1290 Broadway, Suite 1000, Denver, Colorado 80203

(Address of principal executive offices) (Zip code)

(303) 623-2577

(Registrant’s telephone number, including area code)

Patrick Rogers, Secretary

ALPS Series Trust

1290 Broadway, Suite 1000

Denver, CO 80203

(Name and address of agent for service)

Date of fiscal year end: September 30

Date of reporting period: October 1, 2020 – September 30, 2021

Item 1. Reports to Stockholders.

| (a) |

Table of Contents

| Shareholder Letter | 2 |

| Portfolio Update | |

| Beacon Accelerated Return Strategy Fund | 5 |

| Beacon Planned Return Strategy Fund | 7 |

| Disclosure of Fund Expenses | 9 |

| Portfolios of Investments | |

| Beacon Accelerated Return Strategy Fund | 11 |

| Beacon Planned Return Strategy Fund | 14 |

| Statements of Assets and Liabilities | 17 |

| Statements of Operations | 18 |

| Statements of Changes in Net Assets | |

| Beacon Accelerated Return Strategy Fund | 19 |

| Beacon Planned Return Strategy Fund | 20 |

| Financial Highlights | 21 |

| Notes to Financial Statements | 25 |

| Report of Independent Registered Public Accounting Firm | 38 |

| Disclosure Regarding Renewal and Approval of Fund Advisory Agreement | 39 |

| Additional Information | 41 |

| Liquidity Risk Management Program | 42 |

| Privacy Policy | 43 |

| Trustees and Officers | 46 |

| Beacon Funds Trust | Shareholder Letter |

September 30, 2021 (Unaudited)

The S&P 500 squeaked out another positive return for the quarter ended September 30, 2021 rising 0.6%, although it ended on a down note by falling 4.7% in September. Over the course of the 12 months ended September 30, 2021, the S&P 500 was up 30.0%. The September loss was the first since January 2021 and has investors a bit unnerved as the market faces a number of short-term risks as it enters the earnings reporting season. Perhaps the most prominent of these risks is the looming extension of the federal government debt ceiling in December. The U.S. government has never defaulted on its U.S. Treasury bond obligations in its roughly 245 years of existence, but it has gone to the wire on several occasions resulting in investor angst. Treasury Secretary Janet Yellen said a default would be “catastrophic” and send the U.S. economy into another recession. We view a U.S. Treasury default as a low probability, but extremely high impact event, so are watching the situation closely.

Speaking of defaults, perhaps the biggest catalyst for the market’s September drawdown was the slow motion train wreck occurring with Evergrande Group, one of the largest property developers in China and the world. Real estate, and its related ecosystem, is at the heart of the Chinese economy, so the controlled restructuring of Evergrande poses the risk of a collapse and contagion beyond the Chinese real estate sector. Also adding to the September fireworks was the Federal Reserve’s announcement that a tapering of its longstanding bond buying program of $120 billion a month is at hand. We believe the taper is likely to begin in November 2021, but all bets are off if some dramatic events unfold in the interim. The taper talk has sent the yield on the benchmark 10 Year U.S. Treasury Note from roughly 1.25% to 1.65% in short order.

Adding to the risk bonfire is the ongoing supply chain bottlenecks experienced by many firms. These bottlenecks range from companies being unable to get their hands on production inputs, to COVID related lockdowns, to products sitting offshore on massive container ships with no one available to unload them. First, the shortages were confined to computer chips, but now shortages are springing up in areas as far flung as Nike’s sneaker factories in Vietnam. Fortunately, in most of these cases demand is delayed rather than destroyed completely, although the short-term effect is rising prices and dissatisfied customers.

Planned Return Strategy Fund — Performance and Benchmark Comparison

The Planned Return Strategy Fund (“PRS”) performed lower than its benchmark, the CBOE S&P 500 Buy/Write Index, over the past year, but continues to significantly outperform its benchmark over the more relevant 3 year and since inception periods.

PRS Fund Components of Performance

The returns sought to be generated by PRS Fund are derived from three distinct return elements, i.e., returns from Directional/Enhanced market movements, returns from Income (or option premium) and returns from the Hedge that seeks to create constant “downside protection”. Each return driver plays a crucial and sometimes complementary role in the overall performance of the strategy, as further described in greater detail below.

Directional/Enhanced

The Directional/Enhanced return component reflects that the performance of the S&P 500 is usually the main return driver of PRS Fund returns. Market exposure in the PRS Fund is generated by owning a deep-in-the-money call option. The return enhancement is created through the ownership of a long at-the-money call option. The Directional/Enhanced component added to returns over the past 12 months due to the strong increase in the S&P 500.

| 2 | www.beacontrust.com |

| Beacon Funds Trust | Shareholder Letter |

September 30, 2021 (Unaudited)

Income

The Income (or option premium) component represents cash flows received from selling out-of-the-money call and put options. This income generally serves two purposes by enhancing returns during periods of modest market movements and providing additional protection during declining markets. The income component detracted from performance over the past fiscal year since the out of the money call options declined in value, which offset the income gained from selling put options.

Hedge

The Hedge component is always present and provides the PRS Fund with its “downside protection” whenever it may be needed. This permanent “downside protection” is achieved by purchasing an at-the-money put option that rises in value as the market falls. The hedge detracted modestly from value over the year due to the rise in the S&P 500. In essence, it was insurance that was not needed in hindsight, but it reduced the portfolio risk and volatility.

Accelerated Return Strategy Fund — Performance and Benchmark Comparison

The Accelerated Return Strategy Fund (“ARS”) performed lower than its benchmark, the CBOE S&P 500 Buy/Write Index, over the past year, but continues to significantly outperform its benchmark over the more relevant 3 year and since inception periods.

ARS Fund Components of Performance

The returns sought to be generated by ARS Fund are derived from two distinct return elements, i.e. returns from Directional/Enhanced market movements and returns from Income (or option premium). Each return driver plays a crucial, and sometimes complementary role in the overall performance of the strategy.

Directional/Enhanced

The Directional/Enhanced return component reflects that the performance of the S&P 500 is the main return driver of ARS Fund. Market exposure in the ARS Fund is generated by owning a deep in the money call option. The return enhancement is created through the ownership of a long at-the-money call option. The directional component added to value over the past year due to the strong rise in the S&P 500.

Income

The Income (or option premium) component represents cash flows received from selling out-of-the-money call options. This Income component serves two purposes by enhancing returns during periods of modest market movements and providing additional protection during declining markets. The income component detracted from value over the past fiscal year since the premium received from selling the call options was smaller than the amount paid from the exercise of the options due to the strong rise in the S&P 500.

Market Outlook, Risks, and Conclusion

Assuming the federal debt ceiling is increased in December, as it always has in the past, we expect interest rates to gradually trend upward and the supply chain problems to slowly disappear, allowing for synchronized global growth to resume in earnest. In order for the economy to start to resemble what it looked like nearly two years ago, further progress on beating the COVID-19 pandemic must occur. There is good news to report on this front ranging from continued increase in global vaccinations, to a pill from Merck that limits the damage from the virus in most instances, to the impending launch of vaccinations for those at the age of 5 and above.

| Annual Report | September 30, 2021 | 3 |

| Beacon Funds Trust | Shareholder Letter |

September 30, 2021 (Unaudited)

To touch upon some additional risks not covered earlier in our note, we start with inflation, with recent readings of the Consumer Price Index (CPI) coming in at 5%+. The Fed’s longstanding trope of “transitory” inflation is experiencing increasing doubt. “Sticky” inflation may result in spiraling wage inflation creating a double whammy with the surge in most commodity prices this year. It raises the specter of the s word – stagflation – that is usually anathema to financial assets. At Beacon, we are not yet in the stagflation camp, but have it on our collective radar screens.

It seems like we have been saying this for months, but Congress continues to work on an infrastructure package. Our current thinking is that the traditional infrastructure package (e.g., bridges, roads, tunnels, sewers, broadband, etc.) will go through largely as planned, but that the “human services” infrastructure program may have to be slimmed down in order to receive congressional approval. An approved infrastructure package is likely to boost short-term GDP but also raises the possibility of higher taxes in order to pay for it. Geopolitical risk is ever present, with China-U.S. relations leading the list due to the enormous size of their respective economies. Beijing leaders have been cracking down on prominent Chinese firms, such as Alibaba and Tencent, in part to advance their “common prosperity” philosophy. It is not out of the question that Beijing will next target global firms doing business in China, negatively impacting profitability. China’s show of force with naval and air power over the South China Sea and Taiwan adds another dimension to geopolitical risk. Traditional hotspots in Russia, Iran, Afghanistan, and North Korea always have the potential to move from the back pages of the news to the front pages in a heartbeat.

The recent pullback in U.S. equities in September is normal, if not to be expected. We still favor equity-based strategies such as PRS and ARS with defined outcomes over fixed income for the long-term. Prior to the market decline at the end of the third quarter, the biggest drop for the S&P 500 in 2021 was a paltry 5%. This figure compares to an average intra-year decline of roughly 14% over the past 40 years and median decline of 11%. Yet, 75% of the time over this time frame, investors in the S&P 500 have finished the year in positive territory The lesson? During times of market distress, it usually makes sense to act like Rip Van Winkle. Relax, don’t focus on the stress of the short-term market turmoil, and wake up refreshed to discover potentially attractive long-term performance.

Beacon Funds Portfolio Management Team

| 4 | www.beacontrust.com |

| Beacon Accelerated Return Strategy Fund | Portfolio Update |

September 30, 2021 (Unaudited)

Performance of a Hypothetical $1,000,000 Initial Investment

(at Inception* through September 30, 2021)

The graph shown above represents historical performance of a hypothetical investment of $1,000,000 in the Institutional Class. Past performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Performance (as of September 30, 2021)

| 6 Month | 1 Year | 3 Year | Since Inception* | |

| Beacon Accelerated Return Strategy Fund – Institutional Class | 4.29% | 17.42% | 10.83% | 11.56% |

| CBOE S&P 500 BuyWrite Index | 6.50% | 21.10% | 4.15% | 5.51% |

The performance data quoted above represents past performance. Past performance is not a guarantee of future results. Investment return and value of the Fund shares will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Performance may be lower or higher than performance data quoted. Fund performance current to the most recent month end is available by calling (844) 894-9222 or by visiting www.beacontrust.com.

| * | Inception date of October 2, 2017 for Institutional Class. |

The Cboe S&P 500 BuyWrite Index (BXM) is a benchmark index designed to track the performance of a hypothetical buy-write strategy on the S&P 500 Index. The BXM is a passive total return index based on (1) buying an S&P 500 stock index portfolio, and (2) "writing" (or selling) the near-term S&P 500 Index (SPXSM) "covered" call option, generally on the third Friday of each month. The SPX call written will have about one month remaining to expiration, with an exercise price just above the prevailing index level (i.e., slightly out of the money). The SPX call is held until expiration and cash settled, at which time a new one-month, near-the-money call is written.

Returns of less than 1 year are cumulative.

| Annual Report | September 30, 2021 | 5 |

| Beacon Accelerated Return Strategy Fund | Portfolio Update |

September 30, 2021 (Unaudited)

Indices are not actively managed and do not reflect a deduction for fees, expenses or taxes. An investor cannot invest directly in an index.

The returns shown above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares.

The total annual operating expenses and total annual operating expenses after fee waivers and/or reimbursement for the Fund’s Institutional Class shares (as reported in the January 28, 2021 Prospectus), are 1.24% and 1.24%, respectively. The Fund’s investment adviser has contractually agreed to limit expenses through January 31, 2022.

Top Ten Holdings

| Option Contract | Expiration Date | Strike Price | % of Net Assets* |

| S&P 500® Mini Index | 6/14/22 | $0.01 | 11.62% |

| S&P 500® Mini Index | 11/12/21 | $0.01 | 8.99% |

| S&P 500® Mini Index | 12/14/21 | $0.01 | 8.44% |

| S&P 500® Mini Index | 1/14/22 | $0.01 | 8.44% |

| S&P 500® Mini Index | 2/14/22 | $0.01 | 8.43% |

| S&P 500® Mini Index | 3/14/22 | $0.01 | 8.24% |

| S&P 500® Mini Index | 8/12/22 | $0.01 | 8.03% |

| S&P 500® Mini Index | 7/14/22 | $0.01 | 7.86% |

| S&P 500® Mini Index | 10/14/21 | $0.01 | 7.74% |

| S&P 500® Mini Index | 5/13/22 | $0.01 | 7.16% |

| Top Ten Holdings | 84.95% |

| Asset Allocation | % of Net Assets* | ||

| Purchased Option Contracts | 104.62% | ||

| Written Option Contracts | -7.17% | ||

| Cash, Cash Equivalents, & Other Assets in Excess of Liabilities | 2.55% | ||

| Total | 100.00% |

| * | Holdings are subject to change, and may not reflect the current or future position of the portfolio. |

| 6 | www.beacontrust.com |

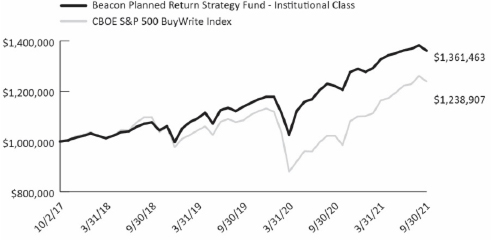

| Beacon Planned Return Strategy Fund | Portfolio Update |

September 30, 2021 (Unaudited)

Performance of a Hypothetical $1,000,000 Initial Investment

(at Inception* through September 30, 2021)

The graph shown above represents historical performance of a hypothetical investment of $1,000,000 in the Institutional Class. Past performance does not guarantee future results. All returns reflect reinvested dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

Performance (as of September 30, 2021)

| 6 Month | 1 Year | 3 Year | Since Inception* | |

| Beacon Planned Return Strategy Fund – Institutional Class | 2.58% | 11.53% | 8.14% | 8.03% |

| CBOE S&P 500 BuyWrite Index | 6.50% | 21.10% | 4.15% | 5.51% |

The performance data quoted above represents past performance. Past performance is not a guarantee of future results. Investment return and value of the Fund shares will fluctuate so that an investor’s shares, when sold or redeemed, may be worth more or less than their original cost. Performance may be lower or higher than performance data quoted. Fund performance current to the most recent month end is available by calling (844) 894-9222 or by visiting www.beacontrust.com.

| * | Inception date of October 2, 2017 for Institutional Class. |

The Cboe S&P 500 BuyWrite Index (BXM) is a benchmark index designed to track the performance of a hypothetical buy-write strategy on the S&P 500 Index. The BXM is a passive total return index based on (1) buying an S&P 500 stock index portfolio, and (2) "writing" (or selling) the near-term S&P 500 Index (SPXSM) "covered" call option, generally on the third Friday of each month. The SPX call written will have about one month remaining to expiration, with an exercise price just above the prevailing index level (i.e., slightly out of the money). The SPX call is held until expiration and cash settled, at which time a new one-month, near-the-money call is written.

Returns of less than 1 year are cumulative.

| Annual Report | September 30, 2021 | 7 |

| Beacon Planned Return Strategy Fund | Portfolio Update |

September 30, 2021 (Unaudited)

Indices are not actively managed and do not reflect a deduction for fees, expenses or taxes. An investor cannot invest directly in an index.

The returns shown above do not reflect the deduction of taxes a shareholder would pay on Fund distributions or redemption of Fund shares.

The total annual operating expenses and total annual operating expenses after fee waivers and/or reimbursement for the Fund’s Institutional Class shares (as reported in the January 28, 2021 Prospectus), 1.20% and 1.20%, respectively. The Fund’s investment adviser has contractually agreed to limit expenses through January 31, 2022.

Top Ten Holdings

| Option Contract | Expiration Date | Strike Price | % of Net Assets* |

| S&P 500® Mini Index | 10/14/21 | $45.30 | 9.56% |

| S&P 500® Mini Index | 1/14/22 | $49.25 | 8.71% |

| S&P 500® Mini Index | 2/14/22 | $51.35 | 8.50% |

| S&P 500® Mini Index | 3/14/22 | $51.25 | 8.38% |

| S&P 500® Mini Index | 11/12/21 | $47.30 | 8.24% |

| S&P 500® Mini Index | 7/14/22 | $56.80 | 8.18% |

| S&P 500® Mini Index | 9/14/22 | $58.40 | 8.13% |

| S&P 500® Mini Index | 6/14/22 | $55.39 | 7.96% |

| S&P 500® Mini Index | 8/12/22 | $58.00 | 7.84% |

| S&P 500® Mini Index | 5/13/22 | $54.25 | 7.84% |

| Top Ten Holdings | 83.34% |

| Asset Allocation | % of Net Assets* | ||

| Purchased Option Contracts | 117.00% | ||

| Written Option Contracts | -19.57% | ||

| Cash, Cash Equivalents, & Other Assets in Excess of Liabilities | 2.57% | ||

| Total | 100.00% |

| * | Holdings are subject to change, and may not reflect the current or future position of the portfolio. |

| 8 | www.beacontrust.com |

| Beacon Funds Trust | Disclosure of Fund Expenses |

September 30, 2021 (Unaudited)

Example. As a shareholder of the Beacon Accelerated Return Strategy Fund or Beacon Planned Return Strategy Fund (the “Funds”), you incur two types of costs: (1) transaction costs; and (2) ongoing costs, including management fees, shareholder service fees, and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 invested on April 1, 2021 and held through September 30, 2021.

Actual Expenses. The first line under each class in the following table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading “Expenses Paid During Period April 1, 2021 – September 30, 2021” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes. The second line under each class in the following table provides information about hypothetical account values and hypothetical expenses based on a Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in a Fund and other mutual funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing Fund costs only and do not reflect any transactional costs. Therefore, the second line under each class in the table below is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Annual Report | September 30, 2021 | 9 |

| Beacon Funds Trust | Disclosure of Fund Expenses |

September 30, 2021 (Unaudited)

| Beginning Account Value April 1, 2021 | Ending Account Value September 30, 2021 | Expense Ratio(a) | Expenses Paid During Period April 1, 2021 - September 30, 2021(b) | |

| Beacon Accelerated Return | ||||

| Strategy Fund | ||||

| Institutional Class | ||||

| Actual | $1,000.00 | $1,042.90 | 1.22% | $ 6.25 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,018.95 | 1.22% | $ 6.17 |

| Beacon Planned Return | ||||

| Strategy Fund | ||||

| Institutional Class | ||||

| Actual | $1,000.00 | $1,025.80 | 1.19% | $ 6.04 |

| Hypothetical (5% return before expenses) | $1,000.00 | $1,019.10 | 1.19% | $ 6.02 |

| (a) | Each Fund's expense ratios have been annualized based on the Fund's most recent fiscal half-year expenses after any applicable waivers and reimbursements. |

| (b) | Expenses are equal to the annualized expense ratio shown above for the applicable class, multiplied by the average account value over the period, multiplied by the number of days in the most recent fiscal half year (183), divided by 365. |

| 10 | www.beacontrust.com |

| Beacon Accelerated Return Strategy Fund | Portfolio of Investments |

September 30, 2021

| Counterparty | Expiration Date | Strike Price | Contracts | Notional Value | Value (Note 2) | |||||||||||||

| PURCHASED OPTION CONTRACTS - (104.62%) | ||||||||||||||||||

| Call Option Contracts (104.62%) | ||||||||||||||||||

| S&P 500® Mini Index: | ||||||||||||||||||

| Goldman Sachs | 10/14/2021 | $ | 0.01 | 215 | $ | 9,261,211 | $ | 9,262,578 | ||||||||||

| Goldman Sachs | 10/14/2021 | 361.68 | 215 | 9,261,211 | 1,491,314 | |||||||||||||

| Goldman Sachs | 11/12/2021 | 0.01 | 250 | 10,768,850 | 10,761,343 | |||||||||||||

| Goldman Sachs | 11/12/2021 | 377.80 | 250 | 10,768,850 | 1,371,659 | |||||||||||||

| Goldman Sachs | 12/14/2021 | 0.01 | 235 | 10,122,719 | 10,102,928 | |||||||||||||

| Goldman Sachs | 12/14/2021 | 393.35 | 235 | 10,122,719 | 1,012,188 | |||||||||||||

| Goldman Sachs | 01/14/2022 | 0.01 | 235 | 10,122,719 | 10,102,651 | |||||||||||||

| Goldman Sachs | 01/14/2022 | 393.09 | 185 | 7,968,949 | 844,909 | |||||||||||||

| Goldman Sachs | 01/14/2022 | 393.35 | 50 | 2,153,770 | 227,280 | |||||||||||||

| Goldman Sachs | 02/14/2022 | 0.01 | 235 | 10,122,719 | 10,093,948 | |||||||||||||

| Goldman Sachs | 02/14/2022 | 393.09 | 125 | 5,384,425 | 595,547 | |||||||||||||

| Goldman Sachs | 02/14/2022 | 416.40 | 110 | 4,738,294 | 327,589 | |||||||||||||

| Goldman Sachs | 03/14/2022 | 0.01 | 230 | 9,907,342 | 9,868,752 | |||||||||||||

| Goldman Sachs | 03/14/2022 | 414.64 | 70 | 3,015,278 | 232,272 | |||||||||||||

| Goldman Sachs | 03/14/2022 | 416.40 | 160 | 6,892,064 | 510,591 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 0.01 | 190 | 8,184,326 | 8,148,278 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 414.64 | 190 | 8,184,326 | 673,508 | |||||||||||||

| Goldman Sachs | 05/13/2022 | 0.01 | 200 | 8,615,080 | 8,568,897 | |||||||||||||

| Goldman Sachs | 05/13/2022 | 424.82 | 200 | 8,615,080 | 608,782 | |||||||||||||

| Goldman Sachs | 06/14/2022 | 0.01 | 325 | 13,999,505 | 13,910,024 | |||||||||||||

| Goldman Sachs | 06/14/2022 | 424.82 | 100 | 4,307,540 | 321,983 | |||||||||||||

| Goldman Sachs | 06/14/2022 | 436.60 | 225 | 9,691,965 | 556,569 | |||||||||||||

| Goldman Sachs | 07/14/2022 | 0.01 | 220 | 9,476,588 | 9,411,015 | |||||||||||||

| Goldman Sachs | 07/14/2022 | 436.60 | 50 | 2,153,770 | 132,687 | |||||||||||||

| Goldman Sachs | 07/14/2022 | 445.40 | 170 | 7,322,818 | 365,093 | |||||||||||||

| Goldman Sachs | 08/12/2022 | 0.01 | 225 | 9,691,965 | 9,616,414 | |||||||||||||

| Goldman Sachs | 08/12/2022 | 445.40 | 100 | 4,307,540 | 229,876 | |||||||||||||

| Goldman Sachs | 08/12/2022 | 447.90 | 125 | 5,384,425 | 270,110 | |||||||||||||

| Goldman Sachs | 09/14/2022 | 0.01 | 125 | 5,384,425 | 5,336,422 | |||||||||||||

| Goldman Sachs | 09/14/2022 | 447.90 | 125 | 5,384,425 | 290,113 | |||||||||||||

| 231,314,898 | 125,245,320 | |||||||||||||||||

| TOTAL PURCHASED OPTION CONTRACTS | ||||||||||||||||||

| (Cost $116,583,602) | $ | 231,314,898 | $ | 125,245,320 | ||||||||||||||

See Notes to Financial Statements.

| Annual Report | September 30, 2021 | 11 |

| Beacon Accelerated Return Strategy Fund | Portfolio of Investments |

September 30, 2021

| 7 Day Yield | Shares | Value (Note 2) | ||||||||||

| SHORT TERM INVESTMENTS (2.67%) | ||||||||||||

| Money Market Funds | ||||||||||||

| Goldman Sachs Financial Square Funds - Treasury Instruments Fund(a) | 0.000 | % | 1,844,318 | $ | 1,844,318 | |||||||

| Invesco Short-Term Investments Trust | ||||||||||||

| Government & Agency Portfolio - Institutional Class | 0.030 | % | 1,355,054 | 1,355,054 | ||||||||

| 3,199,372 | ||||||||||||

| TOTAL SHORT TERM INVESTMENTS | ||||||||||||

| (Cost $3,199,372) | 3,199,372 | |||||||||||

| TOTAL INVESTMENTS (107.29%) | ||||||||||||

| (Cost $119,782,974) | $ | 128,444,692 | ||||||||||

| LIABILITIES IN EXCESS OF OTHER ASSETS (-7.29%) | (8,730,859 | ) | ||||||||||

| NET ASSETS (100.00%) | $ | 119,713,833 | ||||||||||

| (a) | All or a portion is held as collateral at broker for written options. |

See Notes to Financial Statements.

| 12 | www.beacontrust.com |

| Beacon Accelerated Return Strategy Fund | Portfolio of Investments |

September 30, 2021

WRITTEN OPTION CONTRACTS (7.17%)

| Counterparty | Expiration Date | Strike Price | Contracts | Premiums Received | Notional Value | Value (Note 2) | ||||||||||||||||

| Call Option Contracts - (7.17%) | ||||||||||||||||||||||

| S&P 500® Mini Index | ||||||||||||||||||||||

| Goldman Sachs | 10/14/21 | $ | 394.23 | (430 | ) | $ | 435,125 | $ | (18,522,422 | ) | $ | (1,609,020 | ) | |||||||||

| Goldman Sachs | 11/12/21 | 408.97 | (500 | ) | 539,960 | (21,537,700 | ) | (1,377,262 | ) | |||||||||||||

| Goldman Sachs | 12/14/21 | 427.89 | (470 | ) | 575,712 | (20,245,438 | ) | (773,898 | ) | |||||||||||||

| Goldman Sachs | 01/14/22 | 427.05 | (370 | ) | 420,105 | (15,937,898 | ) | (737,519 | ) | |||||||||||||

| Goldman Sachs | 01/14/22 | 430.05 | (100 | ) | 129,392 | (4,307,540 | ) | (179,482 | ) | |||||||||||||

| Goldman Sachs | 02/14/22 | 429.25 | (250 | ) | 299,605 | (10,768,850 | ) | (523,581 | ) | |||||||||||||

| Goldman Sachs | 02/14/22 | 448.20 | (220 | ) | 225,042 | (9,476,588 | ) | (222,304 | ) | |||||||||||||

| Goldman Sachs | 03/14/22 | 445.86 | (140 | ) | 147,409 | (6,030,556 | ) | (187,901 | ) | |||||||||||||

| Goldman Sachs | 03/14/22 | 450.20 | (320 | ) | 340,135 | (13,784,128 | ) | (361,515 | ) | |||||||||||||

| Goldman Sachs | 04/14/22 | 447.89 | (380 | ) | 417,210 | (16,368,652 | ) | (555,060 | ) | |||||||||||||

| Goldman Sachs | 05/13/22 | 456.00 | (400 | ) | 404,778 | (17,230,160 | ) | (508,293 | ) | |||||||||||||

| Goldman Sachs | 06/14/22 | 458.21 | (200 | ) | 211,189 | (8,615,080 | ) | (267,116 | ) | |||||||||||||

| Goldman Sachs | 06/14/22 | 469.43 | (450 | ) | 489,125 | (19,383,930 | ) | (400,488 | ) | |||||||||||||

| Goldman Sachs | 07/14/22 | 471.62 | (100 | ) | 115,995 | (4,307,540 | ) | (95,382 | ) | |||||||||||||

| Goldman Sachs | 07/14/22 | 478.18 | (340 | ) | 376,022 | (14,645,636 | ) | (255,395 | ) | |||||||||||||

| Goldman Sachs | 08/12/22 | 0.01 | (250 | ) | 313,237 | (10,768,850 | ) | (177,091 | ) | |||||||||||||

| Goldman Sachs | 08/12/22 | 480.36 | (200 | ) | 228,989 | (8,615,080 | ) | (162,591 | ) | |||||||||||||

| Goldman Sachs | 08/12/22 | 481.85 | (250 | ) | 300,987 | (10,768,850 | ) | (193,012 | ) | |||||||||||||

| TOTAL WRITTEN OPTION CONTRACTS | $ | 5,970,017 | $ | (231,314,898 | ) | $ | (8,586,910 | ) | ||||||||||||||

See Notes to Financial Statements.

| Annual Report | September 30, 2021 | 13 |

| Beacon Planned Return Strategy Fund | Portfolio of Investments |

September 30, 2021

| Counterparty | Expiration Date | Strike Price | Contracts | Notional Value | Value (Note 2) | |||||||||||||

| PURCHASED OPTION CONTRACTS - (117.00%) | ||||||||||||||||||

| Call Option Contracts (111.96%) | ||||||||||||||||||

| S&P 500® Mini Index: | ||||||||||||||||||

| Goldman Sachs | 10/14/2021 | $ | 45.30 | 900 | $ | 38,767,860 | $ | 34,697,562 | ||||||||||

| Goldman Sachs | 10/14/2021 | 347.50 | 900 | 38,767,860 | 7,515,617 | |||||||||||||

| Goldman Sachs | 11/12/2021 | 47.30 | 780 | 33,598,812 | 29,887,011 | |||||||||||||

| Goldman Sachs | 11/12/2021 | 362.35 | 780 | 33,598,812 | 5,423,152 | |||||||||||||

| Goldman Sachs | 12/14/2021 | 47.85 | 315 | 13,568,751 | 12,035,434 | |||||||||||||

| Goldman Sachs | 12/14/2021 | 48.70 | 450 | 19,383,930 | 17,155,231 | |||||||||||||

| Goldman Sachs | 12/14/2021 | 368.55 | 315 | 13,568,751 | 2,047,879 | |||||||||||||

| Goldman Sachs | 12/14/2021 | 373.25 | 450 | 19,383,930 | 2,732,961 | |||||||||||||

| Goldman Sachs | 01/14/2022 | 49.25 | 830 | 35,752,582 | 31,595,435 | |||||||||||||

| Goldman Sachs | 01/14/2022 | 377.65 | 830 | 35,752,582 | 4,879,524 | |||||||||||||

| Goldman Sachs | 02/14/2022 | 51.35 | 815 | 35,106,451 | 30,823,320 | |||||||||||||

| Goldman Sachs | 02/14/2022 | 393.20 | 815 | 35,106,451 | 3,875,715 | |||||||||||||

| Goldman Sachs | 03/14/2022 | 51.25 | 805 | 34,675,697 | 30,416,833 | |||||||||||||

| Goldman Sachs | 03/14/2022 | 393.00 | 805 | 34,675,697 | 3,986,465 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 54.25 | 680 | 29,291,272 | 25,475,034 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 56.80 | 135 | 5,815,179 | 5,023,129 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 416.85 | 680 | 29,291,272 | 2,300,860 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 435.25 | 135 | 5,815,179 | 293,262 | |||||||||||||

| Goldman Sachs | 05/13/2022 | 54.25 | 760 | 32,737,304 | 28,445,009 | |||||||||||||

| Goldman Sachs | 05/13/2022 | 415.50 | 760 | 32,737,304 | 2,789,499 | |||||||||||||

| Goldman Sachs | 06/14/2022 | 55.39 | 775 | 33,383,435 | 28,879,879 | |||||||||||||

| Goldman Sachs | 06/14/2022 | 424.10 | 775 | 33,383,435 | 2,531,913 | |||||||||||||

| Goldman Sachs | 07/14/2022 | 56.80 | 800 | 34,460,320 | 29,680,829 | |||||||||||||

| Goldman Sachs | 07/14/2022 | 435.25 | 800 | 34,460,320 | 2,188,615 | |||||||||||||

| Goldman Sachs | 08/12/2022 | 58.00 | 770 | 33,168,058 | 28,446,779 | |||||||||||||

| Goldman Sachs | 08/12/2022 | 446.85 | 770 | 33,168,058 | 1,707,848 | |||||||||||||

| Goldman Sachs | 09/14/2022 | 58.40 | 800 | 34,460,320 | 29,485,019 | |||||||||||||

| Goldman Sachs | 09/14/2022 | 448.10 | 800 | 34,460,320 | 1,848,183 | |||||||||||||

| 828,339,942 | 406,167,997 | |||||||||||||||||

See Notes to Financial Statements.

| 14 | www.beacontrust.com |

| Beacon Planned Return Strategy Fund | Portfolio of Investments |

September 30, 2021

| Counterparty | Expiration Date | Strike Price | Contracts | Notional Value | Value (Note 2) | |||||||||||||

| PURCHASED OPTION CONTRACTS - (117.00%) (continued) | ||||||||||||||||||

| Put Option Contracts (5.04%) | ||||||||||||||||||

| S&P 500® Mini Index: | ||||||||||||||||||

| Goldman Sachs | 10/14/2021 | $ | 347.50 | 900 | $ | 38,767,860 | $ | 15,512 | ||||||||||

| Goldman Sachs | 11/12/2021 | 362.35 | 780 | 33,598,812 | �� | 108,443 | ||||||||||||

| Goldman Sachs | 12/14/2021 | 368.55 | 315 | 13,568,751 | 113,351 | |||||||||||||

| Goldman Sachs | 12/14/2021 | 373.25 | 450 | 19,383,930 | 180,824 | |||||||||||||

| Goldman Sachs | 01/14/2022 | 377.65 | 830 | 35,752,582 | 536,943 | |||||||||||||

| Goldman Sachs | 02/14/2022 | 393.20 | 815 | 35,106,451 | 907,451 | |||||||||||||

| Goldman Sachs | 03/14/2022 | 393.00 | 805 | 34,675,697 | 1,073,688 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 416.85 | 680 | 29,291,272 | 1,475,286 | |||||||||||||

| Goldman Sachs | 04/14/2022 | 435.25 | 135 | 5,815,179 | 377,687 | |||||||||||||

| Goldman Sachs | 05/13/2022 | 415.50 | 760 | 32,737,304 | 1,789,887 | |||||||||||||

| Goldman Sachs | 06/14/2022 | 424.10 | 775 | 33,383,435 | 2,215,296 | |||||||||||||

| Goldman Sachs | 07/14/2022 | 435.25 | 800 | 34,460,320 | 2,769,450 | |||||||||||||

| Goldman Sachs | 08/12/2022 | 446.85 | 770 | 33,168,058 | 3,185,835 | |||||||||||||

| Goldman Sachs | 09/14/2022 | 448.10 | 800 | 34,460,320 | 3,518,576 | |||||||||||||

| 414,169,971 | 18,268,229 | |||||||||||||||||

| TOTAL PURCHASED OPTION CONTRACTS | ||||||||||||||||||

| (Cost $391,444,612) | $ | 1,242,509,913 | $ | 424,436,226 | ||||||||||||||

| 7 Day Yield | Shares | Value (Note 2) | ||||||||||

| SHORT TERM INVESTMENTS (2.70%) | ||||||||||||

| Money Market Funds | ||||||||||||

| Goldman Sachs Financial Square Funds - Treasury Instruments Fund(a) | 0.000 | % | 3,836,483 | $ | 3,836,483 | |||||||

| Invesco Short-Term Investments Trust | ||||||||||||

| Government & Agency Portfolio - Institutional Class | 0.030 | % | 5,975,927 | 5,975,928 | ||||||||

| 9,812,411 | ||||||||||||

| TOTAL SHORT TERM INVESTMENTS | ||||||||||||

| (Cost $9,812,411) | 9,812,411 | |||||||||||

| TOTAL INVESTMENTS (119.70%) | ||||||||||||

| (Cost $401,257,023) | $ | 434,248,637 | ||||||||||

| LIABILITIES IN EXCESS OF OTHER ASSETS (-19.70%) | (71,476,023 | ) | ||||||||||

| NET ASSETS (100.00%) | $ | 362,772,614 | ||||||||||

| (a) | All or a portion is held as collateral at broker for written options. |

See Notes to Financial Statements.

| Annual Report | September 30, 2021 | 15 |

| Beacon Planned Return Strategy Fund | Portfolio of Investments |

September 30, 2021

WRITTEN OPTION CONTRACTS (19.57%)

| Counterparty | Expiration Date | Strike Price | Contracts | Premiums Received | Notional Value | Value (Note 2) | ||||||||||||||||

| Put Option Contracts - (2.94%) | ||||||||||||||||||||||

| S&P 500® Mini Index | ||||||||||||||||||||||

| Goldman Sachs | 10/14/21 | $ | 312.75 | (900 | ) | $ | 1,883,627 | $ | (38,767,860 | ) | $ | (5,799 | ) | |||||||||

| Goldman Sachs | 11/12/21 | 326.12 | (780 | ) | 1,513,137 | (33,598,812 | ) | (49,463 | ) | |||||||||||||

| Goldman Sachs | 12/14/21 | 331.70 | (315 | ) | 654,230 | (13,568,751 | ) | (50,197 | ) | |||||||||||||

| Goldman Sachs | 12/14/21 | 335.93 | (450 | ) | 899,064 | (19,383,930 | ) | (78,443 | ) | |||||||||||||

| Goldman Sachs | 01/14/22 | 339.89 | (830 | ) | 1,799,403 | (35,752,582 | ) | (254,935 | ) | |||||||||||||

| Goldman Sachs | 02/14/22 | 353.88 | (815 | ) | 1,895,624 | (35,106,451 | ) | (458,303 | ) | |||||||||||||

| Goldman Sachs | 03/14/22 | 353.70 | (805 | ) | 1,777,375 | (34,675,697 | ) | (579,061 | ) | |||||||||||||

| Goldman Sachs | 04/14/22 | 375.17 | (680 | ) | 1,296,706 | (29,291,272 | ) | (818,553 | ) | |||||||||||||

| Goldman Sachs | 04/14/22 | 391.73 | (135 | ) | 215,453 | (5,815,179 | ) | (205,204 | ) | |||||||||||||

| Goldman Sachs | 05/13/22 | 373.95 | (760 | ) | 1,513,859 | (32,737,304 | ) | (1,028,750 | ) | |||||||||||||

| Goldman Sachs | 06/14/22 | 381.69 | (775 | ) | 1,474,008 | (33,383,435 | ) | (1,315,153 | ) | |||||||||||||

| Goldman Sachs | 07/14/22 | 391.73 | (800 | ) | 1,601,556 | (34,460,320 | ) | (1,670,517 | ) | |||||||||||||

| Goldman Sachs | 08/12/22 | 402.17 | (770 | ) | 1,568,449 | (33,168,058 | ) | (1,951,127 | ) | |||||||||||||

| Goldman Sachs | 09/14/22 | 403.29 | (800 | ) | 1,797,558 | (34,460,320 | ) | (2,204,310 | ) | |||||||||||||

| 19,890,049 | (414,169,971 | ) | (10,669,815 | ) | ||||||||||||||||||

| Call Option Contracts - (16.63%) | ||||||||||||||||||||||

| S&P 500® Mini Index | ||||||||||||||||||||||

| Goldman Sachs | 10/14/21 | 368.20 | (1,800 | ) | 3,268,681 | (77,535,720 | ) | (11,318,520 | ) | |||||||||||||

| Goldman Sachs | 11/12/21 | 381.55 | (1,560 | ) | 2,595,729 | (67,197,624 | ) | (8,021,868 | ) | |||||||||||||

| Goldman Sachs | 12/14/21 | 388.34 | (630 | ) | 1,079,769 | (27,137,502 | ) | (2,984,151 | ) | |||||||||||||

| Goldman Sachs | 12/14/21 | 392.30 | (900 | ) | 1,507,427 | (38,767,860 | ) | (3,956,932 | ) | |||||||||||||

| Goldman Sachs | 01/14/22 | 398.50 | (1,660 | ) | 3,034,366 | (71,505,164 | ) | (6,847,483 | ) | |||||||||||||

| Goldman Sachs | 02/14/22 | 415.89 | (1,630 | ) | 3,276,188 | (70,212,902 | ) | (4,914,955 | ) | |||||||||||||

| Goldman Sachs | 03/14/22 | 415.10 | (1,610 | ) | 3,042,788 | (69,351,394 | ) | (5,289,667 | ) | |||||||||||||

| Goldman Sachs | 04/14/22 | 436.11 | (1,360 | ) | 2,366,298 | (58,582,544 | ) | (2,883,247 | ) | |||||||||||||

| Goldman Sachs | 04/14/22 | 450.05 | (270 | ) | 440,085 | (11,630,358 | ) | (364,939 | ) | |||||||||||||

| Goldman Sachs | 05/13/22 | 434.90 | (1,520 | ) | 2,843,812 | (65,474,608 | ) | (3,627,325 | ) | |||||||||||||

| Goldman Sachs | 06/14/22 | 442.04 | (1,550 | ) | 2,653,515 | (66,766,870 | ) | (3,347,141 | ) | |||||||||||||

| Goldman Sachs | 07/14/22 | 454.75 | (1,600 | ) | 3,084,712 | (68,920,640 | ) | (2,648,701 | ) | |||||||||||||

| Goldman Sachs | 08/12/22 | 466.15 | (1,540 | ) | 2,842,758 | (66,336,116 | ) | (1,996,486 | ) | |||||||||||||

| Goldman Sachs | 09/14/22 | 469.03 | (1,600 | ) | 3,172,717 | (68,920,640 | ) | (2,134,067 | ) | |||||||||||||

| 35,208,845 | (828,339,942 | ) | (60,335,482 | ) | ||||||||||||||||||

| TOTAL WRITTEN OPTION CONTRACTS | $ | 55,098,894 | $ | (1,242,509,913 | ) | $ | (71,005,297 | ) | ||||||||||||||

See Notes to Financial Statements.

| 16 | www.beacontrust.com |

| Beacon Funds Trust | Statements of Assets and Liabilities |

September 30, 2021

| BEACON ACCELERATED RETURN STRATEGY FUND | BEACON PLANNED RETURN STRATEGY FUND | |||||||

| ASSETS: | ||||||||

| Investments, at value (Cost $119,782,974 and $401,257,023) | $ | 128,444,692 | $ | 434,248,637 | ||||

| Receivable for investments sold | 35 | 125 | ||||||

| Receivable for shares sold | 8,506 | 40,886 | ||||||

| Dividends and interest receivable | 1 | 5 | ||||||

| Other assets | 5,818 | 6,407 | ||||||

| Total Assets | 128,459,052 | 434,296,060 | ||||||

| LIABILITIES: | ||||||||

| Written options, at value (premiums received $5,970,017 and $55,098,894) | 8,586,910 | 71,005,297 | ||||||

| Payable for administration and transfer agent fees | 21,624 | 51,916 | ||||||

| Payable for shares redeemed | – | 100,000 | ||||||

| Payable to adviser | 100,221 | 300,547 | ||||||

| Payable for distribution and service fees | 2,984 | 12,518 | ||||||

| Payable for printing fees | 1,321 | 3,718 | ||||||

| Payable for professional fees | 24,479 | 32,111 | ||||||

| Payable for trustees' fees and expenses | 2,558 | 7,580 | ||||||

| Payable to Chief Compliance Officer fees | 679 | 2,013 | ||||||

| Accrued expenses and other liabilities | 4,443 | 7,746 | ||||||

| Total Liabilities | 8,745,219 | 71,523,446 | ||||||

| NET ASSETS | $ | 119,713,833 | $ | 362,772,614 | ||||

| NET ASSETS CONSIST OF: | ||||||||

| Paid-in capital (Note 6) | $ | 100,779,450 | $ | 326,257,435 | ||||

| Total distributable earnings | 18,934,383 | 36,515,179 | ||||||

| NET ASSETS | $ | 119,713,833 | $ | 362,772,614 | ||||

| PRICING OF SHARES | ||||||||

| Institutional Class : | ||||||||

| Net Asset Value, offering and redemption price per share | $ | 11.66 | $ | 11.13 | ||||

| Net Assets | $ | 119,713,833 | $ | 362,772,614 | ||||

| Shares of beneficial interest outstanding | 10,269,360 | 32,603,940 | ||||||

See Notes to Financial Statements.

| Annual Report | September 30, 2021 | 17 |

| Beacon Funds Trust | Statements of Operations |

For the Year Ended September 30, 2021

| BEACON ACCELERATED RETURN STRATEGY FUND | BEACON PLANNED RETURN STRATEGY FUND | |||||||

| INVESTMENT INCOME: | ||||||||

| Dividends | $ | 199 | $ | 2,043 | ||||

| Total Investment Income | 199 | 2,043 | ||||||

| EXPENSES: | ||||||||

| Investment advisory fees (Note 7) | 1,185,438 | 3,445,351 | ||||||

| Administration fees | 101,659 | 275,463 | ||||||

| Shareholder service fees | ||||||||

| Institutional Class | 37,435 | 137,435 | ||||||

| Custody fees | 6,182 | 5,915 | ||||||

| Legal fees | 10,453 | 29,970 | ||||||

| Audit and tax fees | 19,250 | 19,250 | ||||||

| Transfer agent fees | 29,152 | 65,394 | ||||||

| Trustees' fees and expenses | 10,897 | 31,492 | ||||||

| Registration and filing fees | 21,859 | 25,227 | ||||||

| Printing fees | 3,612 | 10,143 | ||||||

| Chief Compliance Officer fees | 8,183 | 23,774 | ||||||

| Insurance fees | 4,272 | 11,833 | ||||||

| Other expenses | 5,642 | 10,753 | ||||||

| Total Expenses | 1,444,034 | 4,092,000 | ||||||

| NET INVESTMENT LOSS | (1,443,835 | ) | (4,089,957 | ) | ||||

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS AND WRITTEN OPTIONS: | ||||||||

| Net realized gain/(loss) on: | ||||||||

| Investments | 60,570,955 | 147,281,843 | ||||||

| Written options | (37,981,708 | ) | (108,238,114 | ) | ||||

| Net realized gain | 22,589,247 | 39,043,729 | ||||||

| Change in unrealized appreciation/(depreciation) on: | ||||||||

| Investments | (7,733,233 | ) | (535,144 | ) | ||||

| Written options | 5,522,204 | 2,096,550 | ||||||

| Net change | (2,211,029 | ) | 1,561,406 | |||||

| NET REALIZED AND UNREALIZED GAIN ON INVESTMENTS AND WRITTEN OPTIONS | 20,378,218 | 40,605,135 | ||||||

| NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS | $ | 18,934,383 | $ | 36,515,178 | ||||

See Notes to Financial Statements.

| 18 | www.beacontrust.com |

| Beacon Accelerated Return Strategy Fund | Statements of Changes in Net Assets |

| For the Year Ended September 30, 2021 | For the Year Ended September 30, 2020 | |||||||

| OPERATIONS: | ||||||||

| Net investment loss | $ | (1,443,835 | ) | $ | (1,370,186 | ) | ||

| Net realized gain on investments and written options | 22,589,247 | 11,547,459 | ||||||

| Net change in unrealized appreciation/(depreciation) on investments and written options | (2,211,029 | ) | 1,267,721 | |||||

| Net increase in net assets resulting from operations | 18,934,383 | 11,444,994 | ||||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Institutional Class | (9,098,504 | ) | (5,021,704 | ) | ||||

| Total distributions | (9,098,504 | ) | (5,021,704 | ) | ||||

| BENEFICIAL SHARE TRANSACTIONS (Note 6): | ||||||||

| Institutional Class | ||||||||

| Shares sold | 5,742,480 | 2,294,251 | ||||||

| Dividends reinvested | 8,904,999 | 4,912,463 | ||||||

| Shares redeemed | (20,810,707 | ) | (16,630,726 | ) | ||||

| Net decrease from beneficial share transactions | (6,163,228 | ) | (9,424,012 | ) | ||||

| Net increase/(decrease) in net assets | 3,672,651 | (3,000,722 | ) | |||||

| NET ASSETS: | ||||||||

| Beginning of year | 116,041,182 | 119,041,904 | ||||||

| End of year | $ | 119,713,833 | $ | 116,041,182 | ||||

See Notes to Financial Statements.

| Annual Report | September 30, 2021 | 19 |

| Beacon Planned Return Strategy Fund | Statements of Changes in Net Assets |

| For the Year Ended September 30, 2021 | For the Year Ended September 30, 2020 | |||||||

| OPERATIONS: | ||||||||

| Net investment loss | $ | (4,089,957 | ) | $ | (3,547,058 | ) | ||

| Net realized gain on investments and written options | 39,043,729 | 22,651,065 | ||||||

| Net change in unrealized appreciation on investments and written options | 1,561,406 | 1,302,816 | ||||||

| Net increase in net assets resulting from operations | 36,515,178 | 20,406,823 | ||||||

| DISTRIBUTIONS TO SHAREHOLDERS | ||||||||

| Institutional Class | (16,088,934 | ) | (19,513,463 | ) | ||||

| Total distributions | (16,088,934 | ) | (19,513,463 | ) | ||||

| BENEFICIAL SHARE TRANSACTIONS (Note 6): | ||||||||

| Institutional Class | ||||||||

| Shares sold | 38,458,035 | 27,902,211 | ||||||

| Dividends reinvested | 14,203,122 | 16,951,434 | ||||||

| Shares redeemed | (25,703,820 | ) | (36,881,950 | ) | ||||

| Net increase from beneficial share transactions | 26,957,337 | 7,971,695 | ||||||

| Net increase in net assets | 47,383,581 | 8,865,055 | ||||||

| NET ASSETS: | ||||||||

| Beginning of year | 315,389,033 | 306,523,978 | ||||||

| End of year | $ | 362,772,614 | $ | 315,389,033 | ||||

See Notes to Financial Statements.

| 20 | www.beacontrust.com |

| Beacon Accelerated | |

| Return Strategy Fund – Institutional Class | Financial Highlights |

For a Share Outstanding Throughout the Period Presented

| For the Year Ended September 30, 2021 | For the Year Ended September 30, 2020 | For the Year Ended September 30, 2019 | For the Period Ended September 30, 2018 (a) | |||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 10.74 | $ | 10.15 | $ | 11.30 | $ | 10.00 | ||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||

| Net investment loss(b) | (0.14 | ) | (0.12 | ) | (0.11 | ) | (0.13 | ) | ||||||||

| Net realized and unrealized gain on investments | 1.93 | 1.15 | 0.37 | 1.49 | ||||||||||||

| Total from investment operations | 1.79 | 1.03 | 0.26 | 1.36 | ||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||

| From net realized gains on investments | (0.87 | ) | (0.44 | ) | (1.41 | ) | (0.06 | ) | ||||||||

| Total Distributions | (0.87 | ) | (0.44 | ) | (1.41 | ) | (0.06 | ) | ||||||||

| NET INCREASE/(DECREASE) IN NET ASSET VALUE | 0.92 | 0.59 | (1.15 | ) | 1.30 | |||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 11.66 | $ | 10.74 | $ | 10.15 | $ | 11.30 | ||||||||

| TOTAL RETURN(c) | 17.42 | % | 10.32 | % | 5.09 | % | 13.70 | % | ||||||||

| SUPPLEMENTAL DATA: | ||||||||||||||||

| Net assets, end of period (in 000s) | $ | 119,714 | $ | 116,041 | $ | 119,042 | $ | 154,518 | ||||||||

| RATIOS TO AVERAGE NET ASSETS | ||||||||||||||||

| Operating expenses (d) | 1.22 | % | 1.22 | % | 1.20 | % | 1.29 | %(e) | ||||||||

| Net investment loss | (1.22 | )% | (1.21) | % | (1.16 | )% | (1.25 | )%(e) | ||||||||

| PORTFOLIO TURNOVER RATE(f) | 0 | % | 0 | % | 0 | % | 0 | % | ||||||||

| (a) | Commenced operations on October 2, 2017. |

| (b) | Calculated using the average shares method. |

| (c) | Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are for the period indicated and have not been annualized. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (d) | According to the Fund's shareholder services plan with respect to the Fund's Institutional Class shares, any amount of fees accrued according to the plan but not paid during the Fund's fiscal year for such service activities shall be reimbursed to the Fund as soon as practical. Fees were reimbursed to the Fund during the period ended September 30, 2021, the period ended September 30, 2020, the period ended September 30, 2019, and the period ended September 30, 2018, respectively, in the amount of 0.00% (annualized), 0.00% (annualized), 0.14% (annualized), and 0.06% (annualized) of average net assets of Institutional Class shares. |

See Notes to Financial Statements.

| Annual Report | September 30, 2021 | 21 |

| Beacon Accelerated | |

| Return Strategy Fund – Institutional Class | Financial Highlights |

For a Share Outstanding Throughout the Period Presented

| (e) | Annualized. |

| (f) | All securities whose maturity or expiration date at time of acquisition were one year or less are excluded from the portfolio turnover calculation. |

See Notes to Financial Statements.

| 22 | www.beacontrust.com |

| Beacon Planned | |

| Return Strategy Fund – Institutional Class | Financial Highlights |

For a Share Outstanding Throughout the Period Presented

| For the Year Ended September 30, 2021 | For the Year Ended September 30, 2020 | For the Year Ended September 30, 2019 | For the Period Ended September 30, 2018 (a) | |||||||||||||

| NET ASSET VALUE, BEGINNING OF PERIOD | $ | 10.49 | $ | 10.44 | $ | 10.73 | $ | 10.00 | ||||||||

| INCOME/(LOSS) FROM OPERATIONS: | ||||||||||||||||

| Net investment loss(b) | (0.13 | ) | (0.12 | ) | (0.11 | ) | (0.13 | ) | ||||||||

| Net realized and unrealized gain on investments | 1.31 | 0.85 | 0.62 | 0.89 | ||||||||||||

| Total from investment operations | 1.18 | 0.73 | 0.51 | 0.76 | ||||||||||||

| LESS DISTRIBUTIONS: | ||||||||||||||||

| From net realized gains on investments | (0.54 | ) | (0.68 | ) | (0.80 | ) | (0.03 | ) | ||||||||

| Total Distributions | (0.54 | ) | (0.68 | ) | (0.80 | ) | (0.03 | ) | ||||||||

| NET INCREASE/(DECREASE) IN NET ASSET VALUE | 0.64 | 0.05 | (0.29 | ) | 0.73 | |||||||||||

| NET ASSET VALUE, END OF PERIOD | $ | 11.13 | $ | 10.49 | $ | 10.44 | $ | 10.73 | ||||||||

| TOTAL RETURN(c) | 11.53 | % | 7.21 | % | 5.77 | % | 7.64 | % | ||||||||

| SUPPLEMENTAL DATA: | ||||||||||||||||

| Net assets, end of period (in 000s) | $ | 362,773 | $ | 315,389 | $ | 306,524 | $ | 351,595 | ||||||||

| RATIOS TO AVERAGE NET ASSETS | ||||||||||||||||

| Operating expenses (d) | 1.19 | % | 1.20 | % | 1.17 | % | 1.25 | %(e) | ||||||||

| Net investment loss | (1.19 | )% | (1.19 | )% | (1.13 | )% | (1.23 | )%(e) | ||||||||

| PORTFOLIO TURNOVER RATE(f) | 0 | % | 0 | % | 0 | % | 0 | % | ||||||||

| (a) | Commenced operations on October 2, 2017. |

| (b) | Calculated using the average shares method. |

| (c) | Assumes an initial investment on the business day before the first day of the fiscal period, with all dividends and distributions reinvested in additional shares on the reinvestment date, and redemption at the net asset value calculated on the last business day of the fiscal period. Total returns are for the period indicated and have not been annualized. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. |

| (d) | According to the Fund's shareholder services plan with respect to the Fund's Institutional Class shares, any amount of fees accrued according to the plan but not paid during the Fund's fiscal year for such service activities shall be reimbursed to the Fund as soon as practical. Fees were reimbursed to the Fund during the period ended September 30, 2021, the period ended September 30, 2020, the period ended September 30, 2019, and the period ended September 30, 2018, respectively, in the amount of 0.00% (annualized), 0.00% (annualized), 0.14% (annualized), and 0.06% (annualized) of average net assets of Institutional Class shares. |

See Notes to Financial Statements.

| Annual Report | September 30, 2021 | 23 |

| Beacon Planned | |

| Return Strategy Fund – Institutional Class | Financial Highlights |

For a Share Outstanding Throughout the Period Presented

| (e) | Annualized. |

| (f) | All securities whose maturity or expiration date at time of acquisition were one year or less are excluded from the portfolio turnover calculation. |

See Notes to Financial Statements.

| 24 | www.beacontrust.com |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

1. ORGANIZATION

ALPS Series Trust (the “Trust”), a Delaware statutory trust, is an open-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Trust consists of multiple separate portfolios or series. This annual report describes the Beacon Accelerated Return Strategy Fund and the Beacon Planned Return Strategy Fund (each, a “Fund” and collectively, the “Funds”). The Funds are non-diversified and the primary investment objectives are to deliver capital appreciation and generate positive alpha for the Beacon Accelerated Return Strategy Fund, and capital preservation and capital appreciation for the Beacon Planned Return Strategy Fund. The Funds currently offer Institutional Class shares. The Board of Trustees (the “Board”) may establish additional funds and classes of shares at any time in the future without shareholder approval.

2. SIGNIFICANT ACCOUNTING POLICIES

The accompanying financial statements were prepared in accordance with accounting principles generally accepted in the United States of America for investment companies (“U.S. GAAP”). The Funds are considered investment companies under U.S. GAAP and follow the accounting and reporting guidance applicable to investment companies in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification Topic 946. The preparation of financial statements in conformity with U.S. GAAP requires management to make certain estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the period. Actual results could differ from those estimates. The following is a summary of significant accounting policies consistently followed by the Funds in preparation of their financial statements.

Investment Valuation: The Funds generally value their securities based on market prices determined at the close of regular trading on the New York Stock Exchange (“NYSE”), normally 4:00 p.m. Eastern Time, on each day the NYSE is open for trading.

FLEX Options are customized option contracts available through the Chicago Board Options Exchange ("CBOE"). Flexible Exchange Options are valued based on prices supplied by an independent third-party pricing service, which utilizes pricing models that incorporate various inputs such as interest rates, credit spreads, currency exchange rates and volatility measurements for in-the-money, at-the-money, and out-of-money contracts on a given strike price.

Redeemable securities issued by open-end registered investment companies are valued at the investment company’s applicable net asset value (“NAV”). Money market funds, representing short-term investments, are valued at their NAV.

When such prices or quotations are not available, or when the Fair Value Committee appointed by the Board believes that they are unreliable, securities may be priced using fair value procedures approved by the Board.

| Annual Report | September 30, 2021 | 25 |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

Fair Value Measurements: The Funds disclose the classification of their fair value measurements following a three-tier hierarchy based on the inputs used to measure fair value. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including assumptions about risk. Inputs may be observable or unobservable. Observable inputs reflect the assumptions market participants would use in pricing the asset or liability that are developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the asset or liability that are developed based on the best information available.

Various inputs are used in determining the value of the Funds’ investments as of the end of the reporting period. When inputs used fall into different levels of the fair value hierarchy, the level in the hierarchy within which the fair value measurement falls is determined based on the lowest level input that is significant to the fair value measurement in its entirety. The designated input levels are not necessarily an indication of the risk or liquidity associated with these investments. These inputs are categorized in the following hierarchy under applicable financial accounting standards:

| Level 1 – | Unadjusted quoted prices in active markets for identical investments, unrestricted assets or liabilities that the Fund has the ability to access at the measurement date; |

| Level 2 – | Quoted prices which are not active, quoted prices for similar assets or liabilities in active markets or inputs other than quoted prices that are observable (either directly or indirectly); and |

| Level 3 – | Significant unobservable prices or inputs (including the Fund’s own assumptions in determining the fair value of investments) where there is little or no market activity for the asset or liability at the measurement date. |

The following is a summary of the inputs used to value the Funds’ investments as of September 30, 2021:

BEACON ACCELERATED RETURN STRATEGY FUND

| Investments in Securities at Value | Level 1 - Unadjusted Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Purchased Option Contracts | $ | – | $ | 125,245,320 | $ | – | $ | 125,245,320 | ||||||||

| Short Term Investments | 3,199,372 | – | – | 3,199,372 | ||||||||||||

| Total | $ | 3,199,372 | $ | 125,245,320 | $ | – | $ | 128,444,692 | ||||||||

| Valuation Inputs | ||||||||||||||||

| Other Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Liabilities | ||||||||||||||||

| Written Option Contracts | $ | – | $ | (8,586,910 | ) | $ | – | $ | (8,586,910 | ) | ||||||

| Total | $ | – | $ | (8,586,910 | ) | $ | – | $ | (8,586,910 | ) | ||||||

| 26 | www.beacontrust.com |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

BEACON PLANNED RETURN STRATEGY FUND

| Investments in Securities at Value | Level 1 - Unadjusted Quoted Prices | Level 2 - Other Significant Observable Inputs | Level 3 - Significant Unobservable Inputs | Total | ||||||||||||

| Purchased Option Contracts | $ | – | $ | 424,436,226 | $ | – | $ | 424,436,226 | ||||||||

| Short Term Investments | 9,812,411 | – | – | 9,812,411 | ||||||||||||

| Total | $ | 9,812,411 | $ | 424,436,226 | $ | – | $ | 434,248,637 | ||||||||

| Valuation Inputs | ||||||||||||||||

| Other Financial Instruments | Level 1 | Level 2 | Level 3 | Total | ||||||||||||

| Liabilities | ||||||||||||||||

| Written Option Contracts | $ | – | $ | (71,005,297 | ) | $ | – | $ | (71,005,297 | ) | ||||||

| Total | $ | – | $ | (71,005,297 | ) | $ | – | $ | (71,005,297 | ) | ||||||

There were no Level 3 securities held during the year ended September 30, 2021.

Cash & Cash Equivalents: The Funds consider their investment in a Federal Deposit Insurance Corporation ("FDIC") insured interest bearing account to be cash and cash equivalents. Cash and cash equivalents are valued at cost plus any accrued interest. The Funds maintain cash balances, which, at times may exceed federally insured limits. The Funds maintain these balances with a high quality financial institution.

Concentration of Credit Risk: The Funds place their cash with a banking institution, which is insured by FDIC. The FDIC limit is $250,000. At various times throughout the year, the amount on deposit may exceed the FDIC limit and subject the Funds to a credit risk. The Funds do not believe that such deposits are subject to any unusual risk associated with investment activities.

Trust Expenses: Some expenses of the Trust can be directly attributed to a fund. Expenses that cannot be directly attributed to a fund are apportioned among all funds in the Trust based on average net assets of each fund, including Trustees' fees and expenses.

Fund Expenses: Some expenses can be directly attributed to a fund and are apportioned among the classes based on average net assets of each class.

Federal Income Taxes: The Funds comply with the requirements under Subchapter M of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies and intend to distribute substantially all of their net taxable income and net capital gains, if any, each year so that they will not be subject to excise tax on undistributed income and gains. The Funds are not subject to income taxes to the extent such distributions are made.

As of and during the year ended September 30, 2021, the Funds did not have a liability for any unrecognized tax benefits in the accompanying financial statements. The Funds recognize interest and penalties, if any, related to tax liabilities as income tax expense in the Statements of Operations. The Funds file U.S. federal, state and local income tax returns as required. The Funds’ tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations, which is generally three years after the filing of the tax return for federal purposes and four years for most state returns. The Funds’ administrator has analyzed the Funds’ tax positions and has concluded that as of September 30, 2021, no provision for income tax is required in the Funds’ financial statements related to these tax positions.

| Annual Report | September 30, 2021 | 27 |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

Investment Transactions and Investment Income: Investment transactions are accounted for on the date the investments are purchased or sold (trade date basis for financial reporting purposes). Realized gains and losses from investment transactions are reported on an identified cost basis. Interest income, which includes accretion of discounts and amortization of premiums, is accrued and recorded as earned. Dividend income is recognized on the ex-dividend date.

Distributions to Shareholders: The Funds normally pay dividends, if any, and distribute capital gains, if any, on an annual basis. Income dividend distributions are derived from interest, dividends and other income the Funds receive from their investments, including short-term capital gains. Long-term capital gain distributions are derived from gains realized when a Fund sells a security it has owned for more than one year. A Fund may make additional distributions and dividends at other times if its portfolio manager or managers believe doing so may be necessary for the Fund to avoid or reduce taxes. Net investment income/(loss) and net realized gain/(loss) may differ for financial statement and tax purposes.

COVID-19 Risk: An outbreak of respiratory disease caused by a novel coronavirus was first detected in December 2019 and has now spread internationally. This coronavirus has resulted in closing borders, enhanced health screenings, partial population vaccination, healthcare service preparation and delivery, quarantines, cancellations, disruptions to supply chains and customer activity, government sponsored fiscal stimulus programs, various moratoria on the applicability of certain laws and regulations, as well as general concern and uncertainty. The impact of this coronavirus, (and the variants of such virus) and other epidemics and pandemics that may arise in the future, could affect the economies of many nations, individual companies, their securities (including equity and debt), and the market in general in ways that cannot necessarily be foreseen at the present time. In addition, the impact of infectious diseases in developing or emerging market countries may be greater due to less established health care systems. Health crises caused by the recent coronavirus outbreak may exacerbate other pre-existing political, social, financial, and economic risks in certain countries. The impact of the outbreak may last for an extended period of time.

3. DERIVATIVE INSTRUMENTS

Each Fund's principal investment strategy permits it to enter into various types of derivatives contracts, including, but not limited to, futures contracts, forward foreign currency contracts, currency swaps and purchased and written options. In doing so, the Funds may employ strategies in differing combinations to permit it to increase, decrease, or change the level or types of exposure to market factors. Central to those strategies are features inherent in derivatives that make them more attractive for this purpose than equity or debt securities; they require little or no initial cash investment, they can focus exposure on only certain selected risk factors, and they may not require the ultimate receipt or delivery of the underlying security (or securities) to the contract. This may allow the Funds to pursue their objectives more quickly and efficiently than if they were to make direct purchases or sales of securities capable of affecting a similar response to market factors.

Risk of Investing in Derivatives: The Funds’ use of derivatives can result in losses due to unanticipated changes in the market risk factors and the overall market. In instances where the Funds are using derivatives to decrease, or hedge, exposures to market risk factors for securities held by the Funds, there are also risks that those derivatives may not perform as expected resulting in losses for the combined or hedged positions.

| 28 | www.beacontrust.com |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

Derivatives may have little or no initial cash investment relative to their market value exposure and therefore can produce significant gains or losses in excess of their cost. This use of embedded leverage allows the Funds to increase their market value exposure relative to their net assets and can substantially increase the volatility of the Funds’ performance.

Additional associated risks from investing in derivatives also exist and potentially could have significant effects on the valuation of the derivative and the Funds. Typically, the associated risks are not the risks that the Funds are attempting to increase or decrease exposure to, per their investment objectives, but are the additional risks from investing in derivatives.

Examples of these associated risks are liquidity risk, which is the risk that the Funds will not be able to sell or close out the derivative in a timely manner, and counterparty credit risk, which is the risk that the counterparty will not fulfill its obligation to the Funds. In addition, use of derivatives may increase or decrease exposure to the following risk factors:

Equity Risk: Equity risk relates to the change in value of equity securities as they relate to increases or decreases in the general market. Associated risks can be different for each type of derivative.

Option Contracts: Each Fund may enter into options transactions for hedging purposes and for nonhedging purposes such as seeking to enhance return. Each Fund may write covered put and call options on any stocks or stock indices, currencies traded on domestic and foreign securities exchanges, or futures contracts on stock indices, interest rates and currencies traded on domestic and, to the extent permitted by the U.S. Commodity Futures Trading Commission, foreign exchanges. A call option on an asset written by a Fund obligates the Fund to sell the specified asset to the holder (purchaser) at a stated price (the exercise price) if the option is exercised before a specified date (the expiration date). A put option on an asset written by a Fund obligates the Fund to buy the specified asset from the purchaser at the exercise price if the option is exercised before the expiration date. Premiums received when writing options are recorded as liabilities and are subsequently adjusted to the current value of the options written. Premiums received from writing options that expire are treated as realized gains. Premiums received from writing options, which are either exercised or closed, are offset against the proceeds received or amount paid on the transaction to determine realized gains or losses.

The Funds use FLEX Options, which are customized equity or index option contracts that trade on an exchange, but that provide investors with the ability to customize key contract terms like exercise prices, styles and expiration dates. Like standardized exchange-traded options, FLEX Options are guaranteed for settlement by The Options Clearing Corporation (“OCC”), a market clearinghouse. The OCC guarantees performance by each of the counterparties to the FLEX Options, becoming the “buyer for every seller and the seller for every buyer,” protecting clearing members and options traders from counterparty risk. FLEX Options provide investors with the ability to customize key terms, while achieving price discovery in competitive, transparent auctions markets and avoiding the counterparty exposure of Over-the-Counter (“OTC”) options positions. The Funds bear the risk that the OCC will be unable or unwilling to perform its obligations under the FLEX Options contracts.

| Annual Report | September 30, 2021 | 29 |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

Additionally, FLEX Options may be less liquid than certain other securities such as standardized options. In a less liquid market for the FLEX Options, the Funds may have difficulty closing out certain FLEX Options positions at desired times and prices.

Purchased Options: When the Funds purchase an option, an amount equal to the premium paid by the Funds are recorded as an investment and is subsequently adjusted to the current value of the option purchased. If an option expires on the stipulated expiration date or if the Funds enter into a closing sale transaction, a gain or loss is realized. If a call option is exercised, the cost of the security acquired is increased by the premium paid for the call. If a put option is exercised, a gain or loss is realized from the sale of the underlying security, and the proceeds from such sale are decreased by the premium originally paid. Purchased options are non-income producing securities.

Written Options: When the Funds write an option, an amount equal to the premium received by the Funds are recorded as a liability and is subsequently adjusted to the current value of the option written. Premiums received from writing options that expire unexercised are treated by the Funds on the expiration date as realized gain from written options. The difference between the premium and the amount paid on effecting a closing purchase transaction, including brokerage commissions, is also treated as a realized gain, or if the premium is less than the amount paid for the closing purchase transaction, as a realized loss. If a call option is exercised, the premium is added to the proceeds from the sale of the underlying security in determining whether the Funds have realized a gain or loss. If a put option is exercised, the premium reduces the cost basis of the securities purchased by the Funds. The Funds, as writers of an option, bear the market risk of an unfavorable change in the price of the security underlying the written option.

The average option contract notional amount during the year ended September 30, 2021, is noted below for each of the Funds.

| Derivative Type | Unit of Measurement | Monthly Average |

| Beacon Accelerated Return Strategy Fund | ||

| Purchased Option Contracts | Notional value of contracts outstanding | $234,547,027 |

| Written Option Contracts | Notional value of contracts outstanding | $234,547,027 |

| Derivative Type | Unit of Measurement | Monthly Average |

| Beacon Planned Return Strategy Fund | ||

| Purchased Option Contracts | Notional value of contracts outstanding | $1,240,449,192 |

| Written Option Contracts | Notional value of contracts outstanding | $1,240,449,192 |

| 30 | www.beacontrust.com |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

Derivative Instruments: The following tables disclose the amounts related to the Funds’ use of derivative instruments.

The effect of derivative instruments on the Statements of Assets and Liabilities as of September 30, 2021:

| Risk Exposure | Statements of Assets and Liabilities Location | Fair Value of Asset Derivatives | Statements of Assets and Liabilities Location | Fair Value of Liability Derivatives | ||||||||

| Beacon Accelerated Return Strategy Fund | ||||||||||||

| Equity Contracts | ||||||||||||

| (Purchased Options/Written Options) | Investments, at value | $ | 125,245,320 | Written Options, at value | $ | 8,586,910 | ||||||

| $ | 125,245,320 | $ | 8,586,910 | |||||||||

| Beacon Planned Return Strategy Fund | ||||||||||||

| Equity Contracts | ||||||||||||

| (Purchased Options/Written Options) | Investments, at value | $ | 424,436,226 | Written Options, at value | $ | 71,005,297 | ||||||

| $ | 424,436,226 | $ | 71,005,297 | |||||||||

| Annual Report | September 30, 2021 | 31 |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

The effect of derivative instruments on the Statements of Operations for the year ended September 30, 2021:

| Risk Exposure | Statements of Operations Location | Realized Gain (Loss) on Derivatives Recognized in Income | Change in Unrealized Gain (Loss) on Derivatives Recognized in Income | |||||||

| Beacon Accelerated Return Strategy Fund | ||||||||||

| Equity Contracts (Purchased Options) | Net realized gain/(loss) on investments/Net change in unrealized appreciation/ (depreciation) on investments | $ | 60,581,497 | $ | (7,733,233 | ) | ||||

| Equity Contracts (Written Options) | Net realized gain/(loss) on written option contracts/Net change in unrealized appreciation/ (depreciation) on written option contracts | (37,981,708 | ) | 5,522,204 | ||||||

| Total | $ | 22,599,789 | $ | (2,211,029 | ) | |||||

| Beacon Planned Return Strategy Fund | ||||||||||

| Equity Contracts (Purchased Options) | Net realized gain/(loss) on investments/Net change in unrealized appreciation/ (depreciation) on investments | $ | 147,306,141 | $ | (535,144 | ) | ||||

| Equity Contracts (Written Options) | Net realized gain/(loss) on written option contracts/Net change in unrealized appreciation/ (depreciation) on written option contracts | (108,238,114 | ) | 2,096,550 | ||||||

| Total | $ | 39,068,027 | $ | 1,561,406 | ||||||

4. TAX BASIS INFORMATION

Tax Basis of Distributions to Shareholders: The character of distributions made during the period from net investment income or net realized gains may differ from its ultimate characterization for federal income tax purposes. Also, due to the timing of dividend distributions, the fiscal year in which amounts are distributed may differ from the fiscal year in which the income or realized gain were recorded by the Funds. The amounts and characteristics of tax basis distributions and composition of distributable earnings/(accumulated losses) are finalized at fiscal year-end.

| 32 | www.beacontrust.com |

| Beacon Funds Trust | Notes to Financial Statements |

September 30, 2021

The tax character of distributions paid during the fiscal year ended September 30, 2021, were as follows:

| Ordinary Income | Long-Term Capital Gains | |||||||

| Beacon Accelerated Return Strategy Fund | $ | 2,817,768 | $ | 6,280,736 | ||||

| Beacon Planned Return Strategy Fund | 4,302,404 | 11,786,530 | ||||||

The tax character of distributions paid during the fiscal year ended September 30, 2020, were as follows:

| Ordinary Income | Long-Term Capital Gains | |||||||

| Beacon Accelerated Return Strategy Fund | $ | 1,155,236 | $ | 3,866,468 | ||||