UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act File Number 811-22920

The Advisors’ Inner Circle Fund III

(Exact name of registrant as specified in charter)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Address of principal executive offices) (Zip code)

SEI Investments

One Freedom Valley Drive

Oaks, PA 19456

(Name and address of agent for service)

Registrant’s telephone number, including area code: (877) 446-3863

Date of fiscal year end: October 31, 2022

Date of reporting period: October 31, 2022

| Item 1. | Reports to Stockholders. |

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Act”) (17 CFR § 270.30e-1), is attached hereto.

The Advisors’ Inner Circle Fund III

MetLife Core Plus Fund

| Annual Report | October 31, 2022 |

Investment Adviser: MetLife Investment Management, LLC

|

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

|

| |||

| 1 | ||||

| 7 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 34 | ||||

| 36 | ||||

| 47 | ||||

| 48 | ||||

Trustees and Officers of the Advisors’ Inner Circle Fund III | 50 | |||

| 56 | ||||

The Fund files its complete schedule of investments with the Securities and Exchange Commission (“SEC”) for the first and third quarters of each fiscal year as an exhibit to its report on Form N-PORT. The Fund’s Forms N-Q and N-PORT are available on the SEC’s website at http://www.sec.gov, and may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

A description of the policies and procedures that the Fund uses to determine how to vote proxies relating to fund securities, as well as information relating to how the Fund voted proxies relating to fund securities during the most recent 12-month period ended June 30, will be available (i) without charge, upon request, by calling 1-800-252-4993; and (ii) on the Commission’s website at https://www.sec.gov.

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

Investment Objective

The investment objective of the MetLife Core Plus Fund (the “Fund”) is to seek to maximize capital appreciation and income.

Review

The overweight to spread sectors and underweight allocation to US Treasuries detracted as credit spreads were volatile and widened out during the course of the 12-month period. Rates were also extremely volatile and the curve inverted. A slight underweight to duration and a flattening bias in the portfolio were modestly positive contributors to performance.

Overall, investment grade corporates led the bulk of underperformance with the driver being security selection within Industrials. The Energy, Tobacco, and Cable subsectors were all sources of challenged security selection. In Financials, subordinated holdings drove underperformance, in addition to those holdings in the Banking sector with European exposure. Generically, less liquid and underfollowed credits struggled in 2022, and a number of overweights fall into this category. An allocation to High Yield was also a detractor to performance, as the out-of-benchmark sector was under pressure amidst a turbulent macro environment.

Collateralized Mortgage-Backed Security (“CMBS”) exposure was positive, driven by an overweight to Fixed Rate Non-Agency AAA rated paper. Floating Rate CMBS bonds partially offset relative returns. Asset-Backed Securities (“ABS”) added to relative returns due to sector allocation. In a volatile year within fixed income markets, shorter high-quality sectors such as ABS outperformed nearly all other asset classes. Thus, our overweight to the sector aided performance. Collateralized Loan Obligations (“CLOs”) modestly detracted from performance as index spreads widened and the credit curve steepened. The primary driver was the portfolio’s allocation to AA CLOs. Residential Mortgage-Backed Securities (“RMBS”) drove underperformance due to an overweight to 30-year, low coupon Conventionals in Specified Pools.

Outlook

Looking ahead, it is hard to ignore the irrefutable truth that the Federal Reserve has one goal right now (and one goal only), and that is to temper inflation. To accomplish this will require more restrictive monetary policy and slower growth – which is not supportive of risk assets. To get the pendulum to shift to a more attractive environment for risk taking, the market will need to be able to better grasp both the timing of achieving peak inflation and the duration of the adjustment period necessary to return to the Fed’s targeted level of inflation. Neither of those signposts seem imminent. Brief rallies in the market have generally been accompanied by murmurs of Fed easing. We believe these to be misguided. Fed speakers are going out of their way to emphasize that their job will not be done until inflation is tamed – and we believe them. To us, the inflation battle is the overarching risk factor in the market right now, but that is not to diminish the quantity or severity of the other risks present. The war in Ukraine, the European gas crisis, and COVID lockdowns in China are part of a myriad of “knowns” in the market. What is more troubling are the second, third, fourth derivative “unknowns”. The recent UK pension fund crisis was a sobering reminder of the intertwined nature of markets, with collateral calls in the UK being met by selling of US credit (which is a much deeper market for the long duration

1

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

assets owned in these funds). It is hard enough to assess the value of credit amidst the known issues – but the likelihood of further knock-on effects is too high to not anticipate a further discount for spreads.

It is not all bad news for credit investors. Valuations are getting more attractive by the day. Investment grade corporates ended the quarter at +159 OAS – 67 basis points wider year-to-date. More eye-popping is the 5.69% yield of the Bloomberg US Corporate Index. That is 336 basis points higher on the year. The phrase “There is No Alternative” or “TINA” was in vogue for the last few years when there seemed to be no attractive alternative for equities. We are not creative enough to invent new acronyms, but we feel comfortable suggesting TINA can be retired for now because the alternatives are plentiful. If you wanted 4% yields at the start of 2022 you had to buy high yield. Now you can get 4% from T-Bills. The resetting of valuations in 2022 should ultimately provide some level of support for fixed income assets – though the buyer base is likely to shift. Yield hungry domestic buyers – both institutional (e.g., pension, insurance) and retail are likely to welcome the new paradigm of a higher rate environment, while foreign investors are pulling back. They are pulling back due to the rapidly changing economics of hedged yields which have made US corporates hedged back to their local currency increasingly unattractive. It is too early to decipher which flow dynamic is likely to win out – but there are likely to be periods of uneven transition to add to an already volatile environment.

As we evaluate current valuations, we are reticent to get too mesmerized by spreads and yields that we have not seen since the onset of COVID. Historically there has been no magic ceiling for spreads, but credit has been no stranger to visiting OAS levels in the low 200s during periods of elevated volatility and recession. We may not reach those levels this time around due to the health of consumer and corporate balance sheets, but we believe there is enough global uncertainty that a future moment of capitulation could ultimately propel spreads towards those levels.

This process could take some time. There has been a well-defined trend this year of wider wides and wider tights in credit spreads. We would expect this pattern to persist within a broader widening trend. We recognize the difficulty in picking the lows, and so we will use these backups to gradually add risk back to the portfolio. One area of the market we feel comfortable adding to right now is short-dated credit. Flatter rate and spread curves have created extremely attractive opportunities to allocate capital in a maturity window in which we believe we can get very comfortable with the trajectory of the balance sheet. We believe we can structure portfolios to continue to add some yield advantage to the portfolio (at the expense of cash and Treasuries) while still maintaining a generally conservative risk posture until valuations cheapen further. Away from these front-end opportunities, we are intensely focused on the fundamental outlooks for the credits in which we are invested, and their ability to generate attractive risk adjusted returns in the context of a recessionary environment. To the extent that we can identify better opportunities, we are going to reposition into those more resilient credits. We will also continue to be active in the new issue market. Primary issuance has slowed dramatically as many issuers are waiting for calmer conditions, but elevated volatility has resulted in elevated concessions that offers us an opportunity to allocate to liquid credit at attractive valuations. Liquidity is valuable in this market, and so any tactical trading opportunities will likely be concentrated in the primary market, whereas we recognize that relative value trades into less liquid curve points will take longer to monetize.

The “all clear” for credit remains just a dot in the distance, but we believe this to be an

2

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

environment where fundamental credit research will be critical to not only picking winners, but also avoiding the losers in what is likely to be a period of elevated volatility.

Structured Products

In last quarter’s update, we pointed out the Fed’s desired balance sheet run-off regarding agency MBS was going to fall well short of the targeted $35 billion a month. That has raised the specter of possible asset sales to reach their desired objective. We continue to maintain that MBS sales are a very tenuous proposition, and that active selling of MBS may damage an already challenging liquidity environment, ultimately pressuring mortgage spreads and contributing to even high mortgage rates. With mortgage rates up over 3.50% this year, a dysfunctional mortgage market is not something the Fed can easily solve given the current inflationary environment. However, high interest rate volatility combined with a technical backdrop where banks and REITs are dealing with an inverted curve, duration extension, and book value losses, make it difficult to construct a picture that improves the outlook for agency MBS – especially one that doesn’t involve more clarity into the Fed’s ultimate end game.

Over most of the Covid related recovery in asset prices, we maintained an underweight to agency MBS, as spreads were artificially suppressed by the Fed’s asset purchase program. Now that they have embarked on a passive quantitative tightening program, their support is no longer present and valuations are more compelling, making us much more constructive on spreads. Thus, we took advantage of the recent volatility to move to a modest overweight position. We continue to rotate out of TBA mortgages as roll specialness diminishes, and instead favor specified pools, a trend we expect to continue. We continue to focus on specified pools in lower coupons that have the propensity to pay faster than generic collateral, enhancing their yield profile. In higher coupons where negative convexity is more of a concern, our strategy it to buy call protection in the event interest rates fall, allowing portfolios to hold onto that high coupon for longer. With valuations as of this writing sitting on the cheaper side for the first time in years, we expect to move further overweight the basis. However, with volatility at extreme levels, we are operating under a regime where we are going to take what the market gives us in the quarter ahead.

The Non-Agency market has been especially hard hit by the sharp rise in interest rates during the year. While this is not a concern relative to credit quality, it points to the broader slowdown that is hitting the housing market. Underwriting has been strong during the run up in home prices, but with affordability stretched given high prices and high interest rates, we expect some modest stress to start to surface. Unlike the mid 2000’s where ARMs with low teasers were all the rage, the majority of what is in new production Non-Agency pools are loans to high quality borrowers with substantial down payments. In addition, Covid-era home buyers/ refinancers locked in ultra-cheap fixed rate financing, providing them with the ability to weather an economic downturn and incenting them to continue to pay their mortgage debt provided their employment situation remains stable. Unemployment will be the key driver of housing market stress during this cycle. Non-Agency spreads remain volatile taking their que from the broader risk markets. The new issue non-QM market is still pricing to structures we do not prefer given the ongoing uncertainty in the rates market. We continue to be patient in the sub-sector looking for seasoned securities at discount dollar prices. In addition, our focus in the reperforming loan market is on discount securities where speeds are supported by the seasoned nature of the collateral. We are focused on the AAA portion of the capital structure within the sector.

3

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

We remain overweight CMBS and are comfortable with this positioning as the majority of this exposure is to shorter duration cashflows of seasoned deals; despite current headwinds much of the collateral properties within the deals have entrenched valuation improvements to allow for continued good performance and the ability to refinance. We favor bonds with stable cashflows such as front cash flow discount AAAs, which will not extend but are also protected from prepay risk due to their discount nature. We also are overweight AAA rated floating rate SASB and CRE CLO paper trading with spreads greater than 200. We find valuations attractive but also at the whim of increased secondary supply.

The ABS spread movements wider both this quarter and year to date have been immense. With these now wider spreads, we find several high-quality areas of ABS to be attractive, notably top of the credit stack paper within private student loans, subprime auto, equipment loans, and fleet lease auto paper. Tiering between issuers can be steep and we likely will invest primarily in first and second tier names to maintain liquidity as we enter a part of the year with likely diminished trading activity. We are avoiding unsecured consumer loans and subprime auto mezzanine bonds due to elevated credit risks.

In CLOs, we maintained our exposure throughout the quarter. Like other asset classes, spreads were volatile but ended the quarter off the wides. Higher coupons, because of the Fed’s aggressive hiking campaign, have kept high quality CLO floaters supported. However, these rate hikes will start to weigh on levered loans as the cost of capital increases to the end borrower. Defaults are expected to climb, but off very low levels. Even if defaults were to rise unexpectedly, the portfolio’s focus on the top of the capital structure (AAA/AA) will mitigate potential downgrade risks via robust credit enhancement and structural protections.

High Yield

As fixed income spreads have continued to widen out, coupled with rising rates, there has been renewed value in the High Yield universe. HY yields are nearing the peaks of 2011 and 2016, on pace to reach levels last seen in 2009. The spread differential relative to US Investment Grade assets has continued to widen, offering opportunities with additional compensation for down in quality risk. HY fundamentals appear strong with net leverage decreasing off the peaks, therefore we are comfortable going out the curve from a credit risk perspective. However, with lingering recession concerns, we continue to prefer securities within the BB portion of the market as well as stable, less cyclical single-B issuers, to buffer against potential declining corporate fundamentals in a broad sell-off. Dispersion and inflationary pressures will be continued themes, so we will look to shorter duration holdings to limit the downside risk, as a higher yielding environment will compensate us through shorter breakevens amid increased dispersion.

Emerging Markets

Macro uncertainty will continue to present challenges in the near term for Emerging Markets; however, as inflation peaks and interest rate volatility subsides, opportunities will likely arise in the space. We believe this current environment presents opportunities in the EM space, where yields on the indices are at levels not seen since 2009. Security selection has proven to be more important than ever in identifying issuers with strong fundamentals despite a sell-off due to market technicals. With EM corporates down 16% year-to-date and on track for the second worst year on record since the inception of the index, this weakness could drive performance over the next year horizon. EM Sovereigns, down 24% year-to-date, are also poised for strong

4

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

upside if inflation peaks, if countries are able to stabilize currencies, and if IMF support remains strong for lower quality issuers.

The views present are MIM’s only, are subject to change, and may not reflect the manager’s current views. There can be no assurance that the views expressed above will prove accurate and should not be relied upon as a reliable indicator of future events. Any securities mentioned are for informational purposes only and do not represent a recommendation or an offer to buy, hold or sell any securities, and may not be held in client portfolios. Any performance or portfolio holdings cited here were current as of the date stated and are subject to change.

Definition of Comparative Index and Other Investment Terms

Bloomberg US Aggregate Bond Index is an index generally representing fixed rate, investment-grade government bonds, corporate debt securities, mortgage-backed securities, and asset-backed securities with minimum maturity dates of at least one year.

Bloomberg US Corporate Index measures the investment grade, fixed-rate, taxable corporate bond market. It includes USD-denominated securities publicly issued by US and non-US industrial, utility and financial issuers.

5

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

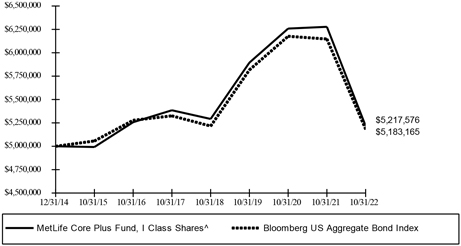

Comparison of Change in the Value of a $5,000,000 Investment in the MetLife Core Plus Fund, I Class Shares versus the Bloomberg US Aggregate Bond Index.

TOTAL RETURN FOR THE YEAR ENDED OCTOBER 31, 2022 | ||||||||

| One Year Return | Three Year Return | Five Year Return | Annualized Inception to Date* | |||||

I Class Shares | -16.88% | -3.99% | -0.63% | 0.54% | ||||

R Class Shares** | -16.96% | -5.10% | -2.13% | -0.43% | ||||

Bloomberg US Aggregate Bond Index | -15.68% | -3.77% | -0.54% | 0.46% | ||||

* The MetLife Core Plus Fund, I Class and R Class Shares, commenced operations on December 31, 2014.

** As R Class Shares only held seed money, Class R Shares did not incur distribution fees due to low net assets. If these fees were incurred the performance disclosed would have been lower.

^ The graph is based on only the I Class Shares.

The Fund’s performance assumes the reinvestment of dividends and capital gains. Index returns assume reinvestment of dividends and, unlike a portfolio’s returns, do not reflect any fees or expenses. If such fees and expenses were included in the index returns, the performance would have been lower. Please note that one cannot invest directly in an unmanaged index.

There are no assurances that the Fund will meet its stated objectives. The Fund’s holdings and allocations are subject to change because it is actively managed and should not be considered recommendations to buy individual securities.

Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares.

See definition of comparative index on page 5.

6

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

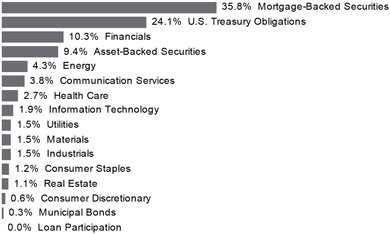

SECTOR WEIGHTING † (unaudited)

† Percentages are based on total investments.

The accompanying notes are an integral part of the financial statements.

7

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| MORTGAGE-BACKED SECURITIES — continued

| ||||||||

| Face Amount | Value | |||||||

| AGENCY MORTGAGE-BACKED OBLIGATIONS — continued | ||||||||

FHLMC Multifamily Structured Pass-Through Certificates, Ser X3FX, Cl A2FX | ||||||||

3.000%, 06/25/27 | $ | 910,000 | $ | 849,939 | ||||

FHLMC, Ser 2006-R006, Cl ZA | ||||||||

6.000%, 04/15/36 | 7,097 | 7,302 | ||||||

FHLMC, Ser 2010-3632, Cl PK | ||||||||

5.000%, 02/15/40 | 20,350 | 20,113 | ||||||

FHLMC, Ser 2012-271, Cl 30 | ||||||||

3.000%, 08/15/42 | 37,932 | 34,133 | ||||||

FHLMC, Ser 2015-4479, Cl HA | ||||||||

3.750%, 05/15/39 | 18,341 | 18,145 | ||||||

FHLMC, Ser 2017-356, Cl 300 | ||||||||

3.000%, 09/15/47 | 156,736 | 141,447 | ||||||

FNMA | ||||||||

6.000%, 09/01/39 | 676 | 700 | ||||||

5.500%, 04/01/36 to 07/01/40 | 136,647 | 136,269 | ||||||

5.000%, 02/01/31 | 15,650 | 15,561 | ||||||

4.500%, 04/01/35 to 06/01/52 | 904,736 | 864,877 | ||||||

4.000%, 06/01/42 to 05/01/52 | 4,975,184 | 4,608,871 | ||||||

3.500%, 07/01/30 to 04/01/52 | 4,357,015 | 3,911,032 | ||||||

3.040%, 01/01/28 | 165,000 | 151,292 | ||||||

3.000%, 12/01/31 to 12/01/51 | 10,218,970 | 8,948,776 | ||||||

2.500%, 06/01/50 to 04/01/52 | 11,947,368 | 9,911,211 | ||||||

2.000%, 05/01/36 to 12/01/51 | 18,401,944 | 14,749,163 | ||||||

1.850%, 09/01/35 | 281,089 | 231,360 | ||||||

FNMA, Ser 2001-T4, Cl A1 | ||||||||

7.500%, 07/25/41 | 1,426 | 1,419 | ||||||

FNMA, Ser 2005-24, Cl ZE | ||||||||

5.000%, 04/25/35 | 3,798 | 3,746 | ||||||

FNMA, Ser 2012-121, Cl TB | ||||||||

7.000%, 11/25/42 | 19,494 | 20,708 | ||||||

FNMA, Ser 2012-411, Cl A3 | ||||||||

3.000%, 08/25/42 | 421,841 | 373,002 | ||||||

The accompanying notes are an integral part of the financial statements.

8

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| MORTGAGE-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

| AGENCY MORTGAGE-BACKED OBLIGATIONS — continued | ||||||||

GNMA | ||||||||

5.500%, 07/20/43 to 09/20/43 | $ | 4,081 | $ | 4,205 | ||||

4.690%, 06/20/62 (A) | 356 | 346 | ||||||

4.548%, 01/20/67 (A) | 51,732 | 50,730 | ||||||

4.500%, 03/15/42 | 45,992 | 44,828 | ||||||

3.000%, 04/20/45 | 72,335 | 64,676 | ||||||

2.500%, 04/20/51 to 11/20/51 | 1,924,759 | 1,634,554 | ||||||

GNMA TBA | ||||||||

4.000%, 11/01/35 | 1,059,000 | 975,753 | ||||||

3.500%, 11/15/41 | 889,000 | 795,576 | ||||||

3.000%, 11/15/52 | 912,000 | 793,796 | ||||||

GNMA, Ser 2010-H14, Cl BI, IO | ||||||||

1.388%, 07/20/60 (A) (B) | 1,554 | 57 | ||||||

GNMA, Ser 2017-H16, Cl PT | ||||||||

4.709%, 05/20/66 (A) | 228 | 226 | ||||||

UMBS TBA | ||||||||

5.000%, 11/01/37 | 1,910,000 | 1,841,732 | ||||||

4.500%, 11/15/34 | 4,767,346 | 4,471,622 | ||||||

4.000%, 11/12/39 | 2,265,997 | 2,059,543 | ||||||

3.500%, 11/01/40 | 2,172,000 | 1,908,792 | ||||||

3.000%, 11/15/42 | 1,023,000 | 869,310 | ||||||

2.500%, 11/25/27 to 11/15/52 | 5,054,253 | 4,285,987 | ||||||

2.000%, 11/15/37 to 11/15/52 | 3,684,620 | 3,066,665 | ||||||

|

| |||||||

| 83,212,189 | ||||||||

|

| |||||||

NON-AGENCY MORTGAGE-BACKED OBLIGATIONS — 8.6% |

| |||||||

1345 Avenue of the Americas & Park Avenue Plaza Trust, Ser 2005-1, Cl A3 | ||||||||

5.278%, 08/10/35 (C) | 331,081 | 317,372 | ||||||

Alen Mortgage Trust, Ser 2021-ACEN, Cl A | ||||||||

4.562%, ICE LIBOR USD 1 Month + 1.150%, 04/15/34 (C) | 585,000 | 556,072 | ||||||

Arbor Multifamily Mortgage Securities Trust, Ser 2021-MF2, Cl B | ||||||||

2.560%, 06/15/54 (A) (C) | 360,000 | 261,974 | ||||||

The accompanying notes are an integral part of the financial statements.

9

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| MORTGAGE-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

NON-AGENCY MORTGAGE-BACKED OBLIGATIONS — continued |

| |||||||

BANK, Ser 2022-BNK40, Cl A4 | ||||||||

3.394%, 03/15/64 (A) | $ | 340,000 | $ | 285,514 | ||||

Bayview Commercial Asset Trust, Ser 2004-3, Cl A1 | ||||||||

4.141%, ICE LIBOR USD 1 Month + 0.555%, 01/25/35 (C) | 47,392 | 47,017 | ||||||

BBCMS Mortgage Trust, Ser 2020-C6, Cl AS | ||||||||

2.840%, 02/15/53 | 340,000 | 268,134 | ||||||

BBCMS Trust, Ser 2015-SRCH, Cl A1 | ||||||||

3.312%, 08/10/35 (C) | 581,925 | 540,127 | ||||||

Benchmark Mortgage Trust, Ser 2021-B31, Cl A5 | ||||||||

2.669%, 12/15/54 | 635,000 | 498,389 | ||||||

Benchmark Mortgage Trust, Ser 2022-B33, Cl A5 | ||||||||

3.458%, 03/15/55 | 525,000 | 444,367 | ||||||

Benchmark Mortgage Trust, Ser 2022-B35, Cl AS | ||||||||

4.445%, 05/15/55 (A) | 445,000 | 387,066 | ||||||

BMO Mortgage Trust, Ser 2022-C3, Cl AS | ||||||||

5.504%, 09/15/54 (A) | 410,000 | 387,064 | ||||||

BPR Trust, Ser 2022-OANA, Cl A | ||||||||

5.274%, TSFR1M + 1.898%, 04/15/37 (C) | 630,000 | 610,394 | ||||||

BWAY Mortgage Trust, Ser 2015-1740, Cl A | ||||||||

2.917%, 01/10/35 (C) | 1,185,000 | 1,055,966 | ||||||

BX Commercial Mortgage Trust, Ser 2019-XL, Cl A | ||||||||

4.332%, ICE LIBOR USD 1 Month + 0.920%, 10/15/36 (C) | 596,787 | 584,825 | ||||||

BX Mortgage Trust, Ser 2022-MVRK, Cl B | ||||||||

5.332%, TSFR1M + 1.916%, 03/15/39 (C) | 950,000 | 903,736 | ||||||

BX Trust, Ser 2019-MMP, Cl A | ||||||||

4.412%, ICE LIBOR USD 1 Month + 1.000%, 08/15/36 (C) | 497,510 | 481,315 | ||||||

BX Trust, Ser 2022-PSB, Cl A | ||||||||

5.827%, TSFR1M + 2.451%, 08/15/39 (C) | 100,000 | 99,689 | ||||||

CG-CCRE Commercial Mortgage Trust, Ser 2014-FL2, Cl A | ||||||||

5.266%, ICE LIBOR USD 1 Month + 1.854%, 11/15/31 (C) | 18,121 | 17,511 | ||||||

The accompanying notes are an integral part of the financial statements.

10

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| MORTGAGE-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

NON-AGENCY MORTGAGE-BACKED OBLIGATIONS — continued |

| |||||||

CIM Trust, Ser 2021-R6, Cl A1 | ||||||||

1.425%, 07/25/61 (A) (C) | $ | 845,904 | $ | 738,149 | ||||

CIM Trust, Ser 2022-R2, Cl A1 | ||||||||

3.750%, 12/25/61 (A) (C) | 499,208 | 464,643 | ||||||

Citigroup Mortgage Loan Trust, Ser 2021-INV1, Cl A3A | ||||||||

2.500%, 05/25/51 (A) (C) | 734,242 | 566,083 | ||||||

COMM Mortgage Trust, Ser 2013-LC6, Cl AM | ||||||||

3.282%, 01/10/46 | 1,010,000 | 1,006,281 | ||||||

COMM Mortgage Trust, Ser 2015-CR26, Cl C | ||||||||

4.469%, 10/10/48 (A) | 715,000 | 645,166 | ||||||

COMM Mortgage Trust, Ser 2020-CBM, Cl A2 | ||||||||

2.896%, 02/10/37 (C) | 145,000 | 132,327 | ||||||

Commercial Mortgage Trust, Ser 2022-LPFL, Cl B | ||||||||

5.271%, TSFR1M + 1.896%, 03/15/39 (C) | 195,000 | 186,770 | ||||||

CSAIL Commercial Mortgage Trust, Ser 2015-C3, Cl A3 | ||||||||

3.447%, 08/15/48 | 112,615 | 106,024 | ||||||

CSAIL Commercial Mortgage Trust, Ser 2015-C3, Cl ASB | ||||||||

3.448%, 08/15/48 | 319,449 | 310,367 | ||||||

CSAIL Commercial Mortgage Trust, Ser 2016-C7, Cl ASB | ||||||||

3.314%, 11/15/49 | 424,419 | 408,078 | ||||||

CSMC Trust, Ser 2016-NXSR, Cl A4 | ||||||||

3.795%, 12/15/49 (A) | 430,000 | 397,766 | ||||||

CSMC Trust, Ser 2021-RPL3, Cl A1 | ||||||||

2.000%, 01/25/60 (A) (C) | 751,858 | 646,797 | ||||||

CSMC, Ser 2014-USA, Cl A2 | ||||||||

3.953%, 09/15/37 (C) | 610,000 | 548,433 | ||||||

CSMC, Ser 2021-NQM8, Cl A1 | ||||||||

1.841%, 10/25/66 (A) (C) | 820,865 | 648,335 | ||||||

DBCCRE Mortgage Trust, Ser 2014-ARCP, Cl A | ||||||||

4.238%, 01/10/34 (C) | 300,000 | 288,005 | ||||||

DBCCRE Mortgage Trust, Ser 2014-ARCP, Cl C | ||||||||

4.935%, 01/10/34 (A) (C) | 450,000 | 421,543 | ||||||

The accompanying notes are an integral part of the financial statements.

11

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| MORTGAGE-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

NON-AGENCY MORTGAGE-BACKED OBLIGATIONS — continued |

| |||||||

EQUS Mortgage Trust, Ser 2021-EQAZ, Cl B | ||||||||

4.512%, ICE LIBOR USD 1 Month + 1.100%, 10/15/38 (C) | $ | 455,000 | $ 428,226 | |||||

FHLMC Whole Loan Securities Trust, Ser 2016-SC01, Cl 2A | ||||||||

3.500%, 07/25/46 | 31,798 | 29,683 | ||||||

Finance of America Structured Securities Trust, Ser 2021-JR1, Cl A2 | ||||||||

2.000%, 04/25/51 | 840,539 | 785,150 | ||||||

Finance of America Structured Securities Trust, Ser 2021-S2 | ||||||||

1.750%, 09/25/51 | 948,744 | 867,917 | ||||||

FREMF Mortgage Trust, Ser 2013-K31, Cl C | ||||||||

3.632%, 07/25/46 (A) (C) | 25,000 | 24,602 | ||||||

FWD Securitization Trust, Ser 2019-INV1, Cl A1 | ||||||||

2.810%, 06/25/49 (A) (C) | 47,628 | 42,916 | ||||||

GPMT, Ser 2021-FL3, Cl A | ||||||||

4.693%, ICE LIBOR USD 1 Month + 1.250%, 07/16/35 (C) | 315,596 | 307,319 | ||||||

JPMBB Commercial Mortgage Securities Trust, Ser 2013- C15, Cl AS | ||||||||

4.420%, 11/15/45 | 535,000 | 523,981 | ||||||

JPMBB Commercial Mortgage Securities Trust, Ser 2014- C21, Cl AS | ||||||||

3.997%, 08/15/47 | 825,000 | 788,955 | ||||||

JPMBB Commercial Mortgage Securities Trust, Ser 2014- C25, Cl B | ||||||||

4.347%, 11/15/47 (A) | 330,000 | 305,907 | ||||||

JPMorgan Chase Commercial Mortgage Securities Trust, Ser 2018-BCON, Cl B | ||||||||

3.756%, 01/05/31 (A) (C) | 145,000 | 143,650 | ||||||

JPMorgan Mortgage Trust, Ser 2021-INV2, Cl A2 | ||||||||

2.500%, 12/25/51 (A) (C) | 1,101,716 | 849,398 | ||||||

MFA Trust, Ser 2022-NQM2, Cl A1 | ||||||||

4.000%, 05/25/67 (C) | 657,831 | 600,816 | ||||||

The accompanying notes are an integral part of the financial statements.

12

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| MORTGAGE-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

NON-AGENCY MORTGAGE-BACKED OBLIGATIONS — continued |

| |||||||

Mill City Mortgage Loan Trust, Ser 2021-NMR1, Cl A1 | ||||||||

1.125%, 11/25/60 (A) (C) | $ | 449,863 | $ 414,074 | |||||

Morgan Stanley Bank of America Merrill Lynch Trust, Ser 2015-C24, Cl C | ||||||||

4.332%, 05/15/48 (A) | 210,000 | 189,998 | ||||||

Morgan Stanley Capital I Trust, Ser 2022-L8, Cl AS | ||||||||

3.795%, 04/15/55 (A) | 405,000 | 335,856 | ||||||

MortgageIT Trust, Ser 2005-1, Cl 1A1 | ||||||||

4.226%, ICE LIBOR USD 1 Month + 0.640%, 02/25/35 | 1,692 | 1,617 | ||||||

MSCG Trust, Ser 2015-ALDR, Cl A2 | ||||||||

3.462%, 06/07/35 (A) (C) | 380,000 | 343,067 | ||||||

OBX Trust, Ser 2020-EXP3, Cl 2A1A | ||||||||

4.486%, ICE LIBOR USD 1 Month + 0.900%, 01/25/60 (C) | 7,450 | 7,423 | ||||||

OBX Trust, Ser 2022-NQM1, Cl A1 | ||||||||

2.305%, 11/25/61 (A) (C) | 917,705 | 730,195 | ||||||

Sequoia Mortgage Trust, Ser 2018-CH4, Cl B1B | ||||||||

4.993%, 10/25/48 (A) (C) | 697,986 | 647,921 | ||||||

Towd Point Mortgage Trust, Ser 2018-2, Cl A1 | ||||||||

3.250%, 03/25/58 (A) (C) | 28,962 | 27,638 | ||||||

Towd Point Mortgage Trust, Ser 2019-4, Cl A1 | ||||||||

2.900%, 10/25/59 (A) (C) | 91,422 | 83,336 | ||||||

Towd Point Mortgage Trust, Ser 2020-3, Cl A1 | ||||||||

3.088%, 02/25/63 (A) (C) | 104,763 | 97,453 | ||||||

UBS Commercial Mortgage Trust, Ser 2017-C4, Cl A3 | ||||||||

3.301%, 10/15/50 | 273,308 | 244,193 | ||||||

UBS Commercial Mortgage Trust, Ser 2017-C7, Cl A3 | ||||||||

3.418%, 12/15/50 | 290,000 | 266,519 | ||||||

Wells Fargo Commercial Mortgage Trust, Ser 2022-C62,Cl A4 | ||||||||

4.000%, 04/15/55 (A) | 575,000 | 497,843 | ||||||

WFRBS Commercial Mortgage Trust, Ser 2013-C12, Cl C | ||||||||

4.314%, 03/15/48 (A) | 50,000 | 49,243 | ||||||

The accompanying notes are an integral part of the financial statements.

13

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| MORTGAGE-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

NON-AGENCY MORTGAGE-BACKED OBLIGATIONS — continued |

| |||||||

WFRBS Commercial Mortgage Trust, Ser 2014-C22, Cl B | ||||||||

4.371%, 09/15/57 (A) | $ | 425,000 | $ | 403,206 | ||||

|

| |||||||

| 25,299,401 | ||||||||

|

| |||||||

TOTAL MORTGAGE-BACKED SECURITIES | ||||||||

(Cost $121,124,814) | 108,511,590 | |||||||

|

| |||||||

CORPORATE OBLIGATIONS — 31.5% |

| |||||||

COMMUNICATION SERVICES — 3.9% |

| |||||||

AT&T | ||||||||

6.000%, 11/15/34 | 20,000 | 18,995 | ||||||

3.550%, 09/15/55 | 1,290,000 | 820,907 | ||||||

3.500%, 06/01/41 | 505,000 | 356,789 | ||||||

1.700%, 03/25/26 | 820,000 | 723,160 | ||||||

Charter Communications Operating | ||||||||

3.900%, 06/01/52 | 710,000 | 439,662 | ||||||

Cox Communications | ||||||||

4.800%, 02/01/35 (C) | 710,000 | 614,230 | ||||||

Nokia | ||||||||

6.625%, 05/15/39 | 350,000 | 319,305 | ||||||

Paramount Global | ||||||||

6.375%, US Treas Yield Curve Rate T Note Const Mat 5 Yr + 3.999%, 03/30/62 | 880,000 | 743,969 | ||||||

6.250%, ICE LIBOR USD 3 Month + 3.899%, 02/28/57 | 225,000 | 188,384 | ||||||

5.900%, 10/15/40 | 455,000 | 369,441 | ||||||

4.750%, 05/15/25 | 474,000 | 462,898 | ||||||

Sprint | ||||||||

7.875%, 09/15/23 | 515,000 | 523,448 | ||||||

Sprint Spectrum | ||||||||

5.152%, 03/20/28 (C) | 1,955,000 | 1,902,359 | ||||||

Time Warner Cable | ||||||||

5.875%, 11/15/40 | 790,000 | 640,820 | ||||||

T-Mobile USA | ||||||||

4.500%, 04/15/50 | 845,000 | 669,488 | ||||||

The accompanying notes are an integral part of the financial statements.

14

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

COMMUNICATION SERVICES — continued |

| |||||||

Verizon Communications | ||||||||

5.250%, 03/16/37 | $ | 760,000 | $ | 704,498 | ||||

4.016%, 12/03/29 | 251,000 | 226,225 | ||||||

3.550%, 03/22/51 | 255,000 | 172,124 | ||||||

Warnermedia Holdings | ||||||||

5.141%, 03/15/52 (C) | 2,150,000 | 1,501,170 | ||||||

|

| |||||||

| 11,397,872 | ||||||||

|

| |||||||

CONSUMER DISCRETIONARY — 0.6% |

| |||||||

Lowe’s | ||||||||

5.625%, 04/15/53 | 500,000 | 450,271 | ||||||

Resorts World Las Vegas | ||||||||

4.625%, 04/06/31 (C) | 670,000 | 454,155 | ||||||

Volkswagen Group of America Finance | ||||||||

1.250%, 11/24/25 (C) | 1,115,000 | 973,660 | ||||||

|

| |||||||

| 1,878,086 | ||||||||

|

| |||||||

CONSUMER STAPLES — 1.3% |

| |||||||

Altria Group | ||||||||

10.200%, 02/06/39 | 40,000 | 47,648 | ||||||

5.800%, 02/14/39 | 785,000 | 670,738 | ||||||

Anheuser-Busch InBev Worldwide | ||||||||

5.450%, 01/23/39 | 750,000 | 704,600 | ||||||

BAT Capital | ||||||||

4.390%, 08/15/37 | 670,000 | 485,309 | ||||||

3.557%, 08/15/27 | 370,000 | 322,123 | ||||||

Constellation Brands | ||||||||

4.400%, 11/15/25 | 445,000 | 433,225 | ||||||

JBS USA LUX | ||||||||

6.500%, 12/01/52 (C) | 790,000 | 693,367 | ||||||

Land O’ Lakes | ||||||||

7.250%, (C) (D) | 65,000 | 60,450 | ||||||

Reynolds American | ||||||||

8.125%, 05/01/40 | 45,000 | 46,342 | ||||||

7.250%, 06/15/37 | 220,000 | 209,695 | ||||||

|

| |||||||

| 3,673,497 | ||||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

15

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

ENERGY — 4.5% |

| |||||||

Cheniere Corpus Christi Holdings | ||||||||

3.700%, 11/15/29 | $ | 1,073,000 | $ | 934,523 | ||||

Continental Resources | ||||||||

2.268%, 11/15/26 (C) | 1,370,000 | 1,164,705 | ||||||

Devon Energy | ||||||||

7.875%, 09/30/31 | 195,000 | 214,933 | ||||||

Diamondback Energy | ||||||||

6.250%, 03/15/33 | 1,070,000 | 1,074,162 | ||||||

Energy Transfer | ||||||||

5.250%, 04/15/29 | 1,315,000 | 1,232,314 | ||||||

4.000%, 10/01/27 | 70,000 | 63,320 | ||||||

Eni | ||||||||

4.000%, 09/12/23 (C) | 1,370,000 | 1,344,996 | ||||||

Galaxy Pipeline Assets Bidco | ||||||||

1.750%, 09/30/27 (C) | 604,933 | 548,369 | ||||||

Hess | ||||||||

6.000%, 01/15/40 | 740,000 | 693,128 | ||||||

HF Sinclair | ||||||||

5.875%, 04/01/26 | 365,000 | 354,985 | ||||||

Hilcorp Energy I | ||||||||

6.250%, 04/15/32 (C) | 1,127,000 | 1,033,718 | ||||||

MPLX | ||||||||

4.950%, 03/14/52 | 805,000 | 622,313 | ||||||

4.800%, 02/15/29 | 625,000 | 578,496 | ||||||

Reliance Industries | ||||||||

3.625%, 01/12/52 (C) | 755,000 | 443,175 | ||||||

Sabine Pass Liquefaction | ||||||||

5.000%, 03/15/27 | 1,145,000 | 1,103,434 | ||||||

Saudi Arabian | ||||||||

Oil 1.625%, 11/24/25 (C) | 590,000 | 527,082 | ||||||

Tennessee Gas Pipeline | ||||||||

8.375%, 06/15/32 | 135,000 | 148,962 | ||||||

2.900%, 03/01/30 (C) | 690,000 | 561,745 | ||||||

Tullow Oil | ||||||||

10.250%, 05/15/26 (C) | 510,000 | 434,020 | ||||||

|

| |||||||

| 13,078,380 | ||||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

16

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

FINANCIALS — 10.6% |

| |||||||

Apollo Management Holdings | ||||||||

4.400%, 05/27/26 (C) | $ | 160,000 | $ | 150,282 | ||||

Athene Global Funding | ||||||||

2.950%, 11/12/26 (C) | 990,000 | 866,151 | ||||||

Athene Holding | ||||||||

4.125%, 01/12/28 | 1,205,000 | 1,073,171 | ||||||

Banco Santander | ||||||||

1.722%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 0.900%, 09/14/27 | 1,000,000 | 816,173 | ||||||

Banco Santander Mexico Institucion de Banca Multiple Grupo Financiero Santand | ||||||||

5.375%, 04/17/25 (C) | 365,000 | 354,050 | ||||||

Bank of America | ||||||||

4.571%, U.S. SOFR + 1.830%, 04/27/33 | 1,615,000 | 1,431,200 | ||||||

3.366%, ICE LIBOR USD 3 Month + 0.810%, 01/23/26 | 1,220,000 | 1,149,881 | ||||||

2.572%, U.S. SOFR + 1.210%, 10/20/32 | 845,000 | 637,503 | ||||||

Bank of Nova Scotia | ||||||||

4.900%, US Treas Yield Curve Rate T Note Const Mat 5 Yr + 4.551%, (D) | 870,000 | 805,987 | ||||||

Barclays | ||||||||

4.375%, 01/12/26 | 1,070,000 | 993,343 | ||||||

Blackstone Secured Lending Fund | ||||||||

3.625%, 01/15/26 | 590,000 | 531,505 | ||||||

Cantor Fitzgerald | ||||||||

4.500%, 04/14/27 (C) | 775,000 | 712,682 | ||||||

CI Financial | ||||||||

4.100%, 06/15/51 | 600,000 | 337,343 | ||||||

3.200%, 12/17/30 | 1,215,000 | 879,024 | ||||||

Citigroup | ||||||||

8.125%, 07/15/39 | 415,000 | 478,663 | ||||||

5.610%, U.S. SOFR + 1.546%, 09/29/26 | 655,000 | 646,322 | ||||||

4.910%, U.S. SOFR + 2.086%, 05/24/33 | 815,000 | 740,389 | ||||||

Citigroup Capital III | ||||||||

7.625%, 12/01/36 | 15,000 | 15,540 | ||||||

Cooperatieve Rabobank UA | ||||||||

3.758%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 1.420%, 04/06/33 (C) | 875,000 | 704,527 | ||||||

The accompanying notes are an integral part of the financial statements.

17

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

FINANCIALS — continued |

| |||||||

F&G Global Funding | ||||||||

1.750%, 06/30/26 (C) | $ | 475,000 | $ | 410,266 | ||||

Farmers Exchange Capital III | ||||||||

5.454%, ICE LIBOR USD 3 Month + 3.454%, 10/15/54 (C) | 615,000 | 544,594 | ||||||

Finance of America Funding | ||||||||

7.875%, 11/15/25 (C) | 1,245,000 | 753,225 | ||||||

Goldman Sachs Group | ||||||||

3.272%, ICE LIBOR USD 3 Month + 1.201%, 09/29/25 | 1,025,000 | 972,214 | ||||||

3.102%, U.S. SOFR + 1.410%, 02/24/33 | 915,000 | 716,619 | ||||||

HSBC Bank | ||||||||

7.650%, 05/01/25 | 75,000 | 75,699 | ||||||

Intercontinental Exchange | ||||||||

4.950%, 06/15/52 | 240,000 | 205,527 | ||||||

Intesa Sanpaolo | ||||||||

4.198%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 2.600%, 06/01/32 (C) | 650,000 | 440,006 | ||||||

Jackson Financial | ||||||||

3.125%, 11/23/31 | 800,000 | 589,746 | ||||||

JPMorgan Chase | ||||||||

1.045%, U.S. SOFR + 0.800%, 11/19/26 | 950,000 | 818,334 | ||||||

KKR Group Finance III | ||||||||

5.125%, 06/01/44 (C) | 120,000 | 101,317 | ||||||

Macquarie Bank | ||||||||

3.624%, 06/03/30 (C) | 550,000 | 434,430 | ||||||

Massachusetts Mutual Life Insurance | ||||||||

3.375%, 04/15/50 (C) | 700,000 | 452,364 | ||||||

Mercury General | ||||||||

4.400%, 03/15/27 | 819,000 | 754,940 | ||||||

Midcap Financial Issuer Trust | ||||||||

5.625%, 01/15/30 (C) | 775,000 | 596,750 | ||||||

Mitsubishi UFJ Financial Group | ||||||||

5.063%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 1.550%, 09/12/25 | 1,155,000 | 1,138,216 | ||||||

Morgan Stanley | ||||||||

1.593%, U.S. SOFR + 0.879%, 05/04/27 | 745,000 | 637,538 | ||||||

Morgan Stanley MTN | ||||||||

2.511%, U.S. SOFR + 1.200%, 10/20/32 | 795,000 | 598,547 | ||||||

The accompanying notes are an integral part of the financial statements.

18

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

FINANCIALS — continued |

| |||||||

Mutual of Omaha Insurance | ||||||||

4.297%, ICE LIBOR USD 3 Month + 2.640%, 07/15/54 (C) | $ | 73,000 | $ | 69,198 | ||||

NatWest Group | ||||||||

1.642%, US Treas Yield Curve Rate T Note Const Mat 1 Yr + 0.900%, 06/14/27 | 750,000 | 623,136 | ||||||

Ohio National Financial Services | ||||||||

6.050%, 01/24/30 (C) | 590,000 | 532,107 | ||||||

Principal Life Global Funding II | ||||||||

2.250%, 11/21/24 (C) | 990,000 | 926,896 | ||||||

Prospect Capital | ||||||||

3.706%, 01/22/26 | 290,000 | 248,216 | ||||||

Santander Holdings USA | ||||||||

3.450%, 06/02/25 | 690,000 | 644,264 | ||||||

Societe Generale | ||||||||

3.625%, 03/01/41 (C) | 435,000 | 246,228 | ||||||

Societe Generale MTN | ||||||||

2.625%, 01/22/25 (C) | 1,050,000 | 962,966 | ||||||

SVB Financial Group | ||||||||

4.700%, US Treas Yield Curve Rate T Note Const Mat 10 Yr + 3.064%, (D) | 885,000 | 590,738 | ||||||

Toronto-Dominion Bank MTN | ||||||||

4.456%, 06/08/32 | 990,000 | 889,701 | ||||||

US Bancorp | ||||||||

4.967%, U.S. SOFR + 2.110%, 07/22/33 | 660,000 | 601,008 | ||||||

Validus Holdings | ||||||||

8.875%, 01/26/40 | 115,000 | 138,400 | ||||||

Wells Fargo MTN | ||||||||

3.196%, ICE LIBOR USD 3 Month + 1.170%, 06/17/27 | 1,040,000 | 942,181 | ||||||

Westpac Banking | ||||||||

2.668%, US Treas Yield Curve Rate T Note Const Mat 5 Yr + 1.750%, 11/15/35 | 580,000 | 410,876 | ||||||

|

| |||||||

| 31,389,983 | ||||||||

|

| |||||||

HEALTH CARE — 2.9% |

| |||||||

Advocate Health & Hospitals | ||||||||

2.211%, 06/15/30 | 395,000 | 314,302 | ||||||

The accompanying notes are an integral part of the financial statements.

19

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

HEALTH CARE — continued |

| |||||||

Amgen | ||||||||

6.375%, 06/01/37 | $ | 535,000 | $ | 554,653 | ||||

3.000%, 01/15/52 | 855,000 | 526,685 | ||||||

Bayer US Finance | ||||||||

3.375%, 10/08/24 (C) | 30,000 | 28,841 | ||||||

Bayer US Finance II | ||||||||

4.700%, 07/15/64 (C) | 765,000 | 545,113 | ||||||

Bon Secours Mercy Health | ||||||||

3.464%, 06/01/30 | 220,000 | 192,879 | ||||||

2.095%, 06/01/31 | 440,000 | 334,336 | ||||||

Bristol-Myers Squibb | ||||||||

3.700%, 03/15/52 | 715,000 | 530,317 | ||||||

2.950%, 03/15/32 | 345,000 | 291,858 | ||||||

Cigna | ||||||||

4.800%, 08/15/38 | 594,000 | 523,423 | ||||||

CommonSpirit Health | ||||||||

4.350%, 11/01/42 | 45,000 | 34,849 | ||||||

4.187%, 10/01/49 | 70,000 | 49,568 | ||||||

3.910%, 10/01/50 | 740,000 | 496,660 | ||||||

Royalty Pharma | ||||||||

1.200%, 09/02/25 | 740,000 | 652,710 | ||||||

Smith & Nephew | ||||||||

2.032%, 10/14/30 | 595,000 | 437,108 | ||||||

Takeda Pharmaceutical | ||||||||

5.000%, 11/26/28 | 750,000 | 723,816 | ||||||

Teva Pharmaceutical Finance Netherlands III | ||||||||

2.800%, 07/21/23 | 1,055,000 | 1,025,703 | ||||||

UnitedHealth Group | ||||||||

5.875%, 02/15/53 | 1,035,000 | 1,056,315 | ||||||

|

| |||||||

| 8,319,136 | ||||||||

|

| |||||||

INDUSTRIALS — 1.5% |

| |||||||

AerCap Ireland Capital DAC | ||||||||

3.000%, 10/29/28 | 830,000 | 670,533 | ||||||

Boeing | ||||||||

2.196%, 02/04/26 | 920,000 | 812,999 | ||||||

CoStar Group | ||||||||

2.800%, 07/15/30 (C) | 765,000 | 603,035 | ||||||

The accompanying notes are an integral part of the financial statements.

20

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

INDUSTRIALS — continued |

| |||||||

GE Capital International Funding Unlimited | ||||||||

4.418%, 11/15/35 | $ | 424,000 | $ | 374,092 | ||||

Raytheon Technologies | ||||||||

3.950%, 08/16/25 | 595,000 | 577,067 | ||||||

Triton Container International | ||||||||

2.050%, 04/15/26 (C) | 450,000 | 380,051 | ||||||

Union Pacific | ||||||||

4.950%, 09/09/52 | 500,000 | 449,795 | ||||||

United Airlines | ||||||||

4.375%, 04/15/26 (C) | 615,000 | 561,285 | ||||||

|

| |||||||

| 4,428,857 | ||||||||

|

| |||||||

INFORMATION TECHNOLOGY — 1.9% |

| |||||||

Apple | ||||||||

4.100%, 08/08/62 | 560,000 | 434,998 | ||||||

Broadcom | ||||||||

4.926%, 05/15/37 (C) | 327,000 | 269,615 | ||||||

4.150%, 11/15/30 | 242,000 | 208,137 | ||||||

3.419%, 04/15/33 (C) | 364,000 | 276,587 | ||||||

Kyndryl Holdings | ||||||||

2.050%, 10/15/26 | 675,000 | 527,864 | ||||||

Marvell Technology | ||||||||

1.650%, 04/15/26 | 972,000 | 839,706 | ||||||

Oracle | ||||||||

3.800%, 11/15/37 | 990,000 | 719,575 | ||||||

3.600%, 04/01/40 | 650,000 | 439,806 | ||||||

2.950%, 04/01/30 | 120,000 | 97,716 | ||||||

PayPal Holdings | ||||||||

5.050%, 06/01/52 | 840,000 | 727,914 | ||||||

TSMC Arizona | ||||||||

1.750%, 10/25/26 | 750,000 | 647,205 | ||||||

Vontier | ||||||||

2.950%, 04/01/31 | 285,000 | 199,993 | ||||||

1.800%, 04/01/26 | 330,000 | 273,389 | ||||||

|

| |||||||

| 5,662,505 | ||||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

21

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

MATERIALS — 1.6% | ||||||||

Celanese US Holdings | ||||||||

6.379%, 07/15/32 | $ | 620,000 | $ | 564,127 | ||||

6.330%, 07/15/29 | 695,000 | 646,496 | ||||||

6.050%, 03/15/25 | 1,700,000 | 1,653,160 | ||||||

Freeport-McMoRan | ||||||||

5.450%, 03/15/43 | 110,000 | 90,365 | ||||||

Industrias Penoles | ||||||||

4.150%, 09/12/29 (C) | 800,000 | 694,535 | ||||||

Newcrest Finance Pty | ||||||||

3.250%, 05/13/30 (C) | 545,000 | 440,448 | ||||||

Sealed Air | ||||||||

1.573%, 10/15/26 (C) | 465,000 | 389,243 | ||||||

|

| |||||||

| 4,478,374 | ||||||||

|

| |||||||

REAL ESTATE — 1.2% | ||||||||

Essential Properties | ||||||||

2.950%, 07/15/31 | 760,000 | 540,728 | ||||||

Newmark Group | ||||||||

6.125%, 11/15/23 | 550,000 | 548,207 | ||||||

Sabra Health Care | ||||||||

3.900%, 10/15/29 | 585,000 | 464,340 | ||||||

Scentre Group Trust | ||||||||

1 3.625%, 01/28/26 (C) | 185,000 | 170,881 | ||||||

Scentre Group Trust 2 | 960,000 | 811,699 | ||||||

Simon Property Group | ||||||||

2.450%, 09/13/29 | 1,020,000 | 817,130 | ||||||

|

| |||||||

| 3,352,985 | ||||||||

|

| |||||||

UTILITIES — 1.5% | ||||||||

Enel Finance International | ||||||||

6.800%, 10/14/25 (C) | 420,000 | 421,747 | ||||||

Oncor Electric Delivery | ||||||||

2.750%, 05/15/30 | 815,000 | 685,065 | ||||||

Pacific Gas and Electric | ||||||||

2.500%, 02/01/31 | 150,000 | 112,081 | ||||||

2.100%, 08/01/27 | 1,035,000 | 851,032 | ||||||

1.700%, 11/15/23 | 1,125,000 | 1,078,196 | ||||||

The accompanying notes are an integral part of the financial statements.

22

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| CORPORATE OBLIGATIONS — continued | ||||||||

| Face Amount | Value | |||||||

UTILITIES — continued |

| |||||||

Texas Electric Market Stabilization Funding N | ||||||||

4.265%, 08/01/34 (C) | $ | 1,165,000 | $ | 1,097,490 | ||||

Vistra Operations | ||||||||

4.300%, 07/15/29 (C) | 415,000 | 362,041 | ||||||

|

| |||||||

| 4,607,652 | ||||||||

|

| |||||||

TOTAL CORPORATE OBLIGATIONS | ||||||||

(Cost $111,274,939)

| 92,267,327 | |||||||

|

| |||||||

U.S. TREASURY OBLIGATIONS — 25.0%

|

| |||||||

U.S. Treasury Bills | ||||||||

3.204%, 12/27/22(E) | 9,805,000 | 9,746,698 | ||||||

2.506%, 11/10/22(E) | 8,575,000 | 8,569,382 | ||||||

U.S. Treasury Bonds | ||||||||

3.375%, 08/15/42 | 3,340,000 | 2,881,272 | ||||||

3.000%, 08/15/52 | 1,315,000 | 1,053,027 | ||||||

2.875%, 05/15/52 | 3,415,000 | 2,650,360 | ||||||

2.375%, 02/15/42 | 9,485,000 | 6,925,532 | ||||||

2.000%, 11/15/41 | 845,000 | 576,052 | ||||||

1.750%, 08/15/41 | 7,870,000 | 5,136,405 | ||||||

1.375%, 08/15/50 | 10,855,000 | 5,786,648 | ||||||

U.S. Treasury Notes | ||||||||

4.250%, 10/15/25 | 3,475,000 | 3,456,539 | ||||||

4.125%, 09/30/27 | 10,370,000 | 10,313,289 | ||||||

3.875%, 09/30/29 | 400,000 | 392,875 | ||||||

3.250%, 06/30/29 | 2,275,000 | 2,148,098 | ||||||

3.000%, 07/15/25 | 1,005,000 | 967,941 | ||||||

2.750%, 08/15/32 | 685,000 | 612,968 | ||||||

2.375%, 03/31/29 | 13,415,000 | 12,020,049 | ||||||

|

| |||||||

TOTAL U.S. TREASURY OBLIGATIONS | ||||||||

(Cost $85,121,898) | 73,237,135 | |||||||

|

| |||||||

ASSET-BACKED SECURITIES — 9.7% |

| |||||||

AccessLex Institute, Ser 2007-A, Cl A3 | 292,444 | 282,344 | ||||||

The accompanying notes are an integral part of the financial statements.

23

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| ASSET-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

Affirm Asset Securitization Trust, Ser 2022-A, Cl A | ||||||||

4.300%, 05/17/27 (C) | $ | 380,000 | $ | 358,552 | ||||

Antares CLO, Ser 2021-1A, Cl A1R | ||||||||

5.785%, ICE LIBOR USD 3 Month + 1.460%, | 285,000 | 268,716 | ||||||

ARI Fleet Lease Trust, Ser 2022-A, Cl A2 | ||||||||

3.120%, 01/15/31 (C) | 575,000 | 562,028 | ||||||

Arivo Acceptance Auto Loan Receivables Trust, Ser 2021-1A, Cl A | ||||||||

1.190%, 01/15/27 (C) | 122,438 | 117,751 | ||||||

Carlyle US CLO, Ser 2021-1A, Cl A2R | ||||||||

5.893%, ICE LIBOR USD 3 Month + 1.650%, 07/20/34 (C) | 920,000 | 862,299 | ||||||

CARS-DB5 LP, Ser 2021-1A, Cl A2 | ||||||||

2.280%, 08/15/51 (C) | 602,260 | 458,804 | ||||||

Chesapeake Funding II, Ser 2019-1A, Cl A1 | ||||||||

2.940%, 04/15/31 (C) | 665 | 665 | ||||||

Chesapeake Funding II, Ser 2020-1A, Cl B | ||||||||

1.240%, 08/15/32 (C) | 295,000 | 284,791 | ||||||

Chesapeake Funding II, Ser 2020-1A, Cl D | ||||||||

2.830%, 08/15/32 (C) | 160,000 | 153,487 | ||||||

CNH Equipment Trust, Ser 2022-B, Cl A3 | ||||||||

3.890%, 08/16/27 | 475,000 | 455,963 | ||||||

College Avenue Student Loans, Ser 2021-B, Cl B | ||||||||

2.420%, 06/25/52 (C) | 280,000 | 237,326 | ||||||

DataBank Issuer, Ser 2021-1A, Cl A2 | ||||||||

2.060%, 02/27/51 (C) | 1,070,000 | 913,273 | ||||||

DLLST, Ser 2022-1A, Cl A3 | ||||||||

3.400%, 01/21/25 (C) | 300,000 | 290,162 | ||||||

Donlen Fleet Lease Funding 2, Ser 2021-2, Cl A2 | 305,797 | 294,250 | ||||||

Donlen Fleet Lease Funding 2, Ser 2021-2, Cl B | 340,000 | 315,930 | ||||||

Donlen Fleet Lease Funding 2, Ser 2021-2, Cl C | 600,000 | 555,462 | ||||||

Dryden 77 CLO, Ser 2021-77A, Cl BR | 875,000 | 814,335 | ||||||

Enterprise Fleet Financing, Ser 2022-3, Cl A2 | 460,000 | 451,619 | ||||||

The accompanying notes are an integral part of the financial statements.

24

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| ASSET-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

Enterprise Fleet Funding, Ser 2021-1, Cl A3 | ||||||||

0.700%, 12/21/26 (C) | $ | 285,000 | $ | 261,838 | ||||

Flagship Credit Auto Trust, Ser 2021-3, Cl A | ||||||||

0.360%, 07/15/27 (C) | 403,437 | 387,852 | ||||||

Goodgreen Trust, Ser 2021-1A, Cl A | ||||||||

2.660%, 10/15/56 (C) | 525,905 | 458,765 | ||||||

Hertz Vehicle Financing III, Ser 2022-1A, Cl A | ||||||||

1.990%, 06/25/26 (C) | 520,000 | 471,700 | ||||||

Hertz Vehicle Financing, Ser 2022-5A, Cl B | ||||||||

4.280%, 09/25/28 (C) | 475,000 | 433,454 | ||||||

Hilton Grand Vacations Trust, Ser 2020-AA, Cl A | ||||||||

2.740%, 02/25/39 (C) | 71,192 | 66,479 | ||||||

HIN Timeshare Trust, Ser 2020-A, Cl A | ||||||||

1.390%, 10/09/39 (C) | 483,993 | 438,415 | ||||||

Hotwire Funding, Ser 2021-1, Cl A2 | ||||||||

2.311%, 11/20/51 (C) | 470,000 | 400,895 | ||||||

John Deere Owner Trust, Ser 2022-A, Cl A3 | ||||||||

2.320%, 09/16/26 | 330,000 | 313,673 | ||||||

JPMorgan Chase, Ser 2020-2, Cl B | ||||||||

0.840%, 02/25/28 (C) | 144,562 | 140,562 | ||||||

JPMorgan Chase, Ser 2021-2, Cl B | ||||||||

0.889%, 12/26/28 (C) | 281,609 | 270,038 | ||||||

JPMorgan Chase, Ser 2021-3, Cl B | ||||||||

0.760%, 02/26/29 (C) | 136,636 | 129,359 | ||||||

LoanCore Issuer, Ser 2021-CRE6, Cl A | ||||||||

4.712%, ICE LIBOR USD 1 Month + 1.300%, 11/15/38 (C) | 610,000 | 579,784 | ||||||

Master Credit Card Trust, Ser 2022-4A, Cl B | ||||||||

6.240%, 04/21/29 (C) | 380,000 | 379,087 | ||||||

MF1, Ser 2021-FL7, Cl A | ||||||||

4.523%, ICE LIBOR USD 1 Month + 1.080%, 10/16/36 (C) | 510,000 | 486,233 | ||||||

MVW, Ser 2021-1WA, Cl A | ||||||||

1.140%, 01/22/41 (C) | 342,395 | 307,125 | ||||||

MVW, Ser 2022-1A, Cl A | ||||||||

4.150%, 11/21/39 (C) | 345,507 | 330,101 | ||||||

Navient Private Education Refi Loan Trust, Ser 2018-CA,Cl A2 | ||||||||

3.520%, 06/16/42 (C) | 79,847 | 78,205 | ||||||

The accompanying notes are an integral part of the financial statements.

25

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| ASSET-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

Navient Private Education Refi Loan Trust, Ser 2019-FA,Cl A2 | ||||||||

2.600%, 08/15/68 (C) | $ | 43,566 | $ | 39,972 | ||||

Navient Private Education Refi Loan Trust, Ser 2020-DA,Cl A | ||||||||

1.690%, 05/15/69 (C) | 442,366 | 397,988 | ||||||

Navient Private Education Refi Loan Trust, Ser 2021-CA,Cl A | ||||||||

1.060%, 10/15/69 (C) | 143,157 | 122,104 | ||||||

Navient Private Education Refi Loan Trust, Ser 2022-A,Cl A | ||||||||

2.230%, 07/15/70 (C) | 258,616 | 220,629 | ||||||

Navient Private Education Refi Loan Trust, Ser 2022-BA,Cl A | ||||||||

4.160%, 10/15/70 (C) | 468,514 | 433,790 | ||||||

Nelnet Student Loan Trust, Ser 2021-CA, Cl AFX | ||||||||

1.320%, 04/20/62 (C) | 691,936 | 604,126 | ||||||

NovaStar Mortgage Funding Trust, Ser 2003-3, Cl A1 | ||||||||

4.296%, ICE LIBOR USD 1 Month + 0.710%, 12/25/33 | 9,321 | 8,914 | ||||||

Orange Lake Timeshare Trust, Ser 2018-A, Cl A | ||||||||

3.100%, 11/08/30 (C) | 73,857 | 71,262 | ||||||

Orange Lake Timeshare Trust, Ser 2019-A, Cl A | ||||||||

3.060%, 04/09/38 (C) | 140,450 | 132,412 | ||||||

Santander Consumer Auto Receivables Trust, Ser 2021- AA, Cl A3 | ||||||||

0.330%, 10/15/25 (C) | 925,288 | 905,575 | ||||||

Santander Drive Auto Receivables Trust, Ser 2021-2, Cl C | ||||||||

0.900%, 06/15/26 | 595,000 | 576,807 | ||||||

Santander Drive Auto Receivables Trust, Ser 2022-3,Cl A3 | ||||||||

3.400%, 12/15/26 | 560,000 | 547,937 | ||||||

Santander Drive Auto Receivables Trust, Ser 2022-5,Cl A3 | ||||||||

4.110%, 08/17/26 | 915,000 | 894,025 | ||||||

Santander Drive Auto Receivables Trust, Ser 2022-6,Cl A3 | ||||||||

4.490%, 11/16/26 | 660,000 | 648,420 | ||||||

SBA Small Business Investment, Ser 2018-10B, Cl 1 | ||||||||

3.548%, 09/10/28 | 45,323 | 42,243 | ||||||

The accompanying notes are an integral part of the financial statements.

26

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| ASSET-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

SBA Small Business Investment, Ser 2022-10A, Cl 1 | ||||||||

2.938%, 03/10/32 | $ | 598,412 | $ | 537,888 | ||||

SBA Small Business Investment, Ser 2022-10B, Cl 1 | ||||||||

4.262%, 09/10/32 | 325,000 | 313,670 | ||||||

Scholar Funding Trust, Ser 2011-A, Cl A | ||||||||

5.274%, ICE LIBOR USD 3 Month + 0.900%, 10/28/43 (C) | 360,303 | 351,322 | ||||||

Sequoia Infrastructure Funding I, Ser 2021-1A, Cl A | ||||||||

5.479%, ICE LIBOR USD 3 Month + 1.400%, 04/15/31 (C) | 283,499 | 280,621 | ||||||

SLM Private Credit Student Loan Trust, Ser 2004-B, Cl A3 | ||||||||

3.623%, ICE LIBOR USD 3 Month + 0.330%, 03/15/24 | 2,559 | 2,550 | ||||||

SMB Private Education Loan Trust, Ser 2021-B, Cl A | ||||||||

1.310%, 07/17/51 (C) | 418,390 | 370,521 | ||||||

SMB Private Education Loan Trust, Ser 2021-B, Cl B | ||||||||

2.650%, 07/17/51 (C) | 295,000 | 229,919 | ||||||

SMB Private Education Loan Trust, Ser 2021-D, Cl A1A | ||||||||

1.340%, 03/17/53 (C) | 552,639 | 485,210 | ||||||

SoFi Professional Loan Program Trust, Ser 2021-A,Cl AFX | ||||||||

1.030%, 08/17/43 (C) | 249,626 | 208,990 | ||||||

South Carolina Student Loan, Ser 2015-A, Cl A | ||||||||

5.086%, ICE LIBOR USD 1 Month + 1.500%, 01/25/36 | 545,490 | 541,952 | ||||||

Southwick Park CLO, Ser 2021-4A, Cl A1R | ||||||||

5.303%, ICE LIBOR USD 3 Month + 1.060%, 07/20/32 (C) | 1,490,000 | 1,446,924 | ||||||

Stack Infrastructure Issuer, Ser 2019-1A, Cl A2 | ||||||||

4.540%, 02/25/44 (C) | 481,667 | 469,008 | ||||||

Stack Infrastructure Issuer, Ser 2020-1A, Cl A2 | ||||||||

1.893%, 08/25/45 (C) | 415,000 | 367,772 | ||||||

Strata CLO II, Ser 2021-1A, Cl A1 | ||||||||

5.833%, ICE LIBOR USD 3 Month + 1.590%, 10/20/33 (C) | 1,100,000 | 1,065,184 | ||||||

STWD, Ser 2019-FL1, Cl A | ||||||||

4.610%, TSFR1M + 1.194%, 07/15/38 (C) | 291,875 | 288,778 | ||||||

Tesla Auto Lease Trust, Ser 2021-B, Cl B | ||||||||

0.910%, 09/22/25 (C) | 925,000 | 855,250 | ||||||

Towd Point Mortgage Trust, Ser 2019-MH1, Cl A1 | ||||||||

3.000%, 11/25/58 (A) (C) | 333,115 | 325,212 | ||||||

The accompanying notes are an integral part of the financial statements.

27

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| ASSET-BACKED SECURITIES — continued | ||||||||

| Face Amount | Value | |||||||

United States Small Business Administration, Ser 2022-25F, Cl 1 | ||||||||

4.010%, 06/01/47 | $ | 505,000 | $ | 476,016 | ||||

Wheels SPV 2, Ser 2020-1A, Cl A2 | ||||||||

0.510%, 08/20/29 (C) | 71,529 | 70,523 | ||||||

Z Capital Credit Partners CLO, Ser 2021-1A, Cl A1R | ||||||||

5.589%, ICE LIBOR USD 3 Month + 1.510%, 07/16/31 (C) | 555,000 | 546,947 | ||||||

|

| |||||||

TOTAL ASSET-BACKED SECURITIES | ||||||||

(Cost $30,463,027) | 28,491,783 | |||||||

|

| |||||||

MUNICIPAL BONDS — 0.3% |

| |||||||

GEORGIA — 0.3% |

| |||||||

Georgia State, Municipal Electric Authority, RB, Ser 2010-A | ||||||||

7.055%, 04/01/57 | 204,000 | 197,075 | ||||||

6.637%, 04/01/57 | 616,000 | 620,282 | ||||||

|

| |||||||

TOTAL MUNICIPAL BONDS | ||||||||

(Cost $1,193,753) | 817,357 | |||||||

|

| |||||||

LOAN PARTICIPATION — 0.0% |

| |||||||

Sungard AS New Holdings III LLC, Initial Loan (2020), 1st Lien | ||||||||

8.500%, 07/01/24 | 4,361 | 2,987 | ||||||

|

| |||||||

TOTAL LOAN PARTICIPATION | ||||||||

|

| |||||||

(Cost $4,345) | 2,987 | |||||||

|

| |||||||

COMMON STOCK — 0.0% |

| |||||||

| Shares | ||||||||

INFORMATION TECHNOLOGY — 0.0% |

| |||||||

Sungard AS * | 190 | 2 | ||||||

|

| |||||||

TOTAL COMMON STOCK | ||||||||

(Cost $4,750) | 2 | |||||||

|

| |||||||

TOTAL INVESTMENTS — 103.5% | ||||||||

(Cost $349,187,526) | $ | 303,328,181 | ||||||

|

| |||||||

The accompanying notes are an integral part of the financial statements.

28

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

Percentages are based on Net Assets of $293,029,714.

| * | Non-income producing security. |

| (A) | Variable or floating rate security, the interest rate of which adjusts periodically based on changes in current interest rates and prepayments on the underlying pool of assets. |

| (B) | Securities considered illiquid. The total value of such securities as of October 31, 2022 was $57 and represented 0.0% of Net Assets. |

| (C) | Securities sold within terms of a private placement memorandum, exempt from registration under Section 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “accredited investors.” The total value of these securities at October 31, 2022 was $66,282,349 and represents 22.6% of Net Assets. |

| (D) | Perpetual security with no stated maturity date. |

| (E) | The rate reported on the Schedule of Investments is the effective yield at time of purchase. |

Cl — Class

CLO — Collateralized Loan Obligation

DAC — Designated Activity Company

FHLMC — Federal Home Loan Mortgage Corporation

FNMA — Federal National Mortgage Association

FREMF — Freddie Mac Multi-Family

GNMA — Government National Mortgage Association

ICE — Intercontinental Exchange

IO — Interest Only - face amount represents notional amount

LIBOR — London Interbank Offered Rates

LLC — Limited Liability Company

MTN — Medium Term Note

Pty — Proprietary

RB — Revenue Bond

Ser — Series

SOFR — Secured Overnight Financing Rate

TBA — To Be Announced

TSFR1M — One Month Term SOFR

UMBS — Uniform Mortgage-Backed Security

USD — U.S. Dollar

As of October 31, 2022, all of the Fund’s investments were considered Level 2 in accordance with the authoritative guidance on fair value measurements and disclosure under U.S. generally accepted accounting principles.

For more information on valuation inputs, see Note 2 — Significant Accounting Policies in the Notes to Financial Statements.

The accompanying notes are an integral part of the financial statements.

29

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| * | Net Assets divided by Shares do not calculate to the stated NAV because Net Assets are shown rounded. |

The accompanying notes are an integral part of the financial statements.

30

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund For the Year Ended October 31, 2022

|

The accompanying notes are an integral part of the financial statements.

31

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund

|

| STATEMENTS OF CHANGES IN NET ASSETS | ||||||

| | Year Ended October 31, 2022 | | | Year Ended October 31, 2021 | | |||

|

| |||||||

Operations: | ||||||||

Net Investment Income | $ | 6,642,743 | $ | 3,433,995 | ||||

Net Realized Loss on Investments and Foreign Currency Transactions | (22,081,367 | ) | (2,368,732) | |||||

Net Change in Unrealized Depreciation on Investments and Foreign Currency Translation | (45,150,475 | ) | (1,801,160) | |||||

|

| |||||||

Net Decrease in Net Assets Resulting from Operations | (60,589,099 | ) | (735,897) | |||||

|

| |||||||

Distributions | ||||||||

I Class Shares | (6,449,449 | ) | (5,556,617) | |||||

|

| |||||||

Total Distributions | (6,449,449 | ) | (5,556,617) | |||||

|

| |||||||

Capital Share Transactions: | ||||||||

I Class Shares: | ||||||||

Issued | 74,462,320 | 208,711,816 | ||||||

Reinvestment of Dividends | 6,443,612 | 5,552,803 | ||||||

Redeemed | (23,000,327 | ) | (6,094,488) | |||||

|

| |||||||

Increase from I Class Shares Capital Share Transactions | 57,905,605 | 208,170,131 | ||||||

|

| |||||||

R Class Shares: | ||||||||

Issued | — | — | ||||||

Reinvestment of Dividends | — | — | ||||||

Redeemed | — | — | ||||||

|

| |||||||

Increase from R Class Shares Capital Share Transactions | — | — | ||||||

|

| |||||||

Net Increase in Net Assets from Capital Share Transactions | 57,905,605 | 208,170,131 | ||||||

|

| |||||||

Total Increase (Decrease) in Net Assets | (9,132,943 | ) | 201,877,617 | |||||

|

| |||||||

Net Assets: | ||||||||

Beginning of Year | 302,162,657 | 100,285,040 | ||||||

|

| |||||||

End of Year | $ | 293,029,714 | $ | 302,162,657 | ||||

|

| |||||||

Amounts designated as “—” are $0 or have been rounded to $0.

The accompanying notes are an integral part of the financial statements.

32

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund

|

| STATEMENTS OF CHANGES IN NET ASSETS (continued) |

| |||||||

| | Year Ended October 31, 2022 | | | Year Ended October 31, 2021 | | |||

|

| |||||||

Shares Issued and Redeemed: | ||||||||

I Class Shares: | ||||||||

Issued | 7,621,412 | 19,890,196 | ||||||

Reinvestment of Dividends | 707,791 | 538,494 | ||||||

Redeemed | (2,749,151) | (591,278) | ||||||

|

|

|

| |||||

Increase in Shares Outstanding from I Class Share Transactions | 5,580,052 | 19,837,412 | ||||||

|

|

|

| |||||

R Class Shares: | ||||||||

Issued | — | — | ||||||

Reinvestment of Dividends | — | — | ||||||

Redeemed | — | — | ||||||

|

|

|

| |||||

Increase in Shares Outstanding from R Class Share Transactions | — | — | ||||||

|

|

|

| |||||

Net Increase in Shares Outstanding from Share Transactions | 5,580,052 | 19,837,412 | ||||||

|

|

|

| |||||

Amounts designated as “—” are zero or have been rounded to zero.

The accompanying notes are an integral part of the financial statements.

33

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund

|

Selected Per Share Data & Ratios For a Share

Outstanding Throughout the Years

| I Class Shares | ||||||||||||||||||||

| Year Ended October 31, 2022 | Year Ended October 31, 2021 | Year Ended October 31, 2020 | Year Ended October 31, 2019 | Year Ended October 31, 2018 | ||||||||||||||||

Net Asset Value, Beginning of Year | $ | 10.26 | $ | 10.42 | $ | 10.36 | $ | 9.55 | $ | 10.00 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Income from Operations: | ||||||||||||||||||||

Net Investment Income(1) | 0.19 | 0.12 | 0.23 | 0.29 | 0.28 | |||||||||||||||

Net Realized and Unrealized Gain (Loss) on Investments | (1.91) | (0.09) | 0.39 | 0.79 | (0.45) | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total from Operations | (1.72) | 0.03 | 0.62 | 1.08 | (0.17) | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Dividends and Distributions from: | ||||||||||||||||||||

Net Investment Income | (0.18) | (0.13) | (0.26) | (0.27) | (0.28) | |||||||||||||||

Net Realized Gains | — | (0.06) | (0.30) | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Dividends and Distributions | (0.18) | (0.19) | (0.56) | (0.27) | (0.28) | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Net Asset Value, End of Year | $ | 8.36 | $ | 10.26 | $ | 10.42 | $ | 10.36 | $ | 9.55 | ||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Total Return † | (16.88)% | 0.30% | 6.17% | 11.39% | (1.73)% | |||||||||||||||

|

|

|

|

|

|

|

|

|

| |||||||||||

Ratios and Supplemental Data | ||||||||||||||||||||

Net Assets, End of Year (Thousands) | $ | 293,030 | $ | 302,163 | $ | 100,285 | $ | 47,291 | $ | 20,036 | ||||||||||

Ratio of Expenses to Average Net Assets (including waivers, reimbursements, excluding fees paid indirectly) | 0.45 | % | 0.45 | % | 0.45 | % | 0.45 | % | 0.45 | % | ||||||||||

Ratio of Expenses to Average Net Assets (excluding waivers, reimbursements and fees paid indirectly) | 0.62 | % | 0.64 | % | 1.22 | % | 1.38 | % | 3.26 | % | ||||||||||

Ratio of Net Investment Income to Average Net Assets | 2.07 | % | 1.20 | % | 2.24 | % | 2.91 | % | 2.84 | % | ||||||||||

Portfolio Turnover Rate† | 329 | % | 463 | % | 300 | % | 356 | % | 311 | % | ||||||||||

Amounts designated as “—” are $0 or round to $0. |

| (1) | Per share calculations were performed using average shares method. |

| † | Total return and portfolio turnover rate are for the period indicated and have not been annualized. Return shown does not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return would have been lower had the Adviser not waived its fee and/or reimbursed other expenses. |

The accompanying notes are an integral part of the financial statements.

34

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund

|

FINANCIAL HIGHLIGHTS (continued) | ||

Selected Per Share Data & Ratios For a Share

Outstanding Throughout the Years

| R Class Shares | ||||||||||||||||||||

| Year Ended October 31, 2022 | Year Ended October 31, 2021 | Year Ended October 31, 2020 | Year Ended October 31, 2019 | Year Ended October 31, 2018 | ||||||||||||||||

Net Asset Value, Beginning of Year | $ | 9.45 | $ | 9.57 | $ | 9.92 | $ | 9.52 | $ | 9.98 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Income from Operations: | ||||||||||||||||||||

Net Investment Income (Loss)(1) | 0.22 | 0.16 | (0.01) | 0.20 | 0.27 | |||||||||||||||

Net Realized and Unrealized Gain (Loss) on Investments | (1.81) | (0.09) | 0.21 | 0.47 | (0.45) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Total from Operations | (1.59) | 0.07 | 0.20 | 0.67 | (0.18) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Dividends and Distributions from: | ||||||||||||||||||||

Net Investment Income | (0.18) | (0.13) | (0.25) | (0.27) | (0.28) | |||||||||||||||

Net Realized Gains | — | (0.06) | (0.30) | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Total Dividends and Distributions | (0.18) | (0.19) | (0.55) | (0.27) | (0.28) | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Net Asset Value, End of Year | $ | 7.68 | $ | 9.45 | $ | 9.57 | $ | 9.92 | $ | 9.52 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Total Return † | (16.96)% | 0.74% | 2.05% | 7.05% | (1.83)% | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

| ||||||||

Ratios and Supplemental Data | ||||||||||||||||||||

Net Assets, End of Year (Thousands) | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

Ratio of Expenses to Average Net Assets (including waivers, reimbursements, excluding fees paid indirectly)‡ | 0.45% | 0.45% | 0.45% | 0.45% | 0.45% | |||||||||||||||

Ratio of Expenses to Average Net Assets (excluding waivers, reimbursements and fees paid indirectly) | 0.62% | 0.64% | 1.22% | 1.38% | 3.26% | |||||||||||||||

Ratio of Net Investment Income (Loss) | 2.52% | 1.65% | (0.11)% | 2.05% | 2.79% | |||||||||||||||

Portfolio Turnover Rate† | 329% | 463% | 300% | 356% | 311% | |||||||||||||||

Amounts designated as “—” are $0 or round to $0.

| (1) | Per share calculations were performed using average shares method. |

| † | Total return and portfolio turnover rate are for the period indicated and have not been annualized. Return shown does not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return would have been lower had the Adviser not waived its fee and/or reimbursed other expenses. |

| ‡ | The share class is expected to run at the expense limit of 0.70% when assets are contributed. Amounts have been revised to reflect an estimation of expenses based on I Class Shares. |

The accompanying notes are an integral part of the financial statements.

35

| THE ADVISORS’ INNER CIRCLE FUND III | MetLife Core Plus Fund October 31, 2022

|

| NOTES TO FINANCIAL STATEMENTS |

1. Organization: