UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment Company Act file number | 811-22930 |

USCF ETF Trust

(Exact name of registrant as specified in charter)

1850 Mt. Diablo Blvd., Suite 640

Walnut Creek, CA 94596

(Address of principal executive offices) (Zip code)

USCF Advisers LLC

Mr. Stuart Crumbaugh

1850 Mt. Diablo Blvd., Suite 640

Walnut Creek, CA 94596

(Name and address of agent for service)

Registrant's telephone number, including area code: 510-522-9600

Date of fiscal year end: June 30

Date of reporting period: June 30, 2021

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

| (a) | The following is a copy of the report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). |

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the funds’ shareholder reports are no longer sent by mail, unless you specifically request paper copies of the reports from your financial intermediary, such as a broker-dealer or bank. Instead, the reports are made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. Please contact your financial intermediary to elect to receive shareholder reports and other fund communications electronically.

You may elect to receive all future reports in paper free of charge. Please contact your financial intermediary to inform them that you wish to continue receiving paper copies of your shareholder reports and for details about whether your election to receive reports in paper will apply to all funds held with your financial intermediary.

USCF ETF TRUST

TABLE OF CONTENTS

LETTERS TO SHAREHOLDERS (as of June 30, 2021)

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND (“SDCI”)

USCF ETF Trust (the “Trust”) launched the USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund (“SDCI”) on May 2, 2018. SDCI is an innovative approach to commodity investing that uses fundamental signals about underlying physical markets to create an active portfolio for commodity futures investors. The SDCI reflects the performance of a fully collateralized portfolio of 14 commodity futures, selected each month from a universe of 27 eligible commodities based on observable price signals, subject to a diversification requirement across Primary commodity sectors. The Primary commodity sectors for the SDCI include Precious Metals, Industrial Metals, Petroleum and Grains. The Non-Primary sector includes natural gas, softs, and livestock commodities.

For the twelve months ending June 30, 2021, the SDCI Total Return Index increased 54.75%. The large positive return over the last 12-month period is a result of the global economic rebound and market response as COVID-19 vaccinations become available. During that period, the 12-month performance of both SDCI and the SDCI Total Return Index was in line with other commodity benchmarks. For example the BCOM Total Return Index was up 45.61% and the SPGSCI Total Return Index was up 57.37% over the same twelve month period.

The Consumer Price Index (CPI) tracks the average price changes of a basket of goods that consumers buy. The change in CPI is commonly used to measure the rate of inflation. If prices increase quickly, consumers will not be able to buy as many goods on the same budget. In this sense, inflation can erode wealth.

CPI inflation for May 2021 hit 5% compared to one year ago. This figure means that the purchasing power of $1 in May 2020 is equivalent to the purchasing power of $1.05 one year later. In other words, a typical American household will spend several hundred dollars more on just groceries in 2021 compared to 2020.

What is causing inflation to rise, and where will it go next? It turns out that predicting inflation is just as difficult as market-timing in equities and commodities. A recent New York Times story covered research from the Peterson Institute for International Economics on inflation forecasting accuracy, reporting that “nobody forecasts well” including the U.S. Treasury market, TIPS market and well-known economists. Allocators should question any confident prediction for low inflation or transitory inflation when forming diversified portfolios. We believe a prudent investor would position for the unexpected and unpredictable, including positive inflation shocks. Given this uncertainty, we explore the macroeconomic factors underlying current inflationary trends.

Three factors are at work in unison to drive inflation upwards. First, 2020 witnessed an unprecedented monetary event. Money supply as measured by M2 experienced a year-over-year increase of 25%, the highest recorded level in history. Furthermore, money supply has continued to expand in 2021, already logging one of the highest percentage increases only halfway through the year. Compared to the expanding money supply, the U.S. economy has been in a recession since early 2020. With too much money chasing after fewer goods, prices are primed to rise.

| 2 | Annual Report June 30, 2021 |

Second, monetary expansion is matched by an equally grand expansion of the government’s balance sheet as ambitious fiscal policy is unleashed to fight a COVID-19 induced recession. The expansion in government spending through 2020 and 2021 has been the highest in the past 40 years. Greater government spending also contributes to more money in the economy, further causing prices to rise.

While the first two factors have an impact on the current rate of inflation, the third factor has implications for future inflation. During the COVID-19 pandemic, Americans saved at unprecedented rates. From 1980 to 2019, the personal savings rate of Americans never exceeded 15%. In 2020, this figure rose past 15%, and in 2021, it is approaching 20%! This additional savings will be spent at some point – more money chasing goods in the future.

Of the 27 eligible commodities that may be held by the SDCI, all except two have had positive returns in the past year. Furthermore, the rally extends across sectors, with the top performers (50%+ return each) coming from different sectors: grains (corn, soybean complex, wheat, oilseeds), livestock (hogs), and industrial metals (tin, copper, aluminum), energy (crude oil as well as its refined products), and softs (sugar).

Since the Global Financial Crisis (GFC) and the deflationary decade that followed, many investors have positioned their portfolios away from assets that protect against inflation such as commodity futures. This positioning reflects the view that future inflation is likely to remain very low. Investors should be aware that the COVID-19 pandemic is unlike the GFC, and the current economic conditions are unlike those in 2008. An elevated risk of inflation could be painful for unprepared investors.

Definitions:

Bloomberg Commodity Index Total Return (BCOM TR) is an index that tracks the performance of 22 broadly diversified commodity futures contracts. Prior to July 1, 2014, BCOM was known as the Dow Jones-UBS Commodity Index.

S&P GSCI Index (GSCI) is an index that tracks the performance of 24 exchange-traded futures contracts that cover physical commodities spanning five sectors. The S&P GSCI was called the Goldman Sachs Commodity Index (GSCI) before it was purchased by Standard & Poor’s in 2007.

Past performance is no guarantee of future results.

There is no assurance that the investment process will consistently lead to successful investing for each fund.

It is not possible to invest in an index.

| 3 |

Important Considerations:

Commodity and futures trading are highly speculative and generally volatile and is not suitable for all investors.

Investing in SDCI involves risks, including the possible loss of principal. Commodities contain a heightened risk including market and price movements that are outside SDCI’s control and may be influenced by weather and climate conditions, livestock disease, war, terrorism, political conflicts and economic event, interest rates, currency exchange rates, U.S. and non-U.S. government regulation and taxation. Investing in derivatives, including futures and swaps, entails risks relating to liquidity, counterparty, leverage, and credit that may reduce return and increase volatility. Investments held in U.S. government securities and money market instruments can suffer losses. SDCI is exposed to non-diversification risk which results from SDCI’s direct or indirect investment in commodities and futures contracts that are economically identical or substantially similar. For more information about these and other risks including correlation and specific risks regarding each commodity sector and the investment in the Subsidiary, please read SDCI’s prospectus.

| 4 | Annual Report June 30, 2021 |

USCF MIDSTREAM ENERGY INCOME FUND (“UMI”)

USCF ETF Trust (the “Trust”) launched the USCF Midstream Energy Income Fund (“UMI”) on March 24, 2021. Midstream energy has had stellar performance since inception through June 30, 2021. During the same period, UMI posted strong absolute returns and outperformed its benchmark, the Alerian Midstream Energy Select Index. A better U.S. COVID-19 outlook, OPEC+ self-discipline, and increasing travel all contributed to an improving volume outlook. In addition, India and China have seen an uptick in demand, as the world slowly returns to a more normalized state. Although the summer waters are not totally clear due to the looming return of Iranian production and a slower pandemic recovery in some international countries, crude prices have moved steadily upward, and U.S. production volumes are starting to follow.

U.S. crude oil and natural gas production fell significantly during the COVID-19 outbreak and was impacted again this winter by severe weather. However, production has started a V-shaped recovery, which is a positive sign for midstream companies who depend on volumes to support cash flows.

In addition, we have seen a better demand outlook for refined products, as the pandemic impact has lessened in the U.S. and resulted in increased economic activity. We are now in the peak summer driving season and should see continuing positive demand trends, particularly for gasoline and diesel. Jet fuel demand is also headed in the right direction but trails the robust rebound in gasoline and diesel demand. The U.S. Energy Information Administration expects U.S. gasoline consumption to average 8.7 million barrels per day (Mmbpd) in 2021 and 9.0 Mmbpd in 2022. This compares with 8.0 Mmbpd in 2020 and 9.3 Mmbpd in 2019.

All of this adds up to a sunny outlook for midstream volumes, which should enable midstream energy companies to realize their goal of enhancing shareholder returns without the need for increased capital spending.

We believe current management teams at midstream energy companies finally understand their own businesses and what investors want from them. Management teams continue to talk about financial discipline, emphasizing free cash flow and returning capital to shareholders through share buybacks and distribution increases. The companies are also focused on reducing leverage through the payoff of debt, although that goal was slowed somewhat in the tough 2020 environment. We expect de-levering should pick up again over the next few years. We believe these developments better position the sector to handle the inevitable volatility of the energy markets through future cycles.

Contributors (by contribution to returns)

Targa Resources - Results exceeded estimates and raised 2021 EBITDA estimates to 13% higher than 2020.

Energy Transfer - ET is selling at a discount on EV/EBITDA compared with the portfolio and has an attractive 18% FCF yield.

| 5 |

Plains GP Holdings - The company’s assets in the Permian Basin, which has the best return on investment for oil fields in the US, positions the company well for increased demand as the economy rebounds.

Detractors (by contribution to returns)

The portfolio did not have any names detract from absolute returns during the fiscal period.

Definitions:

Alerian Midstream Energy Select Index (AMEIX) is a composite of North American energy infrastructure companies. The capped, float-adjusted, capitalization-weighted index, whose constituents are engaged in midstream activities involving energy commodities, is disseminated real-time on a total-return basis.

Past performance is no guarantee of future results.

There is no assurance that the investment process will consistently lead to successful investing for each fund.

It is not possible to invest in an index.

Important Considerations:

The Fund invests primarily in energy infrastructure companies which may be affected by fluctuations in energy prices and supply and demand of energy fuels. An investment in MLP units involves risks that differ from a similar investment in equity securities, such as common stock, of a corporation.

There is no guarantee that the fund’s objective will be met. Fund concentration generally leads to greater price volatility. Foreign investing involves special risks such as currency fluctuations and political uncertainty. Investment in small companies generally experience greater price volatility.

An investor may lose all or substantially all of an investment. These risks could result in large fluctuations in the price of a particular fund’s respective shares. Funds that focus on a single sector generally experience greater volatility. For further discussion of these and additional risks associated with an investment in UMI, please read the respective fund’s prospectus before investing.

| 6 | Annual Report June 30, 2021 |

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN USCF

SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND (“SDCI”),

SUMMERHAVEN DYNAMIC COMMODITY INDEX TOTAL RETURN SM1 AND

BLOOMBERG COMMODITY INDEX TOTAL RETURNSM2 FROM MAY 2, 2018

(INCEPTION DATE)* TO JUNE 30, 2021.

The following graph shows the value as of June 30, 2021 of a $10,000 investment made on May 1, 2018 (commencement of operations). For comparative purposes, the performance of USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund (Net Asset Value and Market Value), the SummerHaven Dynamic Commodity Index Total ReturnSM1 (“SDCITR”) and the performance of Bloomberg Commodity Index Total ReturnSM2 and S&P Goldman Sachs Commodity Index Total Return®3 are shown.

| One Year Return | Annualized | |||||||

USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund (NAV) | 56.04 | % | (1.58 | )% | ||||

USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund (Market Value) | 55.22 | % | (1.78 | )% | ||||

| SummerHaven Dynamic Commodity Index Total ReturnSM1 | 54.75 | % | (1.18 | )% | ||||

| Bloomberg Commodity Index Total ReturnSM2 | 45.61 | % | 3.03 | % | ||||

| * | The inception date is the date the fund started accruing expenses and commenced operations. Shares of SDCI were listed on the NYSE Arca, Inc. on May 3, 2018. |

| 7 |

| 1 | The SummerHaven Dynamic Commodity Index Total ReturnSM (“SDCITR”) is an index designed to reflect the performance of a fully margined and collateralized portfolio of exchange-traded commodities futures contracts. The total return of the SDCITR is based upon the market price movements of its component futures contracts and the return on the hypothetical investments used to collateralize those futures contracts. At any time, the SDCITR is comprised of 14 commodity futures contracts (the “Component Futures Contracts”), weighted equally by notional amount, selected each month based upon a universe of 27 eligible commodities and futures contracts for those commodities. The eligible futures contracts are traded on the Futures Exchanges in major industrialized countries, and typically have active and liquid markets. The eligible futures contracts are physical non-financial commodity futures contracts traded on the Futures Exchanges in major industrialized countries, and typically have active and liquid markets. The eligible futures contracts are denominated in U.S. dollars. Beginning with the commodity selection process that commenced on December 24, 2020, the universe of eligible commodities is categorized into five commodity sectors. Specifically, there are four primary commodity sectors (petroleum; precious metals; industrial metals; and grains) and a non-primary sector. The SDCITR is rules-based and reconstituted and rebalanced monthly using quantitative formulas, subject to the constraint that each of the four primary commodity sectors must be represented by at least one Component Futures Contract. There is no requirement that the non-primary sector be so represented. Previously, the universe of eligible futures commodities were categorized into six sectors: energy; precious metals; industrial metals; grains; softs; and livestock. |

| 2 | The Bloomberg Commodity Index Total ReturnSM (“BCOM”) is an index that tracks the performance of 22 broadly diversified commodity futures contracts. Prior to July 1, 2014, BCOM was known as the Dow Jones-UBS Commodity Index. |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on distributions or on the sale of shares. Principal value and investments returns will fluctuate and investors’ shares, when sold, may be worth more or less than the original cost. To obtain the most recent month-end performance data visit www.uscfinvestments.com or call 1-800-920-0259.

The Fund’s NAV is calculated by dividing the value of the Fund’s total assets less its total liabilities by the number of shares outstanding. Share price returns are based on closing prices for the Fund and do not represent the returns an investor would receive if shares were traded at other times.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions apply and will reduce returns. Market returns are based upon the midpoint of the bid/ask spread at 4:00 p.m. Eastern time (when NAV is normally determined for most ETFs), and do not represent the returns you would receive if you traded shares at other times.

| 8 | Annual Report June 30, 2021 |

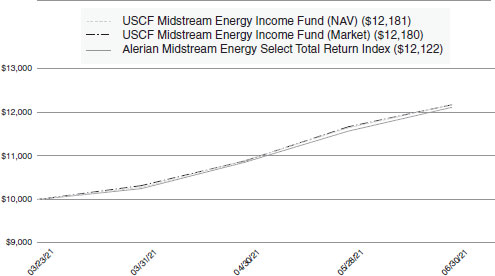

COMPARISON OF CHANGE IN VALUE OF $10,000 INVESTMENT IN USCF

MIDSTREAM ENERGY INCOME FUND (“UMI”) AND ALERIAN MIDSTREAM

ENERGY SELECT TOTAL RETURN INDEX FROM MARCH 23, 2021

(INCEPTION DATE)* TO JUNE 30, 2021.

The following graph shows the value as of June 30, 2021 of a $10,000 investment made on March 23, 2021 (commencement of operations). For comparative purposes, the performance of USCF Midstream Energy Fund (Net Asset Value and Market Value) and the performance of Alerian Midstream Energy Select Total Return Index are shown.

| Since Inception Return^ (3/23/2021) | ||||

| USCF Midstream Energy Income Fund (NAV) | 21.83 | % | ||

| USCF Midstream Energy Income Fund (Market Value) | 21.80 | % | ||

| Alerian Midstream Energy Select Total Return Index | 21.22 | % | ||

| * | The inception date is the date the fund started accruing expenses and commenced operations. Shares of UMI were listed on the NYSE Arca, Inc. on March 24, 2021. |

| ^ | Returns for periods of less than one year are not annualized. |

| 1 | The Alerian Midstream Energy Select Total Return Index is a composite of North American energy infrastructure companies. The capped, float-adjusted, capitalization-weighted index, whose constituents are engaged in midstream activities involving energy commodities, is disseminated real-time on a total-return basis. |

| 9 |

The performance shown represents past performance. Past performance is no guarantee of future results and current performance may be higher or lower than the performance shown. Return calculations assume the reinvestment of distributions and do not reflect taxes that a shareholder would pay on distributions or on the sale of shares. Principal value and investments returns will fluctuate and investors’ shares, when sold, may be worth more or less than the original cost. To obtain the most recent month-end performance data visit www.uscfinvestments.com or call 1-800-920-0259.

The Fund’s NAV is calculated by dividing the value of the Fund’s total assets less its total liabilities by the number of shares outstanding. Share price returns are based on closing prices for the Fund and do not represent the returns an investor would receive if shares were traded at other times.

Shares of ETFs are bought and sold at market price (not NAV) and are not individually redeemed from the Fund. Brokerage commissions apply and will reduce returns. Market returns are based upon the midpoint of the bid/ask spread at 4:00 p.m. Eastern time (when NAV is normally determined for most ETFs), and do not represent the returns you would receive if you traded shares at other times.

| 10 | Annual Report June 30, 2021 |

As a shareholder of one or more of the USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund and the USCF Midstream Energy Income Fund (each a “Fund” and collectively, the “Funds”), each of which is a series of the USCF ETF Trust (the “Trust”), you may incur two potential types of costs: (1) transaction costs, such as brokerage commissions, for purchasing and selling your Fund shares, and (2) ongoing costs, including management fees and other Fund expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other funds. The examples are based on an investment of $1,000 invested at the beginning of the period and held for the entire period from January 1, 2021 until June 30, 2021.

Actual Return. The table below provides information about actual account values and actual expenses. You may use the information in this table, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading “Actual Expenses Paid During the Period” to estimate the expenses you paid on your account during this period.

Hypothetical 5% Return. The table below provides information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare ongoing costs of investing in the Fund and other exchange-traded funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

The expenses shown in the table are meant to highlight ongoing costs only and do not reflect any transaction fees, such as brokerage commission paid on purchases and sales of Fund shares. Therefore, the number under the heading “Hypothetical Expenses Paid During the Period” is useful in comparing ongoing costs only and may not help you determine the relative total costs of owning different funds.

| 11 |

Fund |

Beginning |

Ending |

Annualized | Expenses | ||||||||||||

| USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund | ||||||||||||||||

| Actual(a) | $ | 1,000.00 | $ | 1,264,60 | 0.60 | % | $ | 3.37 | ||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,021.82 | 0.60 | % | $ | 3.01 | ||||||||

| USCF Midstream Energy Income Fund | ||||||||||||||||

| Actual(b) | $ | 1,000.00 | $ | 1,218.30 | 0.85 | % | $ | 2.56 | ||||||||

| Hypothetical (5% return before expenses) | $ | 1,000.00 | $ | 1,020.58 | 0.85 | % | $ | 4.26 | ||||||||

| (a) | Expenses (net of fee waivers and/or expense reimbursements) are equal to the Funds’ annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days (181 days) in the most recent fiscal half-year, then divided by 365 (to reflect the one-half year period). |

| (b) | Expenses (net of fee waivers and/or expense reimbursements) are equal to the Funds’ annualized expense ratio multiplied by the average account value over the period, multiplied by the number of days (99 days) in the most recent fiscal half-year, then divided by 365 (to reflect the one-half year period). |

| 12 | Annual Report June 30, 2021 |

USCF ETF TRUST

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND

CONSOLIDATED SCHEDULE OF INVESTMENTS

AT JUNE 30, 2021

Besides the following listed commodity futures contracts and money market funds of the Fund and its wholly-owned subsidiary, there were no additional investments held by the Fund at June 30, 2021.

The following commodity futures contracts of the Fund’s wholly-owned subsidiary were open at June 30, 2021 (see Security Valuation in the Notes to Financial Statements):

| Number of Contracts | Notional Amount | Expiration Date | Fair Value/ Unrealized Gain (Loss) on Open Commodity Contracts | % of Total Net Assets | ||||||||||||||||

| Open Commodity Futures Contracts – Long | ||||||||||||||||||||

| Foreign Contracts | ||||||||||||||||||||

| LME Nickel Futures LN, July 2021 contracts | 6 | $ | 633,987 | Jul-21 | $ | 21,429 | 0.3 | % | ||||||||||||

| LME Tin Futures LT, July 2021 contracts | 4 | 619,040 | Jul-21 | 38,560 | 0.5 | % | ||||||||||||||

| LME Zinc Futures LX, July 2021 contracts | 3 | 208,896 | Jul-21 | 13,873 | 0.2 | % | ||||||||||||||

| LME Nickel Futures LN, August 2021 contracts | 5 | 550,068 | Aug-21 | (3,828 | ) | (0.1 | )% | |||||||||||||

| LME Tin Futures LT, August 2021 contracts | 4 | 646,020 | Aug-21 | 1,580 | 0.0 | %(a) | ||||||||||||||

| ICE Brent Crude Futures CO, December 2021 contracts | 8 | 506,900 | Oct-21 | 72,060 | 0.9 | % | ||||||||||||||

| 30 | 3,164,911 | 143,674 | 1.8 | % | ||||||||||||||||

| United States Contracts | ||||||||||||||||||||

| CME Lean Hogs Futures LH, August 2021 contracts | 14 | 573,800 | Aug-21 | 4,400 | 0.0 | %(a) | ||||||||||||||

| CME Live Cattle Futures LC, August 2021 contracts | 12 | 586,860 | Aug-21 | 2,220 | 0.0 | %(a) | ||||||||||||||

| CBOT Corn Futures C, September 2021 contracts | 22 | 620,088 | Sep-21 | 39,087 | 0.5 | % | ||||||||||||||

| CBOT Soybean Oil Futures BO, September 2021 contracts | 16 | 583,362 | Sep-21 | 22,494 | 0.3 | % | ||||||||||||||

| COMEX Copper Futures HG, September 2021 contracts | 5 | 560,587 | Sep-21 | (24,462 | ) | (0.3 | )% | |||||||||||||

| COMEX Silver Futures SI, September 2021 contracts | 4 | 560,035 | Sep-21 | (36,155 | ) | (0.5 | )% | |||||||||||||

| CBOT Soybean Meal Futures SM, October 2021 contracts | 16 | 615,800 | Oct-21 | (9,720 | ) | (0.1 | )% | |||||||||||||

| COMEX Gold 100 OZ Futures GC, October 2021 contracts. | 3 | 533,610 | Oct-21 | (1,560 | ) | (0.0 | )%(b) | |||||||||||||

| NYMEX RBOB Gasoline Futures RB, November 2021 contracts | 7 | 572,893 | Oct-21 | 32,365 | 0.4 | % | ||||||||||||||

The accompanying notes are an integral part of the financial statements.

| 13 |

USCF ETF TRUST

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND

CONSOLIDATED SCHEDULE OF INVESTMENTS

AT JUNE 30, 2021 (continued)

| Number of Contracts | Notional Amount | Expiration Date | Fair Value/ Unrealized Gain (Loss) on Open Commodity Contracts | % of Total Net Assets | ||||||||||||||||

| United States Contracts (continued) | ||||||||||||||||||||

| CBOT Soybean Futures, November 2021 contracts | 9 | $ | 594,825 | Nov-21 | $ | 34,725 | 0.4 | % | ||||||||||||

| NYMEX WTI Crude Futures CL, December 2021 contracts | 8 | 473,430 | Nov-21 | 87,610 | 1.1 | % | ||||||||||||||

| 116 | 6,275,290 | 151,004 | 1.8 | % | ||||||||||||||||

| Open Commodity Futures Contracts—Short(c) | ||||||||||||||||||||

| Foreign Contracts | ||||||||||||||||||||

| LME Nickel Futures LN, July 2021 contracts | 6 | (661,452 | ) | Jul-21 | 6,036 | 0.1 | % | |||||||||||||

| LME Tin Futures LT, July 2021 contracts | 4 | (657,680 | ) | Jul-21 | 80 | 0.0 | %(a) | |||||||||||||

| LME Zinc Futures LX, July 2021 contracts | 3 | (208,498 | ) | Jul-21 | (14,271 | ) | (0.2 | )% | ||||||||||||

| 13 | (1,527,630 | ) | (8,155 | ) | (0.1 | )% | ||||||||||||||

| Total Open Commodity Futures Contracts(d) | 159 | $ | 7,912,571 | $ | 286,523 | 3.5 | % | |||||||||||||

The accompanying notes are an integral part of the financial statements.

| 14 | Annual Report June 30, 2021 |

USCF ETF TRUST

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND

CONSOLIDATED SCHEDULE OF INVESTMENTS

AT JUNE 30, 2021 (continued)

| Principal Amount | Market Value | % of Total Net Assets | ||||||||||

| Cash Equivalents | ||||||||||||

| United States – Money Market Funds | ||||||||||||

| Goldman Sachs Financial Square Government Fund – Institutional Shares, 0.03%(e) | 2,092,609 | 2,092,609 | 25.4 | % | ||||||||

| RBC U.S. Government Money Market Fund – Institutional Shares, 0.03%(e) | 4,964,326 | 4,964,326 | 60.4 | % | ||||||||

| Total Money Market Funds (Cost $7,056,935) | $ | 7,056,935 | 85.8 | % | ||||||||

| Total Investments (Cost $7,056,935) | $ | 7,343,458 | 89.3 | % | ||||||||

| Other Assets in Excess of Liabilities | 876,954 | 10.7 | % | |||||||||

| Total Net Assets | $ | 8,220,412 | 100.0 | % | ||||||||

| (a) | Position represents less than 0.05%. |

| (b) | Position represents greater than (0.05)%. |

| (c) | All short contracts are offset by long positions in commodity futures contracts and are acquired solely for the purpose of reducing a long position (e.g., due to a redemption or to reflect a rebalancing of the SDCI). |

| (d) | Collateral amounted to $799,647 on open commodity futures contracts. |

| (e) | Reflects the 7-day yield at June 30, 2021. |

| Summary of Investments by Country^ | ||||

| United States | 98.2 | % | ||

| United Kingdom | 1.8 | |||

| 100.0 | % | |||

| ^ | As a percentage of total investments. |

.

The accompanying notes are an integral part of the financial statements.

| 15 |

USCF ETF TRUST

USCF MIDSTREAM ENERGY INCOME FUND

SCHEDULE OF INVESTMENTS

AT JUNE 30, 2021

| % of Total Net Assets | Shares | Market Value | ||||||||||

| Common Stocks | 75.0 | % | ||||||||||

| Pipelines | 75.0 | % | ||||||||||

| Cheniere Energy, Inc.(a) | 6.4 | % | 74,052 | 6,423,270 | ||||||||

| Enbridge, Inc | 9.0 | % | 223,305 | 8,941,132 | ||||||||

| EnLink Midstream LLC(a) | 2.3 | % | 354,401 | 2,264,622 | ||||||||

| Equitrans Midstream Corp | 2.7 | % | 321,396 | 2,735,080 | ||||||||

| Gibson Energy, Inc. | 3.7 | % | 194,888 | 3,737,858 | ||||||||

| Hess Midstream LP – Class A | 2.6 | % | 103,702 | 2,618,476 | ||||||||

| Inter Pipeline Ltd. | 2.8 | % | 172,352 | 2,804,565 | ||||||||

| Keyera Corp. | 4.7 | % | 172,626 | 4,643,602 | ||||||||

| Kinder Morgan, Inc. | 6.8 | % | 374,231 | 6,822,231 | ||||||||

| ONEOK, Inc. | 4.5 | % | 81,491 | 4,534,159 | ||||||||

| Pembina Pipeline Corp. | 4.4 | % | 136,748 | 4,344,484 | ||||||||

| Plains GP Holdings LP – Class A(a) | 4.6 | % | 382,171 | 4,563,122 | ||||||||

| Targa Resources Corp. | 10.0 | % | 224,264 | 9,968,535 | ||||||||

| TC Energy Corp. | 6.2 | % | 124,780 | 6,179,106 | ||||||||

| Williams Cos., Inc. (The) | 4.3 | % | 160,752 | 4,267,966 | ||||||||

| 74,848,208 | ||||||||||||

| Total Common Stocks | ||||||||||||

| (Cost $65,717,758) | 75.0 | % | 74,848,208 | |||||||||

| Master Limited Partnerships | 24.3 | % | ||||||||||

| Gas | 2.7 | % | ||||||||||

| Western Midstream Partners LP | 2.7 | % | 127,364 | 2,728,137 | ||||||||

| Pipelines | 21.6 | % | ||||||||||

| DCP Midstream LP | 1.8 | % | 59,160 | 1,815,620 | ||||||||

| Energy Transfer LP | 4.5 | % | 424,196 | 4,509,204 | ||||||||

| Enterprise Products Partners LP | 9.2 | % | 378,139 | 9,124,494 | ||||||||

| Holly Energy Partners LP | 0.5 | % | 22,780 | 515,511 | ||||||||

| Magellan Midstream Partners LP | 1.5 | % | 30,786 | 1,505,743 | ||||||||

| MPLX LP | 4.1 | % | 137,088 | 4,059,176 | ||||||||

| 21,529,748 | ||||||||||||

| Total Master Limited Partnerships | ||||||||||||

| (Cost $20,801,816) | 24.3 | % | 24,257,885 | |||||||||

| Money Market Funds | 0.6 | % | ||||||||||

| Dreyfus Government Cash Management Fund, Institutional Shares, 0.03% (Cost $583,532) | 0.6 | % | 583,532 | 583,532 | ||||||||

| Total Investments | ||||||||||||

| (Cost $87,103,106) | 99.9 | % | 99,689,625 | |||||||||

| Other Assets in Excess of Liabilities | 0.1 | % | 95,576 | |||||||||

| Total Net Assets | 100.0 | % | $ | 99,785,201 | ||||||||

| (a) | Non-income producing security. |

The accompanying notes are an integral part of the financial statements.

| 16 | Annual Report June 30, 2021 |

USCF ETF TRUST

USCF MIDSTREAM ENERGY INCOME FUND

SCHEDULE OF INVESTMENTS

AT JUNE 30, 2021 (CONTINUED)

| Summary of Investments by Country^ | ||||

| United States | 69.3 | % | ||

| Canada | 30.7 | |||

| 100.0 | % | |||

| Summary of Investments by Sector^ | ||||

| Energy | 99.4 | % | ||

| Money Market Fund | 0.6 | |||

| 100.0 | % | |||

| ^ | As a percentage of total investments. |

The accompanying notes are an integral part of the financial statements.

| 17 |

USCF ETF TRUST

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND

CONSOLIDATED STATEMENT OF ASSETS AND LIABILITIES

JUNE 30, 2021

| Assets: | ||||

| Investments, at Market Value: | ||||

| Cash and Cash Equivalents | $ | 7,056,935 | ||

| Net Unrealized Appreciation (Depreciation) on Open Commodity Futures Contracts | 286,523 | |||

| Cash | 18,718 | |||

| Receivables: | ||||

| Deposit with broker for futures contracts | 799,647 | |||

| Variation margin on futures contracts | 63,459 | |||

| Dividends and Interest | 135 | |||

| Other Assets | 676 | |||

| Total Assets | 8,226,093 | |||

| Liabilities: | ||||

| Payables: | ||||

| Accrued Management Fees | 5,681 | |||

| Total Liabilities | 5,681 | |||

| Total Net Assets | $ | 8,220,412 | ||

| Net Assets Consist of: | ||||

| Capital Paid In | $ | 7,984,622 | ||

| Total Distributable Earnings (Loss) | 235,790 | |||

| Total Net Assets | $ | 8,220,412 | ||

| Net Asset Value Per Share: | ||||

| Total Net Assets | $ | 8,220,412 | ||

| Shares of Beneficial Interest Outstanding (Unlimited Shares of $0.001 Par Value Authorized) | 400,000 | |||

| Net Asset Value | $ | 20.55 | ||

| Investments, at Cost | $ | 7,056,935 |

The accompanying notes are an integral part of the financial statements.

| 18 | Annual Report June 30, 2021 |

USCF ETF TRUST

USCF MIDSTREAM ENERGY INCOME FUND

STATEMENT OF ASSETS AND LIABILITIES

JUNE 30, 2021

| Assets: | ||||

| Investments, at Market Value | $ | 99,689,625 | ||

| Receivables: | ||||

| Dividends | 164,803 | |||

| Interest | 29 | |||

| Total Assets | 99,854,457 | |||

| Liabilities: | ||||

| Due to custodian | 799 | |||

| Payables: | ||||

| Accrued Management Fees | 68,457 | |||

| Total Liabilities | 69,256 | |||

| Total Net Assets | $ | 99,785,201 | ||

| Net Assets Consist of: | ||||

| Capital Paid In | $ | 87,134,787 | ||

| Total Distributable Earnings (Loss) | 12,650,414 | |||

| Total Net Assets | $ | 99,785,201 | ||

| Net Asset Value Per Share: | ||||

| Total Net Assets | $ | 99,785,201 | ||

| Shares of Beneficial Interest Outstanding (Unlimited Shares of $0.001 Par Value Authorized) | 3,400,000 | |||

| Net Asset Value | $ | 29.35 | ||

| Investments, at Cost | $ | 87,103,106 |

The accompanying notes are an integral part of the financial statements.

| 19 |

USCF ETF TRUST

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND

CONSOLIDATED STATEMENT OF OPERATIONS

FOR THE YEAR ENDED JUNE 30, 2021

| Investment Income: | ||||

| Interest Income | $ | 1,375 | ||

| Total Investment Income | 1,375 | |||

| Expenses: | ||||

| Management Fees | 30,842 | |||

| Total Expenses | 30,842 | |||

| Less Fees Waived (Note 4) | (7,710 | ) | ||

| Net Expenses | 23,132 | |||

| Net Investment Income (Loss) | (21,757 | ) | ||

| Realized and Unrealized Gain (Loss) on Investments: | ||||

| Net Realized Gain (Loss) on Commodity Futures Contracts(a) | 1,248,514 | |||

| Net Change in Unrealized Appreciation (Depreciation) on Commodity Futures Contracts | 246,824 | |||

| Net Change in Realized and Unrealized Gain (Loss) on Commodity Futures Contracts | 1,495,338 | |||

| Net Increase (Decrease) in Net Assets Resulting from Operations | $ | 1,473,581 |

| (a) | Net of commissions of $3,482. |

The accompanying notes are an integral part of the financial statements.

| 20 | Annual Report June 30, 2021 |

USCF ETF TRUST

USCF MIDSTREAM ENERGY INCOME FUND

FOR THE PERIOD ENDED JUNE 30, 2021*

Investment Income: | ||||

| Dividend Income (less net foreign withholding tax $61,126) | $ | 750,386 | ||

| Total Investment Income | 750,386 | |||

| Expenses: | ||||

| Management Fees | 174,897 | |||

| Total Expenses | 174,897 | |||

| Net Investment Income (Loss) | 575,489 | |||

| Realized and Unrealized Gain (Loss) on Investments: | ||||

| Net Realized Gain (Loss) on: | ||||

| Investments | 78,580 | |||

| Foreign currency translations | (6,173 | ) | ||

| Net realized gain (loss) | 72,407 | |||

| Net change in unrealized appreciation (depreciation) on: | ||||

| Investments | 12,586,519 | |||

| Foreign currency translations | 15 | |||

| Net change in unrealized appreciation (depreciation) | 12,586,534 | |||

| Net Change in Realized and Unrealized Gain (Loss) on Investments | 12,658,941 | |||

| Net Increase (Decrease) in Net Assets Resulting from Operations | $ | 13,234,430 |

| * | Inception Date, March 23, 2021. |

The accompanying notes are an integral part of the financial statements.

| 21 |

USCF ETF TRUST

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND

CONSOLIDATED STATEMENTS OF CHANGES IN NET ASSETS

| For the Year Ended June 30, | ||||||||

| 2021 | 2020 | |||||||

| Operations: | ||||||||

| Net Investment Income (Loss) | $ | (21,757 | ) | $ | 33,908 | |||

| Net Realized Gain (Loss) | 1,248,514 | (1,624,675 | ) | |||||

| Net Changes in Unrealized Appreciation (Depreciation) | 246,824 | 60,033 | ||||||

| Net Increase (Decrease) in Net Assets Resulting from Operations | 1,473,581 | (1,530,734 | ) | |||||

| Distributions to Shareholders from: | ||||||||

| Net Investment Income | — | (31,428 | ) | |||||

| Total Distributions to Shareholders | — | (31,428 | ) | |||||

| Shareholder Transactions: | ||||||||

| Proceeds from Shares Sold | 4,112,517 | 1,826,792 | ||||||

| Cost of Shares Redeemed | — | (1,321,701 | ) | |||||

| Net Increase (Decrease) in Net Assets from Shares Transactions | 4,112,517 | 505,091 | ||||||

| Net Increase (Decrease) in Net Assets | 5,586,098 | (1,057,071 | ) | |||||

| Net Assets: | ||||||||

| Beginning of Year | 2,634,314 | 3,691,385 | ||||||

| End of Year | $ | 8,220,412 | $ | 2,634,314 | ||||

| Changes in Shares Outstanding: | ||||||||

| Shares Outstanding, Beginning of Year | 200,000 | 200,000 | ||||||

| Shares Issued | 200,000 | 100,000 | ||||||

| Shares Issued in Reinvestment of Dividends and Distributions | — | — | ||||||

| Shares Redeemed | — | (100,000 | ) | |||||

| Shares Outstanding, End of Year | 400,000 | 200,000 | ||||||

The accompanying notes are an integral part of the financial statements.

| 22 | Annual Report June 30, 2021 |

USCF ETF TRUST

USCF MIDSTREAM ENERGY INCOME FUND

STATEMENTS OF CHANGES IN NET ASSETS

| For the Period Ended June 30, 2021* | ||||

| Operations: | ||||

| Net Investment Income (Loss) | $ | 575,489 | ||

| Net Realized Gain (Loss) | 72,407 | |||

| Net Changes in Unrealized Appreciation (Depreciation) | 12,586,534 | |||

| Net Increase (Decrease) in Net Assets Resulting from Operations | 13,234,430 | |||

| Distributions to Shareholders from: | ||||

| Net Investment Income | (584,016 | ) | ||

| Return of Capital | (221,613 | ) | ||

| Total Distributions to Shareholders | (805,629 | ) | ||

| Shareholder Transactions: | ||||

| Proceeds from Shares Sold | 87,356,400 | |||

| Shares Issued as Reinvestment of Dividends and Distributions | — | |||

| Cost of Shares Redeemed | — | |||

| Net Increase (Decrease) in Net Assets from Shares Transactions | 87,356,400 | |||

| Net Increase (Decrease) in Net Assets | 99,785,201 | |||

| Net Assets: | ||||

| Beginning of Period | — | |||

| End of Period | $ | 99,785,201 | ||

| Changes in Shares Outstanding: | ||||

| Shares Outstanding, Beginning of Period | — | |||

| Shares Issued | 3,400,000 | |||

| Shares Issued in Reinvestment of Dividends and Distributions | — | |||

| Shares Redeemed | — | |||

| Shares Outstanding, End of Period | 3,400,000 | |||

| * | Inception Date, March 23, 2021. |

The accompanying notes are an integral part of the financial statements.

| 23 |

USCF ETF TRUST

USCF SUMMERHAVEN DYNAMIC COMMODITY STRATEGY NO K-1 FUND

CONSOLIDATED FINANCIAL HIGHLIGHTS

SELECTED DATA FOR A SHARE OF COMMON STOCK OUTSTANDING

THROUGHOUT THE PERIOD INDICATED:

| For the | ||||||||||||||||

| Period Ended | ||||||||||||||||

| For the Year Ended June 30, | June 30, | |||||||||||||||

| 2021 | 2020 | 2019 | 2018* | |||||||||||||

| Net Asset Value, Beginning of Period | $ | 13.17 | $ | 18.46 | $ | 21.94 | $ | 22.00 | ||||||||

| Income (Loss) from Operations: | ||||||||||||||||

| Net Investment Income (Loss)(a) | (0.09 | ) | 0.12 | 0.26 | 0.02 | |||||||||||

| Net Realized and Unrealized Gain (Loss) | 7.47 | (5.31 | ) | (3.54 | ) | (0.06 | ) | |||||||||

| Total Income (Loss) from Operations | 7.38 | (5.19 | ) | (3.28 | ) | (0.04 | ) | |||||||||

| Less Distributions From: | ||||||||||||||||

| Net Investment Income (Loss) | — | (0.10 | ) | (0.20 | ) | (0.02 | ) | |||||||||

| Total Distributions | — | (0.10 | ) | (0.20 | ) | (0.02 | ) | |||||||||

| Net Assets Value, End of Period | $ | 20.55 | $ | 13.17 | $ | 18.46 | $ | 21.94 | ||||||||

| Total Return(b) | 56.04 | % | (28.20 | )% | (14.98 | )% | (0.17 | )% | ||||||||

| Net Assets, End of Period (thousands) | $ | 8,220 | $ | 2,634 | $ | 3,691 | $ | 8,774 | ||||||||

| Ratios of Average Net Assets: | ||||||||||||||||

| Gross Expenses | 0.80 | %(c) | 0.94 | %(c) | 0.80 | % | 0.80 | %(d) | ||||||||

| Net Expenses | 0.60 | %(c) | 0.77 | %(c) | 0.80 | % | 0.80 | %(d) | ||||||||

| Net Investment Income (Loss) | (0.56 | )% | 0.73 | % | 1.27 | % | 0.67 | %(d) | ||||||||

| Portfolio Turnover Rate(e) | 0 | % | 0 | % | 123 | % | 19 | % | ||||||||

| * | Inception Date, May 2, 2018. |

| (a) | Per share amounts have been calculated using the average shares method. |

| (b) | Total Return reflects fee waivers and/or expense reimbursement and assumes reinvestment of dividend distributions. In the absence of fee waivers and/or expense reimbursement, the total return would have been lower. Past performance is no guarantee of future results. |

| (c) | Effective August 15, 2019, USCF Advisers, LLC (“the Adviser”) contractually agreed through October 31, 2021 to waive 0.20% of its management fees. |

| (d) | Annualized. |

| (e) | Portfolio turnover rate is not annualized for periods less than one year and does not include securities received or delivered from processing creations or redemptions. |

The accompanying notes are an integral part of the financial statements.

| 24 | Annual Report June 30, 2021 |

USCF ETF TRUST

USCF MIDSTREAM ENERGY INCOME FUND

SELECTED DATA FOR A SHARE OF COMMON STOCK OUTSTANDING

THROUGHOUT THE PERIOD INDICATED:

| For the Period Ended June 30, 2021* | ||||

| Net Asset Value, Beginning of Period | $ | 24.29 | ||

| Income (Loss) from Operations: | ||||

| Net Investment Income (Loss)(a) | 0.21 | |||

| Net Realized and Unrealized Gain (Loss) | 5.09 | |||

| Total Income (Loss) from Operations | 5.30 | |||

| Less Distributions From: | ||||

| Net Investment Income (Loss) | (0.18 | ) | ||

| Return of Capital | (0.06 | ) | ||

| Total Distributions | (0.24 | ) | ||

| Net Assets Value, End of Period | $ | 29.35 | ||

| Total Return(b) | 21.83 | % | ||

| Net Assets, End of Period (thousands) | $ | 99,785 | ||

| Ratios of Average Net Assets: | ||||

| Gross Expenses | 0.85 | %(c) | ||

| Net Expenses | 0.85 | %(c) | ||

| Net Investment Income (Loss) | 2.80 | %(c) | ||

| Portfolio Turnover Rate(d) | 8 | % | ||

| * | Inception Date, March 23, 2021. |

| (a) | Per share amounts have been calculated using the average shares method. |

| (b) | Total Return reflects fee waivers and/or expense reimbursement and assumes reinvestment of dividend distributions. In the absence of fee waivers and/or expense reimbursement, the total return would have been lower. Past performance is no guarantee of future results. |

| (c) | Annualized. |

| (d) | Portfolio turnover rate is not annualized for periods less than one year and does not include securities received or delivered from processing creations or redemptions. |

The accompanying notes are an integral part of the financial statements.

| 25 |

USCF ETF TRUST

NOTES TO FINANCIAL STATEMENTS

JUNE 30, 2021

NOTE 1 – ORGANIZATION

The USCF ETF Trust (the “Trust”) was organized as a Delaware statutory trust in accordance with a Declaration of Trust dated November 6, 2013. The Declaration of Trust was amended and restated on June 16, 2014. The Trust is authorized to have multiple segregated series or portfolios. The Trust is an open-end management investment company registered under the Investment Company Act of 1940 (the “1940 Act”). The Trust currently consists of two investment portfolios, each of which is an exchange-traded fund (“ETF”): the USCF SummerHaven Dynamic Commodity Strategy No K-1 Fund (“SDCI”) and the USCF Midstream Energy Income Fund (“UMI”) (each a “Fund” and collectively, the “Funds”). SDCI commenced operations on May 2, 2018. Shares of SDCI were listed on the NYSE Arca Equity, Inc. (“NYSE Arca”) on May 3, 2018. UMI commenced operations on March 23, 2021. Shares of UMI were listed on NYSE Arca on March 24, 2021. Other series or portfolios may be added to the Trust in the future. The Adviser serves as the investment adviser to each of the Funds and USCF Cayman Commodity 2, the wholly-owned subsidiary of SDCI (the “Subsidiary”). The Adviser has been registered as an investment adviser with the Securities Exchange Commission (the “SEC”) since July 1, 2014 and is a wholly-owned subsidiary of Wainwright Holdings, Inc. SummerHaven Investment Management, LLC serves as the sub-adviser to the Subsidiary. Miller/Howard Investments, Inc. serves as the sub-adviser to UMI.

NOTE 2 – SIGNIFICANT ACCOUNTING POLICIES

The accompanying financial statements were prepared in accordance with U. S. Generally Accepted Accounting Principles (“GAAP”), which require the use of estimates and assumptions made by management. These may affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates. The following is a summary of significant accounting policies consistently followed by the Funds in preparation of their financial statements.

Basis of Presentation

The financial statements have been prepared in conformity with GAAP as detailed in the Financial Accounting Standards Board’s (“FASB”) Accounting Standards Codification (“ASC”). The Funds are investment companies and follow the accounting and reporting guidance in FASB Topic 946.

| 26 | Annual Report June 30, 2021 |

Calculation of Net Asset Value

The Net Asset Value (“NAV”) of a Fund’s shares is calculated each day the national securities exchanges are open for trading. The NAV for SDCI is generally calculated at 2:30 p.m. Eastern Time. For UMI, the NAV is calculated as of the close of regular trading on NYSE Arca, generally 4:00 p.m. Eastern Time. For each Fund, the time at which its NAV is calculated as described herein is it’s “NAV Calculation Time”. If regular trading on NYSE Arca closes earlier than a Fund’s NAV Calculation Time, such Fund’s NAV will be calculated as of that earlier time. NAV per share is calculated by dividing the Fund’s net assets by the number of the Fund’s outstanding shares.

In calculating its NAV, a Fund generally values its assets based on market quotations, last sale prices, or estimates of value furnished by a pricing service or brokers who make markets in such instruments. Debt obligations with maturities of 60 days or less are valued at amortized cost.

Fair value pricing is used by a Fund when reliable market valuations are not readily available or are not deemed to reflect current market values. Securities that may be valued using “fair value” pricing may include, but are not limited to, securities for which there are no current market quotations or whose issuer is in default or bankruptcy, securities subject to corporate actions (such as mergers or reorganizations), securities subject to non-U.S. Investment limits or currency controls, and securities affected by “significant events.” An example of a significant event is an event, occurring after the close of the market in which a security trades but before a Fund’s next NAV Calculation Time that may materially affect the value of the Fund’s investment (e.g., government action, natural disaster, or significant market fluctuation). When fair-value pricing is employed, the prices of securities used by a Fund to calculate its NAV may differ from quoted or published prices for the same securities.

The value of the Funds’ assets that trade in markets outside the United States may fluctuate on days that foreign markets are open (which may include non-Business Days). As such, the value of the Funds’ investments may change on days when you will not be able to purchase or redeem the Funds’ shares.

Security Valuation

i. Securities

Investments by any Fund in securities are carried at market value. All equity securities that are traded on a national securities exchange are valued at the last sale price at the time of the close of the New York Stock Exchange (“NYSE”). If on a particular day an exchange-listed security does not trade, then the mean between the closing bids and asked prices will be used. In the case of securities listed on more than one national securities exchange, the last quoted sale, up to the time of valuation, on the exchange on which the security is principally traded will be used. If there were no sales on that exchange, the last quoted sale on the other exchange will be used.

| 27 |

For securities held by any Fund that are traded on the NASDAQ, the NASDAQ Official Closing Price (e.g., the NASDAQ Closing Cross price, if available) is used. All non- NASDAQ equity securities that are not traded on a listed exchange are valued at the last sale price at the close of the NYSE. If a non-exchange listed security does not trade on a particular day, or if a last sales price or NASDAQ Official Closing Price is not available, then the mean between the closing bid and asked price will be used.

Securities having a remaining maturity of 60 days or less are valued at amortized cost, which approximates market value.

The cost of securities sold is determined on the identified cost basis. When market quotations are not readily available or when events occur that make established valuation methods unreliable, securities of the Funds may be valued at fair value determined in good faith by or under the direction of the Board of Trustees (the “Board”).

Security transactions are recorded on the dates the transactions are entered, which is the trade date.

ii. Master Limited Partnerships

UMI may invest up to 25% of its total assets in certain master limited partnerships (“MLPs”). MLPs are a business venture that exists in the form of a publicly traded limited partnership.

UMI’s ability to meet its investment objective relies in part upon the level of taxable income it receives from the MLPs in which it invests, a factor over which the Fund has no control. The benefit that UMI derives from its investment in MLPs is largely dependent on their being treated as partnerships for U.S. federal income tax purposes. Partnerships do not pay U.S. federal income tax at the partnership level. Rather, each partner is allocated a share of the partnership’s income, gains, losses, deductions and expenses.

An investment in MLP units involves risks that differ from a similar investment in equity securities, such as common stock, of a corporation. As compared to common shareholders of a corporation, holders of MLP units have more limited control and limited rights to vote on matters affecting the partnership.

iii. Treasuries

The Funds may invest in U.S. government obligations. U.S. government obligations include U.S. Treasury obligations and securities issued or guaranteed by various agencies of the U.S. government, or by various instrumentalities which have been established or sponsored by the U.S. government. U.S. Treasury obligations are backed by the “full faith and credit” of the U.S. government. Securities issued or guaranteed by U.S. federal agencies and U.S. government sponsored instrumentalities may or may not be backed by the full faith and credit of the U.S. government.

| 28 | Annual Report June 30, 2021 |

iv. Money Market Instruments

The Funds may invest a portion of their assets in high-quality money market instruments on an ongoing basis. The instruments in which the Funds may invest include: (1) short-term obligations issued by the U.S. government; (2) negotiable certificates of deposit (“CDs”), fixed time deposits and bankers’ acceptances of U.S. and foreign banks and similar institutions; (3) commercial paper rated at the date of purchase “Prime-1” by Moody’s Investors Service, Inc. or “A-1+” or “A-1” by S&P Global, or, if unrated, of comparable quality as determined by the Adviser; and (4) money market mutual funds. CDs are short-term negotiable obligations of commercial banks. Time deposits are non-negotiable deposits maintained in banking institutions for specified periods of time at stated interest rates. Banker’s acceptances are time drafts drawn on commercial banks by borrowers, usually in connection with international transactions.

v. Futures

A commodities futures contract provides for the future sale by one party and the purchase by the other party of a specified amount of a commodity, such as an energy, agricultural or metal commodity, at a specified price, date, time and place. A foreign currency futures contract provides for the future sale by one party and the purchase by the other party of a certain amount of a specified non-U.S. currency at a specified price, date, time and place. An interest rate futures contract provides for the future sale by one party and the purchase by the other party of a certain amount of a specific interest rate sensitive financial instrument (e.g., a debt security) at a specified price, date, time and place. A futures contract on an index is an agreement to be settled by delivery of an amount of cash equal to a specified multiplier times the difference between the value of the index at the close of the last trading day on the contract and the price at which the agreement is made. The clearing house of the exchange on which a futures contract is entered into becomes the counterparty to each purchaser and seller of the futures contract.

SDCI and the Subsidiary may purchase and sell commodity contracts in the form of forwards, futures, and options; may enter into foreign exchange contracts; may enter into swap agreements; may enter into other financial transactions; and may purchase or sell precious metal commodity contracts or options on such contracts in compliance with applicable commodities laws. SDCI and the Subsidiary may also invest in other instruments related to commodities, including structured notes, and securities of commodities finance and operating companies. In the commodity futures market, there are often costs of physical storage associated with purchasing the underlying commodity. The price of the commodity futures contract will reflect the storage costs of purchasing the physical commodity, including the time value of money invested in the physical commodity. To the extent that the storage costs for an underlying commodity change while SDCI and the Subsidiary are invested in futures with respect to that commodity, the value of the futures contract may change proportionately. In the commodity futures markets, producers of the underlying commodity may decide to hedge the price risk of selling the commodity by selling futures contracts today to lock in the price of the commodity at delivery tomorrow. In order to induce speculators to purchase the other side of the same futures contract, the commodity producer generally must sell the futures contract at a lower price than the expected future spot price of the commodity. Conversely, if most hedgers in the futures market are purchasing futures contracts to hedge against a rise in prices, then speculators will only sell the other side of the futures contract at a higher futures price than the expected future spot price of the commodity. The changing nature of the hedgers and speculators in the commodities markets will influence whether futures prices are above or below the expected future spot price, which can have significant implications for SDCI and the Subsidiary. The commodities which underlie commodity futures contracts may be subject to additional economic and non-economic variables, such as drought, floods, weather, livestock disease, embargoes, tariffs, and international economic, political and regulatory developments. These factors may have a larger impact on commodity prices and commodity-linked instruments, including futures contracts, than on traditional securities. Certain commodities are also subject to limited pricing flexibility because of supply and demand factors. Others are subject to broad price fluctuations as a result of the volatility of the prices for certain raw materials and the instability of the supplies of other materials.

| 29 |

When a purchase or sale of a futures contract is made by a fund, the fund is required to deposit with its futures commission merchant (“FCM”) a specified amount of liquid assets (“initial margin”). The margin required for a futures contract is set by the exchange on which the contract is traded and may be modified during the term of the contract. The initial margin is in the nature of a performance bond or good faith deposit on the futures contract that is returned to the fund upon termination of the contract, assuming all contractual obligations have been satisfied. The fund expects to earn taxable interest income on its initial margin deposits.

A futures contract held by a fund is valued daily at the official settlement price on the exchange on which it is traded. Each day the fund pays or receives cash, called “variation margin,” equal to the daily change in value of the futures contract. This process is known as “marking to market.” Variation margin does not represent a borrowing or loan by the fund but is instead a settlement between the fund and the FCM of the amount one would owe the other if the futures contract expired. In accordance with ASC 946-310-45, the variation margin is shown separately on the Consolidated Statement of Assets and Liabilities. In computing daily NAV, the fund will mark to market its open futures positions. Although some futures contracts call for making or taking delivery of the underlying assets, generally these obligations are closed out prior to delivery by offsetting purchases or sales of matching futures contracts (involving the same exchange, underlying security or index and delivery month). If an offsetting purchase price is less than the original sale price, the fund realizes a capital gain, or if it is more, the fund realizes a capital loss. Conversely, if an offsetting sale price is more than the original purchase price, a fund realizes a capital gain, or if it is less, the fund realizes a capital loss. The transaction costs also must be included in these calculations. As discussed below, however, the funds may not always be able to make an offsetting purchase or sale. In the case of a physically settled futures contract, this could result in the funds being required to deliver, or receive, the underlying physical commodity, which could be adverse to the fund.

| 30 | Annual Report June 30, 2021 |

At any time prior to the expiration of a futures contract, the fund may seek to close the position by seeking to take an opposite position, which would operate to terminate the fund’s existing position in the contract. Positions in futures contracts may be closed out only on the exchange on which they were entered into (or through a linked exchange).

No secondary market for such contracts exists. Although the funds may purchase futures contracts only if there is an active market for such contracts, there is no assurance that an active market will exist at any particular time. Most Futures Exchanges limit the amount of fluctuation permitted in futures contract prices during a single trading day. Once the daily limit has been reached in a particular contract, no trades may be made that day at a price beyond that limit or trading may be suspended for specified periods during the day. It is possible that futures contract prices could move to the daily limit for several consecutive trading days with little or no trading, thereby preventing prompt liquidation of futures positions at an advantageous price and subjecting the fund to substantial losses. In such event, and in the event of adverse price movements, the fund would be required to make daily cash payments of variation margin. In such situations, if the fund had insufficient cash, it might have to sell assets to meet daily variation margin requirements at a time when it would be disadvantageous to do so. In addition, if the transaction is entered into for hedging purposes, in such circumstances the fund may realize a loss on a futures contract or option that is not offset by an increase in the value of the hedged position. Losses incurred in futures transactions and the costs of these transactions will affect the performance of the fund. When the fund purchases futures contracts, it will collateralize its position by depositing an amount of cash or liquid securities in an account with the FCM.

When the funds invest in Commodity-Linked Investments (including swaps), they may be required to segregate cash and/or liquid securities to the extent the fund’s obligations are not covered or otherwise offset. Generally, if the fund does not cover its obligations to pay or deliver securities or other assets, the fund will segregate cash or liquid securities in an amount at least equal to the current amount of the obligation. With respect to investments in futures contracts, the fund will deposit initial margin and any applicable daily variation margin in addition to segregating cash or liquid securities sufficient to satisfy its obligation to purchase or provide securities or currencies, or to pay the amount owed at the contract’s expiration.

A summary of the open futures contracts as of June 30, 2021 is included in a table following SDCI’s Schedule of Investments.

| 31 |

The following table summarize the value of SDCI’s derivative instruments held as of June 30, 2021 presented by primary underlying risk exposure:

| Asset Derivatives | Liability Derivatives | |||||||

| Unrealized appreciation on commodity futures contracts* | Unrealized depreciation on commodity futures contracts* | |||||||

| SDCI Commodity Futures Contracts | $ | 376,519 | $ | (89,996 | ) | |||

| * | Included cumulative appreciation or cumulative depreciation of futures contracts as disclosed in the Consolidated Schedule of Investments. Unsettled variation margin is disclosed separately within the Statement of Assets and Liabilities. |

Additionally, the amount of realized and unrealized gains and losses on derivative instruments recognized in SDCI’s earnings during the year ended June 30, 2021 and the related location in the accompanying Consolidated Statement of Operations is summarized in the following tables by primary underlying risk exposure:

The Effect of Derivative Instruments on the Consolidated Statement of Operations

| Year Ended June 30, 2021 | |||||||||||

| Fund | Derivatives not Accounted for as Hedging Instruments | Location of Gain (Loss) on Derivatives | Realized Gain | Change in | |||||||

| SDCI | Open Commodity Futures Contracts | Net Realized Gain (Loss) on Commodity Futures Contracts | $ | 1,248,514 | |||||||

| Net Change in Unrealized Appreciation (Depreciation) on Open Commodity Futures Contracts | $ | 246,824 | |||||||||

For the year ended June 30, 2021, the average monthly volume of derivatives for SDCI was as follows:

| Commodity Futures Contracts (Notional Value) | ||||

| SDCI | $ | 3,797,378 | ||

Fair Value Measurement

The Funds utilize various methods to measure the fair value of most of their investments on a recurring basis. GAAP establishes a hierarchy that prioritizes inputs to valuation methods. The three levels of inputs are:

| 32 | Annual Report June 30, 2021 |

Level 1 – Unadjusted quoted prices in active markets for identical assets or liabilities that the Funds have the ability to access.

Level 2 – Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument or an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level 3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available; representing the Funds’ own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based on the best information available.

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

Futures contracts are generally valued at the settlement prices established each day on the exchange on which they are traded and are categorized as Level 1.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The following tables summarize the valuation of securities at June 30, 2021 for the Funds, using the fair value hierarchy:

SDCI

| Investments, at fair value | Total | Level 1 | Level 2 | Level 3 | ||||||||||||

| Cash Equivalents: | ||||||||||||||||

| United States Money | ||||||||||||||||

| Market Funds | $ | 7,056,935 | $ | 7,056,935 | $ | — | $ | — | ||||||||

| Total Cash Equivalents, at fair value | $ | 7,056,935 | $ | 7,056,935 | $ | — | $ | — | ||||||||

| Exchange-Traded Futures Contracts: | ||||||||||||||||

| Foreign Contracts | 135,519 | 135,519 | — | — | ||||||||||||

| United States Contracts | 151,004 | 151,004 | — | — | ||||||||||||

| Total Exchange-Traded Futures Contracts | $ | 286,523 | $ | 286,523 | $ | — | $ | — | ||||||||

| Total Investments, at fair value | $ | 7,343,458 | $ | 7,343,458 | $ | — | $ | — | ||||||||

| 33 |

UMI

| Investments, at fair value | Total | Level 1 | Level 2 | Level 3 | ||||||||||||

| Common Stocks: | ||||||||||||||||

| Pipelines | $ | 74,848,208 | $ | 74,848,208 | $ | — | $ | — | ||||||||

| Master Limited Partnerships: | ||||||||||||||||

| Gas | 2,728,137 | 2,728,137 | — | — | ||||||||||||

| Pipelines | 21,529,748 | 21,529,748 | — | — | ||||||||||||

| United States Money Market Funds | $ | 583,532 | $ | 583,532 | $ | — | $ | — | ||||||||

| Total Investments, at fair value | $ | 99,689,625 | $ | 99,689,625 | $ | — | $ | — | ||||||||

Income

Dividend income is recorded on the ex-dividend date, as soon as information is available to the Funds. Distributions to shareholders, which are determined in accordance with income tax regulations, are also recorded on the ex-dividend date. Interest income is recorded as earned. Discounts and premiums on securities purchased are amortized over the life of the respective securities.

Commodity futures contracts, forward contracts, physical commodities and related options are recorded on the trade date. All such transactions are recorded on the identified cost basis and marked to market daily. Unrealized gains or losses on open contracts are reflected in the Consolidated Statement of Assets and Liabilities and represent the difference between the original contract amount and the market value (as determined by exchange settlement prices for futures contracts and related options and cash dealer prices at a predetermined time for forward contracts, physical commodities, and their related options) as of the last business day of the period or as of the last date of the consolidated financial statements. Changes in the unrealized gains or losses between periods are reflected in the Consolidated Statement of Operations.

UMI invests in MLPs which make distributions that are primarily attributable to return of capital. UMI records investment income and return of capital in the Consolidated Statement of Operations using management’s estimate of the percentage of income included in the distributions received from each MLP based on historical information from the MLPs and other industry sources. These estimates may be adjusted based on information received from the MLPs after the tax and fiscal year ends.

The return of capital portion of the MLP distributions is a reduction to investment income and a reduction in the cost basis of each investment which increases net realized gain (loss) and net change in unrealized appreciation (depreciation). If the return of capital distributions exceed its cost basis, the distributions are treated as realized gains. The actual amounts of income and return of capital are only determined by each MLP after its fiscal year-end and may differ from the estimated amounts.

| 34 | Annual Report June 30, 2021 |

Federal and Other Taxes

As of and during the year ended June 30, 2021, for SDCI, and the period ended June 30, 2021, for UMI, the Funds did not have a liability for any unrecognized tax benefits in the accompanying financial statements. The Funds file income tax returns in the U.S. federal jurisdiction and Delaware.

The Funds follow ASC 740 “Income Taxes”, which requires that the financial statements effects of a tax position taken or expected to be taken in a tax return be recognized in the financial statements when it is more likely than not, based on the technical merits, that the position will be sustained upon examination. Management has concluded that the Funds have taken no uncertain tax positions that require adjustment to the financial statements.

It is the Trust’s policy to comply with the federal income and excise tax requirements of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, the Funds intend to distribute substantially all of their income and net realized gains on investments, if any, to shareholders each year. Therefore, no federal income tax provision is required in the Funds’ financial statements. Under the applicable foreign tax laws, a withholding tax may be imposed on interest, dividends and capital gains at various rates.

GAAP requires that certain components of net assets be adjusted to reflect permanent differences between financial and tax reporting. These reclassifications have no effect on net assets or NAV per share. The following permanent differences as of June 30, 2021, were reclassified to the following accounts:

| SDCI | UMI | |||||||

| Capital Paid In | $ | 1,248,627 | $ | (221,613 | ) | |||

| Undistributed (Distribution in Excess) Net Investment Income | (113 | ) | 416,669 | |||||

| Undistributed (Accumulated) Net Realized Gain (Loss) | (1,248,514 | ) | (195,056 | ) | ||||

Management has reviewed the tax positions and has concluded that no liability for unrecognized tax benefits should be recorded related to uncertain tax positions taken on returns filed for open tax years or expected to be taken with the 2020 tax returns. SDCI’s federal tax returns for the prior three fiscal years remain subject to examination by the Internal Revenue Service.

| 35 |

Dividends and Distributions

Each Fund intends to pay out dividends on a quarterly basis. Nonetheless, each Fund may not make a dividend payment every quarter. Each Fund intends to distribute its net realized capital gains, if any, to investors annually. Each Fund may occasionally be required to make supplemental distributions at some other time during the year. Distributions in cash may be reinvested automatically in additional whole shares only if the broker through whom you purchased shares makes such option available. Your broker is responsible for distributing the income and capital gain distributions to you.