UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-22933

(Investment Company Act file number)

Apollo Diversified Real Estate Fund

(Exact name of registrant as specified in charter)

Apollo Global Management, Inc.

9 West 57th Street, New York

New York 10019

(Address of principal executive offices)

(212) 515-3200

(Registrant's telephone number, including area code)

ALPS Fund Services, Inc.

1290 Broadway, Suite 1000

Denver, CO 80203

(Name and address of agent for service)

Copy to:

Terrence O. Davis, Esq.

Greenberg Traurig, LLP

Terminus 200

3333 Piedmont Road, NE, Suite 2500

Atlanta, GA 30305

Date of fiscal year end: September 30

Date of reporting period: October 1, 2021 – September 30, 2022

Item 1. Reports to Stockholders.

Apollo Diversified

Real Estate Fund

Annual Report

September 30, 2022

Effective May 2, 2022, Griffin Institutional Access® Real Estate Fund was renamed Apollo Diversified Real Estate Fund.

Table of Contents

| Shareholder Letter | 3 |

| Portfolio Update | 16 |

| Schedule of Investments | 18 |

| Statement of Assets and Liabilities | 23 |

| Statement of Operations | 24 |

| Statements of Changes in Net Assets | 25 |

| Statement of Cash Flows | 27 |

| Financial Highlights | 28 |

| Notes to Financial Statements | 39 |

| Report of Independent Registered Public Accounting Firm | 48 |

| Additional Information | 49 |

| Trustees and Officers | 50 |

| Service Providers | 52 |

| Privacy Notice | 53 |

Dear Fellow Shareholders,

We are pleased to present the Apollo Diversified Real Estate Fund (the “Fund”)1 annual report. We greatly appreciate the support of our shareholders, and we seek to remain true to the Fund’s stated objective of delivering returns comprised of income and appreciation with moderate volatility and low correlation to the broader markets. Despite challenging economic conditions that have characterized most of 2022, the Fund continued to deliver impressive outperformance relative to both stocks and bonds. The Fund’s load-waived Class A shares (NASDAQ: GIREX) returned 10.76% in the one-year period ended September 30, 2022, while the S&P 500 Index and the Bloomberg U.S. Aggregate Bond Index delivered returns of -15.47% and -14.60% respectively, during the same period.2 From the Fund’s inception on June 30, 2014, through September 30, 2022, the Fund’s load-waived Class A shares generated a(n)2:

|

Randy I. Anderson, Ph.D., CRE Portfolio Manager, Apollo Diversified Real Estate Fund |

| ● | Total cumulative return of 77.78% and a 7.22% annualized return |

| ● | Sharpe ratio of 1.60 |

| ● | Standard deviation of 3.99%, which is in line with the standard deviation for the Bloomberg U.S. Aggregate Bond Index (4.12%) |

| ● | Alpha of 4.78% |

| ● | Beta of 0.15 |

The U.S. economy continued to struggle with inflation, slowing economic growth, and the associated monetary policy designed to address the same. Bottlenecks that plagued global supply chains since the start of the pandemic and elevated wage growth have contributed to year-over-year inflation levels not seen in decades. Recently, falling food and energy prices have offered a reprieve from the record high inflation prints, but elevated price levels remain relatively broad based, impacting the core components of inflation. In return, the Federal Reserve (“Fed”) has aggressively implemented tighter monetary policy in an effort to slow inflation and bring price stability to markets. The tightening financial conditions led to a modest decline in gross domestic product (GDP) during the first half of 2022. However, despite this economic contraction, labor markets remained strong with the U.S. unemployment rate at 3.5% in September of 2022.3 Market participants will be carefully watching further policy actions from the Federal Reserve and corresponding impacts on risk assets.

Commercial real estate fundamentals have remained strong, particularly within the Fund’s high-conviction sectors – multifamily, industrial, and specialty (such as life sciences and student housing) properties. These sectors generally consist of property types that benefit from secular growth trends which are fundamental, long-term and may be driven by evolving consumer behavior, demographic changes, or technological innovation. Such secular growth trends benefit from structural demand drivers that persist across macroeconomic regimes and are generally stable over time. Consistent with the broader inflation story, elevated prices for both labor and materials have made adding new supply increasingly difficult, contributing to a favorable supply and demand dynamic that has led to continued rent growth within those sectors benefitting from secular growth trends. In order to potentially capitalize on this dynamic, the Fund’s portfolio management team has been focused on actively positioning the portfolio accordingly. As of October 3, 2022, 88.23% of the Fund’s private equity real estate portfolio is allocated to high-conviction sectors.4

The multifamily sector continued to perform well, driven by healthy releasing spreads. The multifamily occupancy rate, according to CBRE Econometric Advisors, was 96.1% as of Q3 2022, well above the 15-year average national occupancy rate of 95.1%.5 Tight occupancy amidst strong demand contributed to robust growth with rents increasing 10.4% year-over-year across CBRE Econometric Advisors’ national sample of 69 markets as of Q3 2022.5 Sharp increases in mortgage rates coupled with the meteoric rise in residential home prices exhibited post-pandemic have pushed many would-be homebuyers to the rental market, potentially bolstering demand for multifamily assets. Nationally, the U.S. continues to be deeply undersupplied, with some estimates suggesting that it would take millions of new housing units to reach equilibrium.6

Past performance is not indicative of future results. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Investing involves risk, including loss of principal. Fund performance based on load-waived Class A shares and does not reflect any sales charge. The maximum sales charge for Class A shares is 5.75%. If the data reflected the deduction of such charges, the performance would be lower. Performance includes reinvestment of distributions and reflects management fees and other expenses. The Fund offers multiple different classes of shares. An investment in any share class of the Fund represents an investment in the same assets of the Fund. However, the purchase restrictions, ongoing fees, expenses, and performance for each share class are different. For more information on the differences in share classes, refer to the applicable prospectus, which can be found at: www.apollodiversifiedrealestatefund.com.

Due to financial statement adjustments, performance information presented herein for the Fund differs from the Fund’s financial highlights which are prepared in accordance with U.S. GAAP. Such differences generally are attributable to valuation adjustments to certain of the Fund’s investments which are reflected in the financial statements.

3

The industrial sector remained historically strong with broad-based demand and extremely well occupied existing inventory. The national vacancy rate continued to register at a record low of 2.9% as of Q3 2022, down 70 basis points year-over-year according to data from CBRE Econometric Advisors.5 Underlying this strong occupancy at the national level, there are specific markets that remained exceptionally tight on both a relative and absolute basis. Among the leaders in occupancy are Los Angeles, Savannah, and Riverside which have vacancy rates of 0.8%, 0.1%, and 1.2% respectively.5 These conditions have led to outsized rent growth with CBRE Econometric Advisors reporting a 12.1% year-over-year increase as of Q3 2022, marking the fastest growth rate in more than 20 years.5 Year-to-date net absorption of approximately 326 million square feet continues to outpace completions of 267 million square feet during the same period ended Q3 2022, with 71.9% of new deliveries that were completed in the first half of 2022 being either preleased or presold to the ultimate occupier.5, 7 Demand for modern, well-located industrial facilities remained strong from a wide tenant base of businesses and logistics operators seeking to re-tool their supply chains in an effort to reduce both transportation costs (the highest portion of a company’s logistics spend)7 and risk associated with lost sales due to insufficient inventory levels or other supply chain bottlenecks. The continued adoption of e-commerce and omnichannel retailing remained a tailwind for industrial assets and may provide a supportive environment for increased demand and further rent growth.

The specialty sector consists of property types such as life sciences, healthcare, government buildings, and student housing. These assets are highly specialized and are often built for a specific use and have differentiated supply and demand drivers. The largest component of the Fund’s specialty allocation is within the life sciences property type and primarily consists of laboratory facilities which, in many cases, are used by research organizations across various scientific disciplines. The demand for life sciences facilities remained robust, specifically in markets across the country with large, highly educated talent pools. Lab space across the 12 largest life sciences markets in the U.S. saw rental rates increase by 5.8% quarter-over-quarter in Q2 2022 as large pharmaceutical companies continued to lease space.7 Employment growth within Biotech R&D jobs grew at a record rate of 14.0% year-over-year as of Q2 2022. This compares favorably to the broader U.S. employment market which saw expansion of 4.2% during the same period.3 The combination of robust job growth and tight vacancy in many of the top innovation clusters across the country should provide a favorable backdrop for this property type moving forward. The second largest component of the Fund’s specialty allocation is within the student housing property type. Pre-leased occupancy in August 2022 (the last full month in the pre-lease season) continued to break records with 95.7% of student housing beds at the core 175 universities tracked by RealPage being pre-leased for the Fall 2022 academic year. This marked the highest August reading on record and sits 430 bps higher than July’s record pre-leased occupancy.8 Students’ desire for a more traditional educational experience should provide a tailwind in demand for dedicated student housing assets that are in close proximity to top-tier private and public educational institutions throughout the country.

Increased leasing activity within the traditional office sector has led to a modest 1.5% year-over-year increase in rent growth as of Q3 2022 according to data from CBRE Econometric Advisors.5 Vacancy rates across most markets are still below their record highs observed during the pandemic. Office utilization remains well below pre-pandemic levels as most businesses maintain flexibility with hybrid work arrangements. The benefits of working and collaborating in person remains an attractive proposition for companies seeking to develop both a firm culture and an environment that fosters creativity and innovation. Moving forward, the office market is expected to remain bifurcated between aging, commoditized product and modern, well-amenitized assets particularly those in desirable locations.

This bifurcation in asset performance has also been observed in the retail sector with neighborhood, grocery-anchored centers faring better than malls, especially malls in secondary and tertiary markets. Overall, there has been improvement in operating fundamentals for the retail sector with the availability rate falling to 5.0% in Q3 2022, a level not seen in more than 15 years.5 Total retail employment has completely recovered from the pandemic trough and completions remain at historical lows which should aid the sector overall.3, 5 While the retail sector may remain challenged in aggregate, the combination of strong consumer demand and limited new supply has maintained the downward trajectory of availability rates and may provide for resiliency across certain segments of the retail sector moving forward.

Apollo Diversified Real Estate Fund is a closed-end interval fund. Limited liquidity is provided to shareholders only through the Fund’s quarterly repurchase offers for no less than 5% and no more than 25% of the Fund’s shares outstanding at net asset value. The Fund is suitable only for investors who can bear the risks associated with the limited liquidity of the Fund and should be viewed as a long-term investment. There is no secondary market for the Fund’s shares, and none is expected to develop.

Diversification does not eliminate the risk of experiencing investment losses. Holdings and allocations are subject to change without notice.

4

We believe dispersion in sector performance we have observed since the onset of the pandemic will persist, providing potential opportunities for active management. During the trailing one-year period ended June 30, 2022, the Fund’s private portfolio delivered 296bps of outperformance relative to the NCREIF ODCE Index.9 Further, the Fund utilizes an actively managed investment approach with the ability to invest across all four quadrants of the commercial real estate market: private equity, private debt, public equity, and public debt. This flexibility in investment mandate allows for a dynamic allocation strategy to take advantage of relative value discrepancies between public and private markets. As of the time of writing, publicly traded real estate investment trusts (REITs) are trading at significant discounts to net asset value (NAV) (73% Price/NAV as of September 30, 2022).10 Over the last 25 years, when REITs have been priced below 85% Price/NAV, they have delivered an average return of 29% over one year, and 55% over three years.11

Looking ahead to the balance of 2022, the outlook for the economy overall remains relatively opaque with uncertainty around the path of inflation and Fed policy. With the potential for further volatility, portfolio construction and downside protection are of paramount importance. We believe the Fund may offer investors an attractive alternative to traditional fixed income with lower volatility to the broader markets. The Fund’s portfolio management team remains focused on allocating to core, well leased properties in sectors with secular, rather than cyclical, demand drivers that may further grow rent. As of October 3, 2022, the Fund provides exposure to over 3,900 investments representing over $290 billion in gross property value that is 95% occupied.4 The Fund is diversified by property type, geography, and across all four quadrants of the commercial real estate opportunity set. While future economic conditions remain unclear, we believe the Fund’s exposure to high-quality commercial real estate particularly within our high-conviction sectors should continue to deliver attractive risk-adjusted returns to our investors.

We thank you for your continued confidence and support.

Sincerely,

Randy I. Anderson, Ph.D., CRE

Portfolio Manager, Apollo Diversified Real Estate Fund

5

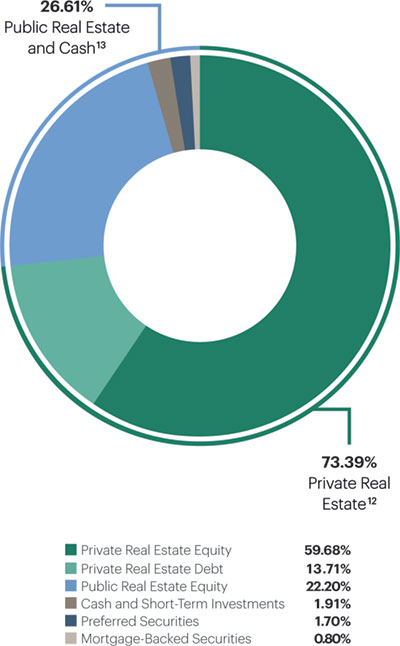

Portfolio Exposure as of October 3, 2022 (Unaudited)

Overall Portfolio Exposure

| Private Real Estate Exposure12 | 73 | % | ||

| Cortland Growth and Income Fund | 6.65 | % | ||

| Clarion Lion Properties Fund | 6.47 | % | ||

| Clarion Lion Industrial Trust | 4.59 | % | ||

| Morgan Stanley Prime Property Fund | 4.19 | % | ||

| Oaktree Real Estate Income Fund | 4.08 | % | ||

| CBRE U.S. Logistics Partners | 4.01 | % | ||

| CBRE U.S. Core Partners | 3.93 | % | ||

| Ventas Life Science and Healthcare Real Estate Fund | 3.41 | % | ||

| Clarion Gables Multifamily Trust | 3.30 | % | ||

| TA Realty Core Property Fund | 3.26 | % | ||

| TA Realty Logistics Fund | 2.89 | % | ||

| Dream US Industrial Fund | 2.39 | % | ||

| Prologis Targeted U.S. Logistics Fund | 1.92 | % | ||

| CA Student Living Income and Growth Fund | 1.77 | % | ||

| Manulife U.S. Real Estate Fund | 1.57 | % | ||

| Sentinel Real Estate Fund | 1.30 | % | ||

| USAA U.S. Government Building Fund | 1.11 | % | ||

| GWL U.S. Property Fund | 0.74 | % | ||

| Prudential PRISA | 0.72 | % | ||

| Stockbridge Smart Markets Fund | 0.61 | % | ||

| Heitman America Real Estate Trust | 0.28 | % | ||

| BGO Diversified U.S. Property Trust | 0.26 | % | ||

| UBS Trumbull Property Fund | 0.23 | % | ||

| Private Real Estate Equity | 59.68 | % | ||

| Brookfield Senior Mezzanine Real Estate Finance Fund | 2.06 | % | ||

| CBRE U.S. Credit Partners | 2.01 | % | ||

| TCM CRE Credit Fund | 2.00 | % | ||

| ARES Real Estate Enhanced Income Fund | 1.66 | % | ||

| JP Morgan U.S. Real Estate Core Mezzanine Debt Fund | 1.64 | % | ||

| Heitman Core Real Estate Debt Income Trust | 1.60 | % | ||

| PGIM Real Estate US Debt Fund | 0.98 | % | ||

| Voya Commercial Mortgage Lending Fund | 0.97 | % | ||

| CrossHarbor Strategic Debt Fund | 0.79 | % | ||

| Private Real Estate Debt | 13.71 | % | ||

| Public Real Estate Exposure and Cash13 | 27 | % | ||

| Public Real Estate Equity | 22.20 | % | ||

| Cash and Short-Term Investments | 1.91 | % | ||

| Preferred Securities | 1.70 | % | ||

| Mortgage-Backed Securities | 0.80 | % |

Portfolio Exposure as of 10/3/22

Past performance is not indicative of future results. Diversification does not eliminate the risk of experiencing investment losses. Holdings and allocations are subject to change without notice.

6

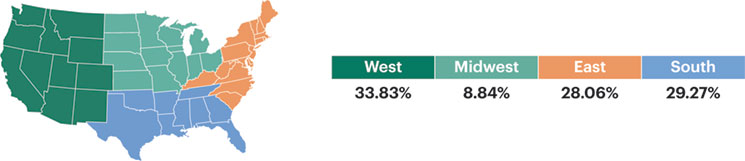

Private Fund Diversification as of October 3, 2022 (Unaudited)

Through its investment in private funds, Apollo Diversified Real Estate Fund offers immediate diversification by property sector, geography, and exposure to real estate equity and debt.

Private Real Estate Exposure: Geographic Diversification14

| Property Sector | Percentage of Total Fund Assets | Percentage of Private Fund Assets14 | Highlights14 |

| Multifamily Private Real Estate Equity Private Real Estate Debt | 26.67% 20.22% 6.45% | 36.34% 27.55% 8.79% | 757 apartment investments comprised of over 287,000 units diversified across high-growth markets. |

| Industrial Private Real Estate Equity Private Real Estate Debt | 25.25% 24.11% 1.14% | 34.40% 32.85% 1.55% | 2,177 investments boasting over 671 million square feet of industrial assets including facilities that support the fast-growing e-commerce logistics industries. |

| Specialty Private Real Estate Equity Private Real Estate Debt | 8.51% 8.33% 0.18% | 11.60% 11.35% 0.25% | 195 investments spanning over 26 million square feet of life sciences facilities, healthcare assets, and government offices, together with more than 24,000 student housing beds across the country. |

| Office Private Real Estate Equity Private Real Estate Debt | 7.59% 4.09% 3.50% | 10.34% 5.57% 4.77% | 234 high-quality office investments in diverse, high- demand metropolitan areas representing over 94 million square feet of space. |

| Other Private Real Estate Equity Private Real Estate Debt | 2.37% 1.25% 1.12% | 3.22% 1.70% 1.52% | 350 investments comprised of self-storage facilities, parking garages, and land. |

| Retail Private Real Estate Equity Private Real Estate Debt | 2.20% 1.66% 0.54% | 3.01% 2.27% 0.74% | 174 investments with more than 44 million square feet of retail space. |

| Hospitality Private Real Estate Equity Private Real Estate Debt | 0.80% 0.02% 0.78% | 1.09% 0.03% 1.06% | 24 investments representing over 6,500 keys across the country. |

Past performance is not indicative of future results. Diversification does not eliminate the risk of experiencing investment losses. Holdings and allocations are subject to change without notice.

7

Private Fund Summaries (Unaudited)

| ARES Real Estate Enhanced Income Fund is an open-end real estate debt fund with a principal objective to generate current income with an emphasis on principal protection by creating a diversified portfolio of first mortgage loans secured by commercial real estate across major property types, which primarily includes multifamily, industrial, retail, office and hospitality properties. The ARES Real Estate Enhanced Income Fund will focus on the disciplined origination of first mortgage loans secured by commercial real estate assets with strong sponsorship and located in major markets within the United States. |

| BGO Diversified US Property Fund is an open-end core real estate private equity fund that invests in a portfolio of institutional-quality real estate assets in the U.S. BGO Diversified’s investment strategy is focused on maintaining stable income, building a diversified modern portfolio, using moderate leverage, and providing superior liquidity. BGO Diversified upholds a strong commitment to the principles of Responsible Property Investing. |

| Brookfield Senior Mezzanine Real Estate Finance Fund is an open-end senior real estate debt fund focused on providing primarily floating rate financing secured by commercial property primarily located in the U.S. and secured by generally well-leased/light transitional commercial real estate properties that generate significant cash flow. Brookfield Senior Mezzanine Real Estate Finance Fund will primarily focus on creating investment positions by originating floating rate whole loans, syndicating the first mortgage and retaining the mezzanine exposure. |

| CA Student Living Income and Growth Fund is an open-end private equity real estate fund that is focused exclusively on the student housing sector. The Fund aims to acquire institutional student housing properties at large public and private universities in the United States. |

| CBRE U.S. Core Partners is an open-end core fund that purchases and operates high-quality, income-producing office, industrial, retail, and multifamily assets in select major U.S. metropolitan markets that exhibit strong growth demographics. |

| | CBRE U.S. Credit Partners is an open-end private debt fund focused on generating current income by constructing a portfolio of first mortgage loans and subordinated debt secured by high-quality income-producing commercial real estate diversified by product type and geography. |

| | CBRE U.S. Logistics Partners is an open-end private equity real estate fund focused exclusively on the industrial sector. The Fund aims to acquire modern, highly-functional, stabilized logistics assets located in major population and consumption centers while simultaneously implementing a build-to-core strategy capitalizing on major metro markets with favorable supply and demand dynamics. |

| Clarion Gables Multifamily Trust provides investors access to a high-quality multifamily portfolio with a best-in-class operator and fund manager. Gables is a market-leading, vertically-integrated multifamily real estate company with a 34 - year history in the management, construction, development, acquisition and disposition of multifamily communities in the United States. |

| | Clarion Lion Industrial Trust is a private REIT focused on the industrial property sector in North America. Clarion Lion Industrial Trust invests primarily in big-box warehouse and distribution centers, with an emphasis on large, core industrial markets throughout the United States. |

| | Clarion Lion Properties Fund is a core private REIT with interests in a diversified portfolio of primarily institutional quality real estate assets and related investments located throughout the U.S. The investment objective is to provide a strong income return with potential for long-term capital appreciation. |

| Cortland Growth and Income Fund, a leading Southern United States focused multifamily owner and operator, is a domestic multifamily open-end core-plus fund focused on acquiring best-in-class, income producing properties in U.S. growth markets. |

| CrossHarbor Strategic Debt Fund is an open-end debt fund that seeks to generate compelling risk-adjusted current and total returns for investors by originating and managing first mortgage loans secured by core, core-plus, and value-add commercial real estate located throughout the United States. |

| Dream US Industrial Fund is an open-end private equity real estate fund focused exclusively on the industrial sector. The Fund seeks to acquire and develop a portfolio of high-quality and functional industrial assets in strategic markets throughout the United States. The Fund will target core and core-plus assets including bulk distribution, last-mile warehousing, business parks, and light industrial assets in secondary interior distribution markets with a primary focus on markets experiencing strong economic and demographic fundamentals. |

| GWL U.S. Property Fund is an open-end real estate fund consisting of a diversified portfolio of institutional quality, income producing assets broadly allocated by property type and geographic location. GWL U.S. Property Fund employs a core plus strategy intertwined with a disciplined risk management process in seeking to achieve its performance objectives. |

| Heitman America Real Estate Trust is an open-end core commingled fund. Heitman America Real Estate Trust’s core strategy encompasses stabilized investments with low to moderate leverage and seeks to objectively minimize risk through diversification in property type, geographic location, and tenant composition. |

| | Heitman Core Real Estate Debt Income Trust is an open-ended, commingled fund, that originates and services first mortgage loans secured by income-producing U.S. commercial real estate. Heitman Core Real Estate Debt Income Trust will seek to originate senior debt financing to high-quality real estate operators in both primary and specialty property sectors. |

Holdings are subject to change without notice.

8

| JP Morgan U.S. Real Estate Core Mezzanine Debt Fund pursues a disciplined, income-producing strategy achieved primarily by investing in a portfolio of real estate and real estate-related assets, consisting of mezzanine debt, B-notes, ALTs by mortgages, and preferred equity investments. It focuses on the four primary property types including office, multifamily, industrial, and retail, owned and operated by experienced and financially capable sponsors with strong performance experience across investment cycles. |

| Manulife U.S. Real Estate Fund is a U.S. open-end core-plus fund that will target properties located in major U.S. markets, with the objective of preserving capital while delivering a combination of income and long-term capital appreciation. The Manulife U.S. Real Estate Fund will target an allocation of 60% core-plus assets and 40% core investments. |

| Morgan Stanley Prime Property Fund is an open-end core fund with a focus on office, retail, multifamily, industrial, self storage and hotel properties located in major real estate markets throughout the United States. |

| Oaktree Real Estate Income Fund is an open-ended fund that targets investments in commercial real estate, primarily office, multifamily and industrial assets. Oaktree Real Estate Income Fund intends to create value by investing in assets that require modest leasing and capital expenditures. |

| Prologis Targeted US Logistics Fund launched in 2004 as an open-ended, co-investment venture formed by Prologis to partner with institutional investors in acquiring, operating, and disposing of high-quality logistics facilities in key target markets across the U.S. The Fund seeks enhanced returns through actively managing, repositioning and renovating portfolio-owned assets. |

| PGIM Real Estate U.S. Debt Fund is an open-end debt fund that seeks to originate and service first mortgage and subordinate debt, fixed and floating rate loans, secured by stable income producing properties or properties exhibiting light transitional characteristics. PGIM Real Estate U.S. Debt Fund will focus on the four main property types in the top 30 MSAs and intends to provide secure income returns from investing in a low risk, low volatility portfolio of real estate debt, with a focus on capital preservation and stability of income. |

| | Prudential PRISA is organized as a perpetual life, open-ended, commingled fund to invest primarily in core, well-leased, operating real estate assets located in the United States, with an emphasis on income. PRISA is Prudential Real Estate Investors (“PREI”) flagship fund, and represents one of the oldest and largest U.S. core real estate funds available in the marketplace. |

| Sentinel Real Estate Fund is a multifamily focused, core private REIT that emphasizes acquisitions of stabilized assets with in-place income with the goal of providing a substantial portion of investor returns in the form of distributed cash. |

| Stockbridge Smart Markets Fund is an open-end core fund that aims to capture performance in excess of the ODCE Index by acquiring assets in “smart markets” characterized by educated, stable and fast-growing employment bases. The Smart Market Fund’s target market strategy is based on the principle that real estate demand is dependent on jobs which are increasingly being created where there are educated work forces in the U.S. |

| TA Realty Core Property Fund invests and operates a diversified portfolio of commercial real estate assets across industrial, multifamily, office and retail property types. TA Realty Core Property Fund has three primary objectives: build and operate a first-class portfolio of institutional quality core real estate assets, generate consistent outperformance versus industry benchmarks and provide outstanding client service to investors. |

| | TA Realty Logistics Fund is an open-end private equity real estate fund focused exclusively on the industrial sector. The Fund seeks to assemble a diversified portfolio of well-located logistics facilities in major distribution hubs and last-mile locations. The Fund targets mainly metropolitan areas of the United States that have population growth, economic growth, market economic diversity, supply constraints, liquidity, volatility, and relative yield necessary to create attractive long-term investment returns. |

| TCM CRE Credit Fund intends to focus primarily on investing in a diversified portfolio of primarily U.S. commercial real estate debt investments, generally within the mezzanine position of the capital stack. Trawler Capital Management Commercial Real Estate Credit Fund will focus on building and maintaining a portfolio of assets that are intended to provide strong risk adjusted returns in all cycles, with emphasis on stable cash flows. |

| UBS Trumbull Property Fund is an open-end, diversified Core fund focusing on the four main property types, with a small exposure to hotels. UBS Trumbull Property Fund focuses on top markets for high-quality Core, institutional real estate assets. |

| USAA U.S. Government Building Fund seeks to provide investors with attractive, risk-adjusted returns generated by the acquisition, build to suit development and operation of buildings located in the United States and leased or intended to be leased to U.S. federal, state and local governments and government agencies and departments. |

| Ventas Life Science and Healthcare Real Estate Fund is an open-ended investment vehicle formed by Ventas, Inc. to invest in high-quality healthcare properties, with a focus on the life science, medical office building, and seniors housing asset classes, in target markets primarily in the United States. The Fund’s primary objective is to generate attractive returns and cash flow with an emphasis on long-term capital growth through investment focused on the healthcare real estate sector. |

| Voya Commercial Mortgage Lending Fund is a perpetual life, open-ended, commercial mortgage debt fund. The Fund’s investment objective is to generate consistent current income with attractive risk-adjusted returns, while seeking to preserve capital through risk management of the portfolio of commercial mortgage loans and balance sheet management at the Fund level. The Fund will seek generally to achieve its investment objective by applying disciplined credit underwriting to identify and originate a diversified pool of commercial real estate loans located throughout the U.S., in primary, secondary and select tertiary markets. |

Holdings are subject to change without notice.

9

Fund Sub-Advisers (Unaudited)

| Aon Investments USA Inc. |  |

Aon Investments USA Inc. (“Aon”), an Aon Company, provides research and advisory services to the portion of the Fund’s investment portfolio that is allocated to private real estate funds. Partnering with Aon, a global leader ($4.1 trillion in assets under advisement as of June 30, 2021) within the institutional advisory services space, provides Apollo Real Estate Fund Adviser with the same level of research and due diligence as the nation’s top endowments, universities and pension funds.

| CenterSquare Investment Management LLC |  |

CenterSquare Investment Management LLC (“CenterSquare”) manages the portion of the Fund’s investment portfolio that is allocated to public real estate securities.

CenterSquare has been managing real estate securities portfolios since 1995, across multiple strategies and market cycles and had approximately $13 billion in real estate assets under management as of September 30, 2022.

Apollo Real Estate Fund Adviser, LLC along with CenterSquare Investment Management have designed a public market strategy in line with the objectives of the Fund with a focus on identifying public real estate securities whose current prices are below their intrinsic values. CenterSquare Investment Management has been managing real estate securities portfolios since 1995 across multiple strategies and market cycles.

10

Glossary (Unaudited)

Alpha: A measure of risk-adjusted return implying how much a fund/manager outperformed its benchmark, given its risk profile.

Annualized Return: Calculated by annualizing cumulative return (i.e., adjusting it for a period of one year). Annualized return includes capital appreciation and assumes a reinvestment of dividends and distributions.

Basis Point (bp): A unit of measure used to describe the percentage change. One basis point is equivalent to 0.01% (1/100th of a percent) or 0.0001 in decimal form.

Beta: A measure of systematic risk (volatility), or the sensitivity of a fund to movements in a benchmark. A beta of 1 implies that you can expect the movement of a fund’s return series to match that of the benchmark used to measure beta. A value of less than 1 implies that the fund is less volatile than the index.

Bloomberg U.S. Aggregate Bond Index: An unmanaged index of domestic investment-grade bonds, including corporate, government and mortgage-backed securities.

Correlation: A statistical measure of how two securities move in relation to each other. A correlation ranges from -1 to 1. A positive correlation of 1 implies that as one security moves, either up or down, the other security will move in lockstep, in the same direction. A negative correlation of -1 indicates that the securities will move in the opposite direction. If the correlation is 0, the movements of the securities are said to have no correlation; they are completely random.

Cumulative Return: The compound return of an investment. It includes capital appreciation and assumes a reinvestment of dividends and distributions.

Net Asset Value (NAV): Represents a fund’s per-share price. NAV is calculated by dividing a fund’s total net assets by its number of shares outstanding.

NCREIF Fund Index – Open End Diversified Core Equity (NFI-ODCE): An index of investment returns reporting on both a historical and current basis the results of certain open-end commingled funds pursuing a core investment strategy. The NFI-ODCE Index is capitalization-weighted.

S&P 500 Index: An index based on market cap of the 500 largest companies having stock listed on the New York Stock Exchange (NYSE) or NASDAQ.

Sharpe Ratio: Measures risk-adjusted returns by calculating the excess return (above the risk-free rate) per unit of risk (standard deviation). The higher the ratio, the better the risk-adjusted returns. The average three-month U.S. Treasury T-bill auction was used as the risk-free rate in this material.

Standard Deviation: Measures the average deviations of a return series from its mean, and is often used as a measure of volatility/risk. A large standard deviation implies that there have been large swings in the return series of the manager.

11

Risk Disclosures and Other Important Information (Unaudited)

This material is neither an offer to sell nor a solicitation to purchase any security. Investors should carefully consider the investment objectives, risks, charges and expenses of Apollo Diversified Real Estate Fund (the “Fund”). This information and other important details about the Fund are contained in the prospectus, which can be obtained by visiting www.apollodiversifiedrealestatefund.com. Please read the prospectus carefully before investing.

All Morningstar calculations and metrics are based on monthly data. CALCULATIONS AND METRICS REFLECT A LOAD-WAIVED, CLASS A SHARE (NASDAQ: GIREX). Investors of the load-waived class A share do not pay a front-end sales load/charge. The Fund offers multiple different classes of shares. An investment in any share class of the Fund represents an investment in the same assets of the Fund. However, the purchase restrictions, ongoing fees, expenses, and performance for each share class are different.

Past performance is not indicative of future results. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Investing involves risk, including loss of principal. Performance includes reinvestment of distributions and reflects management fees and other expenses. The Fund return does not reflect the deduction of all fees, including any applicable Fund share class sales load, third-party brokerage commissions or third-party investment advisory fees paid by investors to a financial intermediary for brokerage services. If the deduction of such fees was reflected, the performance would be lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Investing in the Fund involves risks, including the risk that you may receive little or no return on your investment or that you may lose part or all of your investment. The ability of the Fund to achieve its investment objective depends, in part, on the ability of the Adviser to effectively allocate the assets of the Fund among the various securities and investments in which the Fund invests. There can be no assurance that the actual allocations will be effective in achieving the Fund’s investment objective or delivering positive returns. Current performance may be lower or higher than the performance quoted. The most recent performance is available at www.apollodiversifiedrealestatefund.com or by calling 888.926.2688.

The Fund is a closed-end interval fund, the shares have no history of public trading, nor is it intended that the shares will be listed on a public exchange at this time. No secondary market is expected to develop for the Fund’s shares. Limited liquidity is provided to shareholders only through the Fund’s quarterly repurchase offers for no less than 5% and no more than 25% of the Fund’s shares outstanding at net asset value. There is no guarantee that an investor will be able to sell all the shares that the investor desires to sell in the repurchase offer. The investment return and principal value of an investment will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. Due to these restrictions, an investor should consider an investment in the Fund to be of limited liquidity. The Fund is suitable only for investors who can bear the risks associated with the limited liquidity of the Fund and should be viewed as a long-term investment. Investing in the Fund is speculative and involves a high degree of risk, including the risks associated with leverage and the risk of a substantial loss of investment. There is no guarantee that the investment strategies will work under all market conditions. You should carefully consider which class of shares to purchase.

The Fund’s inception date was June 30, 2014. Per the Fund’s prospectus dated May 2, 2022, the total annual expense ratio is 1.98% for Class A shares. The Adviser and Fund have entered into an expense limitation agreement until at least May 31, 2023 under which the Adviser has contractually agreed to waive its fees and to pay or absorb the ordinary annual operating expenses of the Fund (including offering expenses, but excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses) to the extent that they exceed 1.91% for Class A shares.

Investors in the Fund should understand that the net asset value (“NAV”) of the Fund will fluctuate, which may result in a loss of the principal amount invested. The Fund’s investments may be negatively affected by the broad investment environment and capital markets in which the Fund invests, including the real estate market, the debt market and/or the equity securities market. The value of the Fund’s investments will increase or decrease based on changes in the prices of the investments it holds. This will cause the value of the Fund’s shares to increase or decrease. The Fund is “diversified” under the Investment Company Act of 1940. Diversification does not eliminate the risk of experiencing investment losses. Holdings are subject to change without notice. The Fund is not intended to be a complete investment program.

The Fund will not invest in real estate directly, but, because the Fund will concentrate its investments in securities of REITs and other real estate industry issuers, its portfolio will be significantly impacted by the performance of the real estate market and may experience more volatility and be exposed to greater risk than a more diversified portfolio. The value of companies engaged in the real estate industry is affected by: (i) changes in general economic and market conditions; (ii) changes in the value of real estate properties; (iii) risks related to local economic conditions, overbuilding and increased competition; (iv) increases in property taxes and operating expenses; (v) changes in zoning laws; (vi) casualty and condemnation losses; (vii) variations in rental income, neighborhood values or the appeal of property to tenants; (viii) the availability of financing and (ix) changes in interest rates and leverage. The value of securities of companies in the real estate industry may go through cycles of relative underperformance and outperformance in comparison to equity securities markets in general. By investing in the Fund, a shareholder will not be deemed to be an investor in any underlying fund and will not have the ability to exercise any rights attributable to an investor in any such underlying fund related to their investment. The Fund’s investment in Private Investment Funds will require it to bear a pro rata share of the vehicles’ expenses, including management and performance fees. Also, once an investment is made in a Private Investment Fund, neither the Adviser nor any Sub-Adviser will be able to exercise control over investment decisions made by the Private Investment Fund. The Fund may invest in securities of other investment companies, including ETFs. The Fund will indirectly bear its proportionate share of any management fees and other expenses paid by investment companies in which it invests, in addition to the management fees (and other expenses) paid by the Fund.

The Fund is advised by Apollo Real Estate Fund Adviser, LLC (“AREFA”). AREFA is registered as an investment adviser with the SEC pursuant to the provisions of the 1940 Act, as amended. AREFA is an indirect majority- owned subsidiary of Apollo Global Management, Inc. The Fund’s private real estate funds allocation is sub-advised by Aon Investments USA Inc. (“Aon”), an Aon Company. Aon is registered as an investment adviser with the SEC pursuant to the provisions of the 1940 Act. The Fund’s public real estate securities allocation is sub-advised by CenterSquare Investment Management LLC (“CenterSquare”). CenterSquare is an investment adviser registered with the SEC pursuant to the provisions of the 1940 Act. Registration with the SEC does not constitute an endorsement by the SEC nor does it imply a certain level of skill or training.

This material may not be distributed, transmitted or otherwise communicated to others, in whole or in part, without the express written consent of Apollo Global Management, Inc. (together with its subsidiaries, “Apollo”).

This material has been distributed for informational purposes only and should not be considered as investment advice or a recommendation of any particular security, strategy or investment product or be relied upon for any other purpose. The views expressed represent an assessment of market conditions at a specific point in time, are opinions only and should not be relied upon as investment advice regarding a particular investment or markets in general. Such information does not constitute a recommendation to buy or sell specific securities or investment vehicles. It should not be assumed that any investment will be profitable or will equal the performance of the fund(s) or any securities or any sectors mentioned herein. Information contained herein has been obtained from sources deemed to be reliable, but not guaranteed. Apollo Global Management and its affiliates do not provide tax, legal or accounting advice. This material is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal and accounting advisors before engaging in any transaction. This material represents views as of the date of this presentation and is subject to change without notice of any kind.

12

This annual report may contain certain forward-looking statements. Such forward-looking statements can generally be identified by our use of forward-looking terminology such as “may,” “will,” “expect,” “intend,” “anticipate,” “estimate,” “believe,” “continue,” or other similar words. Because such statements include risks, uncertainties and contingencies, actual results may differ materially from the expectations, intentions, beliefs, plans or predictions of the future expressed or implied by such forward-looking statements. These risks, uncertainties and contingencies include, but are not limited to: uncertainties relating to changes in general economic and real estate conditions; uncertainties relating to the implementation of our investment strategy; uncertainties relating to capital proceeds; and other risk factors as outlined in the Fund’s prospectus, statement of additional information, annual report and semi-annual report filed with the Securities and Exchange Commission.

During the fiscal year ending September 30, 2022, the Fund paid distributions of $289,622,285 to its investors, consisting of distributions of $110,349,489 paid and $179,272,796 that was reinvested through the Fund’s distribution reinvestment program.

During the fiscal year ending September 30, 2022, the Fund recorded dividends and distributions from the Fund’s underlying investments totaling $171,362,333, and realized gain on its investments totaling $68,575,306, and fees and expenses of $111,626,258.

The Fund’s distribution policy is to make quarterly distributions to shareholders. Shareholders should not assume that the source of a distribution from the Fund is net profit. The Fund’s most recent annualized distribution rate as of September 30, 2022 was 5.22%. A portion of the Fund’s distributions includes return of capital. Please refer to the Fund’s most recent Section 19(a) notice for an estimate of the composition of the Fund’s most recent distribution, available at www.apollodiversifiedrealestatefund.com, and the Fund’s semi-annual or annual reports filed with the U.S. Securities and Exchange Commission (the “SEC”) for additional information regarding the composition of distributions. The Fund’s distributions may be affected by numerous factors, including but not limited to changes in Fund expenses, investment performance, realized and projected market returns, fluctuations in market interest rates, and other factors. Distributions paid may exceed and, from time to time, have exceeded the Fund’s total return less fees and expenses of the Fund during some periods due to changes in market conditions affecting components of the Fund’s total return, including unrealized appreciation. Please reference the performance table below to view the Fund’s historical returns. Additionally, the Fund’s performance can always be found on the Apollo Global Management, Inc. website (www.apollo.com). The following chart presents the quarterly changes to the NAV, total return, and cumulative total return for load-waived Class A shares since inception.2 There is no assurance that the Fund’s distribution rate will be sustainable in the future nor are distributions guaranteed.

13

| Period Ending | NAV Return | Total Return | Cumulative Total Return |

6/30/14 | N/A | N/A | N/A |

| 9/30/14 | 0.44% | 1.65% | 1.65% |

| 12/31/14 | 2.11% | 3.40% | 5.10% |

| 3/31/15 | 0.98% | 2.28% | 7.50% |

| 6/30/15 | -1.24% | 0.06% | 7.56% |

| 9/30/15 | 1.13% | 2.47% | 10.21% |

| 12/31/15 | 1.01% | 2.34% | 12.79% |

| 3/31/16 | 1.00% | 2.33% | 15.42% |

| 6/30/16 | 0.95% | 2.28% | 18.05% |

| 9/30/16 | -0.04% | 1.28% | 19.57% |

| 12/31/16 | -0.26% | 1.05% | 20.83% |

| 3/31/17 | -0.15% | 1.17% | 22.24% |

| 6/30/17 | 0.26% | 1.59% | 24.18% |

| 9/30/17 | 0.00% | 1.32% | 25.83% |

| 12/31/17 | 0.90% | 2.23% | 28.64% |

| 3/31/18 | -0.97% | 0.34% | 29.08% |

| 6/30/18 | 1.24% | 2.58% | 32.41% |

| 9/30/18 | 0.11% | 1.43% | 34.31% |

| 12/31/18 | -1.04% | 0.27% | 34.67% |

| 3/31/19 | 2.10% | 3.45% | 39.33% |

| 6/30/19 | 0.15% | 1.47% | 41.38% |

| 9/30/19 | 0.40% | 1.73% | 43.82% |

| 12/31/19 | -0.11% | 1.21% | 45.56% |

| 3/31/20 | -6.70% | -5.46% | 37.61% |

| 6/30/20 | -2.63% | -1.34% | 35.77% |

| 9/30/20 | 0.00% | 1.33% | 37.57% |

| 12/31/20 | 1.41% | 2.76% | 41.37% |

| 3/31/21 | 2.07% | 3.42% | 46.20% |

| 6/30/21 | 3.66% | 5.04% | 53.56% |

| 9/30/21 | 3.15% | 4.52% | 60.51% |

| 12/31/21 | 7.21% | 8.62% | 74.35% |

| 3/31/22 | 2.85% | 4.21% | 81.69% |

| 6/30/22 | -0.92% | 0.38% | 82.39% |

| 9/30/22 | -3.80% | -2.53% | 77.78% |

14

| 1. | Effective May 2, 2022, Griffin Institutional Access® Real Estate Fund has been renamed Apollo Diversified Real Estate Fund. |

| 2. | Past performance is not indicative of future results. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Investing involves risk, including loss of principal. Performance source: Morningstar Direct. Performance includes reinvestment of distributions and reflects management fees and other expenses. The Fund return does not reflect the deduction of all fees, including any applicable Fund share class sales load, third-party brokerage commissions or third-party investment advisory fees paid by investors to a financial intermediary for brokerage services. If the deduction of such fees was reflected, the performance would be lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance may be lower or higher than the performance quoted. The most recent performance is available at www.apollodiversifiedrealestatefund.com or by calling 888.926.2688. As of 9/30/22, the Fund’s load-waived, Class A share had a one-year return of 10.76% and a five-year annualized return of 7.16%, the S&P 500 Index had a one-year return of -15.47% and a five-year annualized return of 9.24%, and the Bloomberg U.S. Aggregate Bond Index had a one-year return of -14.60% and a five-year annualized return of -0.27%. Alpha and beta calculation benchmark: S&P 500 Index. Assets and securities contained within indices are different than the assets and securities contained in Apollo Diversified Real Estate Fund and will therefore have different risk and reward profiles. An investment cannot be made in an index, which is unmanaged and has returns that do not reflect any trading, management or other costs. There are limitations when comparing the Apollo Diversified Real Estate Fund to indices. Many open-end funds which track these indices offer daily liquidity, while closed-end interval funds offer liquidity on a periodic basis. Deteriorating general market conditions will reduce the value of stock securities. Fixed income risks include interest-rate and credit risk, bond values fluctuate in price so the value of your investment can go down depending on market conditions. Real estate securities and debt obligations may decline because of adverse developments affecting the real estate industry and real property values. |

| 3. | Bureau of Labor Statistics; U.S. Department of Labor. |

| 4. | Fund holdings as of October 3, 2022. Fund size based on Gross Asset Value (GAV). Occupancy calculation is based on the Fund’s allocation to private real estate equity funds. Occupancy is the rate of which underlying properties are occupied, typically through leases. Fund holdings are subject to change without notice. Diversification does not eliminate the risk of experiencing investment losses. The Fund is not intended to be a complete investment program. |

| 5. | CBRE Econometric Advisors. |

| 6. | Freddie Mac. |

| 7. | CBRE Research. |

| 8. | Real Page Market Analytics. |

| 9. | Apollo Analysts, NCREIF-ODCE Net Index. |

| 10. | BofA Securities. |

| 11. | Apollo Analysts, CenterSquare, BofA Securities, Morningstar Direct. Past performance is not indicative of future results. |

| 12. | Represents the Fund’s direct holdings in private funds in which the underlying holdings of each respective private fund generally consist of real estate-related interests that are not publicly traded. Holdings and allocations are subject to change without notice. |

| 13. | Represents (i) the Fund’s direct holdings in publicly traded, real estate-related securities; (ii) the Fund’s holdings in private funds and registered investment companies in which the underlying holdings are generally publicly traded; and (iii) cash and short-term investments. Holdings and allocations are subject to change without notice. |

| 14. | Metrics express the Fund’s portfolio allocated to private funds in which the underlying holdings of such private funds generally consist of real estate-related interests that are not publicly traded as of October 3, 2022. Underlying data and statistics of the Fund’s private real estate exposure generally as of June 30, 2022, however, in limited circumstances, data for certain private funds is as of the most recent quarter end. Holdings are subject to change without notice. Diversification does not eliminate the risk of experiencing investment losses. |

15

| Apollo Diversified Real Estate Fund | Portfolio Update |

September 30, 2022 (Unaudited)

Performance (for the periods ended September 30, 2022)

| 6 Month | 1 Year | 3 Year | 5 Year | Since Inception | Inception Date | |

| Apollo Diversified Real Estate Fund – A – With Load* | -9.01% | 3.85% | 5.28% | 5.88% | 6.48% | 6/30/14 |

| Apollo Diversified Real Estate Fund – A – Without Load | -3.45% | 10.19% | 7.38% | 7.15% | 7.25% | 6/30/14 |

| Apollo Diversified Real Estate Fund – C – With Load** | -4.82% | 8.38% | 6.58% | 6.35% | 6.16% | 8/7/15 |

| Apollo Diversified Real Estate Fund – C – Without Load | -3.82% | 9.38% | 6.58% | 6.35% | 6.16% | 8/7/15 |

| Apollo Diversified Real Estate Fund – I – NAV | -3.38% | 10.45% | 7.64% | 7.41% | 7.22% | 8/7/15 |

| Apollo Diversified Real Estate Fund – M – NAV | -3.71% | 9.64% | 6.85% | 6.62% | 6.60% | 11/16/16 |

| Apollo Diversified Real Estate Fund – L – With Load*** | -7.68% | 5.24% | 5.59% | 5.97% | 6.00% | 4/24/17 |

| Apollo Diversified Real Estate Fund – L – Without Load | -3.58% | 9.93% | 7.13% | 6.89% | 6.85% | 4/24/17 |

| S&P 500® Total Return Index | -20.20% | -15.47% | 8.16% | 9.24% | 9.66% | 6/30/14 |

| Bloomberg U.S. Aggregate Bond Index | -9.22% | -14.60% | -3.26% | -0.27% | 0.83% | 6/30/14 |

| * | Adjusted for initial maximum sales charge of 5.75%. |

| ** | Adjusted for contingent deferred sales charge of 1.00%. |

| *** | Adjusted for initial maximum sales charge of 4.25%. |

The S&P 500® Total Return Index is an unmanaged index of 500 common stocks chosen for market size, liquidity and industry group representation. It is a market-value weighted index. The index is not actively managed and does not reflect any deduction for fees, expenses or taxes.

The Bloomberg U.S. Aggregate Bond Index measures the performance of the U.S. investment grade bond market.

Past performance is not indicative of future results. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Investing involves risk, including loss of principal. Fund performance includes reinvestment of distributions and reflects management fees and other expenses. The Fund return does not reflect the deduction of all fees, including third-party brokerage commissions or third-party investment advisory fees paid by investors to a financial intermediary for brokerage services. If the deduction of such fees was reflected, the performance would be lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Current performance may be lower or higher than the performance quoted. The most recent performance is available at www.apollodiversifiedrealestatefund.com or by calling 888.926.2688. An investment cannot be made in an index, which is unmanaged and has returns that do not reflect any trading, management or other costs. Index performance does not represent actual Fund or portfolio performance, nor does it represent actual performance of the Fund’s Adviser or sub-advisers.

Class A shares are offered subject to a maximum sales charge of 5.75% of the offering price. Class L shares are offered subject to a maximum sales charge of 4.25% of the offering price. Class C, Class I and Class M shares are offered at net asset value. Class C shares may be subject to a 1.00% contingent deferred sales charge on shares redeemed during the first 365 days after their purchase. The Fund’s investment adviser has contractually agreed to waive its fees and to pay or absorb the ordinary annual operating expenses of the Fund (including offering expenses, but excluding taxes, interest, brokerage commissions, acquired fund fees and expenses and extraordinary expenses), to the extent that they exceed 1.91%, 2.66%, 1.66%, 2.41% and 2.16% per annum of the Fund’s average daily net assets attributable to Class A, Class C, Class I, Class M and Class L shares, respectively. The Expense Limitation Agreement will remain in effect for Class A, Class C, Class I, Class L and Class M shares, unless and until the Fund's Board of Trustees (the "Board") approves its modification or termination. Per the Fund's most recent prospectus, the total expense ratio after recoupment, if applicable, is 1.98%, 2.73%, 1.73%, 2.47%, and 2.21% for Class A, Class C, Class I, Class M and Class L, respectively. Please review the Fund’s Prospectus for more details regarding the Fund’s fees and expenses. No assurances can be given that the Fund will pay a distribution in the future; or, if any such distribution is paid, the amount or rate of the distribution.

| 16 | 1.888.926.2688 | www.apollo.com |

| Apollo Diversified Real Estate Fund | Portfolio Update |

September 30, 2022 (Unaudited)

Performance of $10,000 Initial Investment (as of September 30, 2022)

The graph shown above represents historical performance of a hypothetical investment of $10,000 in the Fund since inception. Past performance is not indicative of future results. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. Investing involves risk, including loss of principal. Fund performance includes reinvestment of distributions and reflects management fees and other expenses. The Fund return does not reflect the deduction of all fees, including third-party brokerage commissions or third-party investment advisory fees paid by investors to a financial intermediary for brokerage services. If the deduction of such fees was reflected, the performance would be lower. Returns shown do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. The most recent performance is available at www.apollodiversifiedrealestatefund.com or by calling 888.926.2688. An investment cannot be made in an index, which is unmanaged and has returns that do not reflect any trading, management or other costs. Index performance does not represent actual Fund or portfolio performance, nor does it represent actual performance of the Fund’s Adviser or sub-advisers.

Sector Allocation (as a % of Net Assets)

| Private Investment Funds | 78.25% |

| Publicly Traded Securities | 22.54% |

| Preferred Stocks | 1.73% |

| Short Term Investments | 0.01% |

| Liabilities in Excess of Other Assets | -2.53% |

| Total | 100.00% |

| Annual Report | September 30, 2022 | 17 |

| Apollo Diversified Real Estate Fund | Schedule of Investments |

| September 30, 2022 |

| Description | Shares | Value (Note 2) | ||||||

| REAL ESTATE INVESTMENT TRUSTS (100.79%)(a) | ||||||||

| Private Investment Funds (78.25%)* | ||||||||

| Ares Real Estate Enhanced Income Fund, L.P. | N/A | $ | 100,583,854 | |||||

| BGO Diversified US Property Fund, L.P. | 5,252 | 16,577,182 | ||||||

| Brookfield Senior Mezzanine Real Estate Finance Fund | 125,384 | 127,153,578 | ||||||

| CA Student Living Income and Growth Fund | 85,518 | 111,403,883 | ||||||

| CBRE U.S. Core Partners, L.P. | 118,589,710 | 247,688,013 | ||||||

| CBRE U.S. Credit Partners, L.P. | 118,171 | 125,648,341 | ||||||

| CBRE U.S. Logistics Partners, L.P. | 186,538,435 | 248,127,709 | ||||||

| Clarion Gables Multifamily Trust, L.P. | 88,035 | 172,519,534 | ||||||

| Clarion Lion Industrial Trust, L.P. | 70,092 | 295,690,862 | ||||||

| Clarion Lion Properties Fund, L.P. | 200,008 | 410,123,634 | ||||||

| Cortland Growth and Income Fund, L.P. | 282,858 | 488,878,375 | ||||||

| CrossHarbor Strategic Debt Fund, L.P. | N/A | 56,766,103 | ||||||

| Dream U.S. Industrial Fund, L.P. | 87,224 | 149,204,332 | ||||||

| GWL U.S. Property Fund, L.P. | N/A | 46,892,896 | ||||||

| Heitman America Real Estate Trust, L.P. | 11,138 | 17,664,979 | ||||||

| Heitman Core Real Estate Debt Income Trust | 98,436 | 99,002,514 | ||||||

| JPM U.S. Real Estate Mezzanine Debt Fund, L.P. | 975,832 | 101,407,200 | ||||||

| Manulife U.S. Real Estate Fund, L.P. | 54,385 | 106,299,052 | ||||||

| Morgan Stanley Prime Property Fund | 10,956 | 257,123,394 | ||||||

| Oaktree Real Estate Income Fund, L.P. | N/A | 249,372,021 | ||||||

| PGIM Real Estate US Debt Fund, L.P. | 44,692 | 60,718,106 | ||||||

| Principal Real Estate Liquid Debt Fund, L.P. | 2,176,607 | 49,177,843 | ||||||

| PRISA, L.P. | 18,164 | 44,208,454 | ||||||

| Prologis Targeted U.S. Logistics Fund, L.P. | 35,080 | 117,523,465 | ||||||

| Sentinel Real Estate Fund, L.P. | 627 | 82,957,522 | ||||||

| Stockbridge Smart Markets Fund, L.P. | 17,807 | 37,617,088 | ||||||

| TA Realty Core Property Fund, L.P. | 125,724 | 202,983,154 | ||||||

| TA Realty Logistics Fund, L.P. | 144,334 | 180,691,098 | ||||||

| TCM CRE Credit Fund, L.P. | 122,263 | 122,433,054 | ||||||

| UBS Trumbull Property Fund | 1,214 | 14,477,129 | ||||||

| USAA US Government Building Fund, LLC | N/A | 69,700,348 | ||||||

| Ventas Life Science and Healthcare Real Estate Fund | 155,111 | 213,300,358 | ||||||

| Voya Commercial Mortgage Lending Fund, L.P. | N/A | 59,511,100 | ||||||

| 4,683,426,175 | ||||||||

| Publicly Traded Securities (22.54%) | ||||||||

| Acadia Realty Trust | 986,806 | 12,453,492 | ||||||

| Agree Realty Corp. | 488,470 | 33,010,803 | ||||||

| Alexandria Real Estate Equities, Inc. | 181,317 | 25,418,830 | ||||||

| American Homes 4 Rent, Class A | 1,114,754 | 36,575,079 | ||||||

| Americold Realty Trust, Inc. | 675,109 | 16,607,681 | ||||||

| Apartment Investment & Management Co., Class A | 248,791 | 1,816,174 | ||||||

| Apple Hospitality REIT, Inc. | 572,527 | 8,049,730 | ||||||

| AvalonBay Communities, Inc. | 267,160 | 49,208,200 | ||||||

| Boston Properties, Inc. | 25,830 | 1,936,475 | ||||||

| Brixmor Property Group, Inc. | 1,671,619 | 30,874,803 | ||||||

| Broadstone Net Lease, Inc., Class A | 1,112,352 | 17,274,827 | ||||||

| Cousins Properties, Inc. | 564,251 | 13,175,261 | ||||||

| DiamondRock Hospitality Co. | 208,348 | 1,564,693 | ||||||

| Digital Realty Trust, Inc. | 501,130 | 49,702,073 | ||||||

| Douglas Emmett, Inc. | 396,999 | 7,118,192 | ||||||

| 18 | 1.888.926.2688 | www.apollo.com |

| Apollo Diversified Real Estate Fund | Schedule of Investments |

| September 30, 2022 |

| Description | Shares | Value (Note 2) | ||||||

| Publicly Traded Securities (continued) | ||||||||

| Duke Realty Corp. | 759,618 | $ | 36,613,588 | |||||

| Equinix, Inc. | 131,434 | 74,764,916 | ||||||

| Equity Residential | 788,372 | 52,994,366 | ||||||

| Essex Property Trust, Inc. | 48,100 | 11,651,263 | ||||||

| Extra Space Storage, Inc. | 104,225 | 18,000,700 | ||||||

| First Industrial Realty Trust, Inc. | 628,106 | 28,145,430 | ||||||

| Four Corners Property Trust, Inc. | 413,220 | 9,995,792 | ||||||

| Gaming and Leisure Properties, Inc. | 160,448 | 7,098,220 | ||||||

| Healthpeak Properties, Inc. | 898,490 | 20,593,391 | ||||||

| Highwoods Properties, Inc. | 299,180 | 8,065,893 | ||||||

| Host Hotels & Resorts, Inc. | 359,610 | 5,710,607 | ||||||

| Invitation Homes, Inc. | 1,687,253 | 56,978,534 | ||||||

| JBG SMITH Properties | 543,063 | 10,090,111 | ||||||

| Kilroy Realty Corp. | 589,300 | 24,815,423 | ||||||

| Life Storage, Inc. | 315,653 | 34,961,726 | ||||||

| Medical Properties Trust, Inc. | 1,789,119 | 21,218,951 | ||||||

| Mid-America Apartment Communities, Inc. | 160,538 | 24,894,628 | ||||||

| Omega Healthcare Investors, Inc. | 226,711 | 6,685,707 | ||||||

| Outfront Media, Inc. | 679,762 | 10,325,585 | ||||||

| Park Hotels & Resorts, Inc. | 645,765 | 7,271,314 | ||||||

| Prologis, Inc. | 897,109 | 91,146,273 | ||||||

| Public Storage | 265,300 | 77,682,493 | ||||||

| Realty Income Corp. | 739,110 | 43,016,202 | ||||||

| Regency Centers Corp. | 259,530 | 13,975,690 | ||||||

| Rexford Industrial Realty, Inc. | 508,344 | 26,433,888 | ||||||

| RPT Realty | 1,311,431 | 9,914,418 | ||||||

| Ryman Hospitality Properties, Inc. | 77,940 | 5,735,605 | ||||||

| Sabra Health Care REIT, Inc. | 994,664 | 13,049,992 | ||||||

| SBA Communications Corp. | 40,978 | 11,664,388 | ||||||

| Simon Property Group, Inc. | 424,550 | 38,103,362 | ||||||

| Spirit Realty Capital, Inc. | 435,508 | 15,747,969 | ||||||

| Sun Communities, Inc. | 363,300 | 49,165,389 | ||||||

| Sunstone Hotel Investors, Inc. | 207,790 | 1,957,382 | ||||||

| UDR, Inc. | 920,127 | 38,378,497 | ||||||

| Urban Edge Properties | 675,720 | 9,014,105 | ||||||

| Ventas, Inc. | 1,291,519 | 51,880,318 | ||||||

| Veris Residential, Inc. | 895,999 | 10,187,509 | ||||||

| VICI Properties, Inc. | 605,647 | 18,078,563 | ||||||

| Welltower, Inc. | 515,670 | 33,167,894 | ||||||

| Xenia Hotels & Resorts, Inc. | 1,092,217 | 15,061,672 | ||||||

| 1,349,024,067 | ||||||||

| TOTAL REAL ESTATE INVESTMENT TRUSTS | ||||||||

| (Cost $5,042,256,820) | 6,032,450,242 | |||||||

| Description | Coupon Rate | Shares | Value (Note 2) | |||||||||

| PREFERRED STOCKS (1.73%)(b) | ||||||||||||

| Agree Realty Corp., Series A | 4.25 | % | 125,000 | 2,123,750 | ||||||||

| American Homes 4 Rent, Series G | 5.88 | % | 35,000 | 787,500 | ||||||||

| American Homes 4 Rent, Series H | 6.25 | % | 214,000 | 5,131,720 | ||||||||

| Chatham Lodging Trust, Series A | 6.63 | % | 40,177 | 832,869 | ||||||||

| Annual Report | September 30, 2022 | 19 |

| Apollo Diversified Real Estate Fund | Schedule of Investments |

| September 30, 2022 |

| Description | Coupon Rate | Shares | Value (Note 2) | |||||||||

| PREFERRED STOCKS (continued) | ||||||||||||

| DiamondRock Hospitality Co., Series A | 8.25 | % | 126,000 | $ | 3,099,600 | |||||||

| Digital Realty Trust, Inc., Series J | 5.25 | % | 77,000 | 1,653,960 | ||||||||

| Digital Realty Trust, Inc., Series K | 5.85 | % | 171,000 | 3,806,460 | ||||||||

| Digital Realty Trust, Inc., Series L | 5.20 | % | 68,500 | 1,441,925 | ||||||||

| DigitalBridge Group, Inc., Series I | 7.15 | % | 136,345 | 3,048,674 | ||||||||

| DigitalBridge Group, Inc., Series J | 7.13 | % | 47,000 | 1,065,020 | ||||||||

| EPR Properties, Series G | 5.75 | % | 149,000 | 2,673,060 | ||||||||

| Federal Realty Investment Trust, Series C | 5.00 | % | 167,000 | 3,495,310 | ||||||||

| Hersha Hospitality Trust, Series C | 6.88 | % | 135,000 | 2,713,500 | ||||||||

| Hersha Hospitality Trust, Series D | 6.50 | % | 64,287 | 1,202,810 | ||||||||

| Hudson Pacific Properties, Inc., Series C | 4.75 | % | 194,000 | 3,237,860 | ||||||||

| Kimco Realty Corp., Series L | 5.13 | % | 32,658 | 688,431 | ||||||||

| Kimco Realty Corp., Series M | 5.25 | % | 162,000 | 3,478,140 | ||||||||

| National Storage Affiliates Trust, Series A | 6.00 | % | 198,000 | 4,439,160 | ||||||||

| Pebblebrook Hotel Trust, Series E | 6.38 | % | 166,000 | 3,436,200 | ||||||||

| Pebblebrook Hotel Trust, Series F | 6.30 | % | 39,000 | 738,660 | ||||||||

| Pebblebrook Hotel Trust, Series G | 6.38 | % | 69,000 | 1,290,300 | ||||||||

| Pebblebrook Hotel Trust, Series H | 5.70 | % | 89,000 | 1,499,650 | ||||||||

| PS Business Parks, Inc., Series Z | 4.88 | % | 145,000 | 1,979,250 | ||||||||

| Public Storage, Series F | 5.15 | % | 30,000 | 654,600 | ||||||||

| Public Storage, Series G | 5.05 | % | 88,205 | 1,905,228 | ||||||||

| Public Storage, Series H | 5.60 | % | 84,750 | 2,029,762 | ||||||||

| Public Storage, Series J | 4.70 | % | 25,000 | 510,500 | ||||||||

| Public Storage, Series L | 4.63 | % | 165,000 | 3,324,750 | ||||||||

| Rexford Industrial Realty, Inc., Series B | 5.88 | % | 112,000 | 2,602,880 | ||||||||

| Rexford Industrial Realty, Inc., Series C | 5.63 | % | 106,789 | 2,368,580 | ||||||||

| Saul Centers, Inc., Series D | 6.13 | % | 125,000 | 2,653,750 | ||||||||

| Saul Centers, Inc., Series E | 6.00 | % | 73,487 | 1,553,515 | ||||||||

| Seritage Growth Properties, Series A | 7.00 | % | 73,359 | 1,651,318 | ||||||||

| SITE Centers Corp., Series A | 6.38 | % | 212,000 | 4,320,560 | ||||||||

| SL Green Realty Corp., Series I | 6.50 | % | 114,000 | 2,474,940 | ||||||||

| Spirit Realty Capital, Inc., Series A | 6.00 | % | 244,000 | 5,599,800 | ||||||||

| Summit Hotel Properties, Inc., Series E | 6.25 | % | 148,000 | 2,595,920 | ||||||||

| Summit Hotel Properties, Inc., Series F | 5.88 | % | 41,196 | 744,824 | ||||||||

| Sunstone Hotel Investors, Inc., Series H | 6.13 | % | 152,000 | 3,078,000 | ||||||||

| Sunstone Hotel Investors, Inc., Series I | 5.70 | % | 110,431 | 2,047,391 | ||||||||

| Urstadt Biddle Properties, Inc., Series H | 6.25 | % | 116,087 | 2,437,827 | ||||||||

| Urstadt Biddle Properties, Inc., Series K | 5.88 | % | 19,182 | 389,395 | ||||||||

| Vornado Realty Trust, Series L | 5.40 | % | 121,000 | 2,234,870 | ||||||||

| Vornado Realty Trust, Series M | 5.25 | % | 70,000 | 1,220,100 | ||||||||

| Vornado Realty Trust, Series N | 5.25 | % | 93,000 | 1,639,590 | ||||||||

| Vornado Realty Trust, Series O | 4.45 | % | 120,000 | 1,924,800 | ||||||||

| TOTAL PREFERRED STOCKS | ||||||||||||

| (Cost $120,240,302) | 103,826,709 | |||||||||||

| 20 | 1.888.926.2688 | www.apollo.com |

| Apollo Diversified Real Estate Fund | Schedule of Investments |

| September 30, 2022 |

| 7-Day Yield | Shares | Value (Note 2) | ||||||||||

| SHORT TERM INVESTMENT (0.01%) | ||||||||||||

| MSILF Treasury Portfolio | 2.77 | % | 498,555 | $ | 498,555 | |||||||

| TOTAL SHORT TERM INVESTMENT | ||||||||||||

| (Cost $498,555) | 498,555 | |||||||||||

| TOTAL INVESTMENTS (102.53%) | ||||||||||||

| (Cost $5,162,995,677) | $ | 6,136,775,506 | ||||||||||

| Liabilities in Excess of Other Assets (-2.53%) | (151,312,576 | ) | ||||||||||

| NET ASSETS (100.00%) | $ | 5,985,462,930 | ||||||||||

| (a) | A portion of these securities are held as collateral for the outstanding Lines of Credit. At September 30, 2022 outstanding collateral amounted to $5,456,125,895. |

| (b) | These securities have no contractual maturity date, are not redeemable and contractually pay an indefinite stream of dividends. |

Common Abbreviations:

LLC - Limited Liability Company

L.P.- Limited Partnership

REIT - Real Estate Investment Trust

| Annual Report | September 30, 2022 | 21 |

| Apollo Diversified Real Estate Fund | Schedule of Investments |

| September 30, 2022 |

| * | Additional Information on Investments in Private Investment Funds: |

| Value | Fund Name | Redemption Frequency | Redemption Notice (Days) | Unfunded Commitment as of September 30, 2022 | |||||||||

| $ | 100,583,854 | Ares Real Estate Enhanced Income Fund, L.P. | Quarterly | 90 | $ | 0 | |||||||

| 16,577,182 | BGO Diversified US Property Fund, L.P. | Quarterly | N/A** | 0 | |||||||||

| 127,153,578 | Brookfield Senior Mezzanine Real Estate Finance Fund | Quarterly | 90 | 0 | |||||||||

| 111,403,883 | CA Student Living Income and Growth Fund | Quarterly | 90 | 0 | |||||||||

| 247,688,013 | CBRE U.S. Core Partners, L.P. | Quarterly | 60 | 0 | |||||||||

| 125,648,341 | CBRE U.S. Credit Partners, L.P. | Quarterly | 60 | 0 | |||||||||

| 248,127,709 | CBRE U.S. Logistics Partners, L.P. | Quarterly | 90 | 0 | |||||||||

| 172,519,534 | Clarion Gables Multifamily Trust, L.P. | Quarterly | 90 | 35,000,000 | |||||||||

| 295,690,862 | Clarion Lion Industrial Trust, L.P. | Quarterly | 90 | 0 | |||||||||

| 410,123,634 | Clarion Lion Properties Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 488,878,375 | Cortland Growth and Income Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 56,766,103 | CrossHarbor Strategic Debt Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 149,204,332 | Dream U.S. Industrial Fund, L.P. | Quarterly | 60 | 35,000,000 | |||||||||

| 46,892,896 | GWL U.S. Property Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 17,664,979 | Heitman America Real Estate Trust, L.P. | Quarterly | 90 | 0 | |||||||||

| 99,002,514 | Heitman Core Real Estate Debt Income Trust | Quarterly | 90 | 0 | |||||||||

| 101,407,200 | JPM U.S. Real Estate Mezzanine Debt Fund, L.P. | Quarterly | 60 | 0 | |||||||||

| 106,299,052 | Manulife U.S. Real Estate Fund, L.P. | Quarterly | 60 | 0 | |||||||||

| 257,123,394 | Morgan Stanley Prime Property Fund | Quarterly | 90 | 0 | |||||||||

| 249,372,021 | Oaktree Real Estate Income Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 60,718,106 | PGIM Real Estate US Debt Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 49,177,843 | Principal Real Estate Liquid Debt Fund, L.P. | Monthly | 10 | 0 | |||||||||

| 44,208,454 | PRISA, L.P. | Quarterly | 90 | 0 | |||||||||

| 117,523,465 | Prologis Targeted U.S. Logistics Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 82,957,522 | Sentinel Real Estate Fund, L.P. | Quarterly | N/A** | 0 | |||||||||

| 37,617,088 | Stockbridge Smart Markets Fund, L.P. | Quarterly | 45 | 40,000,000 | |||||||||

| 202,983,154 | TA Realty Core Property Fund, L.P. | Quarterly | 45 | 0 | |||||||||

| 180,691,098 | TA Realty Logistics Fund, L.P. | Quarterly | 45 | 0 | |||||||||

| 122,433,054 | TCM CRE Credit Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| 14,477,129 | UBS Trumbull Property Fund | Quarterly | 60 | 0 | |||||||||

| 69,700,348 | USAA US Government Building Fund, LLC | Quarterly | 60 | 0 | |||||||||

| 213,300,358 | Ventas Life Science and Healthcare Real Estate Fund | Quarterly | 90 | 50,000,000 | |||||||||

| 59,511,100 | Voya Commercial Mortgage Lending Fund, L.P. | Quarterly | 90 | 0 | |||||||||

| $ | 4,683,426,175 | $ | 160,000,000 | ||||||||||

| ** | Written notice required for redemption, no minimum timeline required. |

See Notes to Financial Statements.

| 22 | 1.888.926.2688 | www.apollo.com |

| Apollo Diversified Real Estate Fund | Statement of Assets and Liabilities |

| September 30, 2022 |

| ASSETS | ||||