As filed with the Securities and Exchange Commission on 11/04/2022

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

811-23011

Investment Company Act file number

The RBB FUND TRUST

(Exact name of registrant as specified in charter)

615 East Michigan Street

Milwaukee, WI 53202

(Address of principal executive offices) (Zip code)

Steven Plump, President

c/o U.S. Bank Global Fund Services

615 East Michigan Street

Milwaukee, WI 53202

(Name and address of agent for service)

(609) 731-6256

Registrant's telephone number, including area code

Date of fiscal year end: August 31

Date of reporting period: August 31, 2022

Item 1. Reports to Stockholders.

ANNUAL REPORT

August 31, 2022

PENN CAPITAL FLOATING RATE INCOME FUND

PENN CAPITAL MID CAP CORE FUND

PENN CAPITAL OPPORTUNISTIC HIGH INCOME FUND

PENN CAPITAL SHORT DURATION HIGH INCOME FUND

PENN CAPITAL SPECIAL SITUATIONS SMALL CAP EQUITY FUND

Each a series of The RBB Fund Trust (formerly, PENN Capital Funds Trust)

TABLE OF CONTENTS

Advisor’s Letter to Shareholders | 1 | |

Fund Summary | 6 | |

Disclosure of Fund Expenses | 11 | |

Fund | Schedule of Investments | |

Penn Capital Floating Rate Income Fund | 13 | |

Penn Capital Mid Cap Core Fund | 19 | |

Penn Capital Opportunistic High Income Fund | 22 | |

Penn Capital Short Duration High Income Fund | 28 | |

Penn Capital Special Situations Small Cap Equity Fund | 32 | |

Statements of Assets and Liabilities | 35 | |

Statements of Operations | 36 | |

Statements of Changes in Net Assets | 38 | |

Financial Highlights | 40 | |

Notes to the Financial Statements | 44 | |

Additional Information | 58 | |

Report of Independent Registered Public Accounting Firm | 62 | |

Trustees and Officers | 63 | |

Privacy Policy | 68 | |

[THIS PAGE INTENTIONALLY LEFT BLANK.]

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Advisor’s Letter to Shareholders (Unaudited)

Dear Penn Capital Funds Shareholder:

Our investment strategies incorporate Penn Capital’s Complete Capital Structure Analysis®, an in-depth high yield (“HY”) and equity research philosophy used to identify a company’s optimal capital structure. Our investment professionals are capital structure generalists, meaning they are responsible for understanding the entire capital structure of the companies they follow. By following this philosophy, we believe that integrating credit and equity research allows us to construct a more comprehensive investment mosaic. Participating in both credit and equity markets, along with this integrated research process, provides Penn Capital’s investment team with what we believe is an informational advantage. Finding inefficiencies in the market can be challenging, but we remain committed to the pursuit of strong investment returns on behalf of our shareholders.

The following pages review the current market environment and provide additional insight into our funds and their performance over the past fiscal year beginning September 1, 2021 and ended August 31, 2022. Once again, I would like to thank you for your confidence in investing with us.

Overview

Over the past year, capital markets have been navigating a bumpy transition from focusing on the dramatic and immediate impacts of the COVID-19 pandemic, to assessing its long-term ramifications for the global economy and the ways that we live and work every day. The robust fiscal and monetary response to the pandemic supported the economy as activity slowed and people isolated themselves. In retrospect, massive government stimulus combined with the surprising resilience of consumers and businesses drove a faster than expected snapback in growth and increased asset price valuations. Surging consumer demand for goods (given a lack of experiential options) occurred just as global supply chains were hamstrung by COVID-19 outbreaks/restrictions and shortages for labor, raw materials, and components. This drove rapid inflation that has proved to be far more than “transitory” in nature. In 2022, the Federal Reserve has shifted their focus from supporting growth and employment to fighting inflation. Between March and August, the Federal Funds target rate was raised by 2.25%, with market expectations it will close 2022 over 4.00%.

Higher interest rates are a headwind to all risk assets including high yield corporate debt and small to mid-cap equities. Premium valuation, high growth sectors like Health Care and Information Technology have been the most challenged. Commodity-focused companies outperformed the overall market, as their products had pricing power in an inflationary environment. Credit product losses have been a function of higher interest rates, with long duration (low coupon, long maturity bonds) lagging the overall market. Despite significant equity market volatility, high yield credit spreads (risk premium for lower rated debt) have been mostly range bound during the past year. The Federal Reserve rate cycle is raising the total cost of borrowing for companies in our universe when they seek capital. Companies are reluctant to refinance debt at higher interest rates and new issuance has been muted.

As the Federal Reserve continues to raise interest rates, economic growth will slow. High yield credit spreads will be a key indica tor to determine if raising interest rates to combat inflation will ultimately lead to a recession. Shrinking high yield credit spreads is a signal to position portfolios opportunistically, while rising high yield credit spreads is a signal to position portfolios defensively. If a recession occurs, high yield credit spreads can bottom prior to the equity market providing a strong signal to reposition for recovery. During the Global Financial Crisis, the high yield credit spread hit its widest point in November 2008, while the equity market reached its low in March 2009, which provided a large opportunity for our strategy. These relationships drive Penn Capital’s investing philosophy as we navigate into the future.

Performance

The following paragraphs provide more detailed information on the performance of our funds for the fiscal year September 1, 2021 through August 31, 2022, as well as selected holdings.

Penn Capital Floating Rate Income Fund

For the fiscal year ended August 31, 2022, the Penn Capital Floating Rate Income Fund (the “Floating Rate Income Fund”)generated a -1.48% return versus +0.89% for its benchmark, the Credit Suisse Institutional Leveraged Loan Index over the same period.1

(1) | Prior to May 31, 2022, the Floating Rate Income Fund’s primary benchmark was the S&P/LSTA BB Loan Index. |

1

The portfolio benefited from an overweight to the Energy sector as well as solid security selection within Exploration and Production bonds and loans. The portfolio also benefited from gains in both the Industrial Services and Products sectors. Throughout the fiscal year, the Floating Rate Income Fund remained relatively defensively positioned, with minimal exposure to lower- rated CCC securities. This conservative positioning also helped improve performance.

Offsetting these gains was weak performance in the Consumer Discretionary Products, Retail, Media and Technology sectors. In Consumer Discretionary Products and Retail, declines in loans from former COVID winners like Bob’s Discount Furniture, JoAnn Fabrics and Weber were all large contributors to the Floating Rate Income Fund’s underperformance. All three companies experienced downdrafts in their loan prices due to earnings issues related to supply chain log-jams, cost inflation and changing consumer purchasing patterns. In Media and Technology, Dish, Rackspace and Avaya loan declines were also large contributors to the Floating Rate Income Fund’s underperformance. Growing investor trepidation about the large strategic decisions each of these businesses must soon make, combined with declining earnings in the secularly-challenged portions of their operations, drove loan prices for these businesses lower. Finally, the Floating Rate Income Fund’s exposure to mid- and longer-duration fixed rate bonds also hurt performance during the fiscal year, as increases in U.S. Treasury rates drove bond prices lower and caused bond performance to lag that of floating rate loans.

Penn Capital Short Duration High Income Fund

For the fiscal year ended August 31, 2022, the Penn Capital Short Duration High Income Fund (the “Short Duration Fund”) generated a -3.05 % return, outperforming its benchmark, ICE BofA 1-3 Year BB-Rated US Cash Pay High Yield Index, which returned - 3.80% over the same period. The Short Duration Fund maintains an average portfolio maturity of three years or less and excludes CCC-rated bonds. The portfolio will typically underperform the broad short duration market, which includes CCC-rated bonds, during low quality rallies (like 2021), and outperform during low quality selloffs (like 2020).

The portfolio benefitted from an overweight to and good security selection within COVID “re-opening plays”, such as within real estate investment trusts (“REITs”) and the Recreation & Travel and Gaming sectors, mainly via higher-coupon secured paper, including Norwegian Cruise Line Holdings and MGM Resorts International. Additionally, the portfolio benefitted from strong security selection within commodity-oriented industries, such as those in the Chemicals, Metals & Mining and Energy sectors. Strong security selection within the Auto Parts and Aerospace/Defense sectors also contributed to the portfolio, as did an underweight to the Banking sector.

The largest detractor from performance was security selection within the Packaging sector, where the Crown Cork & Seal Co Inc. 7.375% 2026 notes were weaker with higher interest rates, despite being a high quality credit with a non-callable bond structure. Also, structural underweights to Ford (Automotive and Auto Loans sectors) and Sprint (Telecommunications sector) were detractors. As the ICE BofA 1-3 Year BB-Rated US Cash Pay High Yield Index is unconstrained, the Ford and Sprint weightings were over 10%; whereas our portfolio limit on issuer holdings is 5%.

Yield-curve positioning was a net contributor, as the portfolio’s 0–1 year maturity “off-index” allocation more than offset an allocation to the 3-5 year maturity, which underperformed given rising rates. Additionally, off-index credit quality positioning contributed value as the portfolio’s single-B quality bonds allocation outperformed.

During the fiscal year, “off-index” asset allocation contributed value as the Short Duration High Income Fund’s loan allocation performance more than offset weakness from its convertible bond allocation. The fund held an average weighting of 6.3% in bank loan securities via exposure from a combination of individual bank loan holdings and investment in the Penn Capital Floating Rate Income Fund. The allocation to convertible bonds averaged a weighting of less than 1%.

Penn Capital Opportunistic High Income Fund

For the fiscal year ended August 31, 2022, the Penn Capital Opportunistic High Income Fund (the “Opportunistic High Income Fund”) generated a -10.31% return, outperforming its benchmark, the ICE BofA US High Yield Constrained Index, which returned -10.43% over the same period.

The portfolio benefitted from an overweight to and good security selection within the Energy sector, particularly the Exploration & Production sector, as well as an underweight to and strong security selection within the Pharmaceuticals sector. The portfolio avoided significant drawdowns in both Endo (opioids) and Bausch Health (patent challenge). Additionally, the portfolio benefitted from strong security selection within the Financial Services, Retail and Consumer Products sectors.

2

The largest detractor to performance was security selection within the Healthcare Facilities sector, where Community Health Systems, a hospital chain, struggled with higher labor costs. Also, “return-to-work” credits Pitney Bowes and Staples, within the Services sector, underperformed. Longer-dated paper within the Metals & Mining sector, and also an overweight to the Real Estate and Housing-related credit investments underperformed with higher rates.

Yield curve positioning was a slight detractor, as the underweighting of the portfolio’s 0-3 year maturity allocation, more than offset an underweight to the poorly performing 10+ year allocation. Conversely, credit quality positioning contributed value via an underweight to BB-rated bonds, overweight to single-B rated bonds and neutral to CCC-rated bonds.

During the fiscal year, “off-index” asset allocation contributed value as the Opportunistic High Income Fund’s loan allocation performance more than offset weakness from its convertible bond allocation. The fund held an average weighting of 7% in bank loan securities via exposure from a combination of individual bank loan holdings and investment in the Penn Capital Floating Rate Income Fund. The allocation to convertible bonds averaged a weighting of 3.8%.

Penn Capital Mid Cap Core Fund

For the fiscal year ended August 31, 2022, the Penn Capital Mid Cap Core Fund (the “Mid Cap Core Fund”) generated a -17.45 return, slightly underperforming the -16.38% return of its benchmark, the Bloomberg US 2500 Index2 over the same period. Best performing sectors during the period were the Healthcare and the Materials sectors. Within the Healthcare sector, a radiopharmaceutical company launched a highly successful contrast for the detection of prostate cancer. Drug companies that generate strong cash flows from marketed products provided returns in a challenging market. In the Materials sector, a nitrogen producer raised prices and profitability due to a globally advantaged cost structure in the United States. The sectors that hindered performance during the period were Financials and Consumer Discretionary. In the Financial Services sector, a digital marketing company for financial products experienced weakened demand due to rising interest rates. In the Consumer Discretionary sector, retailers lapped tough 2021 comparisons as sales slowed due to 2021 stimulus payments and rising inflation in 2022.

Penn Capital Special Situations Small Cap Equity Fund

For the fiscal year ended August 31, 2022, the Penn Capital Special Situations Small Cap Equity Fund (the “Special Situations Fund”) generated a -14.39% return, outperforming the -17.49% return of its benchmark, the Bloomberg US 2000 Index3, over the same period. Top contributors in the period were the Health Care, Energy, and Materials sectors. Within Health Care, a maker of diagnostic medical imaging products is experiencing surging demand for its new imaging agent for detection of prostate cancer. In the Energy sector, an exploration and production company benefitted from rising commodity prices while its low leverage and robust free-cash-flow will fund accelerating returns to shareholders through dividends and share repurchase. Within Materials, a producer of lithium compounds is capitalizing on growing demand for electric vehicle batteries and a highly favorable pricing environment. The top detractors in the period were the Industrials, Utilities, and Financials sectors. In the Industrials sector, a provider of online recruitment services underperformed due to macro headwinds and investor concerns regarding rising customer acquisition costs and competitive intensity. Underperformance in Utilities stemmed from the allocation effect, as the strategy was underweight the traditionally defensive group and it outperformed amid a risk-off market. Within Financials, a Texas based bank unveiled a strategic plan to establish a broker-dealer/investment bank, which will necessitate significant near-term investments that will weigh on margins and returns.

Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than that shown. To obtain performance current to the most recent month-end please call 844-302 PENN (7366) or visit www.penncapitalfunds.com.

(2) | Prior to May 31, 2022, the Mid Cap Core Fund’s primary benchmark was the Russell 2500® Index. |

(3) | Prior to May 31, 2022, the Special Situations Small Cap Equity Fund’s primary benchmark was the Russell 2000® Index. |

3

Conclusion

We would like to take this opportunity to thank our shareholders for entrusting their investments with our firm. We do not take your faith in us for granted. Our team remains committed to focusing our efforts on behalf of our shareholders, and we value your continued confidence in our vision. We believe the Penn Capital Funds offer a product line-up that embodies our investment philosophy and dedicated research-driven process.

Looking Forward

This report contains performance data and financial information. Please keep in mind that all securities markets, as well as mutual fund prices, fluctuate in value. If you would like more frequent updates, http://www.penncapitalfunds.com provides daily NAV, monthly performance figures, portfolio holdings, and other valuable information. We encourage you to visit penncapitalfunds.com, through which you may access your account, buy and sell sha res, and find other helpful tools.

At Penn Capital Funds, we believe that active management continues to serve as a critical element of investing in HY debt securities and equity securities of smaller and mid-sized companies. Although challenges remain, and markets may continue to be uneven, we are confident that investors with a well-diversified portfolio and a patient, long-term outlook should be well positioned for the years ahead.

We thank you for investing with us and look forward to continuing to serve your investment needs.

Sincerely,

Kirsten Hocker

President

Penn Capital Management Company, LLC

4

Past performance is no guarantee of future results. Unusually favorable market conditions and high returns may not be sustainable or repeated in the future.

This letter reflects Penn Capital’s analysis and opinions as of the most recent fiscal period. The information is not a complete analysis of any market, country, industry, security, or fund and should not be considered as a recommendation to buy, sell or hold any specific security or securities. Portfolio holdings are subject to change at any time. Please see the Schedules of Investments provided in this report for the complete listing of each Fund’s holdings.

All investments involve risk, including possible loss of principal, and there is no guarantee the Funds will achieve their investment objectives. Investments made in small and mid-capitalization companies may be more volatile and less liquid due to limited resources or product lines and more sensitive to economic factors. Investments in ETFs are subject to the same risks as the underlying securities in which the ETF invests as well as entails higher expenses than if invested into the underlying ETF directly. Investments in foreign securities and ADRs involve certain risks such as currency volatility, political and social instability and reduced market liquidity. As interest rates rise the value of bond prices will decline. Credit risk refers to the loss in the value of a security based on a default in the payment of principle and/or interest of the security, or the perception of the market of such default. High-yield bonds have a higher risk of default or other adverse credit events but have the potential to pay higher earnings over investment grade bonds. The value of convertible securities tends to decline as interest rates rise and, because of the conversion feature, tends to vary with fluctuations in the market value of the underlying securities. Bank loans in which the Fund may invest have similar risks to below investment grade fixed income securities. In the event of the insolvency of an agent bank, a loan could be subject to settlement risk as well as the risk of interruptions in the administrative duties performed in the day to day administration of the loan.

Index Definitions

The ICE BofA US High Yield Constrained Index contains all securities in the ICE BofA US High Yield Index but caps issuer exposure at 2%.

The ICE BofA 1-3 Year BB-Rated US Cash Pay High Yield Index is a subset of the ICE BofA US Cash Pay High Yield Index, which tracks the performance of non-investment-grade corporate bonds with a remaining term to final maturity less than three years and rated BB.

The S&P/LSTA BB Ratings Loan Index is a market value-weighted index designed to measure the performance of the US leveraged loan market and is comprised of loans whose rating is BB+, BB, BB-.

The Credit Suisse Institutional Leveraged Loan Index is a sub-index of the Credit Suisse Leveraged Loan Index. The Credit Suisse Leveraged Loan Index is designed to mirror the investable universe of the $US-denominated leveraged loan market. The Credit Suisse Institutional Leveraged Loan Index is designed to more closely reflect the investment criteria of institutional investors by sampling a lower volatility component of the market.

The Bloomberg US 2000 Index is a float market cap weighted benchmark of the lower 2,000 in capitalization of the Bloomberg 3000 Index.

The Bloomberg US 2500 Index is a float market cap weighted benchmark of the lower 2,500 in capitalization of the Bloomberg 3000 Index.

The Russell 2000® Index measures the performance of the small-cap segment of the U.S. equity universe. The Russell 2000 is a subset of the Russell 3000® Index representing approximately 10% of the total market capitalization of that index. It includes approximately 2000 of the smallest securities based on a combination of their market cap and current index membership. The Russell 2000 Index is constructed to provide a comprehensive and unbiased small-cap opportunity barometer and is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set.

The Russell 2500™ Index is composed of the bottom 500 stocks in the Russell 1000® Index and all the stocks in the Russell 2000® Index. The Russell 2500™Index return reflect adjustments for income dividends and capital gains distributions reinvested as of the ex-dividend dates.

An investment cannot be made directly in an index.

Foreside Fund Services, LLC Distributor

5

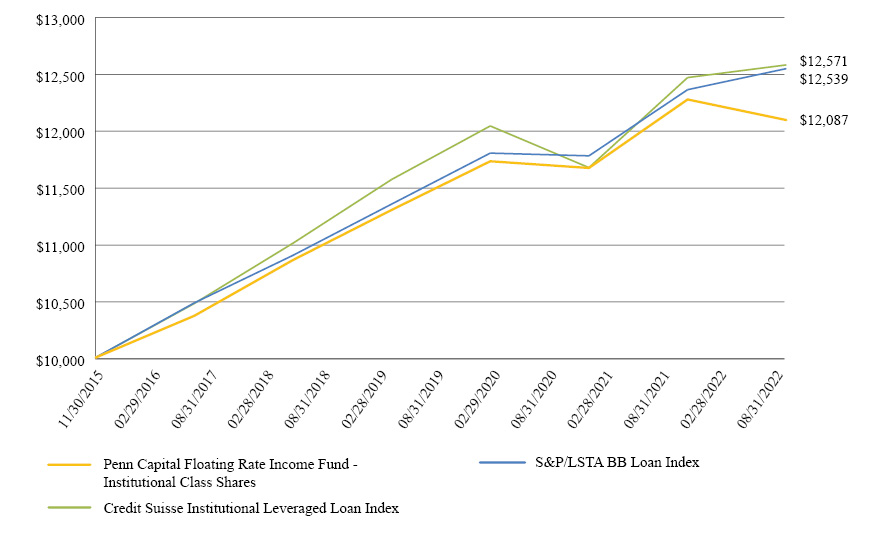

PENN CAPITAL FLOATING RATE INCOME FUND

Fund Summary (UNAUDITED)

This chart assumes a hypothetical initial gross investment of $10,000 made on November 30, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than that shown. To obtain performance current to the most recent month-end please call 844-302 PENN (7366) or visit www.penncapitalfunds.com. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index.

Average Annual Total Returns for the Periods Ended August 31, 2022 | One Year | Three Years | Five Years | Since |

Penn Capital Floating Rate Income Fund | ||||

Institutional Class Shares | -1.48% | 1.02% | 2.17% | 2.85% |

Credit Suisse Institutional Leveraged Loan Index(2) | 0.89% | 1.46% | 2.70% | 3.45% |

S&P/LSTA BB Loan Index | 1.50% | 2.05% | 2.84% | 3.41%(3) |

(1) | Inception date is 11/30/15. |

(2) | Effective May 31, 2022, the Fund changed its primary benchmark from the S&P/LTSA BB Loan Index to the Credit Suisse Institutional Leveraged Loan Index to better reflect the securities in which the Fund invests. |

(3) | The return shown for the S&P/LSTA BB Loan Index is from the inception date of the Institutional Class shares. |

Gross Expense Ratio: 1.16%, Net Expense Ratio: 0.64%, per the most recent Prospectus dated October 31, 2021, as supplemented May 31, 2022 and August 29, 2022.

The Advisor has contractually agreed to waive management fees and/or pay certain Fund expenses through at least April 1, 2023.

6

PENN CAPITAL MID CAP CORE FUND

FUND SUMMARY (UNAUDITED)

This chart assumes a hypothetical initial gross investment of $10,000 made on November 30, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than that shown. To obtain performance current to the most recent month-end please call 844-302 PENN (7366) or visit www.penncapitalfunds.com. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index.

Average Annual Total Returns for the Periods Ended August 31, 2022 | One Year | Three Years | Five Years | Since |

Penn Capital Mid Cap Core Fund | ||||

Institutional Class Shares | -17.45% | 4.21% | 7.05% | 7.52% |

Bloomberg US 2500 Index(2) | -16.38% | 9.50% | 8.23% | 8.98% |

Russell 2500® Index | -15.54% | 9.57% | 8.54% | 9.13%(3) |

(1) | Inception date is 11/30/15. |

(2) | Effective May 31, 2022, the Fund changed its primary benchmark from the Russell 2500® Index to the Bloomberg 2500 Index to better reflect the securities in which the Fund invests. |

(3) | The return shown for the Russell 2500® Index is from the inception date of the Institutional Class shares. |

Gross Expense Ratio: 1.70%, Net Expense Ratio: 1.06%, per the most recent Prospectus dated October 31, 2021, as supplemented May 31, 2022 and August 29, 2022..

The Advisor has contractually agreed to waive management fees and/or pay certain Fund expenses through at least April 1, 2023.

7

PENN CAPITAL OPPORTUNISTIC HIGH INCOME FUND

FUND SUMMARY (UNAUDITED)

This chart assumes a hypothetical initial gross investment of $10,000 made on November 30, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than that shown. To obtain performance current to the most recent month-end please call 844-302 PENN (7366) or visit www.penncapitalfunds.com. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index.

Average Annual Total Returns for the Periods Ended August 31, 2022 | One Year | Three Years | Five Years | Since |

Penn Capital Opportunistic High Income Fund | ||||

Institutional Class Shares | -10.31% | 0.14% | 1.75% | 3.85% |

ICE BofA US High Yield Constrained Index | -10.43% | 0.77% | 2.41% | 4.75%(2) |

50% ICE BofA High Yield Constrained Index -50% S&P/LSTA BB Loan Index | -4.55% | 1.46% | 2.66% | 4.11%(3) |

(1) | Inception date is 11/30/15. |

(2) | The return shown for the ICE BofA US High Yield Constrained Index is from the inception date of the Institutional Class shares. |

(3) | The return for the 50% ICE BofA High Yield Constrained Index -50% S&P/LSTA BB Loan Index is from the inception date of the Institutional Class shares. |

Gross Expense Ratio: 1.65%, Net Expense Ratio: 0.72%, per the most recent Prospectus dated October 31, 2021, as supplemented August 29, 2022.

The Advisor has contractually agreed to waive management fees and/or pay certain Fund expenses through at least April 1, 2023.

8

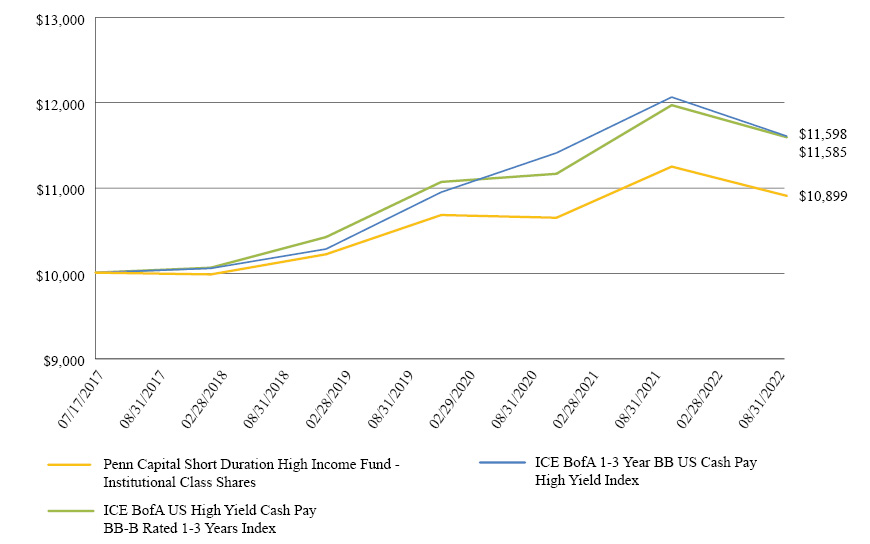

PENN CAPITAL SHORT DURATION HIGH INCOME FUND

FUND SUMMARY (UNAUDITED)

This chart assumes a hypothetical initial gross investment of $10,000 made on July 17, 2017, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Current performance may be lower or higher than that shown. To obtain performance current to the most recent month-end please call 844-302 PENN (7366) or visit www.penncapitalfunds.com. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index.

Average Annual Total Returns for the Periods Ended August 31, 2022 | One Year | Three Years | Five Years | Since |

Penn Capital Short Duration High Income Fund | ||||

Institutional Class Shares | -3.05% | 0.70% | 1.78% | 1.69% |

ICE BofA 1-3 Year BB-Rated US Cash Pay High Yield Index | -3.80% | 1.96% | 2.91% | 2.94%(2) |

ICE BofA US High Yield Cash Pay BB-B Rated 1-3 Years Index | -3.15% | 1.55% | 2.87% | 2.91%(3) |

(1) | Inception date is 7/17/17. |

(2) | The return shown for the ICE BofA. 1-3 Year BB-Rated US Cash Pay High Yield Index is from the inception date of the Institutional Class shares. |

(3) | The return shown for the ICE BofA US High Yield Cash Pay BB-B Rated 1-3 Years Index is from the inception date of the Institutional Class shares. The ICE BofA US High Yield Cash Pay BB-B Rated 1-3 Years Imdex is comprised of bonds within the ICE BofA High Yield Index whose ratings are at or between B1 through BB3, with maturities between 1 and 3 years. |

Gross Expense Ratio: 1.01%, Net Expense Ratio: 0.54%, per the most recent Prospectus dated October 31, 2021, as supplemented August 29, 2022..

The Advisor has contractually agreed to waive management fees and/or pay certain Fund expenses through at least April 1, 2023.

9

PENN CAPITAL SPECIAL SITUATIONS SMALL CAP EQUITY FUND

FUND SUMMARY (UNAUDITED)

This chart assumes a hypothetical initial gross investment of $10,000 made on December 17, 2015, inception of the Institutional Class shares. Returns shown in the chart and table include the reinvestment of all dividends, but do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. In the absence of fee waivers and reimbursements, when they are necessary to keep expenses at the expense cap, total return would be reduced. Past performance is not predictive of future performance. Investment return and principal value will fluctuate so that your shares, when redeemed, may be worth more or less than the original cost. Current performance may be lower or higher than that shown. To obtain performance current to the most recent month-end please call 844-302 PENN (7366) or visit www.penncapitalfunds.com. Index returns do not reflect the effects of fees, transaction costs or expenses. It is not possible to invest directly in an index.

Average Annual Total Returns for the Periods Ended August 31, 2022 | One Year | Three Years | Five Years | Since |

Penn Capital Special Situations Small Cap Equity Fund | ||||

Institutional Class Shares | -14.39% | 18.83% | 12.37% | 12.41% |

Bloomberg US 2000 Index(2) | -17.49% | 10.75% | 7.88% | 8.72% |

Russell 2000® Index | -17.88% | 8.59% | 6.95% | 8.93%(3) |

(1) | Inception date is 12/17/15. |

(2) | Effective May 31, 2022, the Fund changed its primary benchmark from the Russell 2000® Index to the Bloomberg US 2000 Index to better reflect the securities in which the Fund invests. |

(3) | The return shown for the Russell 2000® Index is from the inception date of the Institutional Class shares. |

Gross Expense Ratio: 1.71%, Net Expense Ratio: 1.09%, per the most recent Prospectus dated October 31, 2021, as supplemented May 31, 2022 and August 29, 2022..

The Advisor has contractually agreed to waive management fees and/or pay certain Fund expenses through at least April 1, 2023.

10

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Disclosure of Fund Expenses (Unaudited)

FOR THE PERIOD FROM MARCH 1, 2022 TO AUGUST 31, 2022

Cost in Dollars of a $1,000 Investment

The examples below are intended to describe the fees and expenses borne by shareholders during the six-month period from March 1, 2022 to August 31, 2022, and the impact of those costs on your investment.

Example

As a shareholder of a Fund, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees and other Fund expenses. This example is intended to help you understand your ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. These examples are based on an investment of $1,000 made at the beginning of the six-month period and held for the entire period from March 1, 2022 to August 31, 2022.

These examples illustrate your Fund’s ongoing costs in two ways:

Actual Expenses

The second and third data columns in the table below provide information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that you paid during the six-month period ended August 31, 2022. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number under the heading entitled Expenses Paid During Period to estimate the expenses you paid on your account during this period.

Hypothetical Examples for Comparison Purposes

The fourth and fifth data columns in the table below provide information about hypothetical account values and hypothetical expenses based on each Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not a Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balances or expenses you paid for the six-month period shown. You may use this information to compare the ongoing costs of investing in a Fund with the ongoing costs of investing in other funds. To do so, compare these 5% hypothetical examples with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees. Therefore, the fourth and fifth data columns of the table are useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

11

Beginning | Ending | Expenses Paid | Annualized | Actual Six-Month | |

Penn Capital Floating Rate Income Fund(1) | |||||

Actual | $ 1,000.00 | $ 984.60 | $ 3.20 | 0.64% | -1.54% |

Hypothetical (5% return before expenses) | 1,000.00 | 1,021.98 | 3.26 | 0.64% | N/A |

Penn Capital Mid Cap Core Fund(1) | |||||

Actual | $ 1,000.00 | $ 850.70 | $ 4.94 | 1.06% | -14.93% |

Hypothetical (5% return before expenses) | 1,000.00 | 1,019.86 | 5.40 | 1.06% | N/A |

Penn Capital Opportunistic High Income Fund(1) | |||||

Actual | $ 1,000.00 | $ 922.00 | $ 3.49 | 0.72% | -7.80% |

Hypothetical (5% return before expenses) | 1,000.00 | 1,021.58 | 3.67 | 0.72% | N/A |

Penn Capital Short Duration High Income Fund | |||||

Actual | $ 1,000.00 | $ 979.80 | $ 2.69 | 0.54% | -2.02% |

Hypothetical (5% return before expenses) | 1,000.00 | 1,022.48 | 2.75 | 0.54% | N/A |

Penn Capital Special Situations Small Cap Equity Fund(1) | |||||

Actual | $ 1,000.00 | $ 858.40 | $ 5.11 | 1.09% | -14.16% |

Hypothetical (5% return before expenses) | 1,000.00 | 1,019.71 | 5.55 | 1.09% | N/A |

(1) | Information is for Institutional Class shares. |

(2) | Expenses are equal to each Fund’s annualized expense ratio, net of waivers and excluding acquired fund fees and expenses, if any, multiplied by the average account value over the period, multiplied by the number of days (184) in the most recent fiscal half-year, then divided by 365 to reflect the one-half year period. |

(3) | Ratios reflect expenses waived by the Funds’ investment adviser. Without these waivers, each Fund’s expenses would have been higher and the ending account values would have been lower. |

12

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Floating Rate Income Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

Bank Loans: 83.4%(a)(b) | ||||||||

Advertising & Marketing: 0.6% | ||||||||

Terrier Media Buyer, Inc., 5.166% (1 Month US LIBOR + 3.500%), 12/17/26 | $ | 195,030 | $ | 188,935 | ||||

Apparel & Textile Products: 3.1% | ||||||||

Calceus Acquisition, Inc., 7.075% (1 Month US LIBOR + 5.500%), 3/31/25 | 368,043 | 327,558 | ||||||

Canada Goose, Inc., 4.506% (1 Month US LIBOR + 3.500%), 10/7/27 | 346,251 | 338,785 | ||||||

Crocs, Inc., 4.030% (TSFR1M + 3.500%), 2/20/29 | 299,250 | 287,654 | ||||||

| 953,997 | ||||||||

Asset Management: 3.7% | ||||||||

Fiserv Investment Solutions, Inc., 5.455% (1 Month US LIBOR + 4.000%), 2/26/27 | 196,000 | 188,650 | ||||||

Hightower Holding LLC, 5.098% (1 Month US LIBOR + 4.000%), 4/21/28 | 198,500 | 192,297 | ||||||

Nexus Buyer LLC, 5.416% (1 Month US LIBOR + 3.750%), 10/30/26 | 243,750 | 236,335 | ||||||

Russell Investments US Institutional Holdco, Inc., 5.000%, 5/30/25 | ||||||||

(6 Month US LIBOR + 3.500%) | 138,702 | 130,988 | ||||||

(6 Month US LIBOR + 3.500%) | 59,620 | 56,303 | ||||||

The Edelman Financial Engines Center LLC, 5.166% (1 Month US LIBOR + 3.750%), 4/7/28 | 192,803 | 184,678 | ||||||

Victory Capital Holdings, Inc., 3.219% (1 Month US LIBOR + 2.250%), 7/1/26 | 158,792 | 154,823 | ||||||

| 1,144,074 | ||||||||

Cable & Satellite: 3.3% | ||||||||

Cogeco Communications USA II LP, 3.666% (1 Month US LIBOR + 2.000%), 8/9/24 | 240,430 | 234,821 | ||||||

CSC Holdings LLC, 4.249% (1 Month US LIBOR + 2.250%), 7/17/25 | 237,469 | 229,604 | ||||||

DirecTV Financing LLC, 7.372% (1 Month US LIBOR + 5.000%), 8/2/27 | 329,595 | 314,680 | ||||||

Ziggo Financing Partnership, 4.891% (1 Month US LIBOR + 2.500%), 4/17/28 | 250,000 | 241,095 | ||||||

| 1,020,200 | ||||||||

Principal | Value | |||||||

Chemicals: 4.0% | ||||||||

Avient Corp. T/L B (07/22), 3.750%, 9/30/29(d) | $ | 250,000 | $ | 248,750 | ||||

Diamond BC BV, 3.514%, 10/31/28 | ||||||||

(3 Month US LIBOR + 2.750%) | 248,125 | 238,716 | ||||||

(1 Month US LIBOR + 2.750%) | 625 | 601 | ||||||

Gemini HDPE LLC, 4.240% (1 Month US LIBOR + 3.000%), 12/31/27 | 187,337 | 183,684 | ||||||

Lummus Technology Holdings V LLC, 5.872% (1 Month US LIBOR + 3.500%), 6/30/27 | 187,482 | 180,647 | ||||||

Schweitzer-Mauduit International, Inc., 5.438% (1 Month US LIBOR + 4.000%), 1/27/28 | 198,000 | 188,100 | ||||||

Trinseo Materials Operating SCA, 4.166%, 5/15/28 | ||||||||

(1 Month US LIBOR + 2.500%) | 163,152 | 156,626 | ||||||

(1 Month US LIBOR + 2.500%) | 34,848 | 33,454 | ||||||

| 1,230,578 | ||||||||

Commercial Support Services: 4.2% | ||||||||

Covanta Holding Corp., 4.872% (1 Month US LIBOR + 2.500%), 12/29/28 | 330,272 | 322,980 | ||||||

Covanta Holding Corp., 4.166% (1 Month US LIBOR + 2.500%), 12/29/28 | 24,800 | 24,252 | ||||||

GFL Environmental, Inc., 4.239% (1 Month US LIBOR + 3.000%), 5/30/25 | 197,000 | 195,686 | ||||||

Prime Security Services T/L, 4.463% (1 Month US LIBOR + 2.750%), 9/23/26 | 278,713 | 271,876 | ||||||

R1 RCM T/L B, 4.525%, 5/12/29 | 300,000 | 294,939 | ||||||

TruGreen Limited Parternship T/L, 5.666% (1 Month US LIBOR + 4.000%), 10/29/27 | 197,000 | 188,628 | ||||||

| 1,298,361 | ||||||||

Construction Materials Manufacturing: 1.2% | ||||||||

Quikrete Holdings, Inc., 4.997% (1 Month US LIBOR + 2.625%), 11/15/23 | 376,875 | 362,331 | ||||||

Containers & Packaging Manufacturing: 2.6% | ||||||||

Graham Packaging Co., Inc., 5.372% (1 Month US LIBOR + 3.000%), 8/4/27 | 193,483 | 188,646 | ||||||

Pactiv Evergreen Group Holdings, Inc., 5.166%, 9/20/28 | ||||||||

(1 Month US LIBOR + 3.500%) | 40,327 | 39,175 | ||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

13

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Floating Rate Income Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

(1 Month US LIBOR + 3.500%) | $ | 183,178 | $ | 177,945 | ||||

(1 Month US LIBOR + 3.500%) | 24,620 | 23,916 | ||||||

Pactiv Evergreen Group Holdings, Inc., 4.916%, 2/5/26 | ||||||||

(1 Month US LIBOR + 3.250%) | 27,841 | 27,122 | ||||||

(1 Month US LIBOR + 3.250%) | 45,603 | 44,425 | ||||||

(1 Month US LIBOR + 3.250%) | 123,556 | 120,364 | ||||||

Sabert Corp., 6.875% (1 Month US LIBOR + 4.500%), 11/26/26 | 180,111 | 177,410 | ||||||

| 799,003 | ||||||||

E-Commerce Discretionary: 0.6% | ||||||||

CNT Holdings I Corp., 5.368% (1 Month US LIBOR + 3.750%), 10/16/27 | 197,500 | 192,738 | ||||||

Electric Utilities: 0.6% | ||||||||

Vistra Operations Co. LLC, 3.906%, 12/15/25 | ||||||||

(1 Month US LIBOR + 1.750%) | 38,519 | 37,706 | ||||||

(1 Month US LIBOR + 1.750%) | 156,003 | 152,714 | ||||||

| 190,420 | ||||||||

Engineering & Construction: 1.2% | ||||||||

Centuri Group, Inc., 4.081%, 9/29/28 | ||||||||

(1 Month US LIBOR + 2.500%) | 500 | 487 | ||||||

(3 Month US LIBOR + 2.500%) | 176,166 | 171,487 | ||||||

Pike Corp., 4.670% (1 Month US LIBOR + 3.000%), 1/21/28 | 196,575 | 191,938 | ||||||

| 363,912 | ||||||||

Entertainment Content: 1.8% | ||||||||

Alchemy Copyrights LLC, 4.713% (1 Month US LIBOR + 3.000%), 8/5/27 | 176,857 | 174,204 | ||||||

Playtika Holding Corp., 5.122% (1 Month US LIBOR + 2.750%), 3/13/28 | 197,500 | 192,934 | ||||||

Univision Communications, Inc., 6.254% (TSFR1M + 4.250%), 6/9/29 | 200,000 | 196,000 | ||||||

| 563,138 | ||||||||

Food Production: 3.3% | ||||||||

Chobani LLC, 5.166% (1 Month US LIBOR + 3.500%), 10/20/27(d) | 296,500 | 284,086 | ||||||

Froneri US, Inc., 4.622%, 1/29/27 | ||||||||

(1 Month US LIBOR + 2.250%) | 134,704 | 129,596 | ||||||

(1 Month US LIBOR + 2.250%) | 61,296 | 58,972 | ||||||

Principal | Value | |||||||

HLF Financing Sarl LLC, 4.166% (1 Month US LIBOR + 2.500%), 8/8/25 | $ | 220,625 | $ | 214,145 | ||||

Whole Earth Brands, Inc., 6.125% (1 Month US LIBOR + 4.500%), 2/2/28 | 346,744 | 322,472 | ||||||

| 1,009,271 | ||||||||

Health Care Facilities & Services: 4.9% | ||||||||

ADMI Corp., 5.747% (1 Month US LIBOR + 3.250%), 12/23/27 | 346,744 | 318,942 | ||||||

Cambrex Corp., 5.927% (1 Month US LIBOR + 3.500%), 12/4/26 | 239,209 | 231,959 | ||||||

FC Compassus LLC, 7.127% (1 Month US LIBOR + 4.250%), 12/31/26 | 195,030 | 175,527 | ||||||

Option Care Health, Inc., 5.122% (1 Month US LIBOR + 2.750%), 11/30/28 | 298,500 | 294,957 | ||||||

PetVet Care Centers LLC, 4.416% (1 Month US LIBOR + 2.750%), 2/28/25 | 312,931 | 300,022 | ||||||

Select Medical Corp., 4.170% (6 Month US LIBOR + 2.500%), 3/6/24 | 212,163 | 207,190 | ||||||

| 1,528,597 | ||||||||

Home & Office Products Manufactering: 0.8% | ||||||||

Weber-Stephen Products LLC, 4.916% (1 Month US LIBOR + 3.250%), 11/30/27 | 310,863 | 263,235 | ||||||

Housing: 0.6% | ||||||||

Foundation Building Materials, Inc., 4.489%, 1/31/28 | ||||||||

(3 Month US LIBOR + 3.250%) | 202,438 | 192,568 | ||||||

(1 Month US LIBOR + 3.250%) | 513 | 488 | ||||||

| 193,056 | ||||||||

Industrial Intermediate Products: 0.6% | ||||||||

Gates Global LLC, 4.166% (1 Month US LIBOR + 2.750%), 3/31/27 | 197,805 | 193,623 | ||||||

Insurance: 1.2% | ||||||||

Asurion LLC, 5.622% (1 Month US LIBOR + 3.250%), 12/23/26 | 197,000 | 180,115 | ||||||

HUB International Ltd., 4.214%, 4/18/25 | ||||||||

(2 Month US LIBOR + 3.000%) | 511 | 500 | ||||||

(3 Month US LIBOR + 3.000%) | 195,688 | 191,367 | ||||||

| 371,982 | ||||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

14

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Floating Rate Income Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

Internet Media & Services: 4.9% | ||||||||

Arches Buyer, Inc., 5.622% (1 Month US LIBOR + 3.250%), 12/6/27 | $ | 296,000 | $ | 279,042 | ||||

Buzz Merger Sub Ltd., 5.096% (1 Month US LIBOR + 2.750%), 1/22/27 | 244,375 | 237,655 | ||||||

Endurance International Group Holdings, Inc., 5.291% (1 Month US LIBOR + 3.500%), 2/10/28 | 202,950 | 189,886 | ||||||

Go Daddy Operating Co. LLC, 3.416%, 2/15/24 | ||||||||

(1 Month US LIBOR + 1.750%) | 73,346 | 72,561 | ||||||

(1 Month US LIBOR + 1.750%) | 238,572 | 236,017 | ||||||

Match Group Holdings II LLC, 3.194% (1 Month US LIBOR + 1.750%), 2/7/27 | 200,000 | 194,000 | ||||||

Shutterfly, Inc., 7.250% (1 Month US LIBOR + 5.000%), 9/25/26 | 405,900 | 305,610 | ||||||

| 1,514,771 | ||||||||

Leisure Facilities & Services: 7.2% | ||||||||

Alterra Mountain Co., 5.872% (1 Month US LIBOR + 3.500%), 8/17/28 | 239,441 | 232,557 | ||||||

Caesars Resort Collection LLC, 5.872% (1 Month US LIBOR + 3.500%), 7/21/25 | 112,611 | 111,541 | ||||||

Carnival Corp., 3.750% (1 Month US LIBOR + 3.000%), 6/30/25 | 246,851 | 234,664 | ||||||

Century Casinos T/L (03/22), 7.625%, 3/23/29 | 249,375 | 238,777 | ||||||

Dave & Buster’s, Inc., 7.427% (TSFR1M + 5.000%), 6/22/29 | 300,000 | 292,749 | ||||||

Hilton Grand Vacations LLC, 5.372% (1 Month US LIBOR + 3.000%), 7/31/28 | 248,125 | 242,336 | ||||||

IRB Holding Corp., 5.122% (1 Month US LIBOR + 2.750%), 2/5/25 | 241,309 | 235,981 | ||||||

IRB Holding Corp., 5.437% (SOFR + 3.000%), 12/15/27 | 197,000 | 190,310 | ||||||

Scientific Games Holdings LP, 4.175% (TSFR1M + 3.500%), 2/3/29 | 250,000 | 240,452 | ||||||

Scientific Games International, Inc., 5.044% (TSFR1M + 3.000%), 4/6/29 | 250,000 | 245,625 | ||||||

| 2,264,992 | ||||||||

Machinery Manufacturing: 1.4% | ||||||||

ASP Blade Holdings, Inc., 6.372% (1 Month US LIBOR + 4.000%), 12/31/28 | 248,824 | 231,762 | ||||||

Principal | Value | |||||||

EWT Holdings III Corp., 4.188% (1 Month US LIBOR + 2.500%), 3/10/28 | $ | 198,000 | $ | 195,277 | ||||

| 427,039 | ||||||||

Oil & Gas Producers: 3.1% | ||||||||

AL GCX Holdings (Arclight) T/L B, 5.916% (TSFR1M + 3.750%), 4/20/29 | 300,000 | 296,157 | ||||||

CQP Holdco LP, 6.000% (1 Month US LIBOR + 3.750%), 6/5/28 | 247,500 | 242,364 | ||||||

Freeport LNG Investments LLLP, 4.563% (1 Month US LIBOR + 3.500%), 11/17/28 | 246,674 | 236,329 | ||||||

GIP II Blue Holding LP, 5.506% (1 Month US LIBOR + 4.500%), 9/22/28 | 201,022 | 198,760 | ||||||

| 973,610 | ||||||||

Oil & Gas Services & Equipment: 1.4% | ||||||||

ChampionX T/L B1 (05/22) (Apergy), 5.080%, 5/14/29 | 300,000 | 298,500 | ||||||

Keane Group Holdings LLC, 5.938% (US LIBOR + 3.750%), 6/30/25(d) | 130,000 | 126,263 | ||||||

| 424,763 | ||||||||

Pharmaceuticals: 0.8% | ||||||||

Agiliti Health, Inc., 4.500%, 10/18/25 | ||||||||

(1 Month US LIBOR + 2.750%) | 243,073 | 236,996 | ||||||

(1 Month US LIBOR + 2.750%) | 630 | 614 | ||||||

| 237,610 | ||||||||

Publishing & Broadcasting: 2.8% | ||||||||

Clear Channel Outdoor Holdings, Inc., 6.306% (1 Month US LIBOR + 3.500%), 8/7/26 | 342,869 | 316,821 | ||||||

Cumulus Media New Holdings, Inc., 4.750% (1 Month US LIBOR + 3.750%), 3/30/26 | 145,298 | 139,486 | ||||||

The E.W. Scripps Co., 4.935% (1 Month US LIBOR + 2.563%), 5/1/26 | 242,152 | 237,461 | ||||||

The E.W. Scripps Co., 5.122% (1 Month US LIBOR + 3.000%), 1/7/28 | 165,750 | 163,174 | ||||||

| 856,942 | ||||||||

Retail - Consumer Discretionary: 5.4% | ||||||||

Great Outdoors Group T/L (Bass Pro) LLC, 6.122% (1 Month US LIBOR + 3.750%), 3/31/28 | 347,375 | 335,564 | ||||||

Jo-Ann Stores LLC, 5.964% (1 Month US LIBOR + 4.750%), 7/7/28 | 247,500 | 160,051 | ||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

15

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Floating Rate Income Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

LBM Acquisition LLC, 5.416% (1 Month US LIBOR + 3.750%), 12/17/27(d) | $ | 211,705 | $ | 192,704 | ||||

PetSmart, Inc., 4.500% (1 Month LIBOR USD + 3.750%), 2/11/28 | 198,000 | 193,050 | ||||||

Savers, Inc., 6.506% (1 Month US LIBOR + 5.750%), 4/6/27 | 198,500 | 194,034 | ||||||

Staples, Inc., 5.786% (1 Month US LIBOR + 4.500%), 9/12/24 | 307,569 | 290,173 | ||||||

White Cap Buyer LLC, 5.275% (1 Month US LIBOR + 4.000%), 10/8/27 | 345,386 | 333,063 | ||||||

| 1,698,639 | ||||||||

Semiconductors: 0.9% | ||||||||

II-VI, Inc., 5.123% (1 Month US LIBOR + 2.750%), 12/1/28(d) | 300,000 | 293,124 | ||||||

Software: 6.4% | ||||||||

Azalea TopCo, Inc., 4.739% (1 Month US LIBOR + 3.500%), 7/27/26 | 291,750 | 279,059 | ||||||

McAfee Corp., 6.407% (TSFR1M + 4.000%), 2/2/29 | 300,000 | 283,875 | ||||||

Proofpoint, Inc., 4.825% (1 Month US LIBOR + 3.250%), 6/9/28 | 199,000 | 191,189 | ||||||

Rackspace Technology Global, Inc., 4.160%, 2/15/28 | ||||||||

(3 Month US LIBOR + 2.750%) | 346,242 | 278,677 | ||||||

(1 Month US LIBOR + 2.750%) | 879 | 707 | ||||||

UKG, Inc., 5.535% (1 Month US LIBOR + 3.250%), 5/4/26 | 297,014 | 287,308 | ||||||

Waystar Technologies, Inc., 6.372% (1 Month US LIBOR + 4.000%), 10/31/26(d) | 347,364 | 339,402 | ||||||

Xperi Holding Corp., 5.166% (1 Month US LIBOR + 3.500%), 6/1/25 | 350,604 | 342,936 | ||||||

| 2,003,153 | ||||||||

Specialty Finance: 0.7% | ||||||||

TransUnion LLC, 3.416% (1 Month US LIBOR + 1.750%), 11/13/26 | 237,411 | 232,070 | ||||||

Specialty Retail: 1.3% | ||||||||

BDF Acquisition Corp., 7.622% (1 Month US LIBOR + 5.250%), 8/14/23 | 437,200 | 397,441 | ||||||

Technology Hardware: 0.8% | ||||||||

Maxar Technologies, Inc., 6.677% (TSFR1M + 4.250%), 6/29/29 | 250,000 | 239,625 | ||||||

Principal | Value | |||||||

Technology Services: 2.6% | ||||||||

NAB Holdings T/L, 5.204% (SOFR + 3.000%), 11/17/28 | $ | 348,250 | $ | 335,988 | ||||

Paysafe Holdings US Corp., 4.416% (1 Month US LIBOR + 2.750%), 4/30/25 | 248,120 | 231,372 | ||||||

Sabre GLBL Inc. T/L 8/22, 7.285%, 6/30/28(d) | 250,000 | 240,625 | ||||||

| 807,985 | ||||||||

Telecommnications: 3.2% | ||||||||

Altice France SA, 6.905% (1 Month US LIBOR + 4.000%), 7/13/26 | 235,023 | 227,267 | ||||||

Cincinnati Bell, Inc., 5.677% (SOFR + 3.250%), 12/29/28 | 348,250 | 340,488 | ||||||

Gogo Intermediate Holdings LLC, 4.989% (1 Month US LIBOR + 3.750%), 4/28/28 | 198,000 | 193,751 | ||||||

Lumen Technologies, Inc., 4.622% (1 Month US LIBOR + 2.250%), 3/15/27 | 243,750 | 229,125 | ||||||

| 990,631 | ||||||||

Transportation & Logistics: 1.3% | ||||||||

American Airlines, Inc., 7.460% (1 Month US LIBOR + 4.750%), 4/20/28 | 200,000 | 196,584 | ||||||

SkyMiles IP Ltd., 4.813% (1 Month US LIBOR + 3.750%), 10/20/27 | 200,000 | 202,392 | ||||||

| 398,976 | ||||||||

Wholesale - Consumer Discretionary: 0.9% | ||||||||

Dealer Tire LLC, 5.916%, 12/12/25 | ||||||||

(1 Month US LIBOR + 4.250%) | 100,551 | 99,646 | ||||||

(1 Month US LIBOR + 4.250%) | 170,559 | 169,024 | ||||||

| 268,670 | ||||||||

Total Bank Loans (cost $26,861,925) | 25,897,492 | |||||||

Corporate Bonds: 12.5% | ||||||||

Aerospace & Defense: 0.5% | ||||||||

TransDigm, Inc., 8.000%, 12/15/25(c) | 160,000 | 163,872 | ||||||

Cable & Satellite: 0.4% | ||||||||

Dish DBS Corp., 5.875%, 11/15/24 | 150,000 | 135,750 | ||||||

Containers & Packaging Manufacturing: 0.6% | ||||||||

Matthews International Corp., 5.250%, 12/1/25(c) | 200,000 | 182,110 | ||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

16

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Floating Rate Income Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

Entertainment Content: 0.6% | ||||||||

Univision Communications, Inc., 5.125%, 2/15/25(c) | $ | 195,000 | $ | 188,355 | ||||

Gas & Water Utilities: 0.4% | ||||||||

Rockpoint Gas Storage Canada Ltd., 7.000%, 3/31/23(c) | 138,000 | 136,620 | ||||||

Leisure Facilities & Services: 2.4% | ||||||||

Arrow Bidco LLC, 9.500%, 3/15/24(c) | 115,000 | 114,716 | ||||||

Carnival Corp., 10.500%, 2/1/26(c) | 385,000 | 396,548 | ||||||

International Game Technology PLC, 6.500%, 2/15/25(c) | 200,000 | 198,500 | ||||||

| 709,764 | ||||||||

Oil & Gas Producers: 1.5% | ||||||||

Matador Resources Co., 5.875%, 9/15/26 | 150,000 | 146,828 | ||||||

New Fortress Energy Inc., 6.5% 9/30/26(c) | 188,000 | 170,523 | ||||||

SM Energy Co. 5.625% 06/01/25 | 150,000 | 145,875 | ||||||

| 463,226 | ||||||||

Oil & Gas Services & Equipment: 1.0% | ||||||||

Oceaneering International, Inc., 4.650%, 11/15/24 | 200,000 | 186,584 | ||||||

Weatherford International Ltd., 11.000%, 12/1/24(c) | 124,000 | 125,897 | ||||||

| 312,481 | ||||||||

Home & Office Products Manufacturing: 0.5% | ||||||||

CD&R Smokey Buyer, Inc., 6.750%, 7/15/25(c) | 165,000 | 153,450 | ||||||

Publishing & Broadcasting: 0.4% | ||||||||

Cumulus Media New Holdings, Inc., 6.750%, 7/1/26(c) | 155,000 | 138,647 | ||||||

Real Estate Investment Trusts (REITs): 1.0% | ||||||||

VICI Properties LP / VICI Note Co, Inc., 4.625%, 6/15/25(c) | 150,000 | 145,194 | ||||||

XHR LP, 6.375%, 8/15/25(c) | 160,000 | 155,289 | ||||||

| 300,483 | ||||||||

Specialty Finance: 0.9% | ||||||||

Fortress Transportation and Infrastructure Investors LLC, 6.500%, 10/1/25(c) | 122,000 | 113,662 | ||||||

Principal | Value | |||||||

Starwood Property Trust, Inc., 3.750%, 12/31/24(c) | $ | 190,000 | $ | 177,043 | ||||

| 290,705 | ||||||||

Technology Services: 0.5% | ||||||||

Sabre GLBL, Inc., 9.250%, 4/15/25(c) | 165,000 | 162,573 | ||||||

Tobacco & Cannabis: 0.4% | ||||||||

Turning Point Brands, Inc., 5.625%, 2/15/26(c) | 145,000 | 128,663 | ||||||

Transportation & Logistics: 1.0% | ||||||||

Allegiant Travel Co., 7.250%, 8/15/27(c) | 300,000 | 297,969 | ||||||

Wholesale - Consumer Staples: 0.4% | ||||||||

KeHE Distributors LLC, 8.625%, 10/15/26(c) | 109,000 | 110,363 | ||||||

Total Corporate Bonds (cost $4,049,588) | 3,875,031 | |||||||

Number of | ||||||||

Short-Term Investments: 6.7% | ||||||||

U.S. Bank Money Market Deposit Account, 1.00%(e) | 2,085,171 | 2,085,171 | ||||||

Total Short-Term Investments: (cost $2,085,171) | 2,085,171 | |||||||

Total Investments - 102.6% (cost $32,996,684) | 31,857,694 | |||||||

Liabilities in Excess of Other Assets (2.6)% | (808,878 | ) | ||||||

Net Assets: 100.0% | $ | 31,048,816 | ||||||

Percentages are stated as a percent of net assets.

(a) | Bank Loans typically have rates of interest which are redetermined either daily, monthly, quarterly or semi-annually by reference to a base lending rate, plus a premium. These base lending rates are primarily the London Interbank Offered Rate (“LIBOR”) and secondarily, the prime rate offered by one or more major United States banks (the “Prime Rate”) and the certificate of deposit (“CD”) rate or other base lending rates used by commercial lenders. |

(b) | Senior floating-rate loans (Senior Loans) often require prepayments from excess cash flows or permit the borrowers to repay at their election. The degree to which borrowers repay, whether as a contractual requirement or at their election, cannot be predicted with accuracy. As a result, the actual remaining maturity may be substantially less than the stated maturities shown. However, Senior Loans will typically have an expected average life of approximately two to four years. |

The Accompanying Footnotes are an Integral Part of these Financial Statements

17

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Floating Rate Income Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

(c) | Securities purchased pursuant to Rule 144A of the Securities Act of 1933, as amended, and may be sold only to dealers in that program or other “qualified institutional buyers.” As of August 31, 2022, the value of these investments was $3,259,994, or 10.5% of total net assets. |

(d) | All or a portion of this loan is unfunded - See note. |

(e) | The rate shown is as of August 31, 2022. |

Country Exposure (as a percentage of total investments) | |

United States | 97.4% |

Panama | 1.2% |

United Kingdom | 0.6% |

Canada | 0.4% |

Bermuda | 0.4% |

Asset Type (as a percentage of total investments) (Unaudited) |

The Accompanying Footnotes are an Integral Part of these Financial Statements

18

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Mid Cap Core Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Number of | Value | |||||||

Common Stocks: 88.1% | ||||||||

Aerospace & Defense: 1.3% | ||||||||

Mercury Systems, Inc.* | 3,318 | $ | 159,695 | |||||

Air Freight & Logistics: 1.8% | ||||||||

GXO Logistics, Inc.* | 2,494 | 110,684 | ||||||

XPO Logistics, Inc.* | 2,251 | 117,997 | ||||||

| 228,681 | ||||||||

Banks: 8.1% | ||||||||

Pinnacle Financial Partners, Inc. | 3,623 | 292,412 | ||||||

Seacoast Banking Corp of Florida | 8,137 | 262,988 | ||||||

Texas Capital Bancshares, Inc.* | 4,385 | 258,846 | ||||||

Western Alliance Bancorp | 2,980 | 228,626 | ||||||

| 1,042,872 | ||||||||

Biotechnology: 4.9% | ||||||||

BioMarin Pharmaceutical, Inc.* | 1,921 | 171,353 | ||||||

Halozyme Therapeutics, Inc.* | 4,702 | 191,513 | ||||||

United Therapeutics Corp.* | 1,124 | 254,721 | ||||||

| 617,587 | ||||||||

Building Products: 1.6% | ||||||||

Lennox International, Inc. | 849 | 203,862 | ||||||

Chemicals: 5.3% | ||||||||

CF Industries Holdings, Inc. | 2,304 | 238,372 | ||||||

Livent Corp.* | 7,080 | 227,834 | ||||||

Olin Corp. | 3,735 | 204,155 | ||||||

| 670,361 | ||||||||

Construction Materials: 1.9% | ||||||||

Martin Marietta Materials, Inc. | 701 | 243,745 | ||||||

Consumer Finance: 1.1% | ||||||||

OneMain Holdings, Inc. | 4,169 | 145,623 | ||||||

Electrical Equipment: 1.8% | ||||||||

nVent Electric PLC | 7,063 | 232,796 | ||||||

Food & Staples Retailing: 0.8% | ||||||||

Performance Food Group Co.* | 1,918 | 95,862 | ||||||

Health Care Equipment & Supplies: 3.6% | ||||||||

CONMED Corp. | 2,313 | 204,862 | ||||||

Lantheus Holdings, Inc.* | 3,116 | 245,541 | ||||||

| 450,403 | ||||||||

Number of | Value | |||||||

Hotels, Restaurants & Leisure: 4.6% | ||||||||

MGM Resorts International | $ | 5,054 | $ | 164,963 | ||||

Planet Fitness, Inc. - Class A* | 3,439 | 232,992 | ||||||

Vail Resorts, Inc. | 807 | 181,317 | ||||||

| 579,272 | ||||||||

Independent Power and Renewable Electricity Producers: 2.3% | ||||||||

Vistra Corp. | 11,748 | 290,763 | ||||||

Insurance: 7.0% | ||||||||

Arch Capital Group Ltd.* | 6,709 | 306,736 | ||||||

Axis Capital Holdings Ltd. | 4,361 | 231,787 | ||||||

Lincoln National Corp. | 2,591 | 119,341 | ||||||

Primerica, Inc. | 1,794 | 227,390 | ||||||

| 885,254 | ||||||||

Interactive Media & Services: 0.7% | ||||||||

IAC, Inc.* | 1,340 | 86,122 | ||||||

IT Services: 1.8% | ||||||||

GoDaddy, Inc. - Class A* | 2,984 | 226,247 | ||||||

Life Sciences Tools & Services: 1.9% | ||||||||

Avantor, Inc.* | 9,505 | 236,770 | ||||||

Machinery: 1.8% | ||||||||

Chart Industries, Inc.* | 1,198 | 232,244 | ||||||

Marine: 2.4% | ||||||||

Kirby Corp.* | 4,476 | 300,161 | ||||||

Media: 3.6% | ||||||||

Fox Corp. - Class B | 6,757 | 213,656 | ||||||

Liberty Media Corp.-Liberty SiriusXM - Class A* | 5,877 | 244,131 | ||||||

| 457,787 | ||||||||

Metals & Mining: 3.4% | ||||||||

Constellium SE* | 13,786 | 183,629 | ||||||

Steel Dynamics, Inc. | 3,033 | 244,824 | ||||||

| 428,453 | ||||||||

Oil, Gas & Consumable Fuels: 5.5% | ||||||||

Chesapeake Energy Corp. | 3,212 | 322,774 | ||||||

Diamondback Energy, Inc. | 2,847 | 379,448 | ||||||

| 702,222 | ||||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

19

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Mid Cap Core Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Number of | Value | |||||||

Pharmaceuticals: 2.8% | ||||||||

Catalent, Inc.* | 2,118 | $ | 186,384 | |||||

Perrigo Co Plc | 4,344 | 162,552 | ||||||

| 348,936 | ||||||||

Professional Services: 1.5% | ||||||||

TransUnion | 2,587 | 191,102 | ||||||

Real Estate Management & Development: 1.4% | ||||||||

Kennedy-Wilson Holdings, Inc. | 10,197 | 179,059 | ||||||

Semiconductors & Semiconductor Equipment: 5.5% | ||||||||

Allegro MicroSystems, Inc.* | 10,441 | 243,484 | ||||||

Kulicke & Soffa Industries, Inc. | 4,504 | 189,348 | ||||||

Skyworks Solutions, Inc. | 973 | 95,889 | ||||||

Teradyne, Inc. | 1,975 | 167,164 | ||||||

| 695,885 | ||||||||

Software: 2.6% | ||||||||

RingCentral, Inc. - Class A* | 2,738 | 117,844 | ||||||

Tyler Technologies, Inc.* | 577 | 214,361 | ||||||

| 332,205 | ||||||||

Specialty Retail: 3.4% | ||||||||

Burlington Stores, Inc.* | 975 | 136,685 | ||||||

Five Below, Inc.* | 1,310 | 167,523 | ||||||

Floor & Decor Holdings, Inc. - Class A* | 1,492 | 121,389 | ||||||

| 425,597 | ||||||||

Technology Hardware, Storage & Peripherals: 1.2% | ||||||||

Western Digital Corp.* | 3,715 | 156,996 | ||||||

Trading Companies & Distributors: 2.5% | ||||||||

H&E Equipment Services, Inc. | 4,886 | 154,691 | ||||||

United Rentals, Inc.* | 549 | 160,330 | ||||||

| 315,021 | ||||||||

Total Common Stocks (cost $8,779,943) | 11,161,583 | |||||||

Equity Real Estate Investment Trusts (REITs): 7.4% | ||||||||

Apartment Income REIT Corp. | 6,051 | 247,183 | ||||||

Healthcare Realty Trust, Inc. | 10,493 | 255,190 | ||||||

Pebblebrook Hotel Trust | 9,650 | 170,033 | ||||||

VICI Properties, Inc. | 7,942 | 262,007 | ||||||

| 934,413 | ||||||||

Total REITs (cost $925,013) | 934,413 | |||||||

Number of | Value | |||||||

Short-Term Investments 4.9% | ||||||||

U.S. Bank Money Market Deposit Account, 1.00%(b) | 626,258 | $ | 626,258 | |||||

Total Short-Term Investments (cost $626,258) | 626,258 | |||||||

Total Investments - 100.4% (cost $10,331,214) | 12,722,254 | |||||||

Liabilities in Excess of Other Assets (0.4)% | (45,044 | ) | ||||||

Net Assets: 100.0% | $ | 12,677,210 | ||||||

Percentages are stated as a percent of net assets.

* | Non-income producing security. |

(a) | The rate shown is as of August 31, 2022. |

The Accompanying Footnotes are an Integral Part of these Financial Statements

20

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Mid Cap Core Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Country Exposure (as a percentage of total investments) | |

United States | 91.3% |

Bermuda | 4.2% |

Ireland | 3.1% |

France | 1.4% |

Asset Type (as a percentage of total investments) (Unaudited) |

The industry classifications presented in this report, present the Global Industry Classification Standard (GICS®). GICS® was developed by and/or is the exclusive property of MSCI, Inc. and Standard & Poor Financial Services LLC (“S&P”). GICS® is a service mark of MSCI and S&P and has been licensed for use by U.S. Bank Global Fund Services.

The Accompanying Footnotes are an Integral Part of these Financial Statements

21

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

Penn Capital Opportunistic High Income Fund

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

Convertible Bonds: 3.1% | ||||||||

Cable & Satellite TV: 0.9% | ||||||||

DISH Network Corp., 3.375%, 8/15/26 | $ | 245,000 | $ | 176,293 | ||||

Consumer/Commercial/Lease Financing: 0.4% | ||||||||

Block, Inc., 0.250%, 11/1/27 | 85,000 | 65,628 | ||||||

Food - Wholesale: 0.5% | ||||||||

Herbalife Nutrition Ltd., 2.625%, 3/15/24 | 90,000 | 82,890 | ||||||

Internet: 0.4% | ||||||||

Spotify USA, Inc., 0.000%, 3/15/26 | 85,000 | 69,275 | ||||||

Pharmaceuticals: 0.5% | ||||||||

Tilray Brands, Inc., 5.000%, 10/1/23 | 100,000 | 97,135 | ||||||

Software/Services: 0.4% | ||||||||

RingCentral, Inc., 0.000%, 3/15/26 | 95,000 | 74,290 | ||||||

Total Convertible Bonds (cost $632,354) | 565,511 | |||||||

Corporate Bonds: 85.6% | ||||||||

Advertising: 1.4% | ||||||||

Clear Channel Outdoor Holdings, Inc., 5.125%, 8/15/27(a) | 50,000 | 44,781 | ||||||

Clear Channel Outdoor Holdings, Inc., 7.500%, 6/1/29(a) | 115,000 | 92,457 | ||||||

Stagwell Global LLC, 5.625%, 8/15/29(a) | 135,000 | 114,487 | ||||||

| 251,725 | ||||||||

Aerospace/Defense: 1.3% | ||||||||

Bombardier, Inc., 7.500%, 3/15/25(a) | 95,000 | 92,923 | ||||||

Maxar Technologies, Inc., 7.750%, 6/15/27(a) | 65,000 | 64,512 | ||||||

Triumph Group, Inc., 7.750%, 8/15/25 | 90,000 | 75,796 | ||||||

| 233,231 | ||||||||

Air Transportation: 2.3% | ||||||||

American Airlines, Inc., 5.750%, 4/20/29(a) | 145,000 | 130,897 | ||||||

American Airlines, Inc., 11.750%, 7/15/25(a) | 80,000 | 88,401 | ||||||

United Airlines, Inc., 4.625%, 4/15/29(a) | 90,000 | 78,975 | ||||||

Principal | Value | |||||||

VistaJet Malta Finance PLC / XO Management Holding, Inc., 6.375%, 2/1/30(a) | $ | 60,000 | $ | 51,600 | ||||

VistaJet Malta Finance PLC / XO Management Holding, Inc., 7.875%, 5/1/27(a) | 70,000 | 64,575 | ||||||

| 414,448 | ||||||||

Auto Parts & Equipment: 1.4% | ||||||||

American Axle & Manufacturing, Inc., 6.875%, 7/1/28 | 85,000 | 80,715 | ||||||

American Axle & Manufacturing, Inc., 5.000%, 10/1/29 | 50,000 | 42,104 | ||||||

The Goodyear Tire & Rubber Co., 5.000%, 7/15/29 | 20,000 | 17,929 | ||||||

The Goodyear Tire & Rubber Co., 5.250%, 7/15/31 | 65,000 | 56,020 | ||||||

The Goodyear Tire & Rubber Co., 7.000%, 3/15/28 | 55,000 | 56,017 | ||||||

| 252,785 | ||||||||

Automakers: 1.2% | ||||||||

Ford Motor Co., 6.625%, 10/1/28 | 215,000 | 220,310 | ||||||

Brokerage: 0.5% | ||||||||

StoneX Group, Inc., 8.625%, 6/15/25(a) | 95,000 | 96,662 | ||||||

Building & Construction: 2.6% | ||||||||

Ashton Woods USA LLC, 4.625%, 8/1/29(a) | 95,000 | 74,558 | ||||||

Ashton Woods USA LLC / Ashton Woods Finance Co., 4.625%, 4/1/30(a) | 95,000 | 74,943 | ||||||

Brookfield Residential Properties, Inc., 5.000%, 6/15/29(a) | 85,000 | 67,618 | ||||||

Great Lakes Dredge & Dock Corp., 5.250%, 6/1/29(a) | 100,000 | 85,293 | ||||||

Pike Corp., 5.500%, 9/1/28(a) | 100,000 | 82,671 | ||||||

Taylor Morrison Communities, Inc., 5.125%, 8/1/30(a) | 90,000 | 77,228 | ||||||

| 462,311 | ||||||||

Building Materials: 0.7% | ||||||||

Eco Material Technologies, Inc., 7.875%, 1/31/27(a) | 140,000 | 130,564 | ||||||

Cable & Satellite TV: 3.5% | ||||||||

CCO Holdings LLC, 4.500%, 8/15/30(a) | 135,000 | 113,532 | ||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

22

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

PENN CAPITAL OPPORTUNISTIC HIGH INCOME FUND

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

CSC Holdings LLC, 7.500%, 4/1/28(a) | $ | 200,000 | $ | 177,778 | ||||

CSC Holdings LLC, 6.500%, 2/1/29(a) | 200,000 | 184,047 | ||||||

DIRECTV Holdings LLC, 5.875%, 8/15/27(a) | 105,000 | 96,075 | ||||||

DISH DBS Corp., 5.250%, 12/1/26(a) | 75,000 | 61,922 | ||||||

| 633,354 | ||||||||

Chemicals: 2.2% | ||||||||

Avient Corp., 7.125%, 8/1/30(a) | 70,000 | 69,120 | ||||||

Chemours Co/The, 5.750%, 11/15/28(a) | 55,000 | 49,225 | ||||||

Olin Corp., 5.625%, 8/1/29 | 190,000 | 181,026 | ||||||

Venator Finance Sarl, 5.750%, 7/15/25(a) | 125,000 | 91,875 | ||||||

| 391,246 | ||||||||

Consumer/Commercial/Lease Financing: 2.7% | ||||||||

Enova International, Inc., 8.500%, 9/15/25(a) | 125,000 | 116,607 | ||||||

Fortress Transportation and Infrastructure Investors LLC, 9.750%, 8/1/27(a) | 45,000 | 45,109 | ||||||

Fortress Transportation and Infrastructure Investors LLC, 5.500%, 5/1/28(a) | 65,000 | 55,306 | ||||||

Global Aircraft Leasing Co. Ltd., 7.250% Cash or 7.000% PIK, 9/15/24(a) | 130,000 | 105,173 | ||||||

Navient Corp., 6.750%, 6/25/25 | 95,000 | 91,675 | ||||||

Navient Corp., 4.875%, 3/15/28 | 60,000 | 48,992 | ||||||

OneMain Finance Corp., 6.625%, 1/15/28 | 25,000 | 22,857 | ||||||

| 485,719 | ||||||||

Department Stores: 1.7% | ||||||||

Macy’s Retail Holdings LLC, 5.875%, 4/1/29(a) | 105,000 | 90,878 | ||||||

Neiman Marcus Group LLC, 7.125%, 4/1/26(a) | 225,000 | 210,503 | ||||||

| 301,381 | ||||||||

Diversified Capital Goods: 0.6% | ||||||||

Madison IAQ LLC, 5.875%, 6/30/29(a) | 130,000 | 106,943 | ||||||

Electric - Generation: 1.5% | ||||||||

Leeward Renewable Energy Operations LLC, 4.250%, 7/1/29(a) | 70,000 | 57,700 | ||||||

Principal | Value | |||||||

Sunnova Energy Corp., 5.875%, 9/1/26(a) | $ | 95,000 | $ | 87,638 | ||||

Vistra Corp., 8.000% (5 Year CMT Rate + 6.930%), 4/15/27(a) | 130,000 | 124,475 | ||||||

| 269,813 | ||||||||

Energy - Exploration & Production: 6.9% | ||||||||

Antero Resources Corp., 7.625%, 2/1/29(a) | 90,000 | 91,547 | ||||||

Callon Petroleum Co., 8.250%, 7/15/25 | 120,000 | 118,500 | ||||||

Comstock Resources, Inc., 6.750%, 3/1/29(a) | 145,000 | 138,399 | ||||||

Comstock Resources, Inc., 5.875%, 1/15/30(a) | 145,000 | 132,662 | ||||||

Earthstone Energy Holdings LLC, 8.000%, 4/15/27(a) | 95,000 | 92,566 | ||||||

Hilcorp Energy I LP, 6.250%, 11/1/28(a) | 125,000 | 118,117 | ||||||

Northern Oil and Gas, Inc., 8.125%, 3/1/28(a) | 135,000 | 129,600 | ||||||

Occidental Petroleum Corp., 6.625%, 9/1/30 | 110,000 | 117,513 | ||||||

Occidental Petroleum Corp., 6.125%, 1/1/31 | 90,000 | 93,533 | ||||||

Penn Virginia Holdings LLC, 9.250%, 8/15/26(a) | 130,000 | 127,634 | ||||||

SM Energy Co., 6.750%, 9/15/26 | 65,000 | 63,924 | ||||||

SM Energy Co., 6.500%, 7/15/28 | 35,000 | 33,705 | ||||||

| 1,257,700 | ||||||||

Food - Wholesale: 2.0% | ||||||||

BellRing Brands, Inc., 7.000%, 3/15/30(a) | 140,000 | 133,699 | ||||||

HLF Financing Sarl LLC, 4.875%, 6/1/29(a) | 55,000 | 43,404 | ||||||

KeHE Distributors LLC, 8.625%, 10/15/26(a) | 96,000 | 97,200 | ||||||

Simmons Foods, Inc., 4.625%, 3/1/29(a) | 105,000 | 92,870 | ||||||

| 367,173 | ||||||||

Food & Drug Retailers: 1.1% | ||||||||

Rite Aid Corp., 8.000%, 11/15/26(a) | 100,000 | 81,500 | ||||||

SEG Holding LLC, 5.625%, 10/15/28(a) | 120,000 | 108,487 | ||||||

| 189,987 | ||||||||

Forestry/Paper: 0.4% | ||||||||

Mercer International, Inc., 5.125%, 2/1/29 | 90,000 | 78,575 | ||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

23

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

PENN CAPITAL OPPORTUNISTIC HIGH INCOME FUND

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022

Principal | Value | |||||||

Gaming: 2.2% | ||||||||

Affinity Gaming, 6.875%, 12/15/27(a) | $ | 65,000 | $ | 56,445 | ||||

Boyd Gaming Corp., 4.750%, 12/1/27 | 140,000 | 130,686 | ||||||

CCM Merger, Inc., 6.375%, 5/1/26(a) | 65,000 | 61,085 | ||||||

Scientific Games Holdings LP/Scientific Games US FinCo, Inc., 6.625%, 3/1/30(a) | 100,000 | 88,930 | ||||||

Station Casinos LLC, 4.625%, 12/1/31(a) | 80,000 | 66,841 | ||||||

| 403,987 | ||||||||

Gas Distribution: 5.1% | ||||||||

Antero Midstream Partners LP, 5.375%, 6/15/29(a) | 95,000 | 87,106 | ||||||

Blue Racer Midstream LLC, 6.625%, 7/15/26(a) | 40,000 | 37,864 | ||||||

Blue Racer Midstream LLC, 7.625%, 12/15/25(a) | 40,000 | 39,800 | ||||||

Cheniere Energy, Inc., 4.625%, 10/15/28 | 95,000 | 91,538 | ||||||

Crestwood Midstream Partners LP, 6.000%, 2/1/29(a) | 90,000 | 83,138 | ||||||

DCP Midstream Operating LP, 5.125%, 5/15/29 | 95,000 | 92,597 | ||||||

EnLink Midstream Partners LP, 5.050%, 4/1/45 | 125,000 | 90,055 | ||||||

EnLink Midstream LLC, 6.500%, 9/1/30(a) | 55,000 | 54,725 | ||||||

EQM Midstream Partners LP, 7.500%, 6/1/27(a) | 95,000 | 93,940 | ||||||

New Fortress Energy, Inc., 6.750%, 9/15/25(a) | 125,000 | 120,919 | ||||||

New Fortress Energy, Inc., 6.500%, 9/30/26(a) | 60,000 | 56,841 | ||||||

Solaris Midstream Holdings LLC, 7.625%, 4/1/26(a) | 77,000 | 75,172 | ||||||

| 923,695 | ||||||||

Health Facilities: 2.8% | ||||||||

CHS/Community Health Systems, Inc., 6.875%, 4/1/28(a) | 165,000 | 85,962 | ||||||

CHS/Community Health Systems, Inc., 6.000%, 1/15/29(a) | 105,000 | 86,180 | ||||||

Option Care Health, Inc., 4.375%, 10/31/29(a) | 85,000 | 74,755 | ||||||

Surgery Center Holdings, Inc., 6.750%, 7/1/25(a) | 65,000 | 62,712 | ||||||

Tenet Healthcare Corp., 6.125%, 10/1/28(a) | 65,000 | 59,637 | ||||||

Principal | Value | |||||||

Tenet Healthcare Corp., 4.375%, 1/15/30(a) | $ | 100,000 | $ | 87,500 | ||||

Tenet Healthcare Corp., 6.125%, 6/15/30(a) | 40,000 | 38,404 | ||||||

| 495,150 | ||||||||

Health Services: 1.8% | ||||||||

DaVita, Inc., 4.625%, 6/1/30(a) | 165,000 | 132,831 | ||||||

Modivcare, Inc., 5.875%, 11/15/25(a) | 110,000 | 103,429 | ||||||

Pediatrix Medical Group, Inc., 5.375%, 2/15/30(a) | 100,000 | 85,247 | ||||||

| 321,507 | ||||||||

Hotels: 0.6% | ||||||||

Hilton Grand Vacations LLC, 5.000%, 6/1/29(a) | 75,000 | 66,361 | ||||||

Hilton Grand Vacations LLC, 4.875%, 7/1/31(a) | 45,000 | 37,148 | ||||||

| 103,509 | ||||||||

Investments & Miscellaneous Financial Services: 0.6% | ||||||||

Icahn Enterprises LP, 5.250%, 5/15/27 | 65,000 | 59,134 | ||||||

Icahn Enterprises LP, 4.375%, 2/1/29 | 55,000 | 46,779 | ||||||

| 105,913 | ||||||||

Machinery: 1.0% | ||||||||

Titan International, Inc., 7.000%, 4/30/28 | 190,000 | 180,500 | ||||||

Managed Care: 1.2% | ||||||||

Centene Corp., 4.625%, 12/15/29 | 230,000 | 216,669 | ||||||

Media - Diversified: 1.0% | ||||||||

News Corp., 3.875%, 5/15/29(a) | 135,000 | 117,450 | ||||||

Urban One, Inc., 7.375%, 2/1/28(a) | 70,000 | 62,825 | ||||||

| 180,275 | ||||||||

Media Content: 2.8% | ||||||||

Beasley Mezzanine Holdings LLC, 8.625%, 2/1/26(a) | 105,000 | 81,900 | ||||||

Cumulus Media New Holdings, Inc., 6.750%, 7/1/26(a) | 96,000 | 85,872 | ||||||

Gray Television, Inc., 4.750%, 10/15/30(a) | 115,000 | 94,760 | ||||||

Scripps Escrow II, Inc., 5.375%, 1/15/31(a) | 125,000 | 103,437 | ||||||

Scripps Escrow, Inc., 5.875%, 7/15/27(a) | 50,000 | 45,249 | ||||||

Univision Communications, Inc., 6.625%, 6/1/27(a) | 90,000 | 86,852 | ||||||

| 498,070 | ||||||||

The Accompanying Footnotes are an Integral Part of these Financial Statements

24

THE RBB FUND TRUST (FORMERLY, PENN CAPITAL FUNDS TRUST)

PENN CAPITAL OPPORTUNISTIC HIGH INCOME FUND

SCHEDULE OF INVESTMENTS

AUGUST 31, 2022