Exhibit (C)(8)(C)

|

Independent Evaluation Report

Prepared for the Directors’ Committee of Enersis Américas S.A.

PRELIMINARY VERSION—DRAFT

June 28, 2016

Strictly Private and Confidential

1

|

PRELIMINARY VERSION—DRAFT

Important Information

This document has been prepared by Credicorp Capital Asesorías Financieras S.A. (hereinafter “Credicorp Capital”) at the request of the Directors’ Committee of Enersis Américas S.A. (“ENIA” or the “Company”) for purposes established in Article 147 of Law No. 18,046 on Corporations.

The recommendations and conclusions in this document constitute the best judgment or opinion of Credicorp Capital with respect to the Proposed Operation (as this term is defined below) of ENIA at the time this document is issued, considering the methods used to this end and the information that was available. The conclusions of this document could change if other data or additional information becomes available. Credicorp Capital will have no obligation whatsoever to give notice of such changes or of any modifications to the opinions or information contained in this document.

This document has been prepared by Credicorp Capital on the sole and exclusive basis of the information delivered by ENIA and public information, and Credicorp Capital has assumed that this information is fully complete and accurate without conducting any independent verification. As such, Credicorp Capital assumes no liability with regard to the information reviewed or for the conclusions that may derive from any error, inaccuracy, and/or falsehood in such information.

Likewise, the conclusions in this document may be based on assumptions that are subject to significant uncertainties and economic and market contingencies, such as flows, projections, estimates, and assessments, whose occurrence may be difficult to foresee and many of which may even be outside the control of ENIA, to the extent that there exists no certainty as to the actual fulfillment of these assumptions. Under no circumstance may the use or inclusion of such flows, projections, or estimates be

considered as a representation, guarantee, or prediction of Credicorp Capital with respect to their occurrence or to their underlying assumptions.

Strictly Private and Confidential 2

|

PRELIMINARY VERSION—DRAFT

Contents

1. Executive Summary and Conclusions

2. Background Info and Description of the Proposed Operation

3. General Considerations Used in the Report

4. Analysis of the Economic Terms of the Proposed Operation i. Methods Used for Valuation of ENIA, EOCA, and CHIA ii. Valuation of ENIA, EOCA, and CHIA iii. Estimate of the Exchange Ratios of the Proposed Operation iv. Analysis of the Economic Terms of the Proposed Operation

5. Market and Cash Flow Considerations of the Proposed Operation i. Holding Discount Considerations ii. Liquidity Considerations iii. Considerations on Risk Categorization iv. Impacts on EBITDA

6. Strategic and Management Considerations of the Proposed Operation

Strictly Private and Confidential 3

|

PRELIMINARY VERSION—DRAFT

EXECUTIVE SUMMARY AND CONCLUSIONS

Strictly Private and Confidential

4

|

PRELIMINARY VERSION—DRAFT

Background Info and Description of the Proposed Operation

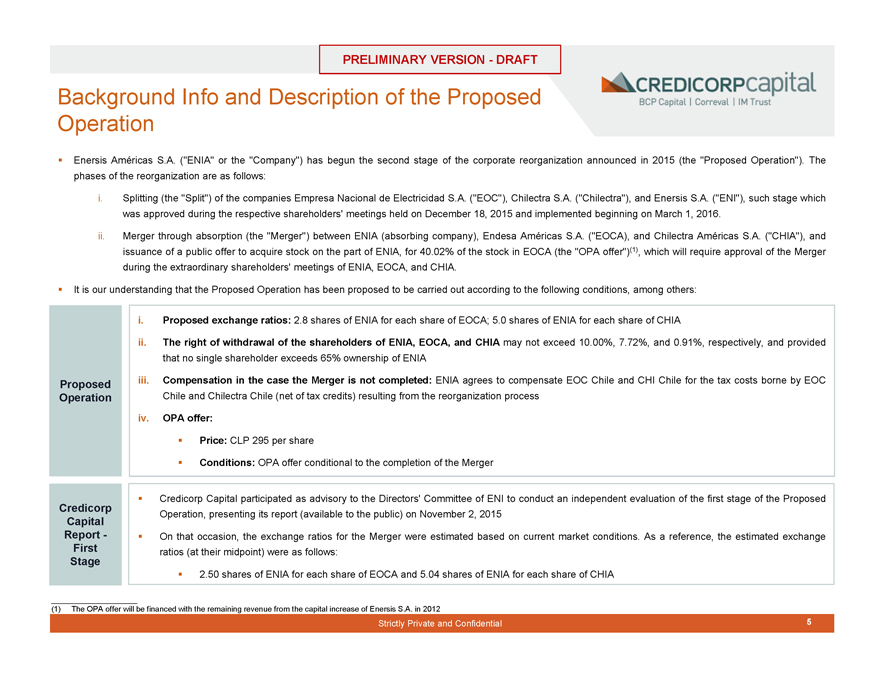

Enersis Américas S.A. (“ENIA” or the “Company”) has begun the second stage of the corporate reorganization announced in 2015 (the “Proposed Operation”). The phases of the reorganization are as follows:

i. Splitting (the “Split”) of the companies Empresa Nacional de Electricidad S.A. (“EOC”), Chilectra S.A. (“Chilectra”), and Enersis S.A. (“ENI”), such stage which was approved during the respective shareholders’ meetings held on December 18, 2015 and implemented beginning on March 1, 2016.

ii. Merger through absorption (the “Merger”) between ENIA (absorbing company), Endesa Américas S.A. (“EOCA), and Chilectra Américas S.A. (“CHIA”), and issuance of a public offer to acquire stock on the part of ENIA, for 40.02% of the stock in EOCA (the “OPA offer”)(1), which will require approval of the Merger during the extraordinary shareholders’ meetings of ENIA, EOCA, and CHIA.

It is our understanding that the Proposed Operation has been proposed to be carried out according to the following conditions, among others:

i. Proposed exchange ratios: 2.8 shares of ENIA for each share of EOCA; 5.0 shares of ENIA for each share of CHIA

ii. The right of withdrawal of the shareholders of ENIA, EOCA, and CHIA may not exceed 10.00%, 7.72%, and 0.91%, respectively, and provided that no single shareholder exceeds 65% ownership of ENIA

iii. Compensation in the case the Merger is not completed: ENIA agrees to compensate EOC Chile and CHI Chile for the tax costs borne by EOC Operation Chile and Chilectra Chile (net of tax credits) resulting from the reorganization process iv. OPA offer:

Price: CLP 295 per share

Conditions: OPA offer conditional to the completion of the Merger

Credicorp Credicorp Capital participated as advisory to the Directors’ Committee of ENI to conduct an independent evaluation of the first stage of the Proposed Operation, presenting its report (available to the public) on November 2, 2015

Capital

Report—On that occasion, the exchange ratios for the Merger were estimated based on current market conditions. As a reference, the estimated exchange First ratios (at their midpoint) were as follows:

Stage

2.50 shares of ENIA for each share of EOCA and 5.04 shares of ENIA for each share of CHIA

(1) The OPA offer will be financed with the remaining revenue from the capital increase of Enersis S.A. in 2012

Strictly Private and Confidential

Credicorp

Capital

Report -

First

Stage

Proposed

Operation

5

|

PRELIMINARY VERSION—DRAFT

Scope of the Independent Evaluation

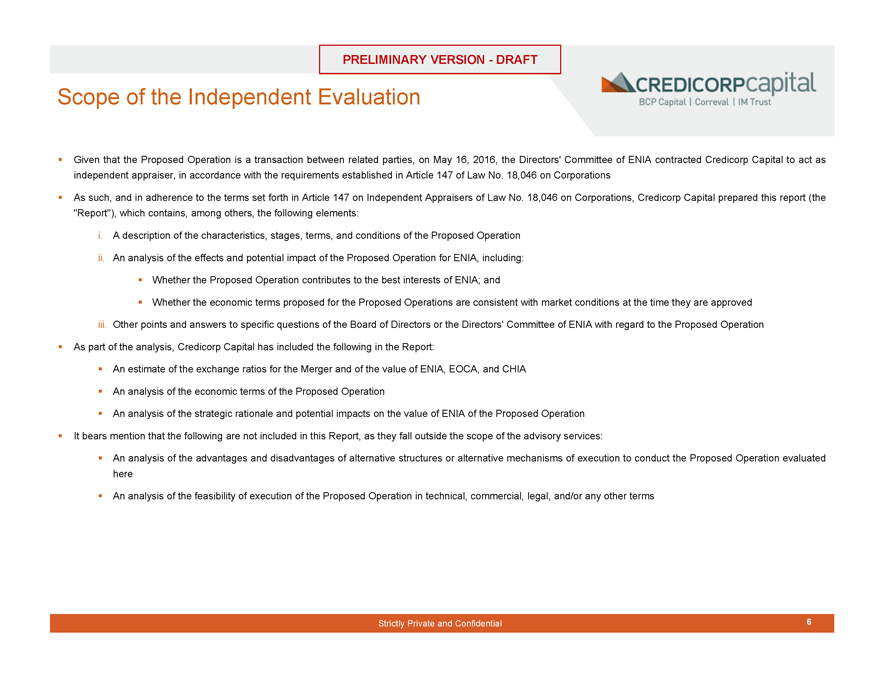

Given that the Proposed Operation is a transaction between related parties, on May 16, 2016, the Directors’ Committee of ENIA contracted Credicorp Capital to act as independent appraiser, in accordance with the requirements established in Article 147 of Law No. 18,046 on Corporations

As such, and in adherence to the terms set forth in Article 147 on Independent Appraisers of Law No. 18,046 on Corporations, Credicorp Capital prepared this report (the “Report”), which contains, among others, the following elements:

i. A description of the characteristics, stages, terms, and conditions of the Proposed Operation ii. An analysis of the effects and potential impact of the Proposed Operation for ENIA, including: Whether the Proposed Operation contributes to the best interests of ENIA; and

Whether the economic terms proposed for the Proposed Operations are consistent with market conditions at the time they are approved iii. Other points and answers to specific questions of the Board of Directors or the Directors’ Committee of ENIA with regard to the Proposed Operation As part of the analysis, Credicorp Capital has included the following in the Report: An estimate of the exchange ratios for the Merger and of the value of ENIA, EOCA, and CHIA

An analysis of the economic terms of the Proposed Operation

An analysis of the strategic rationale and potential impacts on the value of ENIA of the Proposed Operation

It bears mention that the following are not included in this Report, as they fall outside the scope of the advisory services:

An analysis of the advantages and disadvantages of alternative structures or alternative mechanisms of execution to conduct the Proposed Operation evaluated here

An analysis of the feasibility of execution of the Proposed Operation in technical, commercial, legal, and/or any other terms

Strictly Private and Confidential 6

|

PRELIMINARY VERSION—DRAFT

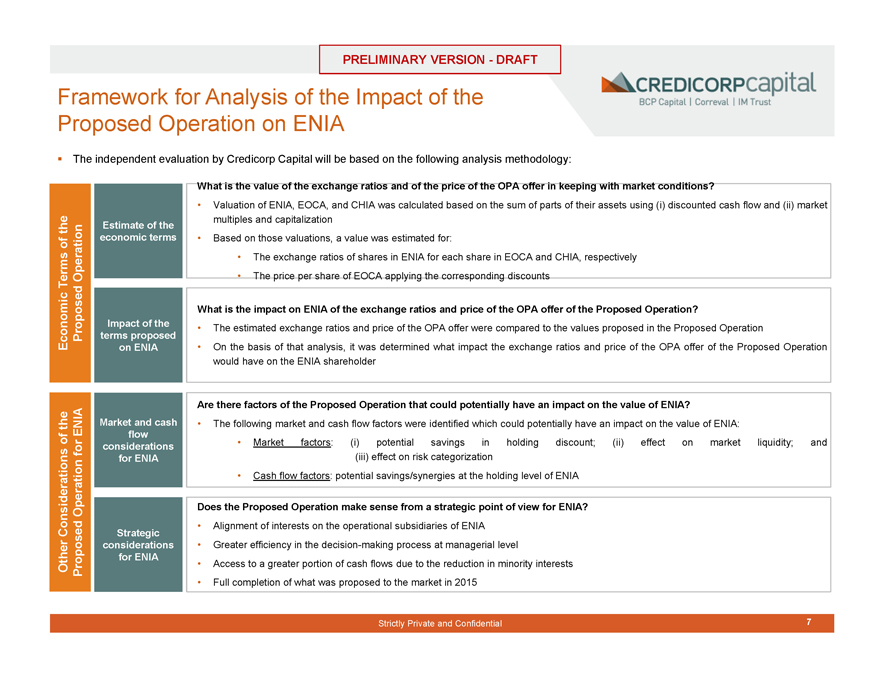

Framework for Analysis of the Impact of the Proposed Operation on ENIA

The independent evaluation by Credicorp Capital will be based on the following analysis methodology:

What is the value of the exchange ratios and of the price of the OPA offer in keeping with market conditions

• Valuation of ENIA, EOCA, and CHIA was calculated based on the sum of parts of their assets using (i) discounted cash flow and (ii) market multiples and capitalization

• Based on those valuations, a value was estimated for:

• The exchange ratios of shares in ENIA for each share in EOCA and CHIA, respectively

• The price per share of EOCA applying the corresponding discounts

What is the impact on ENIA of the exchange ratios and price of the OPA offer of the Proposed Operation

• The estimated exchange ratios and price of the OPA offer were compared to the values proposed in the Proposed Operation

• On the basis of that analysis, it was determined what impact the exchange ratios and price of the OPA offer of the Proposed Operation would have on the ENIA shareholder

Are there factors of the Proposed Operation that could potentially have an impact on the value of ENIA

• The following market and cash flow factors were identified which could potentially have an impact on the value of ENIA:

• Market factors: (i) potential savings in holding discount; (ii) effect on market liquidity; and (iii) effect on risk categorization

• Cash flow factors: potential savings/synergies at the holding level of ENIA

Does the Proposed Operation make sense from a strategic point of view for ENIA

• Alignment of interests on the operational subsidiaries of ENIA

• Greater efficiency in the decision-making process at managerial level

• Access to a greater portion of cash flows due to the reduction in minority interests

• Full completion of what was proposed to the market in 2015

Strictly Private and Confidential

Economic Terms of the Proposed Operation

Other Considerations of the Proposed Operation for ENIA

Estimate of the economic terms

Impact of the terms proposed on ENIA

Market and cash flow considerations for ENIA

Strategic considerations for ENIA

7

|

PRELIMINARY VERSION—DRAFT

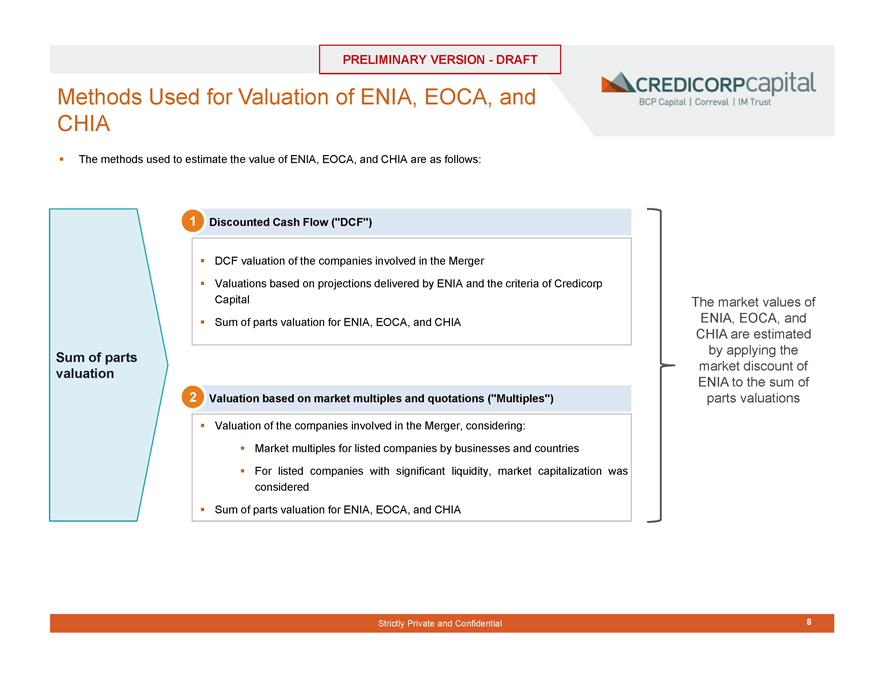

Methods Used for Valuation of ENIA, EOCA, and CHIA

Sum of parts valuation

The methods used to estimate the value of ENIA, EOCA, and CHIA are as follows:

1 Discounted Cash Flow (“DCF”)

DCF valuation of the companies involved in the Merger

Valuations based on projections delivered by ENIA and the criteria of Credicorp Capital Sum of parts valuation for ENIA, EOCA, and CHIA

2 Valuation based on market multiples and quotations (“Multiples”)

Valuation of the companies involved in the Merger, considering:

Market multiples for listed companies by businesses and countries

For listed companies with significant liquidity, market capitalization was considered Sum of parts valuation for ENIA, EOCA, and CHIA

The market values of ENIA, EOCA, and CHIA are estimated by applying the market discount of ENIA to the sum of parts valuations

Strictly Private and Confidential 8

|

PRELIMINARY VERSION—DRAFT

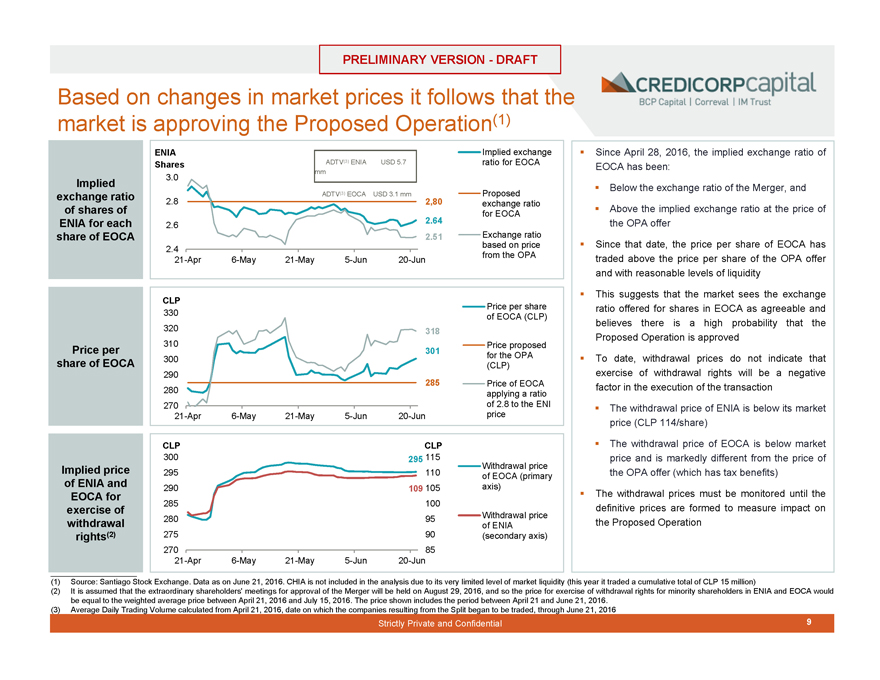

Based on changes in market prices it follows that the market is approving the Proposed Operation(1)

Implied exchange ratio of shares of ENIA for each share of EOCA

Price per share of EOCA

Implied price of ENIA and EOCA for exercise of withdrawal rights(2)

Since April 28, 2016, the implied exchange ratio of EOCA has been:

Below the exchange ratio of the Merger, and

Above the implied exchange ratio at the price of the OPA offer

Since that date, the price per share of EOCA has traded above the price per share of the OPA offer and with reasonable levels of liquidity

This suggests that the market sees the exchange ratio offered for shares in EOCA as agreeable and believes there is a high probability that the Proposed Operation is approved

To date, withdrawal prices do not indicate that exercise of withdrawal rights will be a negative factor in the execution of the transaction

The withdrawal price of ENIA is below its market price (CLP 114/share)

The withdrawal price of EOCA is below market price and is markedly different from the price of the OPA offer (which has tax benefits)

The withdrawal prices must be monitored until the definitive prices are formed to measure impact on the Proposed Operation

(1) Source: Santiago Stock Exchange. Data as on June 21, 2016. CHIA is not included in the analysis due to its very limited level of market liquidity (this year it traded a cumulative total of CLP 15 million)

(2) It is assumed that the extraordinary shareholders’ meetings for approval of the Merger will be held on August 29, 2016, and so the price for exercise of withdrawal rights for minority shareholders in ENIA and EOCA would be equal to the weighted average price between April 21, 2016 and July 15, 2016. The price shown includes the period between April 21 and June 21, 2016.

(3) Average Daily Trading Volume calculated from April 21, 2016, date on which the companies resulting from the Split began to be traded, through June 21, 2016

ENIA Implied exchange

Shares ADTV(3) ENIAUSD 5.7ratio for EOCA

mm

3.0

ADTV(3) EOCAUSD 3.1 mmProposed

2.8 2,80exchange ratio

for EOCA

2.6 2.64

2.51Exchange ratio

2.4 based on price

21-Apr 6-May 21-May5-Jun20-Junfrom the OPA

CLP Price per share

330 of EOCA (CLP)

320 318

310 Price proposed

301

300 for the OPA

(CLP)

290

285Price of EOCA

280 applying a ratio

270 of 2.8 to the ENI

21-Apr 6-May 21-May5-Jun20-Junprice

CLP CLP

300 295 115

Withdrawal price

295 110of EOCA (primary

290 109 105axis)

285 100

280 95Withdrawal price

of ENIA

275 90(secondary axis)

270 85

21-Apr 6-May 21-May5-Jun20-Jun

Strictly Private and Confidential 9

|

PRELIMINARY VERSION—DRAFT

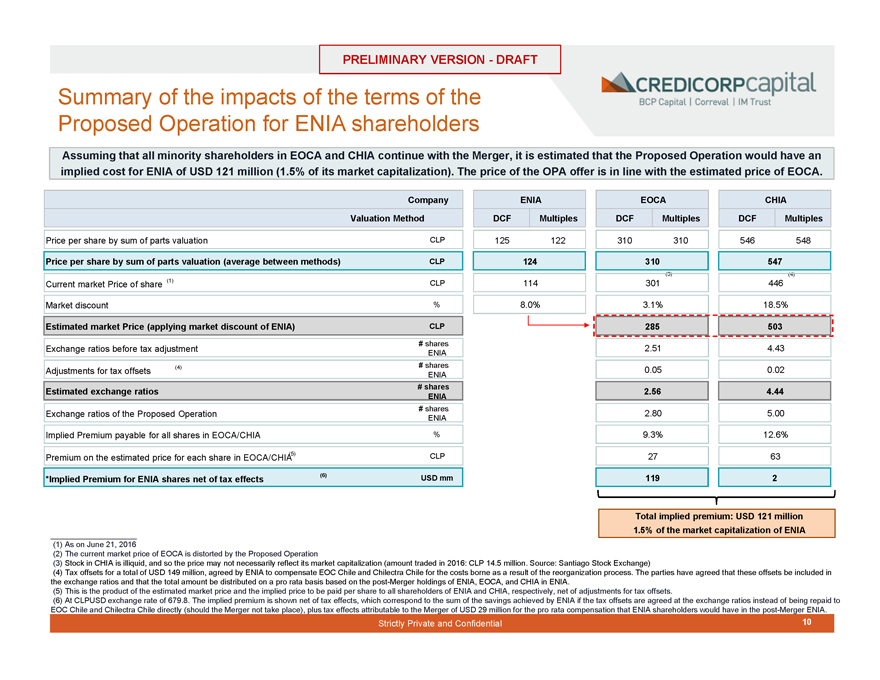

Summary of the impacts of the terms of the Proposed Operation for ENIA shareholders

Assuming that all minority shareholders in EOCA and CHIA continue with the Merger, it is estimated that the Proposed Operation would have an implied cost for ENIA of USD 121 million (1.5% of its market capitalization). The price of the OPA offer is in line with the estimated price of EOCA.

Company

Valuation Method

Price per share by sum of parts valuation CLP

Price per share by sum of parts valuation (average between methods) CLP

Current market Price of share (1) CLP

Market discount %

Estimated market Price (applying market discount of ENIA) CLP

# shares

Exchange ratios before tax adjustment ENIA

(4) # shares

Adjustments for tax offsets ENIA

Estimated exchange ratios # shares

ENIA

# shares

Exchange ratios of the Proposed Operation ENIA

Implied Premium payable for all shares in EOCA/CHIA %

Premium on the estimated price for each share in EOCA/CHIA(5) CLP

*Implied Premium for ENIA shares net of tax effects (6) USD mm

ENIA

DCF

Multiples

125

122

124

114

8.0%

EOCA

DCF

Multiples

310

310

310

(3)

301

3.1%

285

2.51

0.05

2.56

2.80

9.3%

27

CHIA119

DCF

Multiples

546

548

547

(4)

446

18.5%

503

4.43

0.02

4.44

5.00

12.6%

63

2

Total implied premium: USD 121 million 1.5% of the market capitalization of ENIA

(1) As on June 21, 2016

(2) The current market price of EOCA is distorted by the Proposed Operation

(3) Stock in CHIA is illiquid, and so the price may not necessarily reflect its market capitalization (amount traded in 2016: CLP 14.5 million. Source: Santiago Stock Exchange)

(4) Tax offsets for a total of USD 149 million, agreed by ENIA to compensate EOC Chile and Chilectra Chile for the costs borne as a result of the reorganization process. The parties have agreed that these offsets be included in the exchange ratios and that the total amount be distributed on a pro rata basis based on the post-Merger holdings of ENIA, EOCA, and CHIA in ENIA.

(5) This is the product of the estimated market price and the implied price to be paid per share to all shareholders of ENIA and CHIA, respectively, net of adjustments for tax offsets.

(6) At CLPUSD exchange rate of 679.8. The implied premium is shown net of tax effects, which correspond to the sum of the savings achieved by ENIA if the tax offsets are agreed at the exchange ratios instead of being repaid to EOC Chile and Chilectra Chile directly (should the Merger not take place), plus tax effects attributable to the Merger of USD 29 million for the pro rata compensation that ENIA shareholders would have in the post-Merger ENIA.

Strictly Private and Confidential 10

|

PRELIMINARY VERSION—DRAFT

Potential market and cash flow benefits for ENIA resulting from the Proposed Operation (1/2)

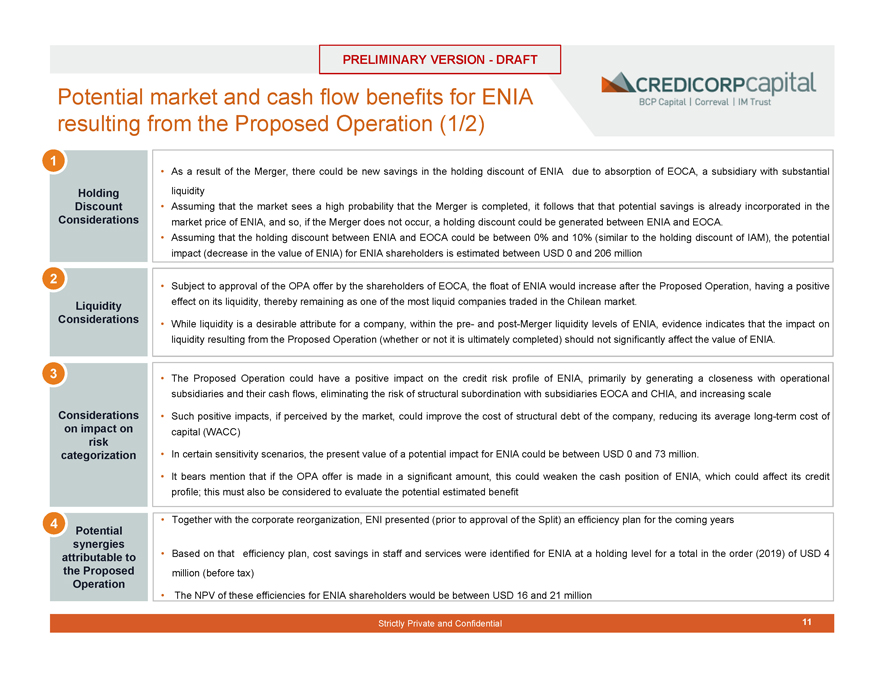

• As a result of the Merger, there could be new savings in the holding discount of ENIA due to absorption of EOCA, a subsidiary with substantial liquidity

• Assuming that the market sees a high probability that the Merger is completed, it follows that that potential savings is already incorporated in the market price of ENIA, and so, if the Merger does not occur, a holding discount could be generated between ENIA and EOCA.

• Assuming that the holding discount between ENIA and EOCA could be between 0% and 10% (similar to the holding discount of IAM), the potential impact (decrease in the value of ENIA) for ENIA shareholders is estimated between USD 0 and 206 million

• Subject to approval of the OPA offer by the shareholders of EOCA, the float of ENIA would increase after the Proposed Operation, having a positive effect on its liquidity, thereby remaining as one of the most liquid companies traded in the Chilean market.

• While liquidity is a desirable attribute for a company, within the pre- and post-Merger liquidity levels of ENIA, evidence indicates that the impact on liquidity resulting from the Proposed Operation (whether or not it is ultimately completed) should not significantly affect the value of ENIA.

• The Proposed Operation could have a positive impact on the credit risk profile of ENIA, primarily by generating a closeness with operational subsidiaries and their cash flows, eliminating the risk of structural subordination with subsidiaries EOCA and CHIA, and increasing scale

• Such positive impacts, if perceived by the market, could improve the cost of structural debt of the company, reducing its average long-term cost of capital (WACC)

• In certain sensitivity scenarios, the present value of a potential impact for ENIA could be between USD 0 and 73 million.

• It bears mention that if the OPA offer is made in a significant amount, this could weaken the cash position of ENIA, which could affect its credit profile; this must also be considered to evaluate the potential estimated benefit

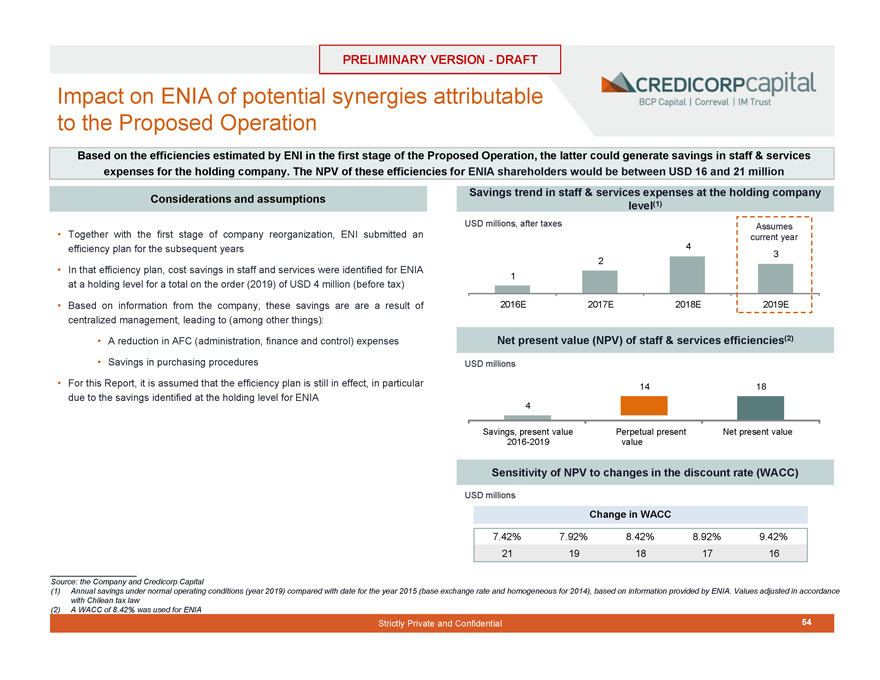

• Together with the corporate reorganization, ENI presented (prior to approval of the Split) an efficiency plan for the coming years

• Based on that efficiency plan, cost savings in staff and services were identified for ENIA at a holding level for a total in the order (2019) of USD 4 million (before tax)

• The NPV of these efficiencies for ENIA shareholders would be between USD 16 and 21 million

1

Holding Discount • Considerations

•

2

•

Liquidity Considerations •

3 •

Considerations • on impact on risk categorization •

•

4

Potential synergies attributable to the Proposed Operation

Strictly Private and Confidential 11

|

PRELIMINARY VERSION—DRAFT

Potential market and cash flow benefits for ENIA resulting from the Proposed Operation (2/2)

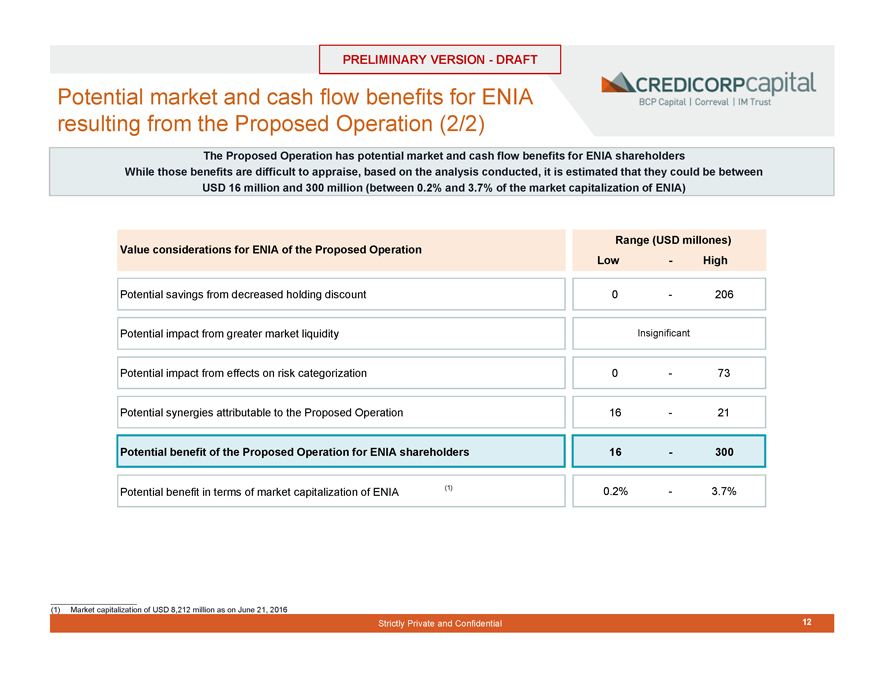

The Proposed Operation has potential market and cash flow benefits for ENIA shareholders

While those benefits are difficult to appraise, based on the analysis conducted, it is estimated that they could be between USD 16 million and 300 million (between 0.2% and 3.7% of the market capitalization of ENIA)

Range (USD millones)

Value considerations for ENIA of the Proposed Operation

Low-High

Potential savings from decreased holding discount 0-206

Potential impact from greater market liquidity Insignificant

Potential impact from effects on risk categorization 0-73

Potential synergies attributable to the Proposed Operation 16-21

Potential benefit of the Proposed Operation for ENIA shareholders 16 -300

Potential benefit in terms of market capitalization of ENIA (1) 0.2%-3.7%

(1) Market capitalization of USD 8,212 million as on June 21, 2016

Strictly Private and Confidential 12

|

PRELIMINARY VERSION—DRAFT

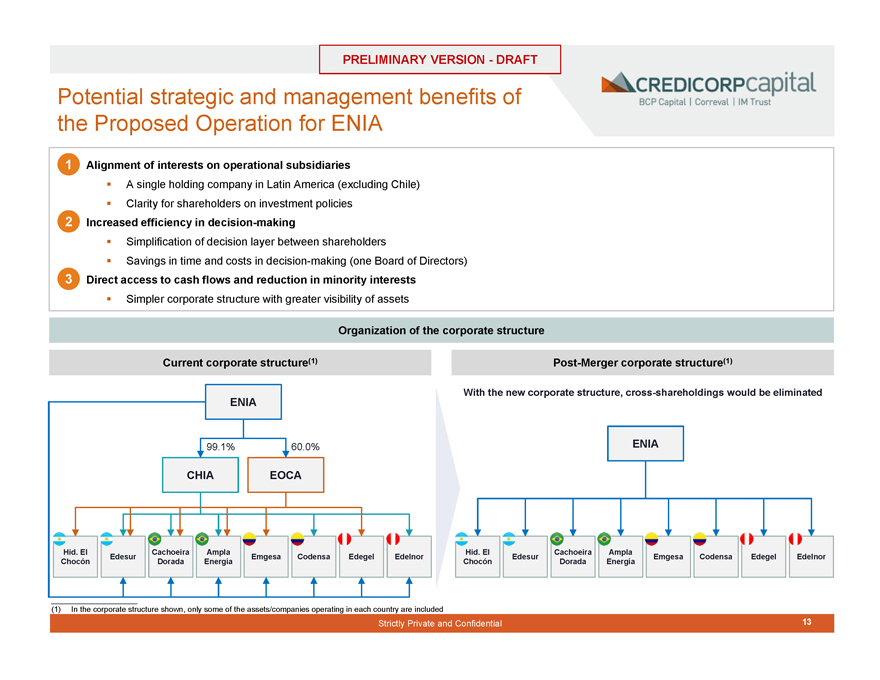

Potential strategic and management benefits of the Proposed Operation for ENIA

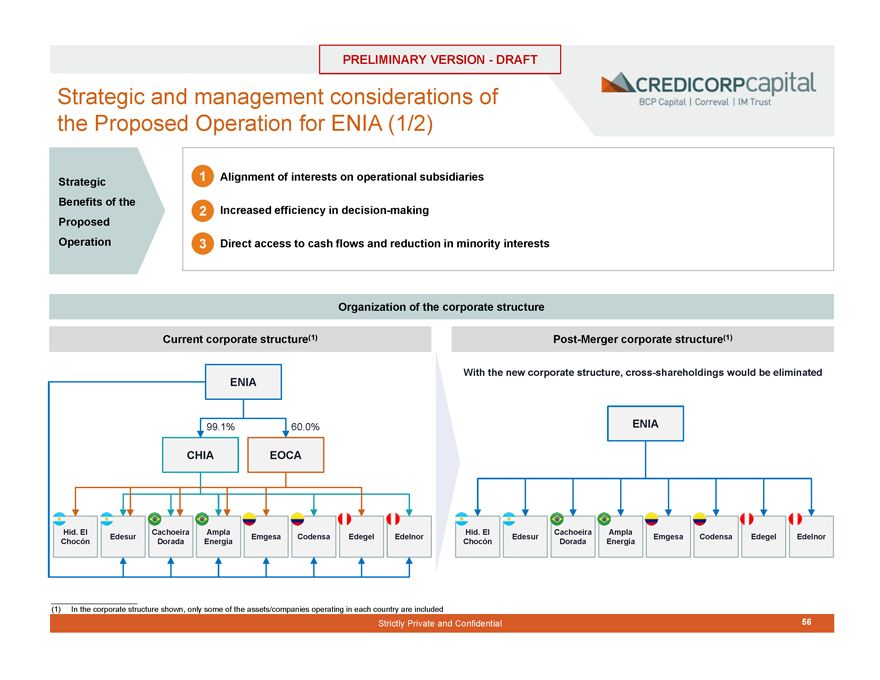

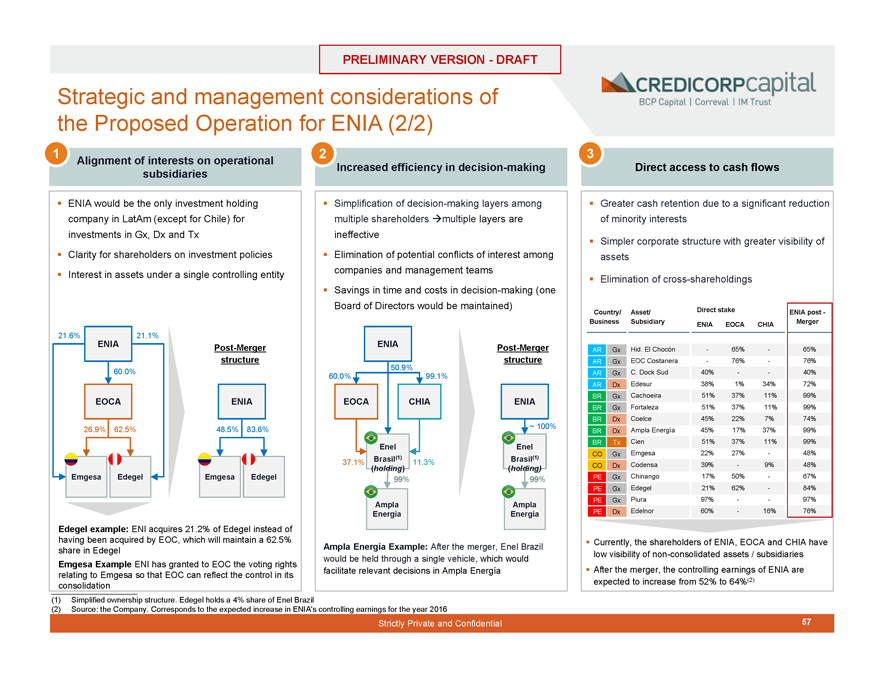

1. Alignment of interests on operational subsidiaries

A single holding company in Latin America (excluding Chile) Clarity for shareholders on investment policies

2. Increased efficiency in decision-making

Simplification of decision layer between shareholders

Savings in time and costs in decision-making (one Board of Directors)

3. Direct access to cash flows and reduction in minority interests

Simpler corporate structure with greater visibility of assets

Organization of the corporate structure

Current corporate structure(1) Post-Merger corporate structure(1)

With the new corporate structure, cross-shareholdings would be eliminated

ENIA

99.1% 60.0%

CHIA EOCA

ENIA

Hid. El Cachoeira Ampla

Edesur Emgesa Codensa Edegel Edelnor Chocón Dorada Energía

Hid. El Cachoeira Ampla

Edesur Emgesa Codensa Edegel Edelnor Chocón Dorada Energía

(1) In the corporate structure shown, only some of the assets/companies operating in each country are included

Strictly Private and Confidential 13

|

PRELIMINARY VERSION—DRAFT

Conclusions

The proposed exchange ratio considers an implied premium for minority shareholders of EOC and CHIA equal to 1.5% of the market capitalization of ENIA

This is derived from exchange ratios (at the midpoint of our estimates) of 2.56 shares of ENIA for each share of EOCA, and 4.44 shares of ENIA for each share of CHIA

With respect to the situation at the time the terms of the Proposed Operation were approved (December 2015), according to our estimates using equivalent methods, that premium has declined

The Proposed Operation has the potential to generate earnings for ENIA that should more than make up for the implied premium deriving from the exchange ratios proposed for the Merger

From a market and cash flow point of view, the benefits include (i) synergies in administration expenses and services, (ii) potential savings in holding discounts, and (iii) potential impacts on risk categorization

From a strategic and management point of view, the Proposed Operation would bring about elimination of cross-shareholdings between the holding companies, allowing (i) alignment of interests over operational subsidiaries, (ii) greater efficiency in costs and times for decision-making, and (iii) direct access to cash flows and a reduction in minority interests at ENIA

With respect to EOCA stock acquired through the OPA offer, our conclusion is that the price offered is in line with the price per share in EOCA that should prevail in the market in the absence of the distortions caused by the Proposed Operation

On the other hand, the market and investors are validating the terms of the Proposed Operation, given that the prices have been fluctuating in ranges that would so indicate and with reasonable levels of liquidity

The exchange ratio of shares in ENIA to shares in EOCA has traded above the implied exchange ratio at the price of the OPA offer and below the exchange ratio offered

Stock in EOCA has traded above the price of the OPA offer

Based on this, we conclude that the Proposed Operation is consistent with market conditions and contributes to the best interests of ENIA

Strictly Private and Confidential 14

|

PRELIMINARY VERSION—DRAFT

BACKGROUND INFO AND DESCRIPTION OF THE PROPOSED OPERATION

Strictly Private and Confidential 15

|

PRELIMINARY VERSION—DRAFT

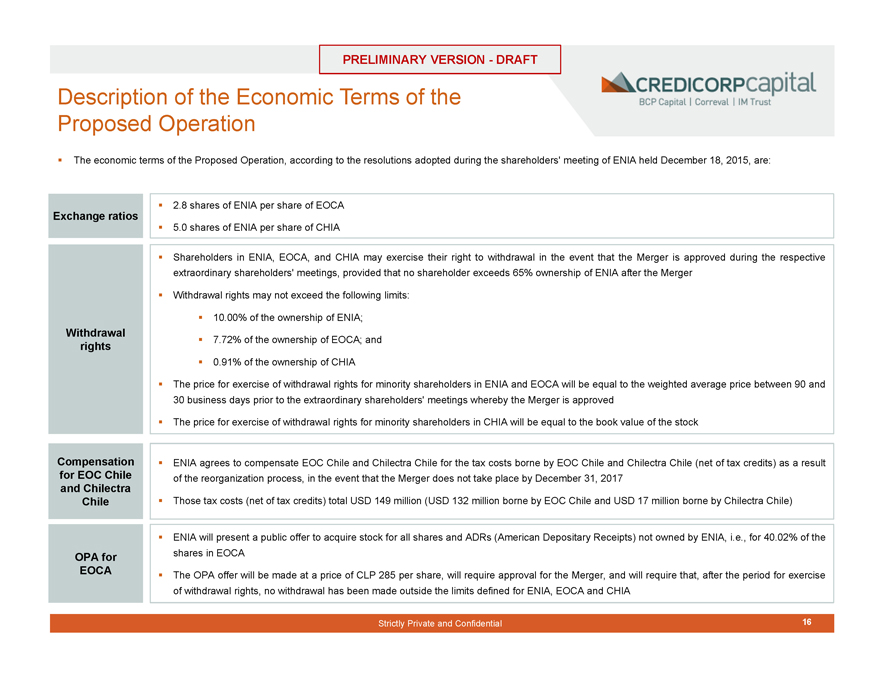

Description of the Economic Terms of the Proposed Operation

The economic terms of the Proposed Operation, according to the resolutions adopted during the shareholders’ meeting of ENIA held December 18, 2015, are:

Exchange ratios

Withdrawal rights

Compensation for EOC Chile and Chilectra Chile

OPA for EOCA

2.8 shares of ENIA per share of EOCA

5.0 shares of ENIA per share of CHIA

Shareholders in ENIA, EOCA, and CHIA may exercise their right to withdrawal in the event that the Merger is approved during the respective extraordinary shareholders’ meetings, provided that no shareholder exceeds 65% ownership of ENIA after the Merger

Withdrawal rights may not exceed the following limits:

10.00% of the ownership of ENIA;

7.72% of the ownership of EOCA; and

0.91% of the ownership of CHIA

The price for exercise of withdrawal rights for minority shareholders in ENIA and EOCA will be equal to the weighted average price between 90 and 30 business days prior to the extraordinary shareholders’ meetings whereby the Merger is approved

The price for exercise of withdrawal rights for minority shareholders in CHIA will be equal to the book value of the stock

ENIA agrees to compensate EOC Chile and Chilectra Chile for the tax costs borne by EOC Chile and Chilectra Chile (net of tax credits) as a result of the reorganization process, in the event that the Merger does not take place by December 31, 2017

Those tax costs (net of tax credits) total USD 149 million (USD 132 million borne by EOC Chile and USD 17 million borne by Chilectra Chile)

ENIA will present a public offer to acquire stock for all shares and ADRs (American Depositary Receipts) not owned by ENIA, i.e., for 40.02% of the shares in EOCA

The OPA offer will be made at a price of CLP 285 per share, will require approval for the Merger, and will require that, after the period for exercise of withdrawal rights, no withdrawal has been made outside the limits defined for ENIA, EOCA and CHIA

Strictly Private and Confidential 16

|

PRELIMINARY VERSION—DRAFT

Structure of the Proposed Operation

Splitting of ENI, EOC, and Chilectra

Enel SpA

100.0%

Enel Enel Iberoamérica Latinoamérica

2

60.6%

ENI Chile

60.6%

ENIA

99.1%

Chilectra Chile

60.0%

EOC Chile

1

99.1%

CHIA

60.0%

EOCA

1. Separation of the assets outside of Chile of Chilectra and EOC into new companies called Chilectra Américas S.A. (CHIA) and Endesa Américas S.A. (EOCA), respectively 2. Splitting of the Chilean assets of ENI into a new company to be called Enersis Chile S.A. (“ENI Chile”)

New companies resulting from the Merger

Merger of EOCA and CHIA into ENIA

Enel SpA

100.0%

Enel Enel Iberoamérica Latinoamérica

60.6%

ENI Chile

99.1%

Chilectra Chile

60.0%

EOC Chile

> 50.0%

ENIA

CHIA EOCA

Merger through absorption

Merger through absorption on the part of ENIA of the companies CHIA and EOCA

The definitive exchange ratios for the Merger must be approved during the respective shareholders’ meetings of ENIA, EOCA, and CHIA

Second stage of the corporate reorganization underway

Strictly Private and Confidential 17

|

PRELIMINARY VERSION—DRAFT

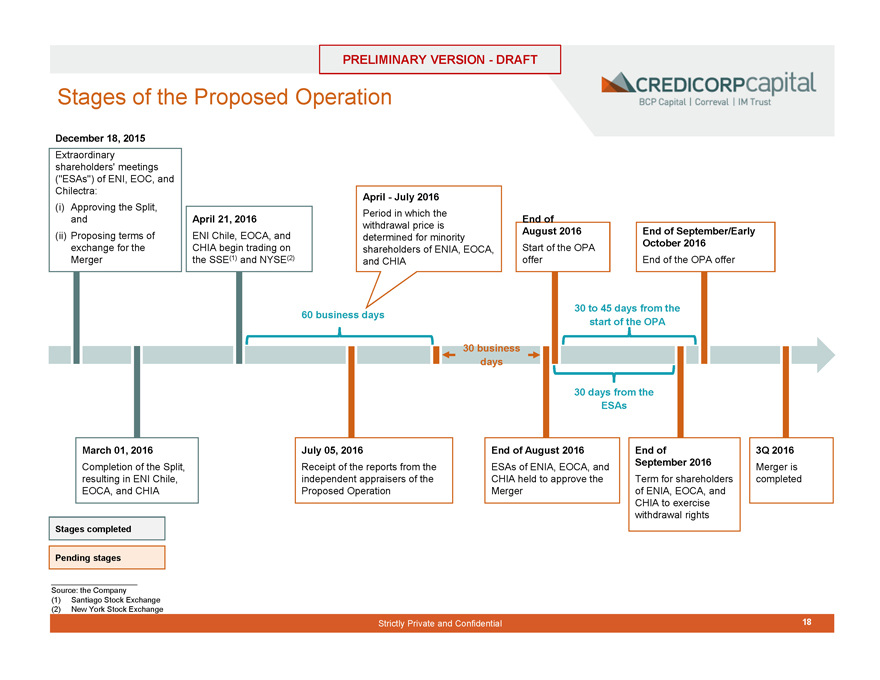

Stages of the Proposed Operation

December 18, 2015

Extraordinary shareholders’ meetings (“ESAs”) of ENI, EOC, and Chilectra: (i) Approving the Split, and (ii) Proposing terms of exchange for the Merger

April 21, 2016

ENI Chile, EOCA, and CHIA begin trading on the SSE(1) and NYSE(2)

April—July 2016

Period in which the withdrawal price is determined for minority shareholders of ENIA, EOCA, and CHIA

End of August 2016

Start of the OPA offer

End of September/Early October 2016

End of the OPA offer

60 business days

30 to 45 days from the start of the OPA

30 business days

30 days from the ESAs

March 01, 2016

Completion of the Split, resulting in ENI Chile, EOCA, and CHIA

July 05, 2016

Receipt of the reports from the independent appraisers of the Proposed Operation

End of August 2016

ESAs of ENIA, EOCA, and CHIA held to approve the Merger

End of

September 2016

Term for shareholders of ENIA, EOCA, and CHIA to exercise withdrawal rights

3Q 2016

Merger is completed

Stages completed

Pending stages

Source: the Company (1) Santiago Stock Exchange (2) New York Stock Exchange

Strictly Private and Confidential 18

|

DRAFT

Strictly Private and Confidential

19

|

PRELIMINARY VERSION—DRAFT

GENERAL CONSIDERATIONS USED IN THE REPORT

Strictly Private and Confidential 20

|

PRELIMINARY VERSION—DRAFT

Information Used

1. The Company launched a virtual data room through which it delivered:

Presentations made to the Board of Directors by the administration of ENIA with regard to the Proposed Operation

Presentations made by the administration of ENIA with regard to the operations it maintains through its subsidiaries in the various markets Historical financial information for the periods March 2016 and May 2016 for each of the companies involved in the Proposed Operation Projected financial information for the 2016-2020 period for each of the companies involved in the Merger, such information which:

• Was updated in June 2016 based on the business plans of each asset and the market conditions in the respective countries

• Was sent to Credicorp Capital on Thursday, June 9, 2016

• Is the same information delivered to the various independent appraisers of ENIA, EOCA, and CHIA as part of the Proposed Operation

• Was approved by the administration of the Company and is known to the Board of Directors of ENIA

Information and estimates on the impacts of the Proposed Operation

2. Meetings with the administration and technical teams of ENIA Work meetings were held with the administration of the Company

Credicorp Capital asked questions of ENIA, which were answered through the virtual data room, together with other questions posed by other ENIA advisors as part of the evaluation process

3. Public information available in the market: financial and market information services, analysts’ reports, etc.

It bears mention that:

ENIA, EOCA, and CHIA are companies publicly traded on the Santiago Stock Exchange (SSE), and additionally, ENIA and EOCA are listed on the New York Stock Exchange (NYSE), and as such, these companies are subject to oversight by domestic and international regulatory entities, including the SVS, the Securities and Exchange Commission (SEC), and other local regulatory bodies in the countries where they operate

The analysis conducted by Credicorp Capital did not include due diligence of ENIA, EOCA, CHIA or any other companies involved in the Proposed Operation. With regard to accounting, legal, tax, and regulatory issues, the Company was asked to provide its best estimate, opinion, or projections with regard to the impacts of the Merger.

These estimates, opinions, and projections have not been independently verified by experts other than those which appeared at the Company to receive initial response, and have not been independently verified by Credicorp Capital

Strictly Private and Confidential 21

|

PRELIMINARY VERSION—DRAFT

General Considerations Used in the Report

According to the information made available by ENIA and the opinions contained in the responses provided by the Company to Credicorp Capital, we have made the following assumptions regarding the Proposed Operation:

That it is permitted under Chilean law and in the rest of the countries where ENIA, EOCA, and CHIA operate (Brazil, Colombia, Peru, and Argentina) and that it does not violate any rules in any jurisdiction applicable to ENIA, EOCA, and CHIA

That it does not generate any adverse regulatory, environmental, or competitive effects for ENIA, EOCA, and/or CHIA, their subsidiaries, and/or any other companies remaining after and/or arising from the Proposed Operation

That it does not affect or violate agreements with partners, providers, customers, or any other counterpart of ENIA, EOCA, and/or CHIA, their subsidiaries, and/or any other companies remaining after and/or arising from the Proposed Operation

That it does not involve accounting or tax effects that could have a negative impact on the earnings of ENIA, EOCA, and/or CHIA, their subsidiaries, and/or any other companies remaining after and/or arising from the Proposed Operation, beyond those considered in this Report on the basis of the information provided by the Company

That it does not generate new contingencies for ENIA, EOCA, and/or CHIA, their subsidiaries, and/or any other companies remaining after and/or arising from the Proposed Operation

That it does not affect or violate the agreements of any lending or credit contracts of ENIA, EOCA, CHIA, and/or their subsidiaries that result in material effects on the earnings of any of those companies, including breach, cross-default or cross-acceleration, and/or increased financial costs.

That no liability management processes are incurred that imply material costs for ENIA, EOCA, and/or CHIA, their subsidiaries, and/or any other companies remaining after and/or arising from the Proposed Operation, which are not included in this Report on the basis of the information provided by the Company

That in the event the Proposed Operation is not carried out, the current situation of ENIA would be maintained, in terms of the consolidation, administration, and political and economic rights over the holdings involved in the Proposed Operation

Strictly Private and Confidential 22

|

ANALYSIS OF THE ECONOMIC TERMS OF THE PROPOSED OPERATION i. Methods Used for Valuation of ENIA, EOCA, and CHIA

PRELIMINARY VERSION—DRAFT

Strictly Private and Confidential 23

|

PRELIMINARY VERSION—DRAFT

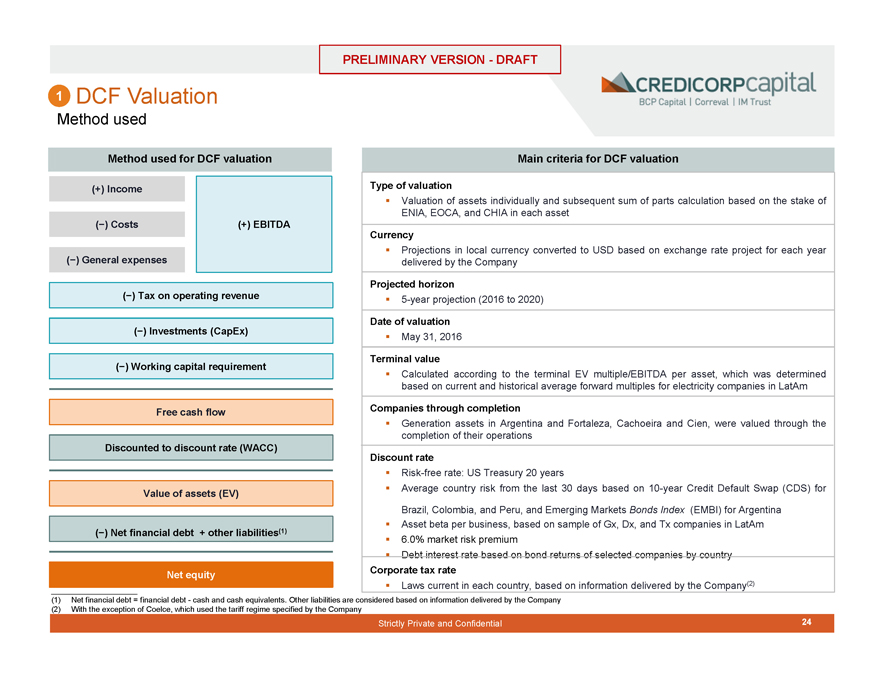

1 DCF Valuation

Method used

Method used for DCF valuation

(+) Income

(-) Costs (+) EBITDA (-) General expenses (-) Tax on operating revenue (-) Investments (CapEx) (-) Working capital requirement

Free cash flow

Discounted to discount rate (WACC)

Value of assets (EV)

(-) Net financial debt + other liabilities(1)

Net equity

Main criteria for DCF valuation

Type of valuation

Valuation of assets individually and subsequent sum of parts calculation based on the stake of ENIA, EOCA, and CHIA in each asset

Currency

Projections in local currency converted to USD based on exchange rate project for each year delivered by the Company

Projected horizon

5-year projection (2016 to 2020)

Date of valuation

May 31, 2016

Terminal value

Calculated according to the terminal EV multiple/EBITDA per asset, which was determined based on current and historical average forward multiples for electricity companies in LatAm

Companies through completion

Generation assets in Argentina and Fortaleza, Cachoeira and Cien, were valued through the completion of their operations

Discount rate

Risk-free rate: US Treasury 20 years

Average country risk from the last 30 days based on 10-year Credit Default Swap (CDS) for

Brazil, Colombia, and Peru, and Emerging Markets Bonds Index (EMBI) for Argentina Asset beta per business, based on sample of Gx, Dx, and Tx companies in LatAm 6.0% market risk premium

Debt interest rate based on bond returns of selected companies by country

Corporate tax rate

Laws current in each country, based on information delivered by the Company(2)

(1) Net financial debt = financial debt—cash and cash equivalents. Other liabilities are considered based on information delivered by the Company (2) With the exception of Coelce, which used the tariff regime specified by the Company

Strictly Private and Confidential 24

|

PRELIMINARY VERSION—DRAFT

PRELIMINARY VERSION—DRAFT

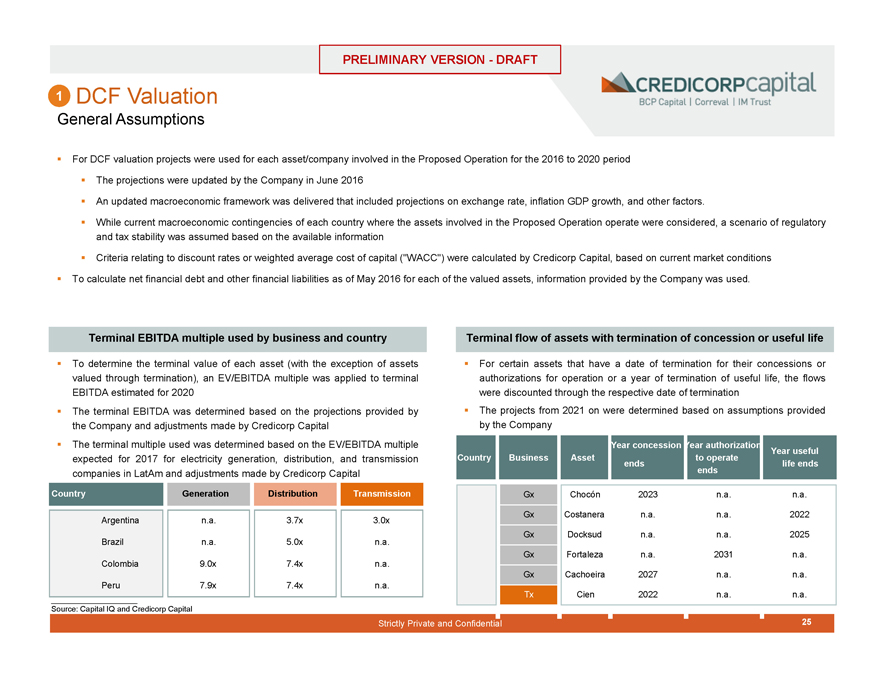

1 DCF Valuation

General Assumptions

For DCF valuation projects were used for each asset/company involved in the Proposed Operation for the 2016 to 2020 period

The projections were updated by the Company in June 2016

An updated macroeconomic framework was delivered that included projections on exchange rate, inflation GDP growth, and other factors.

While current macroeconomic contingencies of each country where the assets involved in the Proposed Operation operate were considered, a scenario of regulatory and tax stability was assumed based on the available information

Criteria relating to discount rates or weighted average cost of capital (“WACC”) were calculated by Credicorp Capital, based on current market conditions

To calculate net financial debt and other financial liabilities as of May 2016 for each of the valued assets, information provided by the Company was used.

Terminal EBITDA multiple used by business and country

To determine the terminal value of each asset (with the exception of assets valued through termination), an EV/EBITDA multiple was applied to terminal EBITDA estimated for 2020 The terminal EBITDA was determined based on the projections provided by the Company and adjustments made by Credicorp Capital The terminal multiple used was determined based on the EV/EBITDA multiple expected for 2017 for electricity generation, distribution, and transmission companies in LatAm and adjustments made by Credicorp Capital

Terminal flow of assets with termination of concession or useful life

For certain assets that have a date of termination for their concessions or authorizations for operation or a year of termination of useful life, the flows were discounted through the respective date of termination The projects from 2021 on were determined based on assumptions provided by the Company

Year concession Year authorization

Country Generation Distribution Transmission

Argentina n.a. 3.7x 3.0x Brazil n.a. 5.0x n.a. Colombia 9.0x 7.4x n.a.

Peru 7.9x 7.4x n.a.

Country GenerationDistributionTransmission

Argentina n.a.3.7x3.0x

Brazil n.a.5.0xn.a.

Colombia 9.0x7.4xn.a.

Peru 7.9x7.4xn.a.

Year concession Year authorizationYear useful

Country Business Assetto operate

endslife ends

ends

Gx Chocón2023n.a.n.a.

Gx Costaneran.a.n.a.2022

Gx Docksudn.a.n.a.2025

Gx Fortalezan.a.2031n.a.

Gx Cachoeira2027n.a.n.a.

Tx Cien2022n.a.n.a.

Source: Capital IQ and Credicorp Capital

Strictly Private and Confidential 25

|

PRELIMINARY VERSION—DRAFT

1 DCF Valuation

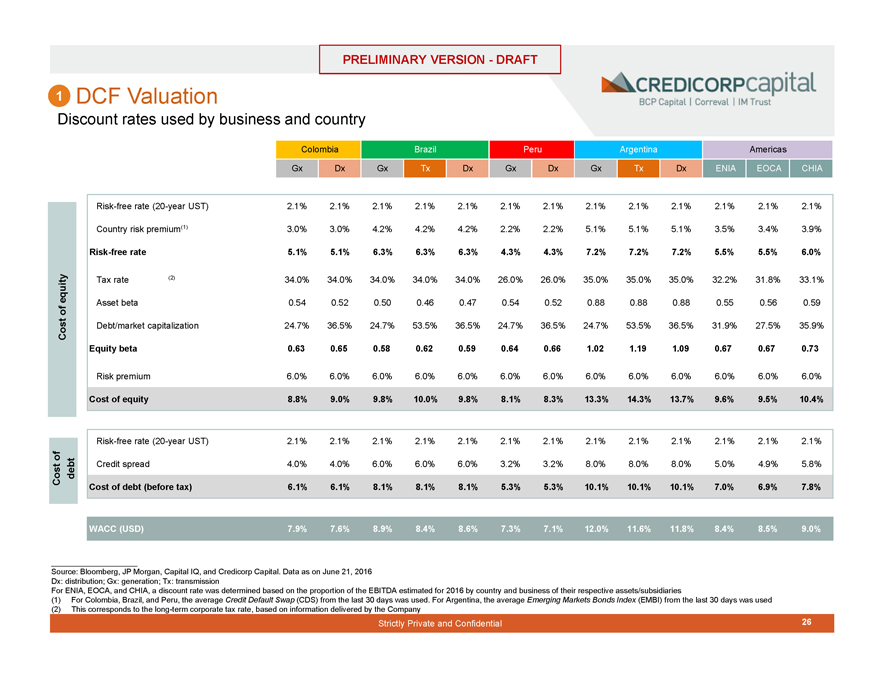

Discount rates used by business and country

Cost of

Cost of equity debt

Colombia Brazil Peru Argentina Americas

Gx Dx Gx Tx Dx Gx Dx Gx Tx Dx ENIA EOCA CHIA

Risk-free rate (20-year UST) 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1%

Country risk premium(1) 3.0% 3.0% 4.2% 4.2% 4.2% 2.2% 2.2% 5.1% 5.1% 5.1% 3.5% 3.4% 3.9%

Risk-free rate 5.1% 5.1% 6.3% 6.3% 6.3% 4.3% 4.3% 7.2% 7.2% 7.2% 5.5% 5.5% 6.0%

Tax rate (2) 34.0% 34.0% 34.0% 34.0% 34.0% 26.0% 26.0% 35.0% 35.0% 35.0% 32.2% 31.8% 33.1% Asset beta 0.54 0.52 0.50 0.46 0.47 0.54 0.52 0.88 0.88 0.88 0.55 0.56 0.59 Debt/market capitalization 24.7% 36.5% 24.7% 53.5% 36.5% 24.7% 36.5% 24.7% 53.5% 36.5% 31.9% 27.5% 35.9%

Equity beta 0.63 0.65 0.58 0.62 0.59 0.64 0.66 1.02 1.19 1.09 0.67 0.67 0.73

Risk premium 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0% 6.0%

Cost of equity 8.8% 9.0% 9.8% 10.0% 9.8% 8.1% 8.3% 13.3% 14.3% 13.7% 9.6% 9.5% 10.4%

Risk-free rate (20-year UST) 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1% 2.1%

Credit spread 4.0% 4.0% 6.0% 6.0% 6.0% 3.2% 3.2% 8.0% 8.0% 8.0% 5.0% 4.9% 5.8%

Cost of debt (before tax) 6.1% 6.1% 8.1% 8.1% 8.1% 5.3% 5.3% 10.1% 10.1% 10.1% 7.0% 6.9% 7.8%

WACC (USD) 7.9% 7.6% 8.9% 8.4% 8.6% 7.3% 7.1% 12.0% 11.6% 11.8% 8.4% 8.5% 9.0%

Source: Bloomberg, JP Morgan, Capital IQ, and Credicorp Capital. Data as on June 21, 2016 Dx: distribution; Gx: generation; Tx: transmission

For ENIA, EOCA, and CHIA, a discount rate was determined based on the proportion of the EBITDA estimated for 2016 by country and business of their respective assets/subsidiaries

(1) For Colombia, Brazil, and Peru, the average Credit Default Swap (CDS) from the last 30 days was used. For Argentina, the average Emerging Markets Bonds Index (EMBI) from the last 30 days was used (2) This corresponds to the long-term corporate tax rate, based on information delivered by the Company

Strictly Private and Confidential 26

|

PRELIMINARY VERSION—DRAFT

2 Valuation through Multiples

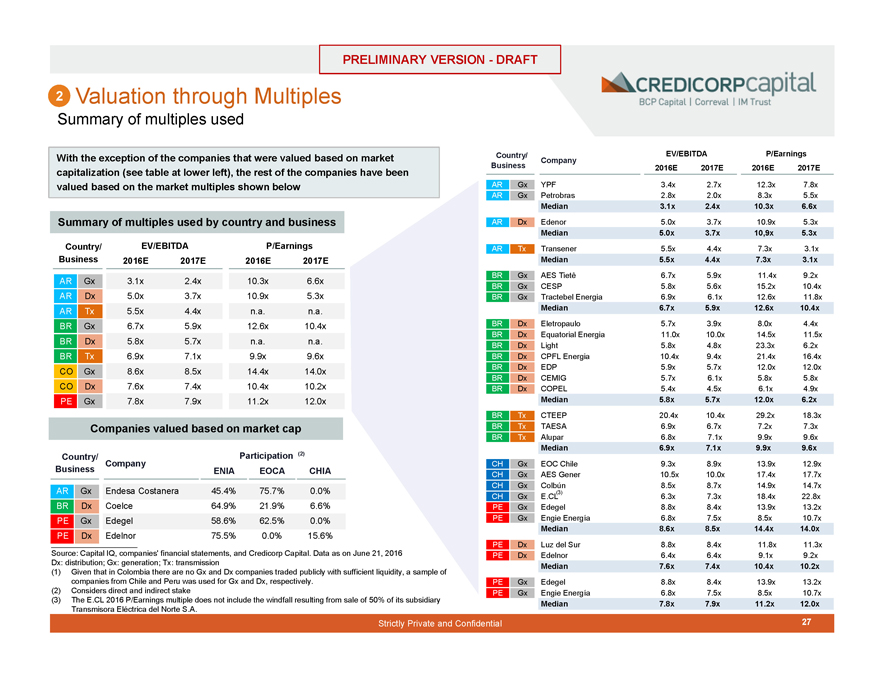

Summary of multiples used

With the exception of the companies that were valued based on market capitalization (see table at lower left), the rest of the companies have been valued based on the market multiples shown below

Summary of multiples used by country and business

Country/ EV/EBITDA P/Earnings

Business 2016E 2017E2016E2017E

AR Gx 3.1x2.4x10.3x6.6x

AR Dx 5.0x3.7x10.9x5.3x

AR Tx 5.5x4.4xn.a.n.a.

BR Gx 6.7x5.9x12.6x10.4x

BR Dx 5.8x5.7xn.a.n.a.

BR Tx 6.9x7.1x9.9x9.6x

CO Gx 8.6x8.5x14.4x14.0x

CO Dx 7.6x7.4x10.4x10.2x

PE Gx 7.8x7.9x11.2x12.0x

Companies valued based on market cap

Country/ Participation (2)

Company

Business ENIAEOCACHIA

AR Gx Endesa Costanera 45.4%75.7%0.0%

BR Dx Coelce 64.9%21.9%6.6%

PE Gx Edegel 58.6%62.5%0.0%

PE Dx Edelnor 75.5%0.0%15.6%

Country/ EV/EBITDAP/Earnings

Company

Business 2016E2017E2016E2017E

AR Gx YPF3.4x2.7x12.3x7.8x

AR Gx Petrobras2.8x2.0x8.3x5.5x

Median3.1x2.4x10.3x6.6x

AR Dx Edenor5.0x3.7x10.9x5.3x

Median5.0x3.7x10,9x5.3x

AR Tx Transener5.5x4.4x7.3x3.1x

Median5.5x4.4x7.3x3.1x

BR Gx AES Tietê6.7x5.9x11.4x9.2x

BR Gx CESP5.8x5.6x15.2x10.4x

BR Gx Tractebel Energia6.9x6.1x12.6x11.8x

Median6.7x5.9x12.6x10.4x

BR Dx Eletropaulo5.7x3.9x8.0x4.4x

BR Dx Equatorial Energia11.0x10.0x14.5x11.5x

BR Dx Light5.8x4.8x23.3x6.2x

BR Dx CPFL Energia10.4x9.4x21.4x16.4x

BR Dx EDP5.9x5.7x12.0x12.0x

BR Dx CEMIG5.7x6.1x5.8x5.8x

BR Dx COPEL5.4x4.5x6.1x4.9x

Median5.8x5.7x12.0x6.2x

BR Tx CTEEP20.4x10.4x29.2x18.3x

BR Tx TAESA6.9x6.7x7.2x7.3x

BR Tx Alupar6.8x7.1x9.9x9.6x

Median6.9x7.1x9.9x9.6x

CH Gx EOC Chile9.3x8.9x13.9x12.9x

CH Gx AES Gener10.5x10.0x17.4x17.7x

CH Gx Colbún8.5x8.7x14.9x14.7x

CH Gx E.CL(3)6.3x7.3x18.4x22.8x

PE Gx Edegel8.8x8.4x13.9x13.2x

PE Gx Engie Energía6.8x7.5x8.5x10.7x

Median8.6x8.5x14.4x14.0x

PE Dx Luz del Sur8.8x8.4x11.8x11.3x

PE Dx Edelnor6.4x6.4x9.1x9.2x

Median7.6x7.4x10.4x10.2x

PE Gx Edegel8.8x8.4x13.9x13.2x

PE Gx Engie Energía6.8x7.5x8.5x10.7x

Median7.8x7.9x11.2x12.0x

Source: Capital IQ, companies’ financial statements, and Credicorp Capital. Data as on June 21, 2016 Dx: distribution; Gx: generation; Tx: transmission

(1) Given that in Colombia there are no Gx and Dx companies traded publicly with sufficient liquidity, a sample of companies from Chile and Peru was used for Gx and Dx, respectively.

(2) Considers direct and indirect stake

(3) The E.CL 2016 P/Earnings multiple does not include the windfall resulting from sale of 50% of its subsidiary Transmisora Eléctrica del Norte S.A.

Strictly Private and Confidential 27

|

PRELIMINARY VERSION—DRAFT

ANALYSIS OF THE ECONOMIC TERMS OF THE PROPOSED OPERATION ii. Valuation of ENIA, EOCA, and CHIA

Strictly Private and Confidential 28

|

PRELIMINARY VERSION—DRAFT

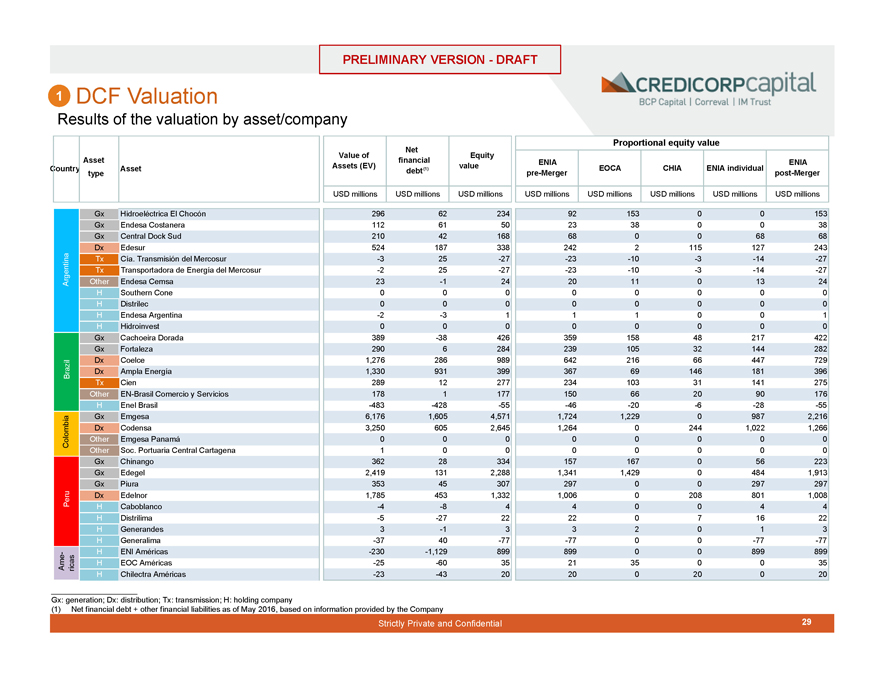

1 DCF Valuation

Results of the valuation by asset/company

Proportional equity value

Net

Value ofEquity

Asset financialENIAENIA

Country type Asset Assets (EV)debt(1)valuepre-MergerEOCACHIAENIA individual post-Merger

USD millionsUSD millionsUSD millionsUSD millionsUSD millionsUSD millionsUSD millionsUSD millions

Gx Hidroeléctrica El Chocón296622349215300153

Gx Endesa Costanera112615023380038

Gx Central Dock Sud2104216868006868

Dx Edesur5241873382422115127243

Tx Cía. Transmisión del Mercosur-325-27-23-10-3-14-27

Tx Transportadora de Energía del Mercosur-225-27-23-10-3-14-27

Argentina Other Endesa Cemsa23-124201101324

H Southern Cone00000000

H Distrilec00000000

H Endesa Argentina-2-3111001

H Hidroinvest00000000

Gx Cachoeira Dorada389-3842635915848217422

Gx Fortaleza290628423910532144282

Dx Coelce1,27628698964221666447729

Brazil Dx Ampla Energía1,33093139936769146181396

Tx Cien2891227723410331141275

Other EN-Brasil Comercio y Servicios1781177150662090176

H Enel Brasil-483-428-55-46-20-6-28-55

Gx Emgesa6,1761,6054,5711,7241,22909872,216

Dx Codensa3,2506052,6451,26402441,0221,266

Colombia Other Emgesa Panamá00000000

Other Soc. Portuaria Central Cartagena10000000

Gx Chinango36228334157167056223

Gx Edegel2,4191312,2881,3411,42904841,913

Gx Piura3534530729700297297

Peru Dx Edelnor1,7854531,3321,00602088011,008

H Caboblanco-4-8440044

H Distrilima-5-272222071622

H Generandes3-1332013

H Generalima-3740-77-7700-77-77

- H ENI Américas-230-1,12989989900899899

Ame ricas H EOC Américas-25-603521350035

H Chilectra Américas-23-432020020020

Gx: generation; Dx: distribution; Tx: transmission; H: holding company

(1) Net financial debt + other financial liabilities as of May 2016, based on information provided by the Company

Strictly Private and Confidential 29

|

PRELIMINARY VERSION—DRAFT

1 DCF Valuation

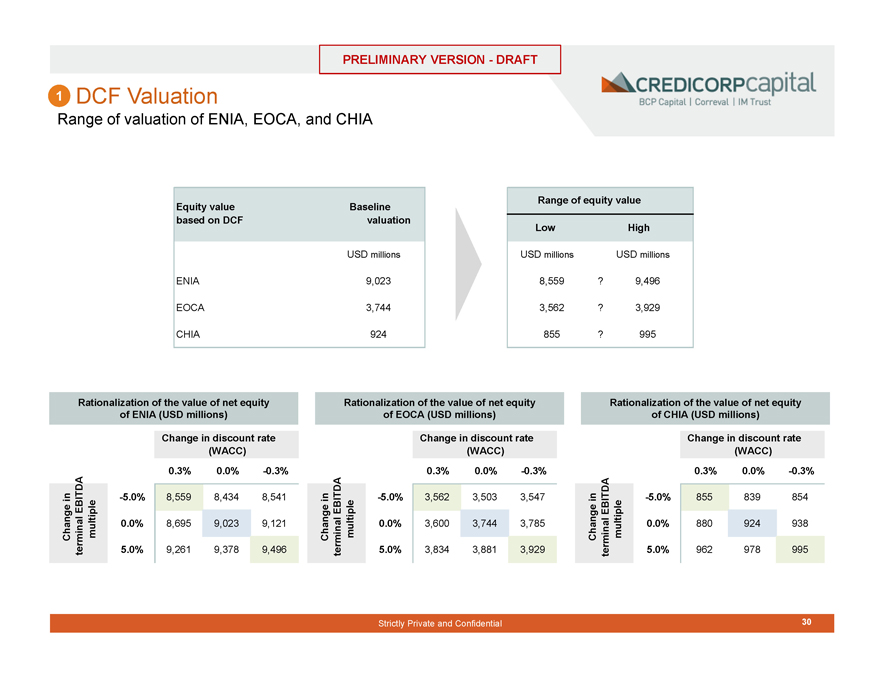

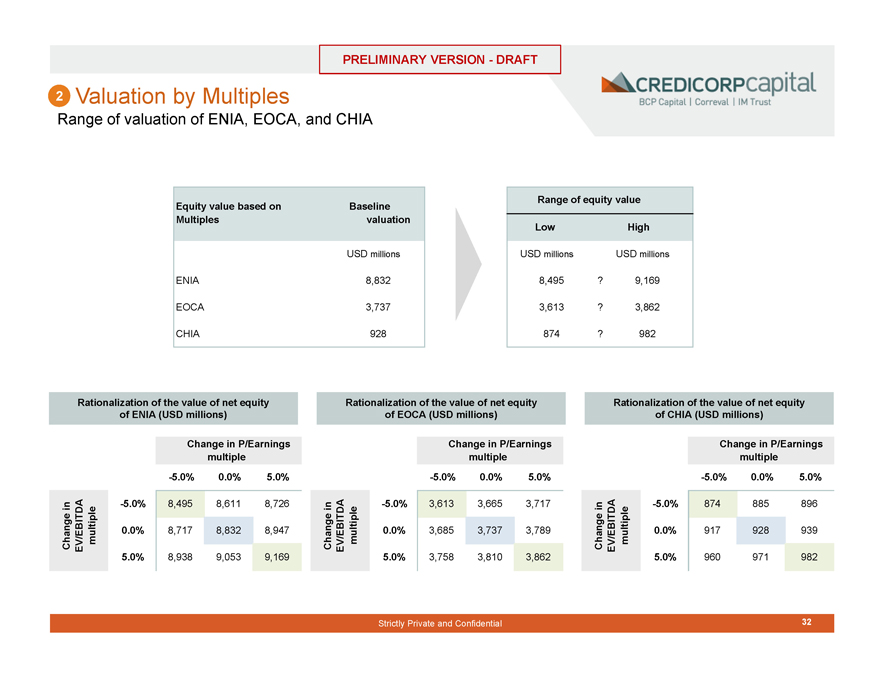

Range of valuation of ENIA, EOCA, and CHIA

Equity value Baseline

based on DCF valuation

USD millions

ENIA 9,023

EOCA 3,744

CHIA 924

Range of equity value

Low High

USD millions USD millions

8,559 ? 9,496

3,562 ? 3,929

855 ? 995

Change in terminal EBITDA multiple

Change in terminal EBITDA multiple

Change in terminal EBITDA multiple

Rationalization of the value of net equity of ENIA (USD millions)

Rationalization of the value of net equity of EOCA (USD millions)

Rationalization of the value of net equity of CHIA (USD millions)

Change in discount rate (WACC)

Change in discount rate (WACC)

Change in discount rate (WACC)

0.3% 0.0%-0.3%

-5.0% 8,559 8,4348,541

0.0% 8,695 9,0239,121

5.0% 9,261 9,3789,496

0.3% 0.0%-0.3%

-5.0% 3,562 3,5033,547

0.0% 3,600 3,7443,785

5.0% 3,834 3,8813,929

0.3% 0.0%-0.3%

-5.0% 855 839854

0.0% 880 924938

5.0% 962 978995

Strictly Private and Confidential 30

|

PRELIMINARY VERSION—DRAFT

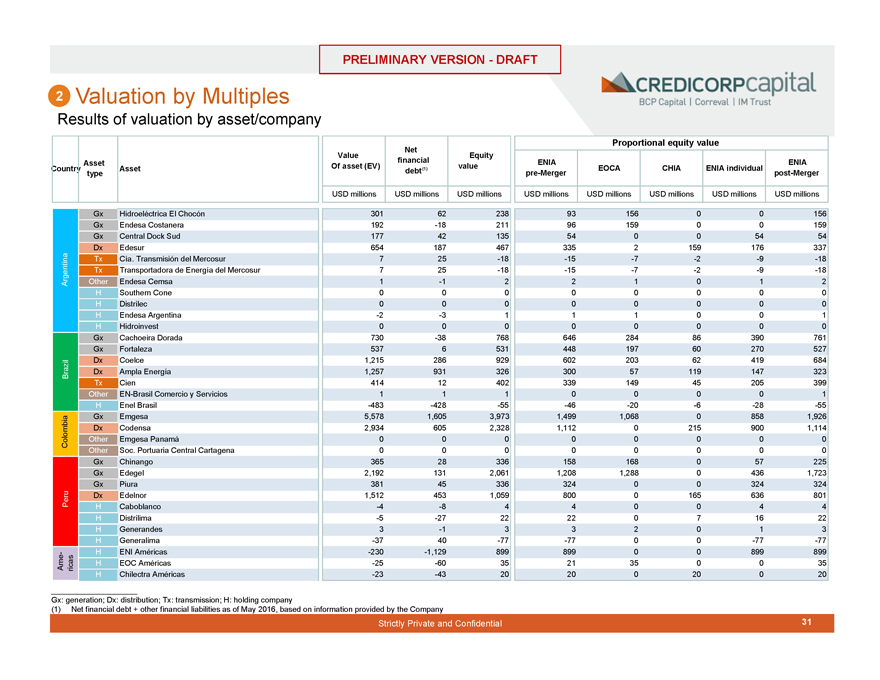

2 Valuation by Multiples

Results of valuation by asset/company

Proportional equity value

Net

ValueEquity

Asset financialENIAENIA

Country type Asset Of asset (EV)debt(1)valuepre-MergerEOCACHIAENIA individual post-Merger

USD millionsUSD millionsUSD millionsUSD millionsUSD millionsUSD millionsUSD millionsUSD millions

Gx Hidroeléctrica El Chocón301622389315600156

Gx Endesa Costanera192-182119615900159

Gx Central Dock Sud1774213554005454

Dx Edesur6541874673352159176337

Tx Cía. Transmisión del Mercosur725-18-15-7-2-9-18

Tx Transportadora de Energía del Mercosur725-18-15-7-2-9-18

Argentina Other Endesa Cemsa1-1221012

H Southern Cone00000000

H Distrilec00000000

H Endesa Argentina-2-3111001

H Hidroinvest00000000

Gx Cachoeira Dorada730-3876864628486390761

Gx Fortaleza537653144819760270527

Dx Coelce1,21528692960220362419684

Brazil Dx Ampla Energía1,25793132630057119147323

Tx Cien4141240233914945205399

Other EN-Brasil Comercio y Servicios11100001

H Enel Brasil-483-428-55-46-20-6-28-55

Gx Emgesa5,5781,6053,9731,4991,06808581,926

Dx Codensa2,9346052,3281,11202159001,114

Colombia Other Emgesa Panamá00000000

Other Soc. Portuaria Central Cartagena00000000

Gx Chinango36528336158168057225

Gx Edegel2,1921312,0611,2081,28804361,723

Gx Piura3814533632400324324

Peru Dx Edelnor1,5124531,0598000165636801

H Caboblanco-4-8440044

H Distrilima-5-272222071622

H Generandes3-1332013

H Generalima-3740-77-7700-77-77

- H ENI Américas-230-1,12989989900899899

Ame ricas H EOC Américas-25-603521350035

H Chilectra Américas-23-432020020020

Gx: generation; Dx: distribution; Tx: transmission; H: holding company

(1) Net financial debt + other financial liabilities as of May 2016, based on information provided by the Company

Strictly Private and Confidential 31

|

PRELIMINARY VERSION—DRAFT

2 Valuation by Multiples

Range of valuation of ENIA, EOCA, and CHIA

Equity value based on

Baseline

Multiples

valuation

USD millions

ENIA

8,832

EOCA

3,737

CHIA

928

Range of equity value

Low

High

USD millions

USD millions

8,495

?

9,169

3,613

?

3,862

874

?

982

Rationalization of the value of net equity Rationalization of the value of net equity Rationalization of the value of net equity of ENIA (USD millions) of EOCA (USD millions) of CHIA (USD millions)

Change in EV/EBITDA multiple

-

Change in EV/EBITDA multiple

Change in EV/EBITDA multiple

Change in P/Earnings multiple

Change in P/Earnings multiple

Change in P/Earnings multiple

-5.0% 0.0%5.0%

-5.0% 8,495 8,6118,726

0.0% 8,717 8,8328,947

5.0% 8,938 9,0539,169

-5.0% 0.0%5.0%

-5.0% 3,613 3,6653,717

0.0% 3,685 3,7373,789

5.0% 3,758 3,8103,862

-5.0% 0.0%5.0%

-5.0% 874 885896

0.0% 917 928939

5.0% 960 971982

Strictly Private and Confidential 32

|

PRELIMINARY VERSION—DRAFT

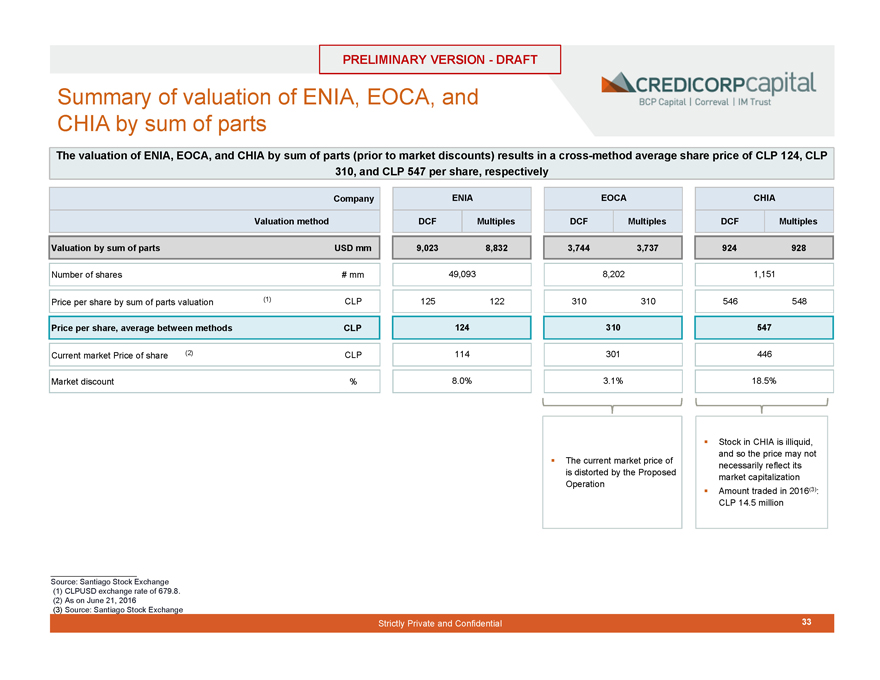

Summary of valuation of ENIA, EOCA, and CHIA by sum of parts

The valuation of ENIA, EOCA, and CHIA by sum of parts (prior to market discounts) results in a cross-method average share price of CLP 124, CLP 310, and CLP 547 per share, respectively

Company

Valuation method

Valuation by sum of parts USD mm

Number of shares # mm

Price per share by sum of parts valuation (1) CLP

Price per share, average between methods CLP

Current market Price of share (2) CLP

Market discount %

ENIA

DCF Multiples

9,023 8,832

49,093

125 122

124

114

8.0%

EOCA

DCF Multiples

3,744 3,737

8,202

310 310

310

301

3.1%

CHIA

DCF Multiples

924 928

1,151

546 548

547

446

18.5%

The current market price of is distorted by the Proposed Operation

Stock in CHIA is illiquid, and so the price may not necessarily reflect its market capitalization Amount traded in 2016(3): CLP 14.5 million

Source: Santiago Stock Exchange (1) CLPUSD exchange rate of 679.8. (2) As on June 21, 2016 (3) Source: Santiago Stock Exchange

Strictly Private and Confidential 33

|

PRELIMINARY VERSION—DRAFT

ANALYSIS OF THE ECONOMIC TERMS OF THE PROPOSED OPERATION iii. Estimate of the Exchange Ratios of the Proposed Operation

Strictly Private and Confidential 34

|

PRELIMINARY VERSION—DRAFT

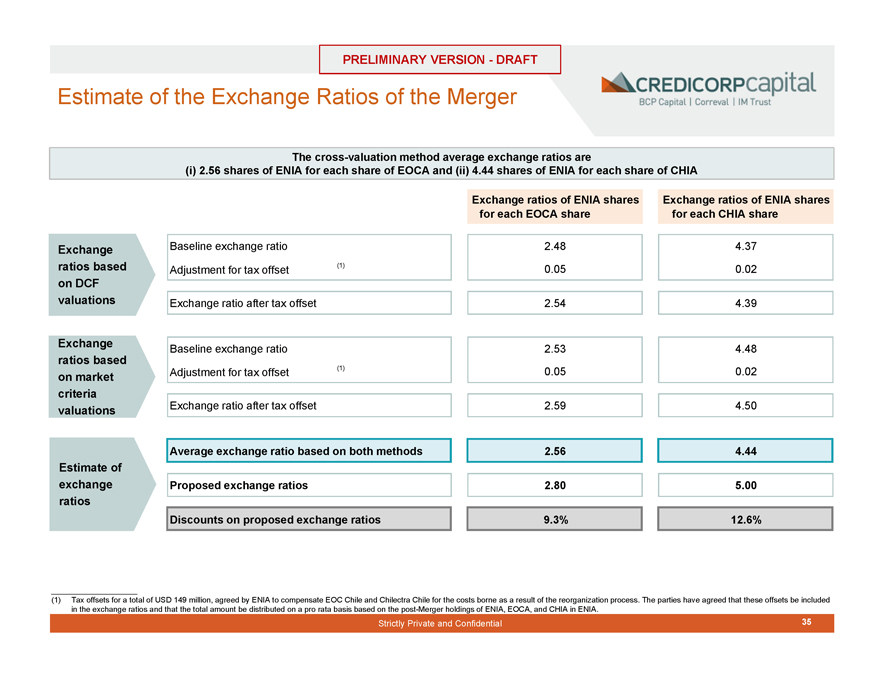

Estimate of the Exchange Ratios of the Merger

The cross-valuation method average exchange ratios are

(i) 2.56 shares of ENIA for each share of EOCA and (ii) 4.44 shares of ENIA for each share of CHIA

Exchange ratios based on DCF valuations

Exchange ratios based on market criteria valuations

Estimate of exchange ratios

Exchange ratios of ENIA shares Exchange ratios of ENIA shares for each EOCA share for each CHIA share

Baseline exchange ratio 2.484.37

Adjustment for tax offset (1) 0.050.02

Exchange ratio after tax offset 2.544.39

Baseline exchange ratio 2.534.48

Adjustment for tax offset (1) 0.050.02

Exchange ratio after tax offset 2.594.50

Average exchange ratio based on both methods 2.56 4.44

Proposed exchange ratios 2.805.00

Discounts on proposed exchange ratios 9.3% 12.6%

(1) Tax offsets for a total of USD 149 million, agreed by ENIA to compensate EOC Chile and Chilectra Chile for the costs borne as a result of the reorganization process. The parties have agreed that these offsets be included in the exchange ratios and that the total amount be distributed on a pro rata basis based on the post-Merger holdings of ENIA, EOCA, and CHIA in ENIA.

Strictly Private and Confidential 35

|

PRELIMINARY VERSION—DRAFT

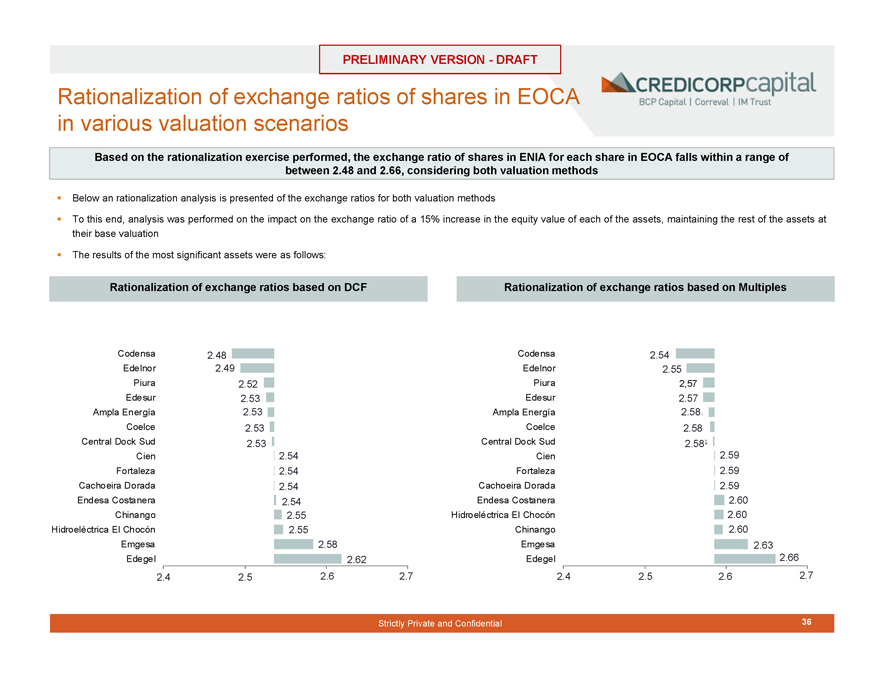

Rationalization of exchange ratios of shares in EOCA in various valuation scenarios

Based on the rationalization exercise performed, the exchange ratio of shares in ENIA for each share in EOCA falls within a range of between 2.48 and 2.66, considering both valuation methods

Below an rationalization analysis is presented of the exchange ratios for both valuation methods

To this end, analysis was performed on the impact on the exchange ratio of a 15% increase in the equity value of each of the assets, maintaining the rest of the assets at their base valuation

The results of the most significant assets were as follows:

Rationalization of exchange ratios based on DCF

Codensa 2.2,48

Edelnor 2.2,49

Piura 2.2,52

Edesur 2.2,53

Ampla Energía 2.2,53

Coelce 2.2,53

Central Dock Sud 2.2,53

Cien 2.2,54

Fortaleza 2.2,54

Cachoeira Dorada 2.2,54

Endesa Costanera 2.2,54

Chinango 2.2,55

Hidroeléctrica El Chocón 2.2,55

Emgesa 2.2,58

Edegel 2.2,62

2.2,4 2.,5 2,2.62.2,77

Rationalization of exchange ratios based on Multiples

Codensa 2.2,54

Edelnor 2.2,55

Piura 2,57

Edesur 2.2,57

Ampla Energía 2.2,588

Coelce 2.2,58

Central Dock Sud 2.2,588

Cien 2.2,59

Fortaleza 2.2,59

Cachoeira Dorada 2.2,59

Endesa Costanera 2.2,60

Hidroeléctrica El Chocón 2.2,60

Chinango 2,2.60

Emgesa 2.2,63

Edegel 2.2,666

2.2,4 2., 5 2.2,62.2,77

Strictly Private and Confidential 36

|

PRELIMINARY VERSION—DRAFT

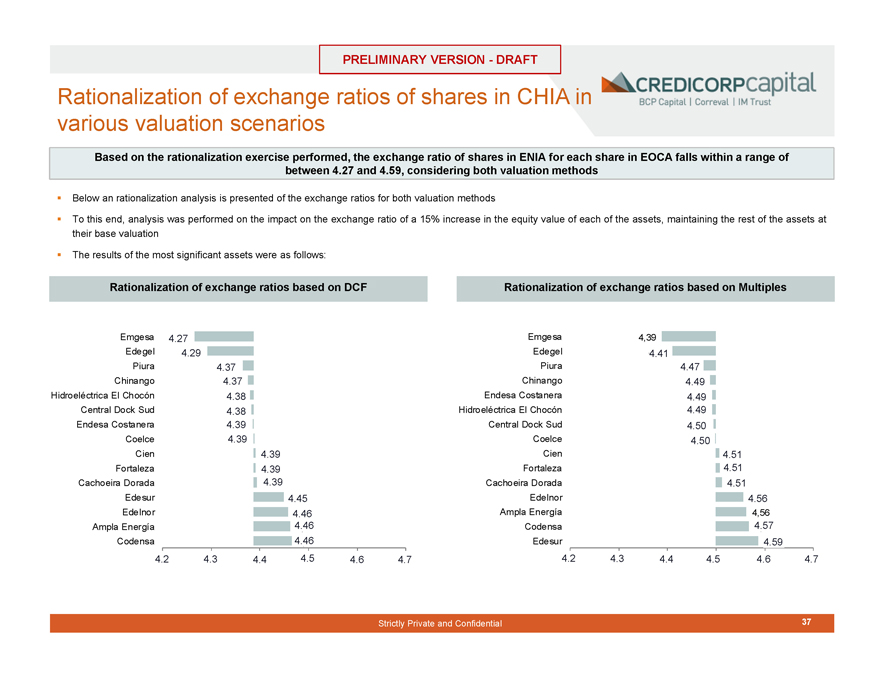

Rationalization of exchange ratios of shares in CHIA in various valuation scenarios

Based on the rationalization exercise performed, the exchange ratio of shares in ENIA for each share in EOCA falls within a range of between 4.27 and 4.59, considering both valuation methods

Below an rationalization analysis is presented of the exchange ratios for both valuation methods

To this end, analysis was performed on the impact on the exchange ratio of a 15% increase in the equity value of each of the assets, maintaining the rest of the assets at their base valuation

The results of the most significant assets were as follows:

Rationalization of exchange ratios based on DCF

Emgesa 4.4,27

Edegel 4.4,29

Piura 4.4,37

Chinango 4.4,3837

Hidroeléctrica El Chocón 4.4, 38

Central Dock Sud 4.4,38

Endesa Costanera 4.4,39

Coelce 4.4,39

Cien 4.4,39

Fortaleza 4.4,39

Cachoeira Dorada 4.4, 39

Edesur 4.4,45

Edelnor 4.4,46

Ampla Energía 4.4,46

Codensa 4.4,46

4.4,2 4.,34.4,44.4,54.,64.,7

Rationalization of exchange ratios based on Multiples

Emgesa 4,39

Edegel 4,4.41

Piura 4,4.47

Chinango 4.494,

Endesa Costanera 4.494,

Hidroeléctrica El Chocón 4.494,

Central Dock Sud 4.504,

Coelce 4.504,

Cien 4.514,

Fortaleza 4.514,

Cachoeira Dorada 4.514,

Edelnor 4.564,

Ampla Energía 4,56

Codensa 4.574,

Edesur 4.594,

4.24,2 4.34,3 4.44,4.54,54.64,4.74,7

Strictly Private and Confidential 37

|

PRELIMINARY VERSION—DRAFT

ANALYSIS OF THE ECONOMIC TERMS OF THE PROPOSED OPERATION iv. Analysis of the Economic Terms of the Proposed Operation

Strictly Private and Confidential 38

|

PRELIMINARY VERSION—DRAFT

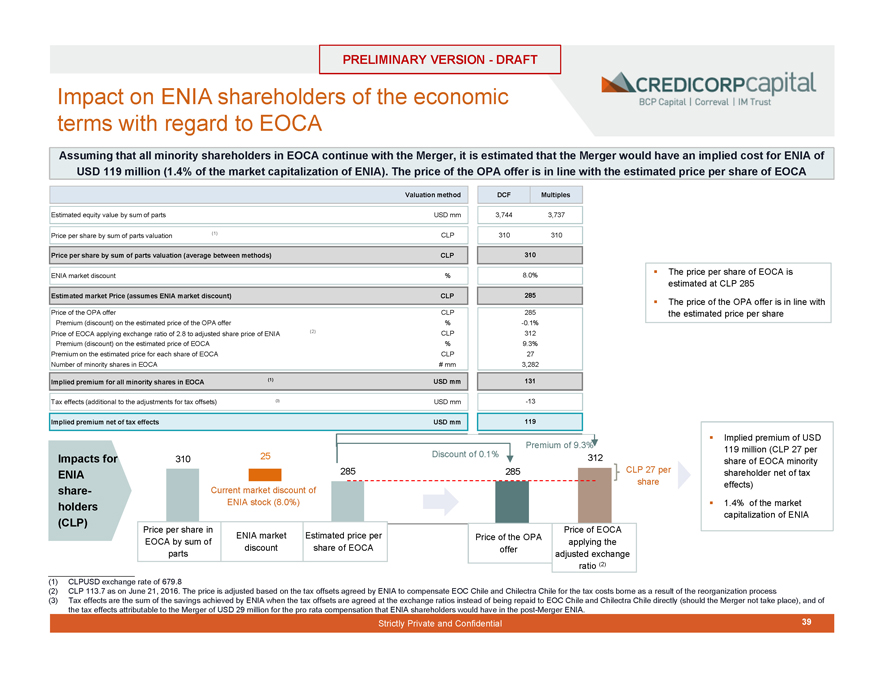

Impact on ENIA shareholders of the economic terms with regard to EOCA

Assuming that all minority shareholders in EOCA continue with the Merger, it is estimated that the Merger would have an implied cost for ENIA of USD 119 million (1.4% of the market capitalization of ENIA). The price of the OPA offer is in line with the estimated price per share of EOCA

Valuation methodDCFMultiples

Estimated equity value by sum of parts USD mm3,7443,737

Price per share by sum of parts valuation (1) CLP310310

Price per share by sum of parts valuation (average between methods) CLP310

ENIA market discount %8.0%

Estimated market Price (assumes ENIA market discount) CLP285

Price of the OPA offer CLP285

Premium (discount) on the estimated price of the OPA offer %-0.1%

Price of EOCA applying exchange ratio of 2.8 to adjusted share price of ENIA (2) CLP312

Premium (discount) on the estimated price of EOCA %9.3%

Premium on the estimated price for each share of EOCA CLP27

Number of minority shares in EOCA # mm3,282

Implied premium for all minority shares in EOCA (1) USD mm131

Tax effects (additional to the adjustments for tax offsets) (3) USD mm-13

Implied premium net of tax effects USD mm119

The price per share of EOCA is estimated at CLP 285

The price of the OPA offer is in line with the estimated price per share

Implied premium of USD 119 million (CLP 27 per share of EOCA minority shareholder net of tax effects)

1.4% of the market capitalization of ENIA

Impacts for 310 25

ENIA 285

share- Current market discount of

holders ENIA stock (8.0%)

(CLP)

Price per share in ENIA marketEstimated price per

EOCA by sum of discountshare of EOCA

parts

Premium of 9.3% Discount of 0.1% 312

285 CLP 27 per share

Price of EOCA Price of the OPA applying the offer adjusted exchange ratio (2)

(1) CLPUSD exchange rate of 679.8

(2) CLP 113.7 as on June 21, 2016. The price is adjusted based on the tax offsets agreed by ENIA to compensate EOC Chile and Chilectra Chile for the tax costs borne as a result of the reorganization process

(3) Tax effects are the sum of the savings achieved by ENIA when the tax offsets are agreed at the exchange ratios instead of being repaid to EOC Chile and Chilectra Chile directly (should the Merger not take place), and of the tax effects attributable to the Merger of USD 29 million for the pro rata compensation that ENIA shareholders would have in the post-Merger ENIA.

Strictly Private and Confidential 39

|

PRELIMINARY VERSION—DRAFT

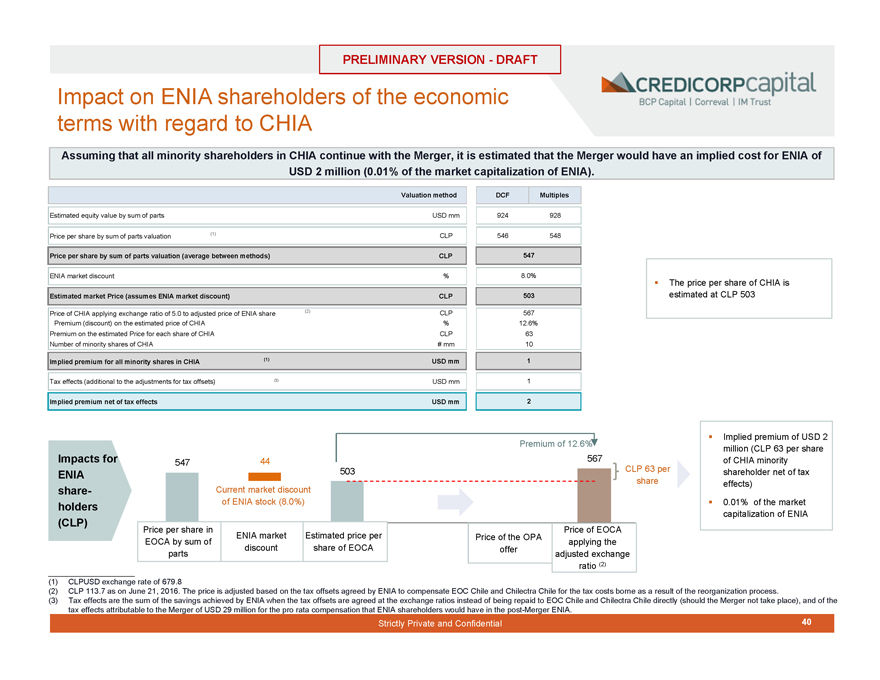

Impact on ENIA shareholders of the economic terms with regard to CHIA

Assuming that all minority shareholders in CHIA continue with the Merger, it is estimated that the Merger would have an implied cost for ENIA of USD 2 million (0.01% of the market capitalization of ENIA).

Valuation methodDCFMultiples

Estimated equity value by sum of parts USD mm924928

Price per share by sum of parts valuation (1) CLP546548

Price per share by sum of parts valuation (average between methods) CLP547

ENIA market discount %8.0%

Estimated market Price (assumes ENIA market discount) CLP503

Price of CHIA applying exchange ratio of 5.0 to adjusted price of ENIA share (2) CLP567

Premium (discount) on the estimated price of CHIA %12.6%

Premium on the estimated Price for each share of CHIA CLP63

Number of minority shares of CHIA # mm10

Implied premium for all minority shares in CHIA (1) USD mm1

Tax effects (additional to the adjustments for tax offsets) (3) USD mm1

Implied premium net of tax effects USD mm2

Impacts for ENIA shareholders (CLP)

The price per share of CHIA is estimated at CLP 503

Implied premium of USD 2 million (CLP 63 per share of CHIA minority shareholder net of tax effects)

0.01% of the market capitalization of ENIA

547 44

503

Current market discount of ENIA stock (8.0%)

Price per share in EOCA by sum of parts

ENIA market discount

Estimated price per share of EOCA

Price of the OPA offer

Price of EOCA applying the adjusted exchange ratio (2)

(1) CLPUSD exchange rate of 679.8

(2) CLP 113.7 as on June 21, 2016. The price is adjusted based on the tax offsets agreed by ENIA to compensate EOC Chile and Chilectra Chile for the tax costs borne as a result of the reorganization process.

(3) Tax effects are the sum of the savings achieved by ENIA when the tax offsets are agreed at the exchange ratios instead of being repaid to EOC Chile and Chilectra Chile directly (should the Merger not take place), and of the tax effects attributable to the Merger of USD 29 million for the pro rata compensation that ENIA shareholders would have in the post-Merger ENIA.

Strictly Private and Confidential 40

|

PRELIMINARY VERSION—DRAFT

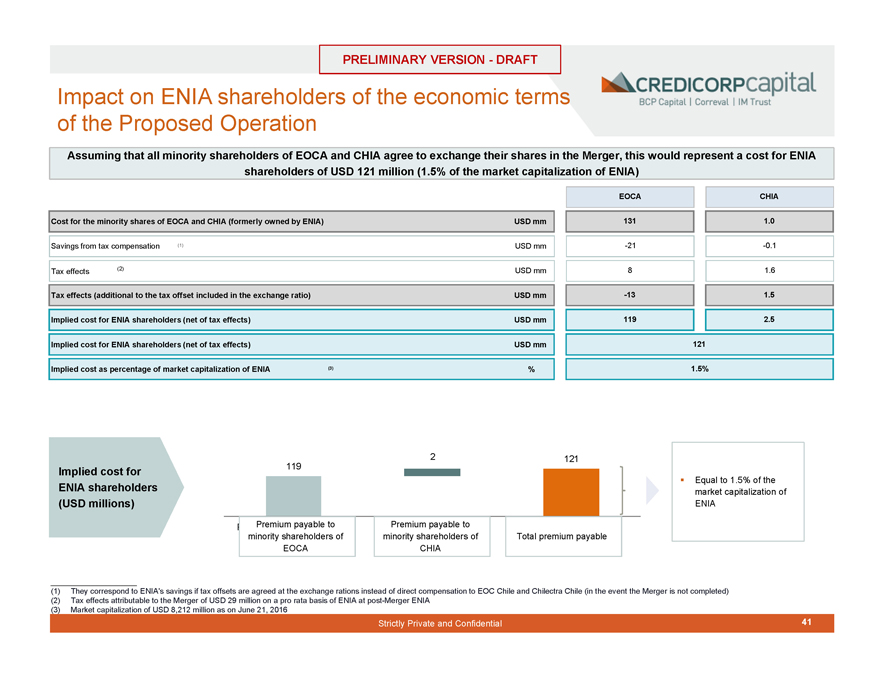

Impact on ENIA shareholders of the economic terms of the Proposed Operation

Assuming that all minority shareholders of EOCA and CHIA agree to exchange their shares in the Merger, this would represent a cost for ENIA shareholders of USD 121 million (1.5% of the market capitalization of ENIA)

EOCACHIA

Cost for the minority shares of EOCA and CHIA (formerly owned by ENIA) USD mm 1311.0

Savings from tax compensation (1) USD mm-21-0.1

Tax effects (2) USD mm81.6

Tax effects (additional to the tax offset included in the exchange ratio) USD mm-131.5

Implied cost for ENIA shareholders (net of tax effects) USD mm1192.5

Implied cost for ENIA shareholders (net of tax effects) USD mm121

Implied cost as percentage of market capitalization of ENIA (3) %1.5%

2121

Implied cost for 119

Equal to 1.5% of the

ENIA shareholders market capitalization of

(USD millions) ENIA

Premium payable to Premium payable to

minority shareholders of minority shareholders ofTotal premium payable

EOCA CHIA

(1) They correspond to ENIA’s savings if tax offsets are agreed at the exchange rations instead of direct compensation to EOC Chile and Chilectra Chile (in the event the Merger is not completed) (2) Tax effects attributable to the Merger of USD 29 million on a pro rata basis of ENIA at post-Merger ENIA

(3) Market capitalization of USD 8,212 million as on June 21, 2016

Strictly Private and Confidential

41

|

PRELIMINARY VERSION—DRAFT

MARKET AND CASH FLOW CONSIDERATIONS OF THE PROPOSED OPERATION i. Holding Discount Considerations

5

Strictly Private and Confidential

42

|

PRELIMINARY VERSION—DRAFT

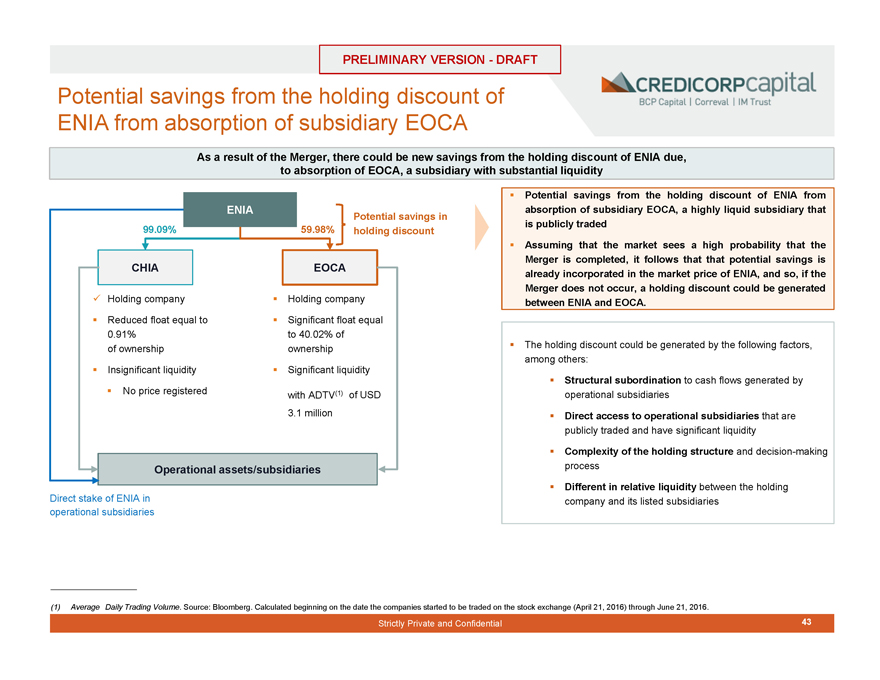

Potential savings from the holding discount of ENIA from absorption of subsidiary EOCA

As a result of the Merger, there could be new savings from the holding discount of ENIA due, to absorption of EOCA, a subsidiary with substantial liquidity

ENIA Potential savings in

99.09% 59.98% holding discount

CHIA EOCA

Holding company Holding company

Reduced float equal to Significant float equal

0.91% to 40.02% of

of ownership ownership

Insignificant liquidity Significant liquidity

No price registered with ADTV(1) of USD

3.1 million

Operational assets/subsidiaries

Direct stake of ENIA in operational subsidiaries

Potential savings from the holding discount of ENIA from absorption of subsidiary EOCA, a highly liquid subsidiary that is publicly traded

Assuming that the market sees a high probability that the Merger is completed, it follows that that potential savings is already incorporated in the market price of ENIA, and so, if the Merger does not occur, a holding discount could be generated between ENIA and EOCA.

The holding discount could be generated by the following factors, among others:

Structural subordination to cash flows generated by operational subsidiaries

Direct access to operational subsidiaries that are publicly traded and have significant liquidity

Complexity of the holding structure and decision-making process

Different in relative liquidity between the holding company and its listed subsidiaries

(1) Average Daily Trading Volume. Source: Bloomberg. Calculated beginning on the date the companies started to be traded on the stock exchange (April 21, 2016) through June 21, 2016.

Strictly Private and Confidential

43

|

PRELIMINARY VERSION—DRAFT

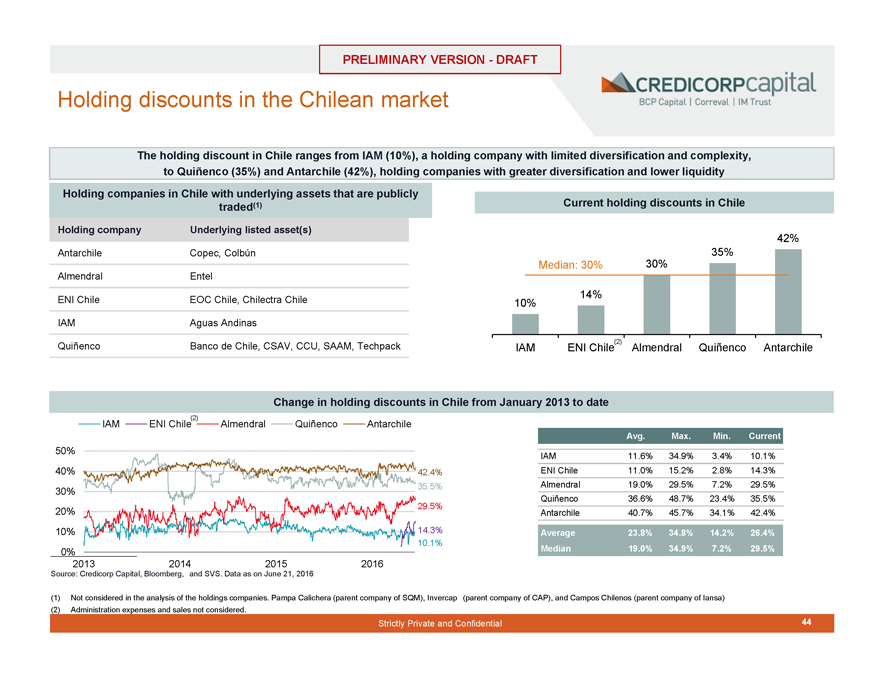

Holding discounts in the Chilean market

The holding discount in Chile ranges from IAM (10%), a holding company with limited diversification and complexity, to Quiñenco (35%) and Antarchile (42%), holding companies with greater diversification and lower liquidity

Holding companies in Chile with underlying assets that are publicly

traded(1)

Holding company Underlying listed asset(s)

Antarchile Copec, Colbún

Almendral Entel

ENI Chile EOC Chile, Chilectra Chile

IAM Aguas Andinas

Quiñenco Banco de Chile, CSAV, CCU, SAAM, Techpack

Current holding discounts in Chile

42%

35%

Median: 30% 30%

14%

10%

IAM ENI Chile(2) Almendral QuiñencoAntarchile

Change in holding discounts in Chile from January 2013 to date

IAM ENI Chile(2) AlmendralQuiñencoAntarchile

50%

40% 42.4%

30% 35.5%

20% 29.5%

10% 14.3%

10.1%

0%

2013 2014 20152016

Source: Credicorp Capital, Bloomberg, and SVS. Data as on June 21, 2016

Avg. Max.Min.Current

IAM 11.6% 34.9%3.4%10.1%

ENI Chile 11.0% 15.2%2.8%14.3%

Almendral 19.0% 29.5%7.2%29.5%

Quiñenco 36.6% 48.7%23.4%35.5%

Antarchile 40.7% 45.7%34.1%42.4%

Average 23.8% 34.8%14.2%26.4%

Median 19.0% 34.9%7.2%29.5%

(1) Not considered in the analysis of the holdings companies. Pampa Calichera (parent company of SQM), Invercap (parent company of CAP), and Campos Chilenos (parent company of Iansa) (2) Administration expenses and sales not considered.

Strictly Private and Confidential

44

|

PRELIMINARY VERSION—DRAFT

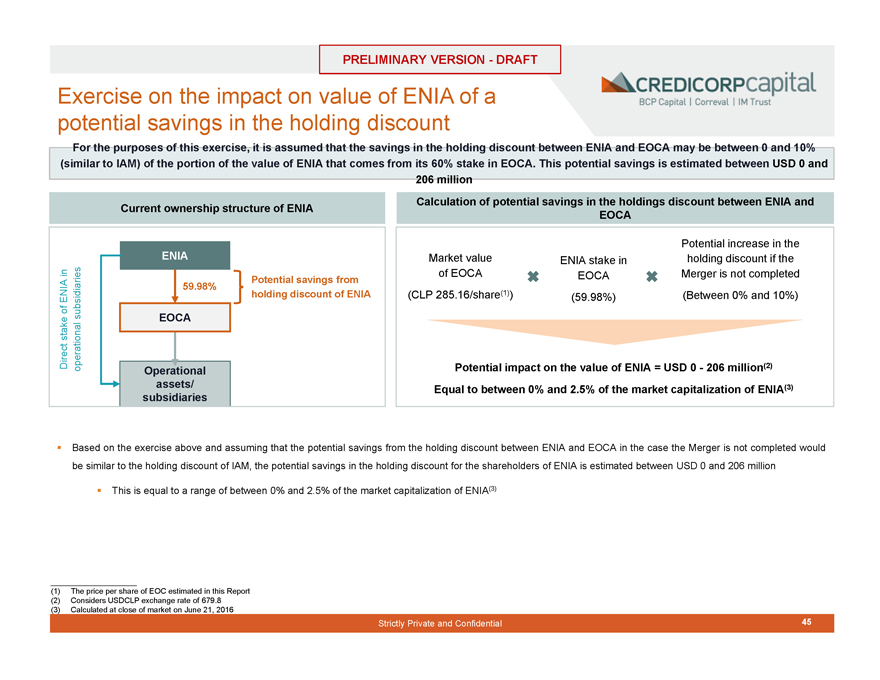

Exercise on the impact on value of ENIA of a potential savings in the holding discount

For the purposes of this exercise, it is assumed that the savings in the holding discount between ENIA and EOCA may be between 0 and 10% (similar to IAM) of the portion of the value of ENIA that comes from its 60% stake in EOCA. This potential savings is estimated between USD 0 and 206 million

Direct stake of ENIA in operational subsidiaries

Current ownership structure of ENIA

ENIA

59.98%

Potential savings from holding discount of ENIA

EOCA

Operational assets/ subsidiaries

Calculation of potential savings in the holdings discount between ENIA and

EOCA

Potential increase in the

Market value ENIA stake in holding discount if the

of EOCA EOCA Merger is not completed

(CLP 285.16/share(1)) (59.98%) (Between 0% and 10%)

Potential impact on the value of ENIA = USD 0—206 million(2)

Equal to between 0% and 2.5% of the market capitalization of ENIA(3)

Based on the exercise above and assuming that the potential savings from the holding discount between ENIA and EOCA in the case the Merger is not completed would be similar to the holding discount of IAM, the potential savings in the holding discount for the shareholders of ENIA is estimated between USD 0 and 206 million

This is equal to a range of between 0% and 2.5% of the market capitalization of ENIA(3)

(1) The price per share of EOC estimated in this Report (2) Considers USDCLP exchange rate of 679.8 (3) Calculated at close of market on June 21, 2016

Strictly Private and Confidential

45

|

PRELIMINARY VERSION—DRAFT

MARKET AND CASH FLOW CONSIDERATIONS OF THE PROPOSED OPERATION ii. Liquidity Considerations

5

Strictly Private and Confidential

46

|

PRELIMINARY VERSION—DRAFT

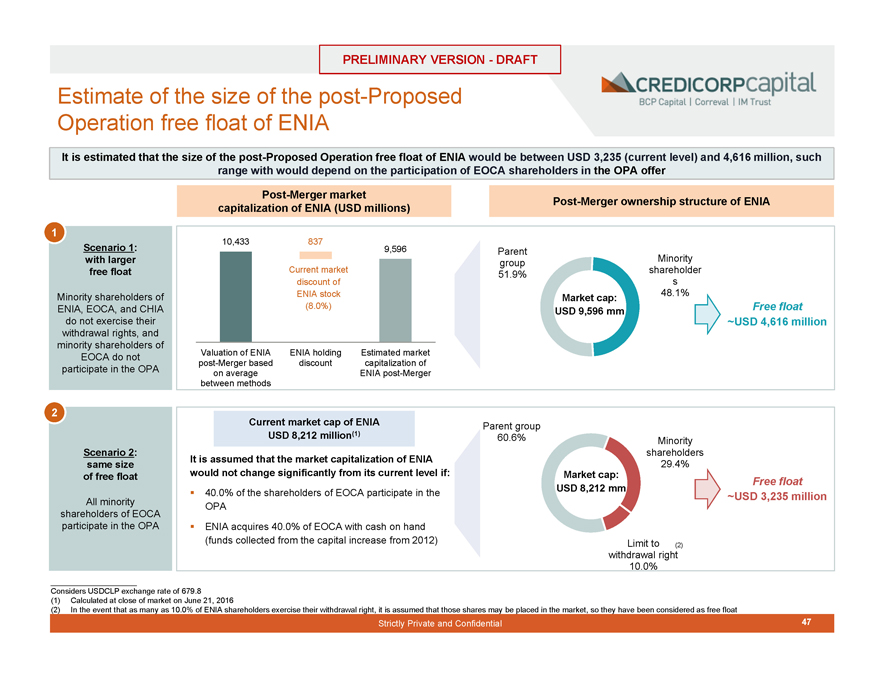

Estimate of the size of the post-Proposed Operation free float of ENIA

It is estimated that the size of the post-Proposed Operation free float of ENIA would be between USD 3,235 (current level) and 4,616 million, such range with would depend on the participation of EOCA shareholders in the OPA offer

1

Scenario 1: with larger free float

Minority shareholders of ENIA, EOCA, and CHIA do not exercise their withdrawal rights, and minority shareholders of EOCA do not participate in the OPA

Post-Merger market capitalization of ENIA (USD millions)

10,433 837

9,596

Current market

discount of

ENIA stock

(8.0%)

Valuation of ENIA ENIA holding Estimated market

post-Merger based discount capitalization of

on average ENIA post-Merger

between methods

Post-Merger ownership structure of ENIA

Parent

group Minority

51.9% shareholder

s

Market cap: 48.1%

USD 9,596 mm Free float

~USD 4,616 million

2

Scenario 2: same size of free float

All minority shareholders of EOCA participate in the OPA

Current market cap of ENIA USD 8,212 million(1)

It is assumed that the market capitalization of ENIA would not change significantly from its current level if:

40.0% of the shareholders of EOCA participate in the OPA

ENIA acquires 40.0% of EOCA with cash on hand (funds collected from the capital increase from 2012)

Parent group

60.6% Minority

shareholders

29.4%

Market cap: Free float

USD 8,212 mm

~USD 3,235 million

Limit to (2)

withdrawal right

10.0%

Considers USDCLP exchange rate of 679.8

(1) Calculated at close of market on June 21, 2016

(2) In the event that as many as 10.0% of ENIA shareholders exercise their withdrawal right, it is assumed that those shares may be placed in the market, so they have been considered as free float

Strictly Private and Confidential

47

|

PRELIMINARY VERSION—DRAFT

Liquidity outlook of ENIA and EOCA in the Chilean market

According to pro forma estimates of ENIA post-Proposed Operation, ENIA would remain as one of the most liquid companies in the Chilean market. If the Proposed Operation is not performed, it would be expected that EOCA would be among the 20 companies with the largest float in the Chilean market, showing reasonable levels of ADTV(1) for this market

Liquidity of leading Chilean companies(2)

ENIA post-ENIA post-

Merger (ScenarioMerger (Scenario

30 ENI Chile2)1)

(pbs) 25

EOCAEOC ChileENIA

20 ITAU CORP.CHILEFALABELLA

E.CLLAN

UDM/Float 15 CCU

AESGENERCMPCSQM-B

10 CENCOSUD

AGUAS-A BCI

QUINENCO

ADTV 5 SM-CHILE BCOLBUNBSANTANDER

COPEC

0

0 5001,0001,5002,0002,5003,0003,5004,0004,5005,000

Free float (USD millions)

Liquidity based on float and ADTV (USD millions) of leading Chilean companies(3)

ADTV UDM (USD millones)ADTV UDM / Float (pbs)

17.6 16.3 17.617.624.417.715.28.215.28.615.511.921.416.013.514.1 12.913.015.99.213.34.17.5

8.1

5.8 5.75.75.45.14.83.93.83.73.53.43.12.92.72.52.42.12.12.01.10.60.4

.

B-AB

-

1) 2)BCICCU. CL

E

post fusión (escenario FALABELLA post fusión (escenarioENIAENI ChileEOC ChileCENCOSUDSQMCHILECOPECCMPCBSANTANDEREOCALANITAU CORPAGUASAESGENERCOLBUNSM—CHILEQUINENCO

ENIA ENIA

Source: Bloomberg. Data as on June 21, 2016. USDCLP exchange rate 679.80.

(1) Average Daily Trading Volume uses data from the last twelve months (UDM). For ENIA and EOC Chile, data were used beginning March 1, 2016, date on which the Split was completed. For ENI Chile and EOCA, data were used beginning April 21, 2016, date on which the companies resulting from the Split began trading (2) The size of the circle represents market capitalization (3) To calculate ADTV of ENIA post-Merger, it was assumed that the ADTV/Float ratio would remain constant after the Merger

Strictly Private and Confidential

48

|

PRELIMINARY VERSION—DRAFT

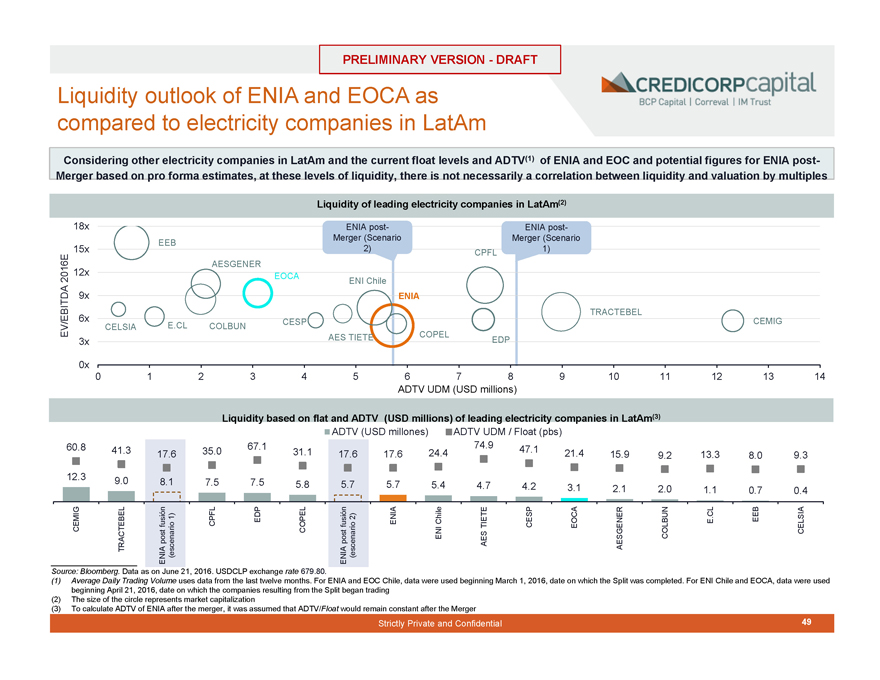

Liquidity outlook of ENIA and EOCA as compared to electricity companies in LatAm

Considering other electricity companies in LatAm and the current float levels and ADTV(1) of ENIA and EOC and potential figures for ENIA post-Merger based on pro forma estimates, at these levels of liquidity, there is not necessarily a correlation between liquidity and valuation by multiples

Liquidity of leading electricity companies in LatAm(2)

18x ENIA post-ENIA post-

EEBMerger (ScenarioMerger (Scenario

15x 2)CPFL1)

AESGENER

2016E 12x EOCA

ENI Chile

9x ENIA

TRACTEBEL

6x CESPCEMIG

EV/EBITDA CELSIA E.CLCOLBUN

3x AES TIETECOPELEDP

0x

0 1234567891011121314

ADTV UDM (USD millions)

Liquidity based on flat and ADTV (USD millions) of leading electricity companies in LatAm(3)

ADTV (USD millones)ADTV UDM / Float (pbs)

60.8 41.3 17.635.067.131.117.617.624.474.947.121.415.99.213.38.09.3

12.3

9.0 8.17.57.55.85.75.75.44.74.23.12.12.01.10.70.4

1)2)EEB

CEMIG fusiónCPFLEDPCOPELfusiónENIAChileTIETECESPEOCACOLBUNECELSIA

TRACTEBEL post (escenariopost (escenarioENIAESAESGENER

ENIAENIA

Source: Bloomberg. Data as on June 21, 2016. USDCLP exchange rate 679.80.

(1) Average Daily Trading Volume uses data from the last twelve months. For ENIA and EOC Chile, data were used beginning March 1, 2016, date on which the Split was completed. For ENI Chile and EOCA, data were used beginning April 21, 2016, date on which the companies resulting from the Split began trading (2) The size of the circle represents market capitalization (3) To calculate ADTV of ENIA after the merger, it was assumed that ADTV/Float would remain constant after the Merger

Strictly Private and Confidential

49

|

PRELIMINARY VERSION—DRAFT

MARKET AND CASH FLOW CONSIDERATIONS OF THE PROPOSED OPERATION iii. Considerations on Risk Categorization

5

Strictly Private and Confidential

50

|

PRELIMINARY VERSION—DRAFT

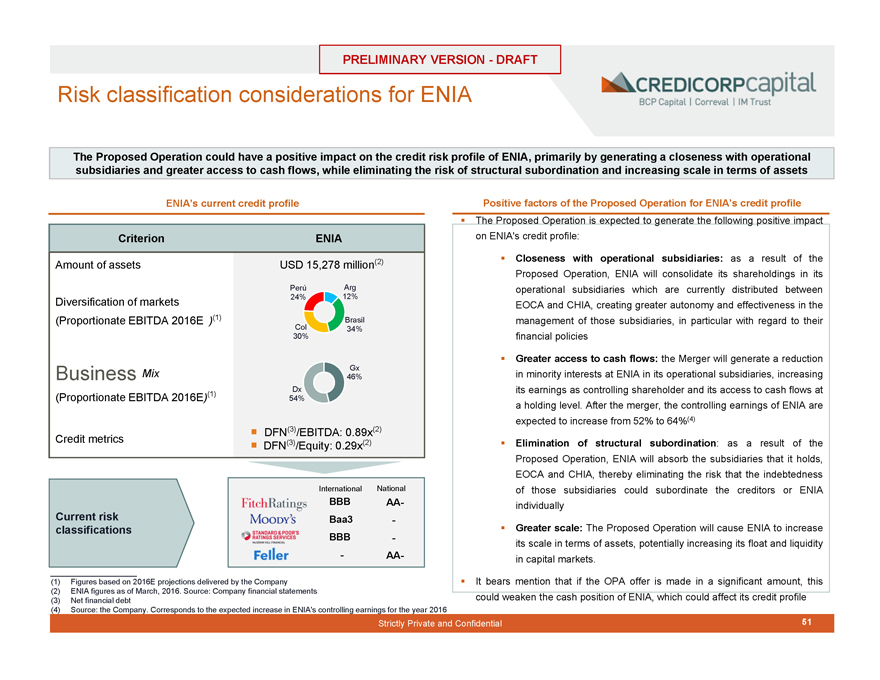

Risk classification considerations for ENIA

The Proposed Operation could have a positive impact on the credit risk profile of ENIA, primarily by generating a closeness with operational subsidiaries and greater access to cash flows, while eliminating the risk of structural subordination and increasing scale in terms of assets

ENIA’s current credit profile

Criterion ENIA

Amount of assets USD 15,278 million(2)

PerúArg

Diversification of markets 24%12%

(Proportionate EBITDA 2016E )(1) Brasil

Col34%

30%

Gx

Business Mix 46%

Dx

(Proportionate EBITDA 2016E)(1) 54%

DFN(3)/EBITDA: 0.89x(2)

Credit metrics DFN(3)/Equity: 0.29x(2)

Current risk classifications

International National

BBB AA-Baa3 -BBB -

- AA-

Positive factors of the Proposed Operation for ENIA’s credit profile

The Proposed Operation is expected to generate the following positive impact on ENIA’s credit profile:

Closeness with operational subsidiaries: as a result of the Proposed Operation, ENIA will consolidate its shareholdings in its operational subsidiaries which are currently distributed between EOCA and CHIA, creating greater autonomy and effectiveness in the management of those subsidiaries, in particular with regard to their financial policies

Greater access to cash flows: the Merger will generate a reduction in minority interests at ENIA in its operational subsidiaries, increasing its earnings as controlling shareholder and its access to cash flows at a holding level. After the merger, the controlling earnings of ENIA are expected to increase from 52% to 64%(4)

Elimination of structural subordination: as a result of the Proposed Operation, ENIA will absorb the subsidiaries that it holds, EOCA and CHIA, thereby eliminating the risk that the indebtedness of those subsidiaries could subordinate the creditors or ENIA individually

Greater scale: The Proposed Operation will cause ENIA to increase its scale in terms of assets, potentially increasing its float and liquidity in capital markets.

It bears mention that if the OPA offer is made in a significant amount, this could weaken the cash position of ENIA, which could affect its credit profile

(1) Figures based on 2016E projections delivered by the Company (2) ENIA figures as of March, 2016. Source: Company financial statements (3) Net financial debt

(4) Source: the Company. Corresponds to the expected increase in ENIA’s controlling earnings for the year 2016

Strictly Private and Confidential

51

|

PRELIMINARY VERSION—DRAFT

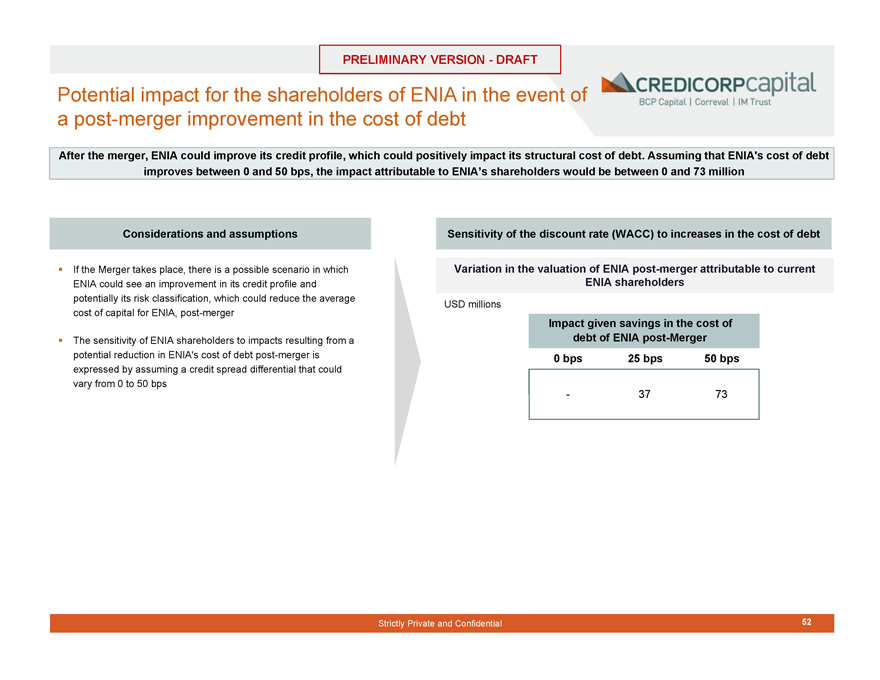

Potential impact for the shareholders of ENIA in the event of a post-merger improvement in the cost of debt

After the merger, ENIA could improve its credit profile, which could positively impact its structural cost of debt. Assuming that ENIA’s cost of debt improves between 0 and 50 bps, the impact attributable to ENIA’s shareholders would be between 0 and 73 million