Exhibit (C)(8)(D)

|

November 2, 2015

Strictly Private and Confidential

Advisory Report on the Reorganization of Enersis S.A.

Prepared for the Enersis S.A. Board of Directors

|

Important information

This document has been prepared by IM Trust consultants financial S.A. (hereinafter “IM Trust”) at the request of the Board of Directors of Enersis S.A. (‘Enersis’, “ENI” or the “Company”) for the exclusive and private use of the company and its Board of Directors.

The recommendations and conclusions of this document constitute the best opinion of IM Trust regarding the Reorganization of Enersis at the time of issuance of this document, considering the methodologies used for this purpose and the information that was available. This document’s conclusions may vary if additional or other background information were available. IM Trust shall be under no obligation to report such variations nor when the opinions or information contained in the document are modified.

For the preparation of the present document, IM Trust has been based solely on information provided by Enersis and public information, for which IM Trust has assumed, without independent verification, its complete and total integrity and accuracy. In this way, IM Trust assumes no responsibility with regard to the information reviewed by the conclusions arising out of any error, inaccuracy, and/or falsity of such information.

Likewise, the conclusions of the document may be based on assumptions that may be subject to significant uncertainties and economic and market contingencies, such as flows, projections, estimates, and interpretations, the occurrence of which can be difficult to predict and many of which could even be beyond the reach of Enersis, so there is no certainty at all about the degree of fulfillment of such assumptions. Under no circumstances may the use or incorporation of such flows, projections or estimates be considered as a representation, warranty, or prediction by IM Trust regarding their occurrence, nor of the assumptions that underlie them.

Strictly Private and Confidential 2

|

Contents

1. Executive summary 4

2. Background and scope of the evaluation 19

3. Description of the Reorganization 23

4. General Considerations and analytical scheme 35

5. Considerations of the business model 39

6. Impact of the Reorganization on the Market Value of Enersis 44 i. Holding Discount Considerations 44 ii. Liquidity Considerations 55 iii. Risk rating considerations 60 iv. Summary 64

7. Cash flow impacts from the reorganization in the value of Enersis 66 i. Impacts on EBITDA 66 ii. Tax impacts 70 iii. Transaction Costs (one-off) 73 iv. Summary 75

8. Estimate of relative holdings in the merger in ENI Americas 77 i. Relative holdings according to discounted cash flow appraisal 79 ii. Relative holdings according to multiples appraisal and market capitalization 86 iii. Relative holdings adjusted by cost disproportionality of the Reorganization 91 iv. Summary 93

9. Answers to questions made by members of the Board of Directors of Enersis 99 10. Attachments 103

Strictly Private and Confidential 3

|

EXECUTIVE SUMMARY 1

Strictly Private and Confidential 4

|

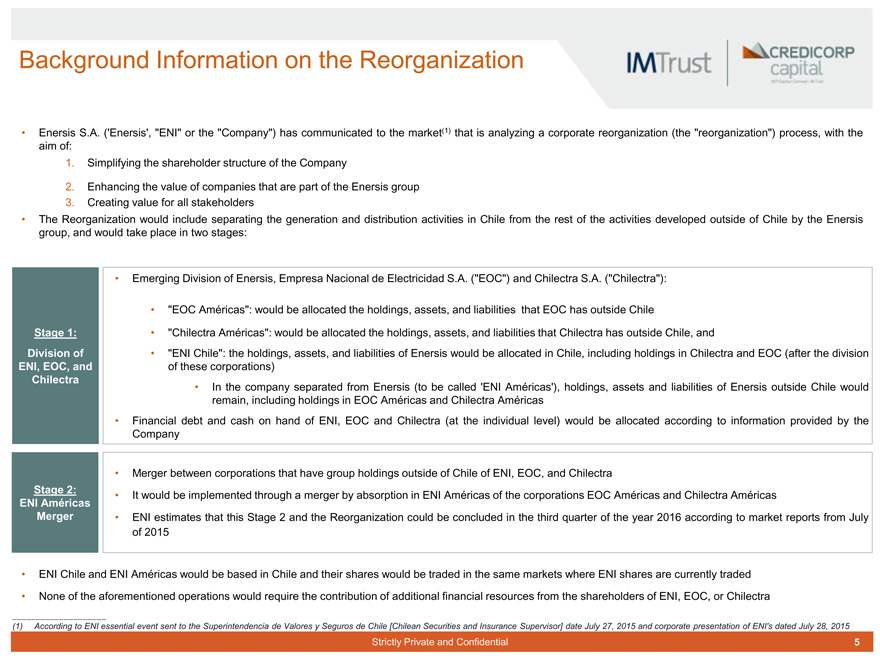

Background Information on the Reorganization

Enersis S.A. (‘Enersis’, “ENI” or the “Company”) has communicated to the market(1) that is analyzing a corporate reorganization (the “reorganization”) process, with the aim of:

1. Simplifying the shareholder structure of the Company

2. Enhancing the value of companies that are part of the Enersis group

3. Creating value for all stakeholders

The Reorganization would include separating the generation and distribution activities in Chile from the rest of the activities developed outside of Chile by the Enersis group, and would take place in two stages:

Emerging Division of Enersis, Empresa Nacional de Electricidad S.A. (“EOC”) and Chilectra S.A. (“Chilectra”):

“EOC Américas”: would be allocated the holdings, assets, and liabilities that EOC has outside Chile

“Chilectra Américas”: would be allocated the holdings, assets, and liabilities that Chilectra has outside Chile, and

“ENI Chile”: the holdings, assets, and liabilities of Enersis would be allocated in Chile, including holdings in Chilectra and EOC (after the division of these corporations)

In the company separated from Enersis (to be called ‘ENI Américas’), holdings, assets and liabilities of Enersis outside Chile would remain, including holdings in EOC Américas and Chilectra Américas

Financial debt and cash on hand of ENI, EOC and Chilectra (at the individual level) would be allocated according to information provided by the Company

Merger between corporations that have group holdings outside of Chile of ENI, EOC, and Chilectra

It would be implemented through a merger by absorption in ENI Américas of the corporations EOC Américas and Chilectra Américas

ENI estimates that this Stage 2 and the Reorganization could be concluded in the third quarter of the year 2016 according to market reports from July of 2015

Stage 1: Division of ENI, EOC, and Chilectra

Stage 2: ENI Américas Merger

ENI Chile and ENI Américas would be based in Chile and their shares would be traded in the same markets where ENI shares are currently traded

None of the aforementioned operations would require the contribution of additional financial resources from the shareholders of ENI, EOC, or Chilectra

(1) According to ENI essential event sent to the Superintendencia de Valores y Seguros de Chile [Chilean Securities and Insurance Supervisor] date July 27, 2015 and corporate presentation of ENI’s dated July 28, 2015

Strictly Private and Confidential 5

|

Scope of the report

IM Trust Asesorías Financieras S.A. [IM Trust Financial Consultants] (“IM Trust”), acting as financial consultant to the Board of Directors of Enersis, with regard to the Reorganization. The scope of such consulting will be equivalent to those provided in the Chilean Companies Act Law No. 18,046 in its Article 147, regarding independent evaluators

In accordance with the above, in its capacity as consultant of the Board of Directors, IM Trust prepared this report (hereinafter the “report”) which contains among others the following elements:

A description of the proposed Reorganization

An assessment of whether the Reorganization helps the best interest of Enersis

An estimate of the relative holdings in the ENI Américas merger, which in our view on today’s date would be consistent with market terms

As part of the analysis, IM Trust has included the following in the report:

An analysis of potential impacts on the value and risks with regard to the reorganization, in order to estimate if it contributes to the best interest of Enersis and the rational strategic

An estimate of relative shares for the merger between ENI Americas, EOC Americas and Chilectra Americas within the framework of the reorganization

Note that for not being within the scope of this advice, this report does not consider:

An analysis of the advantages and disadvantages of alternative structures or alternative implementation mechanisms to carry out the reorganization that is evaluated here

A detailed analysis of the technical, commercial, legal and/or other type of feasibility of the implementation of the Reorganization

Strictly Private and Confidential 6

|

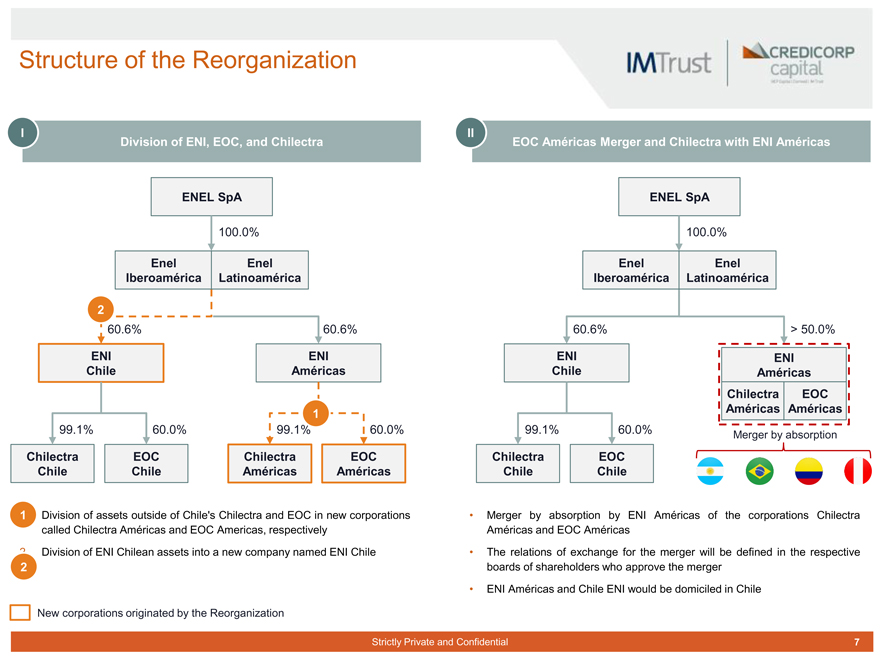

Structure of the Reorganization

I

Division of ENI, EOC, and Chilectra

ENEL SpA

100.0%

Enel Iberoamérica

Enel Latinoamérica

2

60.6% 60.6%

ENI Chile ENI Américas

1

99.1% 60.0% 99.1% 60.0%

Chilectra EOC Chilectra EOC Chile Chile Américas Américas

1. Division of assets outside of Chile’s Chilectra and EOC in new corporations called Chilectra Américas and EOC Americas, respectively

2. Division of ENI Chilean assets into a new company named ENI Chile

2

New corporations originated by the Reorganization

II

EOC Américas Merger and Chilectra with ENI Américas

ENEL SpA

100.0%

Enel Iberoamérica Enel Latinoamérica

60.6% > 50.0%

ENI Chile ENI Américas EOC

Américas Chilectra Américas

99.1% 60.0% Merger by absorption

Chilectra EOC Chile Chile

Merger by absorption by ENI Américas of the corporations Chilectra Américas and EOC Américas

The relations of exchange for the merger will be defined in the respective boards of shareholders who approve the merger

ENI Américas and Chile ENI would be domiciled in Chile

Strictly Private and Confidential 7

|

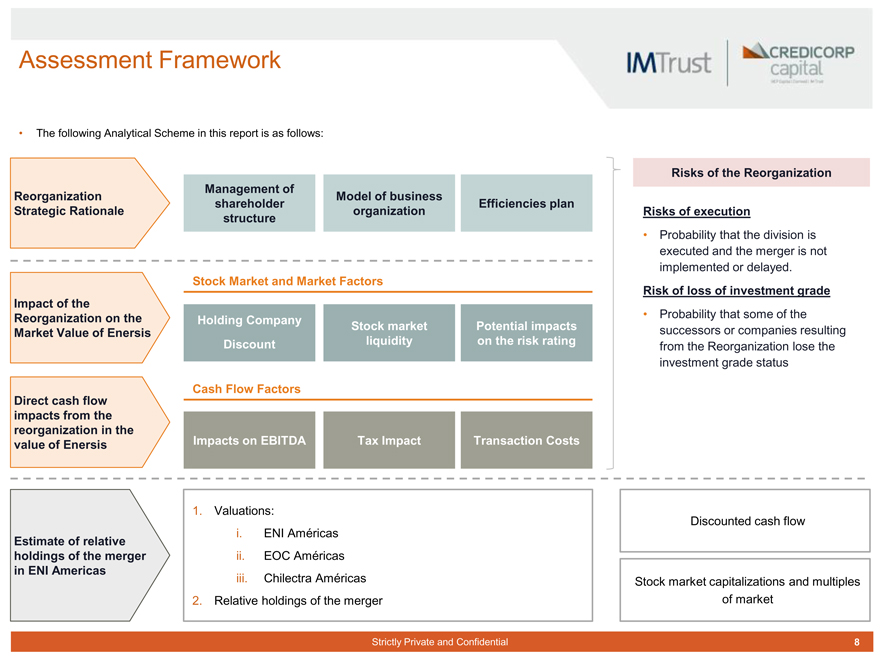

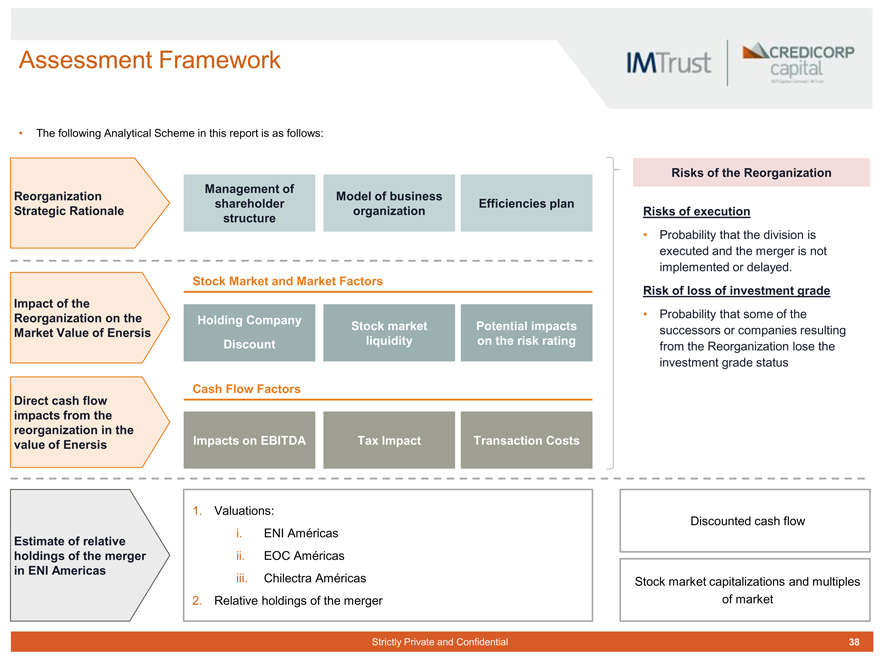

Assessment Framework

The following Analytical Scheme in this report is as follows:

Reorganization Strategic Rationale Management of shareholder structure Model of business organizationEfficiencies plan

Impact of the Reorganization on the Market Value of Enersis Stock Market and Market Factors Holding Company Discount Stock market liquidity

Potential impacts on the risk rating

Direct cash flow impacts from the reorganization in the value of Enersis Cash Flow Factors Impacts on EBITDA Tax ImpactTransaction Costs

Risks of the Reorganization

Risks of execution

Probability that the division is executed and the merger is not implemented or delayed.

Risk of loss of investment grade

Probability that some of the successors or companies resulting from the Reorganization lose the investment grade status

Estimate of relative holdings of the merger in ENI Americas

1. Valuations:

i. ENI Américas

ii. EOC Américas

iii. Chilectra Américas

2. Relative holdings of the merger

Discounted cash flow

Stock market capitalizations and multiples of market

Strictly Private and Confidential 8

|

Reorganization Strategic Rationale

1

Management of shareholder structure

2

Integrated organizational model by geographic area

3

Efficiencies plan

The shareholder structure and management of ENI has been analyzing over time with the existence of cross-ownerships between different Enersis group corporations. The proposed Reorganization pursues the ordering of the shareholder structure and its administration

The separation of ENI in companies with different growth, investment, and dividend offers could result in:

Attracting new investors with different investment preferences, potentially reducing gaps in recovery with its comparables

Greater flexibility to optimize stock market exposure of existing shareholders to the different markets

The reduction of holding administration costs, better management of the structure, and bringing the operational branches to the shareholders, could reduce to some extent the historical holding discount that ENI has had.

It’s only natural that the organization’s structural model will be used as a control device by the controlling shareholder and referred to industrialist or the operator. In this case, Enel has a preference for a model organized primarily by geographic market

In the present consulting analysis, it is not possible to distinguish the existence of a predominant organizational model among the leading integrated electric companies, coexisting in practice with models sorted geographically or by business. Within foreign multinationals operating in Chile and Latin America (“LatAm”) in other industries, it is most common for each country to report directly to the head office

In this regard:

The organization in Chile of ENI is understandable, but the rational becomes less apparent for organizing ENI holdings outside of Chile in a holding based in Chile

In terms of similarity and dynamics of markets, it could also be logical to separate Brazil or group Chile, Peru and Colombia, or even make each market / country depend directly on the Enel parent company. These alternative scenarios have not been evaluated in this Report since they are not within the scope of this advice

In this regard, we believe that it is important that the controlling shareholder and the Directorate of ENI communicate to the market clearly what the long-term structure is and explain the potential future steps and the necessary conditions so that these are given

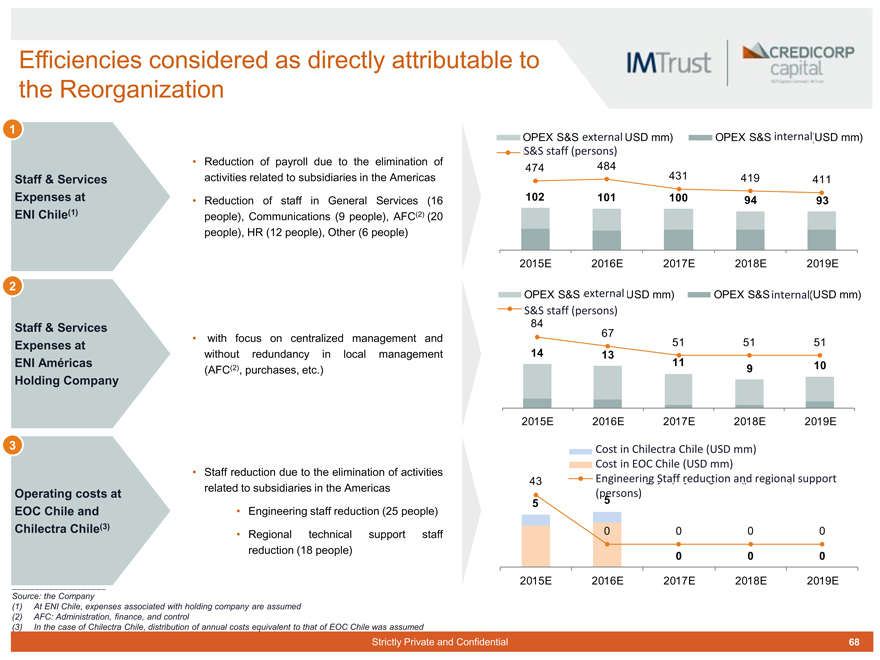

In conjunction with the Reorganization, the company has presented a efficiencies plan at the level of operating costs and expenses in the administration of the holdings

The efficiencies plan presented to the Directorate involves significant savings and that they would be contracted from the year 2019

The efficiencies plan considers savings at the level of the holdings unit as well as at the operational level in which the reorganization would act as catalyst

For purposes of the analysis carried out in this report on the direct impact of the Reorganization on cash flow, only the portion of the savings attributable to the Reorganization as described later has been considered, which does not imply an assessment of the capacity of implementation and the likelihood of success of such a plan

Strictly Private and Confidential 9

|

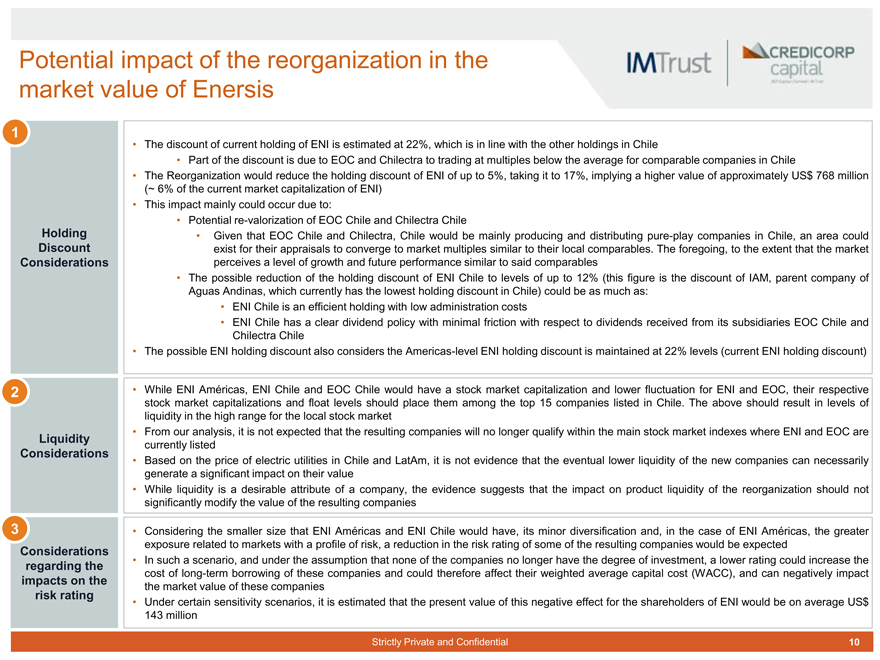

Potential impact of the reorganization in the market value of Enersis

1 Holding Discount Considerations

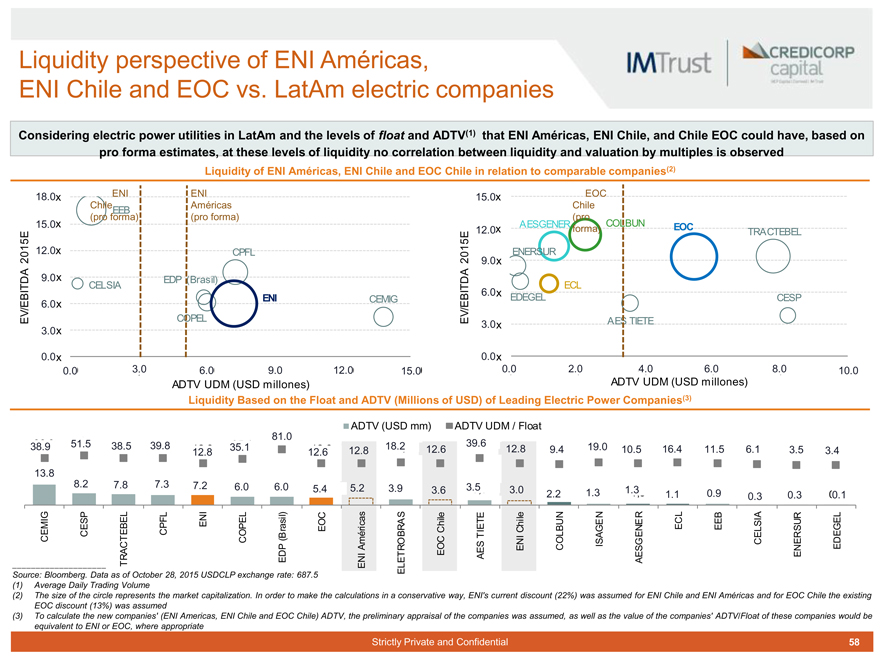

2 Liquidity Considerations

3 Considerations regarding the impacts on the risk rating

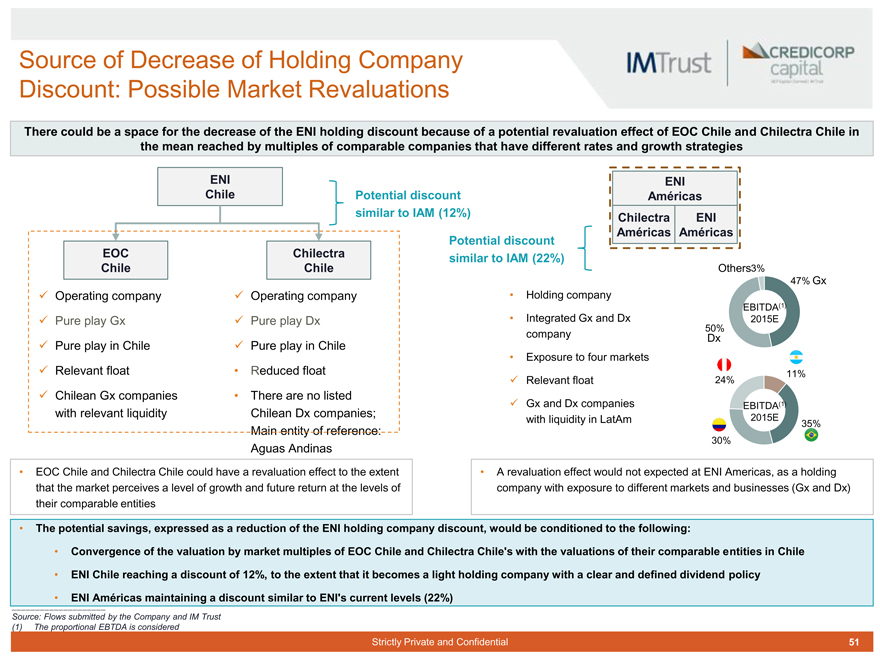

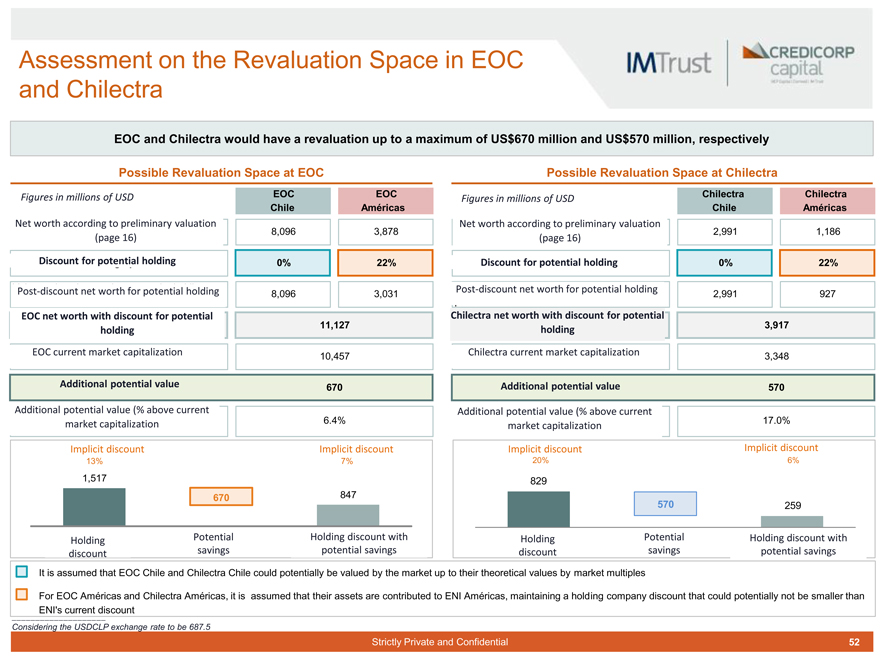

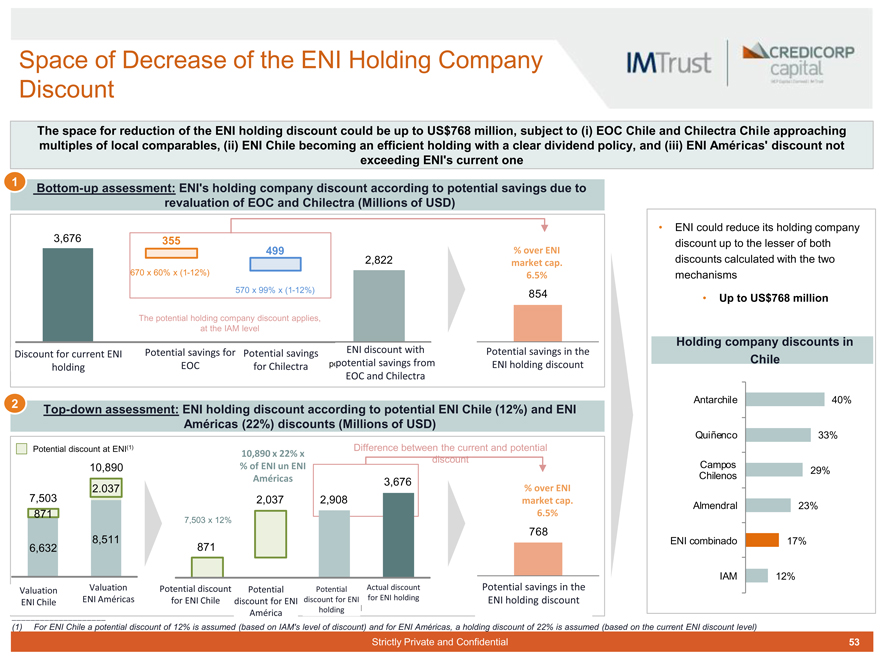

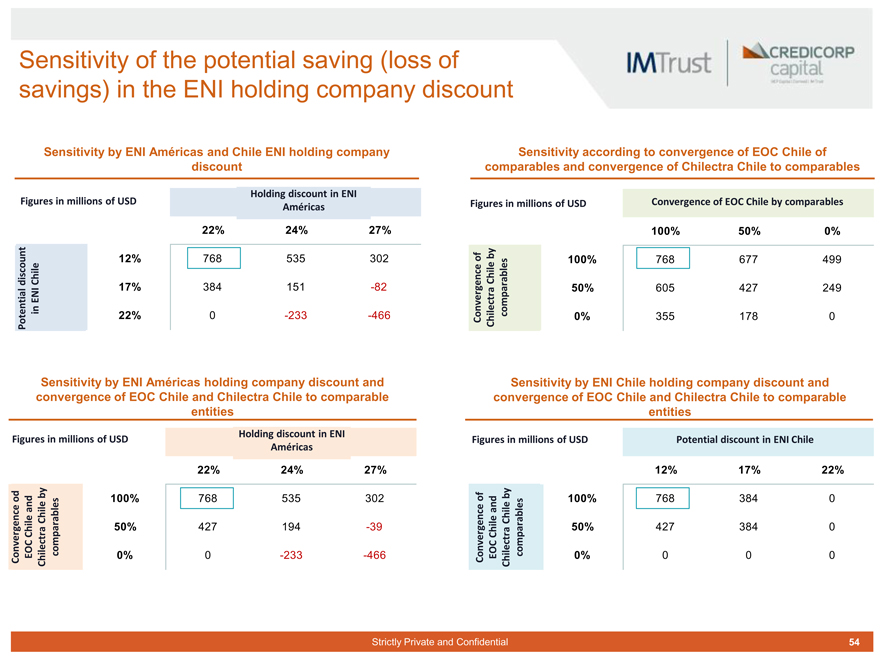

The discount of current holding of ENI is estimated at 22%, which is in line with the other holdings in Chile

Part of the discount is due to EOC and Chilectra to trading at multiples below the average for comparable companies in Chile

The Reorganization would reduce the holding discount of ENI of up to 5%, taking it to 17%, implying a higher value of approximately US$ 768 million

(~ 6% of the current market capitalization of ENI) This impact mainly could occur due to:

Potential re-valorization of EOC Chile and Chilectra Chile

Given that EOC Chile and Chilectra, Chile would be mainly producing and distributing pure-play companies in Chile, an area could exist for their appraisals to converge to market multiples similar to their local comparables. The foregoing, to the extent that the market perceives a level of growth and future performance similar to said comparables

The possible reduction of the holding discount of ENI Chile to levels of up to 12% (this figure is the discount of IAM, parent company of Aguas Andinas, which currently has the lowest holding discount in Chile) could be as much as:

ENI Chile is an efficient holding with low administration costs

ENI Chile has a clear dividend policy with minimal friction with respect to dividends received from its subsidiaries EOC Chile and Chilectra Chile The possible ENI holding discount also considers the Americas-level ENI holding discount is maintained at 22% levels (current ENI holding discount)

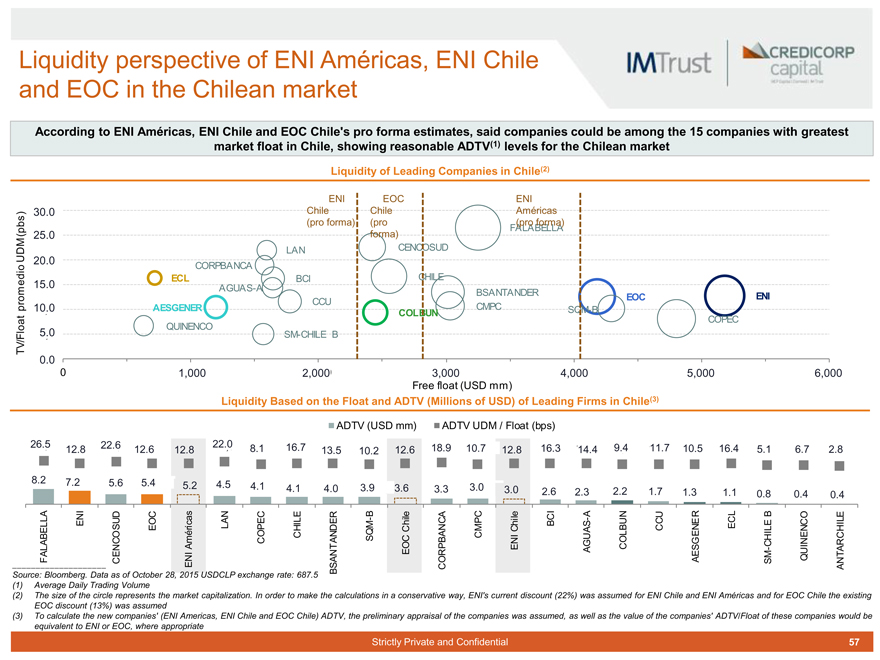

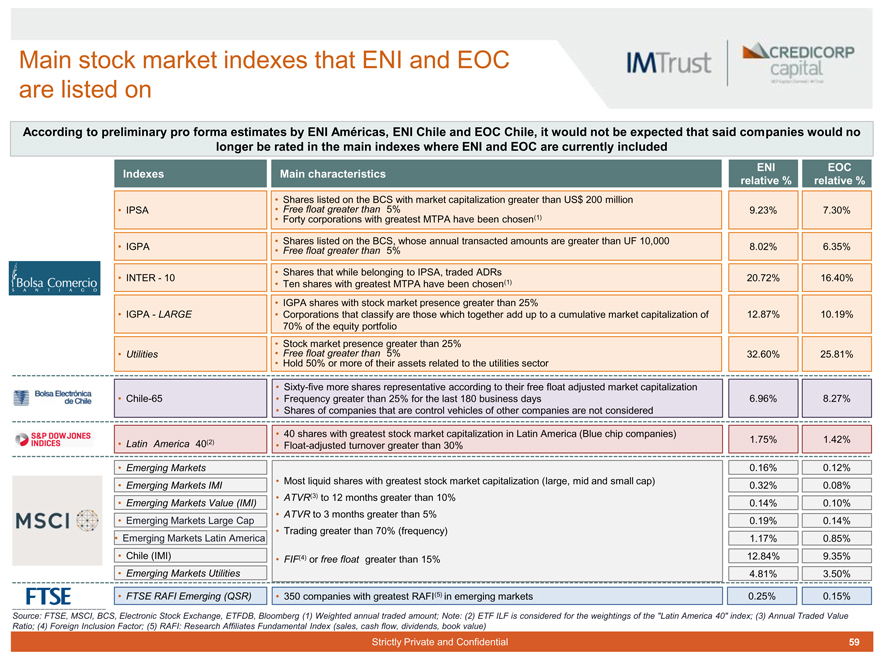

While ENI Américas, ENI Chile and EOC Chile would have a stock market capitalization and lower fluctuation for ENI and EOC, their respective stock market capitalizations and float levels should place them among the top 15 companies listed in Chile. The above should result in levels of liquidity in the high range for the local stock market From our analysis, it is not expected that the resulting companies will no longer qualify within the main stock market indexes where ENI and EOC are currently listed Based on the price of electric utilities in Chile and LatAm, it is not evidence that the eventual lower liquidity of the new companies can necessarily generate a significant impact on their value While liquidity is a desirable attribute of a company, the evidence suggests that the impact on product liquidity of the reorganization should not significantly modify the value of the resulting companies

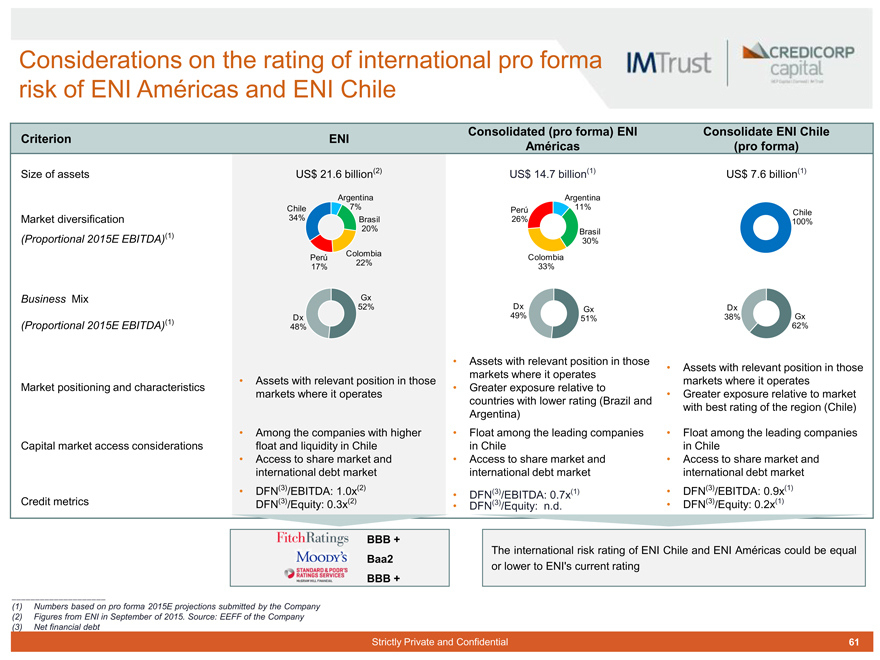

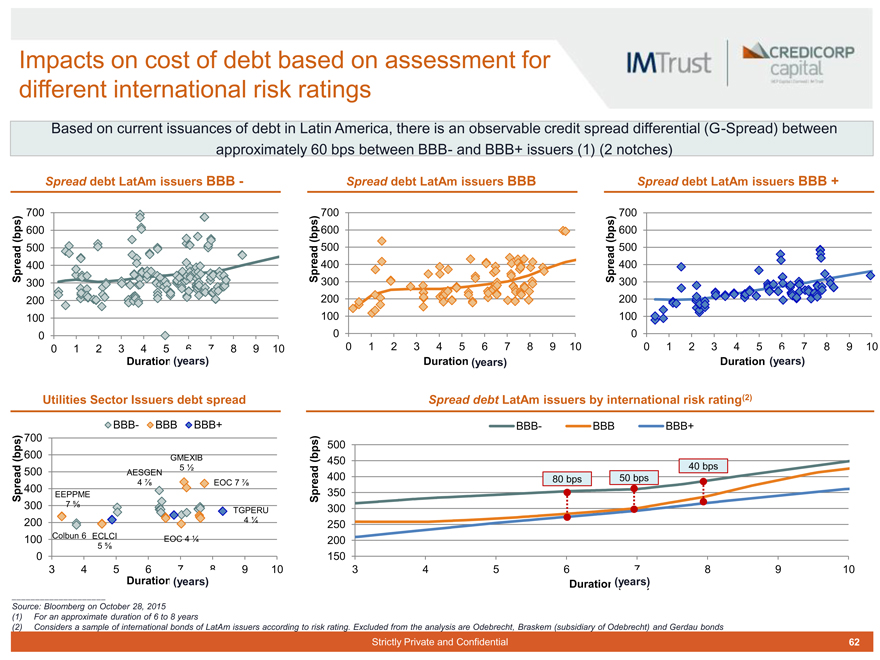

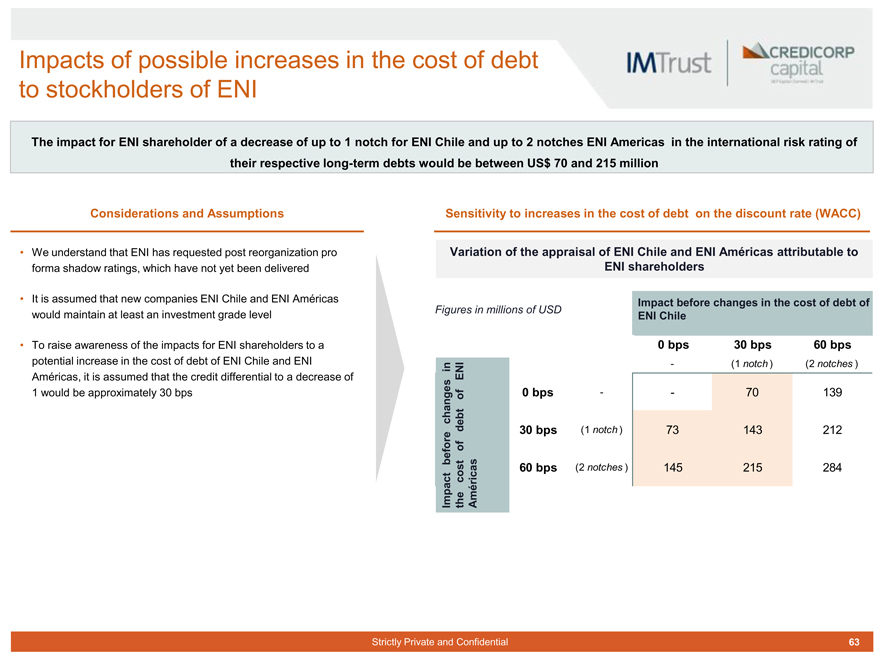

Considering the smaller size that ENI Américas and ENI Chile would have, its minor diversification and, in the case of ENI Américas, the greater exposure related to markets with a profile of risk, a reduction in the risk rating of some of the resulting companies would be expected In such a scenario, and under the assumption that none of the companies no longer have the degree of investment, a lower rating could increase the cost of long-term borrowing of these companies and could therefore affect their weighted average capital cost (WACC), and can negatively impact the market value of these companies Under certain sensitivity scenarios, it is estimated that the present value of this negative effect for the shareholders of ENI would be on average US$ 143 million

Strictly Private and Confidential 10

|

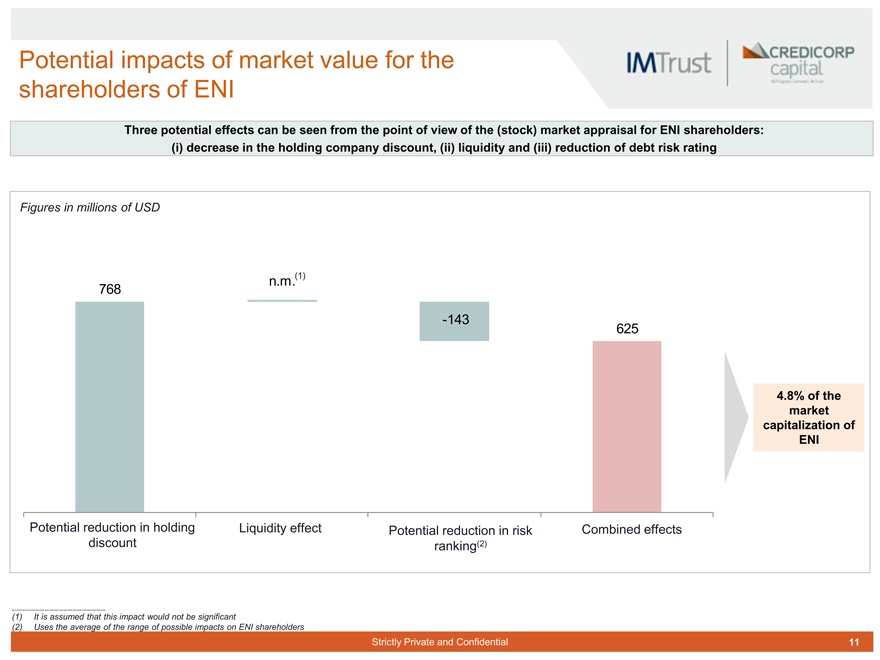

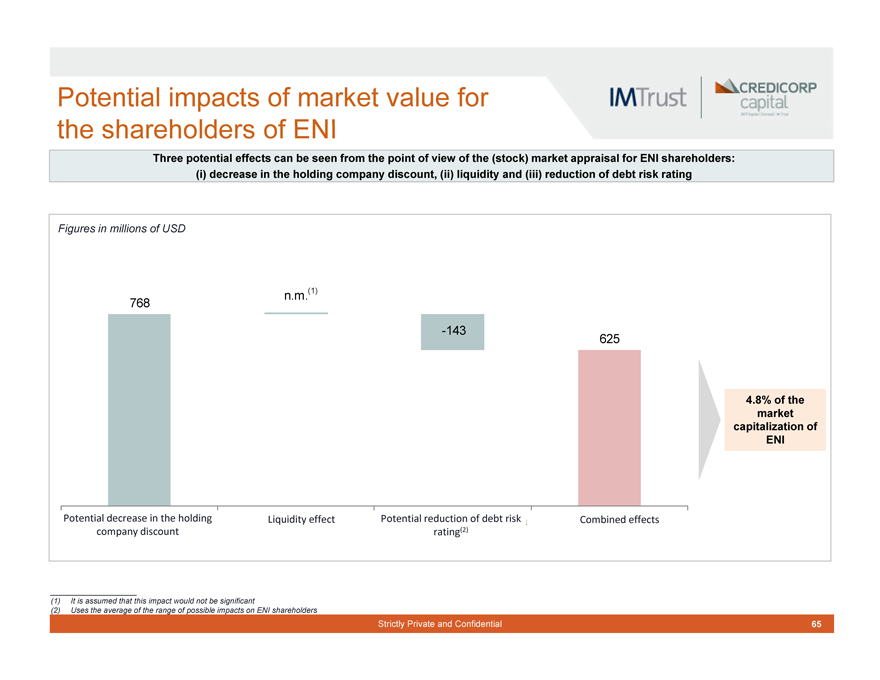

Potential impacts of market value for the shareholders of ENI

Three potential effects can be seen from the point of view of the (stock) market appraisal for ENI shareholders: (i) decrease in the holding company discount, (ii) liquidity and (iii) reduction of debt risk rating

Figures in millions of USD

n.m.(1) 768

-143

625

4.8% of the market capitalization of ENI

Potential reduction in holding Liquidity effect Potential reduction in risk Combined effects discount ranking(2)

(1) It is assumed that this impact would not be significant

(2) Uses the average of the range of possible impacts on ENI shareholders

Strictly Private and Confidential 11

|

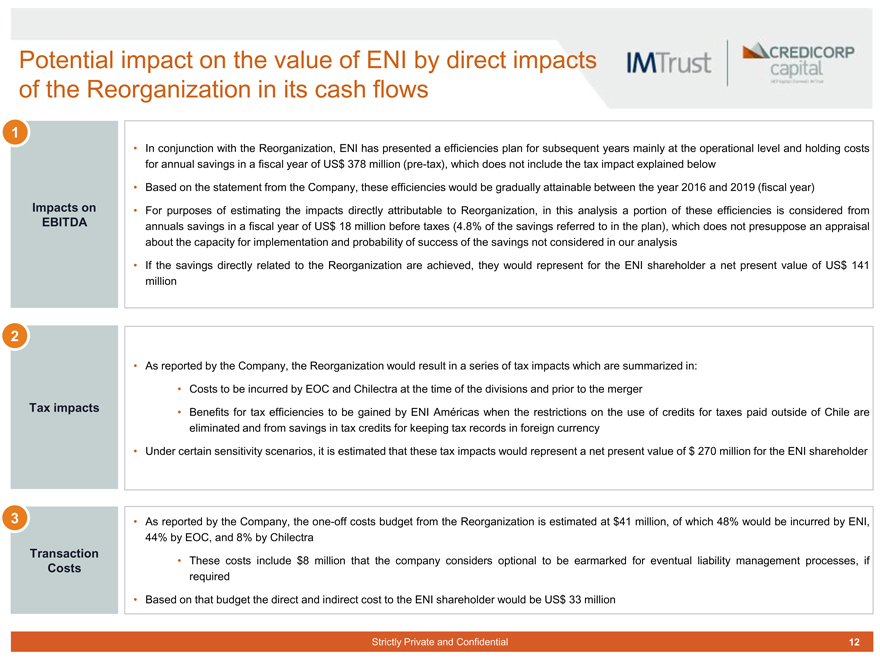

Potential impact on the value of ENI by direct impacts of the Reorganization in its cash flows

1

Impacts on EBITDA

2

Tax impacts

3

Transaction Costs

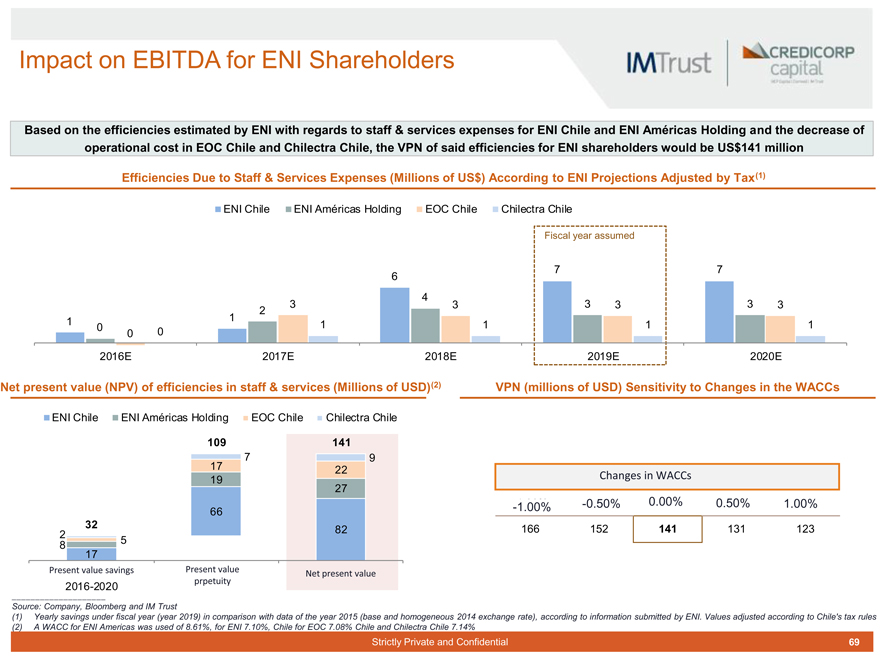

In conjunction with the Reorganization, ENI has presented a efficiencies plan for subsequent years mainly at the operational level and holding costs for annual savings in a fiscal year of US$ 378 million (pre-tax), which does not include the tax impact explained below

Based on the statement from the Company, these efficiencies would be gradually attainable between the year 2016 and 2019 (fiscal year)

For purposes of estimating the impacts directly attributable to Reorganization, in this analysis a portion of these efficiencies is considered from annuals savings in a fiscal year of US$ 18 million before taxes (4.8% of the savings referred to in the plan), which does not presuppose an appraisal about the capacity for implementation and probability of success of the savings not considered in our analysis

If the savings directly related to the Reorganization are achieved, they would represent for the ENI shareholder a net present value of US$ 141 million

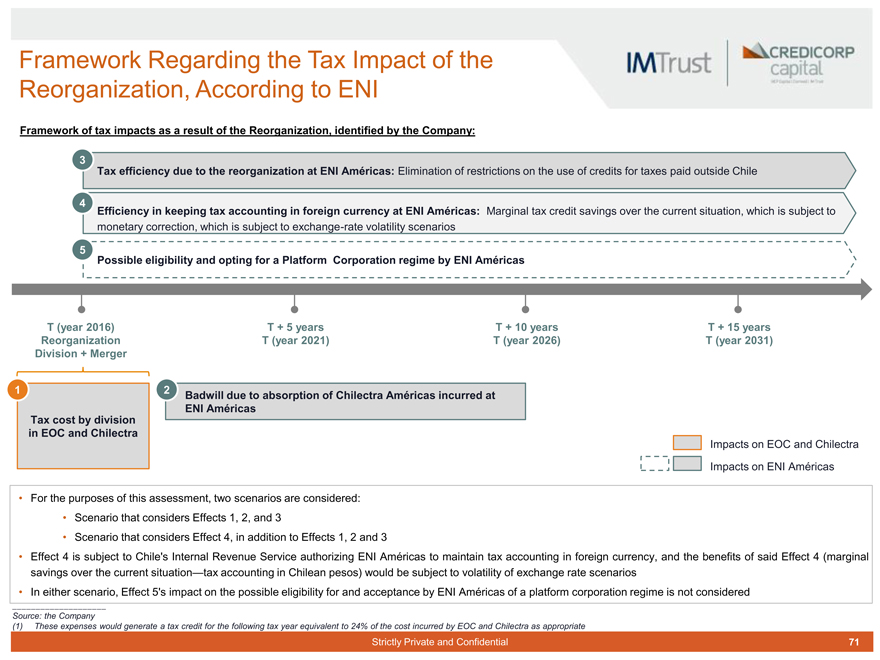

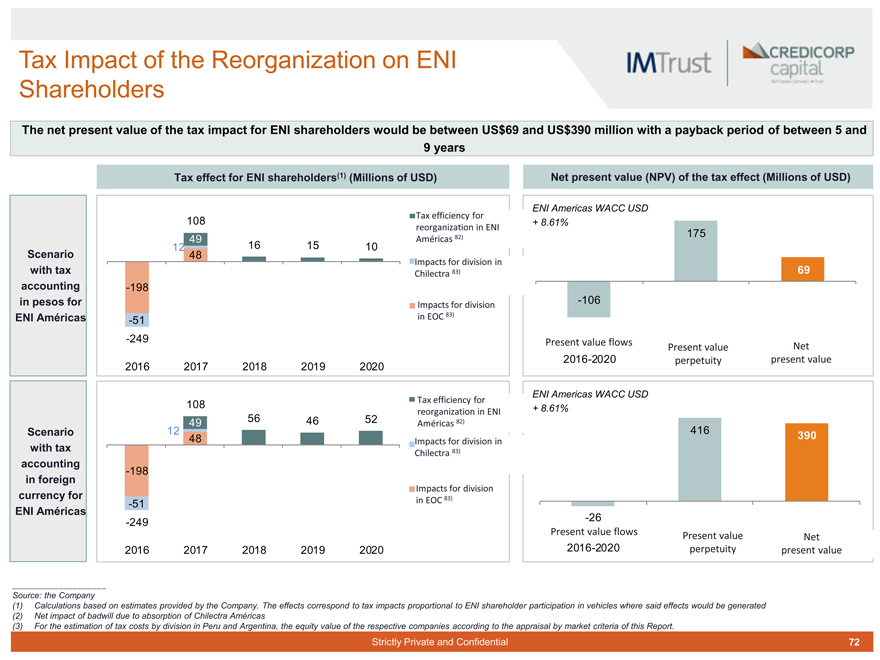

As reported by the Company, the Reorganization would result in a series of tax impacts which are summarized in:

Costs to be incurred by EOC and Chilectra at the time of the divisions and prior to the merger

Benefits for tax efficiencies to be gained by ENI Américas when the restrictions on the use of credits for taxes paid outside of Chile are eliminated and from savings in tax credits for keeping tax records in foreign currency

Under certain sensitivity scenarios, it is estimated that these tax impacts would represent a net present value of $ 270 million for the ENI shareholder

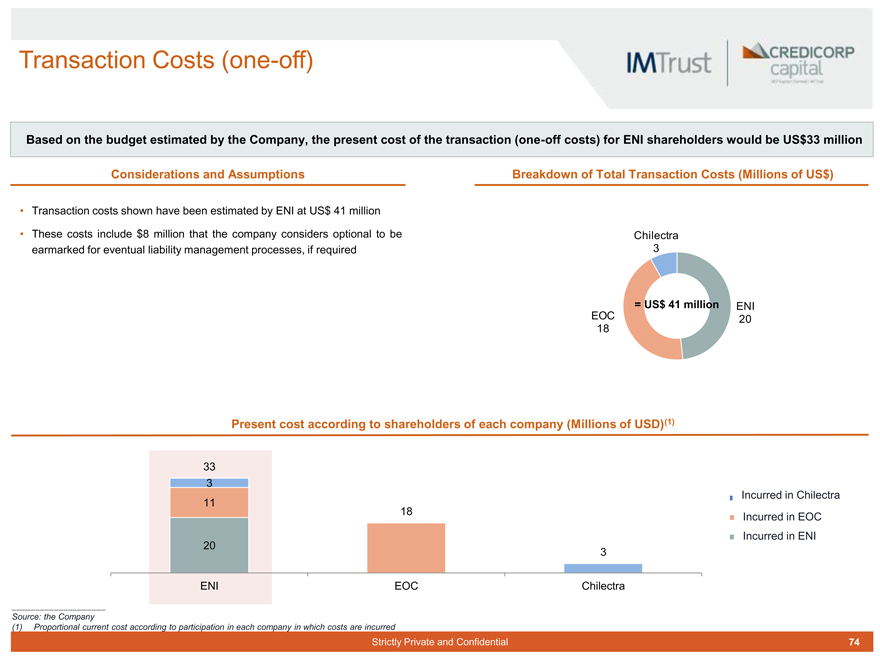

As reported by the Company, the one-off costs budget from the Reorganization is estimated at $41 million, of which 48% would be incurred by ENI, 44% by EOC, and 8% by Chilectra

These costs include $8 million that the company considers optional to be earmarked for eventual liability management processes, if required

Based on that budget the direct and indirect cost to the ENI shareholder would be US$ 33 million

Strictly Private and Confidential 12

|

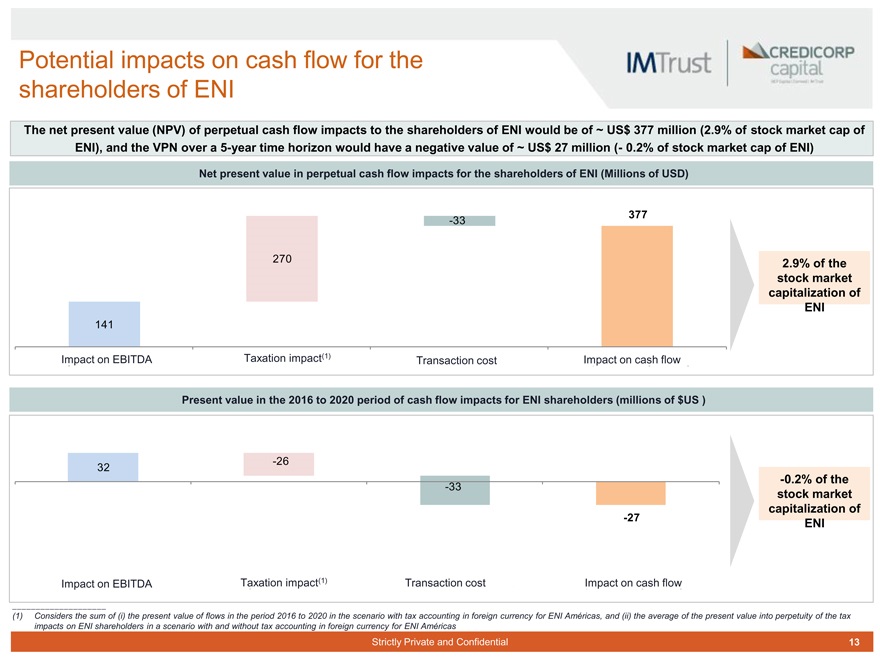

Potential impacts on cash flow for the shareholders of ENI

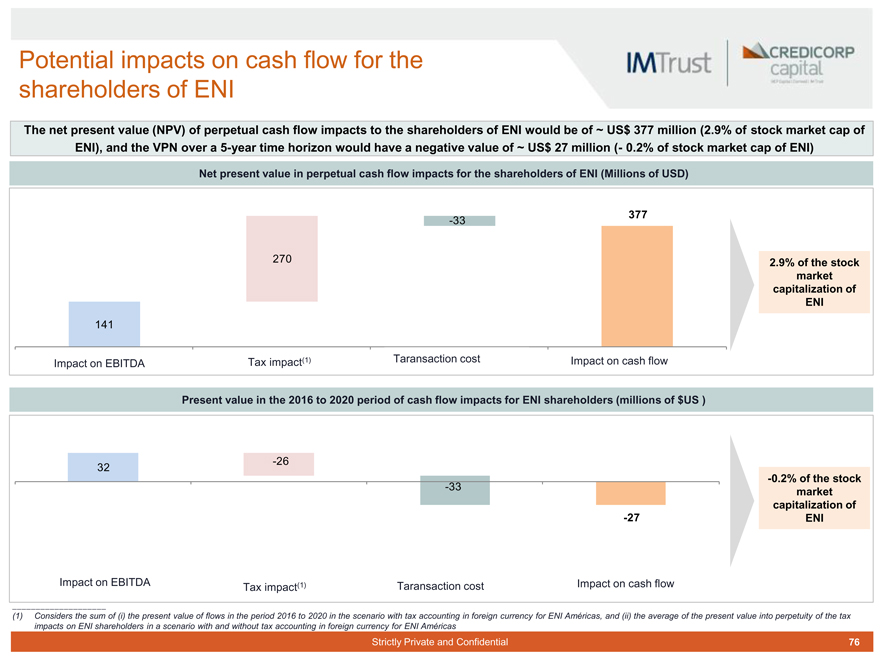

The net present value (NPV) of perpetual cash flow impacts to the shareholders of ENI would be of ~ US$ 377 million (2.9% of stock market cap of ENI), and the VPN over a 5-year time horizon would have a negative value of ~ US$ 27 million (- 0.2% of stock market cap of ENI)

Net present value in perpetual cash flow impacts for the shareholders of ENI (Millions of USD)

377

-33

270 2.9% of the stock market capitalization of ENI

141

Impact on EBITDA Taxation impact(1) Transaction cost

Impact on cash flow

2.9% of the stock market capitalization of ENI

Present value in the 2016 to 2020 period of cash flow impacts for ENI shareholders (millions of $US )

-0.2% of the stock market capitalization of ENI

-26 32

-33

-27

Impact on EBITDA Taxation impact(1) Transaction cost

(1) Considers the sum of (i) the present value of flows in the period 2016 to 2020 in the scenario with tax accounting in foreign currency for ENI Américas, and (ii) the average of the present value into perpetuity of the tax impacts on ENI shareholders in a scenario with and without tax accounting in foreign currency for ENI Américas

Strictly Private and Confidential 13

|

Main risks of the Reorganization

There are risks that are inherent to the businesses that participate Enersis, such as market, regulatory, climatic risks, etc., and that are not directly related or attributable to the Reorganization

Within the risks that are attributable to the Reorganization, we have identified two that could significantly affect the results of not being adequately mitigated and whose probability of occurrence is not considered in the analysis results

Risk of execution

Risk of executing the division of ENI, EOC and Chilectra, and the merger of the resulting companies of this division will fail to materialize or there is more than a reasonable delay

The scenario in which the divisions are executed and the merger does not take place, among others, by any of the following events:

No approval of the merger by the shareholders of ENI Américas, EOC Américas and/or Chilectra Américas

Exercise the right to withdrawal by the shareholders of ENI Américas, EOC Américas and/or Chilectra Americas for an amount greater than that established as a condition of the merger, or if there is no such condition, is not financially affordable.

Not granting or excessive delay of approvals or regulatory requirements (free competition, SVS, etc.)

Prosecution of the process

Such a scenario could affect the Reorganization in at least the following aspects:

Not achieving the proposed shareholder structure system to maintain the cross-ownerships of the ENI subsidiaries

Greater difficulty in implementing the efficiencies plan presented by the Company in conjunction with the Reorganization, even incurring higher costs by having to maintain a greater number of open market holding companies

Insufficient stock market liquidity, product of the smaller size of the ENI Américas, EOC Américas and Chilectra Américas corporations separately (not merged), which may affect the market value of such corporations

Greater likelihood of investment grade credit rating loss of some of the resulting holding companies that may affect their financial condition and market value

Risk of loss of investment grade

Risk that, as a result of the Reorganization, ENI Américas, ENI Chile and/or EOC Chile lose the international investment-grade credit condition Such a scenario could affect the Reorganization in at least the following aspects:

Increase in the cost of long-term borrowing that may have a significant effect on the market value of the affected companies and their future competitiveness

Potential exclusion from the universe of investors that may invest in these corporations both in terms of capital and debt

Activation of investment degree maintenance clauses in current debt agreements

Strictly Private and Confidential 14

|

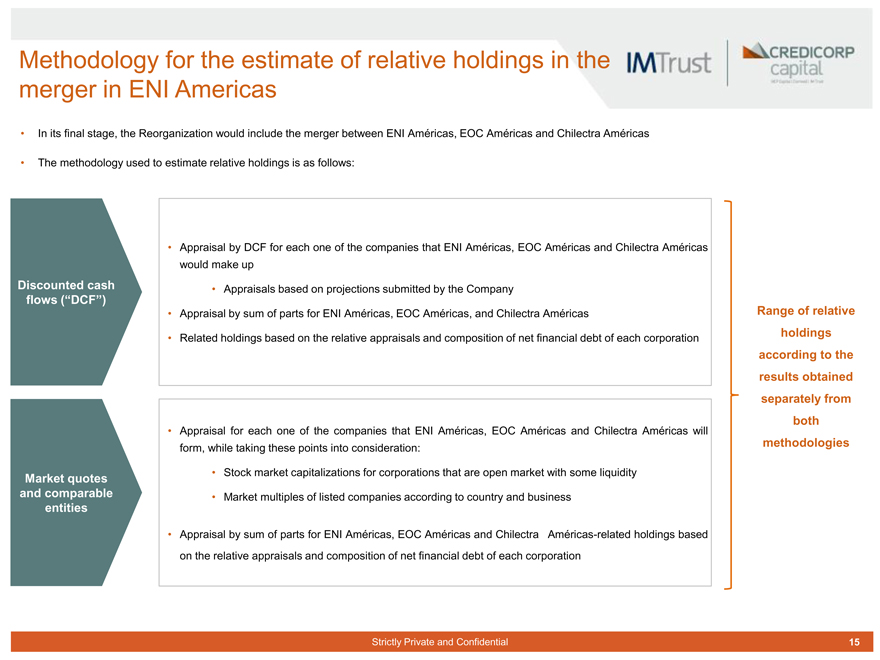

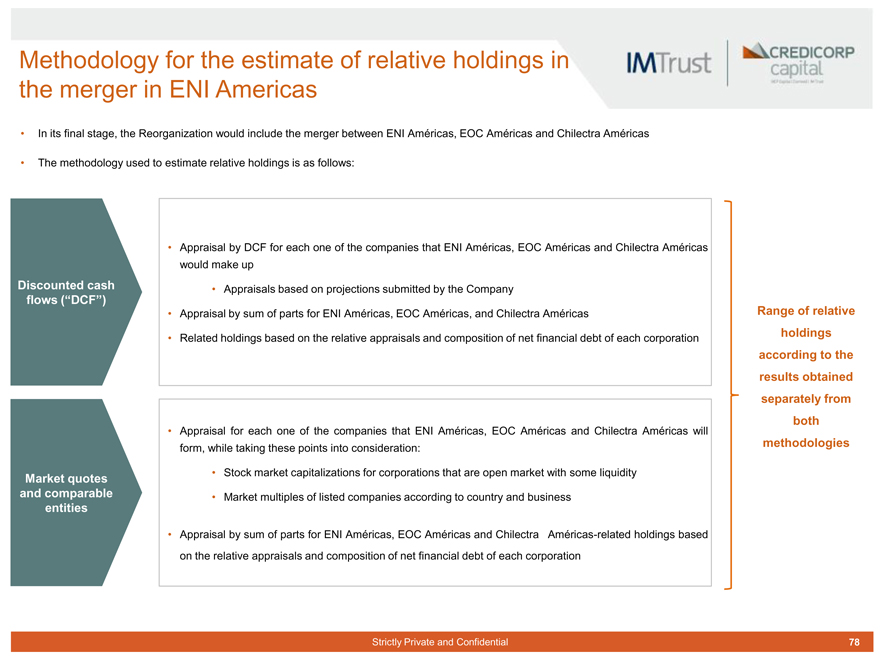

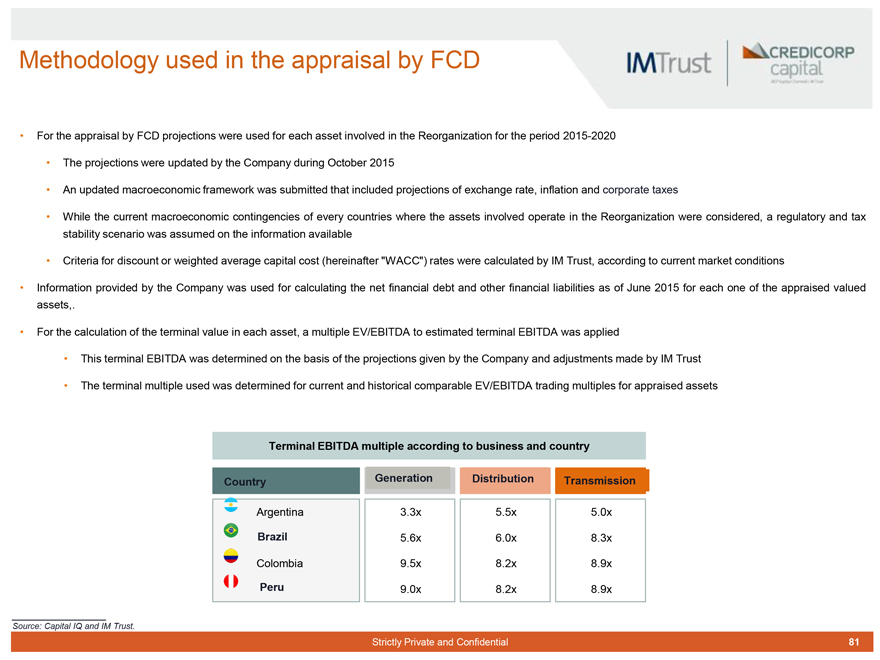

Methodology for the estimate of relative holdings in the merger in ENI Americas

In its final stage, the Reorganization would include the merger between ENI Américas, EOC Américas and Chilectra Américas

The methodology used to estimate relative holdings is as follows:

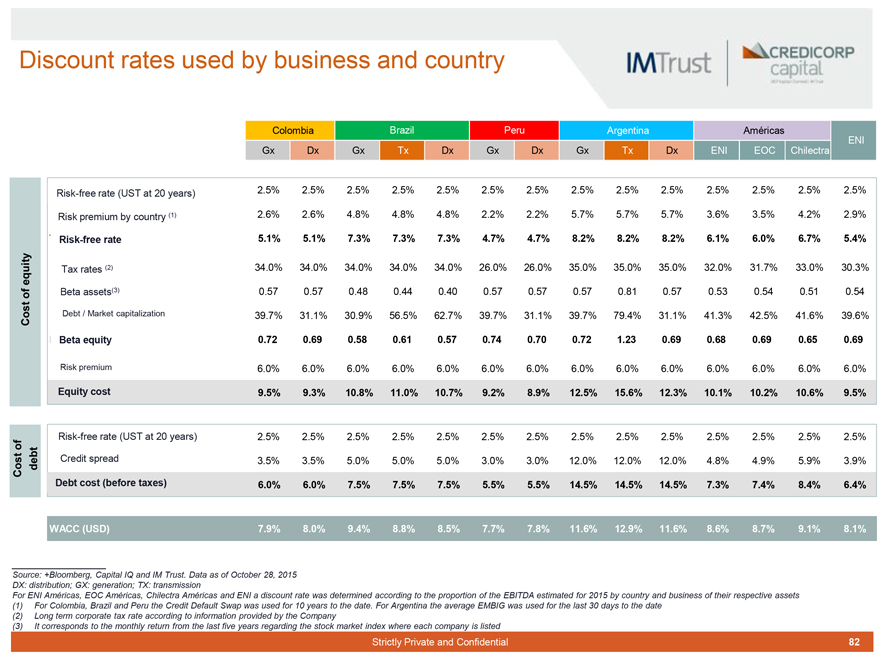

Discounted cash flows (“DCF”)

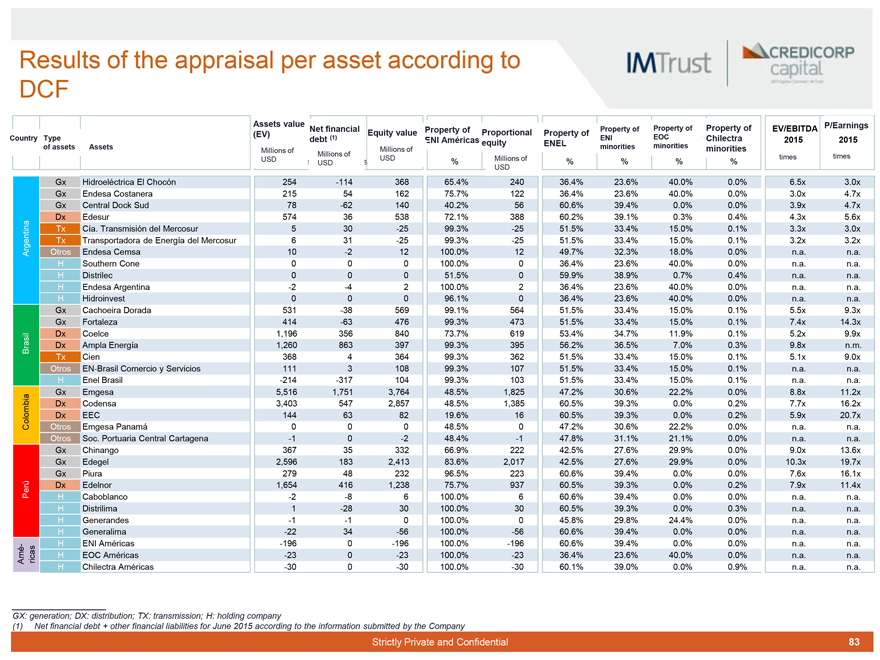

Appraisal by DCF for each one of the companies that ENI Américas, EOC Américas and Chilectra Américas would make up

Appraisals based on projections submitted by the Company

Appraisal by sum of parts for ENI Américas, EOC Américas, and Chilectra Américas

Related holdings based on the relative appraisals and composition of net financial debt of each corporation

Market quotes and comparable entities

Appraisal for each one of the companies that ENI Américas, EOC Américas and Chilectra Américas will form, while taking these points into consideration:

Stock market capitalizations for corporations that are open market with some liquidity

Market multiples of listed companies according to country and business

Appraisal by sum of parts for ENI Américas, EOC Américas and Chilectra Américas-related holdings based on the relative appraisals and composition of net financial debt of each corporation

Range of relative holdings according to the results obtained separately from both methodologies

Strictly Private and Confidential 15

|

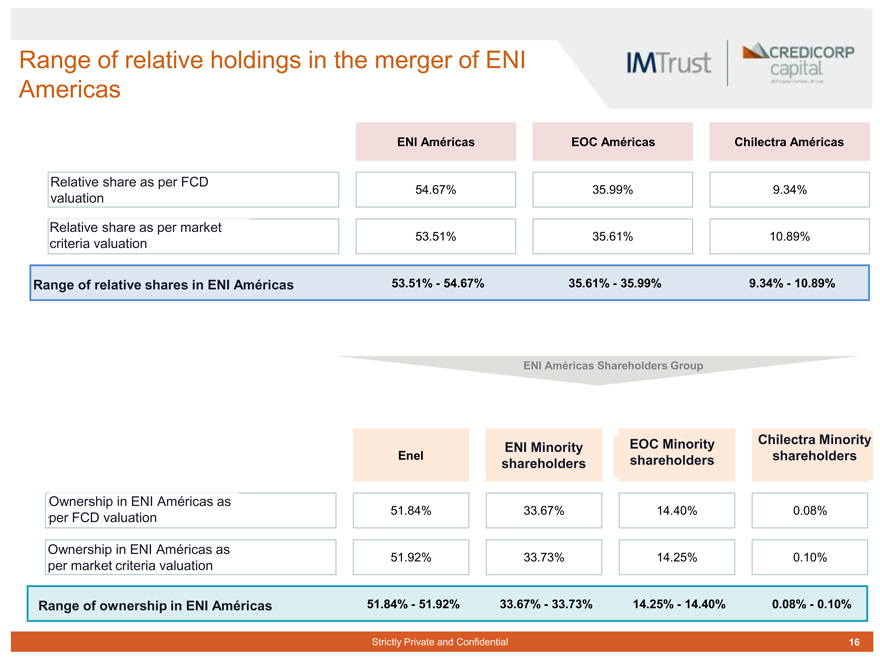

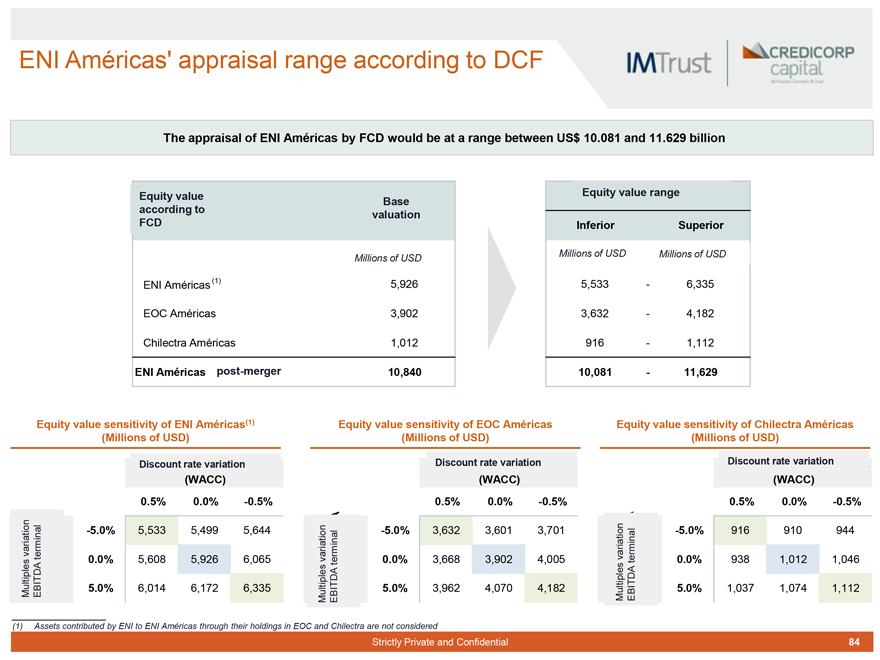

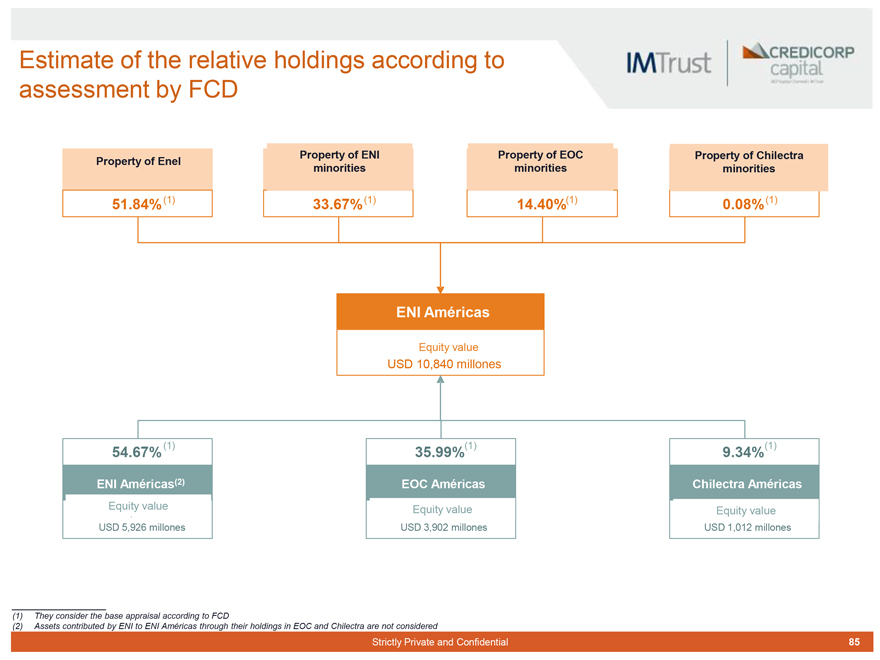

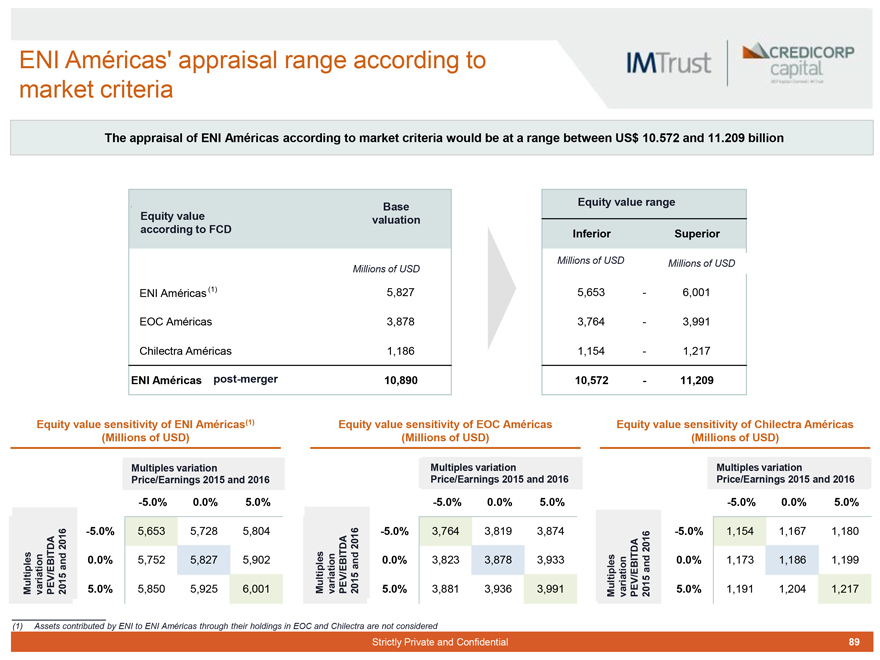

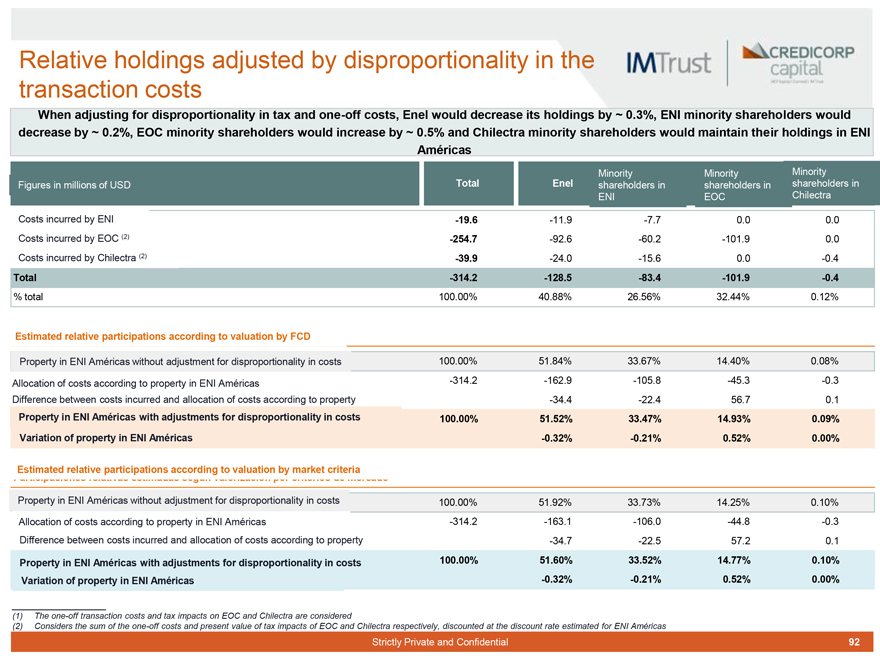

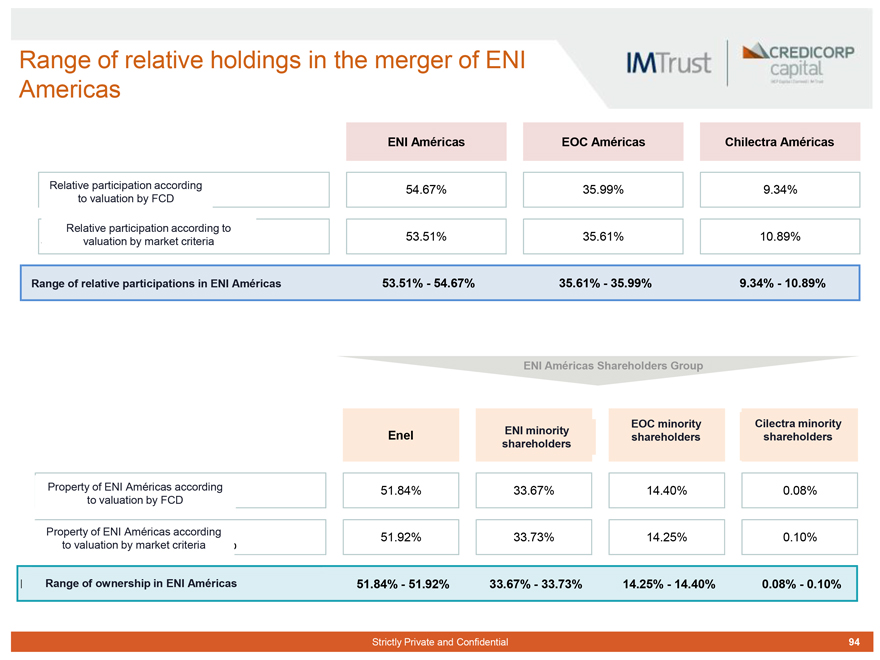

Range of relative holdings in the merger of ENI Americas

ENI Américas EOC AméricasChilectra Américas

Relative share as per FCD valuation 54.67% 35.99%9.34%

Relative share as per market criteria valuation 53.51% 35.61%10.89%

Range of relative shares in ENI Américas 53.51% - 54.67% 35.61% - 35.99%9.34% - 10.89%

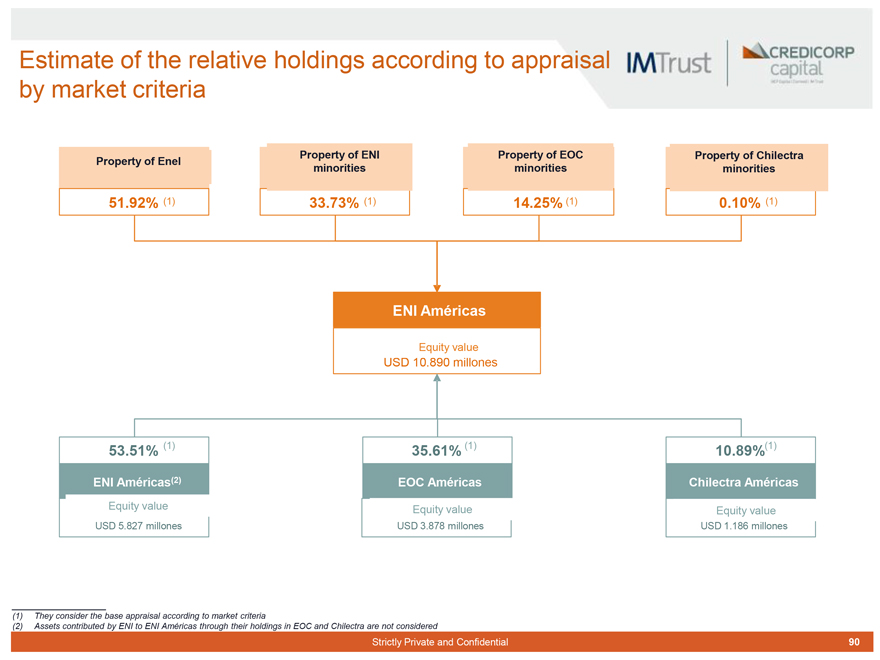

ENI Américas Shareholders Group

Enel ENI Minority shareholdersEOC Minority shareholdersChilectra Minority shareholders

Ownership in ENI Américas as per FCD valuation 51.84% 33.67%14.40%0.08%

Ownership in ENI Américas as per market criteria valuation 51.92% 33.73%14.25%0.10%

Range of ownership in ENI Américas 51.84% - 51.92% 33.67% - 33.73%14.25% - 14.40%0.08% - 0.10%

Strictly Private and Confidential 16

|

Conclusions (1/2)

The proposed Reorganization has positive aspects that could generate benefits for the shareholders of Enersis in the medium and long term:

It leans toward a shareholder structure system according to a by geographic market scheme, eliminating cross-ownership of holdings and facilitating the decision making and execution thereof

It gives existing shareholders greater flexibility and increases the investment alternatives for potential investors who prefer to risk profiles, investment strategies and more targeted dividend policies

Under the assumptions that they are detailed in the report and two alternative approaches, in our opinionit produces potentially positive effects in the appraisal of Enersis due to the following concepts (which are not necessarily additive effects):

Potential adjustment of the (stock) market value of potential re-appraisals of assets and decreases ENI holding discounts of up to US$ 625 million (~ 5% of the current stock market capitalization of ENI)

From the perspective of cash flow impacts, net present value for the shareholders of Enersis of up to US$ 377 million (~ 3% of the current stock market capitalization of ENI) derived mainly from efficiency plans to the holding level, tax impacts and costs of the transaction

For the indicated effects to occur, we have assumed that certain conditions have been met, which might not necessarily take place and therefore their occurrence and risk must be verified and monitored by the Directorate of Enersis, since its noncompliance would make the Reorganization very onerous or even inconvenient. These conditions are:

That the Reorganization be carried out fully on all its stages, from the division of ENI, EOC and Chilectra, and until the merger of ENI Américas, EOC Américas and Chilectra Américas, under the proposed terms and at a reasonable amount of time

As a result of the Reorganization, it is not foreseeable to expect ENI Américas, ENI Chile and/or EOC Chile to have an international credit rating less than investment grade

That a clear and defined policy of dividends for ENI Chile be established and report business plans for EOC Chile and Chilectra Chile with growth and profitability projections justifying appraisal levels that are at least comparable with local peers

That the efficiency plans submitted to the Directorate be approved and implemented, at least in part directly related to the administration of the holdings in Chile, as is considered in this Report

In addition, we consider relevant to the market and to Enersis shareholders:

That the long-term evolution of the organizational structure of the Enersis group be communicated to the market clearly and the potential future steps future and the conditions for its implementation be explained

That the efficiency plans approved by the Directorate in conjunction with the Reorganization be submitted and explained

Strictly Private and Confidential 17

|

Conclusions (2/2)

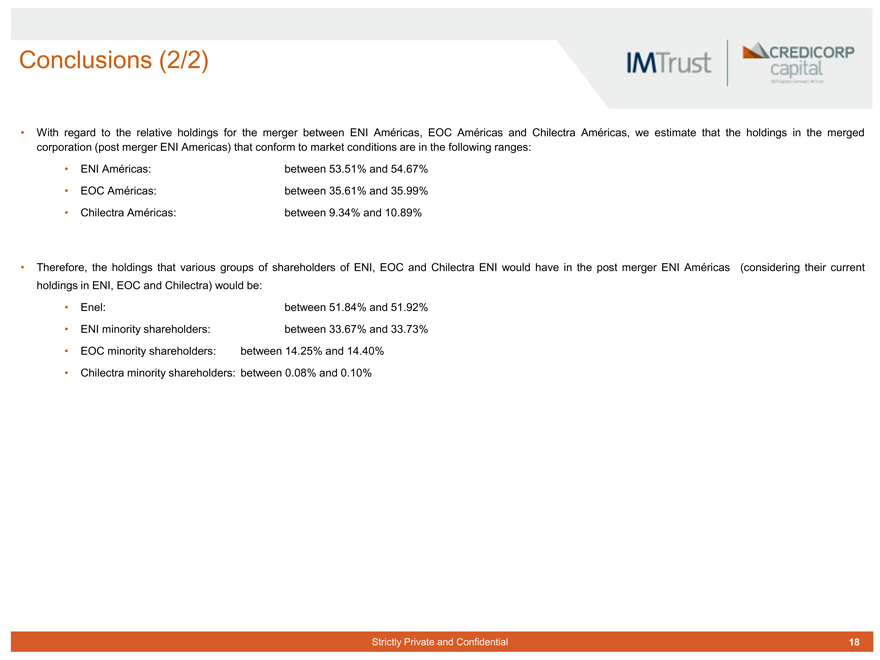

With regard to the relative holdings for the merger between ENI Américas, EOC Américas and Chilectra Américas, we estimate that the holdings in the merged corporation (post merger ENI Americas) that conform to market conditions are in the following ranges:

ENI Américas: between 53.51% and 54.67%

EOC Américas: between 35.61% and 35.99%

Chilectra Américas: between 9.34% and 10.89%

Therefore, the holdings that various groups of shareholders of ENI, EOC and Chilectra ENI would have in the post merger ENI Américas (considering their current holdings in ENI, EOC and Chilectra) would be:

Enel: between 51.84% and 51.92%

ENI minority shareholders: between 33.67% and 33.73%

EOC minority shareholders: between 14.25% and 14.40%

Chilectra minority shareholders: between 0.08% and 0.10%

Strictly Private and Confidential 18

|

BACKGROUND AND SCOPE OF THE EVALUATION 2

Strictly Private and Confidential 19

|

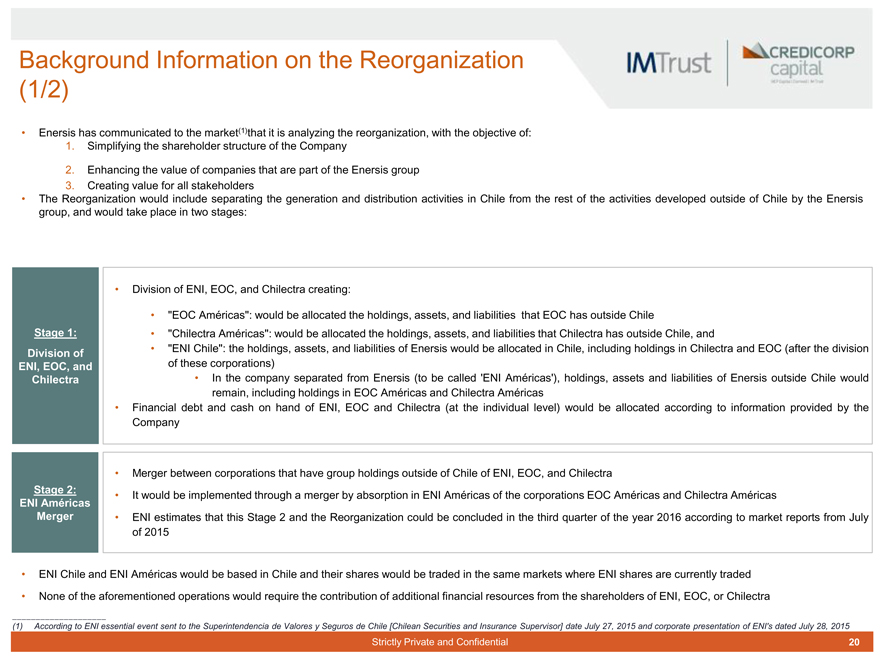

Background Information on the Reorganization (1/2)

Enersis has communicated to the market(1) that it is analyzing the reorganization, with the objective of:

1. Simplifying the shareholder structure of the Company

2. Enhancing the value of companies that are part of the Enersis group

3. Creating value for all stakeholders

The Reorganization would include separating the generation and distribution activities in Chile from the rest of the activities developed outside of Chile by the Enersis group, and would take place in two stages:

Stage 1: Division of ENI, EOC, and Chilectra

Division of ENI, EOC, and Chilectra creating:

“EOC Américas”: would be allocated the holdings, assets, and liabilities that EOC has outside Chile

“Chilectra Américas”: would be allocated the holdings, assets, and liabilities that Chilectra has outside Chile, and

“ENI Chile”: the holdings, assets, and liabilities of Enersis would be allocated in Chile, including holdings in Chilectra and EOC (after the division of these corporations)

In the company separated from Enersis (to be called ‘ENI Américas’), holdings, assets and liabilities of Enersis outside Chile would remain, including holdings in EOC Américas and Chilectra Américas Financial debt and cash on hand of ENI, EOC and Chilectra (at the individual level) would be allocated according to information provided by the Company

Stage 2: ENI Américas Merger

Merger between corporations that have group holdings outside of Chile of ENI, EOC, and Chilectra

It would be implemented through a merger by absorption in ENI Américas of the corporations EOC Américas and Chilectra Américas

ENI estimates that this Stage 2 and the Reorganization could be concluded in the third quarter of the year 2016 according to market reports from July of 2015

ENI Chile and ENI Américas would be based in Chile and their shares would be traded in the same markets where ENI shares are currently traded

None of the aforementioned operations would require the contribution of additional financial resources from the shareholders of ENI, EOC, or Chilectra

(1) According to ENI essential event sent to the Superintendencia de Valores y Seguros de Chile [Chilean Securities and Insurance Supervisor] date July 27, 2015 and corporate presentation of ENI’s dated July 28, 2015

Strictly Private and Confidential 20

|

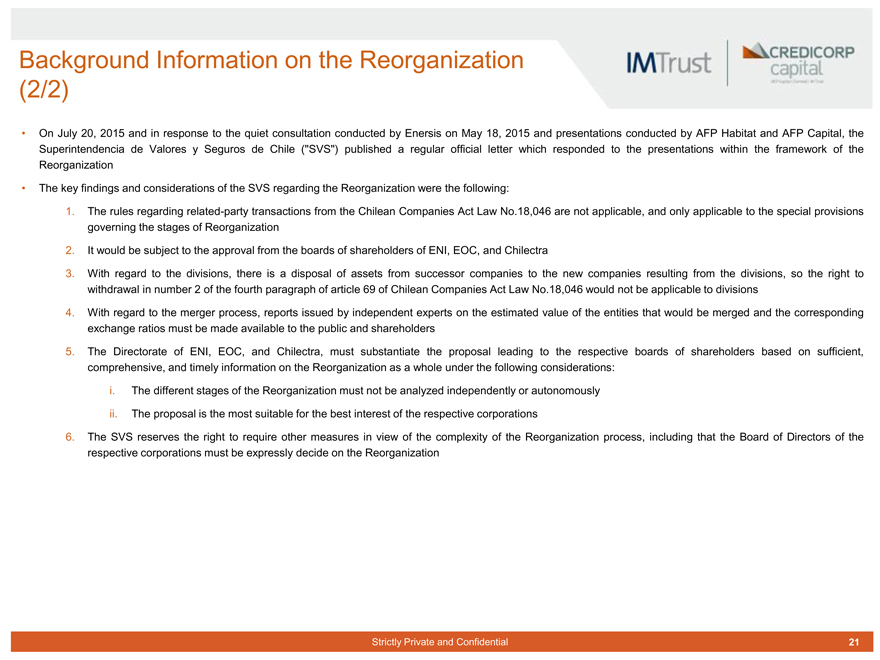

Background Information on the Reorganization (2/2)

On July 20, 2015 and in response to the quiet consultation conducted by Enersis on May 18, 2015 and presentations conducted by AFP Habitat and AFP Capital, the Superintendencia de Valores y Seguros de Chile (“SVS”) published a regular official letter which responded to the presentations within the framework of the Reorganization

The key findings and considerations of the SVS regarding the Reorganization were the following:

1. The rules regarding related-party transactions from the Chilean Companies Act Law No.18,046 are not applicable, and only applicable to the special provisions governing the stages of Reorganization

2. It would be subject to the approval from the boards of shareholders of ENI, EOC, and Chilectra

3. With regard to the divisions, there is a disposal of assets from successor companies to the new companies resulting from the divisions, so the right to withdrawal in number 2 of the fourth paragraph of article 69 of Chilean Companies Act Law No.18,046 would not be applicable to divisions

4. With regard to the merger process, reports issued by independent experts on the estimated value of the entities that would be merged and the corresponding exchange ratios must be made available to the public and shareholders

5. The Directorate of ENI, EOC, and Chilectra, must substantiate the proposal leading to the respective boards of shareholders based on sufficient, comprehensive, and timely information on the Reorganization as a whole under the following considerations:

i. The different stages of the Reorganization must not be analyzed independently or autonomously

ii. The proposal is the most suitable for the best interest of the respective corporations

6. The SVS reserves the right to require other measures in view of the complexity of the Reorganization process, including that the Board of Directors of the respective corporations must be expressly decide on the Reorganization

Strictly Private and Confidential 21

|

Scope of the report

IM Trust acts as financial consultant to the Board of Directors of Enersis with regard to the Reorganization. The scope of such consulting will be equivalent to those provided in the Chilean Companies Act Law No. 18,046 in its Article 147, regarding independent evaluators

In accordance with the above, in its capacity as consultant of the Board of Directors, IM Trust prepared this report which contains among others the following elements:

A description of the proposed Reorganization

An assessment of whether the Reorganization helps the best interest of Enersis

An estimate of the relative holdings in the ENI Américas merger, which in our view on today’s date would be consistent with market terms As part of the analysis, IM Trust has included the following in the report:

An analysis of potential impacts on the value and risks with regard to the reorganization, in order to estimate if it contributes to the best interest of Enersis and the rational strategic

An estimate of relative shares for the merger between ENI Americas, EOC Americas and Chilectra Americas within the framework of the reorganization Note that for not being within the scope of this advice, this report does not consider:

An analysis of the advantages and disadvantages of alternative structures or alternative implementation mechanisms to carry out the reorganization that is evaluated here

A detailed analysis of the technical, commercial, legal and/or other type of feasibility of the implementation of the Reorganization

Strictly Private and Confidential 22

|

DESCRIPTION OF THE REORGANIZATION 3

Strictly Private and Confidential 23

|

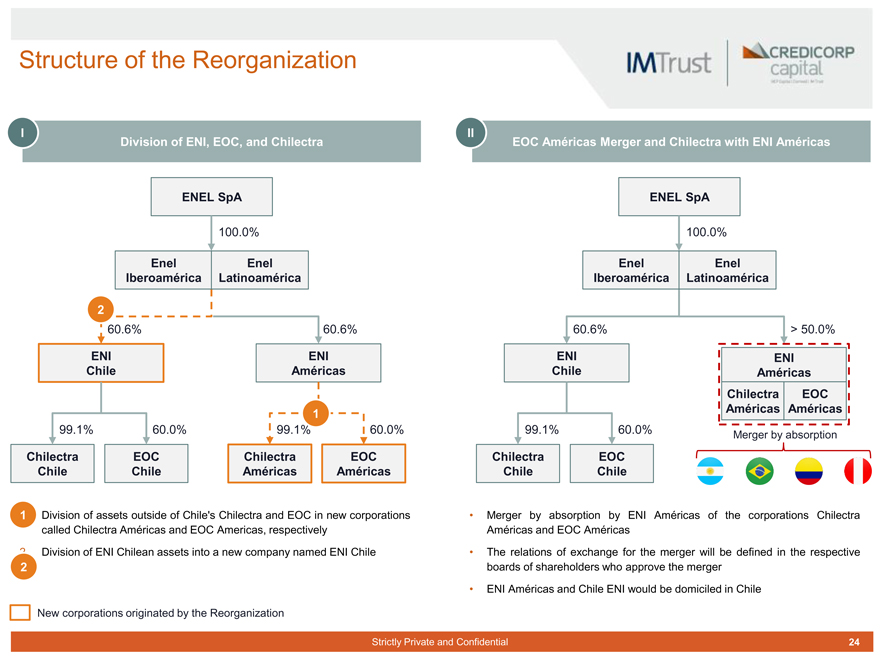

Structure of the Reorganization

1 Division of ENI, EOC, and Chilectra

ENEL SpA

100.0%

Enel Iberoamérica Enel Latinoamérica

2

60.6% 60.6%

ENI Chile ENI Américas

1

99.1% 60.0% 99.1% 60.0%

Chilectra Chile EOC Chile Chilectra Américas EOC Américas

1 Division of assets outside of Chile’s Chilectra and EOC in new corporations called Chilectra Américas and EOC Americas, respectively

2 Division of ENI Chilean assets into a new company named ENI Chile

New corporations originated by the Reorganization

II EOC Américas Merger and Chilectra with ENI Américas

ENEL SpA

100.0%

Enel Iberoamérica Enel Latinoamérica

60.6% > 50.0%

ENI Chile ENI Américas Chilectra

Américas EOC Américas

99.1% 60.0% Merger by absorption

Chilectra Chile EOC Chile

Merger by absorption by ENI Américas of the corporations Chilectra Américas and EOC Américas

The relations of exchange for the merger will be defined in the respective boards of shareholders who approve the merger

ENI Américas and Chile ENI would be domiciled in Chile

Strictly Private and Confidential 24

|

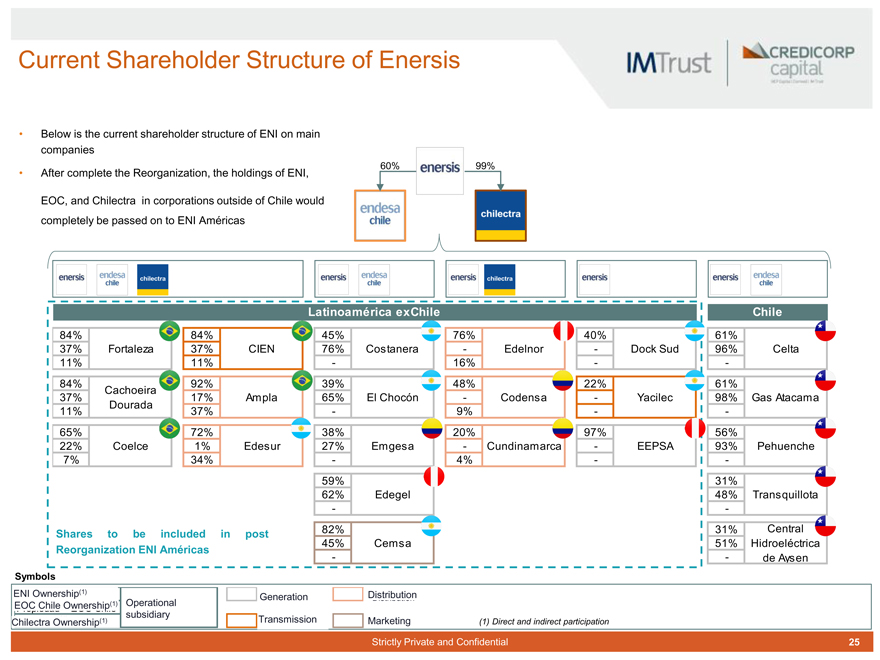

Current Shareholder Structure of Enersis

Below is the current shareholder structure of ENI on main companies

60% 99%

After complete the Reorganization, the holdings of ENI, EOC, and Chilectra in corporations outside of Chile would completely be passed on to ENI Américas

Latinoamérica exChile Chile

84% 84% 45% 76% 40% 61%

37% Fortaleza 37% CIEN 76% Costanera - Edelnor - Dock Sud 96% Celta 11% 11% - 16% - 84% 92% 39% 48% 22% 61% Cachoeira 37% 17% Ampla 65% El Chocón - Codensa - Yacilec 98% Gas Atacama Dourada 11% 37% - 9% - 65% 72% 38% 20% 97% 56% 22% Coelce 1% Edesur 27% Emgesa - Cundinamarca - EEPSA 93% Pehuenche

7% 34% - 4% - 59% 31%

62% Edegel 48% Transquillota

- 82% 31% Central Shares to be included in post 45% Cemsa 51% Hidroeléctrica

Reorganization ENI Américas - de Aysen

Symbols ENI Ownership (1) (1) Propiedad ENI Generation Generatio Distribution Distribution EOC Chile(1) Ownership(1) Operational

Propiedad EOC Chile subsidiary

(1) Transmission Other

Chilectra Propiedad Ownership Chilectra (1) Transmissi Marketing (1) Direct and indirect participation

Strictly Private and Confidential 25

|

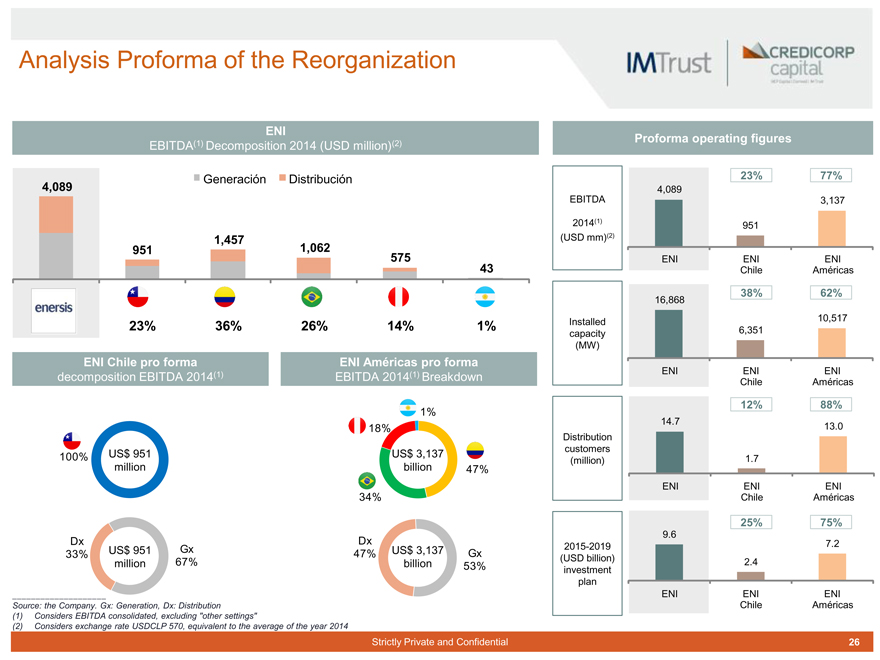

Analysis Proforma of the Reorganization

ENI

EBITDA(1) Decomposition 2014 (USD million)(2)

Generación Distribución

4,089

1,457

951 1,062

575 43

23% 36% 26% 14% 1%

ENI Chile pro forma ENI Américas pro forma decomposition EBITDA 2014(1) EBITDA 2014(1) Breakdown

1% 18%

100% US$ 951 US$ 3,137 million billion 47%

34%

Dx Dx

US$ 951 Gx 47% US$ 3,137 Gx 33% million 67% billion 53%

Source: the Company. Gx: Generation, Dx: Distribution

(1) Considers EBITDA consolidated, excluding “other settings”

(2) Considers exchange rate USDCLP 570, equivalent to the average of the year 2014

Strictly Private and Confidential

Proforma operating figures

23% 77%

4,089

EBITDA 3,137 2014(1) 951 (USD mm)(2)

ENI ENI ENI Chile Américas

38% 62%

16,868

Installed 10,517 capacity 6,351 (MW)

ENI ENI ENI Chile Américas

12% 88%

14.7

13.0 Distribution customers (million) 1.7

ENI ENI ENI Chile Américas

25% 75%

9.6 7.2 2015-2019 (USD billion) 2.4 investment plan ENI ENI ENI

Chile Américas

26

|

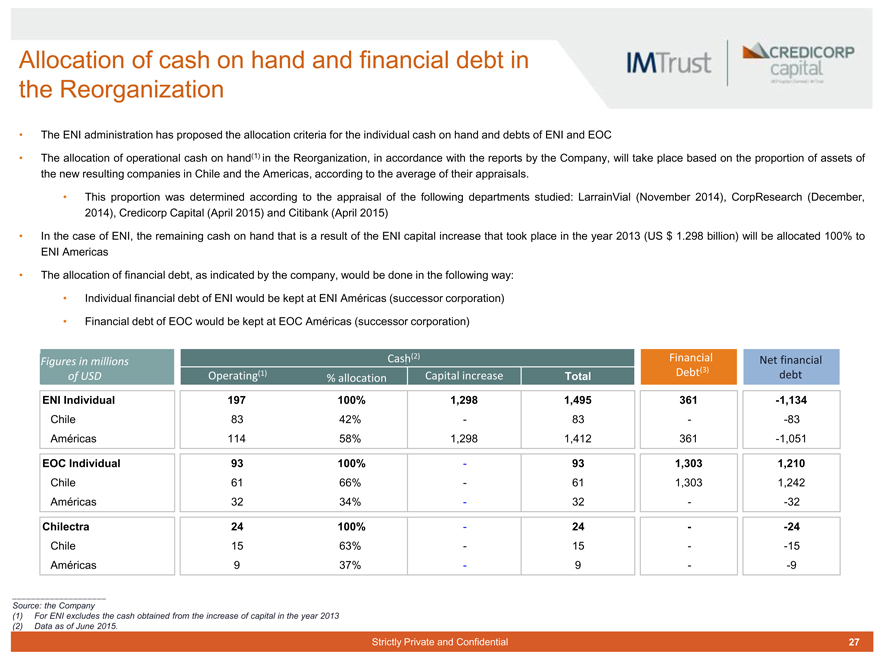

Allocation of cash on hand and financial debt in the Reorganization

The ENI administration has proposed the allocation criteria for the individual cash on hand and debts of ENI and EOC

(1)

The allocation of operational cash on hand(1) in the Reorganization, in accordance with the reports by the Company, will take place based on the proportion of assets of the new resulting companies in Chile and the Americas, according to the average of their appraisals.

This proportion was determined according to the appraisal of the following departments studied: LarrainVial (November 2014), CorpResearch (December, 2014), Credicorp Capital (April 2015) and Citibank (April 2015)

In the case of ENI, the remaining cash on hand that is a result of the ENI capital increase that took place in the year 2013 (US $ 1.298 billion) will be allocated 100% to ENI Americas

The allocation of financial debt, as indicated by the company, would be done in the following way:

Individual financial debt of ENI would be kept at ENI Américas (successor corporation)

Financial debt of EOC would be kept at EOC Américas (successor corporation)

Figures in millions of USD Operating(1) %%asignaallocationióCashCaja(2)(2)Capital increaseTotalFinancial Debt(3)Net financial debt

ENI Individual 197 100%1,2981,495361-1,134

Chile 83 42%-83--83

Américas 114 58%1,2981,412361-1,051

EOC Individual 93 100%-931,3031,210

Chile 61 66%-611,3031,242

Américas 32 34%-32--32

Chilectra 24 100%-24--24

Chile 15 63%-15--15

Américas 9 37%-9--9

Source: the Company

(1) For ENI excludes the cash obtained from the increase of capital in the year 2013 (2) Data as of June 2015.

Strictly Private and Confidential 27

|

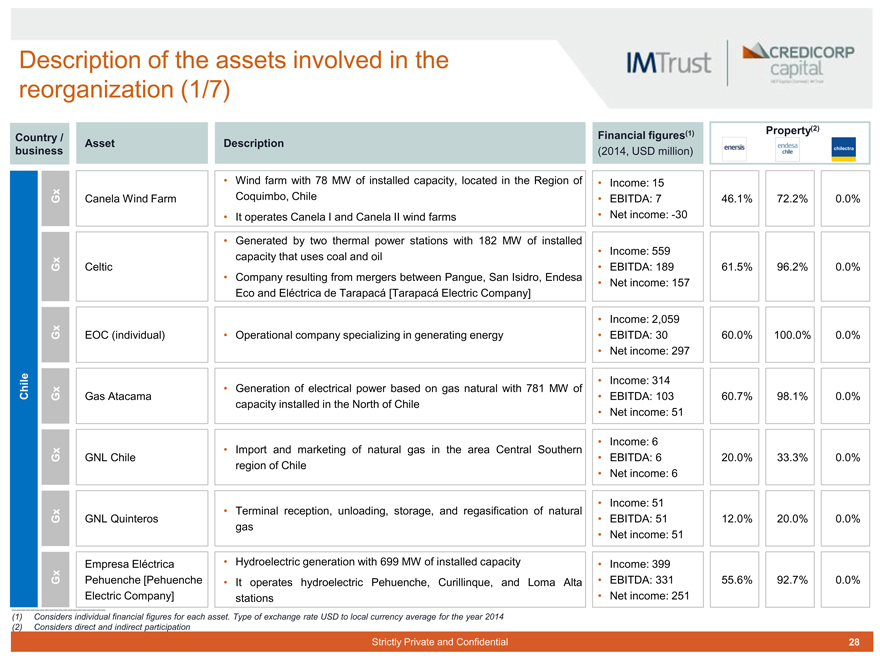

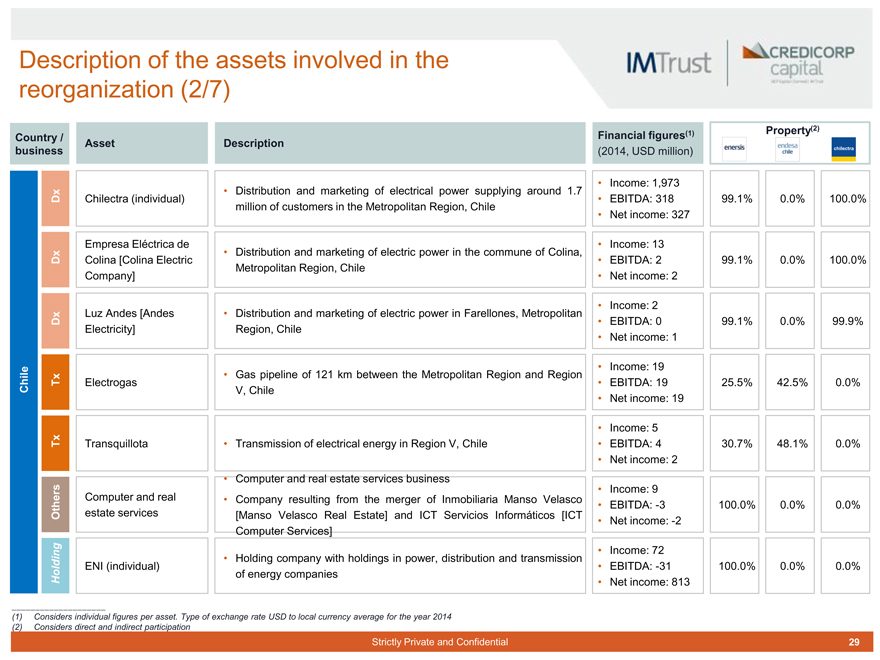

Description of the assets involved in the

reorganization (1/7)

Country / business Asset Description

Gx Canela Wind FarmWind farm with 78 MW of installed capacity, located in the Region of Coquimbo, Chile It operates Canela I and Canela II wind farms Generated by two thermal power stations with 182 MW of installed capacity that uses coal and oil

Gx CelticCompany resulting from mergers between Pangue, San Isidro, Endesa Eco and Eléctrica de Tarapacá [Tarapacá Electric Company]

Gx EOC (individual)Operational company specializing in generating energy

Chile Gx Gas AtacamaGeneration of electrical power based on gas natural with 781 MW of capacity installed in the North of Chile

Gx GNL ChileImport and marketing of natural gas in the area Central Southern region of Chile

Gx GNL QuinterosTerminal reception, unloading, storage, and regasification of natural gas

Gx Empresa Eléctrica Pehuenche [Pehuenche Electric Company]Hydroelectric generation with 699 MW of installed capacity It operates hydroelectric Pehuenche, Curillinque, and Loma Alta stations

Financial figures(1) Property(2)

(2014, USD million)

Income: 15

EBITDA: 7 46.1%72.2%0.0%

Net income: -30

Income: 559

EBITDA: 189 61.5%96.2%0.0%

Net income: 157

Income: 2,059

EBITDA: 30 60.0%100.0%0.0%

Net income: 297

Income: 314

EBITDA: 103 60.7%98.1%0.0%

Net income: 51

Income: 6

EBITDA: 6 20.0%33.3%0.0%

Net income: 6

Income: 51

EBITDA: 51 12.0%20.0%0.0%

Net income: 51

Income: 399

EBITDA: 331 55.6%92.7%0.0%

Net income: 251

(1) Considers individual financial figures for each asset. Type of exchange rate USD to local currency average for the year 2014 (2) Considers direct and indirect participation

Strictly Private and Confidential 28

|

Description of the assets involved in the reorganization (2/7)

Country / business Asset Description

Dx Chilectra (individual)Distribution and marketing of electrical power supplying around 1.7 million of customers in the Metropolitan Region, Chile

Dx Empresa Eléctrica de Colina [Colina Electric Company]Distribution and marketing of electric power in the commune of Colina, Metropolitan Region, Chile

Dx Luz Andes [Andes Electricity]Distribution and marketing of electric power in Farellones, Metropolitan Region, Chile

Chile Tx ElectrogasGas pipeline of 121 km between the Metropolitan Region and Region V, Chile

Tx Transquillota Computer and realTransmission of electrical energy in Region V, Chile Computer and real estate services business Company resulting from the merger of Inmobiliaria Manso Velasco

Others Holding estate services ENI (individual)[Manso Velasco Real Estate] and ICT Servicios Informáticos [ICT Computer Services] Holding company with holdings in power, distribution and transmission of energy companies

Financial figures(1) Property(2)

(2014, USD million)

Income: 1,973

EBITDA: 318 99.1%0.0%100.0%

Net income: 327

Income: 13

EBITDA: 2 99.1%0.0%100.0%

Net income: 2

Income: 2

EBITDA: 0 99.1%0.0%99.9%

Net income: 1

Income: 19

EBITDA: 19 25.5%42.5%0.0%

Net income: 19

Income: 5

EBITDA: 4 30.7%48.1%0.0%

Net income: 2

Income: 9

EBITDA: -3 100.0%0.0%0.0%

Net income: -2

Income: 72

EBITDA: -31 100.0%0.0%0.0%

Net income: 813

(1) Considers individual figures per asset. Type of exchange rate USD to local currency average for the year 2014 (2) Considers direct and indirect participation

Strictly Private and Confidential 29

|

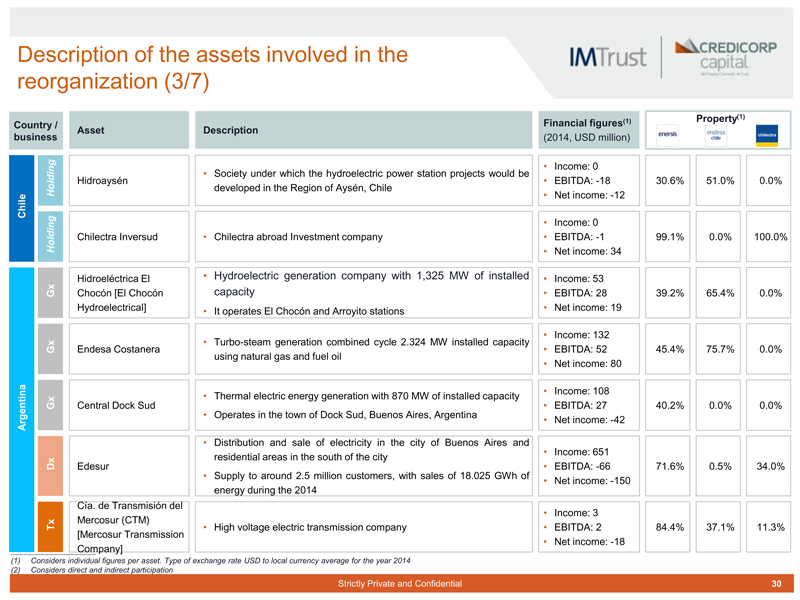

Description of the assets involved in the reorganization (3/7)

Country /

Asset Description business

Holding Hidroaysén Society under which the hydroelectric power station projects would be developed in the Region of Aysén, Chile

Chile Holding Chilectra Inversud Chilectra abroad Investment company

Gx Hidroeléctrica El Chocón [El Chocón Hydroelectrical] Hydroelectric generation company with 1,325 MW of installed capacity It operates El Chocón and Arroyito stations

Gx Endesa Costanera Turbo-steam generation combined cycle 2.324 MW installed capacity using natural gas and fuel oil

Gx Central Dock Sud Thermal electric energy generation with 870 MW of installed capacity

Argentina Operates in the town of Dock Sud, Buenos Aires, Argentina Distribution and sale of electricity in the city of Buenos Aires and residential areas in the south of the city

Dx Edesur Supply to around 2.5 million customers, with sales of 18.025 GWh of energy during the 2014

Tx Cía. de Transmisión del Mercosur (CTM) [Mercosur Transmission Company] High voltage electric transmission company

(1) (2) Considers individual figures per asset. Type of exchange rate USD to local currency average for the year 2014 Considers direct and indirect participation

Strictly Private and Confidential

Financial figures(1) Property(1)

(2014, USD million)

Income: 0

EBITDA: -18 30.6%51.0%0.0%

Net income: -12

Income: 0

EBITDA: -1 99.1%0.0%100.0%

Net income: 34

Income: 53

EBITDA: 28 39.2%65.4%0.0%

Net income: 19

Income: 132

EBITDA: 52 45.4%75.7%0.0%

Net income: 80

Income: 108

EBITDA: 27 40.2%0.0%0.0%

Net income: -42

Income: 651

EBITDA: -66 71.6%0.5%34.0%

Net income: -150

Income: 3

EBITDA: 2 84.4%37.1%11.3%

Net income: -18

30

|

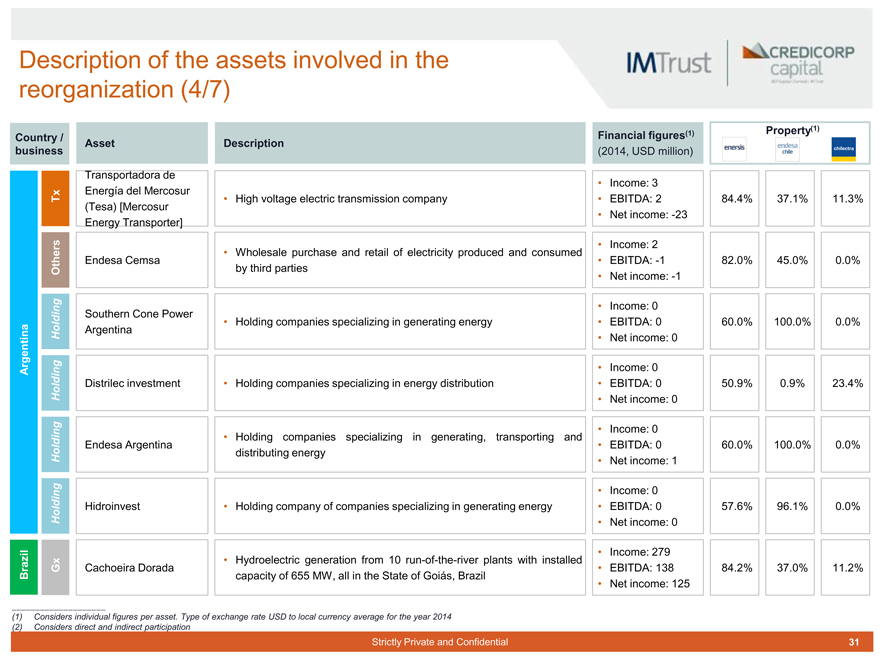

Description of the assets involved in the reorganization (4/7)

Country / business Asset Description

Tx Transportadora de Energía del Mercosur (Tesa) [Mercosur Energy Transporter] High voltage electric transmission company

Others Endesa Cemsa Wholesale purchase and retail of electricity produced and consumed by third parties

Holding Southern Cone Power Argentina Holding companies specializing in generating energy

Argentina Holding Distrilec investment Holding companies specializing in energy distribution

Holding Endesa Argentina Holding companies specializing in generating, transporting and distributing energy

Holding Hidroinvest Holding company of companies specializing in generating energy

Gx Brazil Cachoeira Dorada Hydroelectric generation from 10 run-of-the-river plants with installed capacity of 655 MW, all in the State of Goiás, Brazil

Financial figures(1) Property(1)

(2014, USD million)

Income: 3

EBITDA: 2 84.4%37.1%11.3%

Net income: -23

Income: 2

EBITDA: -1 82.0%45.0%0.0%

Net income: -1

Income: 0

EBITDA: 0 60.0%100.0%0.0%

Net income: 0

Income: 0

EBITDA: 0 50.9%0.9%23.4%

Net income: 0

Income: 0

EBITDA: 0 60.0%100.0%0.0%

Net income: 1

Income: 0

EBITDA: 0 57.6%96.1%0.0%

Net income: 0

Income: 279

EBITDA: 138 84.2%37.0%11.2%

Net income: 125

(1) Considers individual figures per asset. Type of exchange rate USD to local currency average for the year 2014 (2) Considers direct and indirect participation

Strictly Private and Confidential 31

|

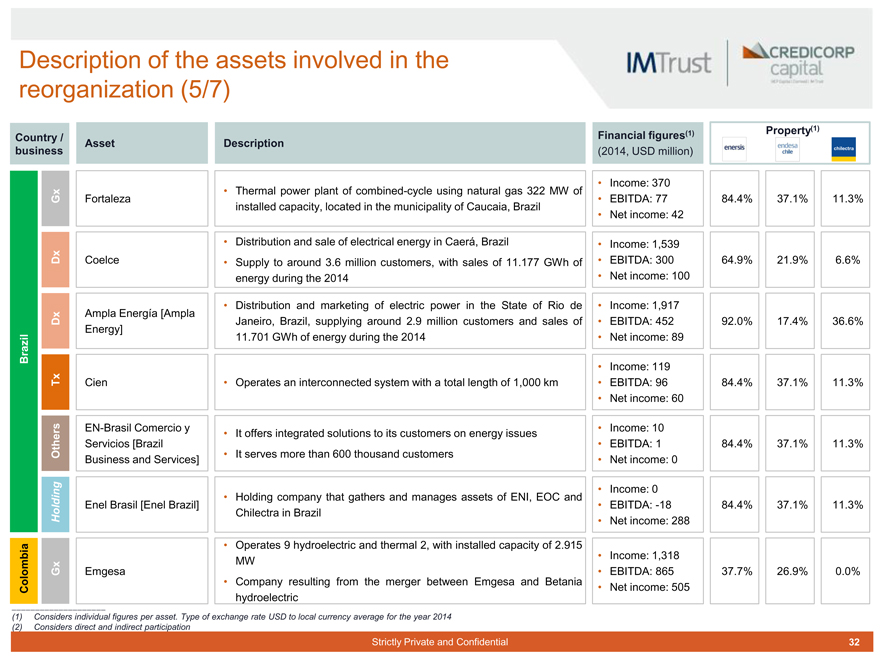

Description of the assets involved in the reorganization (5/7)

Country / business Asset Description

Gx Fortaleza Thermal power plant of combined-cycle using natural gas 322 MW of installed capacity, located in the municipality of Caucaia, Brazil

Dx Coelce Distribution and sale of electrical energy in Caerá, Brazil Supply to around 3.6 million customers, with sales of 11.177 GWh of energy during the 2014

Dx Ampla Energía [Ampla Energy] Distribution and marketing of electric power in the State of Rio de Janeiro, Brazil, supplying around 2.9 million customers and sales of 11.701 GWh of energy during the 2014

Brazil Tx Cien Operates an interconnected system with a total length of 1,000 km

Others EN-Brasil Comercio y Servicios [Brazil Business and Services] It offers integrated solutions to its customers on energy issues It serves more than 600 thousand customers

Holding company that gathers and manages assets of ENI, EOC and

Holding Enel Brasil [Enel Brazil] Chilectra in Brazil Operates 9 hydroelectric and thermal 2, with installed capacity of 2.915 MW

Gx Colombia Emgesa Company resulting from the merger between Emgesa and Betania hydroelectric

Financial figures(1) Property(1)

(2014, USD million)

Income: 370

EBITDA: 77 84.4%37.1%11.3%

Net income: 42

Income: 1,539

EBITDA: 300 64.9%21.9%6.6%

Net income: 100

Income: 1,917

EBITDA: 452 92.0%17.4%36.6%

Net income: 89

Income: 119

EBITDA: 96 84.4%37.1%11.3%

Net income: 60

Income: 10

EBITDA: 1 84.4%37.1%11.3%

Net income: 0

Income: 0

EBITDA: -18 84.4%37.1%11.3%

Net income: 288

Income: 1,318

EBITDA: 865 37.7%26.9%0.0%

Net income: 505

(1) Considers individual figures per asset. Type of exchange rate USD to local currency average for the year 2014 (2) Considers direct and indirect participation

Strictly Private and Confidential 32

|

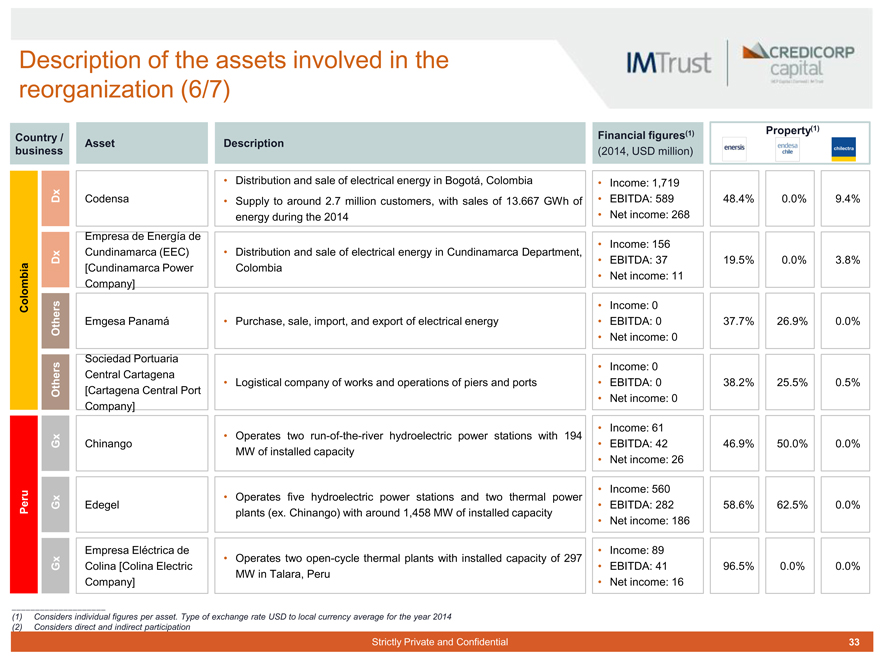

Description of the assets involved in the reorganization (6/7)

Country / business Asset Description

Dx Codensa Distribution and sale of electrical energy in Bogotá, Colombia Supply to around 2.7 million customers, with sales of 13.667 GWh of energy during the 2014

Colombia Dx Empresa de Energía de Cundinamarca (EEC) [Cundinamarca Power Company] Distribution and sale of electrical energy in Cundinamarca Department, Colombia

Others Emgesa Panamá Purchase, sale, import, and export of electrical energy

Others Sociedad Portuaria Central Cartagena [Cartagena Central Port Company] Logistical company of works and operations of piers and ports

Gx Chinango Operates two run-of-the-river hydroelectric power stations with 194 MW of installed capacity

Peru Gx Edegel Operates five hydroelectric power stations and two thermal power plants (ex. Chinango) with around 1,458 MW of installed capacity

Gx Empresa Eléctrica de Colina [Colina Electric Company] Operates two open-cycle thermal plants with installed capacity of 297 MW in Talara, Peru

Financial figures(1) Property(1)

(2014, USD million)

Income: 1,719

EBITDA: 589 48.4%0.0%9.4%

Net income: 268

Income: 156

EBITDA: 37 19.5%0.0%3.8%

Net income: 11

Income: 0

EBITDA: 0 37.7%26.9%0.0%

Net income: 0

Income: 0

EBITDA: 0 38.2%25.5%0.5%

Net income: 0

Income: 61

EBITDA: 42 46.9%50.0%0.0%

Net income: 26

Income: 560

EBITDA: 282 58.6%62.5%0.0%

Net income: 186

Income: 89

EBITDA: 41 96.5%0.0%0.0%

Net income: 16

(1) Considers individual figures per asset. Type of exchange rate USD to local currency average for the year 2014 (2) Considers direct and indirect participation

Strictly Private and Confidential 33

|

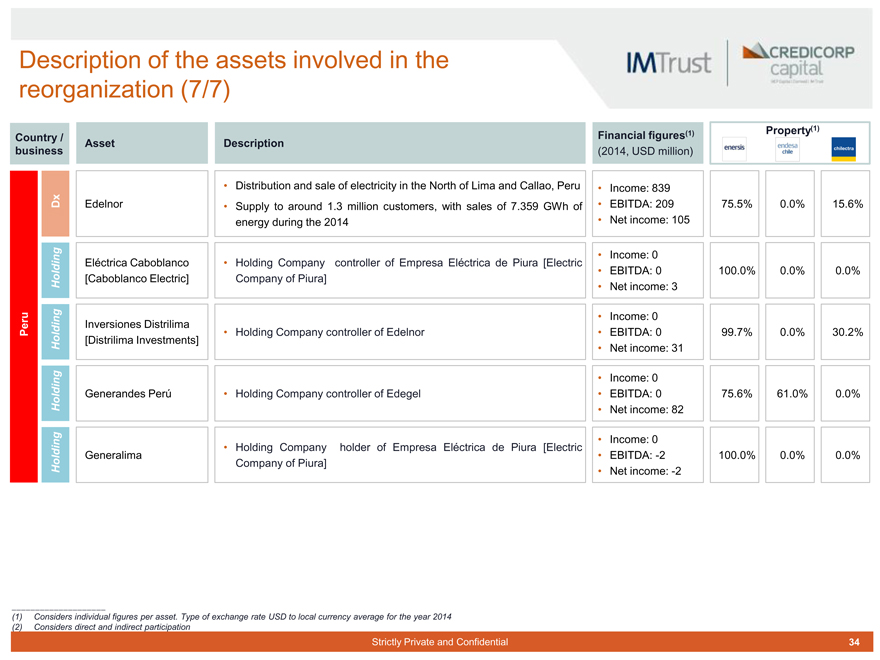

Description of the assets involved in the reorganization (7/7)

Country / business Asset DescriptionFinancial figures(1) (2014, USD million)Property(1)

Dx Edelnor Distribution and sale of electricity in the North of Lima and Callao, Peru Supply to around 1.3 million customers, with sales of 7.359 GWh of energy during the 2014 Income: 839 EBITDA: 209 Net income: 10575.5%0.0%15.6%

Holding Eléctrica Caboblanco [Caboblanco Electric] Holding Company controller of Empresa Eléctrica de Piura [Electric Company of Piura] Income: 0 EBITDA: 0 Net income: 3100.0%0.0%0.0%

Peru Holding Inversiones Distrilima [Distrilima Investments] Holding Company controller of Edelnor Income: 0 EBITDA: 0 Net income: 3199.7%0.0%30.2%

Holding Generandes Perú Holding Company controller of Edegel Income: 0 EBITDA: 0 Net income: 8275.6%61.0%0.0%

Holding Generalima Holding Company holder of Empresa Eléctrica de Piura [Electric Company of Piura] Income: 0 EBITDA: -2 Net income: -2100.0%0.0%0.0%

(1) Considers individual figures per asset. Type of exchange rate USD to local currency average for the year 2014 (2) Considers direct and indirect participation

Strictly Private and Confidential 34

|

GENERAL CONSIDERATIONS AND ANALYTICAL

SCHEME 4

Strictly Private and Confidential 35

|

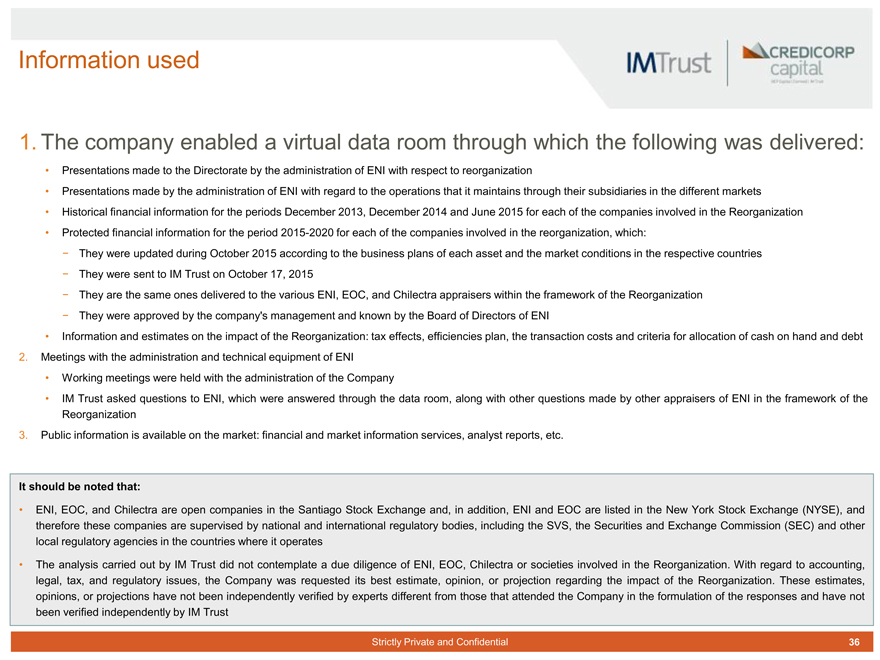

Information used

1. The company enabled a virtual data room through which the following was delivered:

Presentations made to the Directorate by the administration of ENI with respect to reorganization

Presentations made by the administration of ENI with regard to the operations that it maintains through their subsidiaries in the different markets

Historical financial information for the periods December 2013, December 2014 and June 2015 for each of the companies involved in the Reorganization

Protected financial information for the period 2015-2020 for each of the companies involved in the reorganization, which:

- They were updated during October 2015 according to the business plans of each asset and the market conditions in the respective countries

- They were sent to IM Trust on October 17, 2015

- They are the same ones delivered to the various ENI, EOC, and Chilectra appraisers within the framework of the Reorganization

- They were approved by the company’s management and known by the Board of Directors of ENI

Information and estimates on the impact of the Reorganization: tax effects, efficiencies plan, the transaction costs and criteria for allocation of cash on hand and debt

2. Meetings with the administration and technical equipment of ENI

Working meetings were held with the administration of the Company

IM Trust asked questions to ENI, which were answered through the data room, along with other questions made by other appraisers of ENI in the framework of the Reorganization

3. Public information is available on the market: financial and market information services, analyst reports, etc.

It should be noted that:

ENI, EOC, and Chilectra are open companies in the Santiago Stock Exchange and, in addition, ENI and EOC are listed in the New York Stock Exchange (NYSE), and therefore these companies are supervised by national and international regulatory bodies, including the SVS, the Securities and Exchange Commission (SEC) and other local regulatory agencies in the countries where it operates

The analysis carried out by IM Trust did not contemplate a due diligence of ENI, EOC, Chilectra or societies involved in the Reorganization. With regard to accounting, legal, tax, and regulatory issues, the Company was requested its best estimate, opinion, or projection regarding the impact of the Reorganization. These estimates, opinions, or projections have not been independently verified by experts different from those that attended the Company in the formulation of the responses and have not been verified independently by IM Trust

Strictly Private and Confidential 36

|

General considerations used in the report

According to information made available by Enersis and the views contained in the replies provided by Enersis IM Trust, with regard to the Reorganization we have assumed the following:

It is permitted by Chilean legislation and the other countries where ENI, EOC, and Chilectra operates (Brazil, Colombia, Peru, and Argentina) and it does not violate any rule in any jurisdiction applicable to ENI, EOC, and Chilectra

It does not cause regulatory, environmental effects, or adverse competition for ENI, EOC and/or Chilectra, its subsidiaries and/or successors and/or those arising on the occasion of the Reorganization

It does affect or violate agreements with associates, providers, clients or any counterpart of ENI, EOC and/or Chilectra, its subsidiaries and/or successors and/or those arising on the occasion of the Reorganization

It does not involve accounting or tax effects which could negatively impact the results of ENI, EOC and/or Chilectra, its subsidiaries and/or successor companies and/or those arising on the occasion of the reorganization beyond those considered in the present report on the basis of the information provided by the company

It does create not new contingencies for ENI, EOC and/or Chilectra, its subsidiaries and/or successors and/or those arising on the occasion of the Reorganization

It does not affect or violate agreements in credit or creditor contracts of ENI, EOC, Chilectra and/or their subsidiaries that originate material effects in the results of any of these corporations, among which are breach, cross-default, or cross-acceleration events, and/or increases of financial costs

It is not incurred in liability management processes which mean material costs for ENI, EOC, and/or Chilectra, its subsidiaries and/or successor companies and/or arising on the occasion of the reorganization, beyond those considered in the present report on the basis of the information provided by the company

In terms of its stages, it is carried out in it entirety from the division of ENI, EOC and Chilectra, and until the merger of ENI Américas, EOC Américas and Chilectra Américas, under the proposed terms and at a reasonable amount of time

This analysis does not include a scenario in which once the division of ENI, EOC and Chilectra has taken place, the merger in ENI Americas is not completed in the time and manner as planned by Enersis

As a result of the Reorganization, ENI Américas, ENI Chile, and/or EOC Chile will not have an international credit rating below investment grade by any of the following risk classifiers: Moody’s, Standard & Poor’s and/or Fitch Ratings

Divided, successor and merged corporations are still listed and traded in the same markets and stock exchanges where ENI, EOC, and Chilectra are listed and traded, as appropriate

None of the operations involved or that arise due to the Reorganization would require the contribution of additional financial resources from the shareholders of ENI, EOC, and/or Chilectra

The fact that the Reorganization is carried out or does not affect the commitment of Endesa, S.A. and Enel S.p.A., to maintain Enersis and Endesa, S.A. (or the successor company(ies) or those arising from it), except for Enel Green Power S.p.A.(1), as a unique vehicle for investment in South America.

If the Reorganization does not take place, the current situation at Enersis would be maintained in terms of the consolidation, management, and political and economic rights of the holdings involved in the Reorganization

(1) This commitment was established by the Enersis shareholders on December 20, 2012

Strictly Private and Confidential 37

|

Assessment Framework

The following Analytical Scheme in this report is as follows:

Reorganization Strategic Rationale Management of shareholder structure Model of business organizationEfficiencies plan

Impact of the Reorganization on the Market Value of Enersis Stock Market and Market Factors Holding Company Discount Stock market liquidity

Potential impacts on the risk rating

Direct cash flow impacts from the reorganization in the value of Enersis Cash Flow Factors Impacts on EBITDA Tax ImpactTransaction Costs

Risks of the Reorganization

Risks of execution

Probability that the division is executed and the merger is not implemented or delayed.

Risk of loss of investment grade

Probability that some of the successors or companies resulting from the Reorganization lose the investment grade status

Discounted cash flow

Stock market capitalizations and multiples of market

Estimate of relative holdings of the merger in ENI Americas

1. Valuations: i. ENI Américas ii. EOC Américas iii. Chilectra Américas

2. Relative holdings of the merger

Strictly Private and Confidential 38

|

CONSIDERATIONS OF THE BUSINESS MODEL 5

Strictly Private and Confidential 39

|

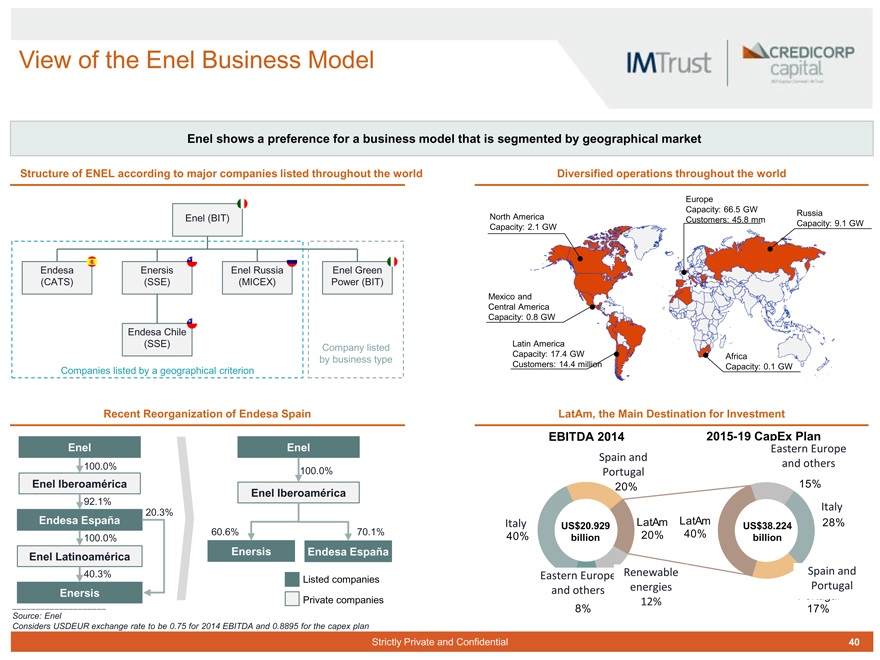

View of the Enel Business Model

Enel shows a preference for a business model that is segmented by geographical market

Structure of ENEL according to major companies listed throughout the world

Enersis (SSE)

Enel (BIT)

Endesa (CATS)

Enel Russia (MICEX)

Enel Green Power (BIT)

Company listed by business type

Companies listed by a geographical criterion

Endesa Chile (SSE)

Diversified operations throughout the world

Africa

Capacity: 0.1 GW

Latin America Capacity: 17.4 GW Customers: 14.4 million

Mexico and Central America Capacity: 0.8 GW

North America Capacity: 2.1 GW

Europe

Capacity: 66.5 GW Customers: 45.8 mm

Russia

Capacity: 9.1 GW

Recent Reorganization of Endesa Spain

Enel

100.0%

Enel Iberoamérica

92.1%

20.3%

Endesa España

100.0%

Enel Latinoamérica

40.3%

Enersis

Enel

100.0%

Enel Iberoamérica

60.6% 70.1%

Enersis Endesa España

Listed companies

Private companies

LatAm, the Main Destination for Investment

Italy

40%

Eastern Europe Renewable and others energies 12%

8%

15%

Italy

28%

Spain and Portugal

17%

US$38.224 billion

LatAm LatAm 20% 40%

Spain and Portugal

20%

EBITDA 2014

2015-19 CapEx Plan

Eastern Europe and others

Source: Enel

Considers USDEUR exchange rate to be 0.75 for 2014 EBITDA and 0.8895 for the capex plan

Strictly Private and Confidential 40

|

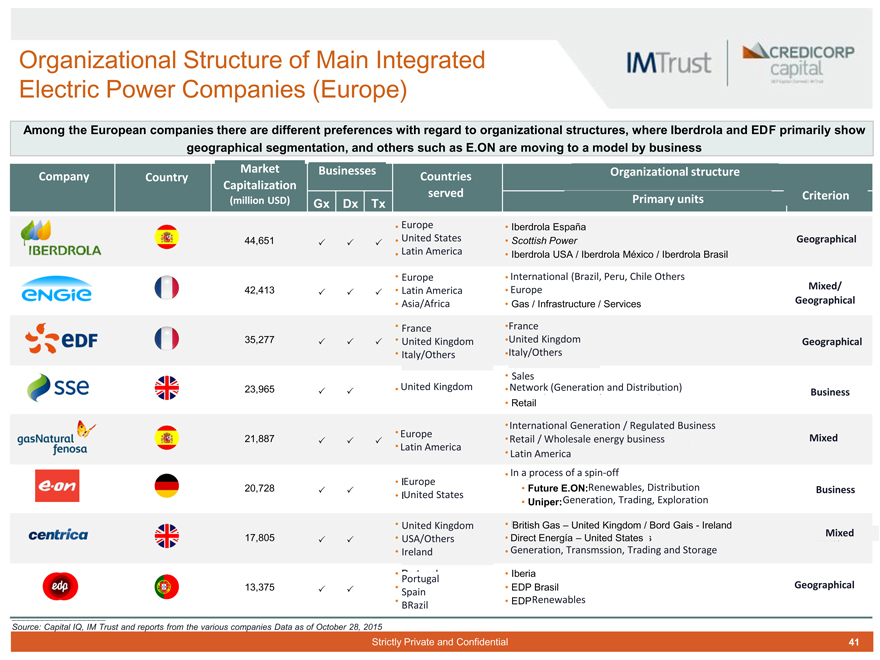

Organizational Structure of Main Integrated Electric Power Companies (Europe)

Among the European companies there are different preferences with regard to organizational structures, where Iberdrola and EDF primarily show geographical segmentation, and others such as E.ON are moving to a model by business

Company Country Market Capitalization (million USD)Businesses Gx Dx TxCountries servedOrganizational structure Primary unitsCriterion

44,651 Europe United States Latin America Iberdrola España Scottish Power Iberdrola USA / Iberdrola México / Iberdrola BrasilGeographical

42,413 Europe Latin America Asia/Africa International (Brazil, Peru, Chile Others Europe Gas / Infrastructure / ServicesMixed/ Geographical

35,277 France United Kingdom Italy/Others France United Kingdom Italy/OthersGeographical

23,965 United Kingdom VSalesntas NetworkRedes (Generación(Generationy Distribución)and Distribution) RetailBusiness

21,887 Europe Latin America InternationalGener ción IntGenerationrnacional / NRegulatedocios ReguladosBusiness RetailNegocios/ Wholesaleminoristas/mayoristasenergy businessde energía LatinL inoaAmericaé ica InEnaprprocessceso deof aspin-offspin-offMixed

20,728 Europe United States Future E.ON:Renewables,Renov les, Distributionis ibución Uniper:Generation, Trading, ExplorationBusiness

17,805 United Kingdom USA/Others Ireland Britishr Gas -–ReinoUnitedUnidoKingdom/ Bord/ BordGaisGais- Irlanda- Ireland Directt EnergíaEne í –- EstadosUnited StatesUnidos Generation, Transmssion, Trading and StorageMixed

13,375 Spain Portugal BRazil Iberia EDP Brasil EDPRenewablesGeographical

Source: Capital IQ, IM Trust and reports from the various companies Data as of October 28, 2015

Strictly Private and Confidential 41

|

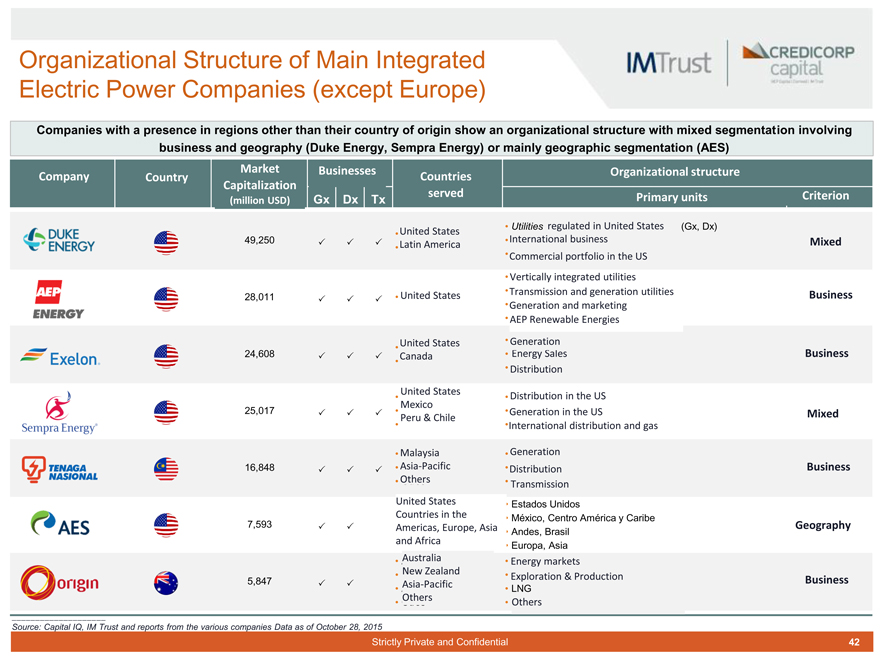

Organizational Structure of Main Integrated Electric Power Companies (except Europe)

Companies with a presence in regions other than their country of origin show an organizational structure with mixed segmentation involving business and geography (Duke Energy, Sempra Energy) or mainly geographic segmentation (AES)

Company Country Market Capitalization (million USD) Businesses Gx Dx TxCountries served Organizational structure Primary units Criterion

49,250 United States Latin America Utilities regulatedreguladasinenUnitedEs a osStatesUnidos (Gx, Dx) International business Commercial portfolio in the USMixed

28,011 United States Vertically integrated utilities Transmission and generation utilities Generation and marketing AEP Renewable EnergiesBusiness

24,608 United States Canada Generation Energy Sales Distribution Business

25,017 United States Mexico Peru & Chile Distribution in the US Generation in the US International distribution and gas Mixed

16,848 Malaysia Asia-Pacific Others Generation Distribution Transmission Business

7,593 United States Countries in the Americas, Europe, Asia and Africa Estados Unidos México, Centro América y Caribe Andes, Brasil Europa, AsiaGeography

5,847 Australia New Zealand Asia-Pacific Others Energy markets Explorationxplor ción & Productionción LNG Others Business

Source: Capital IQ, IM Trust and reports from the various companies Data as of October 28, 2015

Strictly Private and Confidential 42

|

Multinational companies with stock market presence in Chile and LatAm

Multinational companies with presence in Latin America mainly have a geographic segmentation, with companies listed by country and América Móvil being the only holding company listed with subsidiaries in other LatAm countries

Companies - Description

Spanish bank with a presence in 23 countries in Europe and America

It has 117 million customers

Market capitalization of US$ 81.455 billion

Spanish bank with a presence in 31 countries throughout the world

It has 51 million customers

Market capitalization of US$ 56.159 billion

Spanish company dedicated to the management of water and the environment with activities in 24 countries

Company not listed on the stock exchange

Mexican telecommunications company with presence in 18 countries in America and 7 in Europe

Market capitalization of US$ 56.836 billion

Spanish telecommunications company with a presence in 21 countries in Europe and America

Market capitalization of US$ 63.295 billion

Presence in LatAm

Stock market presence

Santander-Chile (SSE)

Santander Brasil (BOVESPA)

Santander México (BMV)

Santander Río (BASE)

BBVA Chile (SSE)

BBVA Bancomer (BMV)

BBVA Colombia (BVC)

BBVA Continental (BVL)

BBVA Francés (BASE)

BBVA Provincial (CCSE)

Aguas Andinas (SSE)

Corporation only for its Chile operation

América Móvil (BMV)

Holding company in Mexico that has as subsidiaries with the rest of the companies in LatAm

Telefónica Chile (SSE)

Telefónica Brasil (BOVESPA)

Telefónica del Perú (BVL)

Source: Information published by various companies and Capital IQ. Data as of October 28, 2015

Strictly Private and Confidential 43

|

IMPACT OF THE REORGANIZATION ON THE

MARKET VALUE OF ENERSIS 6 i. Holding Discount Considerations

Strictly Private and Confidential 44

|

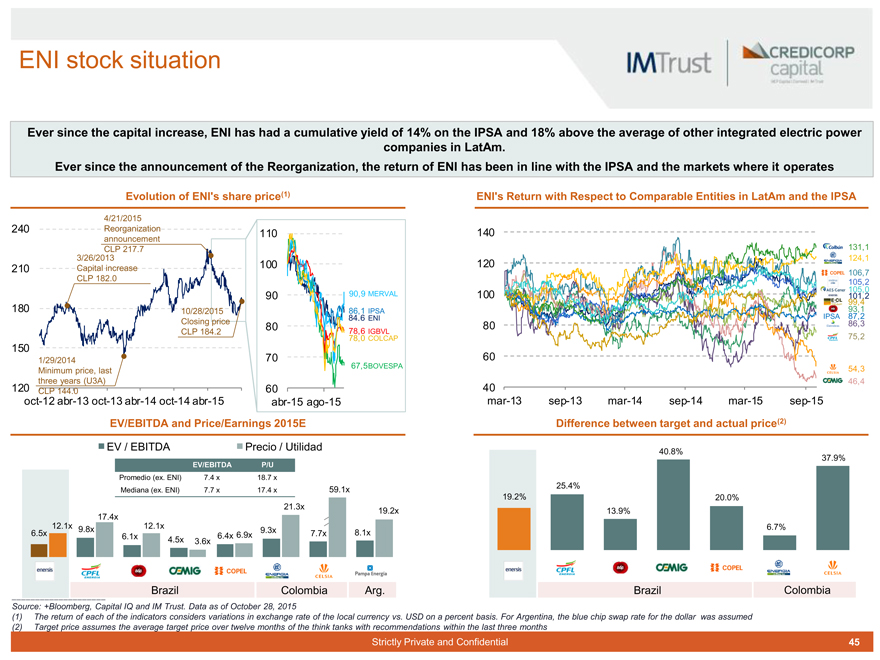

ENI stock situation

Ever since the capital increase, ENI has had a cumulative yield of 14% on the IPSA and 18% above the average of other integrated electric power companies in LatAm.

Ever since the announcement of the Reorganization, the return of ENI has been in line with the IPSA and the markets where it operates

Evolution of ENI’s share price(1)

4/21/2015

240 Reorganization 110 announcement CLP 217.7 3/26/2013 210 Capital increase 100 CLP 182.0

90 90,9 MERVAL

180 10/28/2015 86,1 IPSA Closing price 80 84,6 ENI

CLP 184.2 78,6 78,0 COLCAP IGBVL

150 70

1/29/2014

67,5BOVESPA

Minimum price, last three years (U3A)

120 CLP 144.0 60

oct-12 abr-13 oct-13 abr-14 oct-14 abr-15 abr-15 ago-15

ENI’s Return with Respect to Comparable Entities in LatAm and the IPSA

140

131,1 124,1

120

106,7

105,0 105,2 100 101,2 93,1 99,4

IPSA 86,3 87,2

80

75,2

60

54,3

46,4

40 mar-13 sep-13 mar-14 sep-14 mar-15 sep-15

EV/EBITDA and Price/Earnings 2015E

EV / EBITDA Precio / Utilidad

EV/EBITDA P/U

Promedio (ex. ENI) 7.4 x 18.7 x

Mediana (ex. ENI) 7.7 x 17.4 x 59.1x

21.3x

19.2x 17.4x 12.1x 9.8x 12.1x 6.5x 9.3x 7.7x 8.1x 6.1x 6.4x 6.9x 4.5x 3.6x

Brazil Colombia Arg.

Difference between target and actual price(2)

40.8%

37.9%

25.4%

19.2% 20.0% 13.9%

6.7%

Brazil Colombia

Source: +Bloomberg, Capital IQ and IM Trust. Data as of October 28, 2015

(1) The return of each of the indicators considers variations in exchange rate of the local currency vs. USD on a percent basis. For Argentina, the blue chip swap rate for the dollar was assumed (2) Target price assumes the average target price over twelve months of the think tanks with recommendations within the last three months

Strictly Private and Confidential 45

|

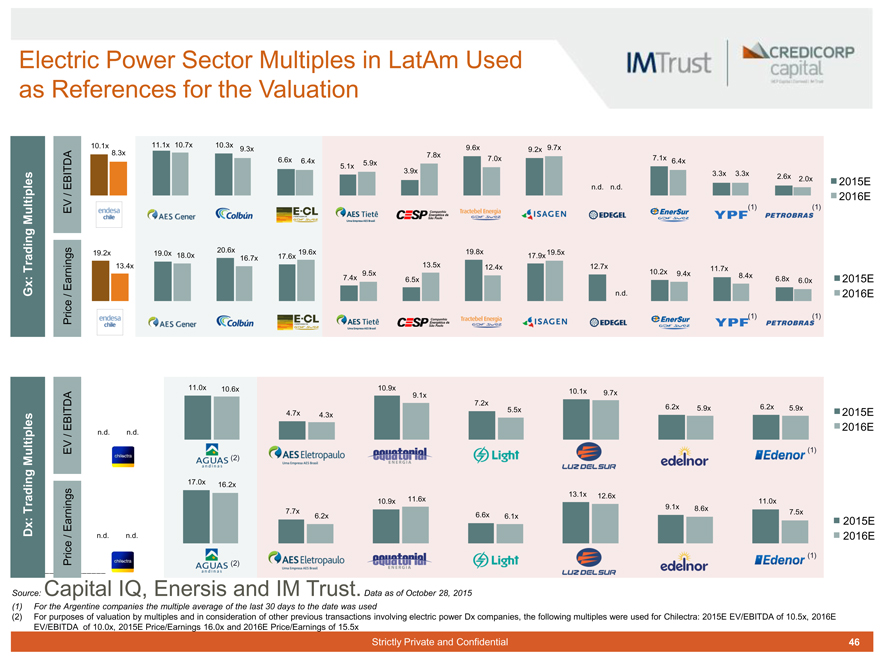

Electric Power Sector Multiples in LatAm Used as References for the Valuation

10.1x 11.1x 10.7x 10.3x 9.6x 9.7x

9.3x 9.2x

8.3x 7.8x

6.6x 6.4x 7.0x 7.1x 6.4x

5.1x 5.9x

3.9x 3.3x 3.3x

2.6x 2.0x

2015E

EBITDA n.d. n.d.

/ 2016E

Multiples EV (1) (1)

19.2x 20.6x 19.6x 19.8x 19.5x 19.0x 18.0x 17.6x 17.9x 16.7x 13.5x

Trading 13.4x 12.4x 12.7x 10.2x 11.7x

9.5x 9.4x 8.4x

Earnings 7.4x 6.5x 6.8x 6.0x 2015E

Gx: / n.d. 2016E

Price (1) (1)

11.0x 10.6x 10.9x

10.1x 9.7x

9.1x

7.2x

4.7x 5.5x 6.2x 5.9x 6.2x 5.9x

4.3x 2015E

EBITDA 2016E

n.d. n.d.

/

EV (1)

Multiples (2)

17.0x 16.2x

13.1x 12.6x

10.9x 11.6x 11.0x

9.1x 8.6x

Trading 7.7x 7.5x

6.2x 6.6x 6.1x

Earnings 2015E

Dx: / n.d. n.d. 2016E (1)

Price (2)

Source: Capital IQ, Enersis and IM Trust. Data as of October 28, 2015 (1) For the Argentine companies the multiple average of the last 30 days to the date was used

(2) For purposes of valuation by multiples and in consideration of other previous transactions involving electric power Dx companies, the following multiples were used for Chilectra: 2015E EV/EBITDA of 10.5x, 2016E EV/EBITDA of 10.0x, 2015E Price/Earnings 16.0x and 2016E Price/Earnings of 15.5x

Strictly Private and Confidential 46

|

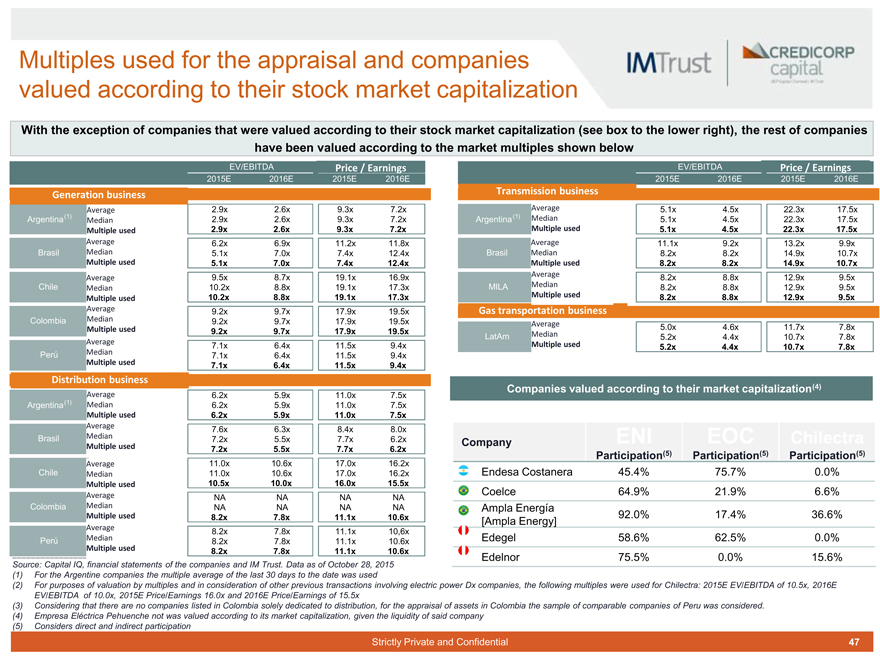

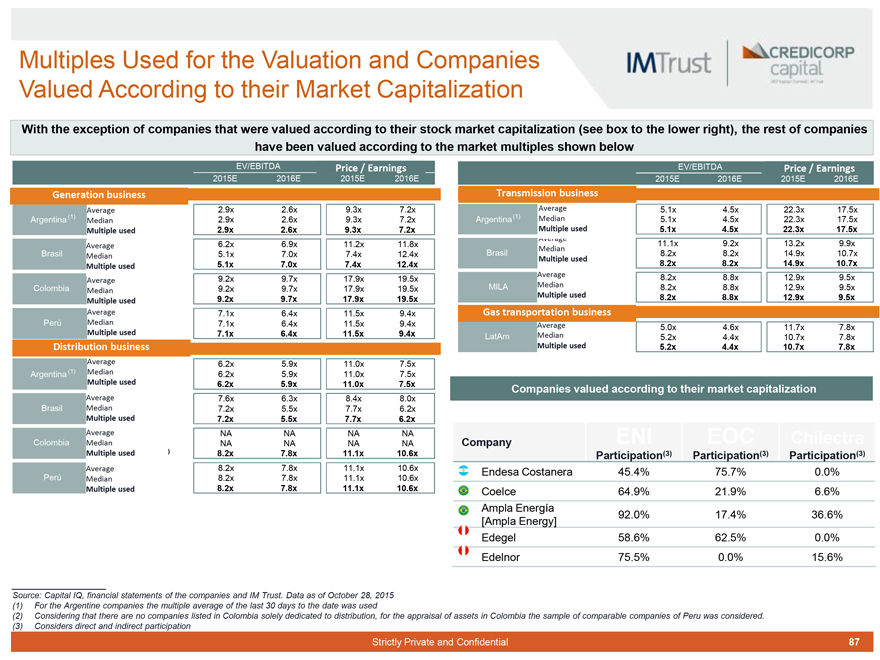

Multiples used for the appraisal and companies valued according to their stock market capitalization

With the exception of companies that were valued according to their stock market capitalization (see box to the lower right), the rest of companies have been valued according to the market multiples shown below

EV/EBITDAPricePr cio/Utilidad/ Earnings

2015E2016E2015E2016E

Generation business

Average 2.9x2.6x9.3x7.2x

Argentina(1) Median 2.9x2.6x9.3x7.2x

Multiple used 2.9x2.6x9.3x7.2x

Average 6.2x6.9x11.2x11.8x

Brasil Median 5.1x7.0x7.4x12.4x

Multiple used 5.1x7.0x7.4x12.4x

Average 9.5x8.7x19.1x16.9x

Chile Median 10.2x8.8x19.1x17.3x

Multiple used 10.2x8.8x19.1x17.3x

Average 9.2x9.7x17.9x19.5x

Colombia Median 9.2x9.7x17.9x19.5x

Multiple used 9.2x9.7x17.9x19.5x

Average 7.1x6.4x11.5x9.4x

Perú Median 7.1x6.4x11.5x9.4x

Multiple used 7.1x6.4x11.5x9.4x

Distribution business

Average 6.2x5.9x11.0x7.5x

Argentina(1) Median 6.2x5.9x11.0x7.5x

Multiple used 6.2x5.9x11.0x7.5x

Average 7.6x6.3x8.4x8.0x

Brasil Median 7.2x5.5x7.7x6.2x

Multiple used 7.2x5.5x7.7x6.2x

Average 11.0x10.6x17.0x16.2x

Chile Median 11.0x10.6x17.0x16.2x

Multiple used 10.5x10.0x16.0x15.5x

Average NANANANA

Colombia Median NANANANA

Multiple used 8.2x7.8x11.1x10.6x

Average 8.2x7.8x11.1x10,6x

Perú Median 8.2x7.8x11.1x10.6x

Multiple used 8.2x7.8x11.1x10.6x

EV/EBITDAPricePrecio/Utilidad/ Earnings

2015E2016E2015E2016E

Transmission business

Average 5.1x4.5x22.3x17.5x

Argentina(1) Median 5.1x4.5x22.3x17.5x

Multiple used 5.1x4.5x22.3x17.5x

Average 11.1x9.2x13.2x9.9x

Brasil Median 8.2x8.2x14.9x10.7x

Multiple used 8.2x8.2x14.9x10.7x

Average 8.2x8.8x12.9x9.5x

MILA Median 8.2x8.8x12.9x9.5x

Multiple used 8.2x8.8x12.9x9.5x

NegocioGasttransportationa s rte de gasbusiness

Average 5.0x4.6x11.7x7.8x

LatAm Median 5.2x4.4x10.7x7.8x

Multiple used 5.2x4.4x10.7x7.8x

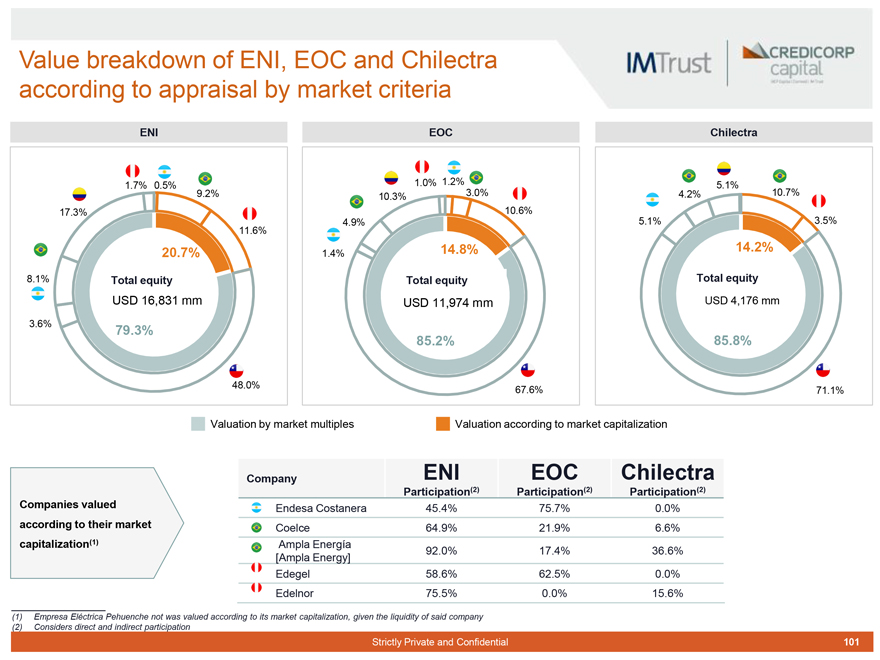

Companies valued according to their market capitalization(4)

Company ENIEOCChilectra

Participation(5) Participation(5)Participation(5)

Endesa Costanera 45.4% 75.7%0.0%

Coelce 64.9%21.9%6.6%

Ampla Energía

[Ampla Energy] 92.0% 17.4%36.6%

Edegel 58.6%62.5%0.0%

Edelnor 75.5%0.0%15.6%

Source: Capital IQ, financial statements of the companies and IM Trust. Data as of October 28, 2015 (1) For the Argentine companies the multiple average of the last 30 days to the date was used

(2) For purposes of valuation by multiples and in consideration of other previous transactions involving electric power Dx companies, the following multiples were used for Chilectra: 2015E EV/EBITDA of 10.5x, 2016E EV/EBITDA of 10.0x, 2015E Price/Earnings 16.0x and 2016E Price/Earnings of 15.5x (3) Considering that there are no companies listed in Colombia solely dedicated to distribution, for the appraisal of assets in Colombia the sample of comparable companies of Peru was considered.

(4) Empresa Eléctrica Pehuenche not was valued according to its market capitalization, given the liquidity of said company (5) Considers direct and indirect participation

Strictly Private and Confidential 47

|

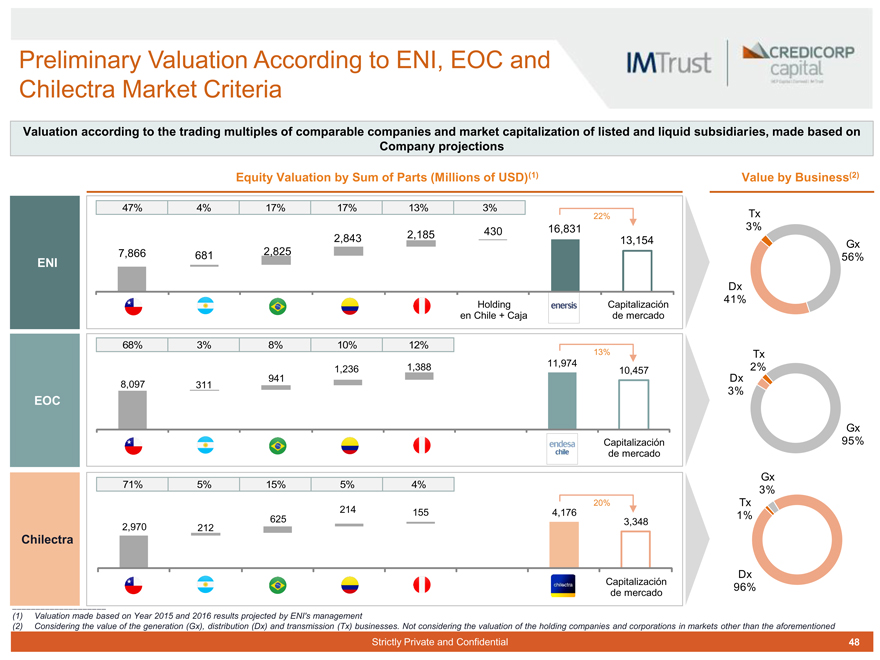

Preliminary Valuation According to ENI, EOC and Chilectra Market Criteria

Valuation according to the trading multiples of comparable companies and market capitalization of listed and liquid subsidiaries, made based on Company projections

Equity Valuation by Sum of Parts (Millions of USD)(1) Value by Business(2)

47% 4% 17% 17% 13% 3%

22% Tx

16,831 3% 2,185 430 2,843 13,154

Gx 7,866 681 2,825 56%

ENI

Dx 41%

Holding Capitalización en Chile + Caja de mercado

68% 3% 8% 10% 12%

13% Tx

1,388 11,974 2% 1,236 10,457 Dx 941 8,097 311

EOC 3%

Gx

Capitalización 95% de mercado

Gx

71% 5% 15% 5% 4%

3%

20% Tx

214 155 4,176

625 1% 3,348 2,970 212

Chilectra

Dx

Capitalización

96% de mercado

(1) Valuation made based on Year 2015 and 2016 results projected by ENI’s management

(2) Considering the value of the generation (Gx), distribution (Dx) and transmission (Tx) businesses. Not considering the valuation of the holding companies and corporations in markets other than the aforementioned

Strictly Private and Confidential 48

|

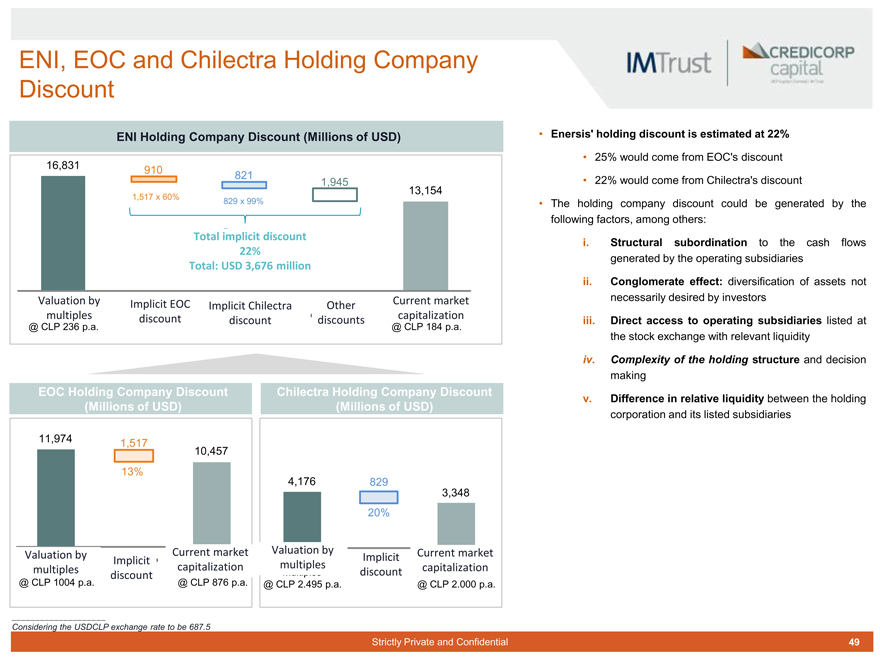

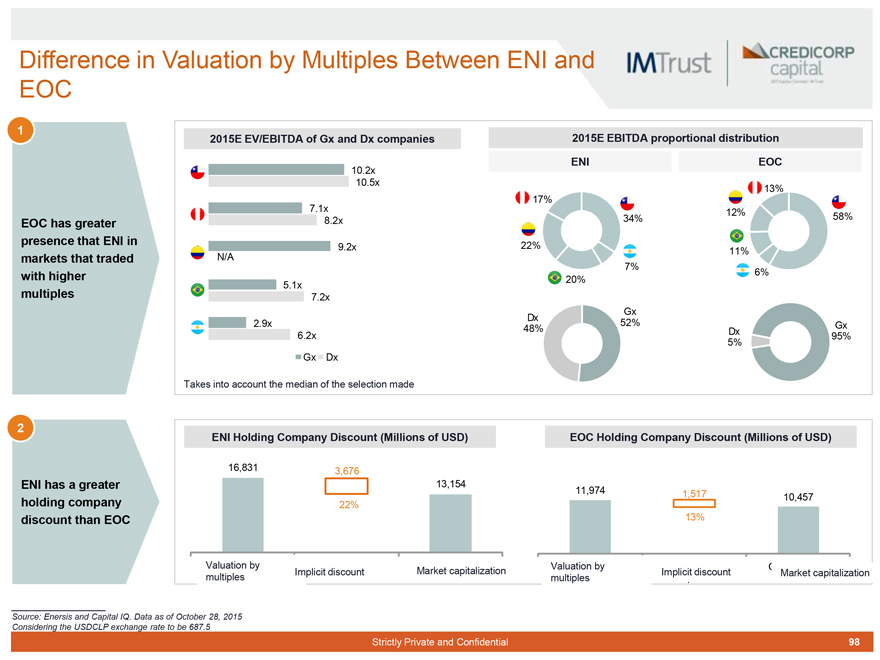

ENI, EOC and Chilectra Holding Company Discount

Enersis’ holding discount is estimated at 22%

25% would come from EOC’s discount

22% would come from Chilectra’s discount

The holding company discount could be generated by the following factors, among others:

i. Structural subordination to the cash flows generated by the operating subsidiaries

ii. Conglomerate effect: diversification of assets not necessarily desired by investors

iii. Direct access to operating subsidiaries listed at the stock exchange with relevant liquidity

iv. Complexity of the holding structure and decision making

v. Difference in relative liquidity between the holding corporation and its listed subsidiaries

ENI Holding Company Discount (Millions of USD)

16,831 910 821

1,945

13,154

1,517 x 60%

829 x 99%

Total implicit discount 22% Total: USD 3,676 million

Valuation by Implicit EOC Current market Implicit Chilectra Other multiples discount capitalization discount discounts

@ CLP 236 p.a. @ CLP 184 p.a.

EOC Holding Company Discount Chilectra Holding Company Discount (Millions of USD) (Millions of USD)

11,974 1,517

10,457

13% 4,176

829

3,348 20%

Current market Valuation by Current market Valuation by Implicit Implicit multiples multiples capitalization capitalization discount discount

@ CLP 1004 p.a. @ CLP 876 p.a. @ CLP 2.495 p.a. @ CLP 2.000 p.a.

Considering the USDCLP exchange rate to be 687.5

Strictly Private and Confidential 49

|

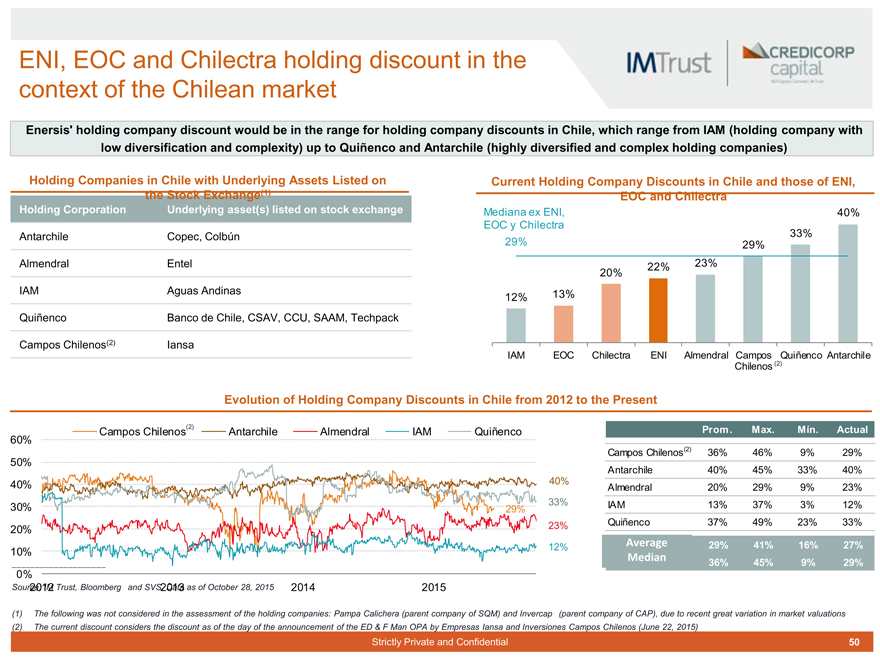

ENI, EOC and Chilectra holding discount in the context of the Chilean market

Enersis’ holding company discount would be in the range for holding company discounts in Chile, which range from IAM (holding company with low diversification and complexity) up to Quiñenco and Antarchile (highly diversified and complex holding companies)

Holding Companies in Chile with Underlying Assets Listed on

the Stock Exchange(1)

Holding Corporation Underlying asset(s) listed on stock exchange

Antarchile Copec, Colbún

Almendral Entel

IAM Aguas Andinas

Quiñenco Banco de Chile, CSAV, CCU, SAAM, Techpack

Campos Chilenos(2) Iansa

Current Holding Company Discounts in Chile and those of ENI, EOC and Chilectra

Mediana ex ENI, 40% EOC y Chilectra 33% 29% 29% 20% 22% 23% 12% 13%