Table of Contents

As filed with the Securities and Exchange Commission on March 14, 2018

Registration No. 333-223261

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FormF-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

GreenTree Hospitality Group Ltd.

(Exact name of Registrant as specified in its charter)

| Cayman Islands | 7011 | Not Applicable | ||

(State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

2451 Hongqiao Road, Changning District

Shanghai 200335

People’s Republic of China

+86-21-3617-4886

(Address and Telephone Number of Registrant’s Principal Executive Offices)

Law Debenture Corporate Services Inc.

801 2nd Avenue, Suite 403

New York, NY 10017, United States

+1-212-750-6474

(Name, address and telephone number of agent for service)

| Chris K.H. Lin, Esq. | Allen C. Wang, Esq. | |

| Daniel Fertig, Esq. | Zheng Wang, Esq. | |

| Simpson Thacher & Bartlett LLP | Latham & Watkins | |

| 35th Floor, ICBC Tower | 18th Floor, One Exchange Square | |

| 3 Garden Road | 8 Connaught Place, Central | |

| Central, Hong Kong | Hong Kong | |

| +852-2514-7600 | +852-2912-2500 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933.

Emerging growth company ☒

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

CALCULATION OF REGISTRATION FEE

| ||||||||

Title of Each Class of Securities to be Registered(1)(2) | Amount to be Registered(2)(3) | Proposed Maximum Offering Price per Share(3) | Proposed Maximum Aggregate Offering Price(3) | Amount of | ||||

Class A ordinary shares, par value US$0.50 per share | 22,310,000 | US$18.00 | US$401,580,000 | US$49,997 | ||||

| ||||||||

| ||||||||

| (1) | American depositary shares, or ADSs, evidenced by American depositary receipts issuable upon deposit of the Class A ordinary shares registered hereby will be registered under a separate registration statement on FormF-6. Each ADS represents one (1) Class A ordinary share. |

| (2) | Includes (a) Class A ordinary shares represented by ADSs that may be purchased by the underwriters pursuant to their option to purchase additional ADSs and (b) all Class A ordinary shares represented by ADSs initially offered and sold outside the United States that may be resold from time to time in the United States. Offers and sales of shares outside the United States are being made pursuant to Regulation S under the Securities Act of 1933, as amended, and are not covered by this Registration Statement. |

| (3) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(a) under the Securities Act of 1933, as amended. |

| (4) | Of which US$24,900 was previously paid. |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to such Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the U.S. Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting any offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

PROSPECTUS (subject to completion)

Issued , 2018

19,400,000 American Depositary Shares

GreenTree Hospitality Group Ltd.

REPRESENTING 19,400,000 CLASS A ORDINARY SHARES

GreenTree Hospitality Group Ltd. is offering 19,400,000 American depositary shares, or ADSs. Each ADS represents one (1) Class A ordinary share, par value US$0.50 per share. This is our initial public offering and no public market currently exists for our ADSs or shares.

We are an “emerging growth company” under applicable U.S. federal securities laws and are eligible for reduced public company reporting requirements. Immediately prior to the completion of this offering, our outstanding share capital will consist of 56,589,300 Class A ordinary shares and 34,762,909 Class B ordinary shares, all of which will be owned by our parent company, GreenTree Inns Hotel Management Group, Inc., a Cayman Islands company, or GTI. Holders of Class A ordinary shares and Class B ordinary shares have the same rights except for voting and conversion rights. Each Class A ordinary share is entitled to one (1) vote. Each Class B ordinary share is entitled to three (3) votes if such Class B ordinary share is owned by GTI, Mr. Alex S. Xu, our founder, chairman and chief executive officer, Mr. Alex S. Xu’s family trusts or his or the family trust’s designated transferees, and is convertible into one (1) Class A ordinary share at any time if such Class B ordinary share is owned by any other holder. Class A ordinary shares are not convertible into Class B ordinary shares under any circumstances.

GTI will beneficially own 74.5% of our Class A ordinary shares and 100% of our Class B ordinary shares immediately after the completion of this offering and 89.2% of the aggregate voting power of our total issued and outstanding share capital immediately after the completion of this offering. The voting power of our company owned by GTI is indirectly owned by Mr. Alex S. Xu, our founder, chairman and chief executive officer, as he owns 83.9% of voting power of GTI, which entitles Mr. Xu to nominate or replace all directors of GTI, and determine how GTI exercises the voting power in our company. Following the completion of this offering and as long as GTI or Mr. Alex S. Xu owns at least 50% of the voting power of our company, we will be a “controlled company” as defined under the NYSE Listed Company Manual. We have no current intention to rely on the controlled company exemption.

Prior to this offering, there has been no public market for the ADSs or our shares. It is currently estimated that the initial public offering price per ADS will be between US$16.00 and US$18.00. We have applied to list our ADSs on the New York Stock Exchange under the symbol “GHG.”

Investing in the ADSs involves risks. See “Risk Factors” beginning on page 14.

PRICE US$ AN ADS

| Price to public | Underwriting Discounts and Commissions(1) | Proceeds before expense to Company | ||||||||||

Per ADS | US$ | US$ | US$ | |||||||||

Total | US$ | US$ | US$ | |||||||||

| (1) | For a description of compensation payable to the underwriters, see “Underwriting.” |

We have granted the underwriters the right to purchase up to 2,910,000 additional ADSs to cover over-allotments within 30 days after the date of this prospectus.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved of these securities, or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the ADSs to purchasers on or about , 2018.

MORGAN STANLEY | BofA Merrill Lynch | UBS INVESTMENT BANK |

| ICBC International |

Prospectus dated , 2018.

Table of Contents

Table of Contents

| 1 | ||||

| 14 | ||||

| 51 | ||||

| 52 | ||||

| 53 | ||||

| 54 | ||||

| 55 | ||||

| 57 | ||||

| 58 | ||||

| 60 | ||||

| 62 | ||||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 66 | |||

| 96 | ||||

| 101 | ||||

| 125 | ||||

| 139 | ||||

| 146 | ||||

| 148 | ||||

| 151 | ||||

| 161 | ||||

| 171 | ||||

| 173 | ||||

| 181 | ||||

| 191 | ||||

| 192 | ||||

| 193 | ||||

| 194 | ||||

| F-1 | ||||

This prospectus contains estimates and information concerning our industry, including market position, market size, and growth rates of the markets in which we participate, that are based on industry publications and reports. This prospectus contains statistical data and estimates published by various sources. This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to these estimates. We have not independently verified the accuracy or completeness of the data contained in these industry publications and reports. The industry in which we operate is subject to a high degree of uncertainty and risk due to variety of factors, including those described in the “Risk Factors” section. These and other factors could cause results to differ materially from those expressed in these publications and reports.

i

Table of Contents

No dealer, salesperson or other person is authorized to give any information or to represent as to anything not contained in this prospectus or in any free writing prospectus we may authorize to be delivered or made available to you. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell, and we are seeking offers to buy, only the ADSs offered hereby, and only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date, regardless of the time of delivery of this prospectus or any sale of the ADSs.

Neither we nor the underwriters have done anything that would permit this offering or the possession or distribution of this prospectus or any filed free writing prospectus in any jurisdiction where other action for that purpose is required, other than in the U.S. persons outside the U.S. who come into possession of this prospectus or any free writing prospectus filed with the U.S. Securities and Exchange Commission, or SEC, must inform themselves about, and observe any restrictions relating to, the offering of the ADSs and the distribution of this prospectus or any filed free writing prospectus outside of the U.S.

Until , 2018 (the 25th day after the date of this prospectus), all dealers that buy, sell or trade ADSs, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

ii

Table of Contents

This summary highlights selected information contained in greater detail elsewhere in this prospectus. This summary may not contain all of the information that you should consider before investing in our ADSs. You should carefully read the entire prospectus, including “Risk Factors” and the financial statements, before making an investment decision.

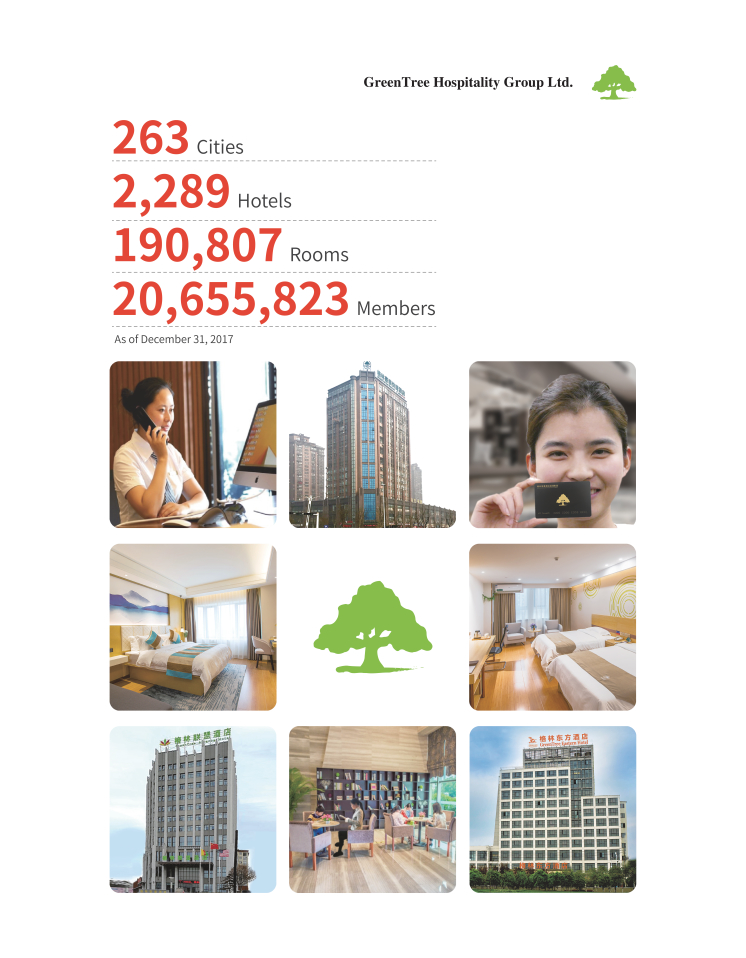

We are the leading pure play franchised hotel operator in China as franchised-and-managed hotels represent almost all of the hotels in our hotel network. In 2016, we were the fourth largest economy tomid-scale hotel group in China in terms of number of hotel rooms according to China Hospitality Association. As of December 31, 2017, we had the highest proportion of franchised-and-managed hotels among the top four economy tomid-scale hotel networks in China, with 98.9% of hotels in our network as of those dates being franchised-and-managed hotels. As of December 31, 2017, our hotel network comprised 2,289 hotels with 190,807 rooms in China, covering all four centrally-administrated municipalities and 263 cities throughout all 27 provinces and autonomous regions in China, as well as an additional 306 hotels with 23,157 rooms that were contracted for or under development. Out of those 306 hotels, 129 hotels were contracted for, and the remaining 177 hotels were under development and are expected to commence operation by June 2018.

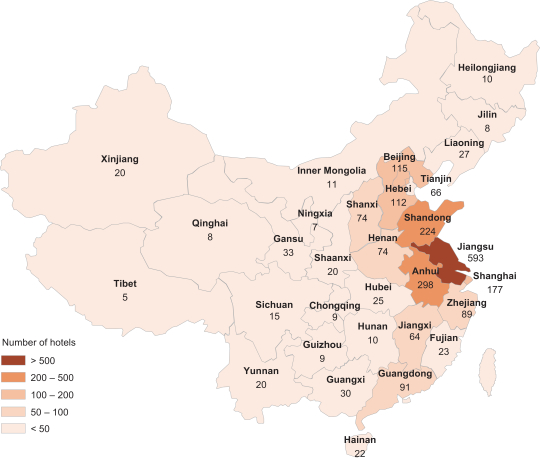

We operate one of the fastest growing economy tomid-scale hotel networks in China, with over 13 years of proven results and experience. Furthermore, we achieved the 2,000-hotel milestone through organic growth. From December 31, 2012 to December 31, 2017, we grew from 792 to 2,289 hotels at a CAGR of 23.7% and from 70,934 rooms to 190,807 rooms at a CAGR of 21.9%. As a result of our strategic focus on building a dense network of hotels in the most affluent regions in China with high growth potential, 50.5% of our hotels were located in Shanghai Municipality, Jiangsu, Zhejiang and Anhui Provinces, or the Greater Yangtze River Delta region, while 12.8% of our hotels were located in Beijing/Tianjin/Hebei region as of December 31, 2017.

We sell a predominant proportion of our room nights through our strong direct sales channels comprising our website and mobile app. In 2015, 2016 and 2017, we sold approximately 97% of our room nights through our direct sales channels, while online travel agencies, or OTAs, only contributed approximately 3% of our room nights. Our strong direct sales channels, combined with a loyal customer base, have contributed to our financial success. Over the years, we have grown a strong base of loyal members at a CAGR of approximately 42% from approximately 1.8 million members as of December 31, 2010. As of December 31, 2017, we had over 820,000 corporate clients who were able to settle directly with us or our franchisees and enjoy a preferential room rate and approximately 21 million members who registered with us and enjoyed a range of different benefits, including discounts on room rates, priority in making hotel reservations. In 2015, 2016 and 2017, our corporate clients and loyal members booked 72.9%, 72.9% and 73.0%, respectively, of our room nights.

We have built a strong “GreenTree Inns” brand as a result of our long-standing dedication in the hospitality industry in China and consistent quality of our services, signature hotel designs, broad geographic coverage and convenient locations. We have positioned our brands to appeal to value- and quality-conscious business travelers and leisure travelers. Starting from our GreenTree Inns hotels in 2004, we have successfully rolled out a number of brands to establish a full product suite, which we believe enables us to capture a wide spectrum of market opportunities. Our current brand portfolio comprises (i)mid- toup-scale brands including GreenTree Eastern founded in 2012, and newly launched Gme, Gya and VX brands with an aggregate of nine hotels being contracted;(ii) mid-scale brands including GreenTree Inns founded in 2004 and GreenTree Alliance founded in 2008; and (iii) economy brands including Vatica founded in 2013 and Shell founded in 2016.

We have established a highly effective and scalable franchise management system that enables us to win franchisees and grow rapidly. This platform not only ensures quality service be consistently delivered to our guests, but also helps our franchisees integrate into our hotel network smoothly and quickly. Our strong and

1

Table of Contents

supportive franchise platform and disciplined return-driven model enable our franchisees to generate highly attractive investment returns, which we believe is both a strong attraction for prospective franchisees and a strong incentive for existing franchisees to open multiple hotels.

As a result of our pure play franchise business model, strong direct sales channels, loyal hotel guests and effective management and operational platform, we have consistently achieved highly attractive profitability, as evidenced by our Adjusted EBITDA of RMB323.1 million, RMB338.5 million and RMB440.8 million (US$67.8 million), Adjusted EBITDA margin of 50.9%, 52.3% and 56.6%, net income of RMB235.7 million, RMB265.8 million and RMB285.1 million (US$43.8 million), net margin of 37.1%, 41.0% and 36.6% and return on equity of 34.5%, 29.5% and 32.4% for 2015, 2016 and 2017, respectively. See “Summary Consolidated Financial and Operating Data — Non-GAAP Financial Data.” We have also been able to grow our network substantially and generate strong cash flow consistently since inception in 2004 with minimal debt and equity financing. In 2015, 2016 and 2017, we generated net operating cash inflow of RMB357.3 million, RMB443.6 million and RMB476.7 million (US$73.3 million) and did not have any outstanding indebtedness as of December 31, 2017.

Our Strengths

We have achieved a leading position in China’s economy tomid-scale hotel industry through our dedication in addressing the needs of our hotel guests and franchisees. We believe that we possess the following strengths which contribute to our success and differentiate us from our competitors:

| • | leading pure play franchise hotel operator in China with attractive returns; |

| • | one of the largest hotel networks in China through rapid organic growth; |

| • | 97% of room nights sold through direct sales channels with loyal membership base; |

| • | strong brand recognition with a diverse product suite; |

| • | effective management and operational system with people-first philosophy; and |

| • | guests and franchisees-focused and service-oriented culture with an experienced management team. |

Our Strategies

Our goal is to become a leading economy tomid-scale hotel network globally for business and leisure travelers. We intend to achieve this goal by executing on the following strategies:

| • | enhance our leading position by expanding our hotel network; |

| • | enhance profitability and performance of our hotels in operations; |

| • | strengthen brand recognition and expand our membership base by leveraging our membership program; |

| • | meet evolving market demand through brand portfolio mix diversification; and |

| • | attract, retain and promote well-trained employees. |

Our Challenges

We believe some of the major risks and uncertainties that may materially and adversely affect us include the following:

| • | our results of operations are subject to conditions typically affecting the hospitality industry; |

2

Table of Contents

| • | we are subject to various risks inherent in the franchised-and-managed business model; |

| • | we may not be able to renew our existing franchise agreements or renegotiate new franchise agreements when they expire; |

| • | failure to comply with government regulations relating to the franchise, hospitality industry, construction, fire prevention, food hygiene, safety and environmental protection could materially and adversely affect our business and results of operations; |

| • | the legal rights of our franchisees and us to use certain leased properties could be challenged by property owners or other third parties, which could prevent our franchisees or us from continuing to operate the affected hotels or increase the costs associated with operating these hotels; |

| • | we may not be able to successfully attract new franchisees and compete for franchise agreements and, as a result, we may not be able to achieve our planned growth; |

| • | the leases of our franchisees and us could be terminated early, we or our franchisees may not be able to renew the existing leases on commercially reasonable terms and the rents could increase substantially, which could materially and adversely affect our operations; |

| • | our financial condition and results of operations may be materially affected if our strategy to diversify our brand portfolio and mix of hospitality offerings is not successfully implemented; and |

| • | our results of operations may fluctuate significantly due to seasonality and other factors. |

We also face other challenges, risks and uncertainties that may materially and adversely affect our business, financial condition, results of operations and prospects. You should consider the risks discussed in “Risk Factors” and elsewhere in this prospectus before investing in our ADSs.

Corporate Structure and History

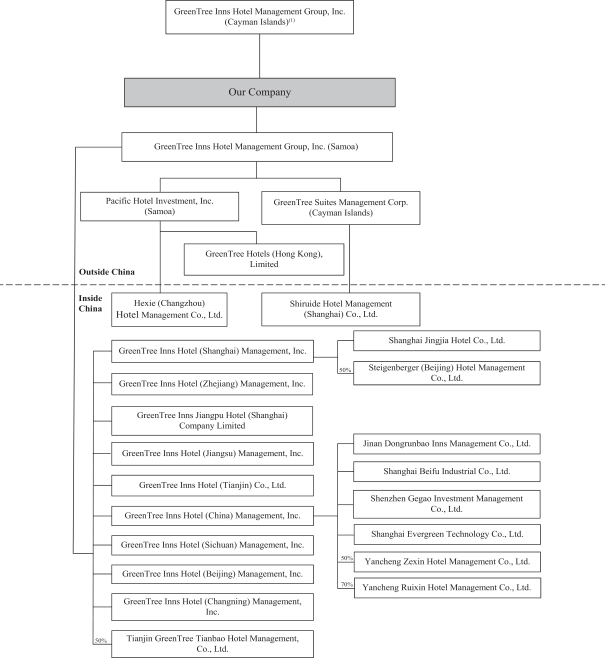

We are a Cayman Islands holding company and conduct our operations in China through our PRC subsidiaries. GreenTree Inns Hotel Management Group, Inc., a company incorporated in Samoa, or GreenTree Samoa, was formed to be the holding company of all but two of our PRC subsidiaries that operate our hotels in the PRC. GreenTree Samoa also owns 100% of the equity interest in Pacific Hotel Investment, Inc. and GreenTree Suites Management Corp., which owns 100% of the equity interest in the other two of our PRC subsidiaries.

Following the completion of this offering and as long as GTI or Mr. Alex S. Xu owns at least 50% of the voting power of our company, we will be a “controlled company” as defined under the NYSE Listed Company Manual. We have no current intention to rely on the controlled company exemption.

The following diagram illustrates our ownership structure immediately before our initial public offering. It omits all our subsidiaries and joint ventures. See “Our History and Corporate Structure” for our corporate structure showing the material subsidiaries and joint ventures.

Note:

| (1) | GTI holds 56,589,300 Class A ordinary shares and 34,762,909 Class B ordinary shares in our company. GTI is entitled to cast 160,878,027 votes. Class A ordinary shares are entitled to one (1) vote per share and |

3

Table of Contents

| holders of Class B ordinary shares are entitled to three (3) votes per share, in respect of matters requiring the votes of shareholders of our company. Holders of our Class A and Class B ordinary shares have the same rights to dividend and other distributions. |

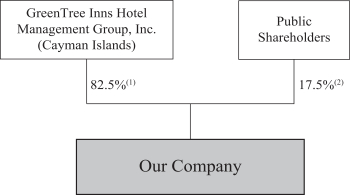

Immediately after the completion of this offering, 56,589,300 of our Class A ordinary shares and 34,762,909 of our Class B ordinary shares will be owned by GTI, our parent company. The following diagram illustrates our ownership structure immediately after the completion of this offering.

Notes:

| (1) | GTI holds 56,589,300 Class A ordinary shares, 34,762,909 Class B ordinary shares and is entitled to cast 160,878,027 votes. Mr. Alex S. Xu is considered to beneficially own these shares and has power to direct these votes. See “Principal Shareholder.” |

| (2) | In aggregate, the public shareholders hold 19,400,000 Class A ordinary shares and are entitled to cast an aggregate of 19,400,000 votes. |

After the completion of this offering, GTI intends to register and distribute to each of its shareholders not more than 60% of the number of our shares that represent the percentage of such shareholder’s ownership in GTI as of the closing date of this offering. As a condition to receive our shares, GTI’s shareholders will be required to enter into lock-up agreements with us to agree, among others, not to offer, sell, contract to sell, pledge, grant any option to purchase, purchase any option or contract to sell, grant any right or warrant to purchase, lend, make any short sale, file a registration statement, or make any demand for or exercise any right to file a registration statement, under the Securities Act or otherwise dispose of any of our shares prior to the expiry of a six-month period following the date of this prospectus. The number of our shares subject to such lock-up agreements will be reduced by 25% at the end of the six month period following the date of this prospectus and each six month period thereafter through the two-year anniversary of the date of this prospectus.

Our Corporate Information

Our principal executive offices are located at 2451 Hongqiao Road, Changning District, Shanghai 200335, People’s Republic of China. Our telephone number at this address is+86-21-3617-4886. Our registered office in the Cayman Islands is located at the offices of Maples Corporate Services Limited, PO Box 309, Ugland House, Grand Cayman,KY1-1104, Cayman Islands. Investors should submit any inquiries to the address and telephone number of our principal executive offices set forth above.

Our corporate website iswww.998.com. The information contained on our websites is not a part of this prospectus. Our agent for service of process in the United States is Law Debenture Corporate Services Inc., located at 801 2nd Avenue, Suite 403, New York, NY 10017.

4

Table of Contents

Implications of Being an Emerging Growth Company

As a company with less than US$1.07 billion in revenue for the last fiscal year, we qualify as an “emerging growth company” pursuant to the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company may take advantage of specified reduced reporting and other requirements that are otherwise applicable generally to public companies. These provisions include exemption from the auditor attestation requirement under Section 404 of theSarbanes-Oxley Act of 2002, or Section 404, in the assessment of the emerging growth company’s internal control over financial reporting. The JOBS Act also provides that an emerging growth company does not need to comply with any new or revised financial accounting standards until such date that a private company is otherwise required to comply with such new or revised accounting standards. We will take advantage of the extended transition period. As a result of this election, our financial statements may not be comparable to other public companies that comply with the public company effective dates for these new or revised accounting standards.

We will remain an emerging growth company until the earliest of (i) the last day of our fiscal year during which we have total annual revenues of at least US$1.07 billion; (ii) the last day of our fiscal year following the fifth anniversary of the completion of this offering; (iii) the date on which we have, during the previous three year period, issued more than US$1.07 billion innon-convertible debt; or (iv) the date on which we are deemed to be a “large accelerated filer” under the Securities Exchange Act of 1934, as amended, or the Exchange Act, which would occur if the market value of our ADSs that are held bynon-affiliates exceeds US$700 million as of the last business day of our most recently completed second fiscal quarter. Once we cease to be an emerging growth company, we will not be entitled to the exemptions provided in the JOBS Act discussed above.

Conventions That Apply to This Prospectus

Unless we indicate otherwise, references in this prospectus to:

| • | “ADR” or “ADRs” are to the American depositary receipts, which, if issued, evidence our ADSs; |

| • | “ADSs” are to our American depositary shares, each of which represents one (1) Class A ordinary share; |

| • | “Adjusted EBITDA” are to Adjusted EBITDA as calculated and presented in the “Summary Consolidated Financial and Operating Data”, “Selected Consolidated Financial and Operating Data”, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” sections and elsewhere in this prospectus; |

| • | “China” and the “PRC” are to the People’s Republic of China, excluding, for the purposes of this prospectus only, Taiwan, the Hong Kong Special Administrative Region and the Macao Special Administrative Region; |

| • | “GreenTree Inns” brand are to hotels operated under the GreenTree Inns and GreenTree Inns Express brands; |

| • | “leased-and-operated hotels” are to hotels that we lease or own the premises and operate; |

| • | “RMB” or “Renminbi” are to the legal currency of China; |

| • | “ramp up stage” are to hotels in operation that have been open for six or fewer months; |

| • | “RevPAR” are to revenue per available room, which is calculated by multiplying our hotels’ average daily room rate, or ADR, by its occupancy rate; |

| • | “shares” are to, collectively, our Class A ordinary shares and Class B ordinary shares, par value US$0.50 per share; |

| • | “Tier 1 cities” are to the term used by the National Bureau of Statistics of China and refer to Beijing, Shanghai, Shenzhen and Guangzhou; |

5

Table of Contents

| • | “Tier 2 cities” are to the 32 major cities, other than Tier 1 cities, as categorized by the National Bureau of Statistics of China, including provincial capitals, administrative capitals of autonomous regions, direct-controlled municipalities and other major cities designated as “municipalities with independent planning” by the State Council; |

| • | “US$,” “U.S. dollars,” or “dollars” are to the legal currency of the United States; |

| • | “U.S. GAAP” are to accounting principles generally accepted in the United States; and |

| • | “we,” “us,” “our company” and “our” are to GreenTree Hospitality Group Ltd., our Cayman Islands holding company, and its subsidiaries, as the context requires. |

Our reporting currency is the Renminbi. This prospectus also contains translations of certain foreign currency amounts into U.S. dollars for the convenience of the reader. Unless otherwise stated, all translations of Renminbi into U.S. dollars were made at RMB6.5063 to US$1.00, the exchange rate set forth in the H.10 statistical release of the Federal Reserve Board on December 29, 2017. We make no representation that the Renminbi or U.S. dollar amounts referred to in this prospectus could have been or could be converted into U.S. dollars or Renminbi, as the case may be, at any particular rate or at all. On March 9, 2018, the noon buying rate for Renminbi was RMB6.3285 to US$1.00.

The number of our shares that will be outstanding after this offering is calculated based on 91,352,209 shares outstanding as of the date of this prospectus, and excludes:

| • | 1,703,000 Class A ordinary shares issuable upon the exercise of options to purchase Class A ordinary shares that were outstanding as of the date of this prospectus; and |

| • | an additional 7,297,000 Class A ordinary shares reserved for future issuance under our 2018 share incentive plan. |

Except as otherwise indicated, all information in this prospectus assumes:

| • | no exercise by the underwriters of their option to purchase up to an additional 2,910,000 ADSs representing 2,910,000 Class A ordinary shares from us. |

6

Table of Contents

THE OFFERING

ADSs Offered by Us | 19,400,000 ADSs |

Public Offering Price | We estimate that the initial public offering price will be between US$16.00 and US$18.00 per ADS. |

ADSs Outstanding Immediately After This Offering | 19,400,000 ADSs. |

Shares Outstanding Immediately After This Offering | 110,752,209 shares, comprising 75,989,300 Class A ordinary shares, and 34,762,909 Class B ordinary shares, excluding shares issuable upon the exercise of options outstanding under our 2018 share incentive plan as of the date of this prospectus. |

Over-Allotment Option | We have granted to the underwriters an option, exercisable for 30 days from the date of this prospectus, to purchase up to an aggregate of 2,910,000 additional ADSs at the initial public offering price, less underwriting discounts and commissions, solely for the purpose of covering over-allotments. |

The ADSs | Each ADS represents one (1) Class A ordinary share. |

| The depositary will be the holder of the Class A ordinary shares underlying the ADSs and you will have the rights as provided in the deposit agreement among us, the depositary and holders and beneficial owners of ADSs from time to time. |

| You may surrender your ADSs to the depositary to withdraw the Class A ordinary shares underlying your ADSs. The depositary will charge you a fee for such an exchange. |

| We may amend or terminate the deposit agreement for any reason without your consent. Any amendment that imposes or increases fees or charges or which materially prejudices any substantial existing right you have as an ADS holder will not become effective as to outstanding ADSs until 30 days after notice of the amendment is given to ADS holders. If an amendment becomes effective, you will be bound by the deposit agreement as amended if you continue to hold your ADSs. |

| To better understand the terms of the ADSs, you should carefully read the section in this prospectus entitled “Description of American Depositary Shares.” We also encourage you to read the deposit agreement, which is an exhibit to the registration statement that includes this prospectus. |

Shares | Our shares will consist of Class A ordinary shares and Class B ordinary shares immediately prior to the completion of this offering. |

7

Table of Contents

Holders of Class A ordinary shares and Class B ordinary shares have the same rights except for voting and conversion rights. Each Class A ordinary share is entitled to one vote; each Class B ordinary share is entitled to three (3) votes if such Class B ordinary share is owned by GTI, Mr. Alex S. Xu, our founder, chairman and chief executive officer, Mr. Alex S. Xu’s family trusts or his or the family trust’s designated transferees, and is convertible into one Class A ordinary share at any time by the holder thereof. Class A ordinary shares are not convertible into Class B ordinary shares under any circumstances. Upon any sale of Class B ordinary shares by a holder thereof to any person or entity which is not an affiliate of such holder, such Class B ordinary shares shall be automatically and immediately converted into the same number of Class A ordinary shares. For a description of Class A ordinary shares and Class B ordinary shares, see “Description of Share Capital.” |

Use of Proceeds | We estimate that we will receive net proceeds of approximately US$301.1 million from this offering, assuming an initial public offering price of US$17.00 per ADS, themid-point of the estimated range of the initial public offering price set forth on the cover of this prospectus, after deducting estimated underwriter discounts, commissions and estimated offering expenses payable by us. We plan to use the net proceeds we will receive from this offering for general corporate purposes in line with our strategies, including for the organic expansion of our hotel chain and the improvement of existing hotel properties, potential acquisitions of domestic and overseas operators that will complement our operations and accelerate our expansion plan, and for working capital and other general corporate purposes. See “Use of Proceeds” for more information. |

Risk Factors | See “Risk Factors” and other information included in this prospectus for a discussion of the risks relating to investing in our ADSs. You should carefully consider these risks before deciding to invest in our ADSs. |

Directed ADS Program | At our request, the underwriters have reserved up to 5% of the ADSs being offered by this prospectus for sale to and purchase by our directors, officers, employees, business associates and related persons at the initial public offering price through a directed share program in accordance with applicable laws. The sales will be made by UBS Financial Services Inc., a selected dealer affiliated with UBS Securities LLC, an underwriter of this offering, through a directed share program. We do not know if these persons will choose to purchase all or a portion of these reserved ADSs, but any purchases they do make will reduce the number of ADSs available to the general public. Any reserved ADSs not so purchased will be offered by the underwriters to the general public on the same terms as the other ADSs. |

Listing | We have applied to list our ADSs on the New York Stock Exchange. |

8

Table of Contents

Proposed Trading Symbol | GHG |

Depositary | Deutsche Bank Trust Company Americas |

Lock-up | We and our sole shareholder, GTI, have agreed with the underwriters to certainlock-up restrictions in respect of our shares, ADSs, and/or any securities convertible into or exchangeable or exercisable for any of our shares or ADSs, during the period ending six months after the completion of this offering, subject to certain exceptions. See “Shares Eligible for Future Sale” and “Underwriting.” |

| After the completion of this offering, GTI intends to register and distribute to each of its shareholders not more than 60% of the number of our shares that represent the percentage of such shareholder’s ownership in GTI as of the closing date of this offering. As a condition to receiving our shares, GTI’s Shareholders will be required to enter into lock-up agreements with us to agree, among others, not to offer, sell, contract to sell, pledge, grant any option to purchase, purchase any option or contract to sell, grant any right or warrant to purchase, lend, make any short sale, file a registration statement, or make any demand for or exercise any right to file a registration statement, under the Securities Act or otherwise dispose of any of our shares prior to the expiry of a six-month period following the date of this prospectus. The number of our shares subject to such lock-up agreements will be reduced by 25% at the end of the six month period following the date of this prospectus and each six month period thereafter through the two-year anniversary of the date of this prospectus. |

9

Table of Contents

Summary Consolidated Financial and Operating Data

The following summary consolidated statements of comprehensive income data for the years ended December 31, 2015, 2016 and 2017 and the summary consolidated balance sheet data as of December 31, 2015, 2016 and 2017 have been derived from our audited consolidated financial statements included elsewhere in this prospectus.

Our consolidated financial statements are prepared and presented in accordance with U.S. GAAP.

Our historical results are not necessarily indicative of results to be expected for any future period. The following summary consolidated financial data for the periods and as of the dates indicated are qualified by reference to and should be read in conjunction with our consolidated financial statements and related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” both of which are included elsewhere in this prospectus.

| Year ended December 31, | ||||||||||||||||

| 2015 | 2016 | 2017 | ||||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| (in thousands) | ||||||||||||||||

Summary Consolidated Statements of Comprehensive Income Data: | ||||||||||||||||

Revenues | ||||||||||||||||

Leased-and-operated hotels | 204,761 | 183,773 | 189,134 | 29,069 | ||||||||||||

Franchised-and-managed hotels | 397,987 | 421,577 | 535,632 | 82,325 | ||||||||||||

Membership fees | 31,972 | 42,439 | 53,365 | 8,202 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total revenues | 634,720 | 647,789 | 778,131 | 119,596 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Operating costs and expenses | ||||||||||||||||

Hotel operating costs | (264,335 | ) | (240,132 | ) | (233,646 | ) | (35,910 | ) | ||||||||

Selling and marketing expenses | (24,643 | ) | (26,609 | ) | (45,032 | ) | (6,921 | ) | ||||||||

General and administrative expenses | (64,308 | ) | (77,933 | ) | (121,657 | )(1) | (18,698 | ) | ||||||||

Other operating expenses | (14,757 | ) | (3,073 | ) | (5,629 | ) | (866 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Total operating costs and expenses | (368,043 | ) | (347,747 | ) | (405,964 | ) | (62,395 | ) | ||||||||

Other operating income | 21,095 | 12,222 | 15,284 | 2,349 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income from operations | 287,772 | 312,264 | 387,451 | 59,550 | ||||||||||||

Interest income and other, net | 19,643 | 22,039 | 26,238 | 4,032 | ||||||||||||

Interest expense | — | — | (1,443 | ) | (221 | ) | ||||||||||

Gains from trading securities | 25,545 | 24,564 | 59,165 | 9,094 | ||||||||||||

Other income (expense), net | — | 1,322 | 1,191 | 183 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Income before income taxes | 332,960 | 360,189 | 472,602 | 72,638 | ||||||||||||

Income tax expense | (80,077 | ) | (83,924 | ) | (186,651 | )(2) | (28,688 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Income before share of loss in equity investees | 252,883 | 276,265 | 285,951 | 43,950 | ||||||||||||

Share of loss in equity investees, net of tax | (17,213 | ) | (10,465 | ) | (900 | ) | (138 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Net income | 235,670 | 265,800 | 285,051 | 43,812 | ||||||||||||

Net loss attributable to noncontrolling interests | 123 | 173 | 349 | 54 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Net income attributable to ordinary shareholders | 235,793 | 265,973 | 285,400 | 43,866 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| (1) | Includes one-time share-based compensation expenses of RMB38.0 million (US$5.8 million) in 2017 for GTI’s shares granted to certain of our directors for their past services as directors. |

| (2) | Includes withholding taxes of RMB67.7 million (US$10.4 million) incurred in connection with a cash dividend distributed by our subsidiaries incorporated in the PRC during the year ended December 31, 2017. |

10

Table of Contents

The following table presents a summary of our consolidated balance sheet data as of December 31, 2015, 2016 and 2017:

| As of December 31, | ||||||||||||||||

| 2015 | 2016 | 2017 | ||||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| (in thousands) | ||||||||||||||||

Summary Consolidated Balance Sheet Data: | ||||||||||||||||

Cash and cash equivalents | 505,857 | 896,783 | 161,964 | 24,893 | ||||||||||||

Property and equipment, net | 141,394 | 110,436 | 96,669 | 14,858 | ||||||||||||

Intangible assets, net | 5,981 | 4,927 | 3,727 | 573 | ||||||||||||

Goodwill | 2,959 | 2,959 | 2,959 | 455 | ||||||||||||

Long-term investments | 81,158 | 35,497 | 122,509 | 18,829 | ||||||||||||

Total assets | 1,407,151 | 1,875,751 | 1,755,983 | 269,890 | ||||||||||||

Deferred revenue | 151,101 | 201,356 | 253,361 | 38,941 | ||||||||||||

Total liabilities | 629,947 | 848,827 | 1,023,378 | 157,291 | ||||||||||||

Total shareholders’ equity | 777,204 | 1,026,924 | 732,605 | 112,599 | ||||||||||||

Total liabilities and shareholders’ equity | 1,407,151 | 1,875,751 | 1,755,983 | 269,890 | ||||||||||||

The following tables present certain unaudited financial data and selected operating data as of and for the years ended December 31, 2015, 2016 and 2017:

| As of December 31, | ||||||||||||

| 2015 | 2016 | 2017 | ||||||||||

Summary Operating Data: | ||||||||||||

Total hotels in operation | 1,651 | 1,964 | 2,289 | |||||||||

Franchised-and-managed hotels | 1,611 | 1,932 | 2,263 | |||||||||

Leased-and-operated hotels | 40 | 32 | 26 | |||||||||

Total hotel rooms in operation | 146,176 | 168,238 | 190,807 | |||||||||

Franchised-and-managed hotels | 141,434 | 164,207 | 187,505 | |||||||||

Leased-and-operated hotels | 4,742 | 4,031 | 3,302 | |||||||||

Number of cities | 210 | 234 | 263 | |||||||||

| Year Ended December 31, | ||||||||||||

| 2015 | 2016 | 2017 | ||||||||||

Occupancy rate (as a percentage)(1) | ||||||||||||

Total hotels in operation | 77.8 | % | 80.4 | % | 82.6 | % | ||||||

Franchised-and-managed hotels | 78.3 | % | 80.9 | % | 82.9 | % | ||||||

Leased-and-operated hotels | 66.8 | % | 66.4 | % | 70.3 | % | ||||||

Average daily rate (in RMB) | ||||||||||||

Total hotels in operation | 152 | 153 | 157 | |||||||||

Franchised-and-managed hotels | 152 | 152 | 156 | |||||||||

Leased-and-operated hotels | 160 | 164 | 186 | |||||||||

RevPAR (in RMB) | ||||||||||||

Total hotels in operation | 118 | 123 | 130 | |||||||||

Franchised-and-managed hotels | 119 | 123 | 129 | |||||||||

Leased-and-operated hotels | 107 | 109 | 131 | |||||||||

11

Table of Contents

| (1) | Based on number of available rooms. |

| Year Ended December 31, | ||||||||||||||||

| 2015 | 2016 | 2017 | ||||||||||||||

| RMB | RMB | RMB | US$ | |||||||||||||

| (in thousands, except for percentage) | ||||||||||||||||

Non-GAAP Financial Data | ||||||||||||||||

Adjusted EBITDA(1) | 323,117 | 338,470 | 440,800 | 67,751 | ||||||||||||

Adjusted EBITDA Margin(2) | 50.9% | 52.3% | 56.6% | |||||||||||||

| (1) | We believe that Adjusted EBITDA, as we present it, is a useful financial metric to assess our operating and financial performance before the impact of investing and financing transactions, income taxes and certain non-core and non-recurring items in our financial statements. |

The presentation of Adjusted EBITDA should not be construed as an indication that our future results will be unaffected by other charges and gains we consider to be outside the ordinary course of our business.

The use of Adjusted EBITDA has certain limitations because it does not reflect all items of income and expenses that affect our operations. Items excluded from Adjusted EBITDA are significant components in understanding and assessing our operating and financial performance. Depreciation and amortization expense for various long-term assets, income tax and share-based compensation have been and will be incurred and are not reflected in the presentation of Adjusted EBITDA. Each of these items should also be considered in the overall evaluation of our results. Additionally, Adjusted EBITDA does not consider capital expenditures and other investing activities and should not be considered as a measure of our liquidity. We compensate for these limitations by providing the relevant disclosure of our depreciation and amortization, interest expense/income, gains/losses from trading securities, income tax expenses, share-based compensation, share of loss in equity investees and other relevant items both in our reconciliations to the corresponding U.S. GAAP financial measures and in our consolidated financial statements, all of which should be considered when evaluating our performance.

The term Adjusted EBITDA is not defined under U.S. GAAP, and Adjusted EBITDA is not a measure of net income, operating income, operating performance or liquidity presented in accordance with U.S. GAAP. When assessing our operating and financial performance, you should not consider this data in isolation or as a substitute for our net income, operating income or any other operating performance measure that is calculated in accordance with U.S. GAAP. In addition, our Adjusted EBITDA may not be comparable to Adjusted EBITDA or similarly titled measures utilized by other companies since such other companies may not calculate Adjusted EBITDA in the same manner as we do.

12

Table of Contents

A reconciliation of Adjusted EBITDA to net income, which is the most directly comparable U.S. GAAP measure, is provided below:

| Year Ended December 31, | ||||||||||||||||

| 2015 | 2016 | 2017 | ||||||||||||||

| (RMB) | (RMB) | RMB | US$ | |||||||||||||

| (in thousands) | ||||||||||||||||

Net income | 235,670 | 265,800 | 285,051 | 43,812 | ||||||||||||

Deduct: | ||||||||||||||||

Other operating income | 21,095 | 12,222 | 15,284 | 2,349 | ||||||||||||

Interest income and other, net | 19,643 | 22,039 | 26,238 | 4,032 | ||||||||||||

Gains from trading securities | 25,545 | 24,564 | 59,165 | 9,094 | ||||||||||||

Other income (expense), net | — | 1,322 | 1,191 | 183 | ||||||||||||

Add: | ||||||||||||||||

Other operating expenses | 14,757 | 3,073 | 5,629 | 866 | ||||||||||||

Income tax expense | 80,077 | 83,924 | 186,651 | 28,688 | ||||||||||||

Share of loss in equity investees, net of tax | 17,213 | 10,465 | 900 | 138 | ||||||||||||

Interest expense | — | — | 1,443 | 221 | ||||||||||||

Share-based compensation | — | — | 38,048 | 5,848 | ||||||||||||

Depreciation and amortization | 41,683 | 35,355 | 24,956 | 3,836 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Adjusted EBITDA (Non-GAAP) | 323,117 | 338,470 | 440,800 | 67,751 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| (2) | Adjusted EBITDA margin is calculated by dividing Adjusted EBITDA by our total revenues. |

13

Table of Contents

You should consider carefully all of the information in this prospectus, including the risks and uncertainties described below, before making an investment in our ADSs. Any of the following risks could have a material adverse effect on our business, financial condition and results of operations. In any such case, the market price of our ADSs could decline, and you may lose all or part of your investment.

Risks Related to Our Business

Our results of operations are subject to conditions typically affecting the hospitality industry.

Our results of operations are subject to conditions typically affecting the hospitality industry, including the following:

| • | changes in national, regional or local economic conditions; |

| • | natural disasters or travelers’ fears of exposure to serious contagious diseases; |

| • | changes in travel patterns; |

| • | changes in governmental regulations that influence or determine wages, prices or construction costs; |

| • | local market conditions such as an oversupply of, or a reduction in demand for, hotel rooms; |

| • | our ability to secure desirable locations for our hotels; |

| • | the attractiveness of our hotels to potential guests and competition from other hotels; |

| • | changes in occupancy and room rates; |

| • | increases in operating costs and expenses due to inflation and other factors; |

| • | our ability to develop and maintain positive relations with current and potential franchisees; and |

| • | the performance of managerial and other employees of our hotels. |

Changes in any of these conditions could adversely affect our occupancy rates, average daily rates and RevPAR or otherwise adversely affect our business, results of operations and financial condition.

We are subject to various operational risks inherent in the franchised-and-managed business model.

Our success could be adversely affected by the performance of our franchised-and-managed hotels. As of December 31, 2017, we franchised-and-managed approximately 98.9% of our hotels, and we derived 62.7%, 65.0% and 68.8% of our revenues from those hotels in 2015, 2016 and 2017, respectively. We plan to increase the number of franchised-and-managed hotels in operation to increase our national presence in China. Our franchisees may not be able to develop hotel properties on a timely basis, which could adversely affect our growth strategy and may impact our ability to collect fees from them on a timely basis.

We oversee and manage the operations of our franchised-and-managed hotels pursuant to various franchise agreements. However, we are not able to control the actions of our franchisees. Under those franchise agreements, our franchisees are typically responsible for developing hotel properties on a timely basis, bearing the costs and expenses of developing and operating the hotels, including costs of renovating the hotels to our standards and recruiting and employing hotel staff. However, if our franchisees have difficulties in accessing capital or are reluctant to make investments for the management or renovation of the hotels, we may not able to force them to secure the required capital and the quality of our franchised-and-managed hotels’ operations may be thereby diminished.

We normally require our franchisees to secure relevant governmental approvals and permits for operating the hotels in our standard franchise agreements and require that our franchisees provide us with some basic

14

Table of Contents

approvals and permits, including business license, special industry license and fire prevention safety inspection certificates. However, some of our franchisees may not be able to obtain such approvals or permits in a timely manner, or at all. See “— Failure to comply with government regulations relating to the franchise, hospitality industry, construction, fire prevention, food hygiene, safety and environmental protection could materially and adversely affect our business and results of operations.”

As many factors affecting the operations of those hotels are beyond our control, we cannot assure you that the quality of the services in our franchised-and-managed hotels are consistent with our standards and requirements. Although we send for routine inspection purposes regional managers and members of our quality control team to franchised-and-managed hotels on a regular basis, we may not be able to identify problems in their operations and make responses on a timely basis. As a result, our image and reputation may suffer, which may have a material adverse effect on our business and results of operations.

In addition to quality standards, safety incidents such as fire accidents may occur at our franchised-and-managed hotels despite our supervision. Any such occurrence may result in substantial reputational harm to us and our brands. In addition, if such safety incidents occur at any of the franchised-and-managed hotels that do not possess the relevant licenses, permits or inspection certificate, there could be substantial negative publicity, thereby triggering large-scale government actions that could impact our entire hotel network, which in turn will have a material adverse impact on our business, results of operations and financial condition.

Although our proprietary information system can collect operational and financial data of each hotel, we may not be able to avoid fraud or manipulation of such data by some franchisees, which may adversely affect the ability to effectively respond to potential issues. In addition, many of our franchisees do not own the hotel land or the property but typically lease the property from landlords who are either a property owner or asub-lessor. We cannot assure you that all landlords who lease the hotel property to our franchisees have good and marketable title, or have unencumbered rights to lease orsub-lease the property to our franchisees. If any third party such as the ultimate property owners or relevant governmental authorities successfully challenge the lease of our franchisees, or if our franchisees fail to renew the leases when they expire, or if the landlords early terminate the lease, or if the properties or lands owned or leased by our franchisees are demolished, acquired or otherwise reclaimed by the government, our franchisees may have to close their hotels and thus terminate the franchise agreements and as a result, our business and results of operations may be adversely affected. Moreover, the term of lease for some of the property of our franchisees is shorter than the typical term of our franchise agreements. We cannot assure you that upon expiration, these franchisees will be able to renew their leases in order to perform their franchise agreements with us.

We may not be able to renew our existing franchise agreements or renegotiate new franchise agreements when they expire.

We franchise hotels to third parties pursuant to franchise agreements. These franchise agreements may be renegotiated or may expire. The versions of franchise agreements we have used during recent years typically have an initial term of 15 to 20 years except for the franchise agreements with our GreenTree Alliance franchisees and Shell franchisees. We plan to renew our existing franchise agreements upon expiration or renegotiate with our franchisees for new franchise agreements. However, we may be unable to retain our franchisees on satisfactory terms, or at all. If a significant number of our existing franchise agreements expire and new franchisees do not cover those expired franchises, our revenue and profit may decrease in the future, and our results of operations could be materially and adversely affected.

As the hospitality industry in China is highly competitive, the terms of our franchise agreements are influenced by contract terms offered by our competitors. We cannot assure you that the terms of franchise agreements for new franchised-and-managed hotels entered into or renewed in the future will be as favorable as the terms under our existing franchise agreements.If such agreements cannot be renewed on satisfactory terms upon expiration, our results of operations could be materially and adversely affected.

15

Table of Contents

Failure to comply with government regulations relating to the franchise business model, hospitality industry, construction, fire prevention, food hygiene, safety and environmental protection could materially and adversely affect our business and results of operations.

Our business is subject to various compliance and operational requirements under PRC laws and regulations, which include public safety, construction, fire prevention, public area hygiene, health and sanitation and environmental protection, as well as requirements related to construction or decoration of hotel premises. The failure of any of our hotels to comply with applicable laws and regulations may incur substantial fines and penalties from the relevant PRC government authorities. Each hotel in our network must hold a basic business license and a special industry license issued by local government authorities and must conduct its hotel operations within the business scope of its business license. These hotels must also obtain various other licenses and permits. For example, if our hotels provide catering service, they are required to obtain a food operation permit. In addition, any project construction undertaken by our hotels may be subject to governmental approvals or filings requirements, and our failure to comply with the aforementioned requirements may subject us to fines or the suspension or even the cessation of operations, which could materially and adversely affect our business, financial condition and results of operations. In any event, we may not be able to obtain all permits, licenses, certificates and other approvals required by government regulations, which could negatively impact our business and significantly harm our reputation.

As of February 27, 2018, out of our 26 leased-and-operated hotels, eight and one have not obtained the fire prevention safety inspection certificates and the public area hygiene permits, respectively, two are applying to have their public area hygiene permits examined and verified, and two of our leased-and-operated hotels engaging in the catering service business as of February 27, 2018 were either in the process of renewing or applying for their food operation permits. Given the significant discretion local government authorities have in the examination of our application as well as other factors beyond our control, we may be unable to renew or obtain our food operation permits at all. In addition, we have only been provided with and reviewed the relevant governmental approvals and permits for the operation of 1,862 out of our 2,263 franchised-and-managed hotels in operation as of December 31, 2017, and have found that:

| • | approximately 1% of these hotels did not provide us with the business license; |

| • | approximately 10% of these hotels did not provide us with the special industry license; |

| • | approximately 16% of these hotels did not provide us with the fire prevention safety inspection certificate; and |

| • | approximately 11% of these hotels did not provide us with the public hygiene license. |

For our leased-and-operated hotels that have not obtained the necessary licenses, and to the extent that the franchisees who did not provide us with the licenses had not obtained the licenses prior to the commencement of their operations, the legal consequences will be as follows:

| • | Business license: fines, suspension of operation, warnings, orders to suspend or cease continuing operations, confiscations of illegal gains or fines, and even up to 15 days of detention; |

| • | Special industry license: warnings or fines of up to RMB1,000, and even up to a 15-days detention. In addition, pursuant to various local regulations, hotels failing to obtain the special industry license may be subject to warnings, orders to suspend or cease continuing business operations, confiscations of illegal gains or fines. |

| • | Fire prevention safety inspection certificate: (i) suspension of construction of projects, and/or use or operation of the business; and (ii) fines between RMB30,000 and RMB300,000; |

| • | Public hygiene license: a range of administrative penalties depending on the seriousness of a hotel’s activities: (i) warnings; (ii) fines between RMB500 and RMB30,000; or (iii) suspension of operations for rectification, or revocation of public hygiene license; and |

| • | Food operation permit: (i) confiscation of illegal gains, food illegally produced for sale and tools, facilities and raw materials used for illegal production; or (ii) fines between RMB50,000 and RMB100,000 if the value of food illegally produced is less than RMB10,000 or fines of 10 to 20 times of the value of food if such value is equal to or greater than RMB10,000. |

16

Table of Contents

If any franchisee is subject to the foregoing legal consequences, whether fines or orders to suspend or even cease operations, due to its failure to obtain necessary licenses and permits or to comply with other requirements, our image and reputation may suffer, and such franchisee may defer making or refuse to make payments in breach of its franchise agreement with us. As we hold equity interests in certain of our franchisees, any regulatory non-compliance by such franchisees may also decrease the value of our investments. In either case, our business and results of operations may be adversely affected. Furthermore, as to certain hotels that are being converted from the leased-and-operated model to the franchised-and-managed model, if any franchisee refuses to return and uses any of our hotels’ permits in breach of their supplementary agreements with us, our company as the registered permit holder could be held liable for any regulatory non-compliance by our franchisees. See “— Our hotels being converted into franchised-and-managed hotels may not be able to obtain their own operational licenses or fail to pay us the rent materially and adversely affect our business and results of operations.”

In respect of our franchising business, we are subject to a comprehensive disclosure requirement when recruiting and managing our franchisees. In the past, we have not received penalties in relation to such requirements. However, our communication with our franchisees could be found in violation of these requirements in the future.

We are also required to file our sample franchise agreements and file annual reports with the provincial level counterpart of the PRC Ministry of Commerce for record-keeping purposes in connection with the execution, withdrawal and renewal of any amendment to franchise agreements in the preceding calendar year. After filing the initial information regarding the operations of our hotel franchise business, the information regarding the execution, withdrawal and renewal of any amendment to franchise agreements for the calendar year 2016 have not been filed with the government authorities. Accordingly, we could be subject to fines of up to an aggregate amount of RMB100,000 for each of our operating subsidiaries which fails to make the filing in a timely manner as required by applicable regulations.

We started to franchise our Shell brand from early 2016. However, we may not satisfy all the prerequisites for franchising our Shell brand under relevant PRC laws and regulations. If the competent government authorities establish that we have no adequate qualification to franchise our Shell brand, we could be subject to penalties including confiscation of relevant gain and fines between RMB100,000 and RMB500,000. We have filed with the competent government authorities to establish these qualifications.

Furthermore, holders of 70% of equity interest in Yibon Hotel Group Co., Ltd., or Yibon, an equity investee of ours, have the right to exchange their equity interest in Yibon into our shares in 2020. See “Description of Share Capital — History of Securities Issuances — Outstanding Right Exchangeable with our Shares.” If we are deemed to acquire control of Yibon after the exchange, Yibon will become one of our subsidiaries and we may bear the legal consequences if any of Yibon’s hotels are not in compliance with applicable PRC laws and regulations. Accordingly, any such non-compliance could adversely affect our results of operations and financial condition. If Yibon becomes one of our subsidiaries, we will also face challenges and related risks of integrating Yibon with the rest of our company. Following the exchange of the equity interests in Yibon, we will consolidate the results of operation of Yibon in our financial statements as a subsidiary. As a result, we will be exposed to the risks of Yibon’s business and financial results, which could negatively impact our results of operation and financial condition.

We may terminate franchise agreements earlier under certain circumstances, and we may have disputes with our franchisees which may materially and adversely affect our business and result of operations.

Our franchisees may terminate our franchise agreements in the event that, among others, the franchised-and-managed hotels’ performance is worse than they expect. Although they are not permitted to do so by our franchise agreements, the franchisees may still attempt to unilaterally terminate their franchise agreements. In such instances, we may have disputes with them, and it will be difficult for us to force them to continue the

17

Table of Contents

performance of our franchise agreements until they expire. If the franchise agreements are eventually terminated either based on a settlement between us and the franchisees or with a judgment or arbitral award which requires the franchisees to compensate us for our losses and costs, such compensation may not cover our losses which we have suffered as a result of the early termination, and we may no longer receive the franchise fees and related management fees from the termination. Furthermore, if our franchisees breach or terminate their franchise agreements with us before the hotel commences operation, we might not be able to grow our hotel network as planned.

Due to our rapid expansion in recent years, we have added a large number of new franchised-and-managed hotels into our hotel network, some of which may not be able to provide consistent and high quality service to meet our standards. To avoid potential damage to our brand name and to ensure the quality of services provided to our guests, we may terminate our franchise agreements with such franchisees. In addition, if any of our franchisees defaults or commits wrongdoing and fails to cure defaults or wrongdoings, we may also need to terminate our franchise agreements. Although our franchise agreements typically allow us to terminate the agreements under many circumstances, our franchisees may dispute our termination or our claim and in such cases we have to submit such disputes for the settlement by courts or arbitration. For example, as of January 31, 2018, we had 29 pending legal proceedings in connection with the franchised-and-managed hotels. Also, we have in the past closed and may close in the future certain franchised-and-managed hotels as a result of disputes with the franchisees for their failure to comply with our requirements on, among other things, the punctual payment of our franchise fees or management fees, the decoration or operation standard, use of our brand, maintenance of the hotel condition and appearance, the avoidance of competition between the franchisees, including keeping appropriate distances between the franchised-and-managed hotels. For example, in 2017, we terminated 65 franchised-and-managed hotels that did not comply with our brand and operating standards. If a significant number of our existing franchise agreements are terminated early, our revenue and profit may decrease in the future.

In case of a dispute with our franchisees, even if such disputes can be resolved in favor of us, the disputes could divert our management attention, affect our brand image, and incur cost for us. There could also be situations where the franchisee is not in a position to sufficiently compensate us for losses which we have suffered as a result of their defaults or wrongdoings. If we eventually terminate any franchisees, we will lose such franchisees and can no longer collect franchise fees and management fees from them. If new franchisees do not cover those terminated franchises, our results of operations and financial conditions could be materially and adversely affected.

Our hotels being converted into franchised-and-managed hotels may not be able to obtain their own operational licenses or fail to pay us the rent materially and adversely affect our business and results of operations.

During the past few years, we have sought to convert some hotels from the leased-and-operated model over to the franchised-and-managed model through selling relevant business assets and handed over the management of such hotels, in most of the cases pursuant to an asset, business and personnel transfer agreement, or Transfer Agreements, to certain individuals or entities that have subsequently entered into franchise agreements with us and have therefore become our new franchisees. According to the Transfer Agreements, such new franchisees shall take over and operate such hotels on their own account and shall take the risks and enjoy the benefit of operating such hotels from the completion of the transfer contemplated by such agreements. However, the Transfer Agreements typically allow our franchisees under such arrangements to continue to use the hotel’s permits that were previously obtained by us and remain in the name of our company for a transitional period. As of December 31, 2017, some of the abovementioned new franchisees were still using our relevant hotels’ permits. However, all but two of these franchisees have executed a supplementary agreement which requires them to stop using and return to us our hotels’ permits upon execution of the supplementary agreements. Such supplementary agreements also require the franchisees to indemnify us against all losses, costs or liabilities incurred by us for their defaults under such agreements. However, if any franchisees refuse to return and continue to use any of our

18

Table of Contents

hotels’ permits, our company could be held liable as the registered permit holder for any regulatory non-compliance on the part of our franchisees. As a result, any breach by our franchisees of relevant regulations could cause us to incur relevant legal liability under PRC law, which may materially affect our brand image and our results of operations. In addition, in such instances, because the relevant leases have not been transferred to our new franchisees, we continued to be the tenants of the relevant hotel premises and we remain liable to pay the rent to our landlords, and may not thereafter be fully compensated by the new franchisees. As a result, our result of operations and financial conditions may be materially and adversely affected by the default of such franchisees. Furthermore, such arrangement between us and the new franchisees could be deemed as a sublease, and our landlords may claim that our subleasing arrangement without our landlords’ consent constitutes a default. In such cases, we may be required by our landlords to terminate sublease arrangements and compensate their losses, if any, which may further increase our costs and risks. Moreover, we may not be able to enforce our rights against the franchisees under the supplementary agreements, which would hinder our ability to prevent the franchisees from using our hotel permits and negatively impact our business and our reputation.

Our leased-and-operated hotels are subject to a number of operational risks.

For hotels under theleased-and-operated model, a significant portion of operating costs, including rent, is fixed. Accordingly, a decrease in revenues could result in a disproportionately larger decrease in earnings because the operating costs and expenses are unlikely to decrease proportionately. For example, the period during both the New Year and Chinese Spring Festival holidays generally accounts for a smaller portion of our annual revenues than the other periods, but the expenses do not vary in proportion to changes in occupancy rates and revenues. Major construction work near our hotel may also have a negative impact on the occupancy rate. We need to continue to pay rent and salaries, make regular repairs, perform maintenance and renovations and invest in other capital improvements for ourleased-and-operated hotels throughout the year to maintain their attractiveness. Therefore, ourleased-and-operated hotels’ costs and expenses may remain constant or increase even if their revenues decline. The operation of eachleased-and-operated hotel goes through the stages of development,ramp-up and mature operation. Our involvement in the development of such properties presents a number of risks, including construction delays or cost overruns, which may result in increased project costs or forgone revenue. During the development stage, significantpre-opening expenses will be incurred, and at theramp-up stage, which is usually six months, when the occupancy rate increases gradually, revenues generated by these hotels may be insufficient to cover their operating costs, which are relatively fixed in nature. As a result, most newly openedleased-and-operated hotels may not achieve profitability until they reach mature operations. We also may be unable to recover development costs we incur for projects that are not completed. Any expansion of ourleased-and-operated hotel portfolio would incur significantpre-opening expenses during the development stage and relatively low revenues during theramp-up stage of such newly openedleased-and-operated hotels, which expenses may have a significant negative impact on our results of operations. Properties that we develop could become less attractive due to market saturation, oversupply or changes in market demand, with the result that we may not be able to recover development costs as we expect, or at all.

We also may acquire or developowned-and-operated hotels on a limited,case-by-case basis to seize unusually attractive business opportunities. Any suchowned-and-operated hotels will be subject to risks similar to those of ourleased-and-operated hotels. Suchowned-and-operated hotels will also be subject to depreciation in the value paid by us for the underlying hotel property, which usually is influenced by macroeconomic and local political and economic factors.

As of December 31, 2017, we were in the process of liquidating five of our PRC subsidiaries and branches which previously operated leased-and-operated hotels. In liquidating such subsidiaries and branches, we need to complete various deregistration procedures, which may be time consuming and therefore we cannot assure you that such subsidiaries and branches can be deregistered in a timely manner. In the future, we may need to liquidate more subsidiaries and branches which have ceased to operate leased-and-operated hotels.

19

Table of Contents

The legal rights of our franchisees and us to use certain leased properties could be challenged by property owners or other third parties, which could prevent our franchisees or us from operating the affected hotels or increase the costs associated with operating these hotels.