Table of Contents

PROXY STATEMENT FOR

EXTRAORDINARY GENERAL MEETING OF LEO HOLDINGS CORP.

PROSPECTUS FOR

36,812,807 SHARES OF CLASS A COMMON STOCK AND 14,000,000 WARRANTS OF LEO HOLDINGS CORP.

(AFTER ITS DOMESTICATION AS A CORPORATION INCORPORATED IN THE STATE OF DELAWARE,

WHICH WILL BE RENAMED DIGITAL MEDIA SOLUTIONS, INC. IN CONNECTION WITH THE

DOMESTICATION DESCRIBED HEREIN)

The board of directors of Leo Holdings Corp., a Cayman Islands exempted company (“Leo”), has unanimously approved the transactions (collectively, the “Business Combination”) contemplated by the Business Combination Agreement, dated April 23, 2020, by and among Leo, Digital Media Solutions Holdings, LLC (“DMS”), certain selling stockholders (the “Sellers”) and the other parties thereto (as hereafter amended, the “Business Combination Agreement”), a copy of which is attached to this proxy statement/prospectus as Annex A, including (a) the domestication of Leo as a Delaware corporation (the “Domestication”) and (b) the reorganization of the combined post-business combination company in an umbrellapartnership-C corporation (or“Up-C”) structure. In connection with the Domestication, Leo will change its name to “Digital Media Solutions, Inc.” and, as used in this proxy statement/prospectus, “New DMS” refers to Leo after the Business Combination. As described in this proxy statement/prospectus, Leo’s shareholders are being asked to consider a vote upon (among other things) the Business Combination.

Immediately prior to the consummation of the Closing, (1) the issued and outstanding Class A ordinary shares, par value $0.0001 per share (the “Class A ordinary shares”), of Leo will convert automatically by operation of law, on aone-for-one basis, into shares of Class A common stock, par value $0.0001 per share, of New DMS (the “New DMS Class A Common Stock”); (2) the issued and outstanding redeemable warrants that were registered pursuant to the Registration Statement on FormS-1(333-222599) of Leo (the “IPO registration statement”) will become automatically redeemable warrants to acquire shares of New DMS Class A Common Stock (no other changes will be made to the terms of any issued and outstanding public warrants as a result of the Domestication); (3) each issued and outstanding unit of Leo that has not been previously separated into the underlying Class A ordinary share and underlying warrant upon the request of the holder thereof, will be cancelled and will entitle the holder thereof to one share of New DMS Class A Common Stock andone-half of one redeemable warrant to acquire one share of New DMS Class A Common Stock; (4) each issued and outstanding Class B ordinary share, par value $0.0001 per share (the “Class B ordinary shares”), of Leo will convert automatically by operation of law, on aone-for-one basis without giving effect to any rights of adjustment or other anti-dilution protections, into shares of New DMS Class A Common Stock; and (5) the issued and outstanding warrants of Leo issued in a private placement will automatically become warrants to acquire shares of New DMS Class A Common Stock (no other changes will be made to the terms of any issued and outstanding private placement warrants as a result of the Domestication). As used herein, “public warrants” shall mean the redeemable warrants to acquire Class A ordinary shares, in each case, that were registered pursuant to the IPO registration statement and the shares of New DMS Class A Common Stock issued on the effective date of the Domestication. As used herein, “Class B ordinary shares” shall mean the 5,000,000 Class B ordinary shares, par value $0.0001 per share, of Leo, of which at least 1,500,000 will be forfeited and surrendered pursuant to the Amended and Restated Sponsor Shares and Warrant Surrender Agreement between Sponsor, Leo and certain holders of Class B ordinary shares (the “Surrender Agreement”), and “private placement warrants” shall mean the 4,000,000 private placement warrants outstanding as of the date of this proxy statement/prospectus (of which 2,000,000 will be forfeited and surrendered pursuant to the Surrender Agreement and 2,000,000 will be issued to the Sellers) which will be automatically converted by operation of law into warrants to acquire shares of New DMS Class A Common Stock in the Domestication.

Accordingly, this prospectus covers 36,812,807 shares of New DMS Class A Common Stock (including shares issuable upon exercise of the warrants described above) and 14,000,000 warrants to acquire shares of New DMS Class A Common Stock to be issued in the Domestication.

Leo’s units, Class A ordinary shares, public warrants and private placement warrants are currently listed on the New York Stock Exchange (the “NYSE”) under the symbols “LHC.U,” “LHC” and “LHC WS,” respectively. Leo will apply for listing, to be effective at the time of the Business Combination, of New DMS’s Class A Common Stock and warrants on the NYSE under the proposed symbols “DMS” and “DMS WS,” respectively. It is a condition of the consummation of the Business Combination that Leo receive confirmation from the NYSE that New DMS has been conditionally approved for listing on the NYSE but there can be no assurance such listing condition will be met or that Leo will obtain such confirmation from the NYSE. If such listing condition is not met or if such confirmation is not obtained, the Business Combination will not be consummated unless the NYSE condition set forth in the Business Combination Agreement is waived by the applicable parties.

The accompanying proxy statement/prospectus provides shareholders of Leo with detailed information about the Business Combination and other matters to be considered at the extraordinary general meeting of Leo. We encourage you to read the entire accompanying proxy statement/prospectus, including the Annexes and other documents referred to therein, carefully and in their entirety. You should also carefully consider the risk factors described in “Risk Factors” beginning on page 39 of the accompanying proxy statement/prospectus.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

The accompanying proxy statement/prospectus is dated June 24, 2020, and

is first being mailed to Leo’s shareholders on or about June 24, 2020.

Table of Contents

LEO HOLDINGS CORP.

A CAYMAN ISLANDS EXEMPTED COMPANY

(COMPANY NUMBER 329879)

21 GROSVENOR PLACE

LONDON SW1X 7HF, UNITED KINGDOM

Dear Leo Holdings Corp. Shareholders:

You are cordially invited to attend the extraordinary general meeting in lieu of the annual meeting (the “extraordinary general meeting”) of Leo Holdings Corp., a Cayman Islands exempted company (“Leo”), at 9:00 a.m., Eastern Time, on July 14, 2020, at the offices of Kirkland & Ellis LLP located at 601 Lexington Avenue, New York, New York 10022, or at such other time, on such other date and at such other place to which the meeting may be adjourned.

At the extraordinary general meeting, Leo shareholders will be asked to consider and vote upon a proposal, which is referred to herein as the “BCA Proposal,” to approve and adopt the Business Combination Agreement, dated as of April 23, 2020, by and among Leo, Digital Media Solutions Holdings, LLC (“DMS”), CEP V DMS US Blocker Company, a Delaware corporation (“Blocker Corp”), Prism Data, LLC, a Delaware limited liability company (“Prism”),CEP V-A DMS AIV Limited Partnership, a Delaware limited partnership (“Clairvest Direct Seller”), Clairvest Equity Partners V Limited Partnership, an Ontario, Canada limited partnership (“Blocker Seller 1”), CEPV Co-Investment Limited Partnership, a Manitoba, Canada limited partnership (“Blocker Seller 2,” and together with Prism, Clairvest Direct Seller and Blocker Seller 1, the “Sellers”), Clairvest GP Manageco Inc., an Ontario corporation (“Clairvest GP”) as a Seller Representative, and, solely for the limited purposes set forth therein, Leo Investors Limited Partnership, a Cayman Islands exempted limited partnership (“Sponsor”) (as hereafter amended, the “Business Combination Agreement”), a copy of which is attached to the accompanying proxy statement/prospectus as Annex A, certain related agreements (including the Subscription Agreements (as defined below), the Amended Partnership Agreement (as defined below), the Tax Receivable Agreement (as defined below) and the Surrender Agreement (as defined below)) and the transactions contemplated thereby.

The Business Combination Agreement provides for the consummation of the following transactions in the following order (collectively, the “Business Combination”), in each case conditional upon each prior transaction having been consummated:

| a) | pursuant to the Amended and Restated Sponsor Shares and Warrant Surrender Agreement between Sponsor, Leo and certain holders of Class B ordinary shares of Leo (the “Surrender Agreement”), Sponsor will surrender and forfeit to Leo 2,000,000 private placement warrants of Leo and, together with certain other holders, at least 1,500,000 Class B ordinary shares of Leo (collectively, the “Surrender”); |

| b) | Leo will change its jurisdiction of incorporation by deregistering as an exempted company in the Cayman Islands and continuing and domesticating as a corporation incorporated under the laws of the State of Delaware (the “Domestication”), upon which Leo will change its name to “Digital Media Solutions, Inc.” (“New DMS”) (for further details, see “Proposal No. 2—The Domestication Proposal”); |

| c) | Leo will consummate the PIPE Investment (as defined below); and |

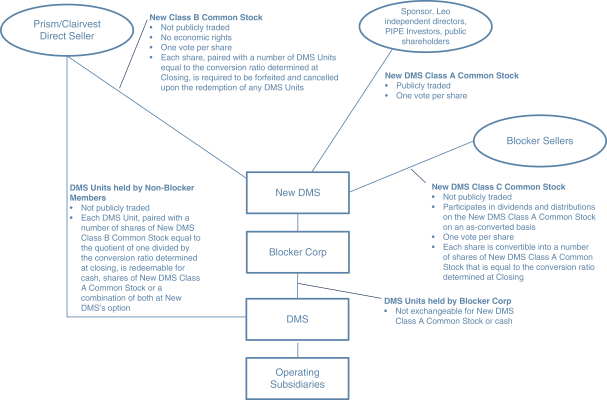

| d) | Leo will purchase the equity interests of Blocker Corp and a portion of the units of DMS held by Prism and Clairvest Direct Seller (which units will be immediately contributed to the capital of Blocker Corp) in exchange for a combination of cash consideration, 2,000,000 private placement warrants of Leo that shall be issued to Sellers (the “Seller Warrants”), shares of Class B common stock, par value $0.0001 per share, of New DMS, which will have no economic value but will entitle the holder thereof to one vote per share (the “New DMS Class B Common Stock”), and shares of Class C common stock, par value $0.0001 per share, of New DMS (the “New DMS Class C Common Stock”), which are convertible into shares of Class A common stock, par value $0.0001 per share, of New DMS (the “New |

Table of Contents

| DMS Class A Common Stock”) pursuant to a conversion ratio to be determined at the closing of the transactions contemplated by the Business Combination Agreement (the “Closing”) (the “Business Combination Consideration”). |

Immediately prior to the consummation of the Closing, (1) the issued and outstanding Class A ordinary shares, par value $0.0001 per share (the “Class A ordinary shares”), of Leo will convert automatically by operation of law, on aone-for-one basis, into shares of New DMS Class A Common Stock, par value $0.0001 per share, of New DMS; (2) the issued and outstanding redeemable warrants that were registered pursuant to the Registration Statement on FormS-1(333-222599) of Leo (the “IPO registration statement”) will become automatically redeemable warrants to acquire shares of New DMS Class A Common Stock (no other changes will be made to the terms of any issued and outstanding public warrants as a result of the Domestication); (3) each issued and outstanding unit of Leo that has not been previously separated into the underlying Class A ordinary share and underlying warrant upon the request of the holder thereof, will be cancelled and will entitle the holder thereof to one share of New DMS Class A Common Stock andone-half of one redeemable warrant to acquire one share of New DMS Class A Common Stock; (4) each issued and outstanding Class B ordinary share, par value $0.0001 per share (the “Class B ordinary shares” and, together with the Class A ordinary shares, the “ordinary shares”), of Leo will convert automatically by operation of law, on aone-for-one basis without giving effect to any rights of adjustment or other anti-dilution protections, into shares of New DMS Class A Common Stock; and (5) the issued and outstanding warrants of Leo issued in a private placement will automatically become warrants to acquire shares of New DMS Class A Common Stock (no other changes will be made to the terms of any issued and outstanding private placement warrants as a result of the Domestication). As used herein, “public shares” shall mean the Class A ordinary shares and “public warrants” shall mean the redeemable warrants to acquire Class A ordinary shares, in each case, that were registered pursuant to the IPO registration statement and the shares of New DMS Class A Common Stock issued as a matter of law upon the conversion thereof on the effective date of the Domestication. As used herein, “Class B ordinary shares” shall mean the 5,000,000 Class B ordinary shares, par value $0.0001 per share, of Leo, of which at least 1,500,000 will be forfeited and surrendered pursuant to the Surrender Agreement, and “private placement warrants” shall mean the 4,000,000 private placement warrants outstanding as of the date of this proxy statement/prospectus (of which 2,000,000 will be forfeited and surrendered pursuant to the Surrender Agreement and 2,000,000 will be the Seller Warrants issued to the Sellers as part of the Business Combination Consideration) which will be automatically converted by operation of law into warrants to acquire shares of New DMS Class A Common Stock in the Domestication. For further details, see “Proposal No. 2—The Domestication Proposal.”

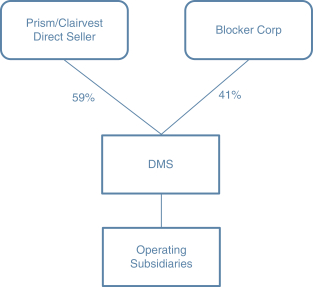

Clairvest Direct Seller and Prism will continue to hold membership interests in DMS (“DMS Units”) subject to and in accordance with the Amended Partnership Agreement (as defined below). Following the Business Combination, the combined company will be organized in an umbrellapartnership-C corporation (or“Up-C”) structure, in which substantially all of the assets and business of New DMS will be held by DMS and continue to operate through the subsidiaries of DMS and New DMS’s sole material asset will be equity interests of DMS indirectly held by it. At the Closing, DMS and its current equity holders will amend and restate the limited liability company agreement of DMS (the “Amended Partnership Agreement”) in its entirety to, among other things, provide Clairvest Direct Seller and Prism the right to redeem their DMS Units for cash or, at New DMS’s option, New DMS may acquire such DMS Units (which DMS Units are expected to be contributed to Blocker Corp) in exchange for cash or shares of New DMS Class A Common Stock, in each case subject to certain restrictions set forth therein. DMS Units acquired by New DMS are expected to be contributed to Blocker Corp.

Concurrent with the Closing, New DMS and Blocker Corp will enter into the tax receivable agreement (the “Tax Receivable Agreement”) with the Sellers. Pursuant to the Tax Receivable Agreement, New DMS will be required to pay the Sellers (i) 85% of the amount of savings, if any, in U.S. federal, state and local income tax that New DMS and Blocker Corp actually realize as a result of (A) certain existing tax attributes of Blocker Corp acquired in the Business Combination, and (B) increases in Blocker Corp’s allocable share of the tax basis of the tangible and intangible assets of DMS and certain other tax benefits related to the payment of the cash consideration pursuant to the Business Combination Agreement and any redemptions of DMS Units or exchanges of DMS Units for cash or shares of New DMS Class A Common Stock after the Business Combination and (ii) 100% of certain refunds ofpre-Closing taxes of DMS and Blocker Corp received during a

Table of Contents

taxable year beginning within two years after the Closing. All such payments to the Sellers will be New DMS’s obligation, and not that of DMS.

Leo has entered into subscription agreements (the “Subscription Agreements”) with certain investors, pursuant to which, among other things, such investors agreed to subscribe for and purchase, and Leo agreed to issue and sell to such investors, including funds managed by Lion Capital LLP, an affiliate of Sponsor, immediately following the Domestication, an aggregate of 10,000,000 shares of New DMS Class A Common Stock for $10.00 per share, which will generate aggregate proceeds of $100.0 million (the “PIPE Investment”). The closing of the PIPE Investment is contingent upon, among other things, the substantially concurrent consummation of the Business Combination.

You will also be asked to consider and vote upon (a) six separate proposals to approve material differences between Leo’s existing amended and restated memorandum and articles of association (the “Existing Organizational Documents”) and the proposed new certificate of incorporation of New DMS (“Proposed Certificate of Incorporation”) and the proposed new bylaws of New DMS upon the Domestication, which are referred to herein as the “Organizational Documents Proposals,” (b) a proposal to approve for purposes of complying with applicable provisions of NYSE Listing Rule 312.03, the issuance of New DMS Class A Common Stock in the PIPE Investment and the issuance of the Seller Warrants, New DMS Class B Common Stock, including the New DMS Class A Common Stock into which the DMS Units are redeemable in accordance with the Amended Partnership Agreement, and New DMS Class C Common Stock, including the New DMS Class A Common Stock into which the New DMS Class C Common Stock is convertible in accordance with the Proposed Certificate of Incorporation, to the Sellers to the extent such issuance would require a shareholder vote under NYSE Listing Rule 312.03, which is referred to herein as the “Security Issuance Proposal,” (c) a proposal to approve and adopt the Digital Media Solutions, Inc. 2020 Omnibus Incentive Plan, a copy of which is attached to the accompanying proxy statement/prospectus as Annex E, which is referred to herein as the “Incentive Award Plan Proposal,” (d) a proposal to approve on a non-binding, advisory basis, the appointment of Robbie Isenberg, James Miller, Fernando Borghese and Mary Minnick to the New DMS Board as of the Closing in accordance with Section 9.14(g) of the Business Combination Agreement, which is referred to herein as the “Seller Nominee Appointment Proposal” and (e) a proposal to approve by ordinary resolution the adjournment of the extraordinary general meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that there are insufficient votes for the approval of one or more proposals at the extraordinary general meeting, which is referred to herein as the “Adjournment Proposal.”

The Business Combination will be consummated only if the BCA Proposal, the Domestication Proposal, certain of the Organizational Documents Proposals (the “Required Organizational Documents Proposals”) and, the Security Issuance Proposal (collectively, the “Condition Precedent Proposals”) are approved at the extraordinary general meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of each other. The Organizational Documents Proposals that are not Required Organizational Documents Proposals, the Seller Nominee Appointment Proposal and the Incentive Award Plan Proposal, are conditioned on the approval of the Condition Precedent Proposals. The Adjournment Proposal is not conditioned upon the approval of any other proposal. Each of these proposals is more fully described in the accompanying proxy statement/prospectus, which each shareholder is encouraged to read carefully and in its entirety.

Concurrent with the execution of the Business Combination Agreement, Sponsor, Leo and certain holders of Class B ordinary shares of Leo entered into the Surrender Agreement, pursuant to which (a) the Surrender will be effectuated in connection with the consummation of the Business Combination and (b) Sponsor and the other holders party thereto agreed to waive any adjustment to the conversion ratio set forth in the Existing Organizational Documents or any other anti-dilution or similar protection with respect to the Class B ordinary shares of Leo held by them that may result from the PIPE Investment and the transactions contemplated by the Business Combination Agreement, in each case on the terms and conditions set forth in the Surrender Agreement. For further details, see “BCA Proposal—Related Agreements”

In connection with the Business Combination, certain related agreements have been, or will be entered into on or prior to the Closing, including the Amended Partnership Agreement, Tax Receivable Agreement, Director

Table of Contents

Nomination Agreement, Amended and Restated Registration Rights Agreement andLock-Up Agreement (each as defined in the accompanying proxy statement/prospectus). See “BCA Proposal—Related Agreements” in the accompanying proxy statement/prospectus for more information.

Pursuant to the Existing Organizational Documents, a holder of Leo’s public shares (a “public shareholder”) may request that Leo redeem all or a portion of such public shares for cash if the Business Combination is consummated. Holders of units must elect to separate the units into the underlying public shares and warrants prior to exercising redemption rights with respect to the public shares. If holders hold their units in an account at a brokerage firm or bank, holders must notify their broker or bank that they elect to separate the units into the underlying public shares and warrants, or if a holder holds units registered in its own name, the holder must contact Continental Stock Transfer & Trust Company (“Continental”), Leo’s transfer agent, directly and instruct it to do so. The redemption rights include the requirement that a holder must identify itself in writing as a beneficial holder and provide its legal name, phone number and address to Continental in order to validly redeem its shares.Public shareholders may elect to redeem their public shares even if they vote “for” the BCA Proposal.If the Business Combination is not consummated, the public shares will be returned to the respective holder, broker or bank. If the Business Combination is consummated, and if a public shareholder properly exercises its right to redeem all or a portion of the public shares that it holds and timely delivers its shares to Continental, New DMS will redeem such public shares for aper-share price, payable in cash, equal to the pro rata portion of the trust account established at the consummation of our initial public offering, calculated as of two business days prior to the consummation of the Business Combination. For illustrative purposes, as of June 18, 2020, this would have amounted to approximately $10.40 per issued and outstanding public share. If a public shareholder exercises its redemption rights in full, then it will be electing to exchange its public shares for cash and will no longer own public shares. The redemption will take place following the Domestication and accordingly it is shares of New DMS Class A Common Stock that will be redeemed immediately after consummation of the Business Combination. See “Extraordinary General Meeting of Leo— Redemption Rights” in the accompanying proxy statement/prospectus for a detailed description of the procedures to be followed if you wish to redeem your public shares for cash.

Notwithstanding the foregoing, a public shareholder, together with any affiliate of such public shareholder or any other person with whom such public shareholder is acting in concert or as a “group” (as defined in Section 13(d)(3) of the Securities Exchange Act of 1934, as amended (“Exchange Act”)), will be restricted from redeeming its public shares with respect to more than an aggregate of 15% of the public shares. Accordingly, if a public shareholder, alone or acting in concert or as a group, seeks to redeem more than 15% of the public shares, then any such shares in excess of that 15% limit would not be redeemed for cash.

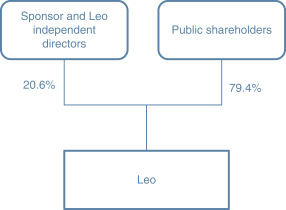

The holders of Class B ordinary shares (the “Class B Shareholders”) have agreed to vote all of their ordinary shares in favor of the proposals being presented at the extraordinary general meeting and waive their redemption rights with respect to such ordinary shares in connection with the consummation of the Business Combination. The Class B ordinary shares will be excluded from the pro rata calculation used to determine theper-share redemption price. As of the date of this proxy statement/prospectus, the Class B Shareholders own 20.0% of the issued and outstanding ordinary shares.

The Business Combination Agreement is subject to the satisfaction or waiver of certain other closing conditions as described in the accompanying proxy statement/prospectus. There can be no assurance that the parties to the Business Combination Agreement would waive any such provision of the Business Combination Agreement. In addition, in no event will Leo redeem public shares in an amount that would cause New DMS’s net tangible assets (as determined in accordance with Rule3a51-1(g)(1) of the Exchange Act) to be less than $5,000,001.

Leo is providing the accompanying proxy statement/prospectus and accompanying proxy card to Leo’s shareholders in connection with the solicitation of proxies to be voted at the extraordinary general meeting and at any adjournments of the extraordinary general meeting. Information about the extraordinary general meeting, the Business Combination and other related business to be considered by Leo’s shareholders at the extraordinary general meeting is included in the accompanying proxy statement/prospectus.Whether or not you plan to

Table of Contents

attend the extraordinary general meeting, all of Leo’s shareholders are urged to read the accompanying proxy statement/prospectus, including the Annexes and other documents referred to therein, carefully and in their entirety. You should also carefully consider the risk factors described in “Risk Factors” beginning on page39 of the accompanying proxy statement/prospectus.

After careful consideration, the board of directors of Leo has unanimously approved the Business Combination and unanimously recommends that shareholders vote “FOR” the adoption of the Business Combination Agreement and approval of the transactions contemplated thereby, including the Business Combination, and “FOR” all other proposals presented to Leo’s shareholders in the accompanying proxy statement/prospectus. When you consider the recommendation of these proposals by the board of directors of Leo, you should keep in mind that Leo’s directors and officers have interests in the Business Combination that may conflict with your interests as a shareholder. See the section entitled “BCA Proposal—Interests of Leo’s Directors and Executive Officers in the Business Combination” in the accompanying proxy statement/prospectus for a further discussion of these considerations.

The approval of each of the Domestication Proposal and Organizational Documents Proposals requires a special resolution under Cayman Islands law, being the affirmative vote of holders of at leasttwo-thirds of the ordinary shares represented in person or by proxy and entitled to vote thereon and who vote at the extraordinary general meeting. The approval of each of the BCA Proposal, Incentive Award Plan Proposal, the Security Issuance Proposal, the Seller Nominee Appointment Proposal. and the Adjournment Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of a majority of the ordinary shares represented in person or by proxy and entitled to vote thereon and who vote at the extraordinary general meeting.

Your vote is very important.Whether or not you plan to attend the extraordinary general meeting, please vote as soon as possible by following the instructions in the accompanying proxy statement/prospectus to make sure that your shares are represented at the extraordinary general meeting. If you hold your shares in “street name” through a bank, broker or other nominee, you will need to follow the instructions provided to you by your bank, broker or other nominee to ensure that your shares are represented and voted at the extraordinary general meeting. The Business Combination will be consummated only if the Condition Precedent Proposals are approved at the extraordinary general meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of each other. The Organizational Documents Proposals that are not Required Organizational Documents Proposals, the Seller Nominee Appointment Proposal and the Incentive Award Plan Proposal, are conditioned on the approval of the Condition Precedent Proposals. The Adjournment Proposal is not conditioned on the approval of any other proposal set forth in the accompanying proxy statement/prospectus.

If you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted FOR each of the proposals presented at the extraordinary general meeting. If you fail to return your proxy card or fail to instruct your bank, broker or other nominee how to vote, and do not attend the extraordinary general meeting in person, the effect will be, among other things, that your shares will not be counted for purposes of determining whether a quorum is present at the extraordinary general meeting. If you are a shareholder of record and you attend the extraordinary general meeting and wish to vote in person, you may withdraw your proxy and vote in person.

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST DEMAND IN WRITING THAT YOUR PUBLIC SHARES ARE REDEEMED FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT AND TENDER YOUR SHARES TO LEO’S TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE VOTE AT THE EXTRAORDINARY GENERAL MEETING. IN ORDER TO EXERCISE YOUR REDEMPTION RIGHT YOU NEED TO IDENTIFY YOURSELF AS A BENEFICIAL HOLDER AND PROVIDE YOUR LEGAL NAME, PHONE NUMBER AND ADDRESS IN YOUR WRITTEN DEMAND. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL BE

Table of Contents

RETURNED TO YOU OR YOUR ACCOUNT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

On behalf of Leo’s board of directors, I would like to thank you for your support and look forward to the successful completion of the Business Combination.

| Sincerely, |

|

Lyndon Lea |

| Chairman and Chief Executive Officer |

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE TRANSACTIONS DESCRIBED IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION OR RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THE ACCOMPANYING PROXY STATEMENT/PROSPECTUS. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

The accompanying proxy statement/prospectus is dated June 24, 2020 and is first being mailed to shareholders on or about June 24, 2020.

Table of Contents

LEO HOLDINGS CORP.

A CAYMAN ISLANDS EXEMPTED COMPANY

(COMPANY NUMBER 329879)

21 GROSVENOR PLACE

LONDON SW1X 7HF, UNITED KINGDOM

NOTICE OF EXTRAORDINARY GENERAL MEETING

TO BE HELD ON July 14, 2020

TO THE SHAREHOLDERS OF LEO HOLDINGS CORP.:

NOTICE IS HEREBY GIVEN that an extraordinary general meeting of the shareholders (the “extraordinary general meeting”) of Leo Holdings Corp., a Cayman Islands exempted company (“Leo”), will be held at 9:00 a.m., Eastern Time, on July 14, 2020, at the offices of Kirkland & Ellis LLP located at 601 Lexington Avenue, New York, New York 10022.* You are cordially invited to attend the extraordinary general meeting, which will be held for the following purposes:

| • | Proposal No. 1—The BCA Proposal—to consider and vote upon a proposal to approve by ordinary resolution and adopt the Business Combination Agreement, dated as of April 23, 2020 and as hereafter amended, by and among Leo, Digital Media Solutions Holdings, LLC (“DMS”), CEP V DMS US Blocker Company, a Delaware corporation (“Blocker Corp”), Prism Data, LLC, a Delaware limited liability company (“Prism”),CEP V-A DMS AIV Limited Partnership, a Delaware limited partnership (“Clairvest Direct Seller”), Clairvest Equity Partners V Limited Partnership, an Ontario, Canada limited partnership (“Blocker Seller 1”), CEPV Co-Investment Limited Partnership, a Manitoba, Canada limited partnership (“Blocker Seller 2,” and together with Prism, Clairvest Direct Seller and Blocker Seller 1, the “Sellers”), Clairvest GP Manageco Inc., an Ontario corporation (“Clairvest GP”) as a Seller Representative, and, solely for the limited purposes set forth therein, Leo Investors Limited Partnership, a Cayman Islands exempted limited partnership (“Sponsor”) (the “Business Combination Agreement”) (a copy of which is attached to this proxy statement/prospectus as Annex A), pursuant to which, among other things, following the Domestication of Leo to Delaware as described below, Leo will purchase all of the outstanding stock of Blocker Corp and a portion of the units of DMS held by Prism and Clairvest Direct Seller, which units Leo will immediately contribute to the capital of Blocker Corp, in exchange for a combination of (a) cash consideration, (b) 2,000,000 private placement warrants (the “Seller Warrants”), (c) shares of Class B common stock, par value $0.0001 per share, of New DMS (the “New DMS Class B Common Stock”), which will have no economic value but will entitle the holder thereof to one vote per share, and (d) shares of Class C common stock, par value $0.0001 per share, of New DMS (the “New DMS Class C Common Stock”), which are convertible into shares of Class A common stock, par value $0.0001 per share, of New DMS (the “New DMS Class A Common Stock”) pursuant to a conversion ratio to be determined at the closing of the Business Combination (as defined below), certain related agreements (including the Subscription Agreements, the Amended Partnership Agreement, the Tax Receivable Agreement and the Surrender Agreement, each as defined in this proxy statement/prospectus) and the transactions contemplated thereby (this proposal is referred to herein as the “BCA Proposal”); |

| • | Proposal No. 2—The Domestication Proposal—to consider and vote upon a proposal to approve by special resolution the change of Leo’s jurisdiction of incorporation by deregistering as an exempted |

| * | We intend to hold the extraordinary general meeting in person. However, we are sensitive to the public health and travel concerns our shareholders may have and recommendations that public health officials may issue in light of the evolving coronavirus(COVID-19) situation. As a result, we may impose additional procedures or limitations on meeting attendees or may decide to hold the meeting in a different location or solely by means of remote communication (i.e., a virtual-only meeting). We plan to announce any such updates in a press release filed with the Securities and Exchange Commission and on our proxy websitehttps://www.cstproxy.com/leoholdingscorp/2020, and we encourage you to check this website prior to the meeting if you plan to attend. |

Table of Contents

company in the Cayman Islands and continuing and domesticating as a corporation incorporated under the laws of the State of Delaware (the “Domestication,” and together with the other transactions contemplated by the Business Combination Agreement, the “Business Combination”) (this proposal is referred to herein as the “Domestication Proposal”); |

| • | Organizational Documents Proposals—to consider and vote upon the following six separate proposals (collectively, the “Organizational Documents Proposals”) to approve by special resolution the following material differences between the current amended and restated memorandum and articles of association of Leo (the “Existing Organizational Documents”) and the proposed new certificate of incorporation (“Proposed Certificate of Incorporation”) and the proposed new bylaws (“Proposed Bylaws”) of Leo Holdings Corp. (a corporation incorporated in the State of Delaware, assuming the Domestication Proposal is approved and adopted, and the filing with and acceptance by the Secretary of State of Delaware of the certificate of domestication in accordance with Section 388 of the Delaware General Corporation Law (the “DGCL”)), which will be renamed “Digital Media Solutions, Inc.” in connection with the Domestication (Leo after the Domestication is referred to herein as “New DMS”): |

| (A) | Proposal No. 3—Organizational Documents Proposal A—to authorize the change in the authorized capital stock of Leo from (i) 200,000,000 Class A ordinary shares, par value $0.0001 per share (the “public shares”), 20,000,000 Class B ordinary shares, par value $0.0001 per share (the “Class B ordinary shares” and, together with the Class A ordinary shares, the “ordinary shares”) and 1,000,000 preferred shares, par value $0.0001 per share, to (ii) 600,000,000 shares of common stock, par value $0.0001 per share, of New DMS, consisting of (a) 500,000,000 shares of New DMS Class A Common Stock, (b) 60,000,000 shares of New DMS Class B Common Stock, (c) 40,000,000 shares of New DMS Class C Common Stock, and 100,000,000 shares of preferred stock, par value $0.0001 per share, of New DMS (“New DMS Preferred Stock”) (this proposal is referred to herein as “Organizational Documents Proposal A”); |

| (B) | Proposal No. 4—Organizational Documents Proposal B—to authorize the board of directors of New DMS to issue any or all shares of New DMS Preferred Stock in one or more classes or series, with such terms and conditions as may be expressly determined by New DMS’s board of directors and as may be permitted by the DGCL (this proposal is referred to herein as “Organizational Documents Proposal B”); |

| (C) | Proposal No. 5—Organizational Documents Proposal C—to provide that certain provisions of the certificate of incorporation of New DMS are subject to the Director Nomination Agreement (this proposal is referred to herein as “Organizational Documents Proposal C”); |

| (D) | Proposal No. 6—Organizational Documents Proposal D—to authorize the removal of the ability of New DMS stockholders to take action by written consent in lieu of a meeting, from and after the first date that Prism, Clairvest and any of their respective affiliates cease to collectively own, in the aggregate, at least fifty percent (50%) of the outstanding voting stock of New DMS (this proposal is referred to herein as “Organizational Documents Proposal D”); |

| (E) | Proposal No. 7—Organizational Documents Proposal E—to authorize the grant of an explicit waiver regarding corporate opportunities to New DMS and its directors (this proposal is referred to herein as “Organizational Documents Proposal E” and, together with Organization Documents Proposal A, the “Required Organizational Documents Proposals”); |

| (E) | Proposal No. 8—Organizational Documents Proposal F—to authorize all other changes in connection with the replacement of Existing Organizational Documents with the Proposed Certificate of Incorporation and Proposed Bylaws as part of the Domestication (copies of which are attached to this proxy statement/prospectus as Annex C and Annex D, respectively), including (1) changing the post-Business Combination corporate name from “Leo Holdings Corp.” to “Digital Media Solutions, Inc.” (which is expected to occur upon the Domestication), (2) making New DMS’s corporate existence perpetual, (3) adopting Delaware as the exclusive forum for certain stockholder litigation, (4) electing to not be governed by Section 203 of the DGCL and limiting certain corporate takeovers by interested stockholders and (5) removing certain provisions related to our status as a blank check company that will no longer be applicable upon consummation of the Business Combination, all of |

Table of Contents

| which Leo’s board of directors believes is necessary to adequately address the needs of New DMS after the Business Combination; |

| • | Proposal No. 9—The Security Issuance Proposal—to consider and vote upon a proposal to approve by ordinary resolution for the purposes of complying with the applicable provisions of NYSE Listing Rule 312.03, the issuance of shares of New DMS Class A Common Stock to certain private placement investors, including an affiliate of Sponsor, and the issuance of the Seller Warrants, New DMS Class B Common Stock, including the New DMS Class A Common Stock into which the DMS Units are redeemable in accordance with the Amended Partnership Agreement, and New DMS Class C Common Stock, including the New DMS Class A Common Stock into which the New DMS Class C Common Stock is convertible in accordance with the Proposed Certificate of Incorporation, to the Sellers, and the issuance of to the extent such issuance would require a shareholder vote under NYSE Listing Rule 312.03 (this proposal is referred to herein as the “Security Issuance Proposal” and, collectively with the BCA Proposal, the Domestication Proposal and the Required Organizational Documents Proposals, the “Condition Precedent Proposals”); |

| • | Proposal No. 10—The Seller Nominee Appointment Proposal—to consider and vote on a non-binding, advisory basis upon a proposal to approve by ordinary resolution the appointment of Robbie Isenberg, James Miller, Fernando Borghese and Mary Minnick to the board of directors of New DMS as of the closing of the transactions contemplated by the Business Combination Agreement in accordance with Section 9.14(g) of the Business Combination Agreement (this proposal is referred to herein as the “Seller Nominee Appointment Proposal”); |

| • | Proposal No. 11—The Incentive Award Plan Proposal—to consider and vote upon a proposal to approve by ordinary resolution the Digital Media Solutions, Inc. 2020 Omnibus Incentive Plan, a copy of which is attached to this proxy statement/prospectus as Annex E (this proposal is referred to herein as the “Incentive Award Plan Proposal”); and |

| • | Proposal No. 12—The Adjournment Proposal—to consider and vote upon a proposal to approve by ordinary resolution the adjournment of the extraordinary general meeting to a later date or dates, if necessary, to permit further solicitation and vote of proxies in the event that there are insufficient votes for the approval of one or more proposals at the extraordinary general meeting (this proposal is referred to herein as the “Adjournment Proposal” and together with the BCA Proposal, the Domestication Proposal, the Organizational Documents Proposals, the Security Issuance Proposal, the Seller Nominee Appointment Proposal and the Incentive Award Plan Proposal, the “Proxy Proposals”). |

Each of the BCA Proposal, the Domestication Proposal, the Required Organizational Documents Proposals and the Security Issuance Proposal is conditioned on the approval and adoption of each of the other Condition Precedent Proposals. The Organizational Documents Proposals that are not Required Organizational Documents Proposals, the Seller Nominee Appointment Proposal and the Incentive Award Plan Proposal, are conditioned on the approval of the Condition Precedent Proposals. The Adjournment Proposal is not conditioned on any other proposal.

These items of business are described in this proxy statement/prospectus, which we encourage you to read carefully and in its entirety before voting.

Only holders of record of ordinary shares at the close of business on June 3, 2020 are entitled to notice of and to vote and have their votes counted at the extraordinary general meeting and any adjournment of the extraordinary general meeting.

This proxy statement/prospectus and accompanying proxy card is being provided to Leo’s shareholders in connection with the solicitation of proxies to be voted at the extraordinary general meeting and at any adjournment of the extraordinary general meeting.Whether or not you plan to attend the extraordinary general meeting, all of Leo’s shareholders are urged to read this proxy statement/prospectus, including the Annexes and the documents referred to herein carefully and in their entirety. You should also carefully consider the risk factors described in “Risk Factors” beginning on page39 of this proxy statement/prospectus.

Table of Contents

After careful consideration, the board of directors of Leo has unanimously approved the Business Combination and unanimously recommends that shareholders vote “FOR” the adoption of the Business Combination Agreement and approval of the transactions contemplated thereby, including the Business Combination, and “FOR” all other proposals presented to Leo’s shareholders in this proxy statement/prospectus. When you consider the recommendation of these proposals by the board of directors of Leo, you should keep in mind that Leo’s directors and officers have interests in the Business Combination that may conflict with your interests as a shareholder. See the section entitled “BCA Proposal—Interests of Leo’s Directors and Executive Officers in the Business Combination” in this proxy statement/prospectus for a further discussion of these considerations.

Pursuant to the Existing Organizational Documents, a holder of public shares (a “public shareholder”) may request of Leo that New DMS redeem all or a portion of its public shares for cash if the Business Combination is consummated. As a holder of public shares, you will be entitled to receive cash for any public shares to be redeemed only if you:

| (i) | (a) hold public shares, or (b) if you hold public shares through units, you elect to separate your units into the underlying public shares and warrants prior to exercising your redemption rights with respect to the public shares; |

| (ii) | submit a written request to Continental Stock Transfer & Trust Company (“Continental”), Leo’s transfer agent, in which you (i) request that New DMS redeem all or a portion of your public shares for cash, and (ii) identify yourself as the beneficial holder of the public shares and provide your legal name, phone number and address; and |

| (iii) | deliver your public shares to Continental, Leo’s transfer agent, physically or electronically through The Depository Trust Company. |

Holders must complete the procedures for electing to redeem their public shares in the manner described above prior to 5:00 p.m., Eastern Time, on July 10, 2020 (two business days before the extraordinary general meeting) in order for their shares to be redeemed.

Holders of units must elect to separate the units into the underlying public shares and warrants prior to exercising redemption rights with respect to the public shares. If holders hold their units in an account at a brokerage firm or bank, holders must notify their broker or bank that they elect to separate the units into the underlying public shares and warrants, or if a holder holds units registered in its own name, the holder must contact Continental, Leo’s transfer agent, directly and instruct them to do so. The redemption rights include the requirement that a holder must identify itself in writing as a beneficial holder and provide its legal name, phone number and address to Continental in order to validly redeem its shares. Public shareholders may elect to redeem public shares regardless of if or how they vote in respect of the BCA Proposal. If the Business Combination is not consummated, the public shares will be returned to the respective holder, broker or bank. If the Business Combination is consummated, and if a public shareholder properly exercises its right to redeem all or a portion of the public shares that it holds and timely delivers its shares to Continental, Leo’s transfer agent, New DMS will redeem such public shares for aper-share price, payable in cash, equal to the pro rata portion of the trust account established at the consummation of our initial public offering (the “trust account”), calculated as of two business days prior to the consummation of the Business Combination. For illustrative purposes, as of June 18, 2020, this would have amounted to approximately $10.40 per issued and outstanding public share. If a public shareholder exercises its redemption rights in full, then it will be electing to exchange its public shares for cash and will no longer own public shares. The redemption will take place following the Domestication and accordingly it is shares of New DMS Class A Common Stock that will be redeemed immediately after consummation of the Business Combination. See “Extraordinary General Meeting of Leo—Redemption Rights” in this proxy statement/prospectus for a detailed description of the procedures to be followed if you wish to redeem your public shares for cash.

Notwithstanding the foregoing, a public shareholder, together with any affiliate of such public shareholder or any other person with whom such public shareholder is acting in concert or as a “group” (as defined in

Table of Contents

Section 13(d)(3) of the Securities Exchange Act of 1934, as amended (“Exchange Act”)), will be restricted from redeeming its public shares with respect to more than an aggregate of 15% of the public shares. Accordingly, if a public shareholder, alone or acting in concert or as a group, seeks to redeem more than 15% of the public shares, then any such shares in excess of that 15% limit would not be redeemed for cash.

The Class B Shareholders have agreed to vote all of their ordinary shares in favor of the proposals being presented at the extraordinary general meeting and waive their redemption rights with respect to such ordinary shares in connection with the consummation of the Business Combination. The Class B ordinary shares will be excluded from the pro rata calculation used to determine theper-share redemption price. As of the date of this proxy statement/prospectus, the Class B Shareholders own 20.0% of the issued and outstanding ordinary shares.

The Business Combination Agreement is subject to the satisfaction or waiver of certain other closing conditions as described in the accompanying proxy statement/prospectus. There can be no assurance that the parties to the Business Combination Agreement would waive any such provision of the Business Combination Agreement. In addition, in no event will Leo redeem public shares in an amount that would cause New DMS’s net tangible assets (as determined in accordance with Rule3a51-1(g)(1) of the Exchange Act) to be less than $5,000,001.

The approval of each of the Domestication Proposal and the Organizational Documents Proposals requires a special resolution under Cayman Islands law, being the affirmative vote of holders of at leasttwo-thirds of the ordinary shares represented in person or by proxy and entitled to vote thereon and who vote at the extraordinary general meeting. The approval of each of the BCA Proposal, the Incentive Award Plan Proposal, the Security Issuance Proposal, the Seller Nominee Appointment Proposal and the Adjournment Proposal requires an ordinary resolution under Cayman Islands law, being the affirmative vote of a majority of the ordinary shares represented in person or by proxy and entitled to vote thereon and who vote at the extraordinary general meeting.

Your vote is very important.Whether or not you plan to attend the extraordinary general meeting, please vote as soon as possible by following the instructions in this proxy statement/prospectus to make sure that your shares are represented at the extraordinary general meeting. If you hold your shares in “street name” through a bank, broker or other nominee, you will need to follow the instructions provided to you by your bank, broker or other nominee to ensure that your shares are represented and voted at the extraordinary general meeting. The Business Combination will be consummated only if the Condition Precedent Proposals are approved at the extraordinary general meeting. Each of the Condition Precedent Proposals is cross-conditioned on the approval of each other. The Organizational Documents Proposals that are not Required Organizational Documents Proposals, the Seller Nominee Appointment Proposal and the Incentive Award Plan Proposal, are conditioned on the approval of the Condition Precedent Proposals. The Adjournment Proposal is not conditioned on the approval of any other proposal set forth in this proxy statement/prospectus.

If you sign, date and return your proxy card without indicating how you wish to vote, your proxy will be voted FOR each of the proposals presented at the extraordinary general meeting. If you fail to return your proxy card or fail to instruct your bank, broker or other nominee how to vote, and do not attend the extraordinary general meeting in person, the effect will be, among other things, that your shares will not be counted for purposes of determining whether a quorum is present at the extraordinary general meeting. If you are a shareholder of record and you attend the extraordinary general meeting and wish to vote in person, you may withdraw your proxy and vote in person.

Your attention is directed to the remainder of the proxy statement/prospectus following this notice (including the Annexes and other documents referred to herein) for a more complete description of the proposed Business Combination and related transactions and each of the proposals. You are encouraged to read this proxy statement/prospectus carefully and in its entirety, including the Annexes and other documents referred to herein. If you have any questions or need assistance voting your ordinary shares, please contact Morrow Sodali LLC, our proxy solicitor, by calling (800)662-5200, or banks and brokers can call collect at (203)658-9400, or by emailing LHC.info@investor.morrowsodali.com.

Table of Contents

Thank you for your participation. We look forward to your continued support.

By Order of the Board of Directors of Leo Holdings Corp.,

| ||

| Lyndon Lea | ||

| Chairman and Chief Executive Officer |

TO EXERCISE YOUR REDEMPTION RIGHTS, YOU MUST DEMAND IN WRITING THAT YOUR PUBLIC SHARES ARE REDEEMED FOR A PRO RATA PORTION OF THE FUNDS HELD IN THE TRUST ACCOUNT AND TENDER YOUR SHARES TO LEO’S TRANSFER AGENT AT LEAST TWO BUSINESS DAYS PRIOR TO THE VOTE AT THE EXTRAORDINARY GENERAL MEETING. IN ORDER TO EXERCISE YOUR REDEMPTION RIGHT YOU NEED TO IDENTIFY YOURSELF AS A BENEFICIAL HOLDER AND PROVIDE YOUR LEGAL NAME, PHONE NUMBER AND ADDRESS IN YOUR WRITTEN DEMAND. YOU MAY TENDER YOUR SHARES BY EITHER DELIVERING YOUR SHARE CERTIFICATE TO THE TRANSFER AGENT OR BY DELIVERING YOUR SHARES ELECTRONICALLY USING THE DEPOSITORY TRUST COMPANY’S DWAC (DEPOSIT WITHDRAWAL AT CUSTODIAN) SYSTEM. IF THE BUSINESS COMBINATION IS NOT COMPLETED, THEN THESE SHARES WILL BE RETURNED TO YOU OR YOUR ACCOUNT. IF YOU HOLD THE SHARES IN STREET NAME, YOU WILL NEED TO INSTRUCT THE ACCOUNT EXECUTIVE AT YOUR BANK OR BROKER TO WITHDRAW THE SHARES FROM YOUR ACCOUNT IN ORDER TO EXERCISE YOUR REDEMPTION RIGHTS.

Table of Contents

| Page | ||||

| i | ||||

| i | ||||

| ii | ||||

| vi | ||||

| viii | ||||

| xi | ||||

| 1 | ||||

| 39 | ||||

| 86 | ||||

| 94 | ||||

| 134 | ||||

| 137 | ||||

| 141 | ||||

| 143 | ||||

| 145 | ||||

| 146 | ||||

| 148 | ||||

| 149 | ||||

| 153 | ||||

| 155 | ||||

| 157 | ||||

| 165 | ||||

| 166 | ||||

UNAUDITED PRO FORMA CONDENSED COMBINED FINANCIAL INFORMATION | 176 | |||

| 192 | ||||

LEO’S MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 210 | |||

| 216 | ||||

DMS’S MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 228 | |||

| 250 | ||||

| 253 | ||||

| 257 | ||||

| 263 | ||||

| 267 | ||||

| 269 | ||||

SECURITIES ACT RESTRICTIONS ON RESALE OF NEW DMS CLASS A COMMON STOCK | 282 | |||

| 283 | ||||

| 283 | ||||

| 284 | ||||

| 284 | ||||

Table of Contents

Table of Contents

You may request copies of this proxy statement/prospectus and any other publicly available information concerning Leo, without charge, by written request to our General Counsel at Leo Holdings Corp., 21 Grosvenor Place, London SW1X 7HF, United Kingdom, or by telephone request at +44 20 7201 2200; or Morrow Sodali LLC, our proxy solicitor, by calling (800)662-5200, or banks and brokers can call collect at (203)658-9400, or by emailing LHC.info@investor.morrowsodali.com, or from the SEC through the SEC website at the address provided above.

In order for Leo’s shareholders to receive timely delivery of the documents in advance of the extraordinary general meeting of Leo to be held on July 14, 2020, you must request the information no later than five business days prior to the date of the extraordinary general meeting, by July 7, 2020.

This document contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this proxy statement/prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. We do not intend our use or display of other companies’ trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

i

Table of Contents

Unless otherwise stated in this proxy statement/prospectus or the context otherwise requires, references to:

| • | “Amended and Restated Registration Rights Agreement” are to the amended and restated registration rights agreement to be entered into by New DMS, Prism, Clairvest Direct Seller, Blocker Seller 1, Blocker Seller 2, Sponsor PIPE Entity and the holders of ordinary shares of Leo who are parties to the existing registration rights agreement in respect to ordinary shares held by such holders at the Closing; |

| • | “Amended and Restated Warrant Agreement” are to the amended and restated warrant agreement to be entered into by New DMS and Continental at the Closing; |

| • | “Blocker Corp” are to CEP V DMS US Blocker Company, a Delaware corporation; |

| • | “Blocker Seller 1” are to Clairvest Equity Partners V Limited Partnership, an Ontario, Canada limited partnership; |

| • | “Blocker Seller 2” are to CEPV Co-Investment Limited Partnership, a Manitoba, Canada limited partnership; |

| • | “Blocker Sellers” are to Blocker Seller 1 and Blocker Seller 2; |

| • | “Business Combination” are to the Domestication, the Equity Purchase and other transactions contemplated by the Business Combination Agreement, collectively; |

| • | “Business Combination Consideration” are to a combination of cash consideration, the Seller Warrants, shares of New DMS Class B Common Stock and shares of New DMS Class C Common Stock; |

| • | “Cayman Islands Companies Law” are to the Companies Law (2020 Revision) of the Cayman Islands; |

| • | “Clairvest” are to Clairvest Group Inc., an Ontario corporation; |

| • | “Clairvest Direct Seller” are toCEP V-A DMS AIV Limited Partnership, a Delaware limited partnership; |

| • | “Clairvest GP” are to Clairvest GP Manageco Inc., an Ontario corporation; |

| • | “Class A ordinary shares” are to the Class A ordinary shares, par value $0.0001 per share, of Leo; |

| • | “Class B ordinary shares” or “founder shares” are to the 5,000,000 Class B ordinary shares, par value $0.0001 per share, of Leo (of which at least 1,500,000 Class B ordinary shares shall be surrendered and forfeited pursuant to the Surrender Agreement described in this proxy statement/prospectus); |

| • | “Class B Shareholders” are to Sponsor and the Leo independent directors; |

| • | “Closing” are to the closing of the Business Combination; |

| • | “company,” “we,” “us” and “our” are to Leo prior to its domestication as a corporation in the State of Delaware and to New DMS upon and after Leo’s domestication as a corporation incorporated in the State of Delaware; |

| • | “Condition Precedent Proposals” are to the BCA Proposal, the Domestication Proposal, the Required Organizational Documents Proposals and Security Issuance Proposal, collectively; |

| • | “Continental” are to Continental Stock Transfer & Trust Company; |

| • | “Converted Founder Shares” are to the shares of New DMS Class A Common Stock issued as a matter of law upon the conversion of the Class B ordinary shares at the time of the Domestication; |

| • | “Director Nomination Agreement” are to the director nomination agreement to be entered into by New DMS, Sponsor, Sponsor PIPE Entity, Clairvest Group Inc. and Prism at the Closing; |

| • | “DMS” are to Digital Media Solutions Holdings, LLC, a Delaware limited liability company, and its subsidiaries; |

ii

Table of Contents

| • | “Domestication” are to the domestication of Leo Holdings Corp. as a corporation incorporated in the State of Delaware; |

| • | “Equity Purchase” are to the purchase of all outstanding stock of Blocker Corp and a portion of the units of DMS held by Prism and Clairvest Direct Seller pursuant to the Business Combination Agreement in exchange for the Business Combination Consideration; |

| • | “Existing Organizational Documents” are to the amended and restated memorandum and articles of association of Leo, dated February 14, 2018; |

| • | “initial public offering” are to Leo’s initial public offering that was consummated on February 15, 2018; |

| • | “IPO registration statement” are to the Registration Statement on FormS-1(333-222599) filed by Leo in connection with its initial public offering and declared effective by the SEC on February 12, 2018; |

| • | “Leo” are to Leo Holdings Corp. prior to the Domestication; |

| • | “Leo independent directors” are to Mss. Bush and Minnick, and Mr. Bensoussan; |

| • | “Lion Capital” are to Lion Capital, LLP, an affiliate of Sponsor; |

| • | “Lock-Up Agreement” are to thelock-up agreement to be entered into by New DMS and the Sellers at the Closing; |

| • | “New DMS” are to Digital Media Solutions, Inc. (f.k.a. Leo Holdings Corp.) upon and after the Business Combination; |

| • | “New DMS Board” are to the board of directors of New DMS; |

| • | “New DMS Class A Common Stock” are to the Class A common stock, par value $0.0001 per share, of New DMS; |

| • | “New DMS Class B Common Stock” are to the Class B common stock, par value $0.0001 per share, of New DMS, which will have no economic value but will entitle the holder thereof to one vote per share; |

| • | “New DMS Class C Common Stock” are to the Class C common stock, par value $0.0001 per share, of New DMS, which are convertible into shares of New DMS Class A Common Stock; |

| • | “New DMS Common Stock” are collectively to New DMS Class A Common Stock, New DMS Class B Common Stock and New DMS Class C Common Stock; |

| • | “New DMS public shares” are to the shares of New DMS Class A Common Stock issued as a matter of law upon the conversion at the time of the Domestication of the Class A ordinary shares that were offered and sold by Leo as part of units in its initial public offering and registered pursuant to the IPO registration statement and of the Class B ordinary shares; |

| • | “New DMS public warrants” are to the 10,000,000 warrants of New DMS issued as a matter of law upon the conversion at the time of the Domestication of the public warrants that were offered and sold by Leo as part of units in its initial public offering and registered pursuant to the IPO registration statement; |

| • | the outstanding New DMS Class A Common Stock “on an as-converted and as-redeemed basis” are to the number of shares of New DMS Class A Common Stock that would be outstanding as of immediately after the Closing assuming (i) all shares of New DMS Class C Common Stock were converted into shares of New DMS Class A Common Stock in accordance with the Proposed Certificate of Incorporation and (ii) all DMS Units held by Prism and Clairvest Direct Seller were acquired upon a Redemption by New DMS for shares of New DMS Class A Common Stock in accordance with the Amended Partnership Agreement; |

| • | “ordinary shares” are to the Class A ordinary shares and the Class B ordinary shares, collectively; |

| • | “Plan” are to the Digital Media Solutions, Inc. 2020 Omnibus Incentive Plan to be considered by the shareholders pursuant to the Incentive Award Plan Proposal; |

iii

Table of Contents

| • | “PIPE Investment” are to the transactions contemplated by the Subscription Agreements, pursuant to which the PIPE Investors have collectively committed to subscribe for 10,000,0000 shares of New DMS Class A Common Stock for an aggregate purchase price equal to $100.0 million to be consummated substantially concurrently with the Closing; |

| • | “PIPE Investors” are to the qualified institutional buyers and accredited investors (including Sponsor PIPE Entity) that have committed to purchase New DMS Class A Common Stock in the PIPE Investment; |

| • | “Prism” are to Prism Data, LLC, a Delaware limited liability company; |

| • | “private placement warrants” are to the 4,000,000 private placement warrants outstanding as of the date of this proxy statement/prospectus (of which 2,000,000 private placement warrants shall be surrendered and forfeited pursuant to the Surrender Agreement described in this proxy statement/prospectus), which will be automatically converted by operation of law, on aone-for-one basis without giving effect to any rights of adjustment or other anti-dilution protections which adjustment and protections will have been waived by the holders of the Class B ordinary shares pursuant to the Surrender Agreement, into warrants to acquire shares of New DMS Class A Common Stock in the Domestication; |

| • | “pro forma” are to giving pro forma effect to the Business Combination; |

| • | “Proposed Bylaws” are to the proposed bylaws of New DMS to be effective upon the Domestication attached to this proxy statement/prospectus as Annex D; |

| • | “Proposed Certificate of Incorporation” are to the proposed certificate of incorporation of New DMS to be effective upon the Domestication attached to this proxy statement/prospectus as Annex C; |

| • | “Proposed Organizational Documents” are to the Proposed Certificate of Incorporation and the Proposed Bylaws; |

| • | “public shares” are to the currently outstanding 19,312,807 Class A ordinary shares that were offered and sold as part of units by Leo in its initial public offering and registered pursuant to the IPO registration statement and the New DMS public shares; |

| • | “public shareholders” are to holders of public shares, whether acquired in Leo’s initial public offering or acquired in the secondary market; |

| • | “public warrants” are to the 10,000,000 public warrants that were offered and sold as part of units by Leo in its initial public offering and registered pursuant to the IPO registration statement and the New DMS public warrants; |

| • | “redemption” are to each redemption of public shares for cash pursuant to the Existing Organizational Documents; |

| • | “SEC” are to the Securities and Exchange Commission; |

| • | “Sellers” are to Prism, Clairvest Direct Seller and Blocker Sellers; |

| • | “Seller Warrants” are to the 2,000,000 warrants issued to Sellers as part of the Business Combination Consideration and pursuant to the Amended and Restated Warrant Agreement; |

| • | “Surrender Agreement” are to the Amended and Restated Sponsor Shares and Warrant Surrender Agreement, dated as of June 22, 2020, entered into by Leo, the Sponsor and the Leo independent directors; |

| • | “Sponsor” are to Leo Investors Limited Partnership, a Cayman Islands exempted limited partnership; |

| • | “Sponsor PIPE Entity” are to Lion Capital (Guernsey) Bridgeco Limited, a company organized under the laws of Guernsey; |

| • | “Subscription Agreements” are to the subscription agreements, entered into by Leo and each of the PIPE Investors in connection with the PIPE Investment; |

iv

Table of Contents

| • | “Tax Receivable Agreement” are to the tax receivable agreement to be entered into by New DMS, Blocker Corp and the Sellers at the Closing; |

| • | “transfer agent” are to Continental, Leo’s transfer agent; |

| • | “trust account” are to the trust account established at the consummation of Leo’s initial public offering at JP Morgan Chase Bank, N.A. and maintained by Continental, acting as trustee; |

| • | “units” are to the units of Leo, each unit representing one Class A ordinary share andone-half of one warrant to acquire one Class A ordinary share, that were offered and sold by Leo in its initial public offering and registered pursuant to the IPO registration statement; and |

| • | “warrants” are to the public warrants and the private placement warrants and, with respect to any period of time after the Closing, the Seller Warrants. |

v

Table of Contents

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Certain statements in this proxy statement/prospectus may constitute “forward-looking statements” for purposes of the federal securities laws. Our forward-looking statements include, but are not limited to, statements regarding our or our management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, including those relating to the Business Combination. The information included in this proxy statement/prospectus in relation to DMS has been provided by DMS and its respective management, and forward-looking statements include statements relating to our and its respective management team’s expectations, hopes, beliefs, intentions or strategies regarding the future, including those relating to the Business Combination. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “intends,” “may,” “might,” “plan,” “possible,” “potential,” “predict,” “project,” “should,” “will,” “would” and similar expressions may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements in this proxy statement/prospectus may include, for example, statements about:

| • | our ability to complete the Business Combination with DMS or, if we do not consummate such business combination, any other initial business combination; |

| • | satisfaction or waiver of the conditions to the Business Combination including, among other things: (1) the approval of the BCA Proposal, the Domestication Proposal, the Security Issuance Proposal and certain of the Organizational Documents Proposals being obtained; (2) all required waiting periods or approvals under the Hart-Scott-Rodino Act of 1976 (the “HSR Act”) and all applicable antitrust laws having expired, been received or terminated; (3) the consummation of the Domestication immediately prior to the Closing; (4) the consummation of the PIPE Investment immediately prior to the Closing; (5) 1,500,000 Class B ordinary shares and 2,000,000 private placement warrants of Leo having been surrendered and forfeited by Sponsor and the Leo independent directors, as applicable, in accordance with the Surrender Agreement; (6) the absence of a Material Adverse Effect (as defined in the Business Combination Agreement); (7) the net tangible assets of New DMS (as determined in accordance with Rule3a51-1(g)(1) of the Securities Exchange Act of 1934, as amended (“Exchange Act”)) being at least $5,000,001; (8) cash proceeds from the trust account established for the purpose of holding the net proceeds of Leo’s initial public offering and certain of the proceeds from its concurrent private placement of warrants, together with the proceeds from the PIPE Investment, net of any amounts paid to Leo shareholders that exercise their redemption rights in connection with the Business Combination, equaling no less than $200,000,000 at the Closing; and (9) the shares of New DMS Class A Common Stock to be issued in connection with the Business Combination Agreement having been approved for listing on the NYSE; |

| • | the occurrence of any event, change or other circumstances, including the outcome of any legal proceedings that may be instituted against Leo and DMS following the announcement of the Business Combination Agreement and the transactions contemplated therein, that could give rise to the termination of the Business Combination Agreement; |

| • | our ability to consummate the Business Combination due to the uncertainty resulting from the recentCOVID-19 pandemic; |

| • | the projected financial information, growth rate and market opportunity of New DMS; |

| • | the ability to obtain and/or maintain the listing of the New DMS Class A Common Stock and the warrants on the NYSE, and the potential liquidity and trading of our securities; |

| • | the risk that the proposed Business Combination disrupts current plans and operations of DMS as a result of the announcement and consummation of the proposed Business Combination; |

| • | the ability to recognize the anticipated benefits of the proposed Business Combination, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profitably and retain its key employees; |

vi

Table of Contents

| • | costs related to the proposed Business Combination; |

| • | changes in applicable laws or regulations; |

| • | our ability to raise financing in the future; |

| • | our success in retaining or recruiting, or changes required in, our officers, key employees or directors following the completion of the Business Combination; |

| • | our officers and directors allocating their time to other businesses and potentially having conflicts of interest with our business or in approving the Business Combination; |

| • | factors relating to our business, operations and financial performance following the Business Combination, including: |

| • | our ability to attract consumers to our websites, marketplaces or brand direct solutions and convert them to sales for our advertisers; |

| • | our ability to maintain or increase our share of expenditures from our advertisers and our ability to establish relationships with new advertisers; |

| • | our ability to maintain, grow and protect the data we obtain from consumers and advertisers; |

| • | our dependence on our emails and sites not being treated disadvantageously by internet service providers; |

| • | our ability to provide new product and service offerings that make our marketplaces, brand direct solutions and websites useful for consumers; |

| • | our ability to compete effectively for consumers and advertisers; |

| • | our ability to successfully integrate the operations of companies we acquire; |

| • | the performance of our technology infrastructure; |

| • | our dependence on third-party website publishers for a significant portion of our visitors; |

| • | our ability to protect our intellectual property rights; |

| • | our ability to maintain adequate internal controls over financial and management systems; and |

| • | other factors detailed under the section entitled “Risk Factors.” |

The forward-looking statements contained in this proxy statement/prospectus are based on current expectations and beliefs concerning future developments and their potential effects on us and/or DMS. There can be no assurance that future developments affecting us and/or DMS will be those that we and/or DMS have anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control or the control of DMS) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, those factors described under the heading “Risk Factors”. Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in theseforward-looking statements. Some of these risks and uncertainties may in the future be amplified bythe COVID-19 outbreak and there may be additional risks that we consider immaterial or which are unknown. It is not possible to predict or identify all such risks. We and DMS undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Before any shareholder grants its proxy or instructs how its vote should be cast or vote on the proposals to be put to the extraordinary general meeting, such stockholder should be aware that the occurrence of the events described in the “Risk Factors” section and elsewhere in this proxy statement/prospectus may adversely affect us.

vii

Table of Contents