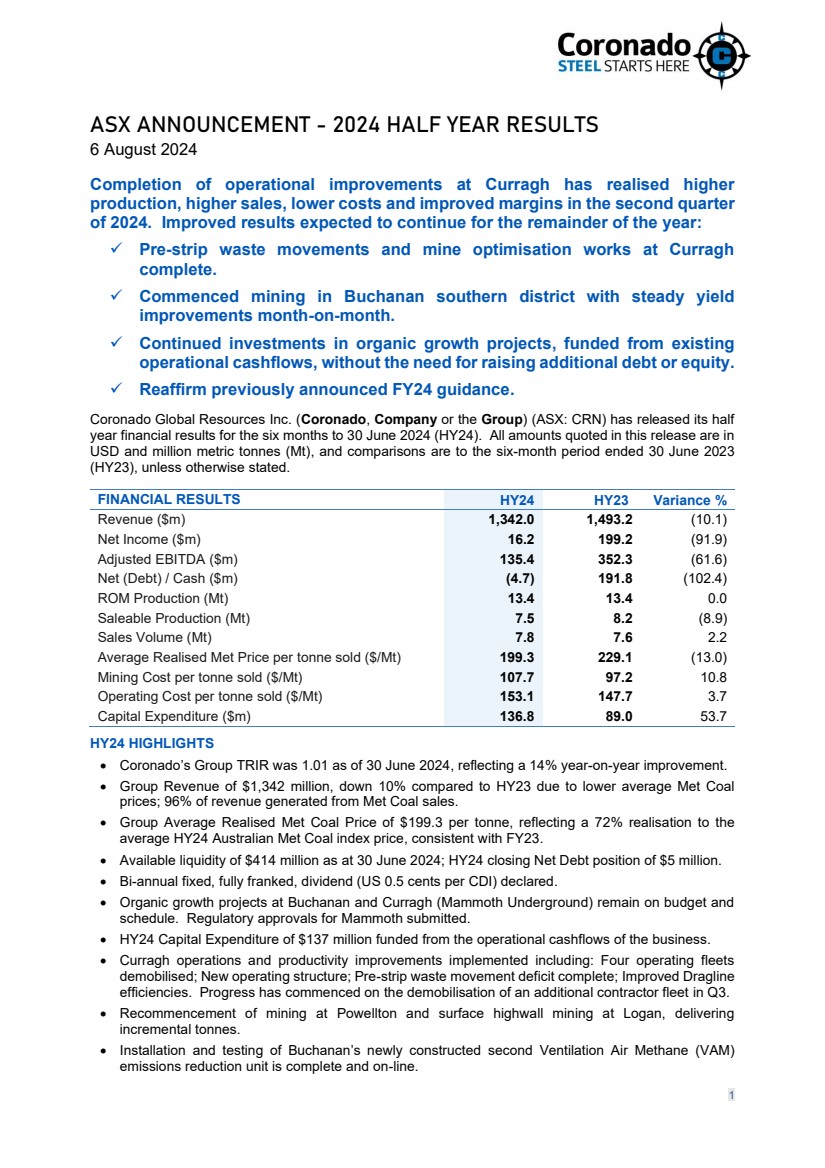

| 1 ASX ANNOUNCEMENT - 2024 HALF YEAR RESULTS 6 August 2024 Completion of operational improvements at Curragh has realised higher production, higher sales, lower costs and improved margins in the second quarter of 2024. Improved results expected to continue for the remainder of the year: ✓ Pre-strip waste movements and mine optimisation works at Curragh complete. ✓ Commenced mining in Buchanan southern district with steady yield improvements month-on-month. ✓ Continued investments in organic growth projects, funded from existing operational cashflows, without the need for raising additional debt or equity. ✓ Reaffirm previously announced FY24 guidance. Coronado Global Resources Inc. (Coronado, Company or the Group) (ASX: CRN) has released its half year financial results for the six months to 30 June 2024 (HY24). All amounts quoted in this release are in USD and million metric tonnes (Mt), and comparisons are to the six-month period ended 30 June 2023 (HY23), unless otherwise stated. HY24 HIGHLIGHTS • Coronado’s Group TRIR was 1.01 as of 30 June 2024, reflecting a 14% year-on-year improvement. • Group Revenue of $1,342 million, down 10% compared to HY23 due to lower average Met Coal prices; 96% of revenue generated from Met Coal sales. • Group Average Realised Met Coal Price of $199.3 per tonne, reflecting a 72% realisation to the average HY24 Australian Met Coal index price, consistent with FY23. • Available liquidity of $414 million as at 30 June 2024; HY24 closing Net Debt position of $5 million. • Bi-annual fixed, fully franked, dividend (US 0.5 cents per CDI) declared. • Organic growth projects at Buchanan and Curragh (Mammoth Underground) remain on budget and schedule. Regulatory approvals for Mammoth submitted. • HY24 Capital Expenditure of $137 million funded from the operational cashflows of the business. • Curragh operations and productivity improvements implemented including: Four operating fleets demobilised; New operating structure; Pre-strip waste movement deficit complete; Improved Dragline efficiencies. Progress has commenced on the demobilisation of an additional contractor fleet in Q3. • Recommencement of mining at Powellton and surface highwall mining at Logan, delivering incremental tonnes. • Installation and testing of Buchanan’s newly constructed second Ventilation Air Methane (VAM) emissions reduction unit is complete and on-line. FINANCIAL RESULTS HY24 HY23 Variance % Revenue ($m) 1,342.0 1,493.2 (10.1) Net Income ($m) 16.2 199.2 (91.9) Adjusted EBITDA ($m) 135.4 352.3 (61.6) Net (Debt) / Cash ($m) (4.7) 191.8 (102.4) ROM Production (Mt) 13.4 13.4 0.0 Saleable Production (Mt) 7.5 8.2 (8.9) Sales Volume (Mt) 7.8 7.6 2.2 Average Realised Met Price per tonne sold ($/Mt) 199.3 229.1 (13.0) Mining Cost per tonne sold ($/Mt) 107.7 97.2 10.8 Operating Cost per tonne sold ($/Mt) 153.1 147.7 3.7 Capital Expenditure ($m) 136.8 89.0 53.7 |

| 2 COMMENTS FROM MANAGING DIRECTOR AND CEO, DOUGLAS THOMPSON “In the first half of FY2024, the substantial investments we have made over the past 18 months to optimise and expand our mining operations in Australia and the U.S. began to deliver tangible and promising results. “The material improvement in production, sales, costs and revenue reported in Q2 are the direct result of the sustained focus on improving every aspect of our business to ensure Coronado remains a competitive, world class provider of metallurgical coal for decades to come. “The dramatic cost and productivity gains at Curragh, were made possible by the successful completion to plan of historical pre-strip waste deficit works and the subsequent removal of four fleets. This allowed for a sustained improvement in dragline productivity and drill and blast performance in Q2, setting new benchmarks for future performance. “Production and cost improvements were also realised in the U.S, with yields increasing as planned at Buchanan, following the installation of the Southern district longwall, and the reopening of the Powellton mine at Logan. “Our preference for organic growth funded by cashflows, rather than bolt-on acquisitions funded by debt and equity, has proven to be prudent in a challenging market characterised by high inflation and increasing taxes and royalties. “Our growth projects in Australia (Mammoth Underground) and the U.S. (Buchanan Expansion) continue to make good progress. First coal from Mammoth is expected in December 2024, subject to receiving regulatory approvals, and the Buchanan expansions are scheduled to complete in Q2 2025. Completion of both projects is expected to deliver incremental tonnages of up to 3 Mtpa once fully ramped up. “Maximising returns from our portfolio of high-quality assets through expansion and ongoing productivity and cost improvement, will further strengthen our balance sheet. With improving results and a positive outlook for the second half of the year, we have reaffirmed our previously announced FY24 guidance.” HEALTH AND SAFETY The safety and well-being of our workforce continue to be Coronado’s highest priority. The Group Total Reportable Incident Rate (TRIR) as of 30 June 2024 was 1.01, compared to 1.18 as of 30 June 2023, reflecting an 14% year-on-year improvement. In Australia, the 12-month rolling average Total Reportable Injury Frequency Rate (TRIFR) as of 30 June 2024 was 1.29, compared to 2.52 as of 30 June 2023, reflecting a 49% year-on-year improvement and the lowest Australia TRIFR since April 2018. In the U.S., the 12-month rolling average TRIR as of 30 June 2024 was 2.26, compared to 2.56 as of 30 June 2023. As reported in prior public announcements, on 31 May 2024 (U.S. Eastern time), the Company temporarily suspended operations at the Buchanan mine following the fatality involving one of its employees, Mr Brock Jackson. Coronado is deeply saddened by this tragic event and extends its deepest sympathies and sincere condolences to the family, friends and colleagues of Mr Jackson. FINANCIAL PERFORMANCE Coronado continues to maintain a strong balance sheet with healthy liquidity levels, allowing for the continued investment in our highly accretive organic growth projects, without the need for raising additional debt or equity. As of 30 June 2024, Coronado has Available Liquidity of $414.4 million, despite the negative impact of a one-off payment on 6 March 2024 to the Queensland Revenue Office, or the QRO, of $51.5 million (A$79.0 million), inclusive of interest, prior to the Company lodging its appeal in the Supreme Court of Queensland on 11 March 2024, against the QRO's assessment of the stamp duty payable on Coronado's acquisition of the Curragh mine in March 2018. Cash generated from operating activities (excluding the QRO payment) was $62.6 million for HY24. HY24 Group Revenues were $1,342.0 million, down 10.1% compared to HY23. Lower revenues are reflective of the fall in Met Coal index prices in HY24, combined with lower PCI coal price relativities compared to the Australian PLV benchmark. Coronado reported Net Income of $16.2 million and Adjusted EBITDA of $135.4 million. HY24 Average Mining Costs Per Tonne Sold for the Group were $107.7 per tonne. While Group mining costs per tonne are higher than HY23, they should be viewed in the context of quarterly performance where Q1 2024 ($125.6 per tonne) and Q2 2024 ($91.1 per tonne) reflect a materially improved cost base at Curragh following significant operational and productivity improvements gains. Q2 2024 mining costs per |

| 3 tonne represent a 27.5% decrease quarter-on-quarter, and at Curragh specifically, were at the lowest level since Q1 2022. The lower costs quarter-on-quarter are attributable to the demobilisation of four fleets from Curragh at the end of March combined with higher Sales volumes. The Company expects costs to be further reduced in the coming quarters following the demobilisation of an additional contractor fleet at Curragh in the September quarter, combined with planned higher production volumes aligned with full year guidance metrics. Coronado paid $261 million in corporate taxes, stamp duty, government royalties and rebates in HY24. HY24 Capital Expenditure of $136.8 million was up 53.7% compared to HY23 ($89.0 million) primarily due to expenditure on organic growth projects at Buchanan and Mammoth Underground. Today, Coronado’s Board of Directors declares a bi-annual fully franked fixed dividend of $8.4 million, or USD 0.5 cents per CDI to Shareholders in accordance with its dividend policy. The dividend record date is 28 August 2024, and payment date is 18 September 2024. No matching offer to Senior Secured Notes holders is required. Coronado reaffirms previously announced FY24 guidance for Saleable Production (16.4 – 17.2 Mt); Mining Costs Per Tonne Sold ($95 - $99/t), and Capital Expenditure ($220 million - $250 million). OPERATIONS Group ROM coal production for HY24 was 13.4 Mt (no change) and Saleable Production was 7.5 Mt (8.9% lower). The Australian operations (Curragh) delivered ROM coal production of 6.5 Mt and Saleable Production of 4.8 Mt in HY24. While these results broadly mirror HY23, the underlying theme is the enhanced performance in Q2 2024 compared to Q1 2024, following the implementation of operational and productivity improvements. In Q2 2024, Curragh delivered ROM coal production and Saleable Production increases of 39.1% and 23.4% respectively compared to Q1 2024. These significantly improved results are principally due to the completion of the historical pre-strip waste deficit works and the subsequent removal of four fleets in late March 2024, combined with improved productivity from our dragline fleet and improved drill and blast performance. The dragline fleet continues to meet improvement targets with the ratio of waste moved by draglines compared to truck/excavator at 44% (up from 37%). HY24 total waste movement increased by 2.8% compared to HY23 (HY24: 94.5 Mbcms vs HY23: 91.9 Mbcms). Operationally, Curragh finished HY24 in a strong position with elevated stockpiles. Coronado is targeting further cost and productivity improvements in the September quarter with the planned removal of an additional contractor fleet. Upon full demobilisation, that will take the number of fleets removed from Curragh to five, plus the introduction of a new Komatsu PC7000 excavator which is increasing coal delivery and contributing to the overall productivity gains at the site. The U.S. operations (Buchanan / Logan) delivered ROM coal production of 6.9 Mt and Saleable Production of 2.7 Mt in HY24. Like Australia, the U.S. business delivered higher tonnages and lower costs in Q2 2024 compared to Q1 2024. Following the commencement of mining in the Southern district of Buchanan in January, yields have steadily improved. The mine continues to experience improved skip efficiencies following maintenance works earlier in the year, and conveyor belt systems continue to work well, with skip counts at their best rates in two years. In Q3 2024, it is currently planned that development of the next panel in the Northern district will be ready for mining, and for a portion of time, we will be running both longwall sections at the same time. This is expected to further increase product yields from Buchanan given the Northern district is a higher yielding section. At Logan, incremental tonnages are being achieved following the reestablishment of mining in the Powellton mine and commencement of highwall mining works at the surface operations in April. Sales volumes for the Group in HY24 were 7.8 Mt, 2.2% higher than HY23. Sales volumes from the Australian and U.S. operations were 5.2 Mt and 2.6 Mt, respectively. Curragh inventory levels at the mine as of 30 June 2024 remained above average with approximately 690 Kt of ROM coal production and 360 Kt of Saleable Production coal on hand. Stockpiles at Buchanan and Logan were at normal levels. As a percentage of total Sales volumes year-to-date, export sales were 69.8%. Coronado’s proportion of Met Coal sales revenue as a percentage of total coal revenues year-to-date was 95.7%. The percentage of Met Coal sales was higher than prior year (HY23: 90.4%) due to the delivery in prior year of certain U.S. thermal coal contracts negotiated when thermal coal pricing was at elevated levels. The HY24 Group Realised Price Per Tonne of Met Coal Sold (mixture of FOB / FOR / Domestic pricing) was $199.3 per tonne equating to a 72.3% realisation on the average Australian Met Coal index price of $275.6 per tonne. This percentage realisation mirrors FY23 despite lower PCI price relativities compared to the Australian benchmark index. |

| 4 ORGANIC GROWTH PLANS AND EMISSIONS REDUCTION In HY24, we have continued to invest in our organic growth and emissions reduction projects, that we believe will ultimately underscore higher sustained returns to Shareholders over time. Our growth projects at both Buchanan and Curragh (Mammoth Underground) remain on target and continue to be funded by the operational cashflows of our existing assets, without the need for raising debt or further equity from the market. The plan to expand Buchanan and implement the Mammoth Underground mine we anticipate will see our Saleable Production levels for our high-quality Met Coal increase overtime, and result in both higher margins and lower costs for our business. Mammoth Underground The Mammoth Underground Project remains on schedule, subject to regulatory approvals. In June, Coronado submitted the relevant statutory approvals on time and the approval process is progressing to schedule. All procurement activities are progressing as planned, including all equipment orders placed and delivery schedules agreed upon with providers before project commencement. Mammoth has a full leadership team in place supporting the construction of the project and expressions of interest for staff and workforce have been released to the market. All required earthworks in S-Pit are complete, and highwall stabilisation works have commenced in preparation for portal development. All engagements with the regulators and community have continued to be positive. Mammoth has substantial high-quality Met Coal reserves of 41 million ROM tonnes. Once fully operational, the project is on target to deliver an incremental 1.5 – 2.0 Mtpa Saleable Production in its first phase. Subject to receipt of regulatory approvals, first coal from Mammoth is expected in December 2024. Buchanan Expansion Organic growth plans at our U.S. operations remain on target to ultimately deliver increased production of 7.0 Mtpa of Met Coal from mid-2025. Capital works continue at Buchanan to invest in the construction of a new surface raw coal storage area to increase the mine’s storage capacity, ultimately reducing the risk of bottlenecks and allowing the longwall equipment to run at a higher capacity. In HY24, excavation works continued with the completion of access roads and bridge extensions, in addition to grading, compaction and surveying of the stockpile area. The scheduled date for the new stockpile facility remains on plan for April 2025. Buchanan also progressed the construction of a second set of skips, to increase the mine’s hoisting capacity to the surface. As at 30 June 2024, the shaft excavation works and concrete lining works were completed, with next stage works continuing as planned. Full completion of the project is expected in May 2025. Buchanan Emissions Reduction Given the proven success of the VAM unit at Vent Shaft 16 to reduce emissions, Coronado undertook a commitment to install a second VAM unit at Vent Shaft 18. The construction of the second VAM unit was completed in April, with testing conducted in May and June. Coronado is pleased to announce that the new VAM unit at Vent Shaft 18 was approved for operations by the Virginia Energy, Oil and Gas Board on 18 June 2024 and is now fully operational and actively reducing emissions at our Buchanan mine. The establishment of this second VAM unit is expected to further reduce Coronado’s emissions, as part of our strategic path to a 30% Group emission reduction target by 2030. Coronado considers itself as an industry leader in implementing this emission reduction technology. Curragh Gas Pilot Project Coronado continued to make progress on its Gas Pilot Project at Curragh in HY24. The project is targeting the capture and beneficial use of open-cut waste mine coal gas from our operations, with downstream use cases for power generation and as a diesel substitute in mining fleets continuing to be explored. Production of Europa 1 and Europa 2 wells commenced in January 2024, and Coronado is continuing to monitor gas flow from these wells to build a data record and our understanding of performance. During the June quarter, Coronado commenced its second gas converted truck trial to assess the performance of a Caterpillar 793F engine with upgraded conversions. Early results are positive and in line with our expectations. The trial will run for eight weeks. |

| 5 METALLURGICAL COAL / STEEL MARKET OUTLOOK 1 Undoubtedly, the long-term growth story for Met Coal is the projected future demand from India. India remains one of Coronado’s largest export destinations and is forecasting GDP growth rates of approx. 6% year-on-year for the next 20 years. Long-term growth in global Met Coal export demand is anticipated to push trade flows up from an estimated 388 Mt in 2024 to an estimated 576 Mt in 2050. India is expected to lead all countries in import demand growth due to its significant potential for urbanisation and industrialisation. Imports are expected to increase to 269 Mt by 2050, up 241% from projected 2024 levels. Indian crude steel production is expected to grow from 152 Mt to 534 Mt by 2050, an increase underpinned by Blast Furnace steel generation methods. In HY24, 22% of all Coronado coal revenues were generated from exports to India. In addition to the Indian growth story, we expect that demand for steel will continue to grow in traditional markets as the world continues to pursue net-zero emission targets by building large scale emissions reduction and renewable energy infrastructure projects requiring steel. In FY24, total global steel production from the blast furnace process is expected to be 1.3 billion tonnes, with this process representing 72% of total crude steel production. This level of steel production sustains current infrastructure development, but the ever-increasing demand for renewable infrastructure, will further drive increased demand for steel over the medium to longer term. To produce 1.3 billion tonnes of blast furnace steel, 1 billion tonnes of mined Met Coal is required, making Met Coal a critical material for the renewables transition. In fact, Met Coal has been declared a critical raw material by the European Union to help build the world’s infrastructure needs and renewable energy transition. Met Coal prices in HY24 were lower than HY23 principally due to a combination of increased supply due to drier operating conditions in the Bowen Basin, and soft global economic confidence with elevated inflation and interest rates. The average benchmark Australian premium low-vol hard coking coal index (PLV HCC FOB AUS) price in HY24 was $275.6 per tonne, down 6.2% compared to the average index price in HY23 of $293.8 per tonne. Despite the year-to-date price reductions, price increases were noted in early July following production issues at peer Met Coal mines in Australia and the U.S. Coronado expects that in the second half of 2024, prices will remain strong on the back of Indian restocking appetite after the monsoon season. In the same period, Met Coal supply is expected to be restricted with mine production issues from our peers. The SGX forward curve, as at 31 July 2024, is projecting PLV HCC FOB AUS average index pricing of $234 per tonne for the remainder of FY24. These pricing projections continue to suggest a higher pricing environment for longer, and a forward pricing environment well above the long-term average price of $199 per tonne. 1 Source: Data sourced from AME Metallurgical Coal Strategic Market Study 2024 Q2; Wood Mackenzie May 2024 Coal Market Service Metallurgical Trade Long-term Outlook H1 2024; Wood Mackenzie May 2024 GDP forecasts; Forward curve estimates reflect the SGX Aus Coking Coal forward curve pricing as of 31 July 2024. Approved for release by the Board of Directors of Coronado Global Resources Inc. For a detailed review of Coronado’s operating and financial performance, investors should refer to the Company’s Quarterly Report on Form 10-Q, Appendix 4D, and the Investor Presentation released to the Australian Securities Exchange and the Securities and Exchange Commission on 6 August 2024 (AEST). For further information please contact: Investors Andrew Mooney Vice President Investor Relations & Communications P: +61 458 666 639 E: amooney@coronadoglobal.com E: investors@coronadoglobal.com Media Helen McCombie Morrow Sodali P: +61 411 756 248 E: helen.mccombie@sodali.com |

| 6 Cautionary Notice Regarding Forward – Looking Statements This report contains forward-looking statements concerning our business, operations, financial performance and condition, the coal, steel and other industries, and our plans, objectives and expectations for our business, operations, financial performance and condition. Forward-looking statements may be identified by words such as "may", "could", "believes", "estimates", "expects", "intends", “plans”, "considers", “forecasts”, “anticipates”, “targets” and other similar words that involve risk and uncertainties. Forward-looking statements provide management's current expectations or predictions of future conditions, events or results. All statements that address operating performance, events or developments that we expect or anticipate will occur in the future are forward-looking statements. They may include estimates of revenues, income, earnings per share, cost savings, capital expenditures, dividend payments, share repurchases, liquidity, capital structure, market share, industry volume, or other financial items, descriptions of management’s plans or objectives for future operations, or descriptions of assumptions underlying any of the above. All forward-looking statements speak only as of the date they are made and reflect the Company's good faith beliefs, assumptions and expectations, but they are not a guarantee of future performance or events. Furthermore, the Company disclaims any obligation to publicly update or revise any forward-looking statement, except as required by law. By their nature, forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those suggested by the forward-looking statements. Factors that might cause such differences include, but are not limited to, a variety of economic, competitive and regulatory factors, many of which are beyond the Company's control, that are described in our Annual Report on Form 10-K for the fiscal year ended 31 December 2023 filed with the ASX and SEC on 20 February 2024 (AEST), our Quarterly Report on Form 10-Q filed with the ASX and SEC on 7 May 2024 (AEST) and our Quarterly Report on Form 10-Q filed with the ASX and SEC on 6 August 2024 (AEST), as well as additional factors we may describe from time to time in other filings with the ASX and SEC. You may get such filings for free at our website at www.coronadoglobal.com. You should understand that it is not possible to predict or identify all such factors and, consequently, you should not consider any such list to be a complete set of all potential risks or uncertainties. Reconciliation of Non-GAAP Measures This report includes a discussion of results of operations and references to and analysis of certain non-GAAP measures (as described below) which are financial measures not recognised in accordance with U.S. GAAP. Non-GAAP financial measures are used by the Company and investors to measure operating performance. Management uses a variety of financial and operating metrics to analyse performance. These metrics are significant in assessing operating results and profitability. These financial and operating metrics include: (i) safety and environmental statistics; (ii) Adjusted EBITDA; (iii) total sales volumes and average realised price per Mt sold, which we define as total coal revenues divided by total sales volume; (iv) Metallurgical coal sales volumes and average realised Metallurgical coal price per tonne sold, which we define as metallurgical coal revenues divided by metallurgical sales volume; (v) Mining costs per Mt sold, which we define as mining cost of coal revenues divided by sales volumes (excluding non-produced coal) for the respective segment; (vi) Operating costs per Mt sold, which we define as operating costs divided by sales volumes for the respective segment. Investors should be aware that the Company’s presentation of Adjusted EBITDA and other non-GAAP measures may not be comparable to similarly titled financial measures used by other companies. We define Net (Debt) / Cash as cash and cash equivalents (excluding restricted cash) less the outstanding aggregate principal amount of the 10.750% senior secured notes due 2026 and less other interest-bearing liabilities. Reconciliations of certain forward-looking non-GAAP financial measures, including our 2024 Mining Cost per Tonne Sold guidance, to the most directly comparable GAAP financial measures are not provided because the Company is unable to provide such reconciliations without unreasonable effort, due to the uncertainty and inherent difficulty of predicting the occurrence and the financial impact of items impacting comparability and the periods in which such items may be recognised. For the same reasons, the Company is unable to address the probable significance of the unavailable information, which could be material to future results. |

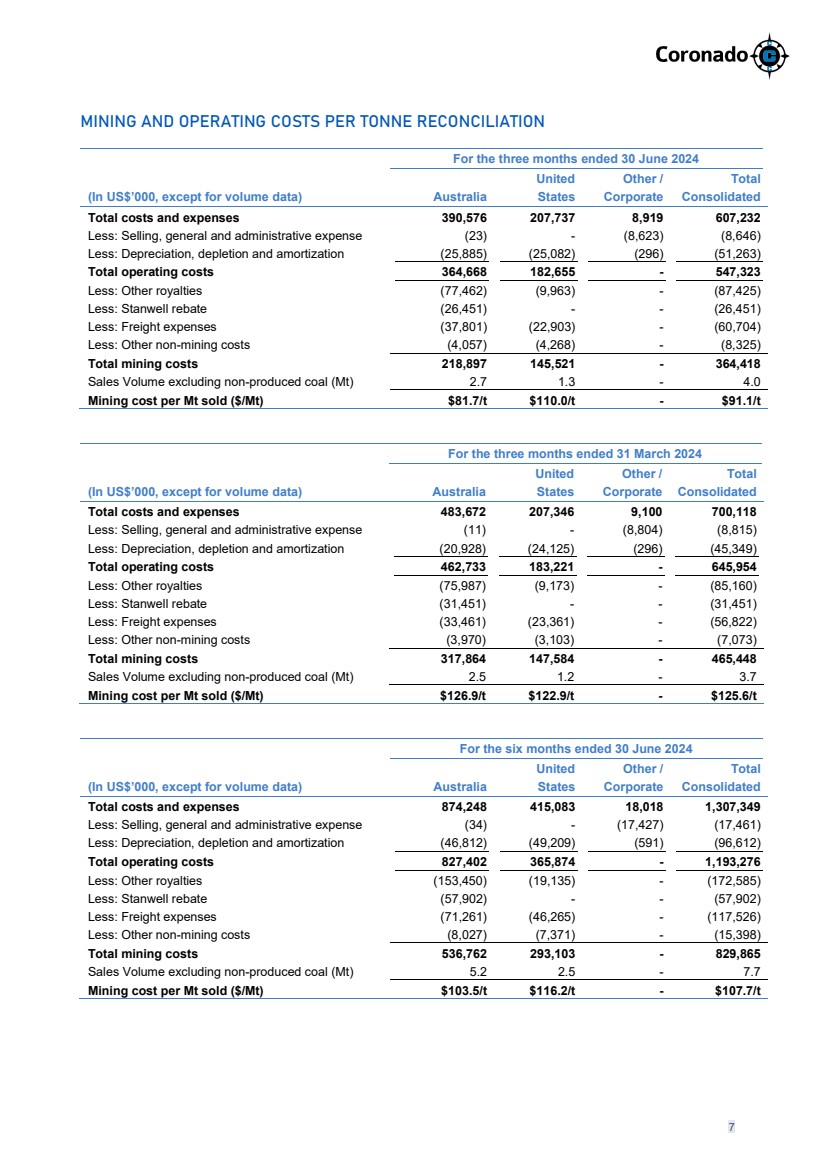

| 7 MINING AND OPERATING COSTS PER TONNE RECONCILIATION For the three months ended 30 June 2024 (In US$’000, except for volume data) Australia United States Other / Corporate Total Consolidated Total costs and expenses 390,576 207,737 8,919 607,232 Less: Selling, general and administrative expense (23) - (8,623) (8,646) Less: Depreciation, depletion and amortization (25,885) (25,082) (296) (51,263) Total operating costs 364,668 182,655 - 547,323 Less: Other royalties (77,462) (9,963) - (87,425) Less: Stanwell rebate (26,451) - - (26,451) Less: Freight expenses (37,801) (22,903) - (60,704) Less: Other non-mining costs (4,057) (4,268) - (8,325) Total mining costs 218,897 145,521 - 364,418 Sales Volume excluding non-produced coal (Mt) 2.7 1.3 - 4.0 Mining cost per Mt sold ($/Mt) $81.7/t $110.0/t - $91.1/t For the three months ended 31 March 2024 (In US$’000, except for volume data) Australia United States Other / Corporate Total Consolidated Total costs and expenses 483,672 207,346 9,100 700,118 Less: Selling, general and administrative expense (11) - (8,804) (8,815) Less: Depreciation, depletion and amortization (20,928) (24,125) (296) (45,349) Total operating costs 462,733 183,221 - 645,954 Less: Other royalties (75,987) (9,173) - (85,160) Less: Stanwell rebate (31,451) - - (31,451) Less: Freight expenses (33,461) (23,361) - (56,822) Less: Other non-mining costs (3,970) (3,103) - (7,073) Total mining costs 317,864 147,584 - 465,448 Sales Volume excluding non-produced coal (Mt) 2.5 1.2 - 3.7 Mining cost per Mt sold ($/Mt) $126.9/t $122.9/t - $125.6/t For the six months ended 30 June 2024 (In US$’000, except for volume data) Australia United States Other / Corporate Total Consolidated Total costs and expenses 874,248 415,083 18,018 1,307,349 Less: Selling, general and administrative expense (34) - (17,427) (17,461) Less: Depreciation, depletion and amortization (46,812) (49,209) (591) (96,612) Total operating costs 827,402 365,874 - 1,193,276 Less: Other royalties (153,450) (19,135) - (172,585) Less: Stanwell rebate (57,902) - - (57,902) Less: Freight expenses (71,261) (46,265) - (117,526) Less: Other non-mining costs (8,027) (7,371) - (15,398) Total mining costs 536,762 293,103 - 829,865 Sales Volume excluding non-produced coal (Mt) 5.2 2.5 - 7.7 Mining cost per Mt sold ($/Mt) $103.5/t $116.2/t - $107.7/t |

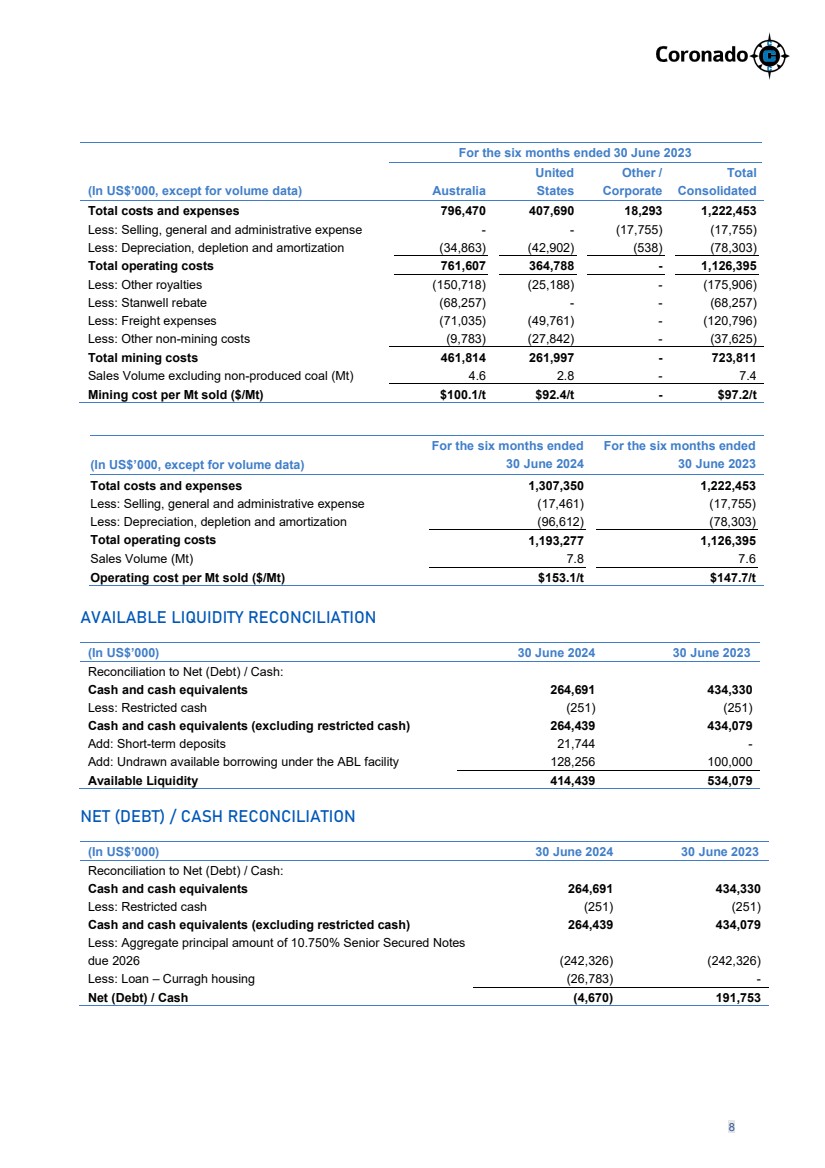

| 8 For the six months ended 30 June 2023 (In US$’000, except for volume data) Australia United States Other / Corporate Total Consolidated Total costs and expenses 796,470 407,690 18,293 1,222,453 Less: Selling, general and administrative expense - - (17,755) (17,755) Less: Depreciation, depletion and amortization (34,863) (42,902) (538) (78,303) Total operating costs 761,607 364,788 - 1,126,395 Less: Other royalties (150,718) (25,188) - (175,906) Less: Stanwell rebate (68,257) - - (68,257) Less: Freight expenses (71,035) (49,761) - (120,796) Less: Other non-mining costs (9,783) (27,842) - (37,625) Total mining costs 461,814 261,997 - 723,811 Sales Volume excluding non-produced coal (Mt) 4.6 2.8 - 7.4 Mining cost per Mt sold ($/Mt) $100.1/t $92.4/t - $97.2/t (In US$’000, except for volume data) For the six months ended 30 June 2024 For the six months ended 30 June 2023 Total costs and expenses 1,307,350 1,222,453 Less: Selling, general and administrative expense (17,461) (17,755) Less: Depreciation, depletion and amortization (96,612) (78,303) Total operating costs 1,193,277 1,126,395 Sales Volume (Mt) 7.8 7.6 Operating cost per Mt sold ($/Mt) $153.1/t $147.7/t AVAILABLE LIQUIDITY RECONCILIATION (In US$’000) 30 June 2024 30 June 2023 Reconciliation to Net (Debt) / Cash: Cash and cash equivalents 264,691 434,330 Less: Restricted cash (251) (251) Cash and cash equivalents (excluding restricted cash) 264,439 434,079 Add: Short-term deposits 21,744 - Add: Undrawn available borrowing under the ABL facility 128,256 100,000 Available Liquidity 414,439 534,079 NET (DEBT) / CASH RECONCILIATION (In US$’000) 30 June 2024 30 June 2023 Reconciliation to Net (Debt) / Cash: Cash and cash equivalents 264,691 434,330 Less: Restricted cash (251) (251) Cash and cash equivalents (excluding restricted cash) 264,439 434,079 Less: Aggregate principal amount of 10.750% Senior Secured Notes due 2026 (242,326) (242,326) Less: Loan – Curragh housing (26,783) - Net (Debt) / Cash (4,670) 191,753 |

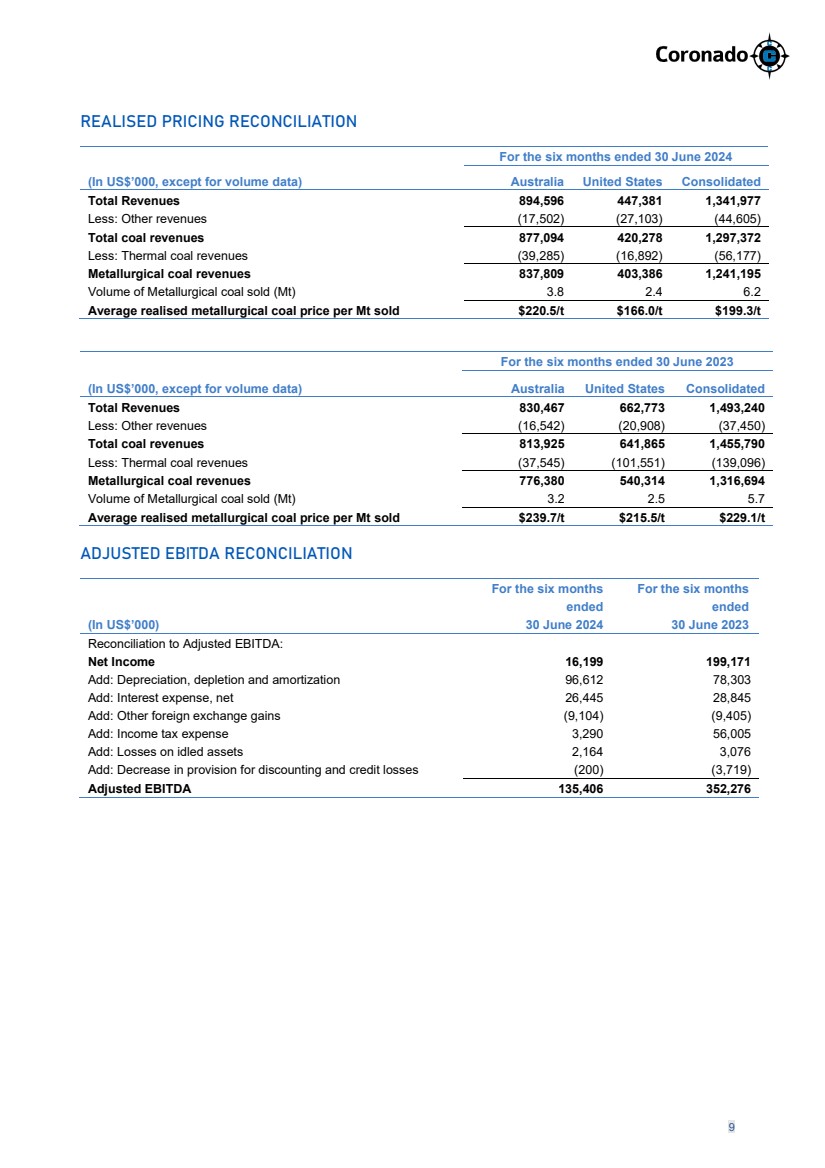

| 9 REALISED PRICING RECONCILIATION For the six months ended 30 June 2024 (In US$’000, except for volume data) Australia United States Consolidated Total Revenues 894,596 447,381 1,341,977 Less: Other revenues (17,502) (27,103) (44,605) Total coal revenues 877,094 420,278 1,297,372 Less: Thermal coal revenues (39,285) (16,892) (56,177) Metallurgical coal revenues 837,809 403,386 1,241,195 Volume of Metallurgical coal sold (Mt) 3.8 2.4 6.2 Average realised metallurgical coal price per Mt sold $220.5/t $166.0/t $199.3/t For the six months ended 30 June 2023 (In US$’000, except for volume data) Australia United States Consolidated Total Revenues 830,467 662,773 1,493,240 Less: Other revenues (16,542) (20,908) (37,450) Total coal revenues 813,925 641,865 1,455,790 Less: Thermal coal revenues (37,545) (101,551) (139,096) Metallurgical coal revenues 776,380 540,314 1,316,694 Volume of Metallurgical coal sold (Mt) 3.2 2.5 5.7 Average realised metallurgical coal price per Mt sold $239.7/t $215.5/t $229.1/t ADJUSTED EBITDA RECONCILIATION (In US$’000) For the six months ended 30 June 2024 For the six months ended 30 June 2023 Reconciliation to Adjusted EBITDA: Net Income 16,199 199,171 Add: Depreciation, depletion and amortization 96,612 78,303 Add: Interest expense, net 26,445 28,845 Add: Other foreign exchange gains (9,104) (9,405) Add: Income tax expense 3,290 56,005 Add: Losses on idled assets 2,164 3,076 Add: Decrease in provision for discounting and credit losses (200) (3,719) Adjusted EBITDA 135,406 352,276 |