0000310158us-gaap:FairValueInputsLevel3Memberus-gaap:ForeignPlanMemberus-gaap:PensionPlansDefinedBenefitMemberus-gaap:OtherInvestmentsMember2023-01-012023-12-31

As filed with the Securities and Exchange Commission on February 25, 2025

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D. C. 20549

_________________________________

FORM 10-K

| | | | | | | | |

| | ☒ | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the Fiscal Year Ended December 31, 2024

OR

| | | | | | | | |

| ☐ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File No. 1-6571

Merck & Co., Inc.

| | | | | | | | | | | | | | |

| 126 East Lincoln Avenue |

| Rahway | New Jersey | 07065 |

(908) 740-4000

| | | | | | | | |

| New Jersey | 22-1918501 |

| (State or other jurisdiction of incorporation) | (I.R.S. Employer Identification No.) |

| | | | | | | | |

| Securities Registered pursuant to Section 12(b) of the Act: |

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on which Registered |

| Common Stock ($0.50 par value) | MRK | New York Stock Exchange |

| 1.875% Notes due 2026 | MRK/26 | New York Stock Exchange |

| 3.250% Notes due 2032 | MRK/32 | New York Stock Exchange |

| 2.500% Notes due 2034 | MRK/34 | New York Stock Exchange |

| 1.375% Notes due 2036 | MRK 36A | New York Stock Exchange |

| 3.500% Notes due 2037 | MRK/37 | New York Stock Exchange |

| 3.700% Notes due 2044 | MRK/44 | New York Stock Exchange |

| 3.750% Notes due 2054 | MRK/54 | New York Stock Exchange |

| | |

| Securities Registered pursuant to Section 12(g) of the Act: None |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Large accelerated filer | ☒ | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | ☐ | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

Number of shares of Common Stock ($0.50 par value) outstanding as of January 31, 2025: 2,526,036,240.

Aggregate market value of Common Stock ($0.50 par value) held by non-affiliates on June 28, 2024 based on the closing price on June 28, 2024, the last business day of the registrant’s most recently completed second fiscal quarter: approximately $313,799,000,000.

| | | | | | | | |

| | |

| Documents Incorporated by Reference: | | |

| Document | | Part of Form 10-K |

Proxy Statement for the Annual Meeting of Shareholders to be held May 27, 2025, to be filed with the Securities and Exchange Commission within 120 days after the close of the fiscal year covered by this report | | Part III |

Table of Contents

| | | | | | | | | | | |

| | | | Page |

|

| Item 1. | | |

| Item 1A. | | |

| | |

| Item 1B. | | |

| Item 1C. | | |

| Item 2. | | |

| Item 3. | | |

| Item 4. | | |

| | |

|

| Item 5. | | |

| Item 6. | | |

| Item 7. | | |

| Item 7A. | | |

| Item 8. | | |

| (a) | | |

| | | |

| | | |

| Item 9. | | |

| Item 9A. | | |

| | |

| Item 9B. | | |

| Item 9C. | | |

|

| Item 10. | | |

| Item 11. | | |

| Item 12. | | |

| Item 13. | | |

| Item 14. | | |

|

| Item 15. | | |

| | |

| Item 16. | | |

| | |

PART I

Item 1.Business.

Merck & Co., Inc. (Merck or the Company) is a global health care company that delivers innovative health solutions through its prescription medicines, including biologic therapies, vaccines and animal health products. The Company’s operations are principally managed on a product basis and include two operating segments, Pharmaceutical and Animal Health, both of which are reportable segments.

The Pharmaceutical segment includes human health pharmaceutical and vaccine products. Human health pharmaceutical products consist of therapeutic and preventive agents, generally sold by prescription, for the treatment of human disorders. The Company sells these human health pharmaceutical products primarily to drug wholesalers and retailers, hospitals, government agencies and managed health care providers such as health maintenance organizations, pharmacy benefit managers and other institutions. Human health vaccine products consist of preventive pediatric, adolescent and adult vaccines. The Company sells these human health vaccines primarily to physicians, wholesalers, distributors and government entities.

The Animal Health segment discovers, develops, manufactures and markets a wide range of veterinary pharmaceutical and vaccine products, as well as health management solutions and services, for the prevention, treatment and control of disease in all major livestock and companion animal species. The Company also offers an extensive suite of digitally connected identification, traceability and monitoring products. The Company sells its products to veterinarians, distributors, animal producers, farmers and pet owners.

All product or service marks appearing in type form different from that of the surrounding text are trademarks or service marks owned, licensed to, promoted or distributed by Merck, its subsidiaries or affiliates, except as noted. All other trademarks or service marks are those of their respective owners.

Product Sales

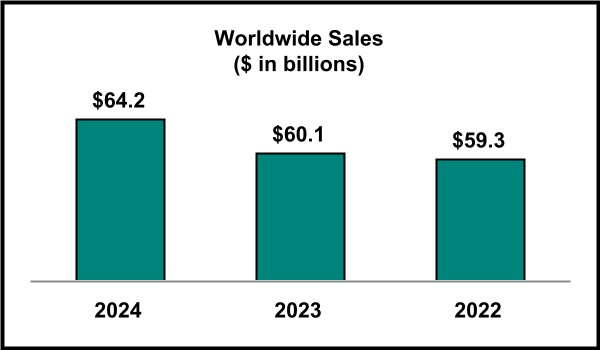

Total Company sales, including sales of the Company’s top pharmaceutical products, as well as sales of animal health products, were as follows:

| | | | | | | | | | | | | | | | | |

| ($ in millions) | 2024 | | 2023 | | 2022 |

| Total Sales | $ | 64,168 | | | $ | 60,115 | | | $ | 59,283 | |

| Pharmaceutical | 57,400 | | | 53,583 | | | 52,005 | |

| Keytruda | 29,482 | | | 25,011 | | | 20,937 | |

Gardasil/Gardasil 9 | 8,583 | | | 8,886 | | | 6,897 | |

ProQuad/M-M-R II/Varivax | 2,485 | | | 2,368 | | | 2,241 | |

| Januvia/Janumet | 2,268 | | | 3,366 | | | 4,513 | |

| Bridion | 1,764 | | | 1,842 | | | 1,685 | |

Alliance revenue - Lynparza(1) | 1,311 | | | 1,199 | | | 1,116 | |

Alliance revenue - Lenvima(1) | 1,010 | | | 960 | | | 876 | |

| Lagevrio | 964 | | | 1,428 | | | 5,684 | |

| Vaxneuvance | 808 | | | 665 | | | 170 | |

| Prevymis | 785 | | | 605 | | | 428 | |

| RotaTeq | 711 | | | 769 | | | 783 | |

| Animal Health | 5,877 | | | 5,625 | | | 5,550 | |

| Livestock | 3,462 | | | 3,337 | | | 3,300 | |

| Companion Animal | 2,415 | | | 2,288 | | | 2,250 | |

Other Revenues(2) | 891 | | | 907 | | | 1,728 | |

(1)Alliance revenue represents Merck’s share of profits, which are product sales net of cost of sales and commercialization costs.

(2)Other revenues are primarily comprised of miscellaneous corporate revenues, including revenue hedging activities, as well as revenue from third-party manufacturing arrangements.

Pharmaceutical

The Pharmaceutical segment includes human health pharmaceutical and vaccine products. Human health pharmaceutical products consist of therapeutic and preventive agents, generally sold by prescription, for the treatment of human disorders. Human health vaccine products consist of preventive pediatric, adolescent and adult vaccines. Certain of the products within the Company’s franchises are as follows:

Oncology

Keytruda is an anti-PD-1 (programmed death receptor-1) therapy that has been approved as monotherapy for the treatment of certain patients with cervical cancer, classical Hodgkin lymphoma (cHL), cutaneous squamous cell carcinoma, esophageal or gastroesophageal junction (GEJ) carcinoma, head and neck squamous cell carcinoma (HNSCC), hepatocellular carcinoma (HCC), melanoma, Merkel cell carcinoma, microsatellite instability-high (MSI-H) or mismatch repair deficient (dMMR) solid tumors (including MSI-H/dMMR colorectal cancer and endometrial carcinoma), non-small-cell lung cancer (NSCLC), primary mediastinal large B-cell lymphoma (PMBCL), tumor mutational burden-high (TMB-H) solid tumors, and urothelial cancer including non-muscle invasive bladder cancer. Keytruda is also approved as monotherapy for the adjuvant treatment of certain patients with melanoma, and for certain patients with renal cell carcinoma (RCC) post-surgery. Keytruda is approved for adjuvant treatment following resection and platinum-based chemotherapy for certain patients with NSCLC. Additionally, Keytruda is approved for patients with certain types of resectable NSCLC in combination with chemotherapy as neoadjuvant treatment, and then continued as a single agent as adjuvant treatment after surgery. Keytruda is also approved for certain patients with high-risk early stage triple-negative breast cancer (TNBC) in combination with chemotherapy as neoadjuvant treatment, and then continued as a single agent as adjuvant treatment after surgery. In addition, Keytruda is approved in combination with chemotherapy for the treatment of certain patients with advanced NSCLC, advanced malignant pleural mesothelioma, HNSCC, advanced biliary tract cancer, advanced esophageal cancer, advanced TNBC, and advanced or recurrent endometrial carcinoma; in combination with chemotherapy with or without bevacizumab, and in combination with chemoradiotherapy, for the treatment of certain patients with advanced cervical cancer; in combination with trastuzumab and chemotherapy for the treatment of certain patients with advanced human epidermal growth factor receptor 2 (HER2)-positive gastric or GEJ adenocarcinoma with programmed death-ligand 1 (PD-L1) (CPS ≥1), and in combination with chemotherapy for the treatment of certain patients with advanced HER2-negative gastric or GEJ adenocarcinoma; in combination with axitinib for the treatment of certain patients with advanced RCC; in combination with Lenvima (lenvatinib) for the treatment of certain patients with advanced RCC or advanced endometrial carcinoma; and in combination with enfortumab vedotin for certain patients with locally advanced or metastatic urothelial cancer. Welireg (belzutifan) is a medication for the treatment of adult patients with certain von Hippel-Lindau (VHL) disease-associated tumors not requiring immediate surgery, and for the treatment of adult patients with advanced RCC following a PD-1 or PD-L1 inhibitor and a vascular endothelial growth factor tyrosine kinase inhibitor. In addition, the Company recognizes alliance revenue related to sales of Lynparza (olaparib), an oral poly (ADP-ribose) polymerase (PARP) inhibitor, for certain types of advanced or recurrent ovarian, early or metastatic breast, metastatic pancreatic, and metastatic castration-resistant prostate cancers; alliance revenue related to sales of Lenvima, an oral receptor tyrosine kinase inhibitor, for certain types of thyroid cancer, RCC, HCC, in combination with everolimus for certain patients with advanced RCC, and in combination with Keytruda for certain patients with advanced endometrial carcinoma or advanced RCC; and alliance revenue related to Reblozyl (luspatercept-aamt) for the treatment of certain types of anemia.

Vaccines

Gardasil (Human Papillomavirus Quadrivalent [Types 6, 11, 16 and 18] Vaccine, Recombinant)/Gardasil 9 (Human Papillomavirus 9-valent Vaccine, Recombinant), vaccines to help prevent certain cancers and diseases caused by certain types of human papillomavirus (HPV); ProQuad (Measles, Mumps, Rubella and Varicella Virus Vaccine Live), a pediatric combination vaccine to help protect against measles, mumps, rubella and varicella; M−M−R II (Measles, Mumps and Rubella Virus Vaccine Live), a vaccine to help prevent measles, mumps and rubella; Varivax (Varicella Virus Vaccine Live), a vaccine to help prevent chickenpox (varicella); Vaxneuvance (Pneumococcal 15-valent Conjugate Vaccine), a vaccine to help prevent invasive pneumococcal disease in individuals 6 weeks of age and older; RotaTeq (Rotavirus Vaccine, Live Oral, Pentavalent), a vaccine to help protect against rotavirus gastroenteritis in infants and children; and Pneumovax 23 (pneumococcal vaccine polyvalent), a vaccine to help prevent pneumococcal disease.

Hospital Acute Care

Bridion (sugammadex), a medication for the reversal of two types of neuromuscular blocking agents used during surgery; Prevymis (letermovir) for the prophylaxis of cytomegalovirus (CMV) infection and disease, or of CMV disease, in certain high risk adult and pediatric recipients of an allogeneic hematopoietic stem cell transplant or of a kidney transplant, respectively; Dificid (fidaxomicin) for the treatment of C. difficile-associated diarrhea; Zerbaxa (ceftolozane and tazobactam) for injection, a combination antibacterial and beta-lactamase inhibitor for the treatment of certain bacterial infections; and Noxafil (posaconazole), an antifungal agent for the prevention of certain invasive fungal infections.

Cardiovascular

Winrevair (sotatercept-csrk), an activin signaling inhibitor indicated for the treatment of adults with pulmonary arterial hypertension (PAH) (World Health Organization [WHO] Group 1) to increase exercise capacity,

improve WHO functional class and reduce the risk of clinical worsening events; Adempas (riociguat), a cardiovascular drug for the treatment of chronic thromboembolic pulmonary hypertension or pulmonary arterial hypertension in certain patients; and Verquvo (vericiguat), a medicine to reduce the risk of cardiovascular death and heart failure hospitalization following a hospitalization for heart failure or need for outpatient intravenous diuretics in certain adults with symptomatic chronic heart failure and reduced ejection fraction.

Virology

Lagevrio (molnupiravir), an investigational oral antiviral COVID-19 medicine available in the U.S. under Emergency Use Authorization (EUA); Isentress/Isentress HD (raltegravir), an HIV integrase inhibitor for use in combination with other antiretroviral agents for the treatment of HIV-1 infection; Delstrigo (doravirine/lamivudine/tenofovir disoproxil fumarate), a complete regimen for the treatment of HIV-1 infection in adult patients with no prior antiretroviral treatment history or to replace the current antiretroviral regime in certain patients who are virologically suppressed on a stable antiretroviral regimen; and Pifeltro (doravirine), a non-nucleoside reverse transcriptase inhibitor for use in combination with other antiretroviral agents for the treatment of HIV-1 infection in adult patients with no prior antiretroviral treatment history or to replace the current antiretroviral regime in certain patients who are virologically suppressed on a stable antiretroviral regimen.

Neuroscience

Belsomra (suvorexant), an orexin receptor antagonist, indicated for the treatment of insomnia, characterized by difficulties with sleep onset and/or sleep maintenance.

Diabetes

Januvia (sitagliptin) and Janumet (sitagliptin/metformin HCl) for the treatment of type 2 diabetes.

Animal Health

The Animal Health segment discovers, develops, manufactures and markets a wide range of veterinary pharmaceuticals, vaccines and health management solutions and services, as well as an extensive suite of digitally connected identification, traceability and monitoring products. Principal products in this segment include:

Livestock Products

Nuflor (Florfenicol) antibiotic range for use in cattle and swine; Bovilis/Vista vaccine lines for infectious diseases in cattle, including Bovilis Cryptium for protection against Cryptosporidium parvum; Banamine (Flunixin meglumine) bovine and swine anti-inflammatory; Estrumate (cloprostenol sodium) for the treatment of fertility disorders in cattle; Matrix (altrenogest) fertility management for swine; Resflor (florfenicol and flunixin meglumine), a combination broad-spectrum antibiotic and non-steroidal anti-inflammatory drug for bovine respiratory disease; Zuprevo (tildipirosin) for bovine respiratory disease; Revalor (trenbolone acetate and estradiol) to improve production efficiencies in beef cattle; Safe-Guard (fenbendazole) de-wormer for cattle; M+Pac (Mycoplasma Hyopneumoniae Bacterin) swine pneumonia vaccine; Porcilis (Lawsonia intracellularis baterin) and Circumvent (Porcine Circovirus Vaccine, Type 2, Killed Baculovirus Vector) vaccine lines for infectious diseases in swine; Nobilis/Innovax (Live Marek’s Disease Vector), vaccine lines for poultry; Paracox and Coccivac coccidiosis vaccines; Exzolt, a systemic treatment for poultry red mite infestations; Slice (emamectin benzoate) parasiticide and Imvixa (lufenuron) for sea lice control in salmon; Clynav vaccine for protection against pancreas disease in salmon; Aquavac (Avirulent Live Culture)/Norvax vaccines against bacterial and viral disease in fish; Aquaflor (florfenicol) antibiotic for farm-raised fish; Flexolt (fluralaner) against lice in sheep; and Allflex Livestock Intelligence solutions for animal identification, monitoring and traceability.

Companion Animal Products

Bravecto, a line of oral, topical and injectable parasitic control products, including the original Bravecto (fluralaner) products for dogs and cats that last up to 12 weeks; Bravecto (fluralaner) One-Month, a monthly product for dogs, Bravecto (fluralaner) Injectable/Quantum, an injectable product for dogs that lasts up to one-year, and Bravecto Plus (fluralaner/moxidectin), a two-month product for cats; Sentinel, a line of oral parasitic products for dogs including Sentinel Spectrum (milbemycin oxime, lufenuron, and praziquantel) and Sentinel Flavor Tabs (milbemycin oxime, lufenuron); Optimmune (cyclosporine), an ophthalmic ointment; Nobivac vaccine lines for flexible dog and cat vaccination, including Nobivac NXT for canine flu and feline leukemia virus; GilvetMab, an immune checkpoint inhibitor monoclonal antibody conditionally licensed for melanoma and mastocytoma tumors; Otomax (gentamicin sulfate, USP; Betamethasone valerate USP; and Clotrimazole USP ointment)/Mometamax (gentamicin sulfate, USP, Mometasone Furoate Monohydrate and Clotrimazole, USP, Otic Suspension)/Mometamax Ultra (gentamicin sulfate, mometasone furoate monohydrate and posaconazole suspension)/Posatex (orbifloxacin, mometasone furoate monohydrate and posaconazole, suspension) ear ointments for acute and chronic otitis; Caninsulin/Vetsulin (porcine insulin zinc suspension) diabetes mellitus treatment for dogs and cats; Panacur (fenbendazole)/Safeguard (fenbendazole) broad-spectrum anthelmintic (de-wormer) for use in many animals; Regumate (altrenogest) fertility management for horses; Prestige vaccine line for horses; Scalibor (Deltamethrin)/Exspot for protecting against bites

from fleas, ticks, mosquitoes and sandflies; and Sure Petcare products for companion animal identification and well-being, including the microchip and pet recovery system Home Again.

For a further discussion of sales of the Company’s products, see Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” below.

Product Approvals

Set forth below is a summary of significant product approvals received by the Company in 2024 and, to date, in 2025.

| | | | | | | | |

| Product | Date | Approval |

| Keytruda | January 2024 | U.S. Food and Drug Administration (FDA) approval in combination with chemoradiotherapy for the treatment of patients with FIGO (International Federation of Gynecology and Obstetrics) 2014 Stage III-IVA cervical cancer, based on the KEYNOTE-A18 trial. |

| January 2024 | FDA full approval for the treatment of patients with HCC secondary to hepatitis B who have received prior systemic therapy other than a PD-1/PD-L1 containing regimen. The conversion from an accelerated to full (regular) approval is based on the KEYNOTE-394 trial. |

| February 2024 | China’s National Medical Products Administration (NMPA) approval in combination with gemcitabine and cisplatin for the first-line treatment of patients with locally advanced or metastatic biliary tract carcinoma, based on the KEYNOTE-966 trial. |

| March 2024 | European Commission (EC) approval in combination with platinum-containing chemotherapy as neoadjuvant treatment, and then continued as monotherapy as adjuvant treatment, for resectable NSCLC at high risk of recurrence in adults, based on the KEYNOTE-671 trial. |

| May 2024 | Japan’s Ministry of Health, Labor and Welfare (MHLW) approval in combination with fluoropyrimidine and platinum-containing chemotherapy for the first-line treatment of patients with locally advanced unresectable or metastatic gastric or GEJ adenocarcinoma, based on the KEYNOTE-859 trial. |

| May 2024 | Japan’s MHLW approval in combination with standard of care chemotherapy (gemcitabine and cisplatin) for the treatment of patients with locally advanced unresectable or metastatic biliary tract cancer, based on the KEYNOTE-966 trial. |

| June 2024 | FDA approval in combination with carboplatin and paclitaxel, followed by Keytruda as a single agent, for the treatment of adult patients with primary advanced or recurrent endometrial carcinoma, based on the KEYNOTE-868 trial. |

| June 2024 | China’s NMPA approval in combination with trastuzumab, fluoropyrimidine and platinum-containing chemotherapy for the first-line treatment of patients with locally advanced unresectable or metastatic HER2 positive gastric or GEJ adenocarcinoma whose tumors express PD-L1 as determined by a fully validated test, based on the KEYNOTE-811 trial. |

| September 2024 | EC approval in combination with Padcev (enfortumab vedotin-ejfv), an antibody-drug conjugate, for the first-line treatment of unresectable or metastatic urothelial carcinoma in adults, based on the KEYNOTE-A39 trial that was conducted in collaboration with Seagen (now Pfizer Inc.) and Astellas. |

| September 2024 | FDA approval in combination with pemetrexed and platinum chemotherapy for the first-line treatment of adult patients with unresectable advanced or metastatic malignant pleural mesothelioma, based on the IND.227/KEYNOTE-483 trial. |

| September 2024 | Japan’s MHLW approval in combination with chemotherapy as a neoadjuvant treatment, then continued as monotherapy as an adjuvant treatment for patients with NSCLC, based on the KEYNOTE-671 trial. |

| | | | | | | | |

| Keytruda | September 2024 | Japan’s MHLW approval in combination with Padcev for the first-line treatment of patients with radically unresectable urothelial carcinoma, based on the KEYNOTE-A39 trial. |

| September 2024 | Japan’s MHLW approval as monotherapy in patients with radically unresectable urothelial carcinoma who are not eligible for any platinum-containing chemotherapy, based on the KEYNOTE-052 trial. |

| September 2024 | China’s NMPA approval for the first-line treatment of adult patients with unresectable or metastatic melanoma, and conversion from conditional to full approval for the second-line treatment of adult patients with unresectable or metastatic melanoma following failure of one prior line of therapy, based on the LEAP-003 trial. |

| October 2024 | EC approval in combination with chemoradiotherapy for the treatment of FIGO 2014 Stage III-IVA locally advanced cervical cancer in adults who have not received prior definitive therapy, based on the KEYNOTE-A18 trial. |

| October 2024 | EC approval in combination with carboplatin and paclitaxel followed by Keytruda as a single agent for the first-line treatment of primary advanced or recurrent endometrial carcinoma in adults who are candidates for systemic therapy, based on the KEYNOTE-868 trial. |

| November 2024 | Japan’s MHLW approval in combination with chemoradiotherapy as treatment for patients with locally advanced cervical cancer, based on the KEYNOTE-A18 trial. |

| December 2024 | Japan’s MHLW approval in combination with carboplatin and paclitaxel as treatment for adult patients with advanced or recurrent endometrial carcinoma, based on the KEYNOTE-868 trial. |

| December 2024 | China’s NMPA approval in combination with platinum-containing chemotherapy as neoadjuvant treatment and then continued as monotherapy as adjuvant treatment after surgery for patients with resectable stage II, IIIA, or IIIB NSCLC, based on the KEYNOTE-671 trial. |

| December 2024 | China’s NMPA approval in combination with chemoradiotherapy for the treatment of patients with FIGO 2014 Stage III-IVA cervical cancer, based on the KEYNOTE-A18 trial. |

| January 2025 | China’s NMPA approval in combination with Padcev for adult patients with locally advanced or metastatic urothelial cancer, based on the KEYNOTE-A39 trial. |

| Bravecto | January 2024 | EC approval of injectable formulation for dogs for the persistent killing of fleas and ticks for 12 months after treatment. |

| Capvaxive | June 2024 | FDA approval for the prevention of invasive pneumococcal disease and pneumococcal pneumonia caused by certain serotypes in individuals 18 years of age and older. |

| Gardasil | January 2025 | China’s NMPA approval for use in males 9-26 years of age to help prevent certain HPV-related cancers and diseases. |

Lynparza(1) | January 2025 | China’s NMPA approval for the adjuvant treatment of adult patients with deleterious or suspected deleterious germline BRCA-mutated, HER2-negative high-risk early breast cancer who have been previously treated with neoadjuvant or adjuvant chemotherapy, based on the OlympiA trial. |

| | | | | | | | |

| Welireg | November 2024 | China’s NMPA approval for the treatment of adult patients with VHL disease who require therapy for associated RCC, central nervous system hemangioblastomas or pancreatic neuroendocrine tumors. |

| February 2025 | EC conditional approval as monotherapy both for the treatment of adult patients with VHL disease who require therapy for associated, localized RCC, central nervous system hemangioblastomas, or pancreatic neuroendocrine tumors, and for whom localized procedures are unsuitable, and for the treatment of adult patients with advanced clear cell RCC that progressed following two or more lines of therapy that included a PD-1 or PD-L1 inhibitor and at least two VEGF targeted therapies. The EC approval of these two indications is based on results from the LITESPARK-004 and LITESPARK-005 trials. |

| Winrevair | March 2024 | FDA approval for the treatment of adults with PAH (WHO Group 1) to increase exercise capacity, improve WHO functional class (FC), and reduce the risk of clinical worsening events. |

| August 2024 | EC approval in combination with other PAH therapies, for the treatment of PAH in adult patients with WHO FC II to III, to improve exercise capacity. |

(1) Being jointly developed and commercialized in a worldwide collaboration with AstraZeneca.

Competition and the Health Care Environment

Competition

The markets in which the Company conducts its business and the pharmaceutical industry in general are highly competitive and highly regulated. The Company’s competitors include other worldwide research-based pharmaceutical companies, smaller research companies with more limited therapeutic focus, generic drug manufacturers, and animal health care companies. The Company’s operations may be adversely affected by generic and biosimilar competition as the Company’s products mature, as well as technological advances of competitors, industry consolidation, patents granted to competitors, competitive combination products, new products of competitors, the generic availability of competitors’ branded products, and new information from clinical trials of marketed products or post-marketing surveillance. In addition, patent rights are increasingly being challenged by competitors, and the outcome can be highly uncertain. An adverse result in a patent dispute can preclude commercialization of products or negatively affect sales of existing products and could result in the payment of royalties or in the recognition of an impairment charge with respect to intangible assets associated with certain products.

Pharmaceutical competition involves a rigorous search for technological innovations and the ability to market these innovations effectively. With its long-standing emphasis on research and development, the Company is well-positioned to compete in the search for technological innovations. The Company is active in acquiring and marketing products through external alliances, such as licensing arrangements and collaborations, and has been refining its sales and marketing efforts to address changing industry conditions. However, the introduction of new products and processes by competitors may result in price reductions and product displacements, even for products protected by patents. For example, the number of compounds available to treat a particular disease typically increases over time and can result in slowed sales growth or reduced sales of the Company’s products in that therapeutic category.

The highly competitive animal health business is affected by several factors including regulatory and legislative issues, scientific and technological advances, product innovation, the quality and price of the Company’s products as well as competitors’ products, effective promotional efforts and the frequent introduction of generic products by competitors.

Health Care Environment and Government Regulation

Global efforts toward health care cost containment continue to exert pressure on product pricing and market access. Changes to the U.S. health care system as part of health care reform, as well as increased purchasing power of entities that negotiate on behalf of Medicare, Medicaid, and private sector beneficiaries, have contributed to pricing pressure. In several international markets, government-mandated pricing actions have reduced prices of generic and patented drugs. In addition, the Company’s sales performance in 2024 was negatively affected by other cost-reduction measures taken by governments and other third parties to lower health care costs. In the U.S., the Executive Branch and Congress continue to discuss legislation designed to control health care costs, including the cost of drugs. The Company anticipates all of these actions and additional actions in the future will continue to negatively affect sales and profits.

In addressing global cost containment pressures, the Company engages in public policy advocacy with policymakers and continues to work to demonstrate that its medicines provide value to patients and to those who pay for health care. The Company advocates with government policymakers to encourage a long-term approach to sustainable health care financing that ensures access to innovative medicines and does not disproportionately target pharmaceuticals as a source of budget savings. In markets with historically low rates of health care spending, the Company encourages those governments to increase their investments and adopt market reforms in order to improve their citizens’ access to appropriate health care, including medicines.

Operating conditions have become more challenging under the global pressures of competition, industry regulation and cost containment efforts. Although no one can predict the effect of these and other factors on the Company’s business, the Company continually takes measures to evaluate, adapt and improve the organization and its business practices to better meet customer needs and believes that it is well-positioned to respond to the evolving health care environment and market forces.

United States

The Company faces increasing pricing pressure from managed care organizations, government agencies and programs that could negatively affect the Company’s sales and profit margins, including, through (i) practices of managed care organizations, federal and state exchanges, and institutional and governmental purchasers, and (ii) federal laws and regulations related to Medicare and Medicaid, including the Medicare Prescription Drug, Improvement, and Modernization Act of 2003, the Patient Protection and Affordable Care Act of 2010 (ACA), the American Rescue Plan Act of 2021 (American Rescue Plan Act), and the Inflation Reduction Act of 2022 (IRA). Additionally, increased utilization of the 340B Federal Drug Discount Program and restrictions on the Company’s ability to identify inappropriate discounts are having a negative impact on Company performance.

In the U.S., federal and state governments for many years have pursued methods to reduce the cost of drugs and vaccines for which they pay. For example, federal and state laws require the Company to pay specified rebates for medicines reimbursed by Medicaid and to provide discounts for medicines purchased by certain state and federal entities such as the Department of Defense, Veterans Affairs, Public Health Service entities and hospitals serving a disproportionate share of low income or uninsured patients.

Additionally in the U.S., consolidation and integration among health care entities is a major factor in the competitive marketplace for pharmaceutical products. Health plans and pharmacy benefit managers have been consolidating into fewer, larger entities, thus enhancing their purchasing strength and importance. Private third-party insurers, as well as governments, employ formularies to control costs by negotiating discounted prices in exchange for formulary inclusion. Failure to obtain timely or adequate pricing or formulary placement for Merck’s products or obtaining such placement at unfavorable pricing could adversely affect revenue. In addition to formulary tier co-pay differentials, private health insurance companies and self-insured employers have been increasing the cost-sharing required from beneficiaries, particularly for branded pharmaceuticals and biotechnology products. Private health insurance companies, as well as governments, also are increasingly imposing utilization management tools, such as clinical protocols, requiring prior authorization for a branded product or requiring the patient to first fail on one or more generic products before permitting access to a branded medicine. These same management tools are also used in treatment areas in which the payor has taken the position that multiple branded products are therapeutically comparable. As the U.S. payor market concentrates further, the Company may face greater pricing pressure from private third-party payors.

Legislative Changes

In 2022, Congress passed the IRA, which makes significant changes to how drugs are covered and paid for under the Medicare program, including the creation of financial penalties for drugs whose prices rise faster than the rate of inflation, redesign of the Medicare Part D program to require manufacturers to bear more of the liability for certain drug benefits, which has taken effect in 2025, and government price setting for certain Medicare Part D drugs, starting in 2026, and Medicare Part B drugs starting in 2028. Government price setting may also impact pricing in the private market negatively affecting the Company’s performance. In August 2023, the U.S. Department of Health and Human Services (HHS), through the Centers for Medicare & Medicaid Services (CMS), selected Januvia for the first year of the IRA’s “Drug Price Negotiation Program” (Program). Pursuant to the IRA’s Program, a government price was set for Januvia, which will become effective on January 1, 2026. In January 2025, HHS announced that Janumet and Janumet XR have been selected for government price setting, which will become effective on January 1, 2027. In addition, the Company expects that Keytruda will be selected in 2026 for government price setting, which would become effective on January 1, 2028 and the Company expects that, as a result, U.S. sales of Keytruda will decline after that time. The Company has sued the U.S. government regarding the IRA’s Program (see Item 8 “Financial Statements and Supplementary Data,” Note 10. “Contingencies and Environmental Liabilities” below). Furthermore,

the Executive Branch and Congress continue to discuss legislation designed to control health care costs, including the cost of drugs.

The long-term implications of the IRA remain uncertain and subject to various factors, including the manner in which HHS decides to implement the statute. Many experts and analysts, both within the industry and outside, have predicted that the law will harm innovation in the pharmaceutical industry and result in fewer new treatments being developed and approved over time. Merck is working to mitigate the potentially harmful effects that the law could have, which could include a detrimental impact on innovation.

In addition, in 2021, Congress passed the American Rescue Plan Act, which included a provision that eliminates the statutory cap on rebates drug manufacturers pay to Medicaid beginning in January 2024. These rebates act as a discount off the list price and eliminating the cap means that manufacturer discounts paid to Medicaid can increase. Prior to this change, manufacturers have not been required to pay more than 100% of the Average Manufacturer Price (AMP) in rebates to state Medicaid programs for Medicaid-covered drugs. As a result of this provision, manufacturers may have to pay state Medicaid programs more in rebates than they received on sales of particular products. This change presents a risk to Merck for drugs that have high Medicaid utilization and rebate exposure that is more than 100% of the AMP.

The Company also faces increasing pricing pressure in the states, which are looking to exert greater influence over the price of prescription drugs. A number of states have passed pharmaceutical price and cost transparency laws. These laws typically require manufacturers to report certain product price information or other financial data to the state. Some laws also require manufacturers to provide advance notification of price increases. The Company expects that states will continue their focus on pharmaceutical pricing and will increasingly shift to more aggressive price control tools such as Prescription Drug Affordability Boards that have the authority to conduct affordability reviews and establish upper payment limits and that Company products may be selected for such reviews. In addition, in 2024, the FDA authorized, for a two-year period, Florida’s application to import prescription drugs from Canada.

Regulatory Changes

The pharmaceutical industry also could be considered a potential source of savings via other legislative and administrative proposals that have been debated but not enacted. These types of revenue generating or cost saving proposals include additional direct price controls.

European Union

Efforts toward health care cost containment remain intense in the European Union (EU). The Company faces competitive pricing pressure resulting from generic and biosimilar drugs. In addition, a majority of countries in the EU attempt to contain drug costs by engaging in reference pricing in which authorities examine pre-determined markets for published prices of drugs. Reference pricing may either compare a product’s prices in other markets (external reference pricing), or compare a product’s price with those of other products in a national class (internal reference pricing). The authorities then use the price data to set new local prices for brand-name drugs, including the Company’s drugs. Reference pricing mechanisms are usually set at the national level and can be changed pursuant to local regulations or guidance.

Some EU Member States have established free-pricing systems, but regulate the pricing for drugs through profit control plans. Others seek to negotiate or set prices based on the cost-effectiveness of a product or an assessment of whether it offers a therapeutic benefit over other products in the relevant class.

The downward pressure on health care costs in general, particularly prescription drugs, has become intense. As a result, increasingly high barriers are being erected to the entry of new products. In some EU Member States, cross-border imports from low-priced markets also exert competitive pressure that may reduce pricing within an EU Member State.

Additionally, EU Member States have the power to restrict the range of pharmaceutical products for which their national health insurance systems provide reimbursement. In the EU, pricing and reimbursement plans vary widely from Member State to Member State. Some EU Member States provide that drug products may be marketed only after a reimbursement price has been agreed. Some EU Member States may require the completion of additional studies that compare the cost-effectiveness of a particular product candidate to already available therapies or a so-called health technology assessment (HTA), in order to obtain reimbursement or pricing approval. The HTA of pharmaceutical products is becoming an increasingly common part of the pricing and reimbursement procedures in most EU Member States. The HTA process, which is currently governed by the national laws of these countries, involves the assessment of the cost-effectiveness, public health impact, therapeutic impact and/or the economic and social impact of use of a given pharmaceutical product in the national health care system of the individual country in

which it is conducted. Ultimately, an HTA measures the added value of a new health technology compared to existing ones.

The EU Health Technology Assessment Regulation 2021/2282 (HTAR) applies in 2025. This provides for the conduct of an EU level comparative Joint Clinical Assessment (JCA) of a new product versus relevant comparators identified by the EU Member States. JCAs will be carried out in parallel with the review of a marketing authorization application, so that a JCA report is available shortly after the product is authorized. The HTAR applies to all new active substance oncology products and advanced therapy medicinal products, including cell and gene therapies, beginning January 1, 2025; to new active substance orphan medicinal products beginning January 1, 2028; and to all products approved via the centralized procedure beginning in 2030.

EU Member States remain responsible for pricing and reimbursement decisions but must take “due consideration” of JCA reports when making national market access decisions. This means that EU Member State pricing and reimbursement processes are likely to evolve and more EU Member States may use HTAs as part of their decision-making.

The outcome of HTAs regarding specific pharmaceutical products will increasingly influence the pricing and reimbursement status granted to these pharmaceutical products by the market access authorities of individual EU Member States. A negative HTA of one of the Company’s products may mean that the product is not reimbursable or may force the Company to reduce its reimbursement price or offer discounts or rebates.

A negative HTA by a leading and recognized HTA body could also undermine the Company’s ability to obtain reimbursement for the relevant product outside a jurisdiction. For example, EU Member States that have not yet developed HTA mechanisms may rely to some extent on JCAs under the HTAR or an HTA performed in other countries with a developed HTA framework, to inform their pricing and reimbursement decisions. HTA procedures require additional data, reviews and administrative processes, all of which increase the complexity, timing and costs of obtaining product reimbursement and exert downward pressure on available reimbursement.

To obtain reimbursement or pricing approval in some EU Member States, the Company may be required to conduct studies that compare the cost-effectiveness of the Company’s product candidates to other therapies that are considered the local standard of care. There can be no assurance that any EU Member State will allow favorable pricing, reimbursement and market access conditions for any of the Company’s products, or that it will be feasible to conduct additional cost-effectiveness studies, if required.

Japan

In Japan, the pharmaceutical industry is subject to government-mandated annual price reductions of pharmaceutical products and certain vaccines. Furthermore, the government can order re-pricings for specific products if it determines that use of such product will exceed certain thresholds defined under applicable re-pricing rules. In addition, if a Merck product has the same medical action or composition of another product that is subject to market expansion re-pricing, the Merck product could also be subject to re-pricing unless it meets exception criteria. The next government-mandated price reduction is scheduled to occur in April 2025.

China

The Company’s business in China has grown in the past few years, and the importance of China to the Company’s overall pharmaceutical and vaccines business has increased accordingly. Continued growth of the Company’s business in China is dependent upon ongoing development of a favorable environment for innovative pharmaceutical products and vaccines, sustained access for the Company’s currently marketed products, and the absence of trade impediments or adverse pricing controls. In recent years, the Chinese government has introduced and implemented a number of structural reforms to accelerate the shift to innovative products and reduce costs. There have been multiple new policies introduced by the government to improve access to new innovation, reduce the complexity of regulatory filings, and accelerate the review and approval process. This has led to a significant increase in the number of new products being approved each year. While the mechanism for drugs being added to the government’s National Reimbursement Drug List (NRDL) evolves, inclusion may require a price negotiation which could impact the outlook in the market for selected brands. A new NRDL was recently completed in which new entries averaged 63% price reductions. While pricing pressure has always existed in China, health care reform has increased this pressure in part due to the acceleration of generic substitution through volume-based procurement (VBP). In 2019, the government implemented the VBP program through a tendering process for mature products which have generic substitutes with a Generic Quality Consistency Evaluation approval. Mature products that have entered into the last five rounds of VBP had, on average, a price reduction of more than 50%. The Company expects VBP to be a semi-annual process that will have a significant impact on mature products moving forward.

Emerging Markets

The Company’s focus on emerging markets, in addition to China, has continued. Governments in many emerging markets are also focused on constraining health care costs and have enacted price controls and measures impacting intellectual property, including in exceptional cases, threats of compulsory licenses, that aim to put pressure on the price of innovative pharmaceuticals or result in constrained market access to innovative medicine. The Company anticipates that pricing pressures and market access challenges will continue in the future to varying degrees in the emerging markets.

Beyond pricing and market access challenges, other conditions in emerging market countries can affect the Company’s efforts to continue to grow in these markets, including potential political instability, changes in trade sanctions and embargoes, significant currency fluctuation and controls, financial crises, limited or changing availability of funding for health care, credit worthiness of health care partners, such as hospitals, and other developments that may adversely impact the business environment for the Company. Further, the Company may engage third-party agents to assist in operating in emerging market countries, which may affect its ability to realize continued growth and may also increase the Company’s risk exposure.

Regulation

The pharmaceutical industry is also subject to regulation by regional, country, state and local agencies around the world focused on standards and processes for determining drug safety and effectiveness, as well as conditions for sale or reimbursement.

Of particular importance is the FDA in the U.S., which administers requirements covering the testing, approval, safety, effectiveness, manufacturing, labeling, and marketing of prescription pharmaceuticals. In some cases, the FDA requirements and practices have increased the amount of time and resources necessary to develop new products and bring them to market in the U.S. At the same time, the FDA has committed to expediting the development and review of products bearing the “breakthrough therapy” designation, which has accelerated the regulatory review process for medicines with this designation. The FDA has also undertaken efforts to bring generic competition to market more efficiently and in a more timely manner.

The EU has adopted directives and other legislation concerning the classification, approval for marketing, labeling, advertising, manufacturing, wholesale distribution, integrity of the supply chain, pharmacovigilance and safety monitoring of medicinal products for human use. These provide mandatory standards throughout the EU, which may be supplemented or implemented with additional regulations by the EU Member States. In particular, EU regulators may approve products subject to a number of post-authorization conditions. Examples of typical post-authorization commitments include additional pharmacovigilance, the conduct of clinical trials, the establishment of patient registries, physician or patient education and controlled distribution and prescribing arrangements. Non-compliance with post-authorization conditions, pharmacovigilance and other obligations can lead to regulatory action, including the variation, suspension or withdrawal of the marketing authorizations, or other enforcement or regulatory actions, including the imposition of financial penalties. The Company’s policies and procedures are already consistent with the substance of these directives; consequently, it is believed that they will not have any material effect on the Company’s business.

The Company believes that it will continue to be able to conduct its operations, including launching new drugs, in this regulatory environment. (See “Research and Development” below for a discussion of the regulatory approval process.)

Access to Medicines

As a global health care company, Merck’s primary role is to discover and develop innovative medicines and vaccines. The Company also recognizes that, in collaboration with key stakeholders, it has a role to play in helping to ensure that its science advances health care, and its products are accessible and affordable globally. The Company is committed to ensuring a high-quality, safe, reliable, supply of its medicines and vaccines, and to implementing innovative solutions that address barriers to sustainable access to its products.

Merck’s approach is designed to enable it to serve the greatest number of patients today, while meeting the needs of patients in the future. The Company's wide-ranging efforts to expand access to health encompass a set of principles embedded in its business strategies and operations. These principles guide its global approach to addressing significant public health burdens and unmet medical needs. The Company systematically evaluates its pipeline candidates to assess their potential in low and middle-income countries and underserved health care settings. Throughout the life cycle of its products, Merck seeks to evaluate their potential and adapt to changes in the external environment. Collaborating with various stakeholders, including private, governmental, multilateral, and non-profit organizations, the Company seeks to design and deliver sustainable access solutions at the payer, provider,

and patient levels. Furthermore, the Company incorporates access to health metrics in its scorecard, making it a component of calculating annual incentive pay for the majority of its global employees.

In addition, through social investments, including philanthropic programs and impact investing, Merck is helping to strengthen health systems and build capacity, particularly in communities underserved by health care. The Merck Patient Assistance Program provides certain medicines and adult vaccines for free to people in the U.S. and U.S. territories who do not have prescription drug or health insurance coverage and who, without the Company’s assistance, cannot afford their Merck medicines and vaccines. Globally, Merck has made substantial contributions to access to health through key initiatives, including product donations for humanitarian assistance in low-income countries through the Medical Outreach Program. The Mectizan Donation Program, the longest running disease-specific drug donation program of its kind, supports the elimination of two neglected tropical diseases – onchocerciasis and lymphatic filariasis. Additionally, through Merck for Mothers, the Company provides funding, and scientific and business acumen to help global health partners strengthen health systems, expand access to critical maternal health services, and end preventable deaths from complications of pregnancy and childbirth. Merck also supports the Merck Foundation, an independent grantmaking organization helping to address systemic barriers to access to health care.

Privacy and Data Protection

The Company is subject to a significant number of privacy and data protection laws and regulations globally, many of which place restrictions on the Company’s ability to collect, transfer, access and use personal data across its business. The legislative and regulatory landscape for privacy and data protection continues to evolve. There has been increased attention to privacy and data protection issues in both developed and emerging markets with the potential to affect directly the Company’s business, including the EU General Data Protection Regulation (GDPR), which imposes penalties of up to 4% of global revenue.

The GDPR and related implementing laws in individual EU Member States govern the collection and use of personal health data and other personal data in the EU. The GDPR increased responsibility and liability in relation to personal data that the Company processes. It also imposes a number of strict obligations and restrictions on the ability to process (which includes collection, analysis and transfer of) personal data, including health data from clinical trials and adverse event reporting. The GDPR also includes requirements relating to the consent of the individuals to whom the personal data relates, the information provided to the individuals prior to processing their personal data or personal health data, notification of data processing obligations to the national data protection authorities, and the security and confidentiality of the personal data. Further, the GDPR prohibits the transfer of personal data to countries outside of the EU that are not considered by the EC to provide an adequate level of data protection, including to the U.S., except if the data controller meets very specific requirements. Following the Schrems II decision of the Court of Justice of the EU in 2020, uncertainty has existed as to the permissibility of international data transfers under the GDPR. In light of the implications of this decision, the Company may face difficulties regarding the transfer of personal data from the EU to third countries. Since then, the Company entered into the EU-approved Standard Contractual Clauses with its vendors, suppliers, collaboration partners and clinical trial sites in order to facilitate the lawful transfer of personal data from the EU to the U.S. In addition, former President Biden issued Executive Order 14086 in October 2022 to address the data privacy concerns raised in the Schrems II decision through introducing, among other measures, further safeguards and oversight of personal data collection by U.S. signals intelligence activities and providing individuals with a redress mechanism in the U.S. for their data protection concerns. Further certainty for the international transfer of personal data from the EU via the EU-U.S. Data Privacy Framework (successor to the invalidated EU-U.S. Privacy Shield) came about by way of a new EU Adequacy Decision, issued by the EC in July 2023. However, the new Adequacy Decision has already been contested by privacy advocates and is subject to legal review.

Failure to comply with the requirements of the GDPR and the related national data protection laws of the EU Member States may result in significant monetary fines and other administrative penalties as well as civil liability claims from individuals whose personal data was processed. Data protection authorities from the different EU Member States may still implement certain variations, enforce the GDPR and national data protection laws differently, and introduce additional national regulations and guidelines, which adds to the complexity of processing personal data in the EU. Guidance developed at both the EU level and at the national level in individual EU Member States concerning implementation and compliance practices is often updated or otherwise revised.

There is, moreover, a growing trend towards required public disclosure of clinical trial data in the EU which adds to the complexity of obligations relating to processing health data from clinical trials. Failing to comply with these obligations could lead to government enforcement actions and significant penalties against the Company, harm to its reputation, and adversely impact its business and operating results. The uncertainty regarding the interplay between

different regulatory frameworks further adds to the complexity that the Company faces with regard to data protection regulation.

In 2021, China passed the Personal Information Protection Law (PIPL) that aims to standardize the handling of personal information in China. The PIPL currently applies to the processing of personal information of natural persons in China, the processing of personal information outside China where the purpose is to provide products and services in China, and to analyze the activities of individuals in China. While similar to the GDPR, the PIPL contains unique requirements not found in the GDPR. The Company has developed and implemented comprehensive plans to ensure compliance with the PIPL, including plans relating to data localization and cross-border transfers.

Additional laws and regulations enacted in Canada, Europe, Asia, Latin America, the Middle East and 19 states in the U.S. have increased enforcement and litigation activity in the U.S. and other developed markets, as well as increased regulatory cooperation among privacy authorities globally. The Company has adopted a comprehensive global privacy program to manage these evolving requirements and risks and to facilitate the transfer of personal information across international borders.

Distribution

The Company sells its human health pharmaceutical products primarily to drug wholesalers and retailers, hospitals, government agencies and managed health care providers, such as health maintenance organizations, pharmacy benefit managers and other institutions. Human health vaccines are sold primarily to physicians, wholesalers, distributors and government entities. The Company’s professional representatives communicate the effectiveness, safety and value of the Company’s pharmaceutical and vaccine products to health care professionals in private practice, group practices, hospitals and managed care organizations. The Company sells its animal health products to veterinarians, distributors, animal producers, farmers and pet owners.

Raw Materials

The Company obtains raw materials essential to its business from numerous suppliers worldwide. Most of the principal materials the Company uses in its manufacturing operations are available from more than one source. However, the Company obtains certain raw or intermediate materials primarily from only one source. The Company attempts, if possible, to mitigate the potential risk associated with raw materials, components and supplies through inventory and appropriate supplier management.

Patents, Trademarks and Licenses

Patent protection is considered, in the aggregate, to be of material importance to the Company’s marketing of its products in the U.S. and in most major foreign markets. Patents may not only cover a product per se, but also pharmaceutical formulations of a product, processes for making a product, including intermediates useful in those processes, and methods of treatment or other uses of a product. Patent protection for individual products extends for varying periods in accordance with the legal life of patents in individual countries. The protection afforded, which may also vary from country to country, depends upon the type of patent and its scope of coverage.

Patent portfolios developed for products introduced by the Company normally provide varying degrees of market exclusivity. Key patents, which generally cover the product per se, may be subject to a patent term restoration (also known as patent term extension or PTE) of up to five years in the U.S., Japan, and certain other jurisdictions. In Europe, up to five years of extended term may be available in the form of a Supplementary Protection Certificate (SPC). PTEs and SPCs are awarded to offset a portion of the patent term lost during the clinical testing and regulatory review process of a product prior to approval. The Food and Drug Administration Modernization Act includes a Pediatric Exclusivity Provision that may provide an additional six months of market exclusivity (added to the patent term for all Orange Book-listed patents, and to the regulatory data exclusivity term for small molecule and biologic products) in the U.S. for indications of new or currently marketed drugs if certain agreed upon pediatric studies are completed by the applicant. The EU also provides an additional six months of pediatric market exclusivity attached to a product’s SPC term for both small molecule and biologic products. Japan attaches the additional term for pediatric studies to market exclusivity and this extension is unrelated to patent term. In some countries, one or more regulatory exclusivities, including data exclusivity, may provide parallel market protection that is complementary to patent protection and, in some cases, may provide more effective or longer lasting marketing exclusivity than a product’s patent portfolio. In the U.S., the regulatory data/marketing protection term generally runs five years from first marketing approval of a new chemical entity, extended to seven years for an orphan drug indication, and twelve years from first marketing approval of a biological product.

The table below provides a list of expiration dates, which include any pending PTE and SPC periods where indicated, for the key patent protection in the U.S., the EU, Japan and China for the following marketed products:

| | | | | | | | | | | | | | | | | | | | | | | |

| Product | Year of Expiration (U.S.) | | Year of Expiration (EU)(1) | | Year of Expiration (Japan)(2) | | Year of Expiration (China) |

| Januvia | 2026(3) | | Expired | | 2025-2026 | | Expired |

| Janumet | 2026(3) | | Expired | | N/A | | Expired |

Janumet XR | 2026(3) | | N/A | | N/A | | Expired |

| Isentress | Expired(4) | | Expired | | 2026(5) | | Expired |

Lenvima(6) | 2026 | | 2026(7) | | 2026 | | Expired |

| Bridion | 2026 | | Expired | | Expired | | Expired |

| Bravecto | 2027 | | 2029 | | 2029 | | 2025 |

| Gardasil | 2028 | | Expired | | Expired | | Expired |

Gardasil 9 | 2028 | | 2030(7) | | 2030 | | 2025 |

| Keytruda | 2028(8) | | 2031 | | 2032-2033 | | 2028 |

Lynparza(9) | 2027(7) (with pending PTE) | | 2029(7) | | 2028-2029 | | Expired |

| Winrevair | 2027(10) | | 2026(10) | | N/A | | N/A |

Adempas(11) | N/A(12) | | 2028(7) | | 2027-2028 | | Expired |

| Belsomra | 2029 | | N/A | | 2031 | | N/A |

| Prevymis | 2029 | | 2029(13) | | 2029 | | Expired |

| Vaxneuvance | 2031(14) | | No Patent(15) | | No Patent(15) | | N/A |

| Welireg | 2035 (with pending PTE) | | N/A | | N/A | | N/A |

| Capvaxive | 2038 | | N/A | | N/A | | N/A |

Note: Compound patent unless otherwise noted. Certain of the products listed may be the subject of patent litigation. See Item 8. “Financial Statements and Supplementary Data,” Note 10. “Contingencies and Environmental Liabilities” below.

N/A: Currently no marketing approval.

(1)The EU date represents the expiration date for the following four countries: France, Germany, Italy, and Spain (Major EU Markets). If SPC applications have been filed but have not been granted in all Major EU Markets, both the patent expiry date and the SPC expiry date are listed.

(2)The PTE system in Japan allows for a patent to be extended more than once provided the later approval is directed to a different indication from that of the previous approval. This may result in multiple PTE approvals for a given patent, each with its own expiration date.

(3)As a result of settlement agreements related to a patent directed to the specific sitagliptin salt form of the products, exclusivity will extend through May 2026 for Januvia and Janumet, and through July 2026 for Janumet XR.

(4)Generic entry is not anticipated in 2025.

(5)Expiry date reflects granted PTE for the 600 mg tablet in Japan.

(6)Part of a global strategic oncology collaboration with Eisai Co., Ltd.

(7)Eligible for six months pediatric market exclusivity.

(8)The compound patent family contains two additional patents that expire in 2029 due to patent term adjustment resulting from patent office delay. These patents are based on the initial discovery of the active ingredient in Keytruda. While these patents may provide additional protection, the Company expects that they will be the subject of litigation in the future.

(9)Part of a global strategic oncology collaboration with AstraZeneca.

(10)Eligible for 12 years of data exclusivity in the U.S. and 10 years in the EU, which will expire in 2036 and 2034, respectively. Granted patents covering methods of treating pulmonary arterial hypertension with Winrevair, which will expire in 2037 (absent PTE or SPC), may provide additional exclusivity.

(11)Commercialized under a worldwide collaboration with Bayer AG.

(12)The Company has no marketing rights in the U.S.

(13)Data exclusivity has also been granted in the EU and expires in January 2028; eligible for two additional years of market exclusivity based on pediatric studies for an orphan product.

(14)PTE pending but is not included in the listed patent expiry date. Data exclusivity has been granted in the U.S. and expires in July 2033.

(15)Data exclusivity has been granted in the EU and Japan, and expires in December 2031 and September 2030, respectively.

The Company has the following key U.S. patent protection for drug candidates under review in the U.S. by the FDA:

| | | | | |

| Under Review in the U.S. | Currently Anticipated

Year of Expiration (in the U.S.) |

MK-1022 (patritumab deruxtecan)(1) | 2035 |

| MK-1654 (clesrovimab) | 2036 |

(1) Being developed in a collaboration with Daiichi Sankyo. The FDA issued a Complete Response Letter for the application in June 2024.

The Company also has the following key U.S. patent protection for drug candidates in Phase 3 development:

| | | | | |

| Phase 3 Drug Candidate | Currently Anticipated

Year of Expiration (in the U.S.) |

MK-8591A (doravirine + islatravir)(1) | 2032 |

MK-2400 (ifinatamab deruxtecan)(2) | 2034 |

| MK-1308A (quavonlimab + pembrolizumab) | 2035 |

| MK-1026 (nemtabrutinib) | 2035 |

V940(2) | 2036 |

| MK-3543 (bomedemstat) | 2036 |

| MK-5684 (opevesostat) | 2037 |

MK-8591D (islatravir + lenacapavir)(1)(2) | 2037 (with pending PTE for lenacapavir patent) |

| MK-2140 (zilovertamab vedotin) | 2038 |

MK-4482 Lagevrio(2)(3) | 2038 |

MK-2870 (sacituzumab tirumotecan)(2) | 2040 |

| MK-3475A (pembrolizumab + hyaluronidase subcutaneous) | 2039 |

| MK-0616 (enlicitide decanoate) | 2040 |

| MK-1084 | 2040 |

| MK-7240 (tulisokibart) | 2040 |

MK-3000(4) | 2041 |

(1)On partial clinical hold for higher doses of islatravir than those used in current clinical trials.

(2)Being developed in a collaboration.

(3)Available in the U.S. under Emergency Use Authorization.

(4)Program is in a Phase 2/3 study.

Unless otherwise noted, the patents in the above tables cover the product per se (also known as compound patents). For those drug candidates under review or in development, the key U.S. patents may be subject to a future PTE of up to five years and/or six months of pediatric market exclusivity. In addition, depending on the circumstances surrounding any final regulatory approval of the product, there may be other granted patents or pending patent applications that could have relevance to the product as finally approved.

While the expiration of the compound patent generally results in loss of market exclusivity for the covered pharmaceutical product, other patents may provide additional market exclusivity associated with certain aspects of the product that extends beyond the compound patent expiration, including those derived from the initial discovery of the product’s active ingredient(s) or from product-related innovation that occurs after this initial discovery. These include later-expiring patents directed to (i) processes and intermediates related to methods of manufacture of the active ingredient(s), (ii) use(s) of the product, and (iii) novel compositions and formulations of the product. The effect of product patent expiration on pharmaceutical product sales may also depend upon many other factors such as the nature of the market and the position of the product in it, the growth of the market, the complexities and economics of the process for manufacture of the active ingredient(s) of the product and the requirements of new drug provisions of the Federal Food, Drug and Cosmetic Act or similar laws and regulations in other countries. In addition, in the U.S. and certain other countries, a variety of different regulatory exclusivities that impact market exclusivity may be available under relevant law.

For further information with respect to the Company’s patents, see Item 1A. “Risk Factors” and Item 8. “Financial Statements and Supplementary Data,” Note 10. “Contingencies and Environmental Liabilities” below.

Worldwide, all of the Company’s important products are sold under trademarks that are considered in the aggregate to be of material importance. Trademark protection continues in some countries as long as used; in other countries, as long as registered. Registration is for fixed terms and can be renewed indefinitely.

Royalty income in 2024 on patent and know-how licenses and other rights amounted to $1.1 billion. Merck also incurred royalty expenses amounting to $1.9 billion in 2024 under patent and know-how licenses it holds.

Research and Development

The Company’s business is characterized by the introduction of new products or new uses for existing products through a strong research and development program. At December 31, 2024, approximately 23,500 people were employed in the Company’s research activities. The Company prioritizes its research and development efforts and focuses on candidates that it believes represent breakthrough science for unmet medical needs that will make a difference for patients and payers.

The Company maintains a number of long-term exploratory and fundamental research programs in biology and chemistry as well as research programs directed toward product development. The Company’s research and development model is designed to increase productivity and improve the probability of success by prioritizing the Company’s research and development resources on candidates the Company believes are capable of providing unambiguous, promotable advantages to patients and payers and delivering the maximum value of its approved medicines and vaccines through new indications and new formulations. Merck is pursuing emerging product opportunities independent of therapeutic area or modality. The Company is committed to ensuring that externally sourced programs remain an important component of its pipeline strategy, with a focus on supplementing its internal research through acquisitions as well as a licensing and external alliance strategy focused on the entire spectrum of collaborations from early research to late-stage compounds, as well as access to new technologies.

The Company’s clinical pipeline includes candidates in multiple disease areas, including cancer, cardiovascular diseases, metabolic diseases, infectious diseases, neurosciences, immunology, ophthalmology, respiratory diseases, and vaccines.

In the development of human health products, industry practice and government regulations in the U.S. and most foreign countries provide for the determination of effectiveness and safety of new chemical compounds through preclinical tests and controlled clinical evaluation. Before a new drug or vaccine may be marketed in the U.S., recorded data on preclinical and clinical experience are included in the New Drug Application (NDA) for a drug or the Biologics License Application (BLA) for a vaccine or biologic submitted to the FDA for the required approval.

Once the Company’s scientists discover a new small molecule compound or biologic that they believe has promise to treat a medical condition, the Company commences preclinical testing with that compound. Preclinical testing includes laboratory testing and animal safety studies to gather data on chemistry, pharmacology, immunogenicity and toxicology. Pending acceptable preclinical data, the Company will initiate clinical testing in accordance with established regulatory requirements. The clinical testing begins with Phase 1 studies, which are designed to assess safety, tolerability, pharmacokinetics, and preliminary pharmacodynamic activity of the compound in humans. If favorable, additional, larger Phase 2 studies are initiated to determine the efficacy of the compound in the affected population, define appropriate dosing for the compound, as well as identify any adverse effects that could limit the compound’s usefulness. In some situations, the clinical program incorporates adaptive design methodology to use accumulating data to decide how to modify aspects of the ongoing clinical study as it continues, without undermining the validity and integrity of the trial. One type of adaptive clinical trial is an adaptive Phase 2a/2b trial design, a two-stage trial design consisting of a Phase 2a proof-of-concept stage and a Phase 2b dose-optimization finding stage. If data from the Phase 2 trials are satisfactory, the Company commences large-scale Phase 3 trials to confirm the compound’s efficacy and safety. Another type of adaptive clinical trial is an adaptive Phase 2/3 trial design, a study that includes an interim analysis and an adaptation that changes the trial from having features common in a Phase 2 study (e.g., multiple dose groups) to a design similar to a Phase 3 trial. An adaptive Phase 2/3 trial design reduces timelines by eliminating activities which would be required to start a separate study. Upon completion of Phase 3 trials, if satisfactory, the Company submits regulatory filings with the appropriate regulatory agencies around the world to have the product candidate approved for marketing. There can be no assurance that a compound that is the result of any particular program will obtain the regulatory approvals necessary for it to be marketed.