QuickLinks -- Click here to rapidly navigate through this document

Management's Discussion and Analysis for the fiscal year ended December 31, 2015,

dated February 25, 2016

MANAGEMENT'S DISCUSSION AND ANALYSIS February 25, 2016 | |

This Management's Discussion and Analysis (this MD&A) should be read in conjunction with Suncor's December 31, 2015 audited Consolidated Financial Statements and the accompanying notes. Additional information about Suncor filed with Canadian securities regulatory authorities and the United States Securities and Exchange Commission (SEC), including quarterly and annual reports and the Annual Information Form dated February 25, 2016 (the 2015 AIF), which is also filed with the SEC under cover of Form 40-F, is available online at www.sedar.com, www.sec.gov and our website, www.suncor.com. Information on or connected to our website, even if referred to in this MD&A, does not constitute part of this MD&A.

References to "we", "our", "Suncor", or "the company" mean Suncor Energy Inc., its subsidiaries, partnerships and joint arrangements, unless the context requires otherwise. For a list of abbreviations that may be used in this MD&A, refer to the Advisories – Common Abbreviations section of this MD&A.

SUNCOR ENERGY INC. ANNUAL REPORT 2015 11

| MD&A – Table of Contents | ||

| 13 | Financial and Operating Summary | |

| 15 | Suncor Overview | |

| 17 | Financial Information | |

| 21 | Segment Results and Analysis | |

| 33 | Fourth Quarter 2015 Analysis | |

| 35 | Quarterly Financial Data | |

| 38 | Capital Investment Update | |

| 41 | Financial Condition and Liquidity | |

| 47 | Accounting Policies and Critical Accounting Estimates | |

| 51 | Risk Factors | |

| 57 | Other Items | |

| 58 | Advisories | |

Basis of Presentation

Unless otherwise noted, all financial information has been prepared in accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board (IASB) and Canadian generally accepted accounting principles (GAAP) as contained within Part 1 of the Canadian Institute of Chartered Professional Accountants Handbook.

All financial information is reported in Canadian dollars, unless otherwise noted. Production volumes are presented on a working-interest basis, before royalties, unless otherwise noted.

Non-GAAP Financial Measures

Certain financial measures in this MD&A – namely operating earnings, cash flow from operations, return on capital employed (ROCE), Oil Sands cash operating costs, free cash flow, and last-in, first-out (LIFO) – are not prescribed by GAAP. Operating earnings, Oil Sands cash operating costs and LIFO are defined in the Advisories – Non-GAAP Financial Measures section of this MD&A and reconciled to GAAP measures in the Financial Information and Segment Results and Analysis sections of this MD&A. Cash flow from operations, ROCE and free cash flow are defined and reconciled to GAAP measures in the Advisories – Non-GAAP Financial Measures section of this MD&A.

Measurement Conversions

Crude oil and natural gas liquids volumes have been converted to mcfe on the basis of one bbl to six mcf in this MD&A. Also, certain natural gas volumes have been converted to boe or mboe on the same basis. Refer to the Advisories – Measurement Conversions section of this MD&A.

Common Abbreviations

For a list of abbreviations that may be used in this MD&A, refer to the Advisories – Common Abbreviations section of this MD&A.

Risks and Forward-Looking Information

The company's financial and operational performance is potentially affected by a number of factors, including, but not limited to, the factors described in the Risk Factors section of this MD&A.

This MD&A contains forward-looking information based on Suncor's current expectations, estimates, projections and assumptions. This information is subject to a number of risks and uncertainties, including those discussed in this MD&A and Suncor's other disclosure documents, many of which are beyond the company's control. Users of this information are cautioned that actual results may differ materially. Refer to the Advisories – Forward-Looking Information section of this MD&A for information on the material risk factors and assumptions underlying our forward-looking information.

12 SUNCOR ENERGY INC. ANNUAL REPORT 2015

1. FINANCIAL AND OPERATING SUMMARY

Financial Summary

| Year ended December 31 ($ millions, except per share amounts) | 2015 | 2014 | 2013 | |||||

| Operating revenues, net of royalties | 29 208 | 39 862 | 39 593 | |||||

| Net (loss) earnings | (1 995 | ) | 2 699 | 3 911 | ||||

| per common share – basic | (1.38 | ) | 1.84 | 2.61 | ||||

| per common share – diluted | (1.38 | ) | 1.84 | 2.60 | ||||

| Operating earnings(1) | 1 465 | 4 620 | 4 700 | |||||

| per common share – basic | 1.01 | 3.15 | 3.13 | |||||

| Cash flow from operations(1) | 6 806 | 9 058 | 9 412 | |||||

| per common share – basic | 4.71 | 6.19 | 6.27 | |||||

| Dividends paid on common shares | 1 648 | 1 490 | 1 095 | |||||

| per common share – basic | 1.14 | 1.02 | 0.73 | |||||

| Weighted average number of common shares in millions – basic | 1 446 | 1 462 | 1 501 | |||||

| Weighted average number of common shares in millions – diluted | 1 447 | 1 465 | 1 502 | |||||

| ROCE(1)(2) (%) | 0.6 | 8.6 | 11.5 | |||||

| Capital Expenditures(3) | 6 220 | 6 530 | 6 380 | |||||

| Sustaining | 2 602 | 3 014 | 3 725 | |||||

| Growth | 3 618 | 3 516 | 2 655 | |||||

| Free cash flow(1) | 139 | 2 097 | 2 635 | |||||

| Balance Sheet (at December 31) | ||||||||

| Total assets | 77 527 | 79 671 | 78 315 | |||||

| Long-term debt(4) | 14 556 | 12 523 | 10 660 | |||||

| Net debt | 11 254 | 7 834 | 6 256 | |||||

| Total liabilities | 38 488 | 38 068 | 37 135 | |||||

- (1)

- Non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

- (2)

- ROCE excludes capitalized costs related to major projects in progress.

- (3)

- Excludes capitalized interest.

- (4)

- Includes current portion of long-term debt.

SUNCOR ENERGY INC. ANNUAL REPORT 2015 13

Operating Summary

| Year ended December 31 | 2015 | 2014 | 2013 | |||||

| Production Volumes (mboe/d) | ||||||||

| Oil Sands | 463.4 | 421.9 | 392.5 | |||||

| Exploration and Production | 114.4 | 113.0 | 169.9 | |||||

| Total | 577.8 | 534.9 | 562.4 | |||||

| Production Mix | ||||||||

| Crude oil and liquids / natural gas (%) | 99/1 | 99/1 | 94/6 | |||||

| Average Price Realizations ($/boe) | ||||||||

| Oil Sands operations | 49.46 | 87.46 | 82.83 | |||||

| Exploration and Production | 60.53 | 103.05 | 91.44 | |||||

| Refinery crude oil processed (mbbls/d) | 432.1 | 427.5 | 431.3 | |||||

| Refinery Utilization(1)(2) (%) | ||||||||

| Eastern North America | 94 | 90 | 91 | |||||

| Western North America | 93 | 95 | 96 | |||||

| 94 | 93 | 94 | ||||||

- (1)

- Refinery utilization is the amount of crude oil run through crude distillation units, expressed as a percentage of the nameplate capacity of these units.

- (2)

- Refinery nameplate capacity increases:

- •

- Effective January 1, 2014, Edmonton refinery from 140,000 bbls/d to 142,000 bbls/d;

- •

- Effective January 1, 2013, Edmonton refinery from 135,000 bbls/d to 140,000 bbls/d;

- •

- Prior years' utilization rates have not been recalculated and reflect the lower nameplate capacities.

Segment Summary

| Year ended December 31 ($ millions) | 2015 | 2014 | 2013 | ||||||

| Net (loss) earnings | |||||||||

| Oil Sands | (856 | ) | 1 776 | 2 040 | |||||

| Exploration and Production | (758 | ) | 653 | 1 000 | |||||

| Refining and Marketing | 2 266 | 1 692 | 2 022 | ||||||

| Corporate, Energy Trading and Eliminations | (2 647 | ) | (1 422 | ) | (1 151 | ) | |||

| Total | (1 995 | ) | 2 699 | 3 911 | |||||

| Operating (loss) earnings(1) | |||||||||

| Oil Sands | (111 | ) | 2 771 | 2 098 | |||||

| Exploration and Production | 7 | 857 | 1 210 | ||||||

| Refining and Marketing | 2 234 | 1 692 | 2 022 | ||||||

| Corporate, Energy Trading and Eliminations | (665 | ) | (700 | ) | (630 | ) | |||

| Total | 1 465 | 4 620 | 4 700 | ||||||

| Cash flow from (used in) operations(1) | |||||||||

| Oil Sands | 2 835 | 5 400 | 4 556 | ||||||

| Exploration and Production | 1 386 | 1 909 | 2 316 | ||||||

| Refining and Marketing | 2 872 | 2 178 | 2 618 | ||||||

| Corporate, Energy Trading and Eliminations | (287 | ) | (429 | ) | (78 | ) | |||

| Total | 6 806 | 9 058 | 9 412 | ||||||

- (1)

- Non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

14 SUNCOR ENERGY INC. ANNUAL REPORT 2015

Suncor is an integrated energy company headquartered in Calgary, Alberta, Canada. We are strategically focused on developing one of the world's largest petroleum resource basins – Canada's Athabasca oil sands. In addition, we explore for, acquire, develop, produce and market crude oil and natural gas in Canada and internationally; we transport and refine crude oil, and we market petroleum and petrochemical products primarily in Canada. Periodically, we market third-party petroleum products. We also conduct energy trading activities focused principally on the marketing and trading of crude oil, natural gas and byproducts.

For a description of Suncor's business segments, refer to the Segment Results and Analysis section of this MD&A.

Suncor's Strategy

We are committed to delivering competitive and sustainable returns to shareholders by focusing on capital discipline, operational excellence and long-term profitable growth, and by leveraging our competitive differentiators: an industry-leading oil sands reserves base, a proven integrated model, financial strength, industry expertise and a commitment to sustainability. Key components of Suncor's strategy include:

- •

- Profitably operate and develop our reserves – Suncor's growth plan is focused on projects, such as Fort Hills and the Canadian Oil Sands Limited (COS) acquisition, that are expected to provide long-term profitability for the company. The company's significant reserves base and industry expertise in oil sands has laid the groundwork for achieving this growth. Suncor's economies of scale have also allowed us to focus on near-term oil sands growth through low-cost debottlenecking and expansion projects.

- •

- Optimize value through integration – From the ground to the gas station, Suncor optimizes its profit through each step of the value chain. As upstream production grows, securing access to global pricing through the company's refining operations and midstream logistics network helps to maximize profit on each upstream barrel.

- •

- Achieve industry-leading unit costs in each business segment – Through a focus on operational excellence, Suncor is aiming to get the most out of our operations. Driving down costs and a continued focus on improved productivity and reliability will help to achieve this.

- •

- Industry leader in sustainable development – Suncor is focused on triple bottom line sustainability, which means leadership and industry collaboration in environmental performance, social responsibility and creating a strong economy.

2015 Highlights

Financial results summary

- •

- Net loss for 2015 was $1.995 billion, compared to net earnings of $2.699 billion in 2014.

- •

- Operating earnings(1) for 2015 were $1.465 billion, compared to $4.620 billion in 2014.

- •

- Cash flow from operations(1) for 2015 was $6.806 billion, compared to $9.058 billion in 2014.

- •

- ROCE(1) (excluding major projects in progress) decreased to 0.6% for the twelve months ended December 31, 2015, compared to 8.6% for the twelve months ended December 31, 2014. ROCE for the twelve months ended December 31, 2015 improves to 4.2% (2014 – 11.5%) when removing the impacts of impairment charges.

Suncor's commitment to capital discipline, operational excellence, and improved reliability generated cash flow from operations which fully funded sustaining capital and dividends in the year.

- •

- Suncor's approach to prudent capital management resulted in the company finishing 2015 with $6.220 billion in capital expenditures, which is within its revised capital guidance range of $5.8 to $6.4 billion, and $1.0 billion below the lower end of initial 2015 guidance.

- •

- In response to the continuing low crude oil price environment, Suncor announced a $750 million reduction to its 2016 capital program, including the deferral of planned Firebag maintenance into 2017. The reduction is not expected to impact the company's safety, reliability, environmental performance, or production targets.

- •

- Continuous improvement and demonstrated reliability of the company's refining facilities resulted in 94% overall refinery utilization while performing planned maintenance.

- (1)

- Operating earnings, cash flow from operations and ROCE, are non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A

SUNCOR ENERGY INC. ANNUAL REPORT 2015 15

- •

- The company continues to focus on improving facility utilization and workforce productivity, achieving Oil Sands upgrading reliability in excess of 90% more than a year ahead of our original plan to upgrade 315,000 bbls/d by 2017.

Continued focus on cost management enabled Suncor to decrease Oil Sands cash operating costs per barrel by 18%.

- •

- Suncor reduced annual cash operating costs per barrel(1) from $33.80/bbl in 2014 to $27.85/bbl in 2015, the lowest since 2007.

- •

- Suncor delivered on the reliability targets and cost reduction measures announced in early 2015 by decreasing companywide operating costs by almost $1 billion. The current pricing environment has reinforced the importance of Suncor's disciplined approach to cost management.

Suncor's strong balance sheet has effectively positioned the company to pursue profitable long-term growth opportunities.

- •

- The company ended the year with $4.0 billion in cash and cash equivalents and had $7.0 billion of credit facilities available at December 31, 2015.

- •

- Suncor acquired an additional 10% working interest in the Fort Hills oil sands project in 2015. The project continues to be on schedule and all critical milestones set for 2015 were achieved, with construction more than 50% complete at the end of the year. First oil is expected in the fourth quarter of 2017, ramping up to 90% of its planned gross production capacity of 180,000 bbls/d within twelve months.

- •

- Construction of the Hebron project continued in 2015, with first oil expected in late 2017.

- •

- Subsequent to year end, Suncor acquired 84.2% of the shares of COS for consideration of 0.28 of a Suncor share for each COS share. Suncor plans to acquire the remaining 15.8% of COS' shares by the end of the first quarter. The transaction valued COS at $6.9 billion at the time of the acquisition.

Continued investment in integration and market access strategies.

- •

- The Refining and Marketing segment continues to reinforce the value of the company's integrated model by generating $2.234 billion of operating earnings, an increase of 32% from the prior year.

- •

- Suncor began shipments of crude oil to the Montreal refinery on Enbridge's Line 9 in the fourth quarter of 2015. The reversal of Enbridge's Line 9 will provide Suncor with the flexibility to supply its Montreal refinery with a full slate of inland-priced crude.

- •

- The company completed a non-cash asset exchange and lease with TransAlta Corporation (TransAlta) in the third quarter of 2015 where Suncor assumed operating control of the Poplar Creek cogeneration facilities, which provide steam and power to the company's Oil Sands operations, in exchange for Suncor's Kent Breeze and its share of the Wintering Hills wind power facilities. Bringing the Poplar Creek assets in-house is expected to improve Suncor's overall Oil Sands operations reliability and profitability.

- •

- The company's integrated model and strong market access position resulted in Suncor capturing global-based pricing on volumes equivalent to 98% of its upstream production in 2015, compared to 97% in 2014.

Oil Sands operations grows production by 11% with strong Oil Sands reliability and record In Situ performance.

- •

- Firebag nameplate capacity increased from 180,000 bbls/d to 203,000 bbls/d as a result of cost-effective debottlenecking activities and sub surface optimizations, and record Firebag production achieved in 2015.

- •

- Strong infill well performance and optimized reservoir management strategies contributed to a record low steam-to-oil ratio (SOR) of 2.6 at Firebag for the year.

- •

- Production at MacKay River increased 14% as a result of the debottlenecking project.

Return of cash to shareholders through dividends, which increased by more than 10%.

- •

- The company paid $1.648 billion in dividends in 2015, reflecting an increase to Suncor's quarterly dividend compared to the prior year, demonstrating our dedication to returning value to shareholders.

- (1)

- Cash operating costs per barrel is a non-GAAP financial measure. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

16 SUNCOR ENERGY INC. ANNUAL REPORT 2015

Net Earnings

Suncor's net loss in 2015 was $1.995 billion, compared to net earnings of $2.699 billion in 2014. The net loss was impacted by the same factors that influenced operating earnings, which are described below. Other items affecting the net loss in 2015 and net earnings in 2014 included:

- •

- In 2015, the company recorded after-tax impairment charges against property, plant and equipment and exploration and evaluation assets of $359 million on White Rose, $331 million on Golden Eagle and $54 million on Terra Nova, primarily as a result of impacts of a decline in the crude oil price forecast. In addition, impairment charges of $290 million were recorded against the Joslyn mining project and $54 million on the Ballicatters well, due to uncertainty on the timing and likelihood of development plans, and $96 million in Oil Sands following a review of certain assets that no longer fit with Suncor's growth strategies, and which could not be repurposed or otherwise deployed.

- •

- In 2015, as a result of shut-in production due to the continued closure of certain Libyan export terminals, escalating political unrest, and increased uncertainty with respect to the company's return to normal operations in the country, the company recorded an after-tax impairment charge of $415 million against property, plant and equipment and exploration and evaluation assets.

- •

- The after-tax unrealized foreign exchange losses on the revaluation of U.S. dollar denominated debt were $1.930 billion for 2015, compared to $722 million for 2014.

- •

- In 2015, the company recorded an after-tax gain of $68 million on the disposal of the company's share of certain assets and liabilities of Pioneer Energy in the Refining and Marketing segment.

- •

- The company recorded a $423 million deferred income tax charge in 2015 related to a 2% increase in the Alberta corporate income tax rate.

- •

- The company recorded a $406 million income tax recovery in 2015 in the Exploration and Production (E&P) segment related to a 12% decrease in the U.K. tax rate.

- •

- Suncor recorded after-tax insurance proceeds of $75 million in 2015 related to a claim on the Terra Nova asset in the E&P segment.

- •

- In 2015, the company recorded after-tax restructuring charges of $57 million related to cost reduction initiatives in the Corporate segment.

- •

- The company recorded an after-tax gain of $61 million in 2014 relating to the sale of its Wilson Creek natural gas assets in the E&P segment.

- •

- Suncor recorded a current income tax expense adjustment and associated interest expense of $54 million in 2014 related to the timing of tax depreciation deductions taken on certain capital expenditures incurred in a prior period in the Oil Sands segment.

- •

- In 2014, Joslyn mining project development activities were scaled back in order to focus on engineering studies to further optimize the Joslyn resource. As a result of Suncor's assessment of expected future net cash flows and the uncertainty of the project, including the timing of the development plans, Suncor recorded an after-tax charge to net earnings of $718 million against property, plant and equipment and exploration and evaluation assets.

- •

- In 2014, as a result of the continued closure of certain Libyan export terminals and the company's view on production plans during the remaining term of the production sharing agreements, the company recorded an after-tax impairment charge of $297 million against property, plant and equipment and exploration and evaluation assets.

- •

- The company recorded after-tax impairment charges of $223 million in the Oil Sands segment in 2014 following a review of certain assets that no longer fit with Suncor's previously revised growth strategies and which could not be repurposed or otherwise deployed. Such assets included a pipeline and related compressor, as well as steam generator components.

- •

- The company recorded after-tax earnings of $32 million in 2014 related to an agreement reached for Suncor to receive a reserves redetermination of 1.2 million barrels of oil related to an interest in a Norwegian asset that Suncor previously owned.

SUNCOR ENERGY INC. ANNUAL REPORT 2015 17

Operating Earnings

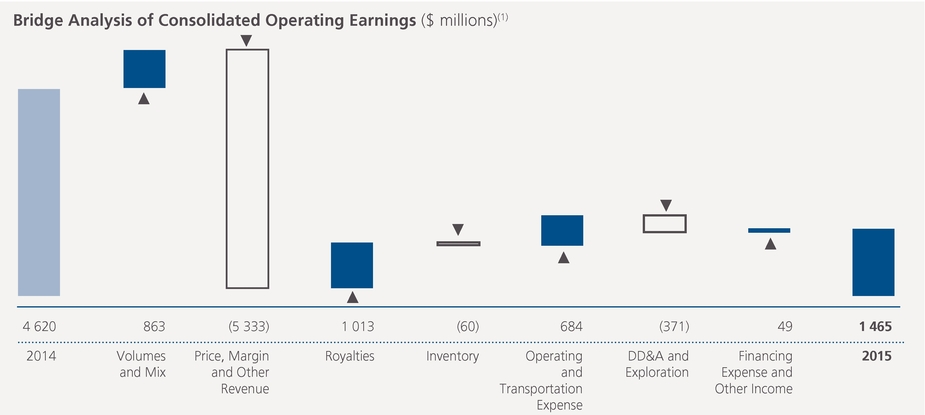

Consolidated Operating Earnings Reconciliation(1)

| Year ended December 31 ($ millions) | 2015 | 2014 | 2013 | |||||

| Net (loss) earnings as reported | (1 995 | ) | 2 699 | 3 911 | ||||

| Unrealized foreign exchange loss on U.S. dollar denominated debt | 1 930 | 722 | 521 | |||||

| Impairments net of reversals and provisions(2) | 1 599 | 1 238 | 563 | |||||

| Restructuring charges | 57 | — | — | |||||

| Recognition of risk mitigation proceeds(2) | (75 | ) | — | (223 | ) | |||

| Net impact of not proceeding with the Voyageur upgrader project(3) | — | — | 58 | |||||

| Gain on significant disposals(4) | (68 | ) | (61 | ) | (130 | ) | ||

| Impact of income tax adjustments on deferred income taxes | 17 | 54 | — | |||||

| Reserves redetermination | — | (32 | ) | — | ||||

| Operating earnings(1) | 1 465 | 4 620 | 4 700 | |||||

- (1)

- Non-GAAP financial measure. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

- (2)

- In 2013, the company recorded after-tax impairment charges of $563 million in the Exploration and Production segment against its assets in Syria, Libya and North America Onshore. Concurrent with the impairment of its Syrian assets, the company recognized after-tax risk mitigation proceeds of $223 million, previously recorded as a long-term provision.

- (3)

- In 2013, the company recorded an after-tax charge of $58 million as a result of not proceeding with the Voyageur upgrader project.

- (4)

- In 2013, the company recorded an after-tax gain of $130 million relating to the sale of the company's conventional natural gas business.

- (1)

- For an explanation of the construction of this bridge analysis, see the Advisories – Non-GAAP Financial Measures section of this MD&A.

Suncor's consolidated operating earnings for 2015 were $1.465 billion, compared to $4.620 billion in 2014. The decrease was primarily due to lower operating earnings in the Oil Sands and E&P segments as a result of significantly lower upstream price realizations consistent with the decline in benchmark crude oil prices, partially offset by increased Oil Sands operations production due to improved reliability, record Refining and Marketing operating earnings due to a strong downstream pricing environment and lower operating costs companywide.

Cash Flow from Operations

Consolidated cash flow from operations for 2015 was $6.806 billion, compared to $9.058 billion in 2014. Cash flow from operations was impacted by the same factors as operating earnings.

18 SUNCOR ENERGY INC. ANNUAL REPORT 2015

Results for 2014 compared with 2013

Net earnings for 2014 were $2.699 billion, compared to $3.911 billion in 2013. The decrease in net earnings was mainly due to the same factors impacting operating earnings described below and by the net earnings adjustments described above.

Operating earnings for 2014 were $4.620 billion, compared to $4.700 billion in 2013. The decrease was primarily due to lower operating earnings from the E&P segment as a result of volume decreases at Buzzard, the sale of the company's conventional natural gas business which took place in 2013, lower price realizations, and lower contributions from Libya. In addition, the Refining and Marketing segment earnings decreased due to the lower downstream pricing environment. These factors were partially offset by higher production from the Oil Sands segment and higher price realizations for Oil Sands sales which benefited from favourable foreign exchange rates.

Consolidated cash flow from operations for 2014 was $9.058 billion, compared to $9.412 billion in 2013. Cash flow from operations decreased primarily due to lower production and price realizations in E&P and lower margins in Refining and Marketing as well as the impacts of settling trading positions in Energy Trading, partially offset by higher production and higher average price realizations from Oil Sands operations.

Business Environment

Commodity prices, refining crack spreads and foreign exchange rates are important factors that affect the results of Suncor's operations.

| Average for the year ended December 31 | 2015 | 2014 | 2013 | ||||

| WTI crude oil at Cushing (US$/bbl) | 48.75 | 93.00 | 97.95 | ||||

| Brent crude oil at Sullom Voe (US$/bbl) | 53.60 | 99.50 | 108.75 | ||||

| Dated Brent/Maya FOB price differential (US$/bbl) | 9.50 | 13.70 | 11.65 | ||||

| MSW at Edmonton (Cdn$/bbl) | 57.60 | 94.85 | 96.80 | ||||

| WCS at Hardisty (US$/bbl) | 35.25 | 73.60 | 72.75 | ||||

| Light/heavy differential for WTI at Cushing less WCS at Hardisty (US$/bbl) | 13.50 | 19.40 | 25.20 | ||||

| Condensate at Edmonton (US$/bbl) | 47.35 | 92.95 | 101.70 | ||||

| Natural gas (Alberta spot) at AECO (Cdn$/mcf) | 2.65 | 4.50 | 3.15 | ||||

| Alberta Power Pool Price (Cdn$/MWh) | 33.40 | 49.65 | 79.95 | ||||

| New York Harbor 3-2-1 crack(1) (US$/bbl) | 19.70 | 19.65 | 23.90 | ||||

| Chicago 3-2-1 crack(1) (US$/bbl) | 18.50 | 17.40 | 21.40 | ||||

| Portland 3-2-1 crack(1) (US$/bbl) | 25.15 | 20.15 | 24.00 | ||||

| Gulf Coast 3-2-1 crack(1) (US$/bbl) | 18.35 | 16.50 | 20.55 | ||||

| Exchange rate (US$/Cdn$) | 0.78 | 0.91 | 0.97 | ||||

| Exchange rate (end of period) (US$/Cdn$) | 0.72 | 0.86 | 0.94 | ||||

- (1)

- 3-2-1 crack spreads are indicators of the refining margin generated by converting three barrels of WTI into two barrels of gasoline and one barrel of diesel. The crack spreads presented here generally approximate the regions into which the company sells refined products through retail and wholesale channels.

Suncor's sweet SCO price realizations are influenced primarily by the price of WTI at Cushing and by the supply and demand of sweet SCO from Western Canada. WTI decreased to US$48.75/bbl in 2015, compared to US$93.00/bbl in 2014.

Suncor produces a specific grade of sour SCO, the price realizations for which are influenced by various crude benchmarks including, but not limited to: MSW at Edmonton and WCS at Hardisty, and which can also be affected by prices negotiated for spot sales. Prices for both MSW at Edmonton and WCS at Hardisty decreased in 2015 compared to 2014, resulting in lower realizations for sour SCO.

Bitumen production that Suncor does not upgrade is blended with diluent to facilitate delivery on pipeline systems. Net bitumen price realizations are therefore influenced by both prices for Canadian heavy crude oil (WCS at Hardisty is a common reference) and prices for diluent (Condensate at Edmonton and SCO). Bitumen price realizations can also be affected by bitumen quality and

SUNCOR ENERGY INC. ANNUAL REPORT 2015 19

spot sales. Average prices for WCS at Hardisty and Condensate at Edmonton decreased significantly in 2015 compared to 2014, resulting in lower realizations for bitumen.

Suncor's price realizations for production from East Coast Canada and E&P International assets are influenced primarily by the price for Brent crude. Brent crude pricing decreased over the prior year and averaged US$53.60/bbl in 2015, compared to US$99.50/bbl in 2014.

Suncor's price realizations for E&P Canada natural gas production are primarily referenced to Alberta spot at AECO. Natural gas is also used in the company's Oil Sands and Refining operations. The average AECO benchmark decreased to $2.65/mcf in 2015, from $4.50/mcf in 2014.

Suncor's refining margins are influenced by 3-2-1 crack spreads, which are industry indicators approximating the gross margin on a barrel of crude oil that is refined to produce gasoline and distillate, and by light/heavy and light/sour crude differentials. More complex refineries can earn greater margins by processing less expensive, heavier crudes. Crack spreads do not necessarily reflect the margins of a specific refinery. Crack spreads are based on current crude feedstock prices whereas actual refining margins are based on first-in, first-out inventory accounting (FIFO), where a delay exists between the time that feedstock is purchased and when it is processed and sold to a third party. Specific refinery margins are further impacted by actual crude purchase costs, refinery configuration and refined products sales markets unique to that refinery. Average market crack spreads increased in 2015 compared to 2014, resulting in a positive impact to refining margins.

Excess electricity produced in Suncor's Oil Sands business is sold to the Alberta Electric System Operator (AESO), with the proceeds netted against the cash operating costs per barrel metric. The Alberta power pool price decreased to an average of $33.40/MWh in 2015 from $49.65/MWh in the prior year.

The majority of Suncor's revenues from the sale of oil and natural gas commodities are based on prices that are determined by or referenced to U.S. dollar benchmark prices. The majority of Suncor's expenditures are realized in Canadian dollars. A decrease in the value of the Canadian dollar relative to the U.S. dollar will increase the revenues received from the sale of commodities. An increase in the value of the Canadian dollar relative to the U.S. dollar will decrease revenue received from the sale of commodities. In 2015, the Canadian dollar weakened in relation to the U.S. dollar as the average exchange rate decreased to 0.78 from 0.91, which had a positive impact on price realizations for the company in 2015.

Conversely, many of Suncor's assets and liabilities, notably the majority of the company's debt, are denominated in U.S. dollars and translated to Suncor's reporting currency (Canadian dollars) at each balance sheet date. A decrease in the value of the Canadian dollar relative to the U.S. dollar from the previous balance sheet date increases the amount of Canadian dollars required to settle U.S. dollar denominated obligations.

Economic Sensitivities(1)(2)

The following table illustrates the estimated effects that changes in certain factors would have had on 2015 net earnings and cash flow from operations if the listed changes had occurred.

| (Estimated change, in $ millions) | Net Earnings | Cash Flow From Operations | ||||

| Crude oil +US$1.00/bbl | 165 | 165 | ||||

| Natural gas +Cdn$0.10/mcf | (15 | ) | (15 | ) | ||

| Light/heavy differential +US$1.00/bbl | 5 | 5 | ||||

| 3-2-1 crack spreads +US$1.00/bbl | 120 | 120 | ||||

| Foreign exchange +$0.01 US$/Cdn$(3) related to operating activities | (135 | ) | (135 | ) | ||

| Foreign exchange on U.S. denominated debt +$0.01 US$/Cdn$(3) | 140 | — | ||||

- (1)

- Each line item in this table shows the effects of a change in that variable only, with other variables being held consistent.

- (2)

- Changes for a variable imply that all such similar variables are impacted, such that Suncor's average price realizations increase uniformly. For instance, "Crude oil +US$1.00/bbl" implies that price realizations influenced by WTI, Brent, SCO, WCS, par crude at Edmonton and condensate all increase by US$1.00/bbl.

- (3)

- The difference between estimates for net earnings and cash flow from operations are due primarily to the revaluation of U.S. dollar denominated debt that is included within net earnings but not within cash flow from operations.

20 SUNCOR ENERGY INC. ANNUAL REPORT 2015

4. SEGMENT RESULTS AND ANALYSIS

Suncor has classified its operations into the following segments:

OIL SANDS

Suncor's Oil Sands segment, with assets located in the Athabasca oil sands of northeast Alberta, recovers bitumen from mining and in situ operations and either upgrades this production into SCO for refinery feedstock and diesel fuel, or blends the bitumen with diluent for direct sale to market. The Oil Sands segment includes:

- •

- Oil Sands operations refer to Suncor's wholly owned and operated mining, extraction, upgrading, in situ and related logistics and storage assets in the Athabasca oil sands region. Oil Sands operations consist of:

- •

- Oil Sands Base operations include the Millennium and North Steepbank mining and extraction operations, integrated upgrading facilities known as Upgrader 1 and Upgrader 2, and the associated infrastructure for these assets – including utilities, energy and reclamation facilities, such as Suncor's Tailings Reduction Operations process (TROTM) assets.

- •

- In Situ operations include oil sands bitumen production from Firebag and MacKay River and supporting infrastructure, such as central processing facilities, cogeneration units and hot bitumen infrastructure, including insulated pipelines, diluent import capabilities and a cooling and blending facility, and related storage assets. In Situ production is either upgraded by Oil Sands Base, or blended with diluent and marketed directly to customers.

- •

- Oil Sands ventures includes Suncor's 50.8% interest in the Fort Hills mining project, where Suncor is the operator, and its 36.75% non-operated interest in the Joslyn North mining project. The company also holds a 12.0% interest in the Syncrude oil sands mining and upgrading joint arrangement and currently holds an additional 30.9% indirectly through its 84.2% ownership of COS, which owns a 36.74% interest in the Syncrude joint venture.

EXPLORATION AND PRODUCTION

Suncor's E&P segment consists of offshore operations off the east coast of Canada and in the North Sea, and onshore assets in North America, Libya and Syria.

- •

- E&P Canada operations include Suncor's 37.675% working interest in Terra Nova, which Suncor operates. Suncor also holds a 20.0% interest in the Hibernia base project and a 19.13% interest in the Hibernia Southern Extension Unit (HSEU) (reset from 19.51%, effective December 1, 2015). Suncor holds a 27.5% interest in the White Rose base project and a 26.125% interest in the White Rose Extensions. Effective January 1, 2016, Suncor's working interest in the Hebron project has been reset from 22.729% to 21.034%. Other than Terra Nova, all of the projects are operated by other companies. Suncor also holds interests in several exploration licences offshore Newfoundland and Labrador and Nova Scotia. E&P Canada also includes Suncor's working interests in unconventional natural gas properties in northeast B.C.

- •

- E&P International operations include Suncor's 29.89% working interest in Buzzard and its 26.69% interest in Golden Eagle. Both operations are located in the U.K. sector of the North Sea and are operated by another company. Suncor also holds interests in several exploration licences offshore the U.K. and Norway. Suncor owns, pursuant to Exploration and Production Sharing Agreements (EPSAs), working interests in the exploration and development of oilfields in the Sirte Basin in Libya. Production in Libya remained impacted by political unrest at the end of 2015, with the timing of a return to normal operations remaining uncertain. Suncor also owns, pursuant to a Production Sharing Contract (PSC), an interest in the Ebla gas development in the Ash Shaer and Cherrife areas in Syria. Suncor's operations in Syria were suspended indefinitely in 2011, due to political unrest in the country.

SUNCOR ENERGY INC. ANNUAL REPORT 2015 21

REFINING AND MARKETING

Suncor's Refining and Marketing segment consists of two primary operations:

- •

- Refining and Supply operations refine crude oil and intermediate feedstock into a broad range of petroleum and petrochemical products. Refining and Supply consists of:

- •

- Eastern North America operations which include a refinery located in Montreal, Quebec, a refinery located in Sarnia, Ontario, and a lubricants business located in Mississauga, Ontario that manufactures and blends products which are marketed worldwide.

- •

- Western North America operations which include refineries located in Edmonton, Alberta and Commerce City, Colorado.

- •

- Other Refining and Supply assets include interests in a sulphur plant, a petrochemical plant, pipelines and product terminals in Canada and the U.S.

- •

- Downstream Marketing operations sell refined petroleum products to retail, commercial and industrial customers through a combination of company-owned, Petro-Canada branded-dealer and other retail stations in Canada and Colorado, a nationwide commercial road transport network in Canada, and a bulk sales channel in Canada. Lubricant products are marketed worldwide through company-operated locations and distributor networks.

CORPORATE, ENERGY TRADING AND ELIMINATIONS

The groupingCorporate, Energy Trading and Eliminations includes the company's investments in renewable energy projects, results related to energy marketing, supply and trading activities, and other activities not directly attributable to any other operating segment.

- •

- Renewable Energy interests include six wind facilities across Canada, including Cedar Point which is the most recent addition to the portfolio, and the St. Clair ethanol plant in Ontario.

- •

- Energy Trading activities primarily involve the marketing, supply and trading of crude oil, natural gas, power and byproducts, and the use of midstream infrastructure and financial derivatives to optimize related trading strategies.

- •

- Corporate activities include stewardship of Suncor's debt and borrowing costs, expenses not allocated to the company's businesses, and the company's captive insurance activities that self-insure a portion of the company's asset base.

- •

- Intersegment revenues and expenses are removed from consolidated results inEliminations. Intersegment activity includes the sale of product between the company's segments and insurance for a portion of the company's operations by theCorporate captive insurance entity.

22 SUNCOR ENERGY INC. ANNUAL REPORT 2015

2015 Highlights

- •

- Oil Sands operations production increased to 433,600 bbls/d, an increase of 11% compared to 2014, driven by strong reliability across all assets and record In Situ production of 217,600 bbls/d.

- •

- The company's continued focus on cost management, combined with increased production, enabled Suncor to decrease its cash operating costs per barrel by 18% to $27.85/bbl in 2015, compared to $33.80/bbl in the prior year and is the lowest achieved since 2007.

- •

- Fort Hills construction continued to ramp up and was more than 50% complete by the end of the year. First oil is expected the fourth quarter of 2017.

- •

- Suncor continues to deliver on its commitment to invest in long-term profitable growth in its core asset areas. The company acquired an additional 10% of the Fort Hills mining project and, subsequent to year end, acquired 84.2% of COS.

- •

- Suncor continues to focus on safely and reliably operating our assets, and optimizing the value chain through integration. The company completed a non-cash asset exchange and lease with TransAlta where Suncor assumed operating control of the Poplar Creek cogeneration facilities, which provide steam and power to the company's Oil Sands operations. Bringing the Poplar Creek assets in-house is expected to improve Suncor's overall Oil Sands operations reliability and profitability.

- •

- Increase to nameplate capacity of Firebag from 180,000 bbls/d to 203,000 bbls/d as a result of cost-effective debottlenecking activities and record Firebag production achieved in 2015. Record low SOR of 2.6 was achieved at Firebag in 2015, primarily due to optimized reservoir management strategies and strong infill well performance.

Strategy and Investment Update

Suncor continues to deliver on its commitment to add shareholder value and invest in long-term profitable growth in its core asset areas. The company acquired an additional 10% working interest in the Fort Hills oil sands project from Total E&P Canada Ltd. (Total E&P) for $360 million. Suncor's share in the project is now 50.8%. In addition, subsequent to December 31, 2015, Suncor acquired 84.2% of COS and plans to acquire the remaining shares by March 21, 2016 at a COS special shareholders meeting to approve the acquisition.

Oil Sands operations has established a large physical asset base providing the opportunity for production growth through low cost debottlenecks, expansions and increased reliability. In 2015, Oil Sands upgrading achieved reliability in excess of 90%, more than a year ahead of our original plan to upgrade 315,000 bbls/d by 2017. Transactions, including the non-cash asset exchange with TransAlta and planned termination of the wastewater treatment facilities operating agreement and lease with a third party to allow for in-house management of those operations, will provide Suncor with increased control over asset reliability.

Oil Sands continues to focus on safe, reliable and sustainable operations. The company's operational excellence initiatives target improving facility utilization and workforce productivity, including a continued focus on upgrader reliability, which are expected to achieve steady production growth while reducing operating costs. Sustaining capital for Oil Sands operations in 2016 is expected to include a turnaround on Upgrader 2.

The primary focus for both cost management and capital discipline in 2016 will be to continue efforts to sustainably reduce controllable operating costs through elimination of non-critical work and close collaboration with suppliers and business partners. Capital discipline continues to focus on managing investment opportunities, including sustainability priorities, through a robust asset development process and realizing turnaround productivity improvements.

Suncor continues to work closely with the Fort Hills mining project co-owners on engineering, procurement and construction activities. As operator of the Fort Hills project, Suncor is developing the mine using traditional open-pit truck and shovel techniques, and paraffinic froth treatment-based extraction technology that will allow the mine to produce a bitumen product that can be sold directly to the market.

SUNCOR ENERGY INC. ANNUAL REPORT 2015 23

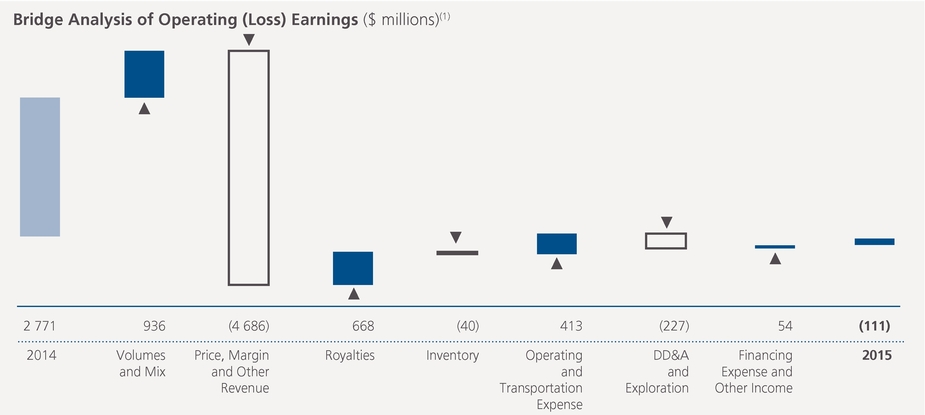

Financial Highlights

| Year ended December 31 ($ millions) | 2015 | 2014 | 2013 | ||||||

| Gross revenues | 9 332 | 14 561 | 13 089 | ||||||

| Less: Royalties | (114 | ) | (982 | ) | (859 | ) | |||

| Operating revenues, net of royalties | 9 218 | 13 579 | 12 230 | ||||||

| Net (loss) earnings | (856 | ) | 1 776 | 2 040 | |||||

| Adjusted for: | |||||||||

| Net impact of not proceeding with the Voyageur upgrader project | — | — | 58 | ||||||

| Impairments | 386 | 941 | — | ||||||

| Impact of income tax adjustments on deferred income taxes | 359 | 54 | — | ||||||

| Operating (loss) earnings(1) | (111 | ) | 2 771 | 2 098 | |||||

| Oil Sands operations | (33 | ) | 2 696 | 1 870 | |||||

| Oil Sands ventures | (78 | ) | 75 | 228 | |||||

| Cash flow from operations(1) | 2 835 | 5 400 | 4 556 | ||||||

- (1)

- Non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

- (1)

- For an explanation of the construction of this bridge analysis, see the Advisories – Non-GAAP Financial Measures section of this MD&A.

Operating losses for Oil Sands operations were $33 million in 2015, compared to operating earnings of $2.696 billion in 2014. The decrease was primarily due to significantly lower price realizations as a result of lower crude oil benchmark prices, partially offset by increased production, lower royalties, and lower operating and transportation expenses as a result of the impact of cost reduction initiatives, lower natural gas prices and lower unplanned maintenance activities.

Operating losses for Oil Sands ventures were $78 million in 2015, compared to operating earnings of $75 million in 2014. The decrease was primarily due to lower price realizations as a result of lower crude oil benchmark prices and lower production, partially offset by lower royalties and operating costs as a result of cost reduction initiatives for Syncrude and the decision to scale back activities at the Joslyn mining project.

Cash flow from operations for the Oil Sands segment was $2.835 billion in 2015, compared to $5.400 billion in 2014. The decrease was largely due to the same factors that impacted operating earnings.

24 SUNCOR ENERGY INC. ANNUAL REPORT 2015

Production Volumes(1)

| Year ended December 31 (mbbls/d) | 2015 | 2014 | 2013 | ||||

| Upgraded product (SCO) | 320.1 | 289.1 | 282.6 | ||||

| Non-upgraded bitumen | 113.5 | 101.8 | 77.9 | ||||

| Oil Sands operations | 433.6 | 390.9 | 360.5 | ||||

| Oil Sands ventures – Syncrude | 29.8 | 31.0 | 32.0 | ||||

| Total | 463.4 | 421.9 | 392.5 | ||||

- (1)

- Bitumen from Oil Sands Base operations is upgraded, while bitumen from In Situ operations is upgraded or sold directly to customers. Yields of SCO from Suncor's upgrading processes are approximately 79% of bitumen feedstock input.

Sales Volumes and Mix

| Year ended December 31 (mbbls/d) | 2015 | 2014 | 2013 | |||||

| Oil Sands operations sales volumes | ||||||||

| Sweet SCO | 107.0 | 99.7 | 91.5 | |||||

| Diesel | 31.3 | 30.7 | 23.5 | |||||

| Sour SCO | 182.5 | 158.9 | 166.0 | |||||

| Upgraded product (SCO) | 320.8 | 289.3 | 281.0 | |||||

| Non-upgraded bitumen | 107.7 | 101.4 | 76.0 | |||||

| Oil Sands operations | 428.5 | 390.7 | 357.0 | |||||

| Oil Sands ventures | 29.8 | 31.0 | 32.0 | |||||

| Total | 458.3 | 421.7 | 389.0 | |||||

Production in Oil Sands operations increased to 433,600 bbls/d in 2015 from 390,900 bbls/d in 2014, due primarily to reliable operations across all assets, with record SCO and In Situ production for 2015. Production in both years was impacted by planned coker maintenance in the spring and fall, while 2014 was also impacted by unplanned maintenance in upgrading and extraction during the third and fourth quarters of 2014, and a weather-related site-wide power outage in the third quarter of 2014. Sweet SCO production in 2015 was impacted by unplanned hydrotreater maintenance in the first half of the year.

Sales volumes for Oil Sands operations increased to 428,500 bbls/d in 2015, compared to 390,700 bbls/d in 2014, reflecting the same factors that led to the overall increase in production volumes. The sales mix improved in 2015, compared to 2014, primarily due to lower unplanned upgrader maintenance activities in the current year.

Sales volumes of non-upgraded bitumen increased in 2015, compared to 2014, mainly due to higher production at Firebag.

The inventory variance factor decreased operating earnings, primarily due to a larger inventory build in 2015 as compared to 2014. Inventory levels in 2015 increased compared to 2014 due to increased production levels and expanded use of midstream assets necessary to access new sales markets.

Suncor's share of Syncrude production and sales volumes averaged 29,800 bbls/d in 2015, compared to 31,000 bbls/d in 2014. Production in both years was impacted by planned and unplanned maintenance events.

Bitumen Production from Operations

| Year ended December 31 | 2015 | 2014 | 2013 | |||||

| Oil Sands Base | ||||||||

| Bitumen production (mbbls/d) | 307.3 | 274.4 | 269.8 | |||||

| Bitumen ore mined (thousands of tonnes/day) | 461.3 | 408.5 | 413.6 | |||||

| Bitumen ore grade quality (bbls/tonne) | 0.67 | 0.67 | 0.65 | |||||

| In Situ bitumen production (mbbls/d) | ||||||||

| Firebag | 186.9 | 172.0 | 143.4 | |||||

| MacKay River | 30.7 | 27.0 | 28.5 | |||||

| Total In Situ production | 217.6 | 199.0 | 171.9 | |||||

| In Situ steam-to-oil ratio | ||||||||

| Firebag | 2.6 | 2.8 | 3.3 | |||||

| MacKay River | 2.9 | 2.9 | 2.6 | |||||

Bitumen production from Oil Sands Base operations increased to an average of 307,300 bbls/d in 2015, compared to 274,400 bbls/d in 2014. The increase was primarily due to reliable operations across all assets, compared to the prior year which was impacted by unplanned extraction, upgrading, and utilities maintenance in the third and fourth quarters that constrained mine production.

In Situ achieved record bitumen production in 2015, increasing to 217,600 bbls/d from 199,000 bbls/d in 2014. The increase was driven by strong production from both Firebag and MacKay River primarily as a result of cost-effective de-bottlenecking and strong infill well performance. Production at Firebag increased to 186,900 bbls/d in 2015 from 172,000 bbls/d in 2014, with nameplate capacity for Firebag increasing to 203,000 bbls/d from 180,000 bbls/d due to sustained production levels in 2015. Production at MacKay River increased to 30,700 bbls/d in 2015 from 27,000 bbls/d in 2014 due to additional production associated with the debottlenecking project.

SUNCOR ENERGY INC. ANNUAL REPORT 2015 25

Firebag attained a record low SOR of 2.6 in 2015, down from 2.8 in 2014, primarily due to strong infill well performance and optimized reservoir management strategies, while SOR at MacKay River remained comparable to 2014.

Price Realizations

| Year ended December 31 Net of transportation costs, but before royalties ($/bbl) | 2015 | 2014 | 2013 | ||||||

| Oil Sands operations | |||||||||

| Sweet SCO and diesel | 66.00 | 109.02 | 104.22 | ||||||

| Sour SCO and non-upgraded bitumen | 41.58 | 76.66 | 72.67 | ||||||

| Crude sales basket (all products) | 49.46 | 87.46 | 82.83 | ||||||

| Crude sales basket, relative to WTI | (12.91 | ) | (15.28 | ) | (18.09 | ) | |||

| Oil Sands ventures | |||||||||

| Syncrude – Sweet SCO | 61.55 | 99.32 | 99.82 | ||||||

| Syncrude, relative to WTI | (0.83 | ) | (3.42 | ) | (1.10 | ) | |||

Price realizations were negatively impacted by the decrease in WTI benchmark prices, partially offset by the weaker Canadian dollar in 2015 and resulted in average price realizations for Oil Sands operations of $49.46/bbl in 2015, compared to $87.46/bbl in 2014.

Suncor's average price realization for Syncrude sales decreased in 2015 to $61.55/bbl, compared to $99.32/bbl in 2014, as the impacts of the decrease in WTI benchmark prices were partially offset by the weaker Canadian dollar in 2015.

Royalties

Royalties were lower in 2015 relative to 2014, primarily due to lower bitumen prices, partially offset by higher production.

Expenses and Other Factors

Operating expenses for 2015 were lower relative to 2014. Factors contributing to the change in operating expenses included:

- •

- A decrease in cash operating costs for Oil Sands operations. See the Cash Operating Costs Reconciliation for further details.

- •

- Operating expenses at Syncrude were lower for 2015 than 2014 as a result of cost reduction initiatives and lower natural gas prices.

- •

- Non-production costs were lower in 2015 compared to 2014, primarily due to cost reduction initiatives, including reductions to discretionary spending, lower expenses related to a gas swap arrangement with a third-party processor, and a decrease in costs associated with future growth activities, partially offset by higher share-based compensation expense.

Transportation expense increased in 2015, relative to 2014, primarily due to the costs related to increased sales volumes.

DD&A expense for 2015 was higher than 2014, mainly due to a larger asset base primarily as a result of assets commissioned in 2015, including well pads and infill wells, as well as the higher production from In Situ in 2015 as compared to 2014.

Cash Operating Costs Reconciliation(1)

| Year ended December 31 | 2015 | 2014 | 2013 | ||||||

| Operating, selling and general expense (OS&G) | 5 220 | 5 940 | 5 852 | ||||||

| Syncrude OS&G | (471 | ) | (593 | ) | (536 | ) | |||

| Non-production costs(2) | (279 | ) | (340 | ) | (282 | ) | |||

| Other items(3) | (63 | ) | (187 | ) | (165 | ) | |||

| Oil Sands cash operating costs ($ millions) | 4 407 | 4 820 | 4 869 | ||||||

| Oil Sands cash operating costs ($/bbl) | 27.85 | 33.80 | 37.00 | ||||||

- (1)

- Cash operating costs and cash operating costs per barrel are non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

- (2)

- Significant non-production costs include share-based compensation adjustments, research and the expense recorded as part of a gas swap arrangement involving a third-party processor.

- (3)

- Other items includes the impacts of changes in inventory valuation and operating revenues associated with excess capacity, primarily power from cogeneration units that was deducted from total cash operating costs.

Oil Sands cash operating costs per barrel averaged $27.85/bbl in 2015, compared to $33.80/bbl in 2014, primarily due to higher production volumes combined with lower cash operating costs in 2015. Total cash operating costs decreased in 2015, primarily due to cost reduction initiatives, lower natural gas input costs and lower unplanned maintenance activities, partially offset by changes in inventory and a decrease in power cogeneration revenues due to the decrease in power price.

Planned Maintenance

The company plans to complete a turnaround on Upgrader 2 commencing at the end of the first quarter of 2016. The impact of this maintenance has been reflected in the company's 2016 guidance.

26 SUNCOR ENERGY INC. ANNUAL REPORT 2015

EXPLORATION AND PRODUCTION

2015 Highlights

- •

- Golden Eagle achieved production of 14,800 boe/d during its first full year of production, and was operating at its peak production rate of approximately 18,000 boe/d by the fourth quarter.

- •

- Construction of the gravity-based structure and topsides at the Hebron project continued with first oil expected in late 2017.

- •

- Exploration drilling at the deepwater Shelburne Basin offshore Nova Scotia commenced in the fourth quarter, and will continue into 2016.

Strategy and Investment Update

The Exploration and Production segment focuses primarily on low-cost projects that deliver significant returns, cash flow and long-term value. Suncor is currently evaluating exploration and development opportunities off the east coast of Canada, offshore Norway and in the U.K. North Sea to provide diverse and lower cost conventional production.

Construction activities continue at the Hebron project, with first oil expected in late 2017. Effective January 1, 2016, Suncor's working interest in the Hebron project has been reset. As a result, the company's working interest in the project decreased from 22.729% to 21.034%, with Suncor to be reimbursed for costs incurred to December 31, 2015.

At Golden Eagle, development drilling activities are planned to continue through 2016. The company also has field extension projects underway which leverage existing facilities and infrastructure. The HSEU and South White Rose Extension (SWRX) projects are expected to provide incremental production and extend the productive life of the existing fields. Drilling activities on both extension projects are planned to continue in 2016. Exploration drilling activities in the Shelburne Basin are also continuing in 2016, along with ongoing appraisal of Norwegian discoveries at Beta and Butch.

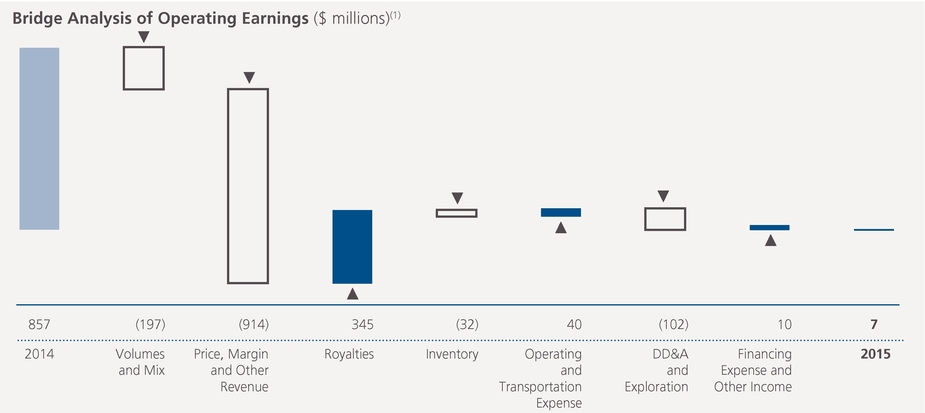

Financial Highlights

| Year ended December 31 ($ millions) | 2015 | 2014 | 2013 | ||||||

| Gross revenues | 2 612 | 4 715 | 6 363 | ||||||

| Less: Royalties | (267 | ) | (672 | ) | (1 146 | ) | |||

| Operating revenues, net of royalties | 2 345 | 4 043 | 5 217 | ||||||

| Net (loss) earnings | (758 | ) | 653 | 1 000 | |||||

| Adjusted for: | |||||||||

| Impairments | 1 213 | 297 | 563 | ||||||

| Recognition of risk mitigation proceeds | (75 | ) | — | (223 | ) | ||||

| Gain on significant disposals | — | (61 | ) | (130 | ) | ||||

| Impact of income tax rate adjustments on deferred income taxes | (373 | ) | — | — | |||||

| Reserves redetermination | — | (32 | ) | — | |||||

| Operating earnings (loss)(1) | 7 | 857 | 1 210 | ||||||

| E&P Canada | (14 | ) | 502 | 643 | |||||

| E&P International | 21 | 355 | 567 | ||||||

| Cash flow from operations(1) | 1 386 | 1 909 | 2 316 | ||||||

- (1)

- Non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

SUNCOR ENERGY INC. ANNUAL REPORT 2015 27

- (1)

- For an explanation of the construction of this bridge analysis, see the Advisories – Non-GAAP Financial Measures section of this MD&A.

E&P operating earnings were $7 million in 2015, compared to operating earnings of $857 million in 2014.

Operating losses in 2015 for E&P Canada were $14 million, compared to operating earnings of $502 million for 2014, with the decrease primarily due to lower price realizations and a decrease in production, partially offset by lower royalties and operating costs. Operating earnings for E&P International were $21 million for 2015, compared to $355 million for 2014, and were lower primarily due to lower price realizations, partially offset by the additional production from Golden Eagle and increased production from Buzzard.

Cash flow from operations was $1.386 billion in 2015, compared to $1.909 billion in 2014. The decrease was largely due to the same factors that impacted operating earnings.

Production Volumes

| Year ended December 31 | 2015 | 2014 | 2013 | |||||

| E&P Canada | ||||||||

| Terra Nova (mbbls/d) | 13.5 | 17.3 | 14.2 | |||||

| Hibernia (mbbls/d) | 18.1 | 23.1 | 27.1 | |||||

| White Rose (mbbls/d) | 12.2 | 14.6 | 14.9 | |||||

| North America Onshore (mboe/d) | 3.2 | 3.6 | 37.3 | |||||

| 47.0 | 58.6 | 93.5 | ||||||

| E&P International | ||||||||

| Buzzard (mboe/d) | 49.8 | 47.1 | 55.8 | |||||

| Golden Eagle (mboe/d) | 14.8 | 0.6 | — | |||||

| Libya (mbbls/d) | 2.8 | 6.7 | 20.6 | |||||

| 67.4 | 54.4 | 76.4 | ||||||

| Total Production (mboe/d) | 114.4 | 113.0 | 169.9 | |||||

| Production Mix (liquids/gas) (%) | 96/4 | 97/3 | 80/20 | |||||

E&P Canada production averaged 47,000 boe/d in 2015, compared to 58,600 boe/d in 2014.

- •

- Production from Terra Nova averaged 13,500 bbls/d in 2015, compared to 17,300 bbls/d in 2014. Production decreased primarily due to higher unplanned maintenance activity in 2015. Production from 2015 was also impacted by natural declines.

- •

- Production from Hibernia averaged 18,100 bbls/d in 2015, compared to 23,100 bbls/d in 2014, with the decrease in 2015 primarily due to natural declines, and the impact of a five-week planned maintenance program in the second half of 2015.

28 SUNCOR ENERGY INC. ANNUAL REPORT 2015

- •

- Production from White Rose averaged 12,200 bbls/d in 2015, compared to 14,600 bbls/d in 2014. Production decreased in 2015 primarily due to natural declines.

- •

- Production from North America Onshore averaged 3,200 boe/d in 2015, compared to 3,600 boe/d in 2014. Production decreased primarily due to the sale of the Wilson Creek assets in the third quarter of 2014.

E&P International production averaged 67,400 boe/d in 2015, compared to 54,400 boe/d in 2014.

- •

- Production from Buzzard averaged 49,800 boe/d in 2015, compared to 47,100 boe/d in 2014. Production increased primarily due to lower maintenance activity in 2015, offset by natural declines.

- •

- Production from Golden Eagle averaged 14,800 boe/d in 2015, compared to 600 boe/d in 2014, as first oil was achieved in the fourth quarter of 2014 and production continued to ramp up throughout 2015.

- •

- Production from Libya averaged 2,800 bbls/d in 2015, compared to 6,700 bbls/d in 2014. Production in Libya remains substantially shut in due to political unrest, with the timing of a return to normal operations remaining uncertain.

Price Realizations

| Twelve months ended December 31 | ||||||||

| Net of transportation costs, but before royalties | 2015 | 2014 | 2013 | |||||

| Exploration and Production | ||||||||

| E&P Canada – Crude oil and natural gas liquids ($/bbl) | 61.78 | 105.98 | 109.71 | |||||

| E&P Canada – Natural gas ($/mcf) | 1.78 | 4.49 | 3.42 | |||||

| E&P International ($/boe) | 61.44 | 104.12 | 107.57 | |||||

| E&P average price ($/boe) | 60.53 | 103.05 | 91.44 | |||||

Average price realizations for crude oil from E&P Canada and E&P International were lower than 2014, consistent with the decrease in benchmark prices for Brent crude in 2015, partially offset by favourable foreign exchange rates.

Royalties

Royalties were lower in 2015, compared with 2014, primarily due to lower price realizations and lower production in East Coast Canada.

Inventory

Inventory movements due to the timing of shuttle tankers in East Coast Canada positively impacted earnings in both years. However, in the decreasing crude oil price environment, the earnings impact was lower than in 2014.

Expenses and Other Factors

Operating expenses were lower in 2015 compared to 2014, primarily due to lower expenses in Libya, lower expenses in North America Onshore following the sale of the Wilson Creek assets in the third quarter of 2014, cost reduction initiatives, and lower maintenance costs in East Coast Canada, partially offset by incremental costs associated with Golden Eagle production, which achieved first oil in the fourth quarter of 2014.

DD&A and exploration expenses were higher in 2015, primarily due to increased production associated with Golden Eagle and Buzzard, partially offset by lower production from East Coast Canada and Libya.

Planned Maintenance of Operated Assets

A planned four-week maintenance event at Terra Nova has been scheduled to commence in the second quarter of 2016. The impact of this maintenance has been reflected in the company's 2016 guidance.

REFINING AND MARKETING

2015 Highlights

- •

- The Refining and Marketing segment continues to be a key component of the company's integrated business model, generating $2.234 billion in operating earnings in 2015.

- •

- Strong refinery utilizations allowed Suncor to reduce the impact of the declining crude price environment by optimizing the profit realized on a portion of Suncor's upstream production.

- •

- Suncor lowered feedstock costs at the Montreal refinery through increased rail shipments of inland crudes and marine shipments of lower priced crudes from the U.S. Gulf Coast when market conditions were favourable.

- •

- Suncor completed the sale of its 50% interest in certain assets and liabilities of Pioneer Energy for $183 million, highlighting the company's continued focus on core assets that are aligned with Suncor's long-term strategy.

- •

- Enbridge's Line 9 reversal was commissioned during the fourth quarter of 2015 and became operational by the end of the year. The reversal will provide Suncor the flexibility of supplying its Montreal refinery with a full slate of inland priced crude.

Strategy and Investment Update

Suncor's downstream is a key component of the integrated business model. The Refining and Marketing network serves to maximize the value of Suncor's oil sands

SUNCOR ENERGY INC. ANNUAL REPORT 2015 29

production by extending the value chain to the end customer. The company operates its refineries at or near maximum capacity to provide reliable offtake and secure international pricing for oil sands production. The strategy also includes selling more volumes than refinery capacity to minimize per unit operating costs and provide a reliable product supply to customers. Feedstock intended for the refineries and finished products that are not expected to be sold by Refining and Marketing are sold at market prices by Suncor's Energy Trading group.

Suncor's Petro-Canada branded outlets maintained their position as a leading retailer by market share in major urban areas of Canada. Suncor will continue to leverage the strong brand to increase non-petroleum revenues through the company's network of convenience stores and car washes, and expand the lubricants product offering, including global expansion in the U.S., Europe and China.

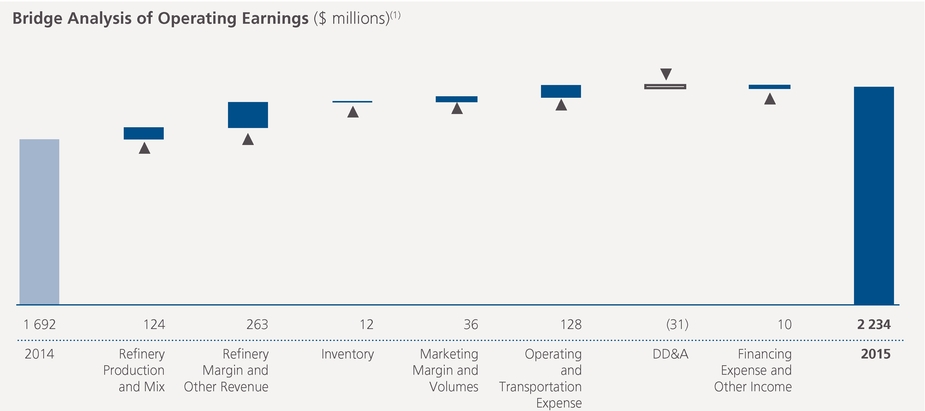

Financial Highlights

| Year ended December 31 ($ millions) | 2015 | 2014 | 2013 | |||||

| Operating revenues | 19 826 | 26 627 | 26 658 | |||||

| Net earnings | 2 266 | 1 692 | 2 022 | |||||

| Adjusted for: | ||||||||

| Impact of income tax rate adjustments on deferred taxes | 36 | — | — | |||||

| Gain on significant disposal | (68 | ) | — | — | ||||

| Operating earnings(1) | 2 234 | 1 692 | 2 022 | |||||

| Refining and Product Supply | 1 864 | 1 385 | 1 758 | |||||

| Marketing | 370 | 307 | 264 | |||||

| Cash flow from operations(1) | 2 872 | 2 178 | 2 618 | |||||

- (1)

- Non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

- (1)

- For an explanation of the construction of this bridge analysis, see the Advisories – Non-GAAP Financial Measures section of this MD&A.

Refining and Product Supply contributed operating earnings of $1.864 billion in 2015, compared with $1.385 billion in 2014. The increase was primarily due to an increase in benchmark gasoline cracking margins and higher refinery production bolstered by the positive impacts of the weaker Canadian dollar, slightly offset by weaker distillate benchmark cracking margins. In addition, 2015 included lower operating expenses driven by lower energy expenses, the impact of cost reduction initiatives, lower environmental expense and lower maintenance activity, partially offset by higher share-based compensation expense.

30 SUNCOR ENERGY INC. ANNUAL REPORT 2015

Marketing operations contributed $370 million to operating earnings in 2015, compared to $307 million in 2014, due mainly to stronger retail and lubricant margins.

Cash flow from operations was $2.872 billion in 2015, compared to $2.178 billion in 2014, due primarily to the same factors that impacted operating earnings.

Volumes

| Year ended December 31 | 2015 | 2014 | 2013 | |||||

| Crude oil processed (mbbls/d) | ||||||||

| Eastern North America | 208.1 | 199.2 | 201.7 | |||||

| Western North America | 224.0 | 228.3 | 229.6 | |||||

| Total | 432.1 | 427.5 | 431.3 | |||||

| Refinery utilization(1)(2) (%) | ||||||||

| Eastern North America | 94 | 90 | 91 | |||||

| Western North America | 93 | 95 | 96 | |||||

| Total | 94 | 93 | 94 | |||||

| Refined Product Sales (mbbls/d) | ||||||||

| Gasoline | 246.2 | 243.4 | 247.4 | |||||

| Distillate | 198.0 | 199.7 | 209.8 | |||||

| Other | 79.1 | 88.6 | 85.7 | |||||

| 523.3 | 531.7 | 542.9 | ||||||

- (1)

- Effective January 1, 2014, the company increased the nameplate capacity of the Edmonton refinery from 140,000 bbls/d to 142,000 bbls/d. Prior year utilization rates have not been recalculated and reflect the lower nameplate capacity.

- (2)

- Refinery utilization is the amount of crude oil run through crude distillation units, expressed as a percentage of the capacity of these units.

Refinery utilization in Eastern North America averaged 94% in 2015, compared with 90% in 2014. The increase from the prior year was primarily due to fewer planned maintenance events at Montreal and Sarnia.

Refinery utilization in Western North America averaged 93% in 2015, compared to 95% in 2014. The decrease from the prior year was primarily due to increased maintenance events in 2015 at the Edmonton refinery and lower demand for refined products in Western North America.

Total sales of refined petroleum products decreased to an average of 523,300 bbls/d in 2015, compared to 531,700 bbls/d in 2014, primarily due to lower demand in Western North America.

Prices and Margins

Refining and Product Supply prices and margins for refined products were higher in 2015 compared to 2014.

- •

- In 2015, the impact of FIFO inventory accounting, as used by the company, relative to an estimated LIFO basis of accounting, had a negative impact on net earnings of approximately $286 million after-tax, compared to $290 million after-tax in 2014.

- •

- Refining margins were also higher due to strong location differentials, the positive impact of the weaker Canadian dollar, partially offset by the impacts of narrower inland crude differentials, relative to WTI, and weaker distillate benchmark margins in 2015.

Marketing margins increased primarily due to higher margins for retail and lubricants channels.

Expenses and Other Factors

Operating expenses were lower in 2015 compared to 2014, primarily due to lower energy costs as a result of lower natural gas prices, the impact of cost reduction initiatives, lower maintenance costs, and lower environmental remediation expense. DD&A expense increased due to a larger asset base, while transportation expense was relatively unchanged between years.

Planned Maintenance

The company has scheduled two planned maintenance events at the Commerce City refinery, both with an expected duration of two weeks in each of the first and second quarters of 2016. The Sarnia refinery has a seven-week planned maintenance event in the second quarter of 2016, a four-week planned maintenance event in the third quarter and a one-week planned maintenance event in the fourth quarter of 2016. The Montreal refinery has a six-week planned maintenance event in the second quarter of 2016. The impacts of this planned maintenance are included in the company's guidance.

CORPORATE, ENERGY TRADING AND ELIMINATIONS

2015 Highlights

- •

- The company completed construction of the 100 MW Cedar Point wind farm in the fourth quarter of 2015.

- •

- The company entered into partnership agreements whereby the Aamjiwnaang First Nation acquired a 25% interest in the 40 MW Adelaide wind facility, and NextEra Energy Canada acquired a 50% interest in the Cedar Point wind facility, which began commercial operations in 2015.

Strategy and Investment Update

The Energy Trading business supports the company's production by securing market access, optimizing price realizations, managing inventory levels and managing the

SUNCOR ENERGY INC. ANNUAL REPORT 2015 31

impacts of external market factors, such as pipeline disruptions or outages at refining customers, while generating trading earnings through established strategies. The Energy Trading business continues to evaluate additional pipeline agreements to support planned production growth.

The Renewables business added 100 MW of gross installed capacity in 2015 through completion of the Cedar Point wind farm and also exchanged its interests in the Kent Breeze and Wintering Hills wind farms with TransAlta for the Poplar Creek cogeneration facilities, which support Oil Sands Base operations. Suncor also invested in a biodiesel plant, which is expected to be producing by the end of the first quarter of 2016.

Financial Highlights

| Year ended December 31 ($ millions) | 2015 | 2014 | 2013 | ||||||

| Net loss | (2 647 | ) | (1 422 | ) | (1 151 | ) | |||

| Adjusted for: | |||||||||

| Unrealized foreign exchange loss (gain) on U.S. dollar denominated debt | 1 930 | 722 | 521 | ||||||

| Restructuring charges | 57 | — | — | ||||||

| Impact of income tax rate adjustments on deferred income taxes | (5 | ) | — | — | |||||

| Operating (loss) earnings(1) | (665 | ) | (700 | ) | (630 | ) | |||

| Renewable Energy | 56 | 78 | 72 | ||||||

| Energy Trading | 36 | 66 | 116 | ||||||

| Corporate | (799 | ) | (850 | ) | (785 | ) | |||

| Eliminations | 42 | 6 | (33 | ) | |||||

| Cash flow used in operations(1) | (287 | ) | (429 | ) | (78 | ) | |||

- (1)

- Non-GAAP financial measures. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

Renewable Energy

| Year ended December 31 | 2015 | 2014 | 2013 | ||||

| Power generation marketed (net gigawatt hours) | 407 | 411 | 430 | ||||

| Ethanol production (thousands of m3) | 418 | 412 | 415 | ||||

Suncor's Renewable Energy assets contributed operating earnings of $56 million in 2015, compared to $78 million in 2014. The decrease was primarily due to narrower margins on ethanol sales driven by lower ethanol fuel prices and higher feedstock costs, partially offset by higher ethanol production.

Energy Trading

Energy Trading activities contributed operating earnings of $36 million in 2015, compared to $66 million in 2014. The decrease in operating earnings was primarily due to lower gains on natural gas strategies due to weaker natural gas prices, lower gains on crude trading strategies as a result of weaker location spreads and the recording of an onerous contract related to the company's rail transportation strategy in 2015.

Corporate

Corporate incurred an operating loss of $799 million in 2015, compared with an operating loss of $850 million in 2014. The decrease in the operating loss was primarily a result of cost reduction initiatives, partially offset by increased share-based compensation expense. Suncor capitalized $447 million of its borrowing costs in 2015 as part of the cost of major development assets and construction projects in progress, compared to $431 million in the prior year. The increase was driven by the ramp up of construction at Fort Hills and the acquisition of an additional 10% working interest in the project.

Eliminations

Eliminations reflect the elimination or realization of profit on crude oil sales from Oil Sands and East Coast Canada to Refining and Marketing. Consolidated profits are only realized when the company sells the products produced from intersegment purchases of crude feedstock to third parties. In 2015, $42 million of after-tax intersegment profit was realized, compared to $6 million of after-tax intersegment profit realized in 2014.

32 SUNCOR ENERGY INC. ANNUAL REPORT 2015

5. FOURTH QUARTER 2015 ANALYSIS

Financial and Operational Highlights

| Three months ended December 31 ($ millions, except as noted) | 2015 | 2014 | |||||

| Net (loss) earnings | |||||||

| Oil Sands | (616 | ) | 180 | ||||

| Exploration and Production | (1 263 | ) | 198 | ||||

| Refining and Marketing | 498 | 173 | |||||

| Corporate, Energy Trading and Eliminations | (626 | ) | (467 | ) | |||

| Total | (2 007 | ) | 84 | ||||

| Operating (loss) earnings(1) | |||||||

| Oil Sands | (230 | ) | 180 | ||||

| Exploration and Production | (50 | ) | 198 | ||||

| Refining and Marketing | 498 | 173 | |||||

| Corporate, Energy Trading and Eliminations | (244 | ) | (165 | ) | |||

| Total | (26 | ) | 386 | ||||

| Cash flow from (used in) operations(1) | |||||||

| Oil Sands | 467 | 875 | |||||

| Exploration and Production | 257 | 401 | |||||

| Refining and Marketing | 596 | 240 | |||||

| Corporate, Energy Trading and Eliminations | (26 | ) | (24 | ) | |||

| Total | 1 294 | 1 492 | |||||

| Production volumes (mboe/d) | |||||||

| Oil Sands | 470.6 | 419.3 | |||||

| Exploration and Production | 112.3 | 138.3 | |||||

| Total | 582.9 | 557.6 | |||||

- (1)

- Non-GAAP financial measures. Operating earnings and cash flow from operations are reconciled below. See the Advisories – Non-GAAP Financial Measures section of this MD&A.

Net Earnings

Suncor's consolidated net loss for the fourth quarter of 2015 was $2.007 billion, compared with net earnings of $84 million for the prior year quarter. Net earnings were primarily affected by the same factors that influenced operating earnings described in the segmented analysis below. Other items affecting net earnings over these periods included:

- •