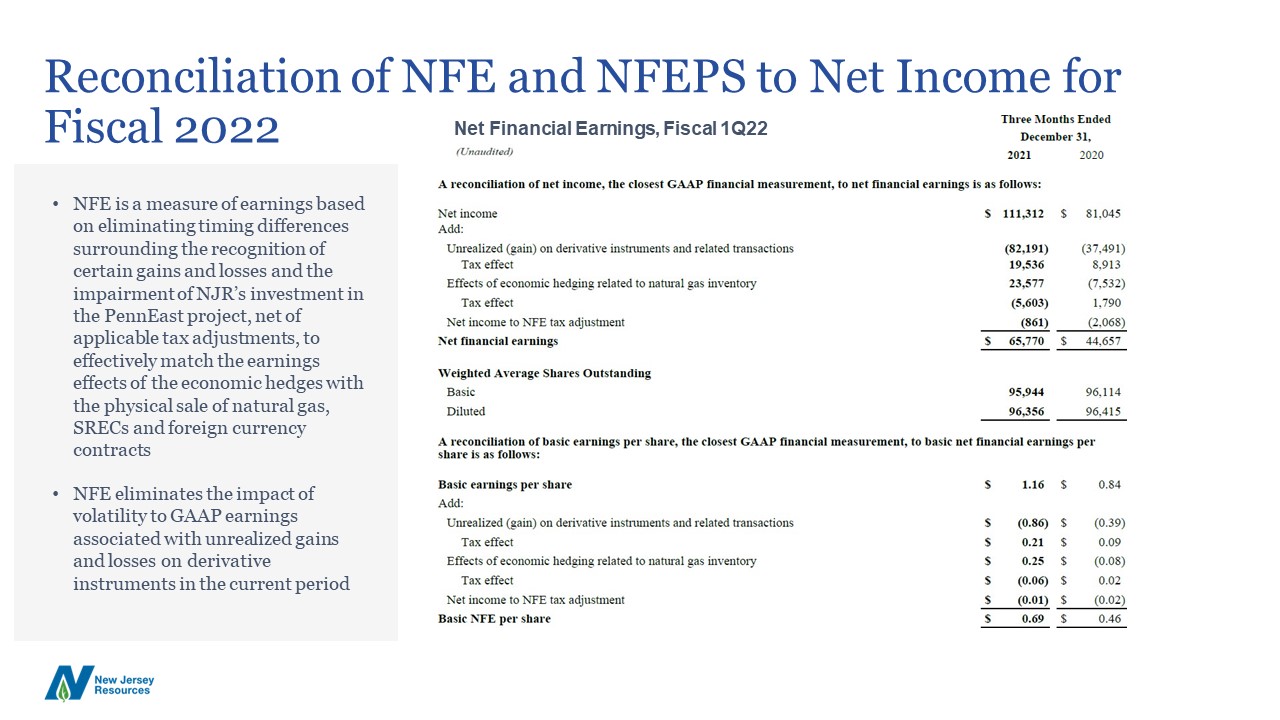

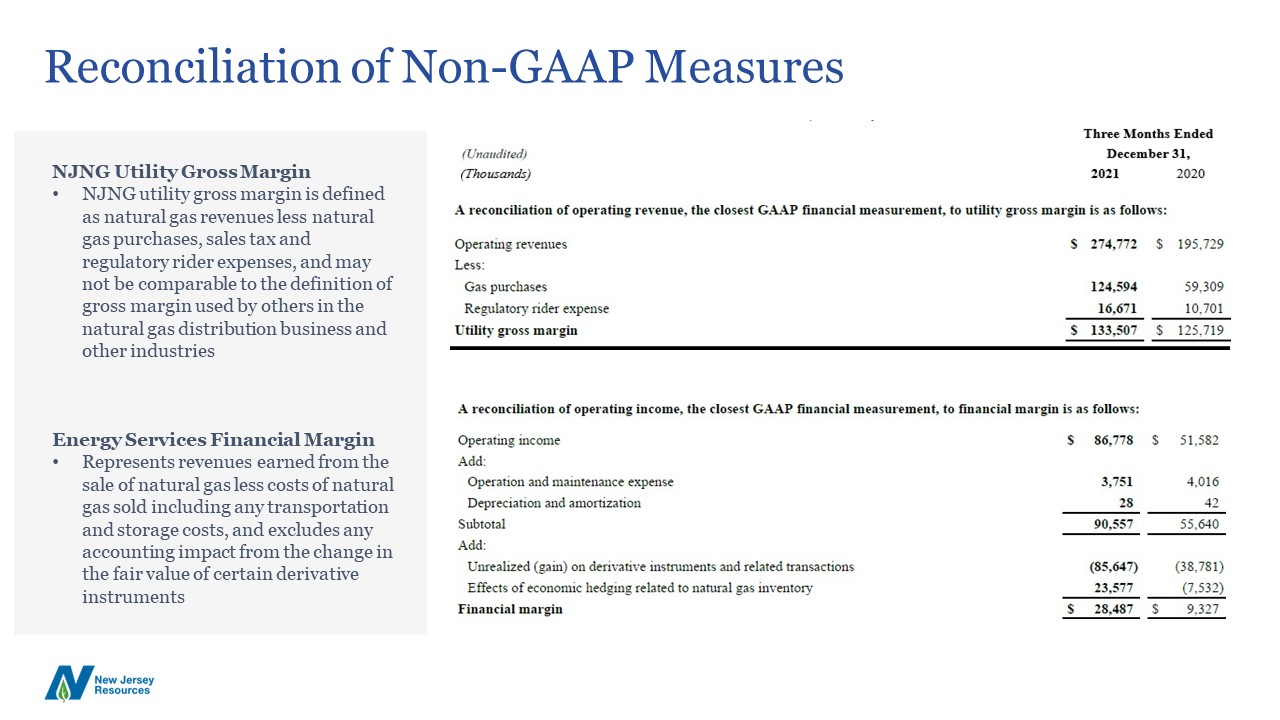

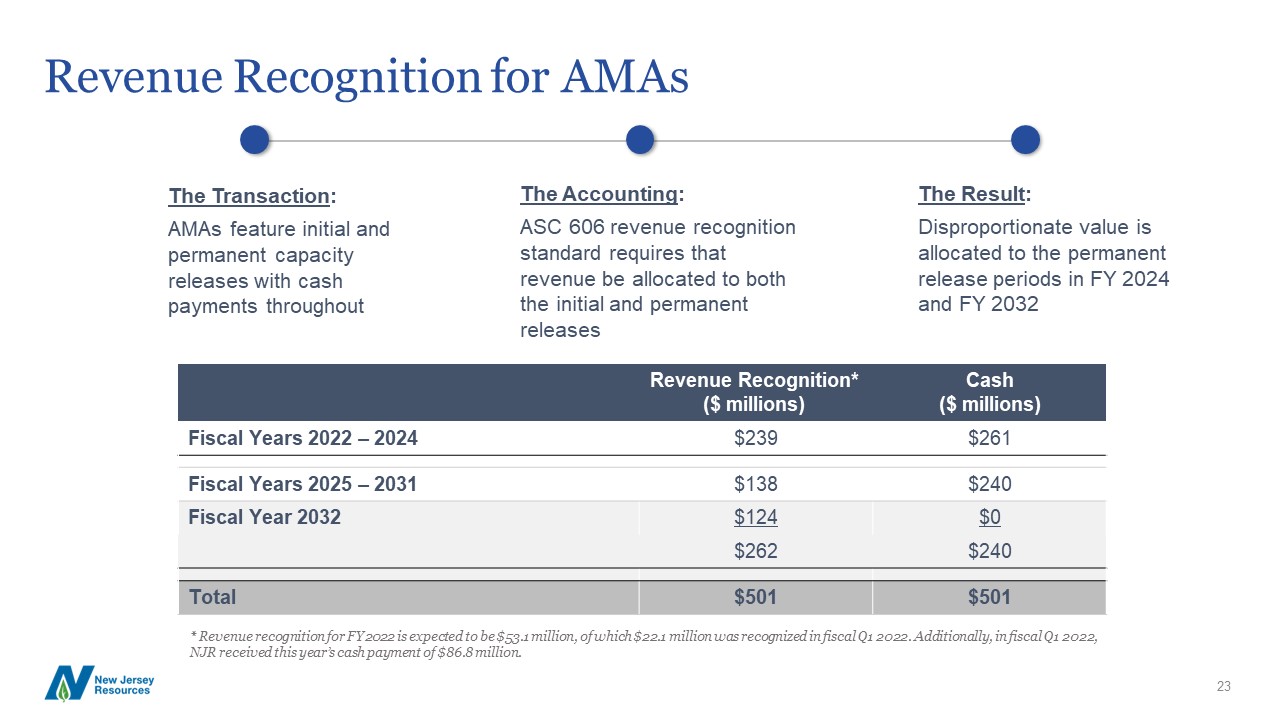

Forward-Looking Statements and Non-GAAP Measures 1 Forward-Looking StatementsThis presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, Section 21E of the Securities Exchange Act of 1934, as amended, and the Private Securities Litigation Reform Act of 1995. New Jersey Resources Corporation (“NJR”, or the “Company”) cautions readers that the assumptions forming the basis for forward-looking statements include many factors that are beyond NJR’s ability to control or estimate precisely, such as estimates of future market conditions and the behavior of other market participants. Words such as “anticipates,” “estimates,” “expects,” “projects,” “may,” “will,” “intends,” “plans,” “believes,” “should” and similar expressions may identify forward-looking statements and such forward-looking statements are made based upon management’s current expectations, assumptions and beliefs as of this date concerning future developments and their potential effect upon NJR. There can be no assurance that future developments will be in accordance with management’s expectations, assumptions and beliefs or that the effect of future developments on NJR will be those anticipated by management. Forward-looking statements in this presentation include, but are not limited to, certain statements regarding NJR’s net financial earnings (“NFE”) per share guidance for fiscal 2022 and beyond, dividend growth goals, capital plans, planned capital expenditures, projected cash flows, impacts of hedging strategies, customer growth rate and timetable and results of future base rates, schedule for completion of infrastructure projects, including but not limited to, New Jersey Natural Gas’s Southern Reliability Link and the Howell Green Hydrogen Project, NJR's environmental sustainability and clean energy goals, emissions reduction strategies, initiatives and targets as well as our related investments in infrastructure, renewables and emerging technologies such as renewable natural gas and hydrogen gas, NJR Clean Energy Ventures’ future capital investment target, projected installed solar capacity, revenue growth, project returns, impacts of Asset Management Agreements, including revenue recognition for fiscal 2022 and beyond, demand for residential and commercial solar energy, and our ability to profitably operate and expand the Adelphia Gateway pipeline and the impairment of NJR’s investment in PennEast.Additional information and factors that could cause actual results to differ materially from NJR’s expectations are contained in NJR’s filings with the U.S. Securities and Exchange Commission (SEC), including NJR’s Annual Reports on Form 10-K and subsequent Quarterly Reports on Form 10-Q, recent Current Reports on Form 8-K, and other SEC filings, which are available at the SEC’s web site, https://www.sec.gov. Information included in this presentation is representative as of today only and while NJR periodically reassesses material trends and uncertainties affecting NJR's results of operations and financial condition in connection with its preparation of management's discussion and analysis of results of operations and financial condition contained in its Quarterly and Annual Reports filed with the SEC, NJR does not, by including this statement, assume any obligation to review or revise any particular forward-looking statement referenced herein in light of future events.Non-GAAP MeasuresThis presentation includes the non-GAAP measures, including, NFE/net financial loss, utility gross margin and financial margin. As an indicator of the Company’s operating performance, these measures should not be considered an alternative to, or more meaningful than, GAAP measures, such as cash flows, net income(loss), operating income or earnings per share.NFE/net financial loss and financial margin exclude unrealized gains or losses on derivative instruments related to the Company’s unregulated subsidiaries and certain realized gains and losses on derivative instruments related to natural gas that has been placed into storage at Energy Services, and the impairment of NJR’s investment in the PennEast project, net of applicable tax adjustments, as described below. Volatility associated with the change in value of these financial and physical commodity contracts is reported in the income statement in the current period. In order to manage its business, NJR views its results without the impacts of the unrealized gains and losses, and certain realized gains and losses, caused by changes in value of these financial instruments and physical commodity contracts prior to the completion of the planned transaction because it shows changes in value currently as opposed to when the planned transaction ultimately is settled. An annual estimated effective tax rate is calculated for NFE purposes, and any necessary quarterly tax adjustment is applied to “NJCEV”, as such adjustment is related to tax credits generated by CEV.NJNG’s utility gross margin represents the results of revenues less natural gas costs, sales and other taxes and regulatory rider expenses, which are key components of the Company’s operations that move in relation to each other. Natural gas costs, sales and other taxes and regulatory rider expenses are passed through to customers and therefore, have no effect on gross margin.Management uses NFE/net financial loss, utility gross margin and financial margin, as supplemental measures to other GAAP results to provide a more complete understanding of the Company’s performance. Management believes these non-GAAP measures are more reflective of the Company’s business model, provide transparency to investors and enable period-to-period comparability of financial performance. In providing NFE guidance, management is aware that there could be differences between reported GAAP earnings and NFE/net financial loss due to matters such as, but not limited to, the positions of our energy-related derivatives. Management is not able to reasonably estimate the aggregate impact or significance of these items on reported earnings and therefore is not able to provide a reconciliation to the corresponding GAAP equivalent for its operating earnings guidance without unreasonable efforts. NFE/net financial loss, utility gross margin and financial margin are discussed more fully in Item 7 of our Report on Form 10-K and, we have provided presentations of the most directly comparable GAAP financial measure and a reconciliation of our non-GAAP financial measure, NFE/net financial loss, to the most directly comparable GAAP financial measure, in the appendix to this presentation. This information has been provided pursuant to the requirements of SEC Regulation G.